Headlines

- US-China trade talks end without extension of tariff truce, as Trump weighs options.

- Australian press reported that the US president threatened to double the baseline tariff on Australian imports.

- A South Korean trade delegation is expected to visit Washington in the coming days for discussions.

- The European Union noted it cannot guarantee that $600 billion will be invested in the United States, clarifying the funds would originate from the private sector.

Global Economics

United States

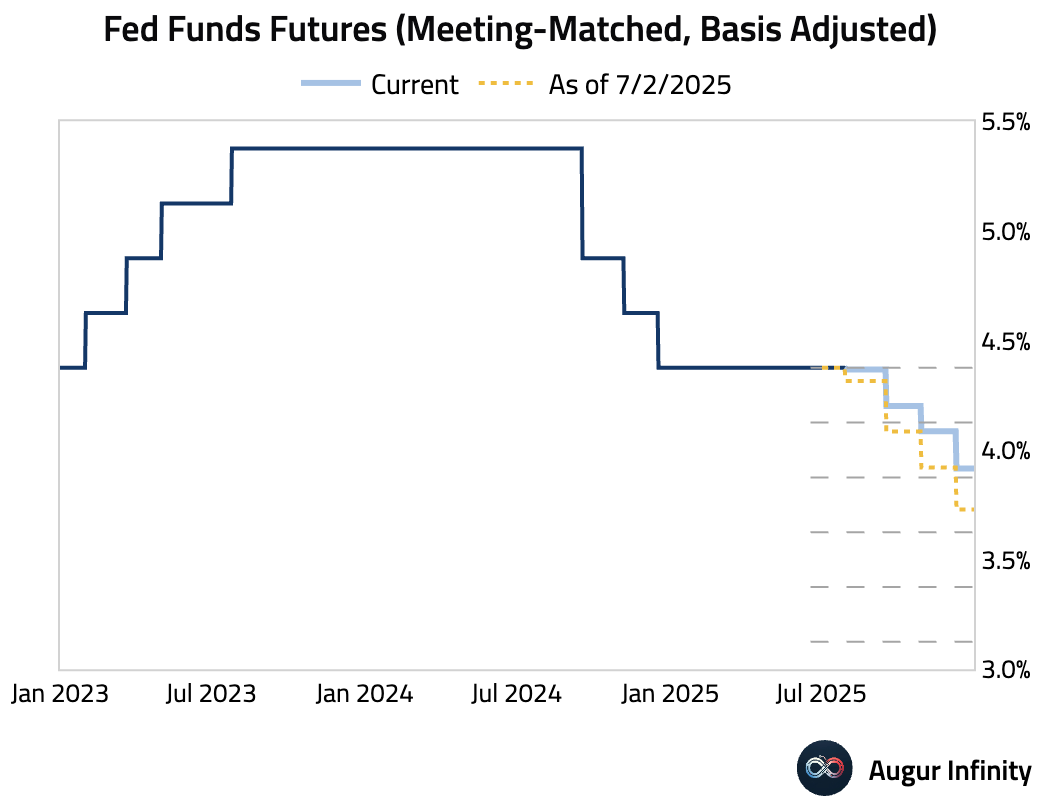

- The market expects the Federal Reserve to hold interest rates steady at the conclusion of its meeting tomorrow.

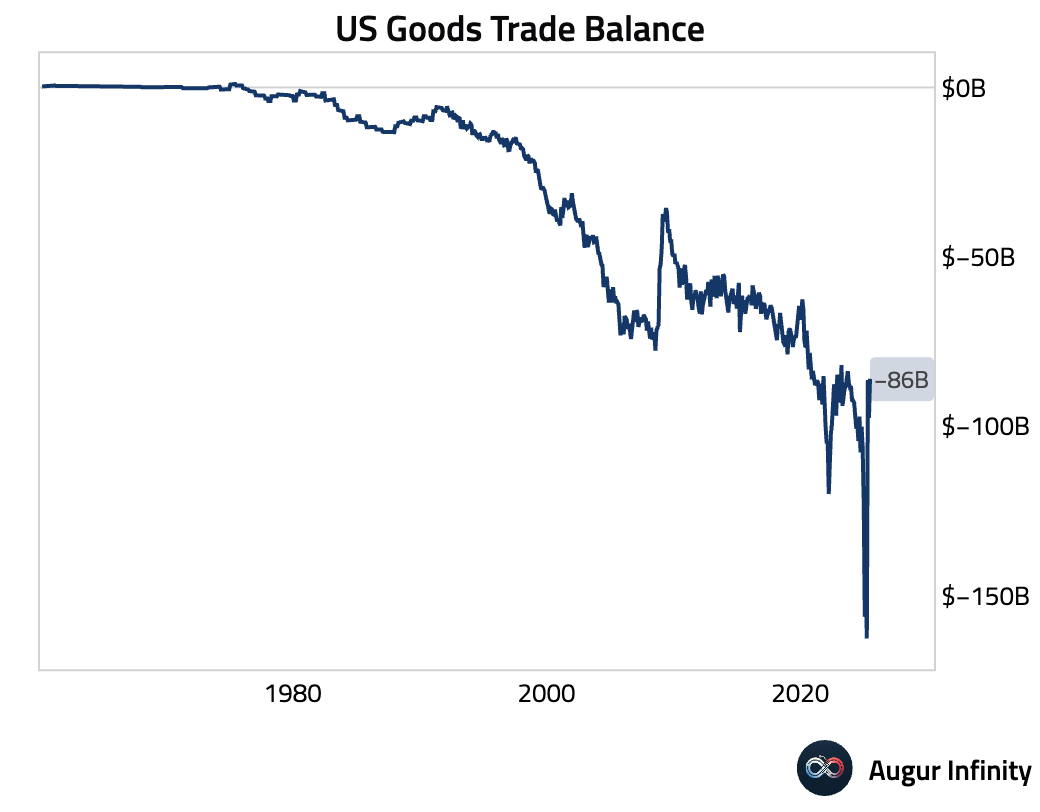

- The advance goods trade deficit for June unexpectedly narrowed to –$86.0 billion, a significant beat compared to the –$98.4 billion consensus and the smallest deficit since September 2023. The improvement was driven by an $11.5 billion drop in imports, led by a steep $8.2 billion decline in consumer goods, signaling softer domestic demand. The smaller trade gap prompted a notable upward revision in Q2 GDP tracking estimates.

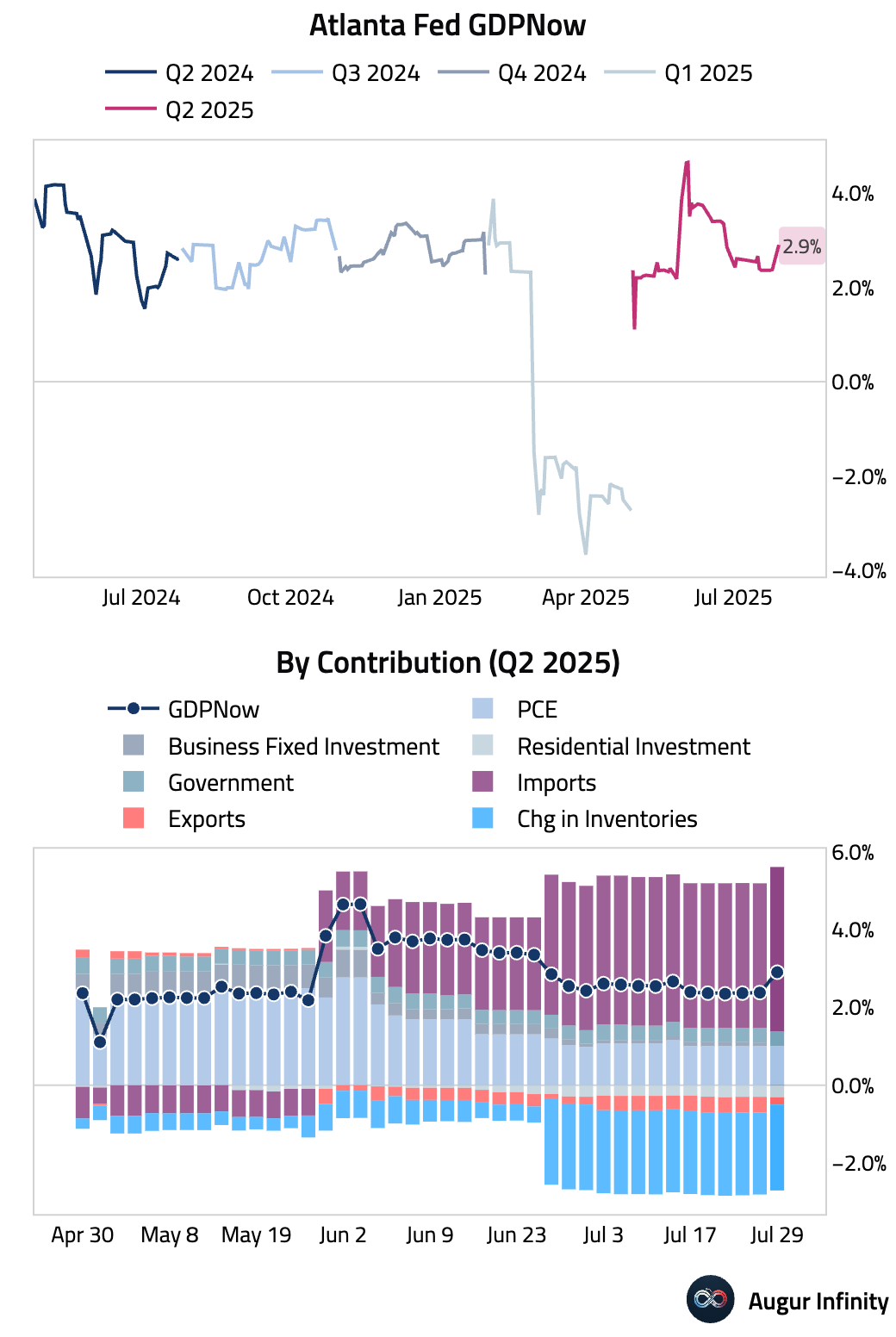

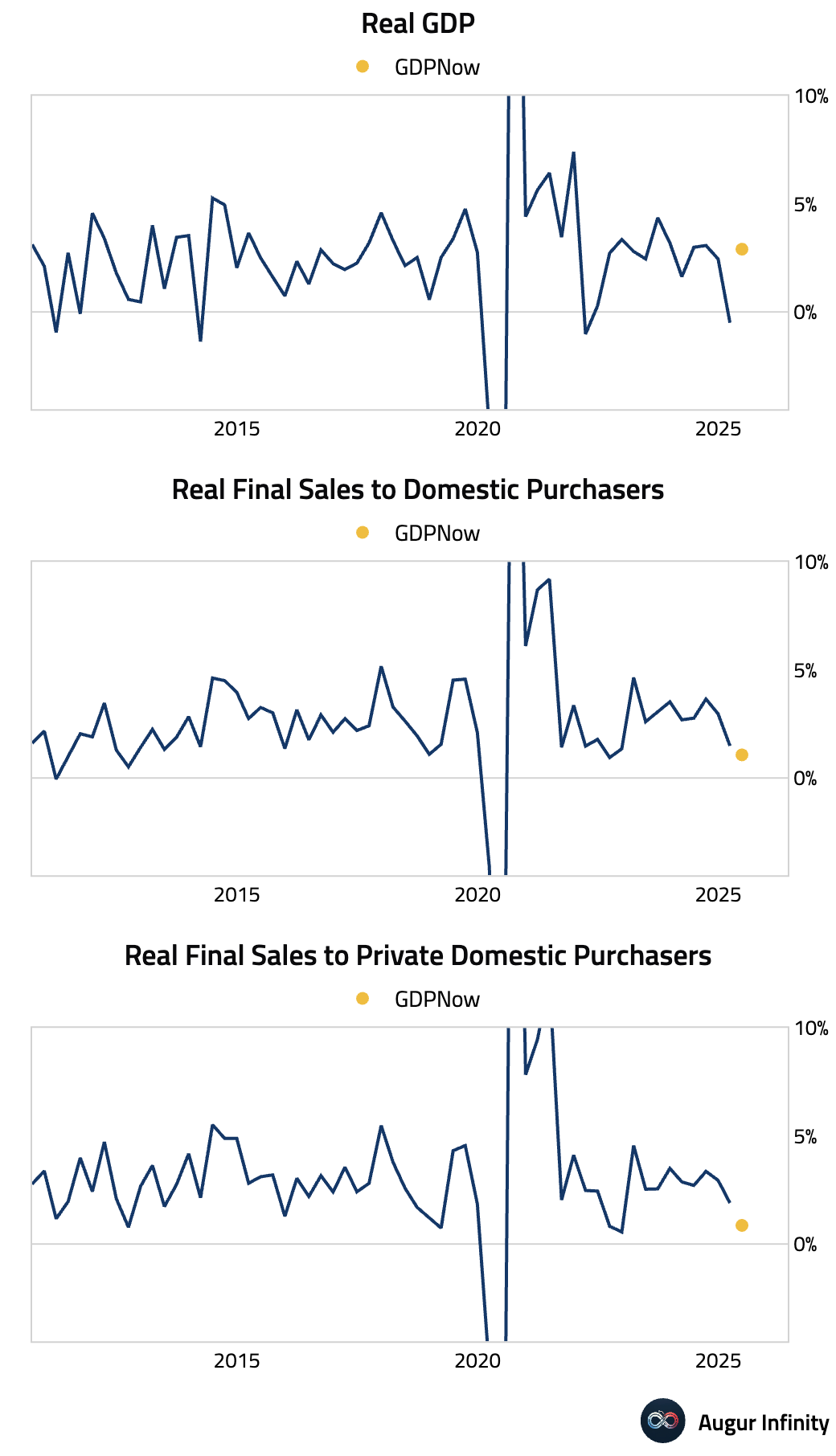

- Reflecting the trade data, the Atlanta Fed's GDPNow model now tracks Q2 2025 GDP growth at 2.9%, a notable increase from 2.4% on July 25.

- Although the headline GDPNow forecast remains strong, underlying growth has weakened. When stripping out net exports and inventories, real final sales to domestic purchasers are tracking at 1.1%. Excluding government spending, real final sales to private domestic purchasers are tracking at an even weaker 0.9%.

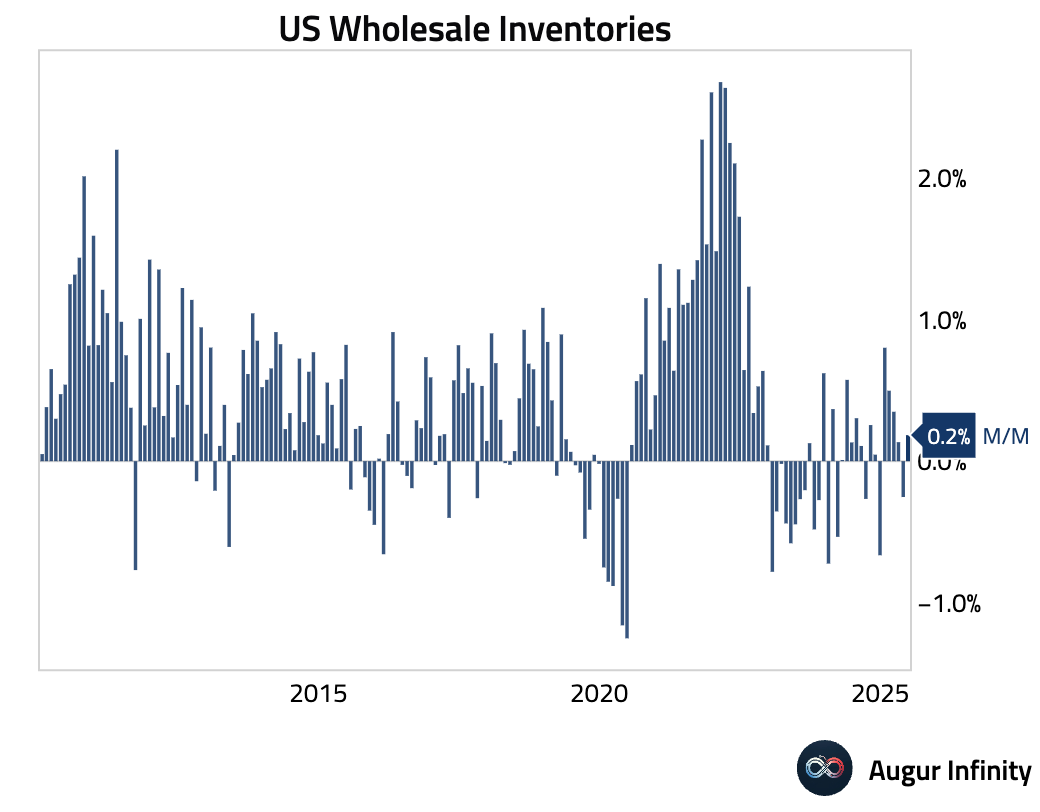

- Wholesale inventories for June rose 0.2% M/M, defying consensus expectations for a 0.1% decline and reversing the prior month's 0.3% drop. Separately, advance retail inventories excluding autos were flat, following a 0.1% increase in May.

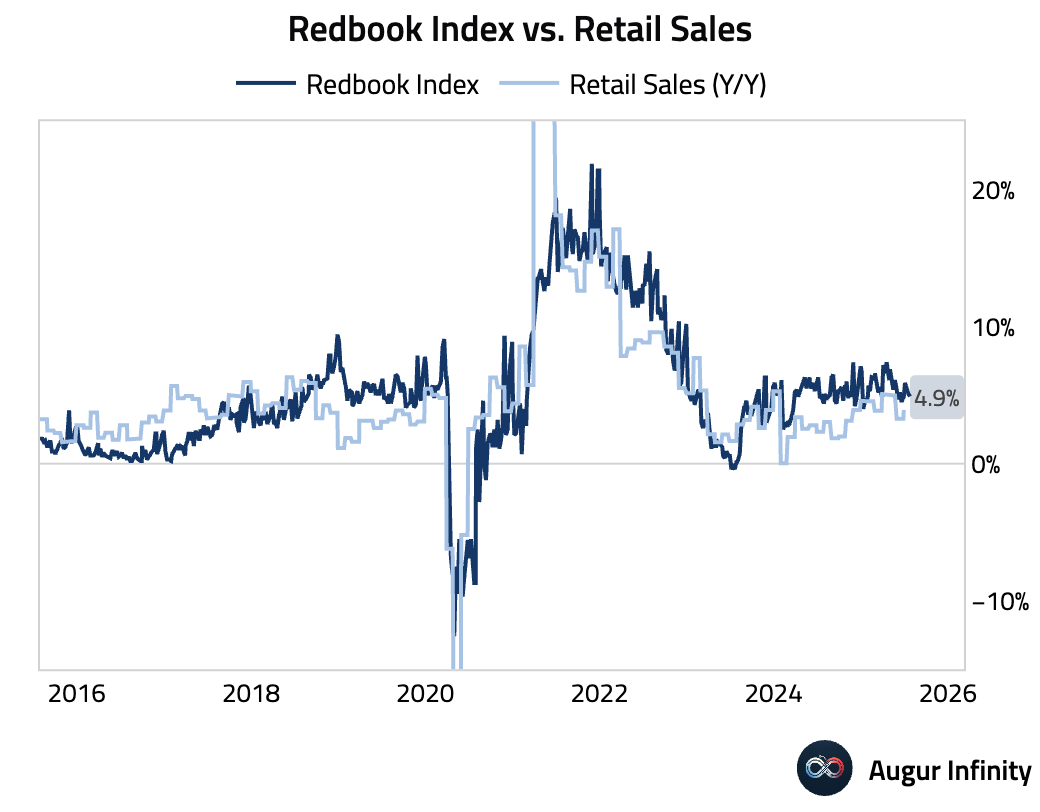

- The Redbook index of same-store sales showed a 4.9% Y/Y increase for the week ending July 26, a slight moderation from the 5.1% gain in the previous week.

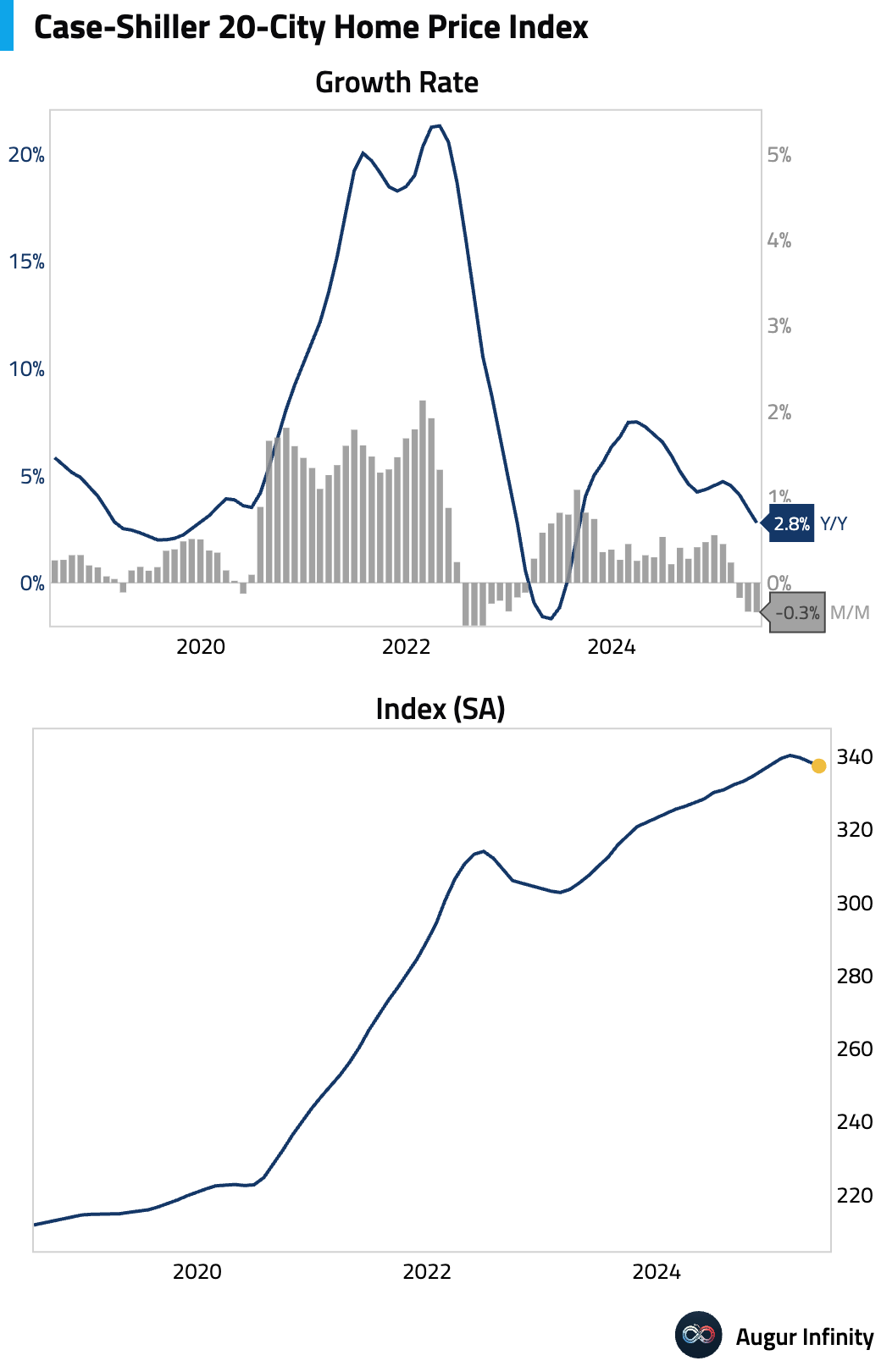

- Home price growth continued to cool in May. The S&P/Case-Shiller 20-City Home Price Index rose 2.8% Y/Y, below the 3.0% consensus and down from 3.4% previously, marking the slowest annual appreciation since August 2023. On a month-over-month and seasonally-adjusted basis, home price declined by 0.3%.

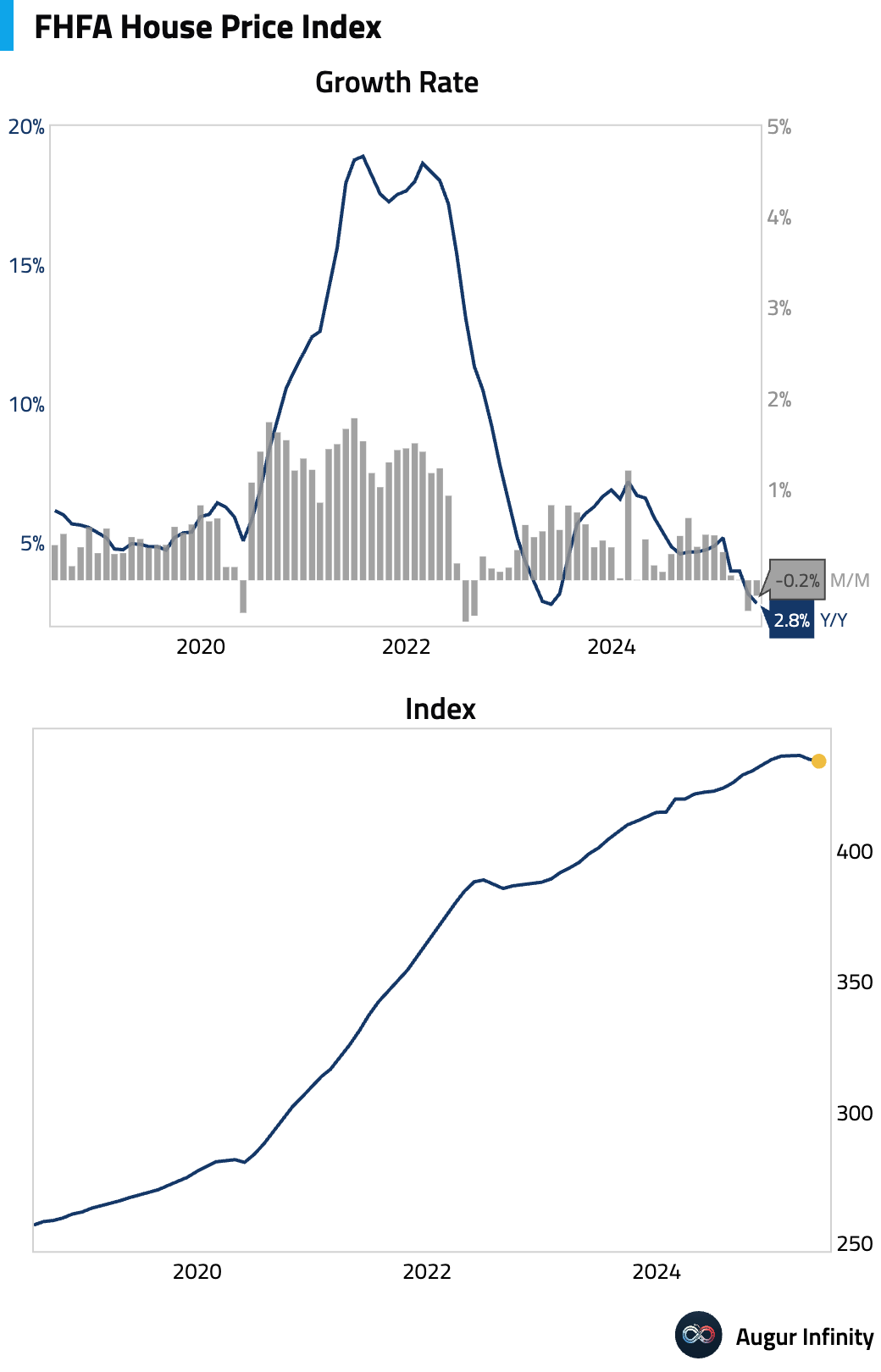

- The FHFA House Price Index for May declined 0.2% M/M, a larger fall than the –0.1% consensus. Year-over-year growth decelerated to 2.8% from 3.2% in April, the weakest reading since May 2023.

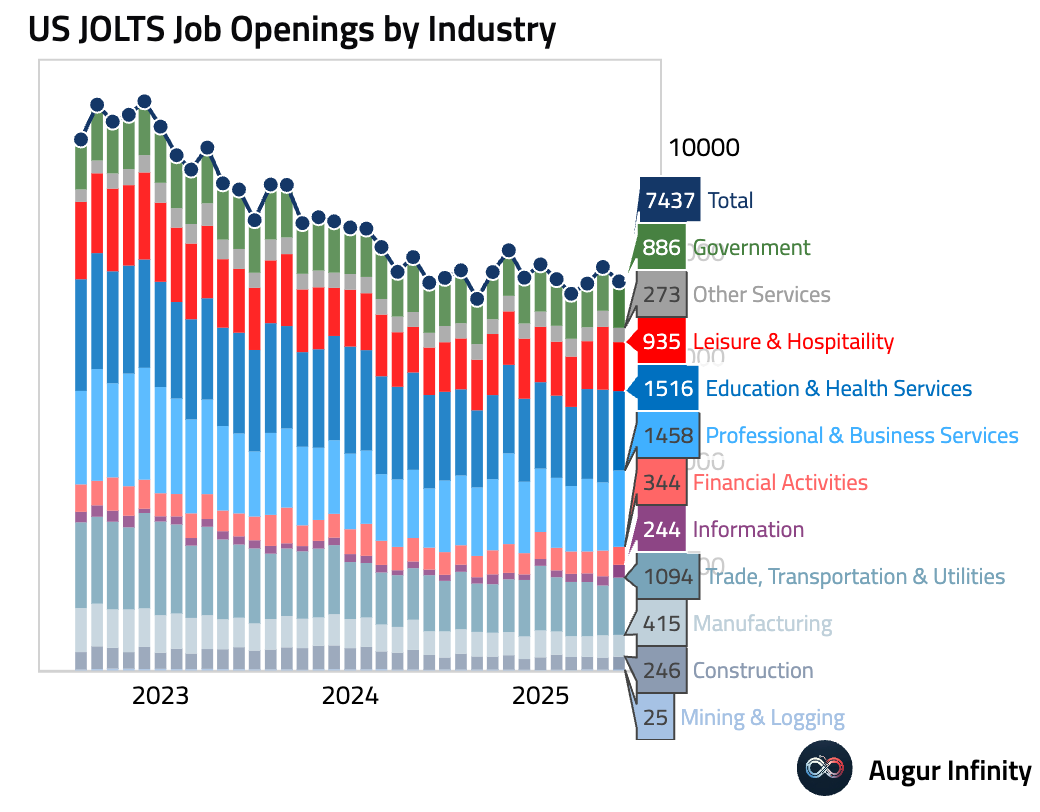

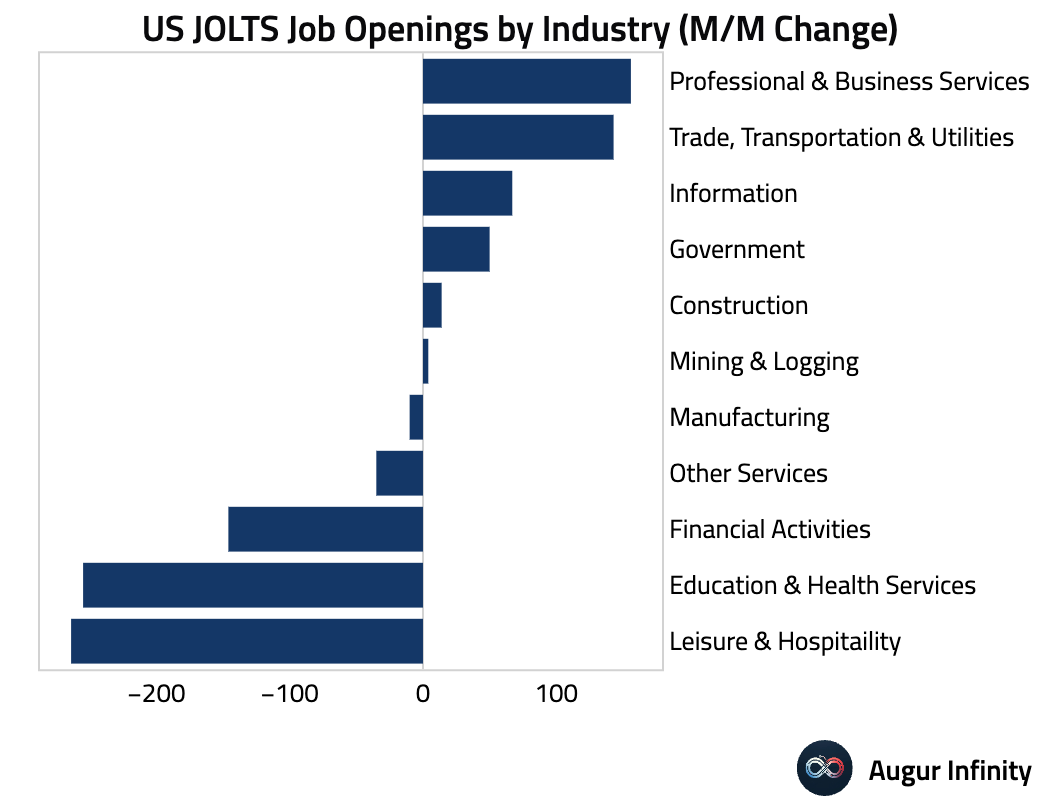

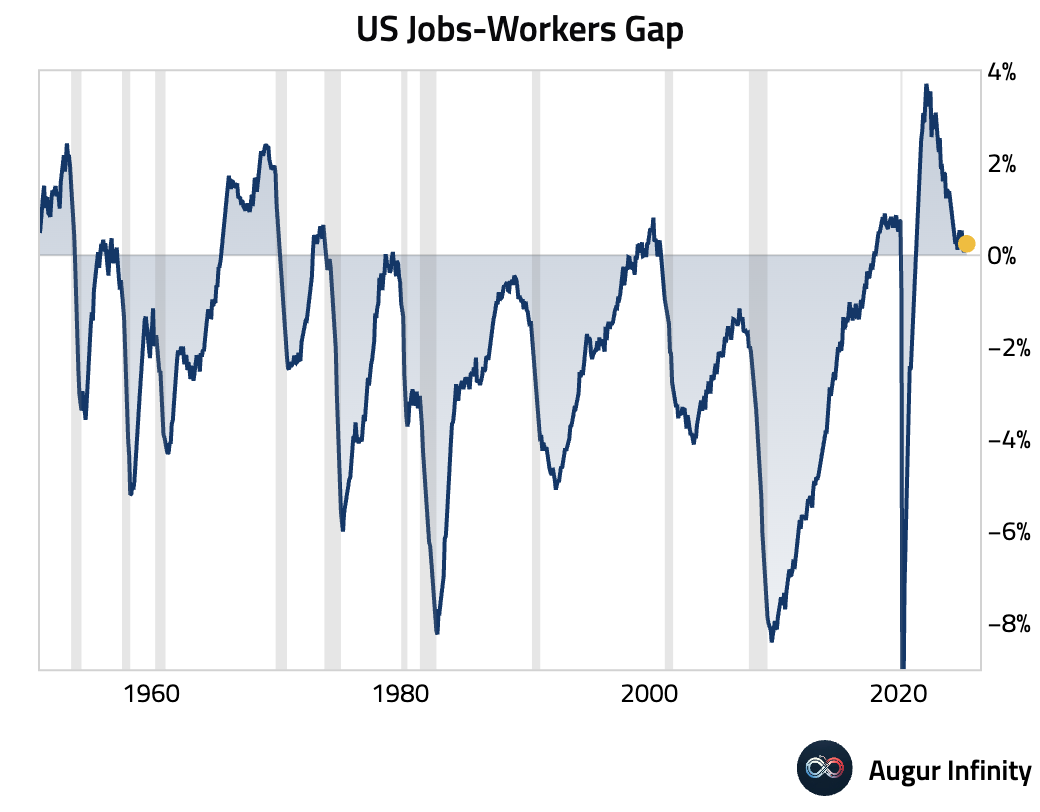

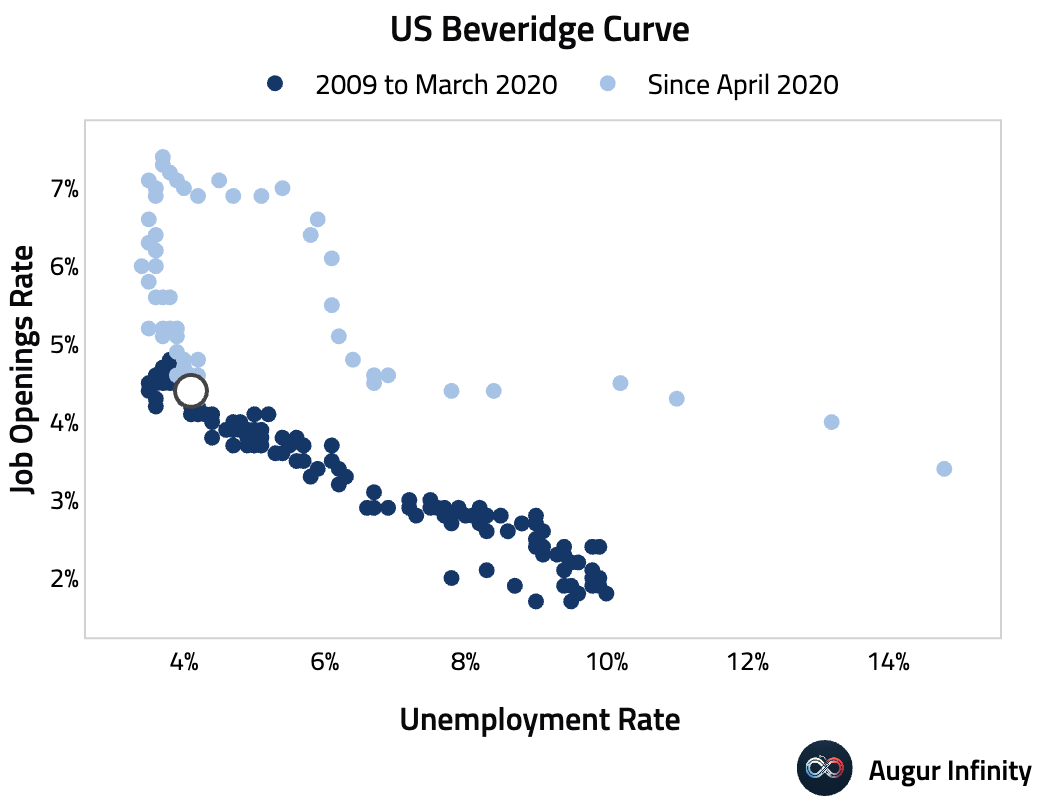

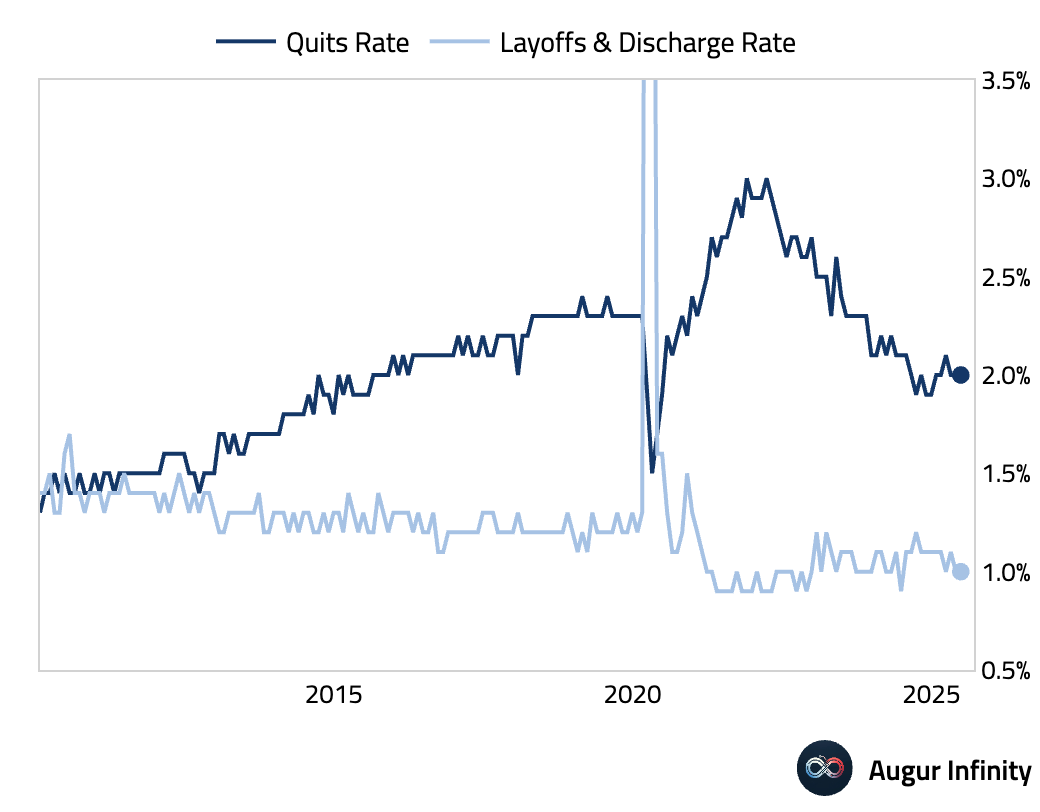

- JOLTs data for June showed job openings fell by 275,000 to 7.44 million, missing consensus of 7.55 million and indicating a continued cooling of labor demand. The decline was concentrated in leisure & hospitality (–264k) and private education & health (–255k).

- Job quits fell to 3.14 million in June from 3.27 million in May, pointing to reduced labor market churn and lower confidence among workers in their ability to find new employment.

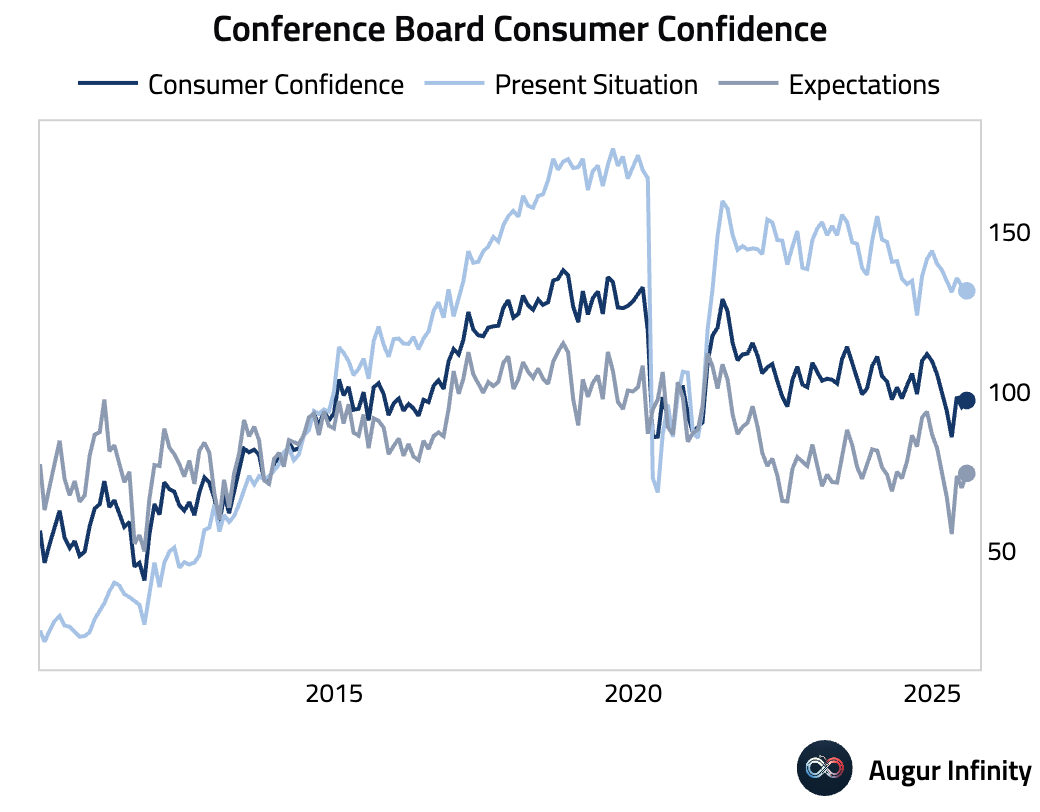

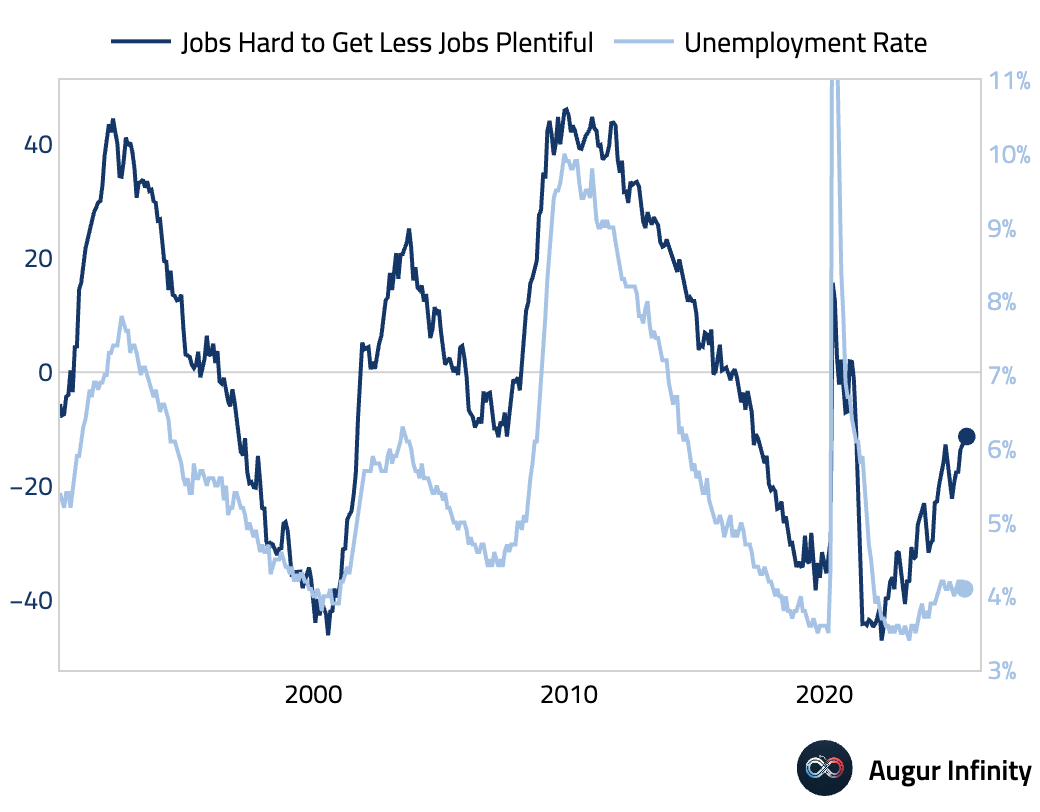

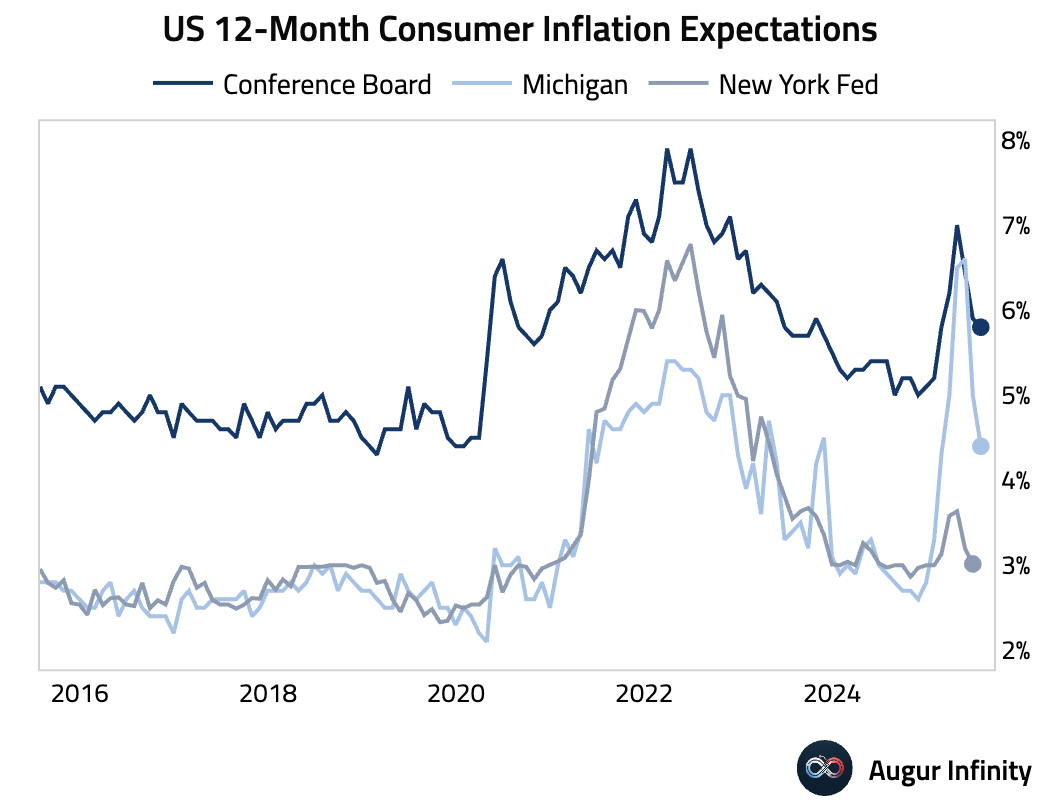

- The Conference Board’s Consumer Confidence Index for July rose to 97.2, beating the 95.8 consensus. The increase was driven entirely by an improved outlook, as the Present Situation component fell to 131.5, its weakest since March 2021. The share of respondents reporting "jobs are hard to get" as opposed to "jobs are plentiful" rose to cycle high. Twelve-month inflation expectations eased to 5.8%, a new low for the survey, though purchasing intentions for big-ticket items weakened.

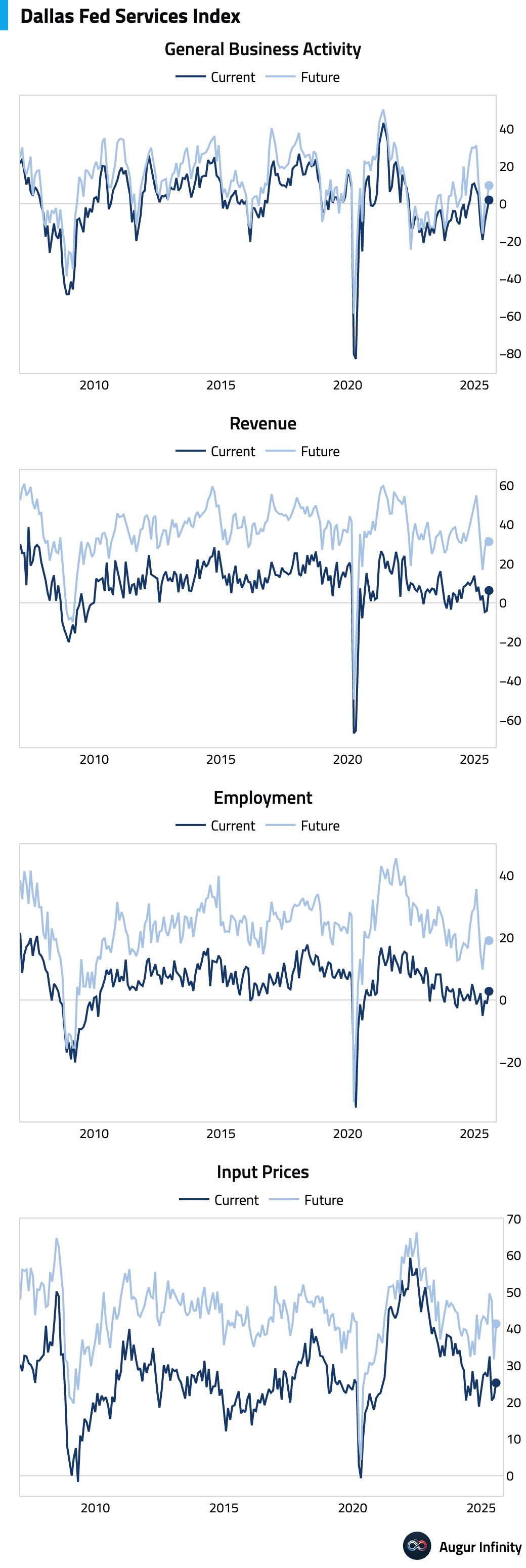

- The Dallas Fed's Services Index for July jumped to 2.0 from –4.4 in June, signaling a return to expansion in the region's service sector. The underlying composition was healthy, with both revenue and employment on the rise.

Europe

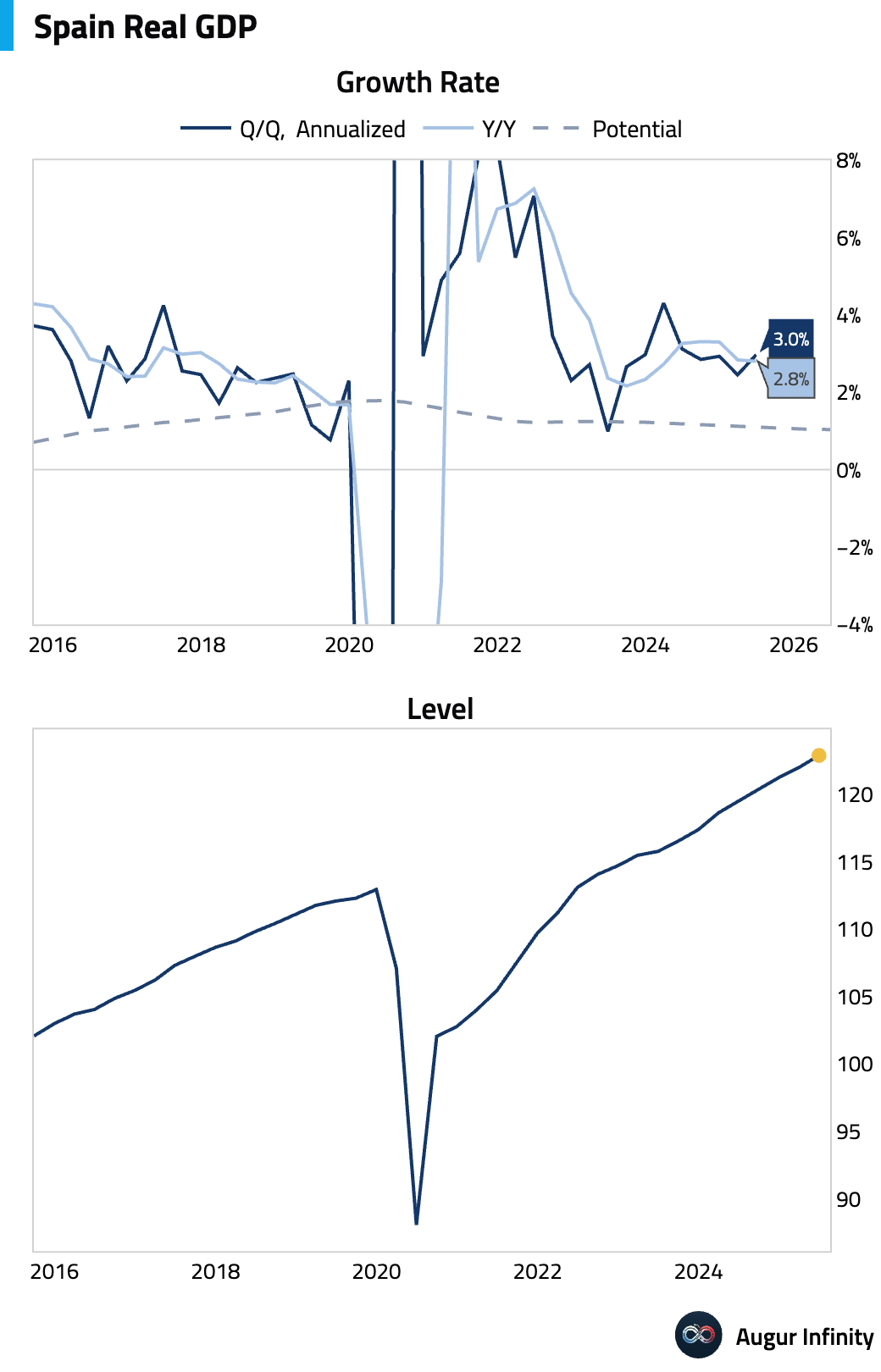

- Spain's economy accelerated in the second quarter, with flash GDP growing 0.7% Q/Q, above the 0.6% consensus and prior reading. This marked the strongest quarterly growth in a year. The Y/Y rate held steady at 2.8%, also beating the 2.5% forecast.

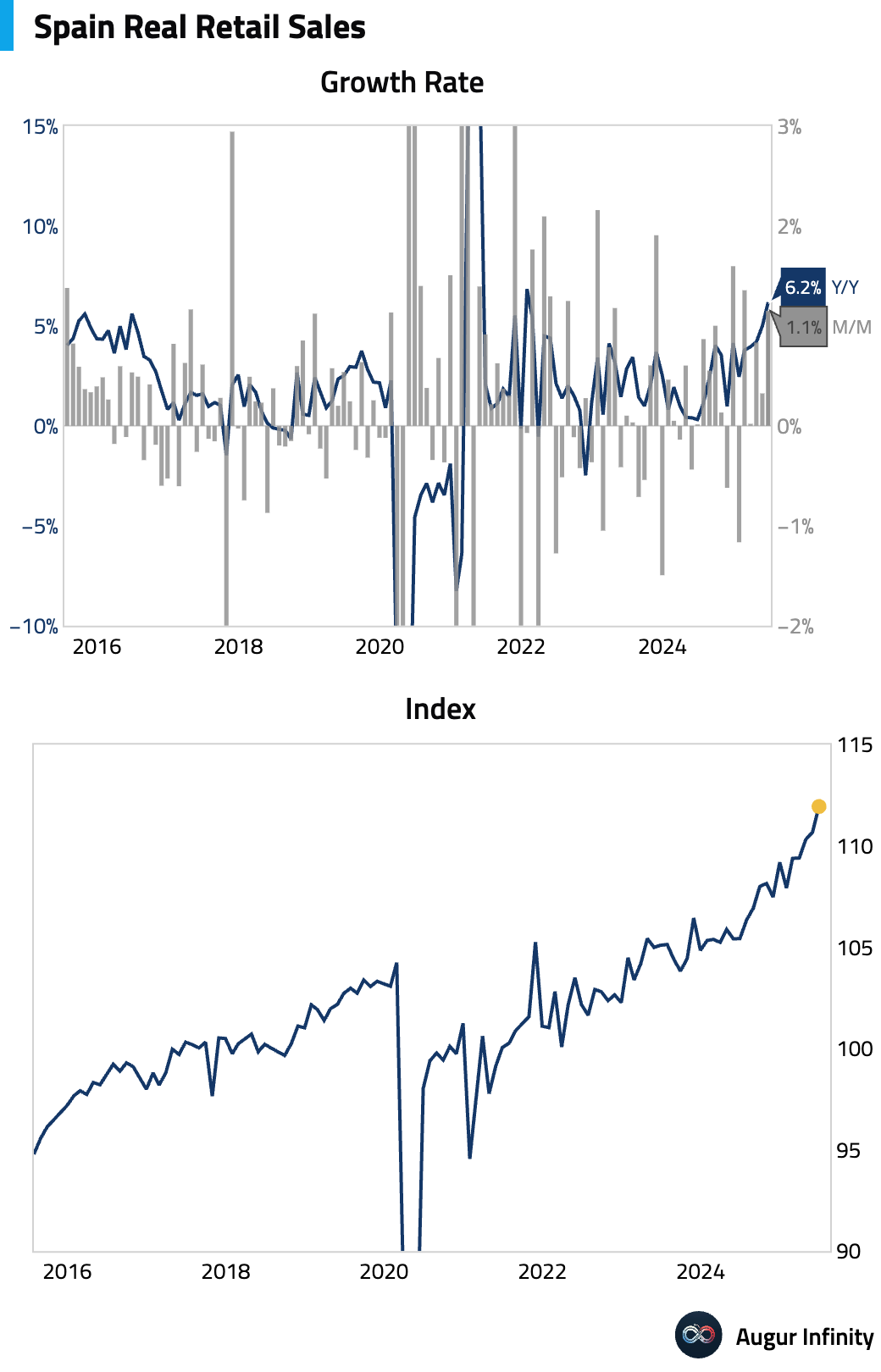

- Spanish retail sales expanded 1.1% M/M in June, a sharp pickup from the 0.2% gain in May. The Y/Y growth rate surged to 6.2% from 5.0%, reaching its highest level since January 2022.

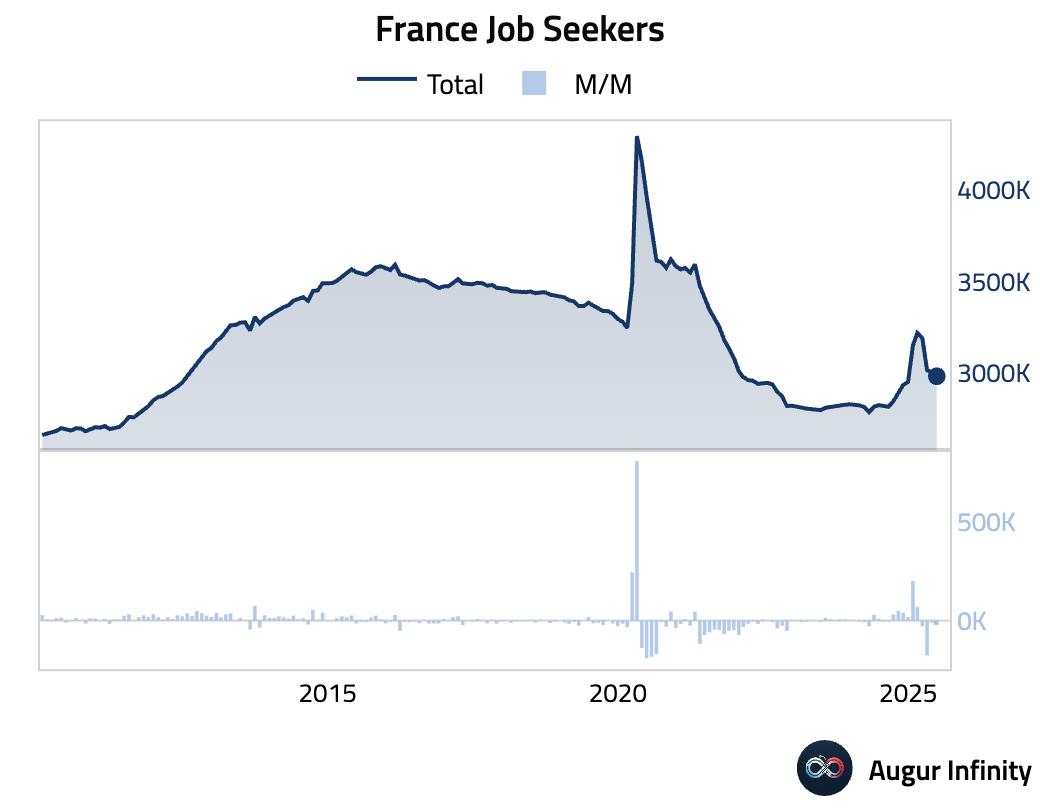

- In France, the number of total jobseekers fell by 21,600 in June to 2.98 million, a larger decline than May's 11,200 drop and the lowest level since December 2024.

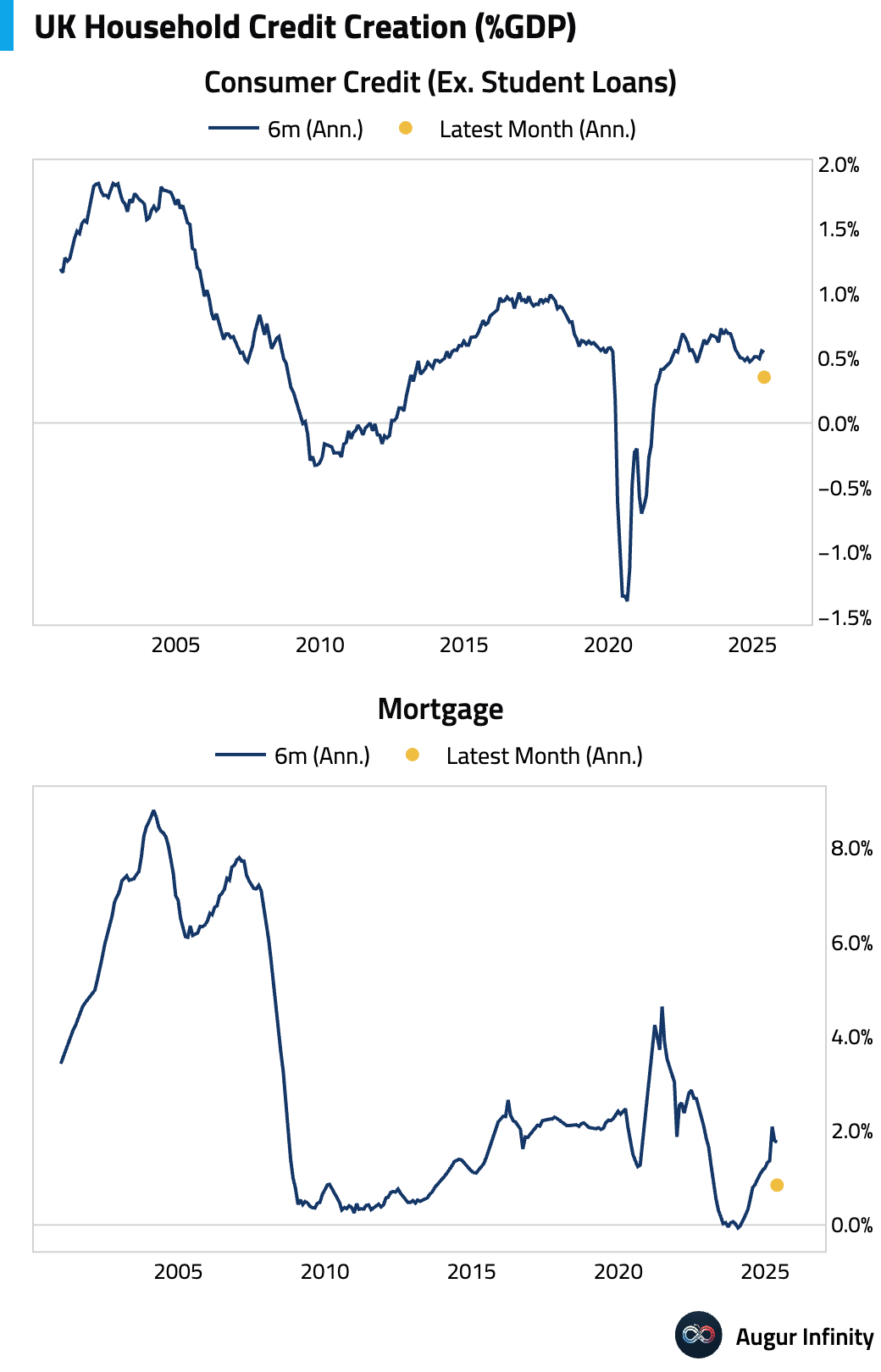

- UK household credit data for June showed strong growth, with net consumer credit rising to £1.42 billion, well above the £1.2 billion consensus. Mortgage lending also saw a notable increase to £5.34 billion from £2.21 billion previously.

- UK mortgage approvals ticked up to 64,170 in June from 63,290 in May, slightly ahead of the 62,500 consensus.

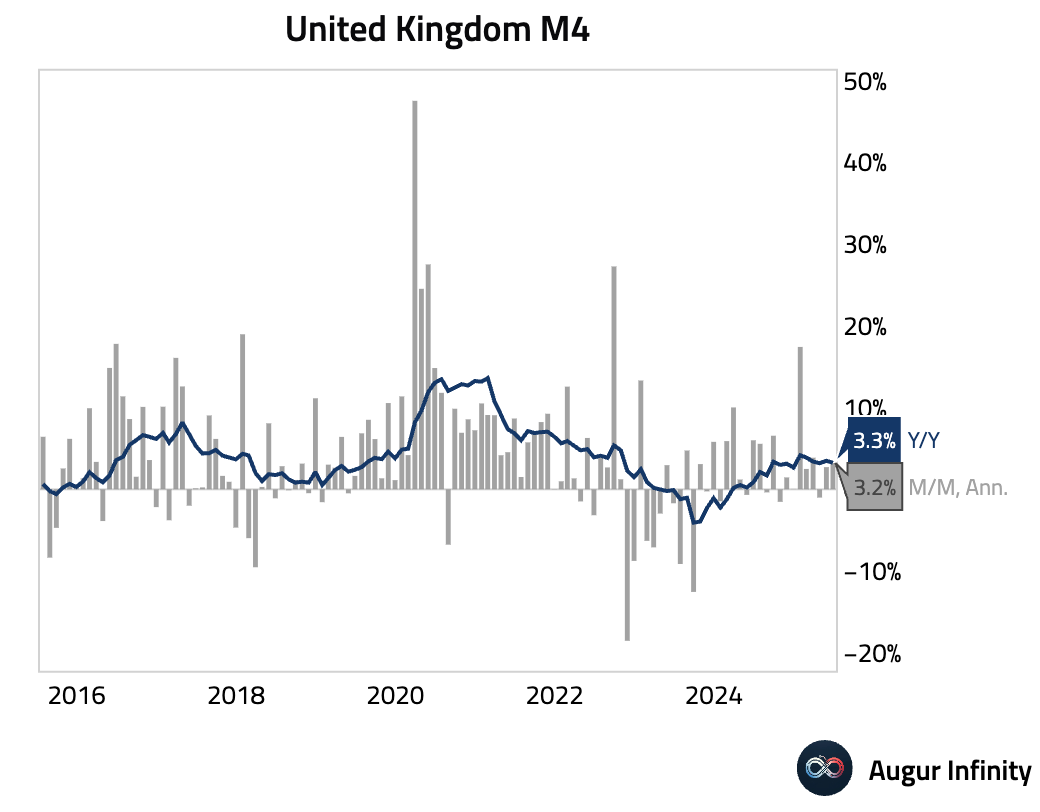

- The UK's M4 money supply grew 0.3% M/M in June, matching consensus and accelerating slightly from the 0.2% pace in May.

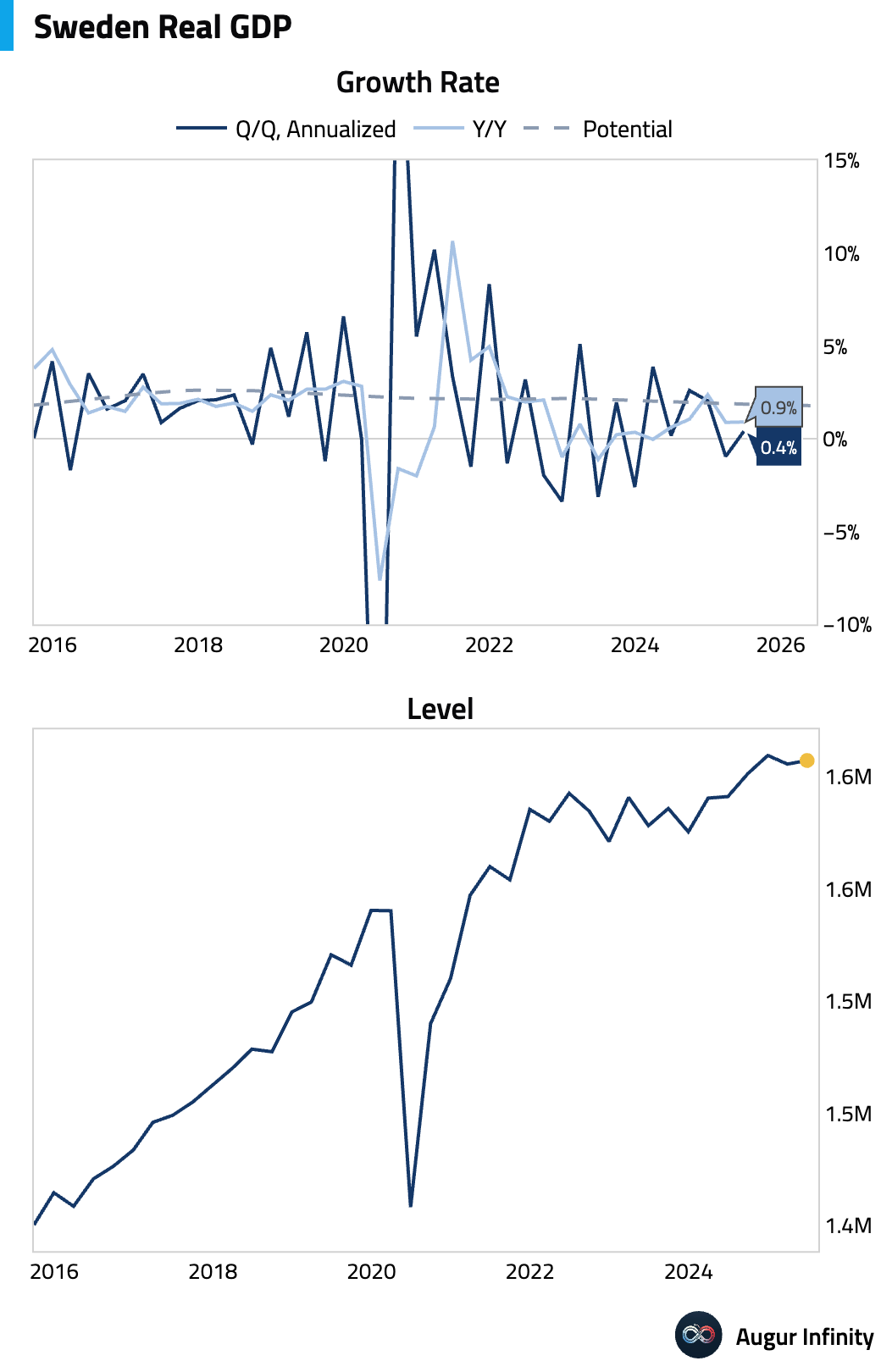

- Sweden’s economy returned to growth in Q2, with the flash GDP estimate showing a 0.1% Q/Q expansion, reversing the 0.2% contraction from Q1. The Y/Y growth rate was stable at 0.9%.

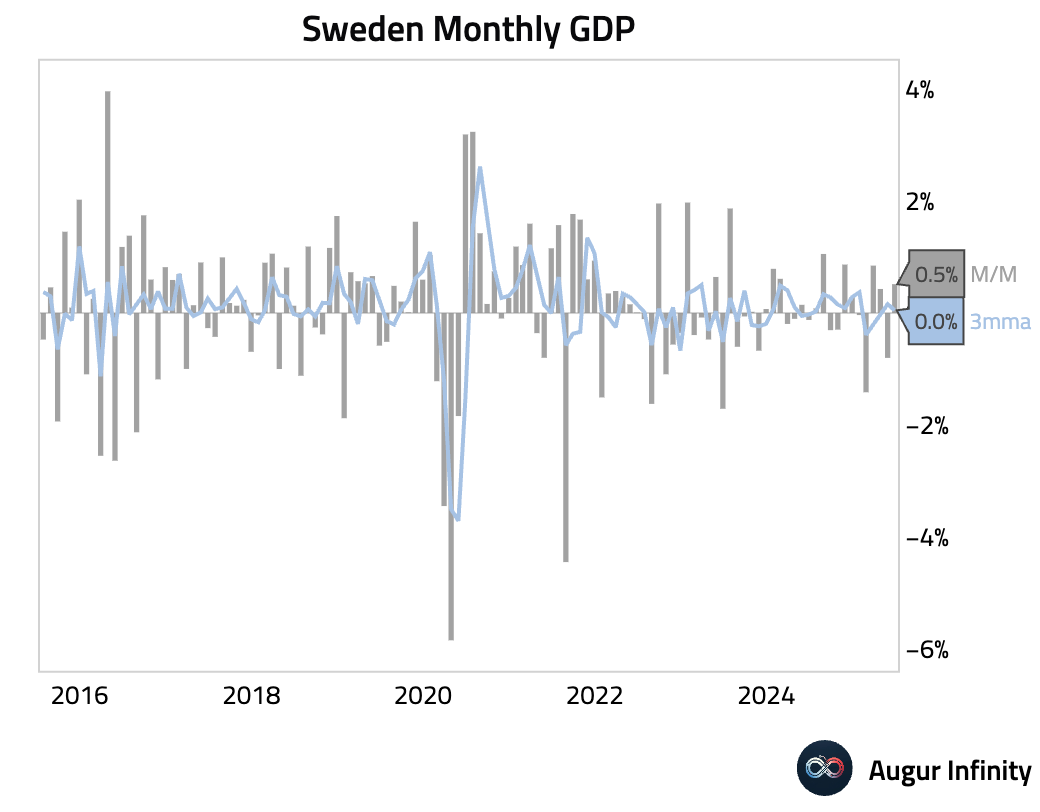

- On a monthly basis, Sweden's GDP rose 0.5% in June, rebounding from a 0.8% contraction in May.

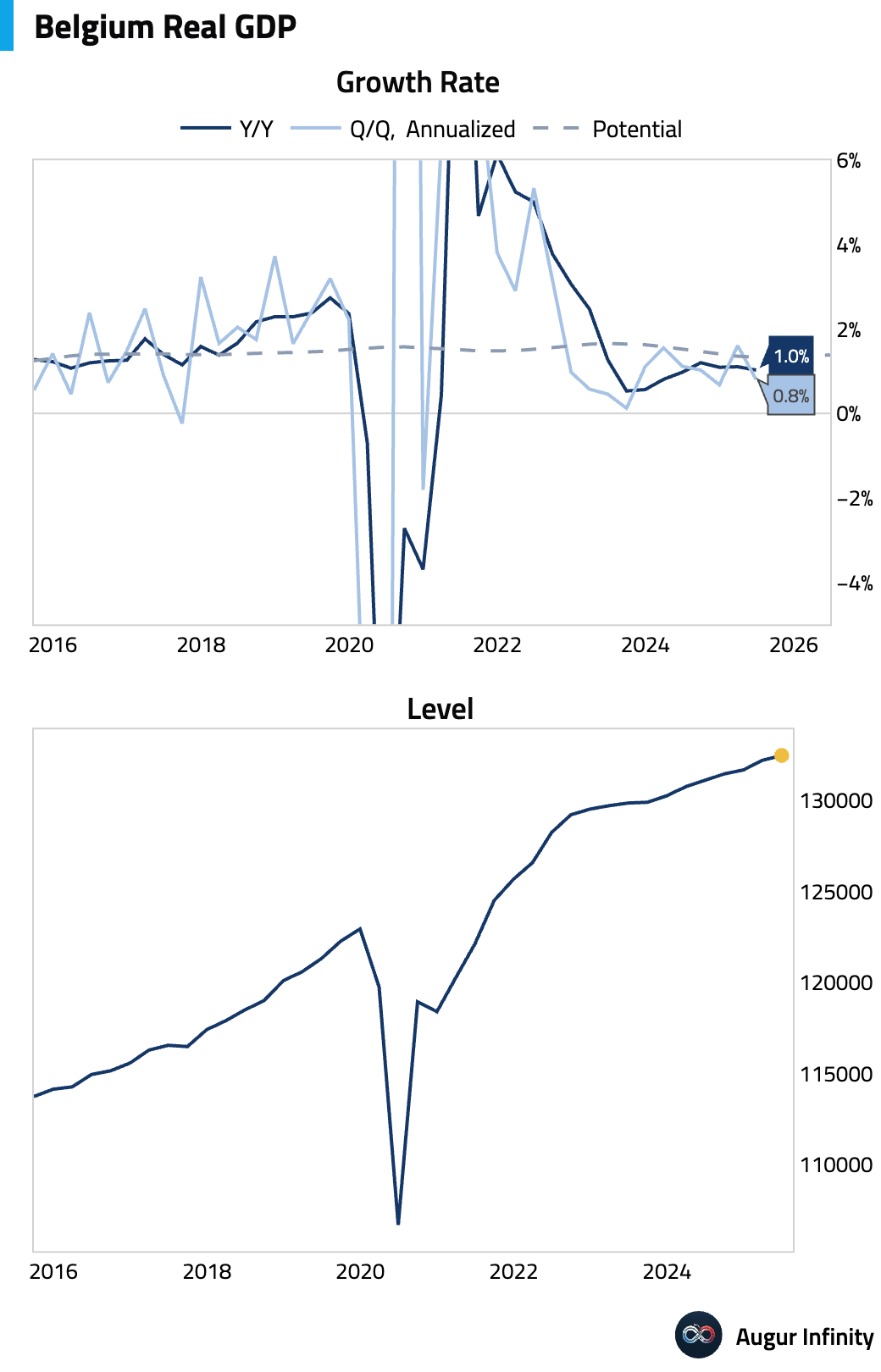

- Belgium's Q2 advance GDP showed growth slowing to 0.2% Q/Q, down from 0.4% in Q1. The Y/Y rate eased to 1.0% from 1.1%.

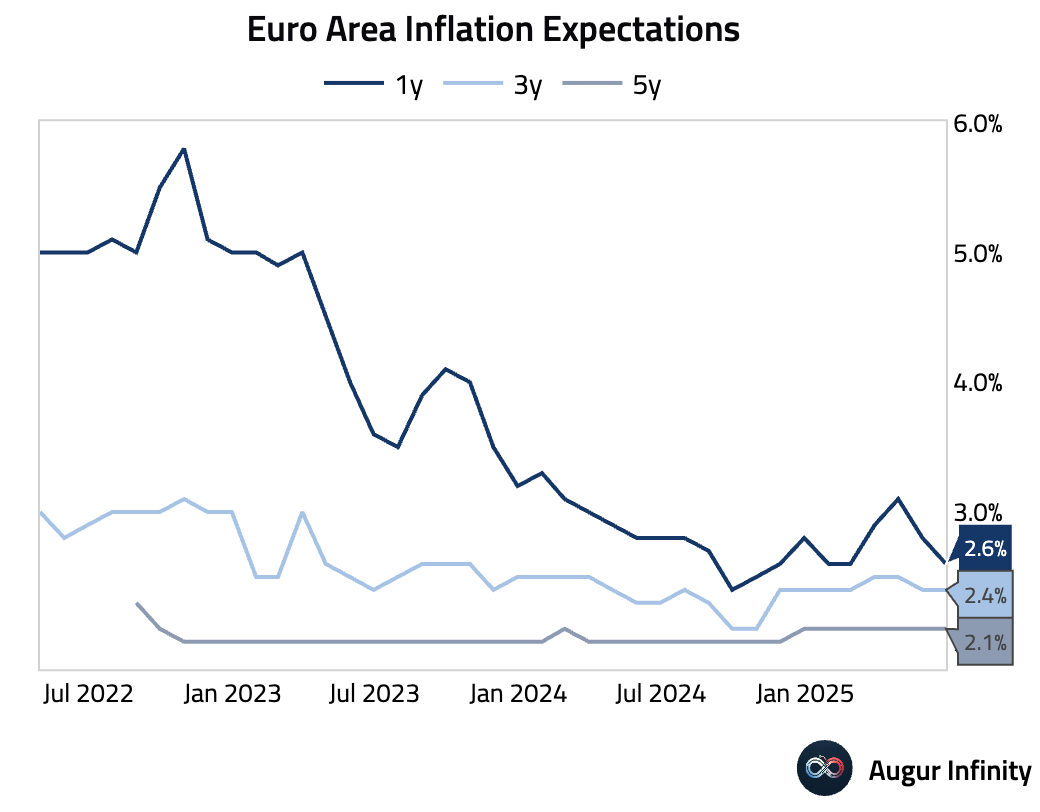

- ECB survey data for June showed consumer inflation expectations for the next 12 months eased to 2.6% from 2.8% in May.

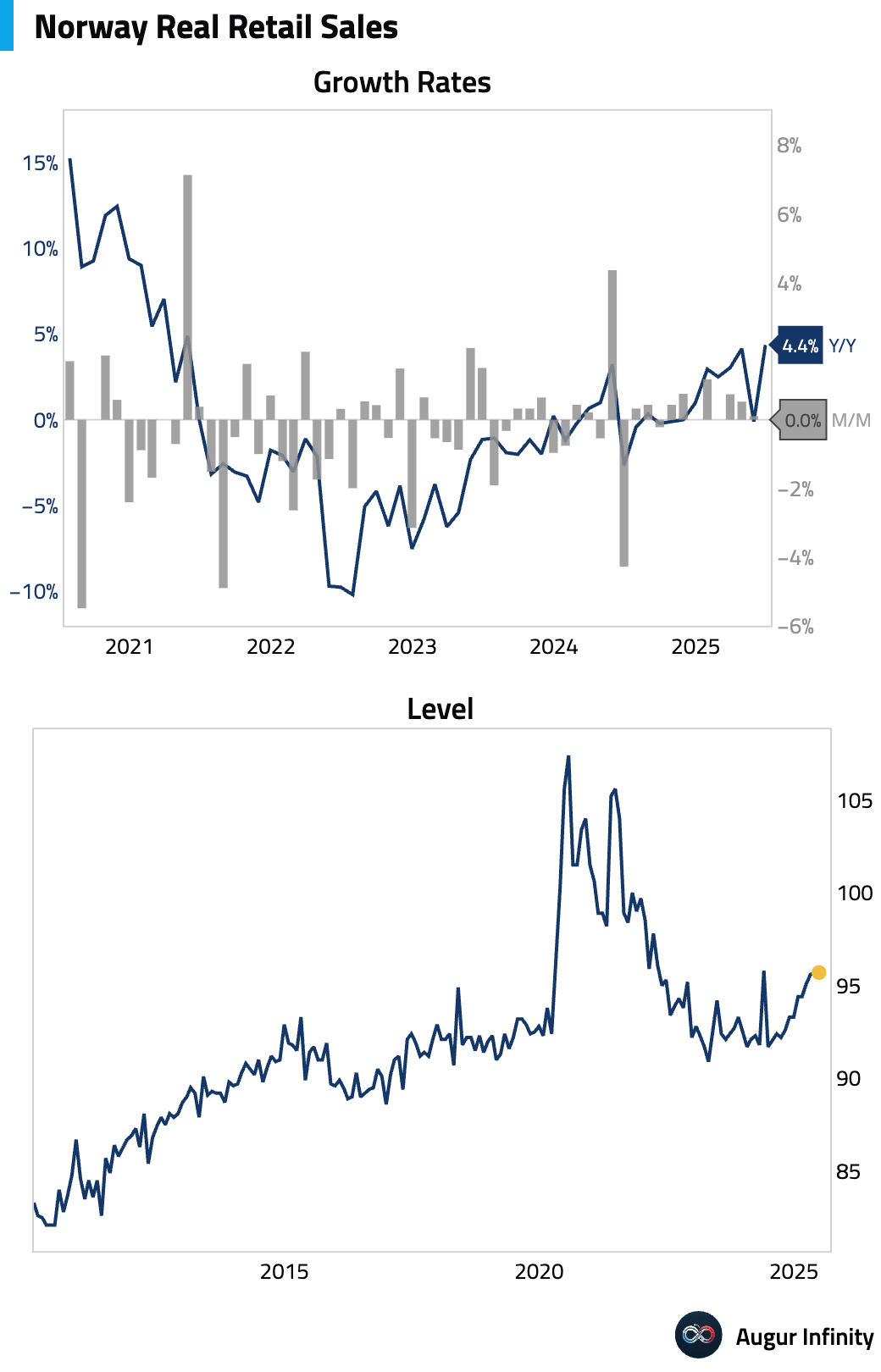

- Norwegian retail sales were flat in June (0.0% M/M), following a 0.1% gain in May, indicating stagnant consumer spending.

Asia-Pacific

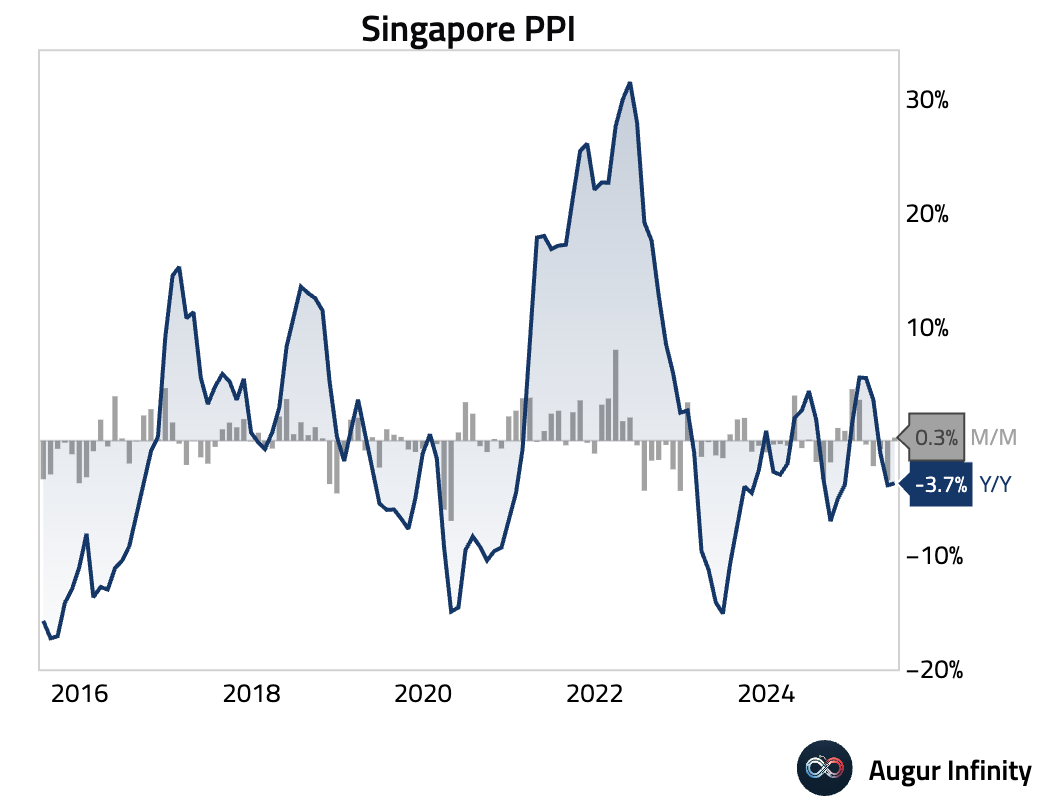

- Singapore’s Producer Price Index (PPI) fell 3.7% Y/Y in June, a slightly slower rate of decline than the 3.9% drop recorded in May.

- Singapore's export prices fell 7.8% Y/Y in June, moderating from an 8.1% decline in the prior month.

- Singapore’s import prices were down 6.5% Y/Y in June, compared to an 8.2% fall in May, indicating easing deflationary pressure from trade.

Emerging Markets ex China

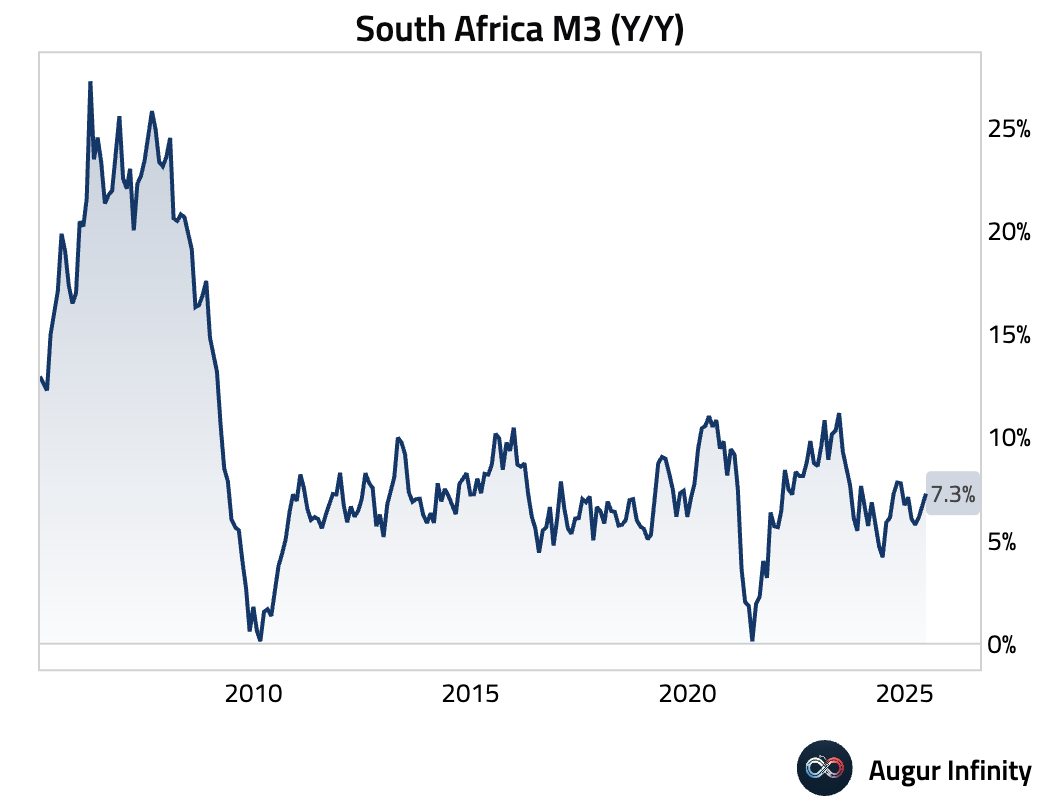

- South Africa's M3 money supply growth accelerated to 7.27% Y/Y in June from 6.86% in May, marking the fastest pace of expansion since November 2024.

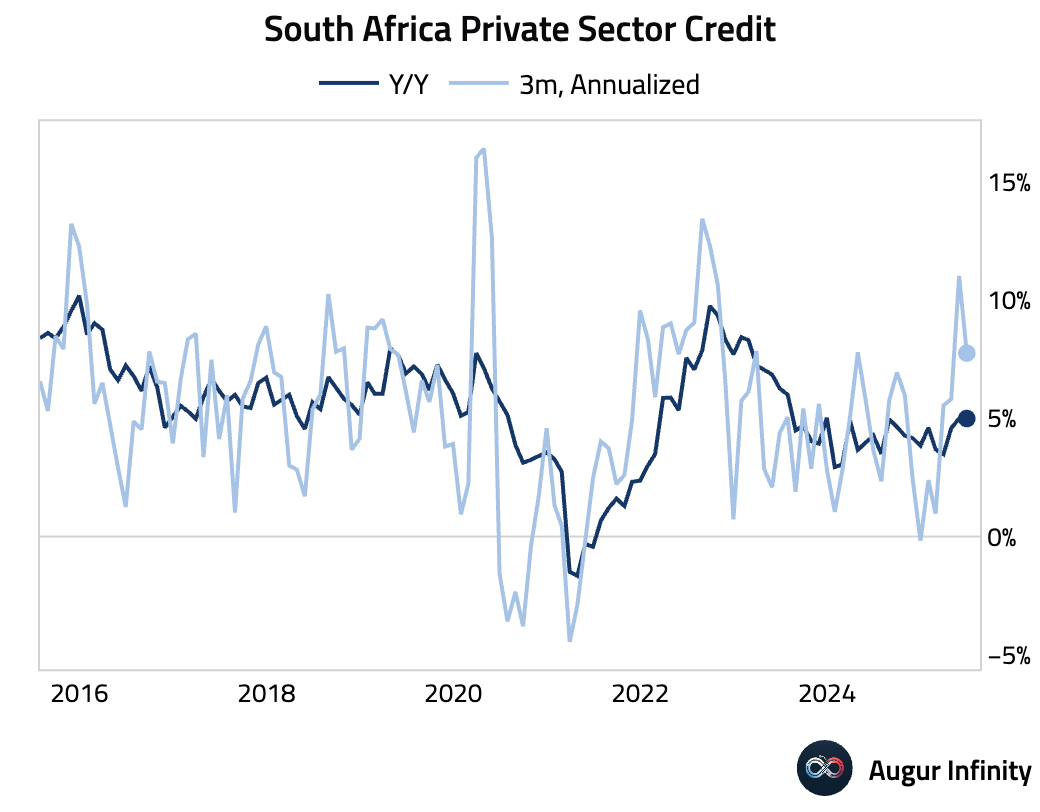

- Private sector credit growth in South Africa was unchanged at 4.98% Y/Y in June.

Global Markets

Equities

- Global equities were mixed as US markets pulled back from recent highs. The S&P 500 and Nasdaq Composite fell 0.3% and 0.4%, respectively. In contrast, European markets posted gains, with Germany up 0.5% and the UK rising 0.7%. In Asia, China's market declined for a fourth consecutive day (–0.7%), while South Korea rallied 1.1%.

Fixed Income

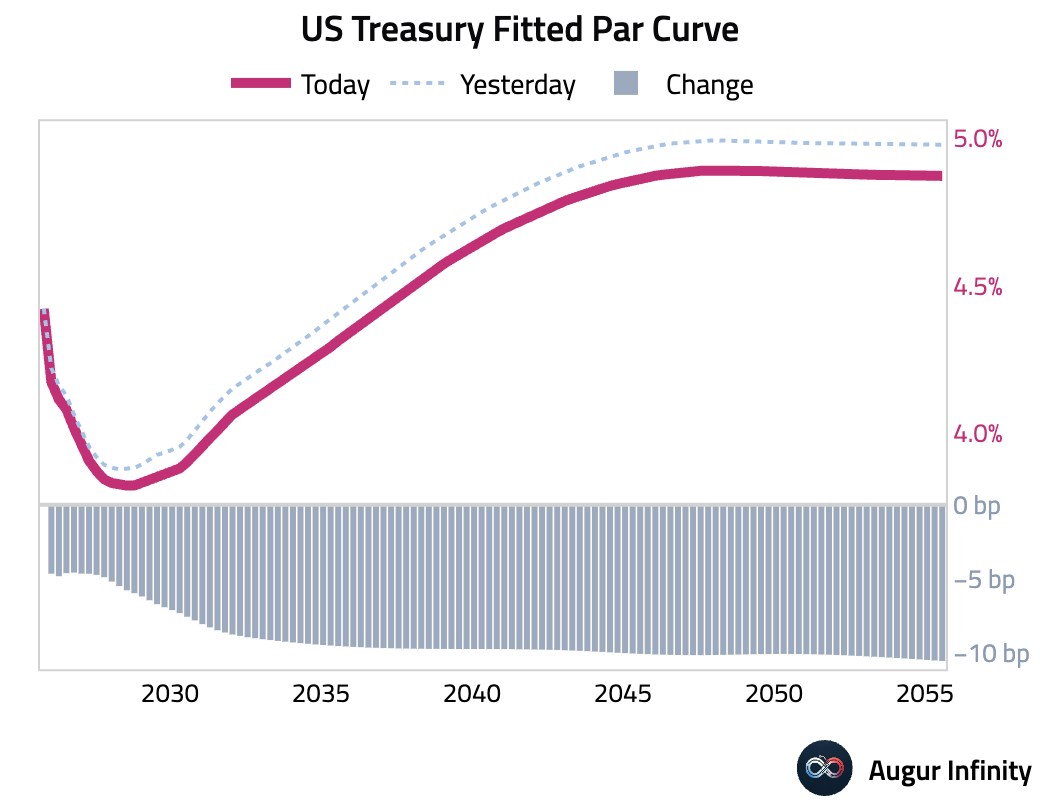

- US Treasury yields fell across the curve ahead of the Federal Reserve's policy decision. The 10-year yield dropped 9.5 basis points to 4.33%, while the 2-year yield fell 4.7 bps to 3.88%, resulting in a bull-flattening of the yield curve.

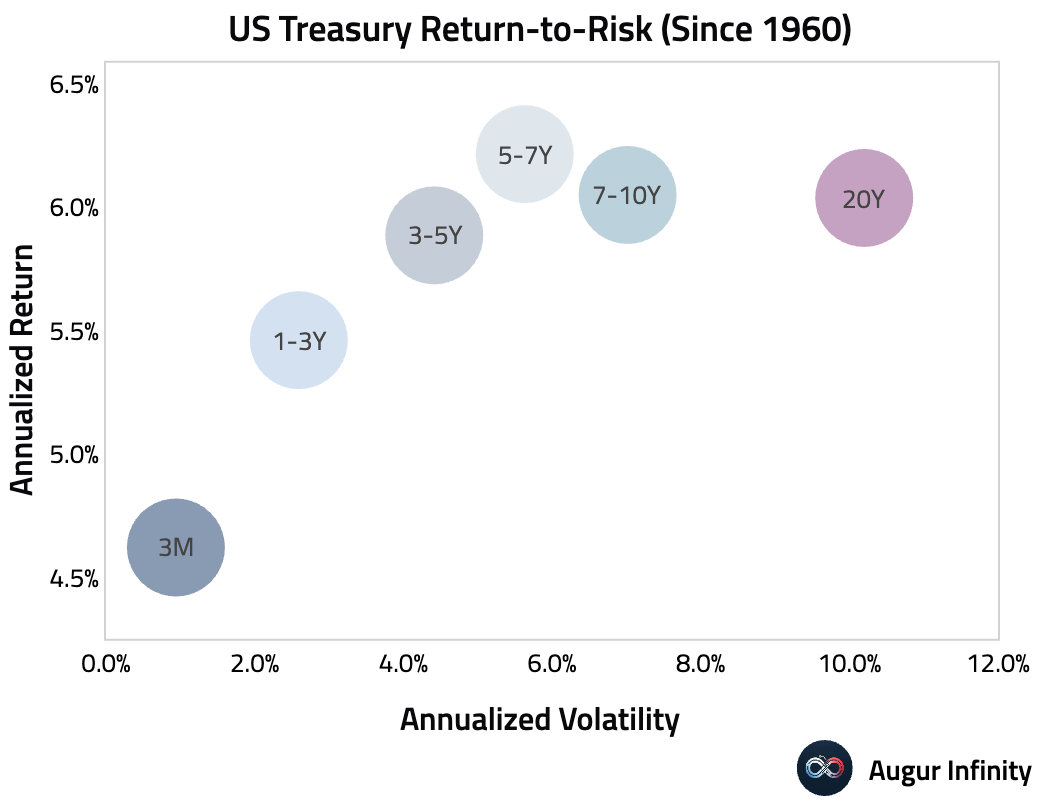

- Analysis of historical returns shows that duration extension is not always rewarded. Since 1960, while moving from cash to short- and intermediate-term bonds improved returns, extending to 7–20-year bonds has historically offered lower risk-adjusted returns than 5–7-year bonds.

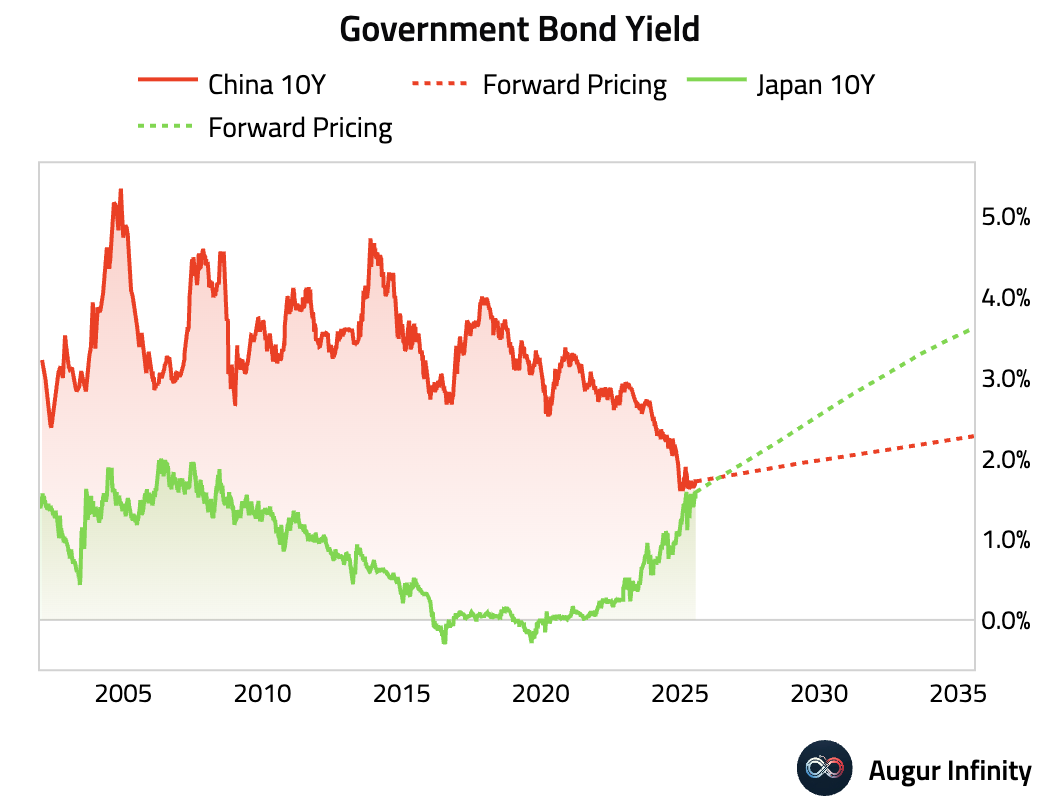

- Forward markets are pricing for Japan's 10-year government bond yield to surpass China's within the next year, with the spread expected to widen further over the coming decade.

Commodities

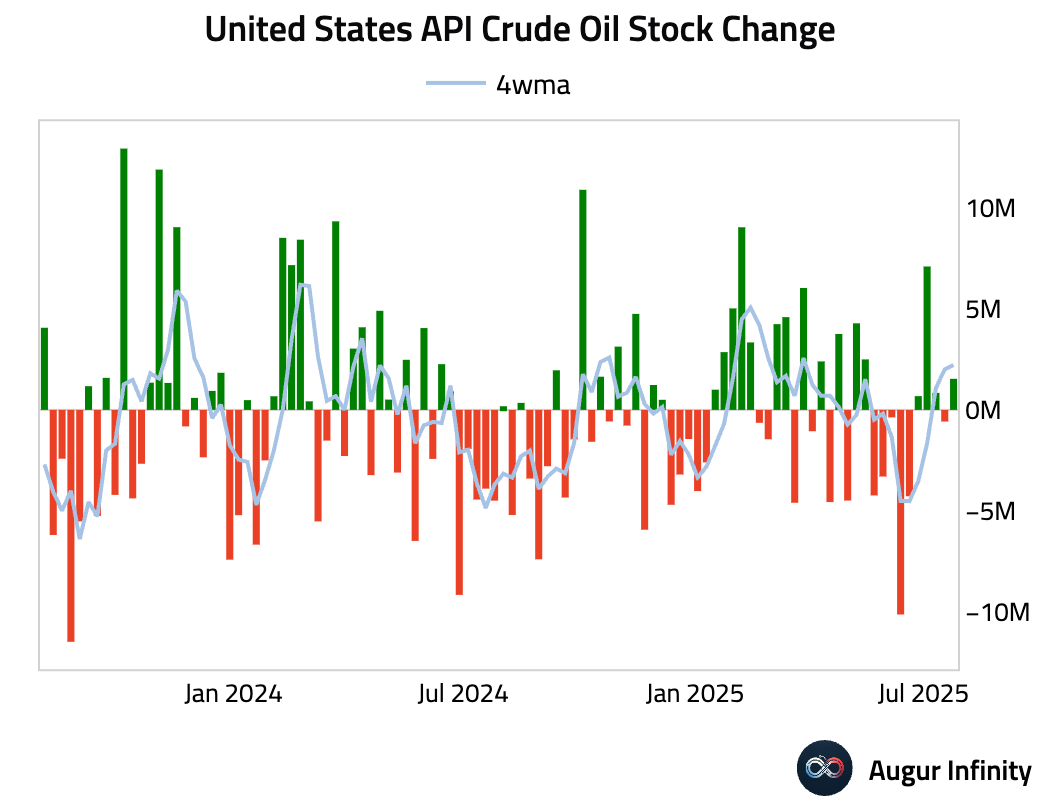

- The American Petroleum Institute (API) reported a surprise build of 1.54 million barrels in US crude oil inventories for the week ending July 25. This contrasted sharply with consensus forecasts for a 2.5 million barrel drawdown.

FX

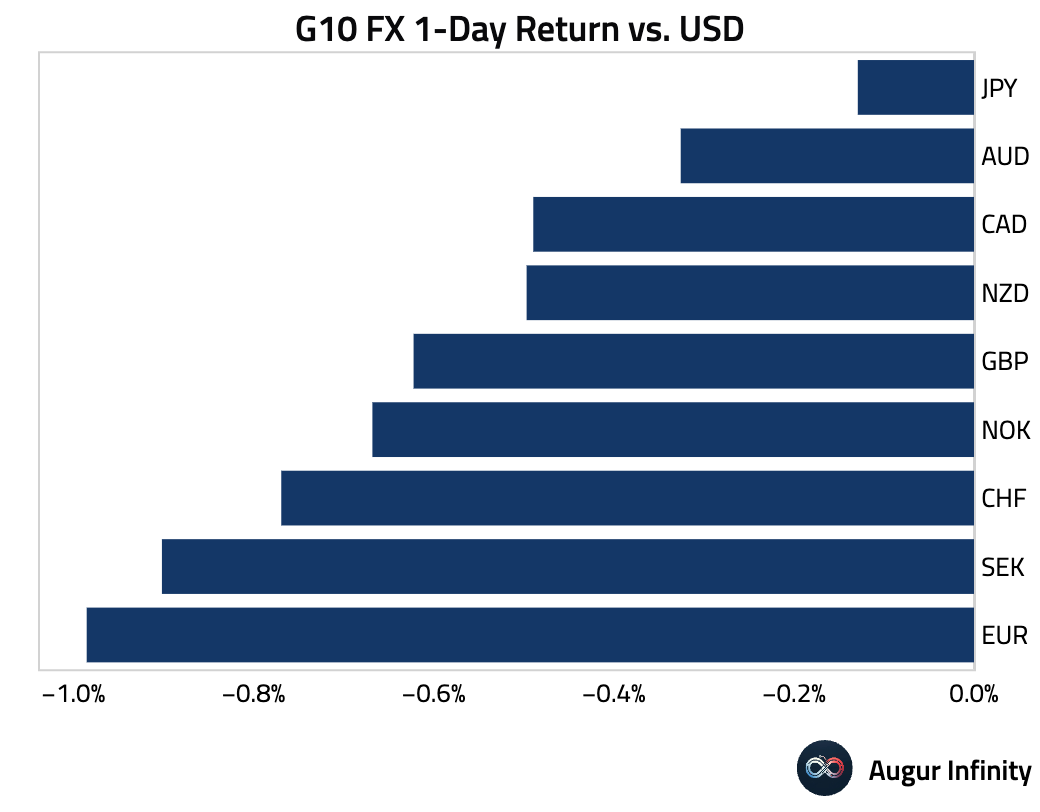

- The US dollar strengthened broadly against all G10 peers, driven by trade developments and positioning ahead of the FOMC meeting. The euro was the weakest performer, falling 1.0% against the dollar. The Canadian dollar, British pound, and Swiss franc all posted their fourth consecutive day of losses against the greenback.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.