The United States and South Korea reached a trade agreement that entails a $350 billion investment and $100 billion in energy purchases by South Korea, in exchange for which South Korean imports will face a 15 percent tariff while US exports will be tariff-free.

The US administration announced it will extend the current tariff rate on goods from Mexico for an additional ninety days to allow for continued negotiations.

A 25 percent tariff on all imports from India is set to take effect on August 1.

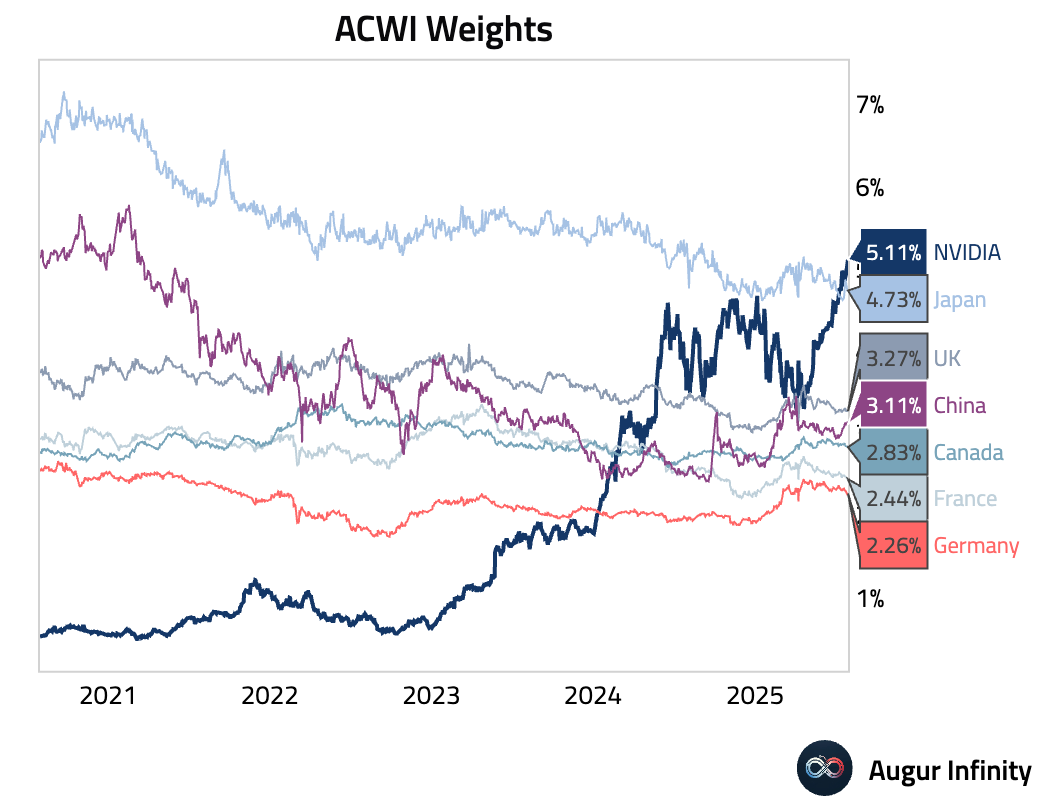

NVIDIA’s weighting in ACWI—the ETF that tracks the MSCI All Country World Index—is now over 5% and 38 bps ahead of Japan's. In other words, if NVIDIA were considered a country, it would rank as the second-largest in ACWI, behind only the United States.

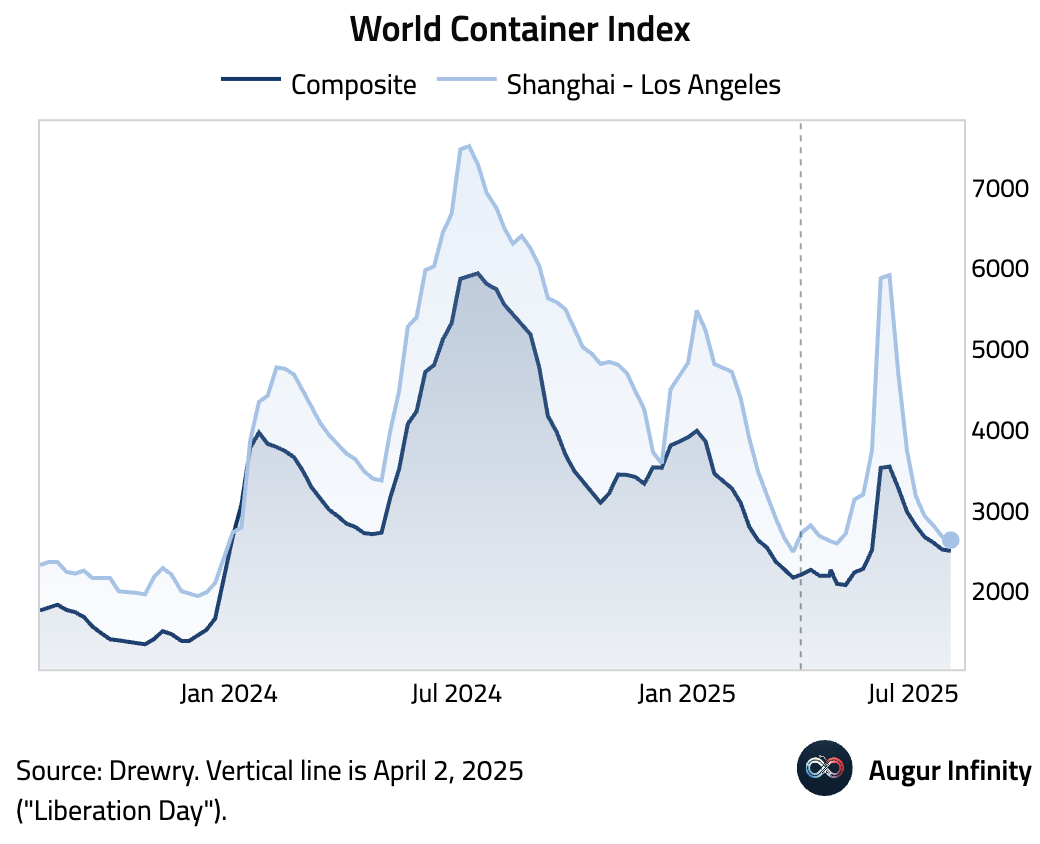

The World Container Index, which measures spot freight rates, declined for the 7th consecutive week.

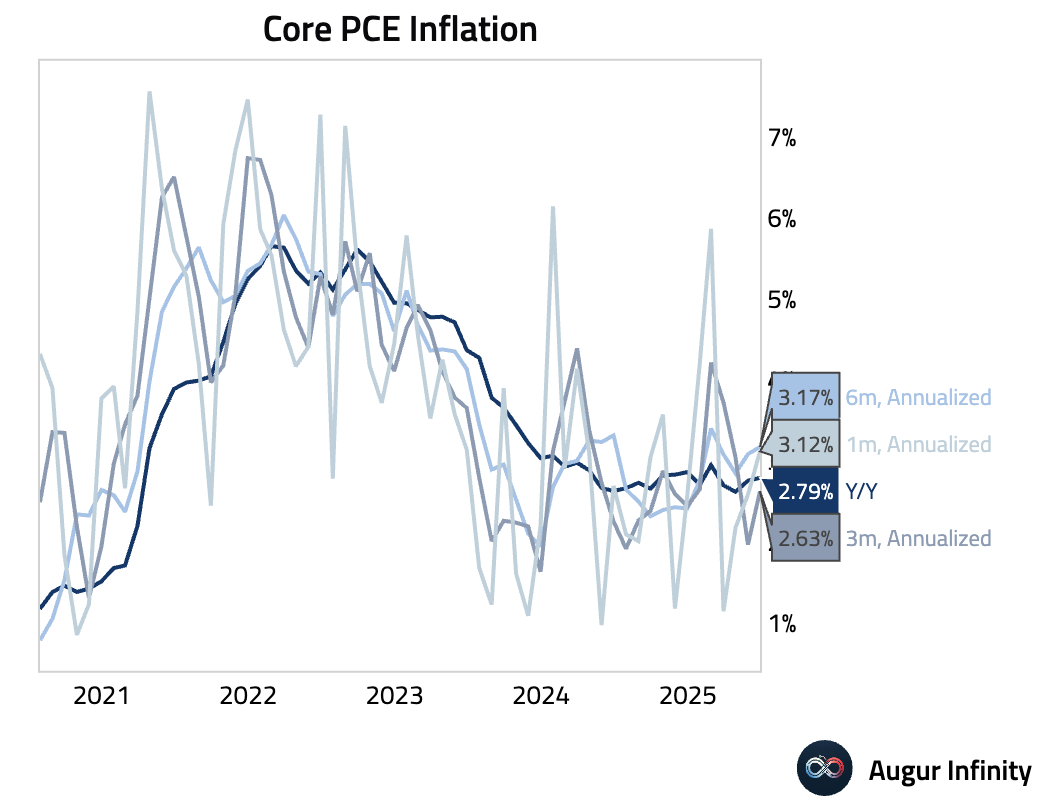

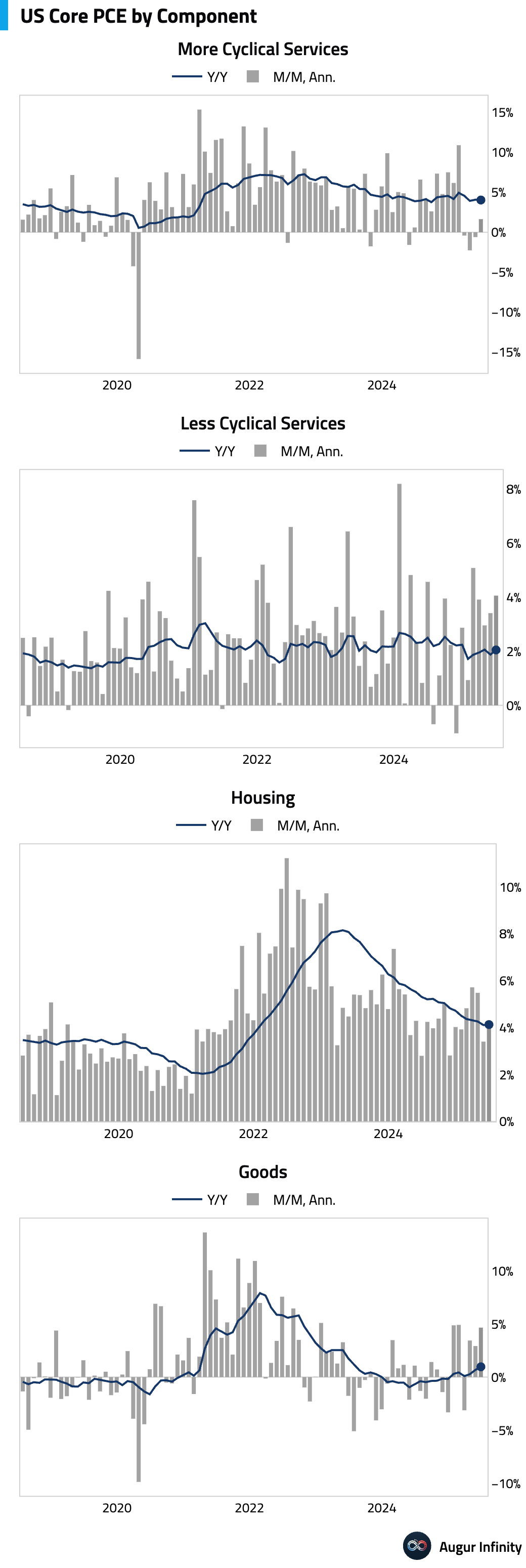

The US Core PCE Price Index rose 0.3% M/M in June, in line with consensus, while prior months were revised higher. Year-over-year, Core PCE held at 2.8%, slightly above the 2.7% consensus. The key “supercore” measure (core services ex-housing) was soft, rising just 0.19%. Headline PCE also rose 0.3% M/M, pushing the annual rate to 2.6% from 2.4%.

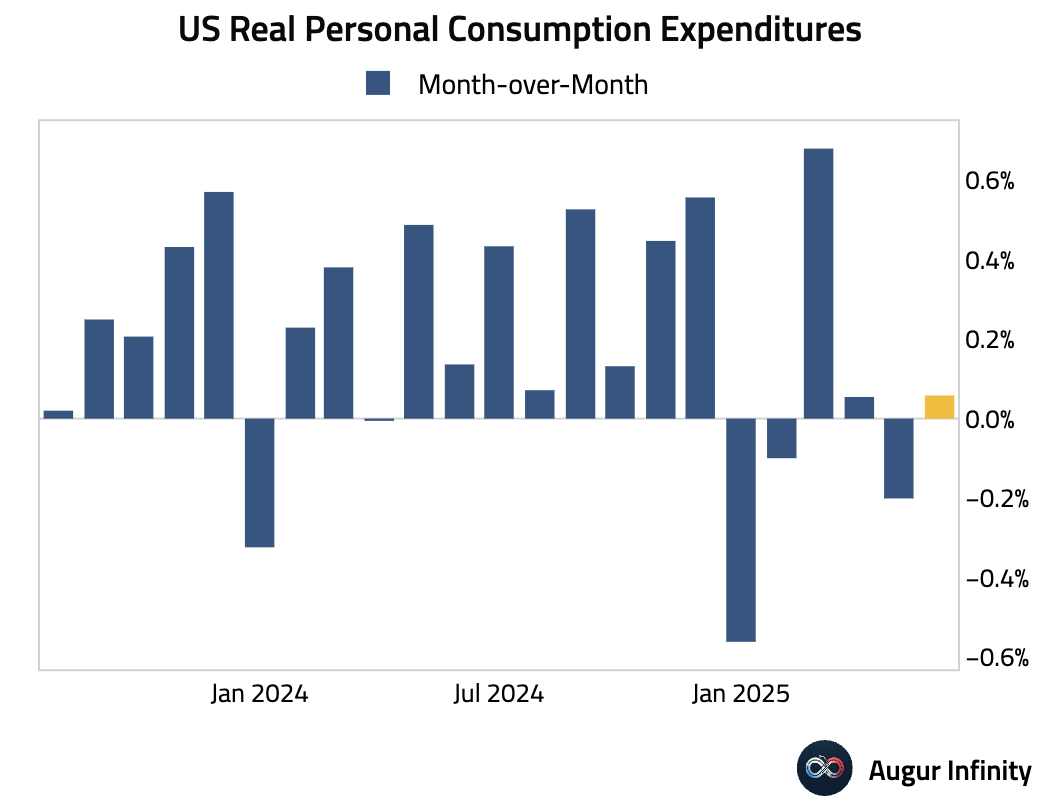

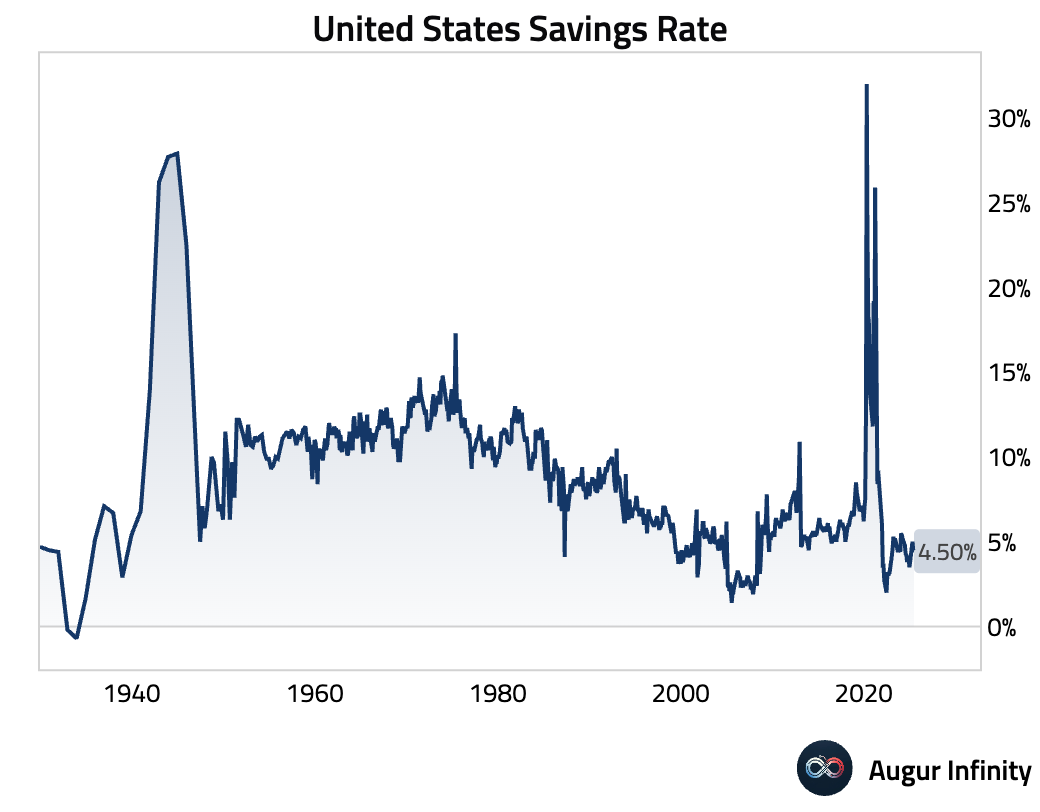

Personal spending increased by 0.3% M/M in June, slightly below the 0.4% consensus but up from a flat reading in May. In real terms, spending rose a tepid 0.1%, with a rotation back towards services consumption. The personal savings rate was unchanged at 4.5%, indicating that consumer momentum remains steady but is not accelerating.

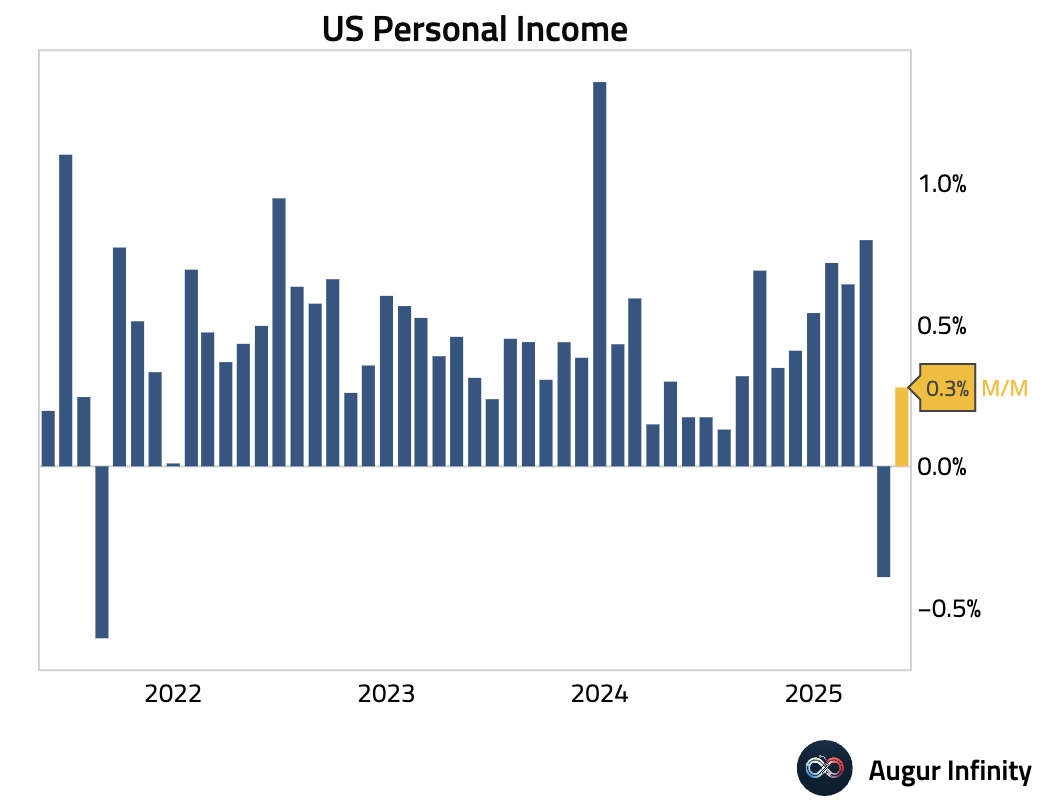

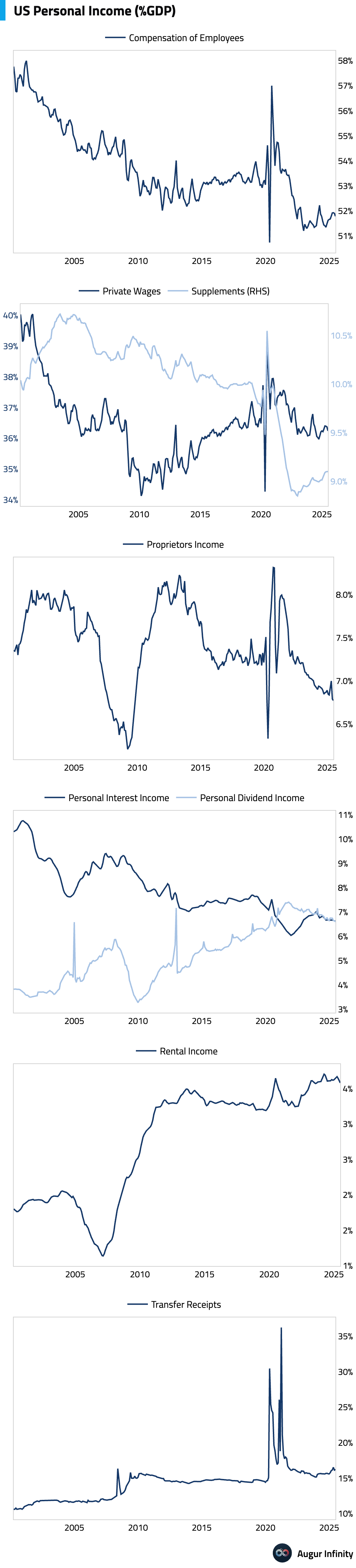

US Personal Income rose 0.3% in June, beating the 0.2% consensus and rebounding from a 0.4% decline in May. The increase was driven by a 1.0% jump in government transfer payments rather than wage growth.

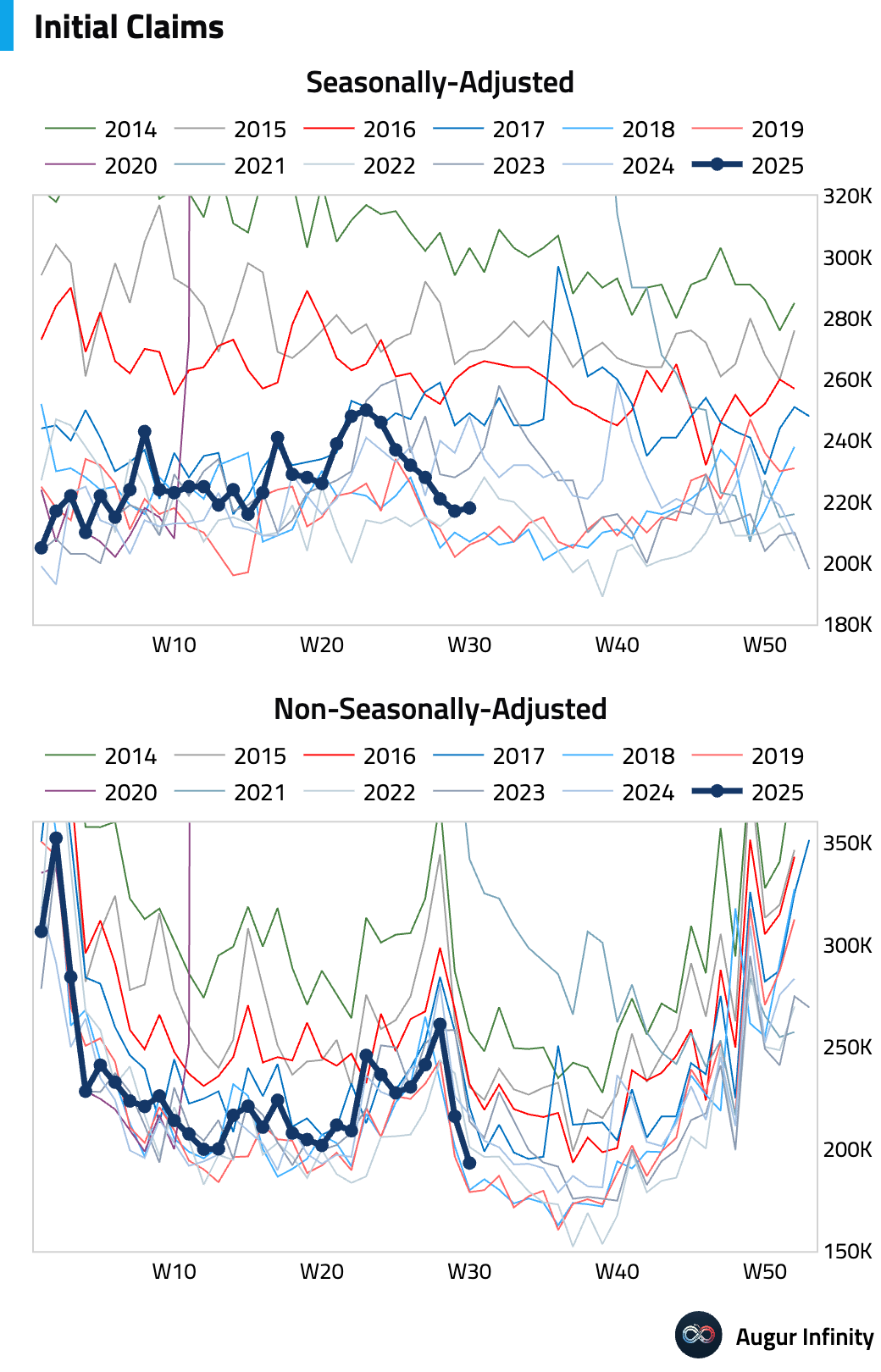

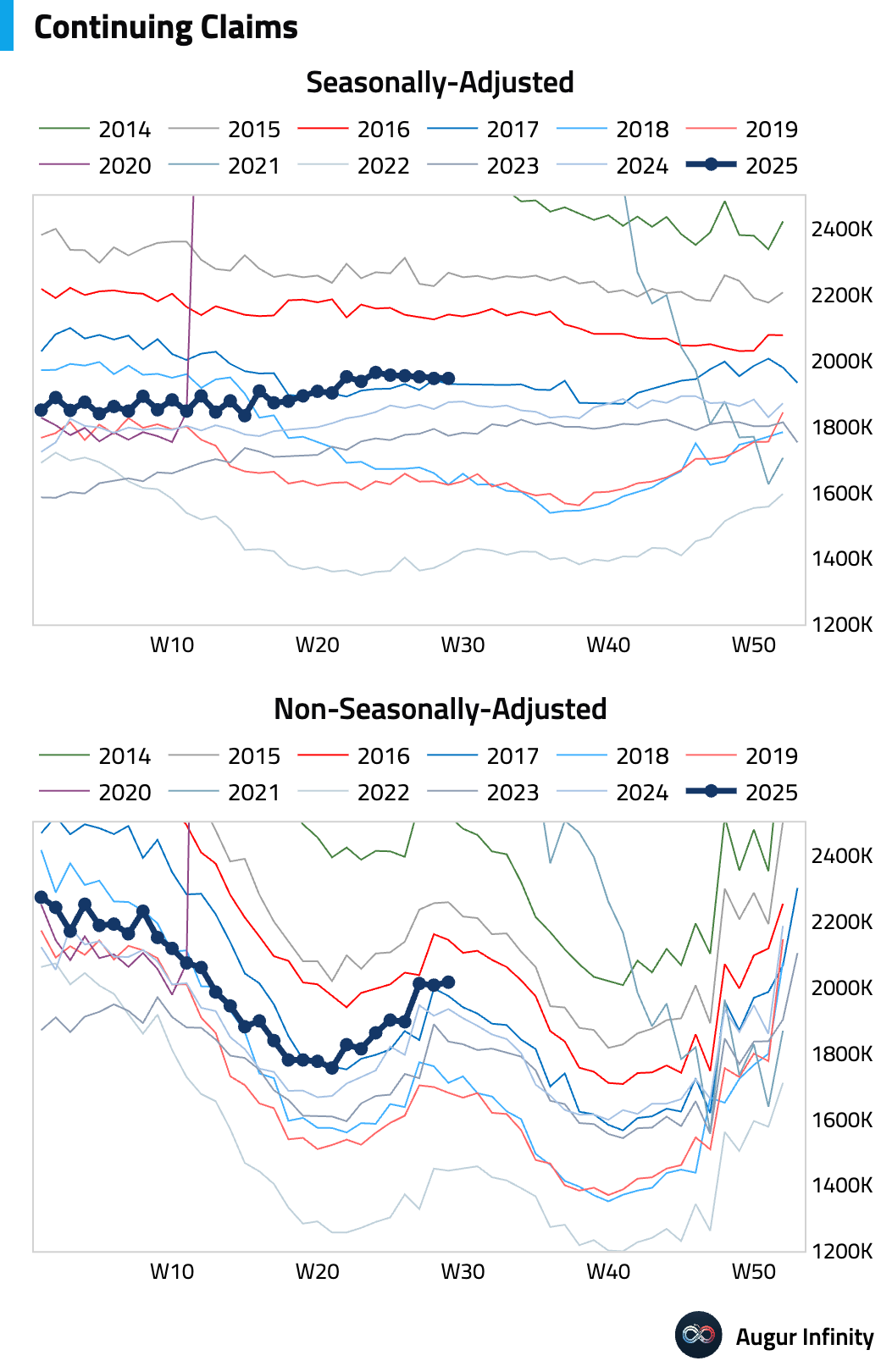

Initial jobless claims for the week ended July 26 were 218,000, below the 224,000 consensus, while the 4-week average fell. Continuing claims were stable at 1.946 million after a downward revision. The data continues to point toward a very tight and resilient labor market with few signs of loosening.

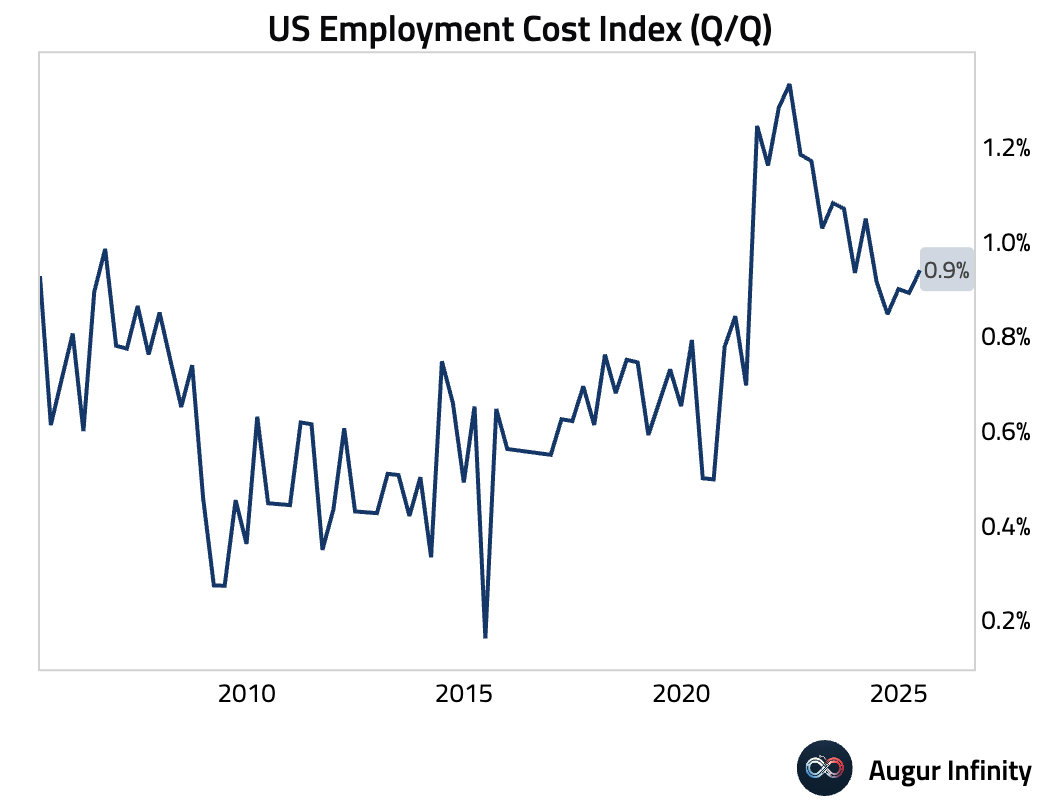

The US Employment Cost Index (ECI) rose 0.9% Q/Q in the second quarter, slightly stronger than the +0.8% consensus.

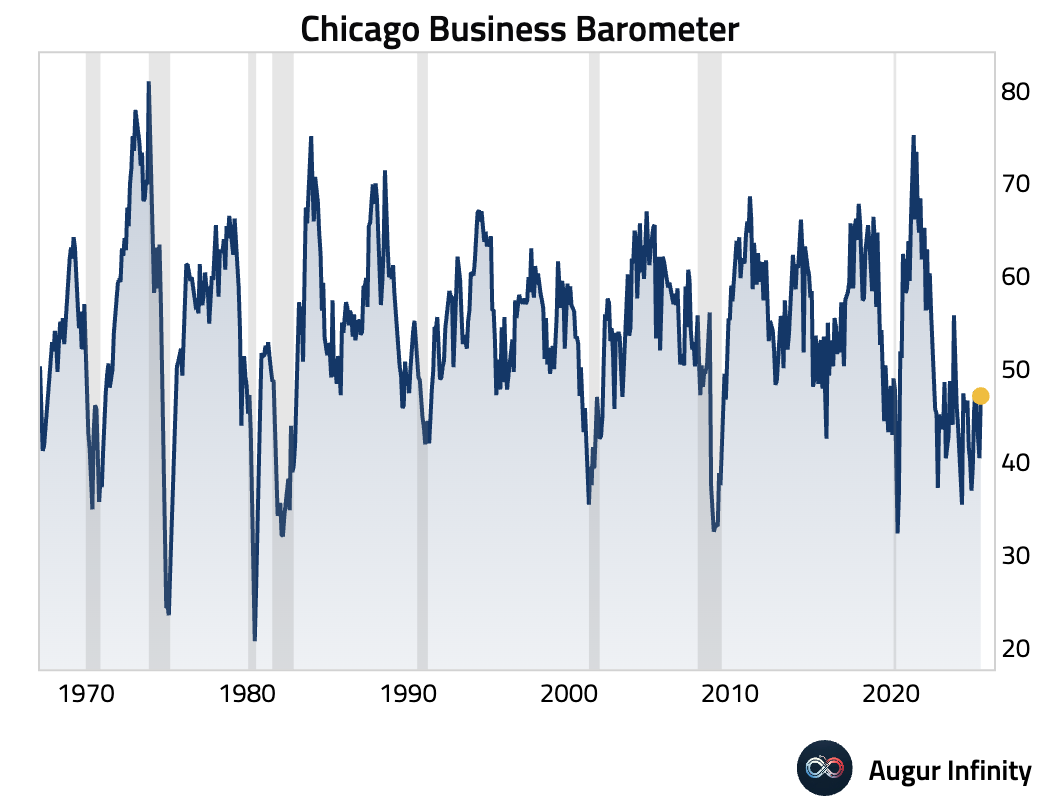

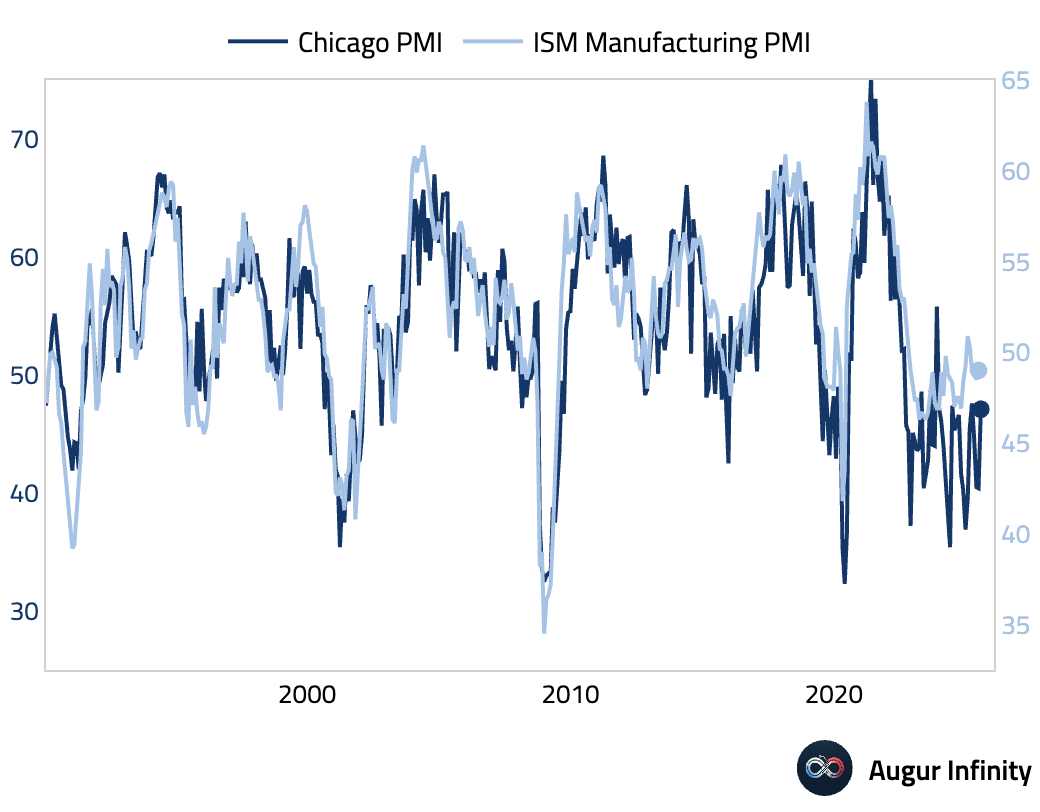

The Chicago PMI rose to 47.1 in July, significantly exceeding the 42.0 consensus and up from 40.4 in June, marking a notable improvement in regional manufacturing activity.

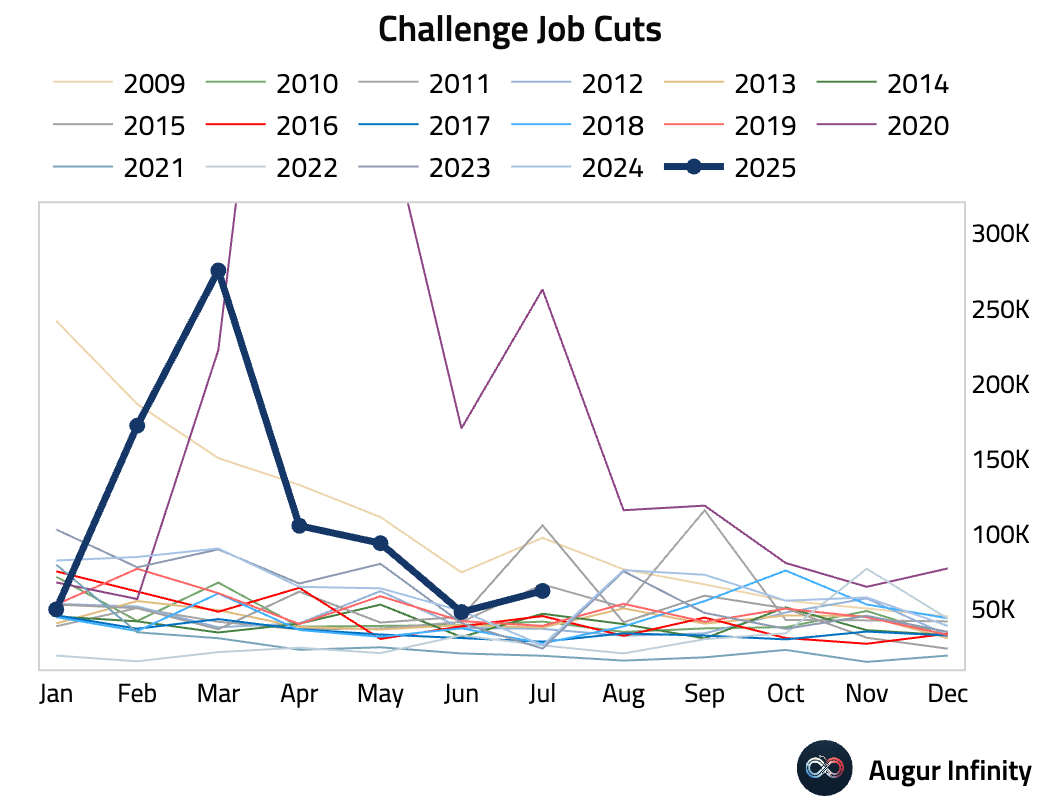

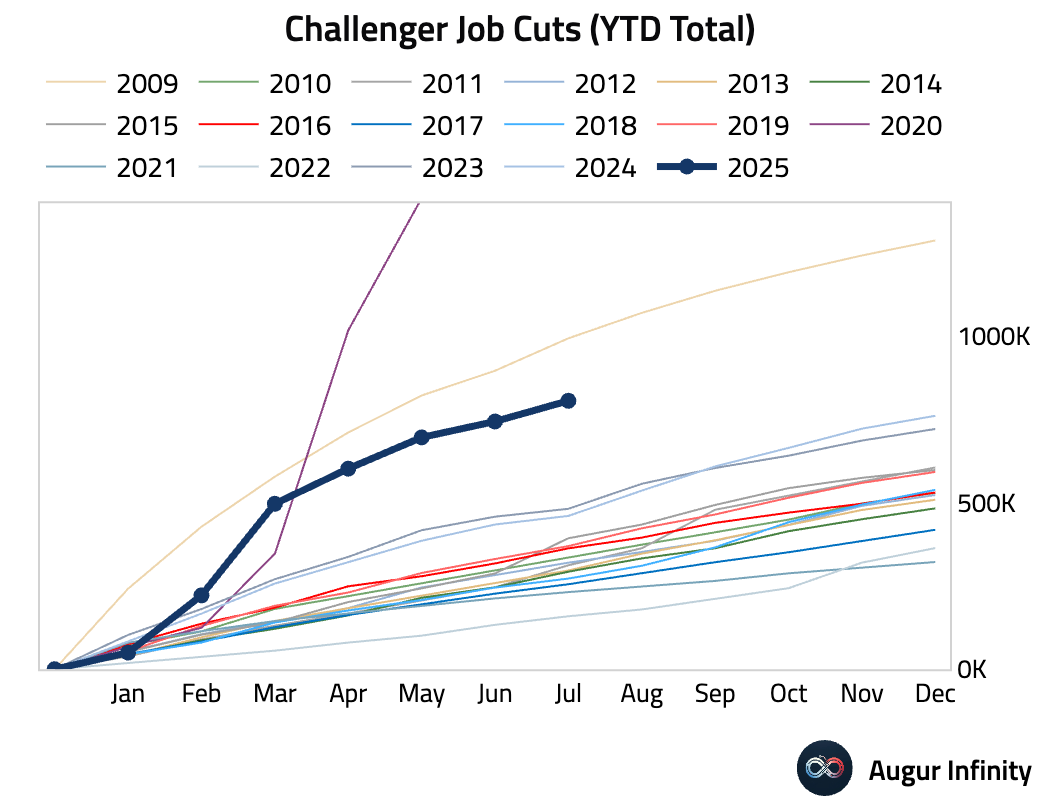

US Challenger Job Cuts rose to 62,075 in July, up from 47,999 in June. Year-to-date, job cuts are the highest they’ve been since 2009.

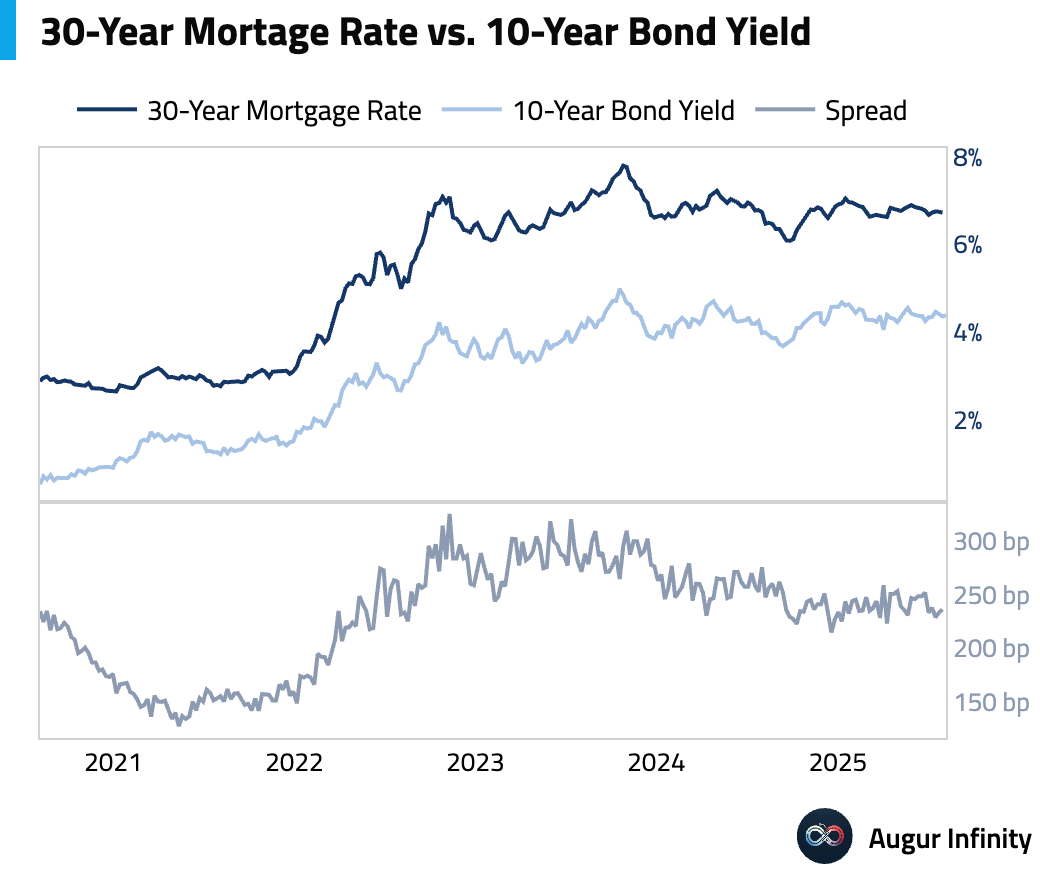

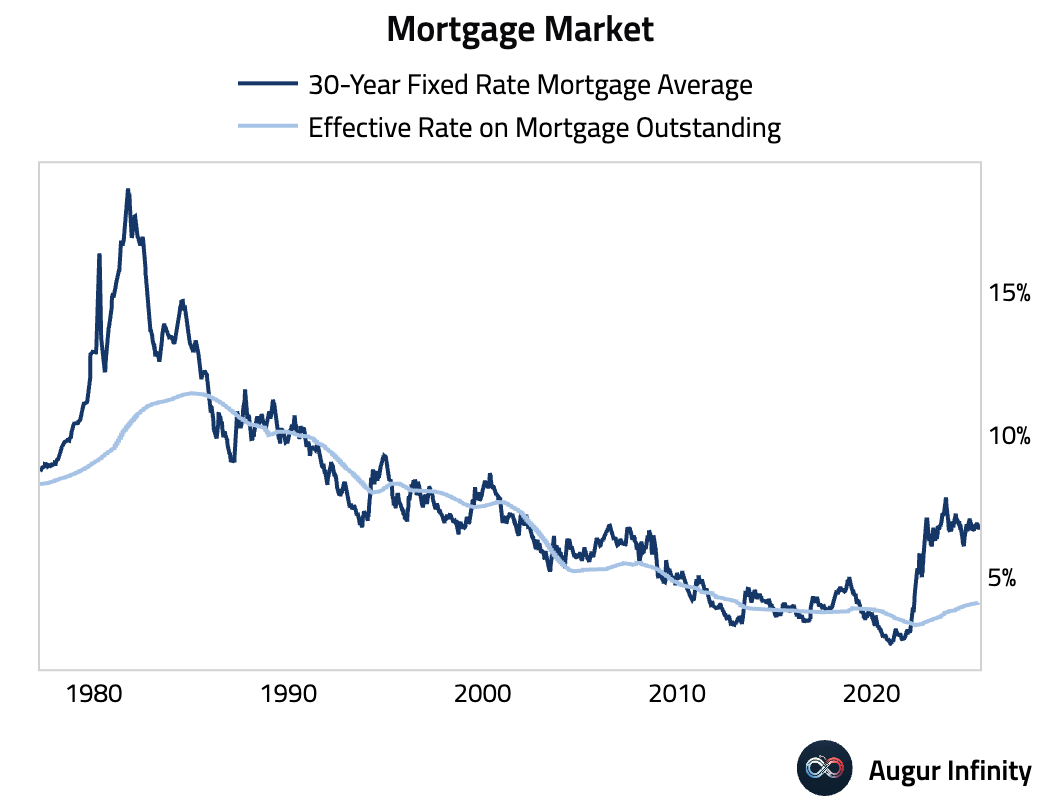

US mortgage rates edged lower week-over-week. The 30-year rate fell to 6.72% from 6.74%, while the 15-year rate declined to 5.85% from 5.87%.

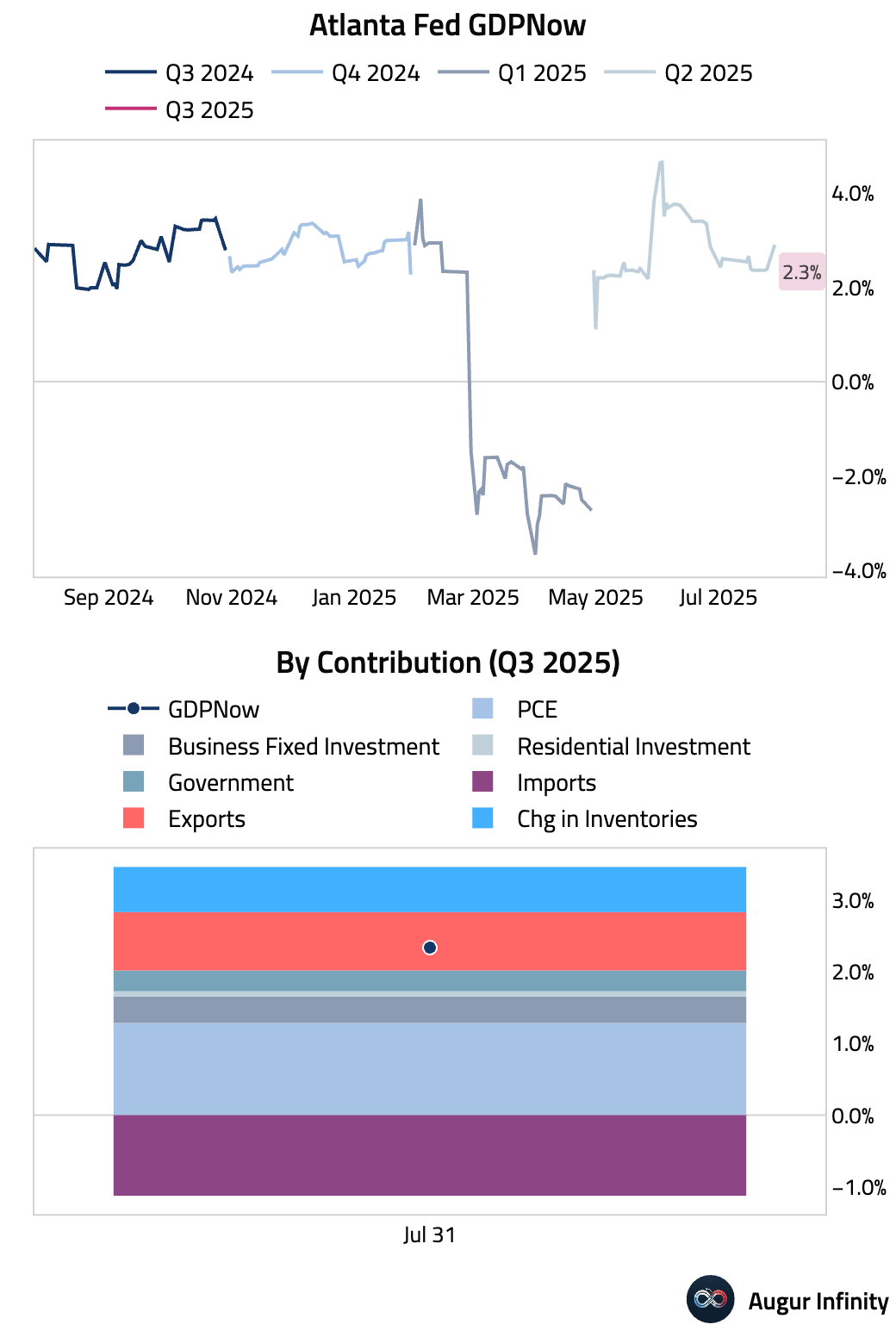

The Atlanta Fed's initial GDPNow model estimate for Q3 GDP is 2.3%.

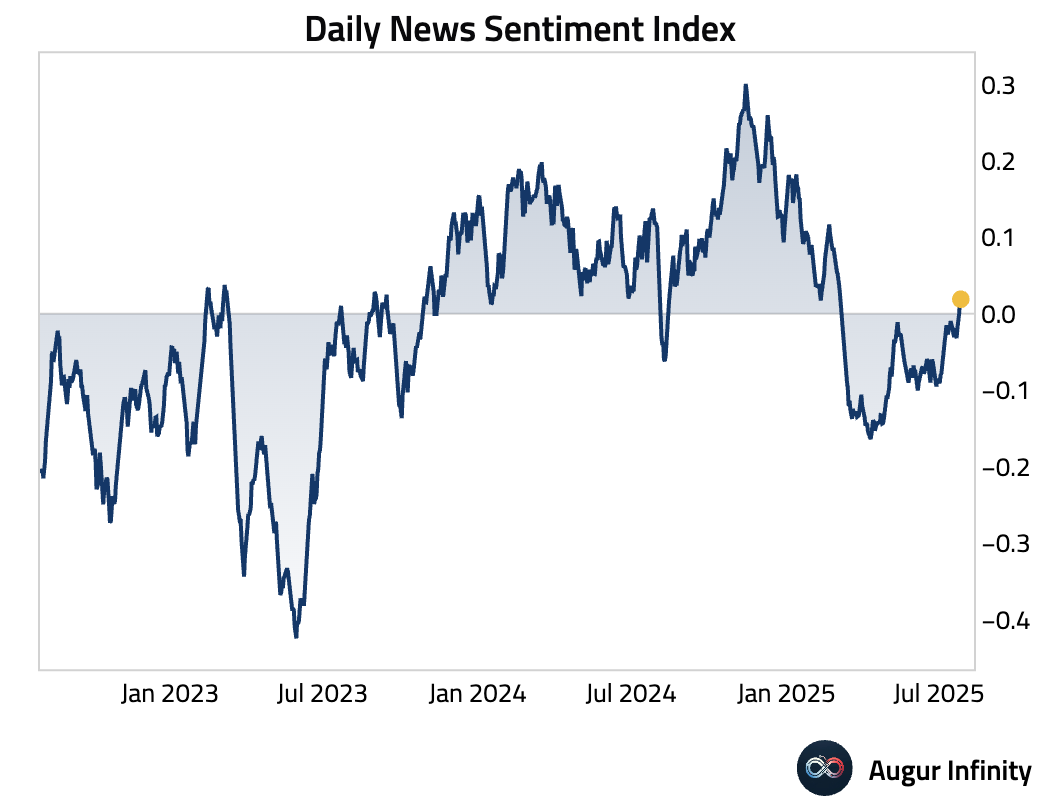

The Dallas Fed's Daily News Sentiment Index has risen to its highest level since March.

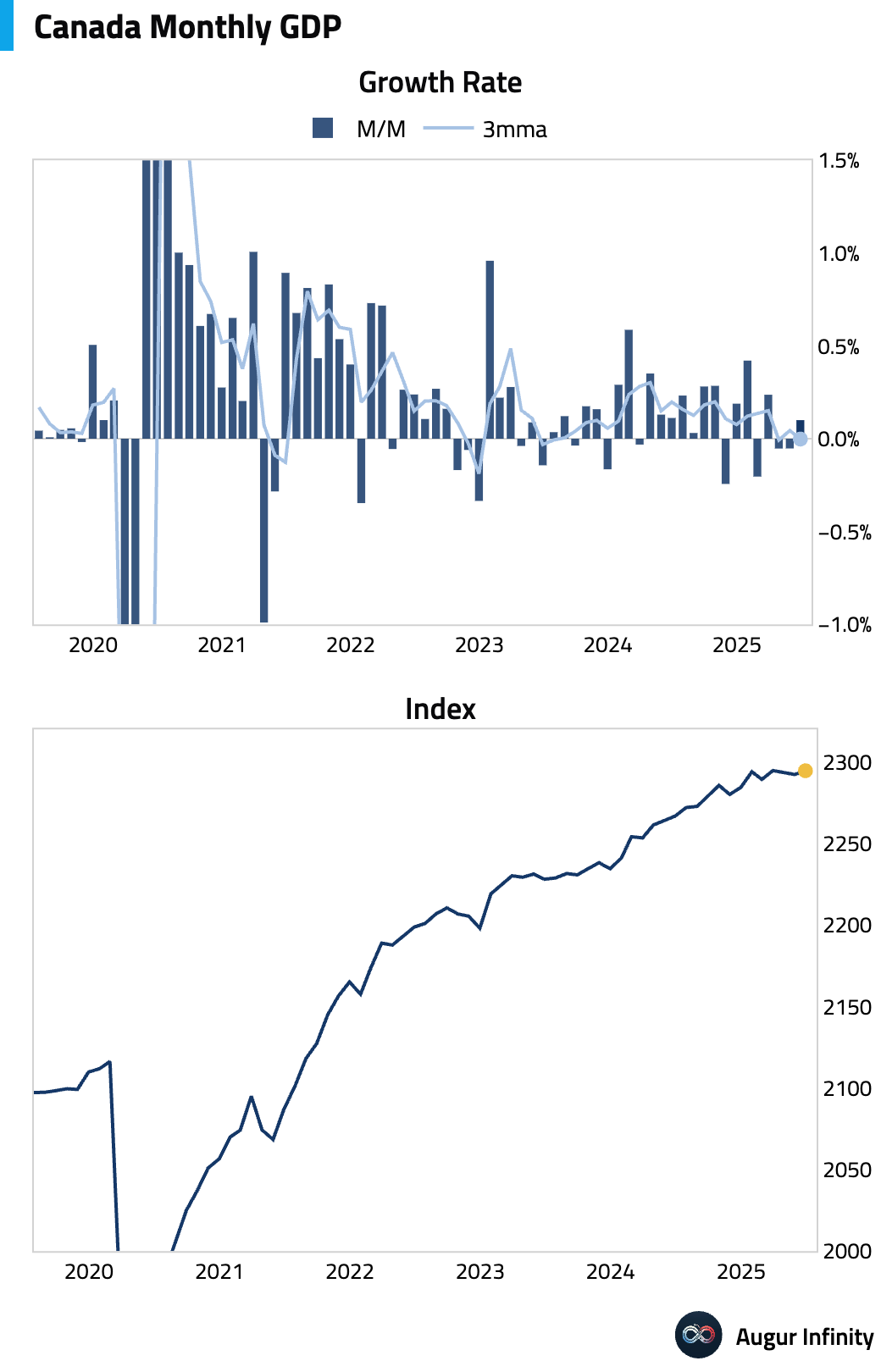

Canada's GDP contracted by 0.1% M/M in May, matching both the consensus and the prior month's reading. Preliminary data for June indicates a modest rebound, with GDP estimated to have grown 0.1% M/M.

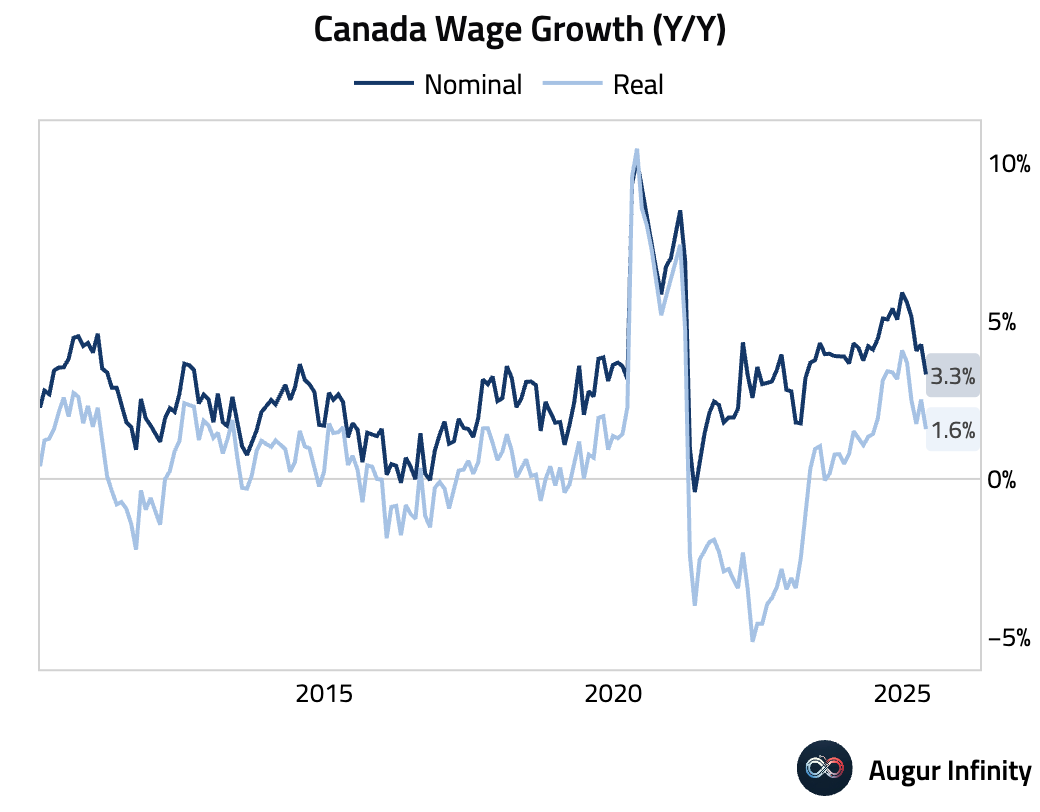

Growth in Canada's average weekly earnings slowed to 3.3% Y/Y in May from 4.26% in April. This marks the lowest reading since April 2023.

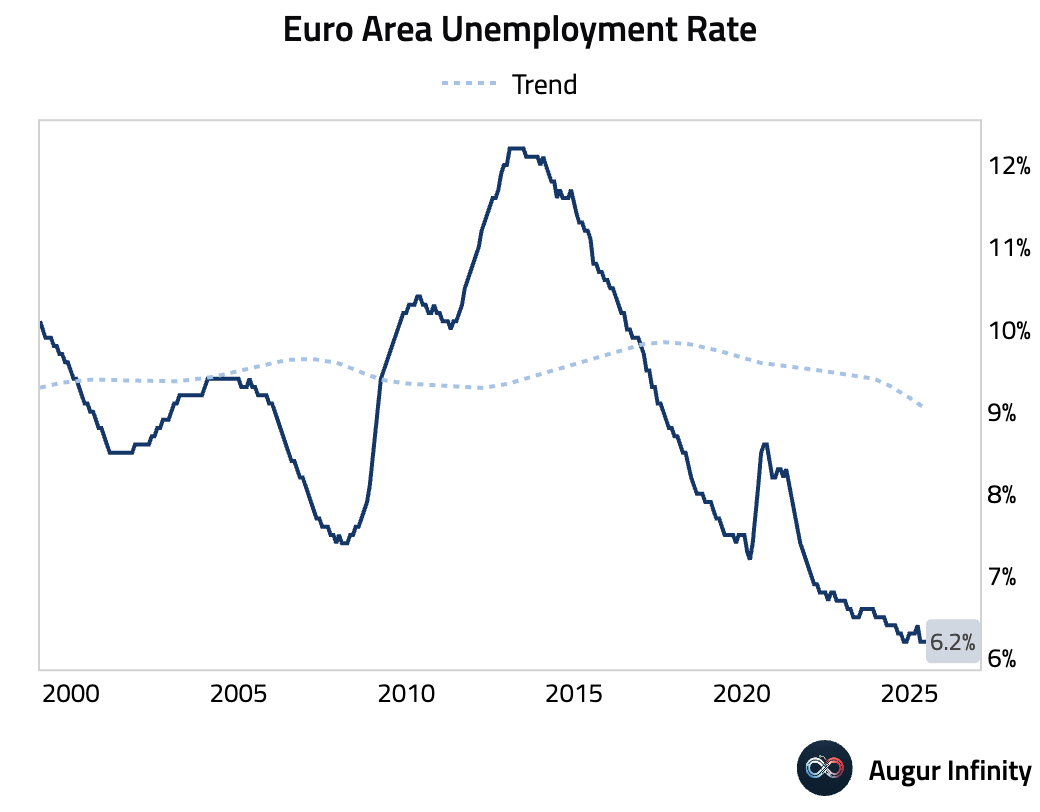

The Euro Area unemployment rate held steady at 6.2% in June, below the 6.3% consensus and matching the all-time low for the series.

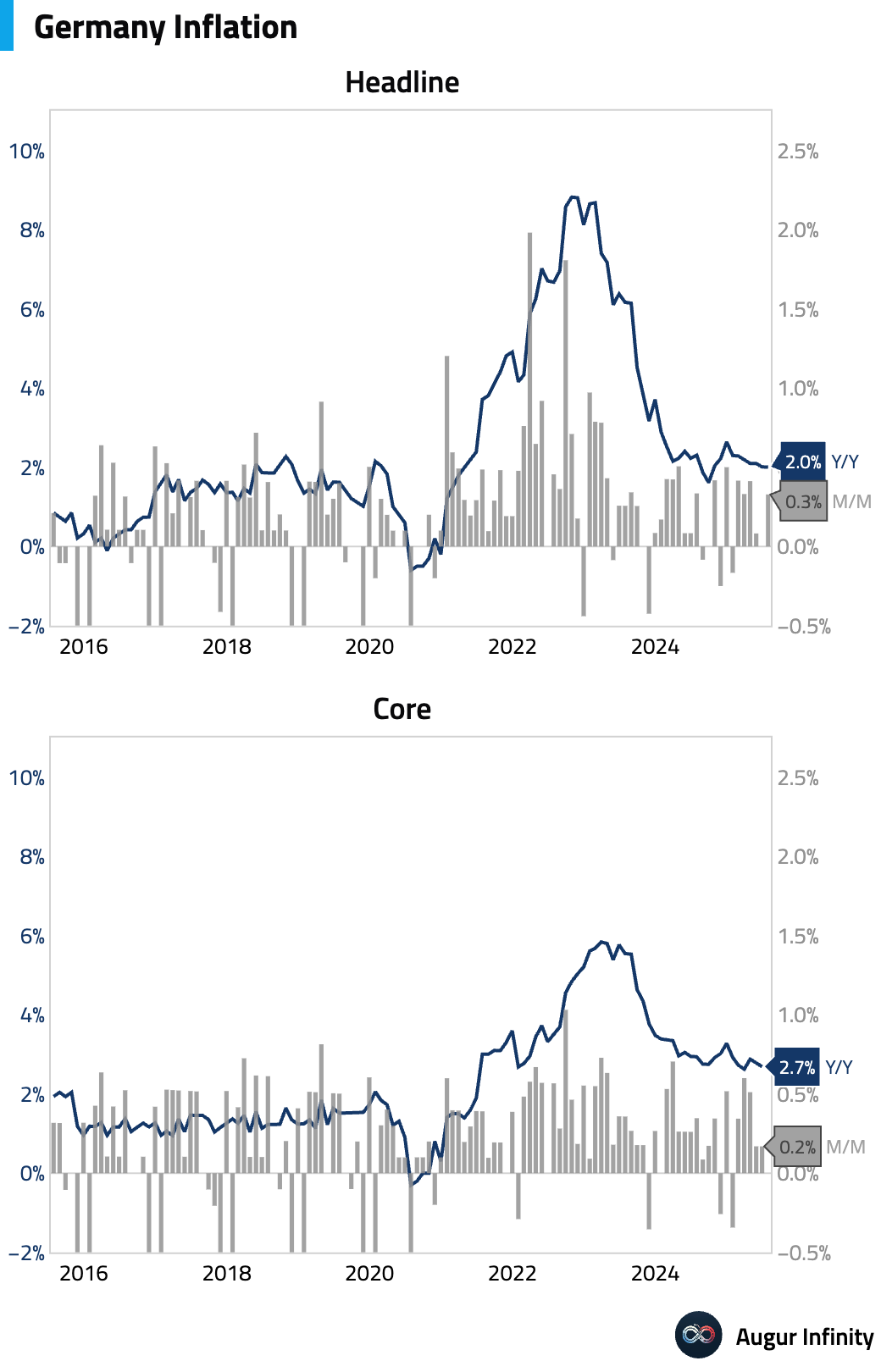

Germany's preliminary inflation rate for July held steady at 2.0% Y/Y, matching the prior month's reading, while M/M inflation accelerated to 0.3% from 0.0%. The HICP measure came in at 1.8% Y/Y, slightly below the 1.9% consensus, with weaker core inflation pressures from package holidays and transport services offsetting higher energy and food costs.

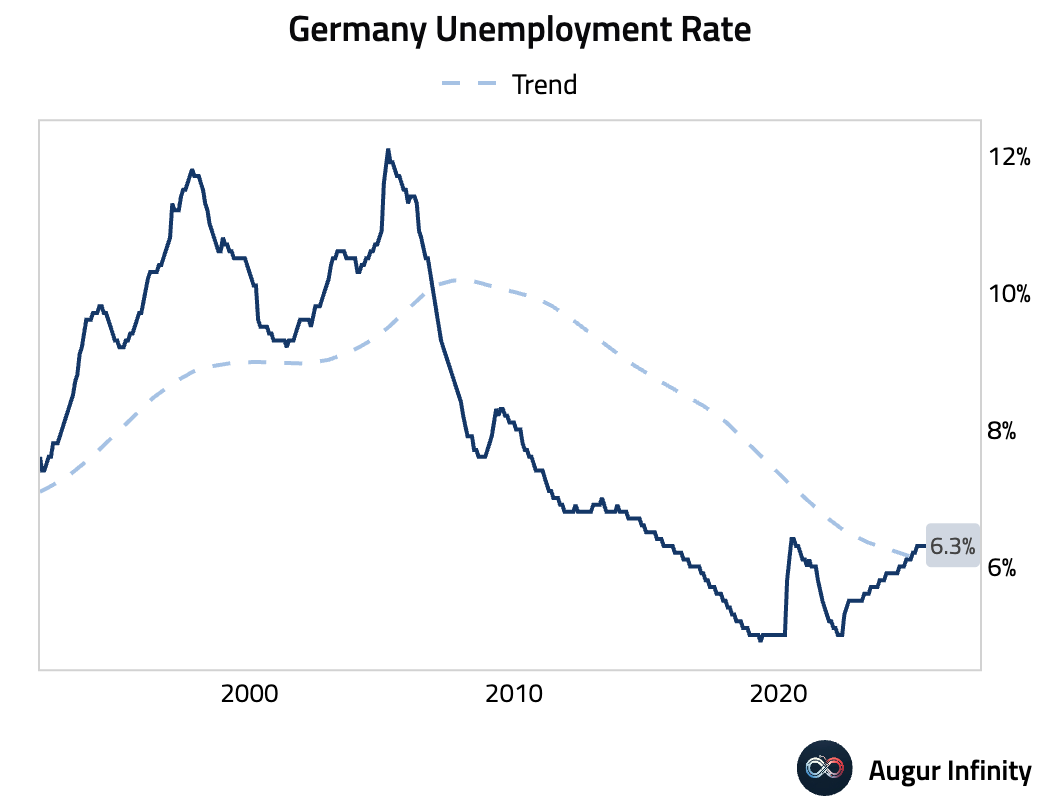

Germany's unemployment rate was unchanged at 6.3% in July, beating the 6.4% consensus. This is the lowest rate since February 2025.

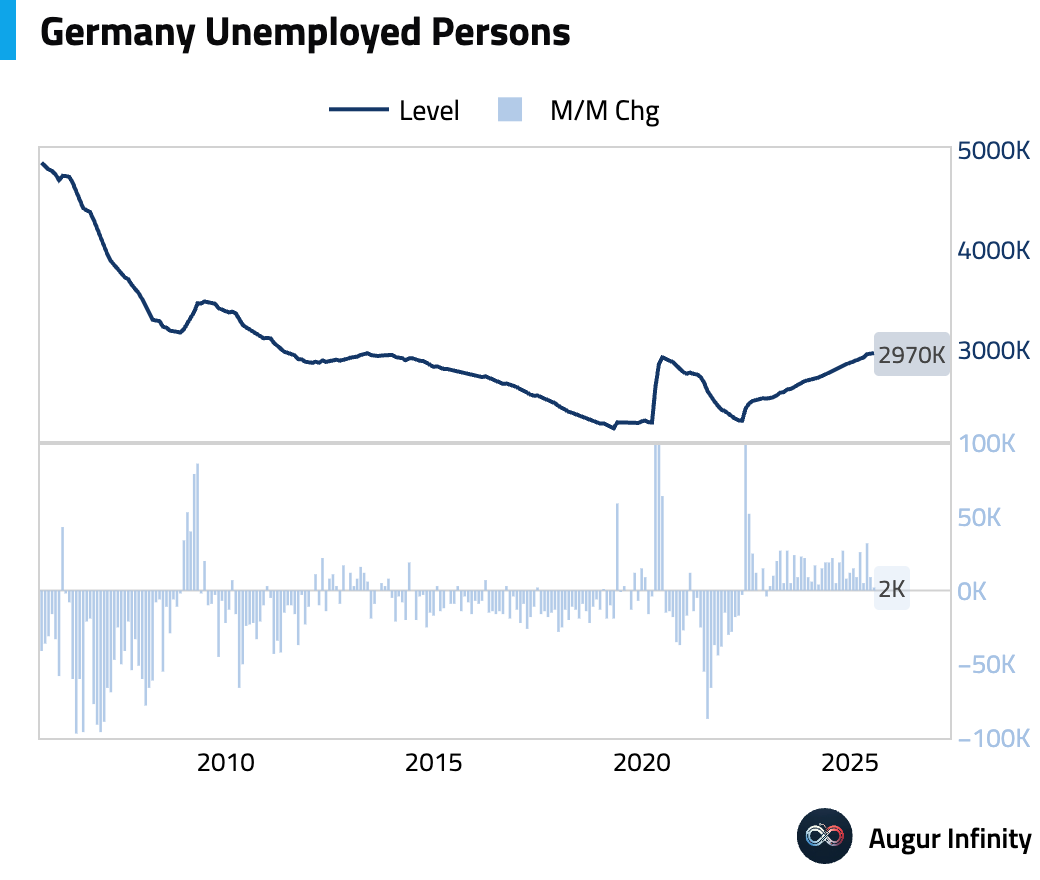

The number of unemployed persons in Germany fell by 2,000 in July to 2.97 million, its lowest level since June 2011.

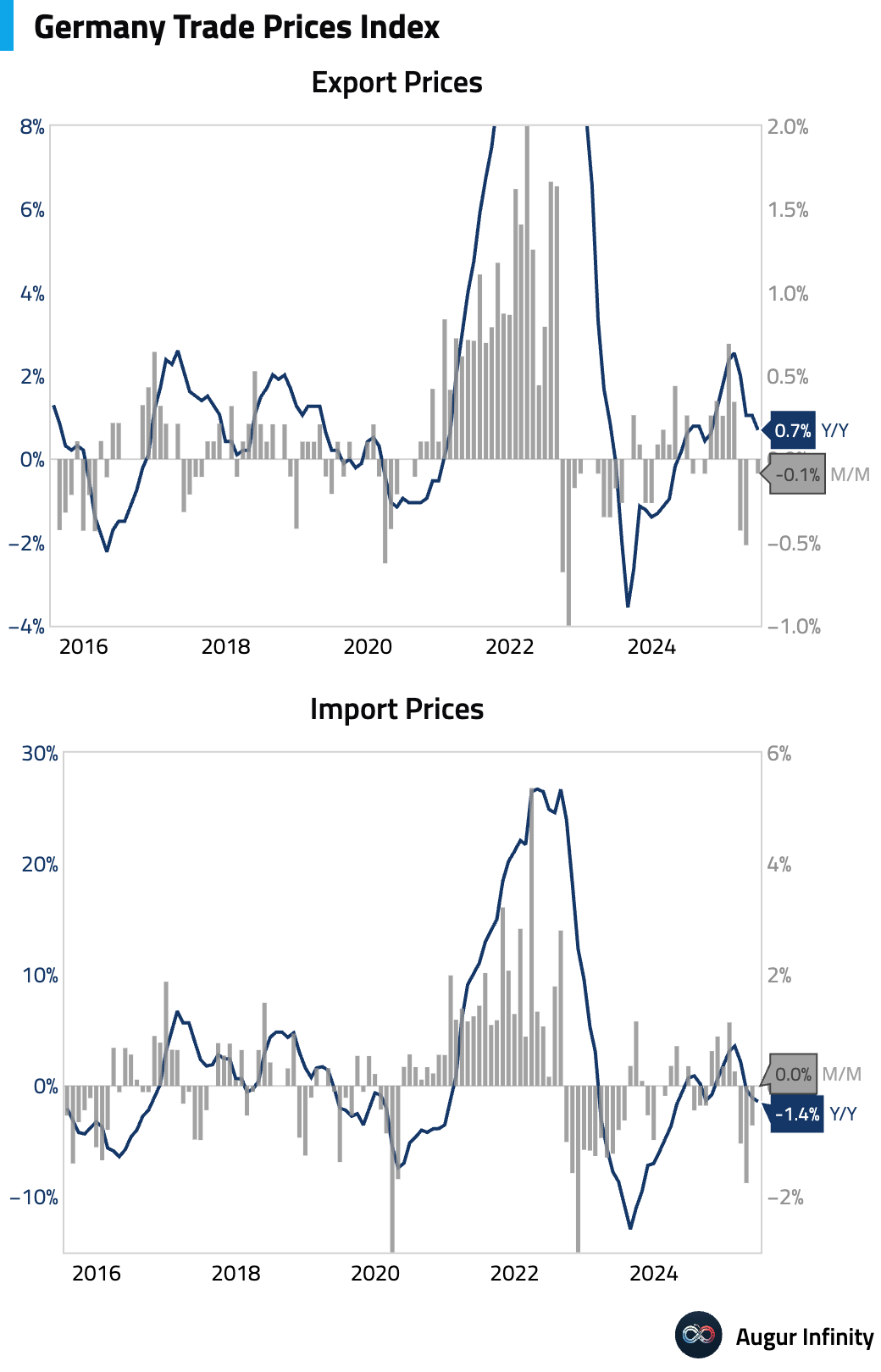

German import prices were flat M/M in June, above the -0.2% consensus. The Y/Y rate fell 1.4%, a deceleration from the prior -1.1% reading.

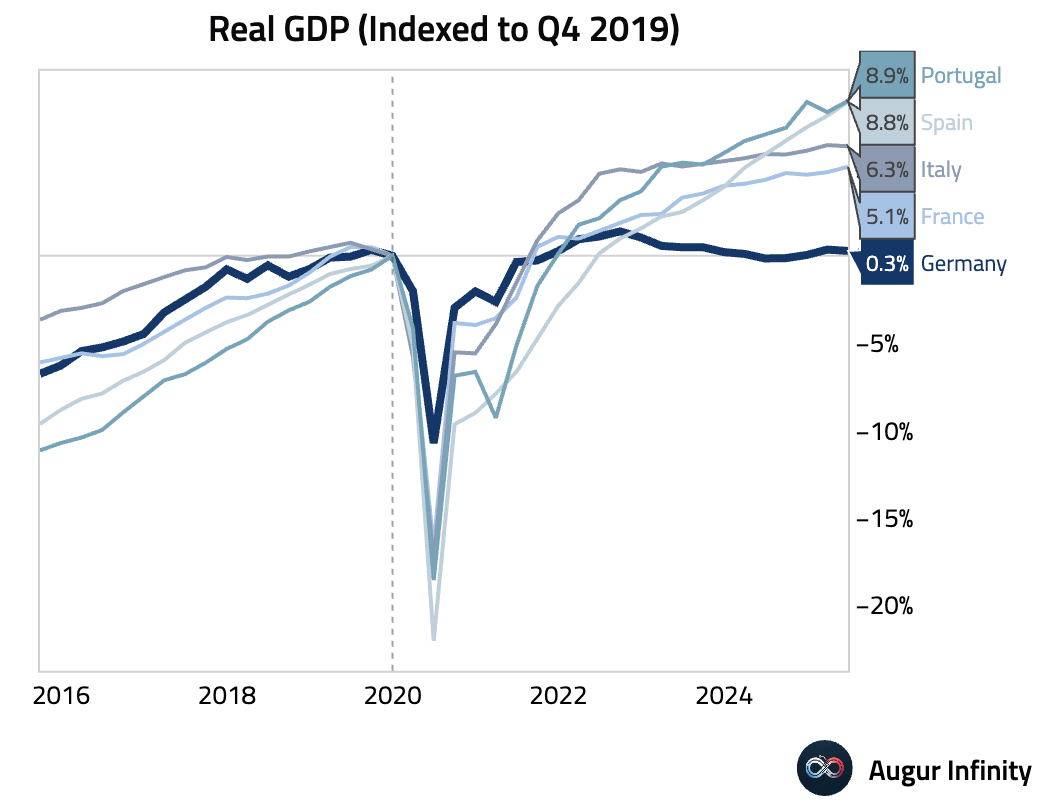

Since the end of 2019, Germany's GDP has risen by just 0.3%, vastly underperforming its peers in the Eurozone.

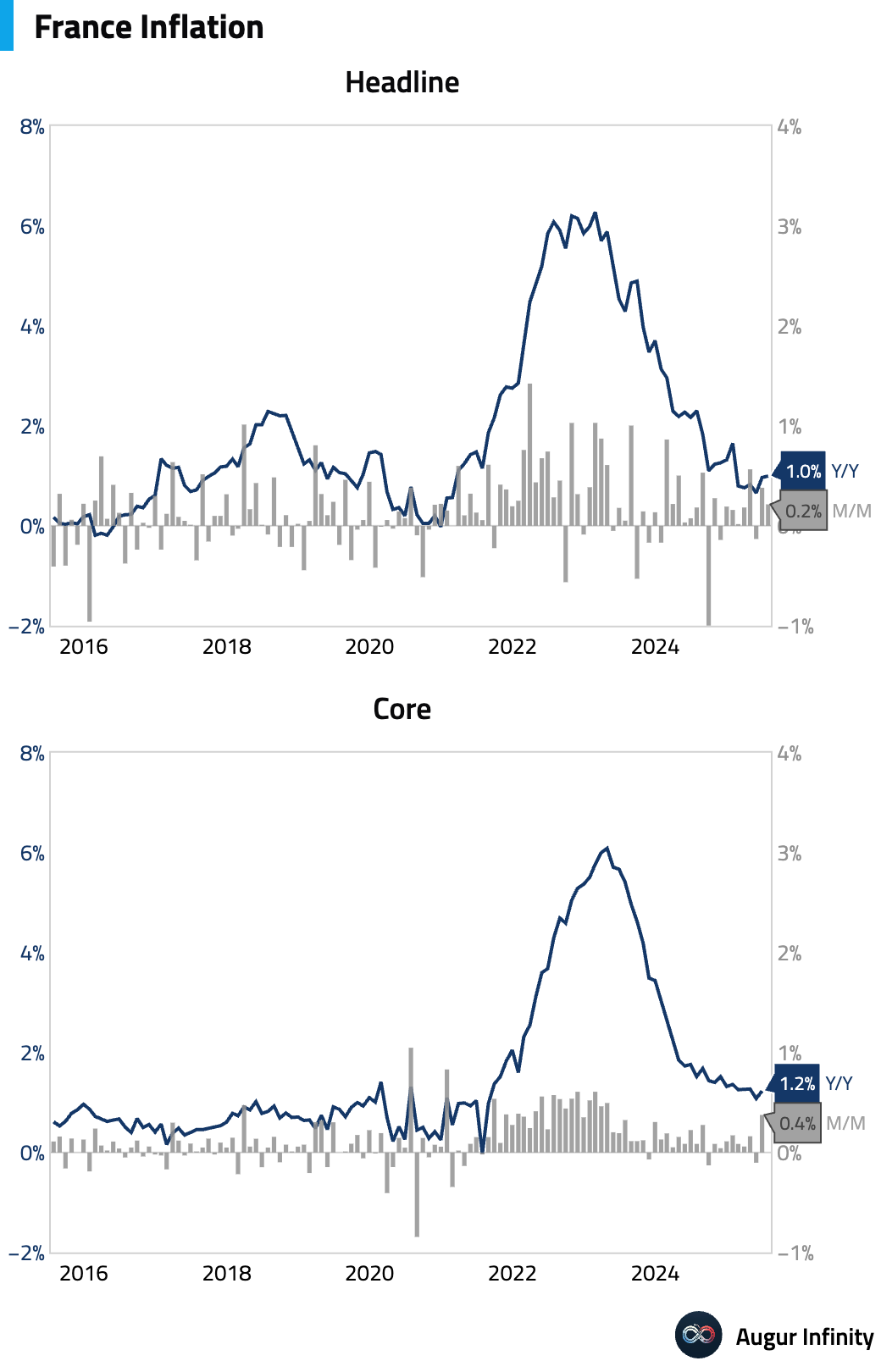

France's preliminary July CPI held steady at 1.0% Y/Y, in line with consensus. The monthly rate rose 0.2%, above the 0.1% forecast. On a harmonized (HICP) basis, the annual rate was 0.9%, with falling energy prices offset by stronger services and food inflation.

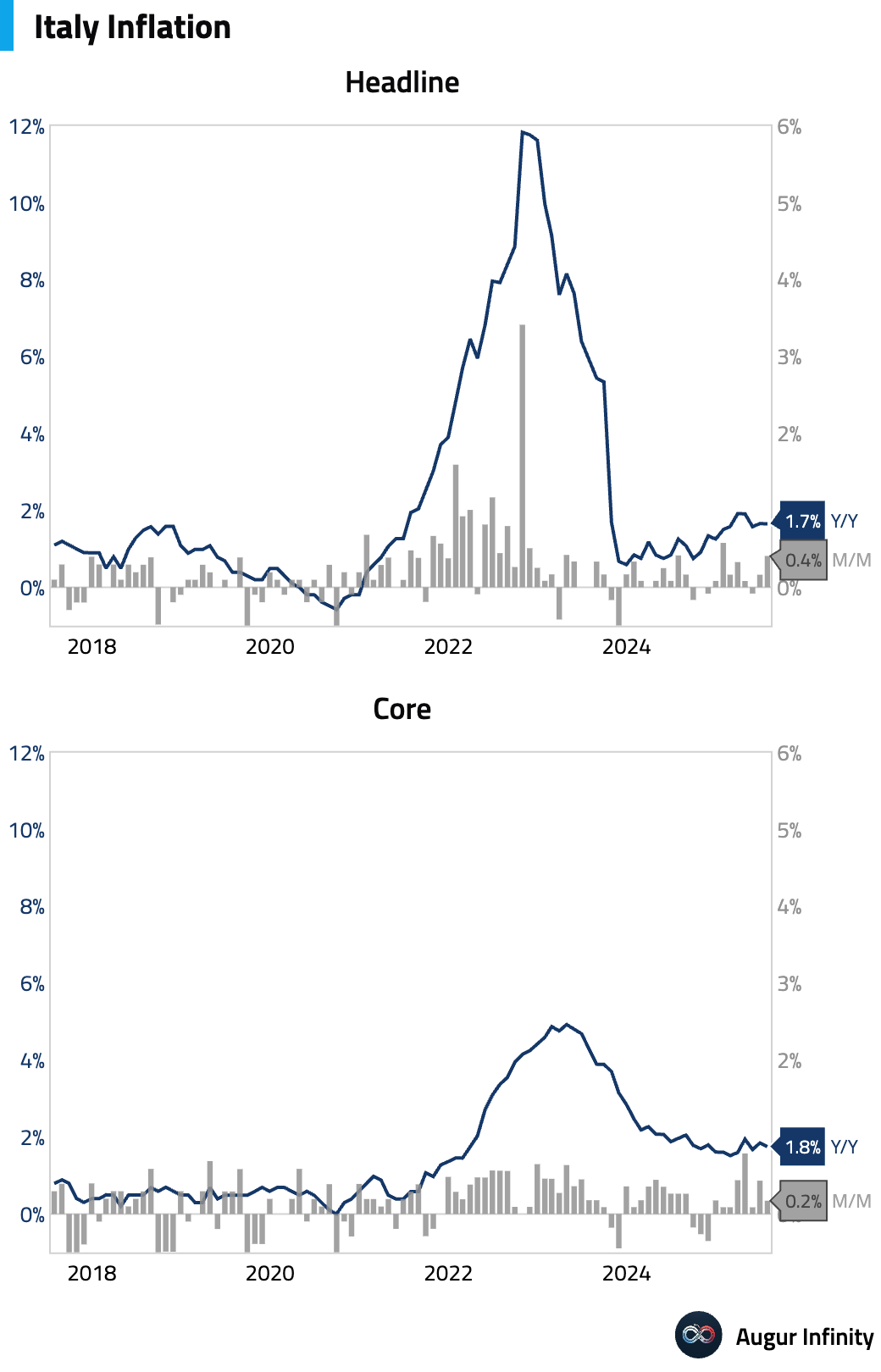

Italy's preliminary July CPI was unchanged at 1.7% Y/Y, above the 1.5% consensus. However, M/M inflation accelerated to 0.4% from 0.2%, beating expectations for a 0.1% rise and marking the strongest monthly reading since January 2025. Sequential core inflation also showed accelerating underlying momentum, rising 0.36% M/M from 0.24% in June.

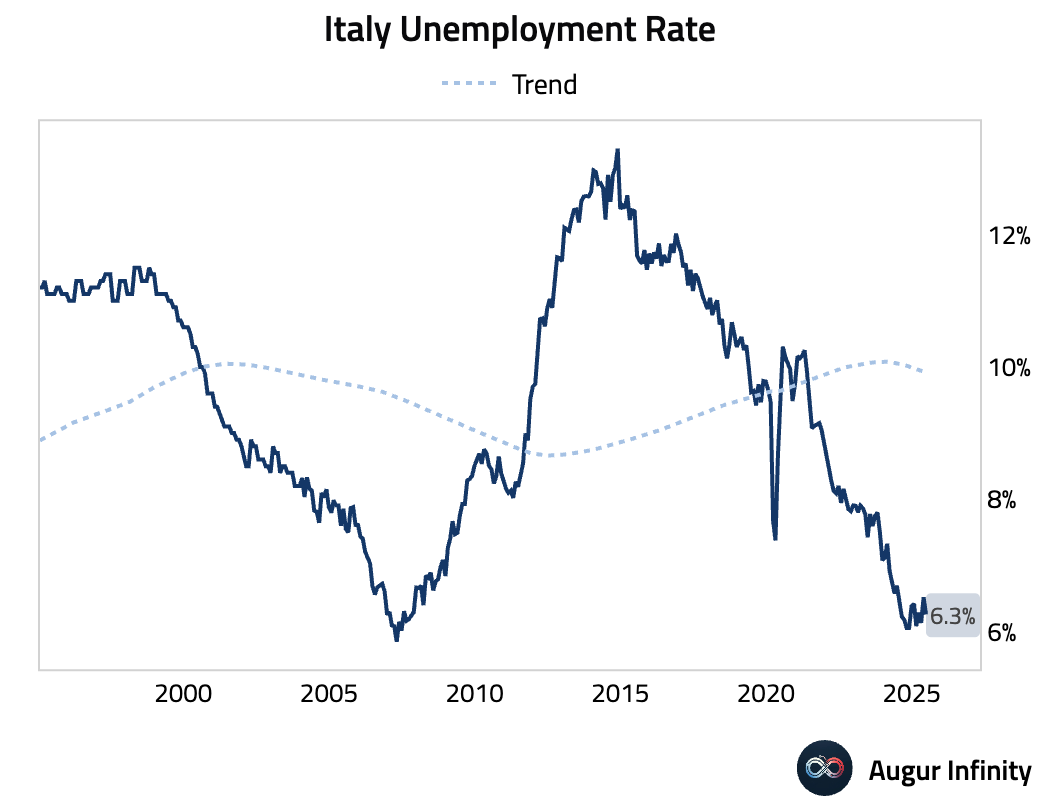

Italy's unemployment rate fell to 6.3% in June from 6.5%, below the 6.4% consensus and marking the lowest reading since April 2025.

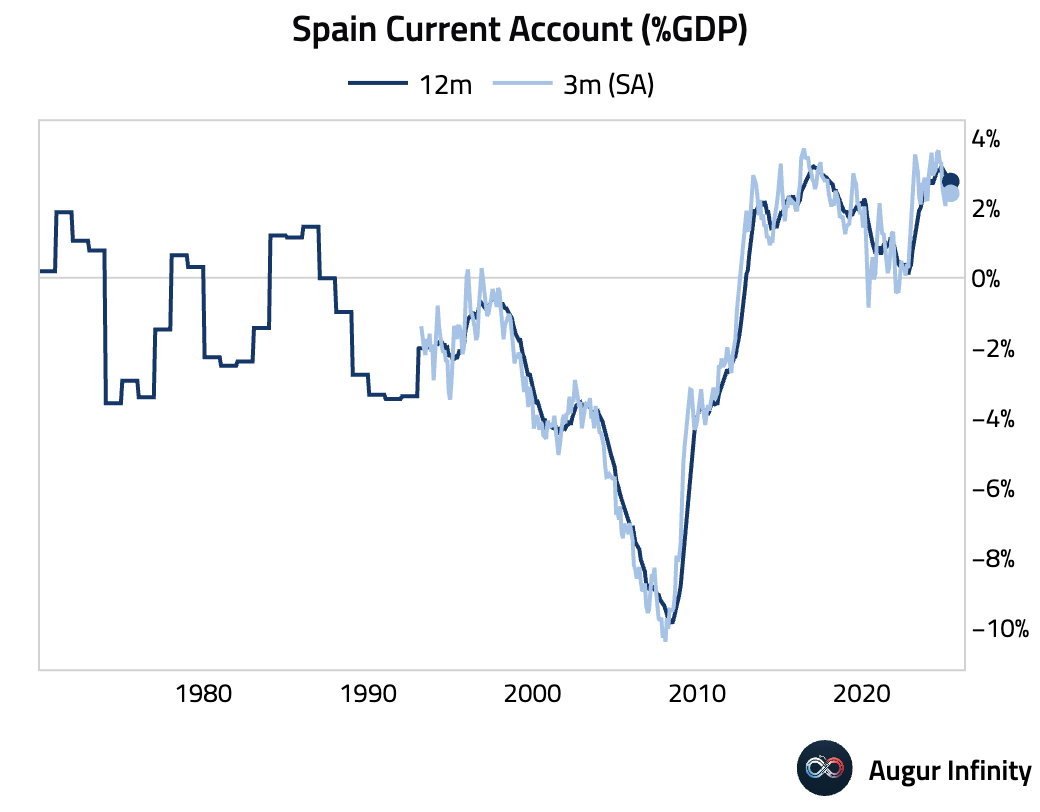

Spain's current account surplus widened to €6.44 billion in May from €1.36 billion in April, marking an all-time record high.

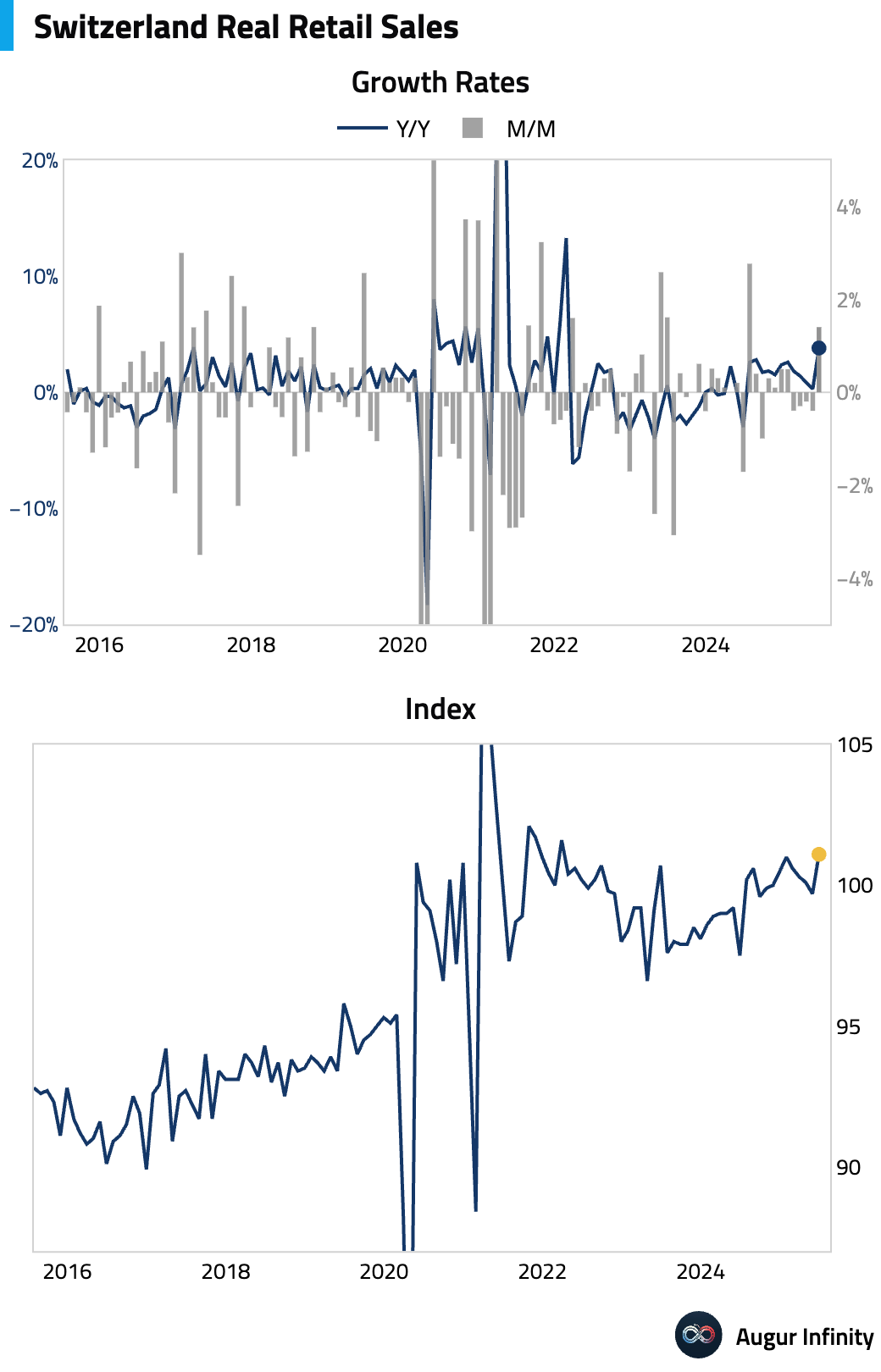

Switzerland's real retail sales surged in June, rising 3.8% Y/Y and 1.5% M/M. The annual figure vastly outpaced the 0.3% prior reading and consensus of 0.2%, reaching its highest level since February 2022.

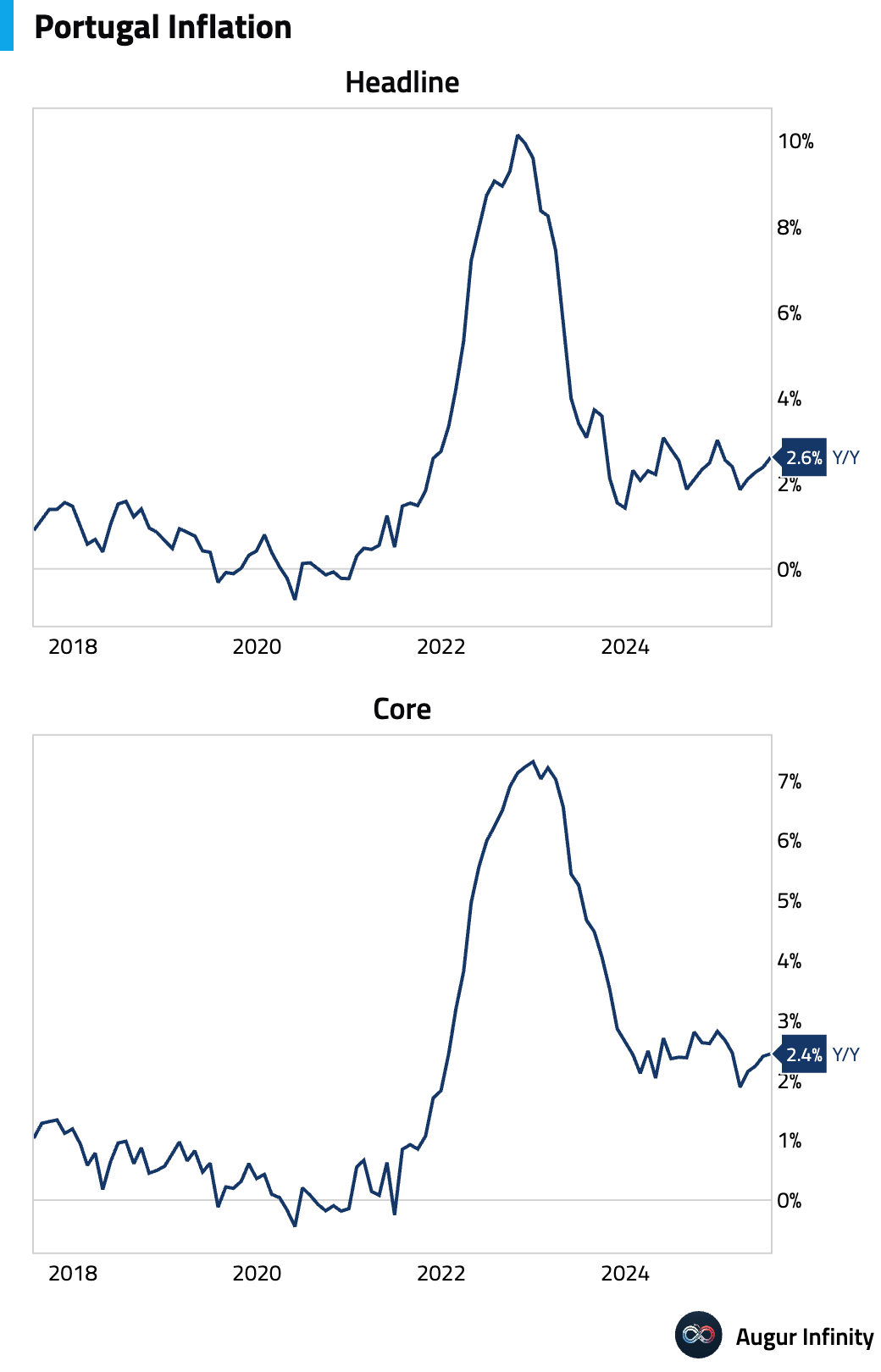

Portugal's preliminary July inflation accelerated to 2.6% Y/Y from 2.4% in June. The M/M reading showed a 0.4% decline.

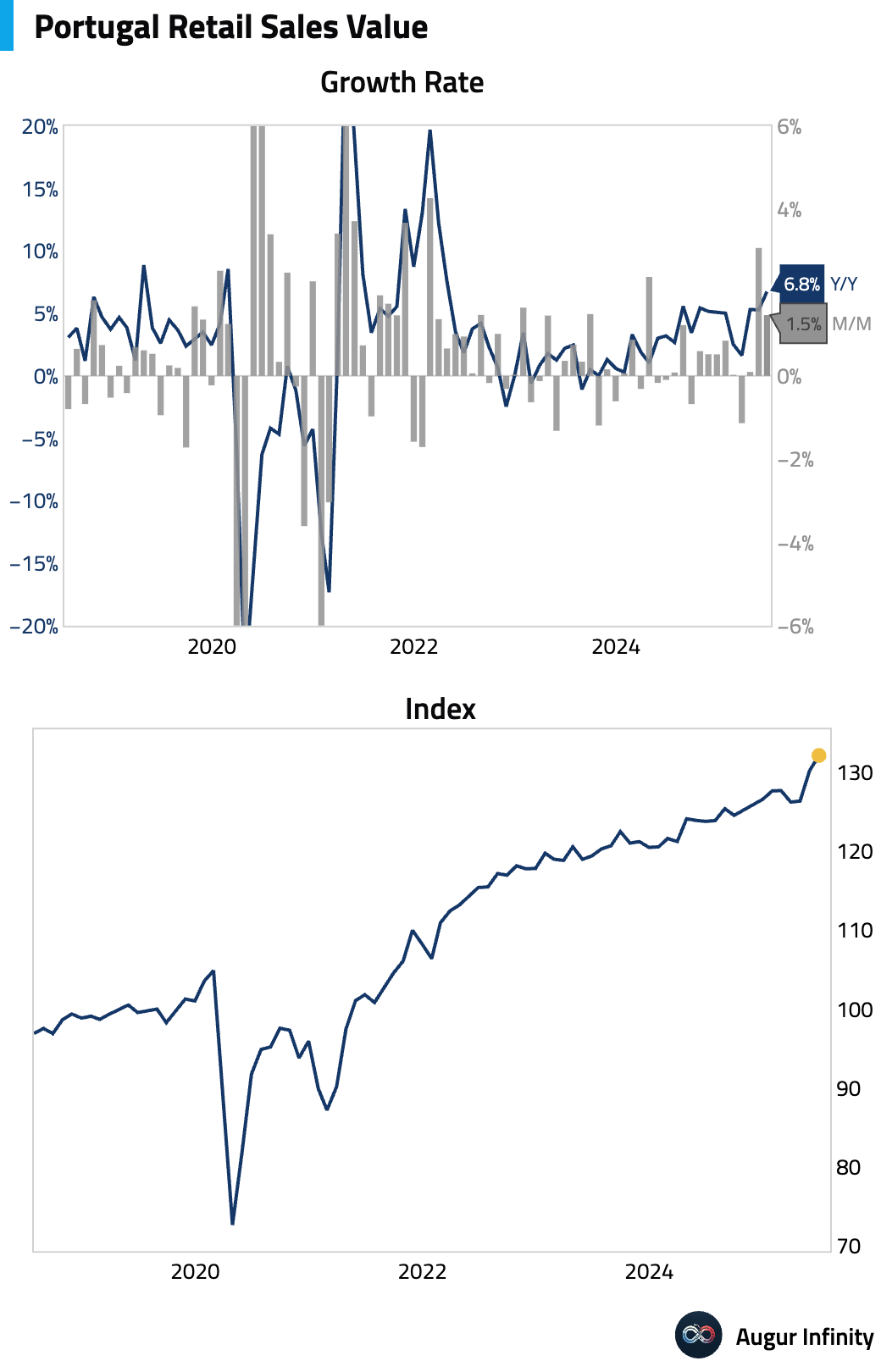

Portugal's retail sales value grew 6.9% Y/Y in June, accelerating from 5.3% in May. The M/M rate, however, slowed to 1.8% from 2.8%.

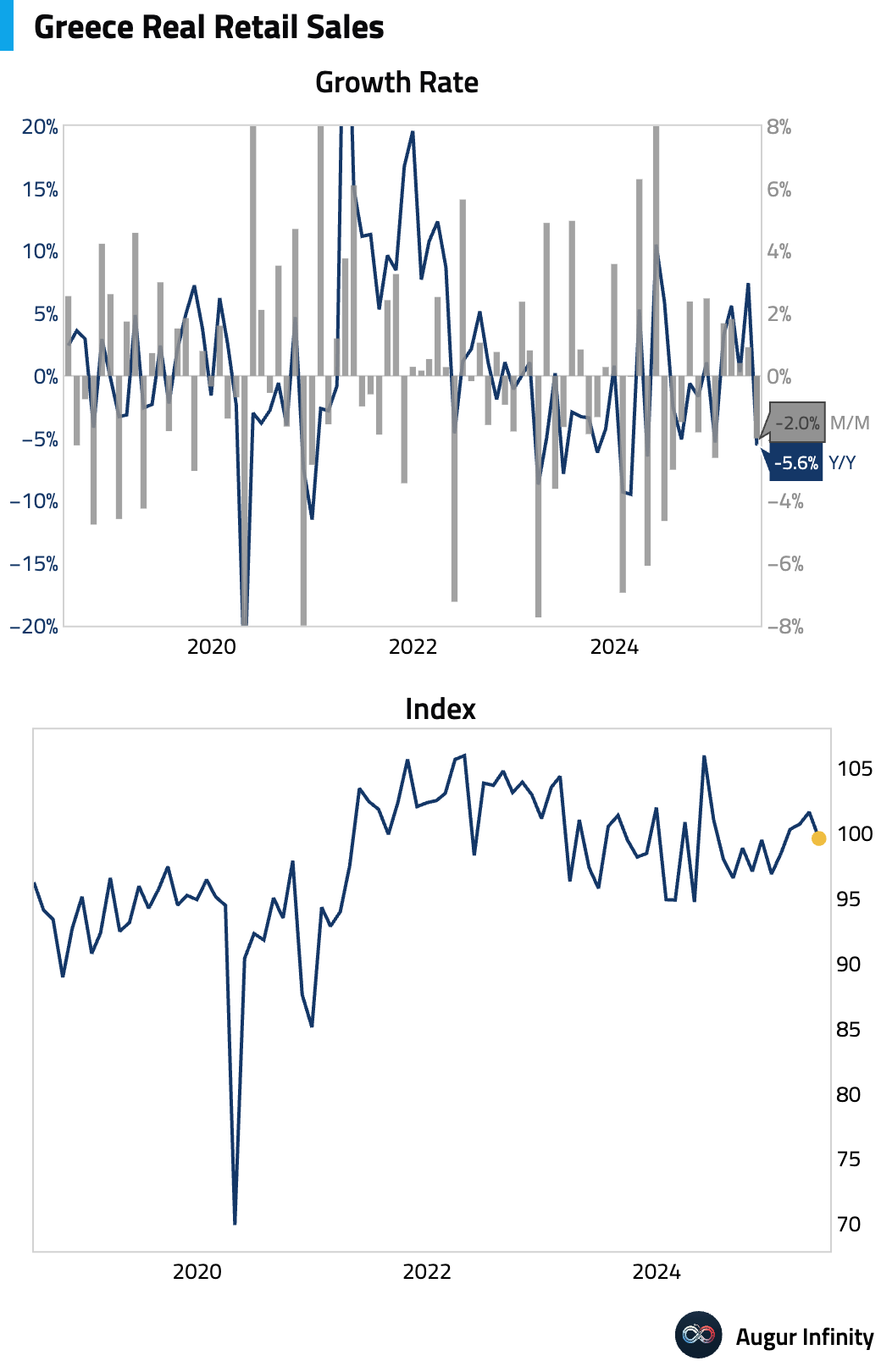

Greek retail sales fell 5.6% Y/Y in May, a sharp reversal from the 7.4% gain in April.

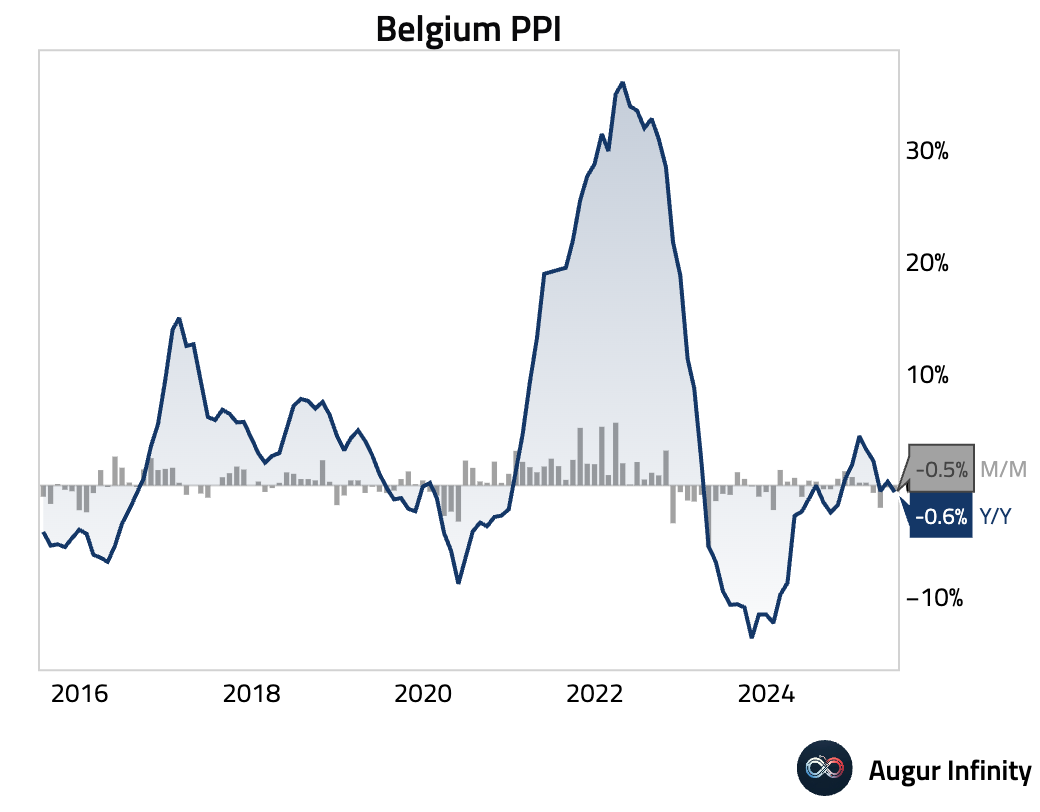

Belgium's producer price index fell 0.6% Y/Y in June, reversing a 0.3% gain in May.

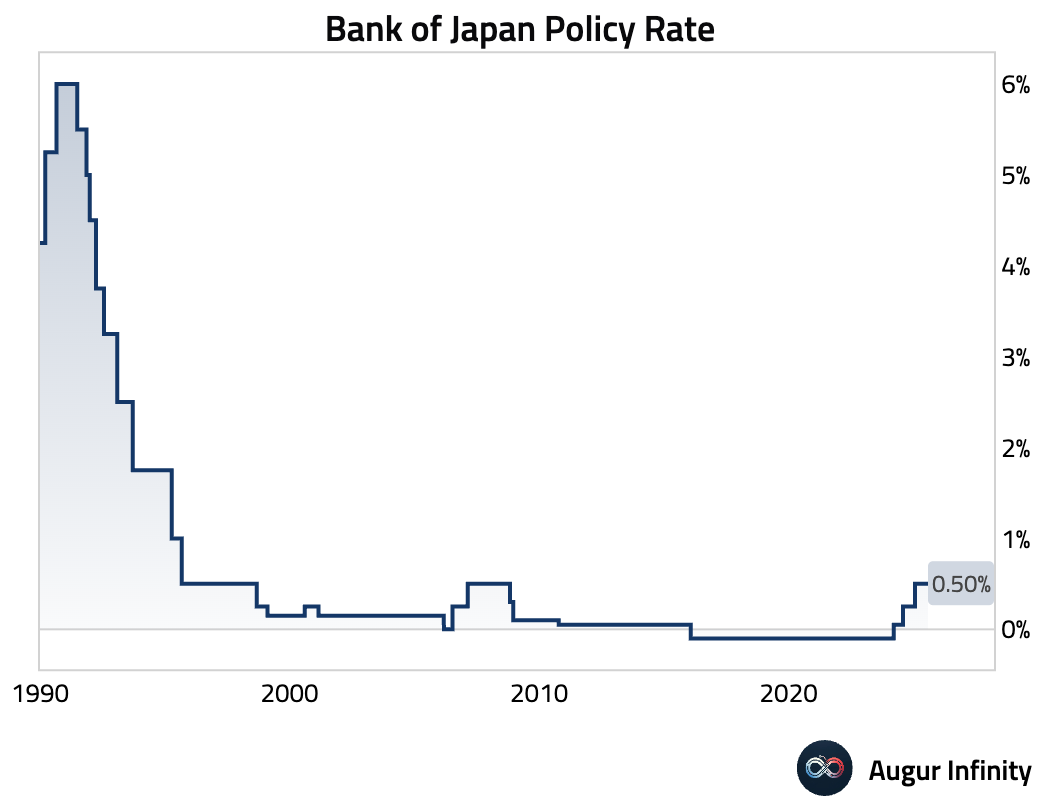

The Bank of Japan held its policy rate at 0.5%, as expected. However, the accompanying outlook was hawkish, with policymakers upgrading the FY2025 Core CPI forecast to 2.8%. The move makes the October meeting “live” for a potential rate hike, with markets now watching for a key board member to signal the next move in a speech beforehand.

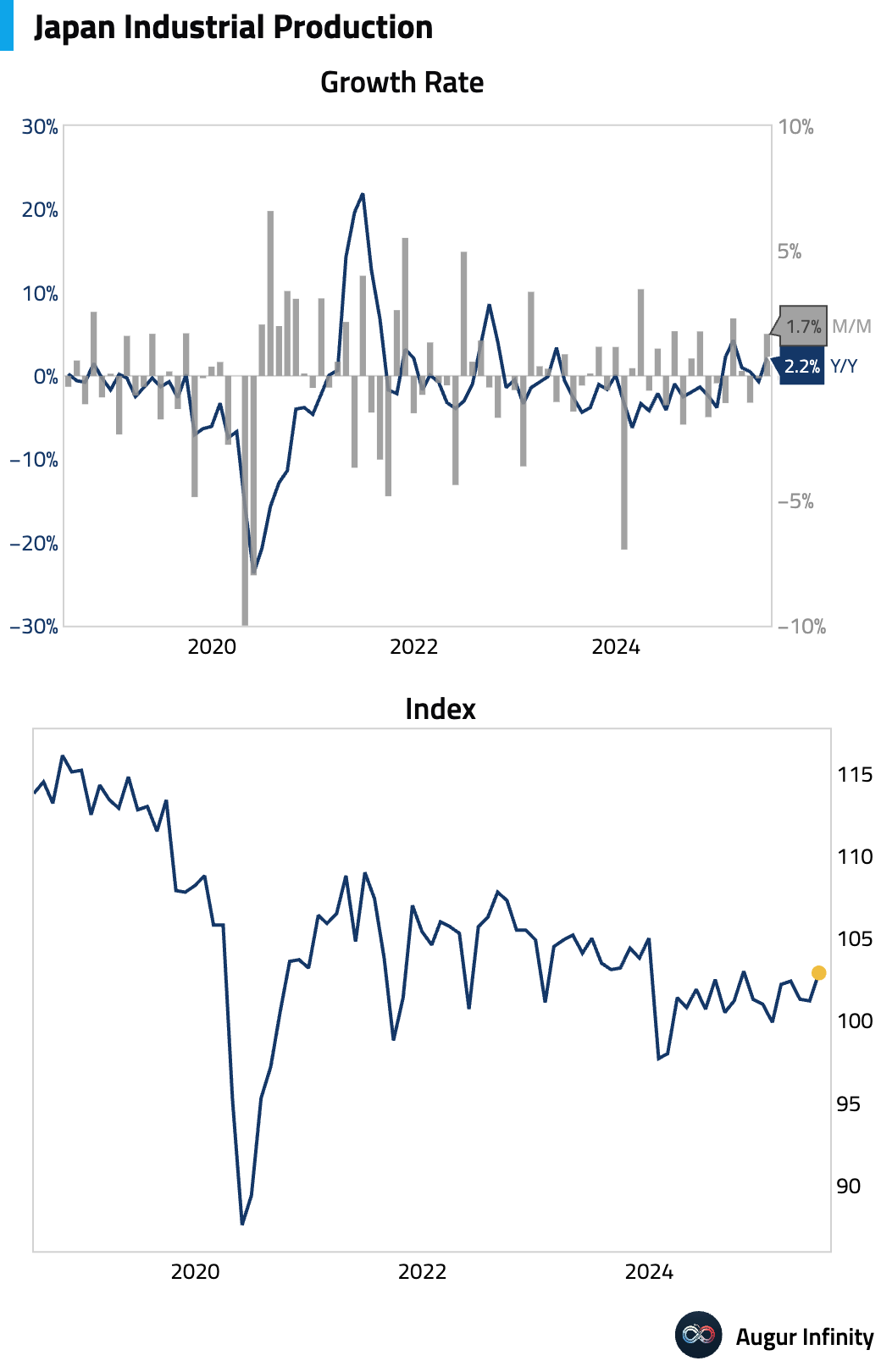

Japan's preliminary industrial production for June unexpectedly rose 1.7% M/M, well ahead of the -0.7% consensus. The monthly strength was led by electronic parts and devices, though it masked an 11.8% M/M fall in passenger vehicle output. Manufacturers' forecasts point to renewed weakness in July and August.

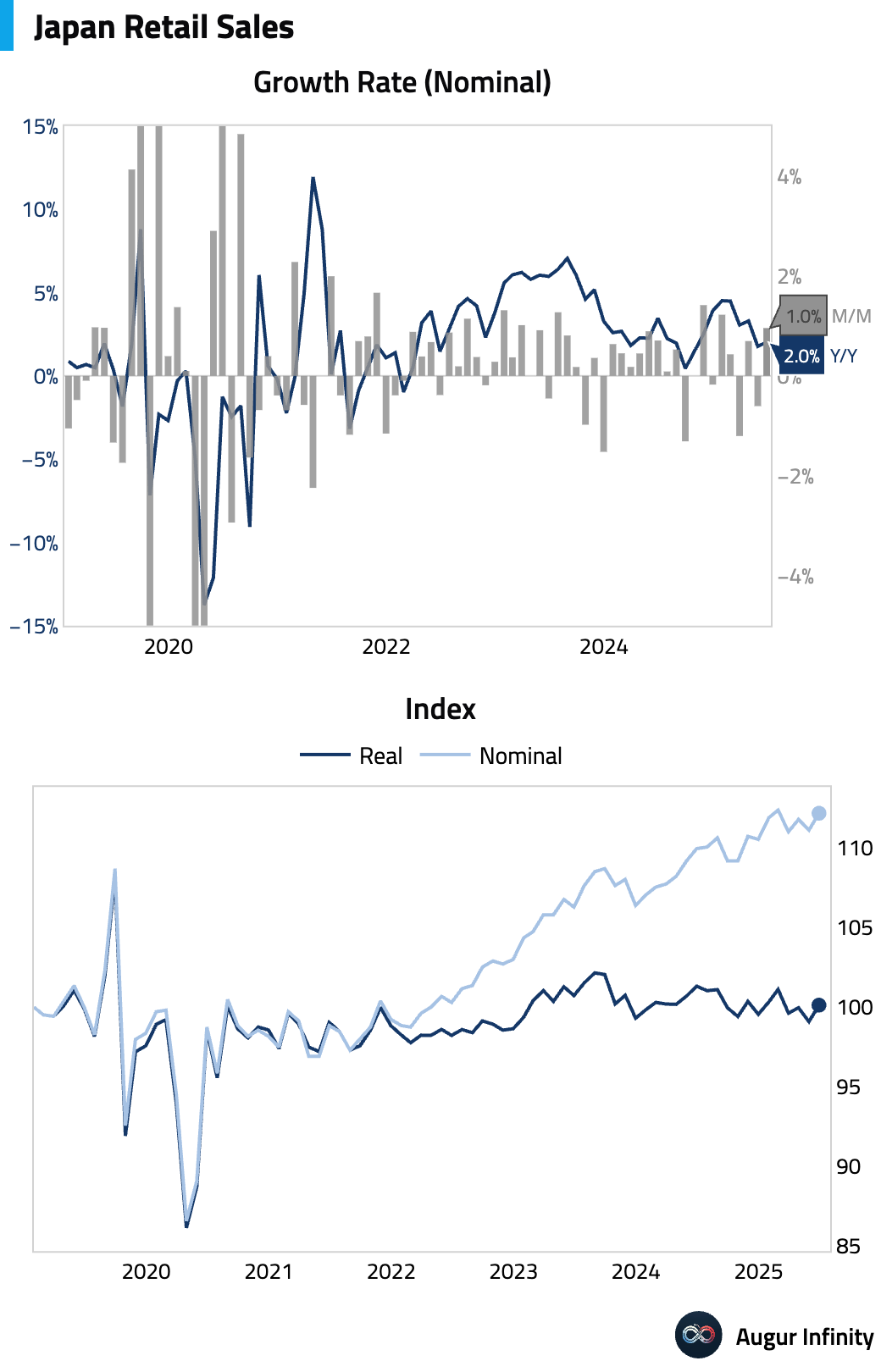

Japanese retail sales rose 2.0% Y/Y in June, slightly beating the 1.8% consensus. Month-over-month sales rebounded 1.0% after a 0.6% decline in May. The annual strength was broad-based, though a 40.6% collapse in duty-free sales dragged down overall department store performance.

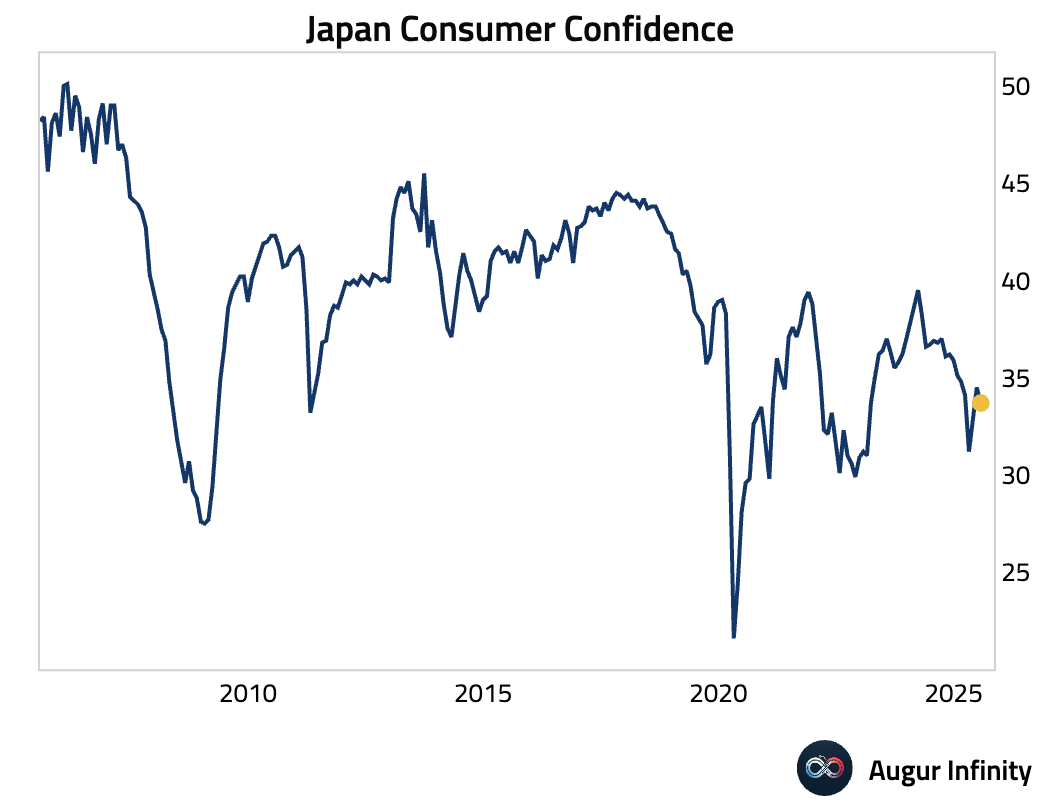

Japan's consumer confidence index fell to 33.7 in July from 34.5 in June, missing the 35.1 consensus and marking its lowest reading since May 2025.

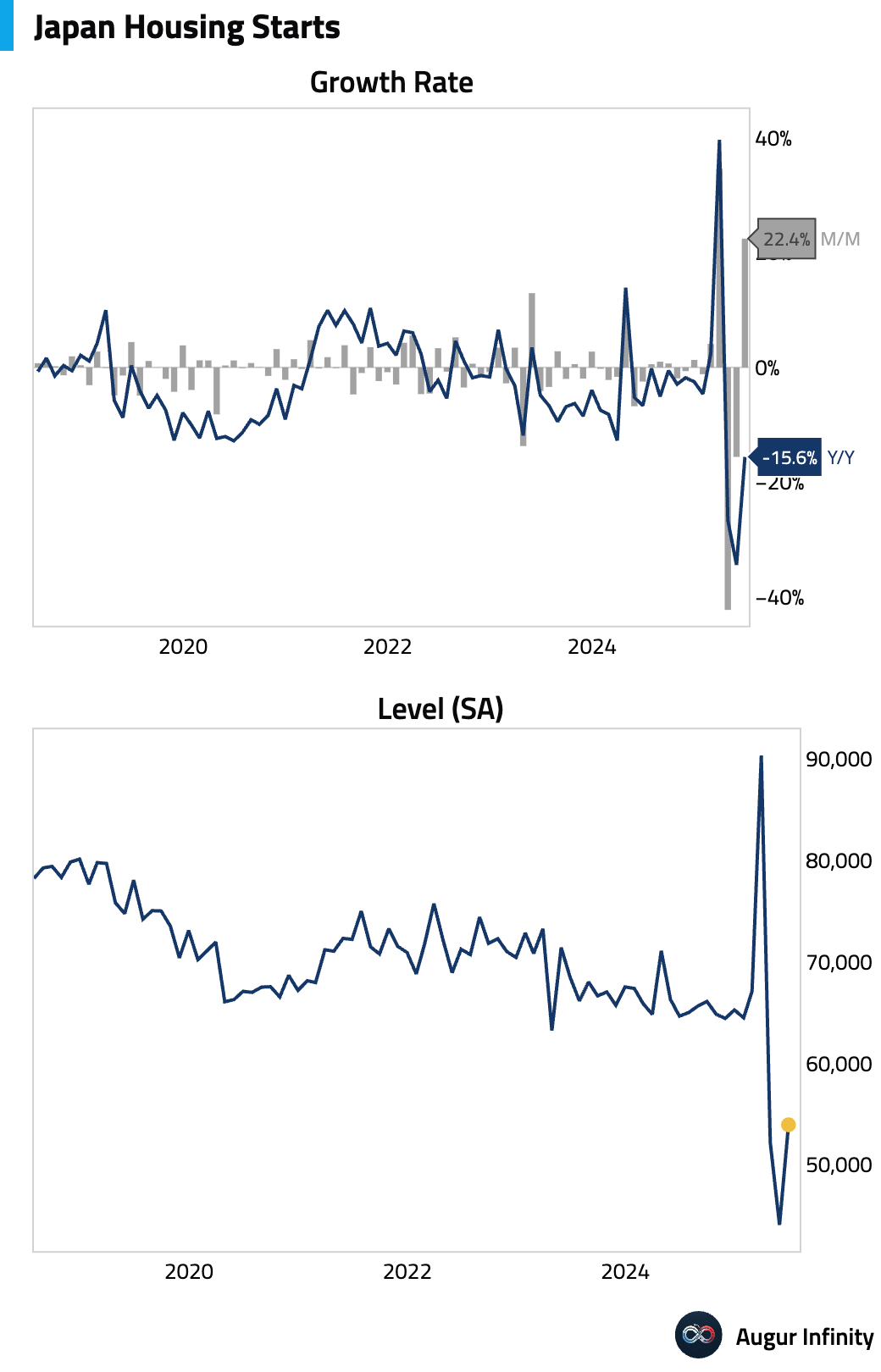

Japanese housing starts improved in June, with the Y/Y decline narrowing to -15.6% from -34.4% in May. The result was slightly better than the -15.8% consensus. The data continues to be heavily distorted by a rush by builders and developers to obtain permits ahead of major changes to Japan's Building Standards Law and the Energy Conservation Act, which took effect on April 1.

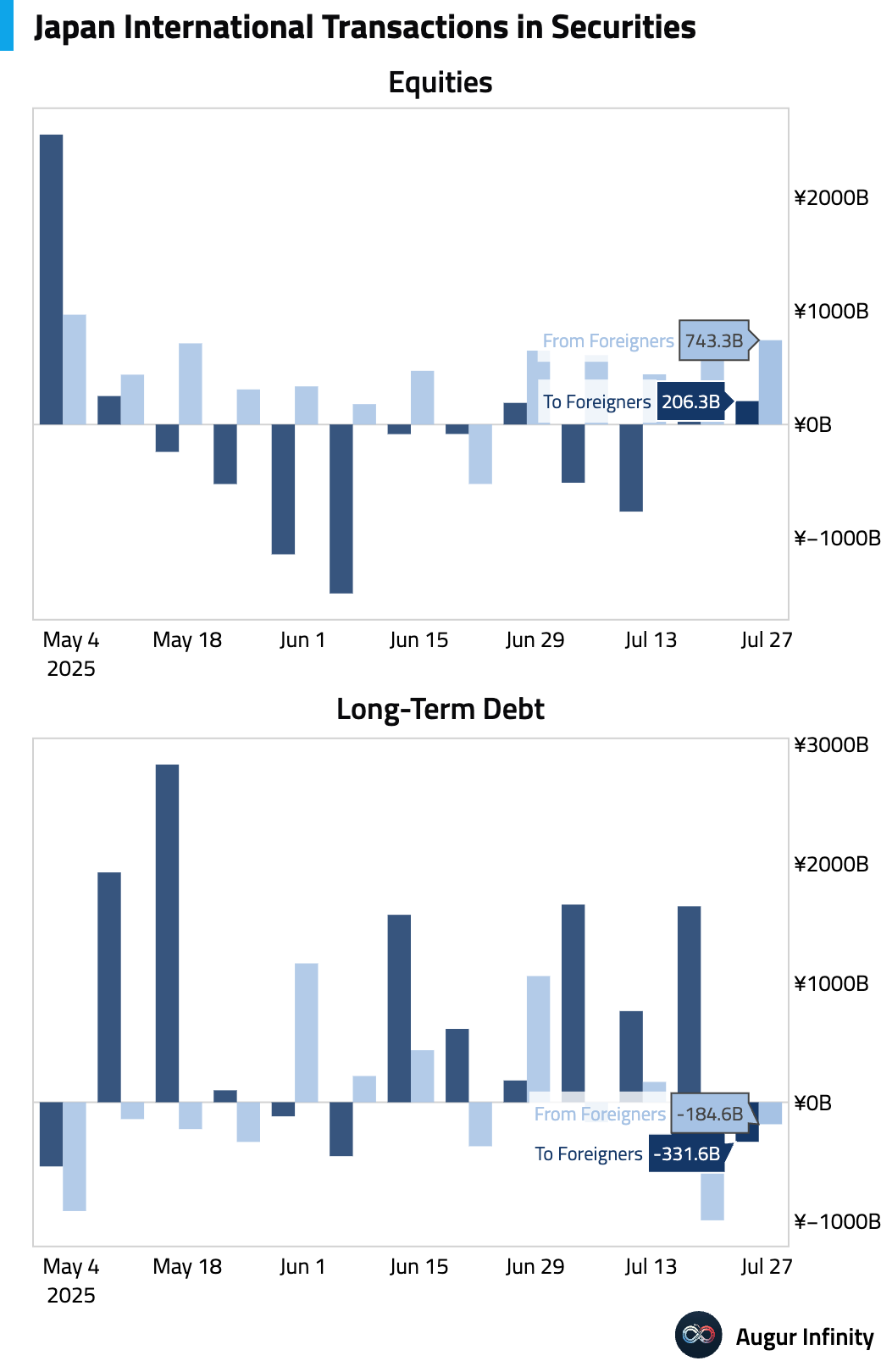

Weekly data showed Japanese investors turned net sellers of foreign bonds to the tune of ¥331.6 billion, while foreign investors were net buyers of Japanese stocks, adding ¥743.3 billion.

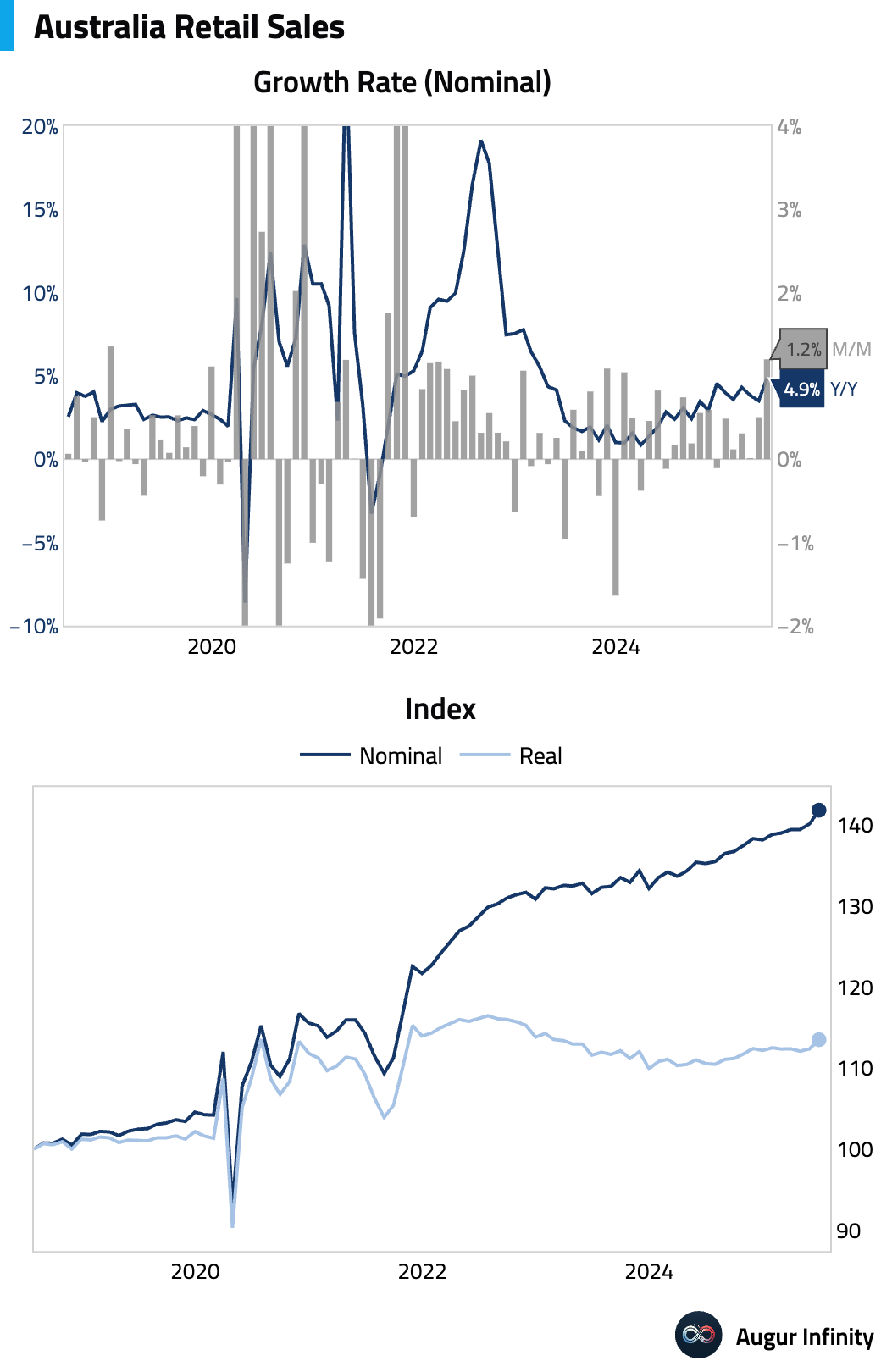

Australian retail sales jumped 1.2% M/M in June, far exceeding the 0.4% consensus. However, the strength was largely driven by a post-flood rebound in Queensland and a major video game console launch, suggesting weak underlying consumer momentum as volumes excluding Queensland grew a much softer 0.1% for the quarter.

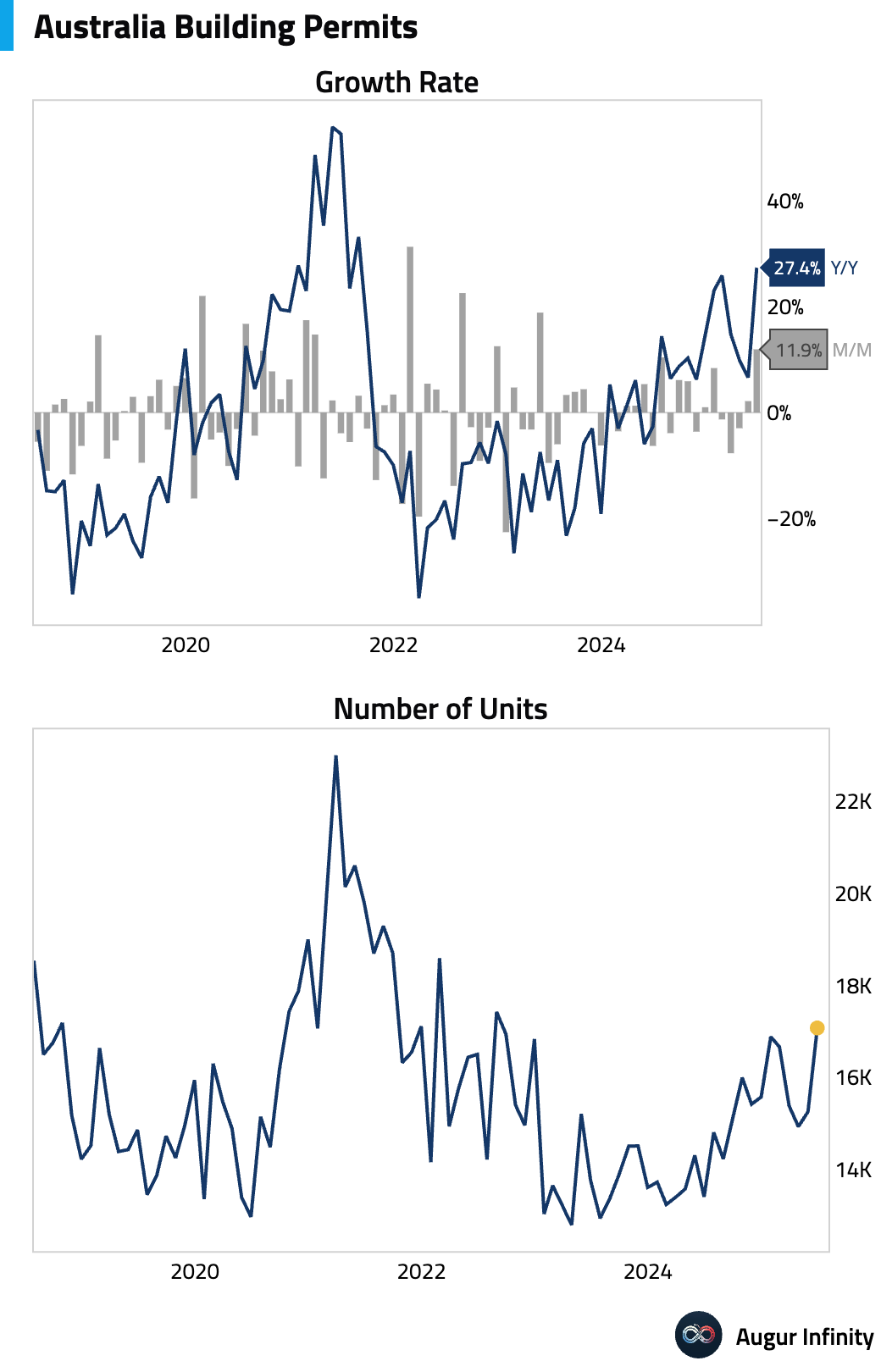

Australian building permits surged 11.9% M/M in June, crushing the 2.0% consensus. The headline strength was driven entirely by a volatile 33.9% jump in high-density dwellings, masking underlying softness as approvals for detached houses fell for a second straight month (-2.0%).

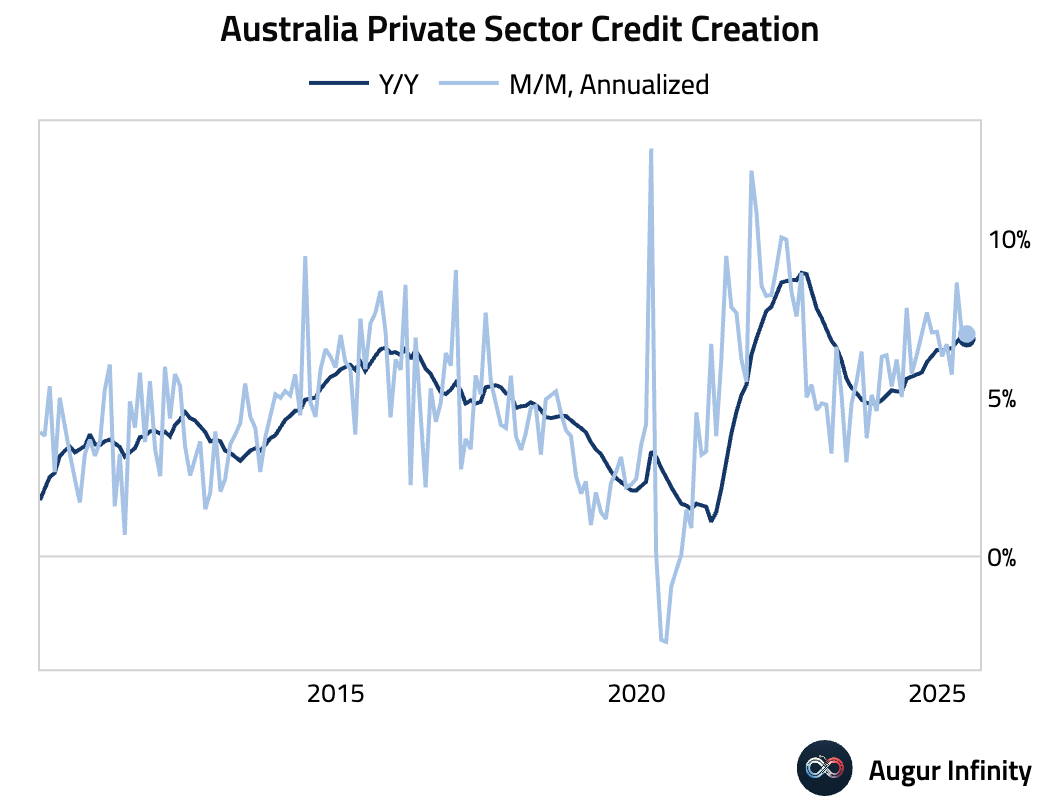

Australia's private sector credit grew 0.6% M/M and 6.8% Y/Y in June. The stable monthly headline figure masked a compositional shift, as a slowdown in business credit was offset by a pickup in personal credit, while housing credit held steady.

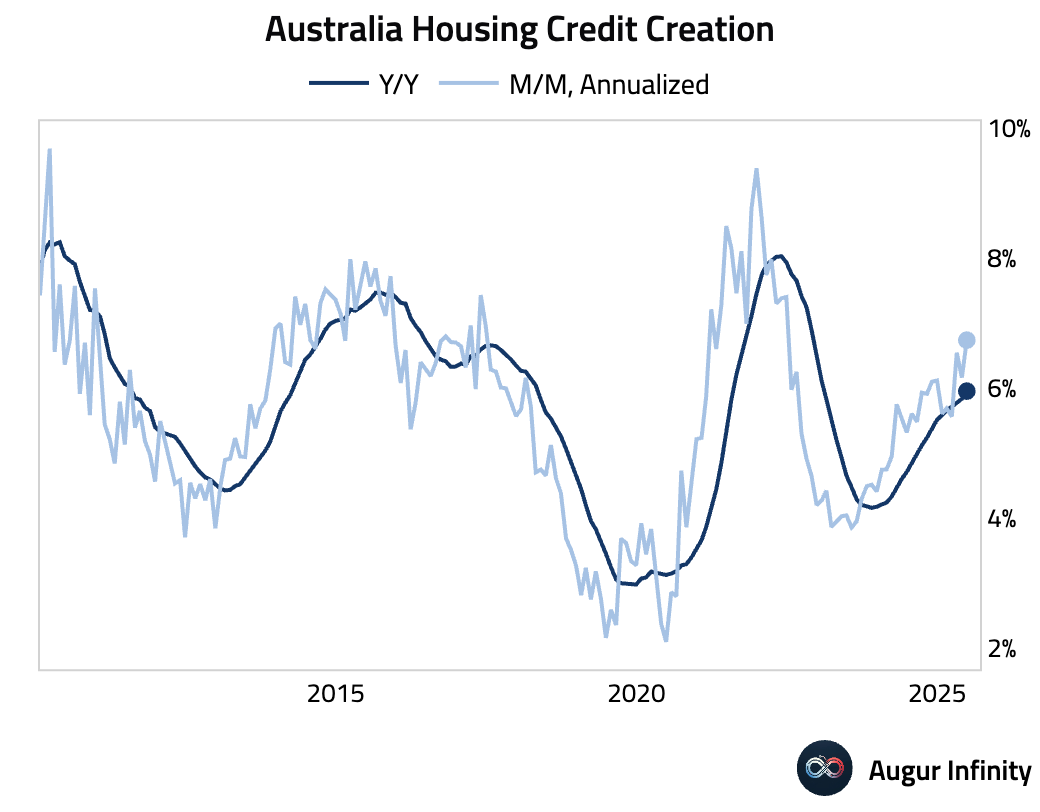

Australian housing credit was unchanged at 0.5% M/M in June, with both owner-occupier and investor lending holding steady.

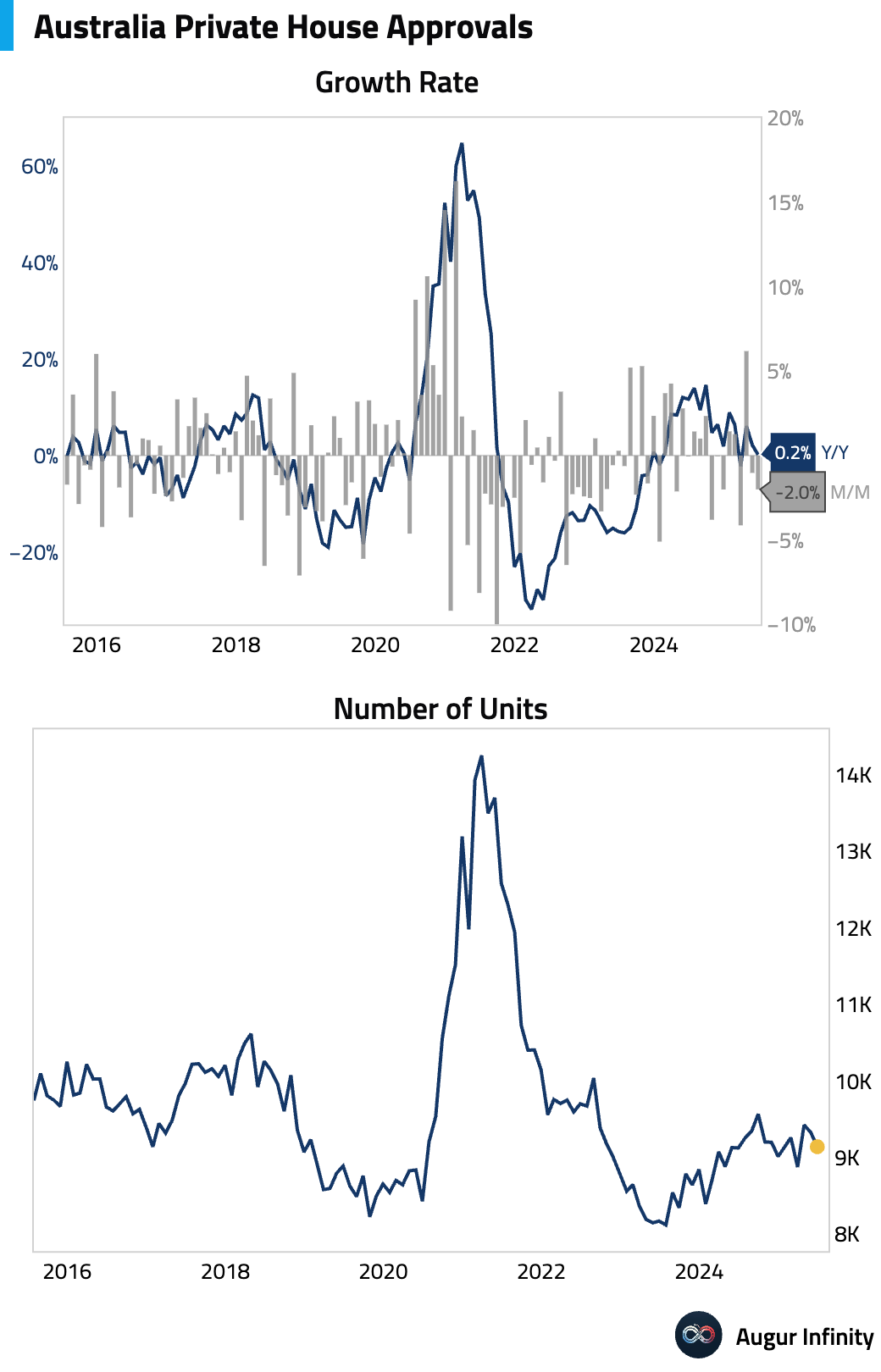

Australian private house approvals fell 2.0% M/M in June, the second consecutive monthly decline.

South Korea's June activity data showed a rebound, but underlying trends were mixed. Industrial production rose 1.6% M/M, driven entirely by strong external demand for semiconductors and autos. Retail sales also gained 0.5%, snapping a three-month losing streak. However, investment was weak, with equipment investment falling for a fourth consecutive month.

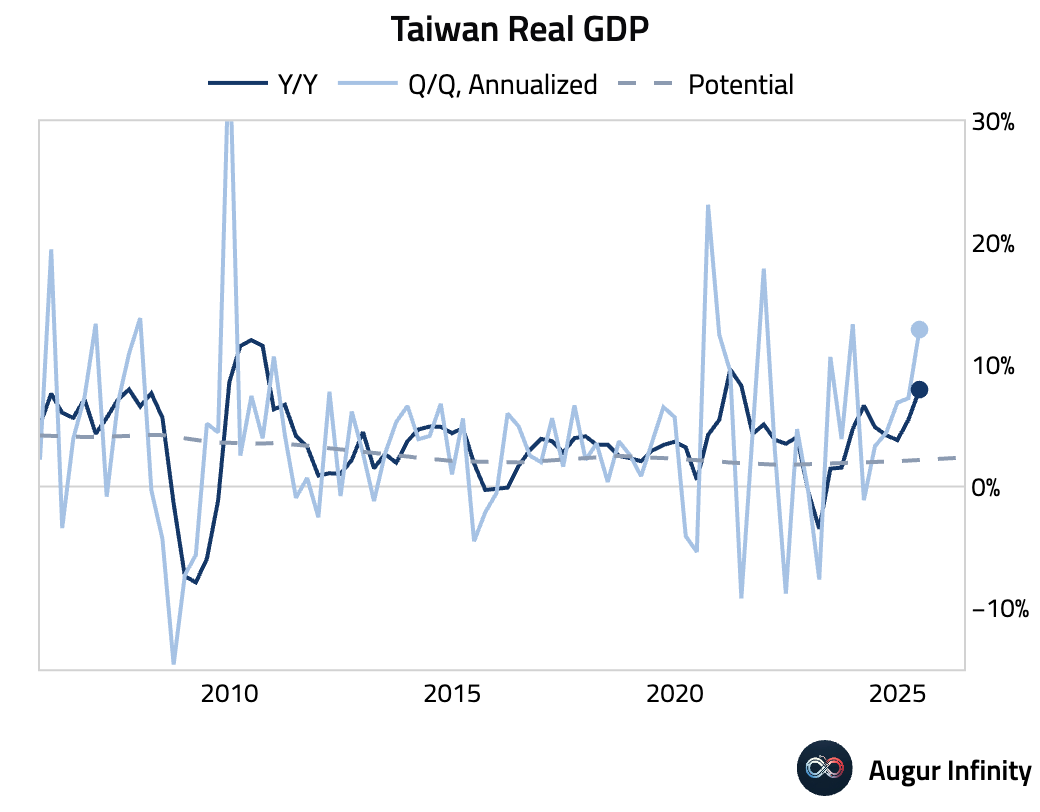

Taiwan's advance estimate for Q2 GDP showed a surge of 7.96% Y/Y, significantly beating the 5.7% consensus and marking the strongest growth since Q2 2021. The boom was driven by a massive 35.1% increase in exports, fueled by AI-related demand and front-loading ahead of US tariffs, which masked weak domestic private consumption (+0.6% Y/Y).

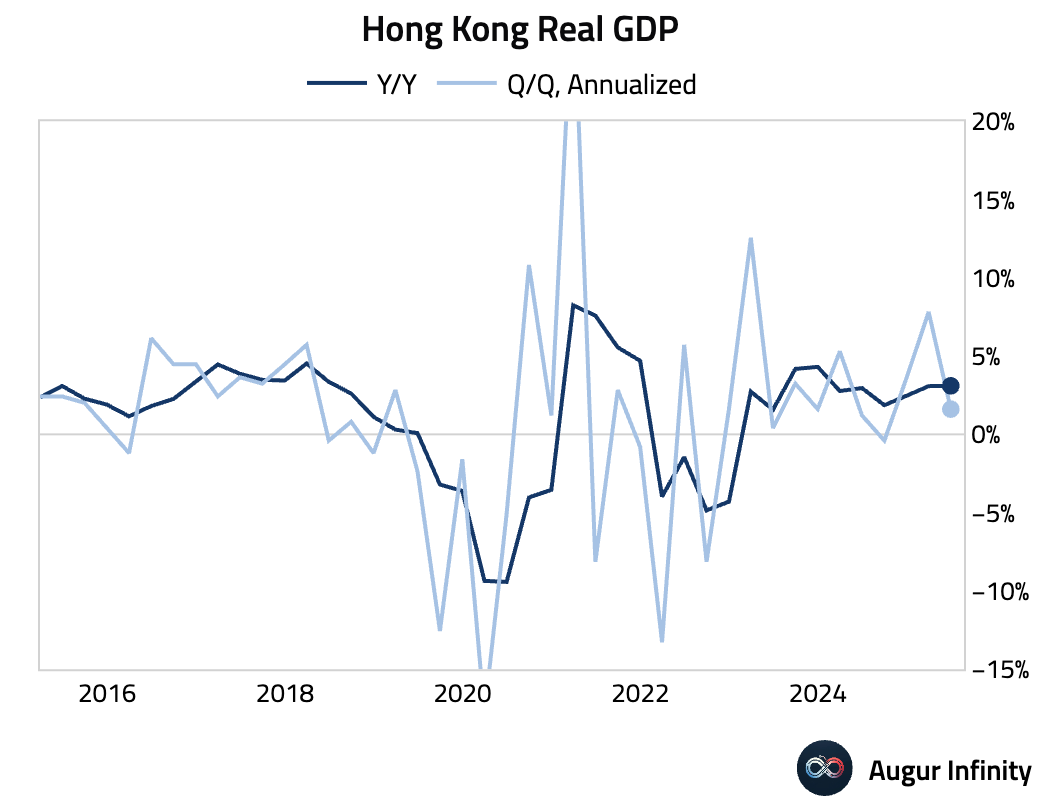

Hong Kong's advance Q2 GDP grew 0.4% Q/Q and 3.1% Y/Y, beating consensus forecasts of -0.2% and 2.8%, respectively. The annual growth was the strongest since Q4 2023.

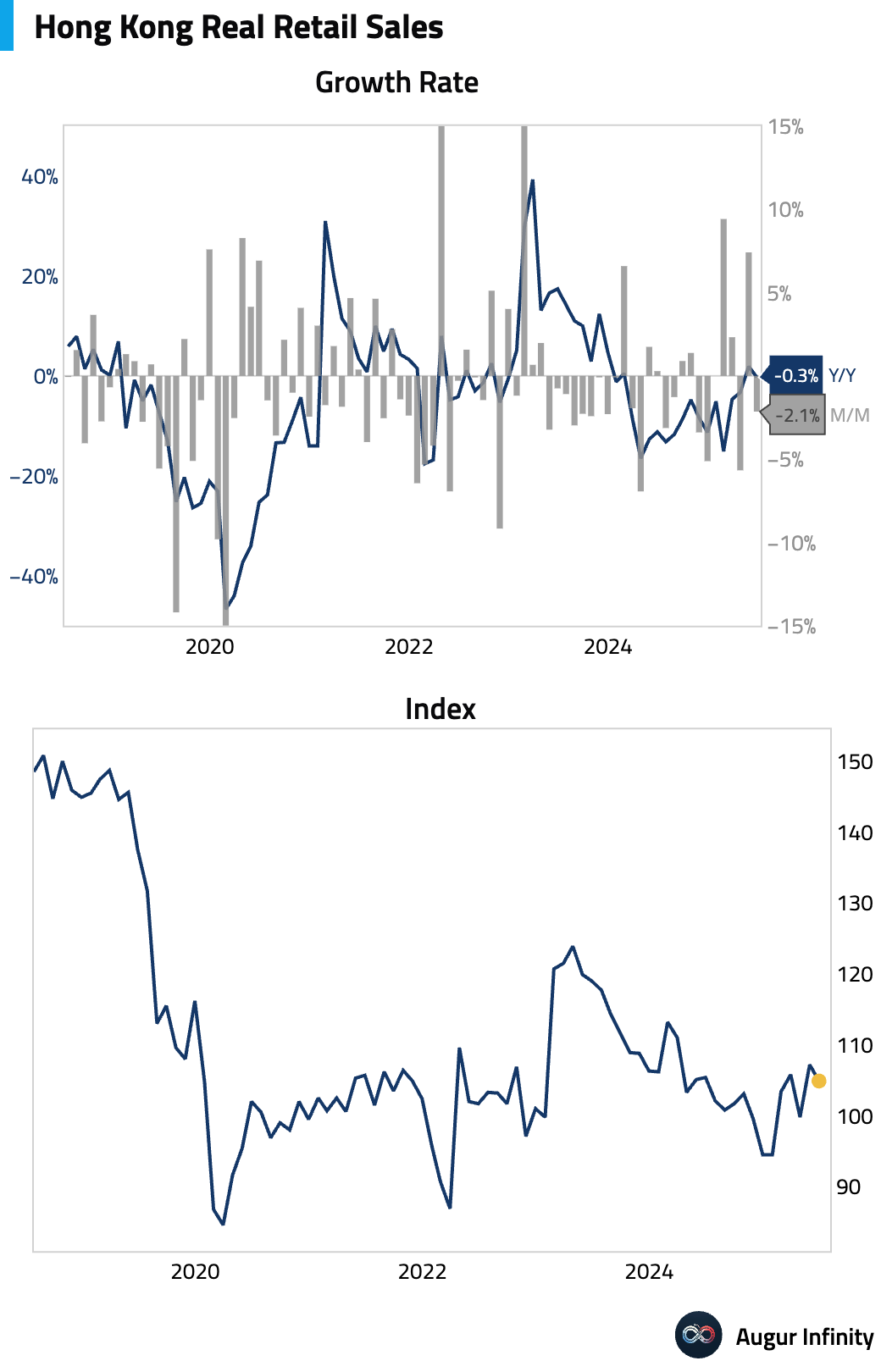

Hong Kong retail sales fell 0.3% Y/Y in June, reversing a 1.9% gain in May. The decline was driven by a sharp drop in consumer durables, and key categories like department store sales remain roughly 50% below pre-pandemic levels, indicating a highly uneven recovery.

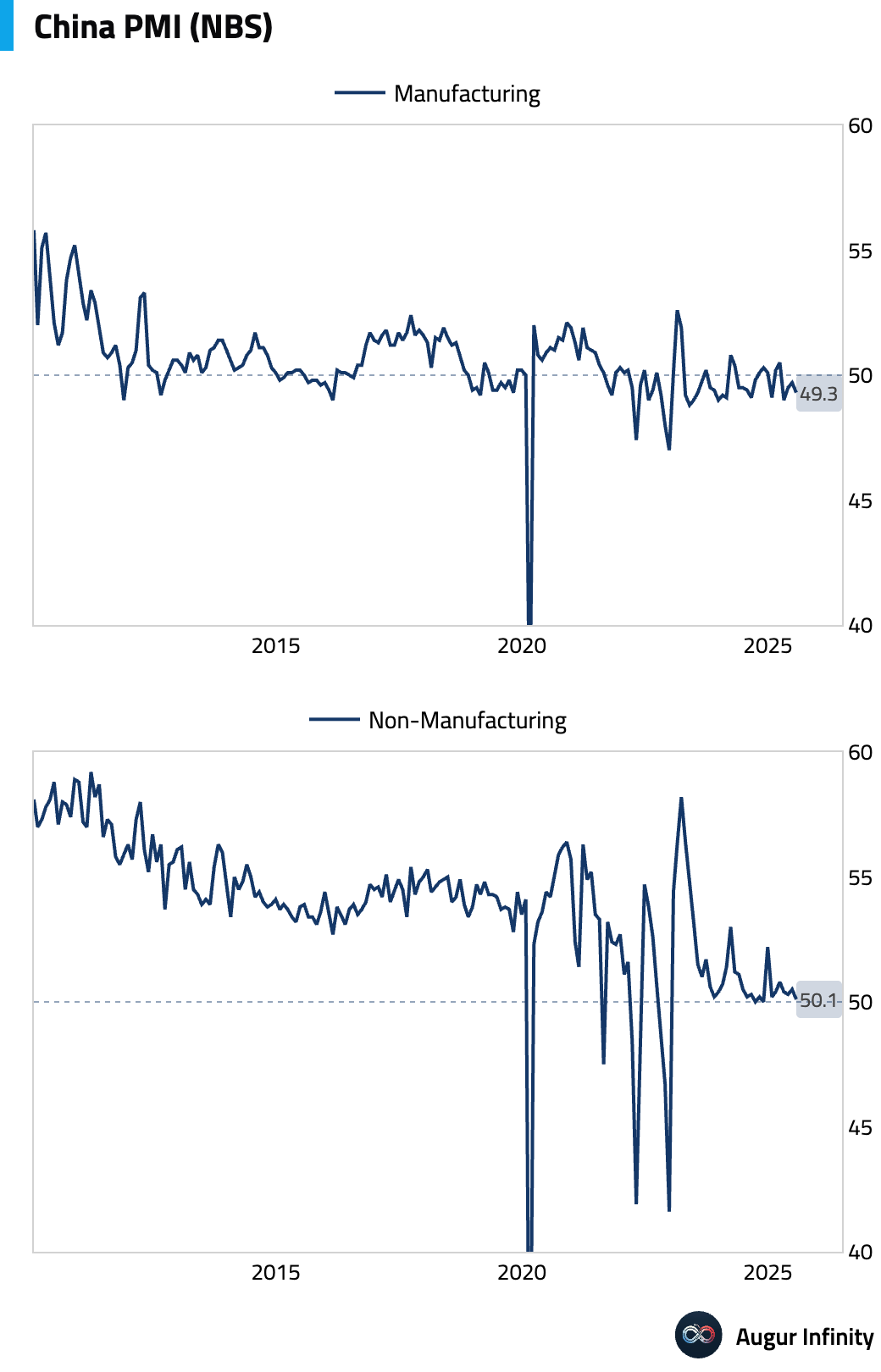

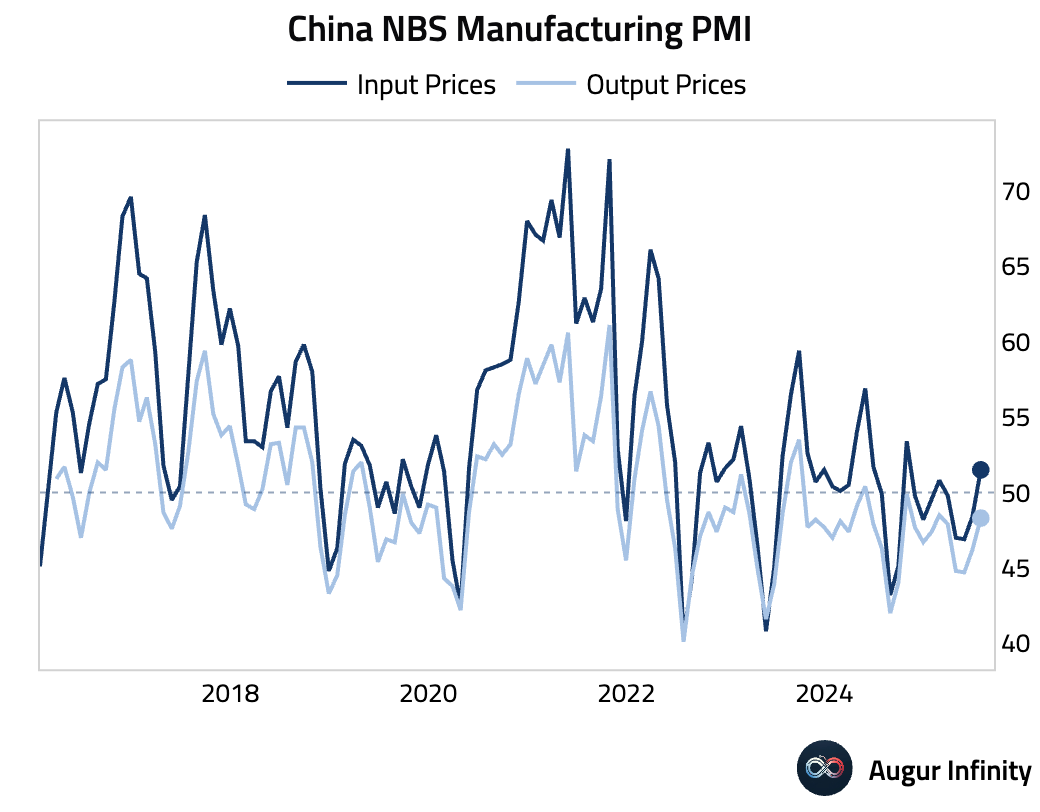

China's official NBS Manufacturing PMI fell to 49.3 in July from 49.7, missing the consensus of 49.7 and indicating a contraction in activity. The decline was driven by lower new orders and output. Notably, despite lower production, both input and output price sub-indexes rose, reflecting government efforts to curb overcapacity and excessive price competition.

Incorporating the latest PMI data, our proprietary tracker for China's underlying growth is running just shy of 5%.

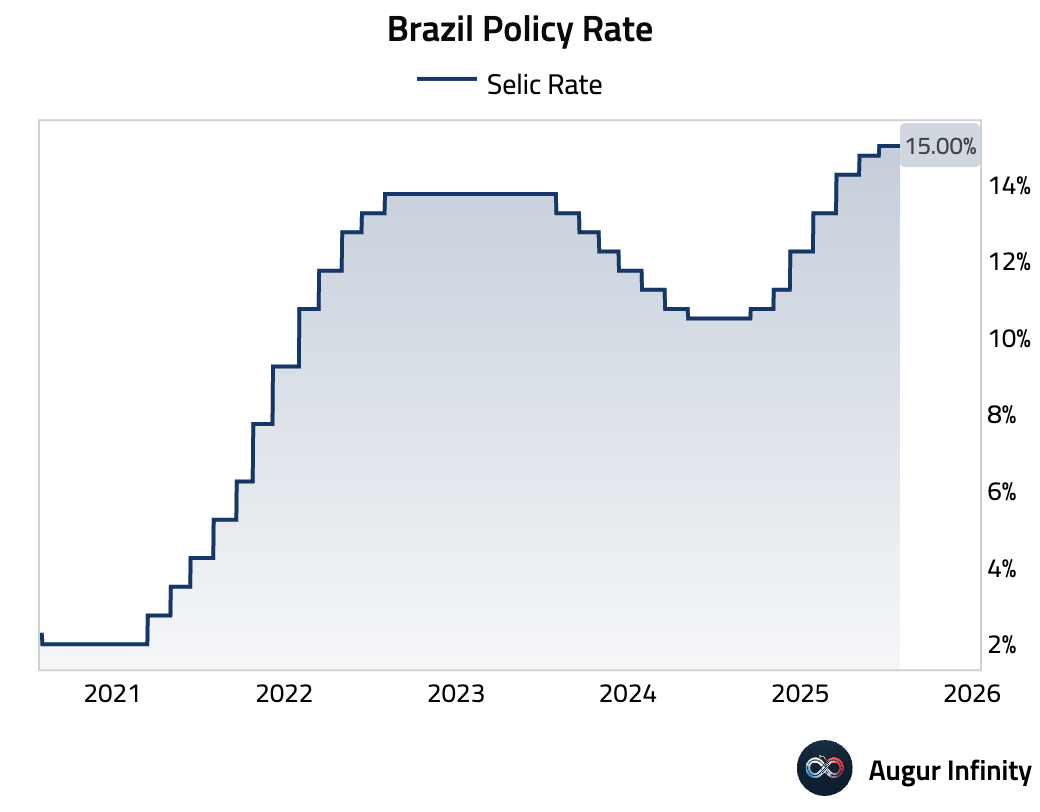

Brazil's central bank held its key interest rate at 15.0%, in line with expectations. The rate remains at its highest level since July 2006.

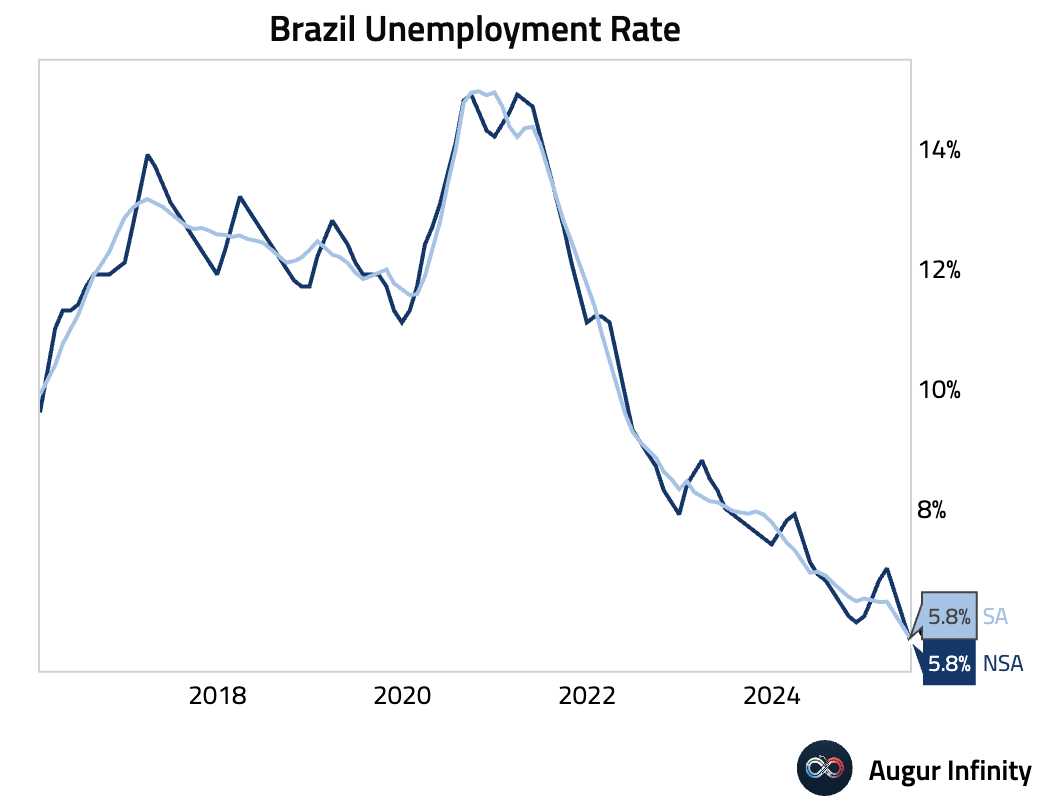

Brazil's unemployment rate fell to 5.8% in June, below the 6.0% consensus and down from 6.2% in May, marking a new all-time low for the series.

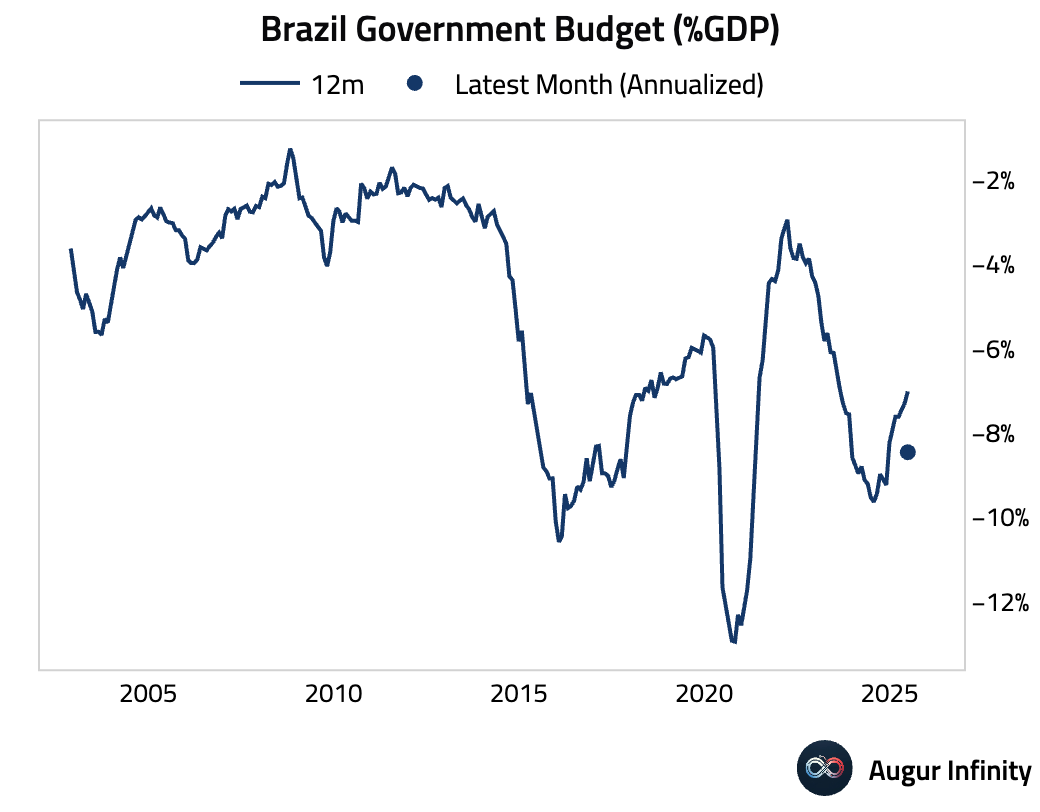

Brazil's nominal budget deficit narrowed to R$108.1 billion in June from R$125.9 billion in May. However, the primary deficit was wider than consensus, and with significant "catch-up" spending expected in H2, the fiscal outlook continues to deteriorate, with the 12-month overall deficit now at 7.3% of GDP.

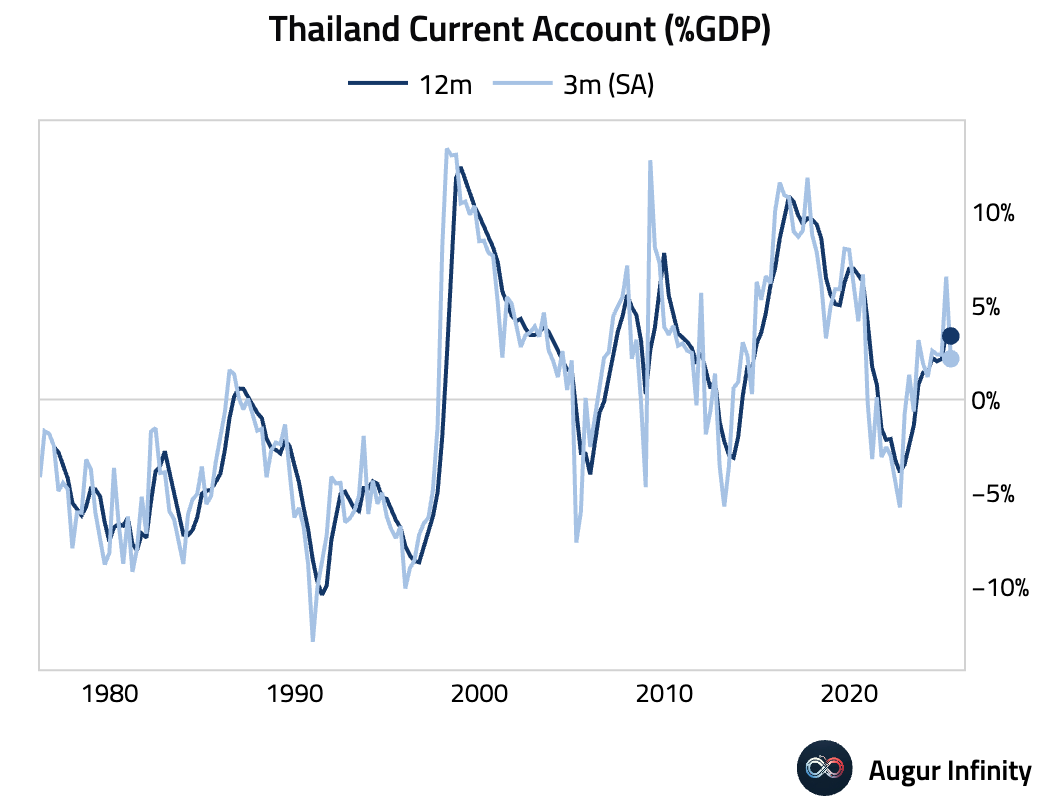

Thailand's current account swung to a $2.4 billion surplus in June from a $0.3 billion deficit in May.

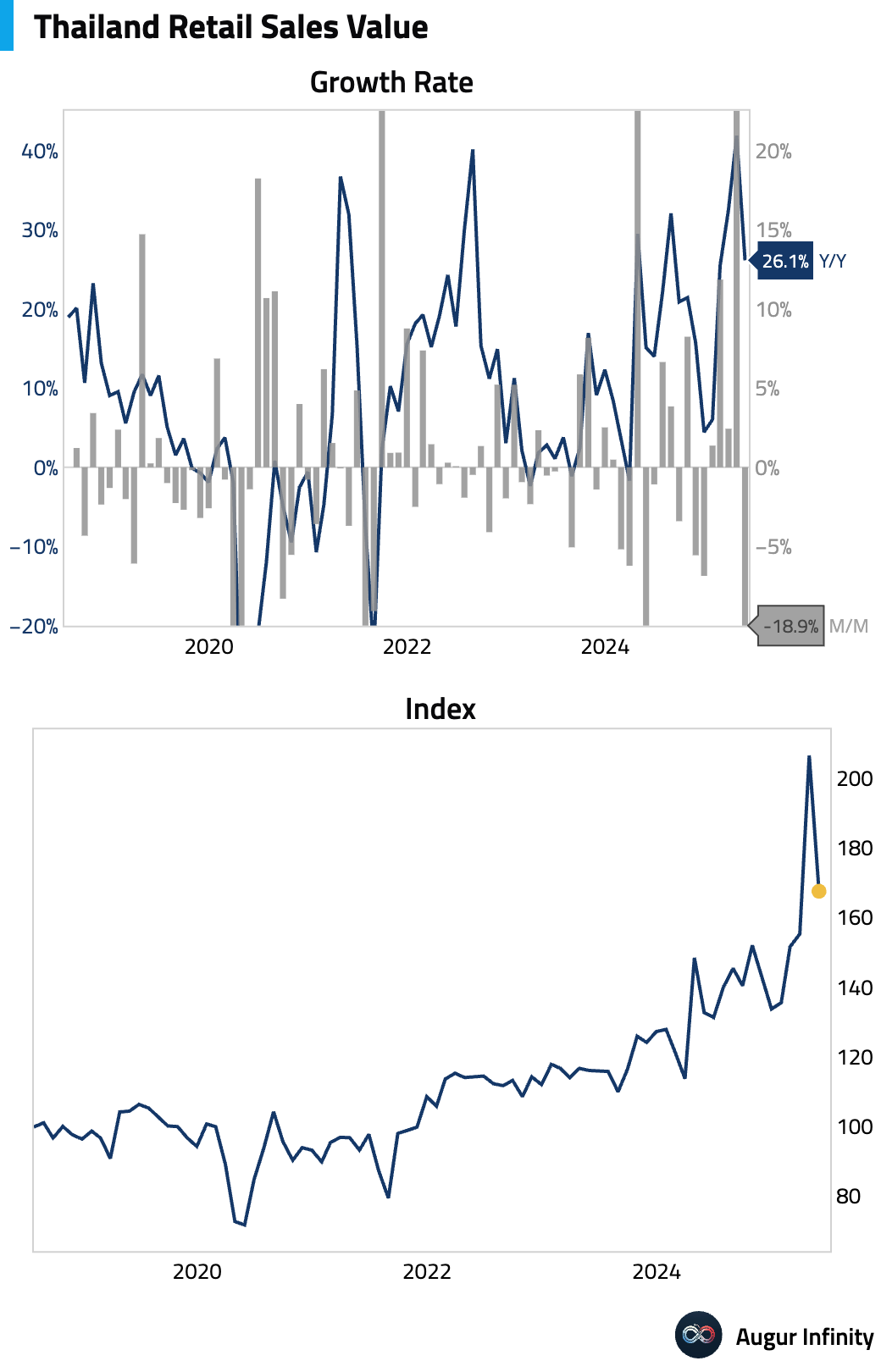

Thailand's private consumption fell 0.3% M/M in June, following a 0.2% rise in May.

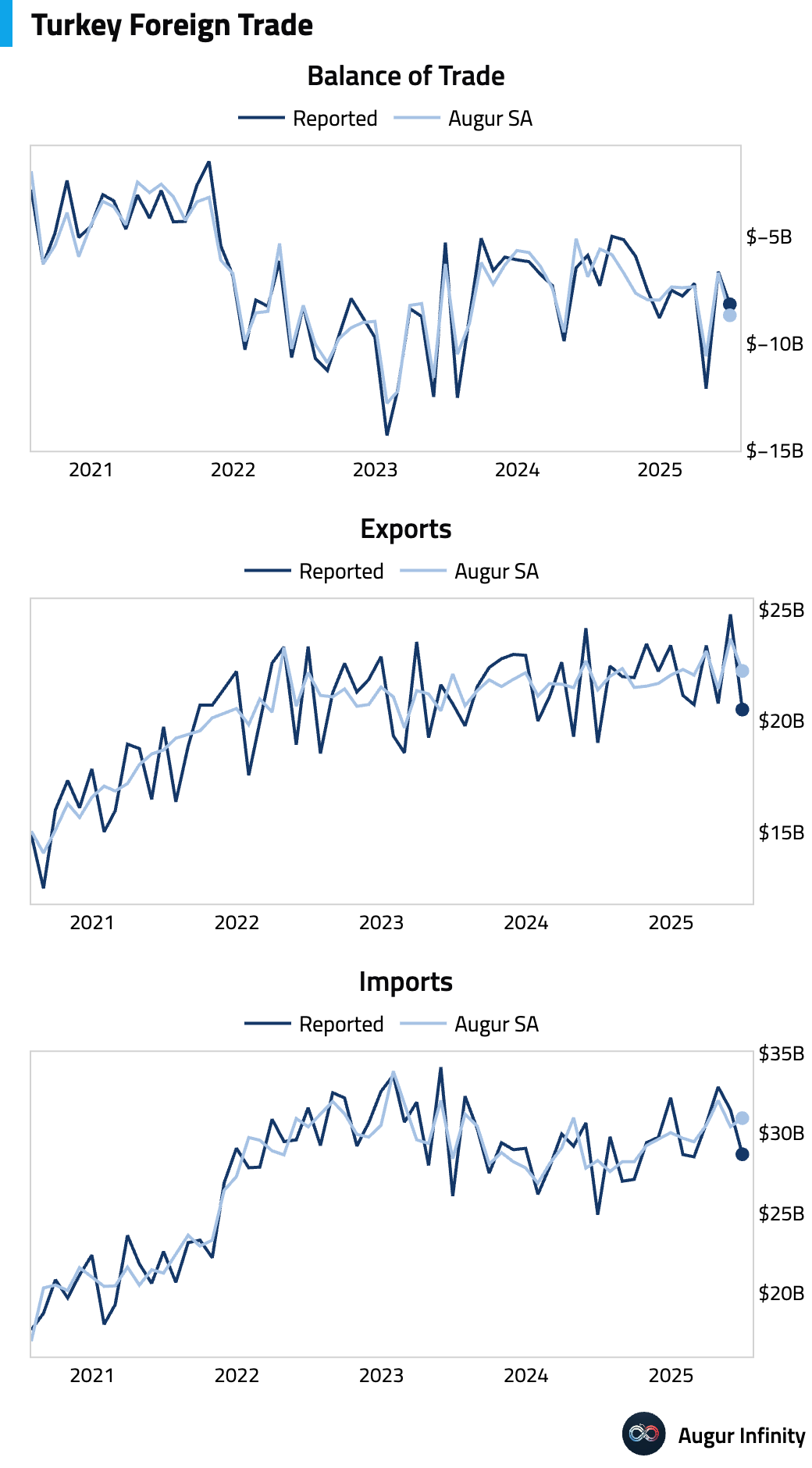

Turkey's trade deficit widened to $8.2 billion in June from a $6.6 billion deficit in May.

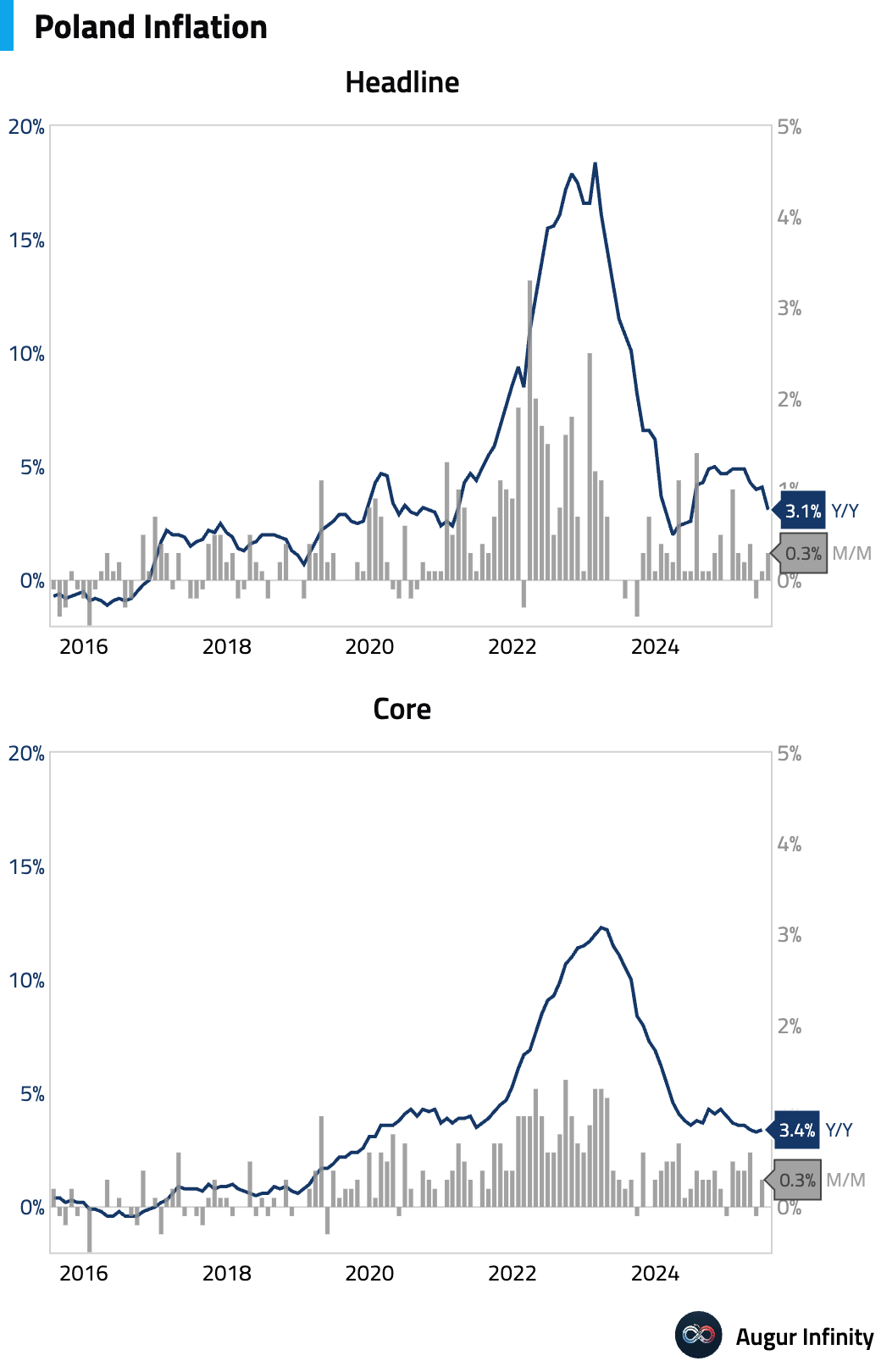

Poland's preliminary July inflation came in at 3.1% Y/Y, a hawkish surprise compared to the 2.8% consensus. The miss was driven by a smaller-than-expected pass-through from a large household gas price cut and stronger food inflation, making a September rate cut less likely. M/M inflation was 0.3%.

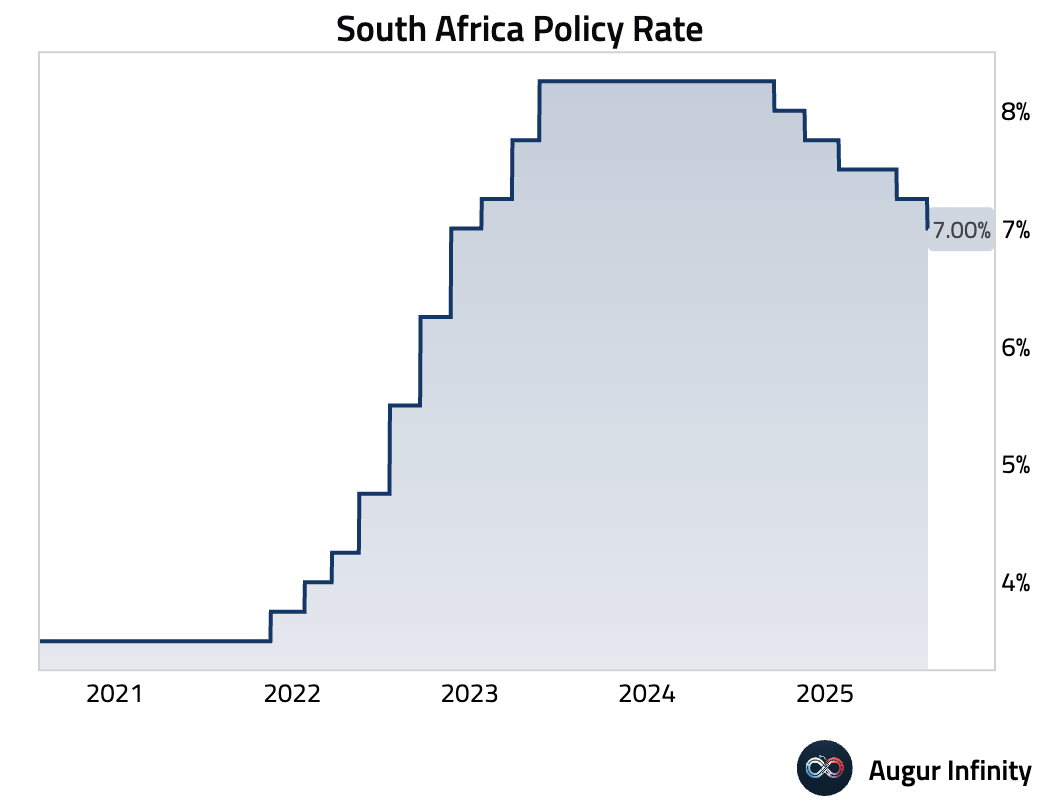

The South African Reserve Bank cut its benchmark interest rate by 25 basis points to 7.0%, in line with consensus. This is the first rate change of the year and brings the policy rate to its lowest level since November 2022.

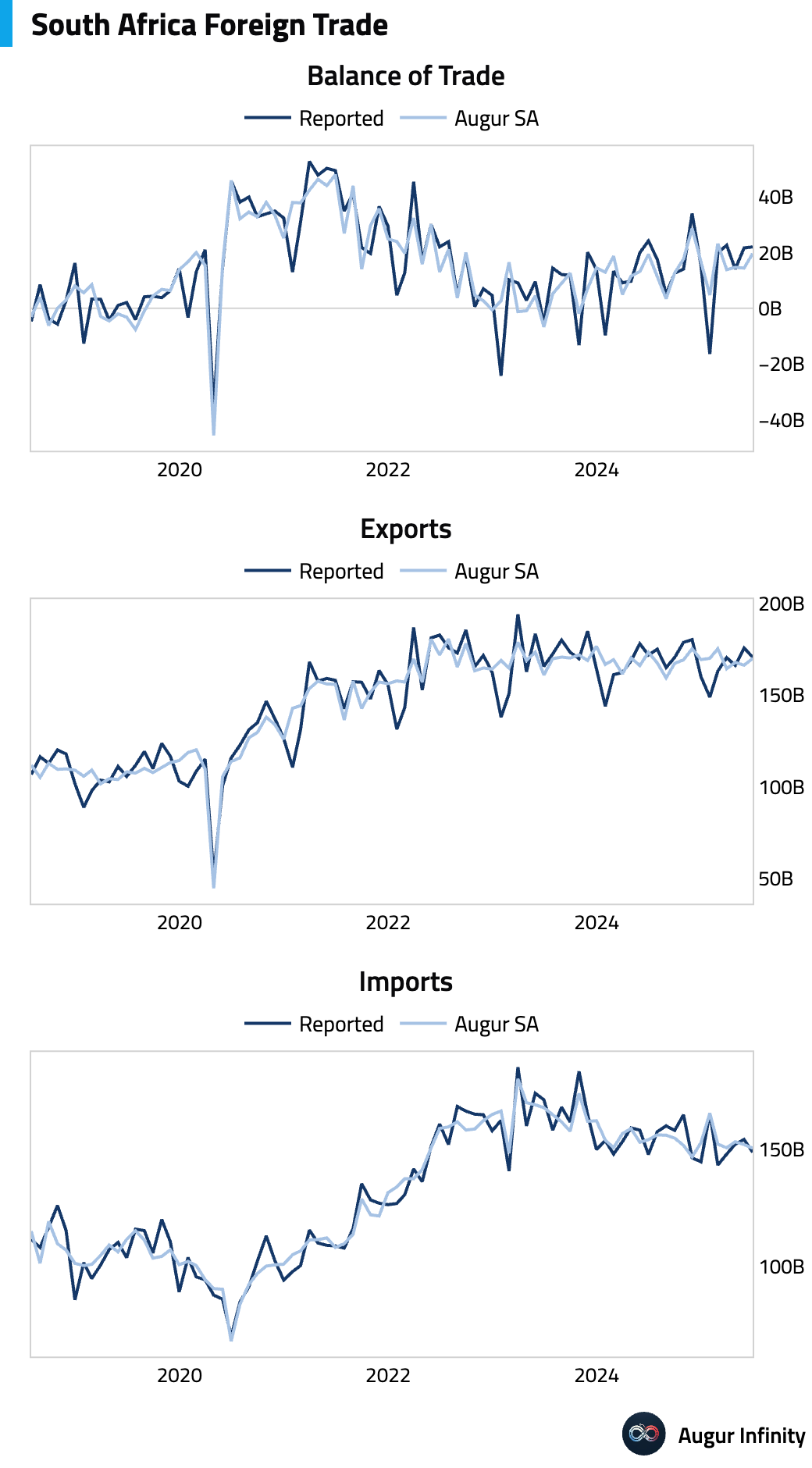

South Africa's trade surplus widened to ZAR 22.04 billion in June from ZAR 20.03 billion in May.

Global equities were mixed, with US markets paring strong pre-market gains to close modestly lower after an initial surge driven by strong tech earnings. The S&P 500 and Dow Jones Industrial Average fell, while the Nasdaq managed a slight gain. US markets finished a third consecutive day lower. European markets were broadly negative, with Germany, France, and the UK all closing down. In Asia, Chinese equities extended their losing streak to six days.

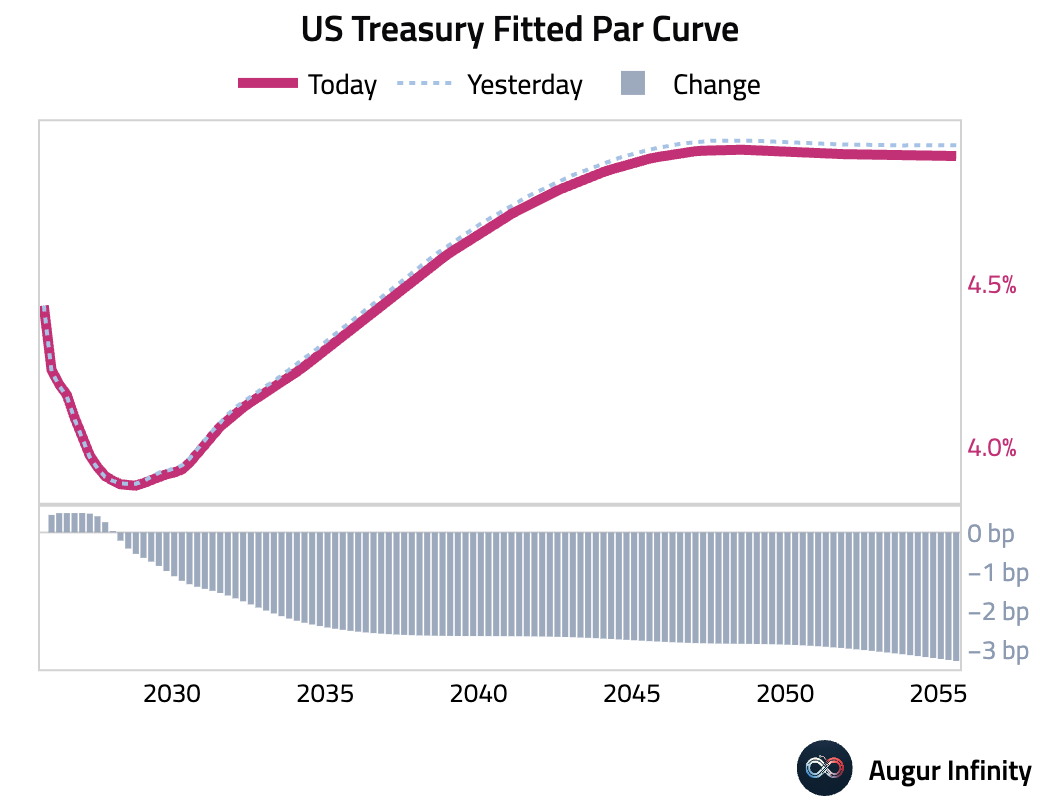

The US Treasury yield curve flattened as the front end rose while longer-dated yields fell. The 2-year yield climbed 0.8 bps, while the 10-year yield fell 1.7 bps and the 30-year yield dropped 1.8 bps. Markets continue to digest the Federal Reserve's hawkish hold from the prior day, where Chair Powell offered no clear signal for a September rate cut and highlighted uncertainty around tariffs' impact on inflation.

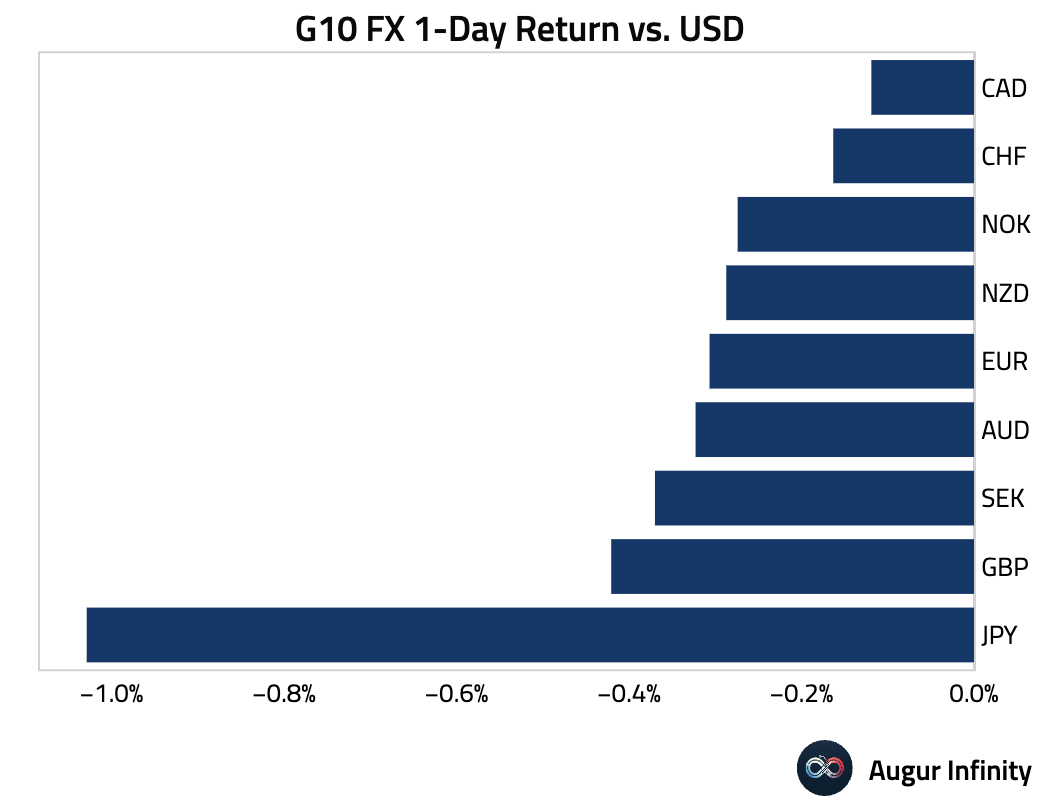

The US dollar strengthened against all G10 peers amid ongoing trade tensions and a hawkish Federal Reserve. The Japanese yen was the weakest performer, falling 1.0% against the dollar. The Australian dollar, Canadian dollar, British pound, Swiss franc, and Japanese yen have all fallen against the USD for at least five consecutive days.