Headlines

• President Trump asserted China violated the preliminary trade agreement, with Treasury Secretary Bessent describing current talks as "a bit stalled."

• The US administration is reportedly considering alternative authority to impose tariffs for 150 days, should a court ruling appeal fail, and is evaluating further technology-related sanctions on China.

• Japan’s chief trade negotiator is in Washington, DC, today for discussions, prompting speculation of a potential trade agreement announcement.

United States

• The Federal Reserve's balance sheet continued to shrink, falling to $6.67 trillion from $6.69 trillion the previous week. This is the lowest level since April 2020.

• Personal income rose by 0.8% M/M in April, accelerating from a 0.7% increase in March and beating the consensus of 0.3%.

• Personal spending increased by 0.2% M/M in April, slowing from 0.7% in March and matching consensus.

• The PCE price index rose 0.1% M/M in April (prev. 0.0%), bringing the Y/Y rate to 2.1% (prev. 2.3%, cons. 2.2%). The core PCE price index also rose 0.1% M/M (prev. 0.1%), with the Y/Y rate declining to 2.5% (prev. 2.7%, cons. 2.5%), its lowest since March 2021.

• The advance goods trade deficit narrowed significantly to $87.62 billion in April from $162.25 billion in March, well below the $141.5 billion consensus.

• Advance retail inventories excluding autos rose 0.3% M/M in April, unchanged from March. Advance wholesale inventories were flat M/M in April (prev. 0.3%, cons. 0.4%).

• The Chicago PMI fell to 40.5 in May from 44.6 in April, missing the consensus of 45.0.

• The final University of Michigan Consumer Sentiment Index for May was 52.2, unchanged from the preliminary reading (prev. month 52.2, cons. 51.0), its lowest since July 2022. Current Conditions fell to 58.9 (prev. 59.8), while Expectations rose to 47.9 (prev. 47.3).

• Final University of Michigan inflation expectations for May showed the 1-year outlook at 6.6% (prev. 6.5%) and the 5-year outlook at 4.2% (prev. 4.4%).

• The Baker Hughes total rig count fell by 3 to 563. Oil rigs decreased by 4 to 461.

Canada

• Q1 GDP grew by 0.5% Q/Q, matching the previous quarter's pace. This translated to an annualized growth rate of 2.2%, up from 2.1% in Q4 2024 and above the 1.7% consensus.

• Monthly GDP rose 0.1% M/M in March, following a 0.2% contraction in February. The preliminary estimate for April GDP also indicates a 0.1% M/M increase.

• The federal government budget balance recorded a deficit of C$23.88 billion in March, a deterioration from the C$7.57 billion surplus in February and the largest deficit since March 2024.

Europe

• Euro Area M3 money supply growth accelerated to 3.9% Y/Y in April from 3.7% in March, slightly above the 3.7% consensus.

• Euro Area loans to companies grew 2.6% Y/Y in April (prev. 2.3%), while loans to households increased 1.9% Y/Y (prev. 1.7%, cons. 1.8%).

• Germany's retail sales fell 1.1% M/M in April (prev. +0.9%, cons. +0.2%), though the Y/Y rate was 2.3% (prev. 3.3%, cons. 1.8%).

• Germany's preliminary inflation for May was 0.1% M/M (prev. 0.4%, cons. 0.1%), with the Y/Y rate unchanged at 2.1% (cons. 2.0%). Harmonized HICP was 0.2% M/M and 2.1% Y/Y.

• UK car production declined 15.8% Y/Y in April, a sharp reversal from the 17.1% increase in March.

• Sweden's final Q1 GDP showed a contraction of 0.2% Q/Q (prev. +0.5%, cons. +0.1%), while Y/Y growth was 0.9% (prev. 2.4%, cons. 1.1%).

• Norway's registered jobless rate remained at 2.0% in May, slightly above the 1.9% consensus.

• Spain's preliminary inflation for May was flat M/M (prev. 0.6%, cons. 0.1%), pulling the Y/Y rate down to 1.9% (prev. 2.2%, cons. 2.1%). Core inflation eased to 2.1% Y/Y (prev. 2.4%).

• Spain's current account surplus narrowed to €1.42 billion in March from €2.31 billion in February.

• Switzerland's KOF leading indicator rose to 98.5 in May from 97.1 in April, beating the consensus of 98.4.

• Italy's final Q1 GDP confirmed 0.3% Q/Q growth (prev. 0.2%, cons. 0.3%), with Y/Y growth at 0.7% (prev. 0.5%, cons. 0.6%).

• Italy's preliminary inflation for May was flat M/M (prev. 0.1%, cons. 0.1%), with the Y/Y rate easing to 1.7% (prev. 1.9%, cons. 1.7%).

• Italy's PPI fell 2.2% M/M in April (prev. -2.4%), with the Y/Y rate slowing to 2.6% from 3.9%.

• Poland's preliminary inflation for May showed a 0.2% M/M decrease (prev. +0.4%), bringing the Y/Y rate to 4.1% (prev. 4.3%, cons. 4.3%).

• Greece's PPI increased 0.5% Y/Y in April, slowing from 2.1% in March.

• Greece's retail sales growth decelerated sharply to 0.3% Y/Y in March from 5.6% in February.

• Greece's unemployment rate fell to 8.3% in April from 8.9% in March, its lowest level since November 2008.

• Greece's total credit growth picked up to 7.3% Y/Y in April from 6.9% in March.

• Portugal's final Q1 GDP showed a contraction of 0.5% Q/Q (prev. +1.4%, cons. -0.5%), with Y/Y growth at 1.6% (prev. 2.8%, cons. 1.6%).

• Portugal's preliminary inflation for May was 0.4% M/M (prev. 0.7%), with the Y/Y rate ticking up to 2.3% from 2.1%.

• Ireland's preliminary HICP for May was flat M/M (prev. 0.4%), with the Y/Y rate slowing to 1.4% from 2.0%.

• Hungary's PPI rose 7.9% Y/Y in April, up from 7.3% in March.

• Czech Republic's Q1 GDP (2nd estimate) grew 0.8% Q/Q (prev. 0.7%), with Y/Y growth at 2.2% (prev. 1.8%).

• Czech Republic M3 money supply growth eased to 4.0% Y/Y in April from 4.5% in March.

• Turkey's Q1 GDP grew 1.0% Q/Q (prev. 1.7%), with Y/Y growth at 2.0% (prev. 3.0%, cons. 2.3%).

• Turkey's unemployment rate rose to 8.6% in April from 8.0% in March.

Japan

• The unemployment rate held steady at 2.5% in April, matching consensus.

• The jobs-to-applications ratio was unchanged at 1.26 in April, in line with consensus.

• Tokyo's CPI for May showed headline inflation steady at 3.4% Y/Y. Core CPI (ex-fresh food) rose to 3.6% Y/Y (prev. 3.4%, cons. 3.5%), and core-core CPI (ex-food and energy) increased to 2.1% Y/Y (prev. 2.0%).

• Preliminary industrial production fell 0.9% M/M in April (prev. +0.2%, cons. -1.4%), with Y/Y growth slowing to 0.7% (prev. 1.0%).

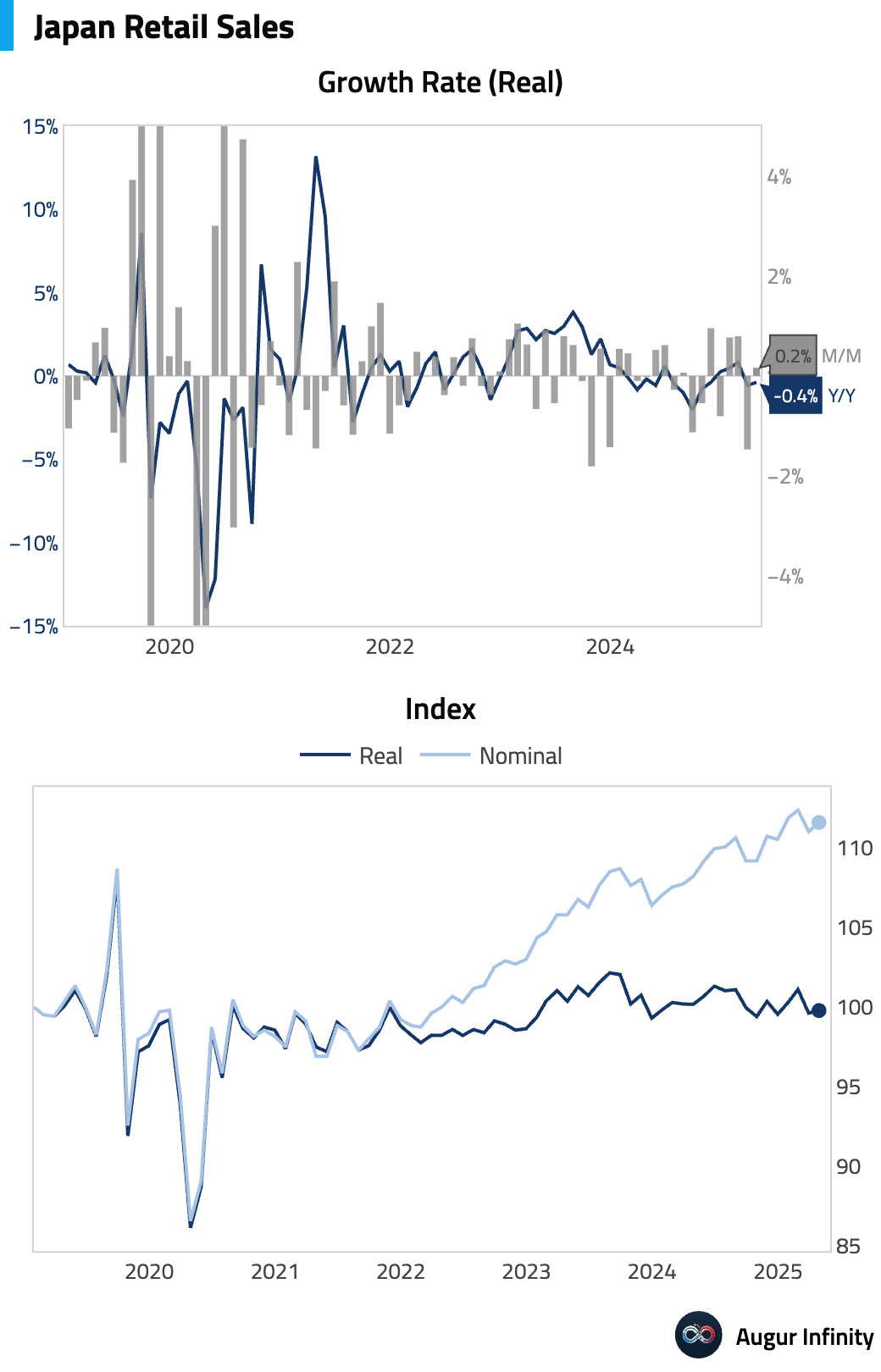

• Retail sales rose 0.5% M/M in April (prev. -1.2%), and Y/Y growth accelerated to 3.3% (prev. 3.1%, cons. 3.1%).

• Housing starts plunged 26.6% Y/Y in April (prev. +39.1%), the largest drop since October 2009.

• Construction orders surged 52.7% Y/Y in April, up from 3.5% in March.

Asia-Pacific

• New Zealand's ANZ Roy Morgan Consumer Confidence fell to 92.9 in May from 98.3 in April.

• New Zealand's building permits dropped 15.6% M/M in April, following a 10.7% rise in March.

• South Korea's industrial production fell 0.9% M/M in April (prev. +2.9%, cons. +0.5%), while Y/Y growth was 4.9% (prev. 5.3%, cons. 4.0%). Retail sales also declined 0.9% M/M (prev. -1.0%).

• Australia's preliminary building permits fell 5.7% M/M in April (prev. -7.1%, cons. +3.1%). Private house approvals, however, rose 3.1% M/M (prev. -1.9%).

• Australia's retail sales edged down 0.1% M/M in April (prev. +0.3%, cons. +0.3%).

• Australia's housing credit growth was 0.5% M/M in April, up from 0.4% in March.

• Australia's private sector credit expanded 0.7% M/M in April (prev. 0.5%, cons. 0.5%), with Y/Y growth accelerating to 6.7% (prev. 6.5%).

• Singapore's bank lending decreased to S$841.9 billion in April from S$846.5 billion in March.

Emerging Markets ex China

• The Philippines' trade deficit narrowed to $3.495 billion in April from $4.512 billion in March. Exports grew 7.0% Y/Y (prev. 8.7%), while imports fell 7.2% Y/Y (prev. +17.8%).

• The Philippines' PPI slowed to 0.1% Y/Y in March from 0.6% in February.

• Thailand's industrial production rose 2.17% Y/Y in April (prev. +0.05%, cons. -3.0%).

• Thailand's current account swung to a deficit of $1.5 billion in April from a $2.3 billion surplus in March.

• Thailand's private consumption fell 1.5% M/M in April (prev. -0.5%), while private investment rose 2.9% M/M (prev. -1.0%).

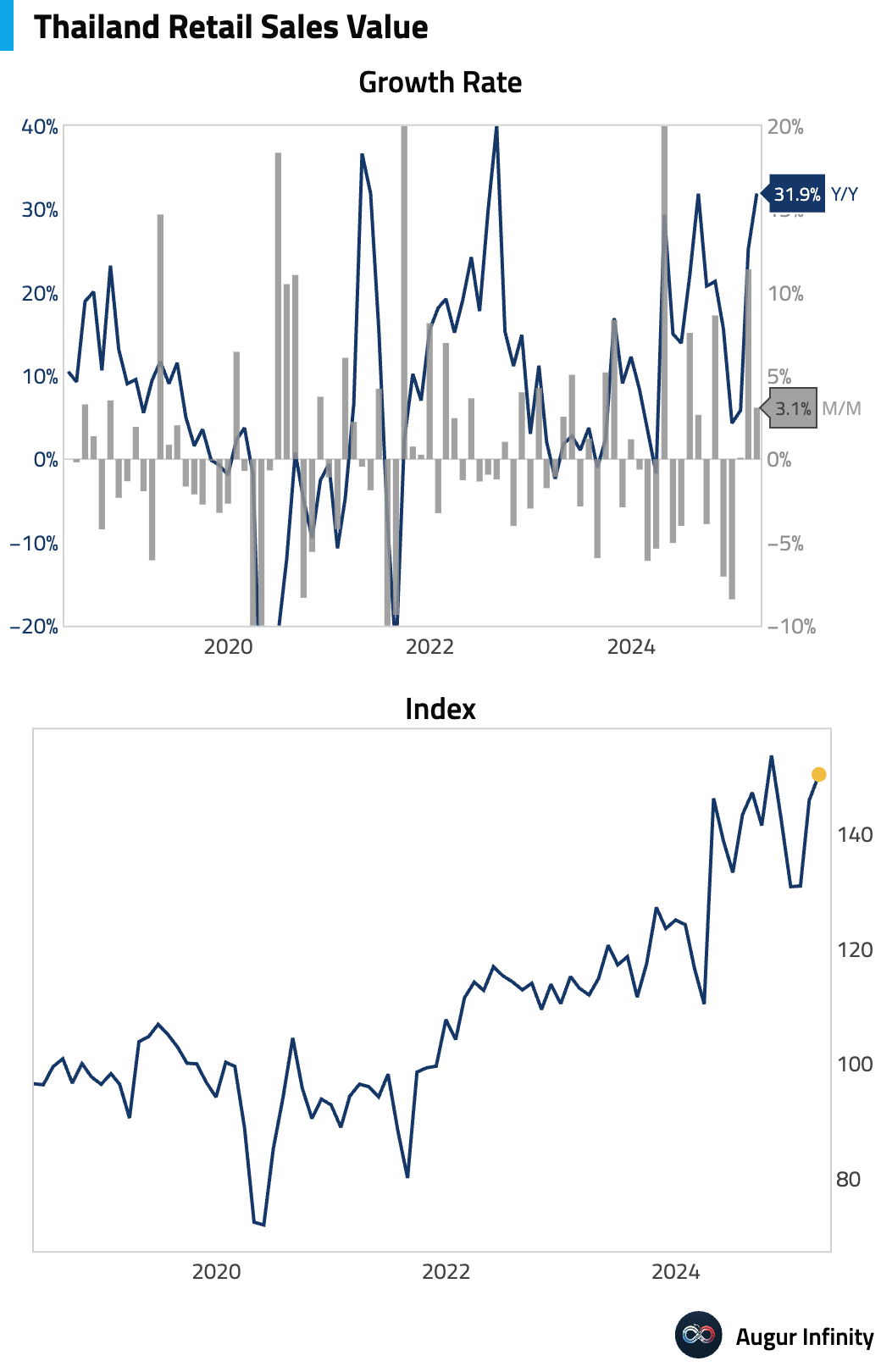

• Thailand's retail sales surged 31.9% Y/Y in April (prev. 25.2%), the highest since August 2022.

• South Africa's M3 money supply growth picked up to 6.12% Y/Y in April from 5.75% in March.

• South Africa's private sector credit growth accelerated to 4.6% Y/Y in April from 3.45% in March.

• South Africa's budget deficit widened to ZAR 64.63 billion in April from ZAR 13.11 billion in March.

• South Africa's trade surplus decreased to ZAR 14.08 billion in April from ZAR 22.65 billion in March.

• Malaysia's M3 money supply grew 3.2% Y/Y in March, up from 2.3% in February.

• India's GDP grew 7.4% Y/Y in Q1 2025 (fiscal Q4 2024-25), accelerating from 6.4% in the previous quarter and beating consensus of 6.7%.

• India's foreign exchange reserves rose to $692.72 billion as of May 23 from $685.73 billion the prior week.

• India's central government budget deficit was INR 1.86 trillion in April, the first month of the new fiscal year, compared to a INR 15.77 trillion deficit in March.

• Brazil's nominal budget deficit narrowed to BRL 55.54 billion in April from BRL 71.62 billion in March, better than the consensus for a BRL 58.1 billion deficit. Gross debt to GDP edged up to 76.2% from 75.9%.

• Brazil's Q1 GDP grew 1.4% Q/Q (prev. 0.1%), with Y/Y growth at 2.9% (prev. 3.6%, cons. 3.2%).

• Mexico's unemployment rate rose to 2.5% in April from 2.2% in March, matching consensus.

• Russia's M2 money supply growth slowed to 14.0% Y/Y in April from 17.0% in March.

Equities

• US equity markets (-0.01%) were little changed, with the Nasdaq down slightly (-0.32%). Emerging markets (-1.2%) saw broader declines, notably in China (-1.7%), South Korea (-1.9%), Mexico (-1.7%), and Brazil (-1.8%). European markets were mixed, with Germany (+0.3%) and the UK (+0.3%) up, while France (-0.6%) declined. Australia (+0.7%) and Canada (+0.4%) posted gains.

Fixed Income

• US Treasury yields fell across the curve. The 2-year yield decreased by 3.6 bps, the 5-year yield by 3.4 bps, the 10-year yield by 2.5 bps, and the 30-year yield by 0.1 bps.

FX

• The US dollar was mixed against G10 currencies. The Canadian dollar (+0.4%) and Swiss franc (+0.3%) gained against the USD. The Norwegian krone (-0.9%) and Swedish krona (-0.5%) weakened most significantly. The Euro and British pound were little changed.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.