Headlines

- President Trump reportedly sent letters to major drug manufacturers requesting a reduction in prices for medicines sold in the United States.

- Japan’s Labor Ministry Council indicated its expectation for a 6 percent increase in the national average minimum wage.

Global Economics

United States

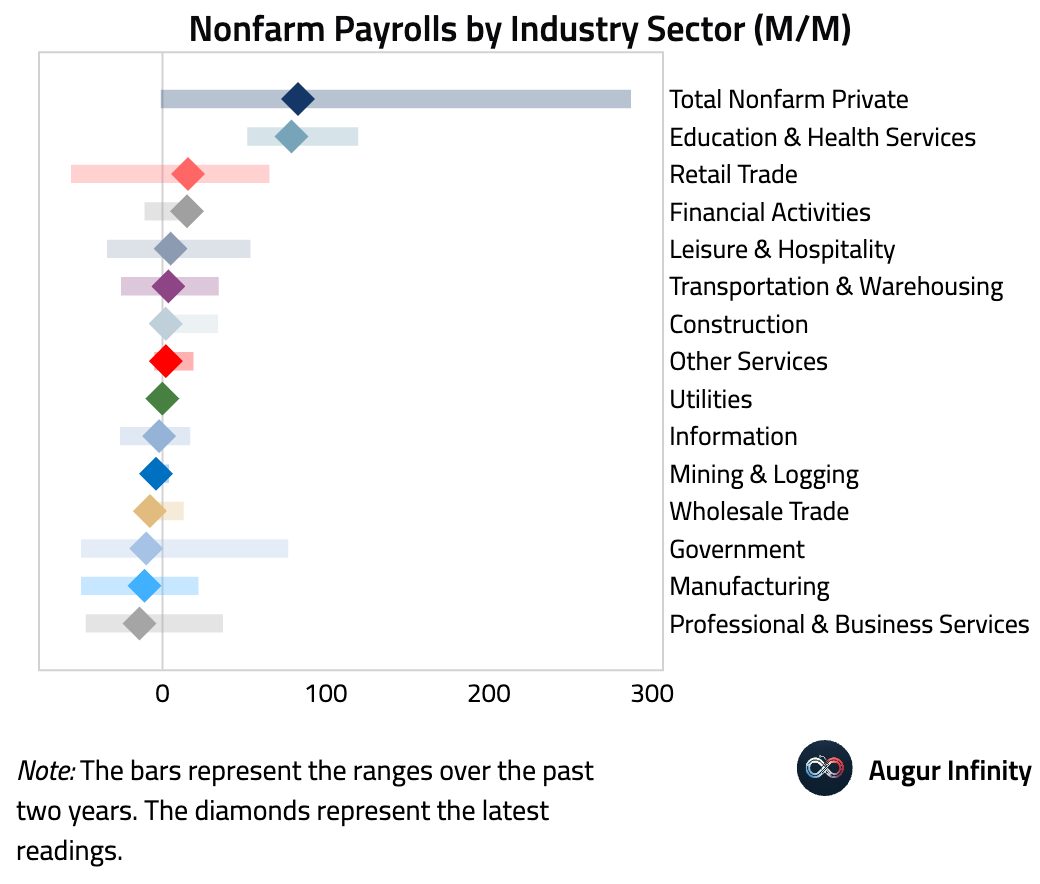

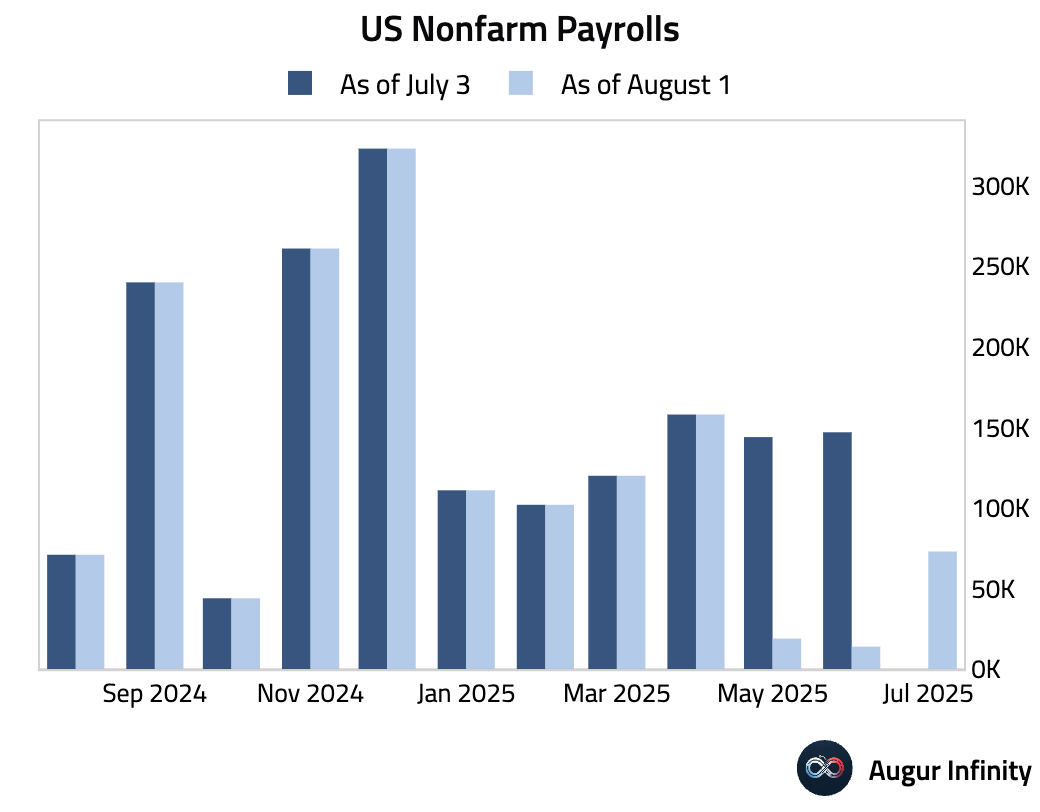

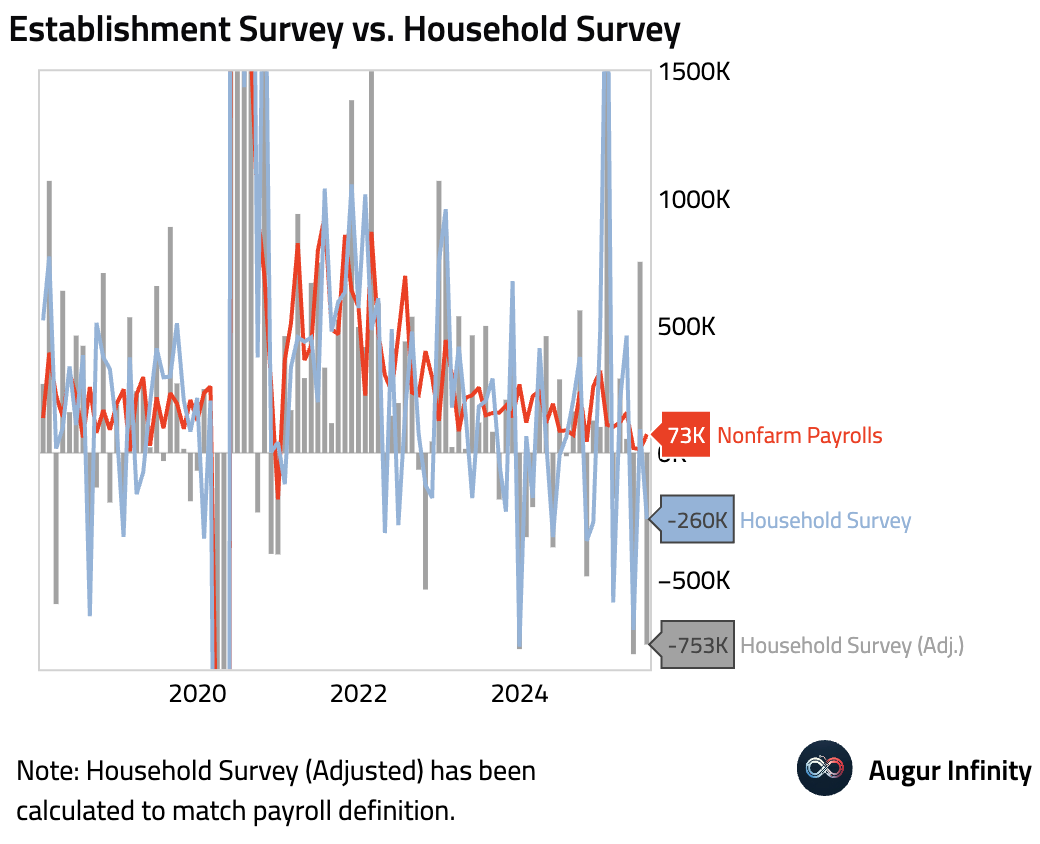

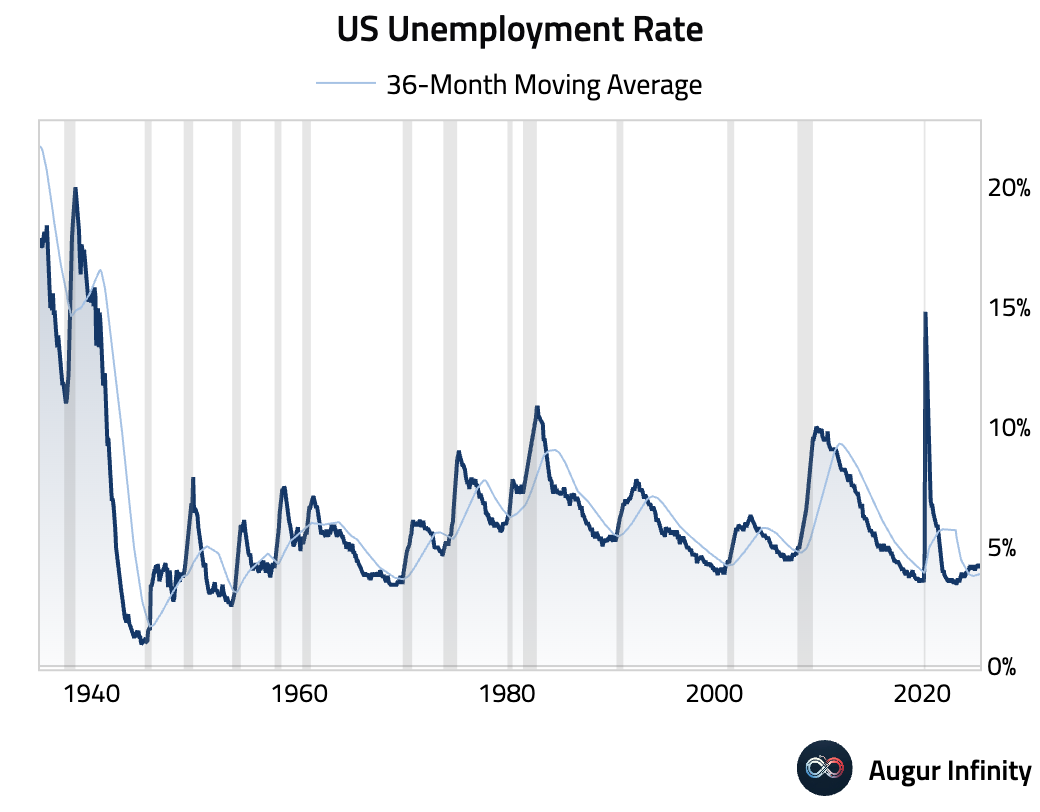

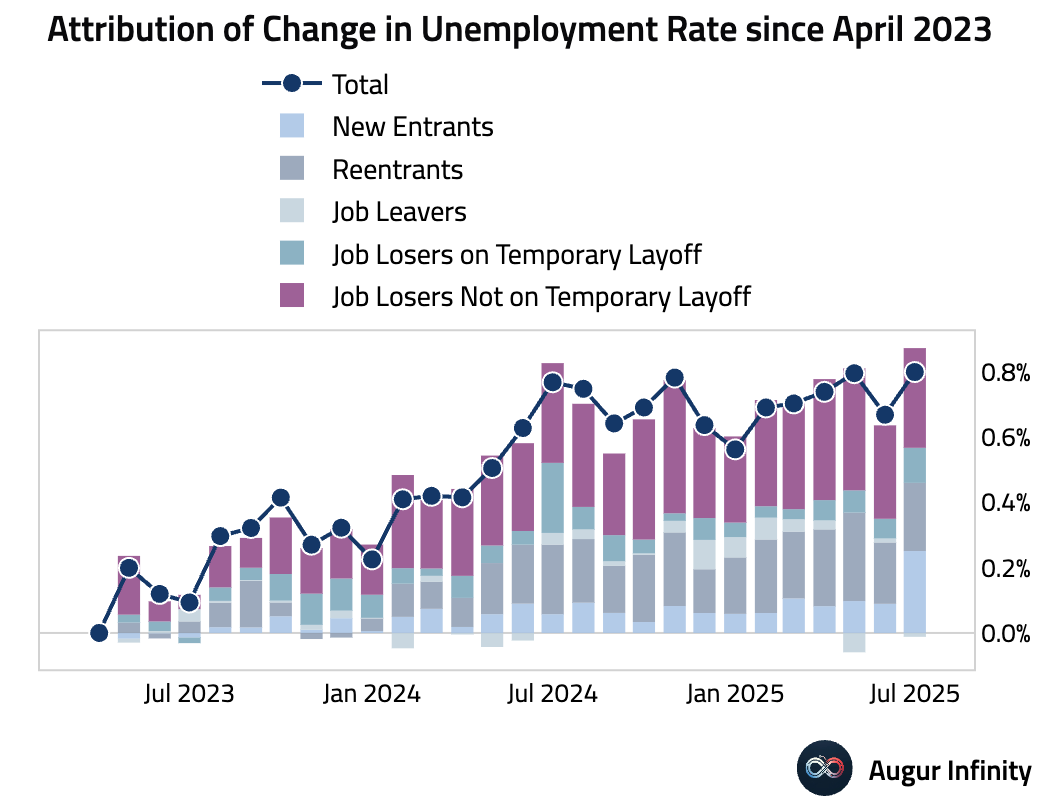

- The July jobs report indicated a significant labor market deceleration. Nonfarm Payrolls rose by only 73k, substantially missing the 110k consensus, and there was a massive -258k cumulative downward revision to the prior two months. The unemployment rate increased to 4.2% from 4.1%, its highest level since October 2021. Job growth was narrow, with the entire net gain coming from healthcare (+73k), slowing the underlying pace of job growth to an estimated 28k. The labor force participation rate edged down to 62.2%.

- The unemployment rate rose to 4.2%, its highest since October 2021.

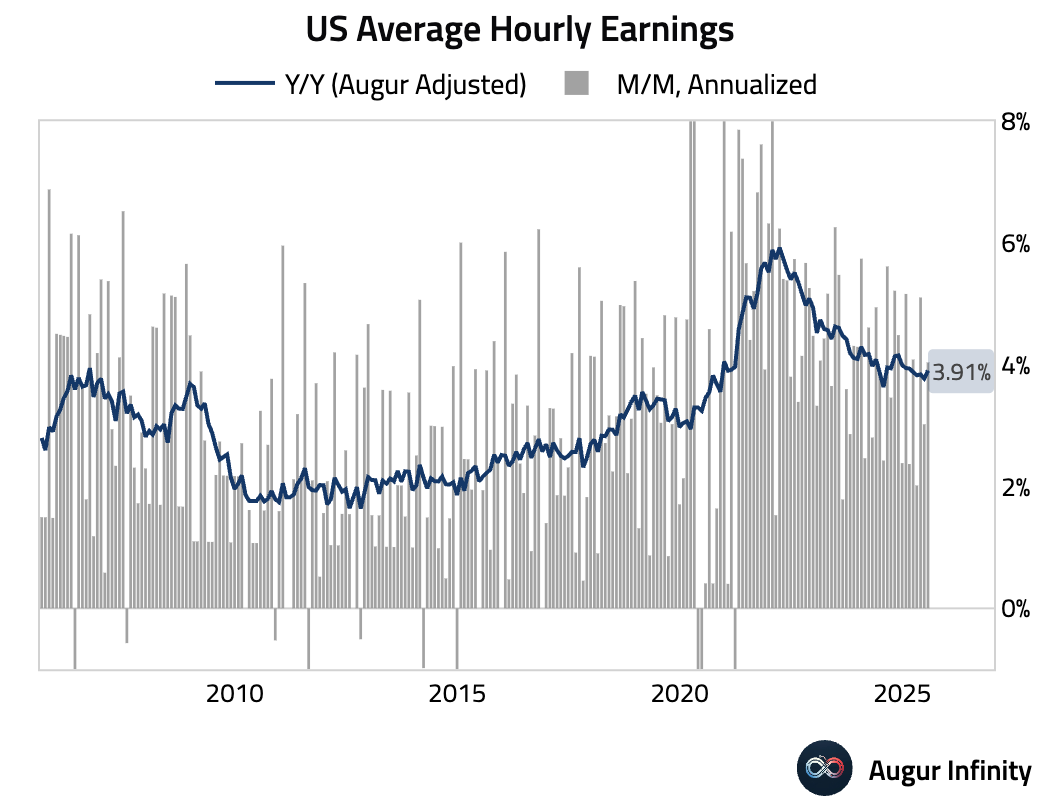

- Average Hourly Earnings rose 0.3% M/M in July, in line with consensus. The year-over-year figure accelerated slightly to 3.9%, beating the 3.8% forecast.

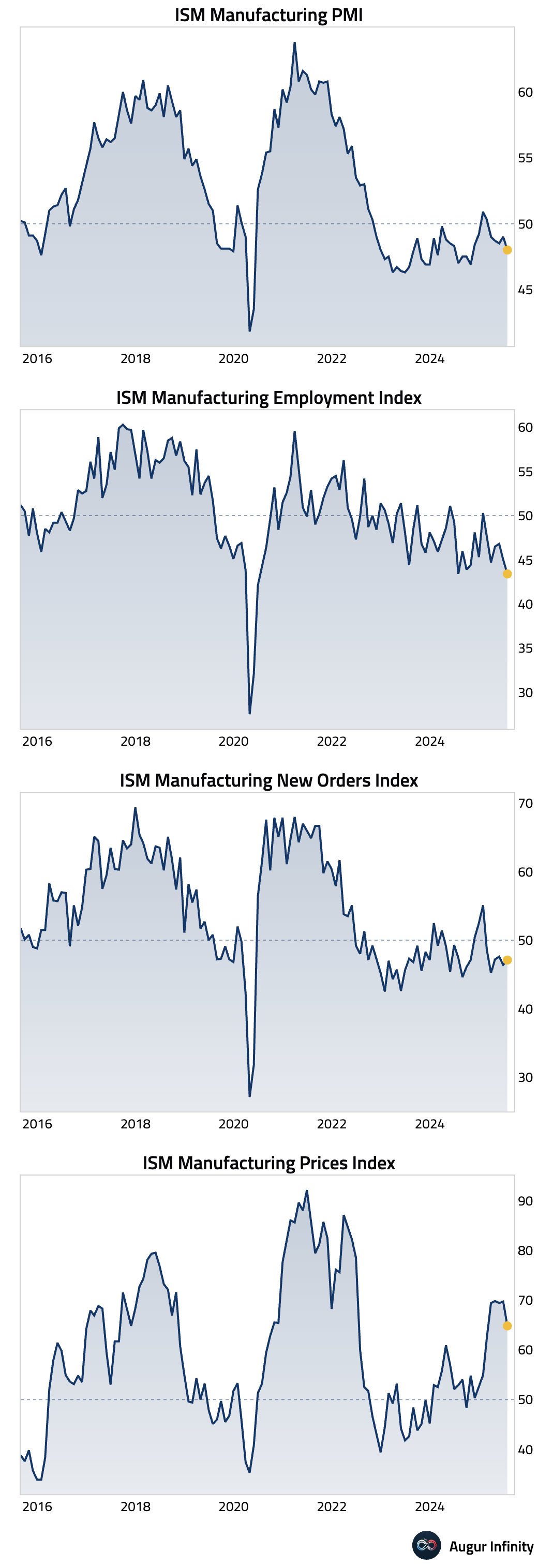

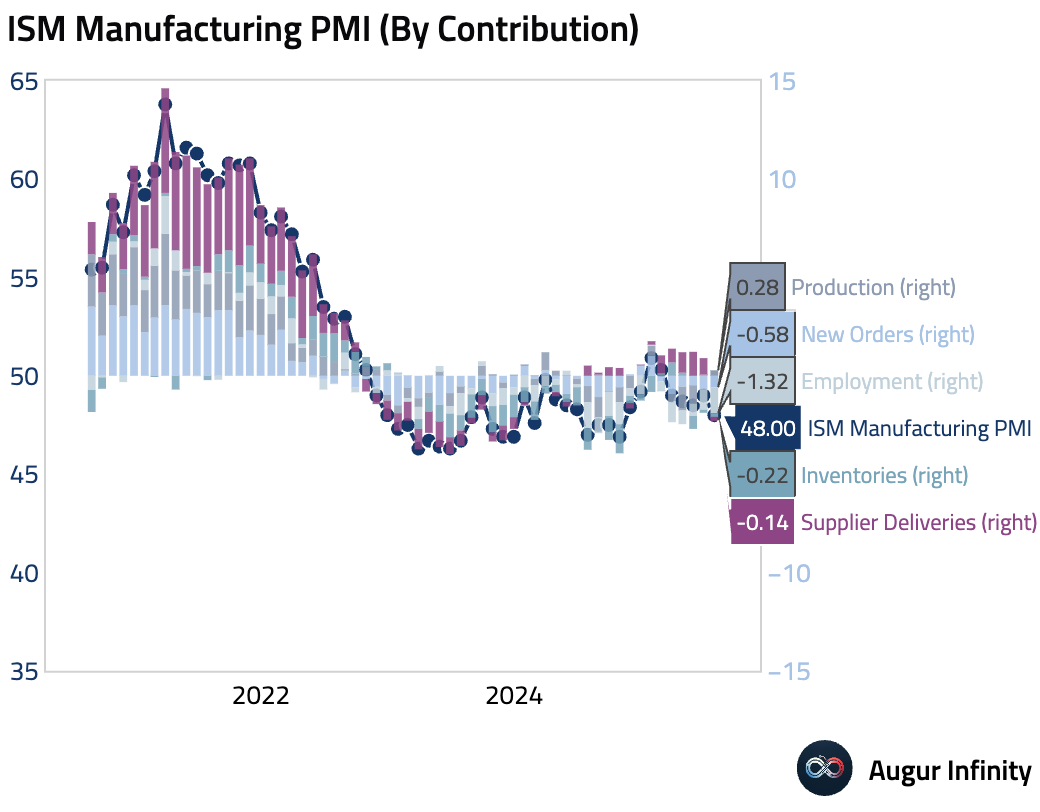

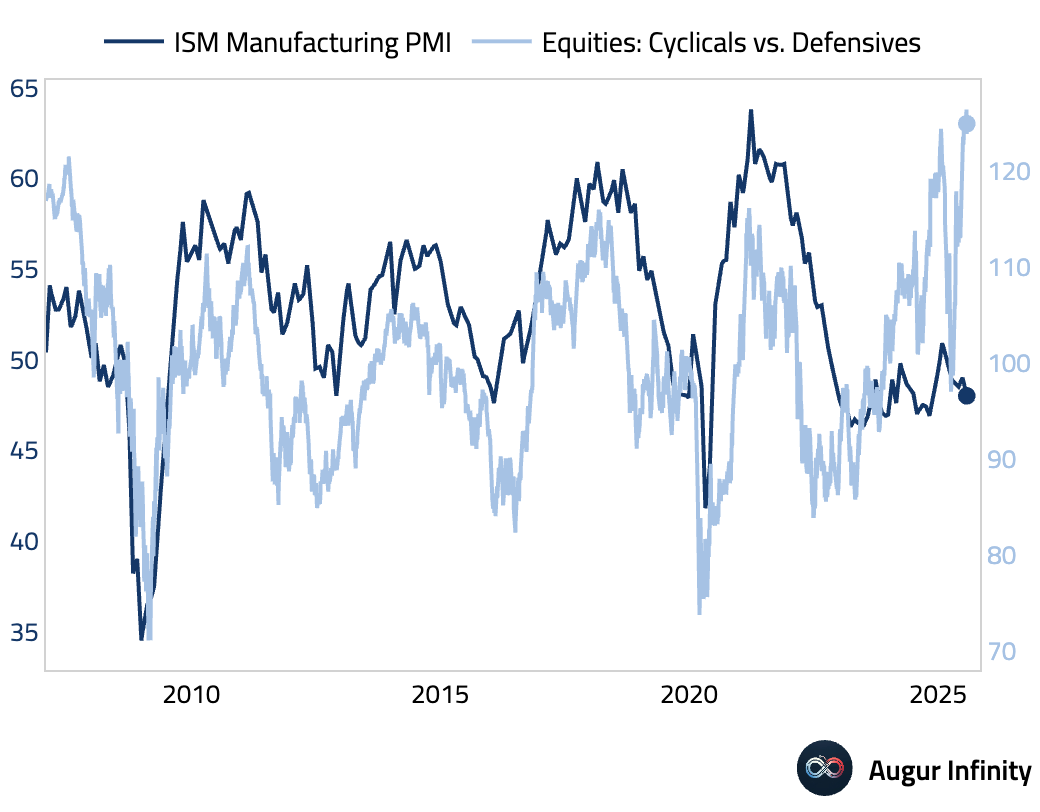

- The ISM Manufacturing PMI fell to 48.0 in July, well below the 49.5 consensus and down from 49.0 in June, marking its weakest reading since October 2024. While new orders (47.1) and production rose, a sharp 1.6-point drop in the employment sub-index to 43.4 drove the headline miss. The prices paid component also eased to 64.8 from 69.7. Respondents noted impacts from tariffs and anticipate higher expenses in the coming quarters.

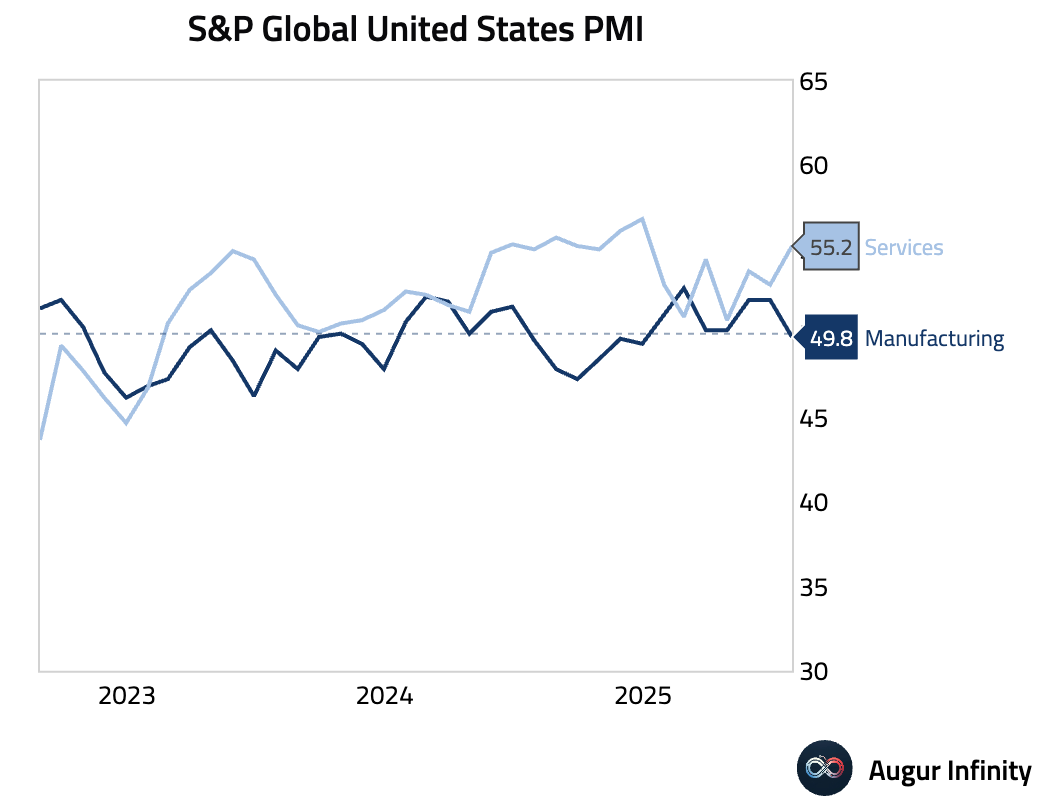

- The final S&P Global Manufacturing PMI for July fell into contraction at 49.8, a sharp decline from June’s 52.9 and the first sub-50 reading of the year. The drop was driven by stagnating new orders amid tariff uncertainty and firms destocking after previously front-running tariff hikes. The employment component was revised down, confirming a theme of weaker factory hiring.

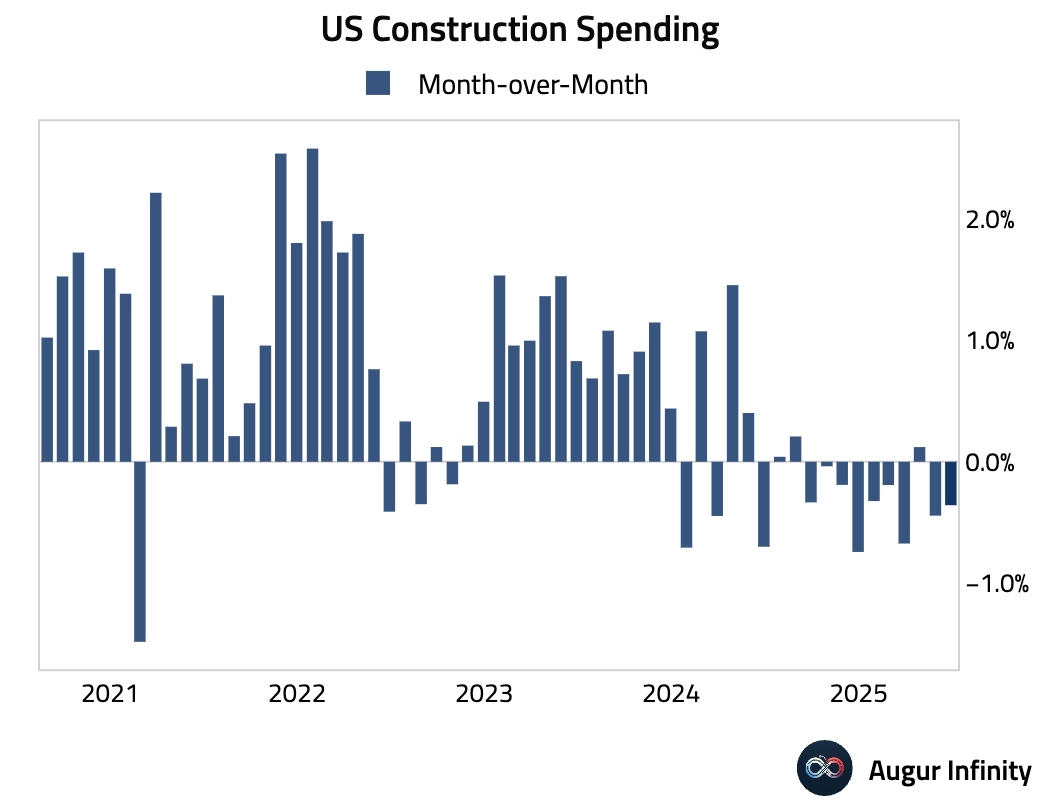

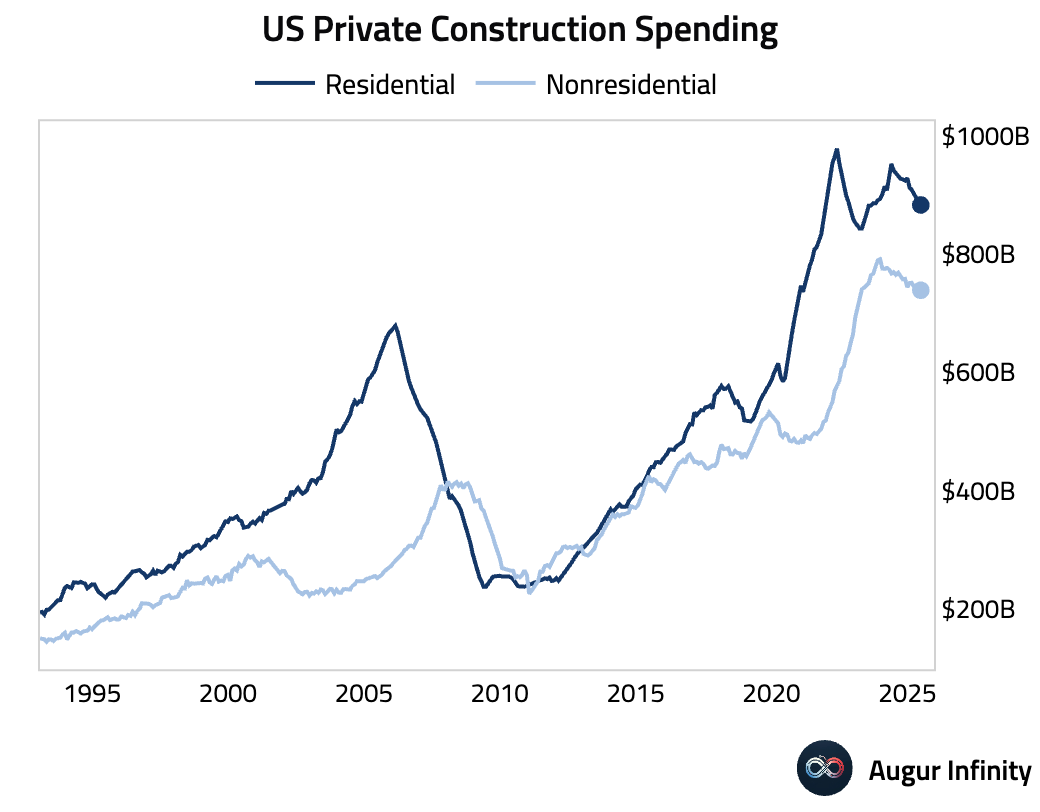

- Construction spending fell 0.4% M/M in June, missing the flat forecast and marking the second consecutive monthly decline. The weakness was driven by both private residential (-0.7%) and nonresidential (-0.3%) spending. In real terms, spending fell by an even larger 0.6%.

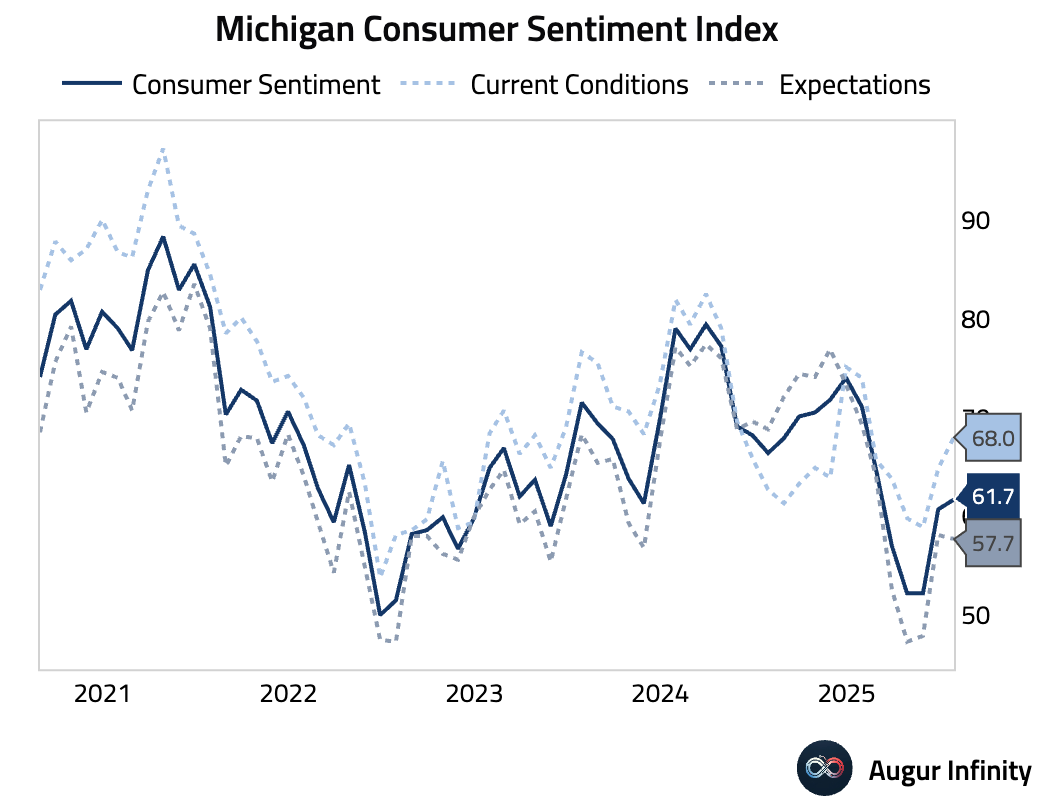

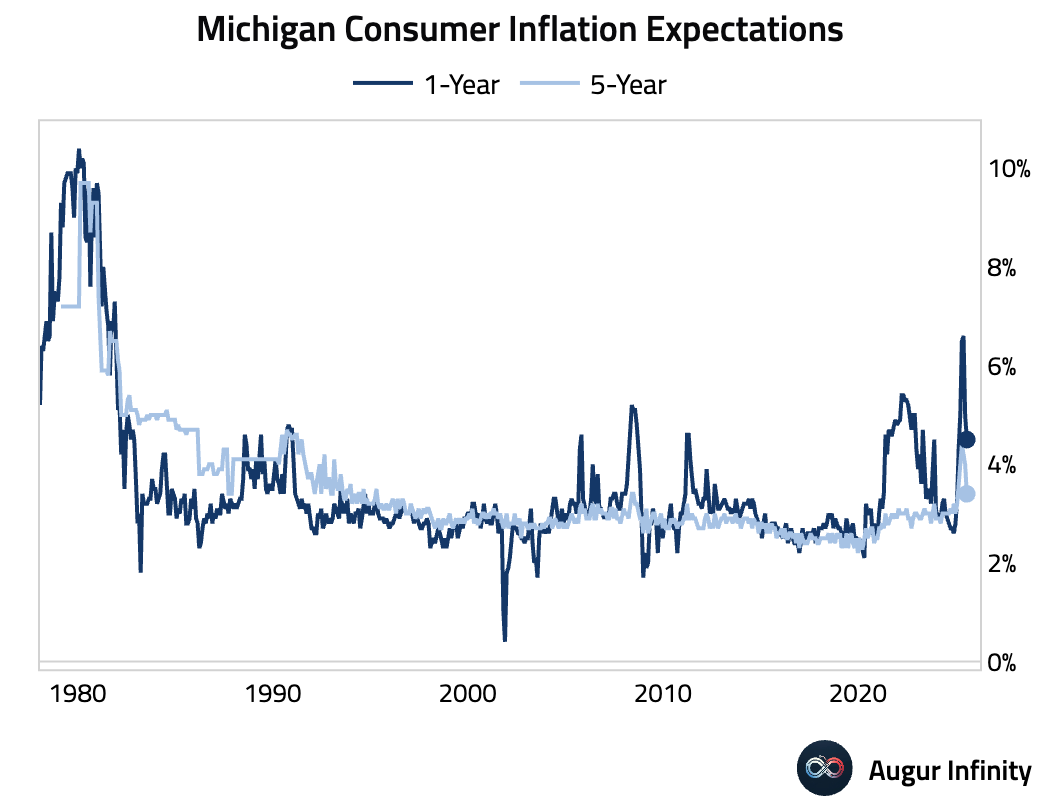

- The final University of Michigan Consumer Sentiment index for July registered 61.7, a modest improvement from 60.7 but slightly below the 62.0 consensus. The Current Conditions component rose to 68.0, its strongest reading since January 2025, while the Expectations index fell to 57.7. Inflation expectations eased, with the 1-year outlook falling to 4.5% and the 5-year outlook at 3.4%.

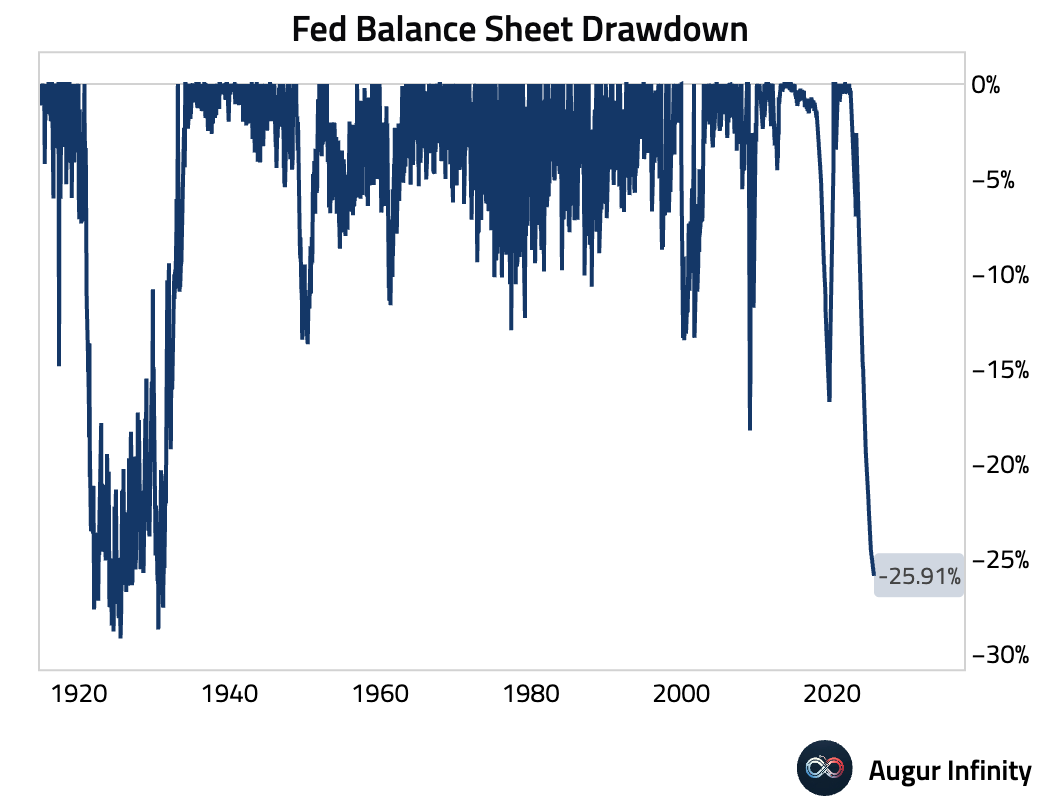

- The Fed’s balance sheet continued its drawdown, falling to $6.64 trillion from $6.66 trillion in the prior week.

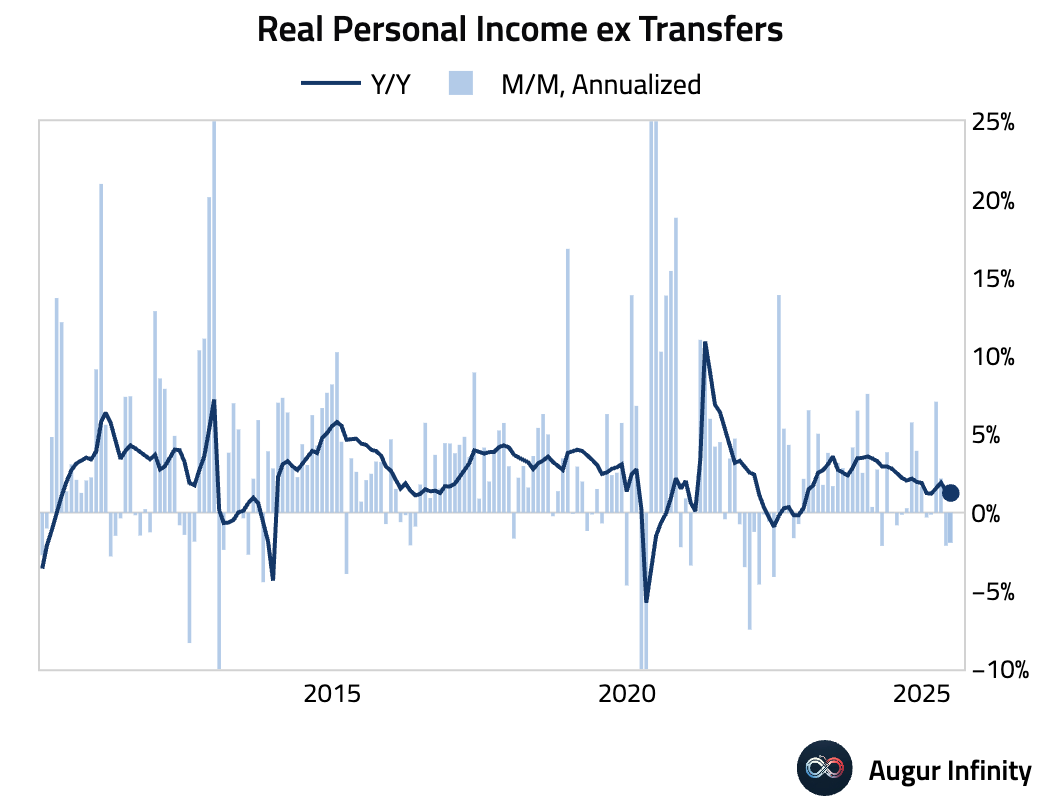

- Excluding transfers, real personal income has declined for two consecutive months.

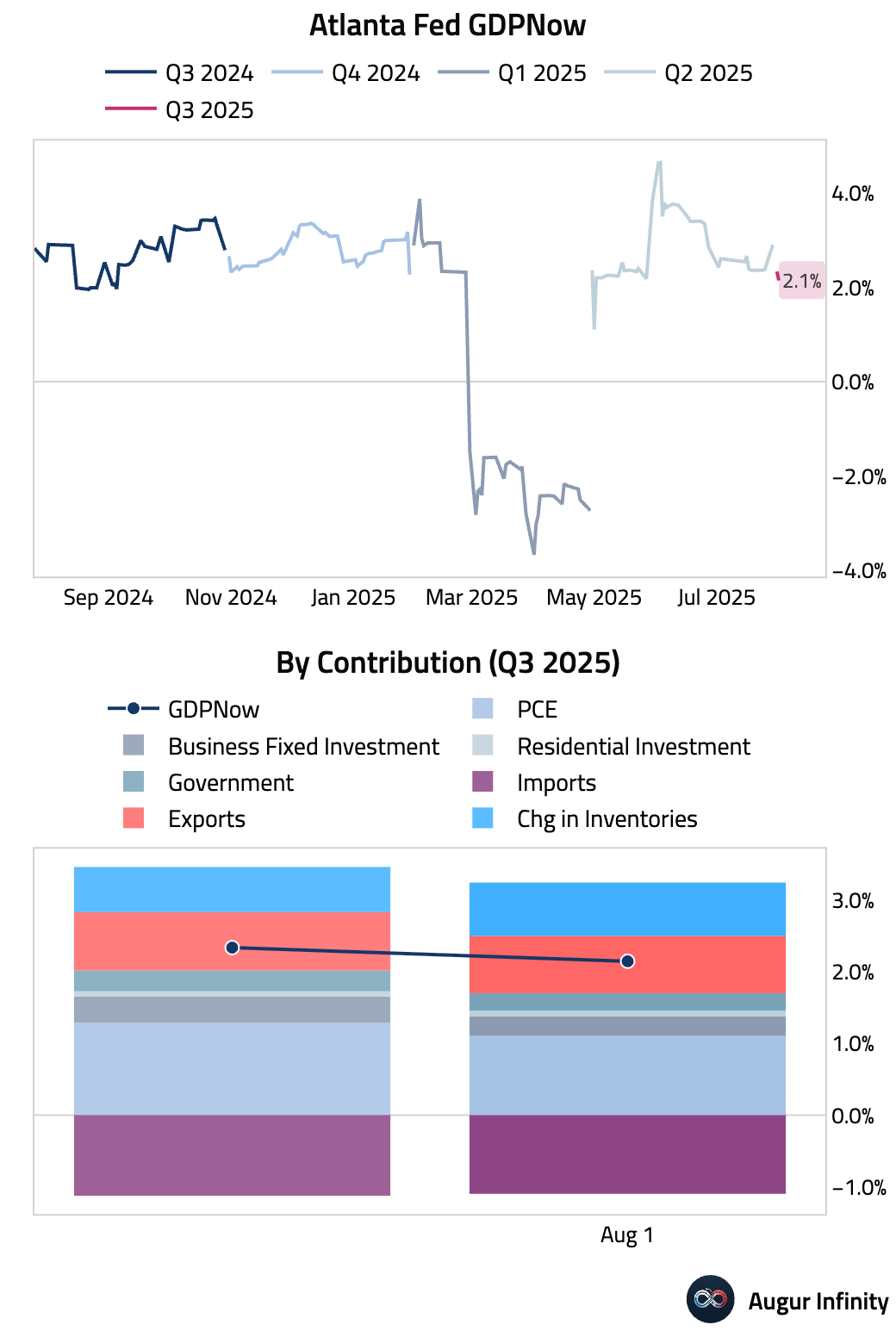

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 2.1%, down from 2.3% yesterday.

Canada

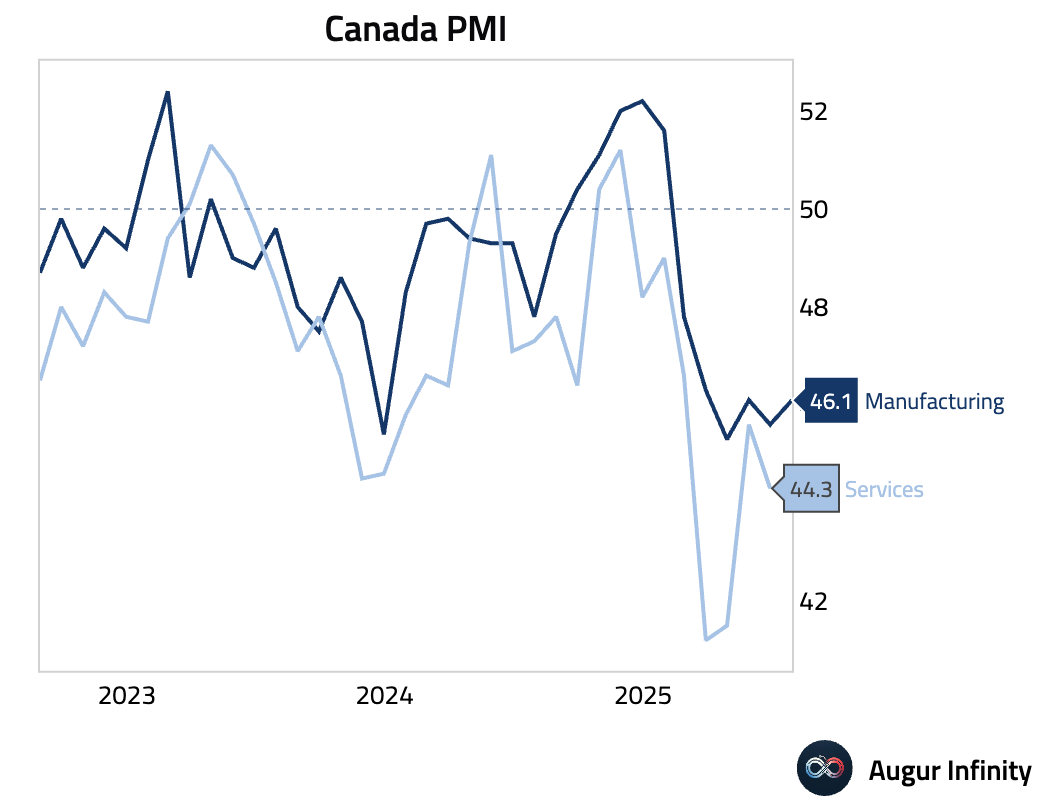

- Canada's S&P Global Manufacturing PMI rose to 46.1 in July from 45.6 but marked its sixth consecutive month of contraction. The persistent weakness was driven by US tariffs hurting demand and new export orders. In response, firms are aggressively destocking, with inventories falling at the fastest rate since 2020, and cutting employment.

Europe

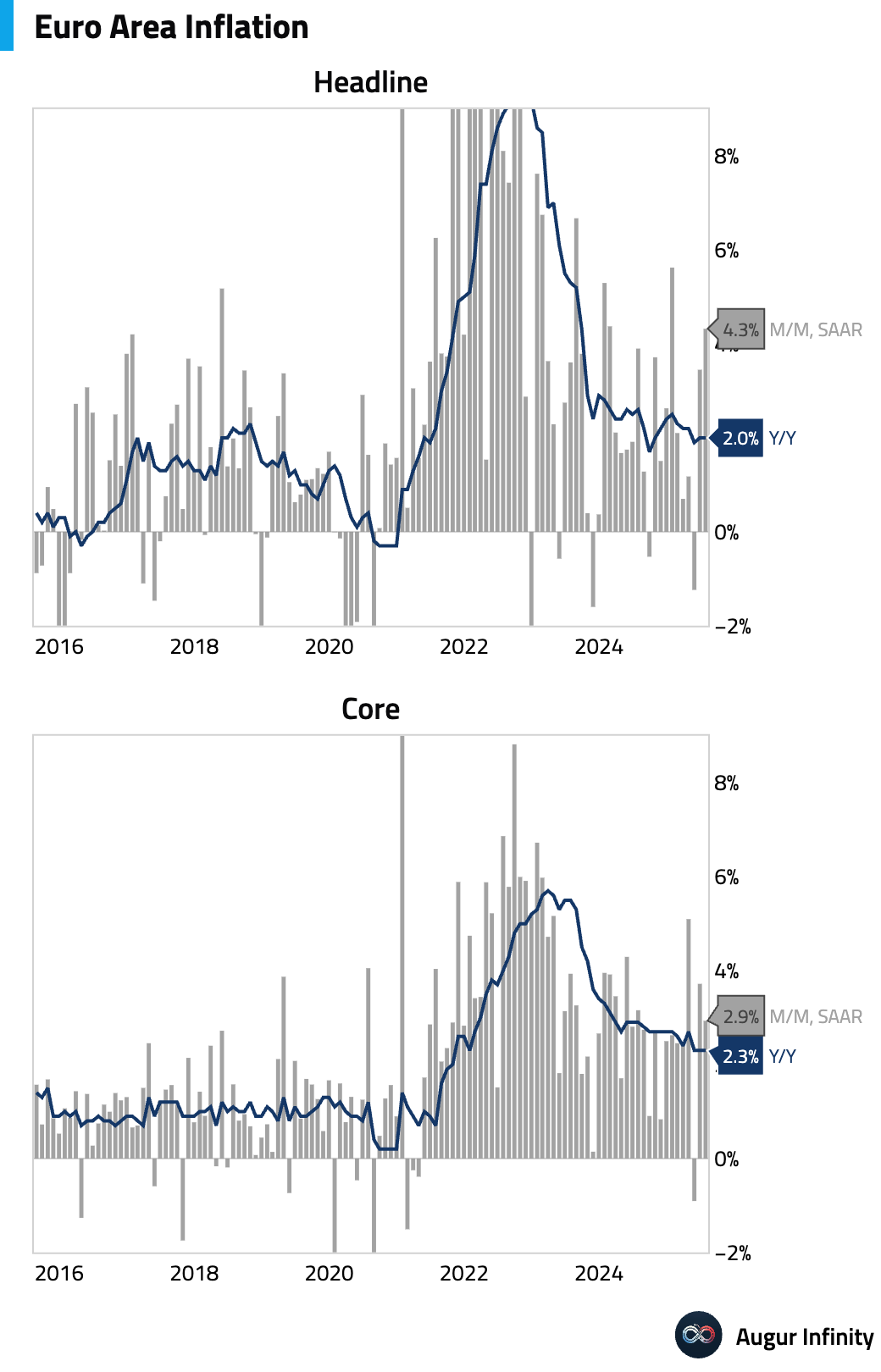

- The Eurozone’s flash inflation rate for July held steady at 2.0% Y/Y, slightly above the 1.9% consensus. The core rate also remained unchanged at 2.3% Y/Y, its lowest since October 2021, driven by slowing services inflation that was nearly offset by a surprisingly strong core goods print. Higher food and energy prices drove the headline beat. Inflation is expected to hover around the 2% target until year-end.

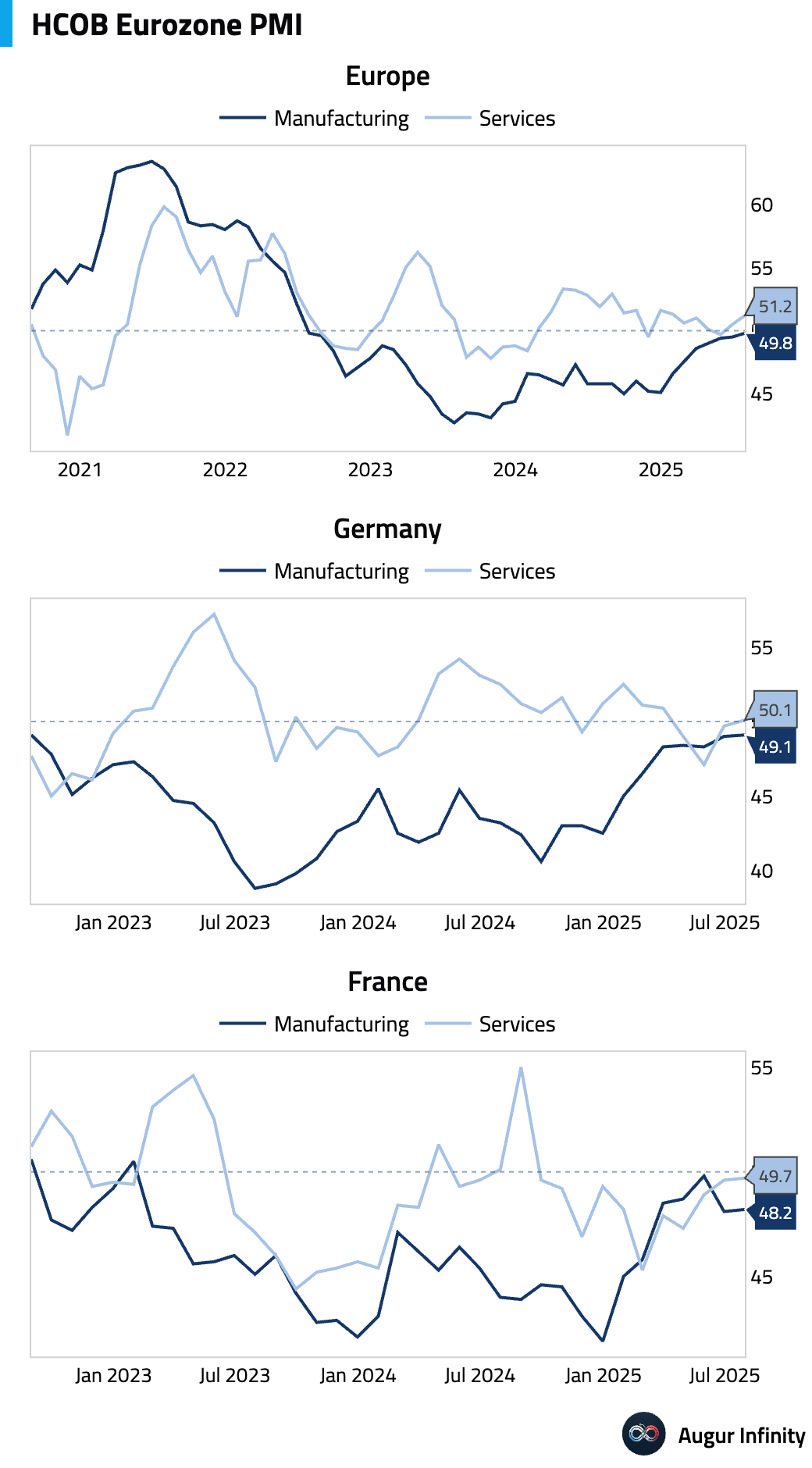

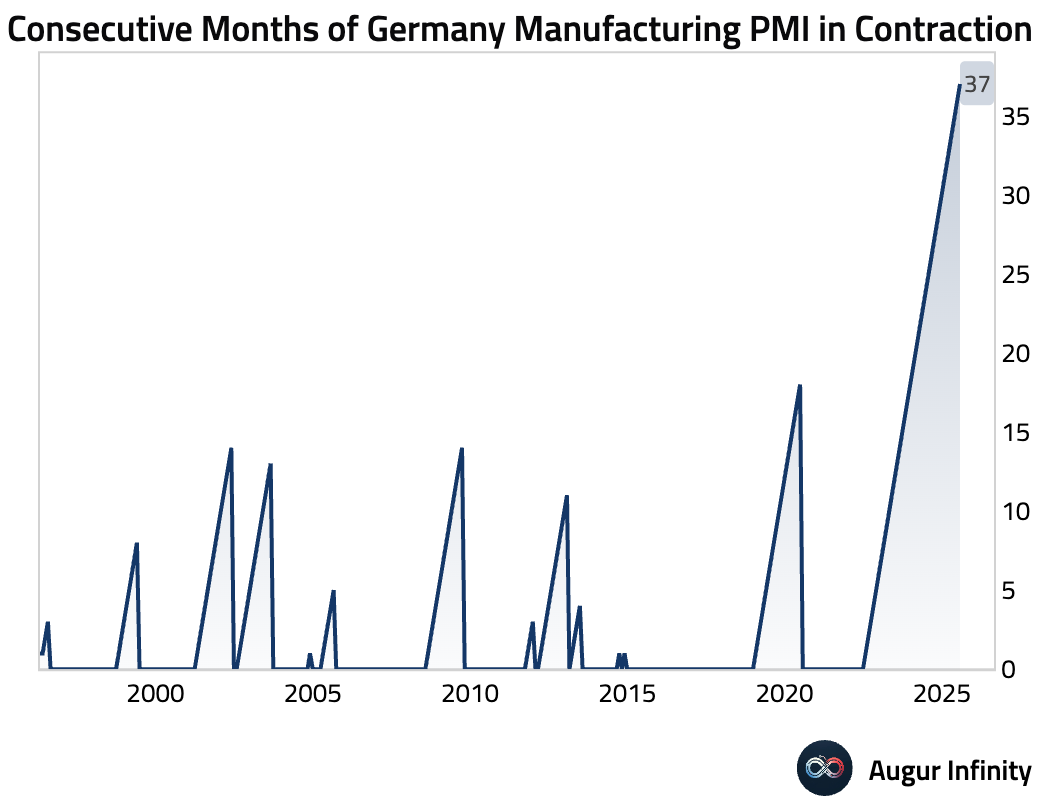

- The final HCOB Manufacturing PMIs for July showed a mixed picture. The Eurozone aggregate rose to a 36-month high of 49.8, nearing stabilization, but this masked underlying weakness as new export orders declined. Germany's PMI hit a 35-month high of 49.1, but upturns in output and new orders lost momentum. France's PMI edged up to 48.2, but the reading was artificially boosted by lengthening supplier delivery times, while new orders fell at the fastest pace since January.

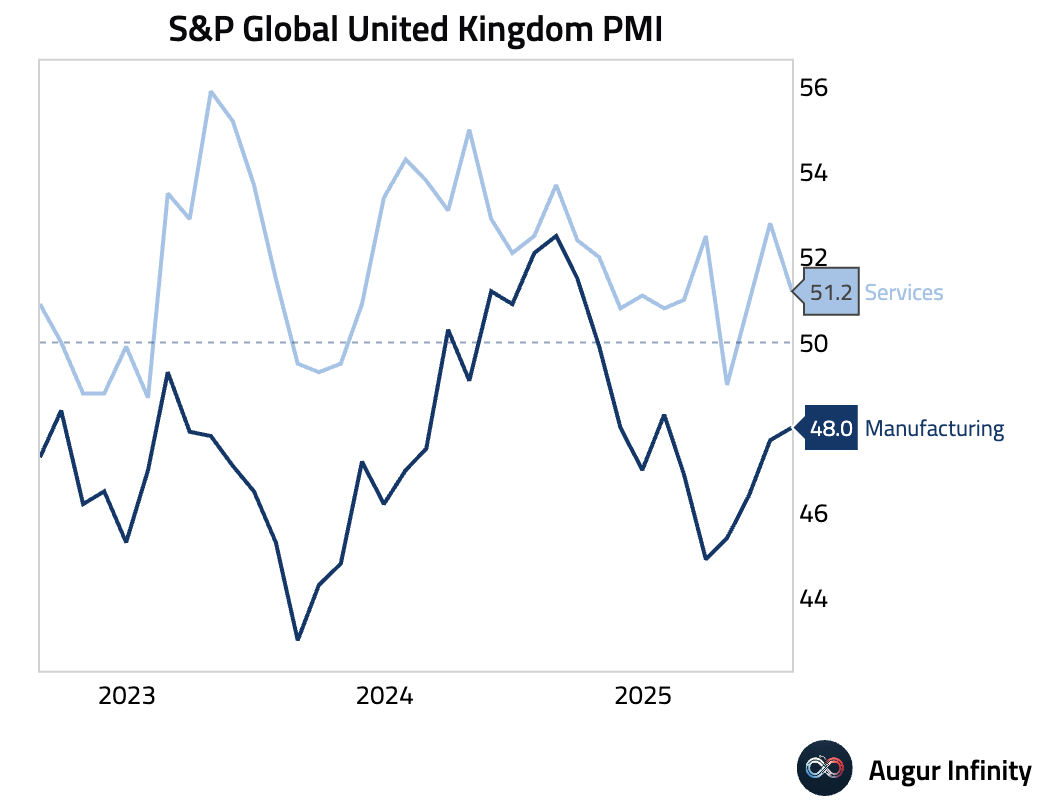

- The UK's final S&P Global Manufacturing PMI rose to a six-month high of 48.0 in July but remained in contraction for the tenth straight month. While the output decline slowed, new orders fell faster. Employment dropped more sharply as firms cited weak demand and the impact of government policy changes on hiring.

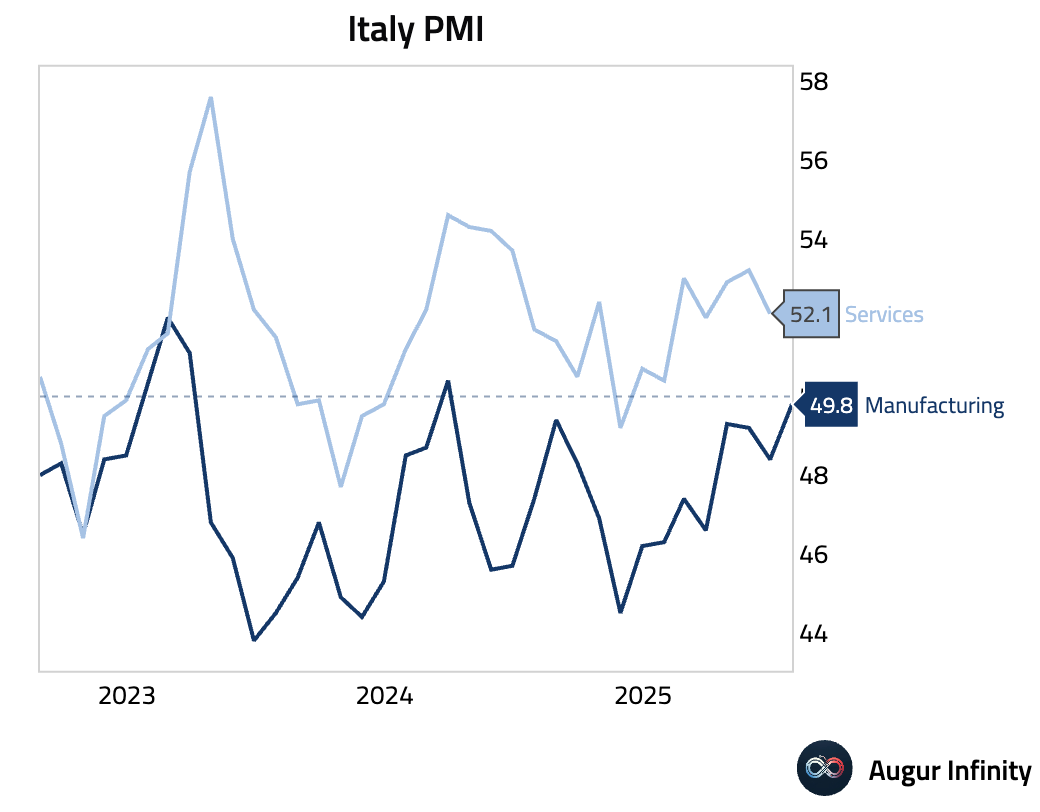

- Italy's HCOB Manufacturing PMI rose to 49.8 in July, beating the 49.0 consensus and reaching its highest level since March 2024. The near-stabilization was notable for a significant shift in inventory management, as firms increased input stocks for the first time in nearly three years, suggesting the downturn may be bottoming.

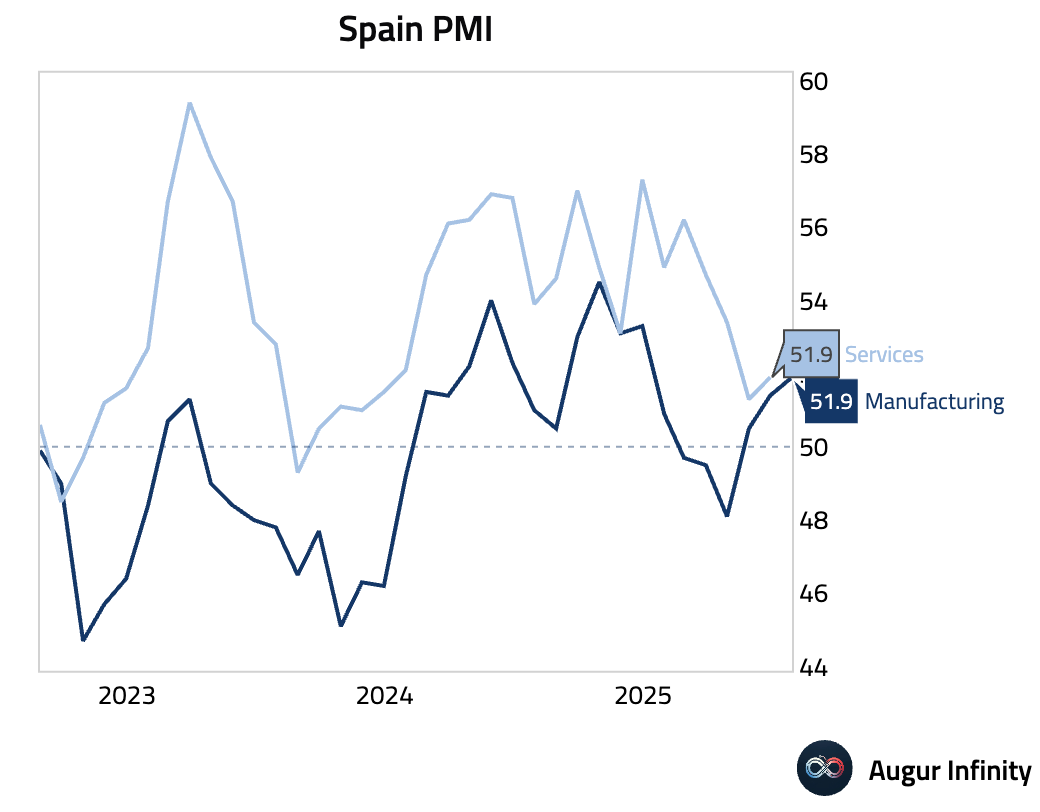

- Spain's HCOB Manufacturing PMI hit a 2025 high of 51.9 in July, exceeding the 51.5 forecast. Production and new orders showed solid growth. However, firms are showing caution by cutting purchases and drawing down inventories amid weakening business confidence.

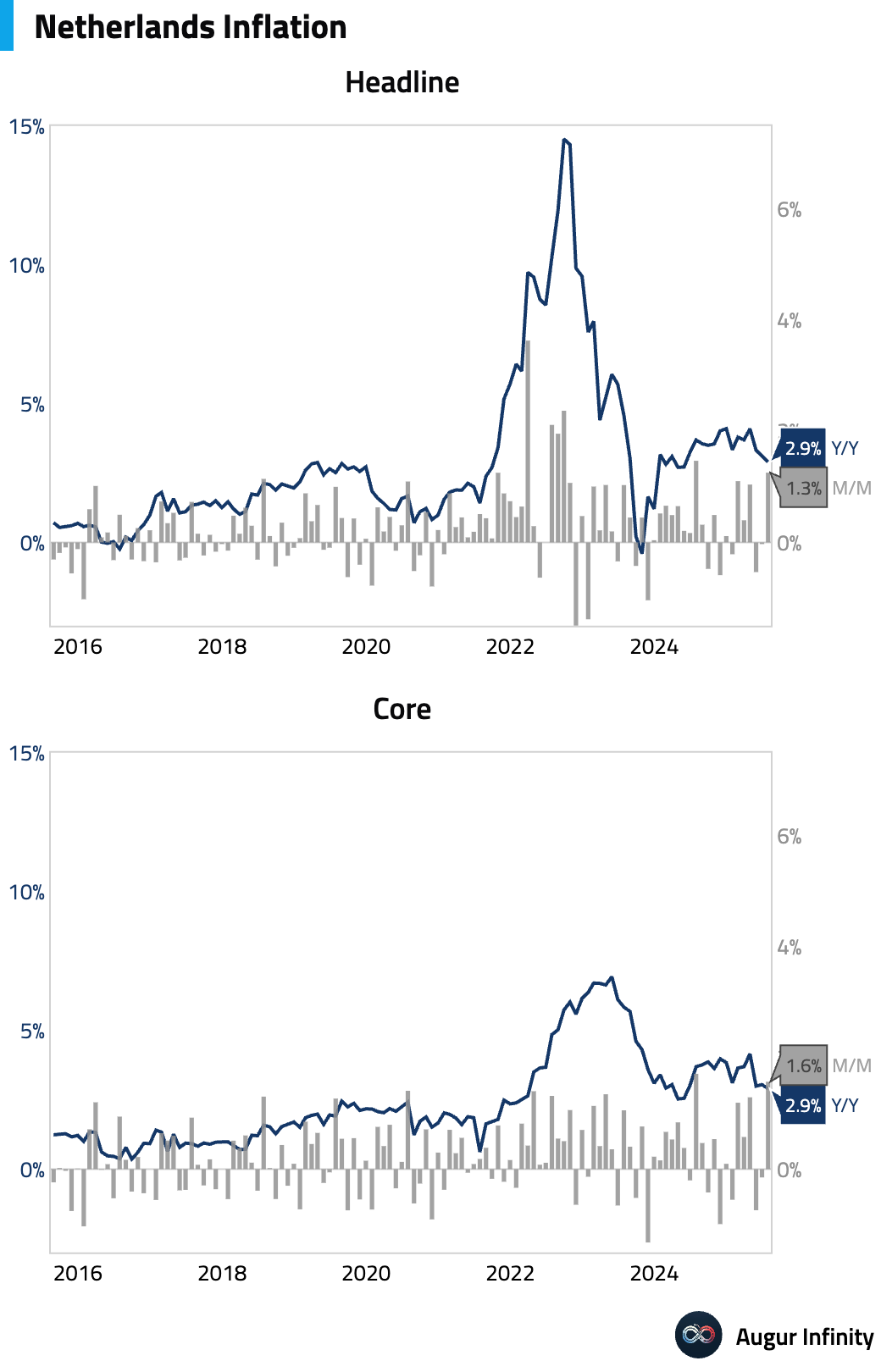

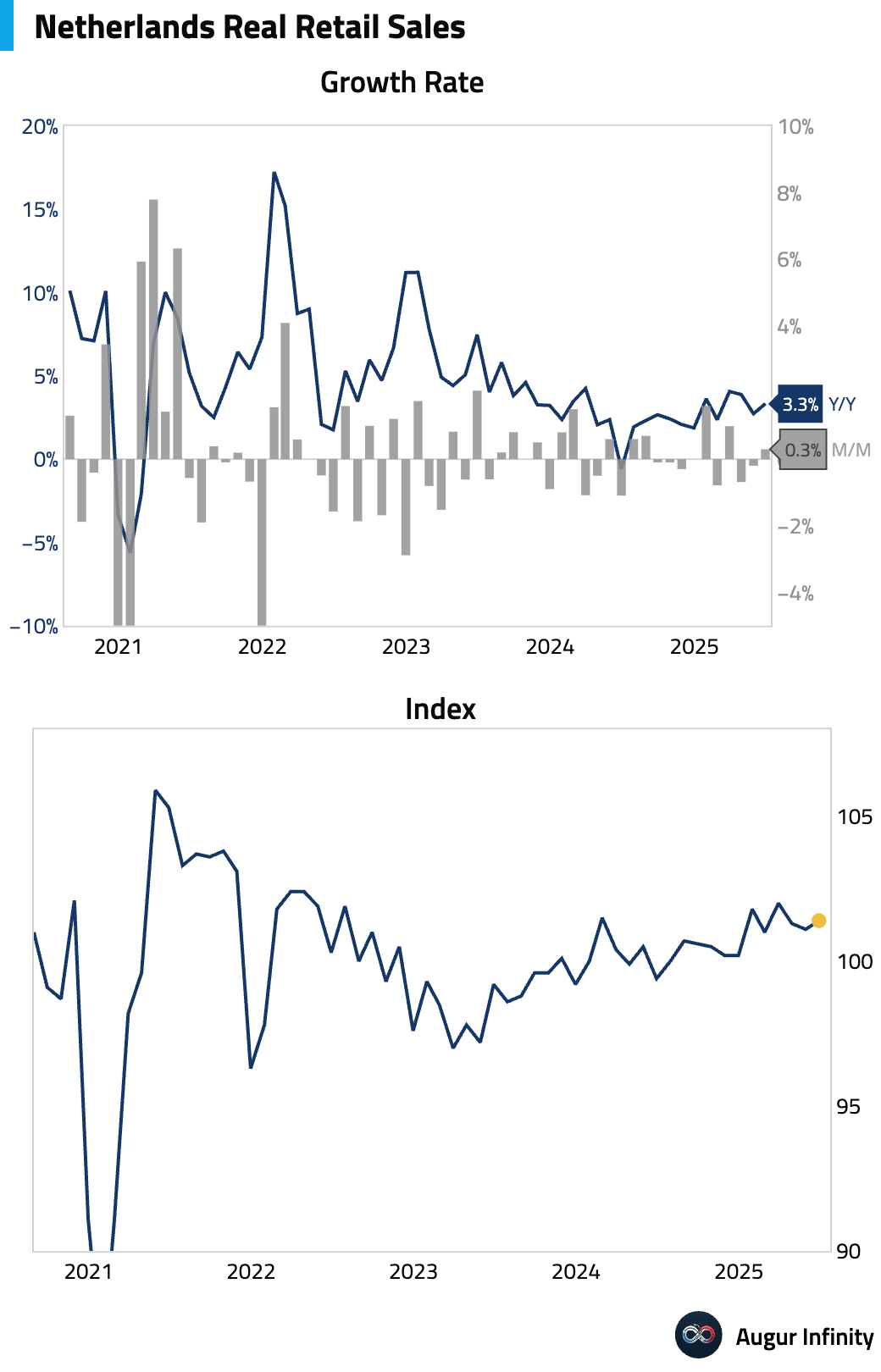

- Dutch preliminary CPI for July eased to 2.9% Y/Y from 3.1%, the lowest since May 2024. Separately, June retail sales rose 3.3% Y/Y, up from 2.7%.

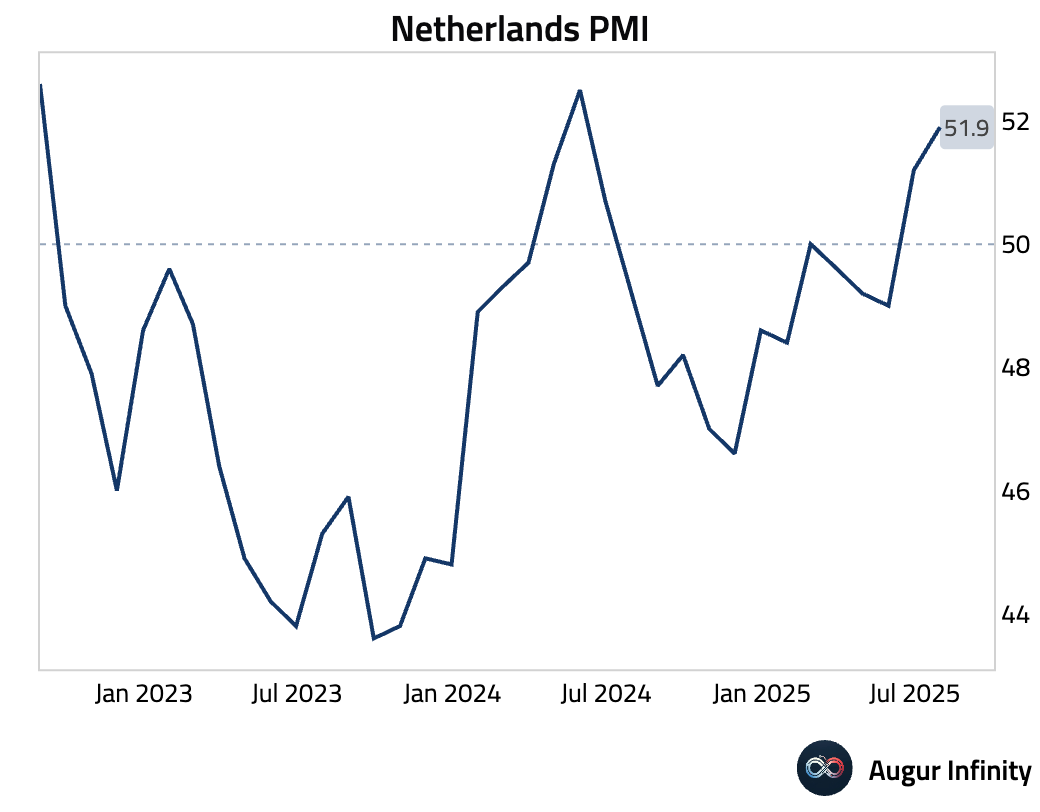

- The Netherlands' NEVI Manufacturing PMI rose to a 14-month high of 51.9 in July, driven by a sharp increase in new orders and the first rise in purchasing activity in nearly three years.

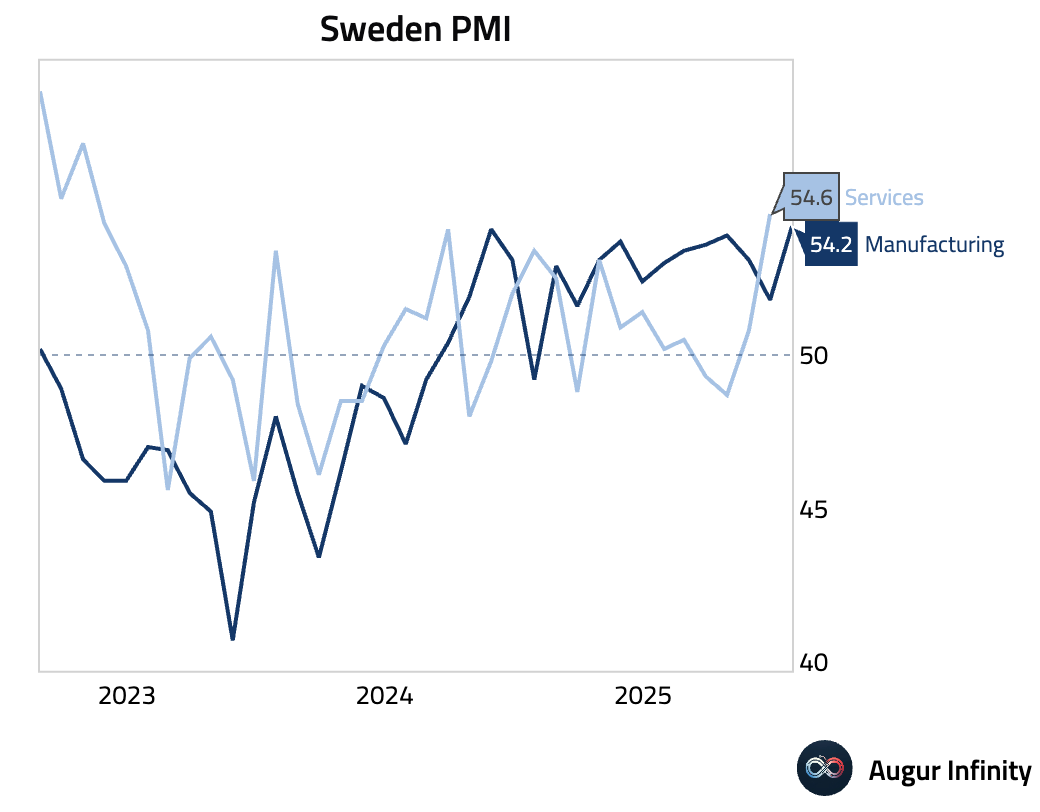

- Sweden's Swedbank Manufacturing PMI jumped to 54.2 in July from 51.8, its highest level since May 2022.

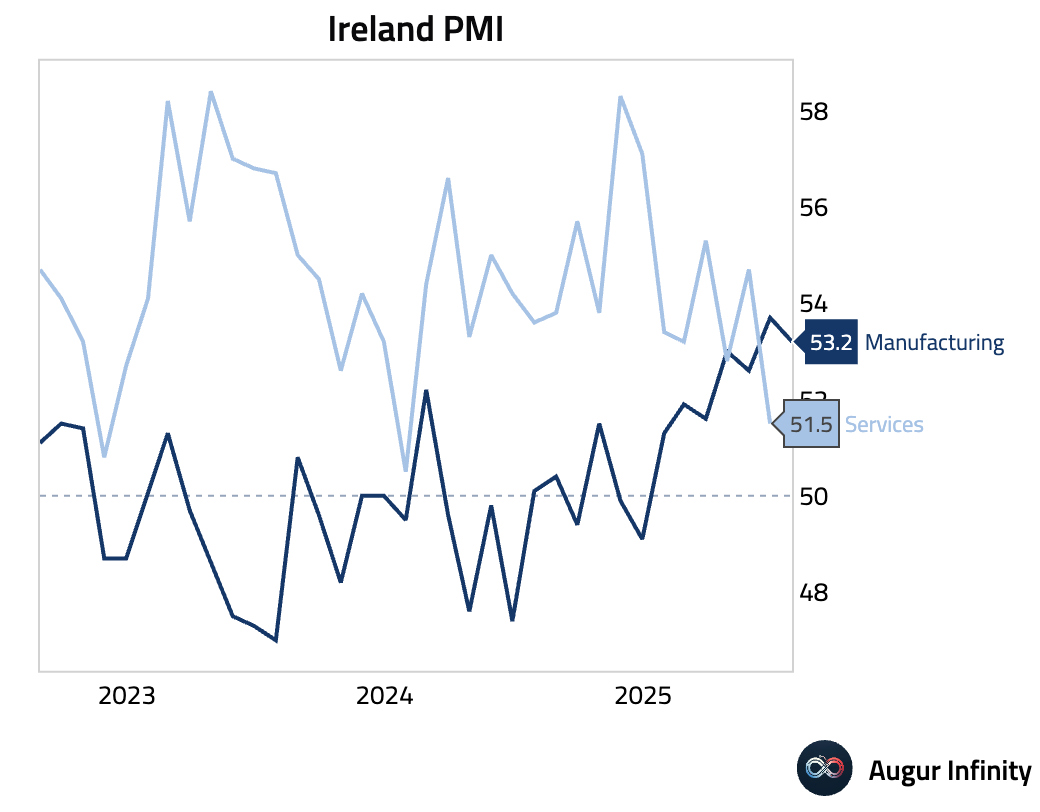

- Ireland’s AIB Manufacturing PMI eased to 53.2 in July but signaled a solid expansion for the seventh straight month. Output growth accelerated, but new orders expanded at the slowest pace since February. Backlogs of work increased for the first time since February, pointing to operational bottlenecks.

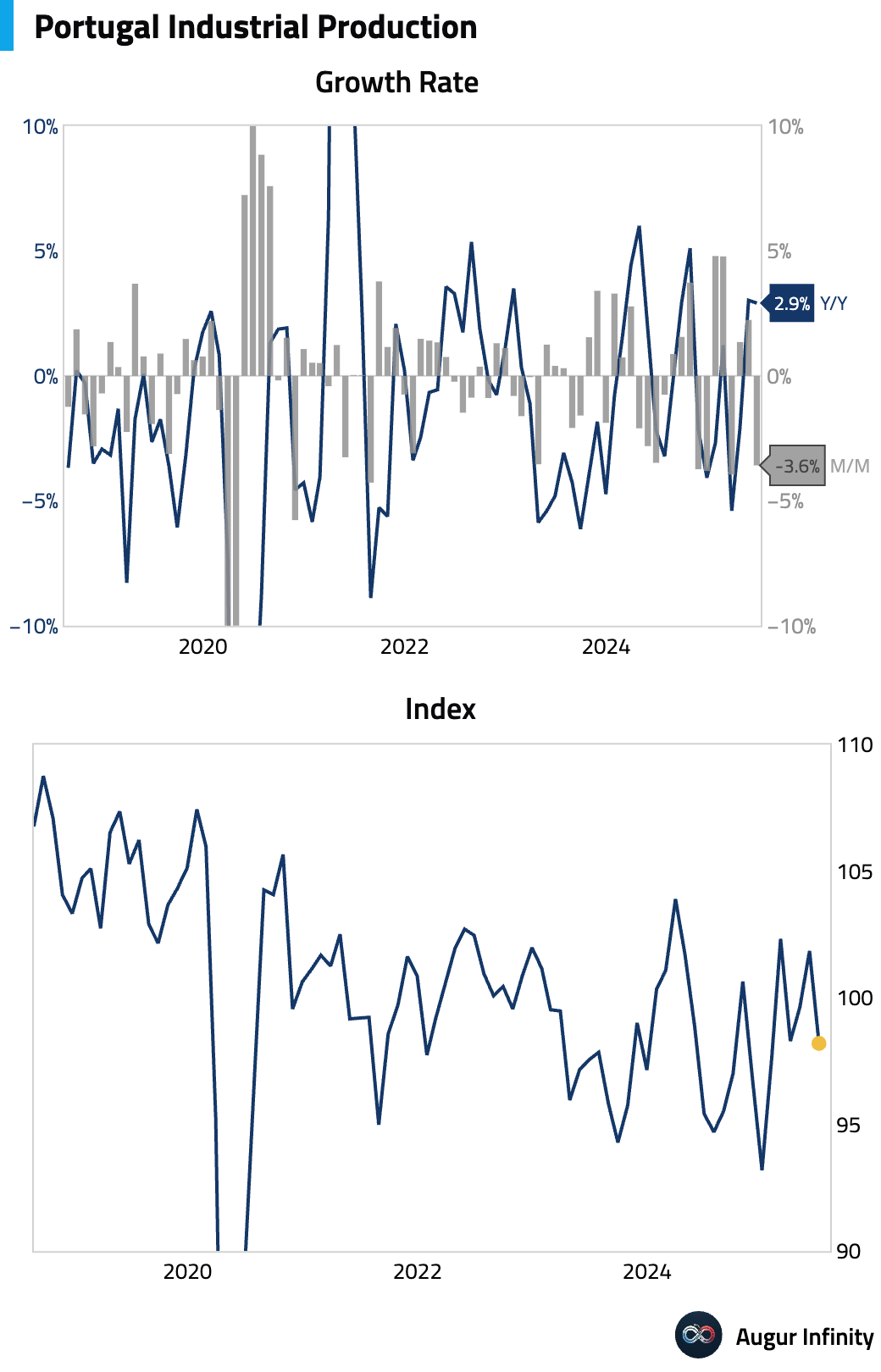

- Portugal's industrial production fell 3.6% M/M in June, though the Y/Y figure was a still-positive 2.9%.

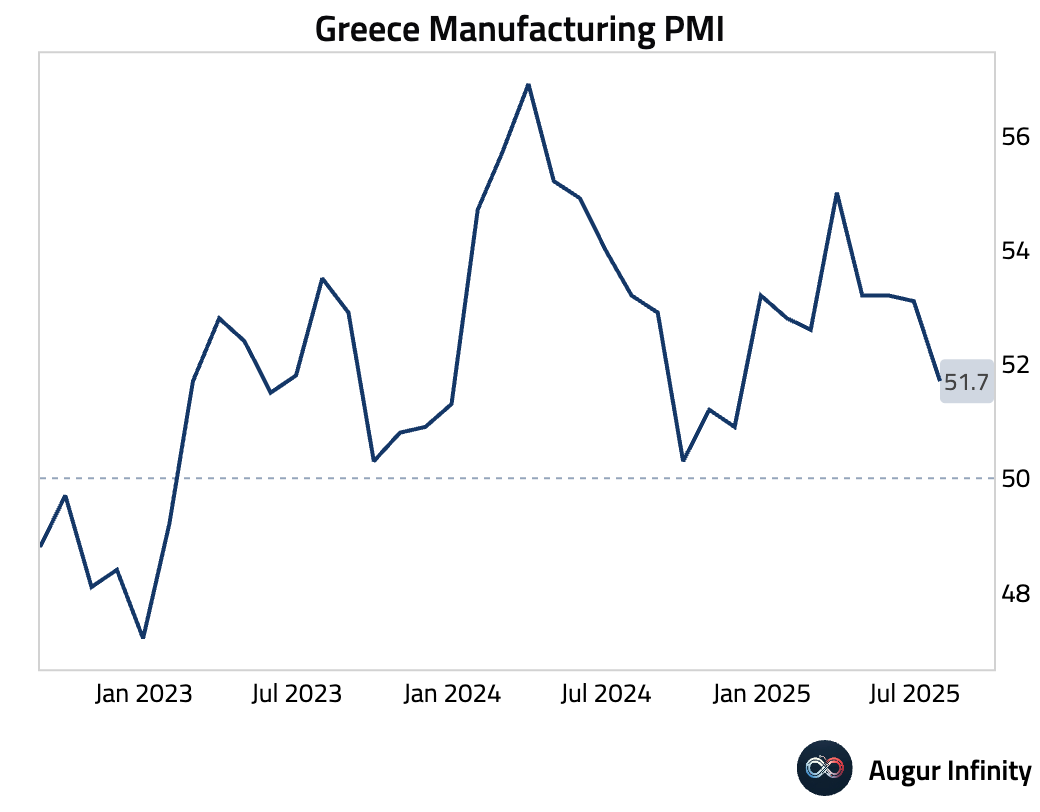

- Greece's S&P Global Manufacturing PMI fell to an 8-month low of 51.7, signaling a loss of momentum. Supply chains were notably disrupted by emergency heatwave policies restricting supplier work hours, leading to the worst vendor performance since January.

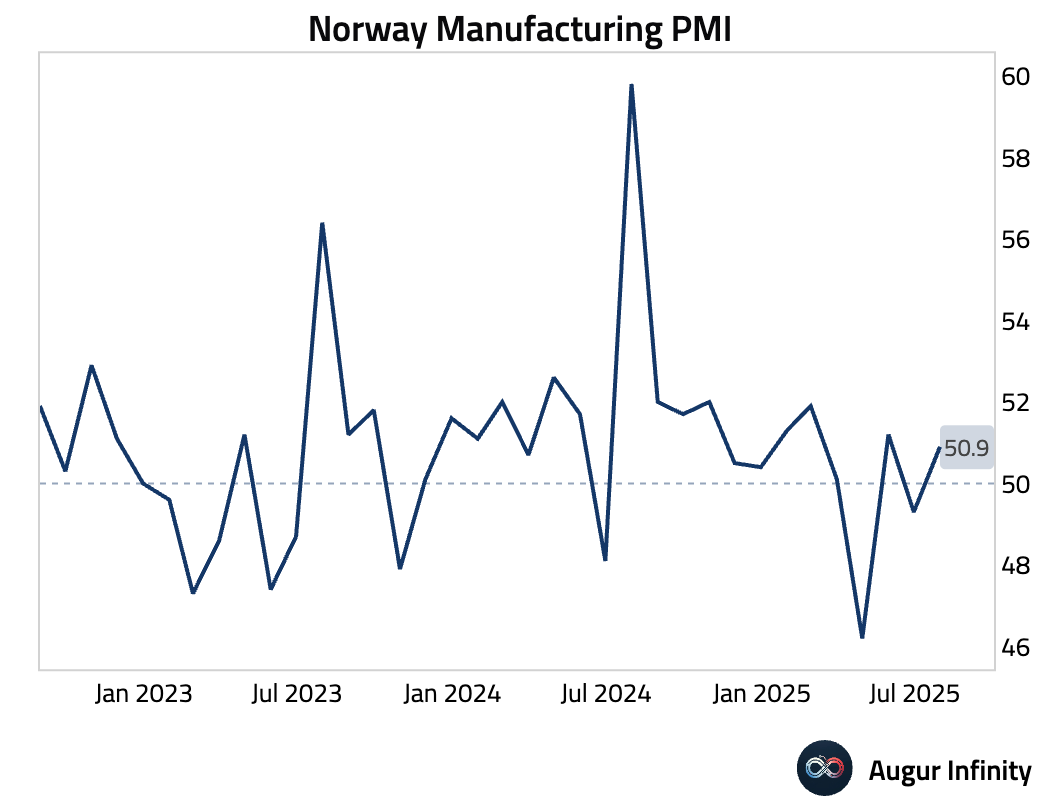

- Norway's DNB Manufacturing PMI returned to expansion, rising to 50.9 in July from 49.3.

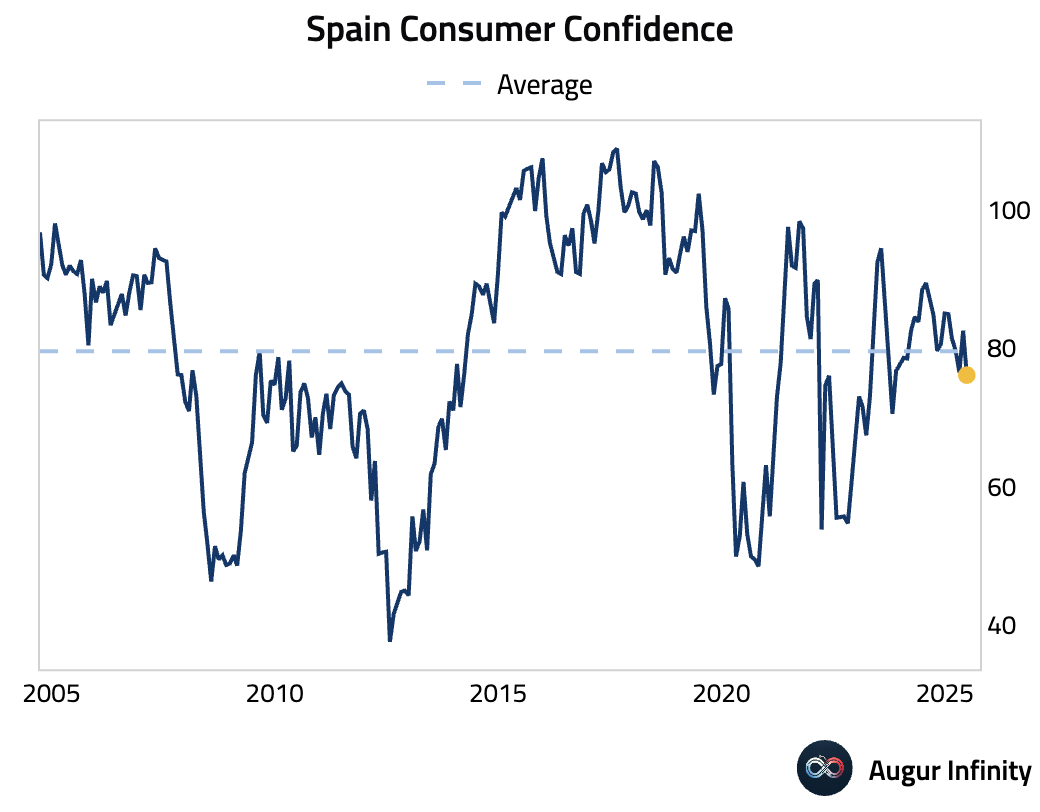

- Spain's consumer confidence dropped sharply to 76.1 in July from 82.5, reaching its lowest level since October 2023.

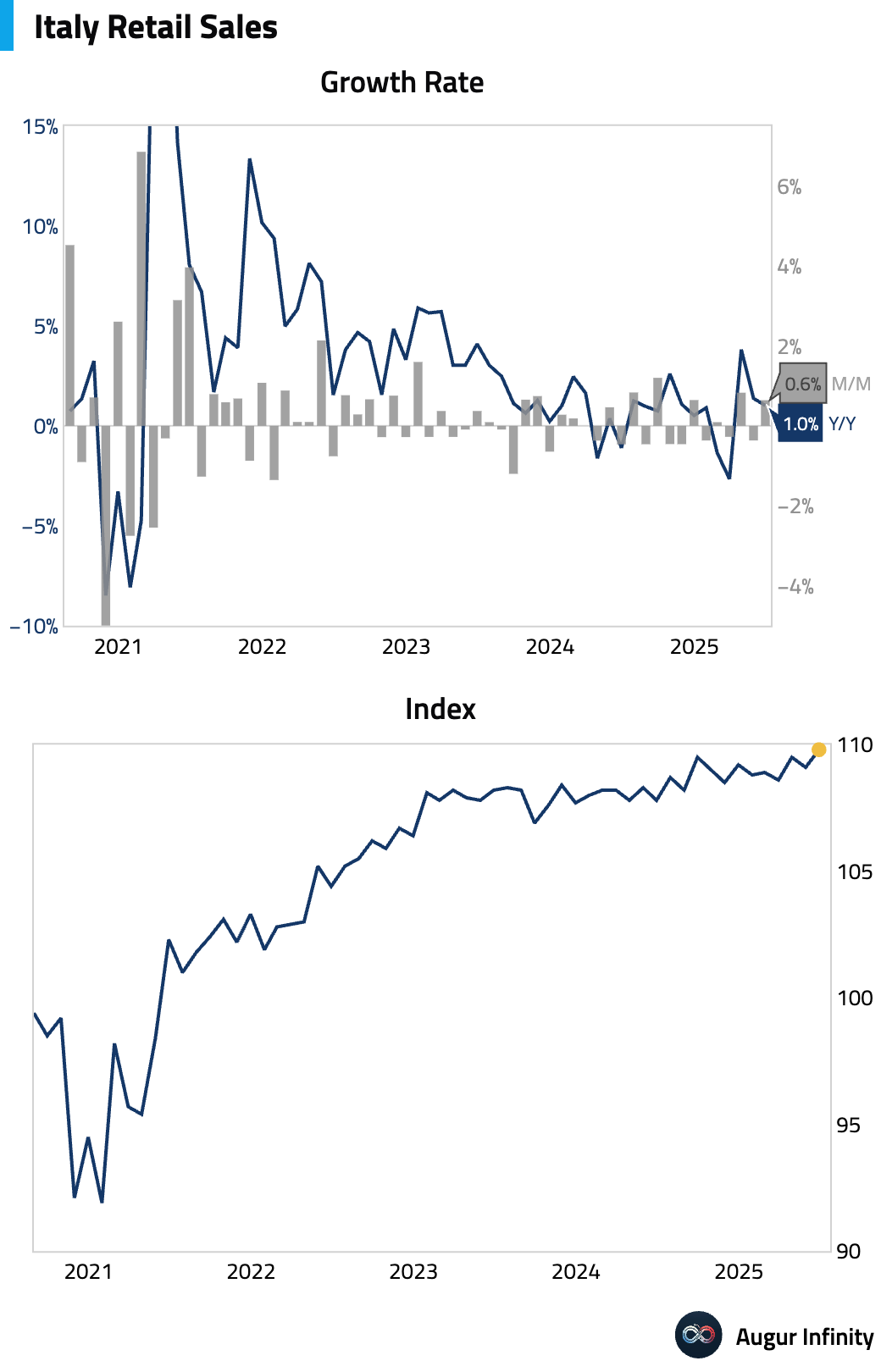

- Italian retail sales rose 0.6% M/M in June, well above the 0.2% consensus and reversing the prior month's decline. The Y/Y rate was 1.0%.

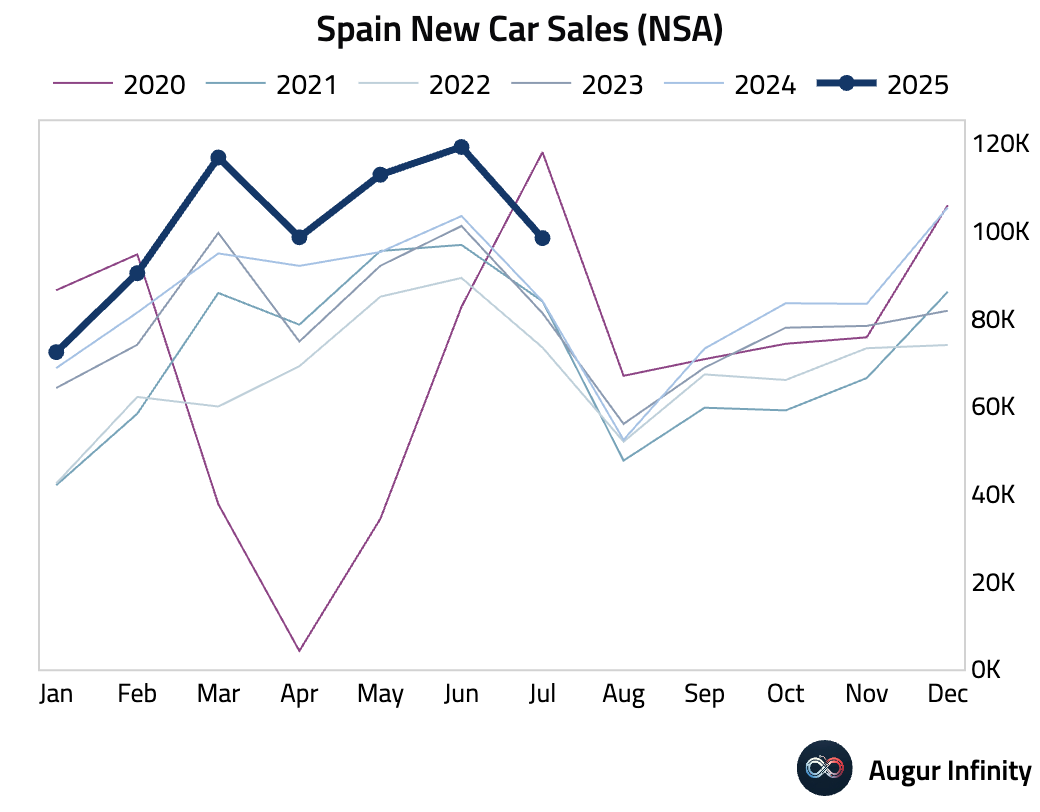

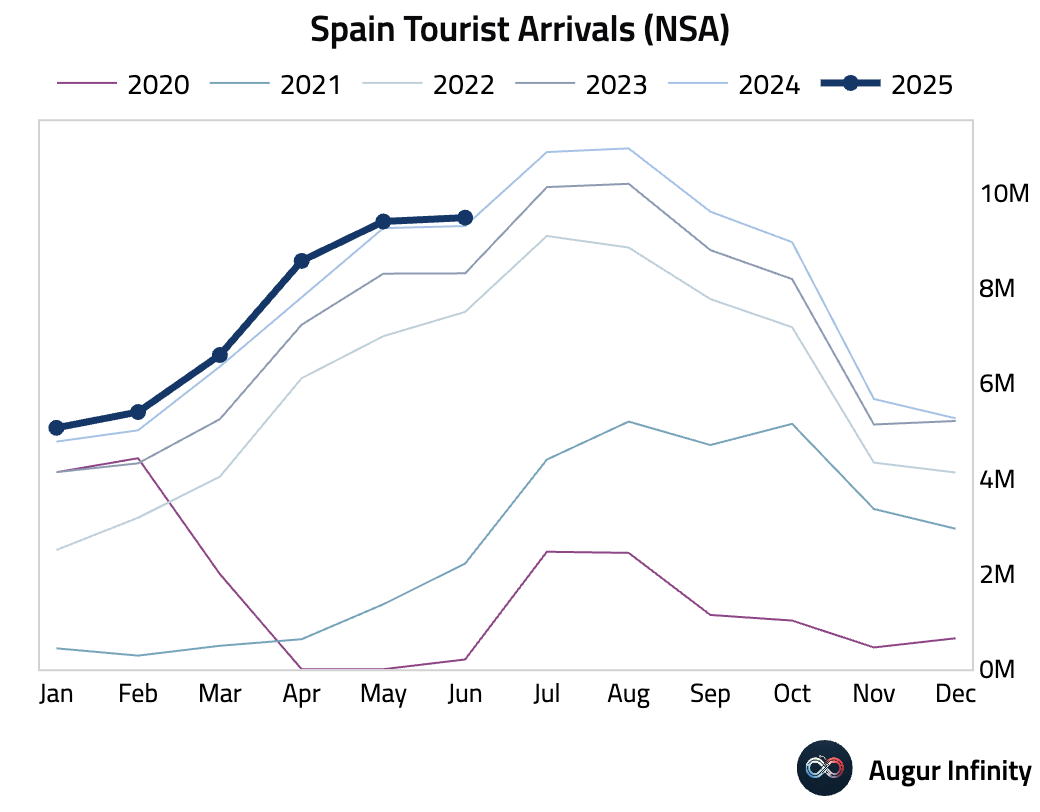

- Spain's new car sales grew 17.1% Y/Y in July, while international tourist arrivals rose 1.9% Y/Y in June.

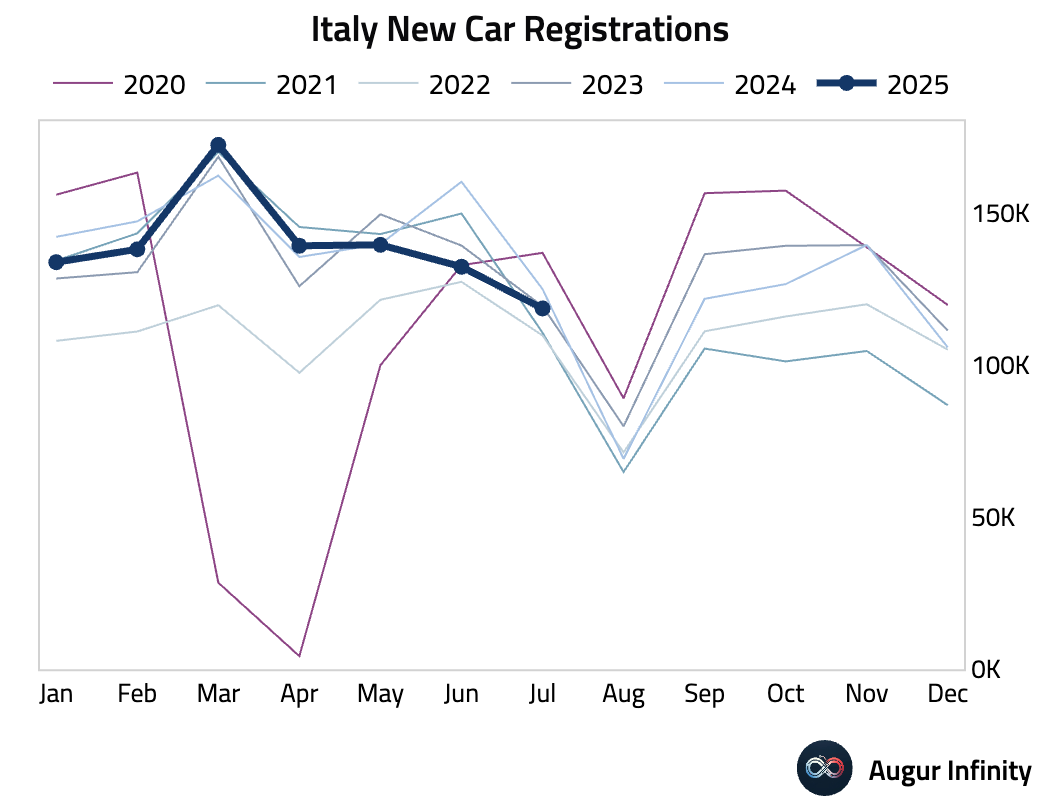

- Italy's new car registrations contracted by 5.1% Y/Y in July, an improvement from the 17.4% fall in June.

Asia-Pacific

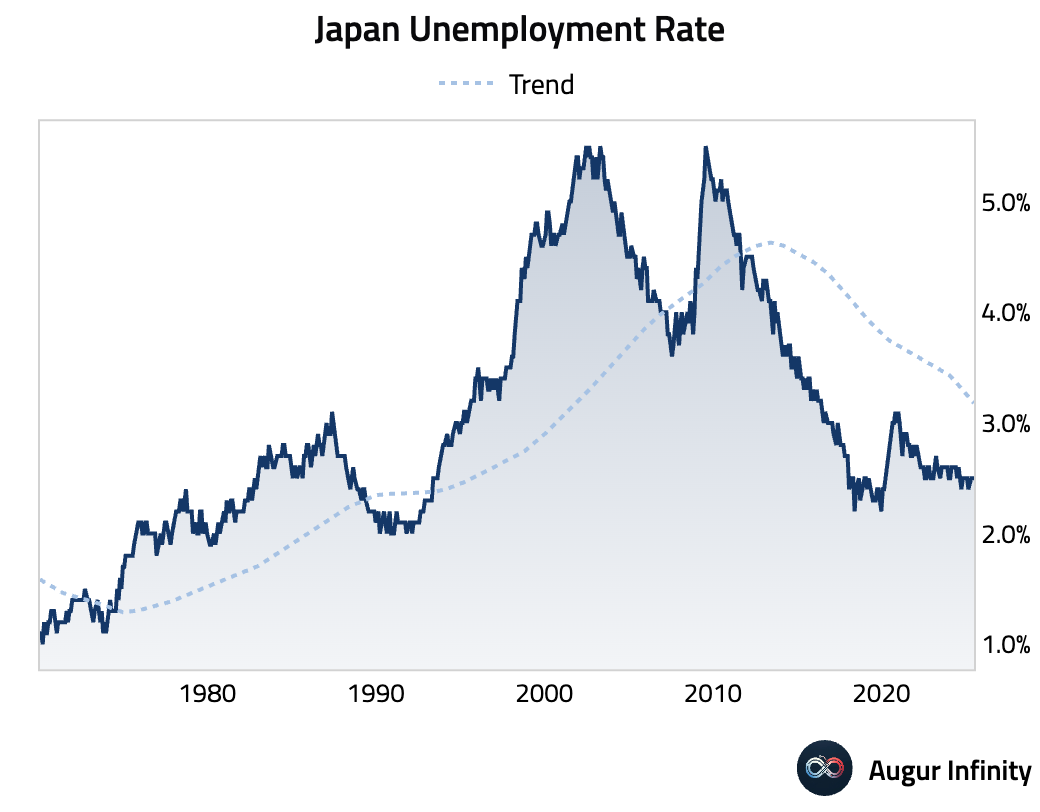

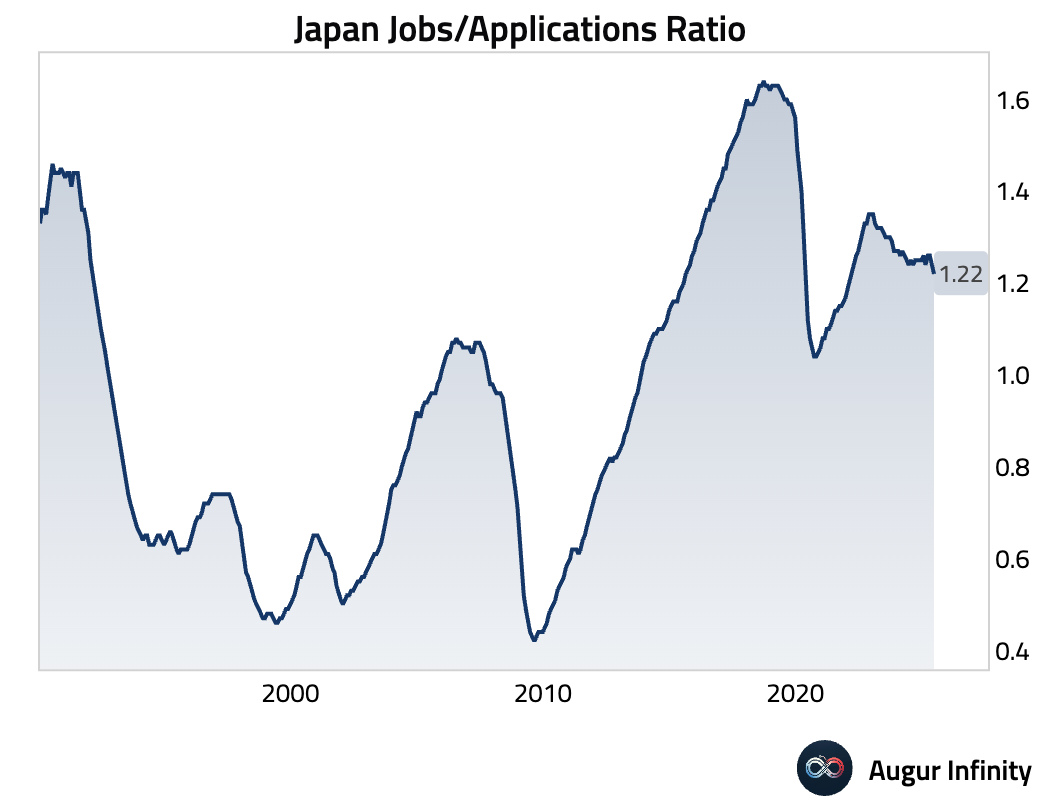

- Japan's unemployment rate held steady at a low 2.5% in June, matching consensus. However, the jobs-to-applications ratio fell to 1.22, its lowest level since February 2022, signaling a softening in labor market demand.

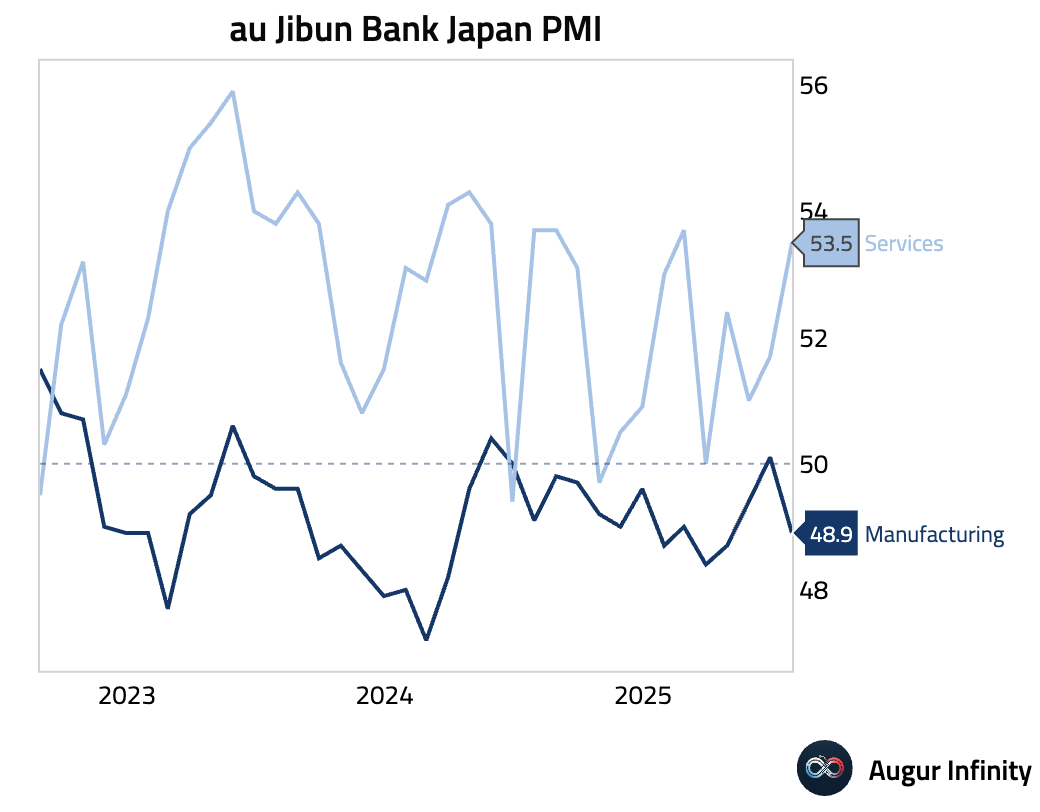

- Japan's S&P Global Manufacturing PMI fell back into contraction at 48.9 for July, a decline from 50.1 in June. The drop was driven by weaker output amid subdued demand, which firms linked to uncertainty before the US-Japan trade deal was announced.

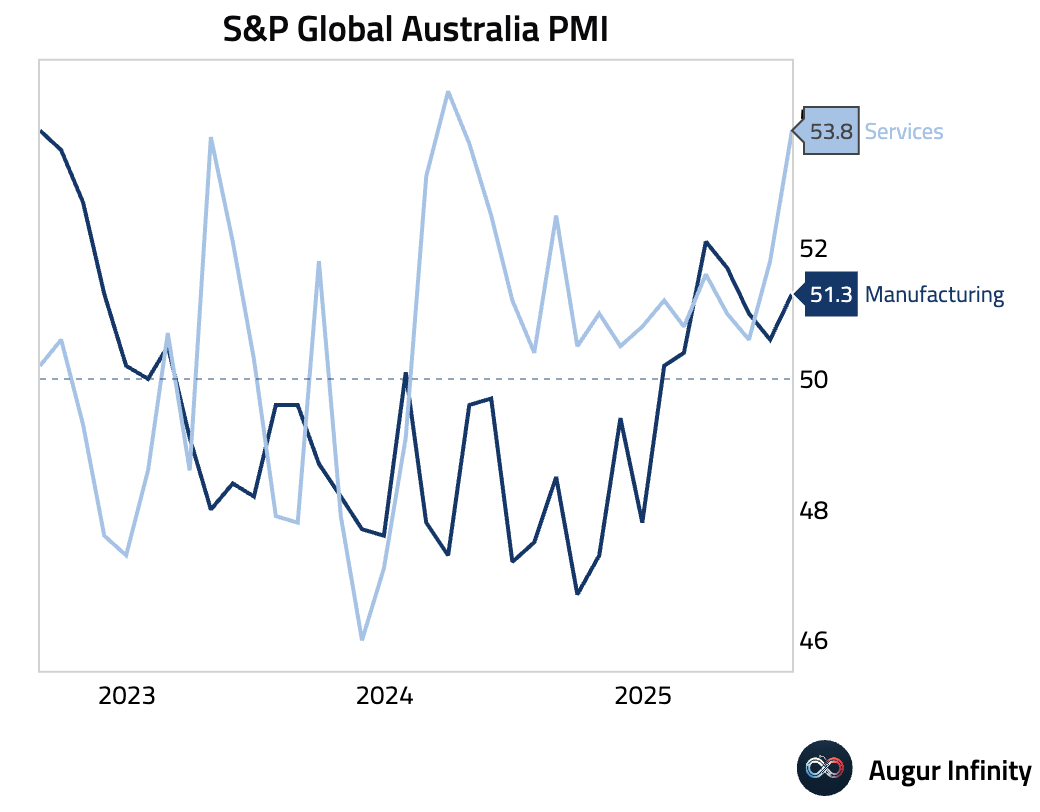

- Australia’s final S&P Global Manufacturing PMI rose to a three-month high of 51.3 in July, driven by a domestic-led return to growth in new orders and output. A key divergence appeared as input cost inflation slowed while firms raised selling prices faster, boosting margin outlooks and pushing business confidence to its highest level in over three years.

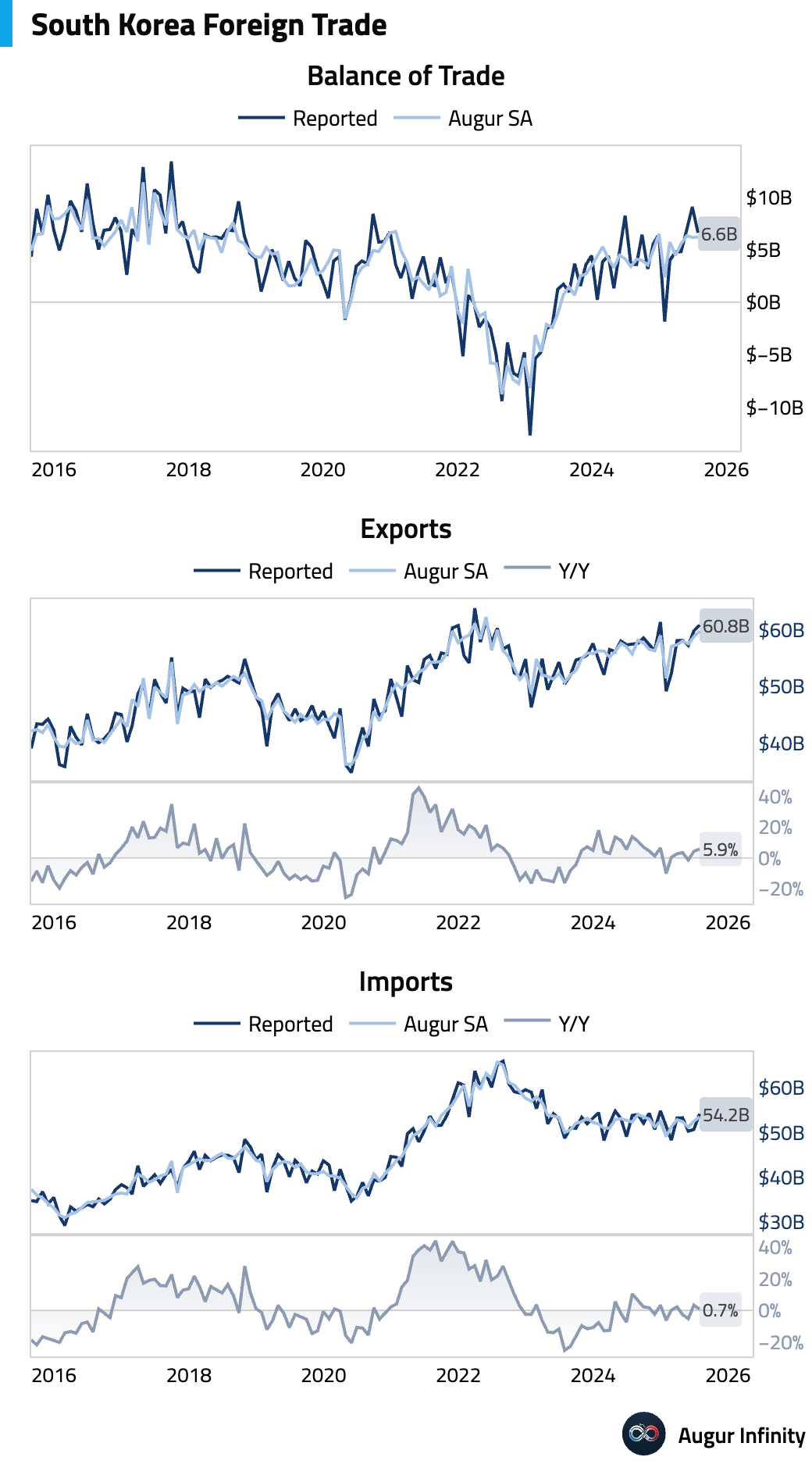

- South Korea's July exports grew 5.9% Y/Y, beating the 4.6% consensus. However, the strength was narrow, as a 13.1% M/M surge in semiconductor exports offset a broad non-tech pullback. The trade surplus narrowed to $6.61 billion from $9.08 billion.

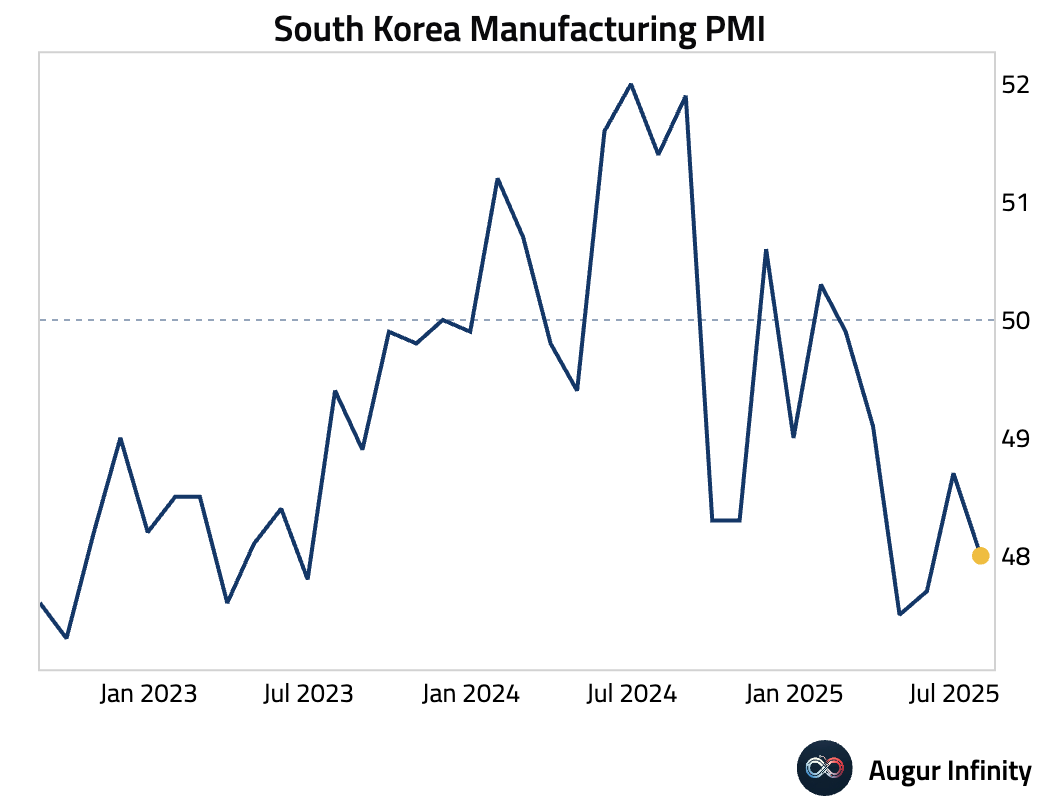

- South Korea's S&P Global Manufacturing PMI fell to 48.0 in July, down from 48.7, marking a faster deterioration and a sixth straight month of contraction. The decline was driven by weak domestic demand, with US tariff policy cited as a factor compounding weakness and pushing business confidence negative.

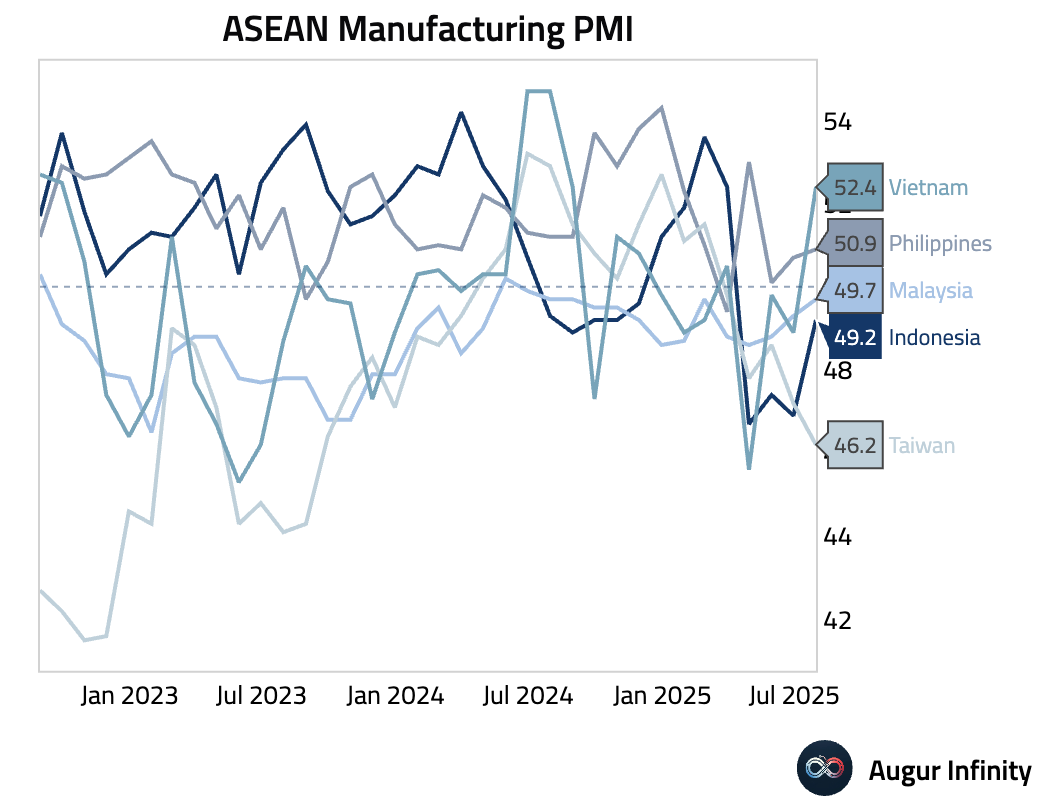

- Manufacturing PMIs across the Asia-Pacific region were mixed. Malaysia’s PMI rose to a 5-month high of 49.7, nearing stabilization on the first rise in new export sales in eight months. The Philippines’ PMI edged up to 50.9, but growth was driven by inventory front-loading ahead of US tariffs. Conversely, Taiwan's PMI dropped to 46.2, its sharpest downturn since August 2023, as trade policy uncertainty hit demand. Indonesia’s PMI rose to 49.2 but remained in contraction as business confidence plunged to a record low.

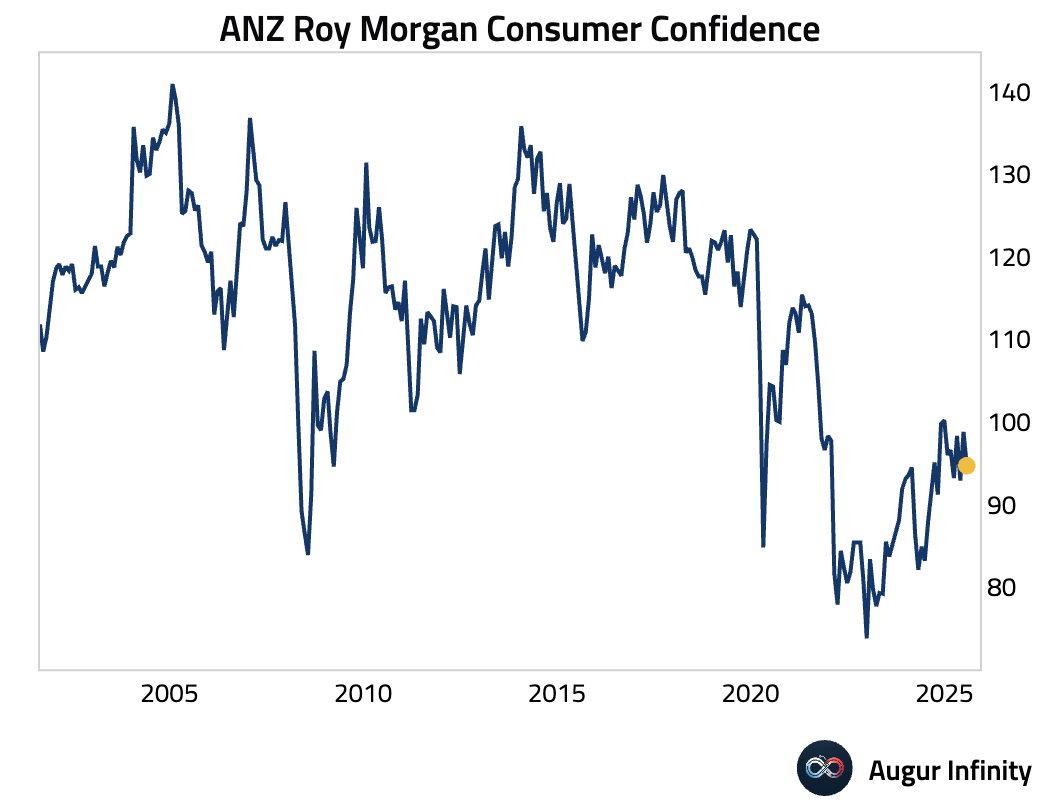

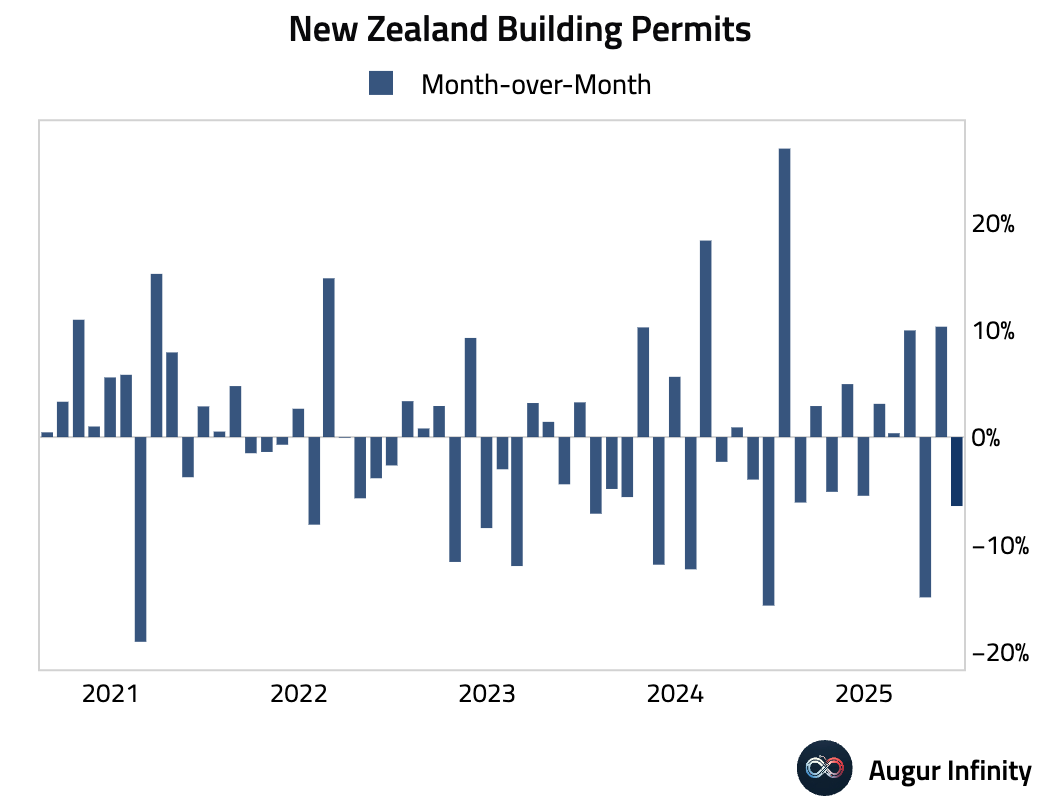

- New Zealand's ANZ-Roy Morgan consumer confidence fell to 94.7 in July from 98.8. Building permits also dropped, contracting 6.4% M/M in June after a 10.3% rise in May.

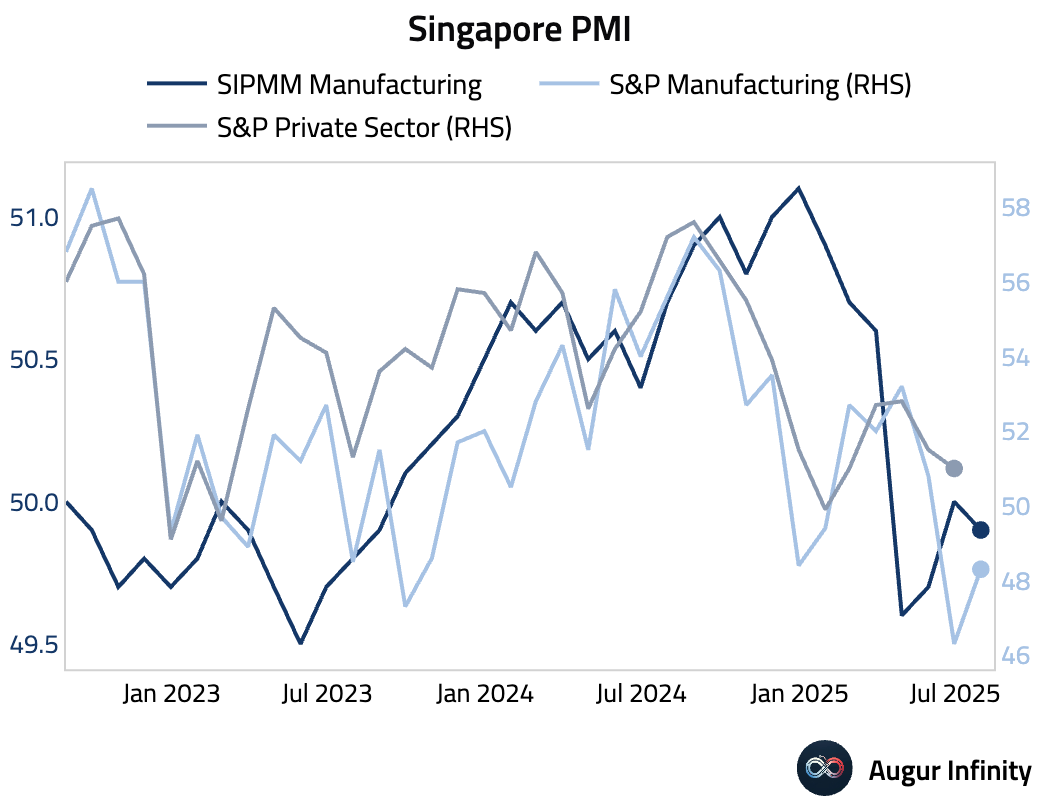

- Singapore's SIPMM Manufacturing PMI slipped to 49.9 in July, dipping back into contraction after a neutral reading of 50.0 in June.

China

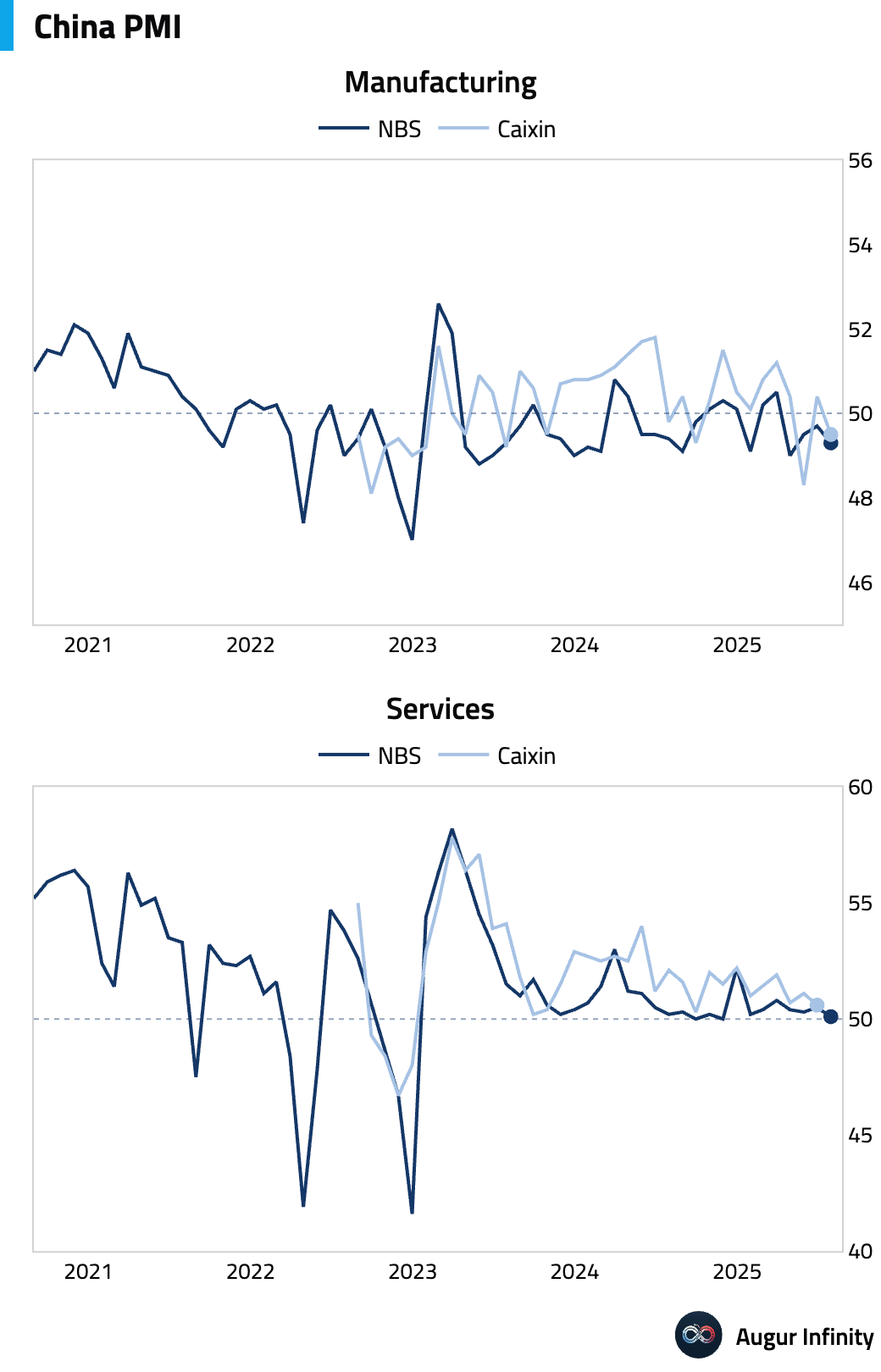

- China’s Caixin Manufacturing PMI unexpectedly fell into contraction at 49.5 in July, significantly missing the 50.2 consensus and declining from 50.4 in June. The drop was led by a renewed decline in output as new order growth slowed and external demand remained weak. Despite rising input costs for the first time in five months, intense competition forced firms to cut selling prices.

Emerging Markets ex China

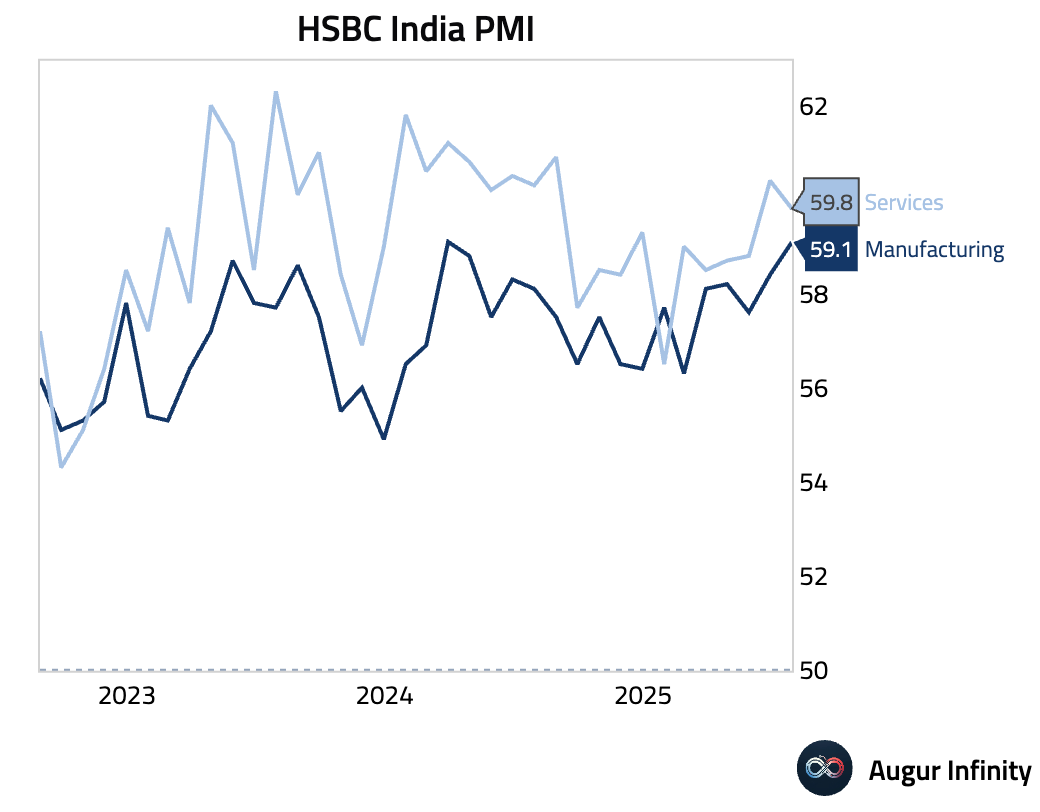

- India's HSBC Manufacturing PMI for July rose to 59.1, its highest in 16 months, driven by the fastest growth in new orders in nearly five years. However, a significant divergence emerged as business confidence fell to a 3-year low on inflation and competition fears, translating into the slowest job creation since November 2024.

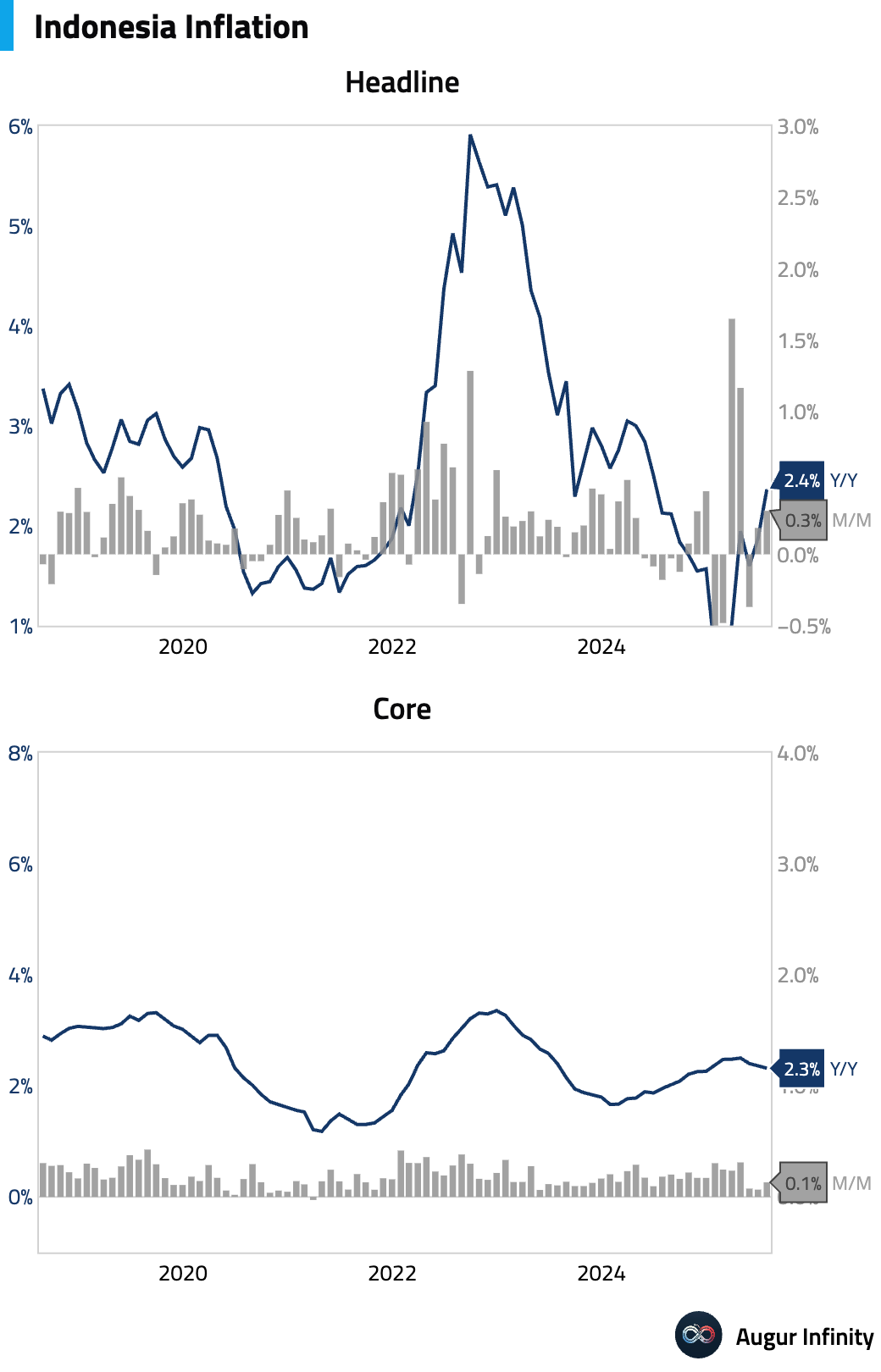

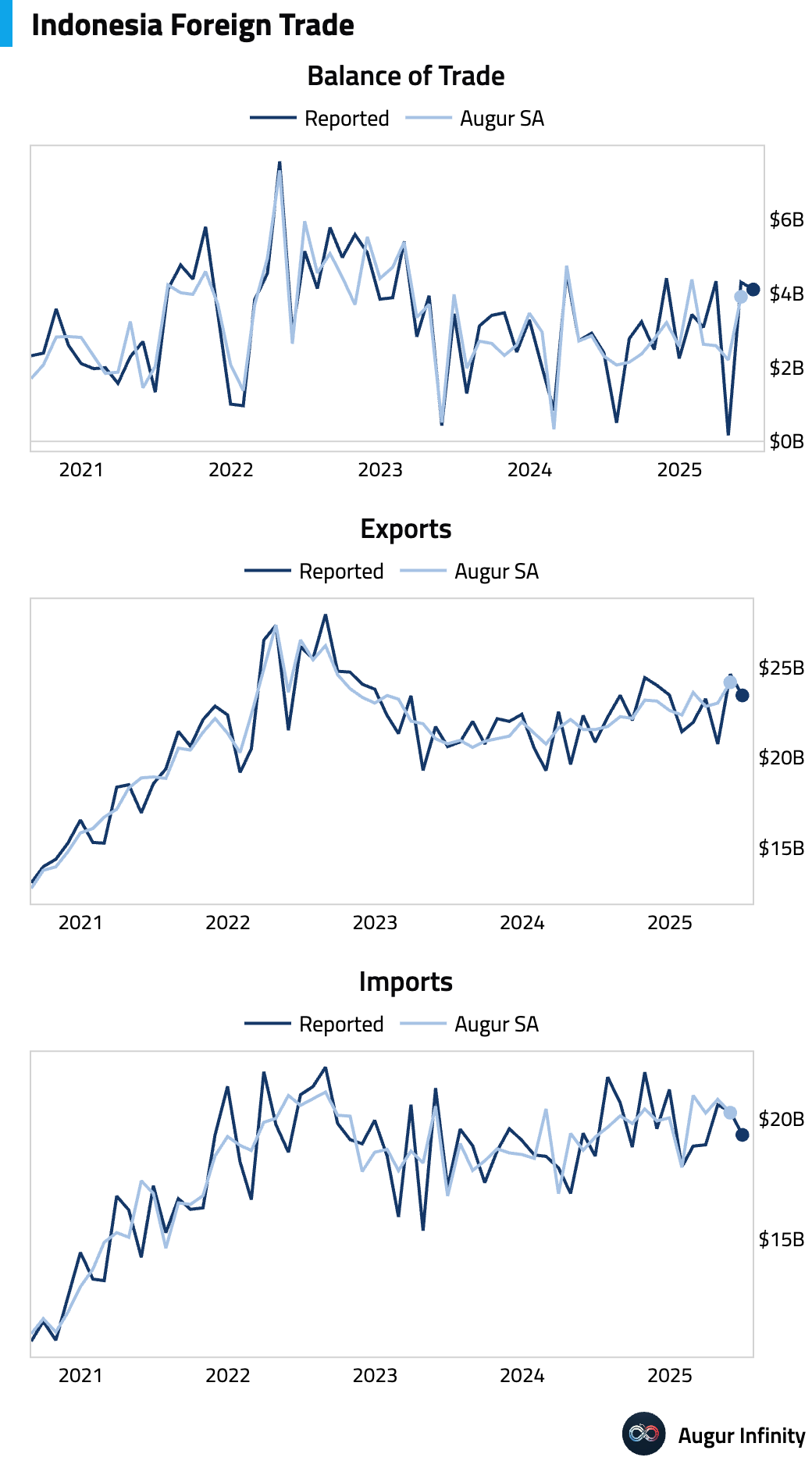

- Indonesia's July inflation rate accelerated to 2.37% Y/Y, above the 2.24% consensus, driven entirely by higher food prices. In contrast, core CPI slowed to 2.32%, suggesting underlying price pressures remain contained. The manageable inflation and soft growth may provide room for Bank Indonesia to cut rates.

- Indonesia's trade surplus for June narrowed to $4.11 billion from $4.3 billion, though it beat the $3.55 billion consensus.

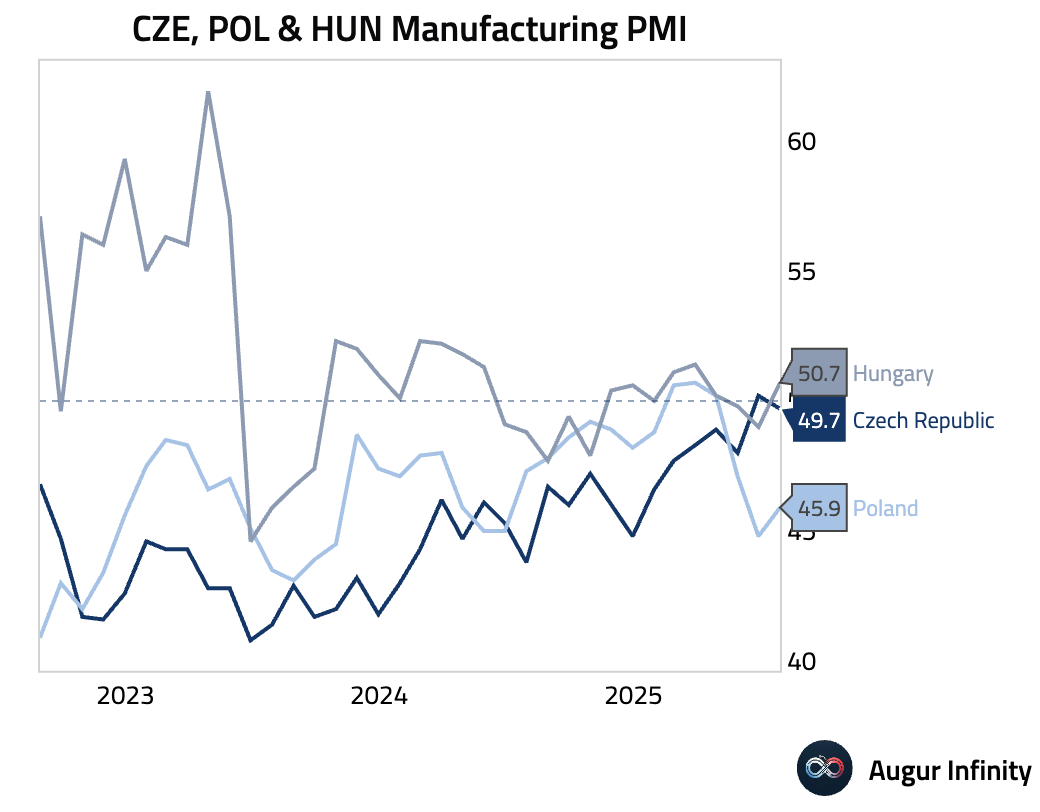

- Central European manufacturing PMIs improved in July, driven by Hungary moving into expansion (50.7) and Poland recovering from a 20-month low (45.9). This was slightly offset by a decline in Czechia to 49.7. Poland continues to underperform, dragged by the steepest drop in new export orders in nearly two years due to weak German demand.

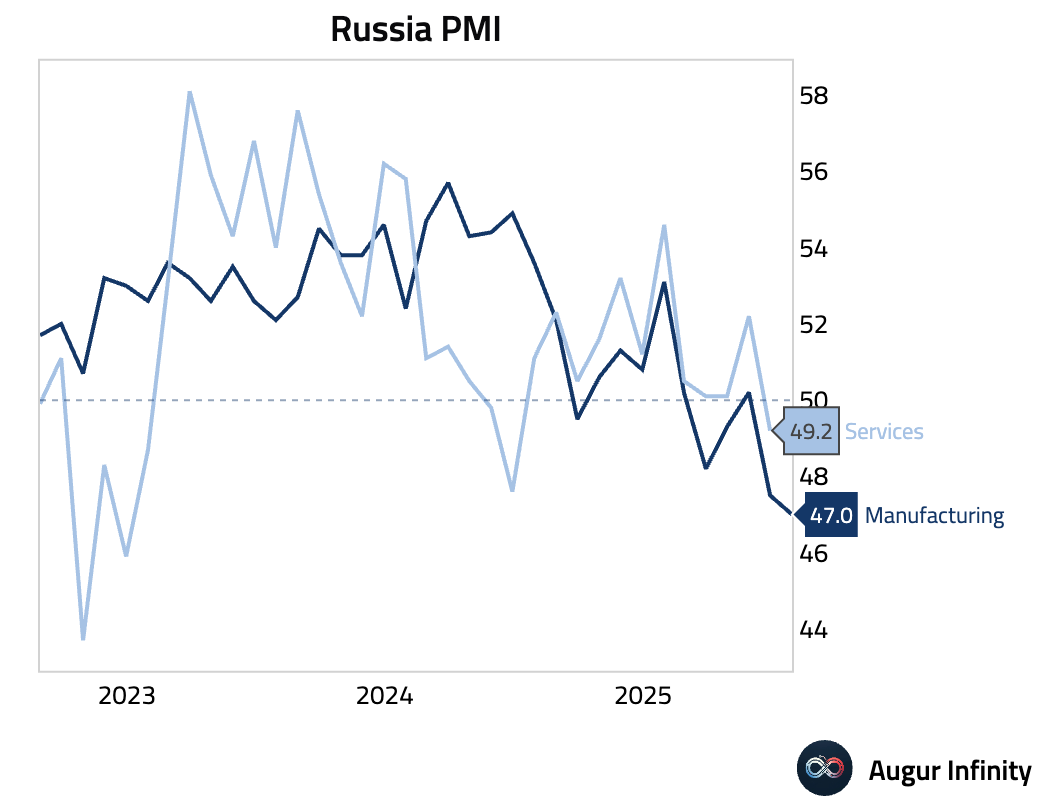

- Russia's S&P Global Manufacturing PMI fell to 47.0 in July, its weakest reading since March 2022. The decline was driven by weak domestic demand, leading to the steepest output drop in three years. In a notable divergence, new export orders rose for the first time in five months.

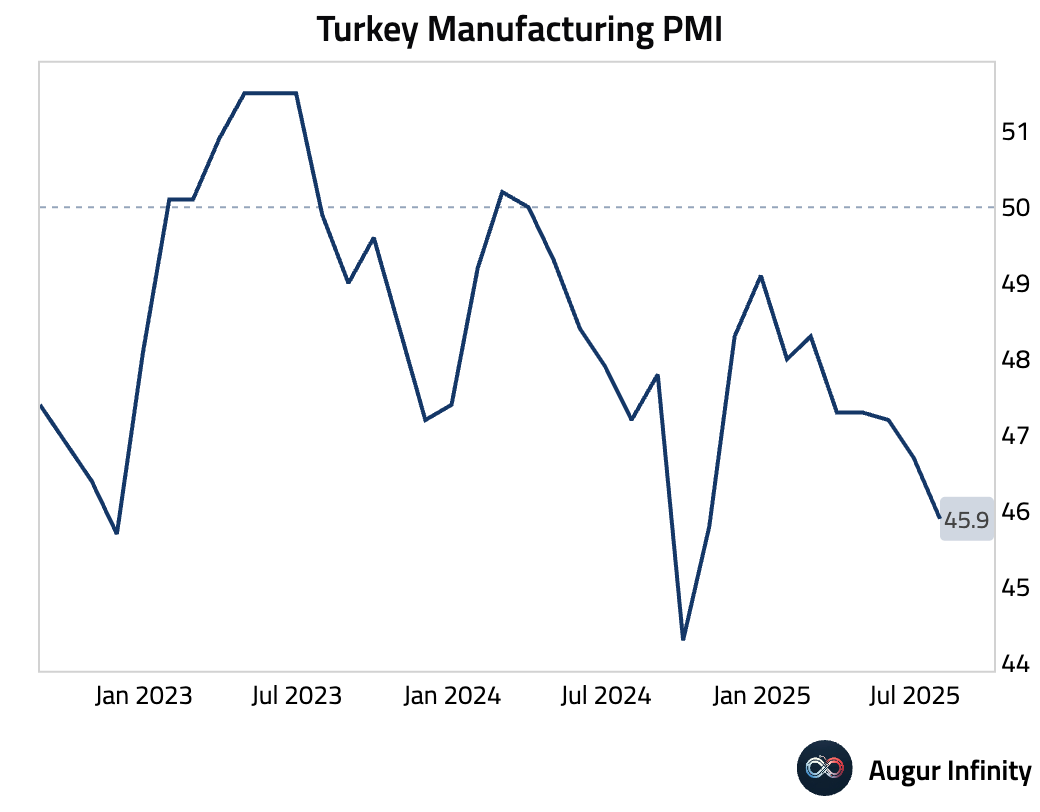

- Turkey’s manufacturing PMI dropped to 45.9 in July, its third consecutive monthly fall and the weakest reading since October 2024. The decline was driven by a 25th straight monthly drop in new orders, prompting firms to scale back output, employment, and purchasing.

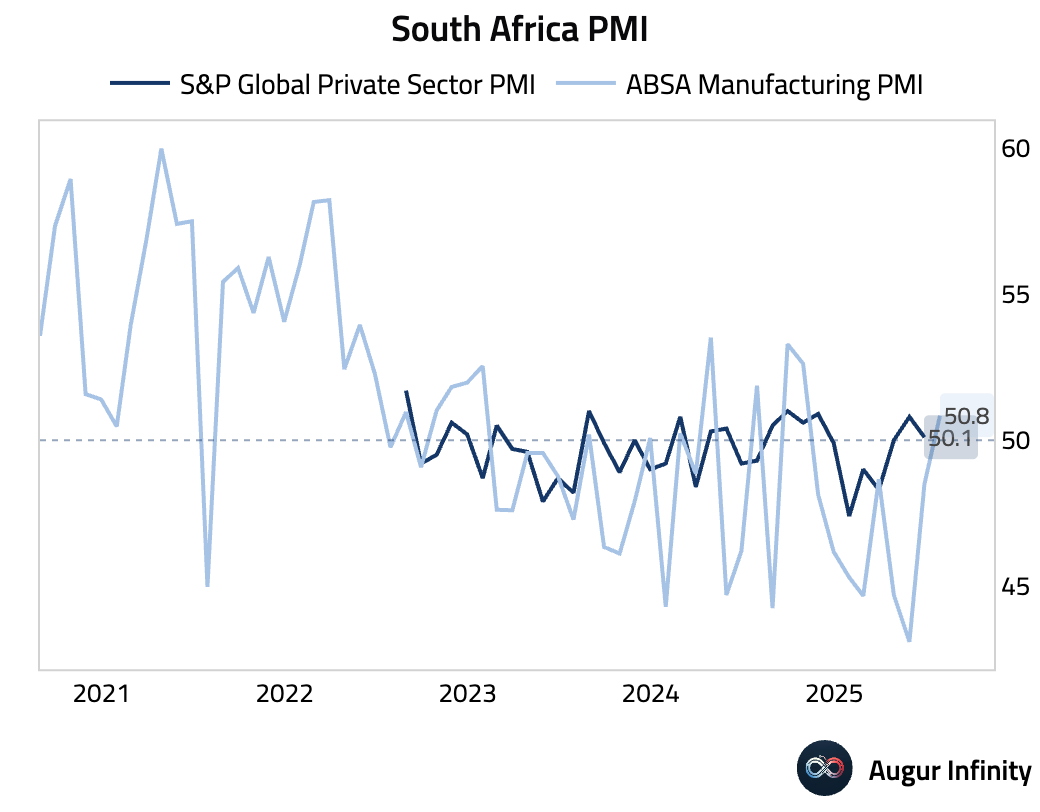

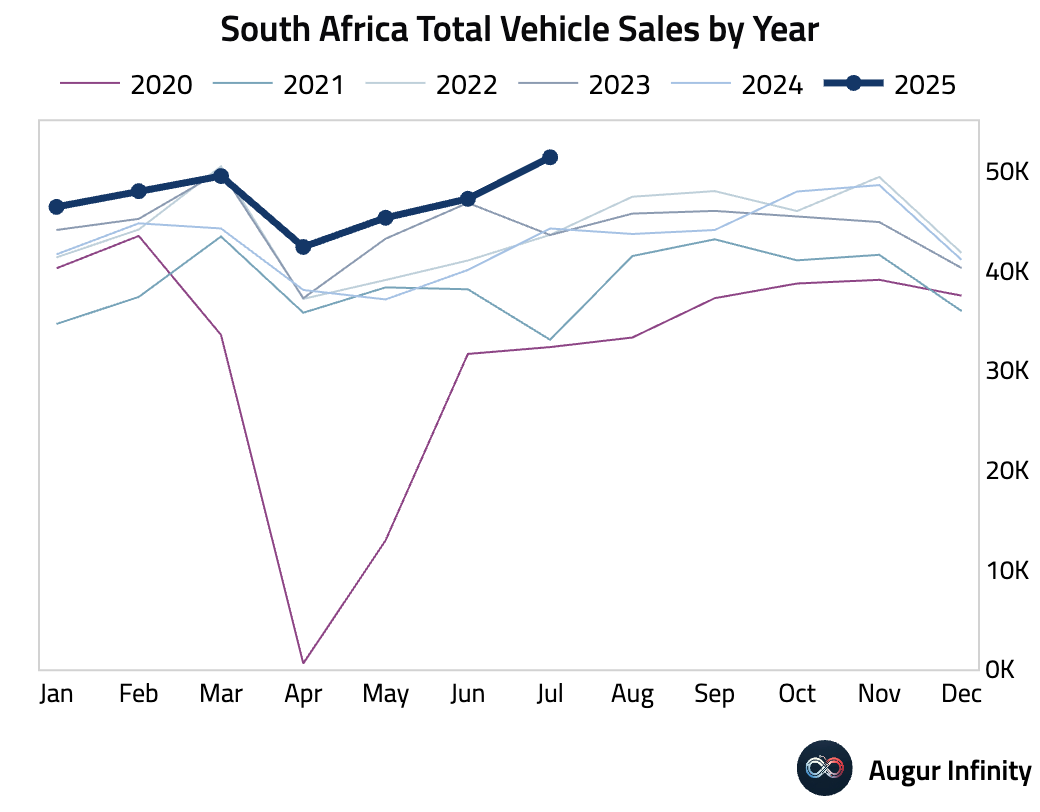

- South Africa's ABSA Manufacturing PMI returned to expansion at 50.8 in July, its strongest reading since October 2024. Separately, total new vehicle sales rose to 51,380, the highest since October 2019.

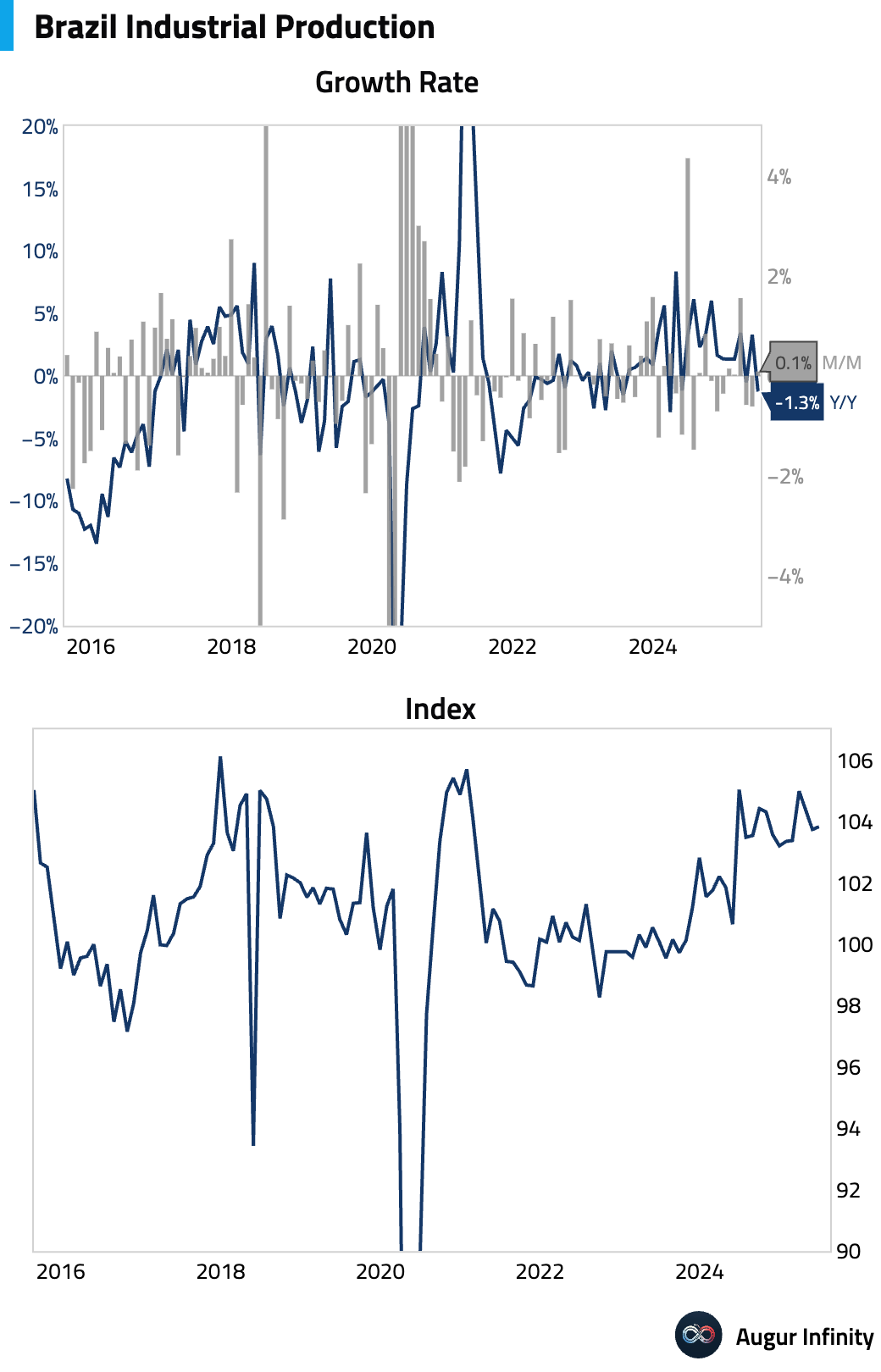

- Brazil's industrial production rose just 0.1% M/M in June, missing the 0.4% consensus. On a Y/Y basis, output declined 1.3%, a significant reversal from the prior 3.3% gain.

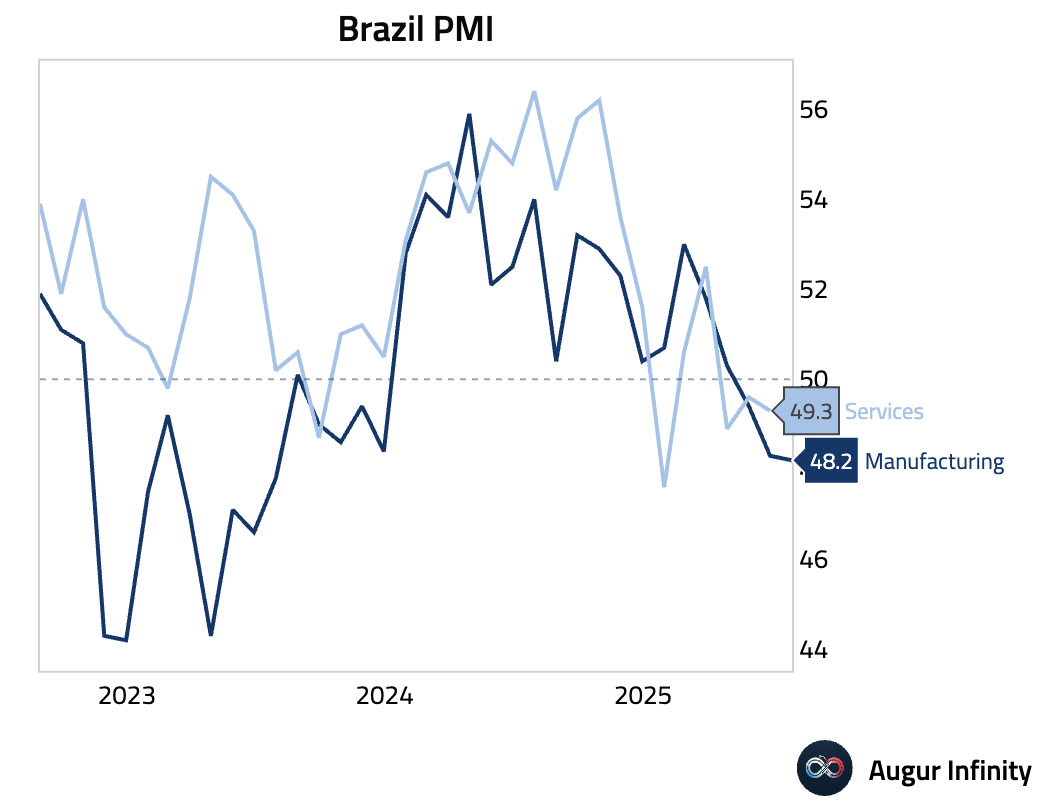

- Brazil's S&P Global Manufacturing PMI edged down to a 24-month low of 48.2, marking a third month of contraction. New orders fell at the fastest pace in over two years, hit by weak domestic demand and a sharp drop in exports, with a new 50% US tariff cited as a significant drag.

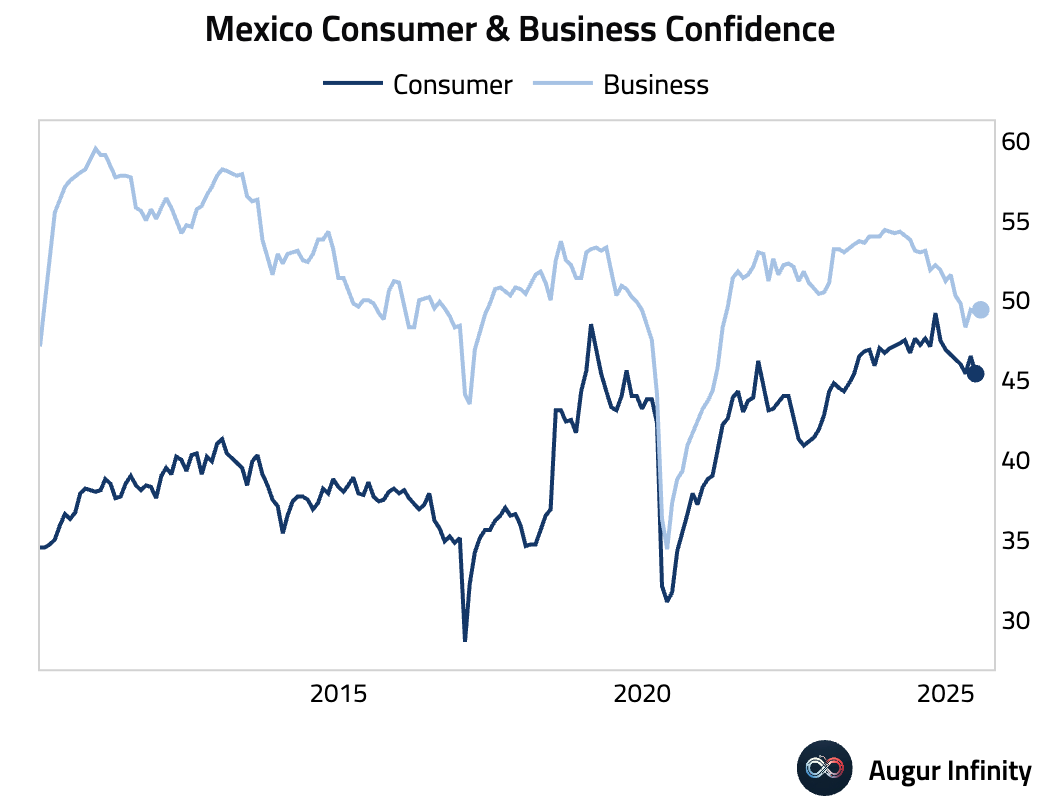

- Mexico's business confidence rose to 49.4 in July, its highest reading since March 2025, though it remains below the neutral 50-mark for the fifth straight month.

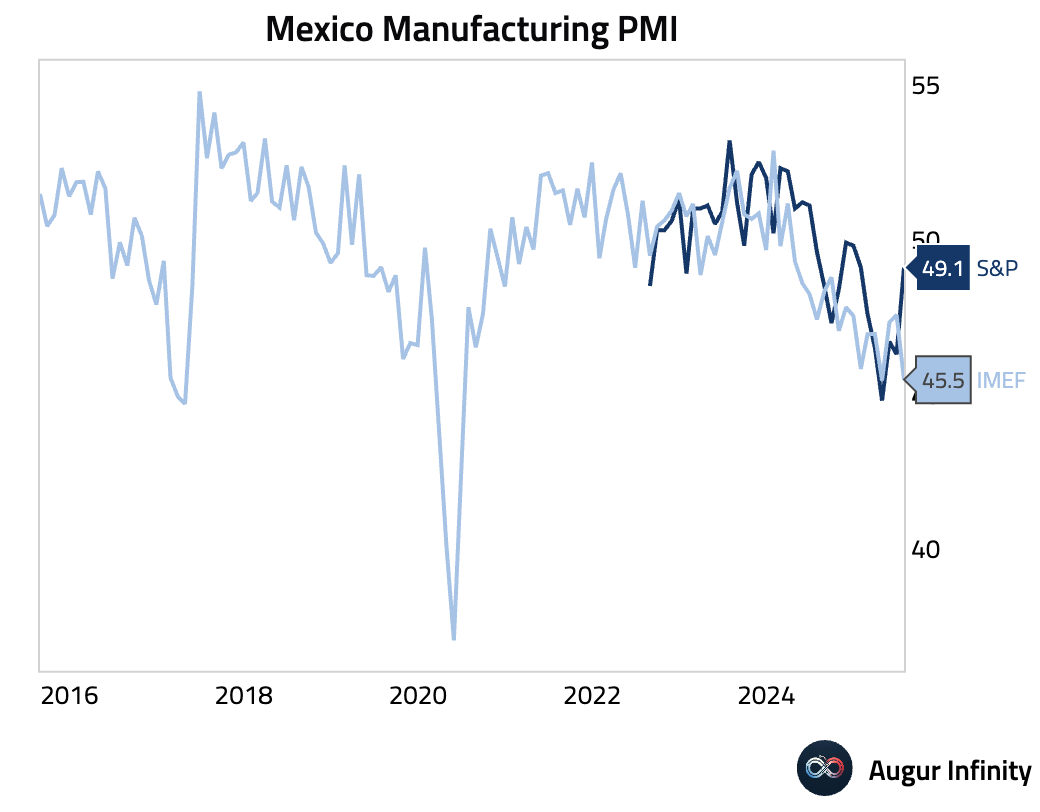

- Mexico’s S&P Global Manufacturing PMI rose to 49.1 in July, up from 46.3 but still in contractionary territory.

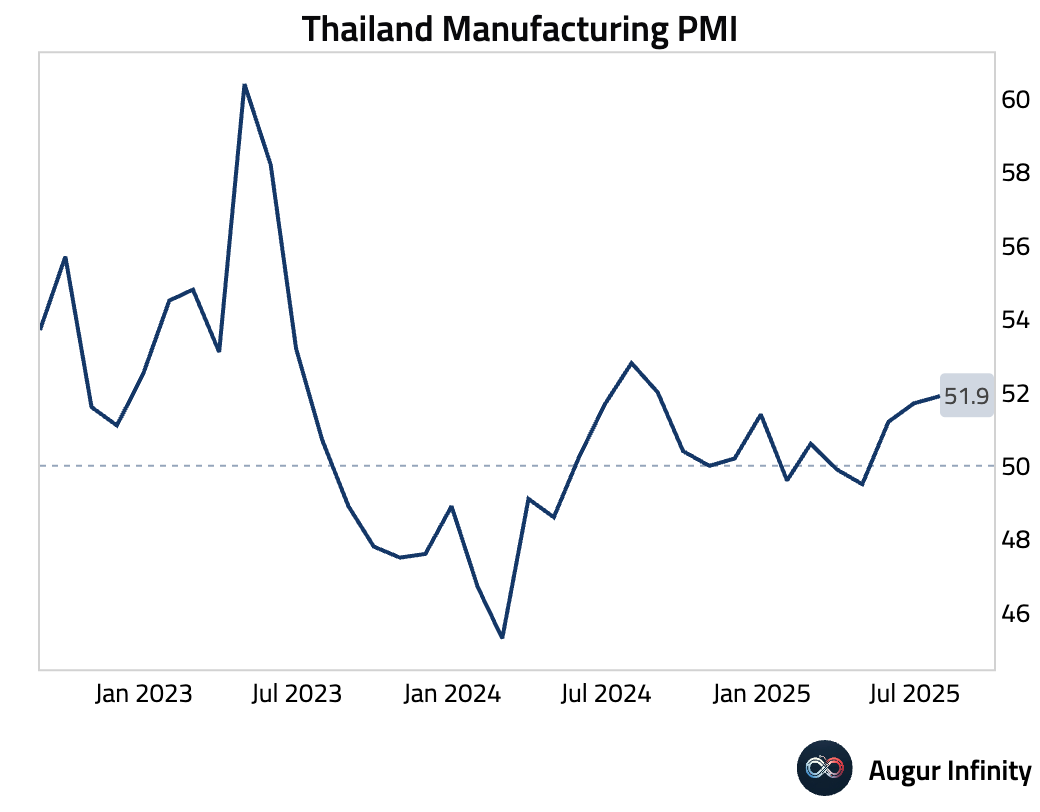

- Thailand's S&P Global Manufacturing PMI rose to 51.9 in July, the fastest improvement in nearly a year, driven by the quickest new order growth in 2025. In contrast, business confidence fell to 45.8, its lowest level since September 2024.

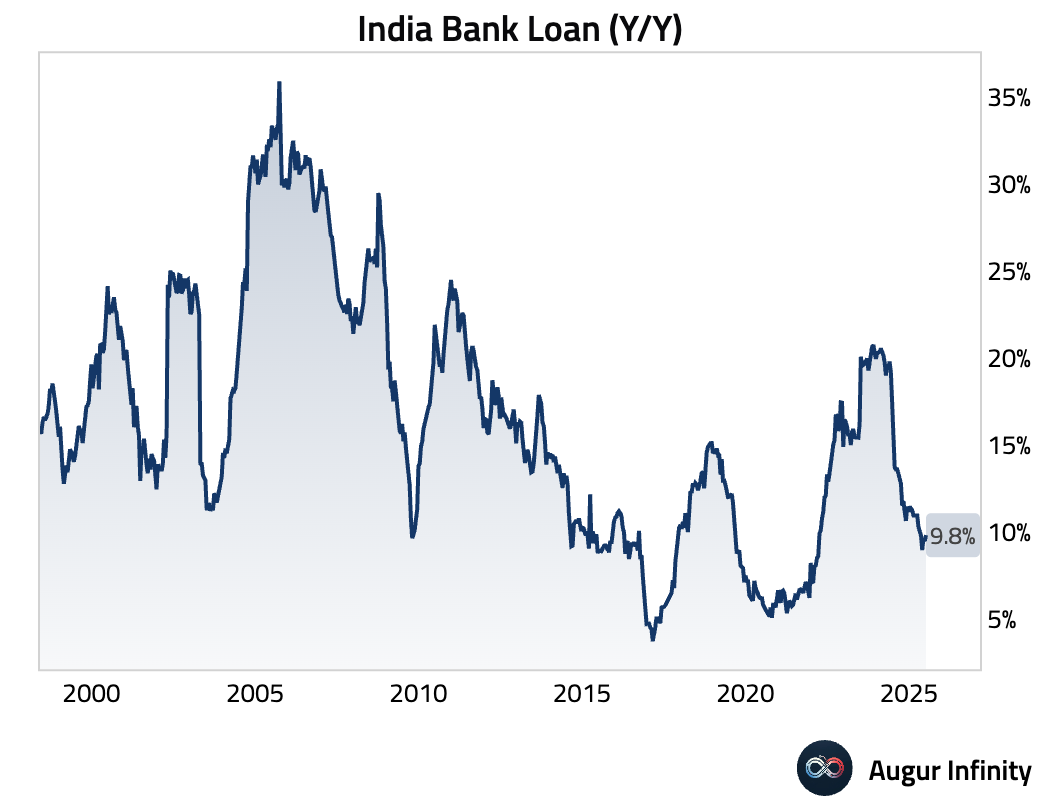

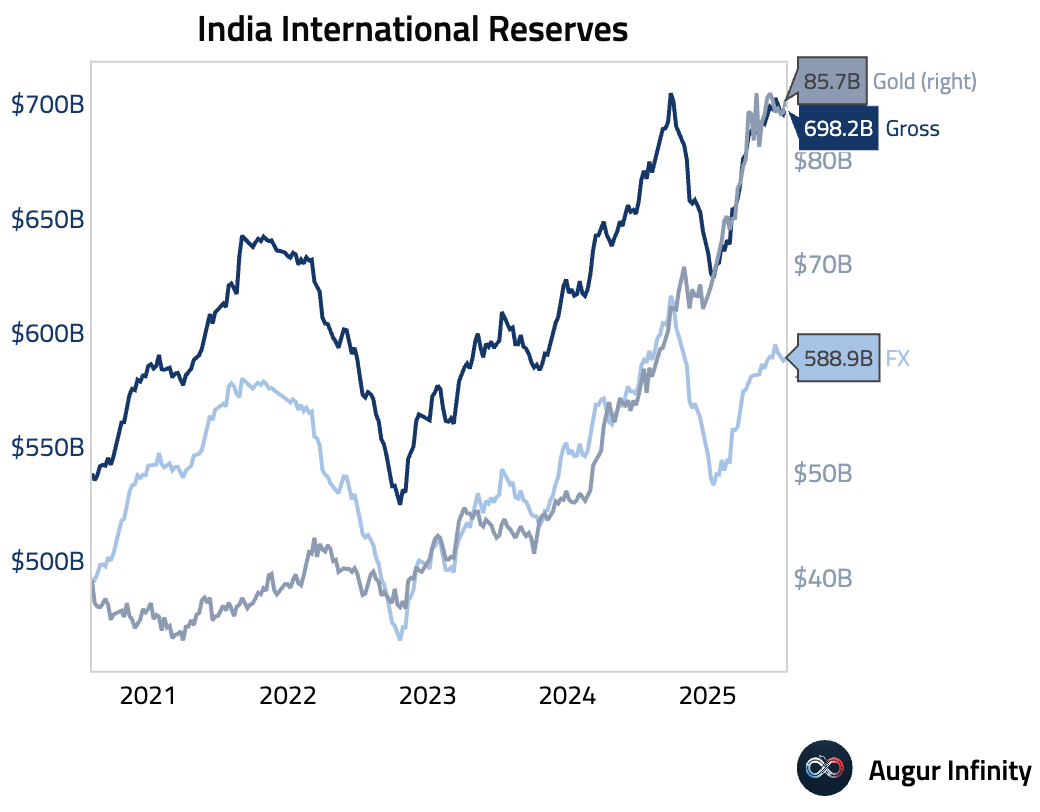

- Indian bank loan growth accelerated to 9.8% Y/Y. Official reserve assets also increased.

Global Markets

Equities

- Global equity markets came under significant pressure, reacting to a much weaker-than-expected US jobs report and tariff headlines. The US market fell 1.6%, with the tech-heavy Nasdaq down 2.2% for its second consecutive loss. US equities have now fallen for four straight days. European markets were also broadly lower, with Germany (-1.0%) and France (-1.2%) posting their third straight day of losses. Chinese equities extended their losing streak to seven days, falling another 1.6%.

- A reminder that the key to wealth compounding over the long run is to avoid catastrophic losses.

Fixed Income

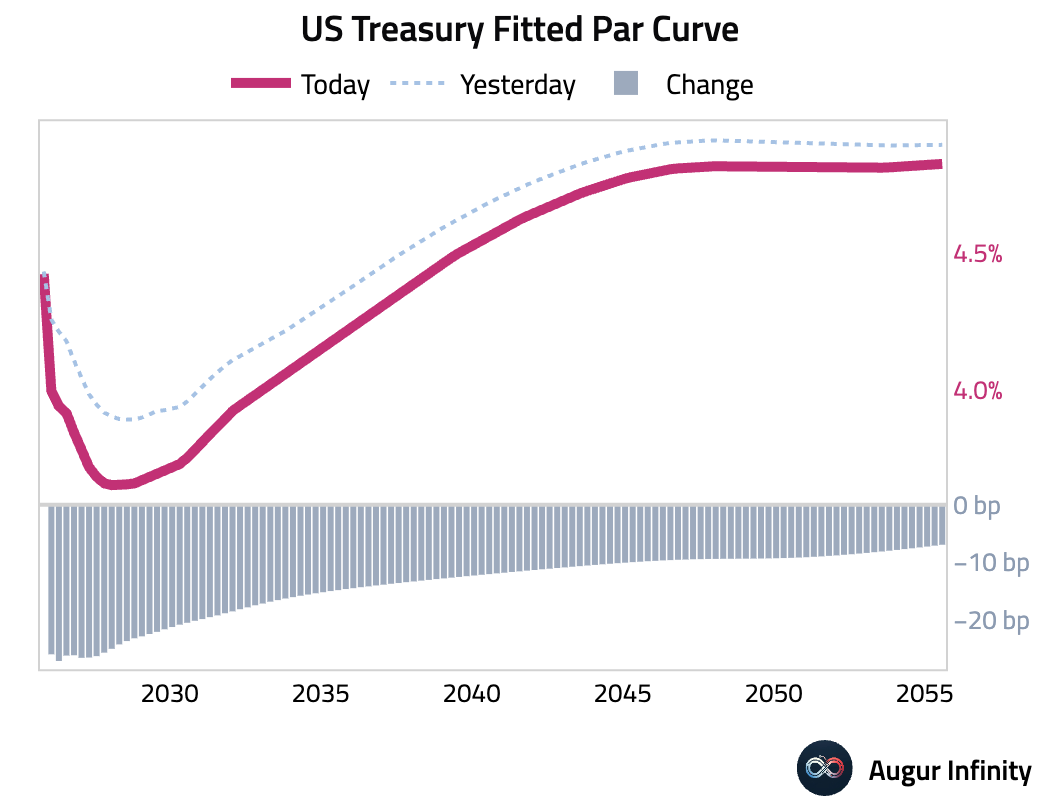

- Treasury bonds rallied sharply as investors fled to safety amid mounting economic concerns. Yields plummeted across the curve, with the 2-year yield dropping 26.4 bps and the 10-year yield falling 14.7 bps to around 4.25%, testing three-month lows. The dramatic move reflects rising expectations for Federal Reserve rate cuts to combat a weakening economy.

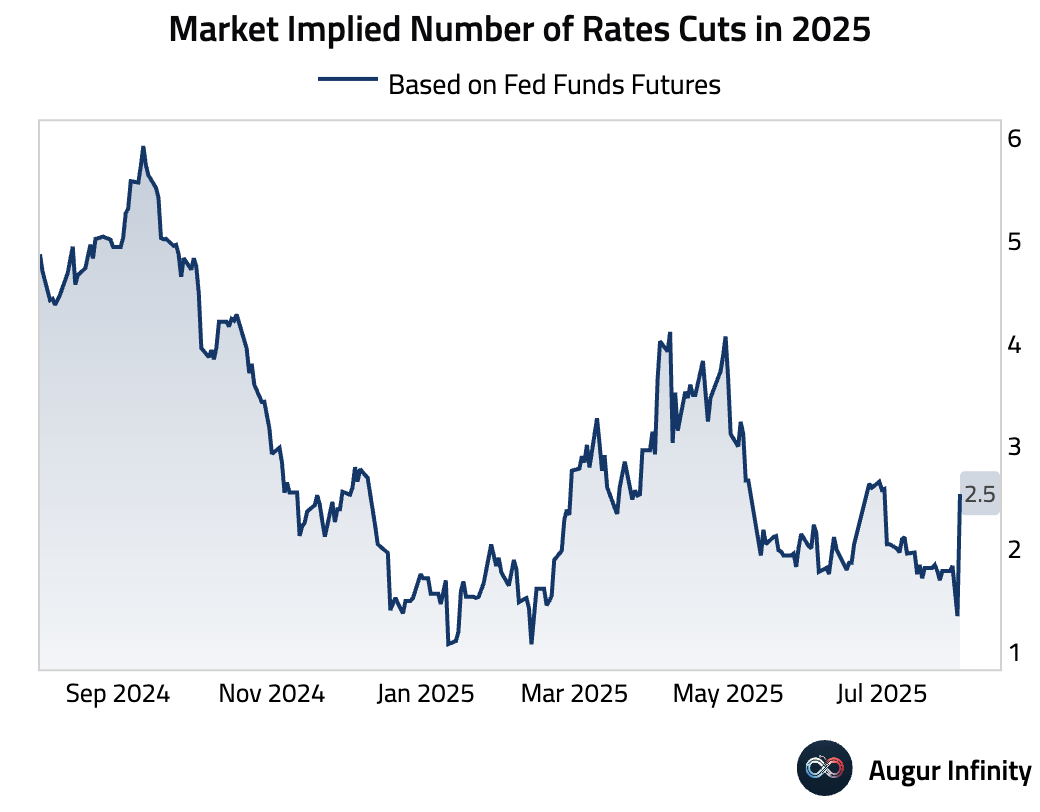

- The market is now pricing for the Fed to deliver 2.5 cuts in 2025, jumping from less than 1.5 yesterday.

Commodities

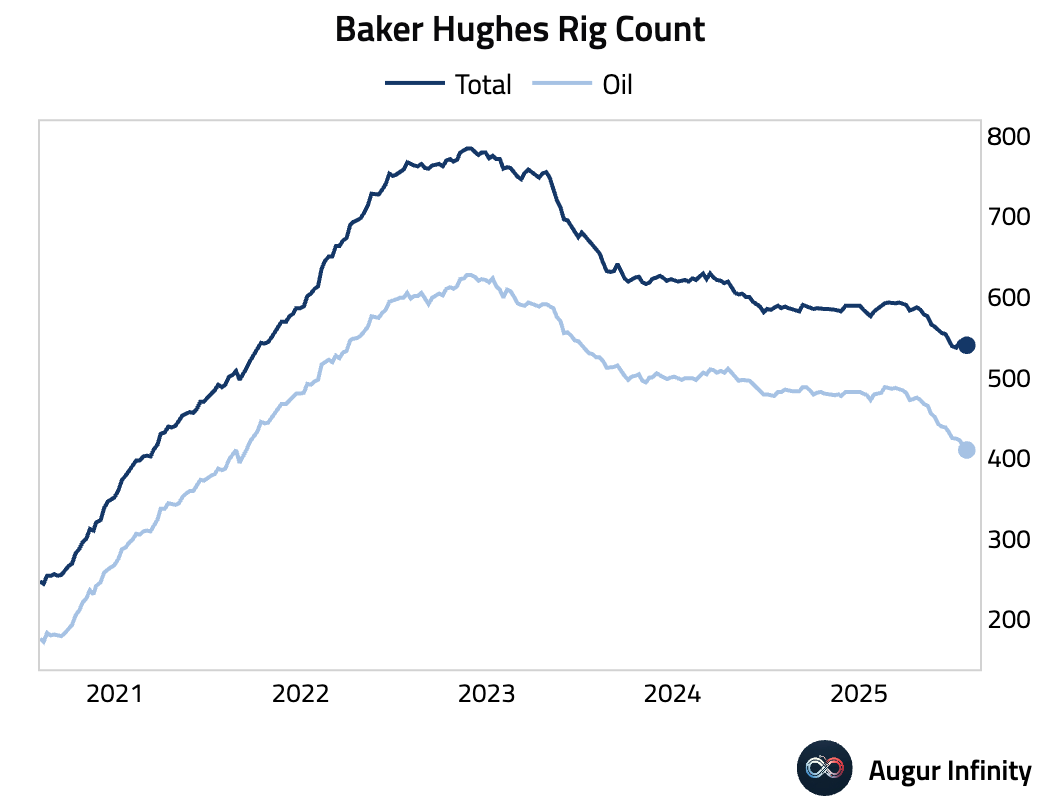

- The US Baker Hughes oil rig count fell to 410 from 415, reaching its lowest level since September 2021. The total rig count also decreased to 540 from 542.

FX

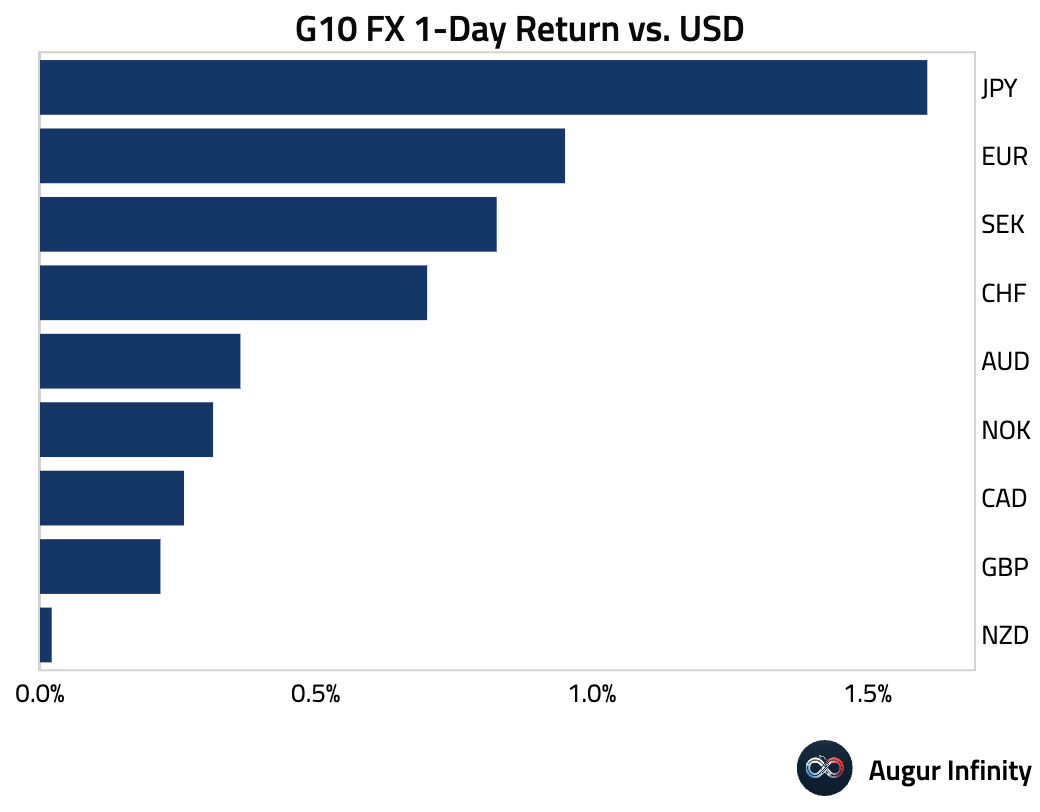

- The greenback lost significant ground to the Japanese yen, which rallied 1.6%, and the euro, which gained 1.0%. The dollar’s safe-haven status was challenged as the weak economic outlook spurred a flight into other traditional havens.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.