Headlines

- The European Union announced Monday that it is suspending for six months its planned countermeasures against the United States’ tariffs, which were set to take effect this week.

- OPEC+ announced an increase in oil output commencing in September.

- The United States implemented a 39 percent tariff on Swiss imports, prompting Switzerland's President Keller-Sutter to engage with the Trump administration.

- President Trump is expected to appoint a new Federal Reserve Governor following Adriana Kugler's resignation, effective August 8.

- Japanese Prime Minister Ishiba indicated the government's readiness to compile an extra budget should economic conditions require it.

- Reports suggest China is restricting the supply of critical minerals to Western defense contractors.

- Officials from Japan and South Korea noted that trade agreements with the United States are not yet finalized, with further details requiring negotiation.

Charts of the Day

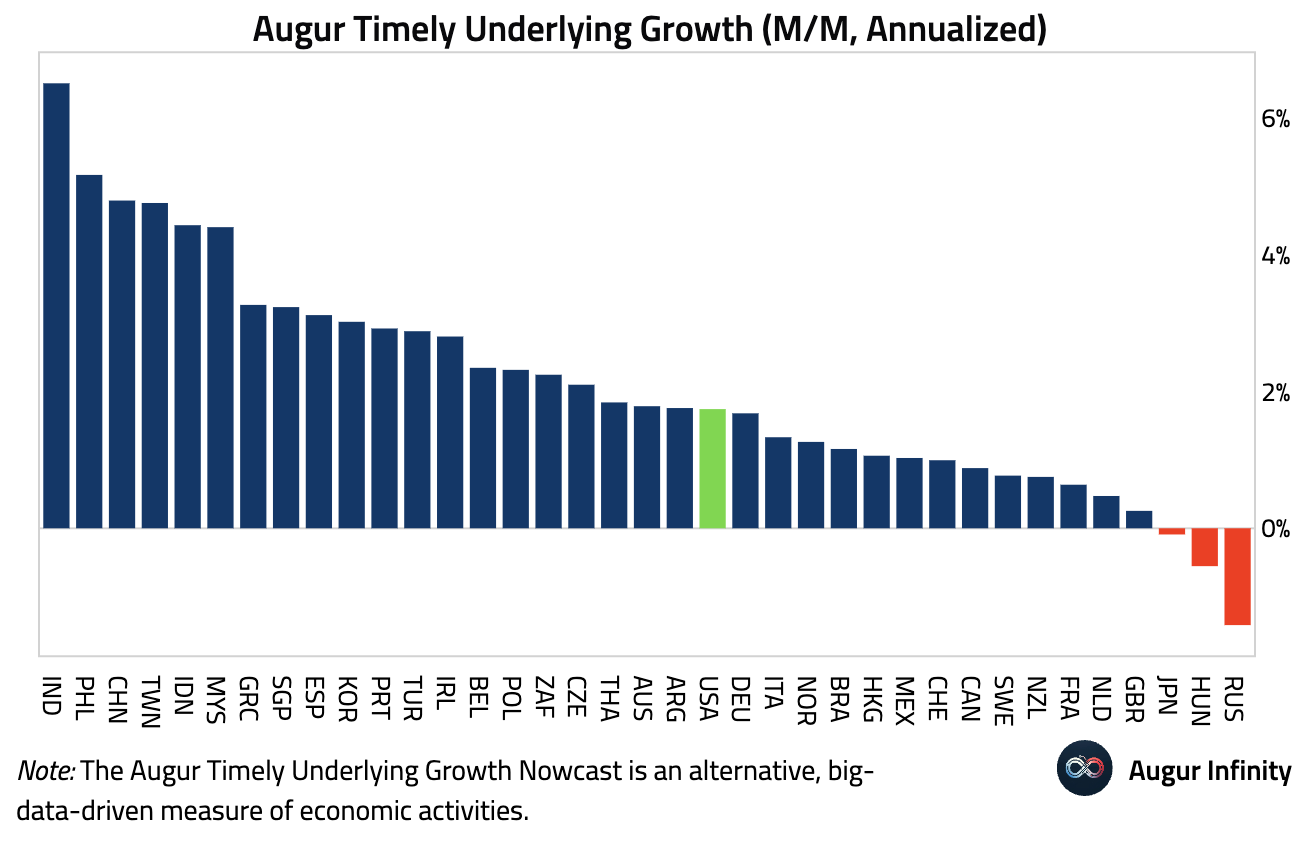

- Augur’s latest daily estimate of global growth rates for the trailing 30 days shows India leading with a growth rate of 6.5%. US growth, at 1.7%, ranks roughly in the middle of the pack, while Japan is the only developed economy with a negative growth rate.

- Here's unemployment rates for major developed countries. The unemployment rate has risen in the US, Germany, the UK, Canada, and Australia, but remains subdued in the rest of the euro area (e.g., France, Italy, and Spain).

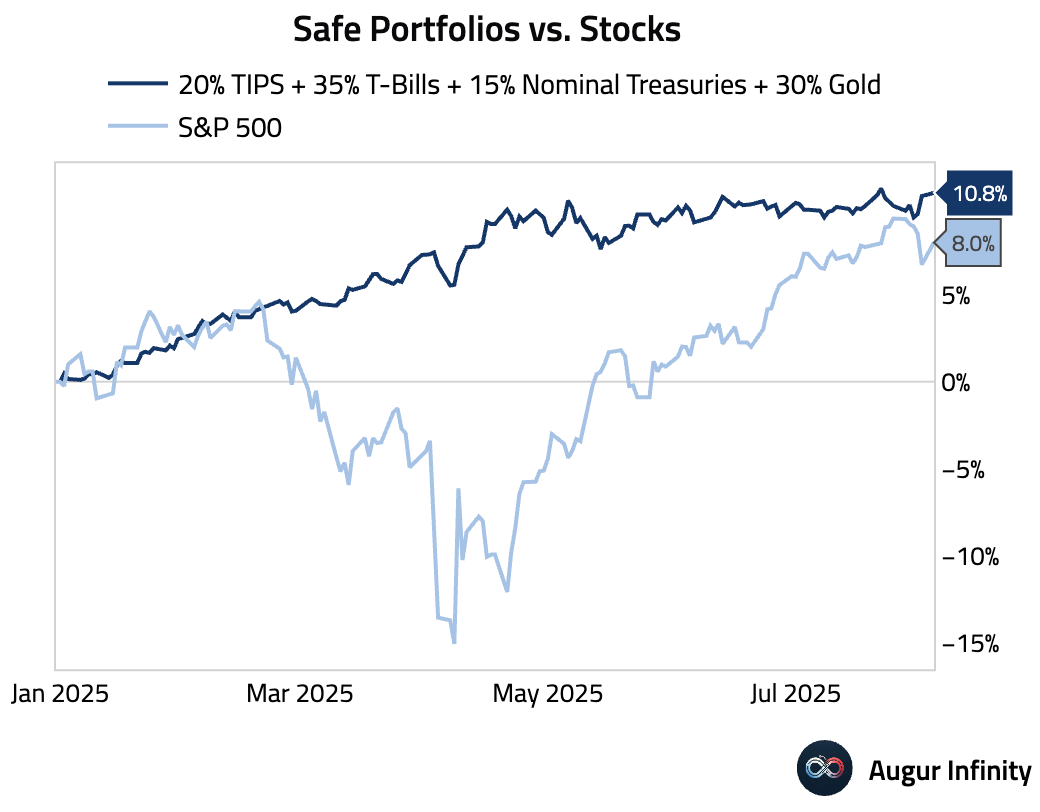

- The outperformance of the “Safe Portfolio” over the S&P 500 year-to-date is widening again.

- Here's how major assets have performed since the 2024 Election day, compared to the 2016 cycle.

Global Economics

United States

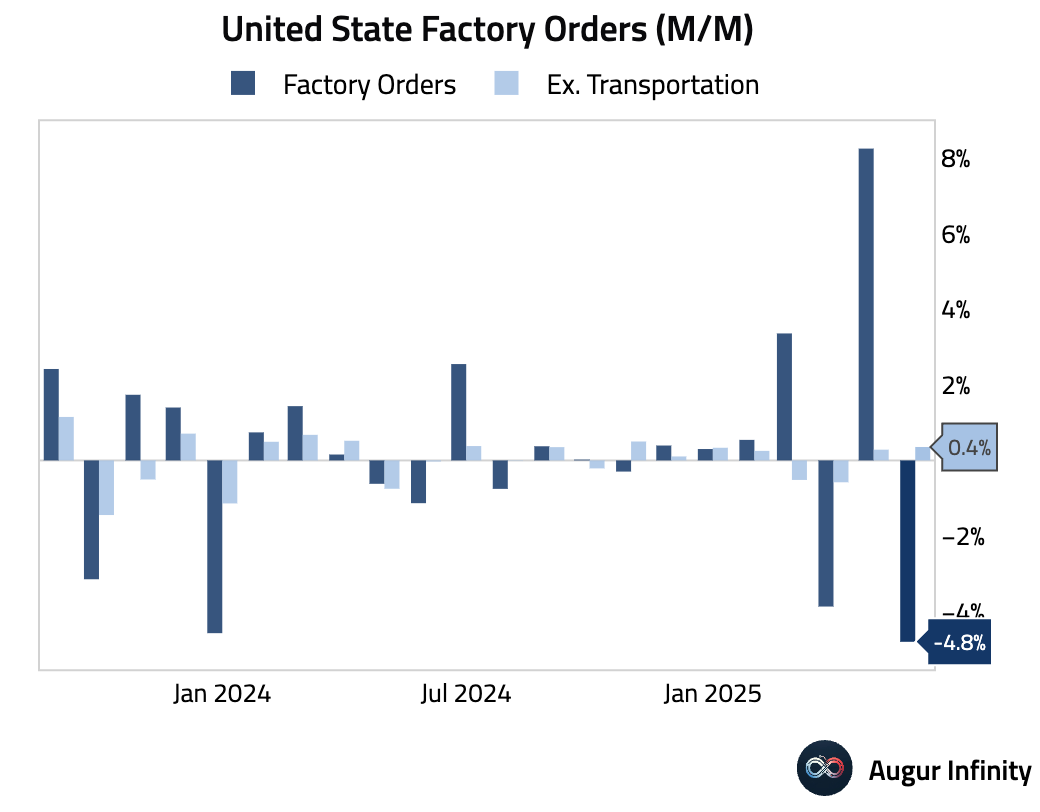

- June Factory Orders fell 4.8% M/M, in line with consensus expectations, following an upwardly revised 8.3% gain in May. The headline reading was the lowest since April 2020. Underlying details were soft, as orders ex-transportation rose 0.4%, but core capital goods orders were revised down to -0.8% and shipments were revised to 0.3%.

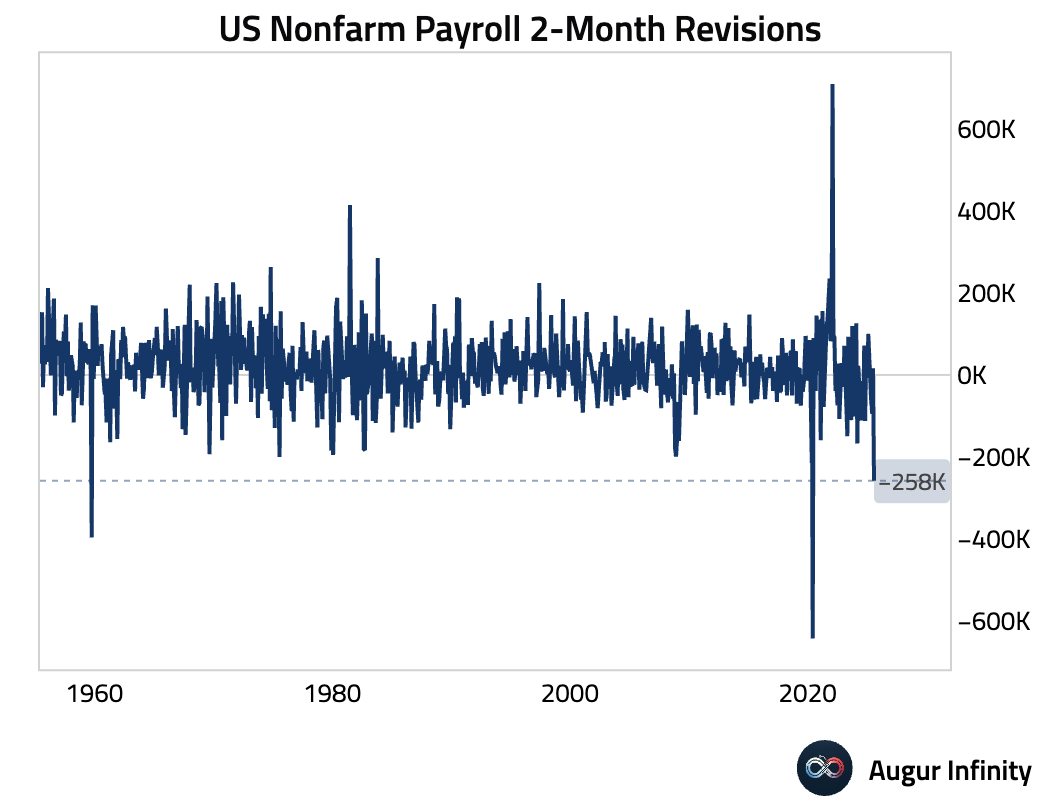

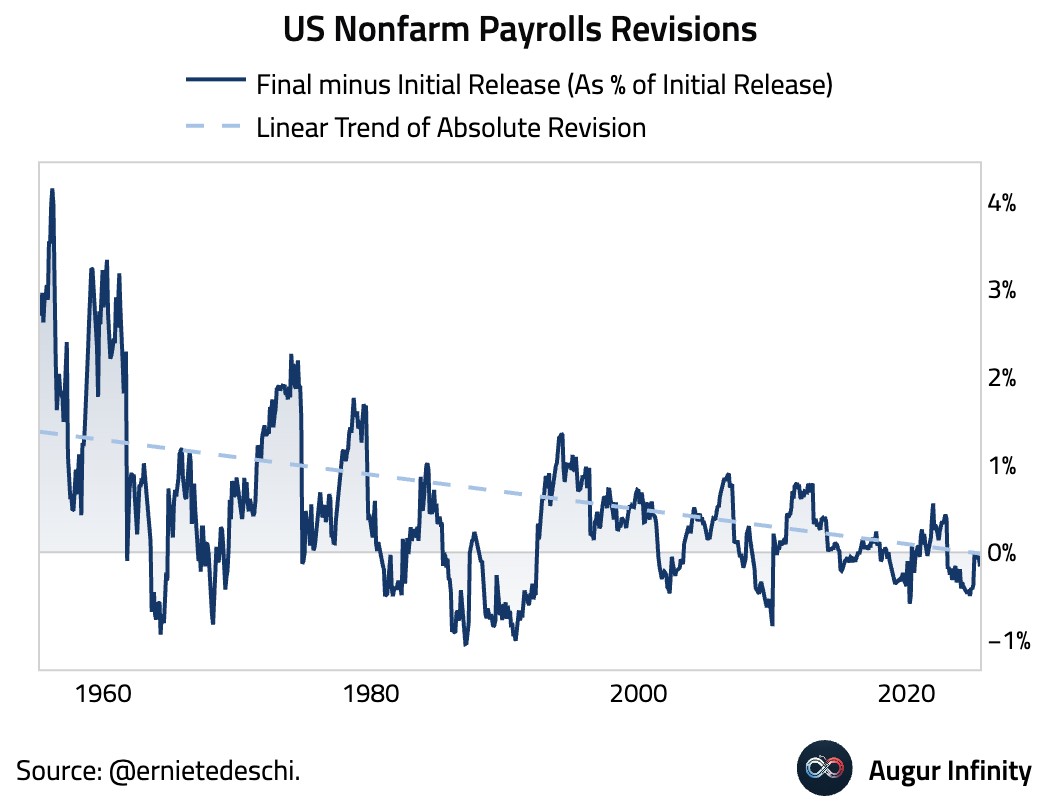

- Nonfarm payrolls were revised down by 258k for May and June. The chart below shows the historical two-month revisions going back to 1955.

- Despite recent large revisions, the magnitude of payroll data revisions from their initial release has declined over time. Since 1955, the linear trend of absolute revisions has effectively fallen to zero.

Source: @ernietedeschi

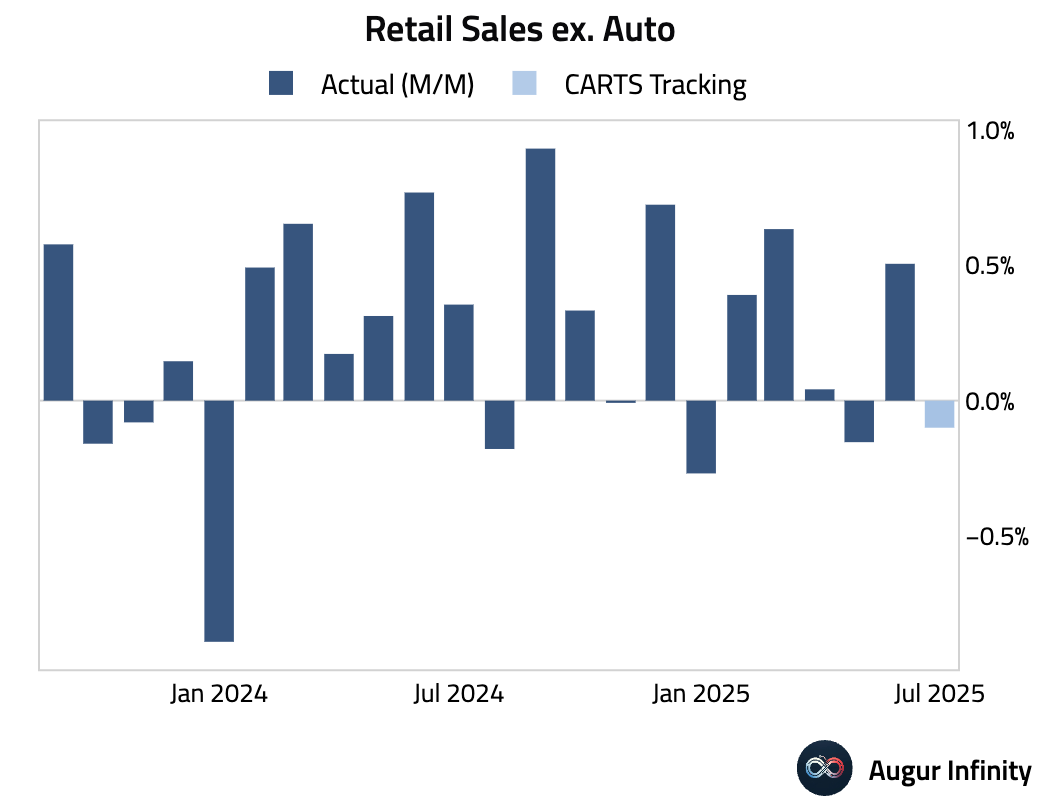

- The Chicago Fed’s CARTS model is projecting a 0.1% M/M decline for July’s retail sales ex-autos.

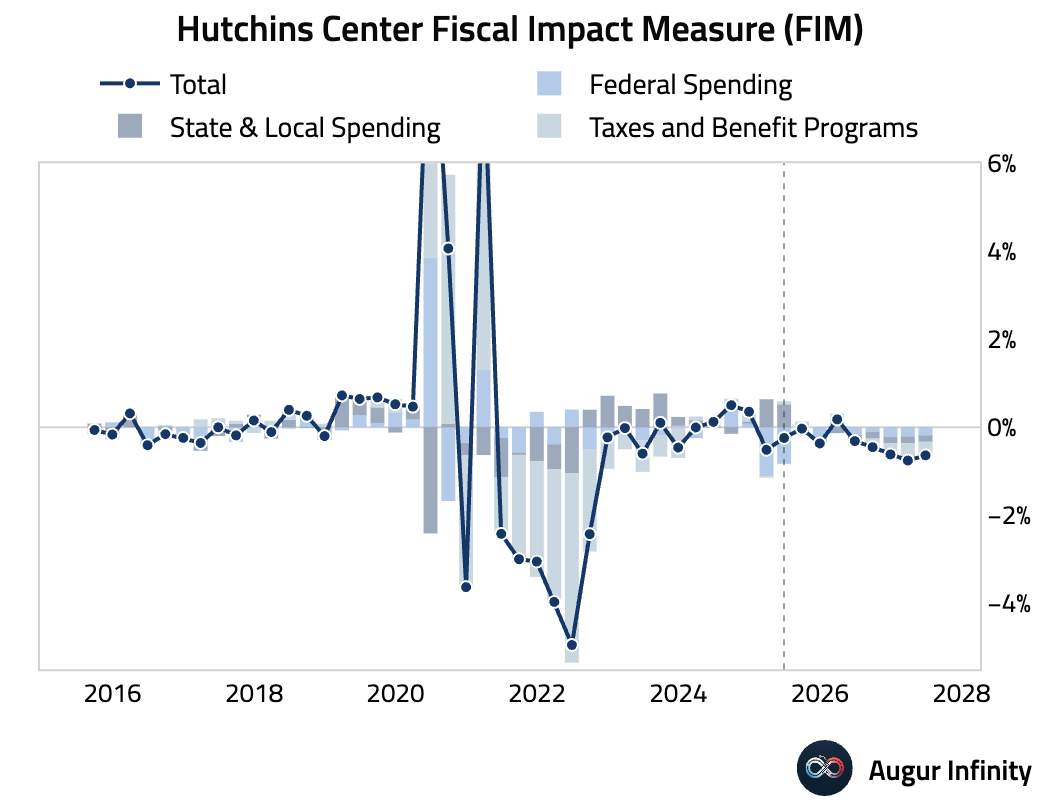

- According to the Hutchins Center Fiscal Impact Measure, fiscal policy subtracted 0.2 percentage points from US GDP growth in Q2 2025 and is expected to remain a headwind. While the One Big Beautiful Bill Act is projected to boost GDP by 0.22 percentage points in 2025 and 0.31 percentage points in 2026 relative to current policy, tariffs and policies related to federal grants to universities are expected to lower GDP by about 0.5 percentage points in each year.

Source: The Brookings Institution

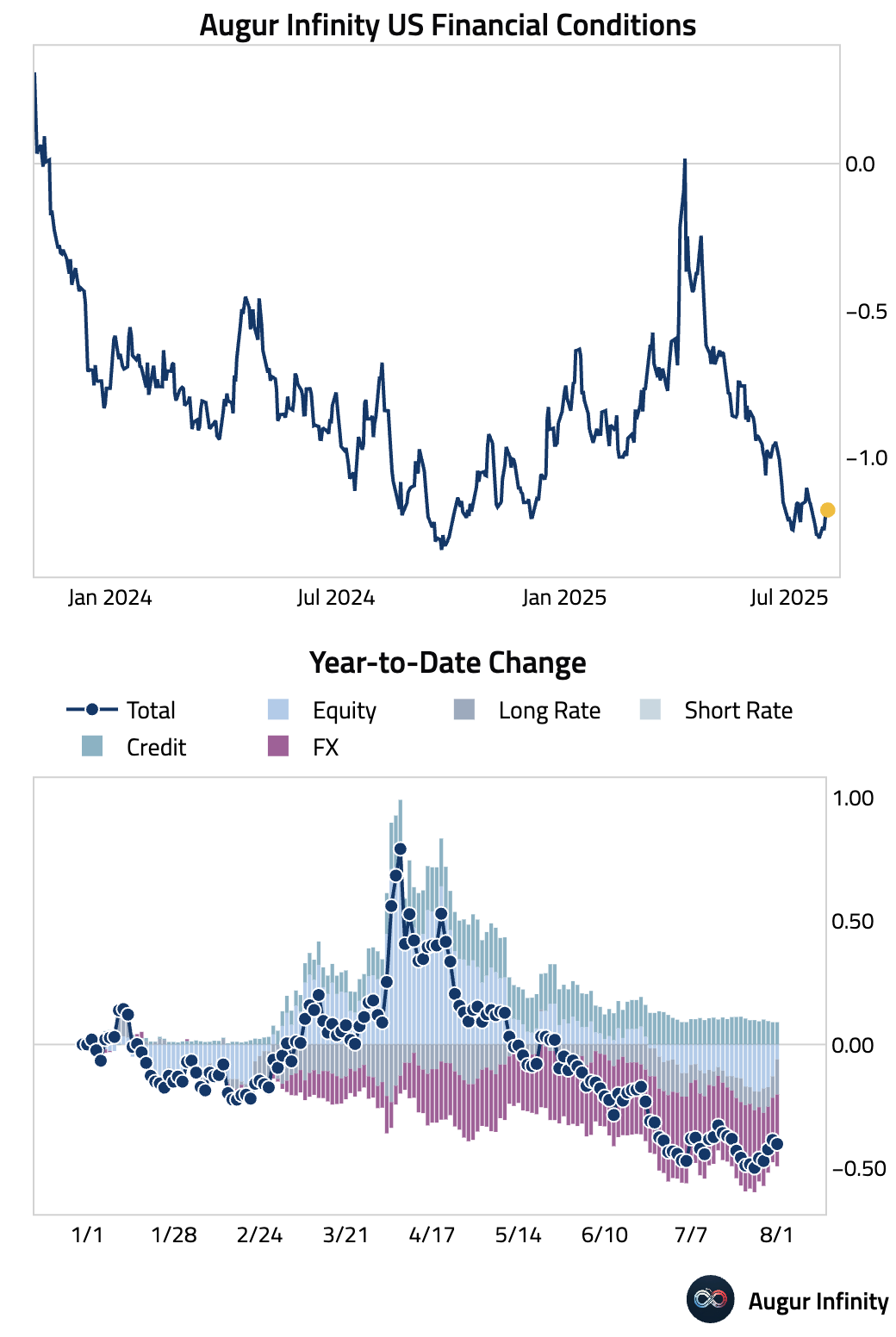

- The US Financial Conditions Index has tightened slightly but remains at very easy levels by historical standards.

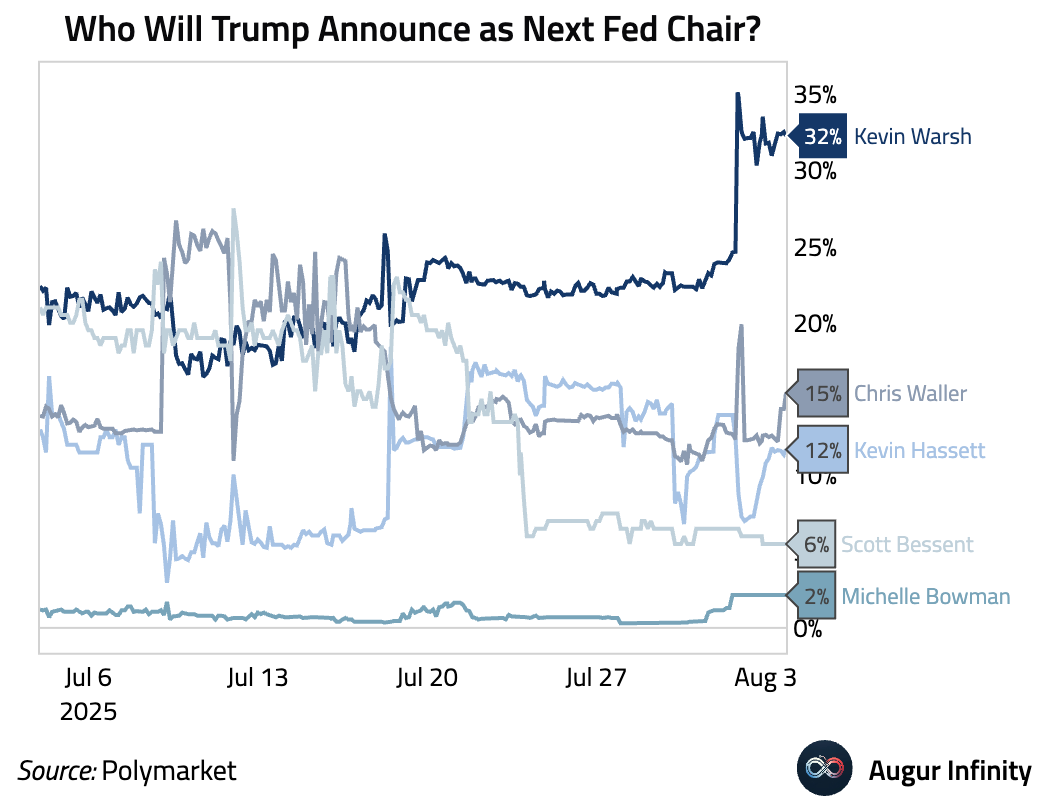

- The probability of Kevin Warsh being announced as the next Fed Chair is on the rise on betting markets.

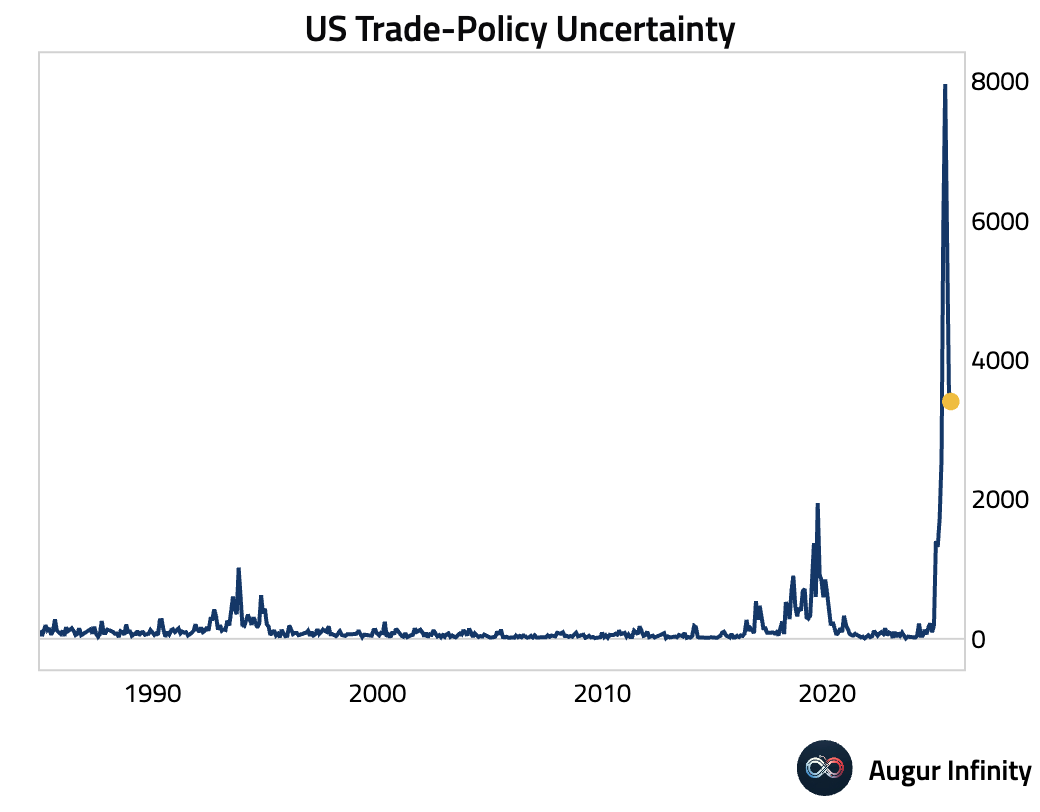

- US trade-policy uncertainty has fallen from its April peak but remains at historically elevated levels.

Europe

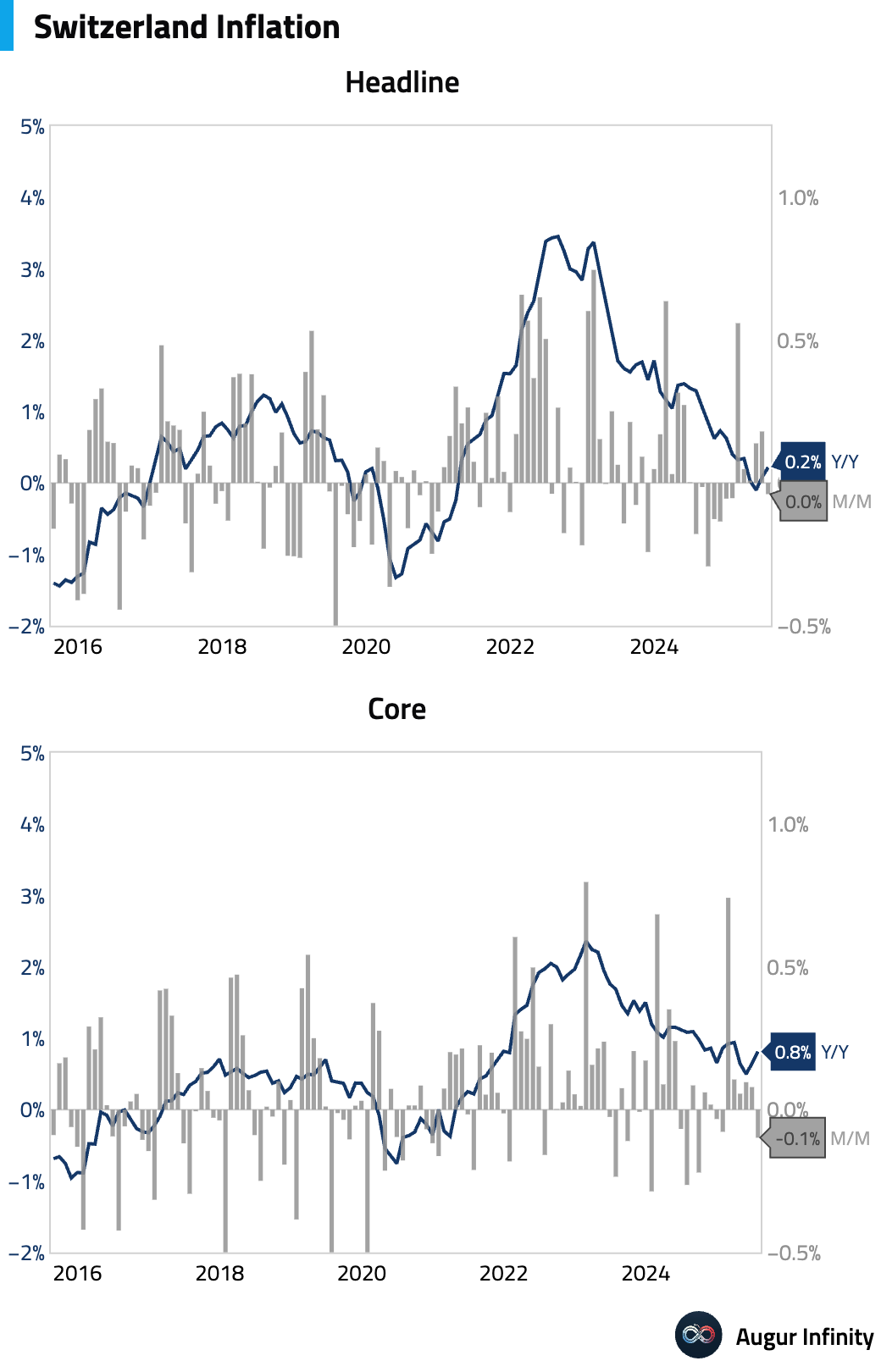

- Switzerland’s inflation rate came in higher than expected in July, with the Y/Y rate rising to 0.2% (consensus: 0.1%) from 0.1% previously. The M/M rate was flat at 0.0% (consensus: -0.2%), arresting a two-month slide.

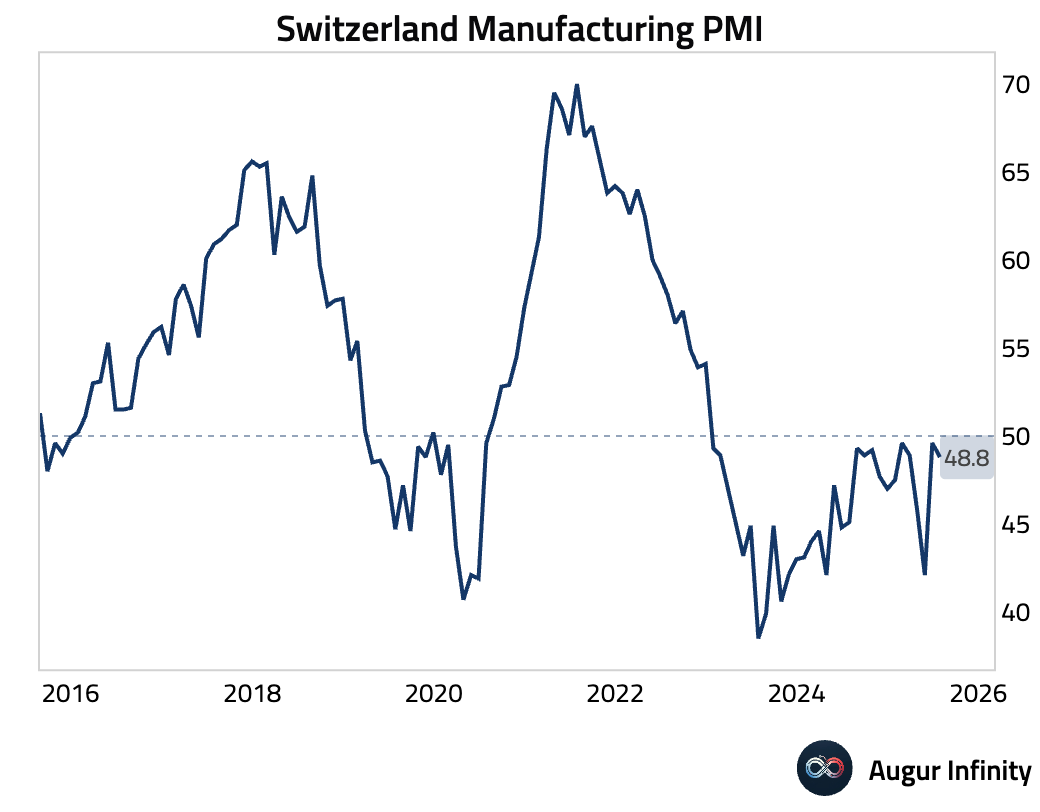

- The Swiss procure.ch Manufacturing PMI fell to 48.8 in July from 49.6, missing the consensus forecast of 49.9 and signaling a faster contraction in the manufacturing sector.

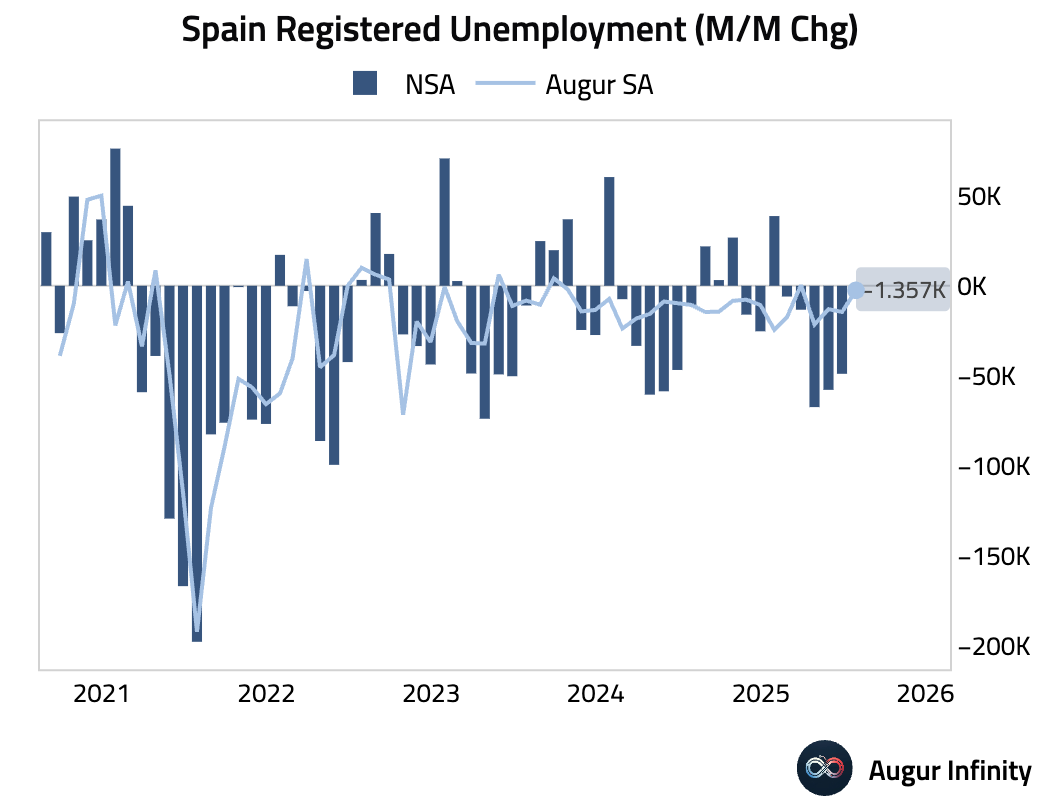

- Spain’s unemployment change for July showed a much smaller-than-expected decline of 1,400, well below the consensus forecast for a 21,300 drop.

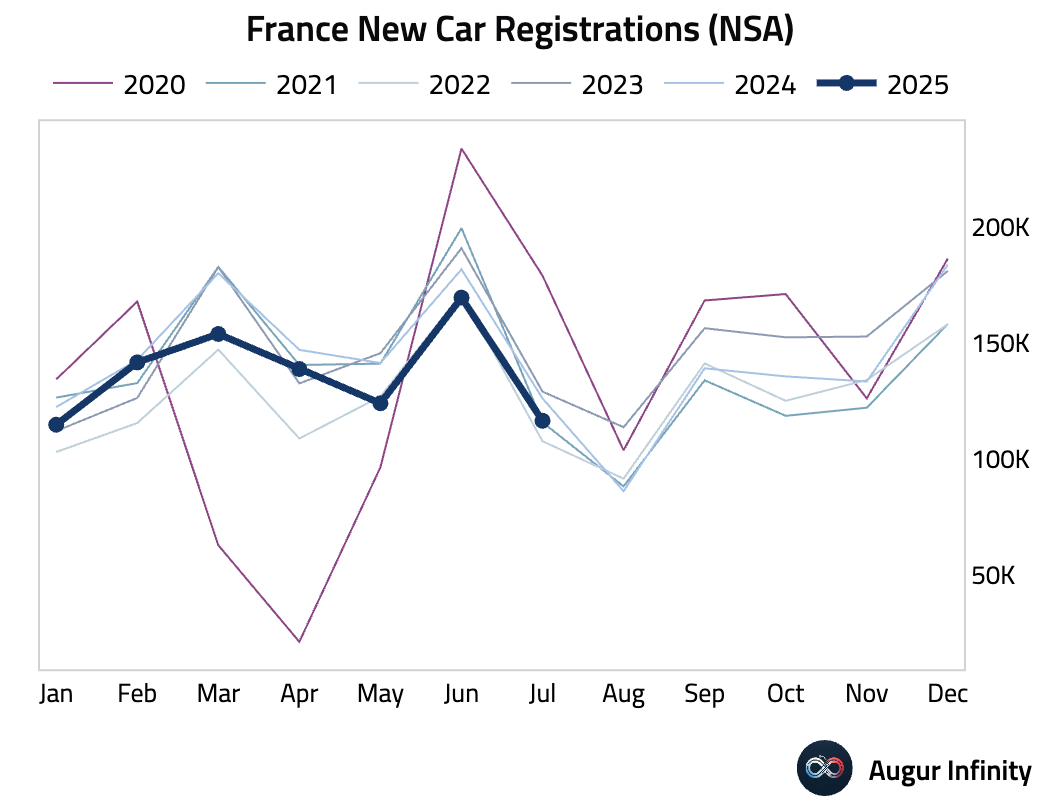

- French new car registrations fell 7.7% Y/Y in July, a further deterioration from the 6.7% decline seen in June.

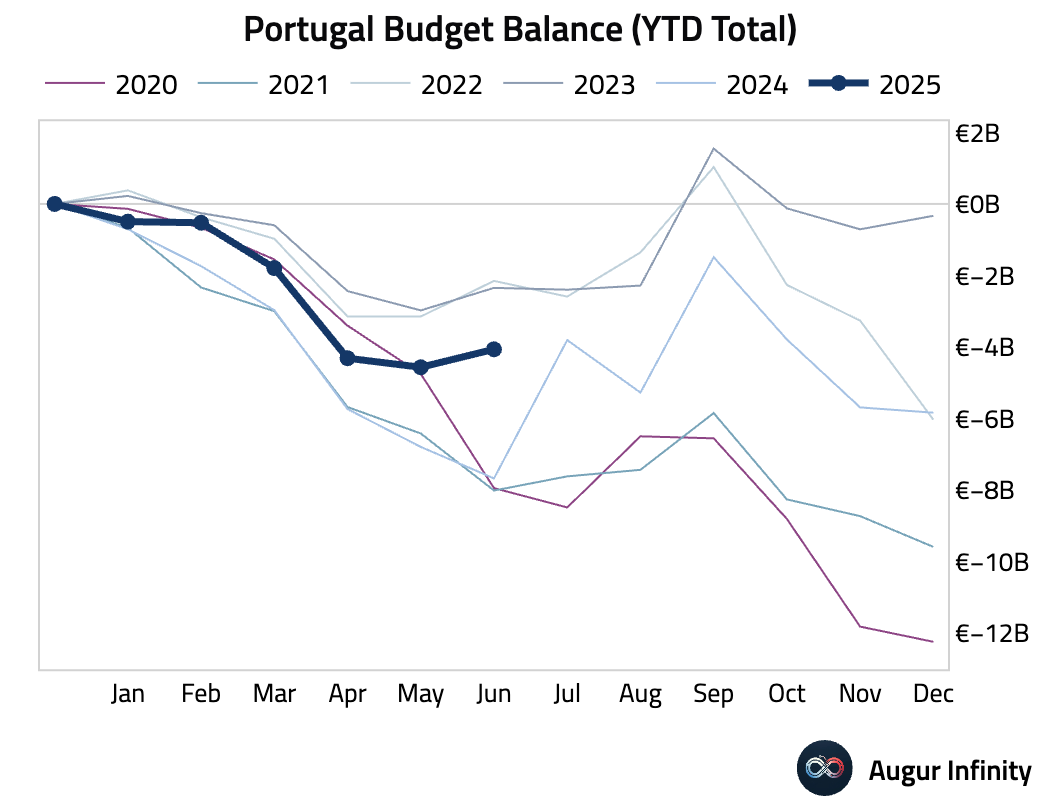

- Portugal’s year-to-date budget balance improved slightly to a deficit of €4.1 billion in July from €4.6 billion in the prior month.

Asia-Pacific

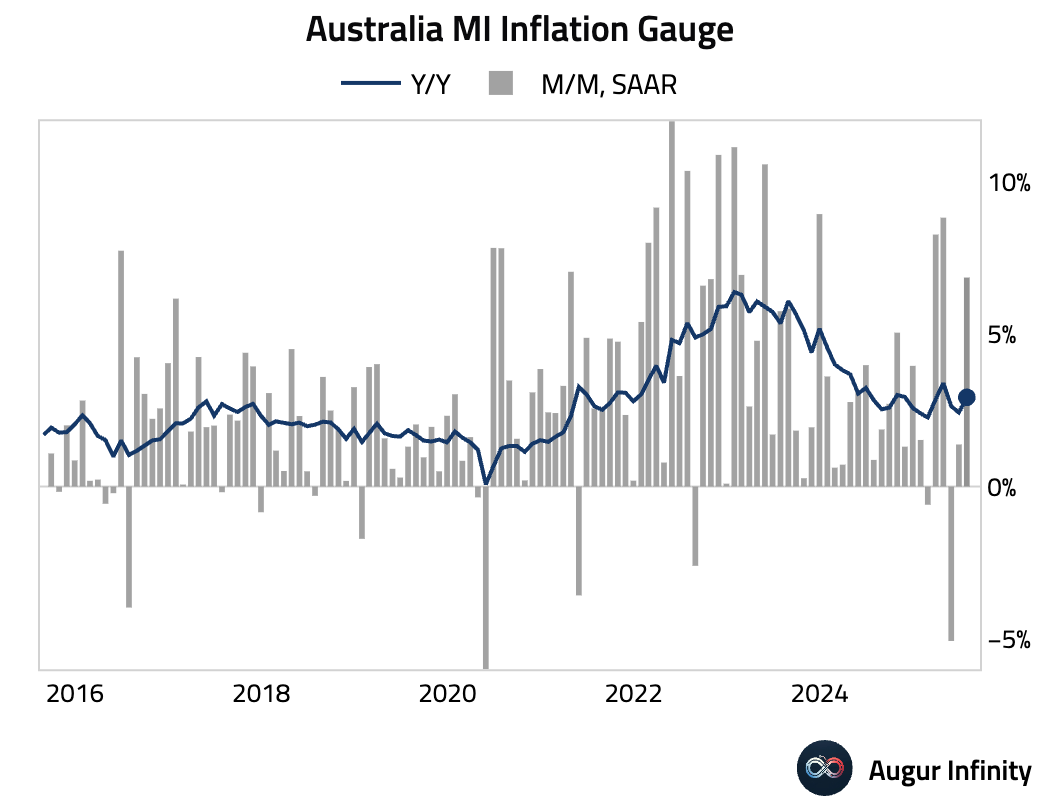

- Australia’s TD-MI Inflation Gauge accelerated to 0.9% M/M in July from 0.1% in June.

Emerging Markets ex China

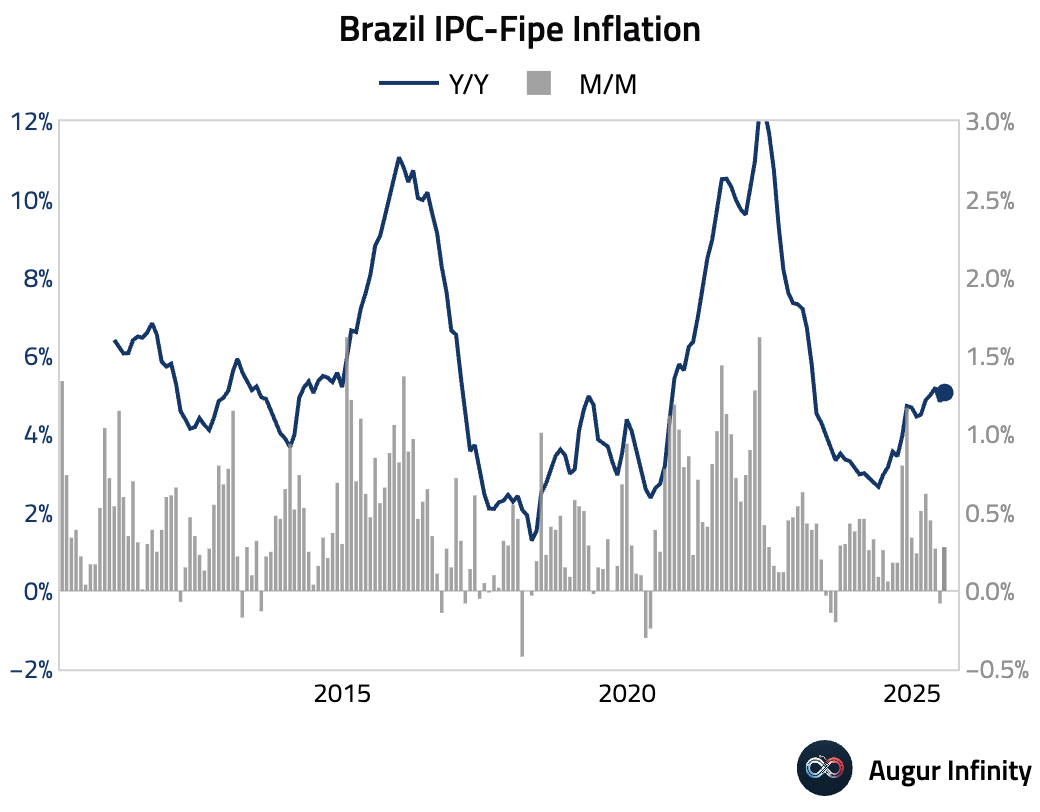

- Brazil’s IPC-Fipe monthly inflation for São Paulo turned positive in July, rising to 0.28% from -0.08% in the previous month.

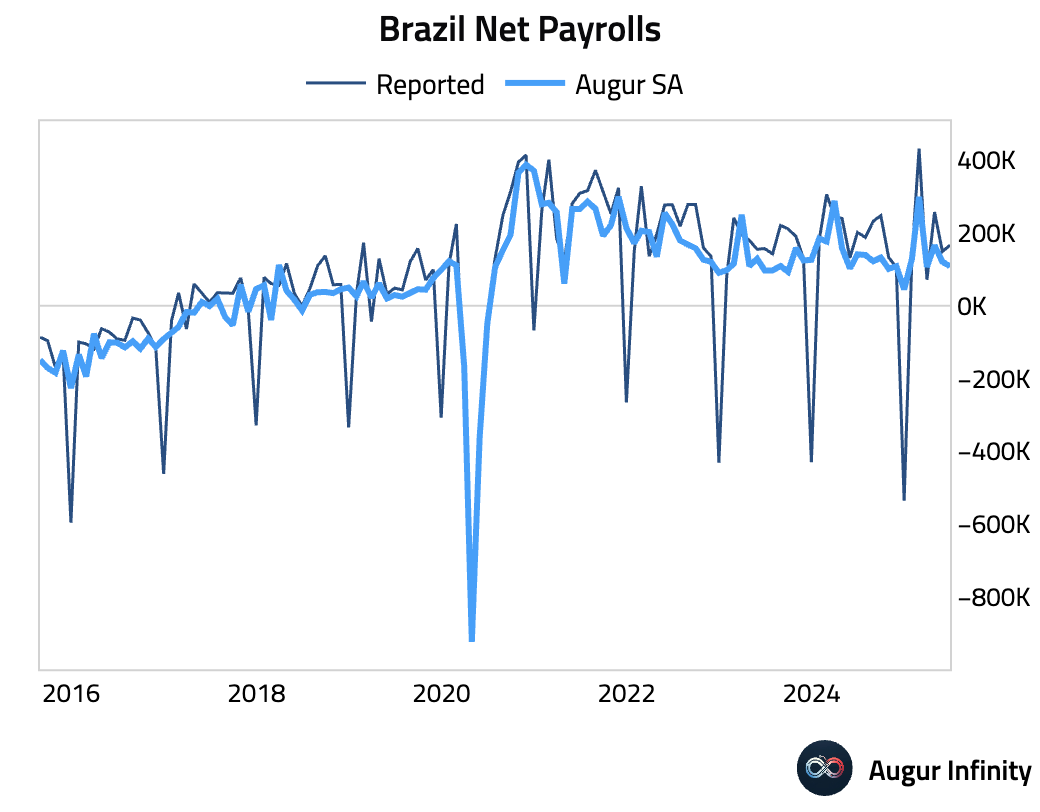

- Brazilian net payroll creation increased to 166,620 in June, up from 148,990 in May. On a seasonally-adjusted basis, however, net payroll declined slightly on the month.

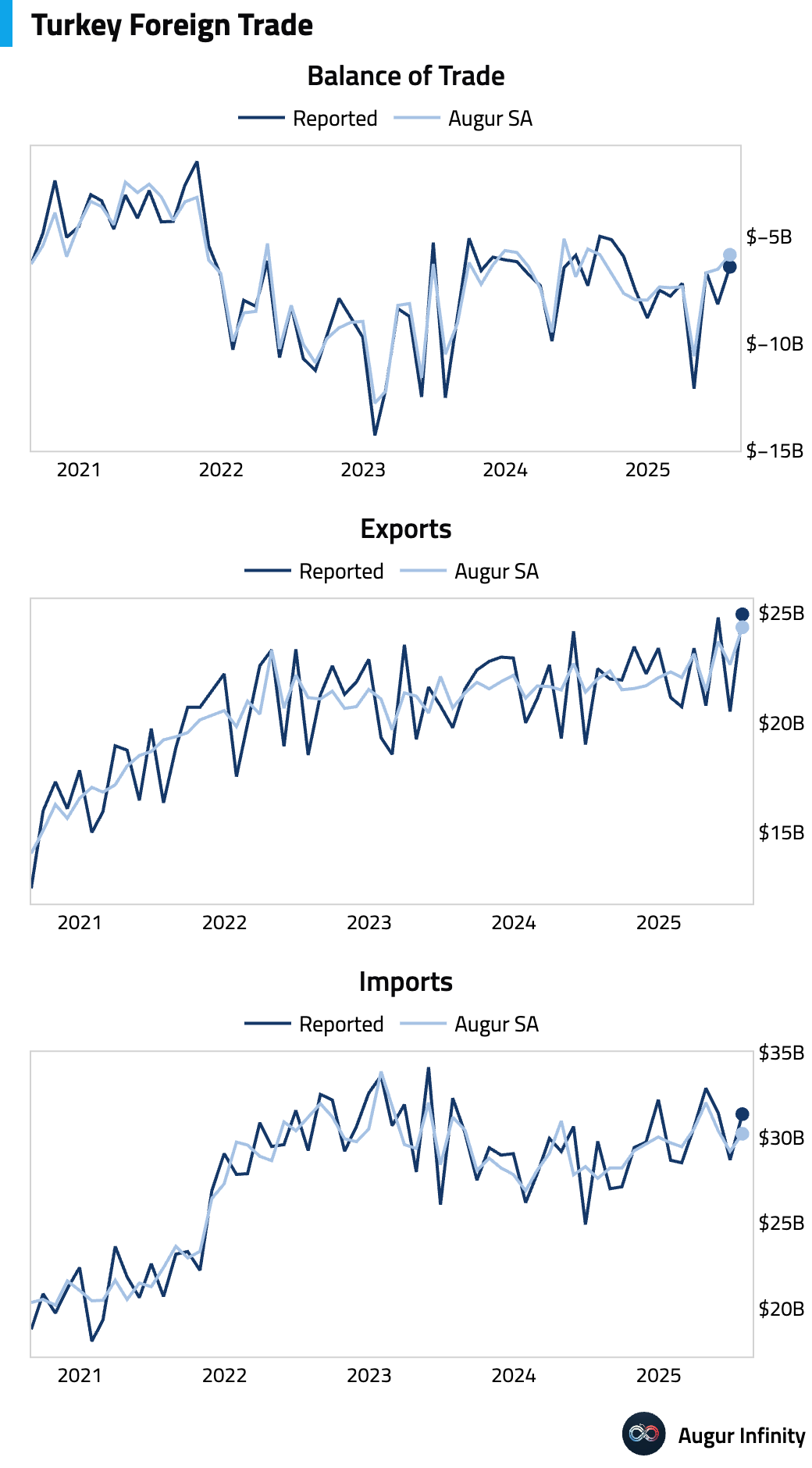

- Turkey’s preliminary trade deficit narrowed to $6.4 billion in July from $8.2 billion in June. Exports surged to an all-time high of $25.0 billion, while imports rose to $31.4 billion.

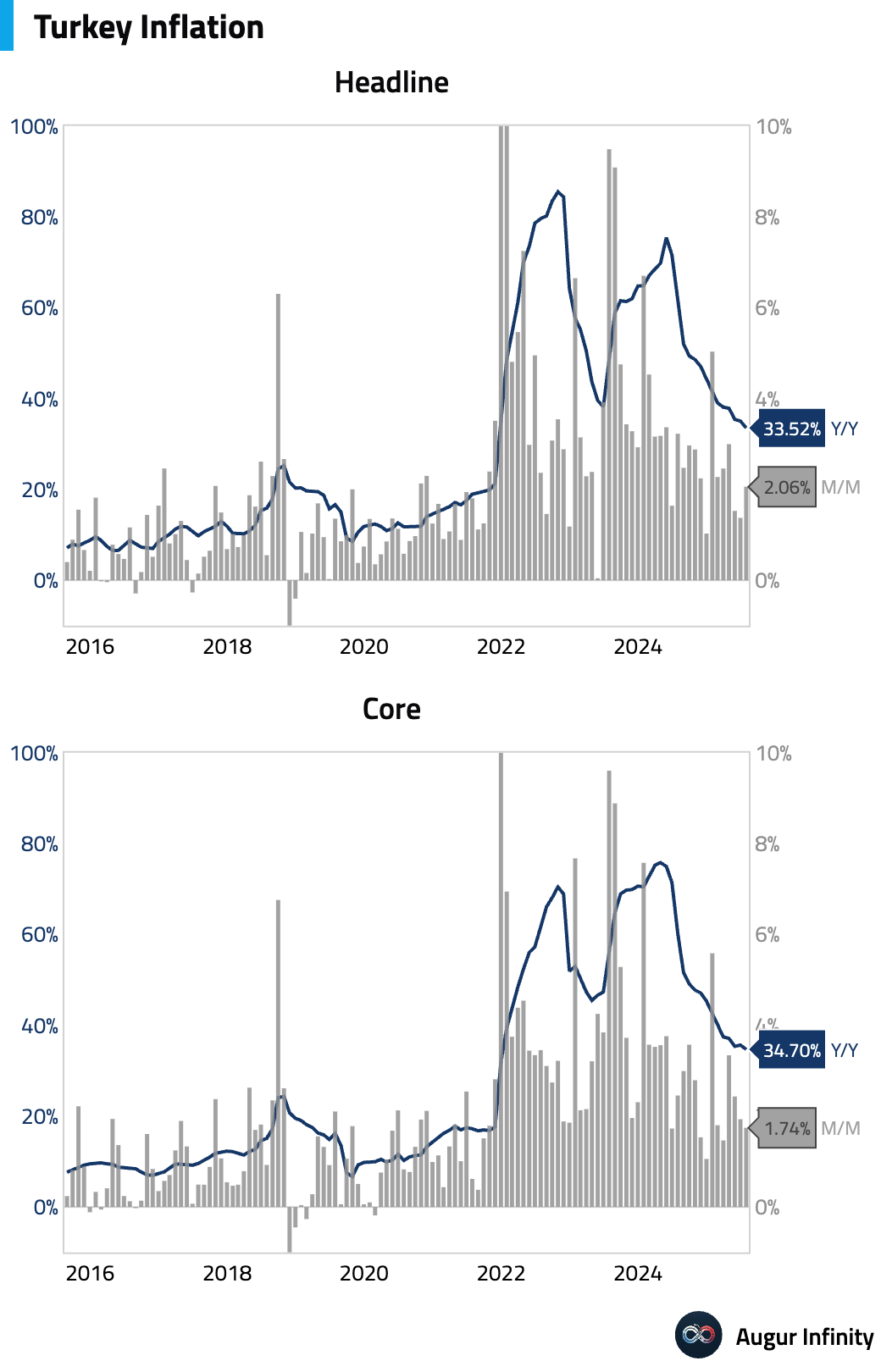

- Turkish inflation decelerated more than expected in July. The Y/Y rate fell to 33.52% (consensus: 34.05%) from 35.05%, marking the lowest annual rate since November 2021. The M/M rate accelerated to 2.06% (consensus: 2.4%) due to regulated price hikes, but a key positive was an unexpected slowdown in services momentum, which helped offset upward pressures from energy and rent.

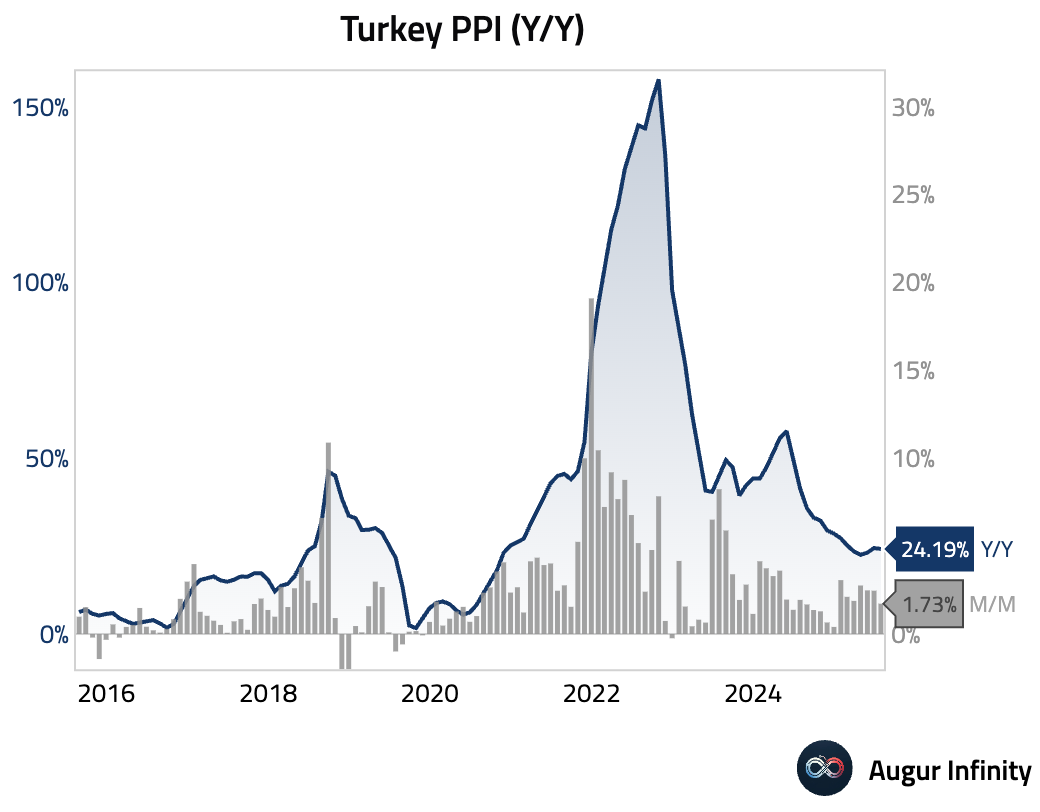

- Turkey’s Producer Price Index (PPI) inflation continued to moderate in July, with the Y/Y rate falling to 24.19% from 24.45% and the M/M rate slowing to 1.73% from 2.46%.

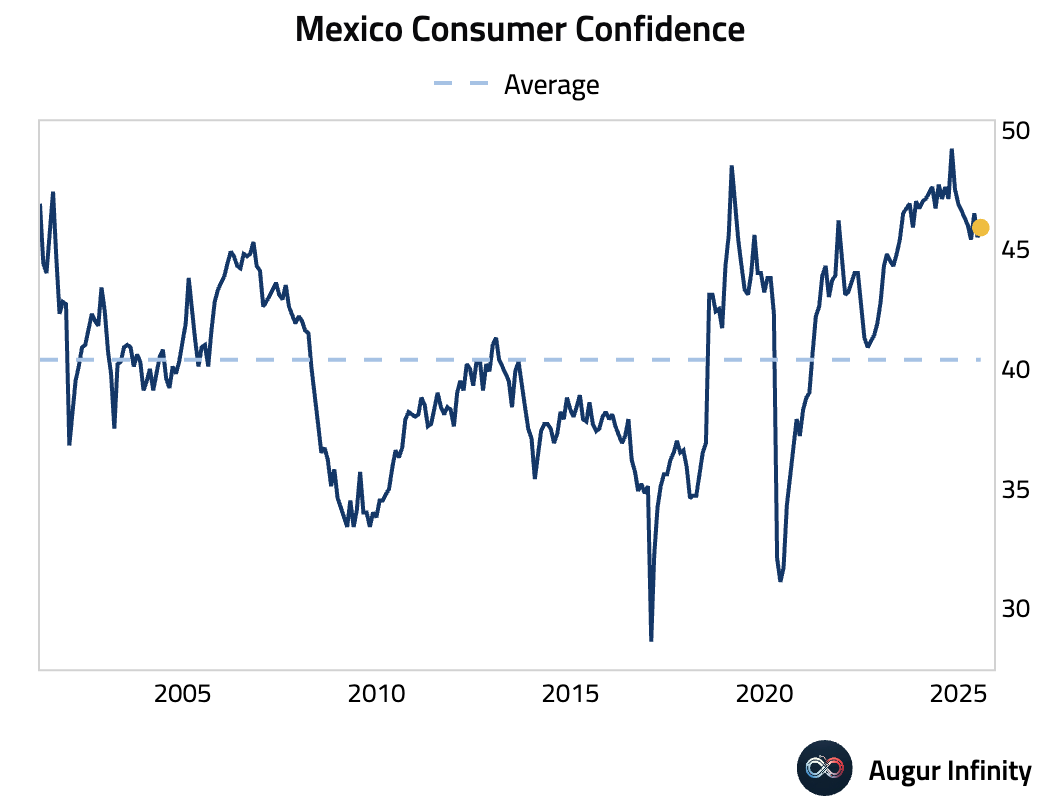

- Mexico’s consumer confidence rose 0.4 points to 45.9 in July, a slight rebound after falling in seven of the prior nine months. The increase was driven by a sharp 2.5-point jump in the durable goods purchase sub-index, though expectations for the future economy and household finances both edged down, suggesting underlying consumer caution.

Global Markets

Equities

- Global equities saw broad gains today, with the overall global market up 1.4%. US equities gained 1.4%, led by the Nasdaq which rose 2%.

- Among other major markets, China rose 1.8% and South Korea saw a significant increase of 2.4%.

- Mexico continued its losing streak, recording its fourth consecutive day of losses.

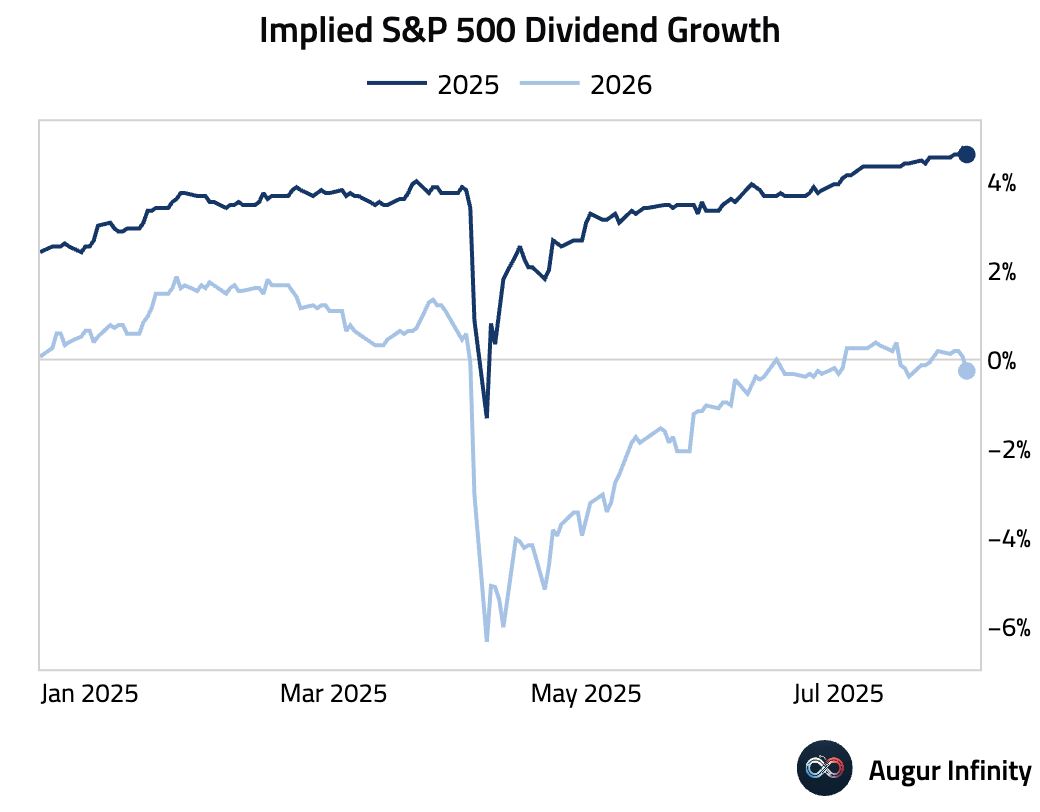

- Implied dividend growth for 2025, based on dividend futures, has risen to roughly the highest level this year. However, implied dividend growth for 2026 has turned negative again.

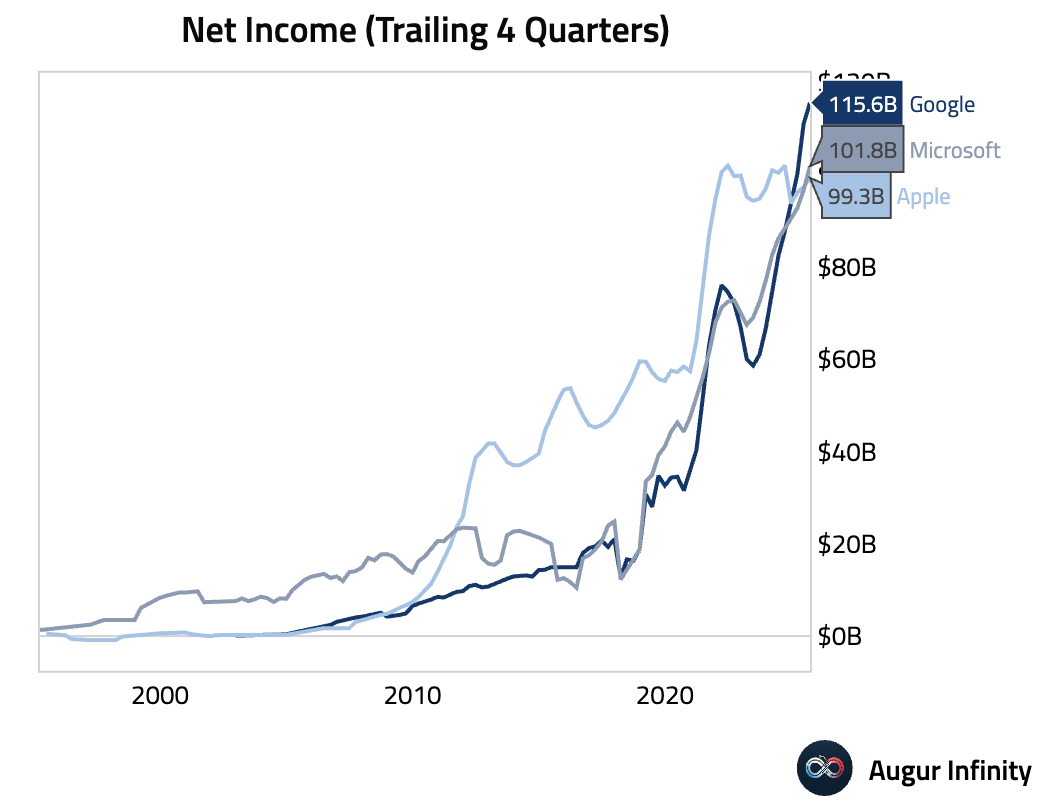

- Google's trailing four-quarter net income has surpassed both Apple and Microsoft, making it the most profitable company in the world.

Source: @StockSavvyShay

Fixed Income

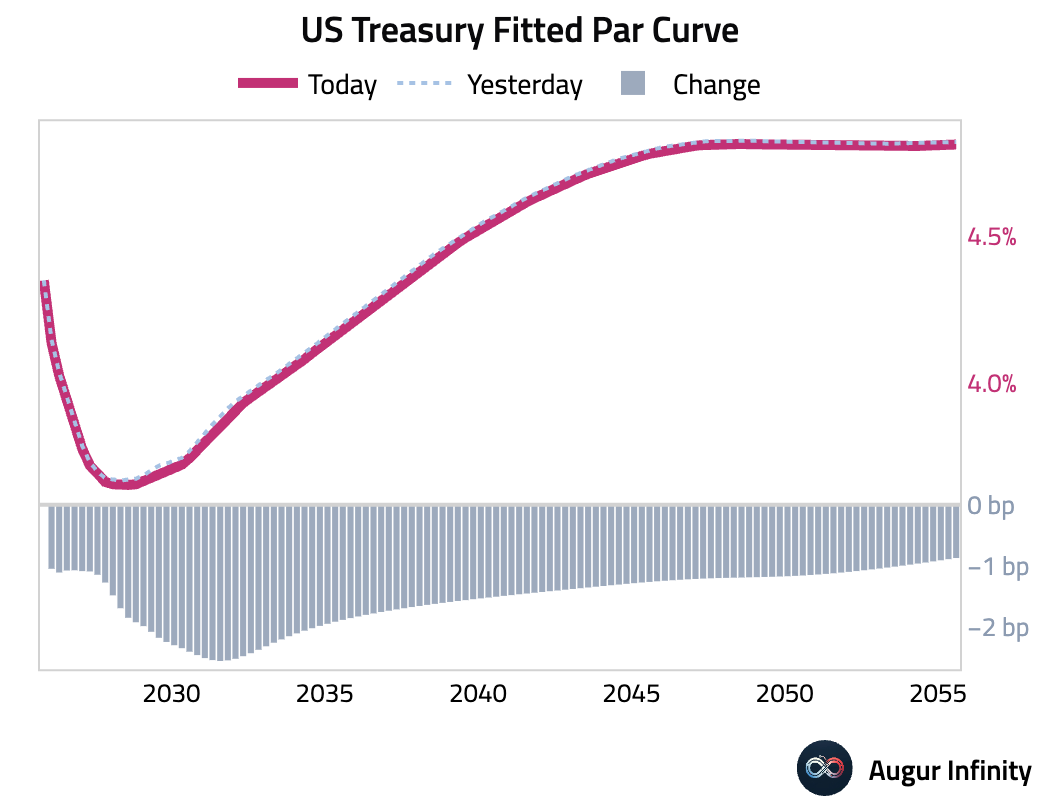

- US Treasury yields declined across the curve today. The 5Y, 10Y, and 30Y Treasury yields each recorded their third consecutive day of decreases, falling by 2.4 bps, 2.2 bps, and 1.2 bps respectively. The 2Y Treasury yield also declined by 1.4 bps.

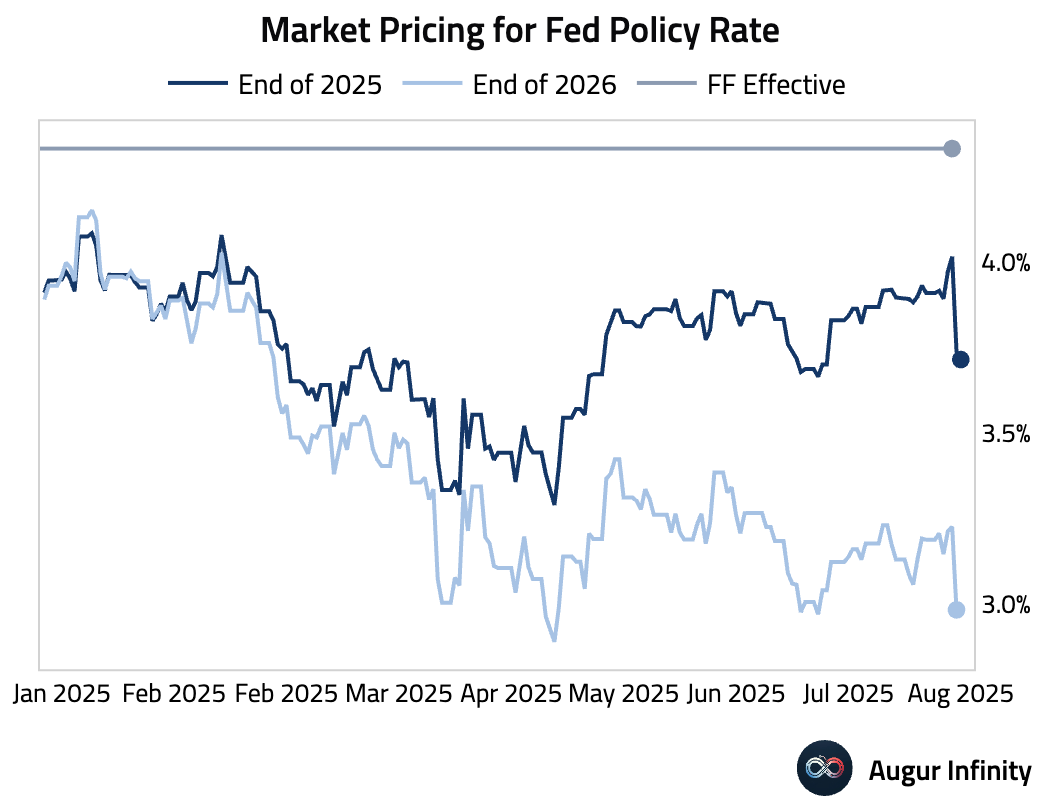

- Market pricing for the Fed policy rate at the end of 2025 and 2026 declined sharply after Friday's nonfarm payroll release.

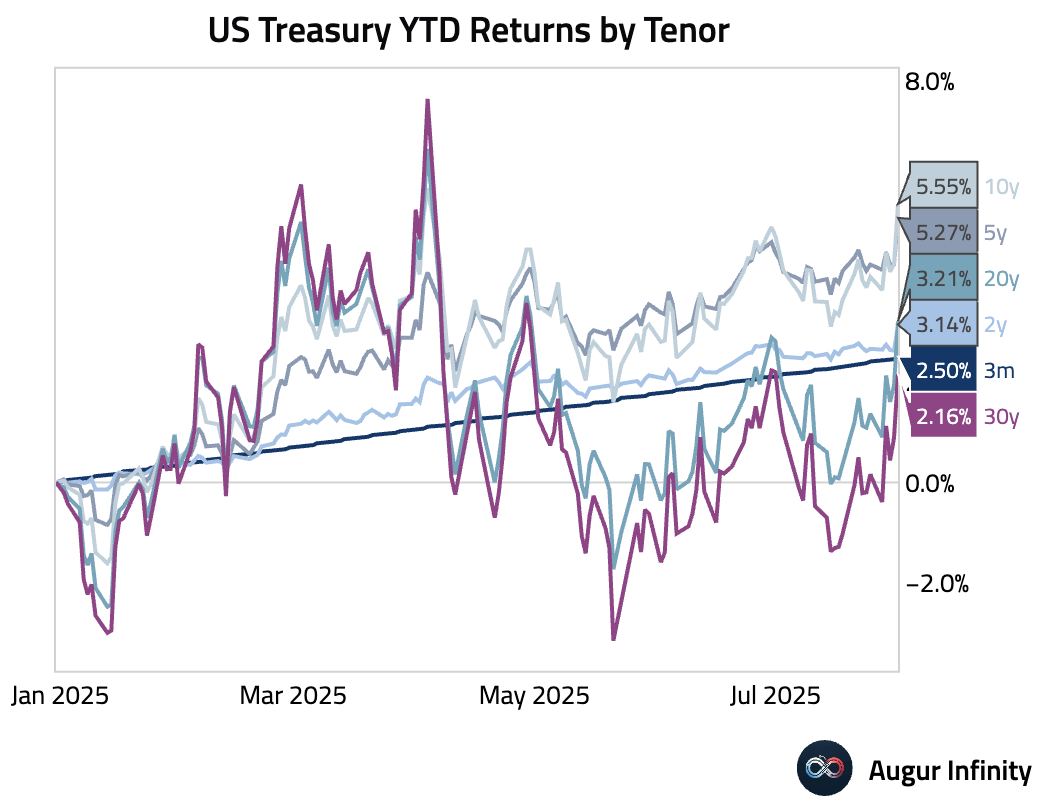

- US Treasuries are now solidly in the black across all tenors.

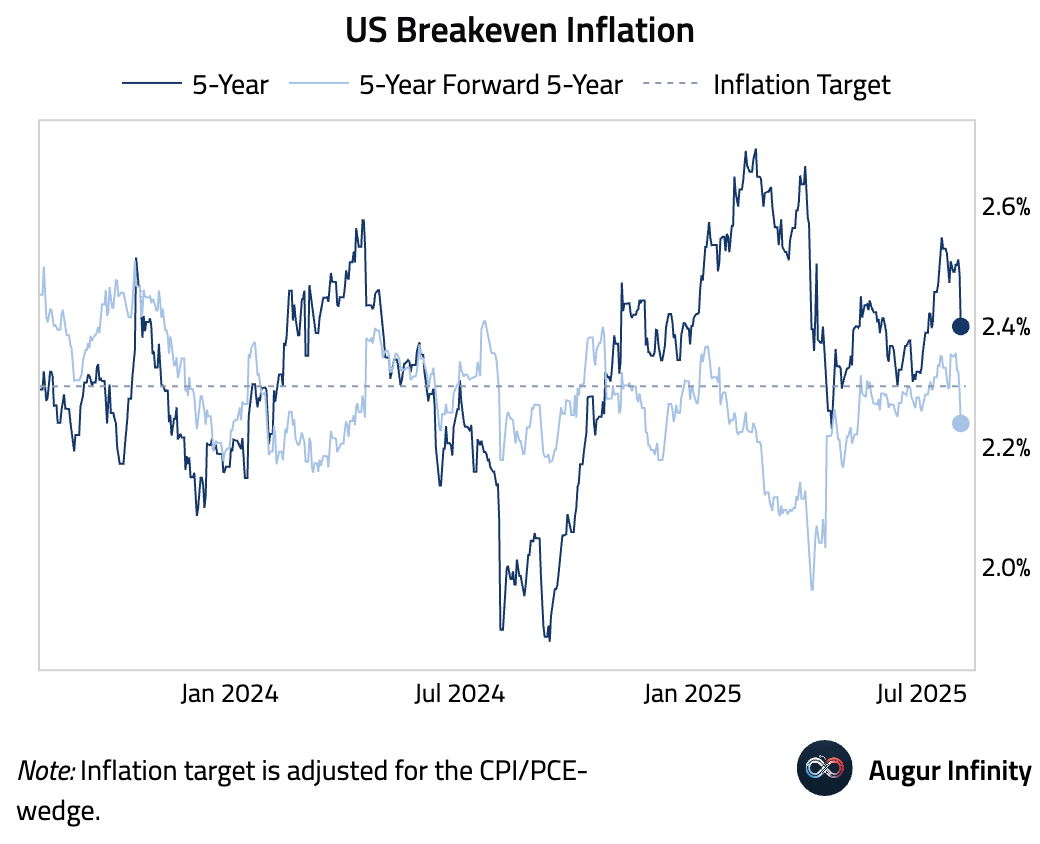

- US breakeven inflation fell meaningfully over the past few sessions.

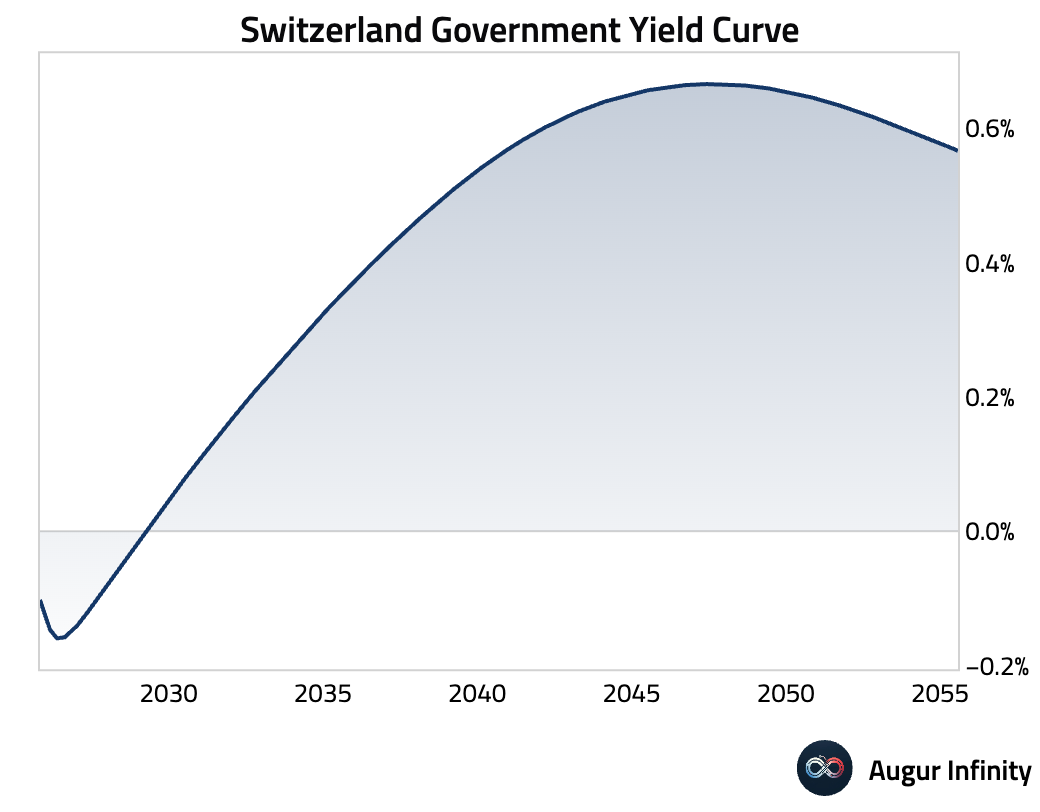

- Switzerland government bond yields are now negative through the 3.5-year point of the curve, amidst increased US trade policy uncertainty following the announcement of new tariffs on Swiss imports.

Commodities

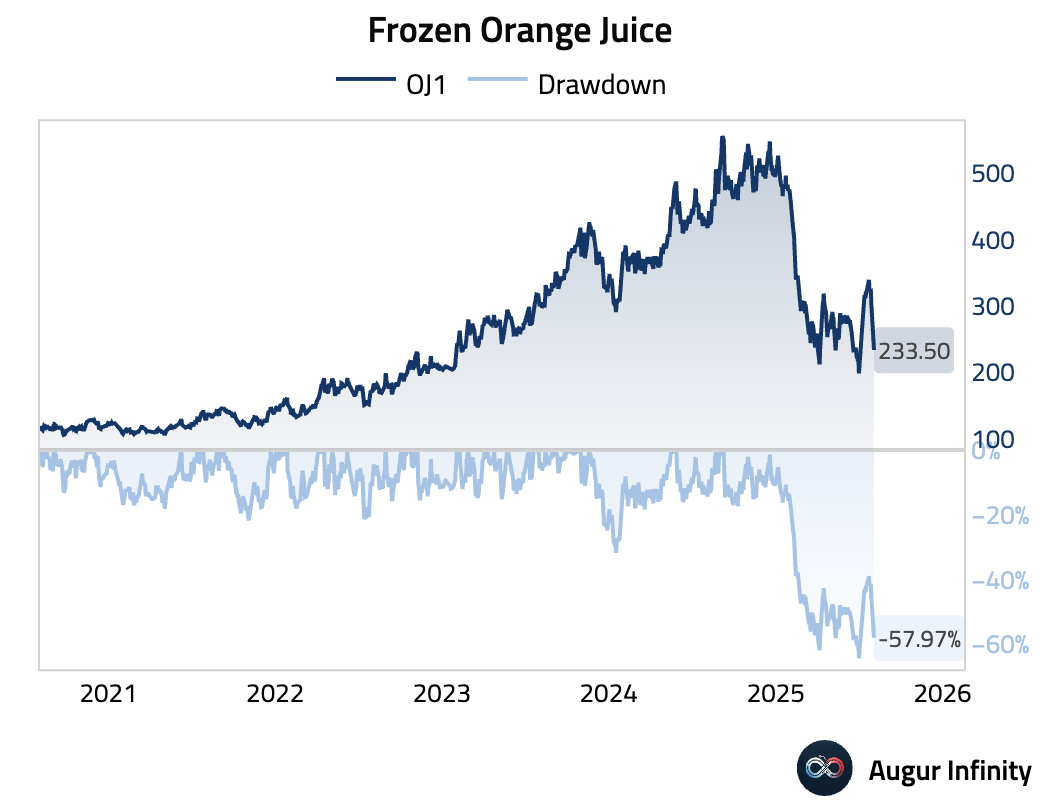

- Frozen orange juice rallied in July due to mounting worries of US tariffs on Brazilian goods curbing supplies. Since then, the price has declined by roughly 30% since its peak.

FX

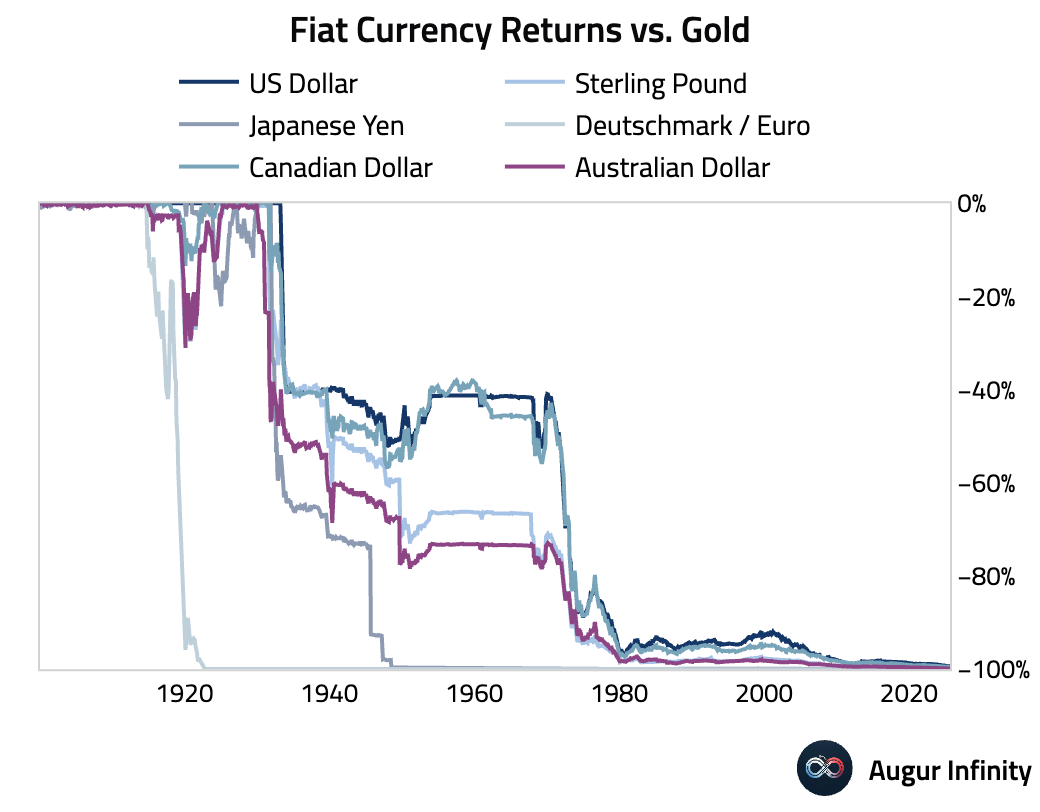

- Over the past 125 years, all major currencies have depreciated by nearly 100% against gold.

- Even after accounting for the fact that cash can earn interest, the long-run performance of fiat currencies against gold has been horrendous.

Disclaimer

Augur Digest is an automated newsletter written by an AI and edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.