Headlines

- President Trump announced that the United States will impose an additional 25 percent tariff on India.

- Germany’s government is reportedly preparing a €100 billion fund for investment in strategic sectors such as defense, energy, and critical materials.

- Scott Bessent has withdrawn from consideration to be the next Federal Reserve Chair, according to an interview with President Trump.

Charts of the Day

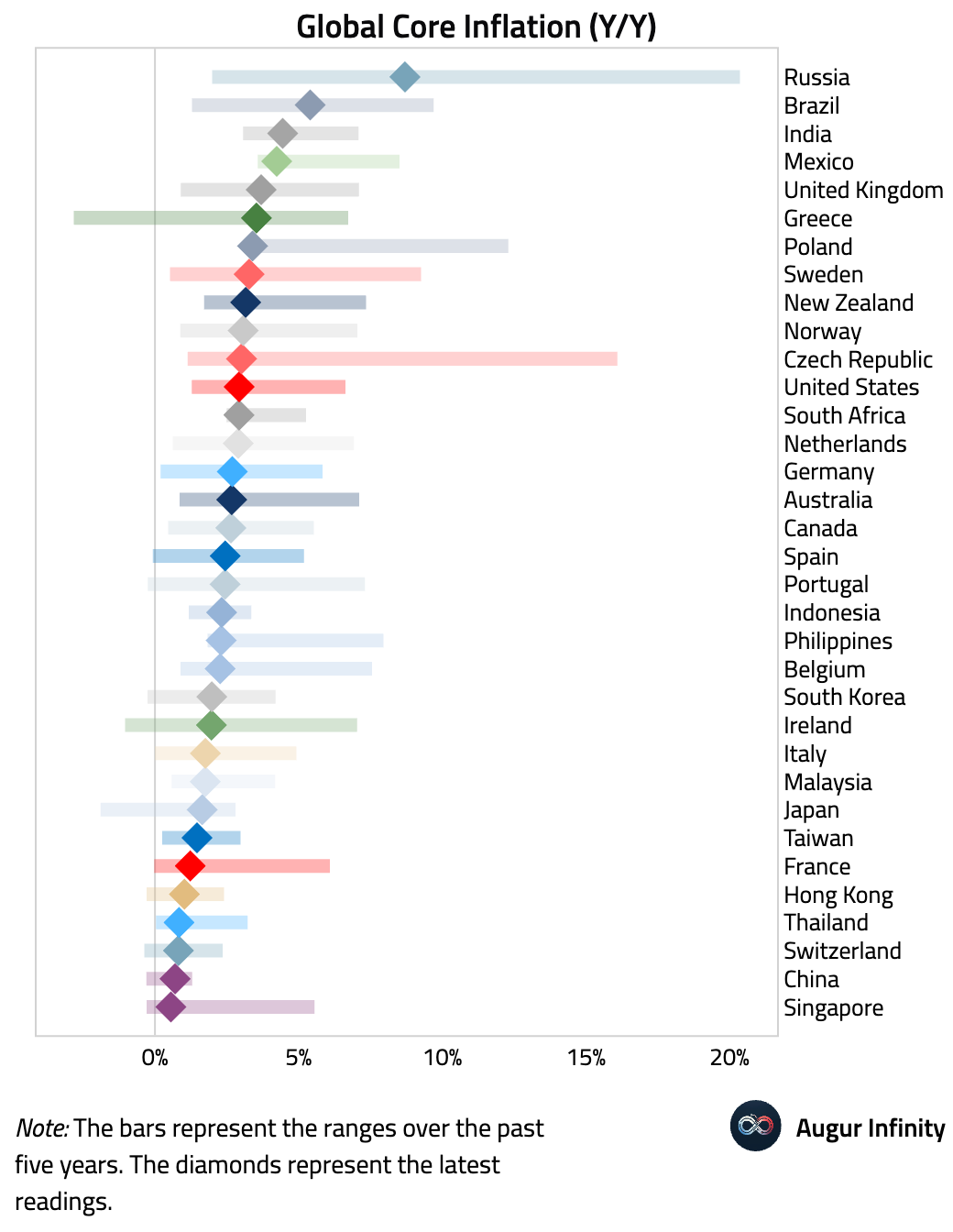

- Here's the latest global core inflation rates vs. trailing five year ranges.

Global Economics

United States

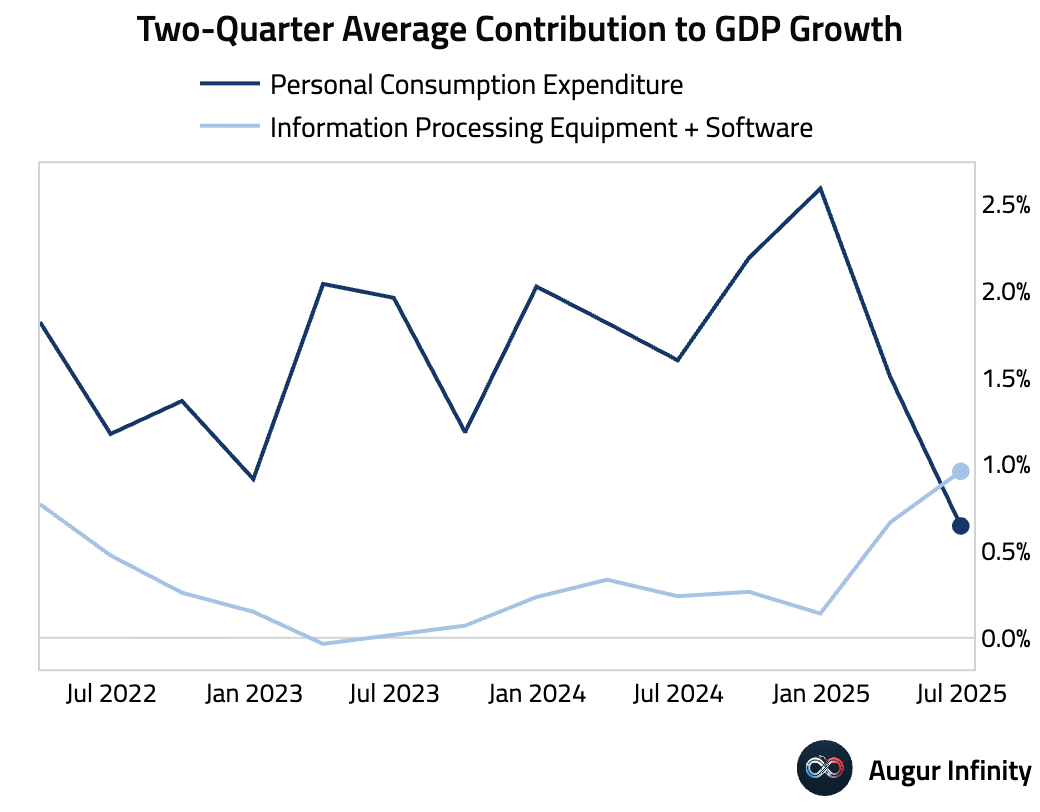

- The contribution of AI-related spending to GDP growth has outpaced that of personal consumption expenditures year-to-date.

Source: @RenMacLLC

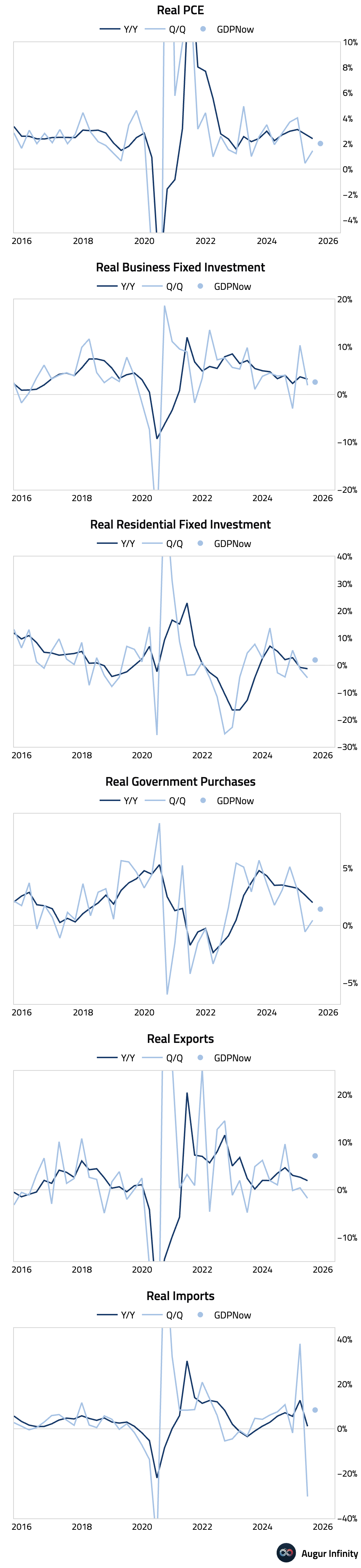

- The Atlanta Fed's GDPNow model is tracking improvements across all major components of GDP for Q3.

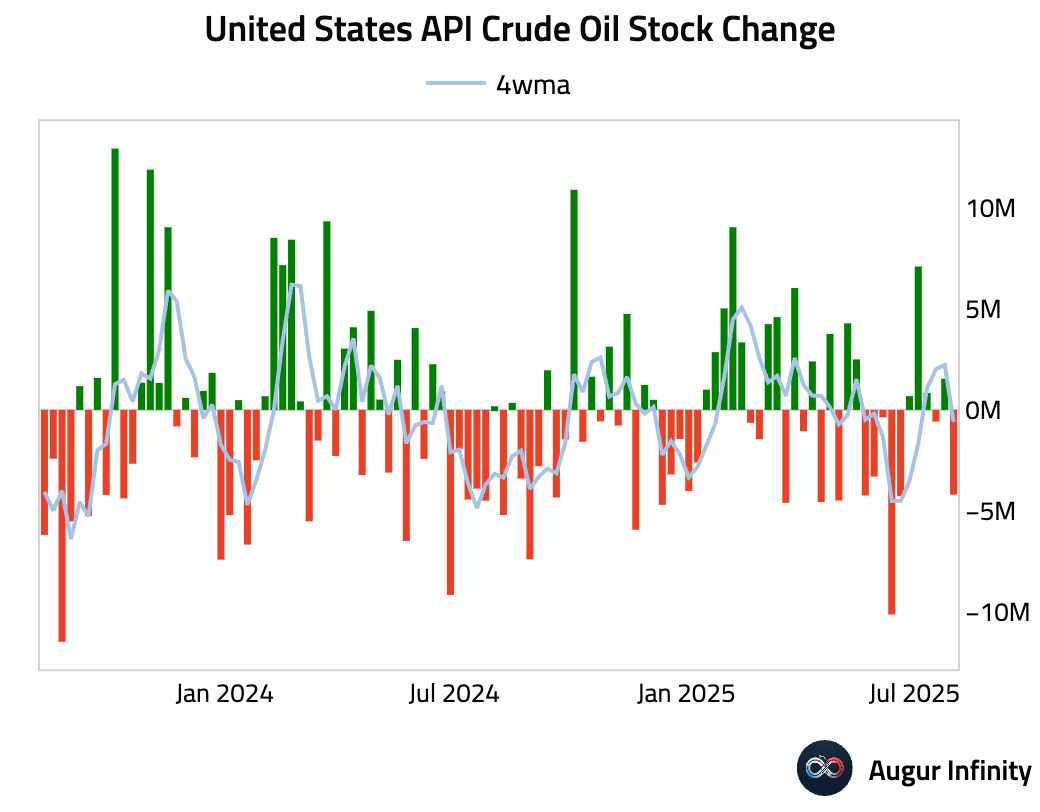

- American Petroleum Institute report showed a crude oil stock drawdown of 4.2 million barrels, more than double the consensus forecast for a 1.8 million barrel draw.

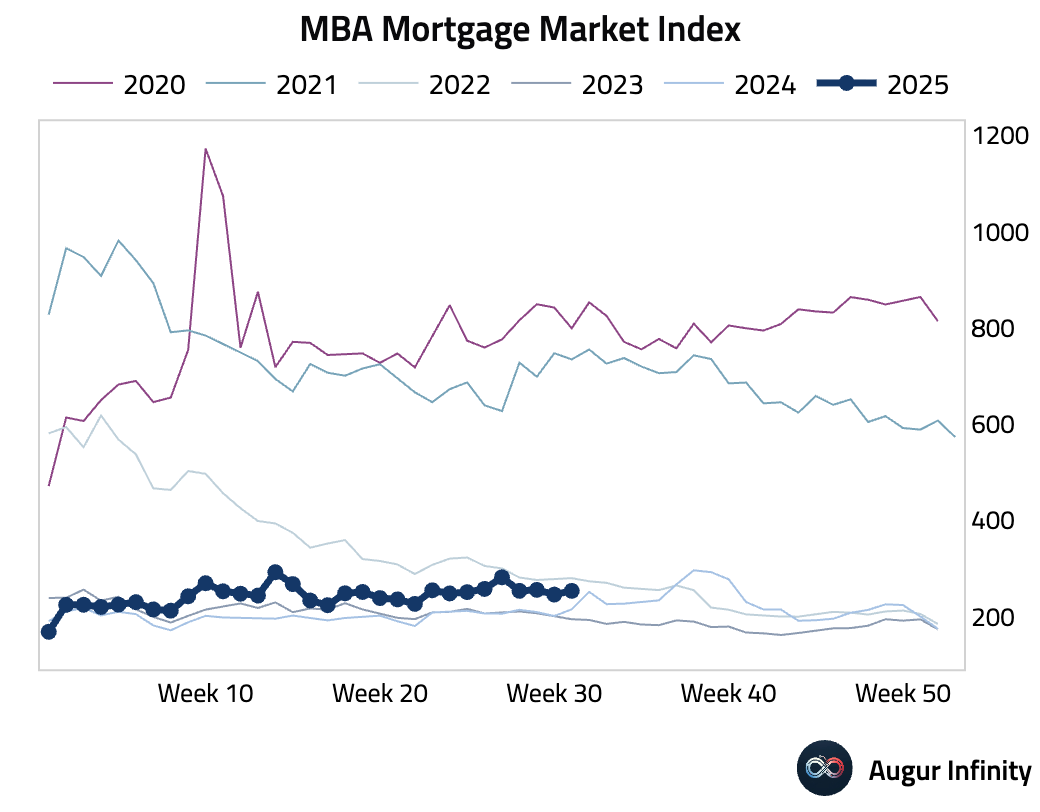

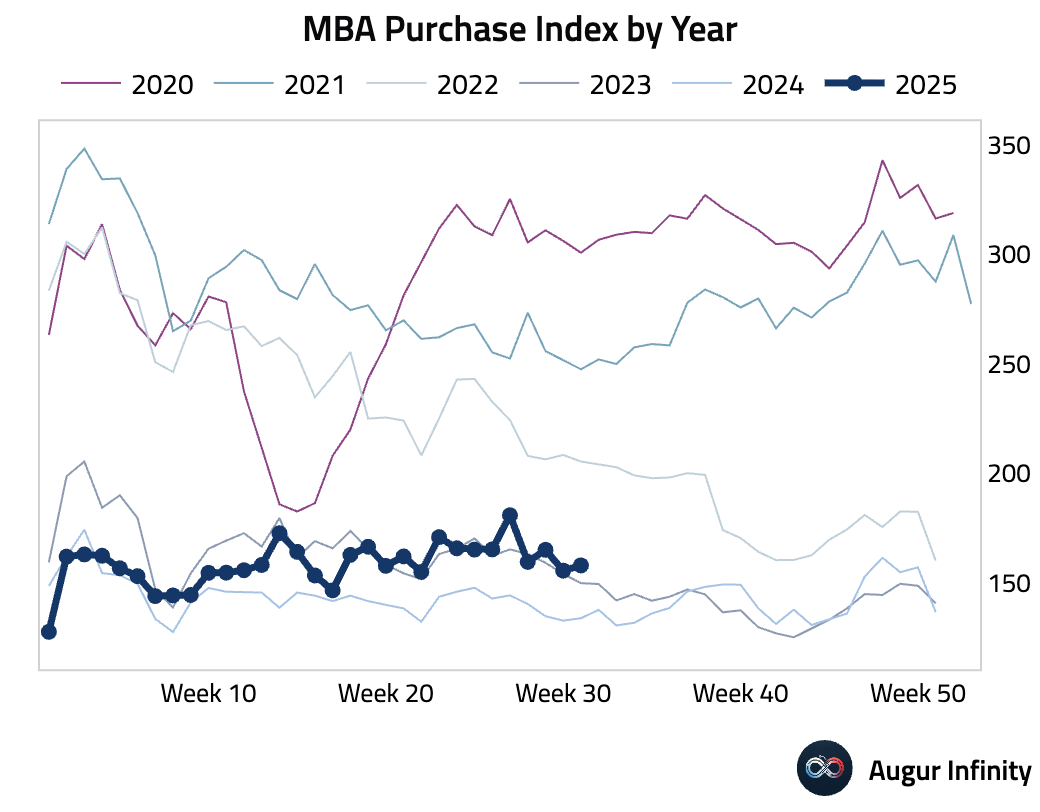

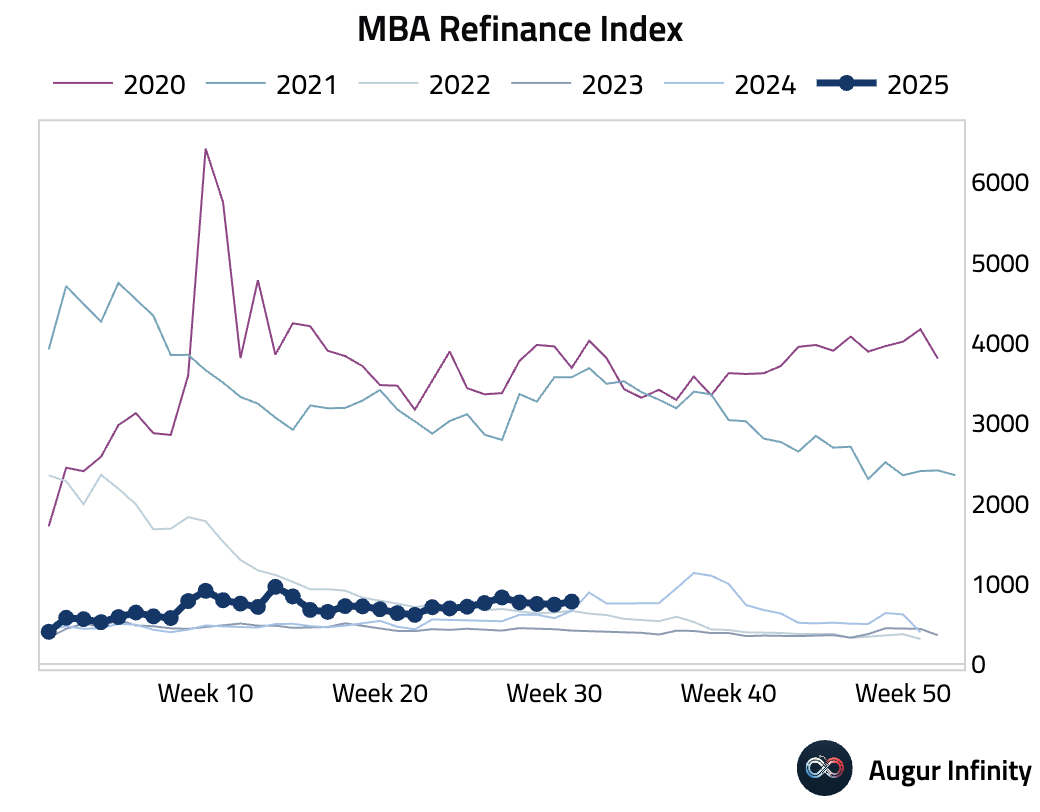

- MBA Mortgage Applications rebounded by 3.1% week-over-week, driven by a 5.2% jump in the Refinance Index. The Purchase Index saw a more modest 1.5% increase. The overall Market Index rose to 253.4.

Canada

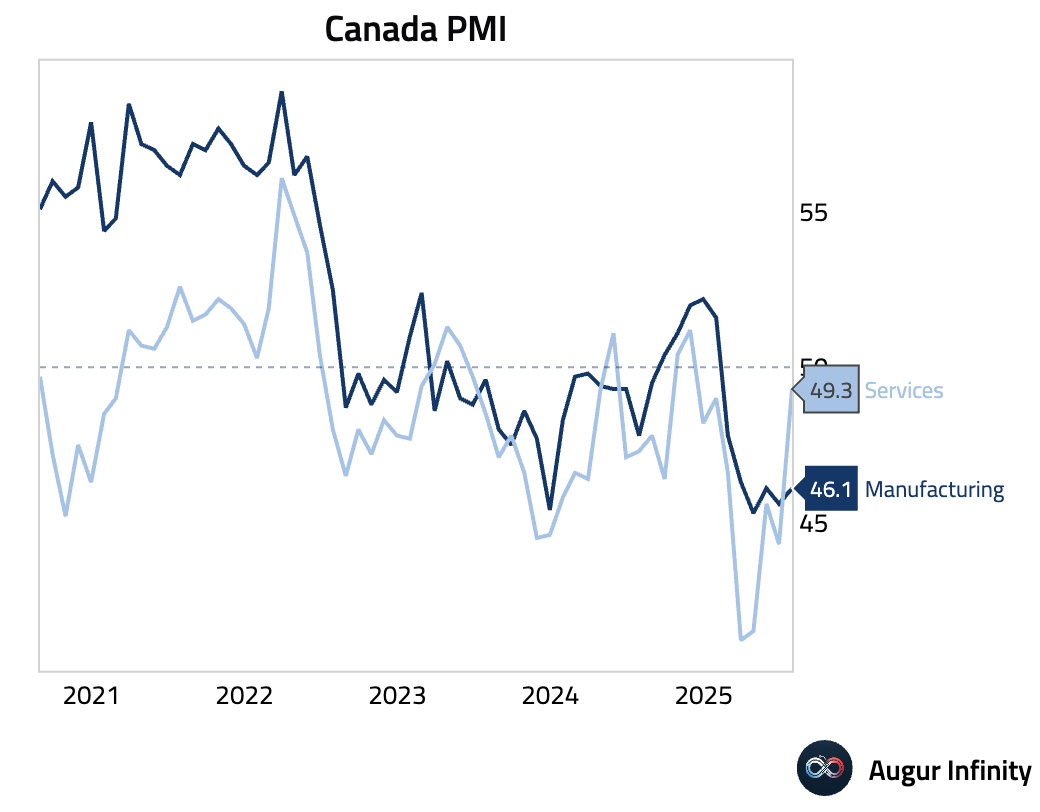

- The S&P Global Services PMI rose to 49.3 in July from 44.3, indicating the slowest pace of contraction in eight months as activity and new orders declined less sharply. Despite headwinds from US tariffs, business confidence improved to a six-month high, partly on optimism related to the 2026 FIFA World Cup.

Europe

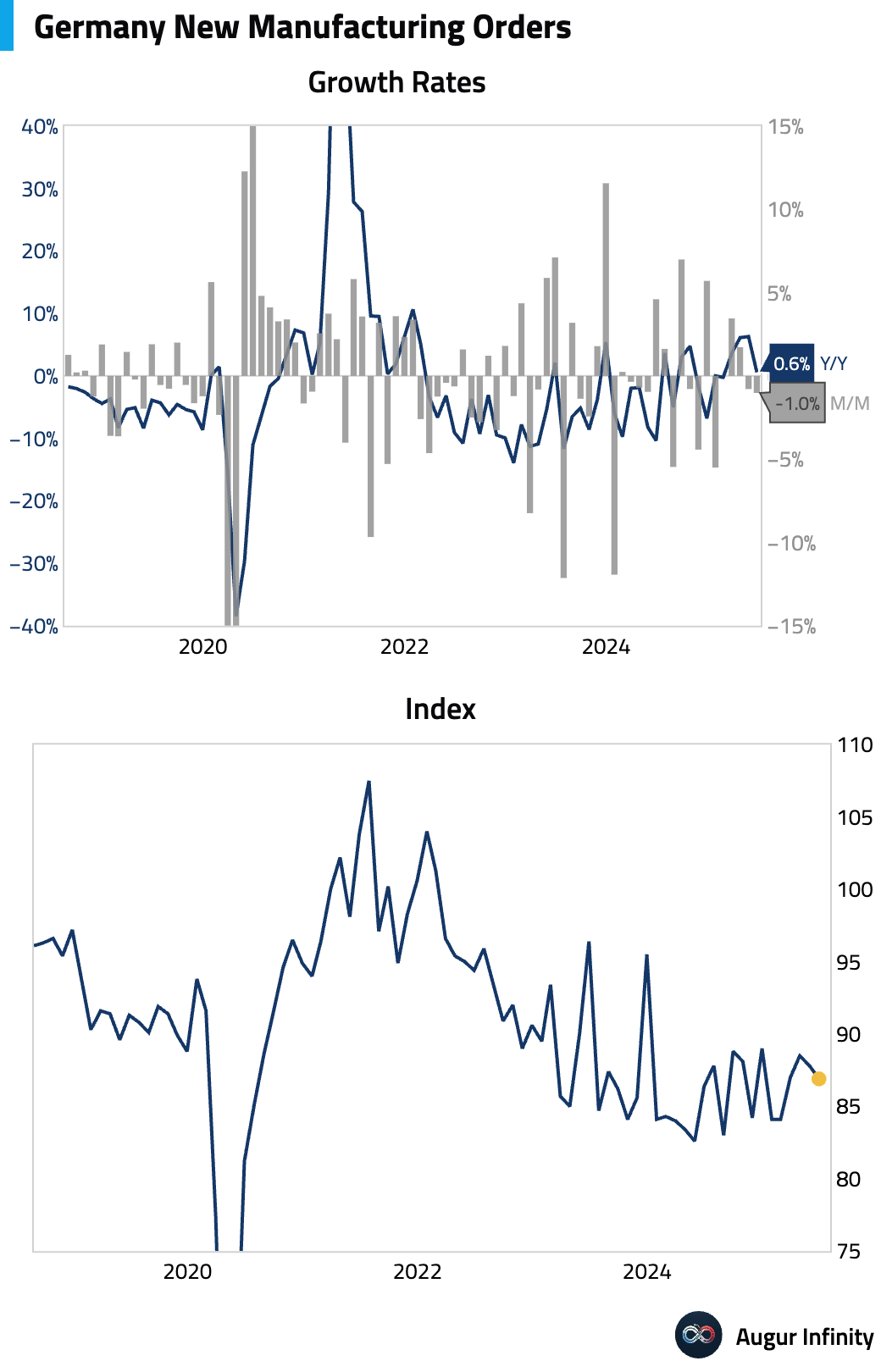

- Germany’s factory orders unexpectedly fell 1.0% M/M in June, a significant disappointment against expectations for a 1.0% rise and a further drop from the prior month's revised -0.8% reading.

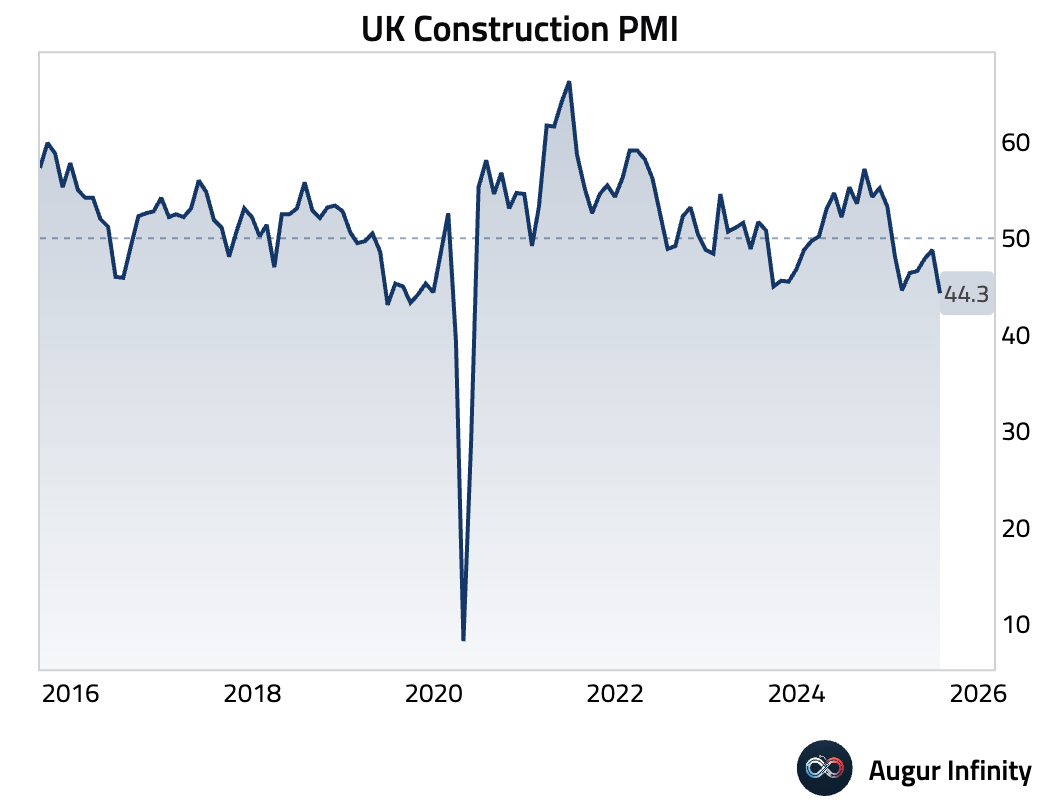

- The UK's S&P Global Construction PMI plunged to 44.3 in July from 48.8, a stark miss of the 49.2 consensus and the sharpest decline since the May 2020 lockdowns. The downturn was broad-based, led by a renewed slump in residential building and a faster decline in civil engineering projects.

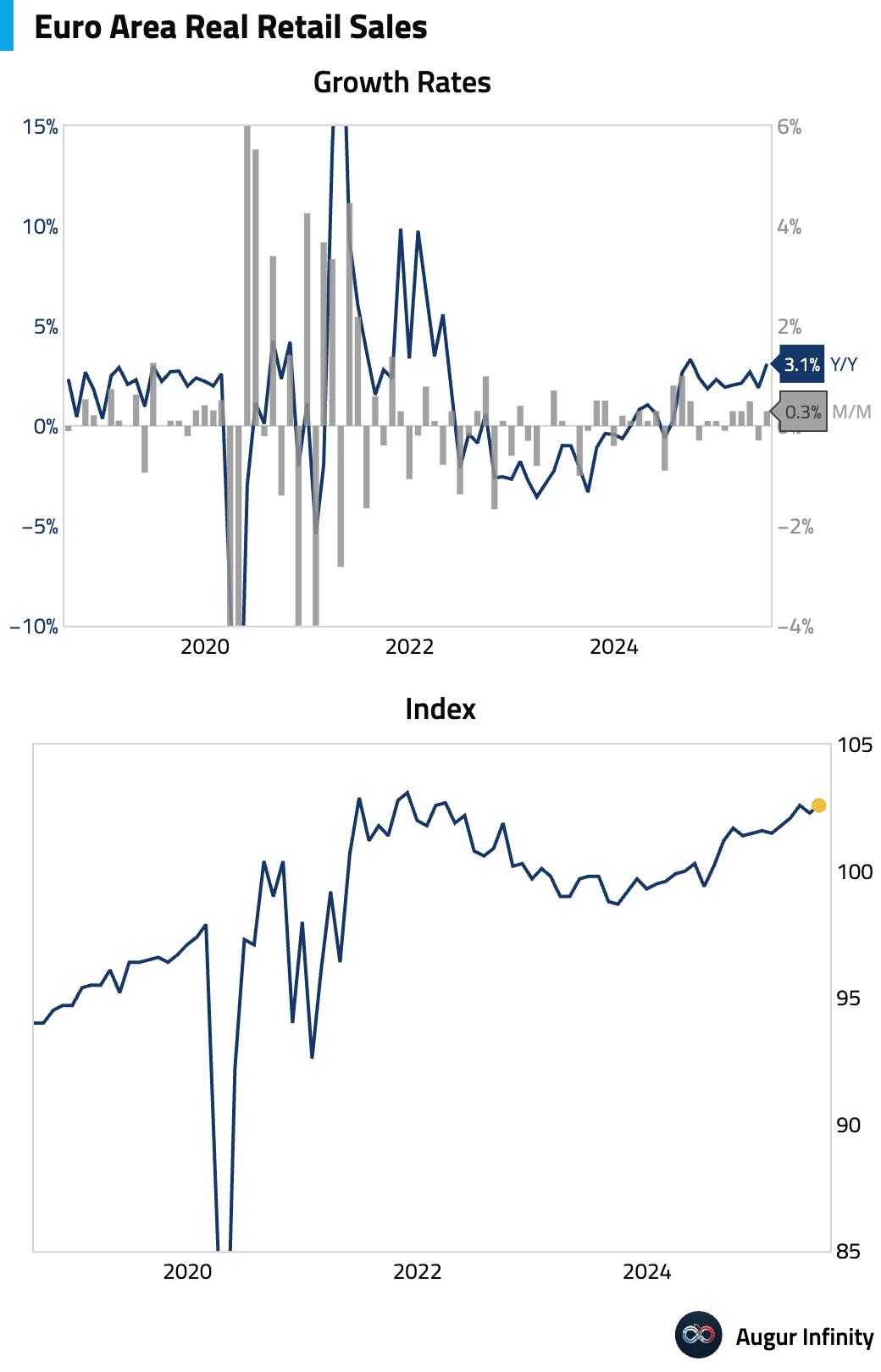

- Eurozone retail sales rose 0.3% M/M in June, slightly below the 0.4% consensus. Year-over-year, sales growth accelerated to 3.1%, beating the 2.6% forecast.

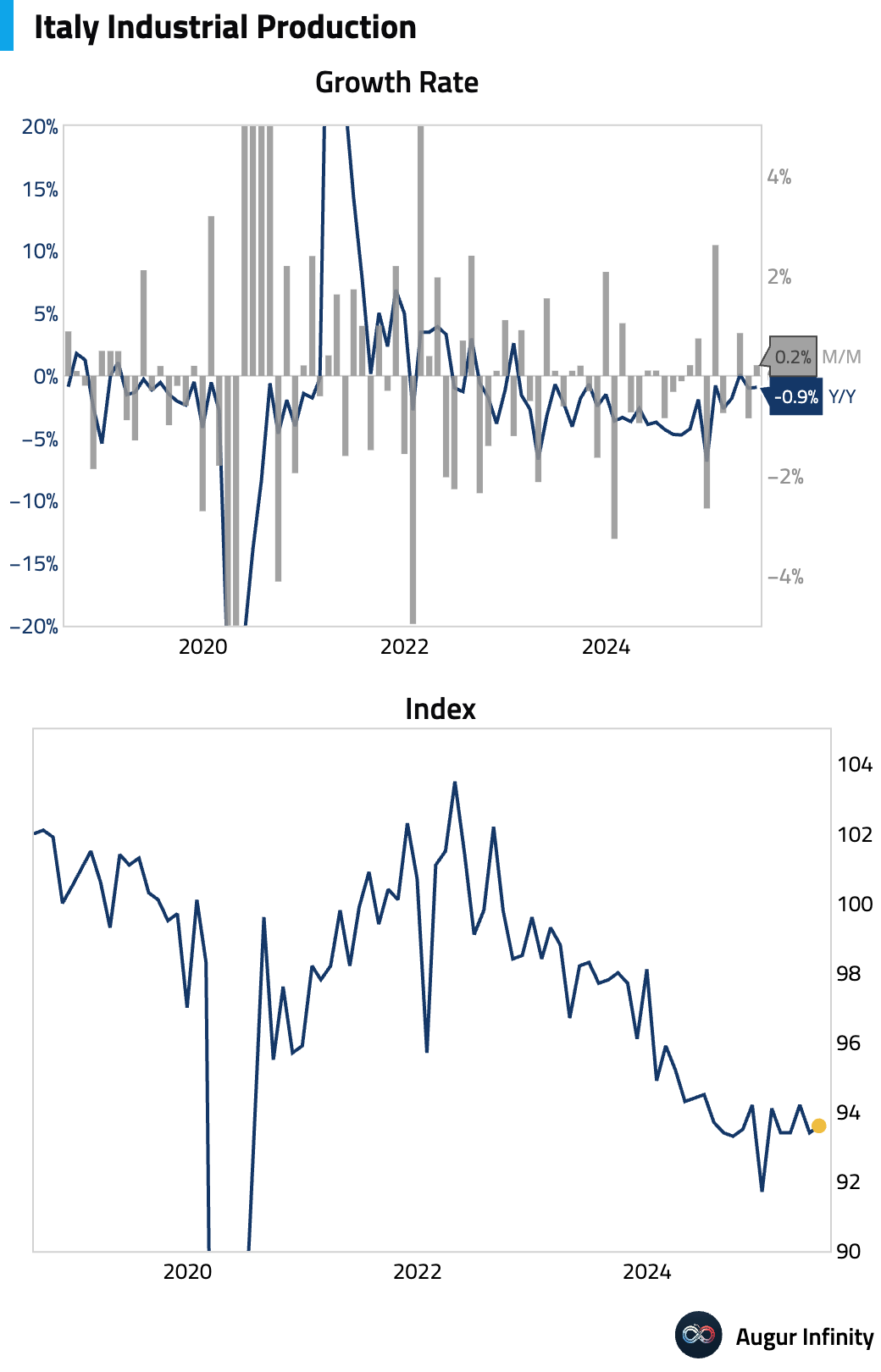

- Italy's industrial production expanded by 0.2% M/M in June, beating the 0.1% consensus and reversing a prior 0.8% decline. On a working-day adjusted basis, output fell 0.9% Y/Y.

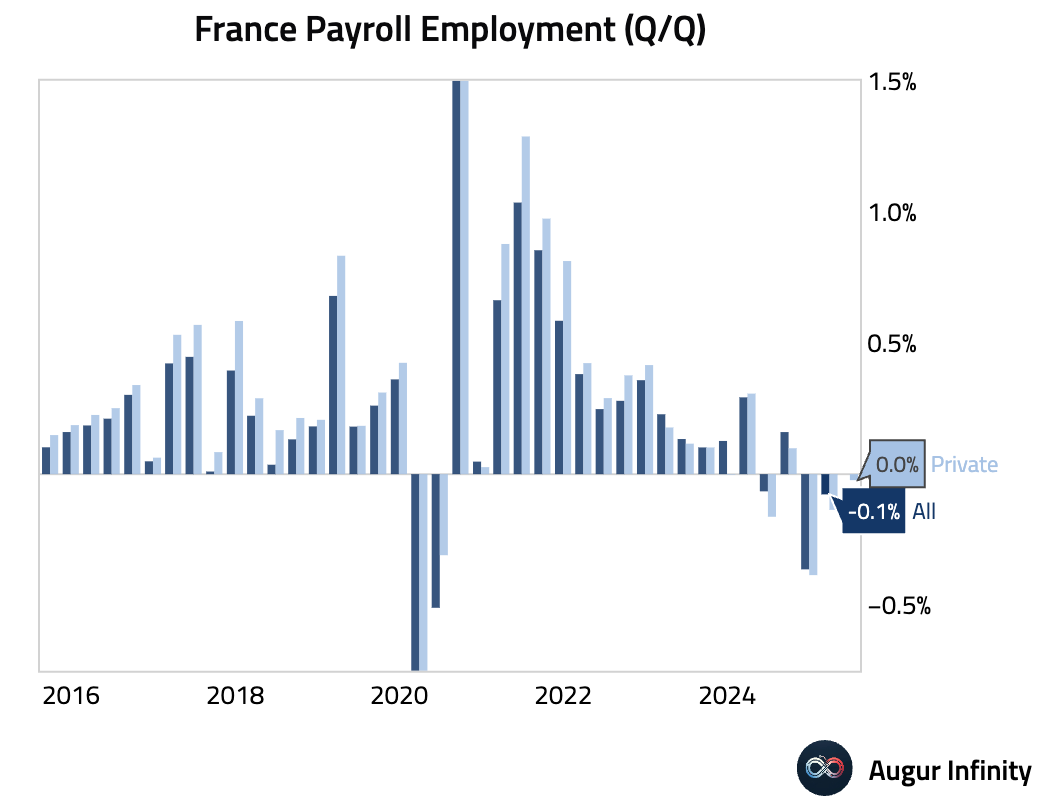

- France’s preliminary Q2 private non-farm payrolls stagnated at 0.0% Q/Q, missing expectations of a 0.1% increase and indicating a stalled job market.

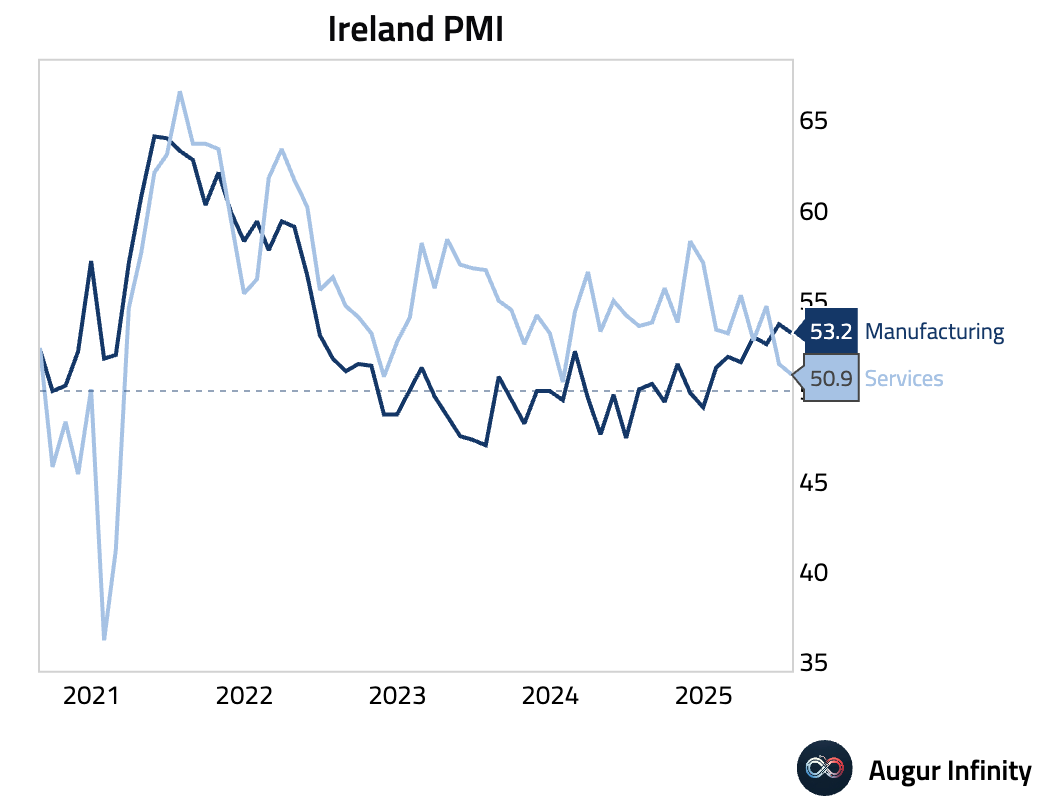

- Ireland’s AIB Services PMI fell to 50.9 in July from 51.5, its weakest reading since January 2024. The slowdown was driven by a near-stall in new business growth and a six-month low in job creation, with the Transport, Tourism & Leisure sector contracting for the fifth straight month.

Asia-Pacific

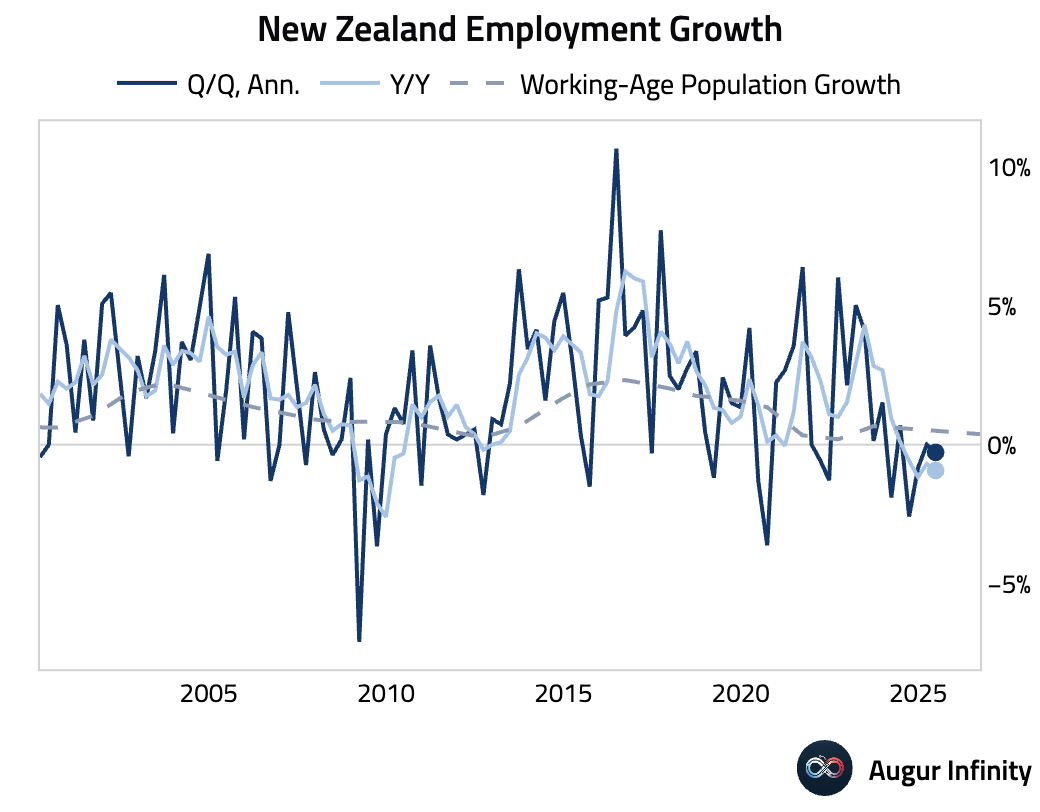

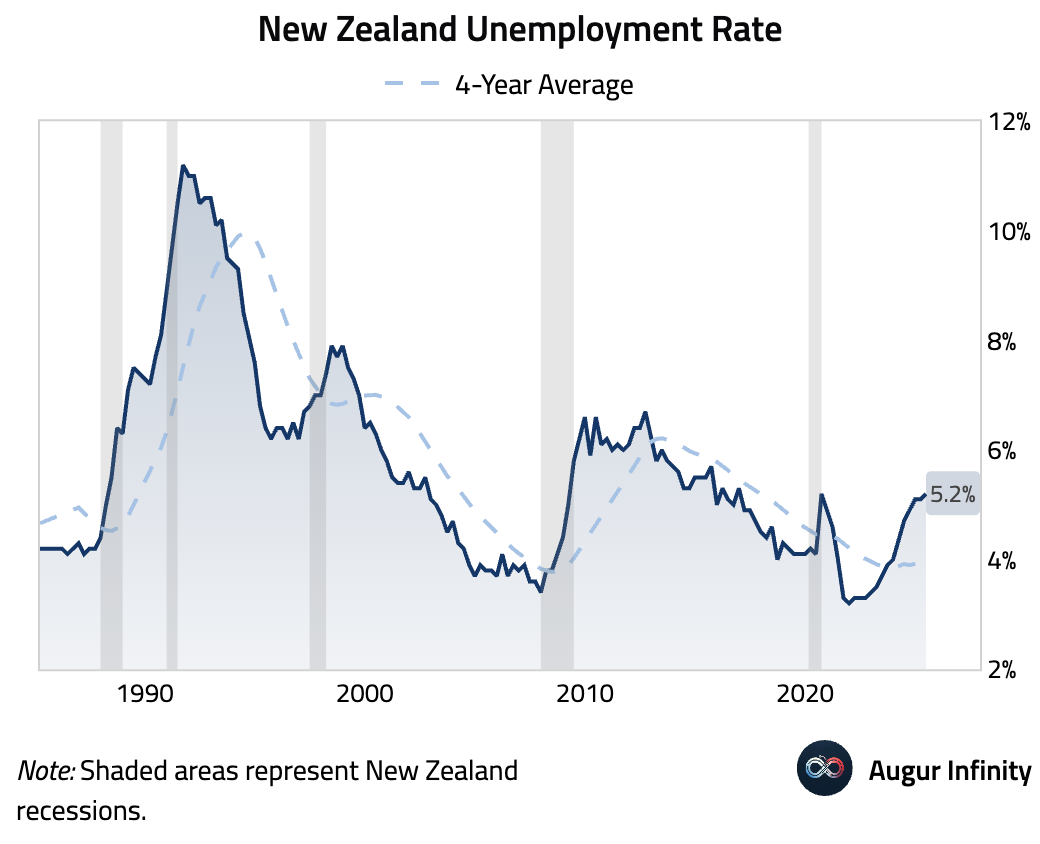

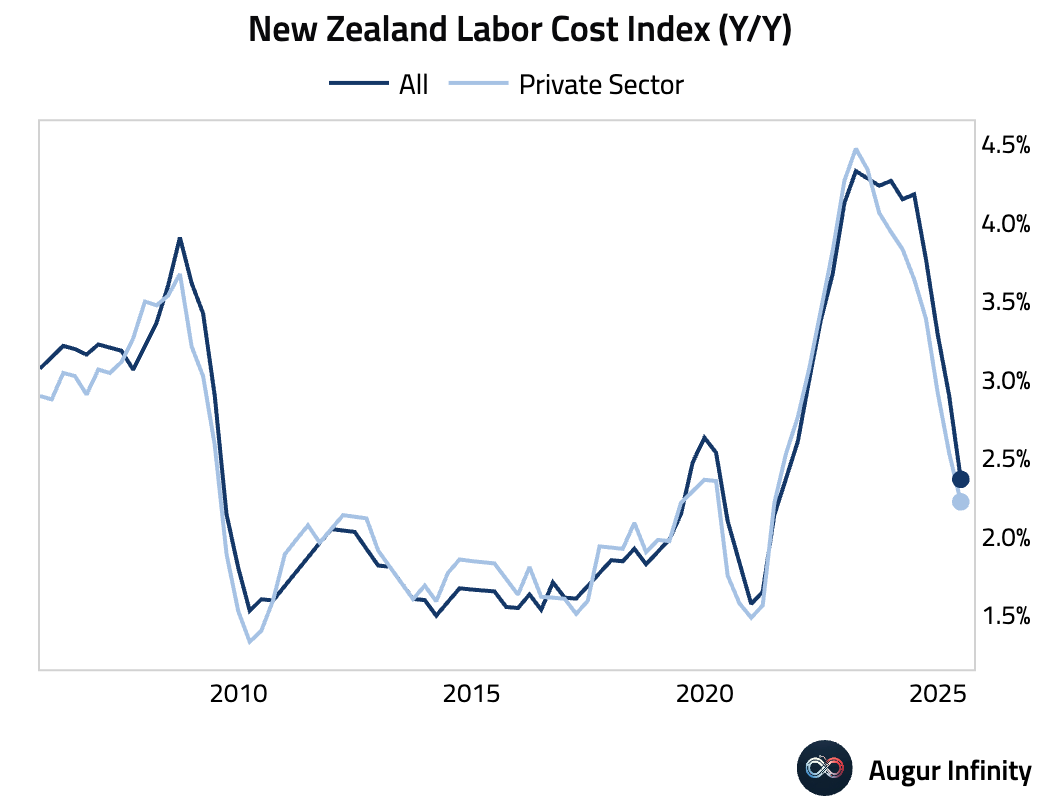

- New Zealand’s Q2 labor market data showed broad weakness. Employment contracted by 0.1% Q/Q, while the unemployment rate rose to 5.2%, its highest level since December 2016. The participation rate also edged down to 70.5%. Wage pressures continued to cool, with the Labor Cost Index slowing to 2.2% Y/Y, the lowest since Q2 2021, supporting the case for RBNZ rate cuts.

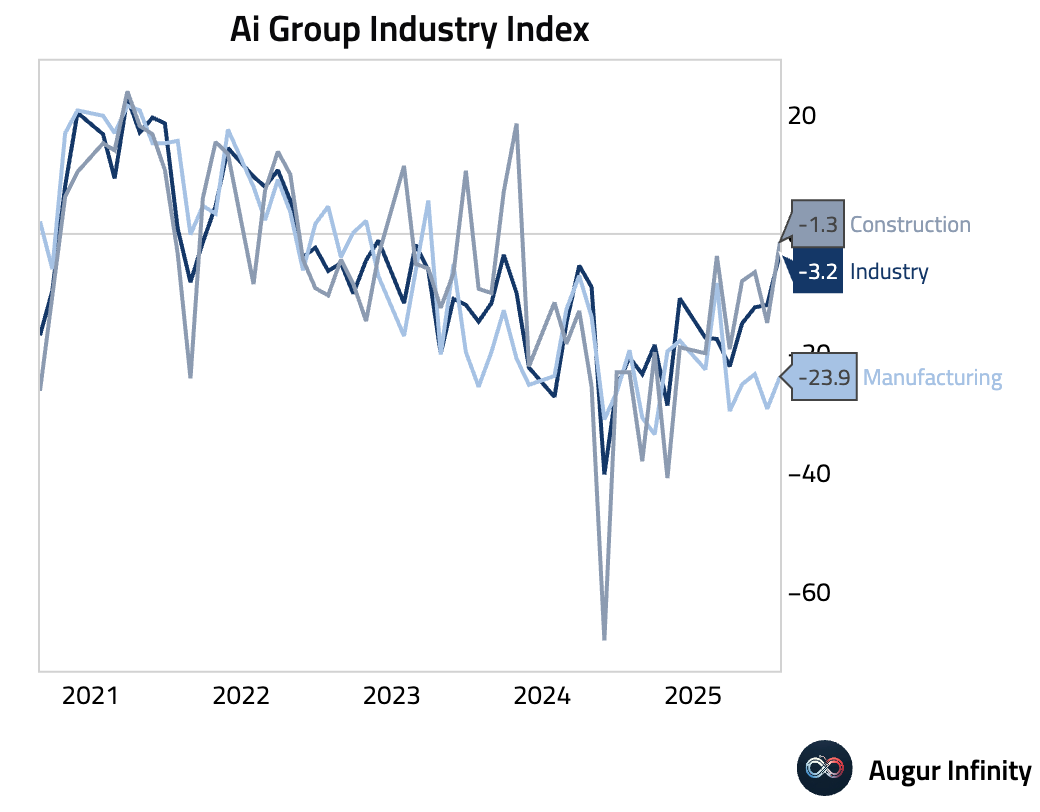

- Australia's Ai Group performance indexes for July showed continued deep contraction across the economy, although the pace of decline moderated from June. The Industry Index rose to -3.2, the Construction Index to -1.3, and the Manufacturing Index to -23.9.

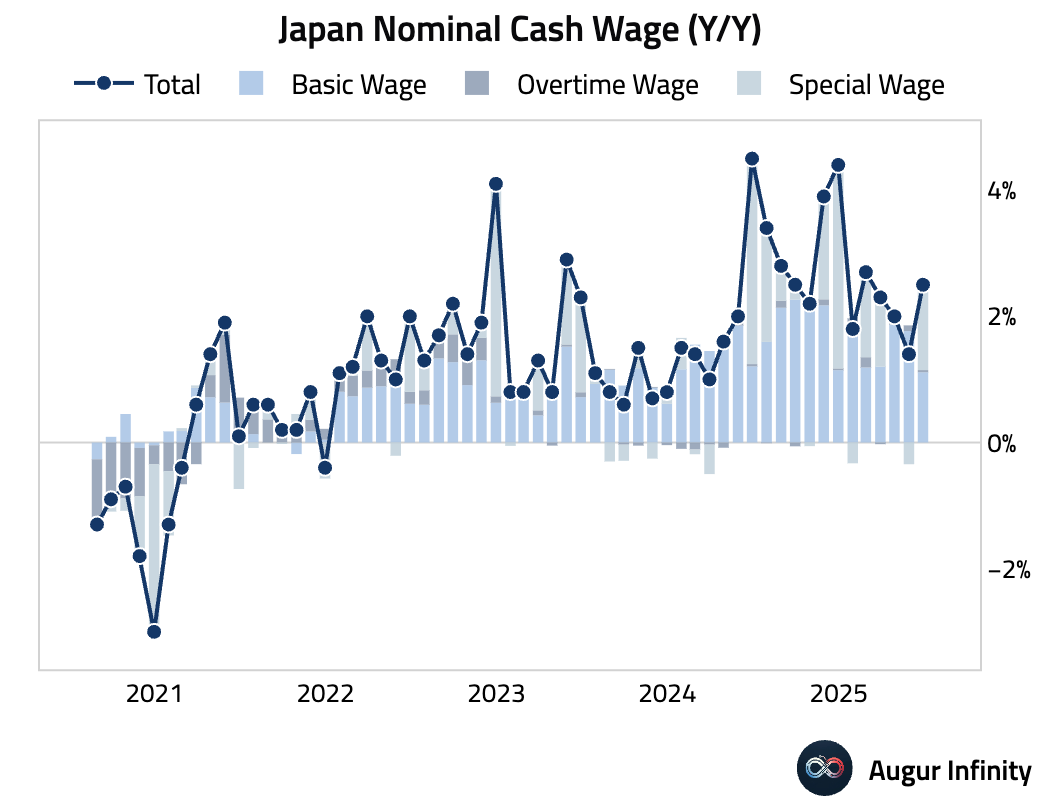

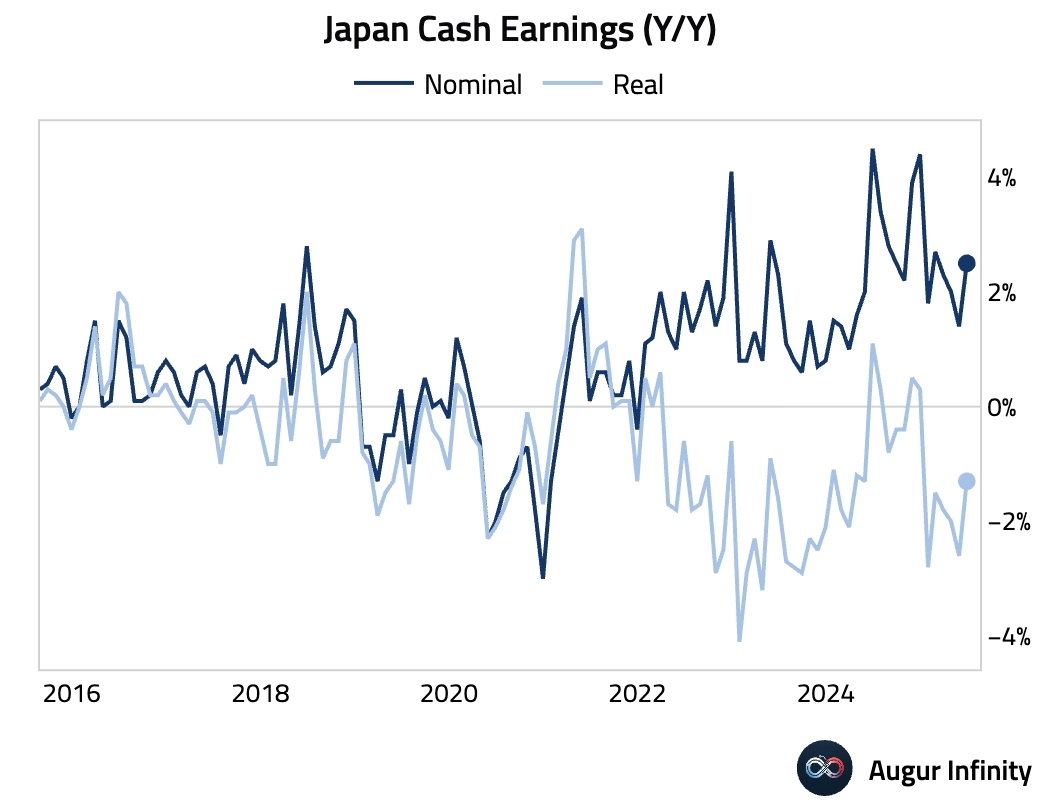

- Japan’s average cash earnings rose 2.5% Y/Y in June, accelerating from May but missing the 3.1% consensus. The increase was driven by summer bonuses, as underlying wage growth for full-time workers slowed slightly. Real wages remained in negative territory, falling 1.3% Y/Y.

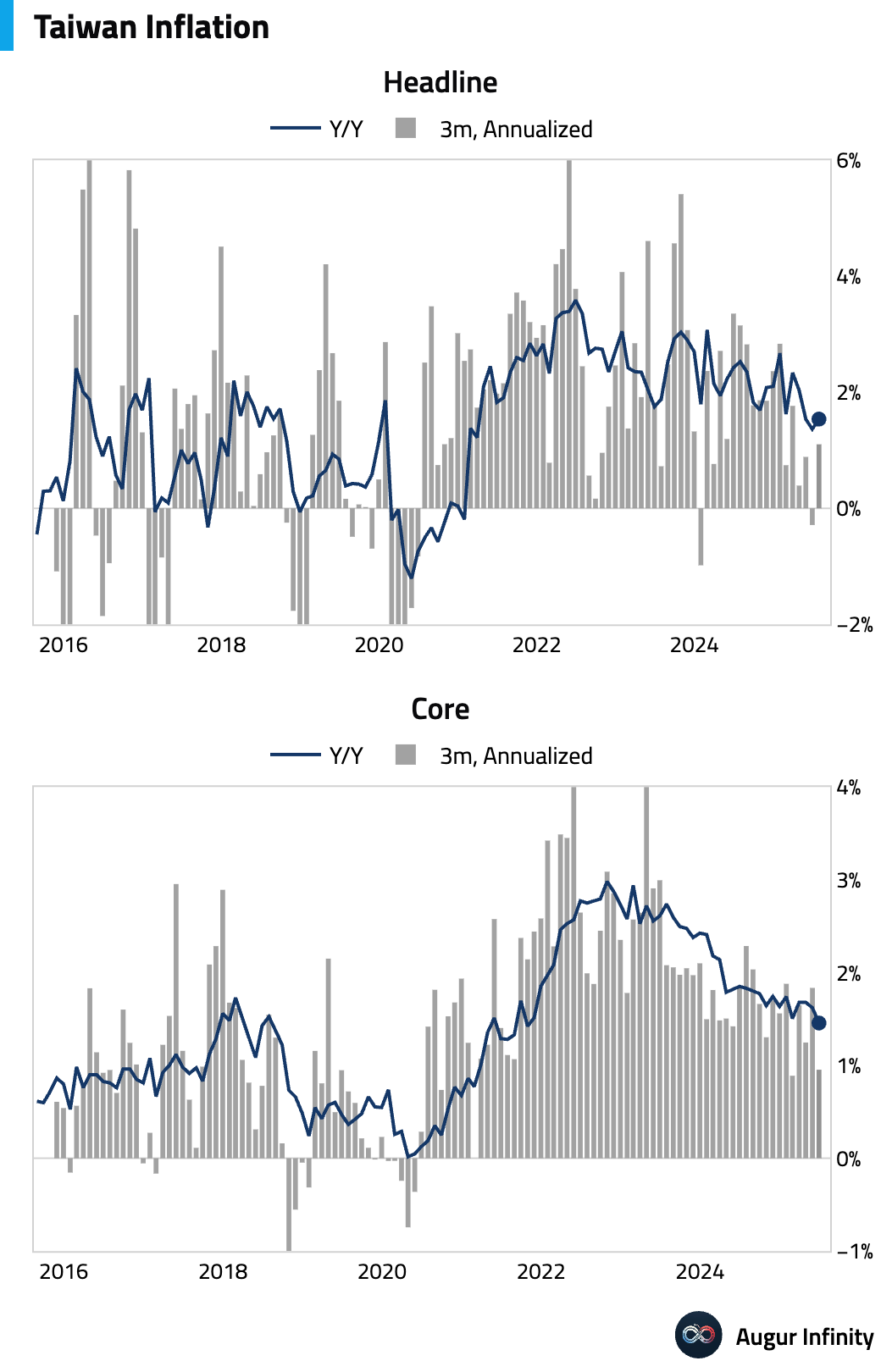

- Taiwan's headline inflation rose to 1.54% Y/Y in July, slightly above consensus. The uptick was driven by typhoon-related food price volatility and higher services costs from train fare hikes. The figures remain within the central bank's comfort zone, supporting expectations for an extended policy pause.

Emerging Markets ex China

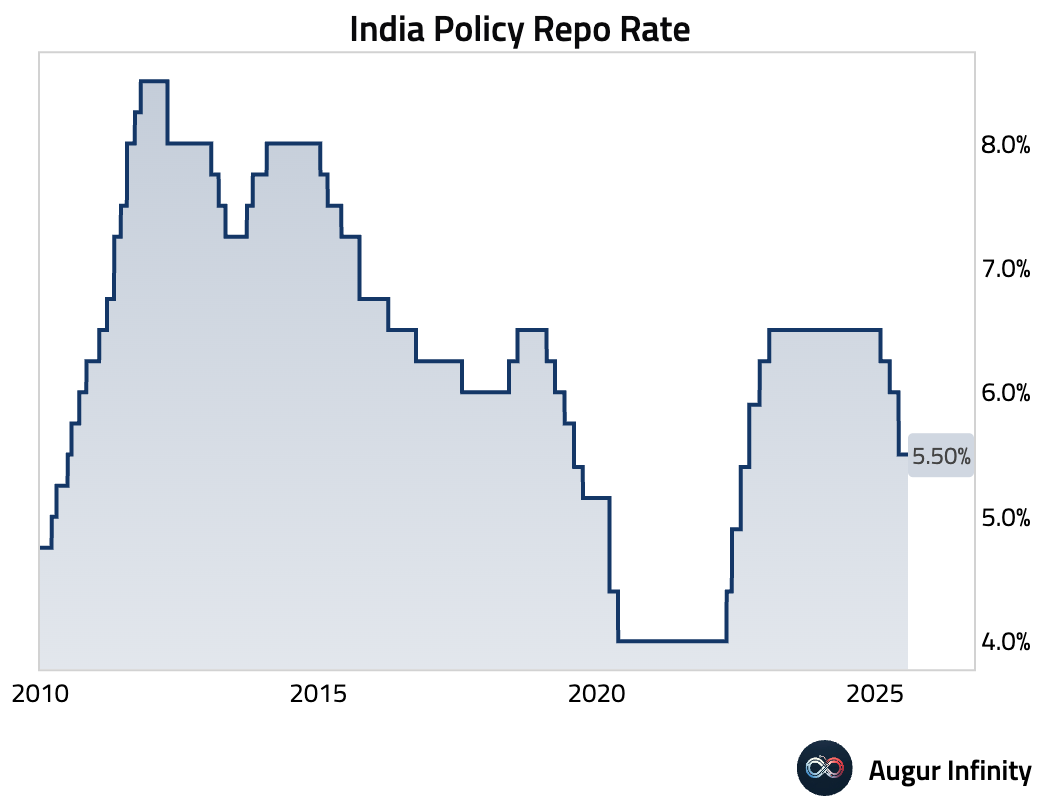

- The Reserve Bank of India held its policy repo rate at 5.5% with a unanimous vote and maintained its “neutral” stance. The decision was a “hawkish hold” relative to market expectations, as the RBI waits to assess the impact of past easing amid geopolitical uncertainty. The bank lowered its FY26 inflation forecast to 3.1% but flagged rising core inflation, while maintaining its 6.5% real GDP growth forecast for FY26.

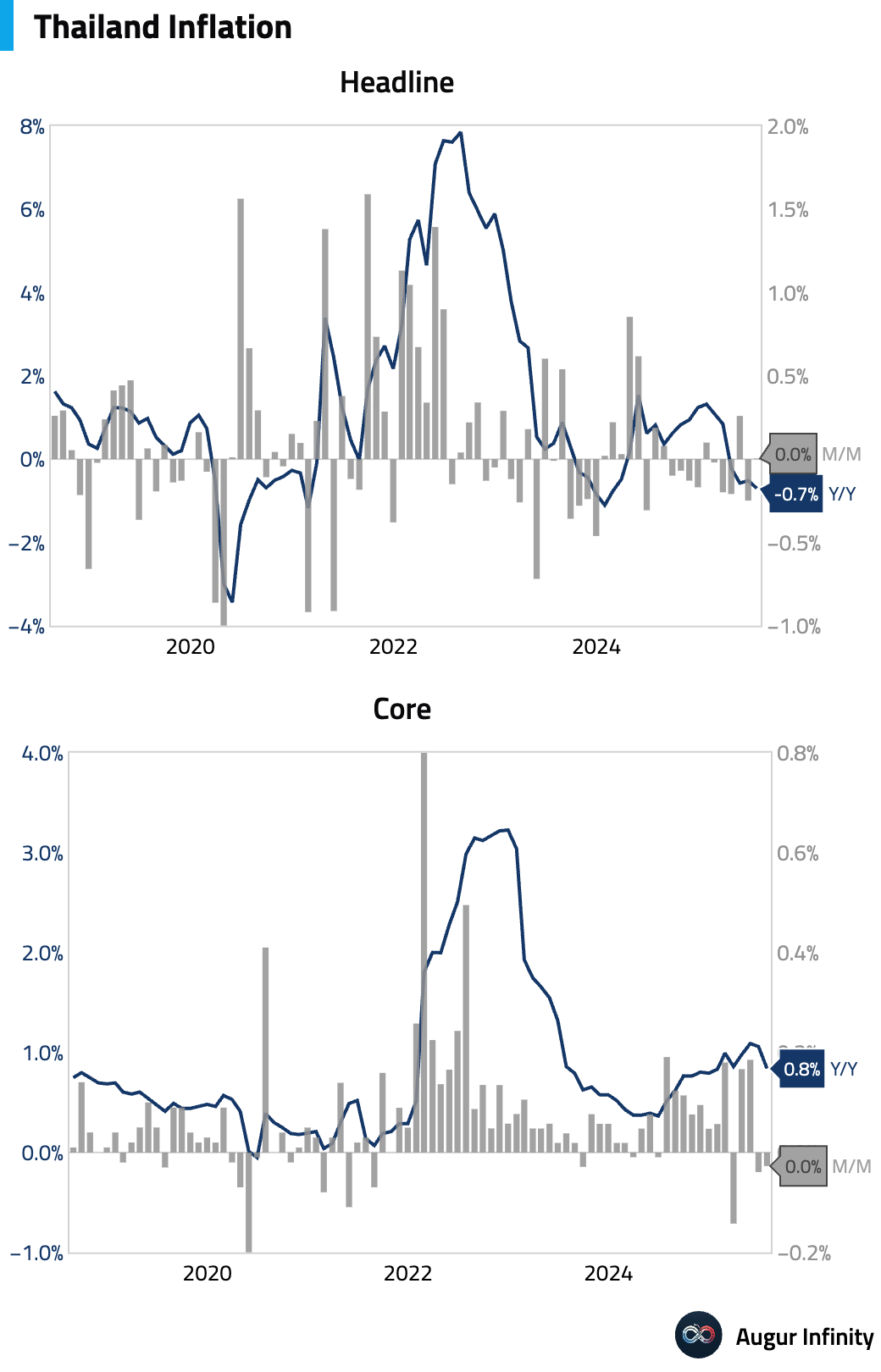

- Thailand entered a deeper state of deflation in July, as the headline inflation rate fell to -0.7% Y/Y, well below the -0.45% consensus, due to steeper declines in raw food and energy prices. Core inflation also slowed to 0.84% Y/Y. The broadening price declines signal very weak domestic demand and increase pressure on the Bank of Thailand to cut rates further.

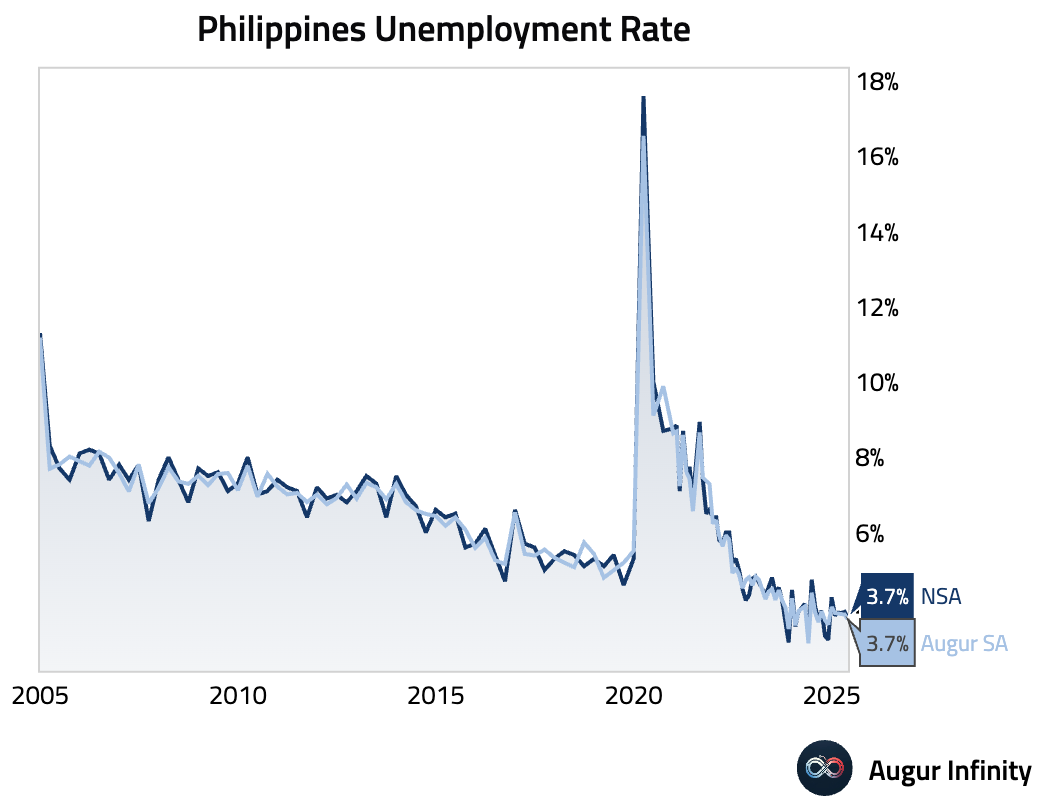

- The Philippines' unemployment rate eased to 3.7% in June from 3.9% in May.

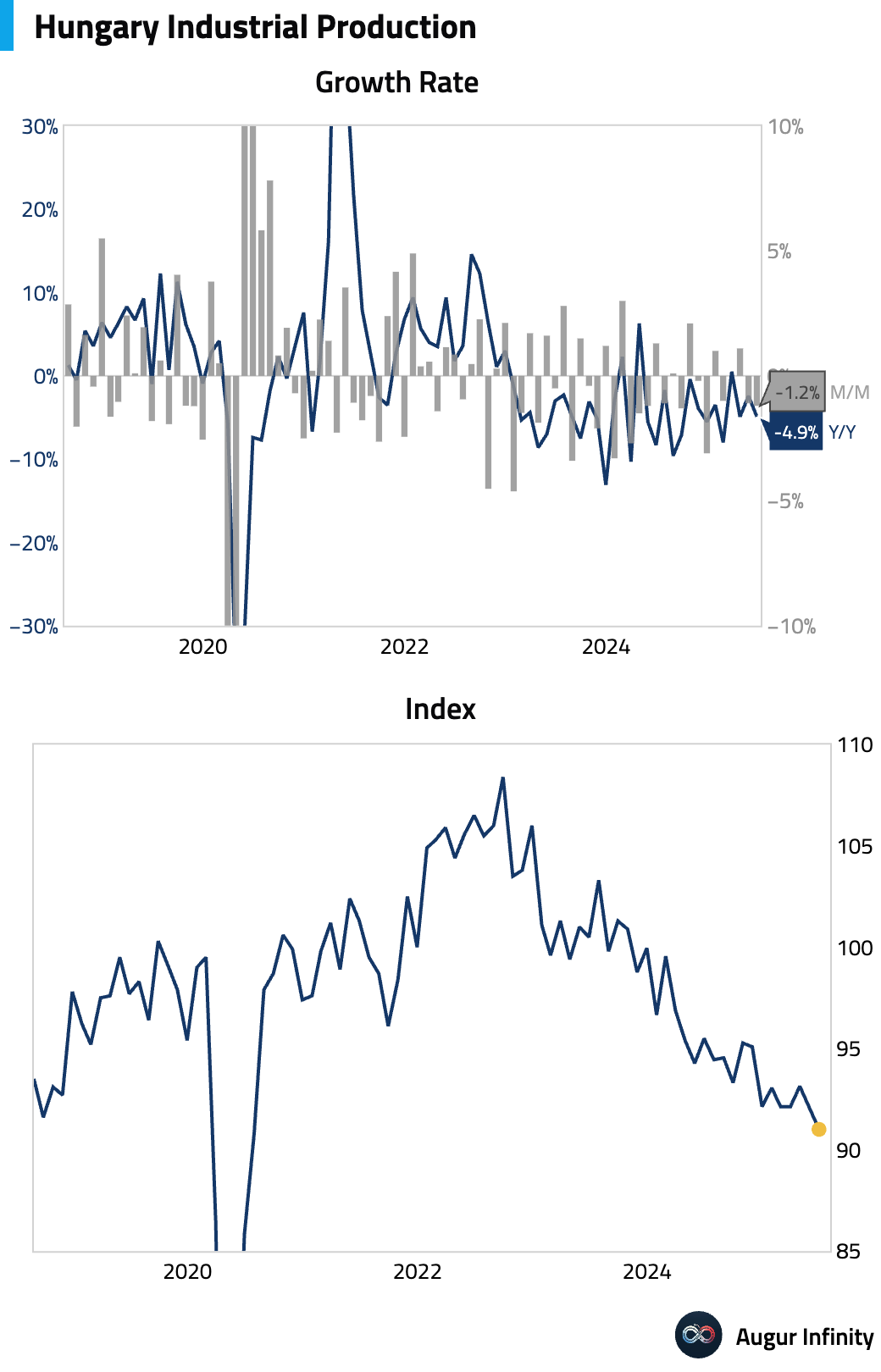

- Hungary’s industrial production contracted by 4.9% Y/Y in June, a steeper decline than the 2.4% drop seen in May.

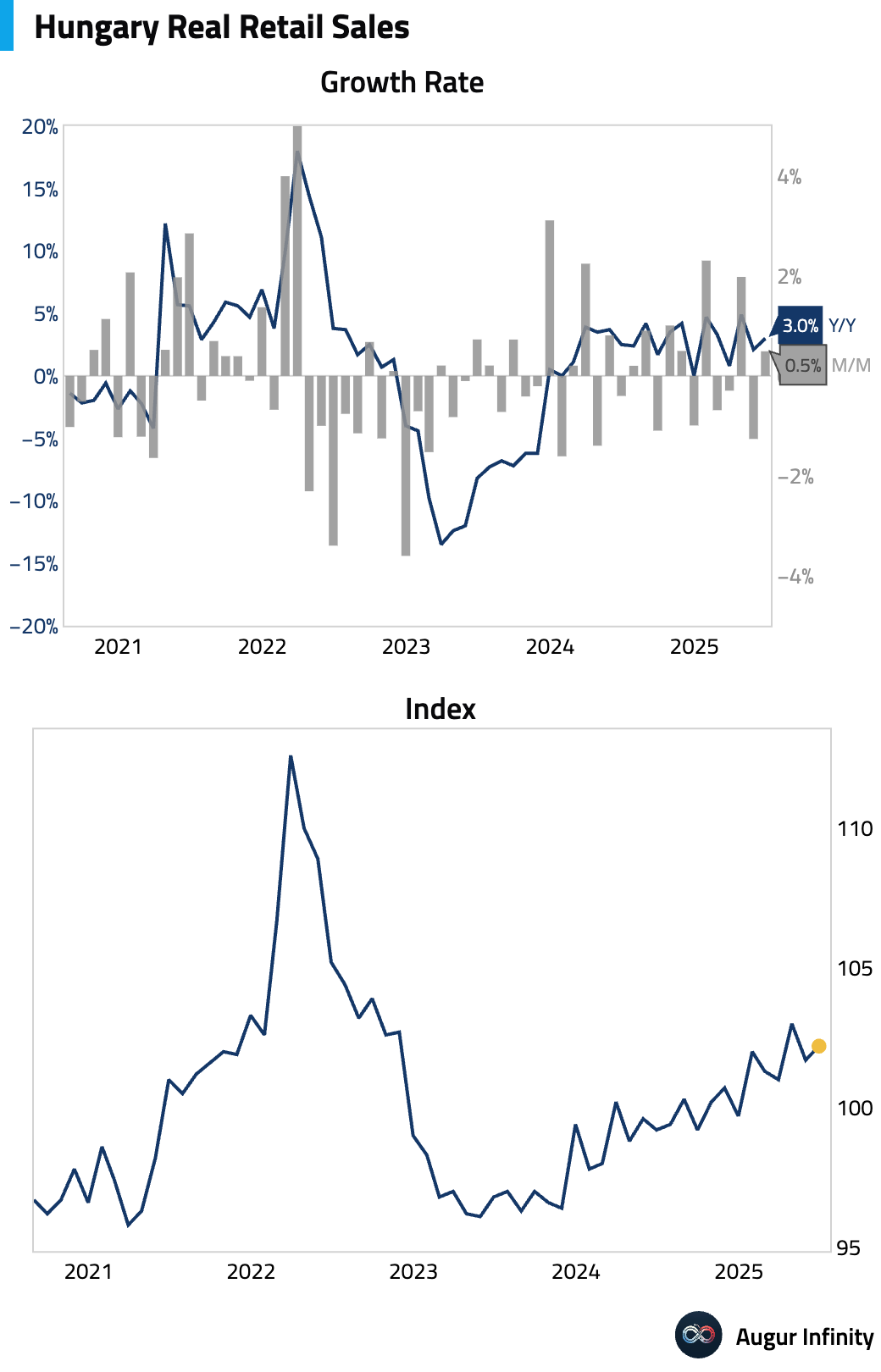

- Hungarian retail sales grew 3.0% Y/Y in June, accelerating from 2.1% growth in the prior month.

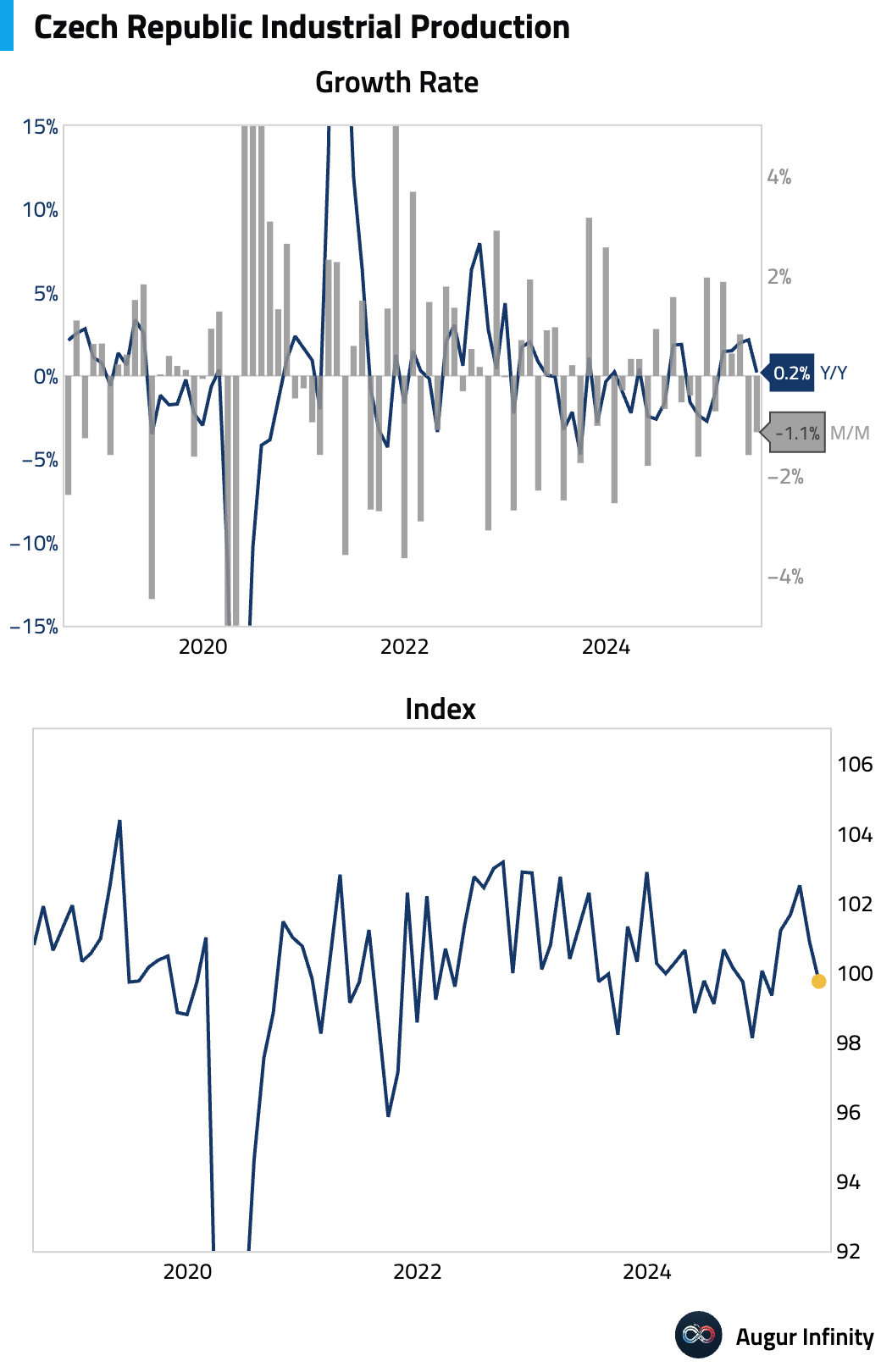

- The Czech Republic's industrial production fell 1.1% M/M in June. The year-over-year figure rose just 0.2%, missing the 1.6% consensus and slowing from the 2.2% pace in May.

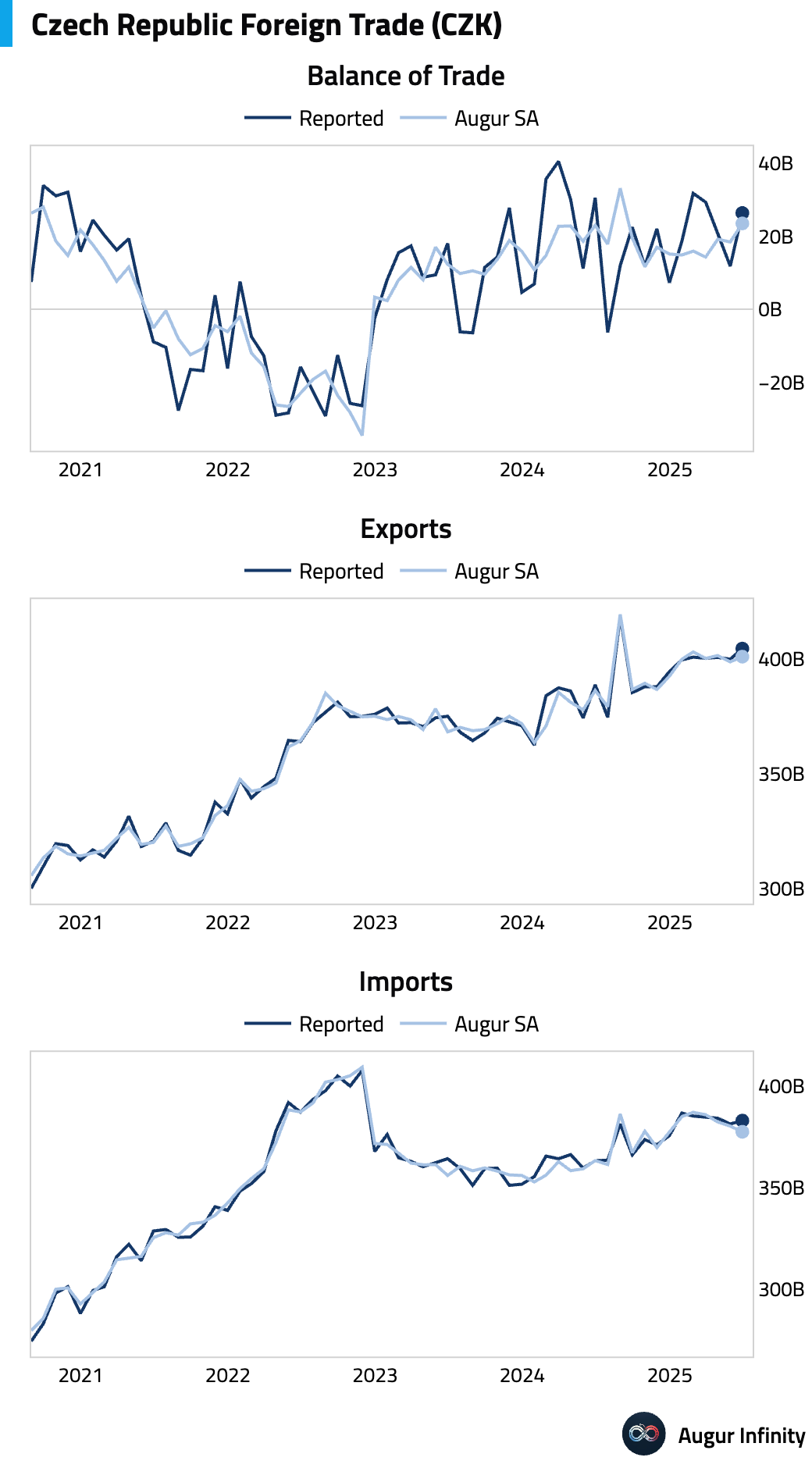

- The Czech Republic's trade surplus widened to CZK 26.3 billion in June, exceeding the previous month's surplus of CZK 13.3 billion.

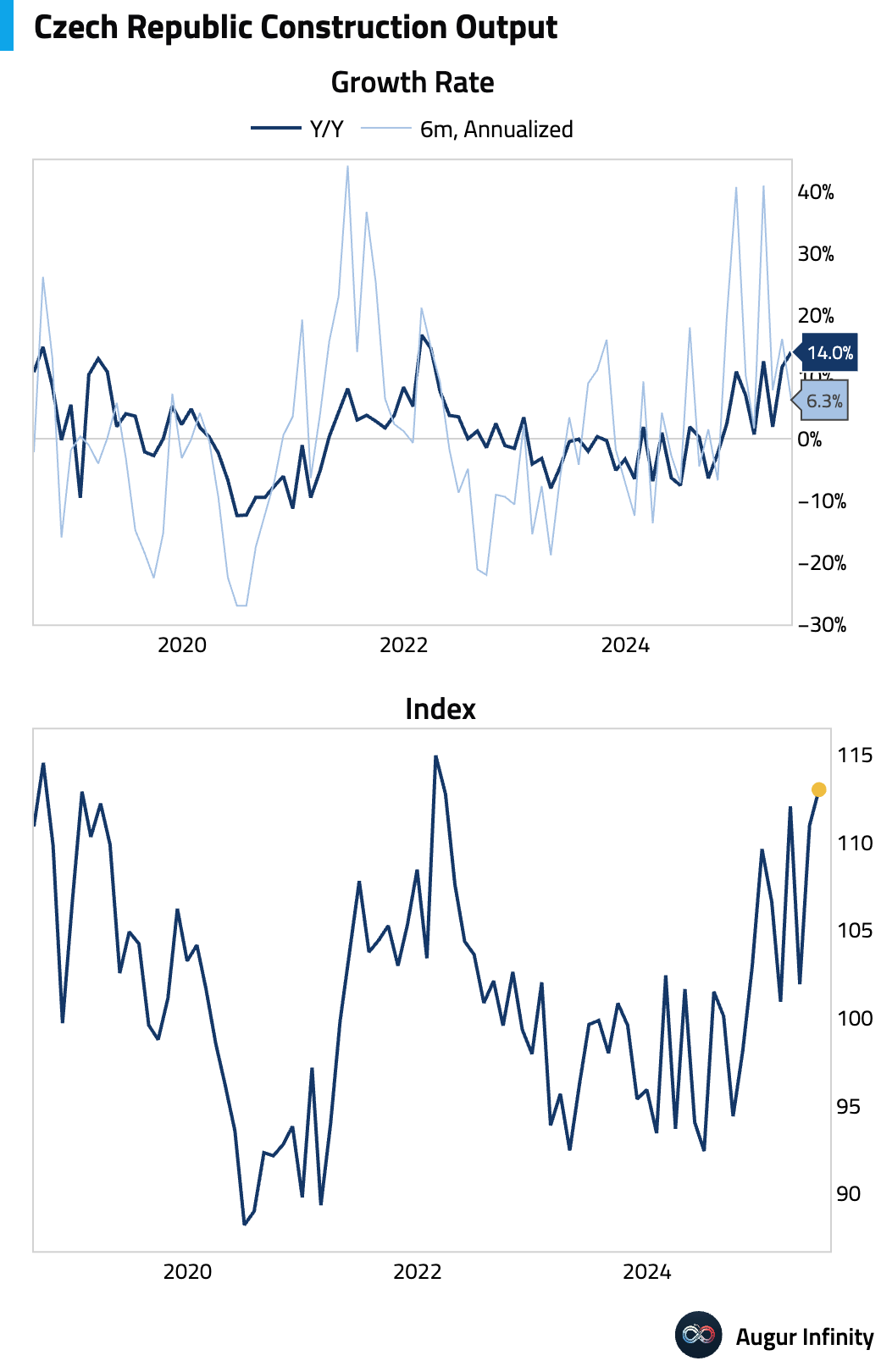

- Construction output in the Czech Republic surged 14.0% Y/Y in June, the fastest pace of growth since March 2022.

Global Markets

Equities

- Global equities advanced on Wednesday, driven by gains in North America and Europe. In the US, equities rose 0.7%, with the tech-heavy Nasdaq climbing 1.2% for its third consecutive day of gains. European markets also posted solid returns, with Germany up 0.8% for its third straight gain. Elsewhere, Canada (+1.7%), Australia (+1.0%), and Brazil (+1.7%) saw strong performance; Canada and Australia recorded their third consecutive advance, while Brazil has now risen for four straight sessions.

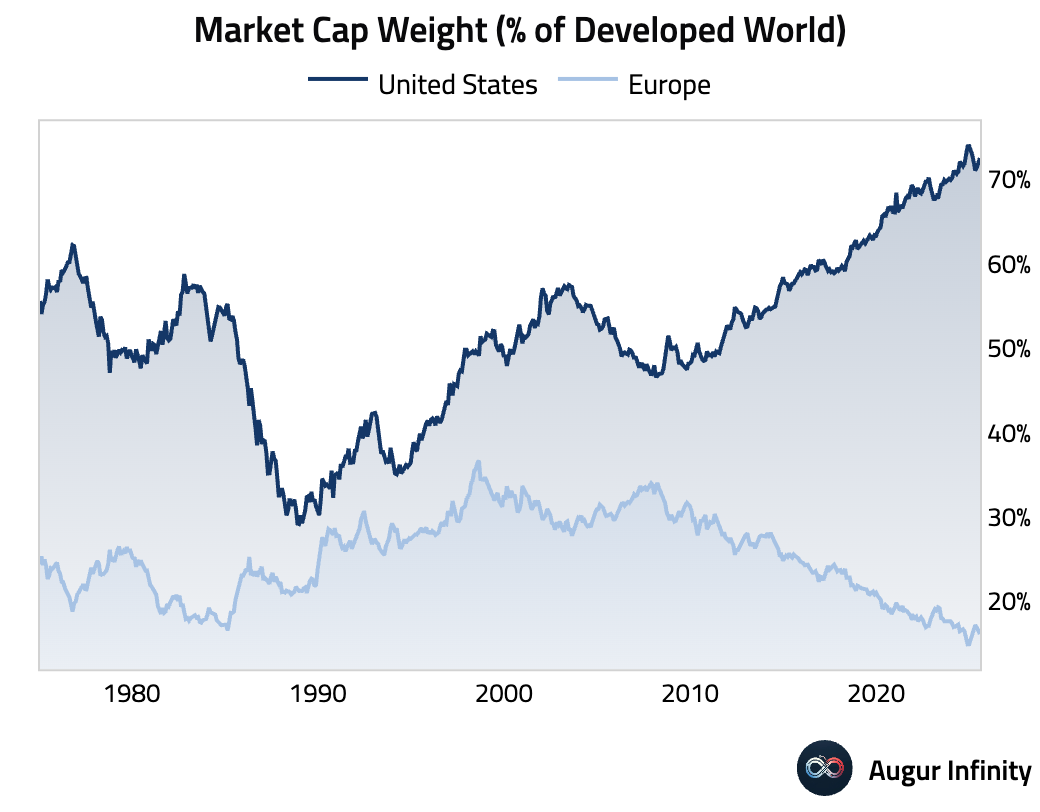

- The US equity market’s share of the developed world’s total market capitalization continued its ascent, rising for a third month to 72.5% at the end of July. In contrast, Europe’s weighting declined to 16.1%, underscoring the ongoing performance divergence between the two regions.

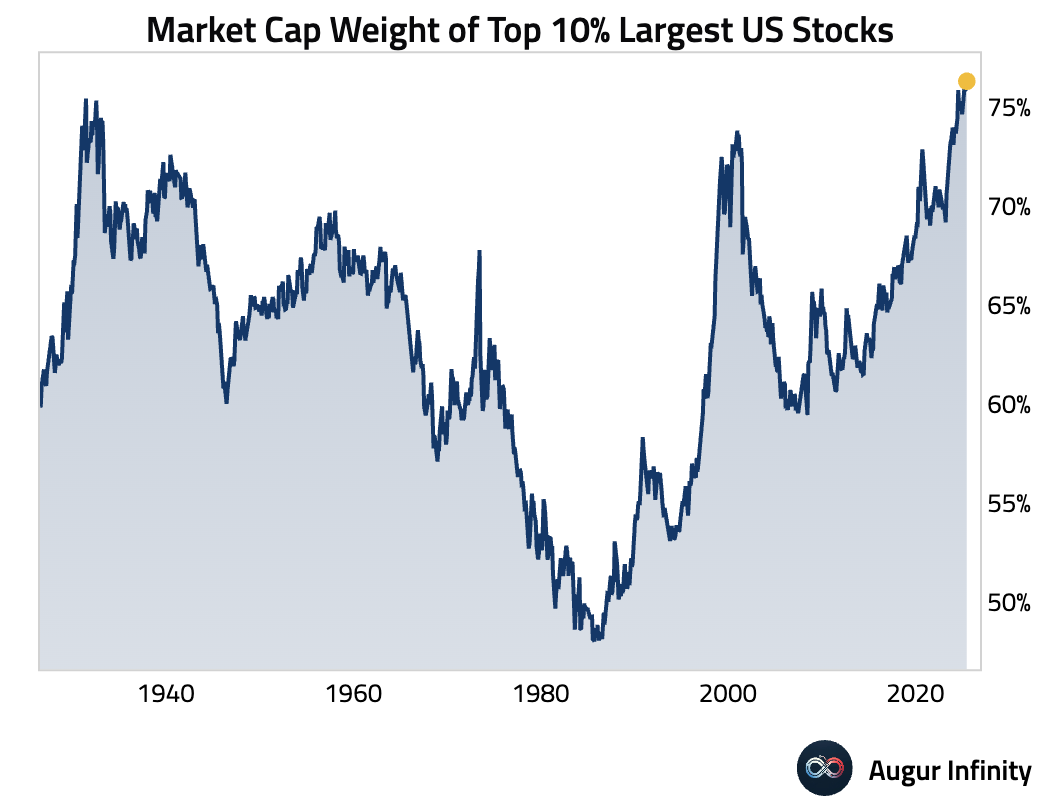

- Market concentration in the US has intensified, as the market capitalization weight of the top 10% of largest US stocks has reached a new record high. This trend highlights the increasing influence of mega-cap companies on broader market performance.

Fixed Income

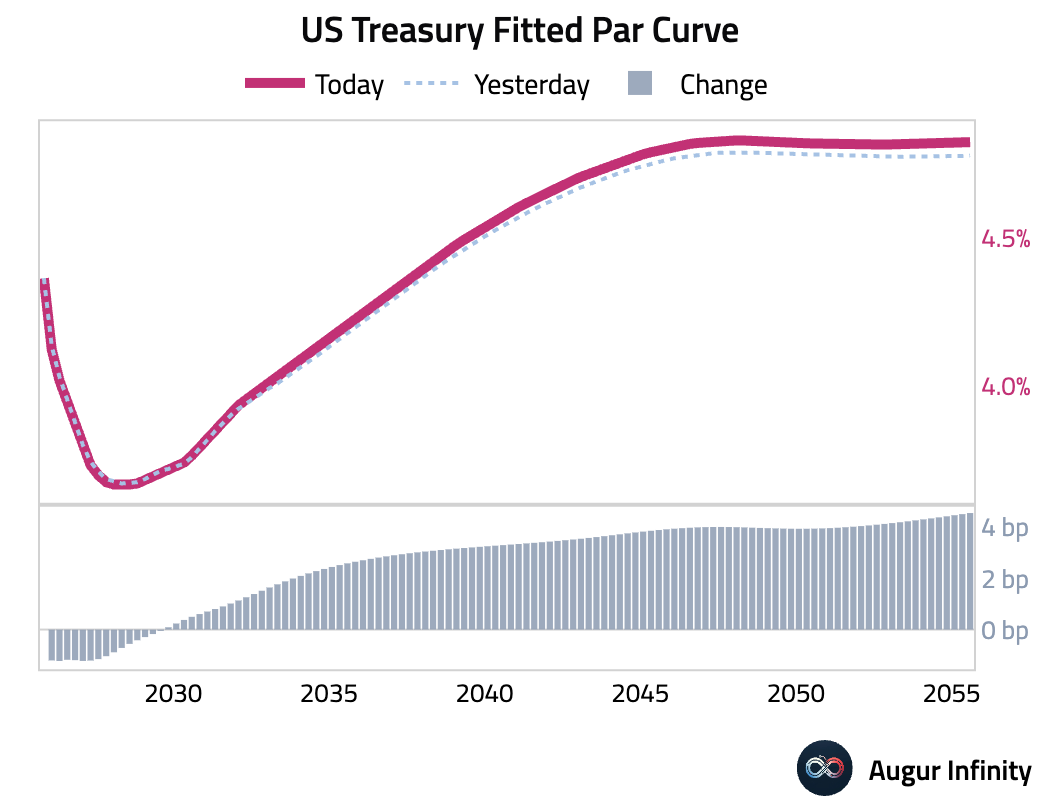

- The US Treasury curve steepened as yields on the long end of the curve rose while the front end declined. The 2-year yield fell 1.0 bps, while the 10-year and 30-year yields increased by 2.6 bps and 4.4 bps, respectively. The moves come as markets continue to price in a high probability of a Federal Reserve rate cut in September, which has kept shorter-term yields anchored.

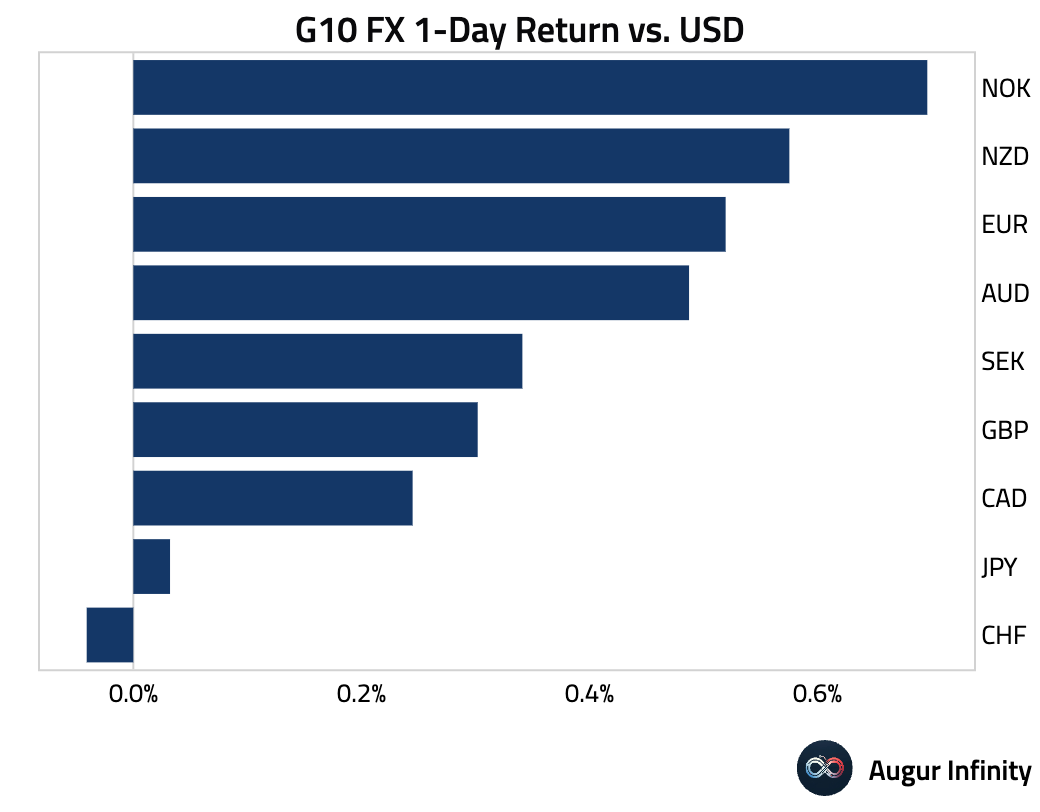

FX

- The US dollar weakened against most G10 peers, reflecting improved risk appetite and expectations for Fed easing. The Norwegian krone was the top performer, gaining 0.7% against the dollar, followed by the New Zealand dollar (+0.6%). The euro and Swedish krona both advanced for a fourth consecutive day, rising 0.5% and 0.3%, respectively.

Disclaimer

Augur Digest is an automated newsletter written by an AI and edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.