Headlines

- The Trump administration is preparing to take Fannie Mae and Freddie Mac public through an initial public offering, according to The Wall Street Journal.

- Bloomberg is reporting, that Washington and Moscow are aiming to reach a deal to halt the war in Ukraine that would lock in Russia’s occupation of territory seized during its military invasion.

- President Trump nominated Stephen Miran, chair of the Council of Economic Advisers, to fill a vacancy on the Federal Reserve’s Board of Governors.

- The White House announced it will clarify that tariffs will not be applied to imports of specific gold bars from Switzerland, according to Bloomberg.

Charts of the Day

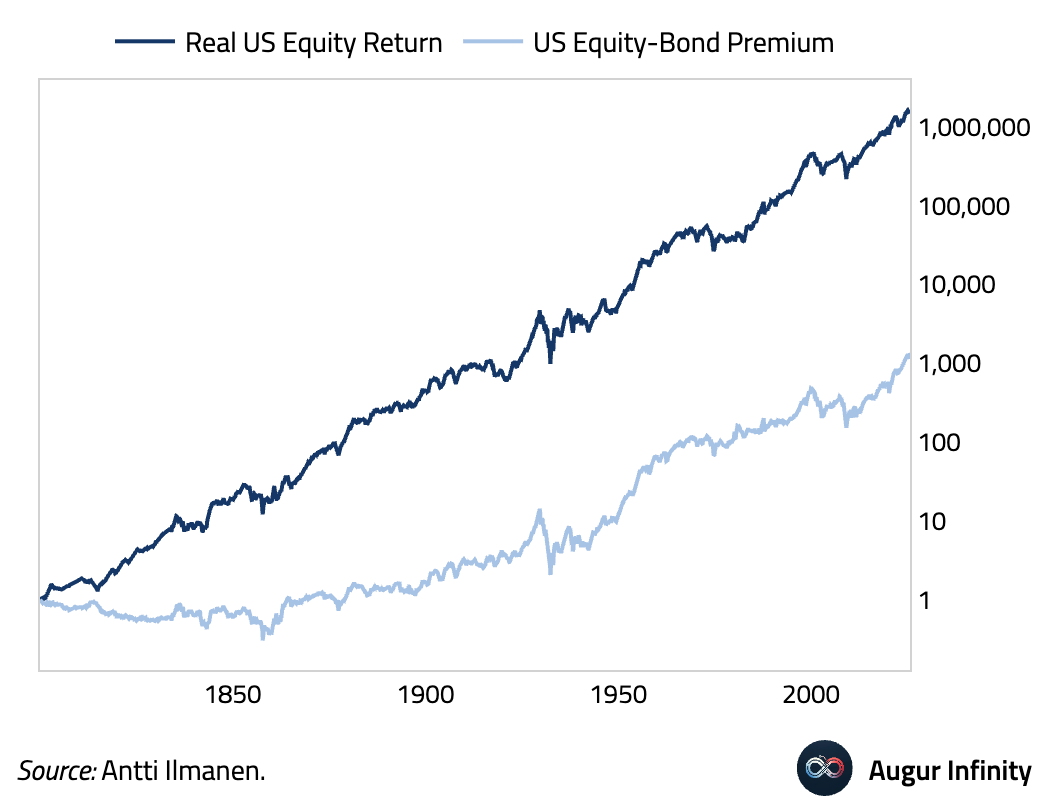

- Cumulative US equity real return has been remarkably stable over the long-run, but a large equity-bond premium is mainly a 20th century phenomenon.

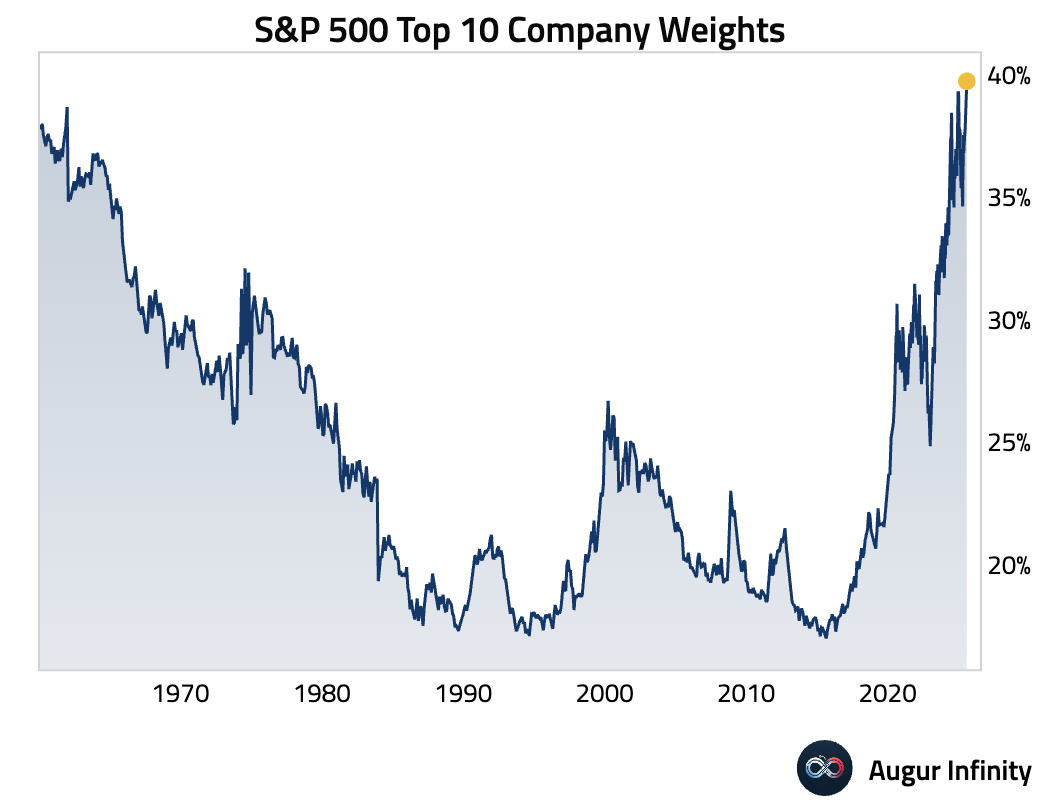

- Market concentration in the US continues to reach new peaks, with the weight of the top 10 companies in the S&P 500 climbing to a record high of 39.7%.

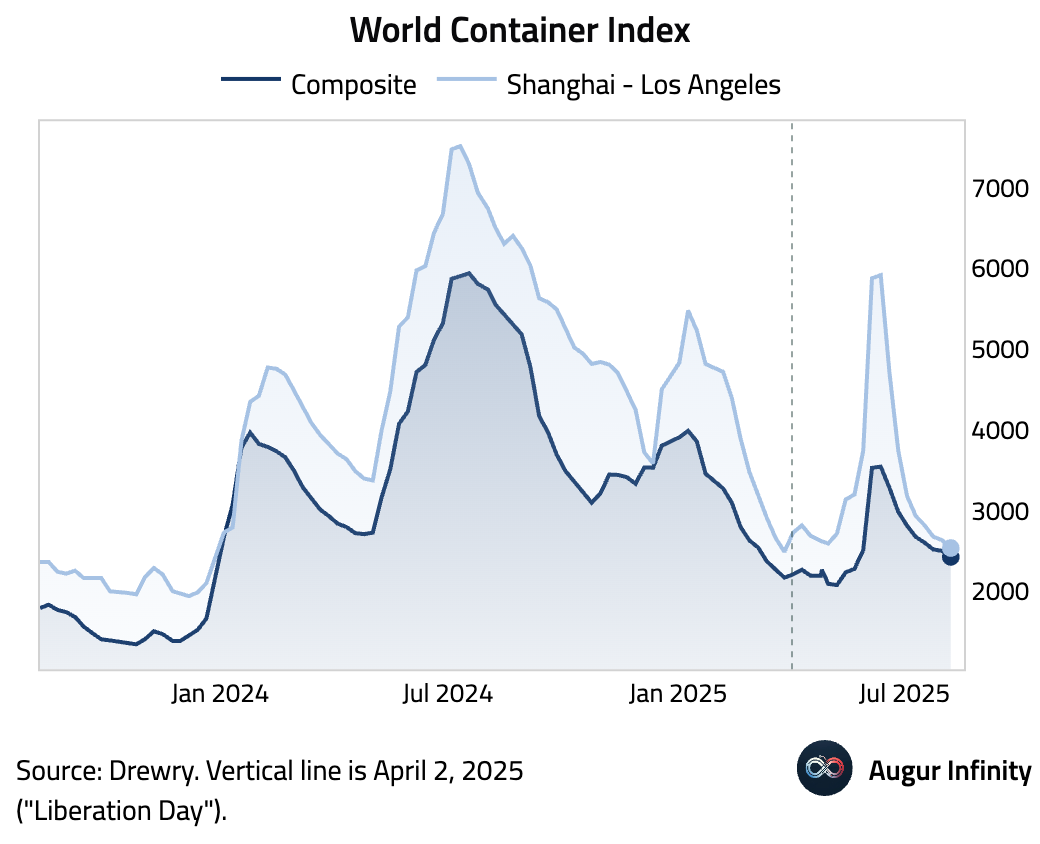

- The World Container Index, which measures spot freight rates, declined for the eighth consecutive week.

Source: Drewry

Global Economics

United States

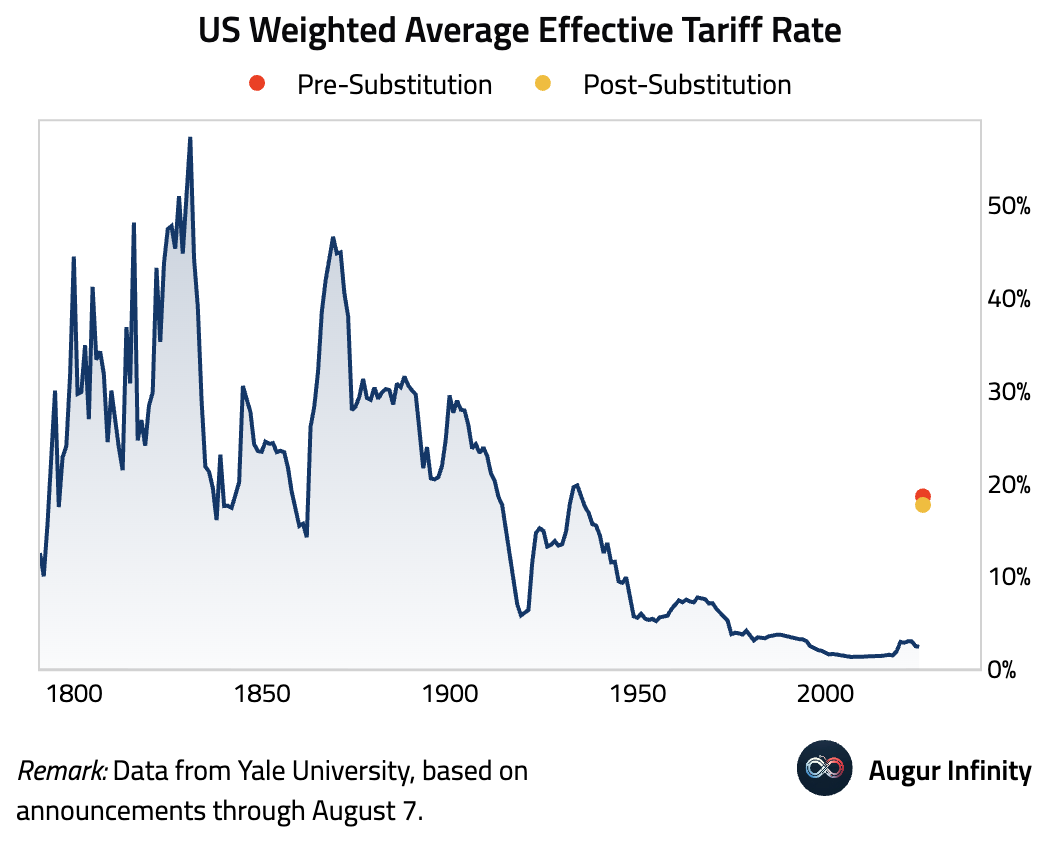

- The Budget Lab estimates that consumers face an overall average effective tariff rate of 18.6%, the highest since 1933. Even if consumption shifts are incorporated, the average tariff rate will still be 17.7%, the highest since 1934.

Source: The Budget Lab

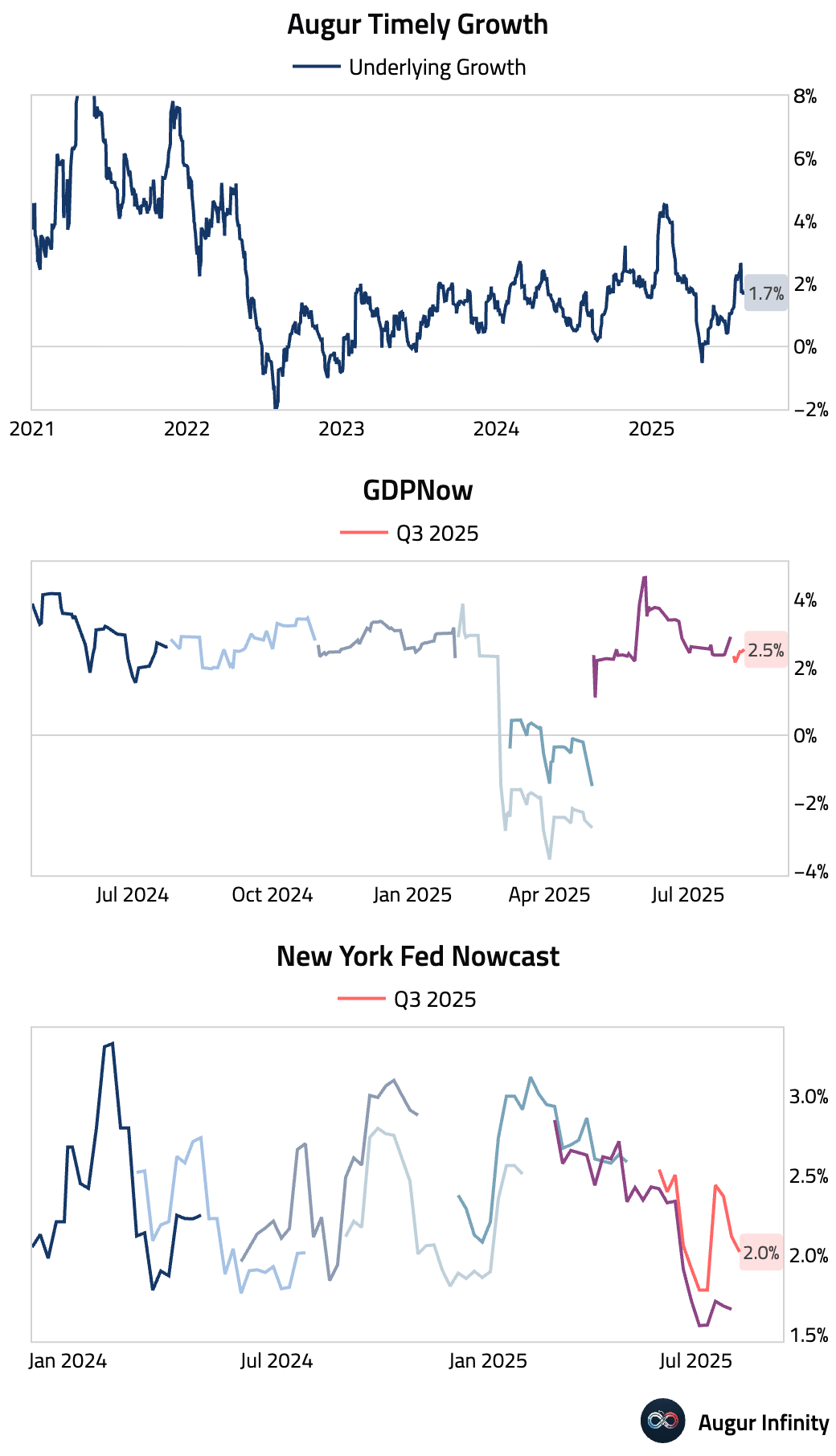

- Here are the latest growth estimates for the US: the Atlanta Fed’s GDPNow model points to 2.5% growth in Q3, the New York Fed Nowcast is at 2.0%, and the Augur Underlying Growth estimate is 1.7% for the last 30 days.

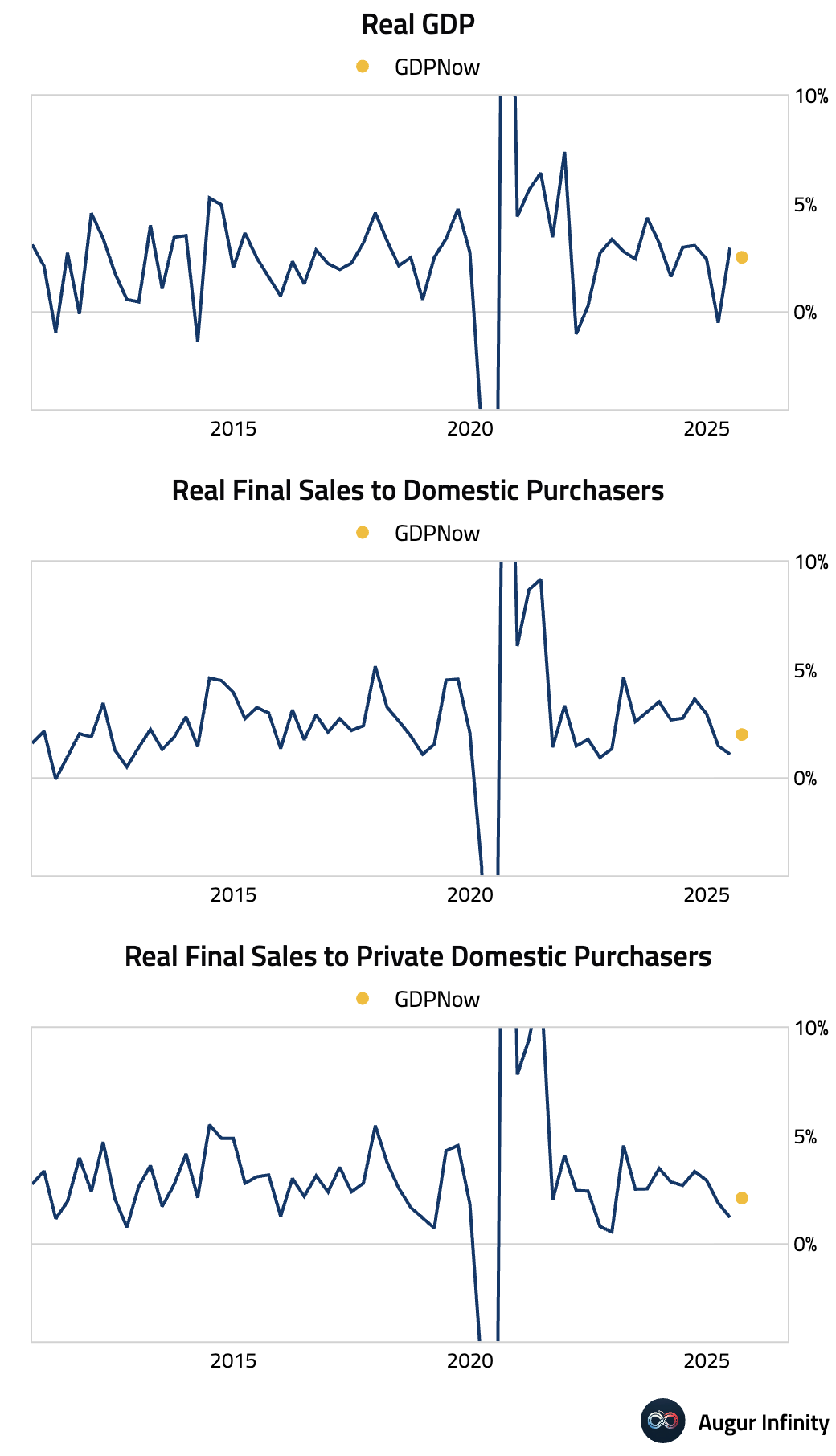

- As shown above, the Atlanta Fed's GDPNow model is tracking headline Q3 real GDP growth at 2.5%. Stripping out net exports and inventories, real final sales to domestic purchasers is tracking at 2%. From there, if we remove government spending, the real final sales to private domestic purchasers is tracking at 2.1%.

Canada

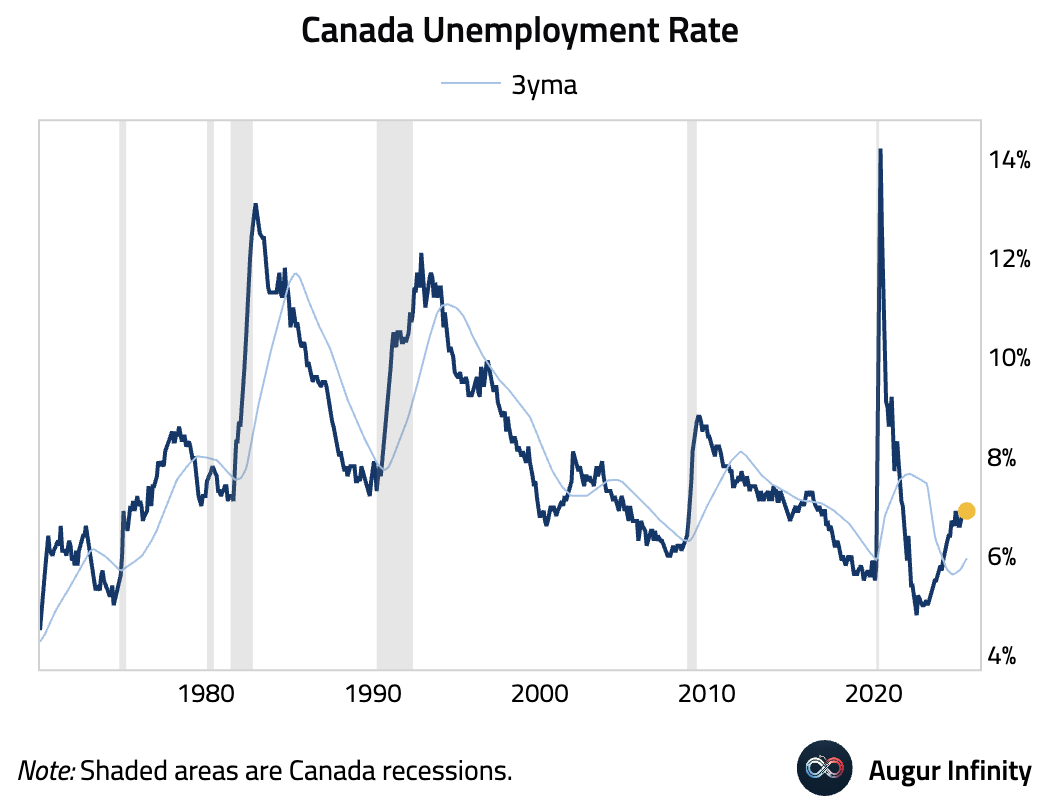

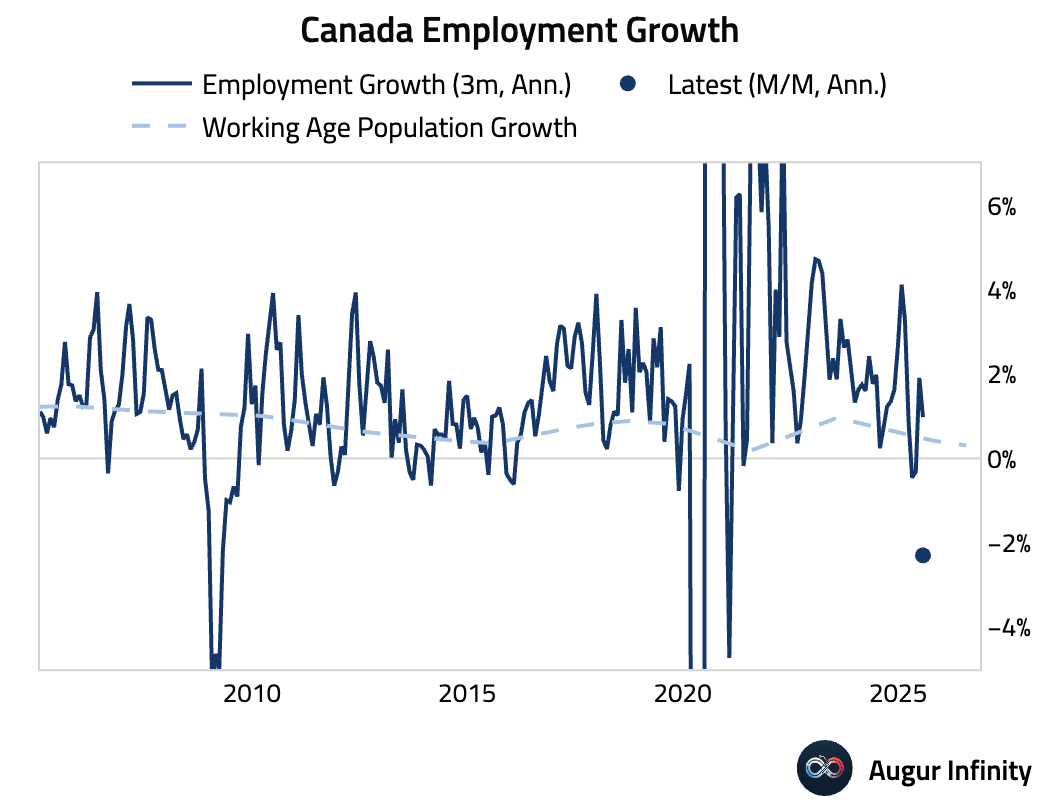

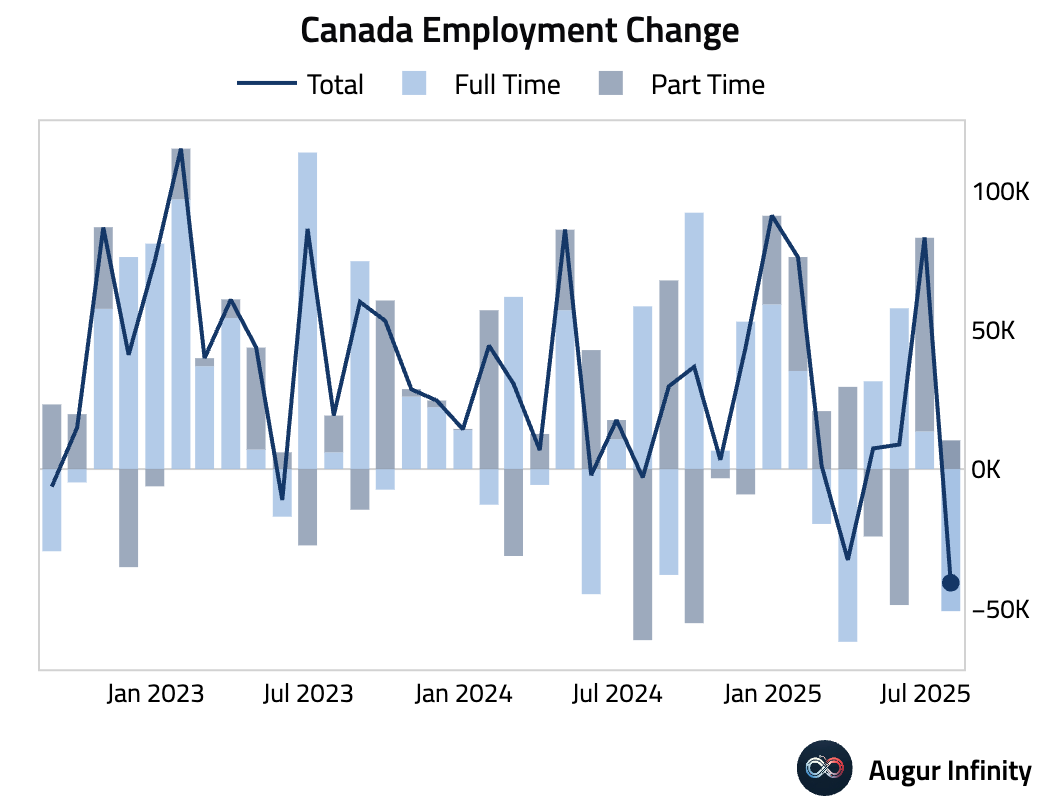

- Canada’s labor market unexpectedly weakened in July, shedding 40,800 jobs, a stark contrast to the 13,500 gain anticipated by consensus. The loss was driven entirely by a 51,000 decline in full-time positions, partially offset by a 10,300 increase in part-time work. The unemployment rate held steady at 6.9%, as the participation rate fell 0.2 percentage points to 65.2%.

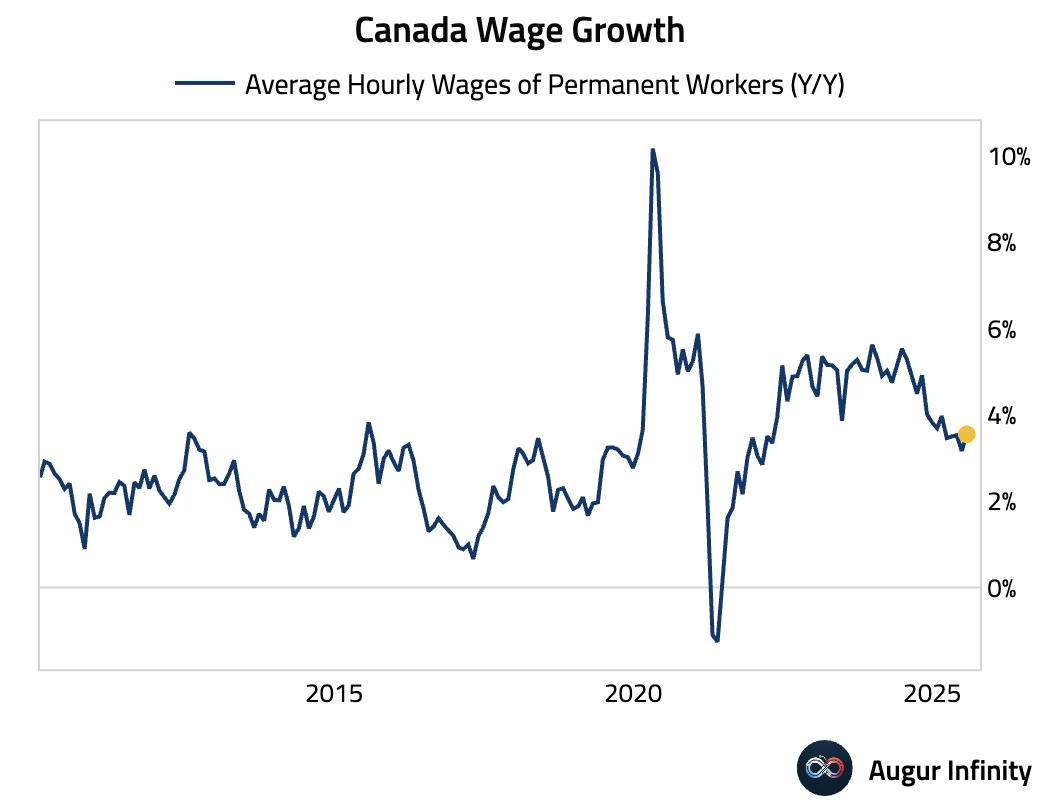

- Average hourly wages accelerated to 3.5% Y/Y in July from 3.2%, marking a six-month high.

Europe

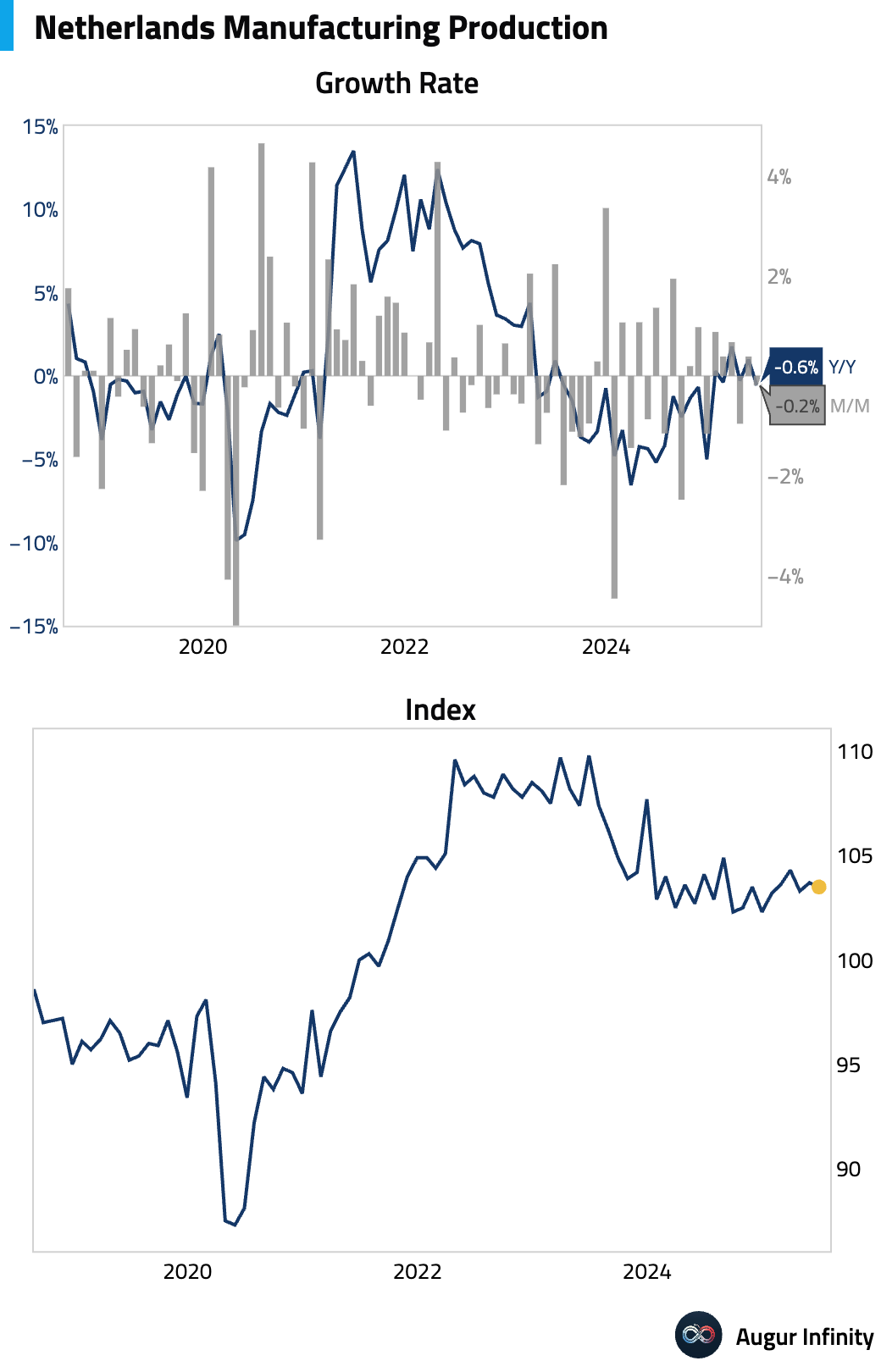

- Dutch manufacturing production slipped 0.1% M/M in June, reversing a 0.4% gain in May.

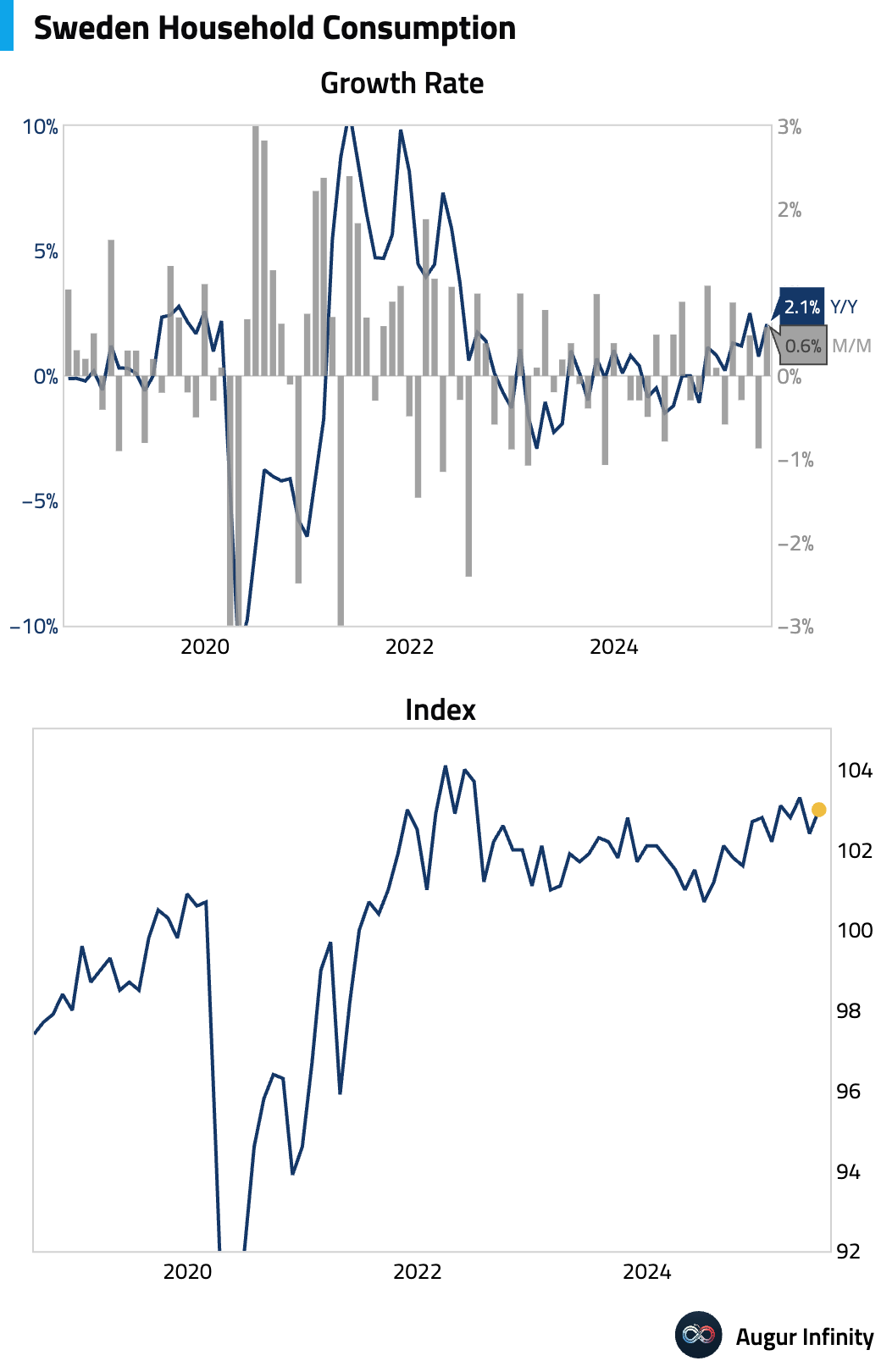

- Swedish household consumption rebounded in June, rising 0.6% M/M and accelerating to 2.1% Y/Y.

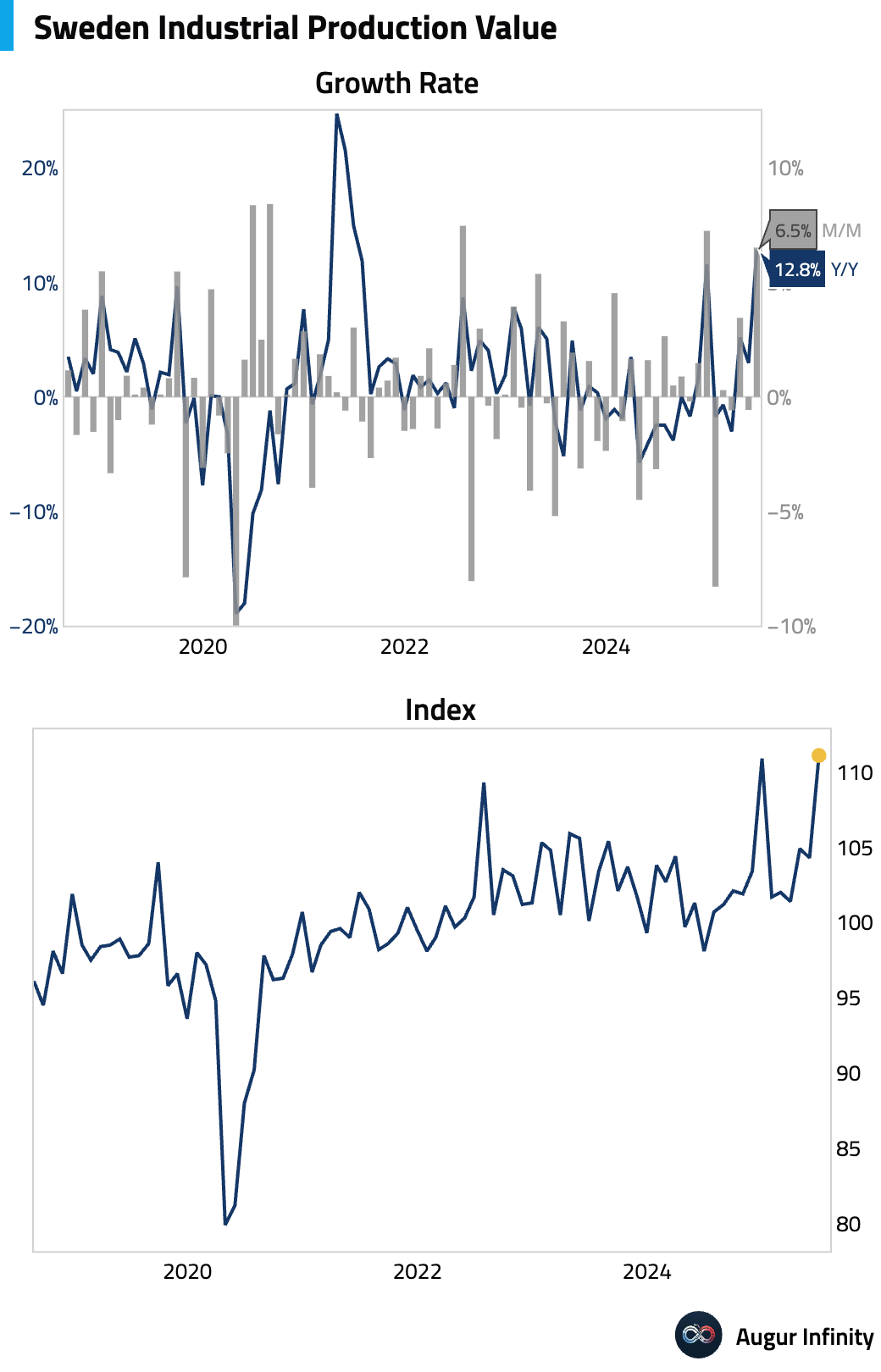

- Swedish industrial production surged in June, with the value index rising 6.5% M/M and 12.8% Y/Y, recovering sharply from May’s declines.

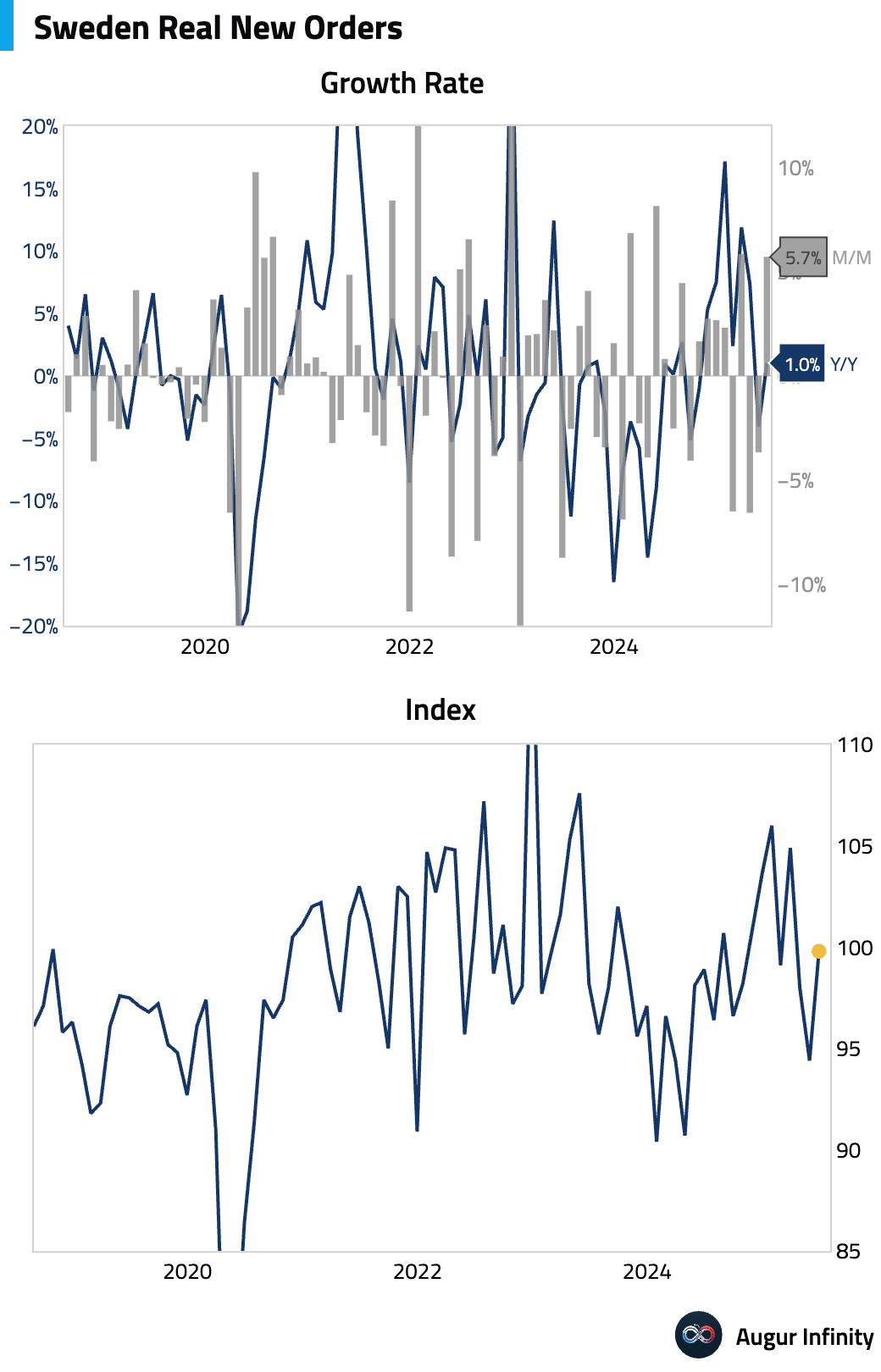

- New orders for Swedish industry returned to growth in June, rising 1.0% Y/Y after a 4.1% fall in May.

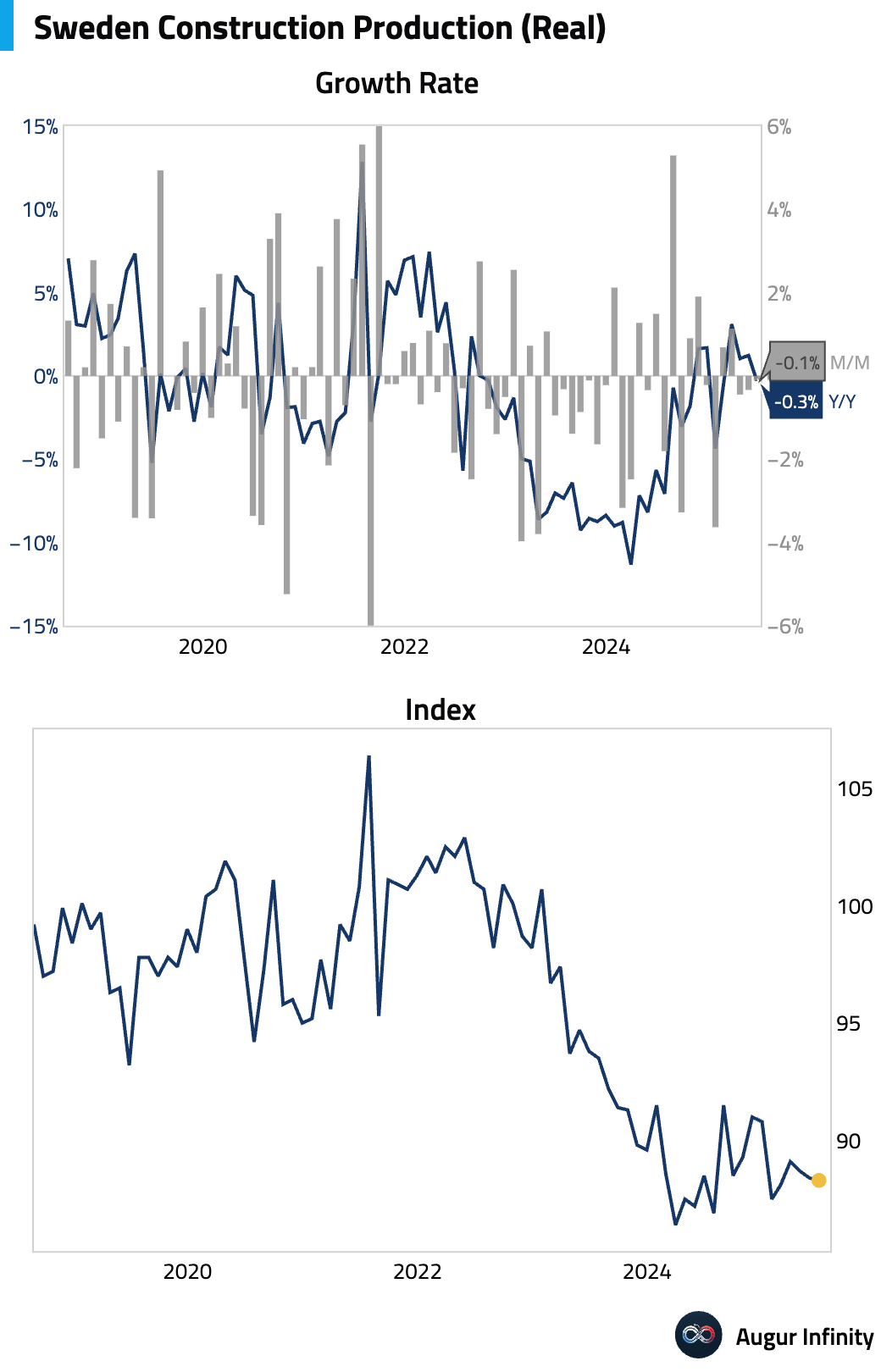

- Swedish construction output fell 0.3% in June, a reversal from the 0.3% increase in May.

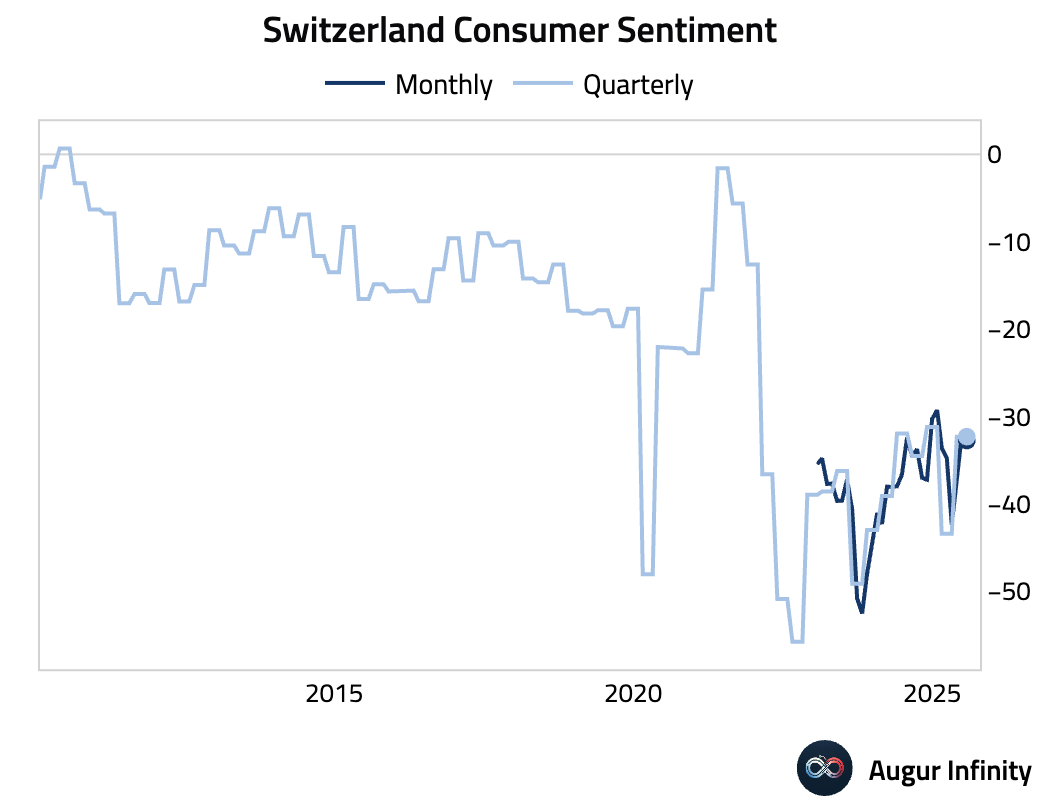

- Swiss consumer confidence deteriorated more than expected in the third quarter, falling to -33 from -32, below the consensus of -30.

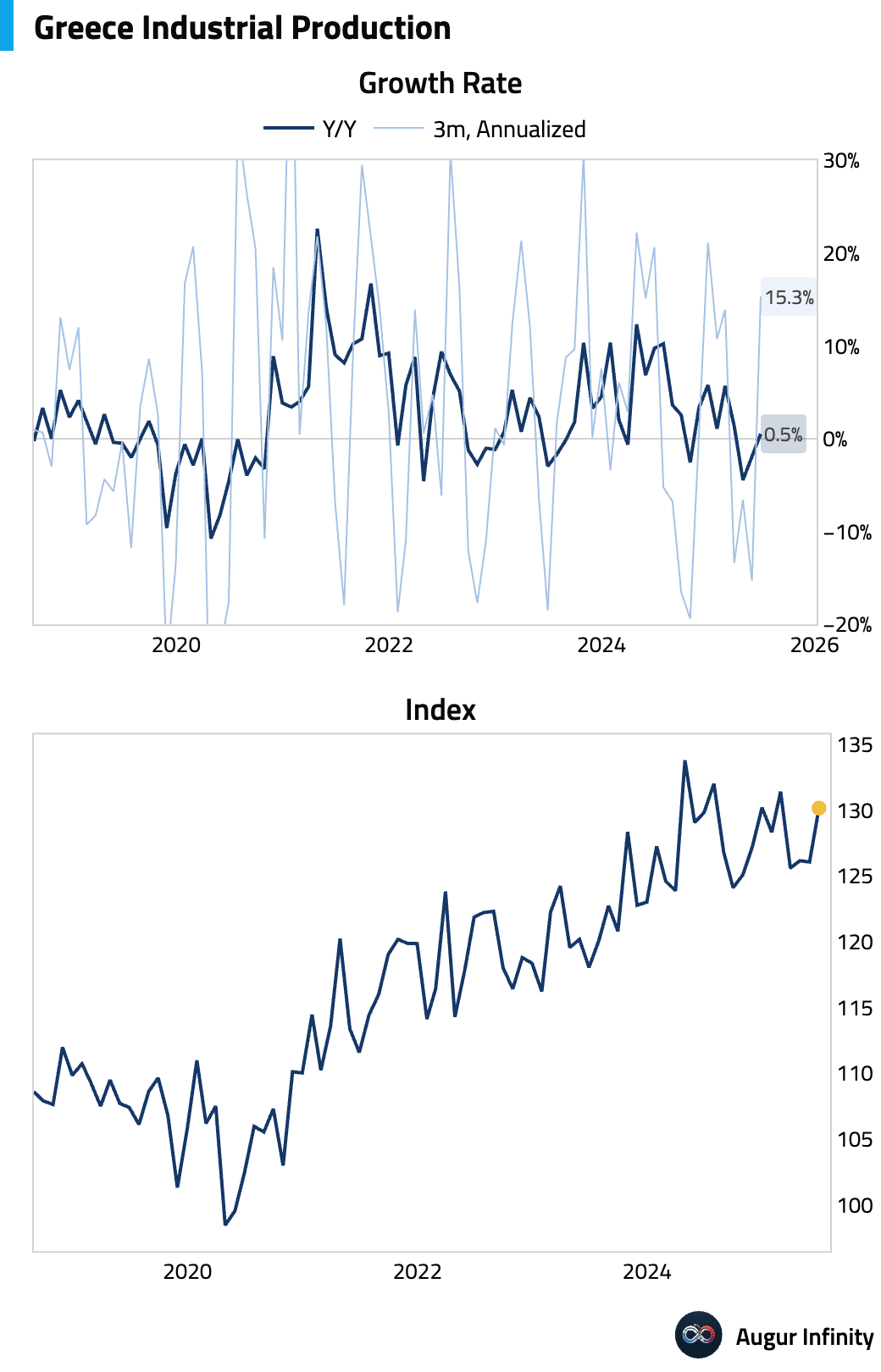

- Greek industrial production returned to growth in June, rising 0.5% Y/Y after a 2.0% decline in May.

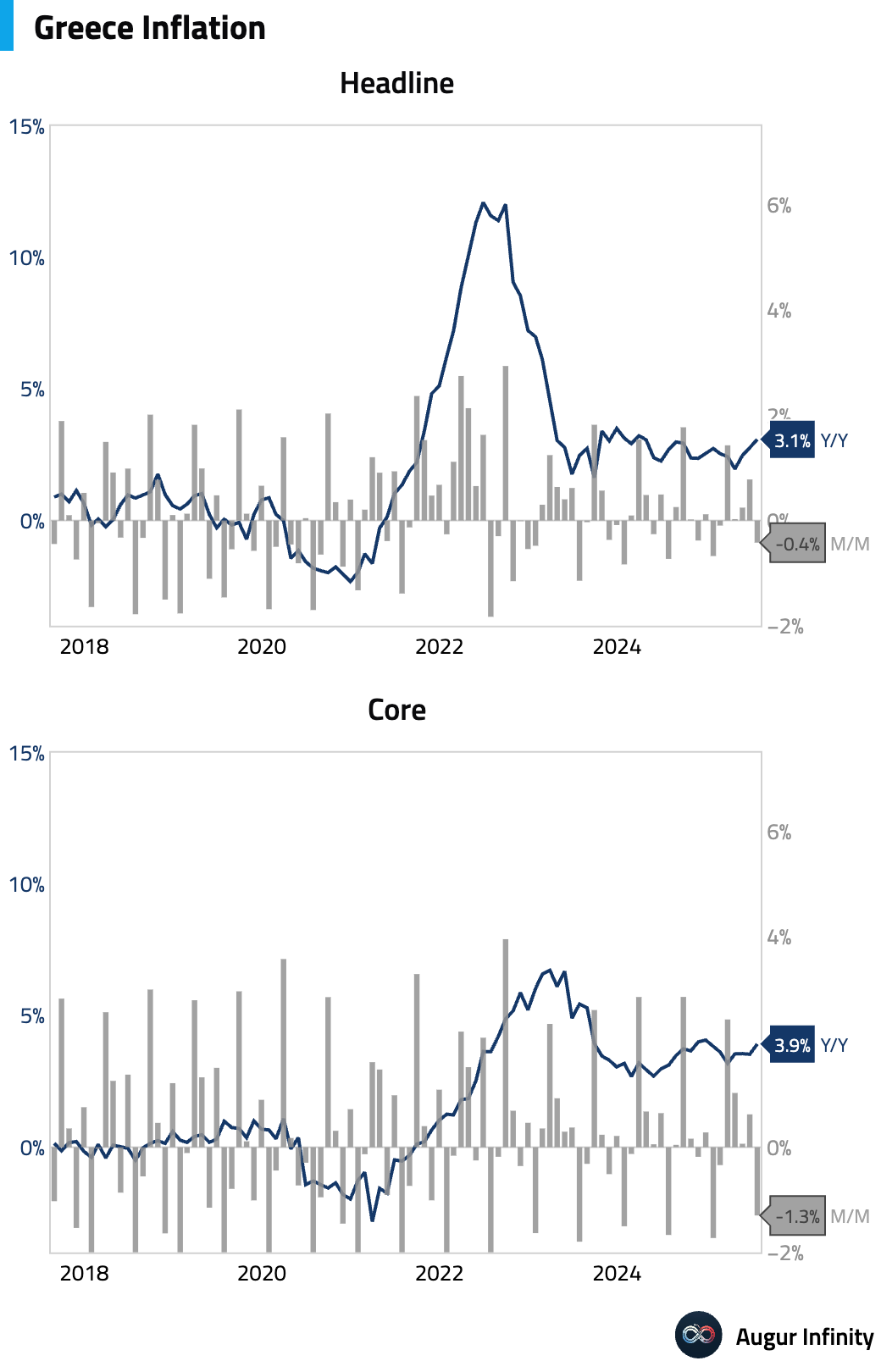

- Greek inflation accelerated in July, with the Y/Y rate rising to 3.1% from 2.8%. On a monthly basis, prices fell 0.4%.

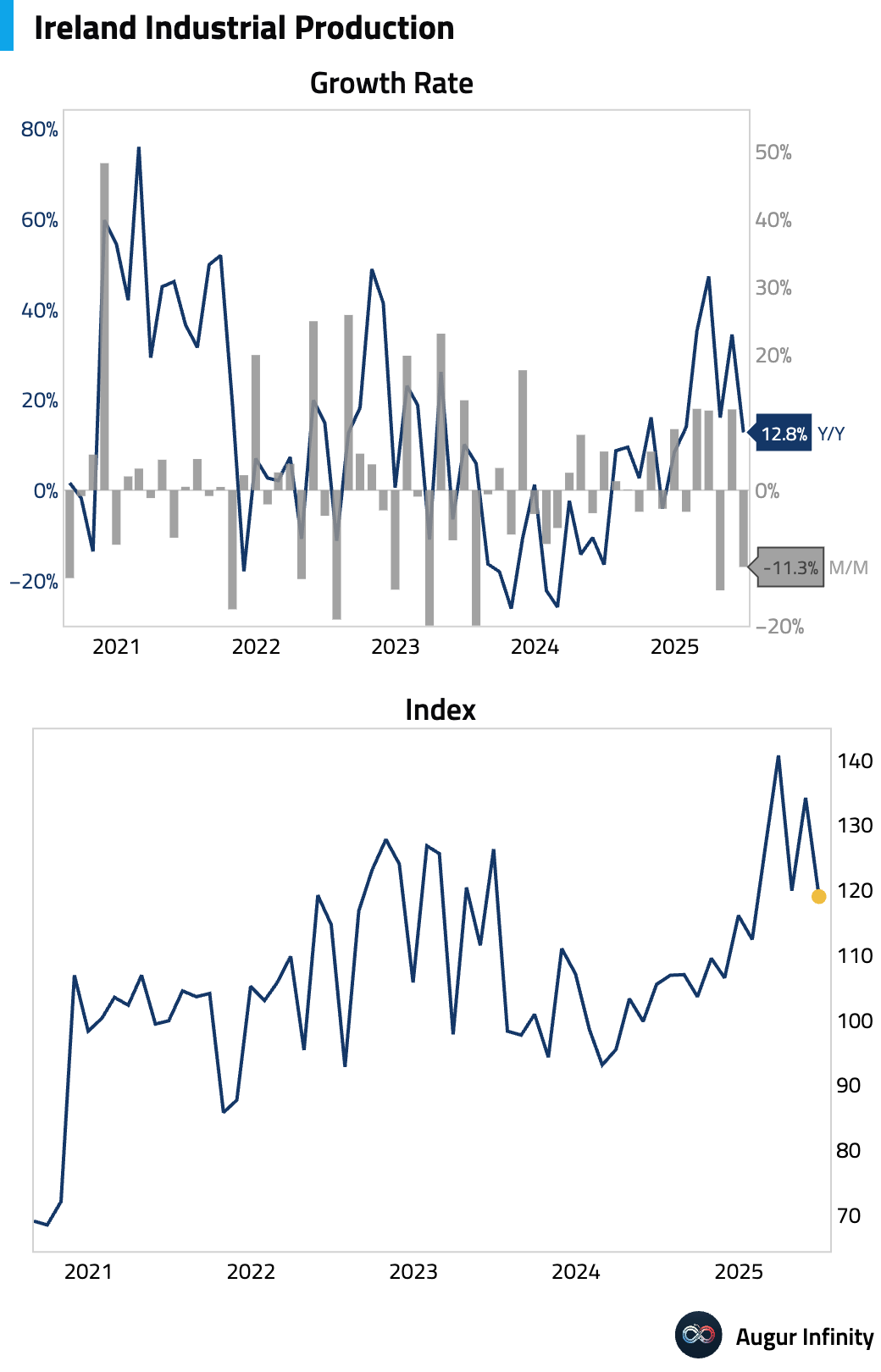

- Irish industrial production growth moderated in June, rising 12.8% Y/Y, down from 34.4% in the prior month.

Asia-Pacific

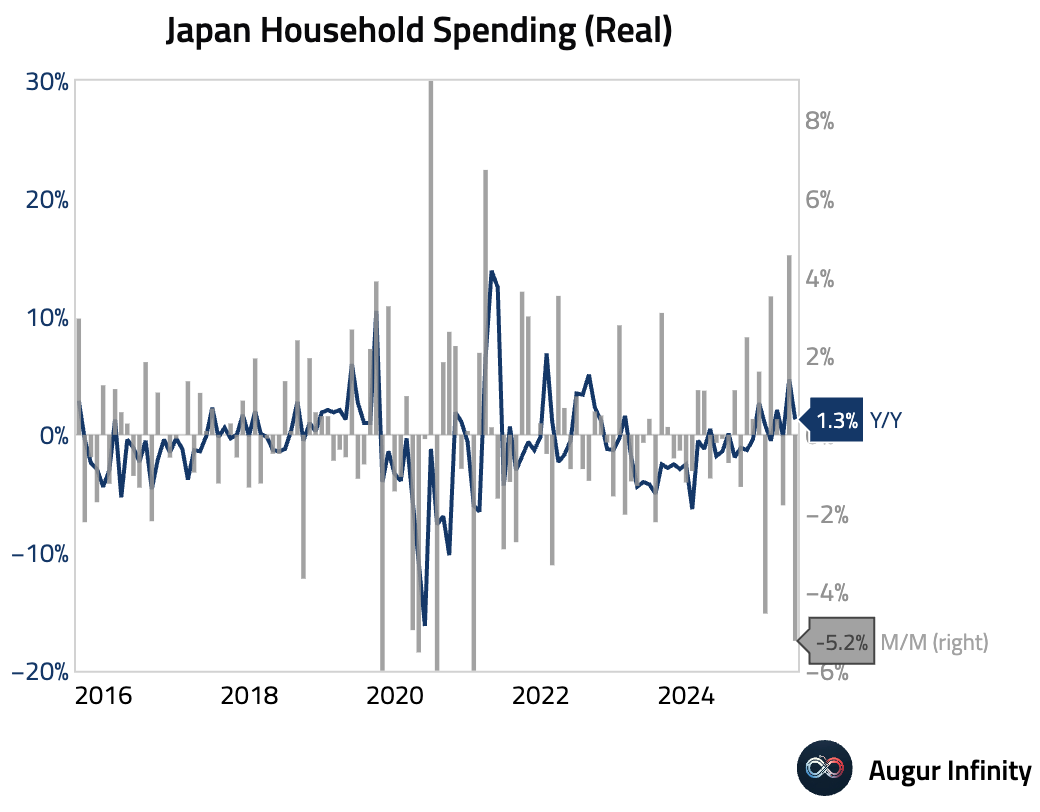

- Japanese household spending unexpectedly plunged 5.2% M/M in June, sharply missing the consensus forecast of a 3.0% decline and reversing the prior month’s 4.6% gain. The year-over-year rate decelerated to 1.3% from 4.7%.

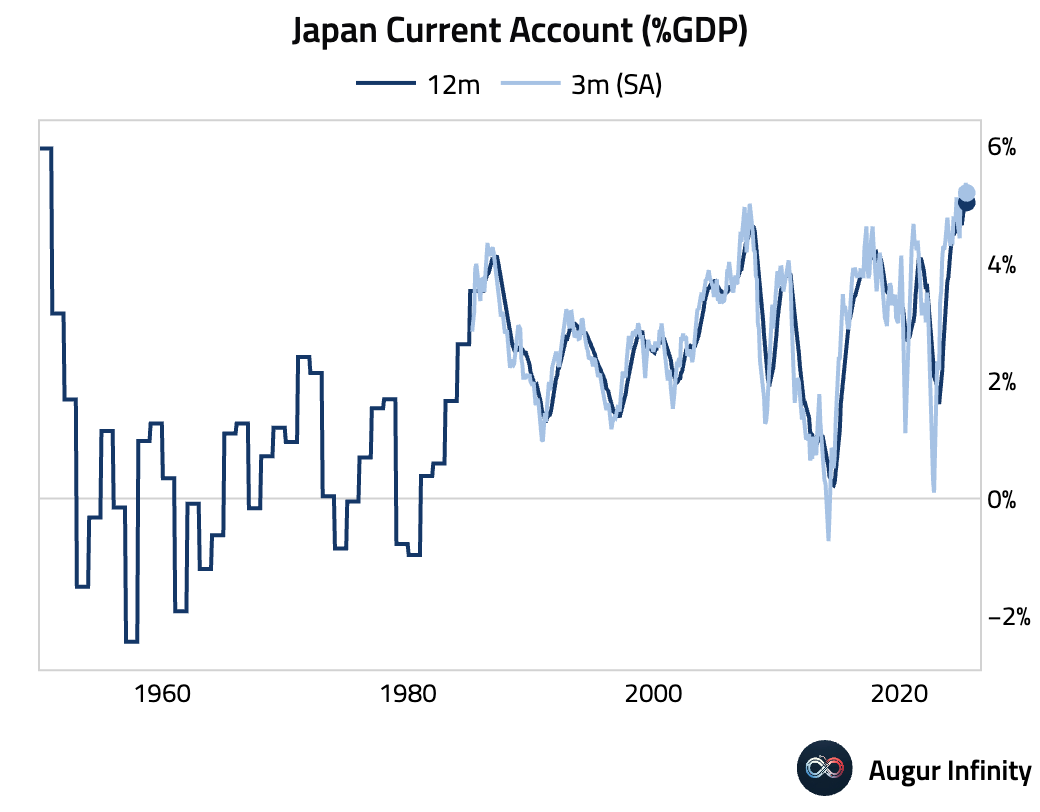

- Japan’s current account surplus narrowed to ¥1.35 trillion in June, missing forecasts. The decline was driven by a smaller trade surplus and a drop in primary income. Inbound travel spending also saw its first year-over-year decline since the post-pandemic reopening. Despite the monthly miss, the Q2 annualized surplus remains strong at 4.8% of GDP.

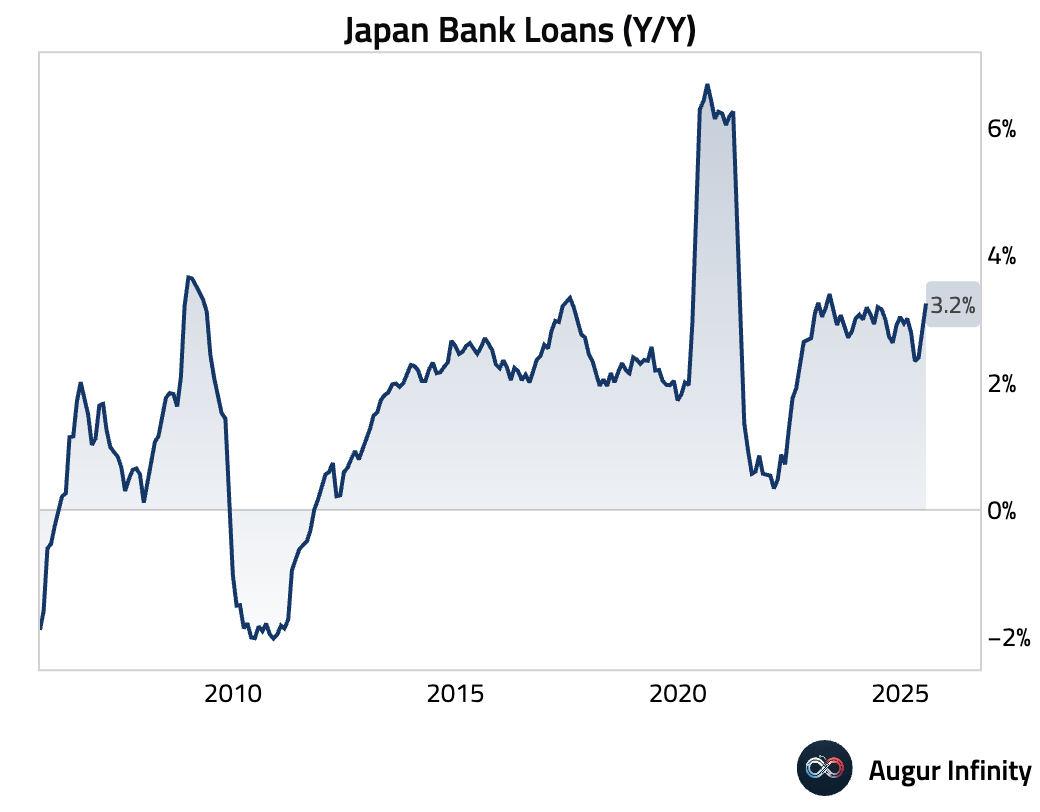

- Japanese bank lending accelerated in July, rising 3.2% Y/Y, its fastest pace since May 2023.

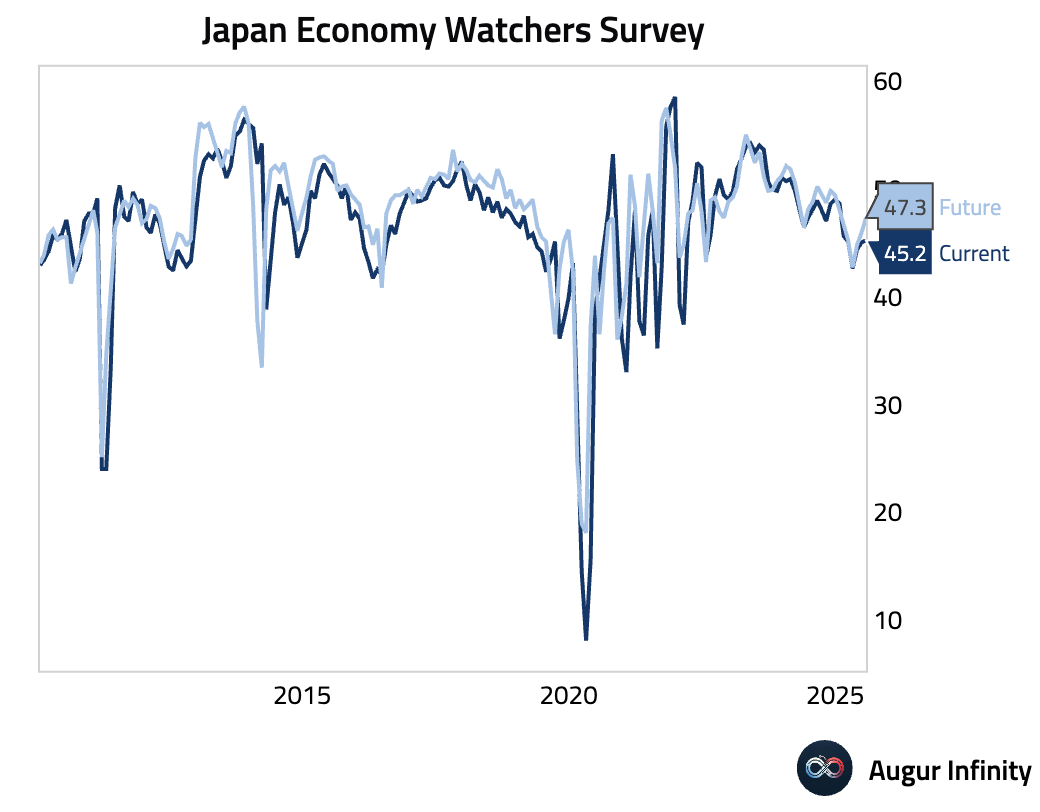

- The Japanese Economy Watchers Survey for July showed an improvement in both current conditions (45.2 from 45.0) and the outlook (47.3 from 45.9), though both remain in pessimistic territory below 50.

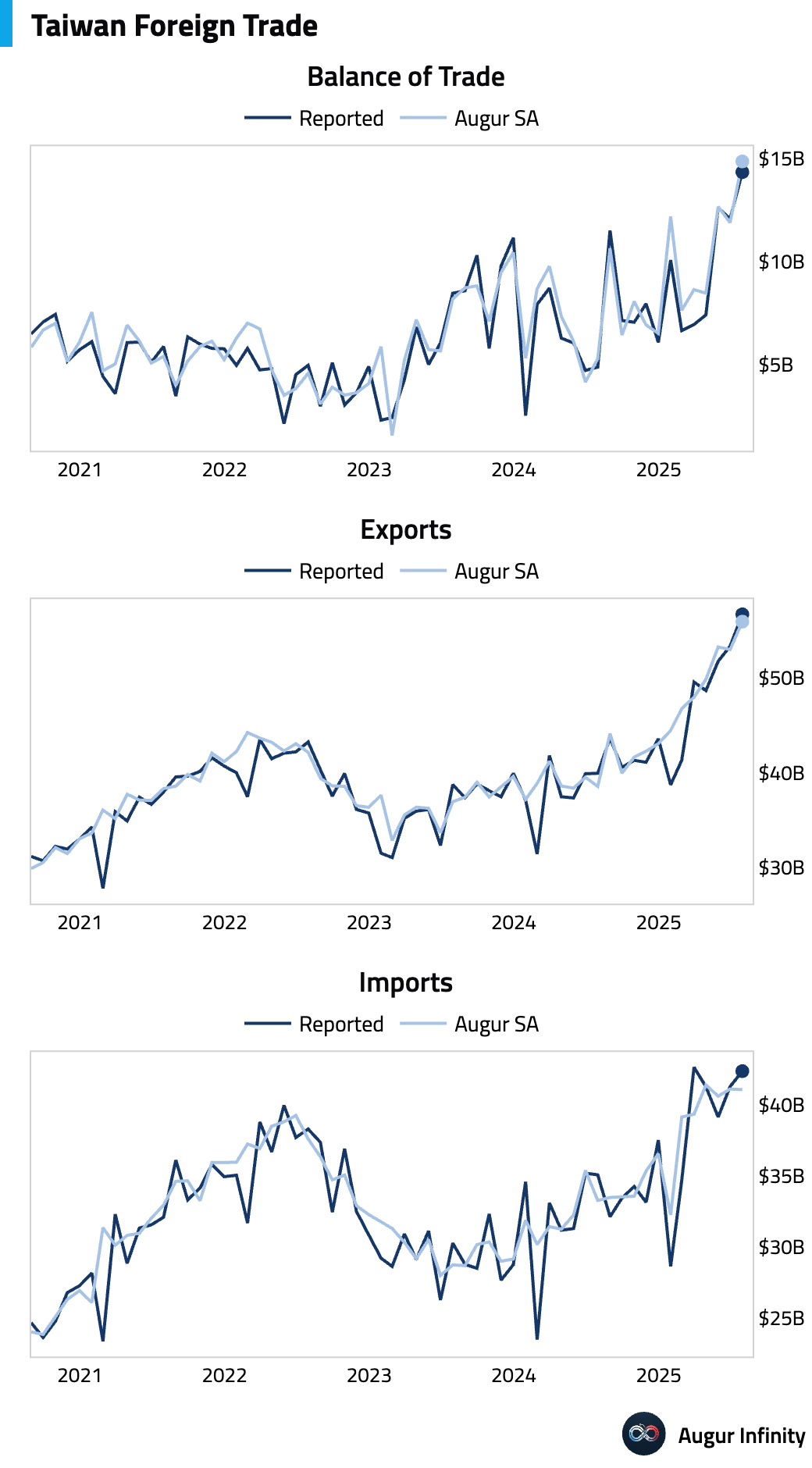

- Taiwan’s trade surplus hit an all-time high of $14.3 billion in July, substantially beating expectations. The result was driven by a record surge in exports, which grew 42.0% Y/Y, far outpacing the 28.7% consensus. The strength was concentrated in info & communication tech exports to ASEAN countries, which masked falling demand from the US, EU, and China. Imports also grew a robust 20.8% Y/Y.

China

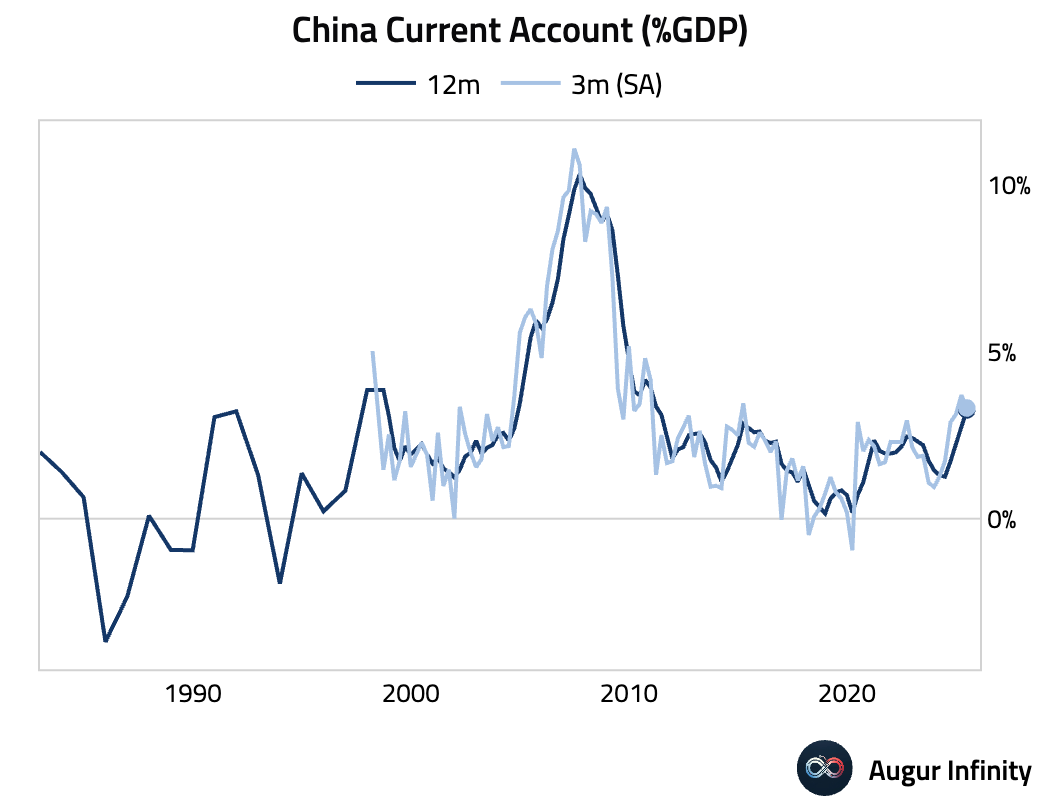

- China’s preliminary current account surplus for Q2 2025 was $135.1 billion, down from $165.4 billion in the first quarter.

Emerging Markets ex China

- Indonesian consumer confidence edged higher to 118.1 in July from 117.8.

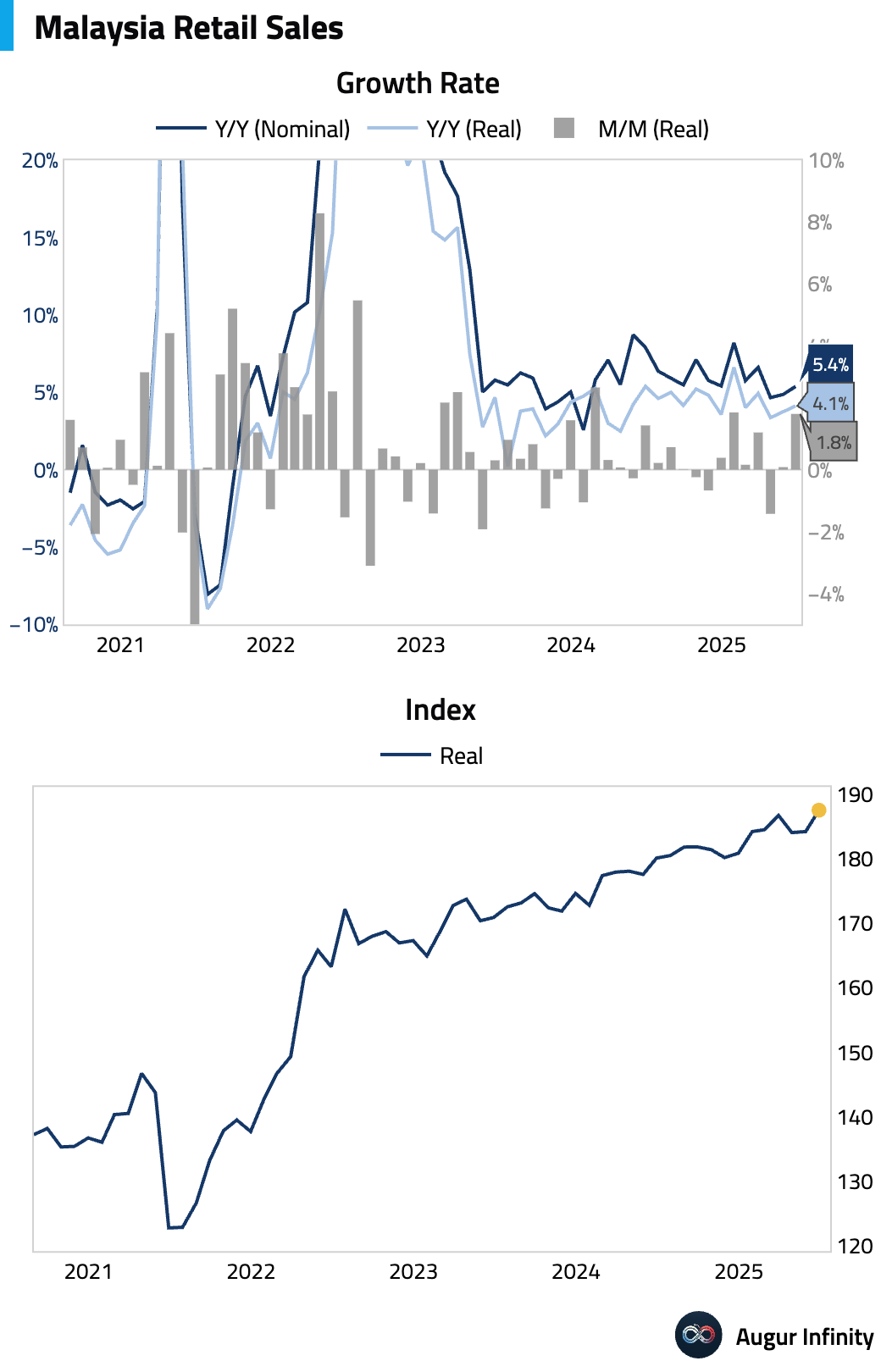

- Malaysian retail sales growth accelerated to 5.4% Y/Y in June from 4.9% in May.

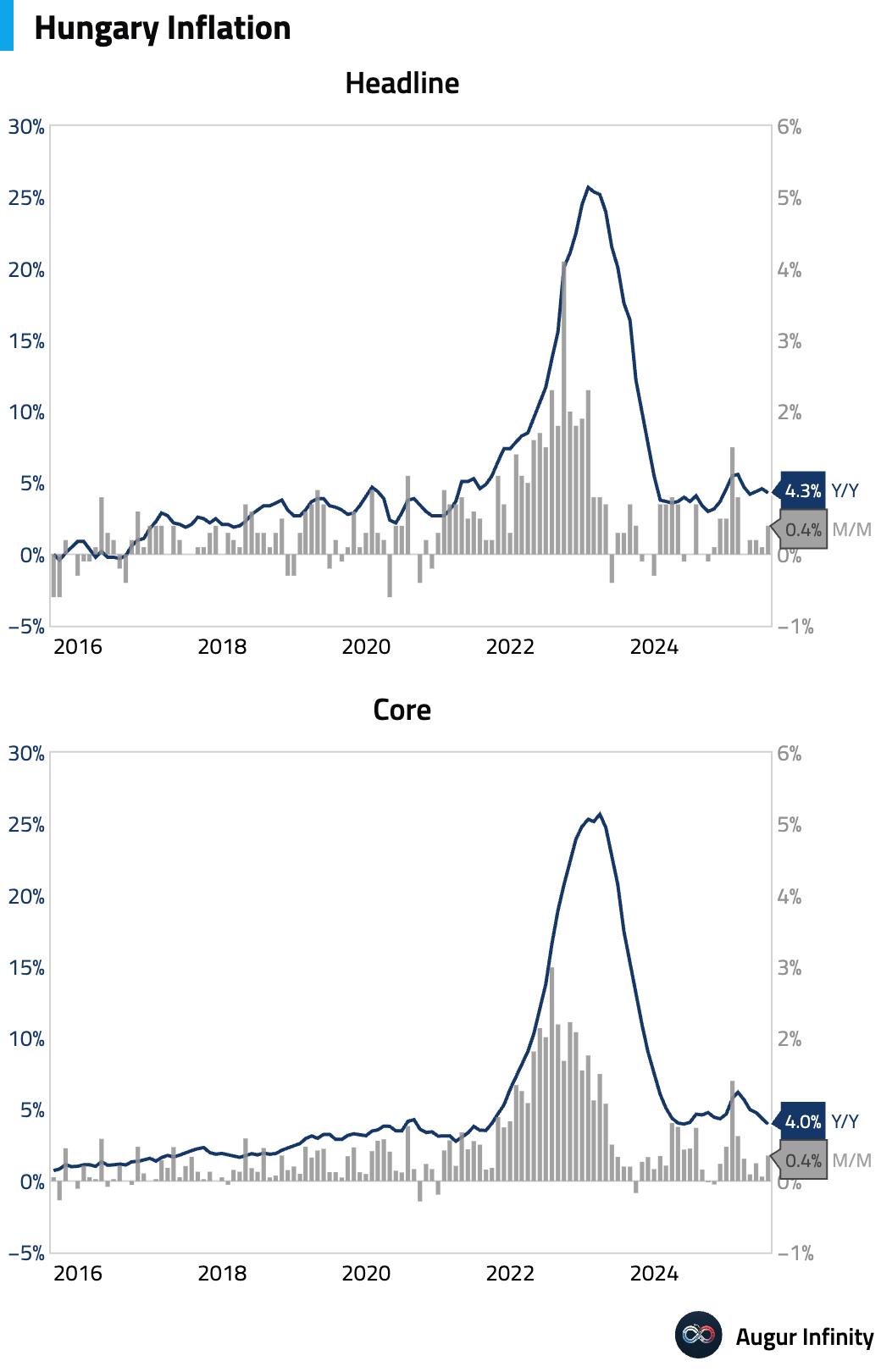

- Hungarian headline inflation surprised to the upside in July at 4.3% Y/Y (consensus: 4.1%), though it decelerated from June’s 4.6% pace. The miss was driven by sticky food and gas prices. Core inflation eased to a near four-year low of 4.0% Y/Y.

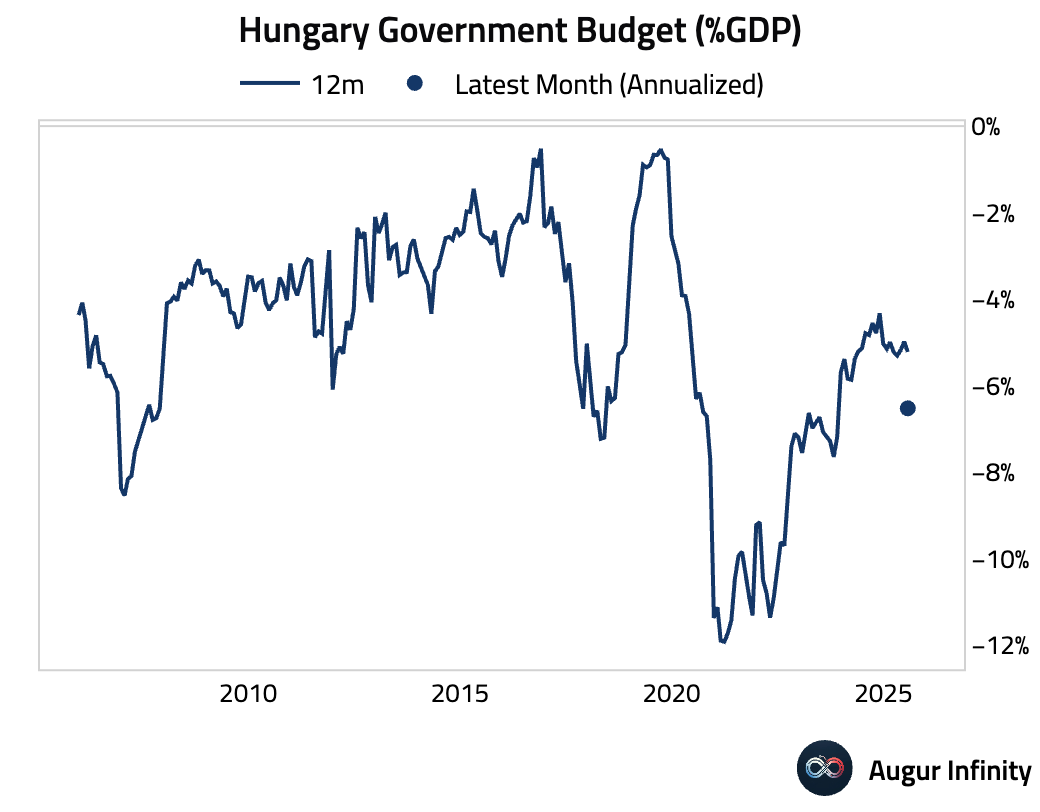

- Hungary posted a budget deficit of 12.8 billion HUF in July, a sharp swing from the 27.4 billion HUF surplus in June.

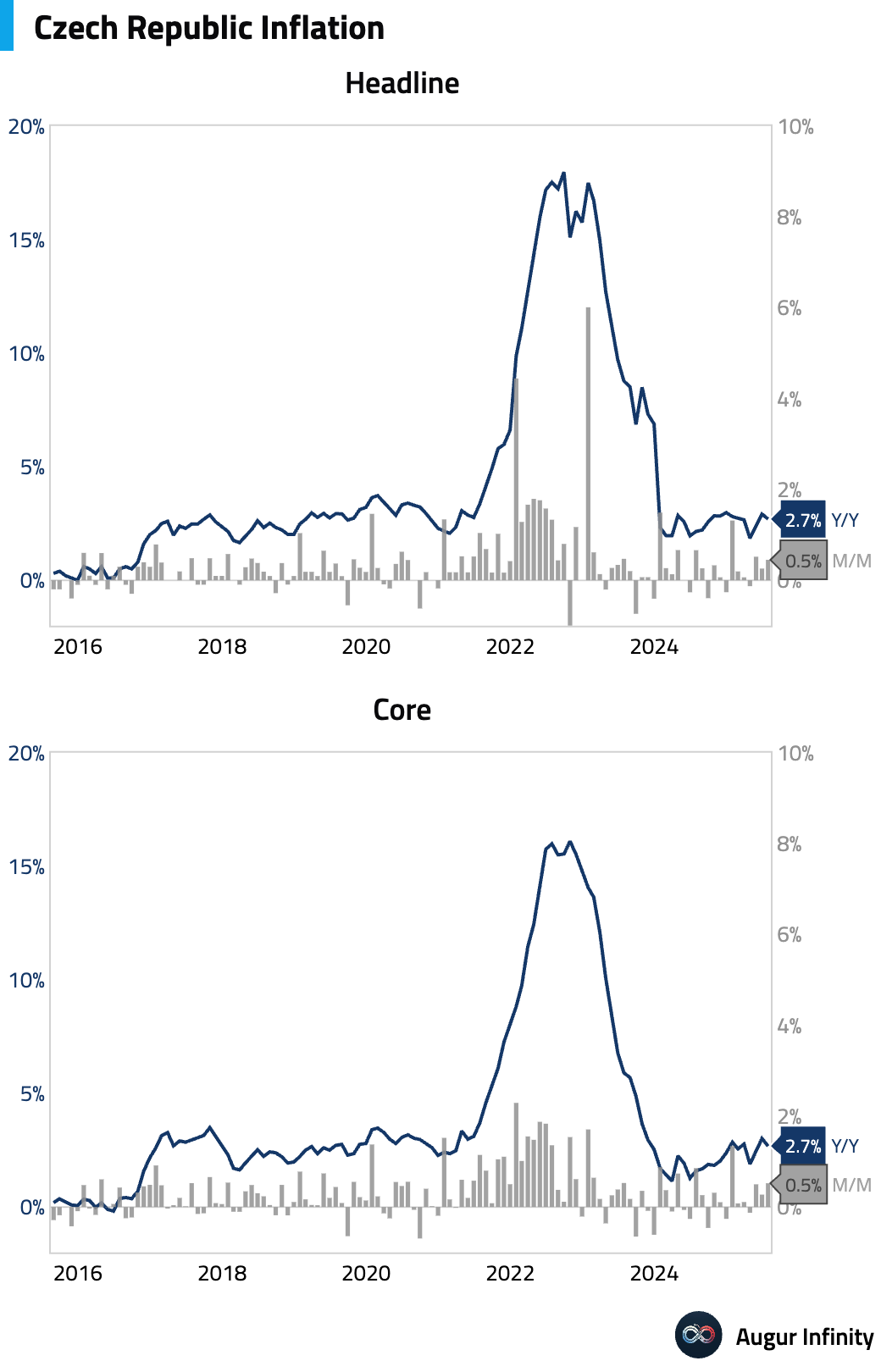

- The final reading for Czech inflation in July was unchanged from the preliminary estimate, with prices rising 0.5% M/M and 2.7% Y/Y.

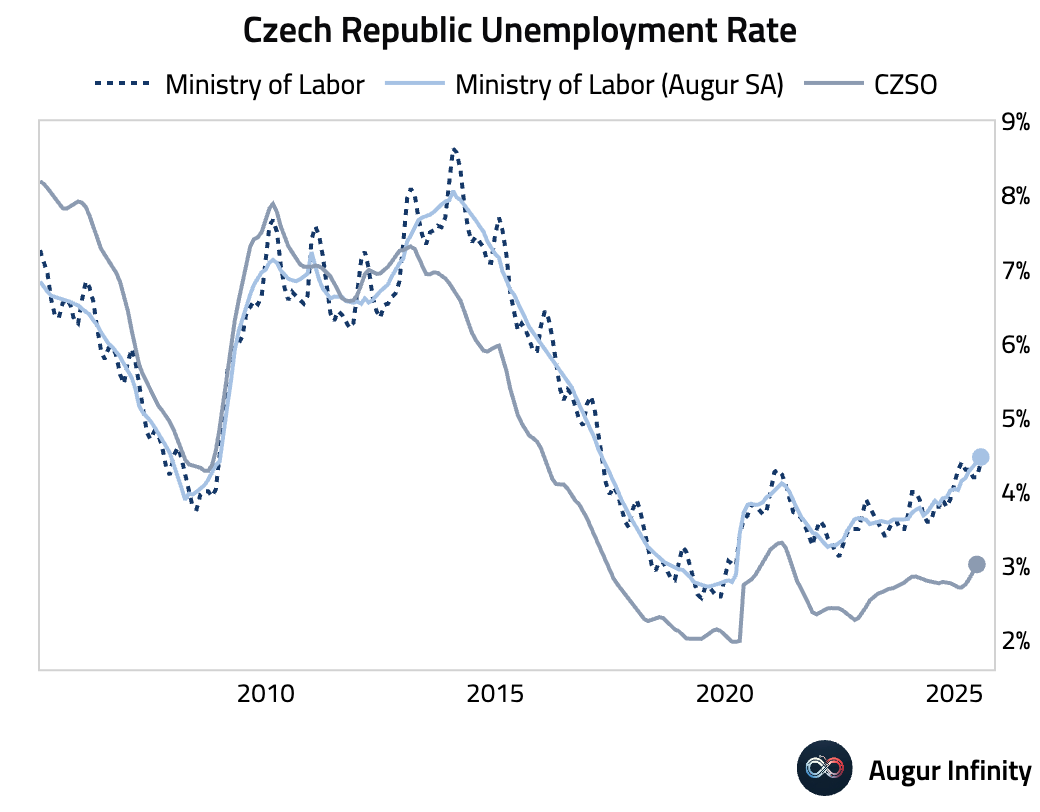

- The Czech unemployment rate rose to 4.4% in July from 4.2% in June, reaching its highest level since March 2017.

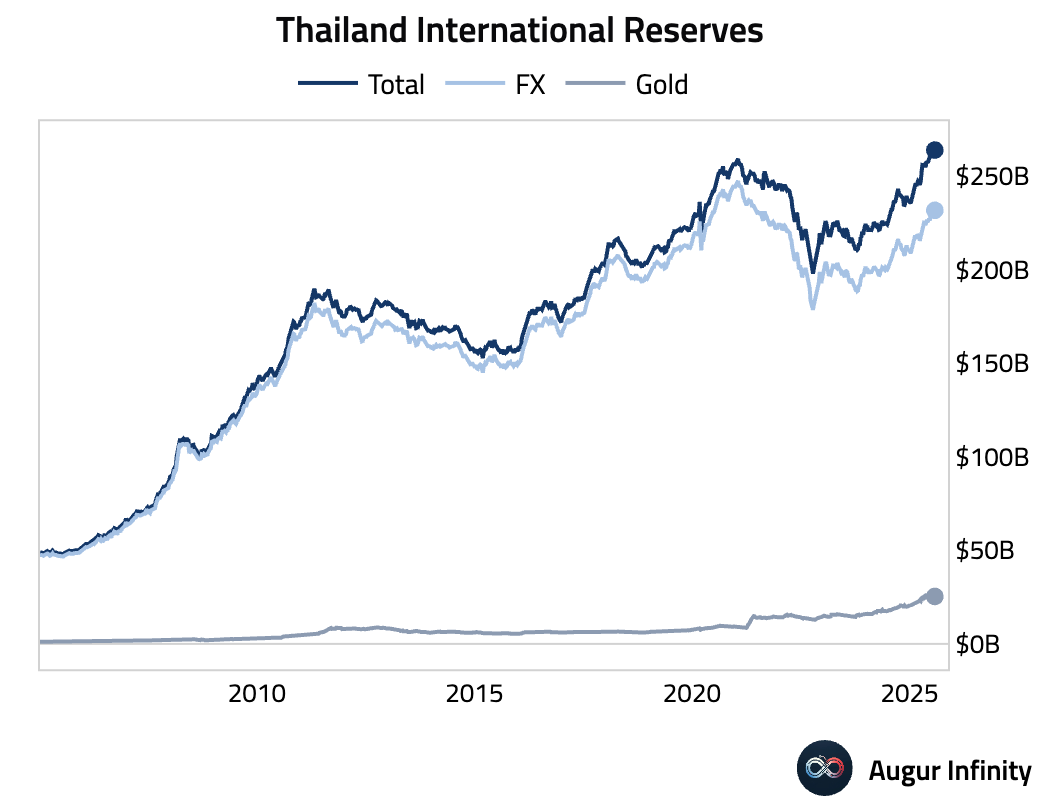

- Thailand’s official reserve assets edged down to $261.9 billion in the week ending August 1st.

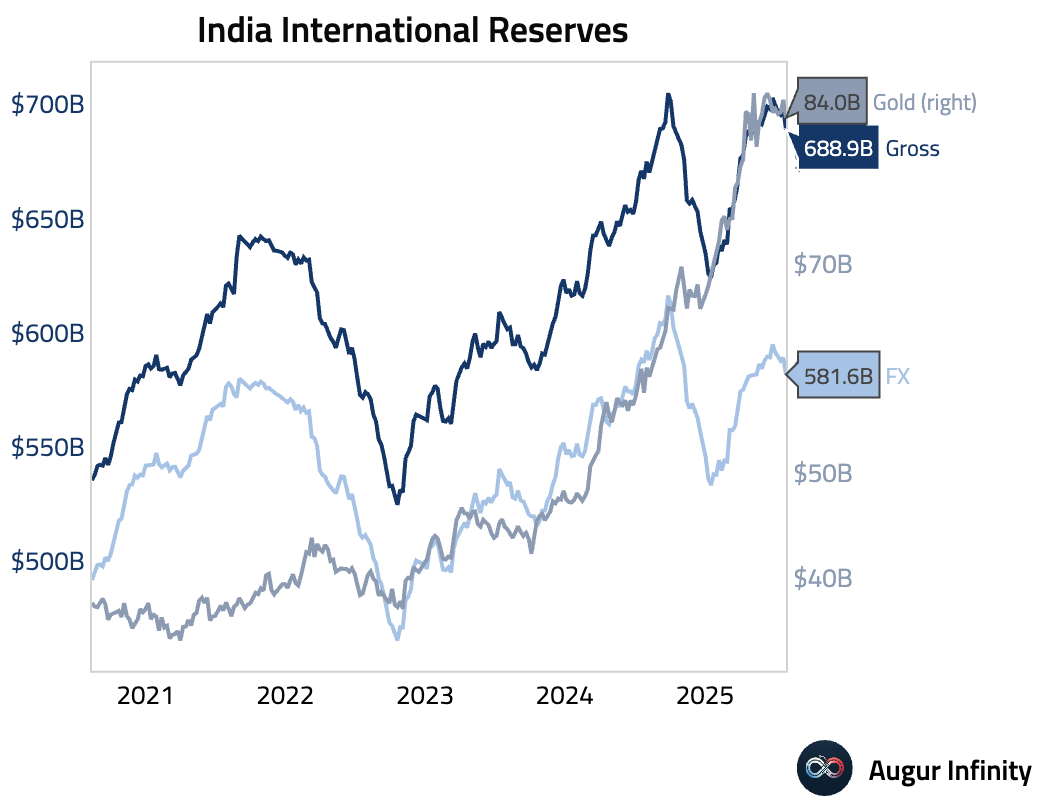

- India's foreign exchange reserves declined to $688.87 billion in the week ending August 1st.

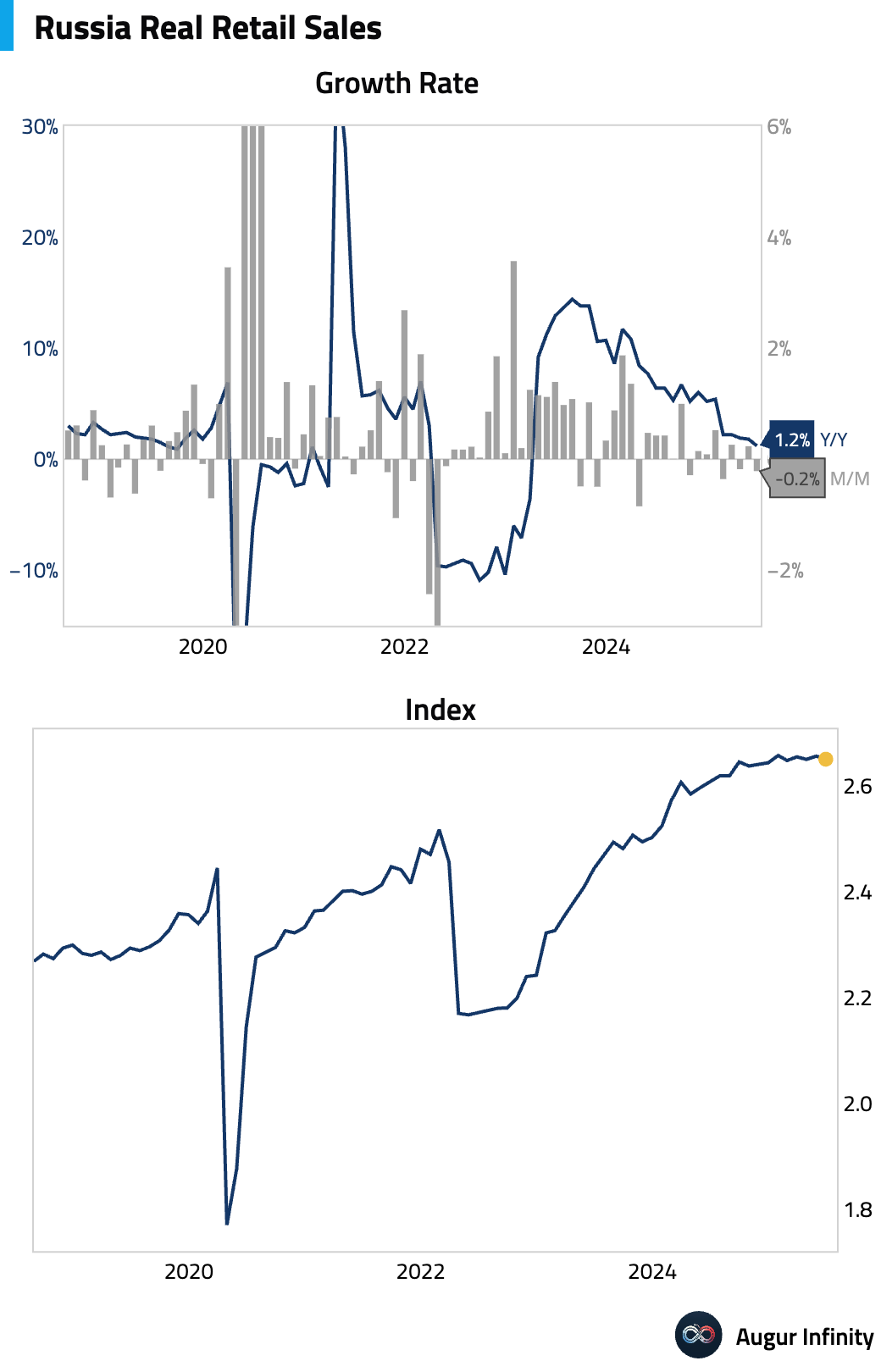

- Russia retail sales moderated to 1.2% Y/Y from 1.8% last month, below consensus of 2.1%. On a seasonally-adjusted basis, retail sales declined by 0.2% M/M based on our estimates.

Global Markets

Equities

- US equities advanced, with the S&P 500 rising 0.78% and the tech-heavy Nasdaq climbing 0.98% for its third consecutive daily gain. The move higher came despite ongoing market digestion of weak employment data from earlier in the week. European markets were also broadly positive, with France up 0.5% for a third straight gain. In the UK, equities rose for the sixth day in a row.

Fixed Income

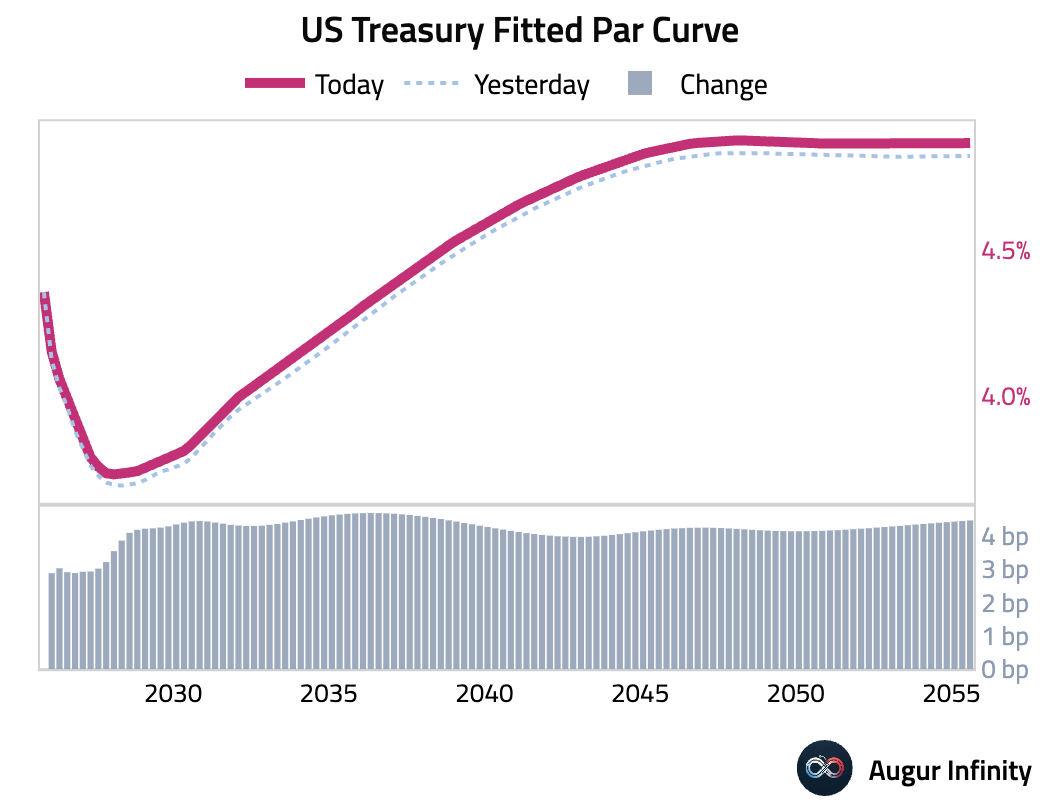

- US Treasury yields rose across the curve, with the 10-year yield climbing 4.2 bps for its third consecutive increase. The 30-year yield added 4.2 bps. Yields have moved higher this week despite a weak jobs report, which markets initially interpreted as increasing the odds of a Fed rate cut. The upward pressure on yields appears linked to concerns over fiscal deficits and weak demand at recent Treasury auctions.

FX

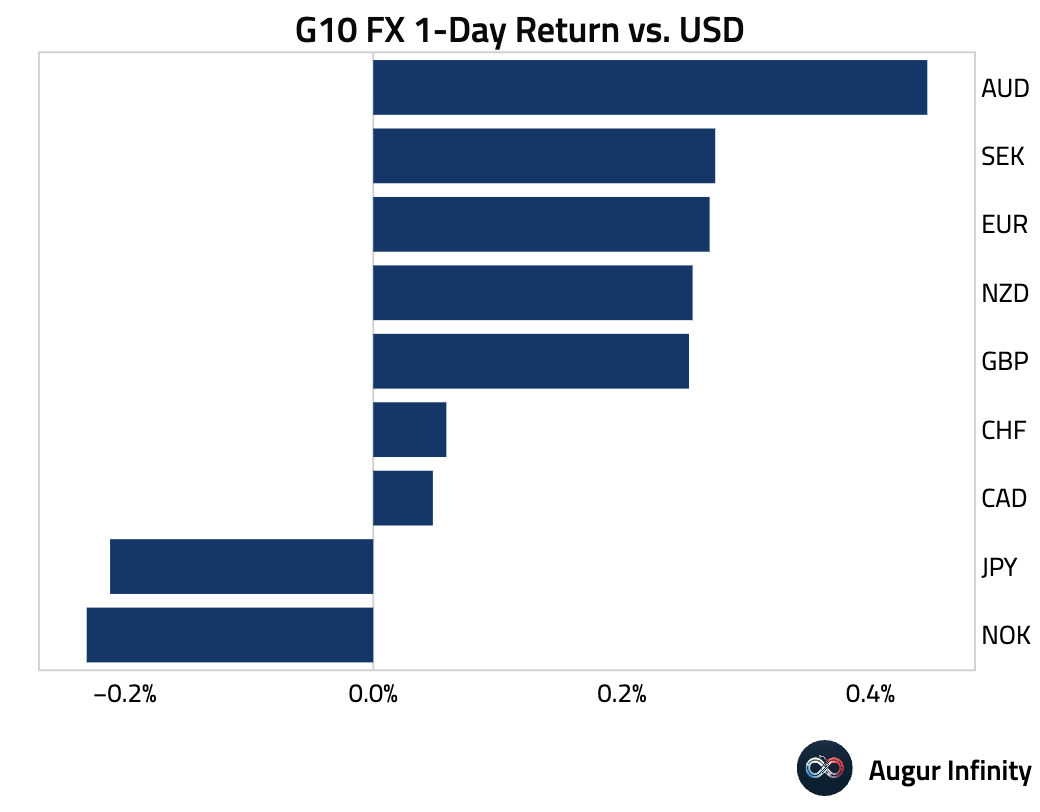

- The US dollar weakened against most G10 peers. The Australian dollar was the top performer, gaining 0.4%, while the British pound and New Zealand dollar each rose 0.3%; all three currencies marked their third straight day of gains. The Swedish krona appreciated for a sixth consecutive session. In contrast, the Japanese yen and Norwegian krone both softened 0.2% against the dollar.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.