Headlines

- Taiwan is seeking to establish a strategic partnership with the United States to obtain a lower tariff rate.

- The European Union is preparing its nineteenth package of sanctions directed at Russia.

Charts of the Day

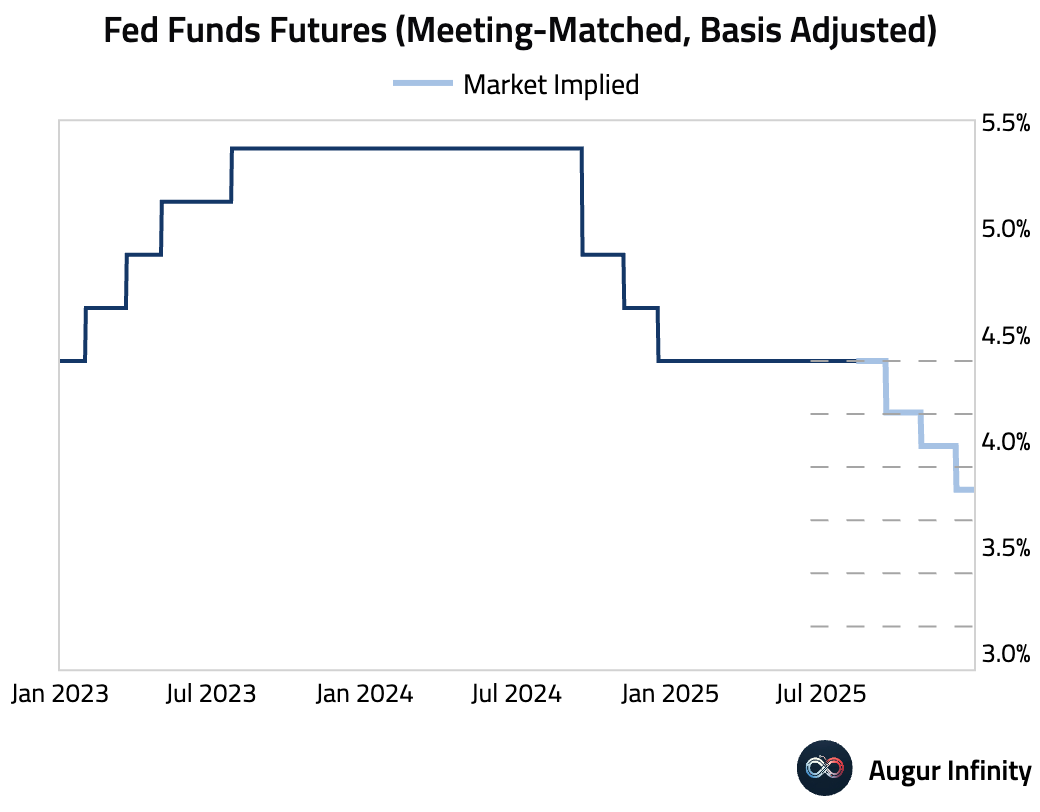

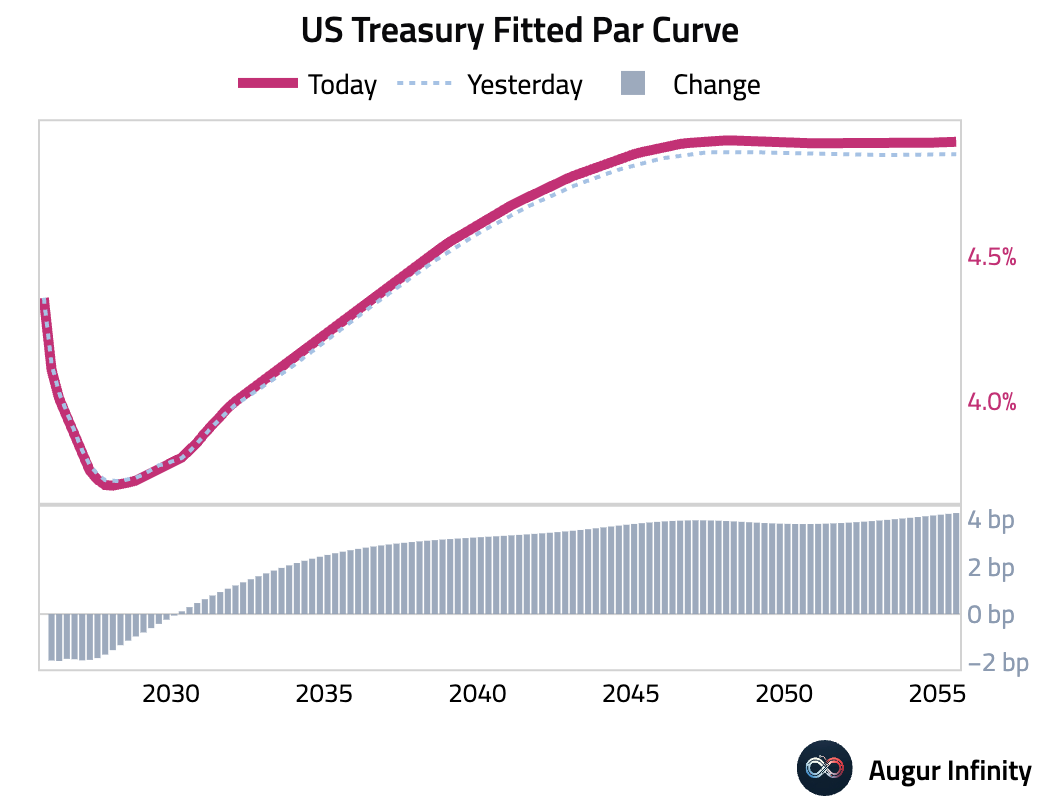

- A 25 bps rate cut at the September FOMC meeting is now pretty much fully priced in, with additional 1.5 cuts in October and December discounted.

Global Economics

United States

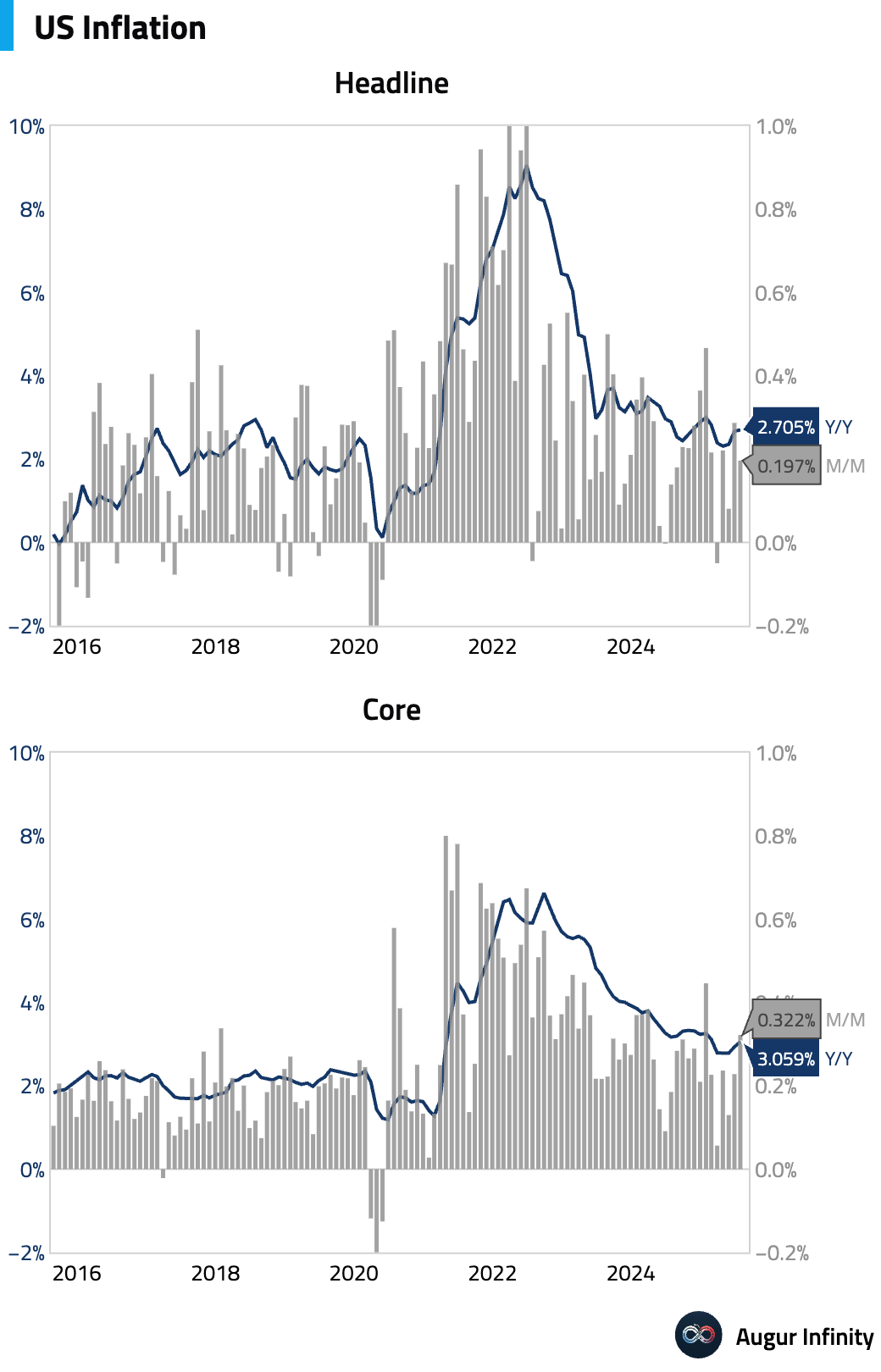

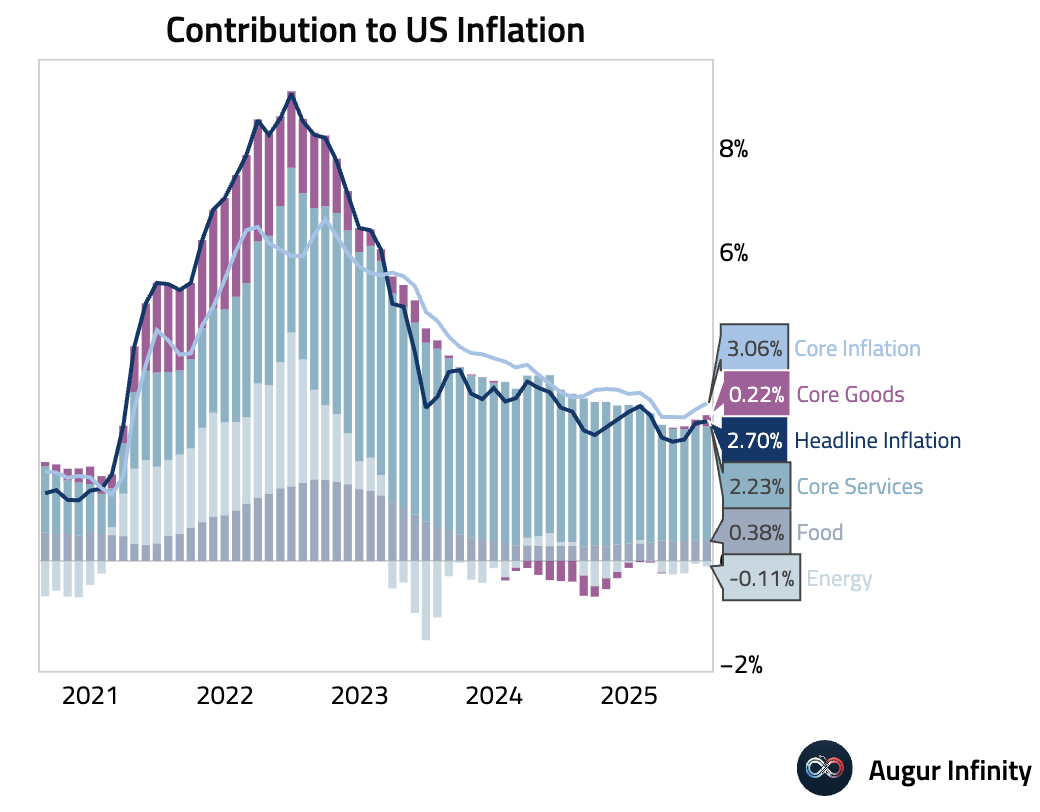

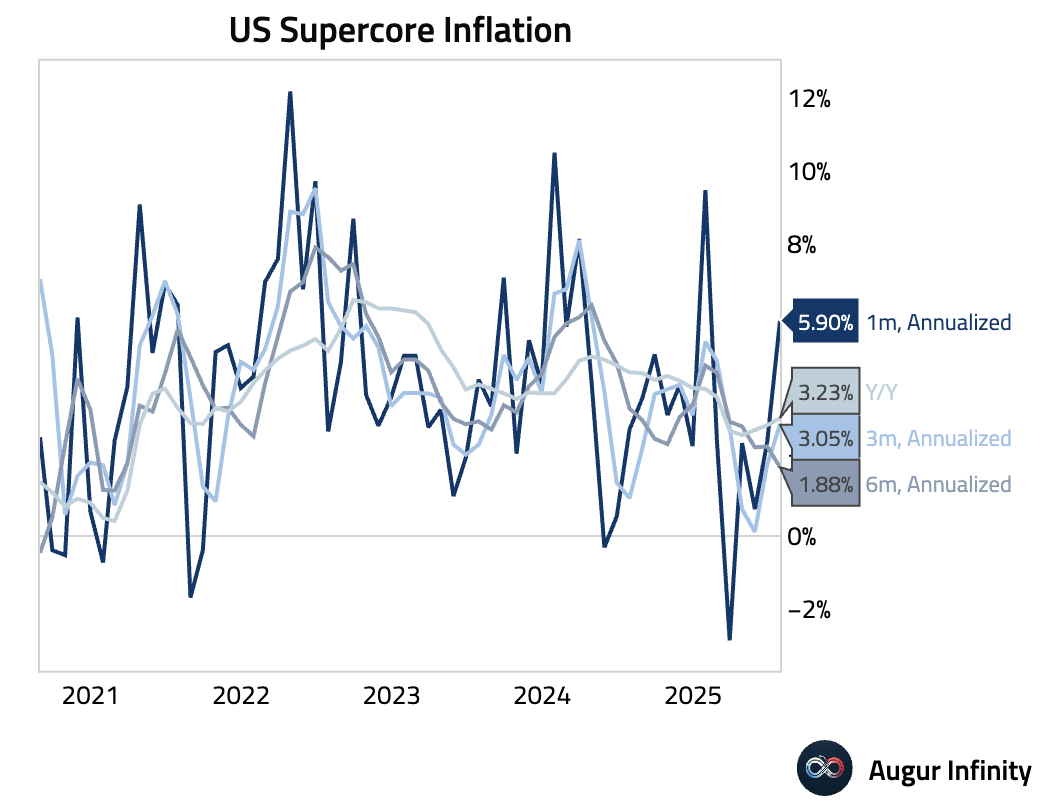

- The July CPI report showed headline inflation steady at 2.7% Y/Y (vs. 2.8% consensus), but core inflation accelerating to 3.1% Y/Y from 2.9% (vs. 3.0% consensus). On a monthly basis, headline CPI rose 0.2% and core CPI rose 0.3%, both matching expectations. The core reading was pushed higher by volatile components, including a 4% M/M jump in airfares and a record 2.6% M/M surge in dental services prices. This drove “supercore” services inflation (ex-rentals) up a sharp 0.5% M/M. However, weaker core goods prices and falling energy costs provided an offset. The specific component mix suggests a softer read for the Fed's preferred metric, with core PCE inflation forecasts for July revised down to around 0.24–0.26%.

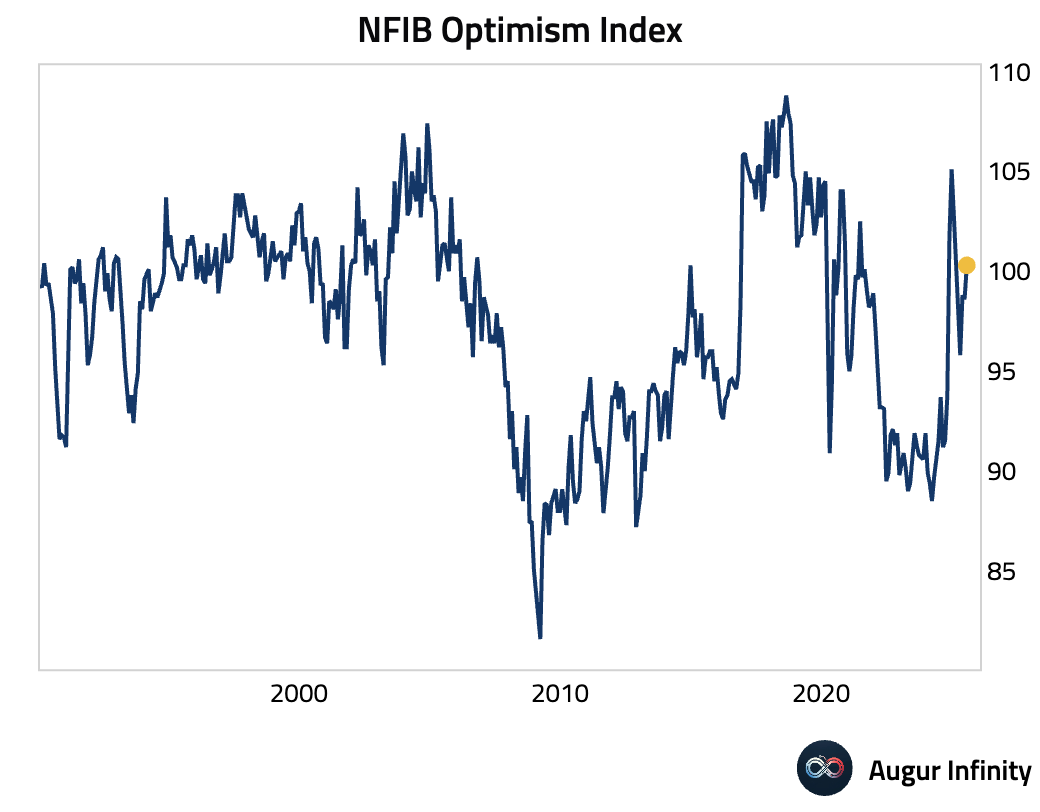

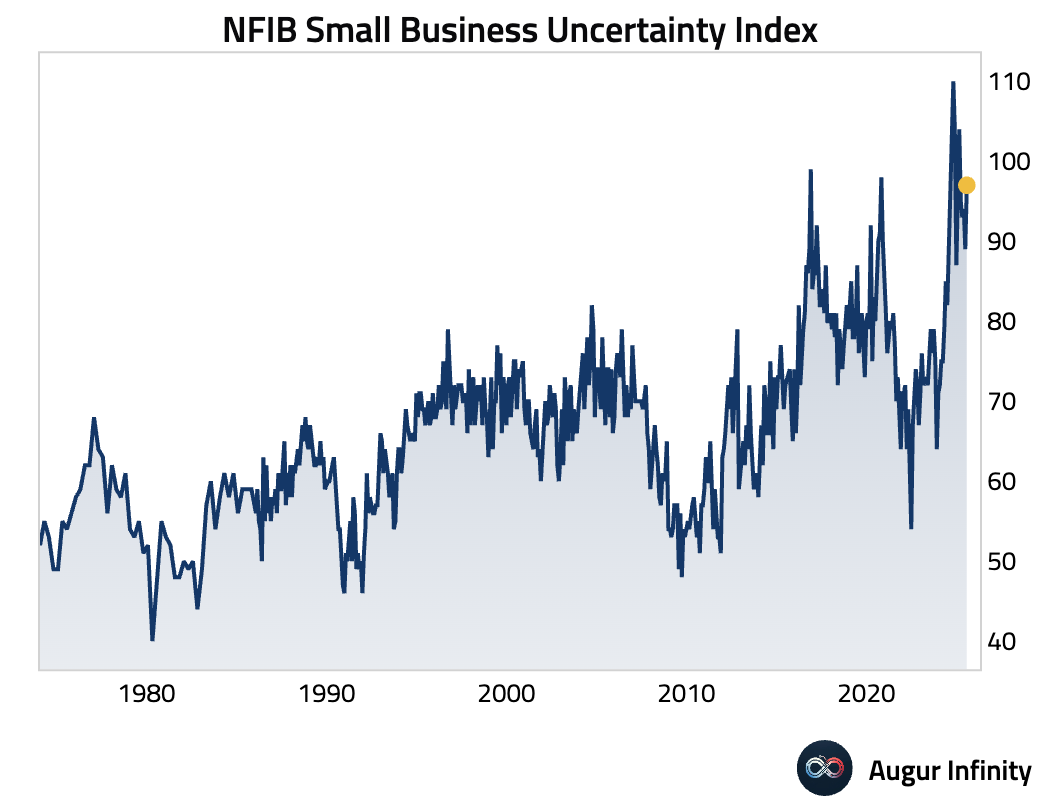

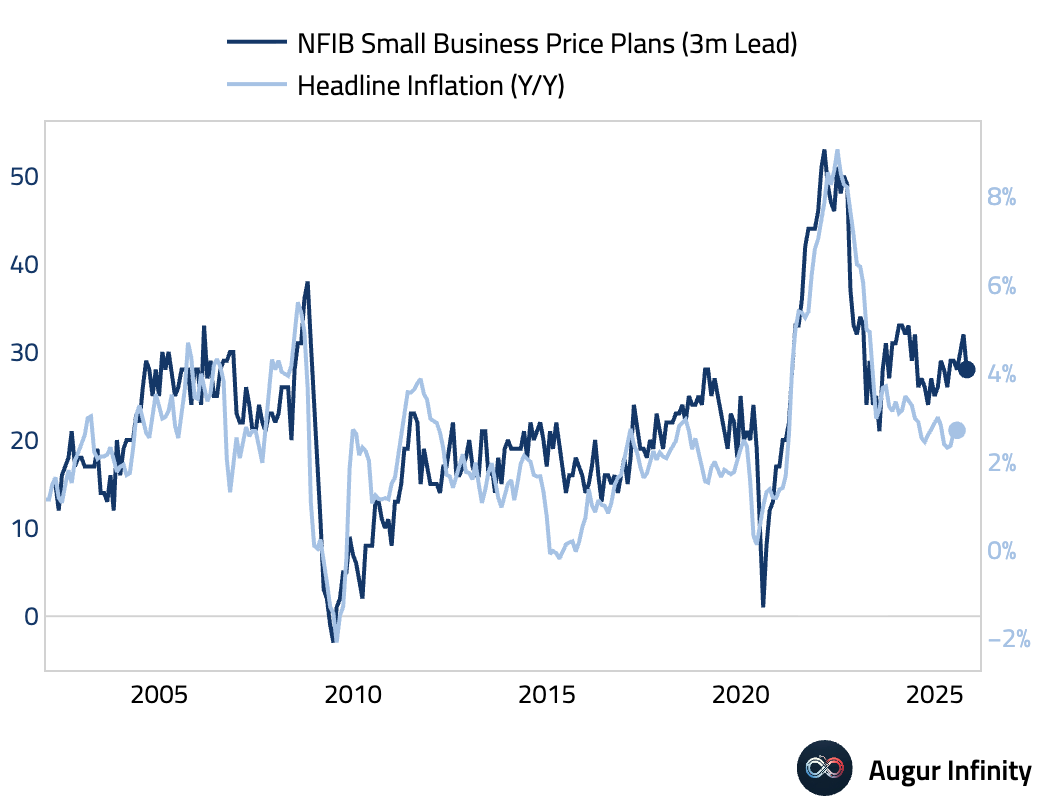

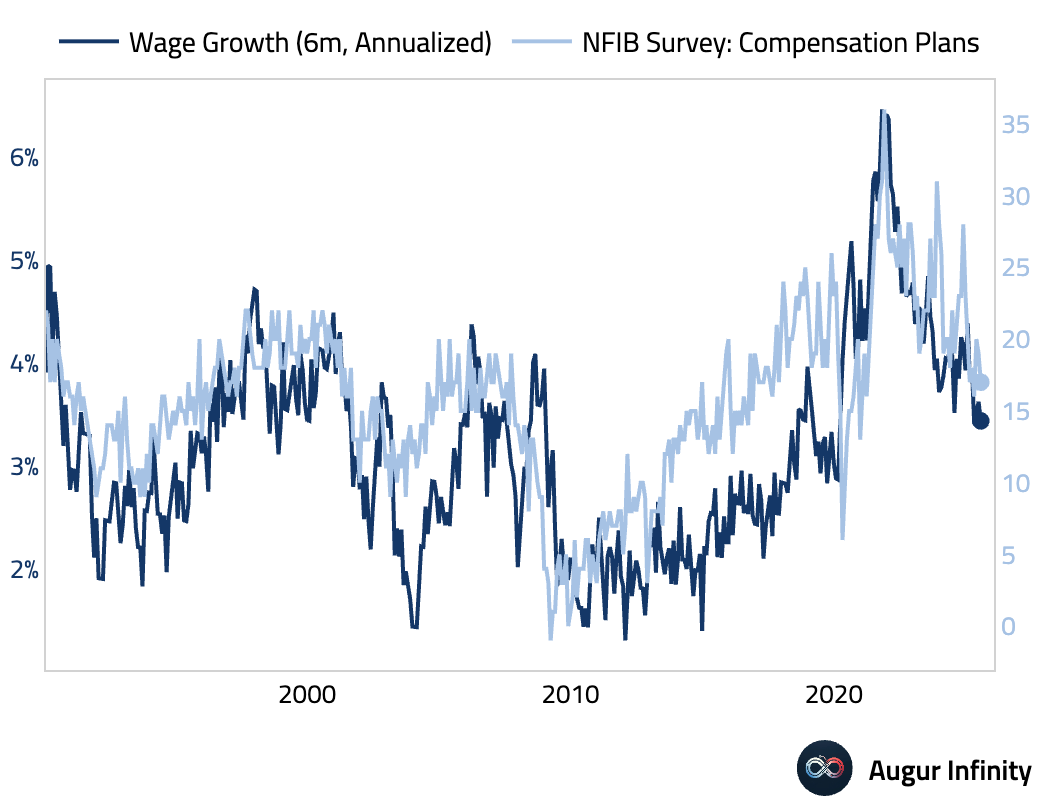

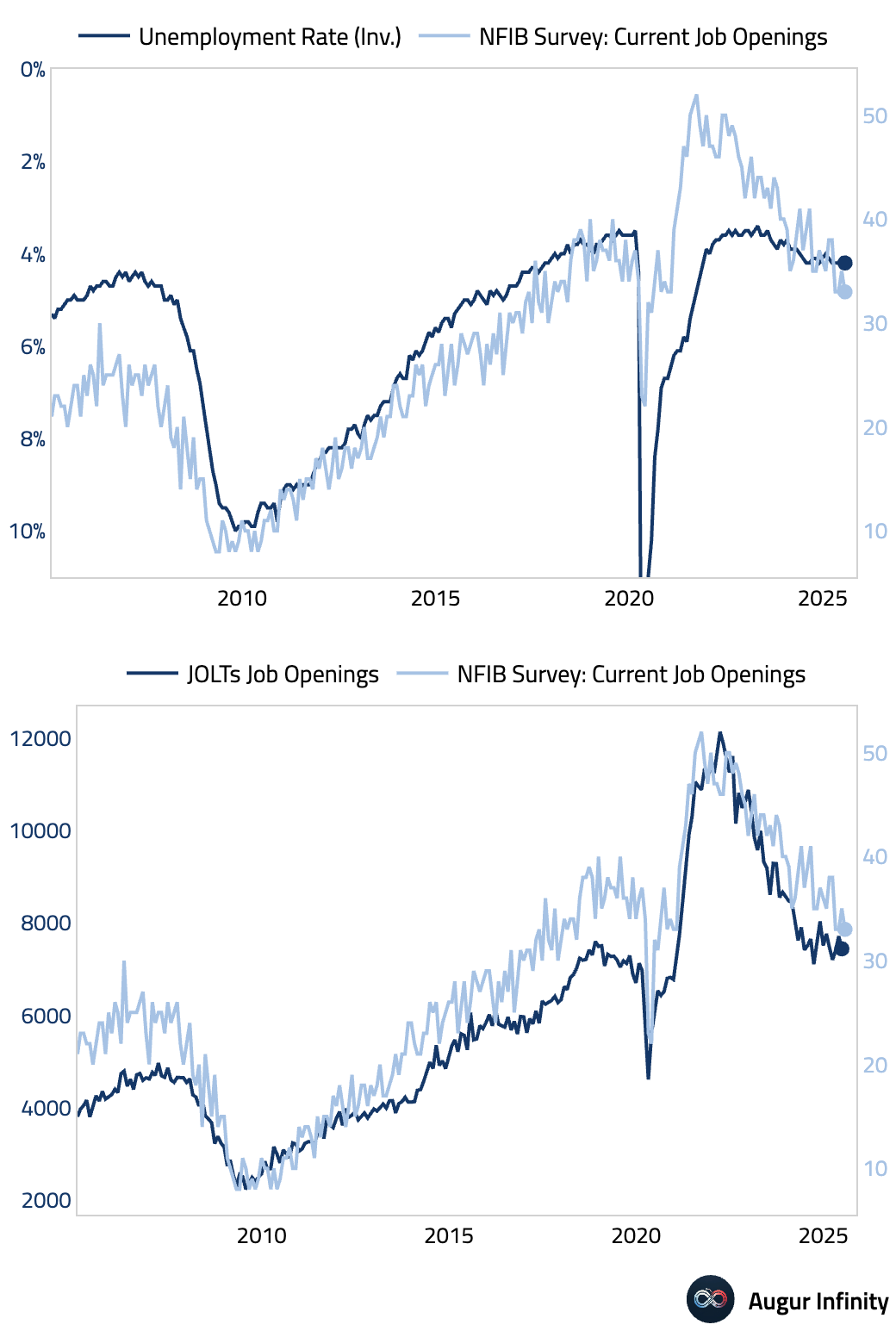

- The NFIB Business Optimism Index for July rose to 100.3 from 98.6, driven by better expectations for business conditions and expansion. However, the Uncertainty Index also spiked, signaling caution. Key disinflationary trends emerged as firms' plans for both price hikes and compensation growth fell. The survey also points to a cooling labor market, with fewer unfilled jobs.

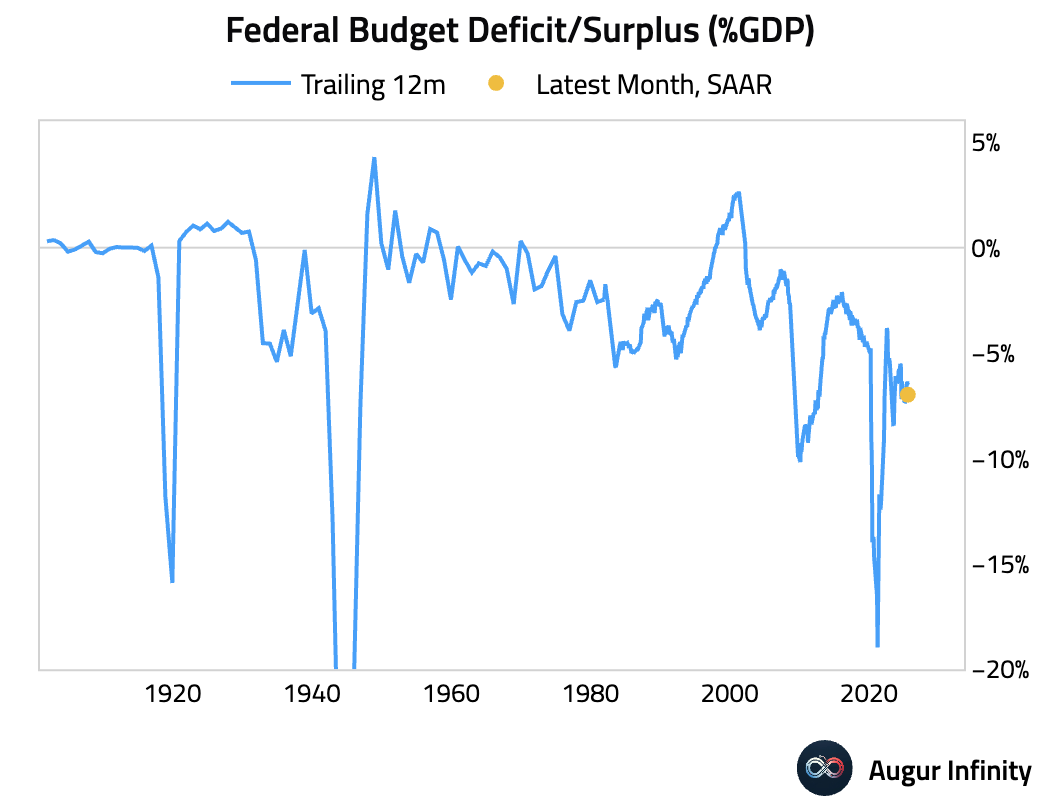

- Federal budget deficit was recorded at $291 billion in July, worse than the consensus estimate of $215 billion. On a seasonally-adjusted basis, this amounts to 7% of GDP.

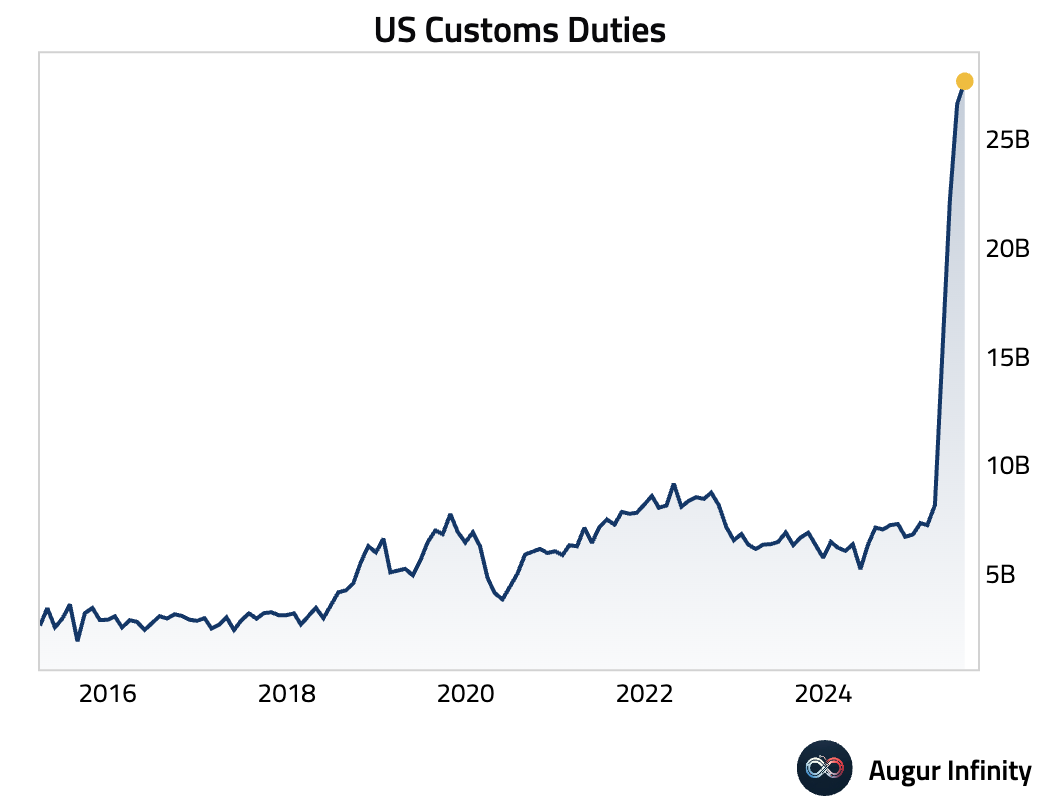

- US customs duties rose further to $27.7B in July.

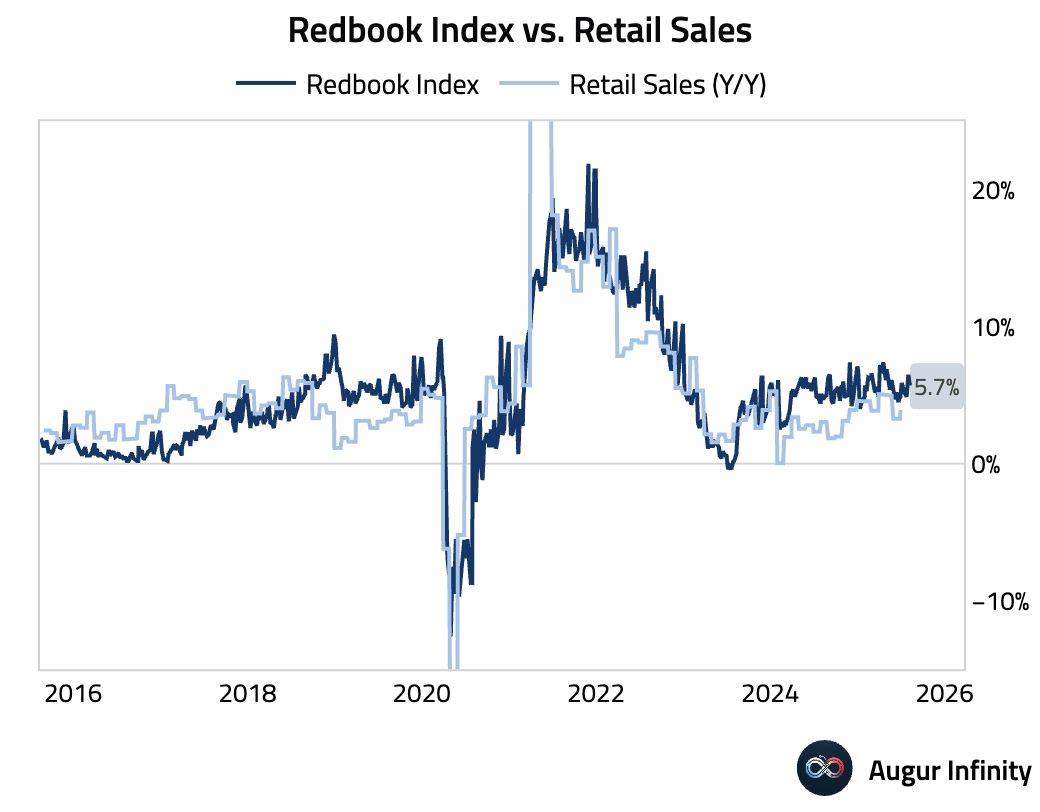

- The Redbook index of weekly retail sales growth slowed to 5.7% Y/Y for the week ending August 9, down from 6.5% in the prior week.

Canada

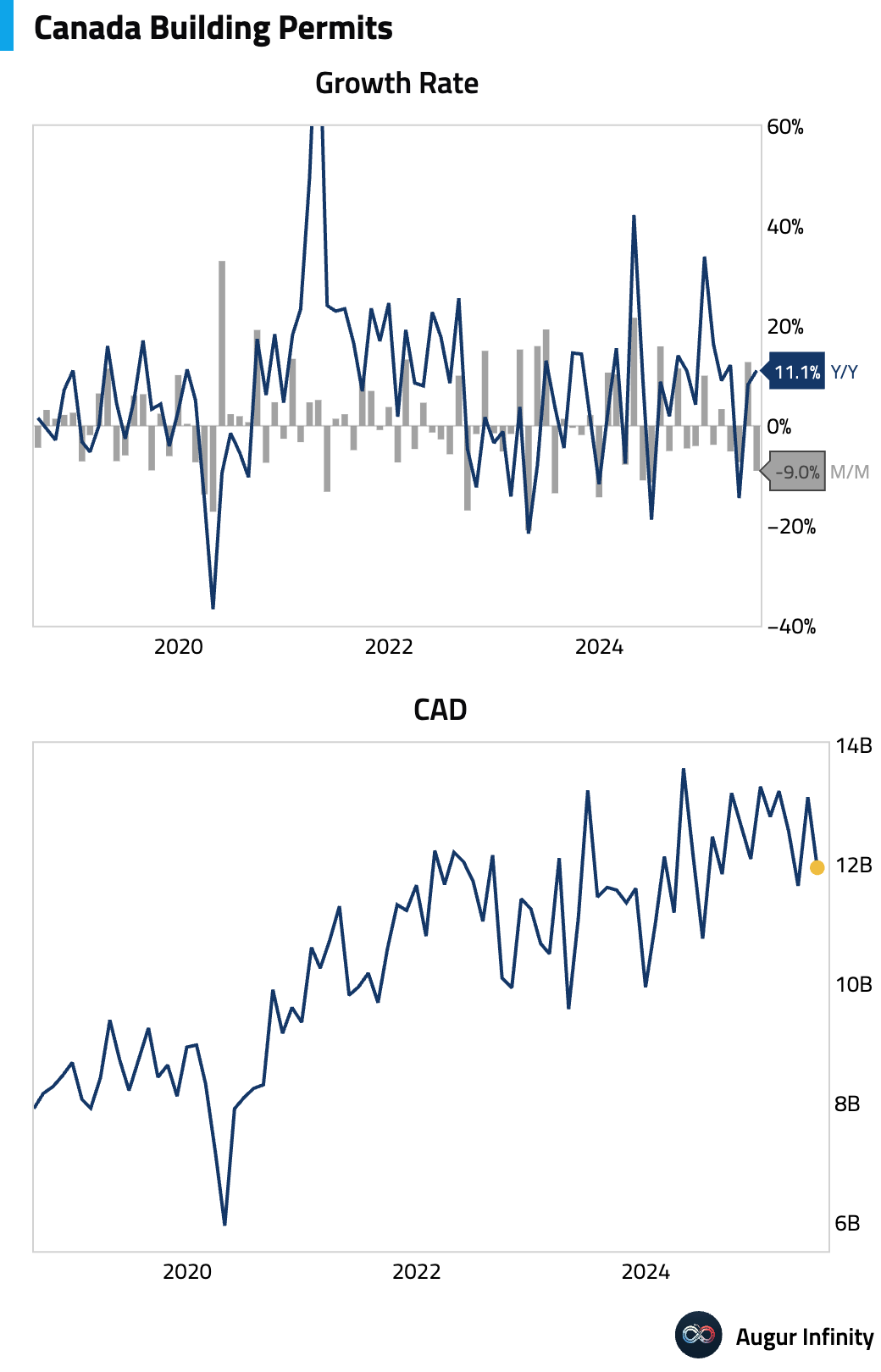

- Canadian building permits fell sharply by 9.0% M/M in June, a significant disappointment against the consensus estimate of a 3.4% decline and a reversal of the 12.8% gain in May. The drop indicates a potential cooling in the construction sector.

Europe

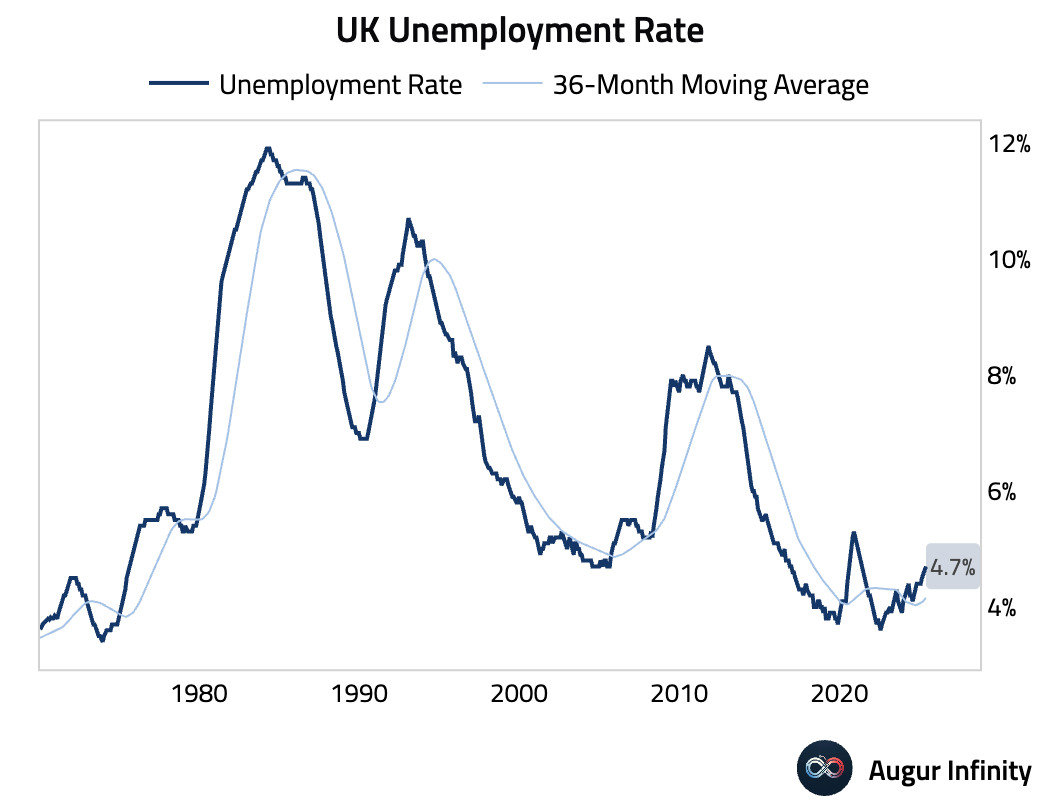

- The UK unemployment rate held steady at 4.7% in the three months to June, meeting expectations. While stable, the rate is already 0.6 percentage points above its 12-month low and above the Bank of England's equilibrium estimate, suggesting the labor market is no longer considered tight.

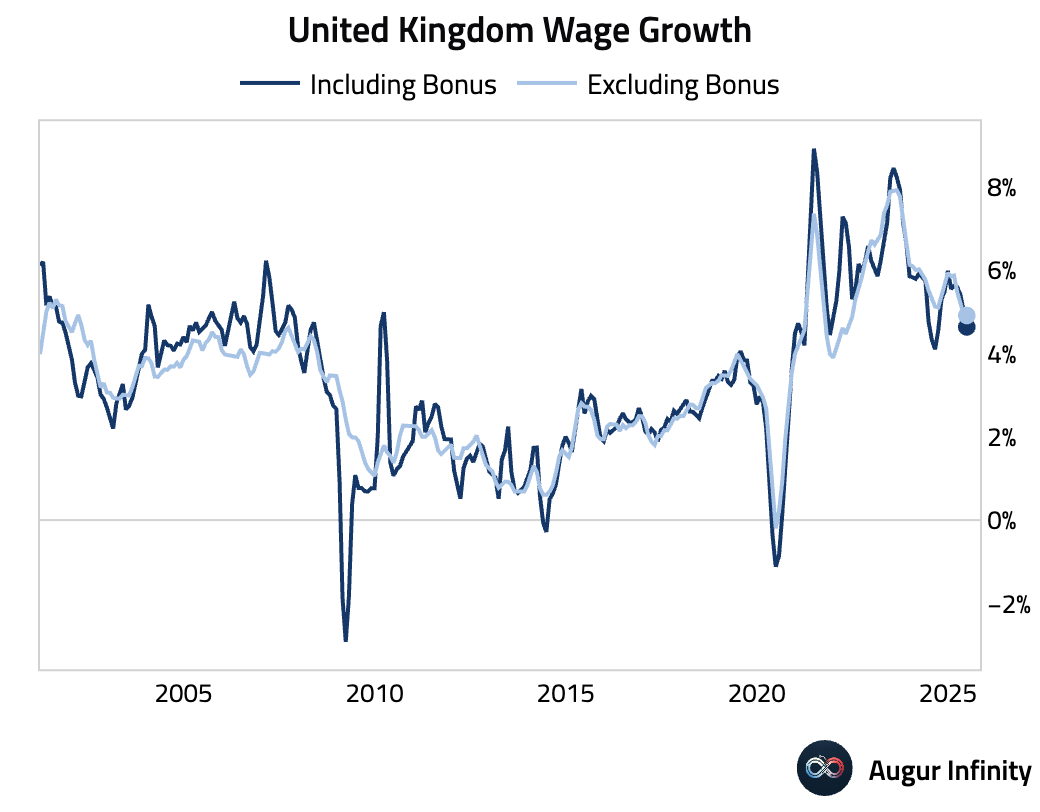

- UK wage growth including bonuses decelerated to 4.6% Y/Y (3-month average) from 5.0% previously, slightly below the 4.7% consensus. Wage growth excluding bonuses, a key metric for the Bank of England, was stable at 5.0% on a 3-month Y/Y basis.

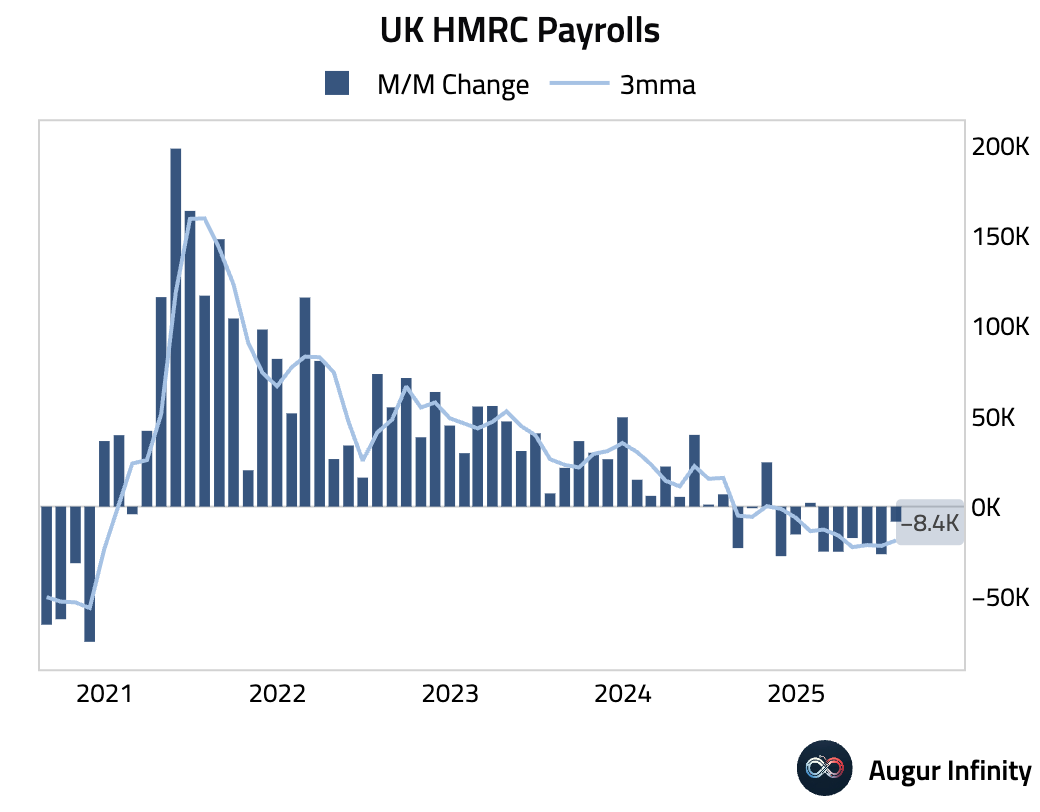

- The UK's flash payrolls for July showed a smaller-than-expected decline of 8,353, while June's figure was revised up significantly to -26k from -41k.

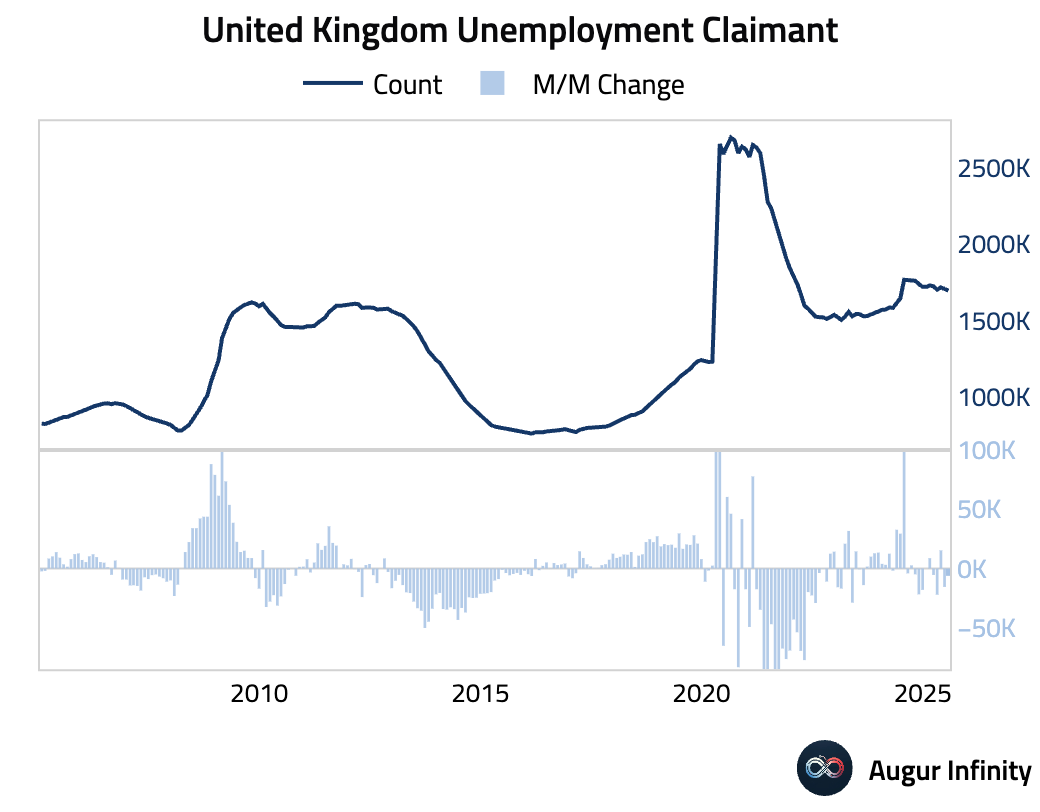

- The UK Claimant Count Change for July registered a drop of 6,200, unexpectedly contracting against a consensus forecast for an increase of 19,700.

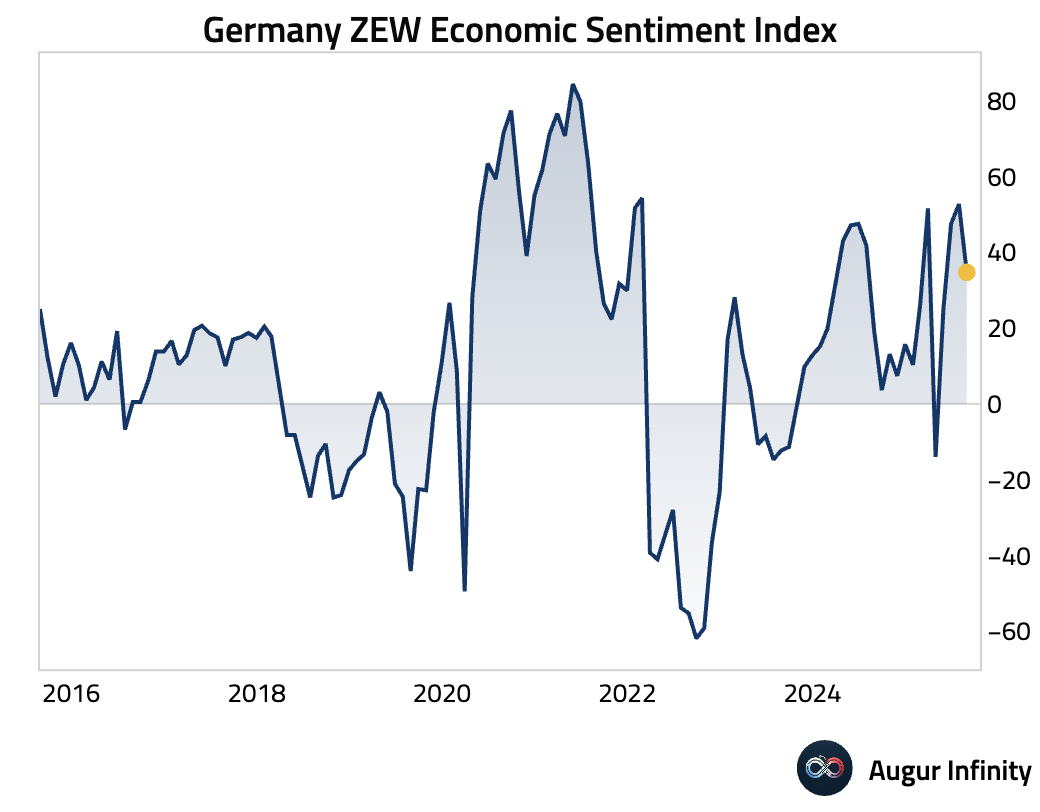

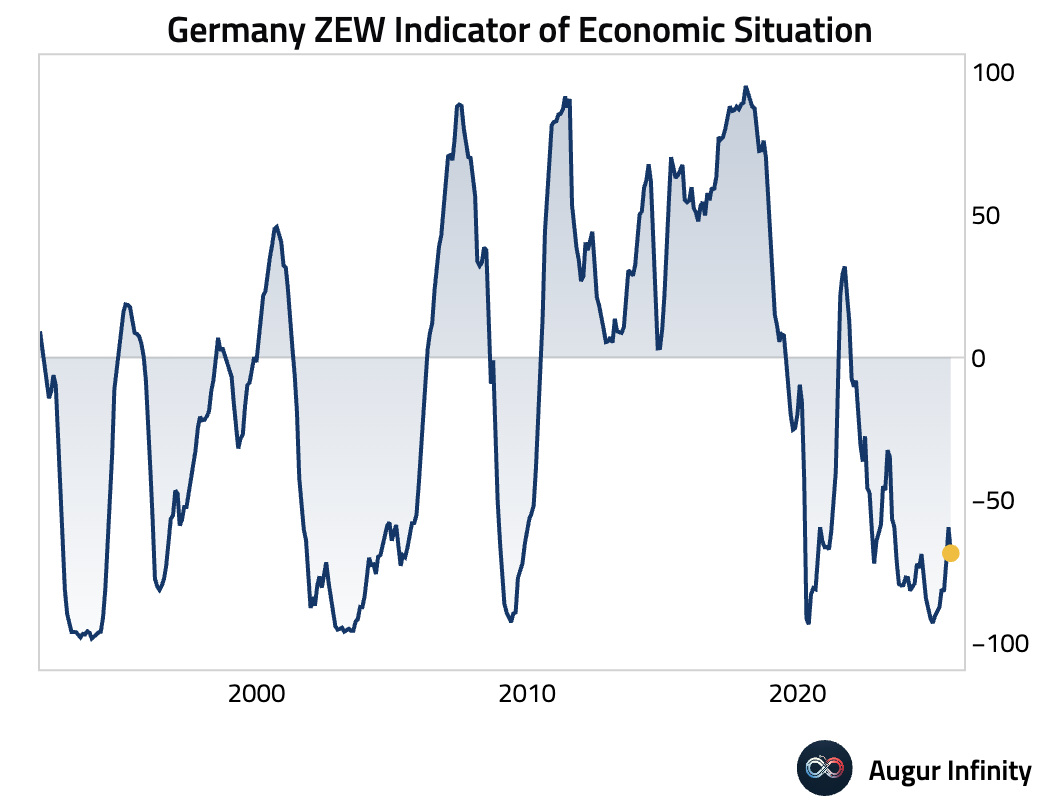

- Germany's ZEW Economic Sentiment Index for August fell sharply to 34.7 from 52.7, missing the consensus of 40.0. The Current Conditions component also deteriorated further, dropping to -68.6 from -59.5, below the -65.0 estimate. The dual decline points to growing pessimism about both the current state and future prospects of the German economy.

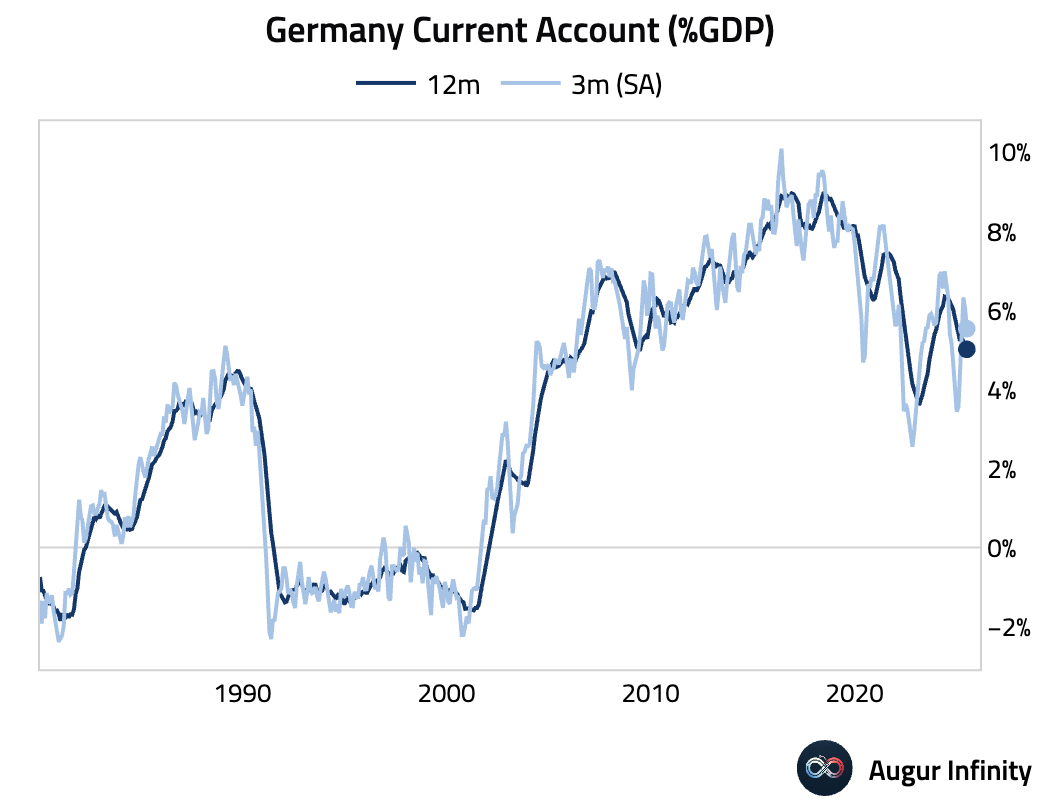

- Germany's current account surplus widened to €18.6 billion in June from €7.5 billion in May, reflecting a recovery in the trade balance.

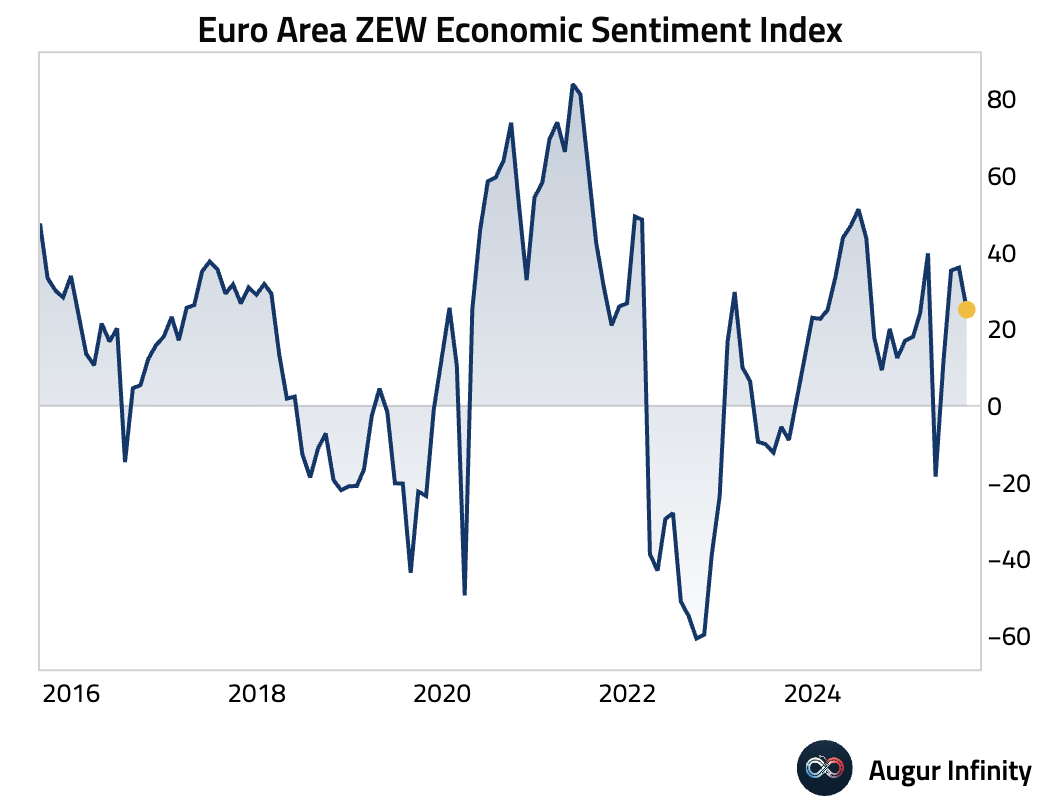

- The Eurozone's ZEW Economic Sentiment Index for August dropped to 25.1 from 36.1 in July, well below the consensus of 28.1.

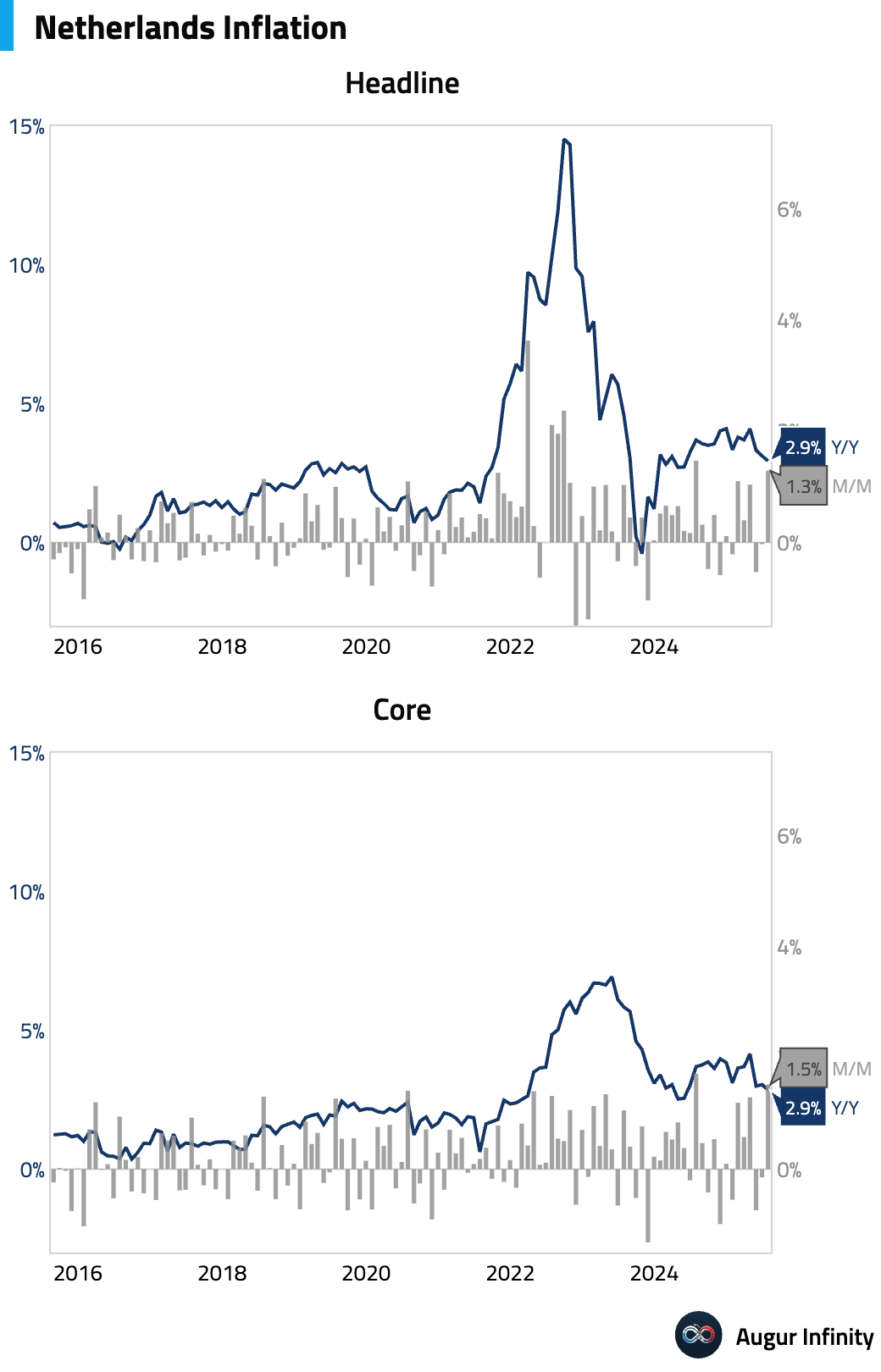

- Final inflation figures for the Netherlands in July confirmed a deceleration, with the Y/Y rate slowing to 2.9% from 3.1%. On a monthly basis, prices rose 1.3% after being flat in June.

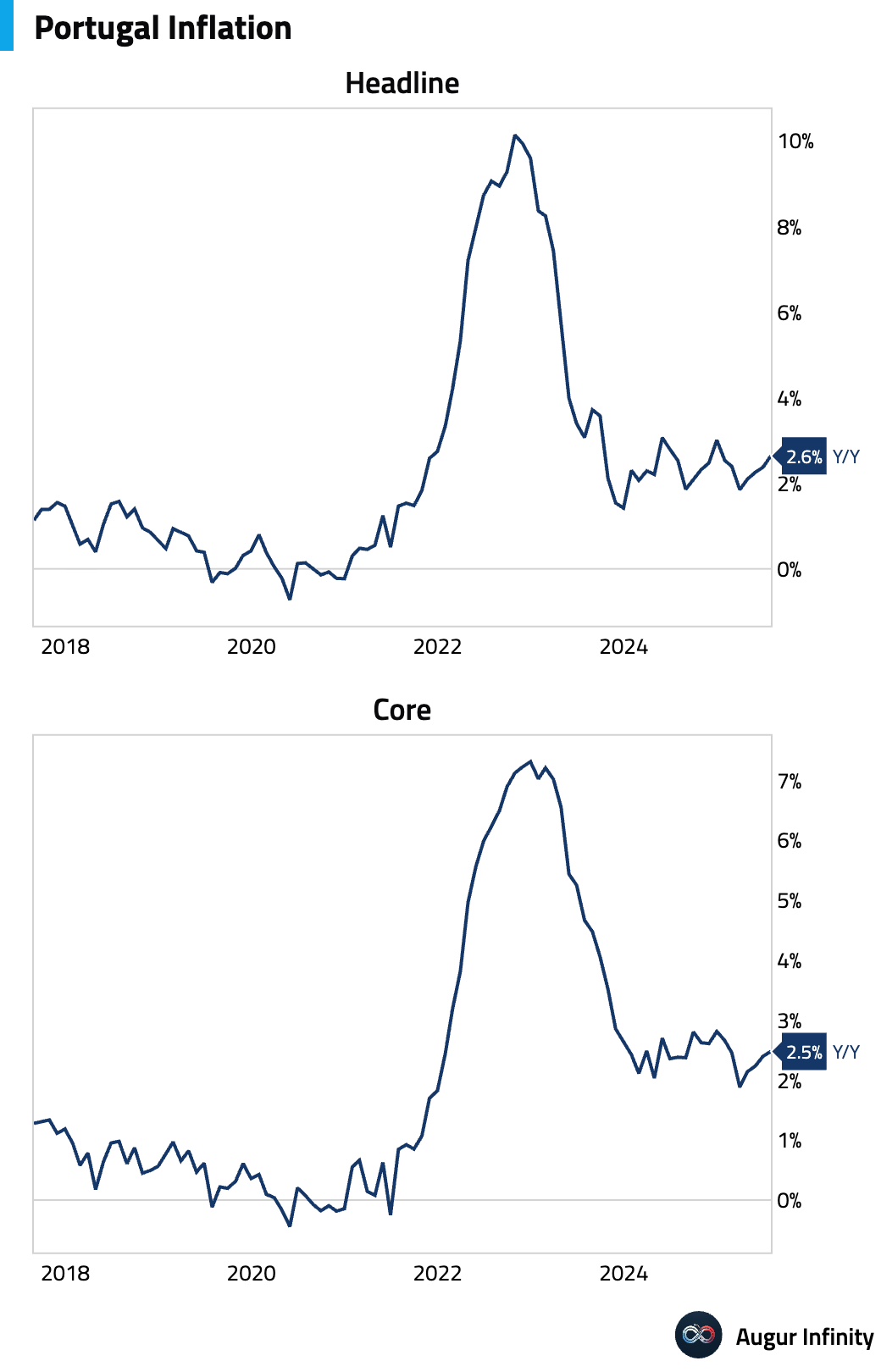

- Portugal's final July inflation rate was confirmed at 2.6% Y/Y, up from 2.4% in June. Prices fell 0.4% M/M.

Asia-Pacific

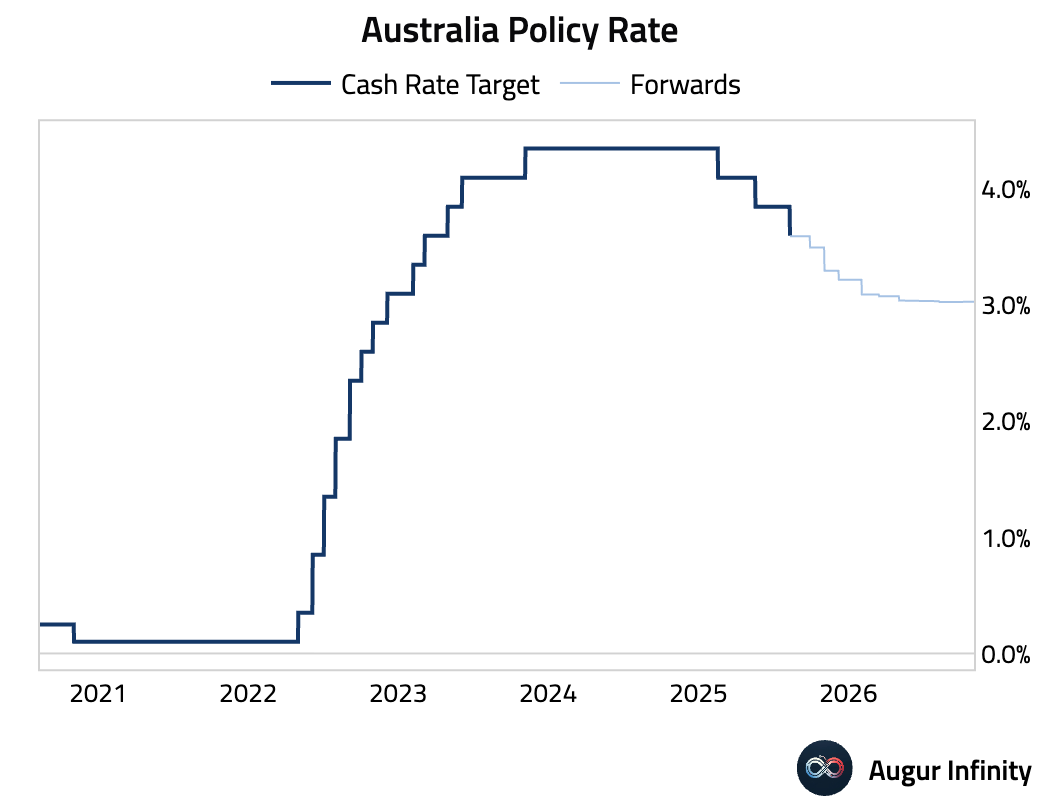

- The Reserve Bank of Australia cut its cash rate by 25 basis points to 3.60% in a unanimous decision, resuming its easing cycle. The communication was more dovish than markets expected, with the RBA toning down its language on labor market tightness. Governor Bullock endorsed market pricing for another "two slash three" rate cuts and signaled that back-to-back cuts are possible, hinging on upcoming data. The central bank's own forecasts are now conditioned on the policy rate falling to 2.9% by the end of 2026, signaling a clear dovish bias.

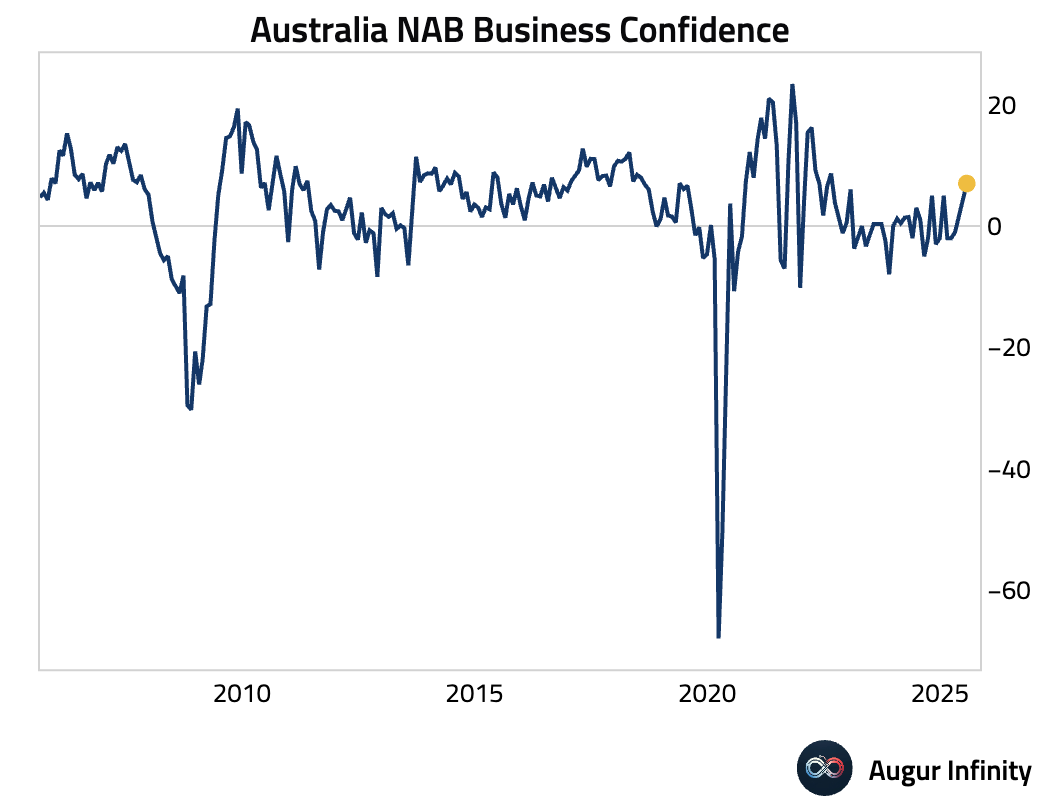

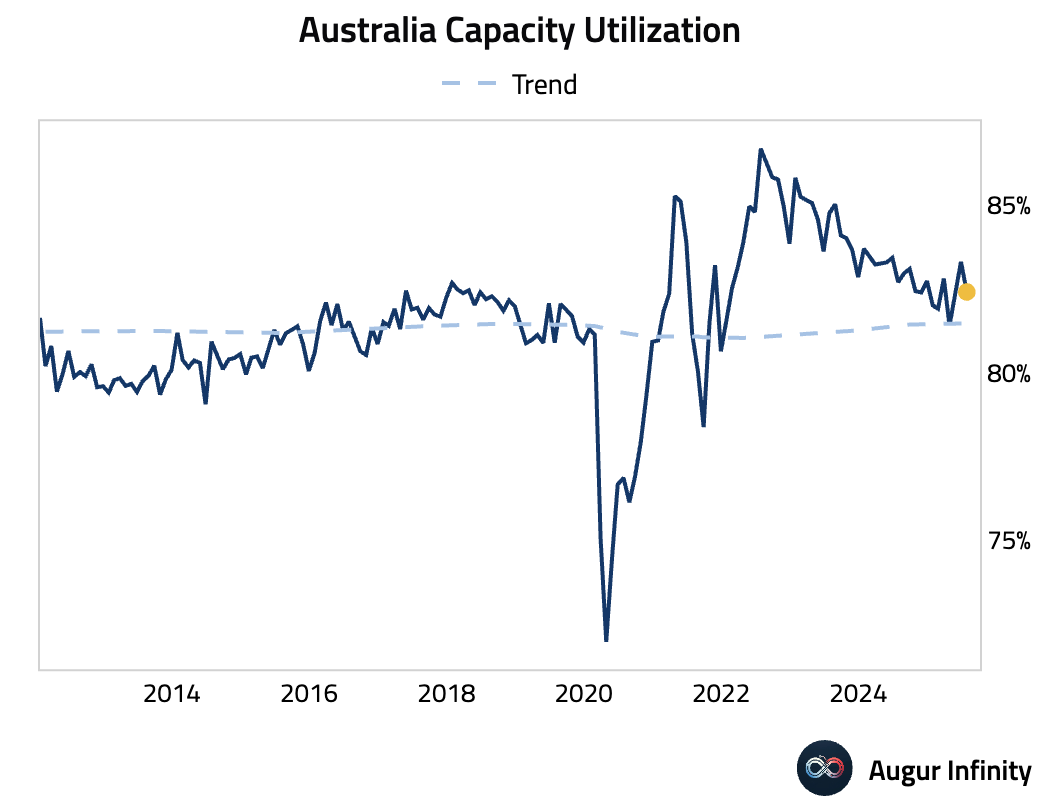

- Australia’s NAB Business Confidence for July unexpectedly rose to +7 from +5, returning to its long-run average. Capacity utilization, however, declined from 83.3 to 82.4. Price pressures rebounded, with labor costs rising, largely due to the July 1 increase in Award wages.

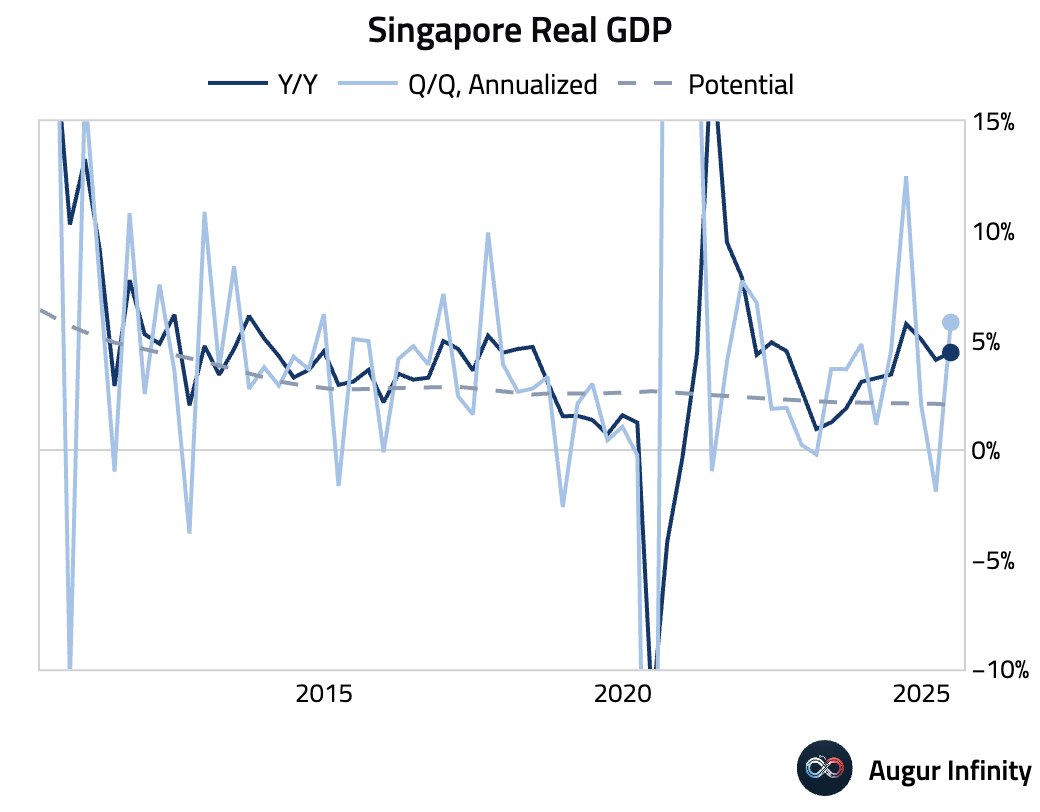

- Singapore's final Q2 GDP growth was revised up, expanding 1.4% Q/Q and 4.4% Y/Y. The upward revision was driven by stronger-than-initially-reported performance in services and construction, which offset manufacturing weakness. Despite the Ministry of Trade and Industry raising its full-year 2025 forecast to a 1.5%–2.5% range, it flagged a sharp second-half slowdown due to external risks and payback effects from front-loaded exports.

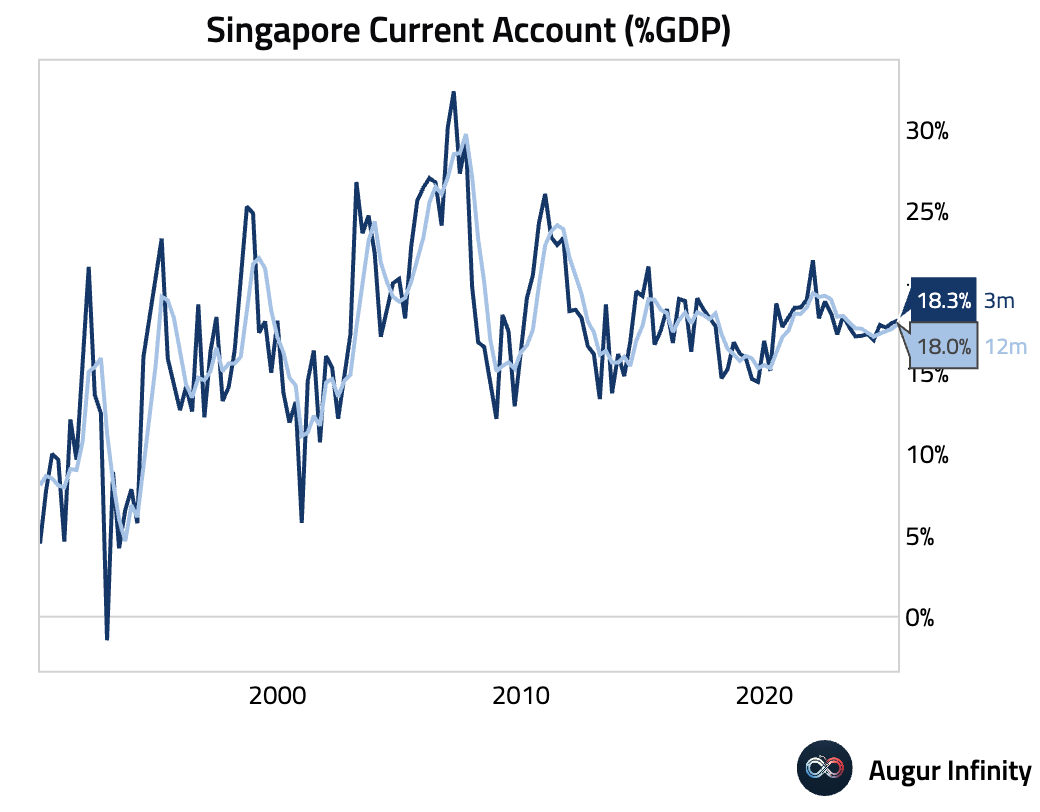

- Singapore’s current account surplus narrowed to S$34.8 billion in Q2 from S$36.6 billion in Q1.

Emerging Markets ex China

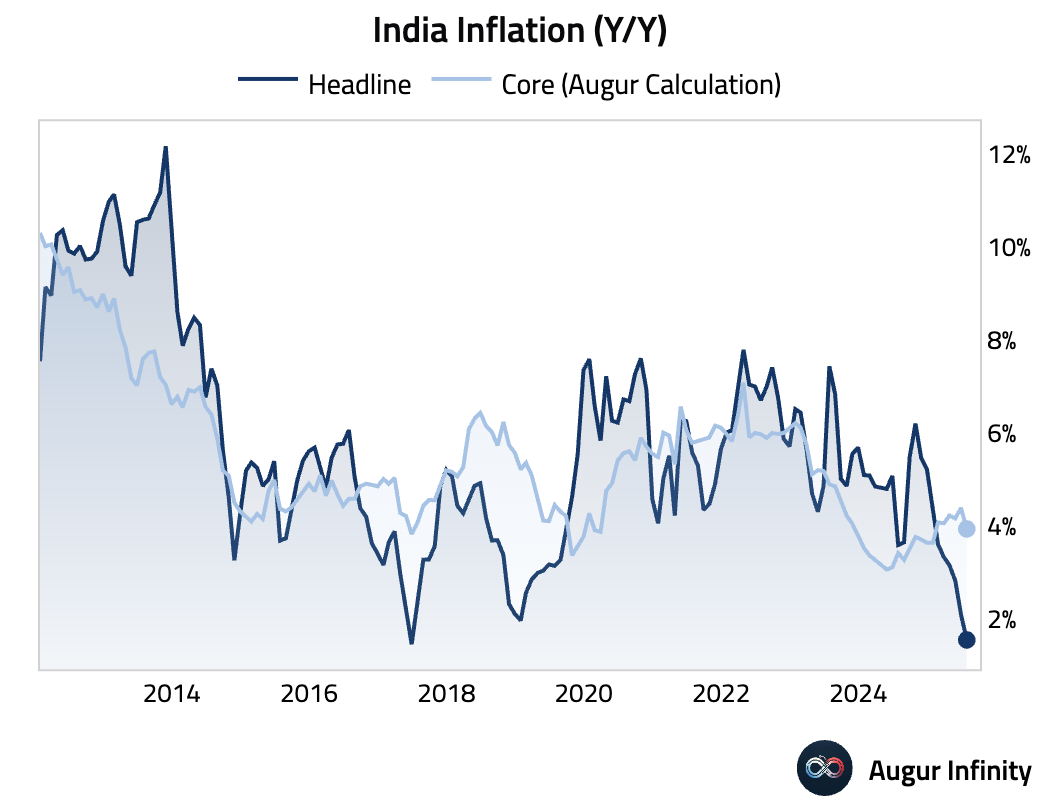

- India's headline CPI inflation slowed to an eight-year low of 1.55% Y/Y in July, significantly below the prior month's 2.1% and below the 1.76% consensus. The decline was driven by continued food price deflation, particularly in vegetables and pulses. Core inflation also moderated to 3.9% Y/Y, confirming a broad disinflationary trend. While the headline weakness is exaggerated by food price base effects, the underlying trend keeps the door open for the RBI to resume rate cuts later this year, with potential for 25 bp cuts in both October and December.

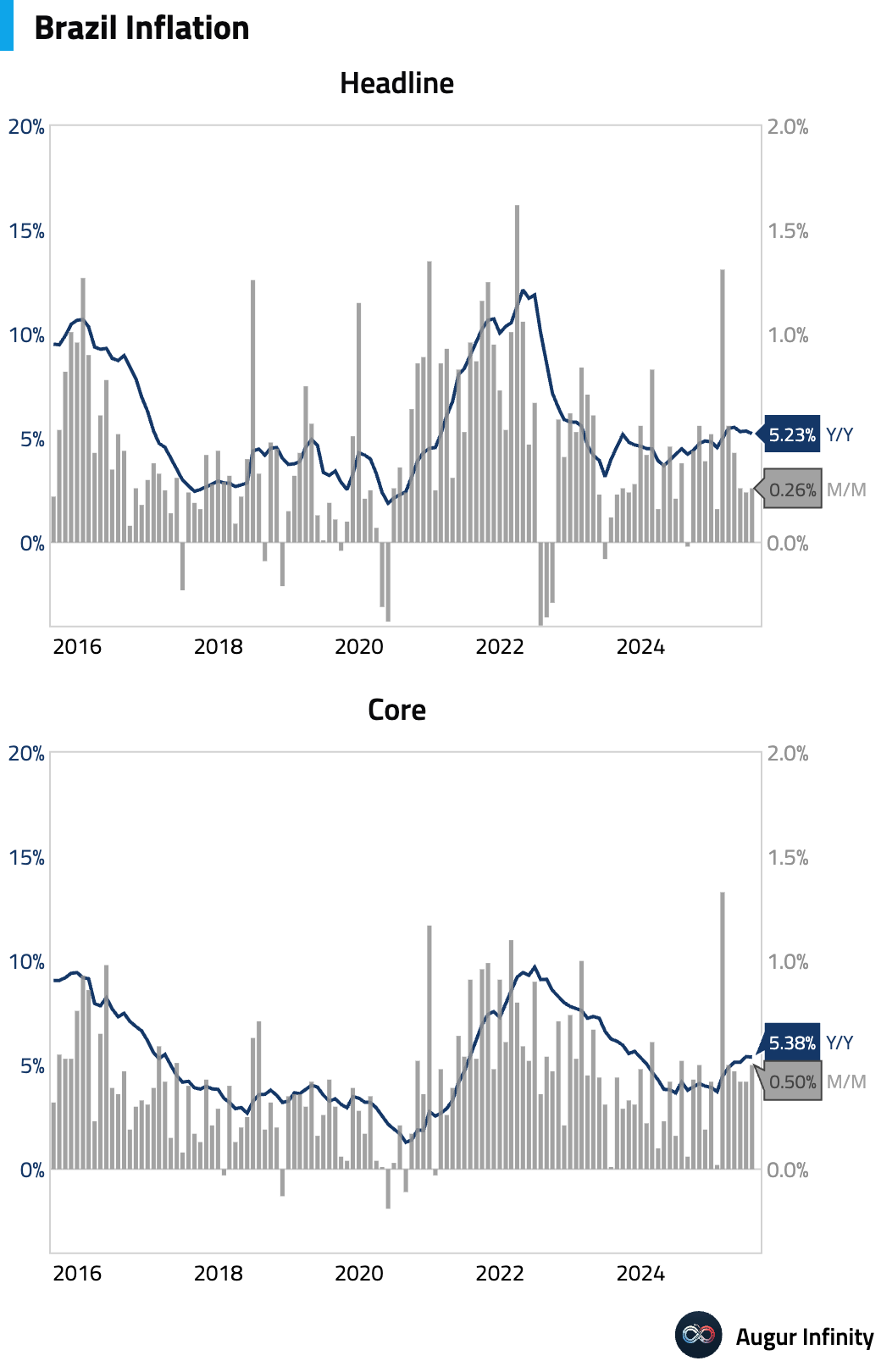

- Brazil’s IPCA inflation rate moderated to 5.23% Y/Y in July from 5.35%, slightly below consensus. The monthly rate was 0.26%. The softer-than-expected headline was driven by food-at-home deflation and weak goods prices. However, policy-sensitive core services inflation remains persistently high, tracking above 6%, which reinforces the need for a conservative monetary policy stance from the central bank. The monthly jump in services was driven almost entirely by a 19.9% surge in airfares.

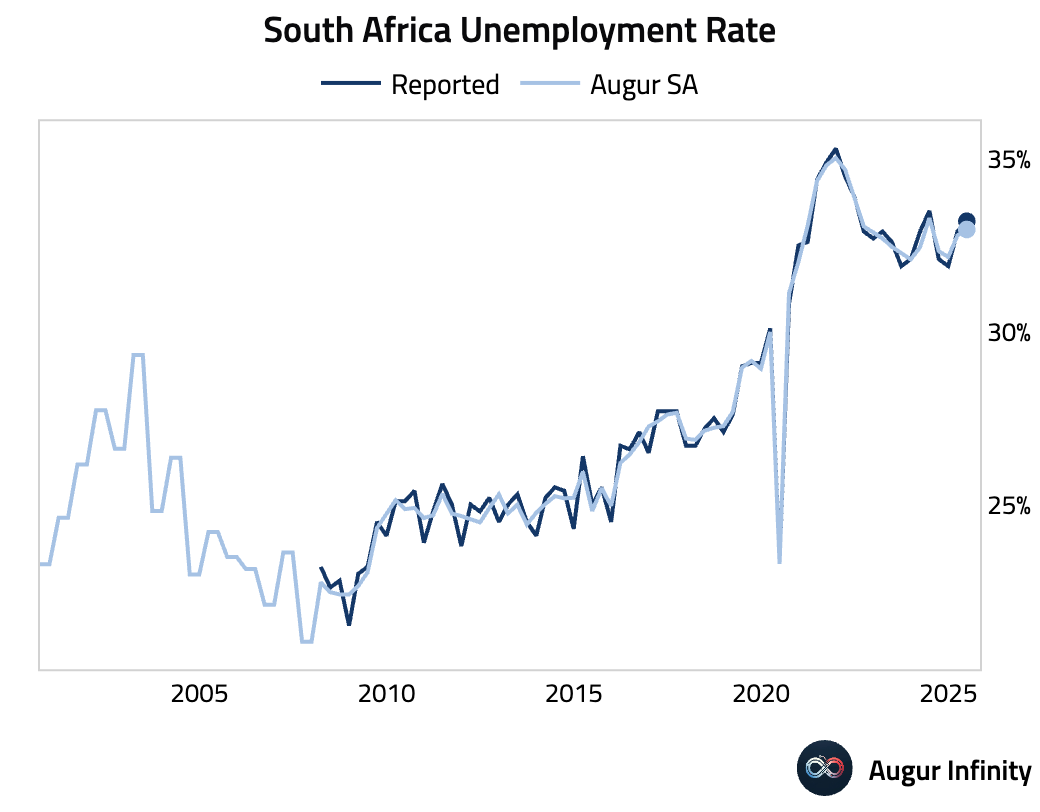

- South Africa's unemployment rate edged up to 33.2% in Q2 from 32.9% in Q1, with the number of unemployed persons rising to 8.367 million.

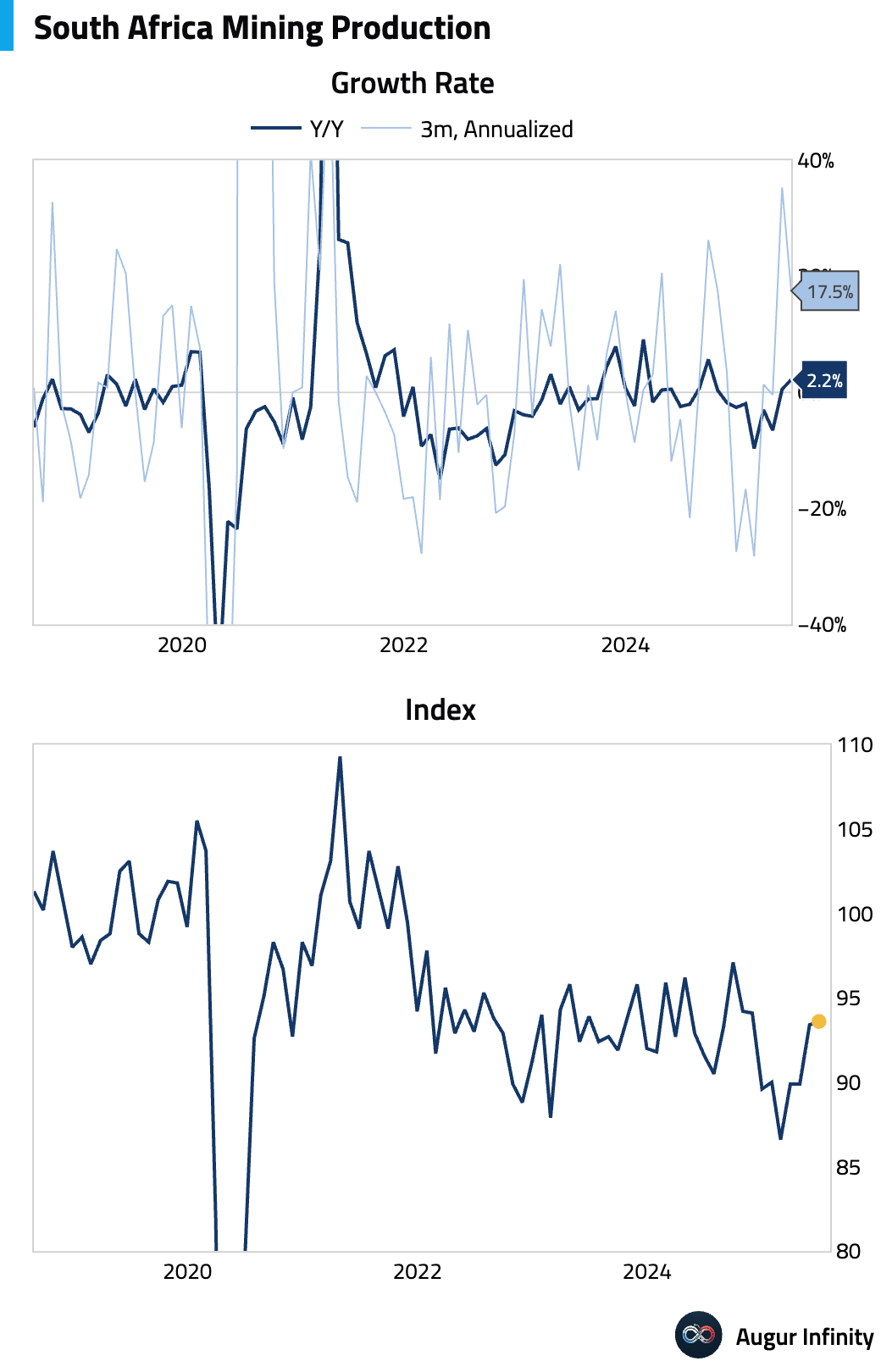

- South Africa’s mining production grew 2.4% Y/Y in June, beating expectations of 1.4% and accelerating from the 0.3% pace in May. M/M, production grew 0.2%.

- South Africa's gold production rose 3.1% Y/Y in June, a significant rebound from the 1.5% growth in May and its best performance in over a year.

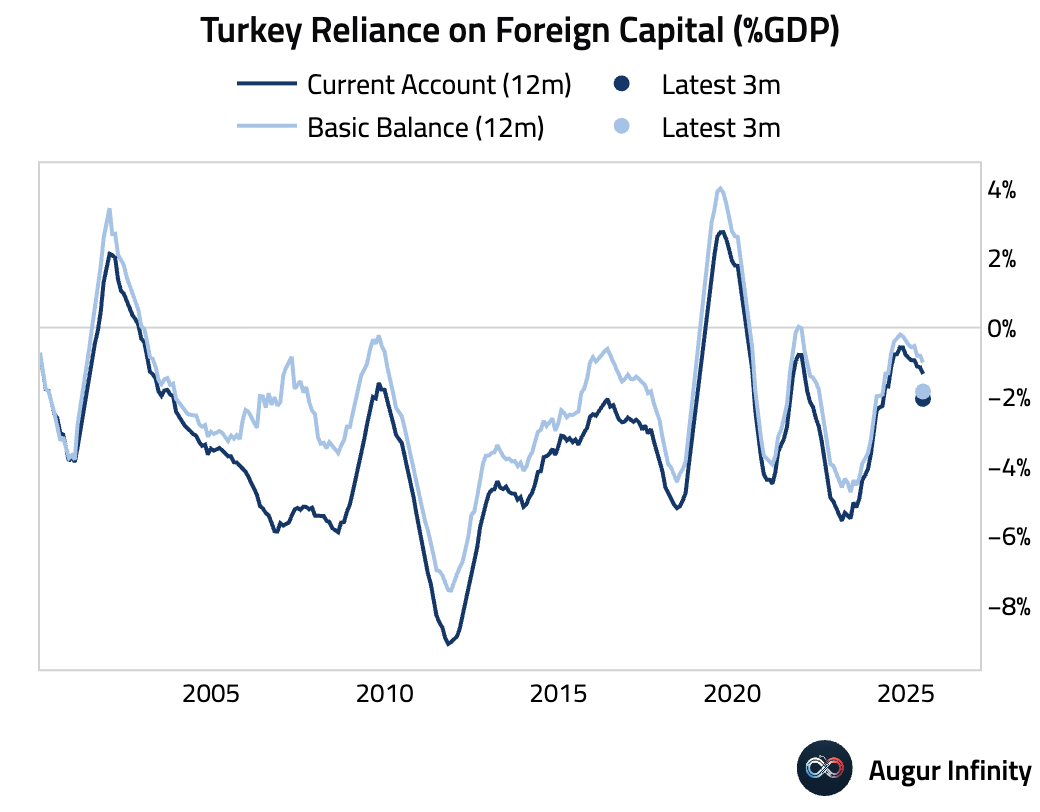

- Turkey's current account deficit widened to $2.01 billion in June, significantly missing the $1.4 billion consensus. The miss was driven by a sharp 16% M/M drop in goods exports. The financial account also flipped to a $2.7 billion outflow, leading to a decline in central bank reserves. However, central bank FX assets have reportedly increased by $21 billion in July, pointing to a substantial rebound in foreign inflows post-period.

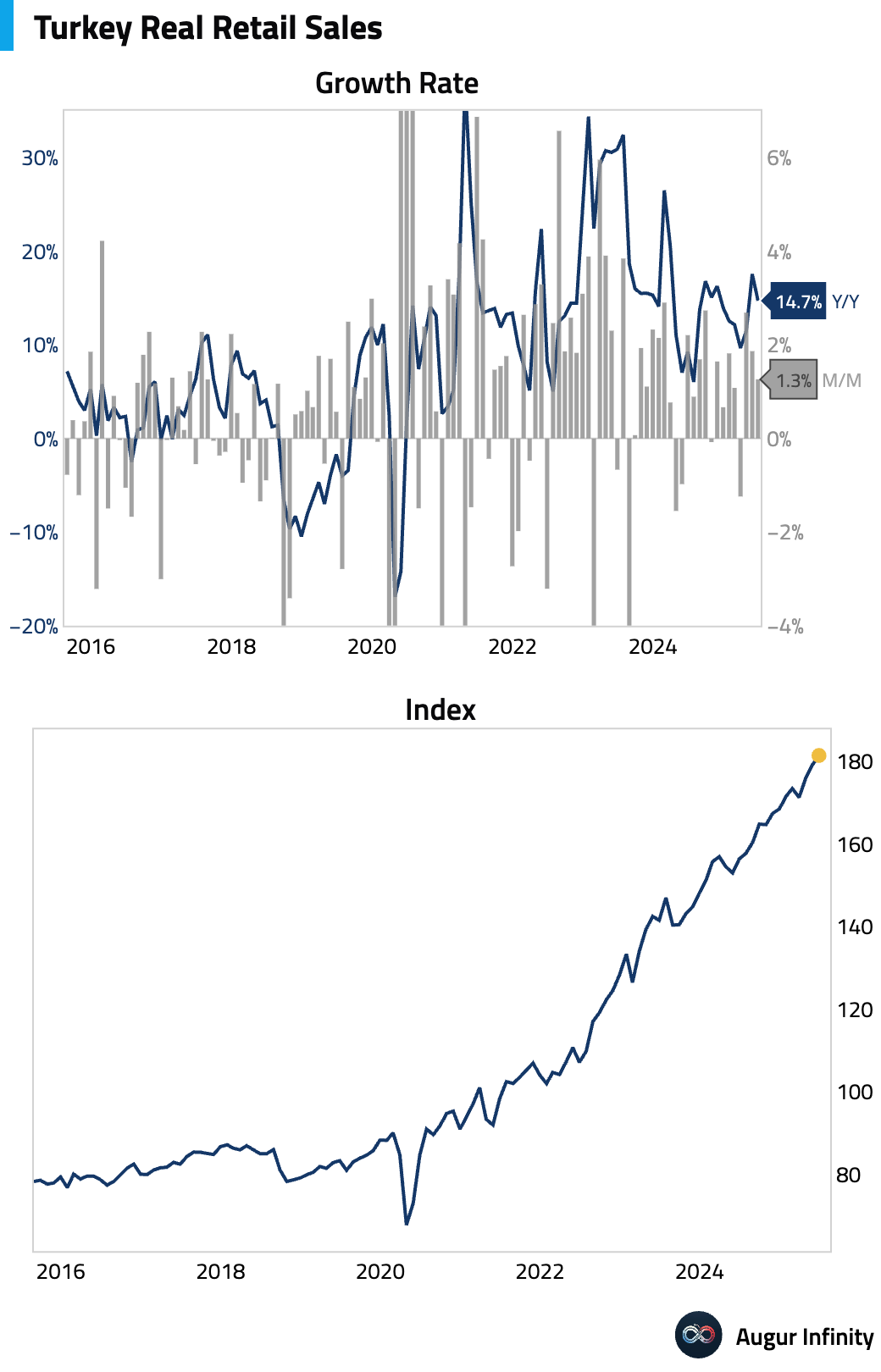

- Turkish retail sales growth decelerated in June, rising 1.3% M/M and 14.7% Y/Y, down from 1.9% and 17.6% respectively in the prior month.

Global Markets

Equities

- Global equity markets posted broad-based gains on Tuesday. In the US, the S&P 500 rose 1.1% and the tech-heavy Nasdaq Composite climbed 1.38%. Emerging markets were particularly strong, with Brazil surging 2.7% and China gaining 1.6%. In developed markets, the United Kingdom recorded its eighth consecutive daily gain (+0.9%), while Australia marked its third straight day of rallies (+1.1%).

Fixed Income

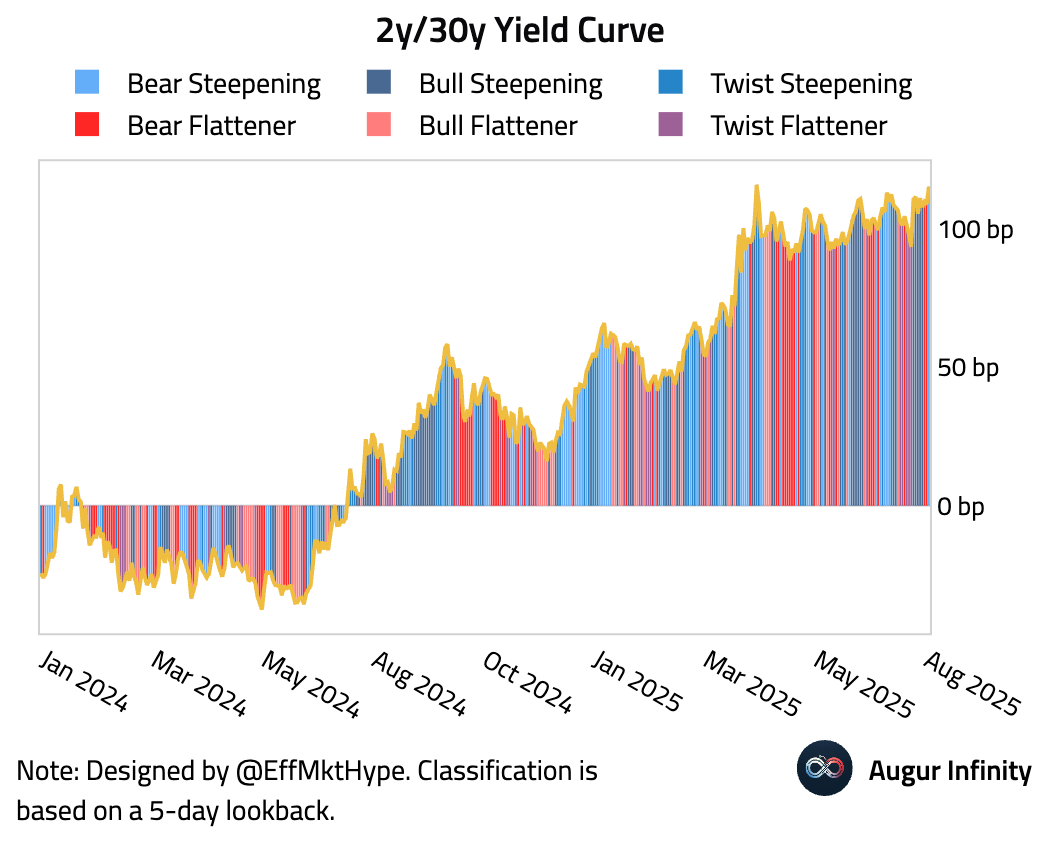

- The US Treasury curve steepened as the front end rallied while the long end sold off. The 2-year yield fell by 2.0 bps, whereas the 10-year and 30-year yields rose by 2.0 bps and 3.9 bps, respectively.

- Accordingly, the 2y/30y curve steepened by over 5.9 bps on the day.

FX

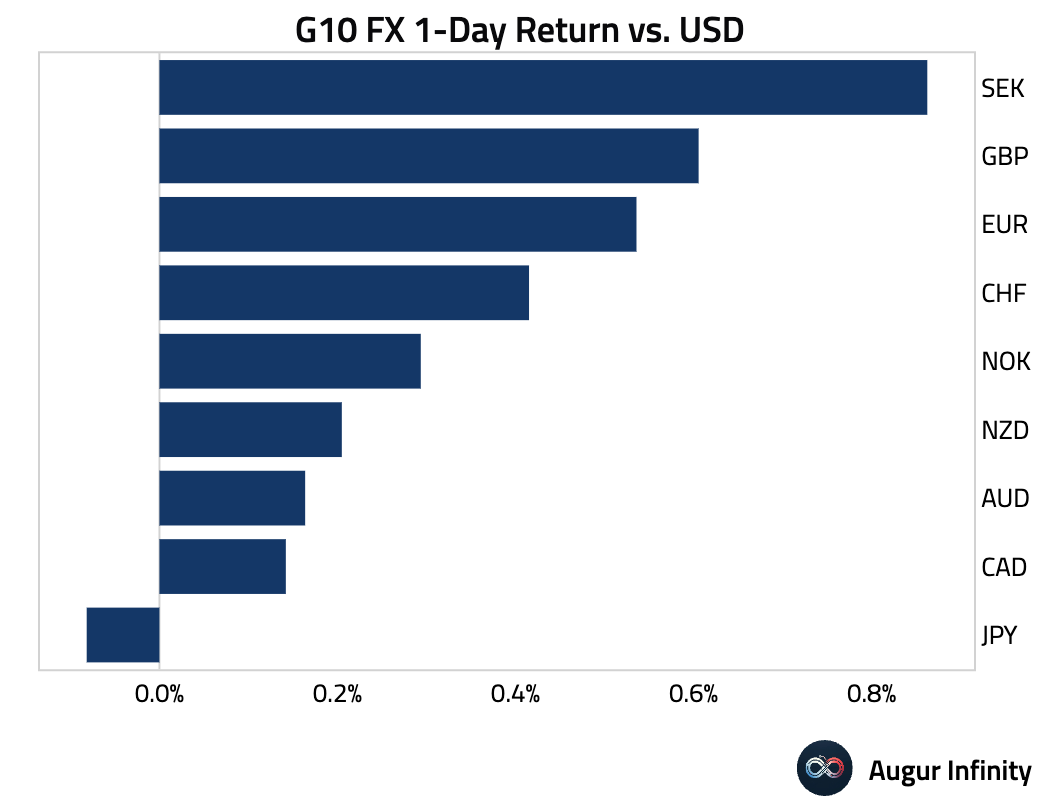

- The US dollar weakened against most G10 currencies, with the euro and British pound gaining 0.5% and 0.6%, respectively. The Japanese yen was an exception, weakening against the dollar for the fourth consecutive session.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.