Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- Diplomatic efforts to resolve the war in Ukraine are expected to continue today, with the Ukrainian president and several European leaders scheduled to meet with the US president.

- Japan’s Financial Services Agency is anticipated to approve yen-denominated stablecoins this month, while reports indicate the government is also considering a potential corporate tax hike.

- South Korea is reportedly contemplating a reduction of its national workweek to four and a half days.

Global Economics

United States

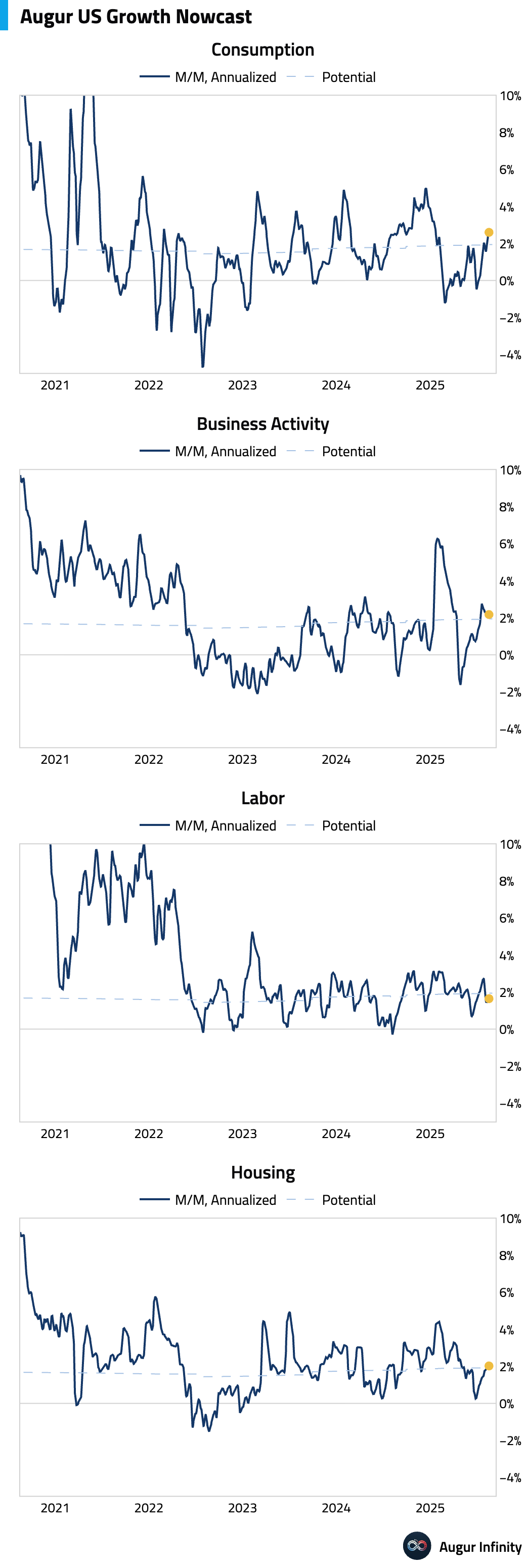

- Our latest tracking shows US growth holding up across sectors. Consumption, business activity, and housing are expanding at or above potential, while the labor market has softened slightly, coming in just below potential.

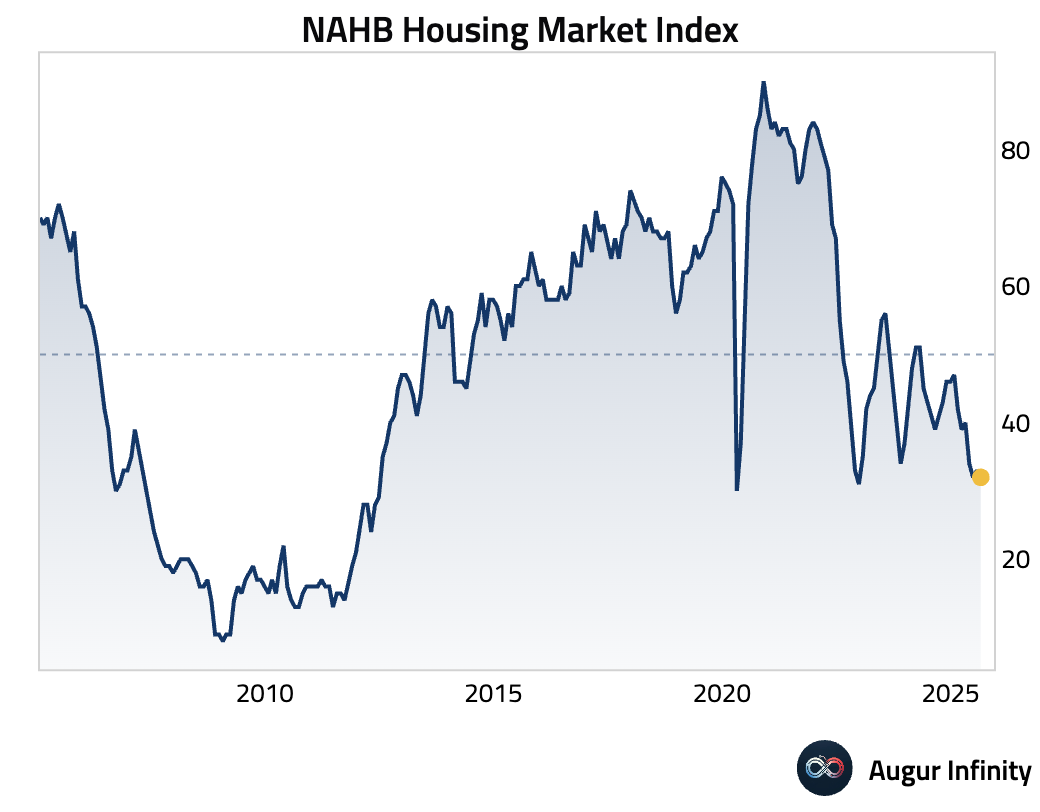

- The NAHB Housing Market Index fell to 32 in August from 33 in July, slightly below the consensus of 34. This marks the lowest reading since December 2022 and indicates continued pessimism among homebuilders.

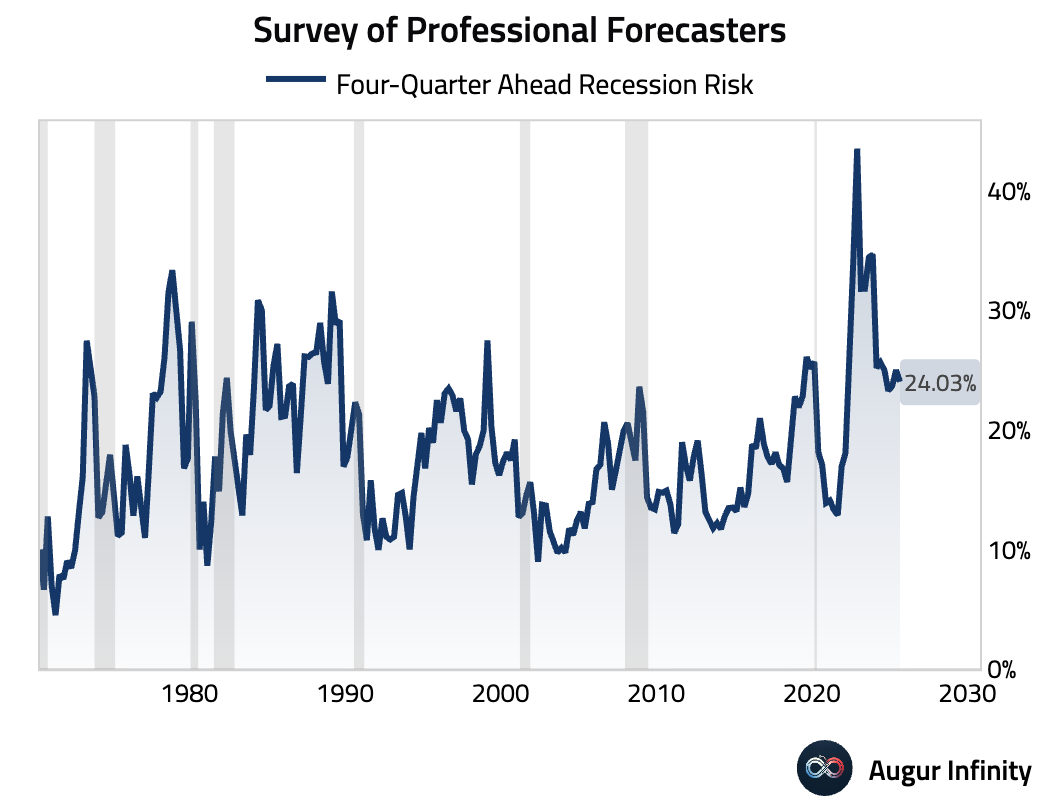

- The Survey of Professional Forecasters places the four-quarter-ahead recession risk at 24%, only 1 percentage point lower than last quarter.

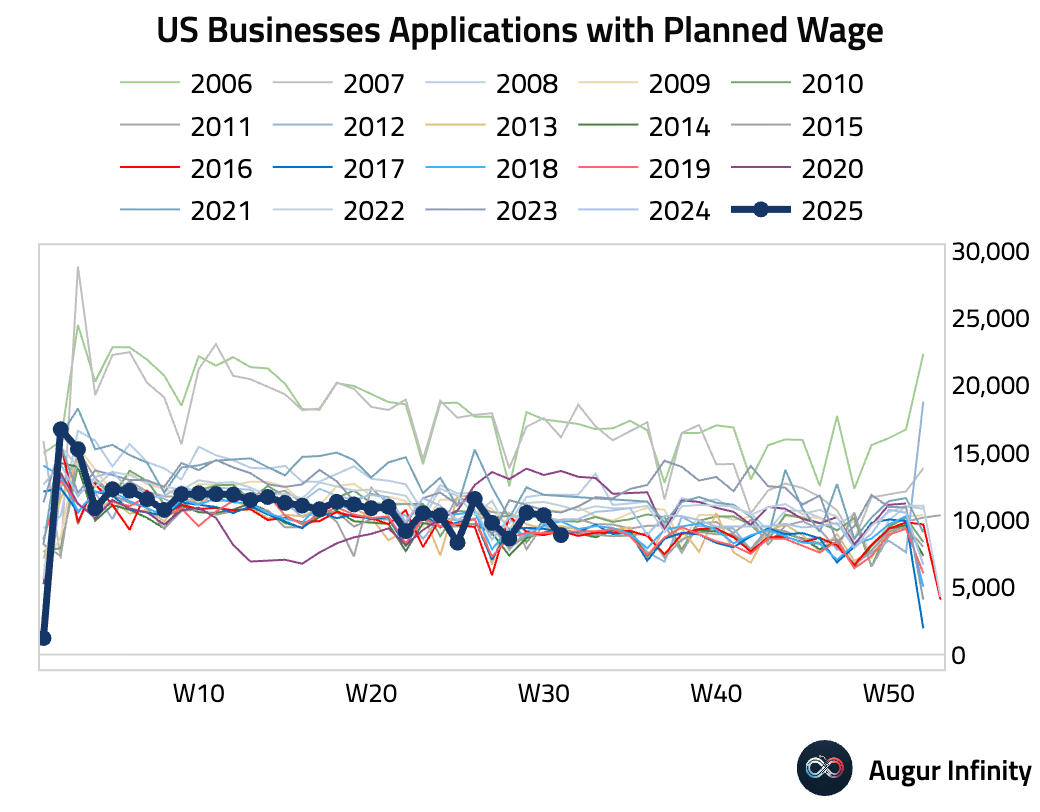

- US business applications with planned wages look weak. The latest reading for week 31 is the lowest on record for this week (i.e., week 31) since the series began.

Canada

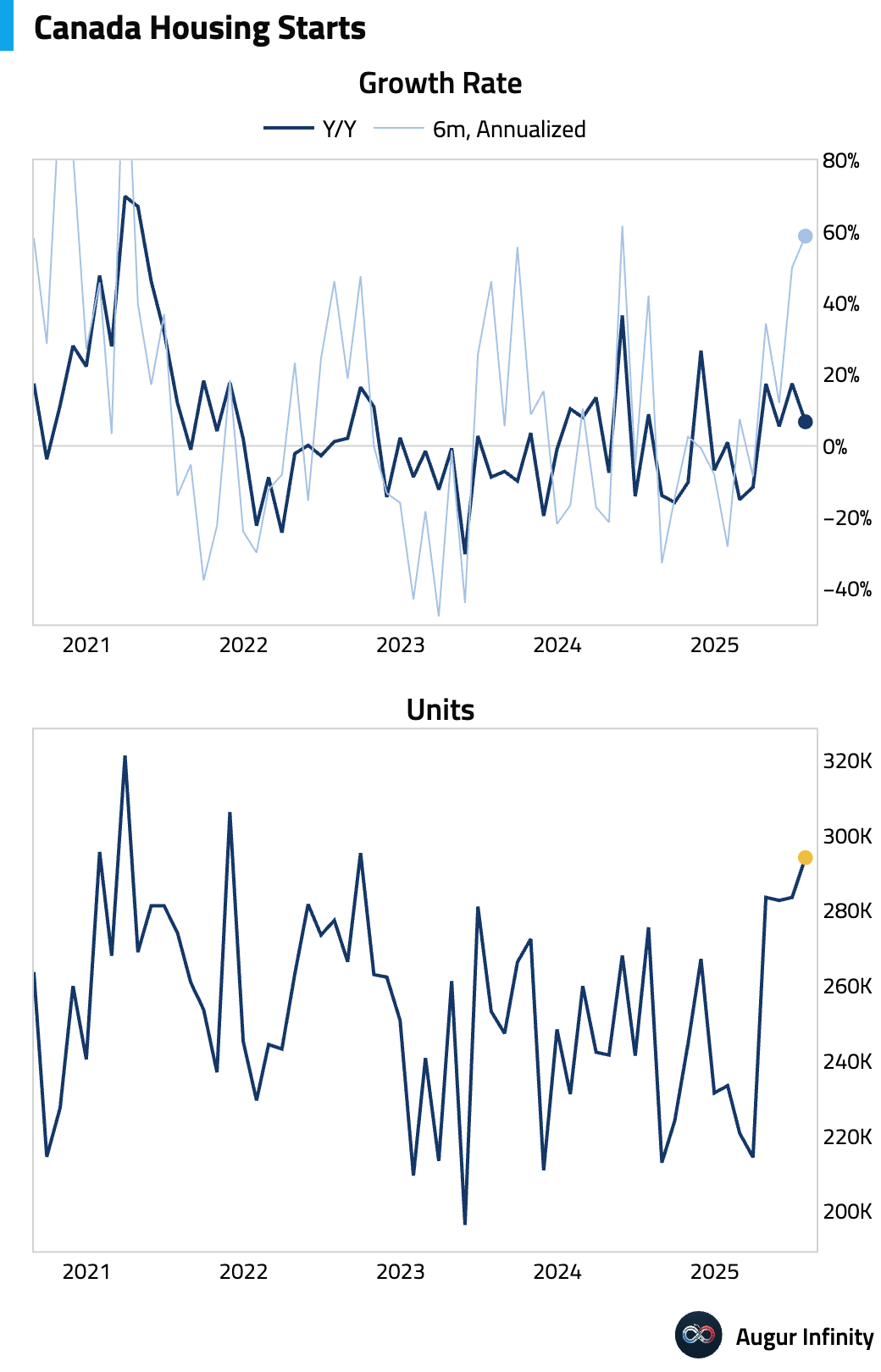

- Housing starts surged to an annualized 294,100 units in July, well above the consensus forecast of 265,000 and up from 283,500 in June. This is the highest level of housing starts since September 2022.

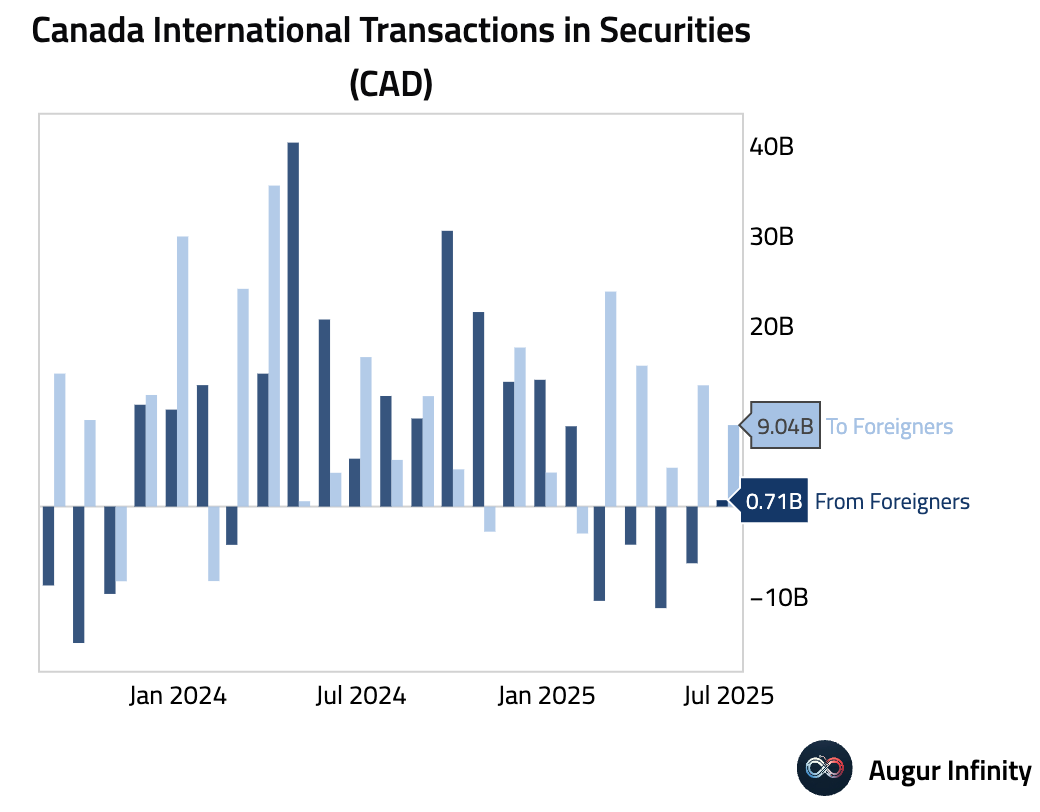

- Foreign investors purchased C$710 million of Canadian securities in June, a sharp reversal from May’s C$6.3 billion divestment and a significant beat of the C$4.75 billion outflow consensus. Meanwhile, Canadian investors’ purchases of foreign securities slowed to C$9.0 billion from C$13.5 billion.

Europe

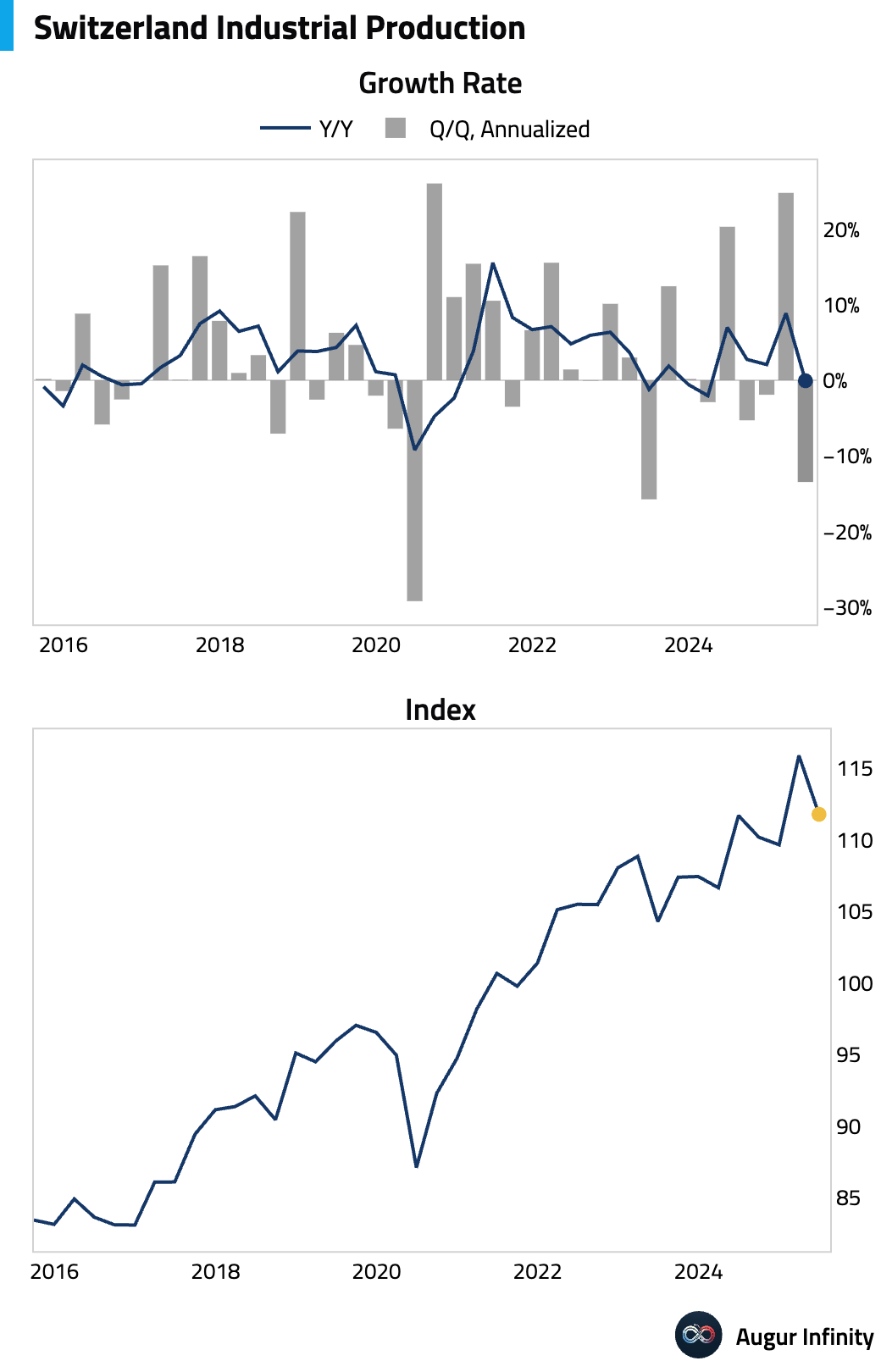

- Switzerland’s industrial production contracted by 0.1% Y/Y in the second quarter, a sharp deceleration from the 8.9% growth recorded in the first quarter and the first decline in over a year.

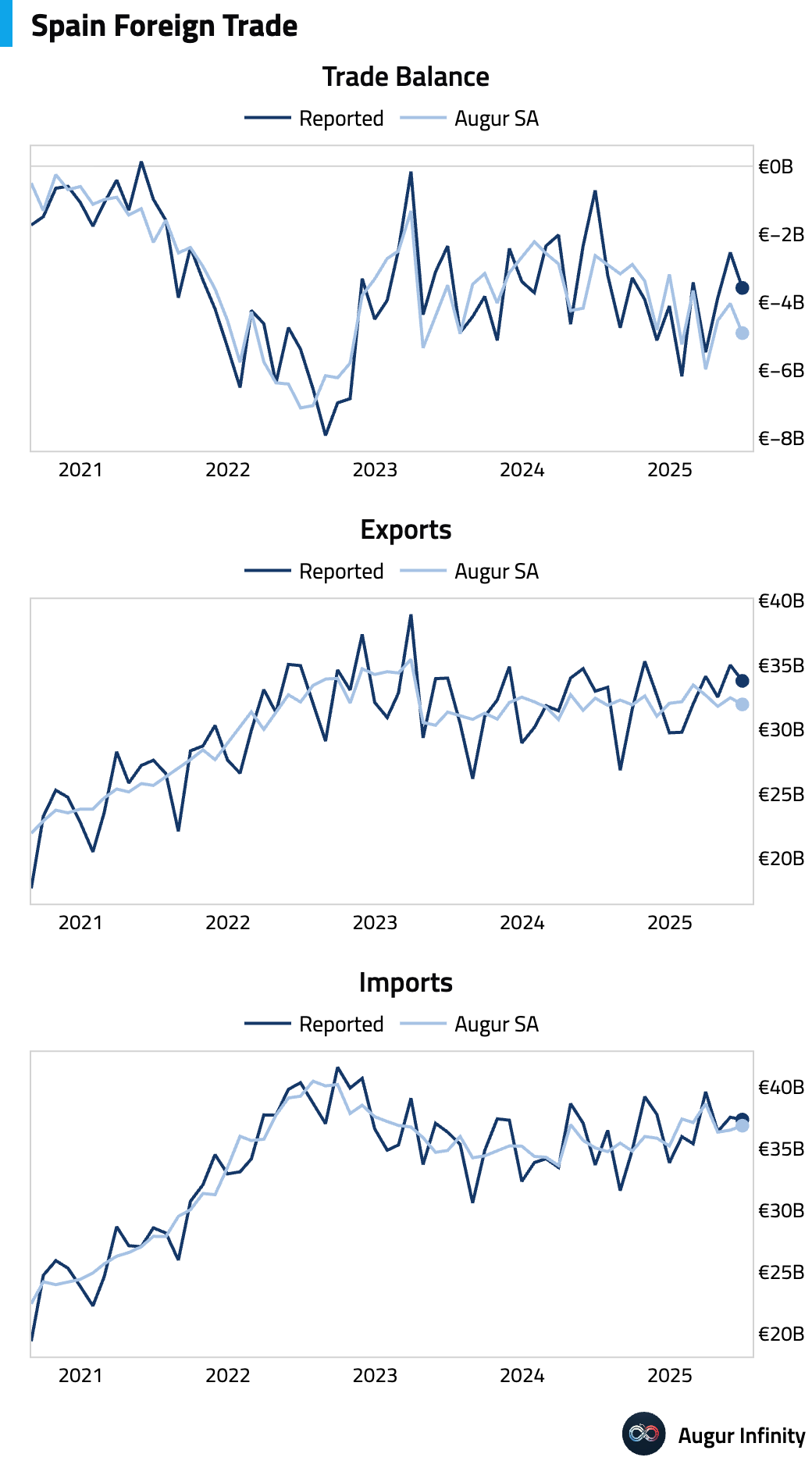

- Spain’s trade deficit widened to €3.59 billion in June from €2.54 billion in May.

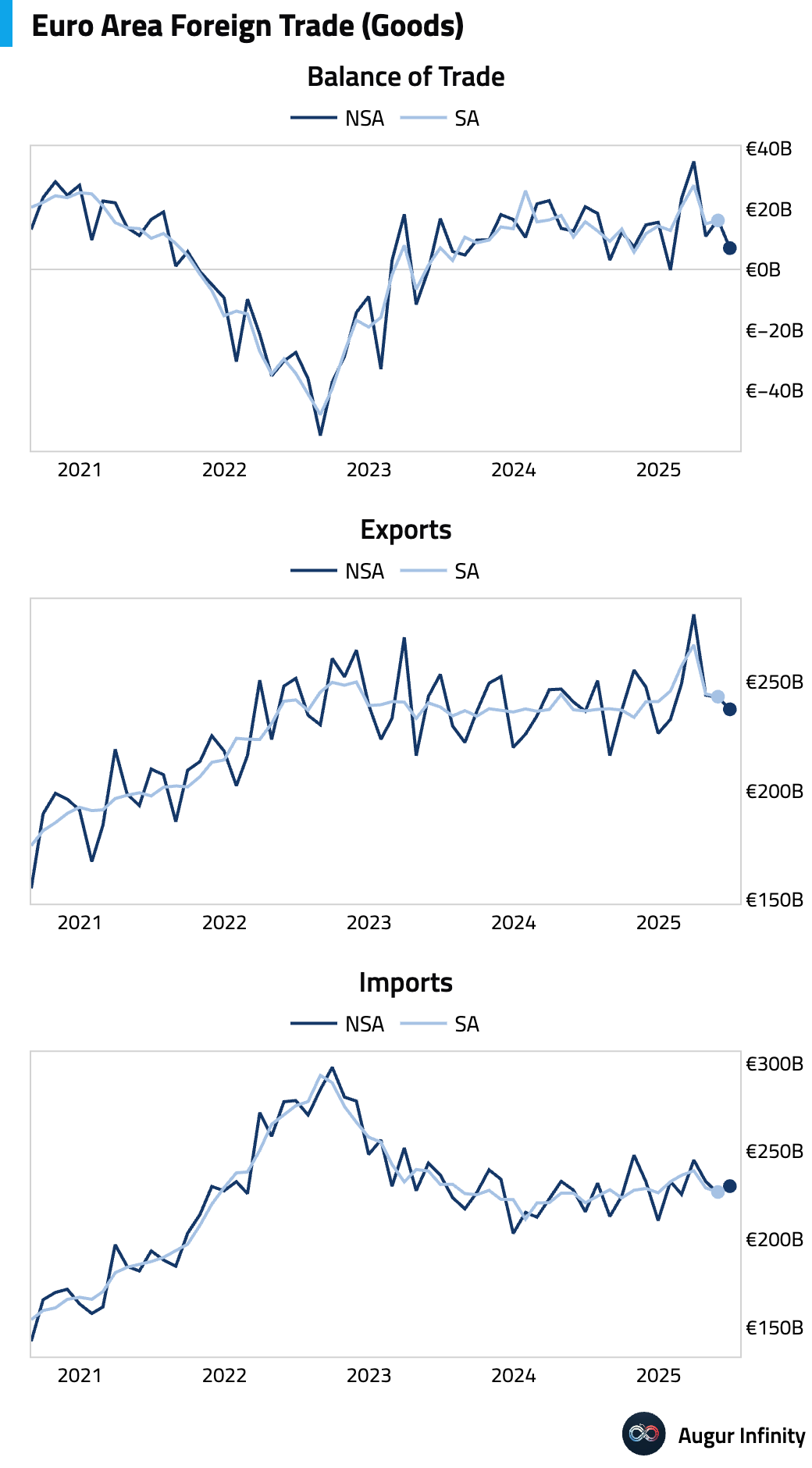

- The Euro Area’s goods trade surplus narrowed significantly to €7.0 billion in June, falling short of the €13.0 billion consensus and down from a revised €16.5 billion in May.

Asia-Pacific

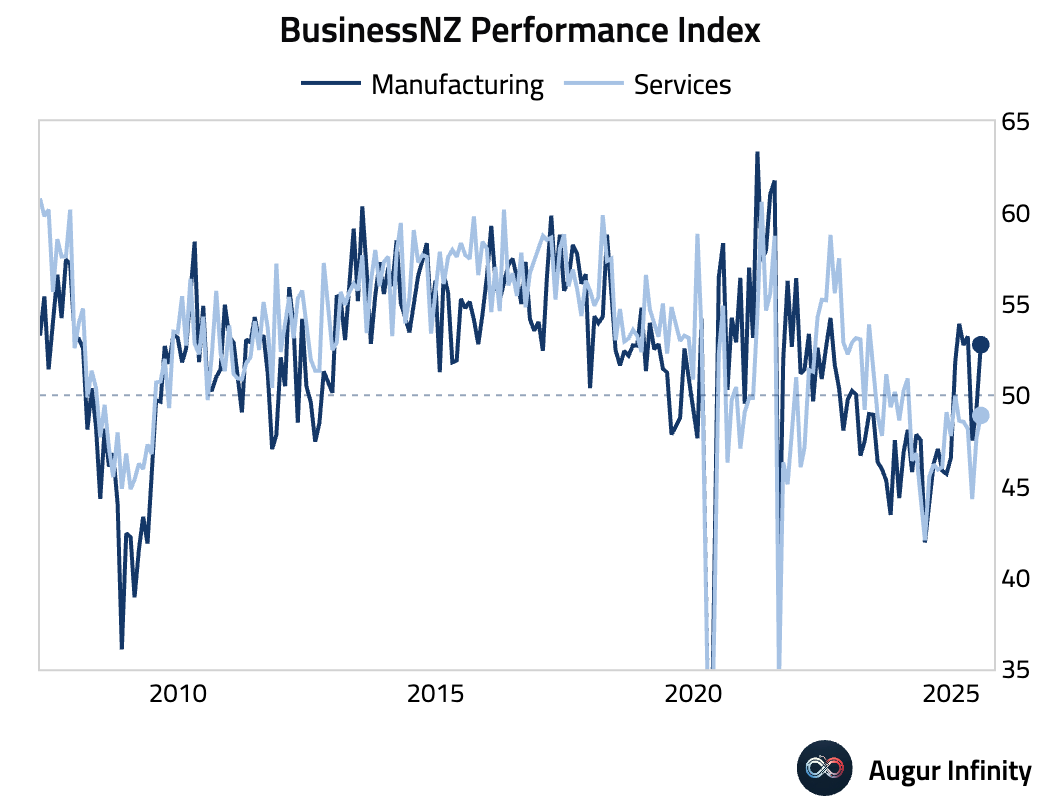

- New Zealand’s services sector showed signs of stabilization as the BusinessNZ Performance of Services Index (PSI) rose to 48.9 in July from 47.6 in June. While still in contractionary territory, it was the strongest reading since January.

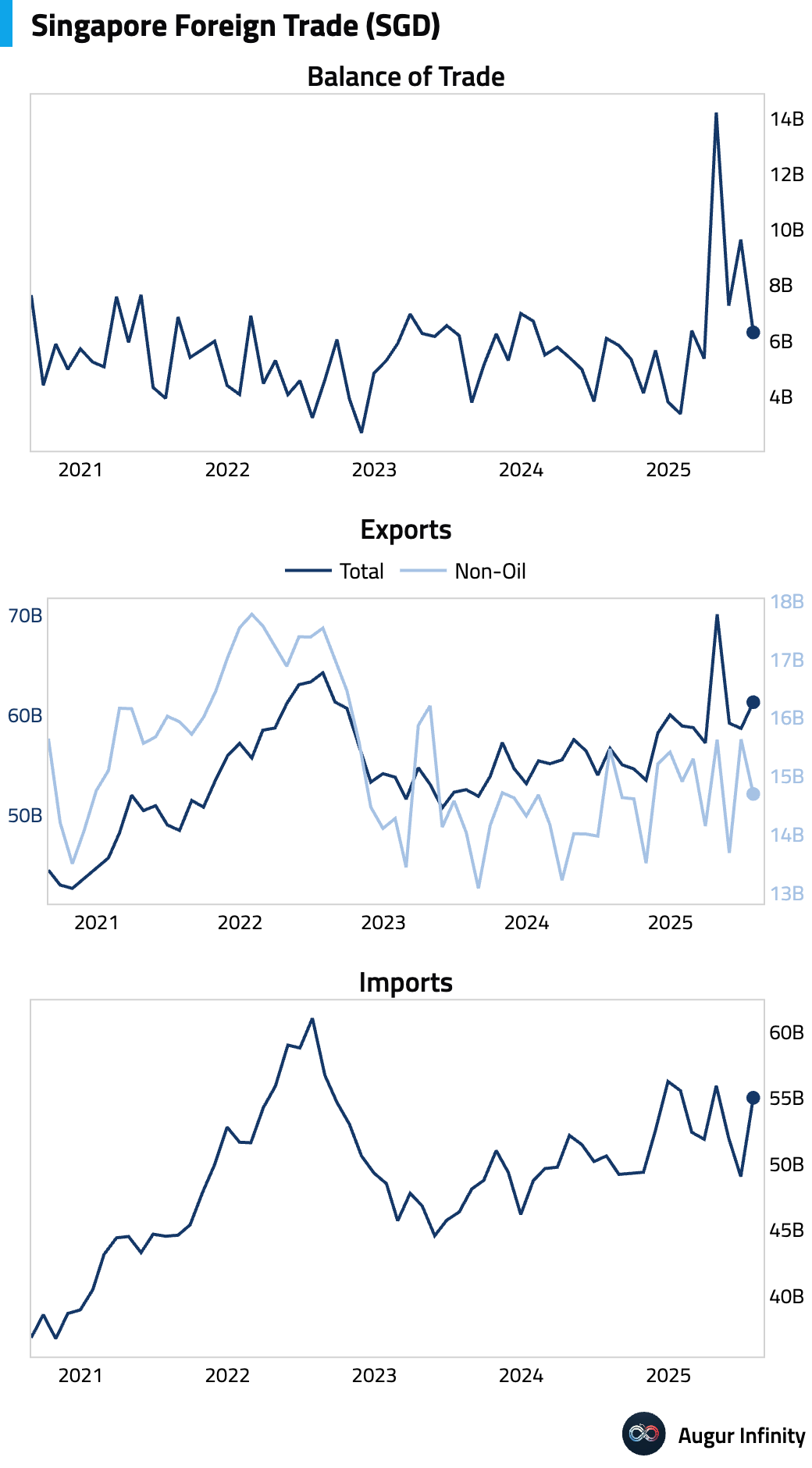

- Singapore’s non-oil exports plunged 6.0% M/M in July, reversing a 14.2% gain in June. On a year-over-year basis, exports fell 4.6%. The trade surplus consequently narrowed to S$6.3 billion from S$9.6 billion.

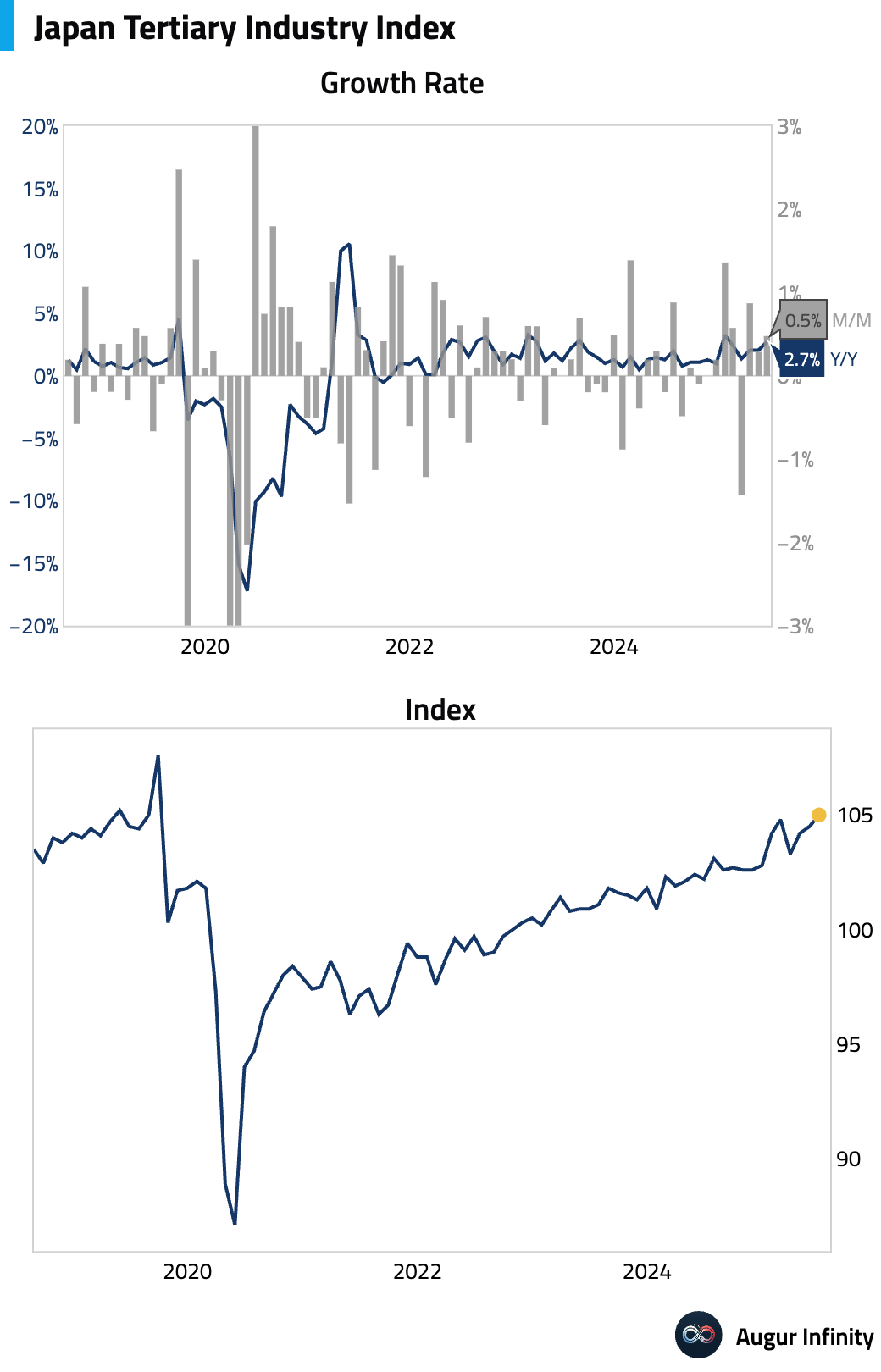

- Japan’s Tertiary Industry Index, a measure of service sector activity, rose 0.5% M/M in June, beating the 0.3% consensus and accelerating from the previous month’s 0.3% increase.

Emerging Markets ex China

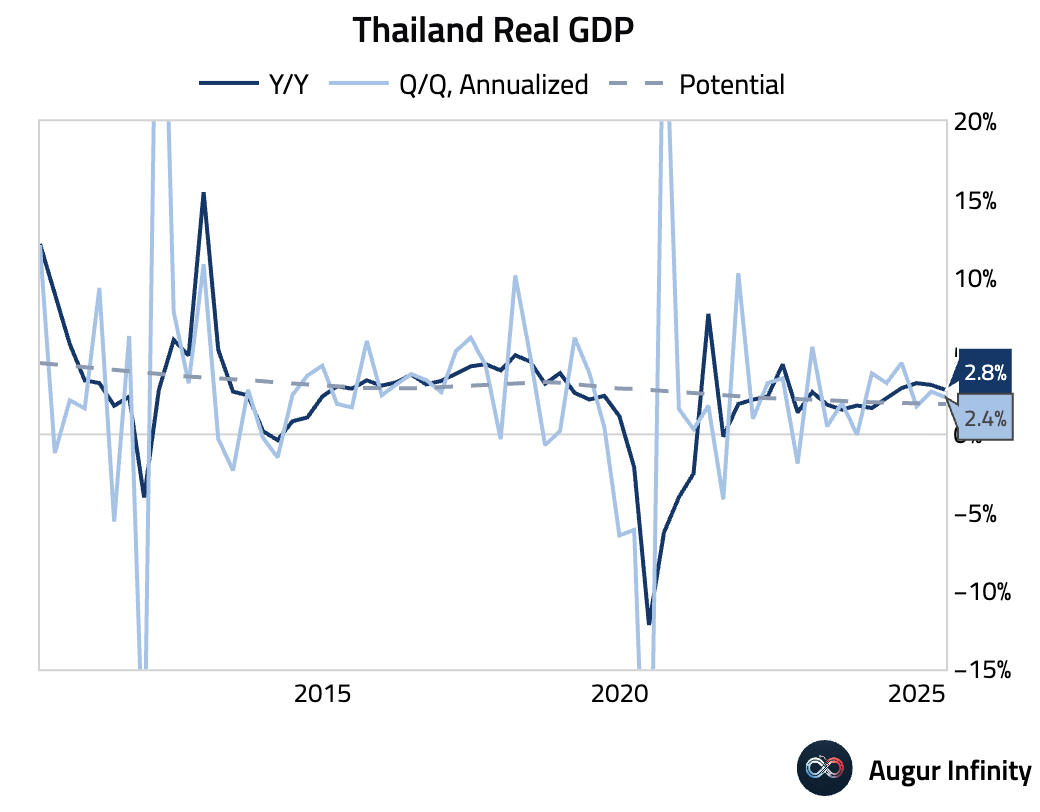

- Thailand’s GDP grew 0.6% Q/Q in the second quarter, doubling the consensus forecast of 0.3%. The year-over-year growth rate slowed to 2.8% from 3.2% in Q1 but still edged past the 2.5% estimate. The slowdown was primarily driven by a significant drag from higher imports (+10.8% Y/Y) and weaker domestic consumption, which was partially offset by a rise in gross fixed capital formation from inventory accumulation.

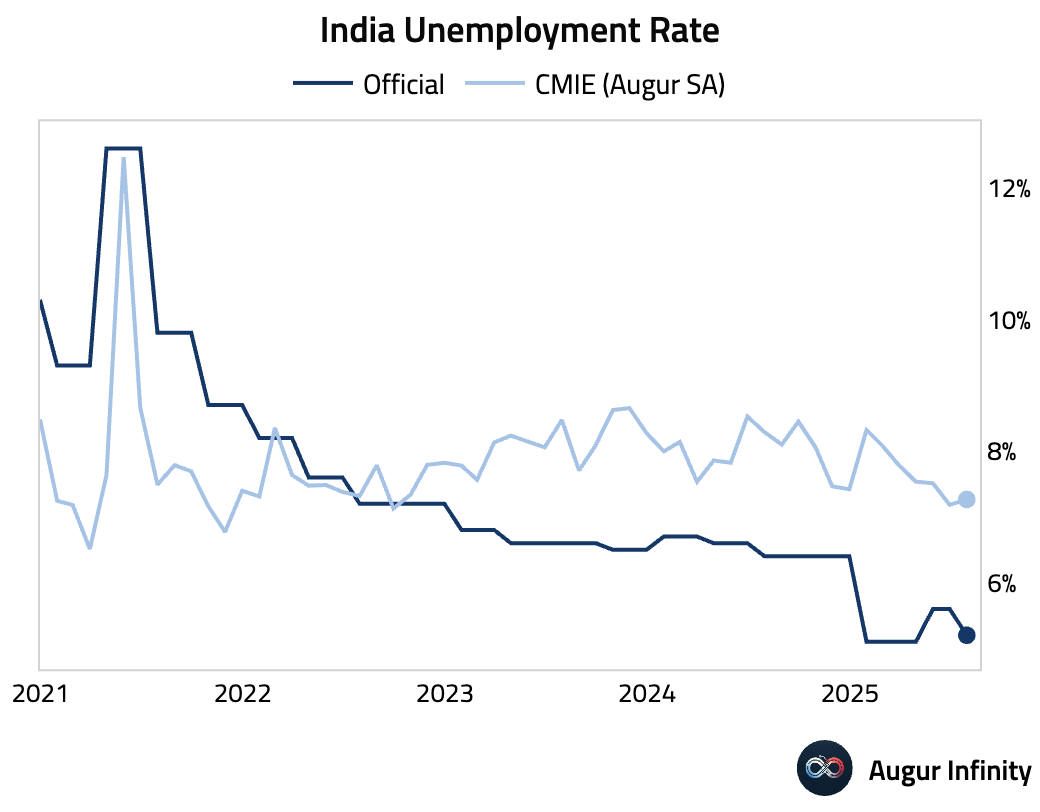

- India’s unemployment rate ticked down to 5.2% in July from 5.6% in June.

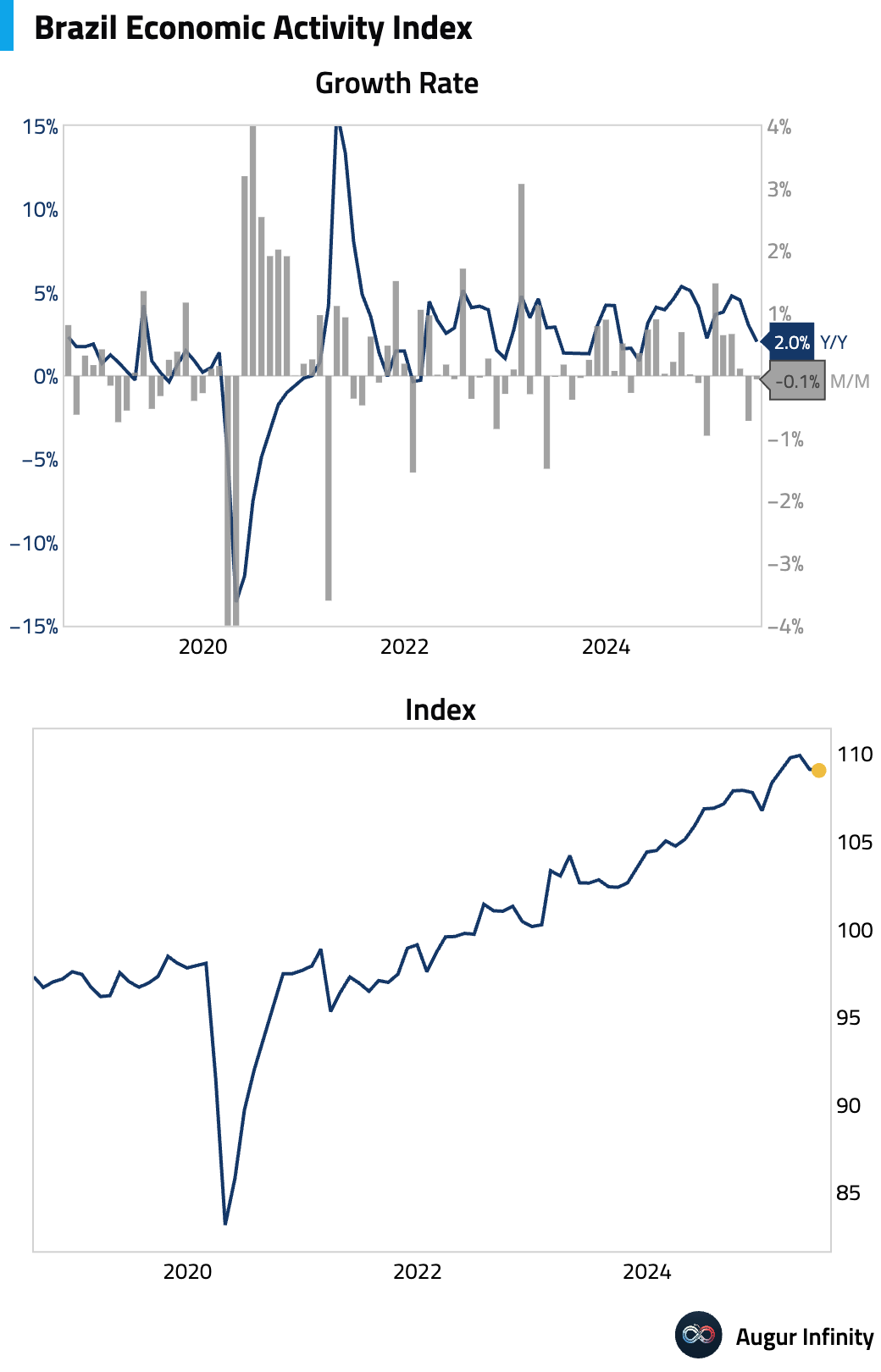

- Brazil’s IBC-Br Economic Activity Index, a monthly proxy for GDP, contracted 0.1% M/M in June, missing the flat consensus estimate. The weakness was driven by sharp declines in agriculture (–2.3%) and a dip in industry (–0.1%), which offset a minor 0.1% gain in services. This result implies Q2 growth of just 0.28% Q/Q, with a negative carry-over of –0.3% into the third quarter.

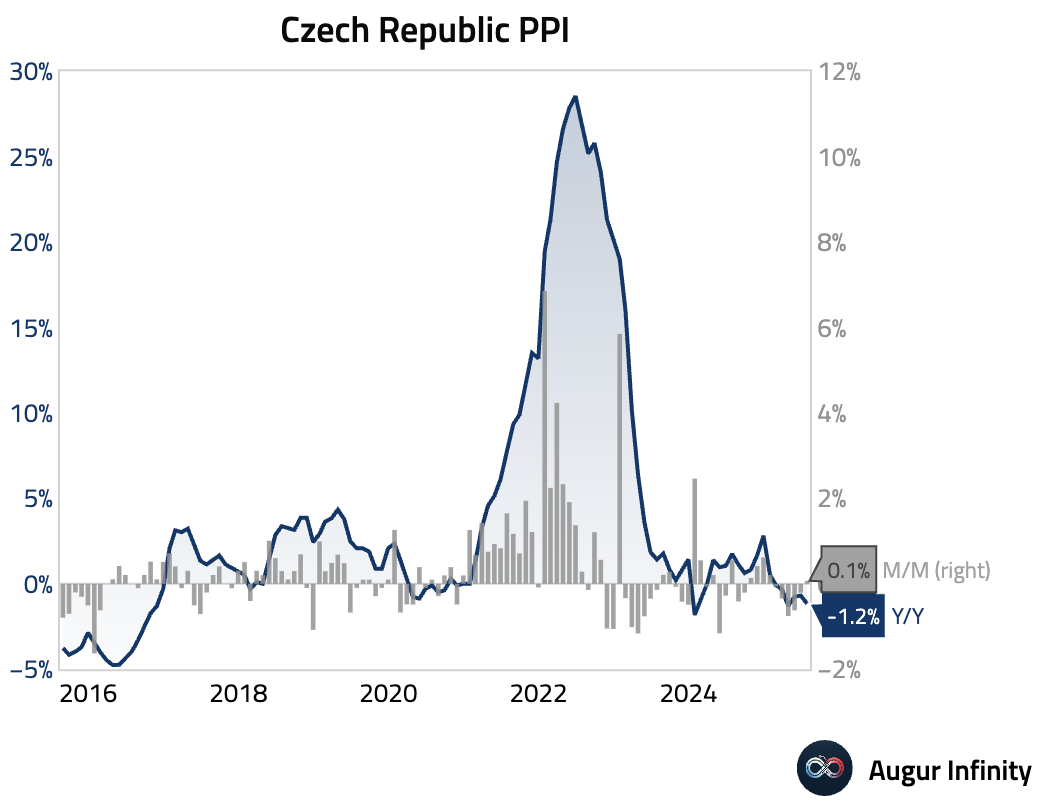

- Czech producer prices fell 1.2% Y/Y in July, a slightly faster decline than the 1.1% consensus. Month-over-month, prices edged up 0.1%, reversing a 0.2% drop in June.

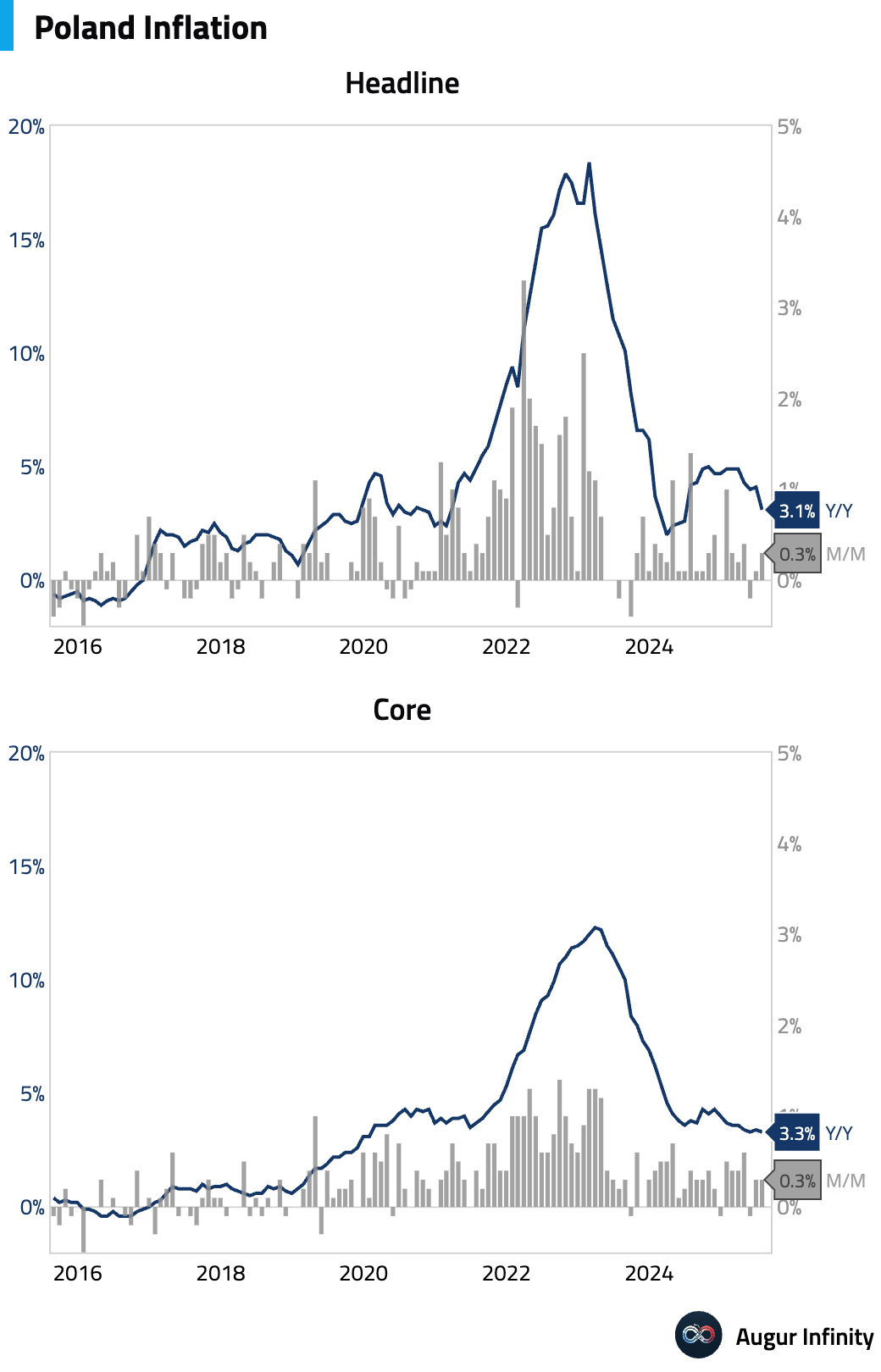

- Poland’s core inflation rate eased to 3.3% Y/Y in July, matching consensus and down from 3.4% in June. This is the lowest core inflation reading since January 2020.

Global Markets

Equities

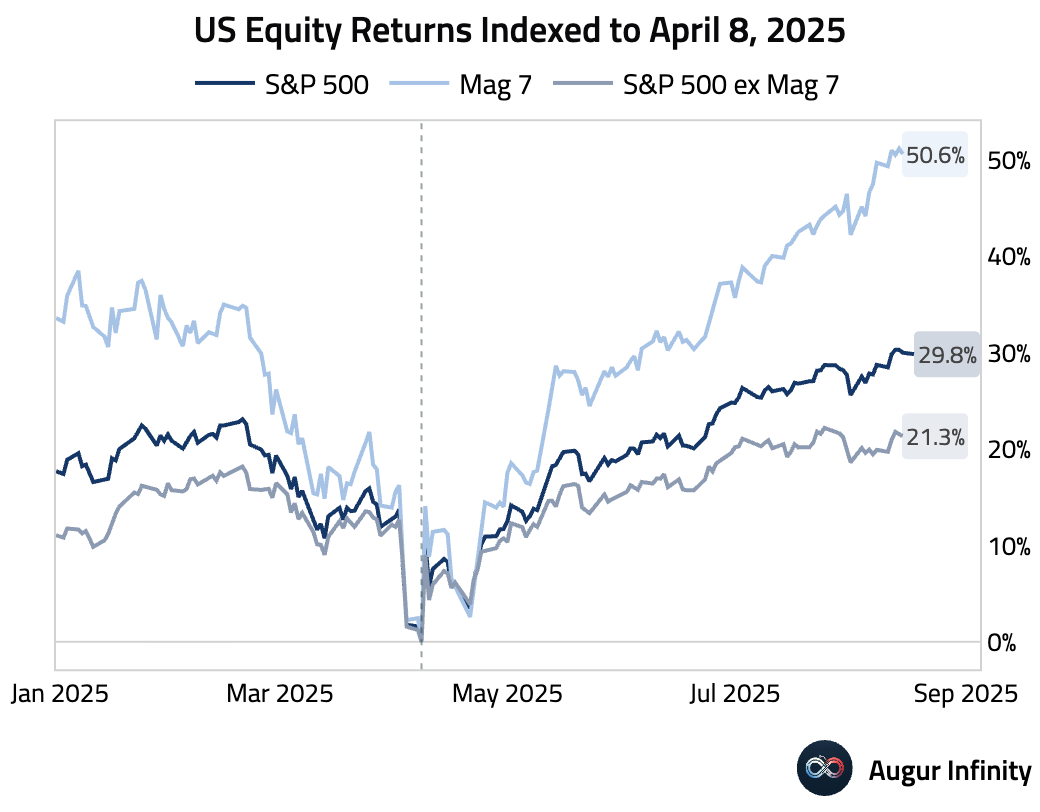

- Since the April 8 low, the S&P 500 has rallied by 30%. This is powered by a 51% surge in Mag-7 stocks, while the rest of the S&P 500 members gained 21%.

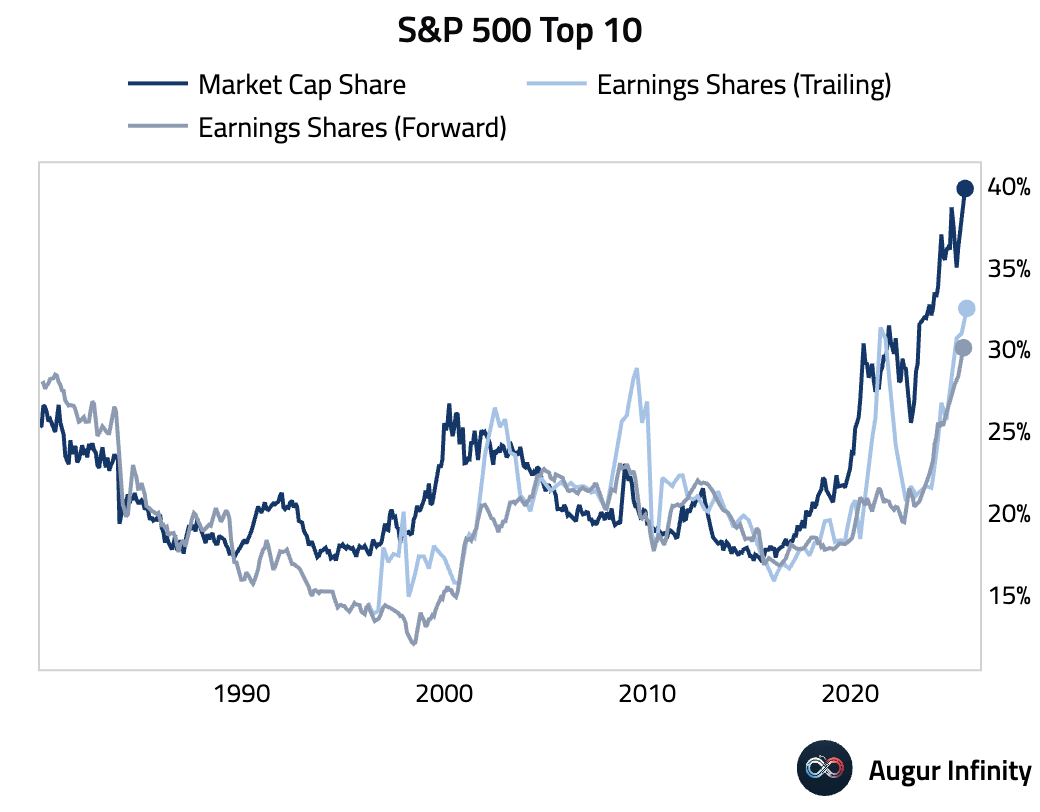

- The market cap weight of the top 10 stocks in the S&P 500 has reached a record high of 40%. The earnings share of these companies has risen as well, with trailing 12-month earnings accounting for 33% of the total and forward earnings (NTM) at 30%.

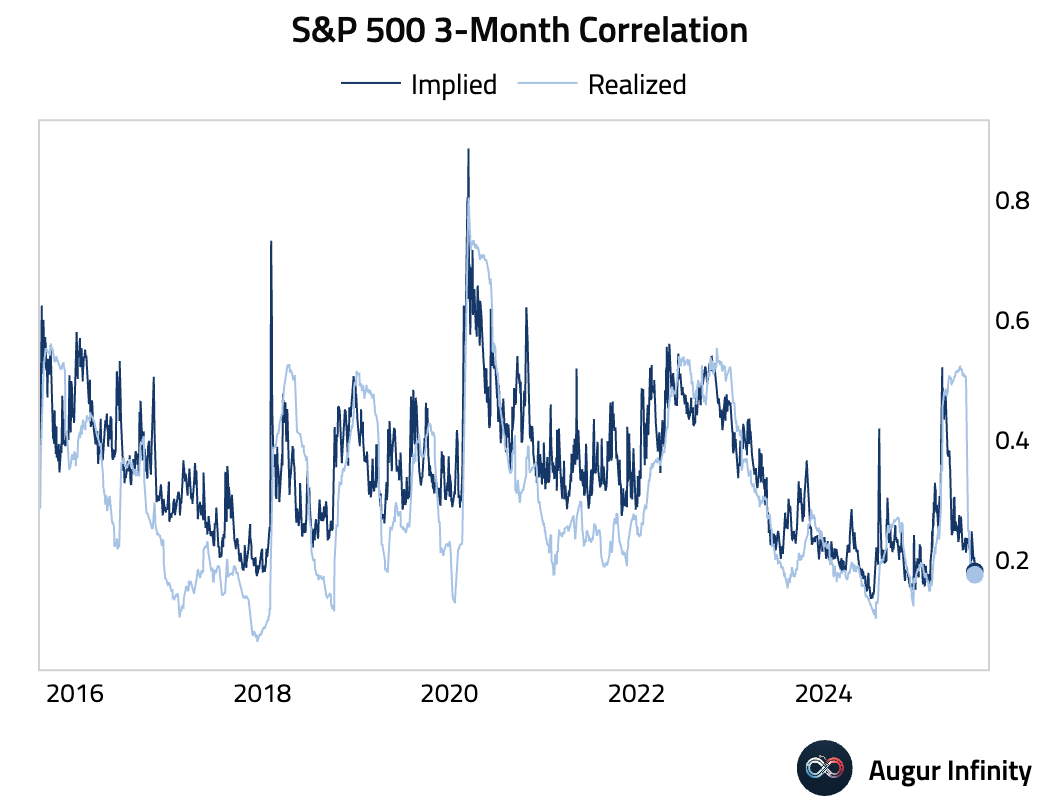

- Both implied and realized correlations amongst S&P 500 members have returned to near record lows.

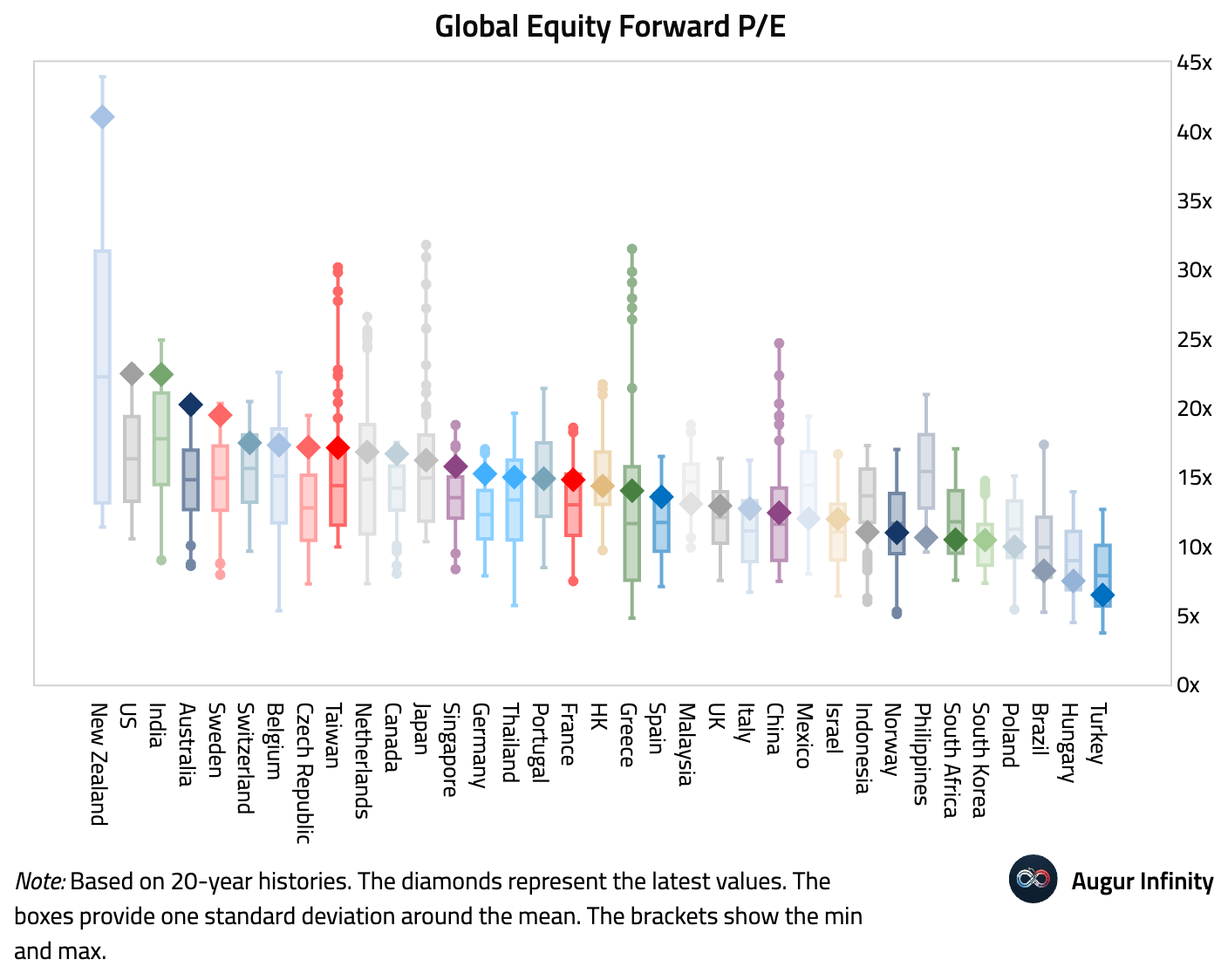

- Valuations remain stretched. The US now has the second-highest forward P/E in our core coverage universe, surpassed only by New Zealand (though the latter is thinly represented).

Fixed Income

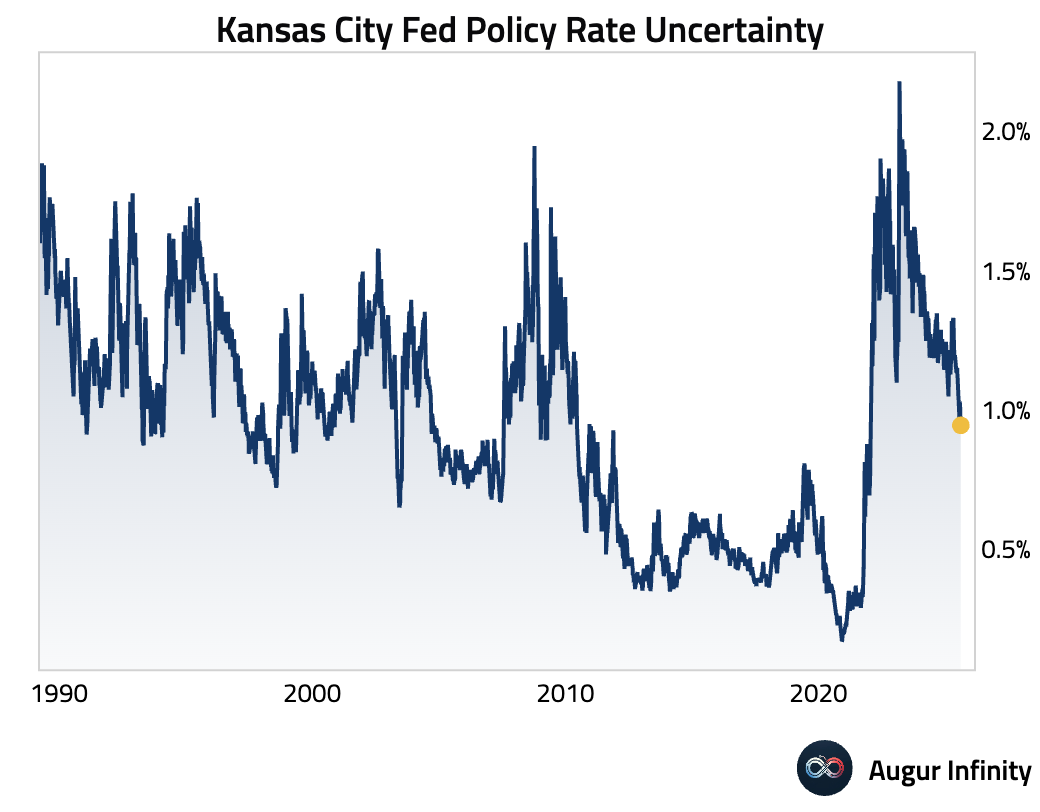

- Amid the debate over whether the Fed should resume rate cuts in the face of a softer labor market but sticky inflation, the Kansas Fed’s policy rate uncertainty gauge has fallen to its lowest level since February 2022.

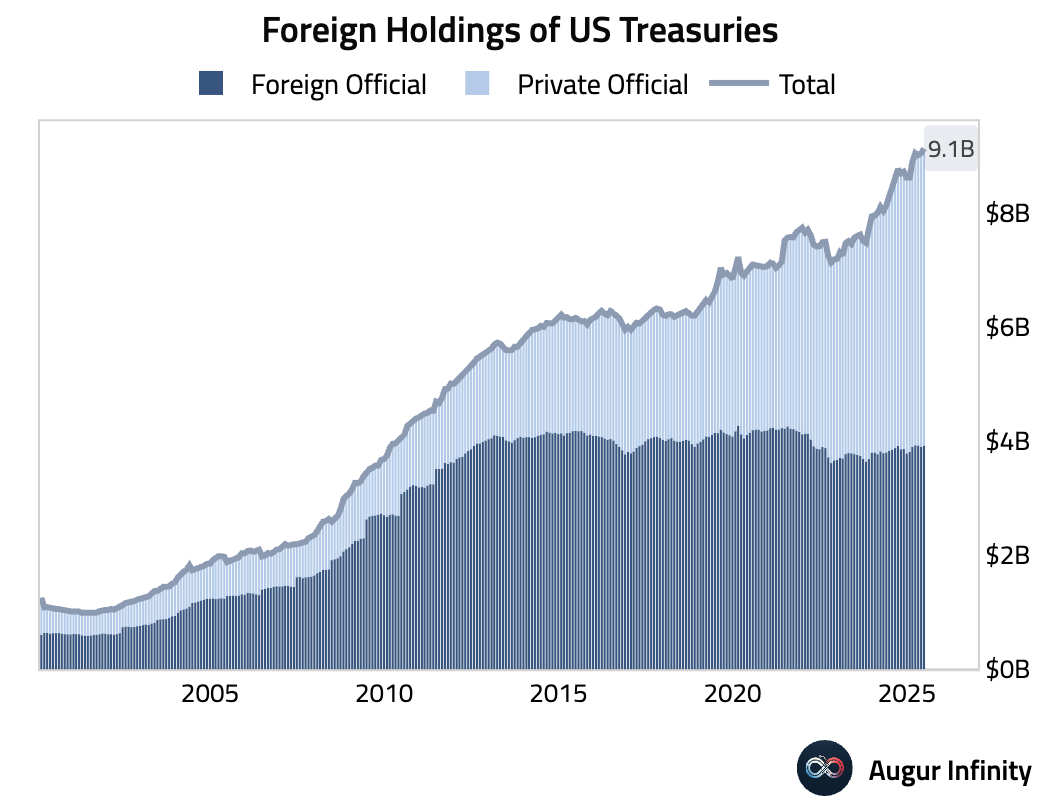

- Foreign holdings of US Treasuries reached a new record high of $9.1 trillion in June.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.