Global Economics

United States

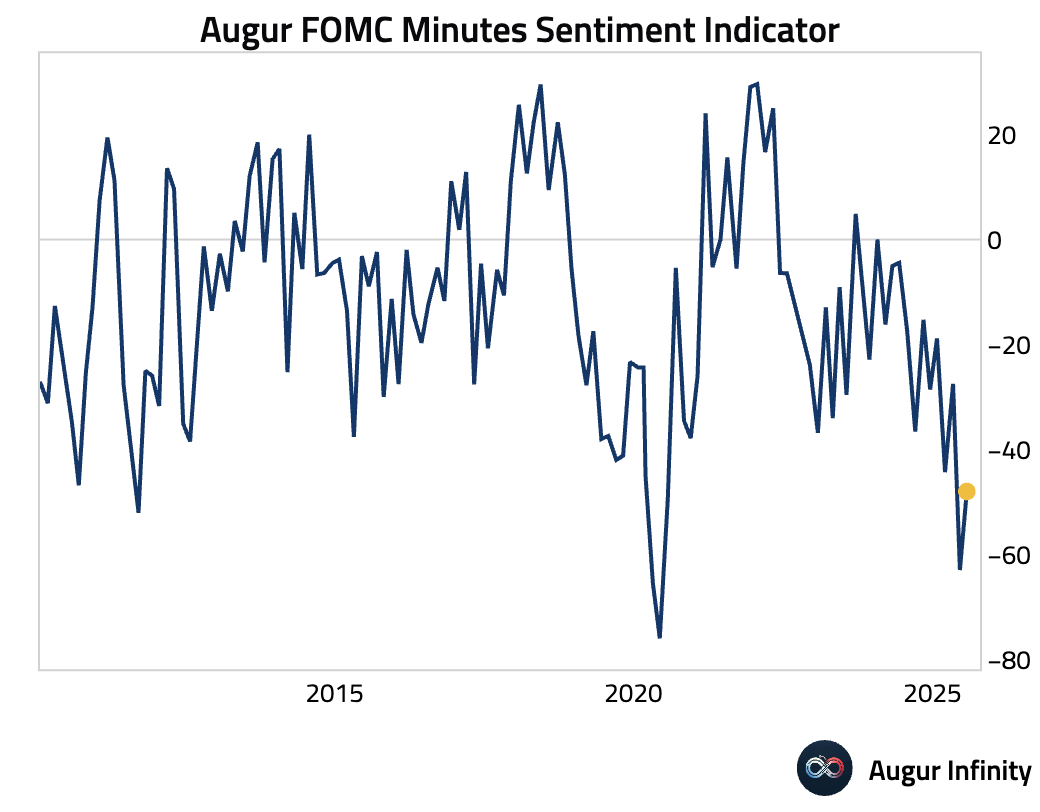

- The sentiment of the July 30th FOMC minutes were less downbeat than in June. The majority of FOMC members saw inflation risk outweighing employment risk. Many noted that the full effect of tariffs could take some time to materialize. Several members flagged the risk of inflation expectations unanchoring.

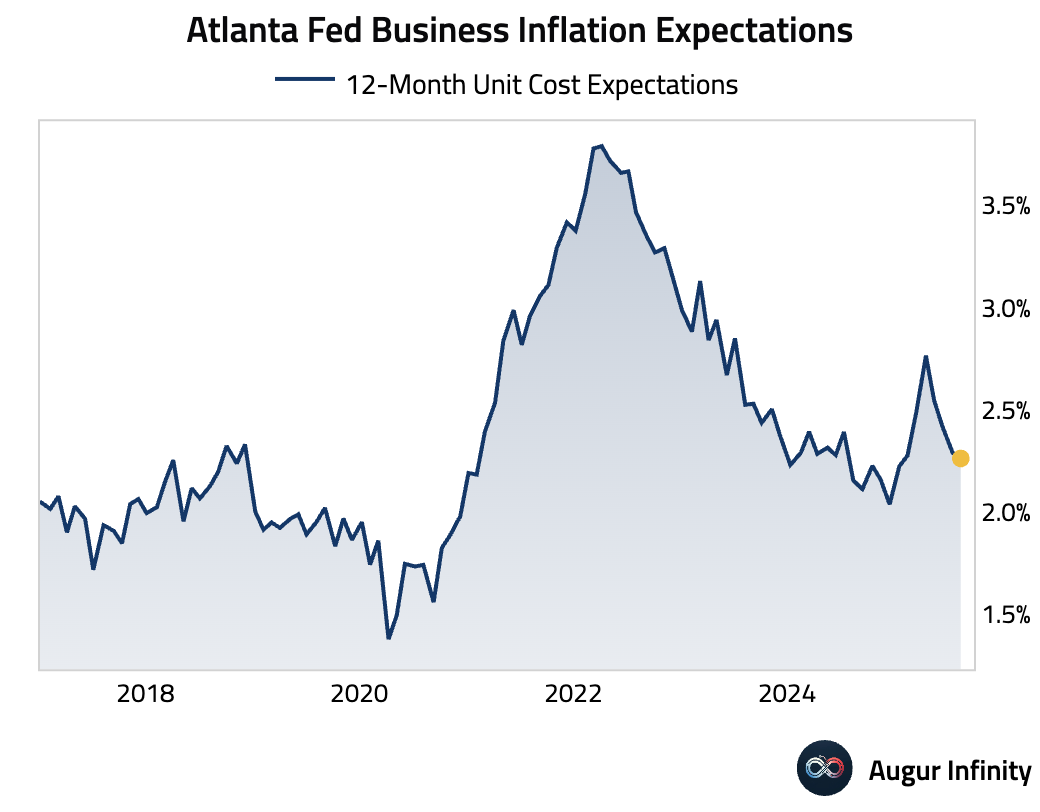

- According to Atlanta Fed survey, firms' inflation expectations for the coming year held steady at 2.3%.

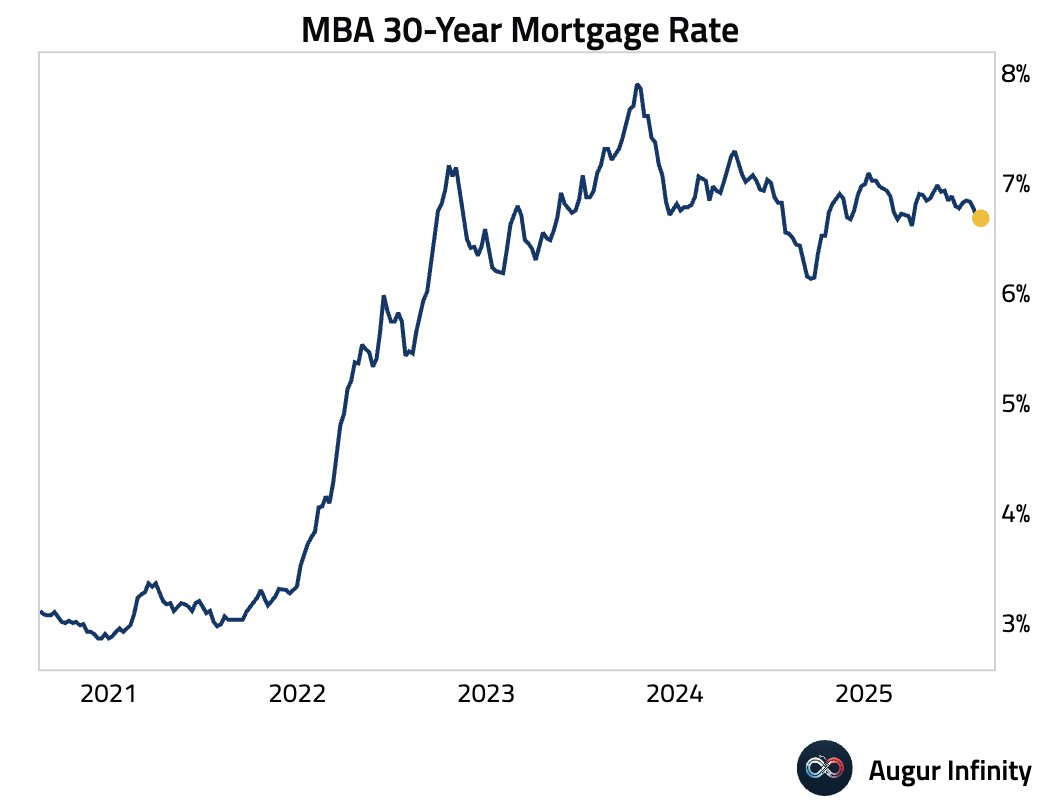

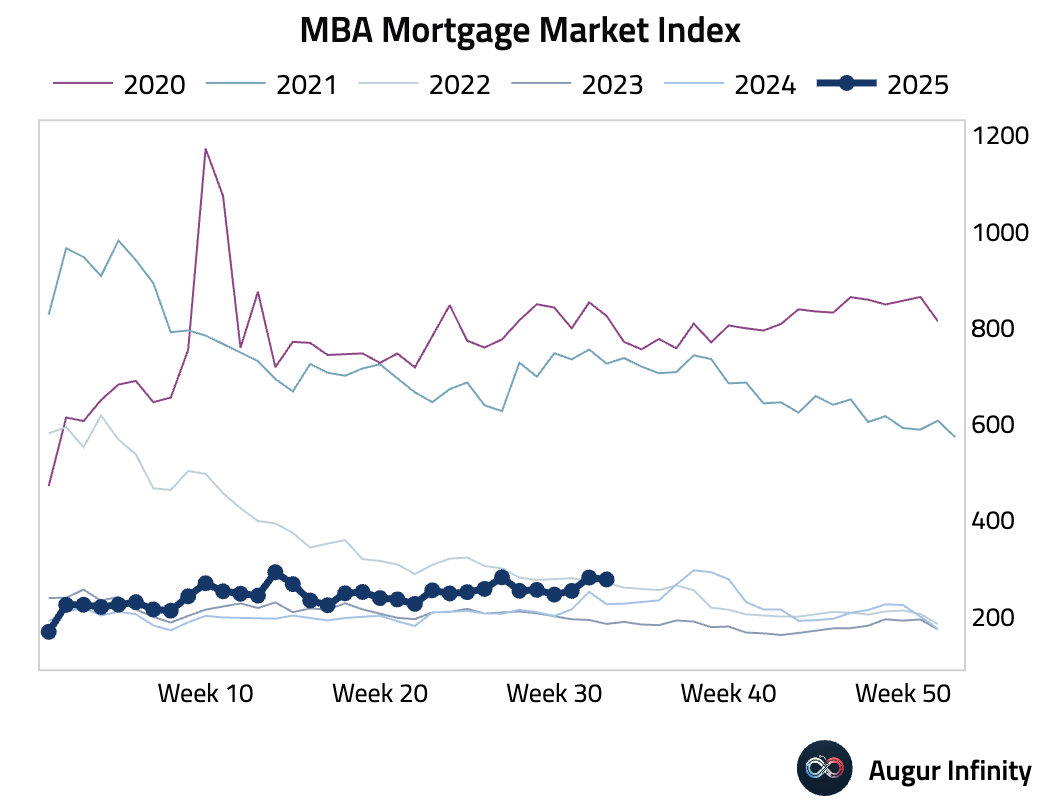

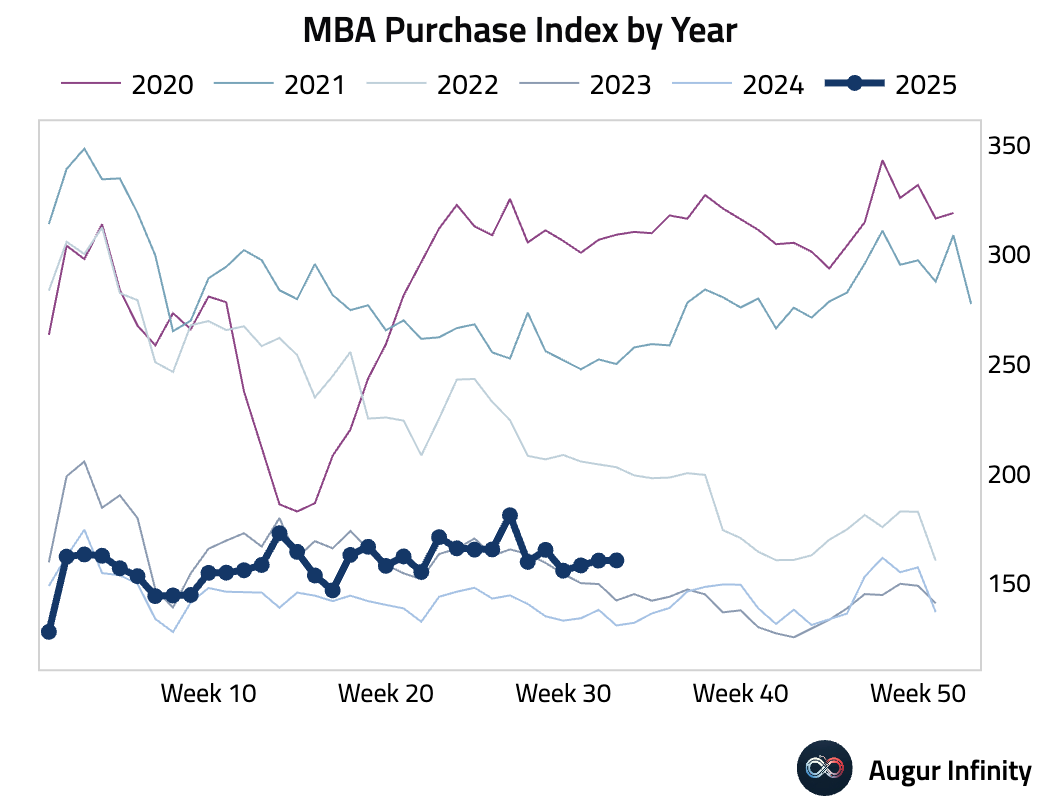

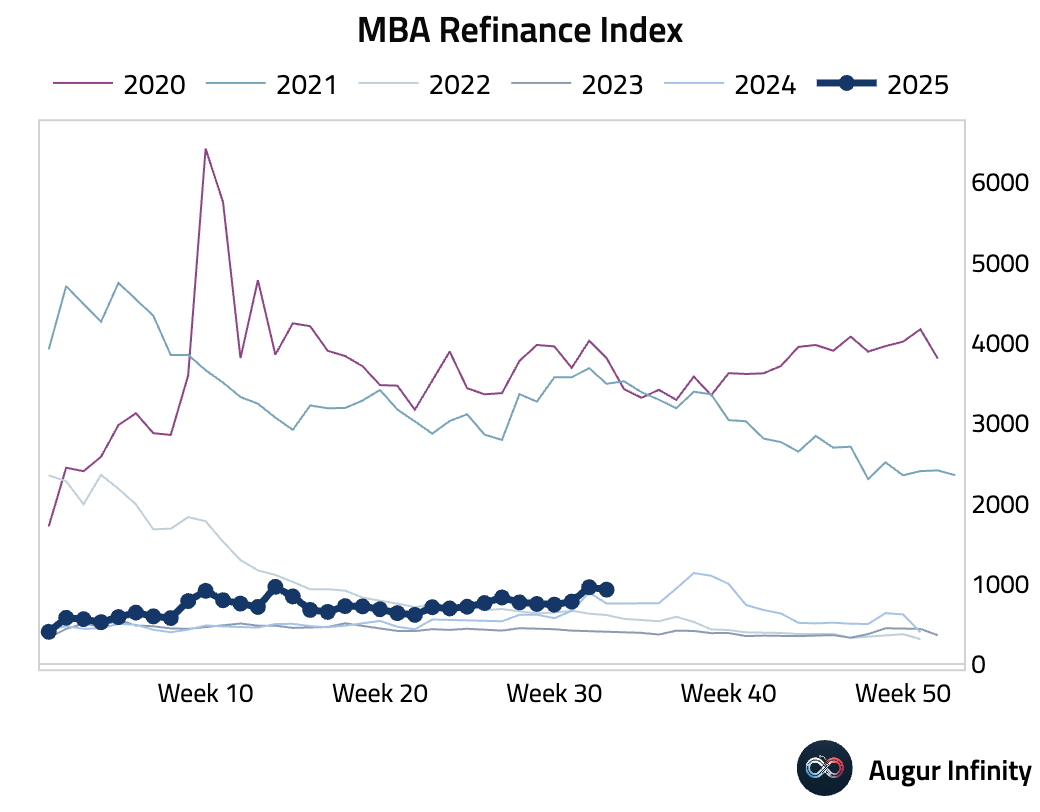

- The MBA 30-year mortgage rate ticked up slightly to 6.68% for the week ending August 15. Mortgage applications fell 1.4% week-over-week, a partial reversal of the prior week’s 10.9% jump. The decline was driven by a 3.1% drop in the Refinance Index, while the Purchase Index edged up by 0.1%.

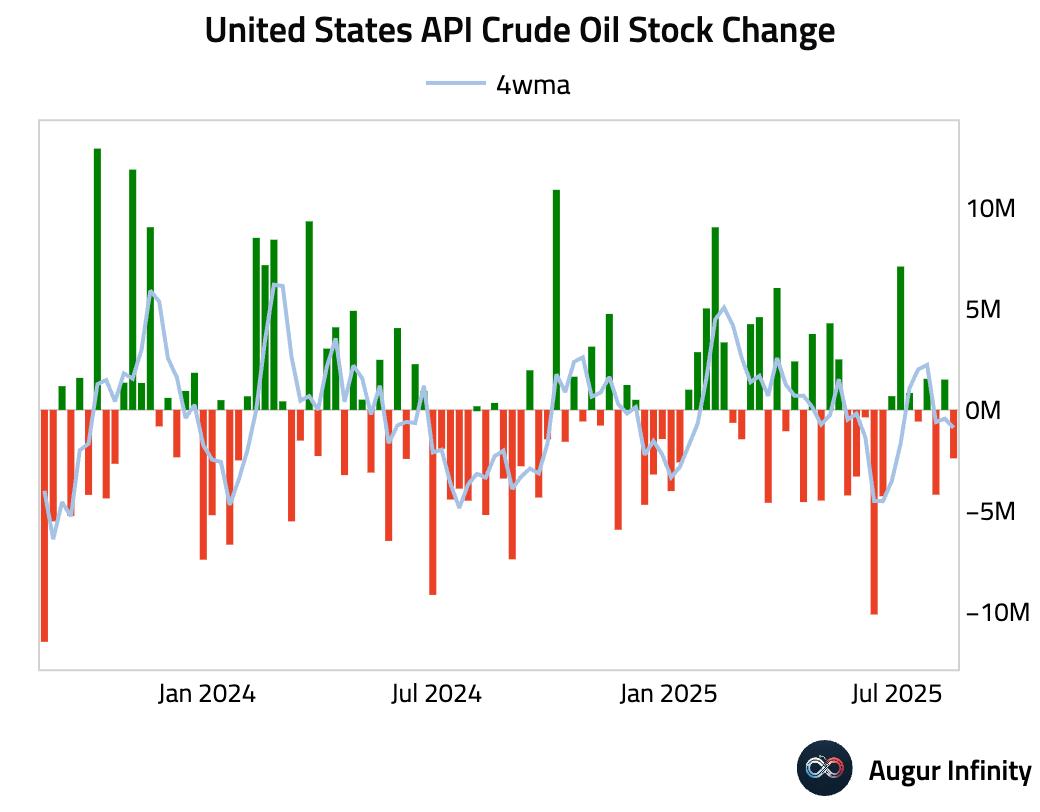

- API data showed a crude oil stock drawdown of 2.4 million barrels for the week, a larger draw than the 1.2 million consensus estimate and a reversal from the prior week’s 1.5 million barrel build.

Canada

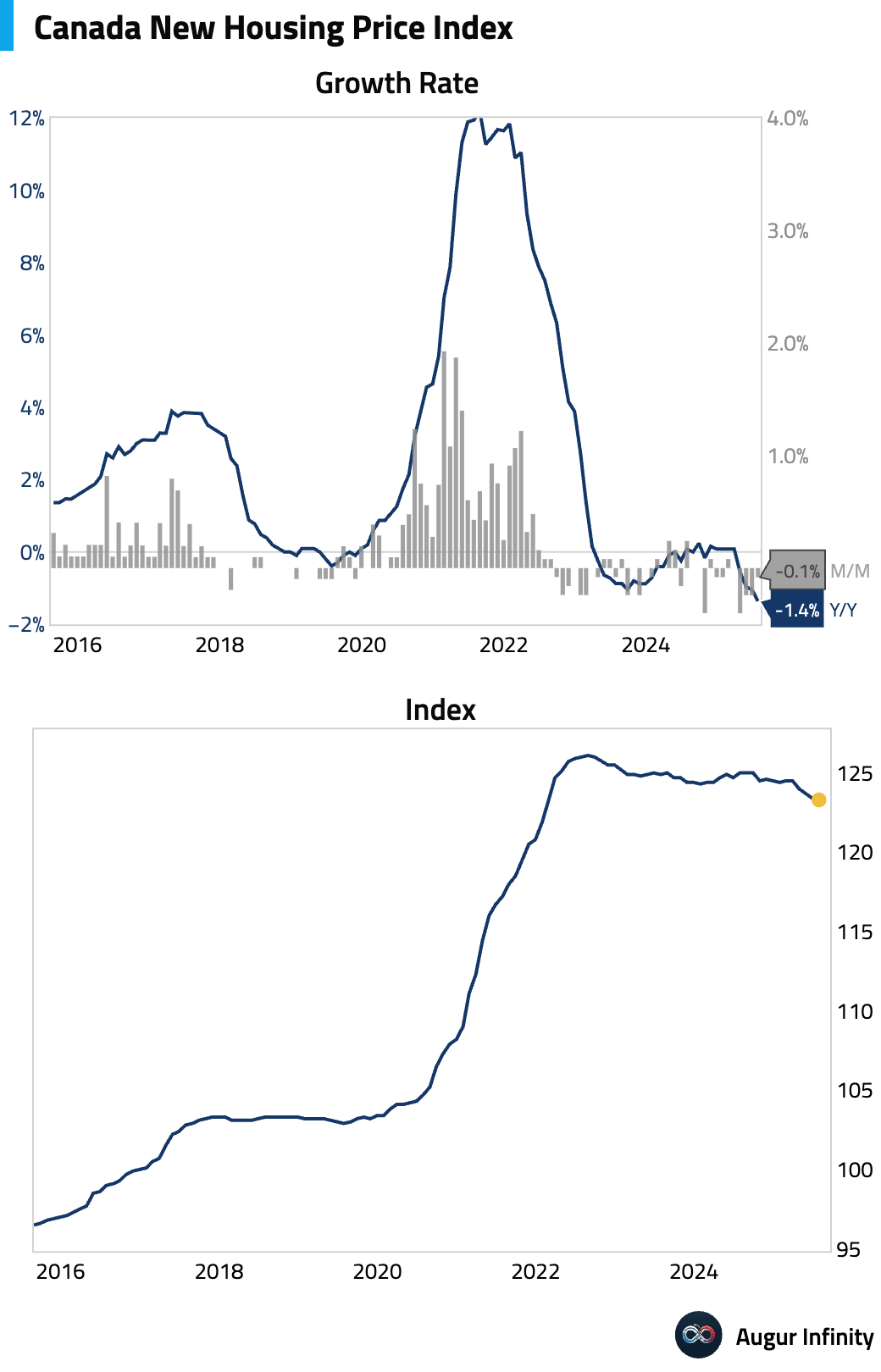

- The New Housing Price Index unexpectedly declined by 0.1% M/M in July, missing the consensus forecast of a 0.1% increase and following a 0.2% drop in June.

Europe

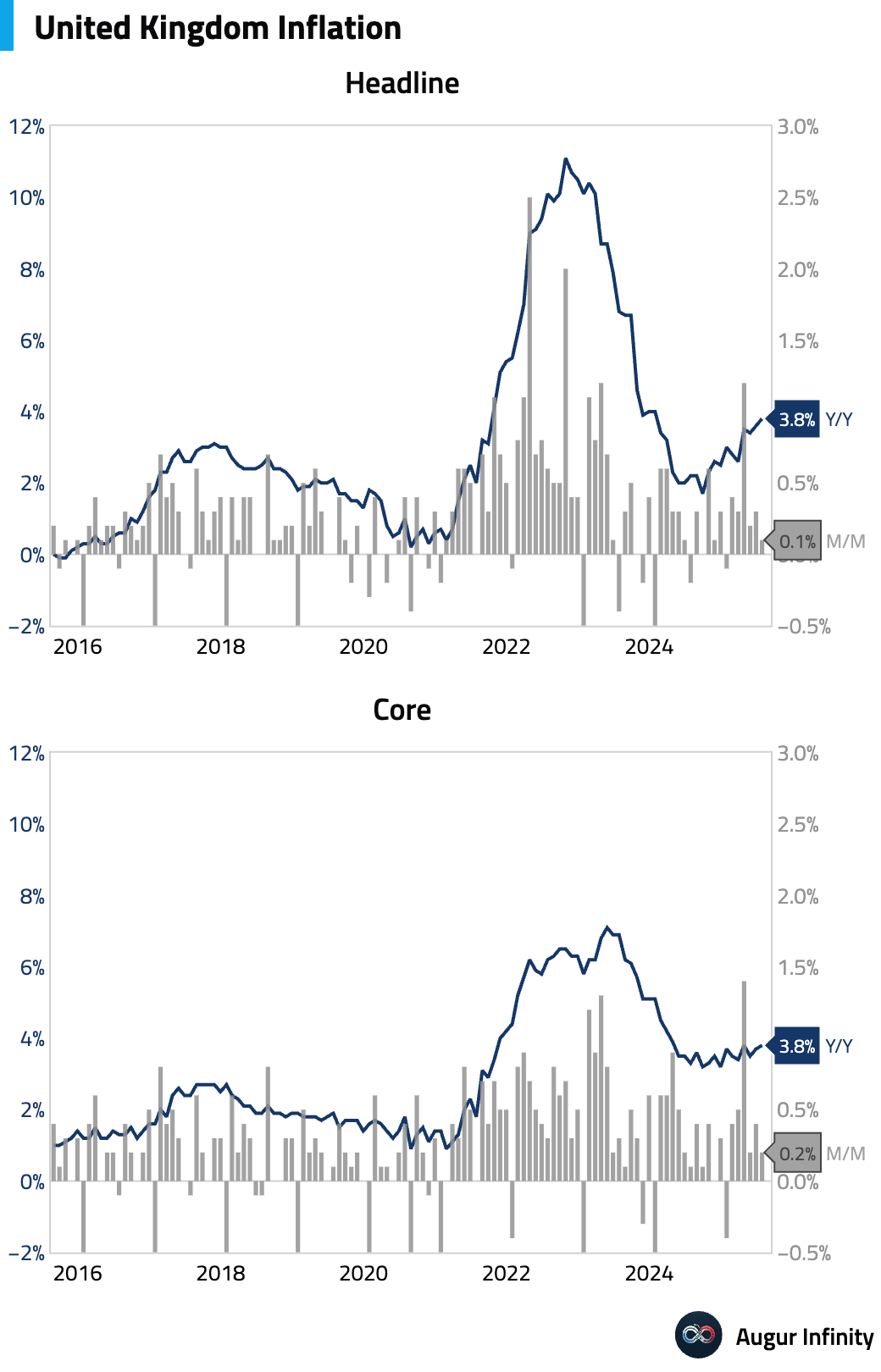

- The UK’s July inflation data came in hotter than expected. Headline CPI rose to 3.8% Y/Y from 3.6%, above the 3.7% consensus. Core CPI also accelerated to 3.8% Y/Y, beating expectations. The upside surprise was driven by services inflation, which climbed to 5.0% Y/Y, largely due to a significant surge in airfares. However, the Bank of England’s preferred measure of underlying services inflation, which excludes volatile items, is estimated to have edged down slightly, tempering the otherwise hawkish print.

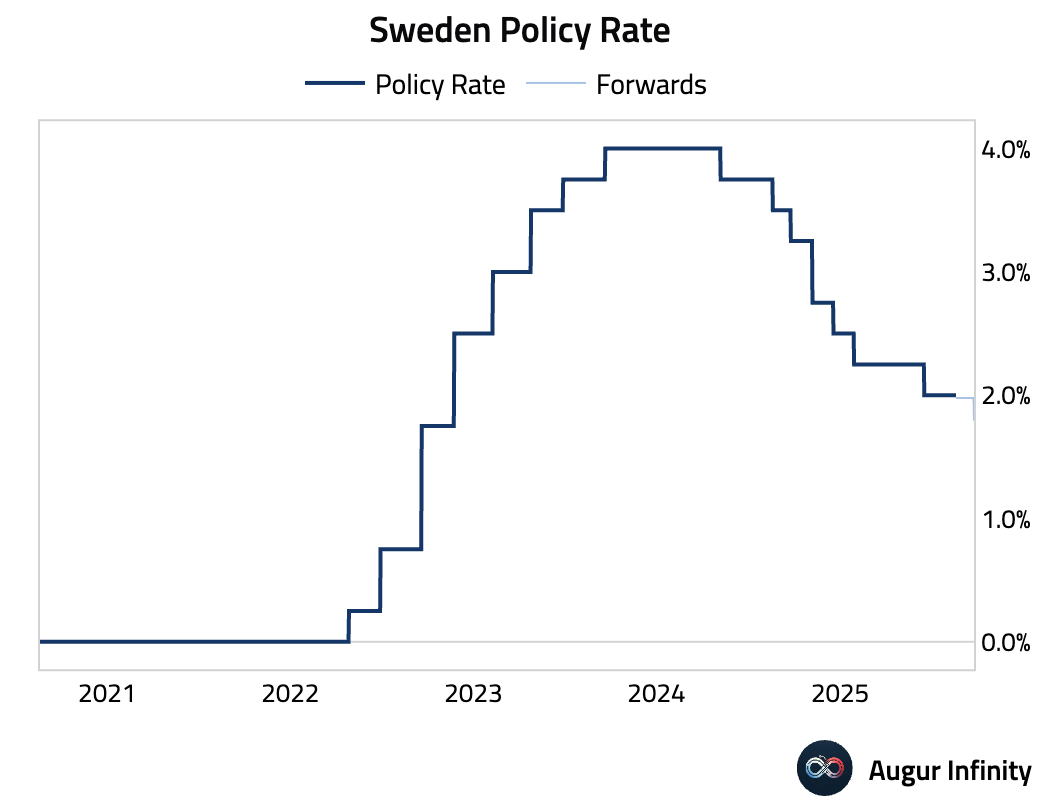

- The Riksbank held its policy rate at 2.00%, in line with market expectations. The board indicated that it views the recent spike in inflation as transitory and described the broader economic recovery as “sluggish.” The central bank remains open to further easing, with a potential cut in September still on the table, though risks are skewed toward later action.

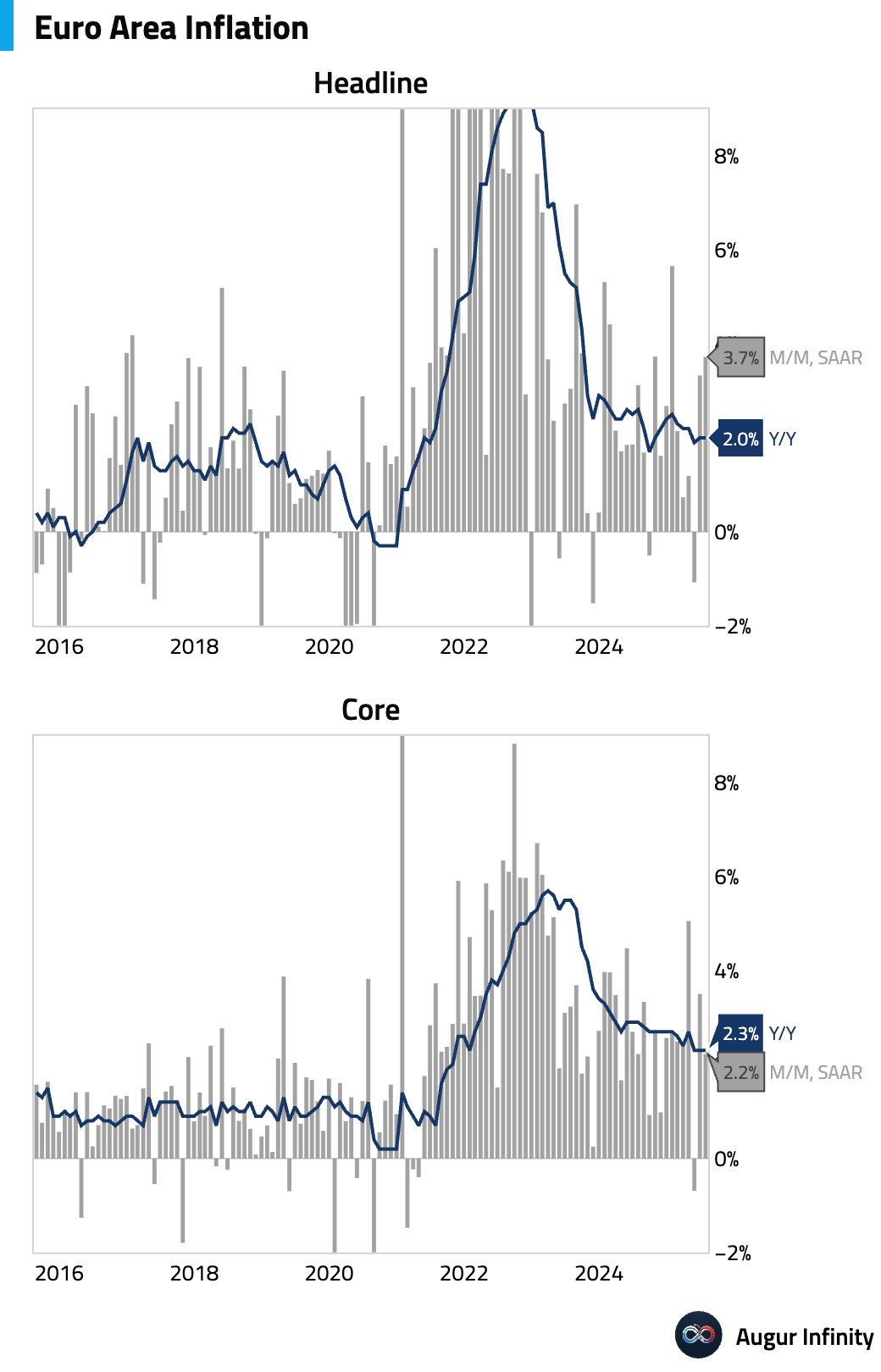

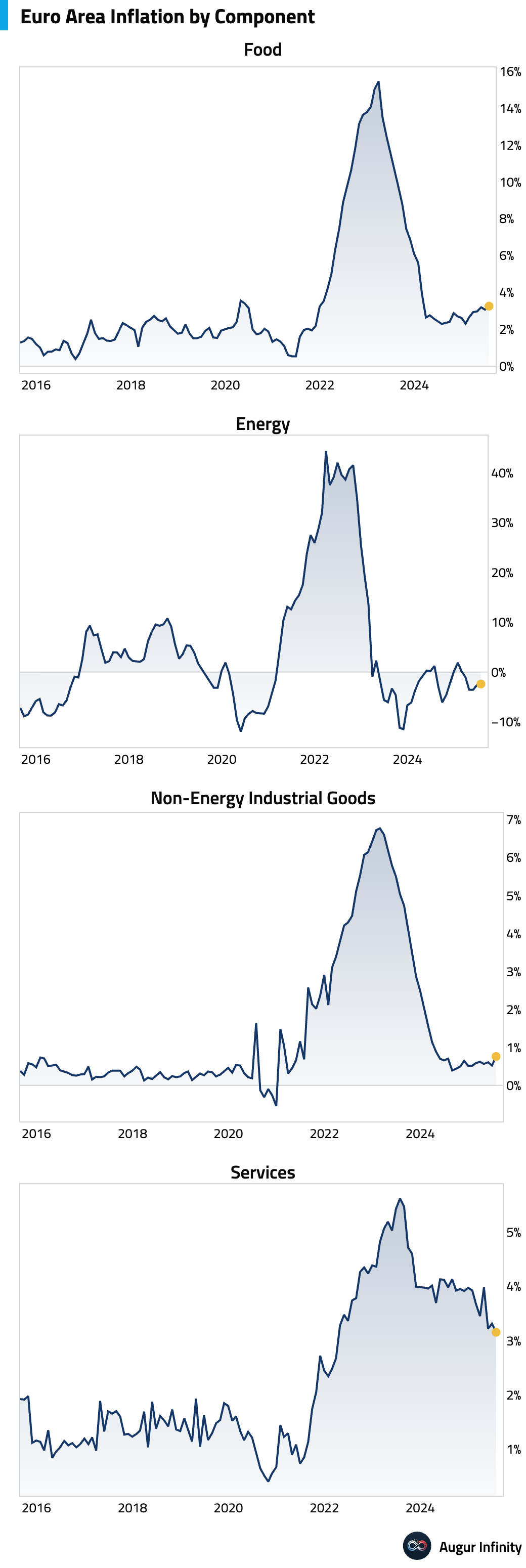

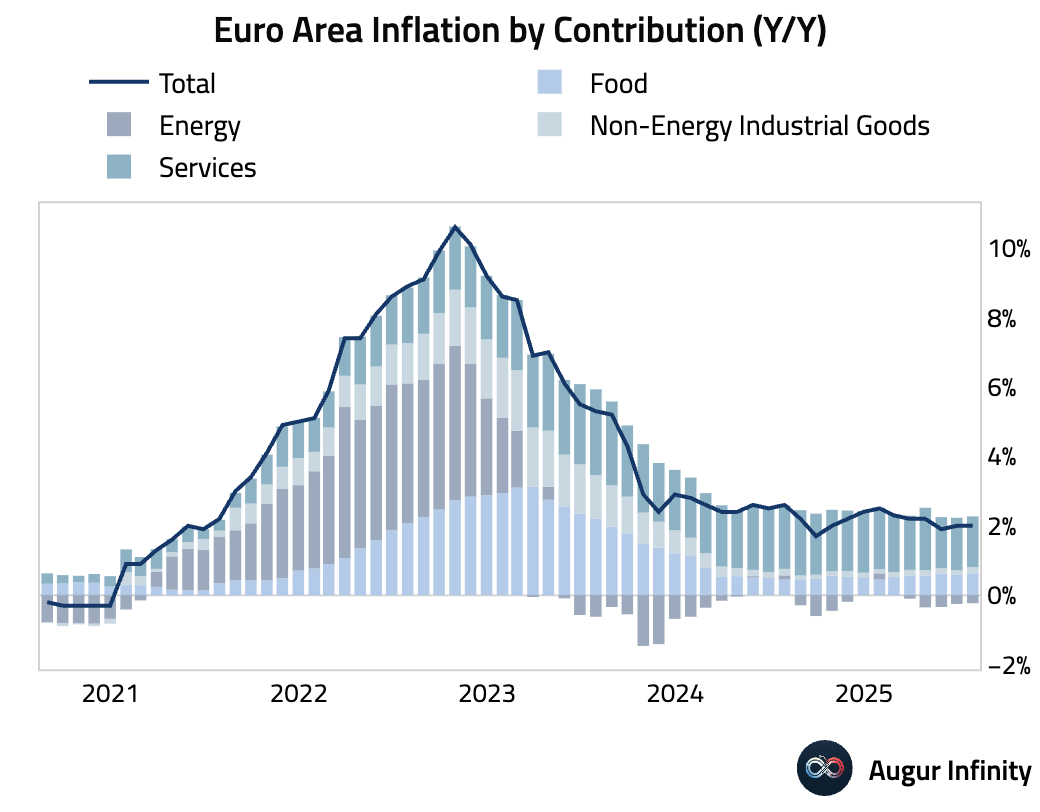

- Final July inflation figures for the Euro Area were revised slightly higher, with the headline rate confirmed at 2.0% Y/Y and the core rate at 2.3% Y/Y. The upward headline revision was driven by food, alcohol, and tobacco prices, whose contribution reached a one-year high. While services inflation remains the main driver, its contribution eased. Despite the higher year-over-year print, underlying momentum softened, with sequential core inflation ticking down.

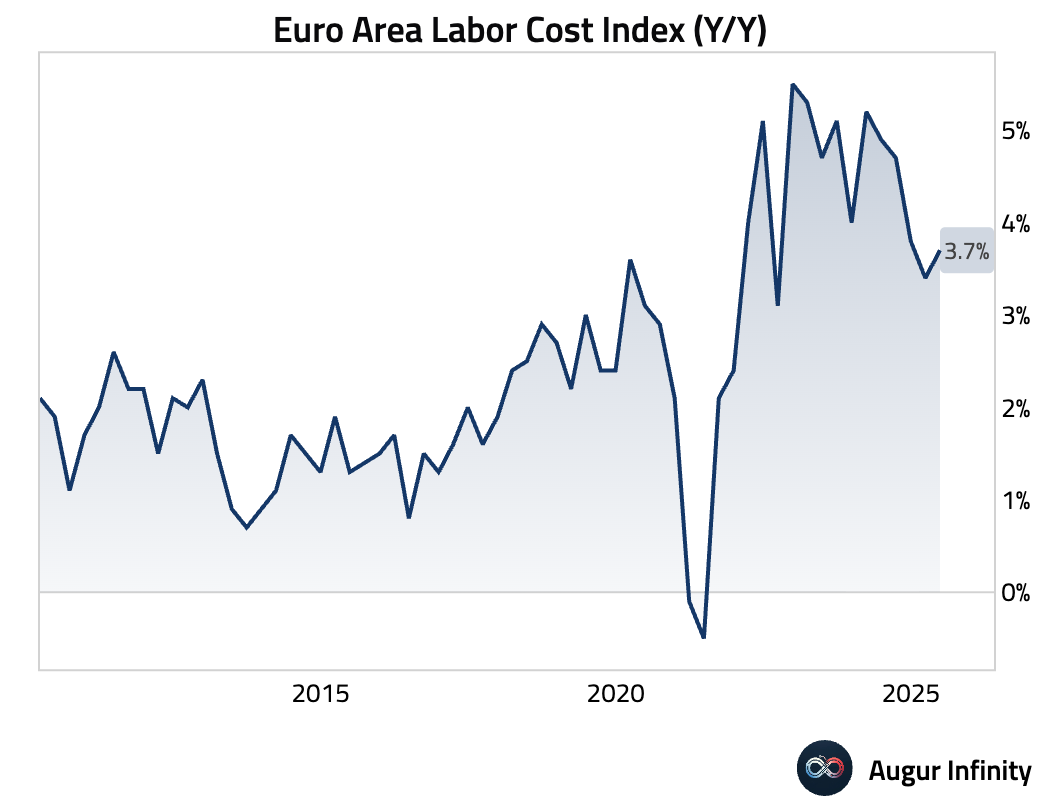

- The Euro Area Labour Cost Index accelerated to 3.7% Y/Y in the second quarter, up from 3.4% in the first quarter, indicating rising wage pressures.

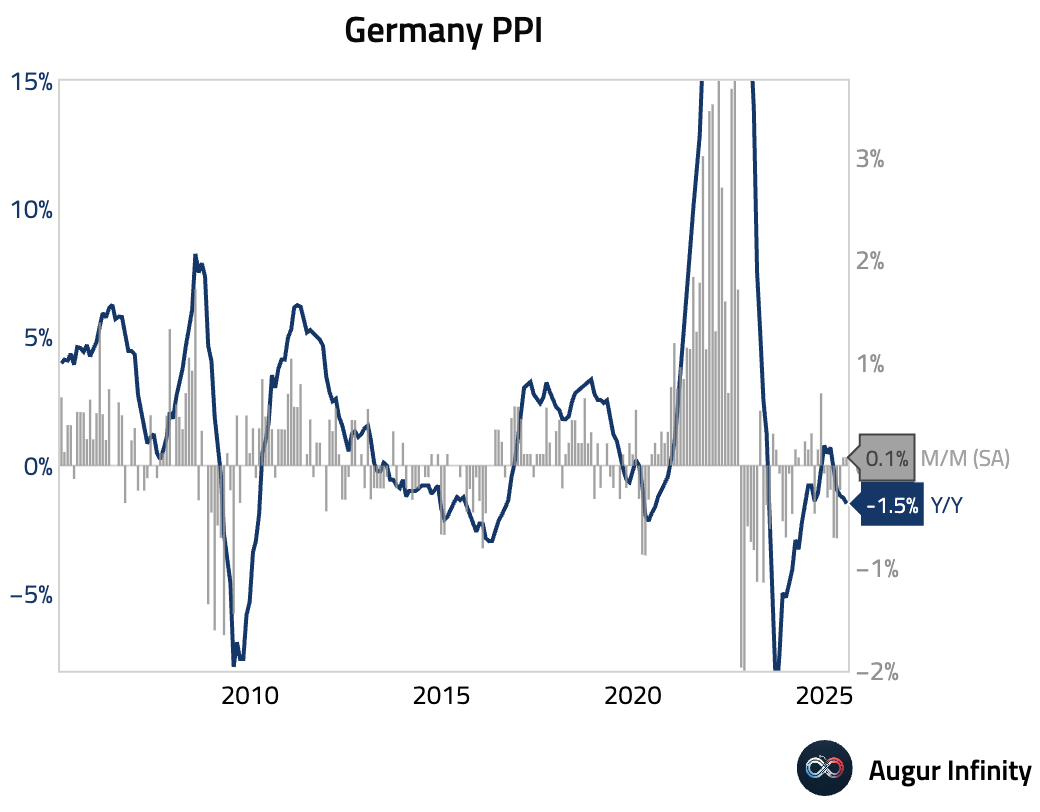

- German Producer Price Index (PPI) fell 1.5% Y/Y in July, a slightly faster pace of decline than the -1.3% consensus and the prior month's reading.

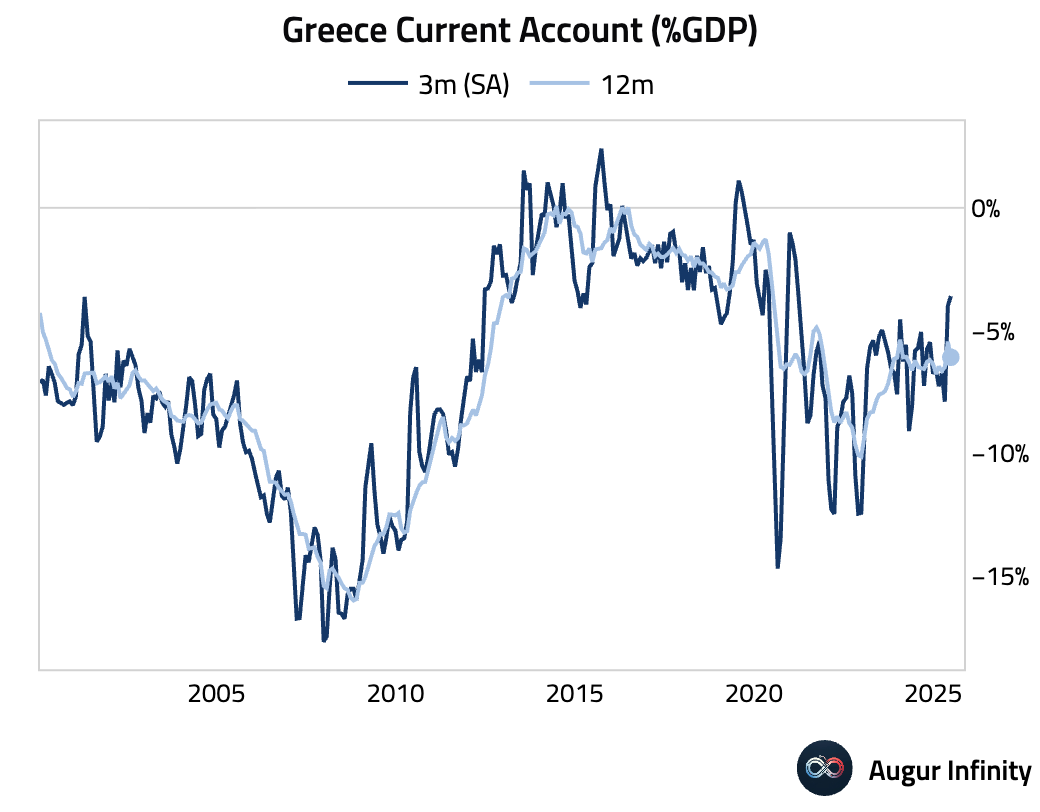

- Greece’s current account balance recorded a deficit of €1.18 billion in June, widening from a €196 million surplus in the prior month.

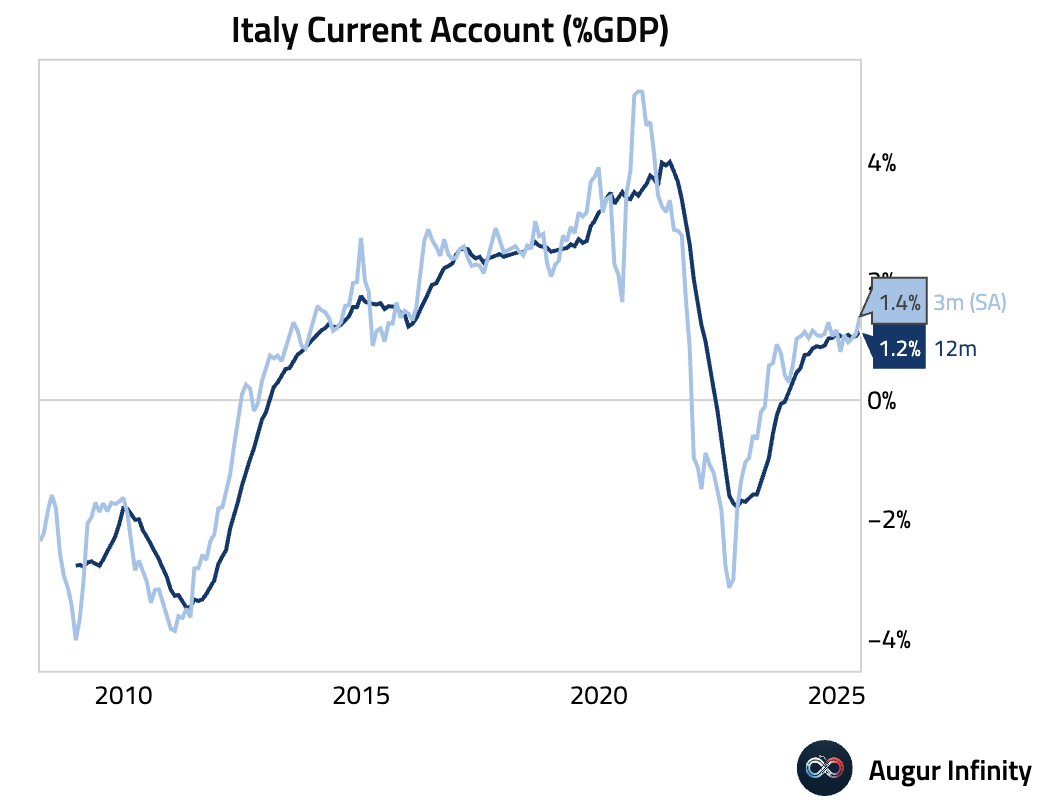

- Italy's current account surplus widened significantly to €5.74 billion in June from €1.72 billion in May.

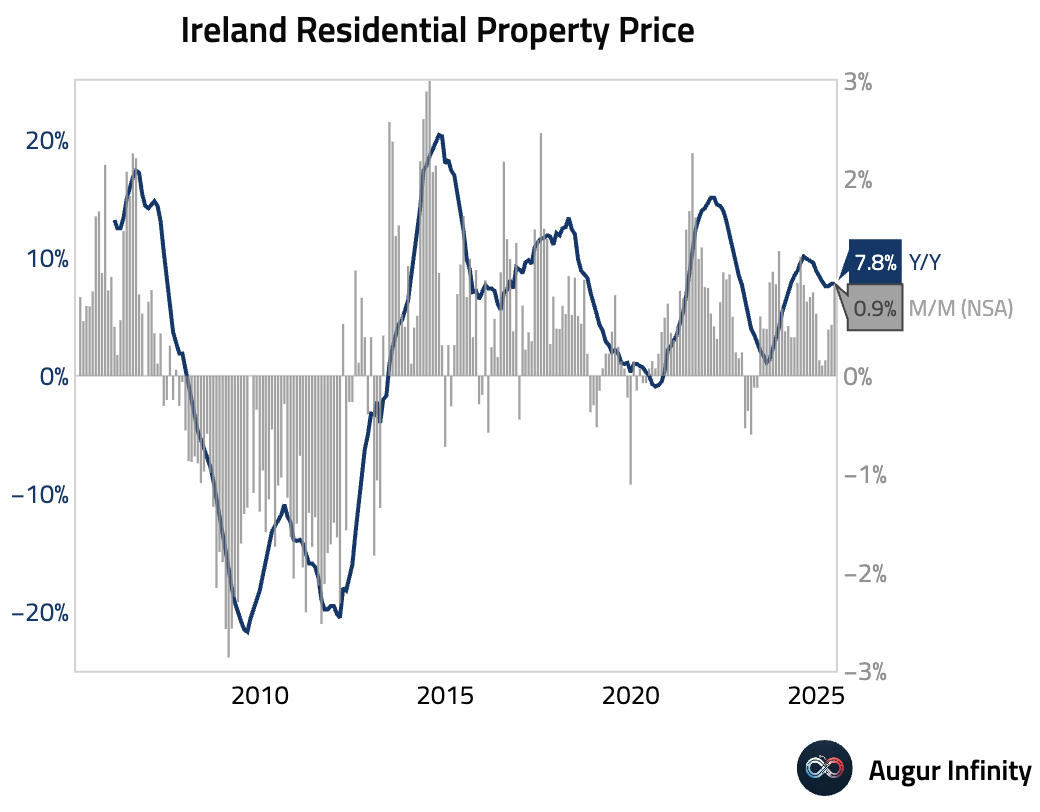

- Irish residential property prices rose 0.9% M/M in July, accelerating from June’s 0.6% pace. The annual rate of price growth held steady at 7.8%.

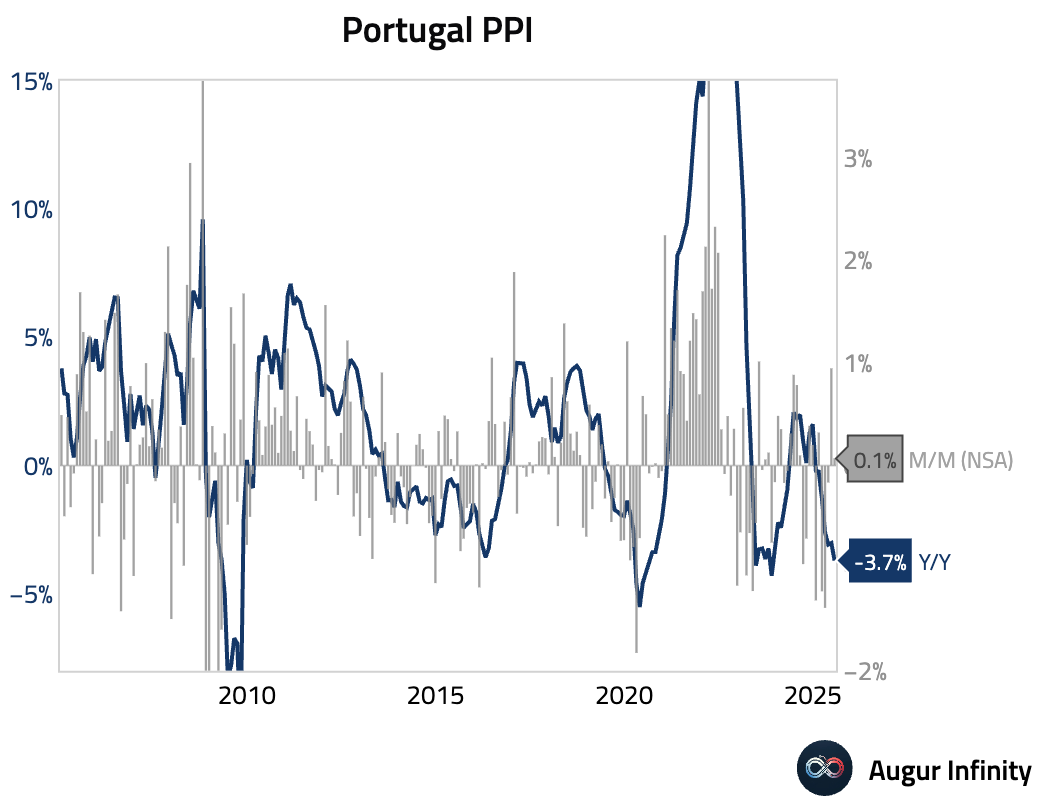

- Portugal’s Producer Price Index (PPI) fell 3.7% Y/Y in July, extending the deflationary trend from the 3.0% decline in June. Prices rose 0.1% M/M.

Asia-Pacific

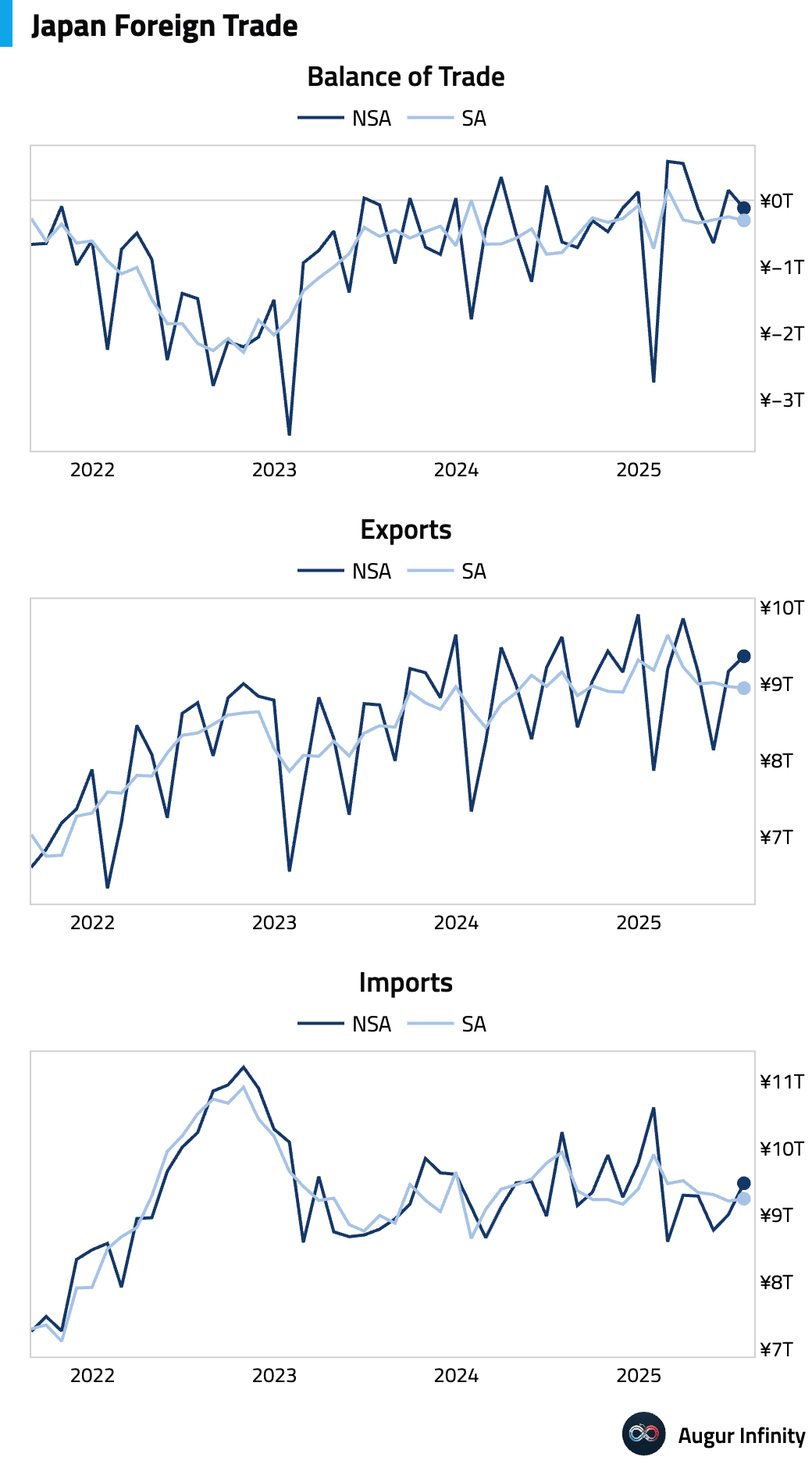

- Japan’s trade balance unexpectedly swung to a deficit of ¥117.5 billion in July, significantly missing the consensus forecast for a ¥196.2 billion surplus. The shift was driven by a 2.6% Y/Y drop in exports, which was worse than the -2.1% consensus. A sharp fall in passenger car export volumes to the United States was a key contributor, signaling that external demand may be peaking and could become a drag on third-quarter GDP.

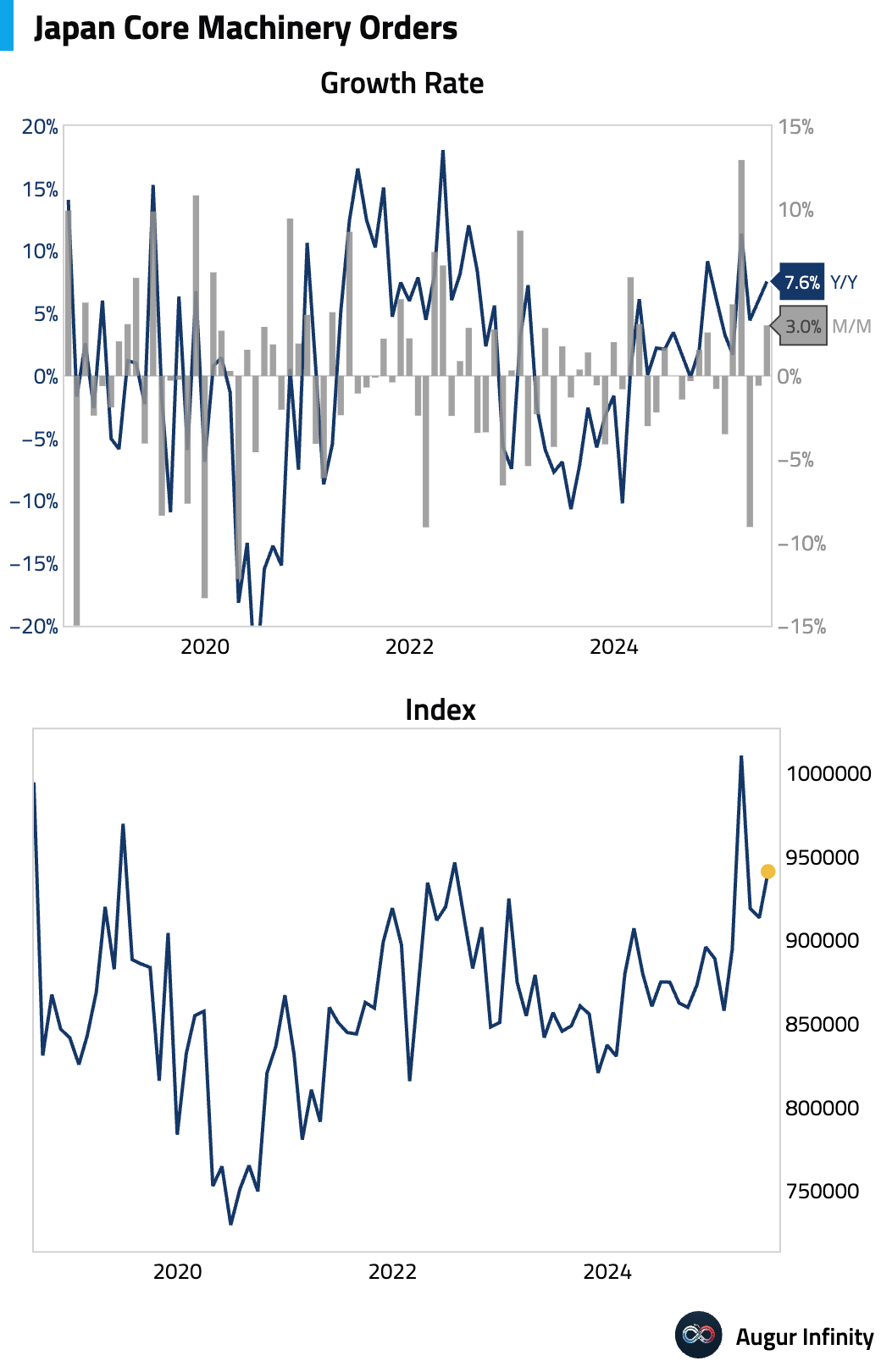

- Japan's core machinery orders surprisingly rose 3.0% M/M in June, beating the -1.0% consensus and marking a third consecutive quarterly gain. The increase was driven by a surge in non-manufacturing orders, which masked a third straight monthly decline in the manufacturing sector. The official outlook for the third quarter is negative, projecting a 4.0% Q/Q decline.

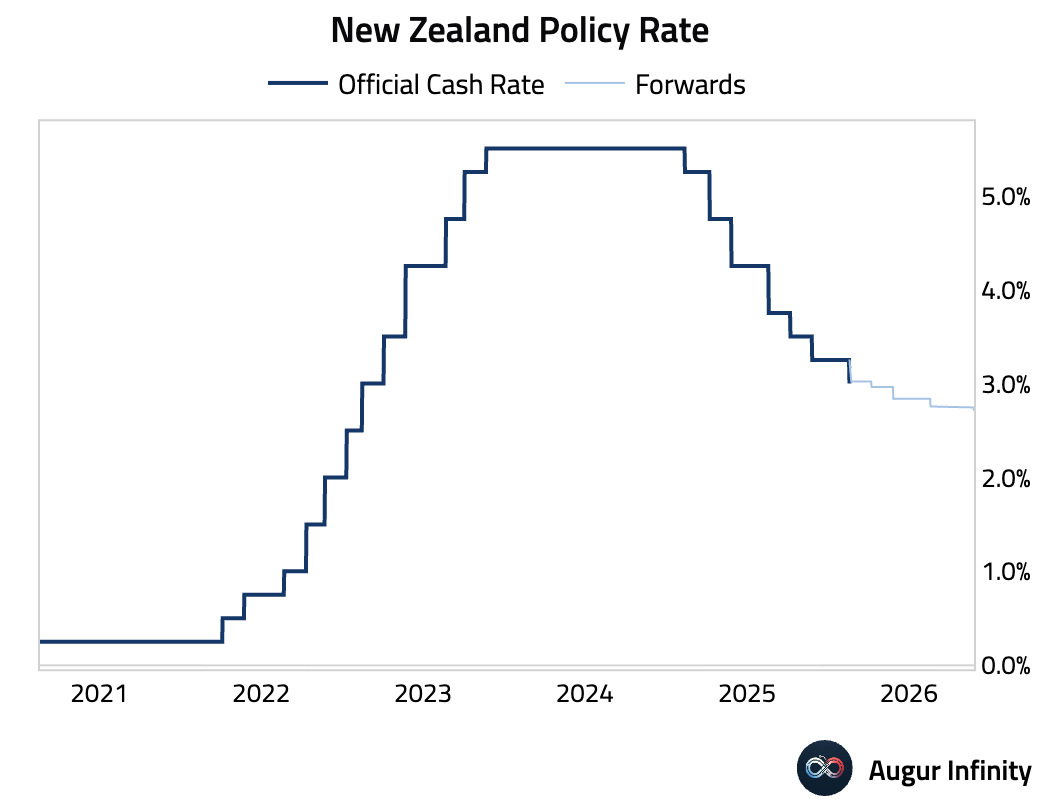

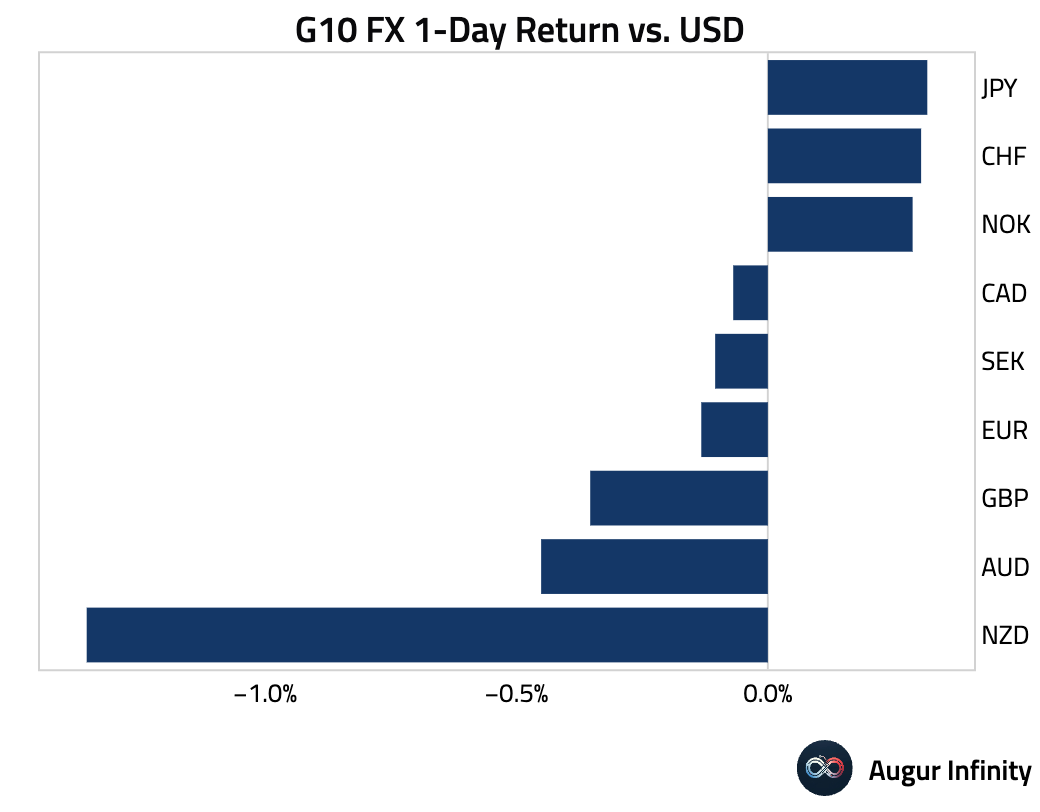

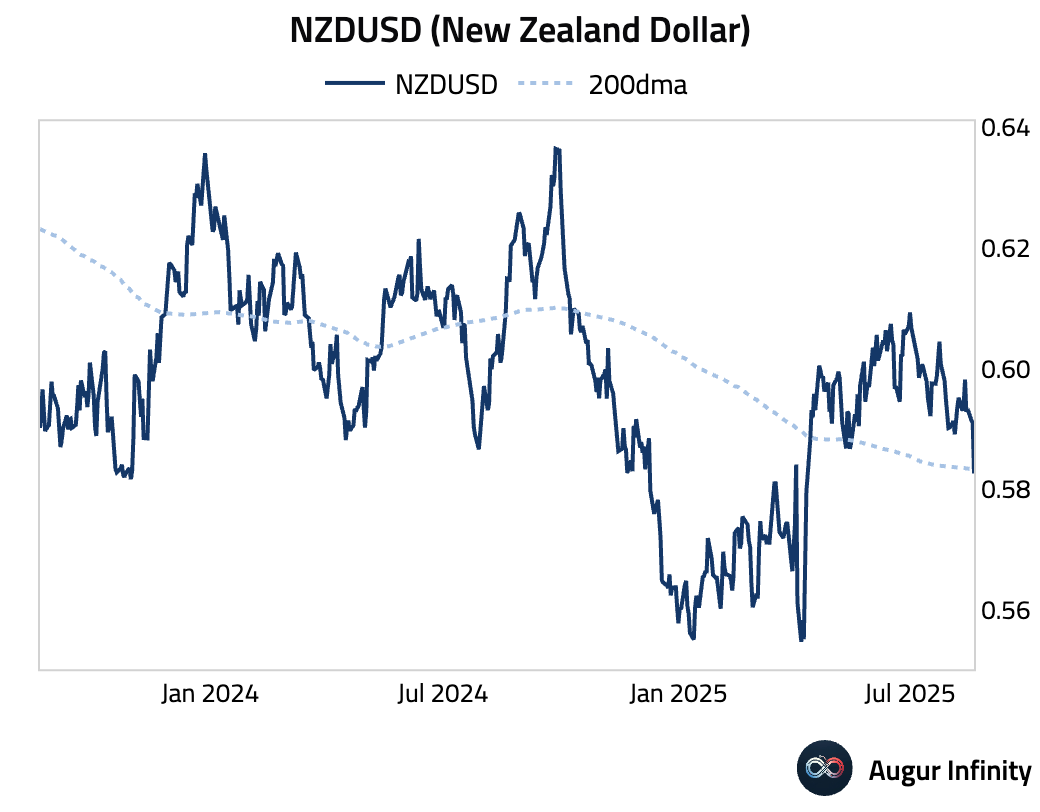

- The Reserve Bank of New Zealand (RBNZ) cut its Official Cash Rate by 25 bps to 3.00%. While the cut was expected, the decision was distinctly dovish. Two members of the monetary policy committee dissented, favoring a larger 50 bps cut. The RBNZ’s forward guidance was also revised materially lower, signaling a strong bias toward further easing due to a weaker economic outlook, despite near-term inflation forecasts being revised higher.

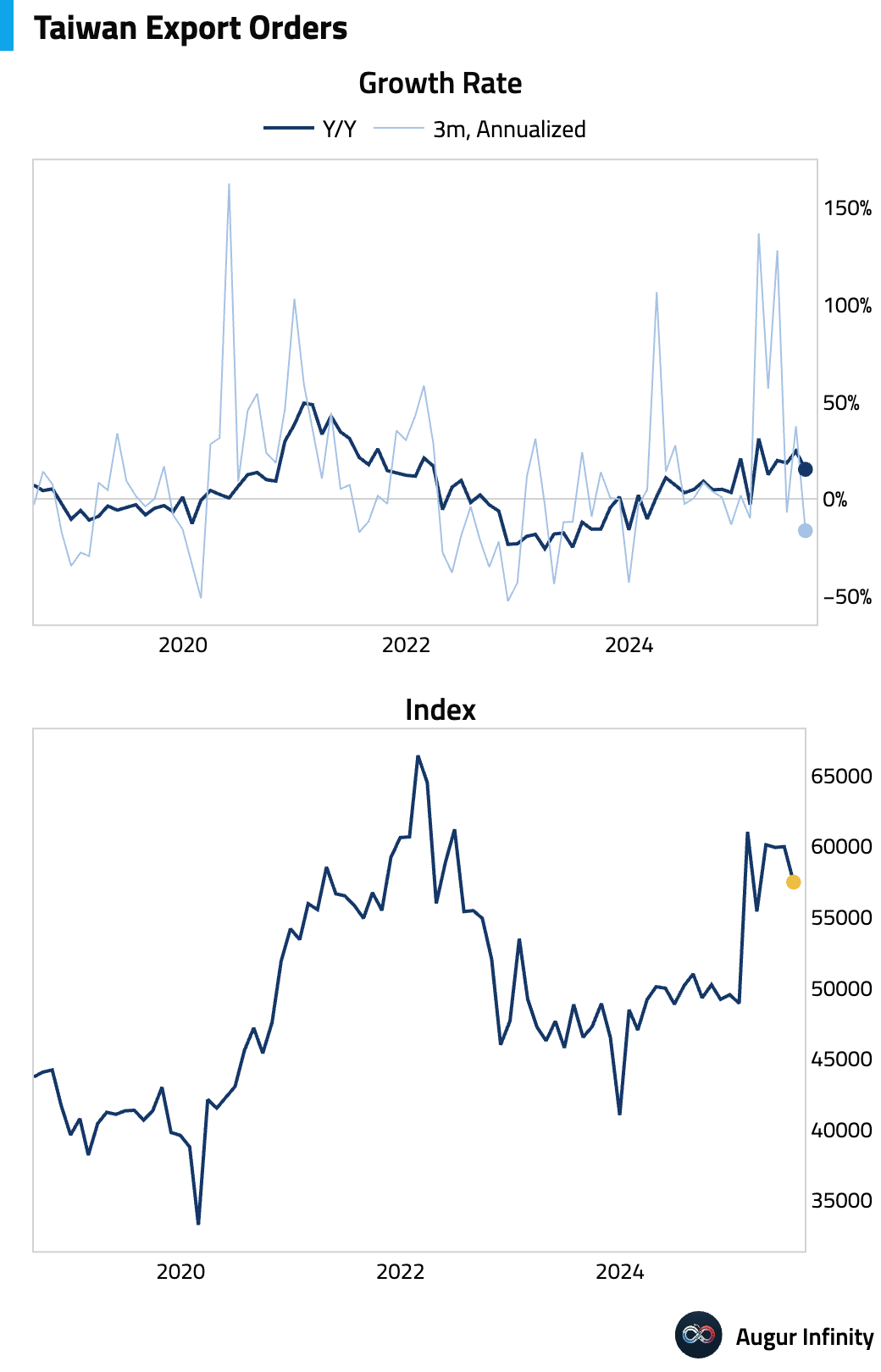

- Taiwan's export orders grew 15.2% Y/Y in July, slightly ahead of the 15.0% consensus but moderating from the 24.6% pace in June.

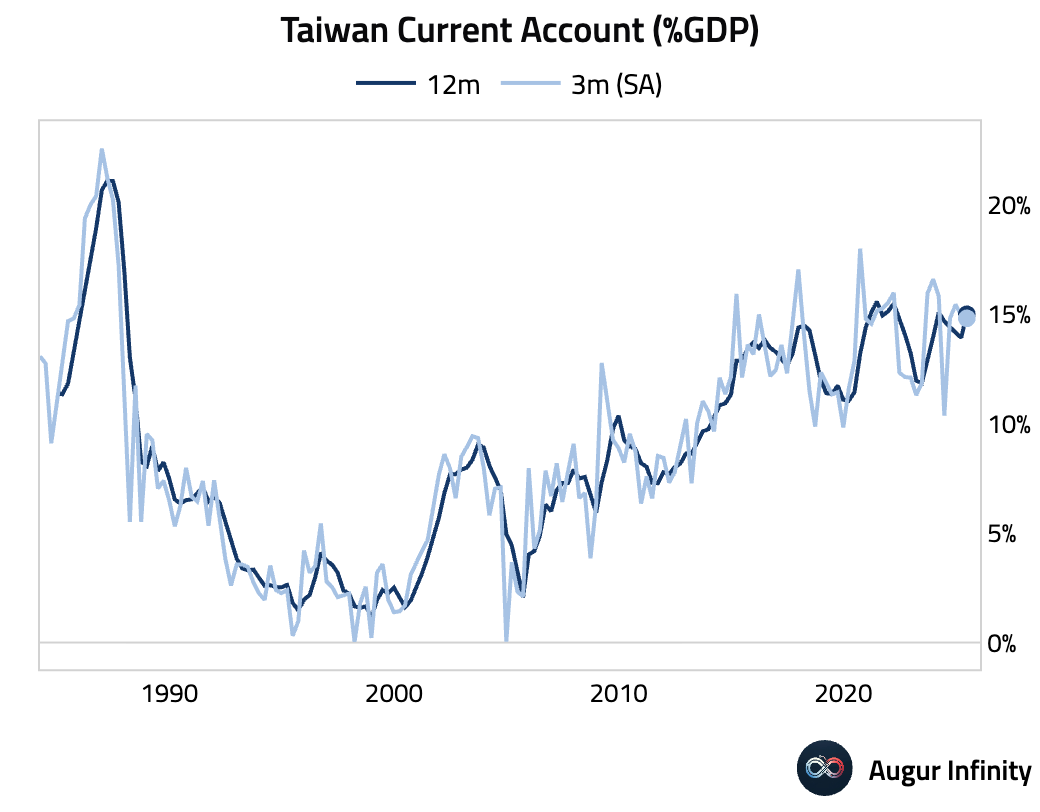

- Taiwan’s current account surplus expanded to an all-time high of $36.23 billion in the second quarter, up from $29.76 billion in the first quarter.

China

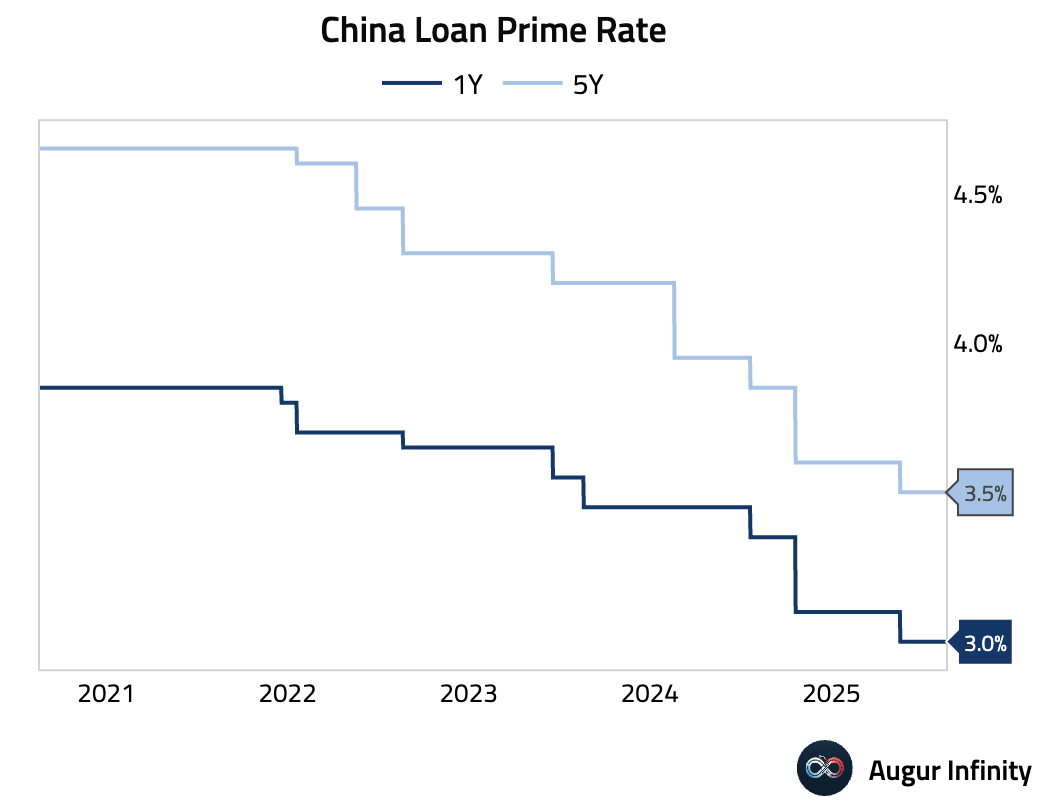

- The People's Bank of China left its key lending rates unchanged, as expected. The 1-year Loan Prime Rate (LPR) was held at 3.00% and the 5-year LPR, a reference for mortgages, was kept at 3.50%. Both rates remain at all-time lows.

Emerging Markets ex China

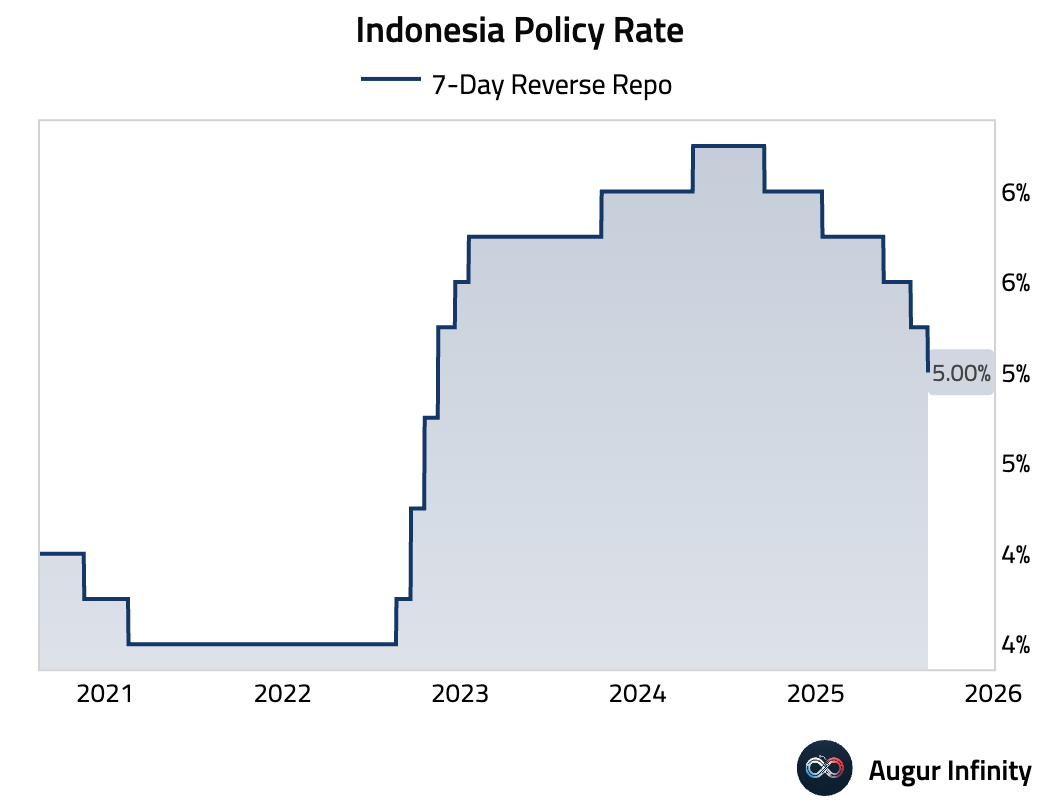

- Bank Indonesia delivered a surprise 25 bps rate cut, lowering its benchmark 7-day reverse repo rate to 5.00%. The consensus was for rates to remain on hold. The central bank cited lower future inflation forecasts, a stable rupiah, and the need to support economic growth as primary reasons for the cut.

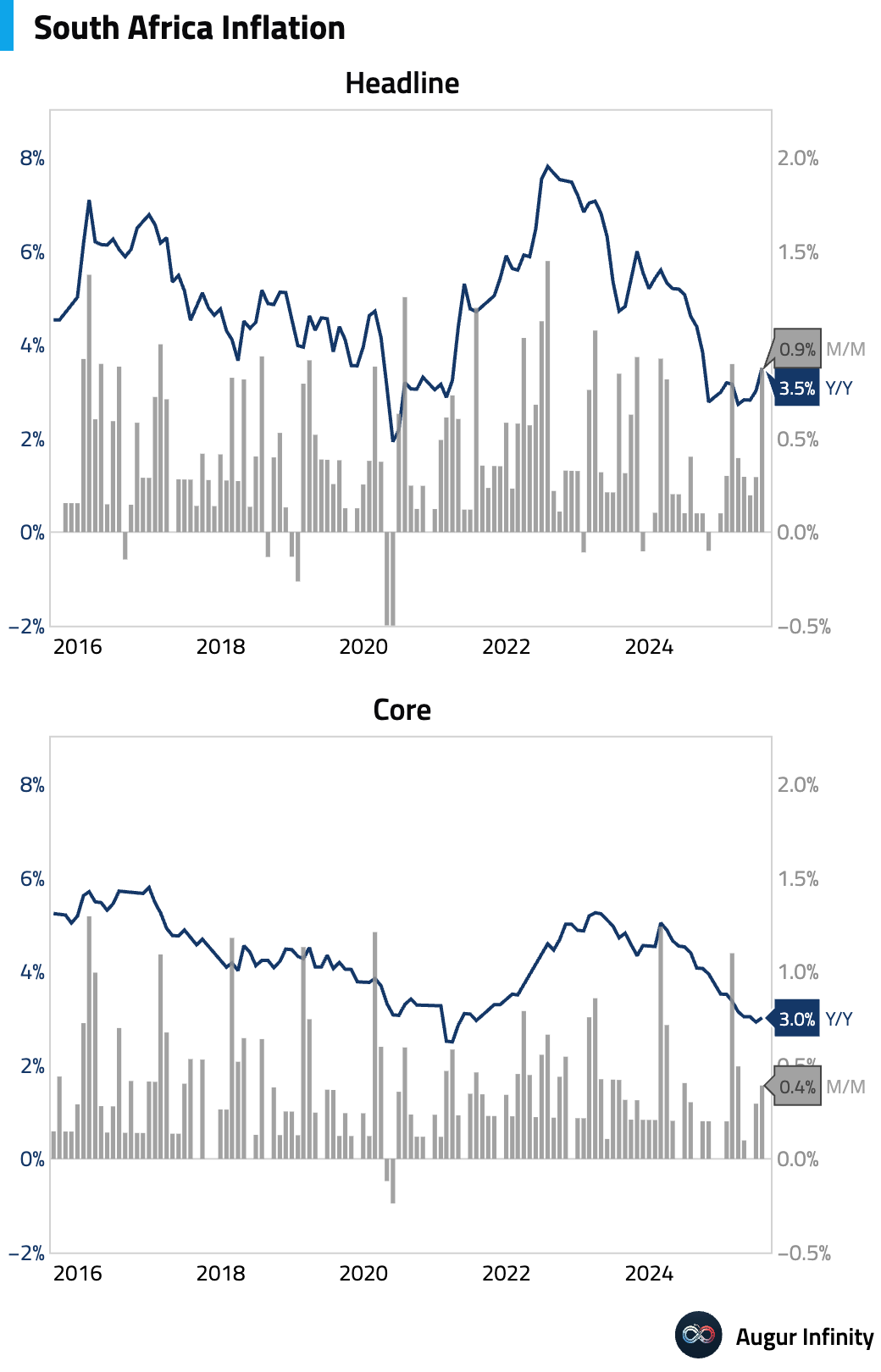

- South Africa's headline inflation accelerated to 3.5% Y/Y in July, in line with consensus, up from 3.0% in June. The rise was driven by accelerating food inflation and easing fuel deflation. Core CPI edged up to 3.0% Y/Y, slightly missing the 3.1% consensus, as a larger-than-expected hike in water tariffs masked continued weakness in other core components.

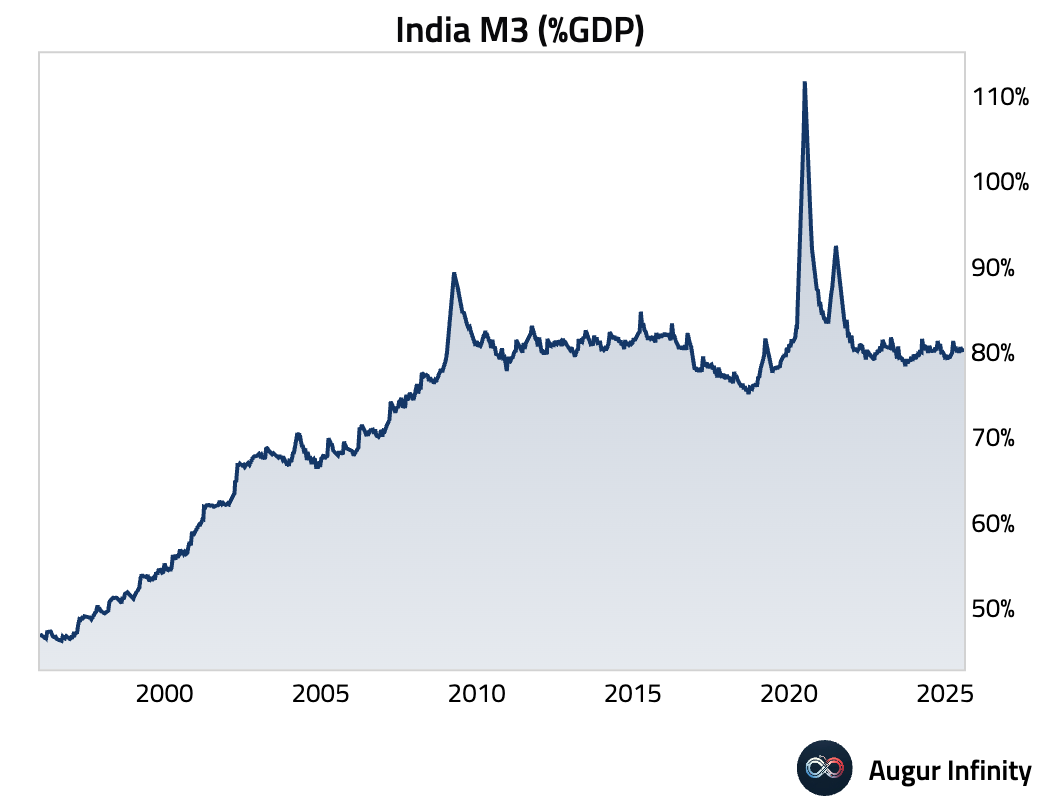

- India’s M3 money supply growth was stable at 9.6% Y/Y for the week ending August 1.

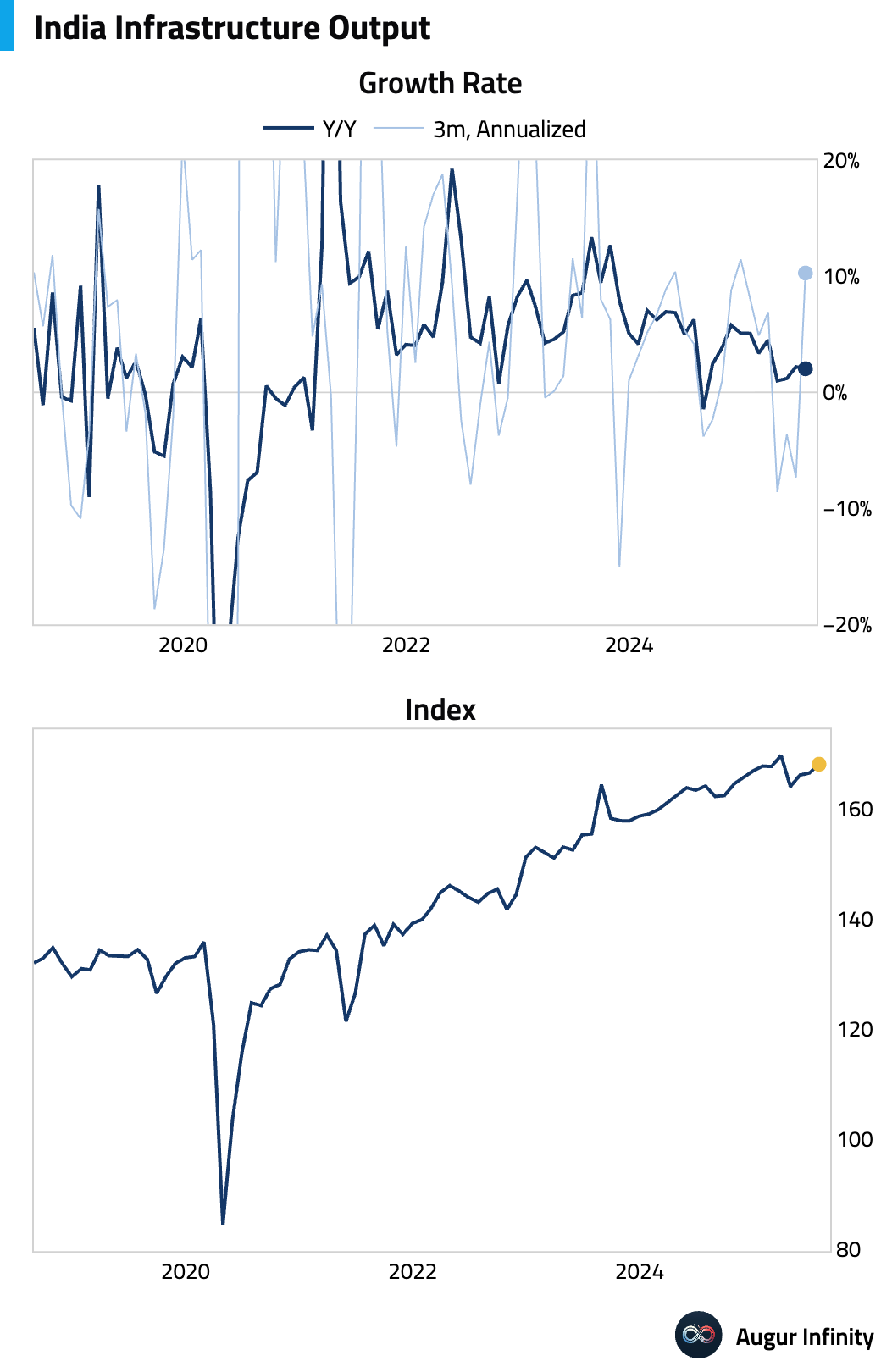

- India's infrastructure output growth slowed to 2.0% Y/Y in July from 2.2% in June.

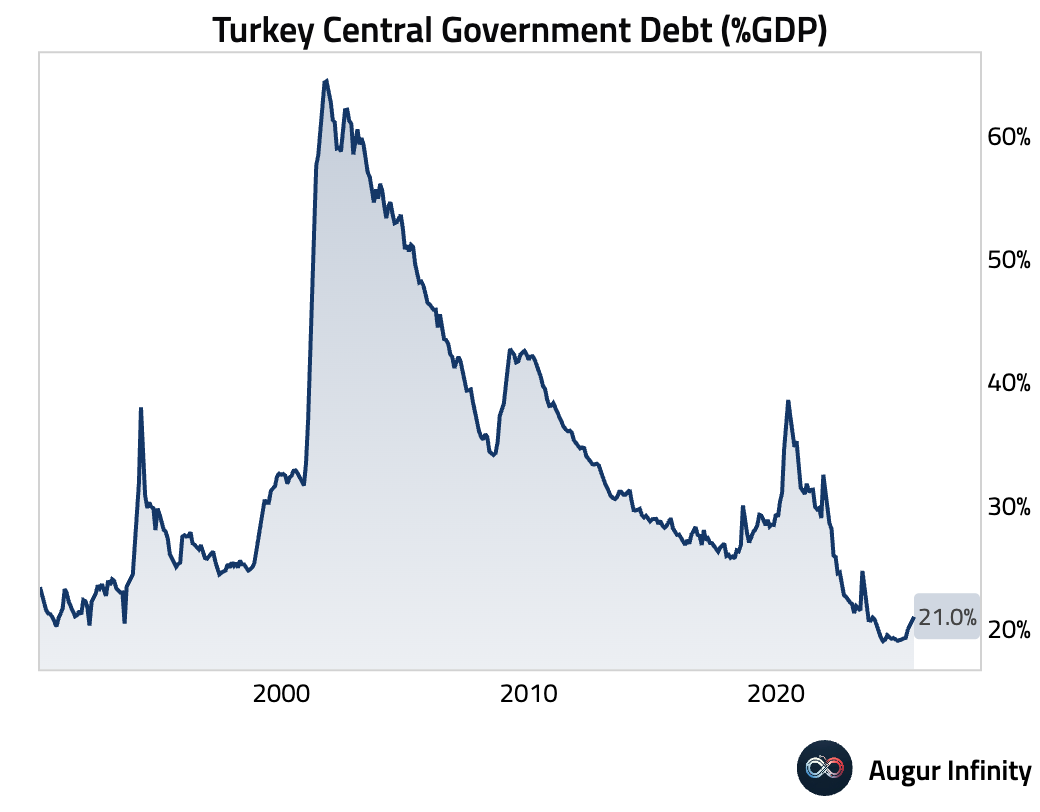

- Turkey's central government debt rose to TRY 12 trillion, or 12% of GDP.

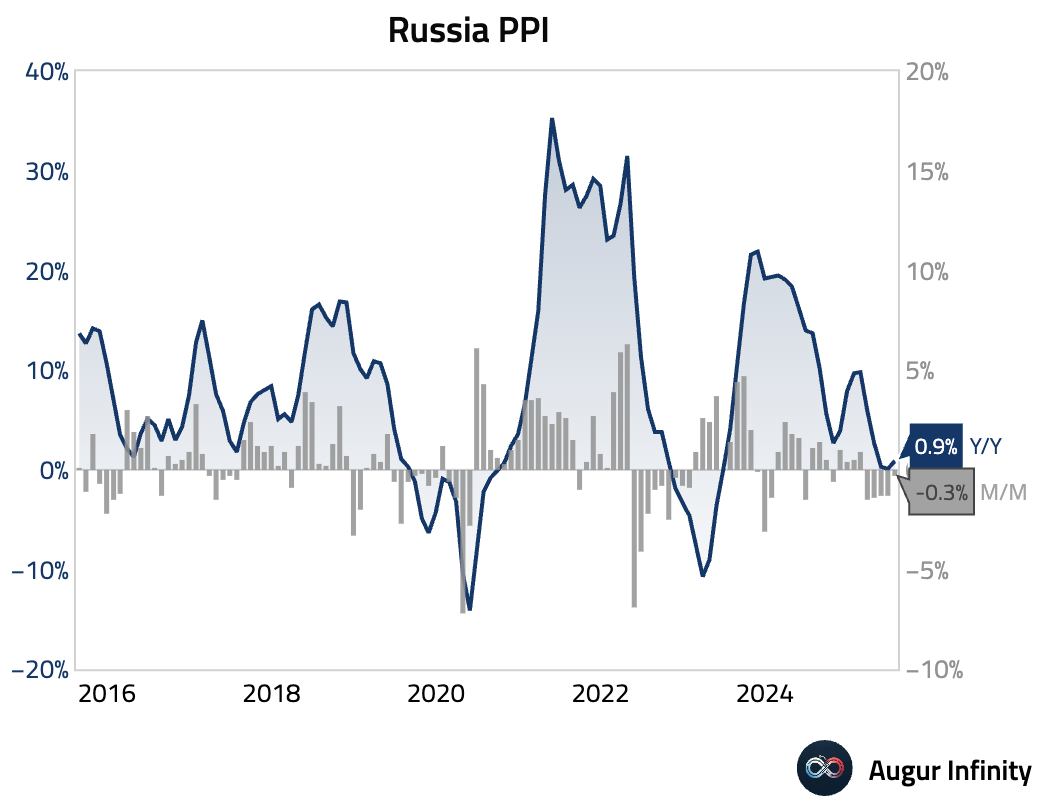

- Russia's Producer Price Index rose 0.9% M/M from -1.3% in June, a sharp rebound.

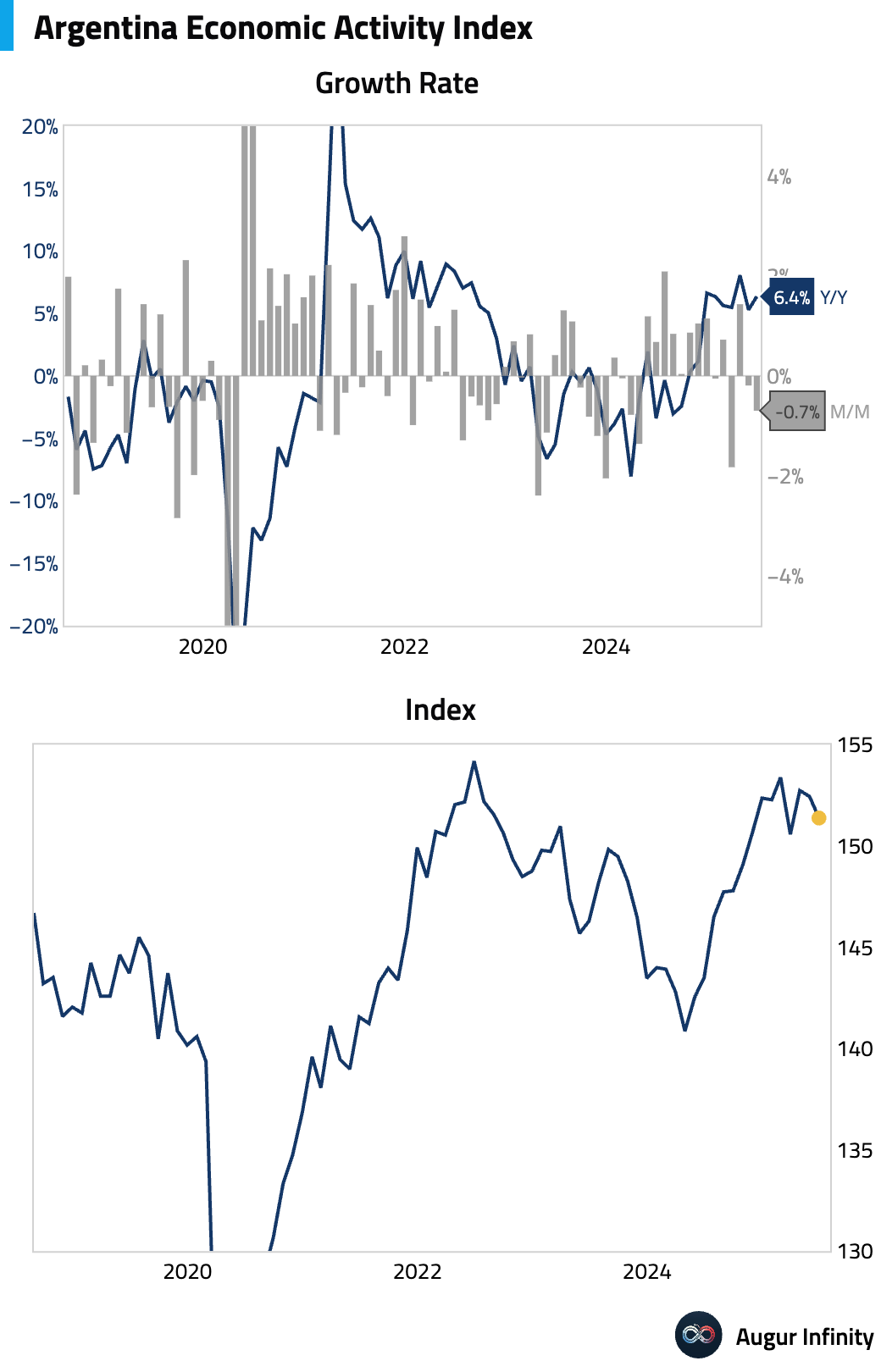

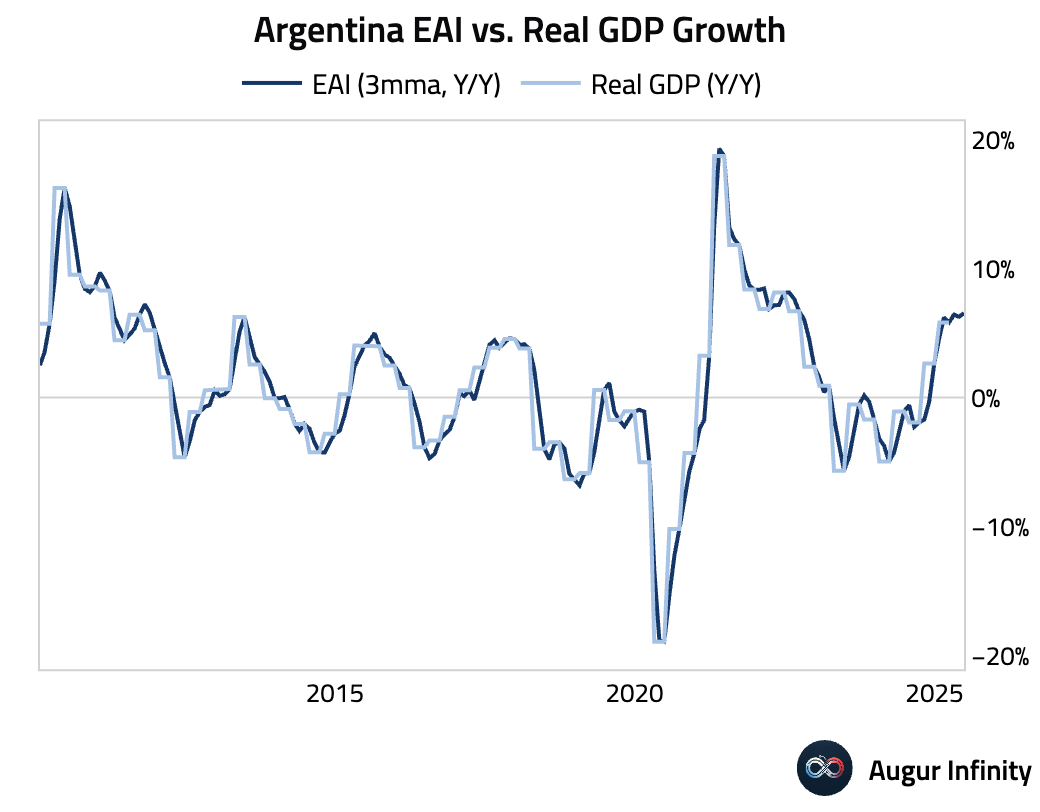

- Argentina Economic Activity rose 6.4% Y/Y in June, matching consensus expectations. This translates into a real GDP growth rate of 6.5% Y/Y in Q2. On a sequential basis, however, economic activity declined for a second month by 0.7% M/M.

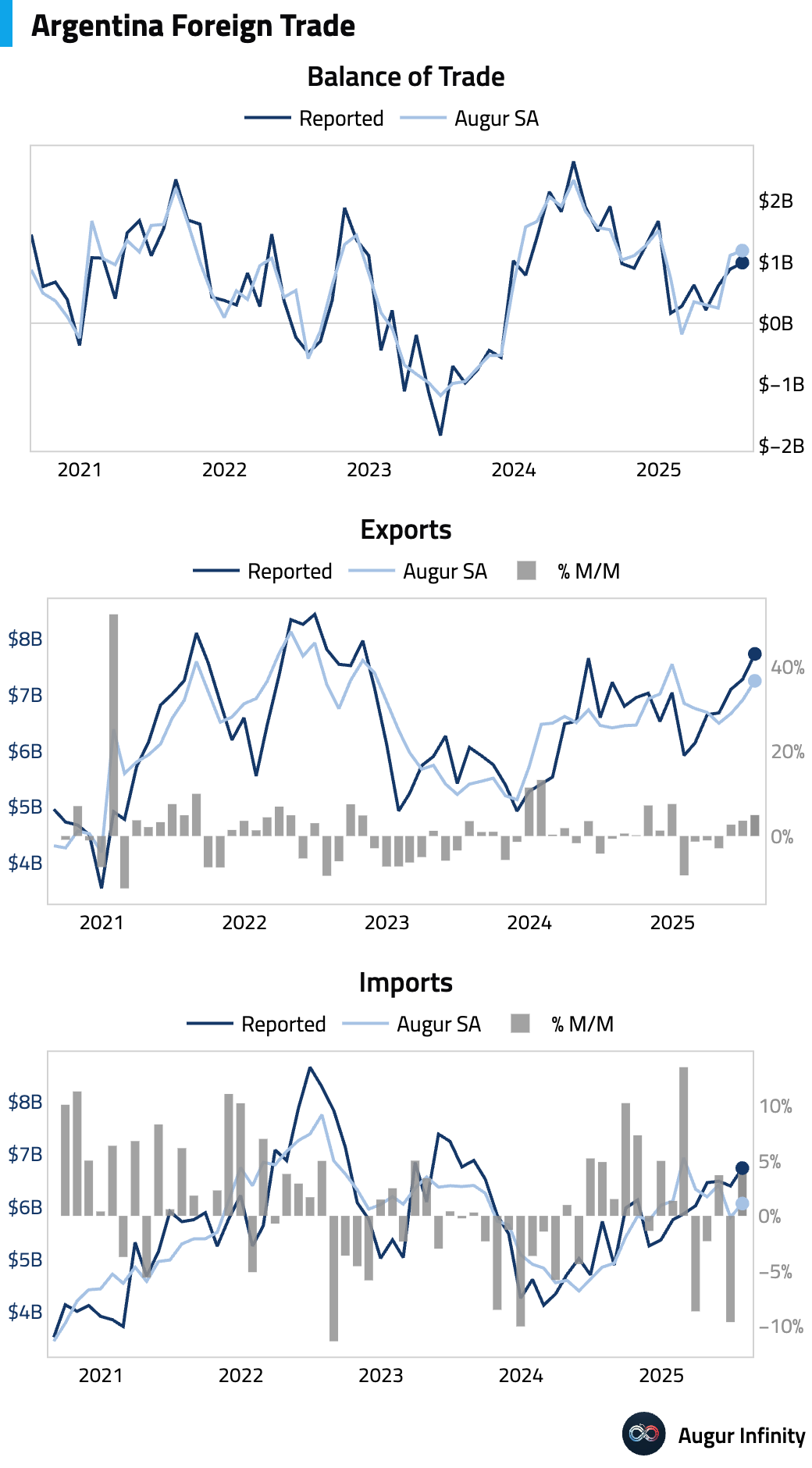

- Argentina's trade balance rose to $988M in July, significantly exceeding the consensus estimate of $690M and up from $906M in June. This marks the highest trade surplus since December 2024.

Global Markets

Equities

- Global equity markets were broadly lower, with US indices extending their losing streak amid a continued technology-led selloff. The tech-heavy Nasdaq fell 0.7%, while the broader US market was down 0.2%, marking the fourth consecutive day of declines for both. South Korean equities also continued their slide, now down for five straight sessions. Bucking the trend, UK stocks rose 1.1%, while Brazil gained 1.0%.

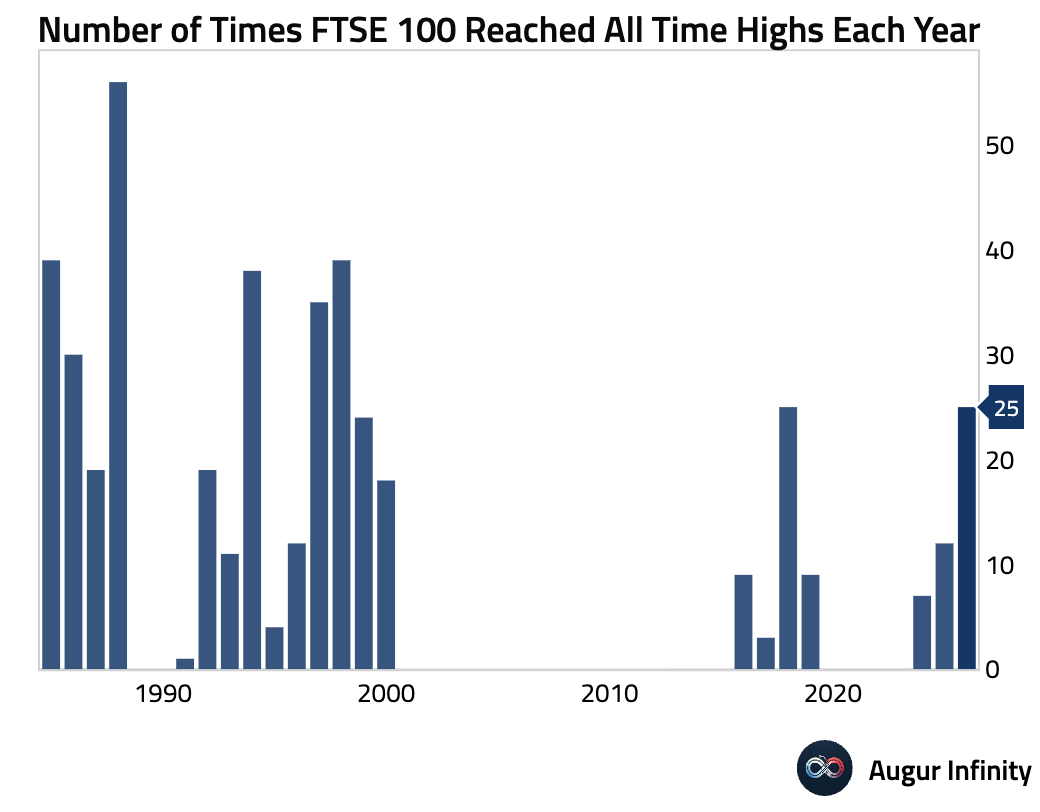

- The FTSE 100 has reached its 25th all-time-high this year. Last time it made this many ATHs in a year was in 2017.

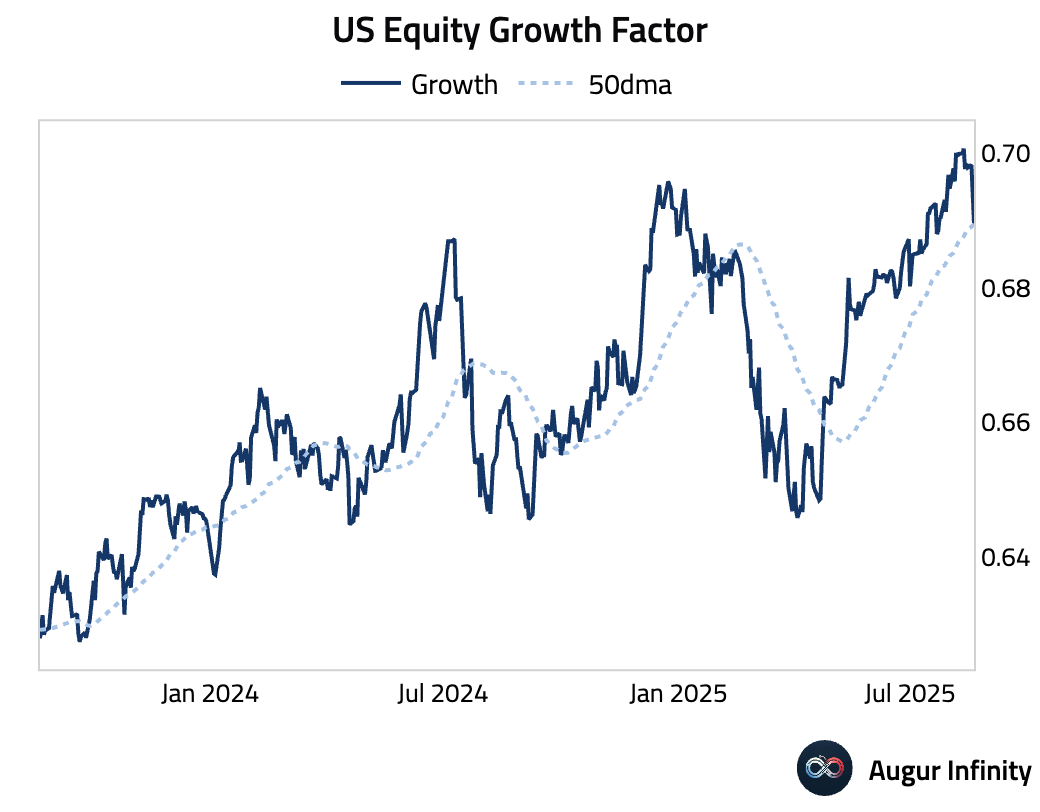

- US Equity Growth Factor slumped below its 50-day moving average.

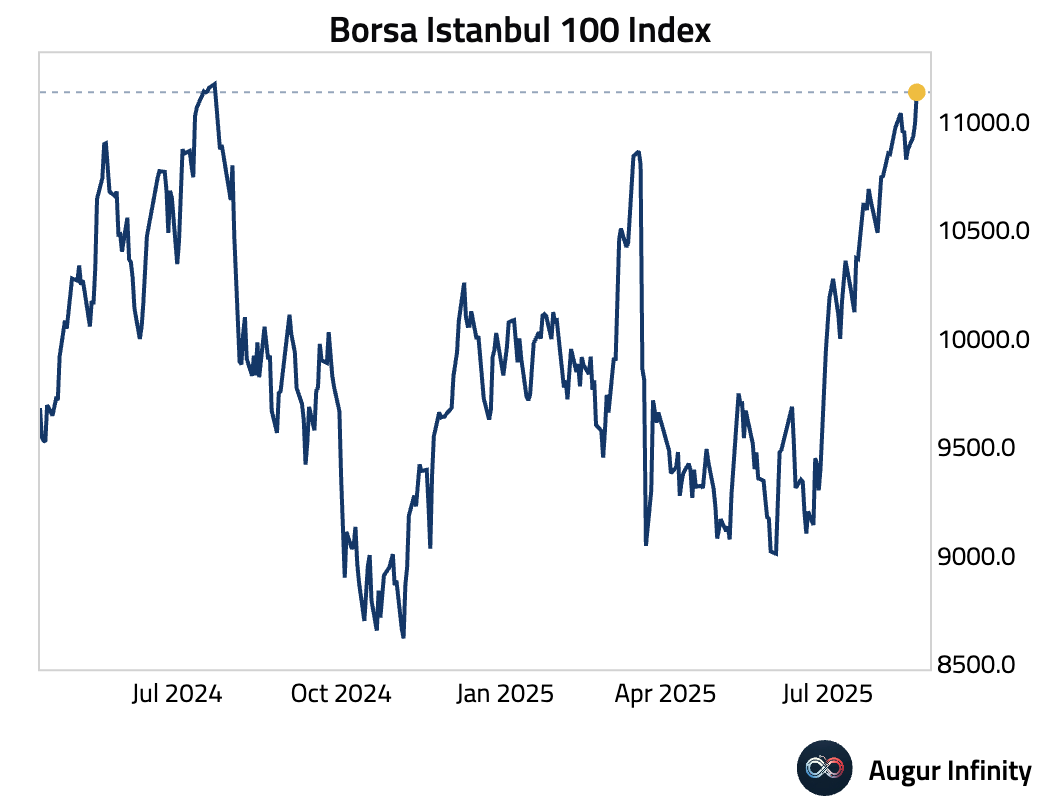

- The Borsa Istanbul 100 Index surged to the highest level since July 2024.

Fixed Income

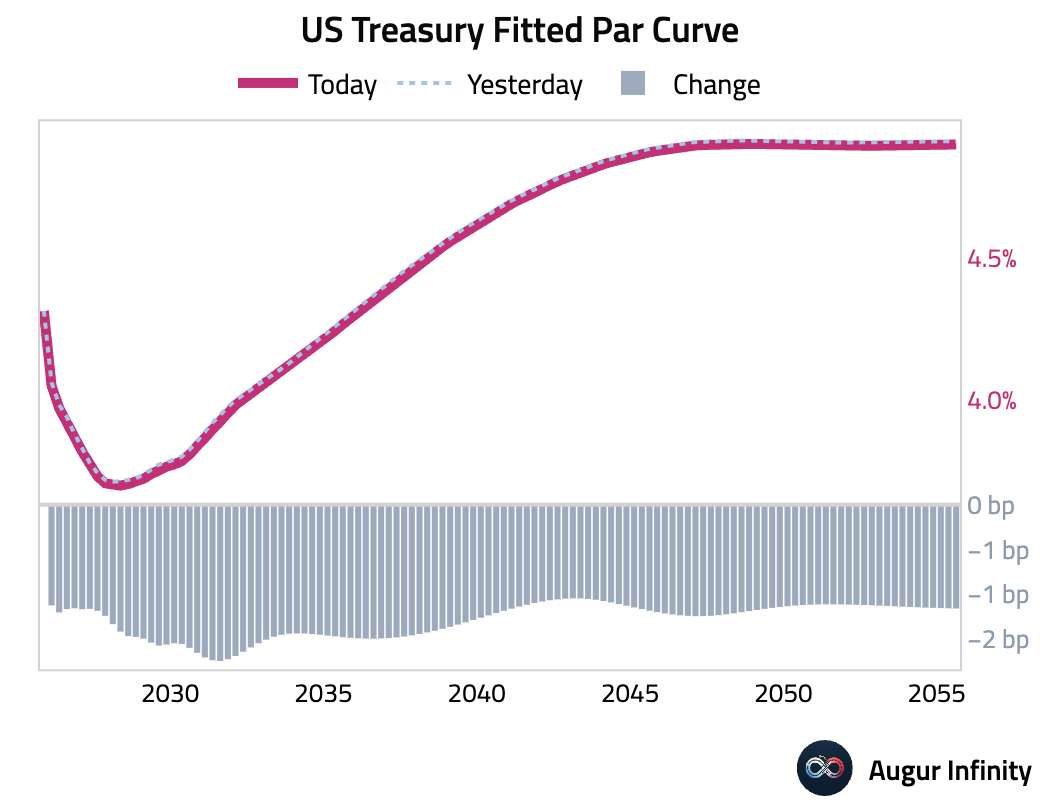

- US Treasury yields declined across the curve as investors sought safety amid equity market weakness and ahead of the Jackson Hole symposium. The 10-year yield fell by 1.4 bps, while the 5-year yield saw the largest drop, declining by 1.5 bps.

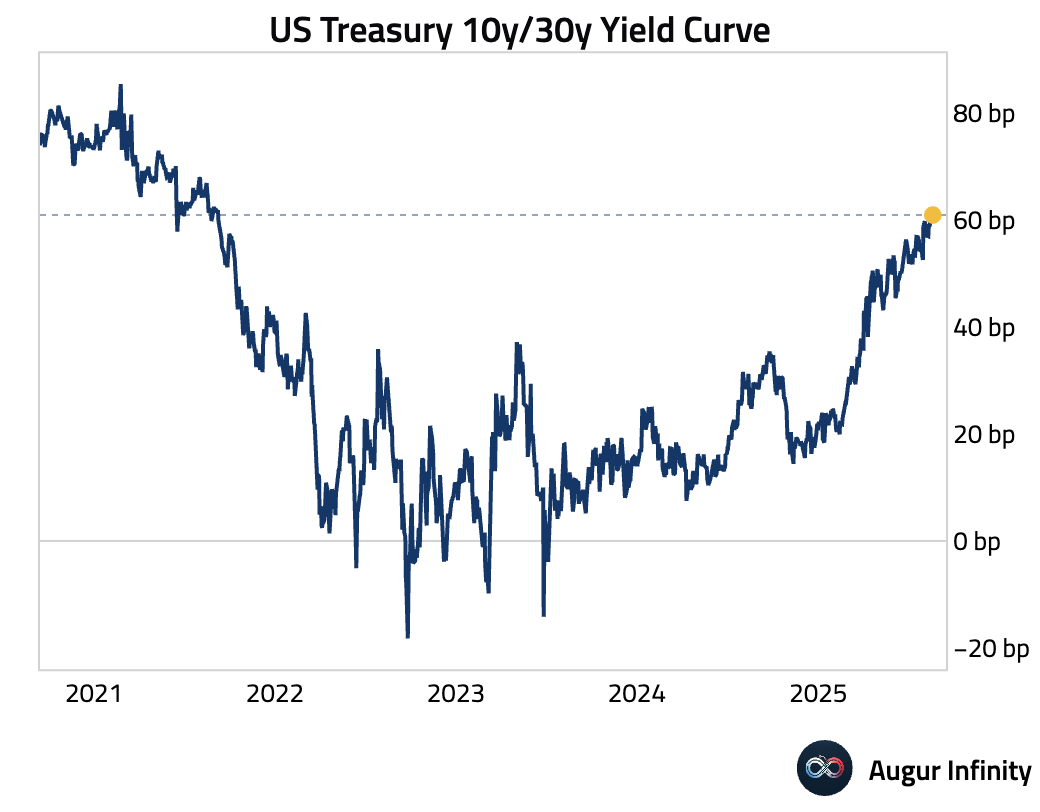

- US Treasury 10y/30y yield curve has reached the steepest level since September 8, 2021.

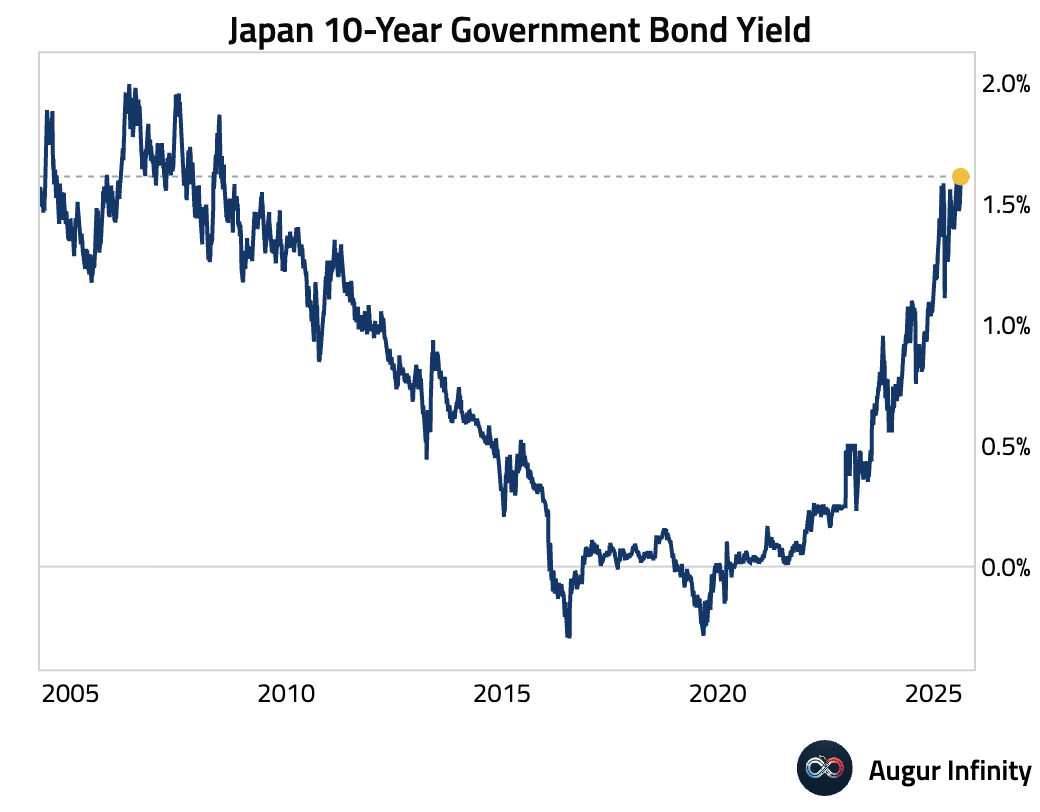

- Japan 10-year government bond yield rose for the eighth day to 1.61%, the highest level since July 2008.

FX

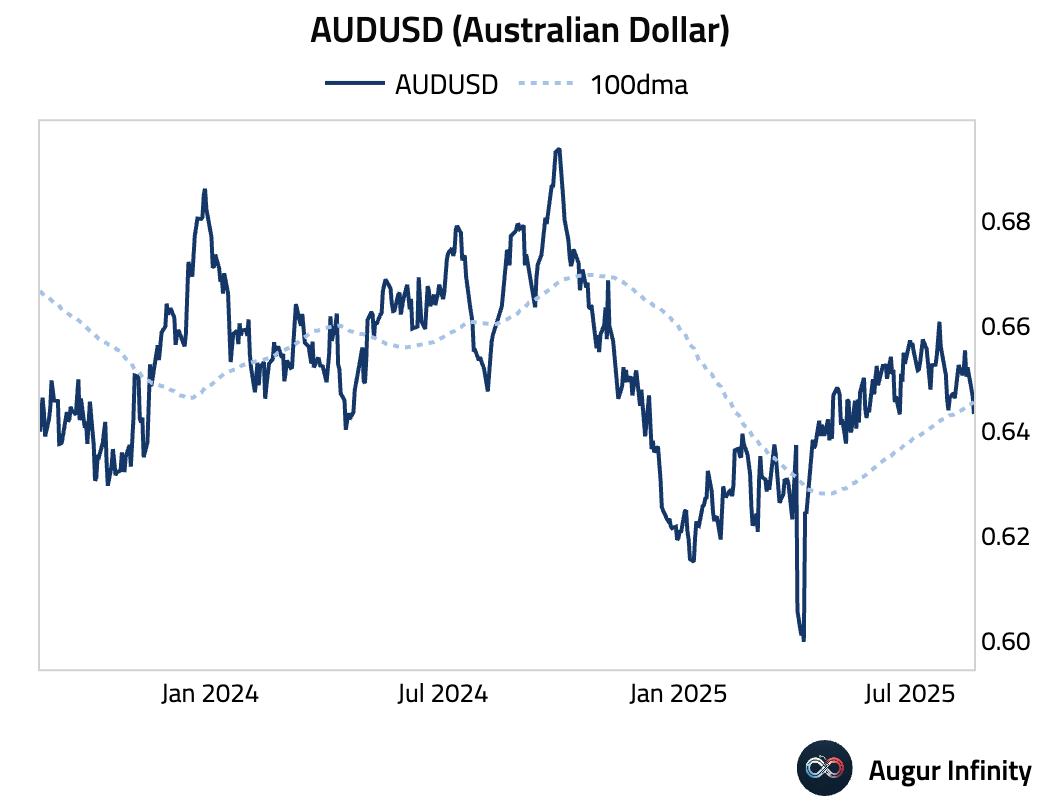

- The US dollar was mixed but showed notable strength against commodity currencies. The New Zealand dollar was the worst performer, plunging 1.4% against the greenback following a dovish interest rate decision from the Reserve Bank of New Zealand. The Australian dollar also weakened, falling 0.5%. The Canadian dollar extended its losses to a fifth consecutive day. In a typical risk-off move, the Japanese yen and Swiss franc both gained against the dollar, rising 0.3%.

- The Aussie dollar fell below its 100-day moving average, while the kiwi fell below its 200-day moving average.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.