Headlines

- China is reportedly considering the use of yuan-backed stablecoins for settling cross-border trade transactions.

- The Wall Street Journal reports that President Trump is contemplating the dismissal of Federal Reserve Governor Lisa Cook following allegations of mortgage fraud.

Charts of the Day

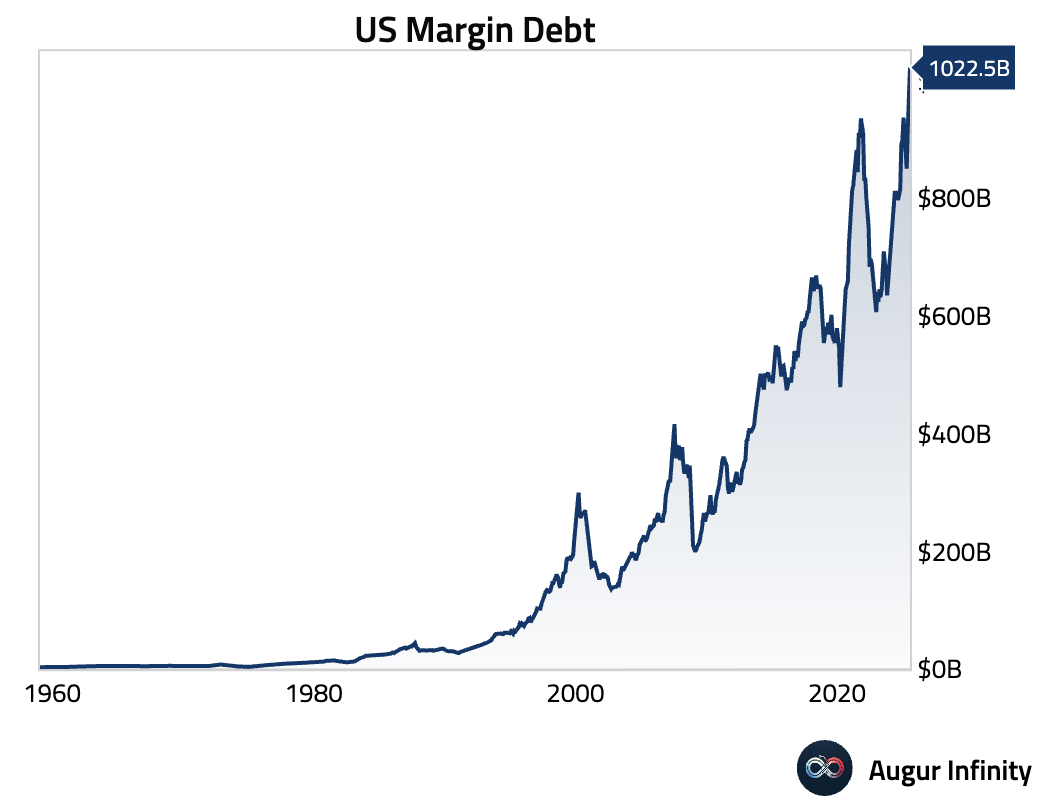

- US margin debt rose another $22 billion in July, after reaching $1 trillion for the time in June.

Global Economics

United States

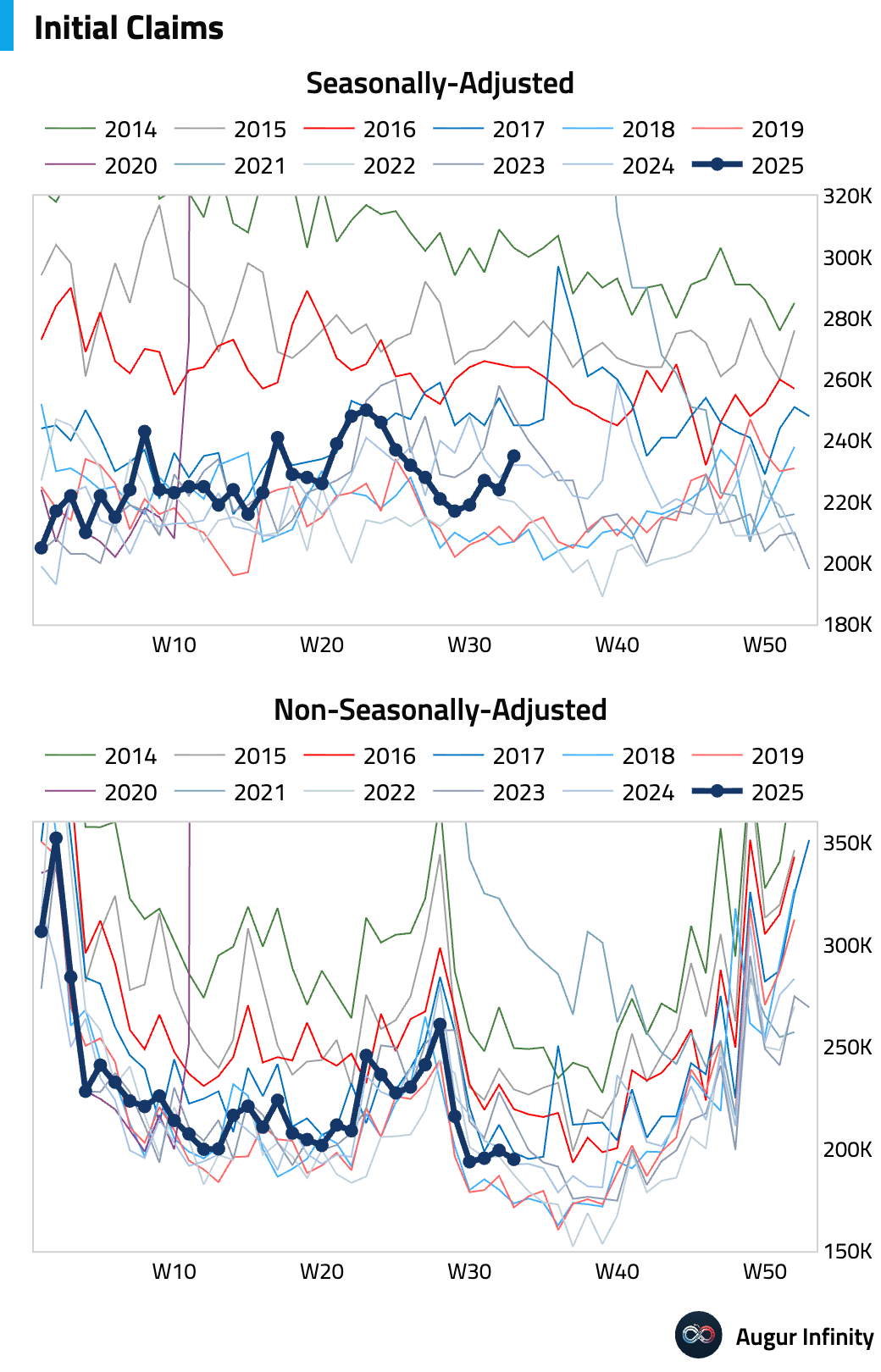

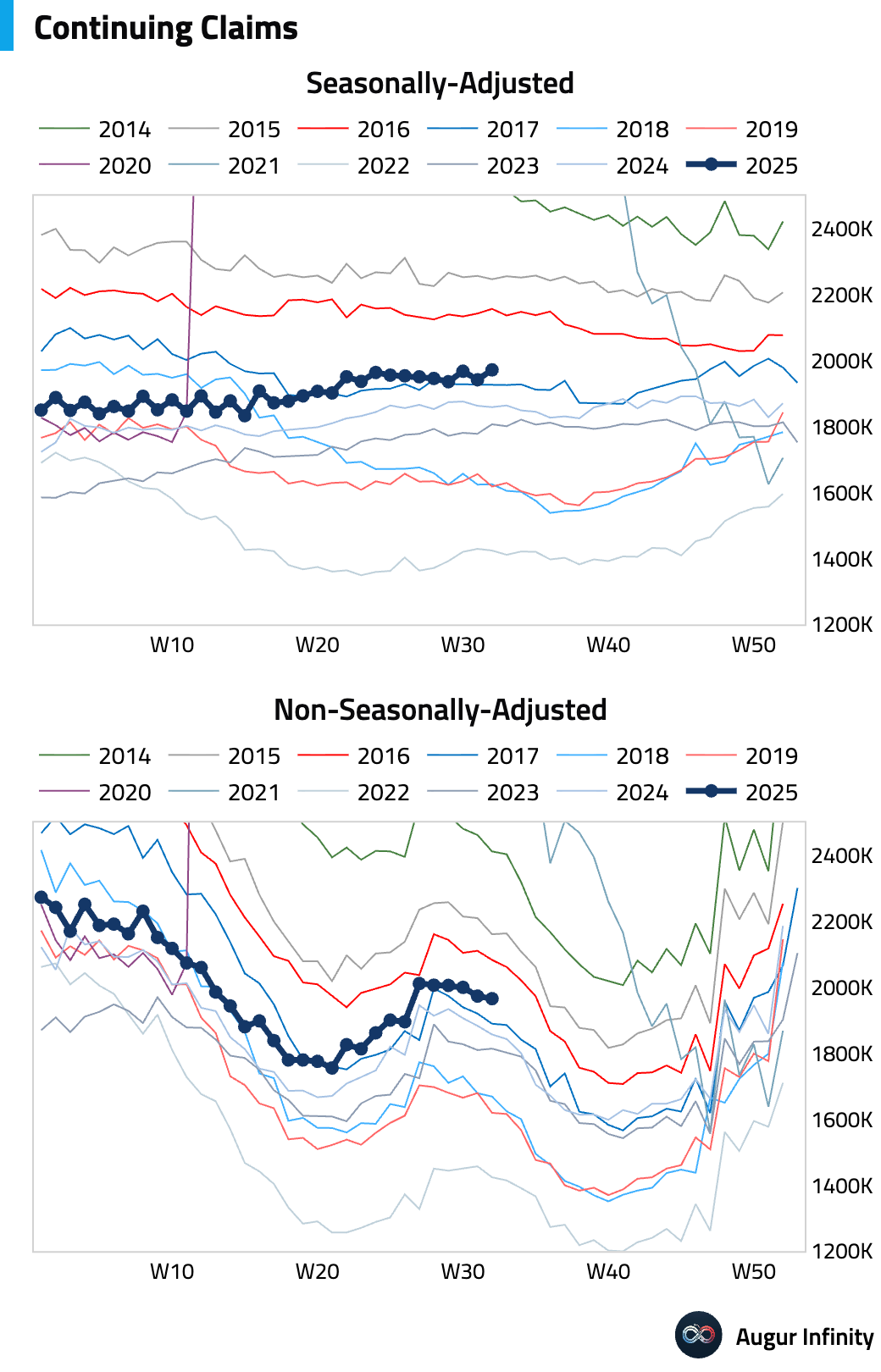

- Weekly jobless claims pointed to some modest softening in the labor market. Initial claims for the week ending August 16 rose 11k to 235,000, above the 225,000 consensus, with the increase partly driven by volatility in Kentucky. Continuing claims for the week ending August 9 also rose more than expected, increasing by 30,000 to 1.972 million, the highest since November 2021.

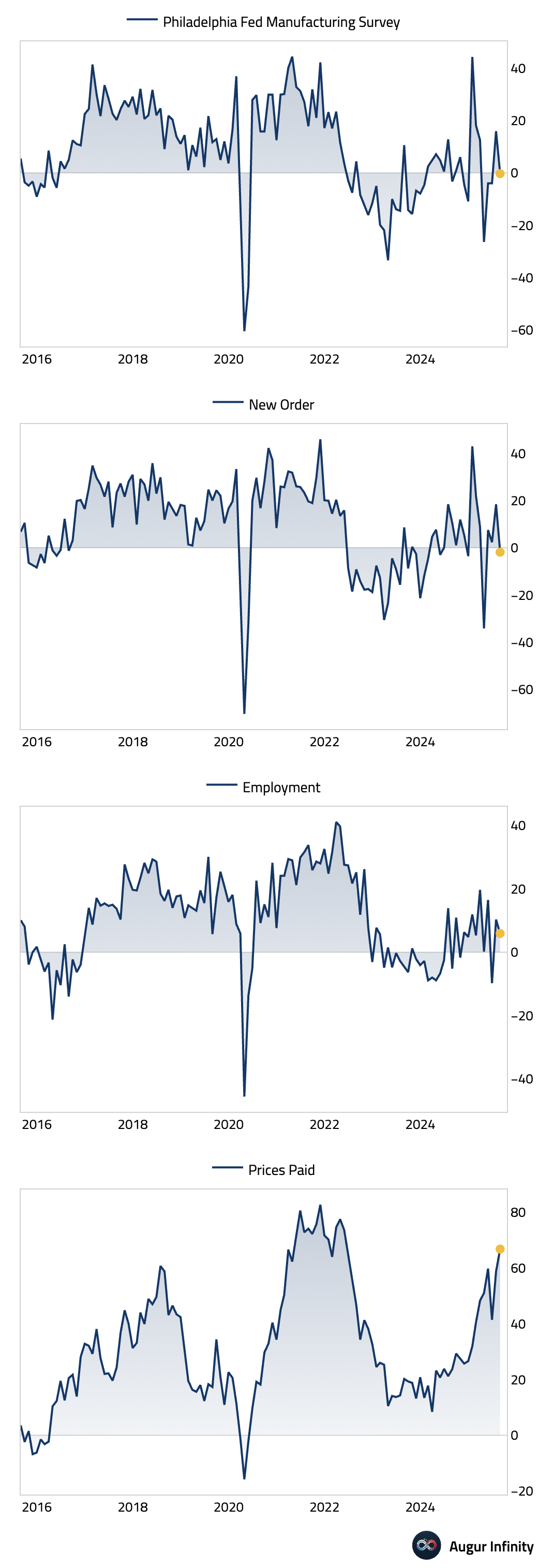

- The Philadelphia Fed Manufacturing Index unexpectedly plunged back into contraction, falling 16.2 points to -0.3 in August, well below the consensus forecast of 7.0. The internals were weak, with the new orders index plummeting 20.3 points to -1.9. In a sign of persistent inflationary pressures despite slowing activity, the prices paid component surged to its highest level since May 2022.

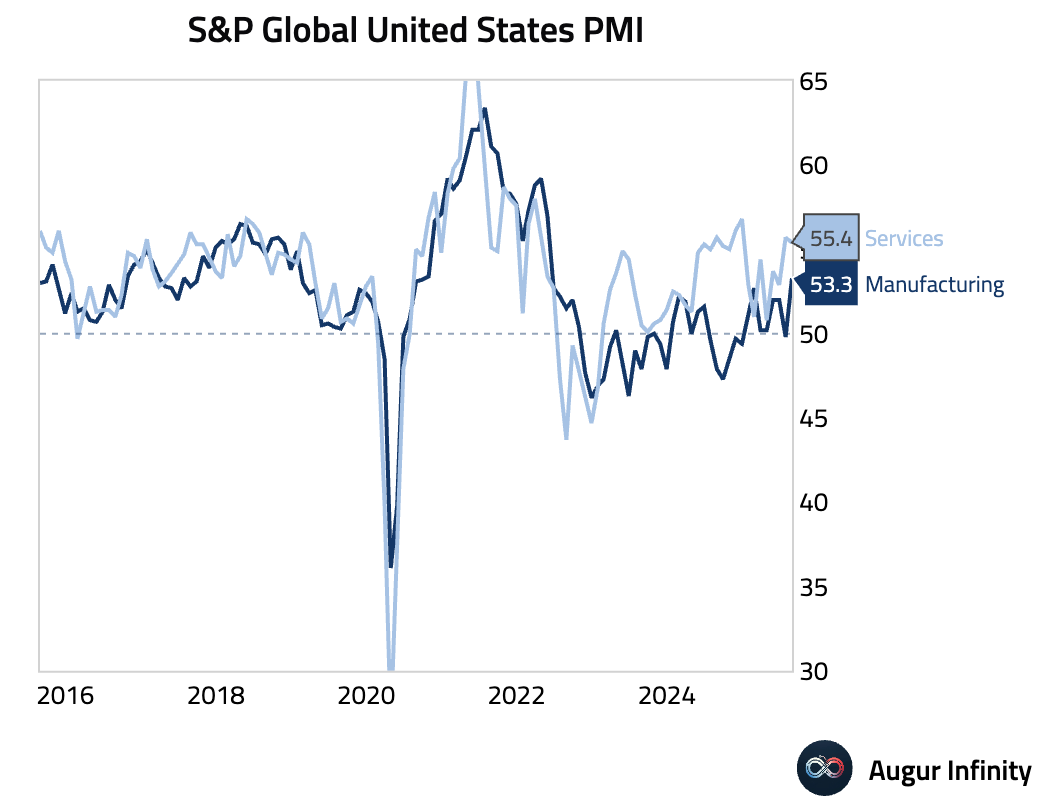

- The S&P Global Flash Manufacturing PMI surged to a 39-month high of 53.3, driven by the steepest rise in production since May 2022. The Services PMI eased slightly to 55.4 but remains in strong expansion. A key takeaway was the 3-year high in selling price inflation, which firms attributed to tariffs, signaling persistent price pressures.

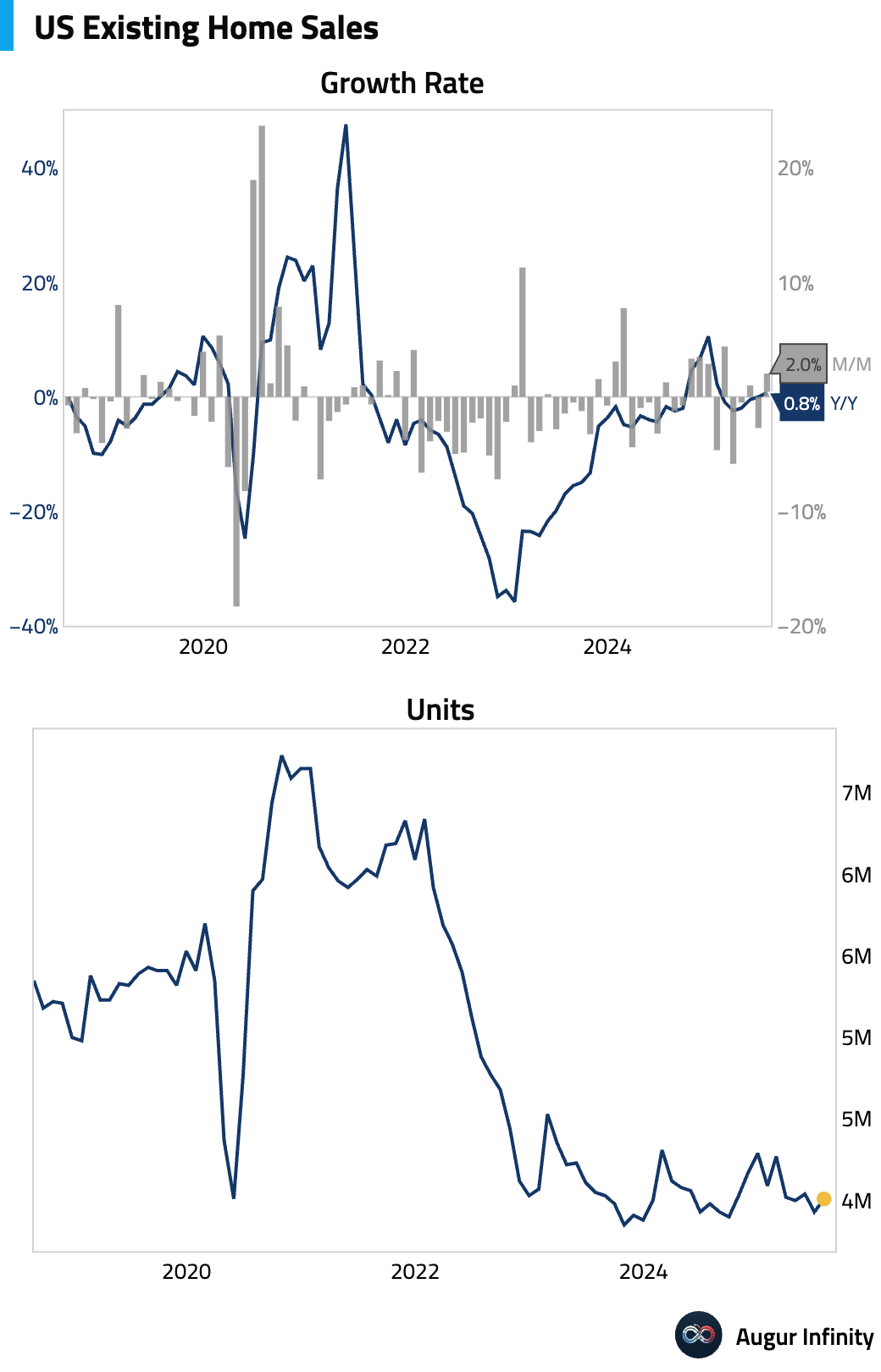

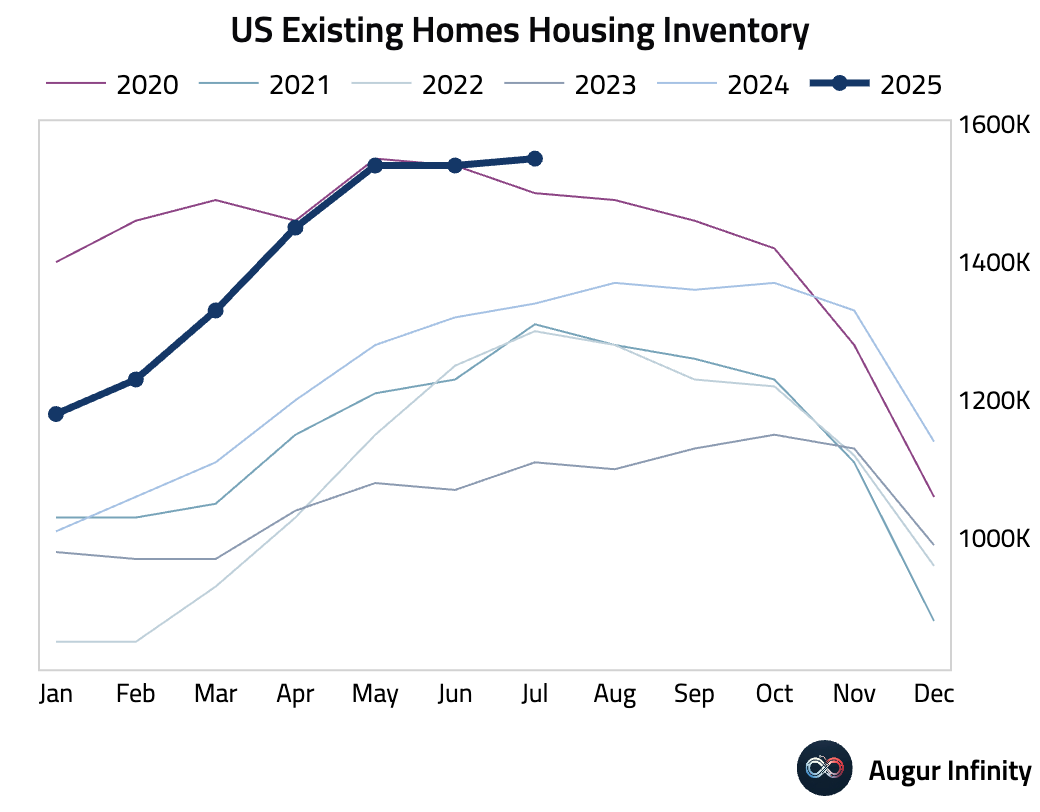

- Existing home sales rebounded in July, rising 2.0% M/M to an annualized rate of 4.01 million, beating the consensus of 3.92 million. This follows a 2.7% decline in June. Existing homes housing inventory, however, rose to the highest since May 2020.

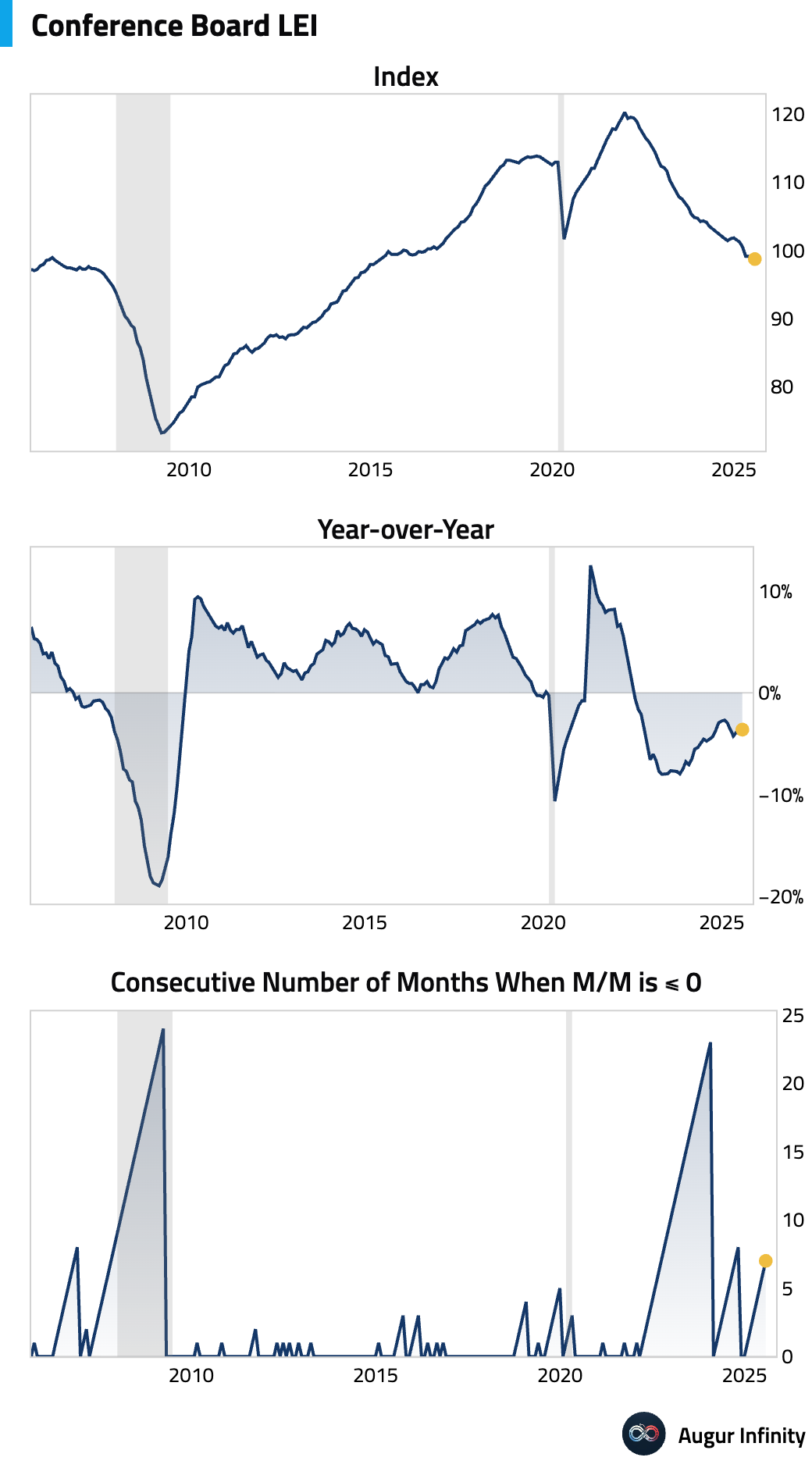

- The Conference Board's Leading Economic Index fell 0.1% M/M in July, its fourth consecutive monthly decline. The reading matched consensus expectations and was a smaller drop than June's 0.3% fall.

Canada

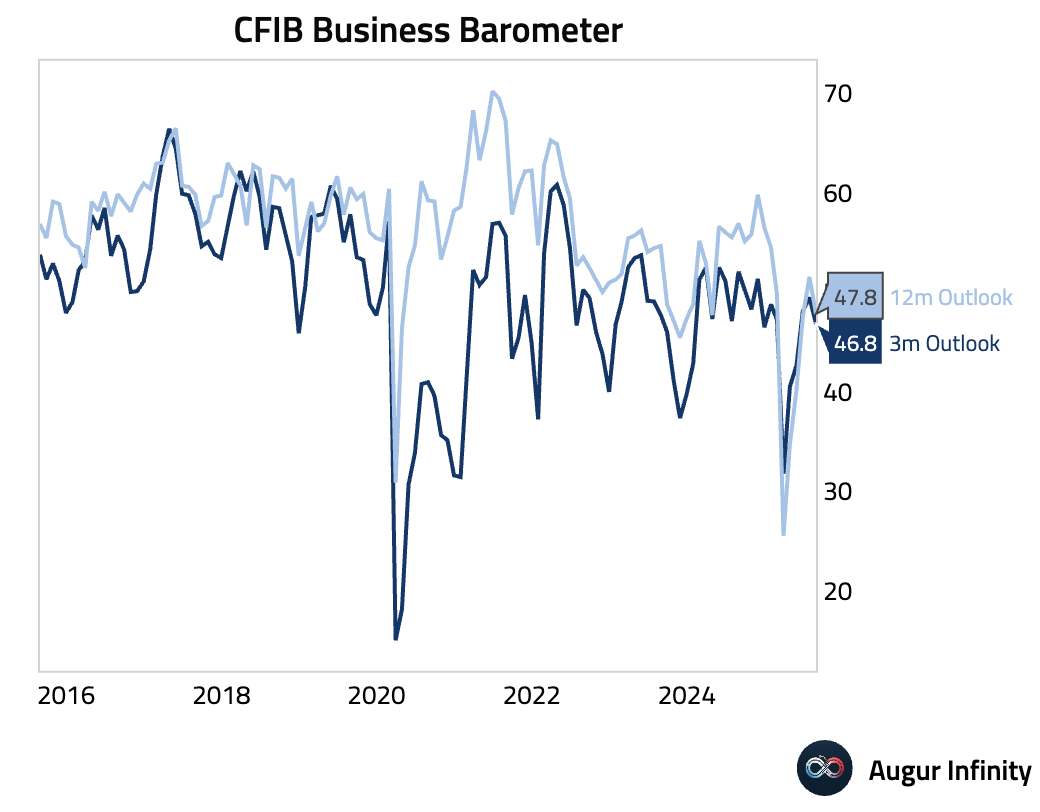

- The CFIB Business Barometer, a measure of small business confidence, fell to 47.8 in August from 50.9, dropping back into contractionary territory.

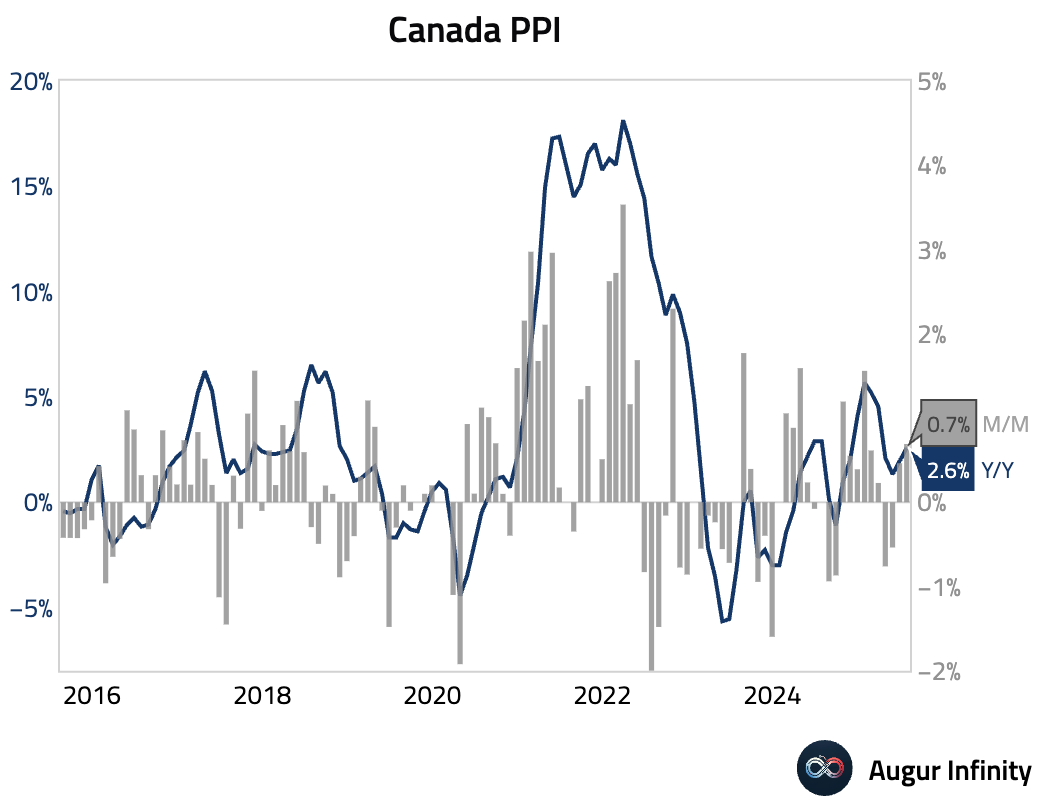

- Producer prices accelerated in July, with the PPI rising 0.7% M/M (vs. 0.5% prior). The year-over-year rate jumped to 2.6% from 1.9%.

Europe

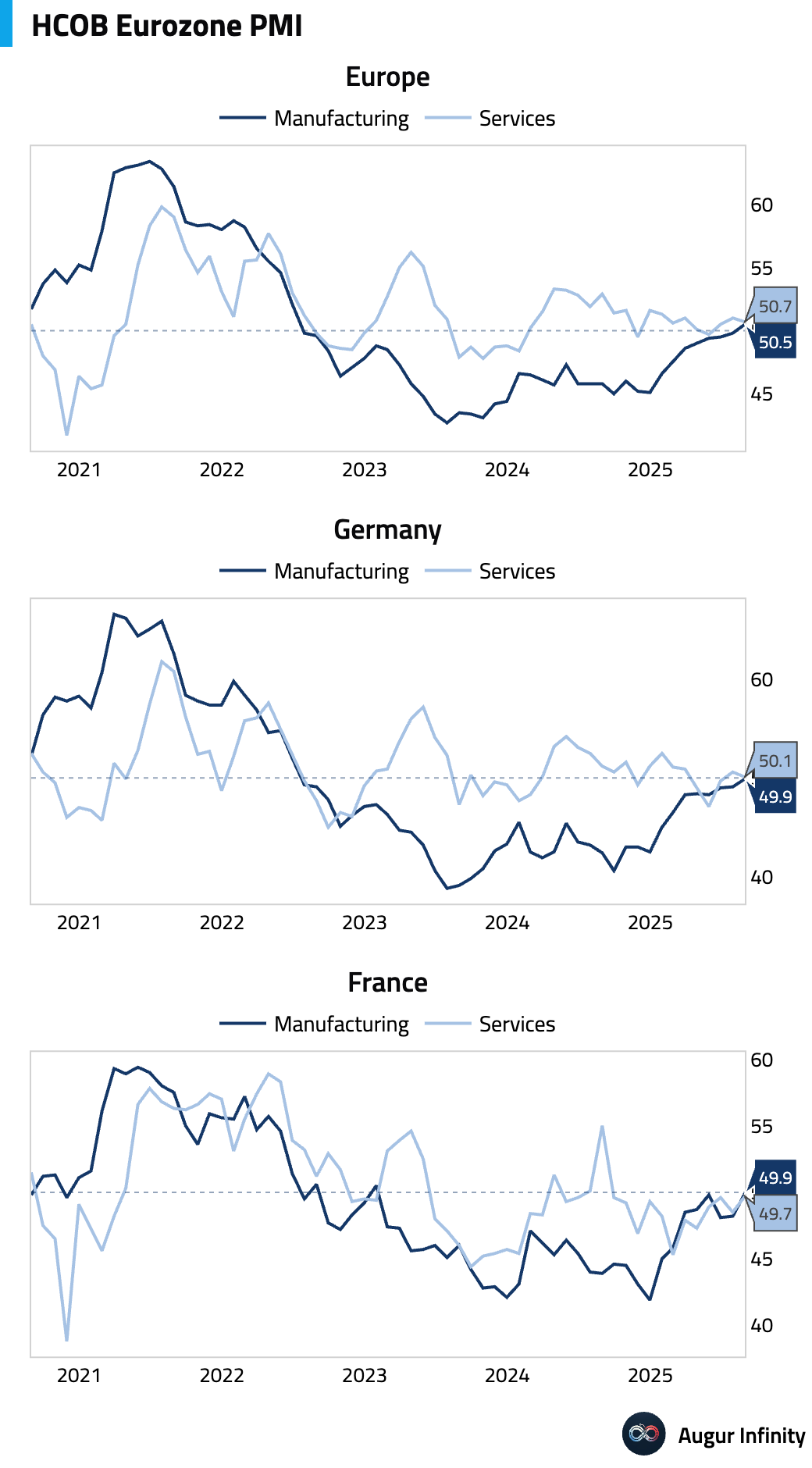

- Germany's HCOB Flash Manufacturing PMI rose to 49.9 in August from 49.1, its highest level since June 2022. The manufacturing output index surged to a 41-month high of 52.6. In France, the manufacturing gauge also improved, hitting a 31-month high of 49.9. The strength in the core economies pushed the broader Eurozone Manufacturing PMI up to 50.5, a 38-month high that marked a return to expansionary territory. The recovery appears domestically driven, as new export orders fell at the sharpest pace in five months.

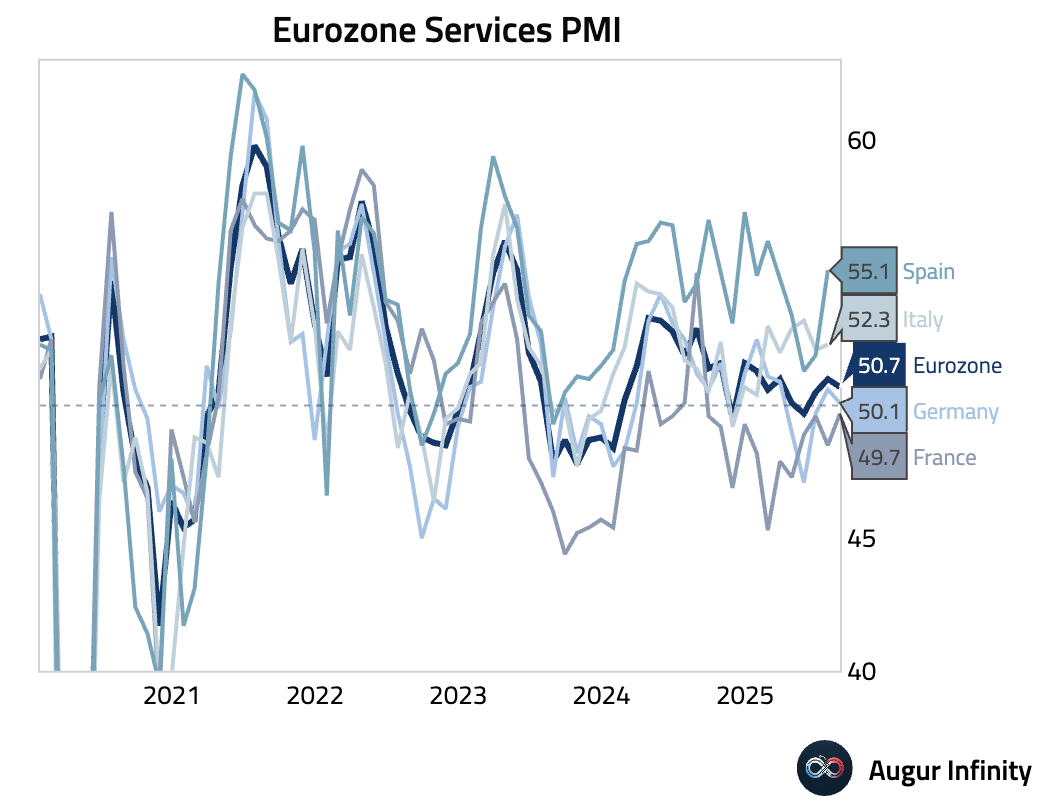

- HCOB Flash Services PMIs softened across the Eurozone in August. The aggregate index for the bloc dipped to 50.7 from 51.0, while Germany's reading fell to a near-stagnant 50.1. France’s Services PMI improved to 49.7 but remained in contraction.

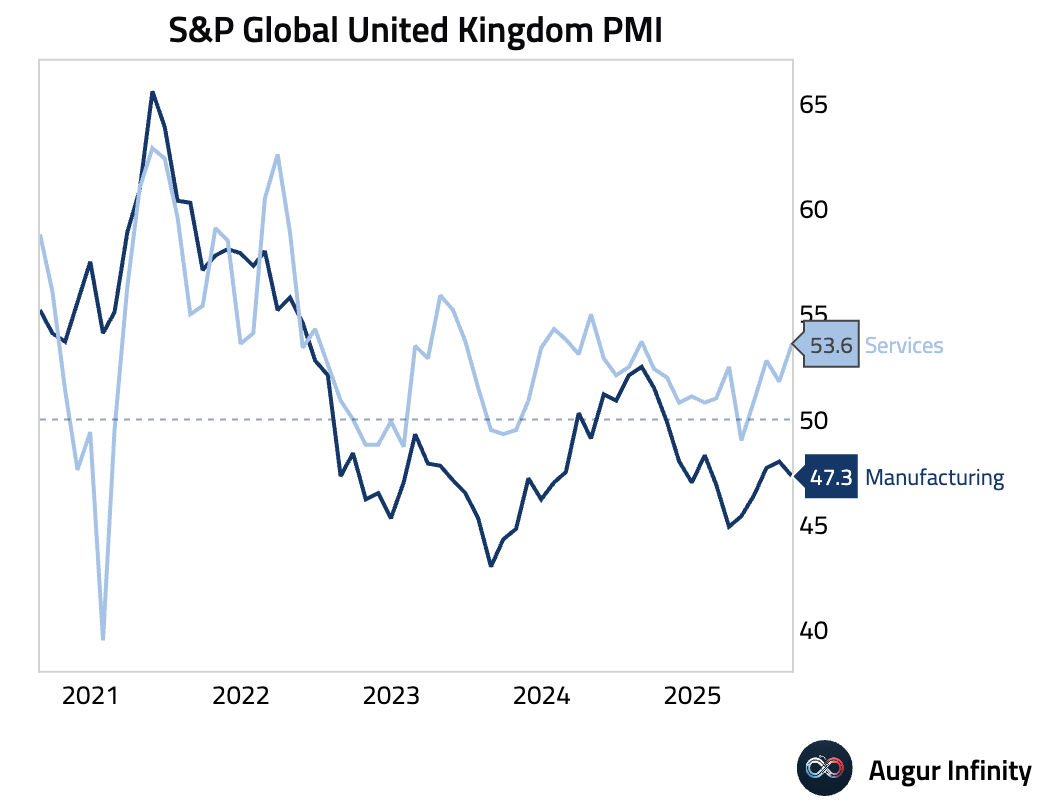

- The UK's S&P Global Flash Composite PMI rose to a 12-month high of 53.0 in August, beating consensus expectations. The strength was entirely driven by the services sector (53.6), which masked a deepening contraction in manufacturing (47.3), its lowest in three months. Despite stronger activity, employment contracted for the 11th straight month. Input cost inflation also accelerated, reducing the likelihood of near-term Bank of England rate cuts.

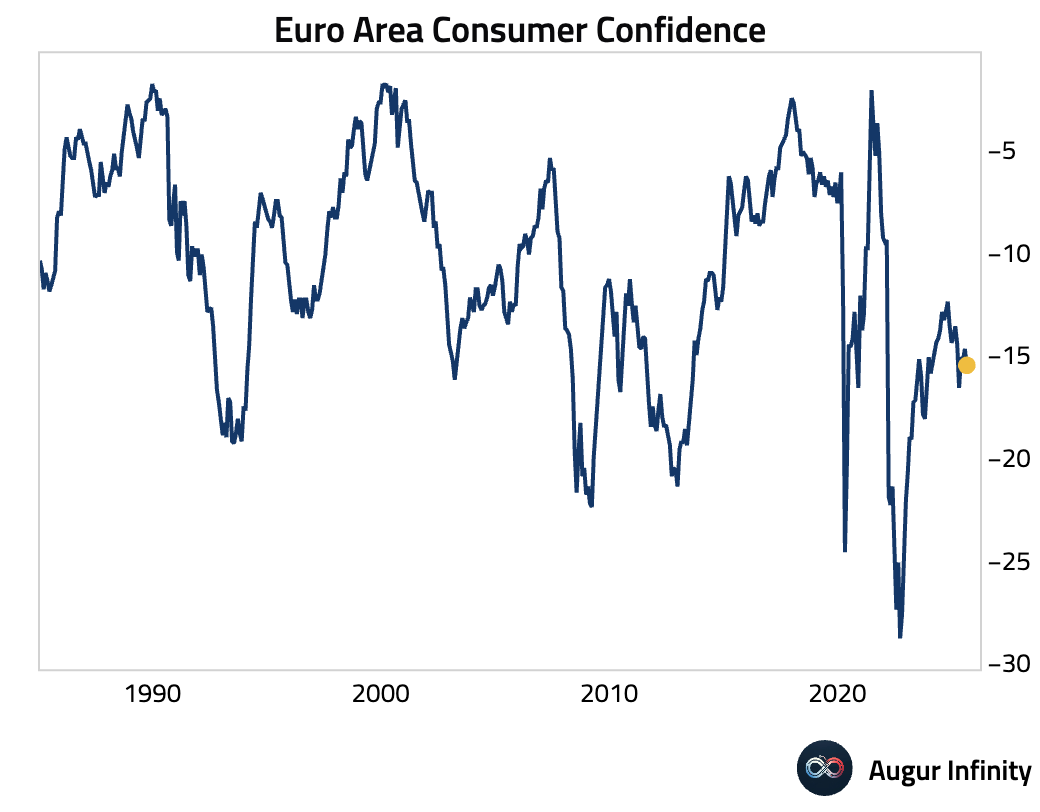

- The Euro Area’s flash Consumer Confidence indicator fell to -15.5 in August from -14.7, missing the consensus forecast of -14.9.

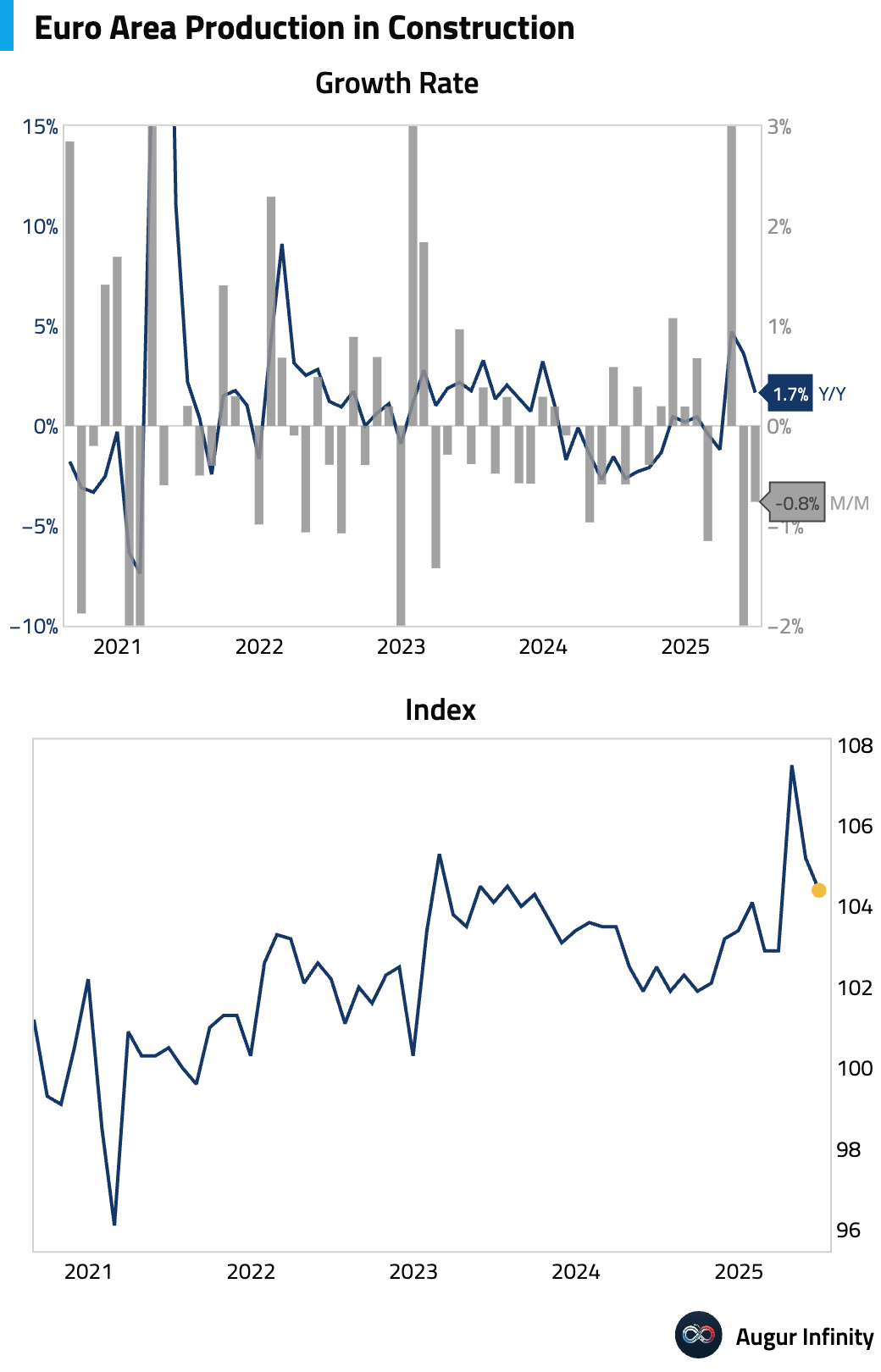

- Euro Area construction output growth slowed to 1.7% Y/Y in June from 3.6% in May.

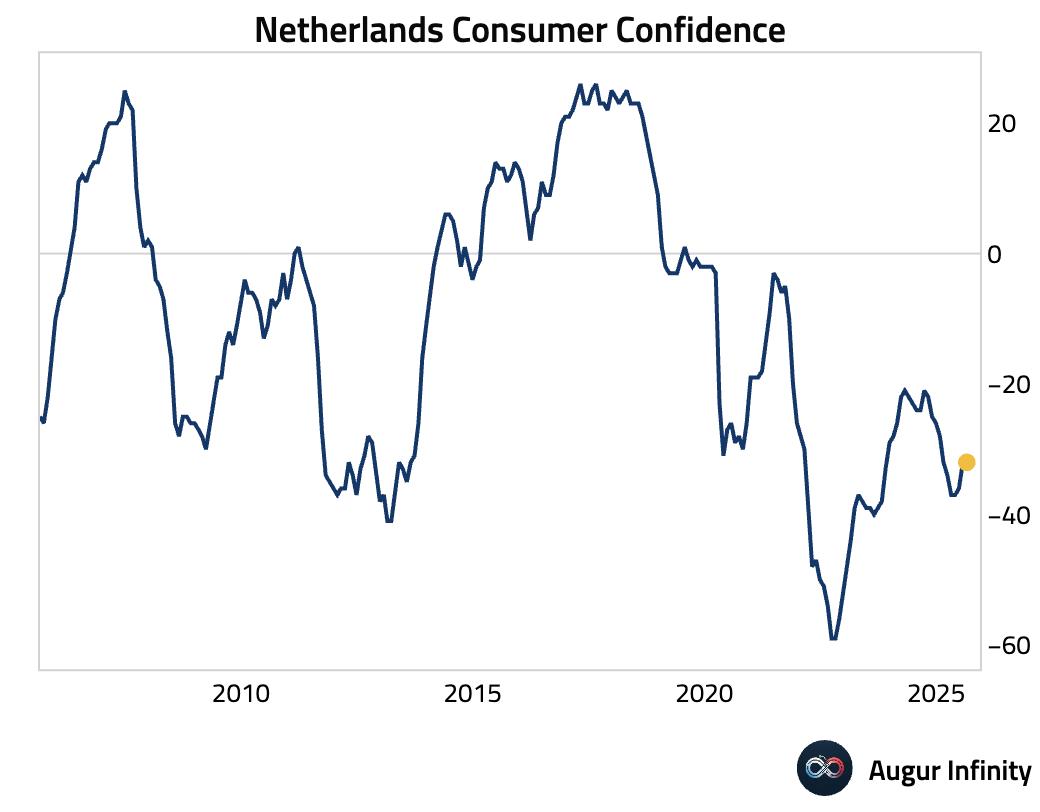

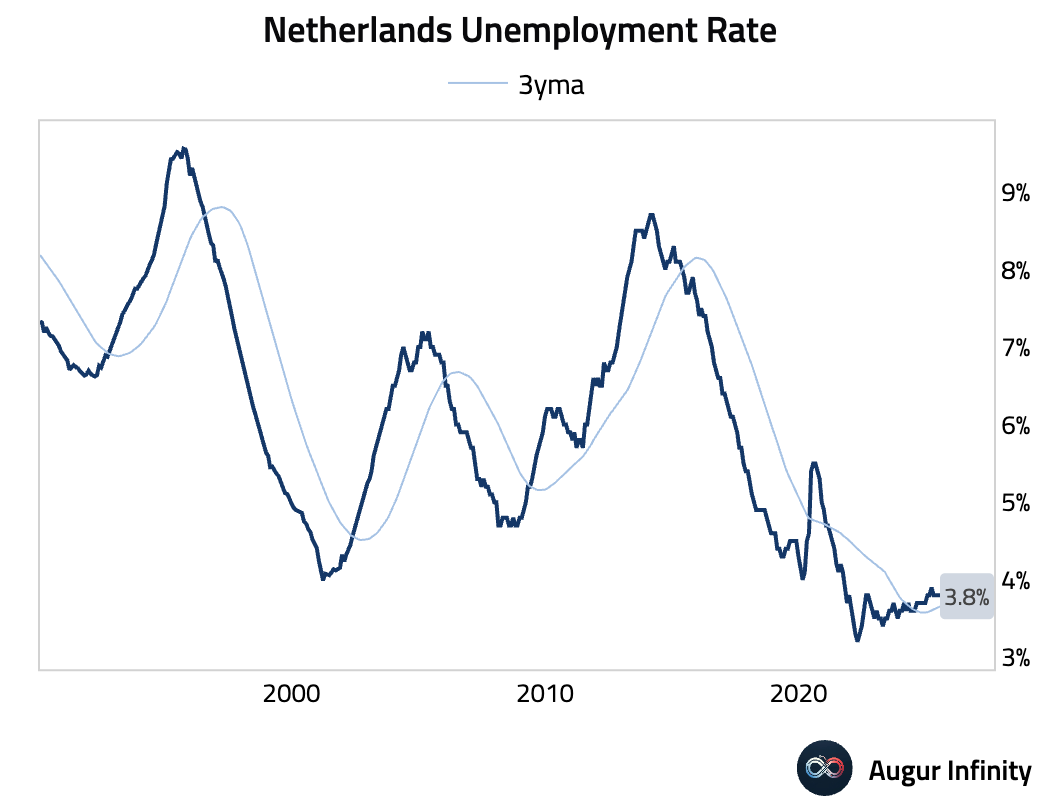

- Dutch consumer confidence was unchanged at -32 in August, while the unemployment rate held steady at 3.8% in July.

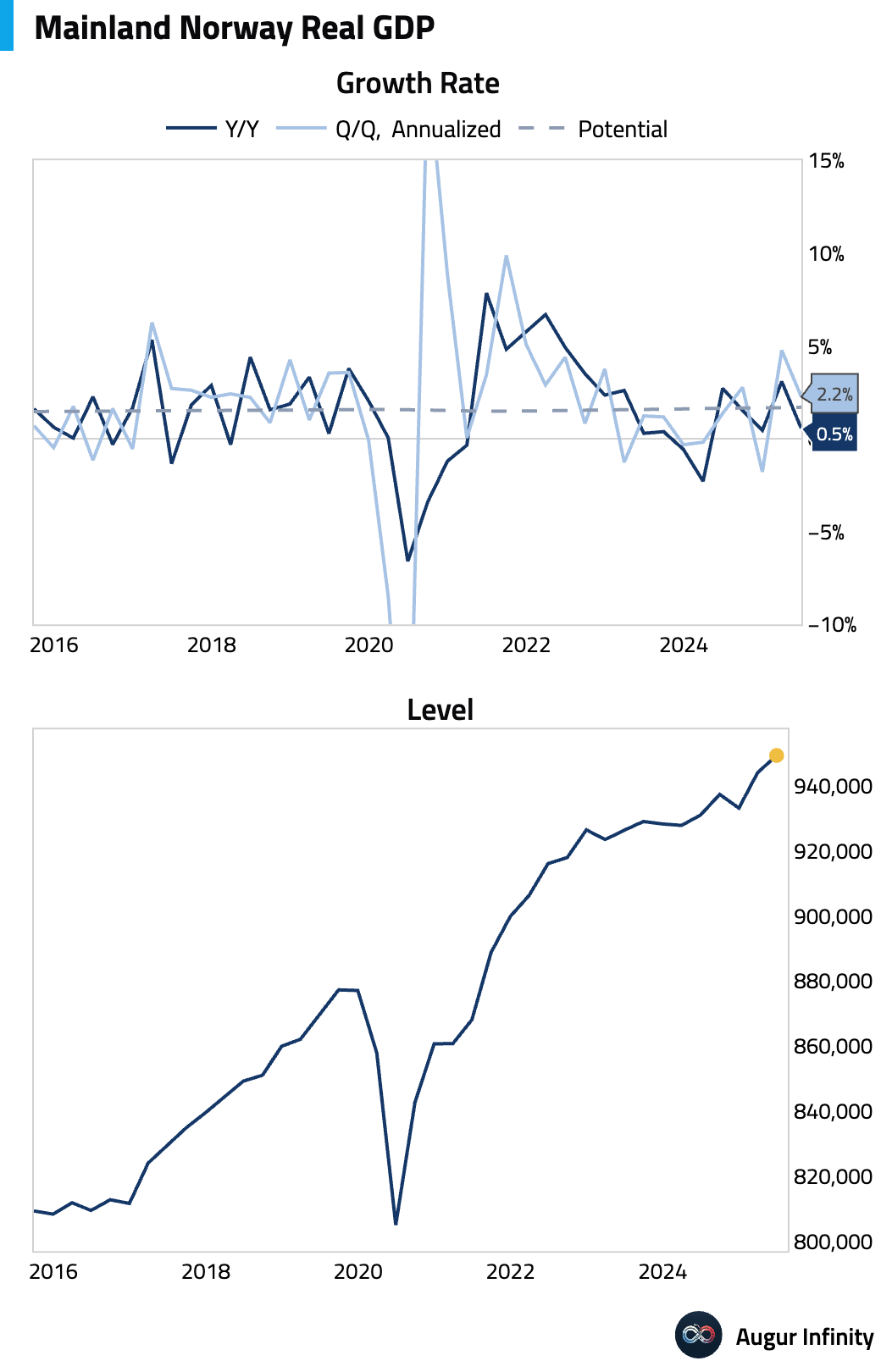

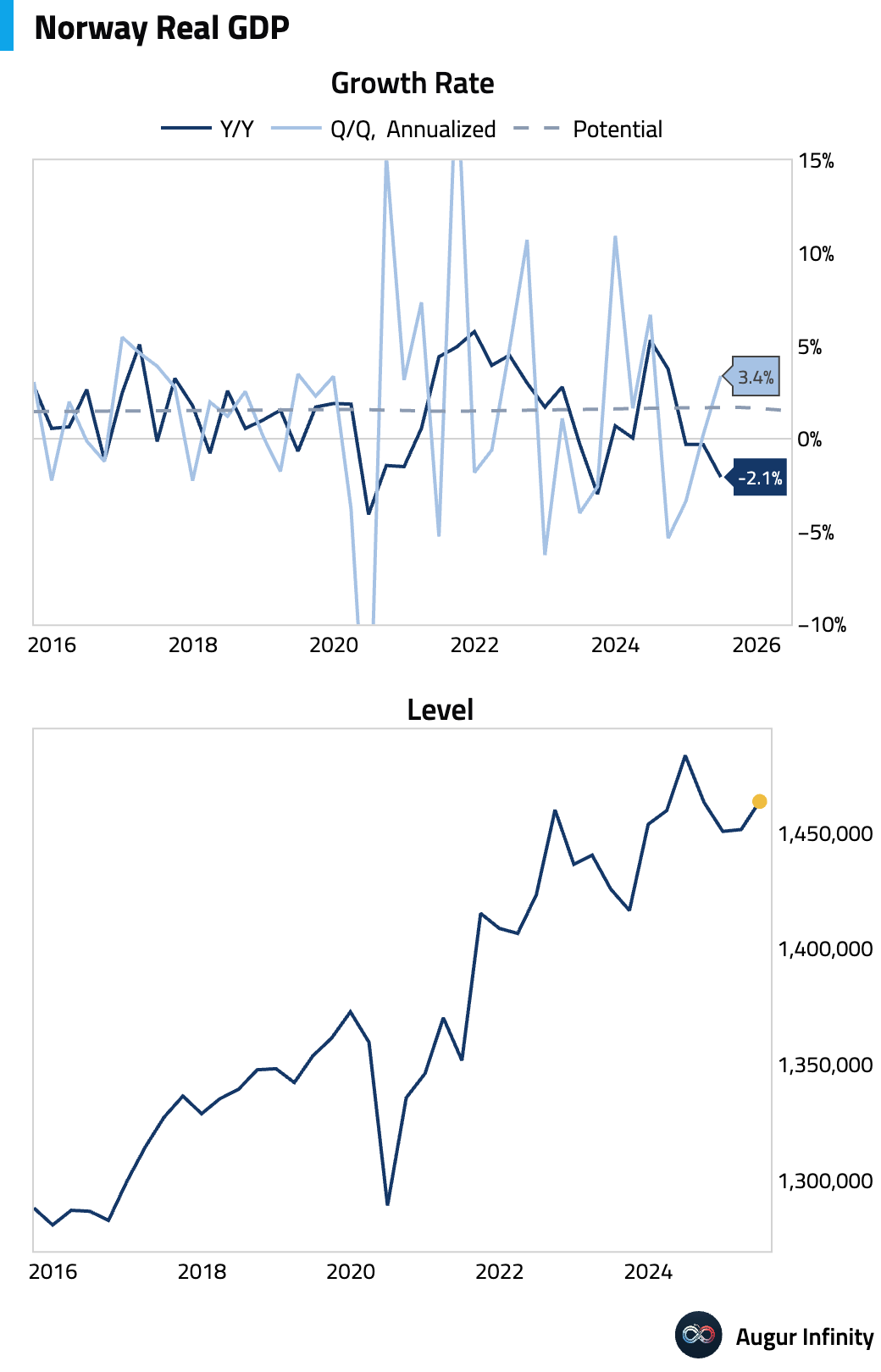

- Norway's mainland GDP grew 0.6% Q/Q (or 2.2% annualized) in Q2, beating expectations of 0.3% and accelerating from Q1's 1.2% revised gain. Total GDP grew 0.8% Q/Q (or 3.4% annualized). The year-over-year rate of total GDP contracted by 2.1%.

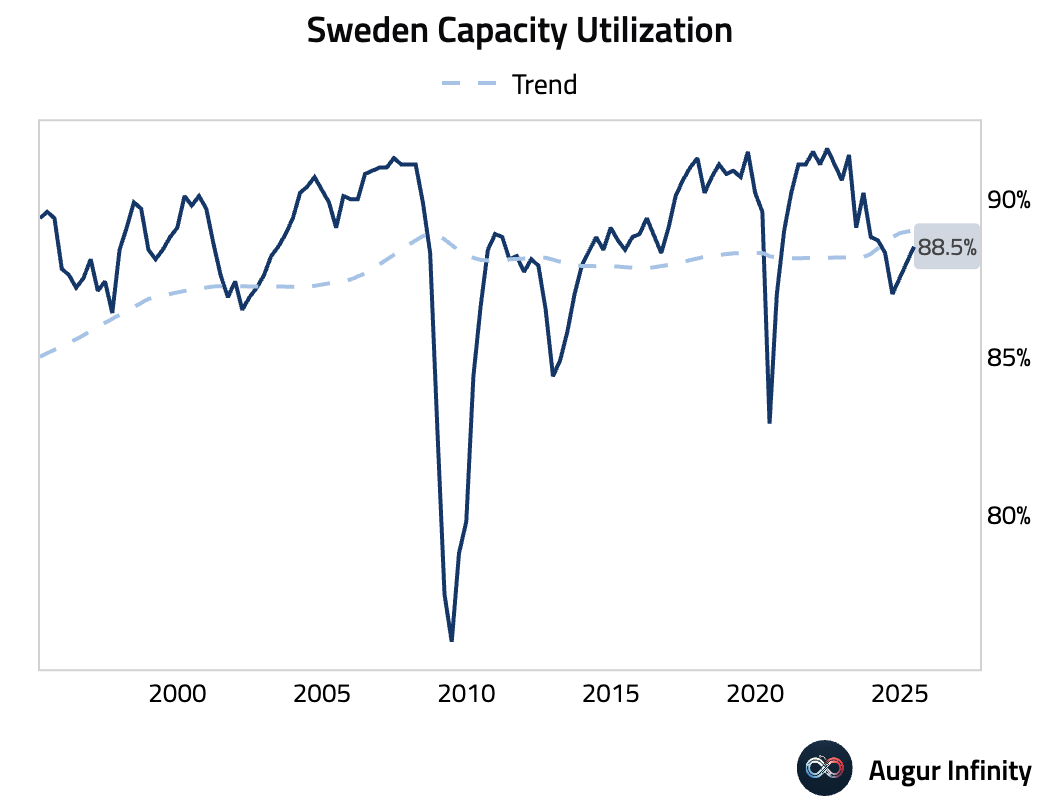

- Swedish industrial capacity utilization increased by 0.4% Q/Q in Q2 2025.

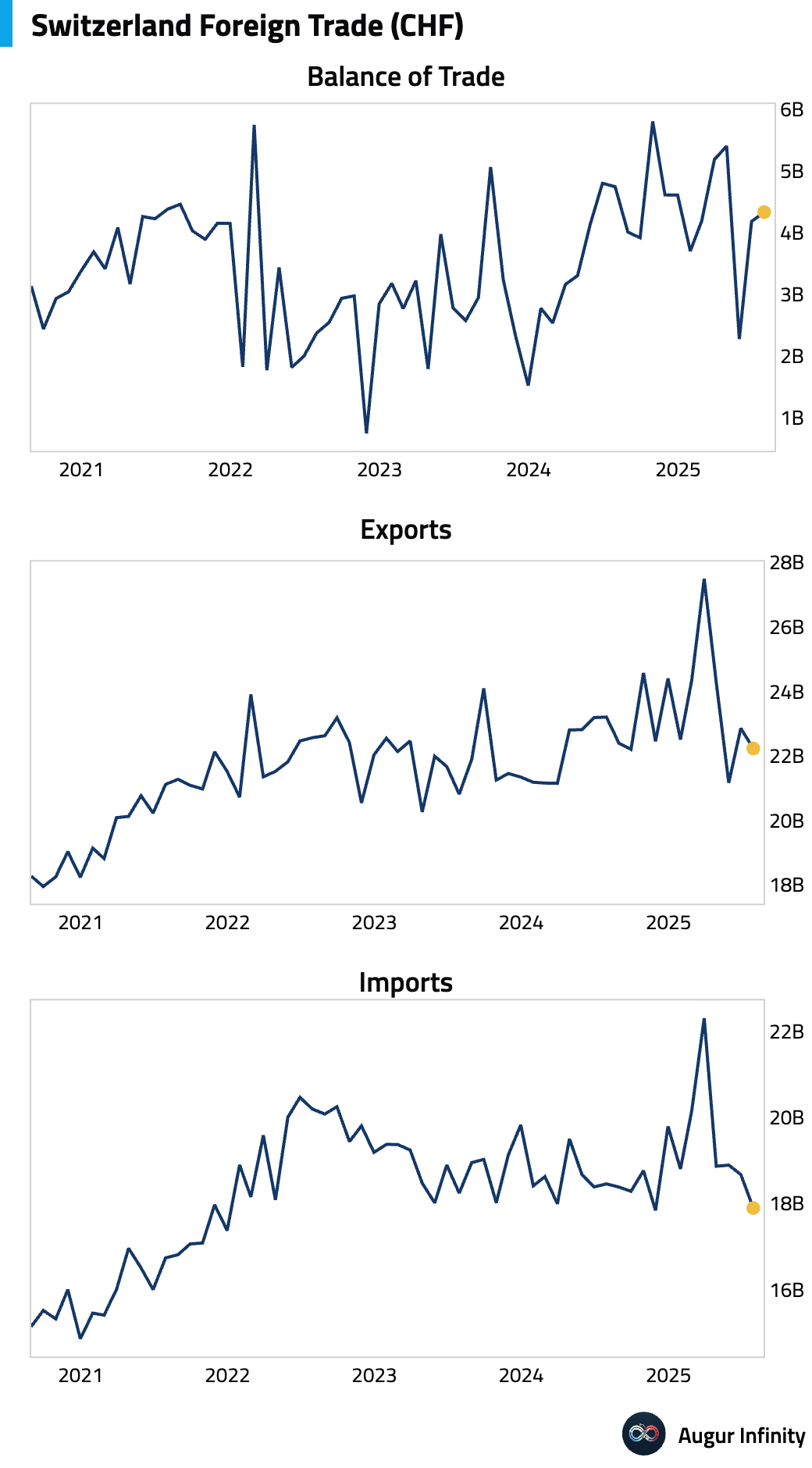

- Switzerland’s trade surplus widened to 4.3 billion CHF in July from 4.2 billion CHF in June.

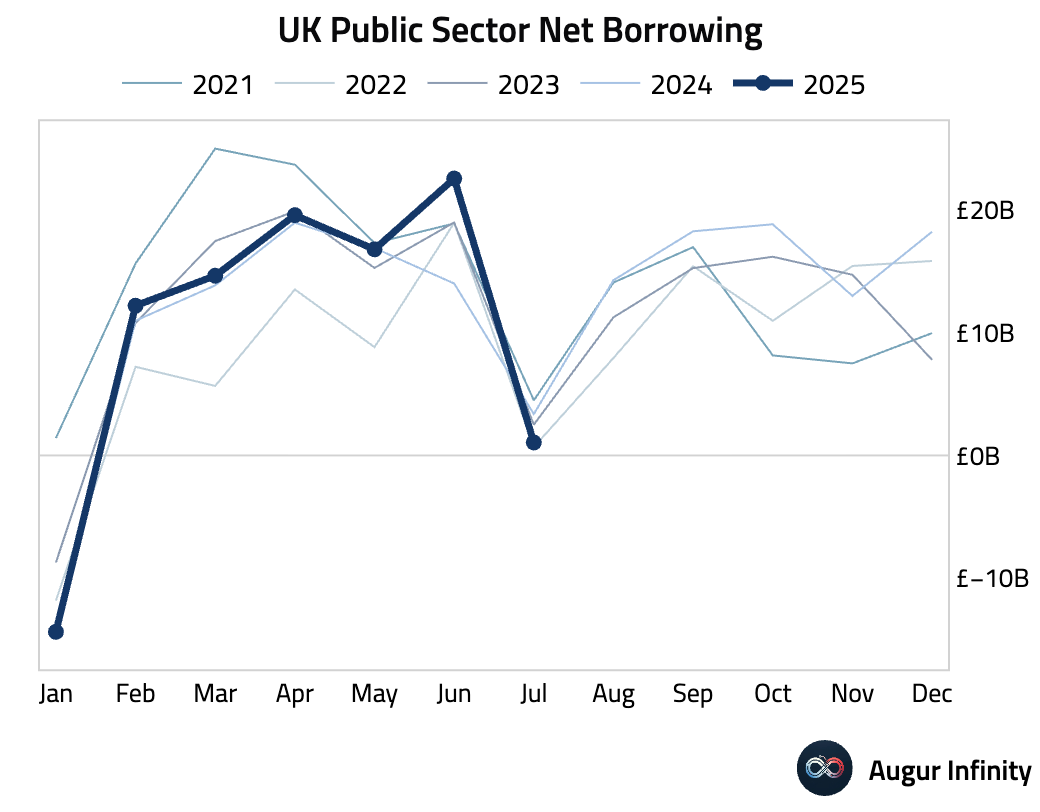

- The UK's public sector net borrowing (ex-banks) was £1.05 billion in July, smaller than the expected £2.6 billion.

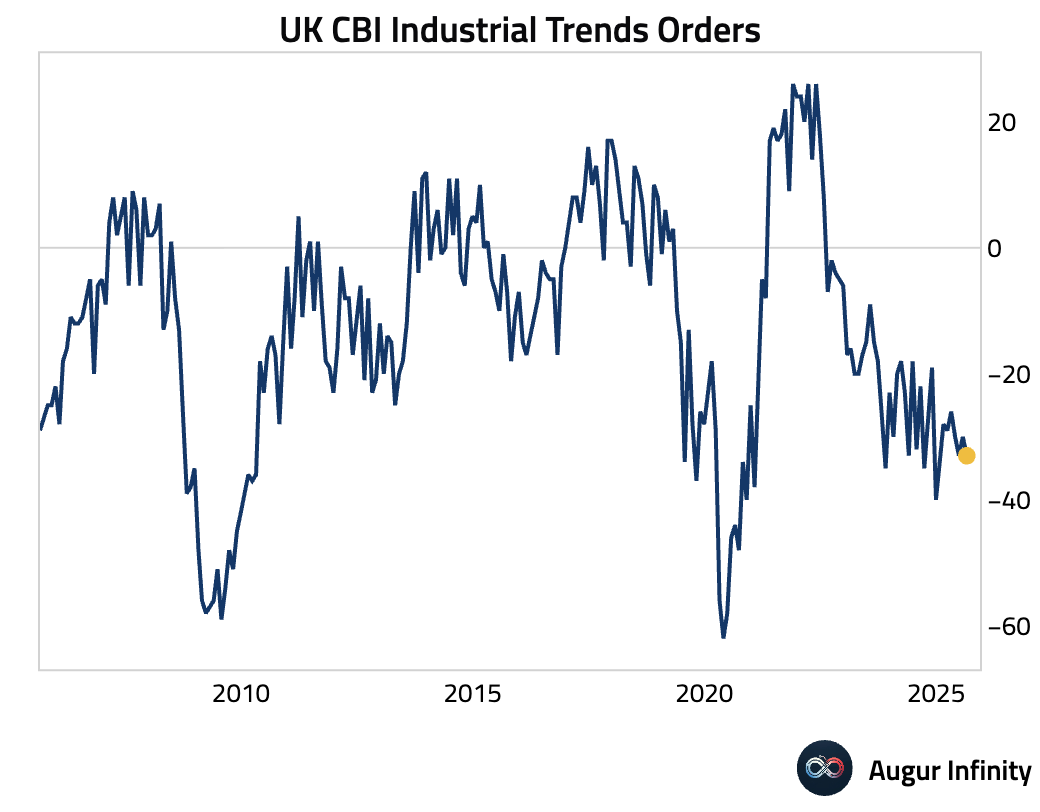

- The UK's CBI Industrial Trends Orders balance deteriorated further in August, falling to -33 from -30 and missing the consensus of -28.

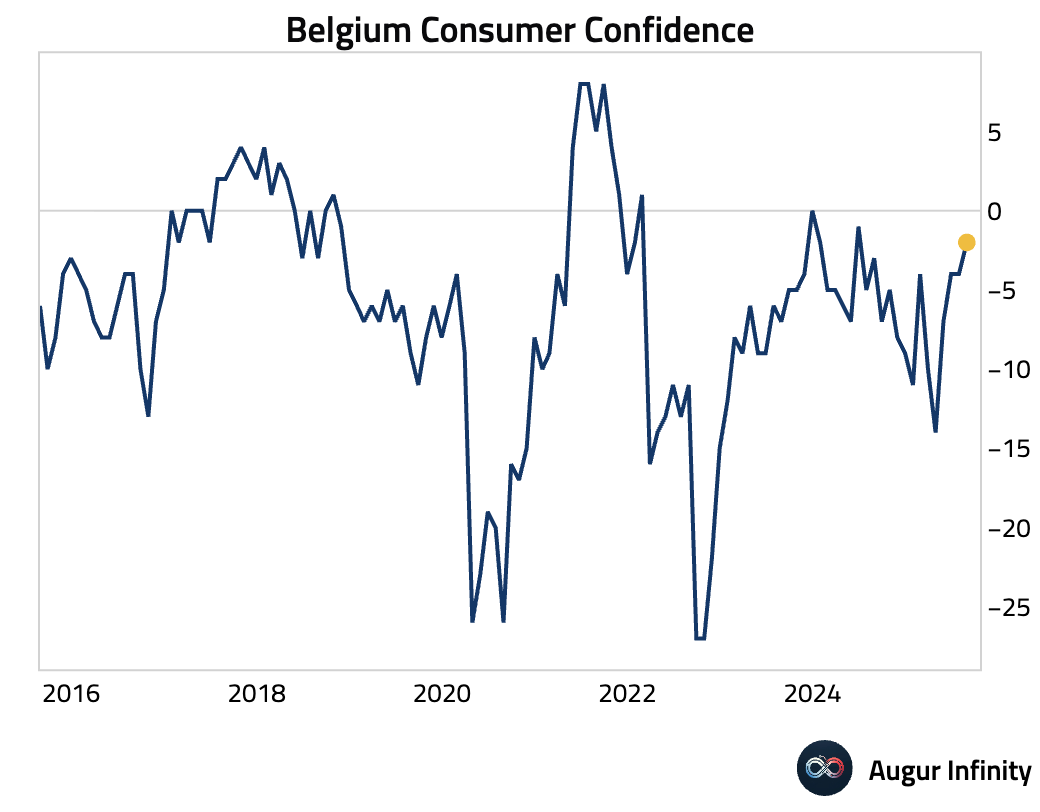

- Belgian consumer confidence improved in August, rising to -2 from -4 in July.

Asia-Pacific

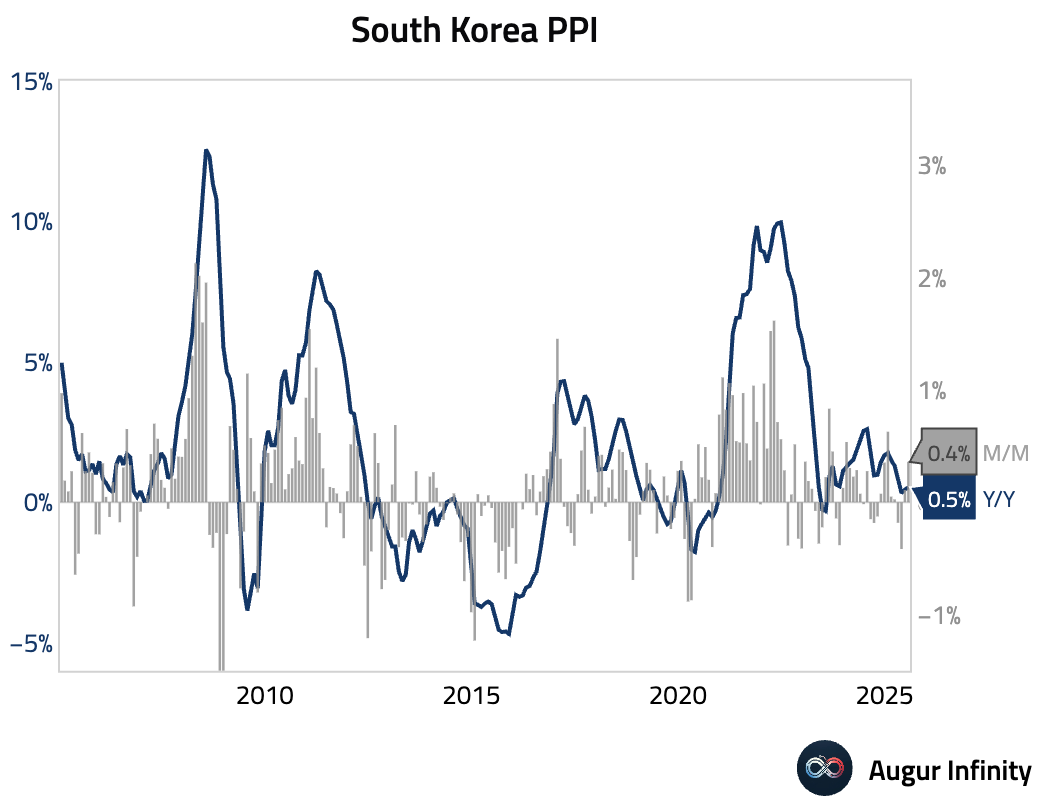

- South Korea’s Producer Price Index rose 0.4% M/M in July, accelerating from June’s 0.1% increase.

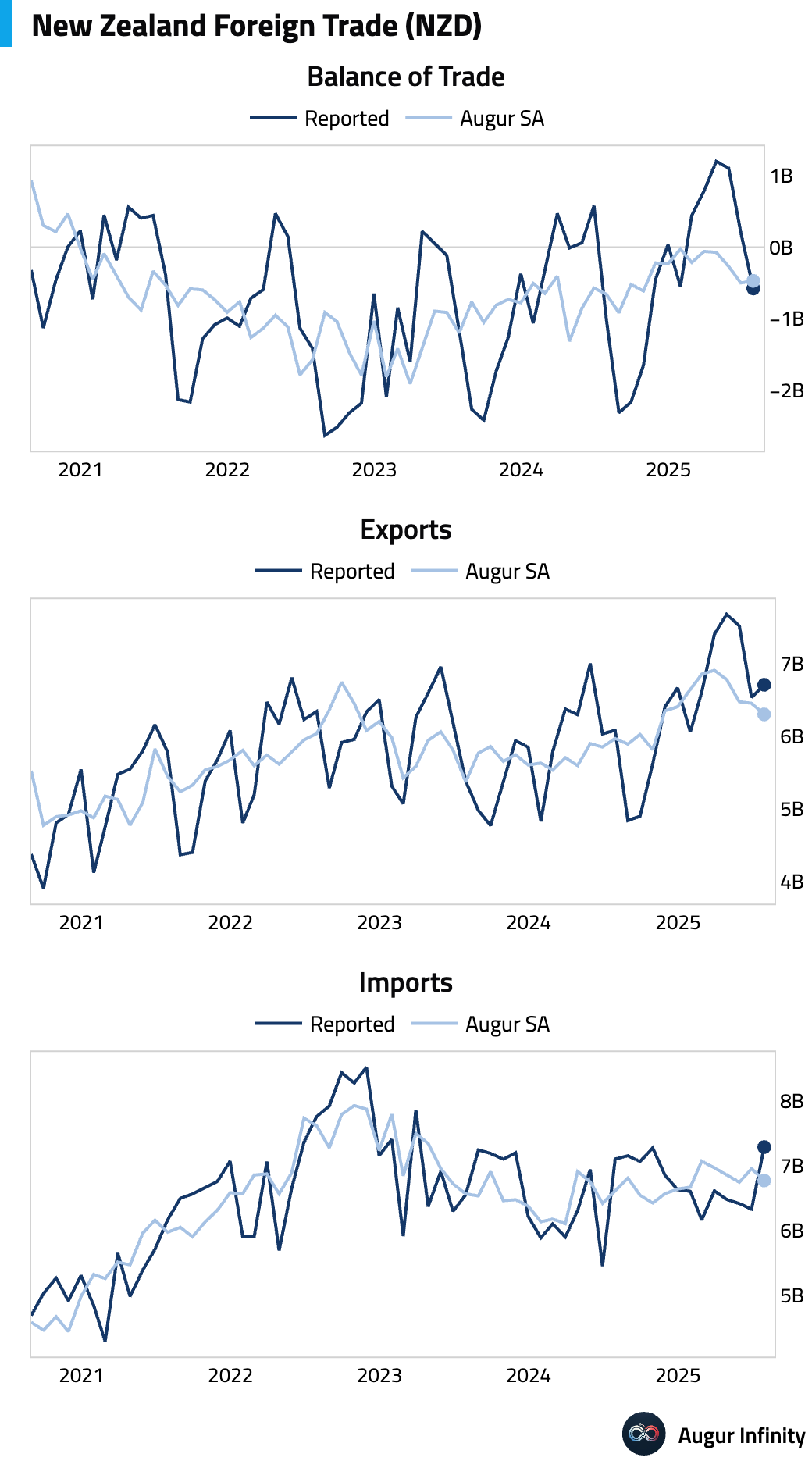

- New Zealand's trade balance swung to a deficit of NZ$578 million in July from a NZ$203 million surplus in June, widely missing the NZ$70 million surplus forecast. On a seasonally-adjusted basis, however, trade balance was roughly unchanged.

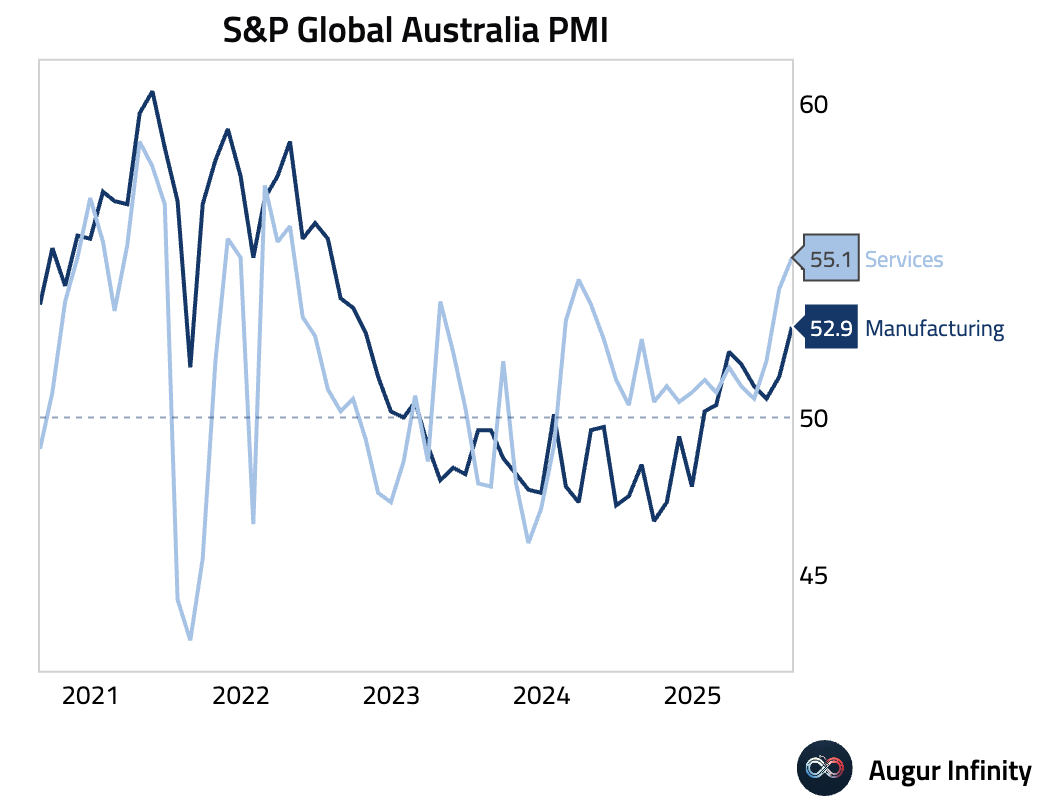

- Australia’s Flash S&P Global Composite PMI surged to 54.9 in August, the fastest expansion since April 2022. The strength was broad-based, with the Services PMI rising to 55.1 and the Manufacturing PMI climbing to 52.9. Growth was driven by solid domestic new orders and the quickest rise in exports in six months.

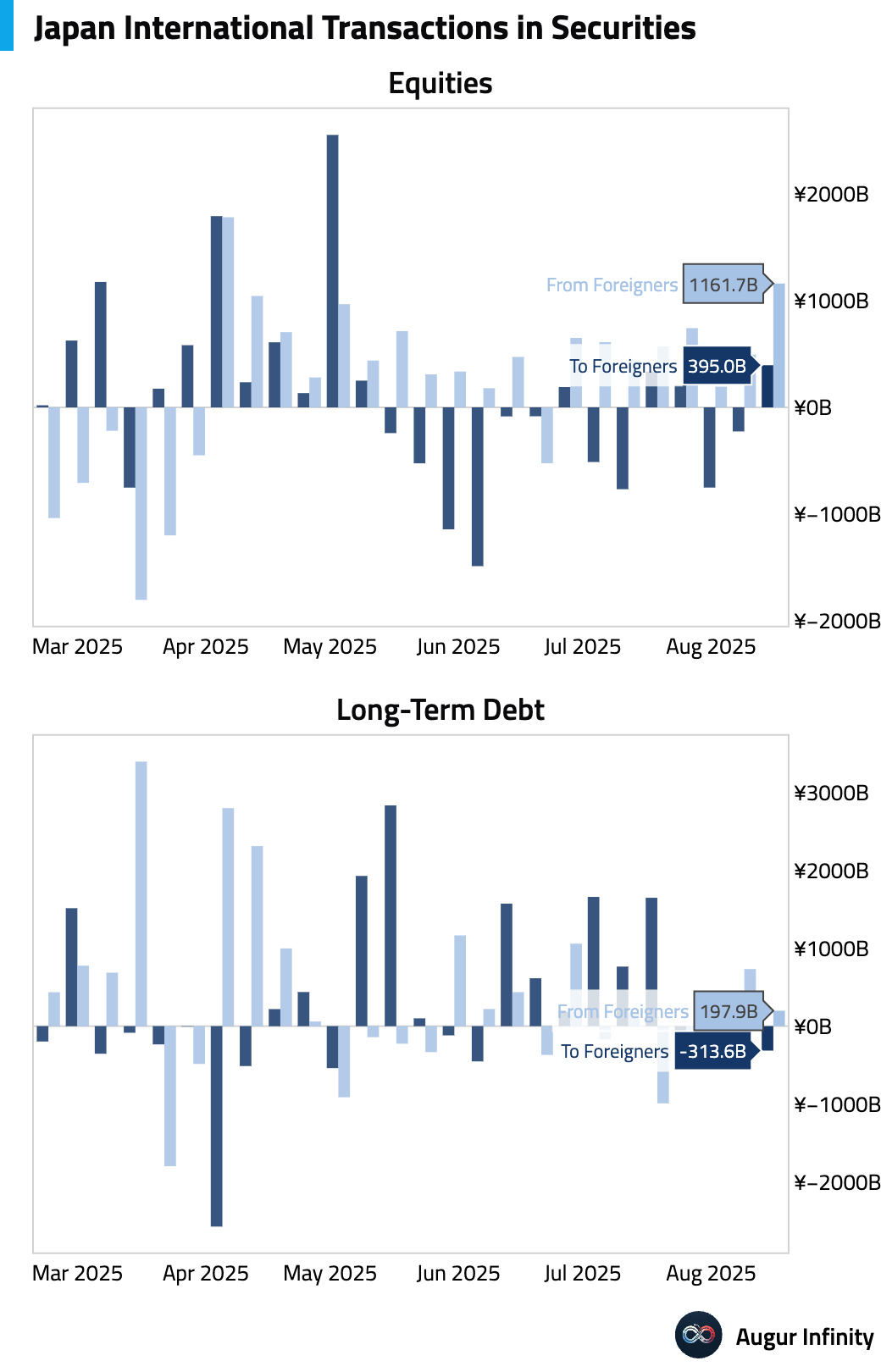

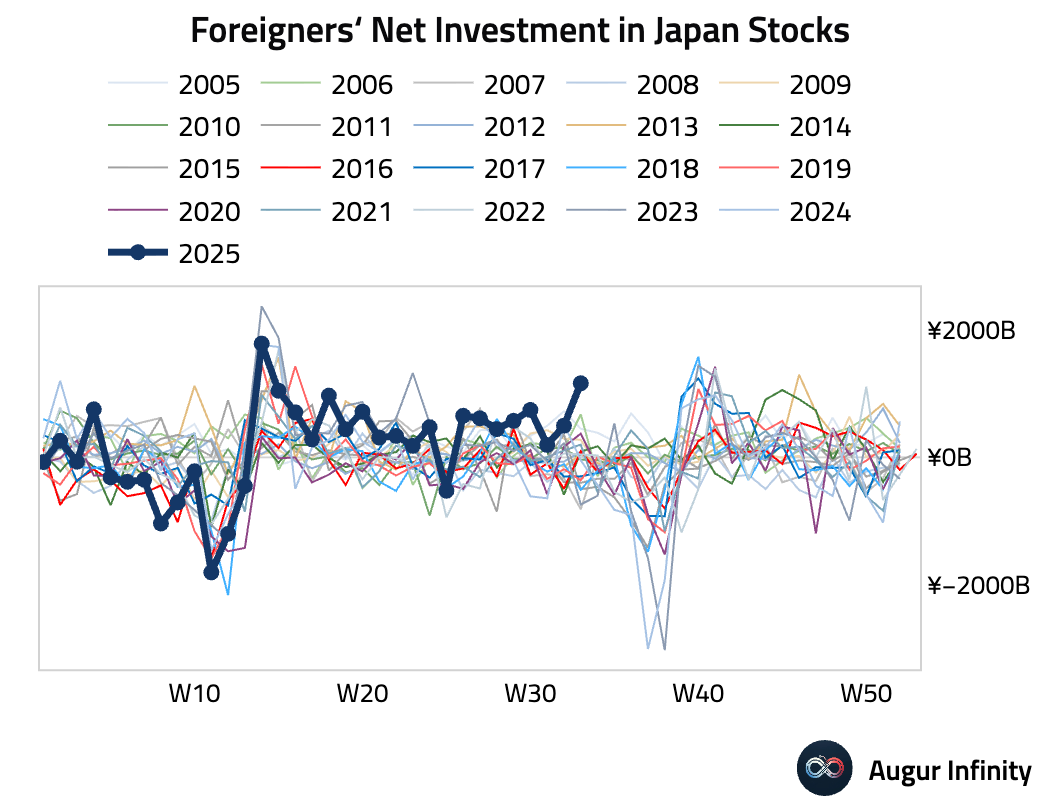

- Japanese investors were heavy net sellers of foreign bonds in the week ending August 16, offloading ¥313.6 billion. By contrast, foreigner's net investment in Japanese stocks surged to ¥1.16 trillion, the highest on record for this week of the year (week 33).

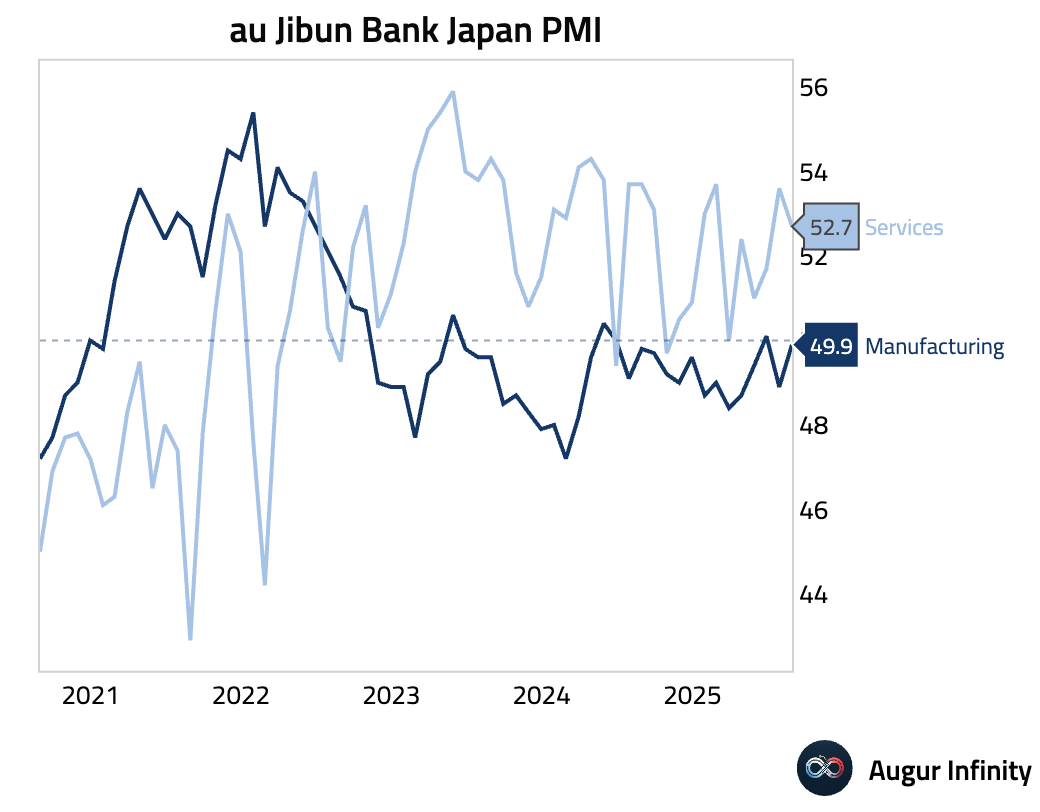

- Japan's S&P Global Flash Composite PMI hit a 6-month high of 51.9 in August. The Manufacturing PMI rose to 49.9, though the recovery remains fragile as new orders fell. The Services PMI eased to 52.7 but continued to be the main driver of growth, supported by domestic demand.

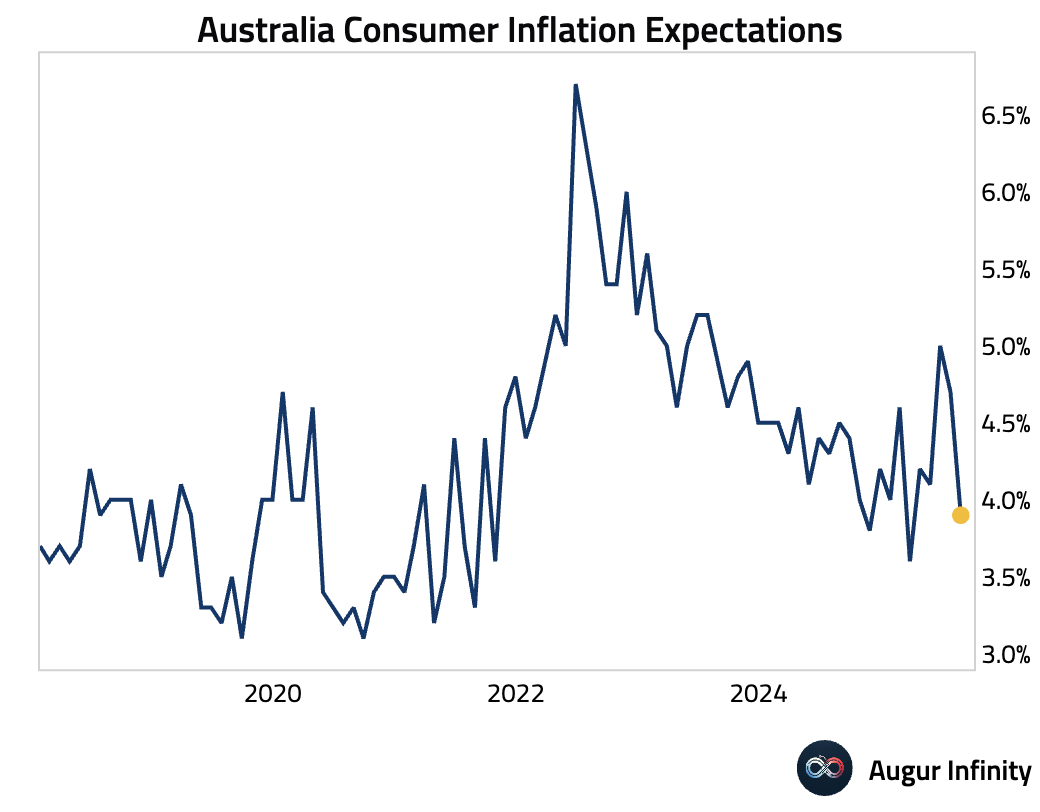

- Australian consumer inflation expectations for August fell sharply to 3.9% from 4.7% in July.

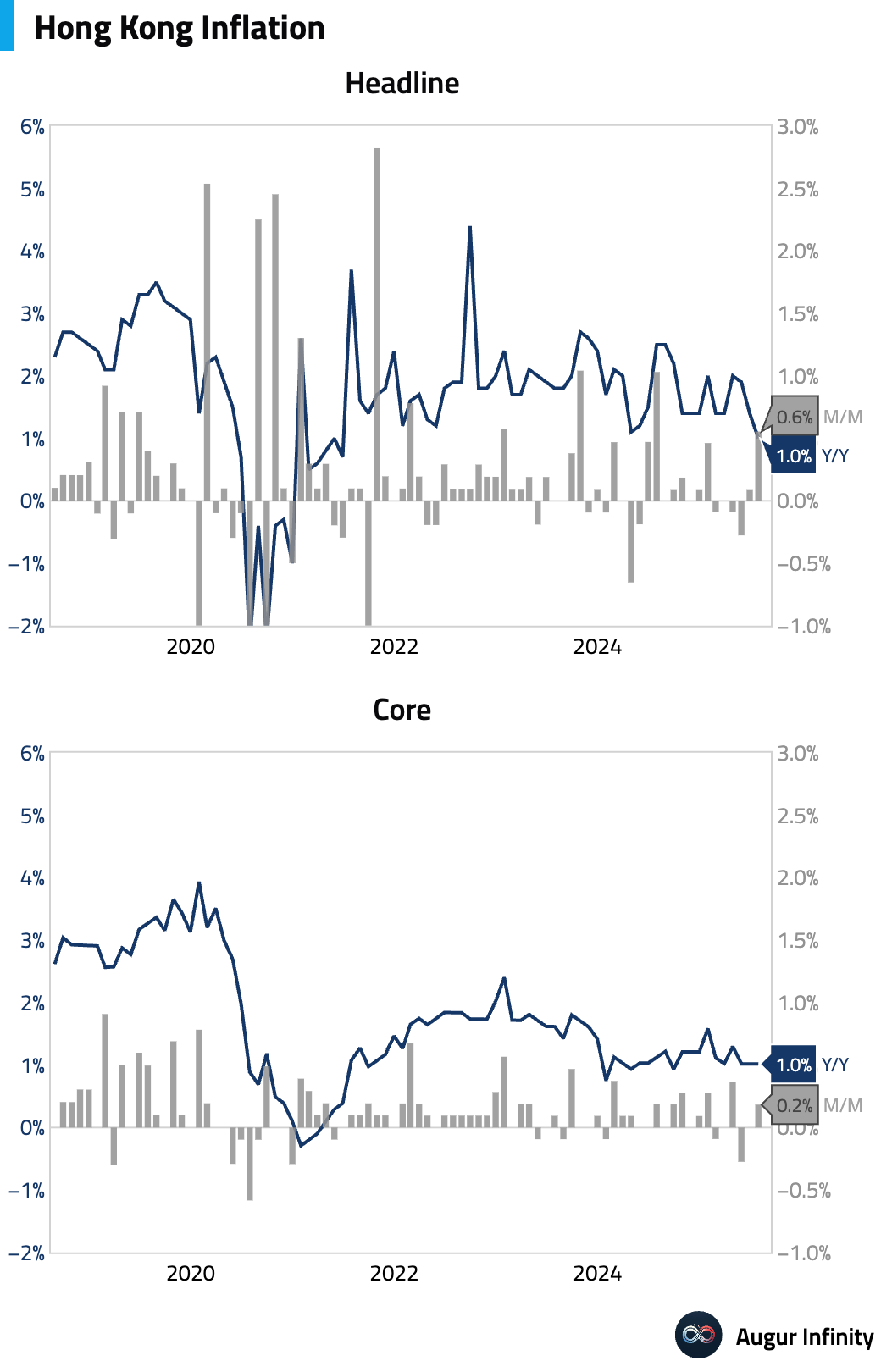

- Hong Kong’s annual inflation rate slowed to 1.0% Y/Y in July from 1.4%, though the M/M inflation accelerated to 0.6%.

Emerging Markets ex China

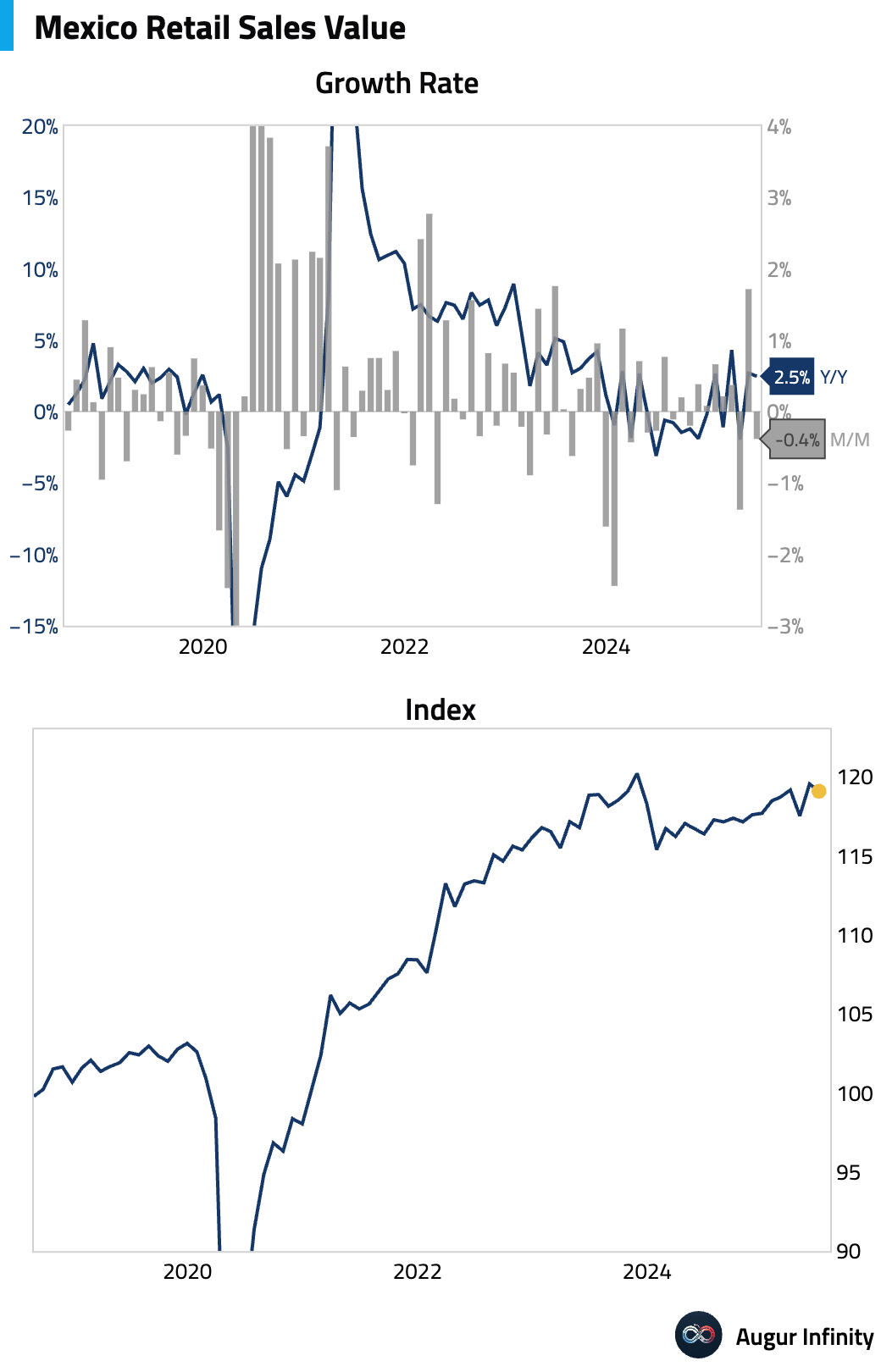

- Mexico's retail sales fell 0.4% M/M in June, weaker than the flat reading expected. The year-over-year growth rate slowed to 2.5% from 2.7%. The decline contributes to a quarterly deceleration, with mixed underlying signals for household spending from a slight dip in employment offset by strong real wage growth.

- Indonesia's current account deficit widened significantly in Q2 to $3.0 billion from $0.2 billion in Q1.

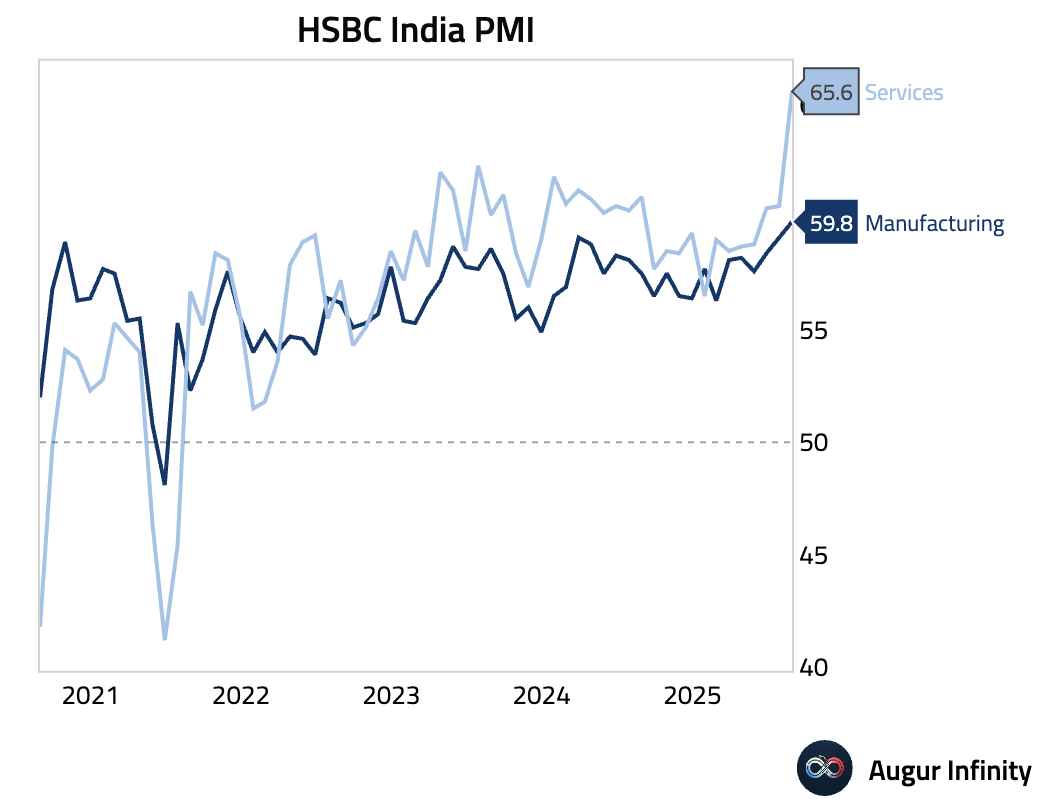

- India’s private sector expanded at a survey-record pace in August, with the HSBC Flash Composite PMI hitting 65.2. The surge was led by the Services PMI reaching an all-time high of 65.6, driven by sharp rises in new domestic and export orders. The Manufacturing PMI also improved to 59.8. Crucially, output price inflation rose faster than input costs, indicating strong pricing power and improving corporate margins.

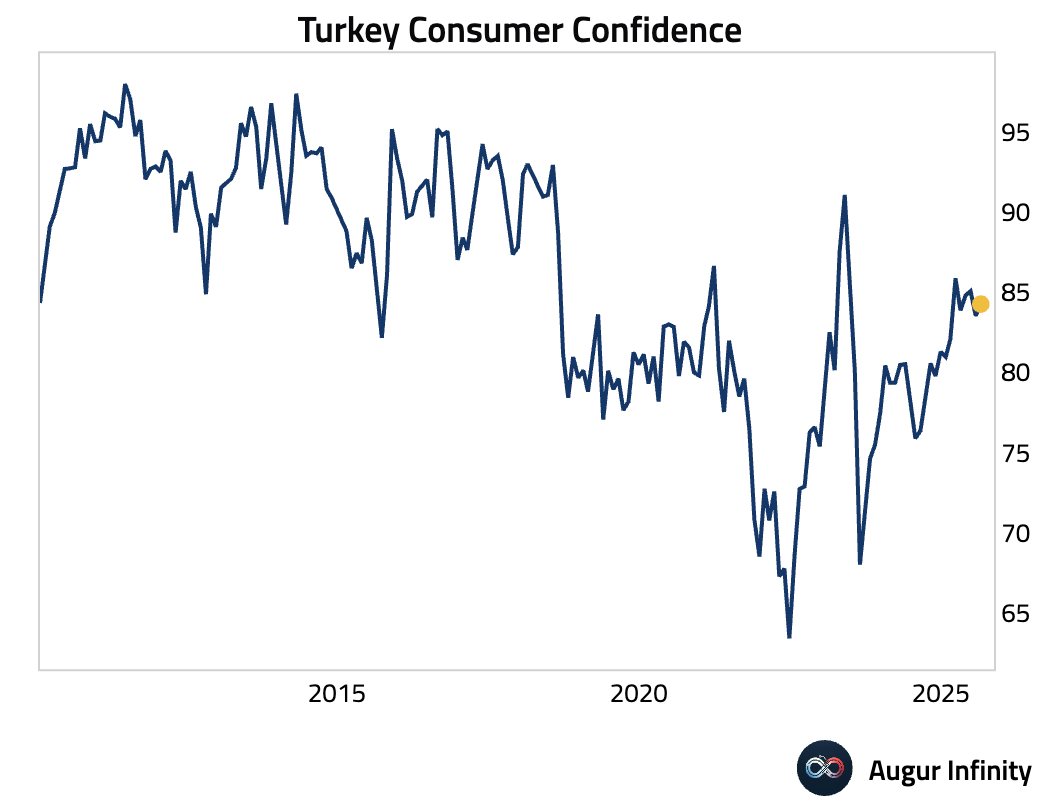

- Turkey's consumer confidence edged up to 84.3 in August from 83.5 in July.

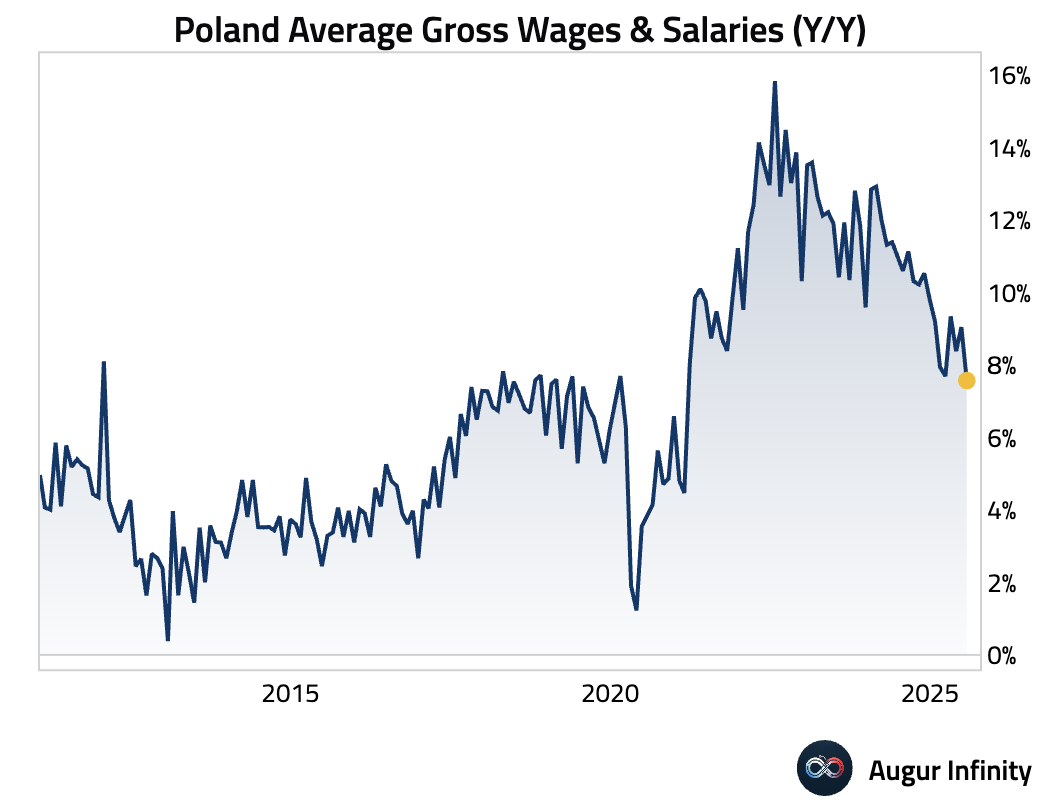

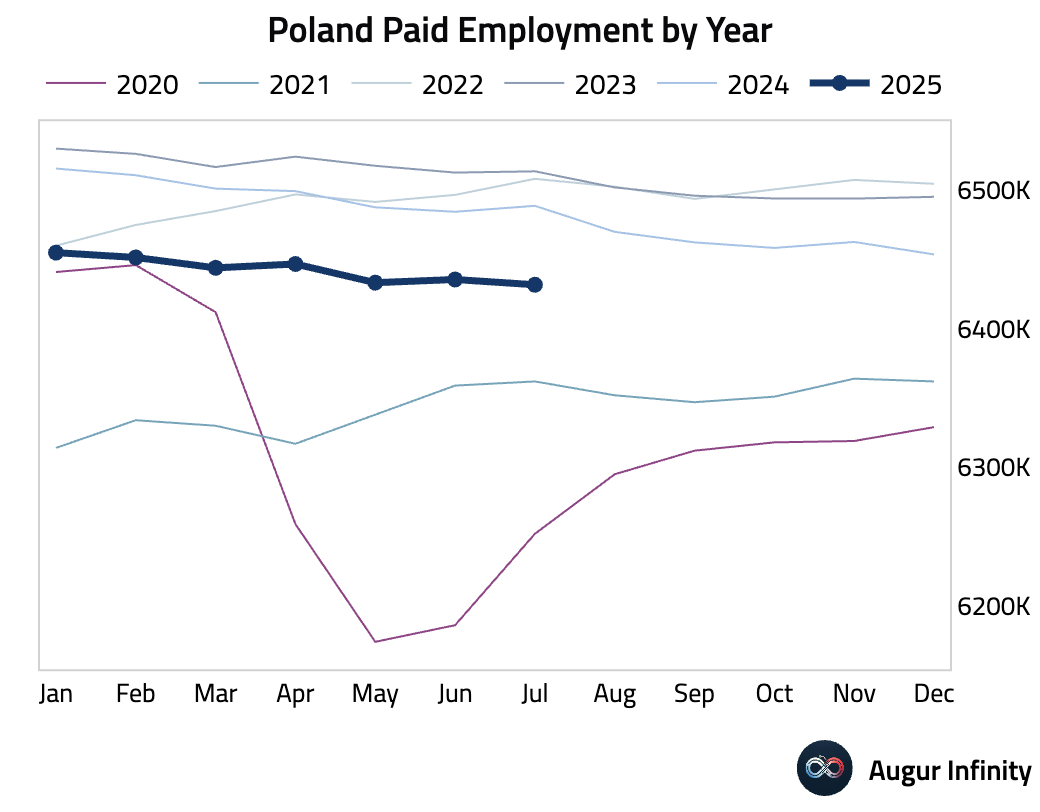

- Poland's corporate sector wage growth slowed significantly to 7.6% Y/Y in July from 9.0%, well below the 8.6% consensus. Employment continued to contract, falling 0.9% Y/Y.

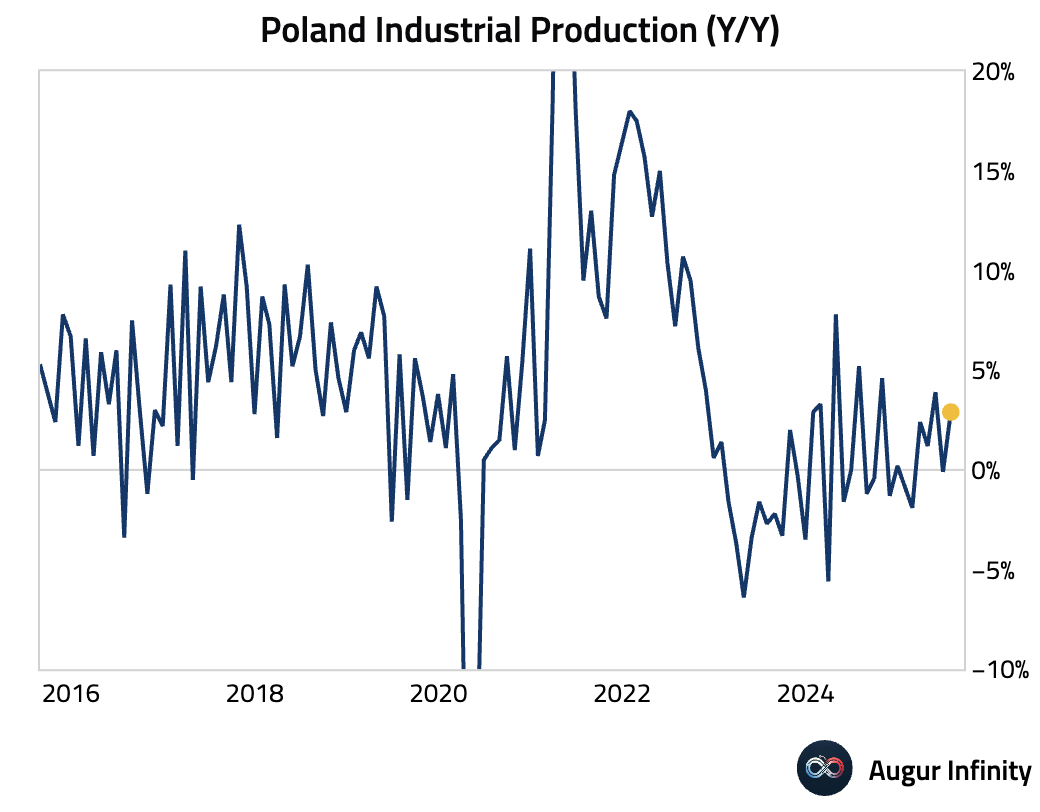

- Polish industrial production rebounded in July, growing 2.9% Y/Y after a 0.4% fall in June and beating the 1.6% consensus.

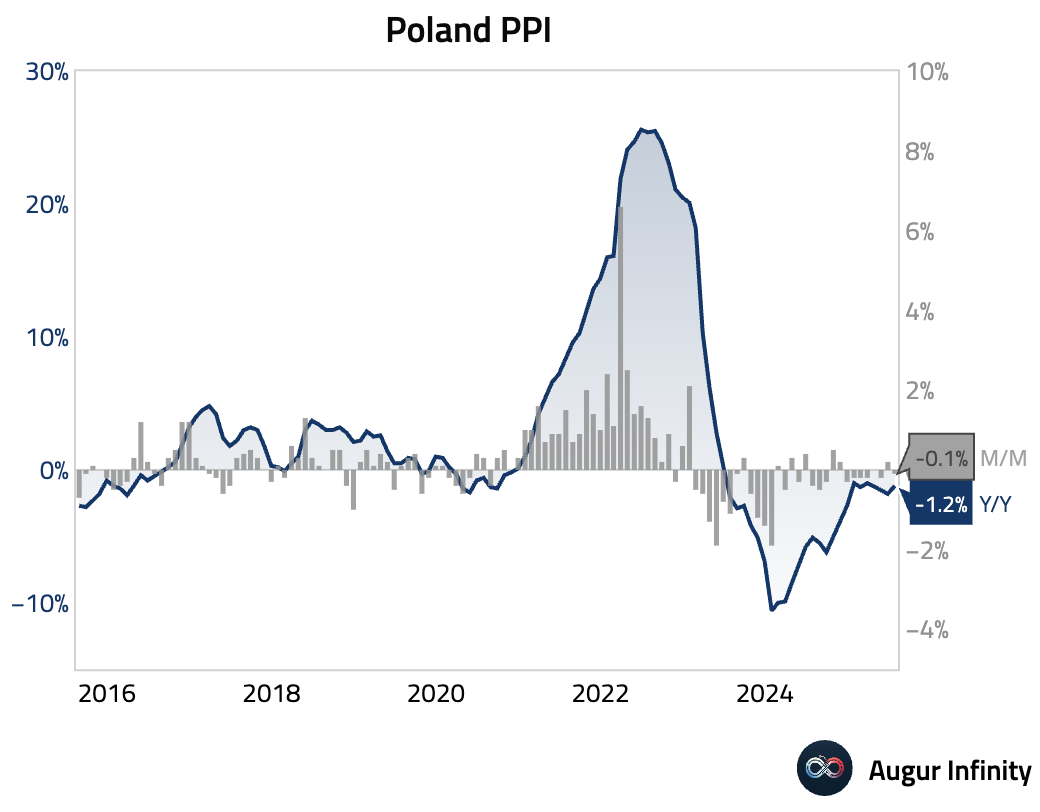

- Poland’s producer prices fell 1.2% Y/Y in July, a slightly smaller decline than the 1.5% drop in June.

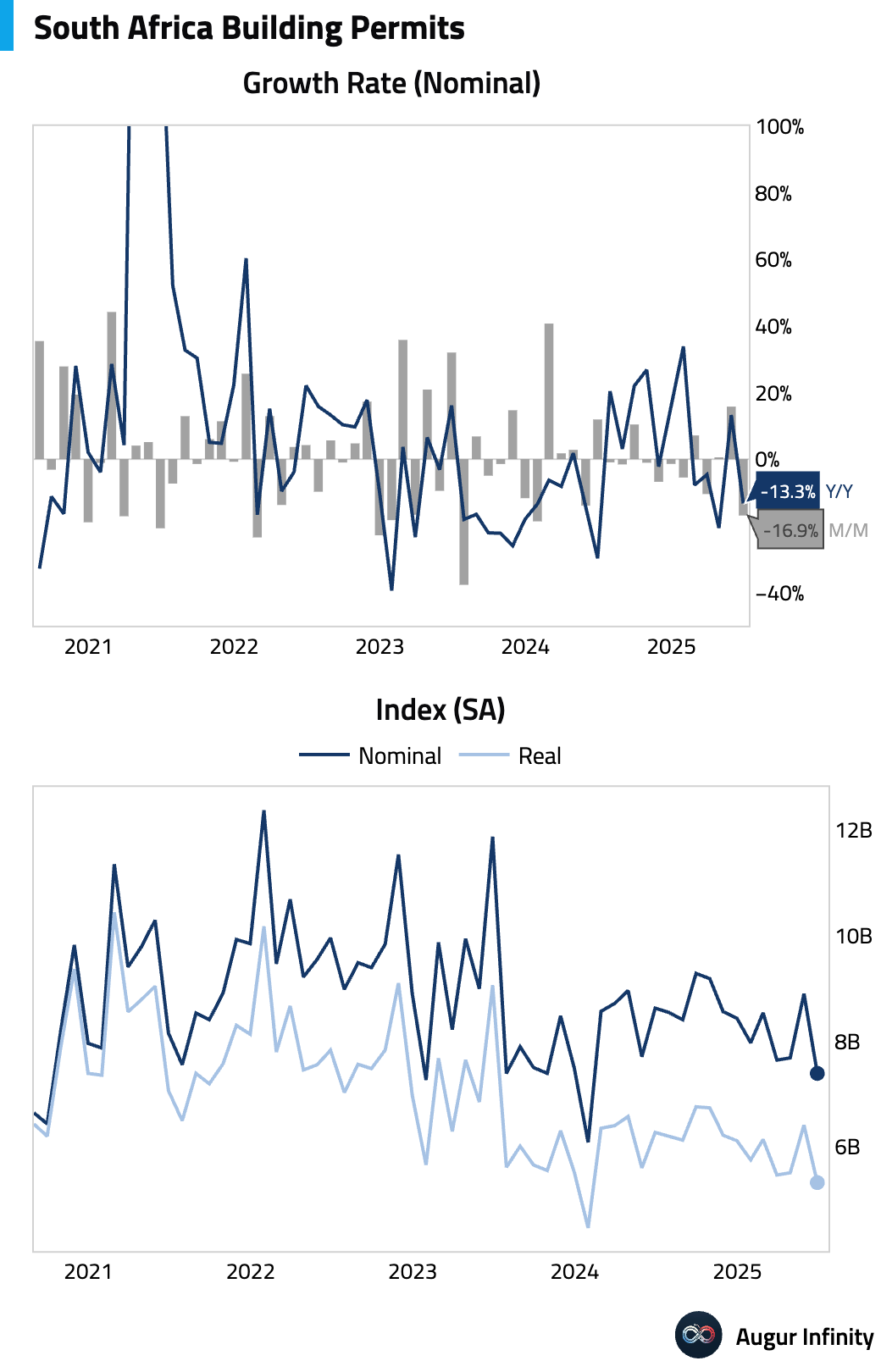

- South Africa’s building permits plunged 13.3% Y/Y in June, reversing a 13.2% gain in May.

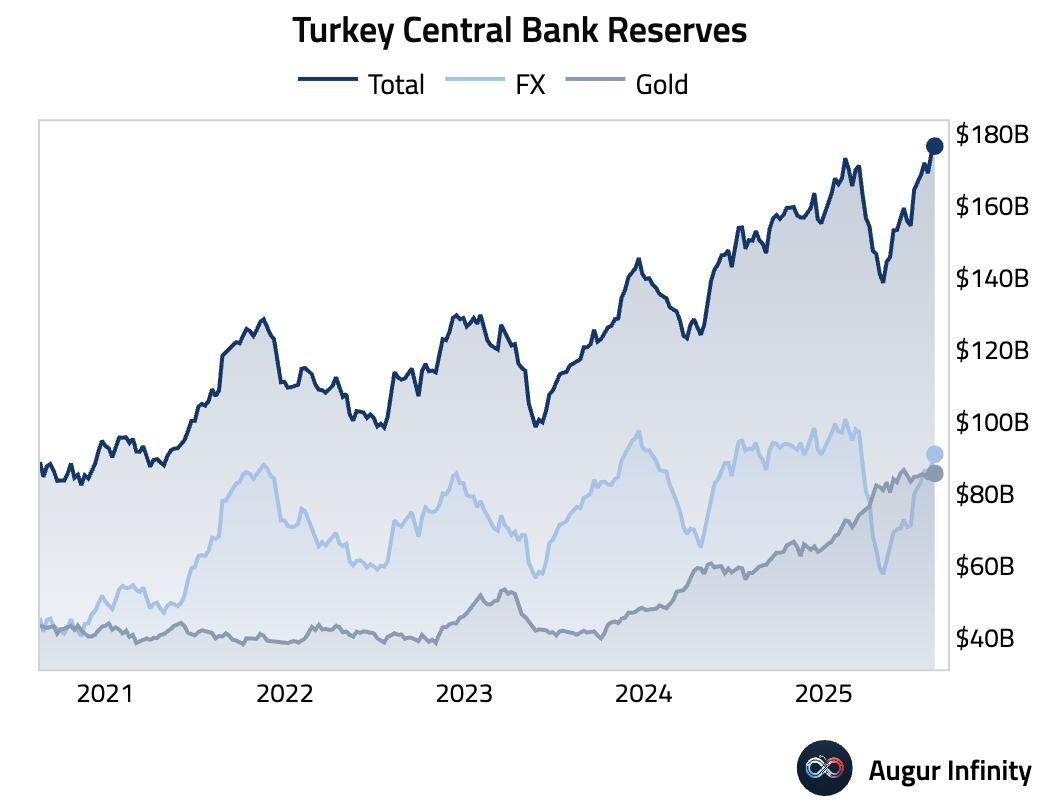

- Turkey’s gross foreign exchange reserves increased to $90.93 billion for the week ending August 15 from $87.61 billion the prior week.

Global Markets

Equities

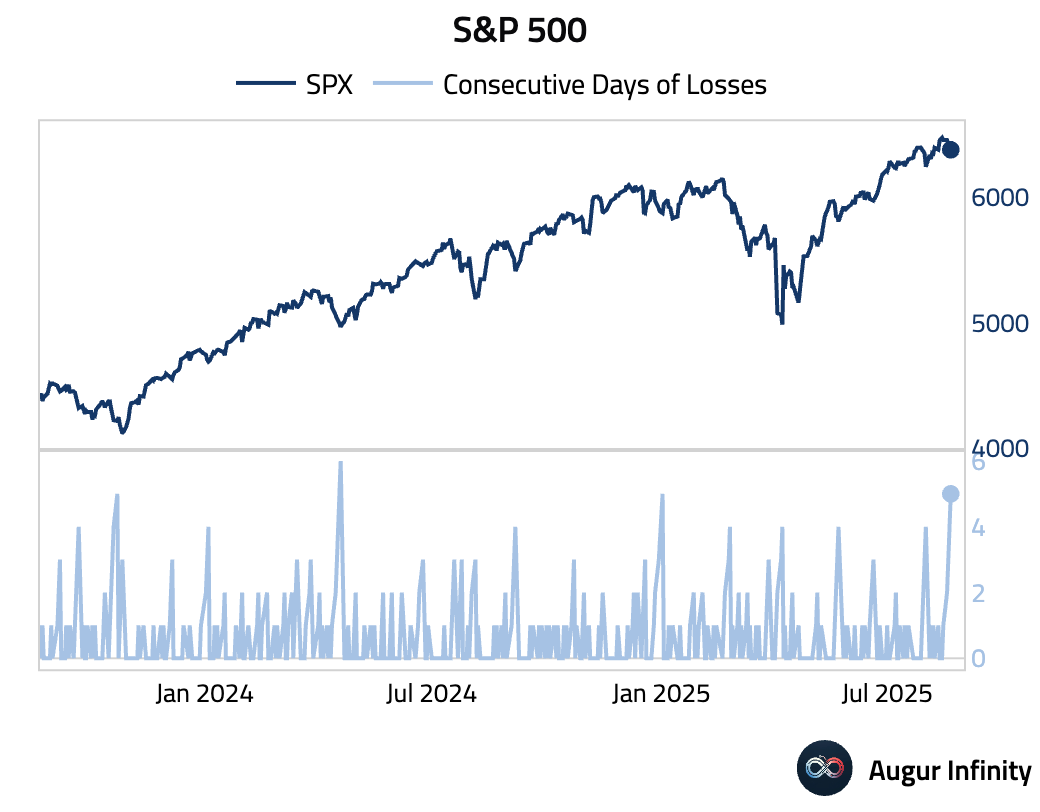

- Global equities declined for a third consecutive session. The broader US market was down 0.4%, while the Nasdaq composite slipped 0.34%, marking its third day of losses. South Korean equities extended their losing streak to six days. In contrast, Australian and Mexican markets posted modest gains.

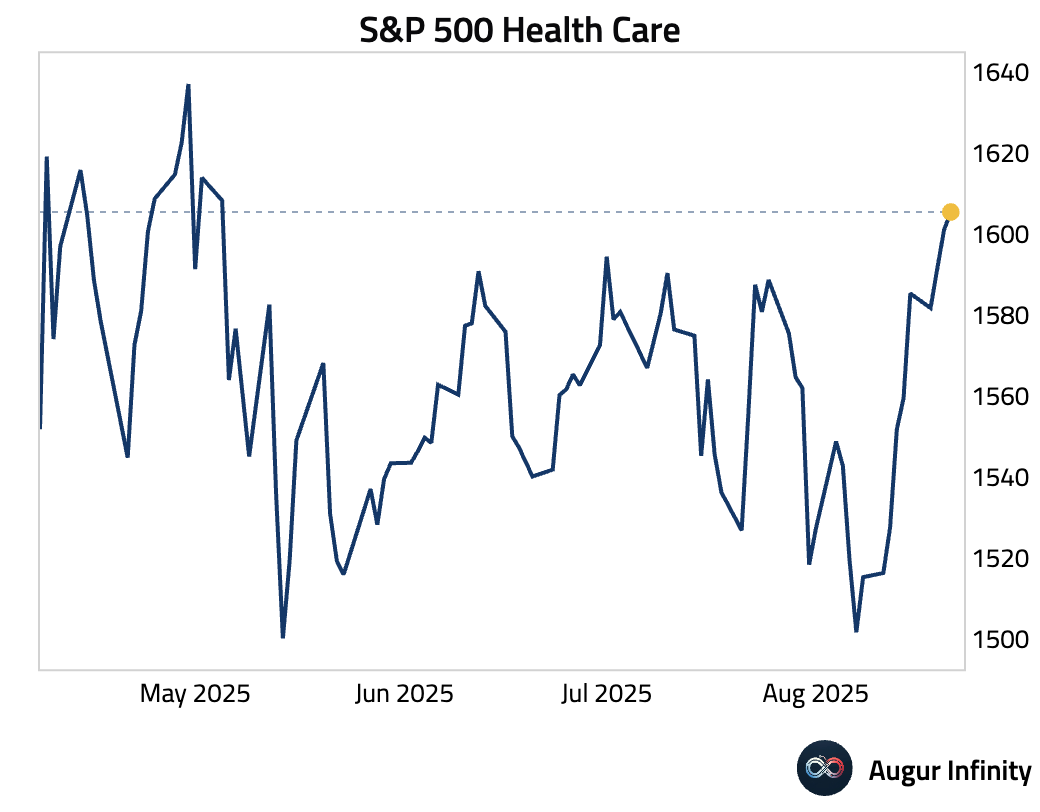

- The S&P 500 Index fell for the fifth consecutive day today. However, the Health Care sector bucked the trend, rising to the highest level in 2.5 months.

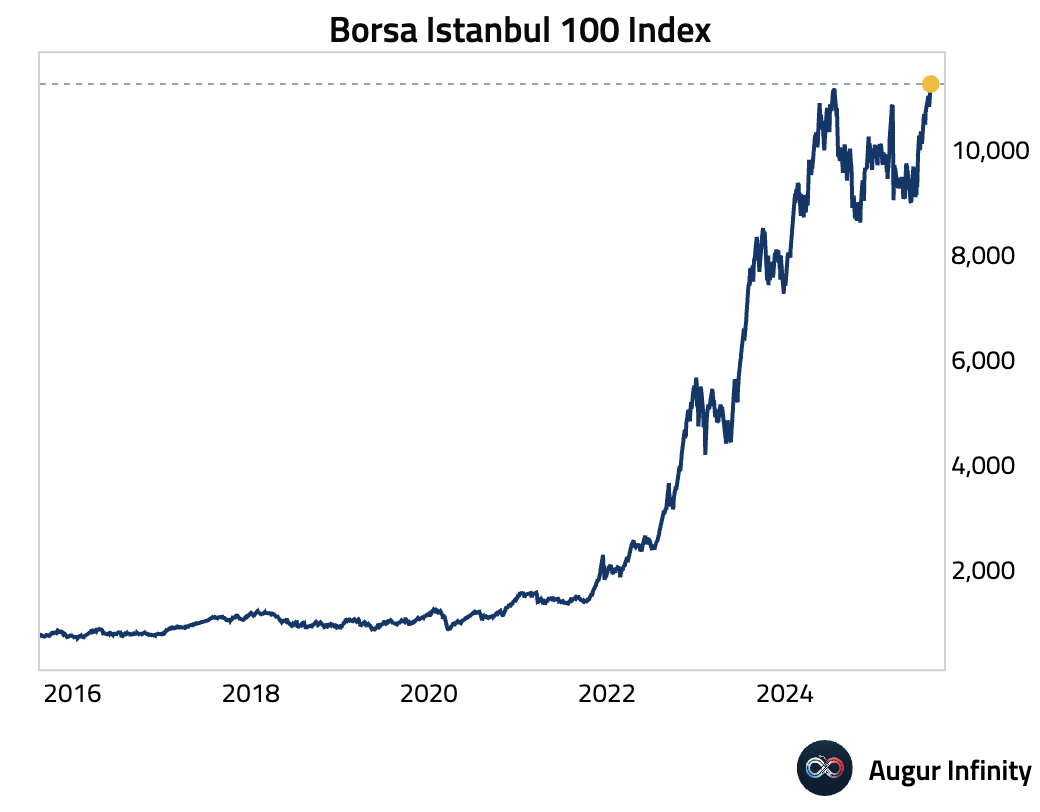

- After five consecutive days of gains, the Borsa Istanbul 100 Index has reached an all-time high.

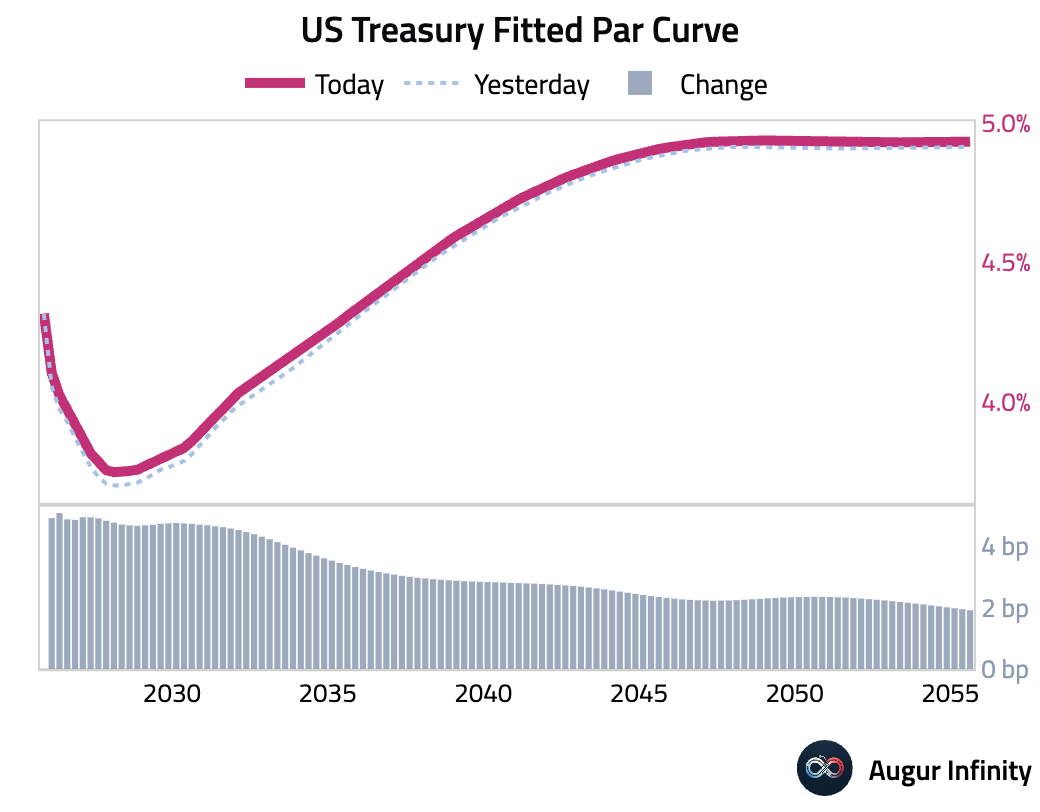

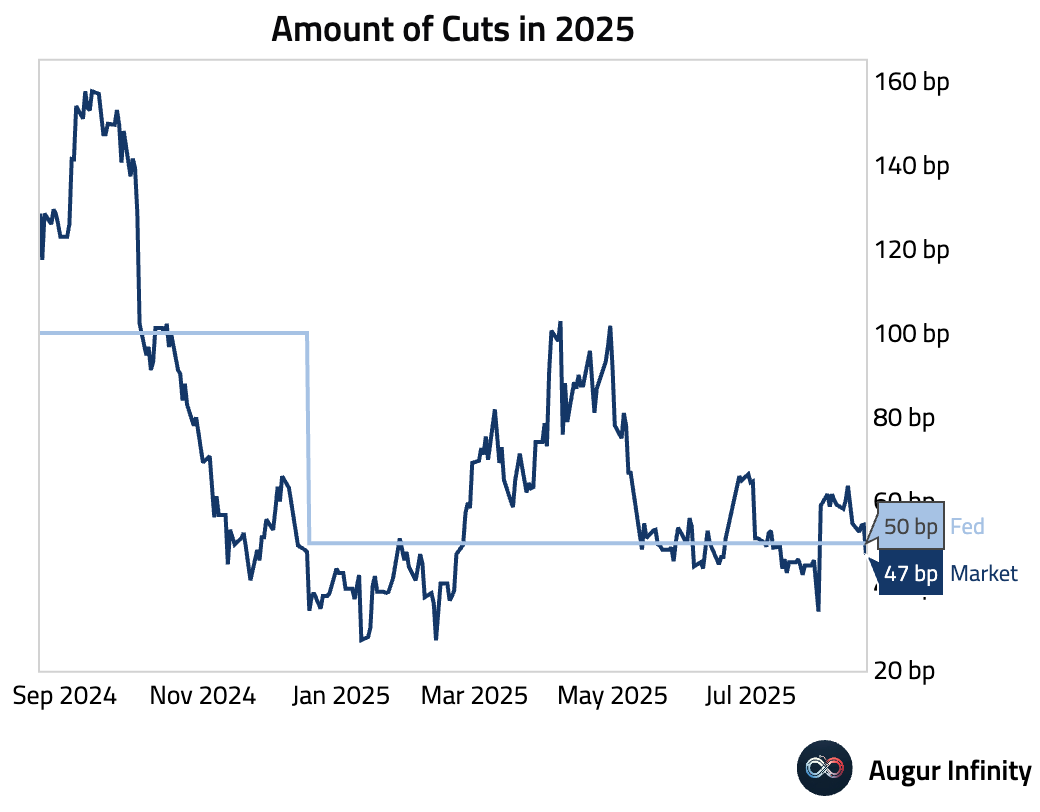

Fixed Income

- US Treasury yields rose across the curve. Yields on the 2-year note climbed 4.7 bps, while the 10-year yield increased by 3.4 bps.

- The amount of rate cuts in 2025 priced by the market fell below 50 bps to 47 bps.

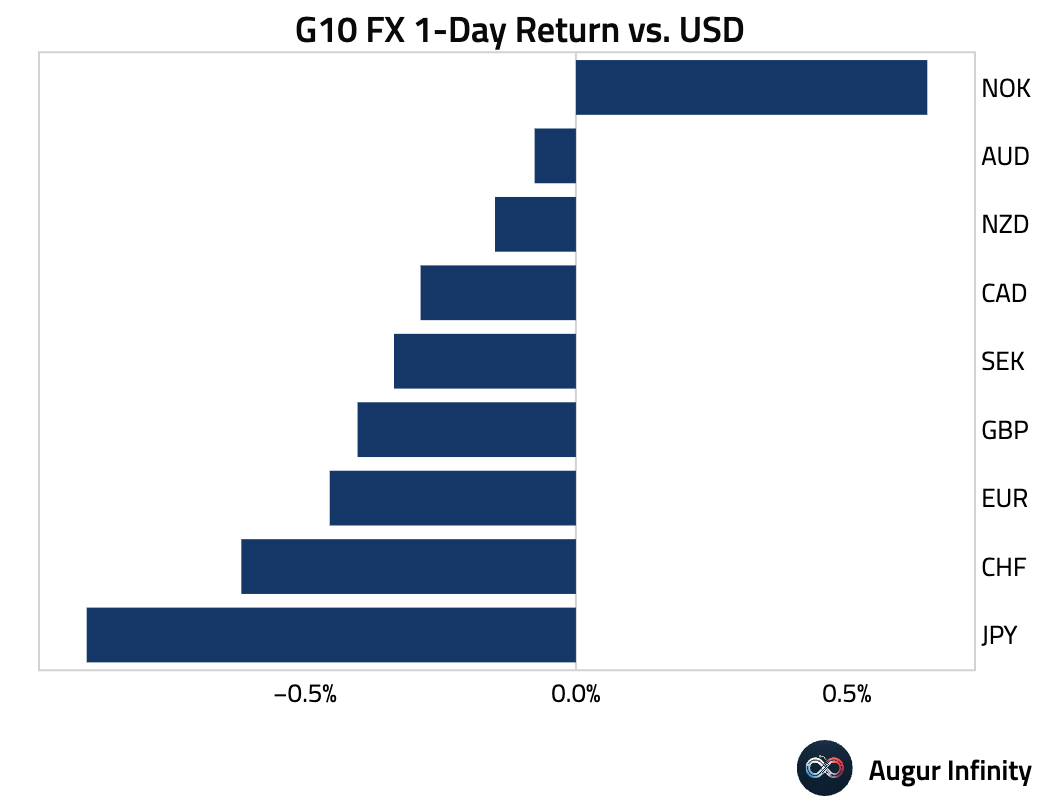

FX

- The US dollar strengthened against most of its G10 peers. The Japanese yen was the most significant underperformer, falling 0.9%. The Canadian dollar weakened for a sixth consecutive session, down 0.3%. The Australian dollar, British pound, New Zealand dollar, and Swedish krona all posted their fourth straight day of losses against the greenback. The Norwegian krone was the notable exception, gaining 0.6%.

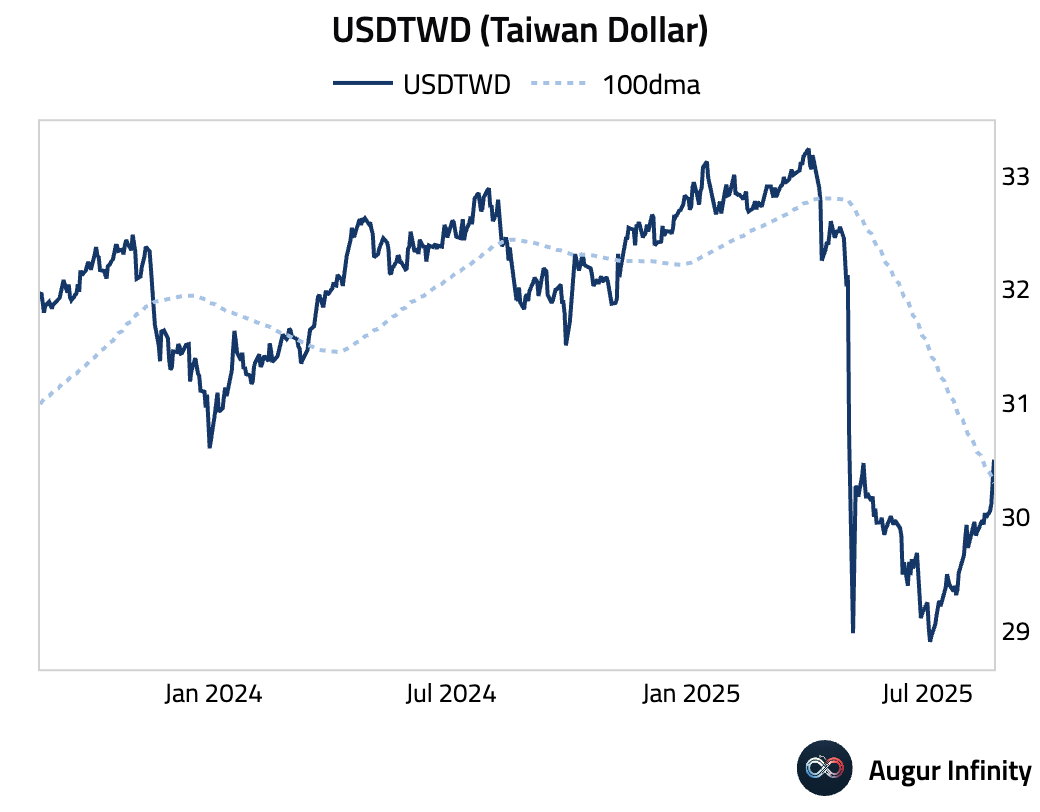

- USDTWD rose above its 100-day moving average.

Commodities

- Coffee futures rallied by over 14% over the past five sessions, the best 5-day run since July 2021.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.