Jackson Hole

- At the Jackson Hole conference, Chair Powell said the “baseline outlook and shifting balance of risks may warrant adjusting our policy stance,” adding that a stable unemployment rate allows the FOMC to “proceed carefully” on policy changes. These remarks support the case for a 25 bps cut in September.

- Chair Powell noted that “downside risks to employment are rising” and GDP growth has "slowed notably." On inflation, he said tariffs likely imply a “one-time shift in the price level,” while inflation expectations “remain well anchored.” He added that sustained inflation from wage-price dynamics seems unlikely as the labor market is “not particularly tight.”

- The FOMC released a new “Statement of Longer-Run Goals and Monetary Policy Strategy,” reverting to flexible inflation targeting rather than tolerating moderate overshoots of 2% after a prolonged period with inflation below the Fed’s 2% target.

- The dovish speech fueled an equity rally, while bond yields and Fed rate expectations declined sharply.

Global Economics

United States

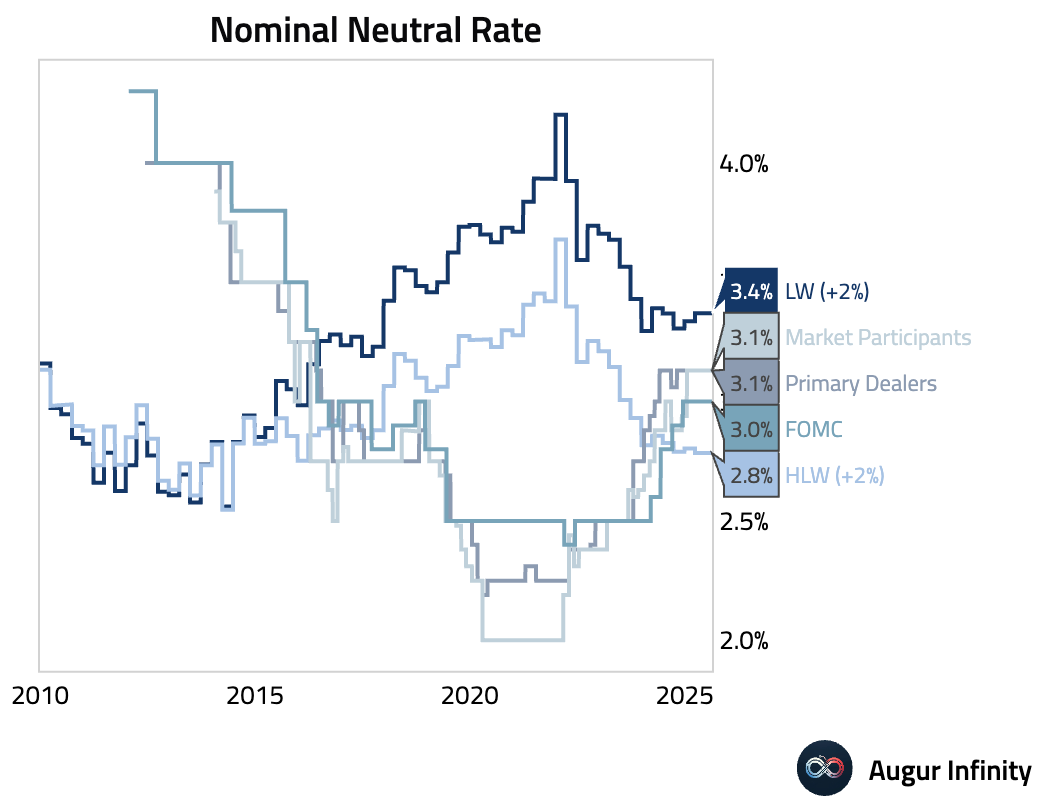

- The latest New York Fed Survey of Market Expectations puts the longer-run Fed funds rate at 3.1%, a touch higher than FOMC’s estimate in June.

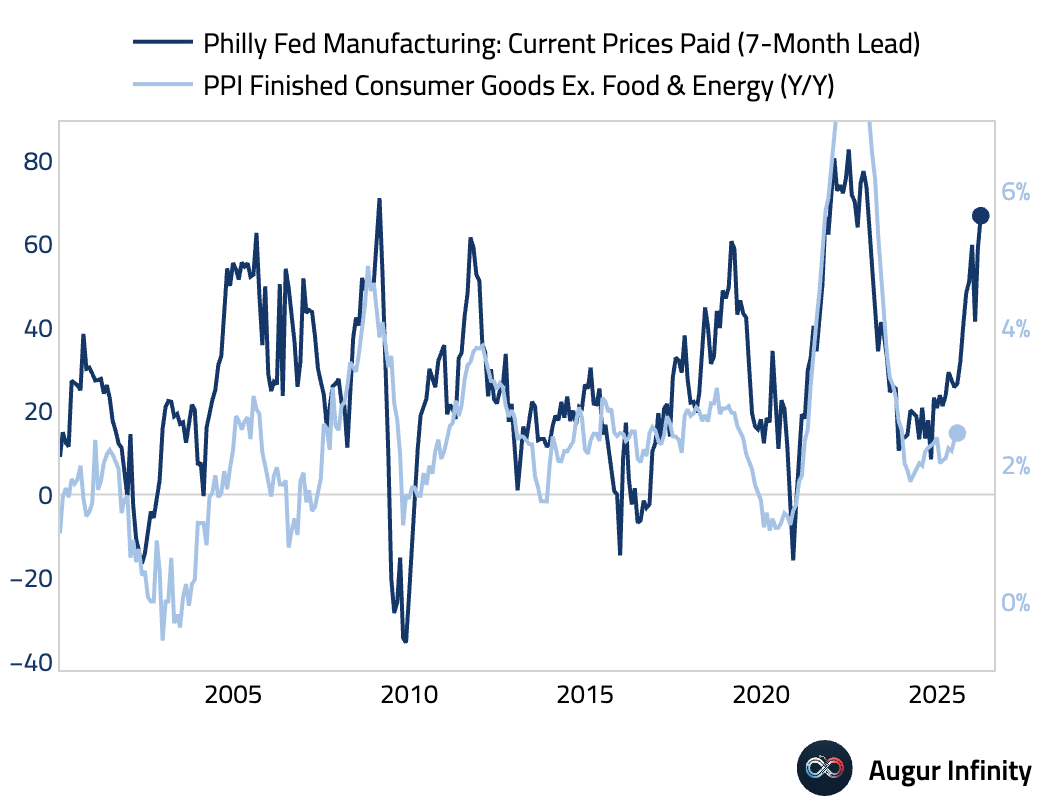

- The prices paid component of the Philadelphia Fed Manufacturing Survey surged to the highest level since May 2022, signaling persistent inflationary pressures.

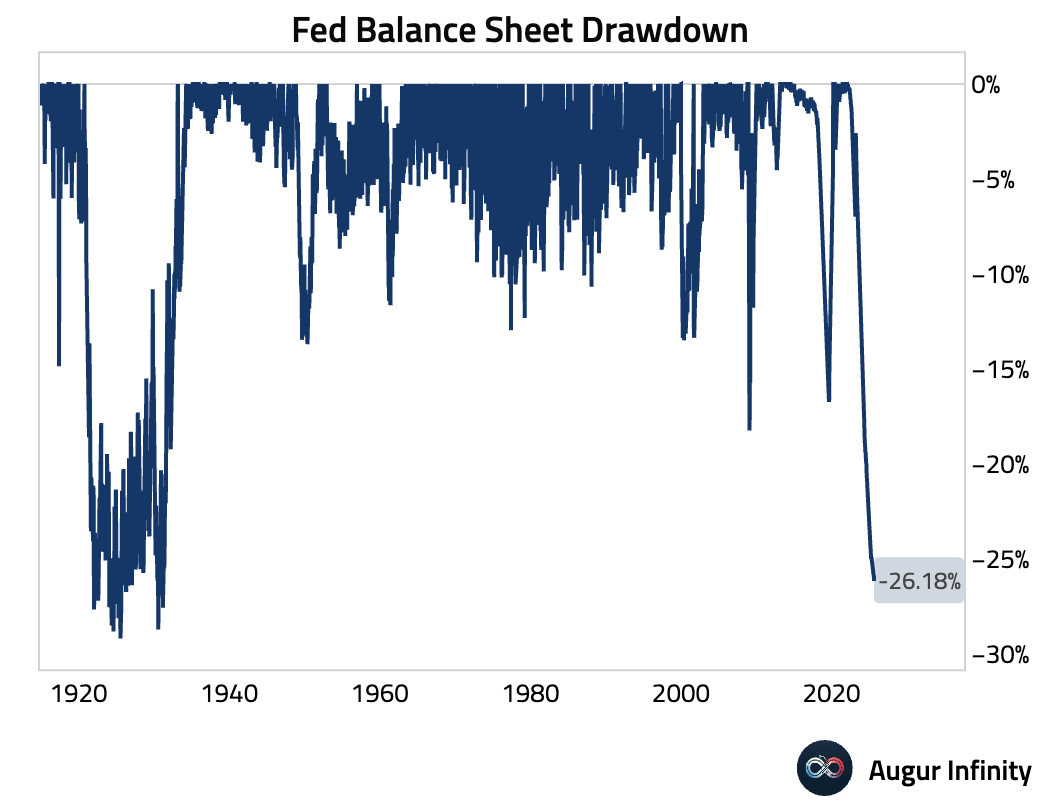

- The Federal Reserve’s balance sheet contracted to $6.62 trillion from $6.64 trillion in the prior week, reaching its lowest level since April 2020. Since the peak, the size of the Fed's balance sheet is down 26.2%.

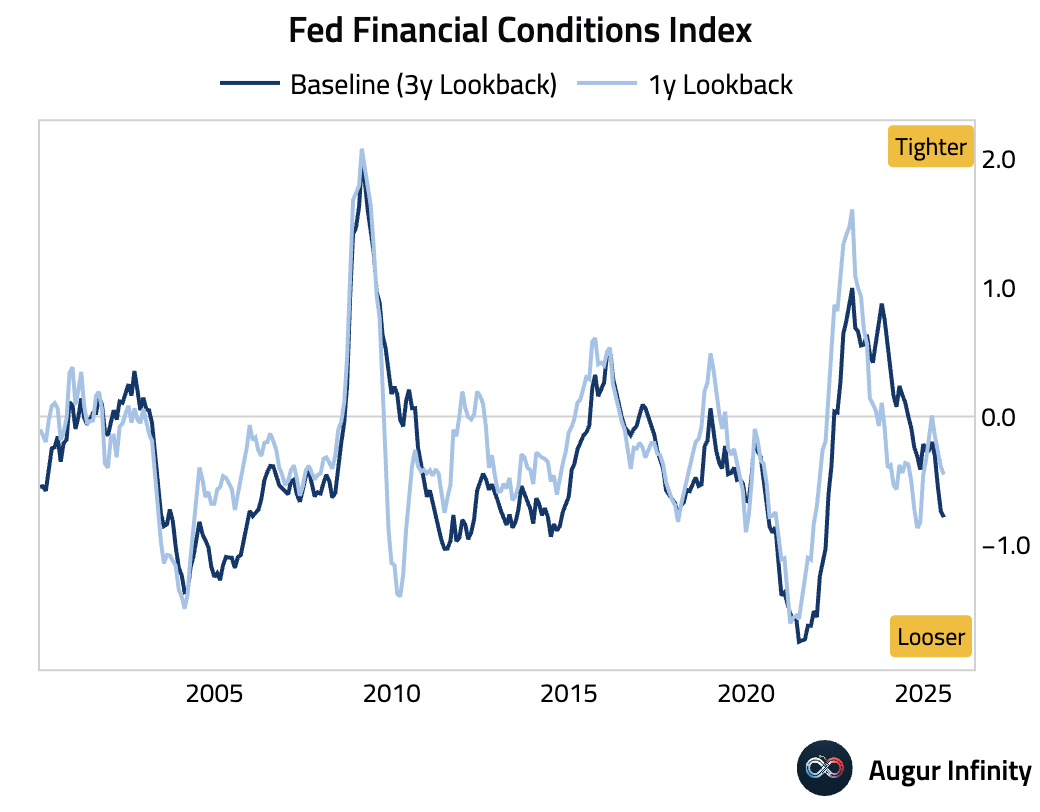

- According to the Fed's Financial Conditions Impulse on Growth (FCI-G) Index, financial conditions loosened further in July, with the baseline index at the easiest level since March 2022.

Canada

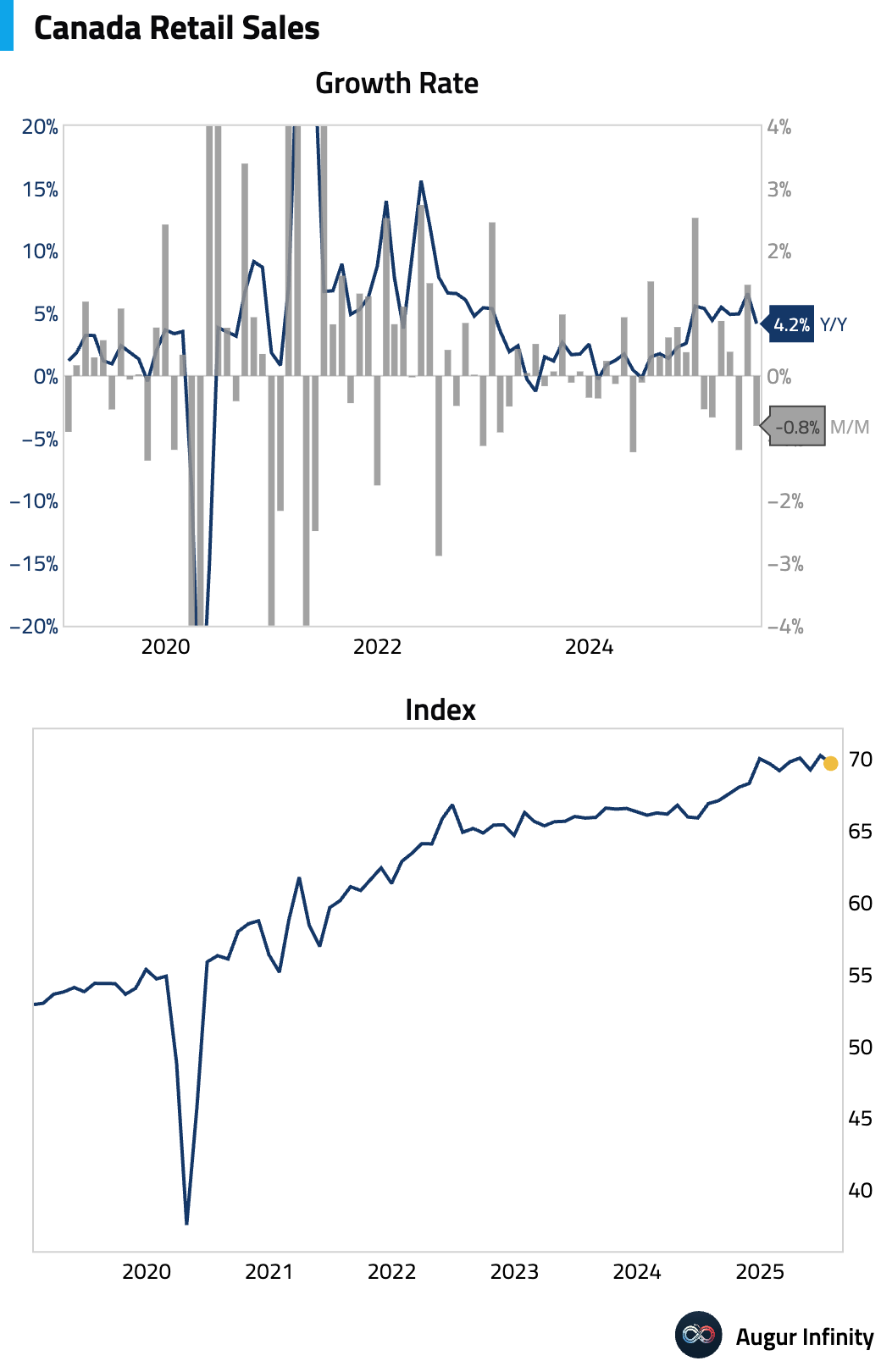

- Canadian retail sales for June rebounded, rising 1.5% M/M (from -1.2%) and accelerating to 6.6% Y/Y (from 4.9%). The ex-autos figure showed even stronger growth at 1.9% M/M, well above the 1.1% consensus and a significant turnaround from the prior -0.3%. However, the preliminary estimate for July suggests a reversal, with sales estimated to have fallen by 0.8%.

Europe

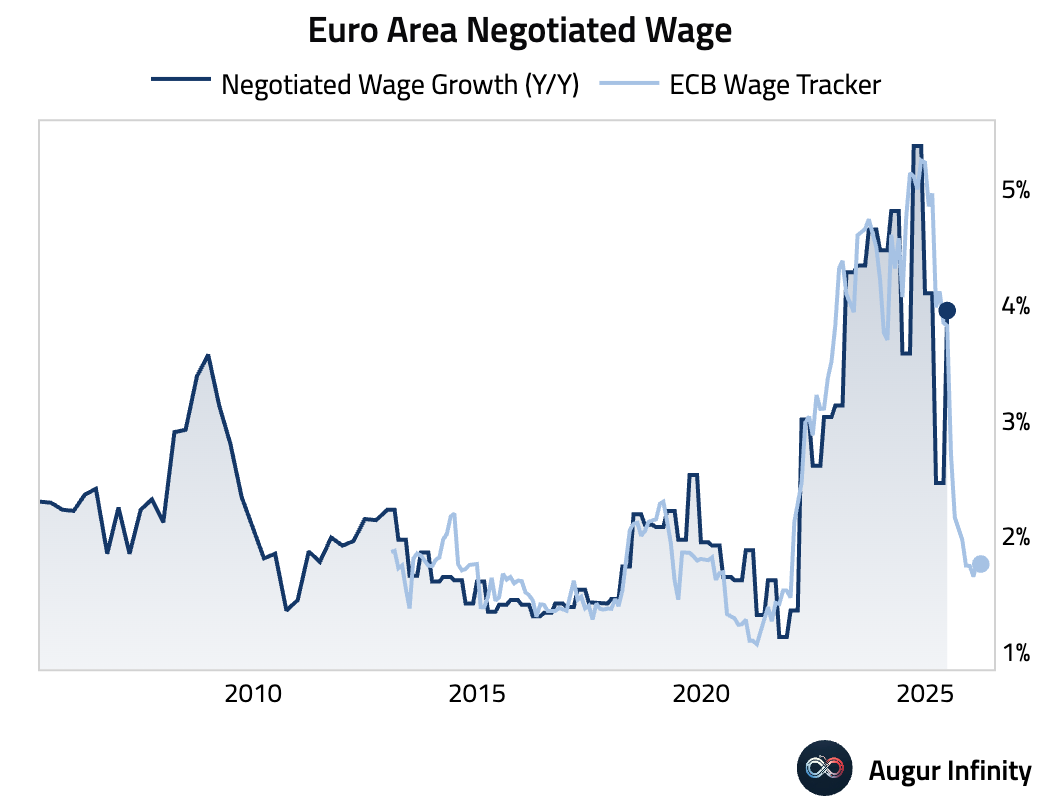

- Eurozone negotiated wage growth accelerated to 3.95% in Q2 from a revised 2.46% in Q1.

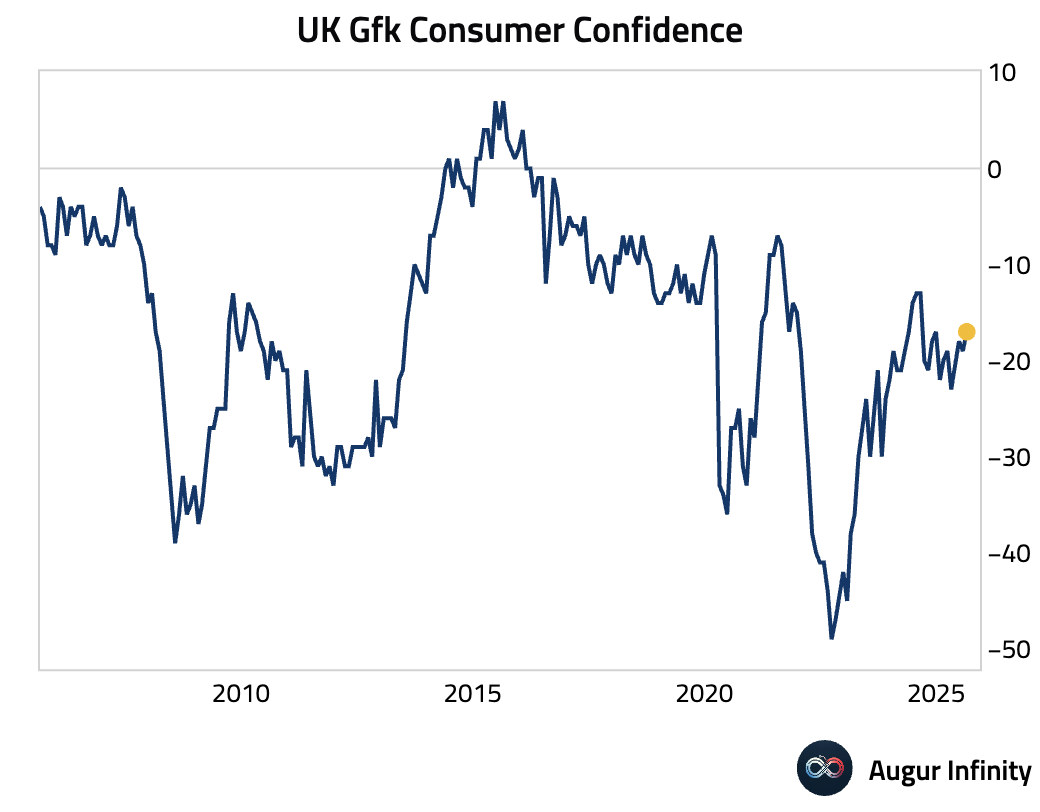

- GfK consumer confidence in the UK improved to -17 in August from -19 in July, beating the consensus estimate of -20.

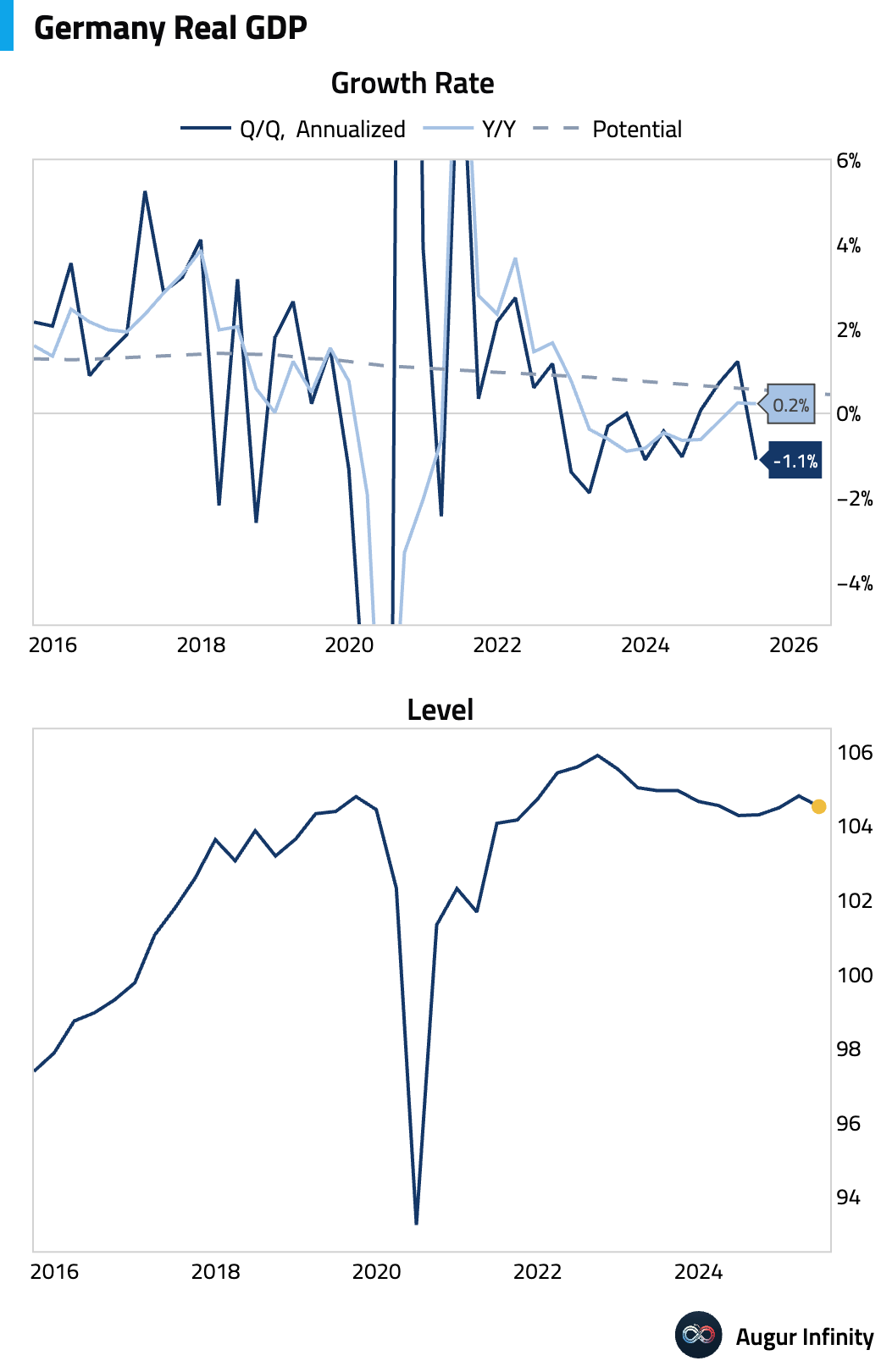

- Germany’s Q2 GDP growth was revised down to -0.3% Q/Q (or -1.1% annualized). Year-over-year, growth slowed to 0.2% from 0.3%, also missing the 0.4% forecast.

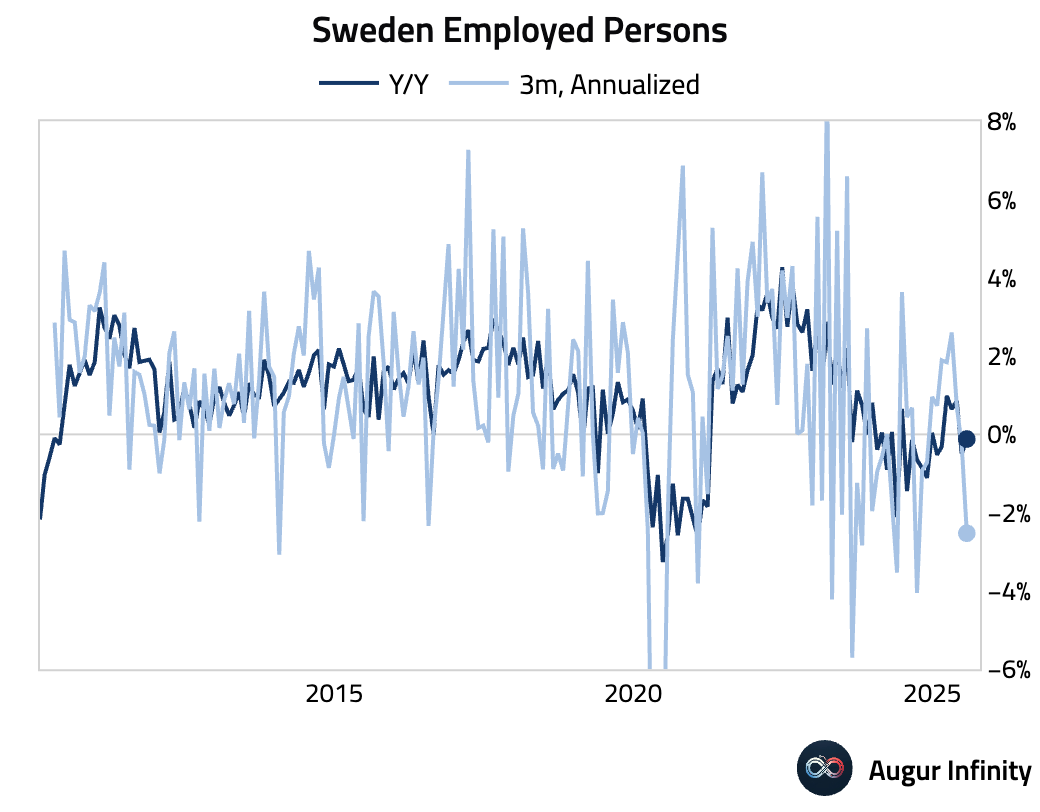

- Sweden’s employed persons rose to 5.438 million in July from 5.402 million in June.

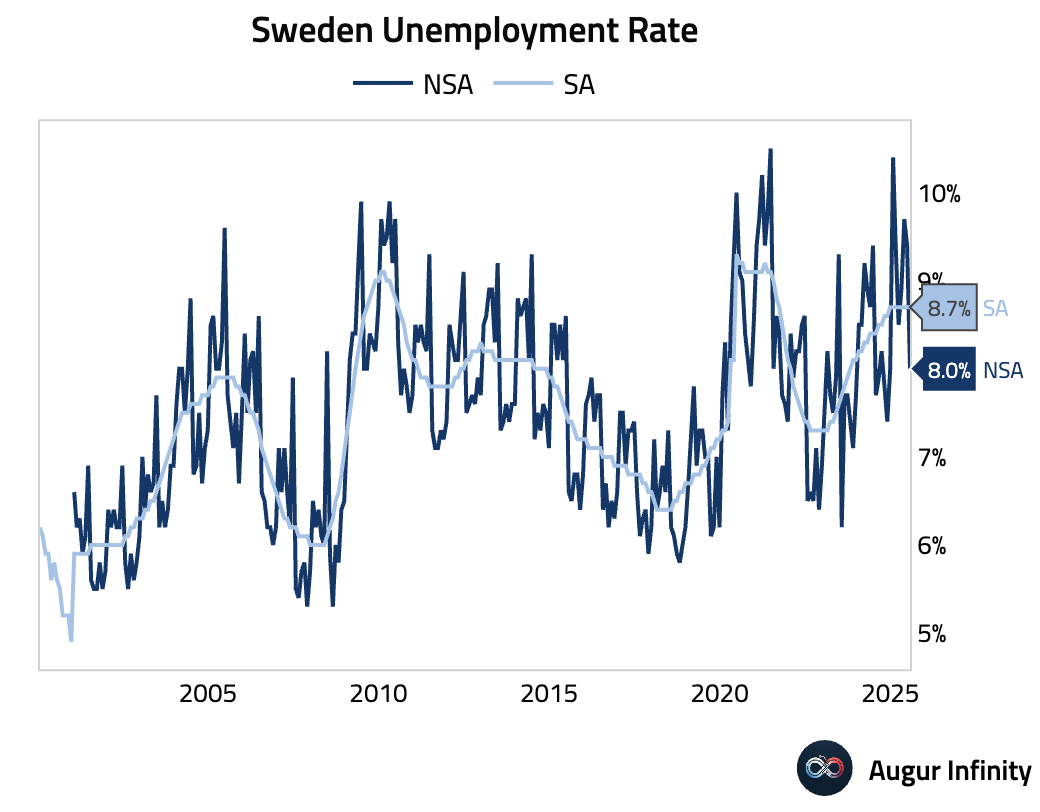

- Sweden’s unemployment rate fell sharply to 8.0% in July from 9.4% in June. On a seasonally-adjusted basis, unemployment held steady at 8.7%.

- France’s business confidence and business climate indicators were both unchanged at 96 in August, matching consensus.

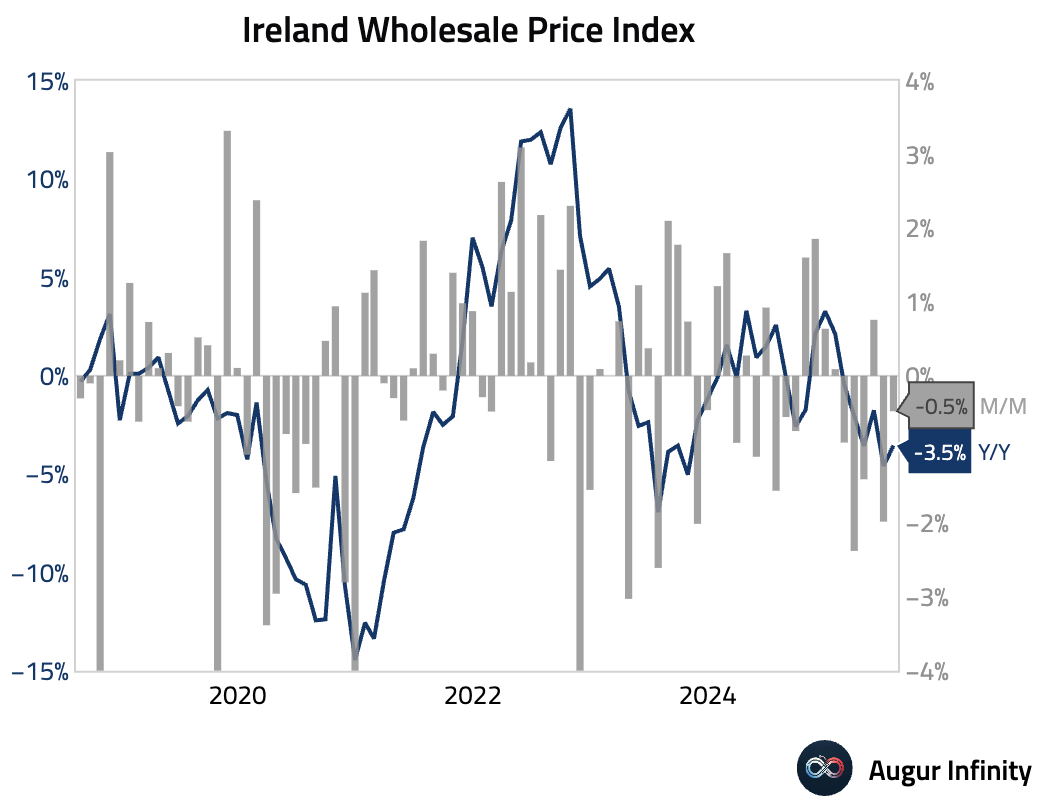

- Irish wholesale prices fell 3.5% Y/Y in July, a slight improvement from the 4.6% decline in June. On a monthly basis, prices were down 0.5% after a 2.0% drop previously.

Asia-Pacific

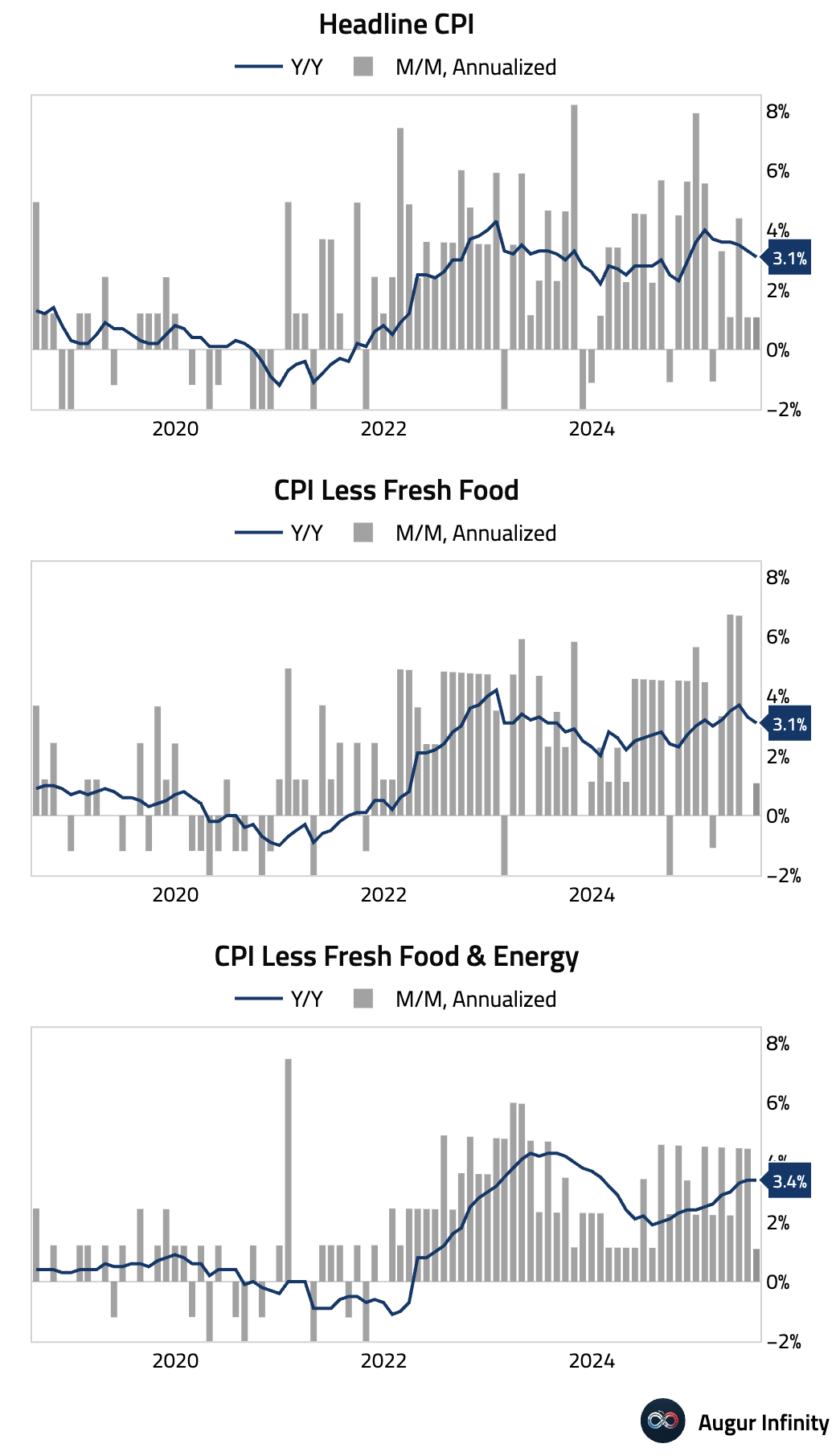

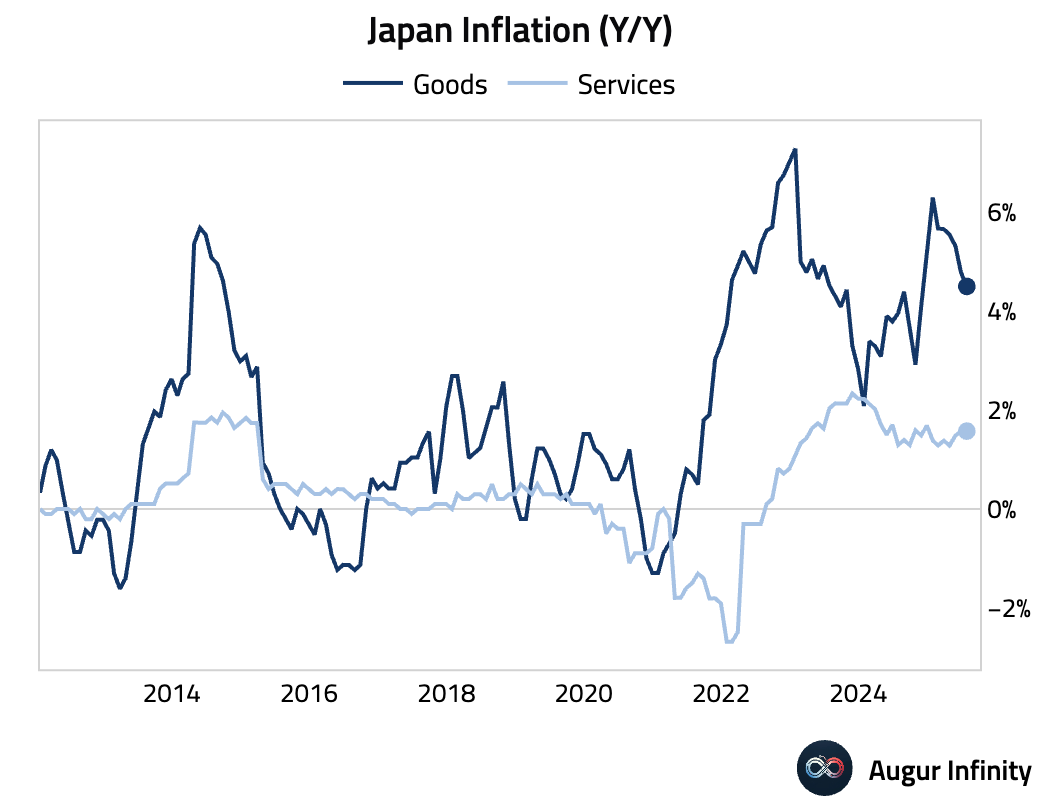

- Japan’s headline inflation for July slowed to 3.1% Y/Y from 3.3% in June, while the core rate (ex-fresh food) also eased to 3.1% from 3.3%, though this was slightly above the 3.0% consensus. The new-core rate (ex-fresh food and energy) held steady at 3.4%. The slowdown in core CPI was driven entirely by energy prices turning negative year-over-year due to lower fuel import costs, which masked stickier inflation elsewhere. Private services inflation, a key indicator for the Bank of Japan, decelerated slightly.

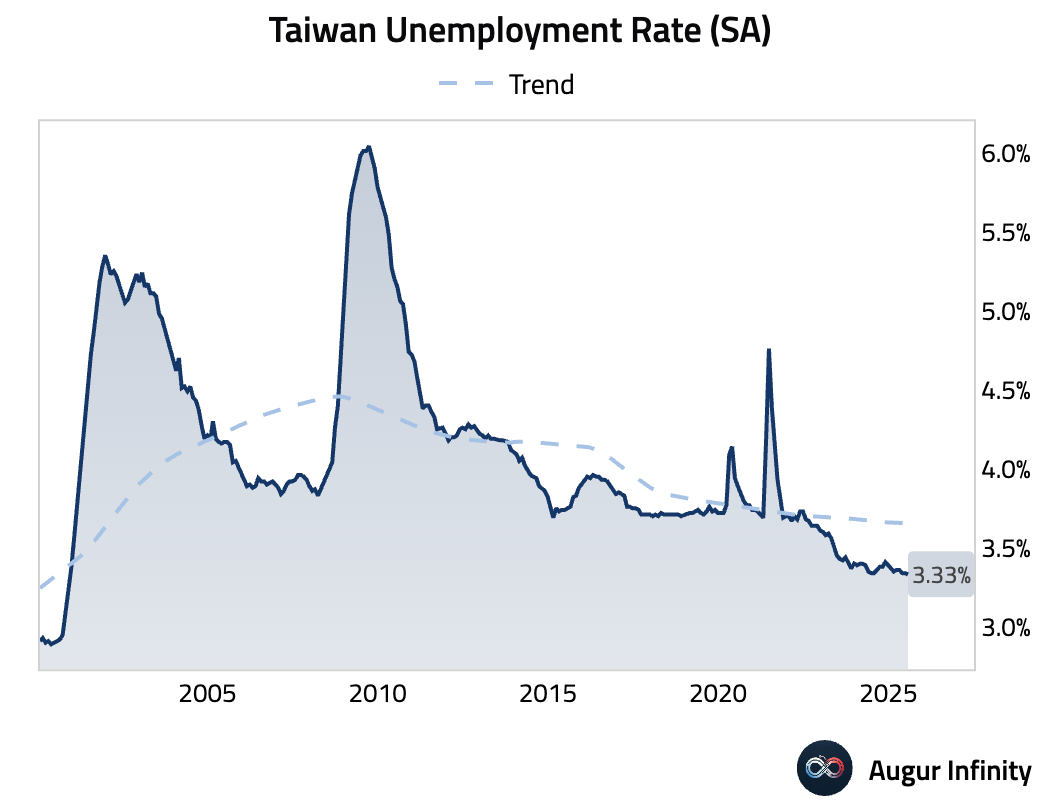

- Taiwan’s unemployment rate edged down to 3.33% in July from 3.34% in June, marking its lowest level since November 2000.

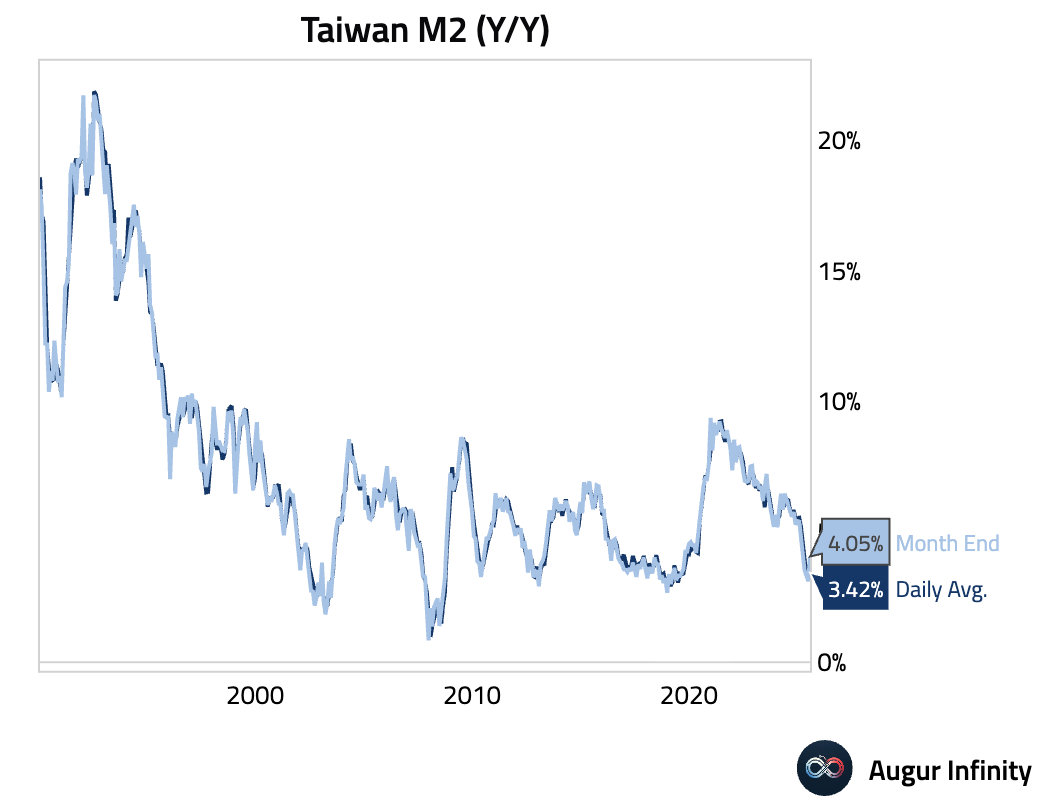

- Taiwan’s M2 money supply growth slowed to 3.42% Y/Y in July from 3.45% in June.

China

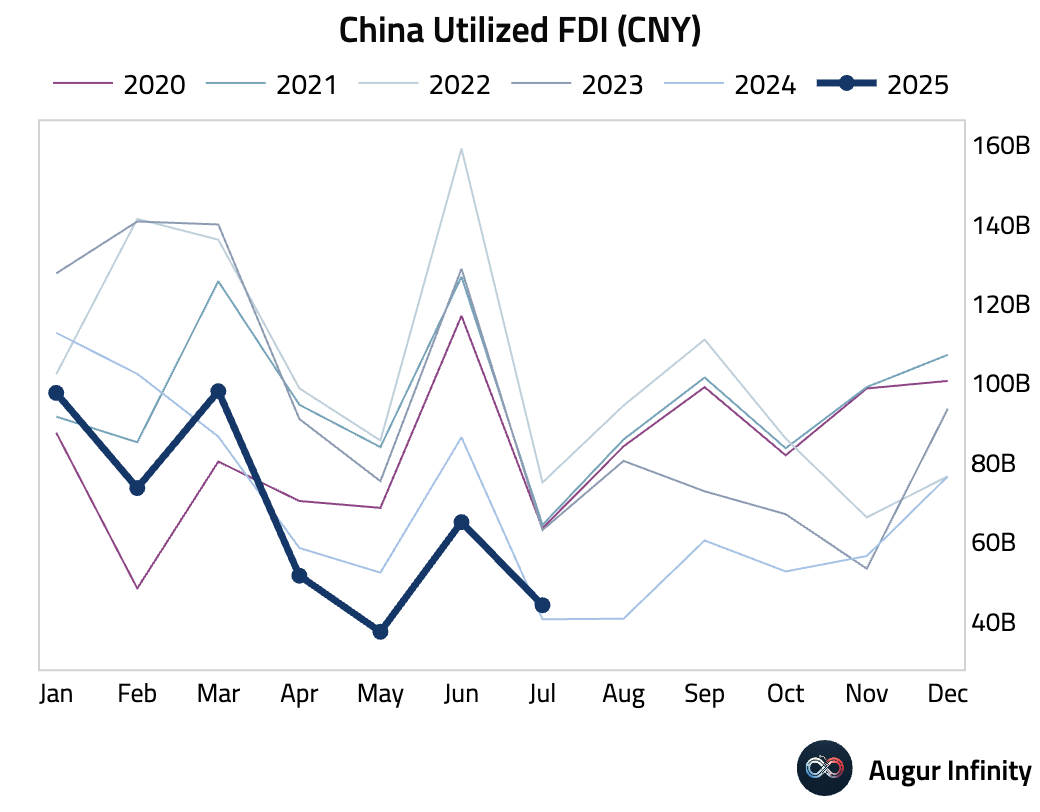

- Utilized foreign direct investment in China for the first seven months (January–July) fell 13.4% Y/Y. However, the single month July FDI rose by 8.8% by our estimate.

Emerging Markets ex China

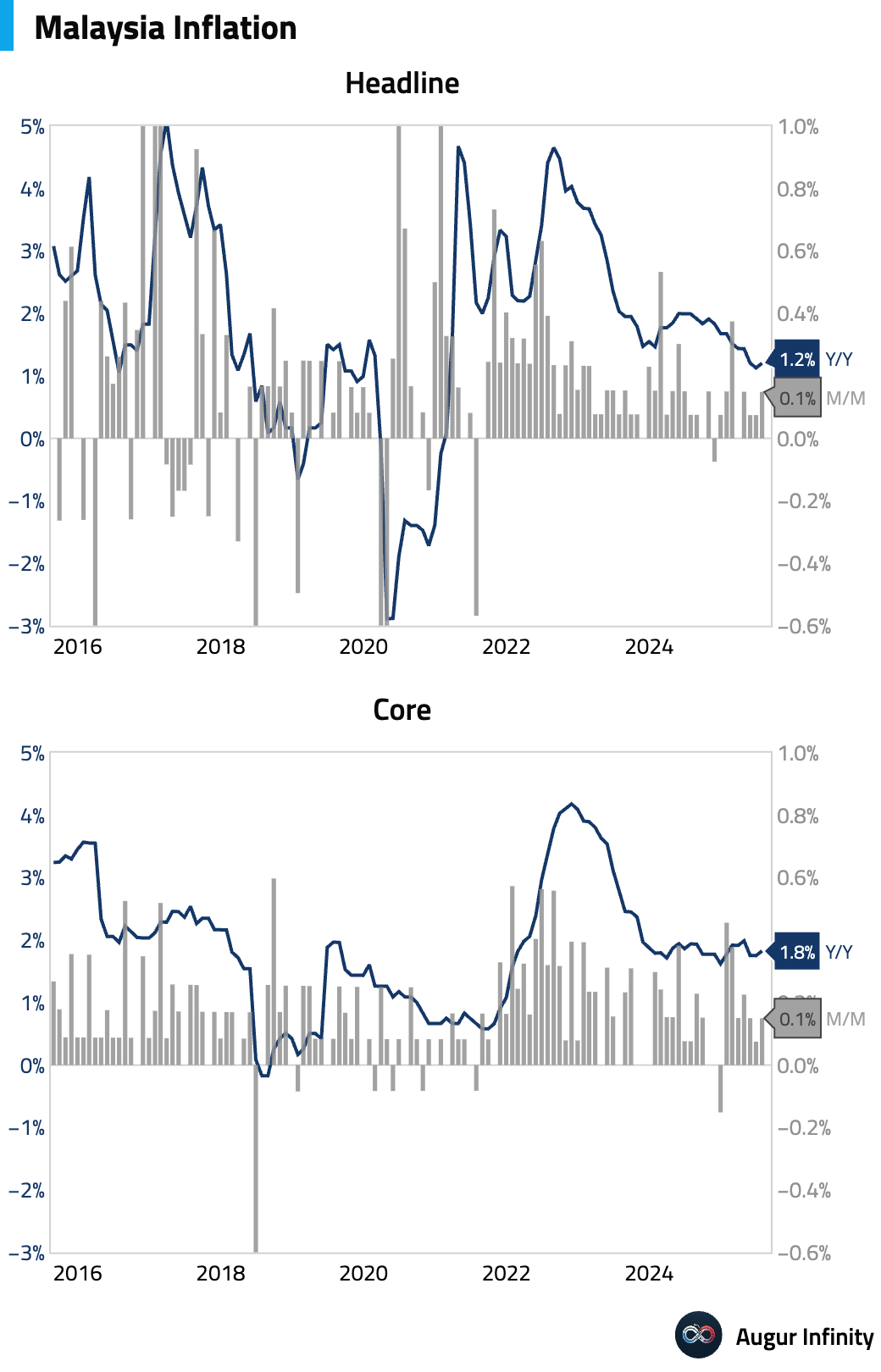

- Malaysia’s inflation rate for July rose to 1.2% Y/Y, in line with consensus and up from 1.1% in June. The monthly rate was stable at 0.1%. A 15% surge in insurance premiums drove the annual increase, while core inflation held steady at 1.8% Y/Y, suggesting the headline move was not broad-based.

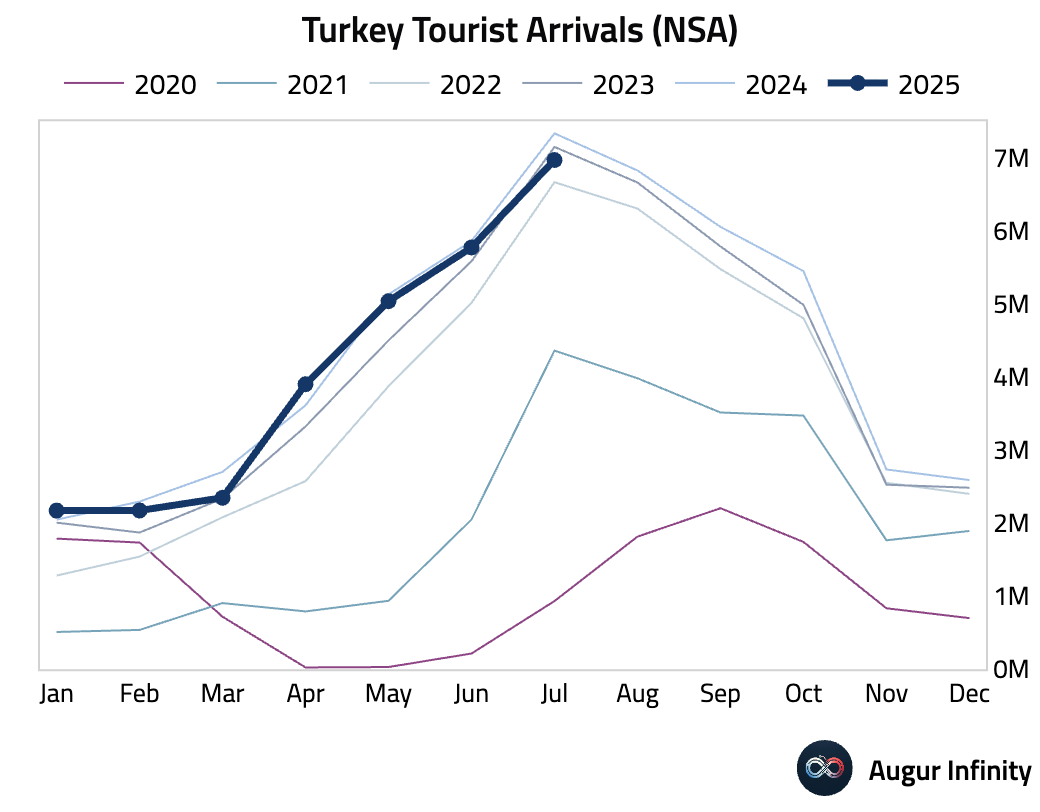

- Tourist arrivals in Turkey dropped 4.97% Y/Y in July, a steeper decline than the 1.5% fall in June.

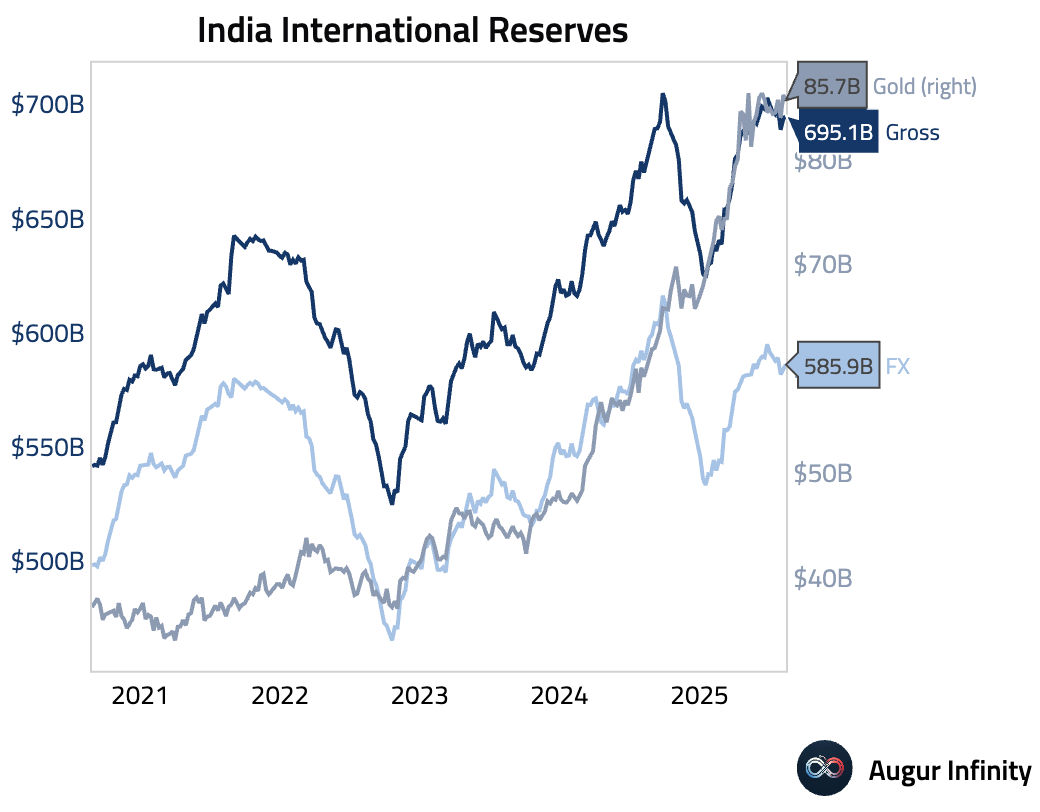

- India's official reserve assets increased to $695.11 billion from $693.62 billion in the previous week.

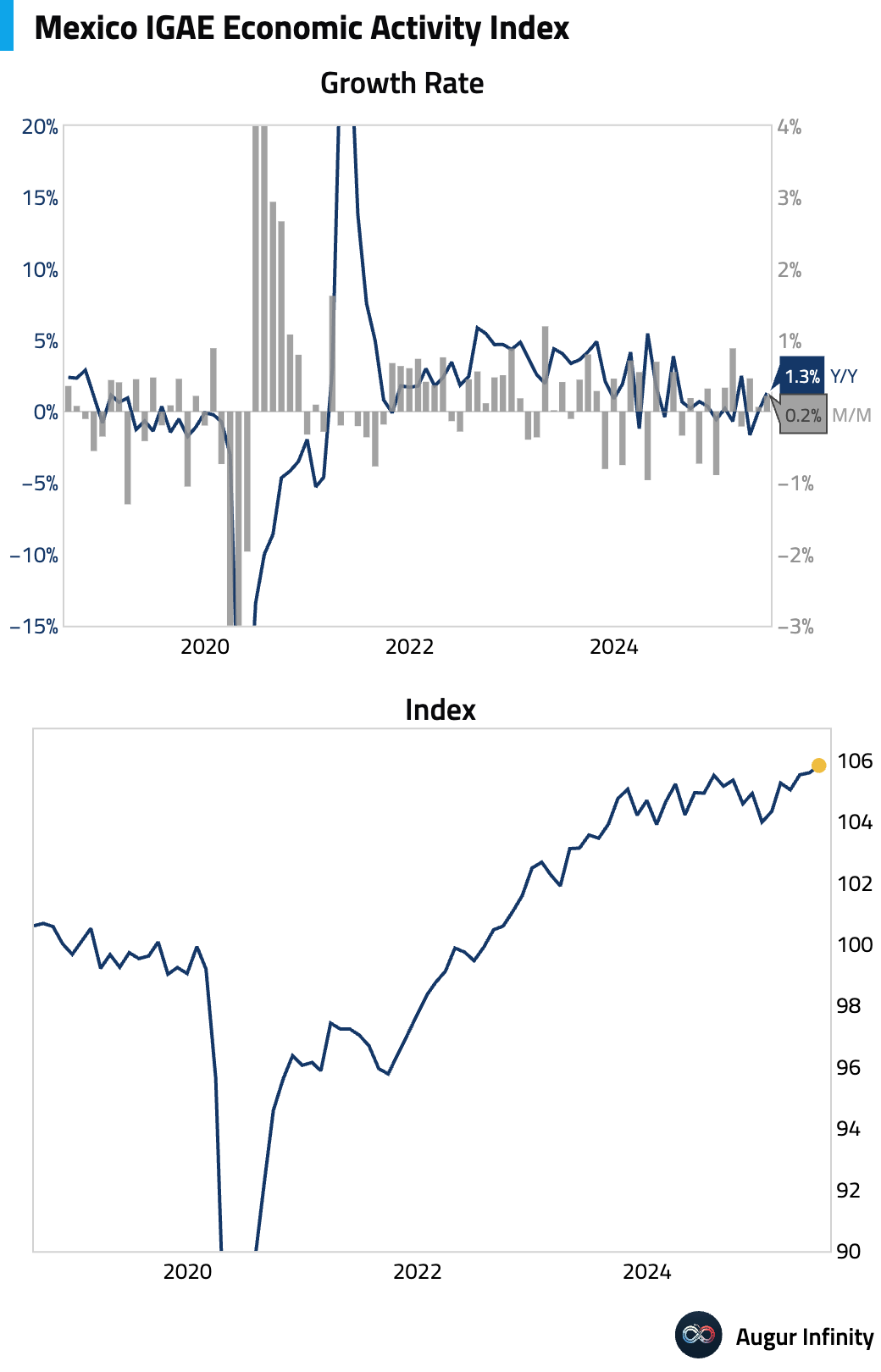

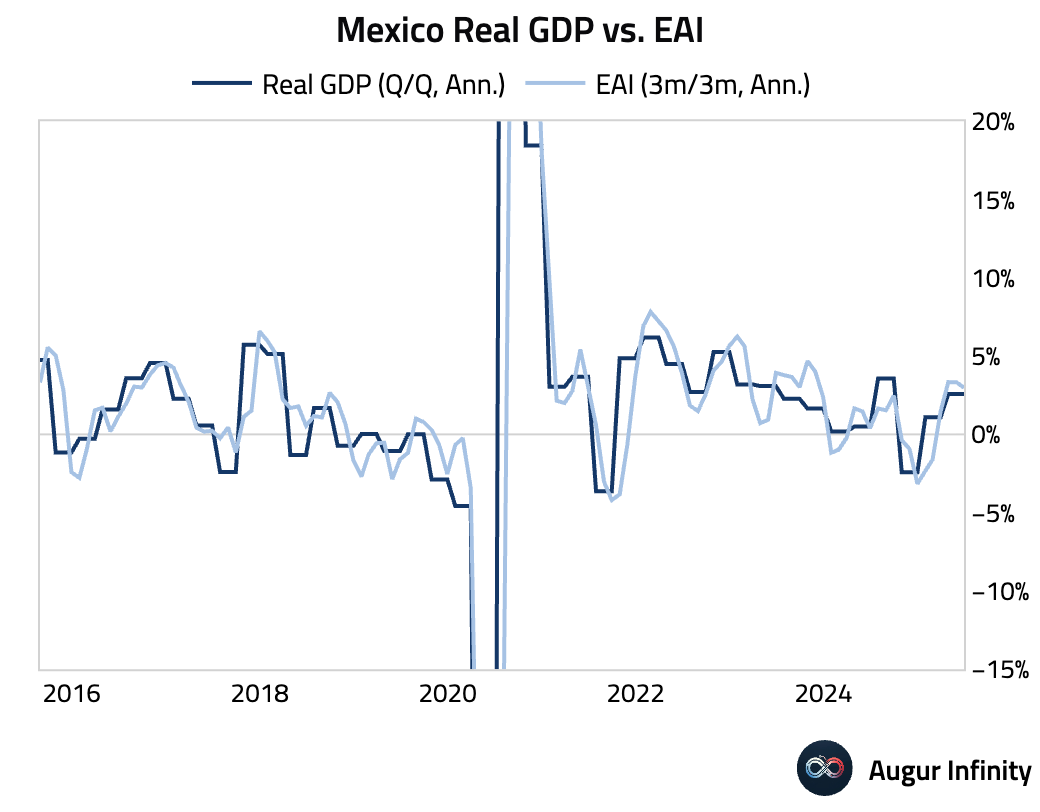

- Mexico’s IGAE economic activity indicator for June rose 0.2% M/M, slightly below the 0.3% consensus, but up from 0.1% previously. Year-over-year, activity expanded 1.3%, missing the 1.5% forecast but improved from May's reading.

- The final estimate for Mexico’s Q2 GDP showed growth of 0.6% Q/Q (or 2.6% annualized), firming from 0.2% in Q1. The print was driven by strong performance in the secondary and services sectors, particularly construction. The year-over-year reading was flat at 0.0%, below the 0.1% consensus.

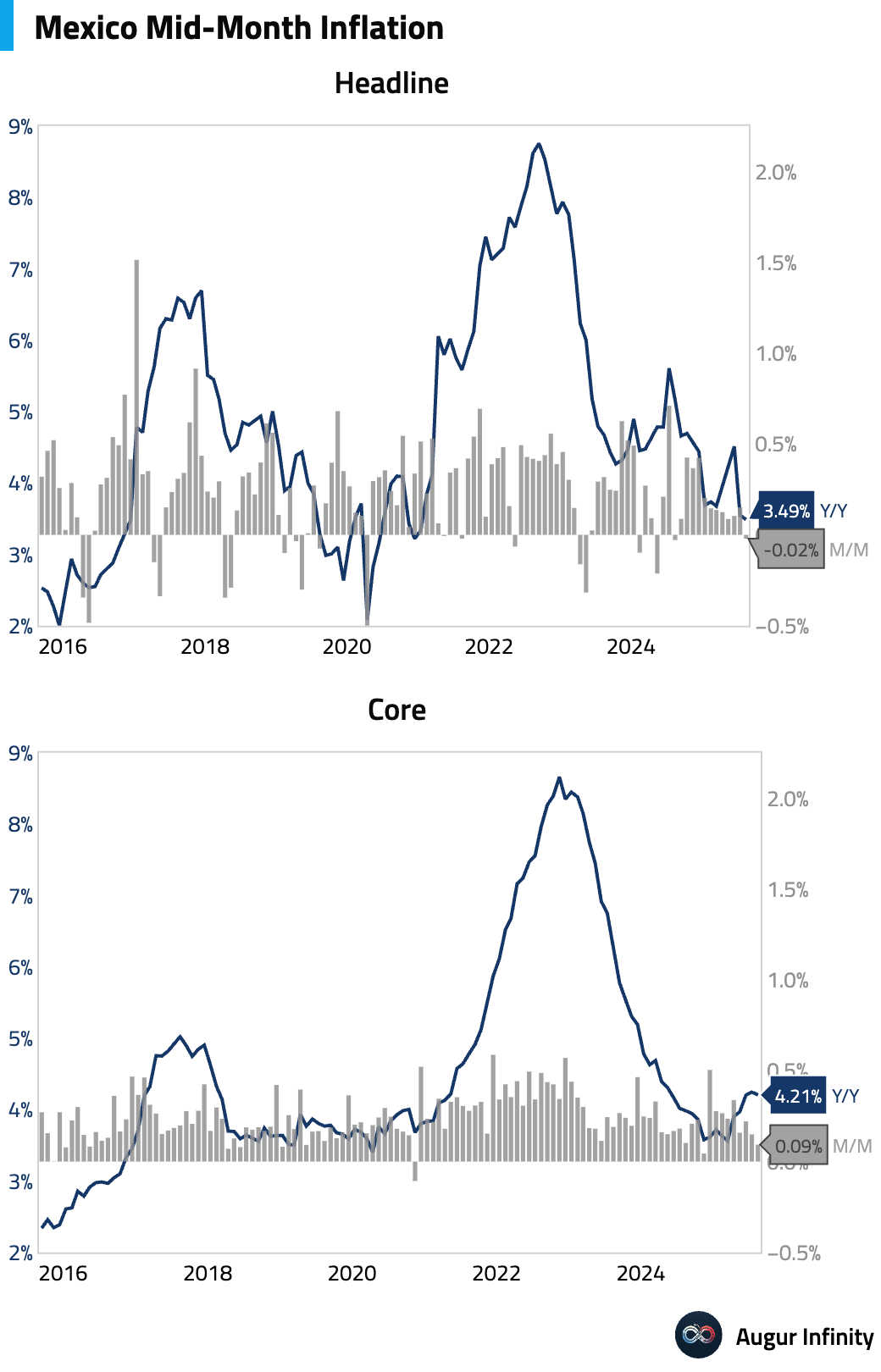

- Mexico’s mid-month inflation for August came in cooler than expected. The headline rate fell 0.02% M/M (vs. +0.12% consensus) and slowed to 3.49% Y/Y (vs. 3.66% consensus), the lowest since January 2021. Core inflation also surprised to the downside, rising 0.09% M/M (vs. +0.14% consensus) and easing to 4.21% Y/Y. The unexpected drop in headline inflation was driven by a sharp fall in non-core food prices, though services inflation remains stubbornly high.

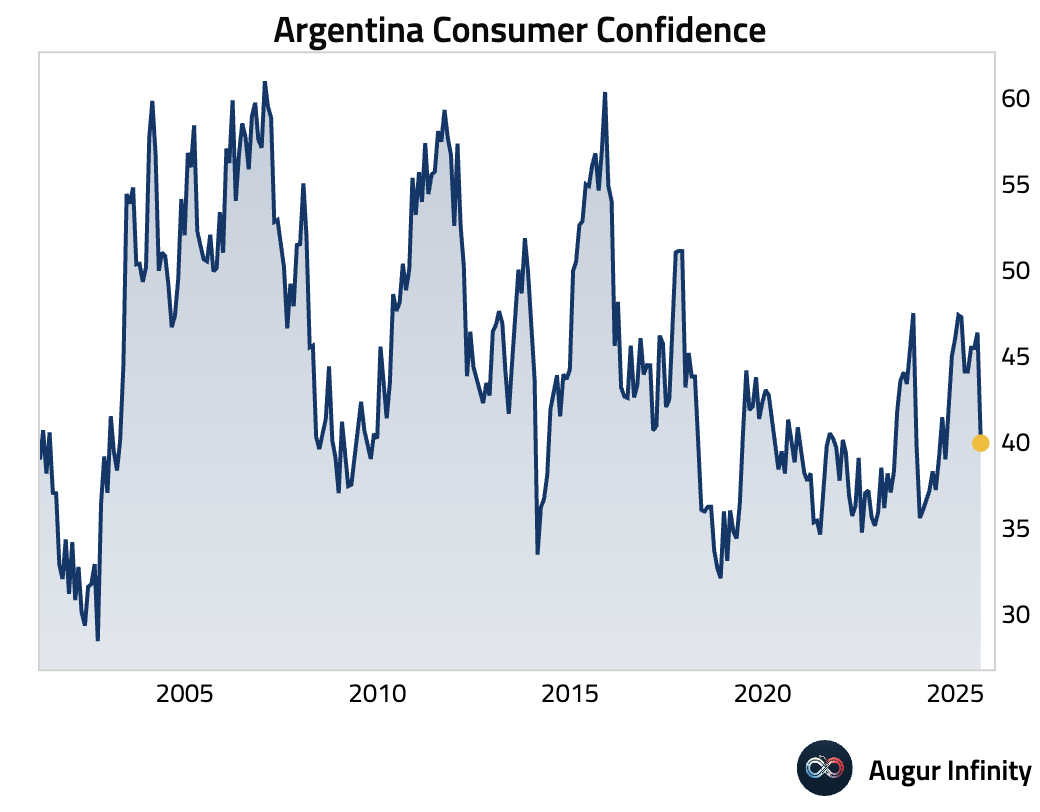

- Argentina’s consumer confidence plunged to 39.94 in August from 46.37 in July.

Global Markets

Equities

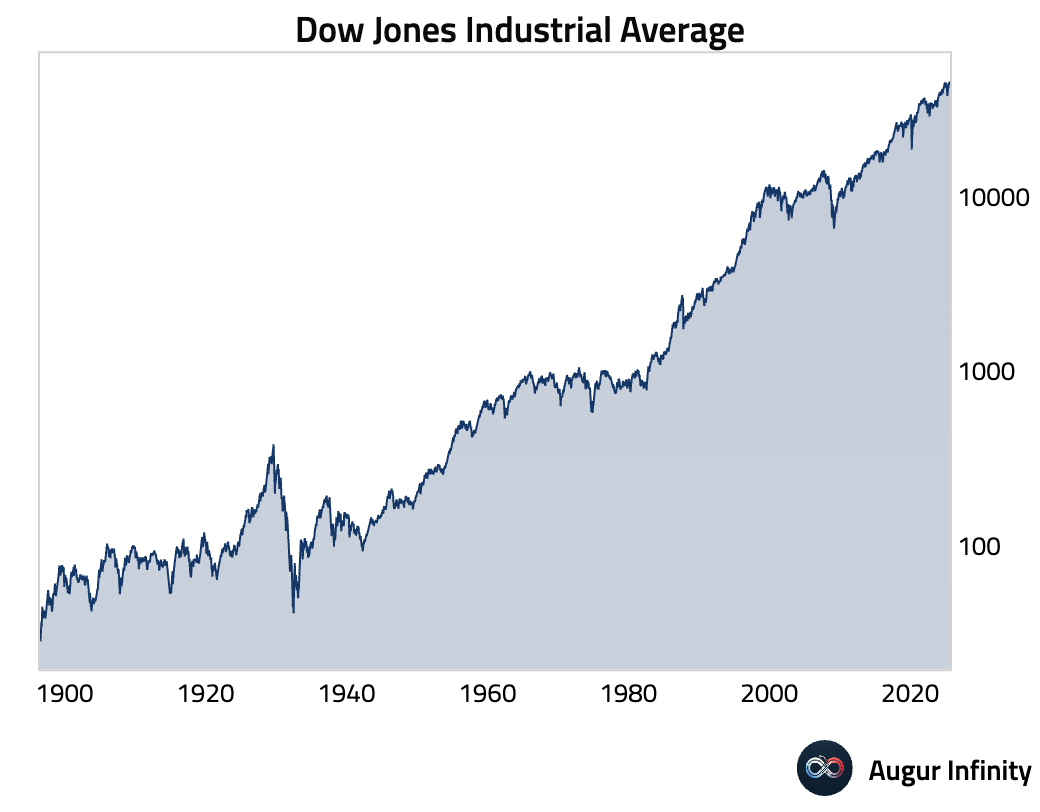

- Global equity markets rallied sharply, catalyzed by dovish commentary from Federal Reserve Chair Jerome Powell at the Jackson Hole symposium that raised expectations for a potential interest rate cut in September. In the US, equities gained 1.5%, with the tech-heavy Nasdaq advancing 1.9%.

- The Dow Jones Industrial Average surged to a new all-time high.

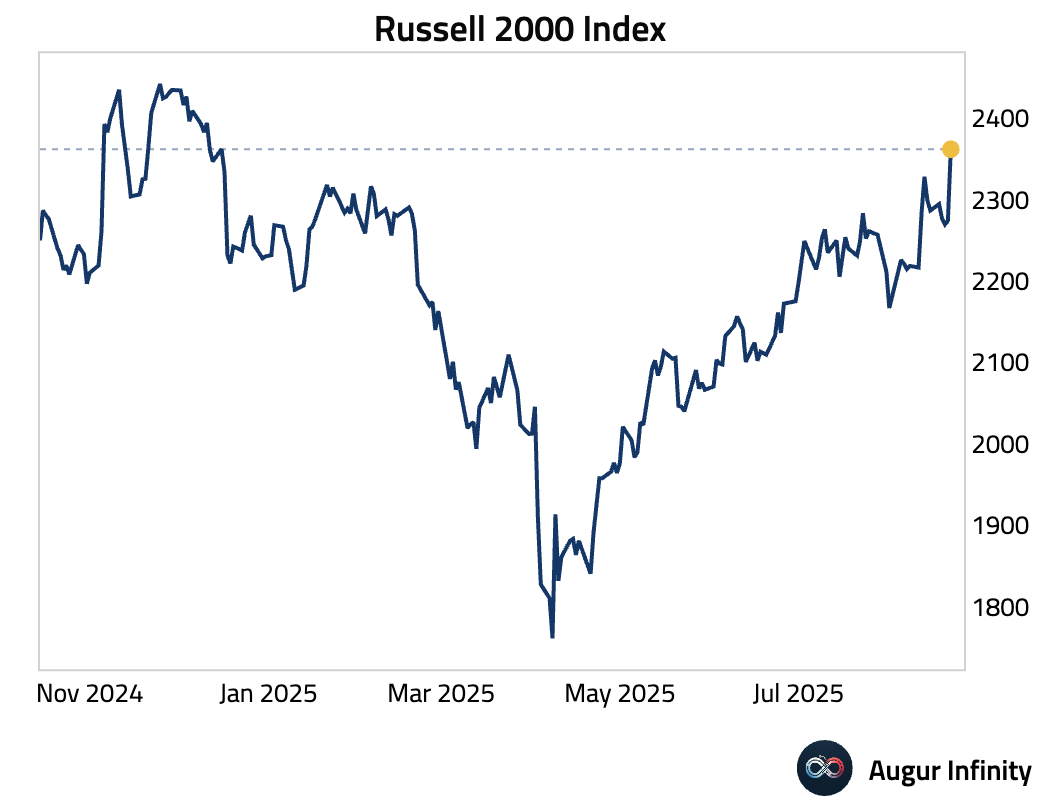

- US small cap equities performed well today, rosing to the highest level since December 2024.

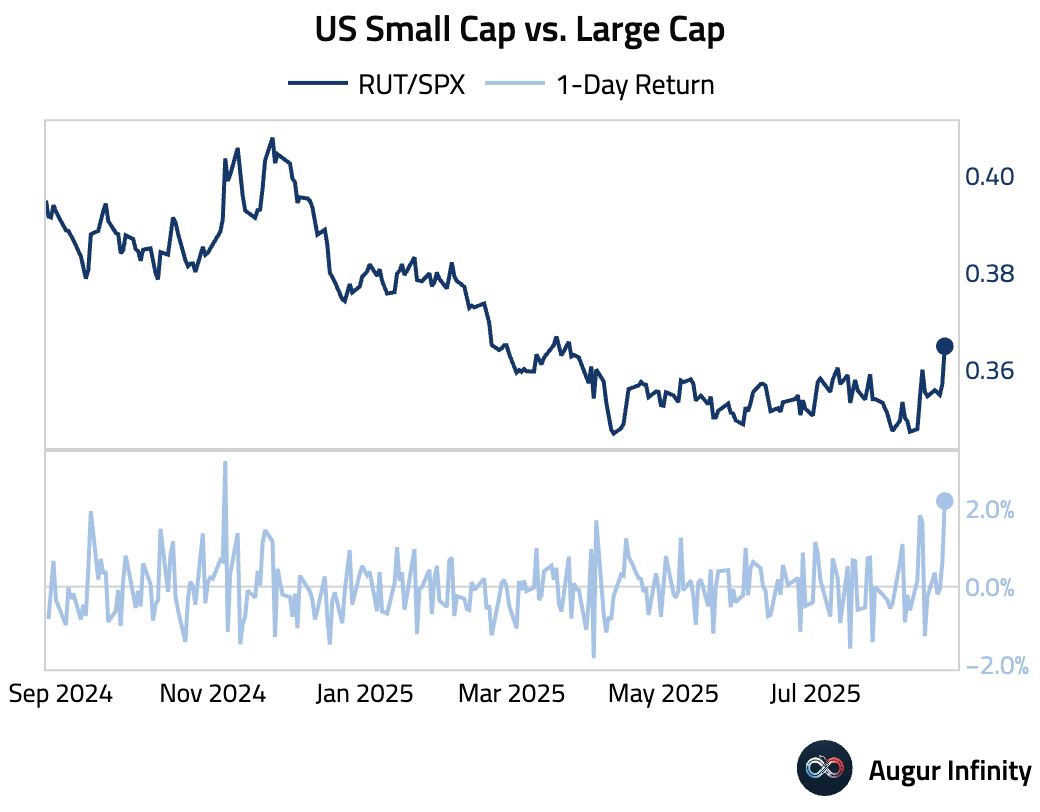

- US small caps also outperformed large caps by over 2%, the largest single-day outperformance since November.

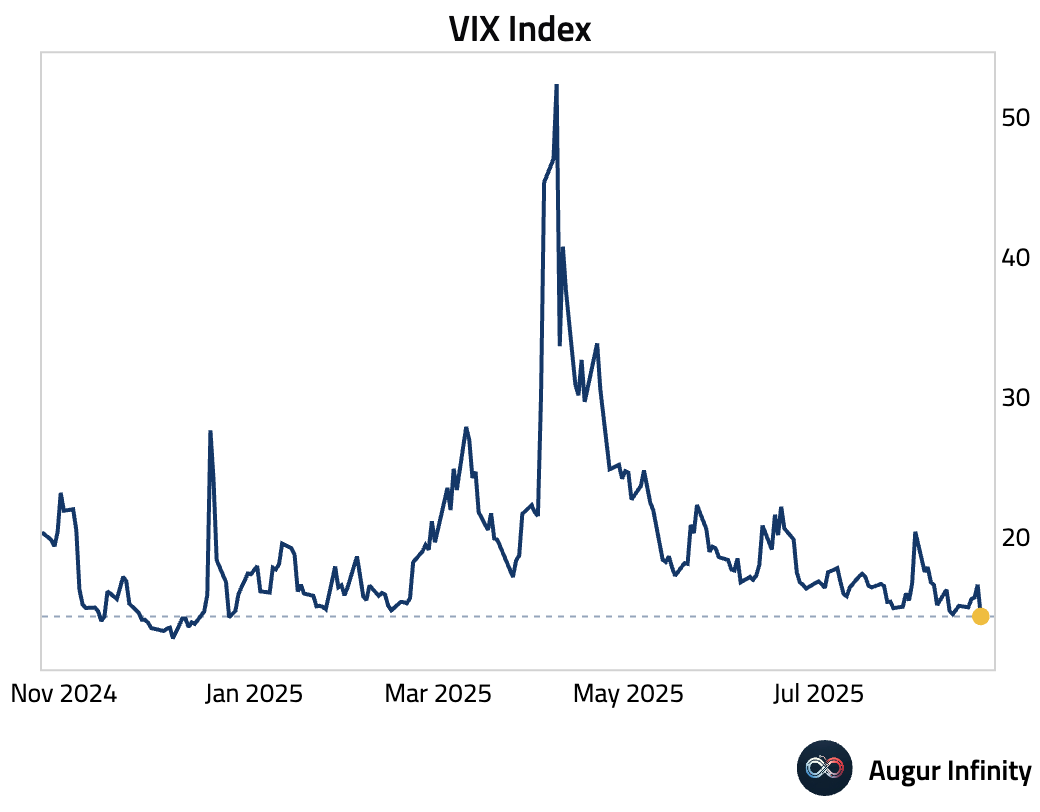

- Market price of risk declined, with the VIX trading down to the lowest level this year.

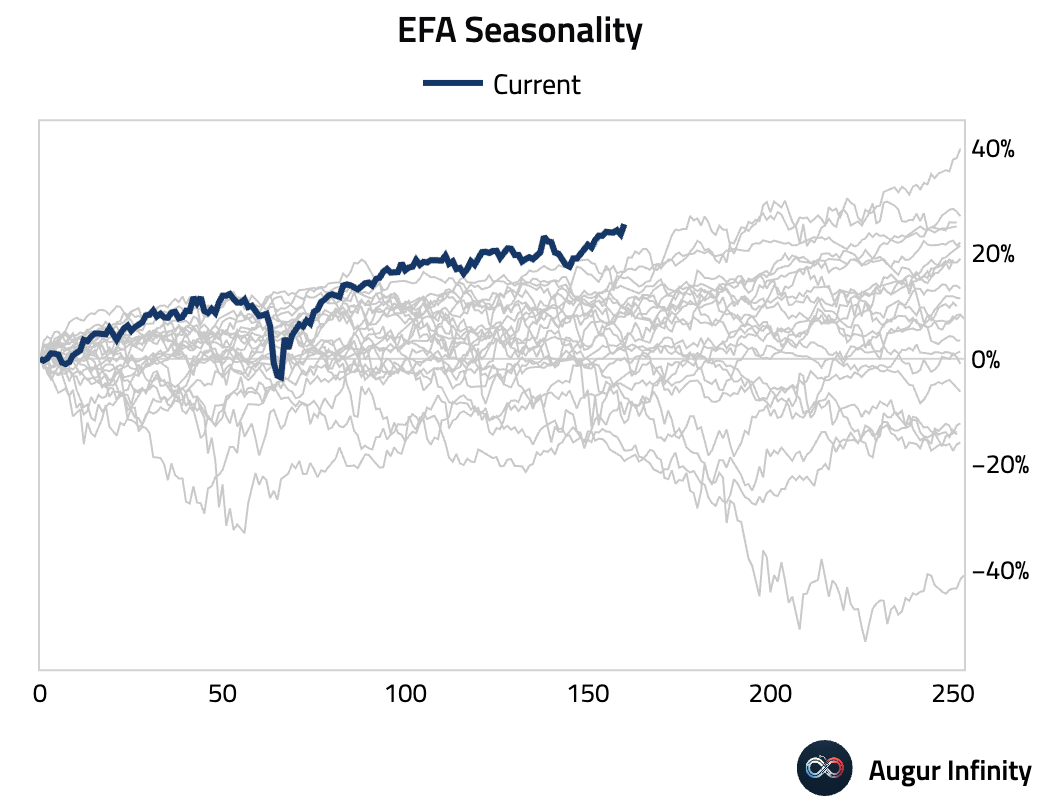

- The year-to-date performance of EFA, the ETF tracking MSCI EAFE, is the strongest since its inception.

Source: @MikeZaccardi

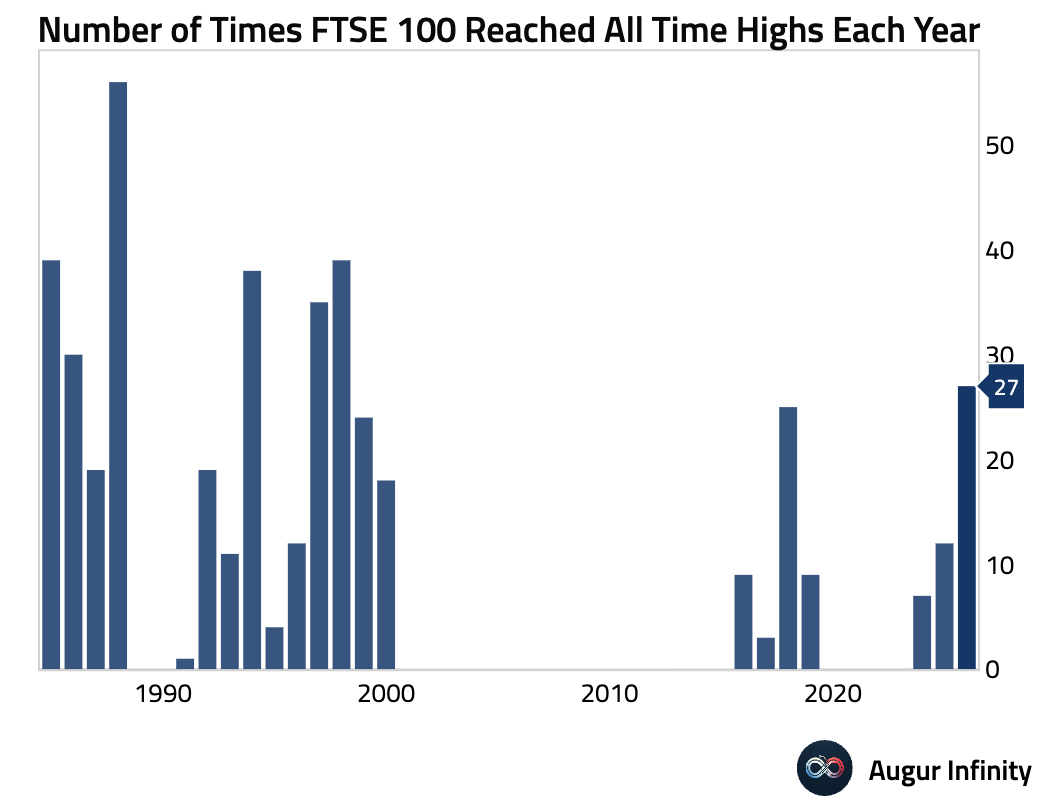

- The FTSE 100 Index rose for the fifth consecutive session to another all-time high. This is the 27th ATH this year so far.

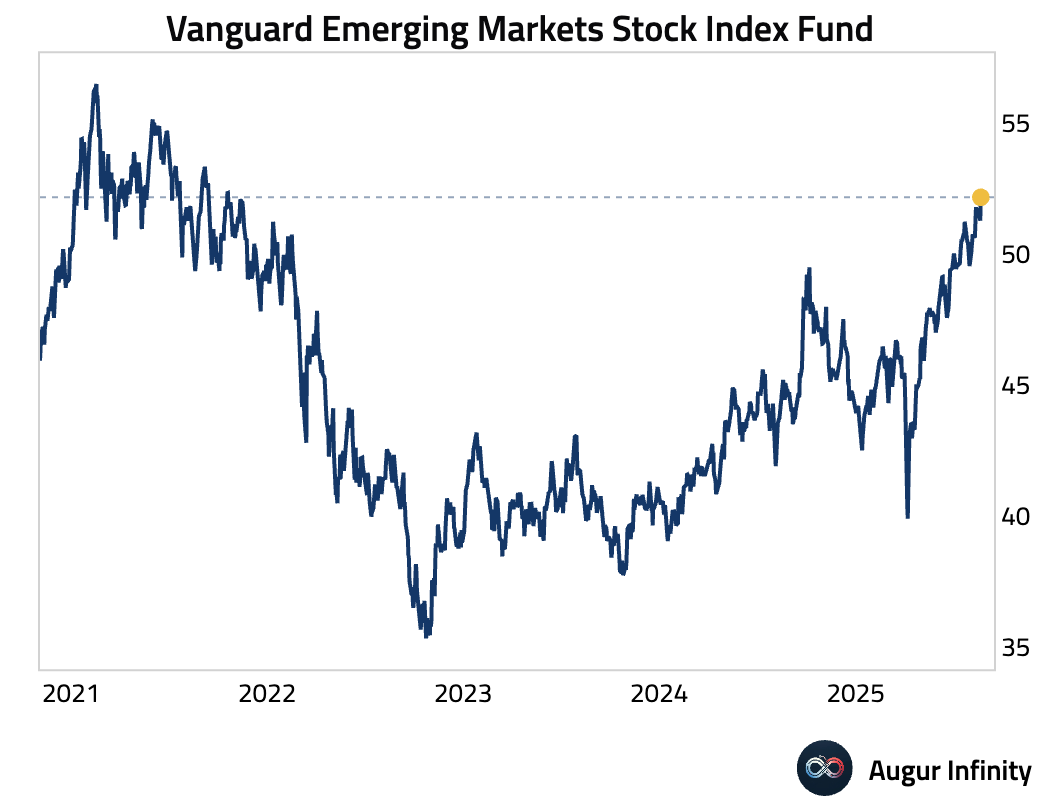

- Vanguard Emerging Markets Index Fund hits its highest level since October 2021.

Fixed Income

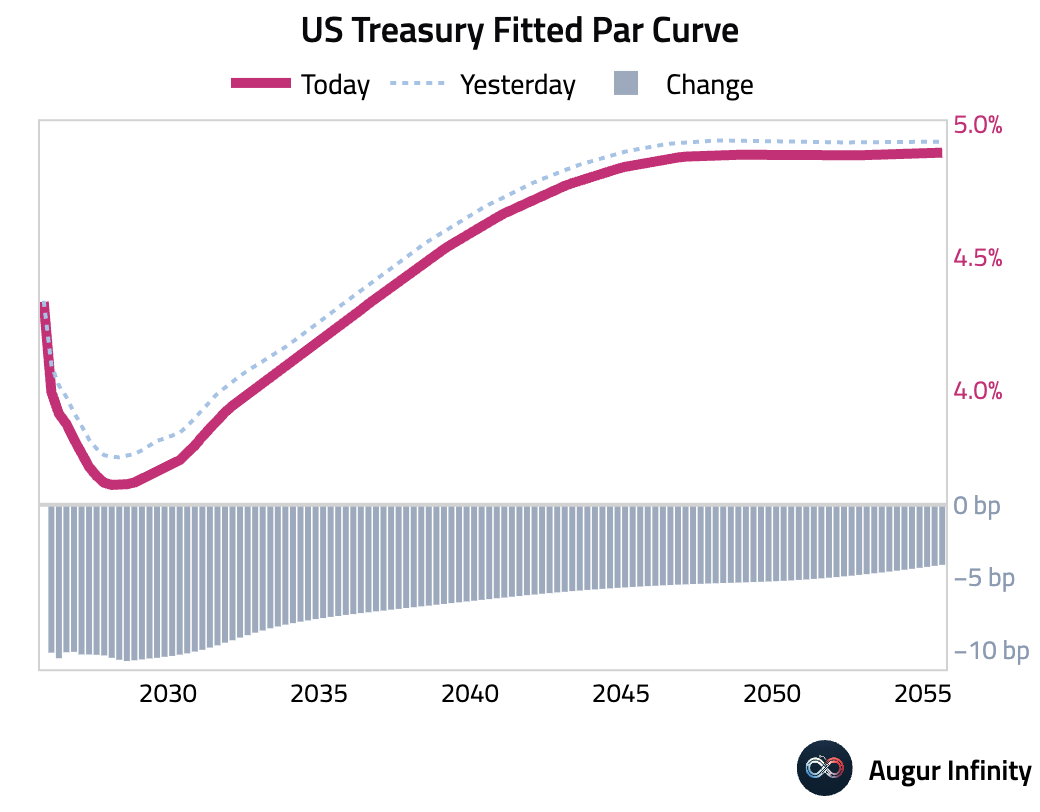

- US Treasury yields fell across the curve following Chair Powell’s remarks, which signaled a potential policy shift. The rate-sensitive 2-year yield dropped 9.4 bps, while the 10-year yield declined by 7.2 bps as markets increased bets on monetary easing.

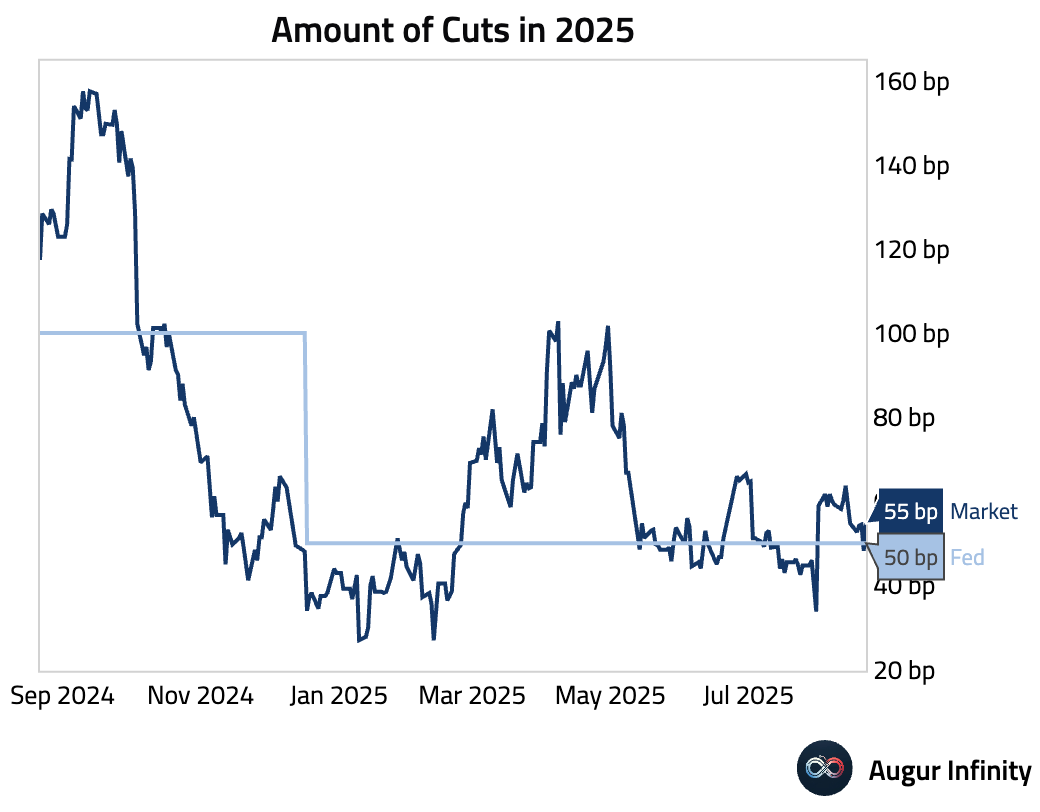

- The rates market now expects 55 bps of rate cut for the rest of 2025, more than reversing yesterday's decline.

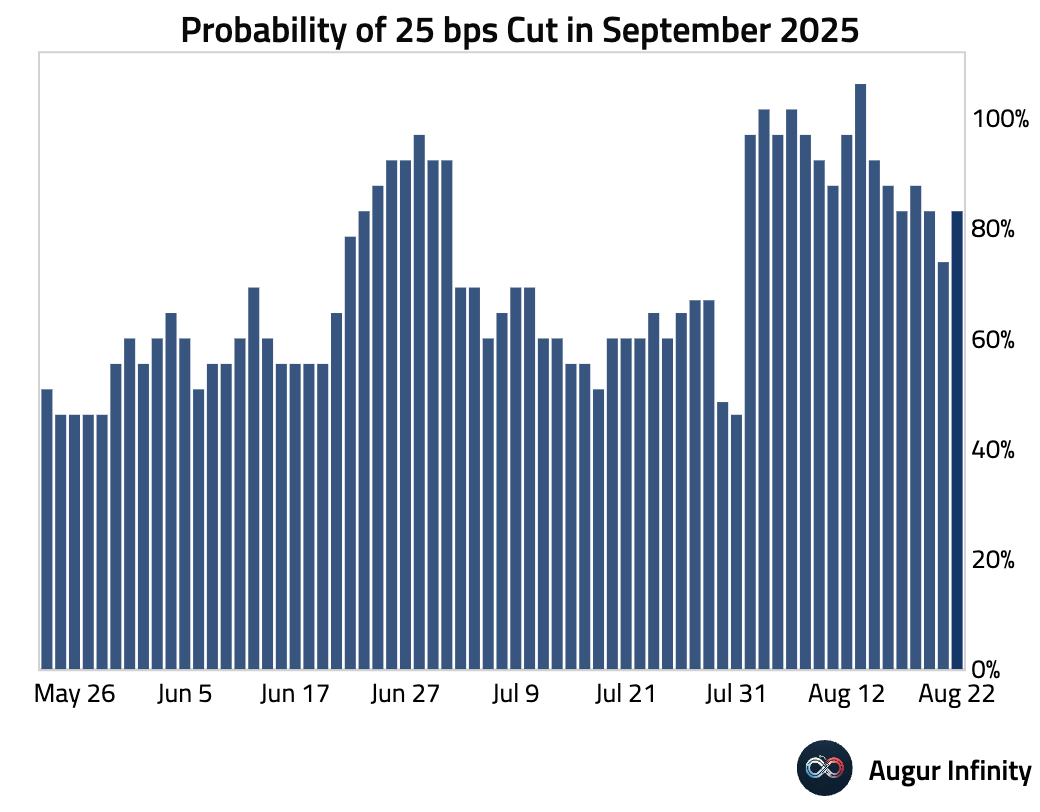

- The probability of a 25 bps rate cut at the September 2025 FOMC meeting increased to about 85%.

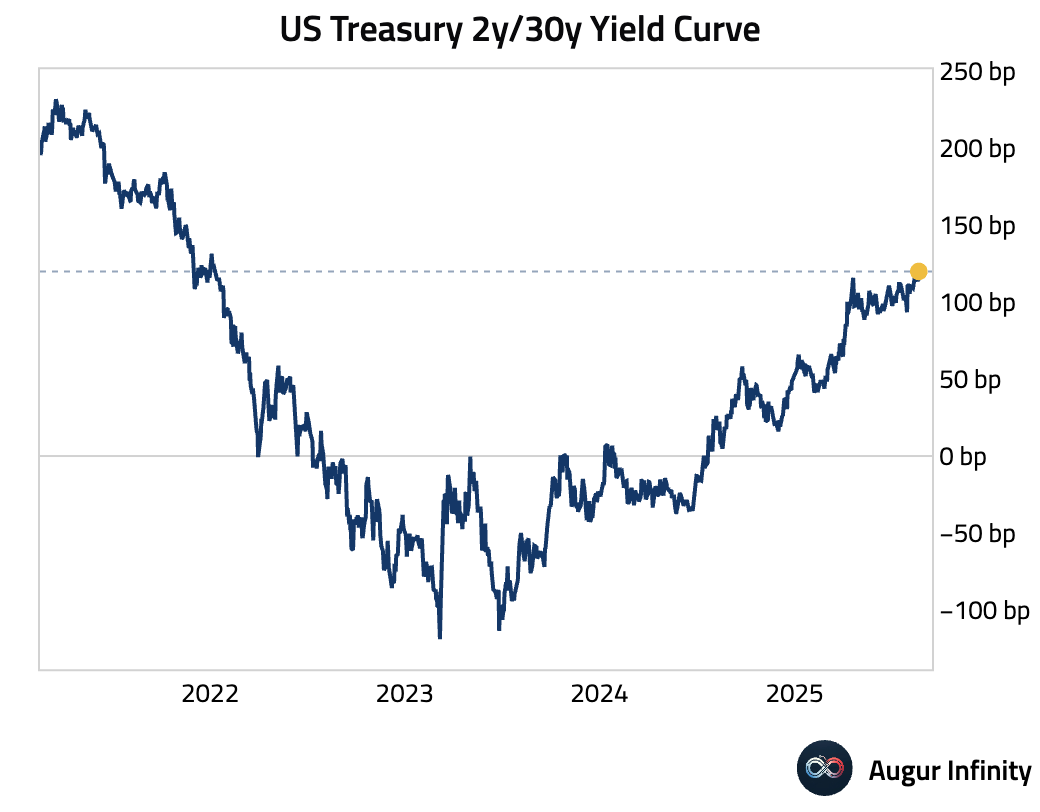

- US Treasury 2y/30y yield curve is at the steepest level since January 2022.

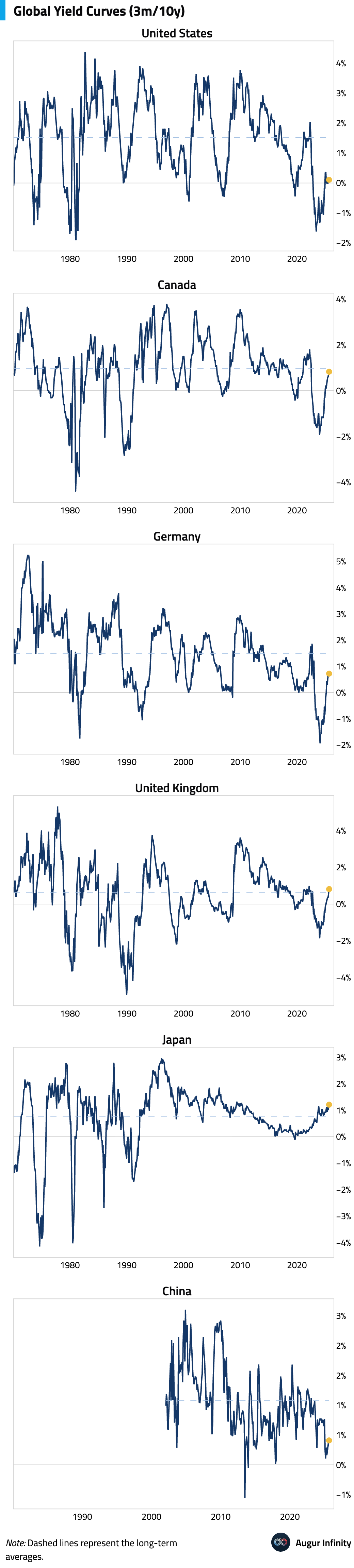

- Japan has the steepest 3m/10y yield curve amongst major economies.

FX

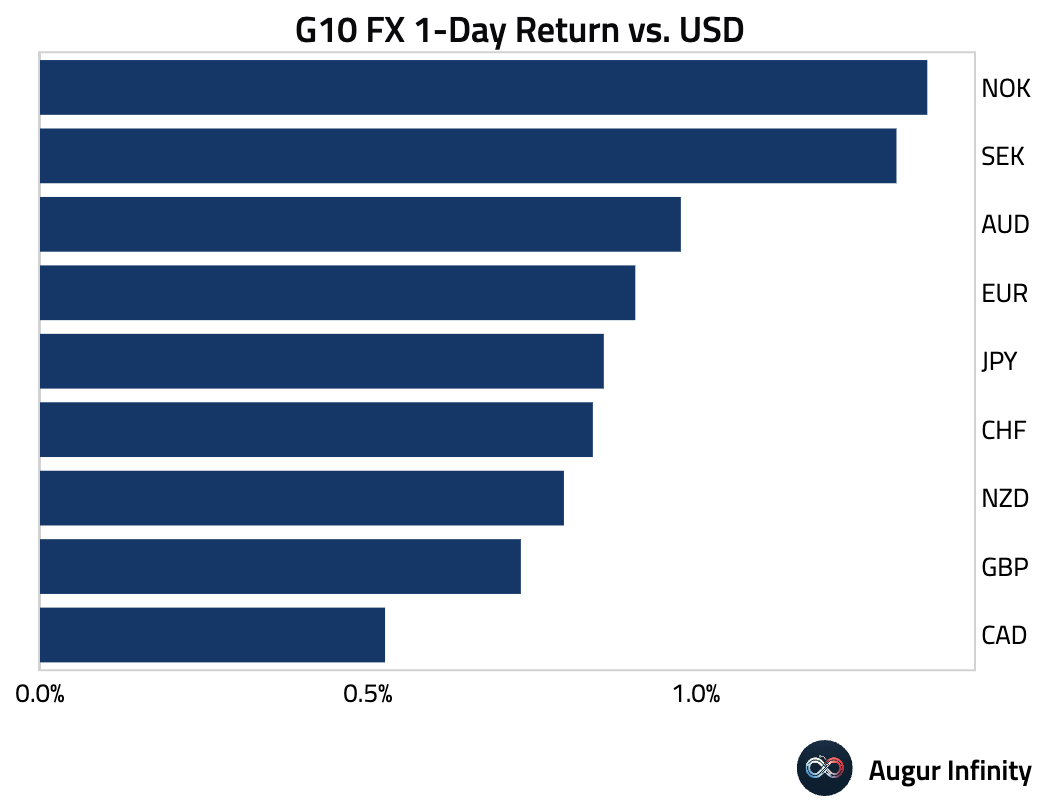

- The US dollar weakened against all G10 peers as rate-cut expectations mounted after Fed Chair Powell’s speech. The Norwegian krone (+1.4%) and Swedish krona (+1.3%) led the gains against the dollar. The krone’s advance marked its third consecutive day of appreciation.

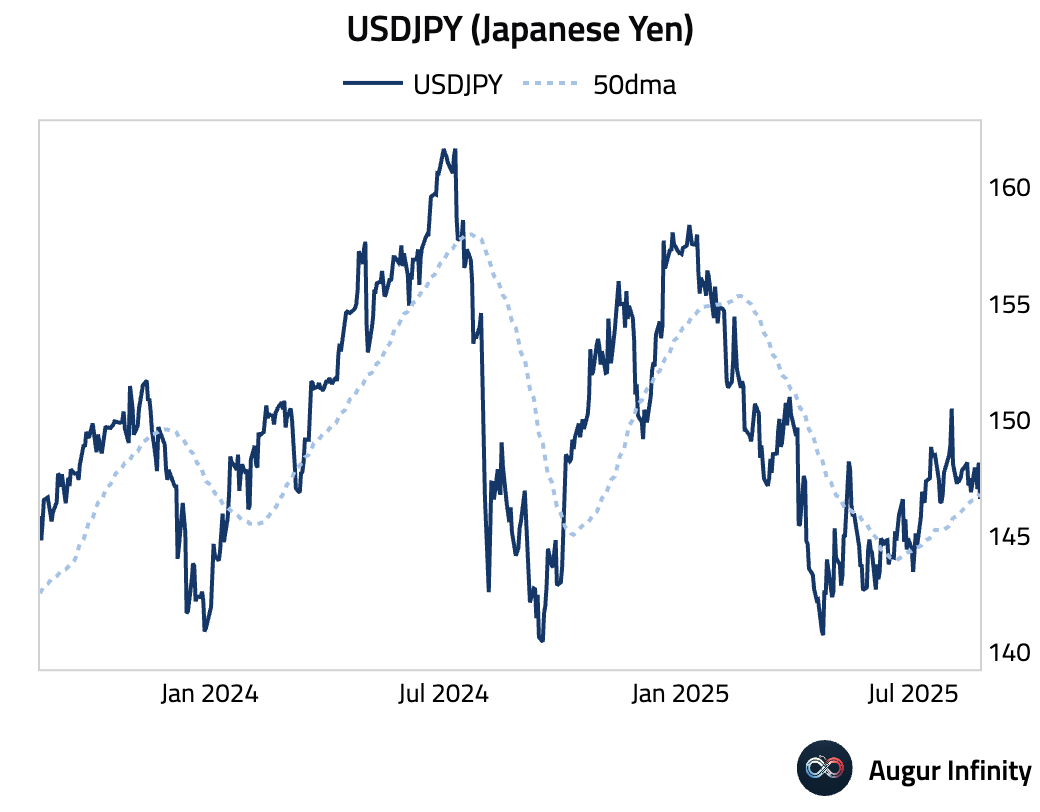

- Dollar yen fell below its 50-day moving average briefly intraday before recovering slightly.

Crypto

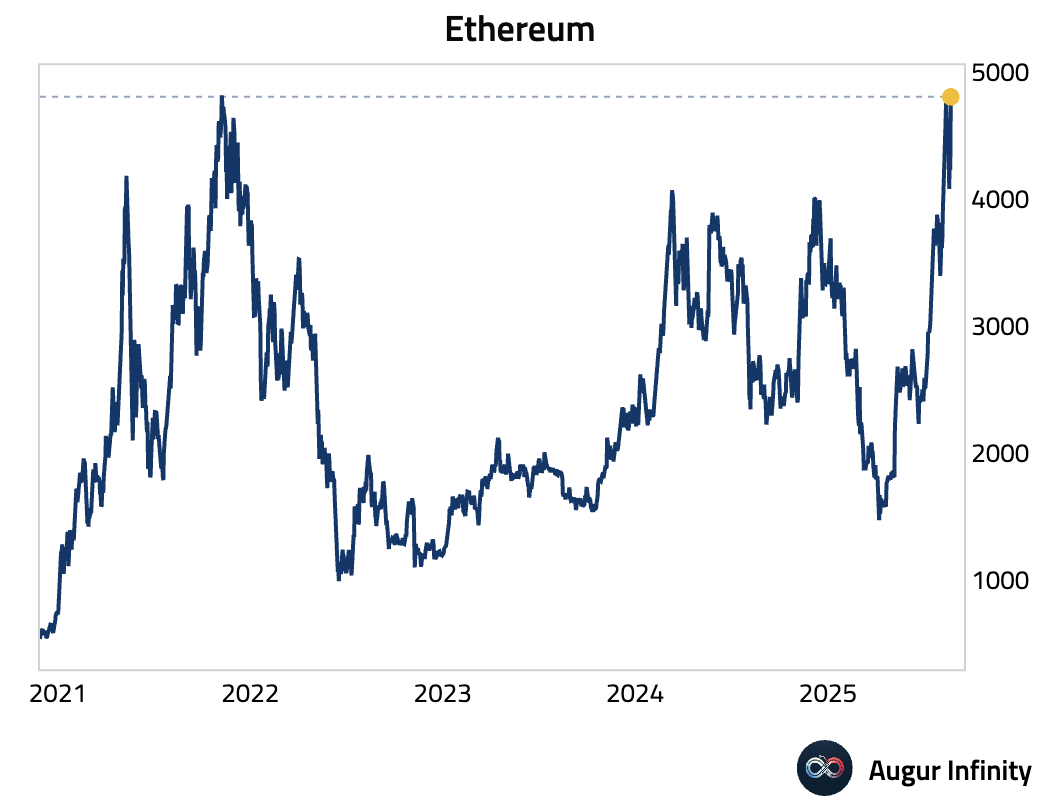

- Ethereum jumped almost 13% (a 3.1σ move), back near all-time highs.

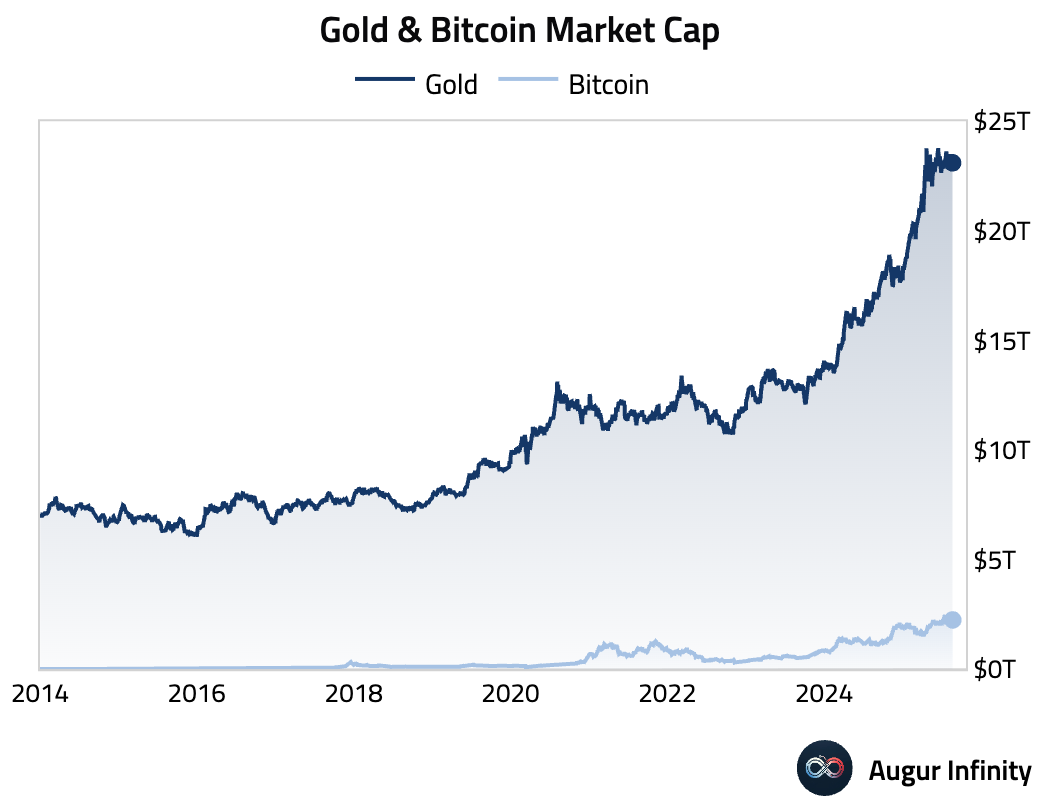

- Bitcoin’s market capitalization is currently about 10% of gold’s total market value.

Source: Bridgewater Associates

Musings

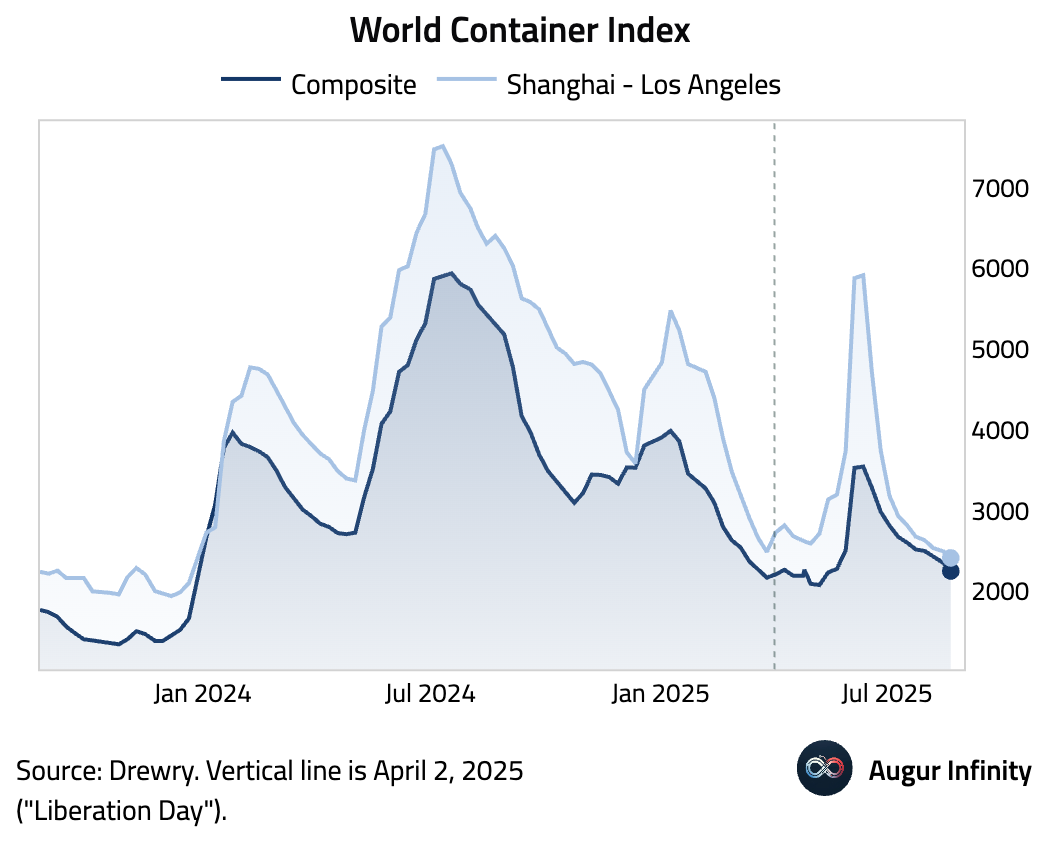

- The World Container Index, which measures spot freight rates, declined for the 10th consecutive week. The index for the Shanghai–Los Angeles route has hit the lowest level since January 2024.

Source: Drewry World Container Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.