Global Economics

United States

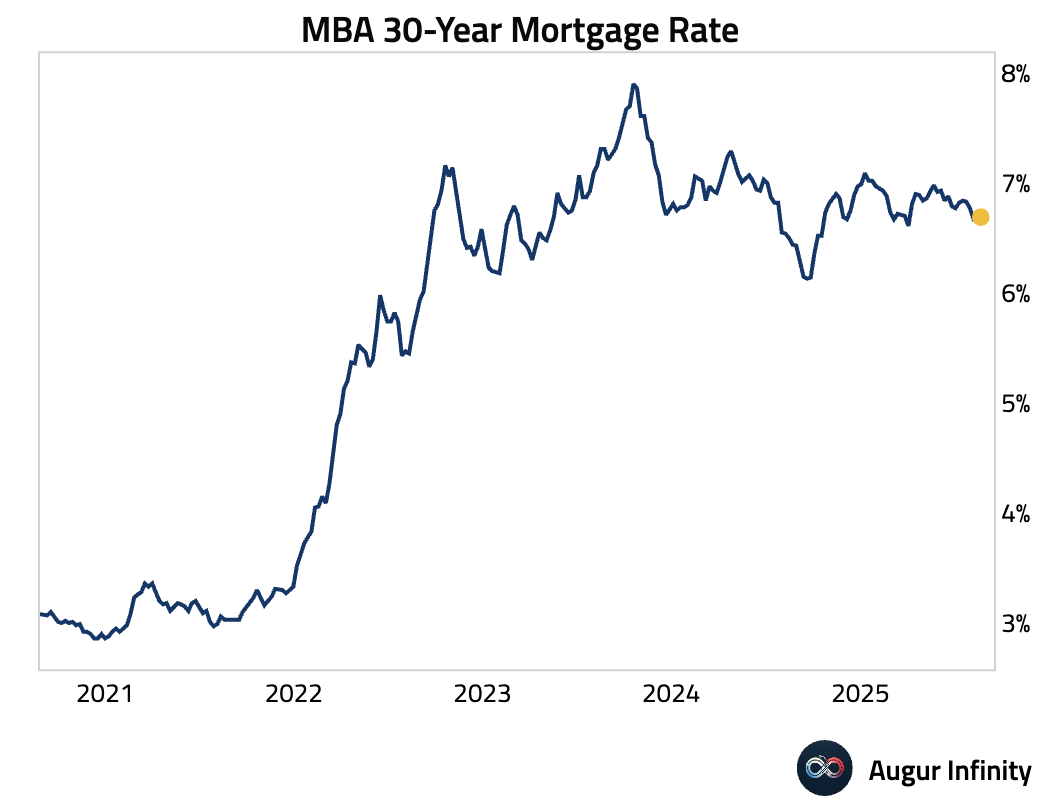

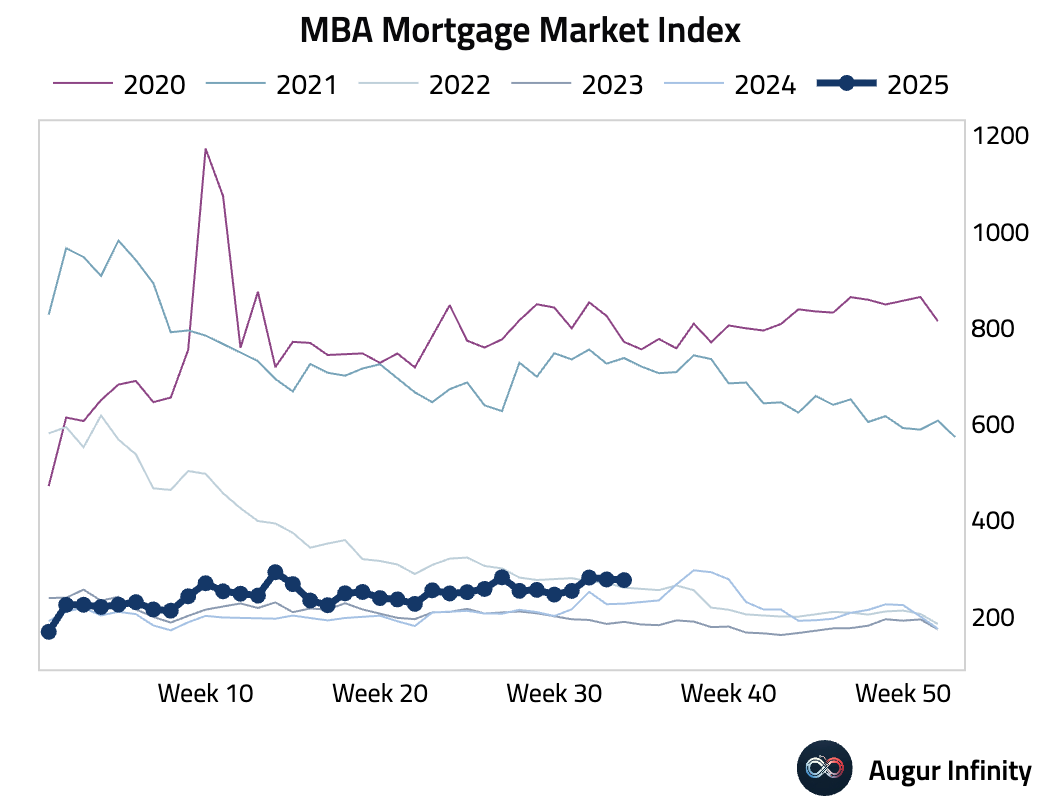

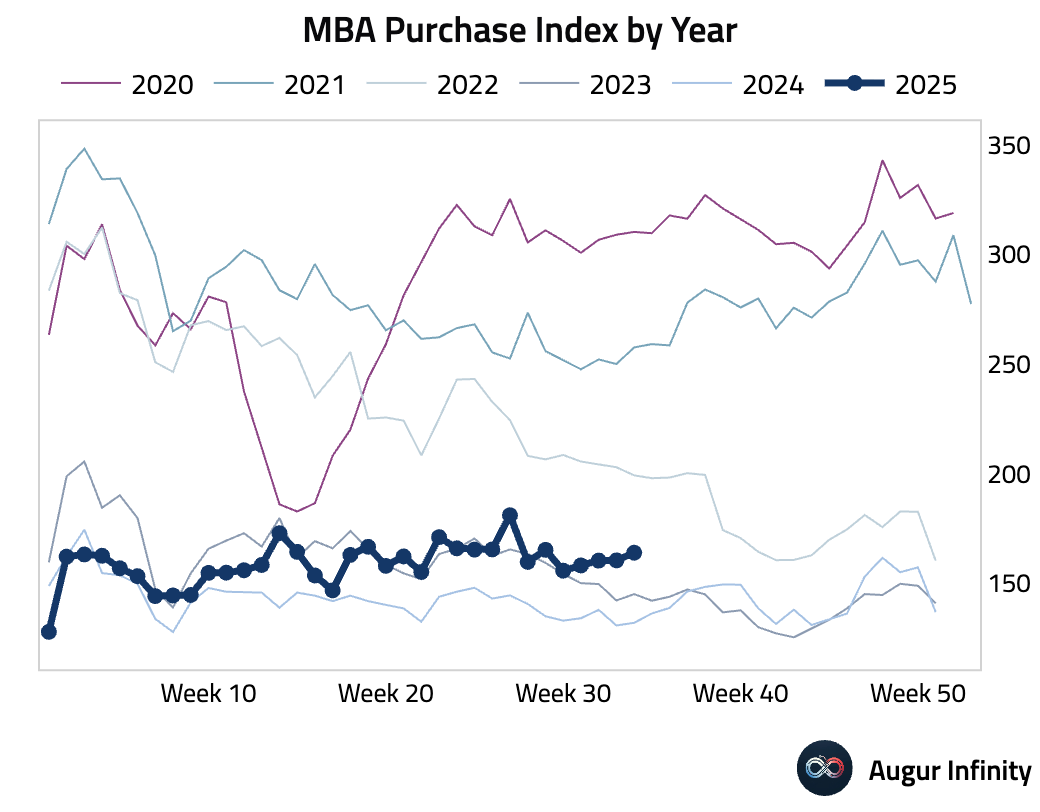

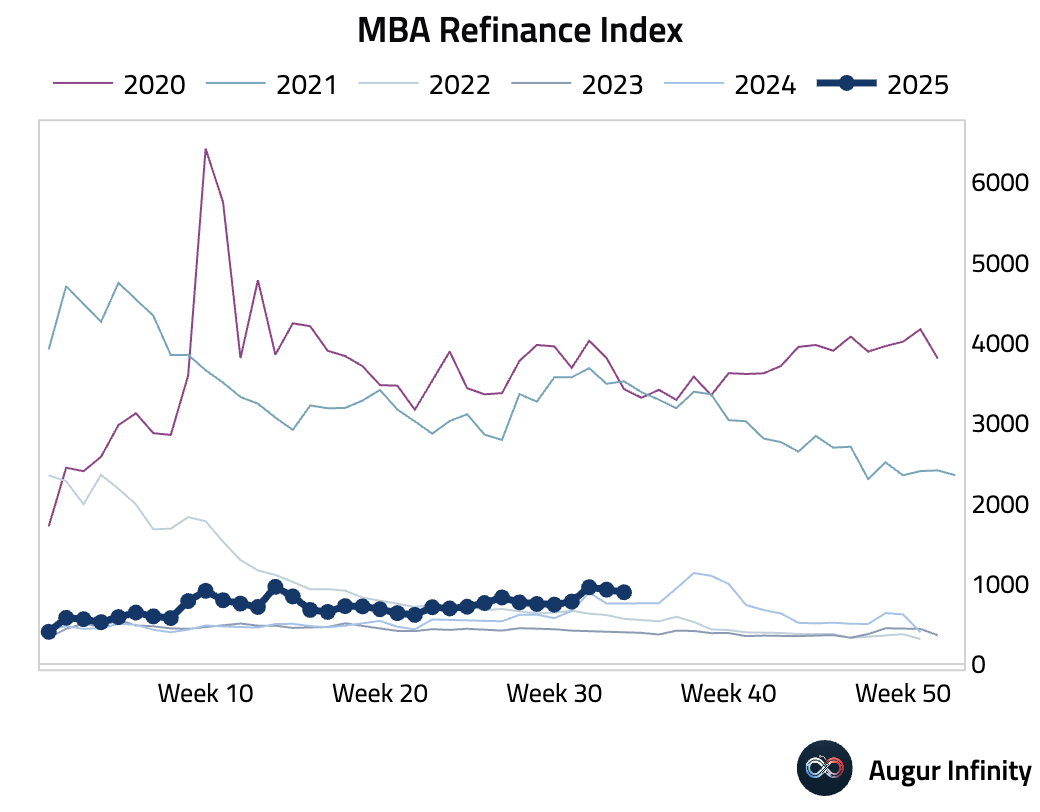

- The MBA 30-year mortgage rate ticked up to 6.69% for the week ending August 22. Overall mortgage applications fell 0.5% week-over-week, a moderation from the prior 1.4% drop. The decline was driven by a fall in the Refinance Index to 894.1, while the Purchase Index rose to 163.8.

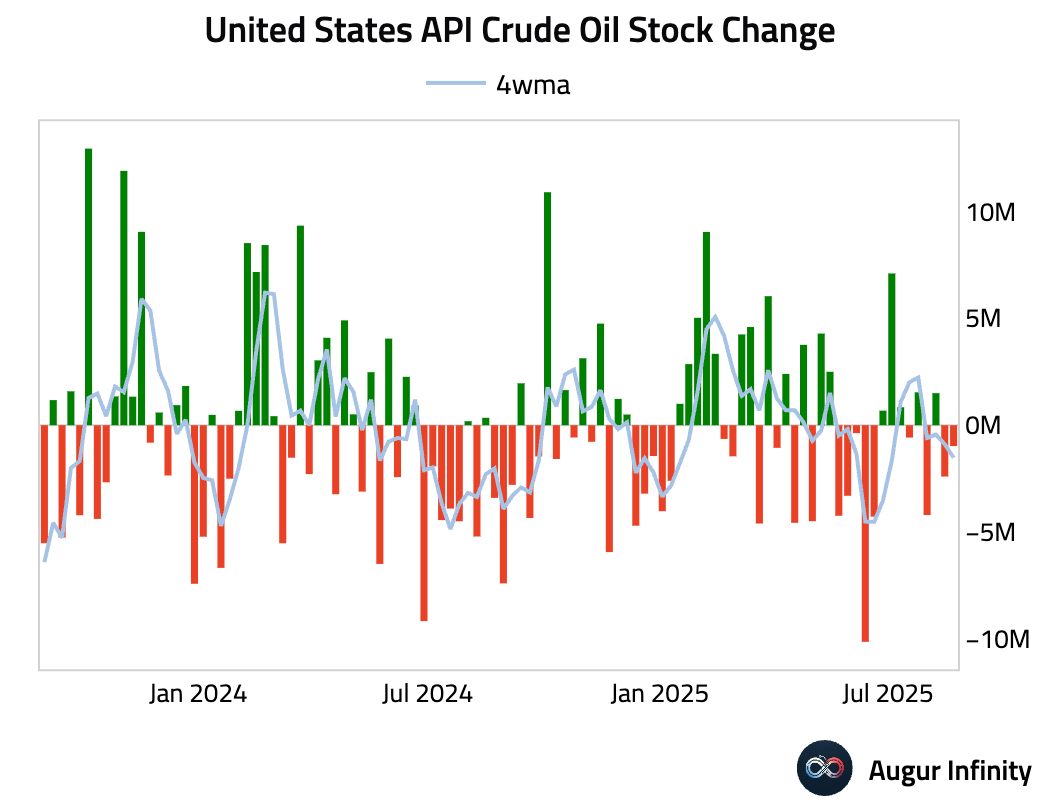

- For the week ending August 22, the API reported a crude oil stock draw of 0.974 million barrels, smaller than the expected 1.7 million barrel draw and the prior week’s 2.4 million barrel decline.

Canada

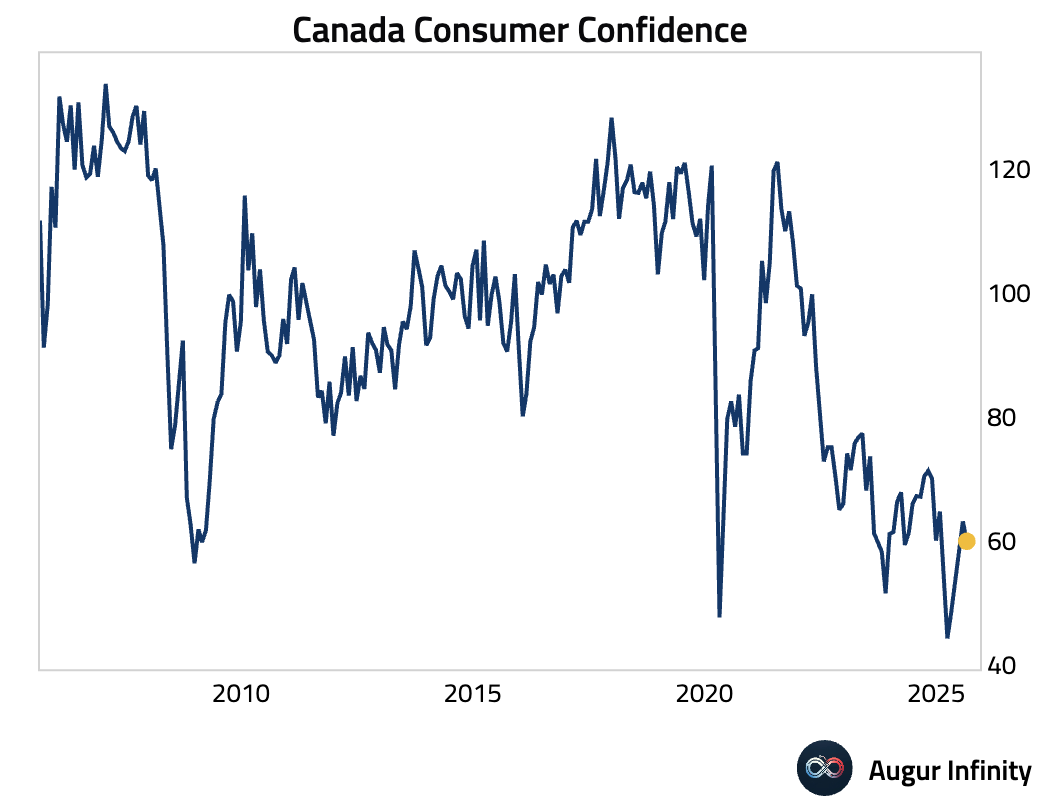

- Consumer confidence in Canada dipped slightly to 59.9 in August, as economic uncertainty keeps consumers on their toes.

Europe

- Germany’s GfK Consumer Confidence for September fell to -23.6, missing the consensus of -22.0 and deteriorating from the prior month’s -21.7. This marks the lowest reading since April 2025, signaling deepening pessimism among consumers.

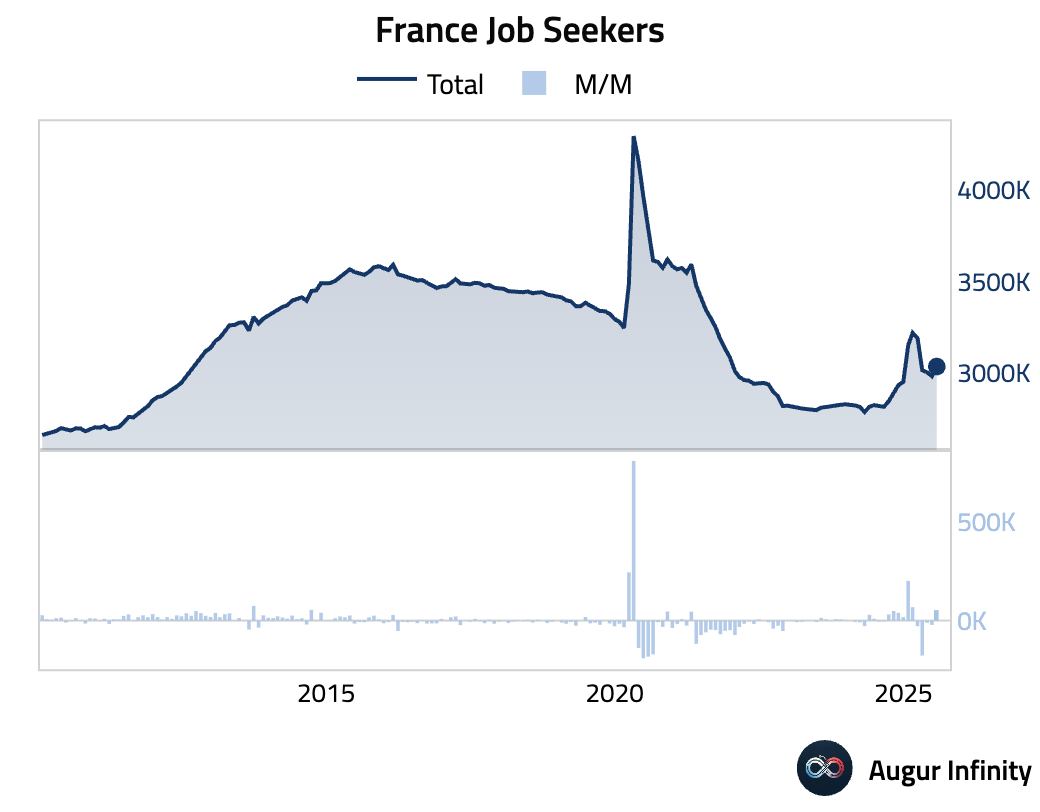

- In France, unemployment benefit claims rose by 52,900 in July, a sharp reversal from June’s 21,600 decline. The total number of jobseekers increased to 3.03 million from 2.98 million.

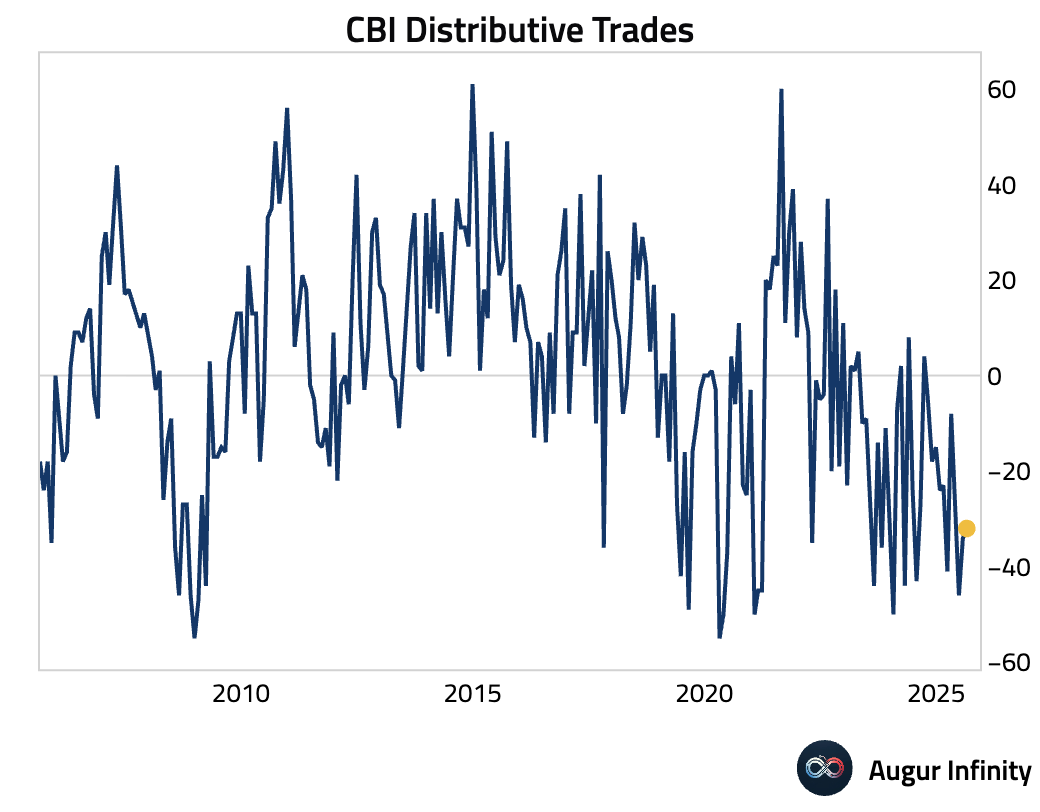

- The UK’s CBI Distributive Trades survey for August registered -32, a slight improvement from July’s -34 and marginally better than the -33 consensus, though still indicating a sharp contraction in retail sales.

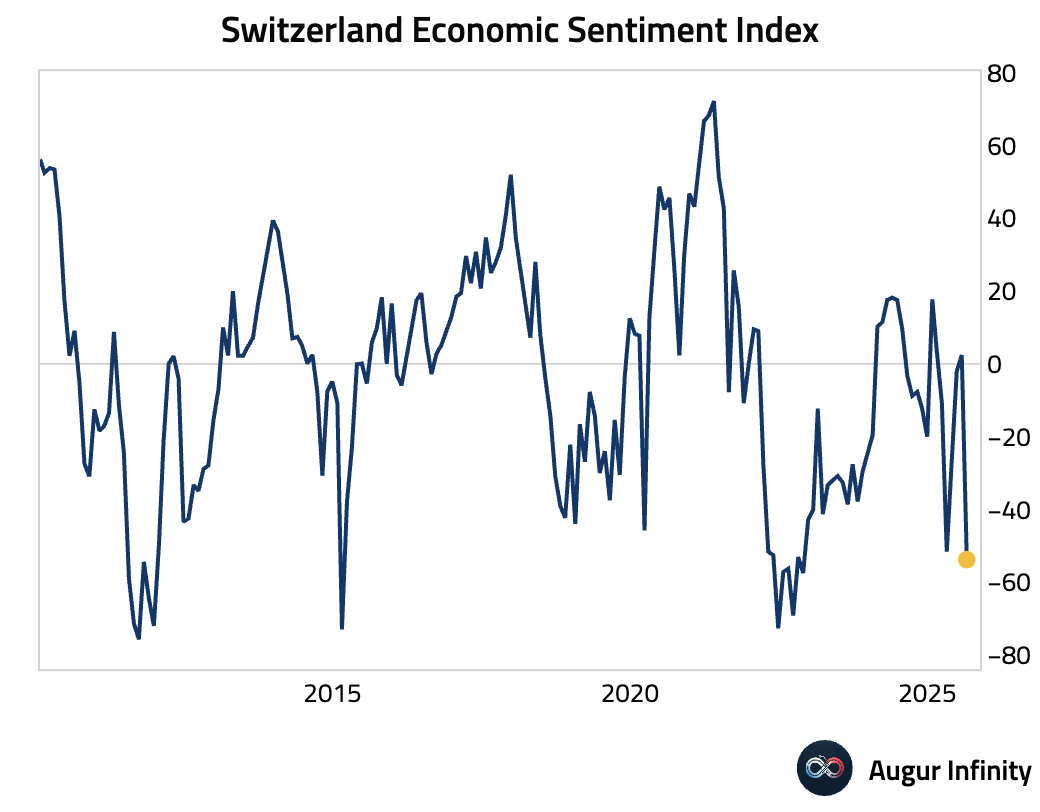

- Switzerland’s Economic Sentiment Index for August plummeted to -53.8 from 2.4 in July, reaching its lowest level since November 2022 and indicating a significant deterioration in economic expectations.

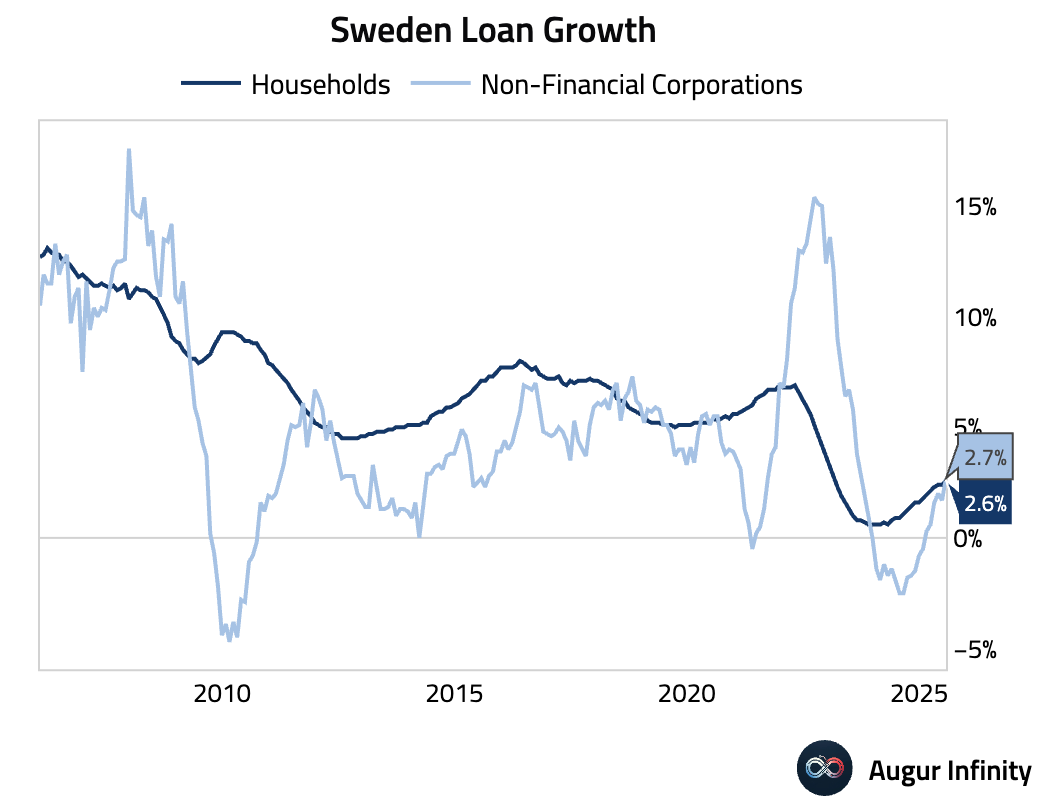

- Sweden’s household lending growth accelerated to 2.6% Y/Y in July from 2.4% in June, marking its highest rate since February 2023.

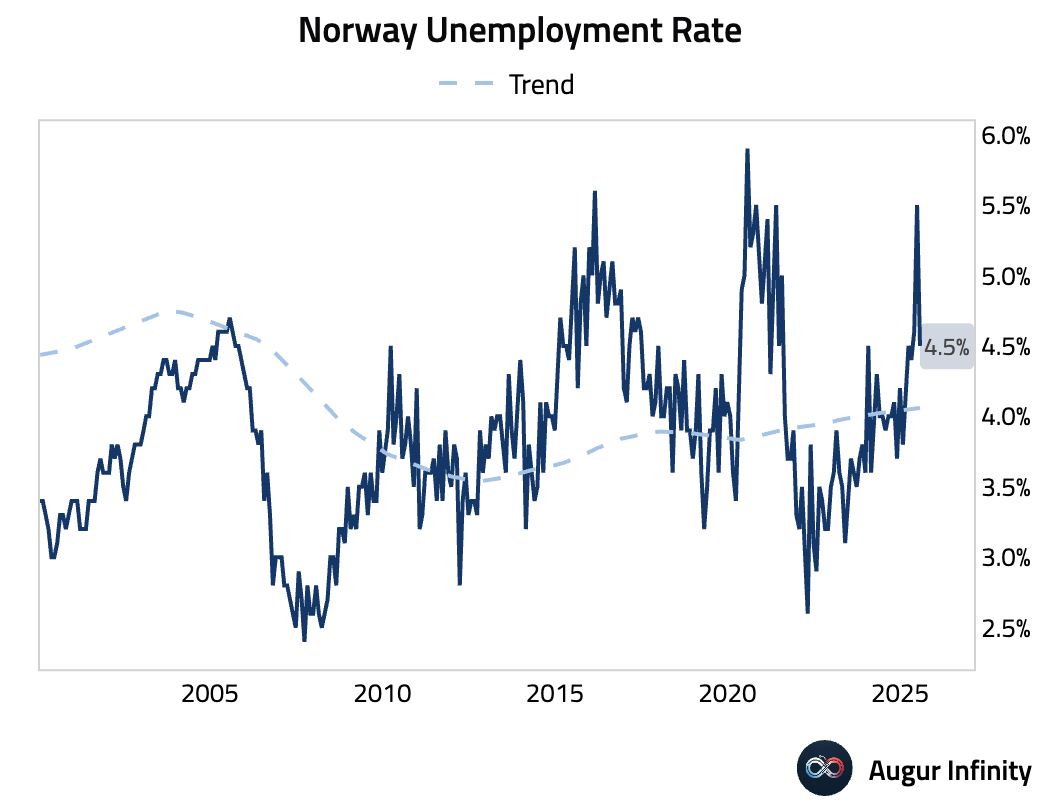

- Norway’s seasonally adjusted unemployment rate fell sharply to 4.5% in June from 5.5% in May.

Asia-Pacific

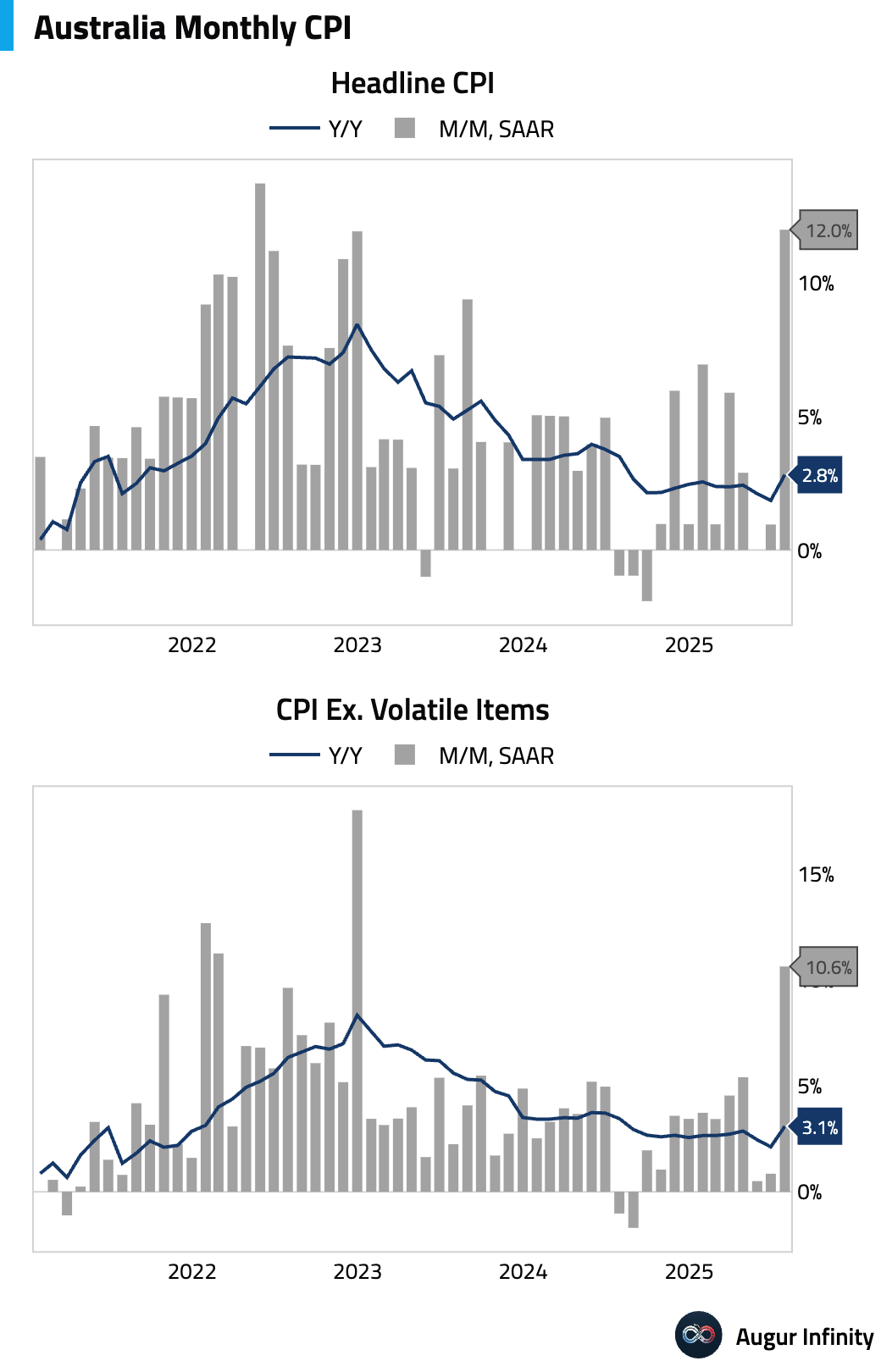

- Australia’s Monthly CPI Indicator accelerated to 2.8% Y/Y in July, significantly above the 2.3% consensus and June’s 1.9% reading. The upside surprise was driven by volatile items, particularly a 13.0% M/M surge in electricity prices following delays in government subsidy payments and a 4.7% M/M jump in holiday travel costs.

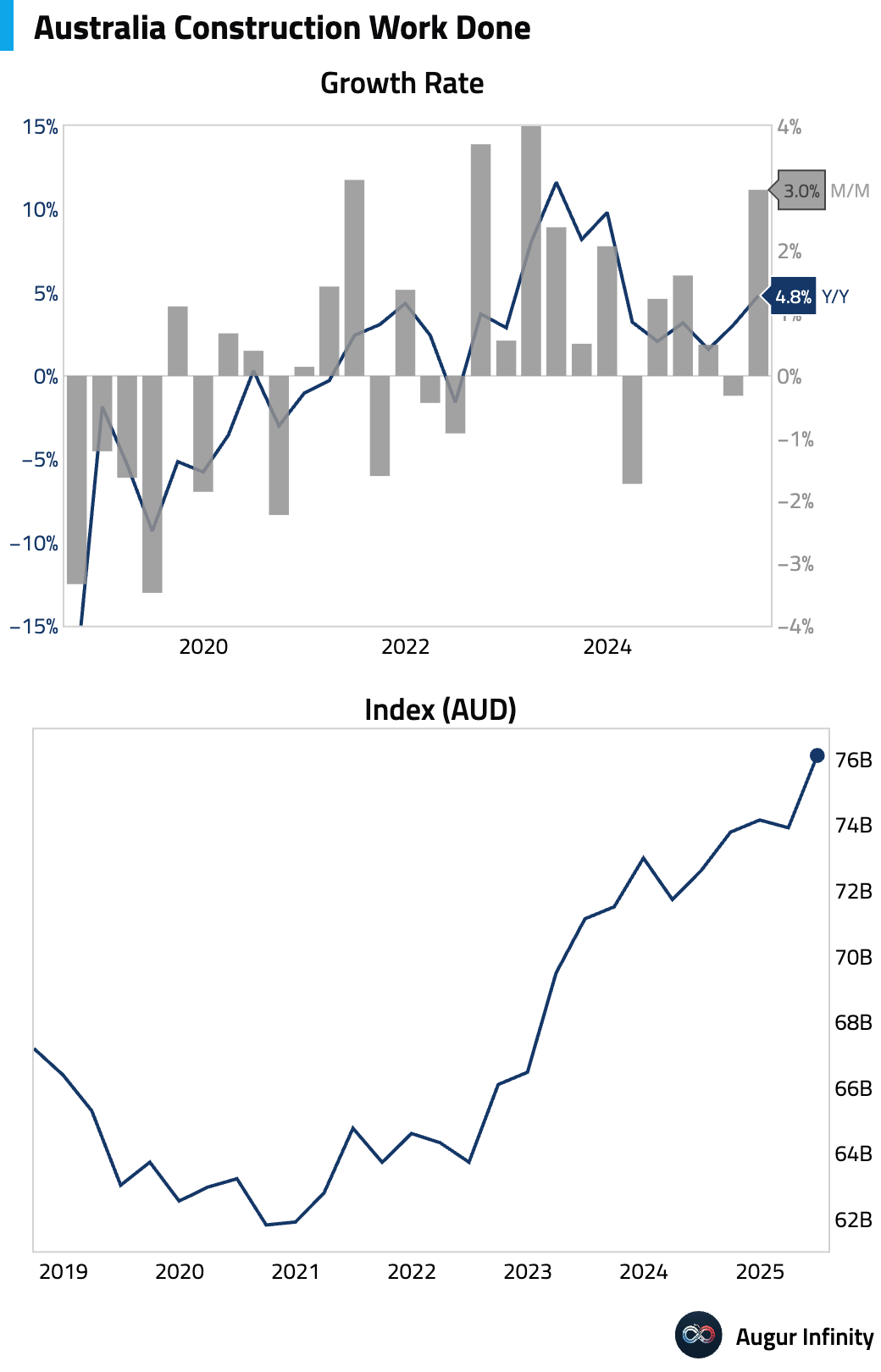

- Australian construction work done surged 3.0% Q/Q in the second quarter, smashing expectations of a 0.7% rise. The beat was driven entirely by a massive 13.5% Q/Q jump in private non-residential engineering. Residential investment was flat (+0.1%) and public construction fell (-0.4%). The headline figure may overstate the impact on GDP, as it may not reflect activity on an accrual basis consistent with National Accounts.

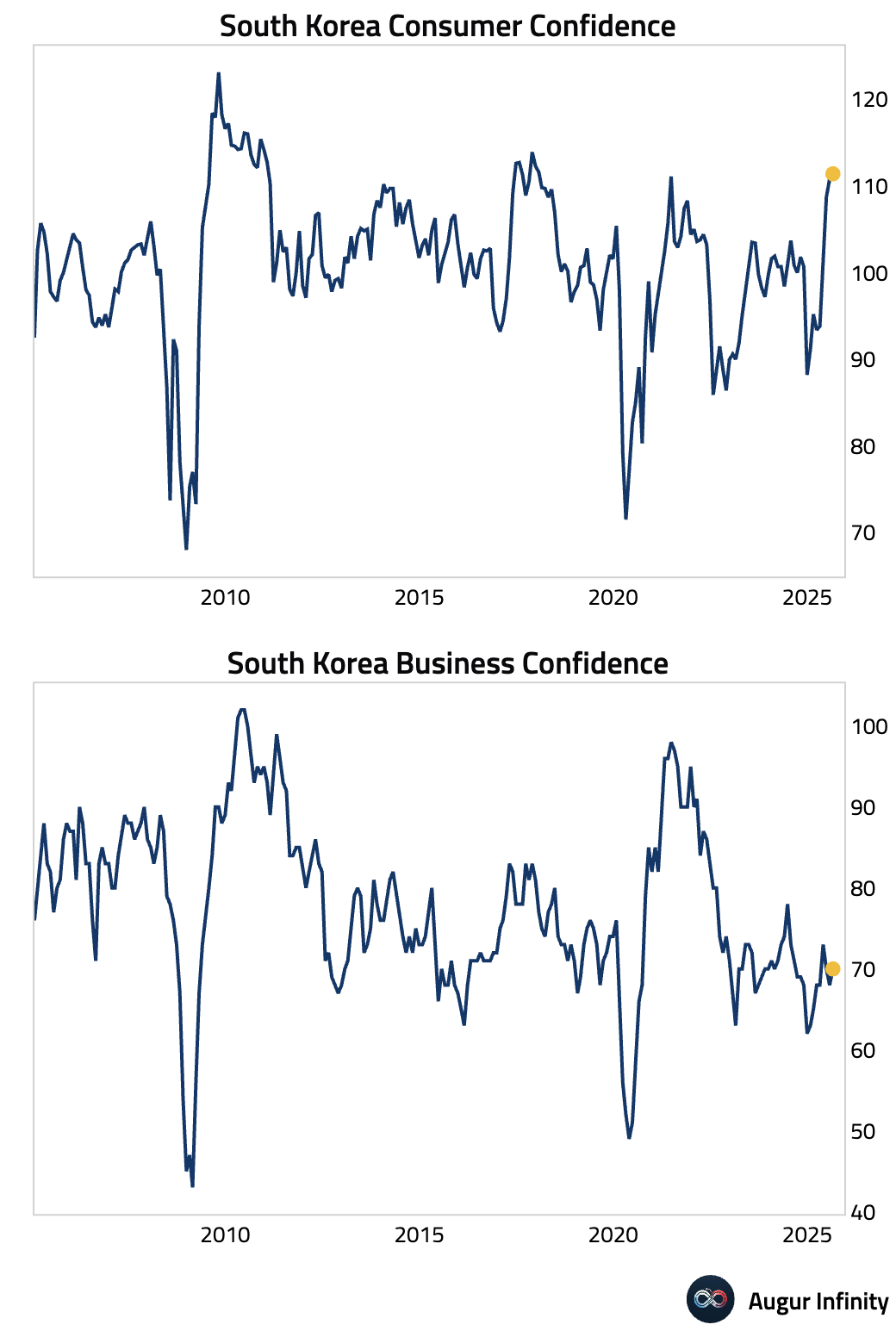

- South Korea’s Business Confidence index for August improved to 70 from 68 in July, its highest reading since May.

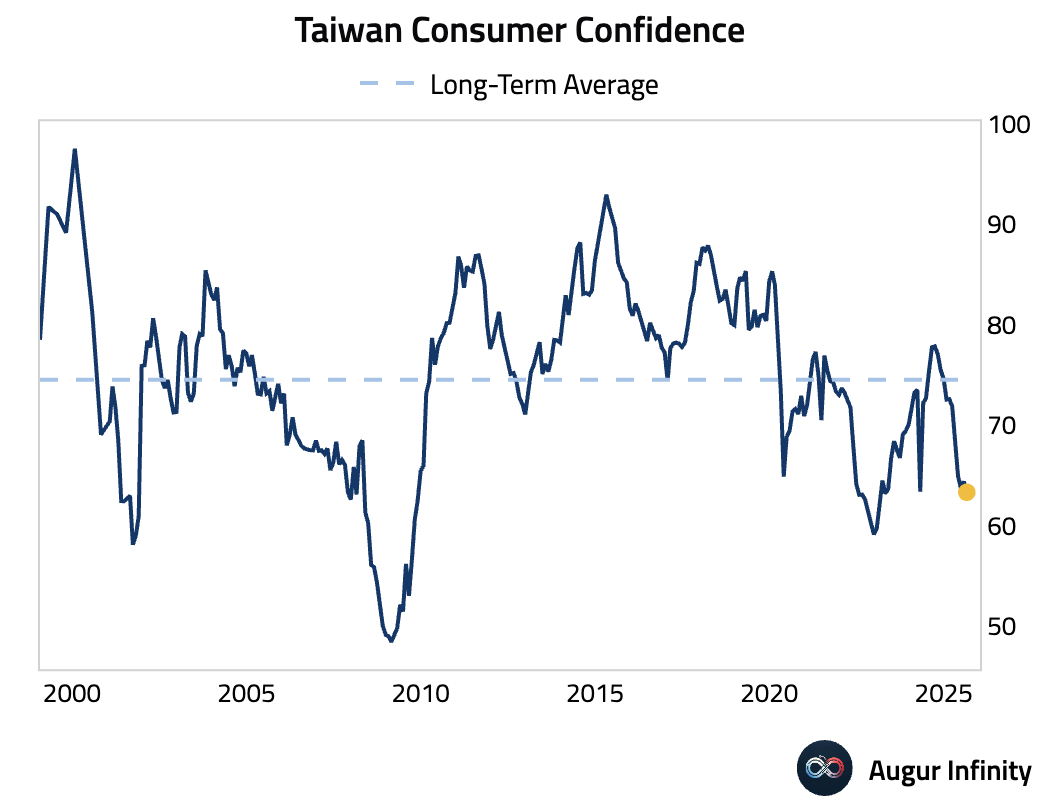

- Taiwan’s consumer confidence index declined to 63.31 in August from 64.38 in July, hitting its lowest level in over two years.

China

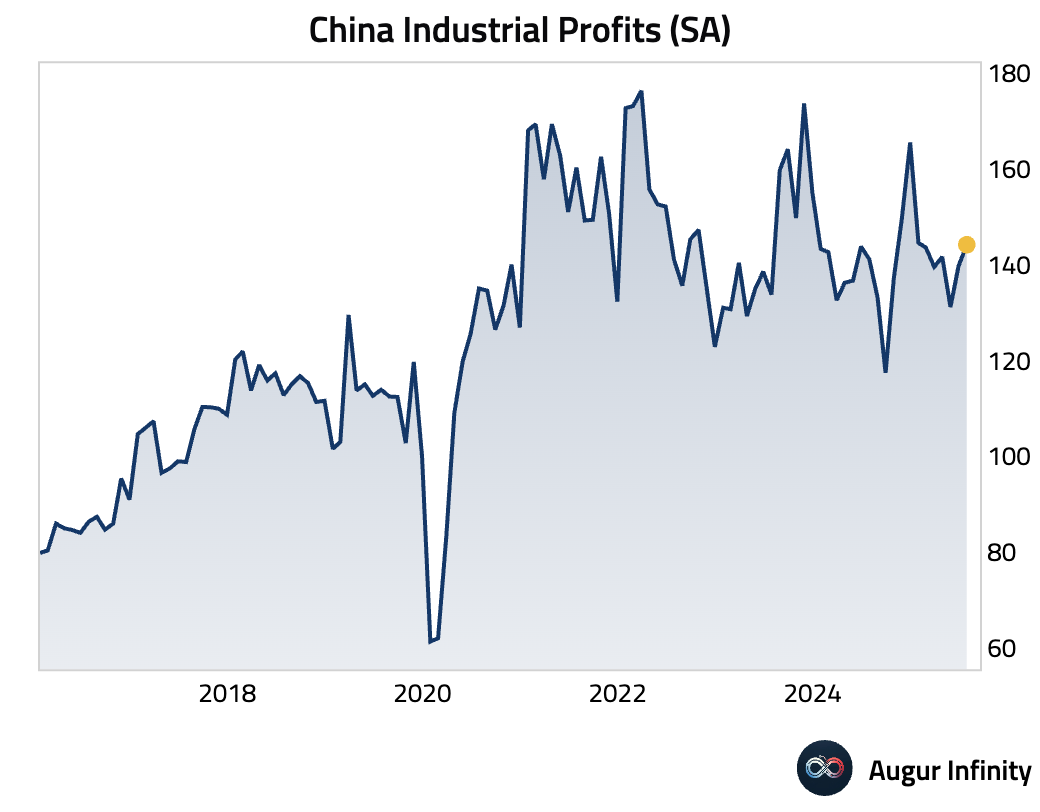

- Year-to-date industrial profits through July contracted by 1.7% Y/Y, a slight improvement from the 1.8% Y/Y decline seen through June. The rebound was driven by a surge in raw material sector profits, which rose 36.9% Y/Y, reflecting higher commodity prices and potentially the early effects of government policies in sectors like steel and coal.

Emerging Markets ex China

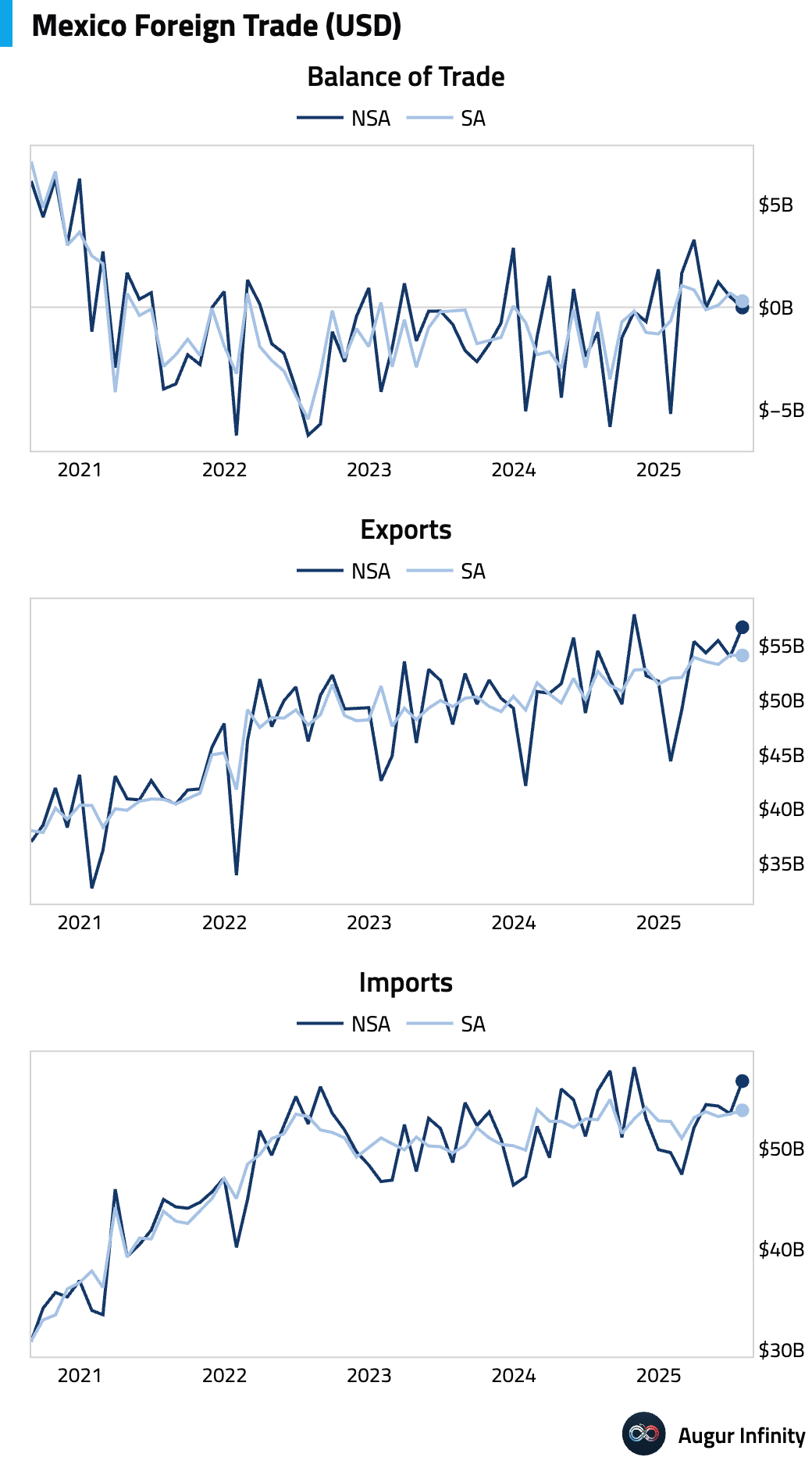

- Mexico posted a trade deficit of $17 million in July, a significant miss compared to the consensus forecast for a $300 million surplus. A strong non-oil surplus more than offset a persistent, widening oil deficit. Auto manufacturing exports were notably soft (-7.0% Y/Y), while non-auto manufacturing exports remained firm (+11.7% Y/Y).

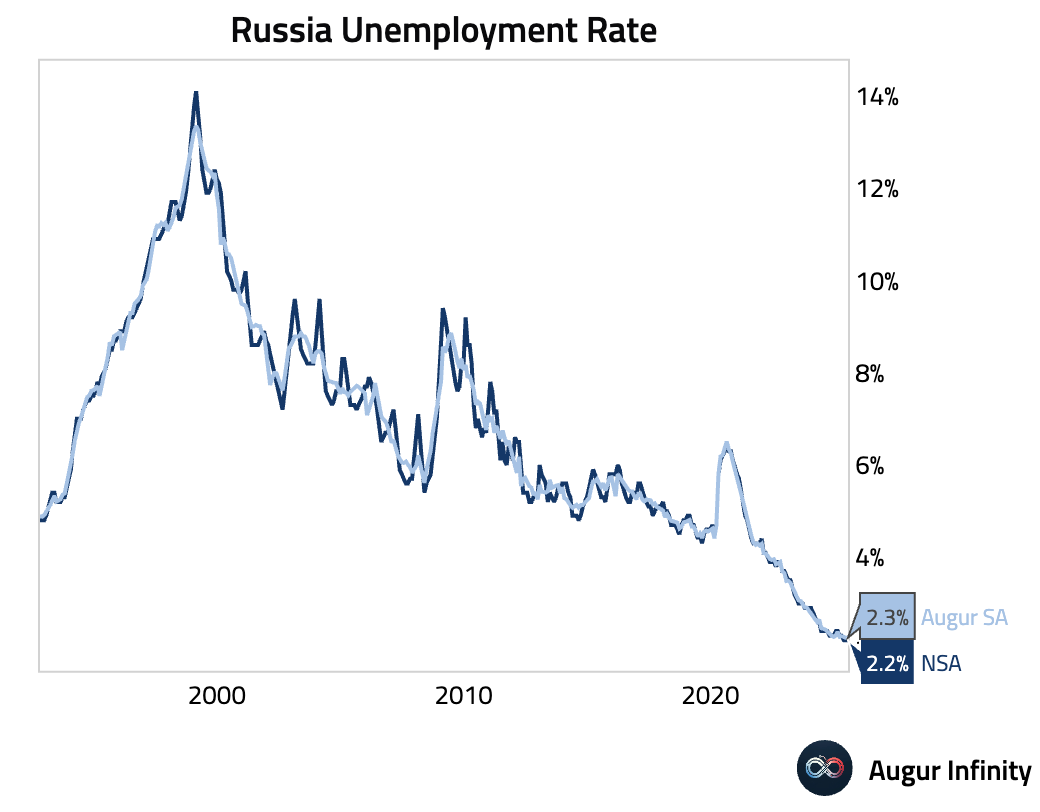

- Russia’s unemployment rate held steady at 2.2% in July, matching the previous month's reading. This level represents a new all-time low for the series.

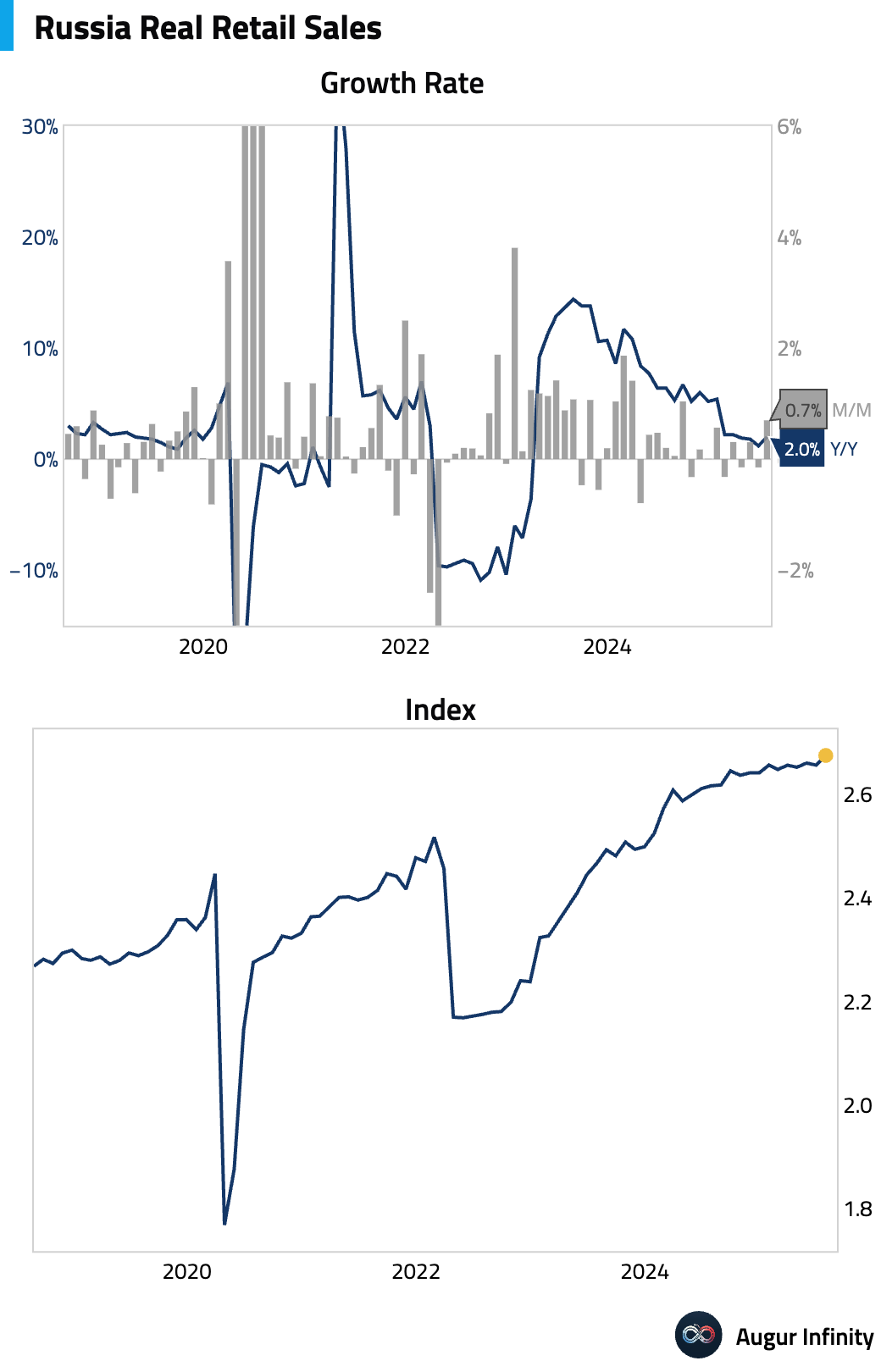

- Russian retail sales growth accelerated to 2.0% Y/Y in July from 1.2% previously, beating the 1.8% consensus.

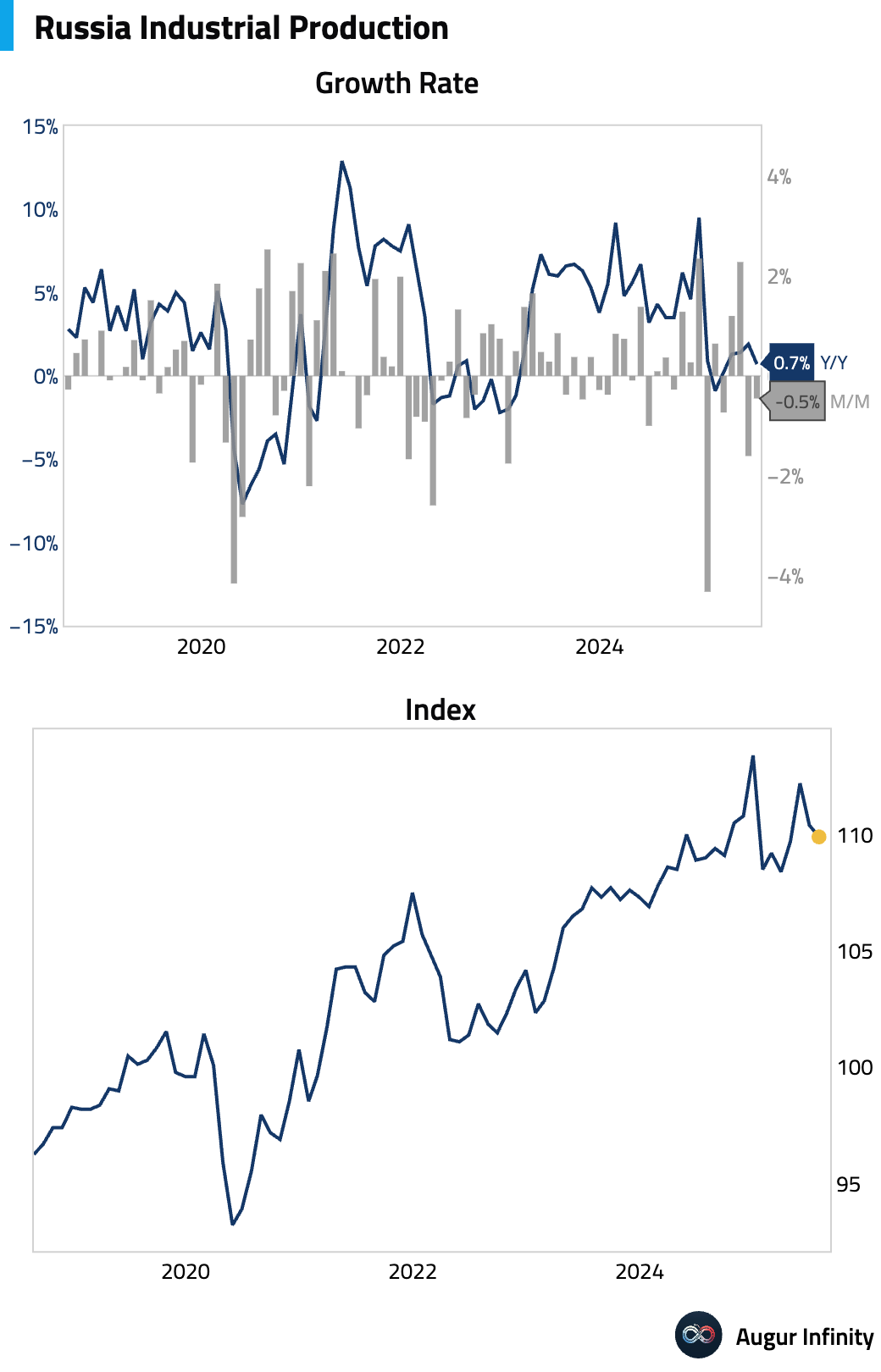

- Russia’s industrial production growth slowed to 0.7% Y/Y in July from 1.9% in June.

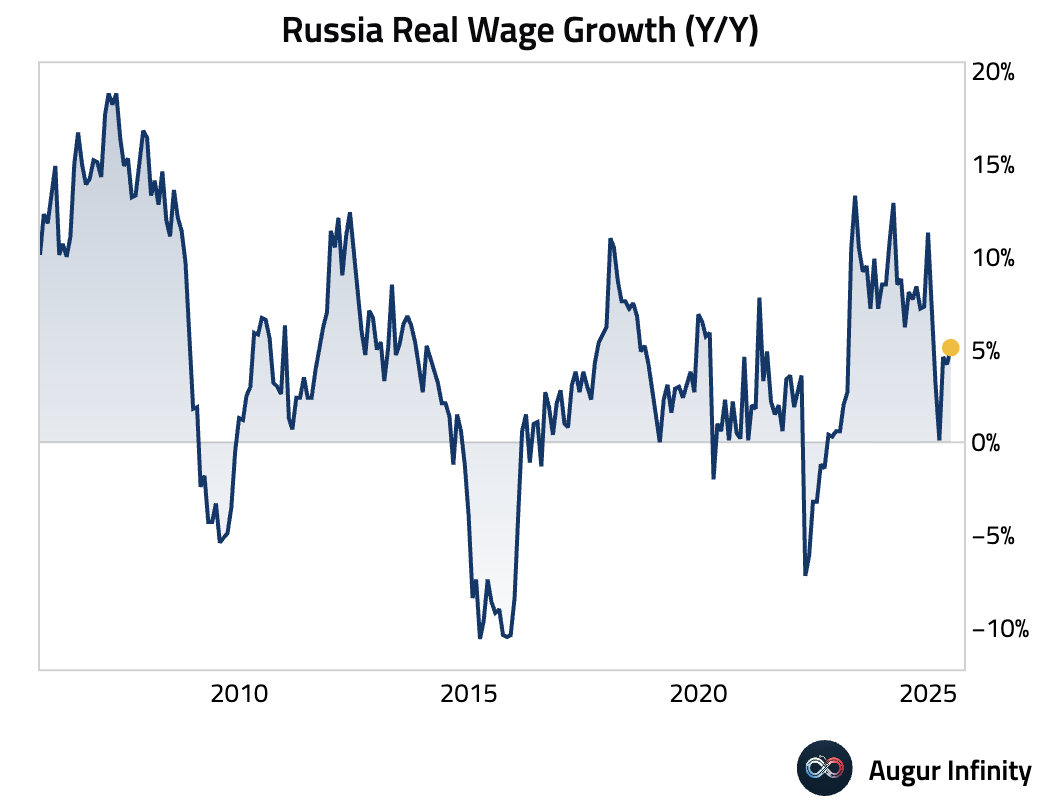

- Real wage growth in Russia increased to 5.1% Y/Y in June, up from 4.2% in May but below the 5.3% consensus.

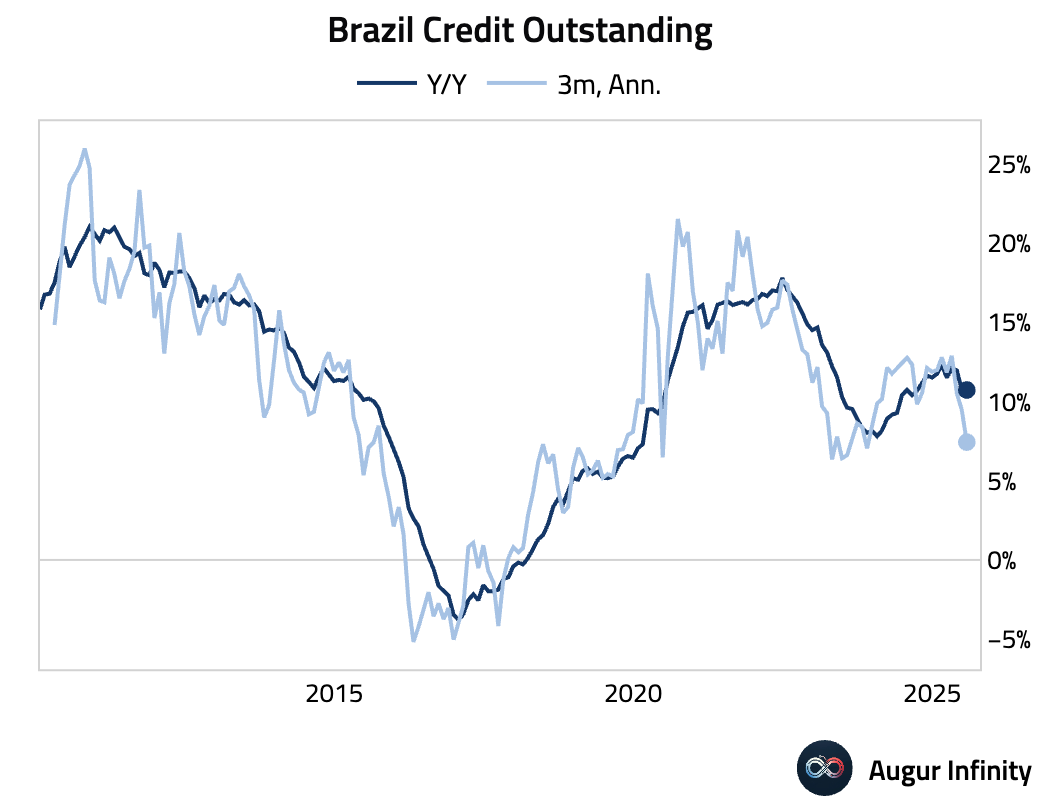

- Brazil’s bank lending growth slowed to 0.4% M/M in July from 0.5% in June, confirming a credit cycle slowdown. The drop was driven by a 2.4% M/M fall in household lending. Credit quality deteriorated, with non-performing loans on freely allocated credit rising 20 basis points to 5.5%.

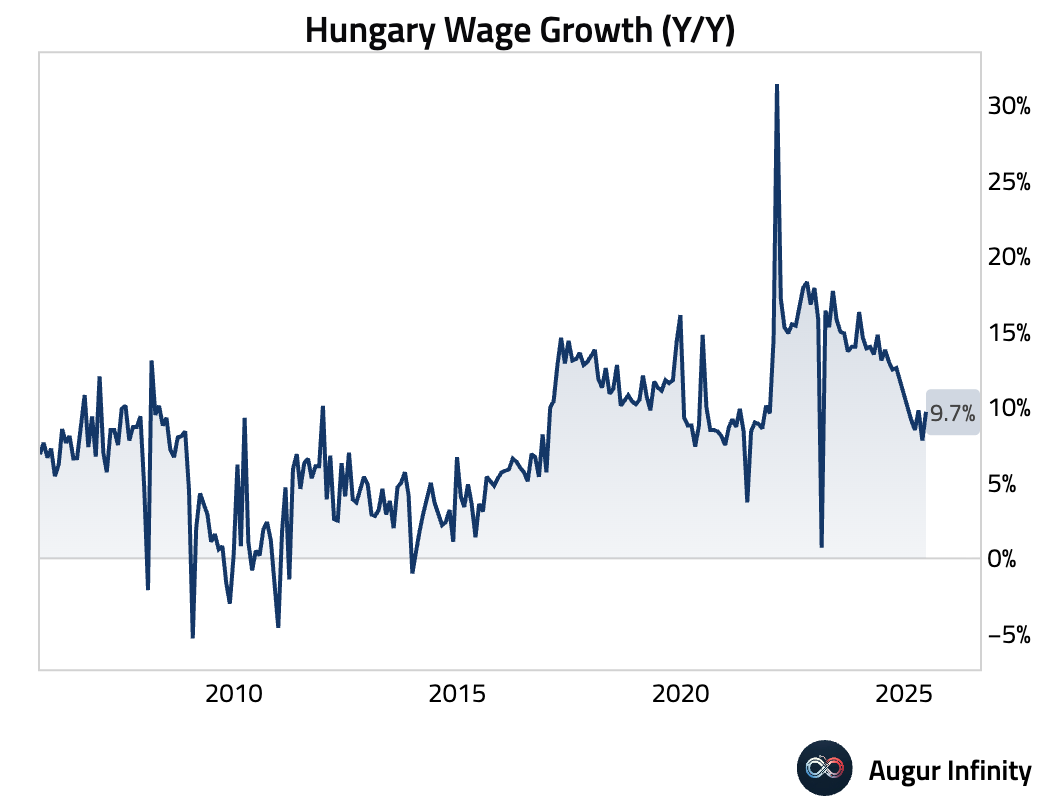

- Hungary’s gross wage growth accelerated to 9.7% Y/Y in June from 7.8% in May.

Global Markets

Equities

- Global equity markets were mixed as investors awaited key corporate earnings. US stocks saw modest gains, with the S&P 500 rising 0.2%. In contrast, Chinese equities fell sharply by 2.5%, contributing to a 0.8% decline in the broader emerging markets index, which has now fallen for three consecutive days. European markets were also broadly lower, with the United Kingdom posting its third straight day of losses. Brazil was a notable outperformer, gaining 1.2%.

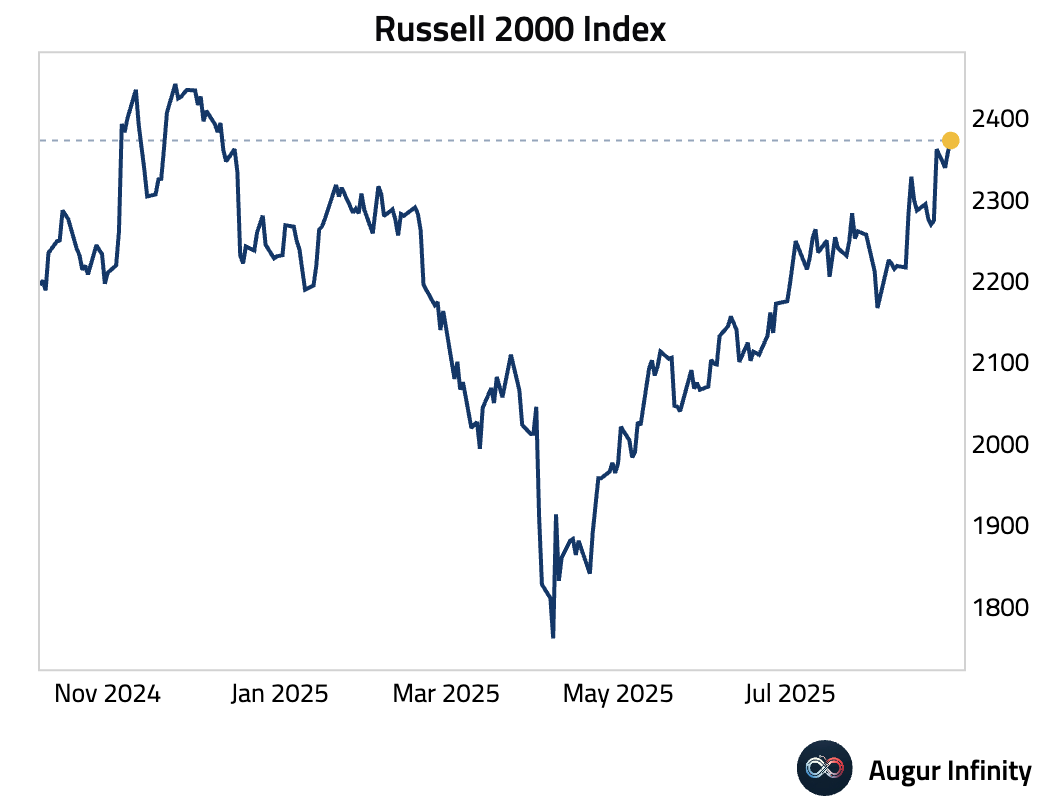

- The Russell 2000 Index hit its highest level since December 2024.

Fixed Income

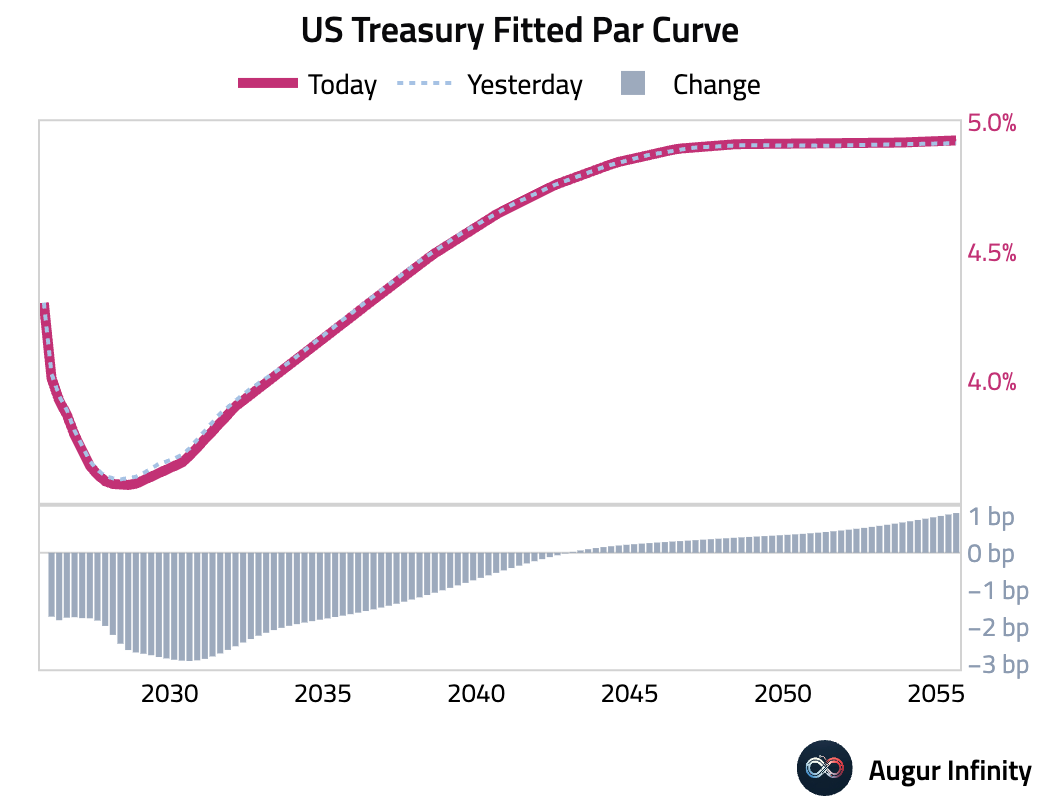

- Yields on the short and intermediate parts of the curve declined while the long end rose. The 2-year and 10-year yields fell by 2.3 bps and 1.9 bps, respectively. In contrast, the 30-year yield increased by 0.6 bps, marking its third consecutive daily rise.

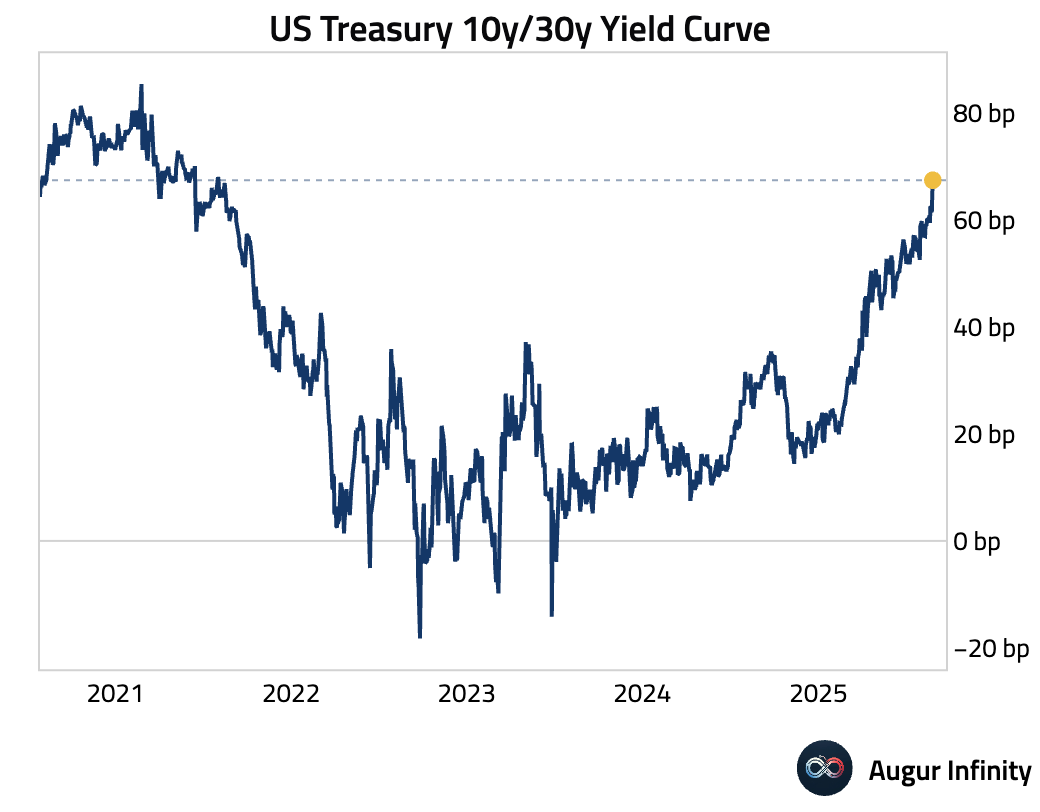

- The Treasury yield curve continues to steepen, with the 10y/30y yield now at the steepest level since August 2021.

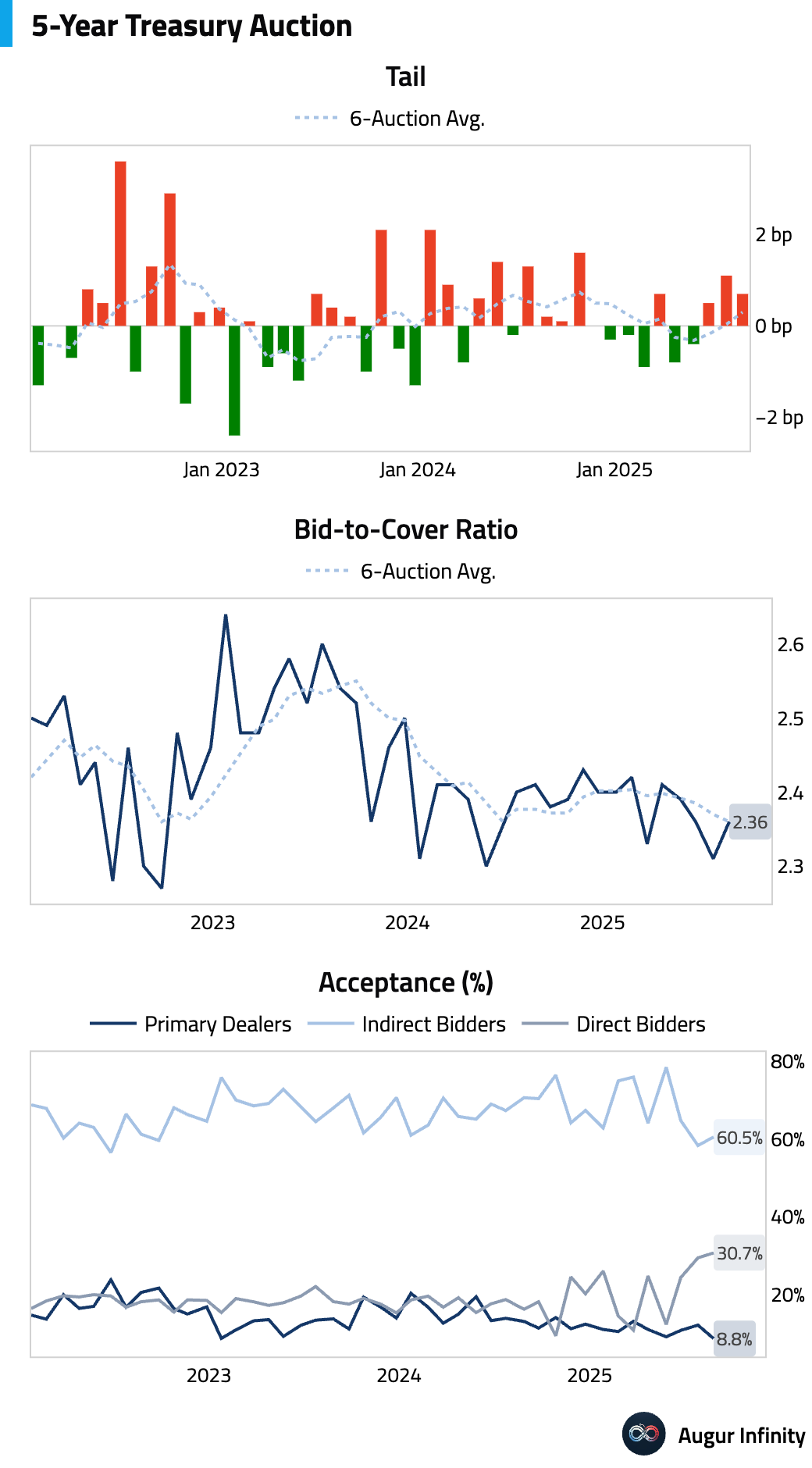

- Today's 5-year Treasury auction tailed by 0.7 bps, the third tail in a row. However, bid-to-cover was solid at 2.36x and dealer acceptance was low at just 8.8%.

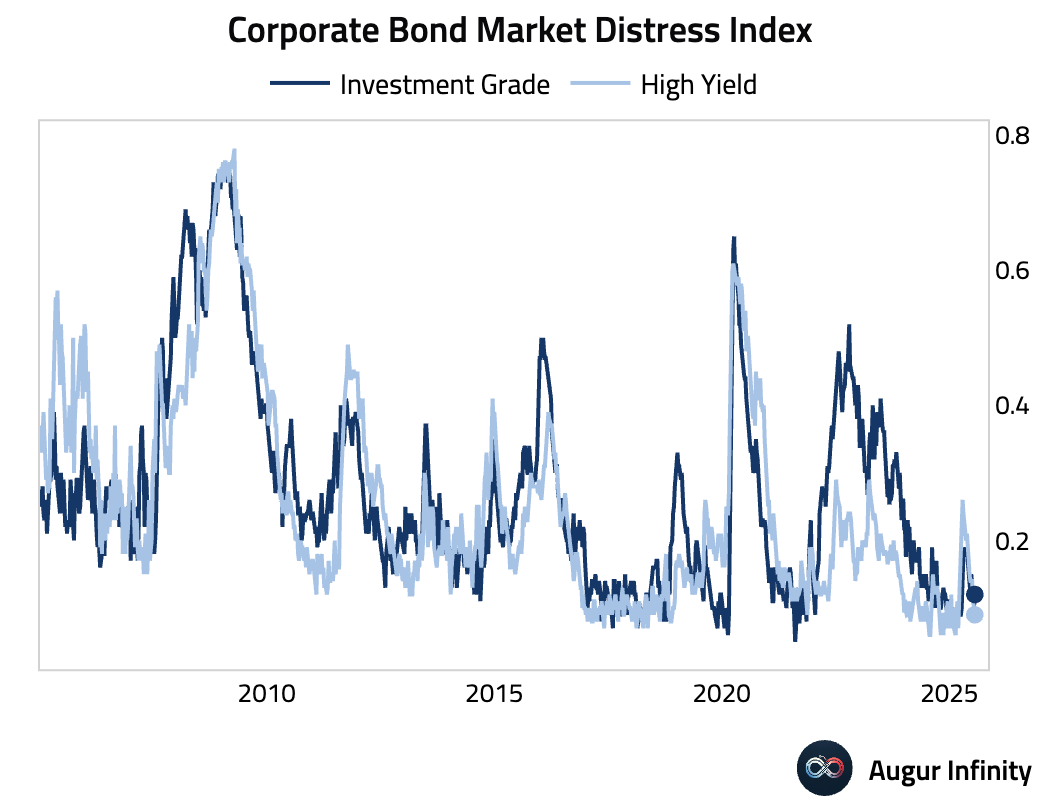

- The New York Fed Corporate Bond Market Distress Index remains very low, with the high yield series at its 11th percentile.

Commodities

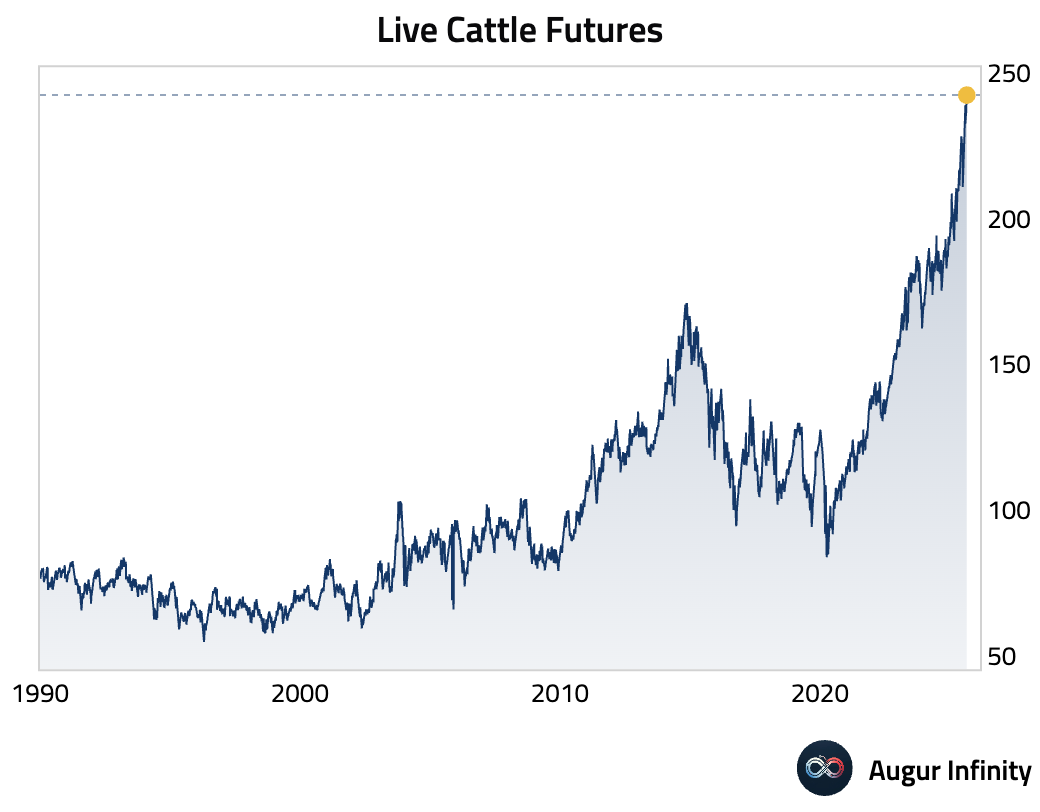

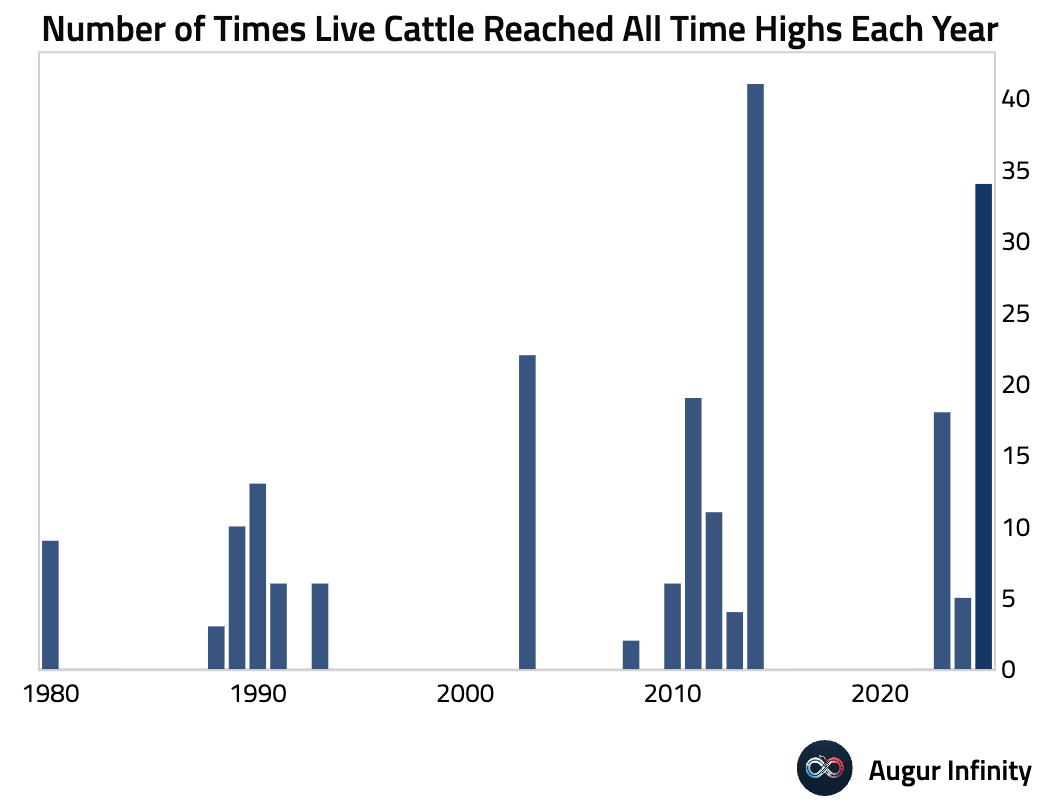

- Live cattle futures reached the 34th all-time-high this year.

FX

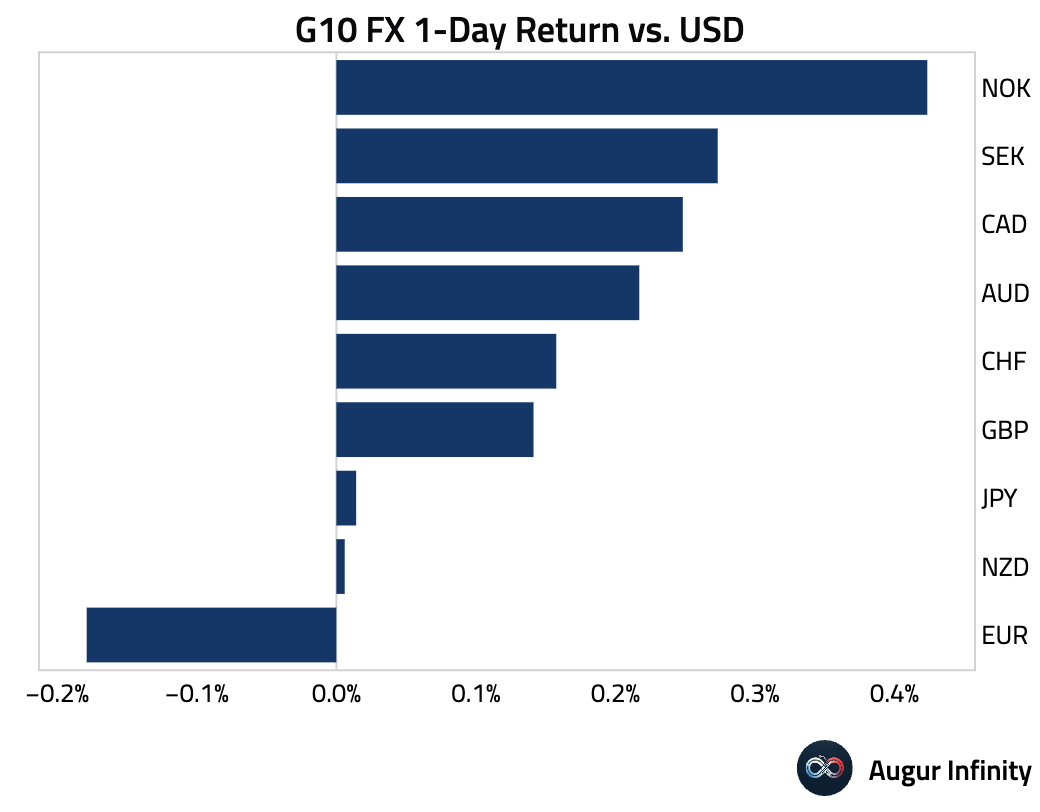

- The US dollar weakened against most of its G10 peers. The Norwegian krone (+0.4%) and Swedish krona (+0.3%) were the strongest performers. The euro was the primary underperformer, declining 0.2% against the dollar for its third consecutive day of losses.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.