Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Global Economics

United States

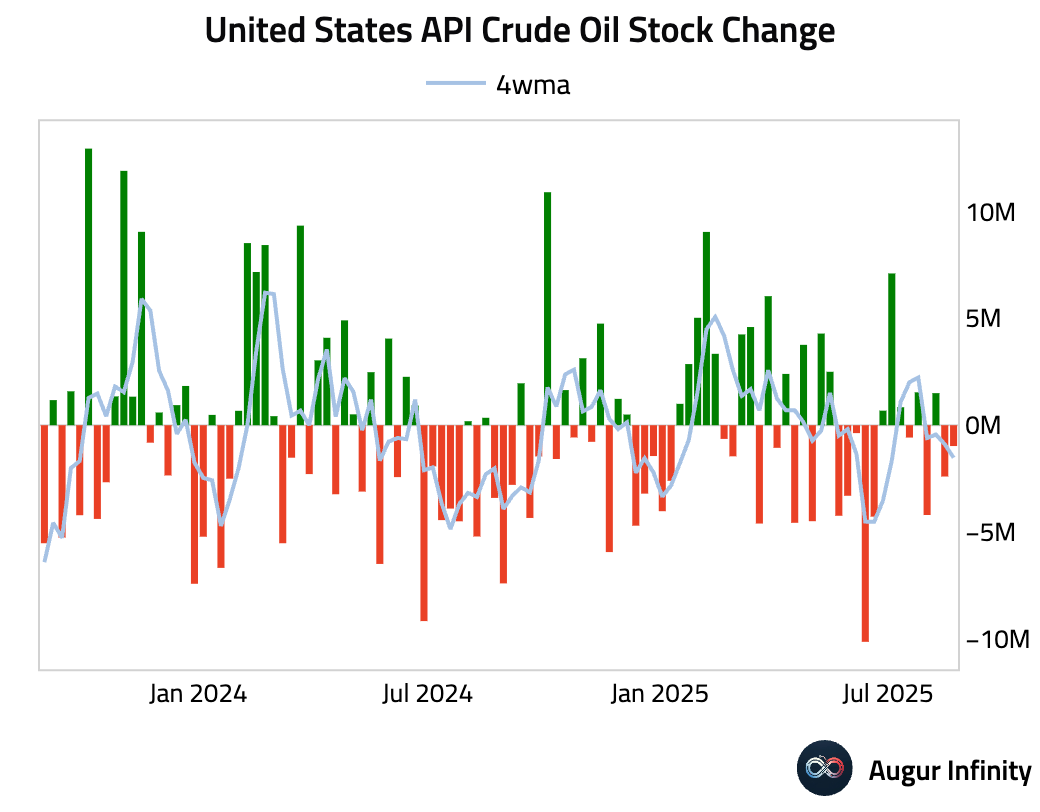

- US crude oil inventories drew down by 0.974 million barrels last week, according to API data. This marks a smaller draw than the previous week’s 2.4 million barrel decline but was larger than the expected 1.7 million barrel draw.

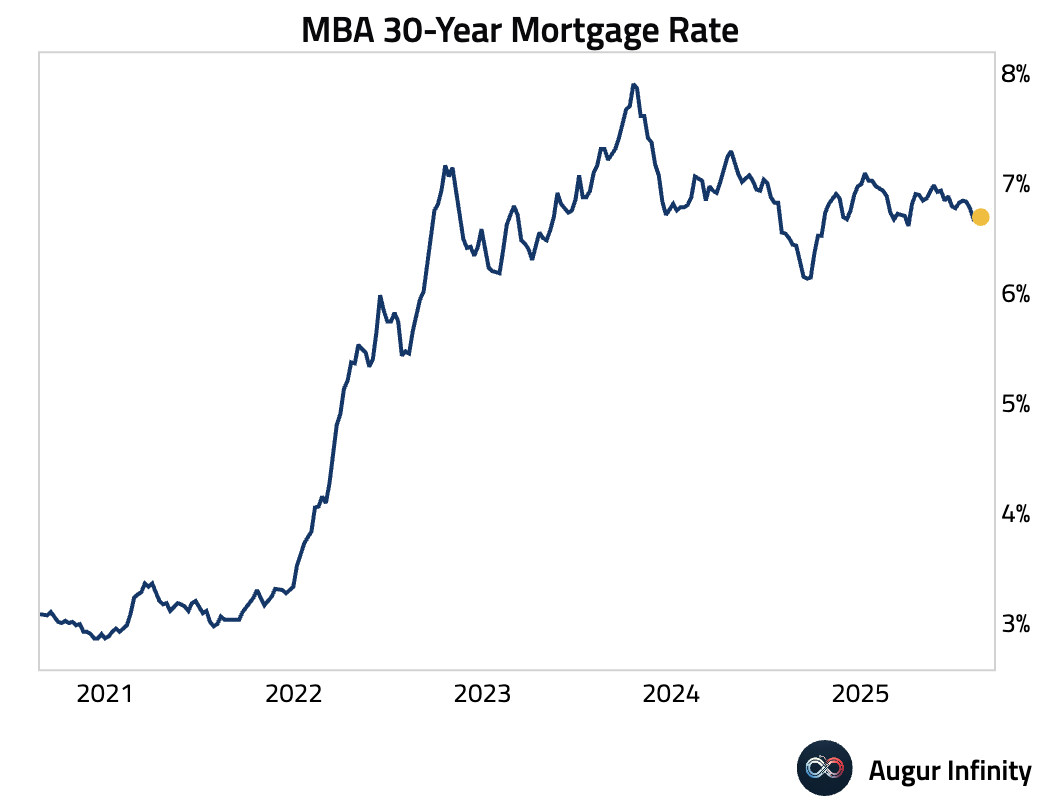

- The MBA 30-Year Mortgage Rate ticked up to 6.69% for the week ending August 22, a slight increase from 6.68% in the prior week.

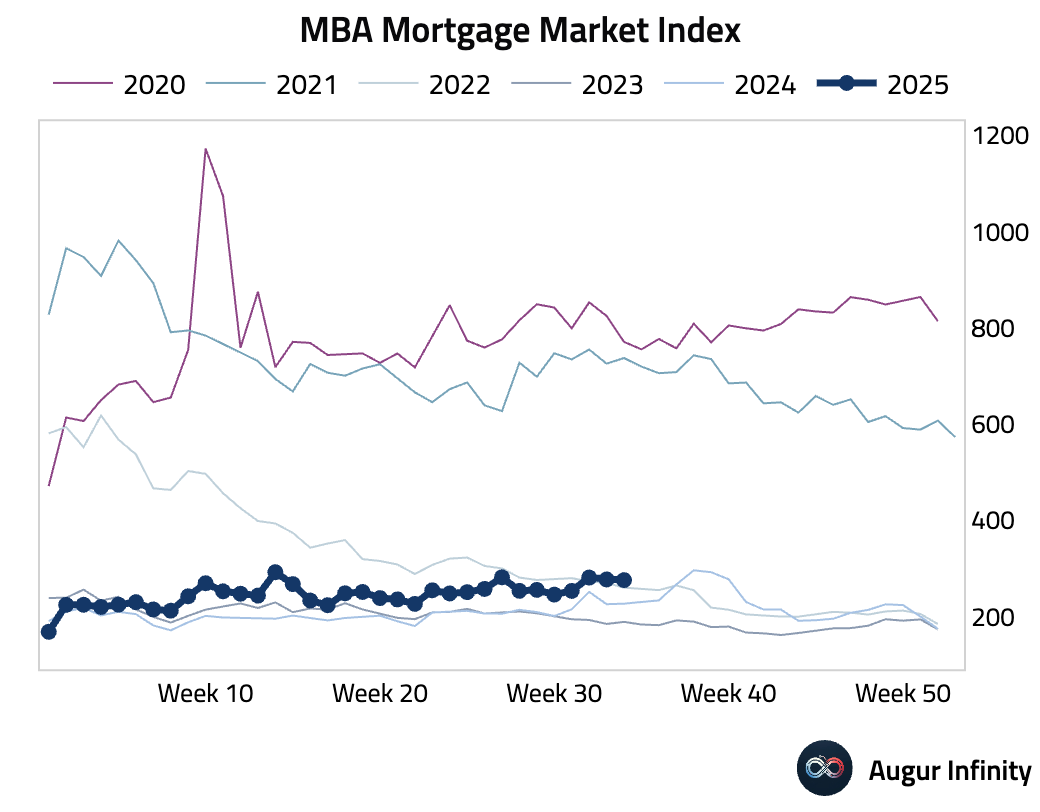

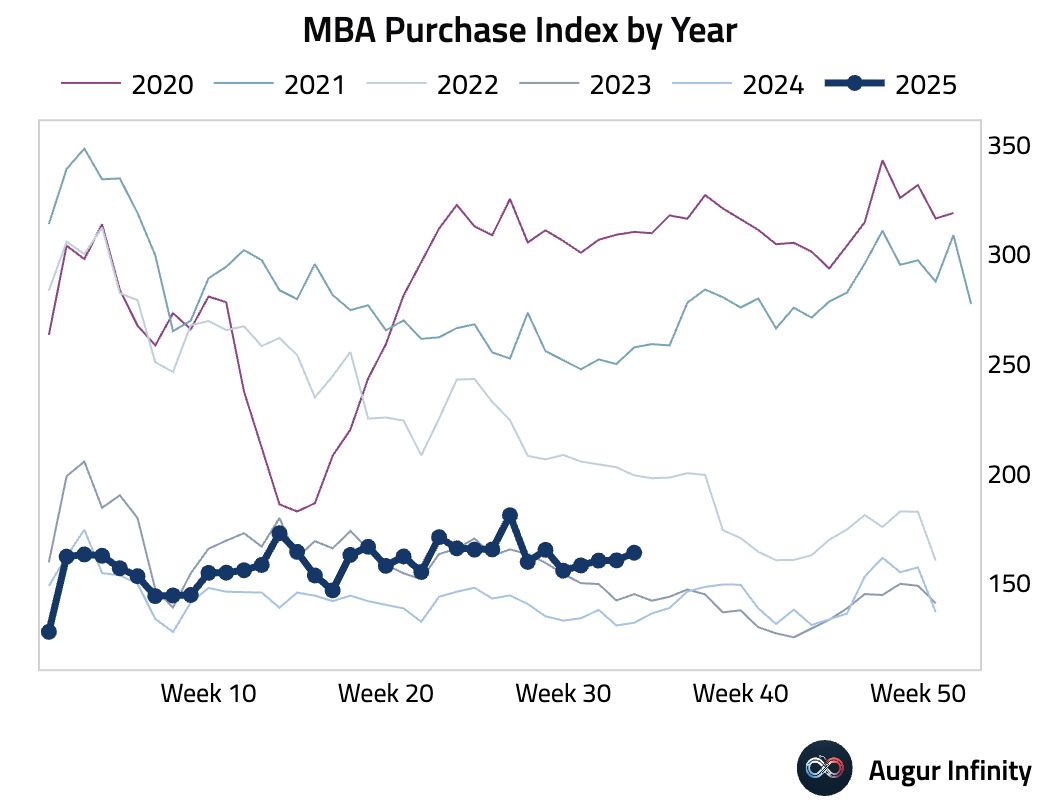

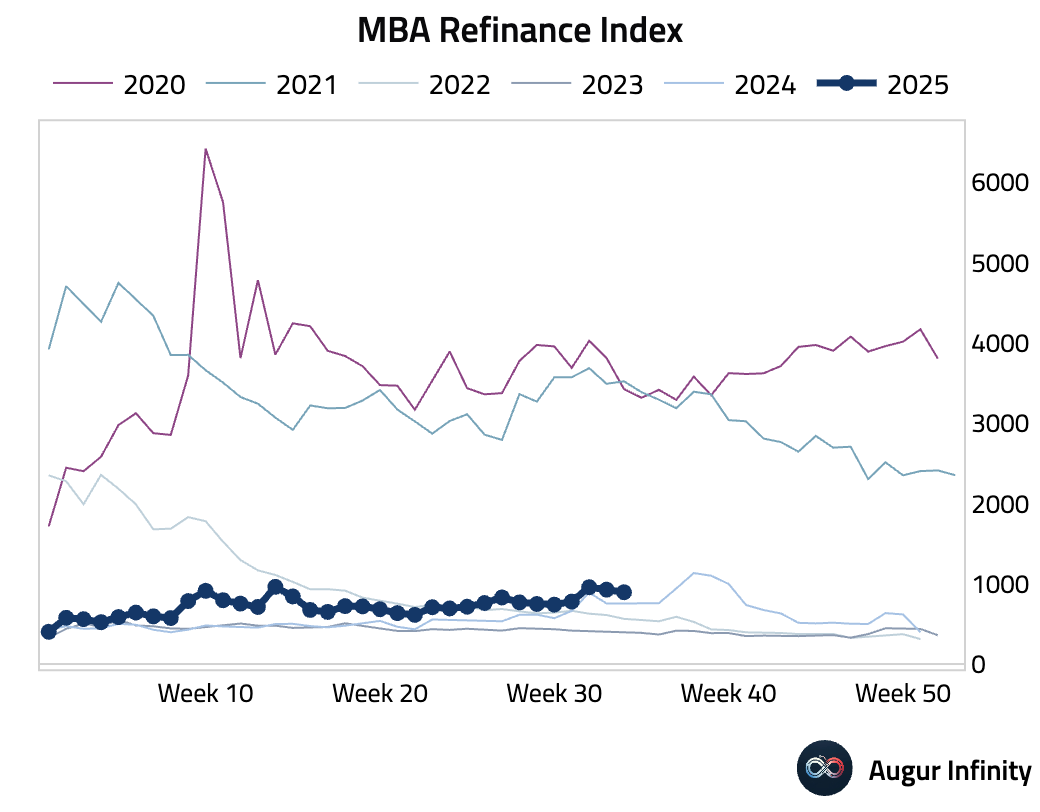

- MBA Mortgage Applications fell 0.5% week-over-week, a moderation from the 1.4% decline previously. The overall Market Index fell to 275.8. The Purchase Index rose to 163.8, while the Refinance Index declined to 894.1.

Europe

- German GfK Consumer Confidence for September fell to -23.6, worse than the -22.0 consensus and down from a revised -21.7 in August. The reading marks the lowest sentiment since April 2025, signaling persistent headwinds for private consumption.

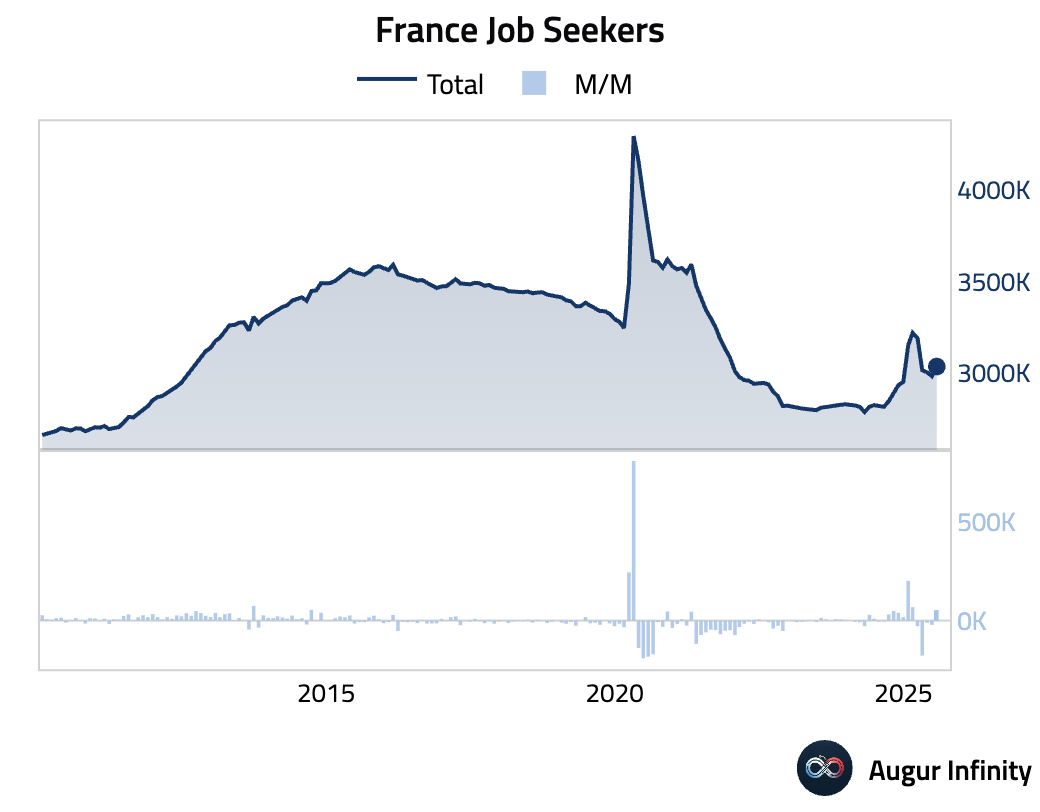

- French jobless claims rose sharply in July, with an additional 52,900 people filing for unemployment benefits. This pushed the total number of jobseekers up to 3.03 million from 2.98 million in the prior month.

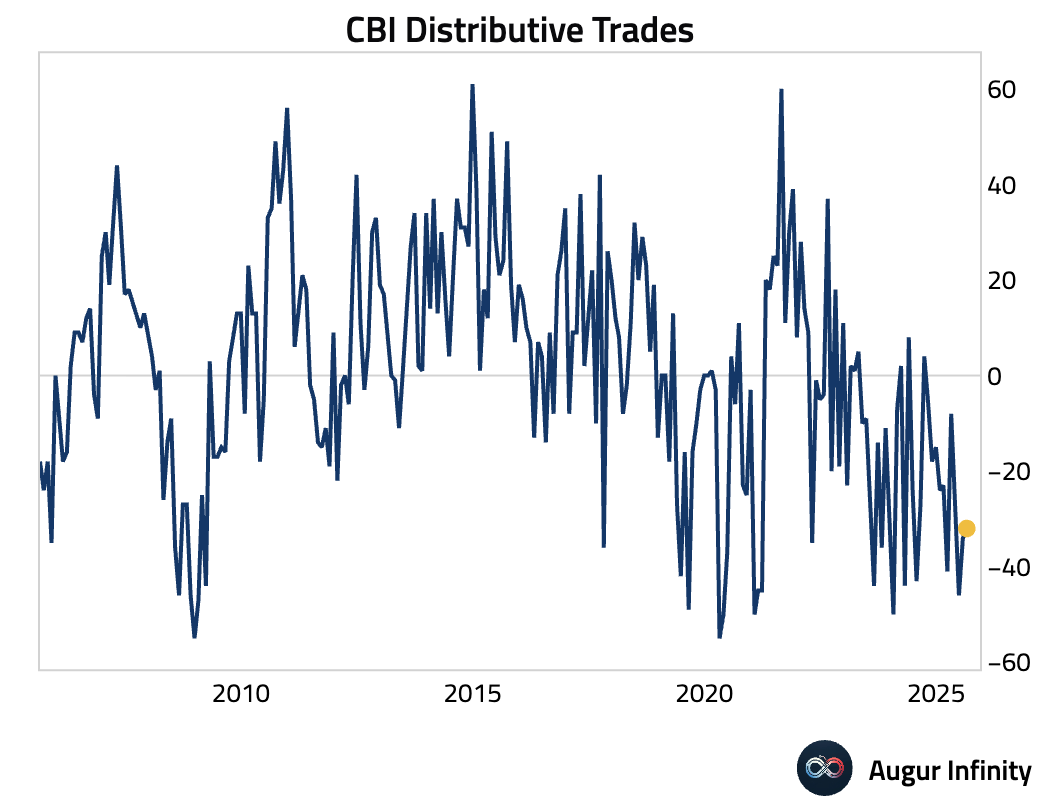

- The UK CBI Distributive Trades survey for August registered -32.0, a slight improvement from -34.0 in July and marginally better than the -33.0 consensus. The reading continues to indicate a deep contraction in the retail sector.

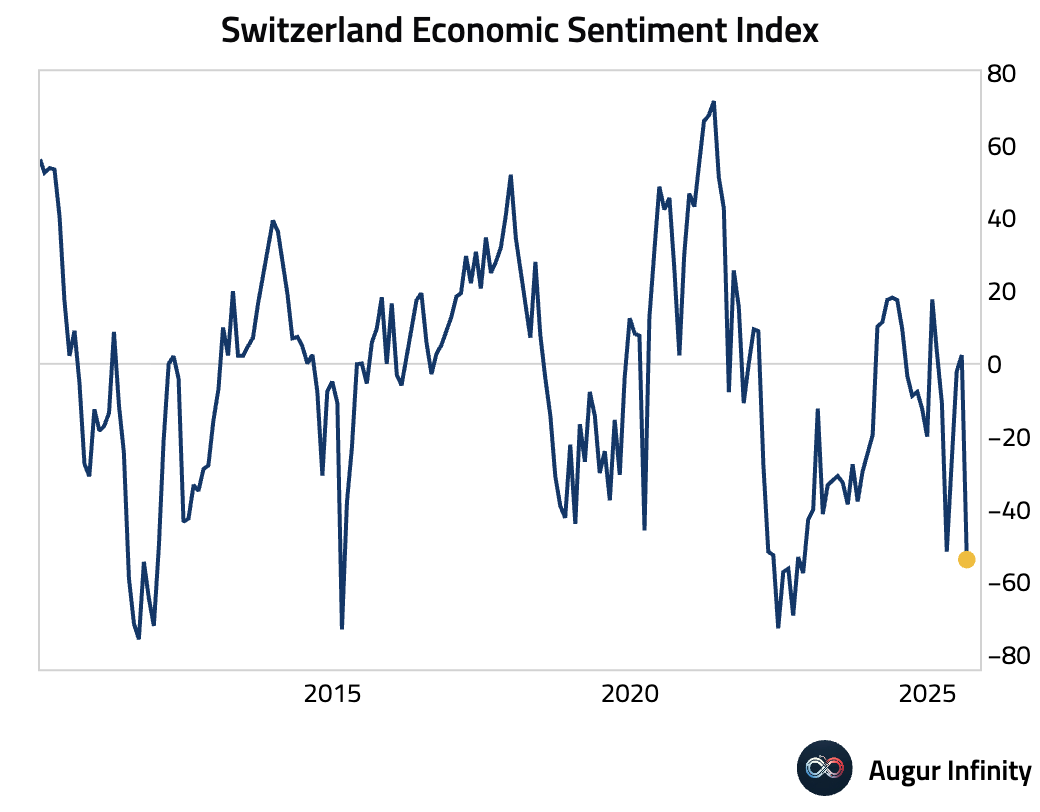

- Swiss Economic Sentiment plunged to -53.8 in August from 2.4 in July, reaching its lowest level since November 2022. The sharp deterioration points to a significant souring of the economic outlook.

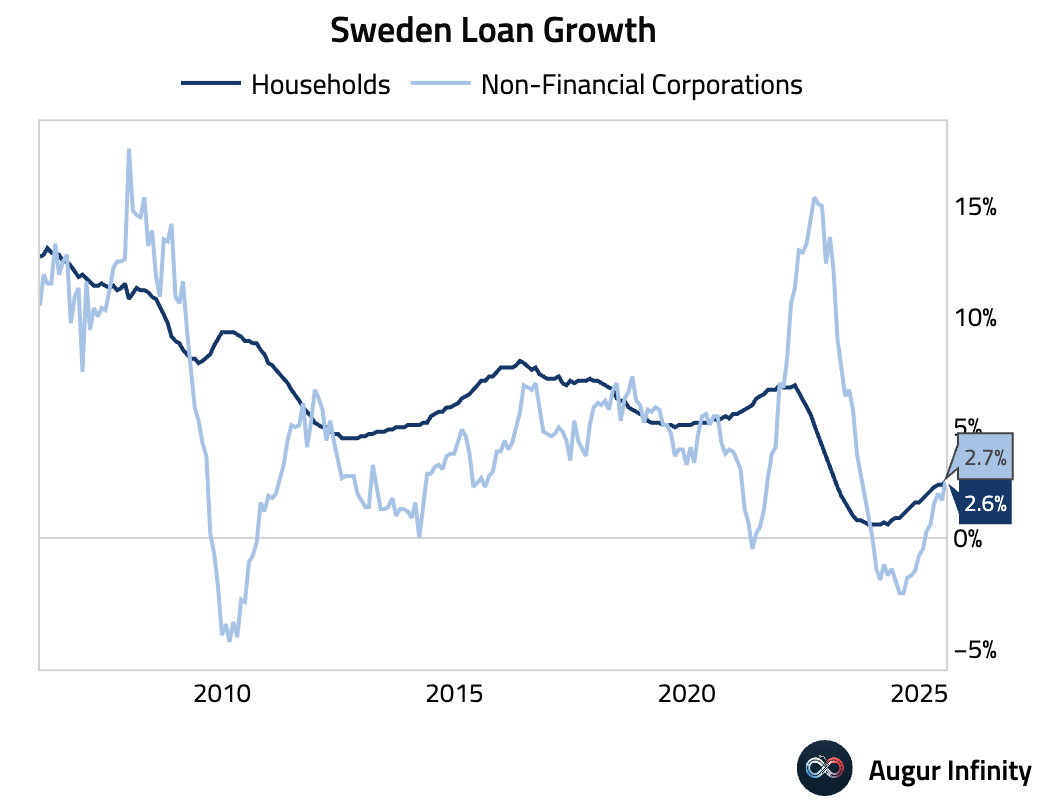

- Sweden’s household lending growth accelerated to 2.6% Y/Y in July from 2.4% previously, hitting its fastest pace since February 2023.

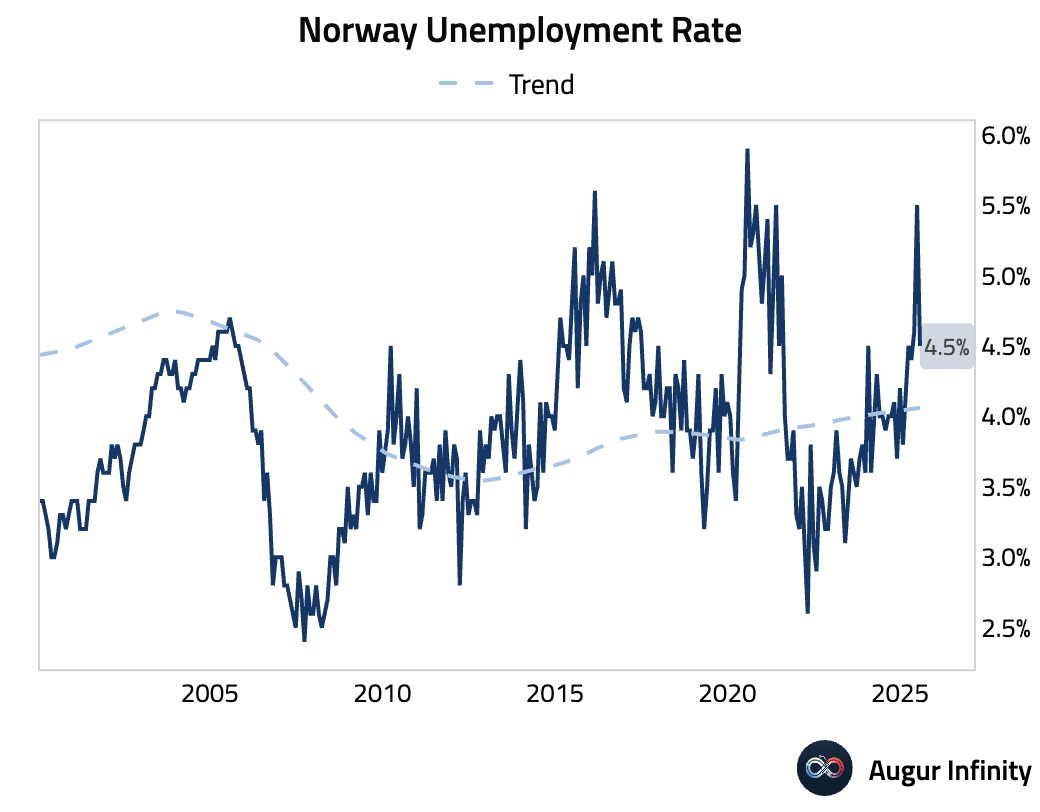

- Norway’s seasonally adjusted unemployment rate fell to 4.5% in June from 5.5% in May.

Asia-Pacific

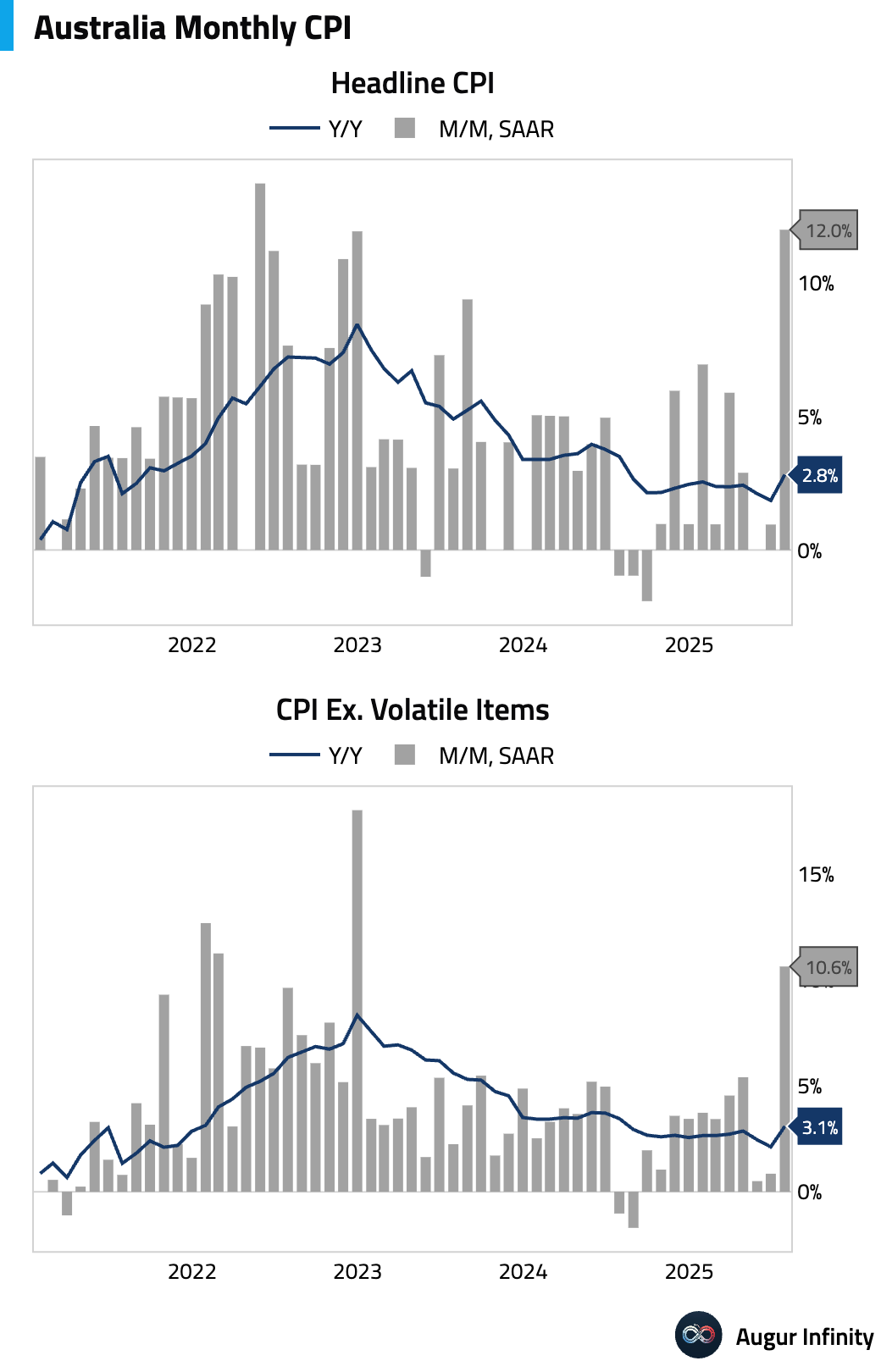

- Australia’s monthly CPI indicator accelerated to 2.8% Y/Y in July, significantly above the 2.3% consensus and up from 1.9% in June. The upside surprise was driven by volatile items, particularly a 13.0% M/M surge in electricity prices and a 4.7% jump in holiday travel costs. A delay in government subsidy payments, which will be received in coming months, artificially boosted the electricity reading. Underlying details were softer, with disinflation in rents and food.

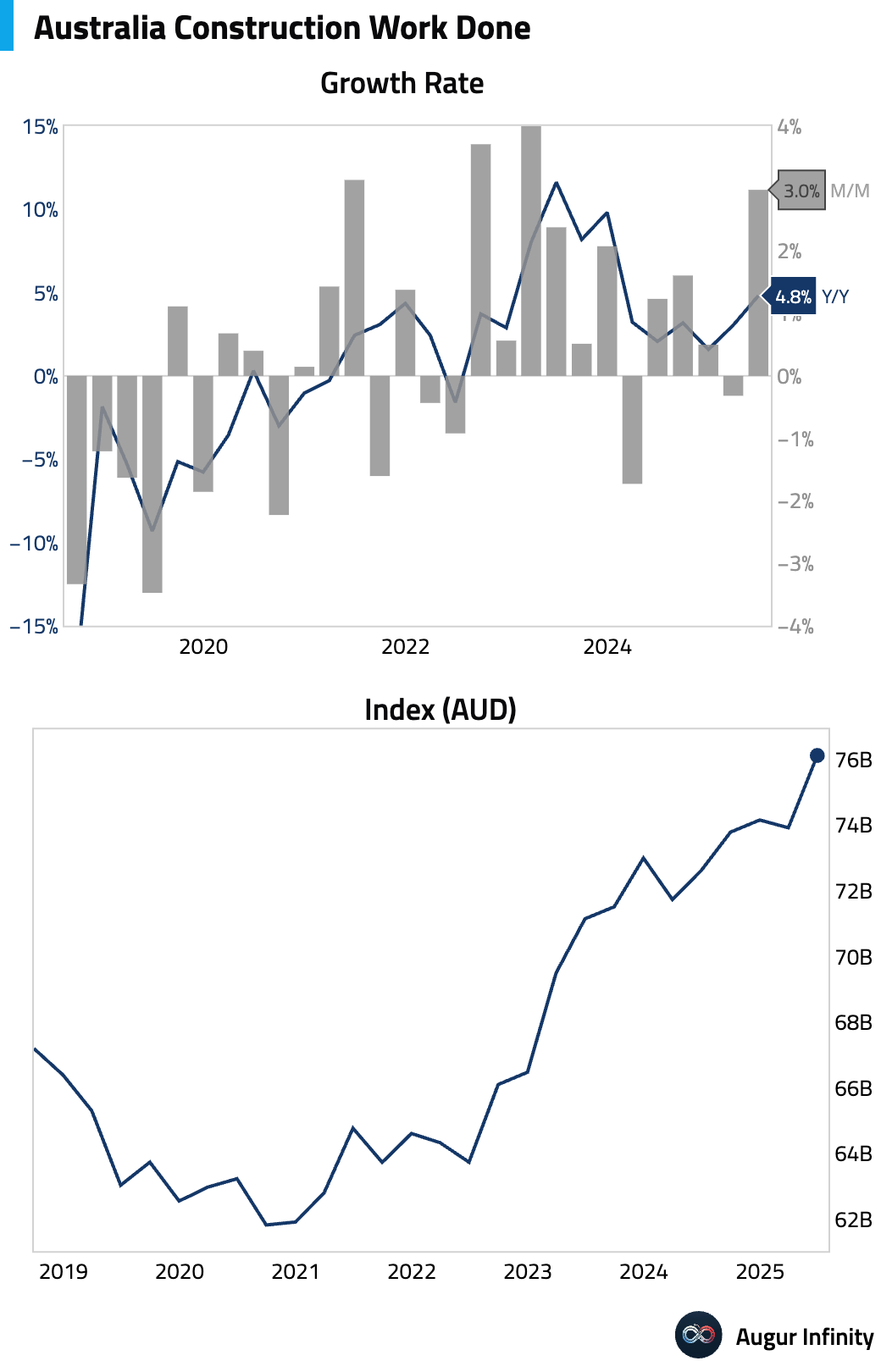

- Australian construction work done surged 3.0% Q/Q in the second quarter, smashing expectations for a 0.7% increase and rebounding from a 0.3% decline in Q1. The beat was driven entirely by a massive 13.5% Q/Q jump in private non-residential engineering. Residential investment was flat at 0.1%, while public construction fell 0.4%. The headline figure may overstate the impact on GDP, as it may not reflect activity on an accruals basis consistent with National Accounts.

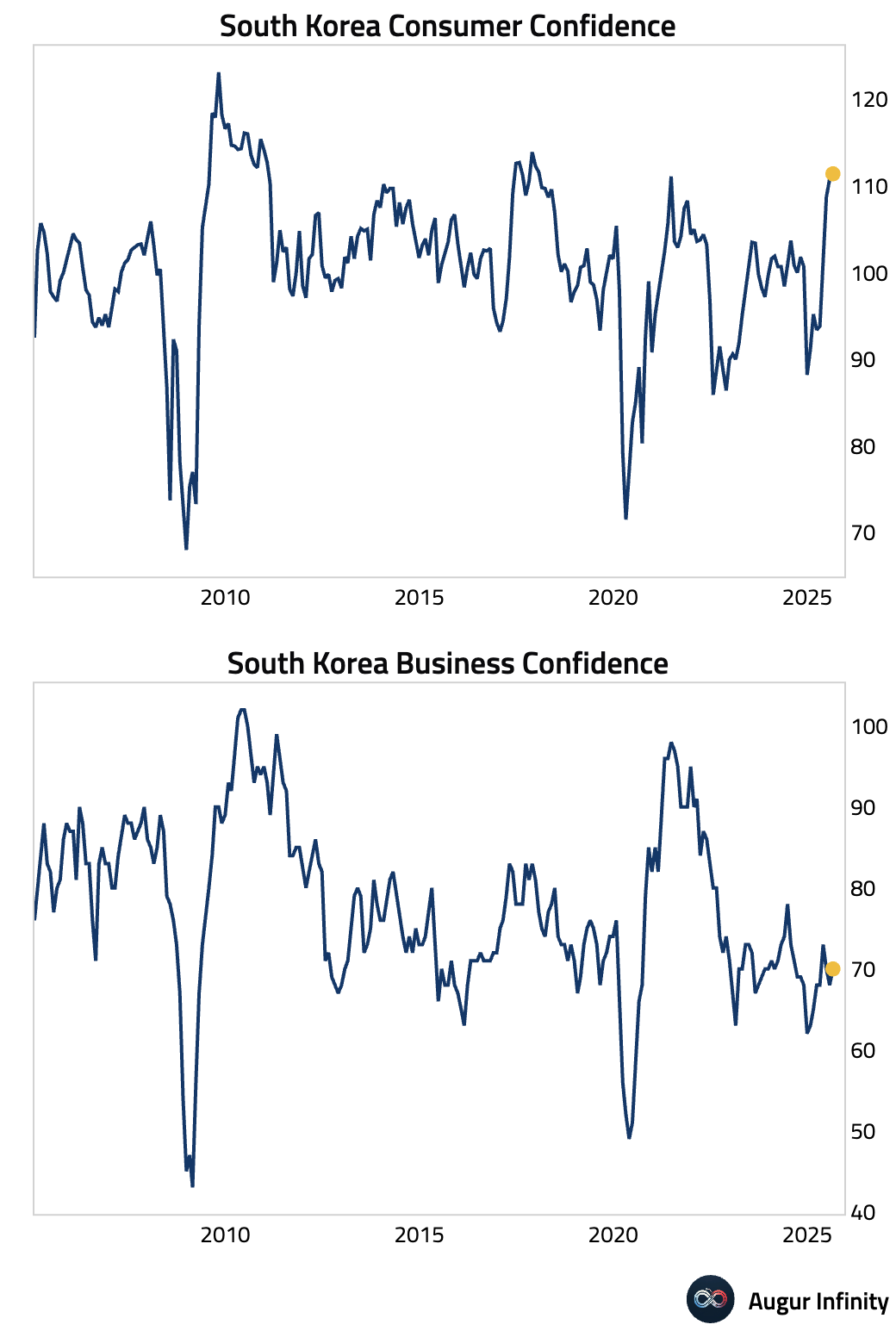

- South Korean business confidence improved in August, with the index rising to 70.0 from 68.0 in July.

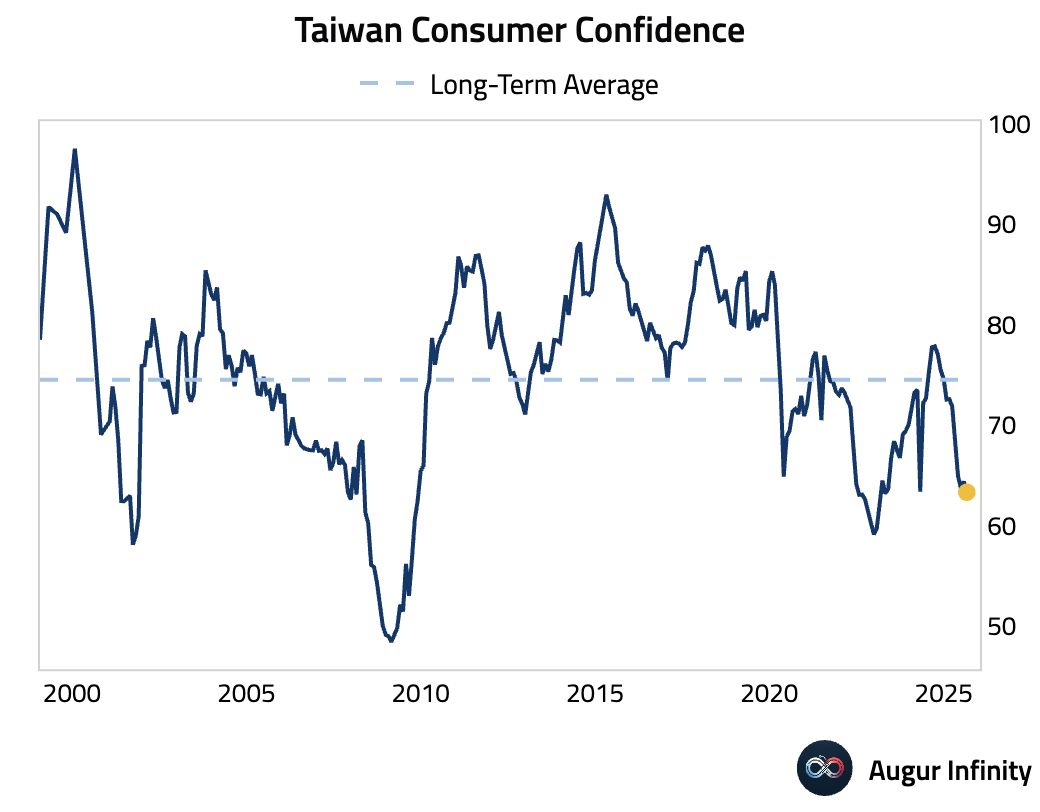

- Taiwan’s consumer confidence index fell to 63.31 in August from 64.38, marking the lowest reading since April 2023.

China

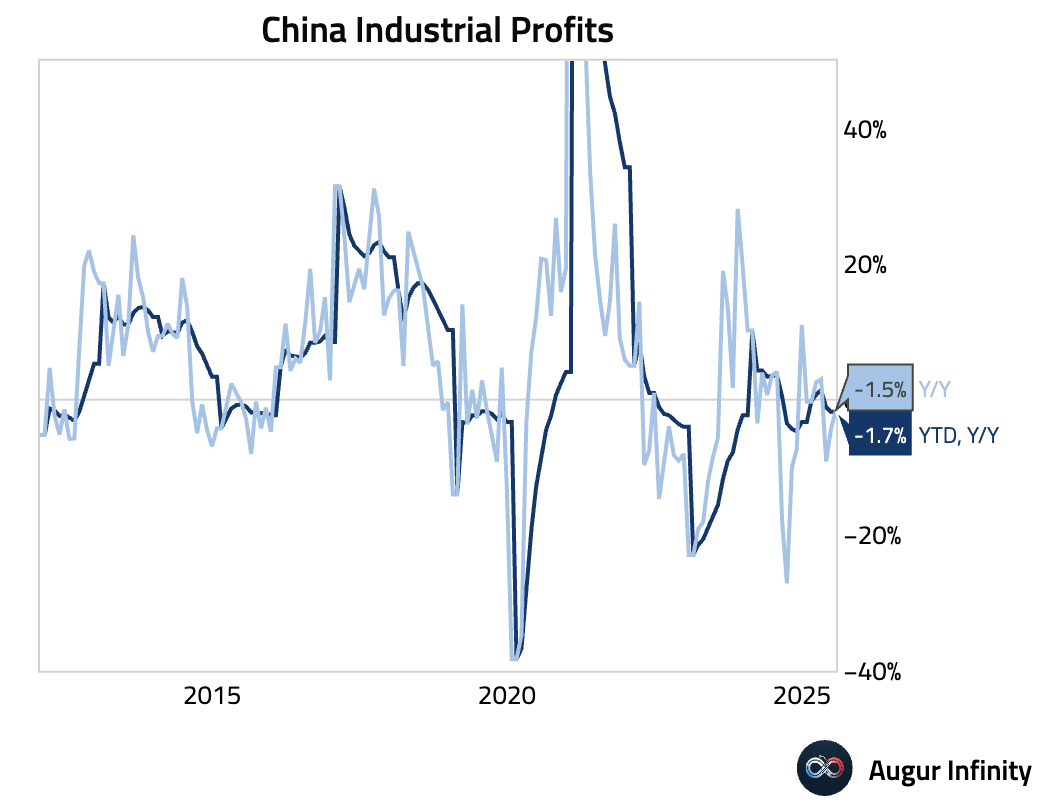

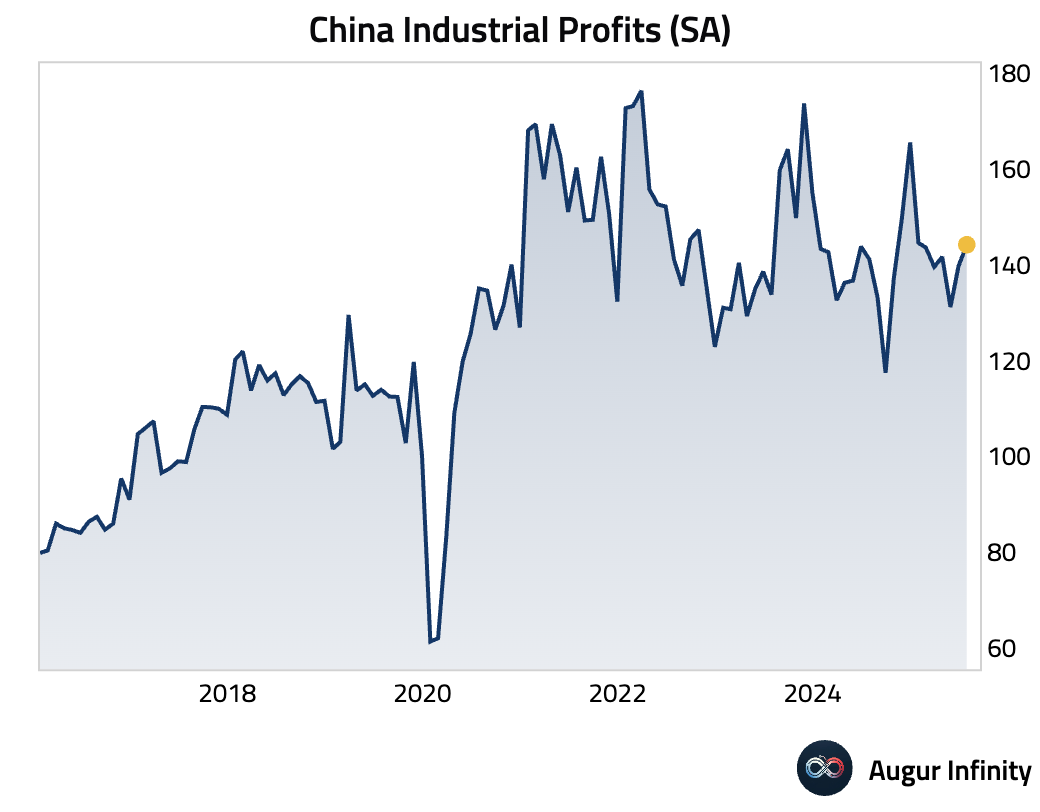

- China's year-to-date industrial profits improved slightly, contracting 1.7% Y/Y through July, compared to a 1.8% decline through June. The rebound was driven by a massive surge in raw material sector profits, which grew 36.9% Y/Y in July versus a 5% decline in June, reflecting higher commodity prices and potentially the early effects of government policies in sectors like steel and coal.

Emerging Markets ex China

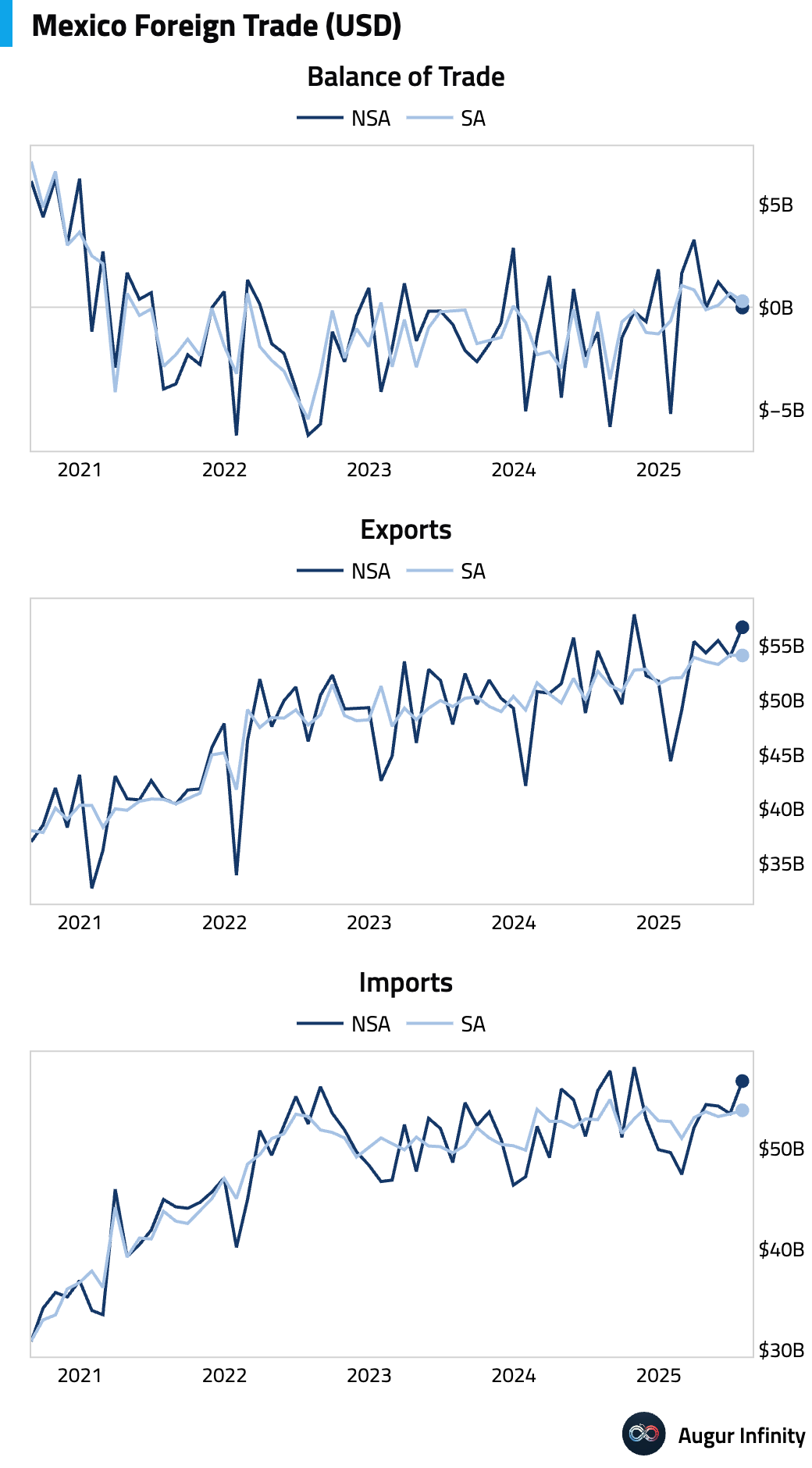

- Mexico posted a negligible trade deficit of $17 million in July, a significant miss compared to the consensus forecast for a $300 million surplus. A strong non-oil surplus more than offset a persistent, widening oil deficit. Within exports, auto manufacturing was very soft (-7.0% Y/Y), while non-auto manufacturing was firm (+11.7% Y/Y). On the import side, capital goods firmed (+6.0% M/M) after seven consecutive monthly declines.

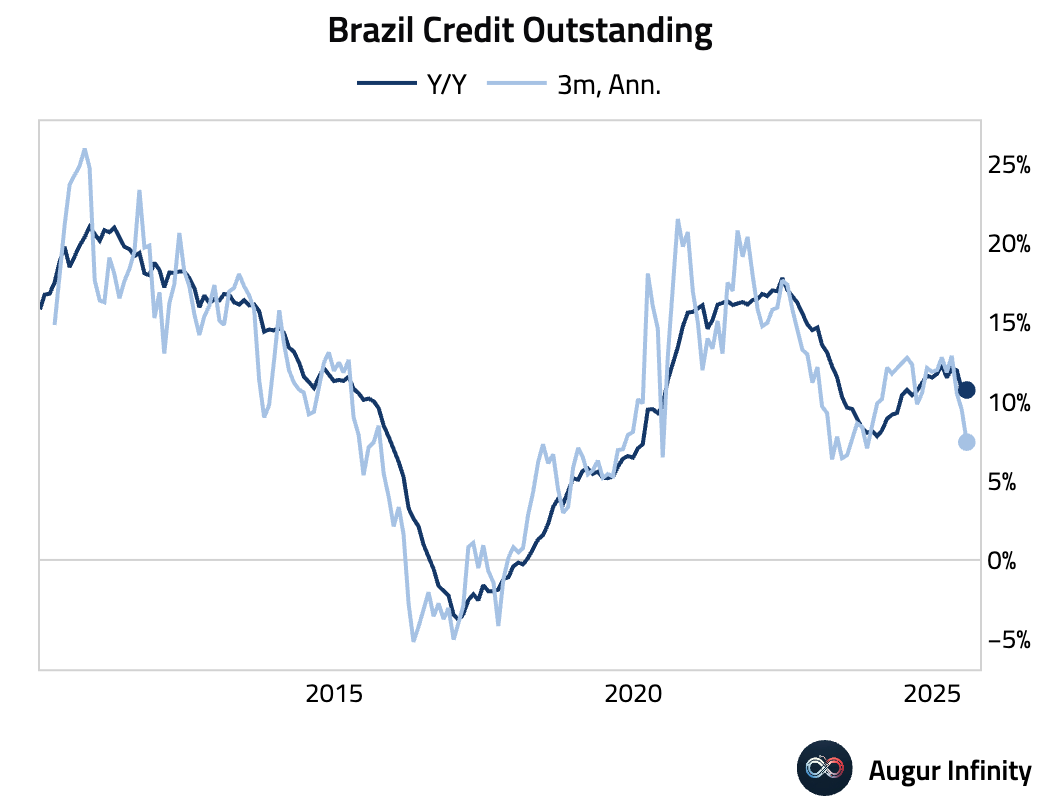

- Brazil’s bank lending growth slowed to 0.4% M/M in July from 0.5% in June. Real credit origination fell for the third consecutive month, confirming a cycle slowdown, driven by a sharp 2.4% fall in household lending. Credit quality deteriorated as non-performing loans on freely allocated credit rose 20 basis points to 5.5%.

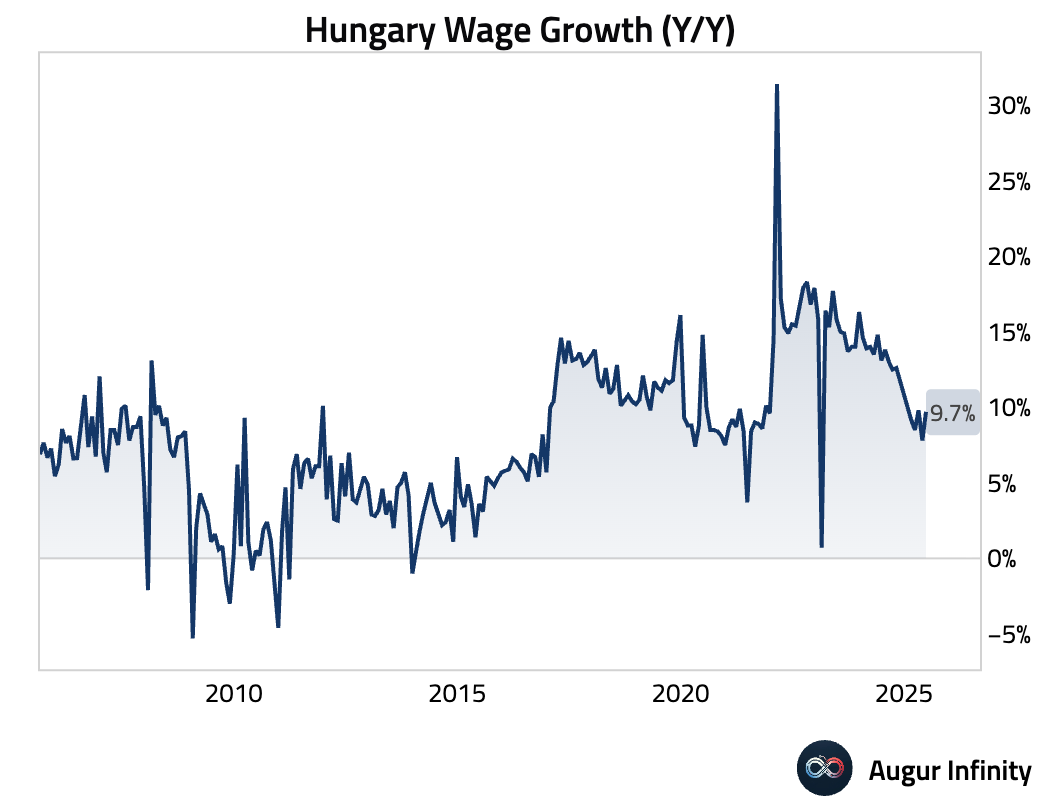

- Hungarian gross wages grew 9.7% Y/Y in June, accelerating from 7.8% in May.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.