Headlines

- Political uncertainty in France is increasing amid growing expectations that Prime Minister Bayrou will lose a parliamentary confidence vote scheduled for September 8.

Charts of the Day

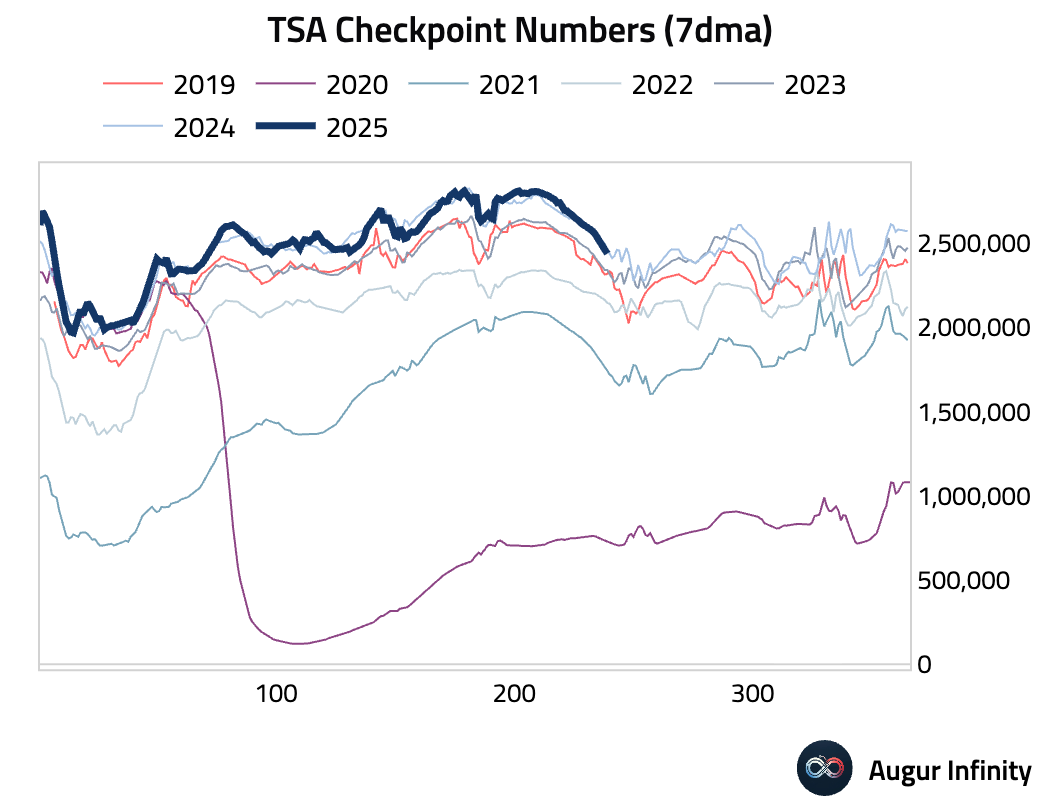

- Travelers transiting through TSA checkpoints have slipped below 2024 levels.

Global Economics

United States

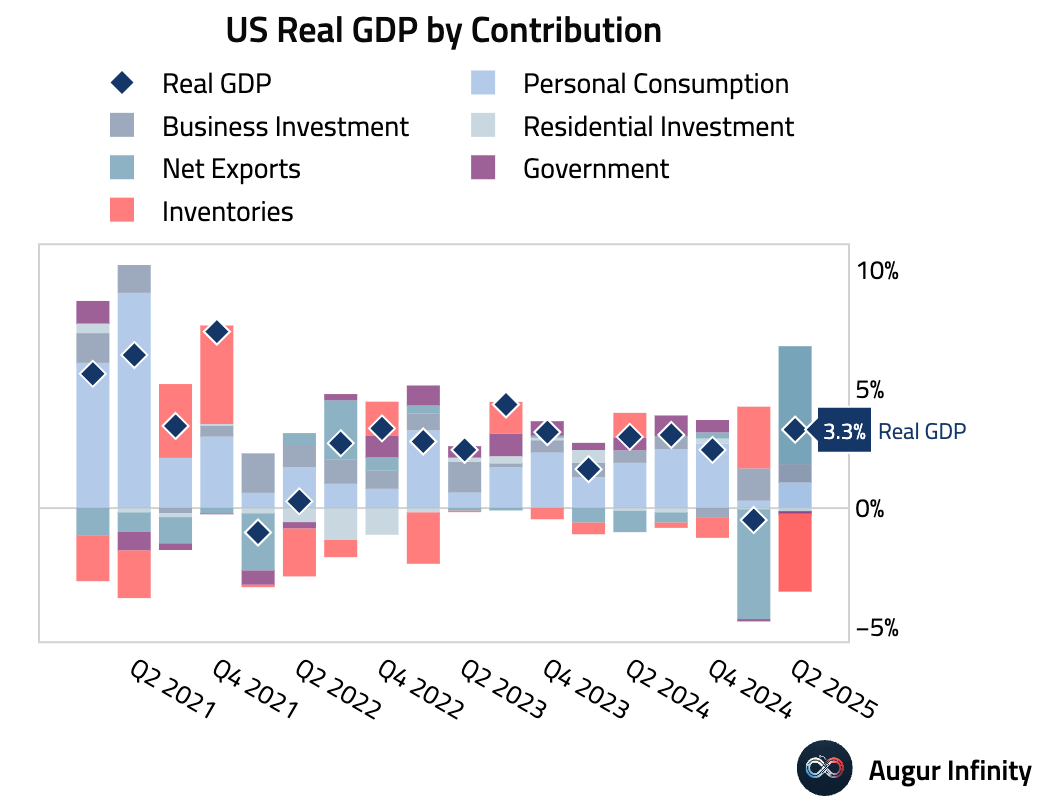

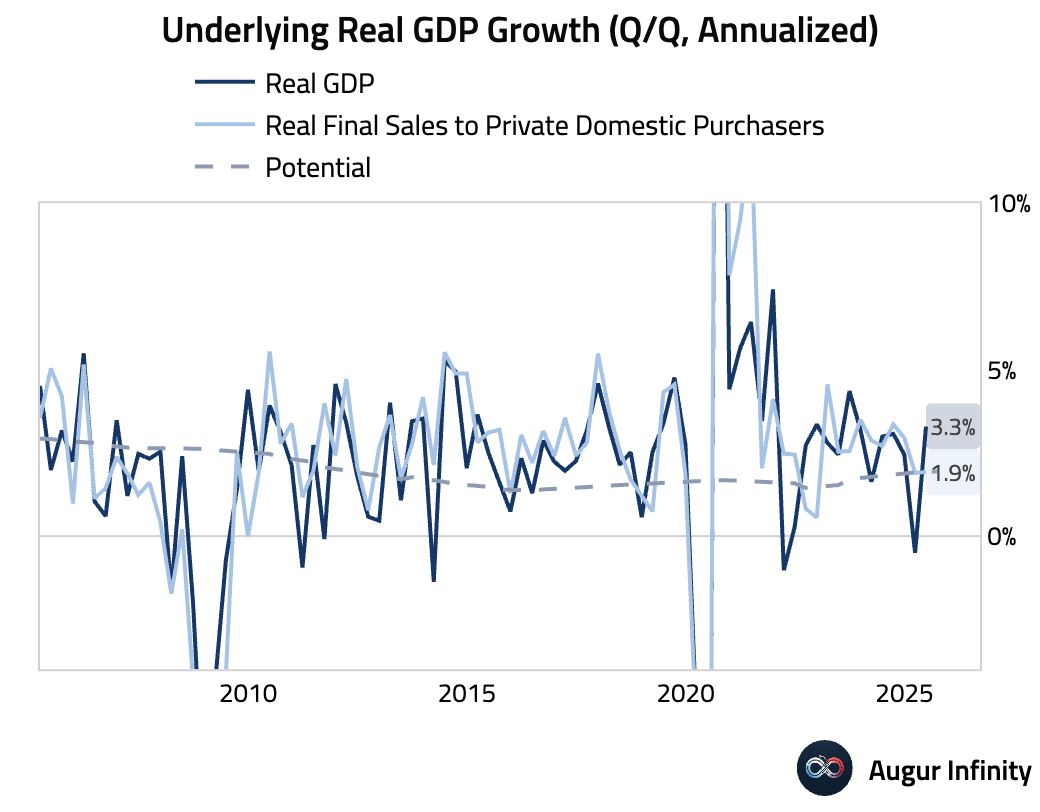

- The second estimate of Q2 GDP was revised up to 3.3% from 3.0%, beating the 3.1% consensus. The composition of the revision was strong, driven by higher consumption (1.6%) and business investment (5.7%). Real private domestic final sales, a core measure of underlying demand, was revised up 0.7pp to 1.9%. Confirming the robust economic picture, Real Gross Domestic Income (GDI) rose a very strong 4.8%. On the inflation front, the Core PCE price index was revised down to 2.5% Q/Q SAAR (from 2.6%).

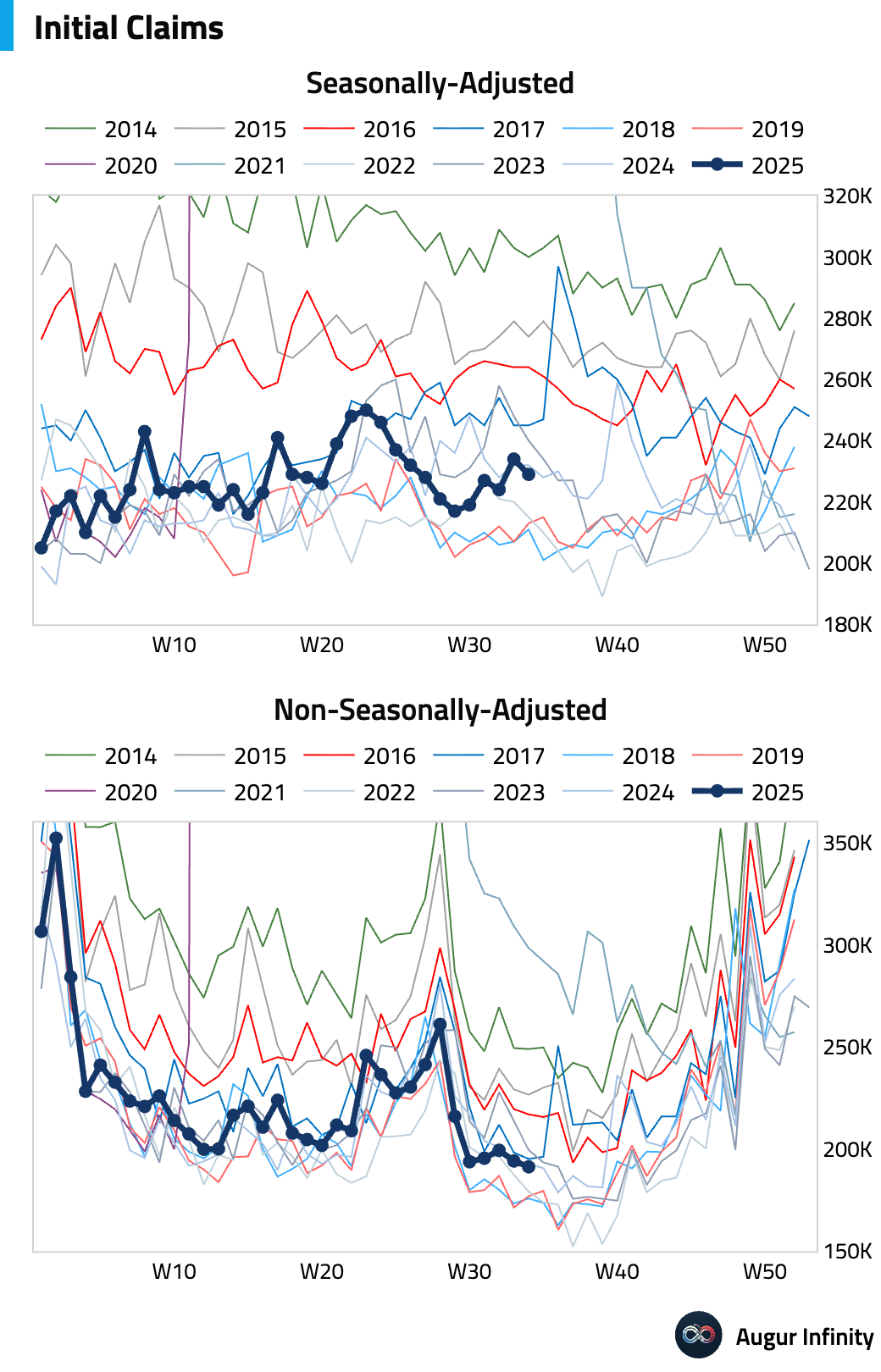

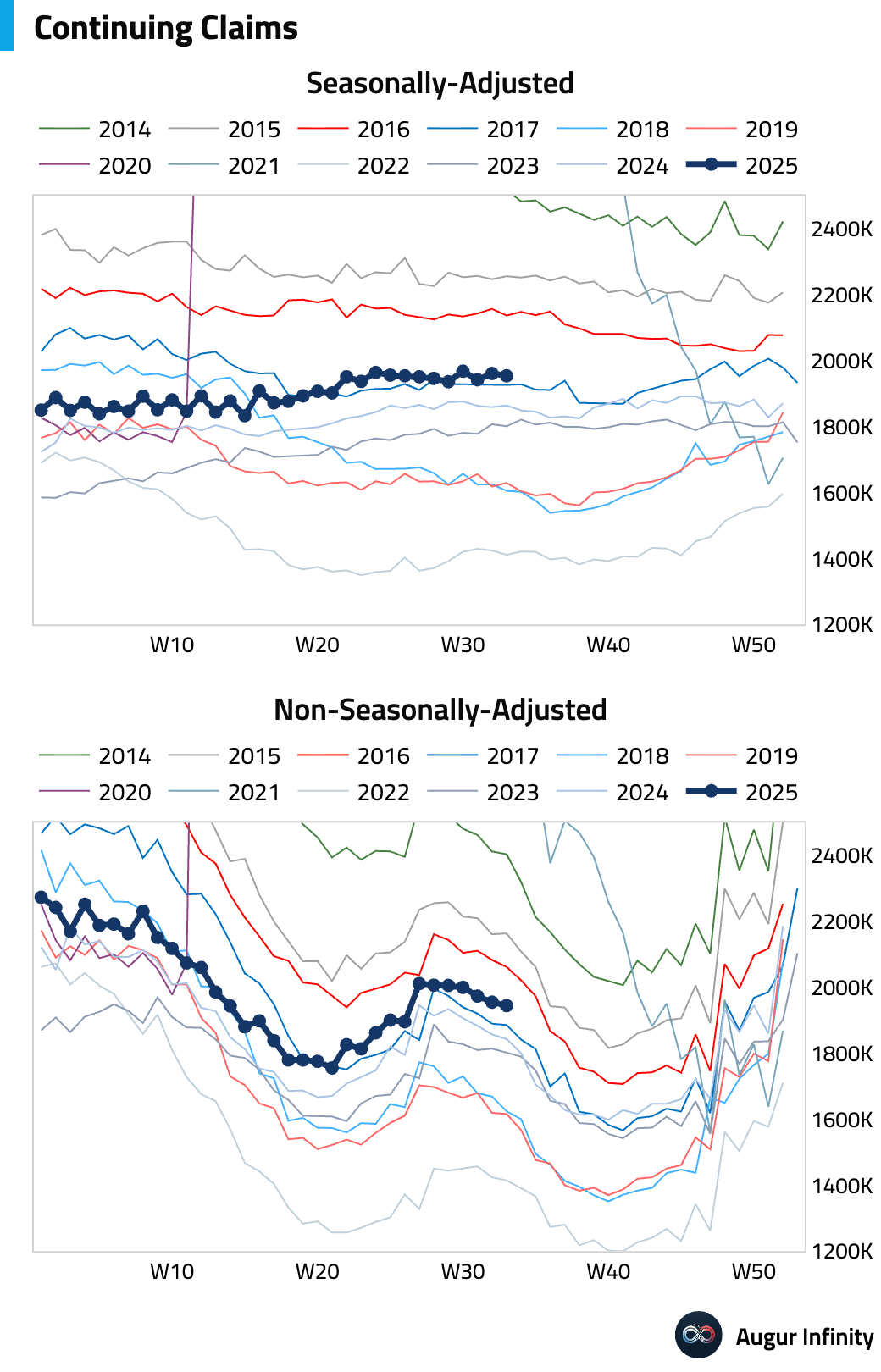

- Initial jobless claims for the week ending August 23 fell to 229k from 234k, just below the 230k consensus. Continuing claims also declined to 1,954k from 1,961k. The four-week moving average of initial claims ticked up slightly to 228.5k. Overall, the data points to continued stability in the labor market.

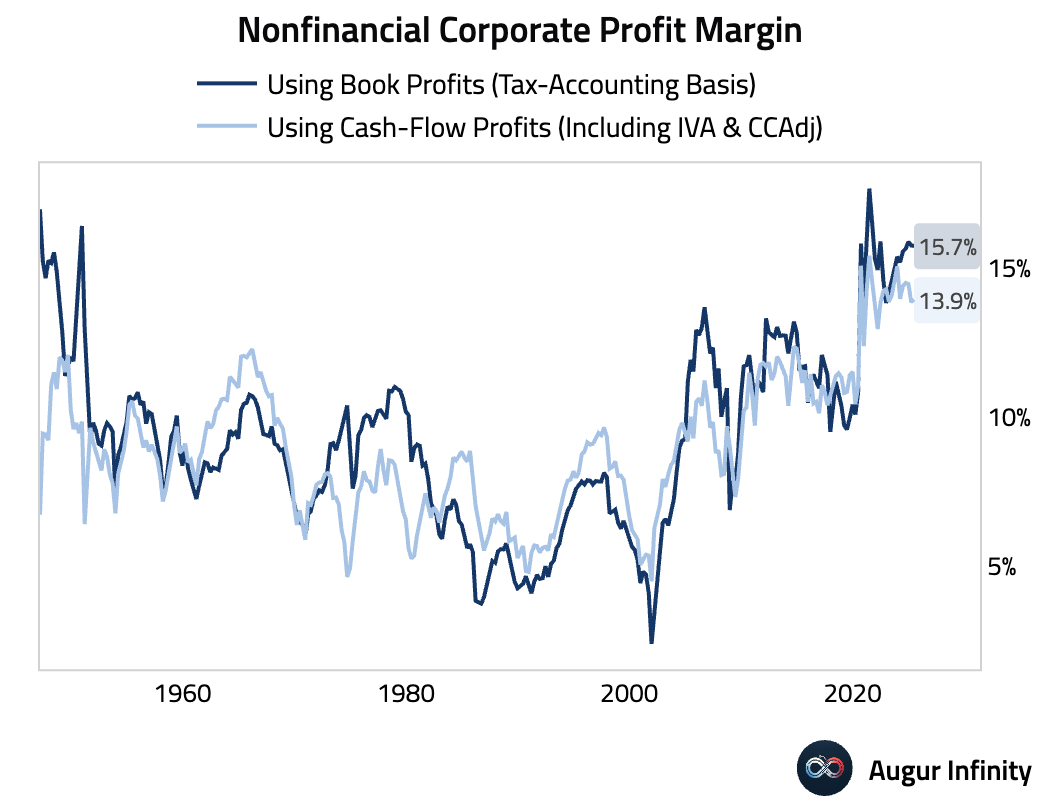

- Corporate profits rose 2.0% Q/Q in the second quarter, rebounding from a 3.3% decline in Q1. Nonfinancial corporate profit margins declined slightly but remained near secular highs.

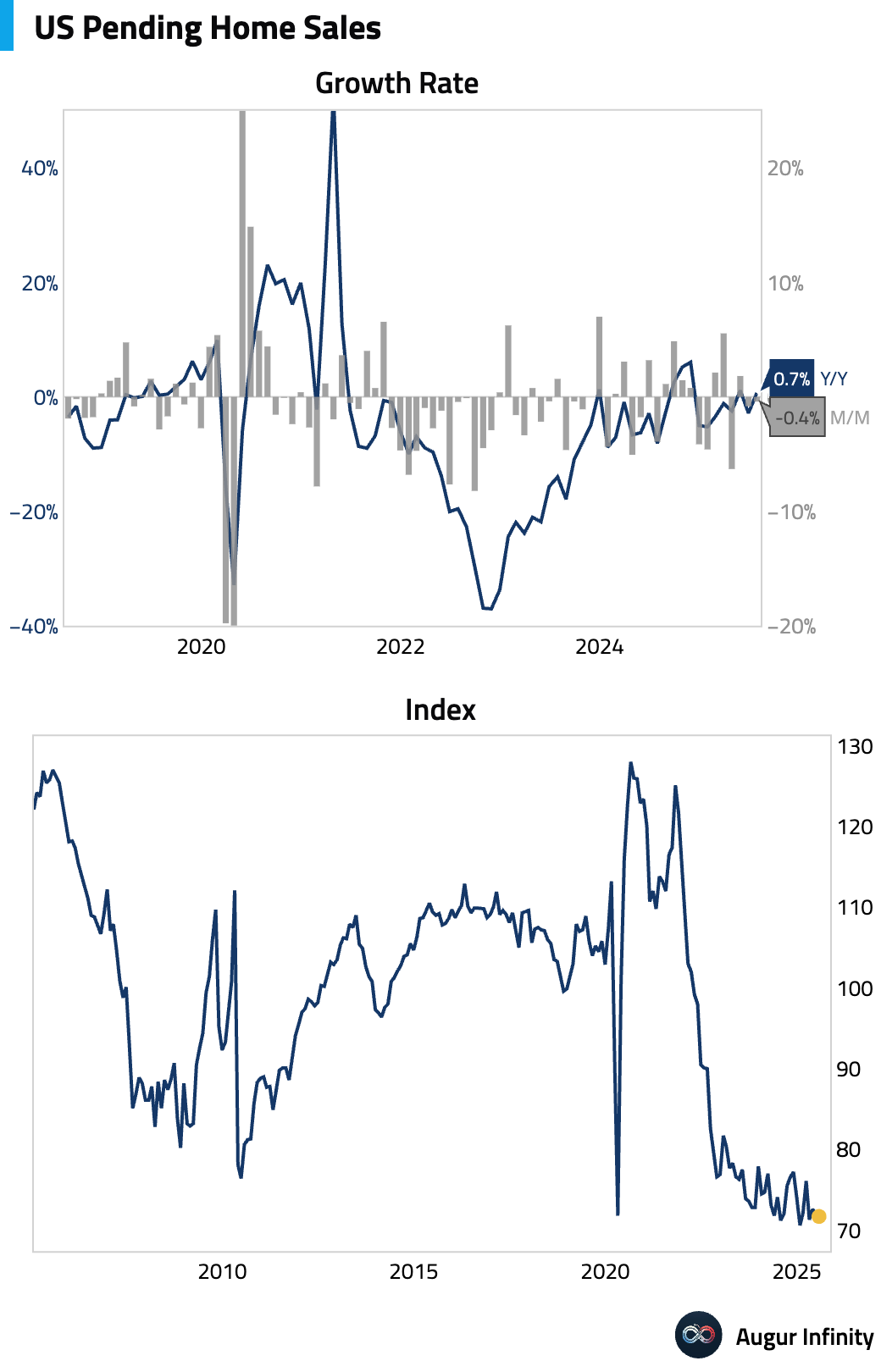

- Pending home sales fell 0.4% M/M in July (vs. -0.1% consensus), following a 0.8% drop in June. Year-over-year, sales rose 0.7%.

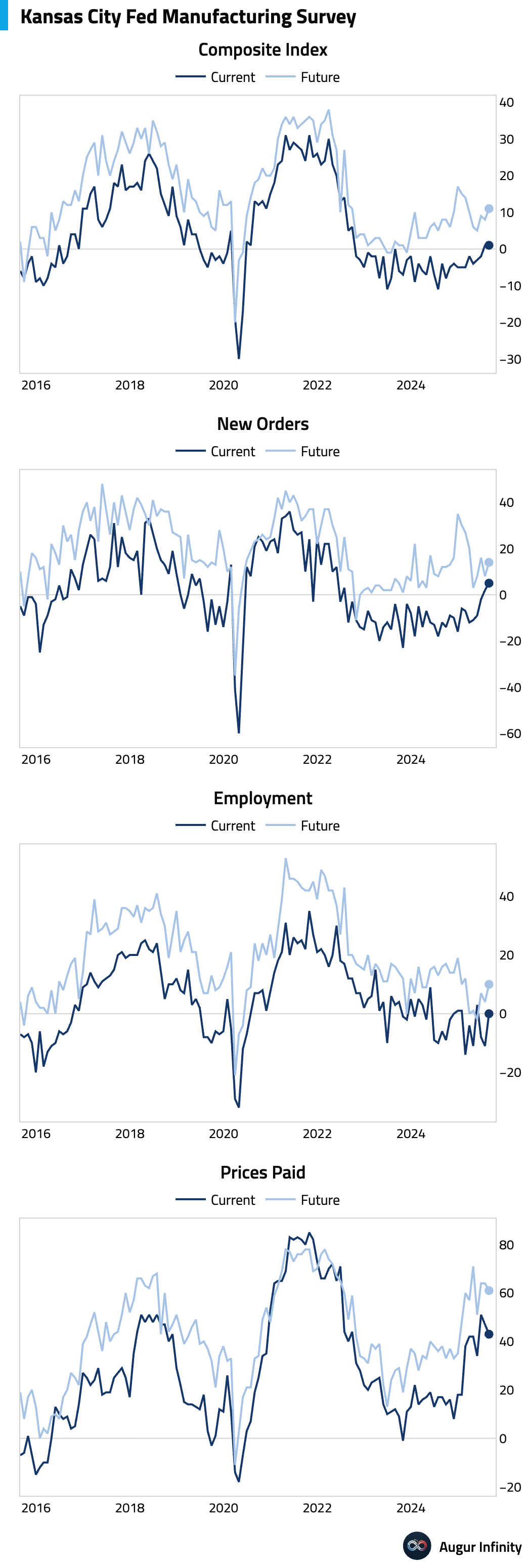

- The Kansas Fed Manufacturing Composite Index was unchanged at 1.0 in August, holding at its highest level since September 2022. The composition was favorable, with new orders and employment rising, while price pressures declined.

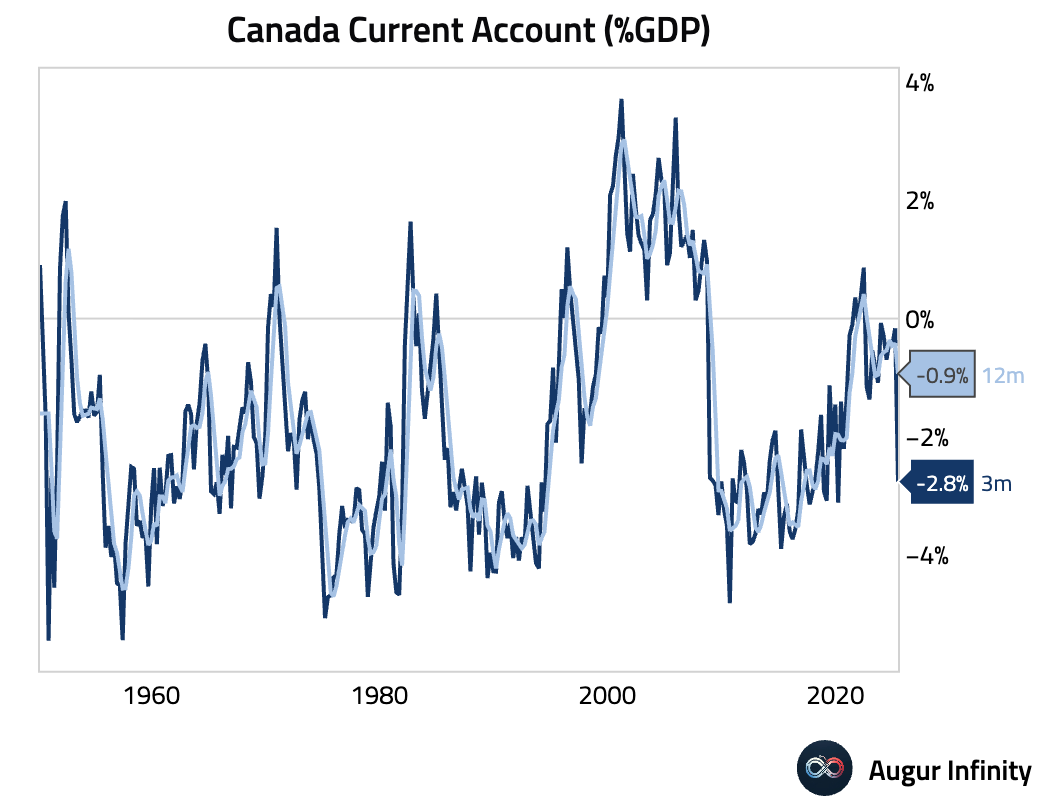

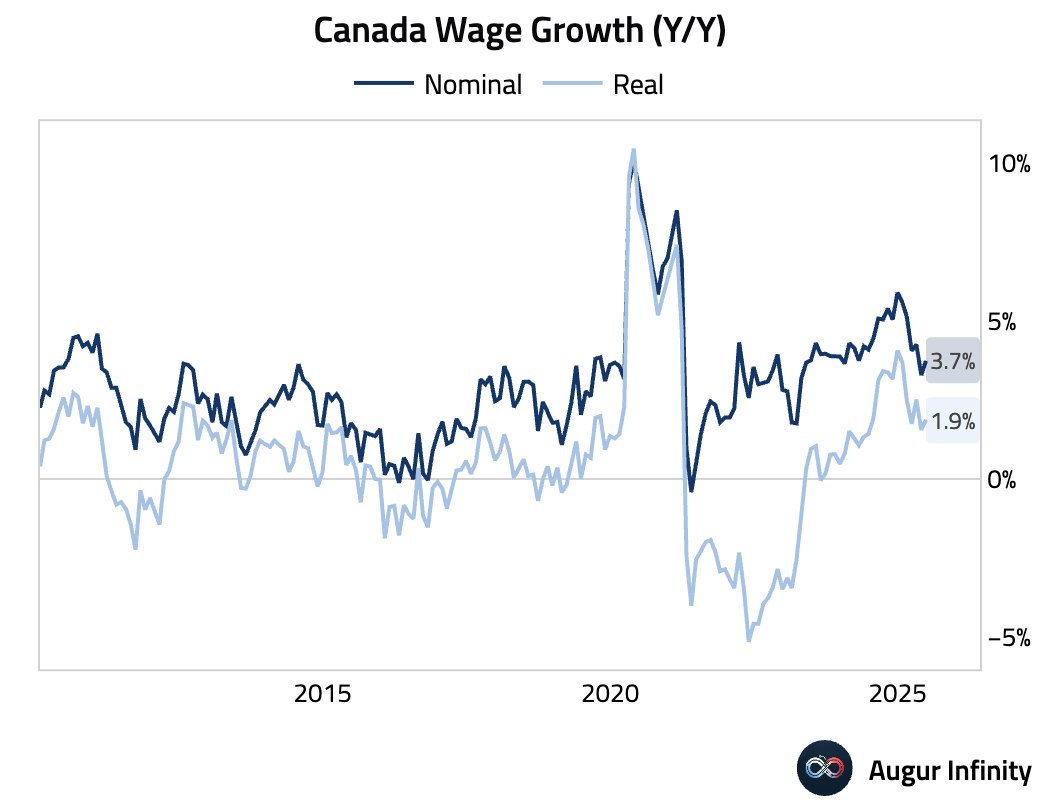

Canada

- Canada’s current account deficit widened sharply to C$21.2 billion in Q2, an all-time record low and significantly worse than the C$19.4 billion consensus. The prior quarter's balance was revised from a C$5.4 billion deficit to a C$1.3 billion deficit.

- Average weekly earnings growth accelerated to 3.7% Y/Y in June from 3.3% in May.

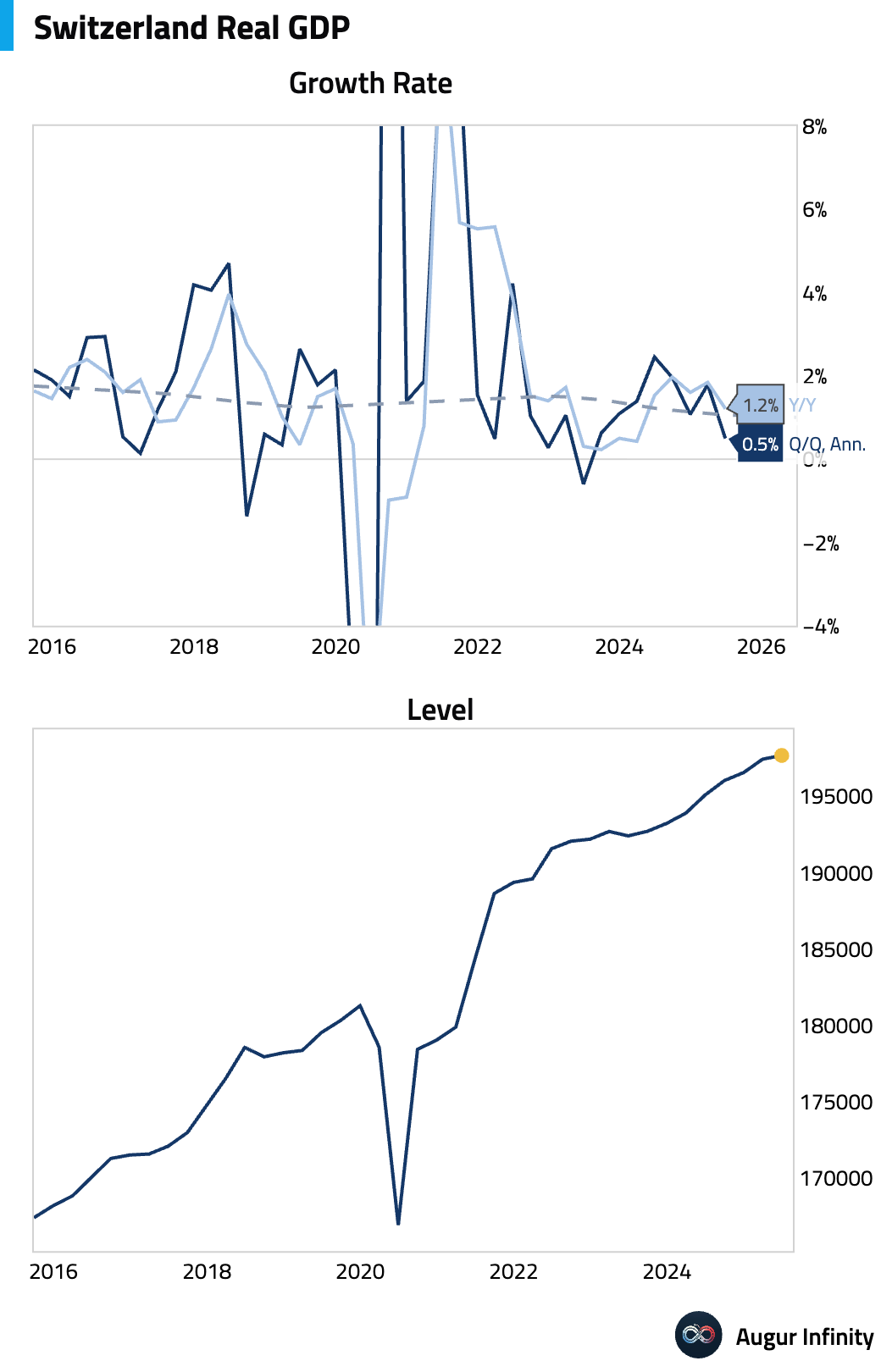

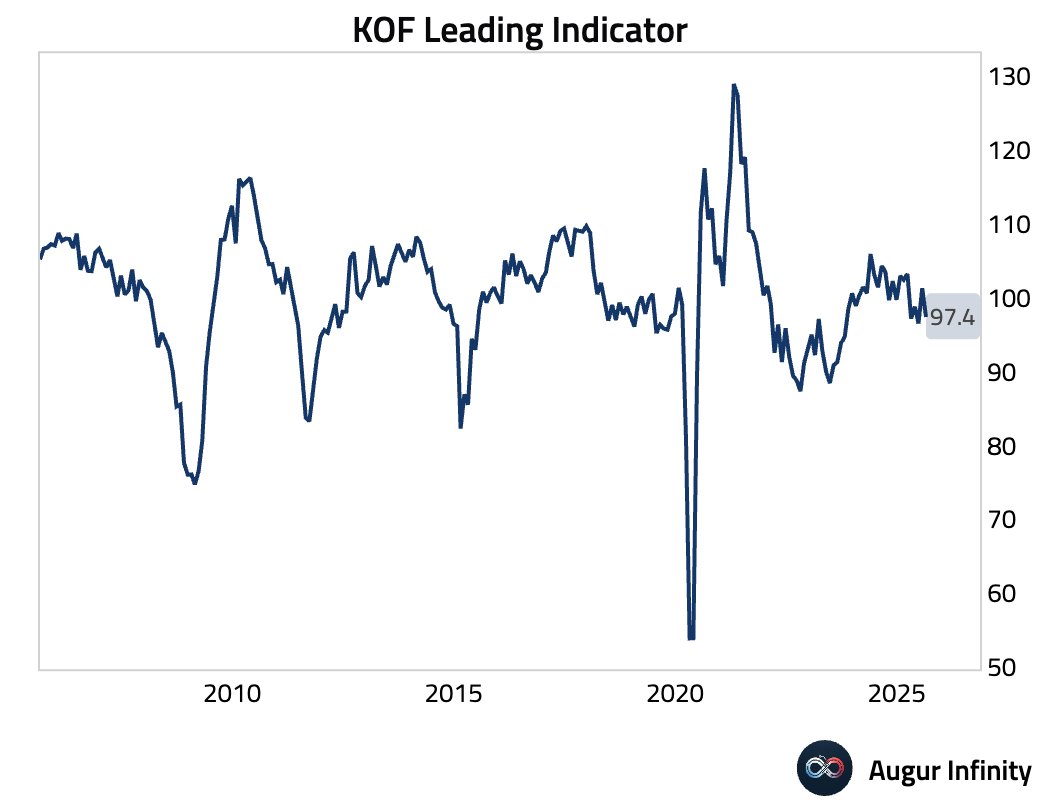

Europe

- Switzerland’s Q2 GDP growth slowed to 0.1% Q/Q, matching consensus, down from 0.7% in Q1. The year-over-year rate decelerated to 1.2% from 1.8%, missing expectations for 1.4% growth.

- The Swiss KOF Leading Indicator fell to 97.4 in August from 101.3, missing the consensus of 98.0 and marking its lowest reading since June.

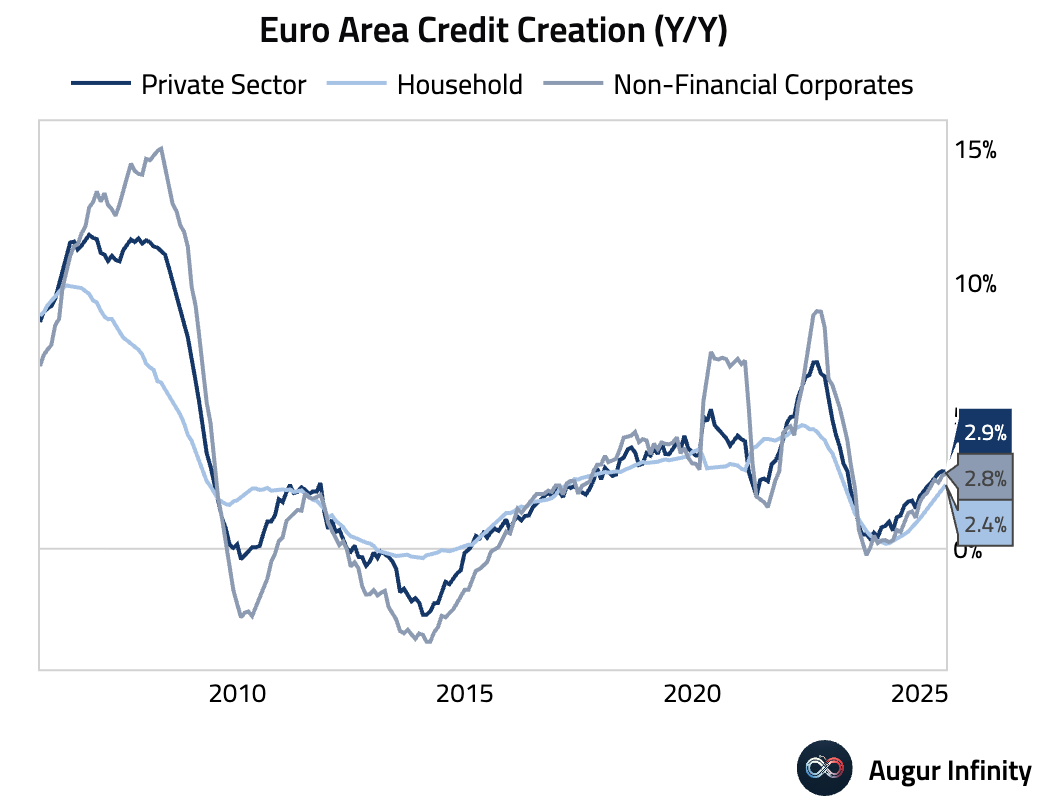

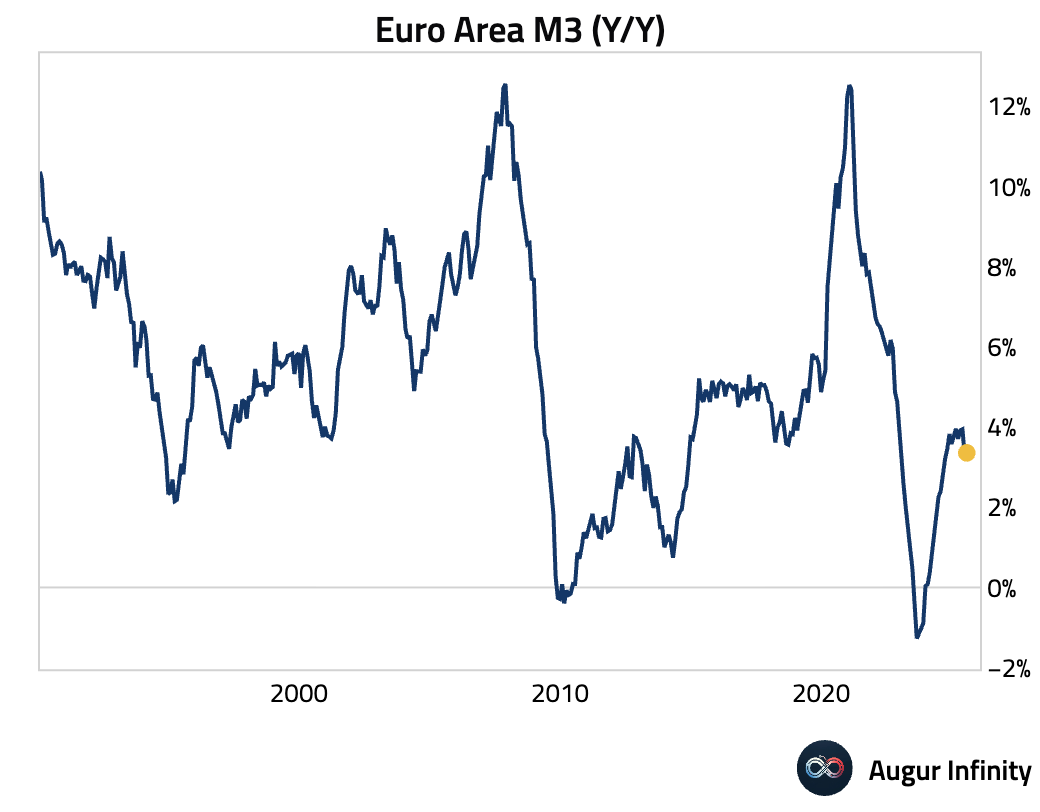

- Euro Area M3 money supply growth edged up to 3.4% Y/Y in July from 3.3%, slightly below the 3.5% consensus. Lending to households accelerated to 2.4% Y/Y, while lending to companies ticked up to 2.8% Y/Y.

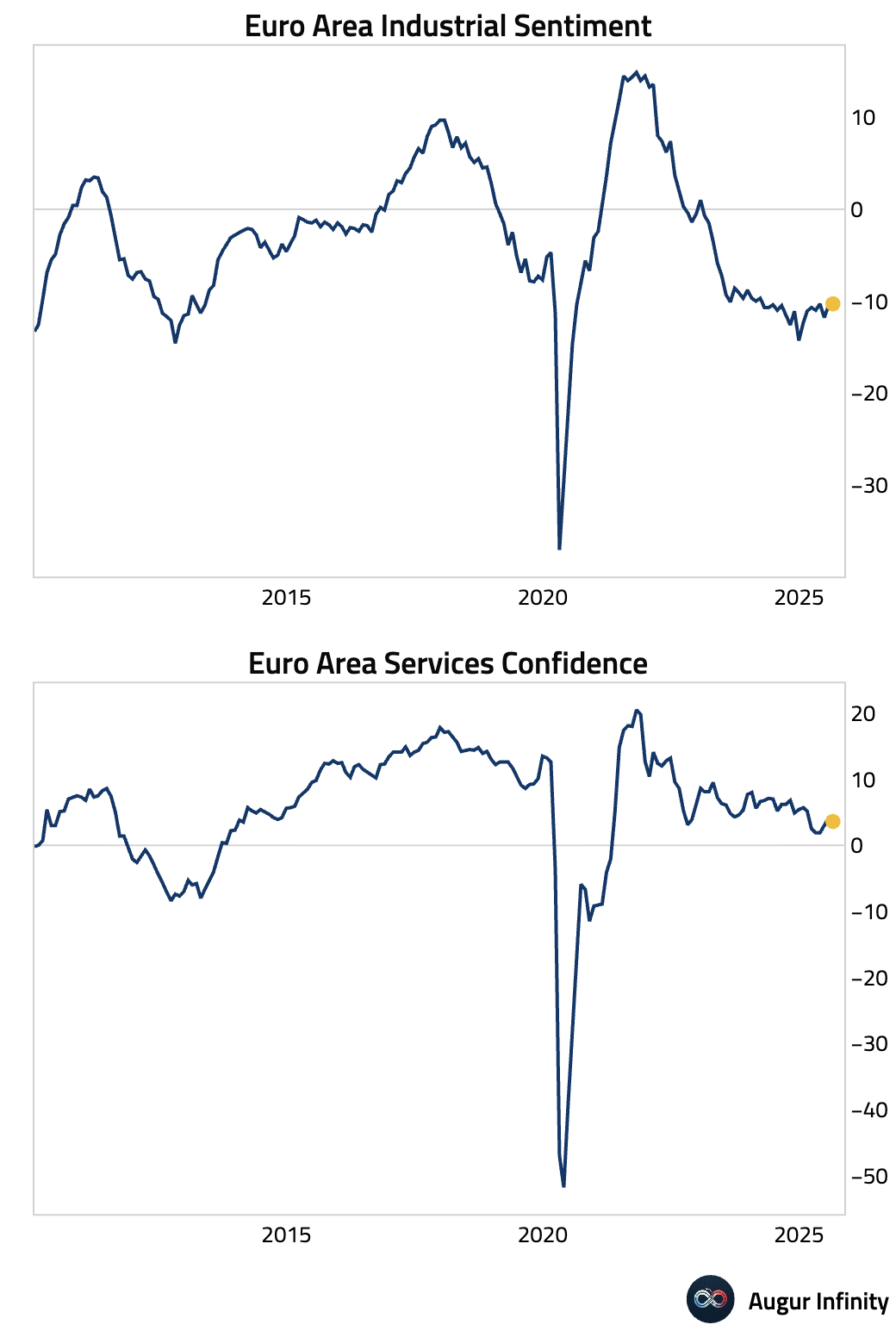

- Eurozone Industrial Sentiment improved slightly to -10.3 (vs. -10.0 consensus), but Services Sentiment dropped to 3.6 (vs. 3.9 consensus).

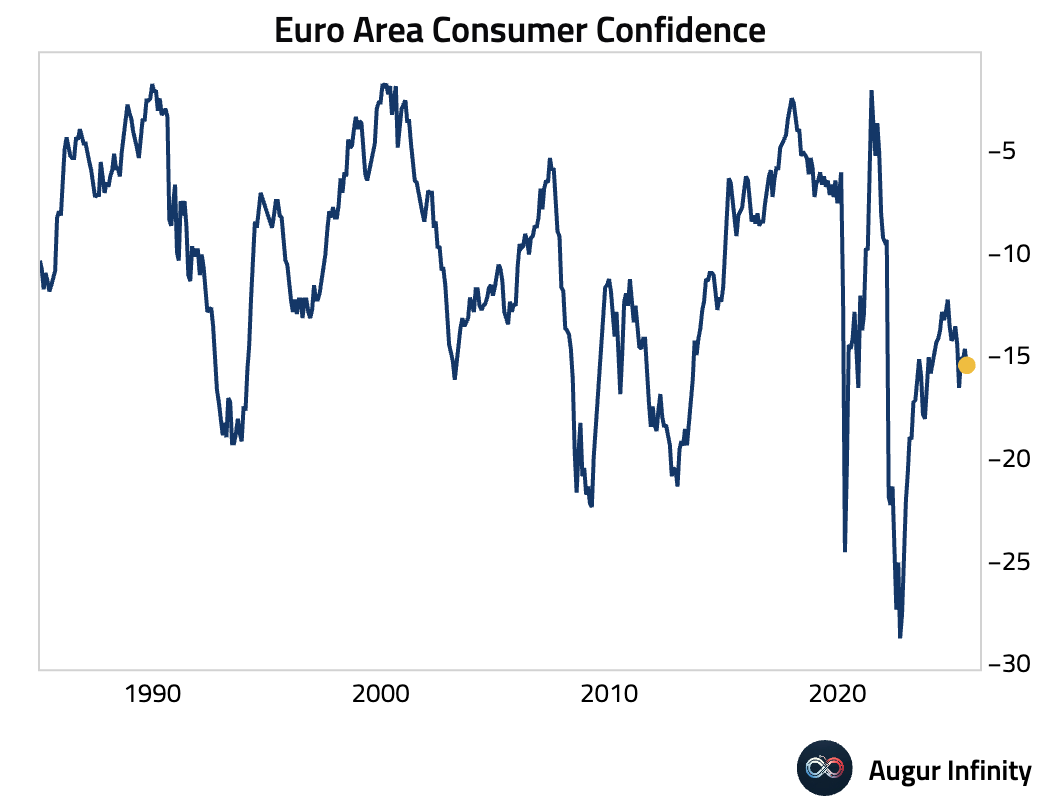

- The final Euro Area Consumer Confidence reading for August was confirmed at -15.5, down from -14.7 in July.

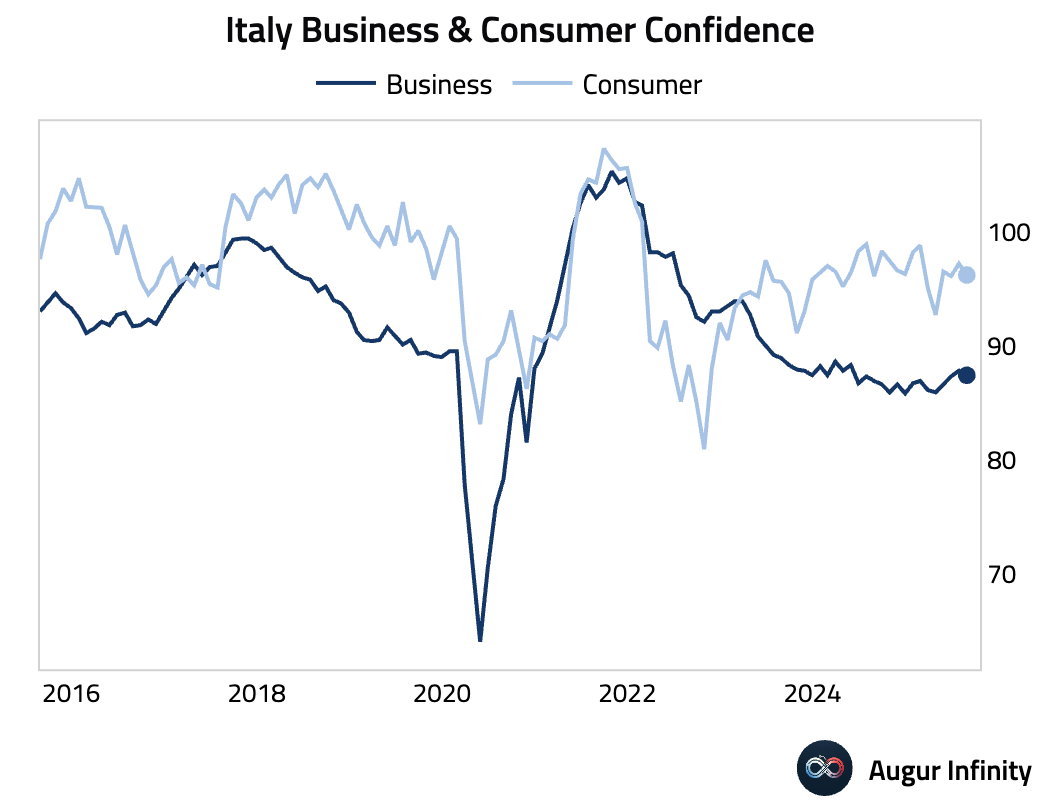

- Italian business and consumer confidence both declined in August. The business confidence index fell to 87.4 (vs. 87.2 consensus) from 87.8, while consumer confidence dropped to 96.2 (vs. 96.6 consensus) from 97.2.

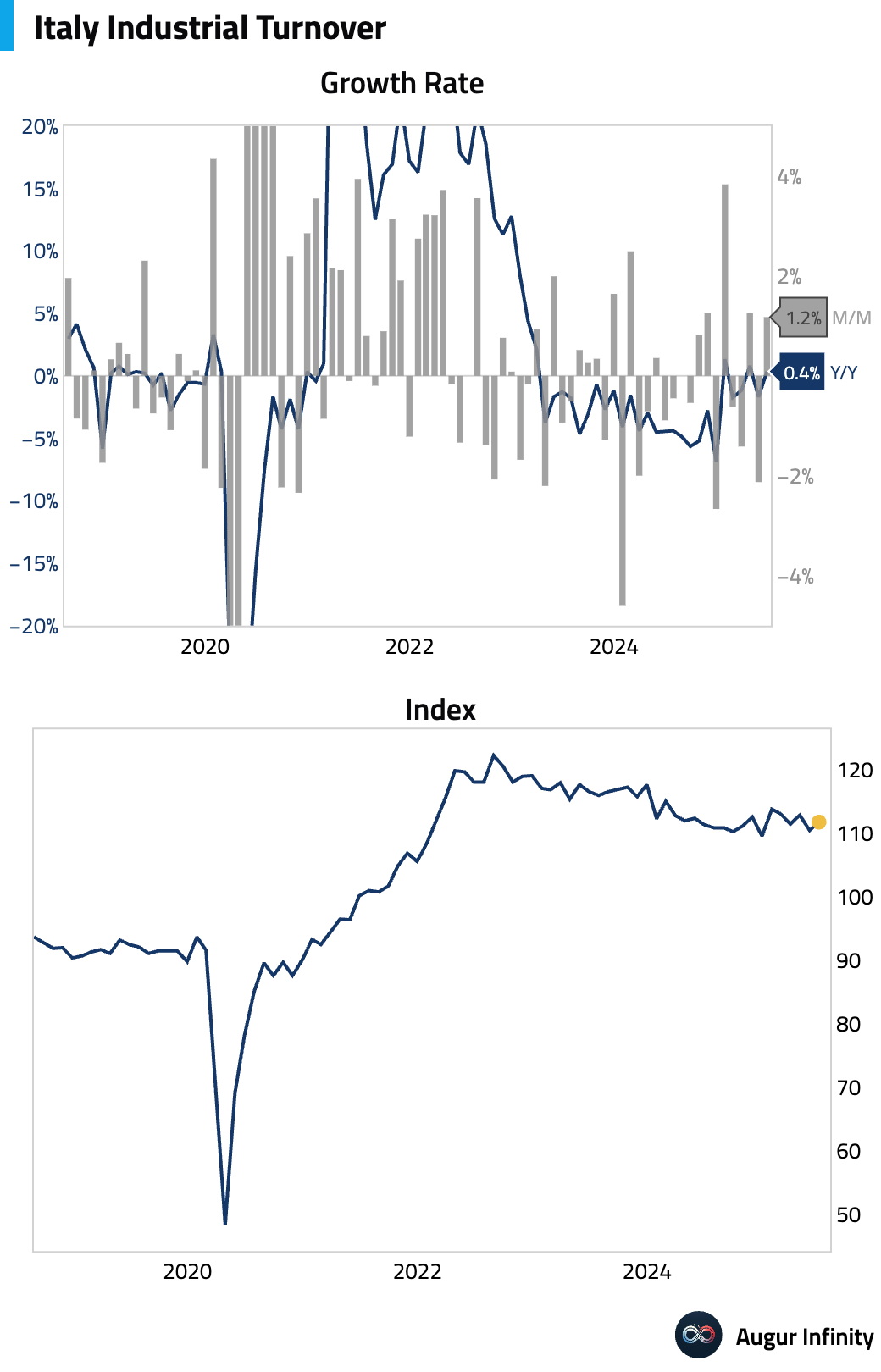

- Italian industrial sales rebounded in June, rising 1.2% M/M after a 2.1% decline in May. On a year-over-year basis, sales rose 0.3%.

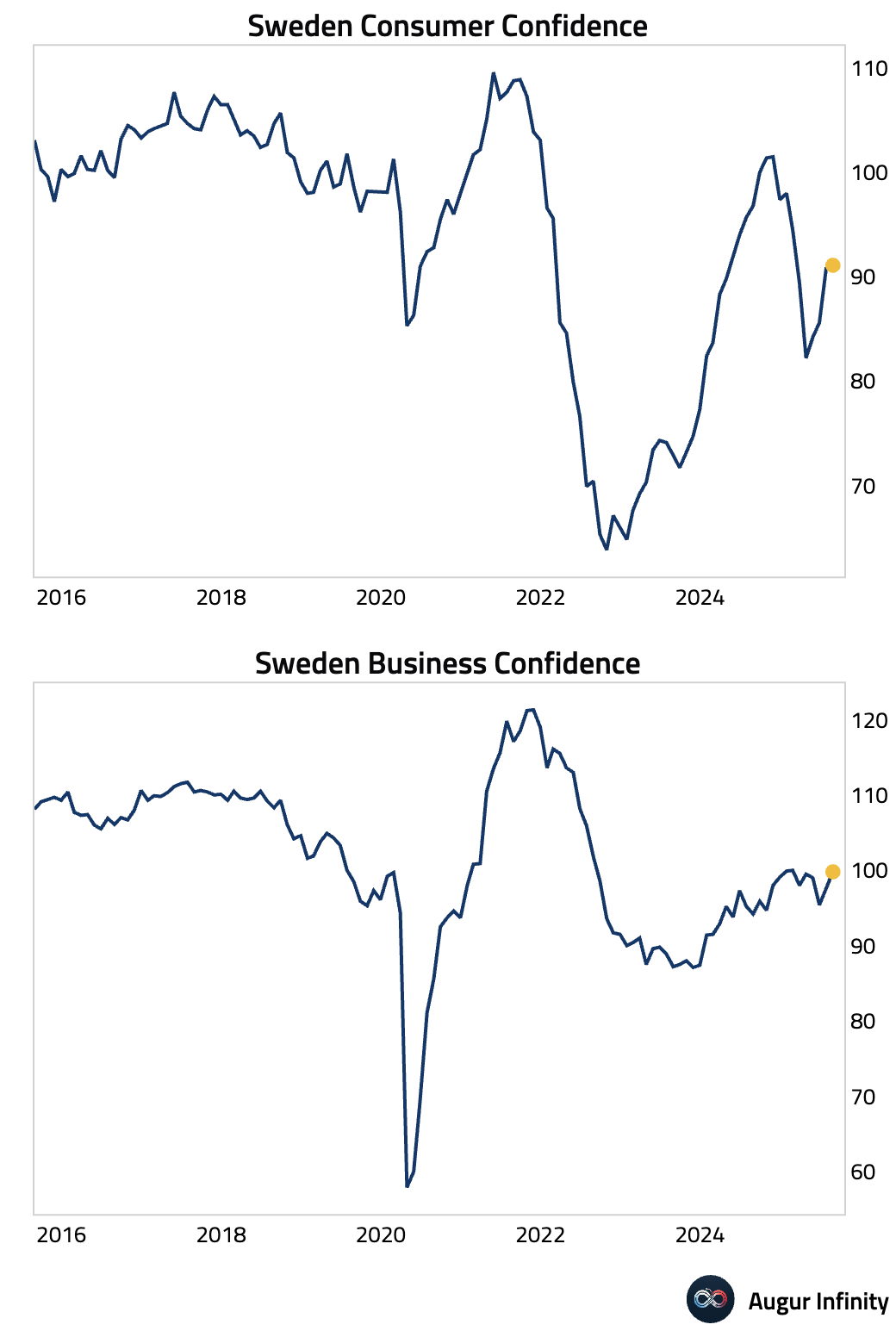

- Swedish consumer and business confidence both improved in August, with the consumer gauge rising to 91.1 from 90.8 and the business metric increasing to 99.8 from 97.4. The broader Economic Tendency Indicator rose to 96.0 from 94.3.

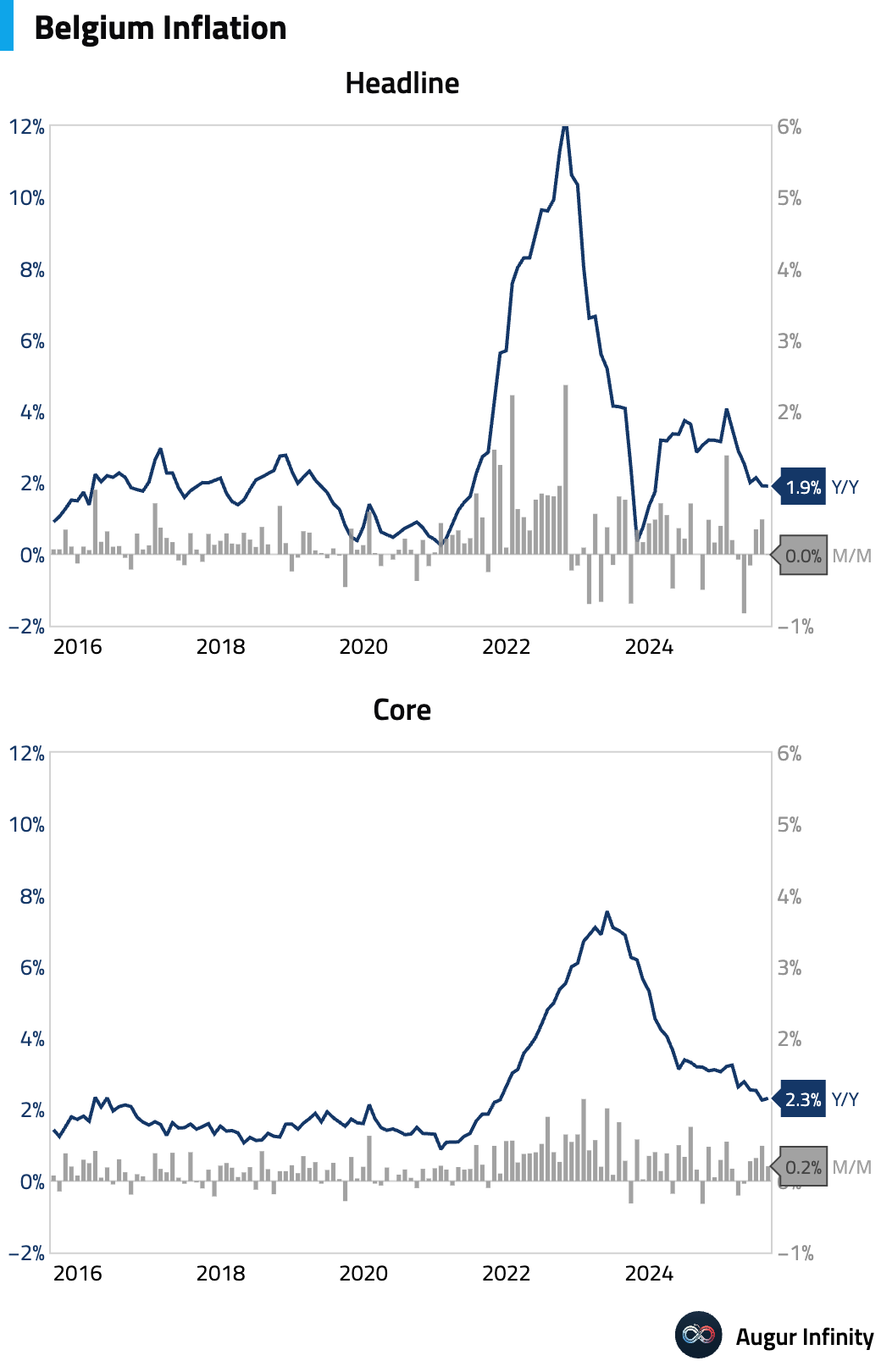

- Belgian inflation eased in August, with the headline rate falling 0.01% M/M. The year-over-year rate ticked down to 1.91% from 1.92%.

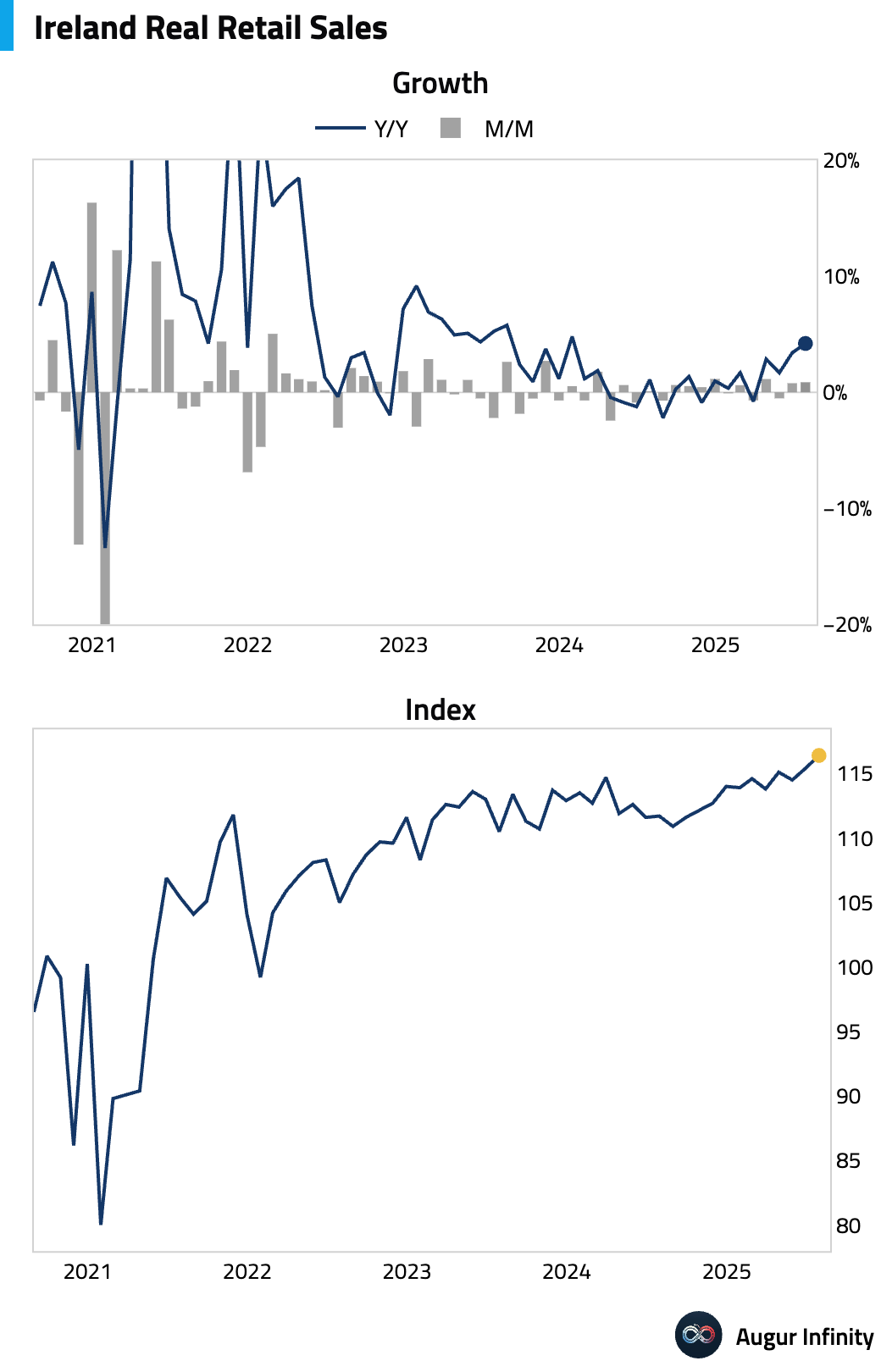

- Irish retail sales rose 0.8% M/M in July, matching June's pace. The year-over-year growth rate accelerated to 4.2% from 3.4%.

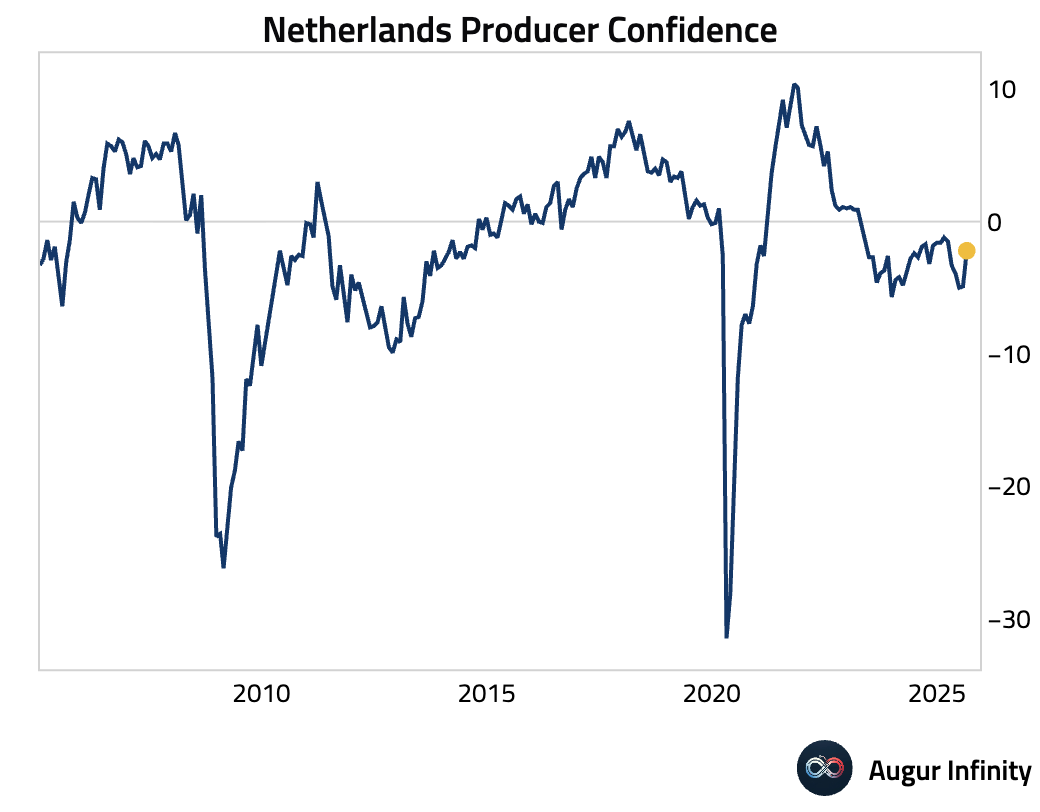

- Dutch business confidence improved in August, rising to -2.2 from -4.9.

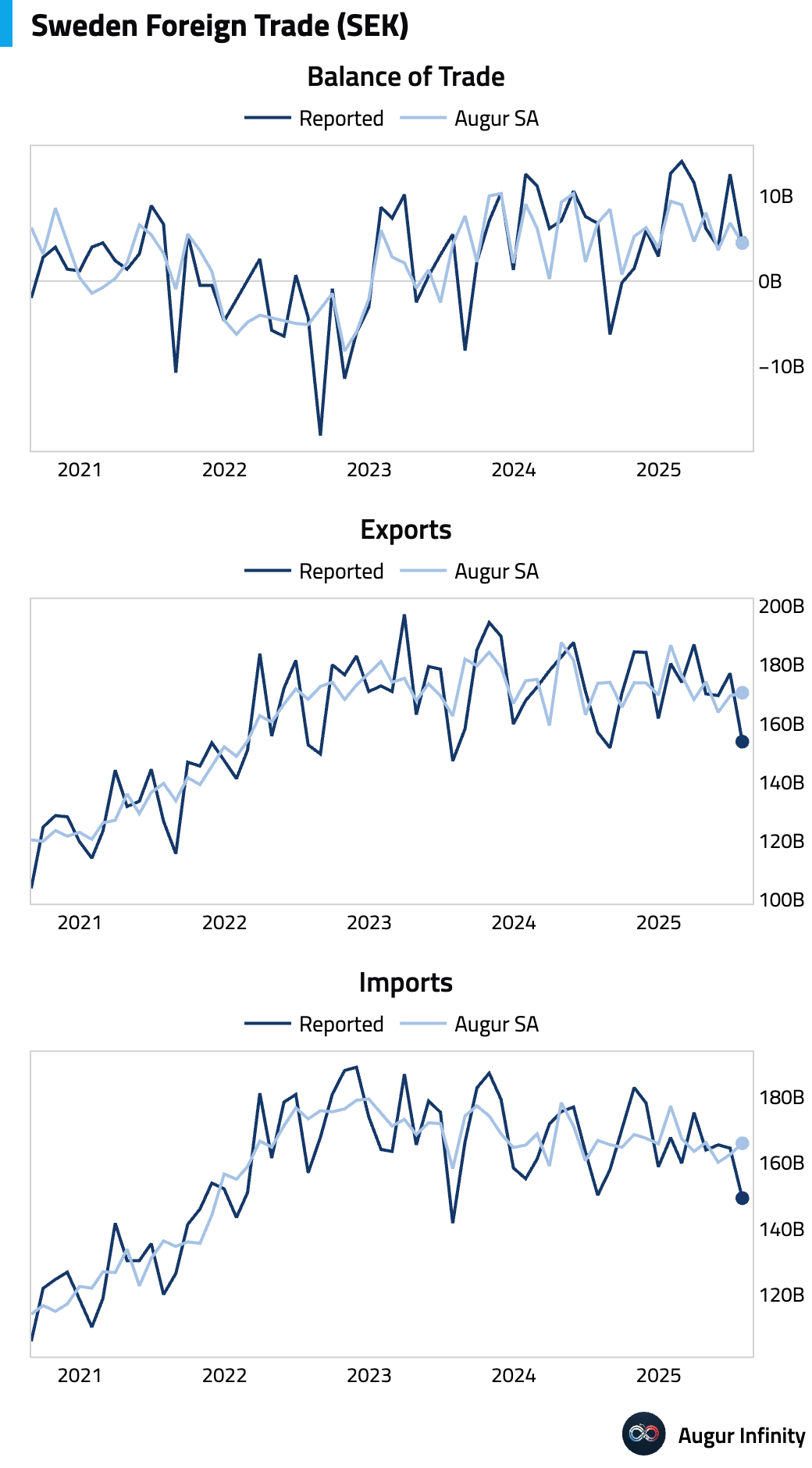

- Sweden’s trade surplus narrowed to SEK 4.5 billion in July from SEK 12.6 billion in June.

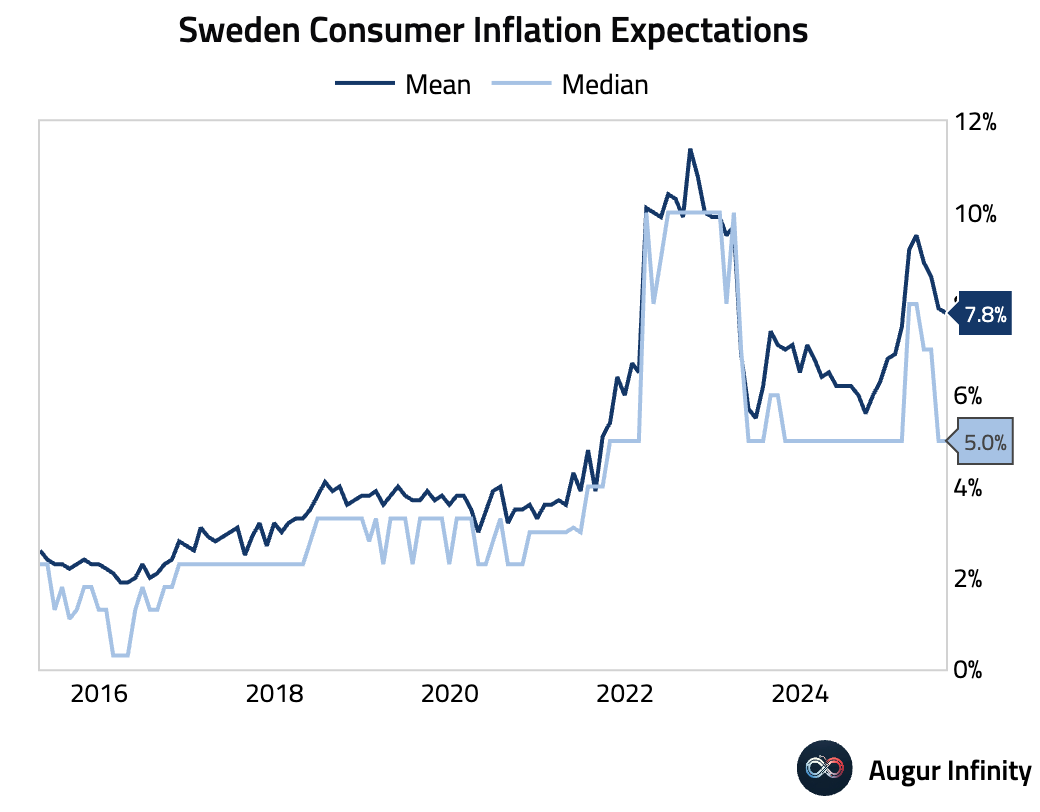

- Swedish consumer inflation expectations for the year ahead eased to 7.8% in August from 7.9% in July.

Asia-Pacific

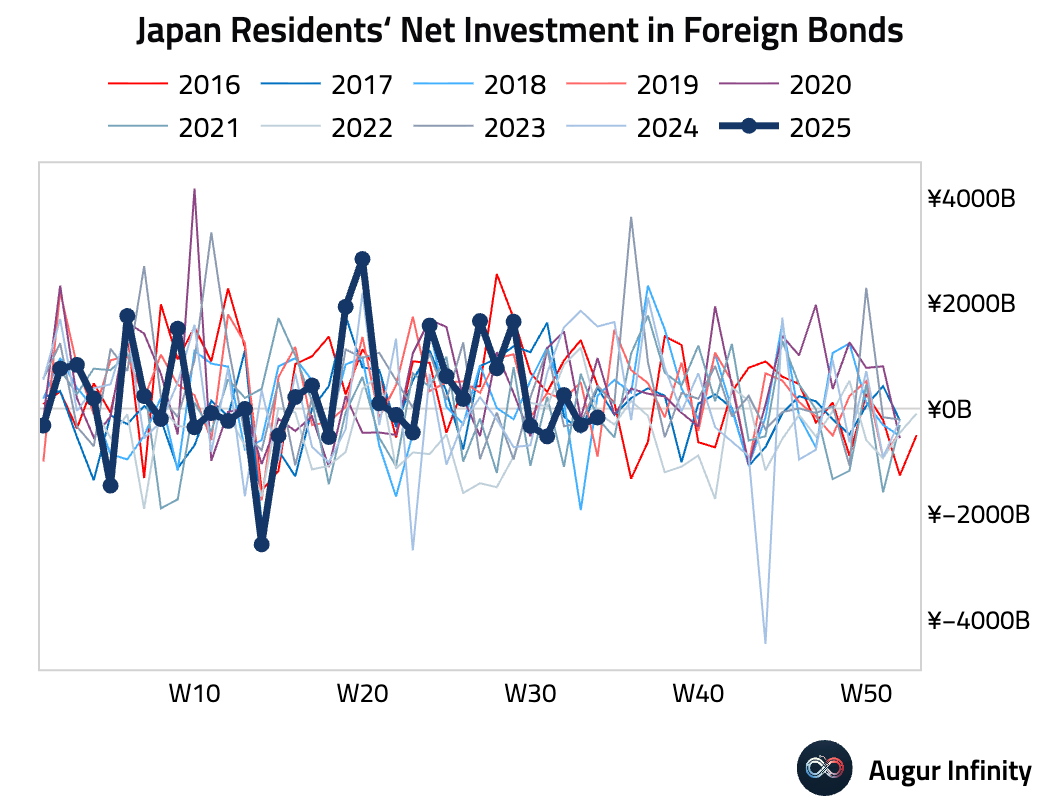

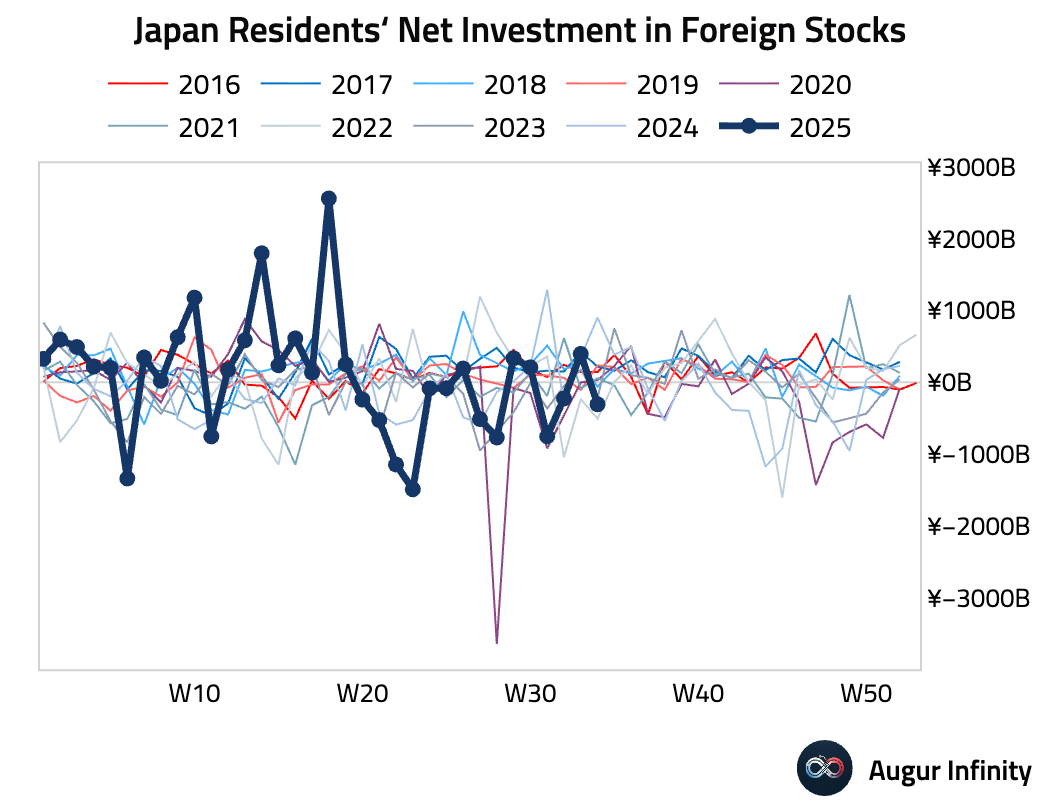

- Japanese investors were net sellers of foreign bonds to the tune of ¥167.2 billion for the week ending August 23, a shift from net selling of ¥310.9 billion in the prior week.

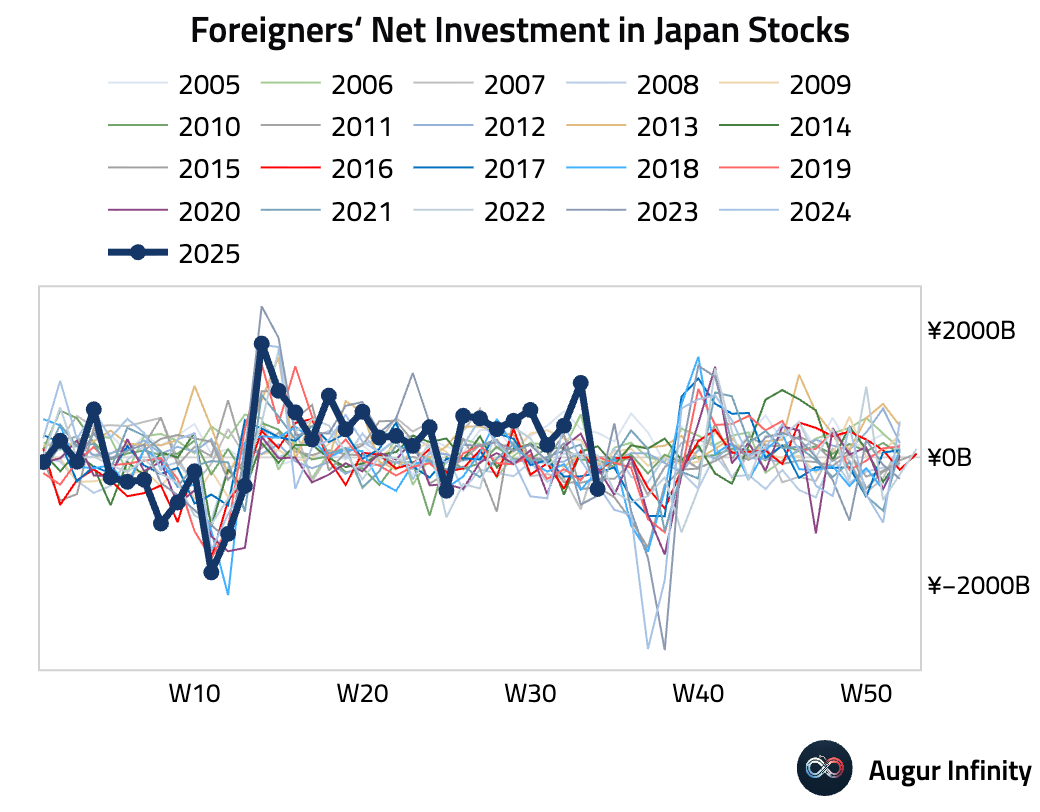

- Foreign investors sold a net ¥496.8 billion of Japanese stocks in the week ending August 23, reversing from a ¥1.17 trillion inflow the week prior.

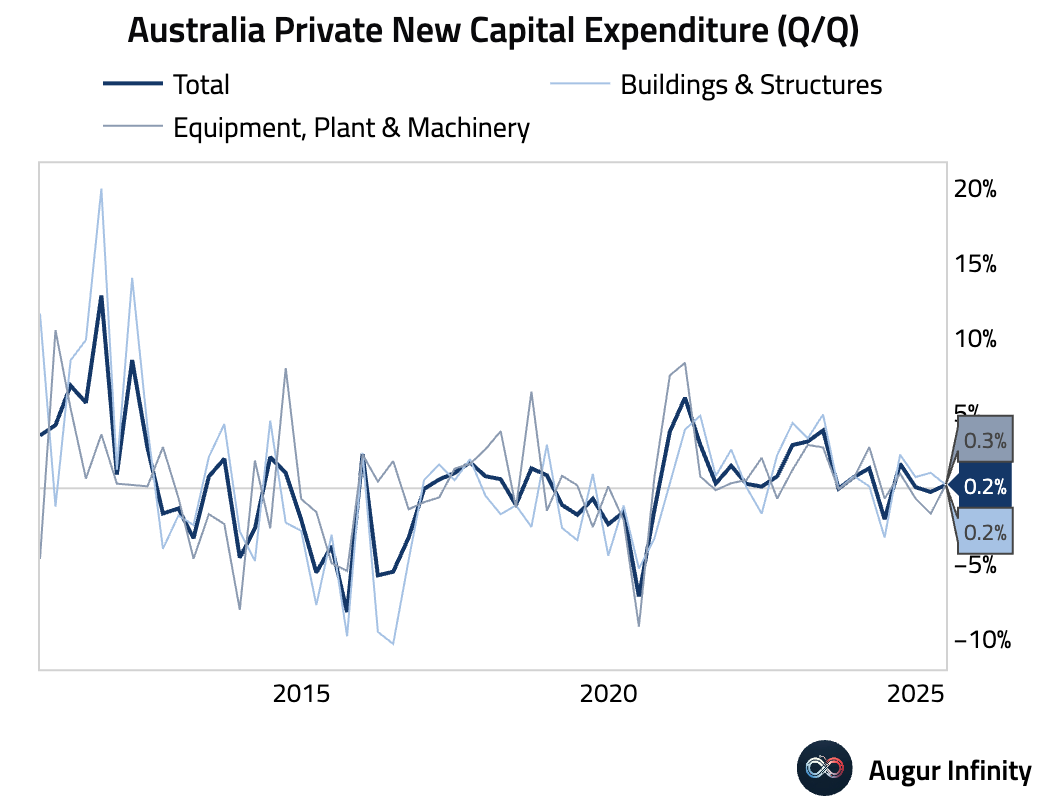

- Australian private capital expenditure rose 0.2% Q/Q in the second quarter, missing the 0.7% consensus forecast. The weakness was broad-based, with spending on buildings and structures up 0.2% and equipment investment rising 0.3%. A rebound in non-mining investment was offset by a decline in the mining sector.

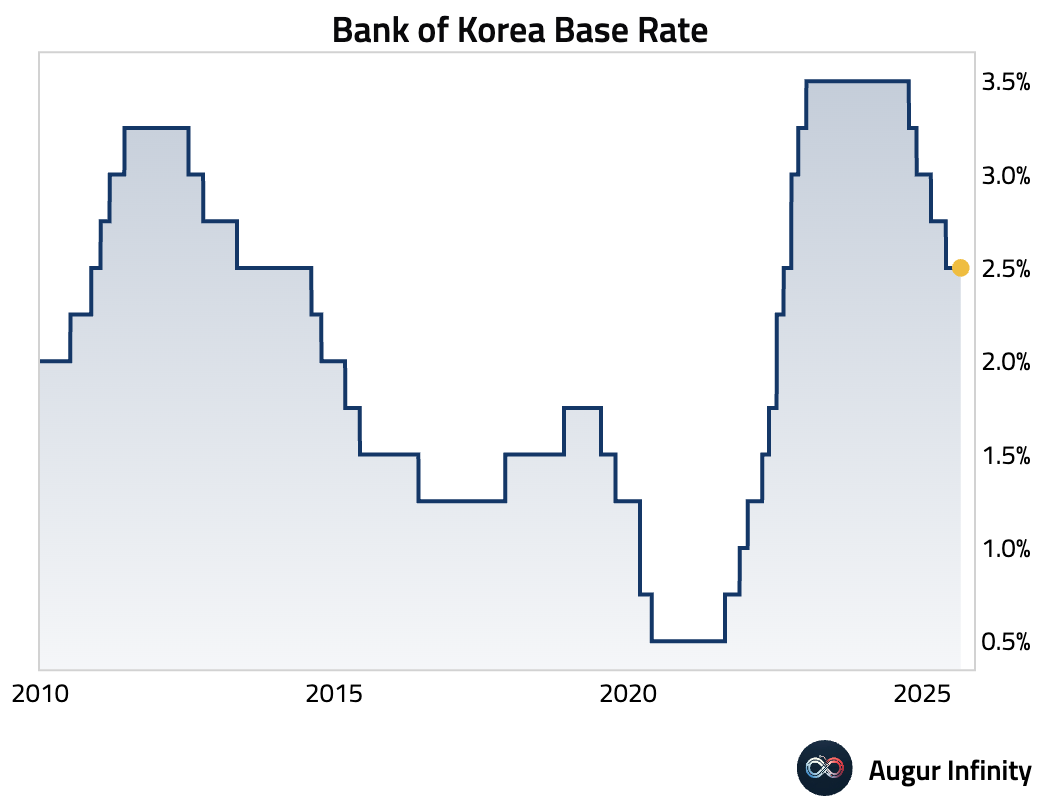

- The Bank of Korea (BOK) held its policy rate at 2.5%, as expected. However, the decision was accompanied by a dovish shift, with one board member dissenting in favor of a 25 bps cut—the first dissent since April. The bank's forward guidance also turned more dovish, with five of six members now open to a rate cut within the next three months, up from four previously. The BOK slightly raised its 2025 GDP forecast to 0.9% but stated it needs more evidence of housing market stability before easing.

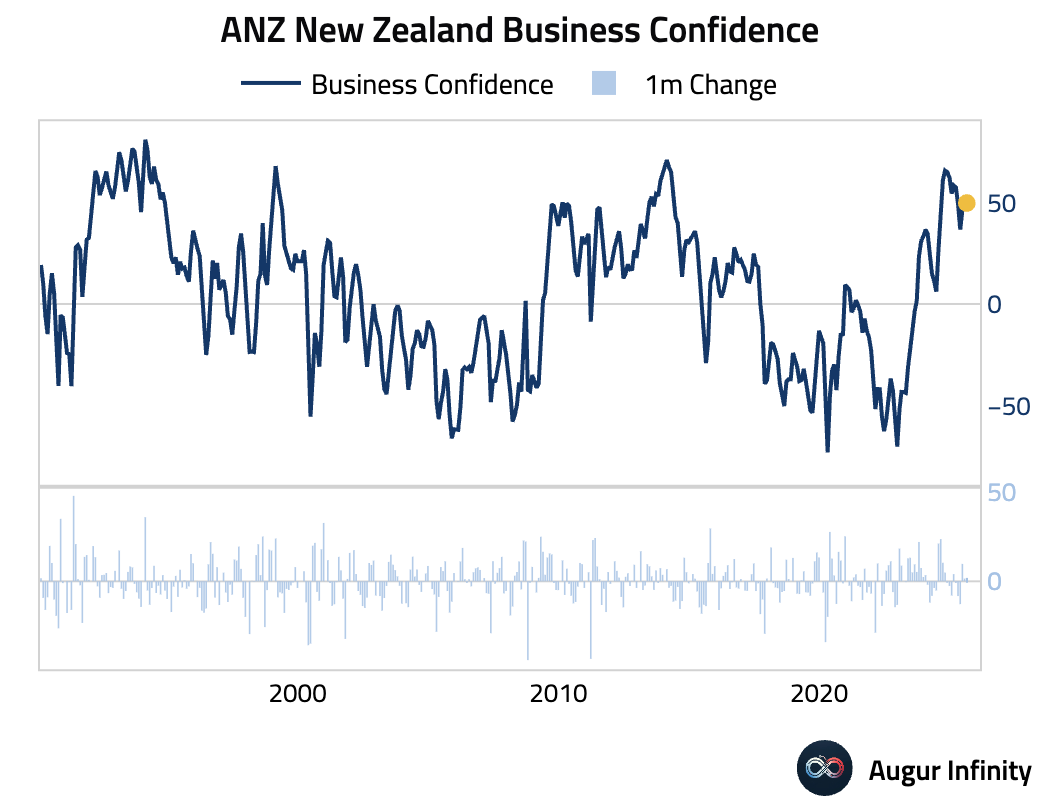

- New Zealand's ANZ Business Confidence index rose to 49.7 in August from 47.8, reaching a five-month high.

Emerging Markets ex China

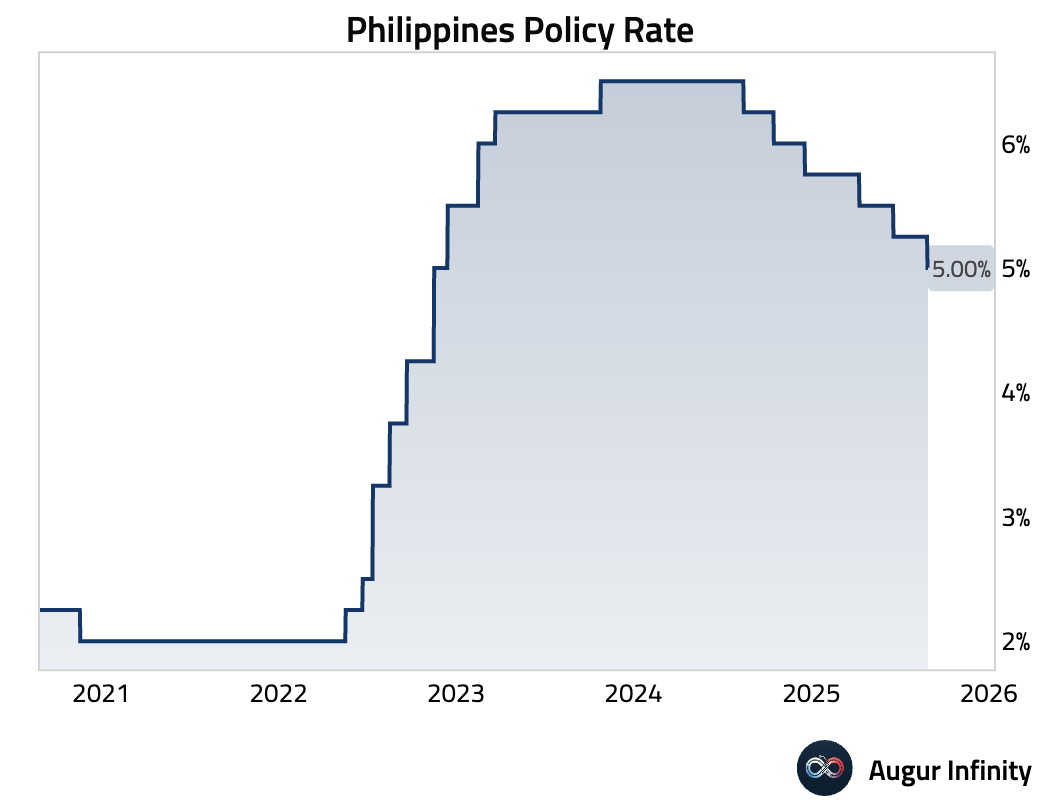

- Bangko Sentral ng Pilipinas (BSP) cut its policy rate by 25 bps to 5.00%, as expected. This brings total easing this cycle to 150 bps. The central bank signaled a pause, with the Governor describing the current rate as a "goldilocks" level, citing upside inflation risks. Any further rate cuts are now conditional on weaker growth data.

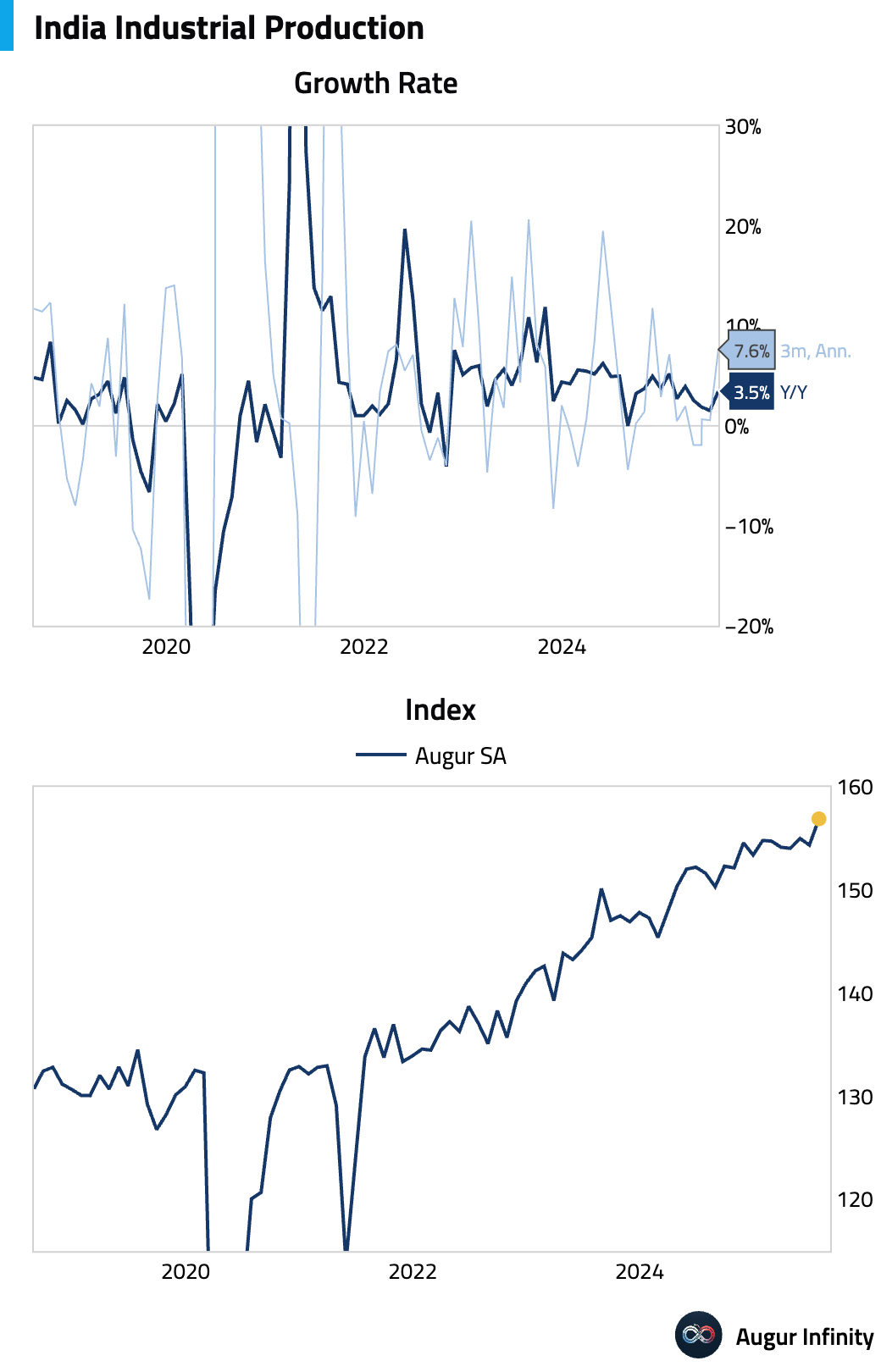

- Indian industrial production grew 3.5% Y/Y in July, accelerating from 1.5% in June and beating the 2.1% consensus. The strength was driven by public capex spending in infrastructure and capital goods. Manufacturing production expanded by 5.4% Y/Y.

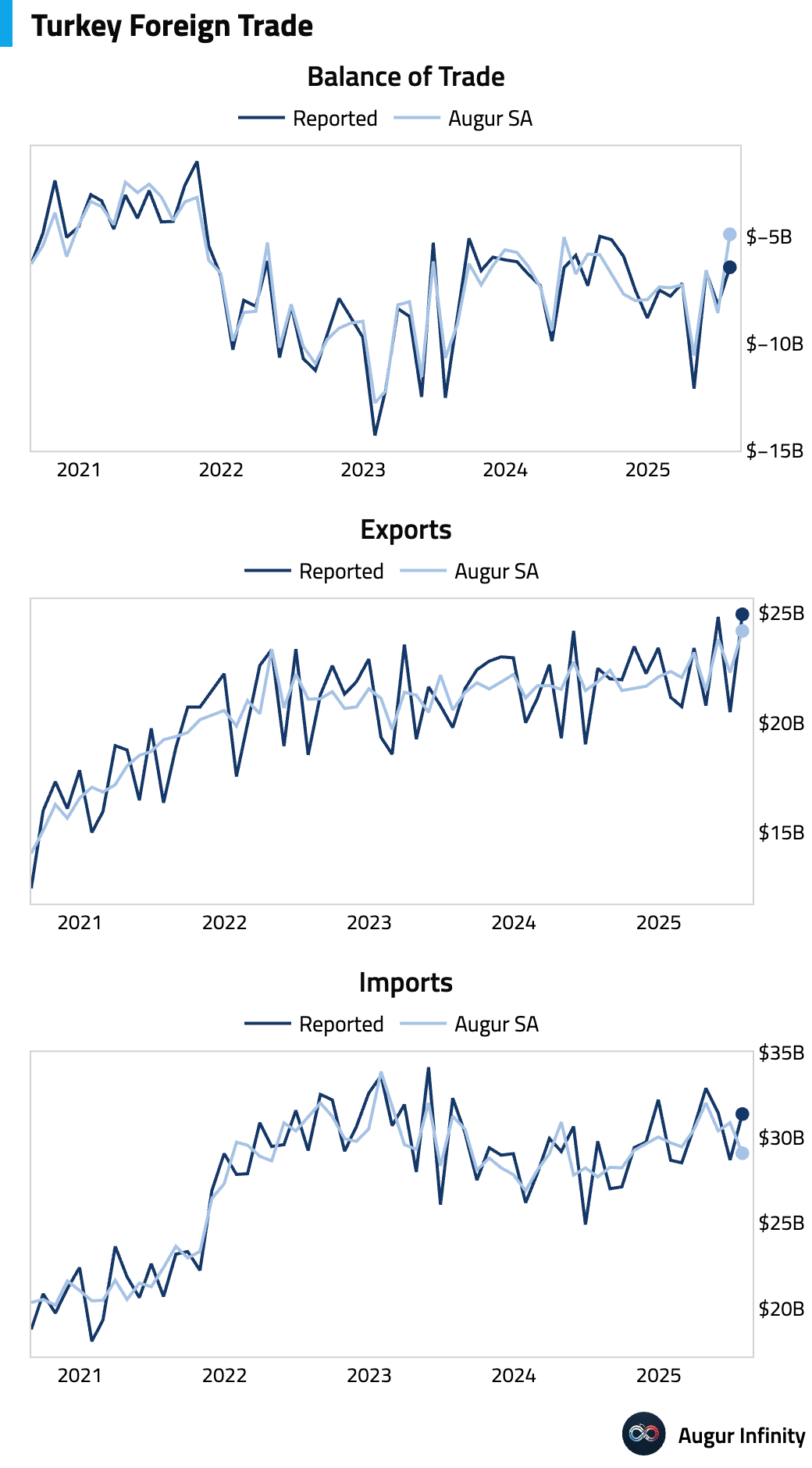

- Turkey’s final trade deficit for July narrowed to $6.4 billion from $8.2 billion in June. Exports rose to an all-time high of $24.9 billion, while imports increased to $31.4 billion.

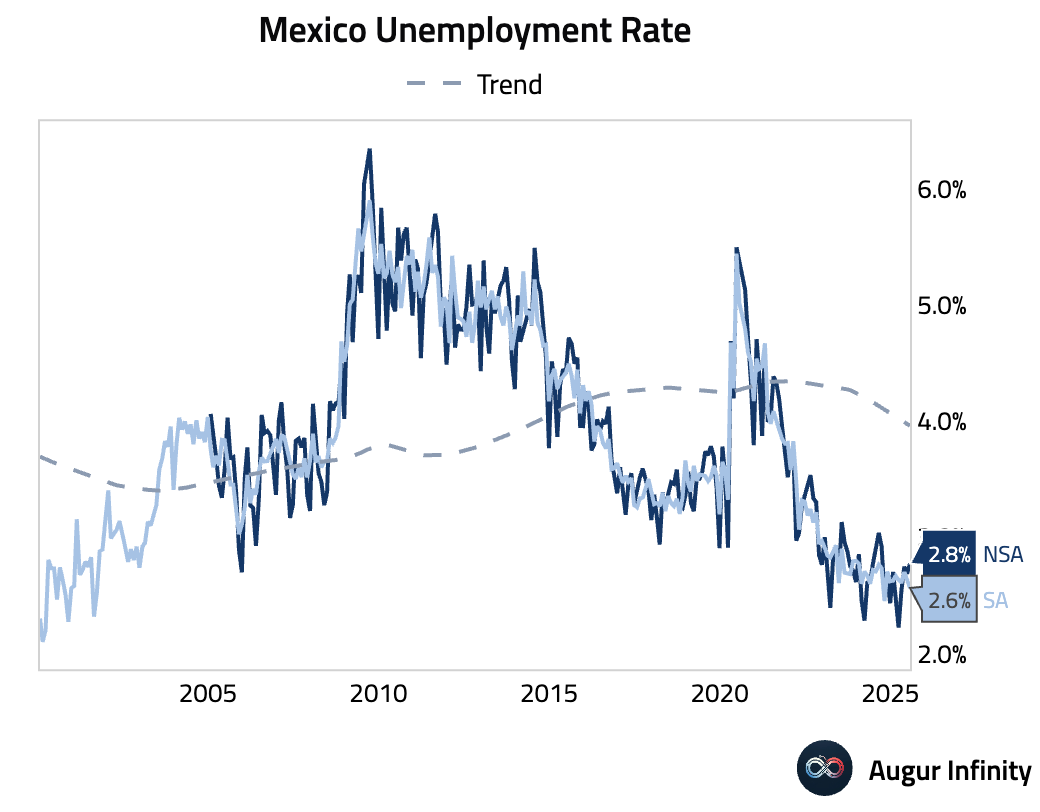

- Mexico’s unemployment rate ticked up to 2.8% in July from 2.7%, slightly below the 2.9% consensus. The seasonally adjusted unemployment rate, however, declined slightly.

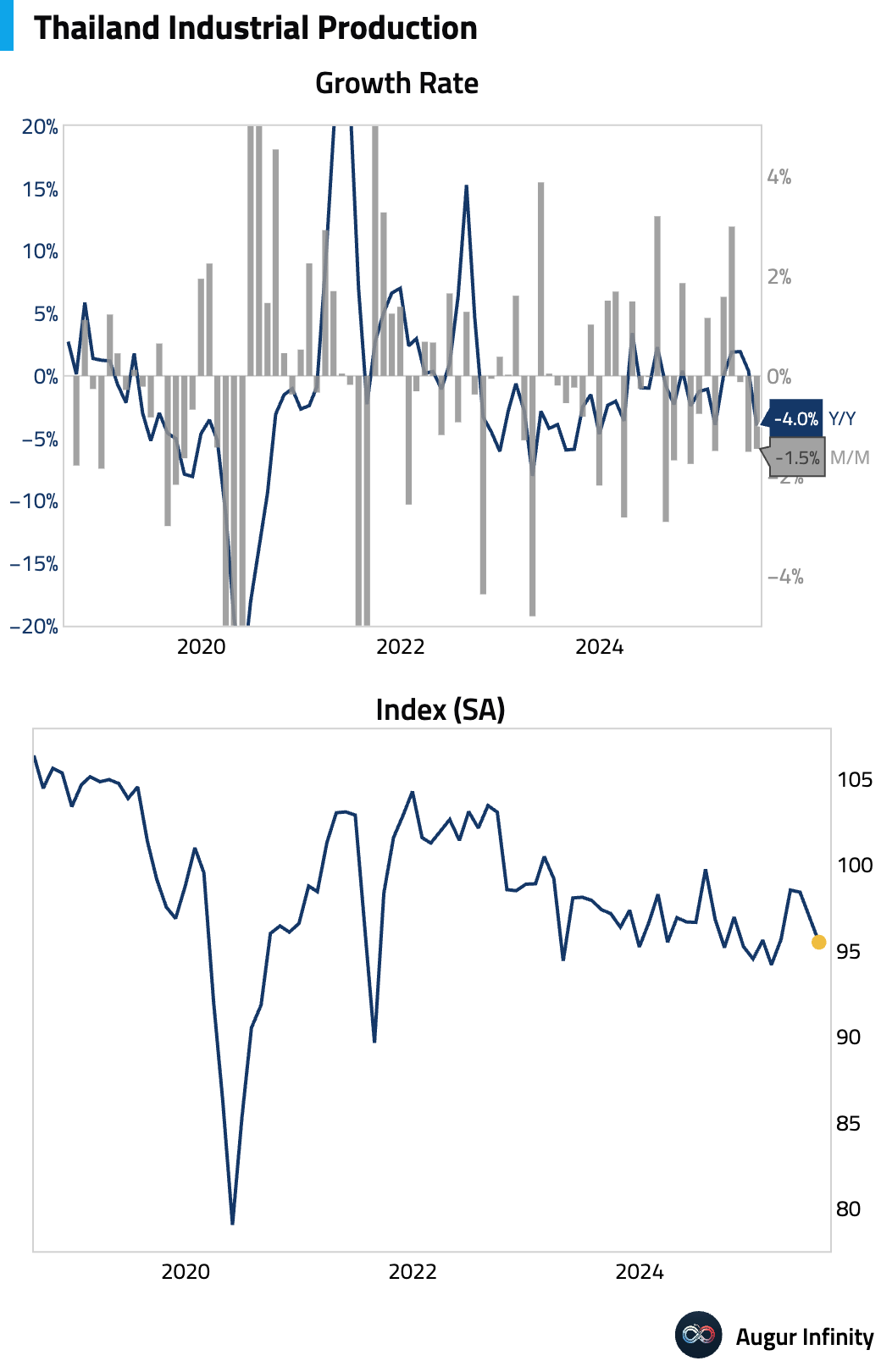

- Thailand's industrial production fell 3.98% Y/Y in July, a sharp contraction compared to the 0.41% growth in June and well below the -1.1% consensus.

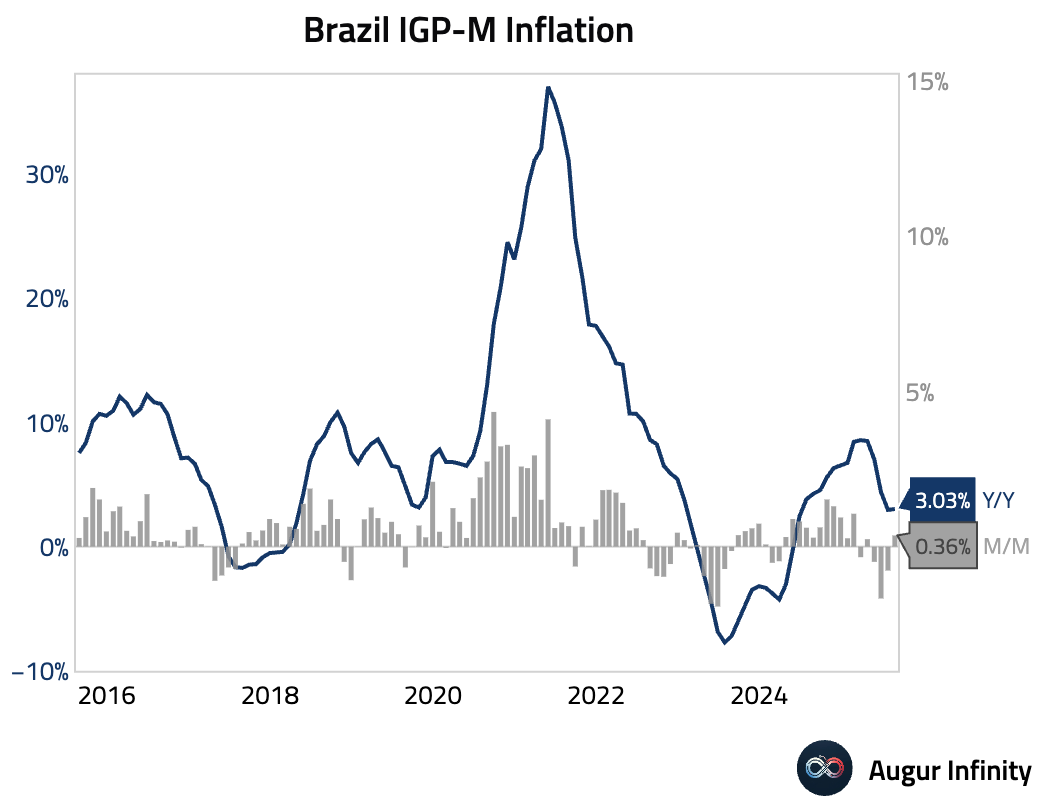

- Brazil’s IGP-M inflation index rose 0.36% M/M in August, rebounding from a 0.77% decline in July and exceeding the 0.21% consensus.

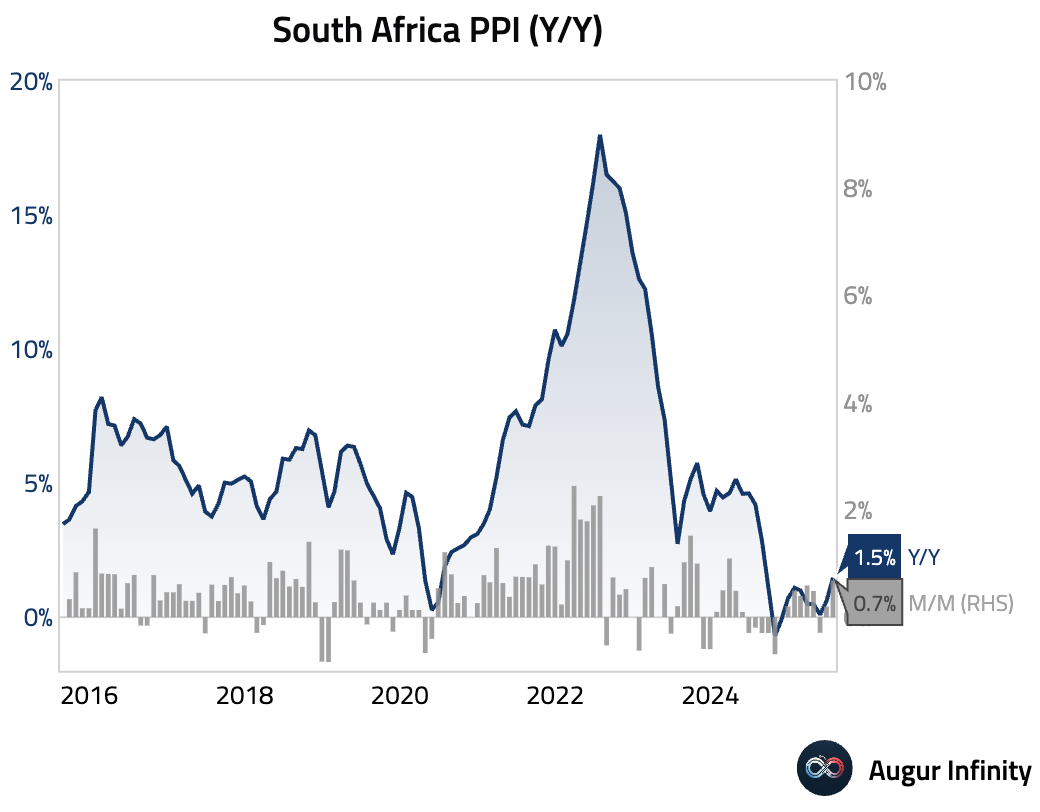

- South African producer prices rose 0.7% M/M in July, pushing the annual rate up to 1.5% from 0.6%.

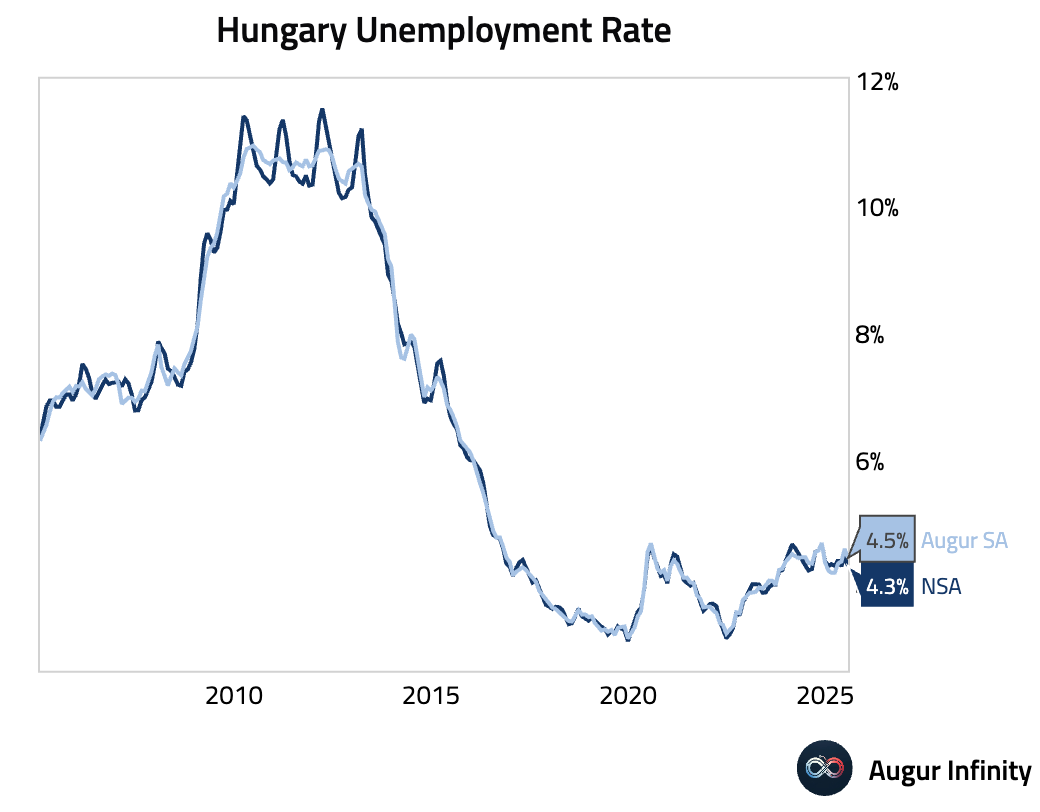

- Hungary’s unemployment rate fell to 4.3% in July from 4.5% in June.

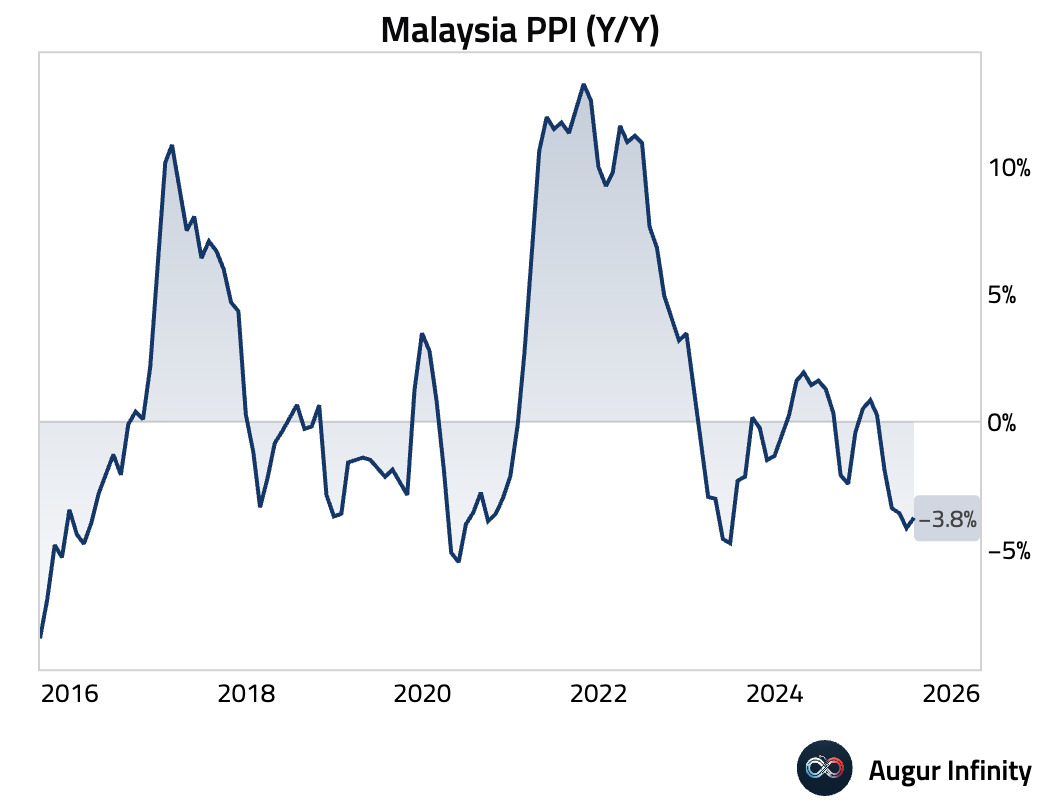

- Malaysia’s producer price deflation eased in July, with the index at -3.8% Y/Y compared to -4.2% in June.

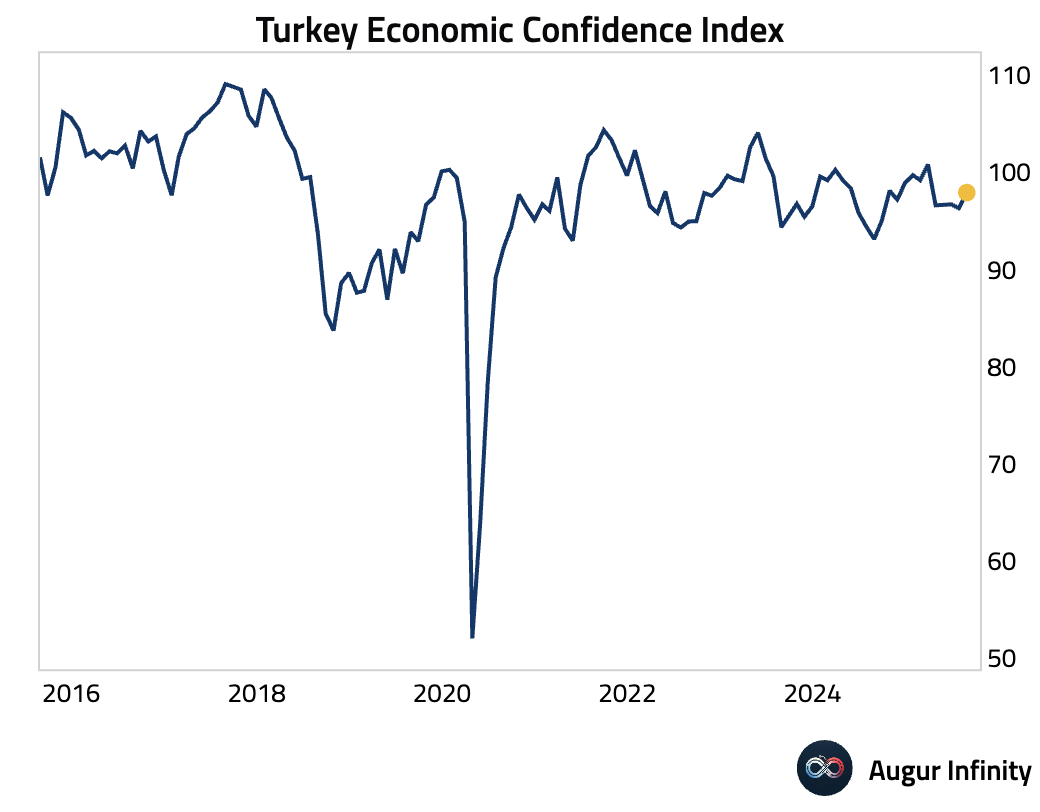

- Turkey’s economic confidence index increased to 97.9 in August from 96.3 in July.

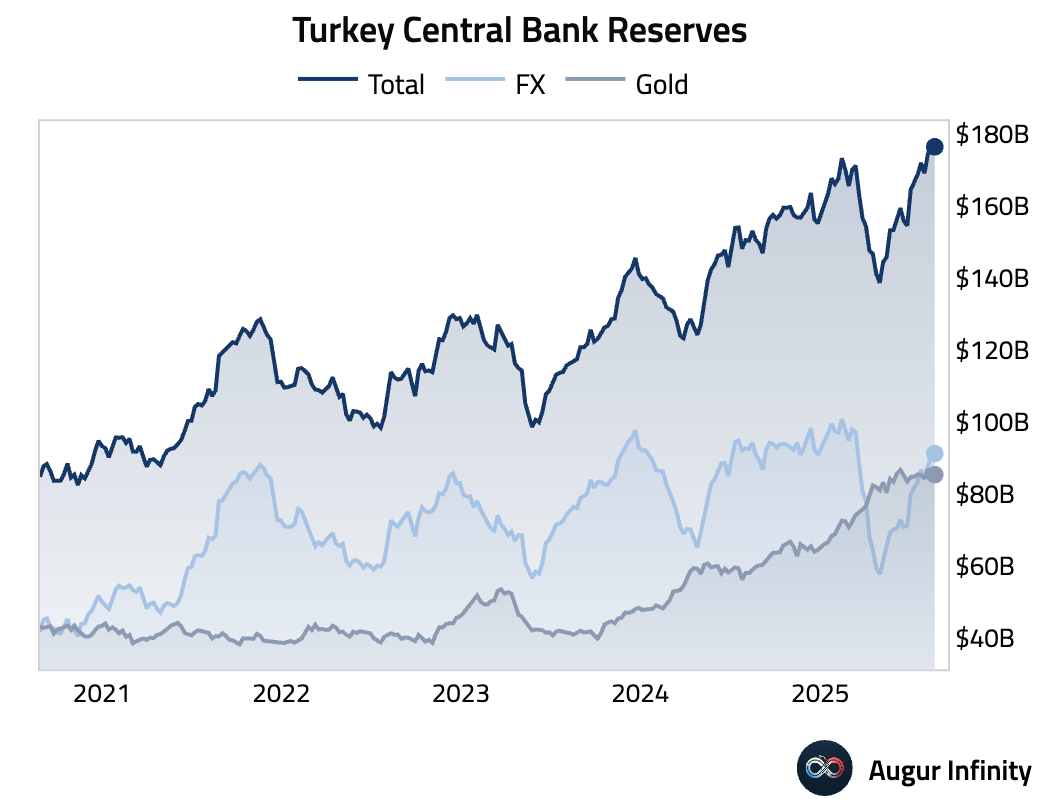

- Turkey’s foreign exchange reserves edged up to $91.09 billion for the week ending August 22 from $90.93 billion previously.

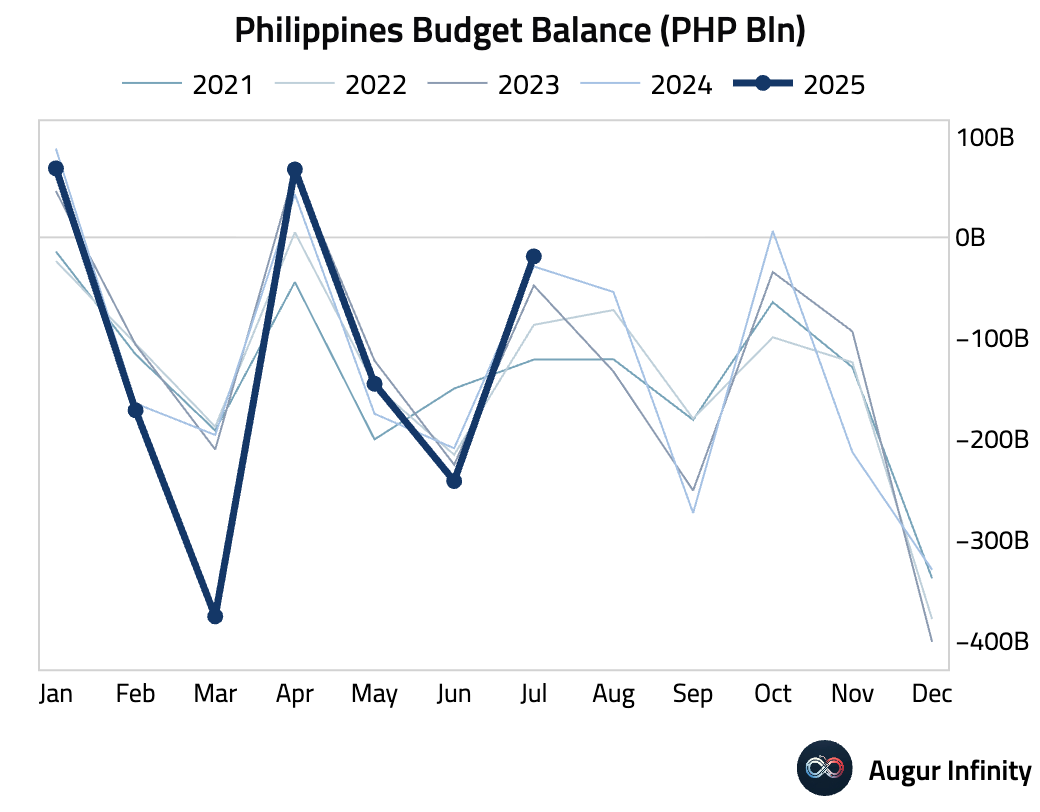

- The Philippines posted a budget deficit of PHP 18.9 billion in July, narrowing significantly from a PHP 241.6 billion deficit in June.

Global Markets

Equities

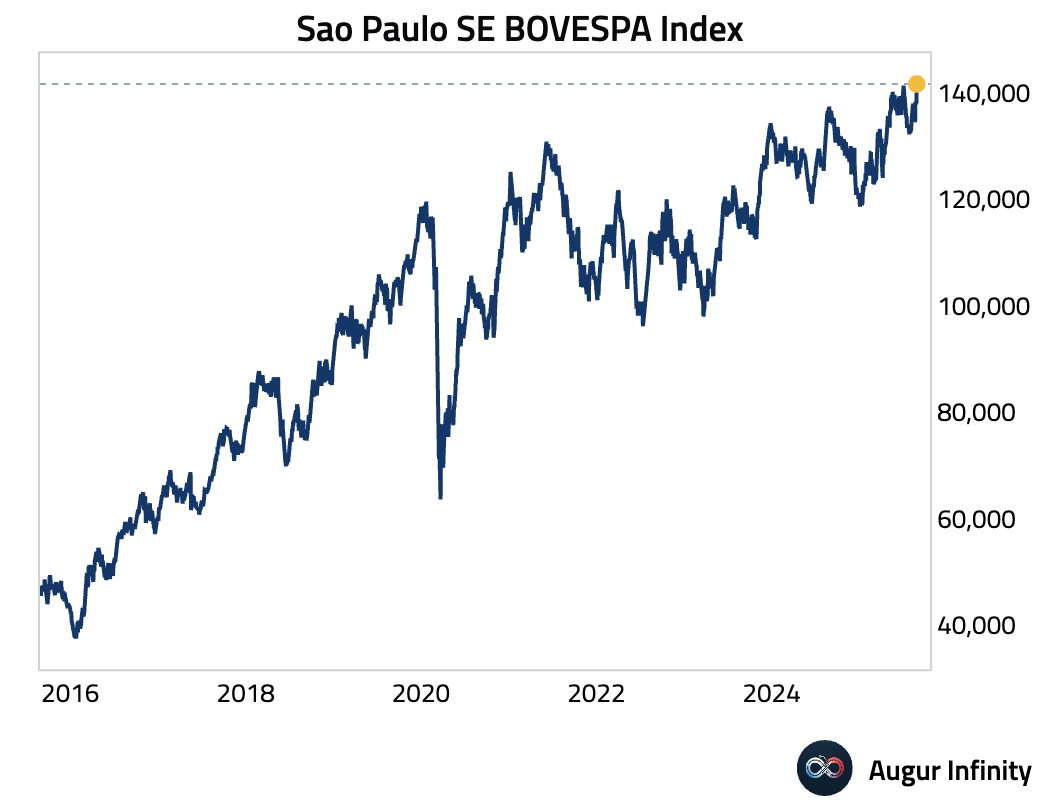

- US equities extended their rally for a third consecutive session, with the S&P 500 closing at a fresh record high. The index rose 0.3%, while the Nasdaq Composite gained 0.5%, also marking its third straight day of gains. The advance was supported by optimism ahead of key technology earnings. Globally, performance was strong; Brazil surged 1.8%, South Korea added 1.6%, and Mexico rose 1.0%. Australia and Canada also posted a third day of gains. Conversely, the UK market declined for a fourth consecutive day, falling 0.2%.

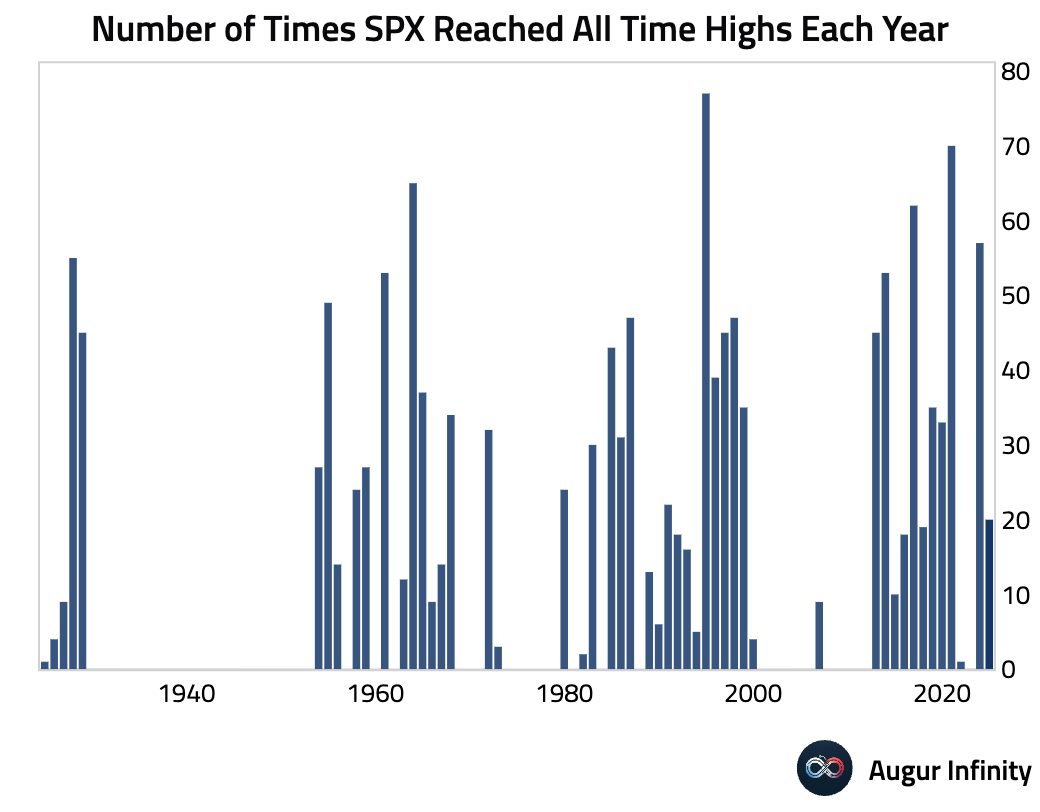

- The S&P 500 notched its 20th all-time-high this year.

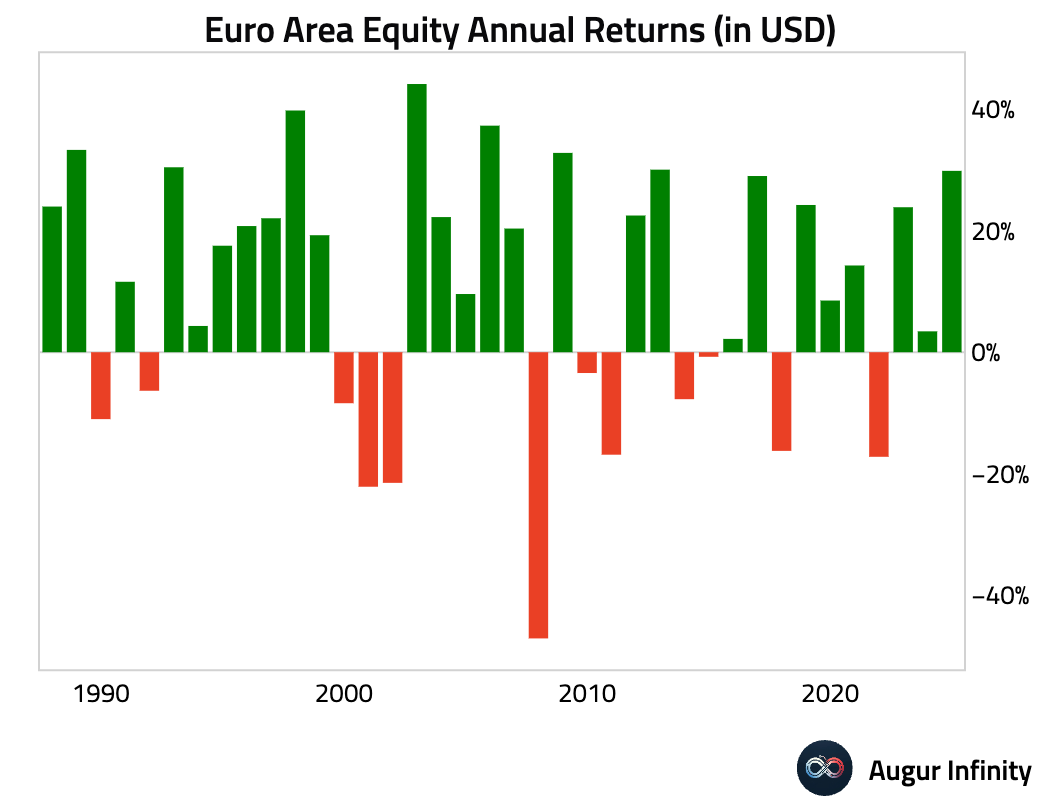

- Eurozone equities have rallied by 30% YTD in USD terms, on track for the best year since 2013.

- BOVESPA, Brazil's main stock market index, also rose to record high.

Fixed Income

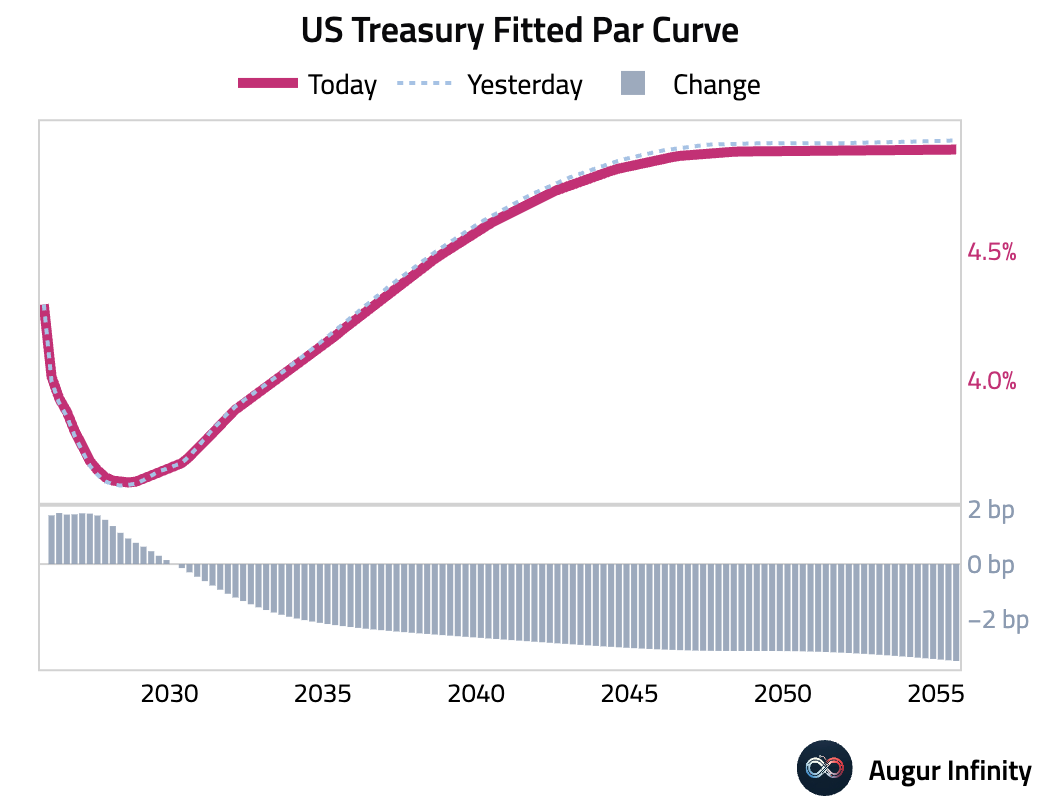

- The 2-year yield rose by 1.7 bps, while the 5-year and 10-year yields fell by 0.4 bps and 2.6 bps, respectively, for their third consecutive day of declines. The 30-year yield decreased by 3.2 bps.

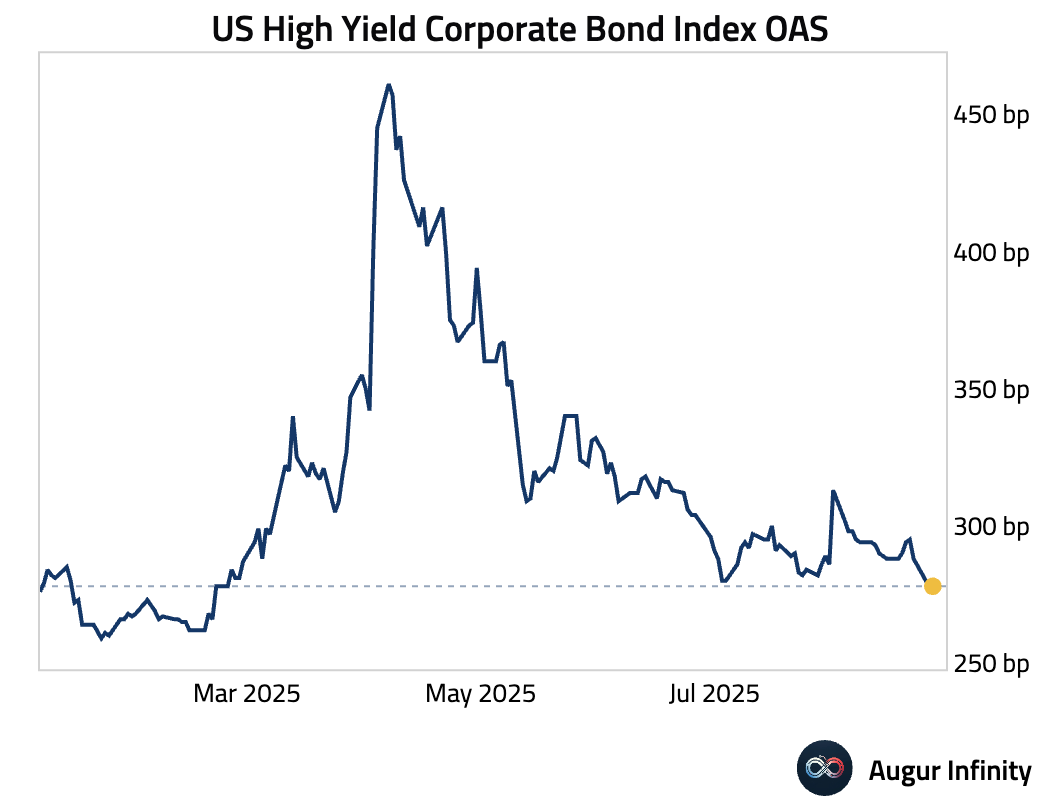

- Credit market continues to demand very little risk premium. The high yield OAS has declined to the lowest level since February.

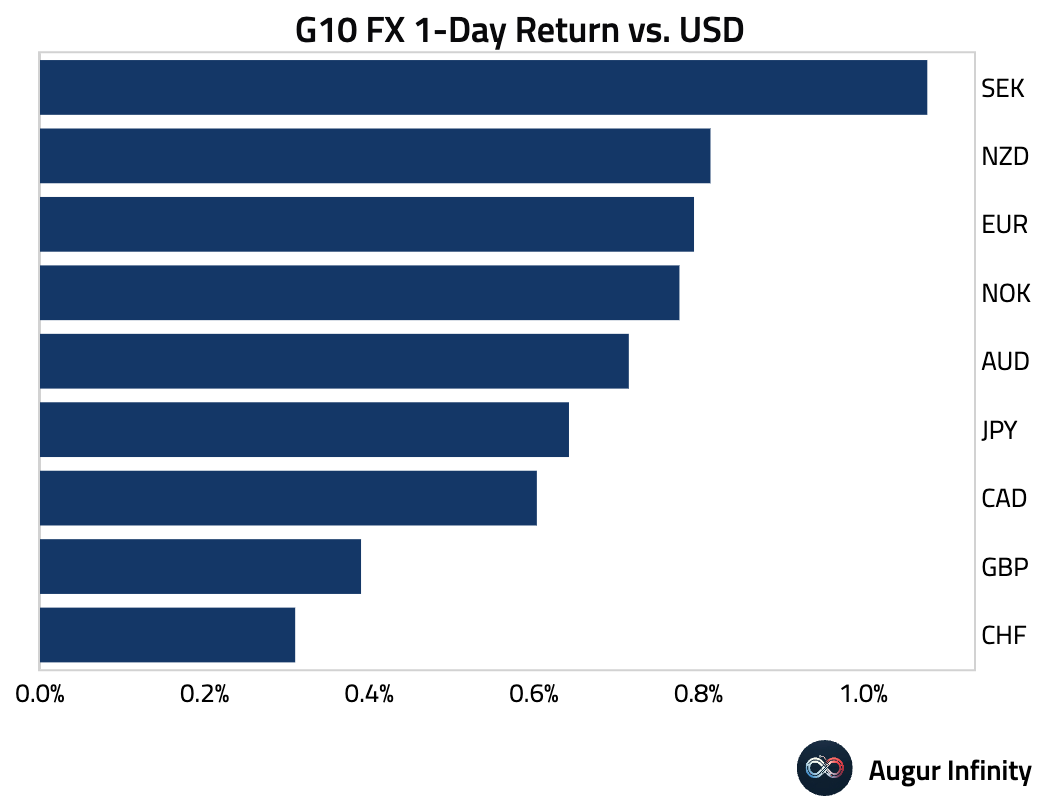

FX

- The US dollar weakened against all G10 peers, influenced by expectations of upcoming Federal Reserve rate cuts. The Swedish krona was the top performer, appreciating 1.1% against the dollar. The euro, New Zealand dollar, and Norwegian krone also posted strong gains of 0.8%. The Japanese yen strengthened 0.6%, supported by hawkish commentary from a Bank of Japan board member that raised expectations for an October rate hike.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.