Headlines

- Federal Housing Finance Agency Director Pulte submitted a second criminal referral against Federal Reserve Governor Cook regarding the alleged mischaracterization of an investment property. Meanwhile, a court hearing in DC ended without a judge ruling on a request by Governor Cook to temporarily bar President Trump from firing her.

- The Financial Times reported that British Chancellor Reeves is considering a surcharge on bank profits or a new bank levy to address a GBP20 billion budget shortfall.

- Thailand's Constitutional Court has dismissed Prime Minister Paetongtarn Shinawatra for an ethics violation. The base case is for a smooth transition with no significant policy disruption, as the ruling coalition is expected to remain intact under a new leader from the same party.

Global Economics

United States

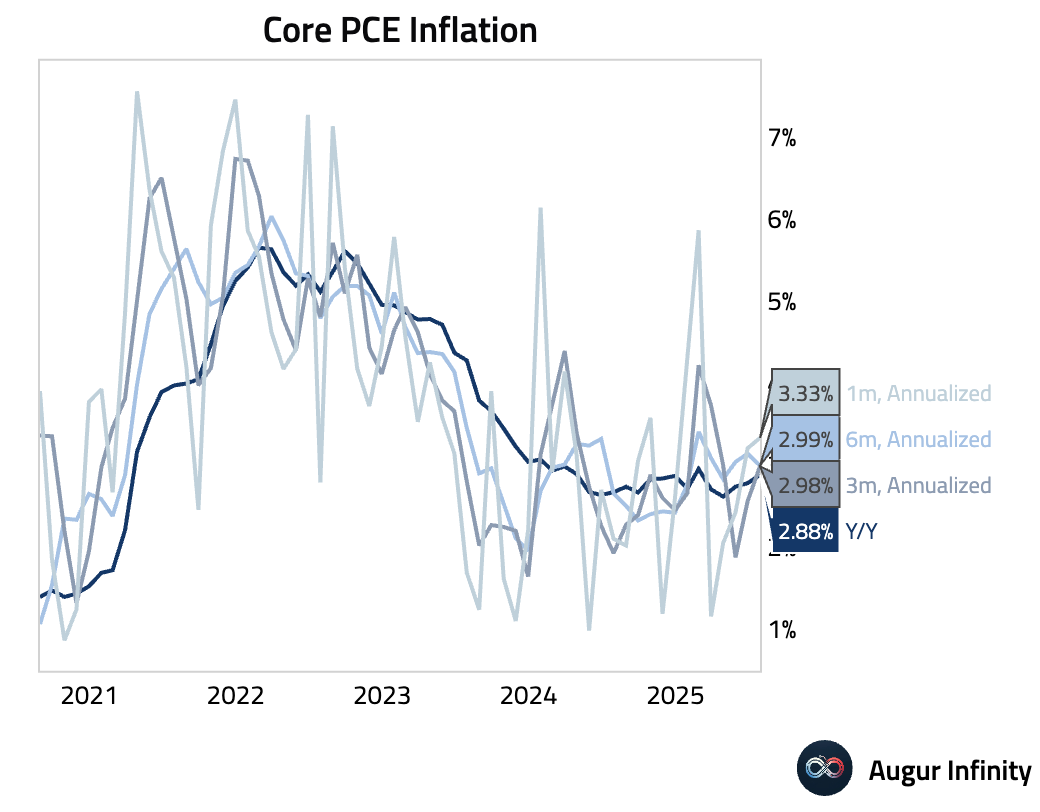

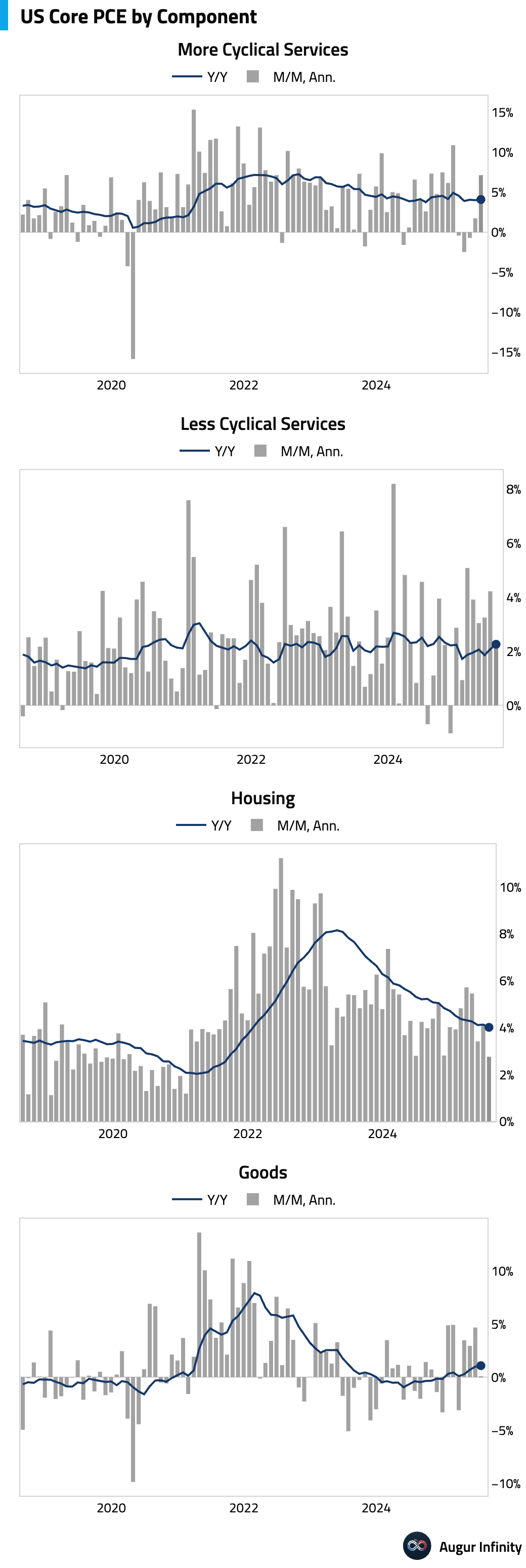

- The Core PCE inflation was in line with consensus in July, rising 0.3% M/M and 2.9% Y/Y, an acceleration from the prior month’s 2.8% pace. The headline PCE inflation also matched consensus, rising 0.2% M/M while holding steady at 2.6% Y/Y. The increase in core was driven by core services (particularly more cyclical services), as goods prices were flat.

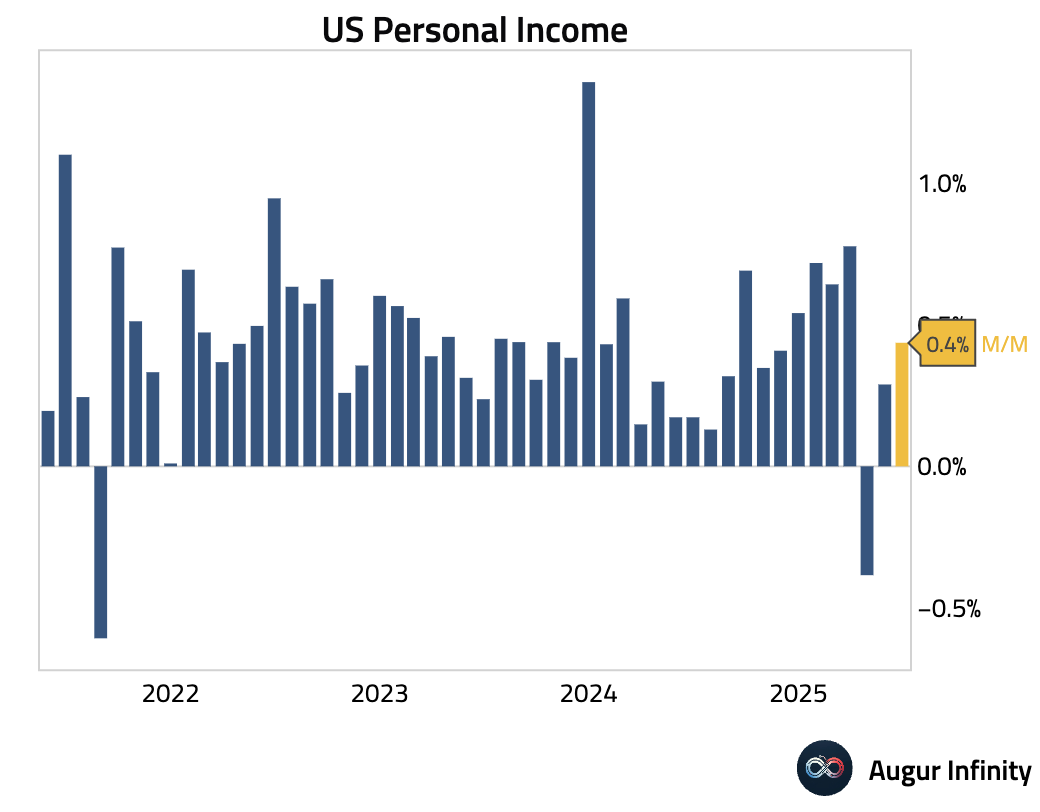

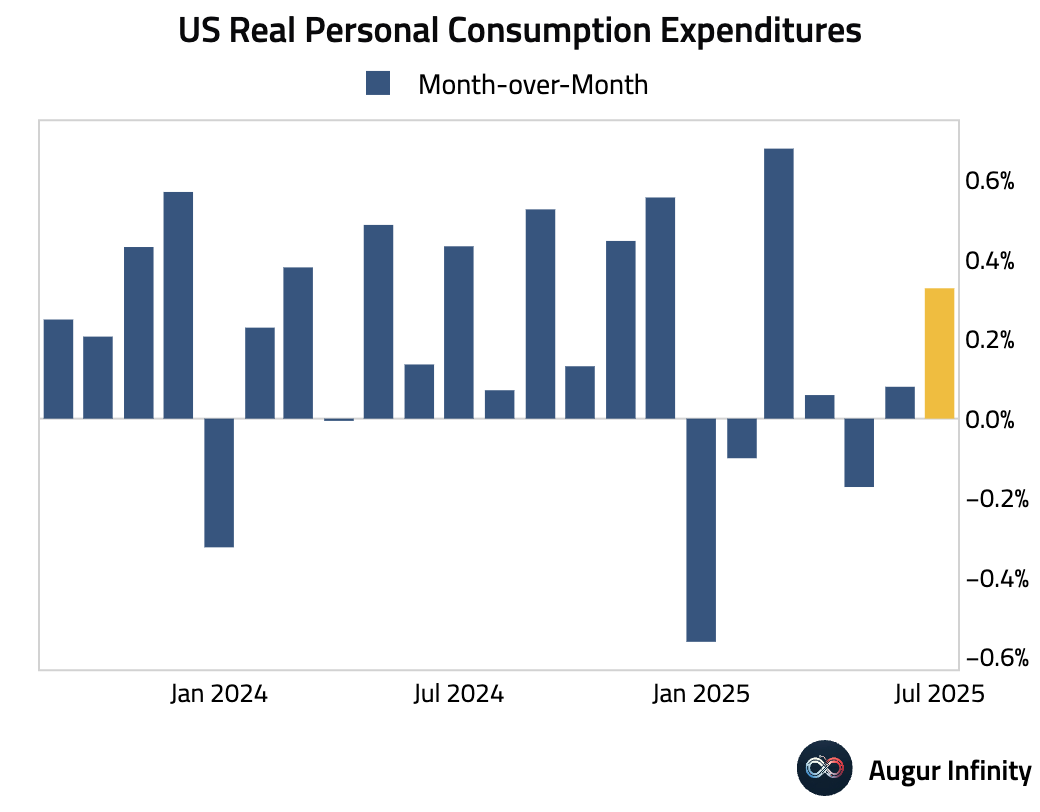

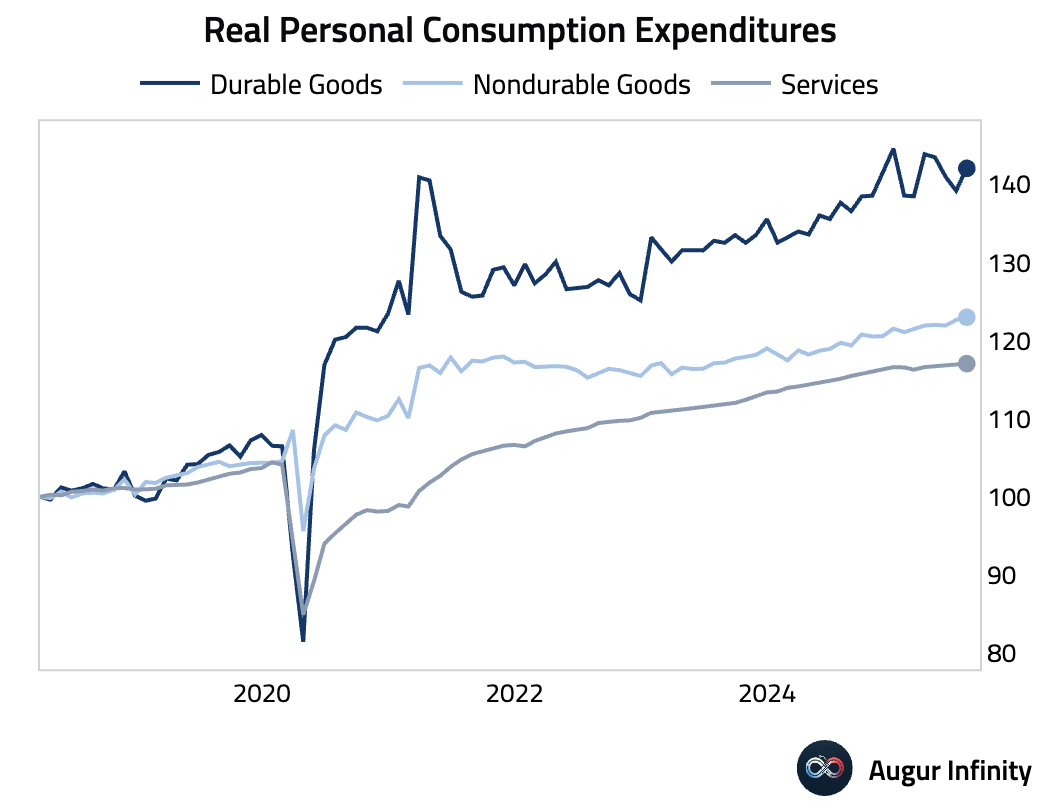

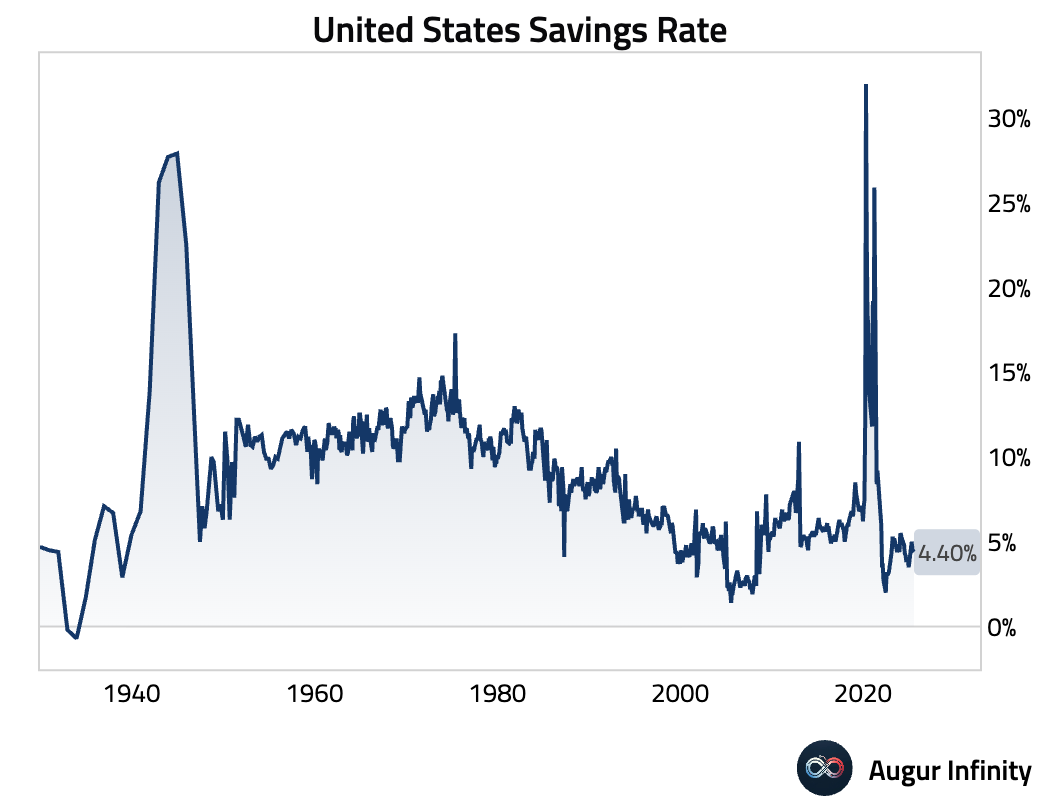

- July personal income and spending both met consensus, rising 0.4% M/M and 0.5% M/M, respectively. The increase in spending was led by a solid 0.9% rise in real goods consumption. The personal saving rate was unchanged but was revised down to 4.4%, suggesting a slightly weaker consumer savings buffer than previously reported.

- The advance goods trade deficit for July widened dramatically to -$103.6 billion, significantly exceeding the -$89.5 billion consensus. The blowout was driven by a surge in imports (+$18.6 billion), particularly in industrial supplies, likely due to companies frontloading imports ahead of new tariffs set to take effect in August.

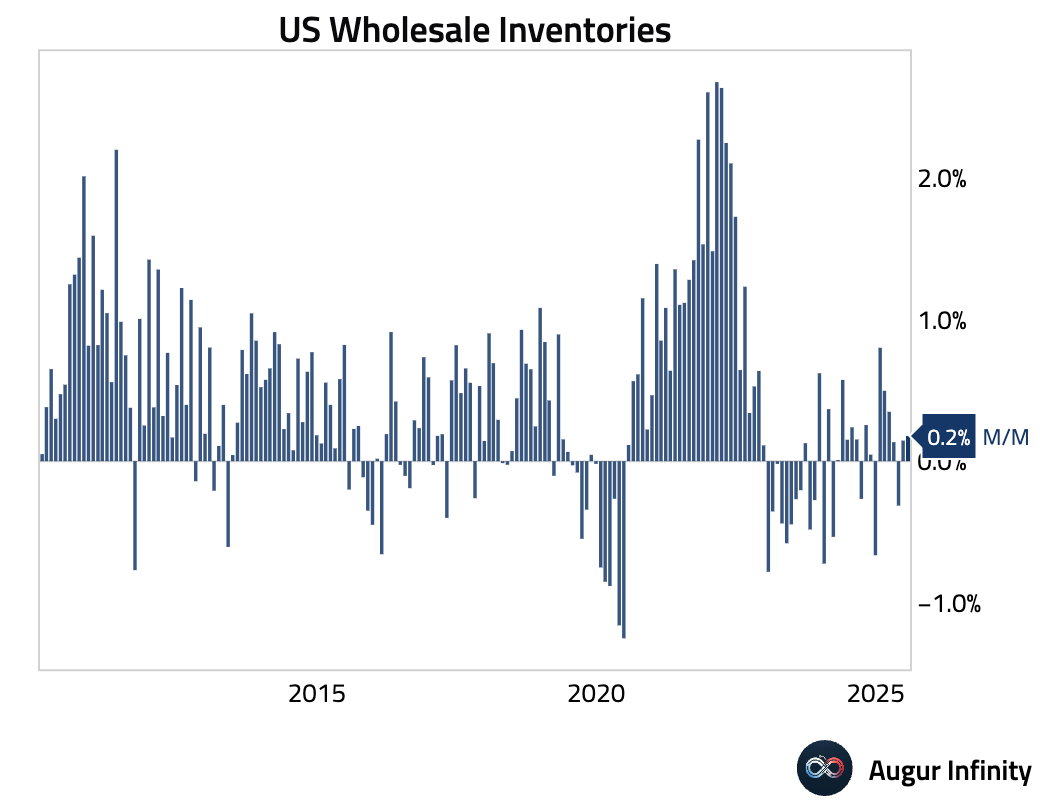

- Advance wholesale inventories rose 0.2% M/M in July, in line with consensus and accelerating from a 0.1% gain in June.

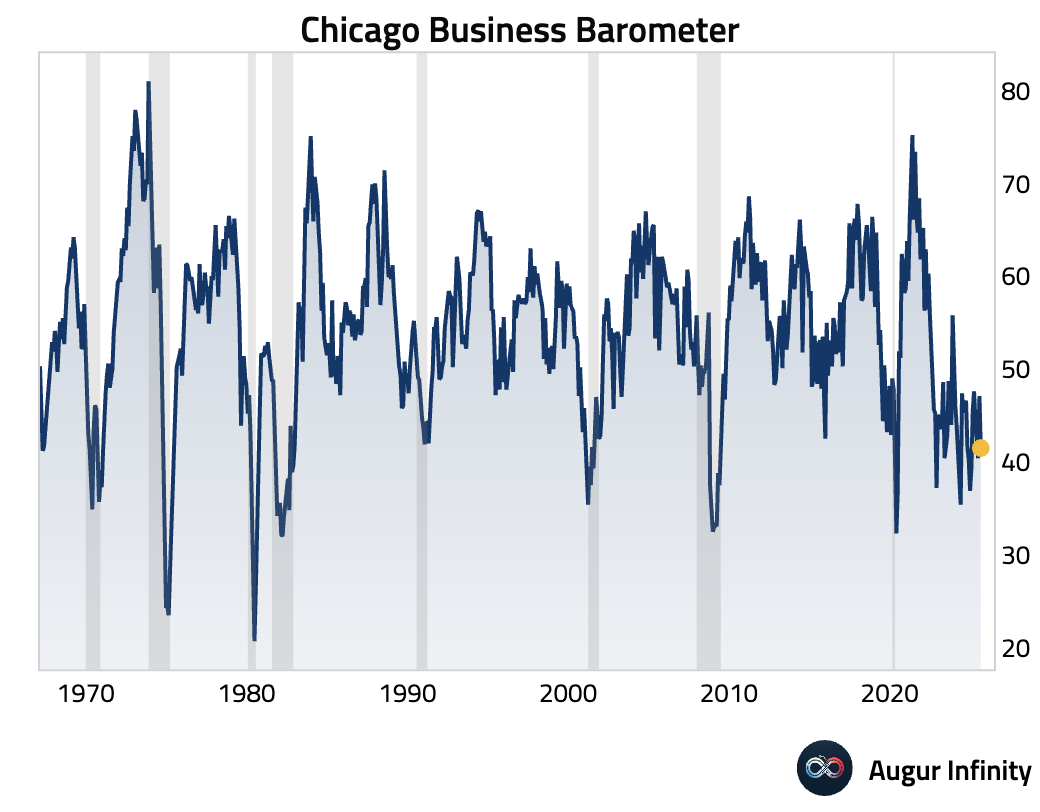

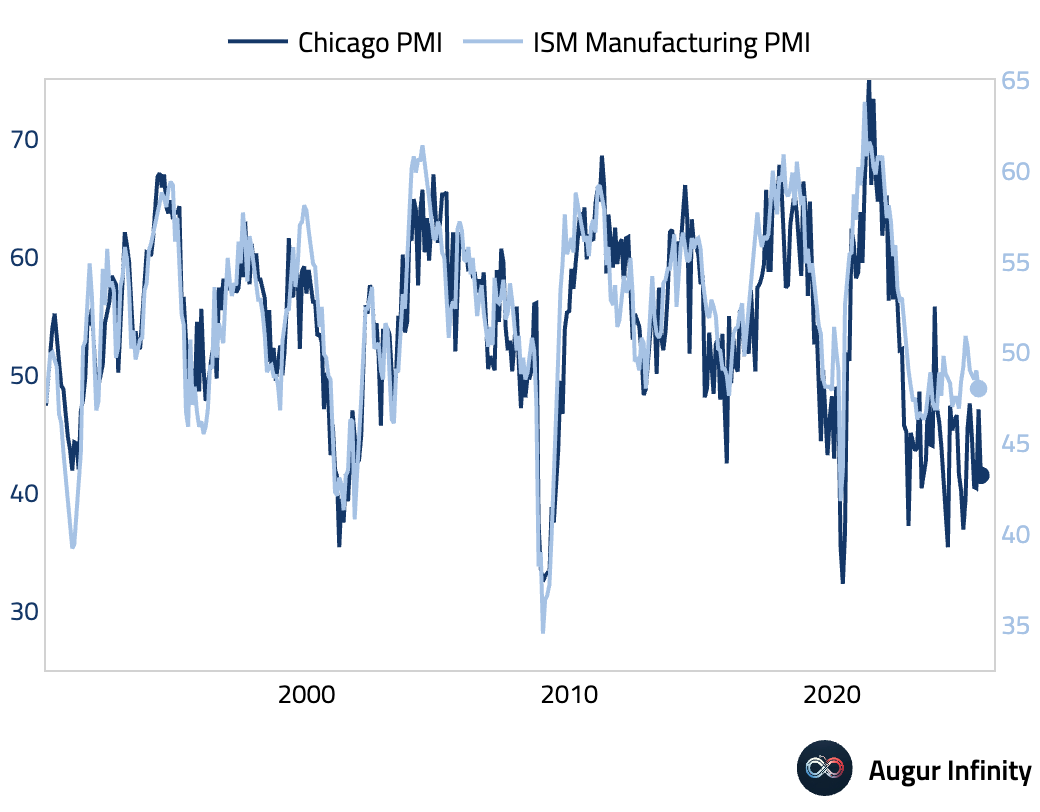

- The Chicago PMI unexpectedly fell to 41.5 in August from 47.1, significantly missing the consensus of 46.0. The reading indicates a deepening contraction in regional business activity.

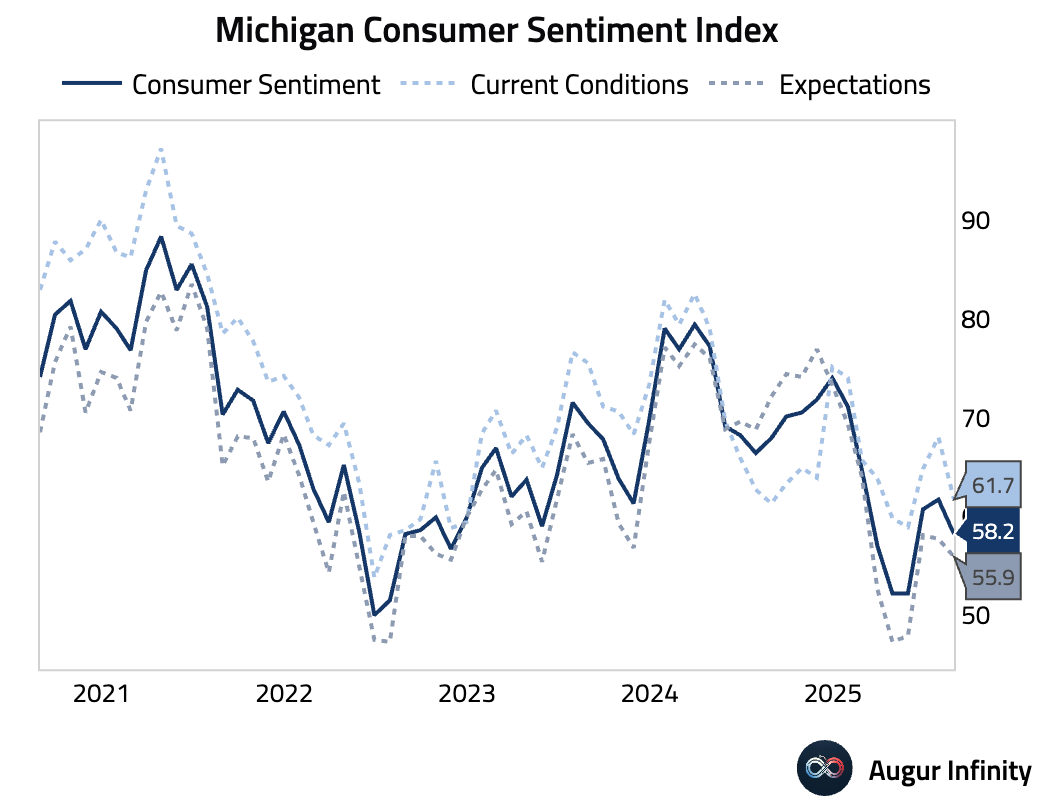

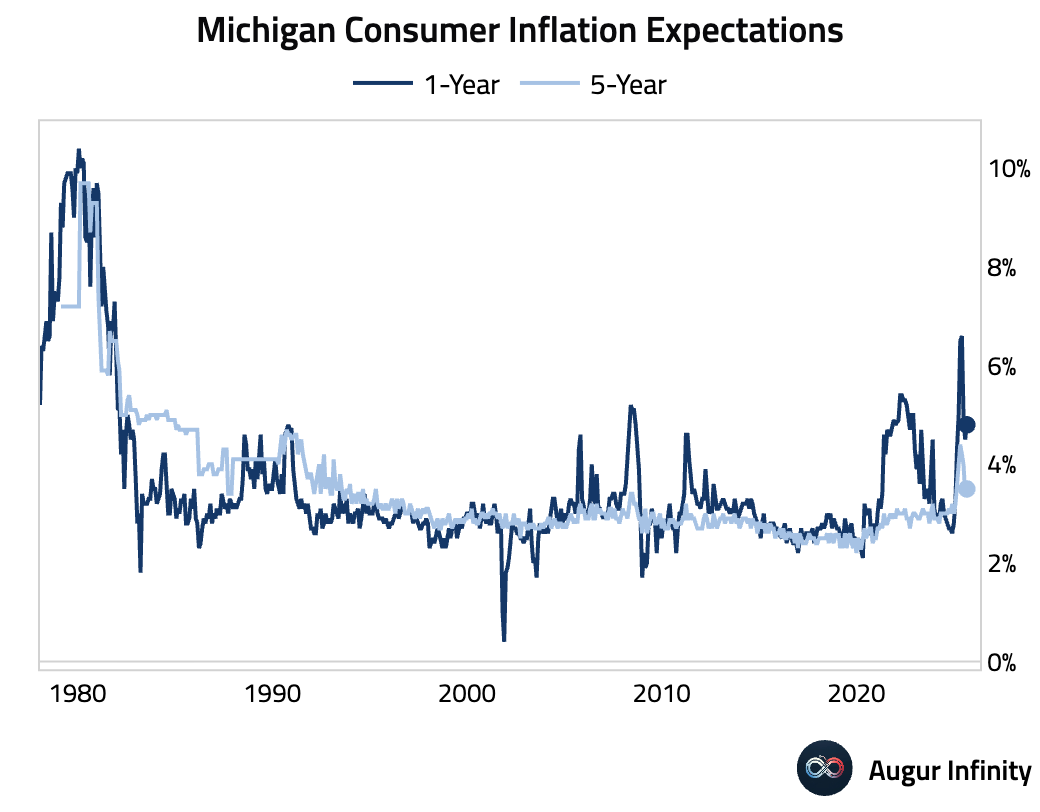

- The final Michigan Consumer Sentiment for August was revised down from 58.6 to 58.2, driven by a sharp downward revision in Consumer Expectations (from 57.2 to 55.9). Current Conditions were revised up from 60.9 to 61.7. Year-ahead inflation expectations ticked up to 4.8% from 4.5% in July (revised down from 4.9%), while the 5-year outlook rose to 3.5% from 3.4% (revised down from 3.9%).

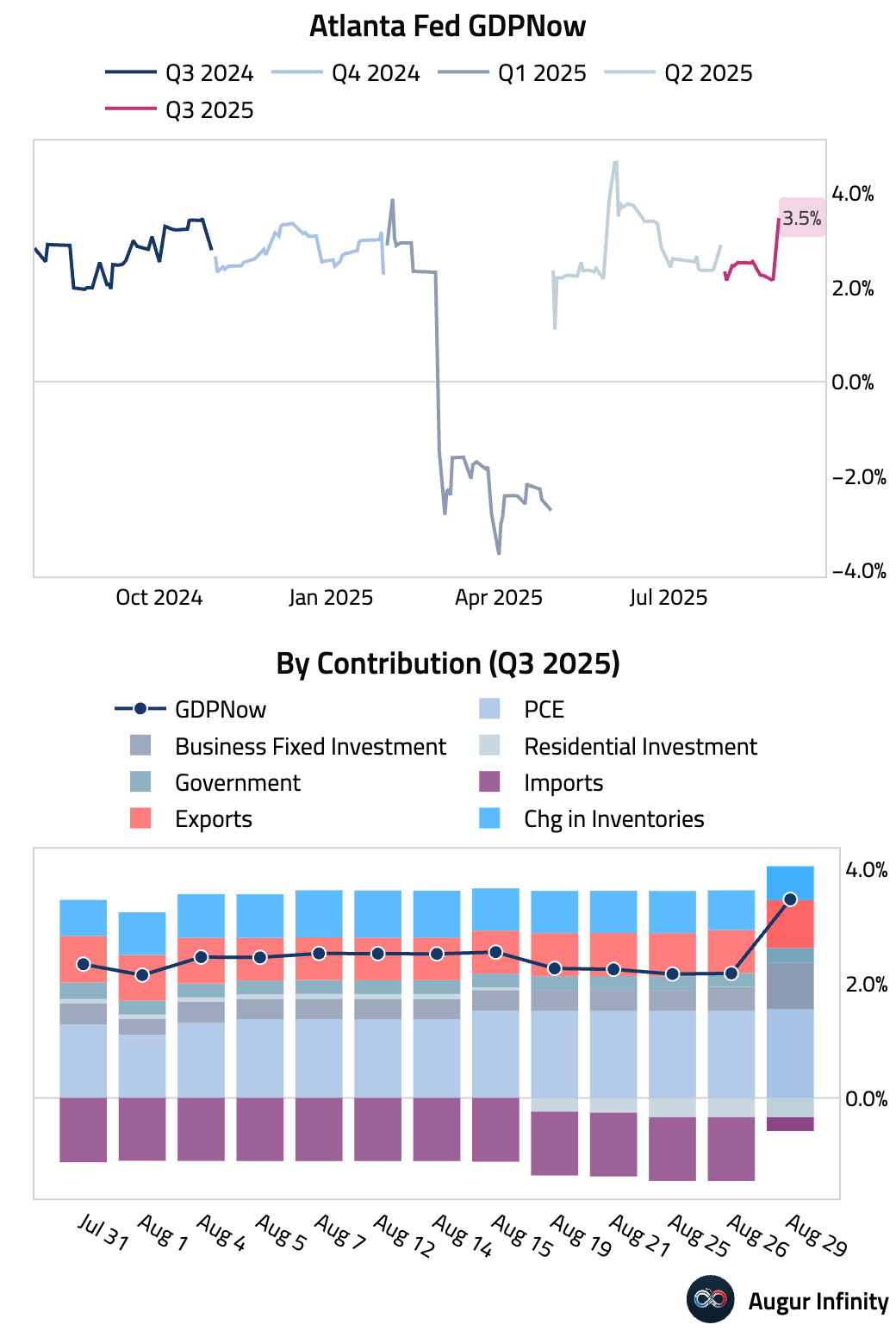

- Incorporating today's data flows, the Atlanta Fed GDPNow model is now tracking Q3 GDP at 3.5%, up sharply from 2.2% on August 26.

Canada

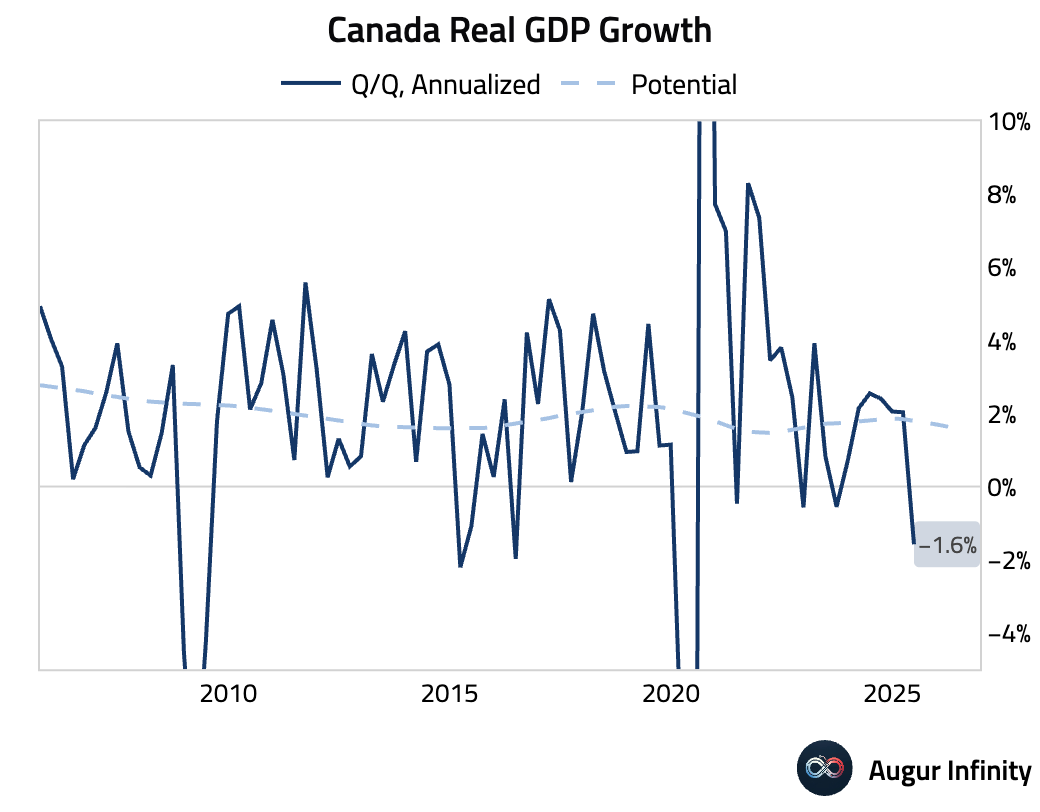

- Canada’s economy contracted in the second quarter, with real GDP falling 0.4% Q/Q (-1.6% annualized), significantly missing the consensus for a 0.6% annualized decline. This marks the weakest performance since the second quarter of 2020.

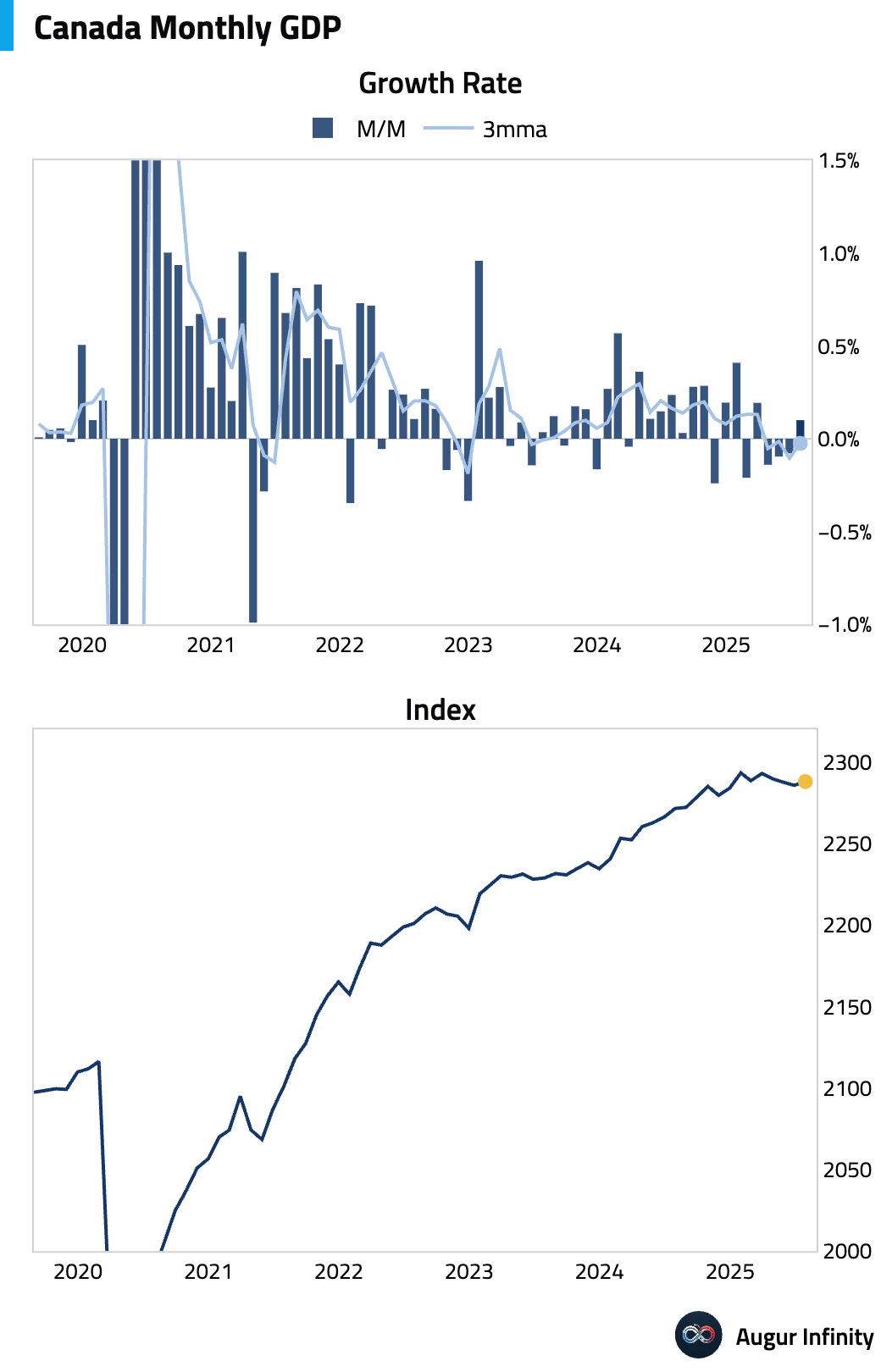

- Monthly GDP for June fell 0.1% M/M, missing expectations for a 0.1% increase. The preliminary estimate for July indicates a rebound of 0.1%.

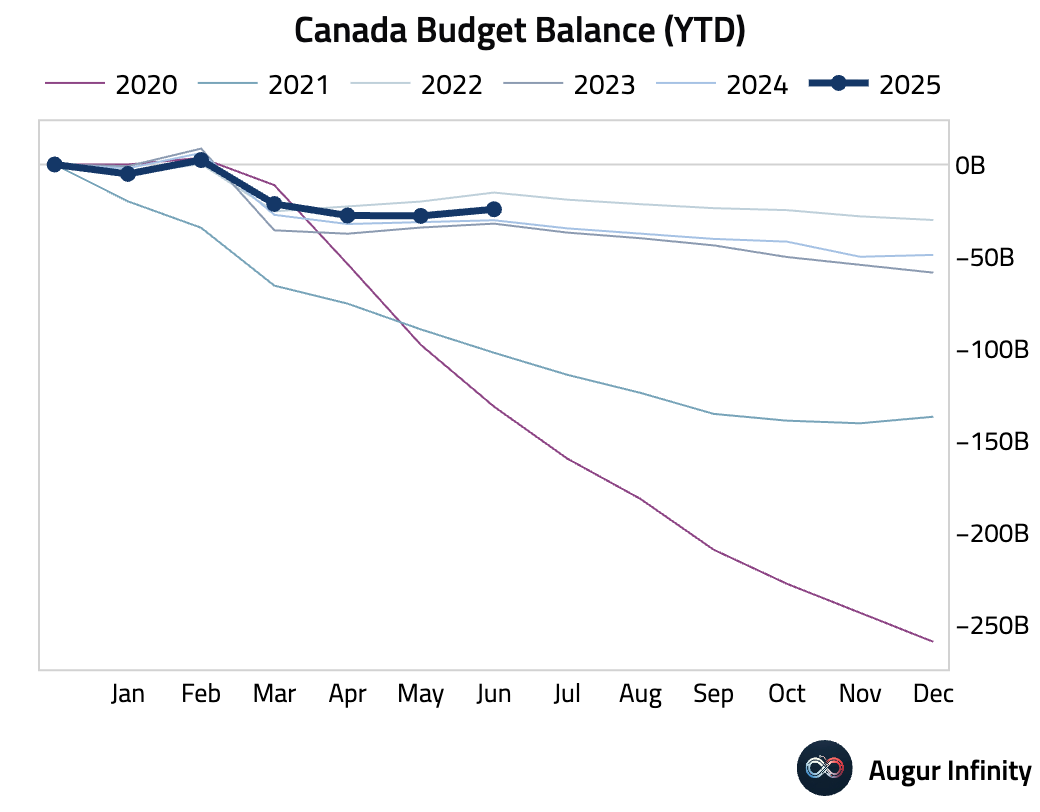

- The federal government posted a budget surplus of C$3.63 billion in June.

Europe

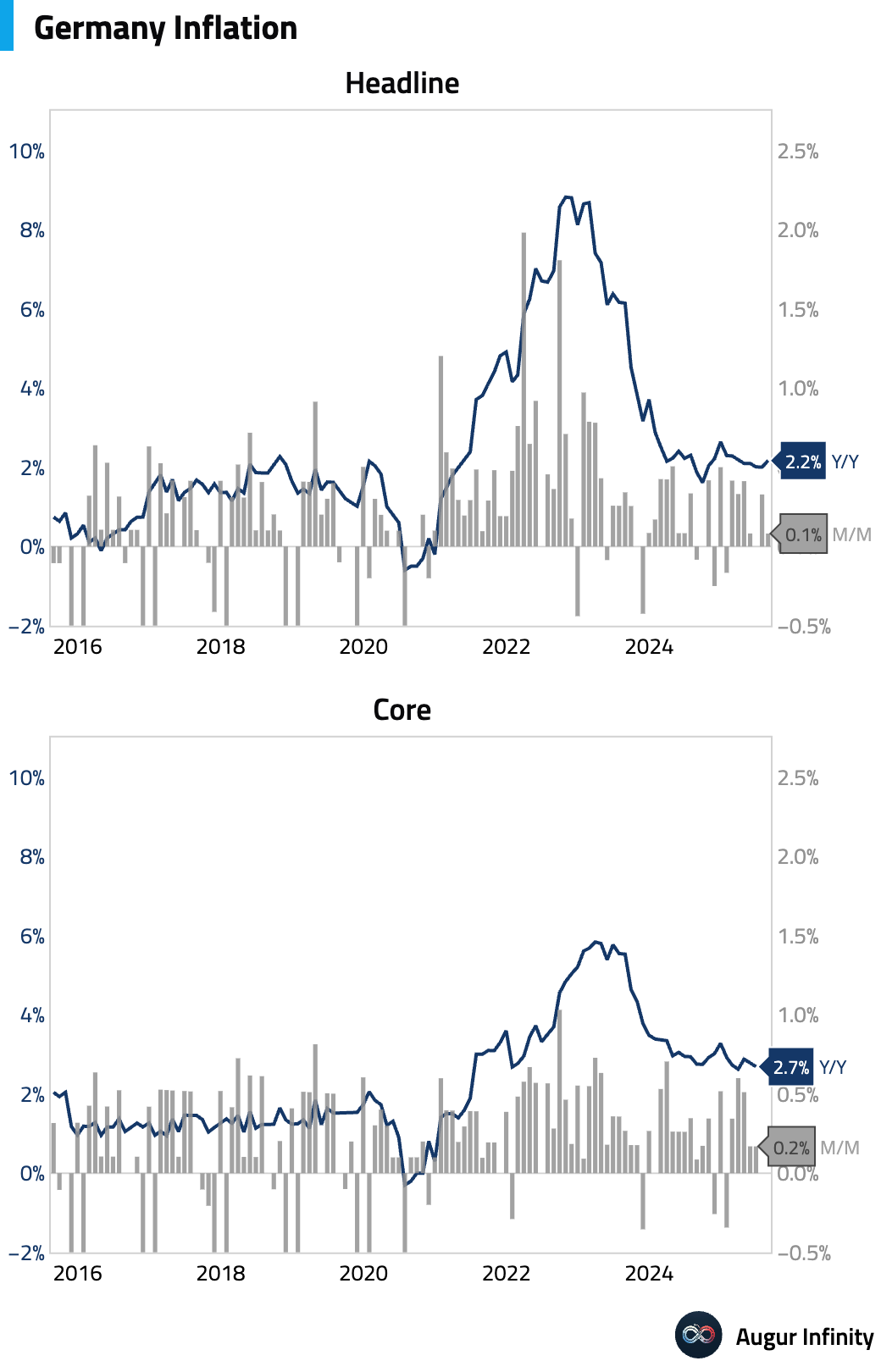

- Germany’s preliminary inflation rate for August accelerated to 2.2% Y/Y, slightly above the 2.1% consensus. The harmonized rate (HICP) also beat expectations at 2.1% Y/Y versus a 2.0% forecast. The higher-than-expected headline was driven by energy prices falling less sharply than in the prior month. However, the underlying picture appears softer, with sequential core inflation slowing.

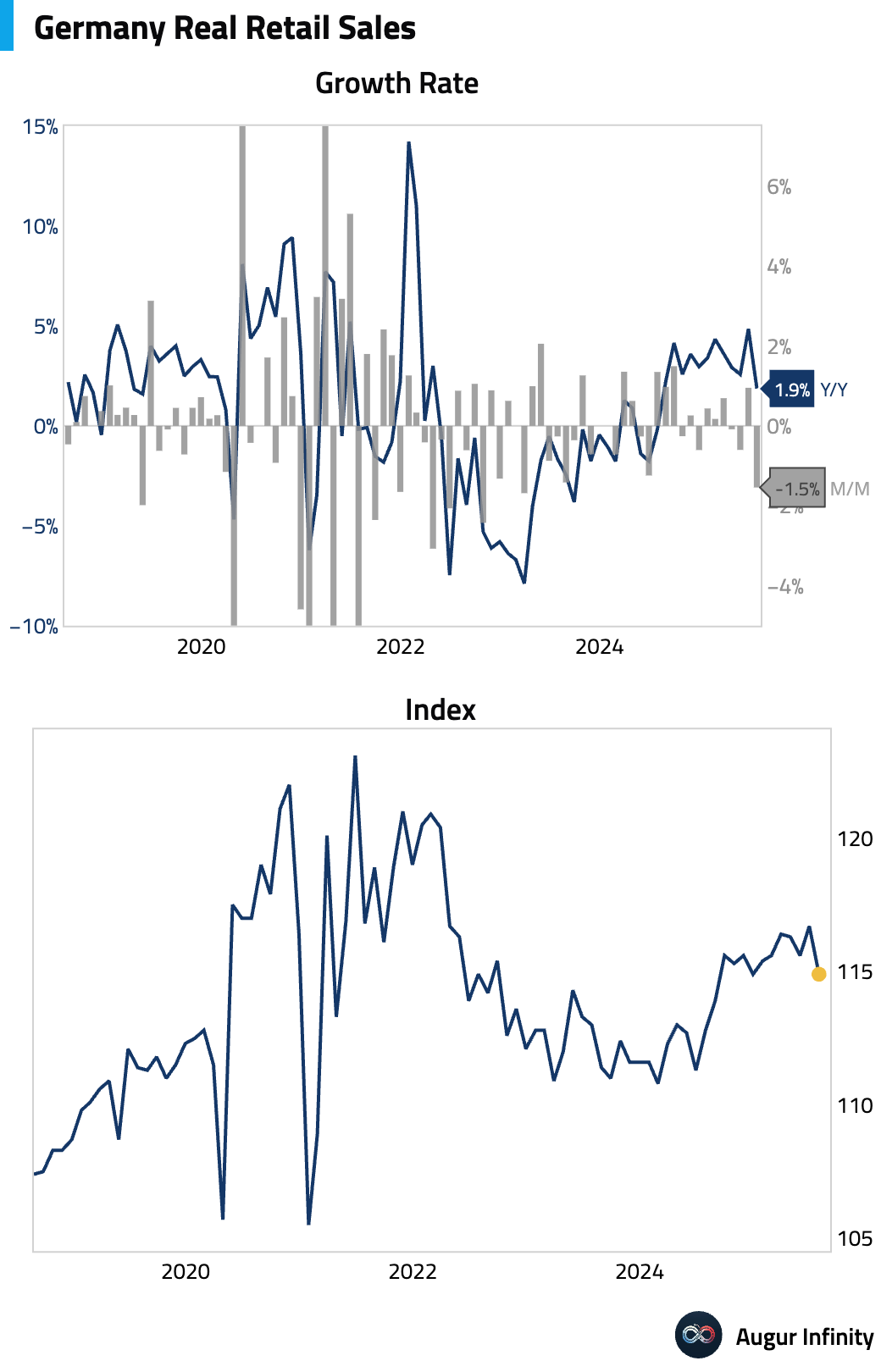

- German retail sales fell 1.5% M/M in July, a much steeper decline than the -0.4% consensus forecast and the weakest reading since March 2023. The year-over-year figure also missed expectations, rising 1.9% against a 2.6% forecast.

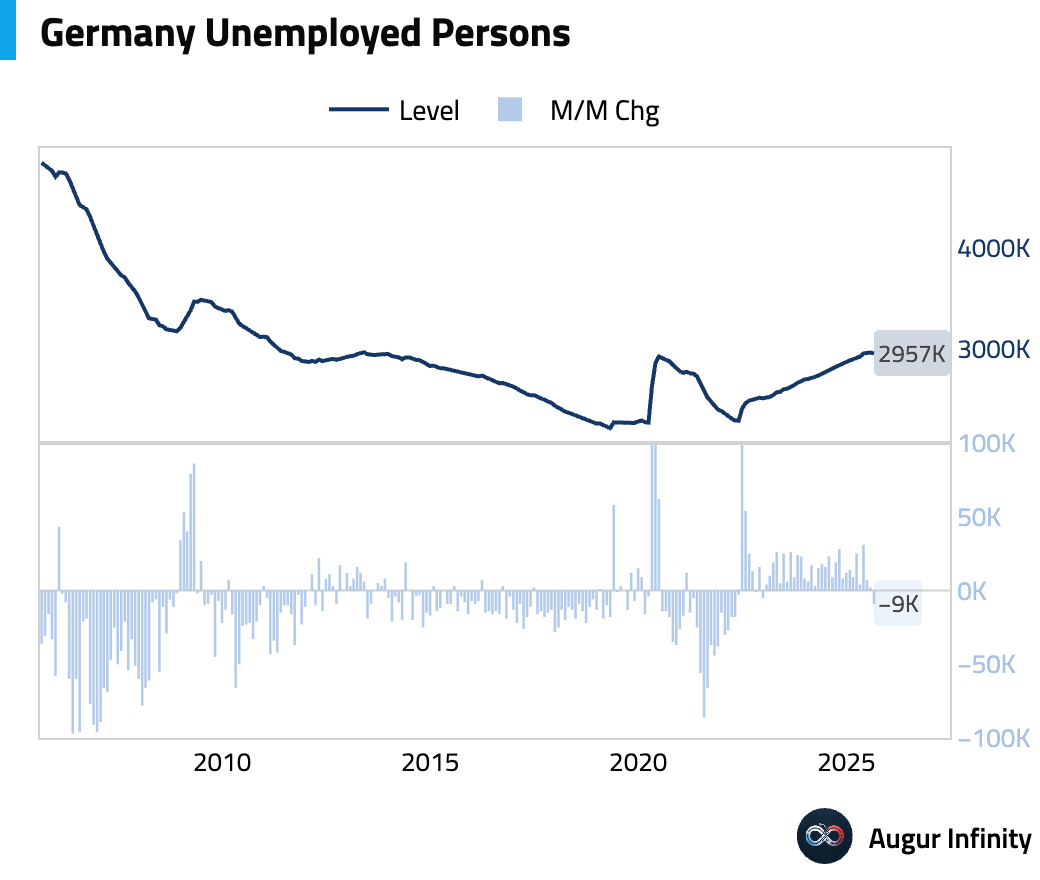

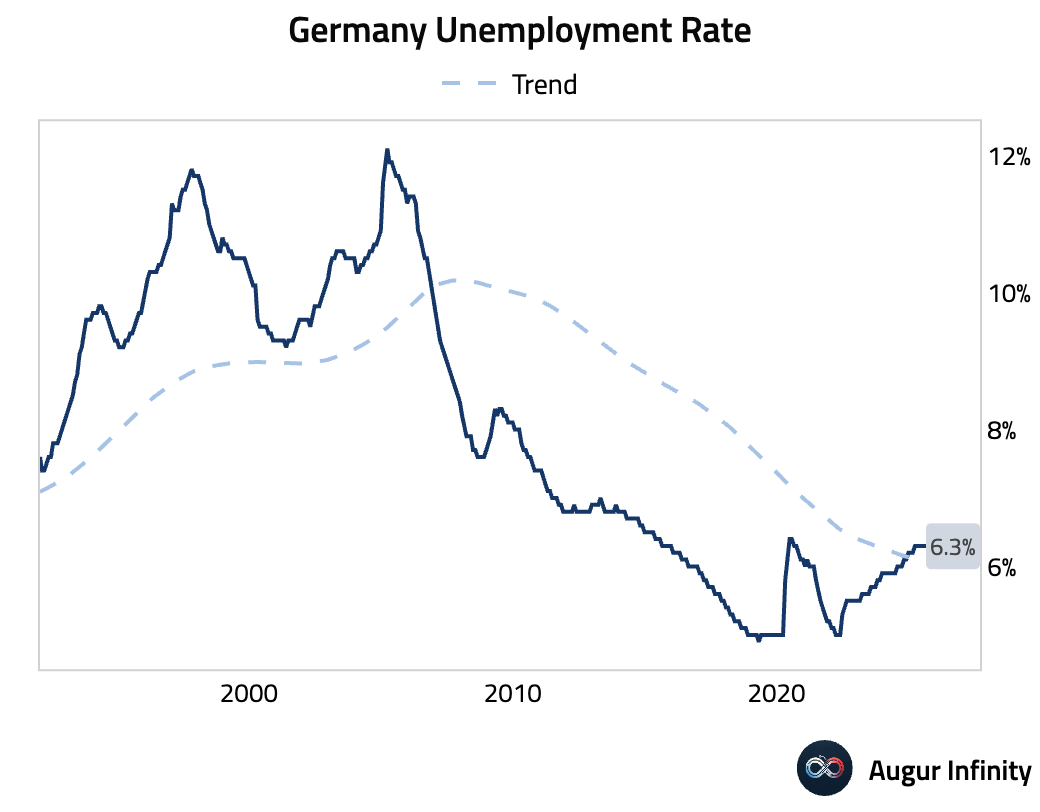

- The German labor market showed unexpected strength in August, with unemployment falling by 9,000, defying consensus expectations for a 10,000 increase. The seasonally adjusted unemployment rate held steady at 6.3%, as expected.

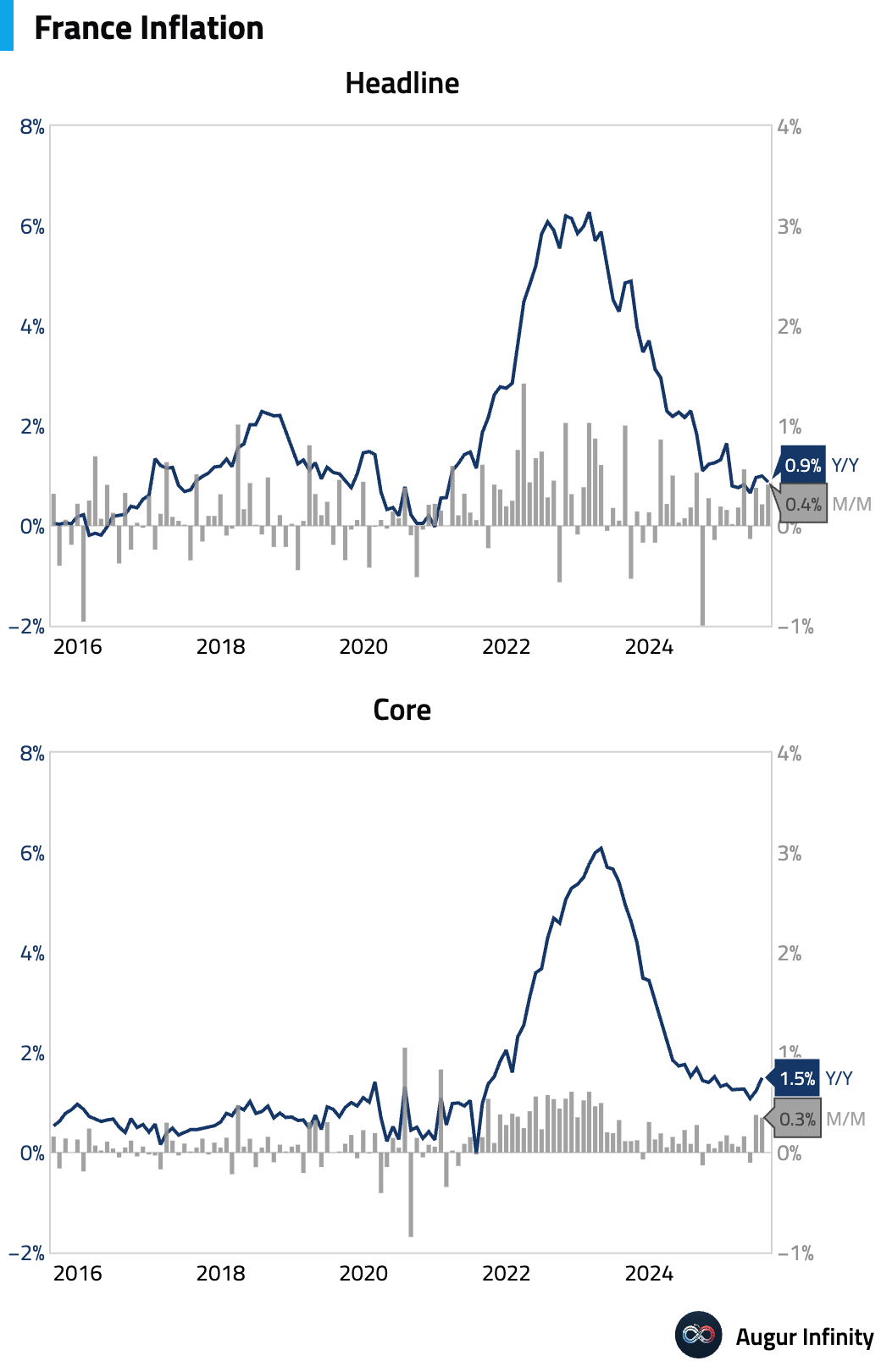

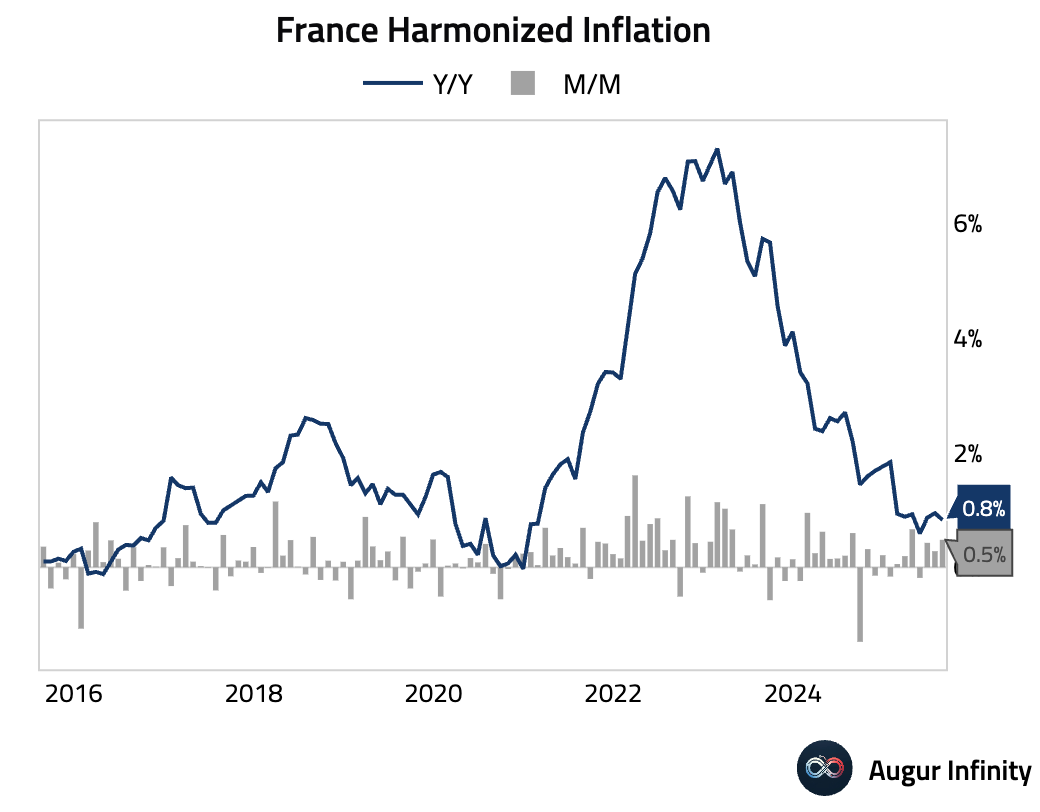

- France’s preliminary inflation rate eased to 0.9% Y/Y in August, below the 1.0% consensus. The harmonized rate (HICP) also missed forecasts, coming in at 0.8% Y/Y versus 0.9% expected. The slowdown was primarily driven by lower services inflation, especially in transport.

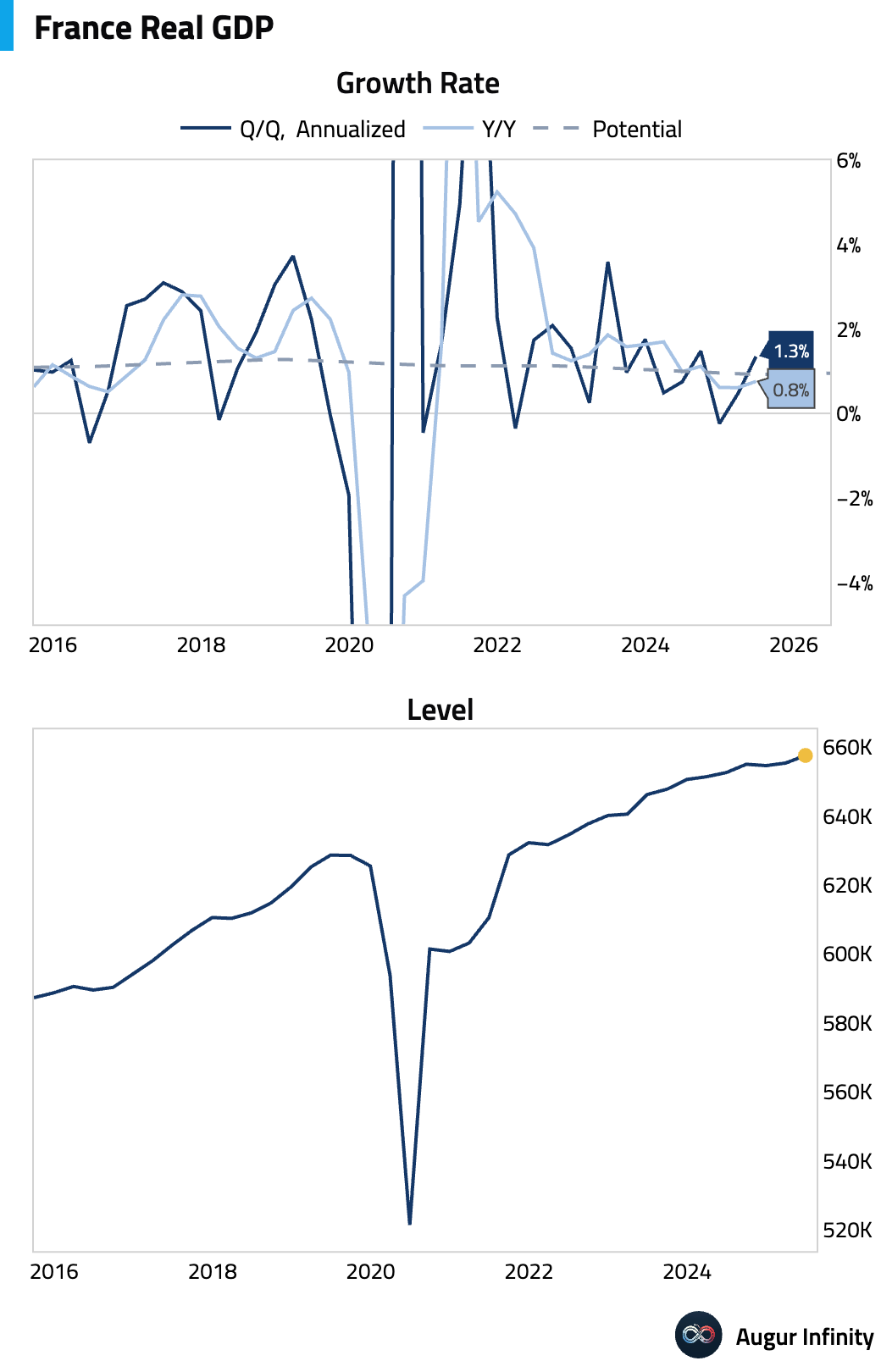

- Final Q2 GDP for France was confirmed at +0.3% Q/Q (or 1.3% annualized) and +0.8% Y/Y, in line with initial estimates.

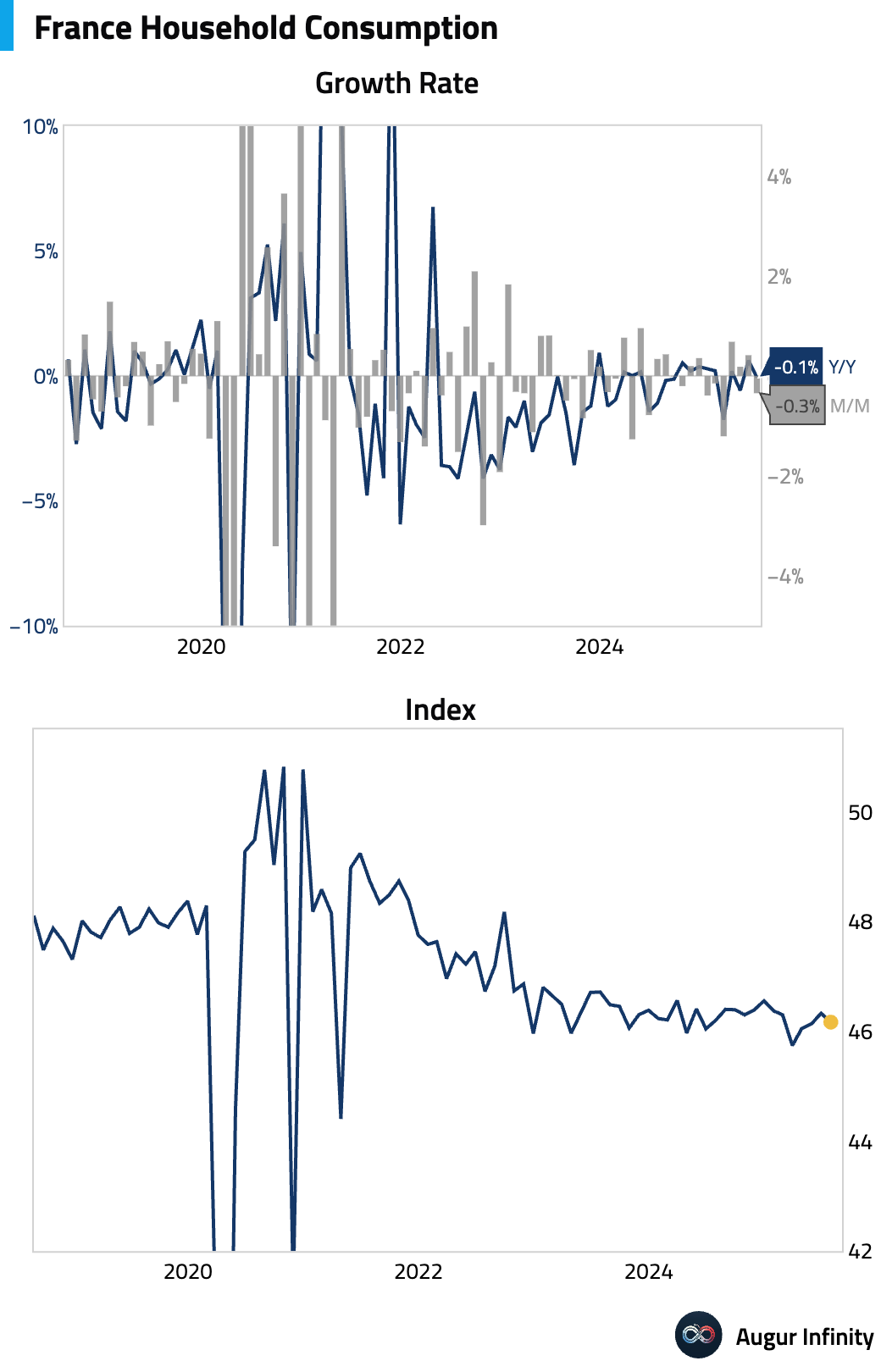

- French household consumption unexpectedly declined by 0.3% M/M in July, missing the consensus of -0.2%.

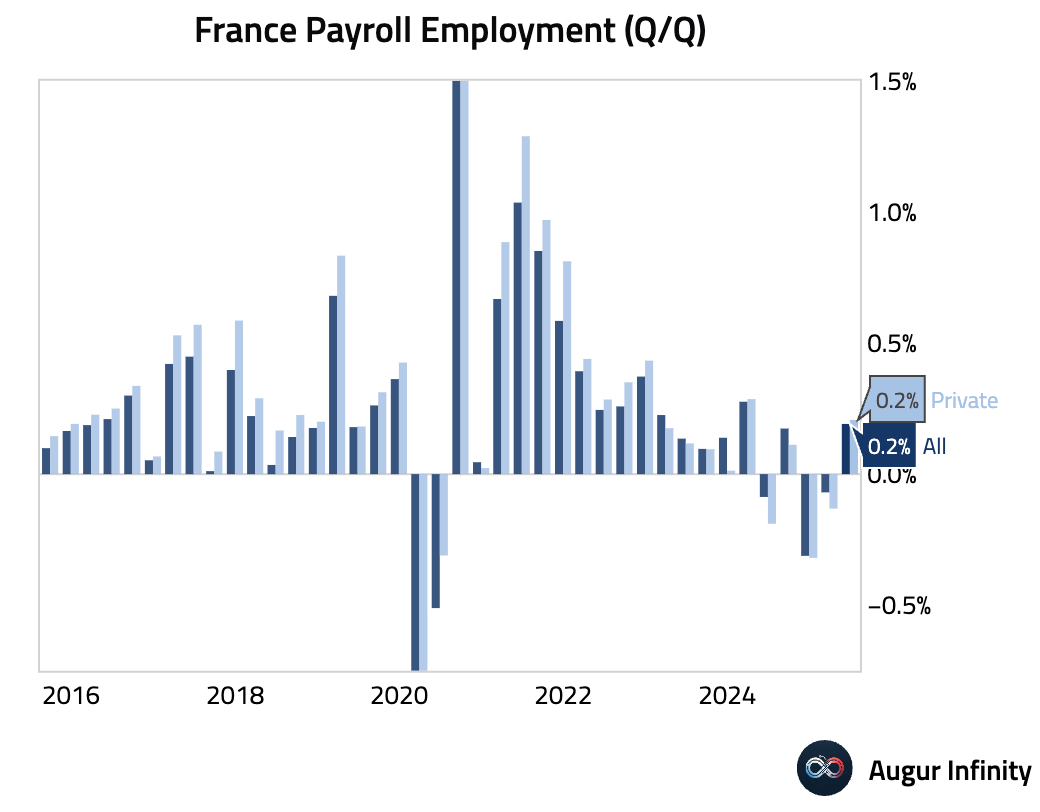

- French non-farm payrolls rose 0.2% Q/Q in Q2, beating expectations of a flat reading.

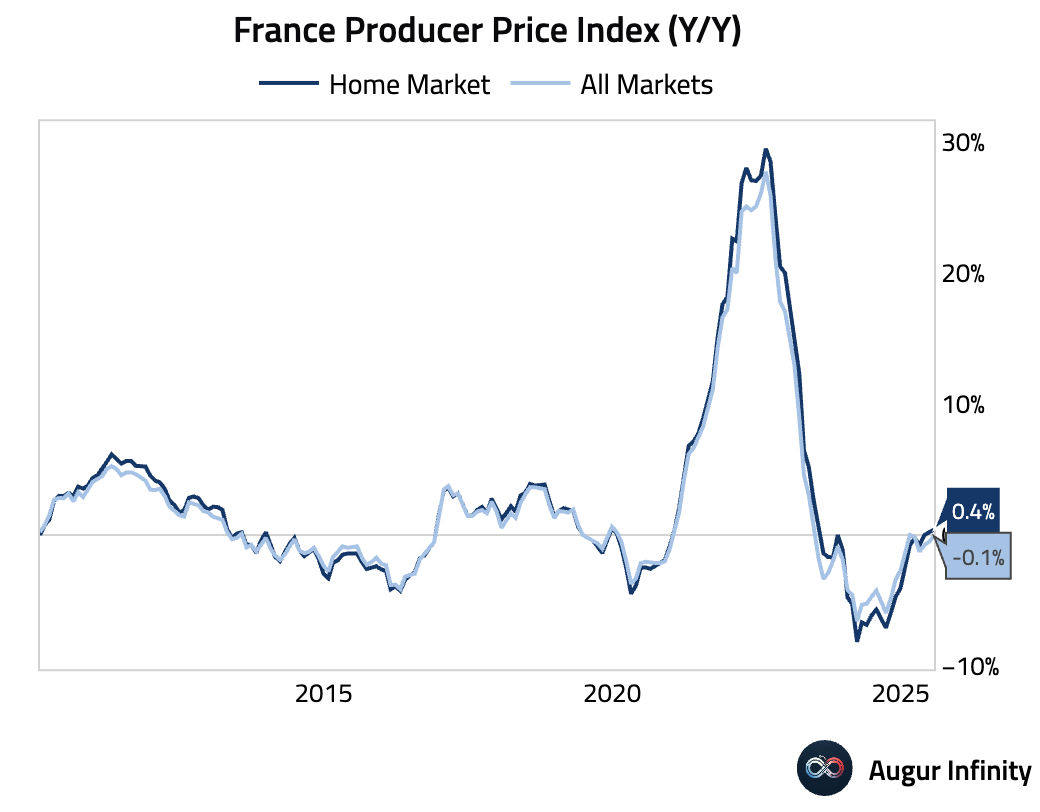

- Producer prices in France rose 0.4% M/M and 0.4% Y/Y in July.

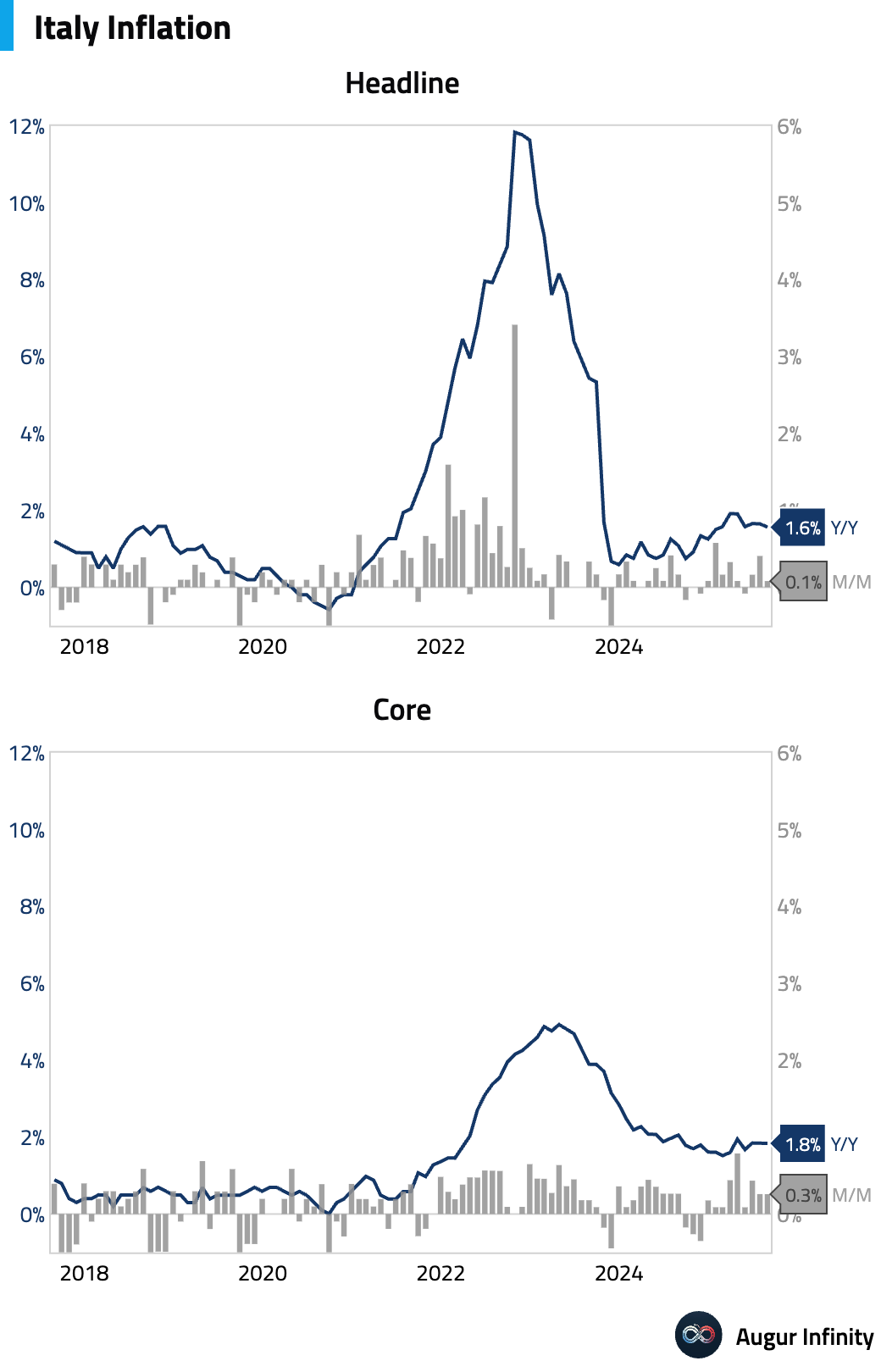

- Italy’s preliminary inflation rate for August eased to 1.6% Y/Y, undershooting the 1.7% consensus. The miss was driven by a larger-than-expected drop in energy inflation and soft core inflation, which showed a notable sequential deceleration, signaling weakening underlying pressures.

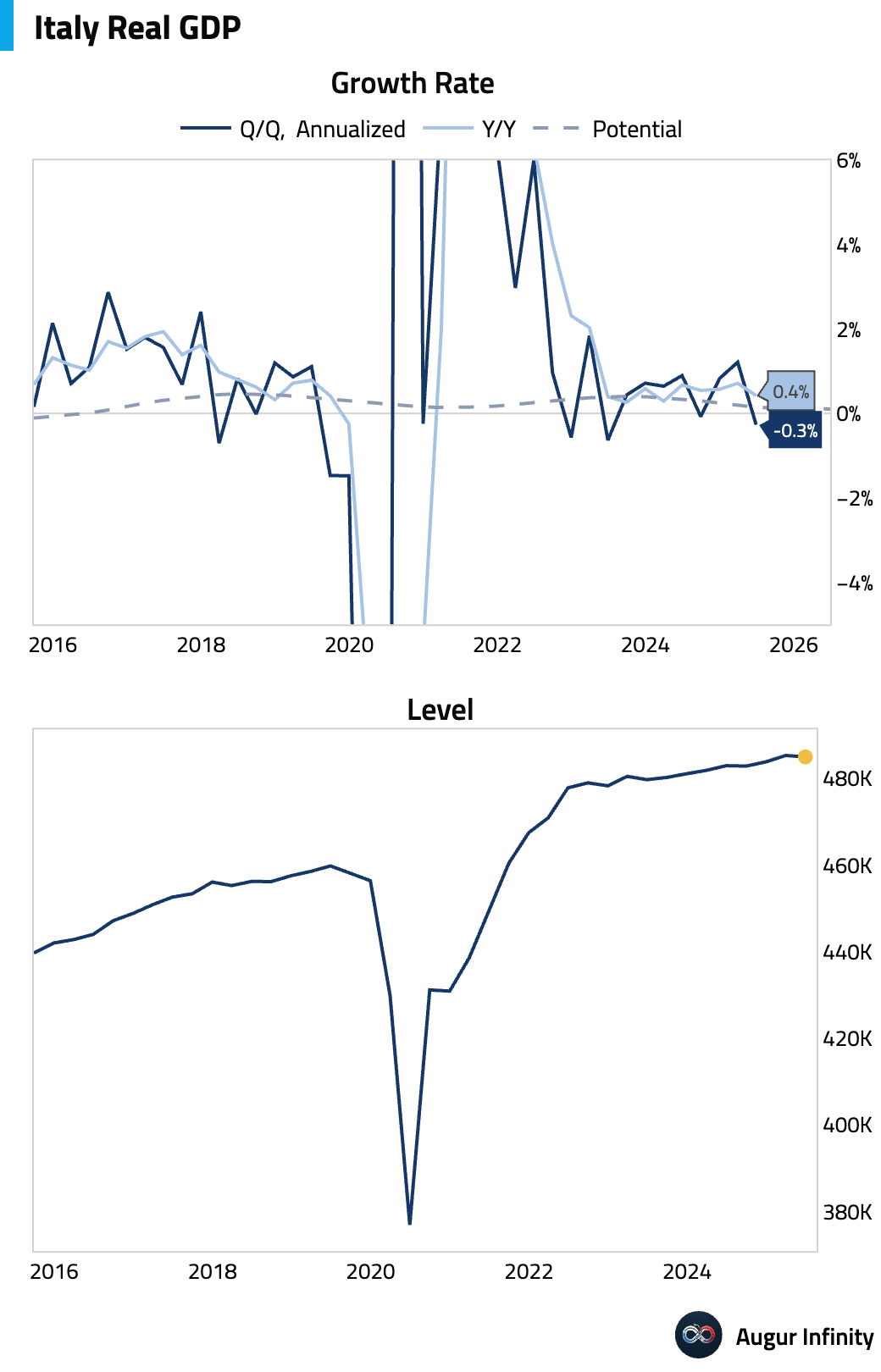

- Italy’s final Q2 GDP growth was confirmed at -0.1% Q/Q (or -0.3% annualized) and +0.4% Y/Y.

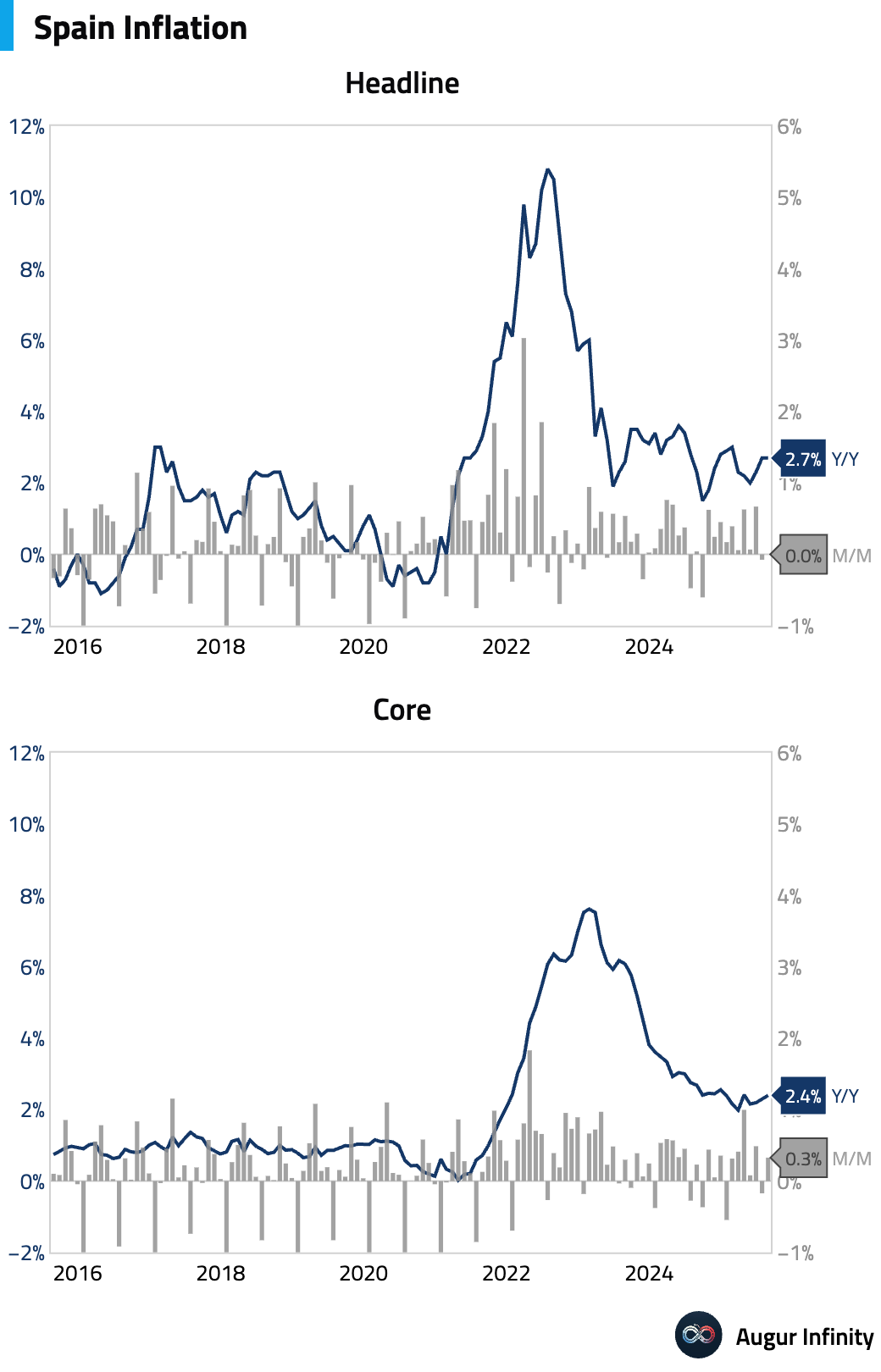

- Spain’s preliminary inflation rate was 2.7% Y/Y in August, slightly below the 2.8% consensus. The main surprise was core CPI, which unexpectedly ticked up to 2.4% Y/Y from 2.3%.

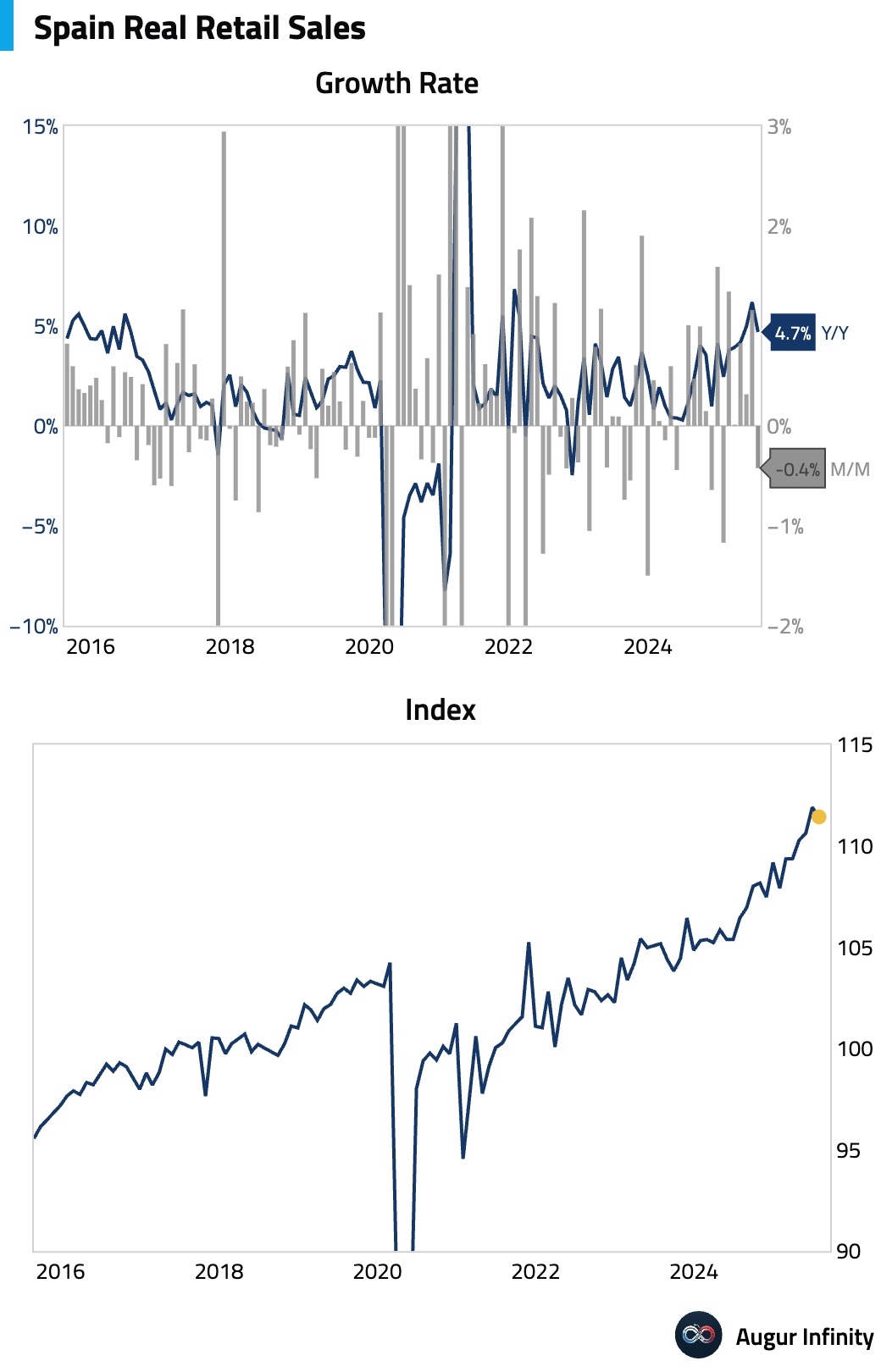

- Spanish retail sales fell 0.4% M/M in July, though the year-over-year rate remained strong at 4.7%.

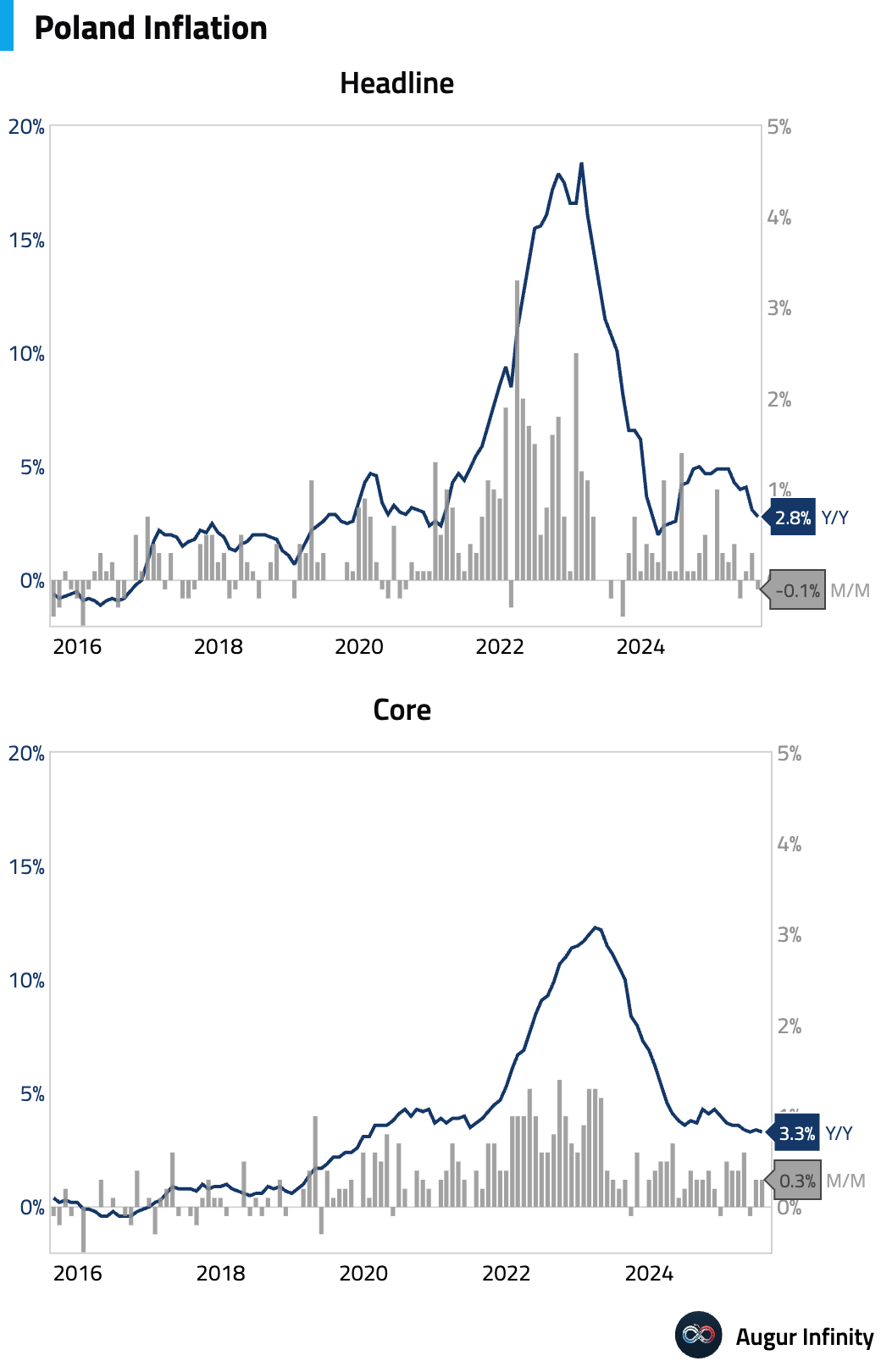

- Poland’s preliminary inflation rate for August fell more than expected to 2.8% Y/Y, below the 2.9% consensus. The decline was driven by increased deflation in transport fuels and a drop in core inflation. This downside surprise solidifies expectations for a National Bank of Poland rate cut next week.

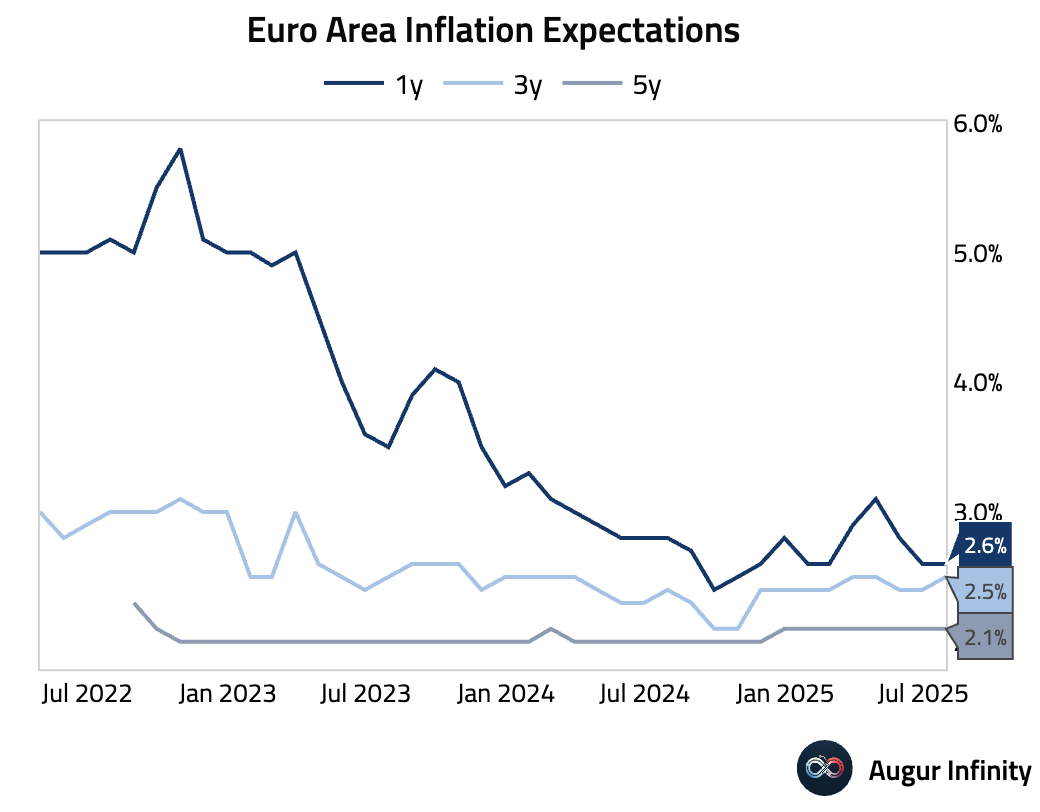

- The Eurozone’s consumer inflation expectations for the next 12 months held steady at 2.6% in July.

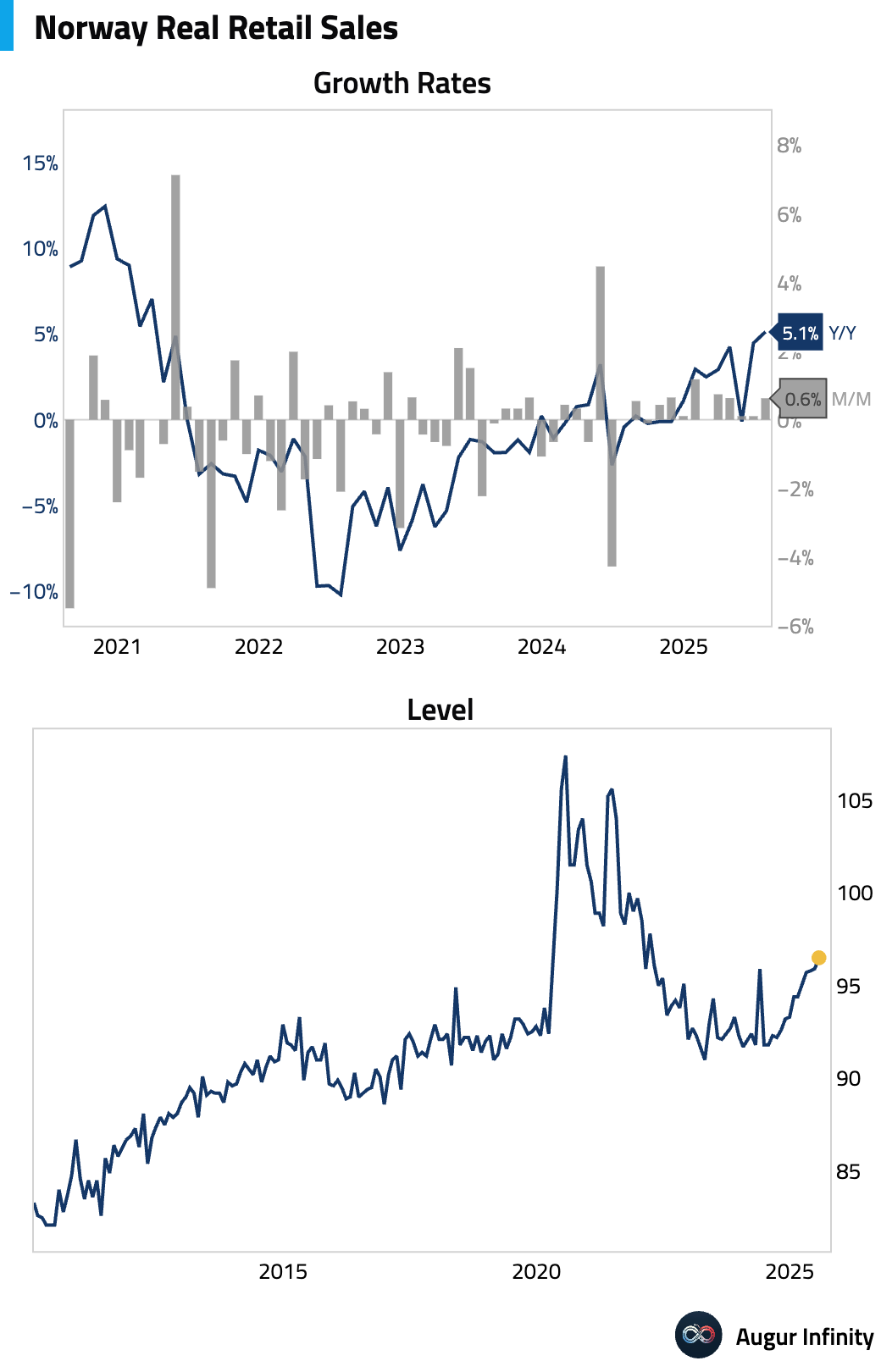

- Norway’s retail sales rose 0.6% M/M in July, accelerating from the prior month’s 0.1% gain.

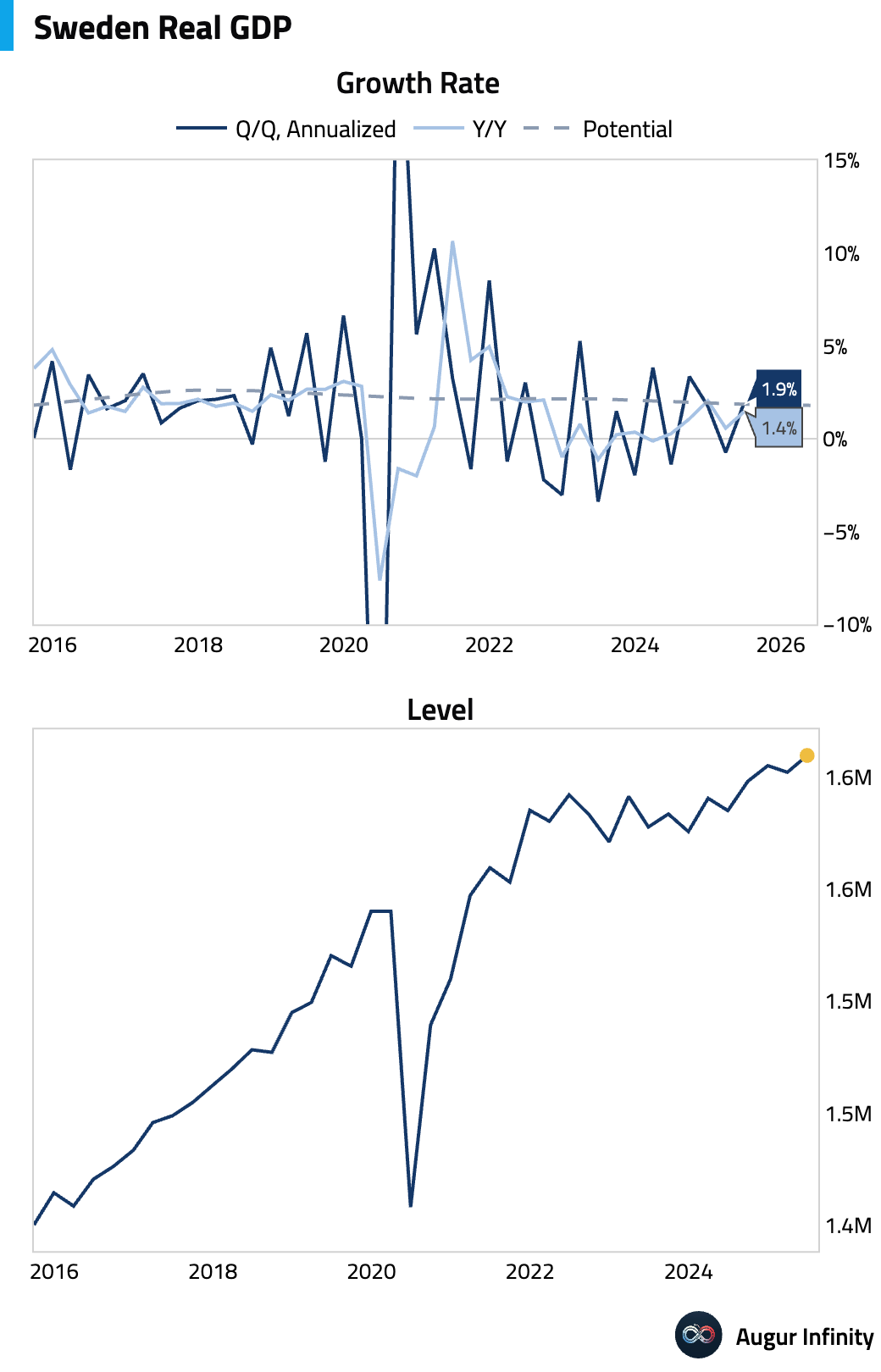

- Sweden’s final Q2 GDP was revised higher to +0.5% Q/Q (or 1.9% annualized) and +1.4% Y/Y.

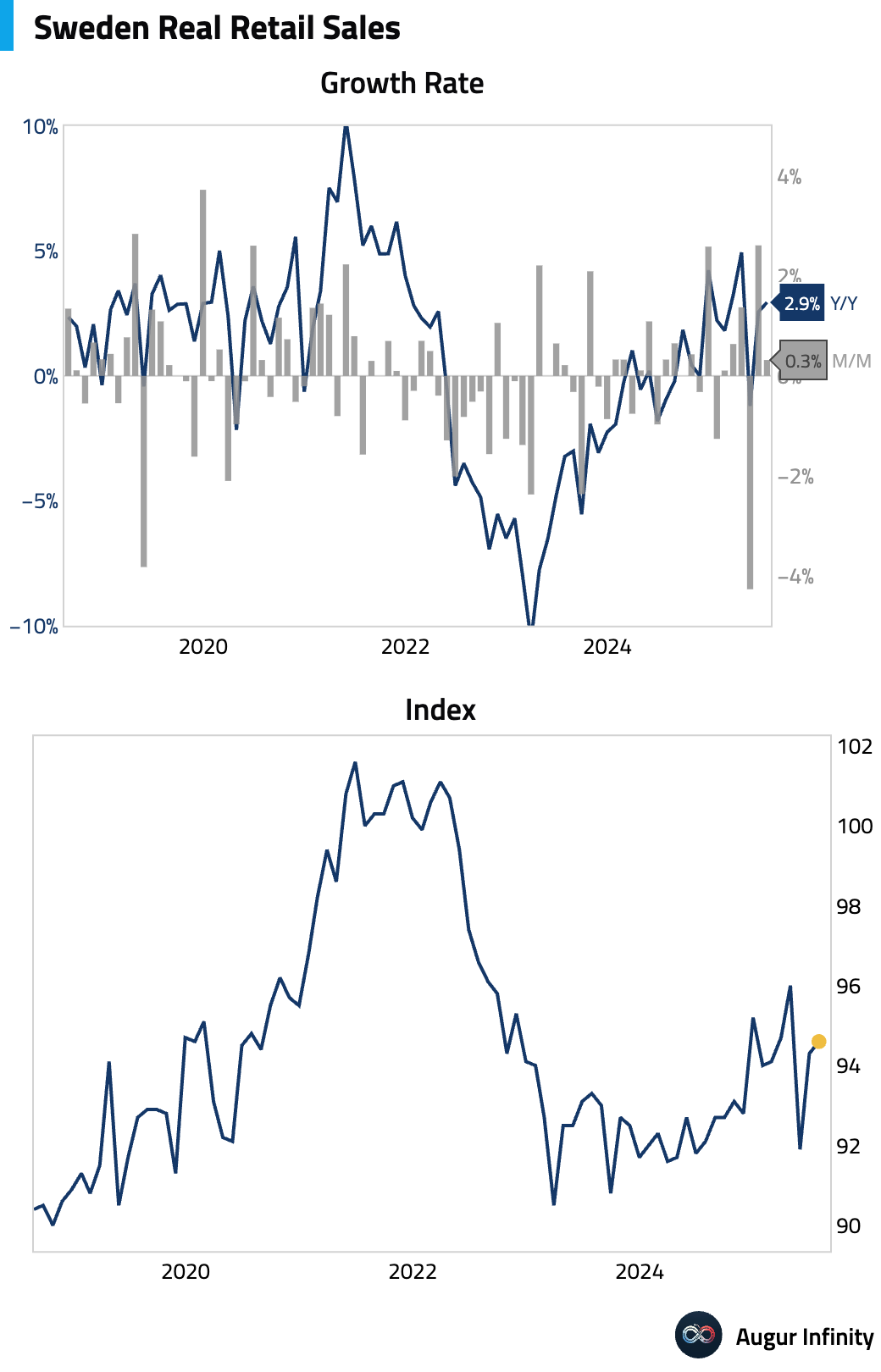

- Swedish retail sales grew 0.3% M/M and 2.9% Y/Y in July.

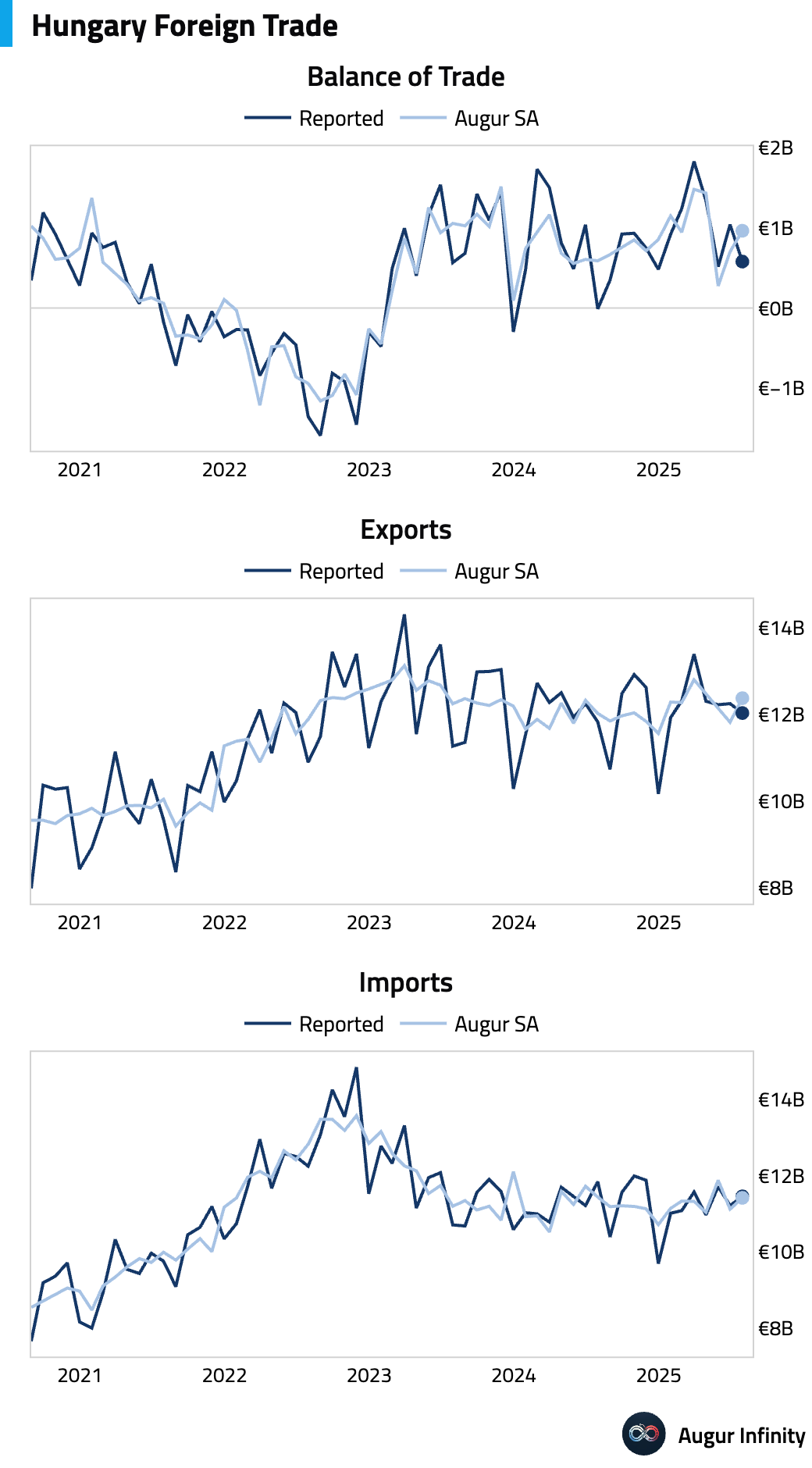

- Hungary’s trade surplus narrowed significantly to €578 million in June, well below the €978 million consensus.

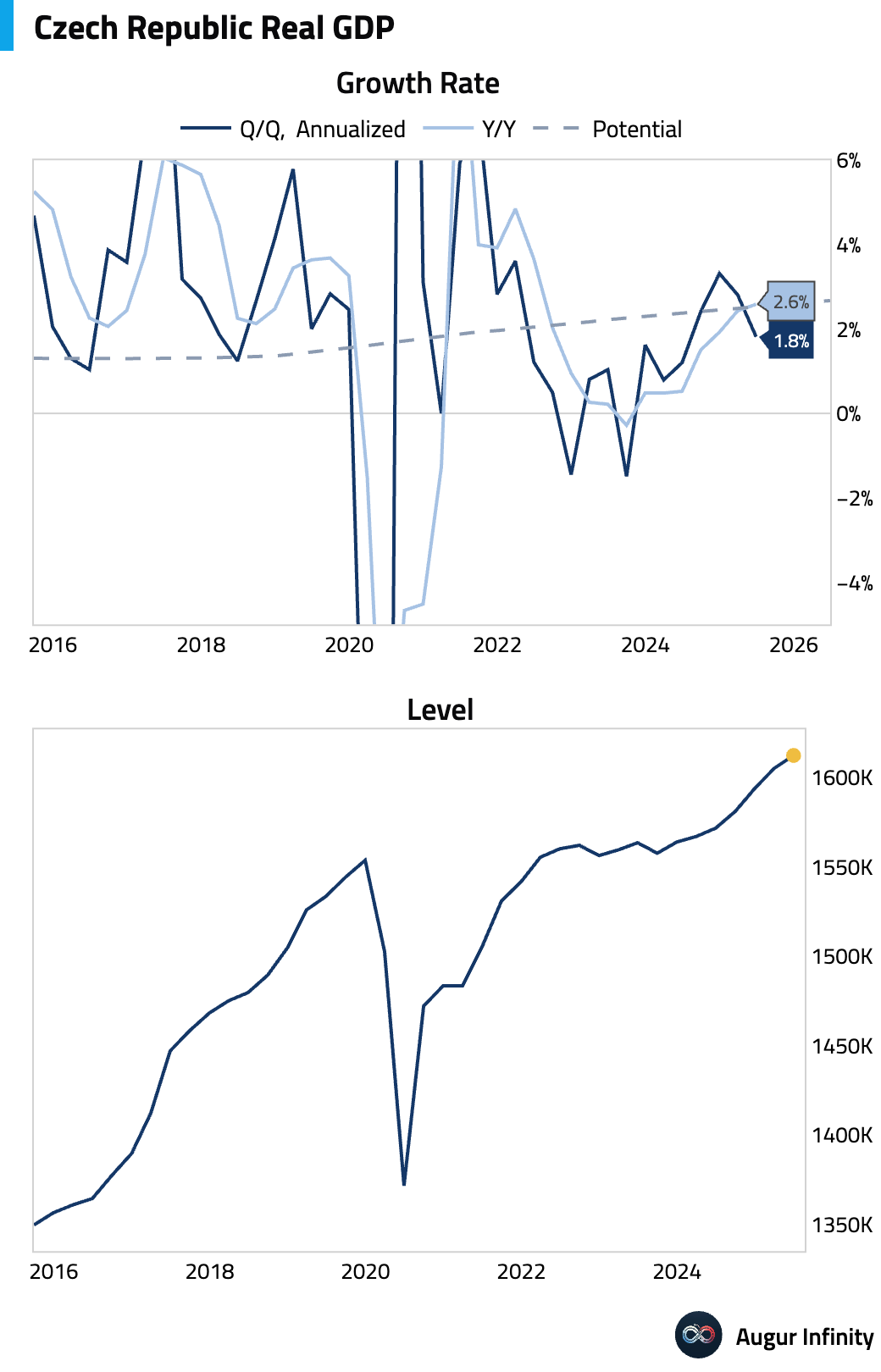

- The Czech Republic’s final Q2 GDP was revised up to +0.5% Q/Q and +2.6% Y/Y, both beating consensus.

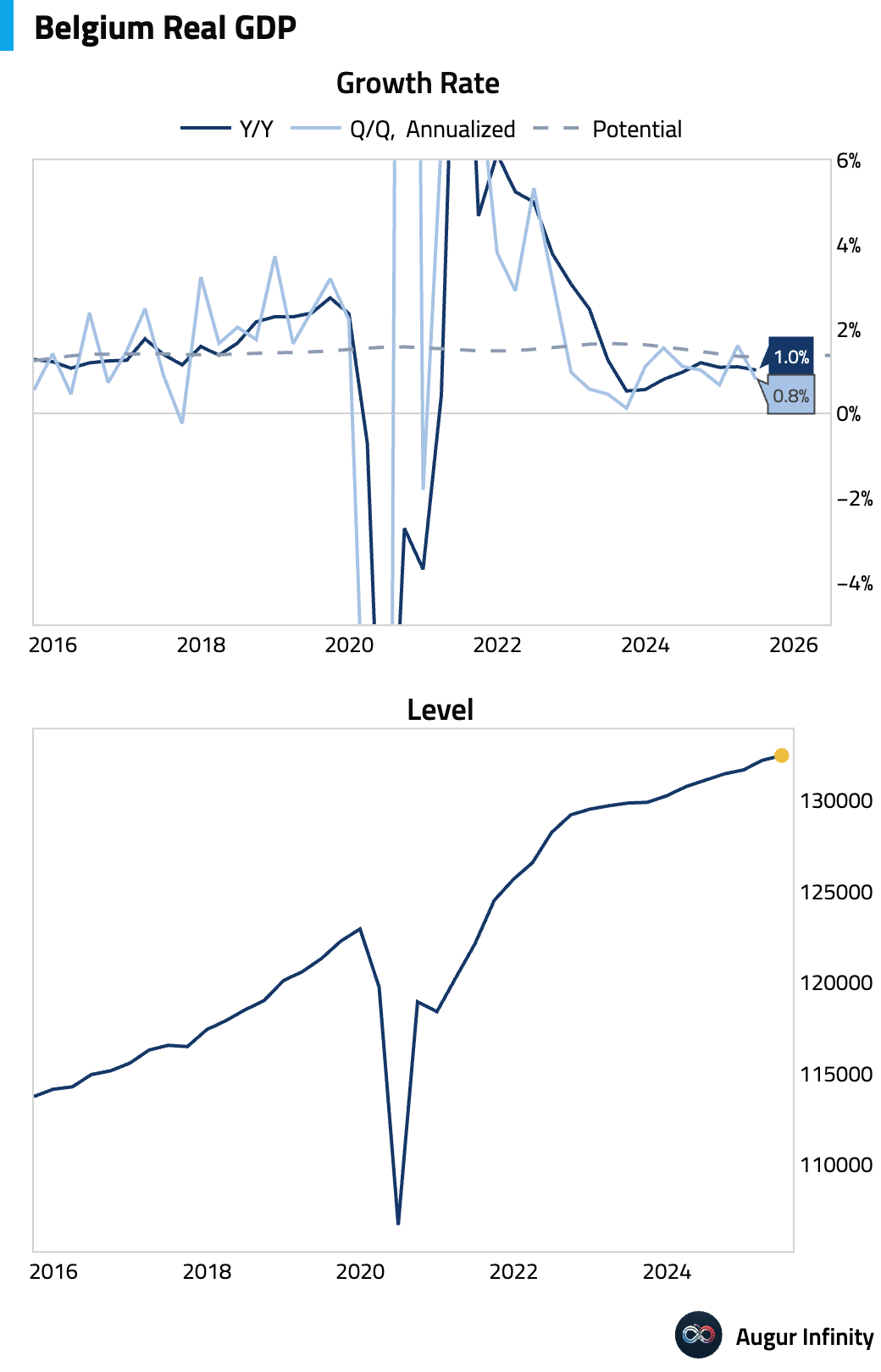

- Final Q2 GDP for Belgium was confirmed at +0.2% Q/Q and +1.0% Y/Y.

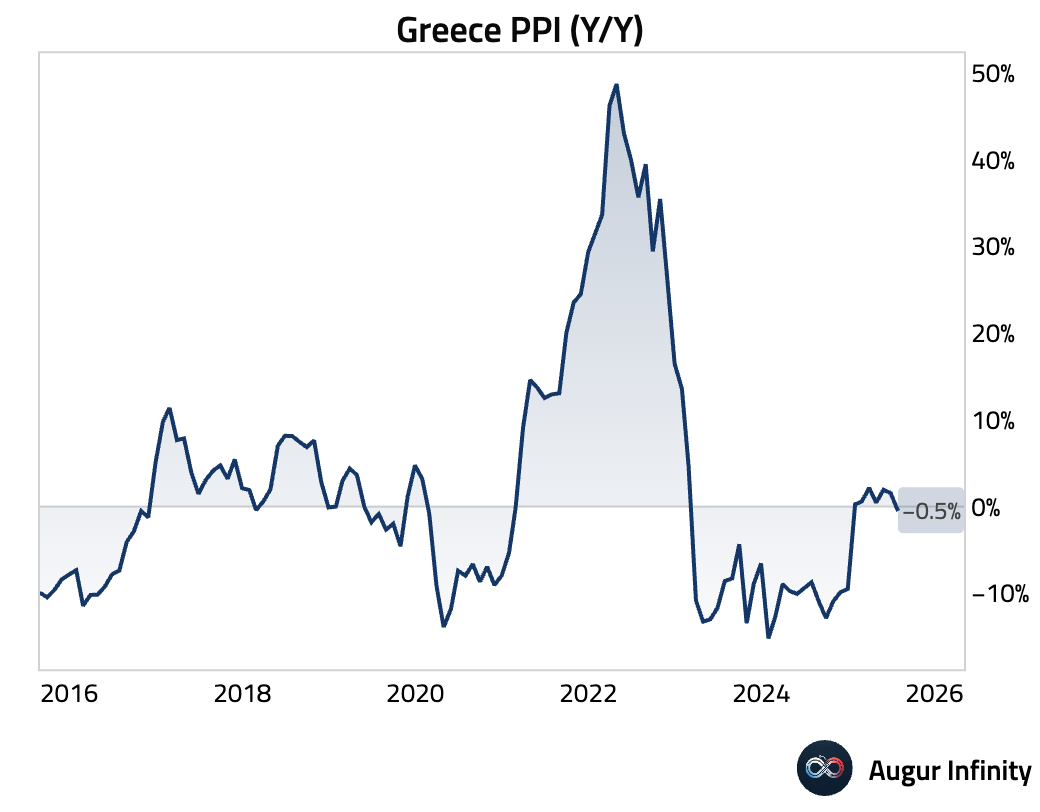

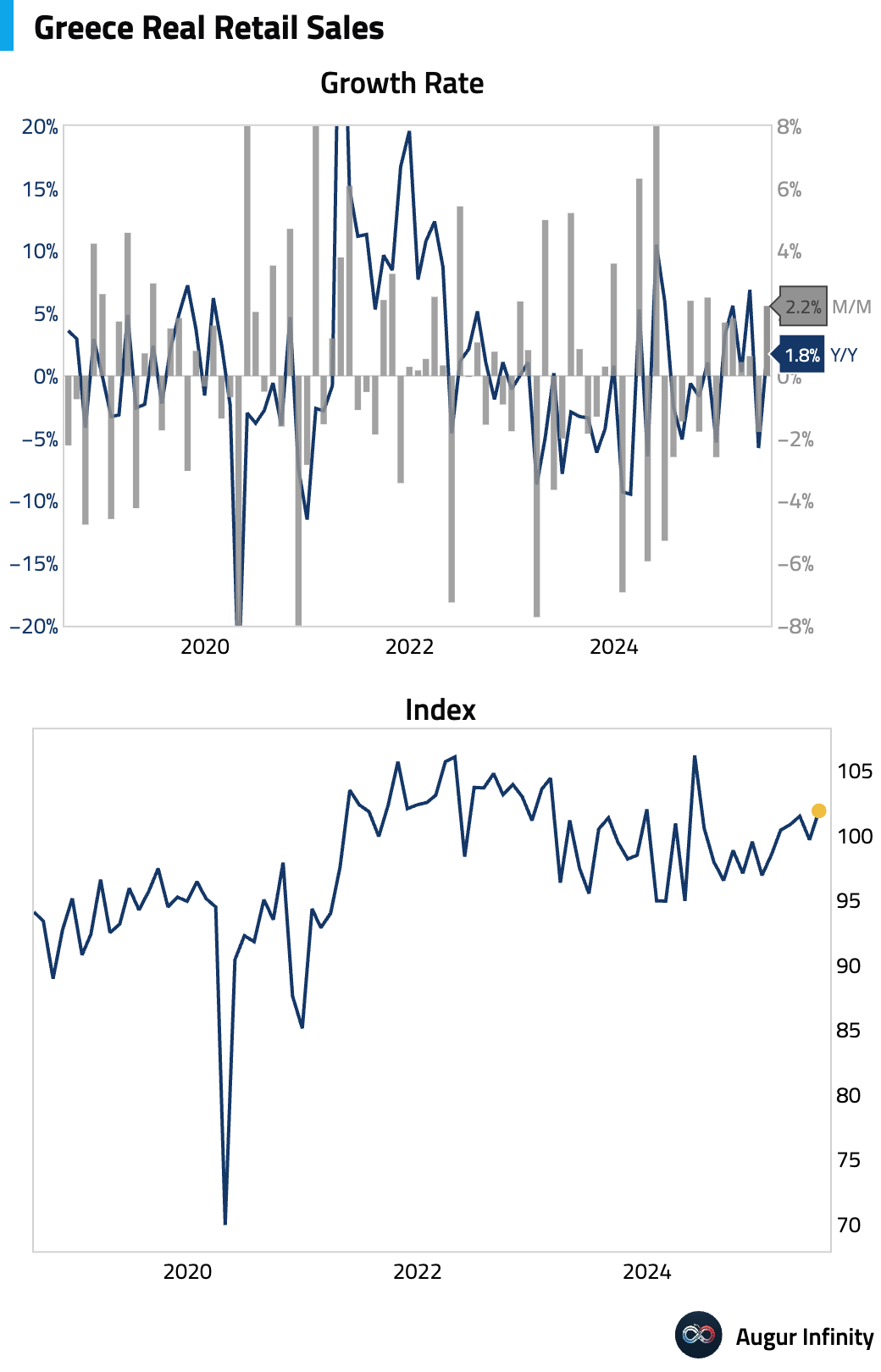

- Greece’s producer prices fell 0.5% Y/Y in July, while retail sales rebounded to +1.8% Y/Y in June.

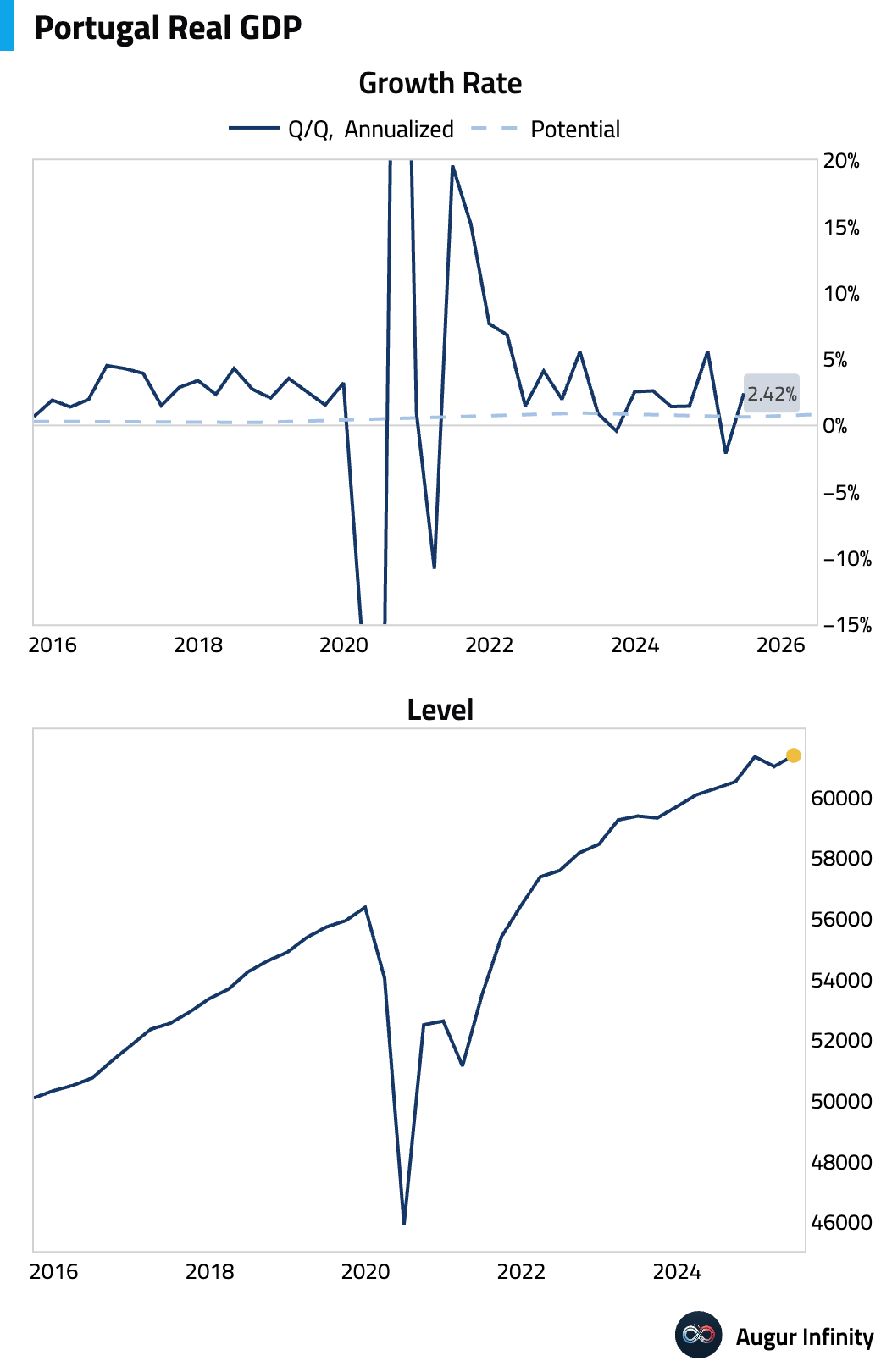

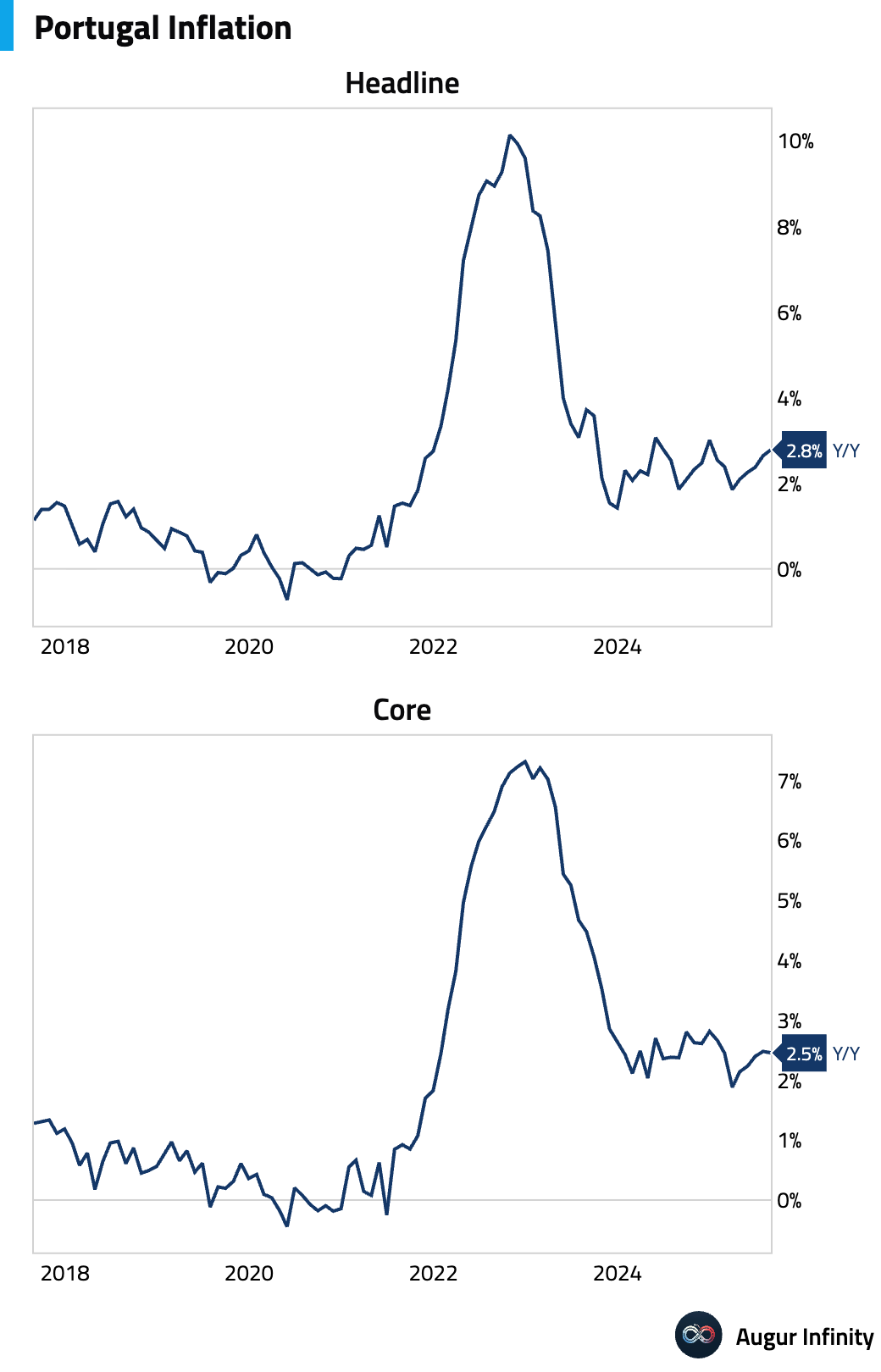

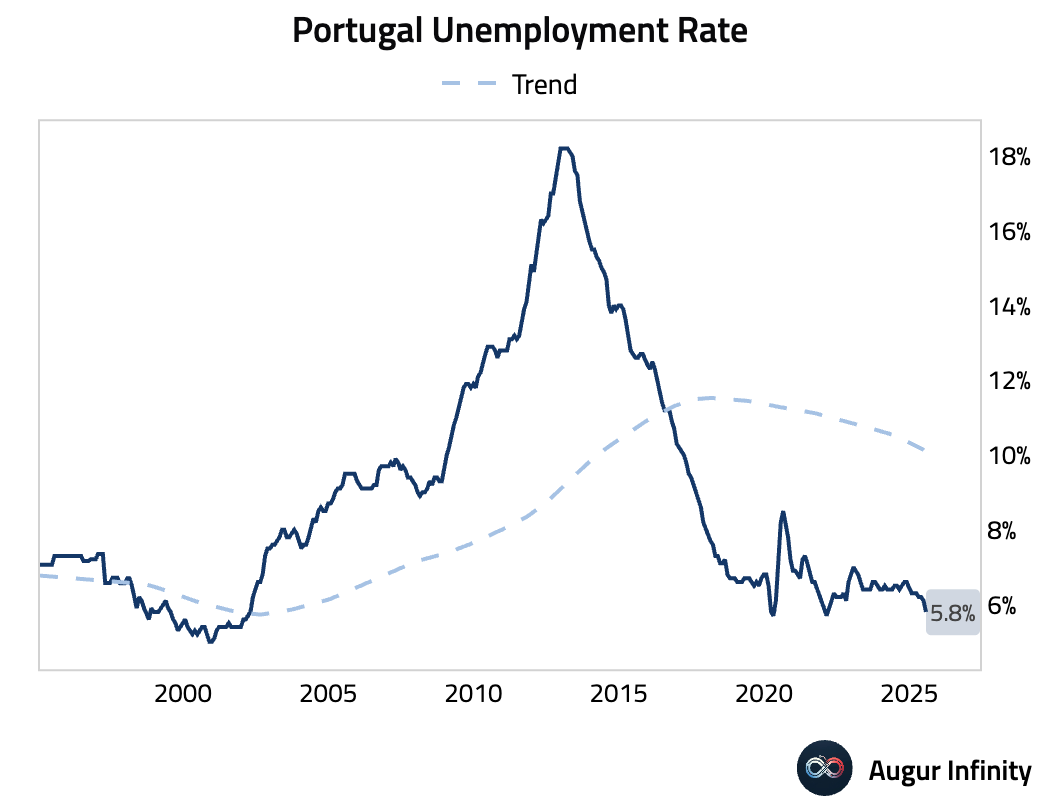

- Portugal’s final Q2 GDP was confirmed at +0.6% Q/Q (or 2.4% annualized) and +1.9% Y/Y. Preliminary August inflation rose to 2.8% Y/Y, and the unemployment rate fell to 5.8%, the lowest since February 2022.

Asia-Pacific

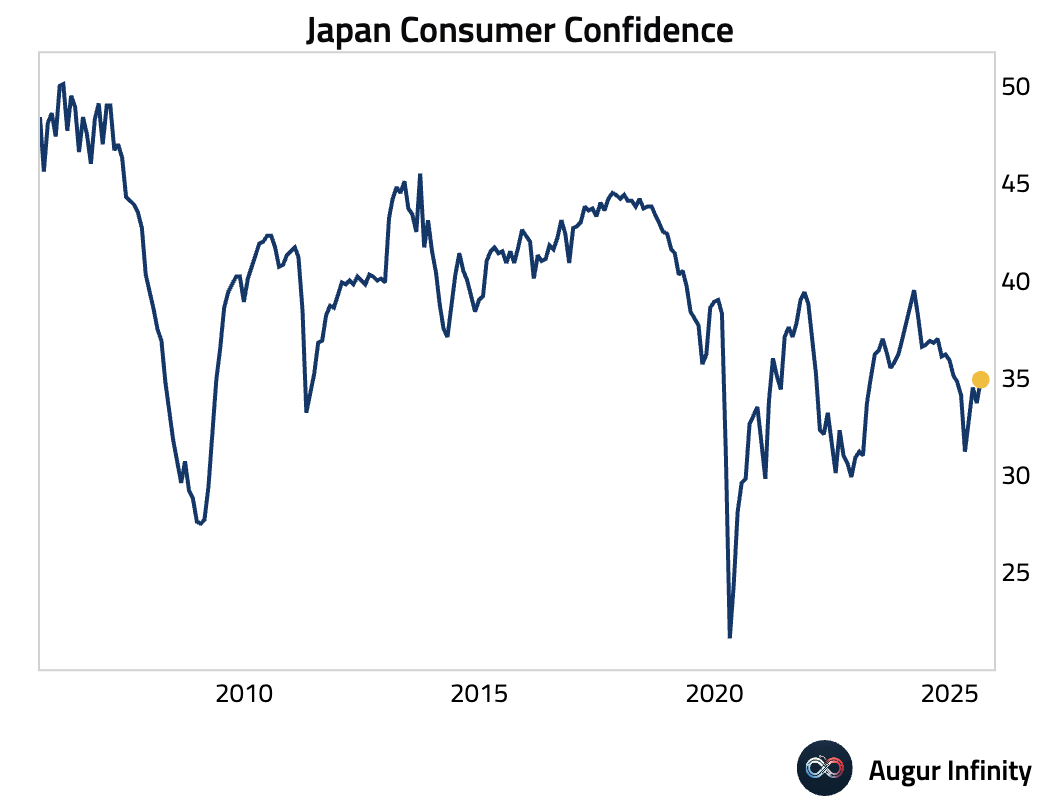

- Japanese consumer confidence rose to 34.9 in August, surpassing the 33.5 consensus.

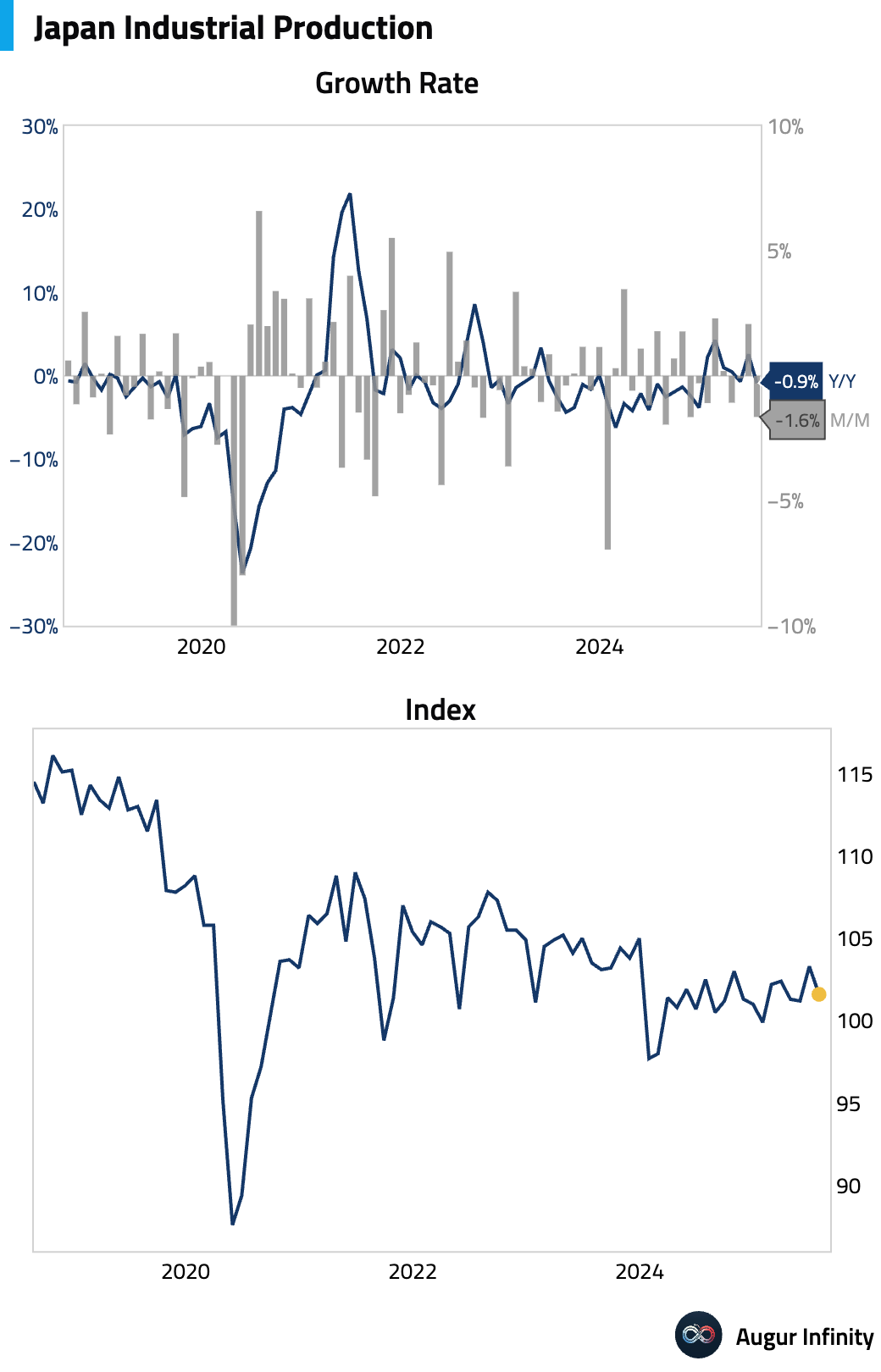

- Japan’s preliminary industrial production for July fell 1.6% M/M, a much sharper drop than the -1.0% consensus and a reversal from June’s 2.1% gain. The decline was driven by weakness in passenger vehicles and semiconductor production equipment, reflecting sluggish exports. The outlook remains weak, with manufacturers forecasting a continued decline in August.

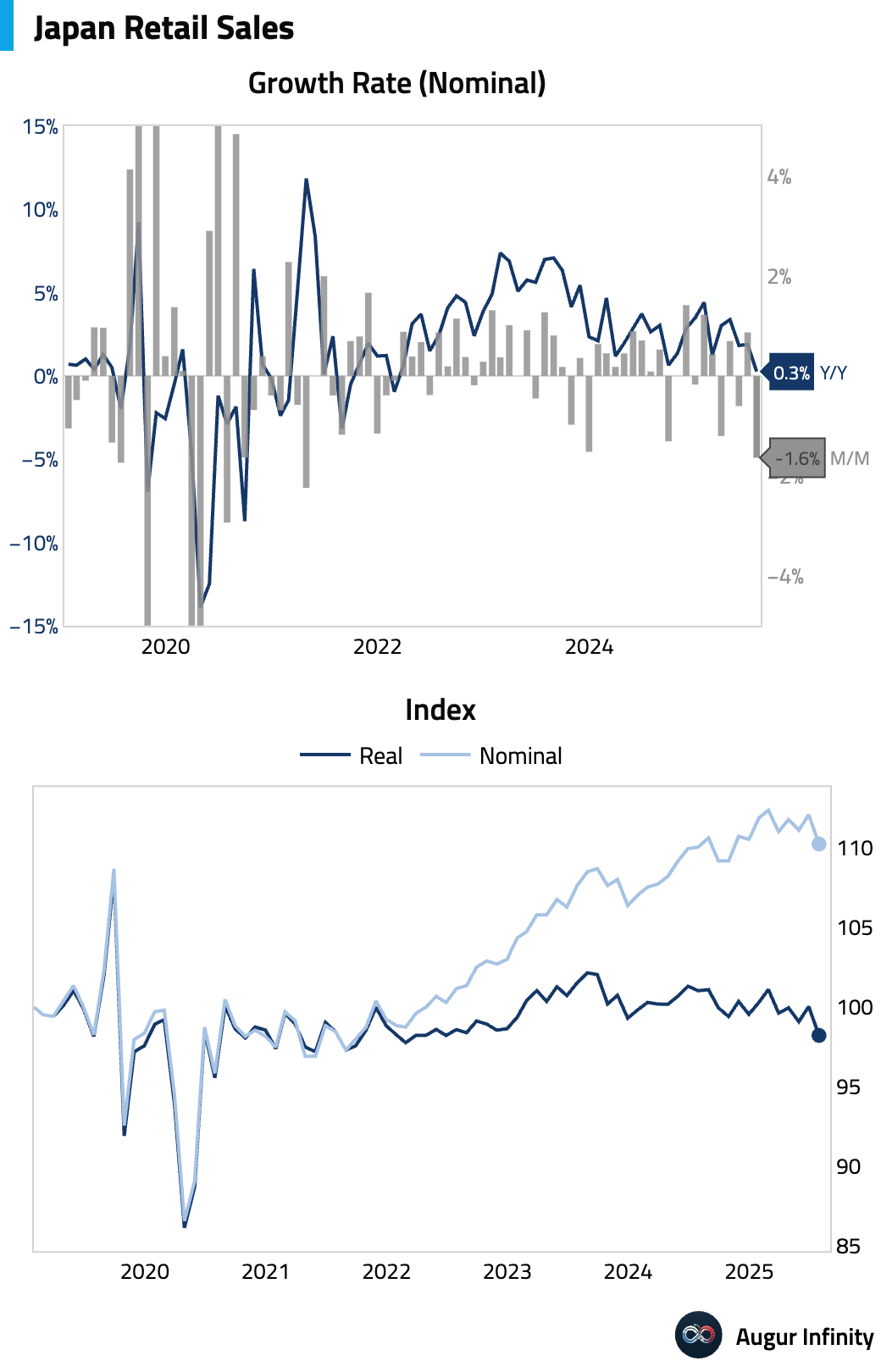

- Japanese retail sales for July disappointed, rising just 0.3% Y/Y against a 1.8% forecast. The M/M figure showed a sharp 1.6% decline. Weakness in department stores was driven by a 36.3% Y/Y plunge in duty-free sales, indicating a slowdown in tourist spending.

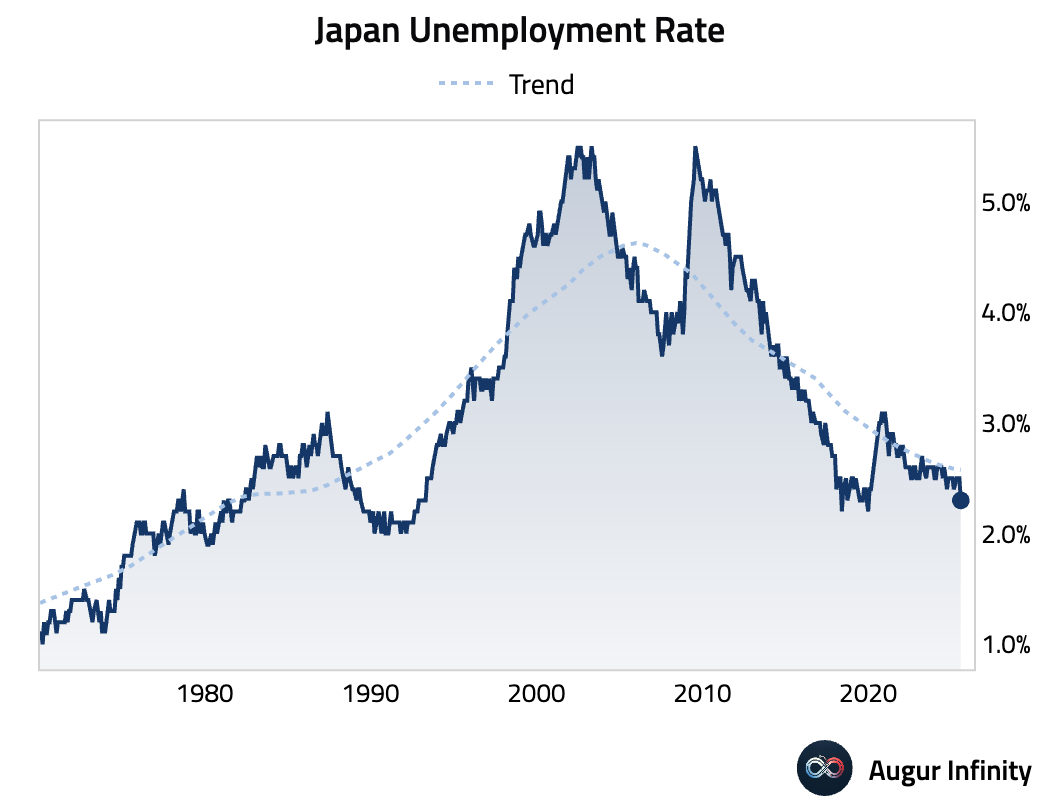

- Japan’s unemployment rate fell to 2.3% in July, better than the 2.5% consensus and the lowest level since December 2019.

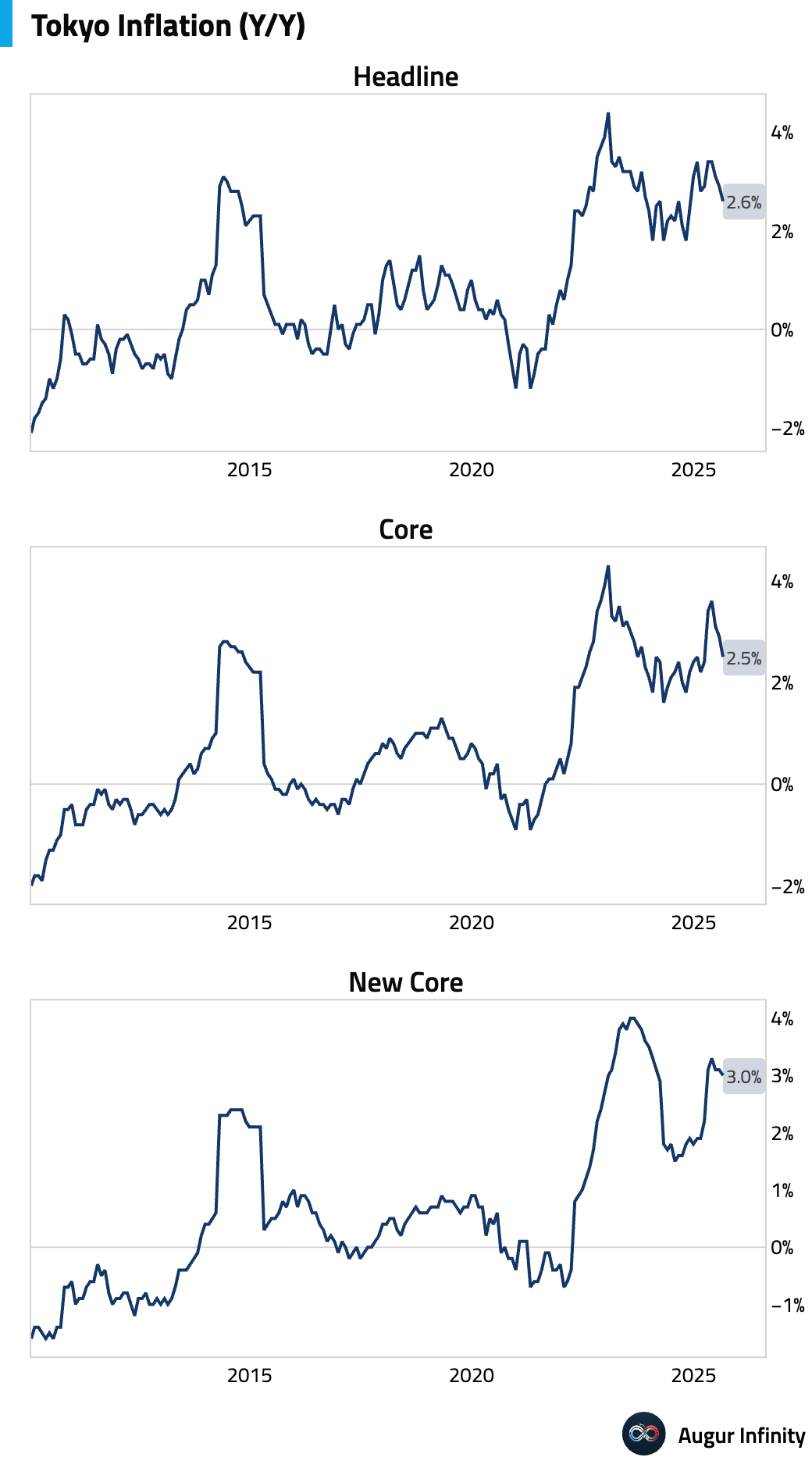

- Tokyo’s Core CPI slowed for a third straight month to 2.5% Y/Y in August, in line with consensus, driven by government energy subsidies. The core-core rate (ex-food & energy) also decelerated to 3.0% Y/Y. While food inflation remained sticky, underlying services inflation remains robust at 3.4% Y/Y, a key focus for the Bank of Japan. A key drag for September will be the rollout of free childcare, expected to depress core CPI by about 0.5 percentage points.

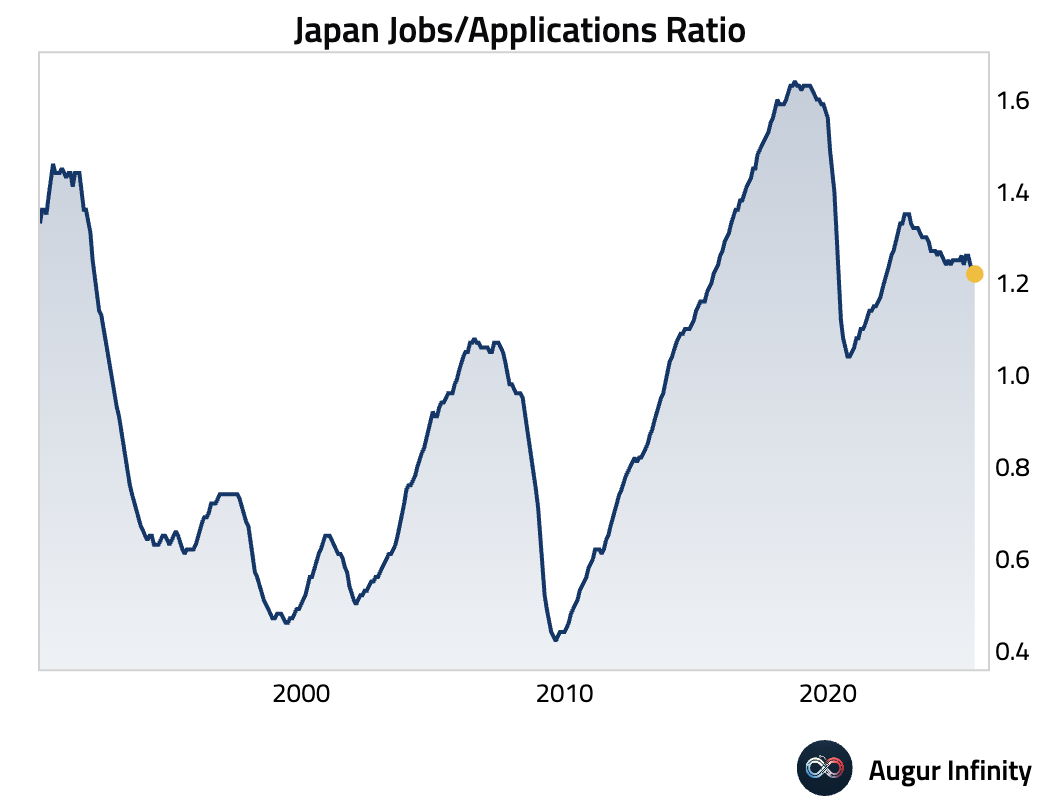

- The jobs-to-applications ratio in Japan held steady at 1.22 in July, matching consensus.

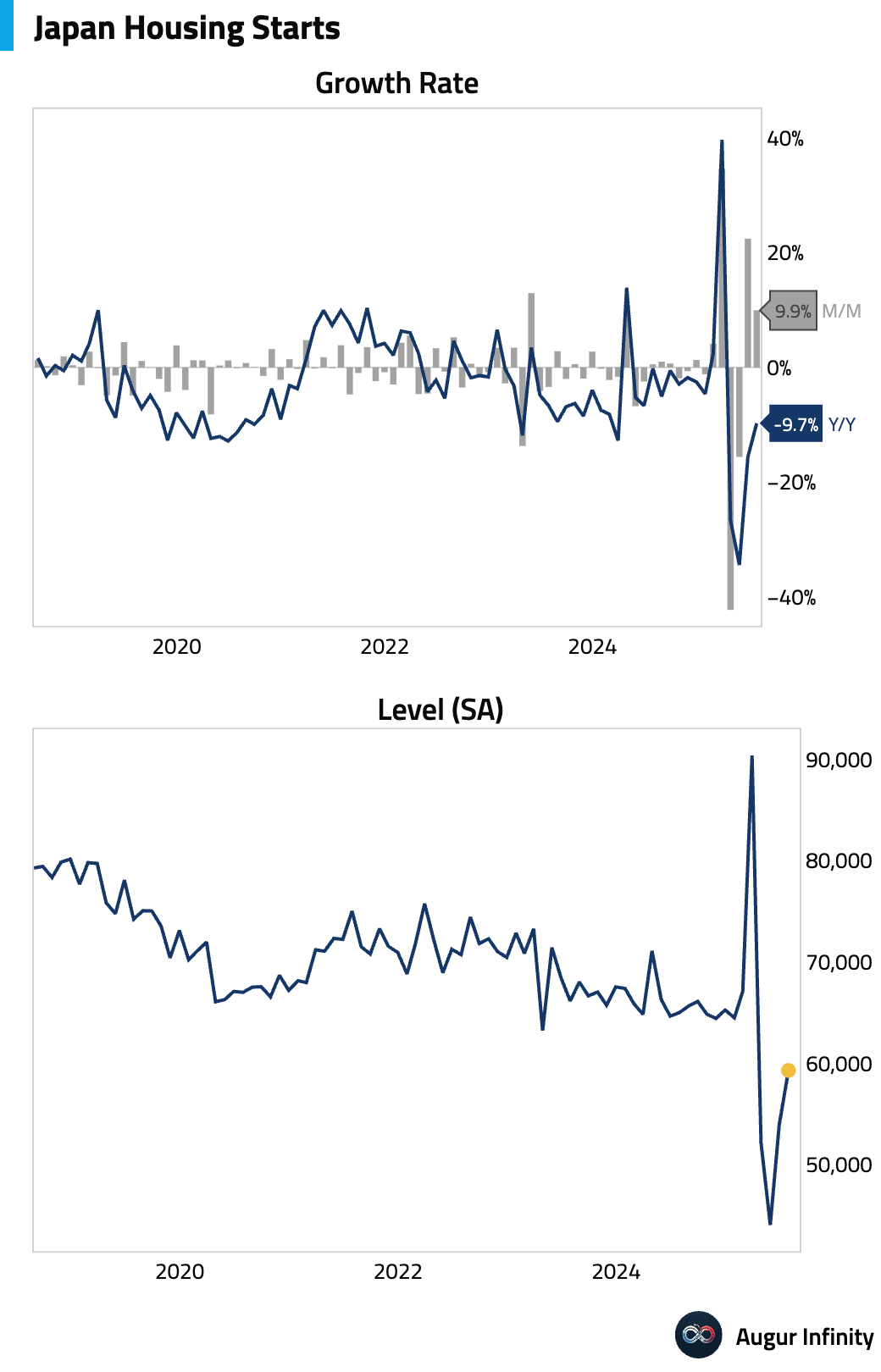

- Japanese housing starts fell 9.7% Y/Y in July, a smaller decline than the 15.6% drop in June and slightly better than the -9.6% consensus.

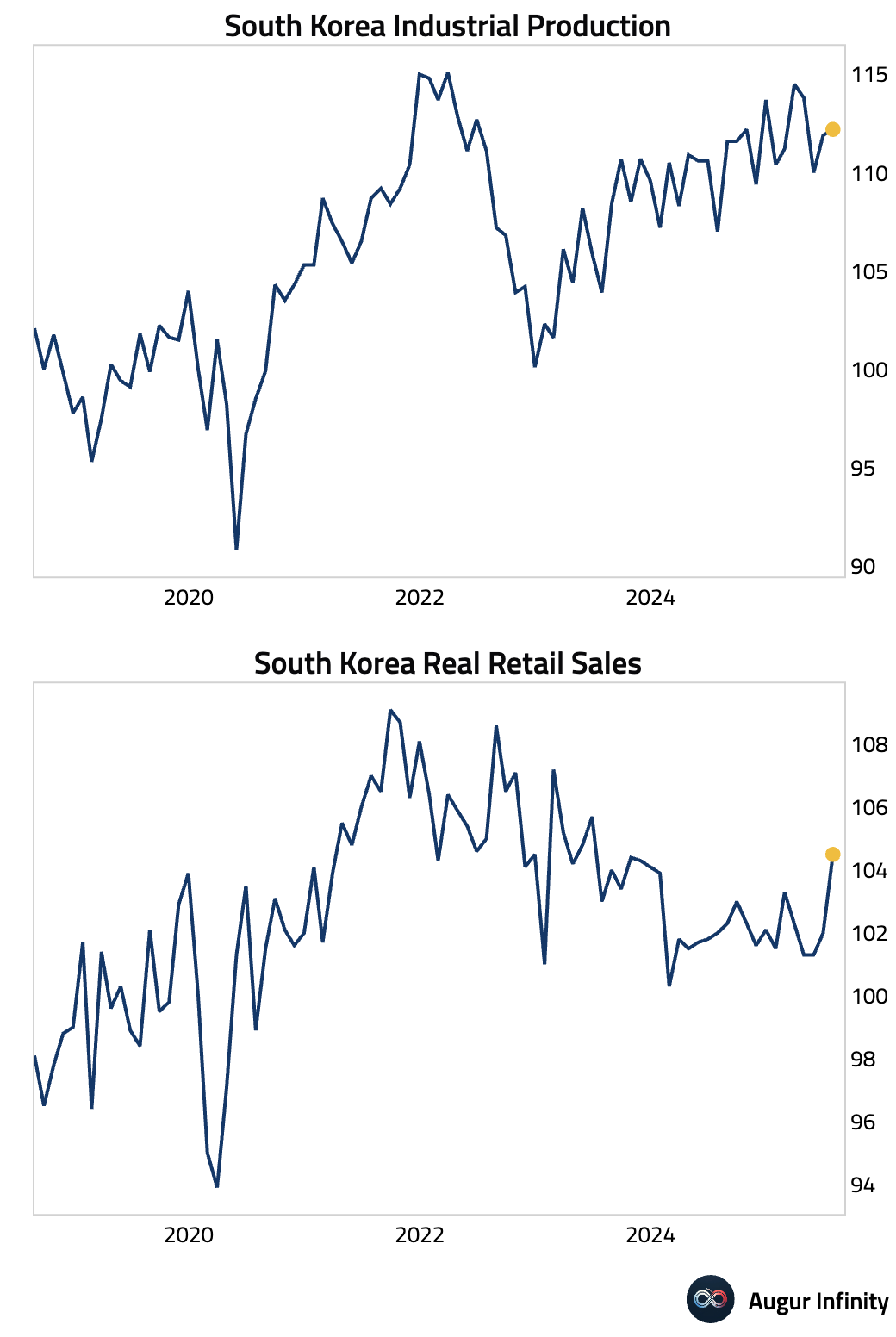

- South Korean industrial production growth slowed to 0.3% M/M in July, dragged down by weaker chip and auto output but cushioned by a surge in electronic parts. In contrast, domestic demand picked up strongly, with retail sales jumping 2.5% M/M, the strongest momentum since February 2023. The sales surge was directly attributed to fiscal stimulus measures, particularly for durable goods. The inventory-to-shipment ratio fell to its lowest since May 2022, a positive signal that inventory destocking is progressing.

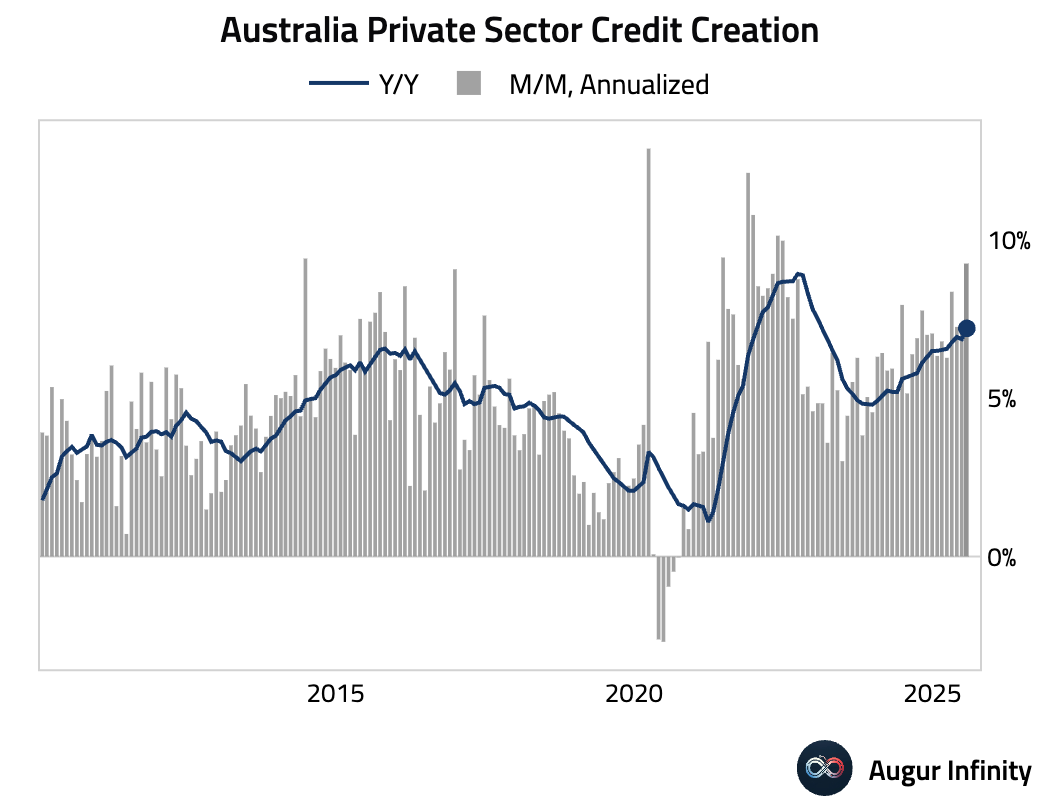

- Australia’s private sector credit grew 0.7% M/M in July, beating the 0.6% consensus. The acceleration was driven by a 1.4% M/M surge in business credit, the fastest monthly pace since November 2021. The annual growth rate accelerated to 7.2% Y/Y, its fastest since February 2023.

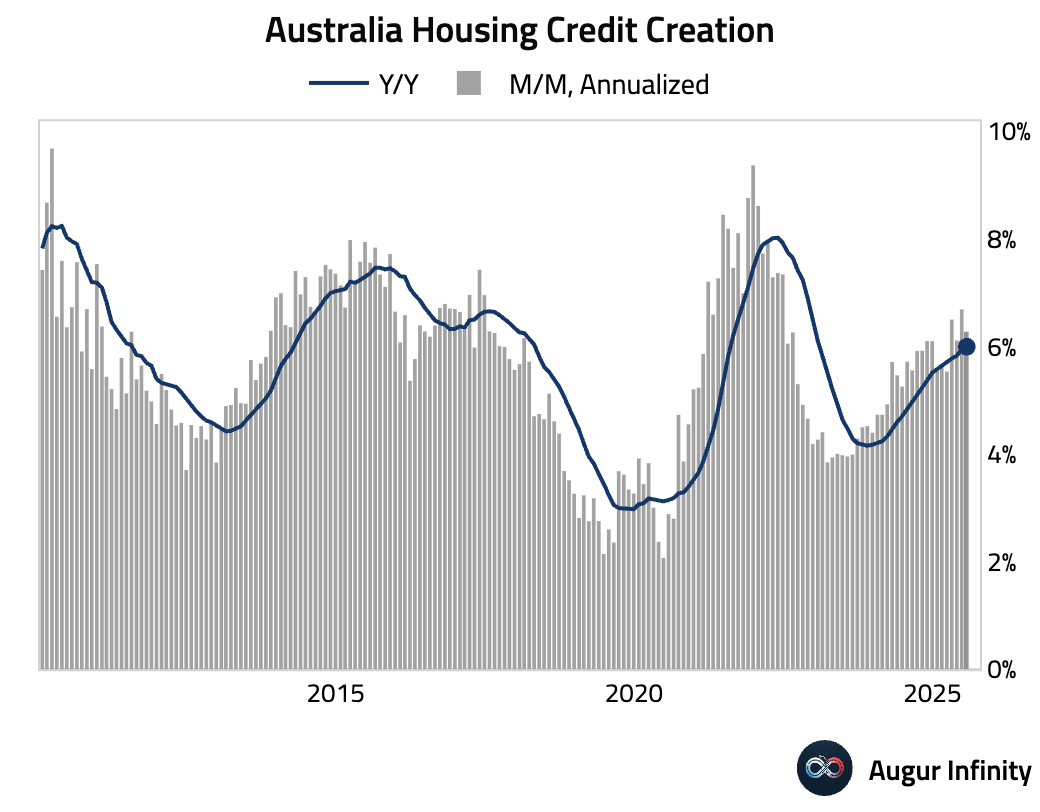

- Australian housing credit growth was steady at 0.5% M/M in July.

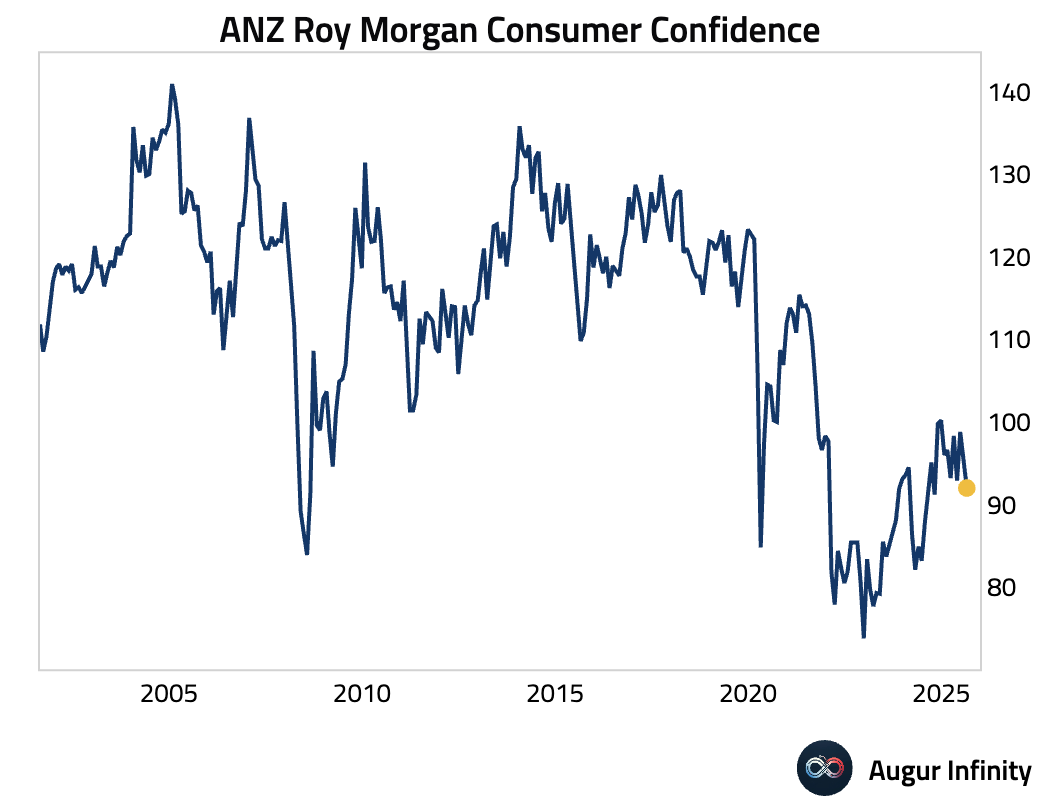

- New Zealand’s ANZ-Roy Morgan consumer confidence index fell to 92.0 in August from 94.7 in July.

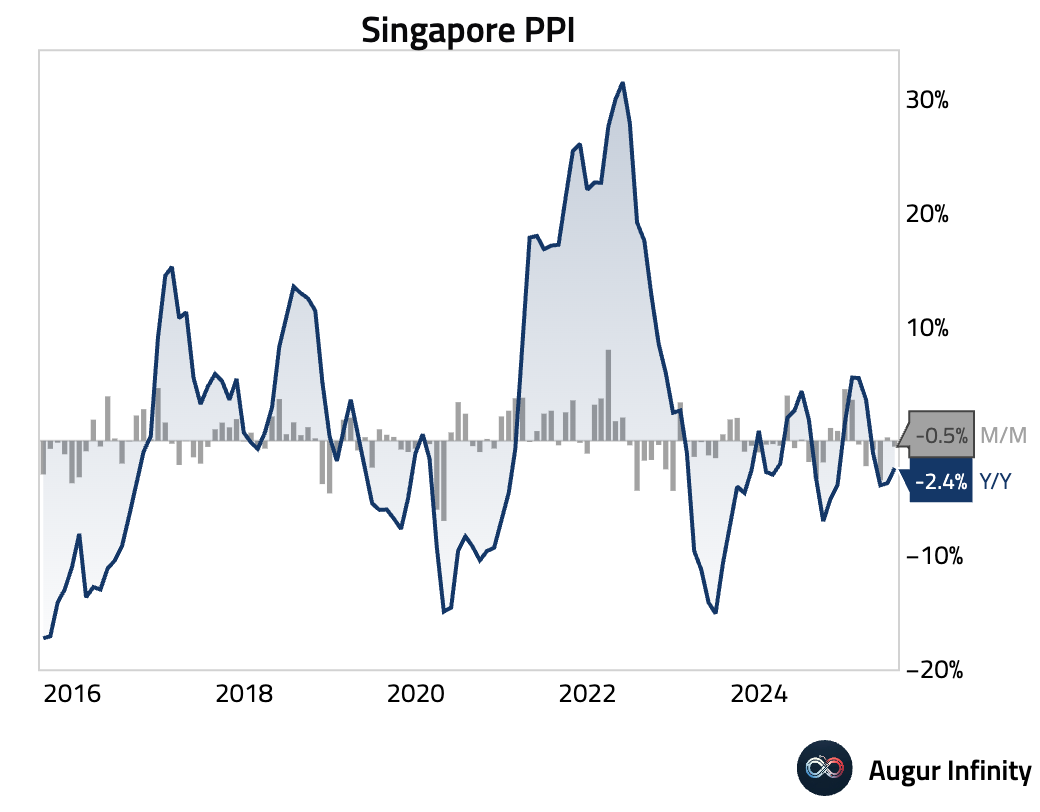

- Singapore’s producer price index fell 2.4% Y/Y in July. Import prices dropped 6.1% Y/Y, while export prices were down 8.0% Y/Y.

Emerging Markets ex China

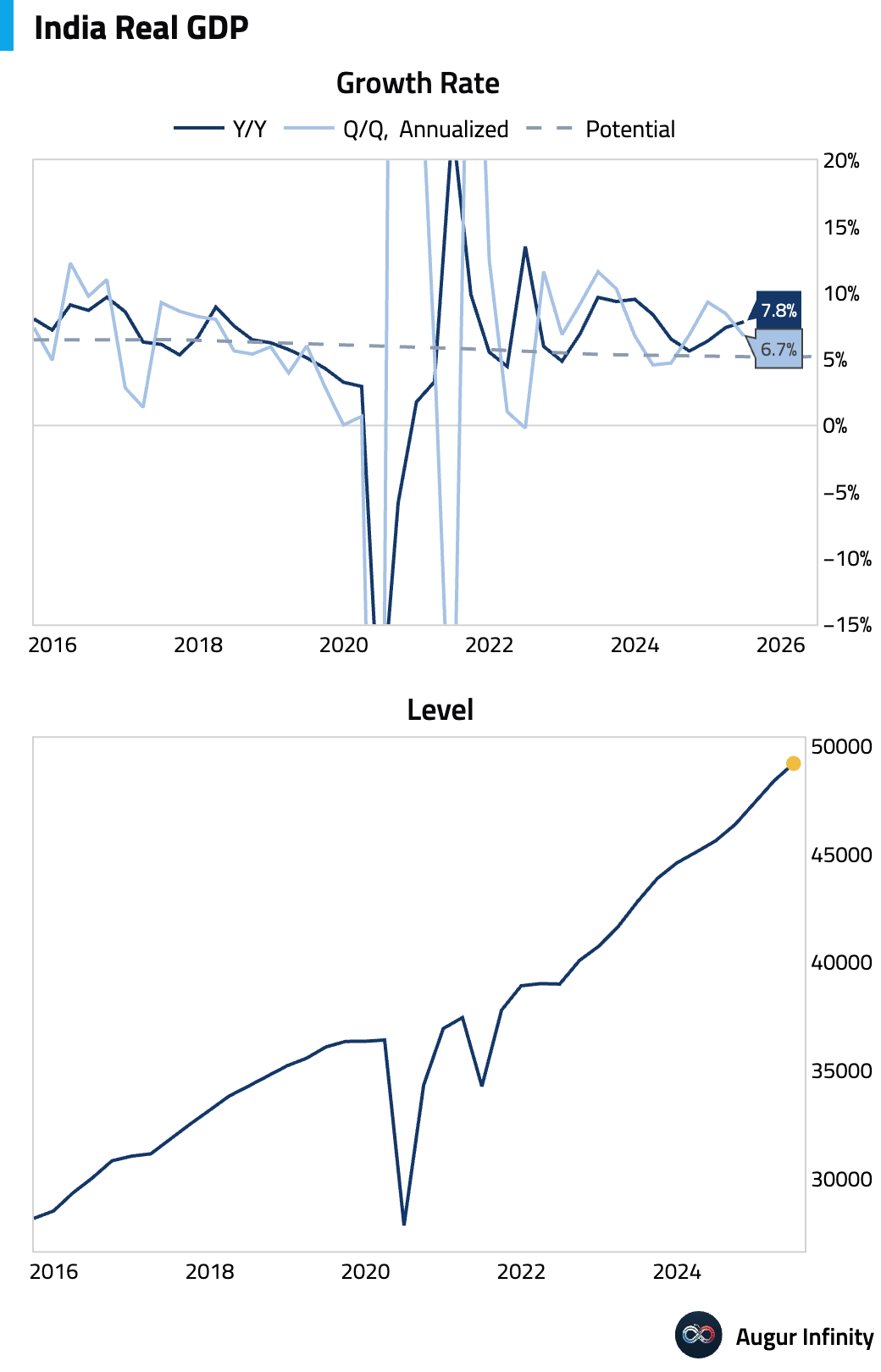

- India’s economy grew 7.8% Y/Y in the second quarter, significantly outperforming the 6.7% consensus forecast.

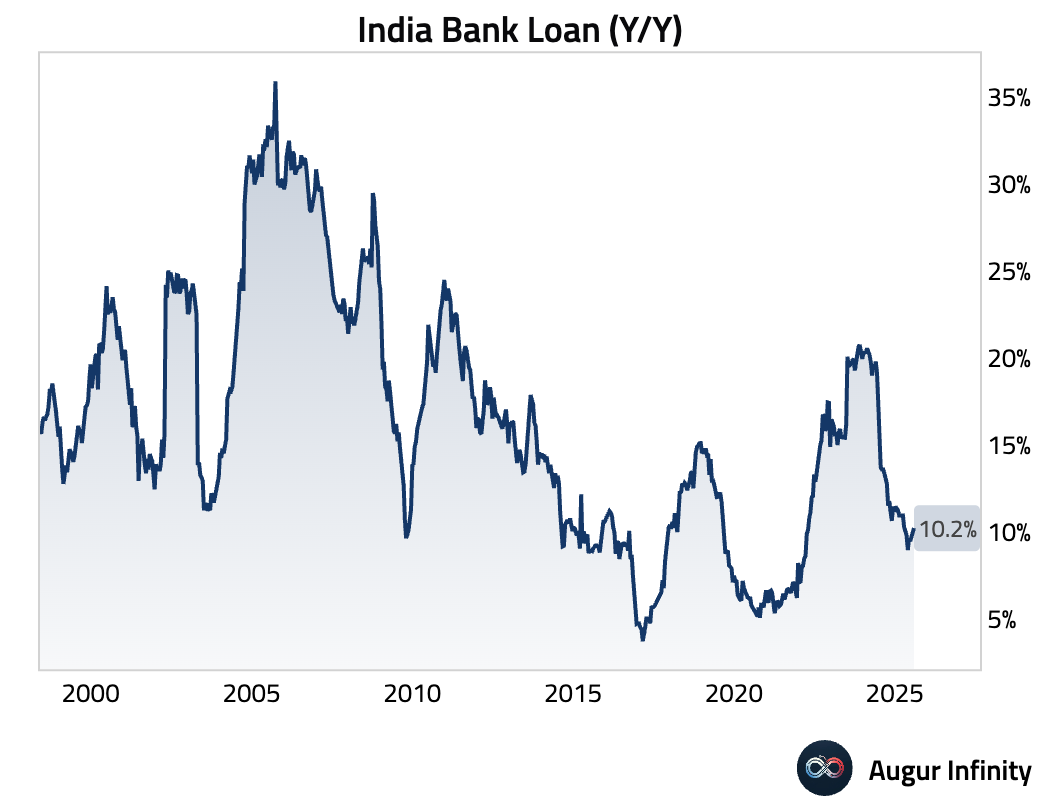

- India’s bank loan growth accelerated to 10.2% Y/Y for the two weeks ending August 15.

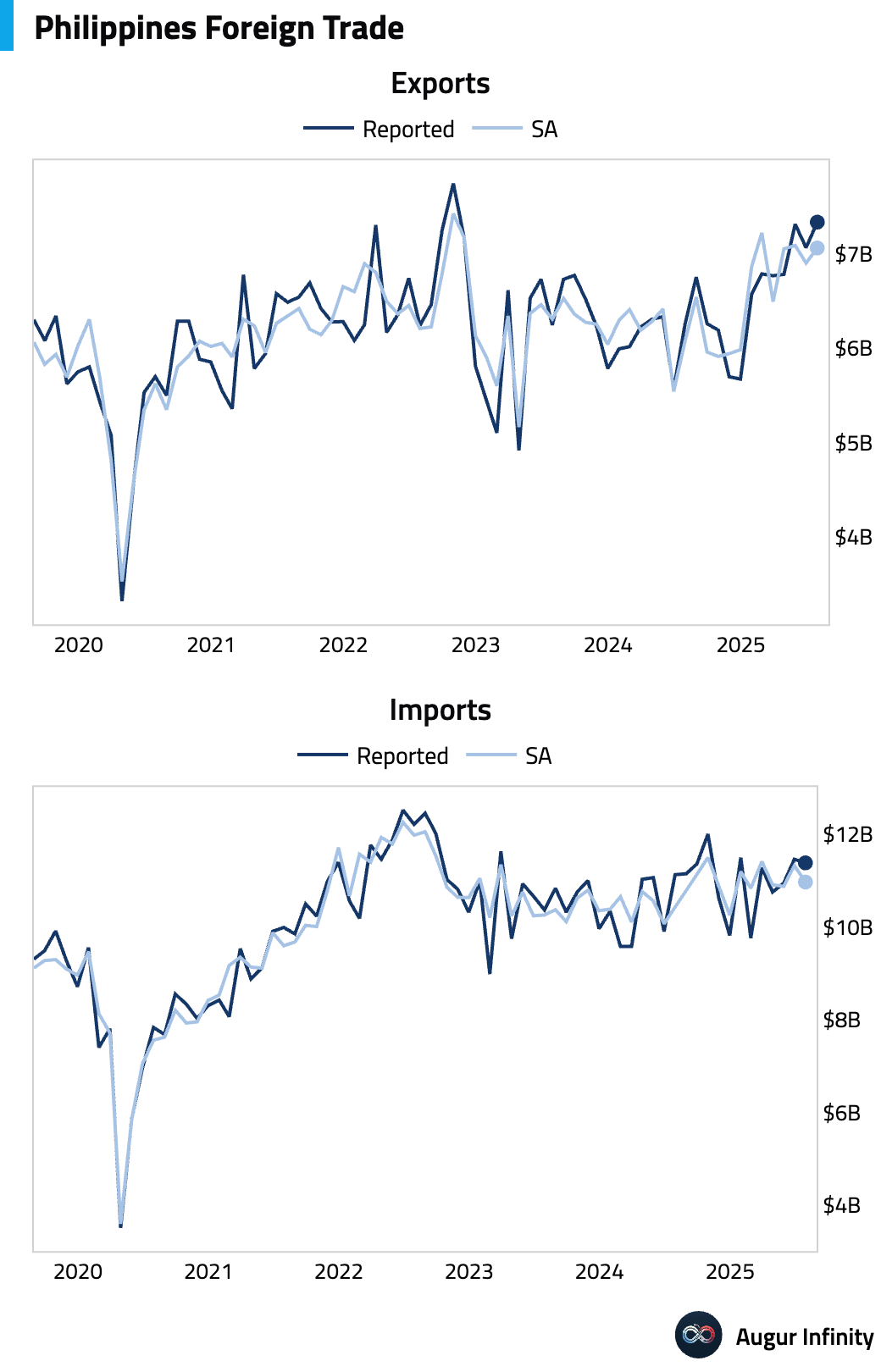

- The Philippines’ trade deficit narrowed to $4.05 billion in July. Exports grew 17.3% Y/Y while imports rose 2.3% Y/Y.

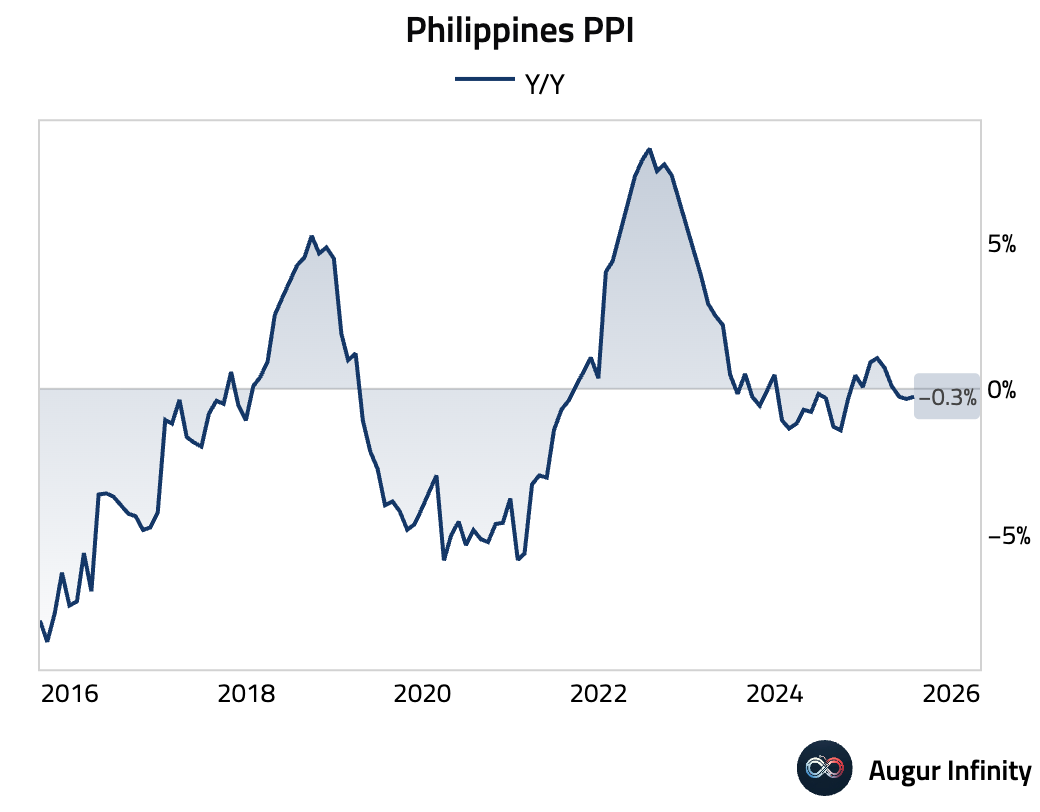

- The Philippines’ producer price index fell 0.27% Y/Y in July.

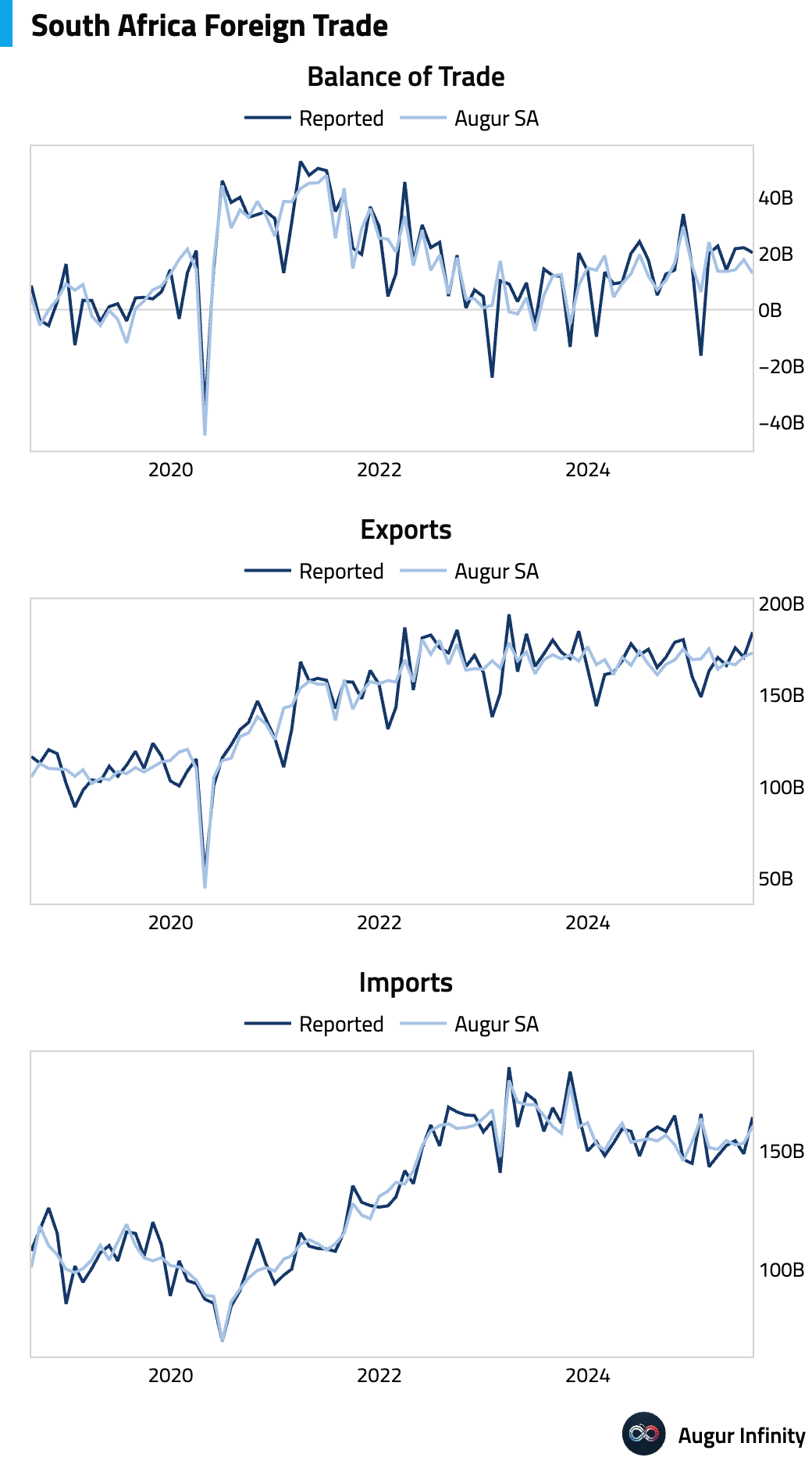

- South Africa’s trade surplus narrowed slightly to R20.29 billion in July.

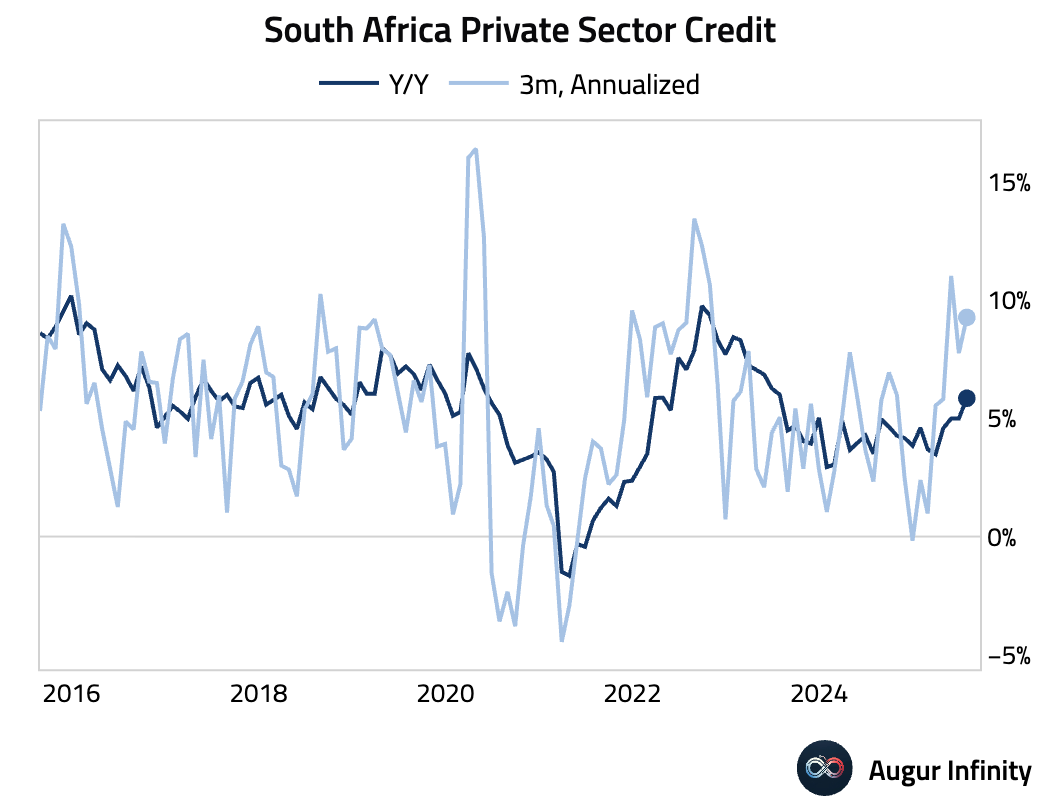

- Private sector credit growth in South Africa accelerated to 5.84% Y/Y in July, the fastest since July 2023.

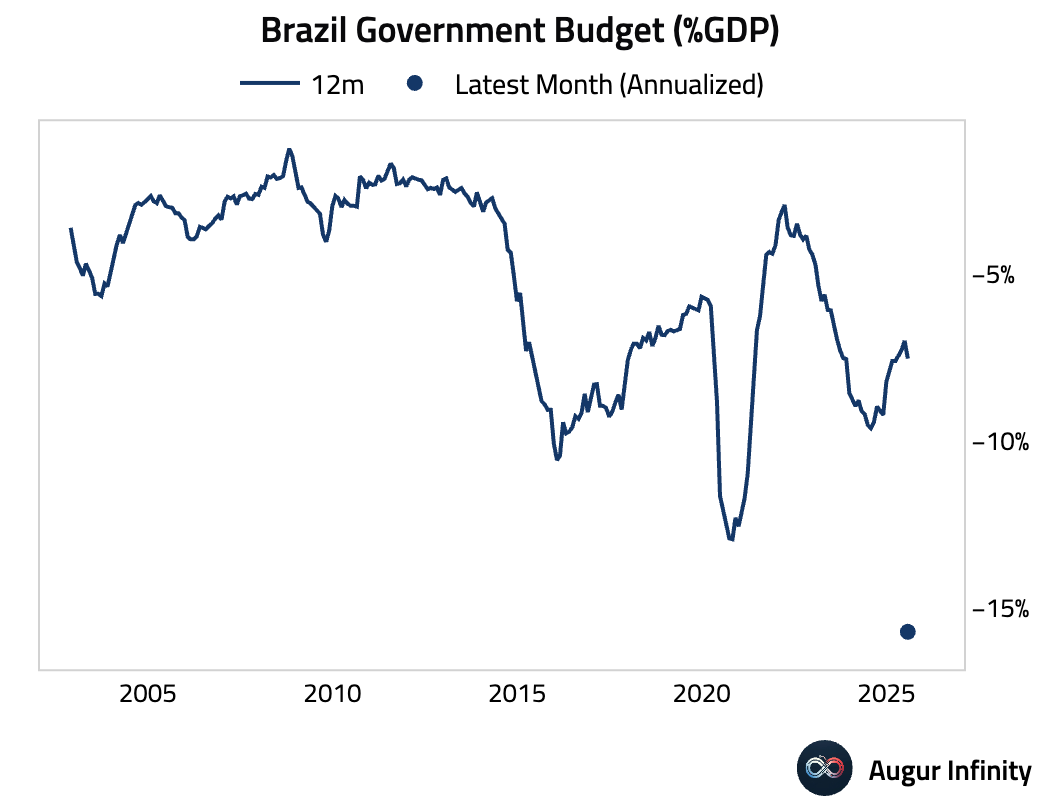

- Brazil’s nominal budget balance posted a deficit of R175.6 billion in July, substantially wider than the R113.7 billion consensus. The miss was driven by a larger-than-expected central government primary deficit, reflecting a sharp fiscal deterioration.

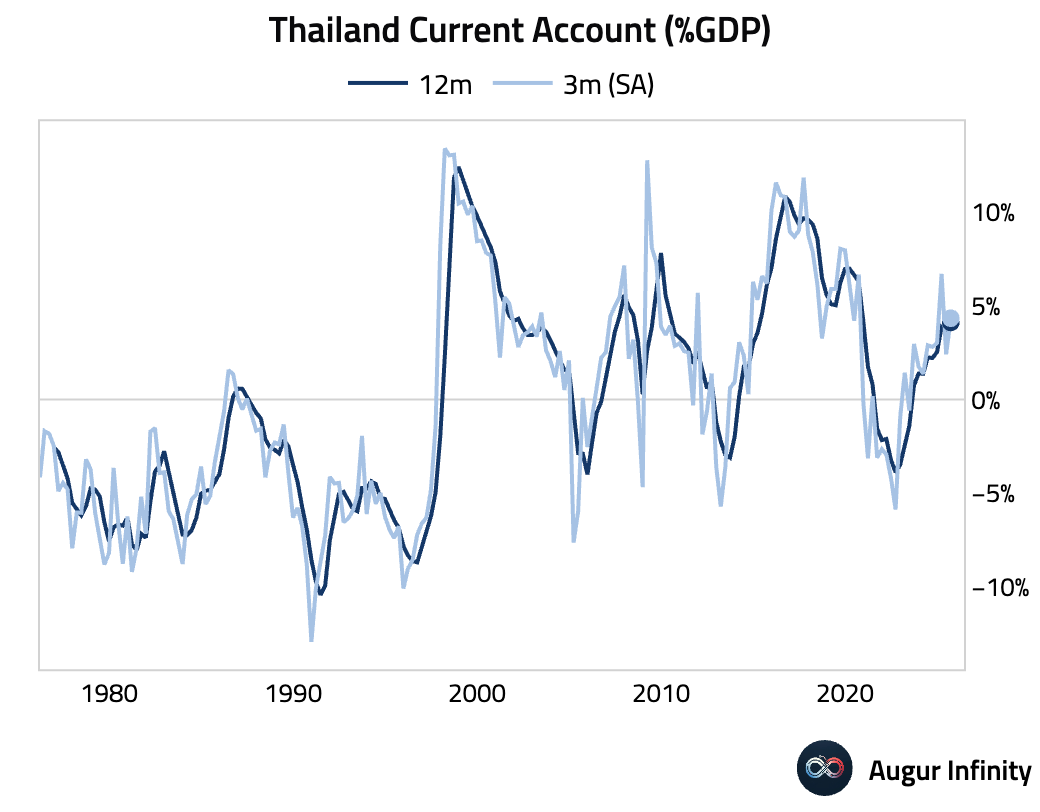

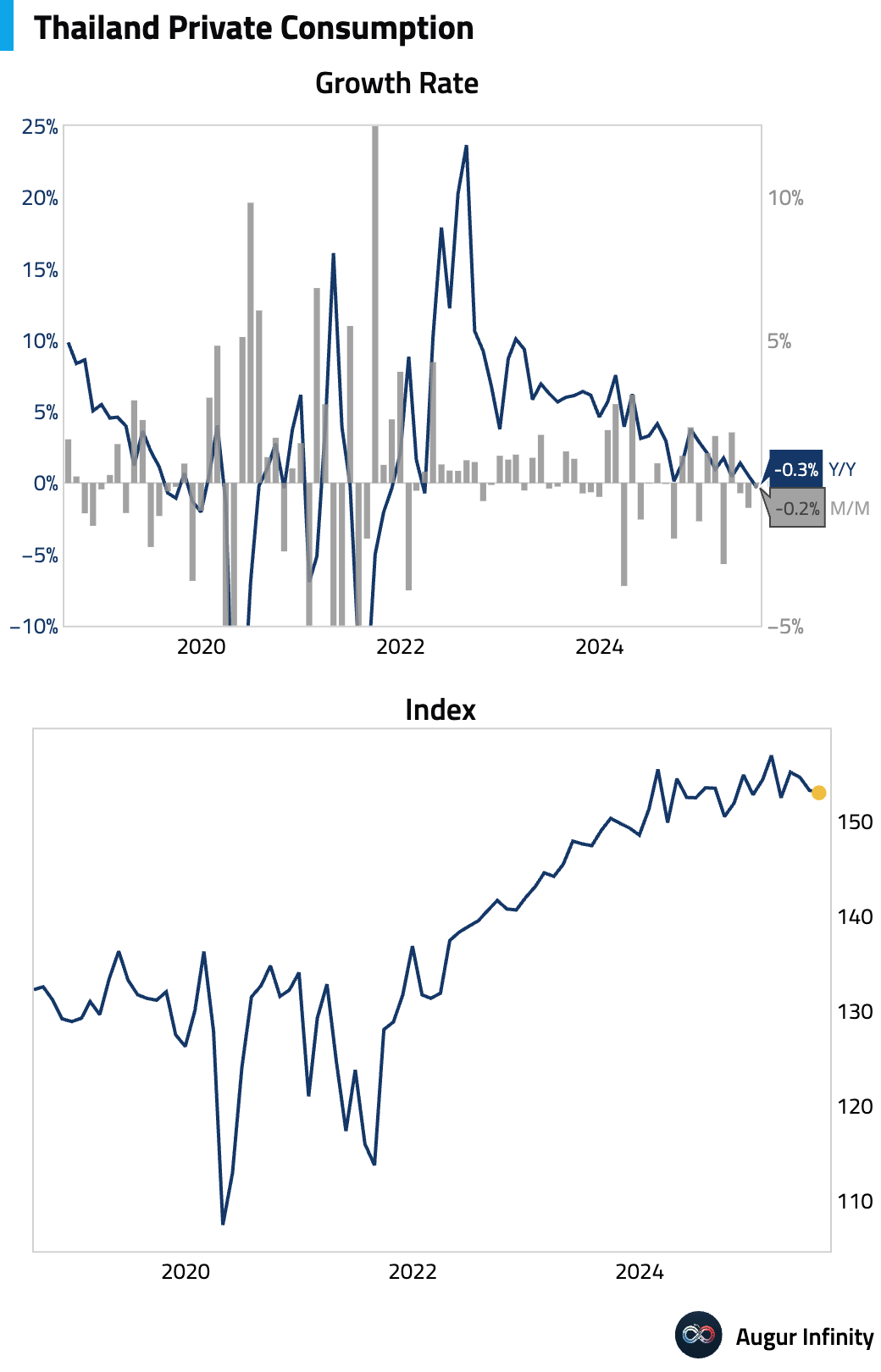

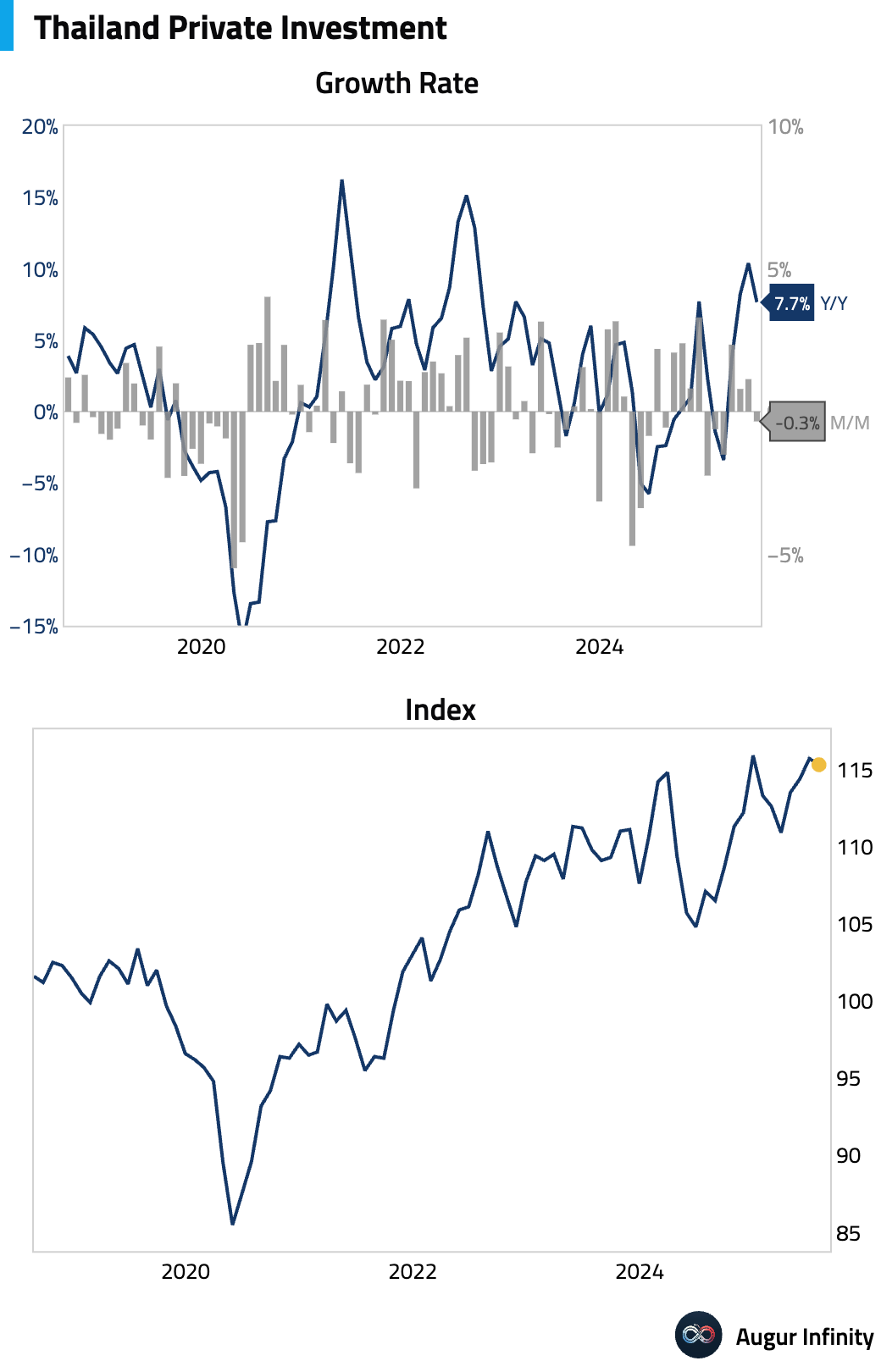

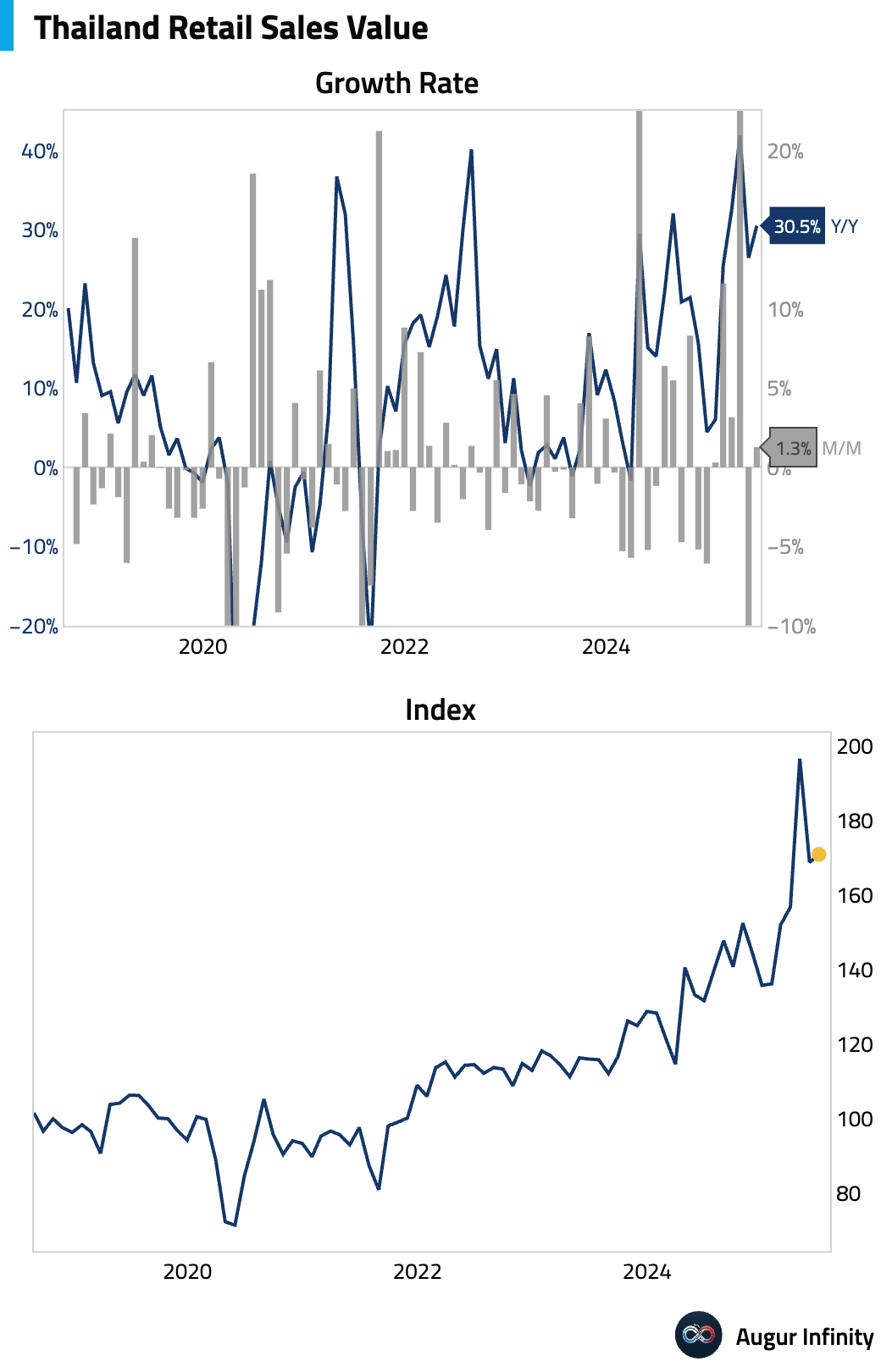

- Thailand’s current account surplus narrowed to $2.2 billion in July. Private consumption fell 0.2% M/M, while private investment dropped 0.4% M/M.

- Thai retail sales growth accelerated to 30.5% Y/Y in June.

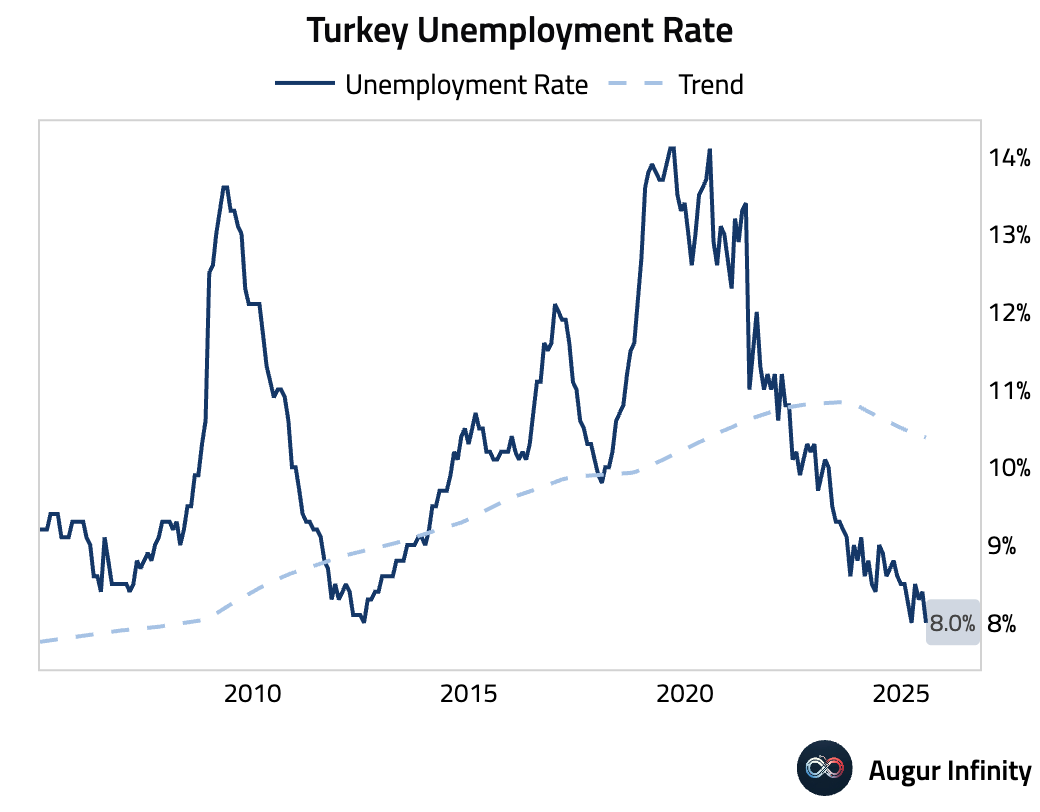

- Turkey’s unemployment rate fell to 8.0% in July, its lowest level since December 2001.

Global Markets

Equities

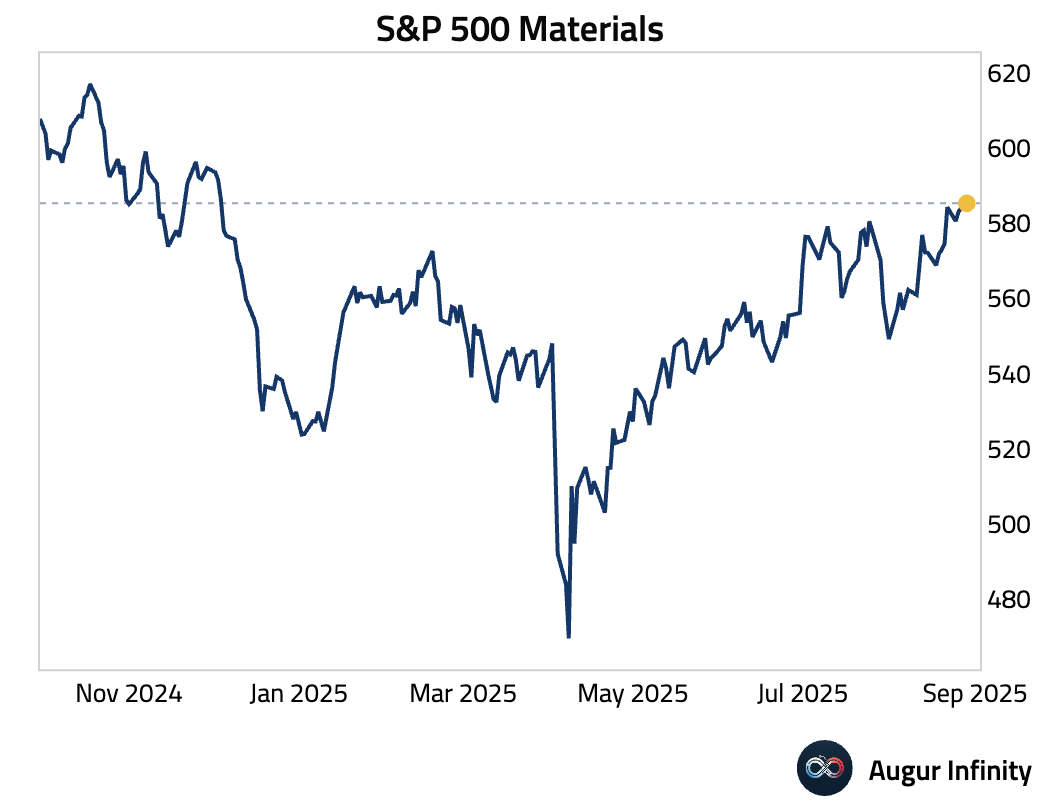

- S&P 500 Materials is at the highest level since December 4, 2024.

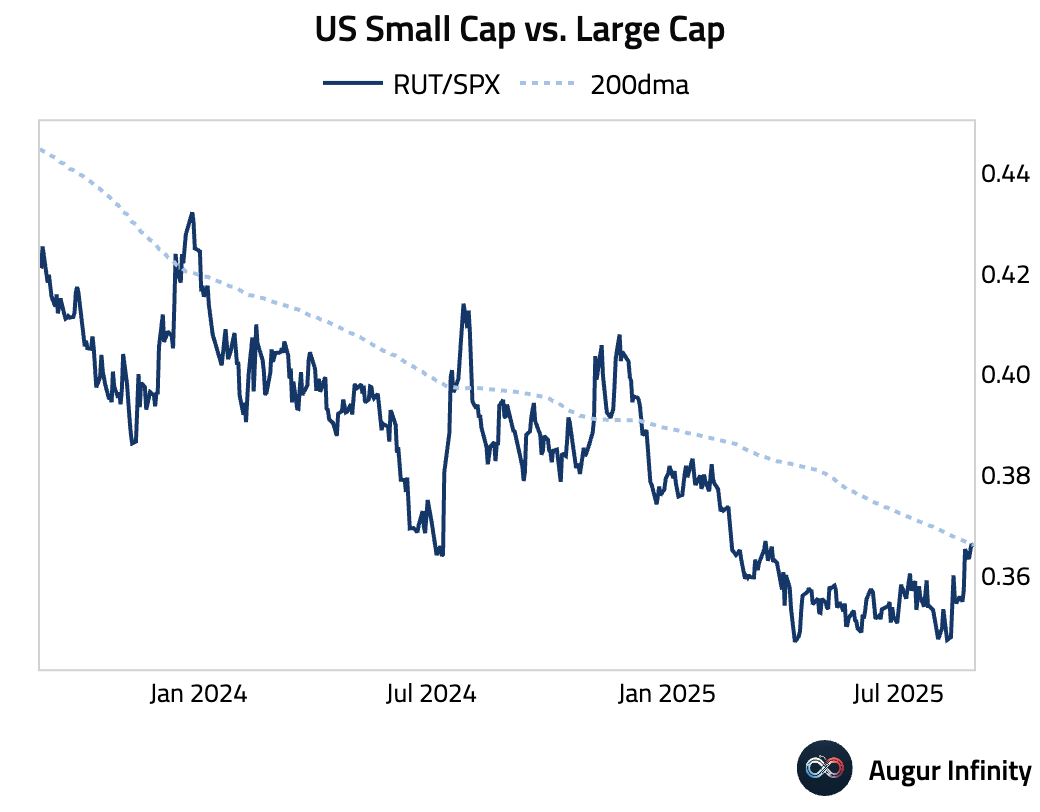

- The US Small Cap vs. Large Cap factor, proxied by Russell 2000 vs. S&P 500, rose above its 200-day moving average.

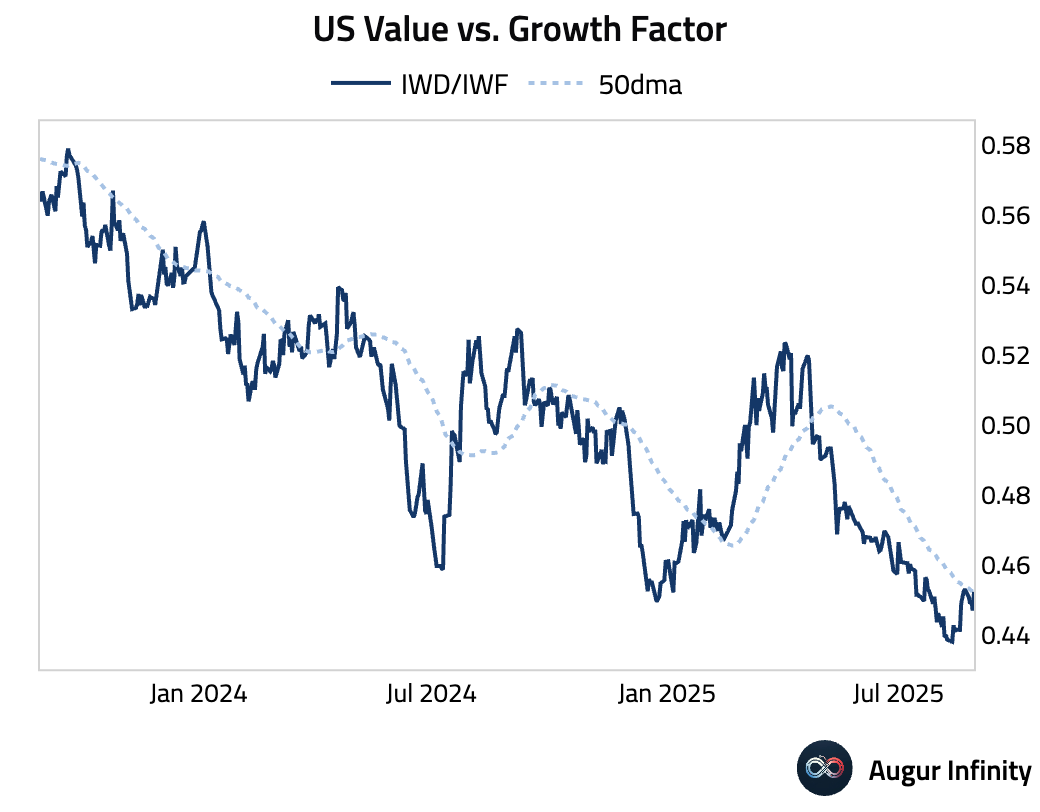

- Meanwhile, the US Value vs. Growth factor rose above its 50-day moving average.

Fixed Income

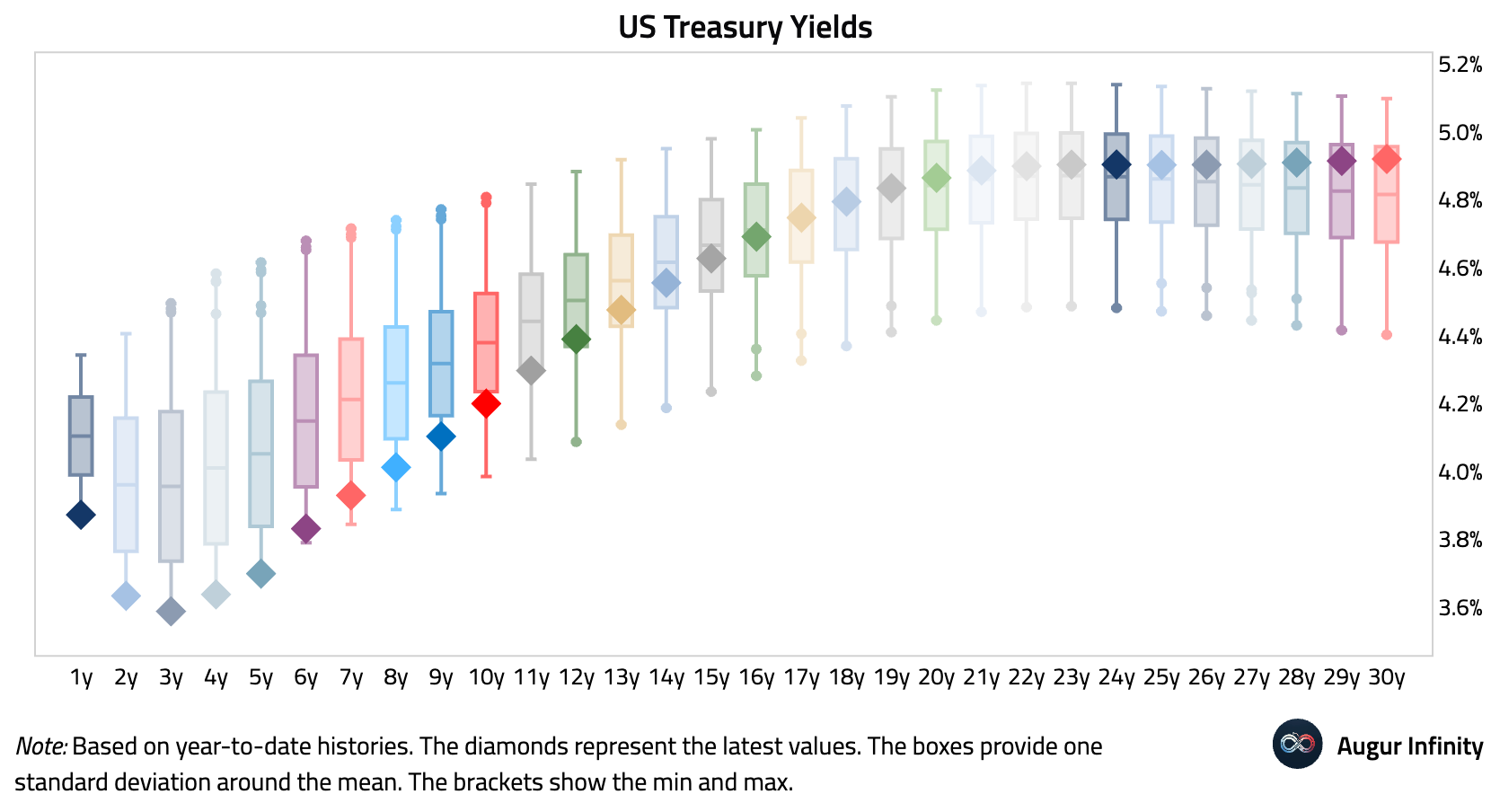

- Here's a year-to-date summary of US Treasury yields across the entire curve. The front end of the curve has fallen to the lowest levels this year, while the long end is trading about one standard deviation above the mean.

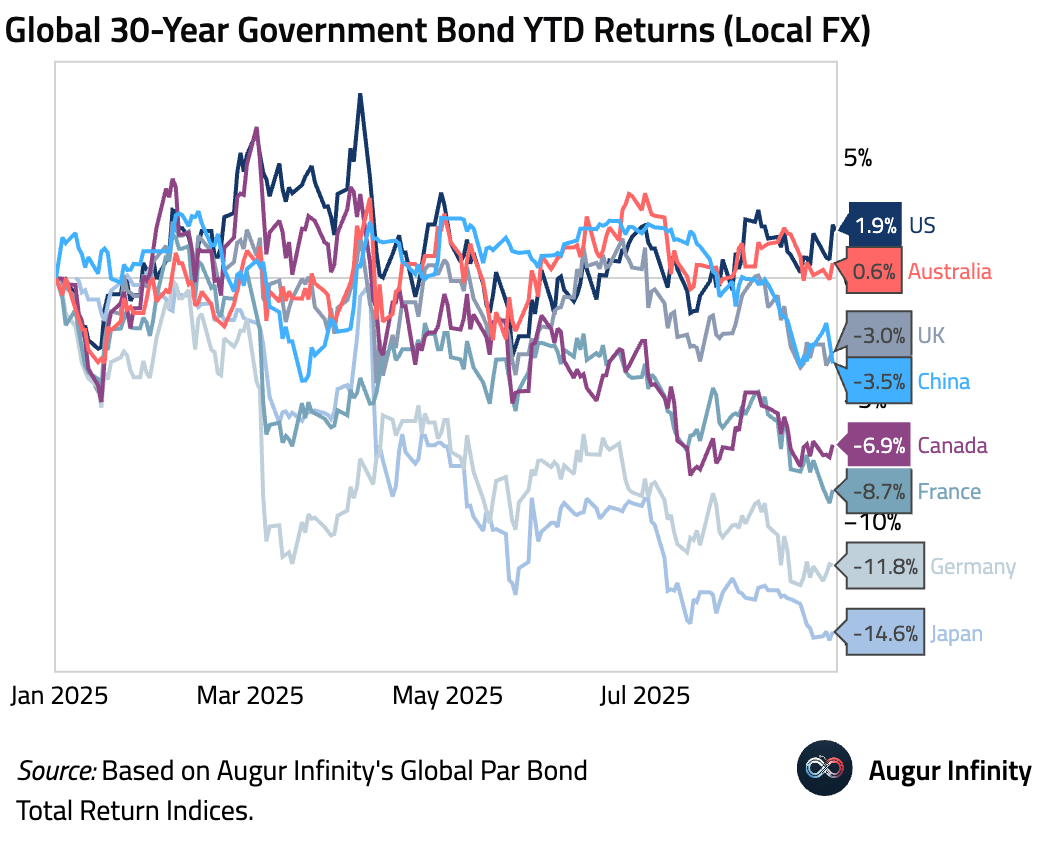

- Japan's 30-year government bonds are down nearly 15% year-to-date, significantly underperforming global peers.

FX

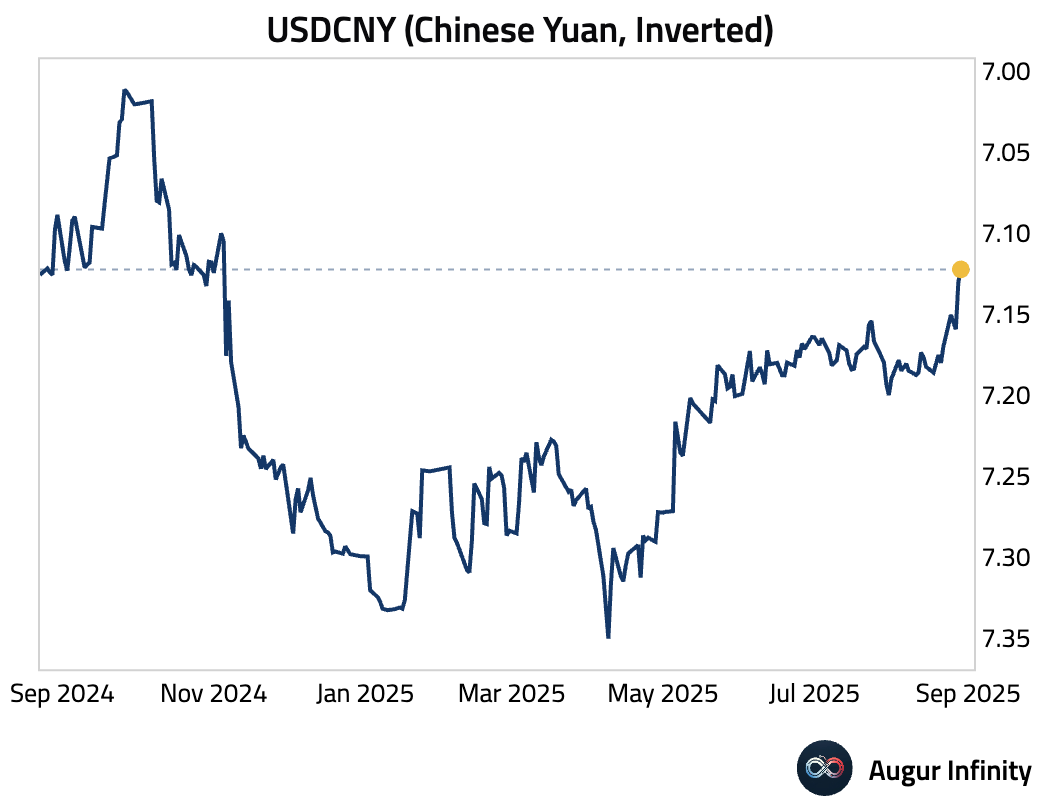

- The Chinese yuan continues to appreciate against the dollar, now at levels last since in November 2024.

Commodities

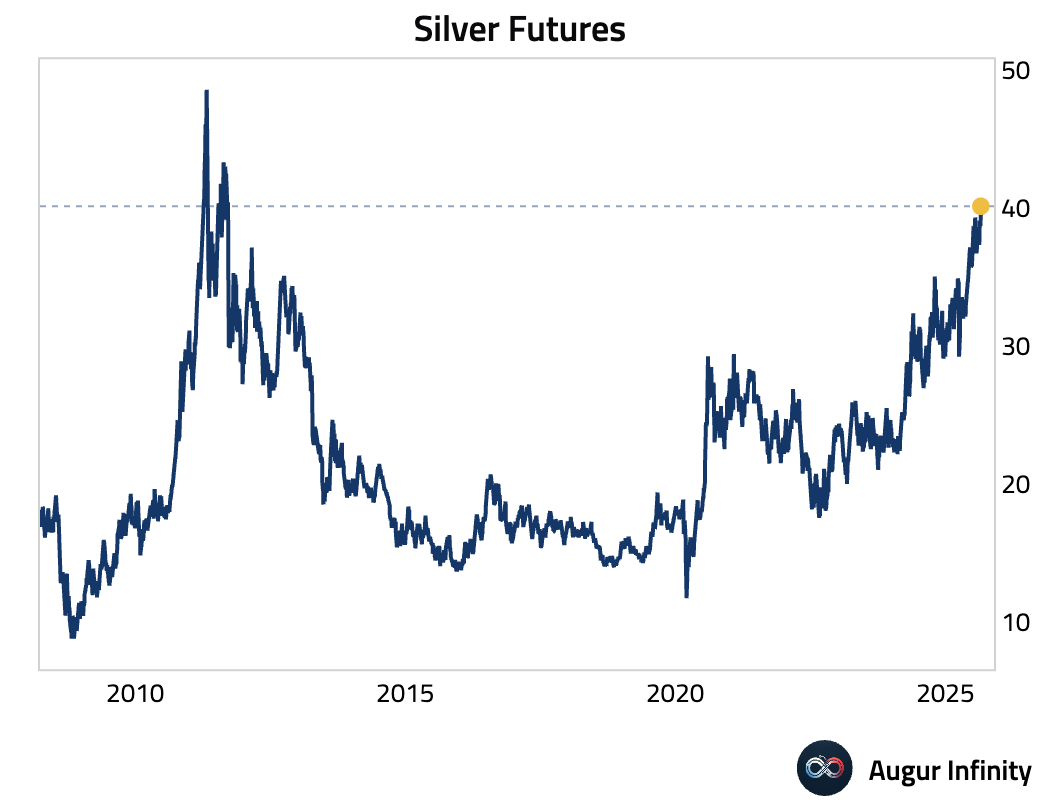

- Silver is trading around the highest level since 2011.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.