Charts of the Day

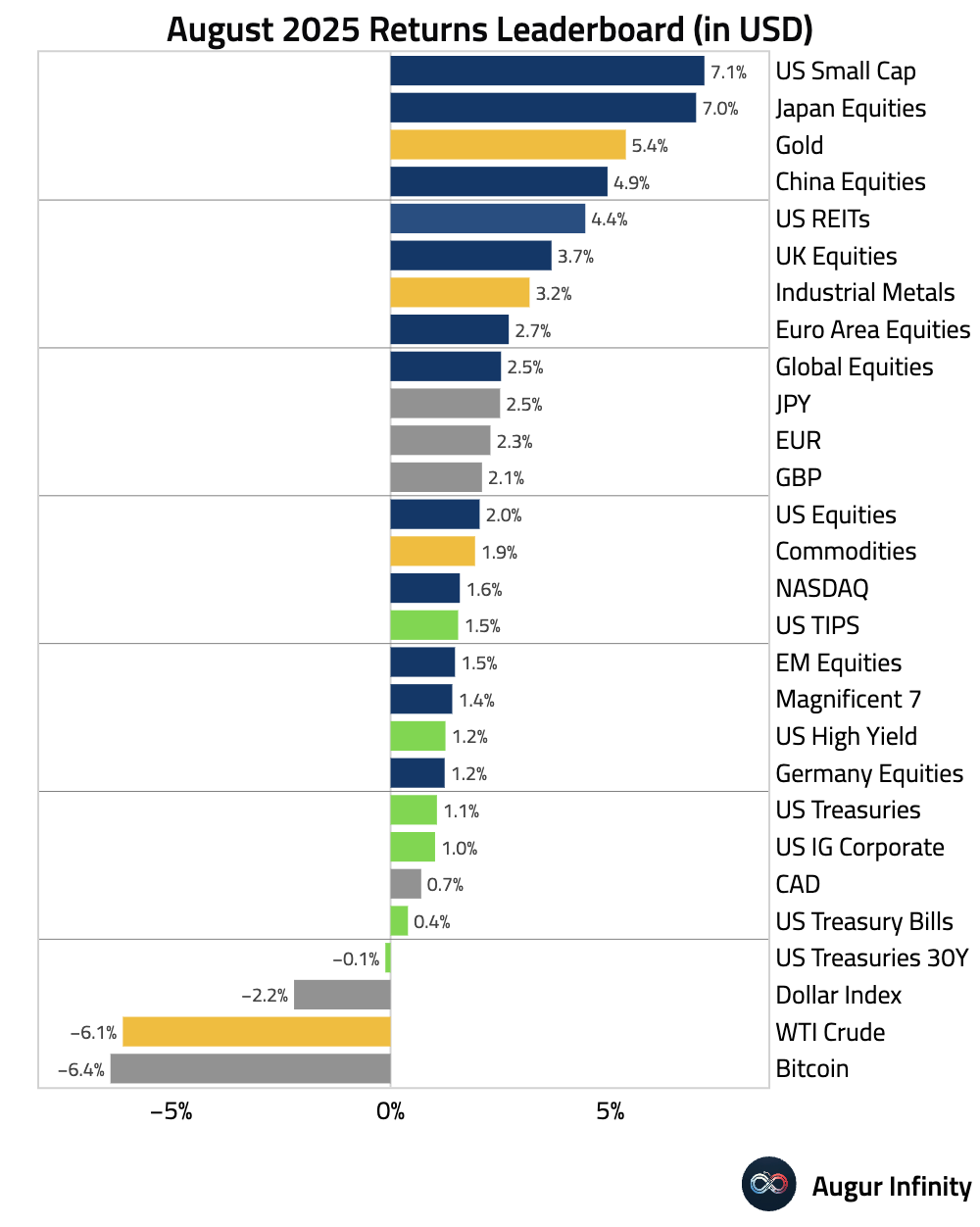

- Here's how global assets performed in August, with US Small Cap equities sitting atop the leaderboard.

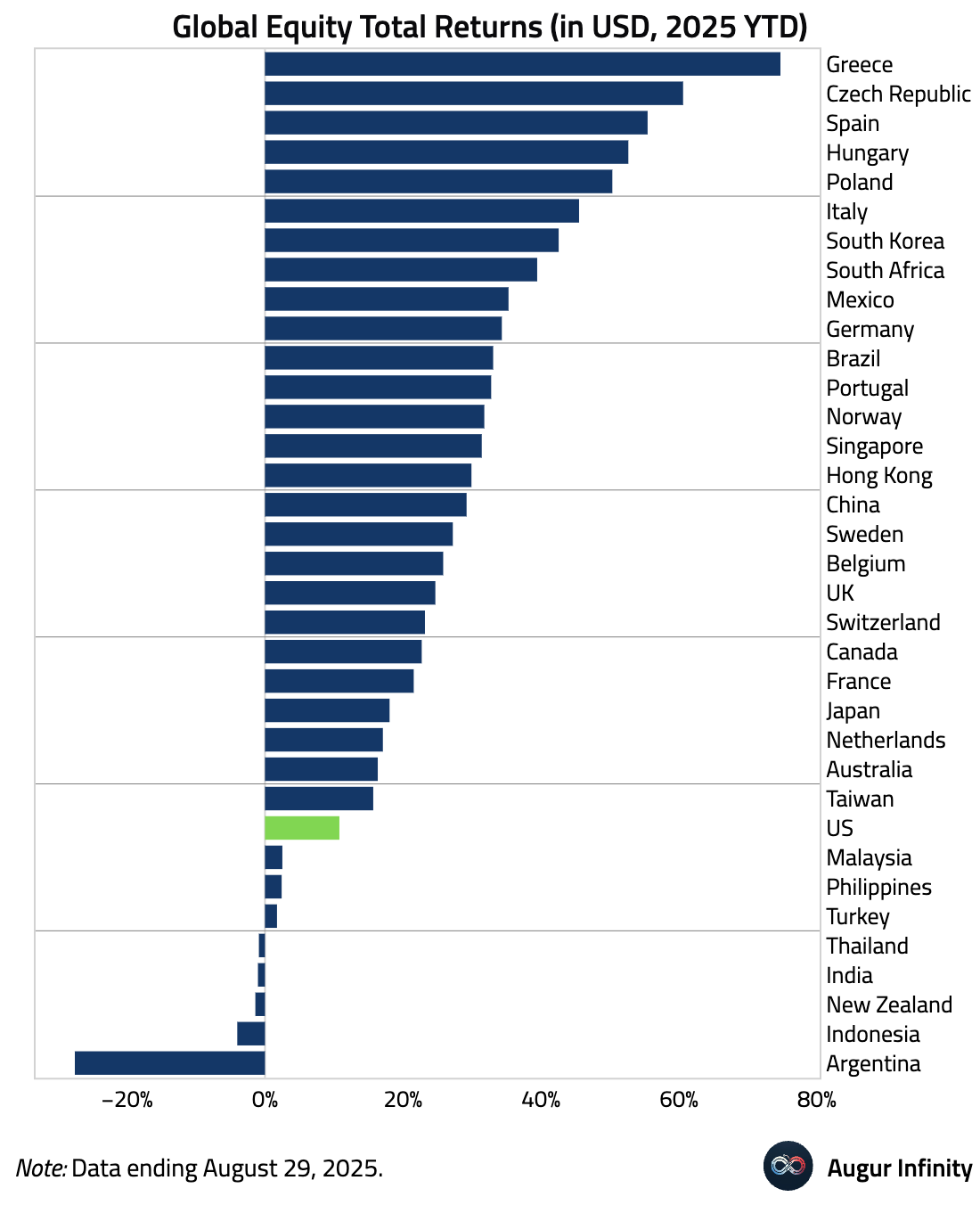

- Below we have the year-to-date returns of global equity markets (in USD). Greece equities toped the leaderboard, returning nearly 75%, while Argentina equities lagged far behind at -28%.

Global Economics

Canada

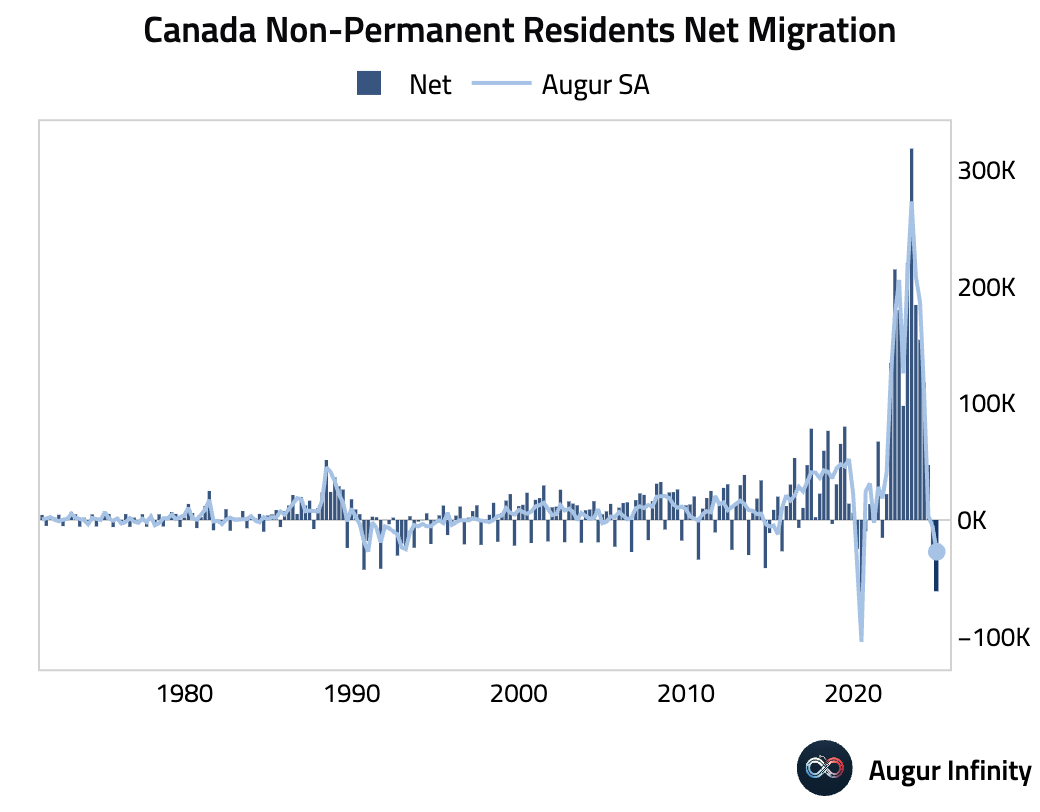

- Canada had the largest quarterly net outflow of non-permanent residents outside of the pandemic.

Source: @daniel_foch

Europe

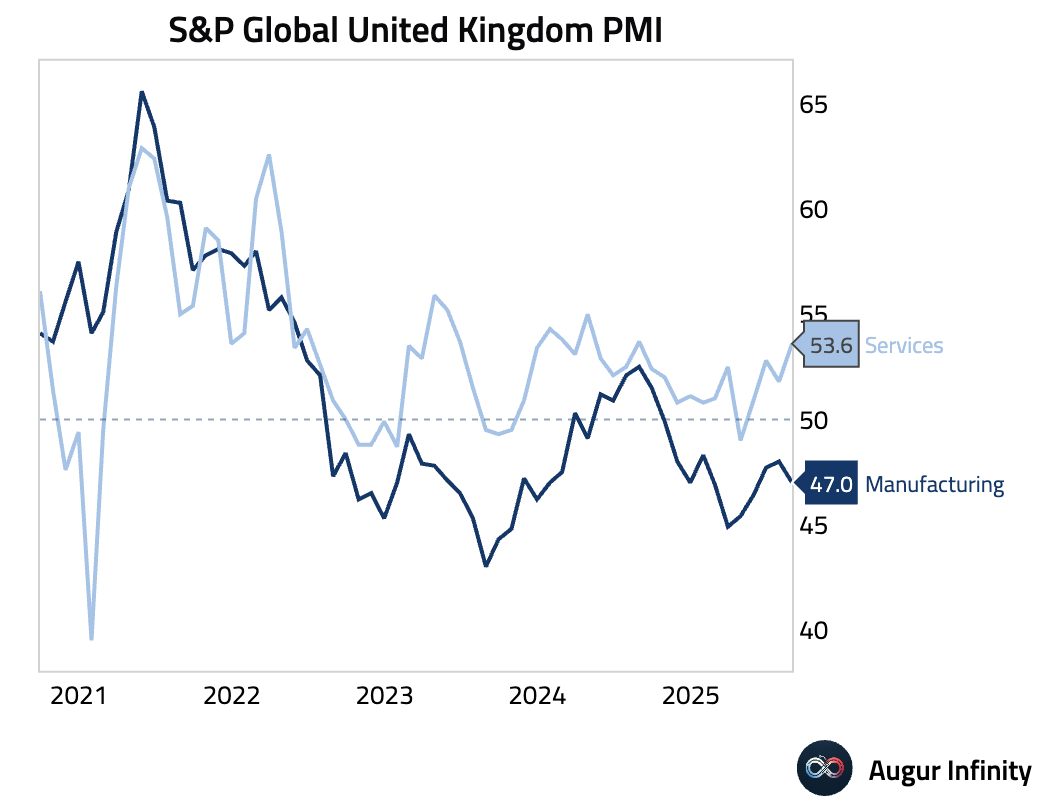

- The UK S&P Global Manufacturing PMI fell to a three-month low of 47.0 in August from 48.0, its 11th consecutive month of contraction. The decline was driven by the fastest drop in new orders in four months due to weak demand and tariff uncertainty. Despite the slowdown, business optimism improved to a six-month high.

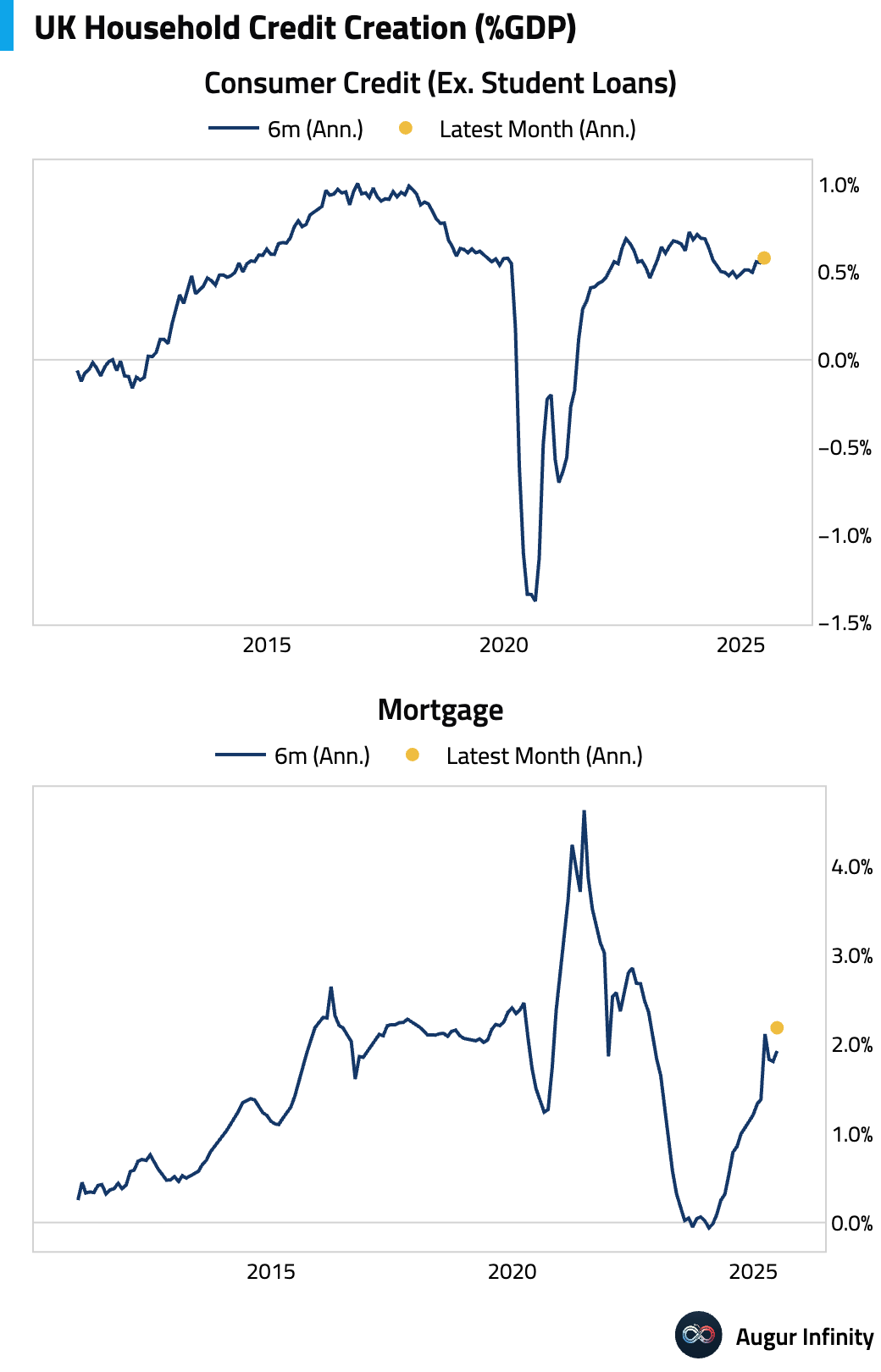

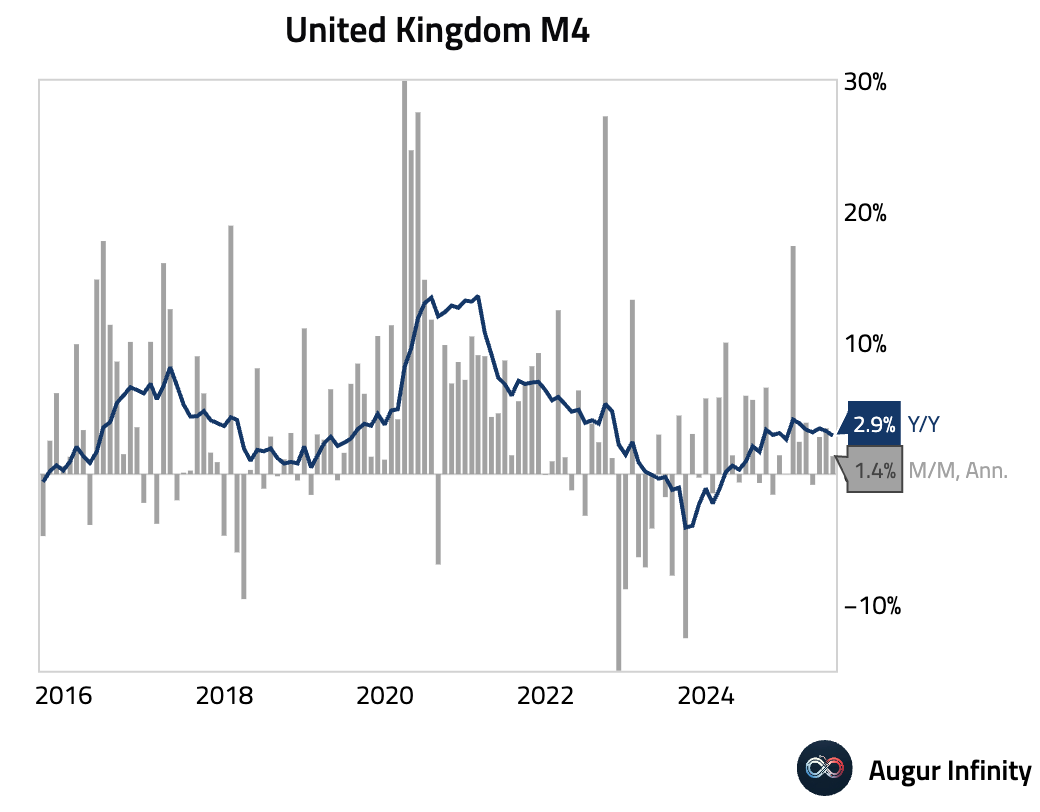

- UK credit growth exceeded expectations in July. Mortgage approvals rose to 65,350 (vs. 64,400 consensus), mortgage lending increased by £4.52 billion (vs. £3.4 billion consensus), and consumer credit expanded by £1.62 billion (vs. £1.35 billion consensus). M4 money supply growth slowed to 0.1% M/M (or 1.4% annualized).

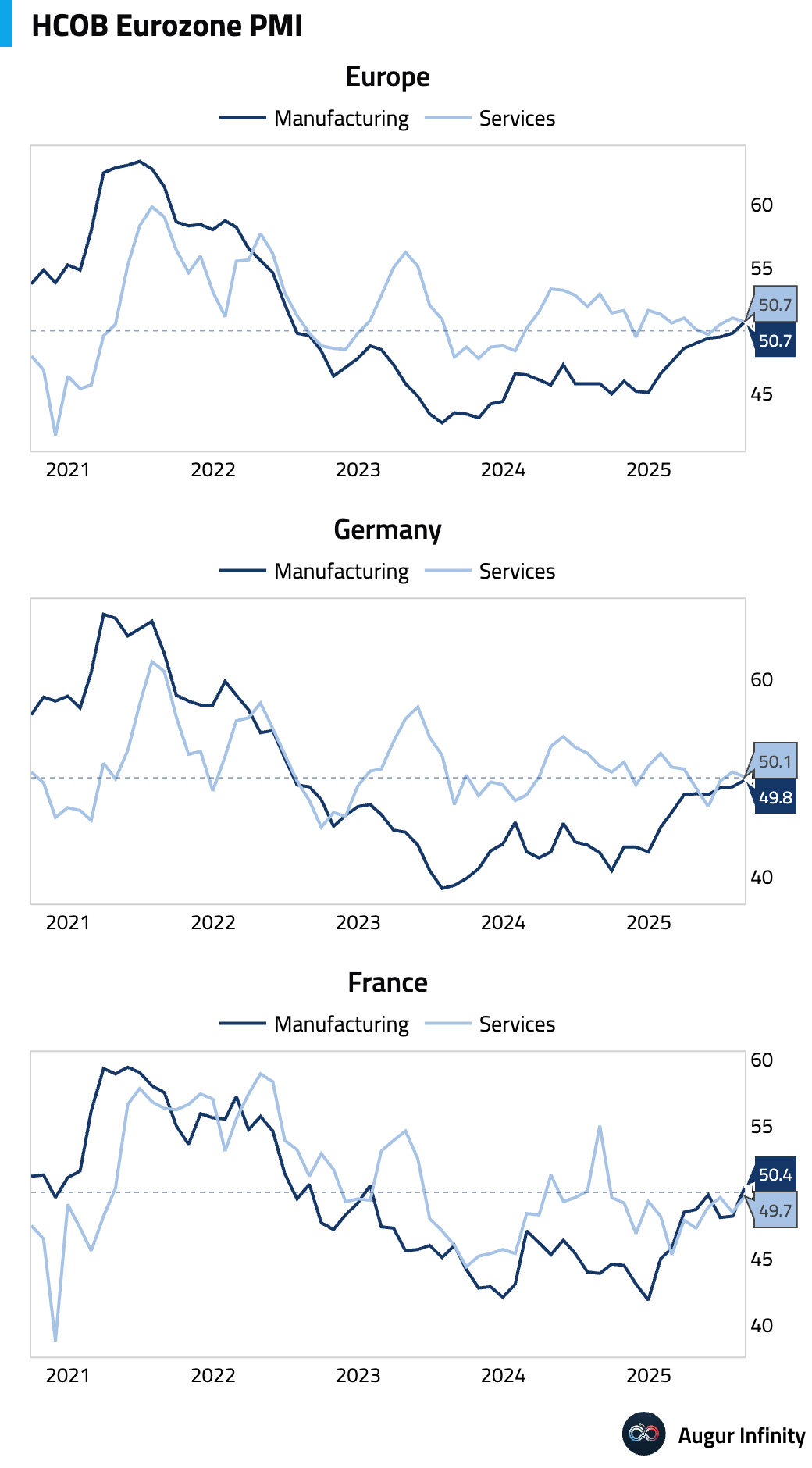

- The Eurozone’s manufacturing sector showed signs of recovery as final August PMIs confirmed a return to expansionary territory for the first time since June 2022. The headline HCOB Manufacturing PMI for the Eurozone rose to 50.7 from 49.8, driven by the sharpest rise in factory output in 41 months. Germany’s PMI reached a 38-month high of 49.8 (from 49.1), nearing stabilization, while France’s PMI registered 50.4 (from 48.2), its first expansionary reading since January 2023. The recovery remains fragile and domestically focused, with new export orders falling for a second consecutive month across the bloc.

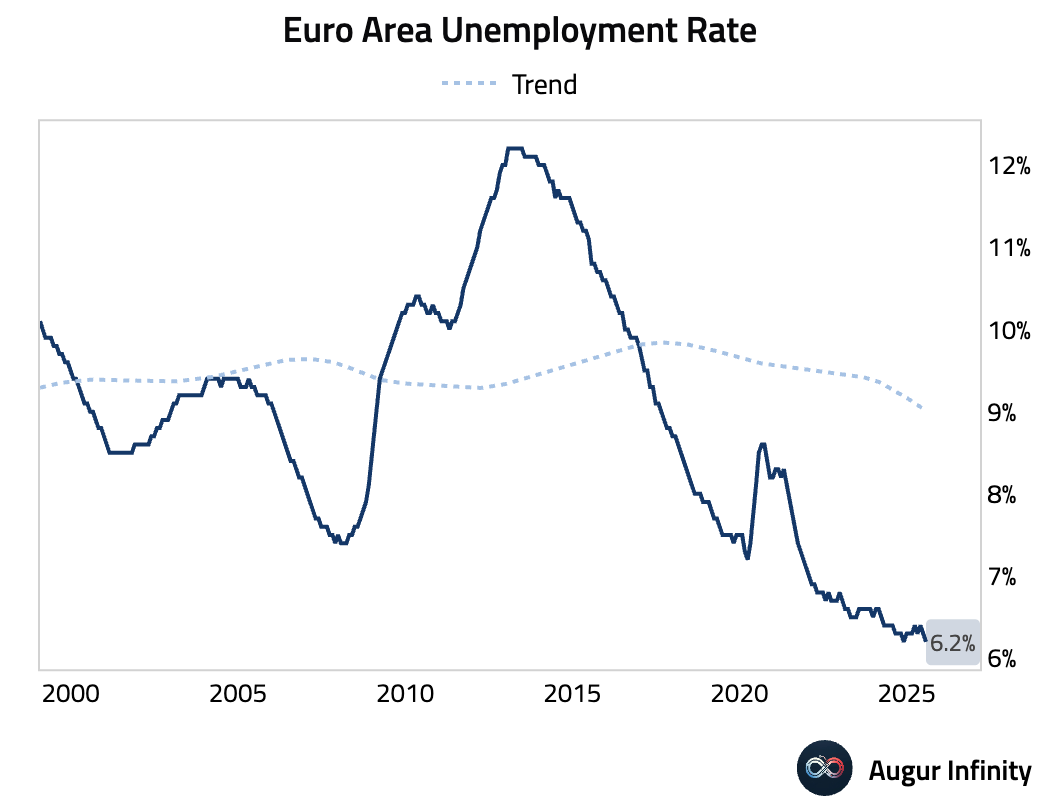

- The Euro Area unemployment rate fell to 6.2% in July, a new all-time low for the series, down from a revised 6.3% in June and in line with consensus.

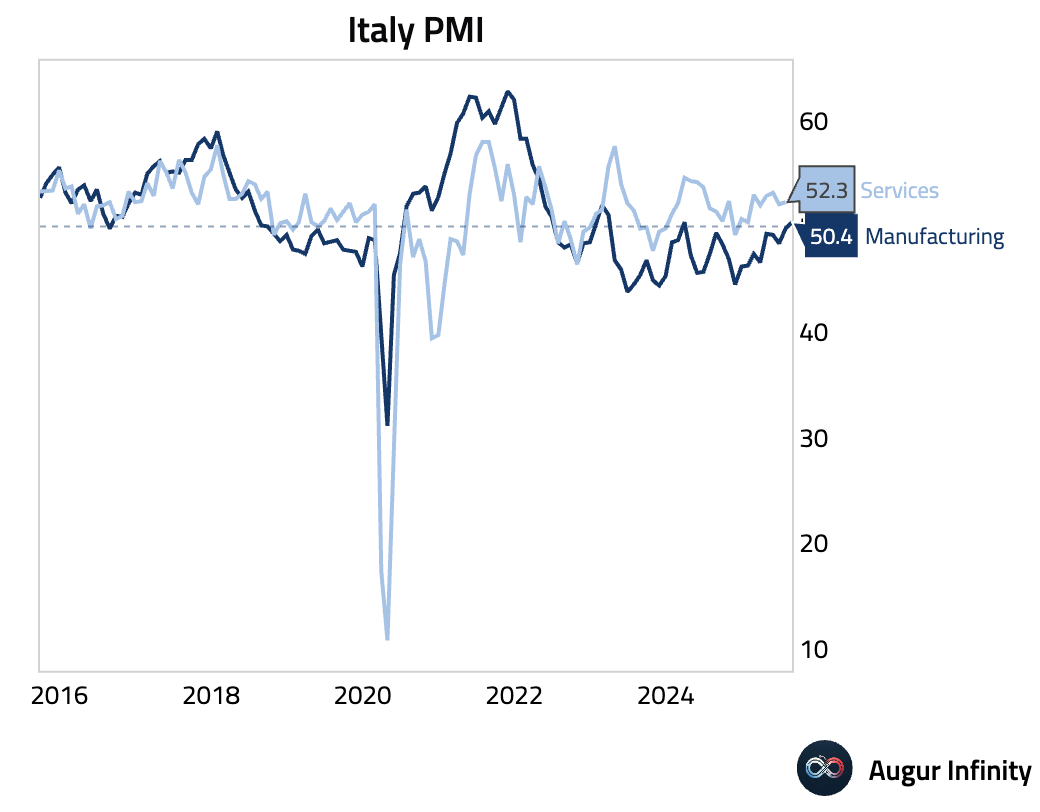

- Italy's HCOB Manufacturing PMI returned to growth in August for the first time in nearly 1.5 years, rising to 50.4 from 49.8 and beating expectations of 49.8. The recovery was driven by the sharpest production increase in almost 2.5 years, though it remains fragile and domestically focused, with a faster decline in export sales offsetting a slight rise in overall orders.

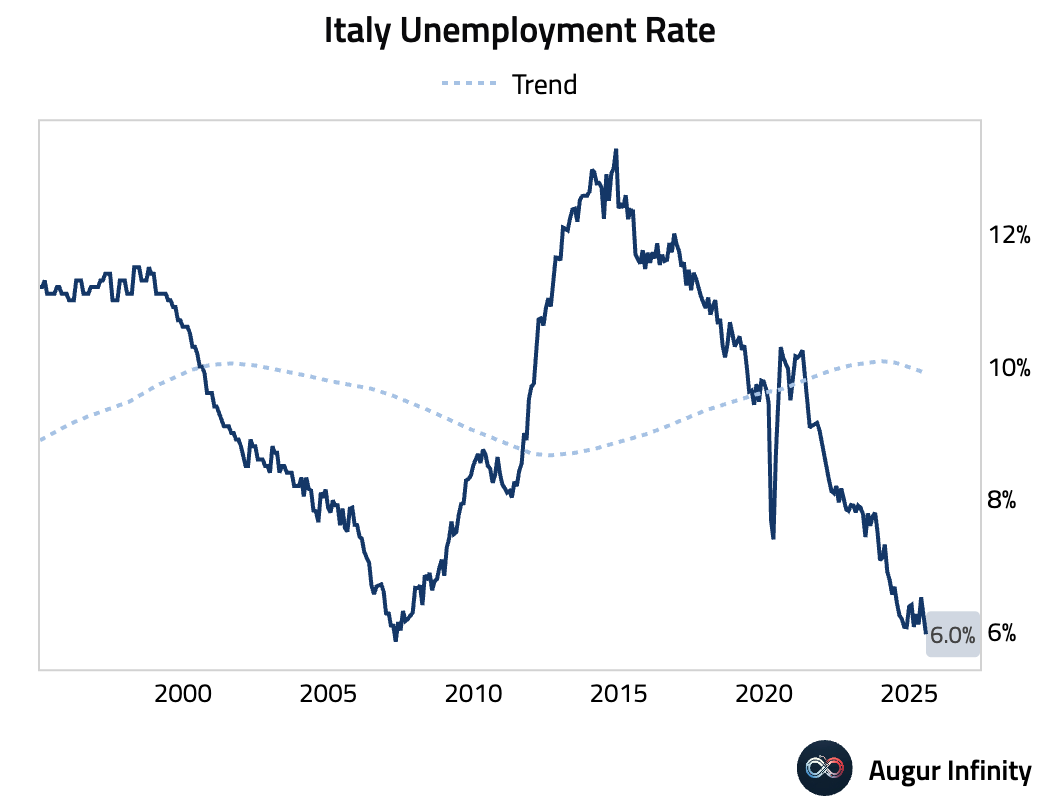

- Italy’s unemployment rate fell to 6.0% in July from 6.2%, below the consensus of 6.2% and marking the lowest level since April 2007.

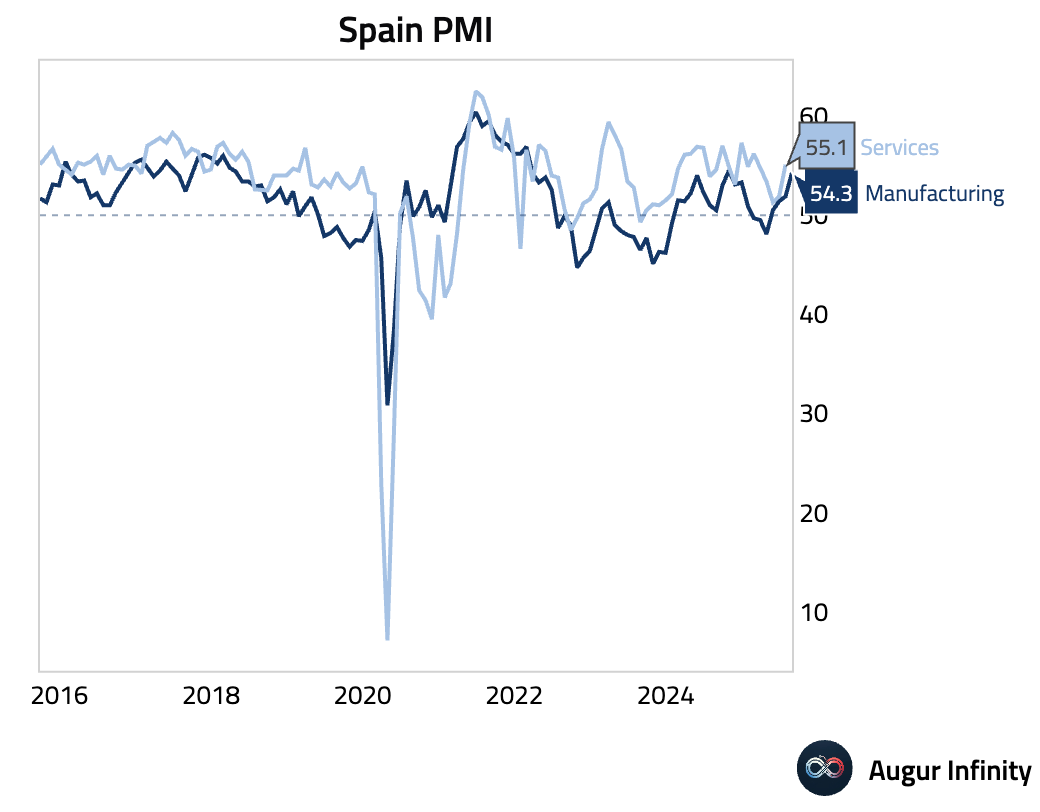

- Spain's HCOB Manufacturing PMI surged to an 11-month high of 54.3 in August, up from 51.9 and well above the 52.0 consensus. The expansion was driven by sharp growth in domestic output and new orders, fueling the strongest job creation since last December.

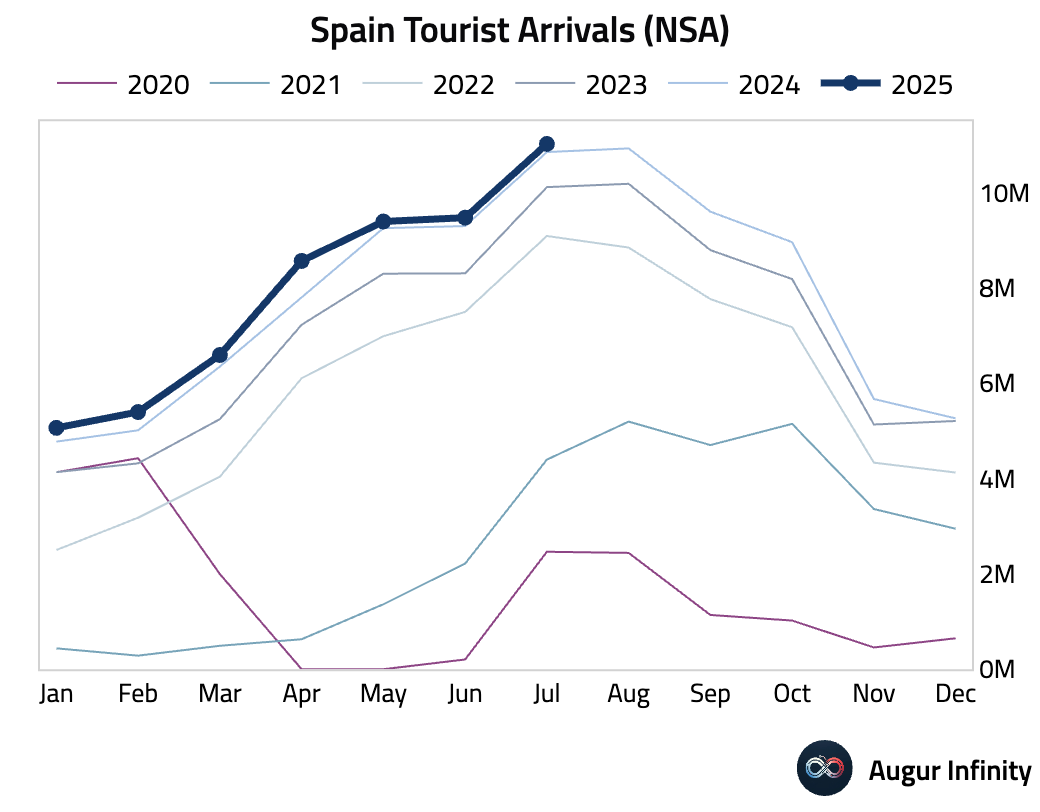

- International tourist arrivals in Spain decelerated in July, growing 1.6% Y/Y, down from 1.9% in June.

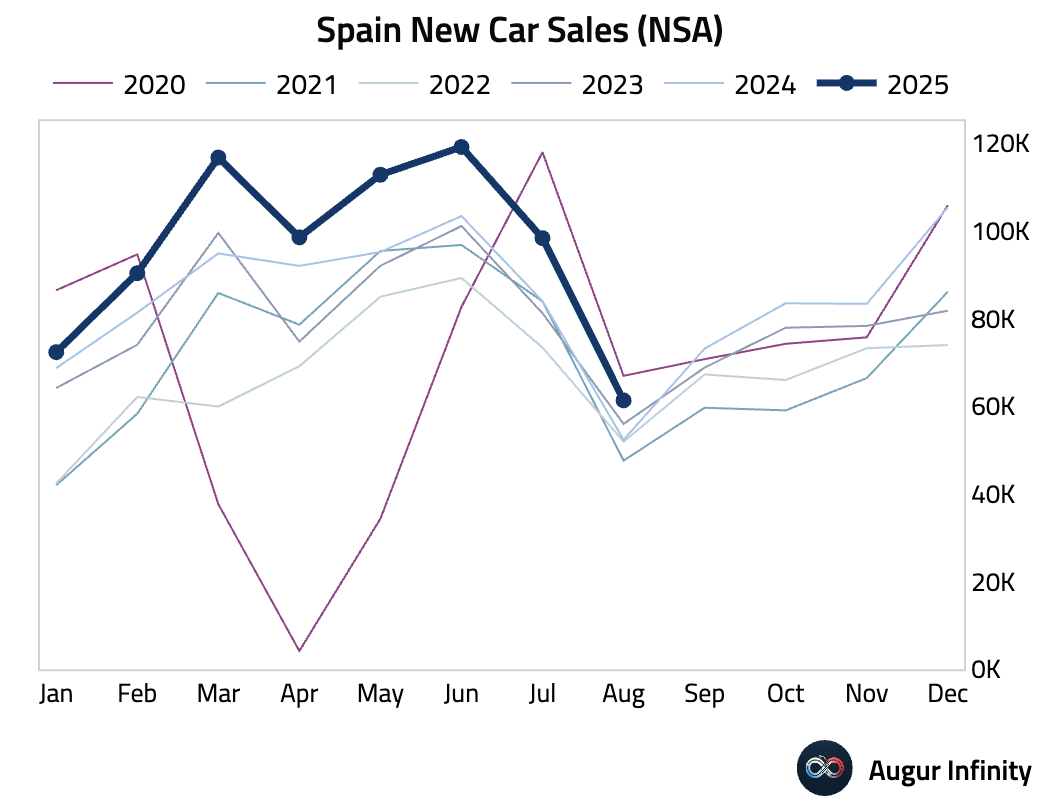

- Spanish new car sales remained robust in August, rising 17.2% Y/Y, slightly faster than July's 17.1% pace.

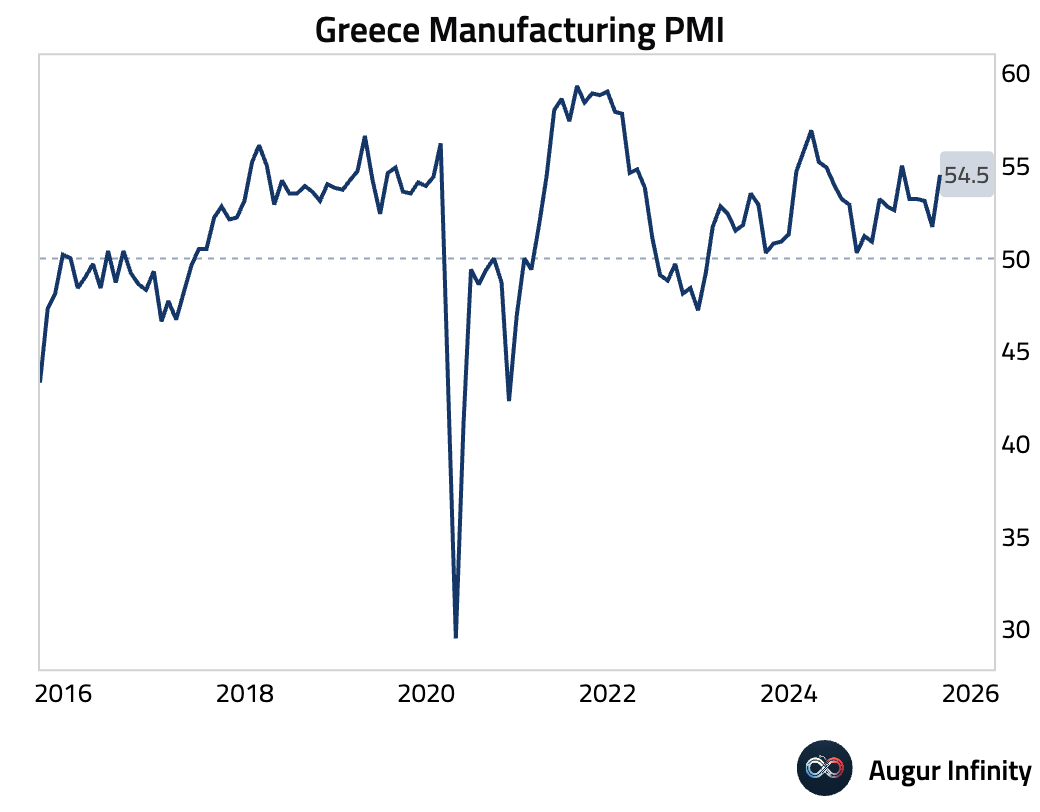

- Greece’s Manufacturing PMI jumped to a five-month high of 54.5 in August from 51.7, driven by the strongest growth in domestic new orders since March 2024. This strength masked a sharp deterioration in exports, which fell at the fastest rate since December 2022.

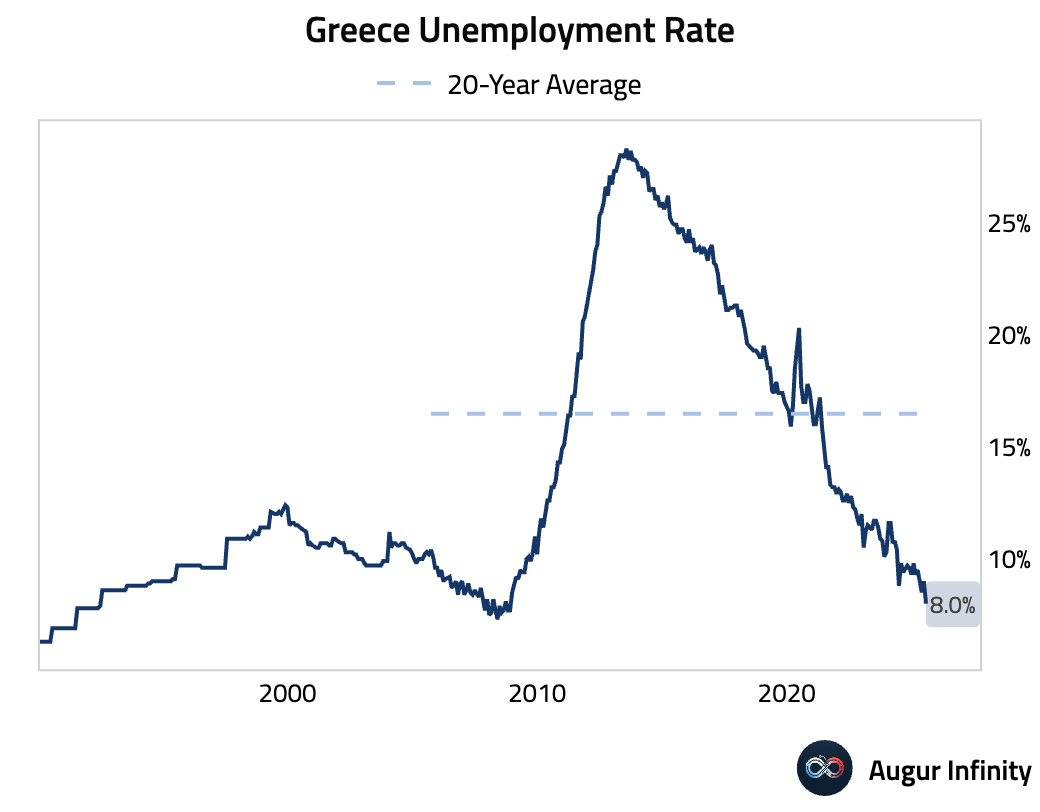

- Greece's unemployment rate fell sharply to 8.0% in July. This is Greece's lowest jobless rate since November 2008.

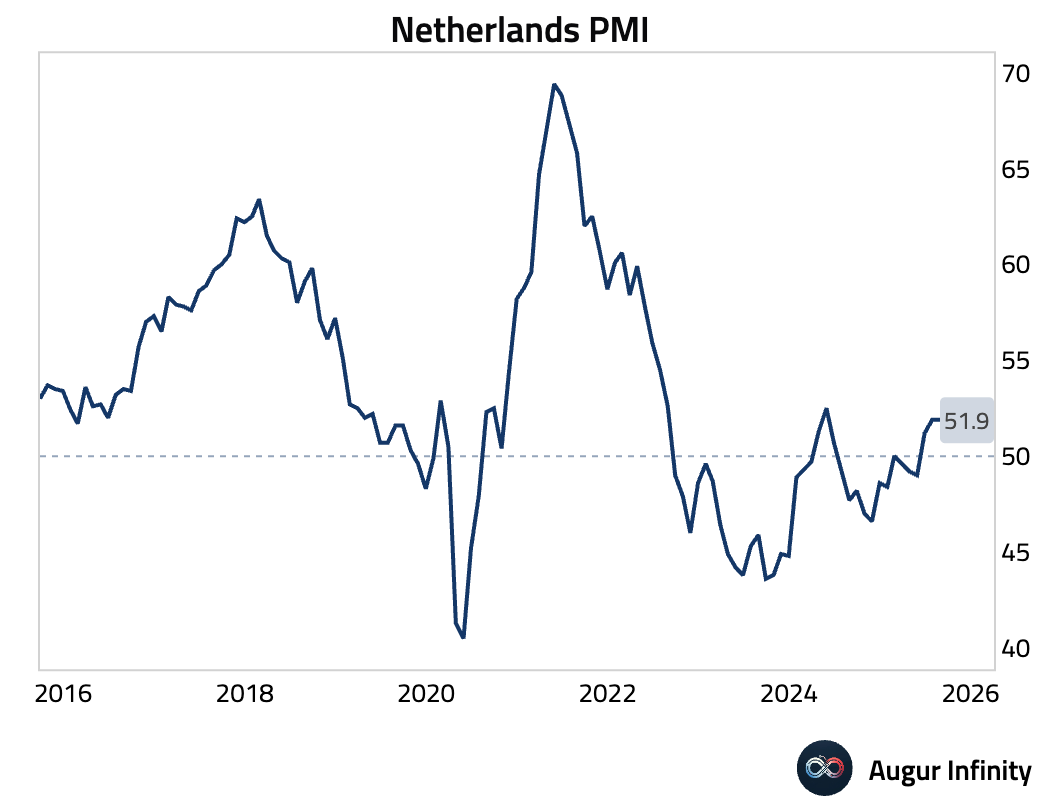

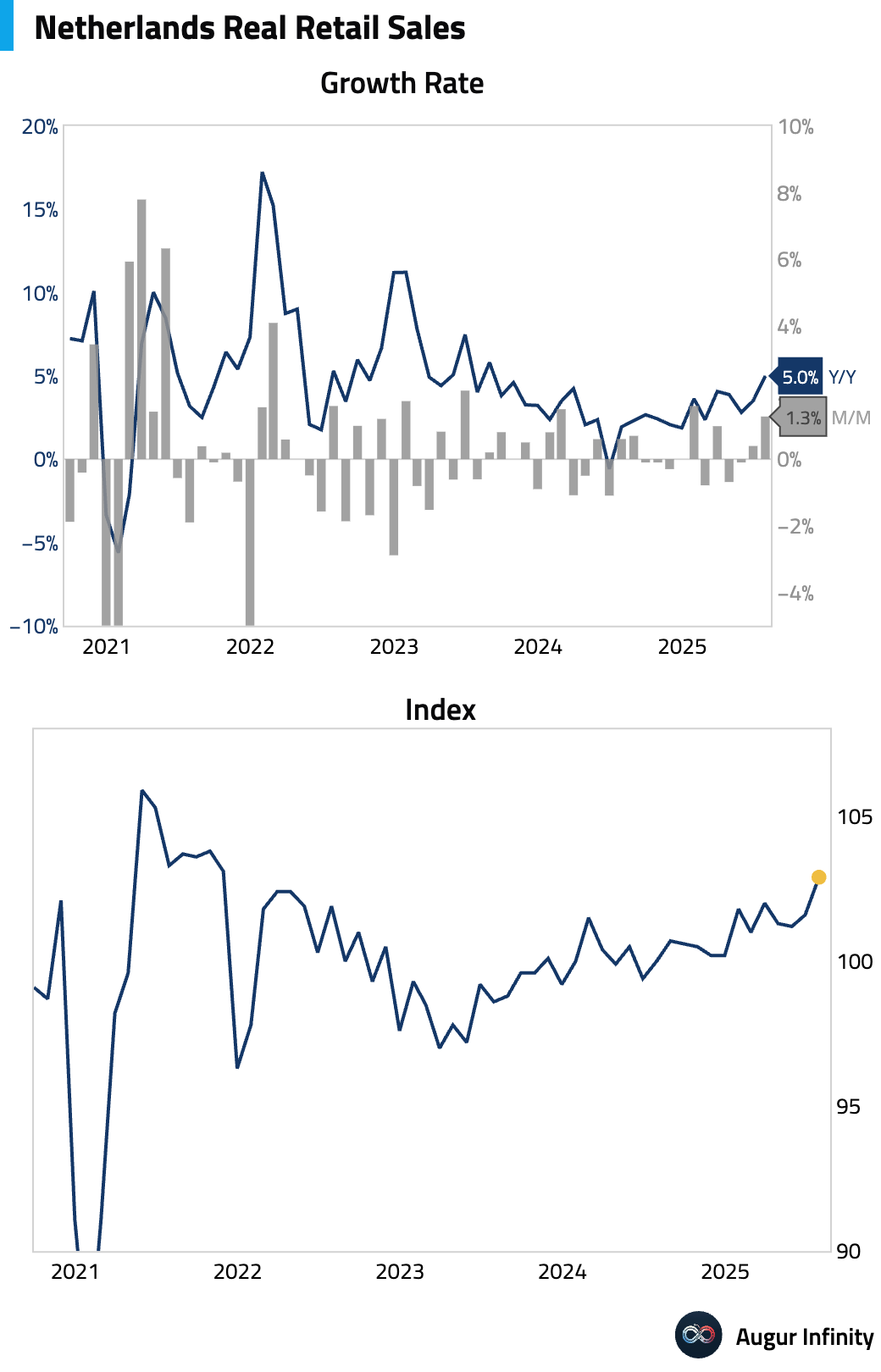

- The Netherlands’ NEVI Manufacturing PMI held steady at 51.9 in August, masking a divergence between soaring output—a 15-month high—and slowing new orders, as export demand nearly stalled. Employment grew at the fastest pace since late 2022 to meet production needs, but business confidence fell to a four-month low amid geopolitical and tariff uncertainty.

- Dutch retail sales accelerated in July, rising 5.0% Y/Y from 3.4% in the prior month. This was the fastest Y/Y growth rate in two years.

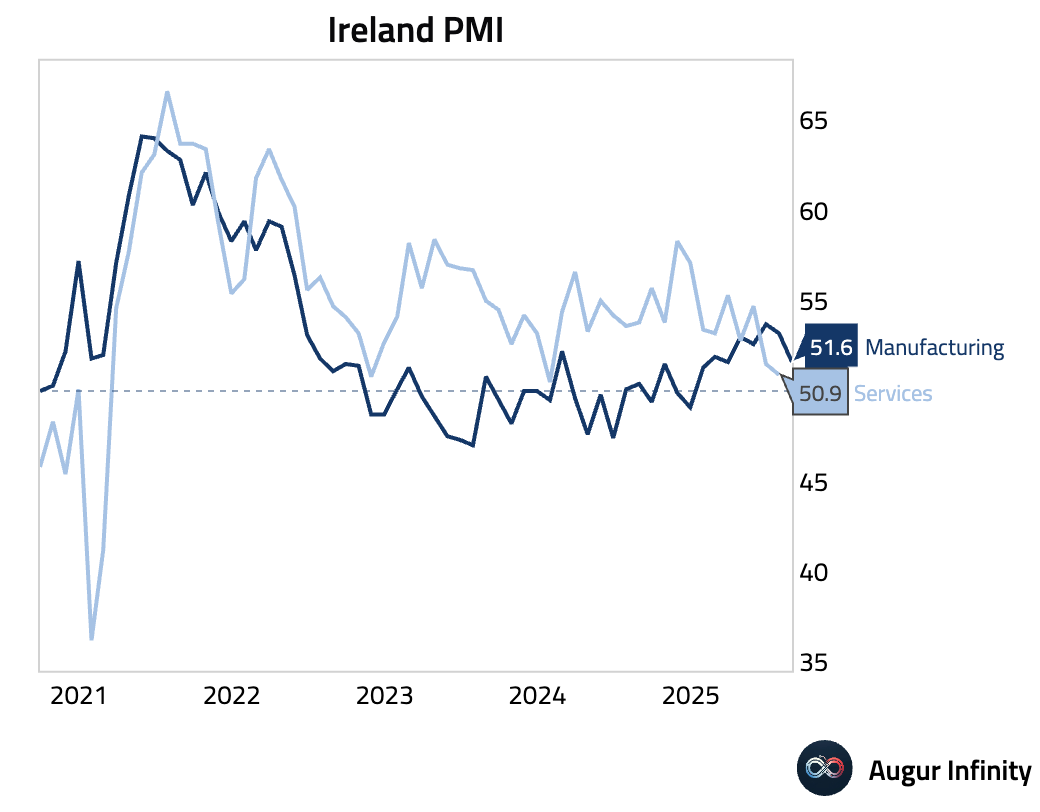

- Ireland’s Manufacturing PMI fell to a five-month low of 51.6 in August from 53.2, as output and new orders hit seven-month lows. The slowdown was driven by weak export demand, particularly from the UK, which offset resilient domestic conditions. Despite this, business optimism reached an eight-month high on hopes for a global rebound.

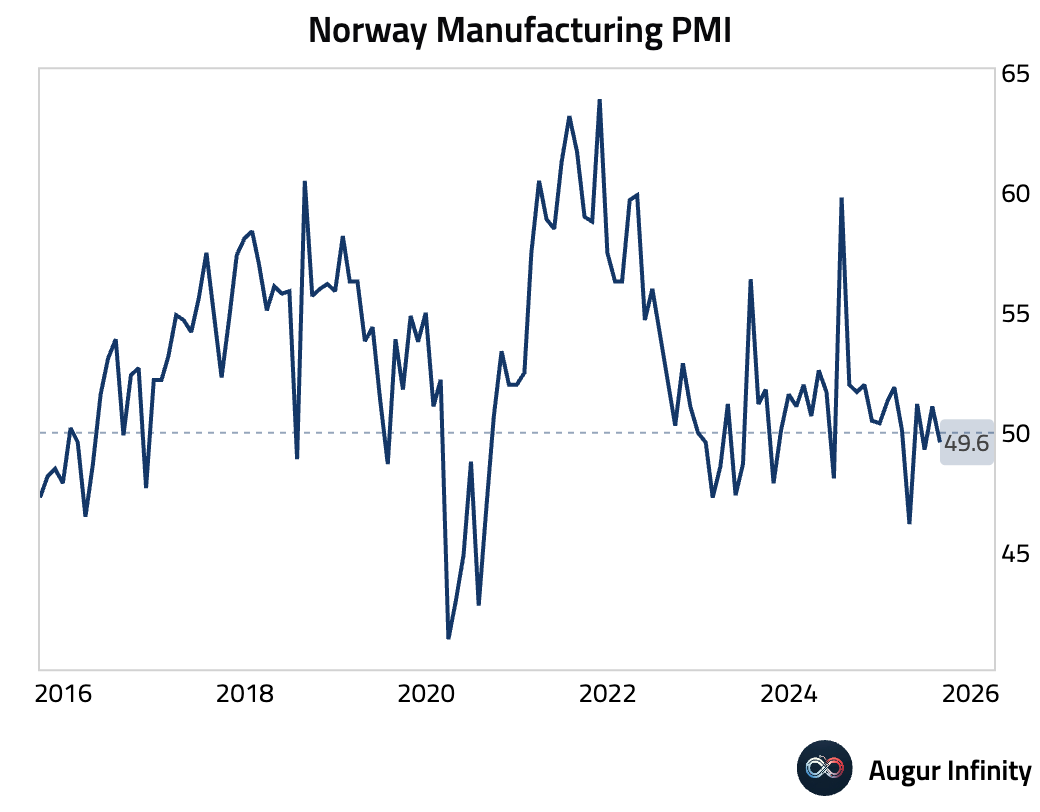

- Norway’s manufacturing sector contracted in August, with the DNB Manufacturing PMI falling to 49.6 from 51.1 in July.

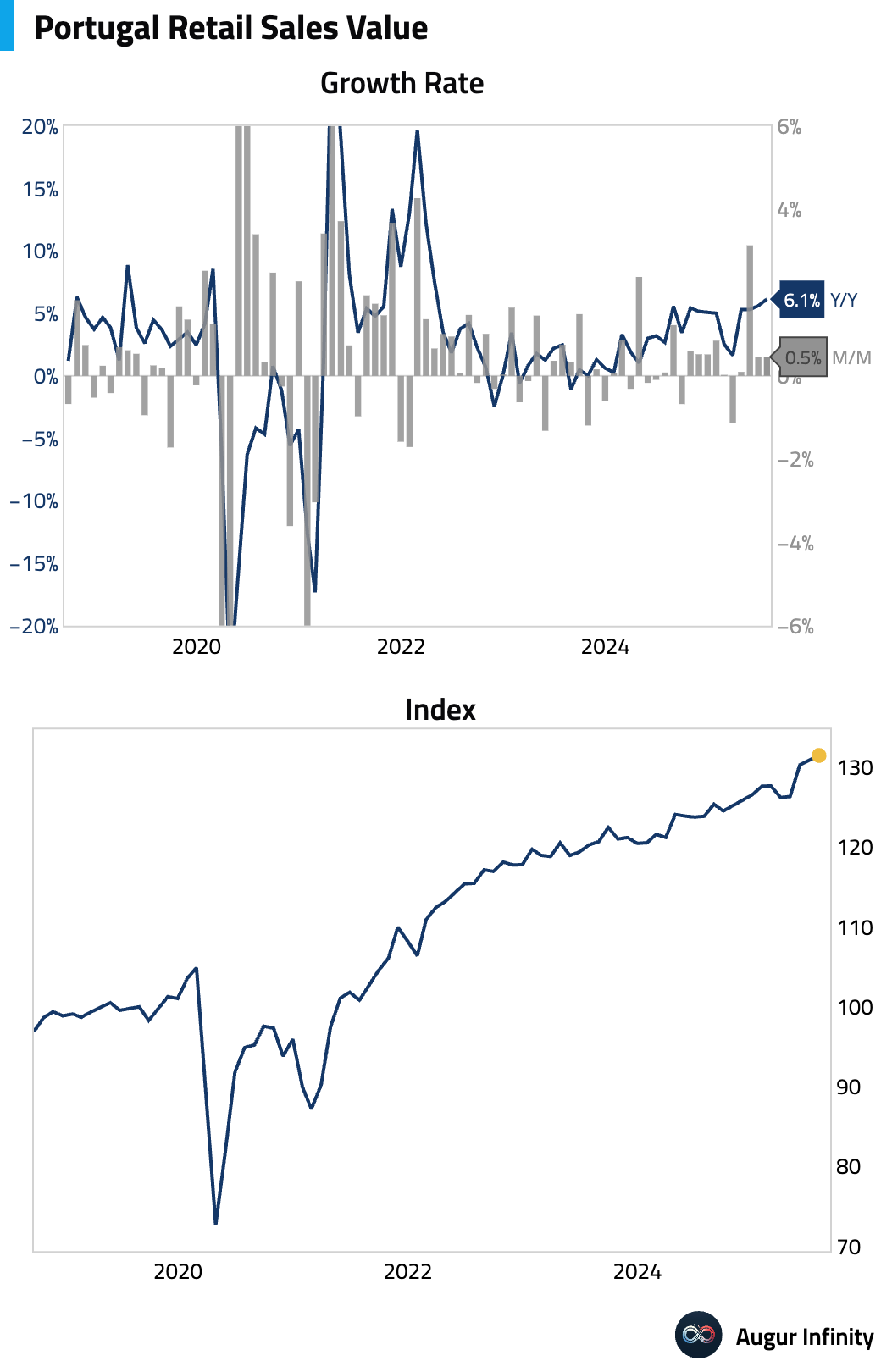

- Portuguese nominal retail sales growth rose to 6.1% Y/Y in July from 5.6% in June.

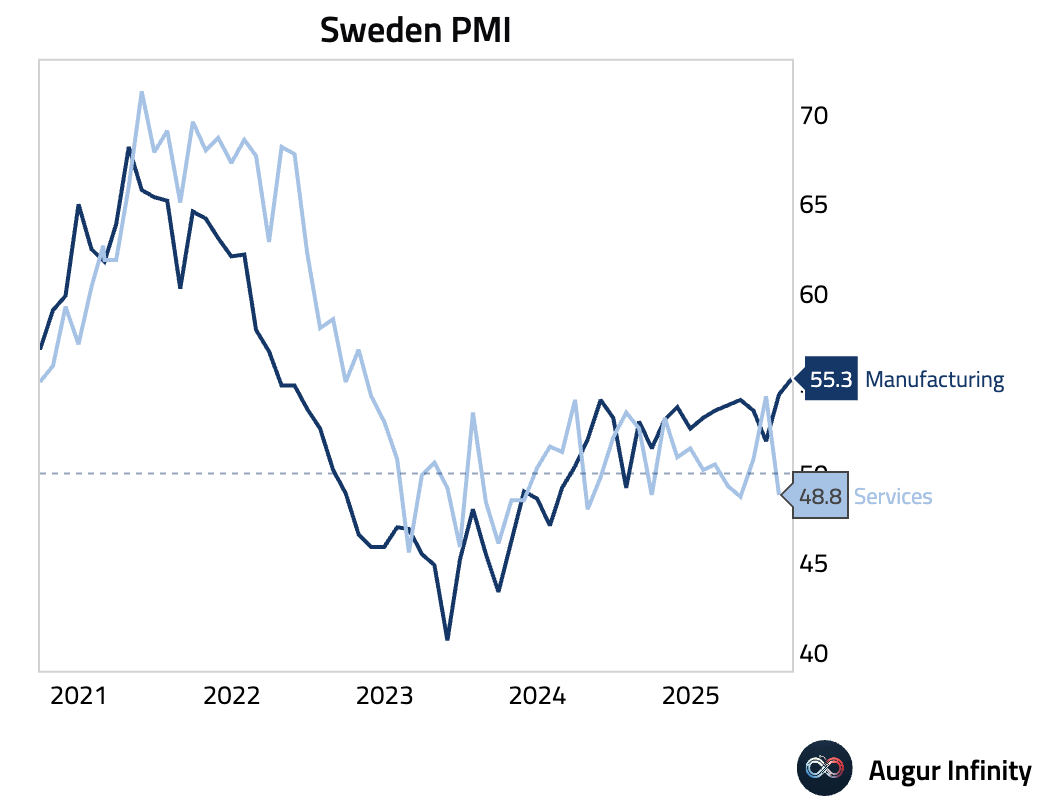

- Sweden’s manufacturing activity strengthened in August, with the Swedbank Manufacturing PMI rising to 55.3 from 54.4. This marks the highest reading since March 2022.

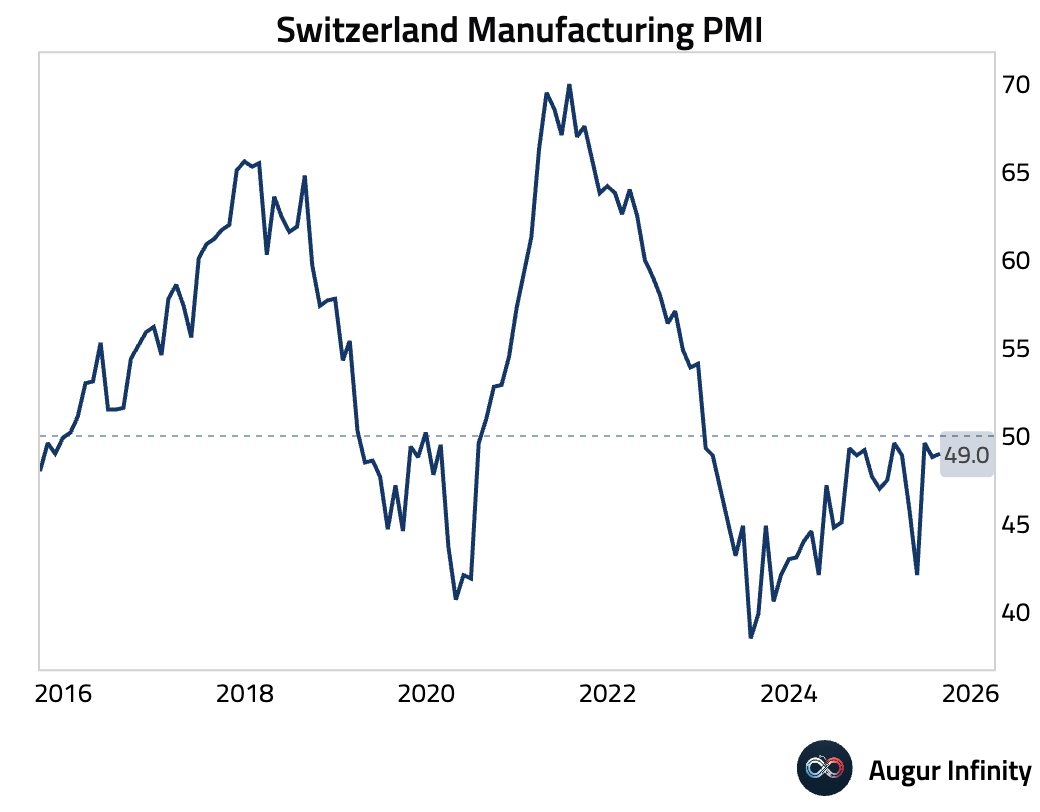

- Switzerland’s procure.ch Manufacturing PMI unexpectedly rose to 49.0 in August, beating the consensus of 47.0 and up from 48.8 in July, though it remains in contractionary territory.

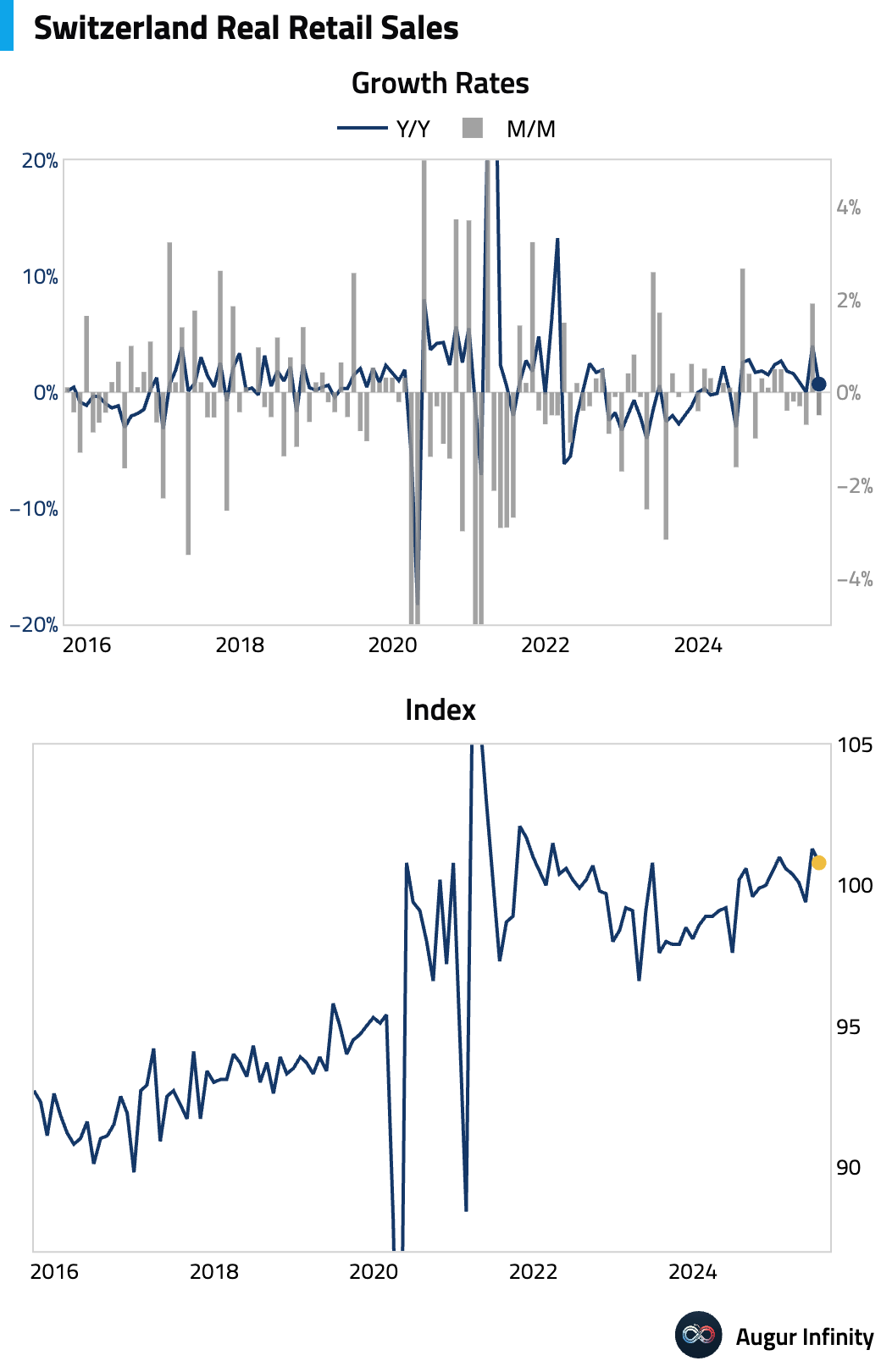

- Swiss real retail sales growth slowed sharply to 0.7% Y/Y in July from 3.9% in June, significantly missing the 3.6% consensus estimate. On a monthly basis, sales fell 0.5%.

Asia-Pacific

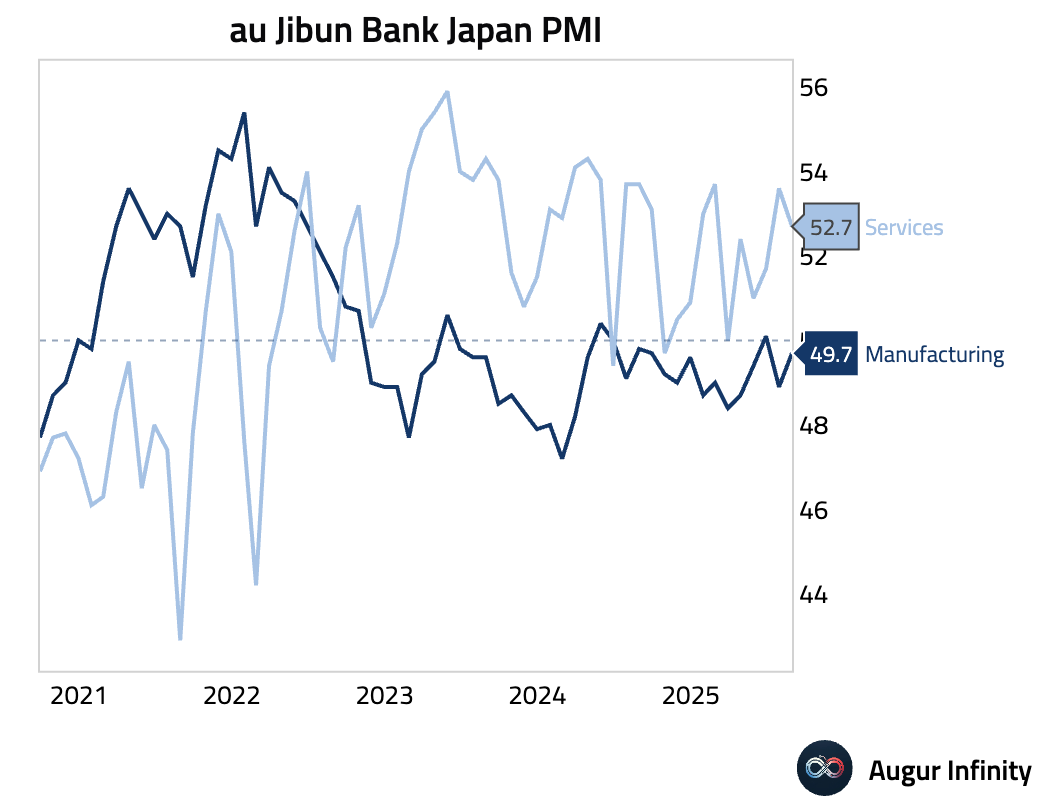

- Japan’s S&P Global Manufacturing PMI edged up to 49.7 in August from 48.9, nearing stabilization as the contraction in output eased. However, new export orders fell at the sharpest pace since March 2024, signaling persistent weakness in global demand. Price pressures cooled significantly, with selling prices rising at the slowest rate in over four years amid intense competition.

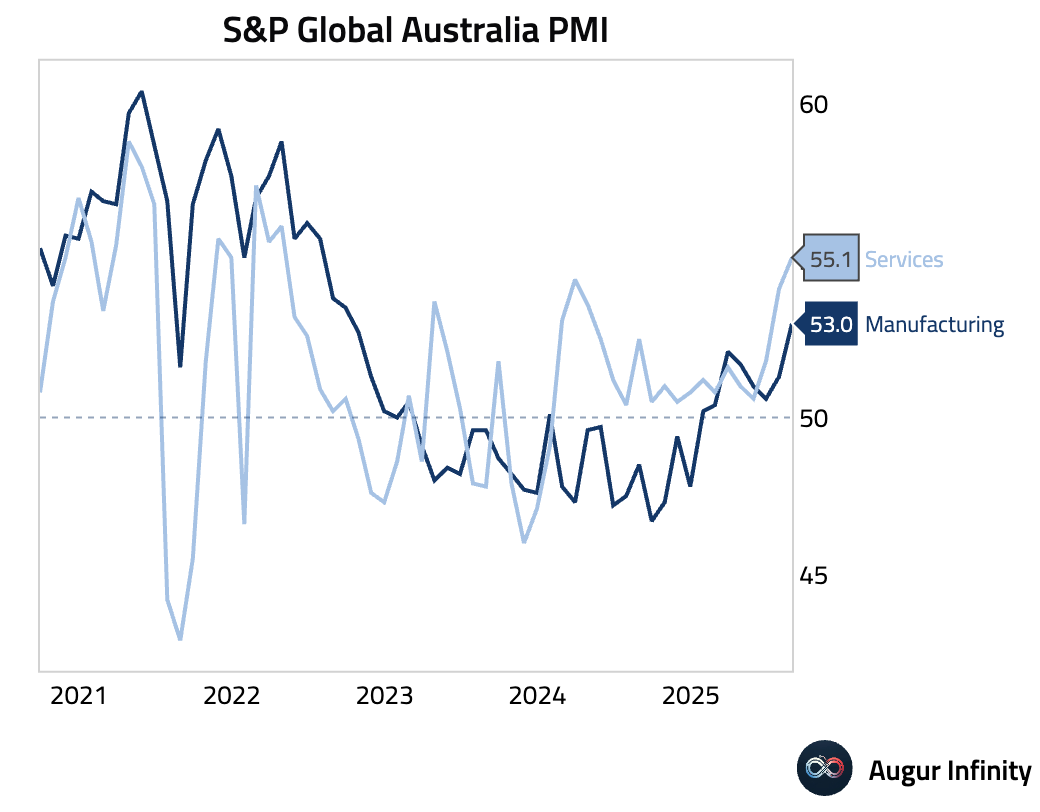

- Australia’s S&P Global Manufacturing PMI rose to 53.0 in August, up from 51.3 and reaching its highest level in nearly three years. The expansion was driven by the fastest growth in new orders in almost three years, reflecting stronger domestic demand and a renewed rise in exports. Easing trade tensions and lower domestic interest rates were cited as key drivers, boosting business confidence to a 3.5-year high.

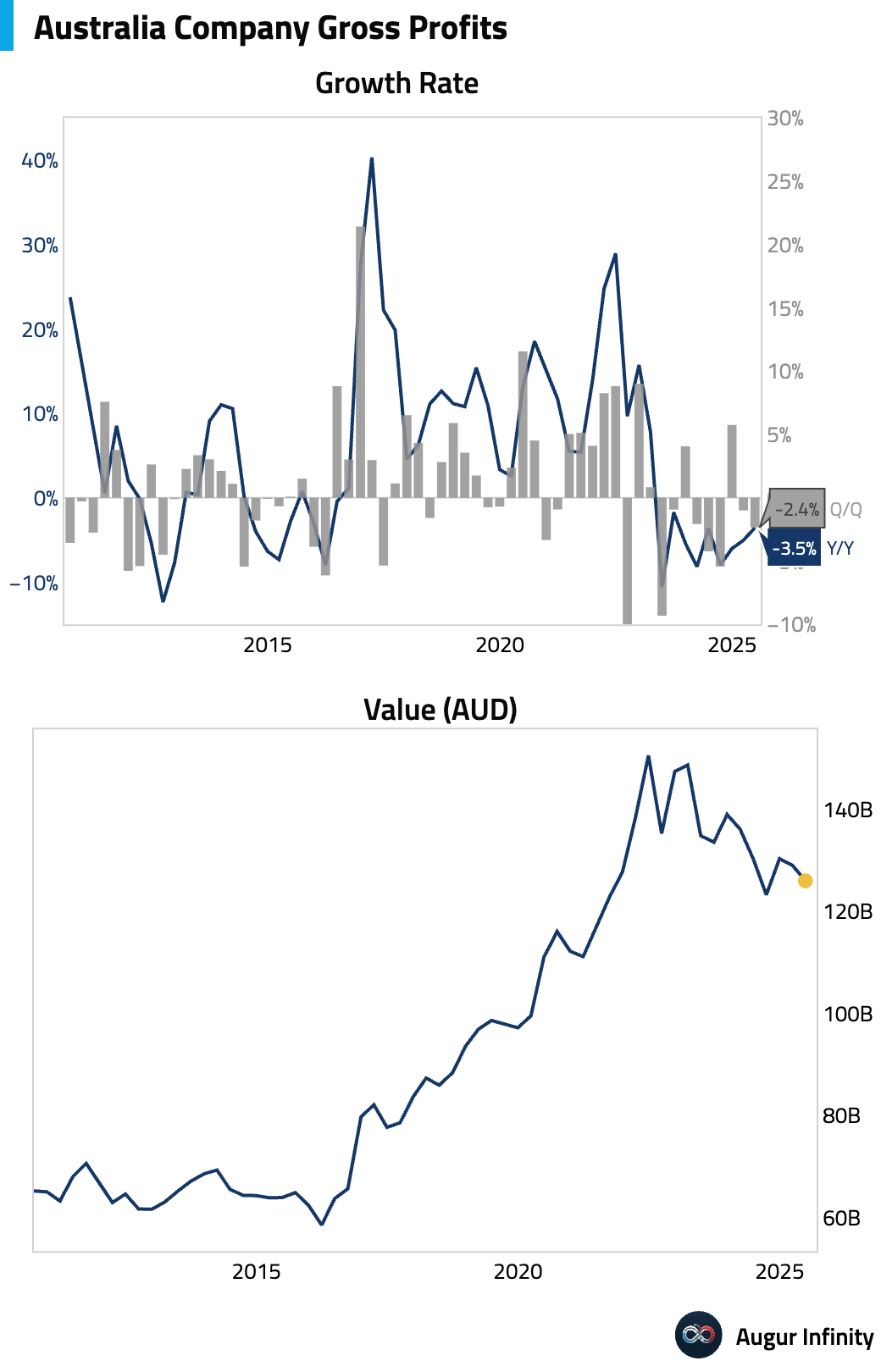

- Australian company gross operating profits unexpectedly fell 2.4% Q/Q in the second quarter, significantly missing the consensus forecast for a 1.2% increase and declining from a 1.0% drop in Q1. Business inventories edged up 0.1% Q/Q, slowing from a 1.2% rise previously.

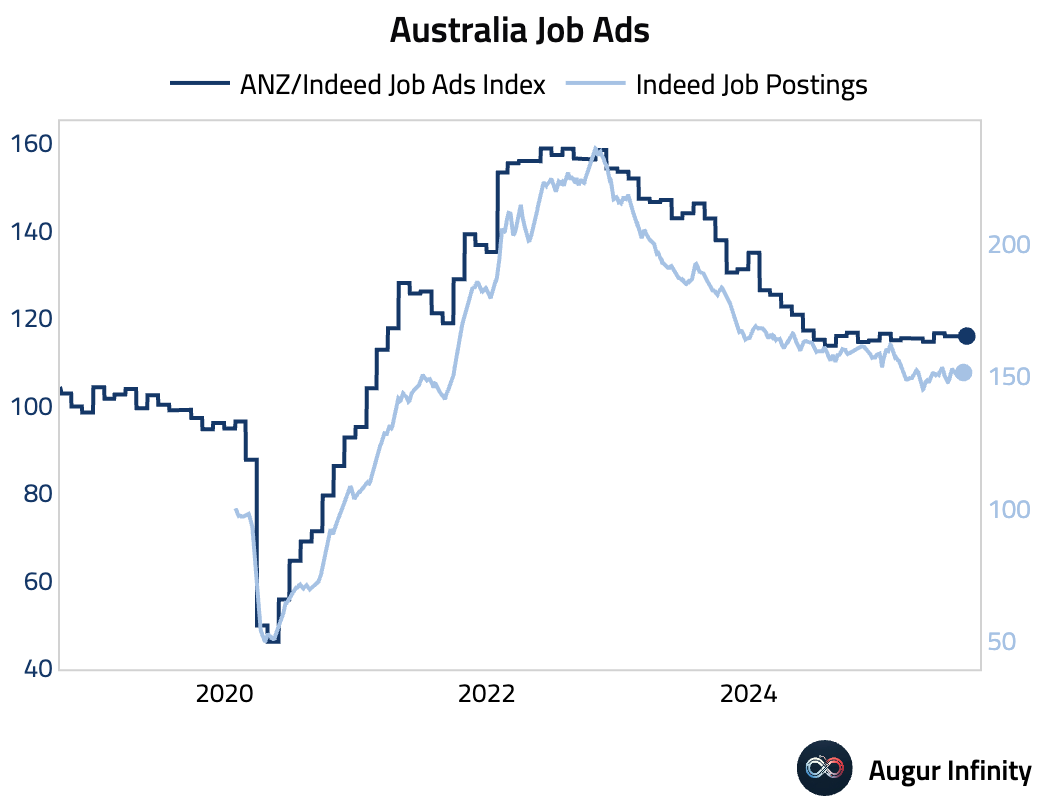

- Australian job advertisements were largely flat in August, with the ANZ-Indeed Job Ads series rising 0.1% M/M following a 0.6% decline in July.

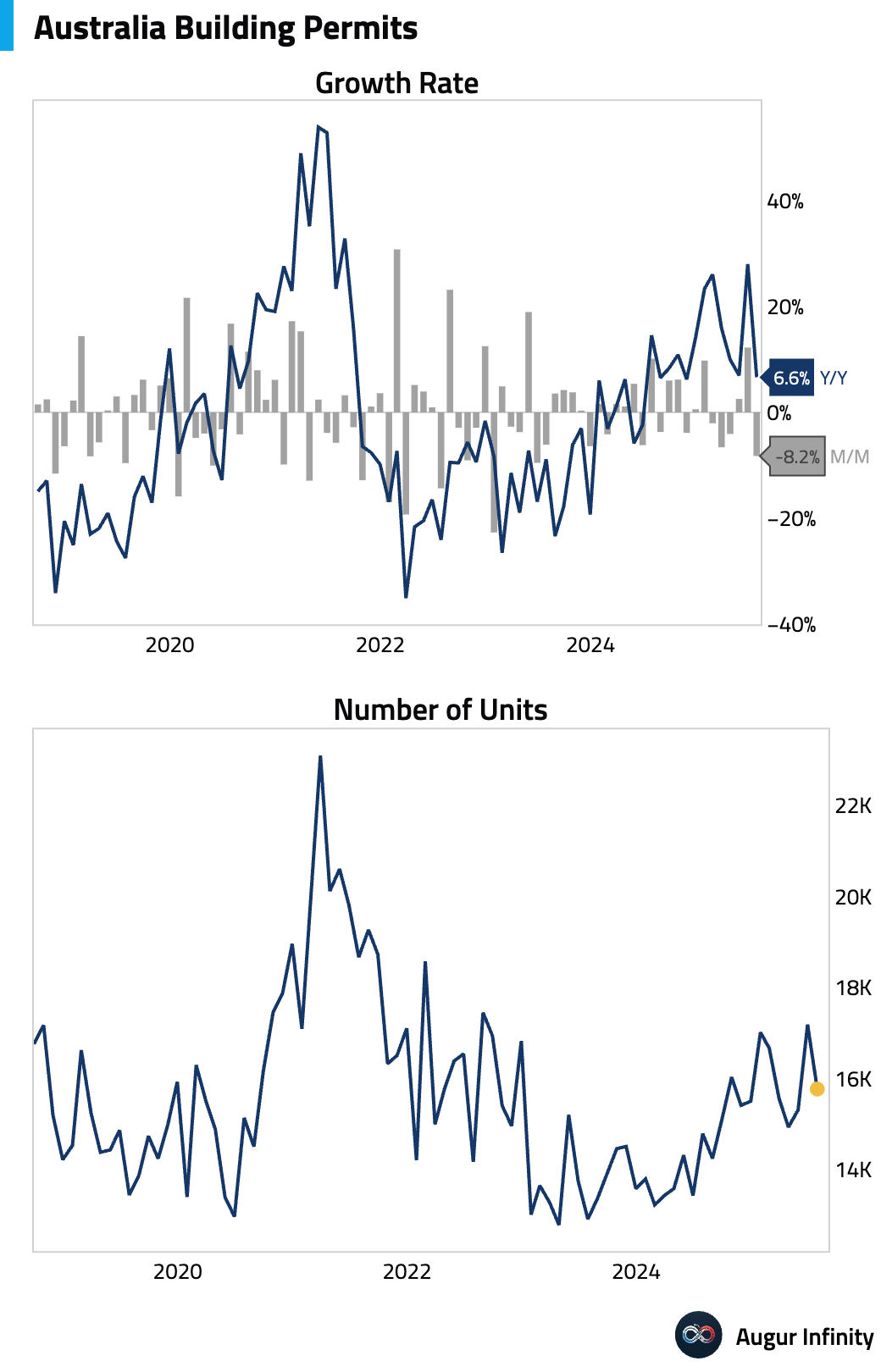

- Australian residential building permits fell 8.2% M/M in July, a much steeper decline than the -4.8% consensus. The drop was driven by a sharp 18.2% fall in the volatile high-density sector, while approvals for detached houses rose slightly by 1.1%. Detached approvals have been flat over the past year, failing to respond to the recent rebound in house prices.

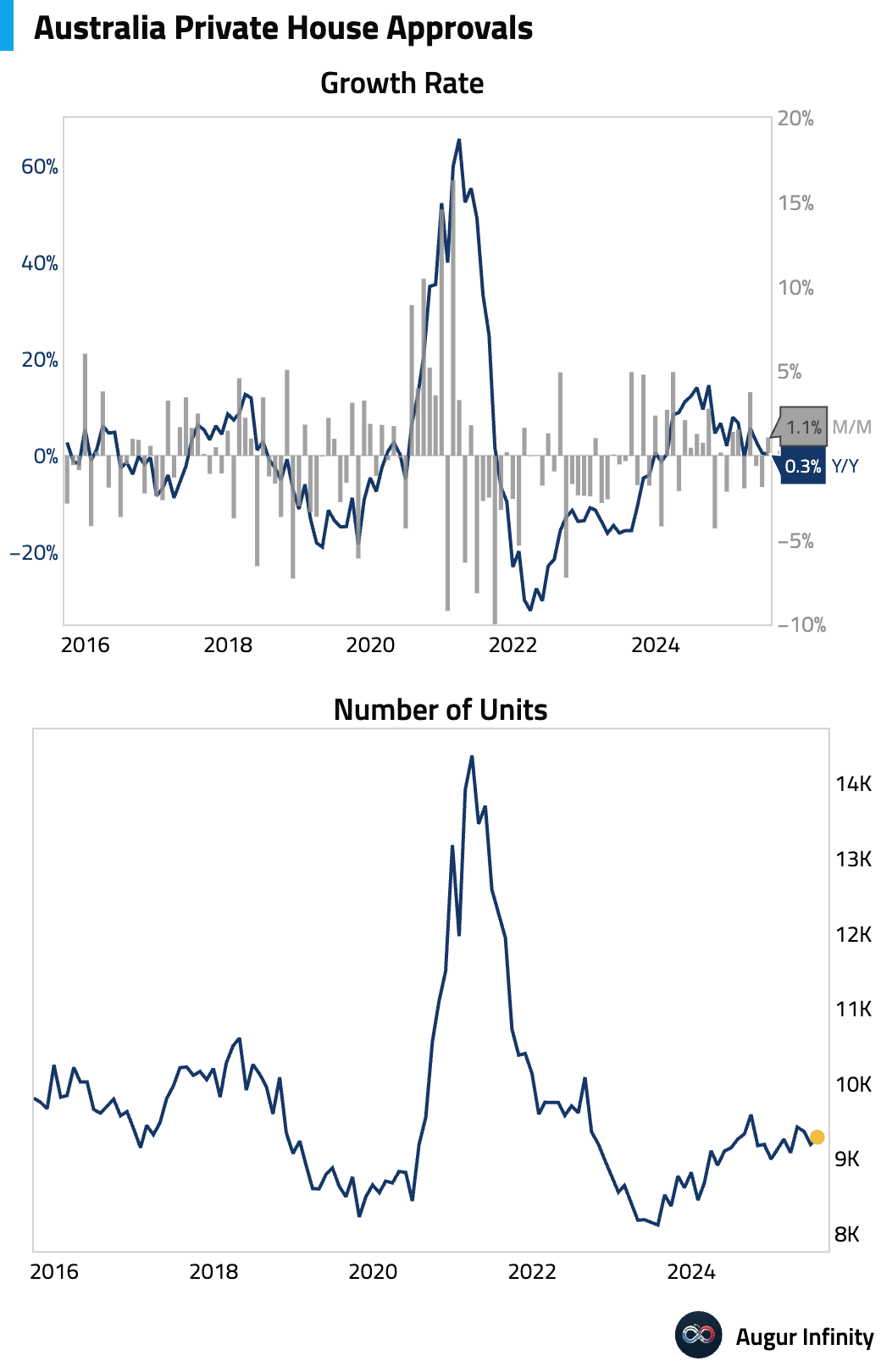

- Australian preliminary private sector house approvals rebounded in July, rising 1.1% M/M after a 1.9% fall in June.

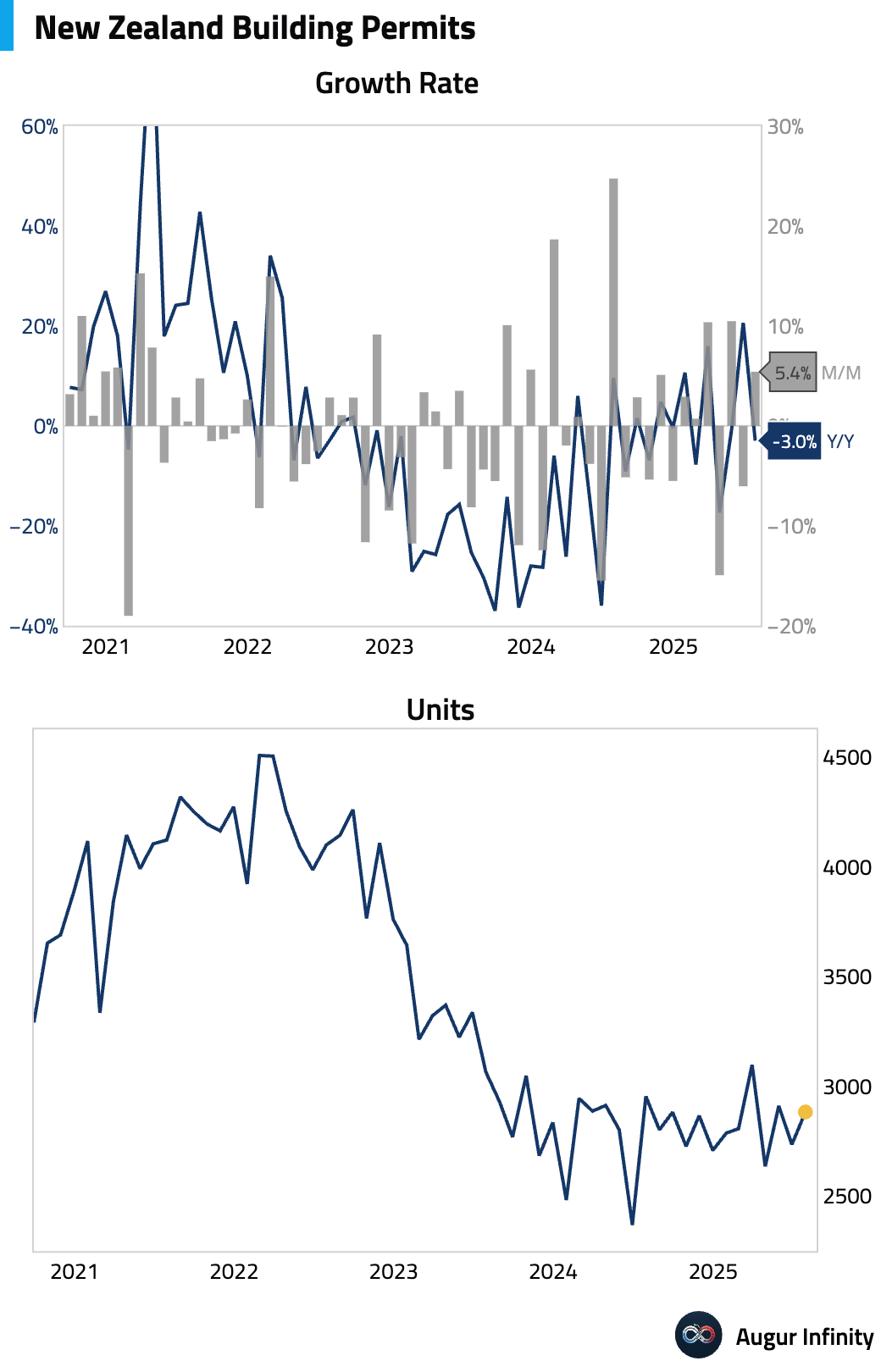

- New Zealand’s building permits rebounded in July, rising 5.4% M/M after a 6.0% decline in June.

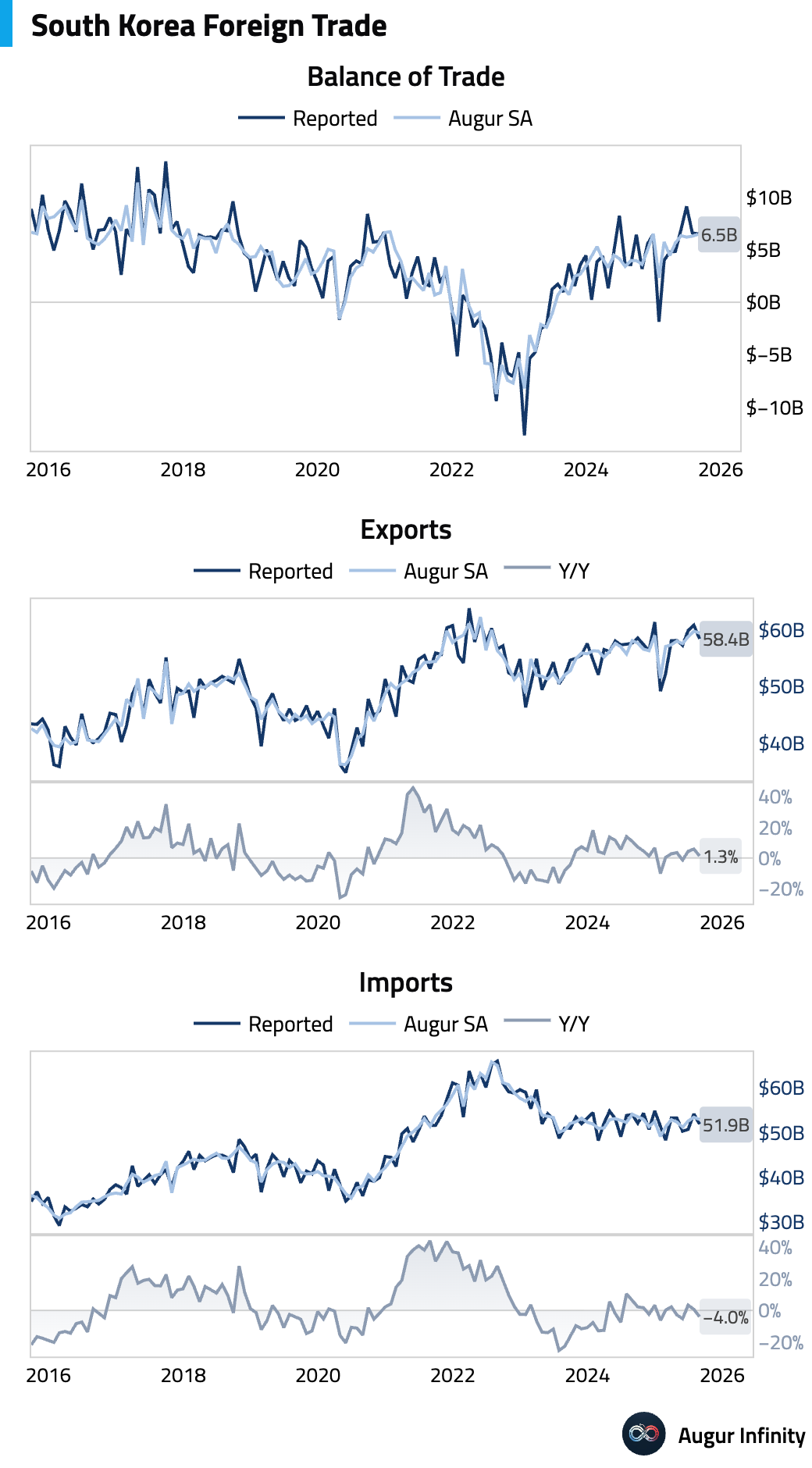

- South Korea’s trade data disappointed in August, with exports growing just 1.3% Y/Y, well below the 3.0% consensus. Imports contracted by 4.0% Y/Y against expectations of a 0.1% decline. Despite the weak trade flows, the trade surplus widened to $6.51 billion from $6.61 billion, beating the $5.4 billion forecast.

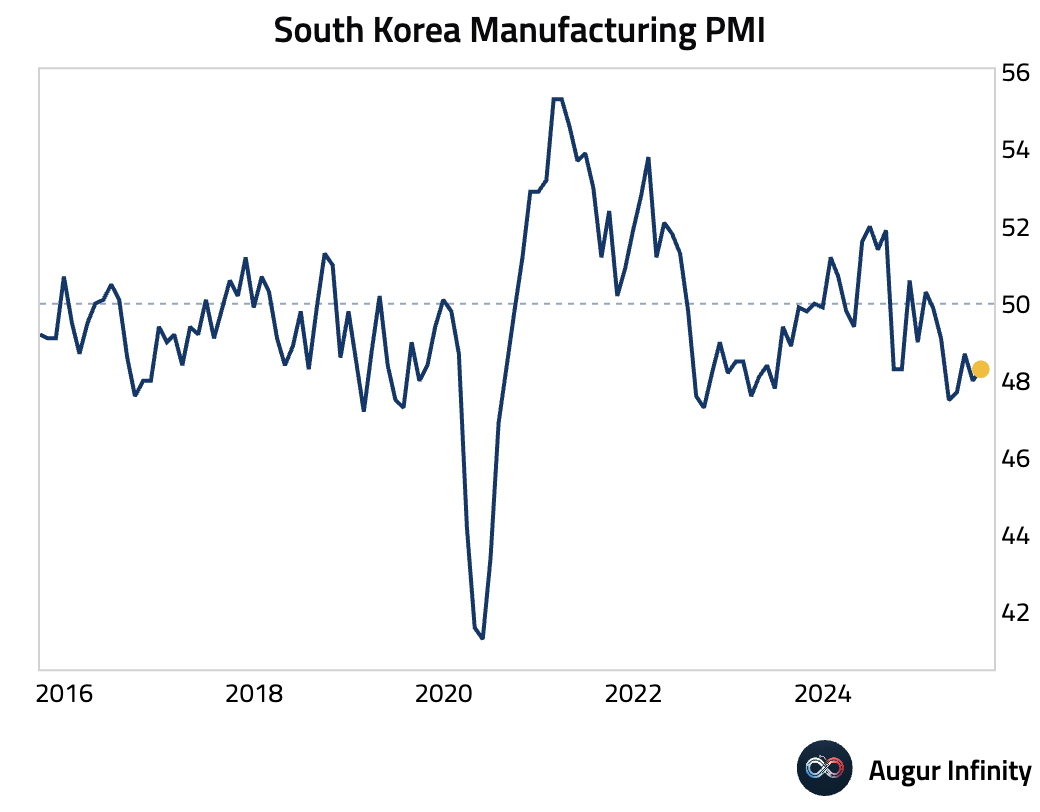

- South Korea’s S&P Global Manufacturing PMI rose to 48.3 in August from 48.0 but remained in contraction for the seventh straight month. Muted domestic demand and the impact of US tariffs drove a sharp fall in new orders and the fastest drop in exports in four months. Despite the weakness, firms turned optimistic, raising employment for the first time in months.

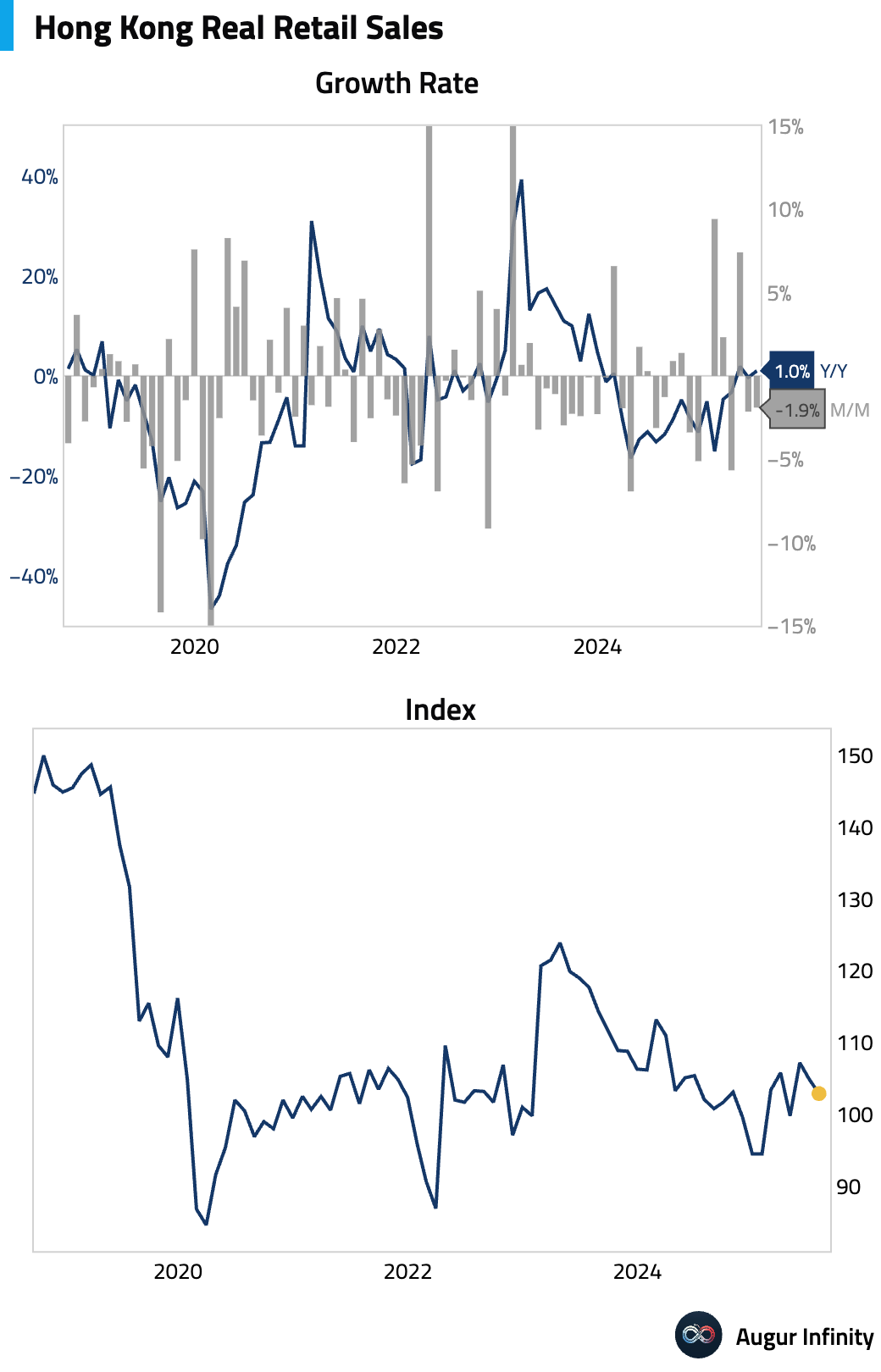

- Hong Kong’s retail sales value rose 1.0% Y/Y in July, accelerating from June’s 0.3% decline but still showing weak momentum on a sequential basis. The monthly decline was broad-based, with sales of department stores and luxury goods remaining nearly 50% below pre-pandemic (2018) levels.

China

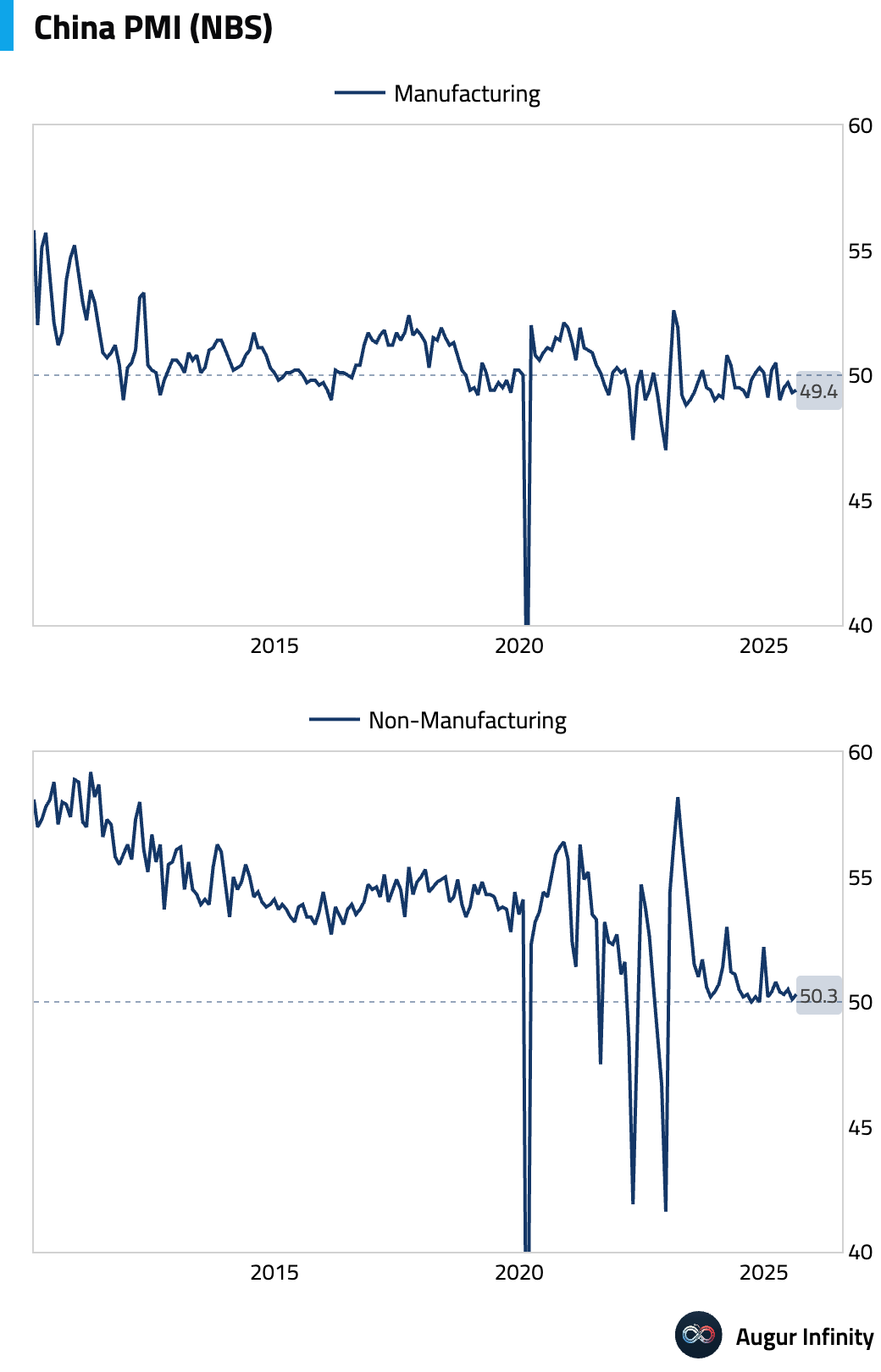

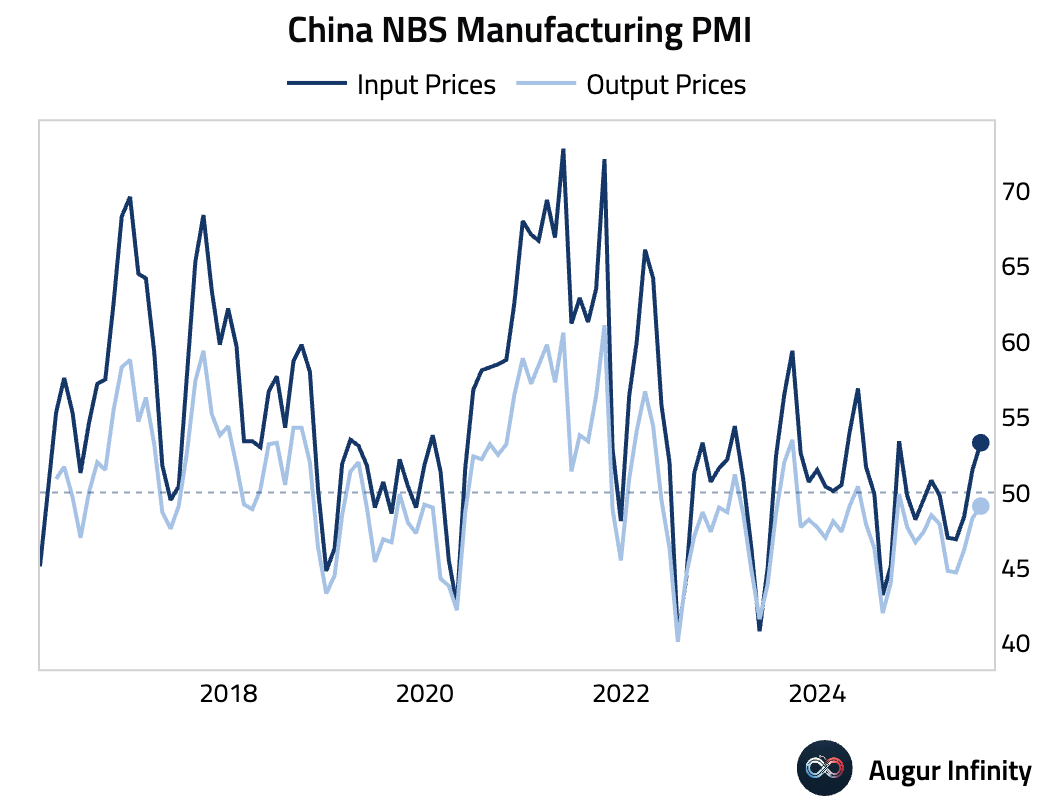

- China’s official NBS Manufacturing PMI edged up to 49.4 in August from 49.3, slightly missing the consensus of 49.5. The modest improvement was led by increases in the output and new orders sub-indexes. A notable jump in input cost (53.3) and output price (49.1) sub-indexes suggests that deflationary pressures continued to ease. The NBS Non-Manufacturing PMI rose to 50.3 in August from 50.1, in line with expectations, driven entirely by the services sector.

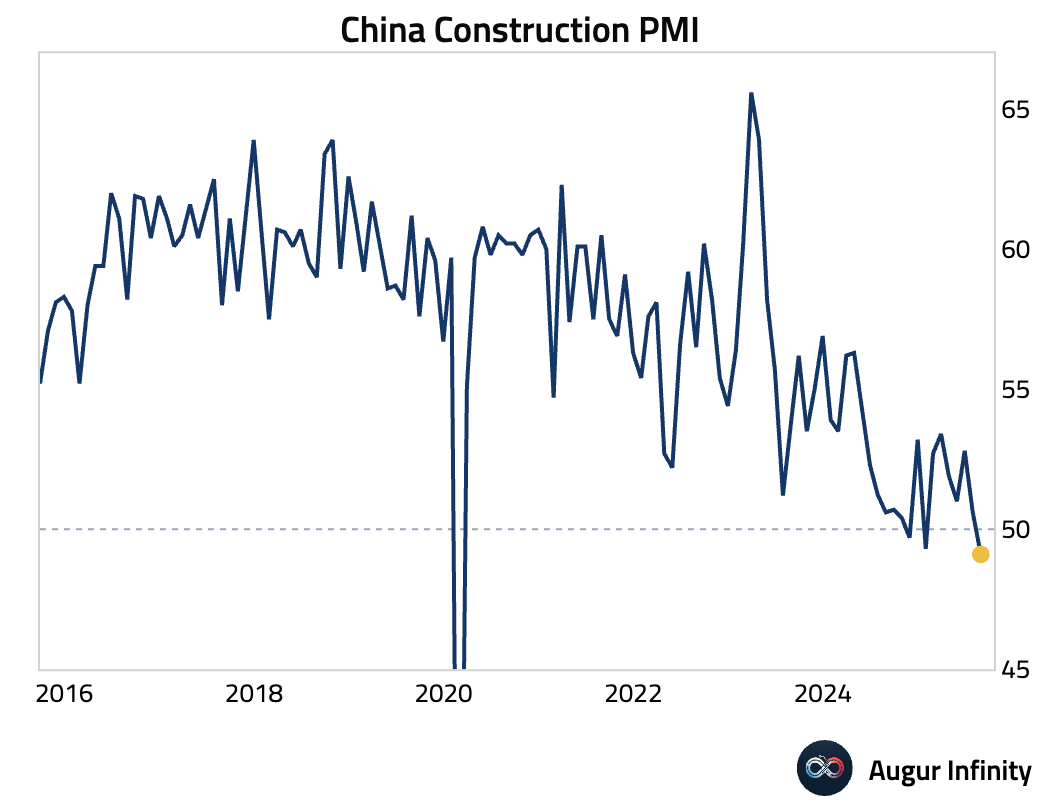

- Construction PMI fell to 49.1—back in contraction and the most pessimistic reading since the pandemic.

- The RatingDog Manufacturing PMI for China returned to expansionary territory in August, rising to a five-month high of 50.5 from 49.5 and beating consensus of 49.5. The rebound was led by the quickest growth in new orders since March, driven by domestic demand, as new export orders remained in contraction. Despite the uptick, firms cut staff for a fifth straight month, suggesting the recovery is patchy.

Emerging Markets ex China

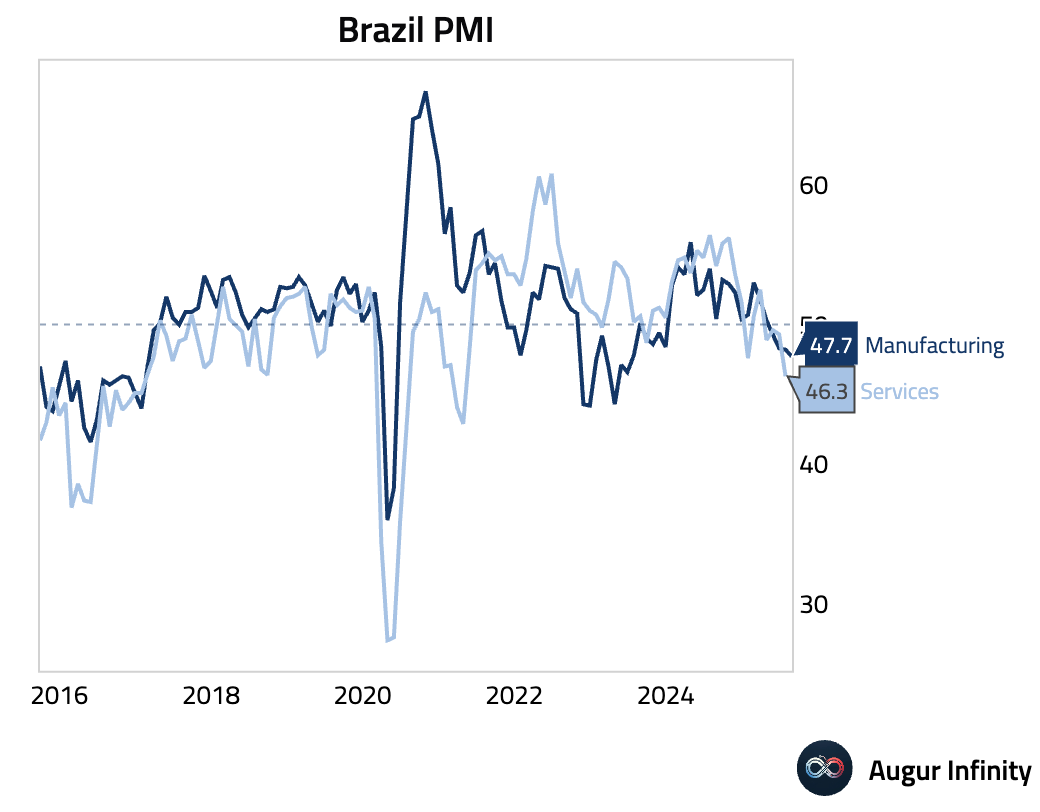

- Brazil's S&P Global Manufacturing PMI declined further into contraction, falling to 47.7 in August from 48.2 in July.

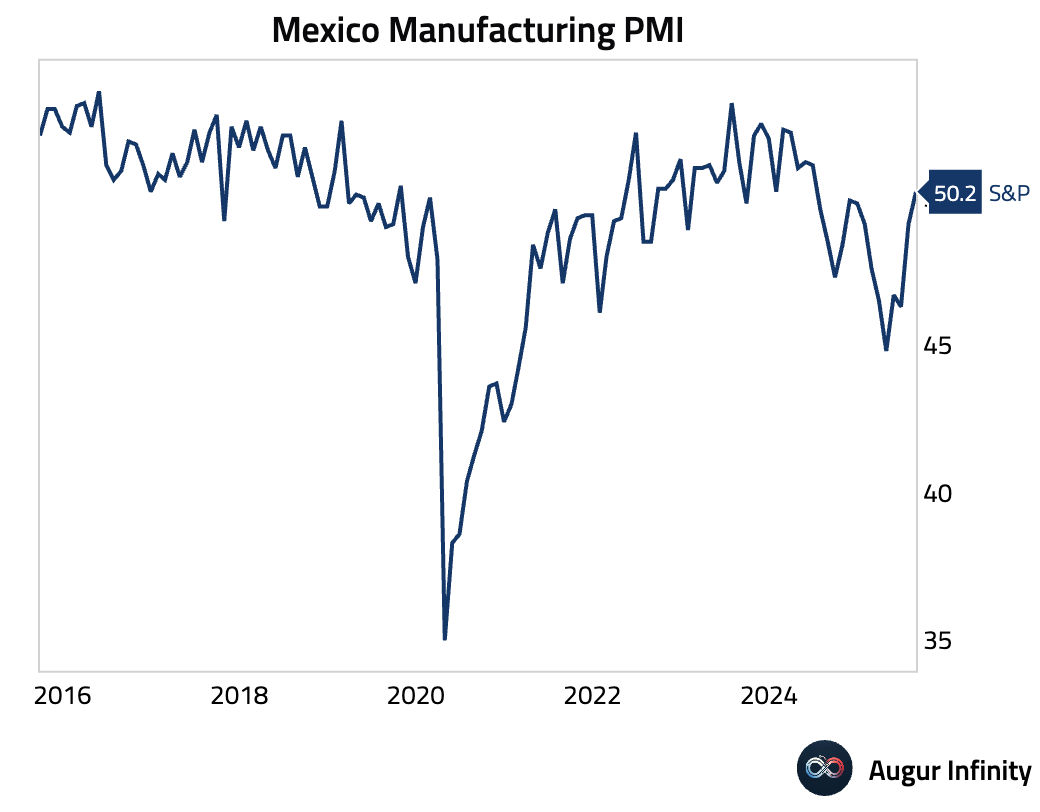

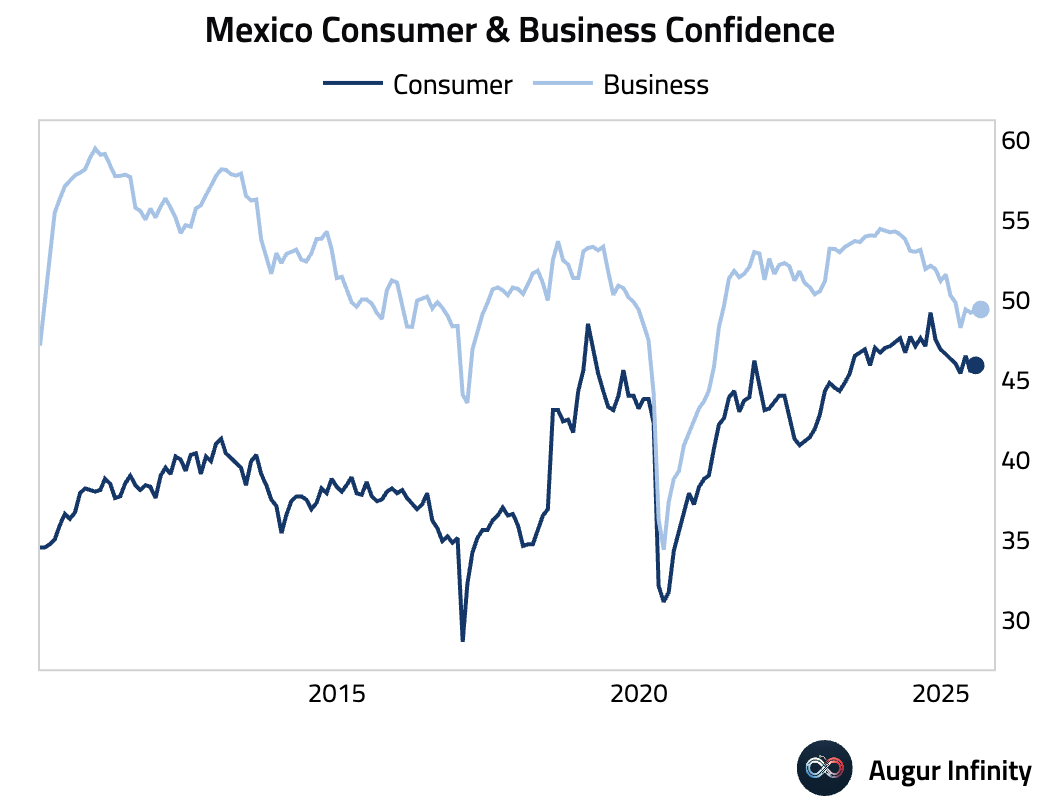

- Mexico PMI rose to 50.2 from 49.1, marking the first expansion in 14 months, driven by a recovery in new orders. However, the expansion is fragile as output and employment continued to contract. Input cost inflation remained historically steep, but firms couldn't pass on costs due to weak demand, squeezing margins.

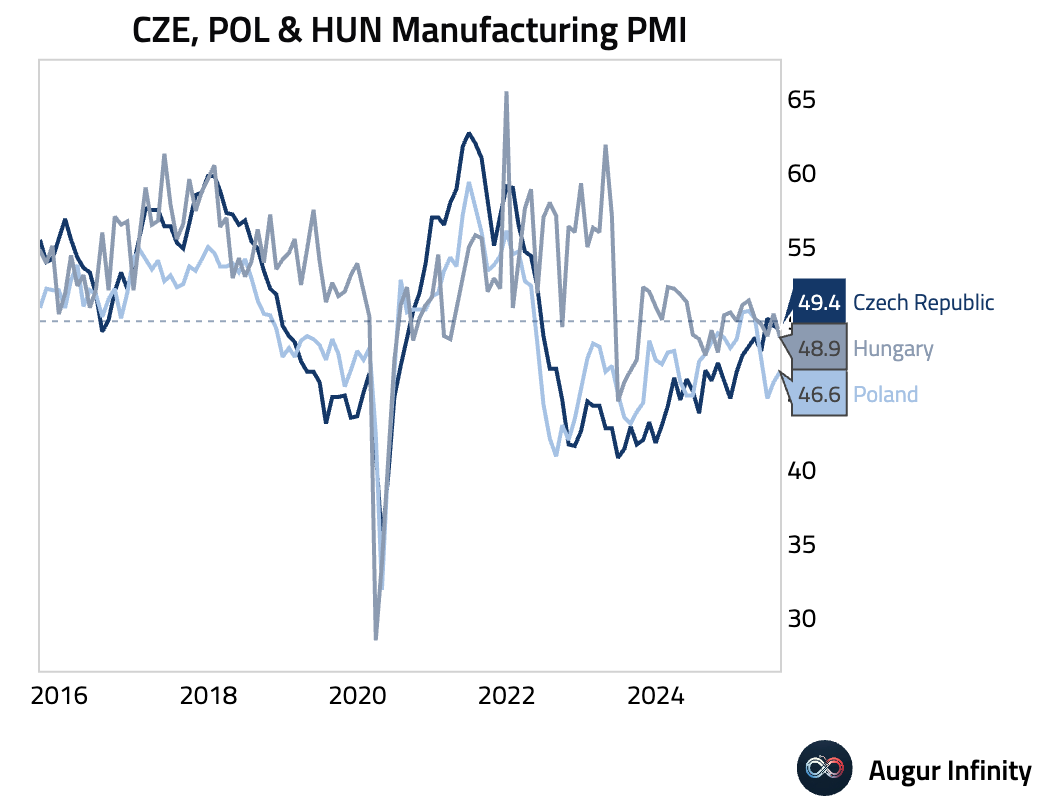

- The Czech manufacturing sector contracted in August as the S&P Global Manufacturing PMI fell to 49.4, below the 50.0 consensus. Poland’s Manufacturing PMI rose to 46.6 in August from 45.9 but remained deep in contraction, lagging the broader Eurozone recovery. Hungary’s HALPIM Manufacturing PMI fell back into contraction in August, dropping to 48.9 from 50.5 in July.

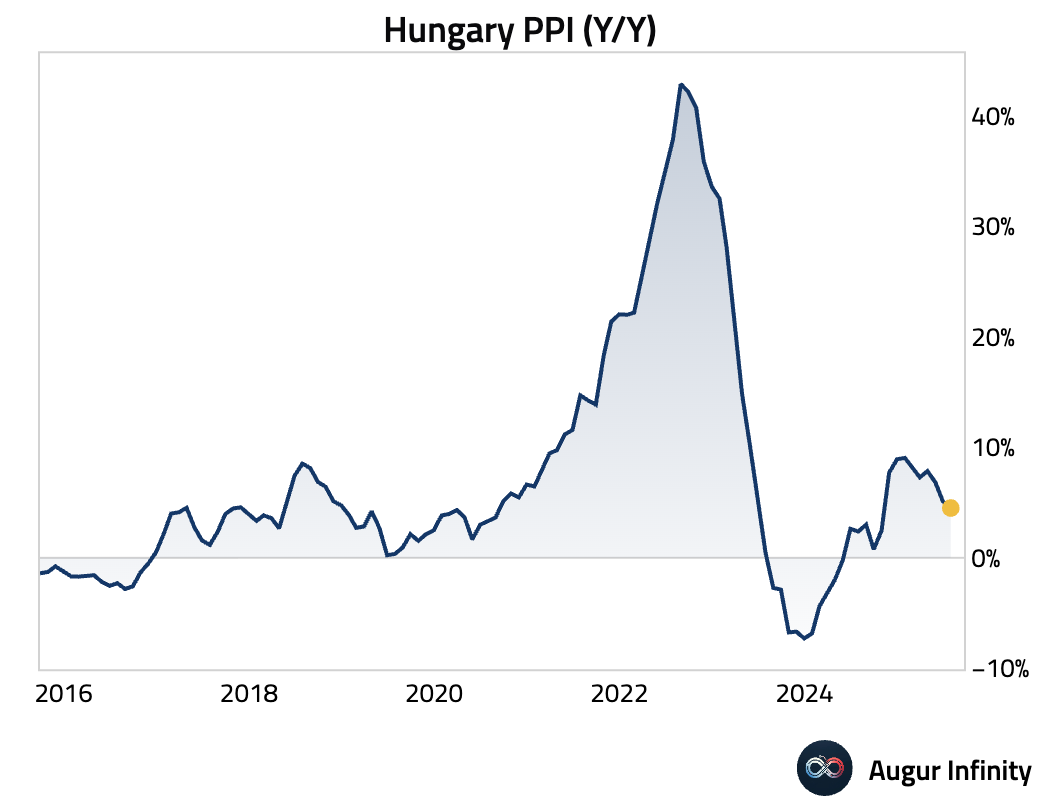

- Hungarian producer price inflation decelerated in July, with the PPI falling to 4.5% Y/Y from 5.1% in June.

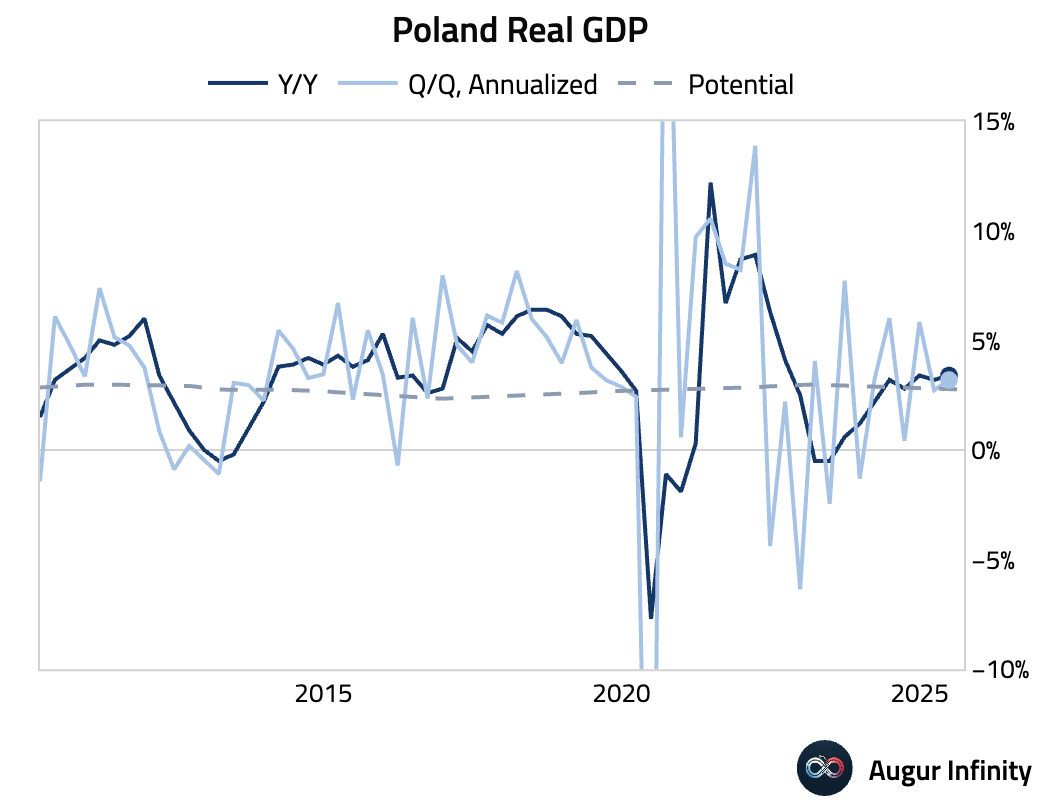

- Final second-quarter GDP data for Poland confirmed growth of 0.8% Q/Q (or 3.2% annualized) and 3.4% Y/Y, matching preliminary estimates.

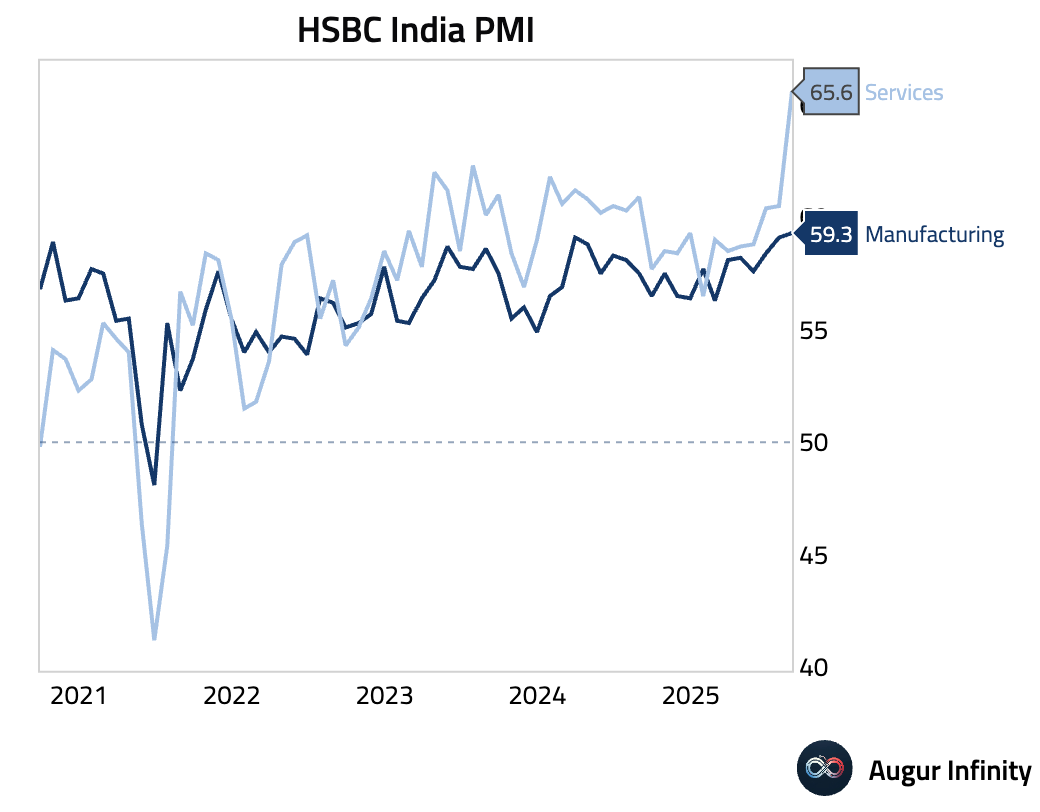

- India's HSBC Manufacturing PMI rose to 59.3 in August from 59.1, reaching its highest level in 17.5 years. The strength was driven by the fastest production growth in nearly five years, fueled by strong domestic demand. However, new export orders slowed to a five-month low, potentially due to the imposition of 50% US tariffs on Indian goods.

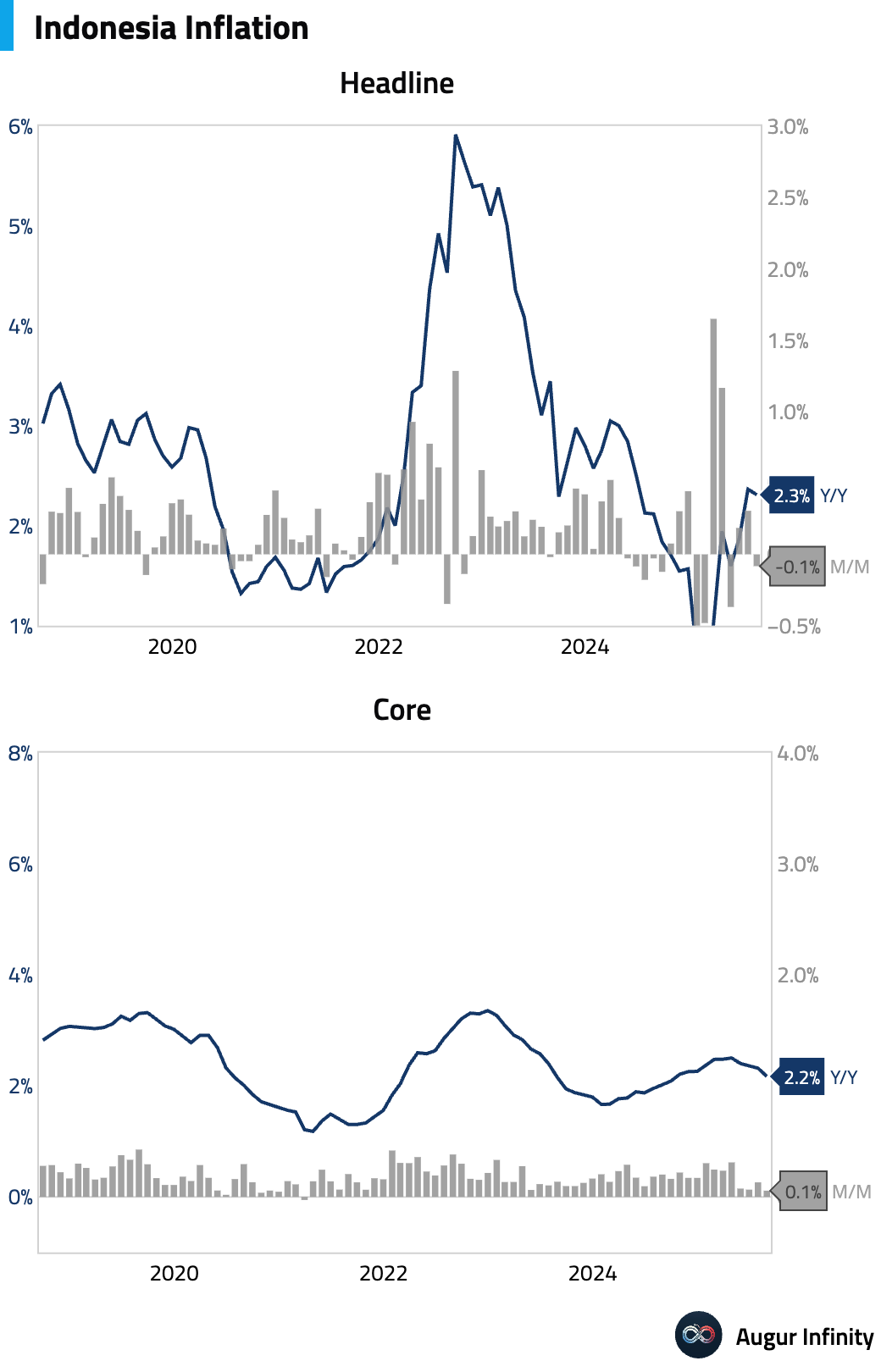

- Indonesian inflation slowed more than expected in August, with the headline rate falling to 2.31% Y/Y (vs. 2.37% prior) and the core rate easing to 2.17% Y/Y (vs. 2.32% prior). The deceleration was mainly driven by lower transportation inflation due to falling fuel prices, potentially giving Bank Indonesia room for further rate cuts. On a monthly basis, prices fell 0.08%.

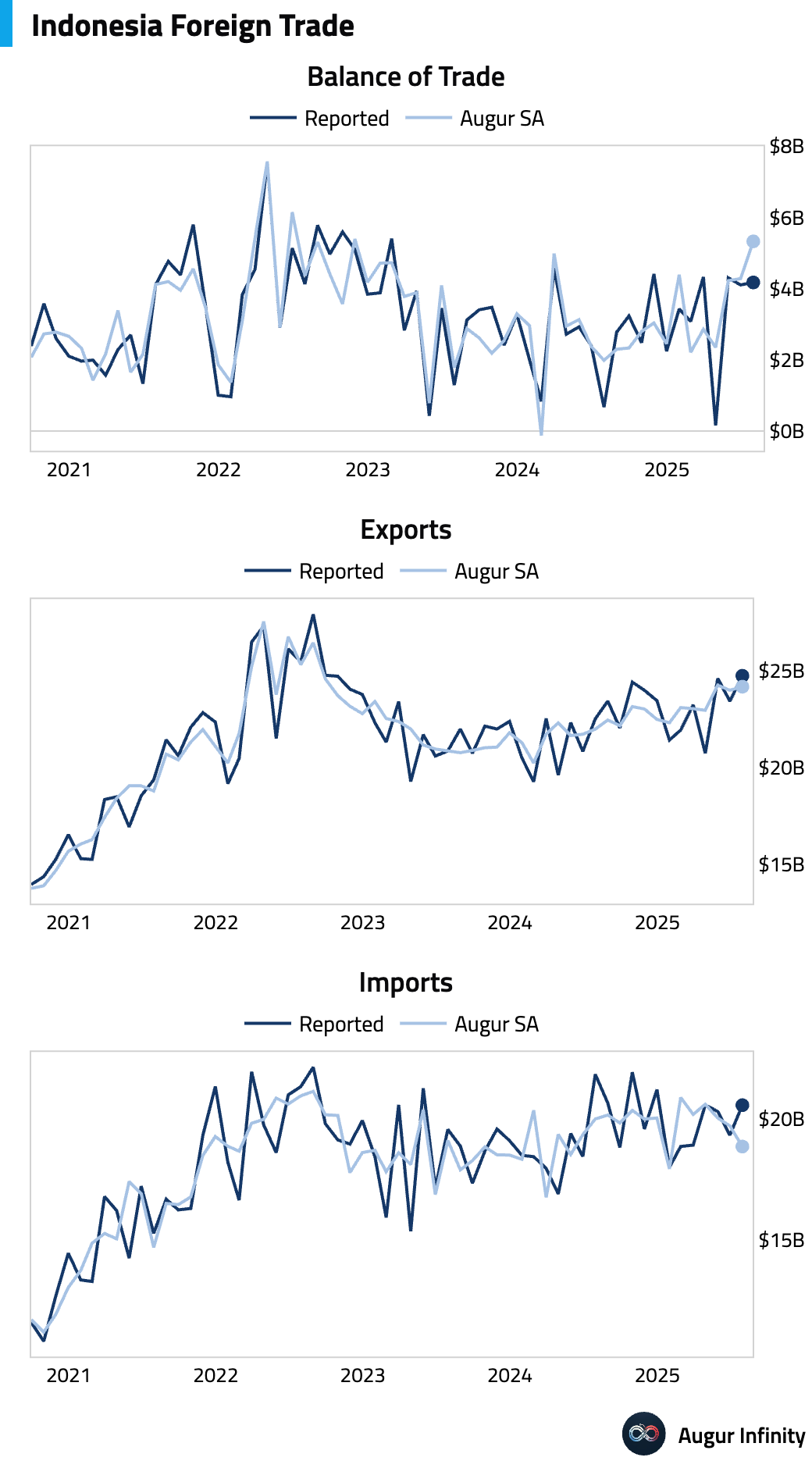

- Indonesia's trade surplus widened to $4.2 billion in August from $4.11 billion in July. Export growth slowed to 9.86% Y/Y from 11.29%, while imports contracted by 5.86% Y/Y after growing 4.28% previously.

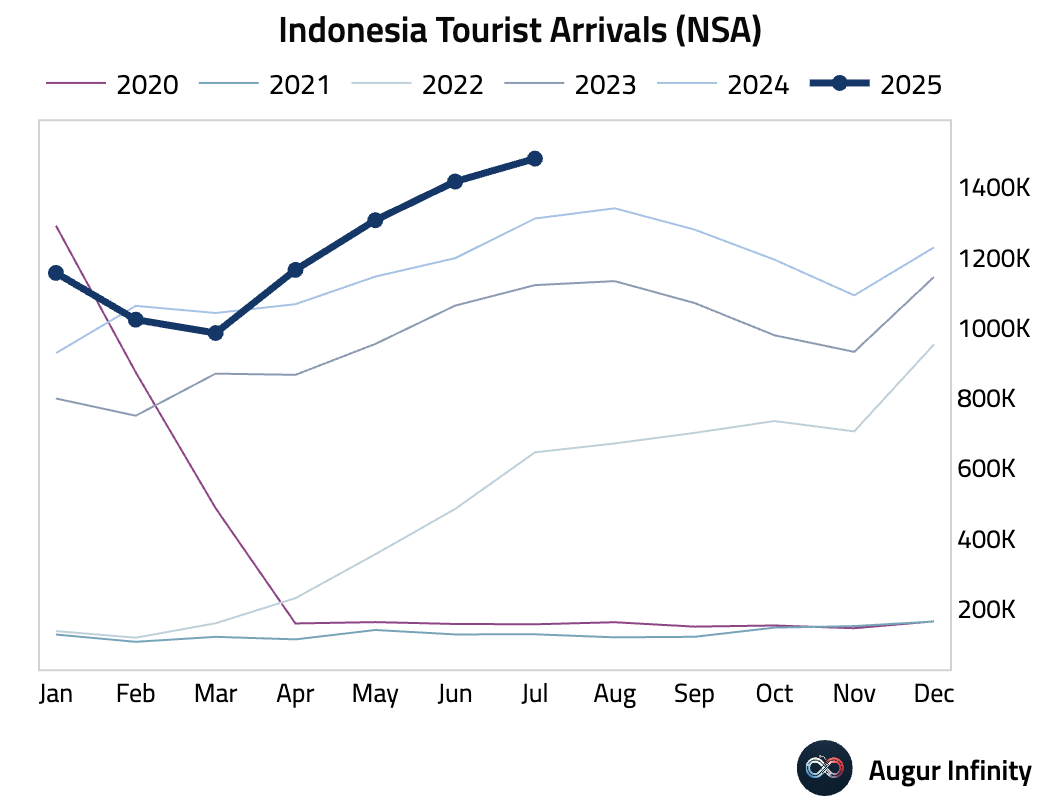

- Growth in tourist arrivals to Indonesia slowed to 13.01% Y/Y in July from 18.2% in June.

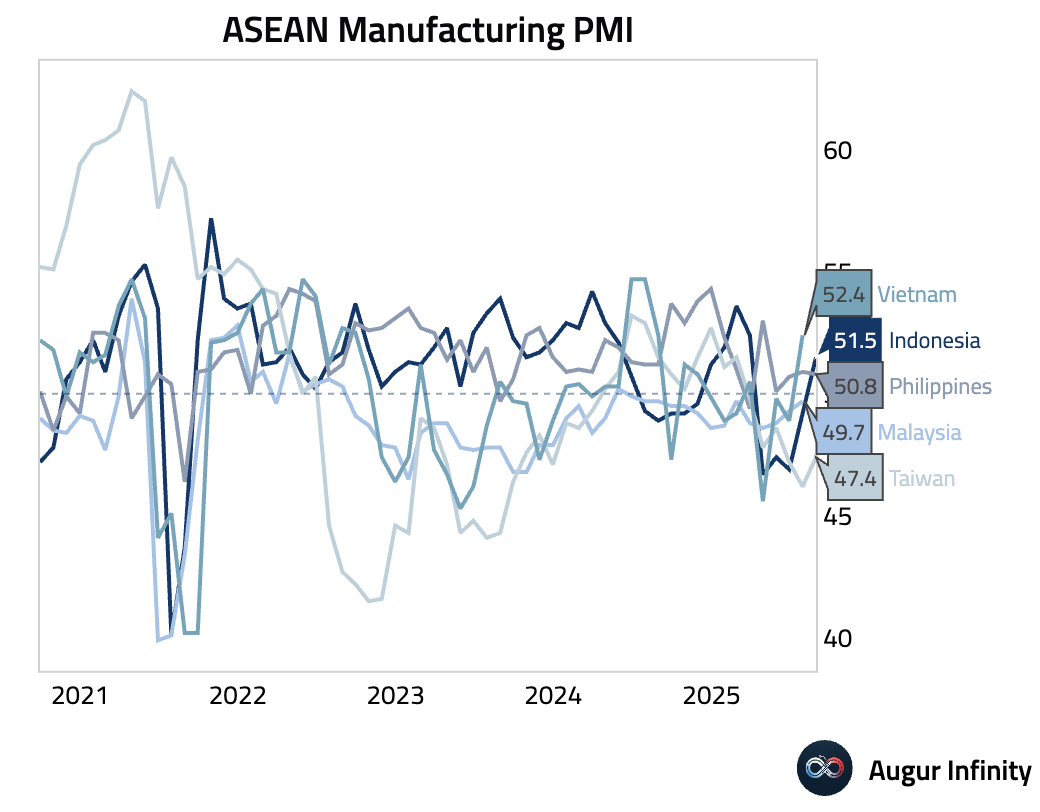

- The Indonesia Manufacturing PMI surged to 51.5 in August from 49.2, returning to expansion for the first time in five months. Philippines’ Manufacturing PMI edged down to 50.8 in August from 50.9, indicating continued but historically subdued growth. Taiwan’s S&P Manufacturing PMI rose to 47.4 in August from 46.2 but still signaled a sixth consecutive month of contraction.

- Mexico's business confidence was unchanged in August, holding steady at 49.4.

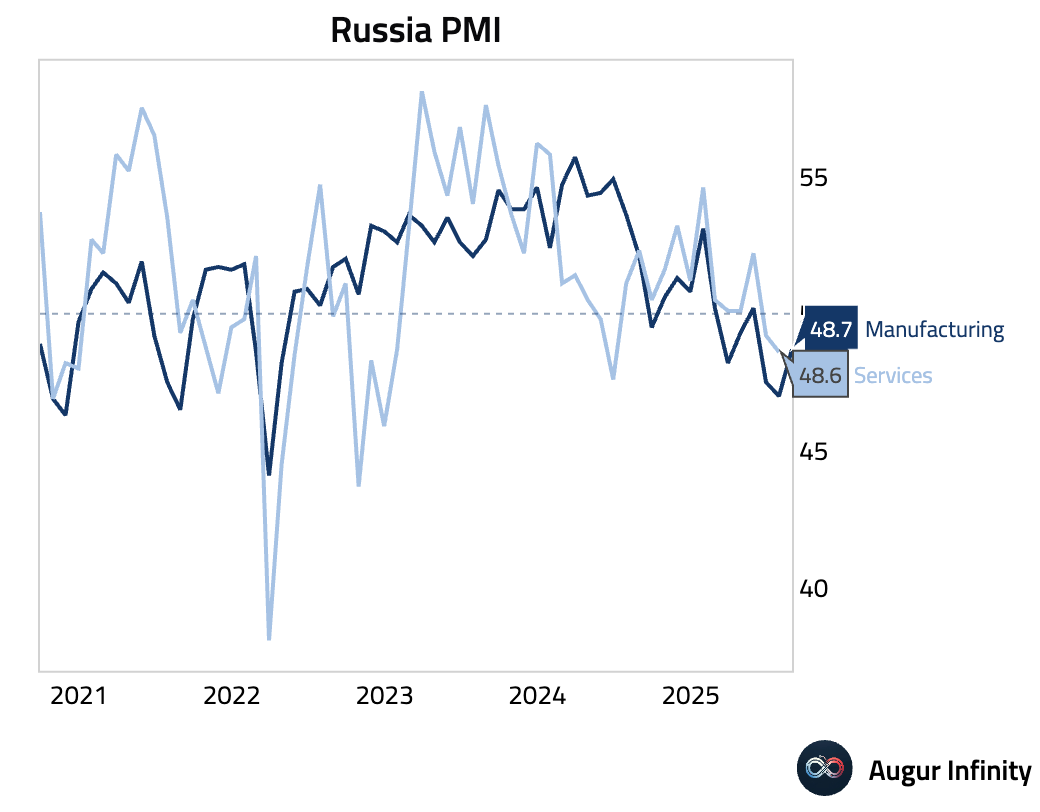

- Russia’s S&P Global Manufacturing PMI rose to 48.7 in August from 47.0, marking a third consecutive month of contraction but at the softest pace in this sequence. To stimulate sales, firms cut selling prices for the first time in nearly three years as input cost inflation hit its weakest level since February 2009.

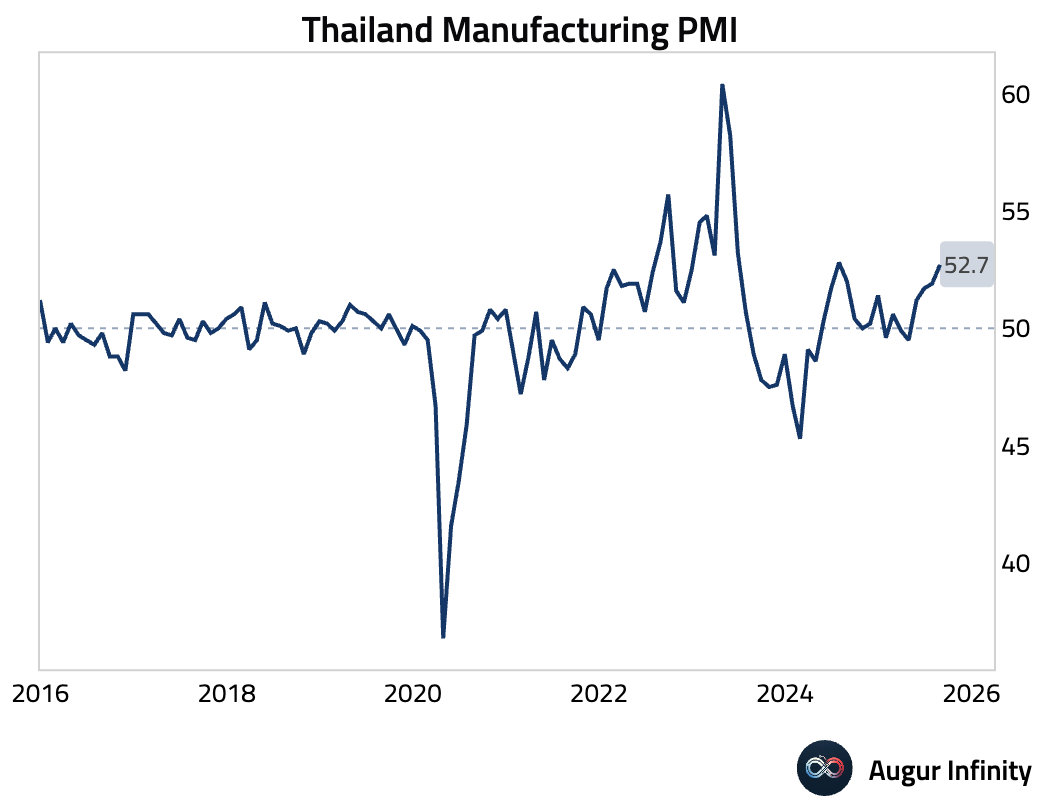

- Thailand's S&P Global Manufacturing PMI rose to 52.7 in August, the fastest expansion since July 2024. The surge was driven by a solid increase in new domestic orders, which lifted production to a 13-month high. However, the strength was entirely domestic, as export orders fell.

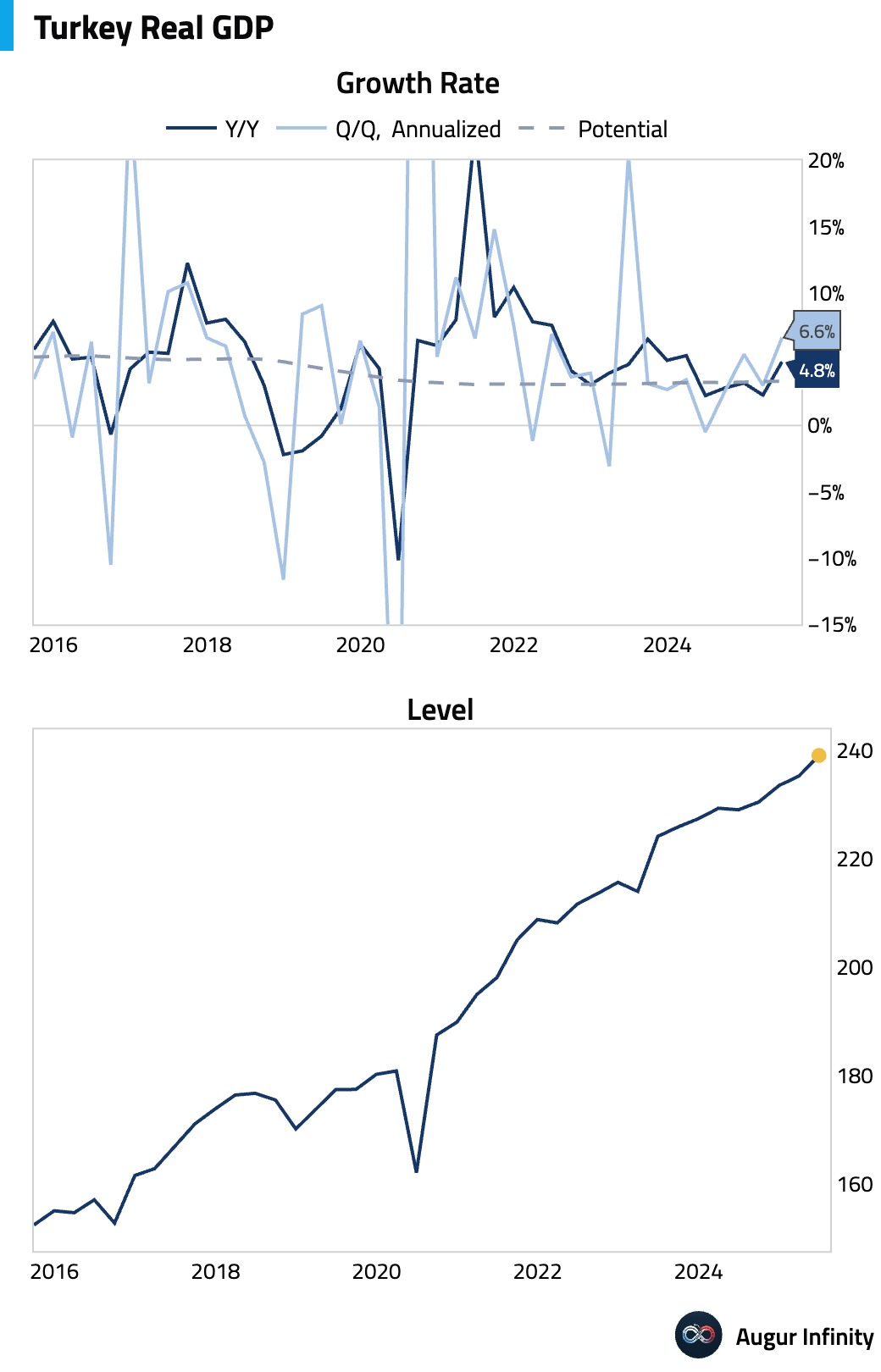

- Turkey's economy accelerated in the second quarter, with GDP growing 4.8% Y/Y, well above the 4.1% consensus and up from 2.3% in Q1. Quarter-over-quarter, growth was 1.6% (or 6.6% annualized), up from 0.7%.

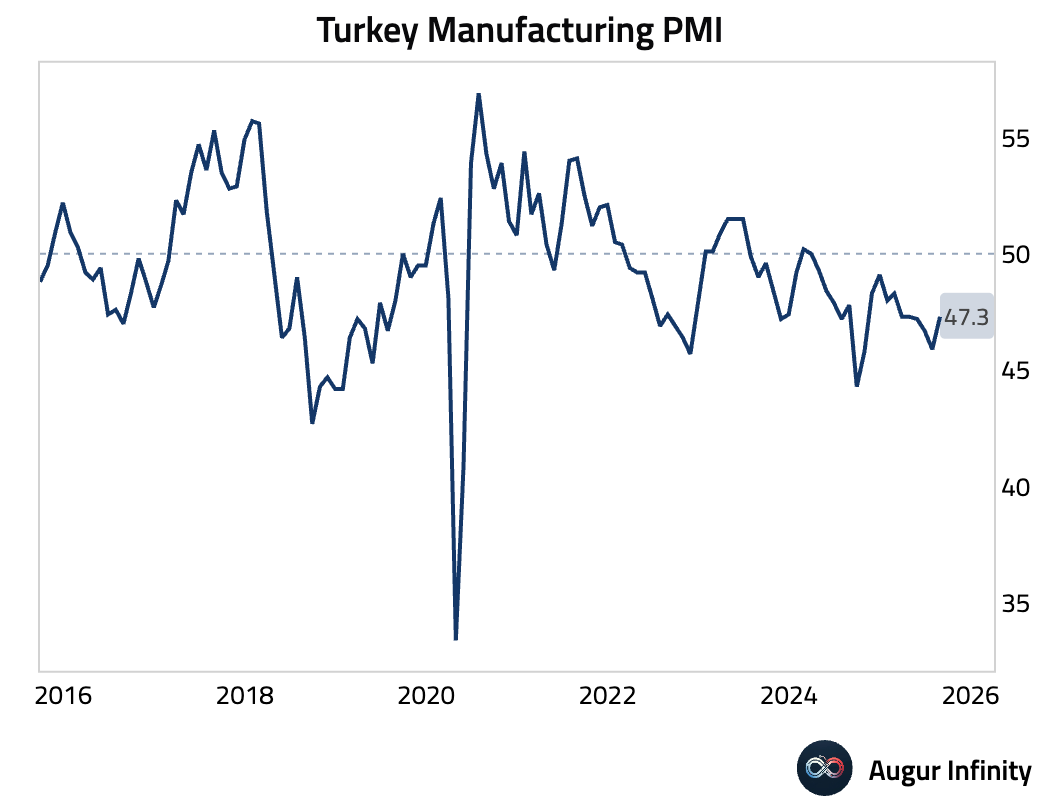

- Turkey’s manufacturing sector continued to contract in August, though at a slower pace. The Istanbul Chamber of Industry Manufacturing PMI rose to 47.3 from 45.9. While slowdowns in output and new orders eased, firms cut employment at the sharpest rate since April 2020. Lira depreciation accelerated input cost inflation, but weak demand limited pricing power, squeezing margins.

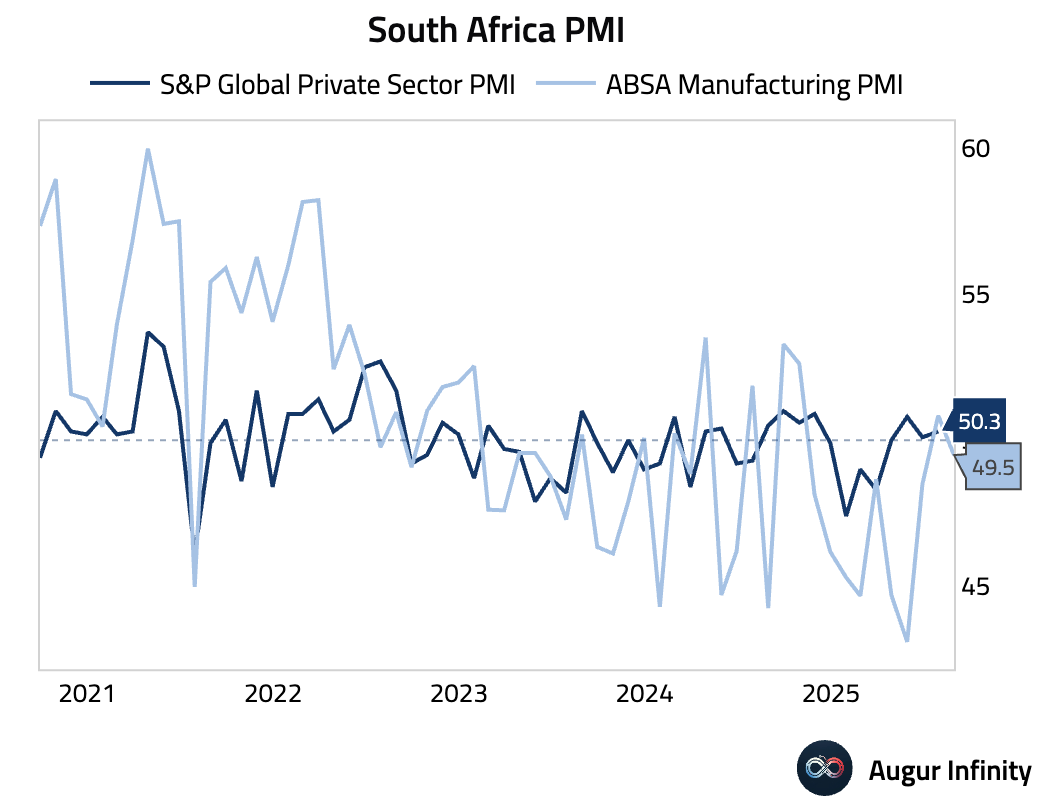

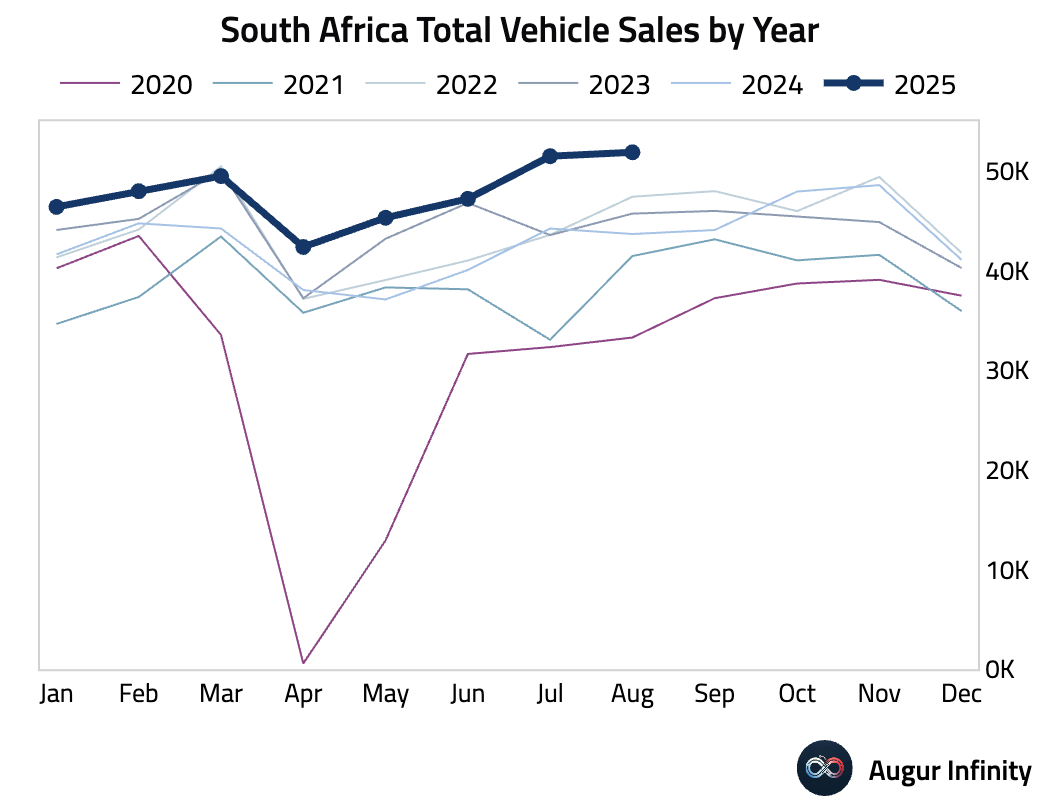

- South Africa's ABSA Manufacturing PMI fell back into contraction in August, declining to 49.5 from 50.9 in July.

- South African new vehicle sales rose to 51,880 in August from 51,490 in July, reaching the highest level since October 2019.

Global Markets

Equities

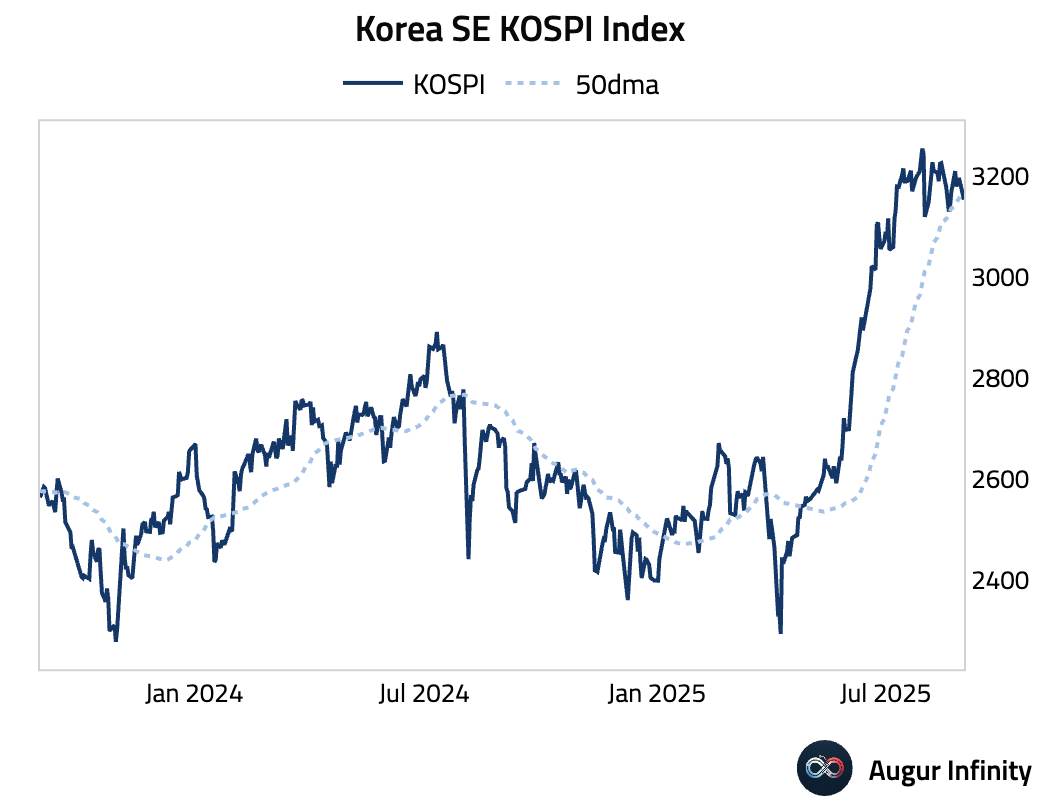

- The Korea SE KOSPI Index fell below its 50-day moving average

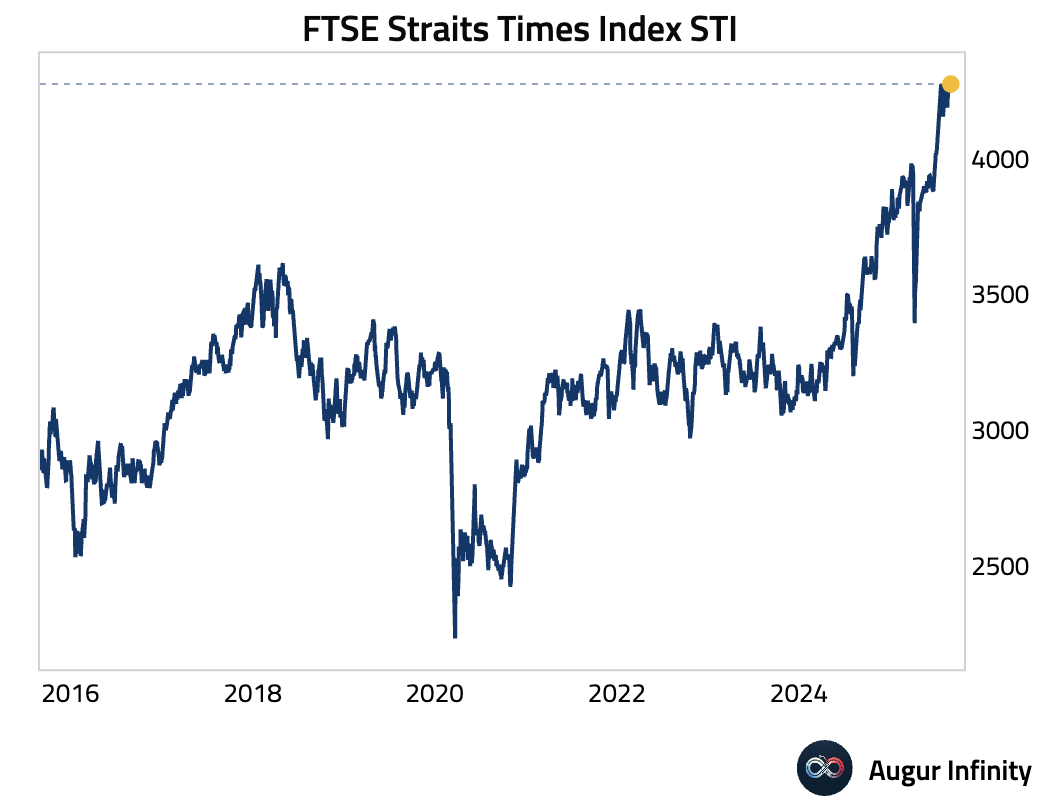

- FTSE Straits Times Index for Singapore has reached an all-time high.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.