Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- An appellate court ruled against many of President Trump’s tariffs, though Treasury Secretary Bessent stated he expects the Supreme Court will ultimately uphold the president’s tariff authority.

- Growing concerns about the United Kingdom’s fiscal stability drove yields on long-term British government bonds to levels not seen in nearly thirty years.

- US Treasury Secretary Bessent indicated that a housing emergency could be declared in the fall.

Global Economics

United States

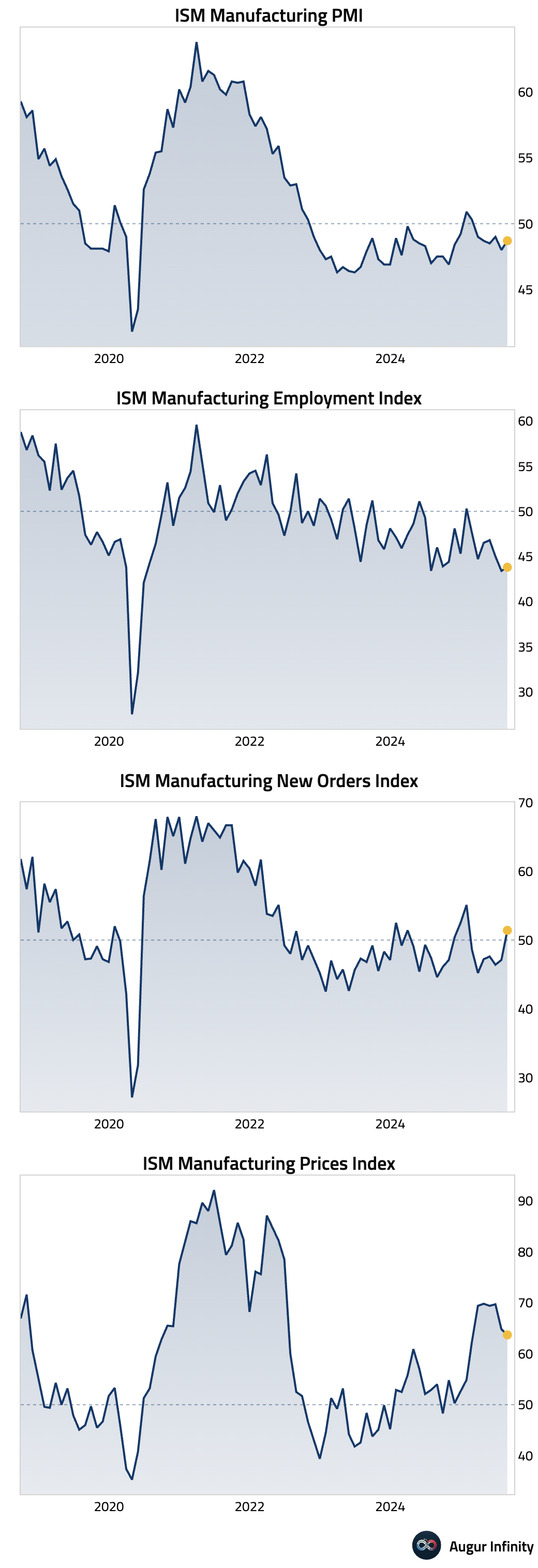

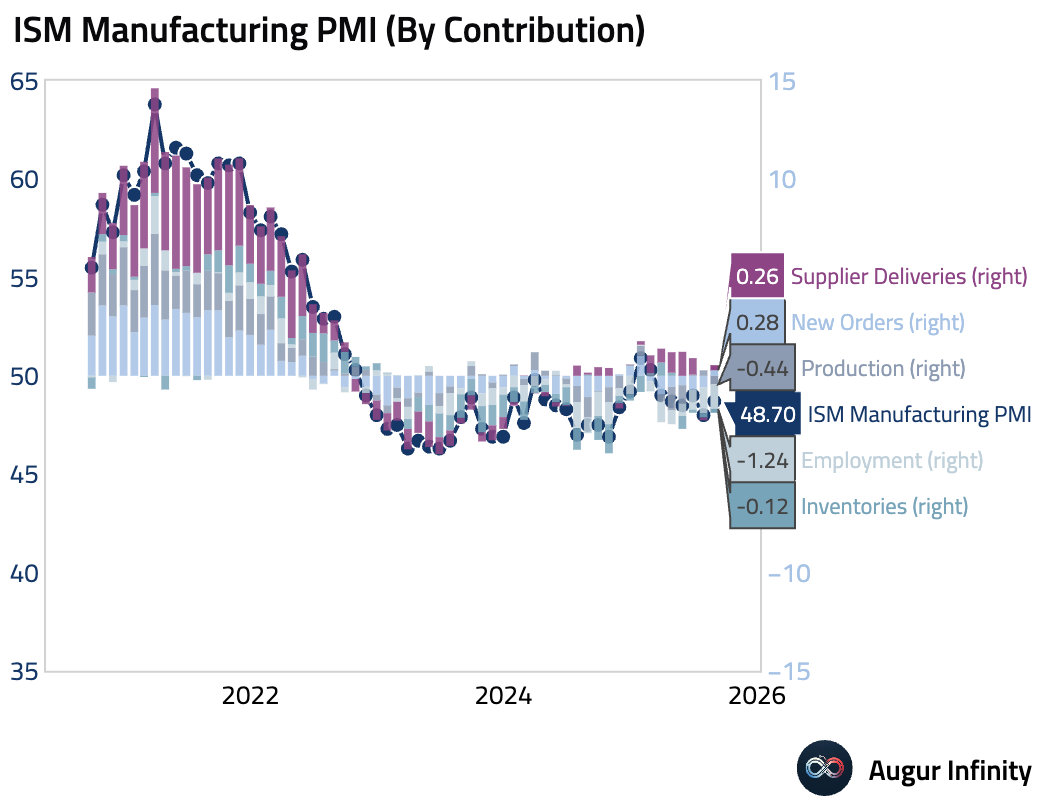

- The ISM Manufacturing PMI for August rose to 48.7 from 48.0, but missed the 49.0 consensus and remained in contraction for the sixth straight month. The report showed a stark divergence: the forward-looking New Orders Index jumped back into expansion at 51.4 for the first time in seven months, while the Production Index fell sharply into contraction at 47.8. The Prices Paid Index eased slightly to 63.7 but remained highly elevated, and the Employment Index stayed deeply contractionary at 43.8, with firms reportedly reducing headcounts.

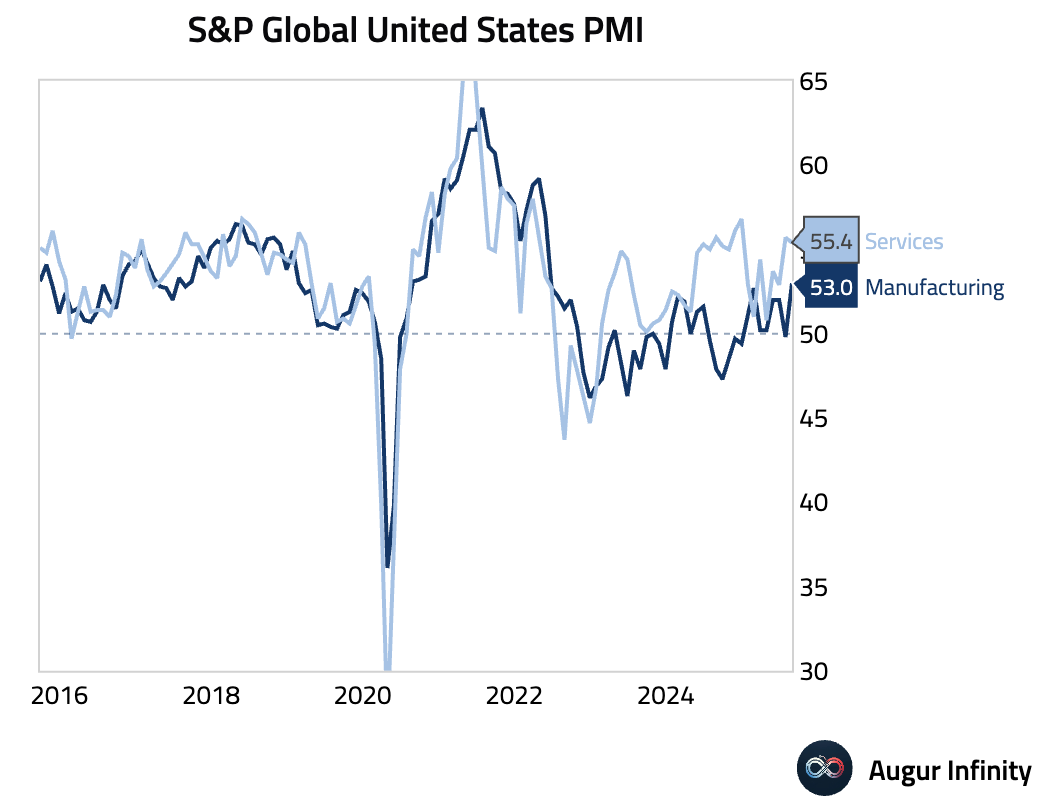

- The final S&P Global US Manufacturing PMI for August was revised down slightly from 53.3 to 53.0, its highest reading since May 2022. The expansion was driven by stronger production fueled by new orders and significant inventory building, as firms stockpiled goods amid concerns over future prices and supply constraints linked to tariffs.

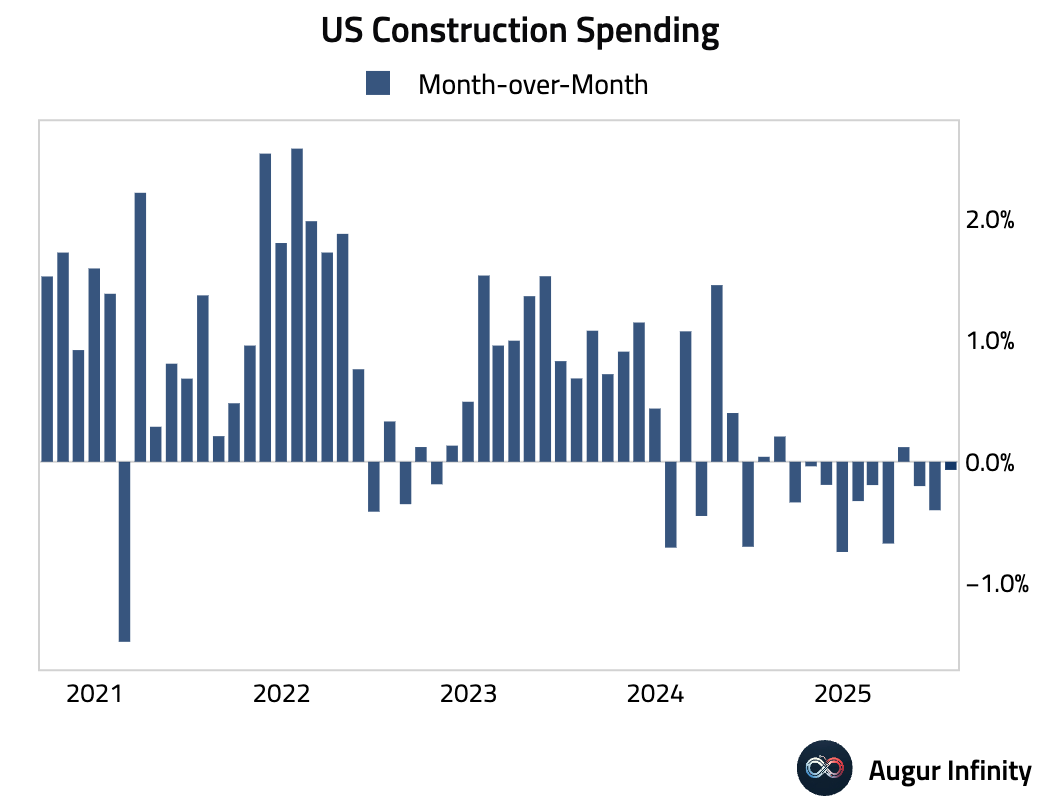

- US construction spending fell 0.1% M/M in July, matching consensus. The decline was driven by private nonresidential projects. After adjusting for a 0.4% M/M rise in construction costs, real spending fell by a more significant 0.5%.

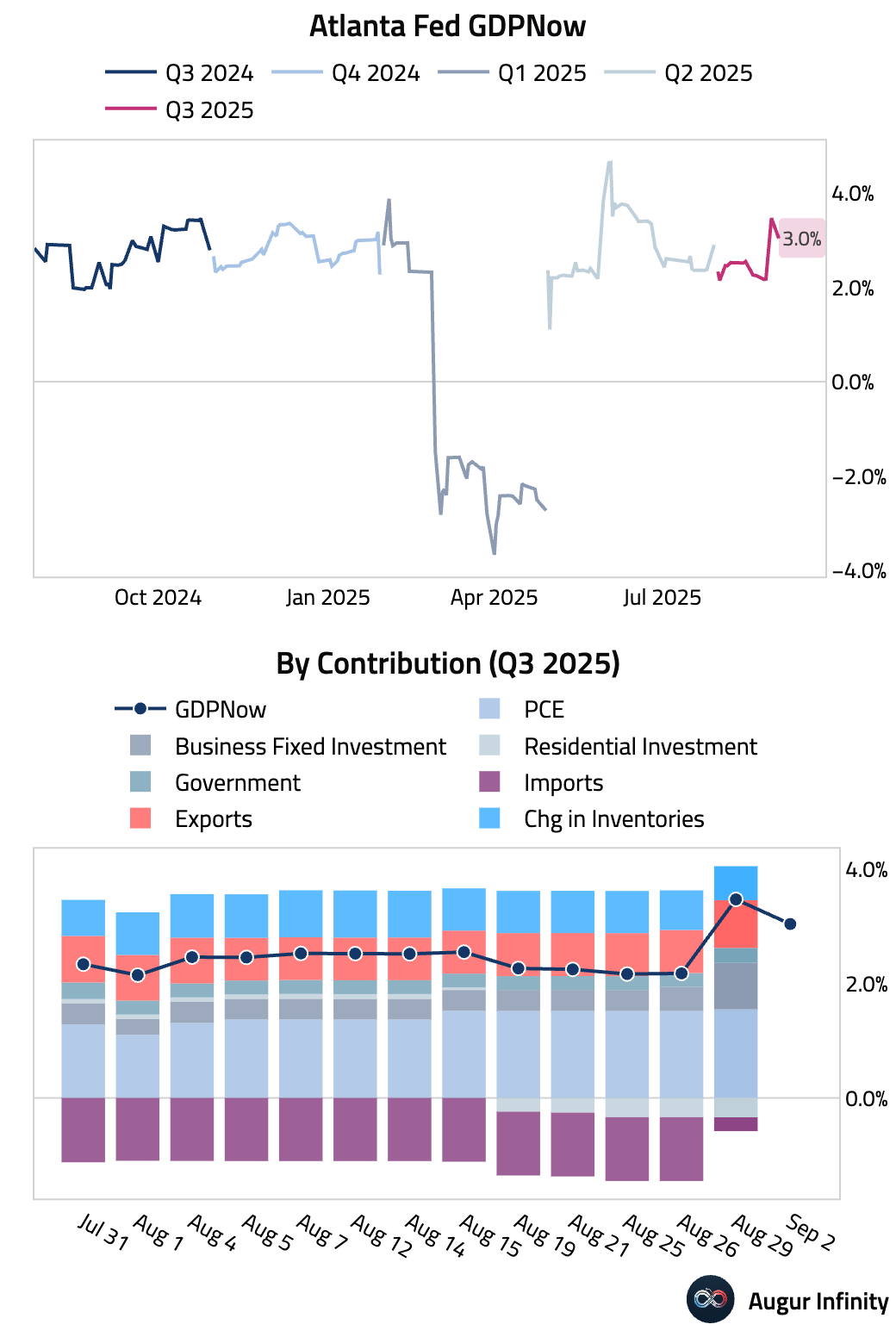

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 3.0%, down from 3.5% on August 29.

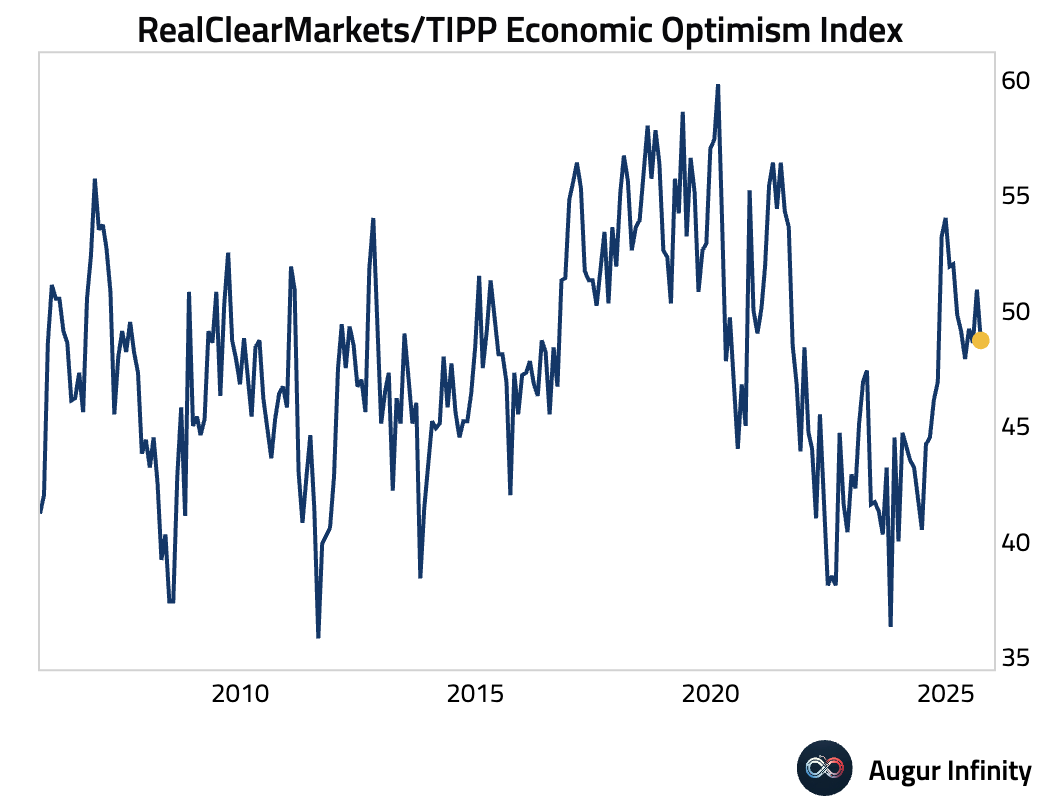

- The RCM/TIPP Economic Optimism Index fell back into pessimistic territory in September, dropping to 48.7 from 50.9.

Canada

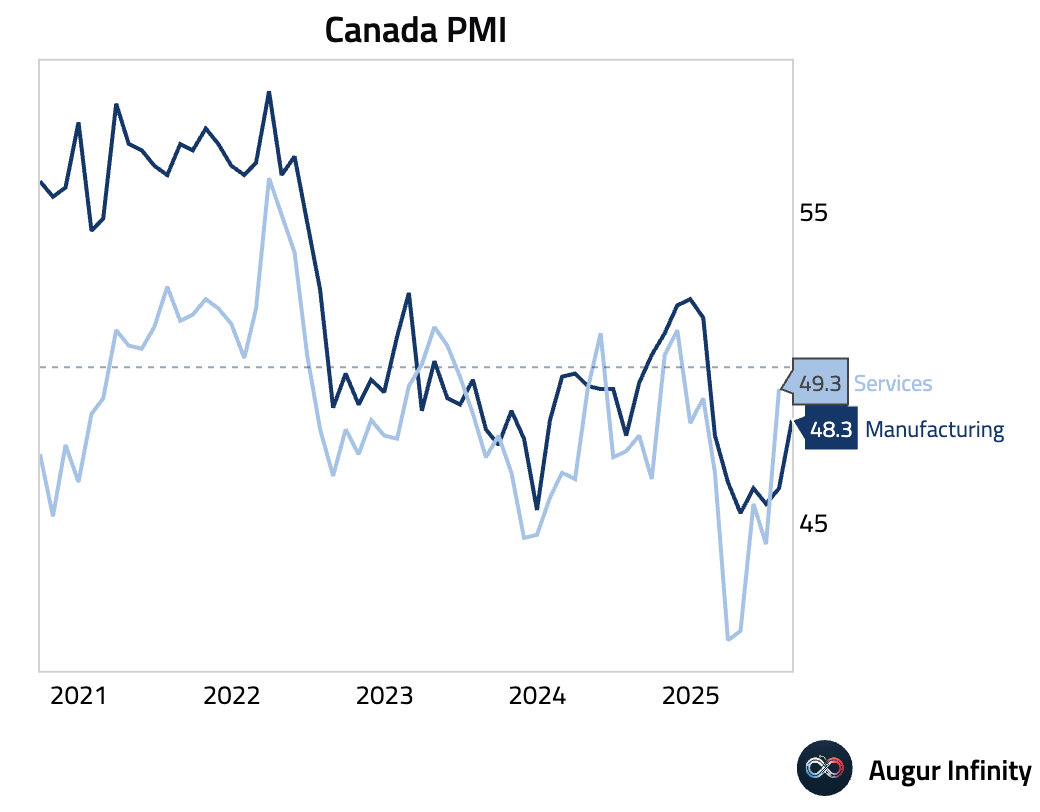

- Canada’s S&P Global Manufacturing PMI rose to a seven-month high of 48.3 in August, up from 46.1. Despite the improvement, the index remained in contractionary territory for the seventh consecutive month, as ongoing trade tariffs continue to suppress demand from US clients and raise input costs.

Europe

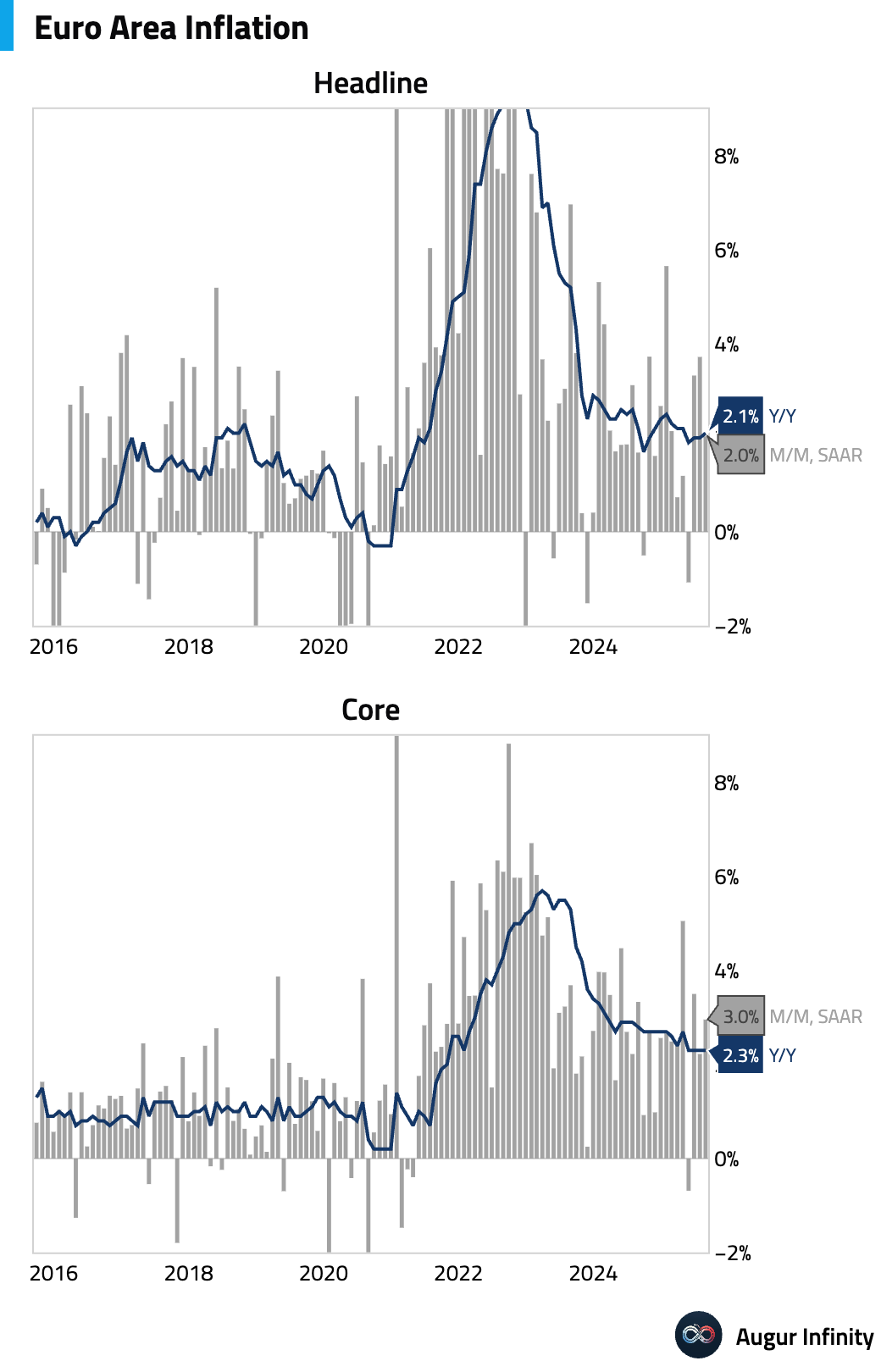

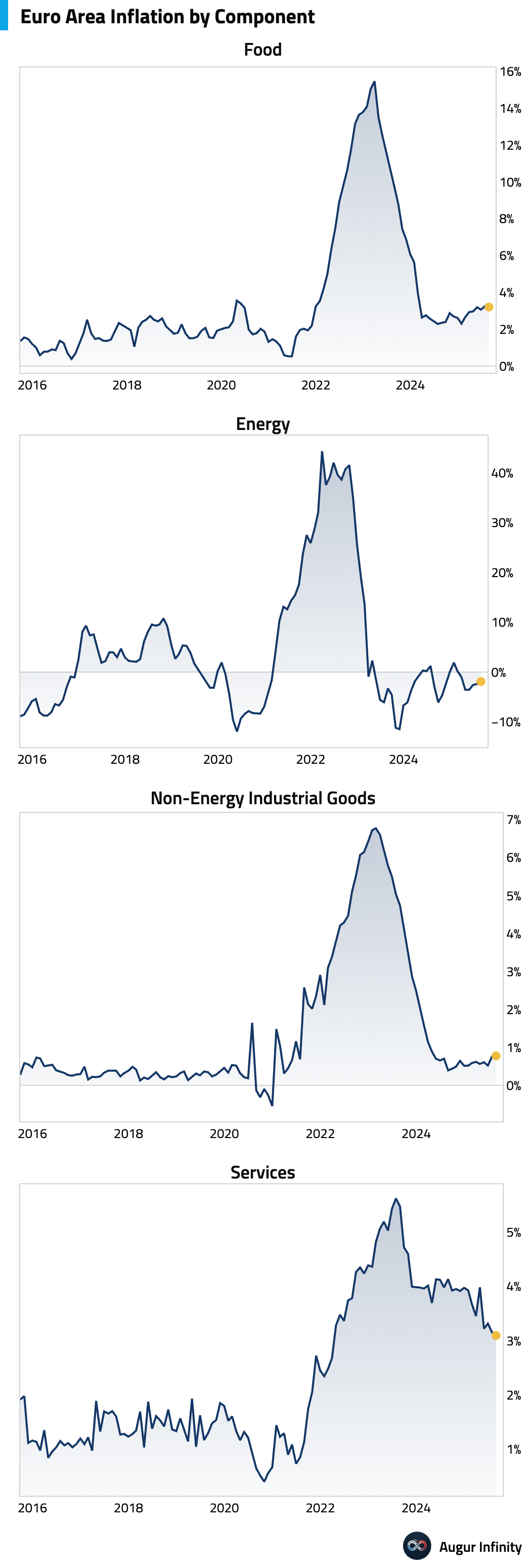

- The flash estimate for Eurozone headline inflation unexpectedly ticked up to 2.1% Y/Y in August, slightly above the 2.0% consensus. Core inflation held steady at 2.3%, also above the 2.2% forecast. The upside surprise in the core reading was driven by stronger-than-expected core goods inflation, which offset an anticipated decline in services inflation.

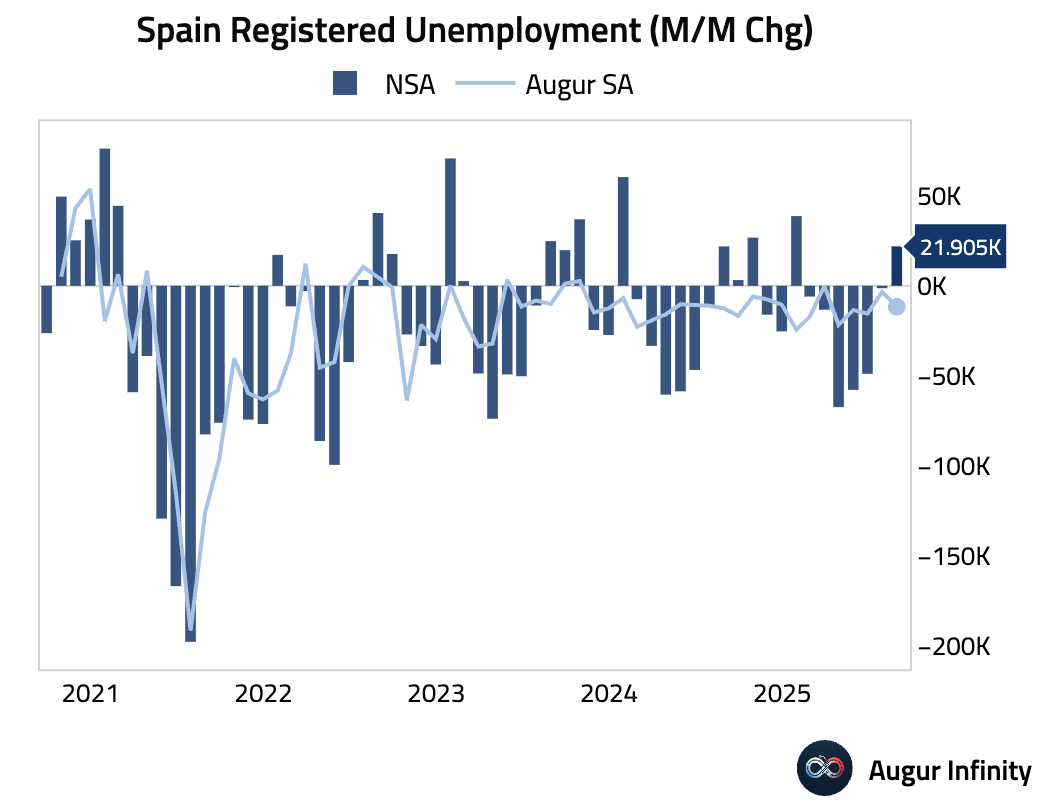

- Spanish unemployment rose by 21.9k in August, a significantly larger increase than the 14.2k consensus, reversing July’s small decline.

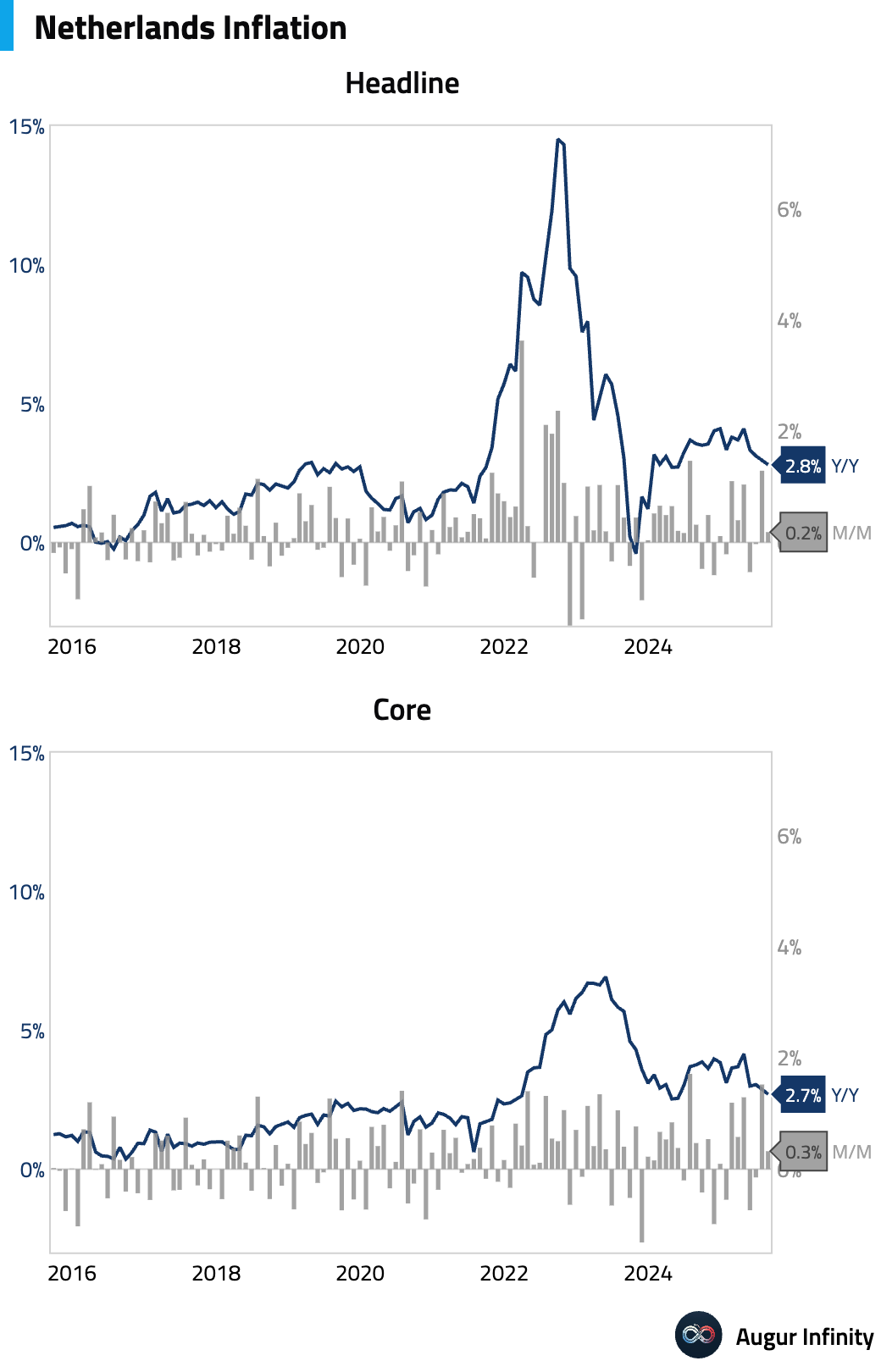

- Preliminary data showed Dutch inflation slowed to 2.8% Y/Y in August from 2.9% in July.

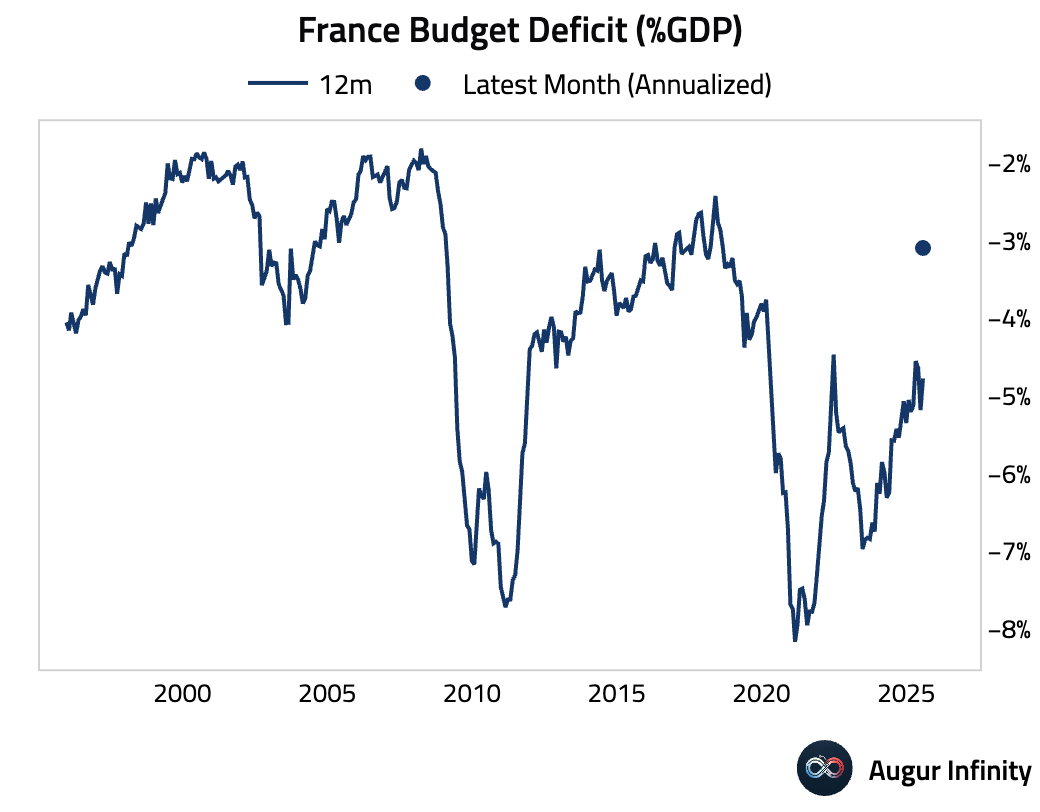

- France’s year-to-date budget deficit widened to €142 billion through July, a larger gap than the €107.2 billion forecast for the period.

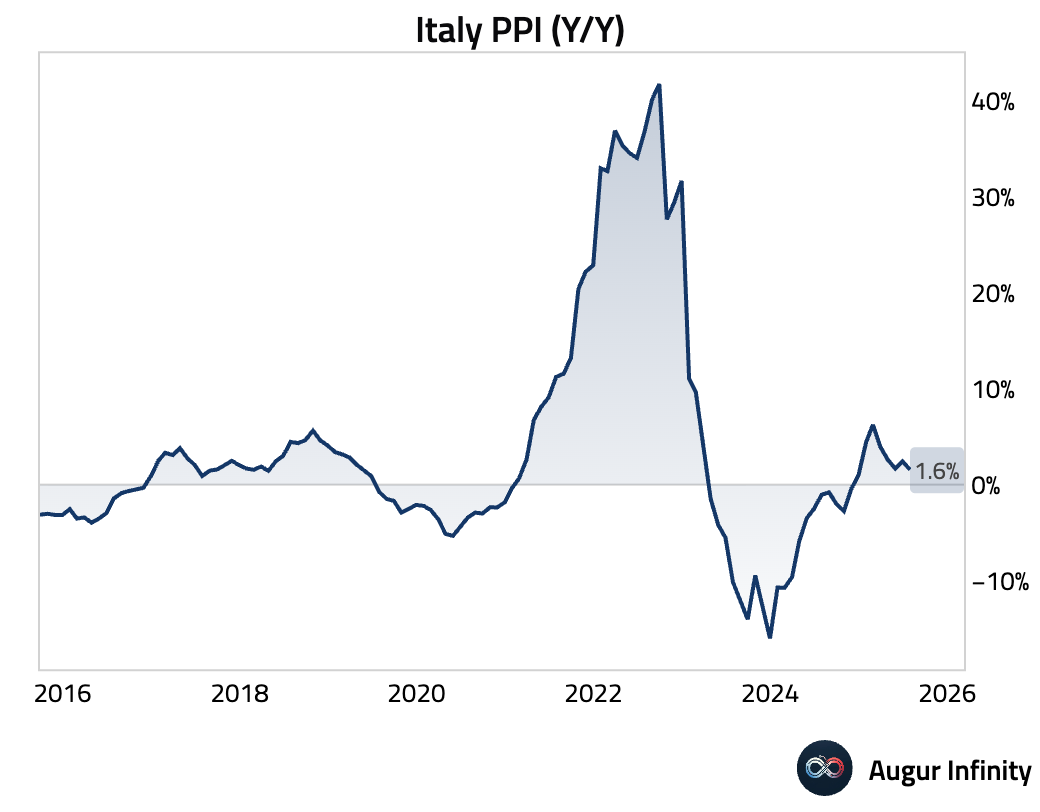

- Italian producer price inflation decelerated in July, with the M/M rate slowing to 0.5% from 1.4% and the Y/Y rate easing to 1.6% from 2.4%.

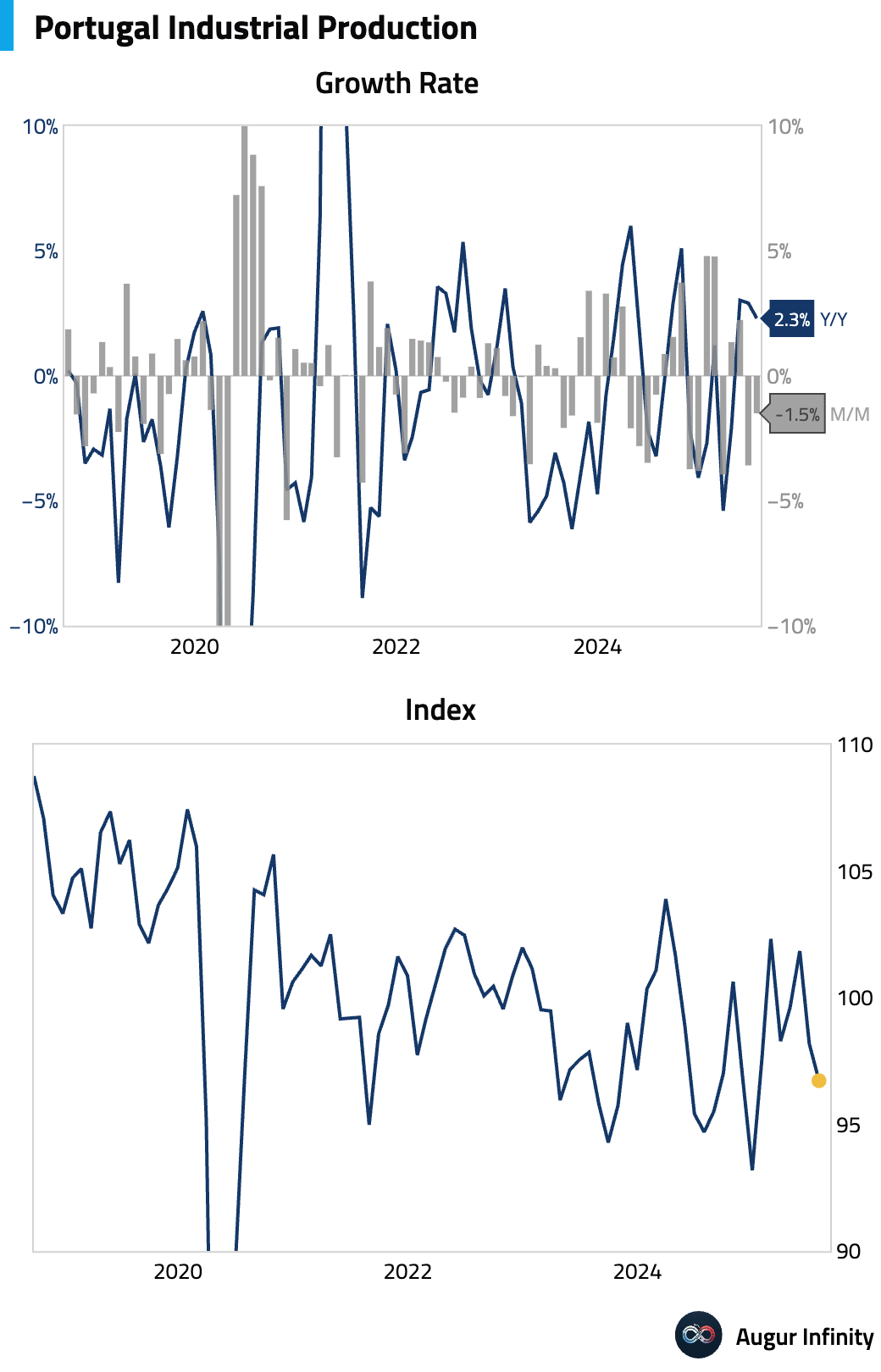

- Portugal’s industrial production fell 1.5% M/M in July, though year-over-year growth remained positive but slowed to 2.3% from 3.0%.

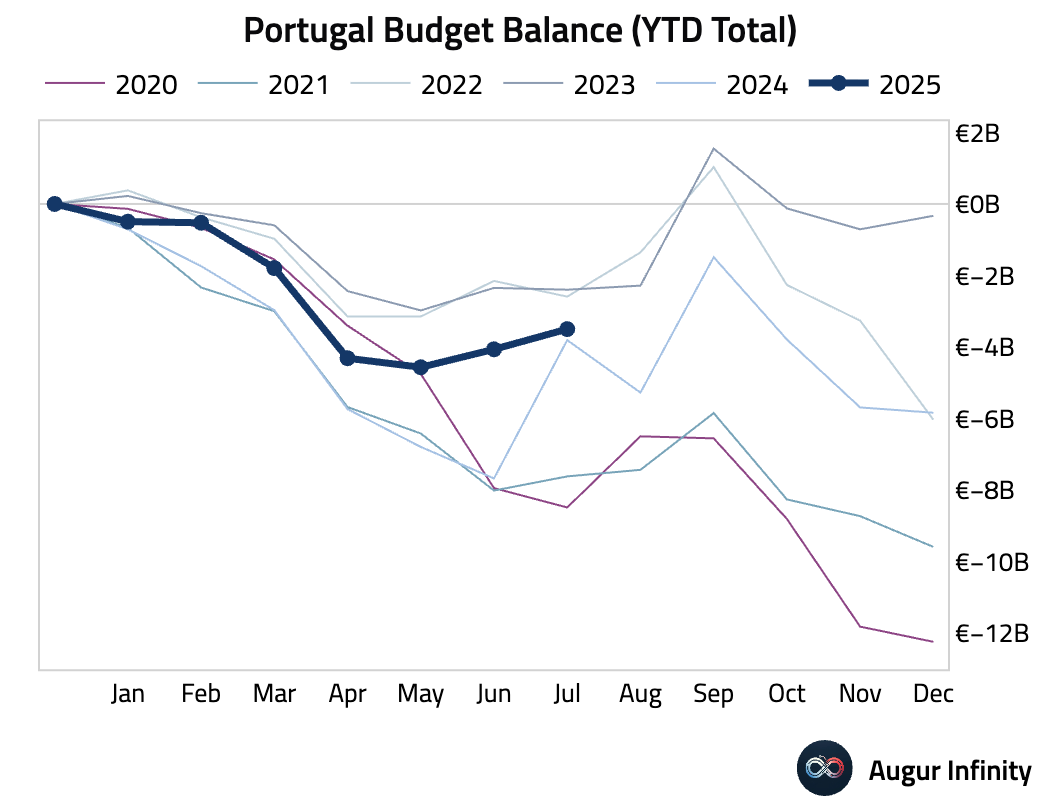

- Portugal's year-to-date budget deficit narrowed to €3.5 billion through July from €4.1 billion in the prior period.

Asia-Pacific

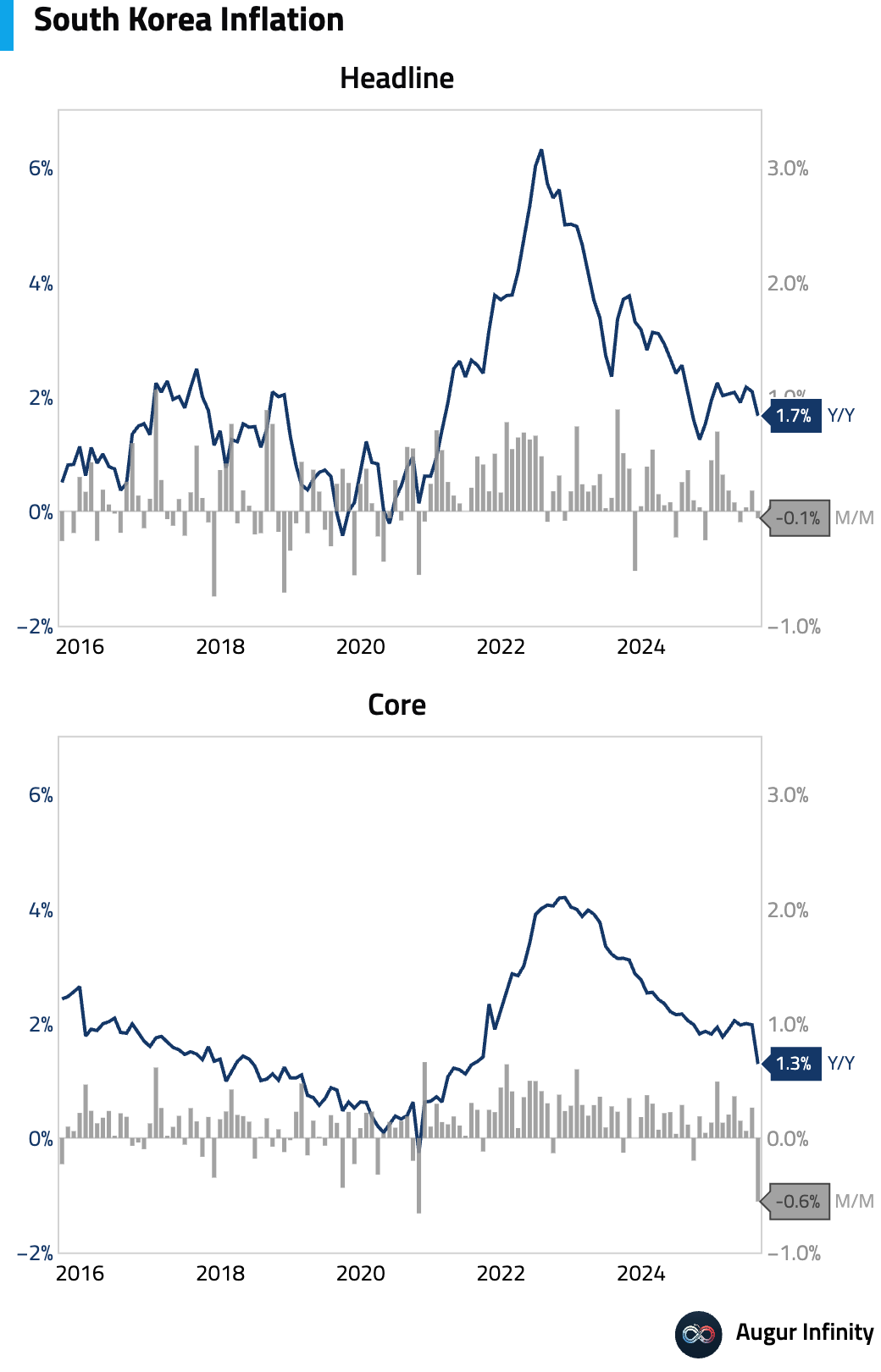

- South Korea’s annual inflation rate fell to 1.7% in August from 2.1%, missing the 2.0% consensus, while the monthly rate unexpectedly declined 0.1%. The drop was driven entirely by a temporary, one-month discount on mobile phone charges from a major telecom provider, an effect that is expected to reverse in September.

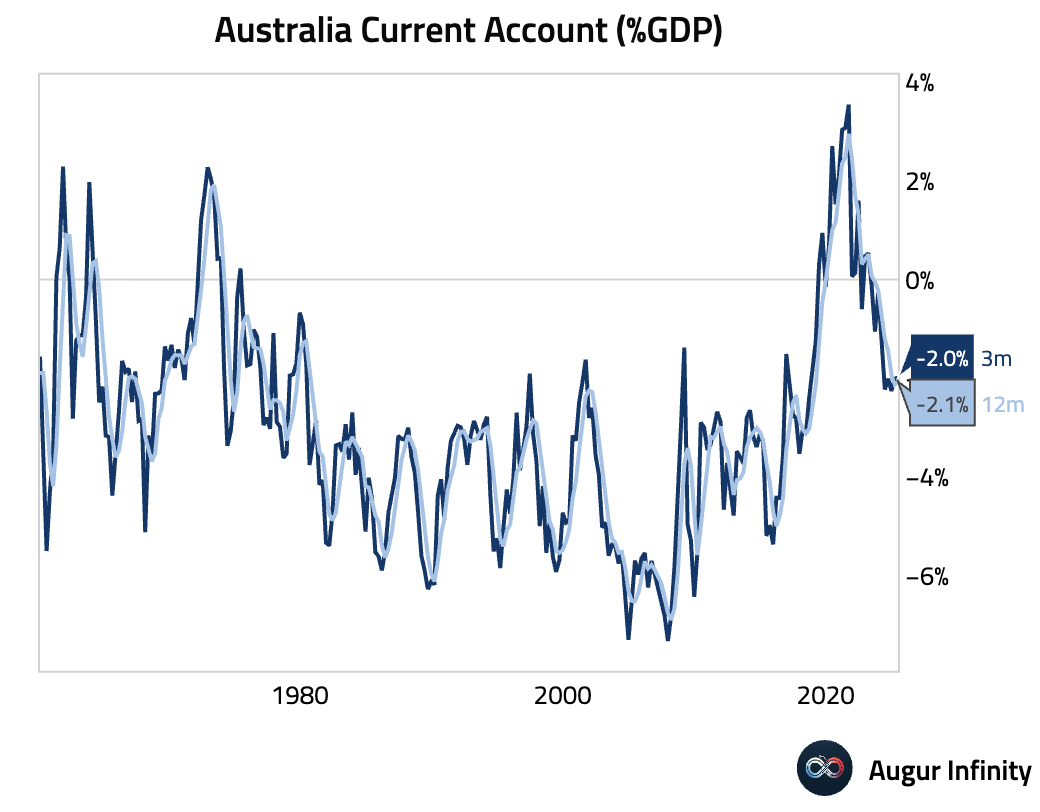

- Australia’s Q2 current account deficit narrowed to A$13.7 billion, smaller than the A$15.1 billion expected. The improvement was driven by a smaller net income deficit, which offset a decline in the goods and services surplus. Net exports are now forecast to add 0.1 percentage points to Q2 GDP.

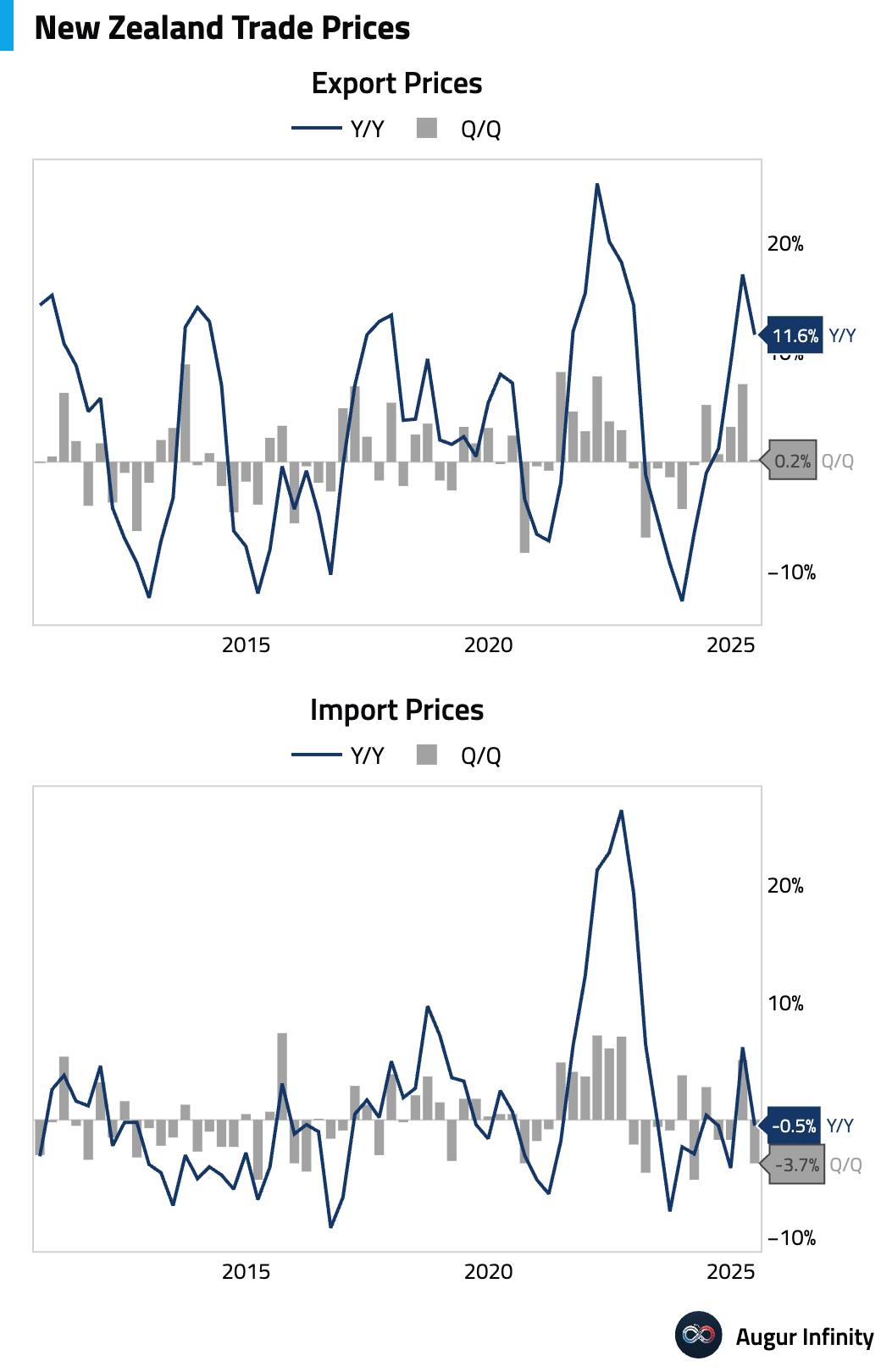

- New Zealand’s terms of trade improved as Q2 export prices edged up 0.2% Q/Q while import prices fell 3.7%.

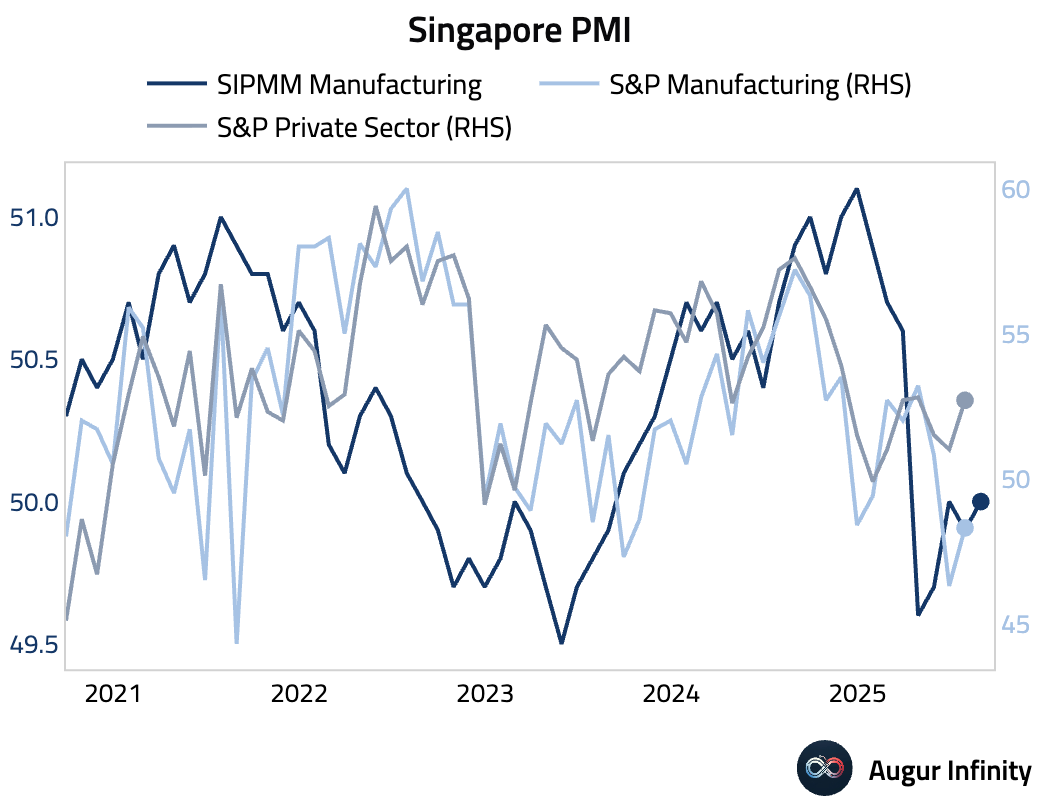

- Singapore’s manufacturing sector reached the neutral threshold in August, with the SIPMM PMI rising to 50.0 from 49.9.

Emerging Markets ex China

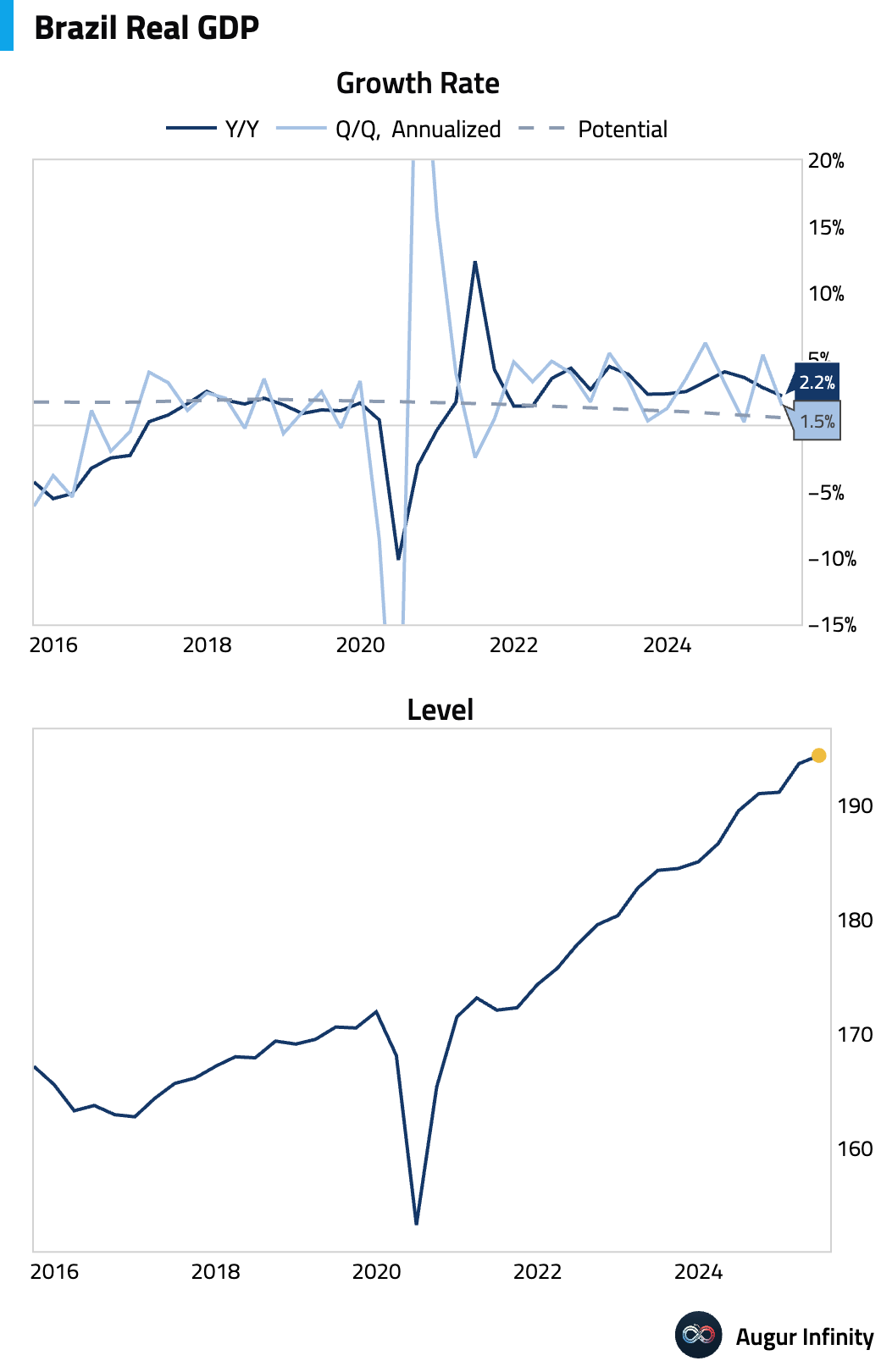

- Brazil’s economy grew 0.4% Q/Q in the second quarter, beating expectations for a 0.3% expansion. However, this represents a sharp slowdown from Q1’s 1.3% growth. The headline figure masked significant domestic weakness, with gross fixed investment plunging 2.2% Q/Q; the quarter was supported by a large positive contribution from net exports as imports fell sharply.

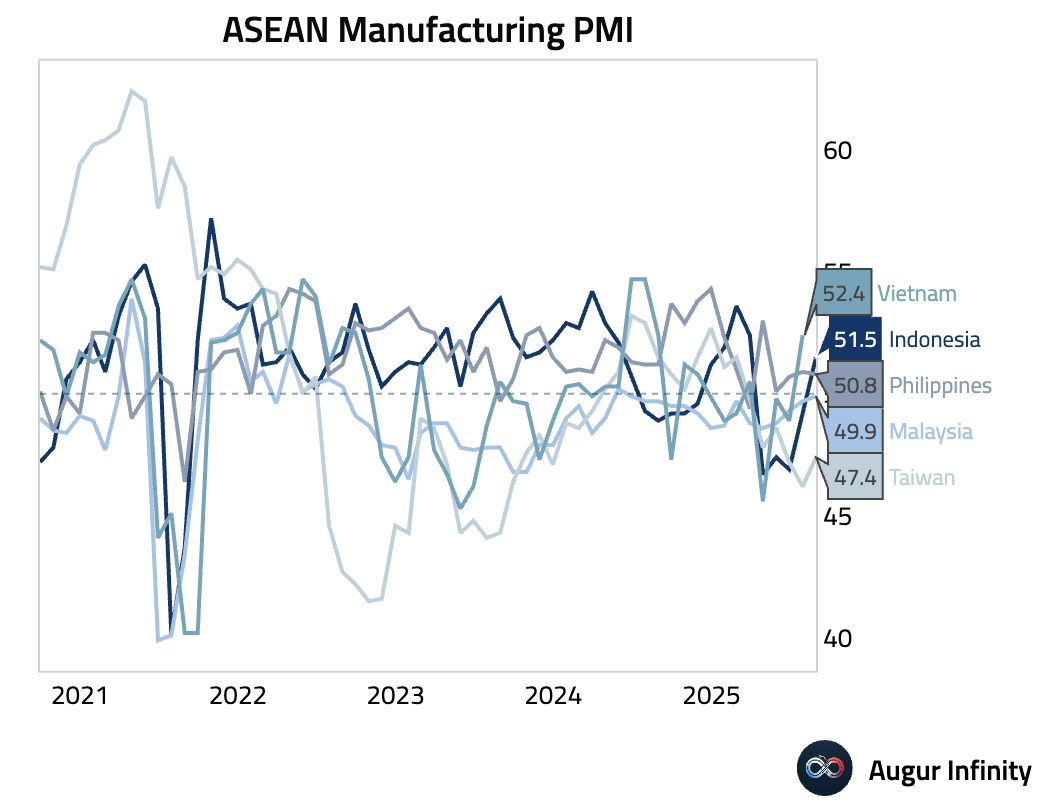

- Malaysia's S&P Global Manufacturing PMI rose to 49.9 in August, its highest level since June 2024 and nearing stabilization. Production grew for the first time in 15 months on the back of the strongest new order growth in three years, though firms cut employment amid concerns about the global economy.

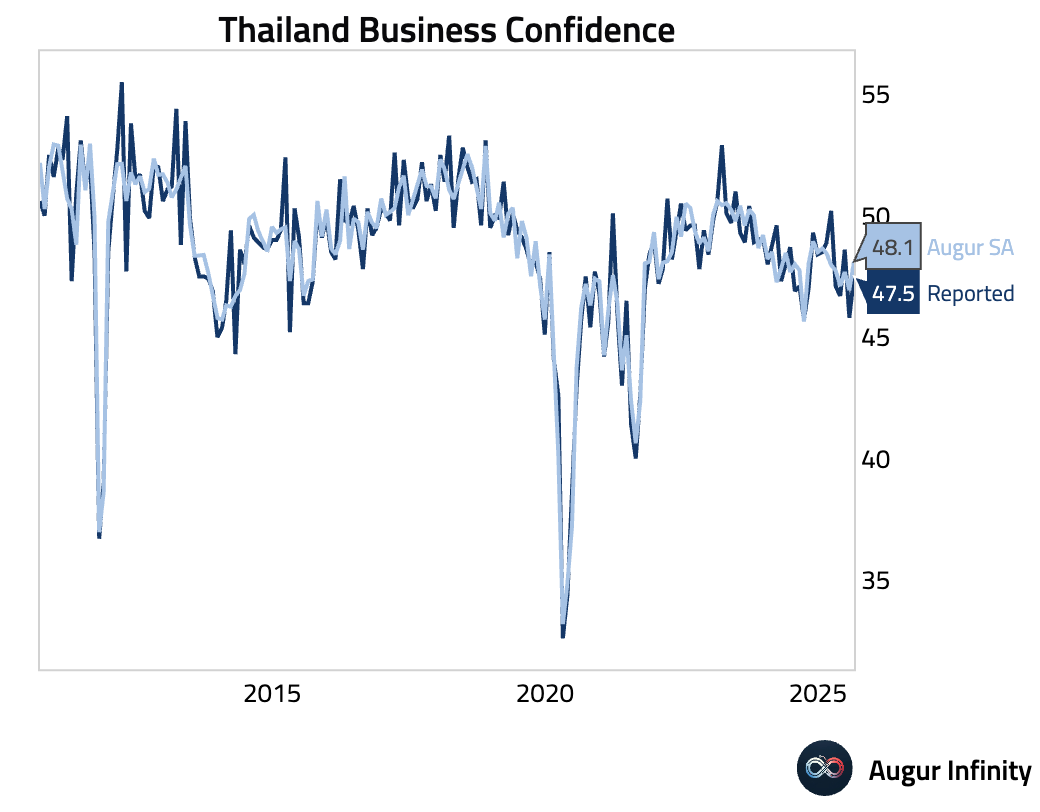

- Thai business confidence improved in August, with the index rising to 47.5 from 45.8, though it remained below the neutral 50-mark.

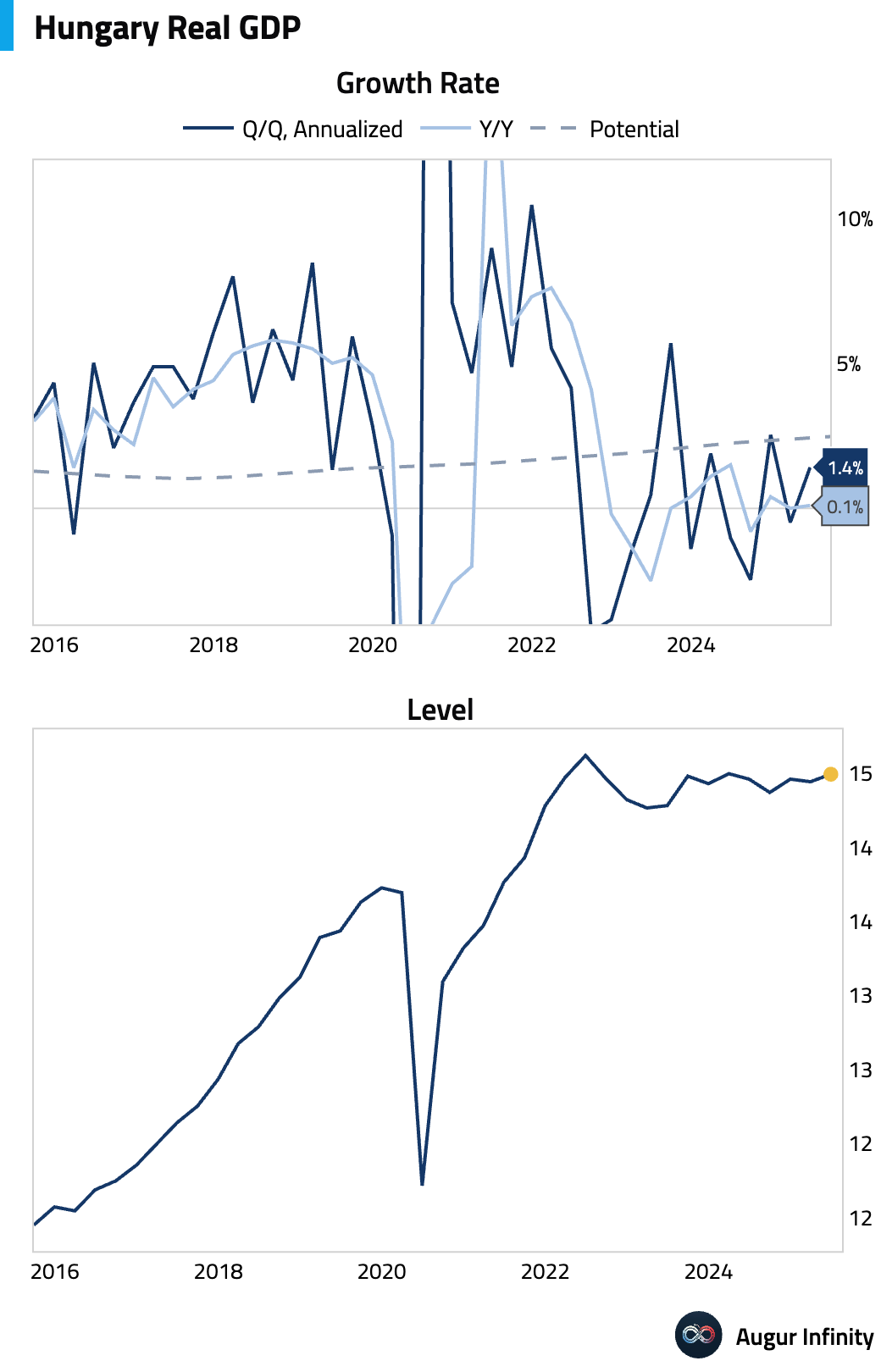

- The final estimate for Hungary’s Q2 GDP confirmed growth of 0.4% Q/Q (or 1.4% annualized) and 0.1% Y/Y.

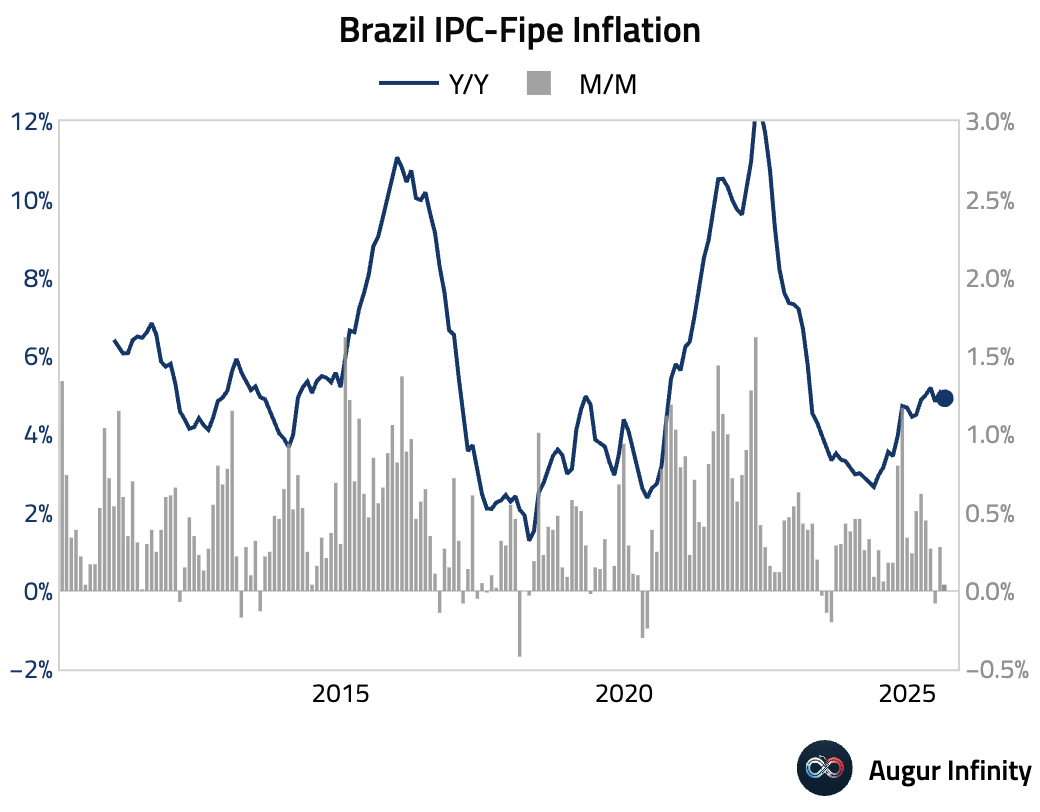

- São Paulo’s IPC-Fipe inflation index showed a sharp deceleration in August, rising just 0.04% M/M compared to 0.28% in July.

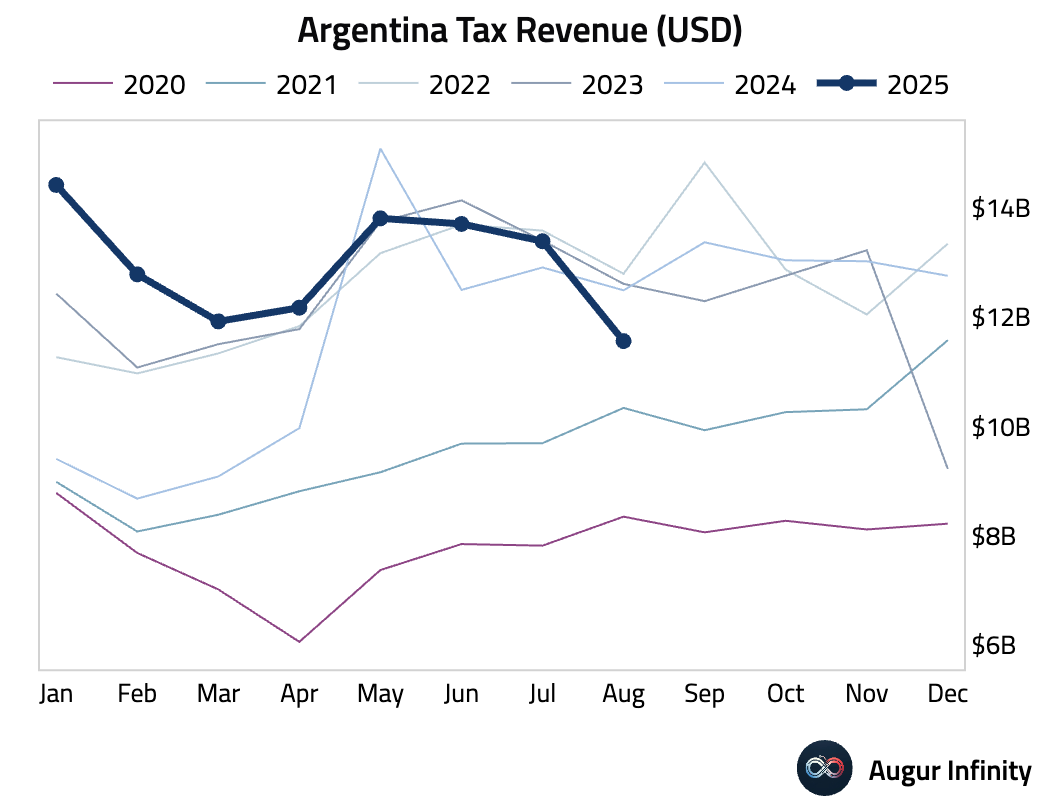

- Argentine tax revenue was ARS 15.36 trillion in August, down from ARS 17.00 trillion in July.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.