Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Global Economics

United States

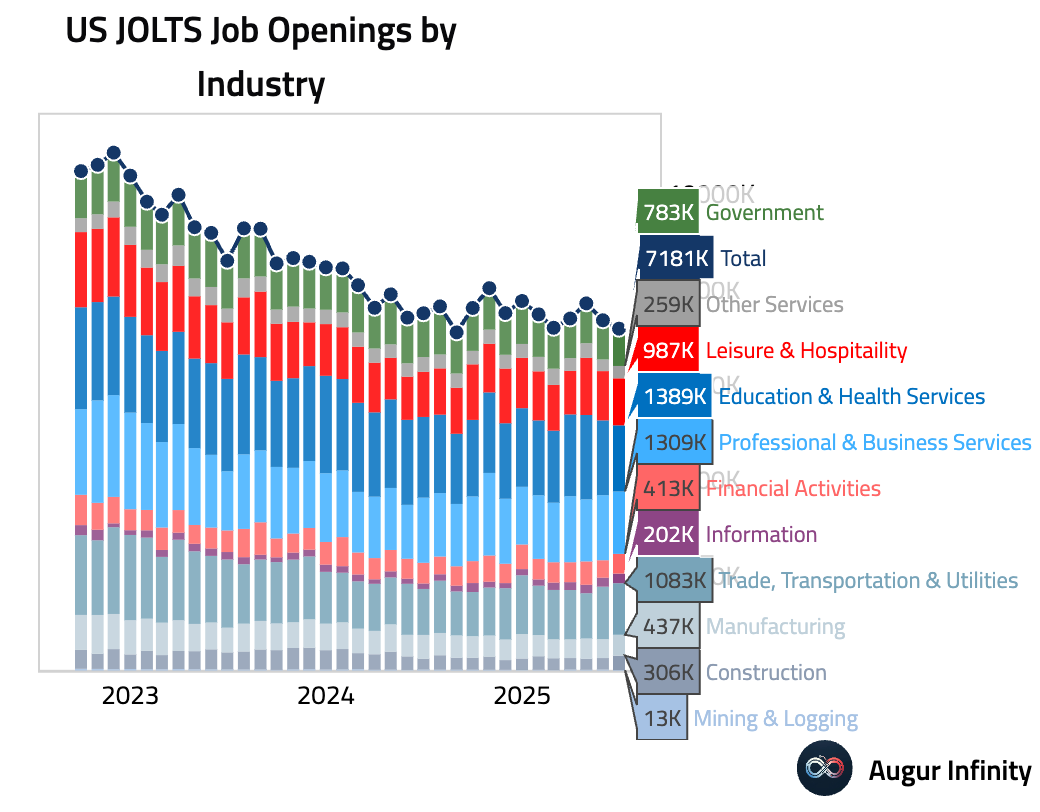

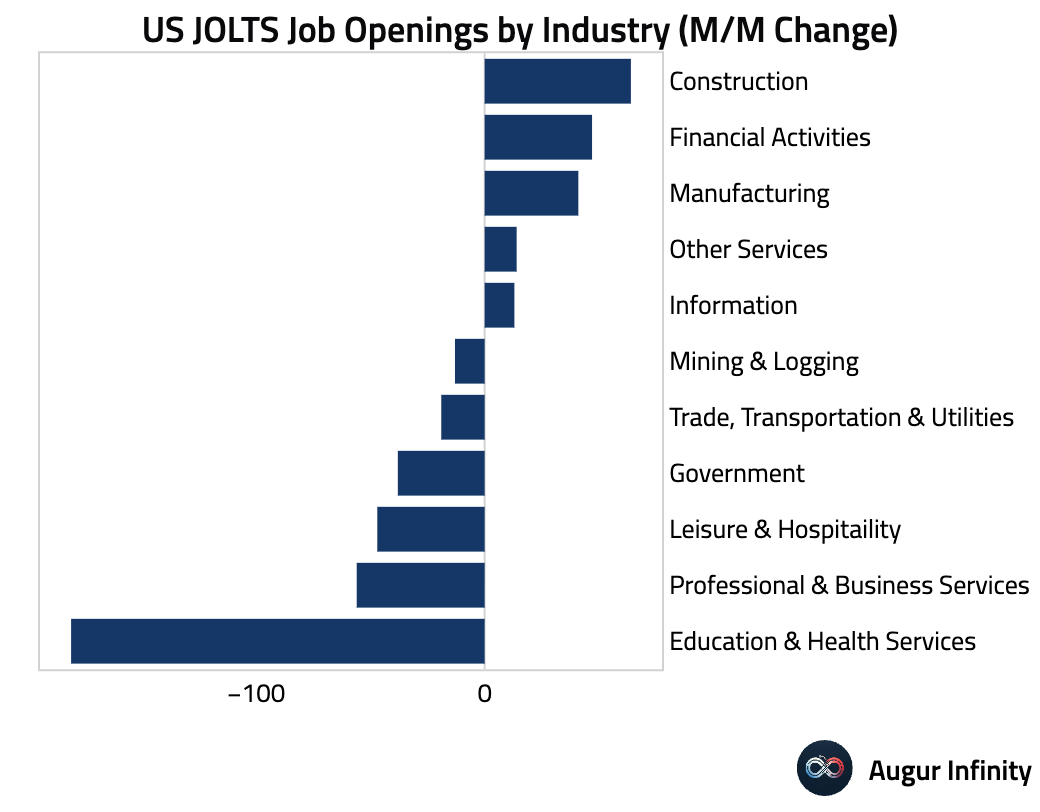

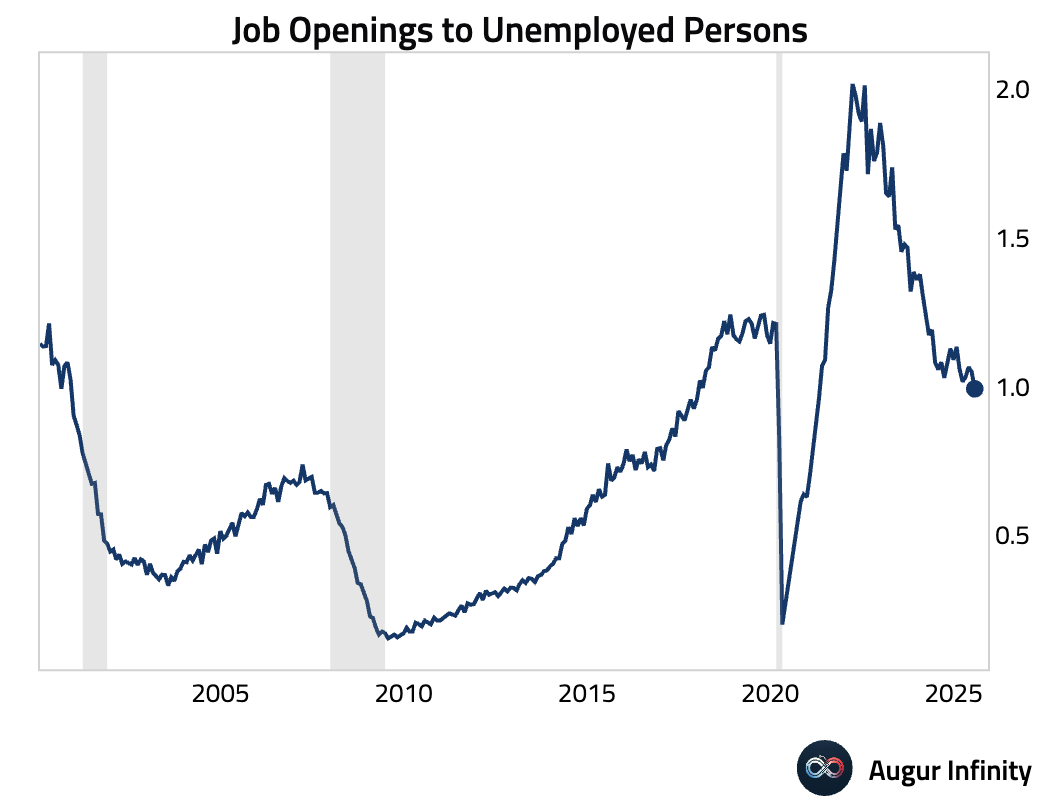

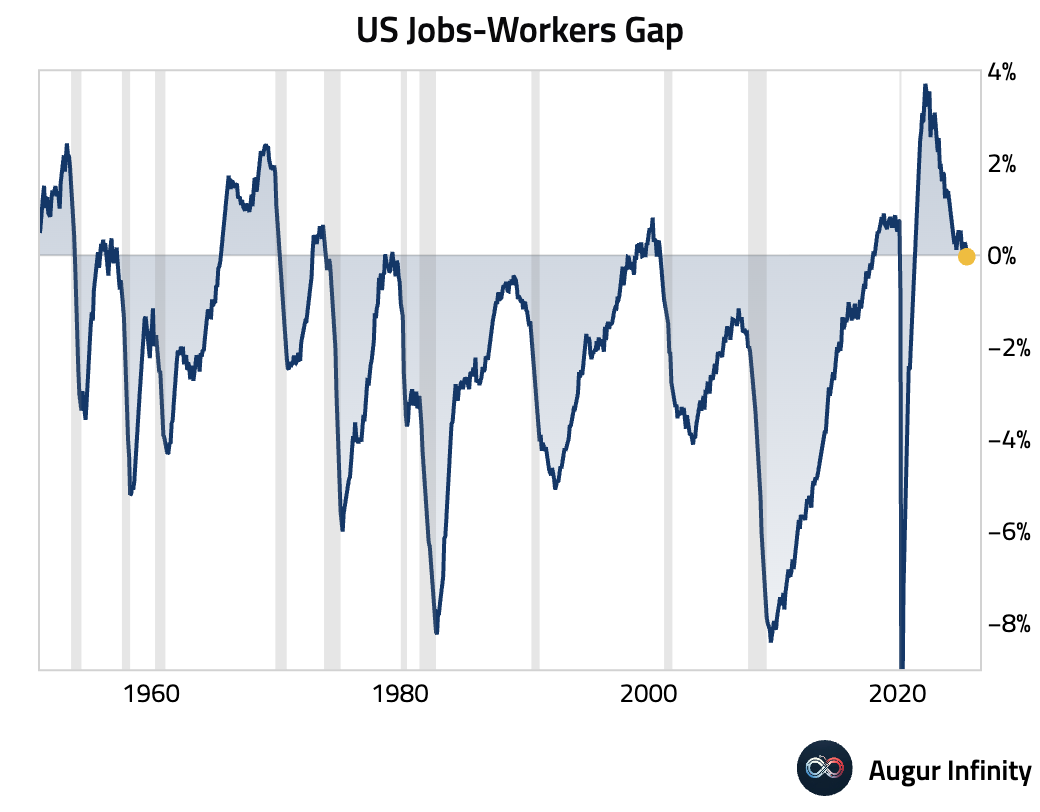

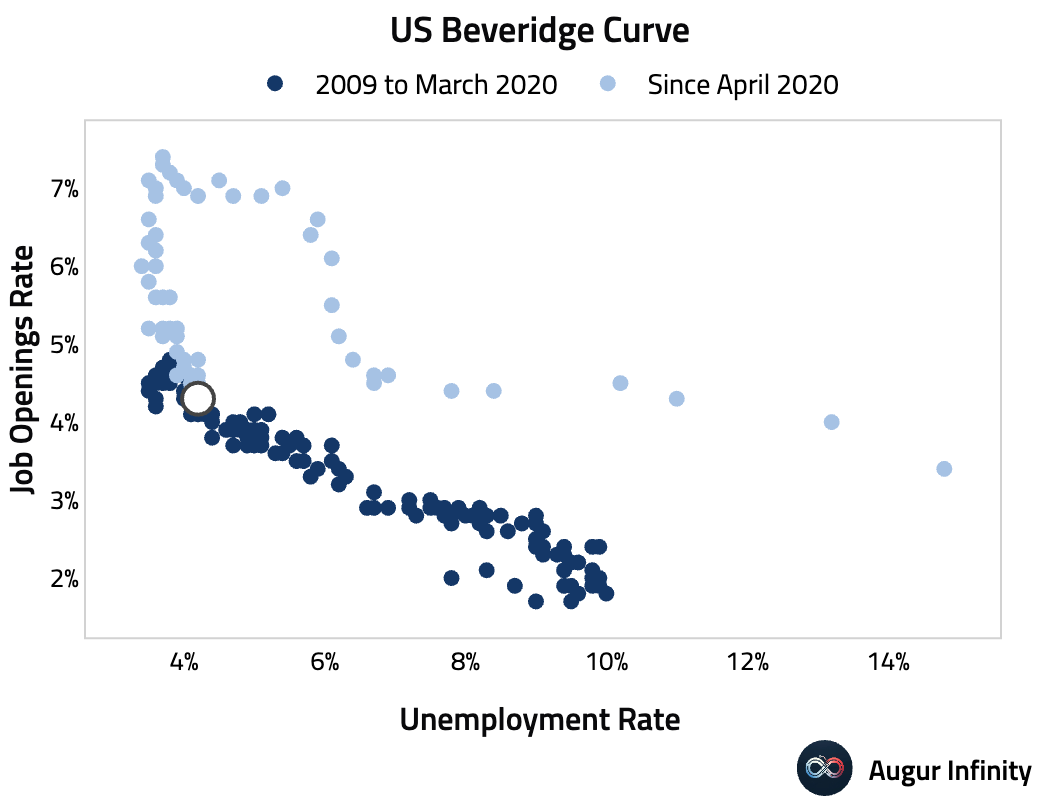

- July’s JOLTS job openings edged down to 7.18 million, below the 7.4 million consensus and a downwardly revised 7.36 million for June. This is the lowest reading since April 2025.

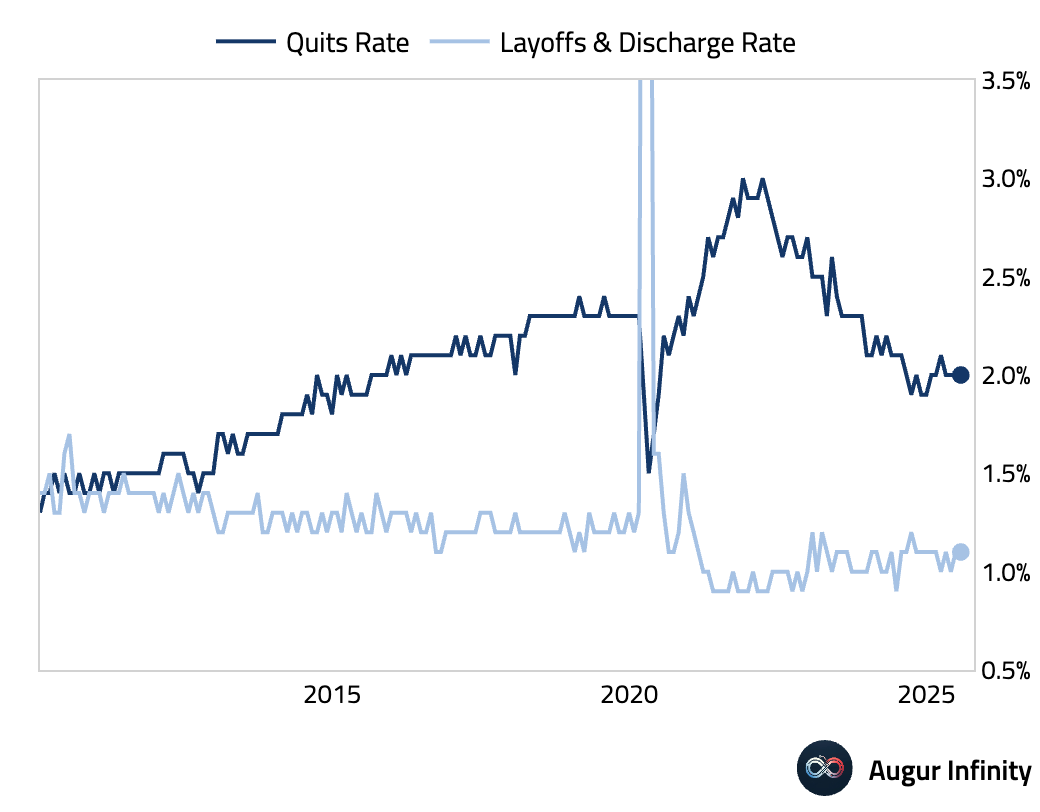

- The JOLTS quits level was effectively unchanged at 3.21 million in July. The quits rate held steady at 2.0%.

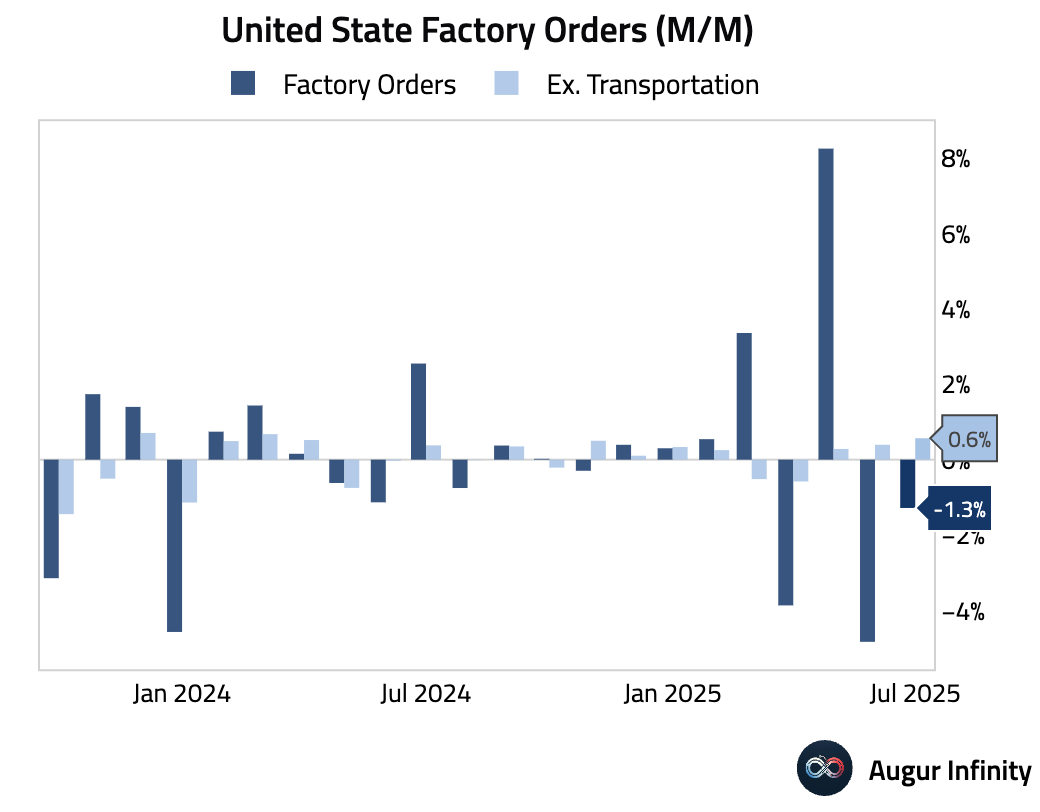

- Factory orders declined 1.3% M/M in July, a modest improvement from June’s 4.8% drop and roughly in line with consensus expectations of -1.4%. Excluding the volatile transportation component, orders rose 0.6%, picking up from the prior month’s 0.4% gain.

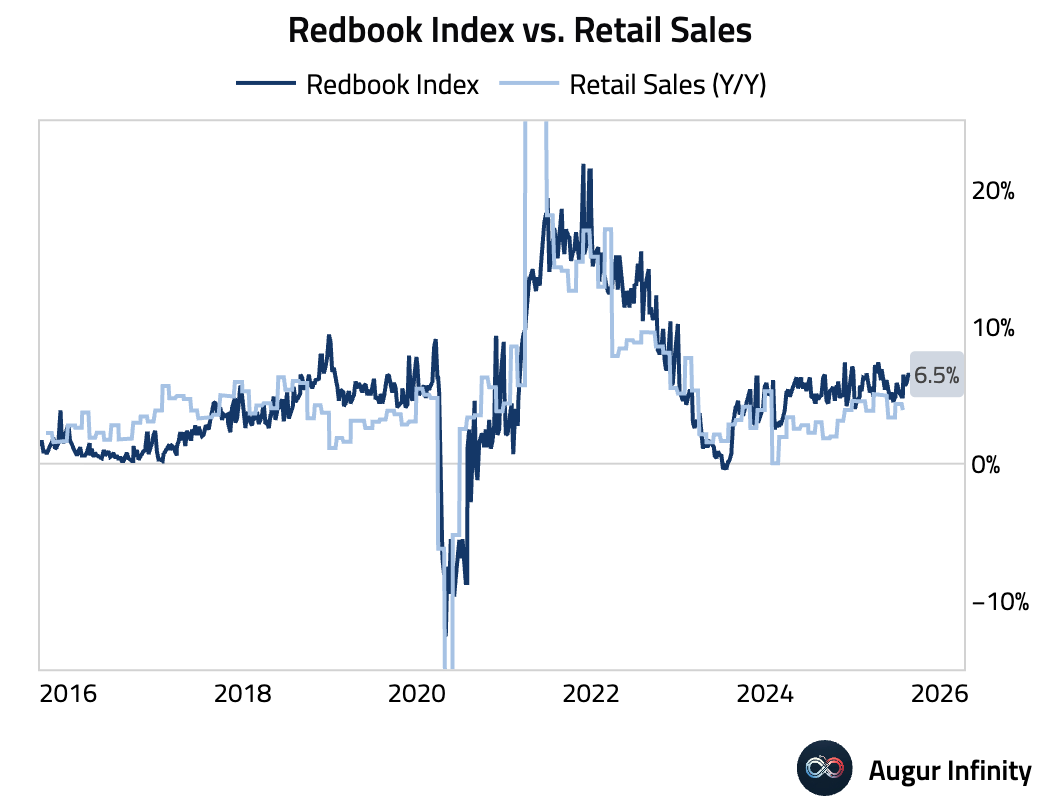

- The Redbook index of same-store sales was unchanged at 6.5% Y/Y for the week ending August 30.

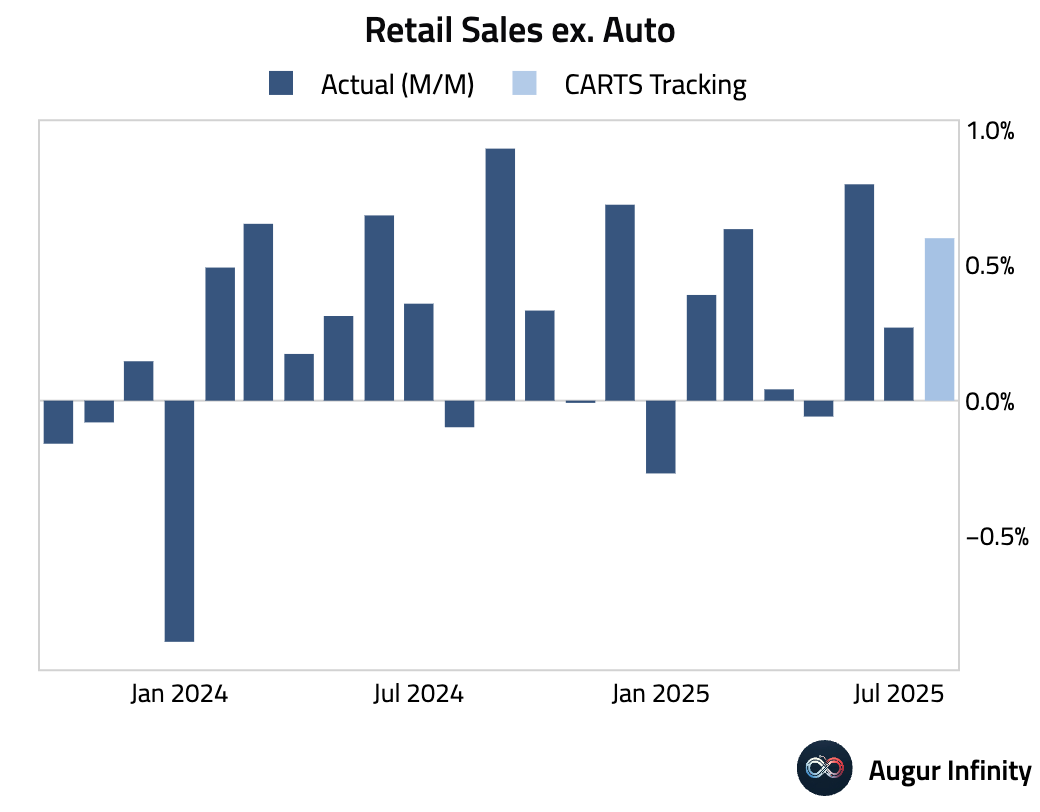

- The Chicago Fed CARTS is projecting retail sales ex auto for August to come in at 0.6% M/M, accelerating from 0.3% in July.

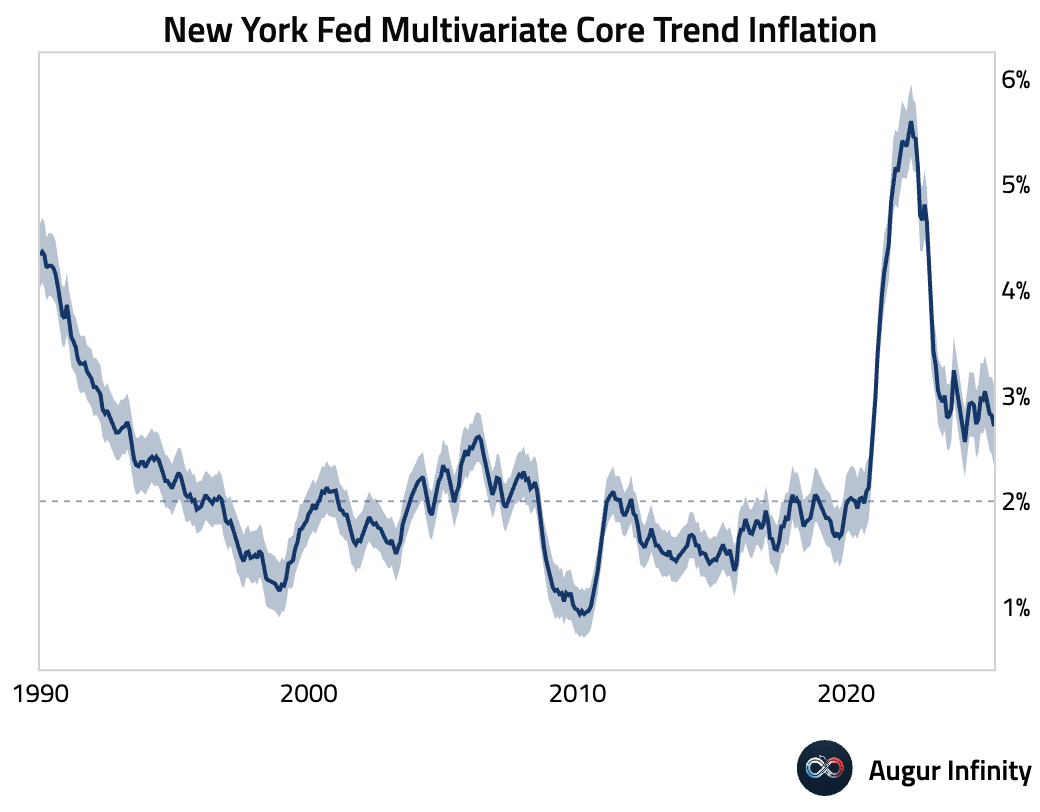

- The New York Fed Multivariate Core Trend (MCT) inflation decreased to 2.7% in July from 2.8%, driven by declines in the common component of the trend in goods and services ex-housing inflation.

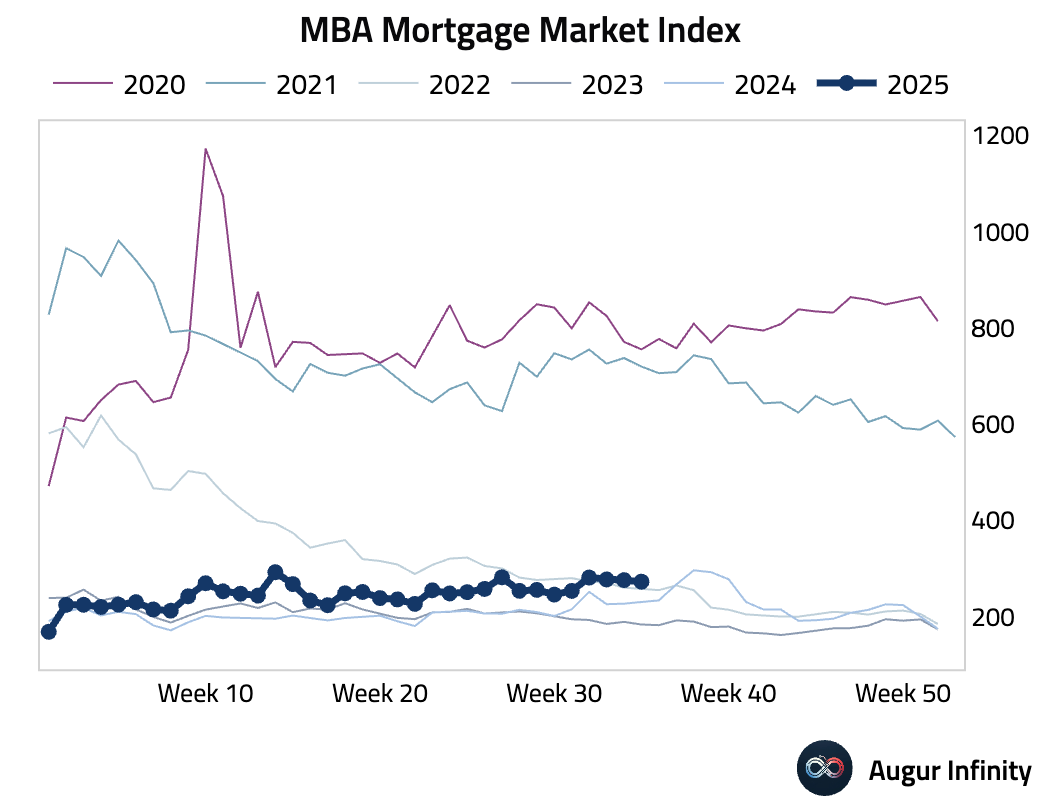

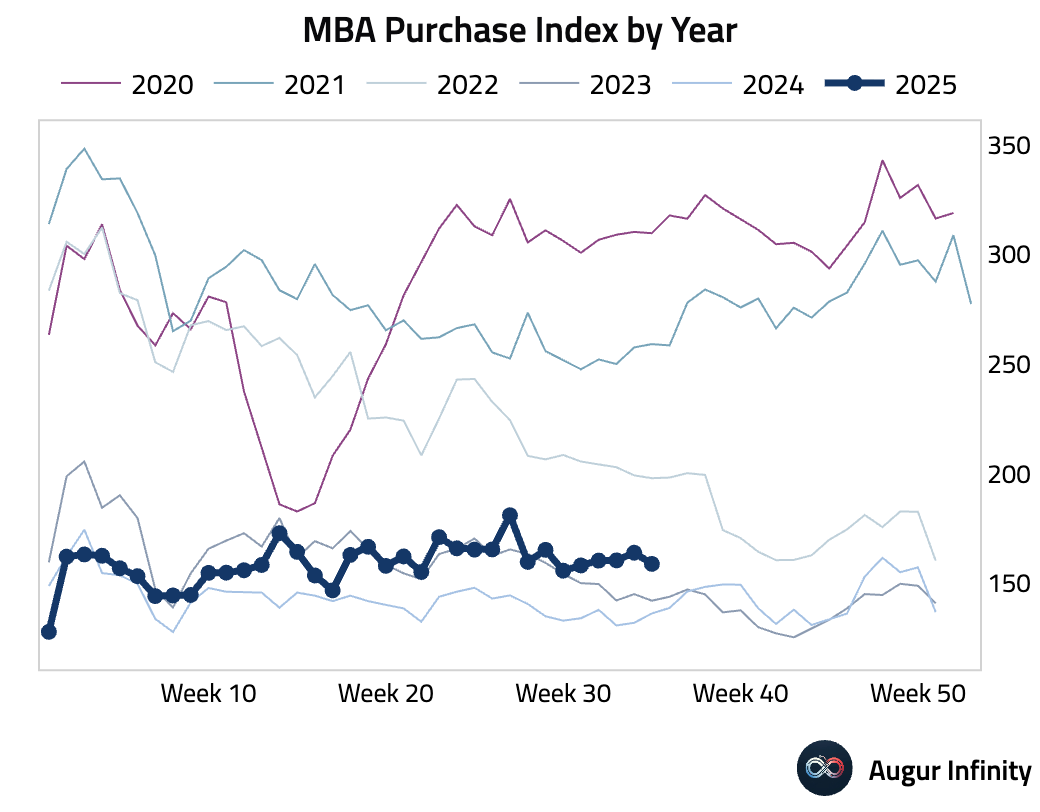

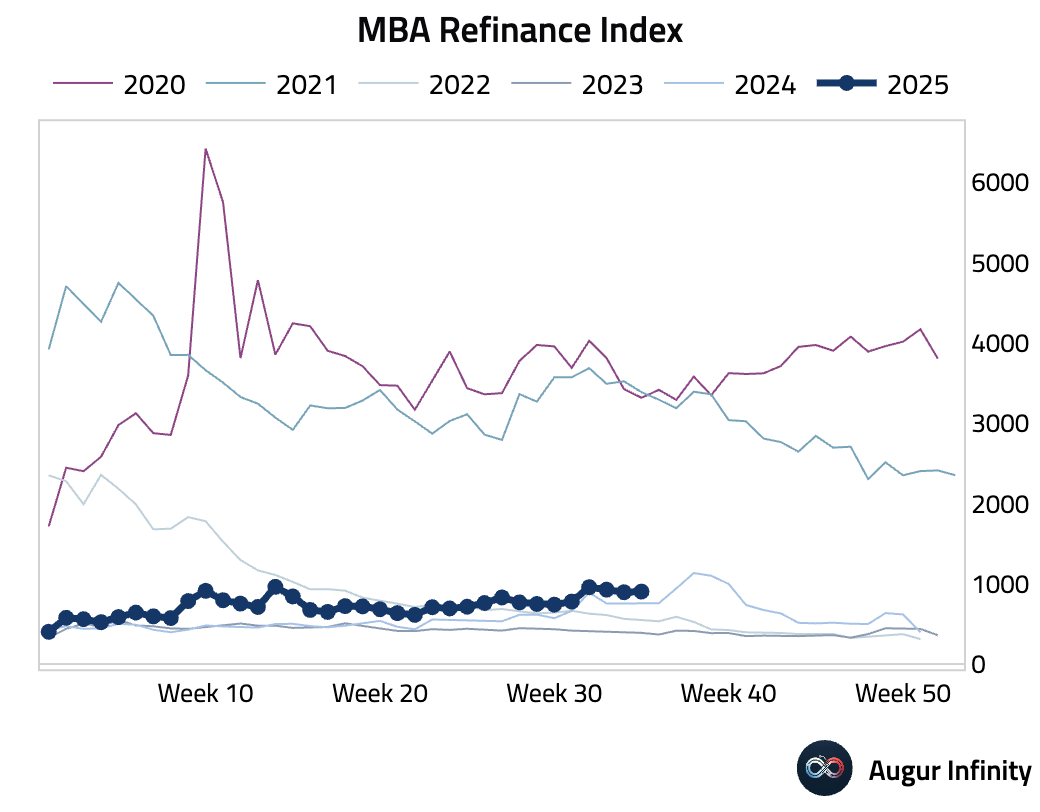

- MBA mortgage applications fell 1.2% week-over-week for the week ending August 29. The decline was driven by a drop in the purchase index, which more than offset a modest gain in the refinance index.

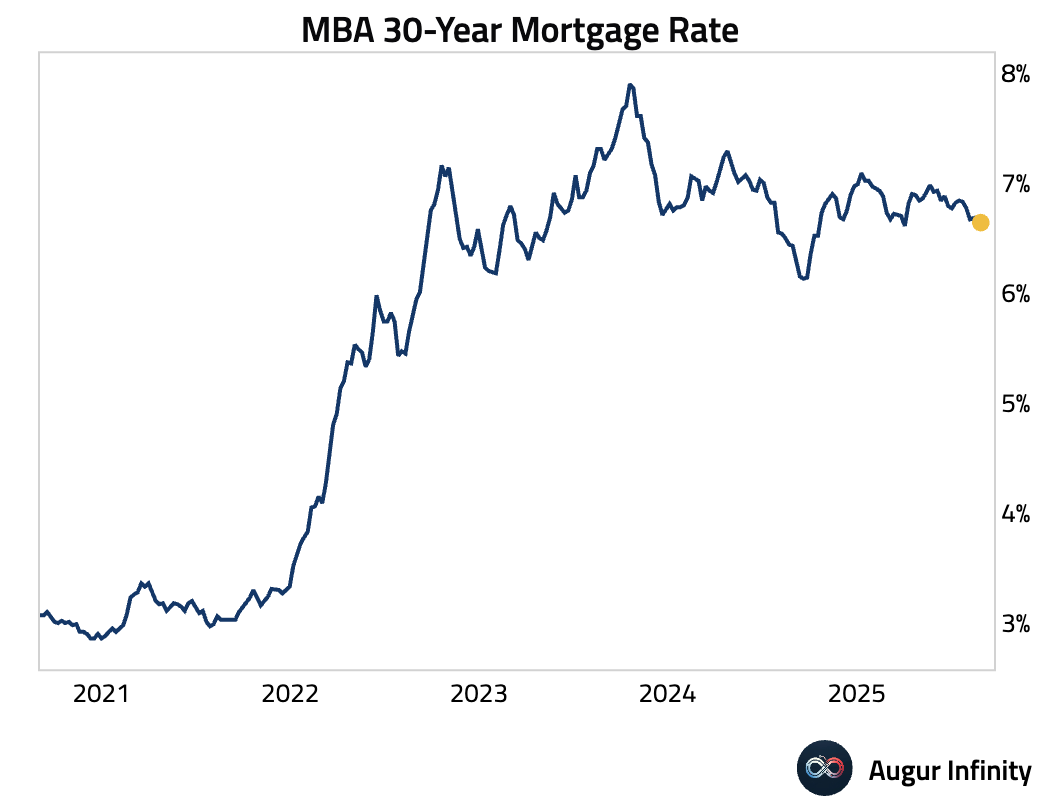

- The MBA 30-year mortgage rate fell 5 basis points to 6.64%, its lowest level since early April.

Canada

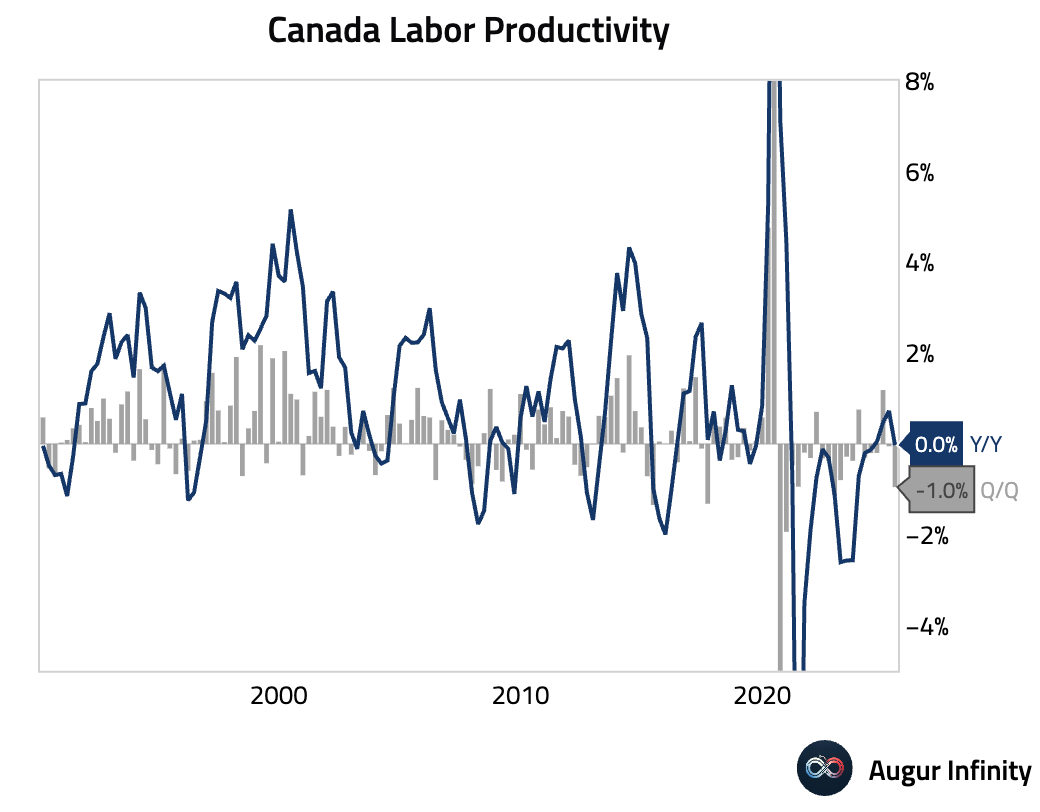

- Labor productivity unexpectedly fell 1.0% Q/Q in the second quarter, missing the +0.2% consensus and marking the worst reading since the fourth quarter of 2022.

Europe

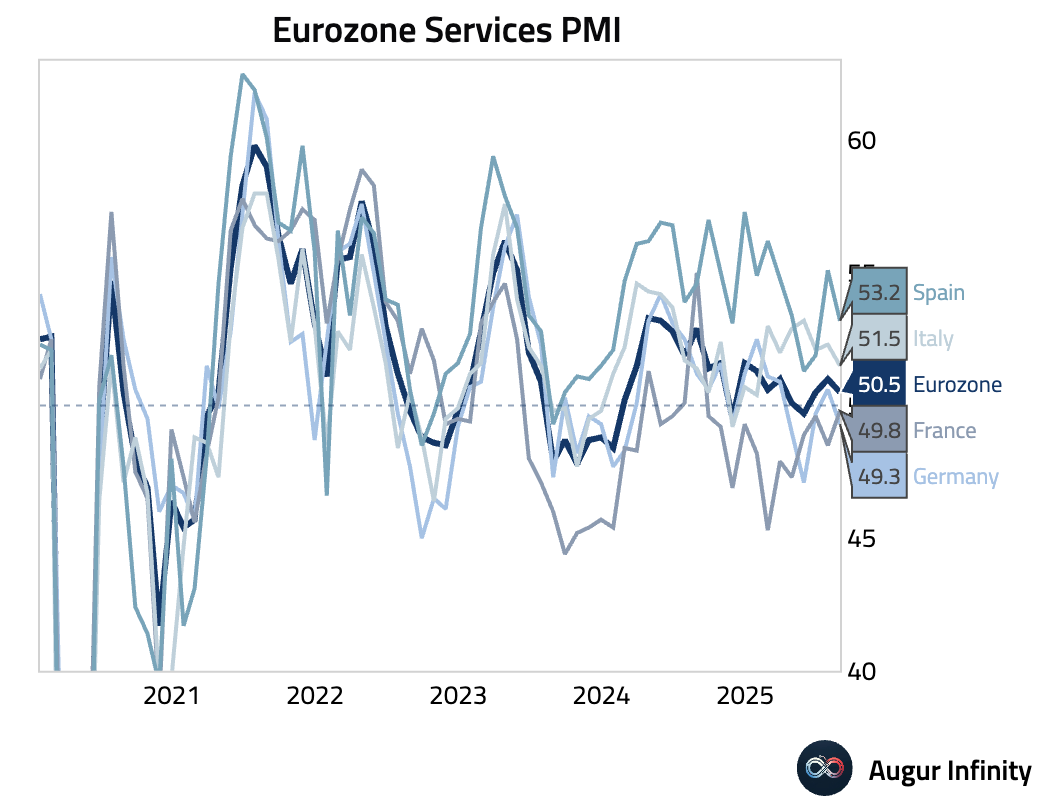

- The final Eurozone HCOB Services PMI for August was revised down slightly to 50.5 from 51.0. The details were mixed: Germany’s PMI fell back into contraction at 49.3 on a renewed decline in new orders and stalled hiring. France’s PMI rose to a 12-month high of 49.8 as emerging capacity constraints drove the strongest job growth in 15 months. In Italy, the PMI fell to a seven-month low of 51.5 as firms slowed price hikes amid sharply rising input costs, compressing margins. Spain’s PMI also softened to 53.2, though still-solid new business gains intensified capacity pressures and pushed output price inflation to a 16-month high.

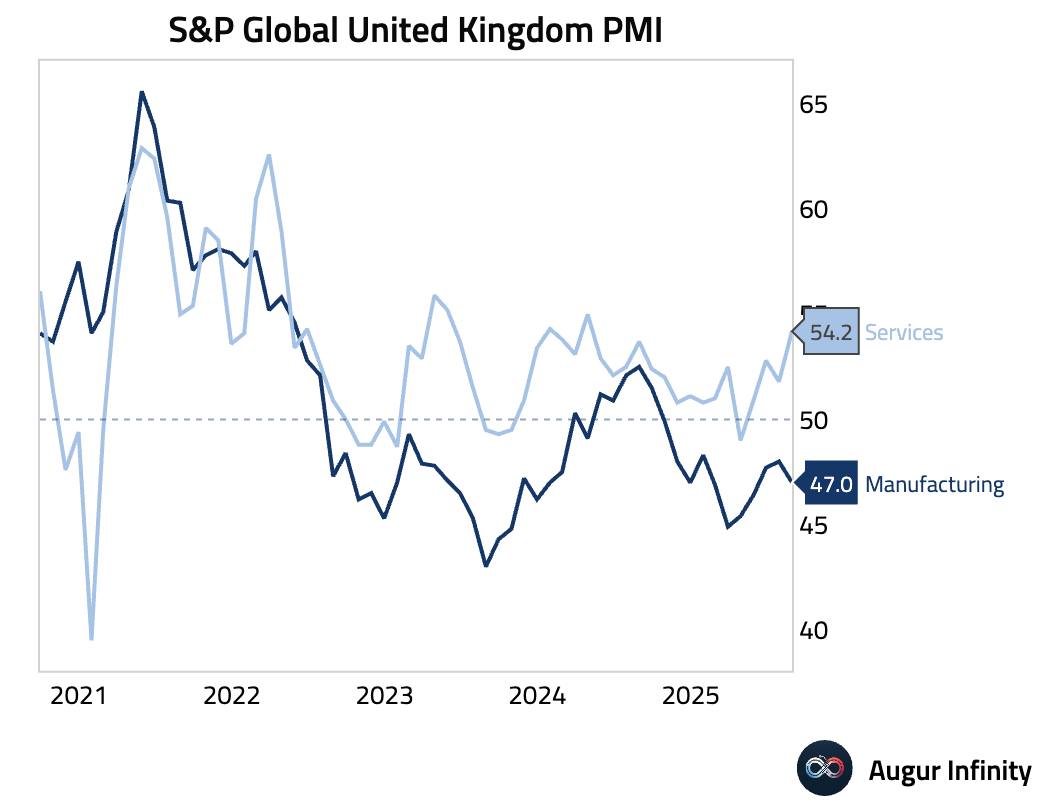

- The UK’s S&P Global Services PMI jumped to 54.2 in August, a 16-month high signaling a solid upturn in activity. The rise was driven by the strongest new order growth since September 2024 and the first increase in export orders since March. Despite the demand pickup, employment fell for the 11th consecutive month as firms focused on productivity gains rather than new hiring.

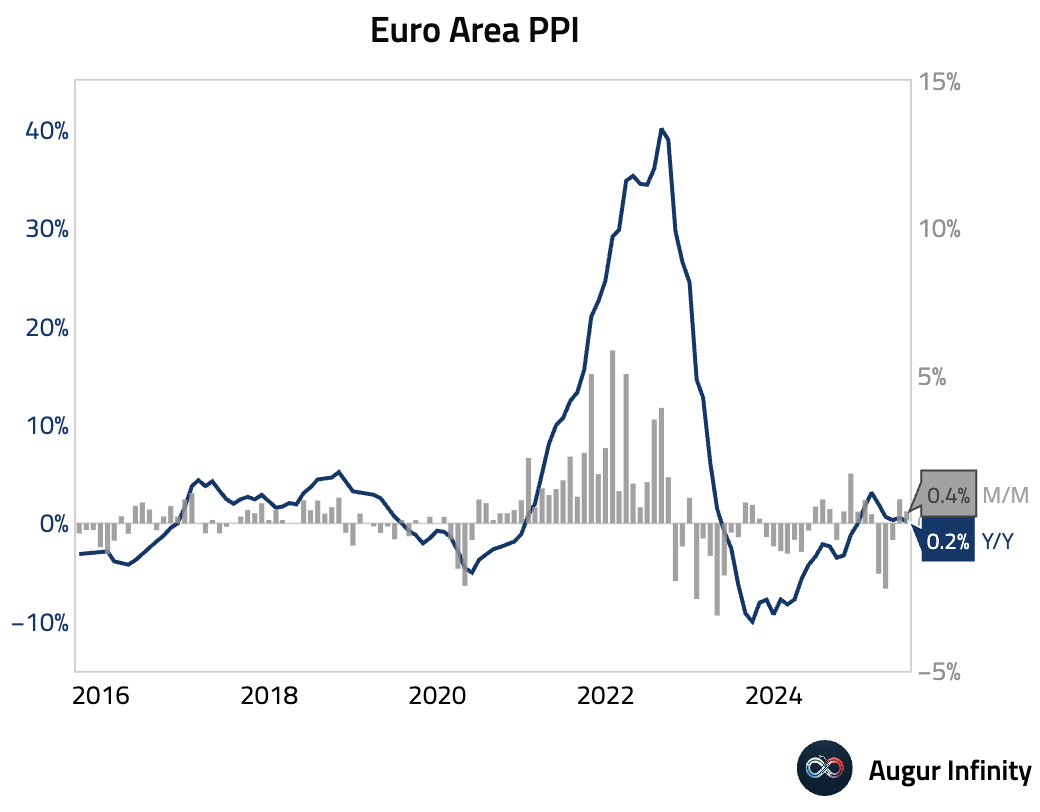

- Eurozone producer prices rose 0.4% M/M in July, accelerating from the prior month and beating the 0.2% consensus. The year-over-year rate fell to 0.2% from 0.6% but was also above expectations.

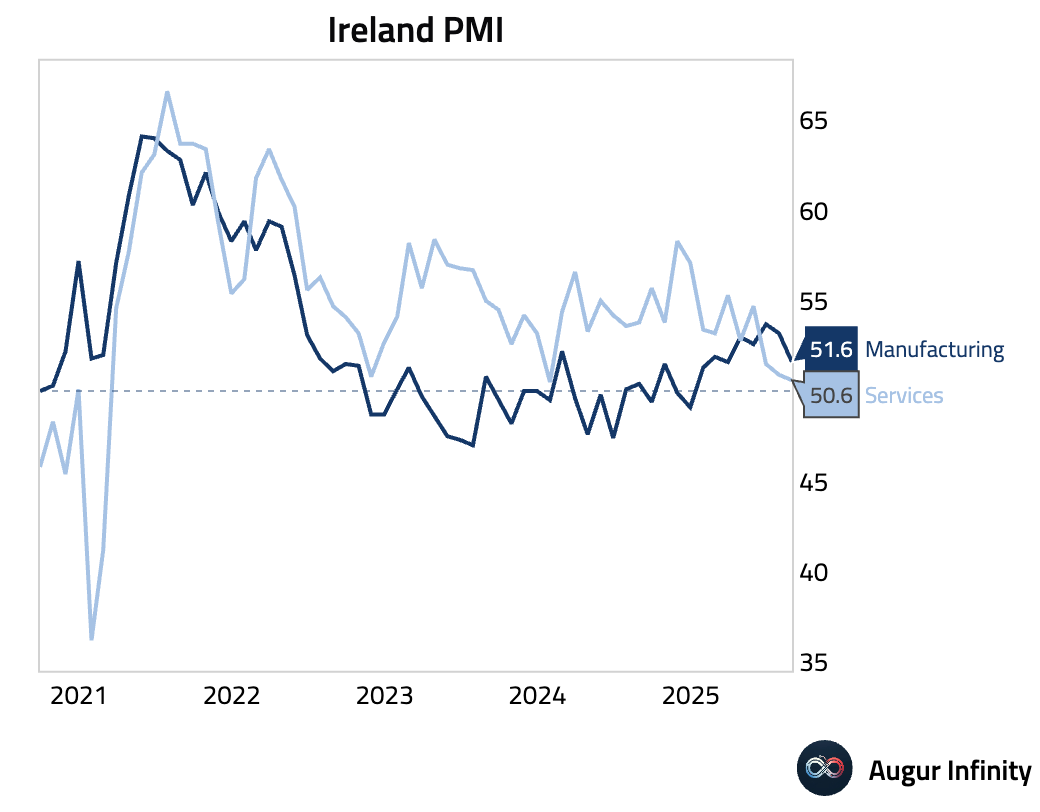

- Ireland’s Services PMI fell to a 19-month low of 50.6 in August, signaling near-stagnation in the sector. The slowdown led to the fastest job cuts since October 2020, with weakness concentrated in the transport and tourism sub-sector.

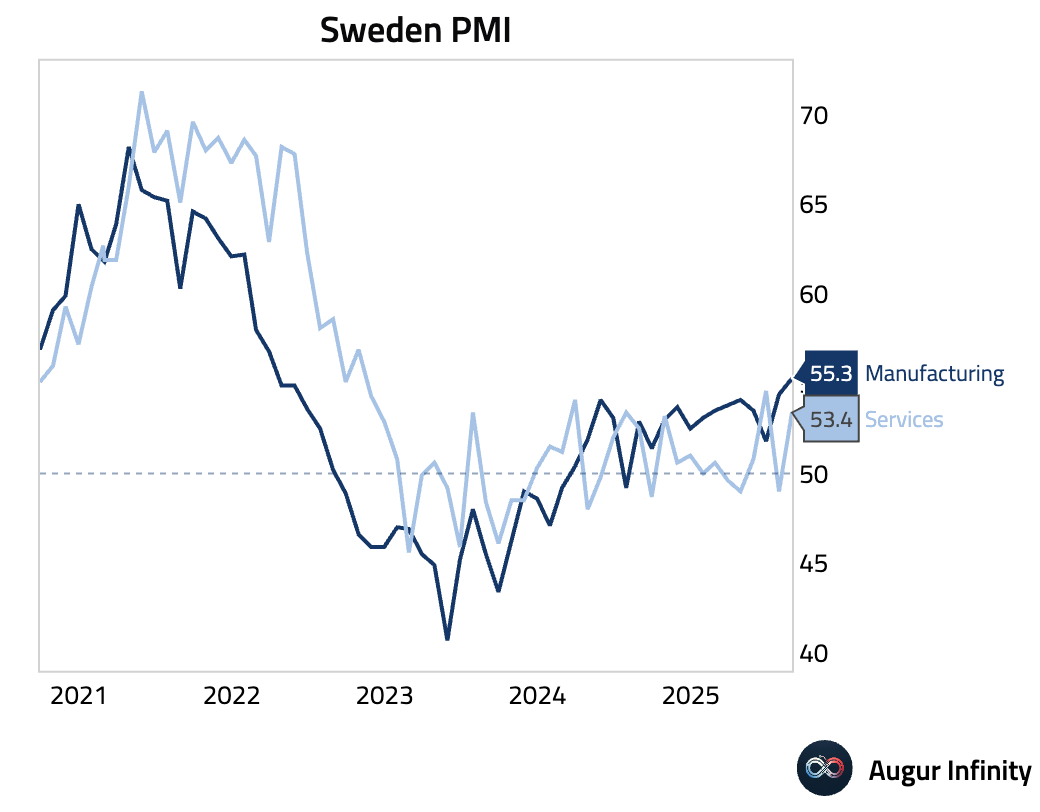

- Sweden’s Services PMI rebounded sharply into expansionary territory in August, rising to 53.4 from 49.0 in July.

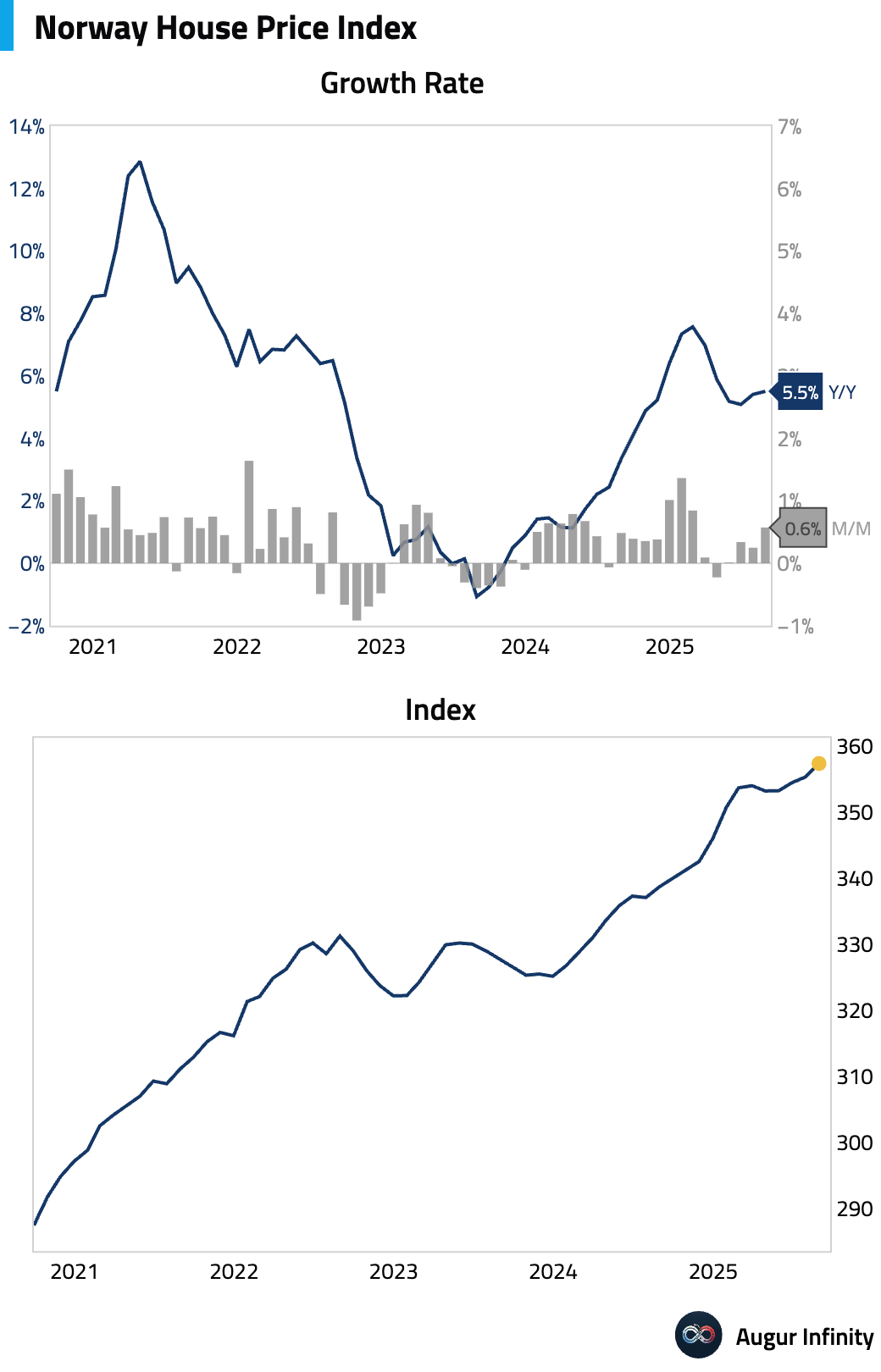

- Norwegian house prices accelerated in August, rising 0.6% M/M and 5.5% Y/Y.

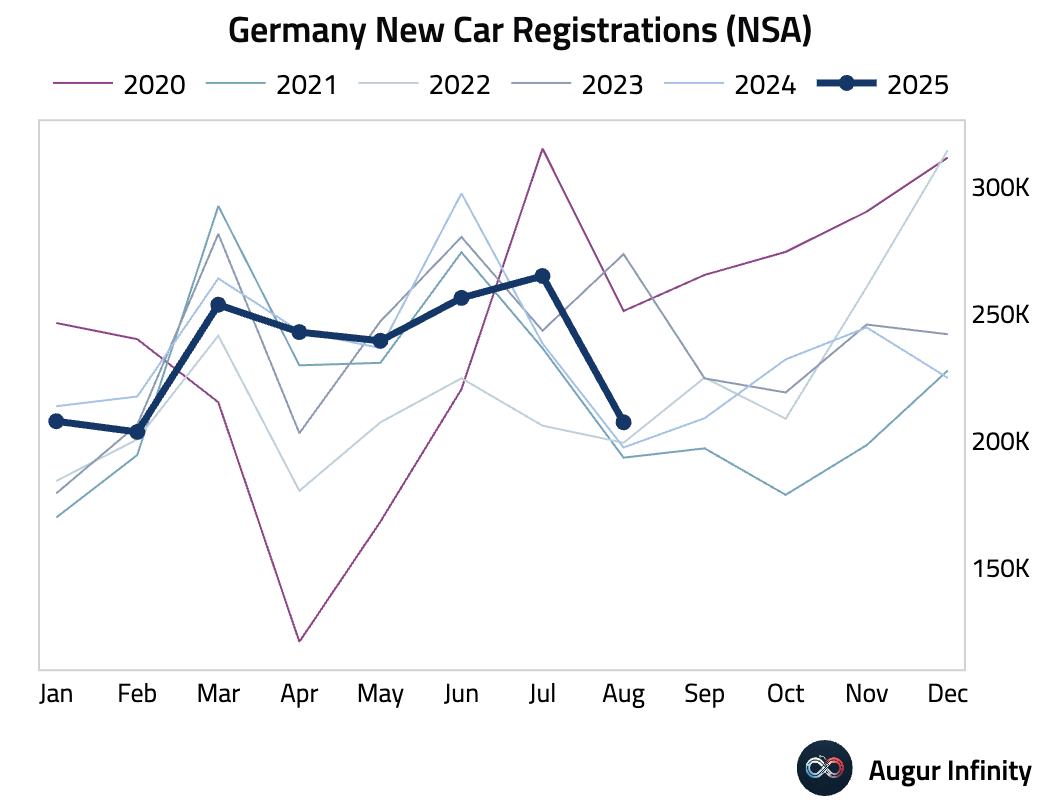

- German new car registrations slowed in August, with growth easing to 5.0% Y/Y from 11.0% in July.

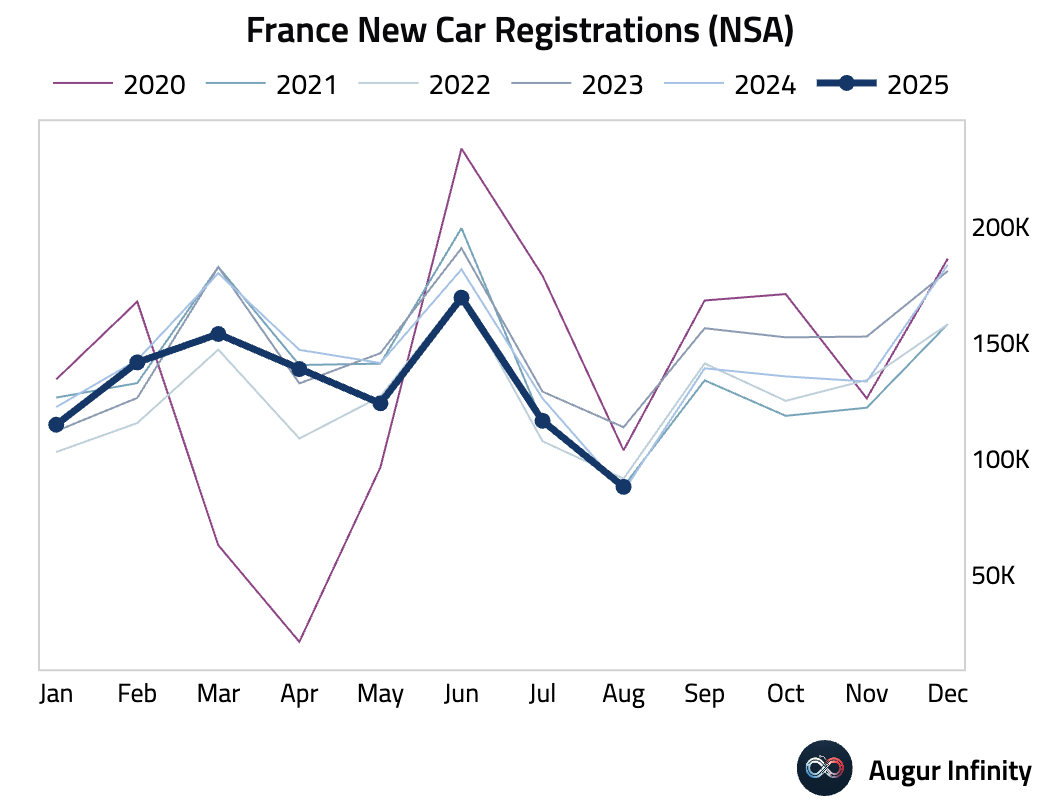

- French new car registrations rebounded in August, rising 2.2% Y/Y after a 7.7% decline in July.

Asia-Pacific

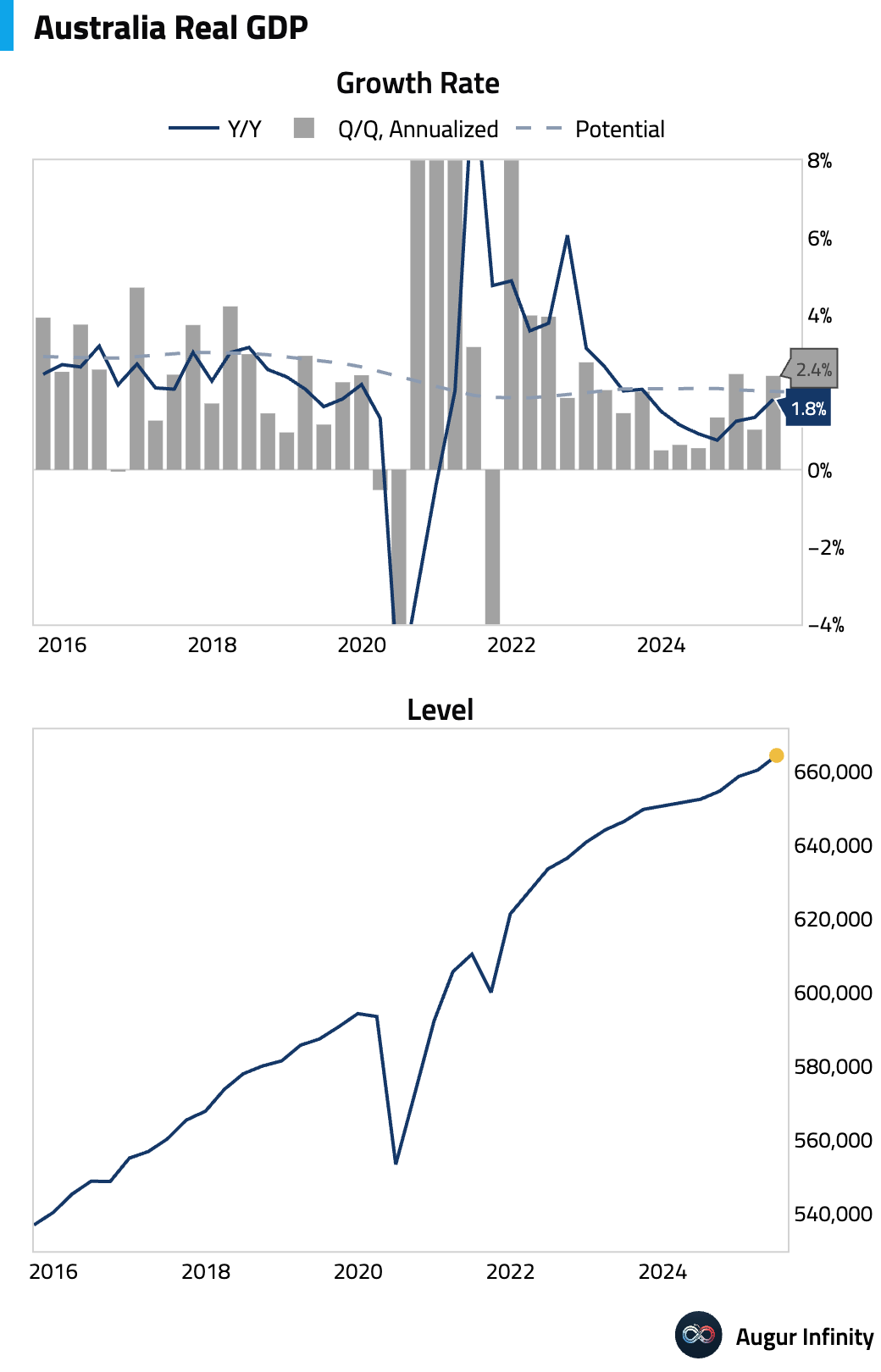

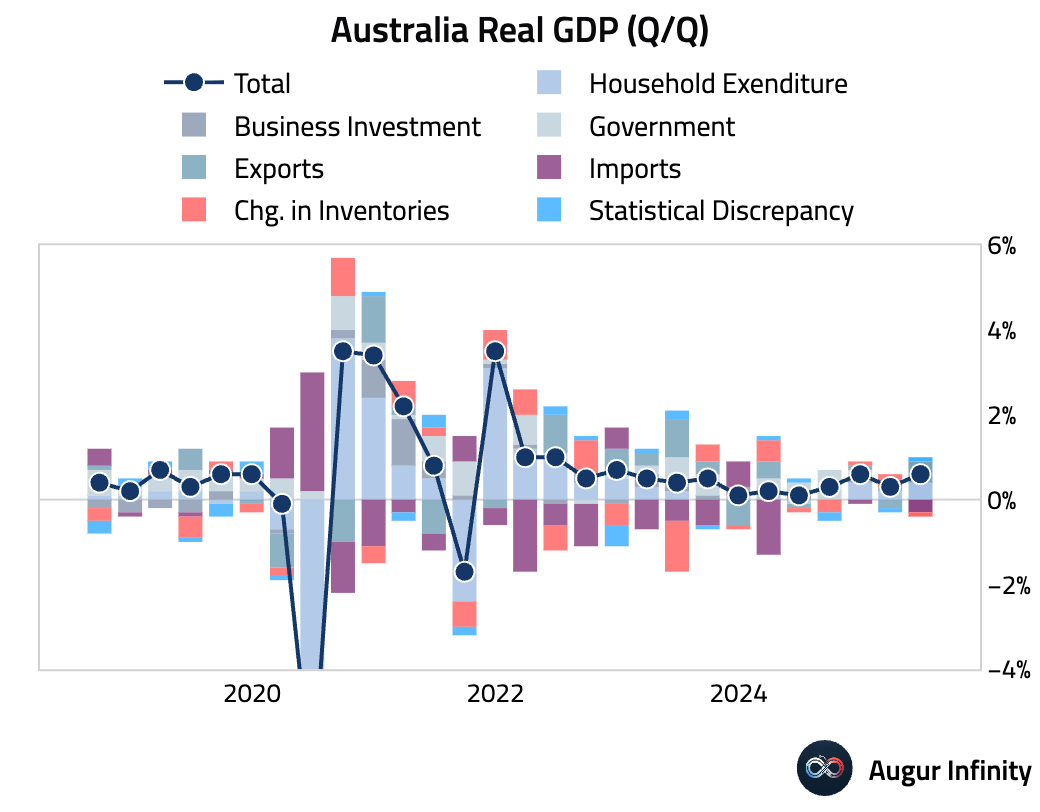

- Australia’s second-quarter GDP grew 0.6% Q/Q (or 2.4% annualized and 1.8% Y/Y), beating consensus estimates of 0.5% (1.6% Y/Y). The upside surprise was driven by a 0.9% Q/Q surge in private consumption, though this was artificially boosted by households extending holiday breaks and is expected to see some payback in the third quarter. Underlying data was more subdued, with business investment falling 0.4% Q/Q and the household savings rate declining 100 bps to 4.2% to fund spending.

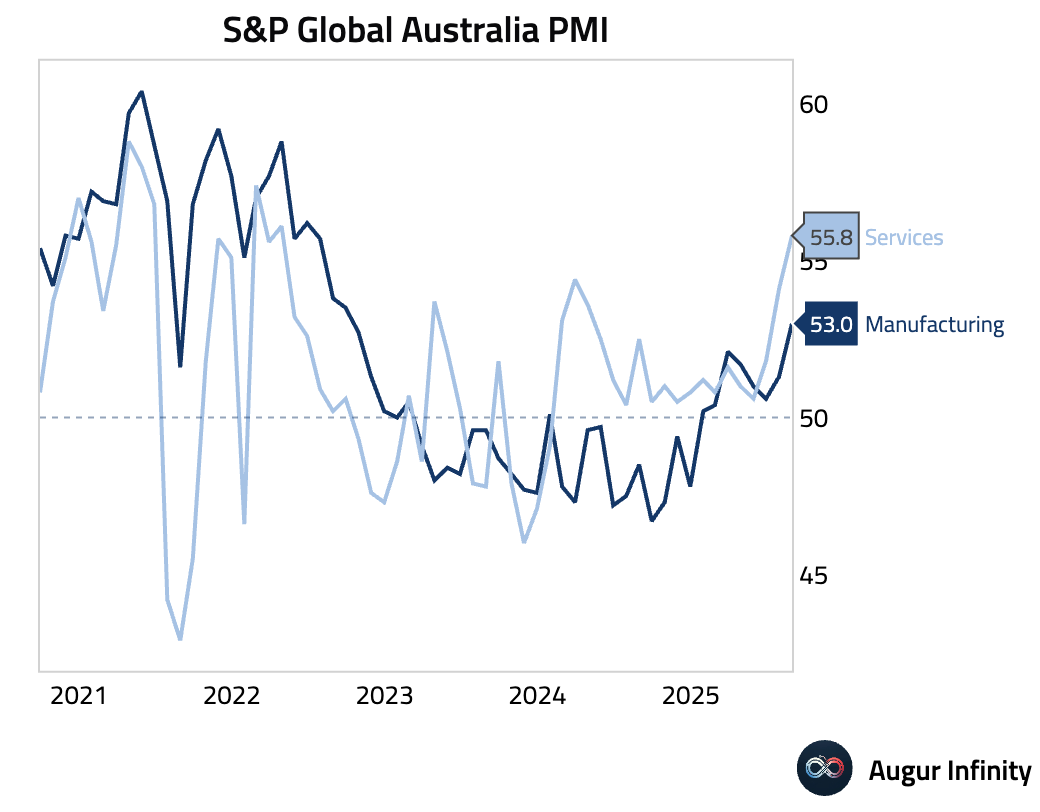

- Australia’s S&P Global Services PMI rose to 55.8 in August, its highest reading since April 2022. The expansion was driven by a sharp rise in new business and the best export gain since June 2022, which spurred the fastest job creation in four months. Both input and output price inflation softened despite the robust demand.

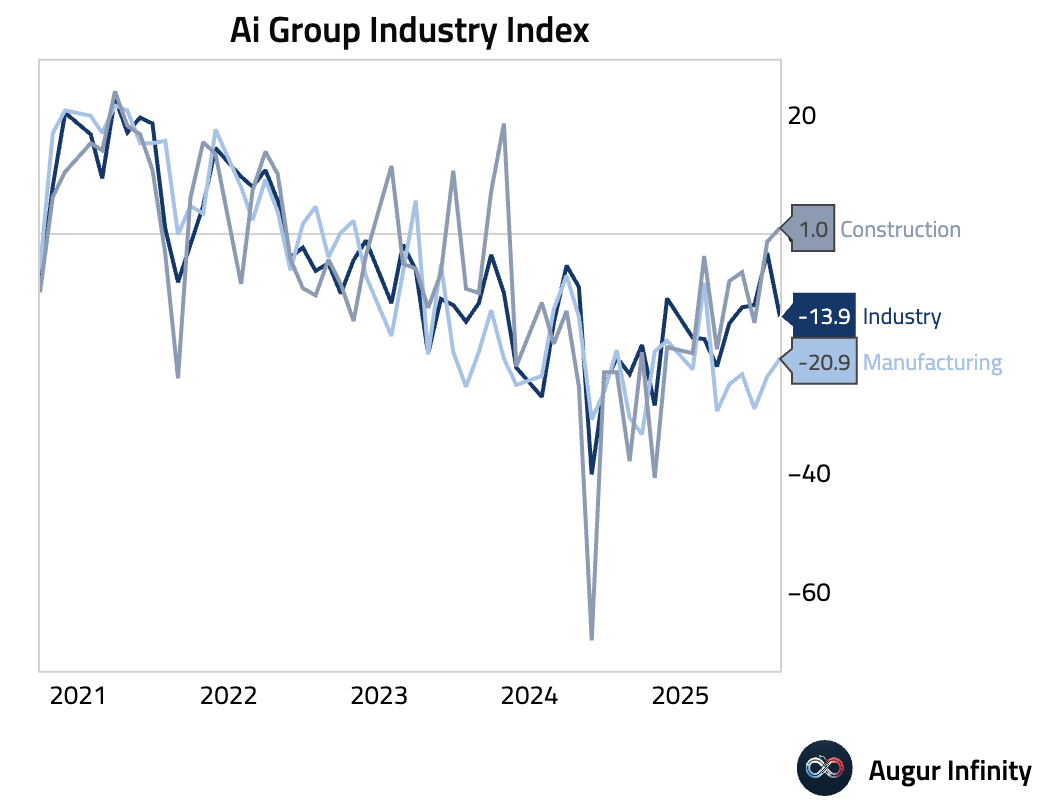

- The Ai Group Industry Index for Australia fell further into contraction in August, declining to -13.9 from -3.2. Weakness was concentrated in manufacturing (-20.9), while construction (1.0) returned to expansion for the first time since October 2023.

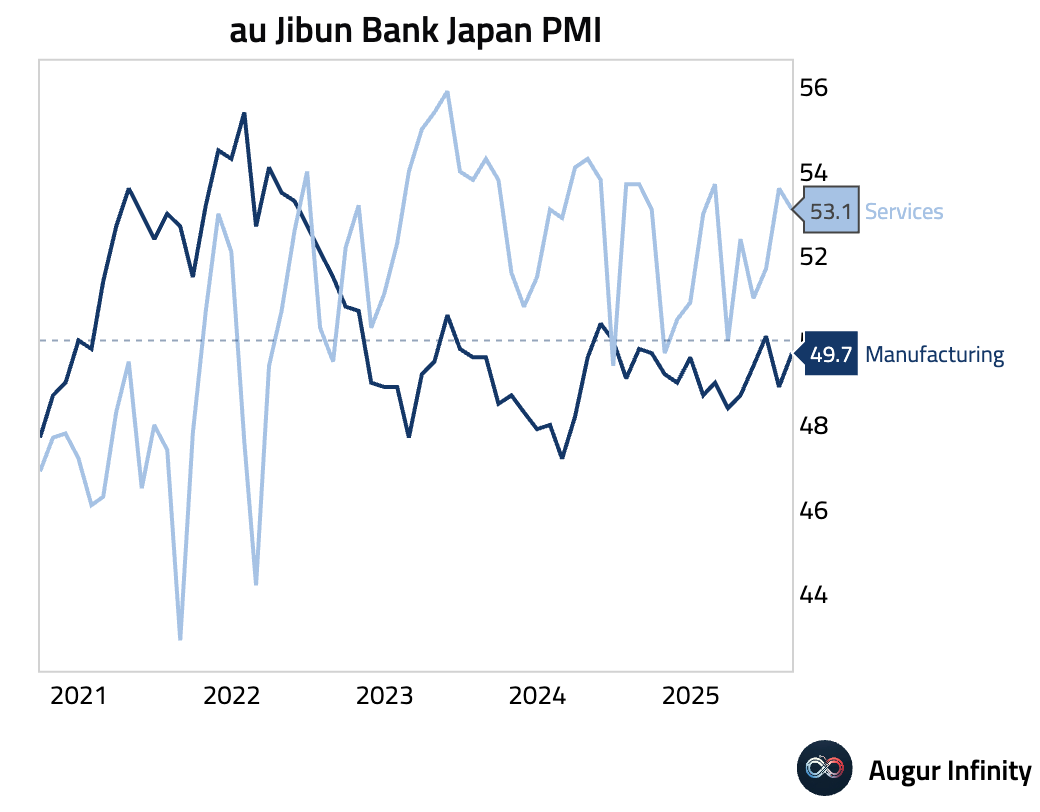

- Japan’s S&P Global Services PMI eased to 53.1 in August but still indicated solid growth. The expansion was driven by the strongest domestic new order growth since February, which masked a sharp contraction in export orders. Notably, firms cut staff for the first time in nearly two years, indicating caution.

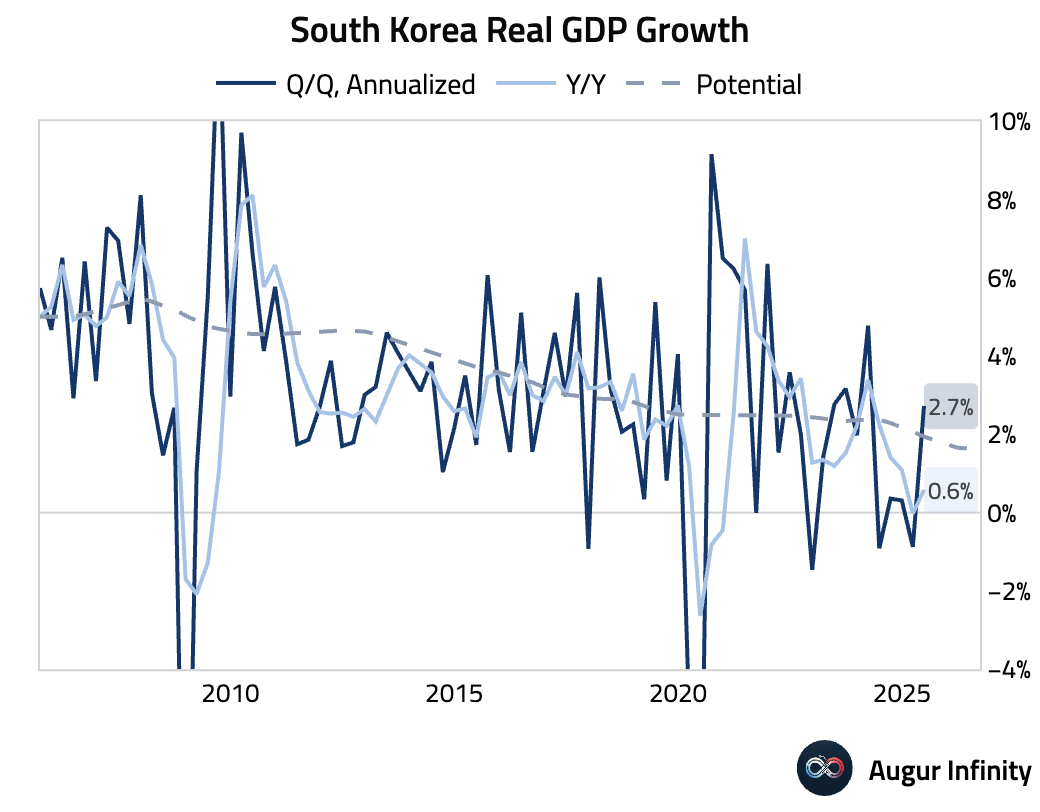

- South Korea’s final second-quarter GDP confirmed a return to growth, with the economy expanding 0.7% Q/Q (or 2.7% annualized and 0.6% Y/Y). The figures were revised slightly higher from preliminary estimates and mark a rebound from the first quarter's mild contraction.

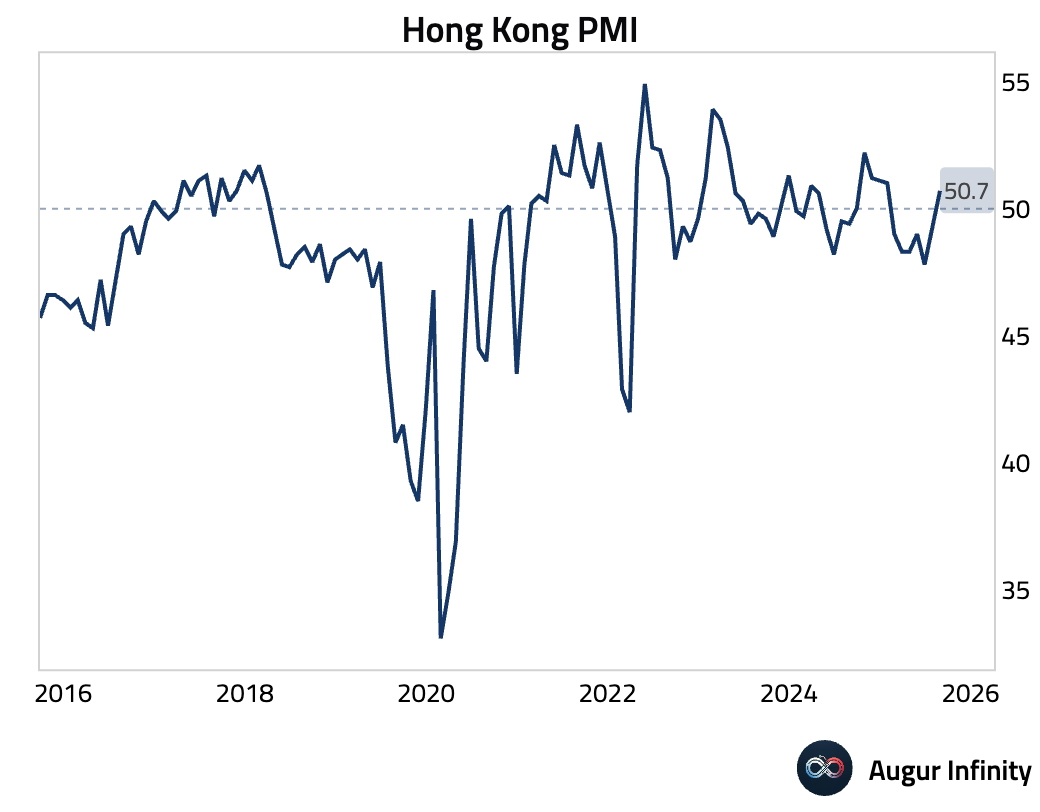

- Hong Kong’s S&P Global PMI rose to a seven-month high of 50.7 in August, returning to expansionary territory for the first time since January. The improvement was driven by a stabilization in domestic demand, as the “new business from China” sub-index fell sharply to 42.0 due to the impact of US tariffs. Firms are offering discounts to support sales despite rising input costs, suggesting pressure on profit margins.

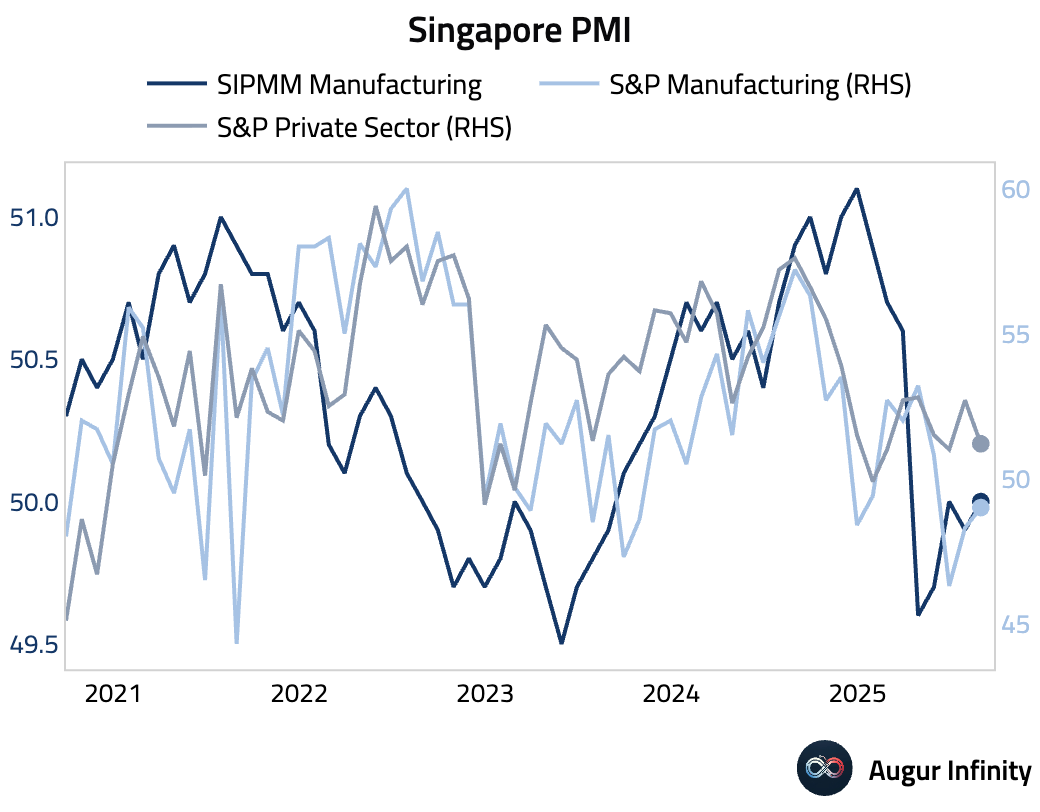

- Singapore’s Private Sector PMI fell to 51.2 in August from 52.7, indicating a slower pace of growth. The deceleration was attributed to US tariffs, which dampened new orders and output to seven- and six-month lows, respectively. In response to intense competition, firms cut jobs and lowered selling prices for the first time in four months, creating significant margin pressure.

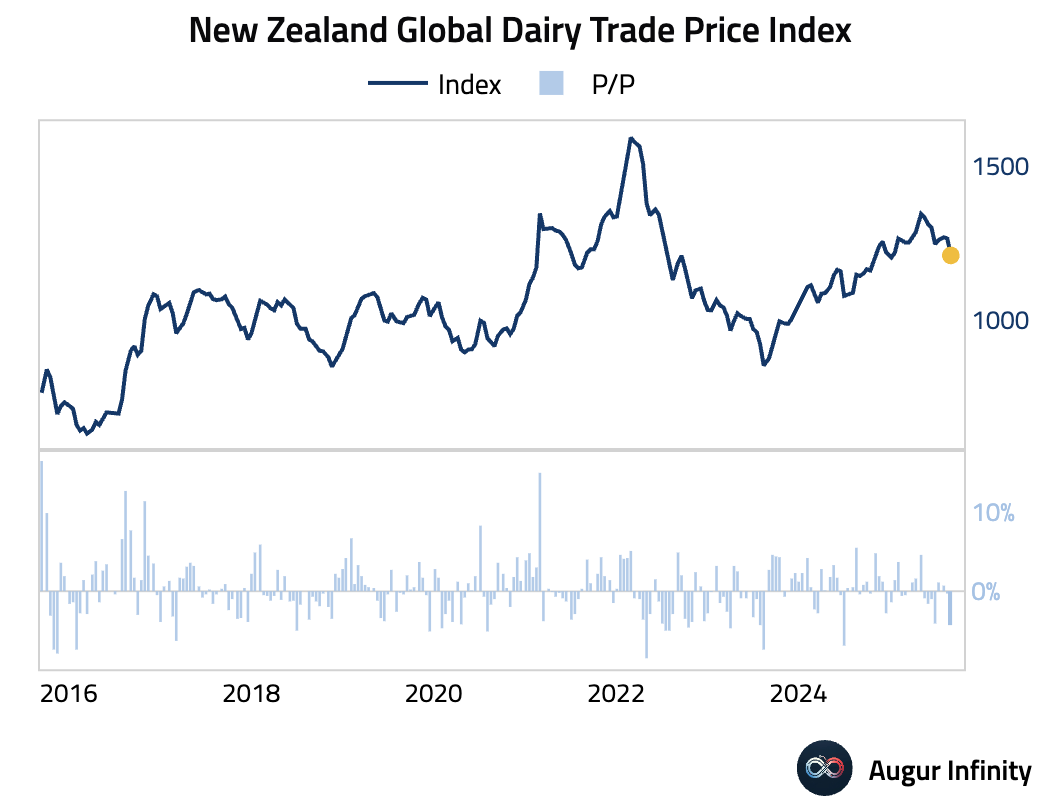

- New Zealand’s Global Dairy Trade Price Index fell 4.3% at the latest auction, its largest drop in over a year.

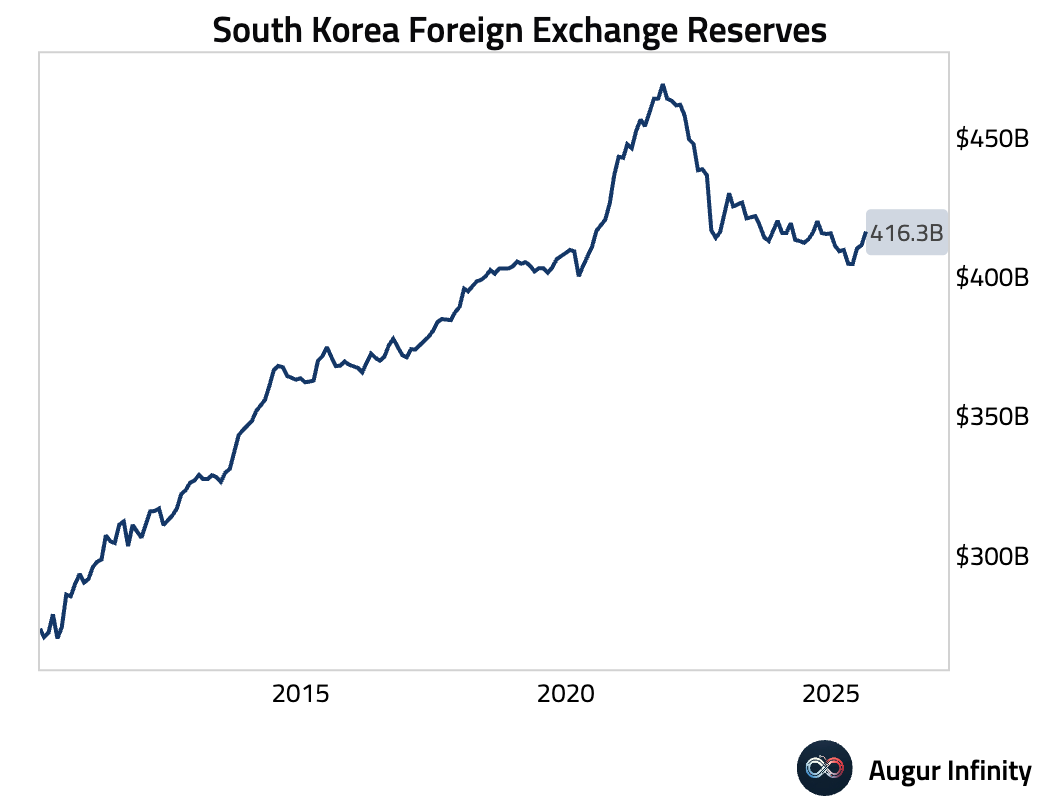

- South Korea’s foreign exchange reserves increased to $416.29 billion in August from $411.33 billion in July.

China

- The RatingDog (formerly Caixin) Services PMI rose to 53.0 in August, beating the 52.5 consensus and marking the fastest expansion since May 2024. The increase was driven by a sharp rise in new business, tourism, and export orders. Despite strong demand, the employment sub-index fell sharply into contraction, and intense competition forced companies to lower output prices while input costs rose, signaling a significant squeeze on profit margins.

Emerging Markets ex China

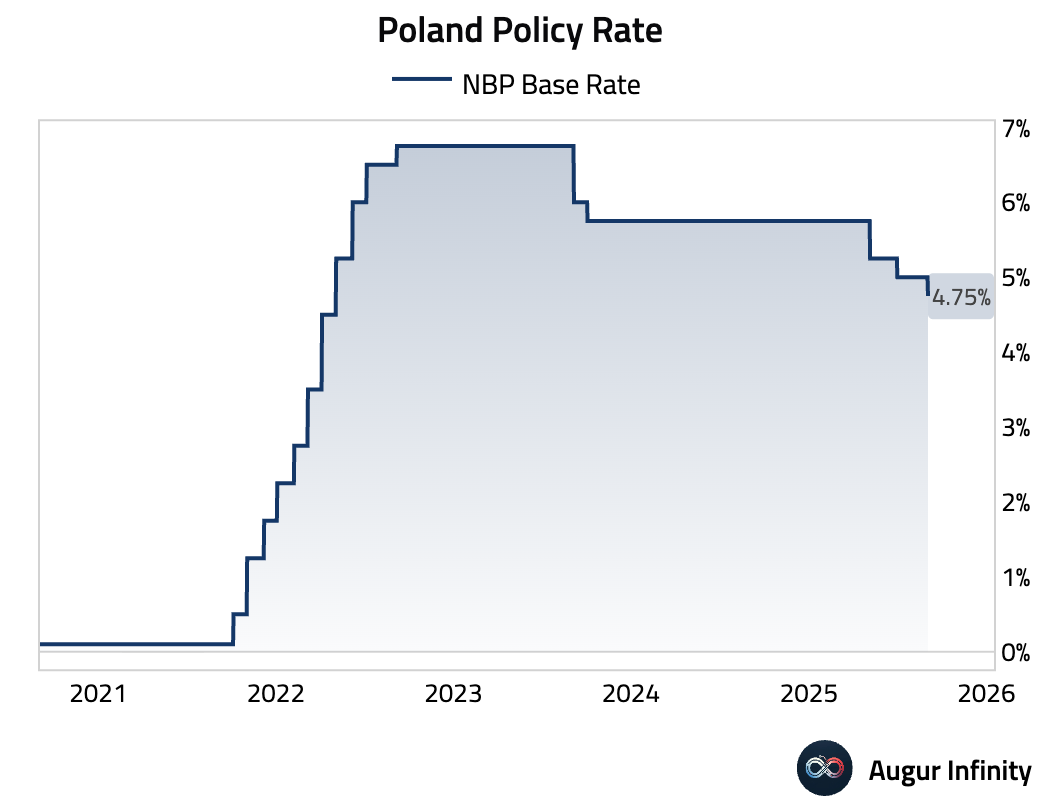

- The National Bank of Poland cut its key interest rate by 25 basis points to 4.75%, in line with market expectations.

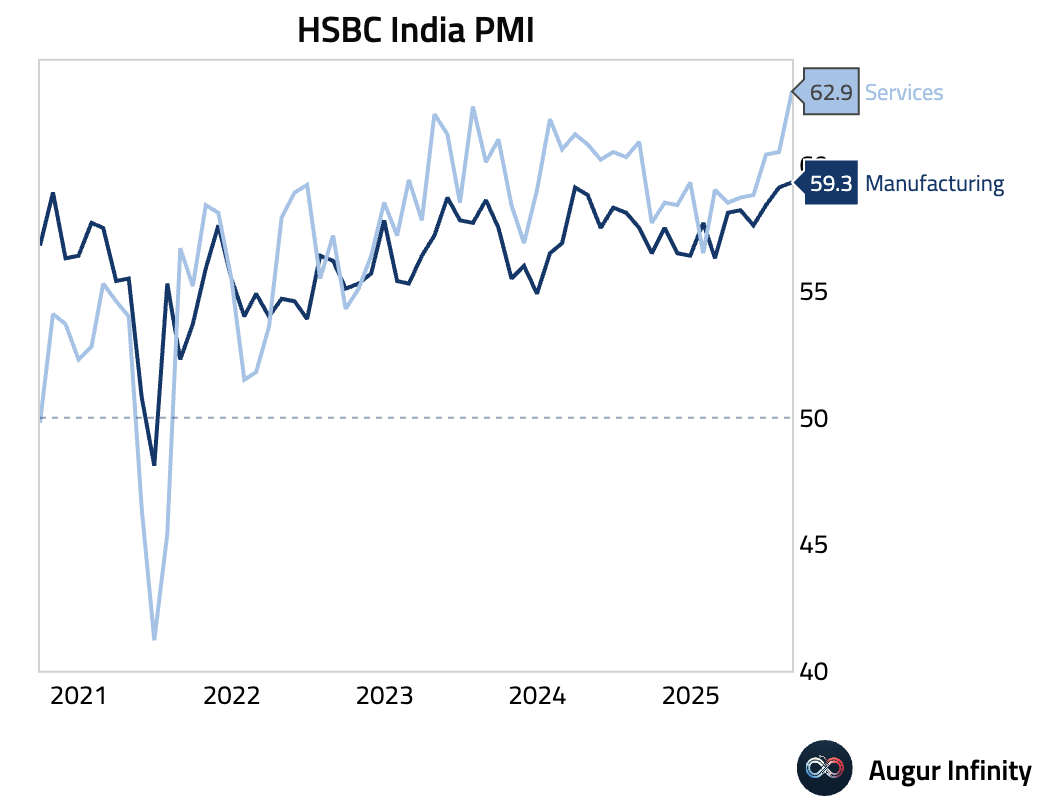

- India’s HSBC Services PMI surged to 62.9 in August from 60.5, hitting a 15-year high. The strength was driven by the fastest new order growth since mid-2010. Robust demand and higher labor costs allowed firms to increase selling prices at the steepest rate in over 13 years, signaling significant inflationary pressures.

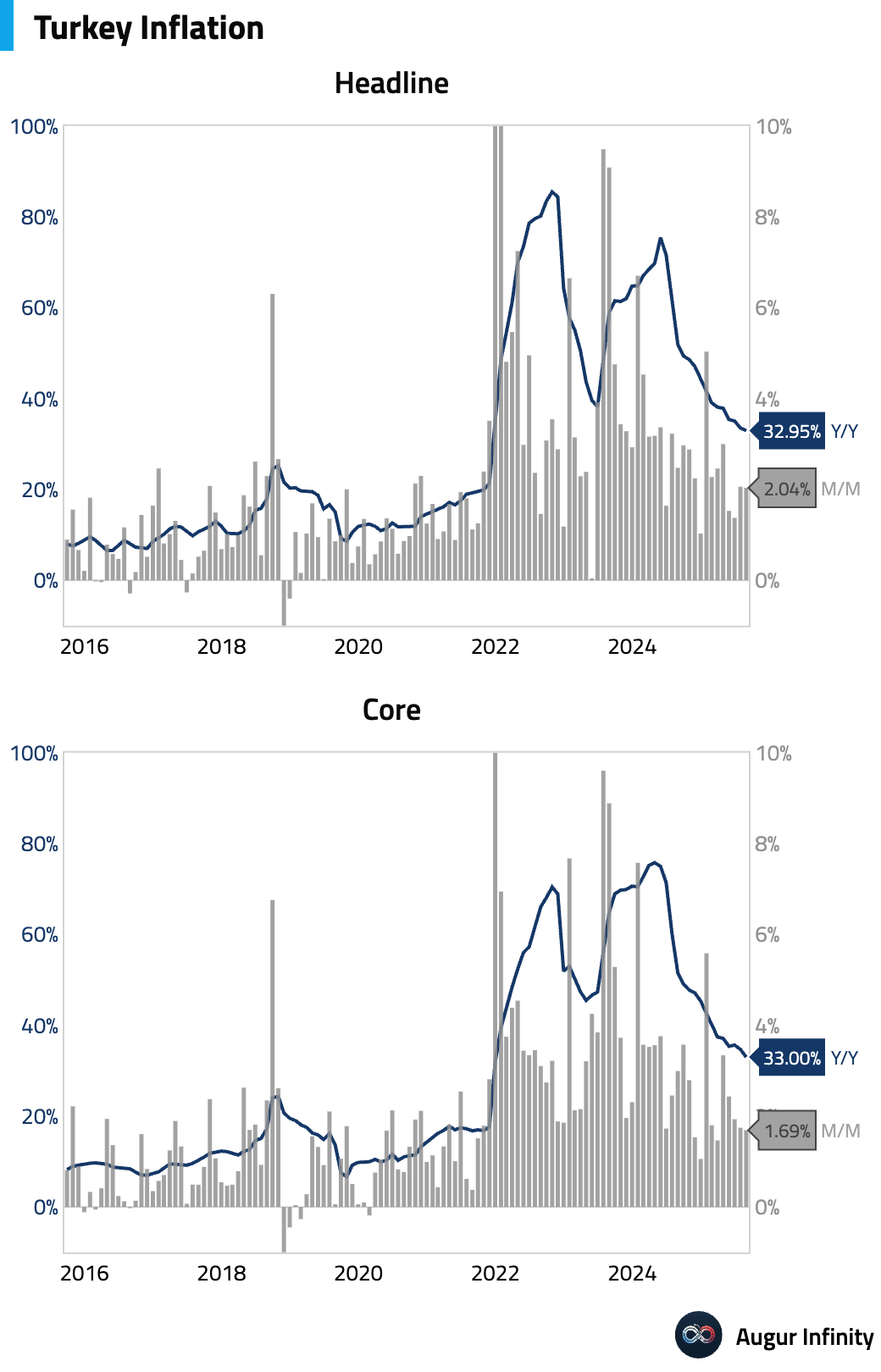

- Turkish inflation came in hotter than expected in August, with consumer prices rising 2.04% M/M (consensus: 1.79%) and 32.95% Y/Y (consensus: 32.6%). The annual rate decelerated from 33.52% in July but remains elevated.

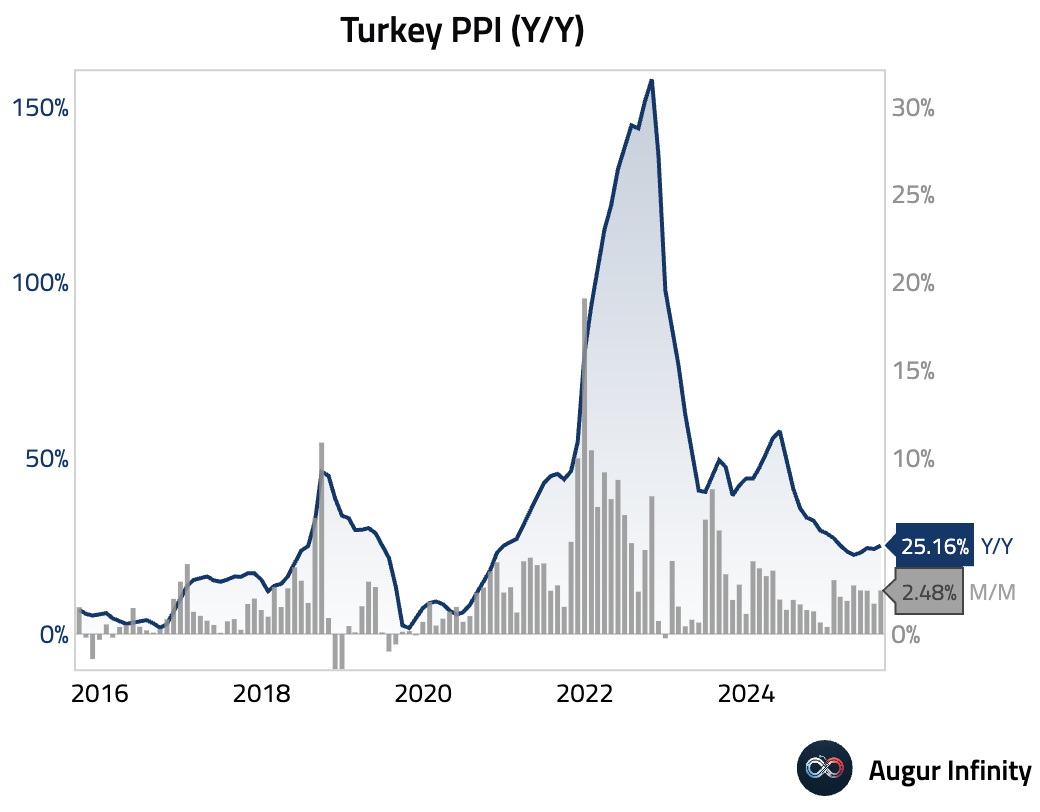

- Turkish producer prices accelerated in August, rising 2.48% M/M and 25.16% Y/Y.

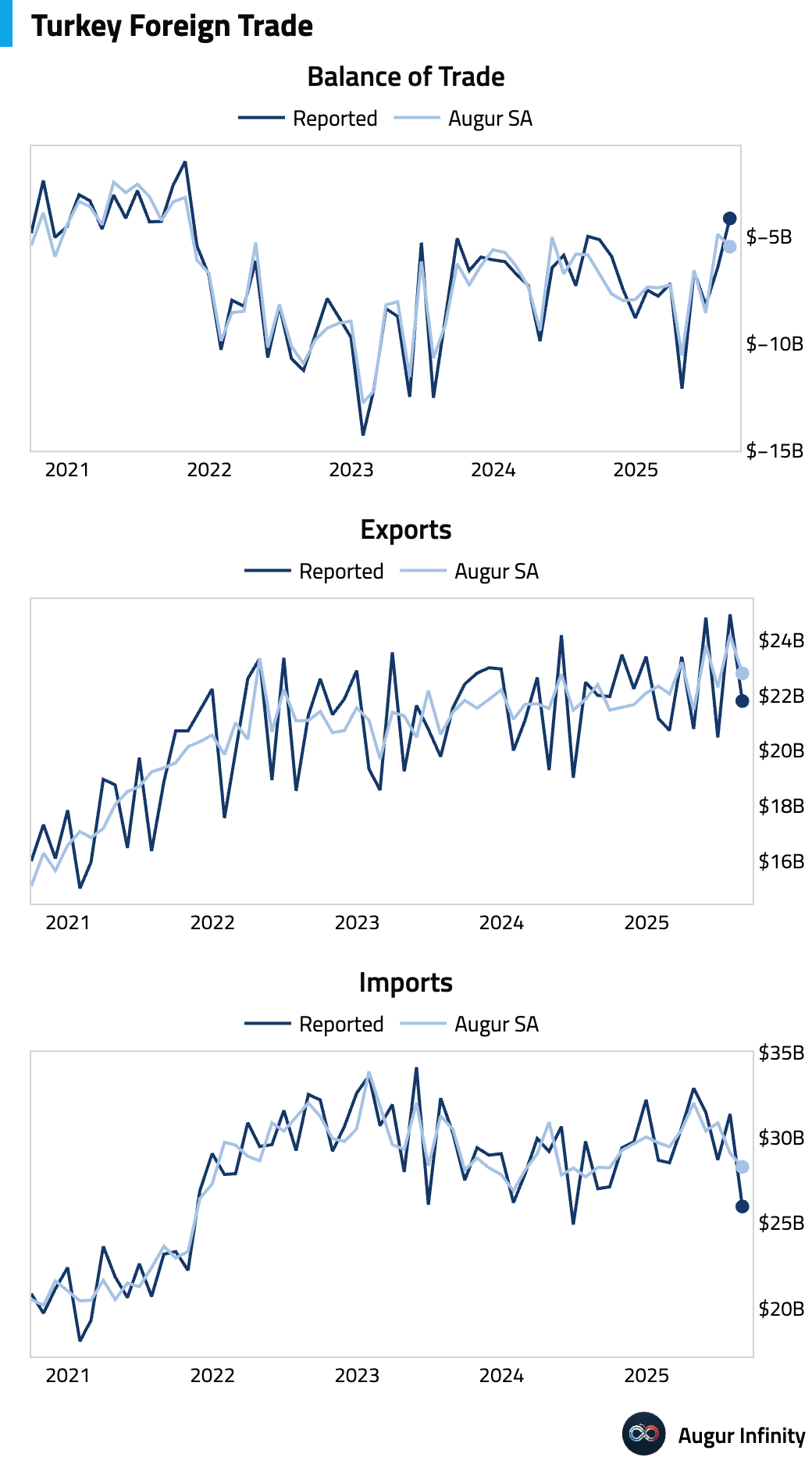

- Turkey’s preliminary trade deficit for August narrowed significantly to $4.2 billion, its smallest gap since October 2021. The improvement was driven by a sharp decline in imports, which fell to $26.0 billion, while exports moderated to $21.8 billion.

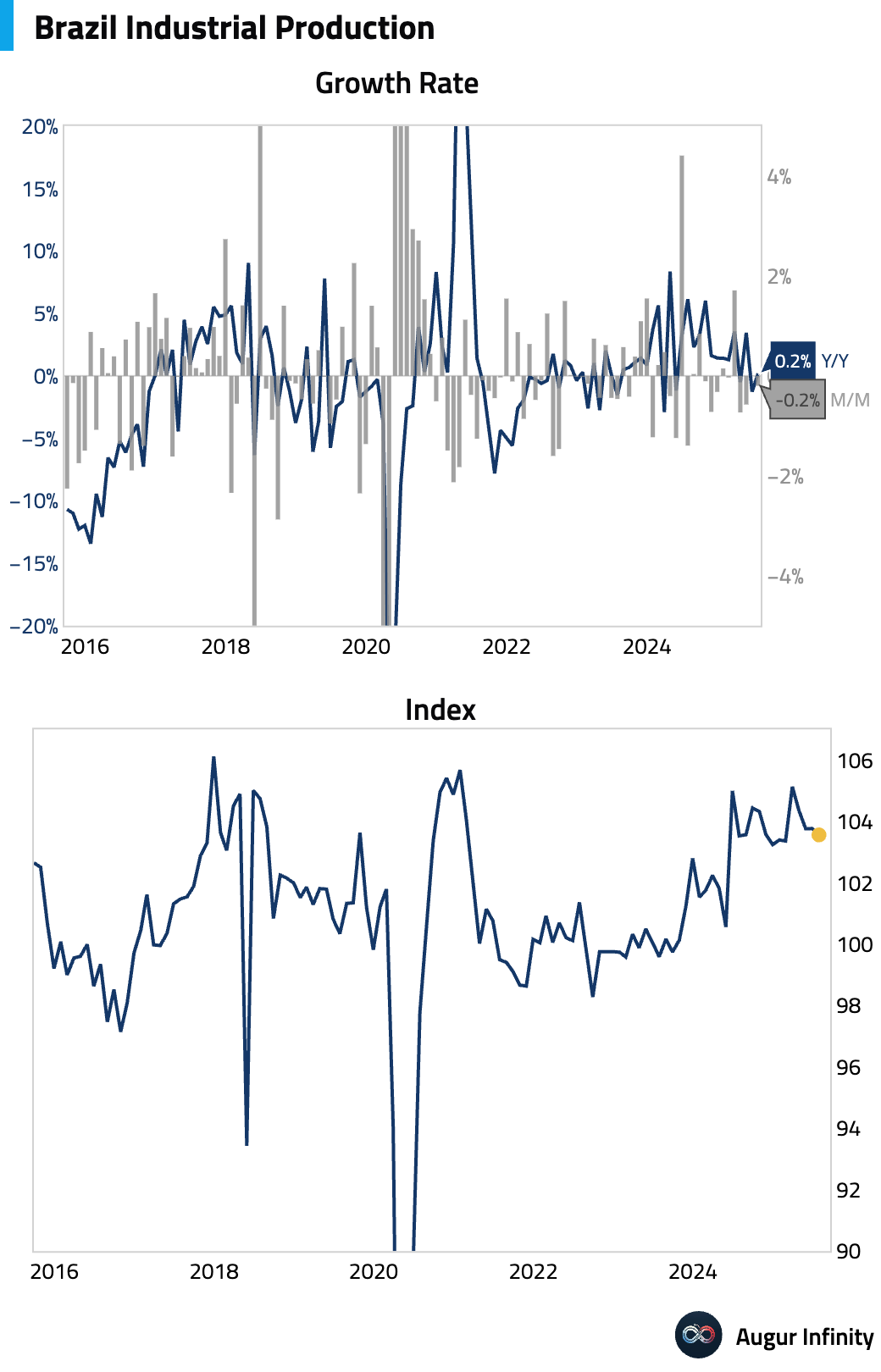

- Brazil’s industrial production fell 0.2% M/M in July, in line with expectations, though the year-over-year rate of 0.2% missed consensus. The decline was driven by weakness in consumer durables and capital goods and signals a soft start to the third quarter with a negative carry-over of -0.4% Q/Q.

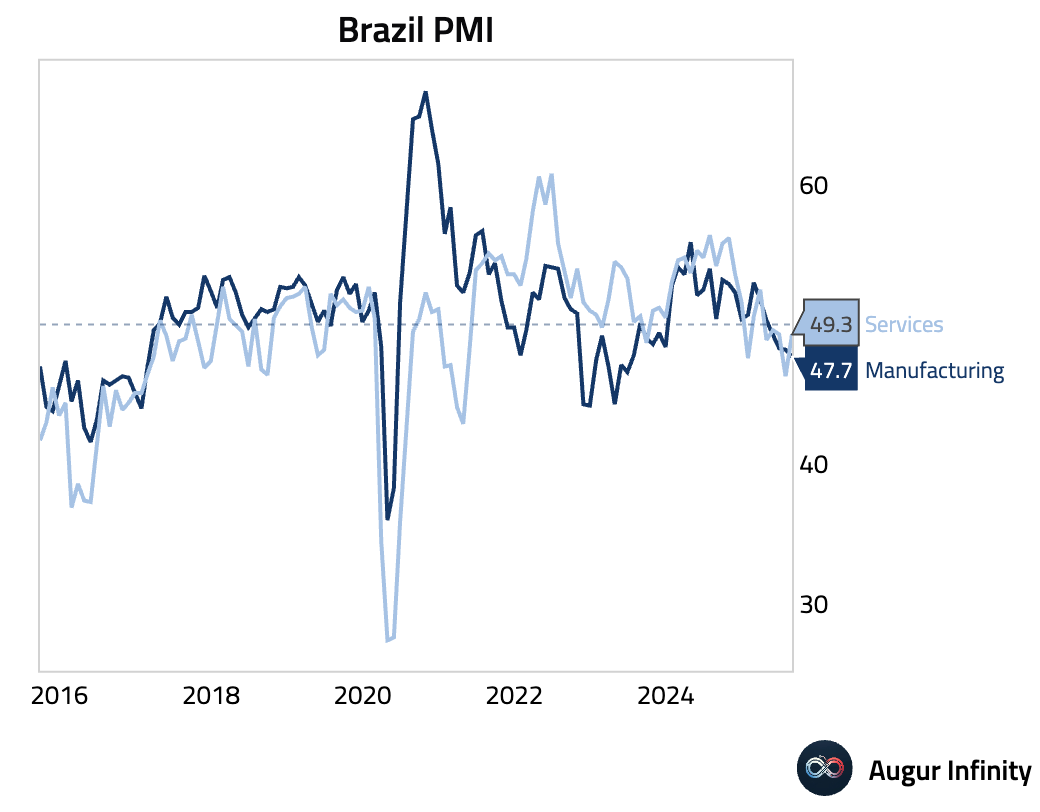

- Brazil’s S&P Global Services PMI rose to 49.3 in August from 46.3, signaling a softer, marginal contraction. Despite an easing in the sales decline, firms accelerated job cuts to the fastest pace in nearly four and a half years due to weak workloads. A sharp rise in input costs contrasted with softer selling price inflation, pointing to a significant margin squeeze.

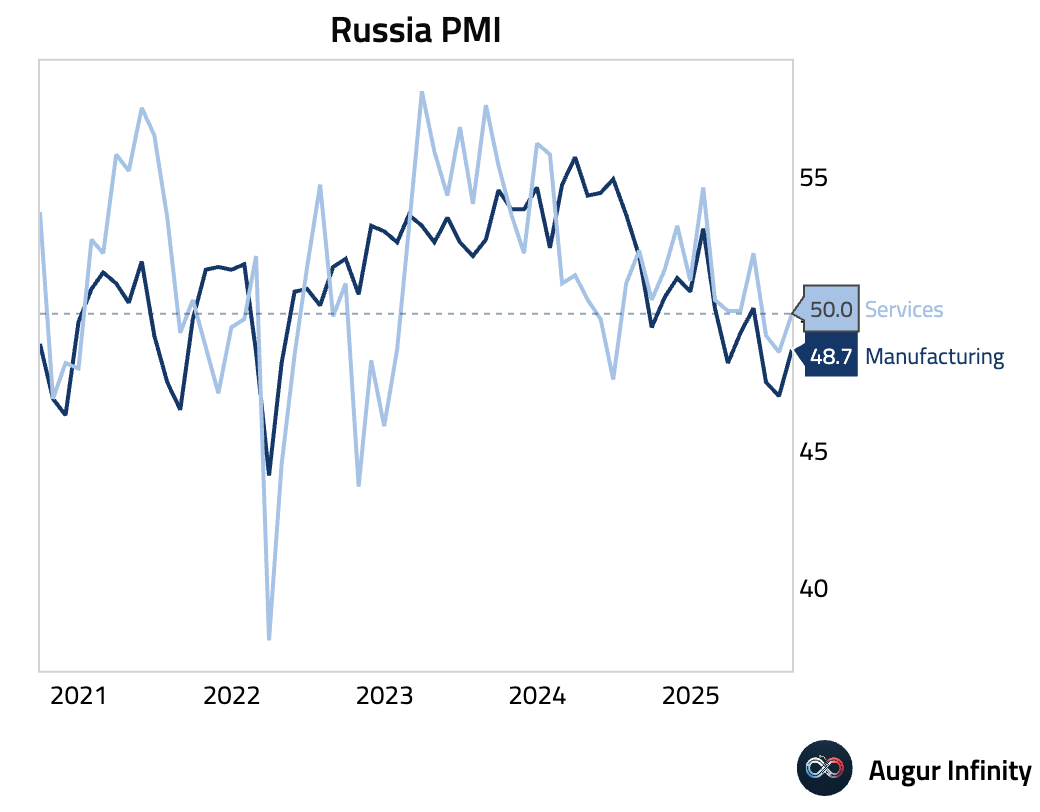

- Russia’s S&P Global Services PMI rose to the neutral 50.0 mark in August, stabilizing after two months of contraction. While new orders fell again, the decline softened, and firms increased hiring in anticipation of future demand. Input cost inflation hit a five-year low, yet companies accelerated output price hikes, suggesting a focus on improving margins.

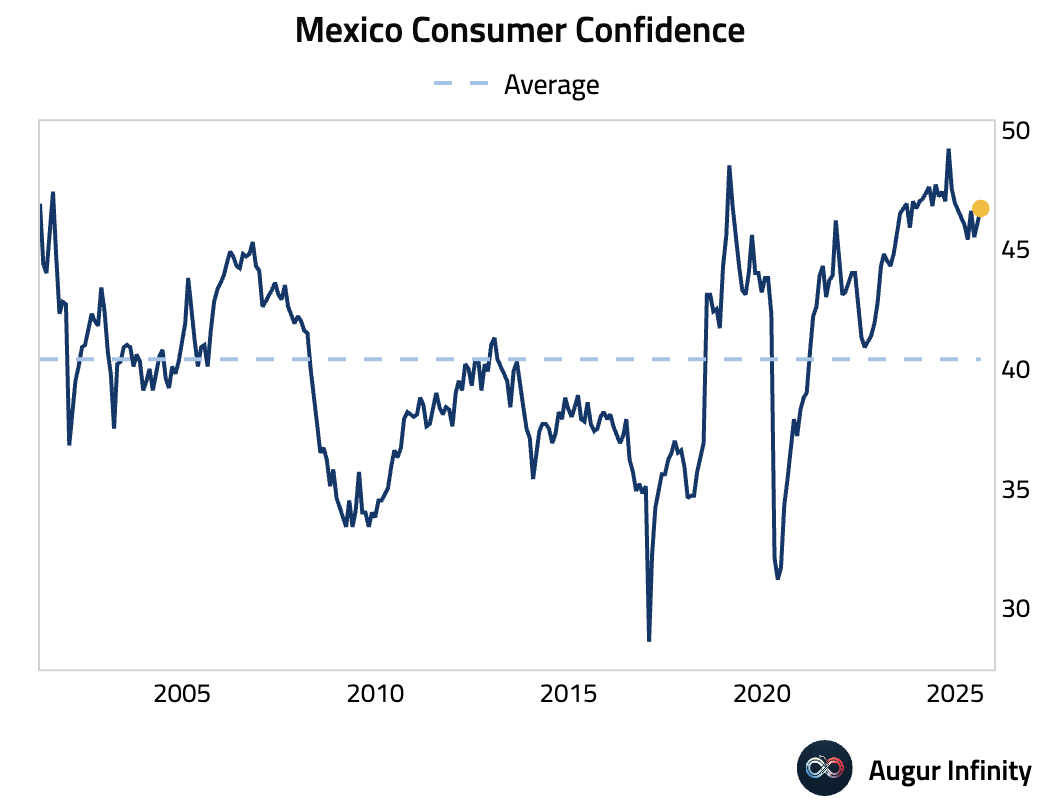

- Mexican consumer confidence rose to 46.7 in August from 46.0. However, the broader trend remains weak, with the index down in seven of the last ten months. The gain was driven by future expectations, while the component measuring capacity to buy durable goods remains very low, signaling continued consumer caution.

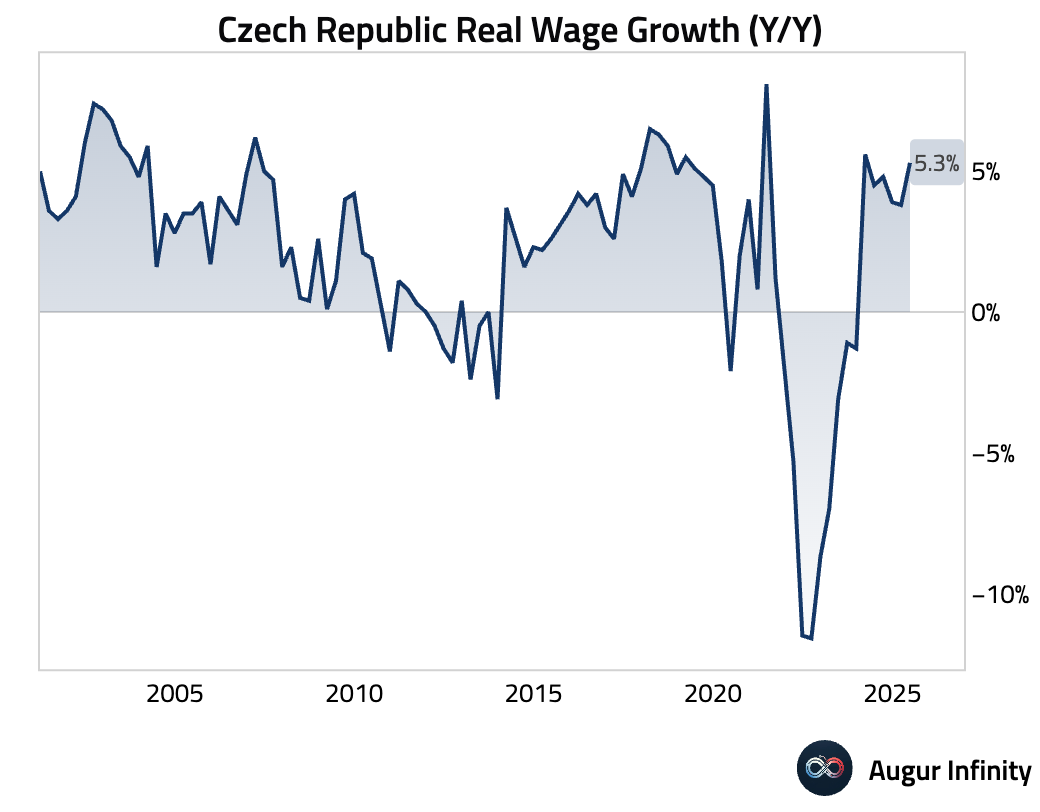

- Real wages in the Czech Republic grew 5.3% Y/Y in the second quarter, accelerating from 3.9% and significantly beating the 4.4% consensus.

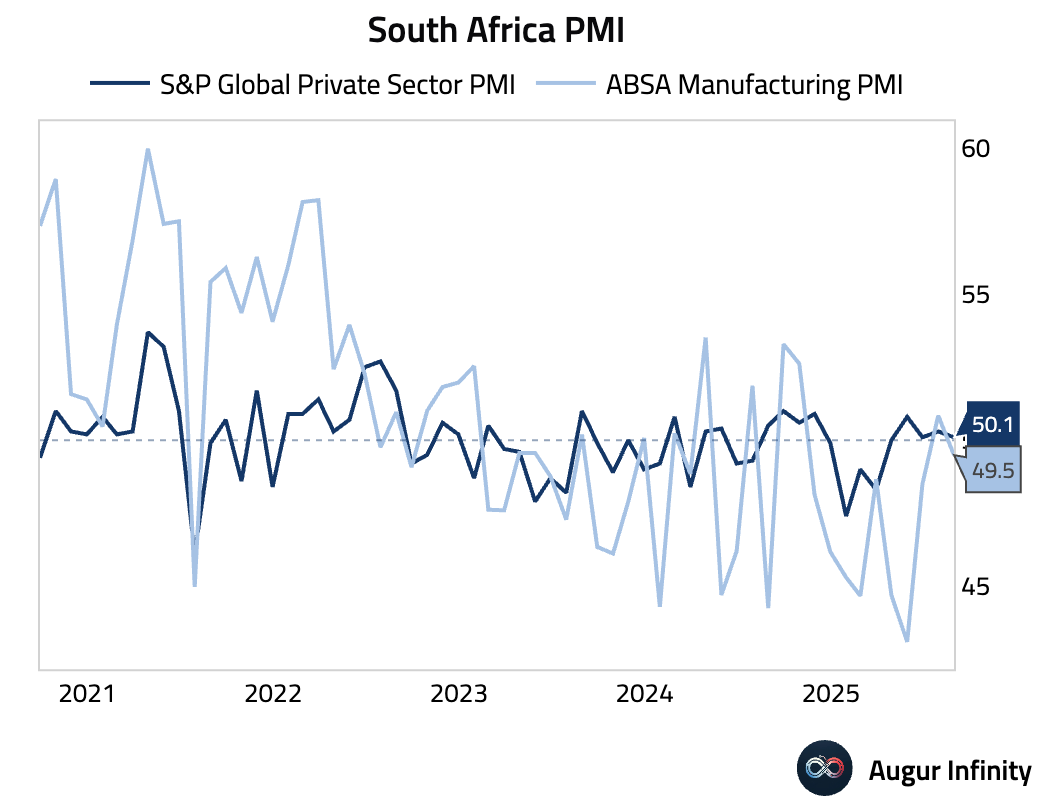

- South Africa’s Private Sector PMI slowed to 50.1 in August from 50.3, marking a fourth month of marginal expansion. Growth was driven by domestic demand, as export orders fell for the fifth consecutive month. Input cost inflation eased to a 10-month low, but firms resumed cutting jobs after two months of growth.

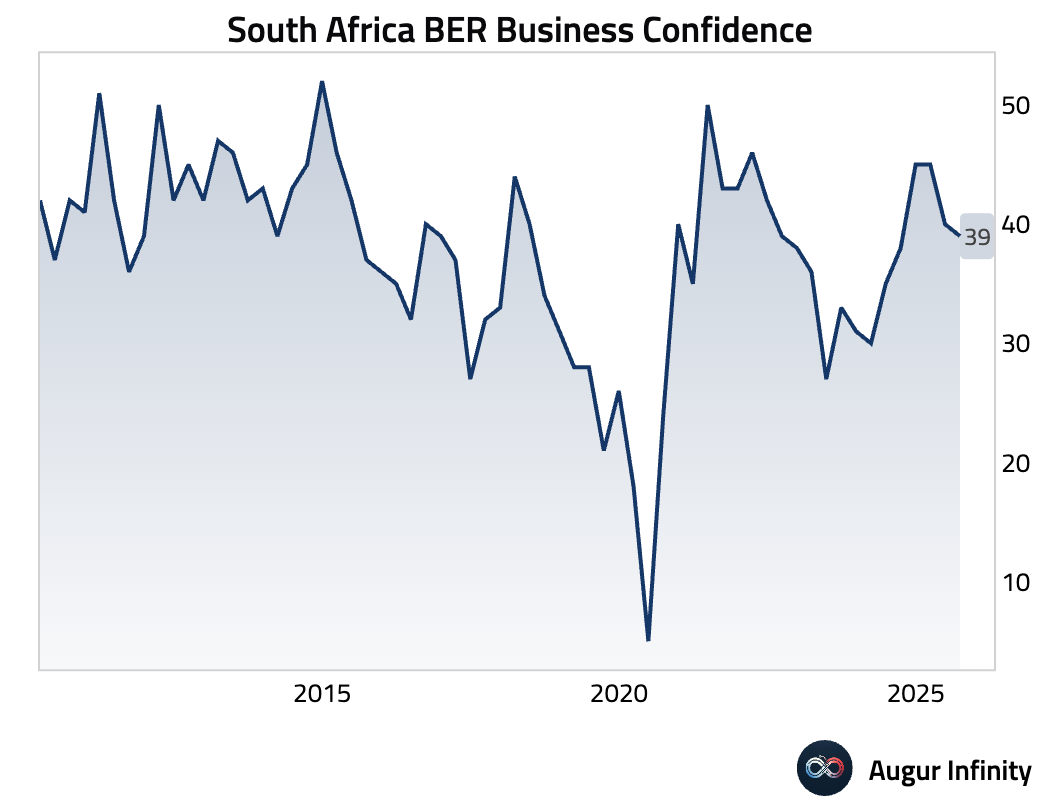

- South African business confidence edged lower in the third quarter, with the index falling to 39 from 40.

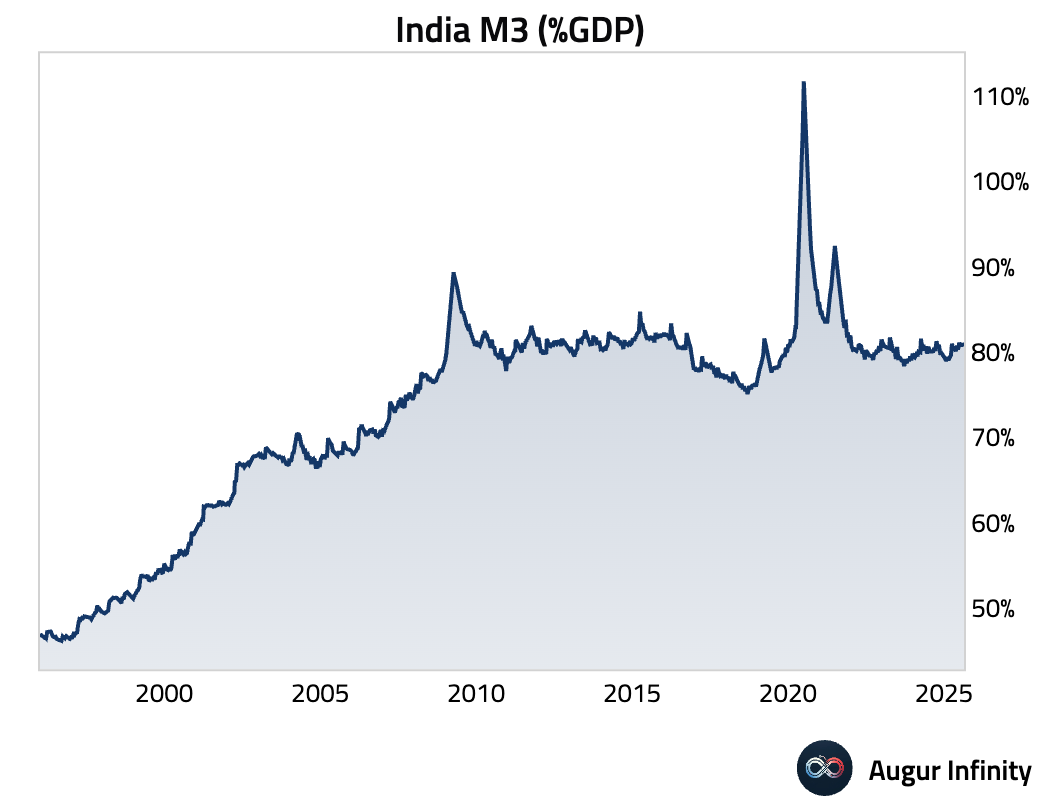

- India’s M3 money supply growth quickened to 9.8% Y/Y for the two weeks ending August 22.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.