Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- China is considering implementing new restrictions on stock speculation after its domestic market reached the best level in a decade.

- Japan’s Ministry of Finance reported that budget requests for the next fiscal year have increased by approximately 6.3 percent year-over-year.

Global Economics

United States

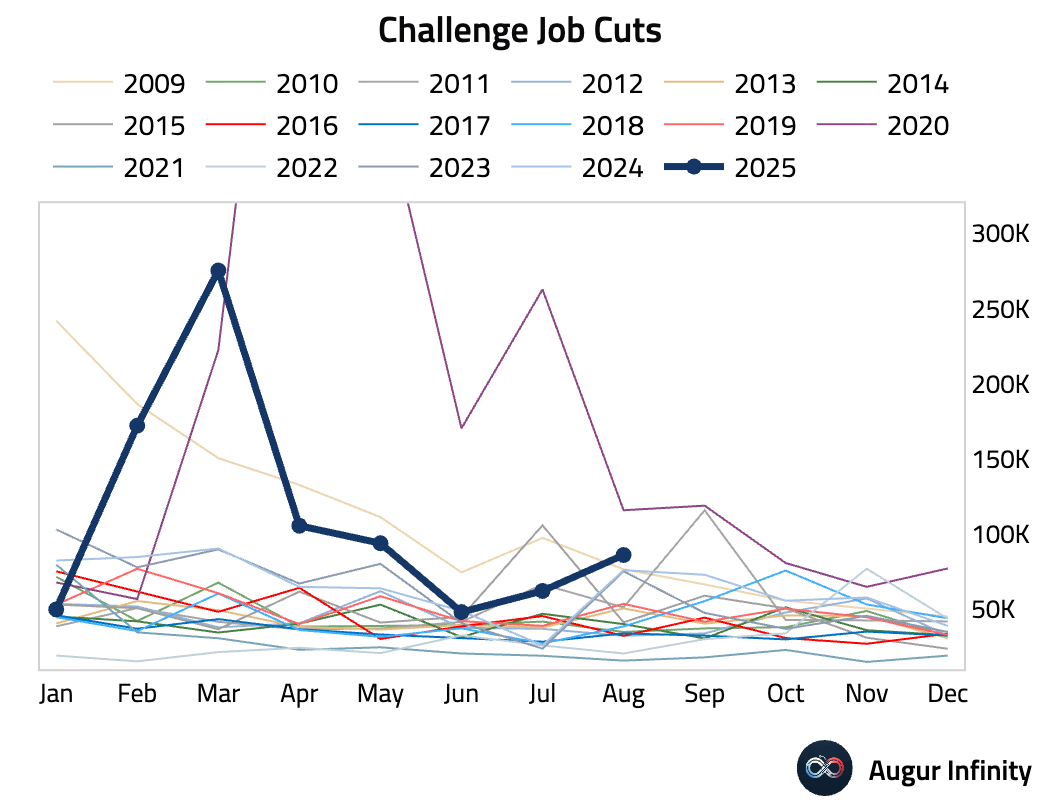

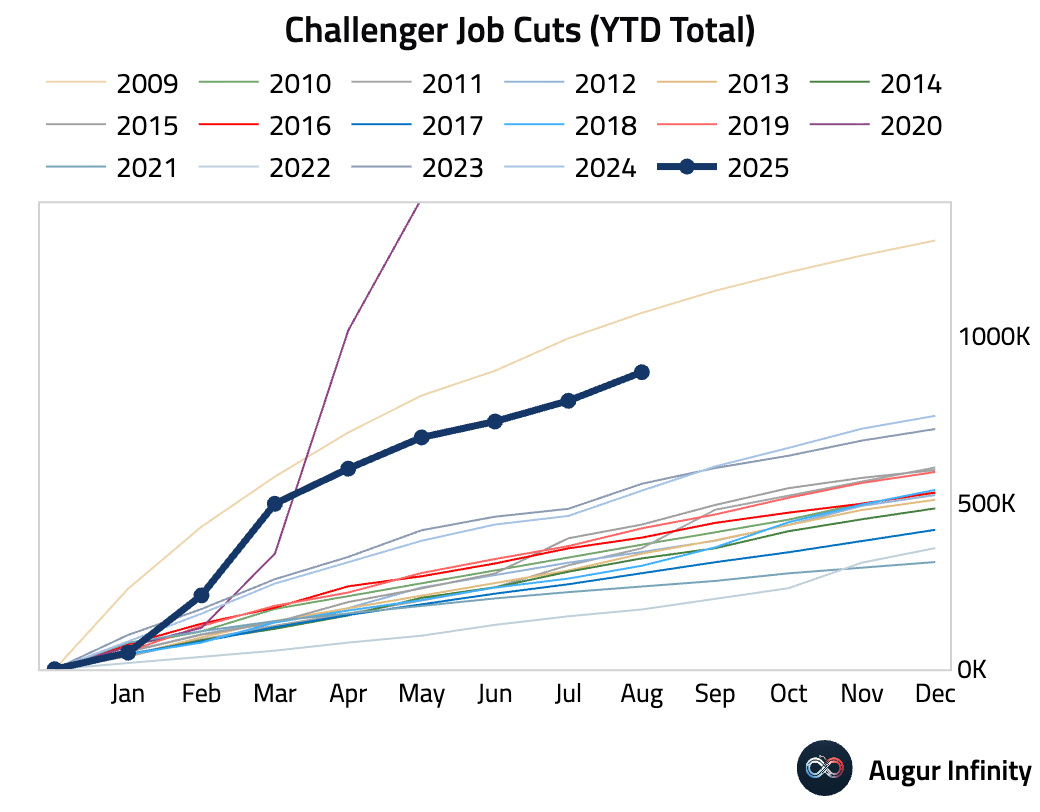

- US companies announced 85,979 job cuts in August, an increase from 62,075 in July and the highest number since May.

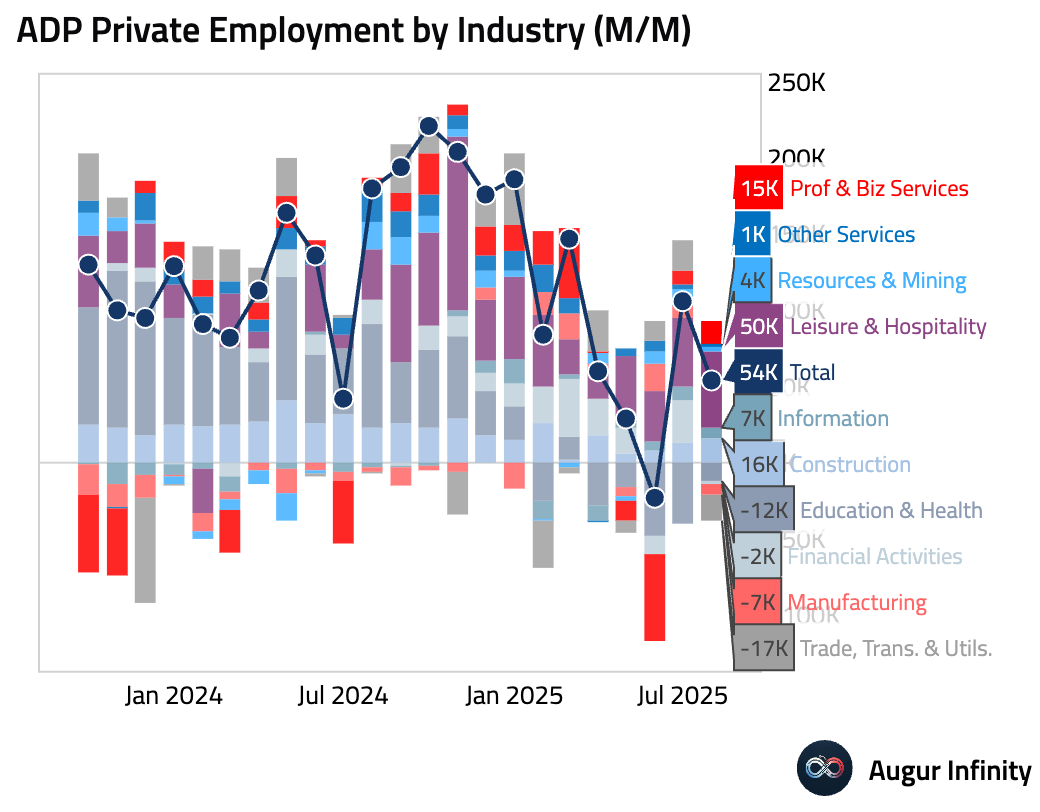

- Private payrolls rose by only 54,000 in August, well below the consensus of 65,000 and a significant slowdown from July’s 106,000. The 50,000 surge in leisure and hospitality was offset by trade and transportation (-17,000) and health and education (-12,000). Pay growth for job-stayers was 4.4%, while job-changers saw a robust 7.1% gain, indicating workers are still being rewarded for switching roles.

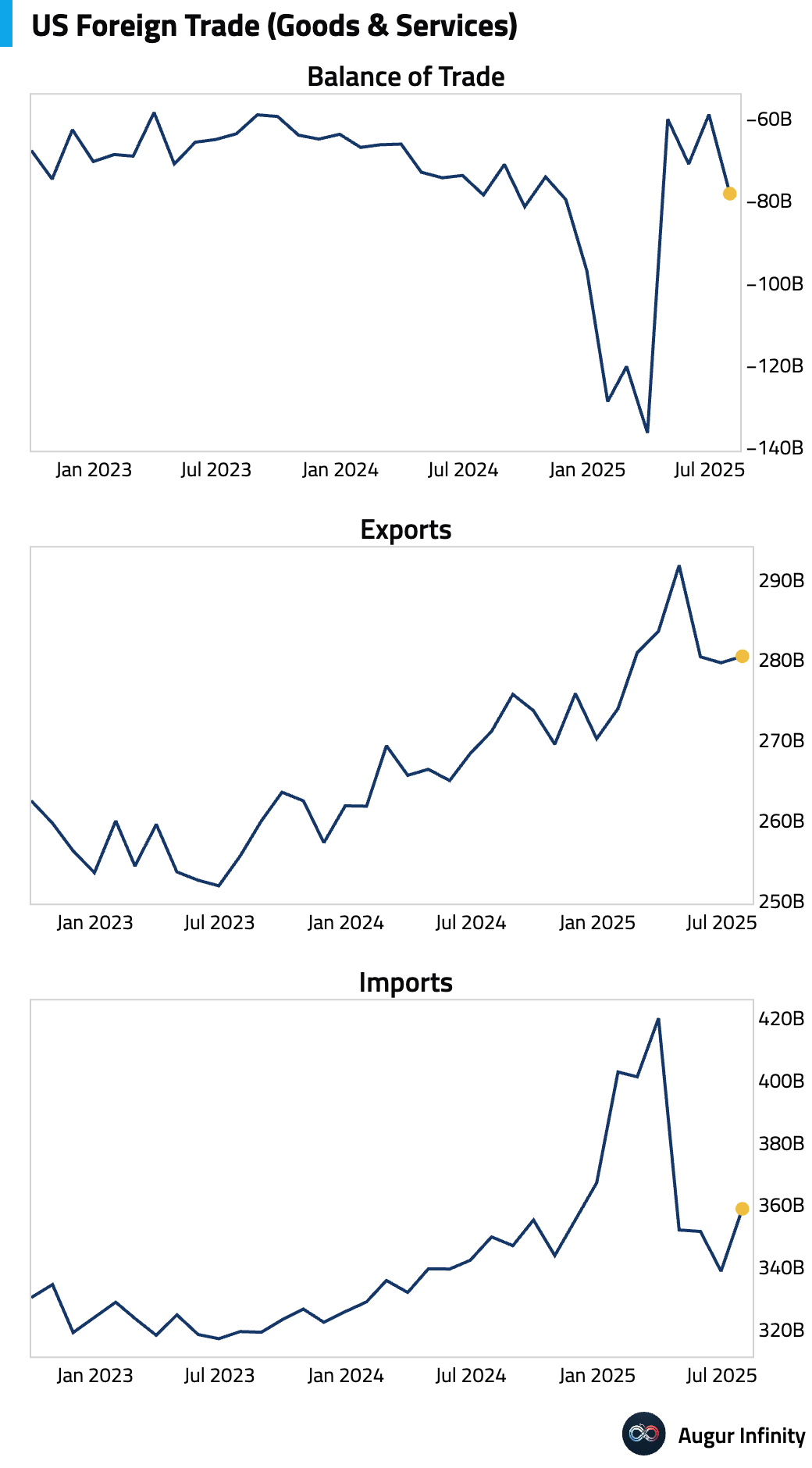

- The US trade deficit widened to $78.3 billion in July from a revised $59.1 billion in June, larger than the $75.7 billion expected. Imports rose to $358.8 billion while exports edged up to $280.5 billion.

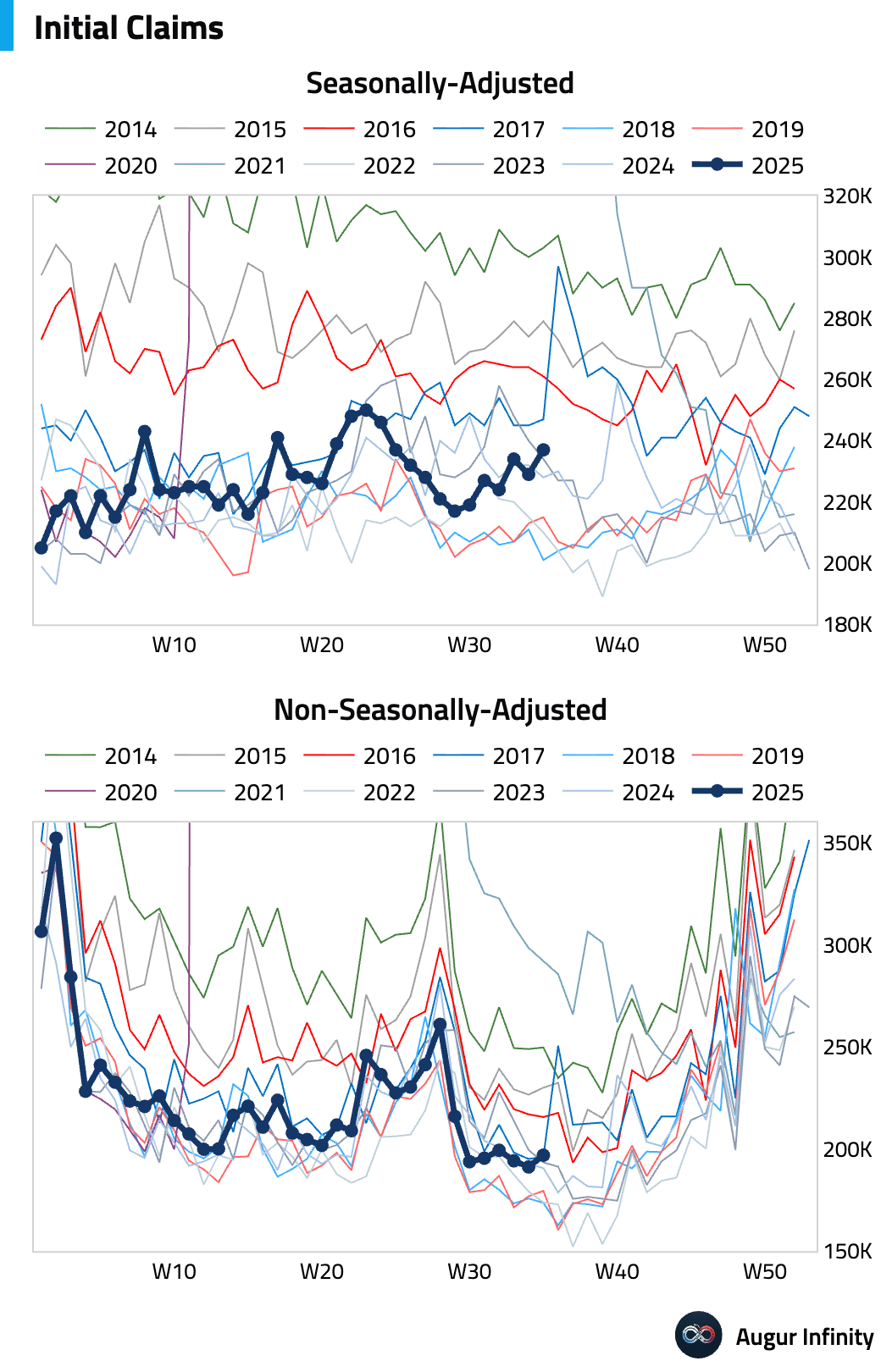

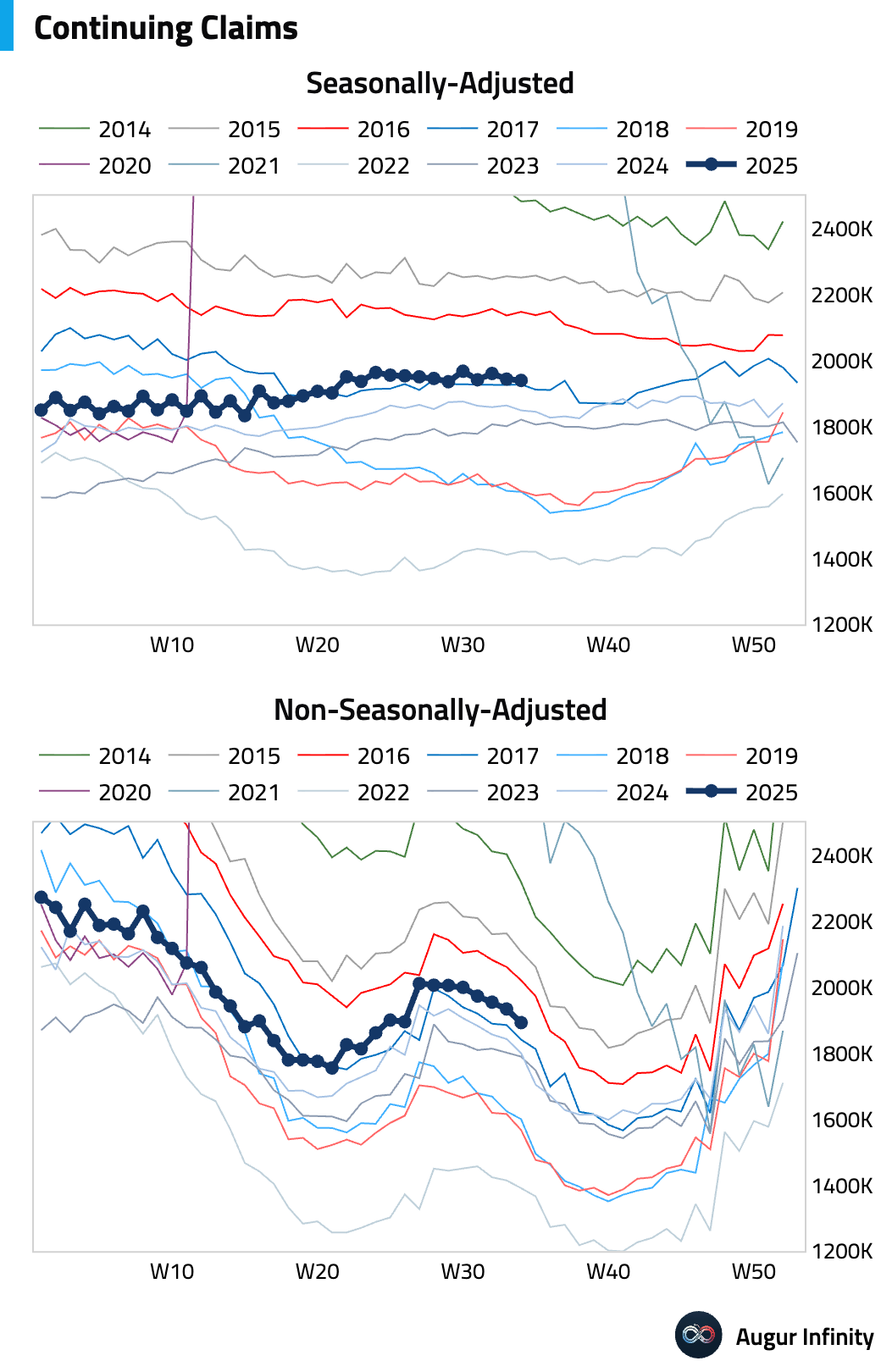

- Initial jobless claims rose to 237,000 for the week ending August 30, slightly above the consensus of 230,000. Continuing claims fell to 1.94 million, while the four-week moving average of initial claims ticked up to 231,000.

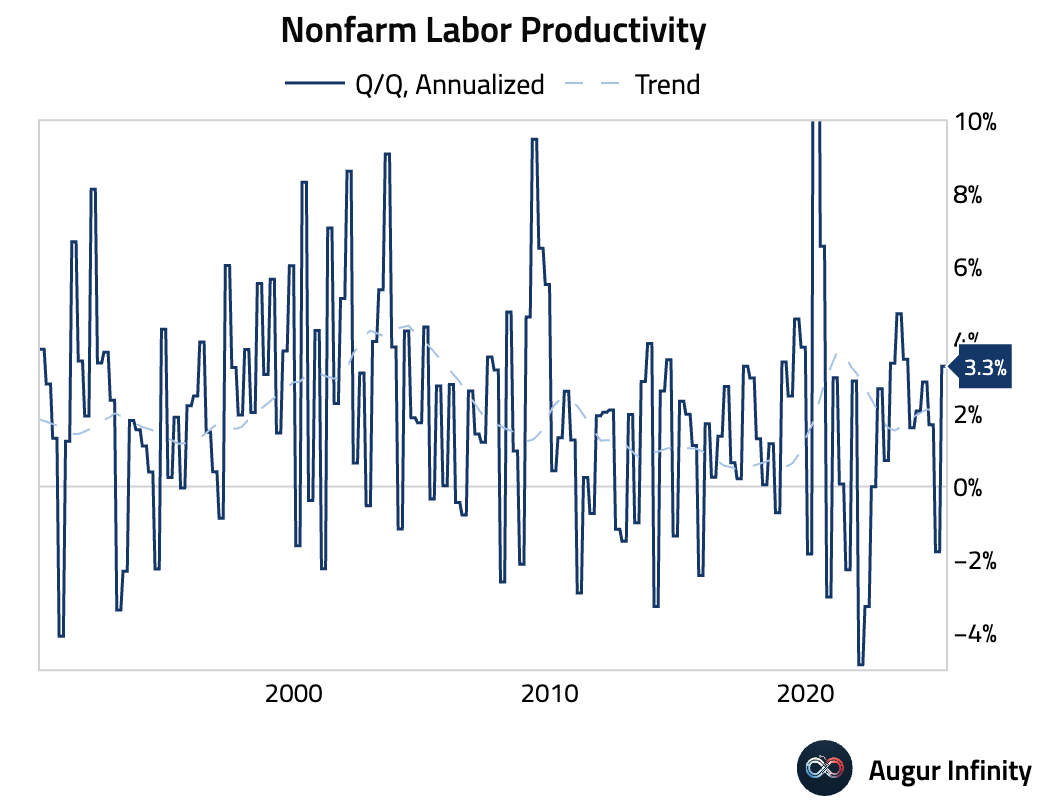

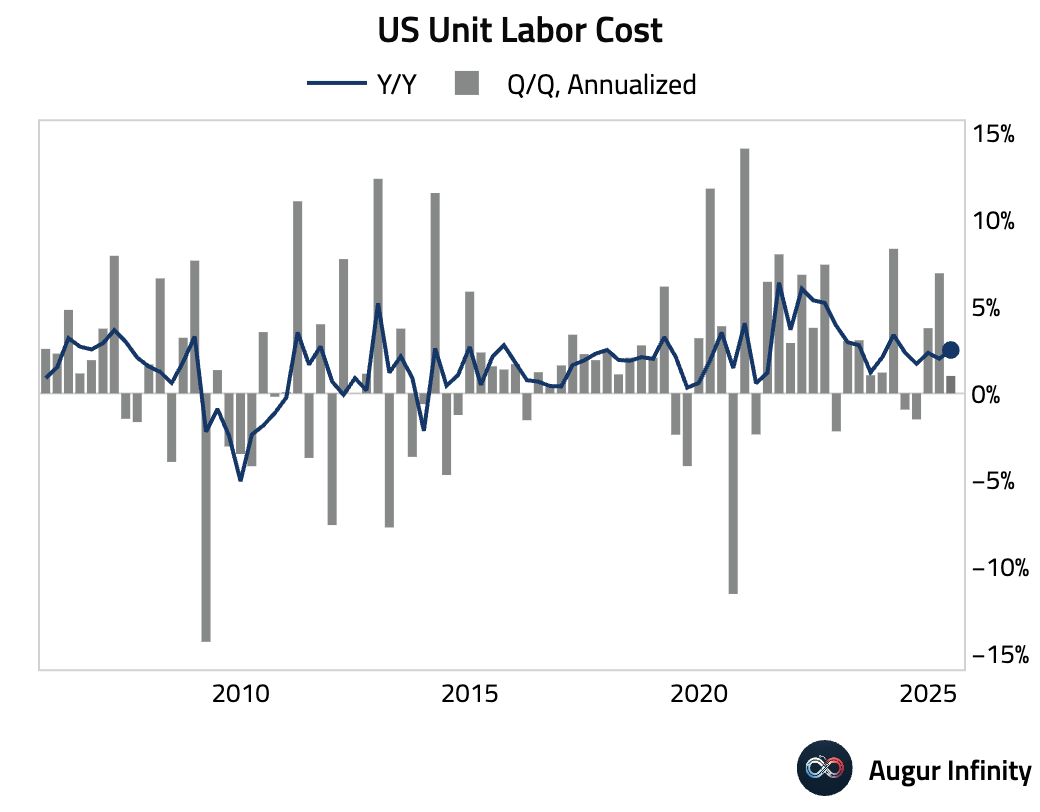

- Final nonfarm productivity for Q2 was revised higher to a 3.3% annualized rate, beating the 2.7% consensus. Unit labor costs were also revised down to a 1.0% annualized increase, below the 1.2% estimate.

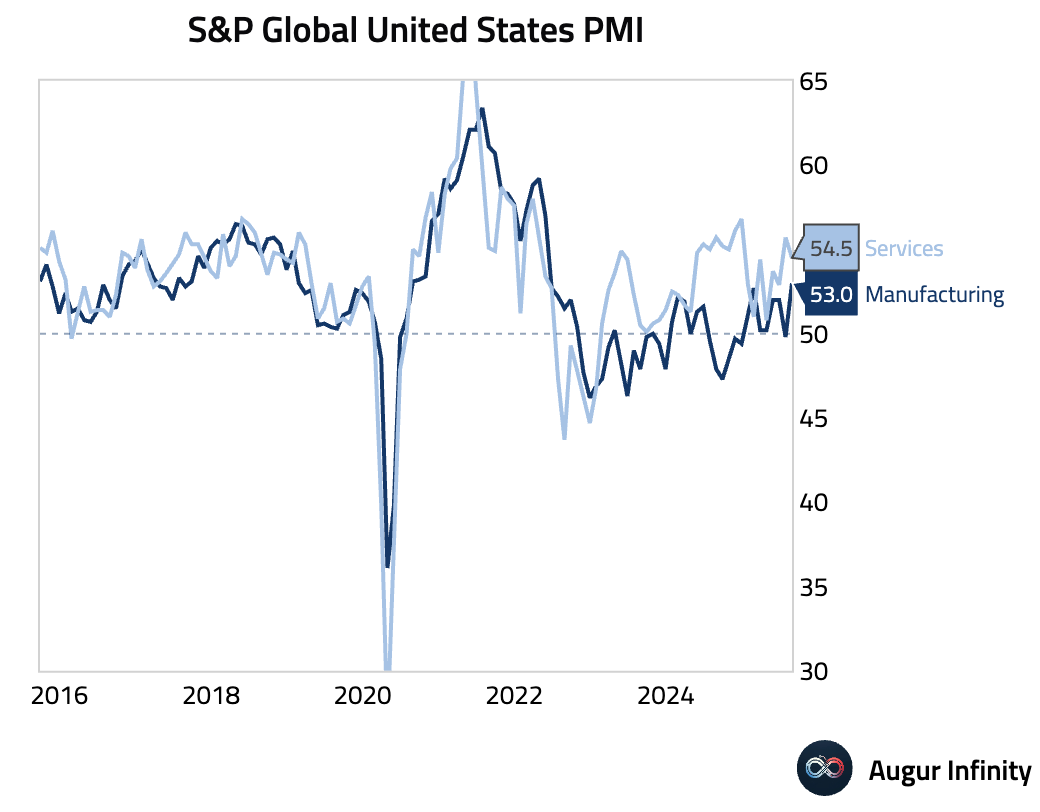

- The final S&P Global Services PMI for August was 54.5, a slight downward revision from the preliminary 55.4 but still indicating strong expansion.

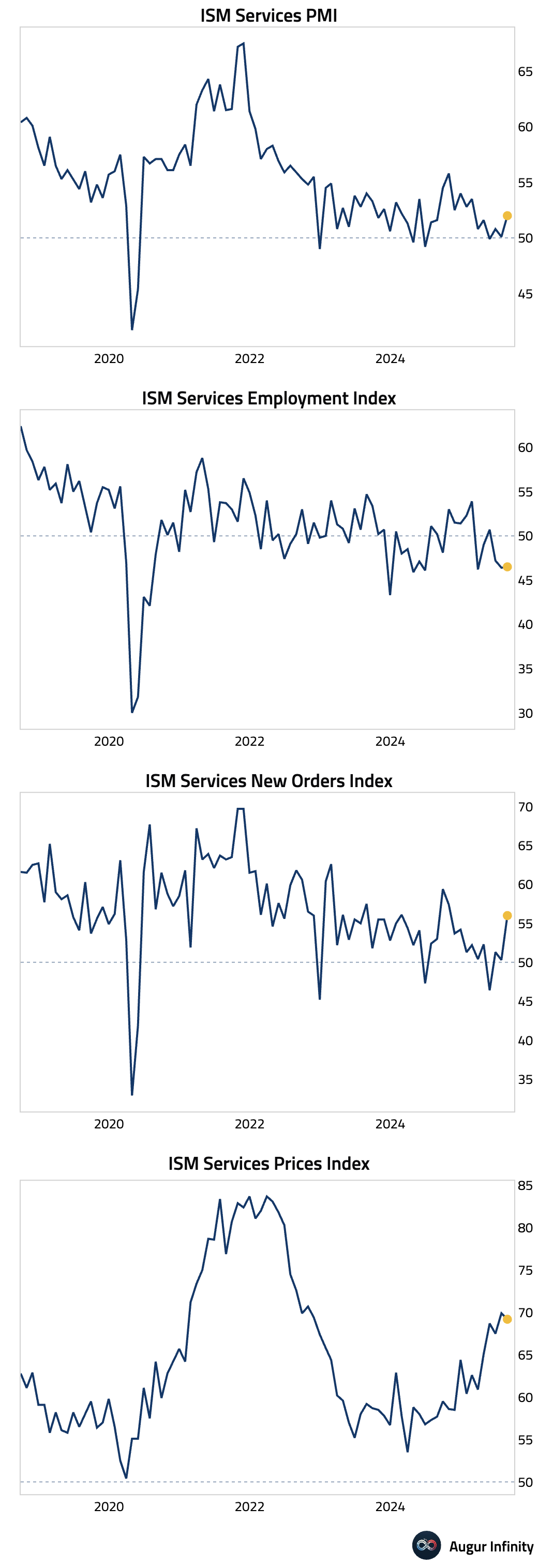

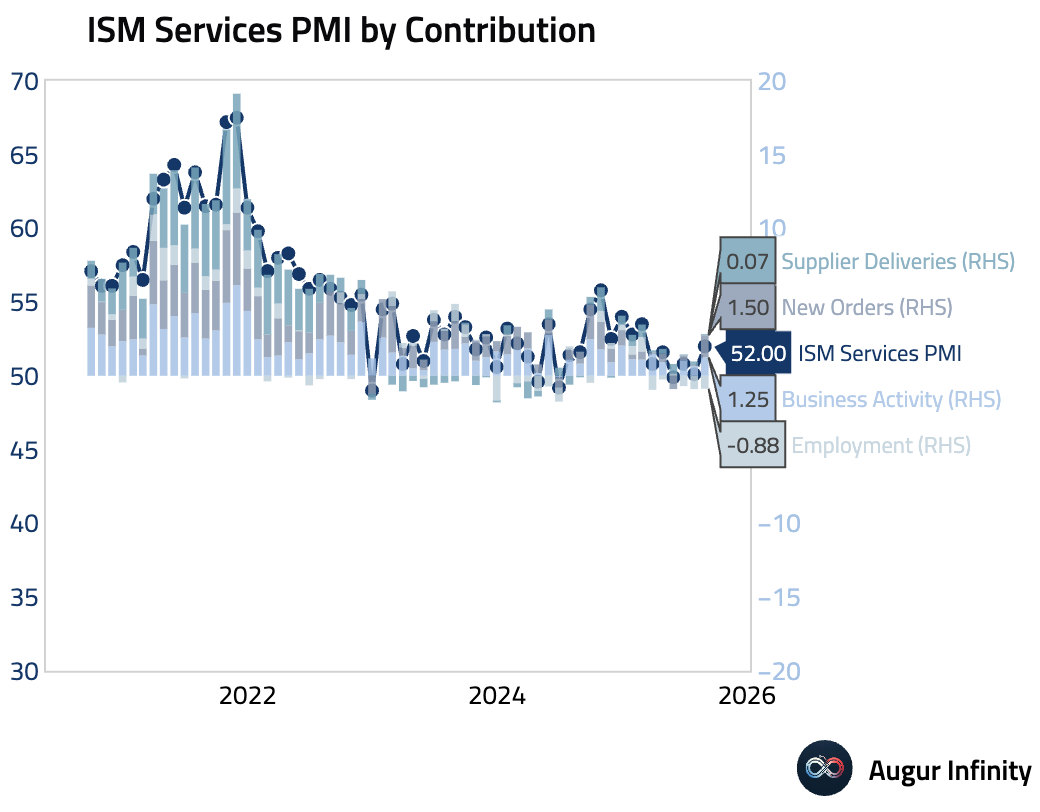

- The ISM Services PMI unexpectedly rose to 52.0 in August from 50.1, beating the consensus estimate of 51.0. The increase was driven by a sharp acceleration in New Orders, which jumped 5.7 points to 56.0, and a rise in Business Activity to 55.0, partly reflecting firms pulling orders forward to get ahead of tariff increases. However, the employment index remained in contraction for a third consecutive month at 46.5, signaling continued softness in the services labor market. The prices paid index remains highly elevated at 69.2, indicating persistent inflationary pressure. Forward-looking indicators were weak, as the backlog of orders index plunged to 40.4, its lowest reading since May 2009.

Canada

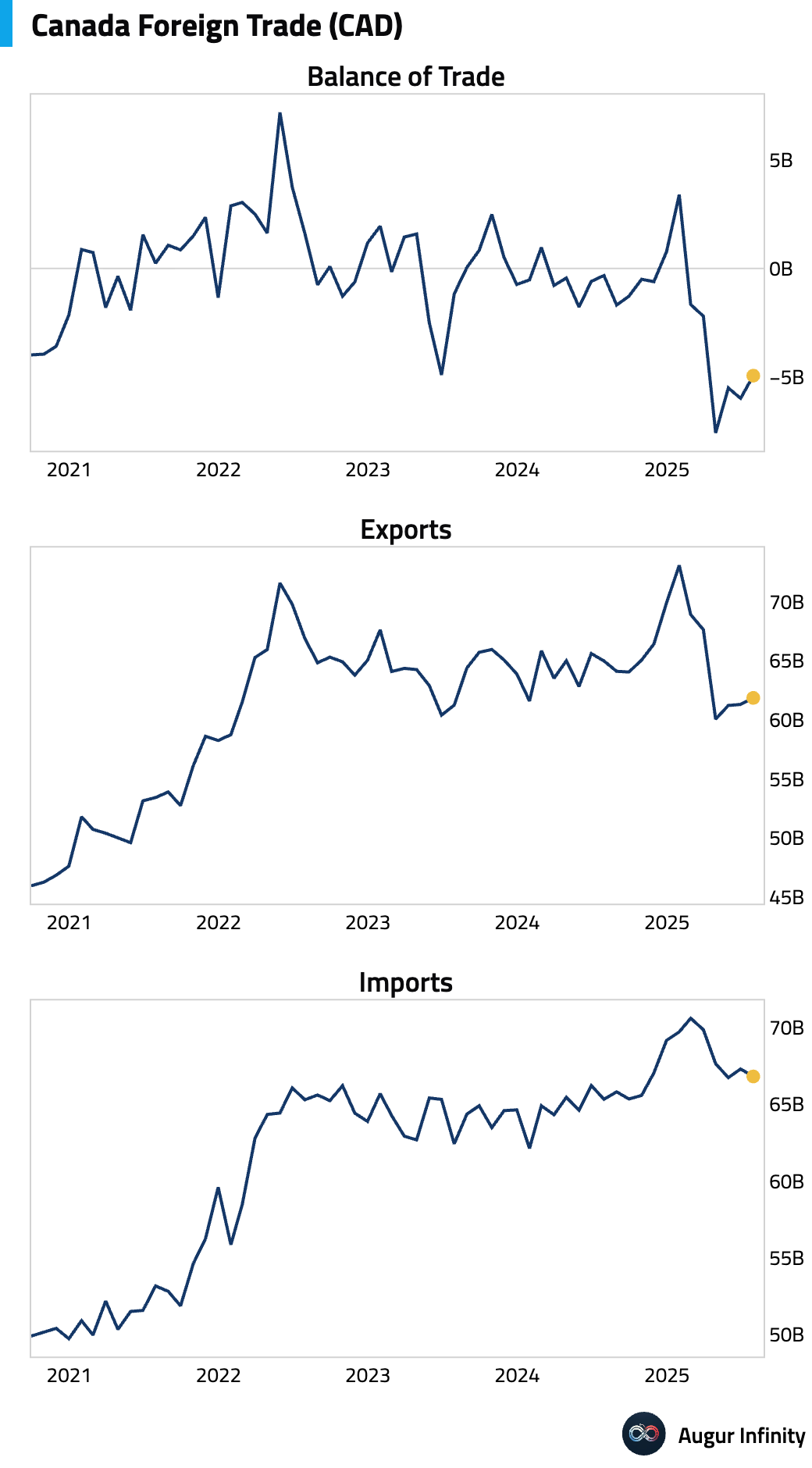

- Canada’s trade deficit narrowed slightly to C$4.94 billion in July from C$5.98 billion in June. Exports rose to C$61.86 billion, while imports decreased to C$66.80 billion.

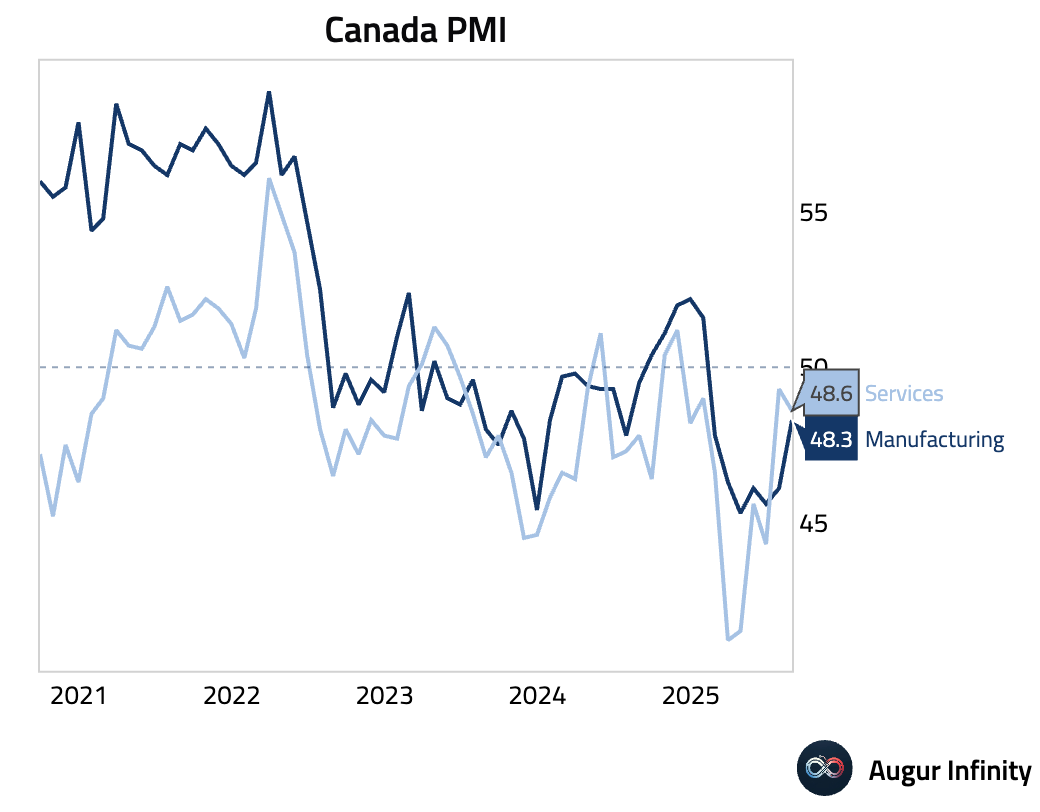

- The S&P Global Services PMI for Canada fell to 48.6 in August from 49.3, indicating a faster pace of contraction in the services sector.

Europe

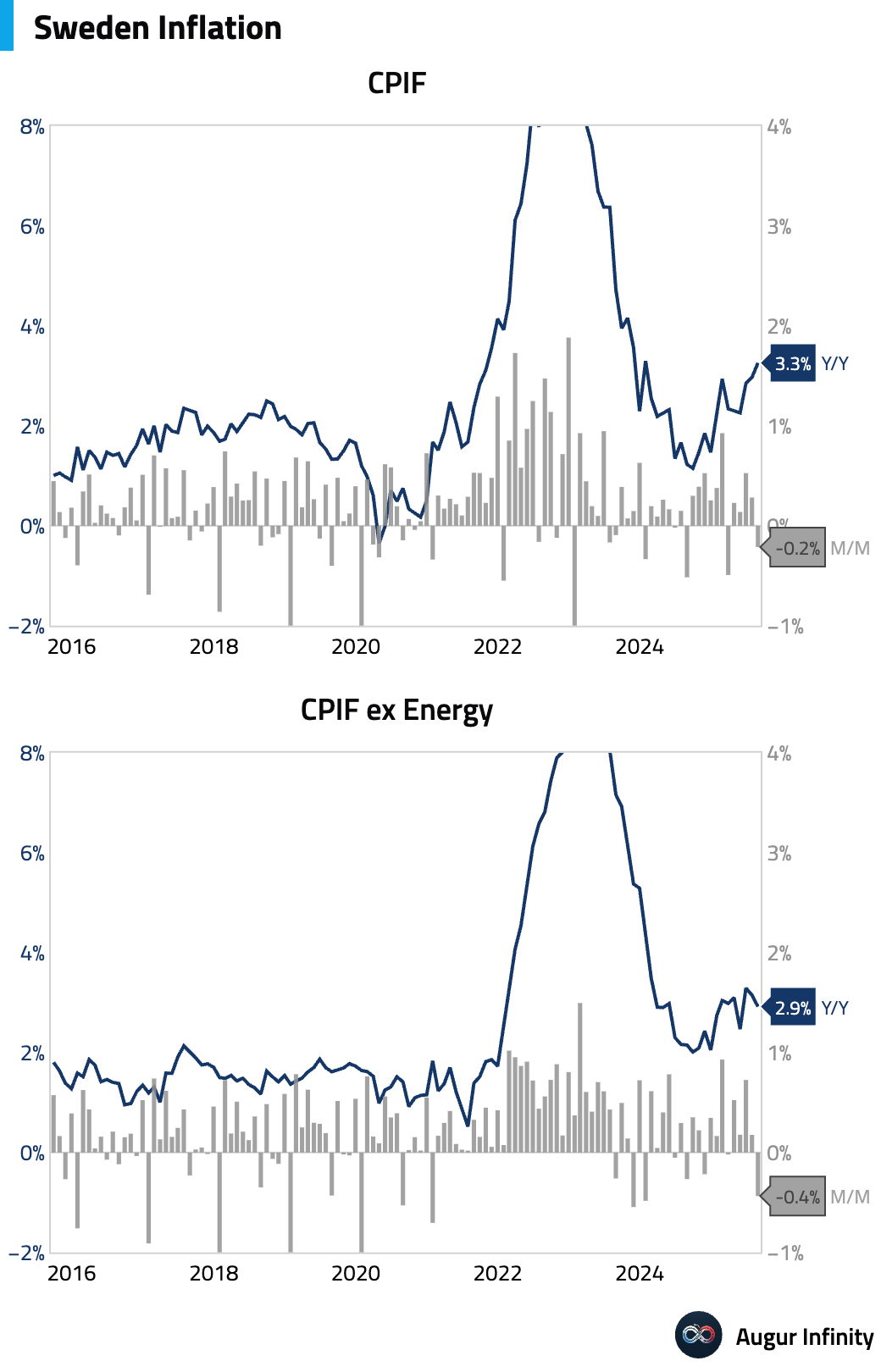

- Preliminary data for August showed Sweden’s CPIF inflation rising to 3.3% Y/Y from 3.0%, while declining 0.2% M/M.

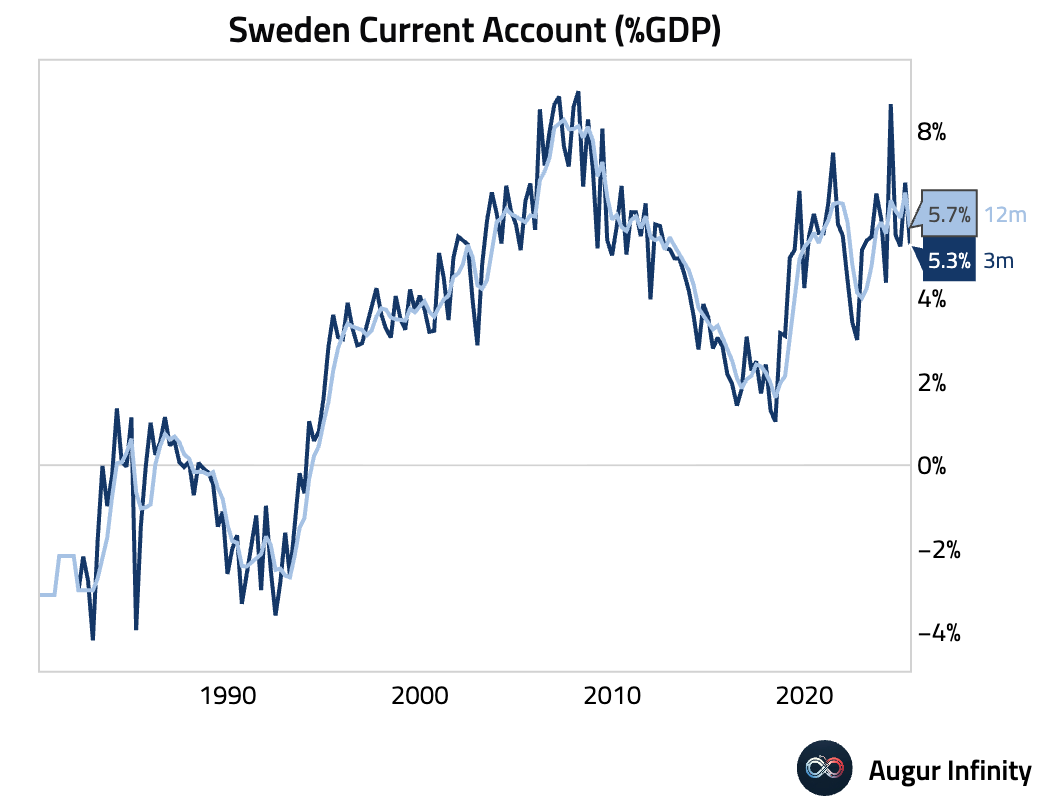

- Sweden’s current account surplus decreased to SEK 84.5 billion in Q2 from SEK 125.4 billion in the prior quarter.

- Sweden’s preliminary headline CPI for August came in at 1.1% Y/Y, up from 0.8%, and -0.4% M/M.

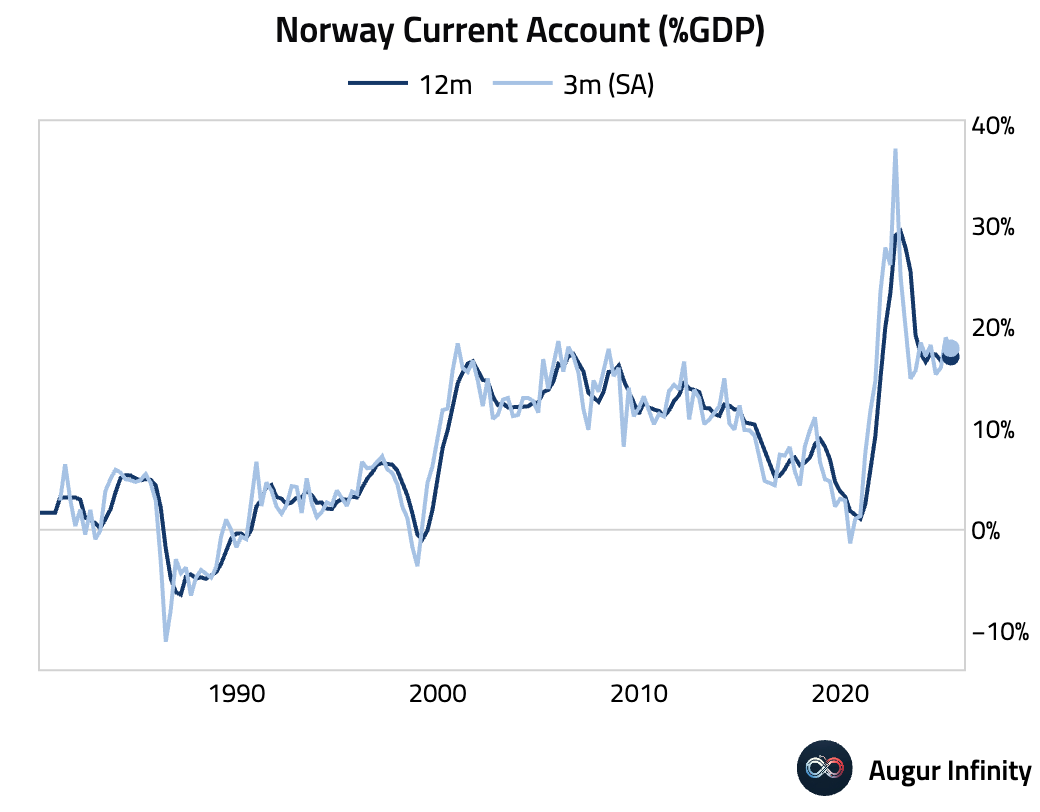

- Norway’s current account surplus narrowed to NOK 217.9 billion in Q2 from NOK 285.3 billion in Q1.

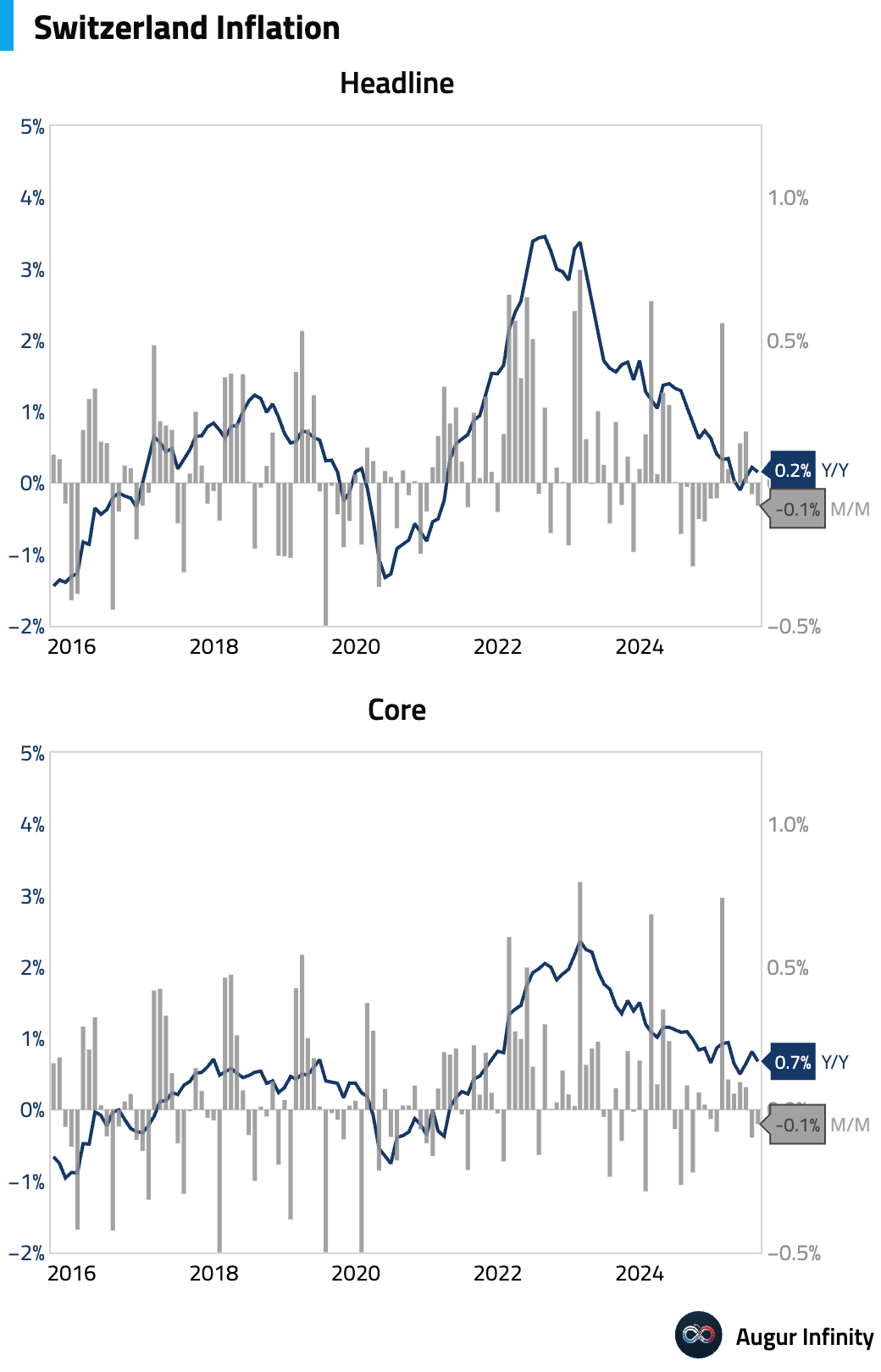

- Switzerland’s annual inflation rate held steady at 0.2% Y/Y in August, matching consensus. On a monthly basis, prices fell 0.1%.

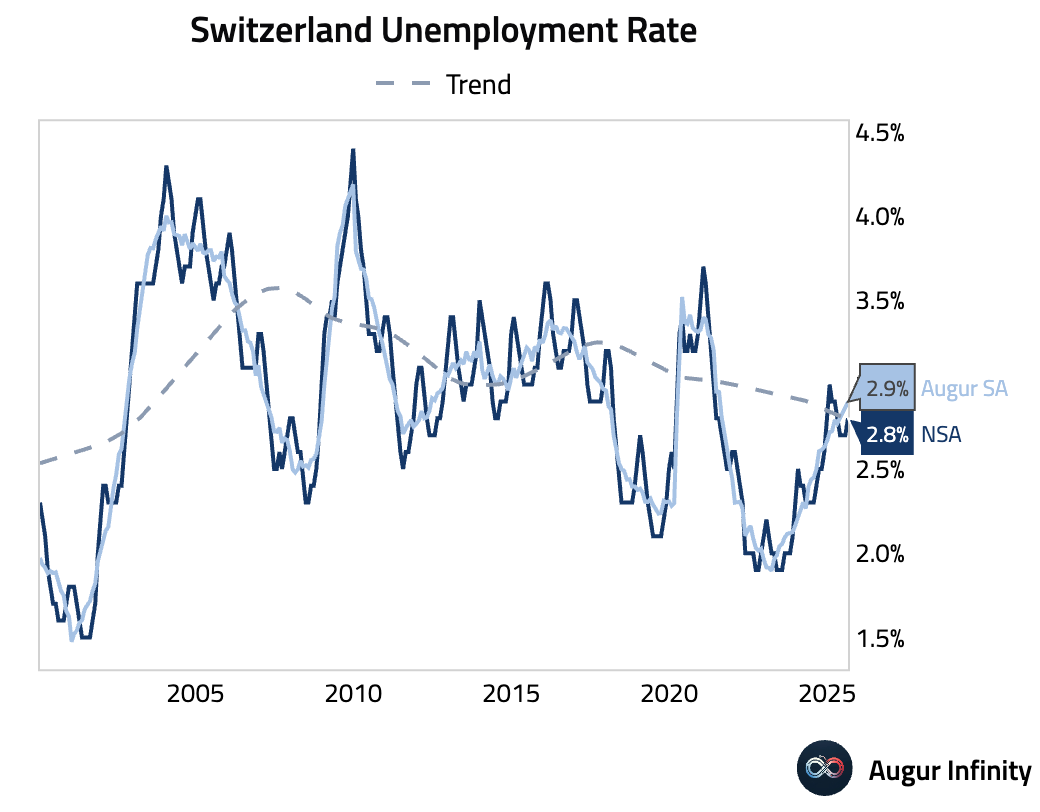

- The Swiss unemployment rate ticked up to 2.8% in August from 2.7%.

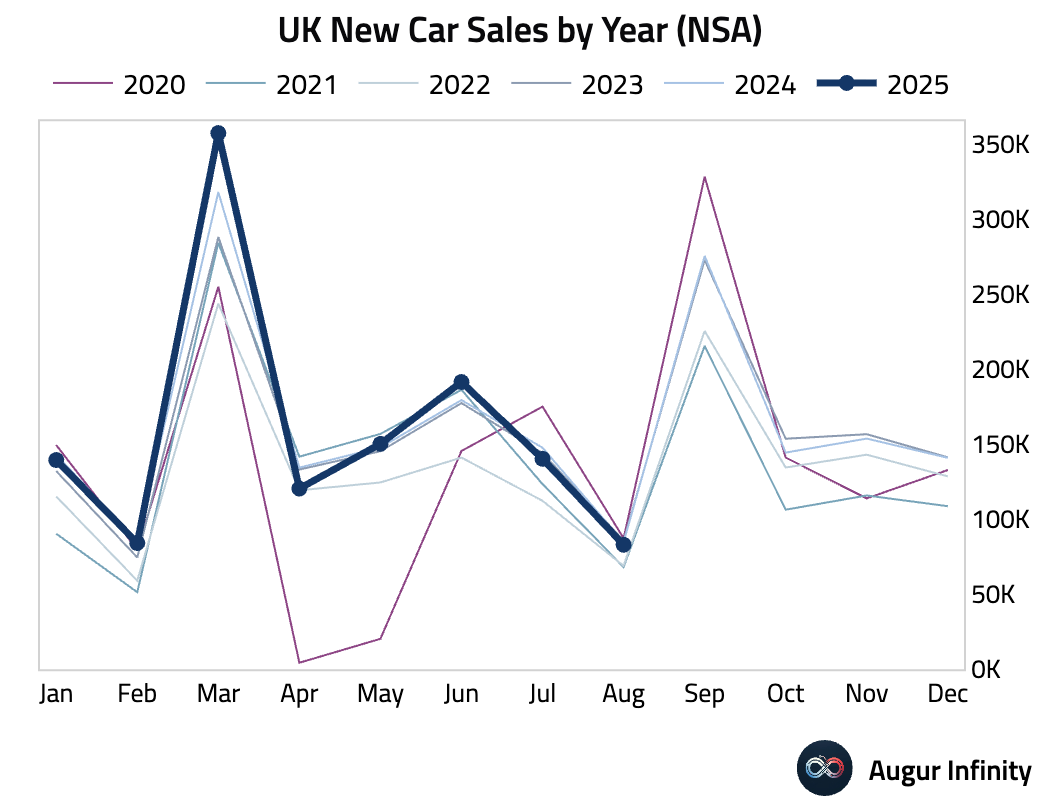

- UK new car sales fell 2.0% Y/Y in August, a smaller decline than the 5.0% drop seen in July.

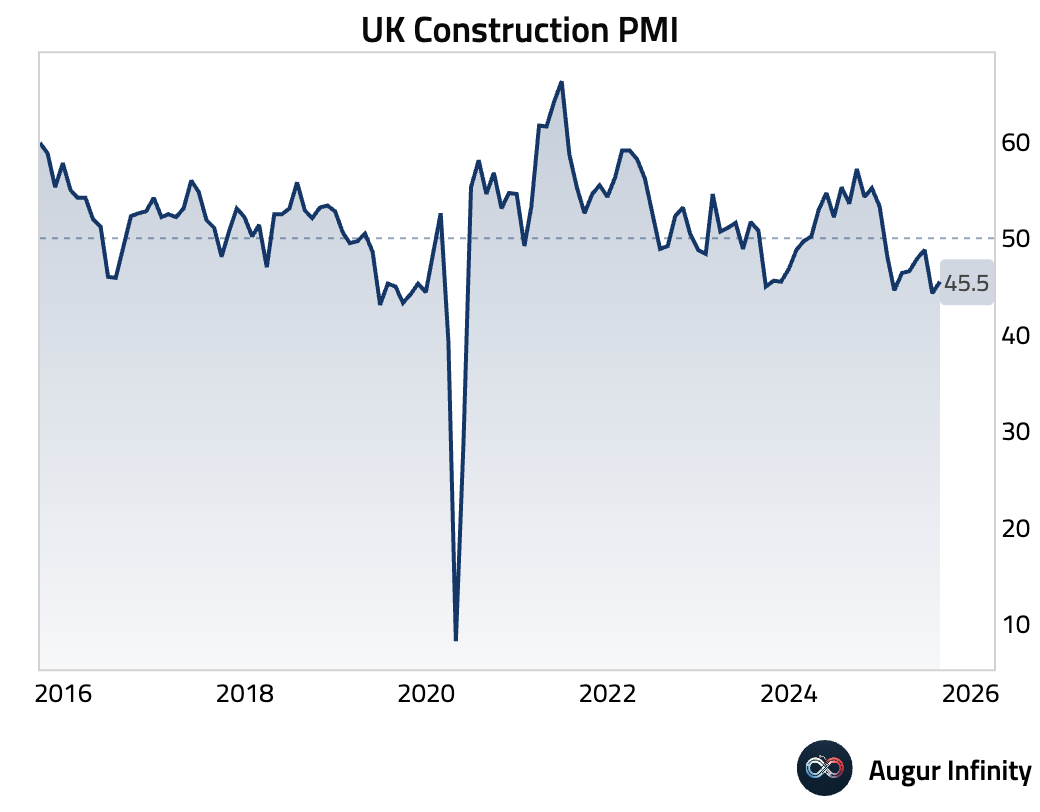

- The S&P Global/CIPS Construction PMI for the UK rose to 45.5 in August from 44.3, slightly beating the consensus of 45.0 but still signaling a contraction in activity.

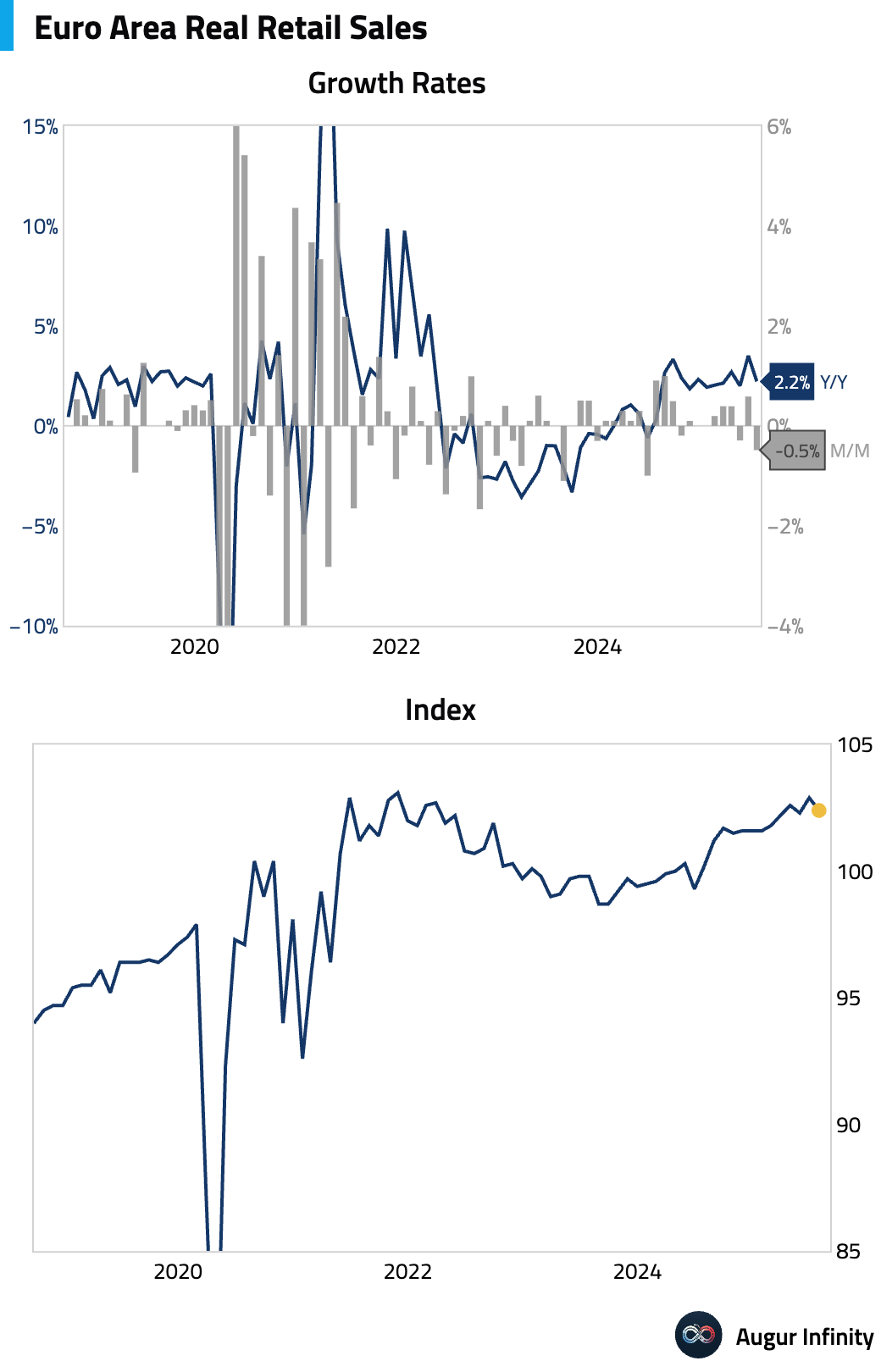

- Retail sales in the Euro Area fell by 0.5% M/M in July, missing the consensus for a 0.2% decline. Year-over-year, sales growth slowed to 2.2% from 3.5% in June.

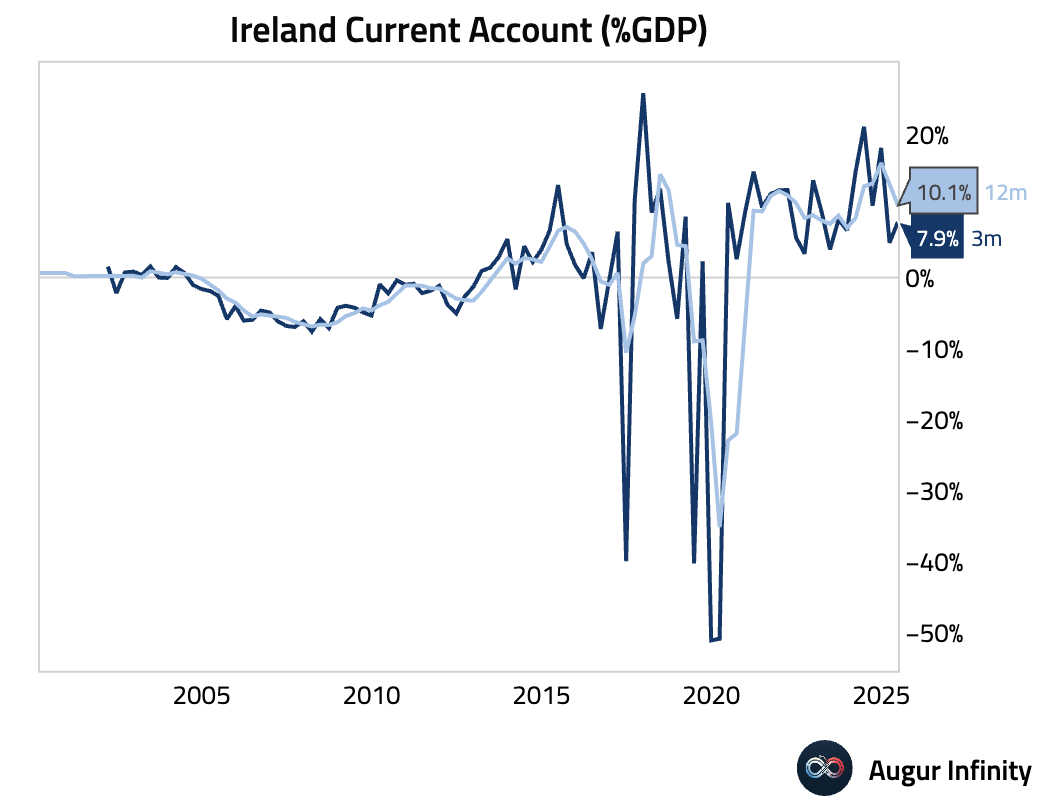

- Ireland’s current account surplus expanded significantly to €19.5 billion in Q2 from €5.8 billion in Q1.

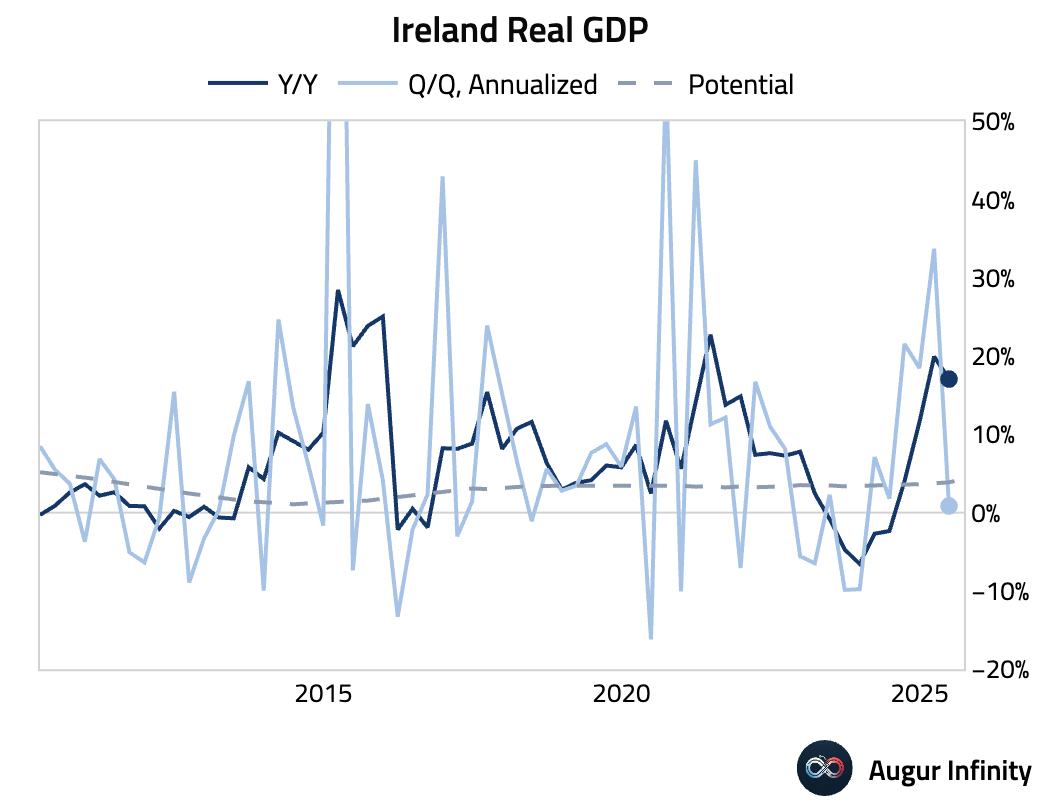

- Ireland’s final Q2 GDP growth was confirmed at 0.2% Q/Q (or 0.9% annualized) and 17.1% Y/Y, well above consensus expectations.

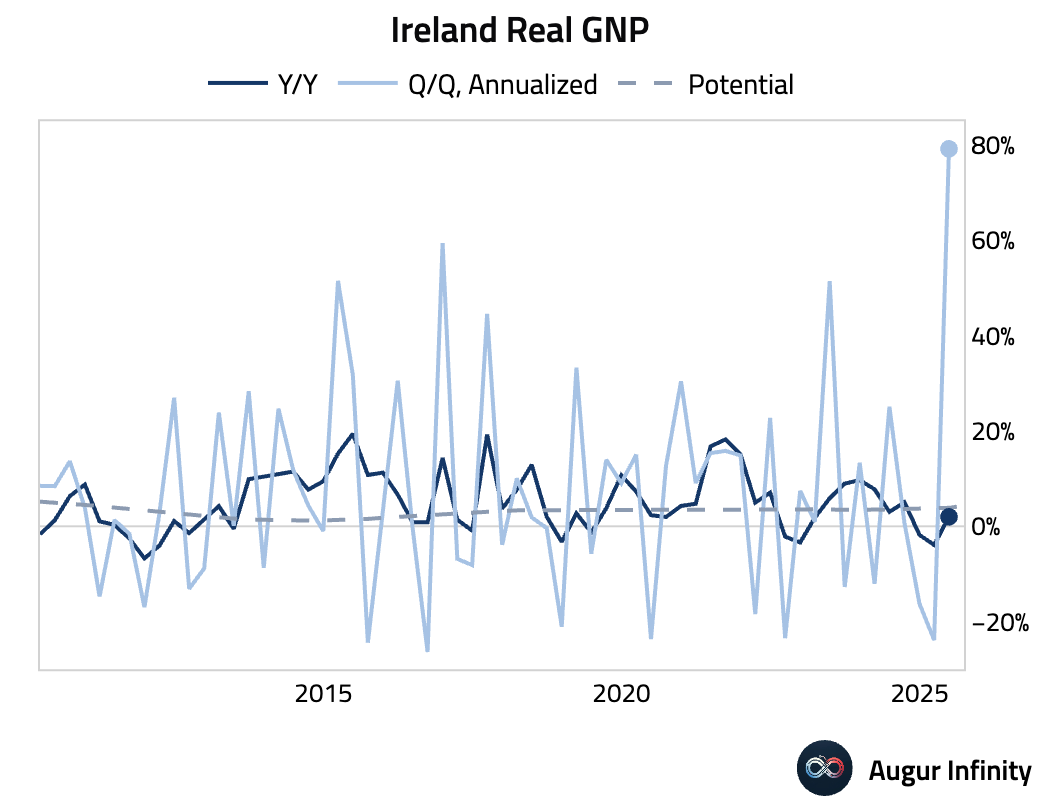

- Ireland’s Gross National Product (GNP) surged in Q2, posting growth of 15.7% Q/Q (or 79% annualized) and 2.0% Y/Y, both all-time highs.

Asia-Pacific

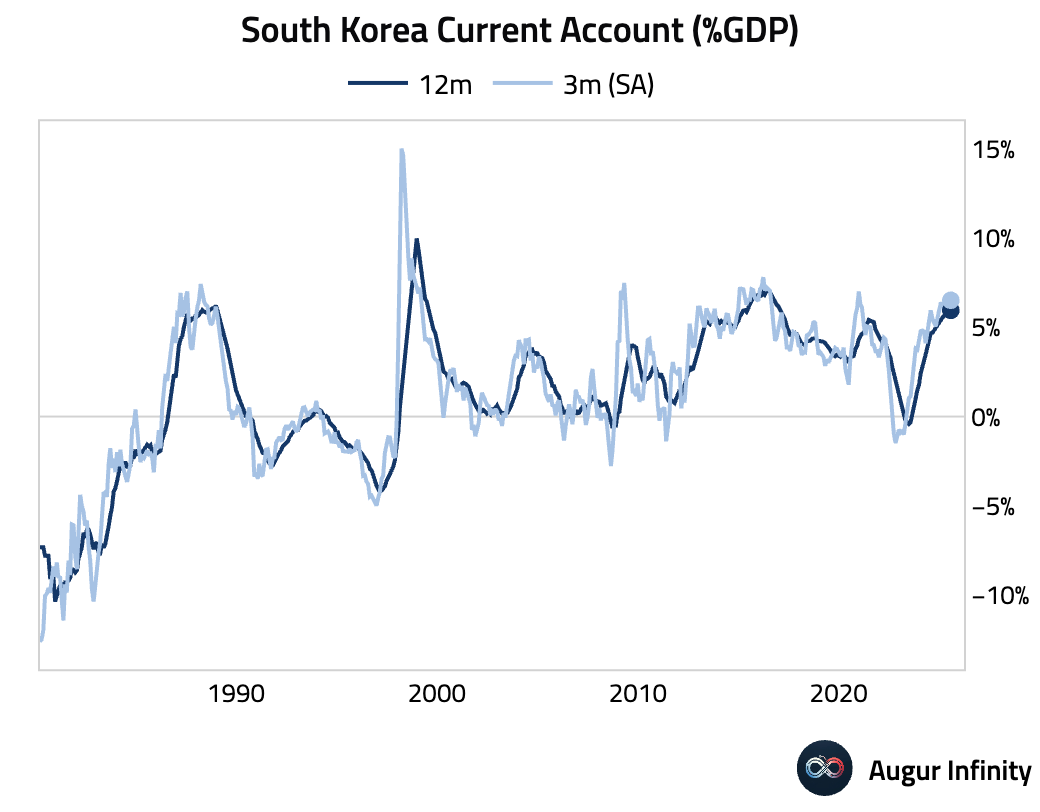

- South Korea’s current account surplus fell to $10.78 billion in July from $14.27 billion in June.

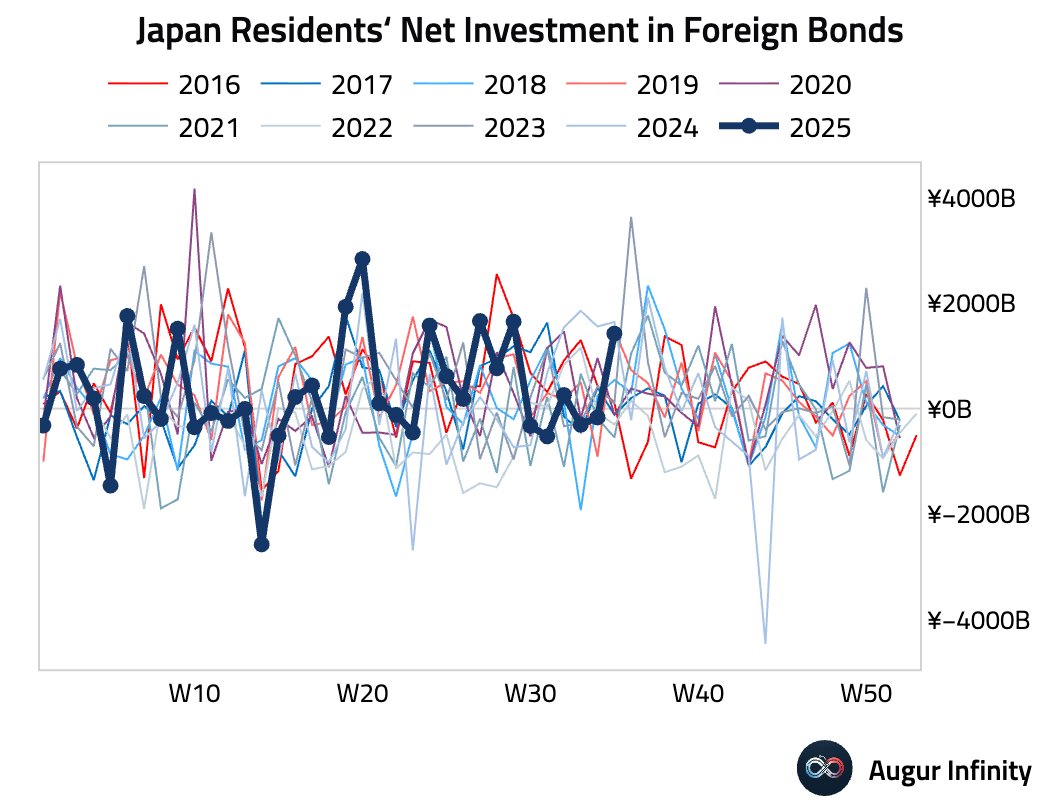

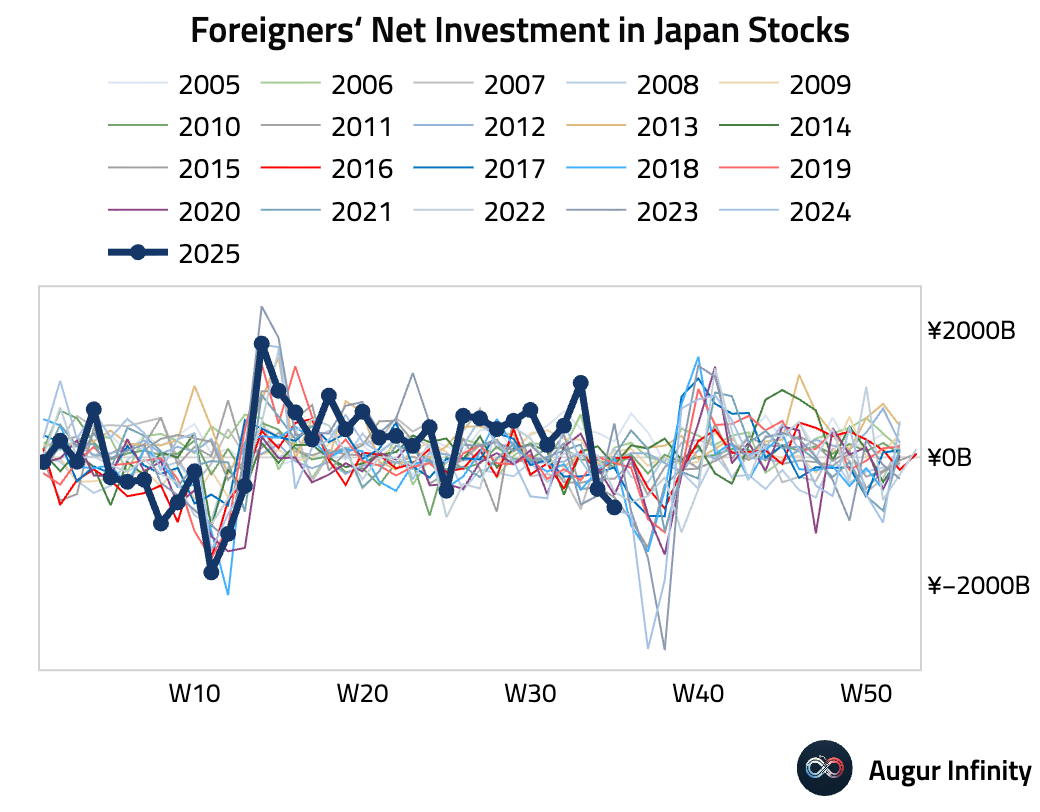

- Japanese investors were net buyers of foreign bonds to the tune of ¥1.42 trillion in the last week of August, while foreign investors were net sellers of Japanese stocks, offloading ¥785.7 billion.

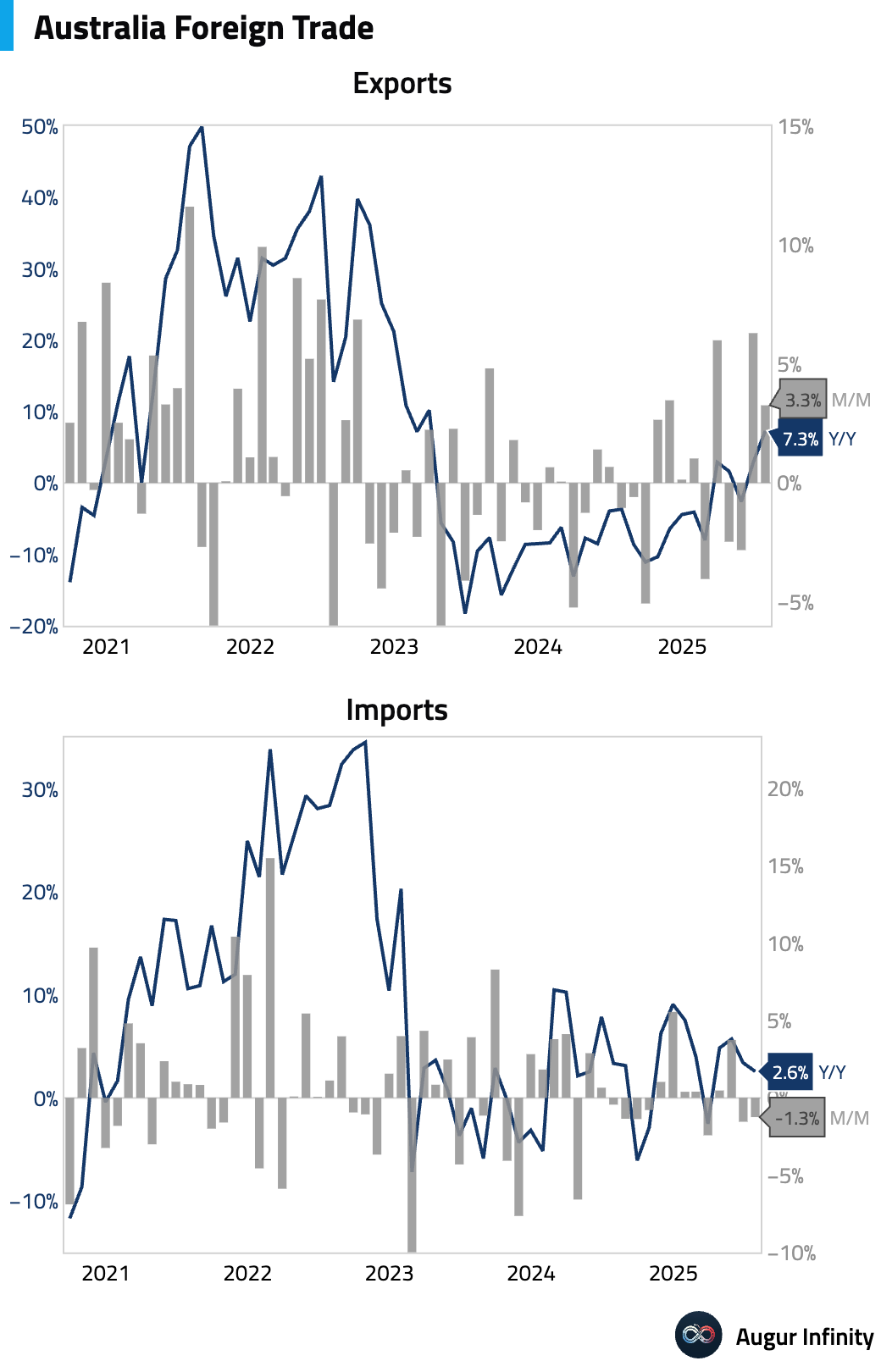

- Australia’s trade surplus widened to A$7.31 billion in July, significantly exceeding the A$5.0 billion consensus. The result was driven by a 3.3% M/M rise in exports, led by strong commodity shipments, while imports fell 1.3% M/M. The drop in imports was notable in consumer goods (-2.6%), suggesting softer domestic demand.

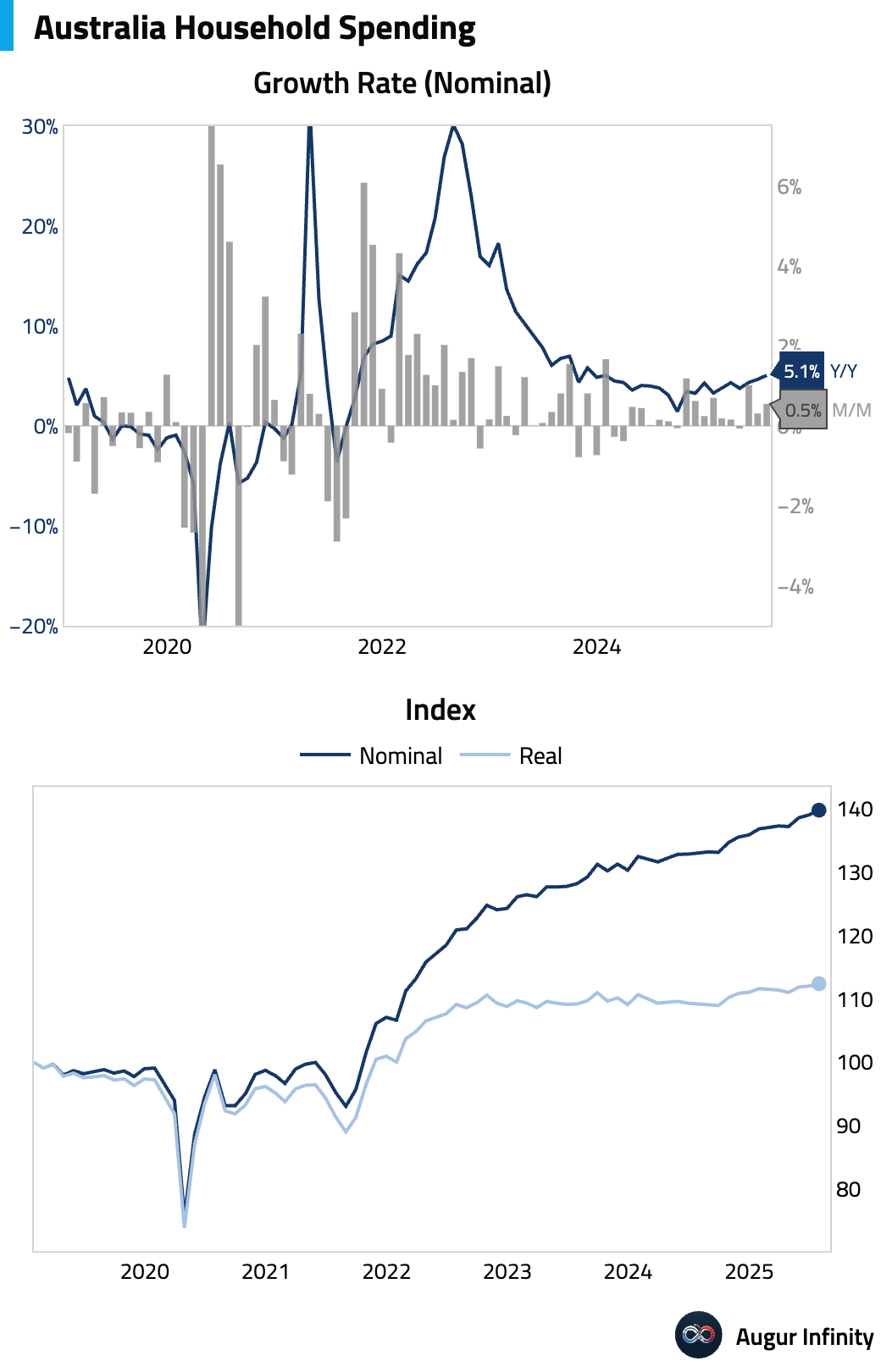

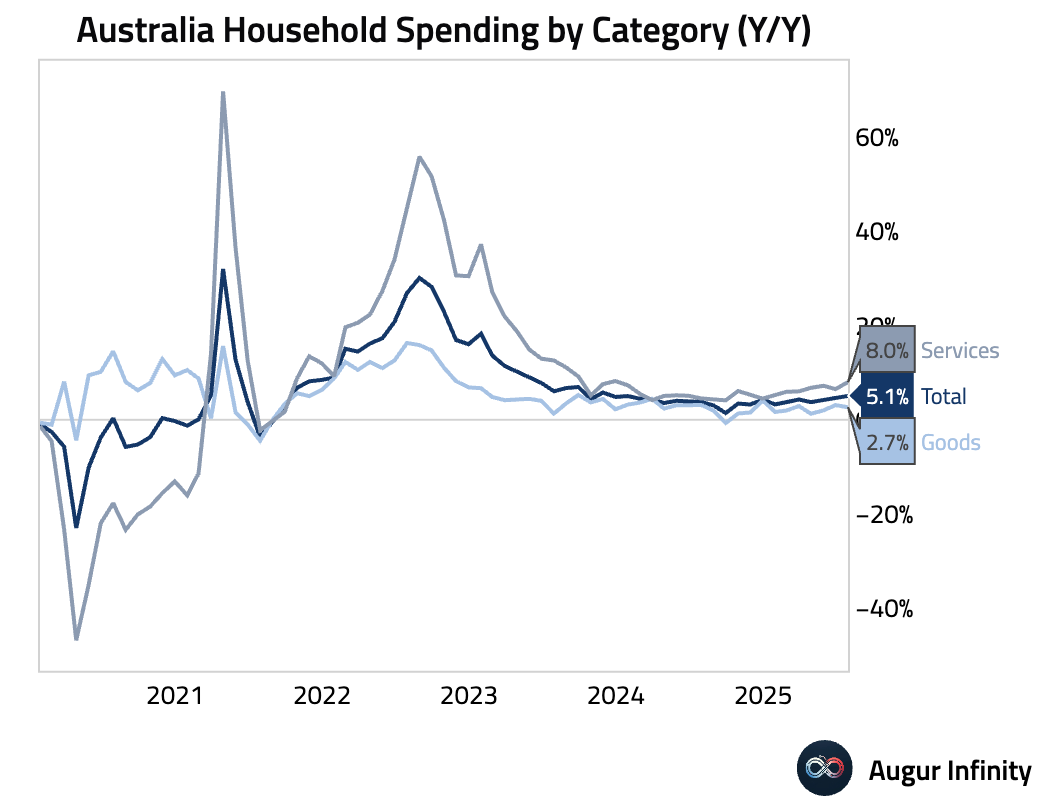

- Australian household spending increased by 0.5% M/M and 5.1% Y/Y in July. The rise was led by non-discretionary spending (+0.8%), while discretionary spending was softer (+0.4%). Spending on clothing (-1.2%) and furnishings (-1.4%) declined, reflecting a pullback after end-of-financial-year sales.

Emerging Markets ex China

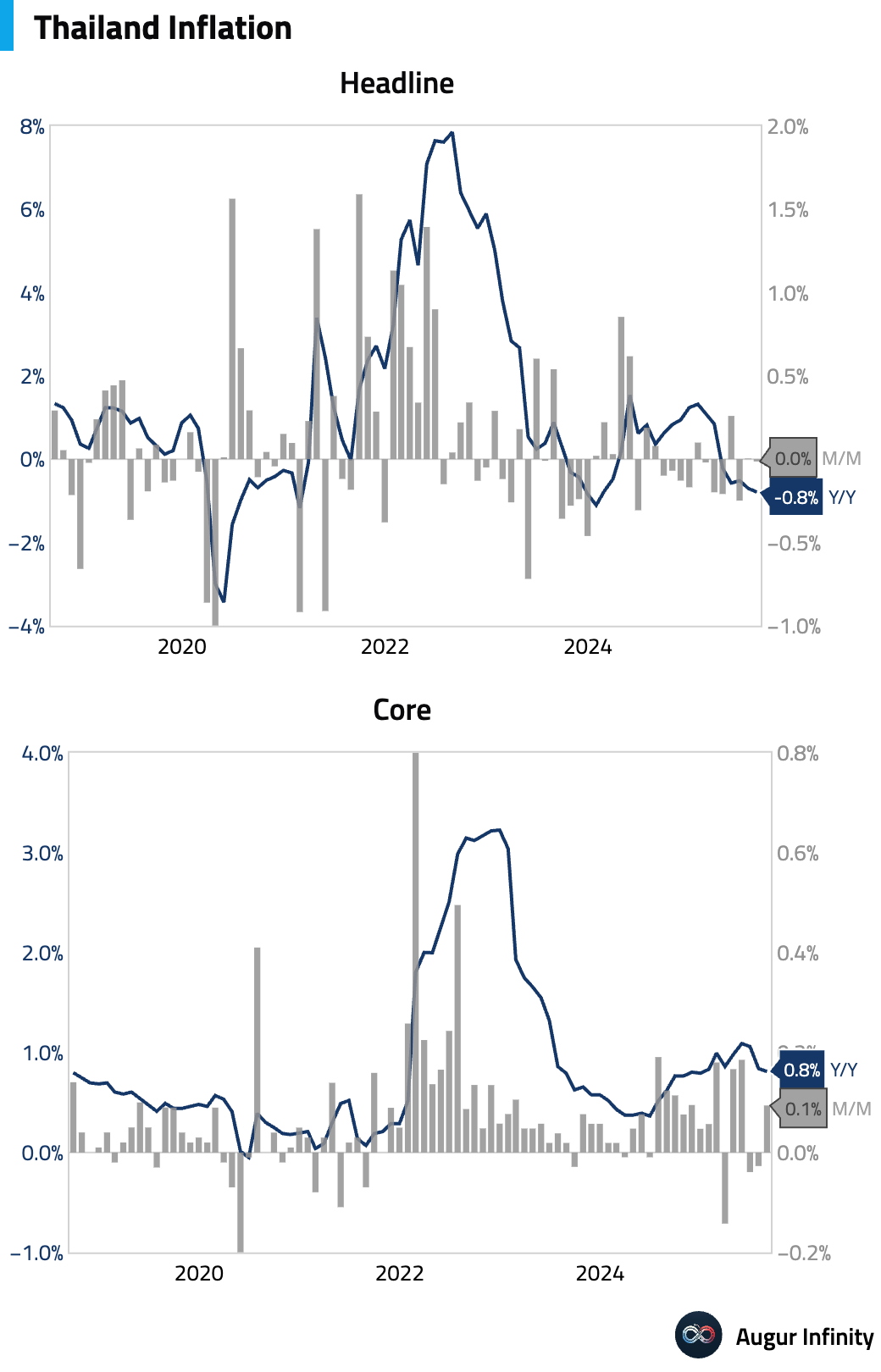

- Thailand’s headline CPI deflation deepened to -0.79% Y/Y in August, driven by a sharp slowdown in food inflation. However, core CPI, which excludes food and energy, was stable at 0.81% Y/Y, suggesting underlying price pressures remain contained.

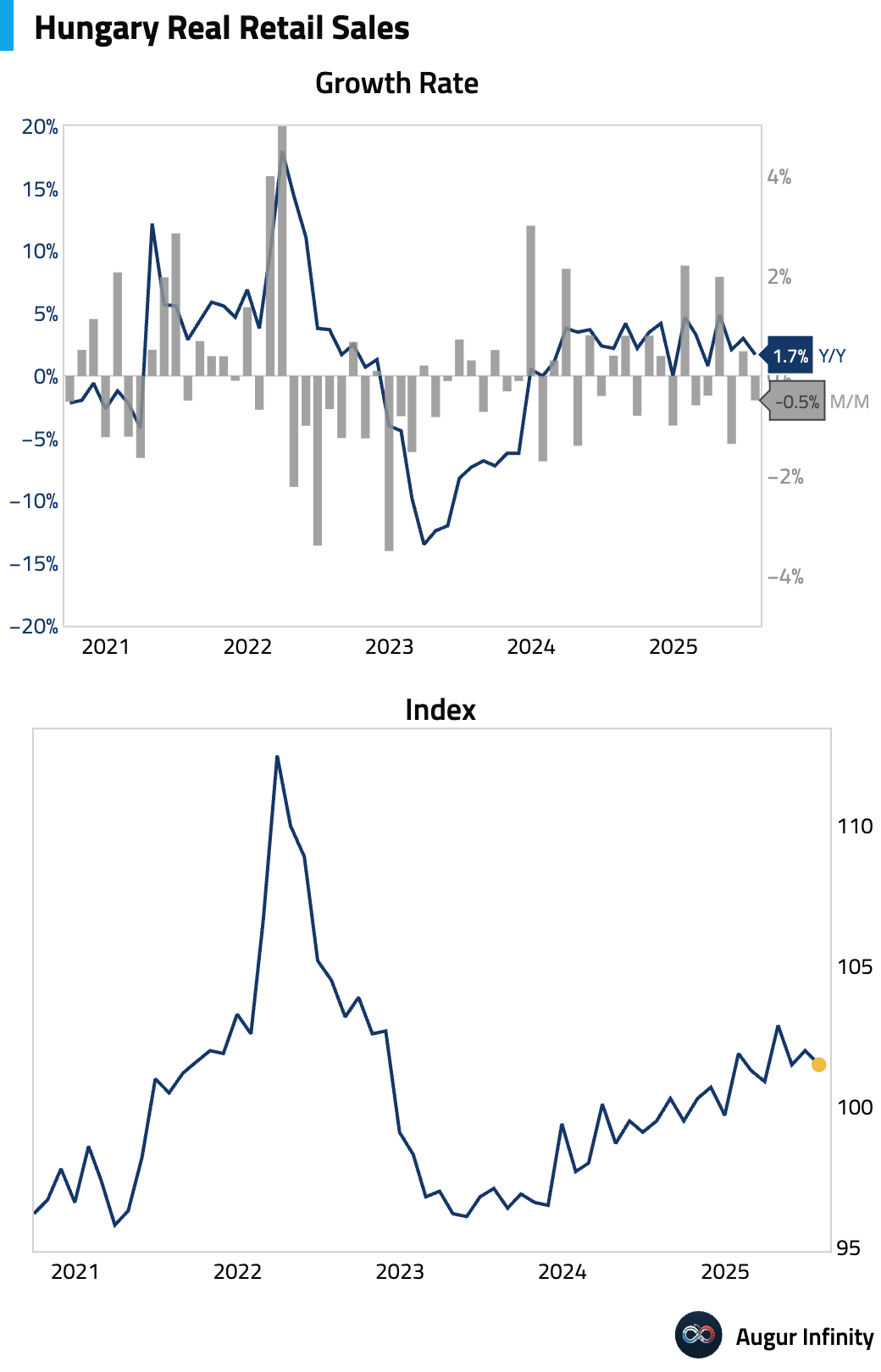

- Hungarian retail sales growth slowed to 1.7% Y/Y in July from 3.0% in June.

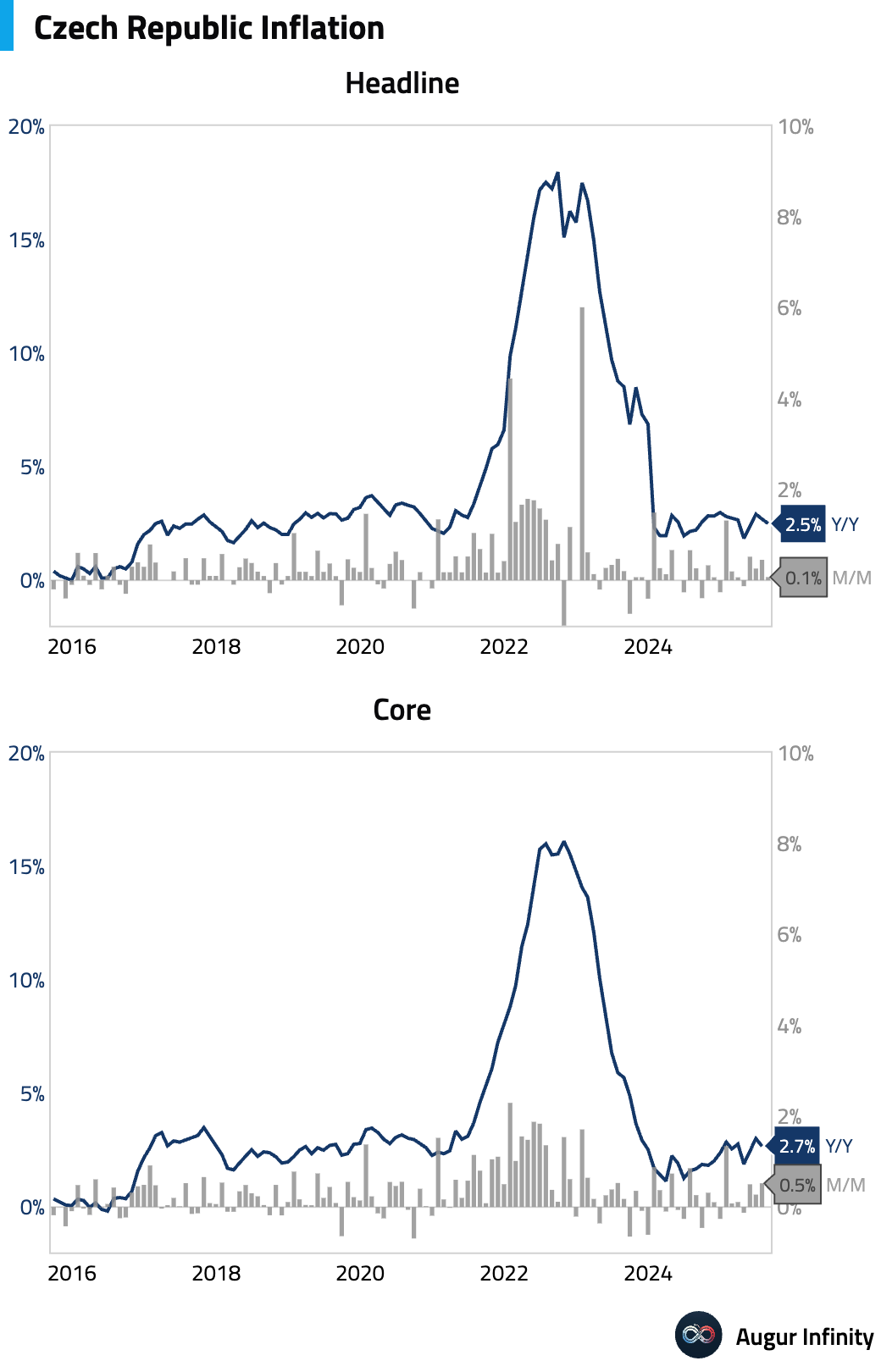

- Preliminary headline CPI in the Czech Republic eased to 2.5% Y/Y in August, down from 2.7% and below the central bank’s forecast of 2.7%. The decline was broad-based, driven by falling goods prices and slowing services momentum, reinforcing expectations for further disinflation.

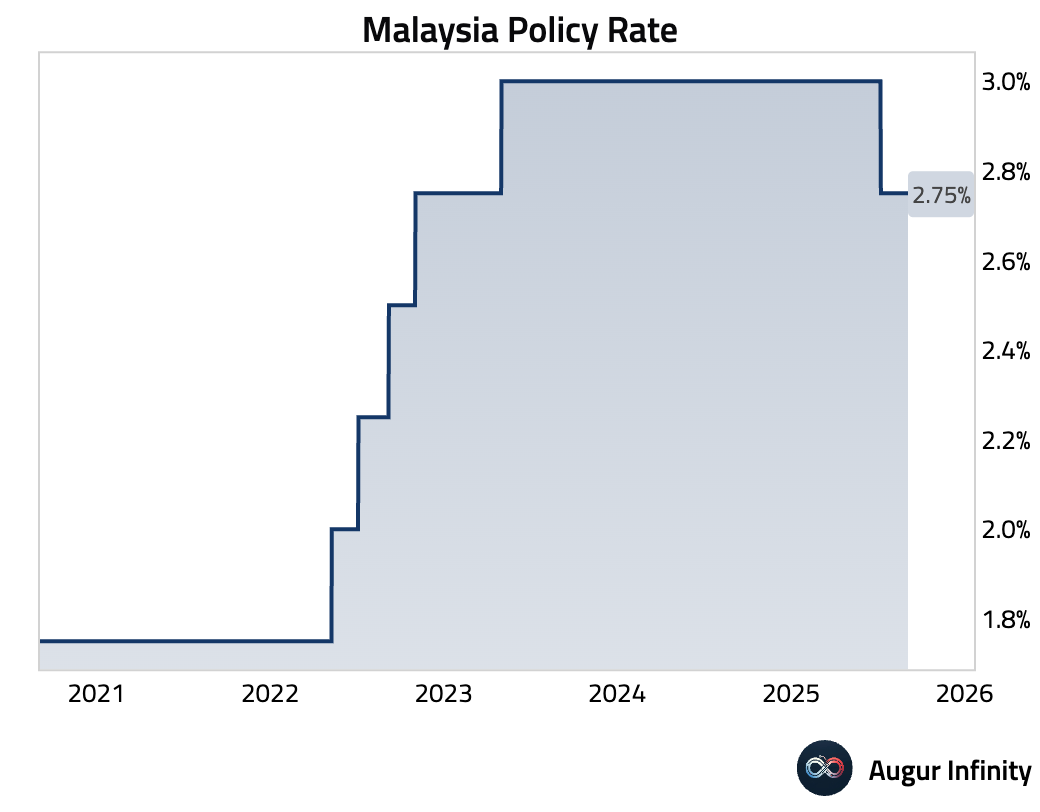

- Bank Negara Malaysia (BNM) held its overnight policy rate at 2.75%, as expected. The central bank adopted a more balanced tone, removing prior warnings of “downside risks” to growth and softening its forward guidance. The statement noted that the current policy stance is “appropriate and supportive,” signaling less urgency for future rate moves.

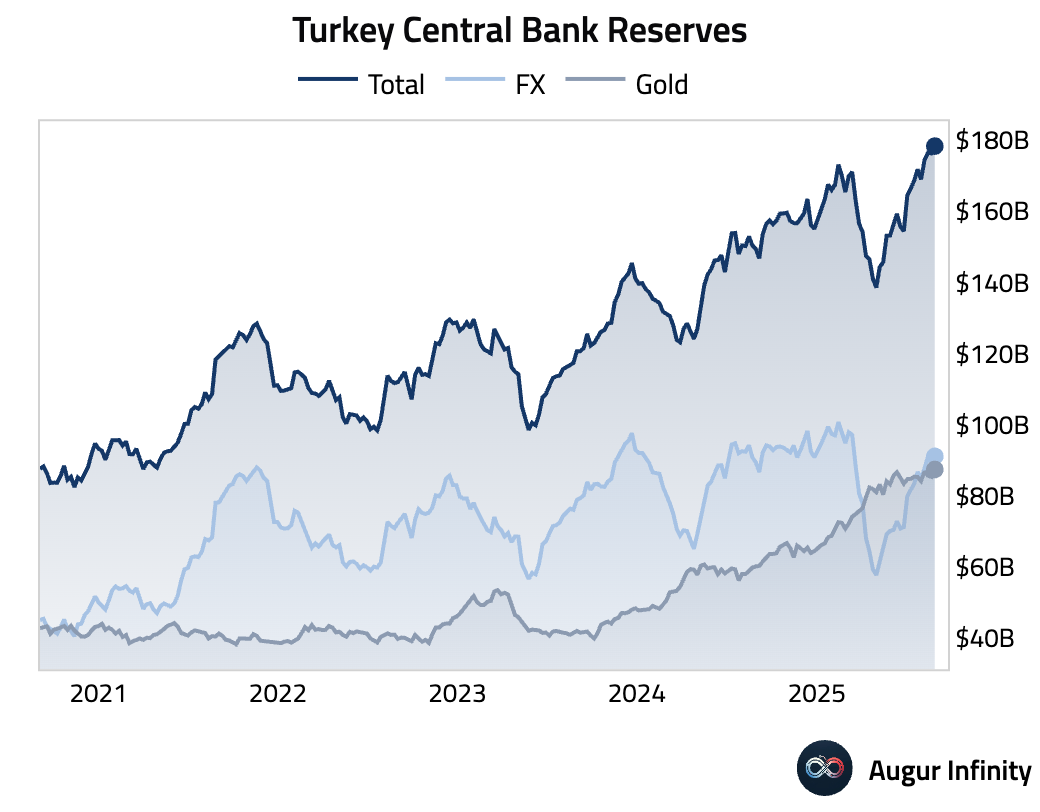

- Turkey’s foreign exchange reserves edged down to $91.03 billion in the week ending August 29 from $91.09 billion the prior week.

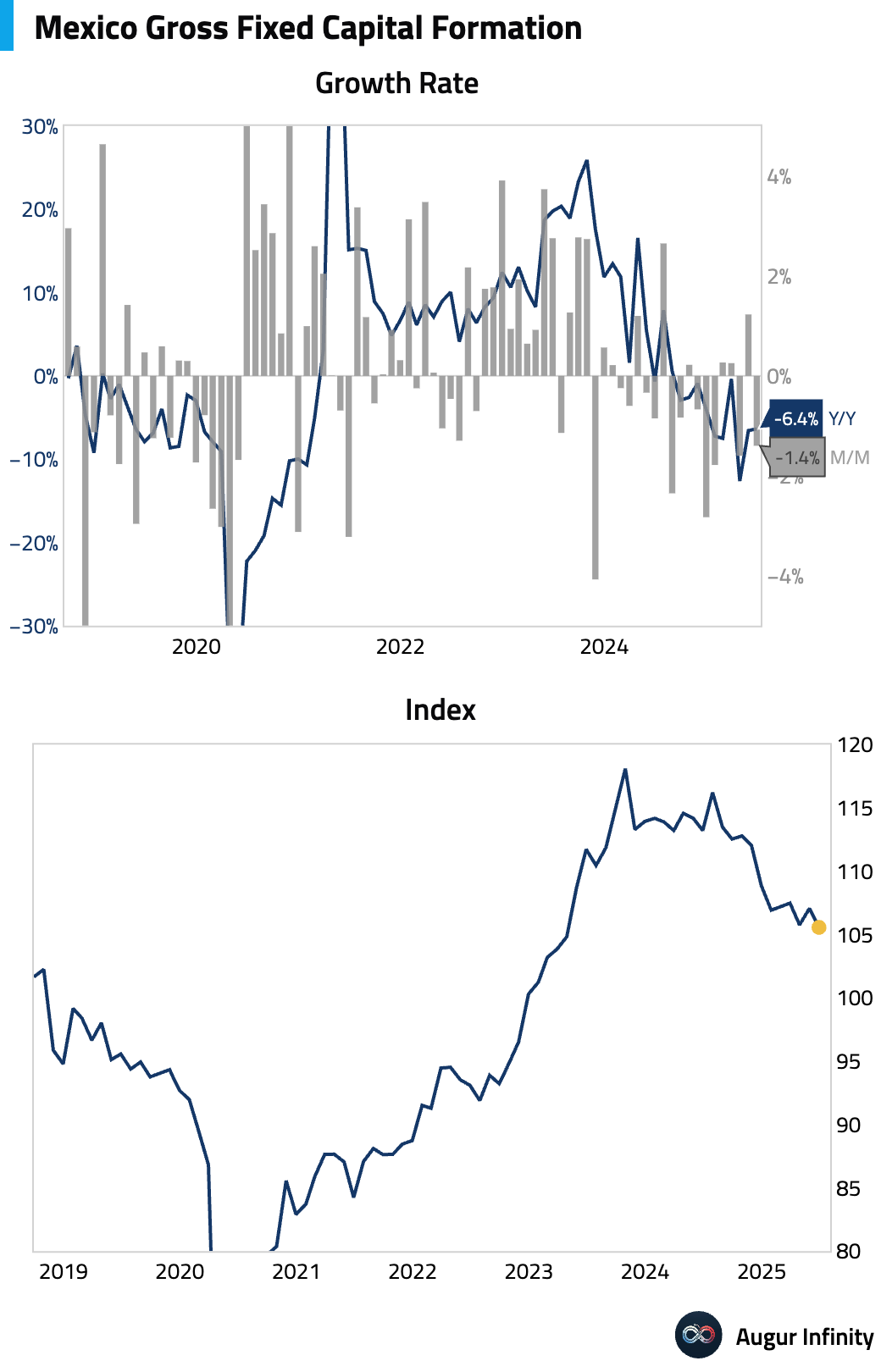

- Mexico’s gross fixed investment unexpectedly fell 1.4% M/M in June, sharply missing expectations for a flat reading. On an annual basis, investment was down 6.4%. The weakness was broad-based, with declines in both construction (-0.8% M/M) and machinery/equipment (-1.6% M/M).

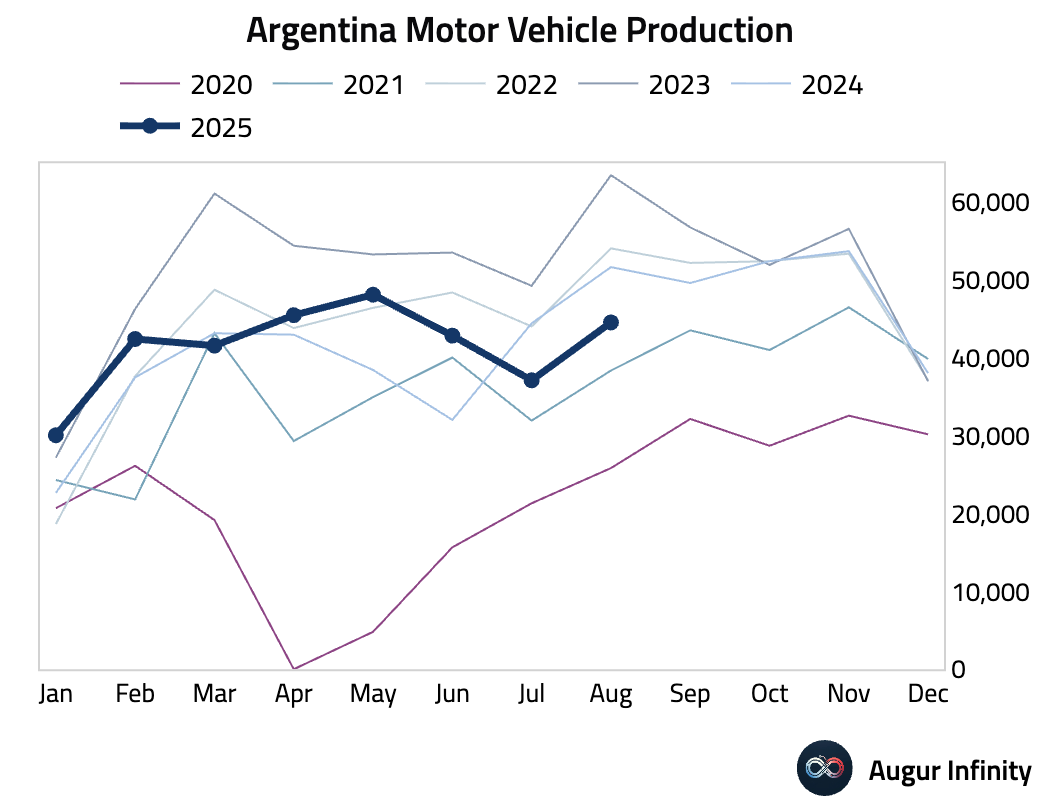

- Argentina motor vehicle production declined by 13.8% Y/Y in August. This is the worst August production level since 2021.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.