Headlines

- The United States and Japan finalized a trade agreement, lowering the US tariff on Japanese auto imports to 15.0 percent from 27.5 percent.

- Trump threatens trade probe after ‘discriminatory’ EU fines against Google, Apple.

- China announced it will implement a 78 percent tariff on imports of US fiber optic products, continuing trade frictions with the United States.

- The US Department of Justice has opened a criminal investigation into governor Lisa Coo regarding allegations of mortgage fraud.

Global Economics

United States

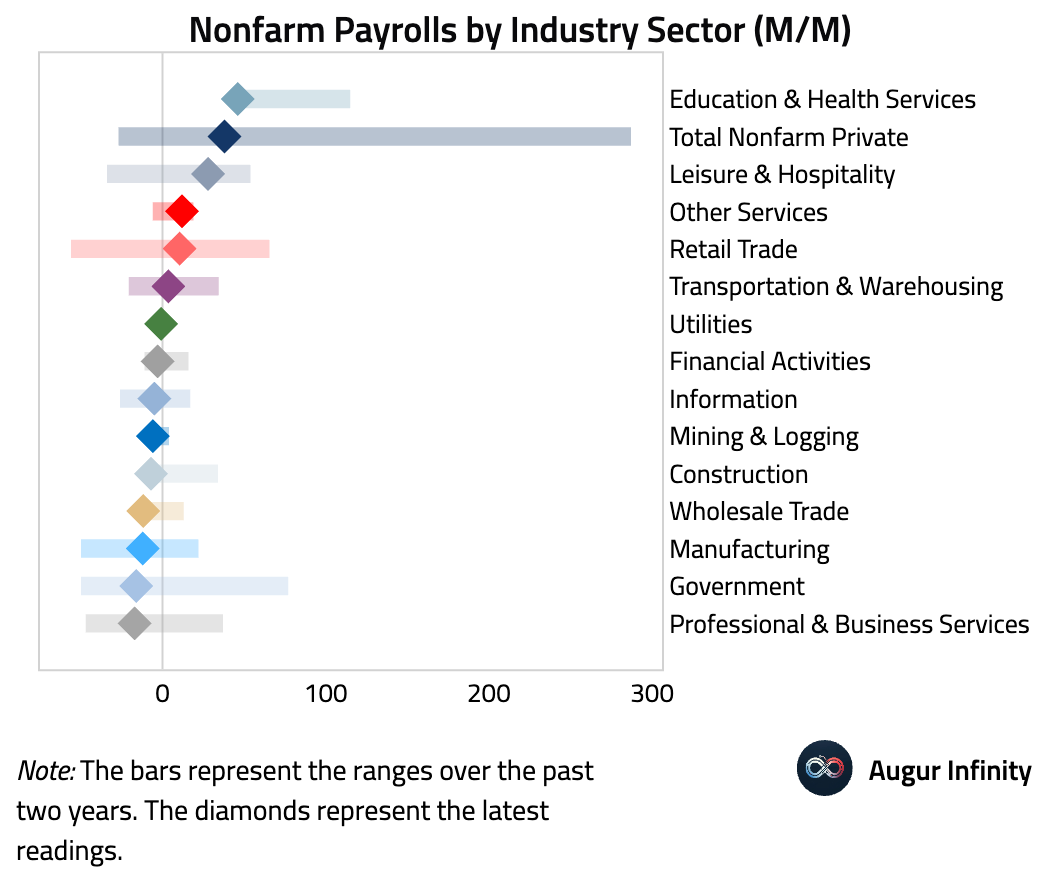

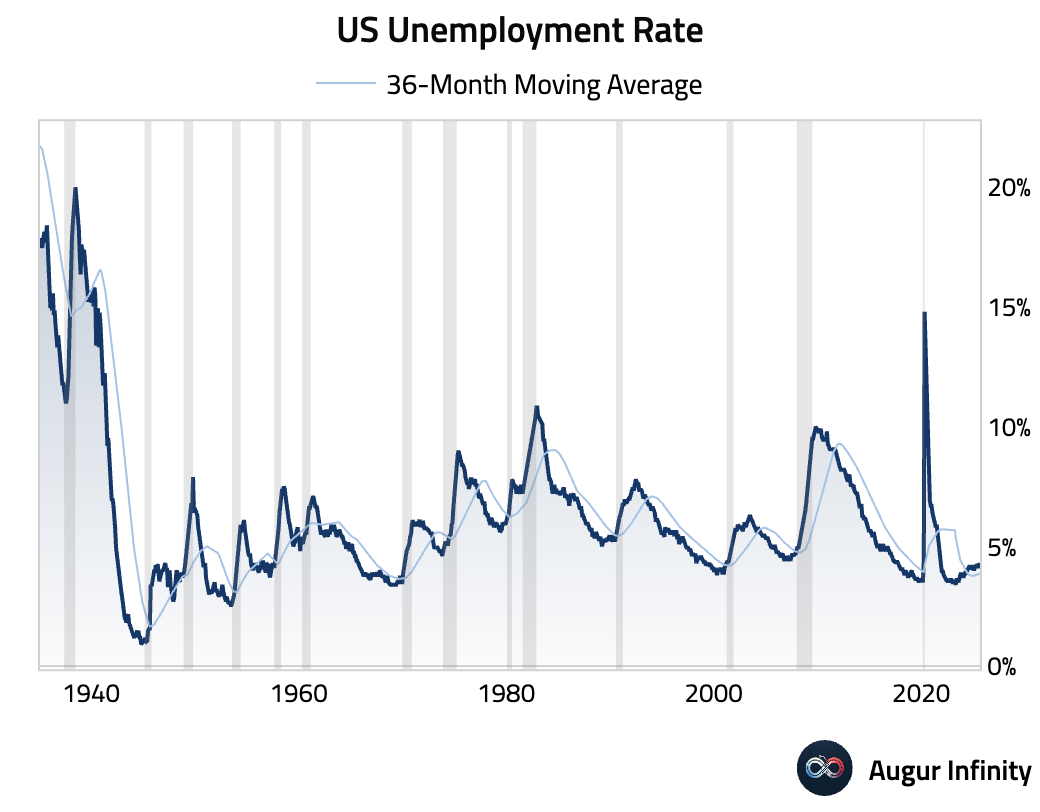

- Headline payrolls rose only +22k, well below the +75k median forecast, with June revised negative to -13k. The weak 3-month average of +29k signals a sharp slowdown. The weakness was driven by a -16k drop in government jobs, while private growth was concentrated in healthcare (+47k) and leisure (+28k), offset by losses in durable goods (-19k) and professional services (-17k). The unemployment rate rose to 4.3%, highest since October 2021. However, the increase was not driven by job losses but by a large +436k influx of workers into the labor force, which outpaced a solid +288k gain in household employment.

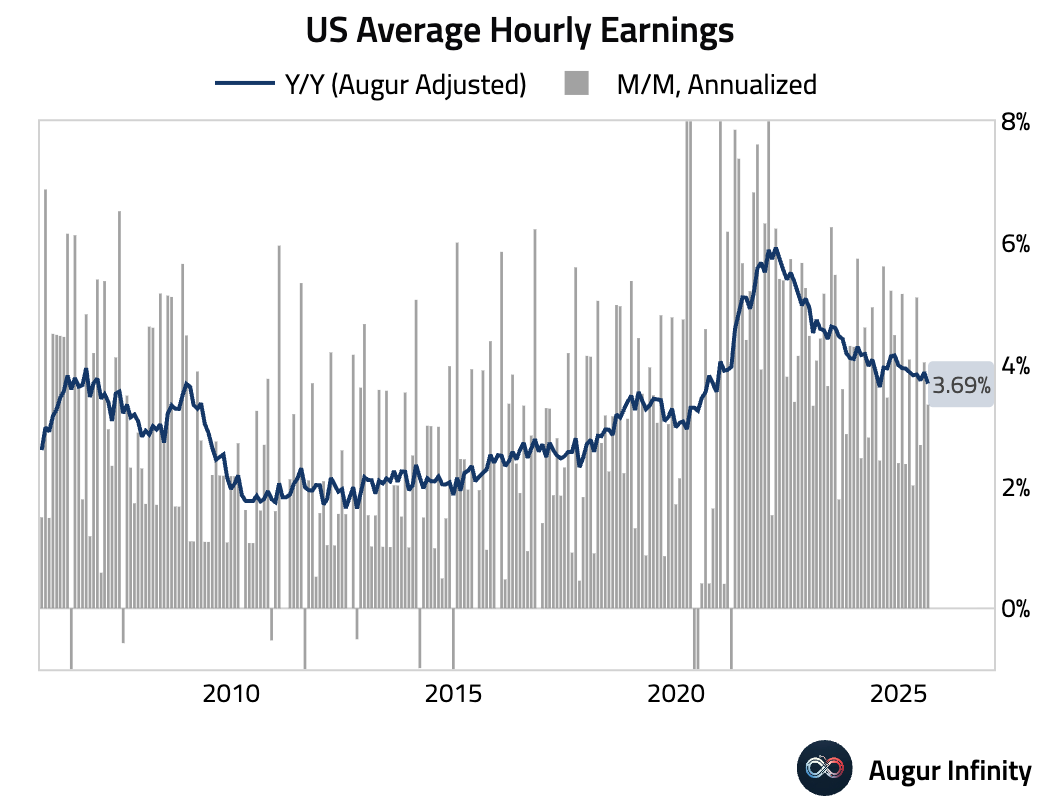

- Average hourly earnings rose 0.3 percent M/M, in line with expectations and the prior month’s pace. Year-over-year, earnings growth decelerated to 3.7 percent from 3.9 percent, matching forecasts.

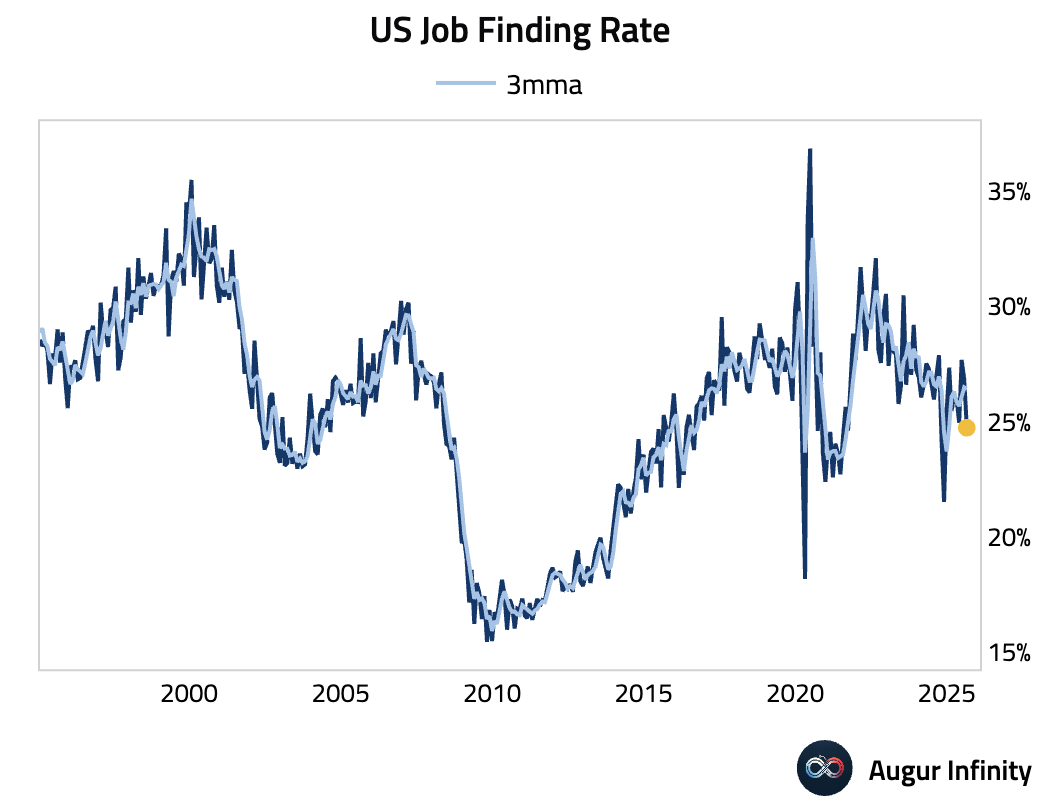

- US job finding rate declined sharply from 26.8% to 24.7%, pulling 3-month moving average down a tad as well.

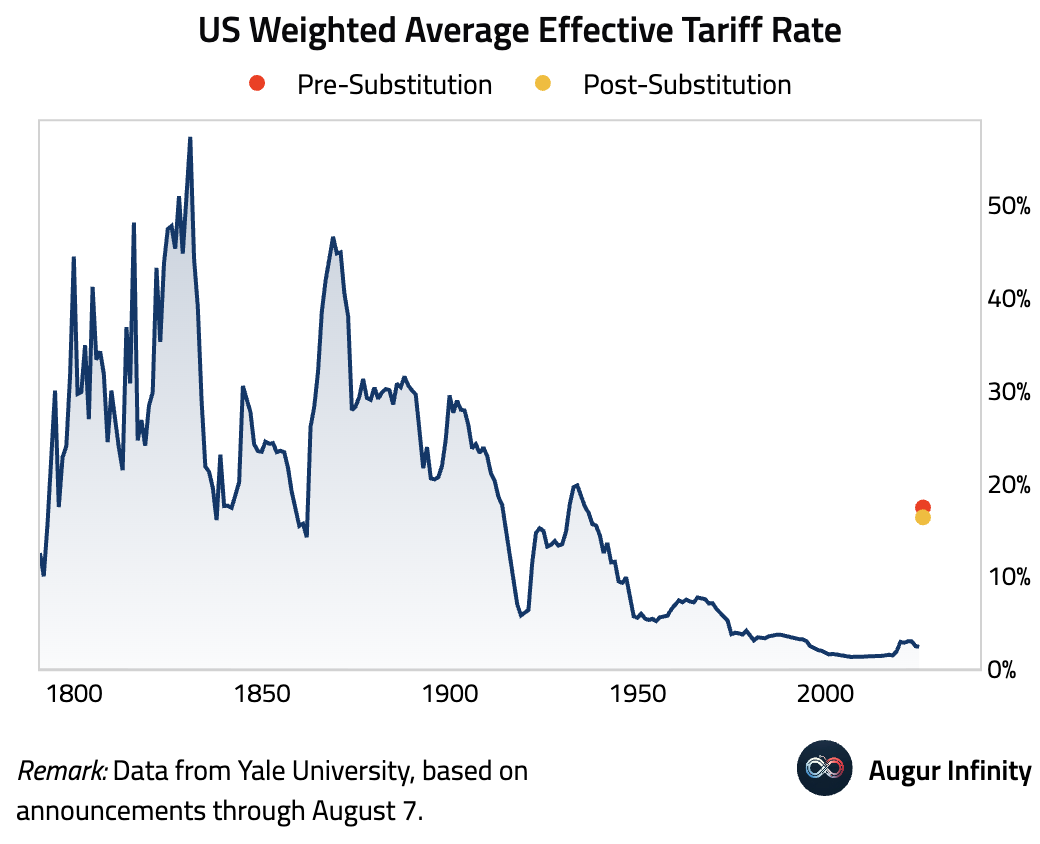

- The Budget Lab estimates consumers face an overall average effective tariff rate of 17.4%, the highest since 1935. After consumption shifts, the average tariff rate is estimated at 16.4%, the highest since 1936.

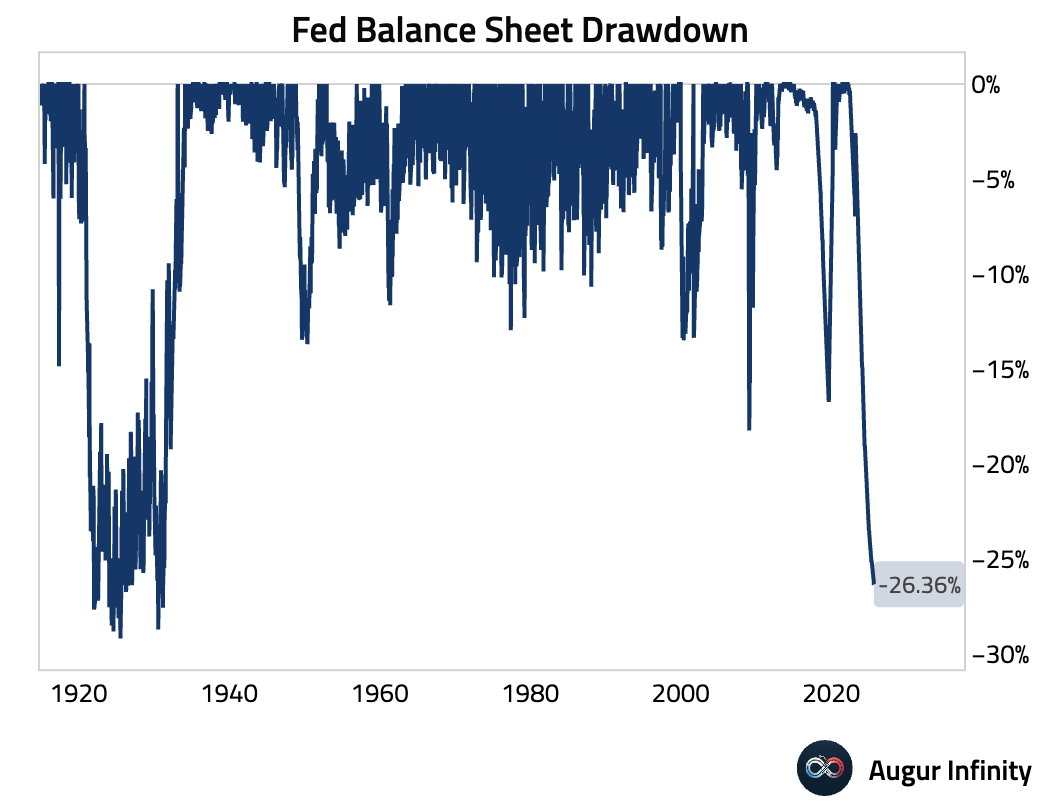

- The Federal Reserve's balance sheet was unchanged at $6.6 trillion for the week ending September 3.

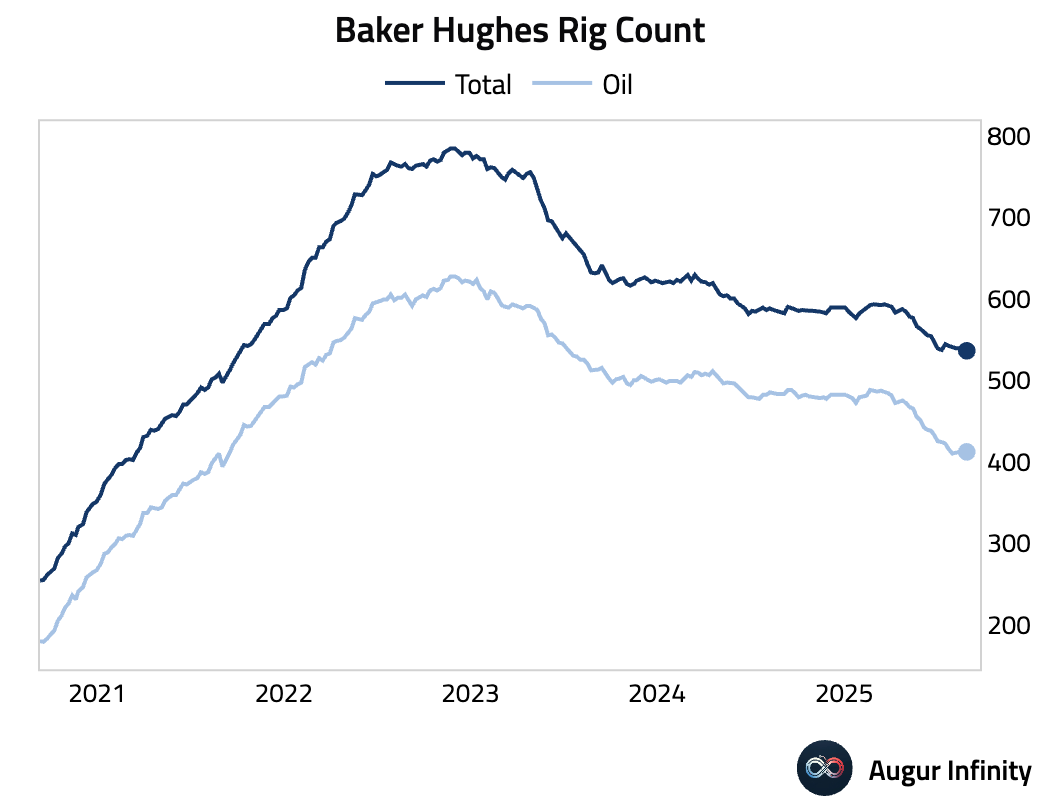

- The Baker Hughes oil rig count increased by two to 414 for the week, suggesting a modest uptick in drilling activity.

Canada

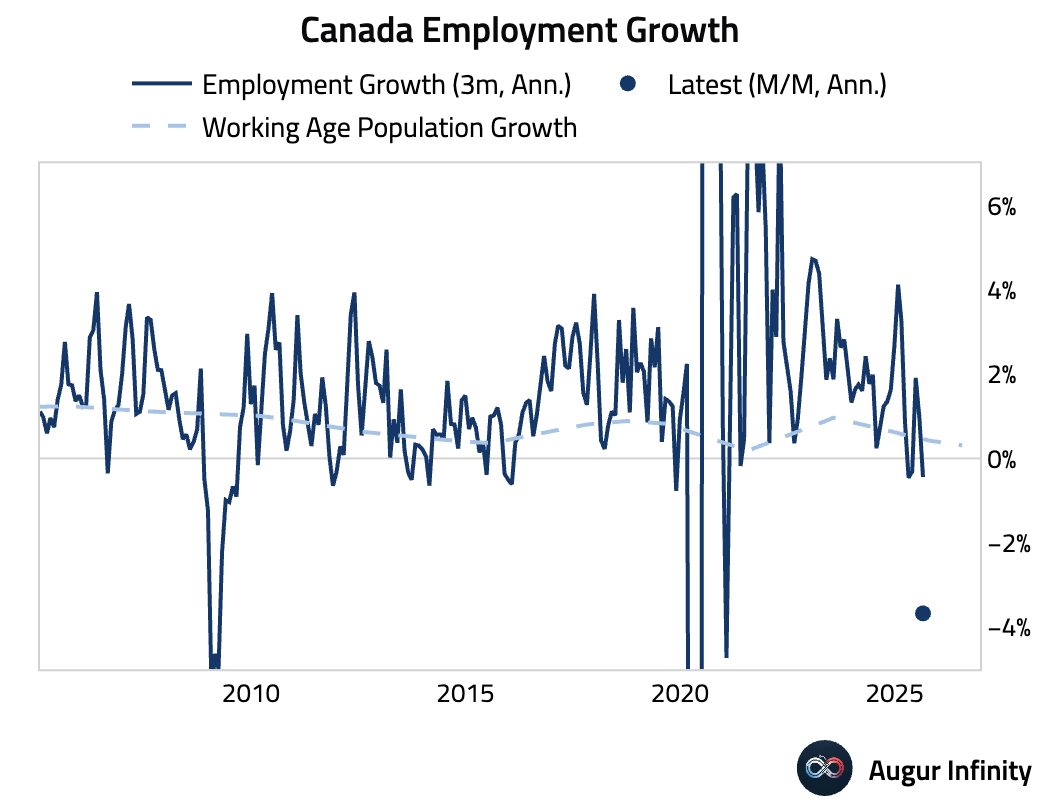

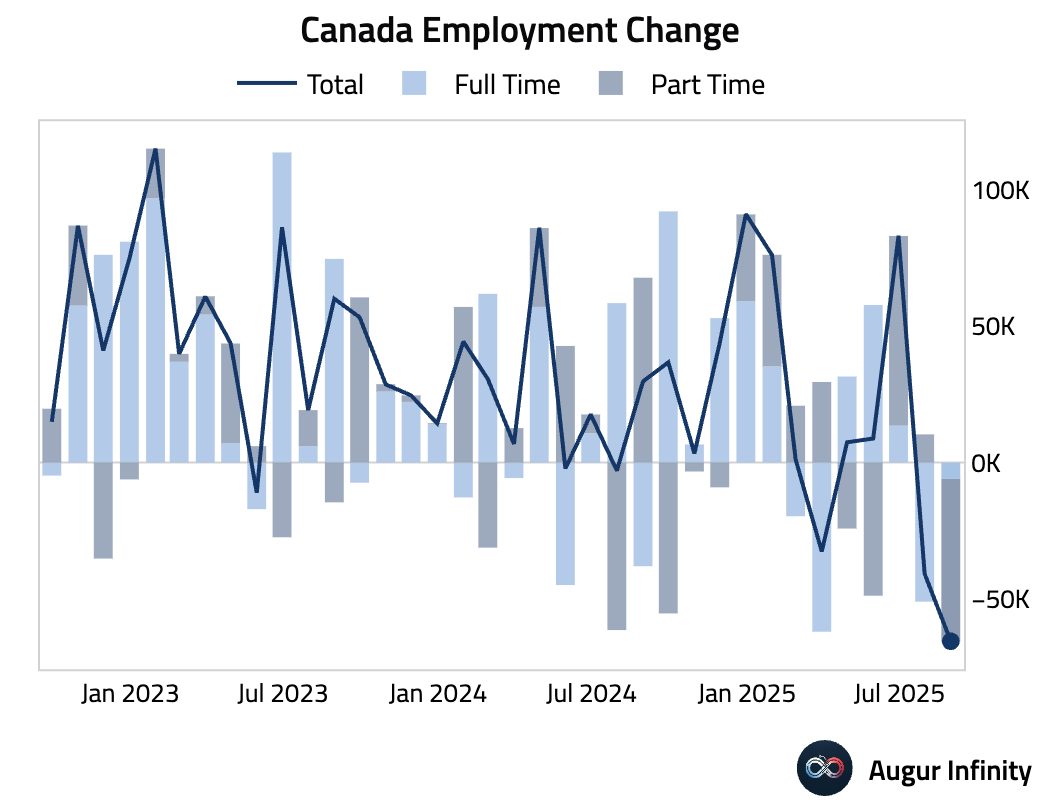

- Canada’s labor market showed significant weakness in August, with employment falling by 65,500, a stark contrast to the expected 7,500 gain. The decline was driven by a loss of 59,700 part-time positions, while full-time employment also fell by 6,000. This pushed the unemployment rate up to 7.1 percent from 6.9 percent , reaching its highest level since July 2021.

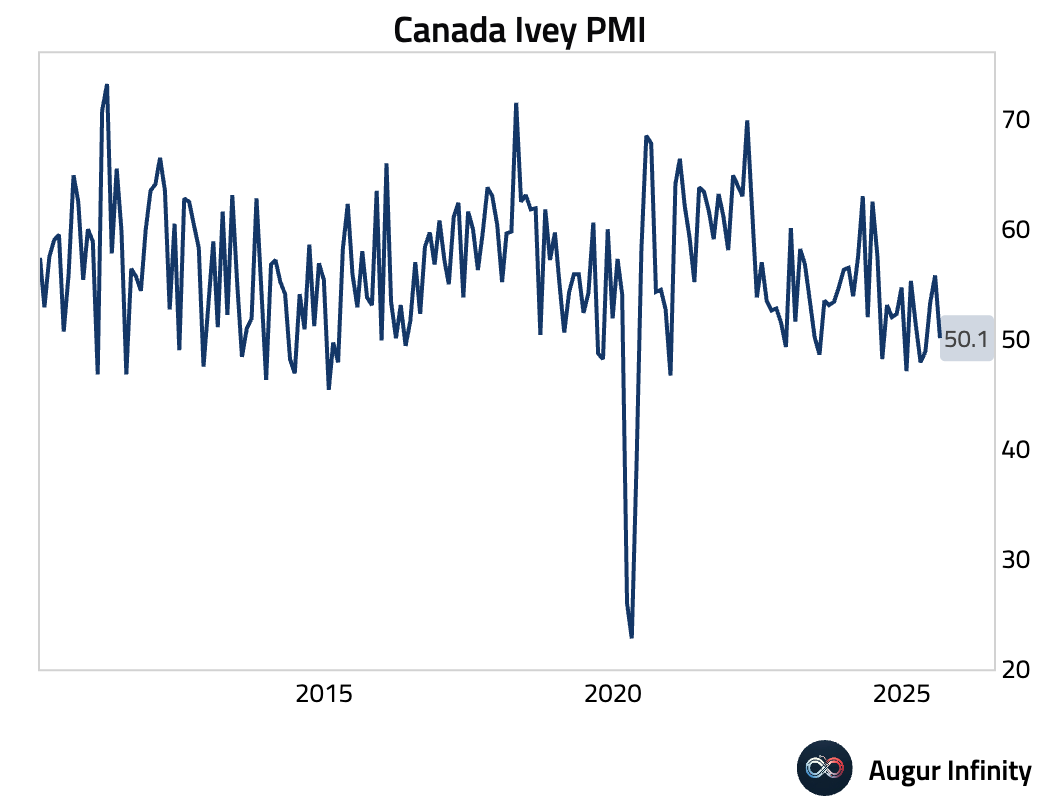

- The Ivey PMI for Canada dropped sharply to 50.1 in August from 55.8, falling well short of the 53.1 consensus. The reading, barely above the 50-point threshold separating expansion from contraction, signals a near-stall in economic activity.

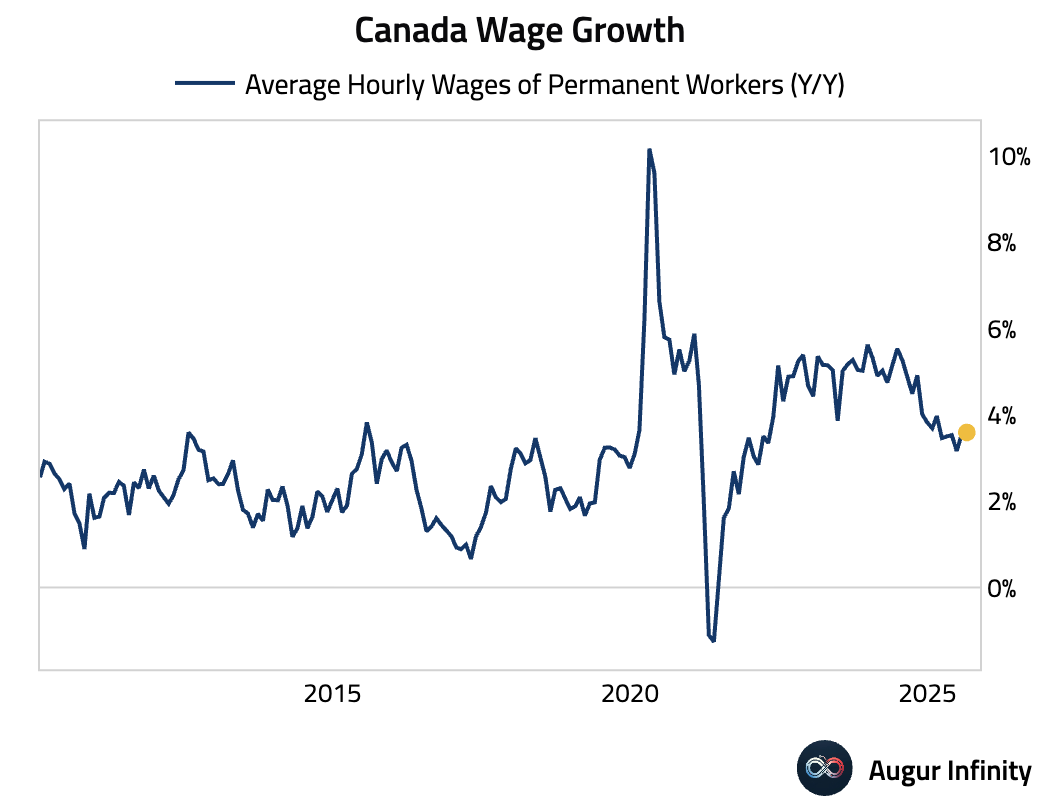

- Average hourly wage growth in Canada accelerated slightly to 3.6 percent Y/Y in August from 3.5 percent in July.

Europe

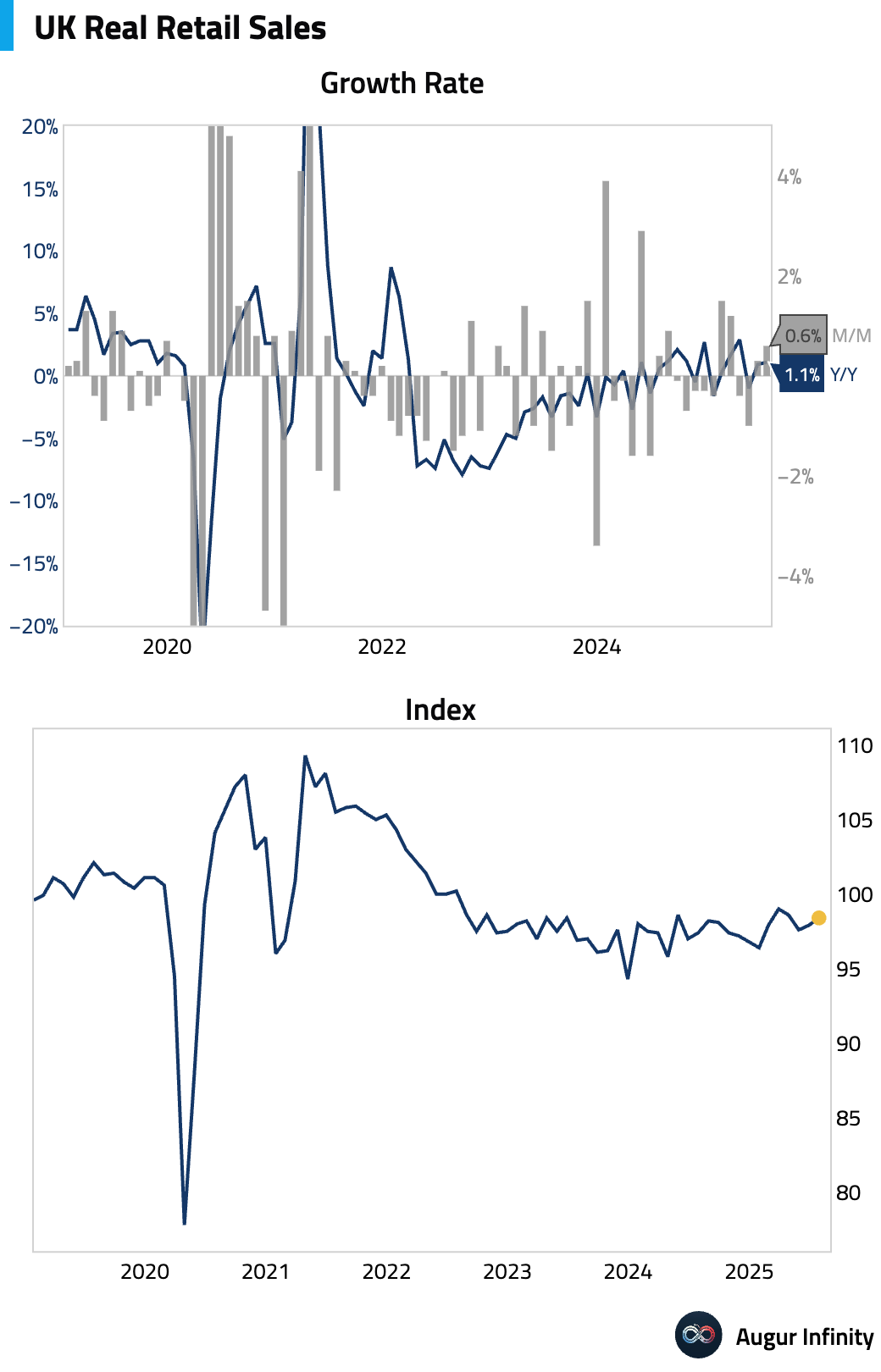

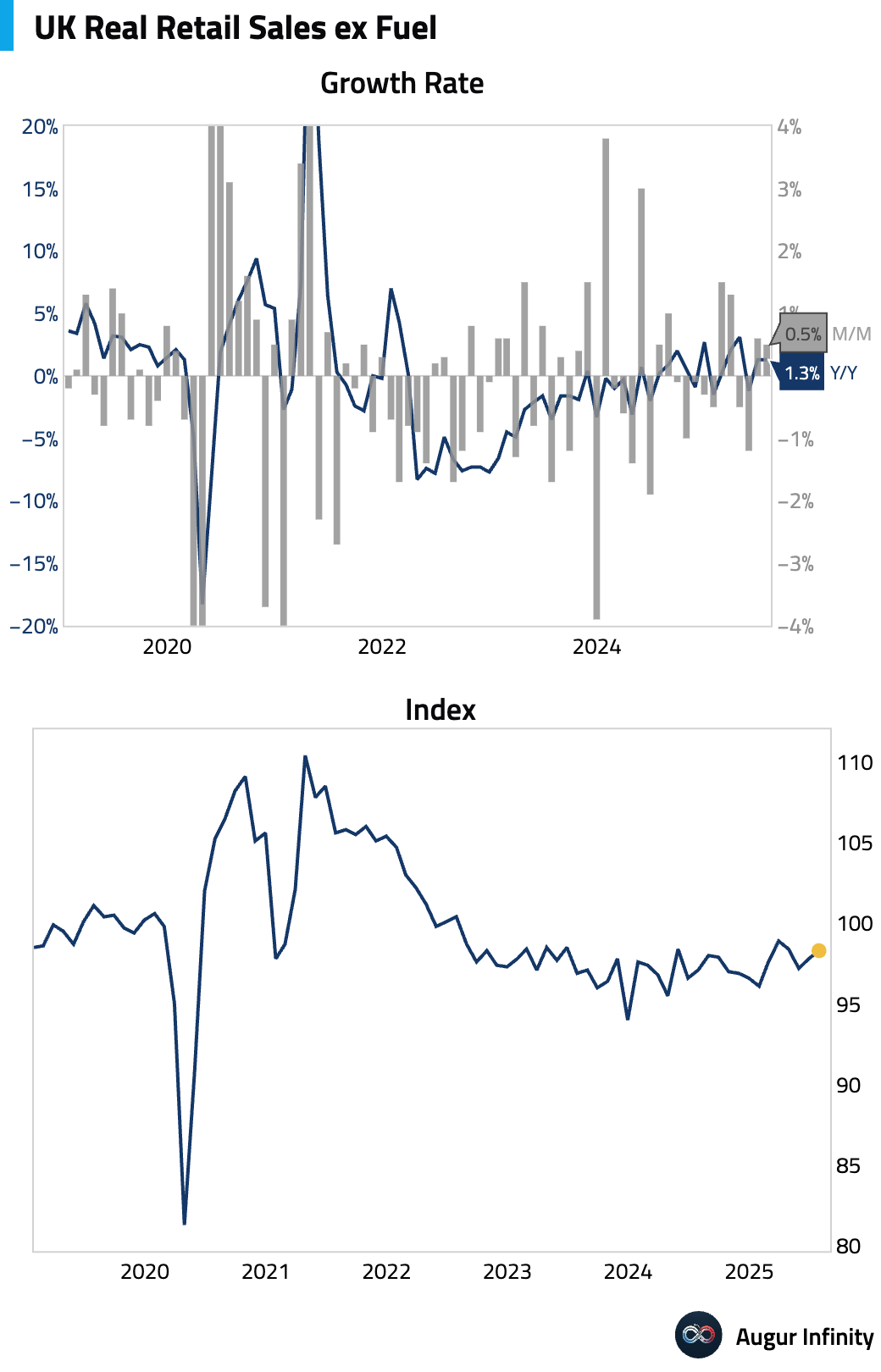

- UK headline retail sales beat expectations, rising +0.6% m/m (vs. +0.2% cons), driven by strong online and clothing sales boosted by good weather and the Women's Euro 2025 tournament. However, this strength is offset by significant downward revisions to H1 data. Due to a seasonal adjustment correction by the ONS, the level of June sales is now 0.5% lower than initially reported, implying weaker cumulative growth in the first half of the year.

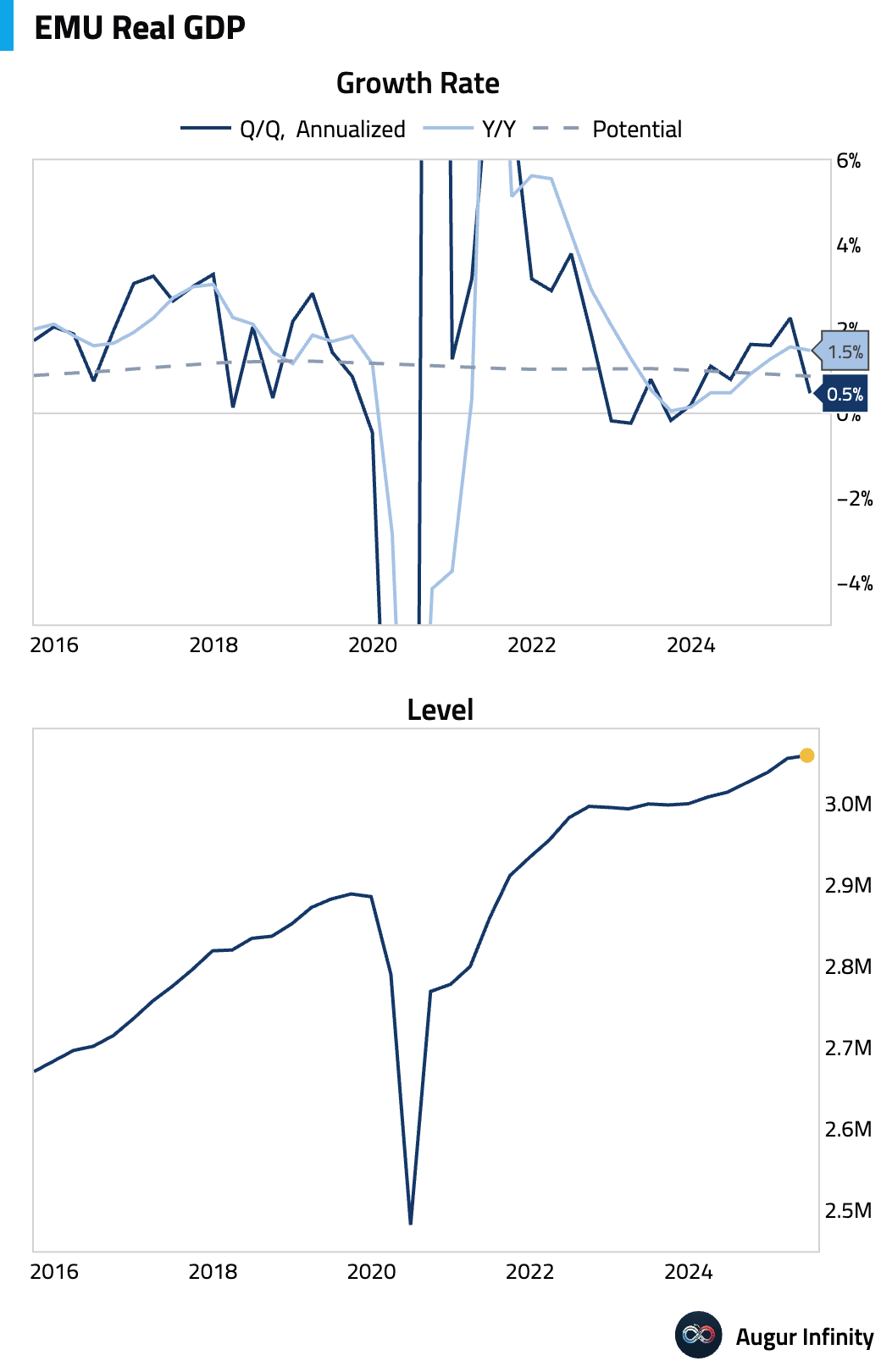

- The third estimate of Eurozone GDP confirmed that the economy expanded by 0.1% Q/Q (or 0.5% annualized) in the second quarter. The year-over-year growth rate was revised slightly higher to 1.5% from 1.4%.

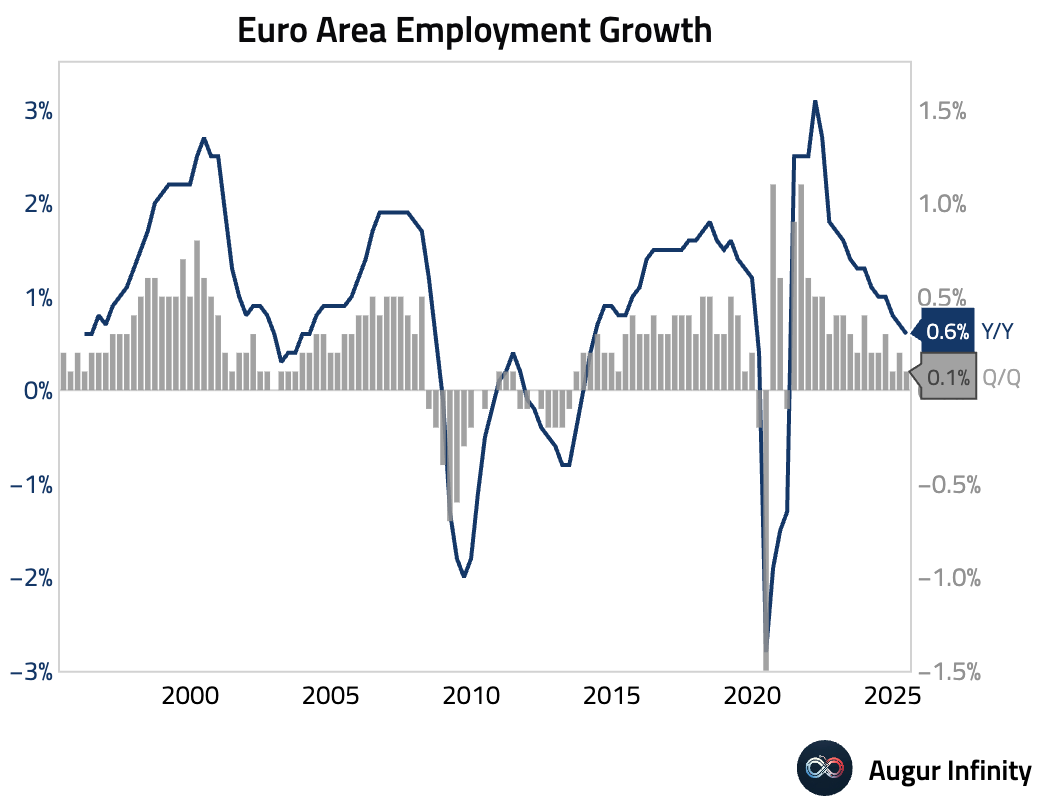

- Final data confirmed that employment in the Eurozone grew by 0.1% Q/Q in the second quarter, slowing from 0.2% in the first quarter. The year-over-year growth rate was 0.6%.

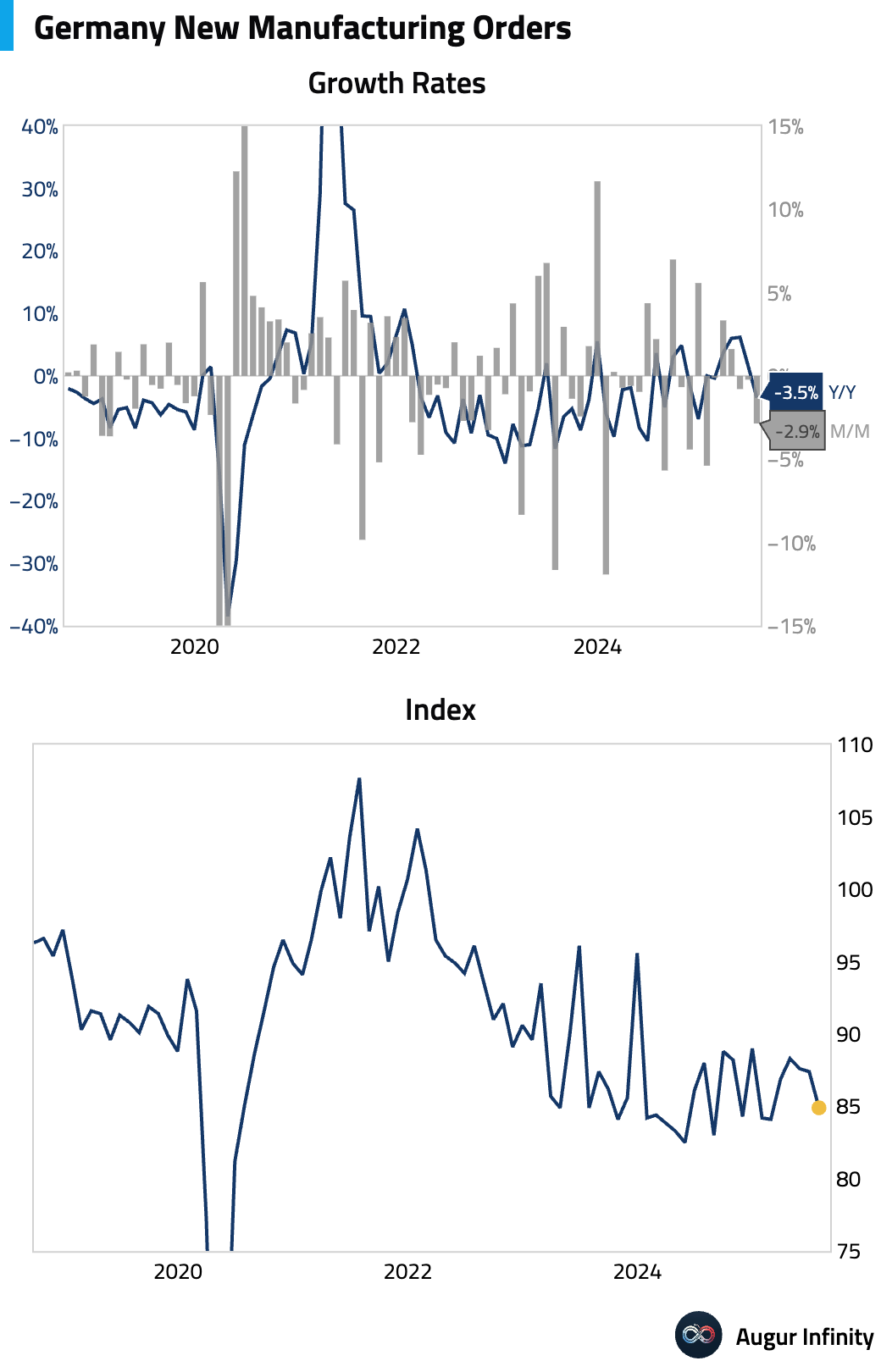

- German factory orders unexpectedly plunged 2.9% M/M in July, a significant deviation from the consensus forecast for a 0.5% increase. The drop follows a revised 0.2% decline in the previous month, pointing to continued weakness in the country's industrial sector.

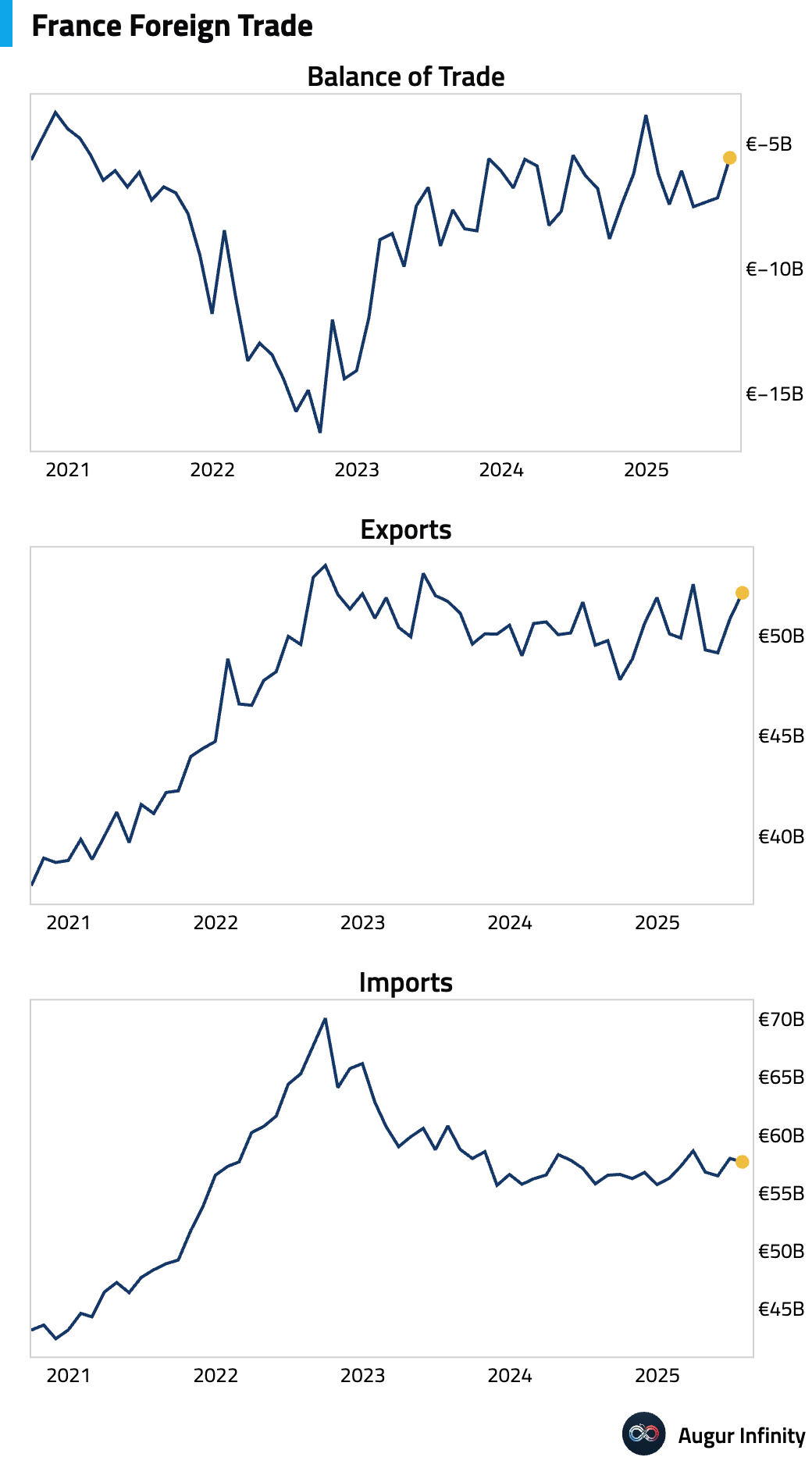

- France’s trade deficit narrowed to €5.6 billion in July from €7.2 billion in June, beating the consensus estimate of a €6.1 billion deficit. The improvement was driven by a rise in exports and a slight decline in imports.

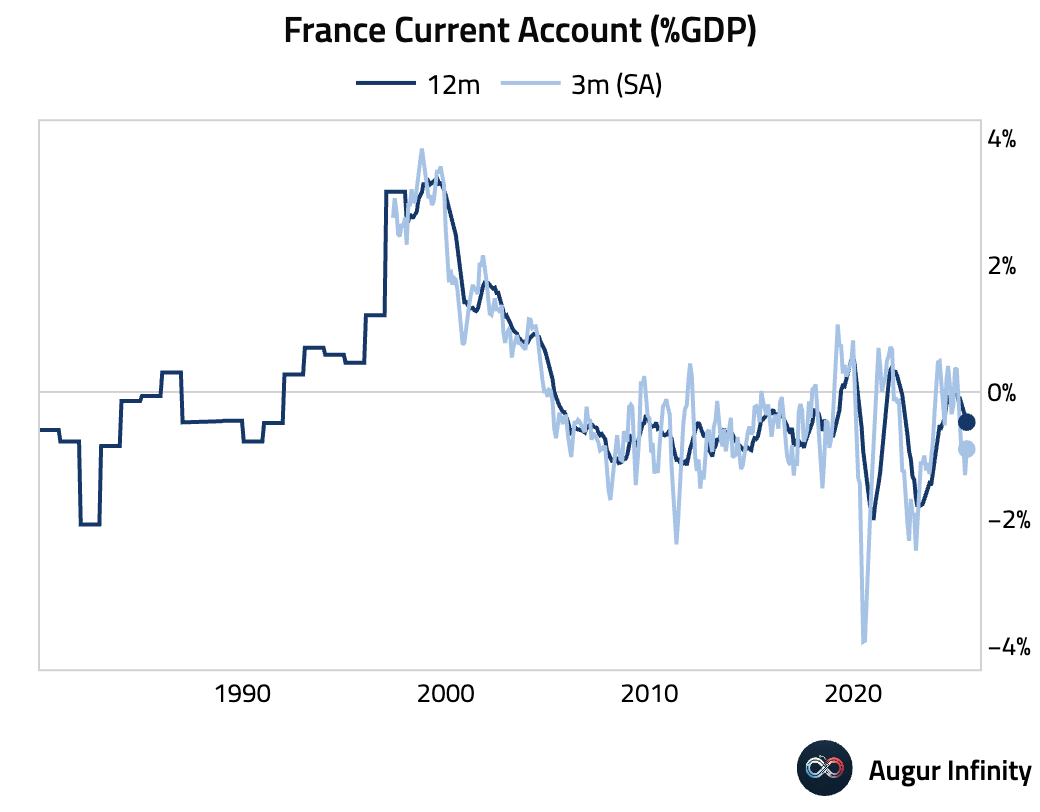

- France posted a current account deficit of €2.5 billion in July, widening slightly from a revised €2.3 billion deficit in June.

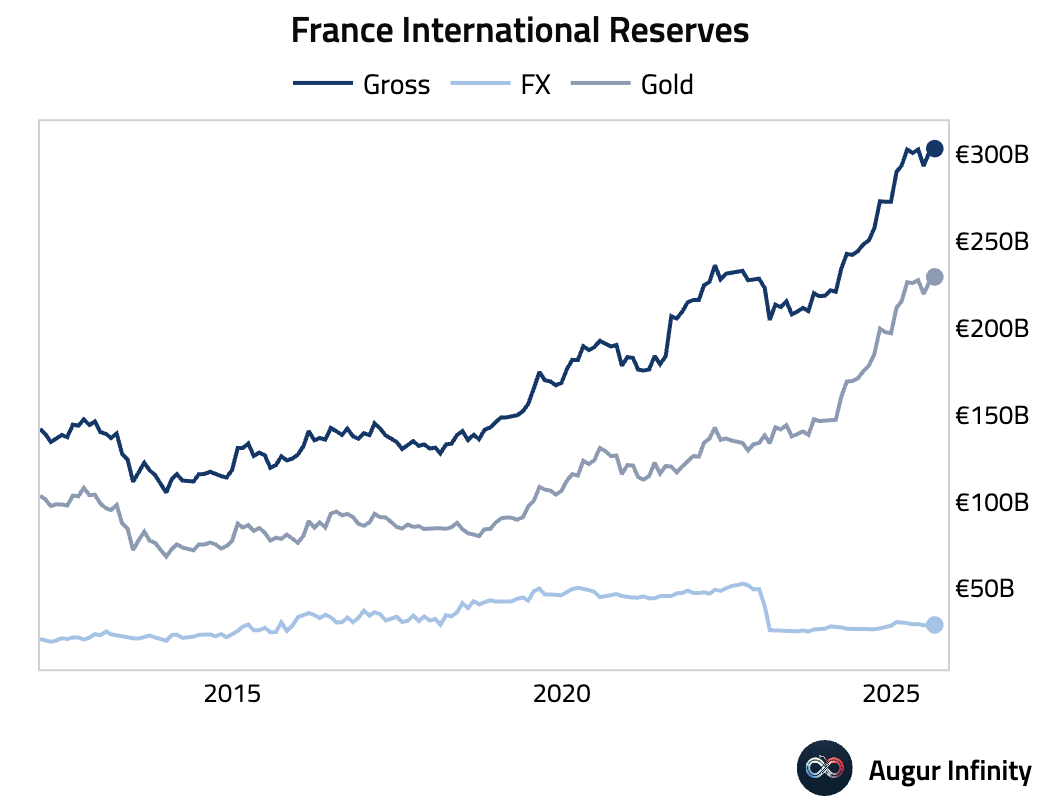

- France's official reserve assets increased to €304.8 billion in August, reaching an all-time high.

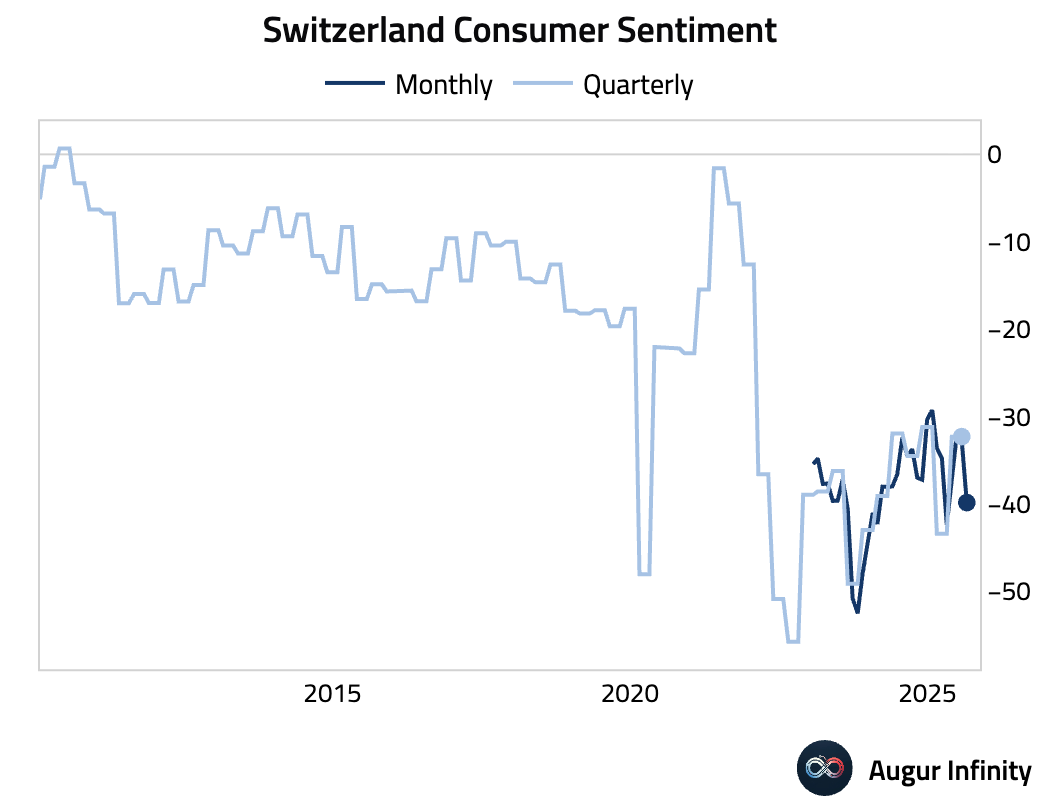

- Swiss consumer confidence deteriorated further in August, falling to -40 from -33, worse than the expected -37. The reading indicates deepening pessimism among households.

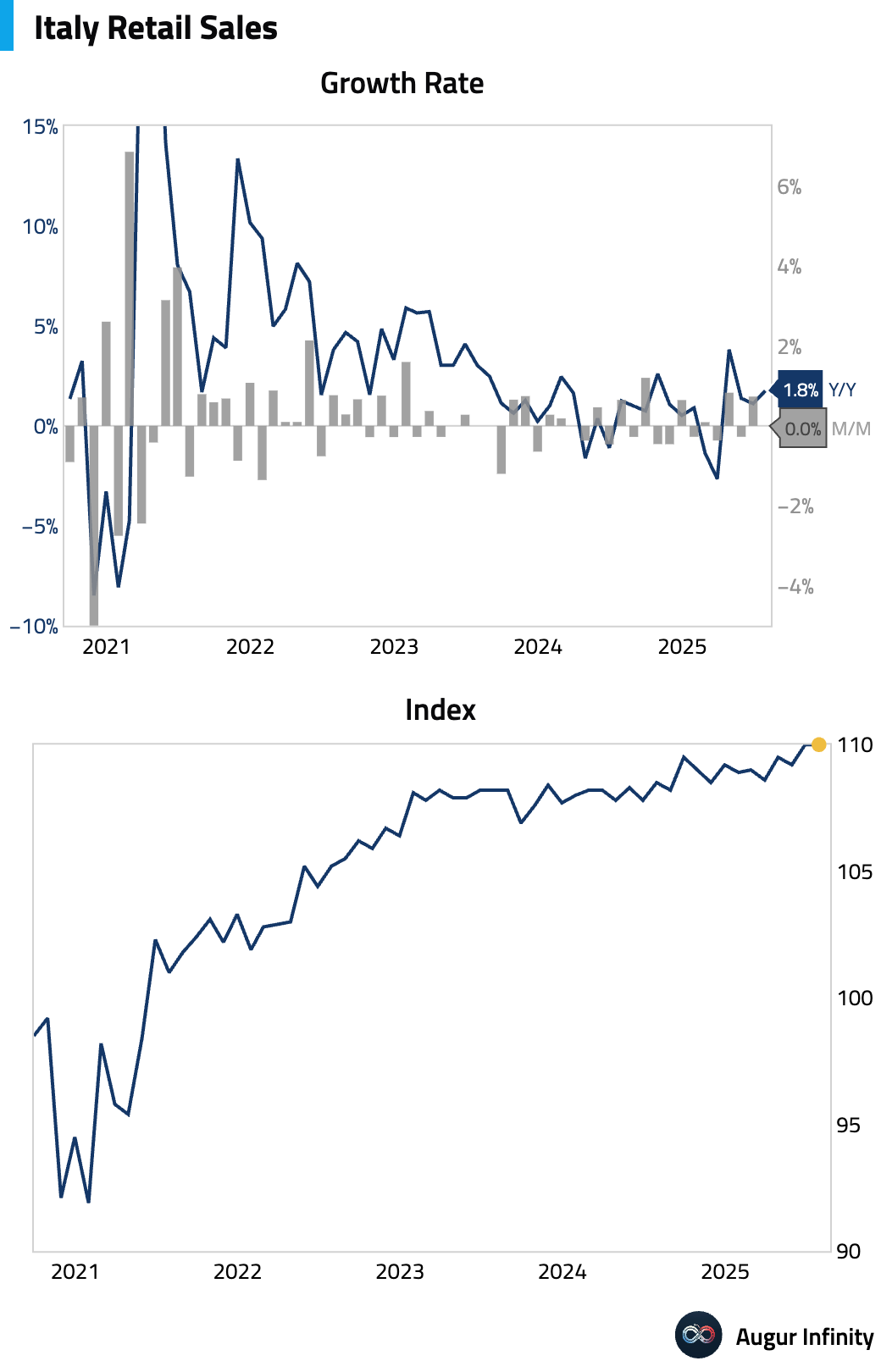

- Italian retail sales were flat in July, missing expectations of a 0.4 percent M/M increase after a 0.7 percent gain in June. The year-over-year growth accelerated to 1.8 percent from 1.1 percent.

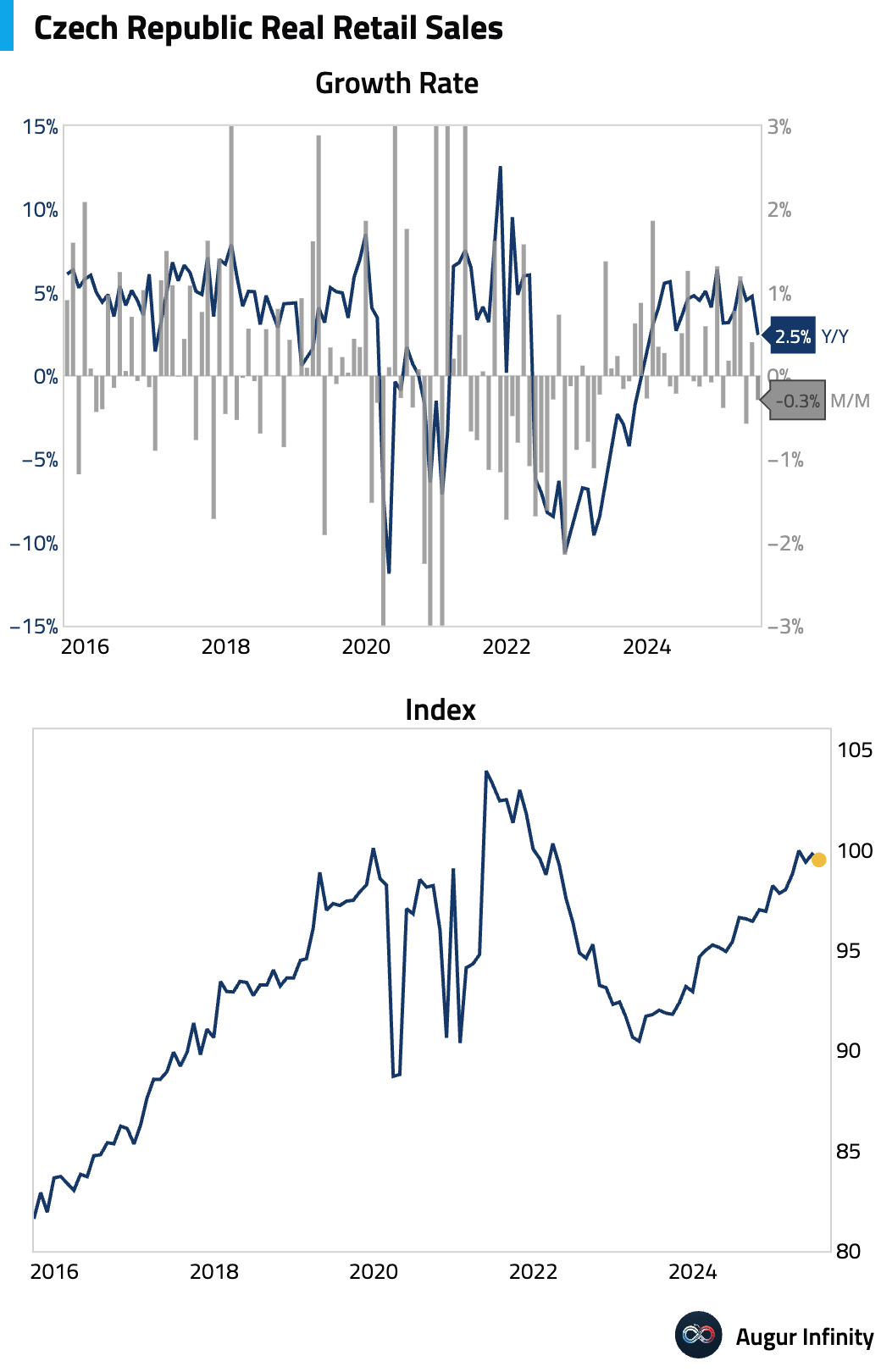

- Retail sales (excluding autos) in the Czech Republic slowed in July, rising 2.5% Y/Y, a significant miss from the 4.3% consensus. The monthly growth was 0.3%.

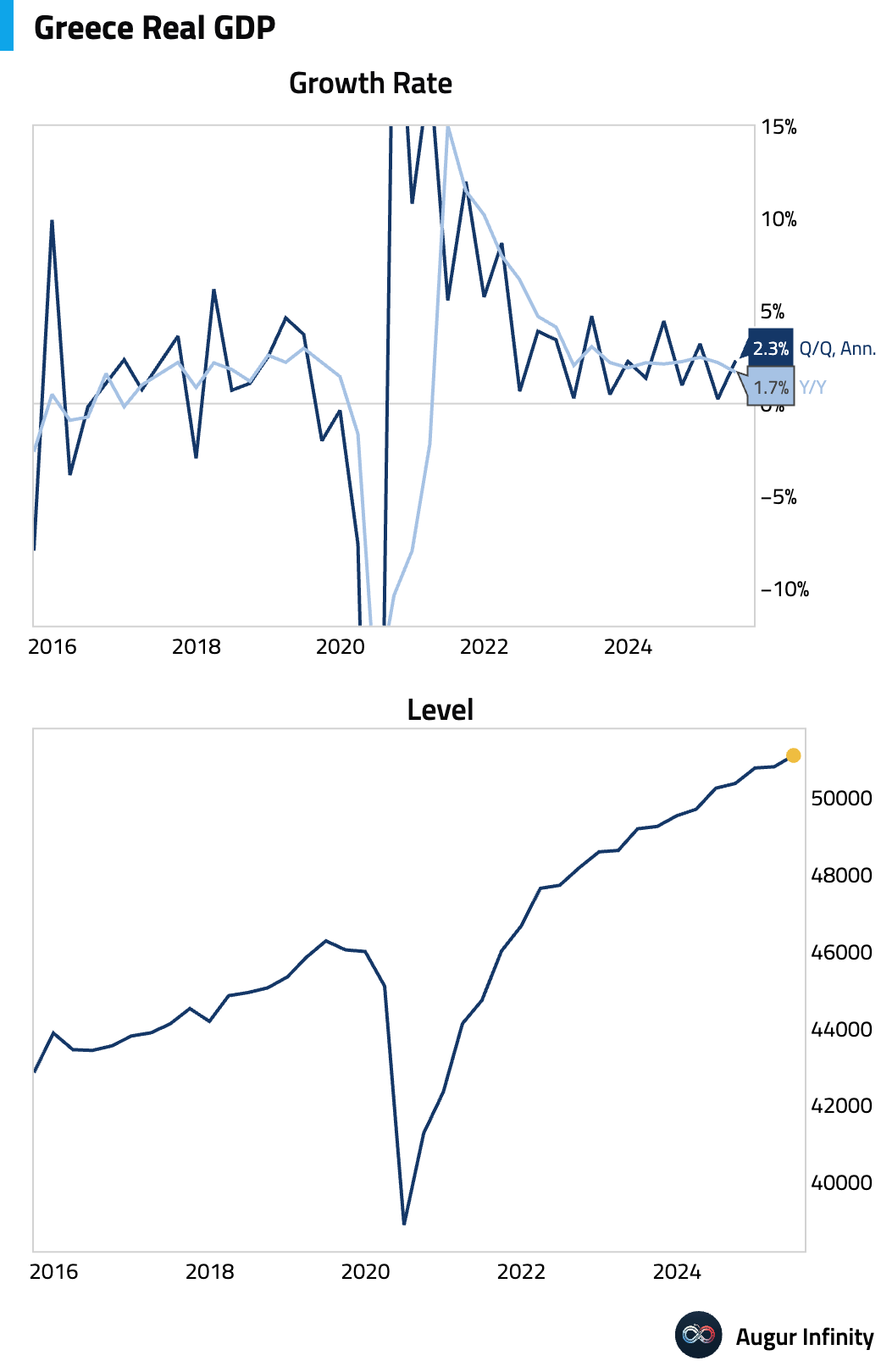

- The Greek economy expanded by 0.6% Q/Q (or 2.3% annualized) in the second quarter, accelerating from a 0.1% gain in Q1. Year-over-year growth was 1.7%.

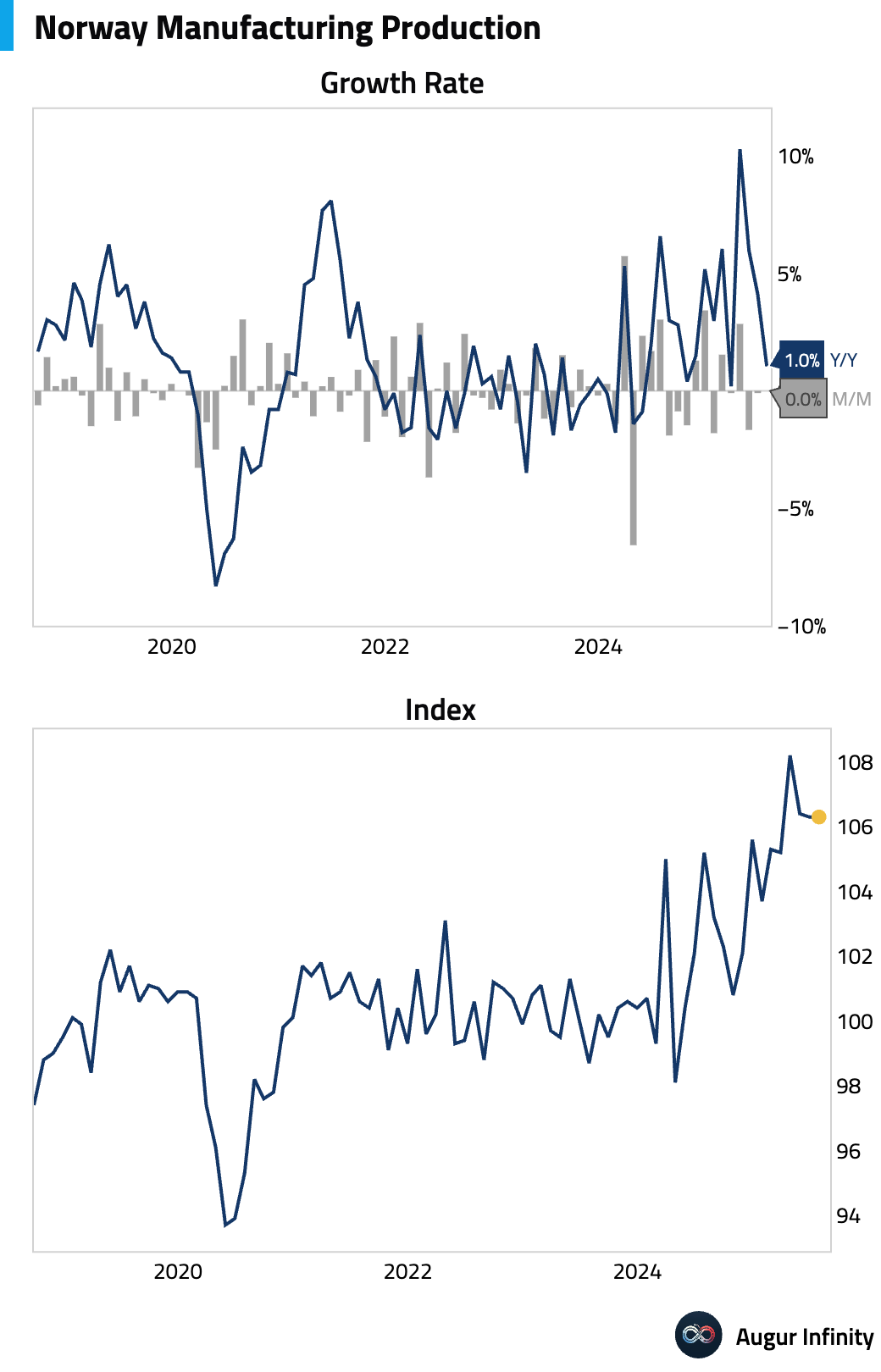

- Norway's manufacturing output was unchanged in July, following a 0.1% decline in June.

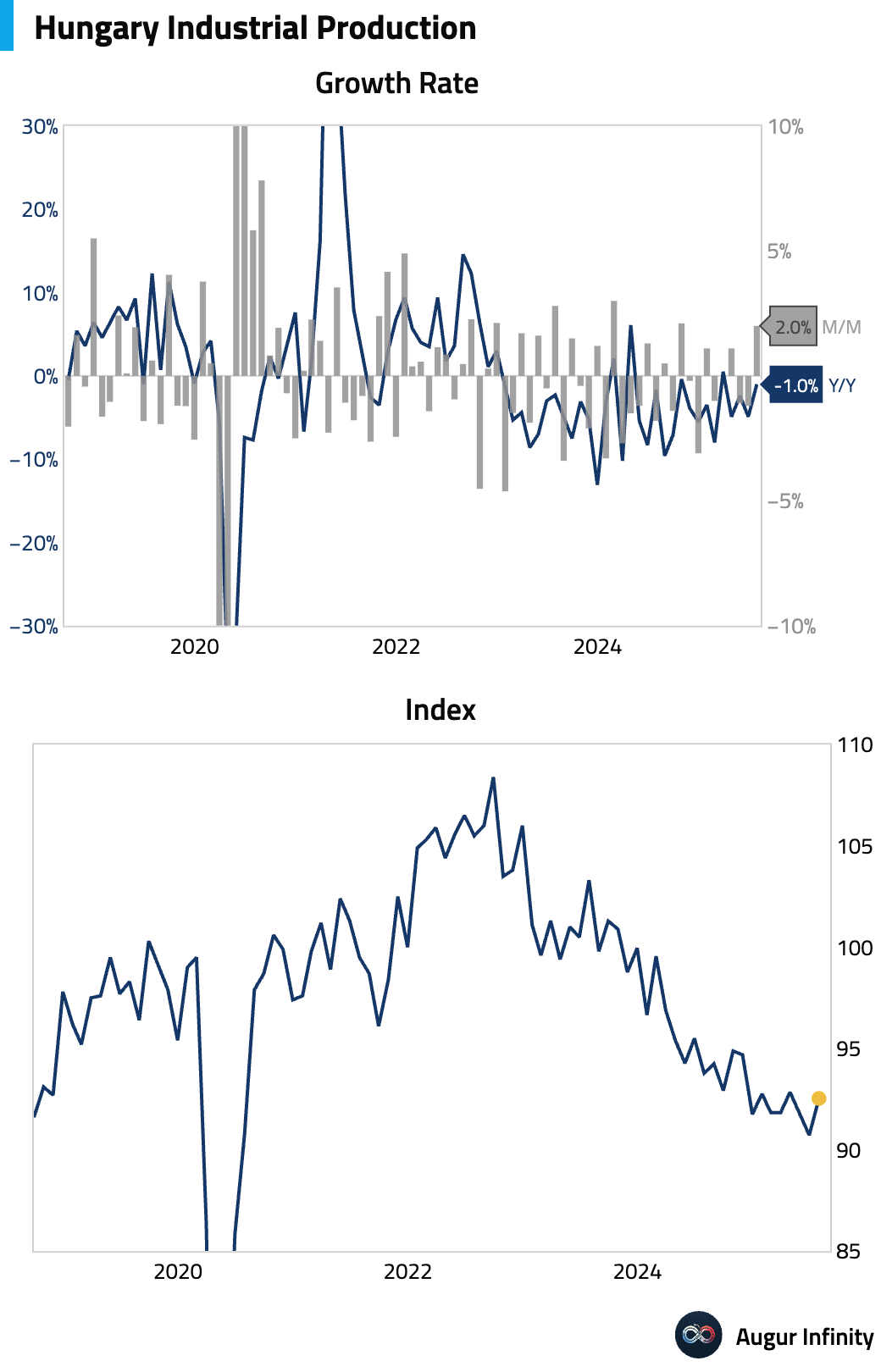

- Hungarian industrial production contracted by 1.0% Y/Y in July, a significant improvement from the 4.9% fall in the prior month.

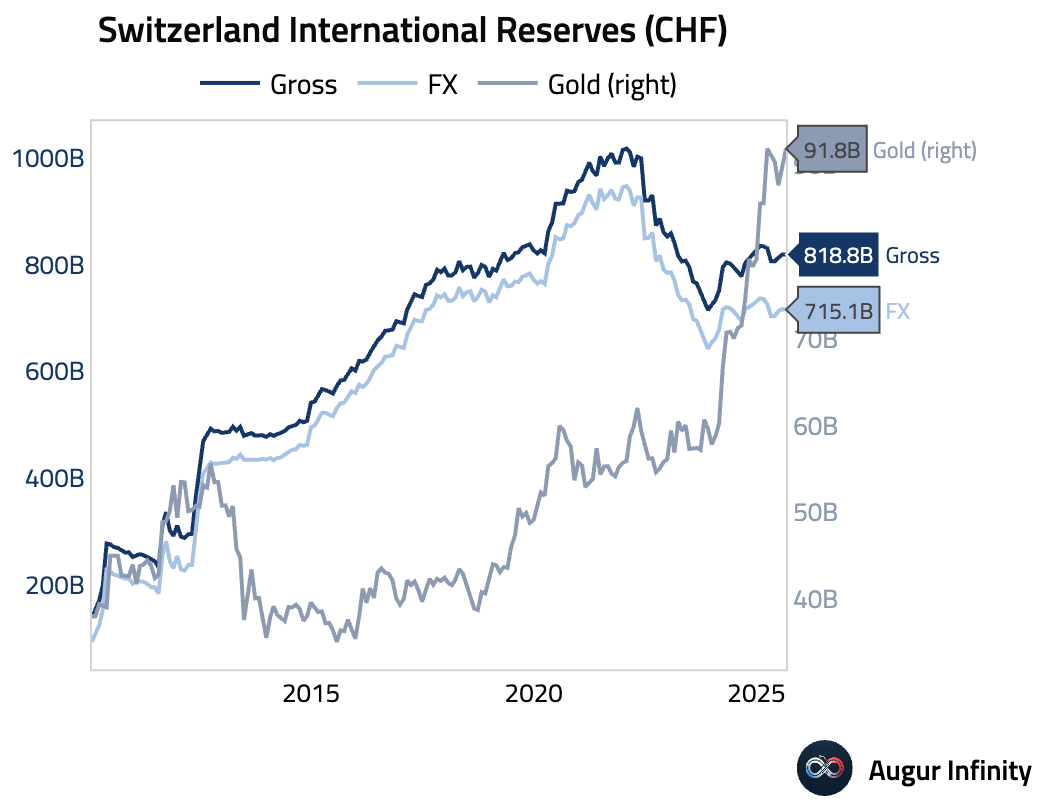

- Switzerland's foreign currency reserves decreased to 715.1 billion francs in August from 716.5 billion in July.

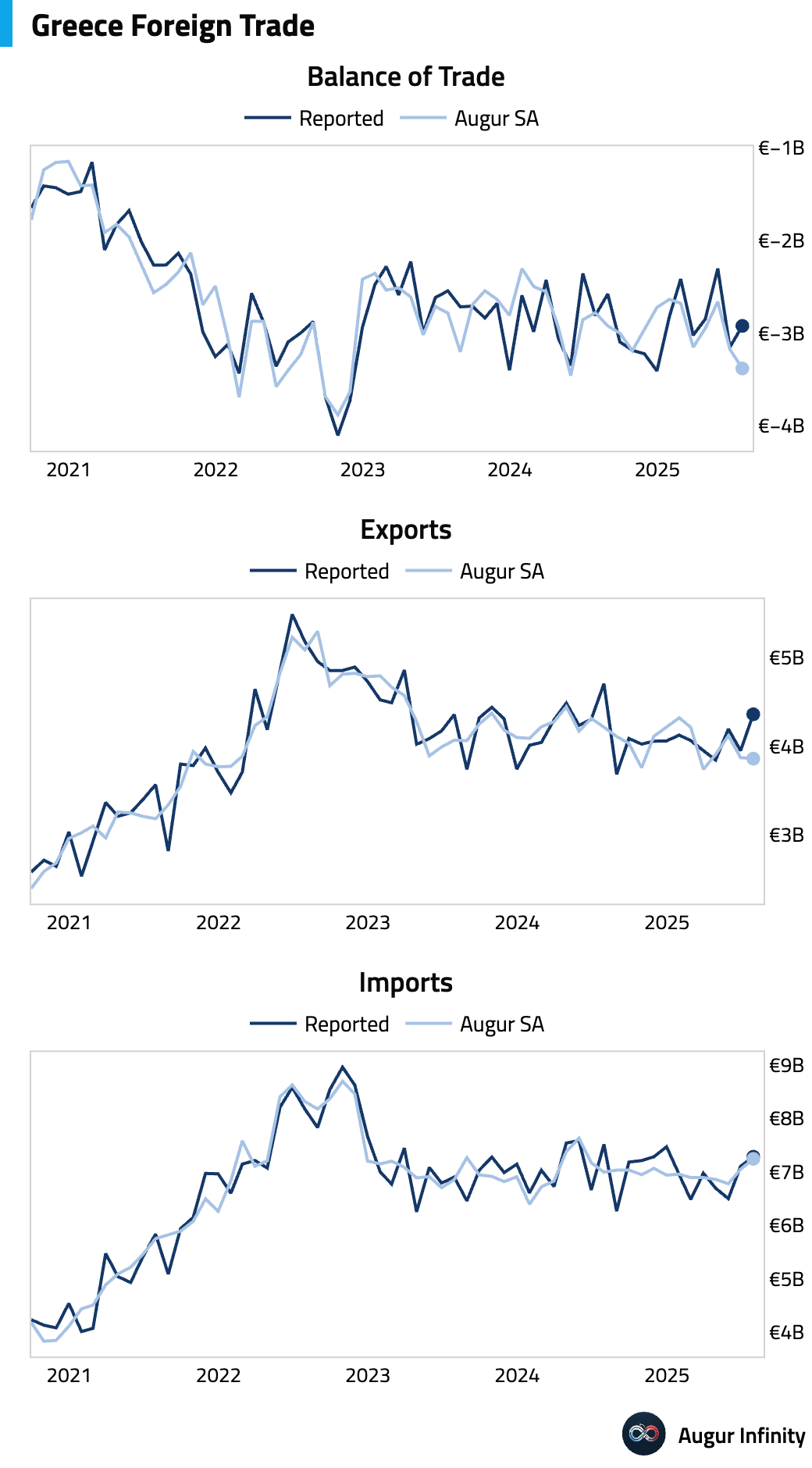

- Greece's trade deficit narrowed to €2.9 billion in July from €3.2 billion in the same month last year.

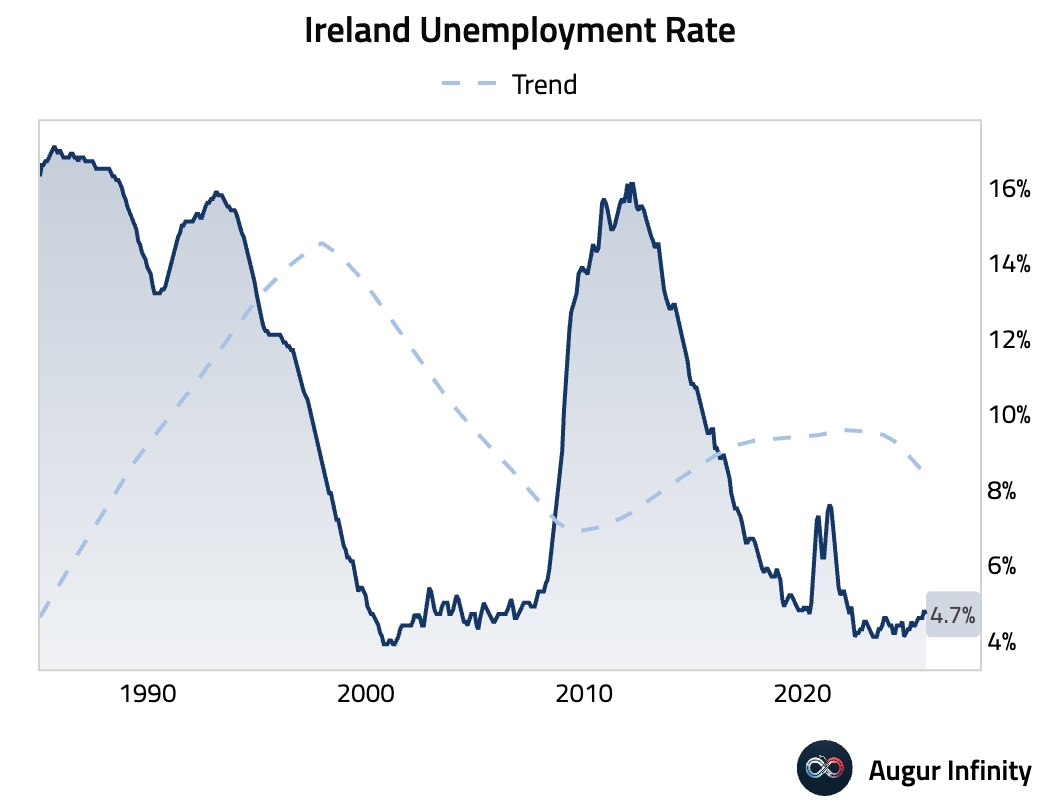

- Ireland’s unemployment rate edged down to 4.7% in August from 4.8% in July.

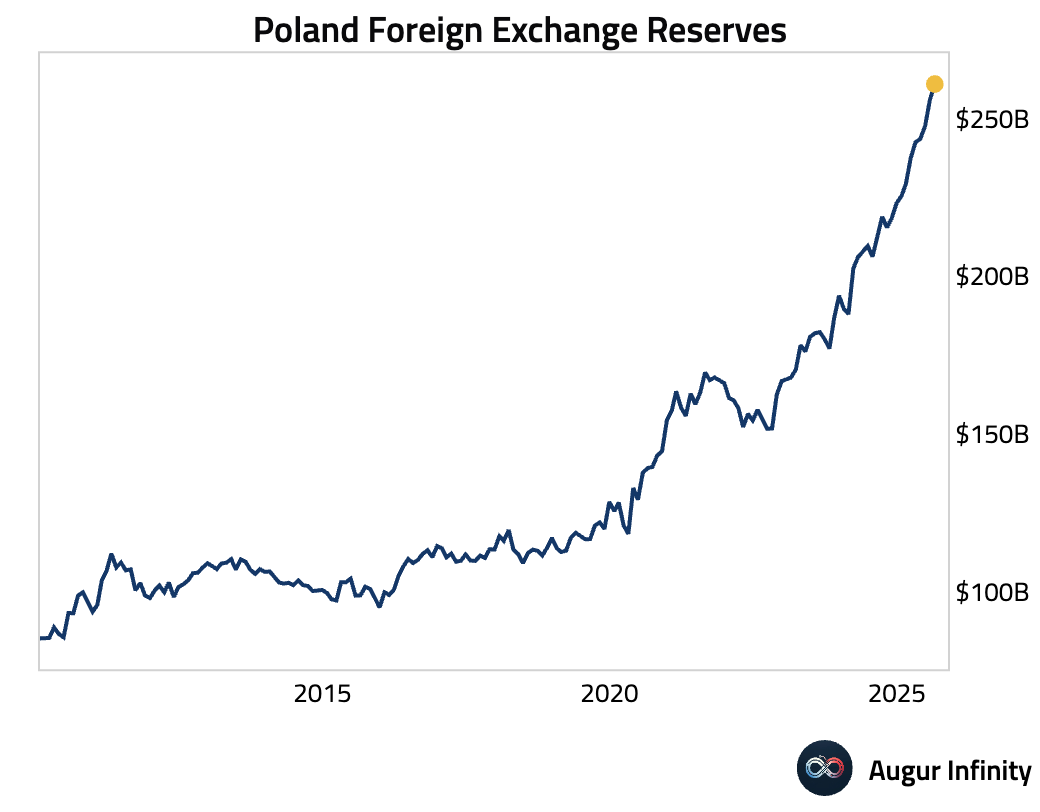

- Poland's foreign exchange reserves climbed to a new record high of $260.9 billion in August.

Asia-Pacific

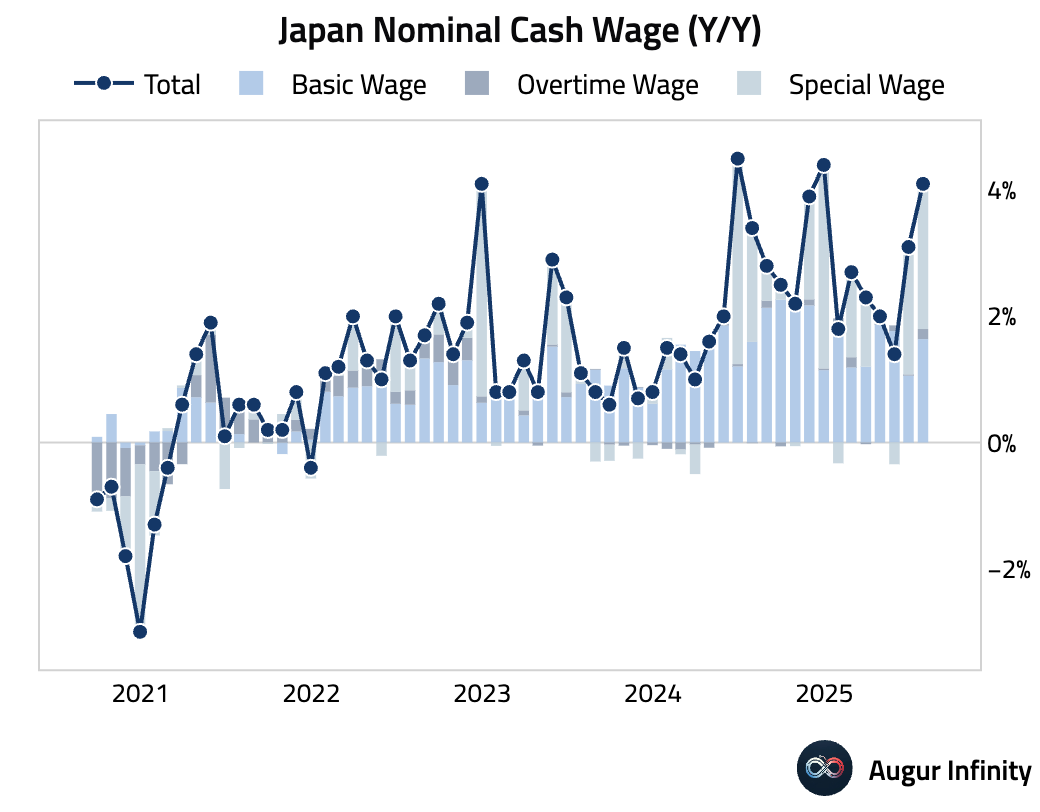

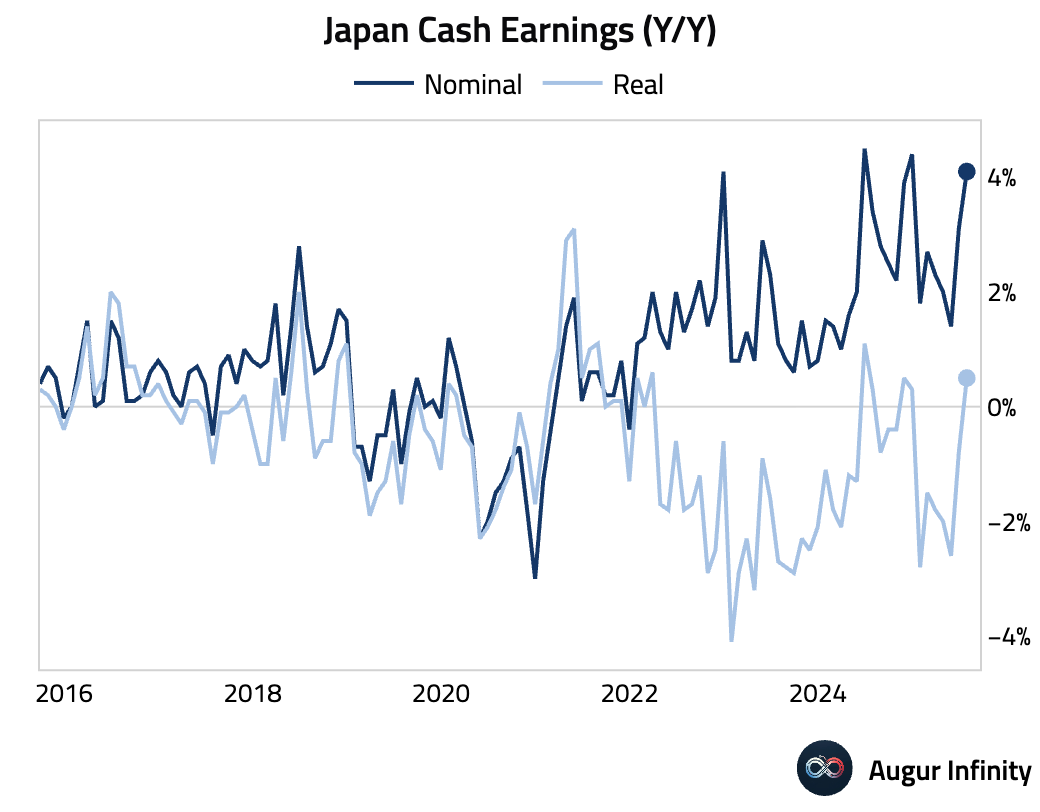

- Japan's July headline nominal wages surged +4.1% Y/Y, driven by a +7.9% jump in summer bonuses, turning real wages positive (+0.5%) for the first time since Dec 2024.

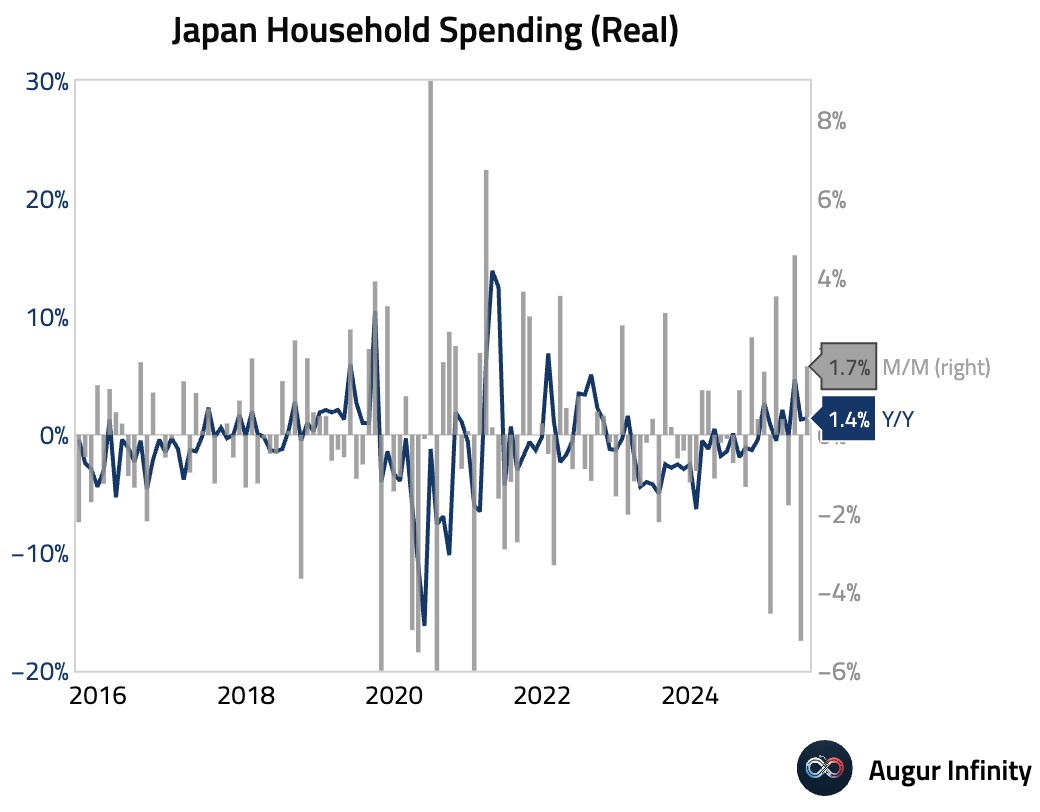

- Japanese household spending rose 1.7% M/M in July, recovering from a 5.2% drop but missing the 1.3% forecast. The year-over-year figure of 1.4% also came in below the expected 2.3%, signaling fragile consumer demand.

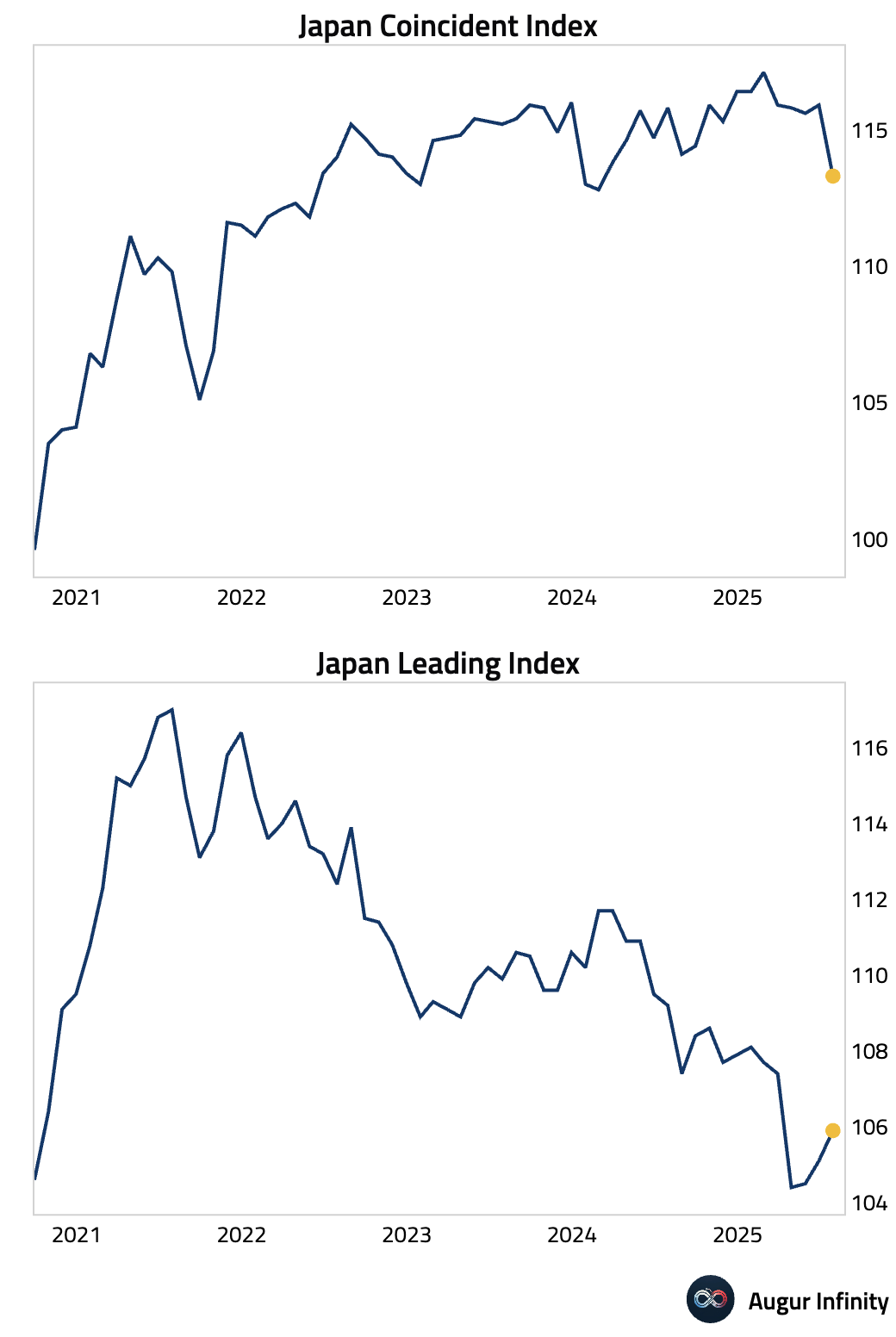

- Japan’s preliminary Coincident Index fell to 113.3 in July from 115.9, while the Leading Economic Index rose to 105.9 from 105.1, matching consensus. The divergence suggests a mixed outlook for the Japanese economy.

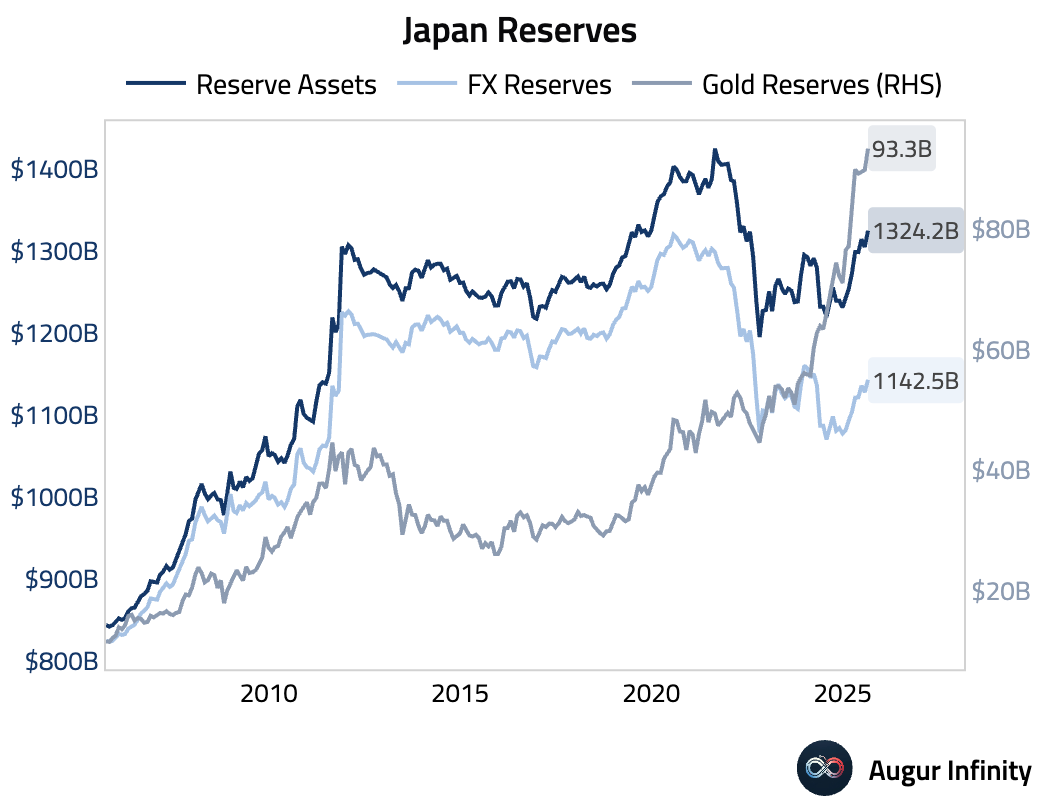

- Japan’s official reserve assets increased to $1.324 trillion in August from $1.304 trillion in July.

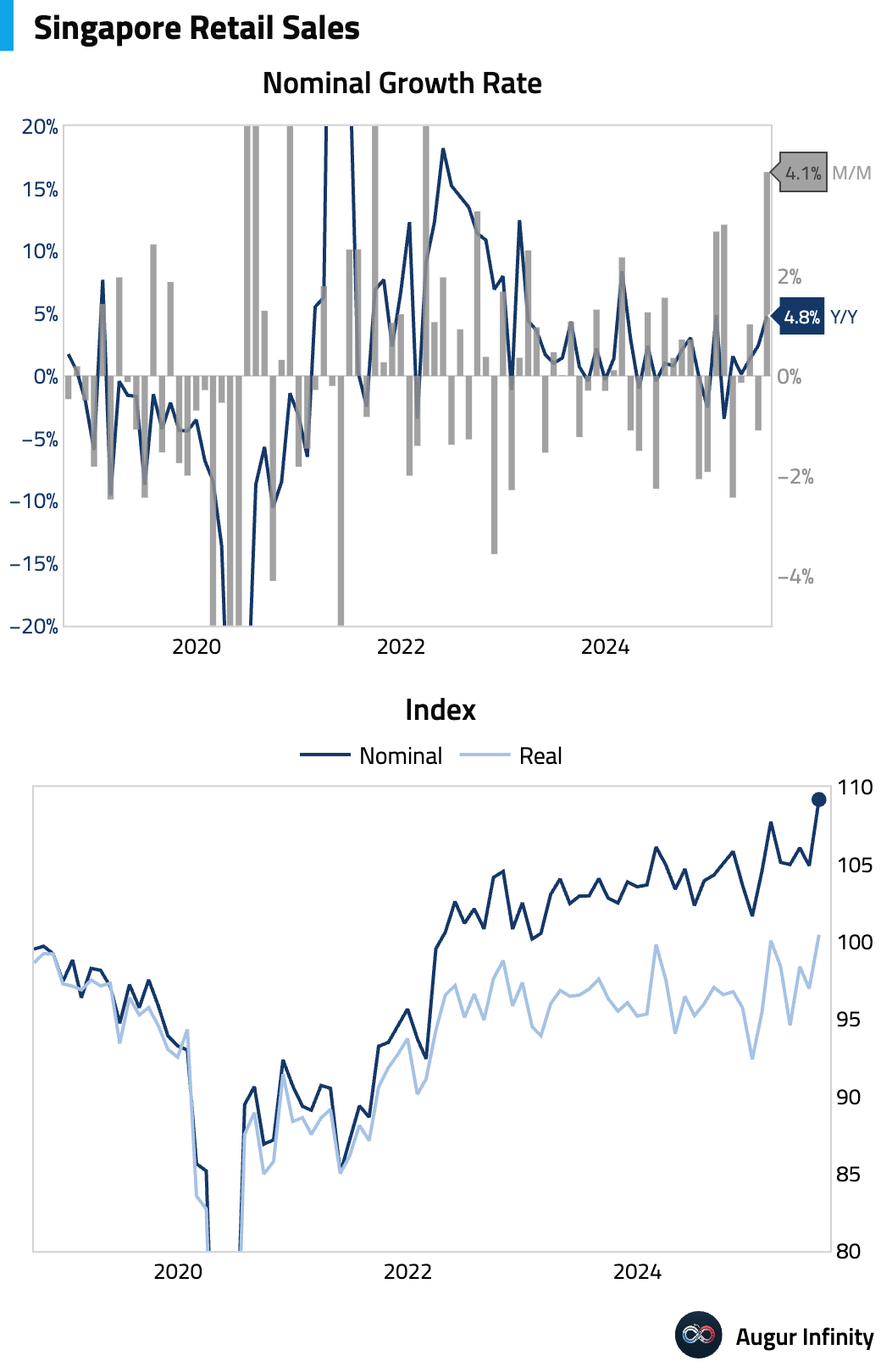

- Singapore's retail sales jumped 4.1% M/M in July, rebounding sharply from a 1.1% decline. Year-over-year, sales growth accelerated to 4.8% from 2.4%

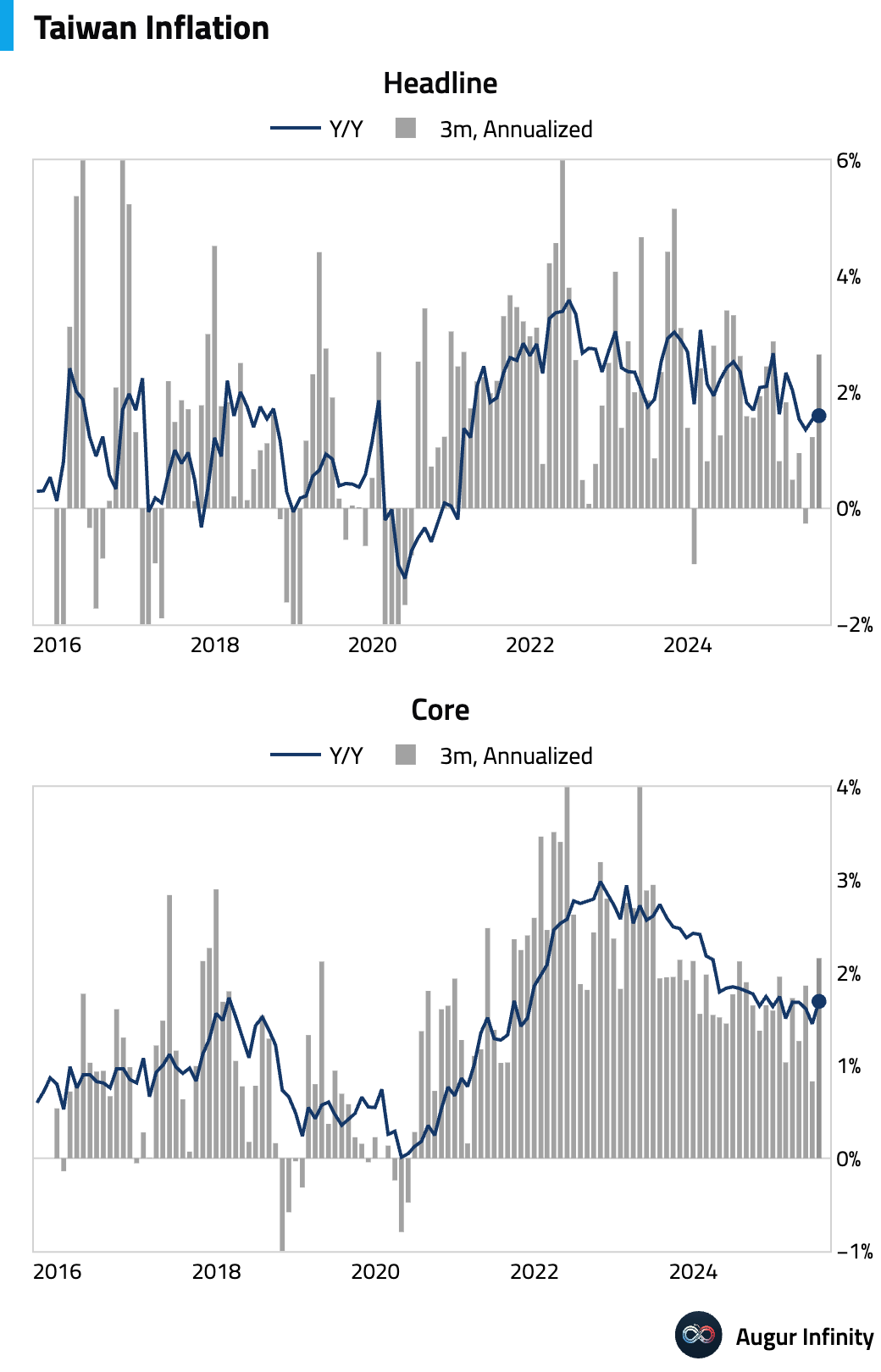

- Taiwan's August CPI rose to +1.6% Y/Y, matching consensus. The increase was driven entirely by a rapid 0.8% M/M rise in food prices, while prices for other goods remained flat for the third consecutive month. Importantly, services inflation slowed significantly to just +0.1% M/M, causing Core CPI to hold steady at +1.7% Y/Y and miss consensus expectations of 1.8%.

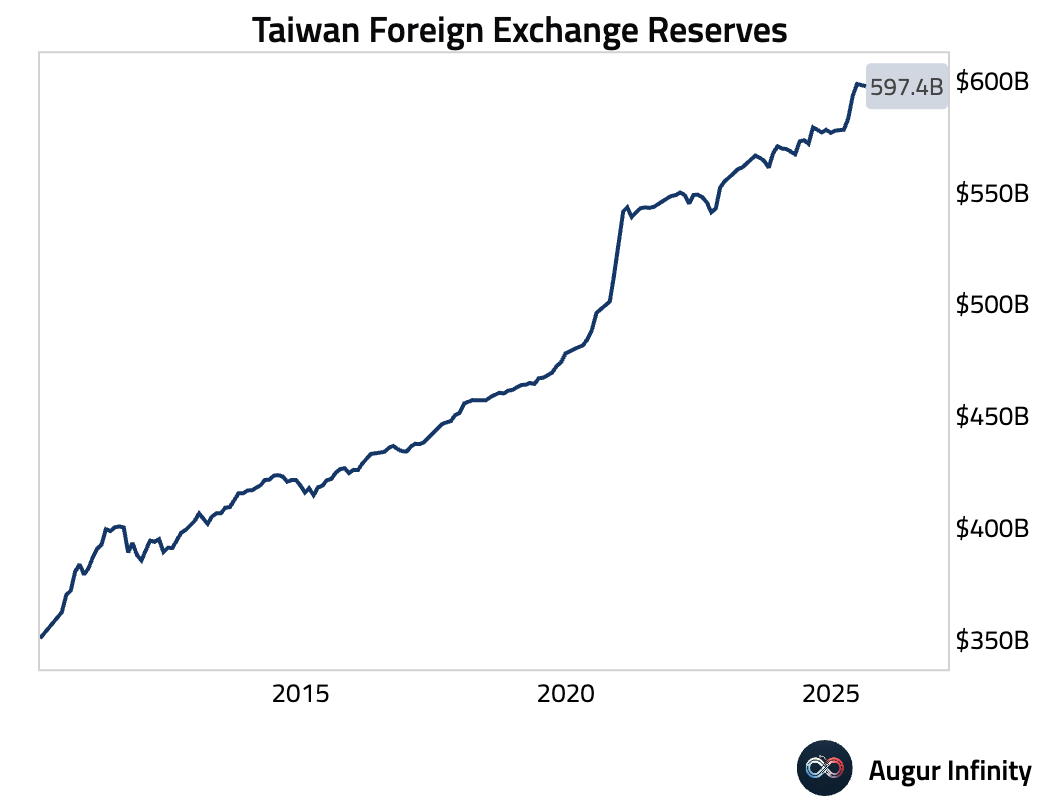

- Taiwan's foreign exchange reserves edged down to $597.43 billion in August from $597.87 billion in the prior month.

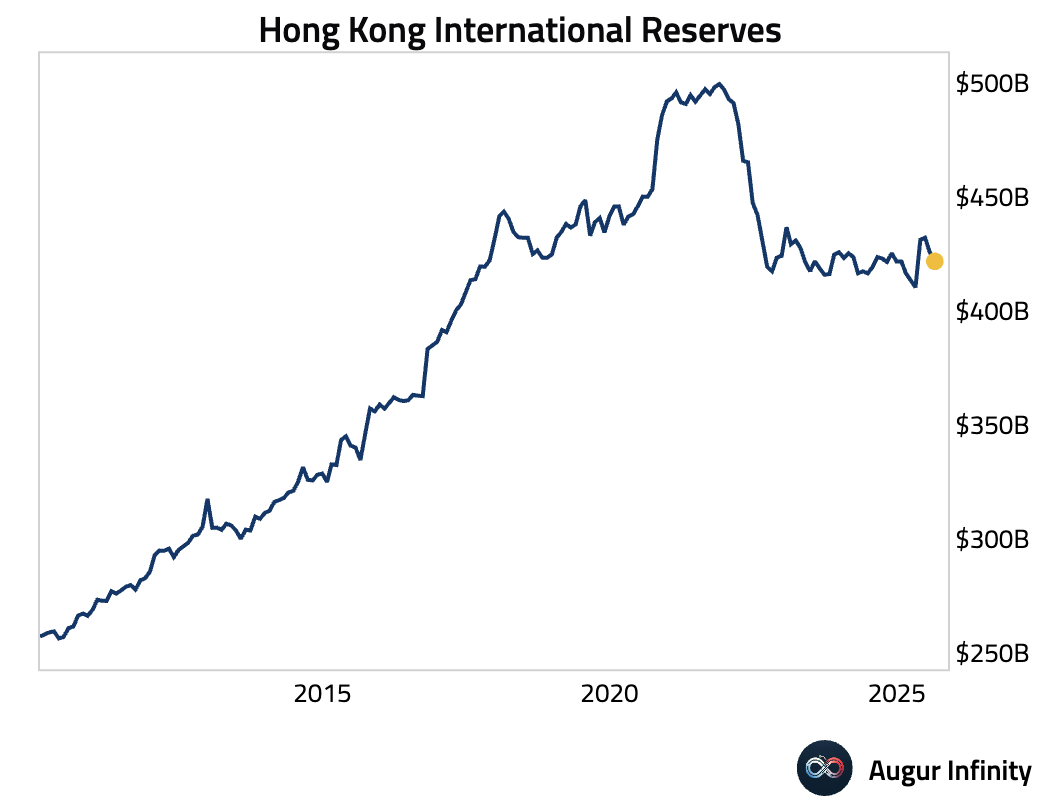

- Hong Kong's official reserve assets declined to $421.6 billion in August from $425.4 billion in July.

Emerging Markets ex China

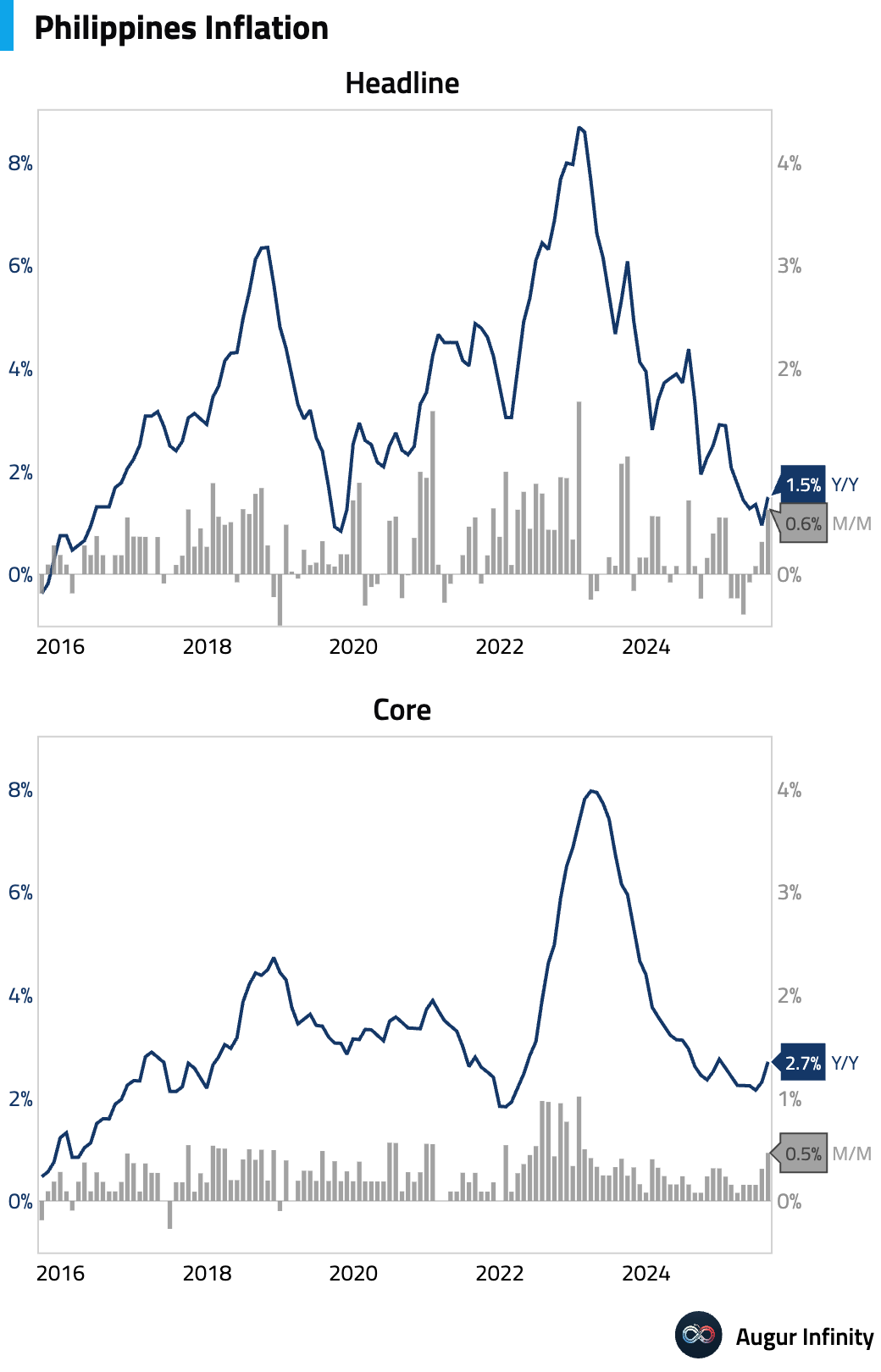

- Philippines' August headline CPI rose to 1.5% Y/Y, beating the 1.2% consensus. The increase from July's 0.9% was driven primarily by a rebound in food inflation to +0.6% from -0.5%, led by higher vegetable, meat, and fish prices. Core inflation also accelerated to 2.7% from 2.3%, indicating broader price pressures.

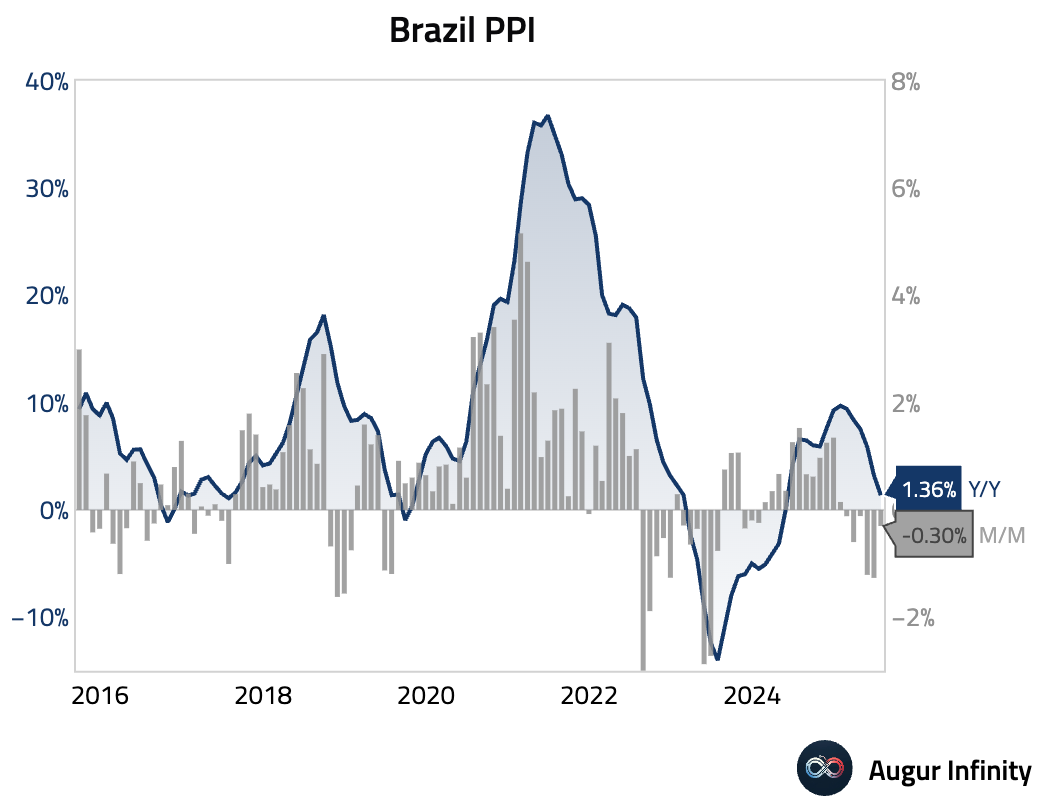

- Brazil's producer price index fell 0.3% M/M in July, a smaller decline than the 1.27% drop in June. The annual rate of producer inflation slowed significantly to 1.36% from 3.22%.

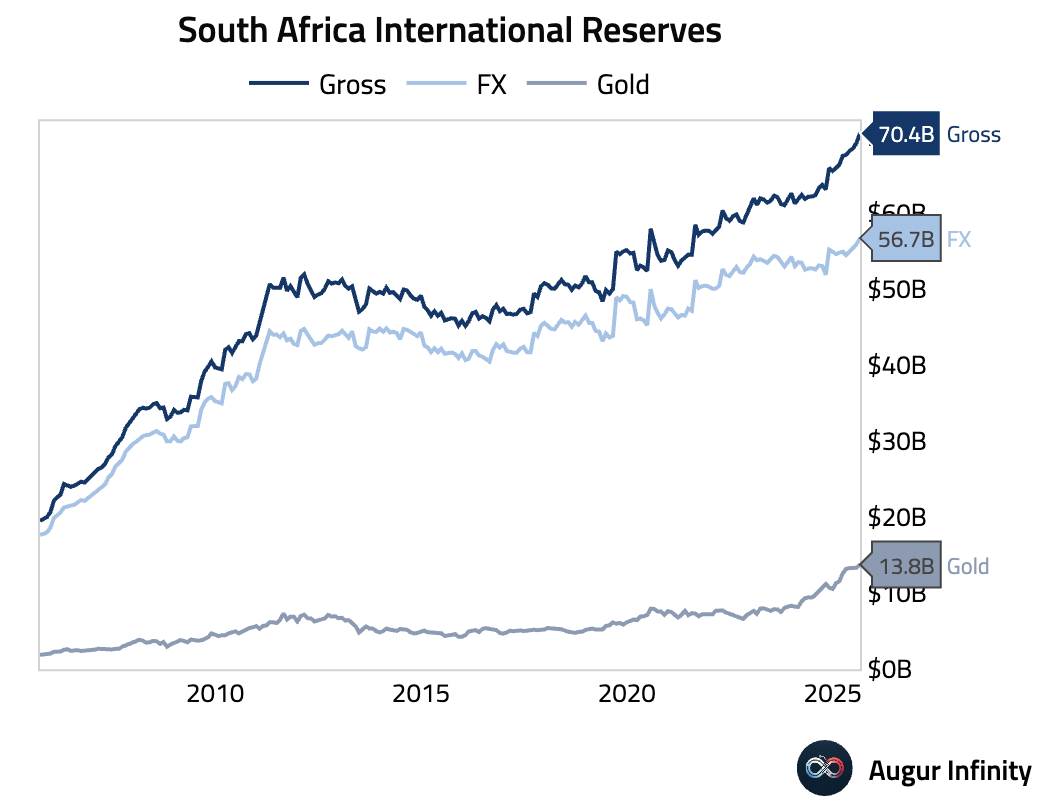

- South Africa's official reserve assets rose to a record high of $70.42 billion in August.

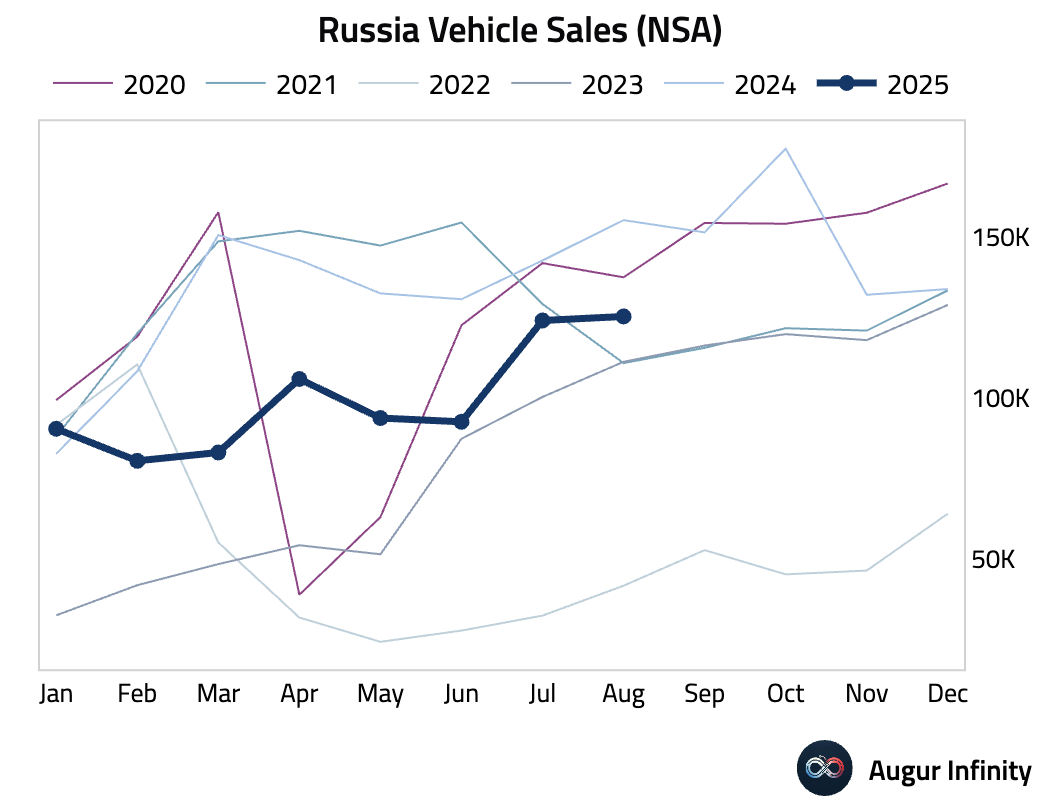

- Russian vehicle sales declined by 19% Y/Y in August, a steeper fall than the 13% drop recorded in July.

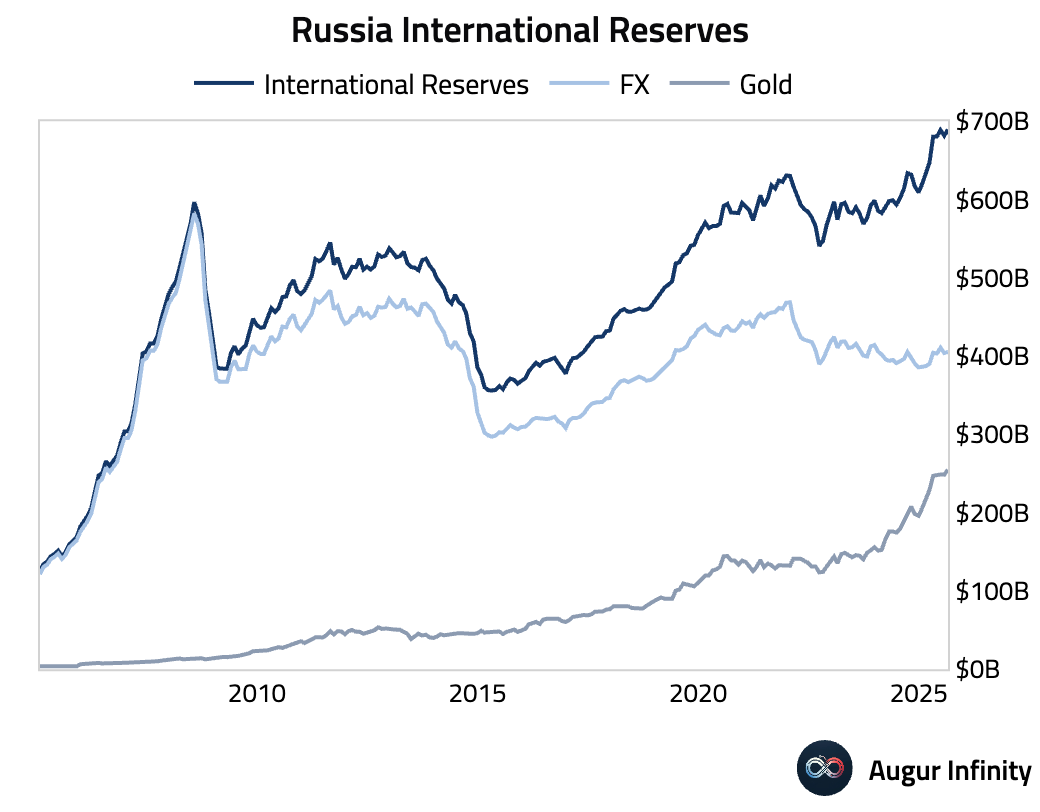

- Russia's official reserve assets increased to a new record high of $689.4 billion in August.

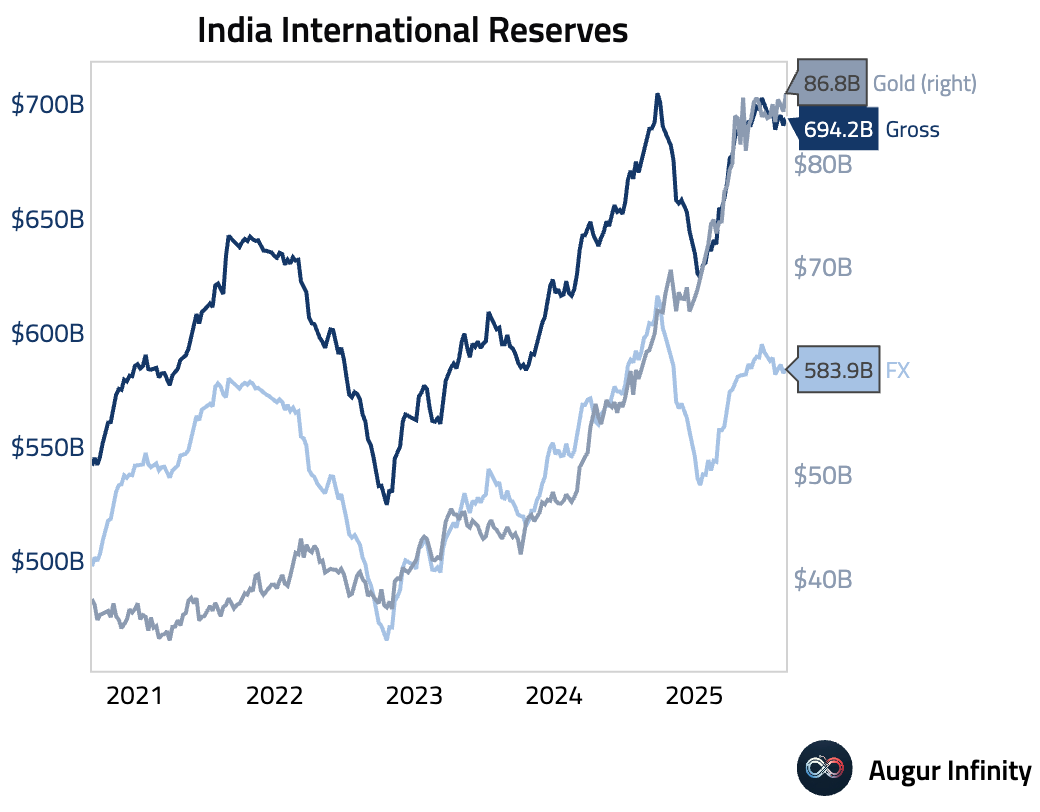

- India's international reserves rose to $694.23 billion in the latest week from $690.72 billion previously.

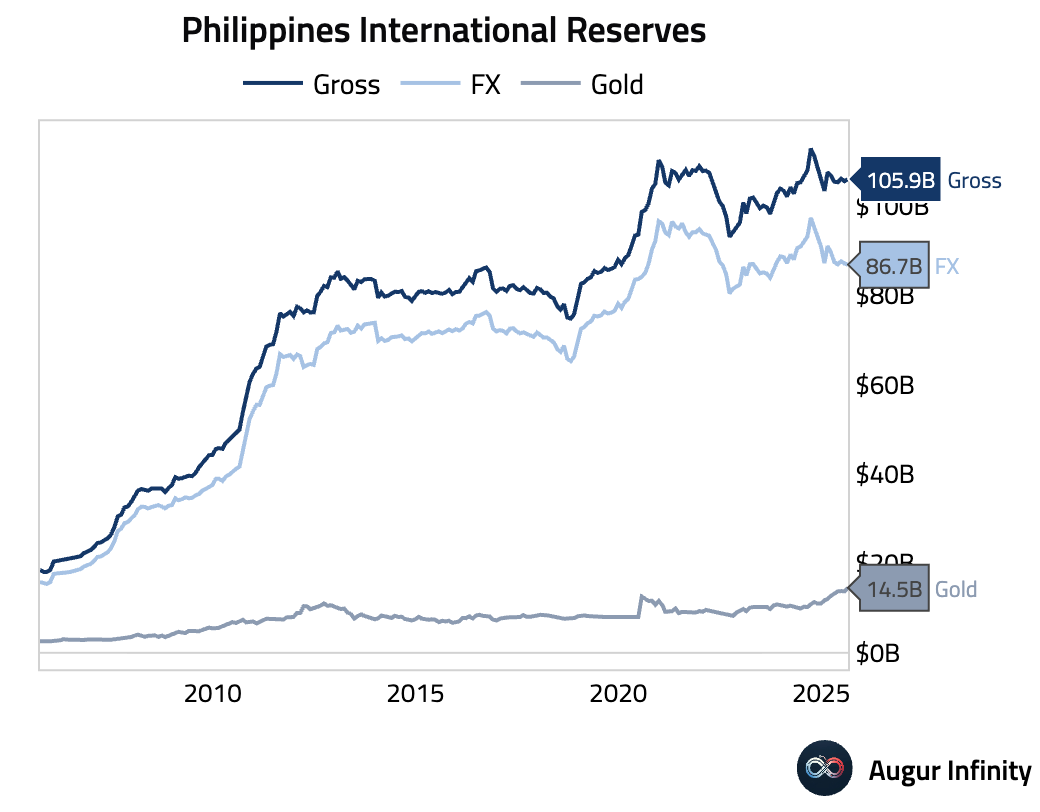

- The Philippines' official reserve assets increased to $105.9 billion in August from $105.4 billion in July.

Global Markets

Equities

- US equities finished lower, with the S&P 500 declining 0.3% following a weaker-than-expected jobs report that intensified expectations for a Federal Reserve rate cut. The Nasdaq also edged down 0.03%. Emerging market equities outperformed, rising 1.2%, led by strong gains in China (+1.3%), Brazil (+1.3%), and Mexico (+1.1%). The United Kingdom, Canada, and South Korea all posted their third consecutive day of gains.

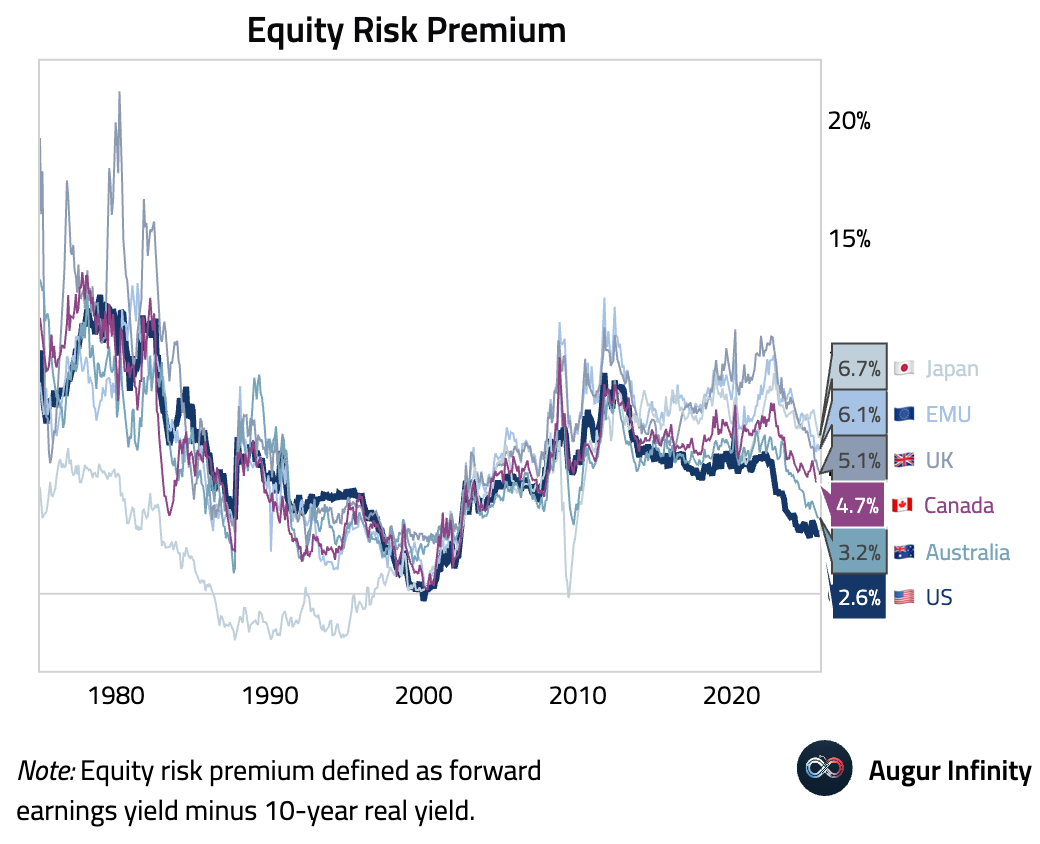

- The US has the lowest equity risk premium amongst major developed economies.

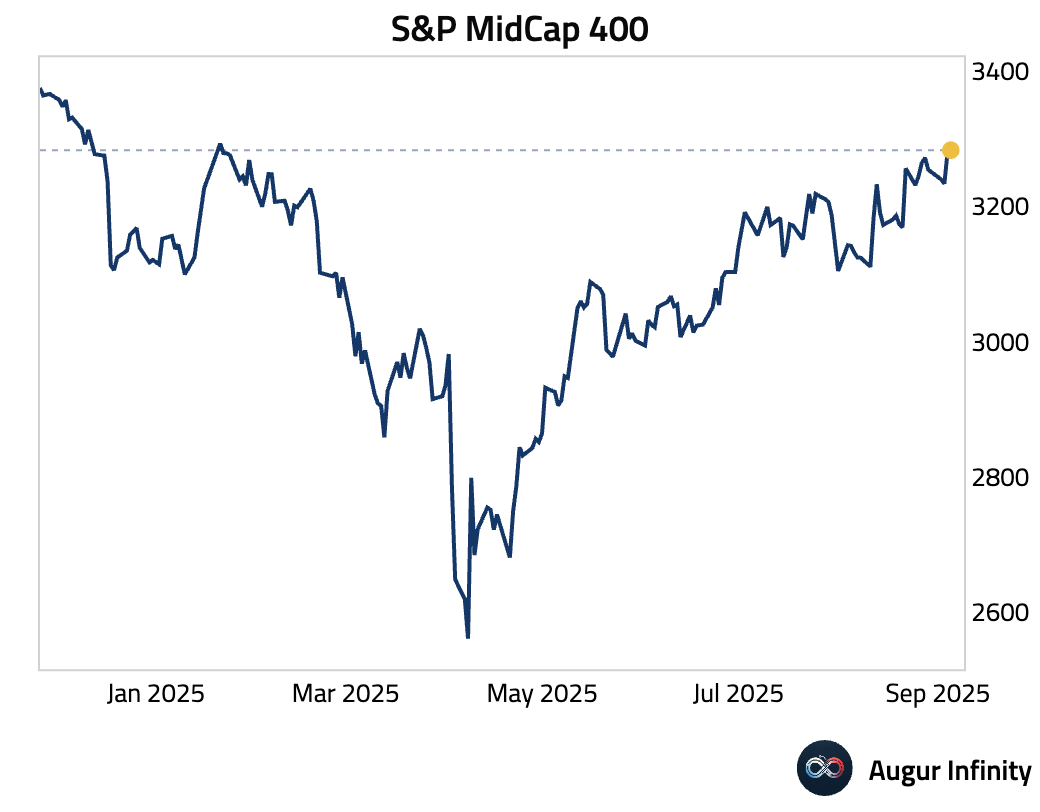

- Although the broader market is down today, the S&P MidCap 400 Index rose to the highest level since January.

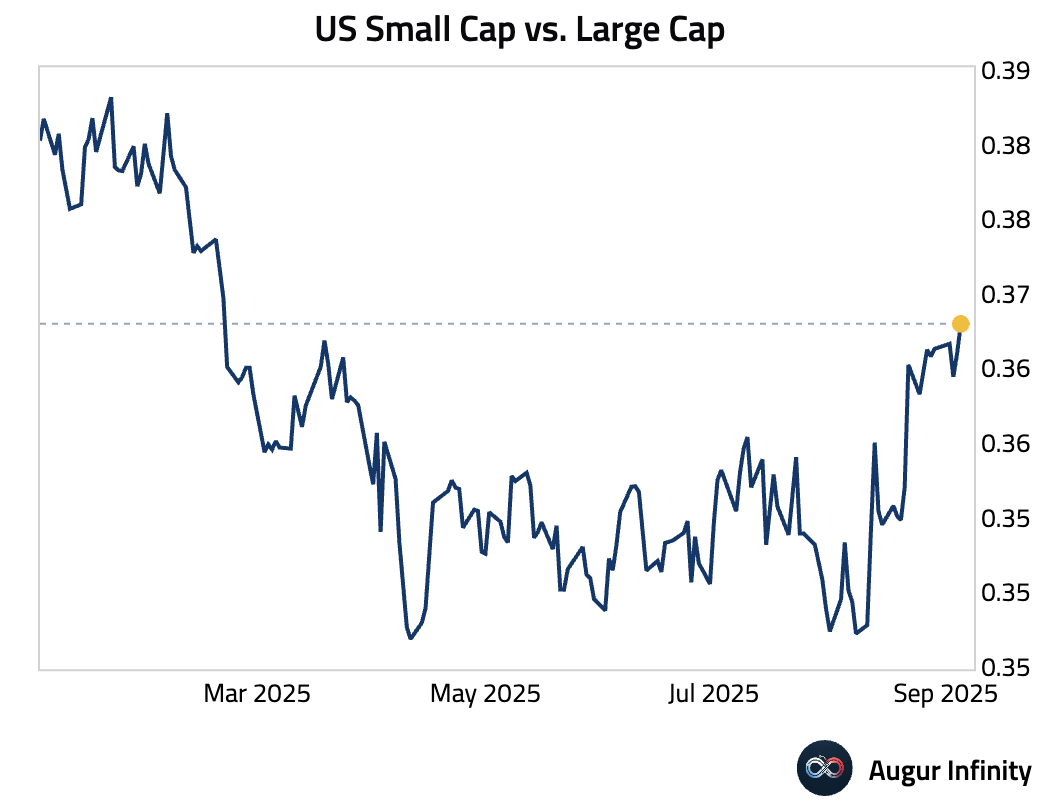

- Meanwhile, US Small Cap vs. Large Cap jumped to the highest since February 2025.

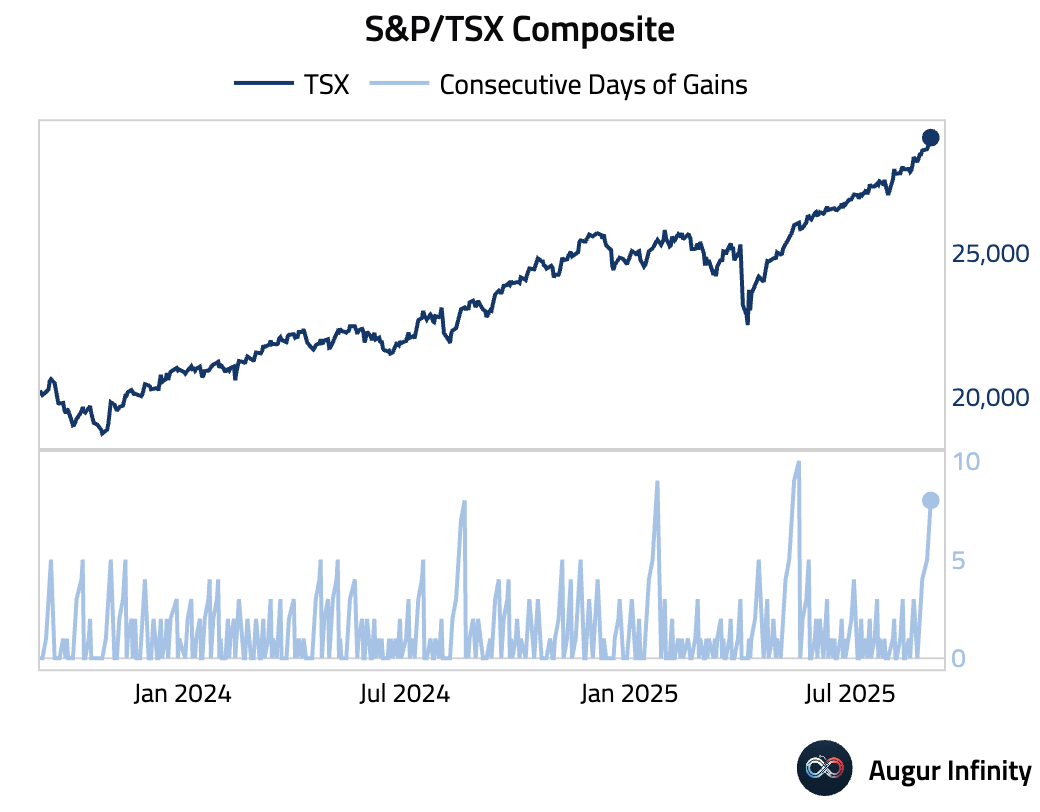

- S&P/TSX Composite for Canada notched its eighth consecutive days of gains.

Fixed Income

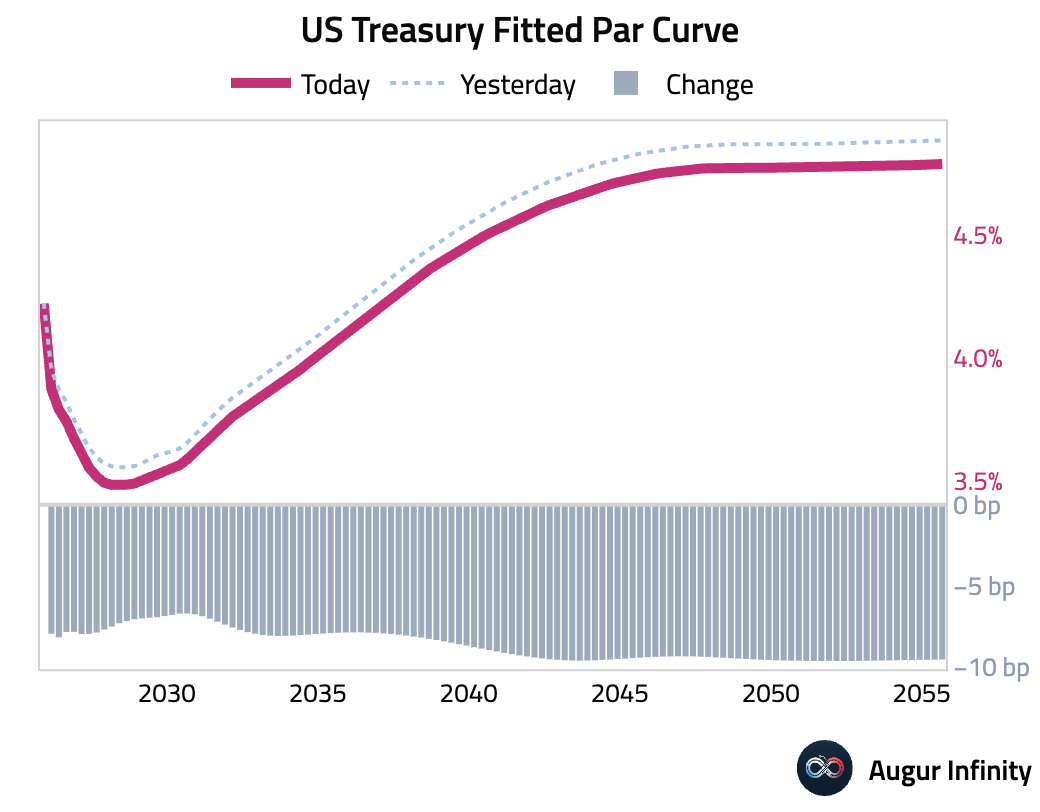

- US Treasury yields fell sharply across the curve for the third consecutive day, driven by disappointing labor market data. The 10-year yield dropped 8.7 bps, while the 30-year yield fell 10.3 bps. The move reflects growing market conviction that the Federal Reserve will begin an easing cycle at its next meeting.

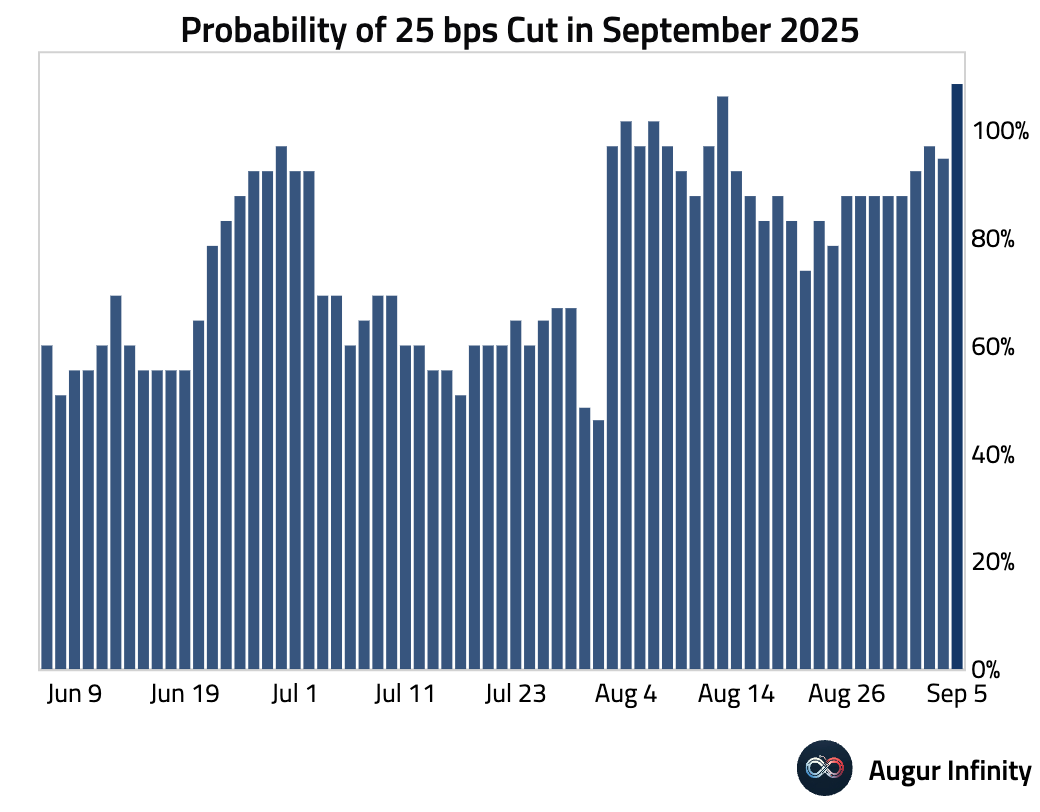

- After the soft NFP print this morning, the probability of a 25 bps rate cut now exceeds 100%. In other words, the market is now pricing in some chance of a 50 bps cut.

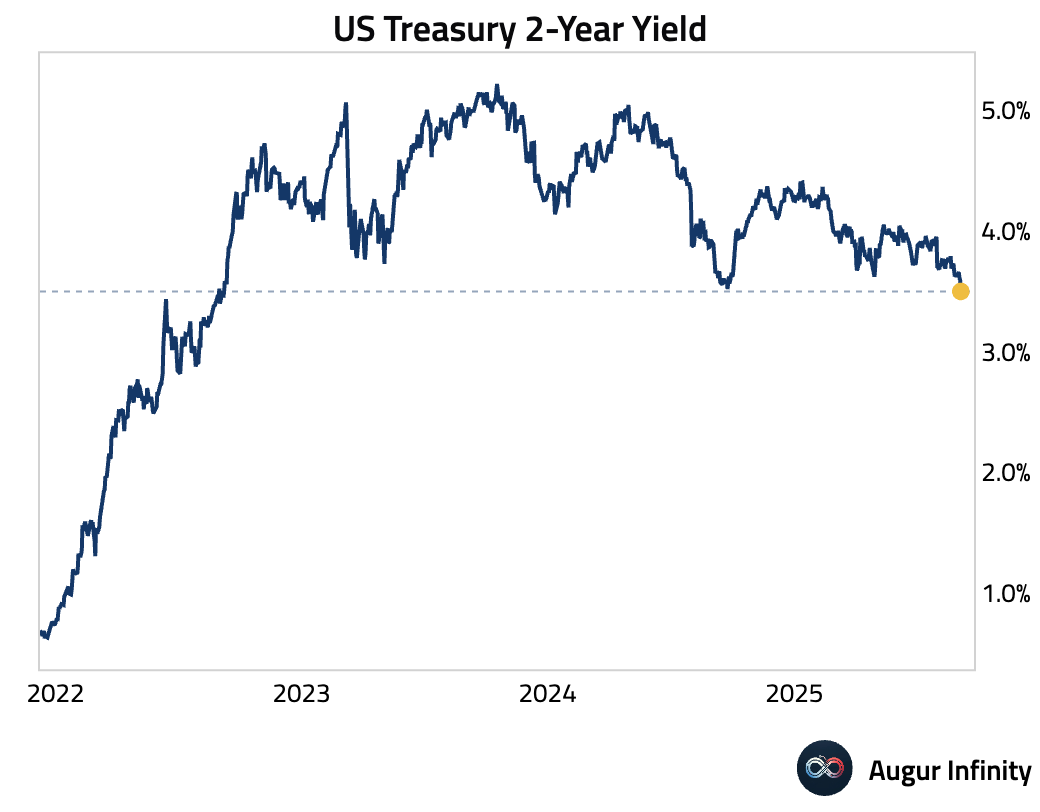

- US Treasury 2-Year yield is now at the lowest level since September 2022.

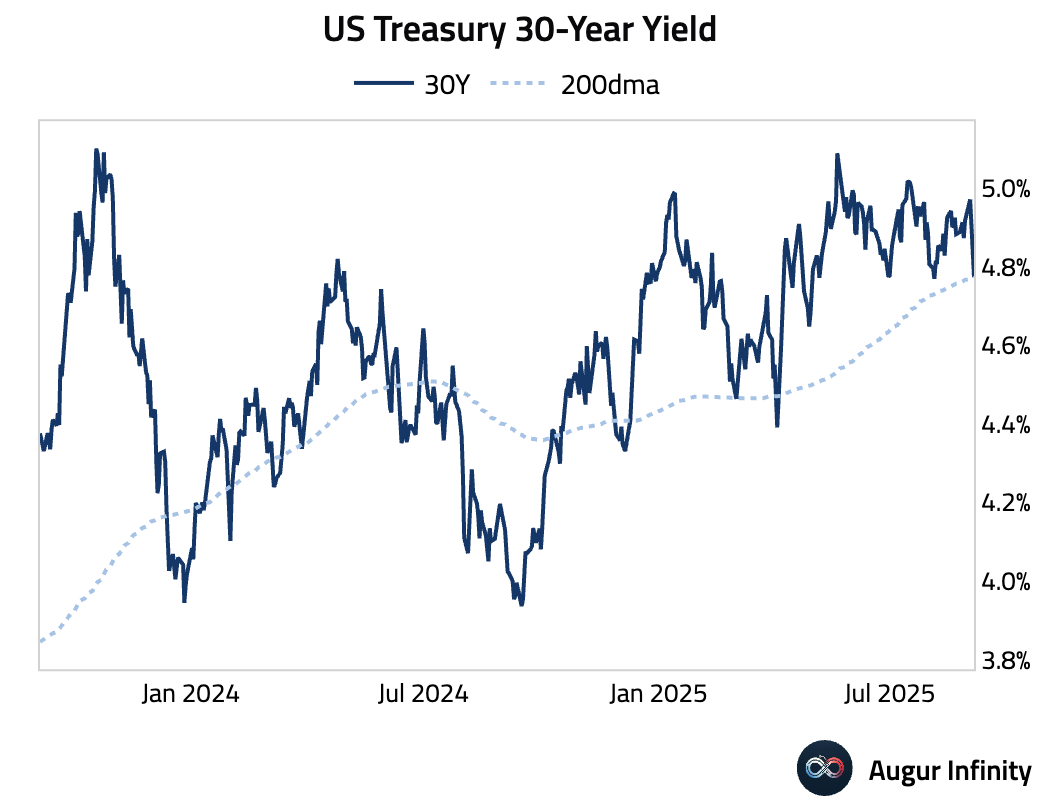

- 30-year Treasury yield fell below its 200-day moving average.

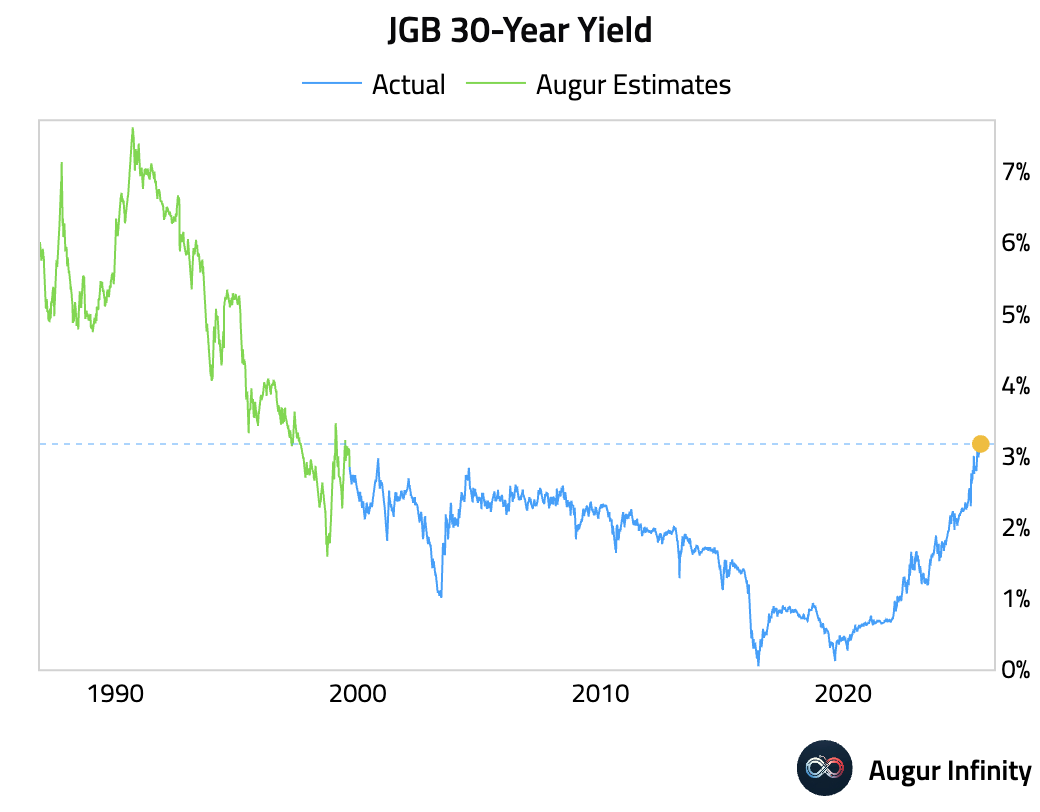

- Japan’s 30-year yield has climbed to the highest level since the MoF began issuing 30-year papers in 1999. The chart below includes our simulated data for an even longer-term perspective.

Commodities

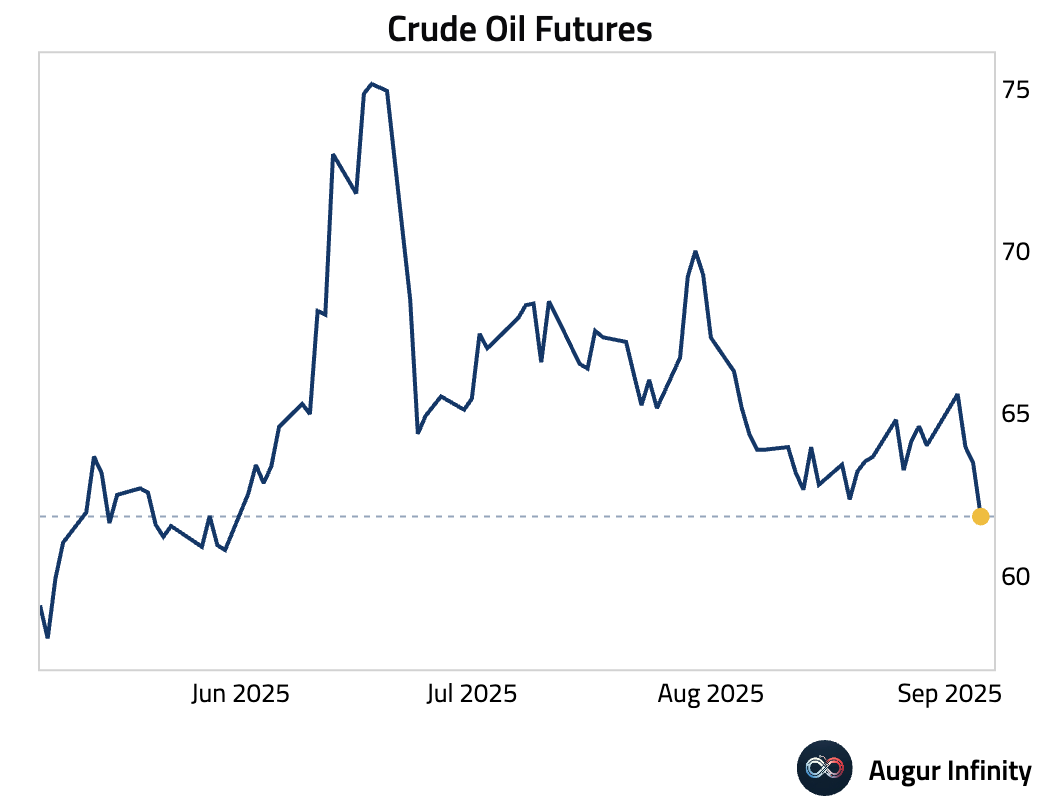

- Crude Oil Futures is at the lowest level since May.

FX

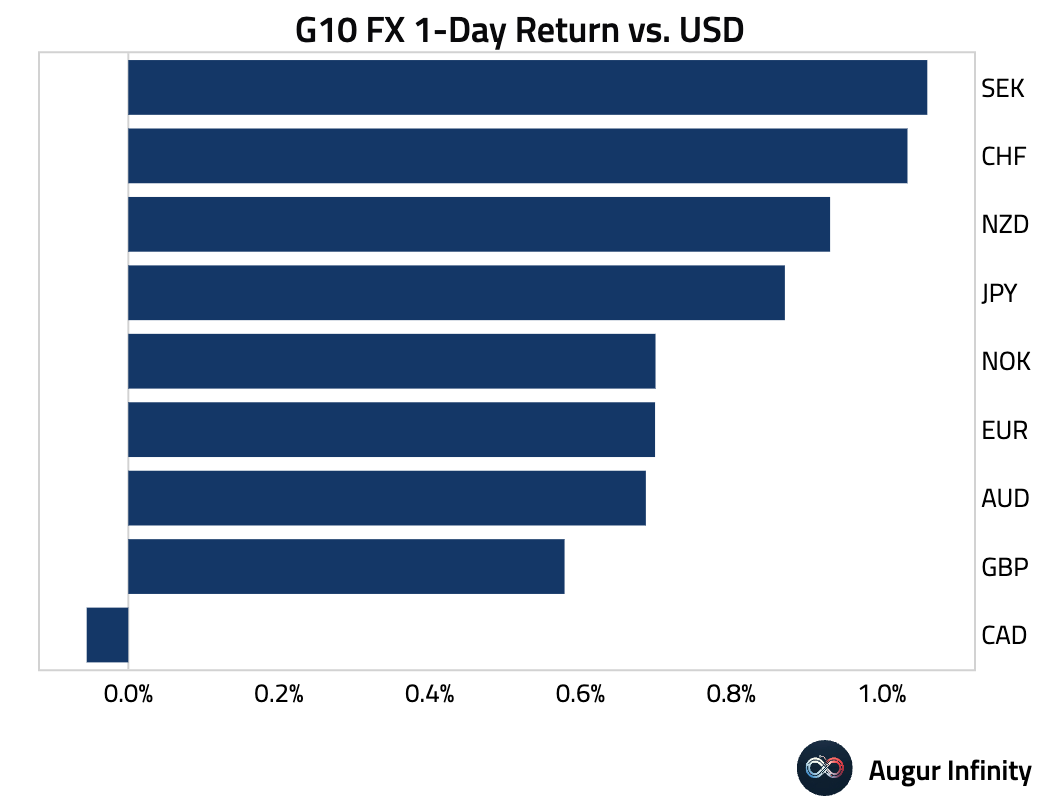

- The US dollar weakened against all G10 peers as expectations for an imminent Fed rate cut solidified. The Swedish krona (+1.1%) and Swiss franc (+1.0%) were the strongest performers. The euro gained 0.7%, while the Japanese yen appreciated by 0.9%.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.