Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- The US president signed an executive order exempting gold, tungsten, and uranium from import tariffs.

- Japanese prime minister Ishiba announced his resignation after twelve months in office, creating political uncertainty in a major Asian economy.

- French prime minister Bayrou is expected to lose a confidence vote, adding to political instability in the eurozone.

- China will reportedly reopen its domestic bond market to Russian energy firms seeking to raise capital.

Global Economics

United States

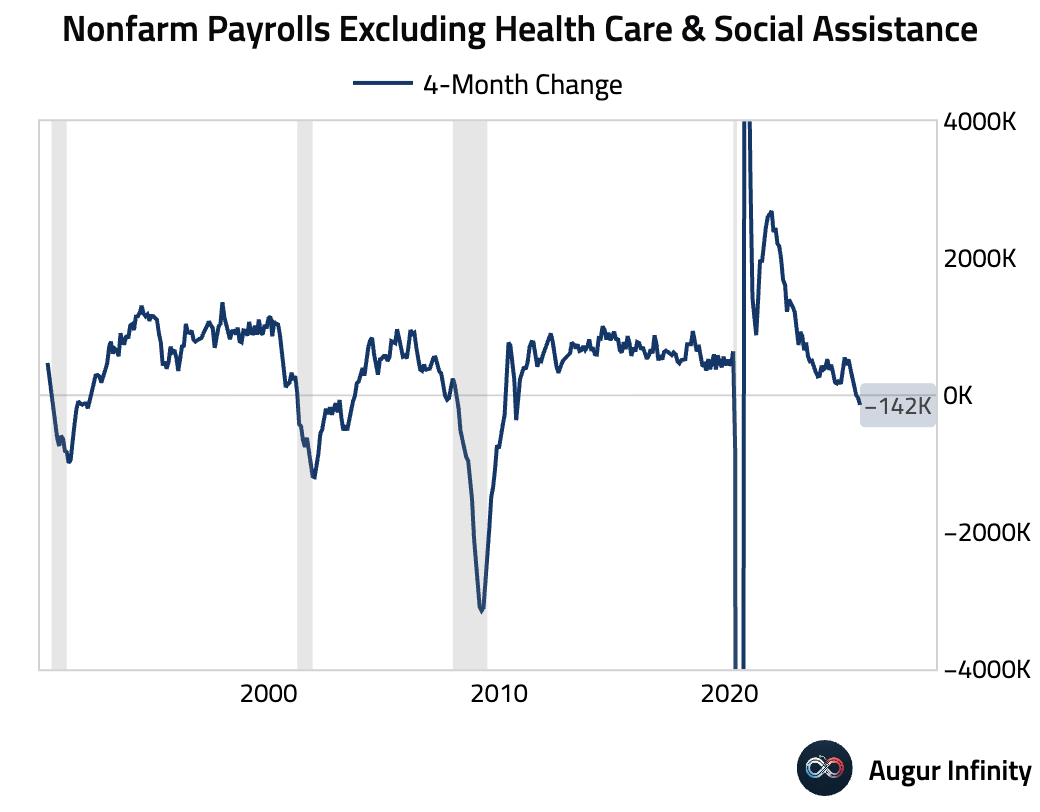

- Excluding health care, more than 142k jobs were lost over the last four months.

Source: @boes_

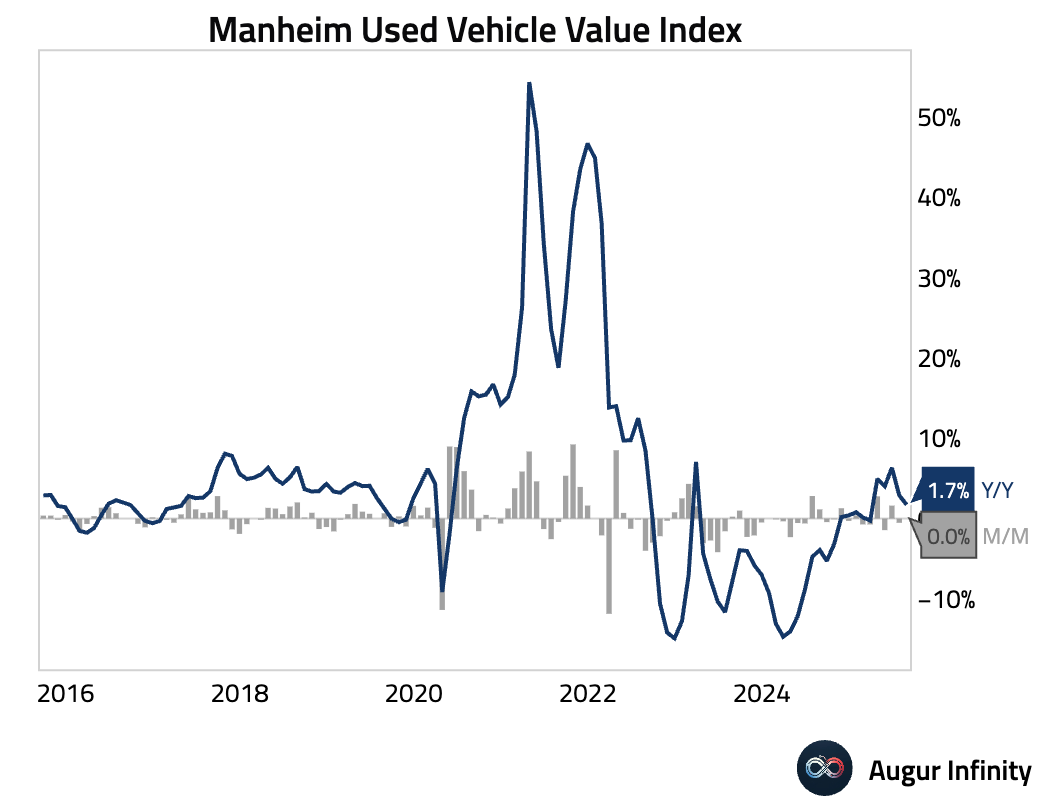

- Used car prices were flat M/M in August after seasonal adjustments, with the year-over-year increase slowing to 1.7% from 2.9%. However, the headline figures mask underlying strength; non-adjusted wholesale prices rose 1.0% against a typical August gain of 0.1%, driven by low inventory and robust demand. Retail conditions tightened, with used-vehicle days' supply falling to 42 from 46 in July.

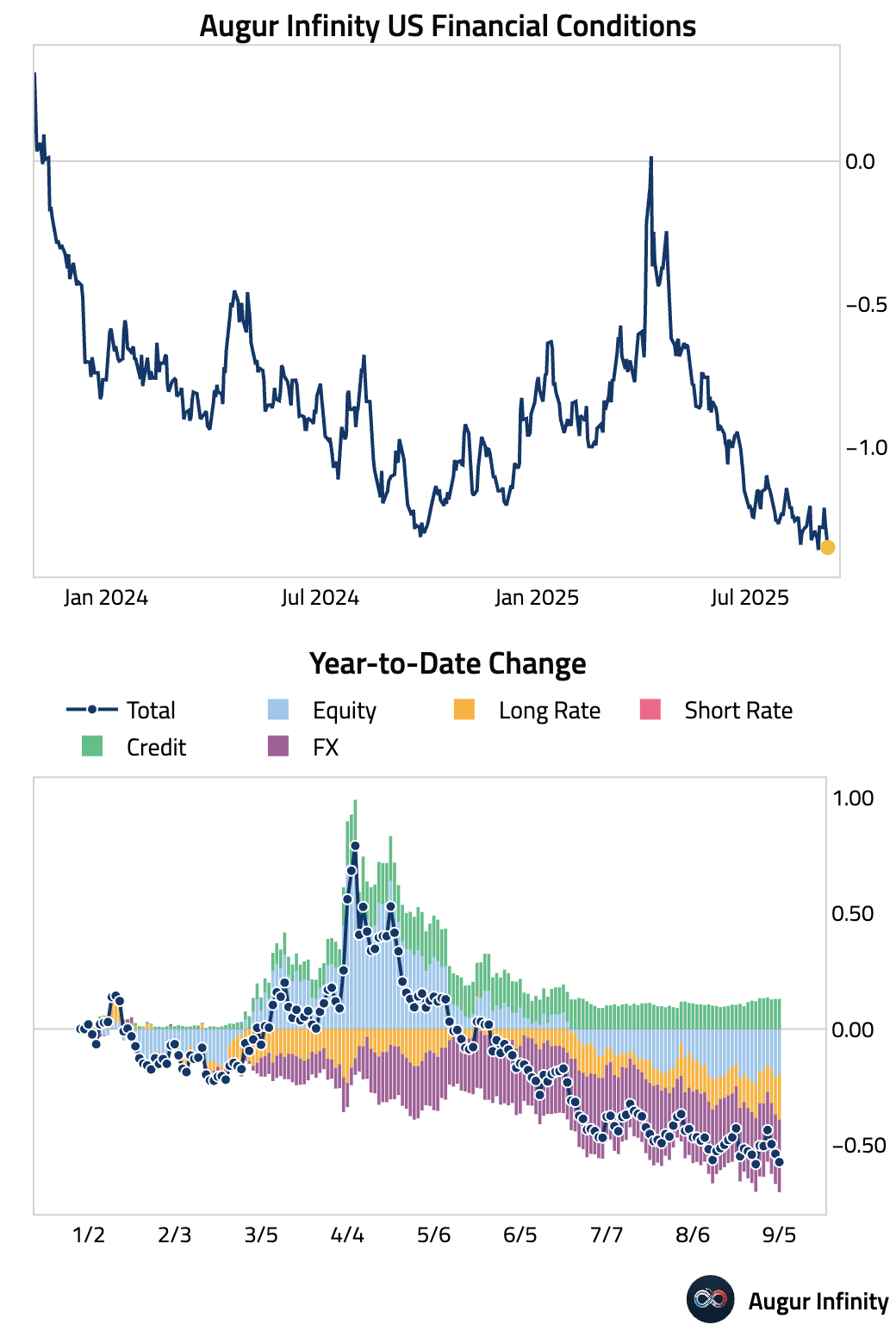

- US financial conditions are now hovering around the easiest level since April 2022.

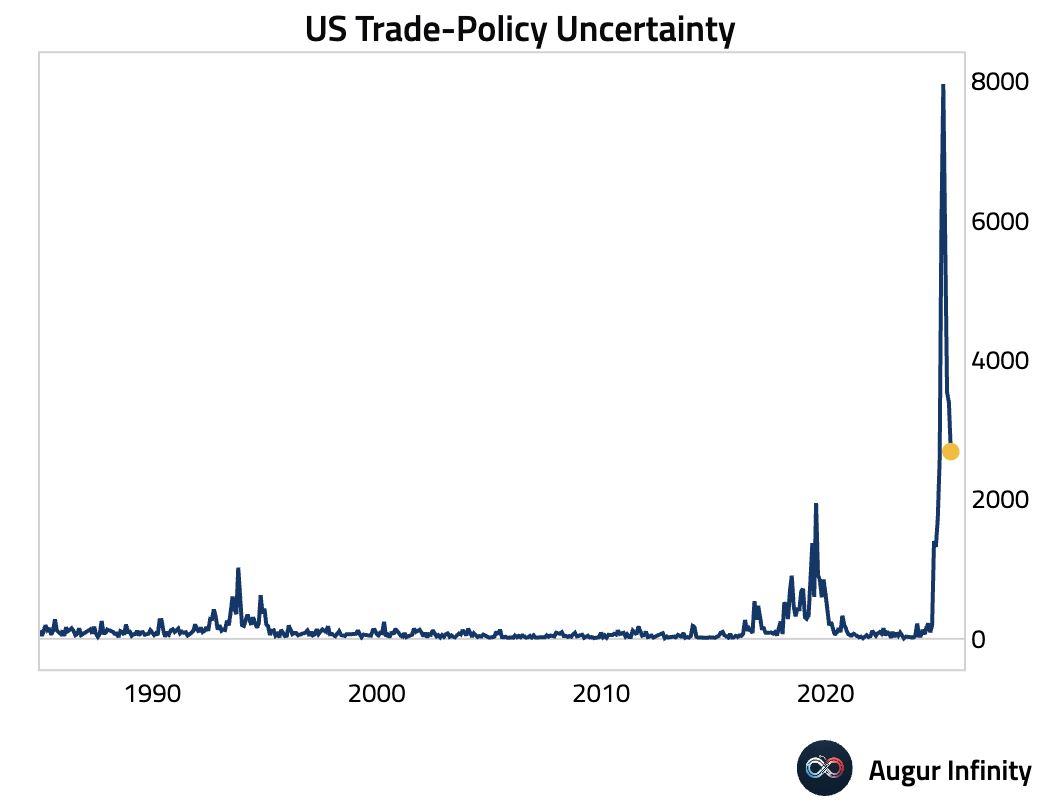

- US trade-policy uncertainty has declined since April, but still hovers around historically elevated levels.

Europe

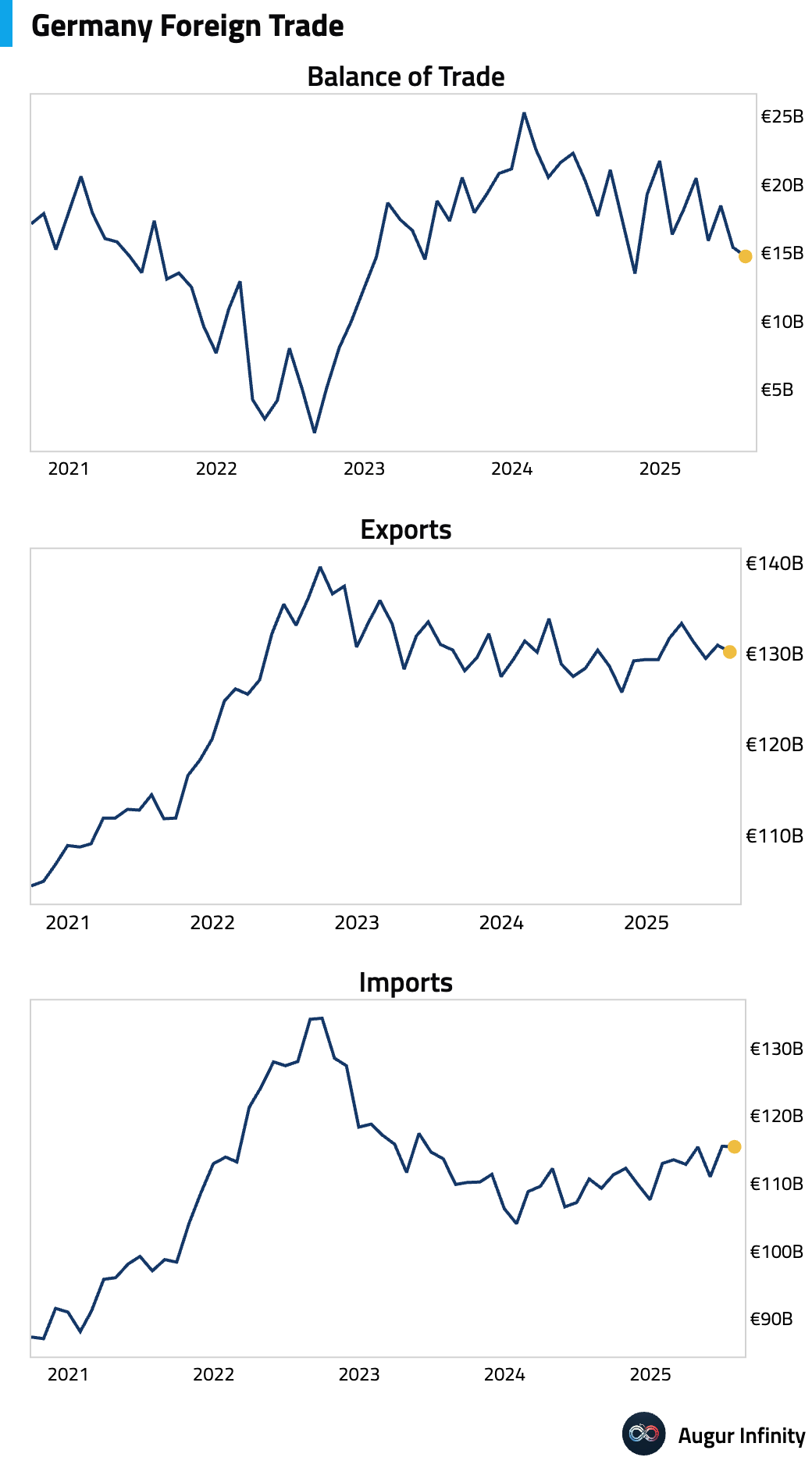

- Germany’s seasonally adjusted trade surplus narrowed to €14.7 billion in July from a revised €15.4 billion, falling short of the €15.4 billion consensus. The decline was driven by a 0.6% M/M drop in exports, while imports contracted by a smaller 0.1%.

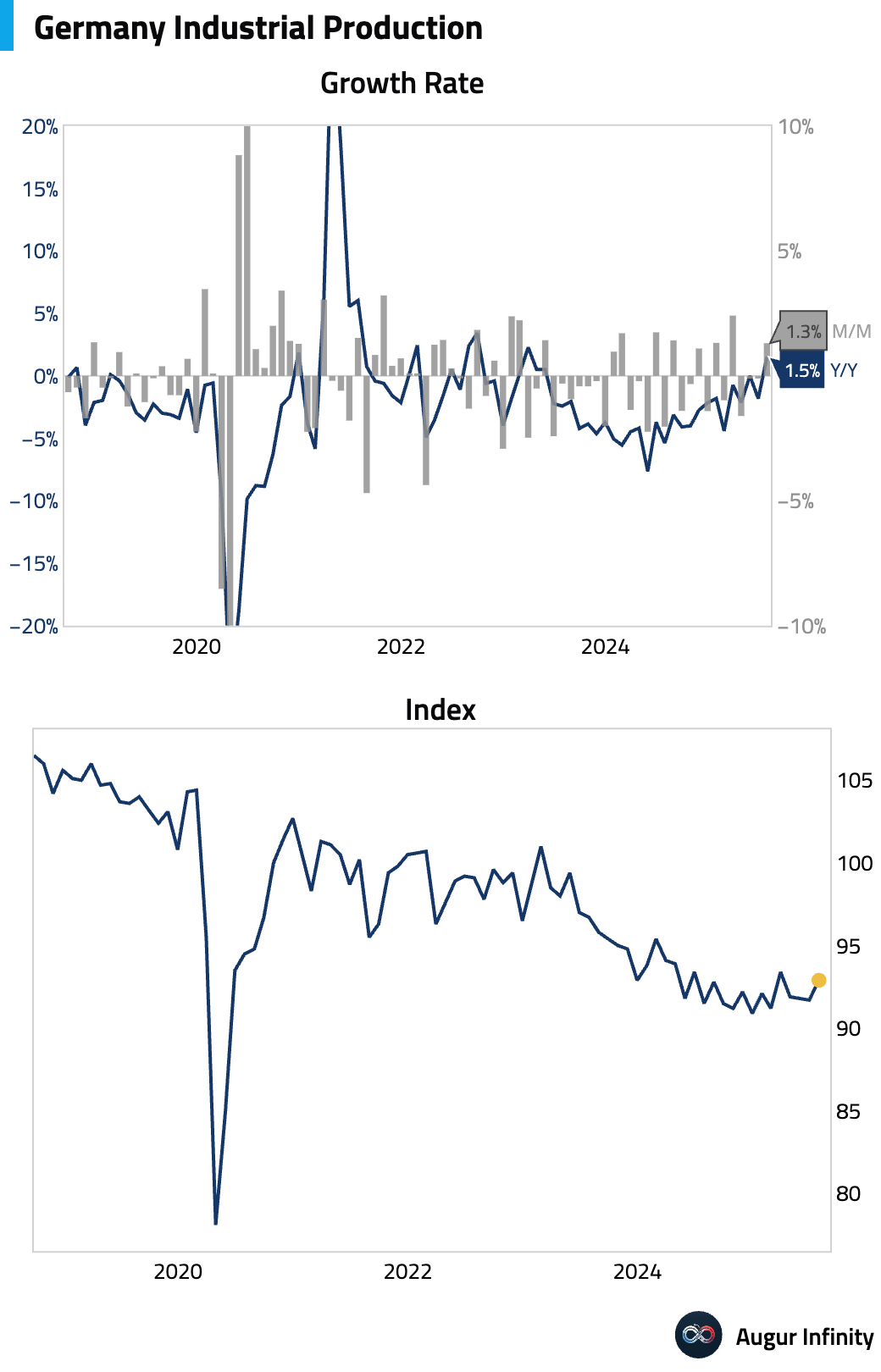

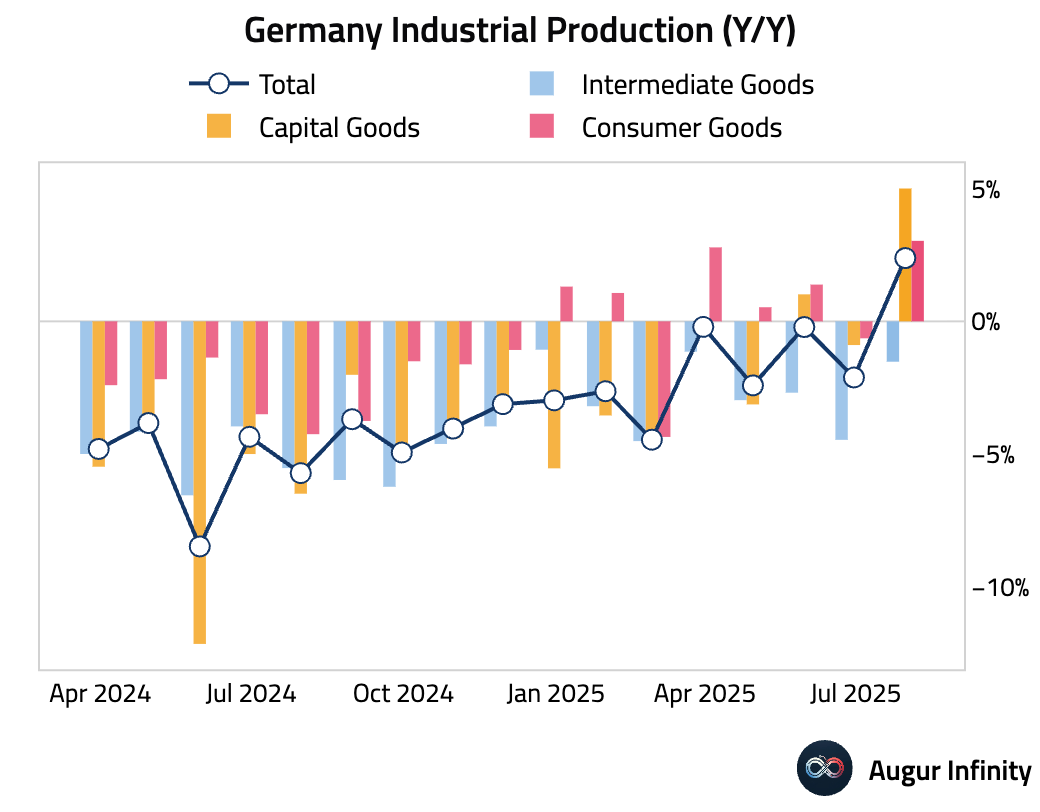

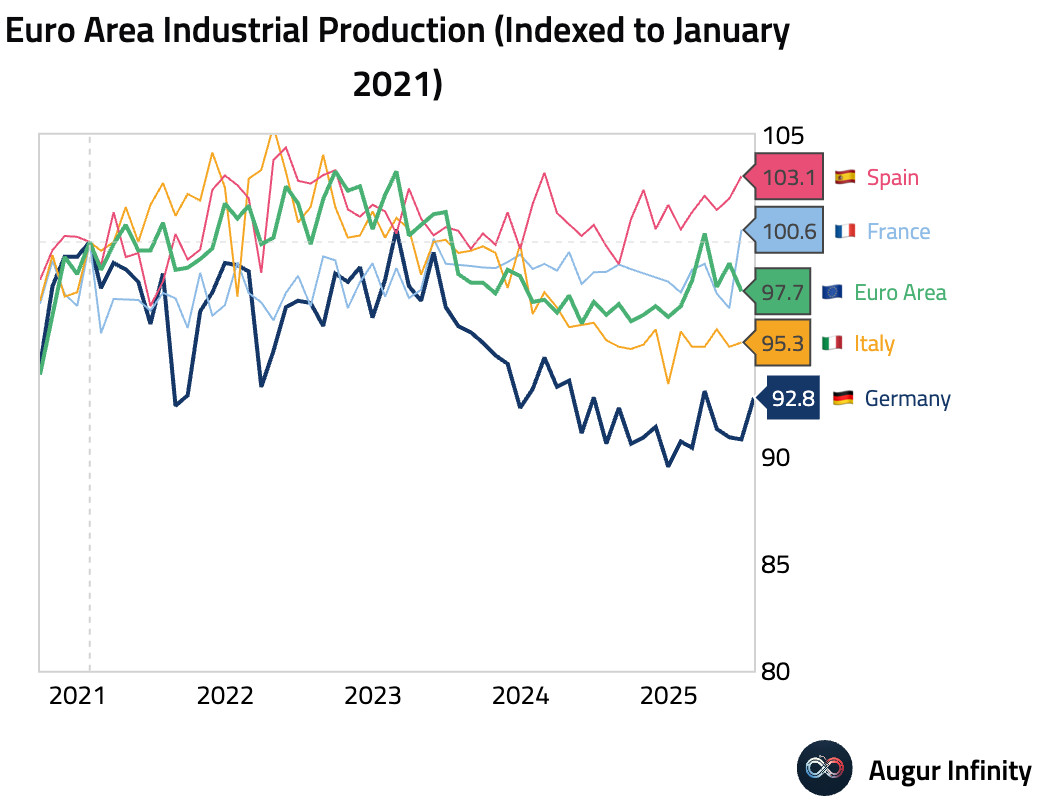

- German industrial production rose by a stronger-than-expected 1.3% M/M in July, rebounding from a 0.1% dip in June.

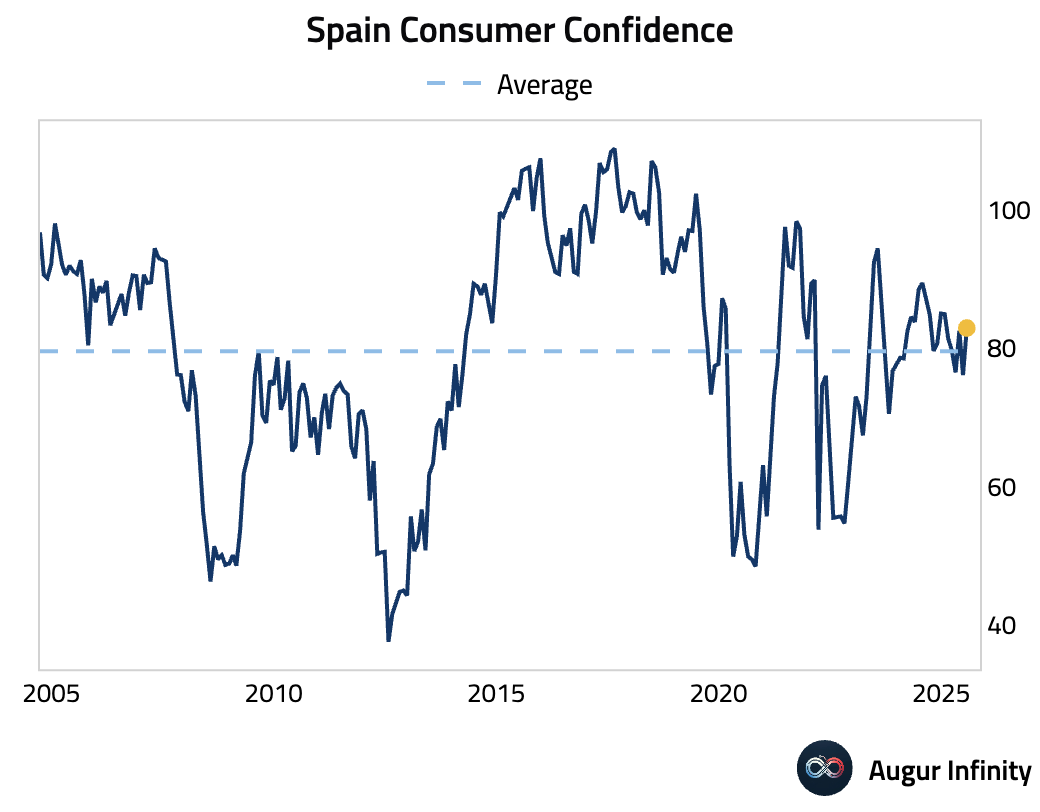

- Spanish consumer confidence jumped to 82.9 in August from 76.1 in July. This marks the highest reading since January, indicating a significant improvement in household sentiment regarding the economic outlook.

Asia-Pacific

- Political uncertainty is rising in Japan after Prime Minister Ishiba announced his resignation following the ruling coalition's failure to secure a majority in the July Upper House election. An internal LDP leadership election is expected in early October. The incoming minority government will necessitate cooperation with the opposition, suggesting a likely expansionary fiscal bias with a potential gasoline tax cut and an autumn inflation package.

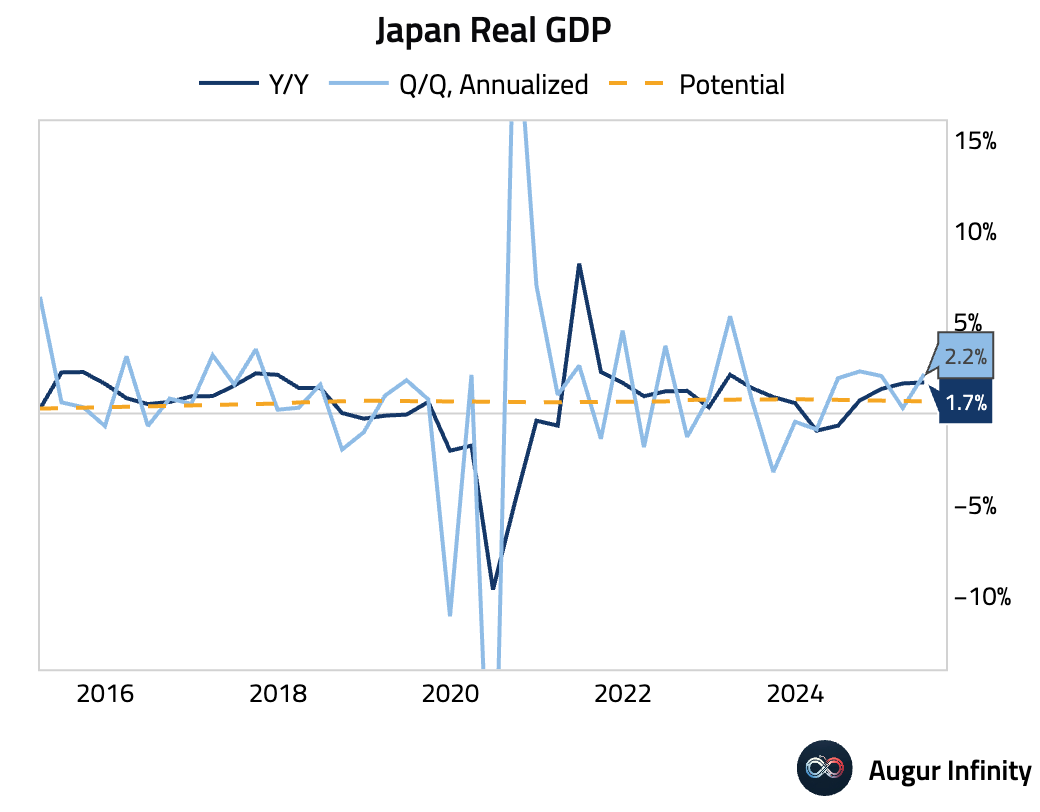

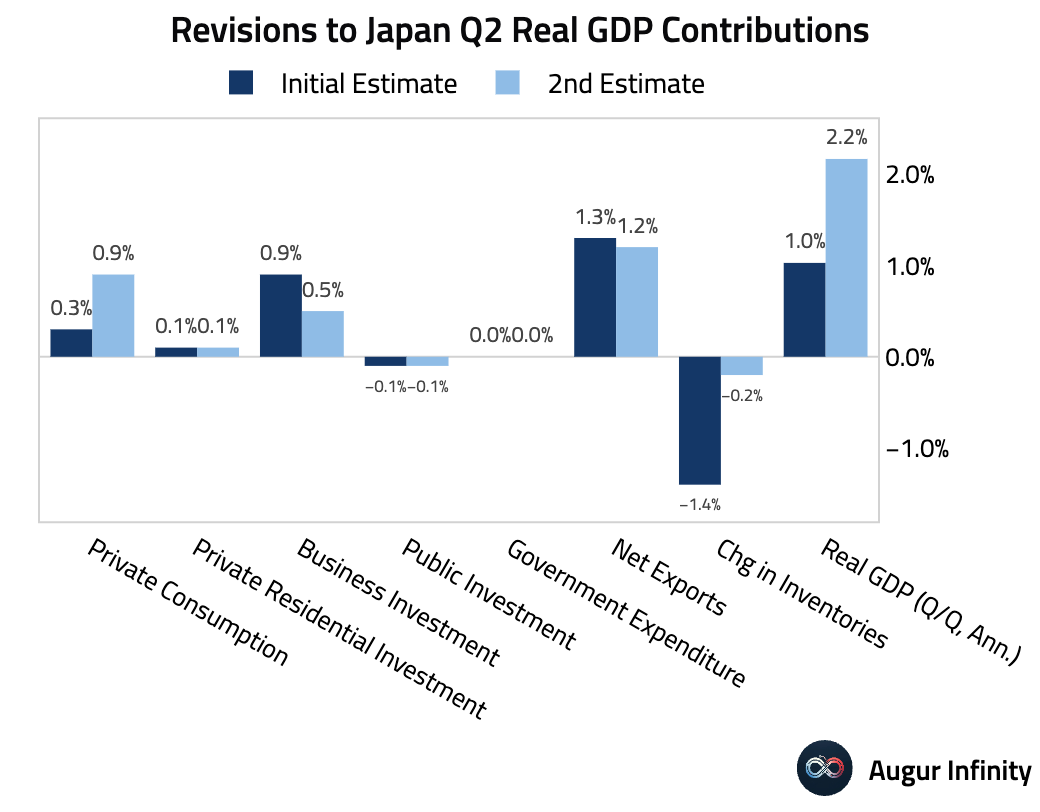

- Japan’s final Q2 GDP growth was revised sharply higher to 2.2% annualized (0.5% Q/Q), more than doubling the 1.0% initial estimate and consensus forecast. The significant upward revision was driven by stronger-than-expected private consumption, which more than offset a large downward revision in capital expenditure and a smaller drag from inventories, signaling a firming of domestic demand.

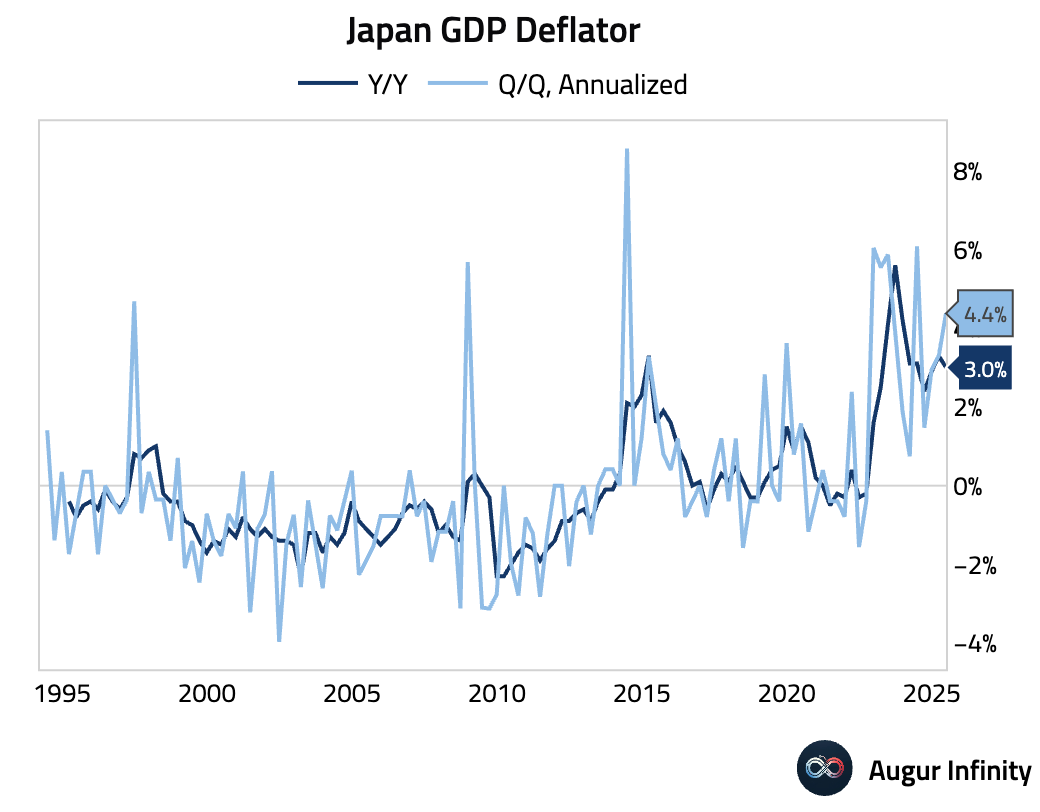

- The final estimate for Japan's Q2 GDP deflator confirmed a 3.0% Y/Y increase, slowing from 3.3% in the prior quarter.

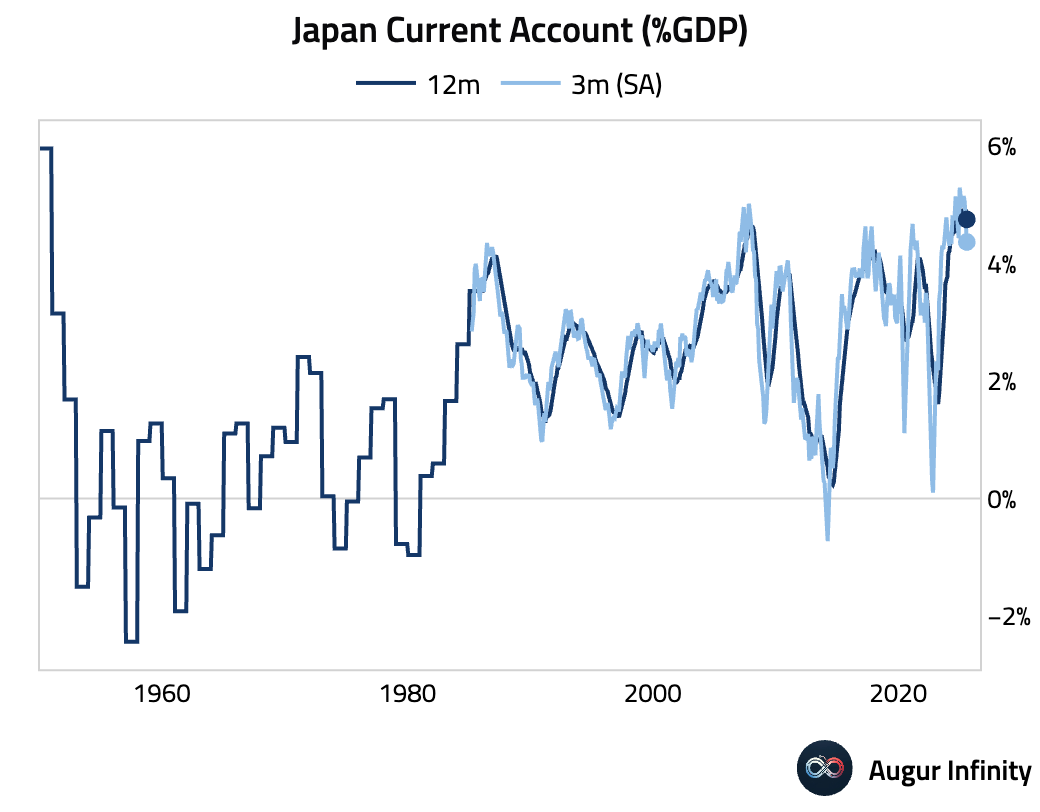

- Japan’s current account surplus narrowed to ¥2.68 trillion in July, well below the ¥3.37 trillion consensus, though up substantially from ¥1.35 trillion in the prior month.

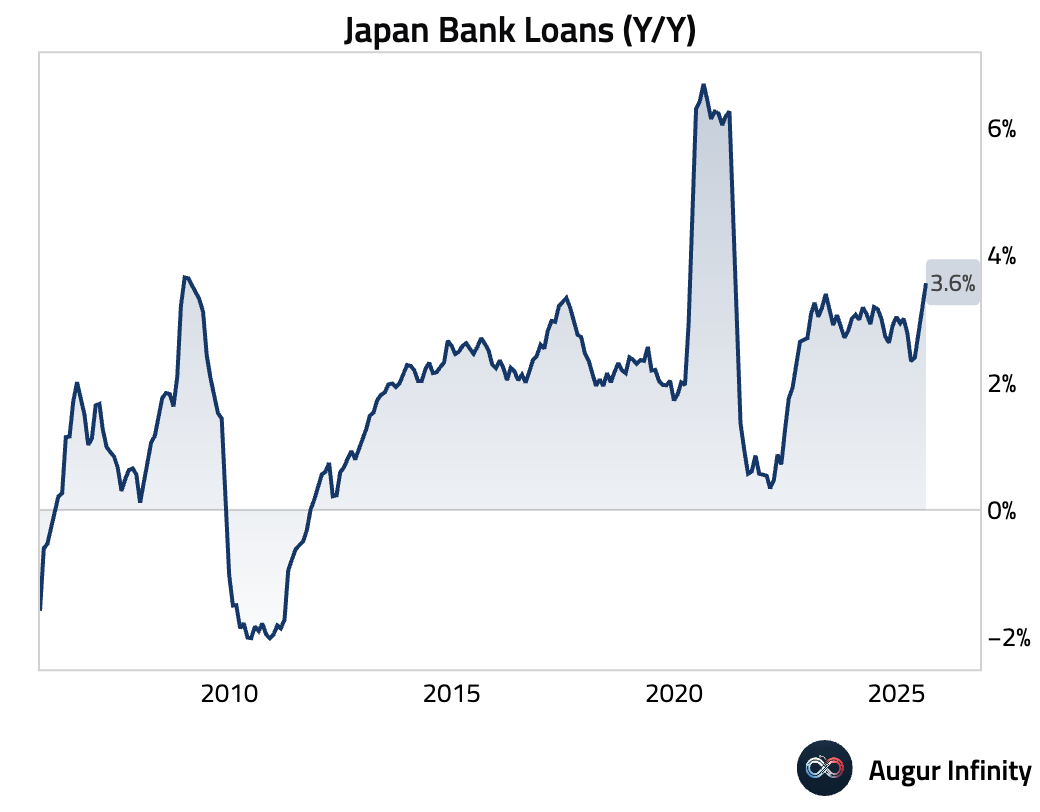

- Bank lending in Japan accelerated to 3.6% Y/Y in August from 3.2% in July, beating the 3.2% consensus. This marks the fastest pace of lending growth since April 2021, suggesting increased credit demand.

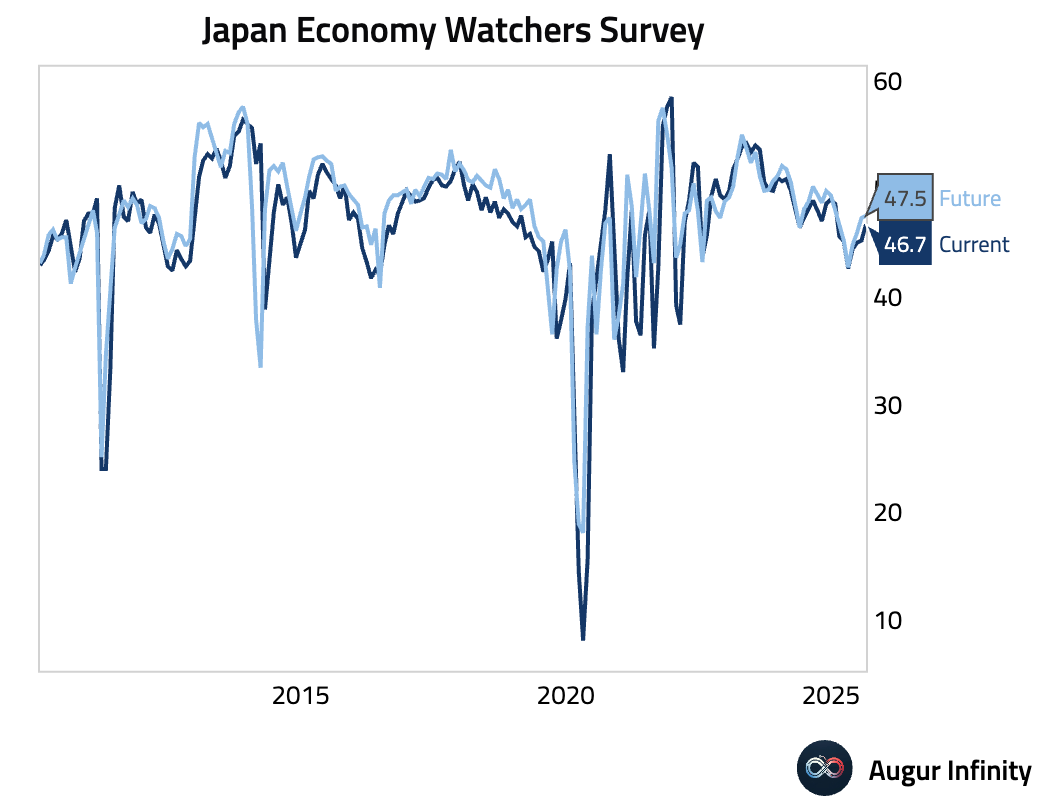

- The Japanese Economy Watchers Survey for August showed a modest improvement in sentiment. The current conditions index rose to 46.7 from 45.2, while the outlook index edged up to 47.5 from 47.3.

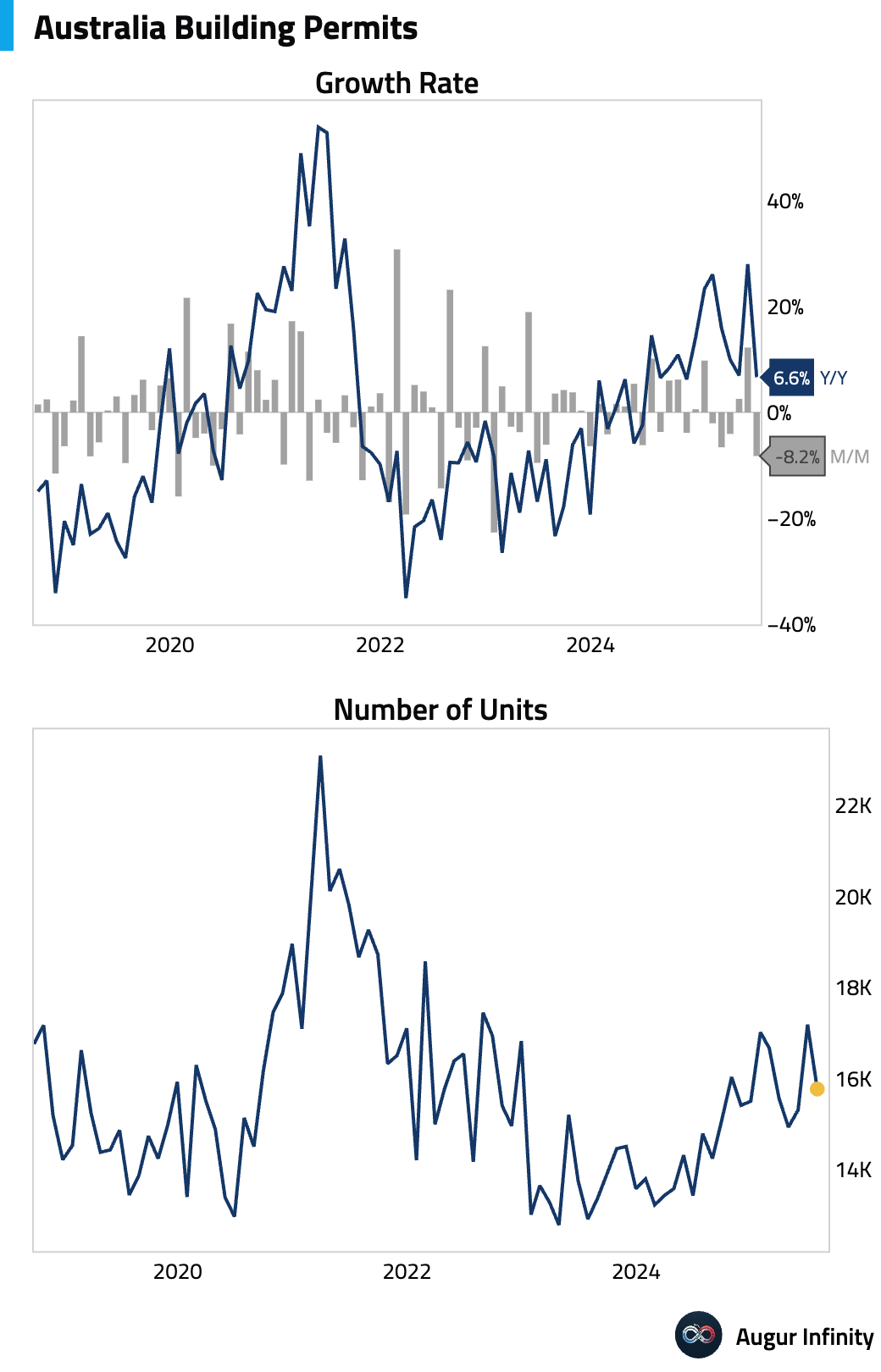

- Australian building permits fell 8.2% M/M in July, partially reversing June’s 12.2% surge and pointing to continued volatility in the construction pipeline.

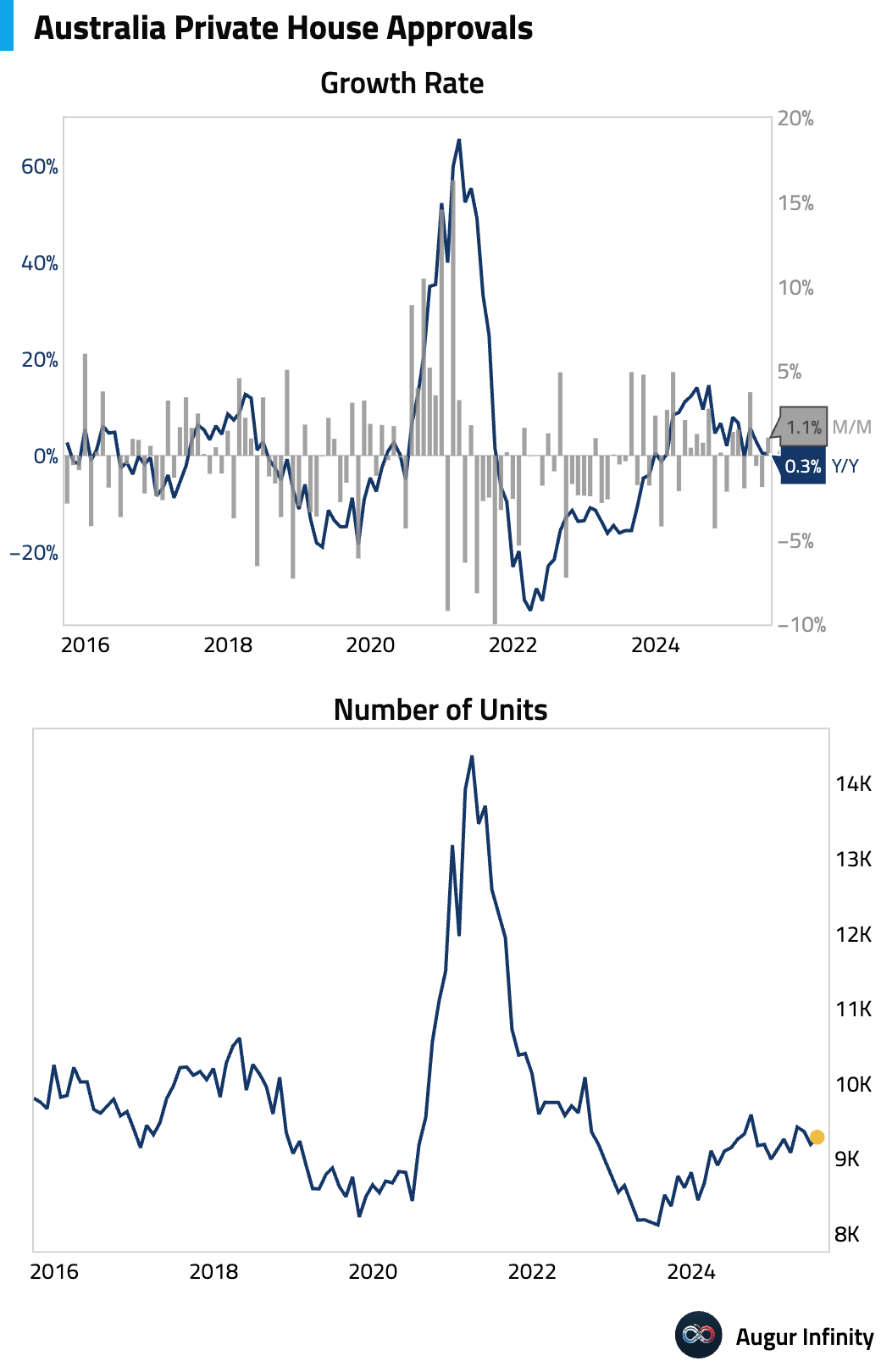

- Approvals for private sector houses in Australia rose 1.1% M/M in July, rebounding from a 1.9% decline in the previous month.

China

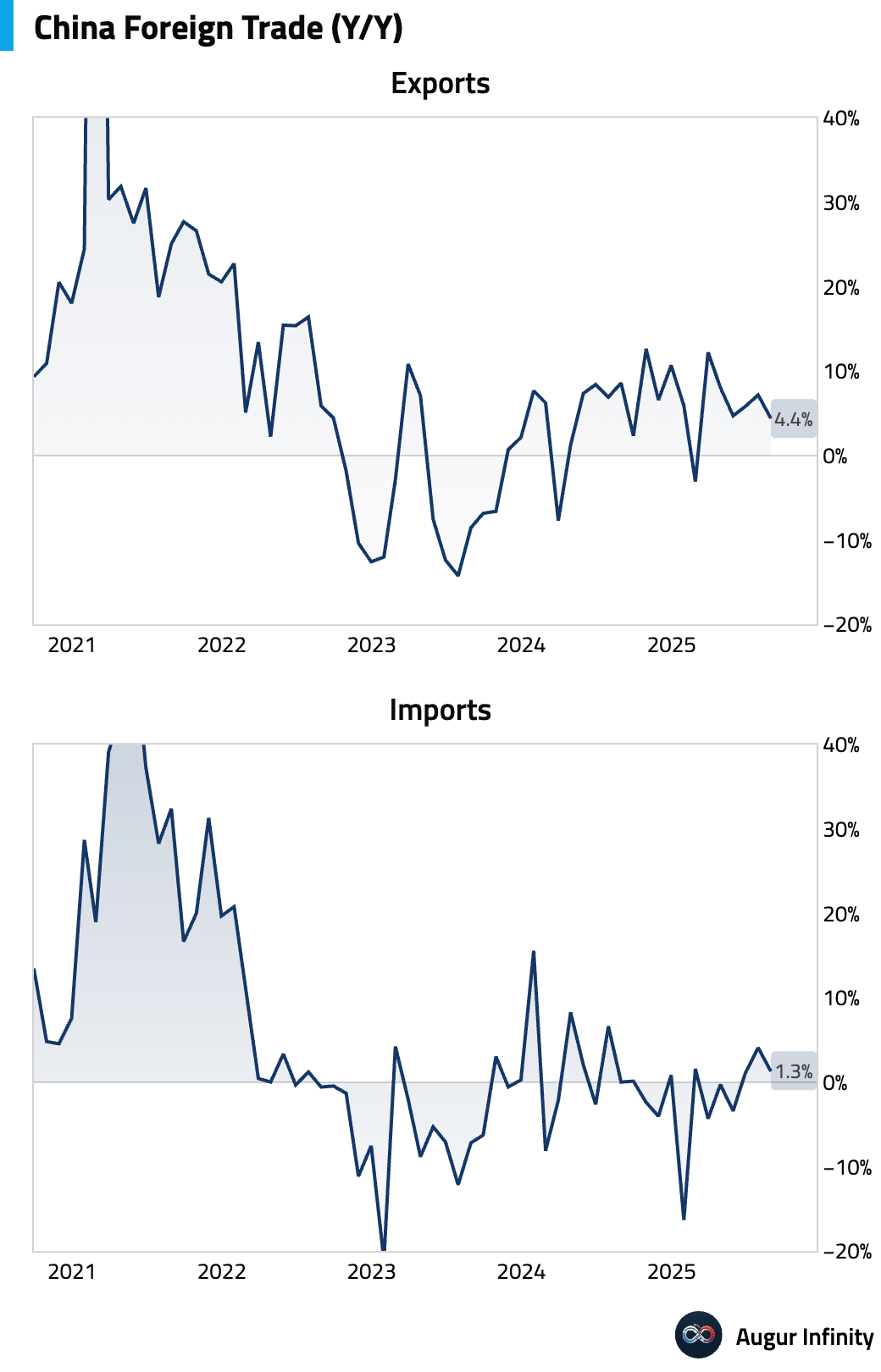

- China’s trade surplus widened to a larger-than-expected $102.3 billion in August. However, underlying growth momentum slowed significantly, with exports rising 4.4% Y/Y (vs. 5.0% consensus) and imports growing just 1.3% Y/Y (vs. 3.0% consensus). The export slowdown was primarily driven by a sharp 33.1% Y/Y decline in shipments to the US, while broad-based import weakness points to soft domestic demand.

Emerging Markets ex China

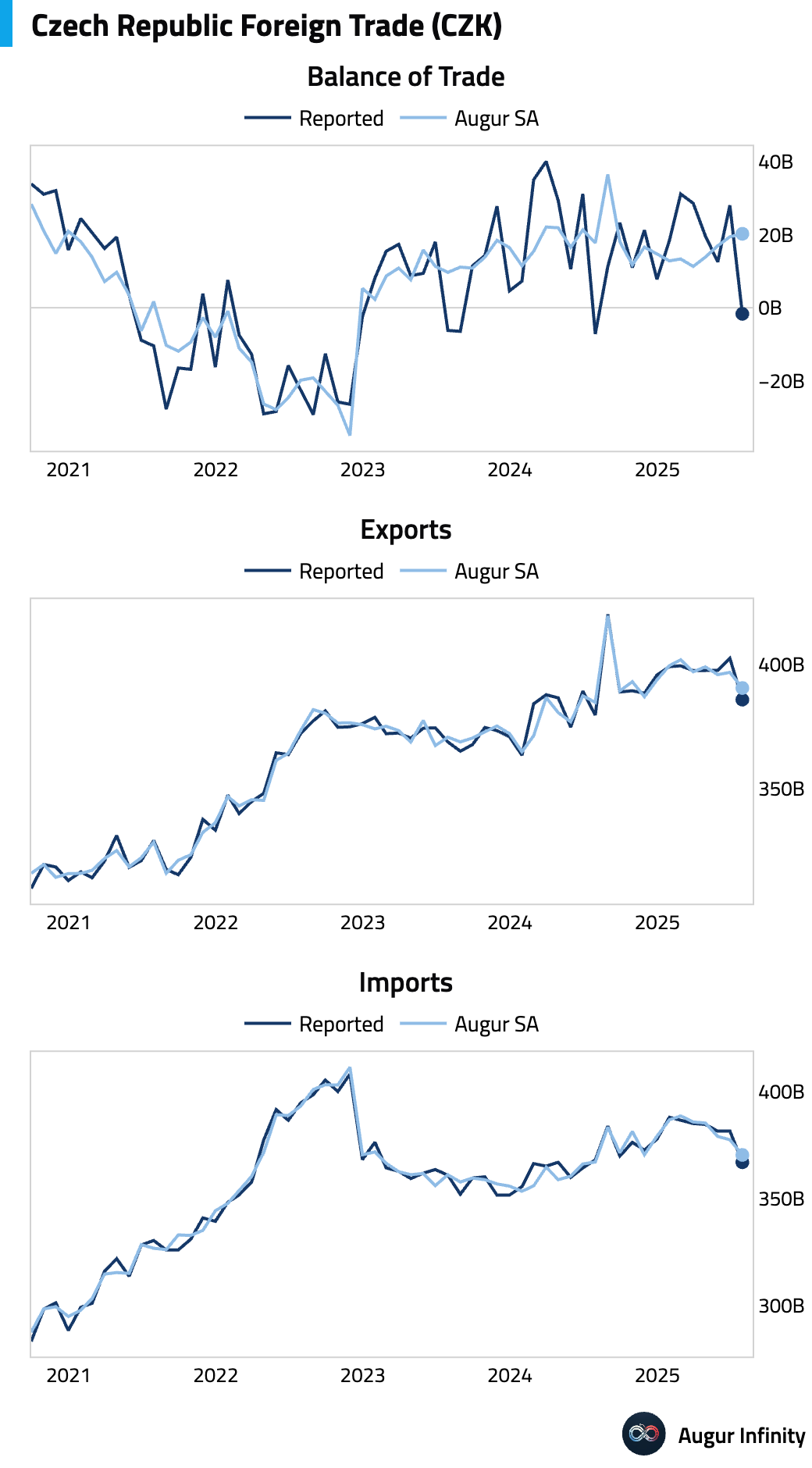

- The Czech Republic's trade balance swung to a deficit of CZK 1.7 billion in July from a surplus of CZK 28.1 billion in June. On a seasonally-adjusted basis, however, trade balance was stable.

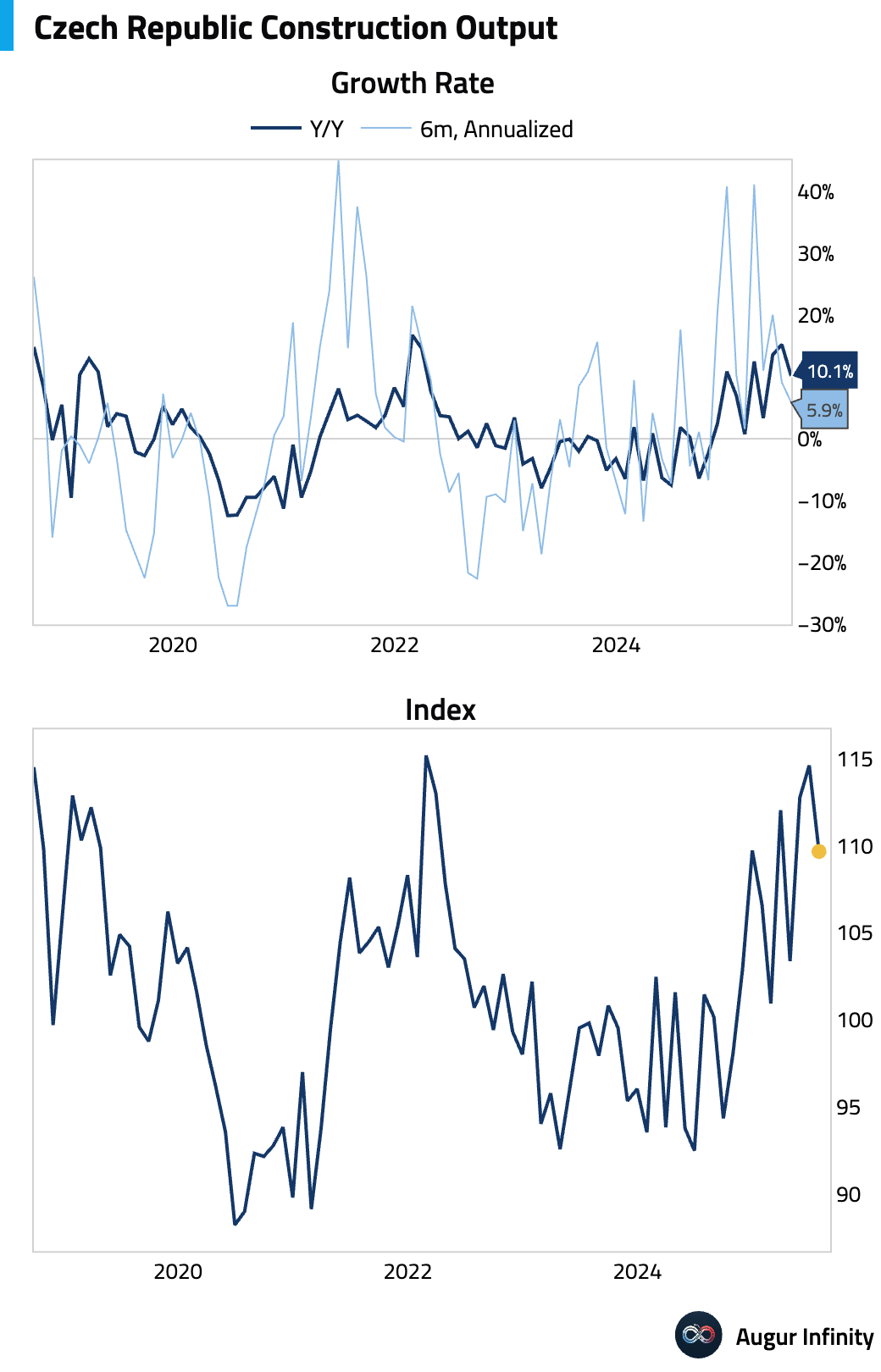

- Construction output in the Czech Republic expanded by 10.1% Y/Y in July. While this represents a slowdown from the 14.0% pace in June, it continues to reflect robust activity in the sector.

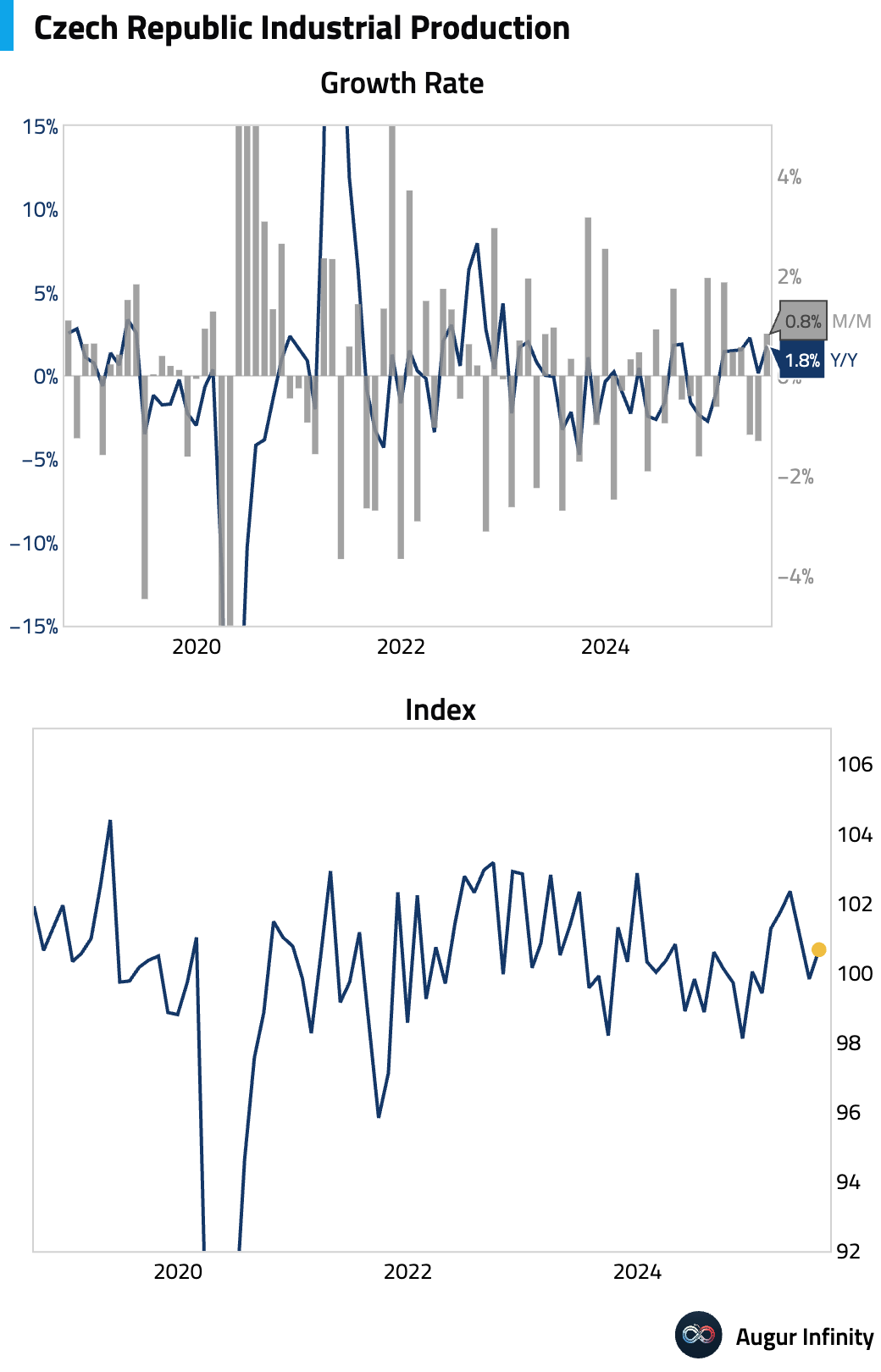

- Czech industrial production rebounded in July, rising 0.8% M/M and accelerating to 1.8% Y/Y from 0.2% previously. The annual figure surpassed the 1.5% consensus estimate.

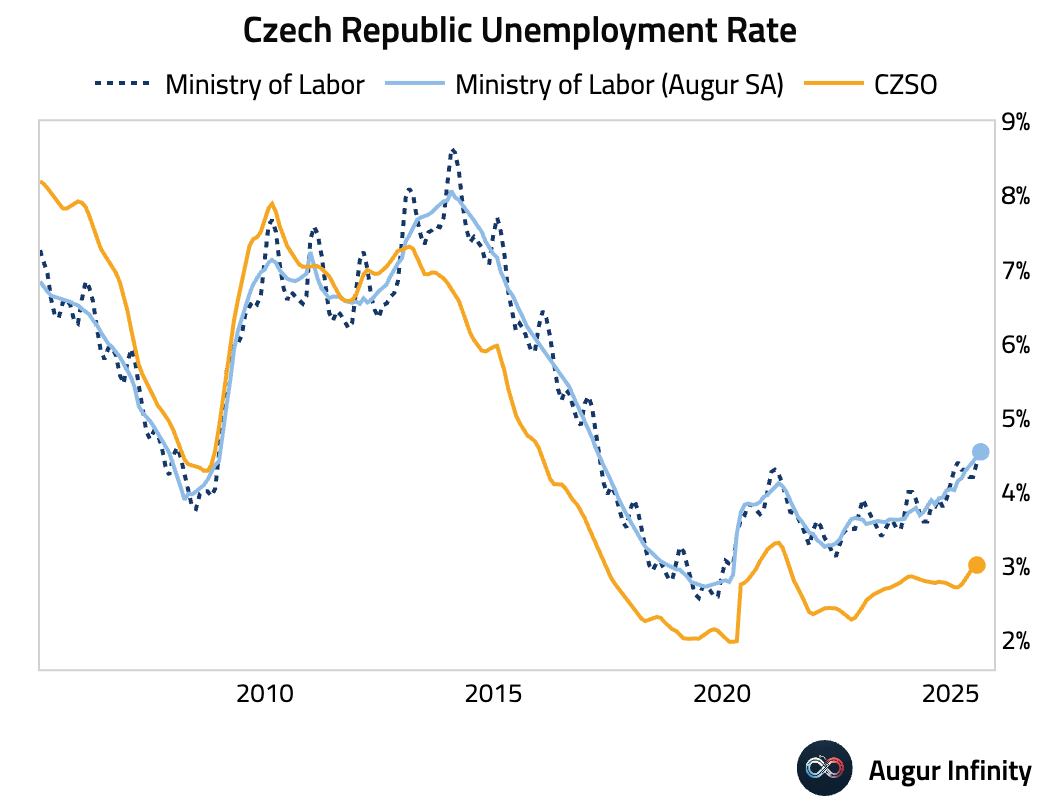

- The unemployment rate in the Czech Republic edged up to 4.5% in August from 4.4% in July, reaching its highest level since March 2017.

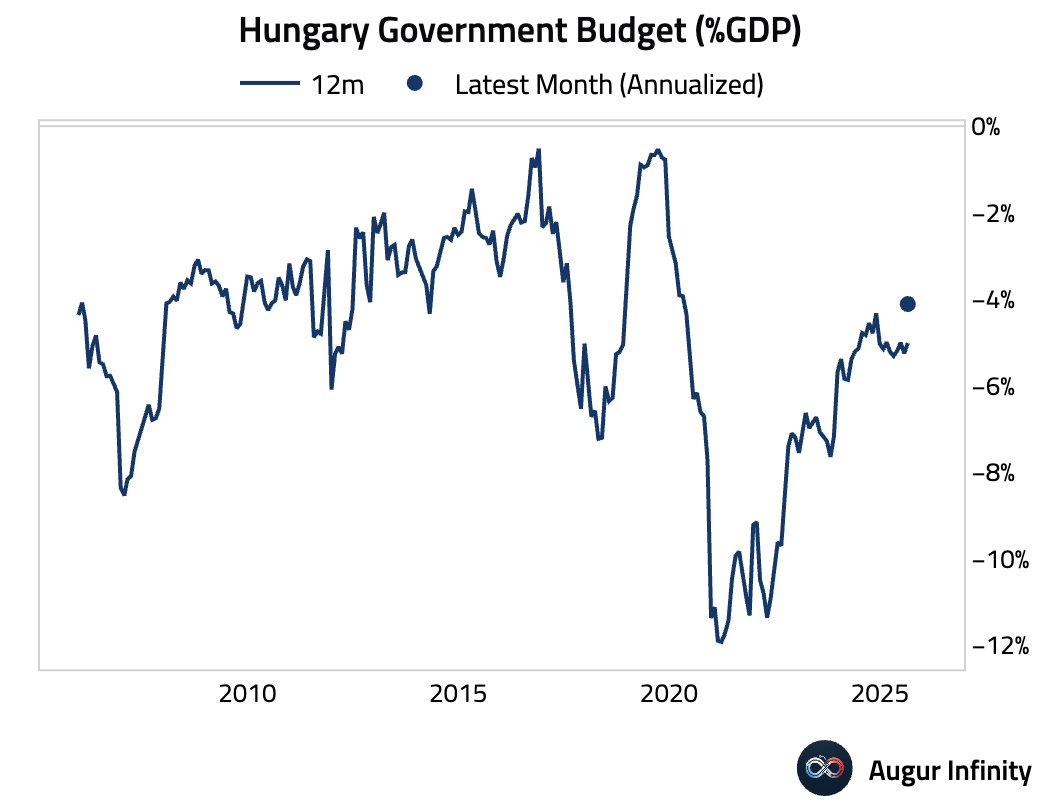

- Hungary recorded a budget deficit of HUF 239.1 billion in August, a significant widening from the HUF 12.8 billion deficit reported in July.

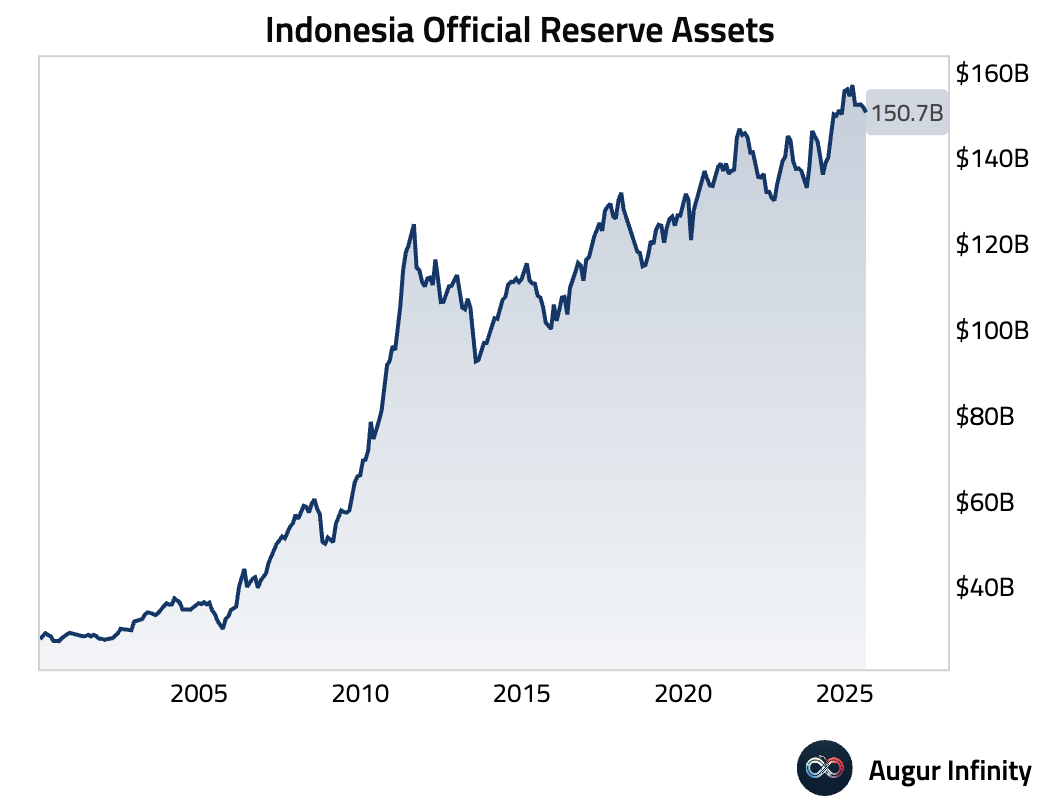

- Indonesia's official foreign reserve assets decreased to $150.7 billion in August from $152.0 billion in the prior month.

Global Markets

Equities

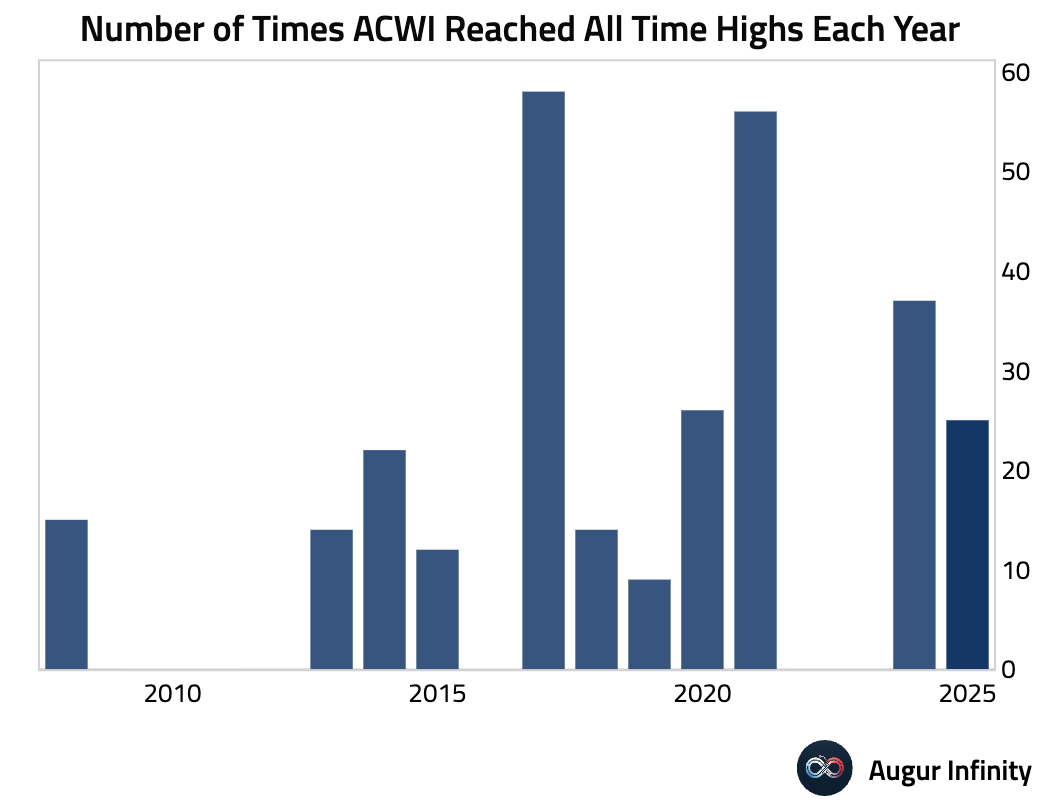

- iShares MSCI ACWI ETF has reached all-time highs 25 times this year.

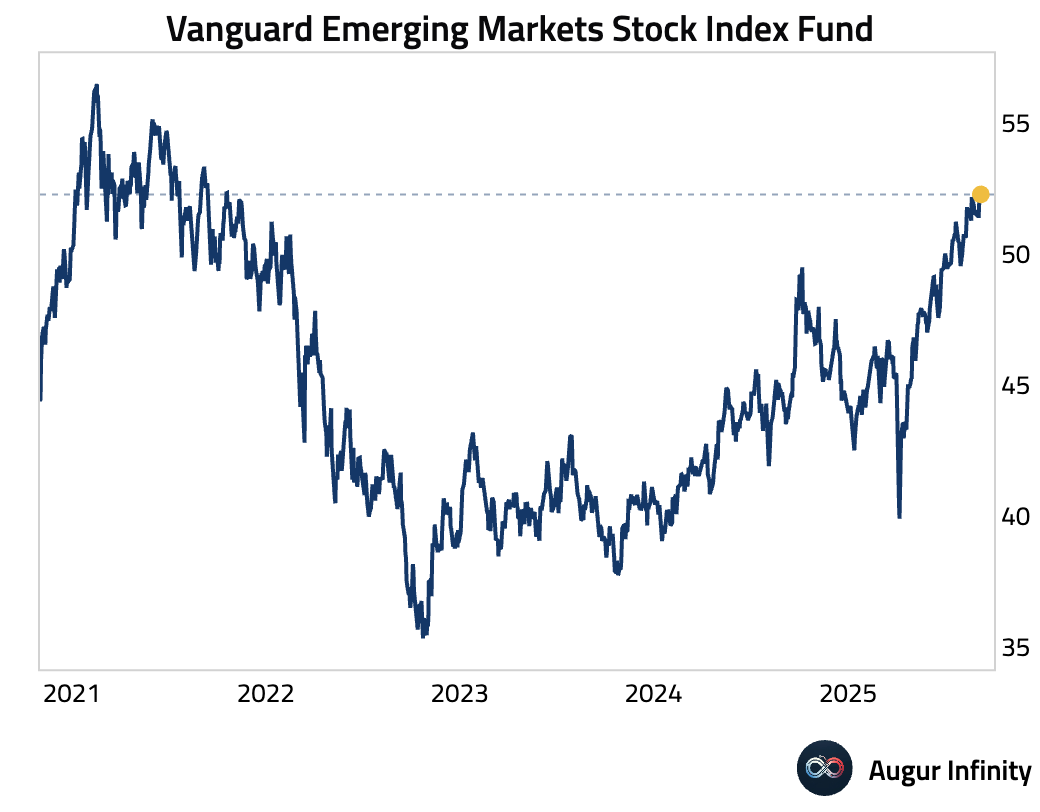

- Vanguard Emerging Markets Stock Index Fund has risen to the highest level since October 2021.

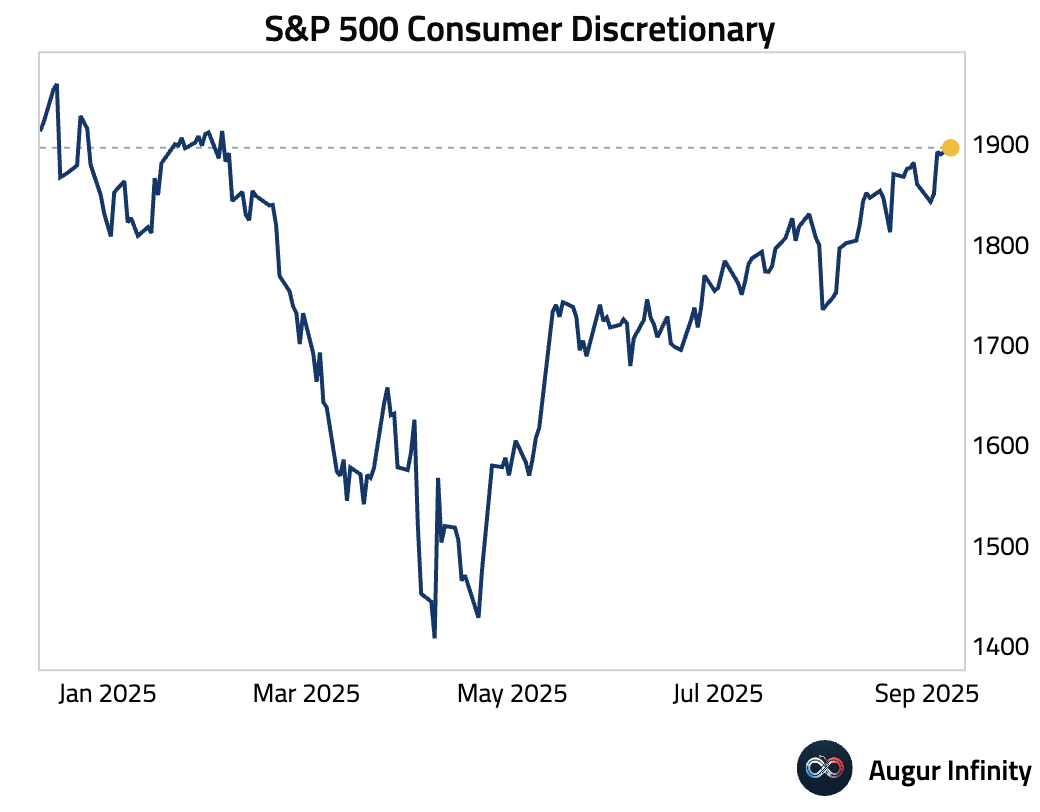

- Turning to the US, S&P 500 Consumer Discretionary has rallied to the highest level since February 2025.

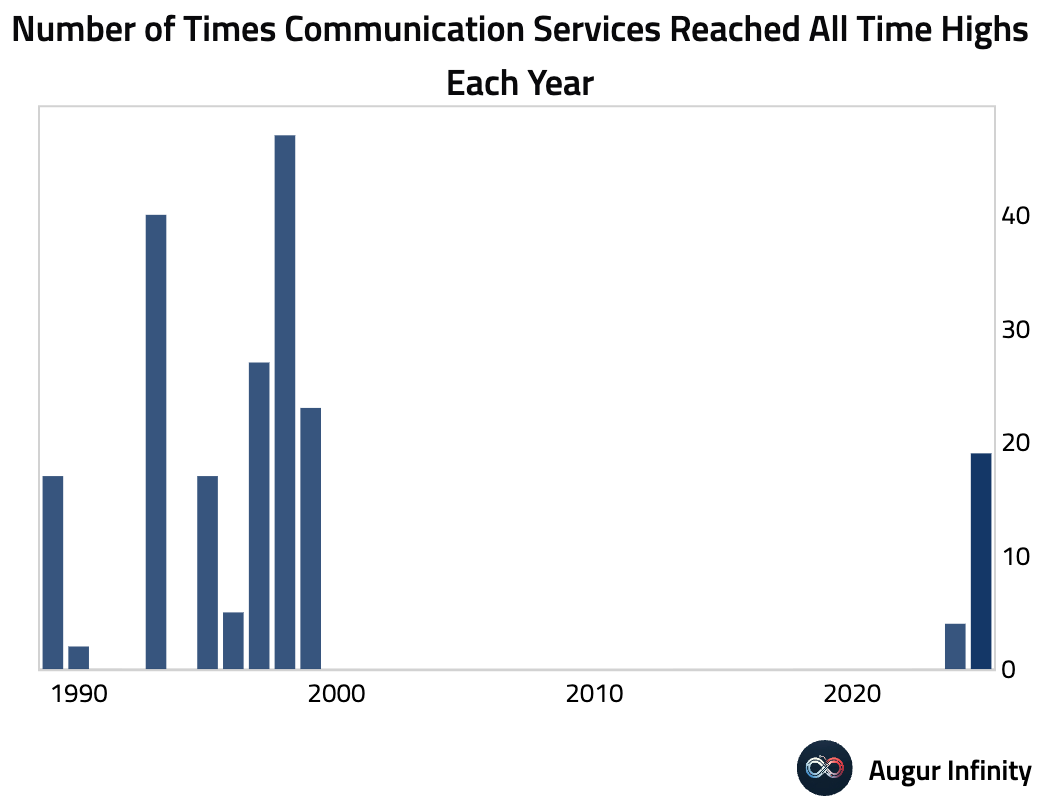

- The S&P 500 Communication Services Index has climbed to a fresh all-time-high, the 19th of the year.

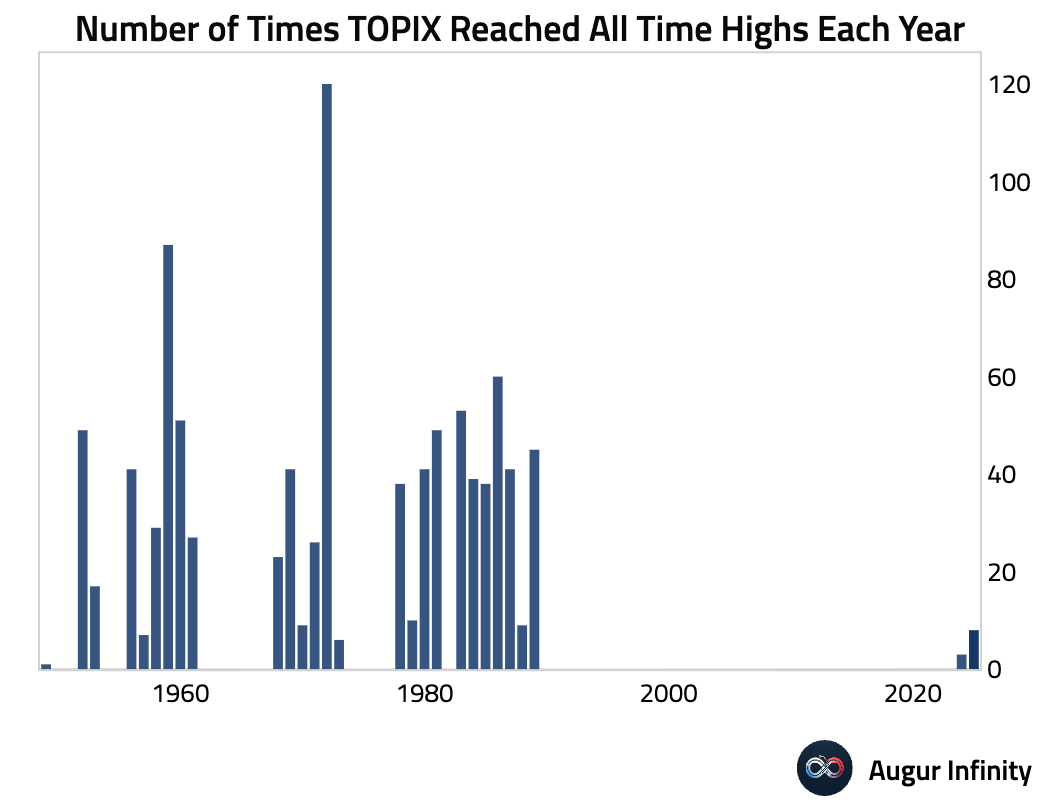

- Japan's TOPIX Index also gained 1%, claiming the 8th all-time-high in 2025.

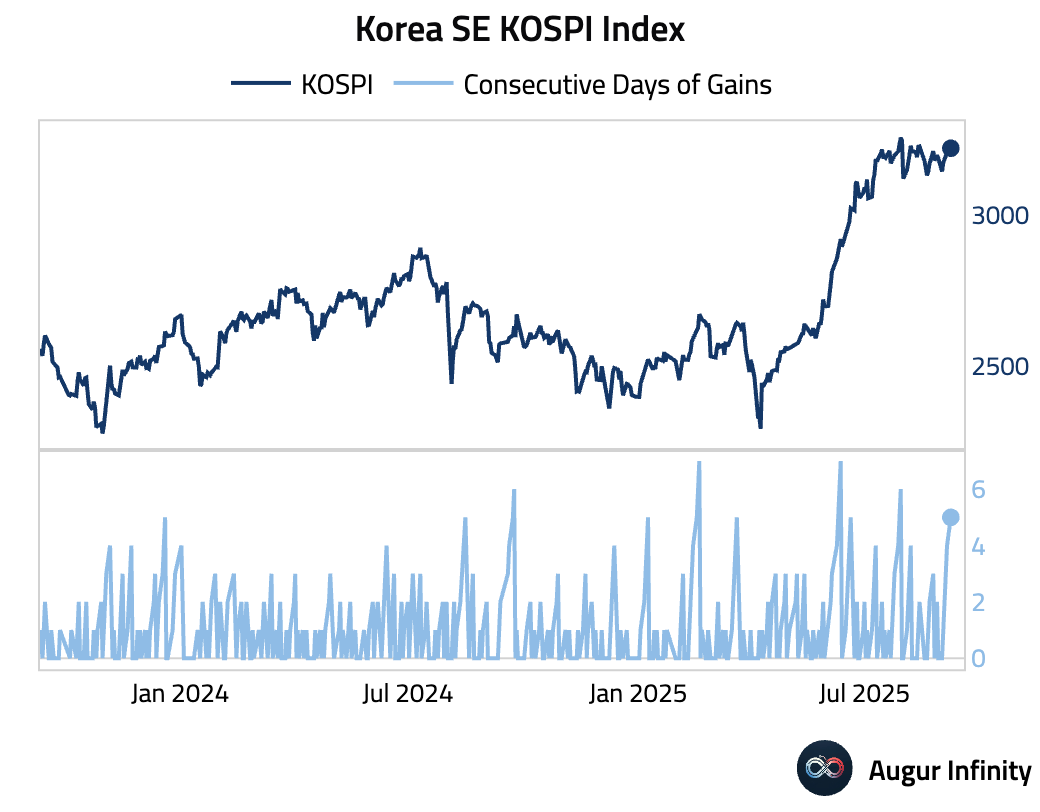

- Korea SE KOSPI Index notched its fifth consecutive gains.

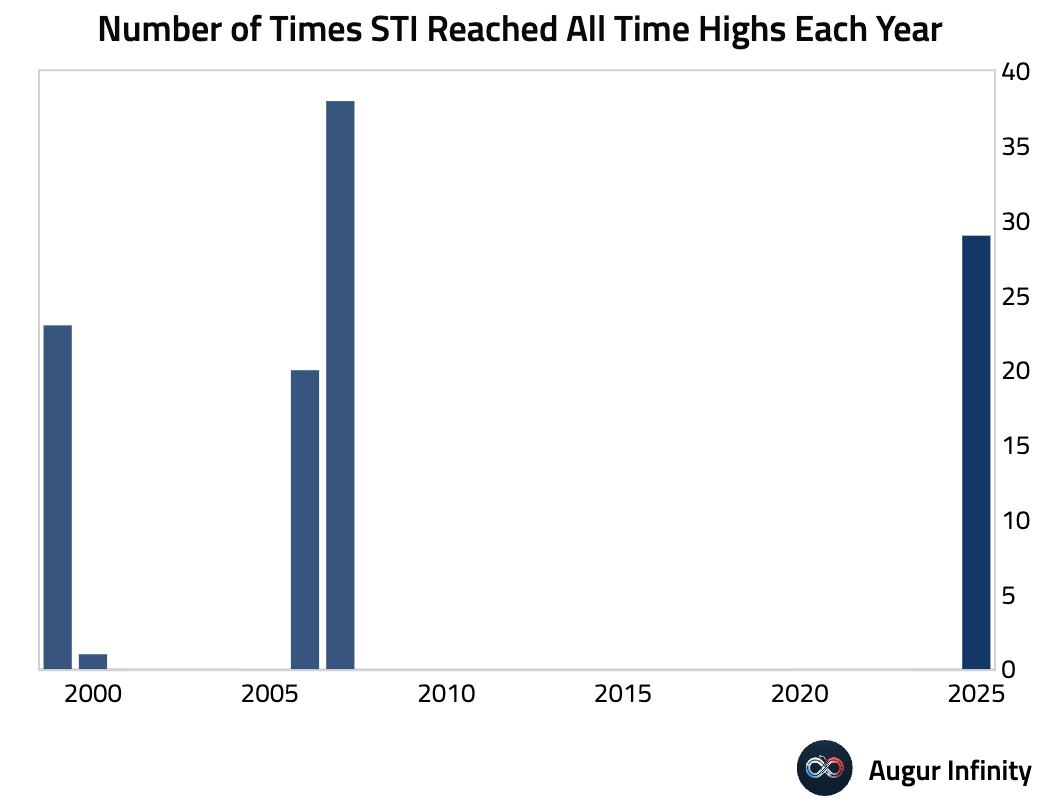

- FTSE Straits Times Index for Singapore reached its 29th all-time-high this year.

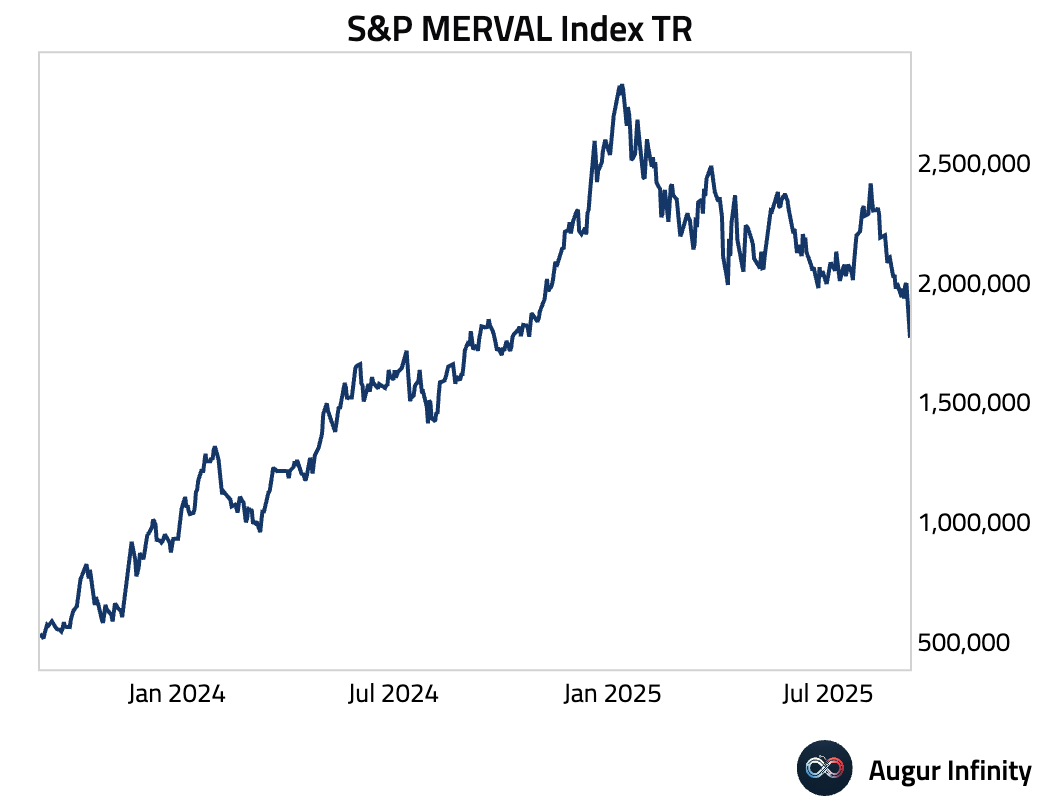

- However, not all global markets are as rosy. The S&P MERVAL Index is down 11.4%, a 3.8σ move. The sharp decline was due to a major political setback suffered by President Javier Milei’s party in this weekend’s provincial election in Buenos Aires, Argentina’s largest and most critical province. The loss, which was far larger than anticipated, has sparked investor fears regarding the stability and future prospects of Milei’s radical reform agenda.

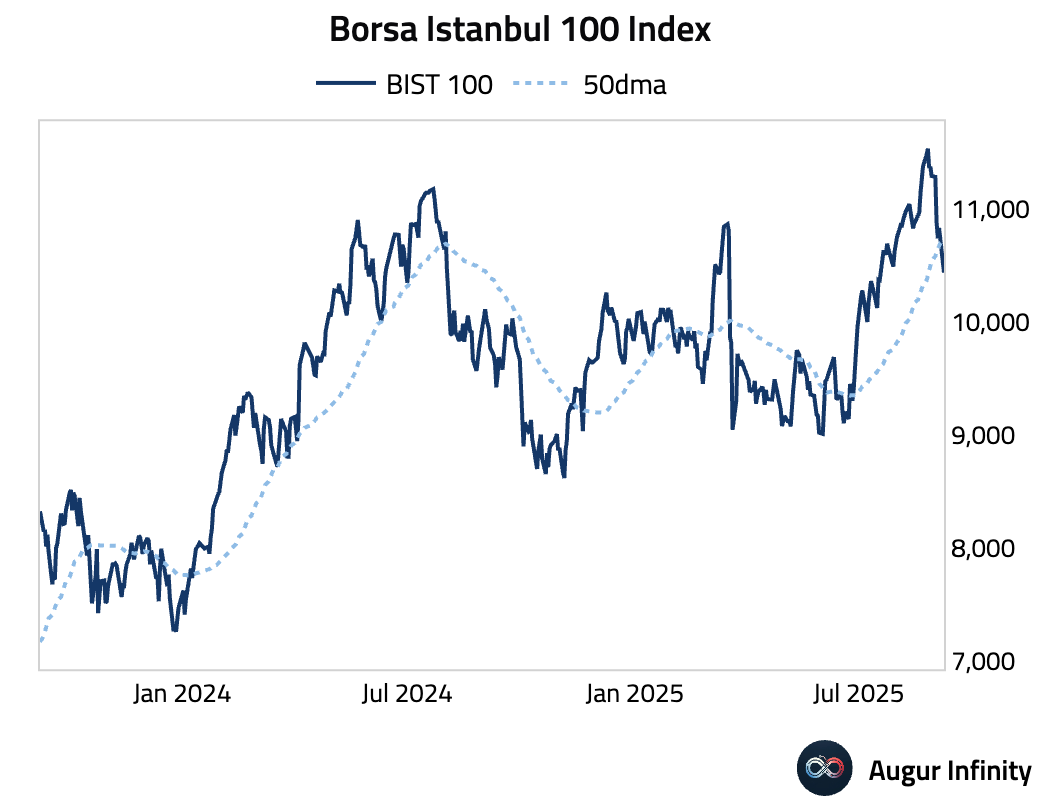

- Borsa Istanbul 100 Index has also performed poorly, down below its 50-day moving average.

Fixed Income

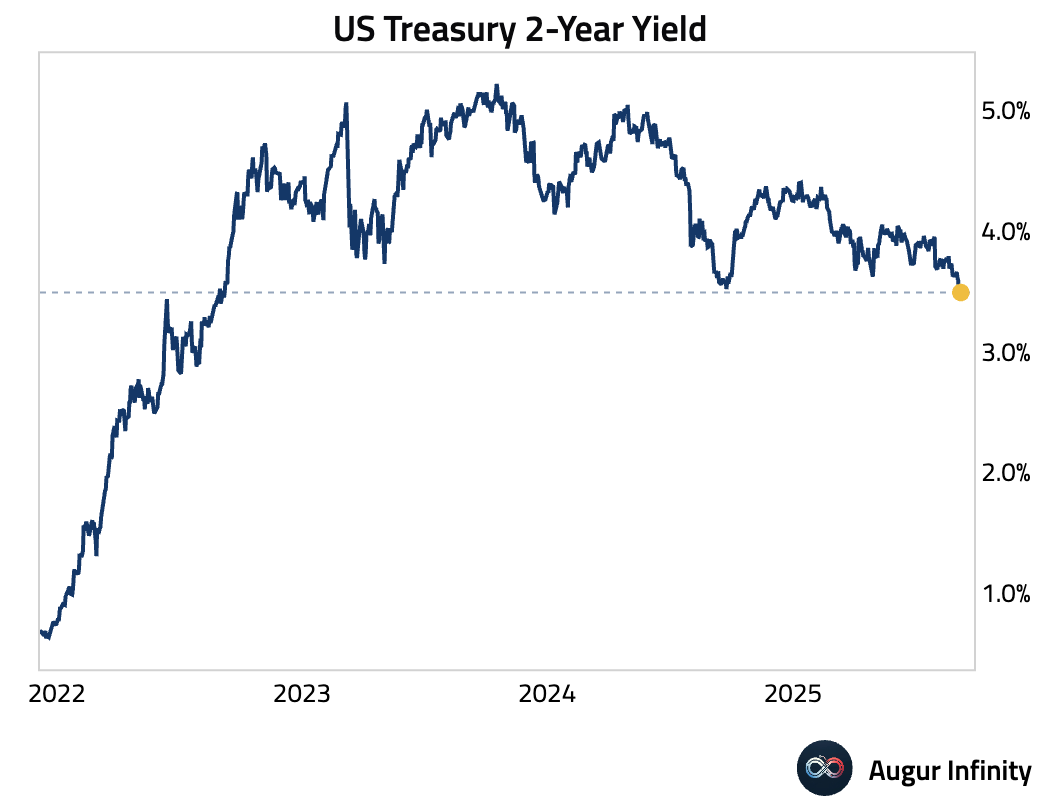

- US Treasury 2-Year Yield is at the lowest level since September 2022.

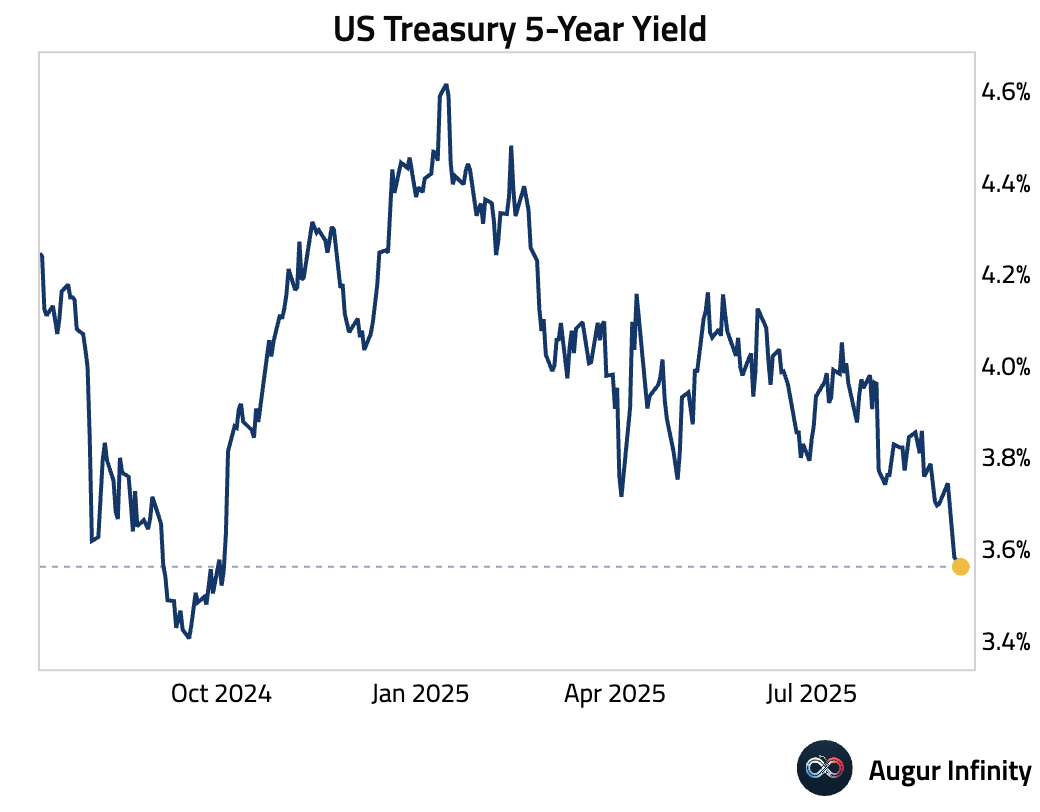

- US Treasury 5-Year Yield is at the lowest level since October 2024.

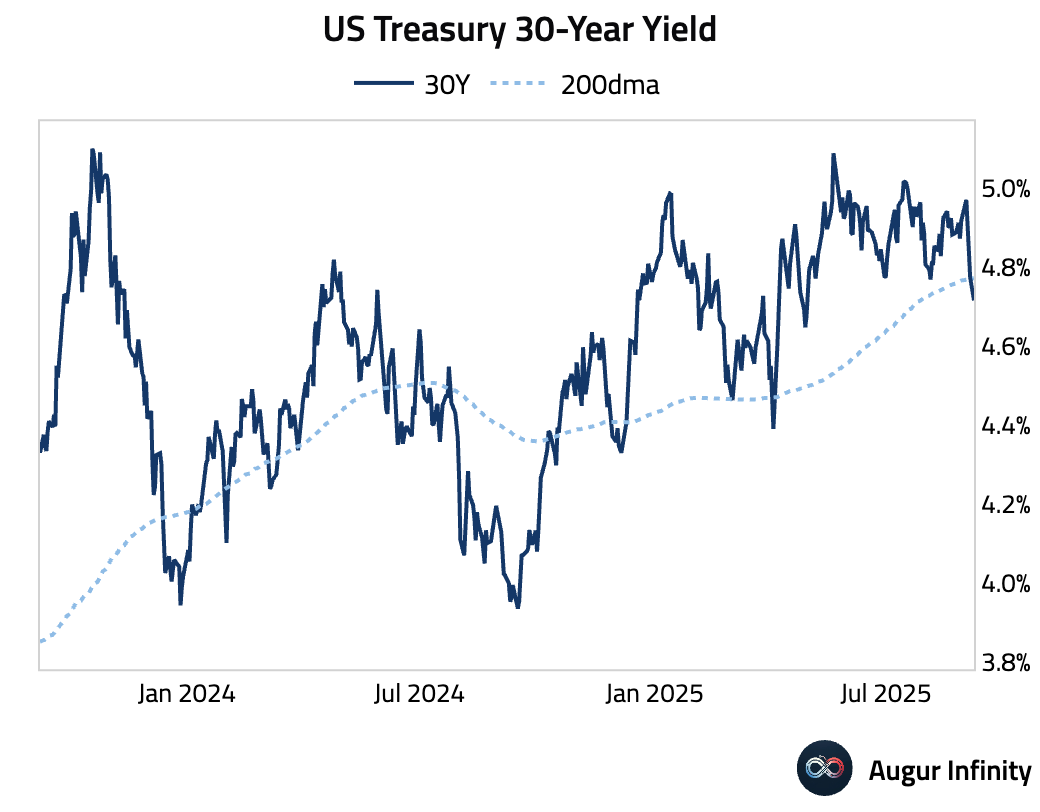

- US Treasury 30-Year Yield is below its 200-day moving average.

FX

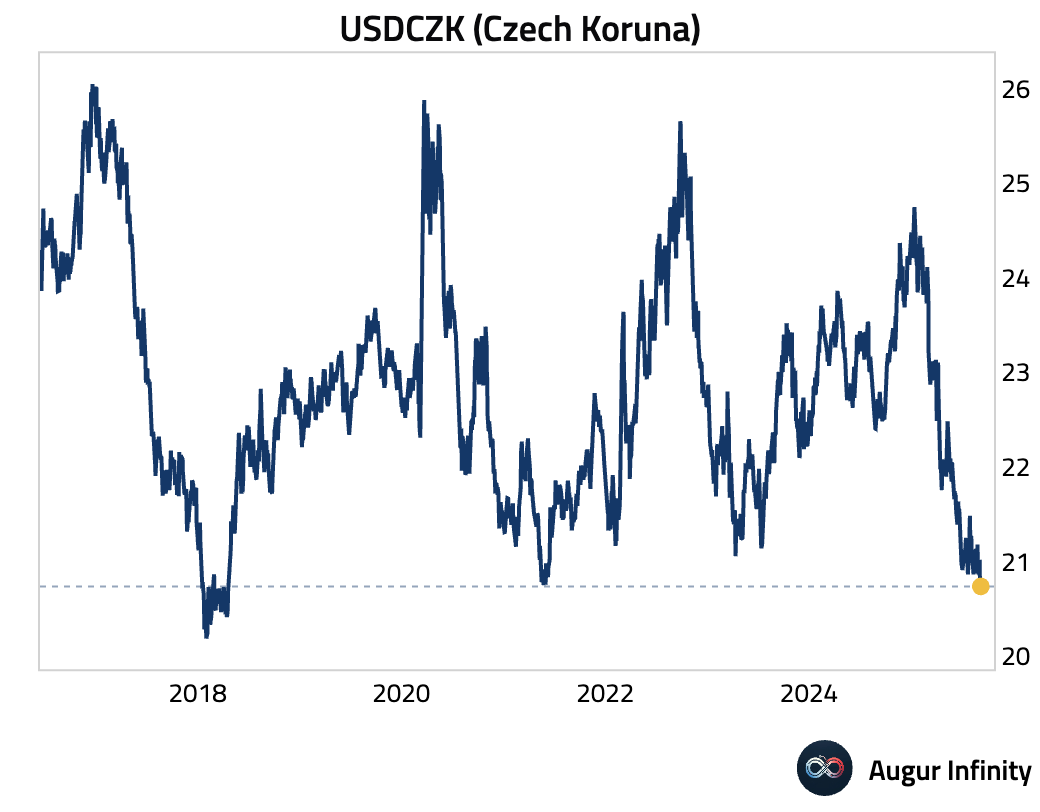

- USDCZK (Czech Koruna) is at the lowest level since April 20, 2018.

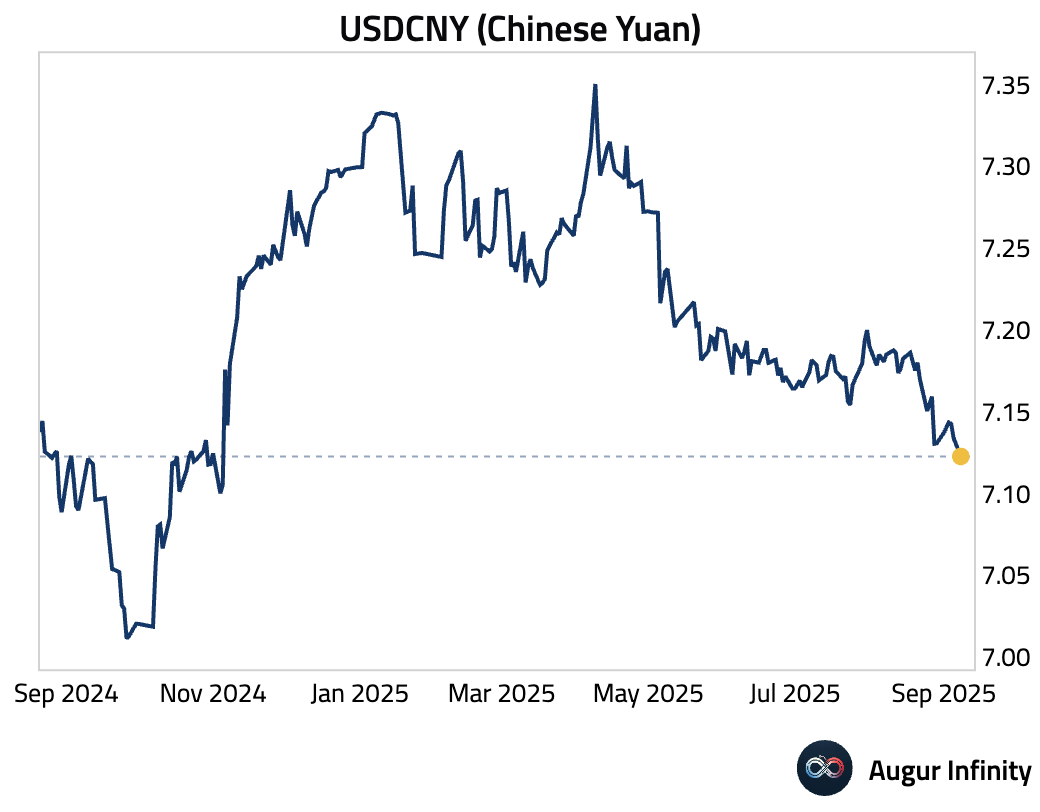

- USDCNY (Chinese Yuan) is at the lowest level since November 5, 2024.

Commodities

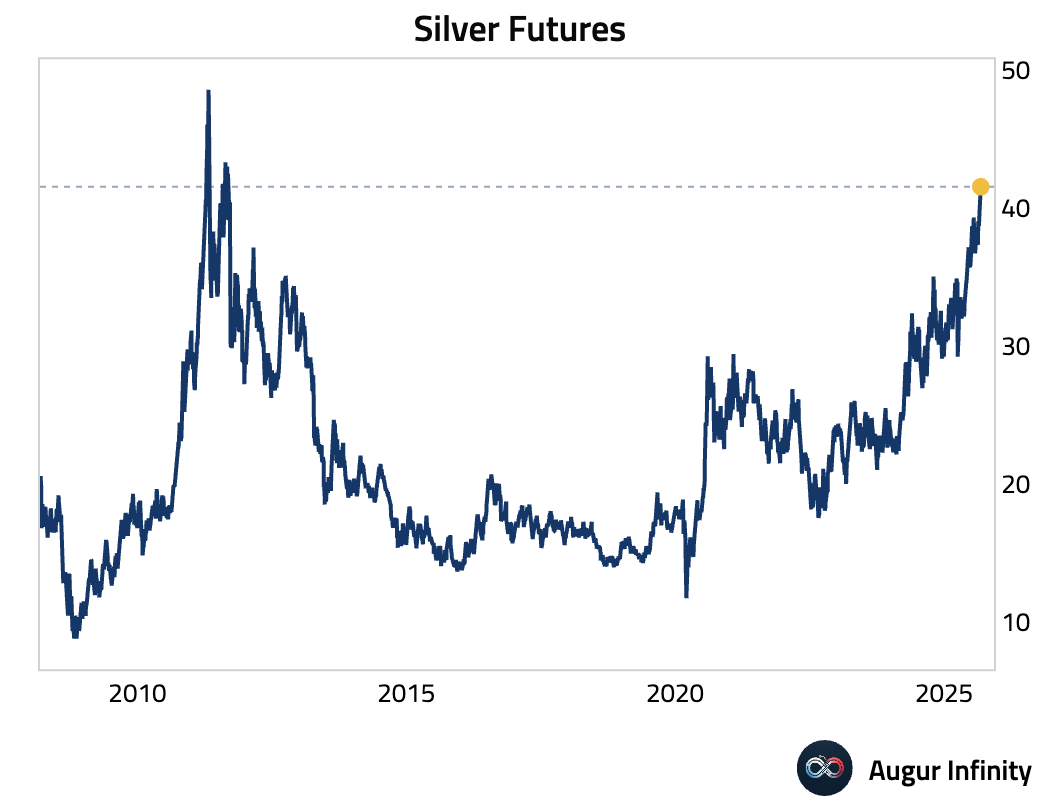

- Silver futures is at the highest level since September 2011.

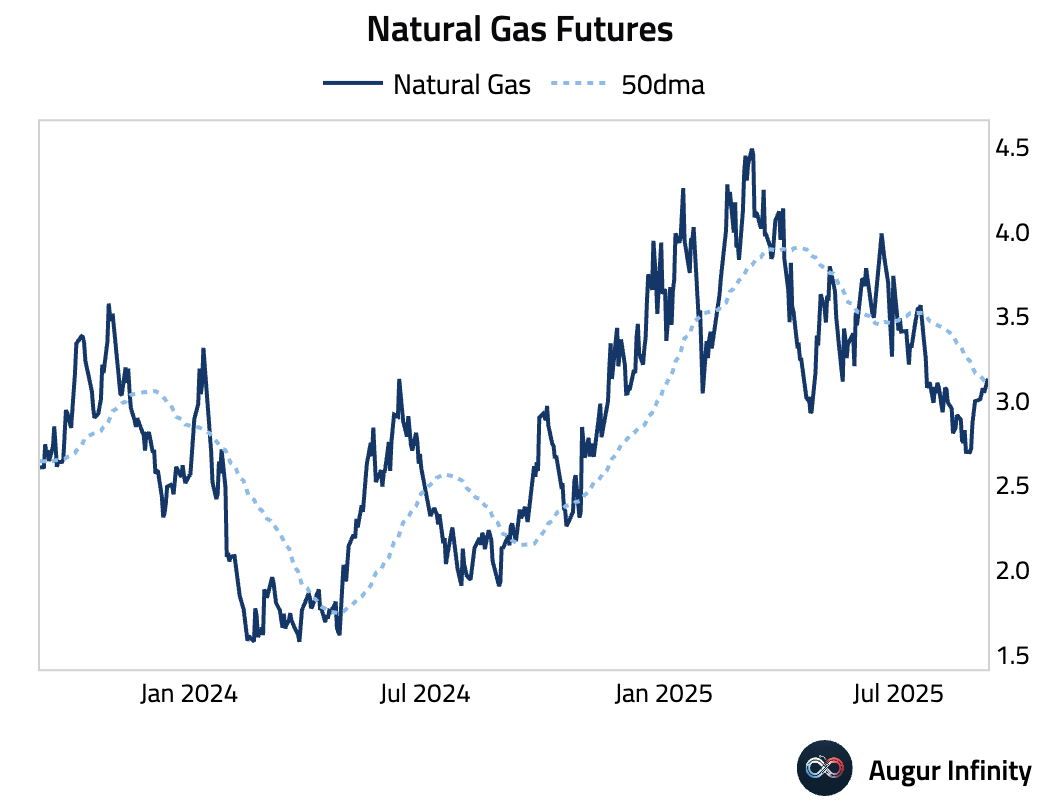

- Natural gas grinded above its 50-day moving average.

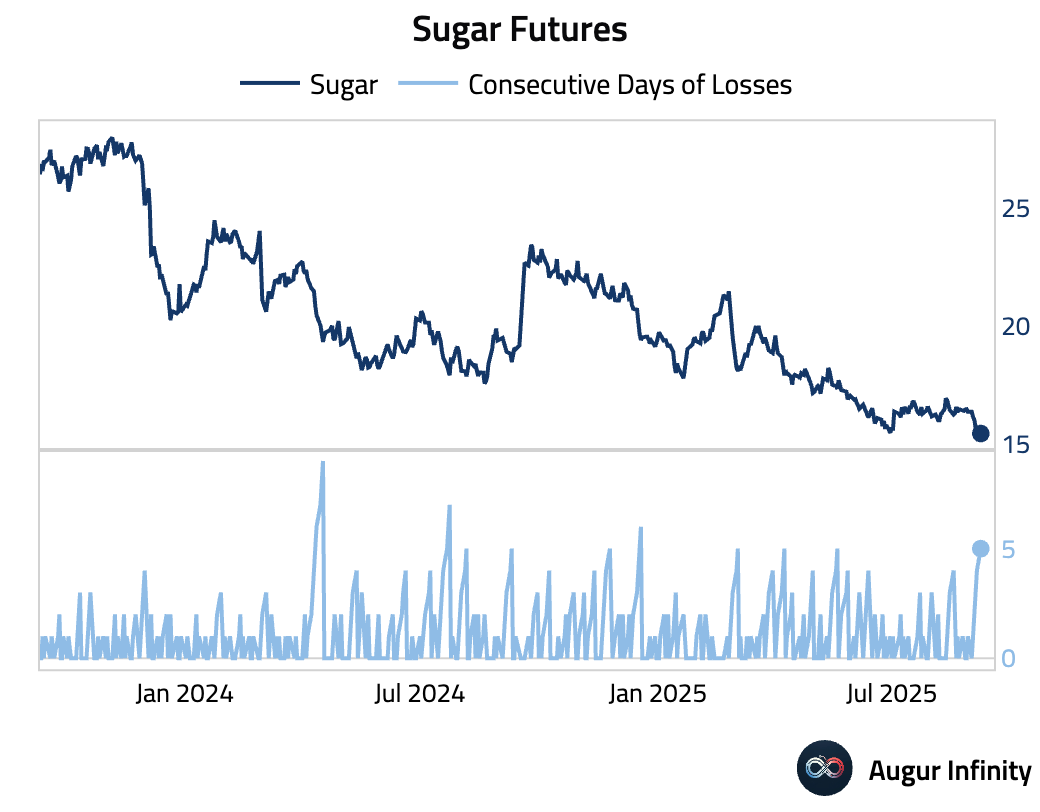

- Sugar futures, however, declined for the fifth consecutive session.

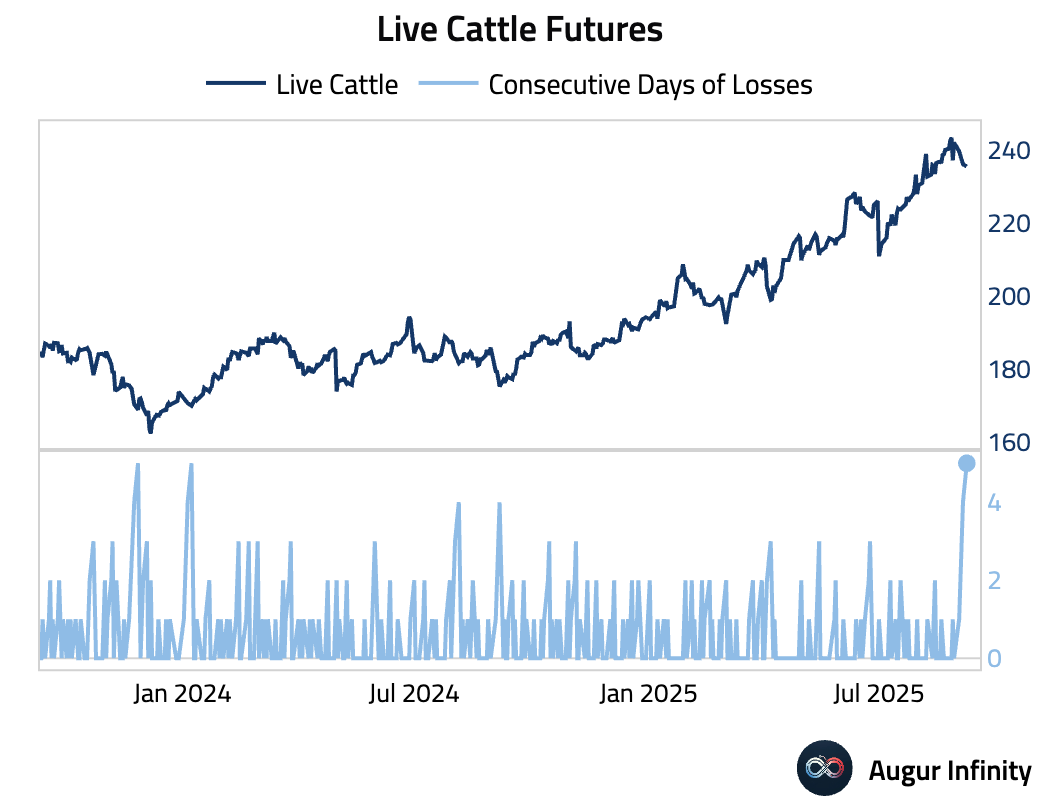

- Live cattle futures also fell for the fifth day.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.