Headlines

- Following Prime Minister Ishiba’s resignation, Japan's ruling Liberal Democratic Party will hold a leadership election on October 4.

- European Union officials are reportedly preparing a new package of sanctions against Russia that could extend to China or other nations for purchasing Russian oil.

- French Prime Minister François Bayrou is expected to submit his resignation after losing a confidence vote, forcing President Emmanuel Macron to name a third prime minister within a year.

- Bank Indonesia intervened in the currency market to support the rupiah after the country’s finance minister was dismissed.

Global Economics

United States

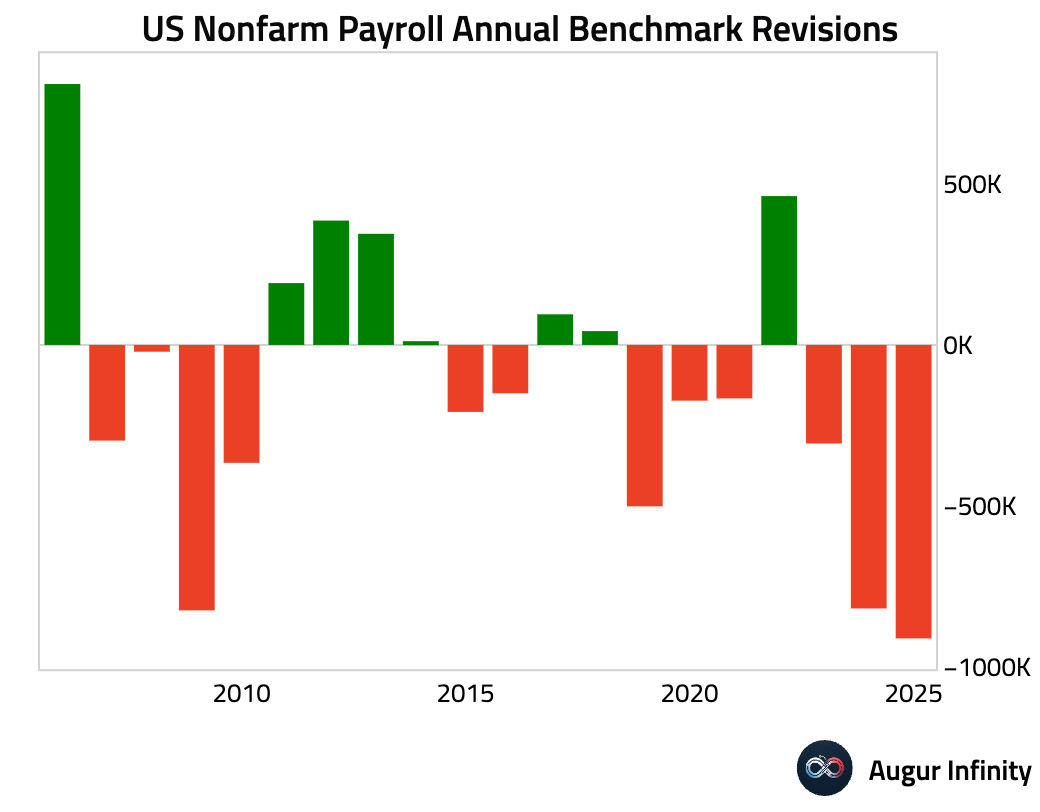

- The BLS's preliminary benchmark revision for April 24 through March 25 payrolls was -911k (-76k/month), marking the largest downward revision in history. This implies actual job growth was only 71k/month, half the initially reported 147k.

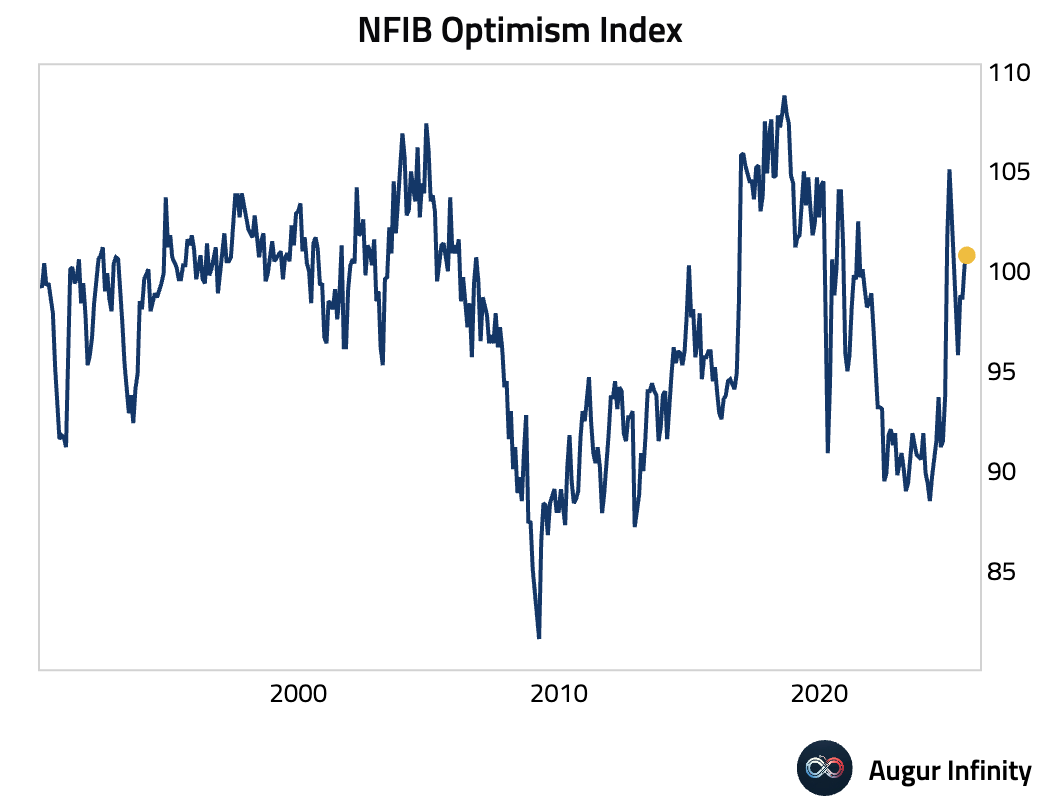

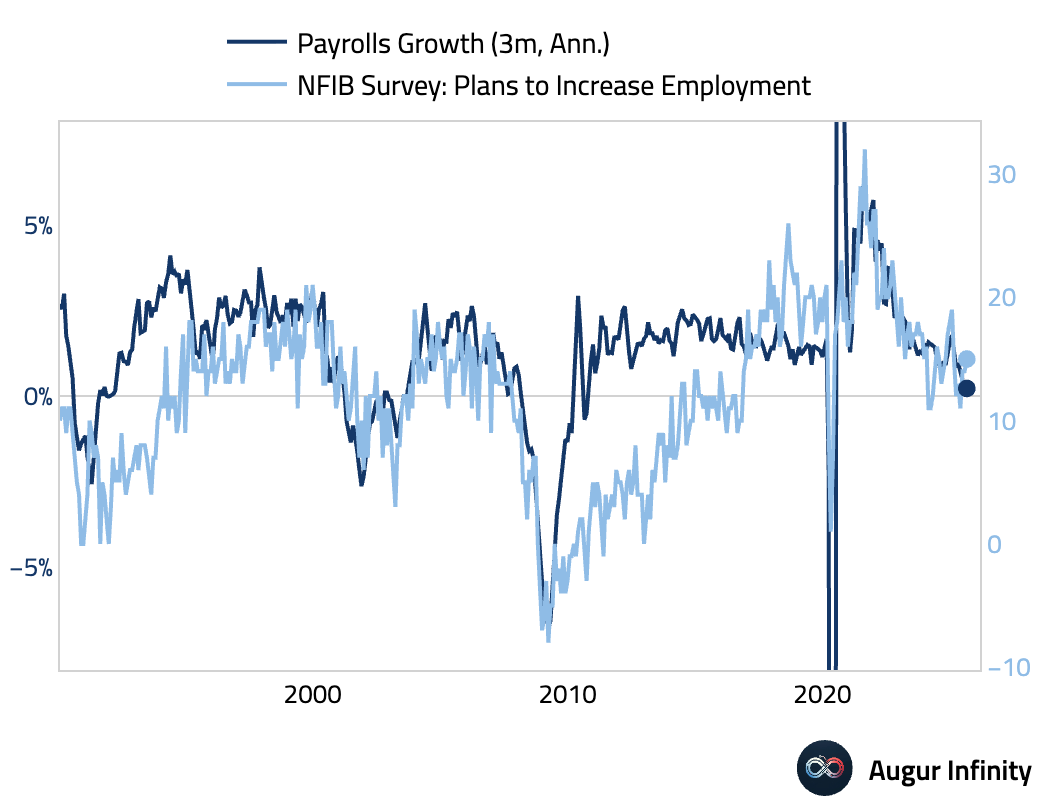

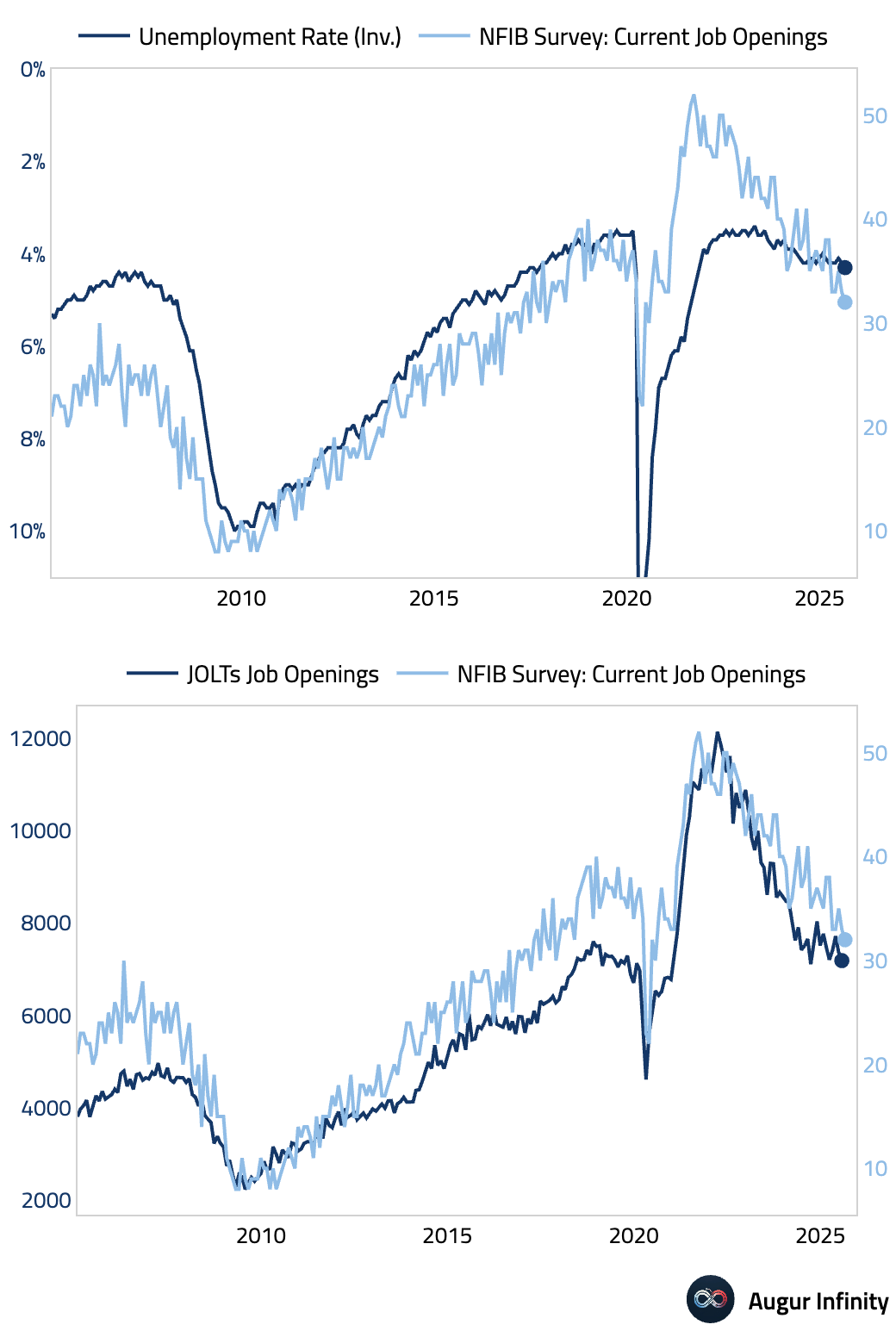

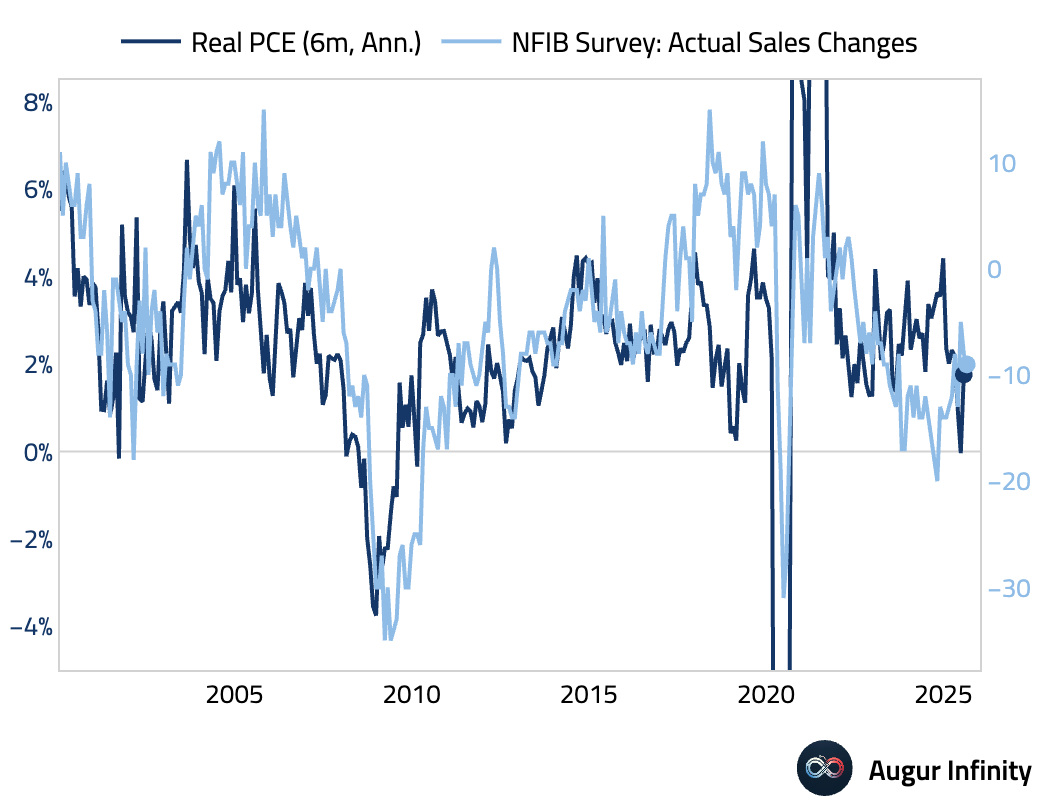

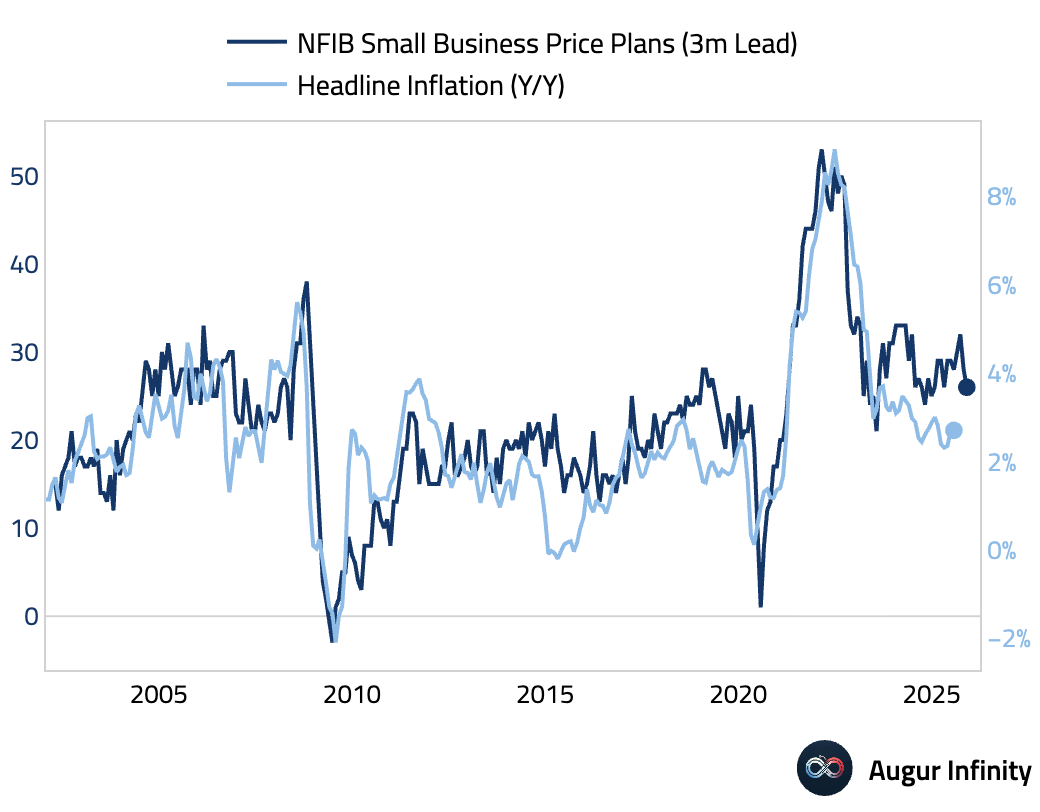

- The NFIB Small Business Optimism Index rose to 100.8 in August, driven by a six-point jump in future sales expectations. However, unfilled job openings fell to the lowest level since July 2020. Price-raising plans also hit a year-to-date low, providing a disinflationary signal.

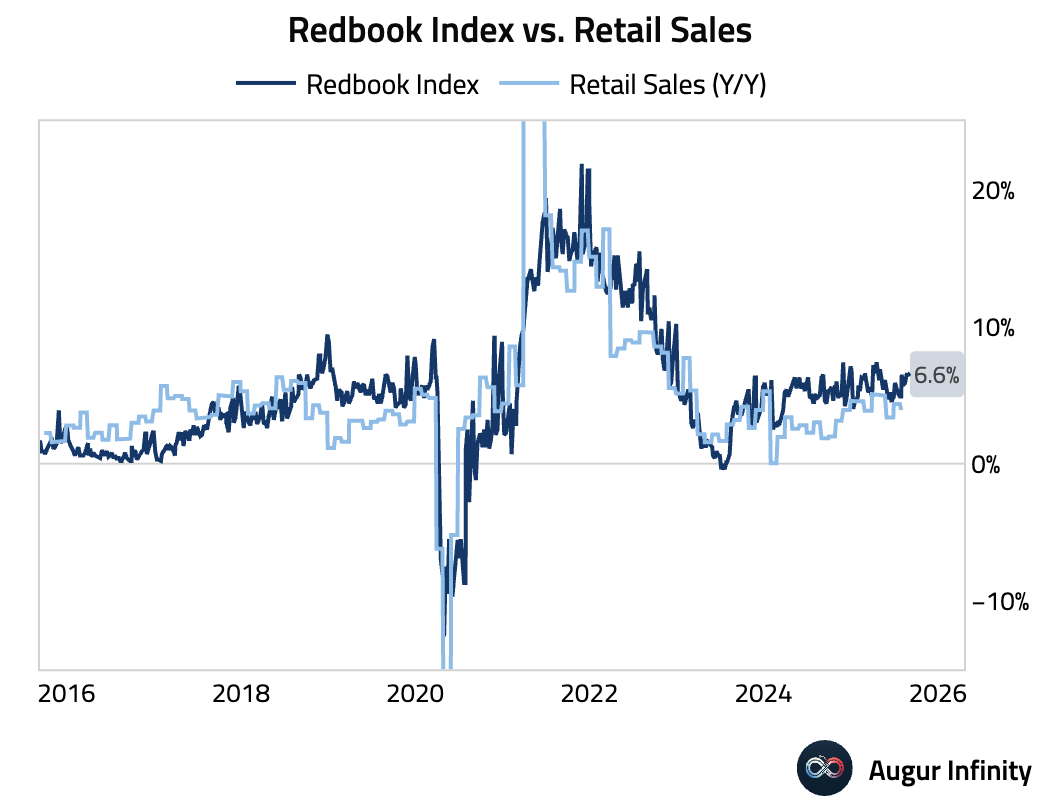

- The Redbook index of same-store retail sales showed year-over-year growth edging up to 6.6% for the week ending September 6, from 6.5% previously.

Europe

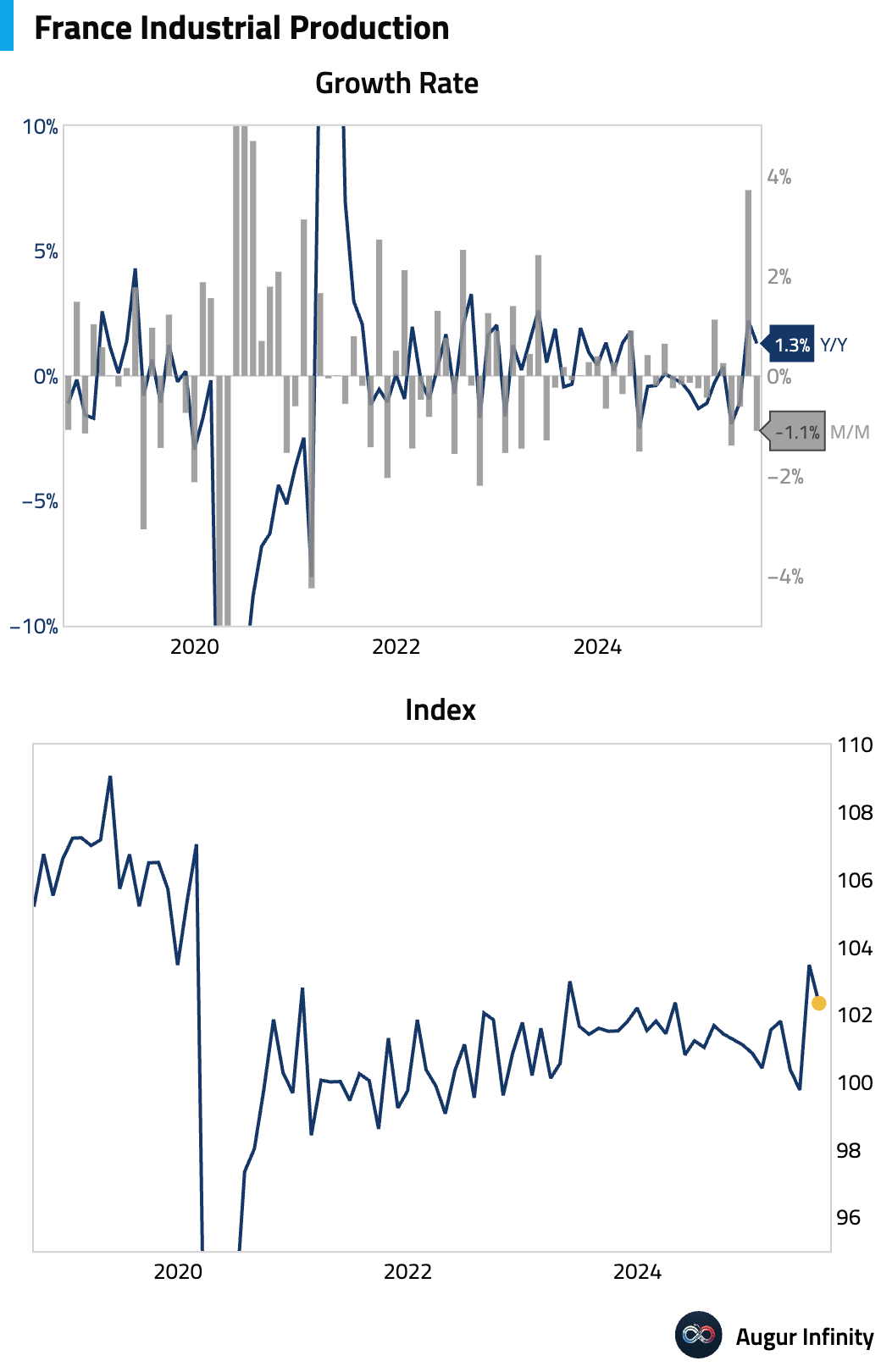

- French industrial production fell 1.1% M/M in July, a smaller contraction than the -1.8% consensus forecast but a reversal from June's strong 3.7% gain.

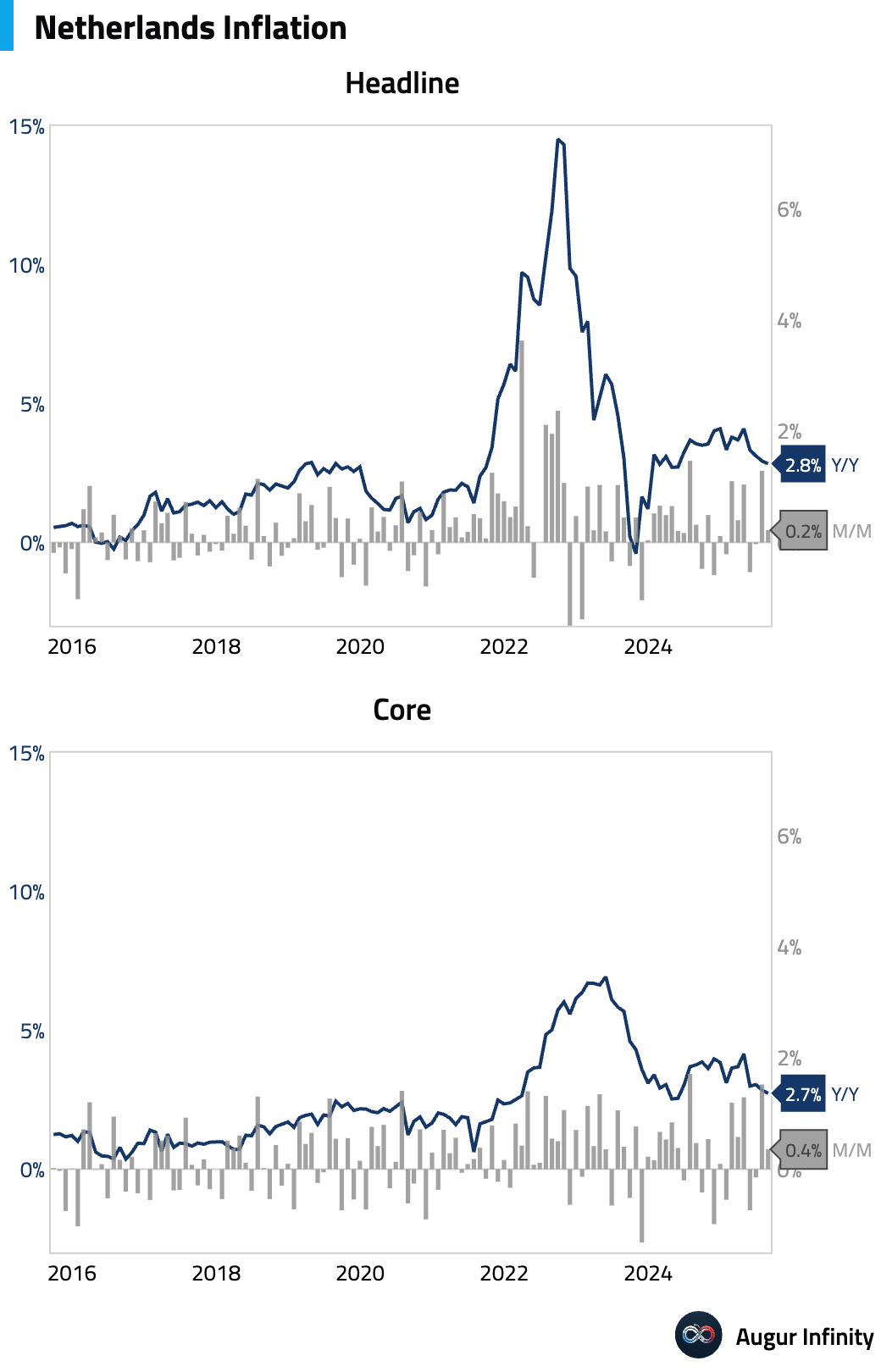

- Final August inflation data from the Netherlands confirmed a slight easing in price pressures, with the annual rate slowing to 2.8% from 2.9% in July. Prices rose 0.2% M/M.

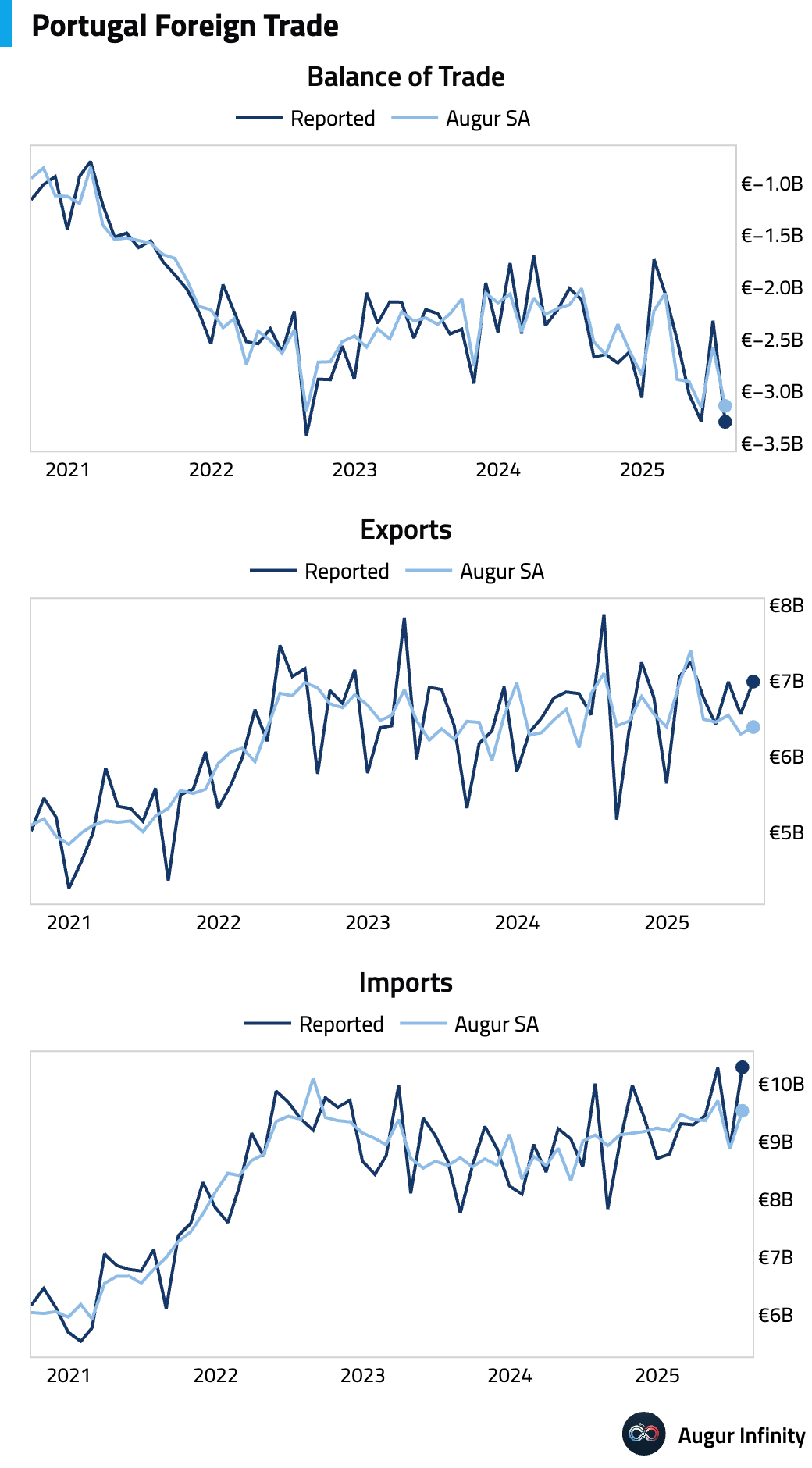

- Portugal's trade deficit widened to €3.29 billion in July from €2.32 billion in June, reaching its largest gap since August 2022.

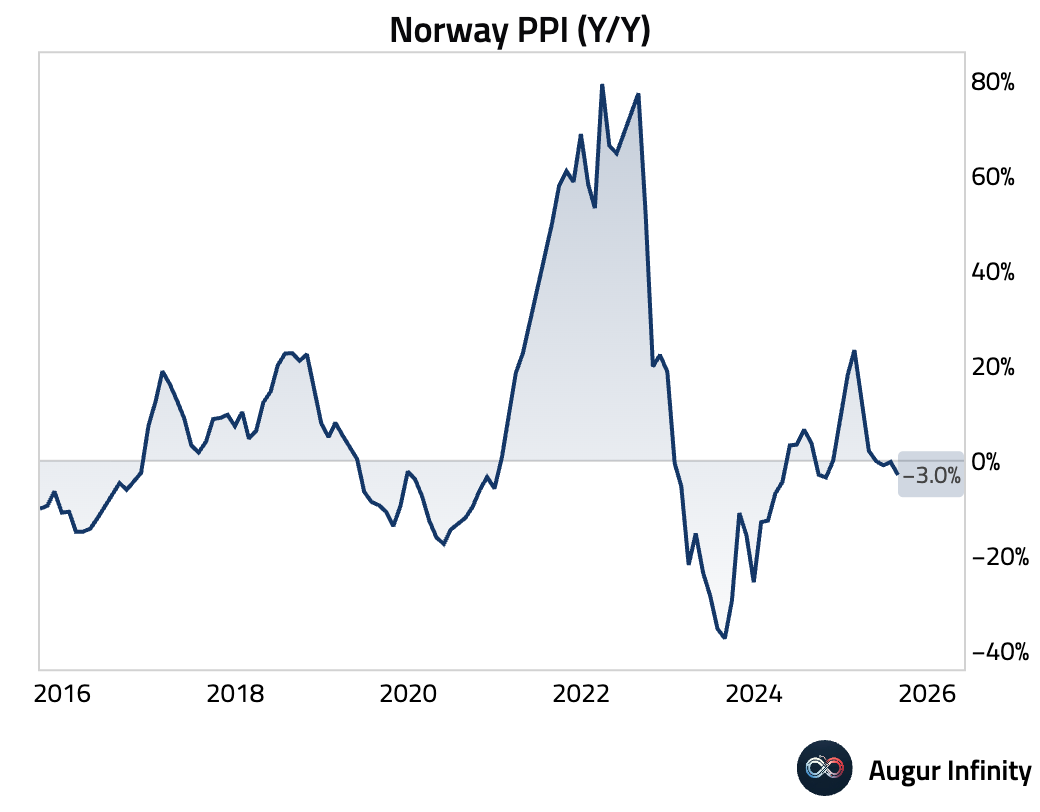

- Norwegian producer prices fell 3.0% Y/Y in August, a steeper decline than the 0.3% drop recorded in July.

Asia-Pacific

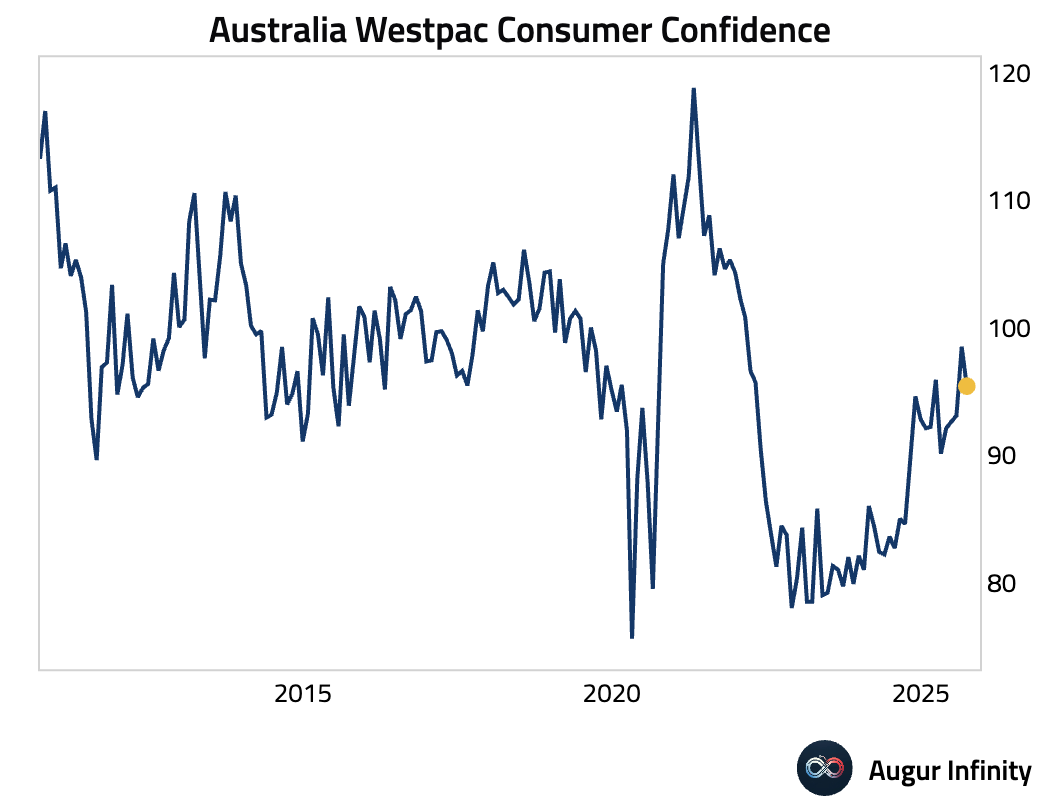

- Australian consumer sentiment deteriorated in September, with the Westpac Consumer Confidence Index falling to 95.4 from 98.5. The monthly change of -3.1% reverses a significant portion of July's 5.7% gain.

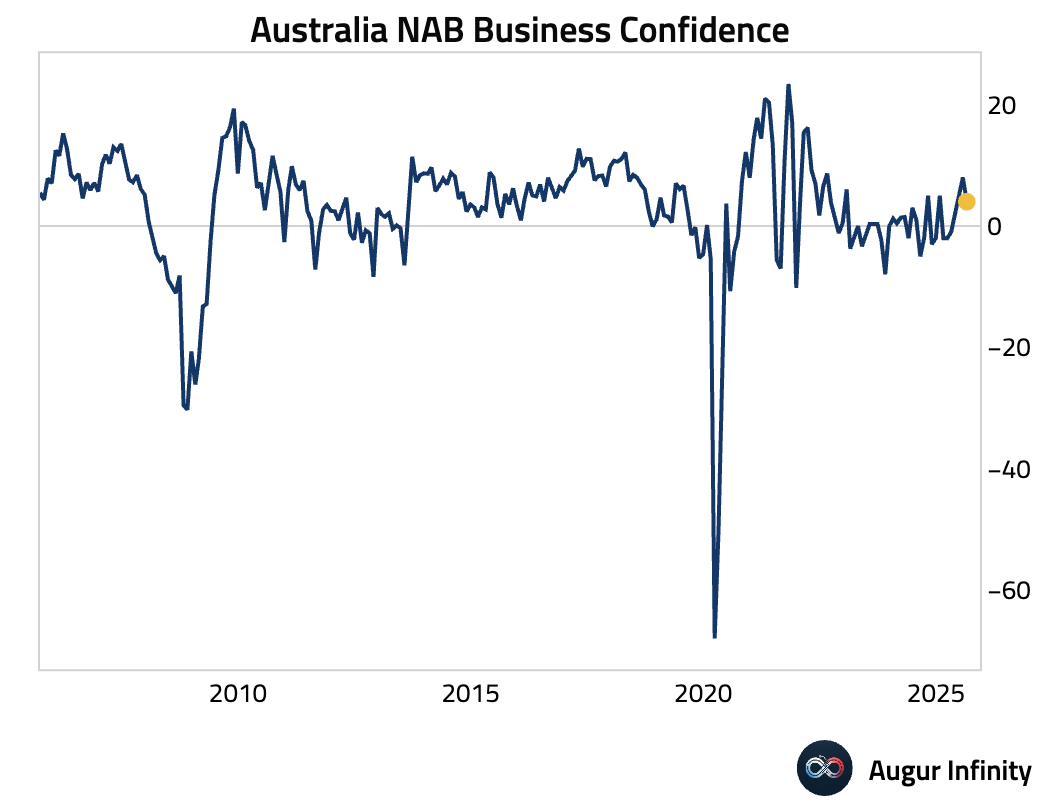

- Australia’s NAB Business Confidence index fell 4 points to +4 in August, diverging from the Business Conditions index, which rose 2 points to +7. The divergence was driven by stronger profitability and employment, but forward-looking sentiment weakened. A key takeaway was a broad easing in price pressures, with retail price growth slowing to its weakest pace since October 2020.

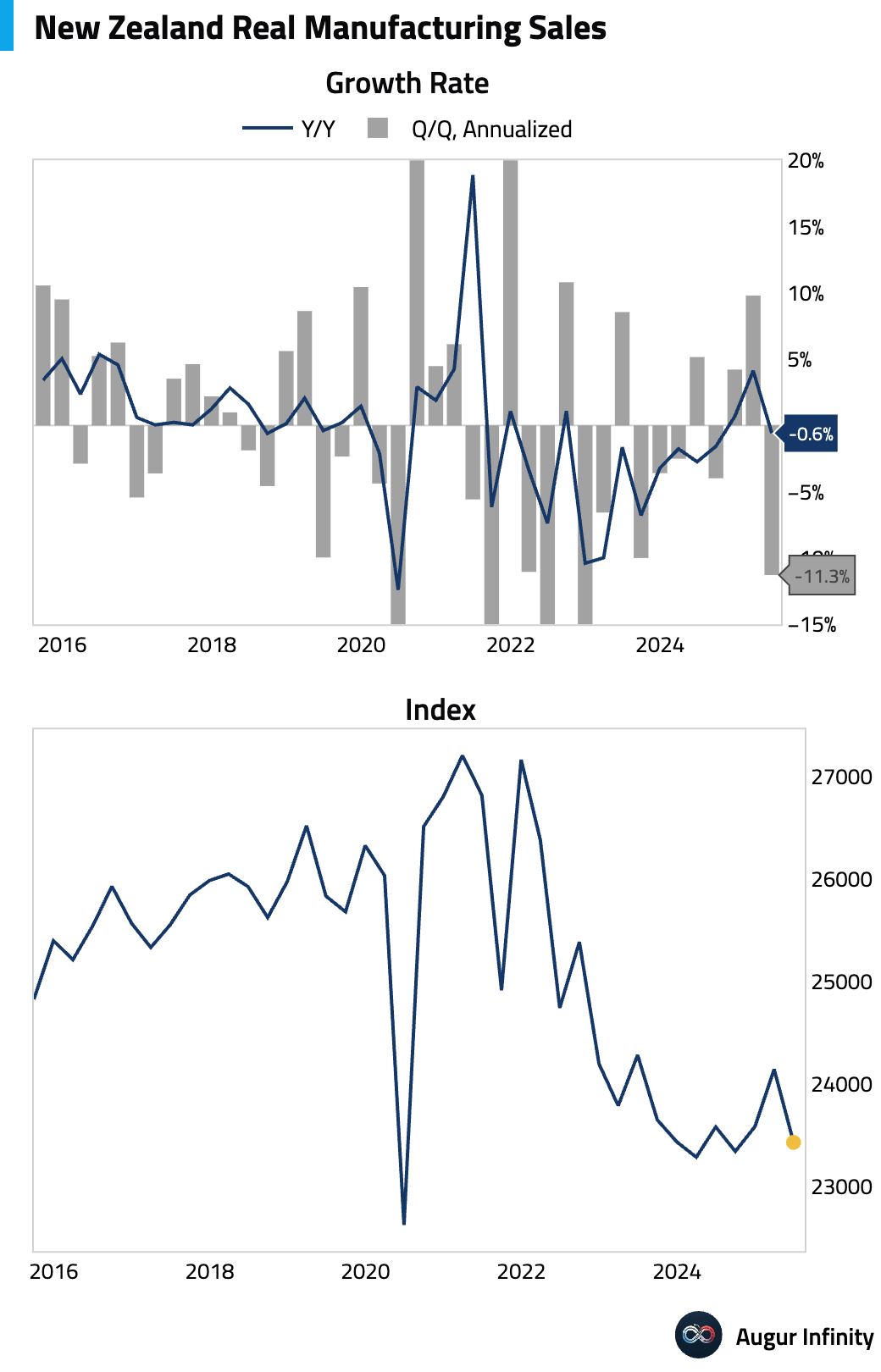

- New Zealand's manufacturing sales fell 0.6% Y/Y in the second quarter. The decline comes amid broader signs of economic weakness, with separate data on nominal business activity showing a quarterly contraction in the manufacturing sector. This has led some analysts to lower Q2 GDP growth forecasts into negative territory.

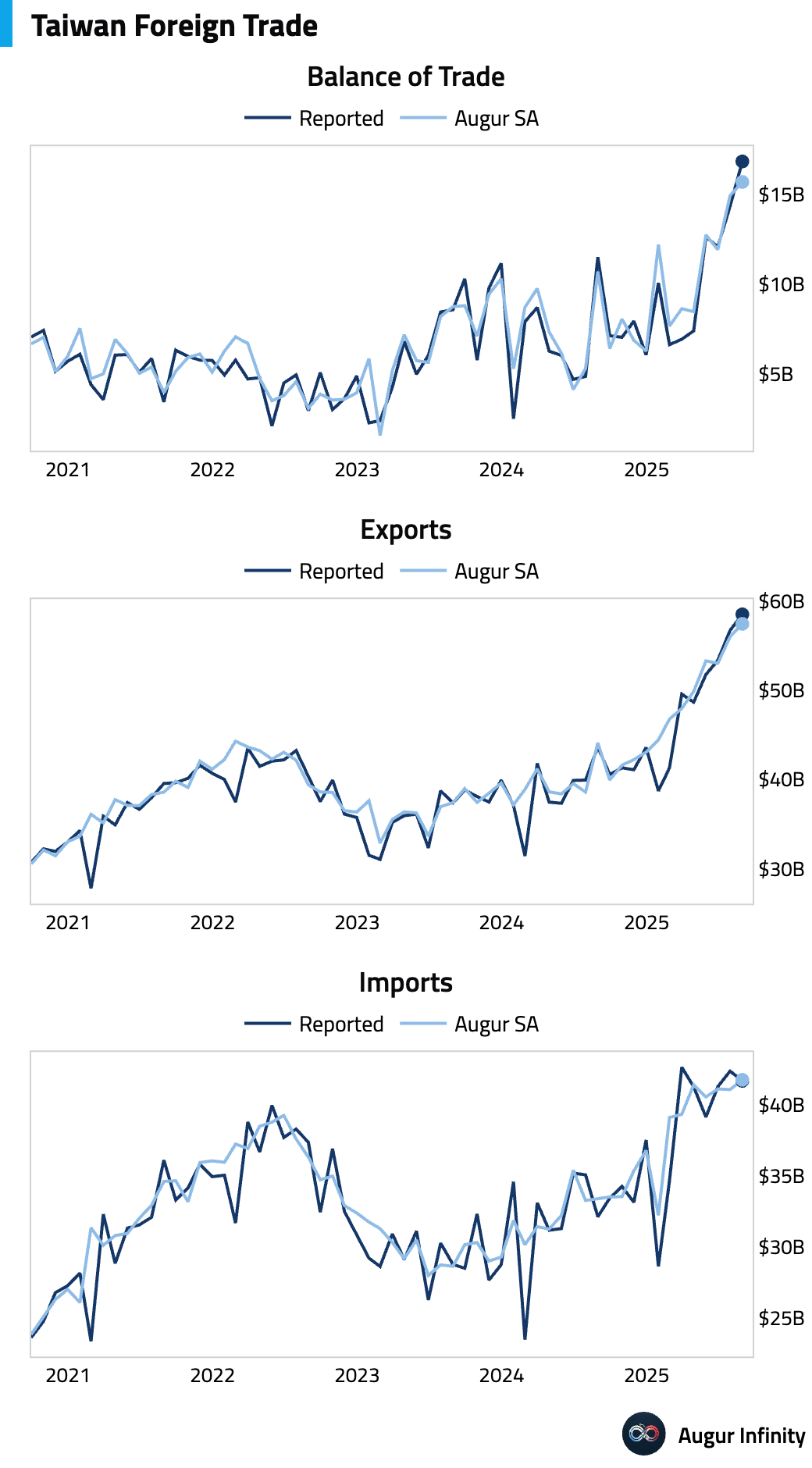

- Taiwan's trade surplus surged to an all-time high of US$16.8 billion in August, driven by a record rebound in US technology demand. Exports jumped 34.1% Y/Y, crushing the 22.3% consensus, while imports rose 29.7% Y/Y. For the third straight month, exports to the US were more than double the amount shipped to mainland China.

Emerging Markets ex China

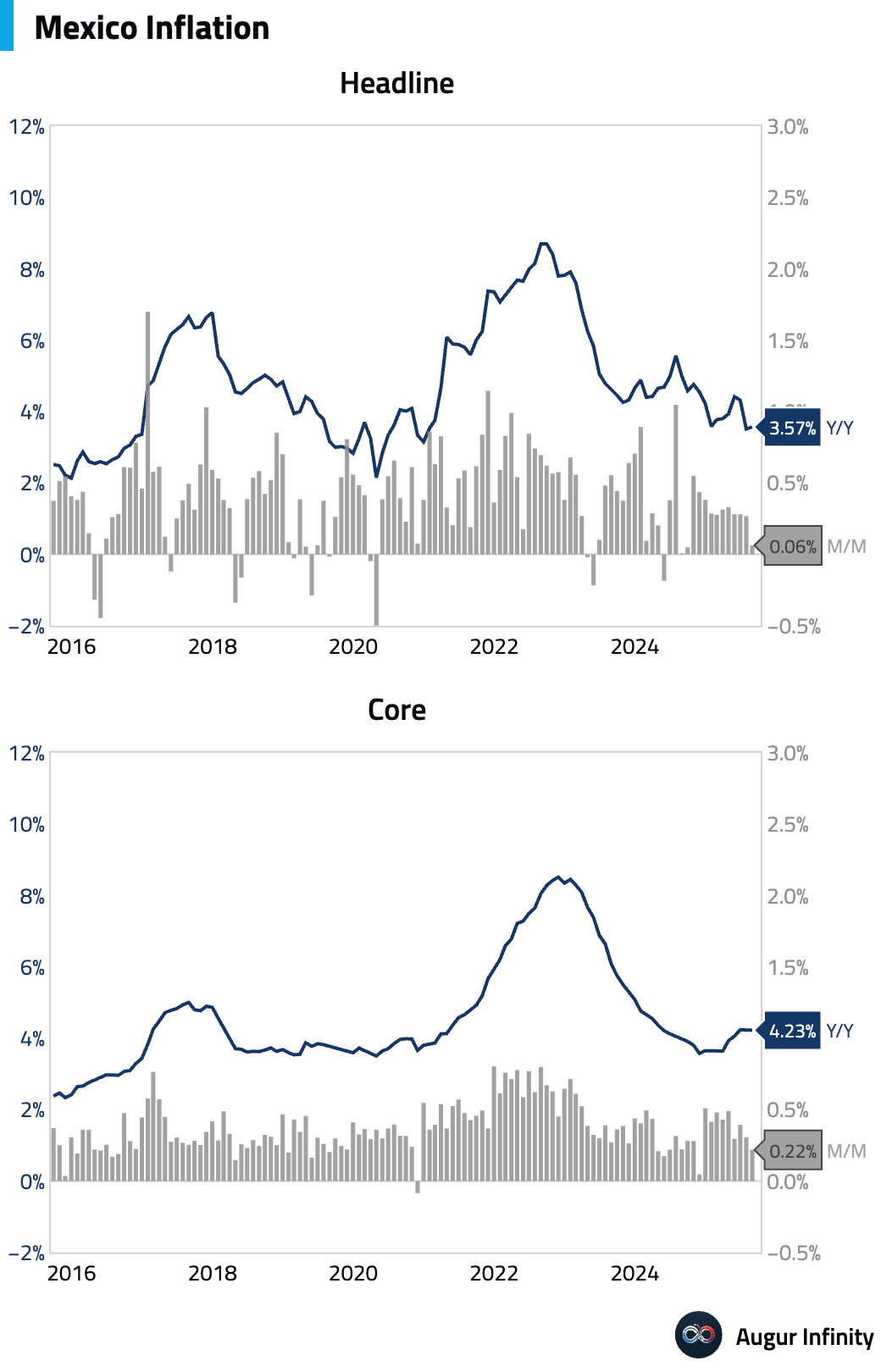

- Mexico's August headline inflation came in slightly hot, with the annual rate ticking up to 3.57% from 3.51%. Core inflation proved sticky, holding at 4.23% Y/Y, above the 4.21% consensus. Persistent services inflation remains a concern, but a downbeat growth outlook and expected Fed rate cuts are anticipated to allow Banxico to continue its easing cycle.

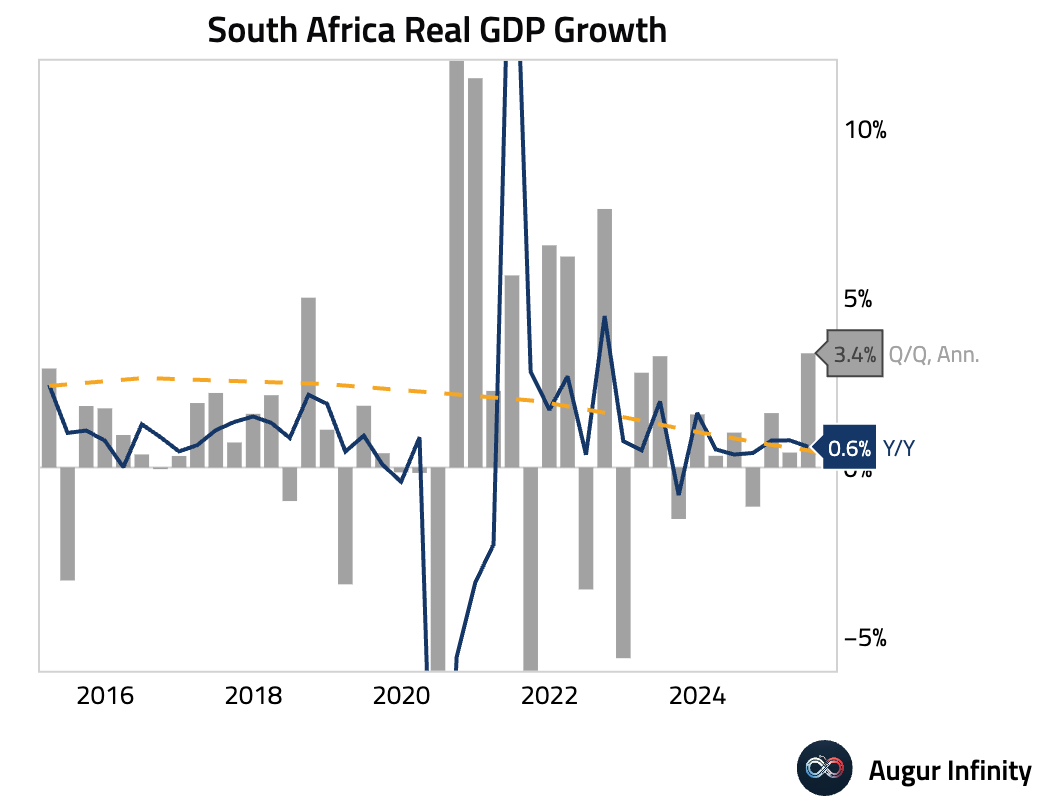

- South Africa's economy grew 0.8% Q/Q (or 3.4% annualized) in the second quarter, significantly beating the 0.5% consensus and accelerating from Q1's 0.1% expansion. The upside surprise was driven by stronger household consumption and a rebound in mining and manufacturing. However, a 1.4% Q/Q contraction in fixed investment highlights persistent business caution and remains a drag on the economy.

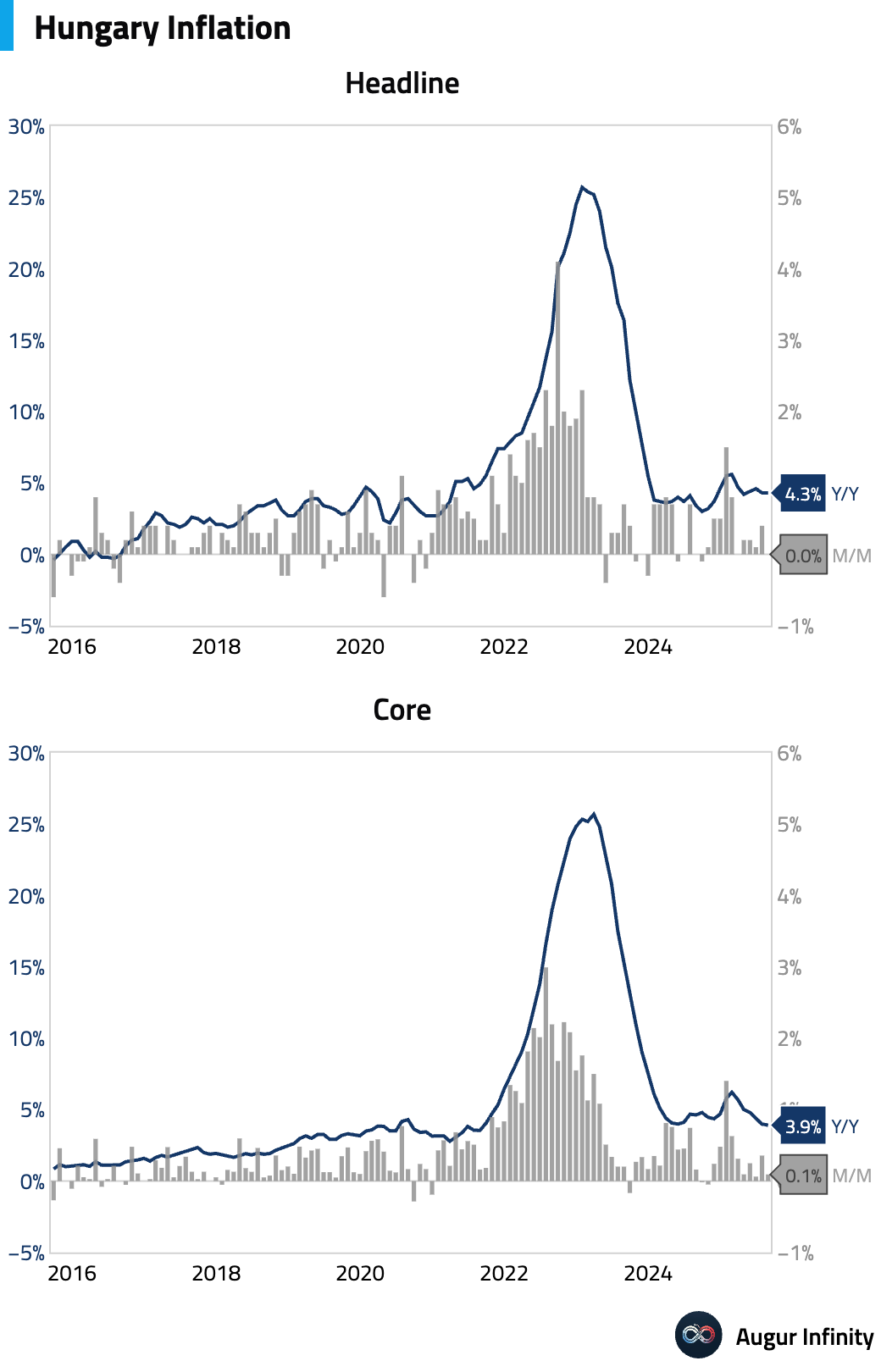

- Hungary's headline inflation held steady at 4.3% Y/Y in August, in line with consensus. Core inflation eased slightly to 3.9% Y/Y from 4.0%. Despite ongoing disinflationary trends, the central bank remains cautious due to external risks, prompting some analysts to raise year-end policy rate forecasts.

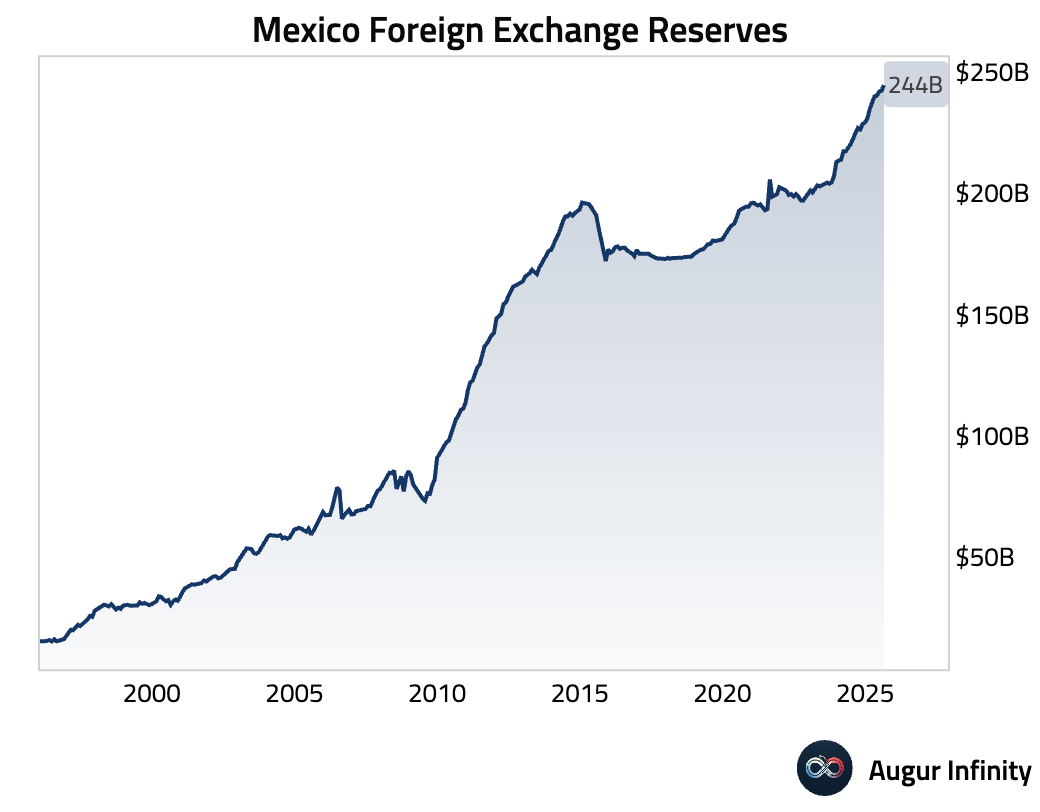

- Mexico's foreign exchange reserves rose to an all-time high of $244.4 billion at the end of August, up from $242.0 billion in July.

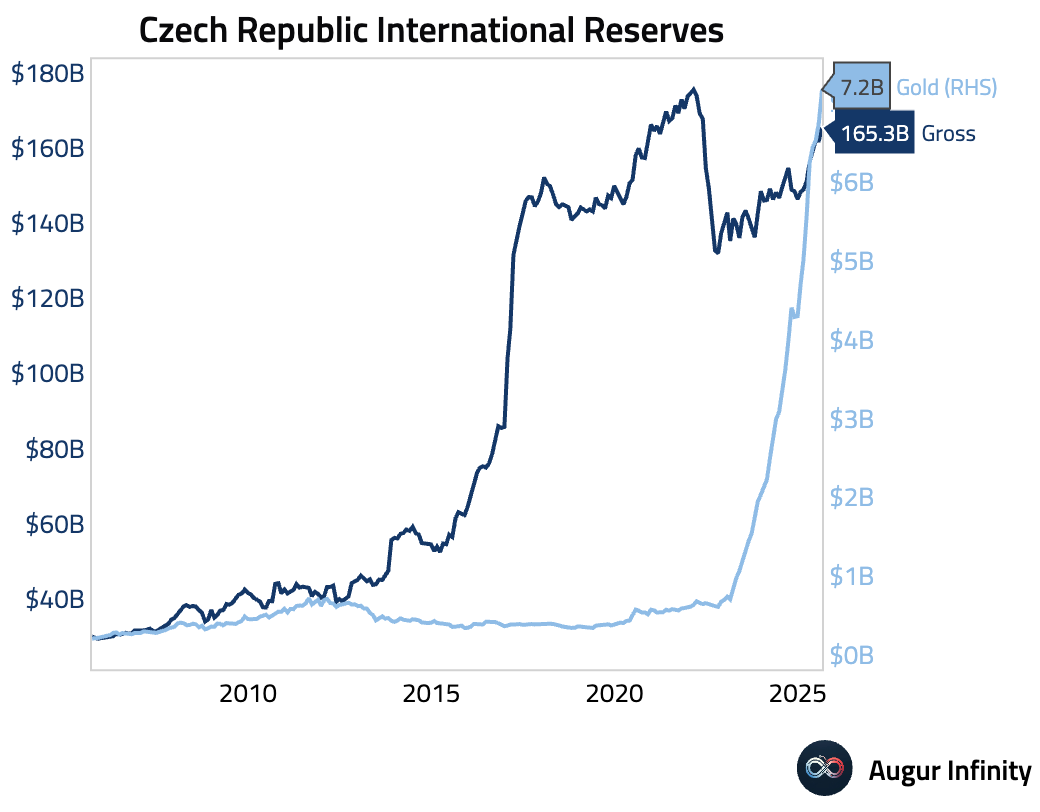

- The Czech Republic's official reserve assets increased to $165.3 billion in August from $161.9 billion in July.

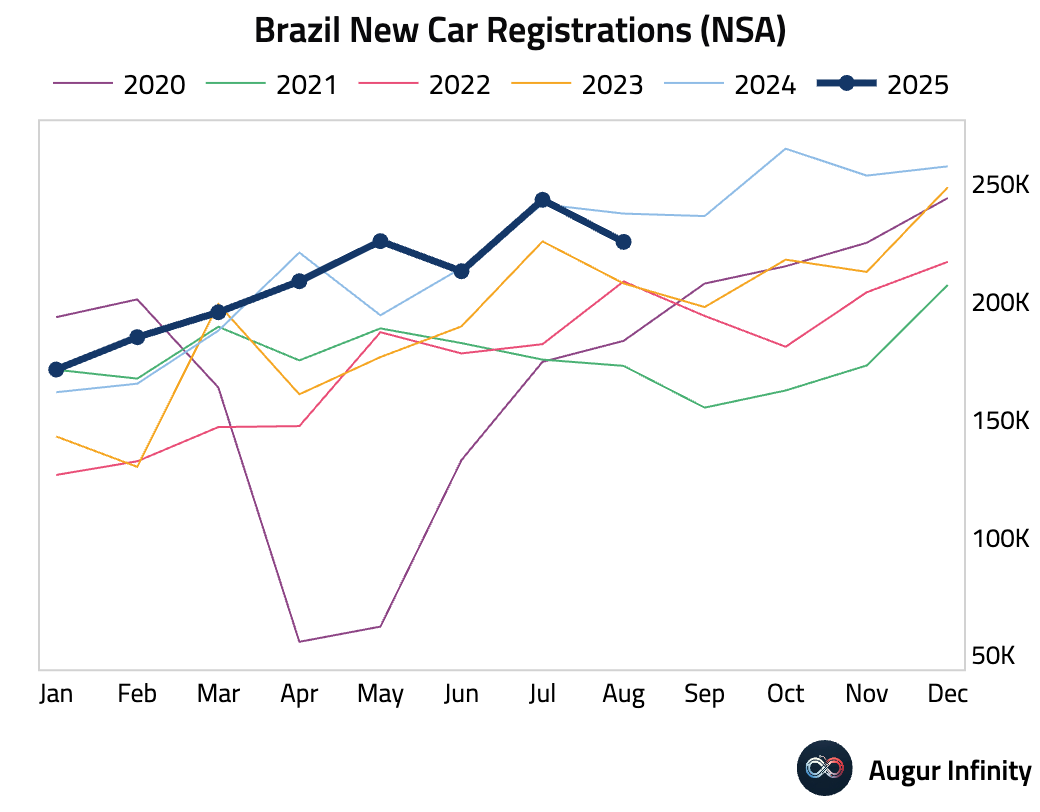

- Brazilian new car registrations declined by 7.3% M/M in August, partially reversing a 14.2% surge in July.

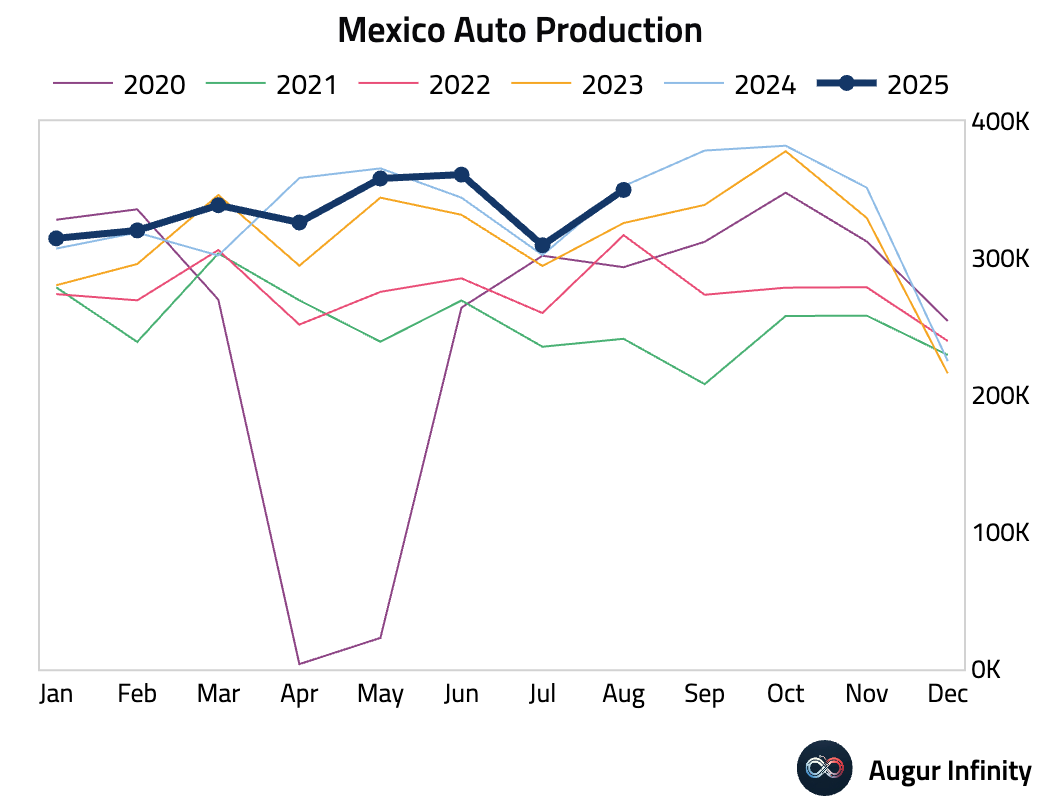

- Mexican auto production contracted 0.8% Y/Y in August, a reversal from the 2.4% growth seen in July.

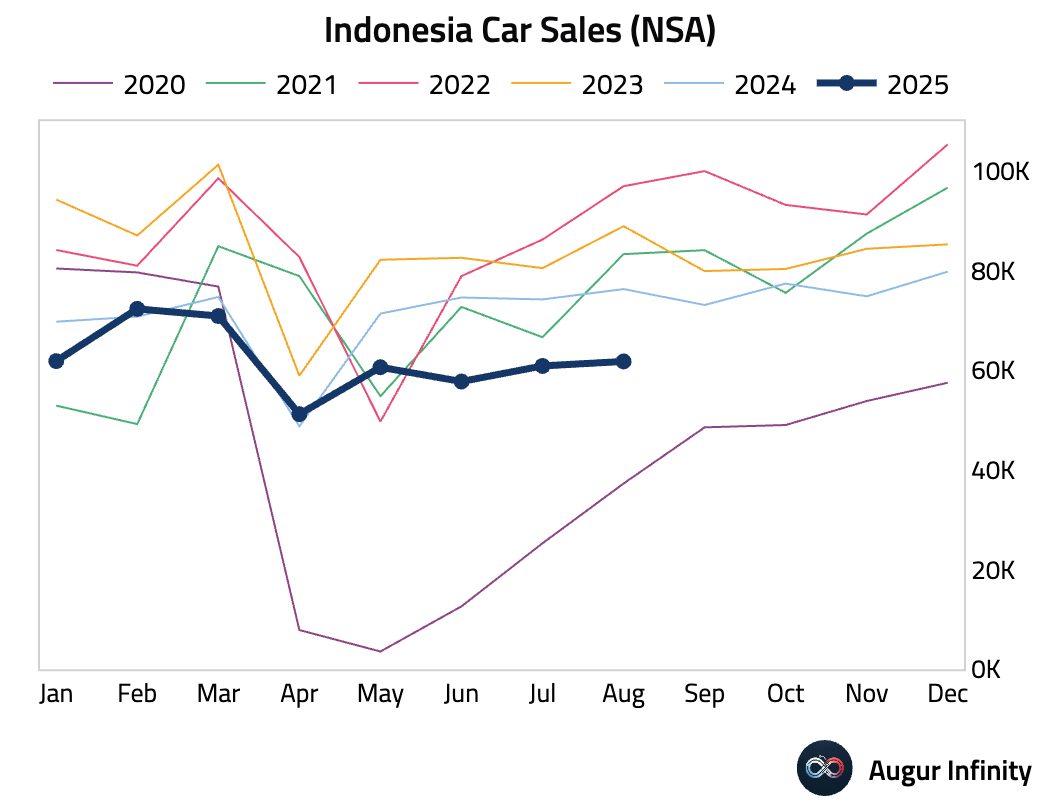

- Indonesian car sales fell 19.0% Y/Y in August, worsening from an 18.0% decline in July and marking the fourth consecutive month of contraction.

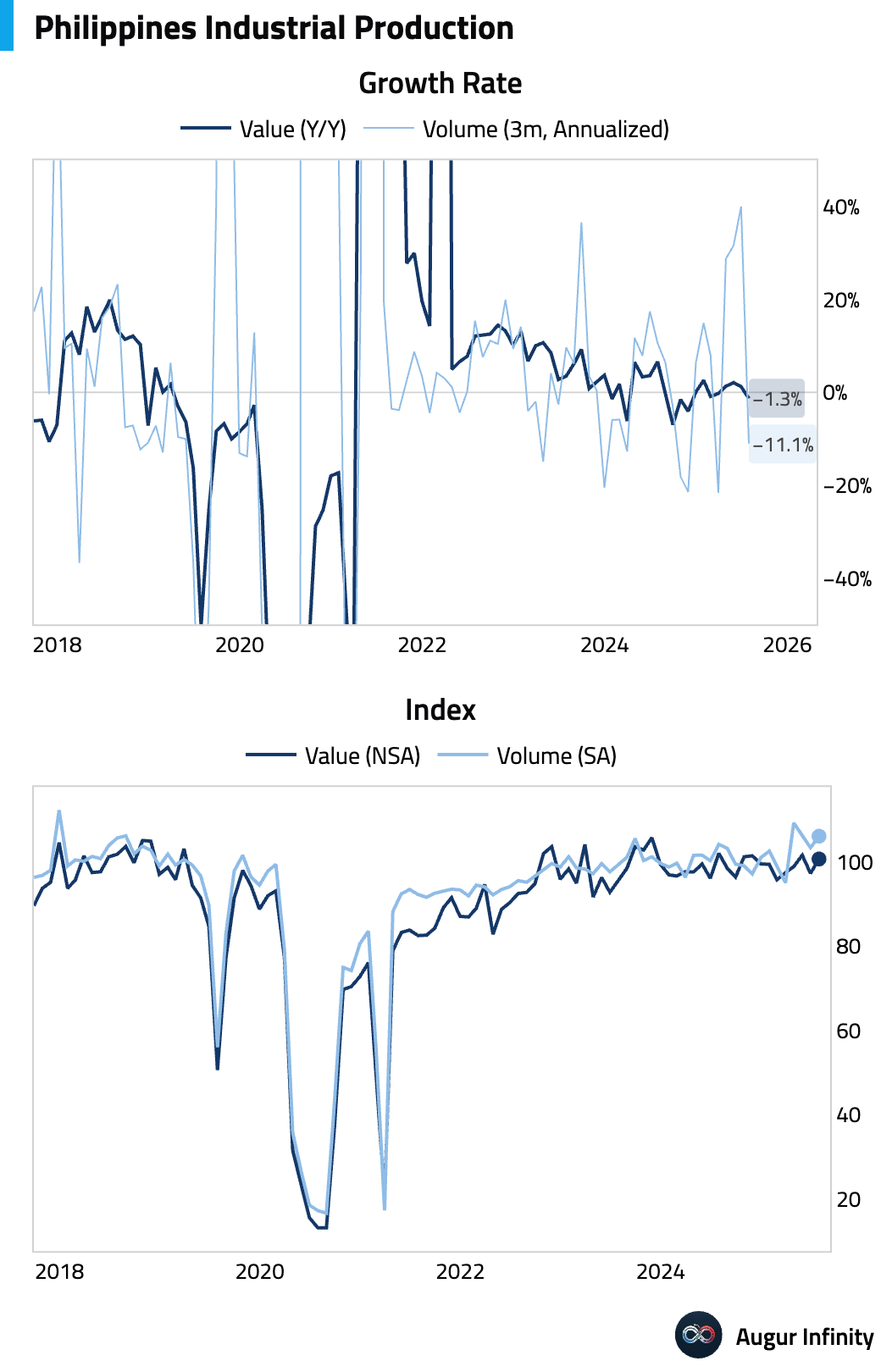

- Industrial production in the Philippines contracted 1.3% Y/Y in July, reversing from a 1.2% gain in June.

Global Markets

Equities

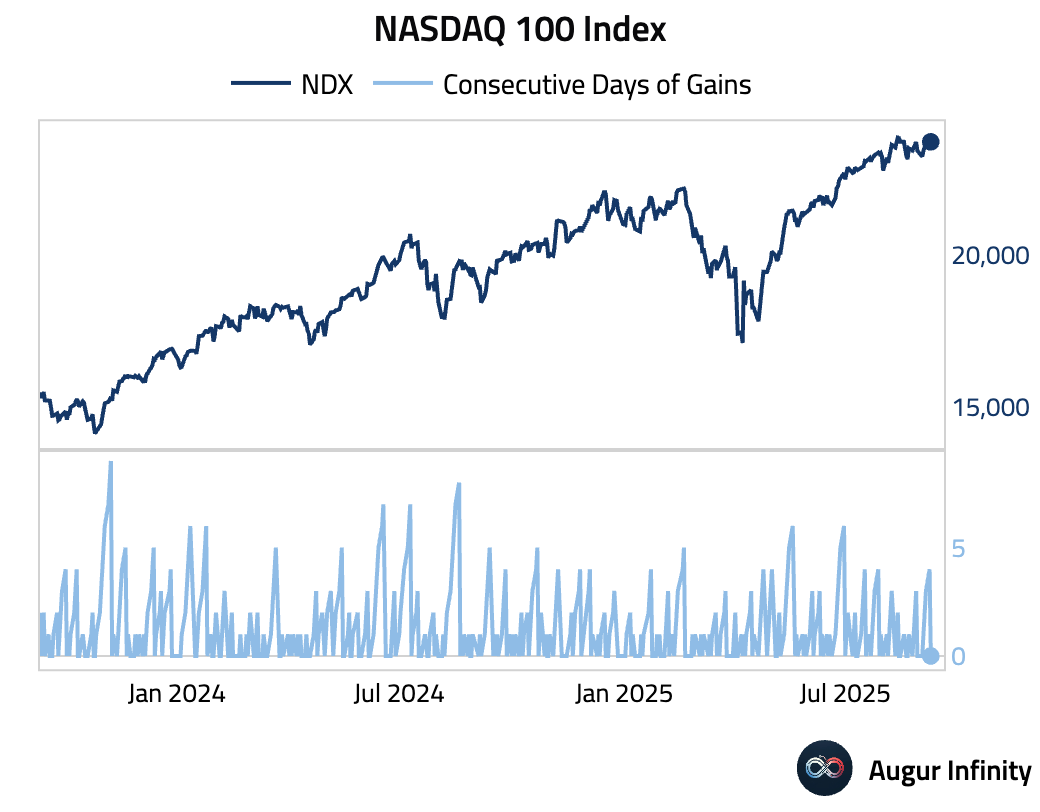

- US equities edged higher, with the S&P 500 up 0.3% and the Nasdaq Composite gaining 0.4%. Asian markets were strong, led by gains in China (+1.3%) and South Korea (+1.0%), while European markets were mixed, with Germany underperforming (-0.6%). Several markets extended winning streaks, including Emerging Markets (3 days), China (3 days), South Korea (5 days), and Mexico (4 days).

- The NASDAQ 100 Index notched its fifth consecutive gain.

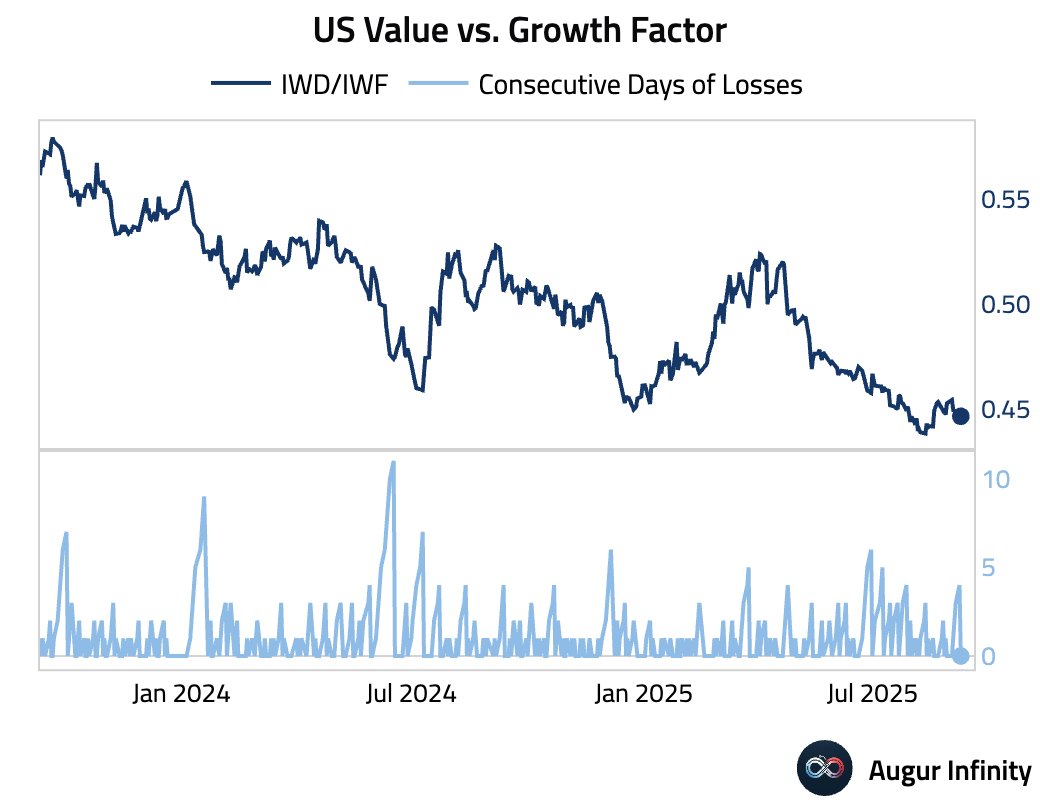

- US Value vs. Growth Factor declined for the fifth day in a row.

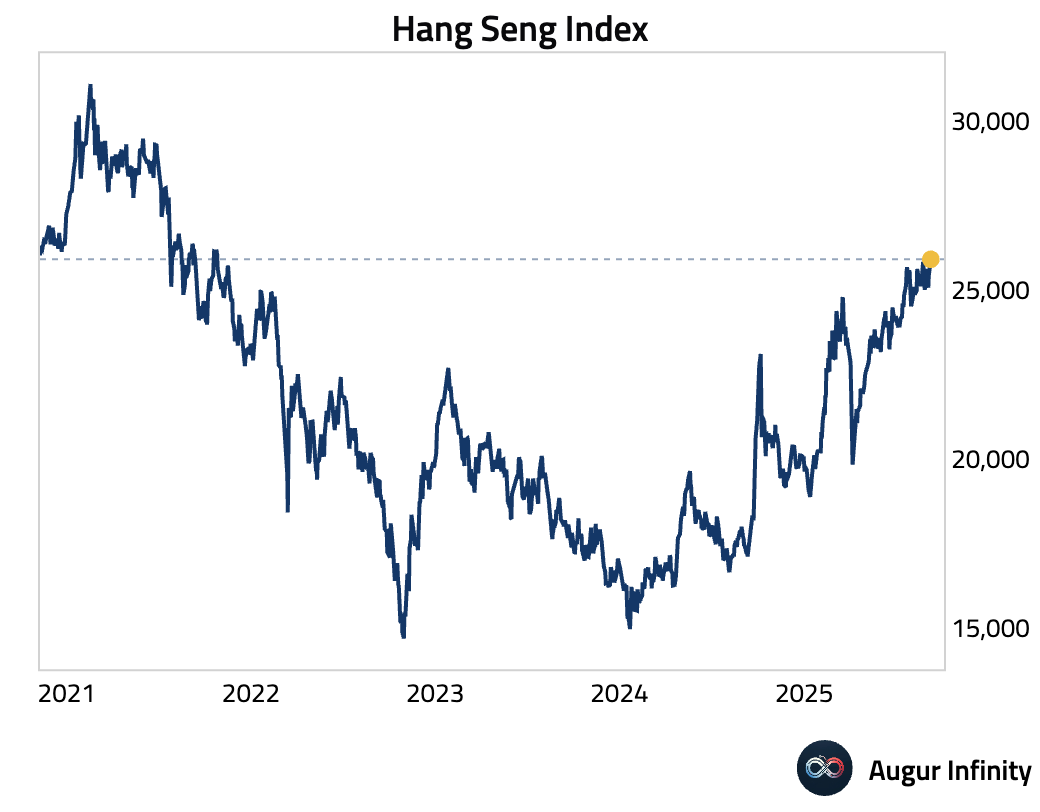

- The Hang Seng Index has climbed to the highest level since October 2021.

Fixed Income

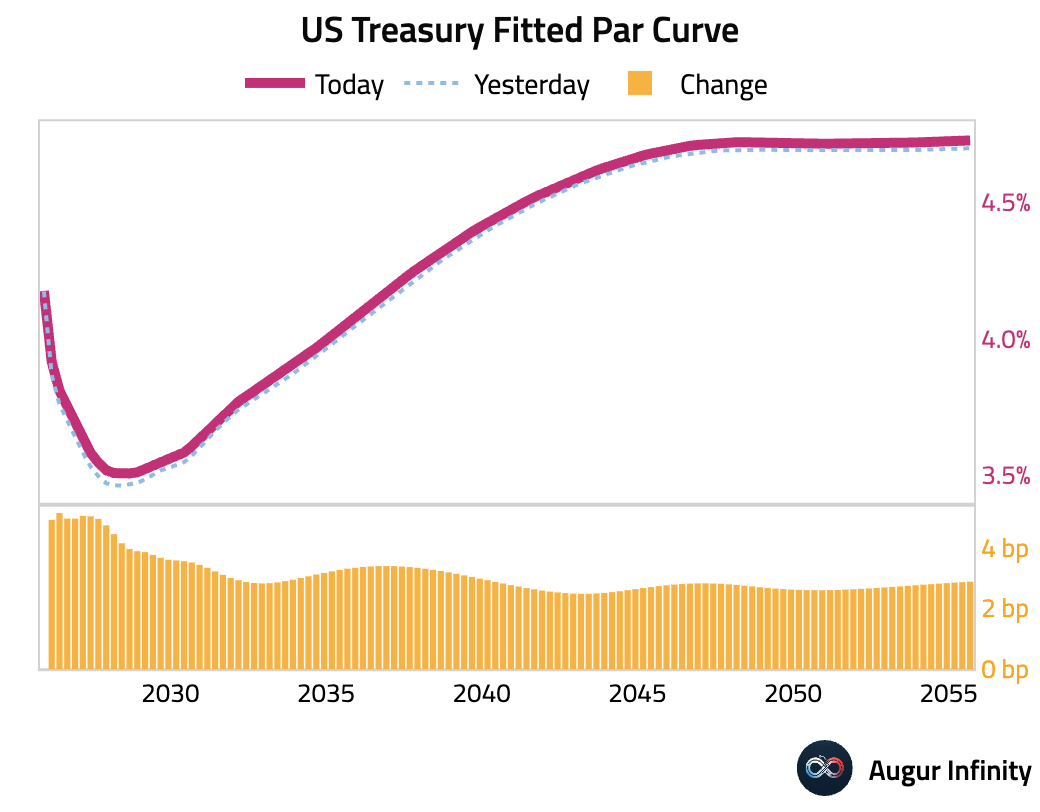

- US Treasury yields increased across the curve, with the 2-year yield climbing 5.9 bps and the 10-year yield rising 3.7 bps, resulting in a slight flattening of the 2s10s spread. The rise in yields occurred despite growing market expectations for a Federal Reserve rate cut at its next meeting, which were bolstered by news of a significant downward revision to historical US employment data.

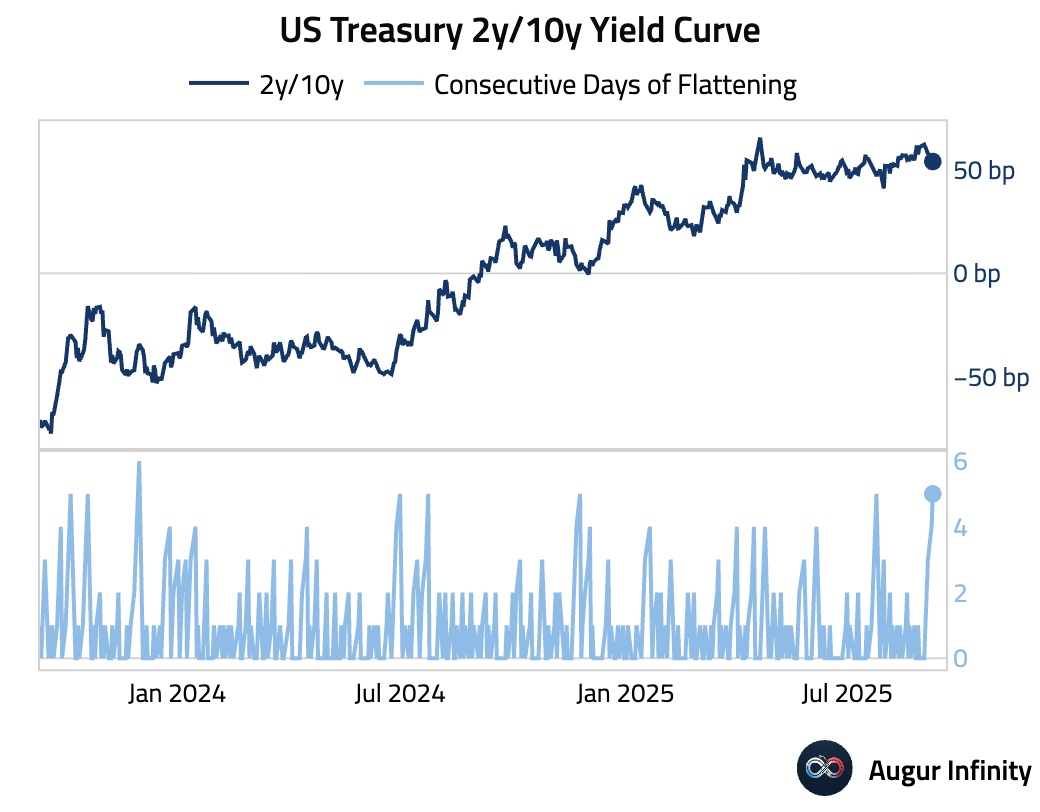

- US Treasury 2y/10y curve has flattened for five consecutive sessions.

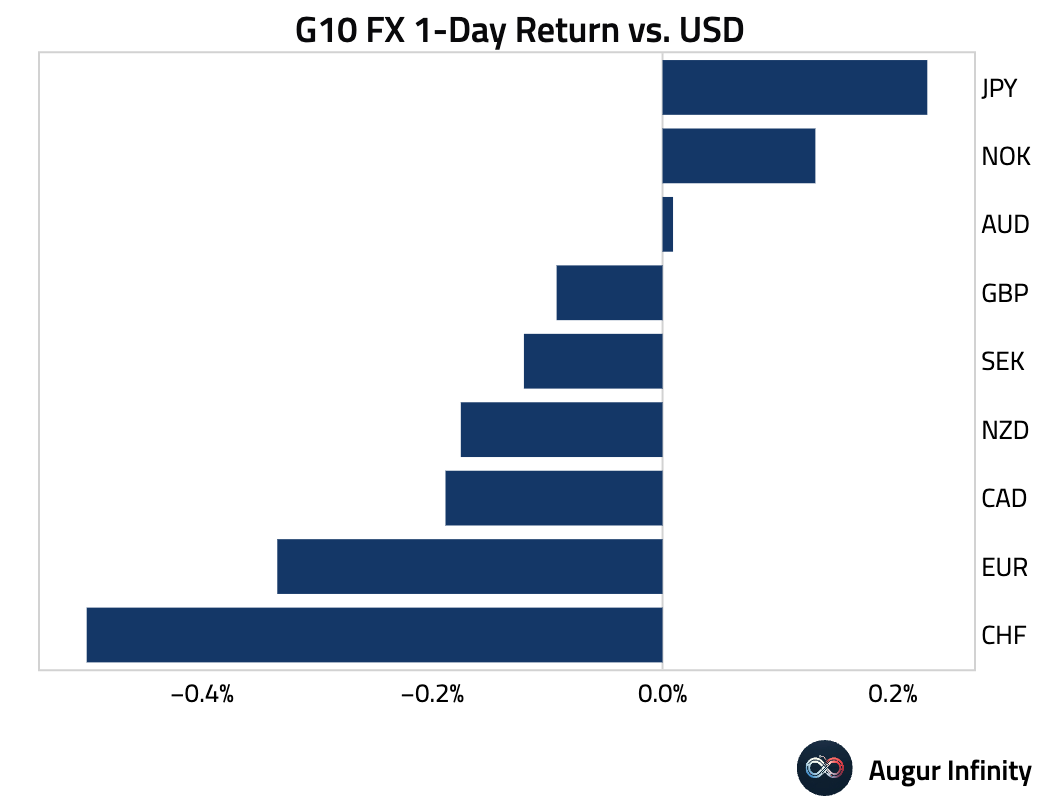

FX

- The US dollar was mixed against its G10 counterparts. The Japanese yen (+0.2%) and Norwegian krone (+0.1%) were the top performers. The Swiss franc (-0.5%) and the euro (-0.3%) were the main laggards. The Norwegian krone extended its winning streak to three days.

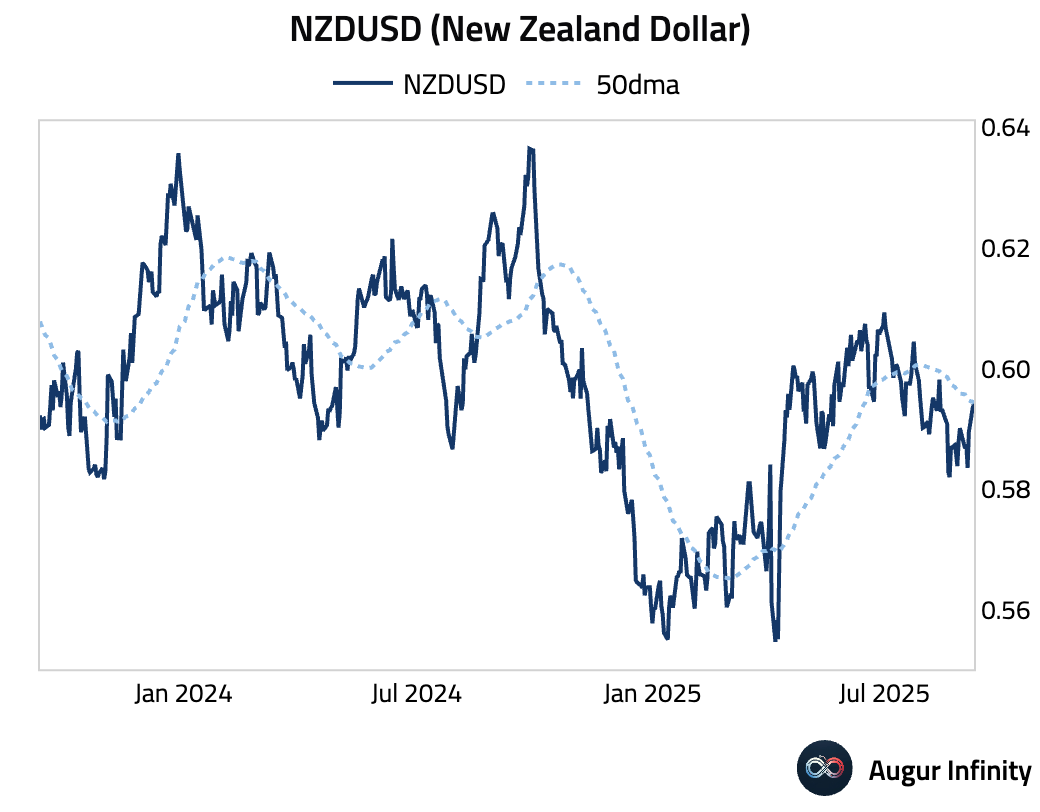

- NZDUSD (New Zealand Dollar) is above its 50-day moving average.

Commodities

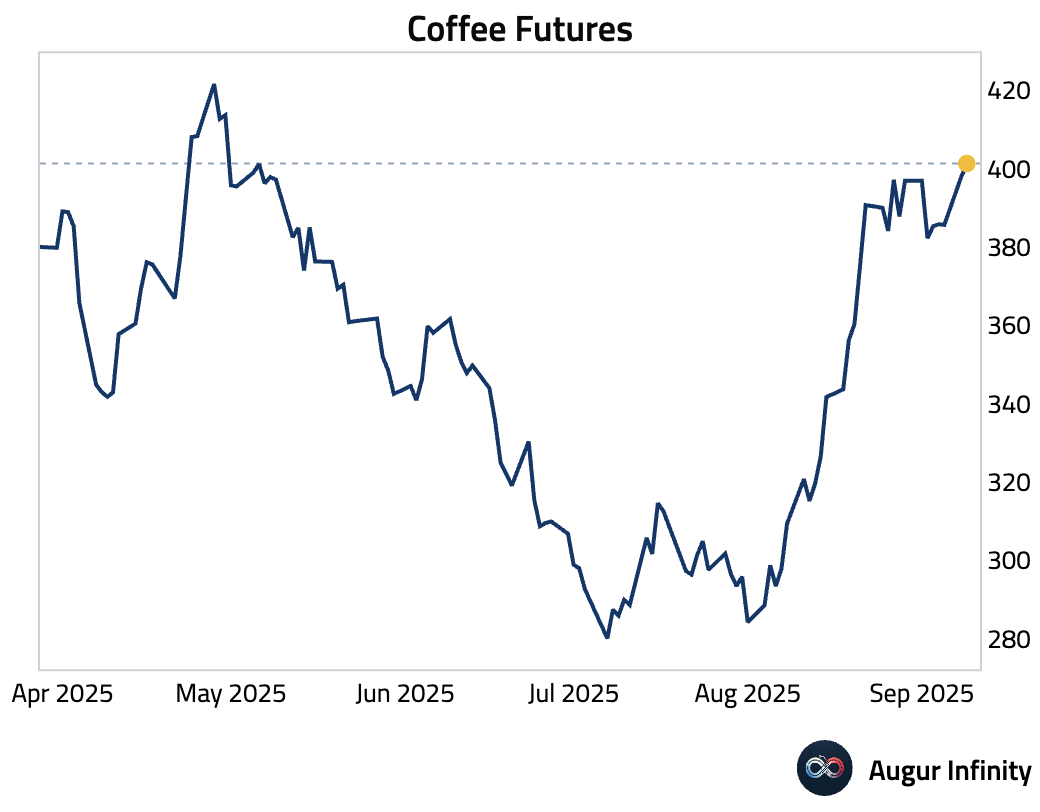

- Coffee Futures is trading at the highest level since April.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.