Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- Reports indicate Russian drones crossed into Poland from Ukraine and were subsequently shot down, marking a significant escalation involving a NATO member state.

- A legal dispute over the presidential firing of a Federal Reserve governor is expected to be elevated to the Supreme Court after a federal judge blocked the dismissal.

- European Union officials are reportedly preparing a new sanctions package against Russia that could extend to nations purchasing Russian oil, potentially including China.

- French president Emmanuel Macron appointed Sebastien Lecornu as the new prime minister following the resignation of his predecessor.

Global Economics

United States

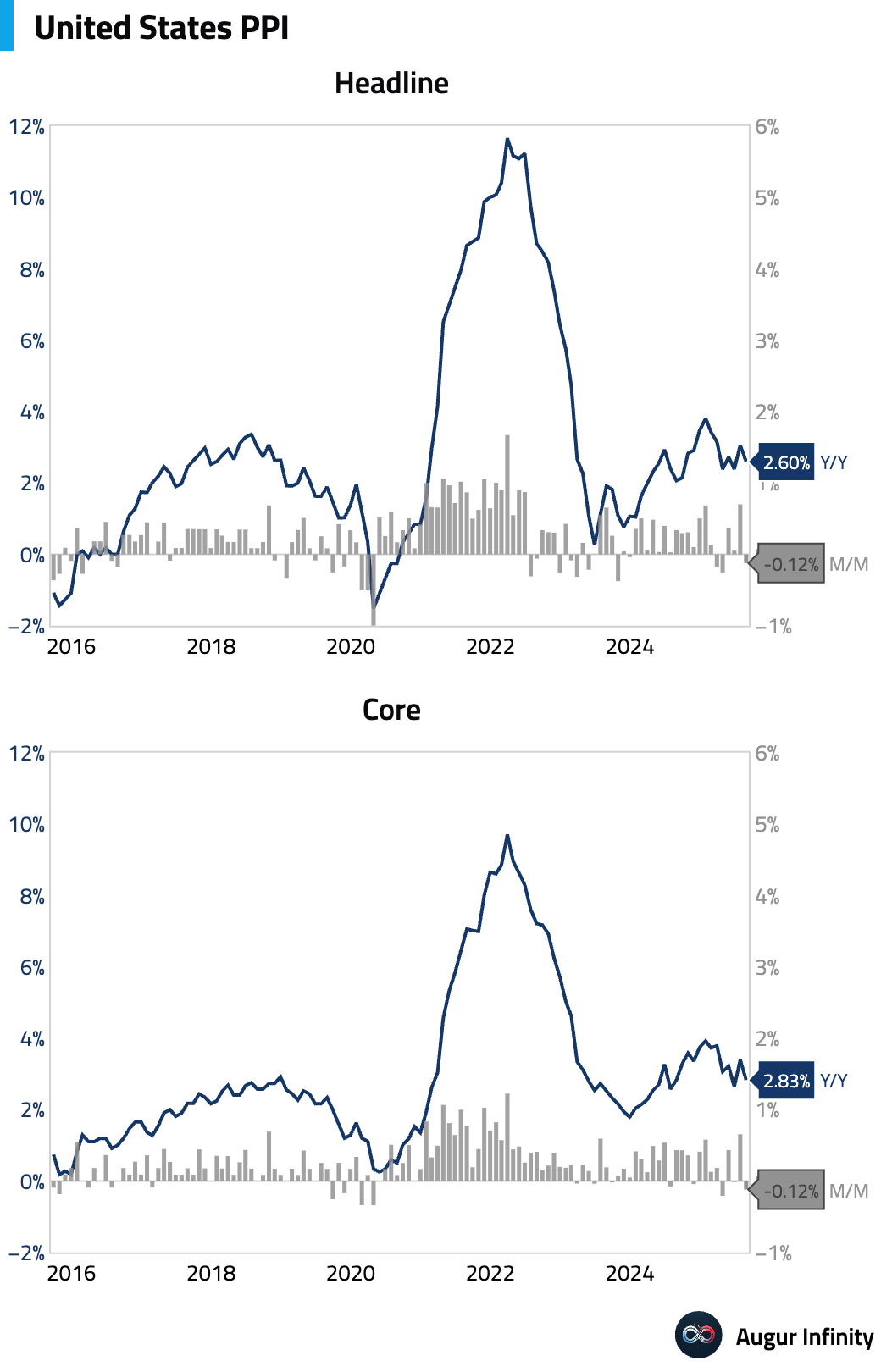

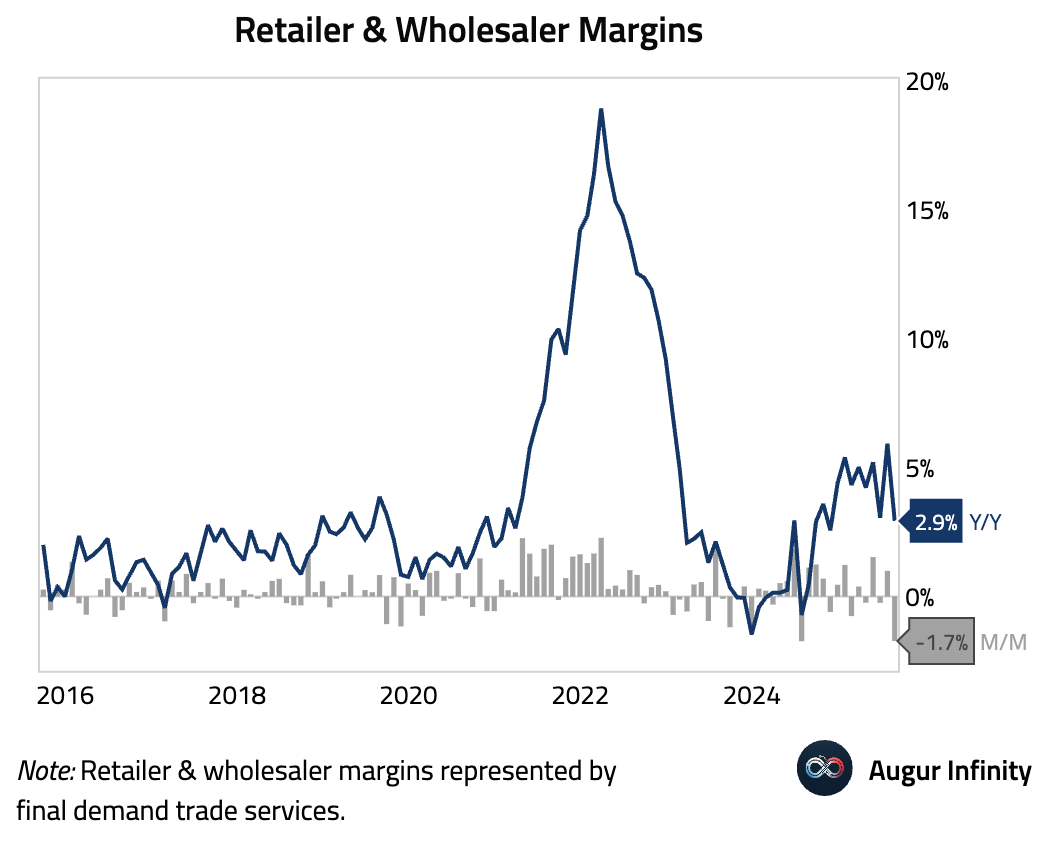

- The Producer Price Index (PPI) unexpectedly declined 0.1% M/M in August, a sharp reversal from July’s 0.7% increase and well below the +0.3% consensus estimate. The headline Y/Y rate decelerated to 2.6% from 3.1%. Core PPI also fell 0.1% M/M, pulling the annual rate down to 2.8% from 3.4%. While the soft headline figures were driven by lower energy prices and trade service margins, underlying details that feed into Core PCE, such as airfares (+1.0%), were firmer.

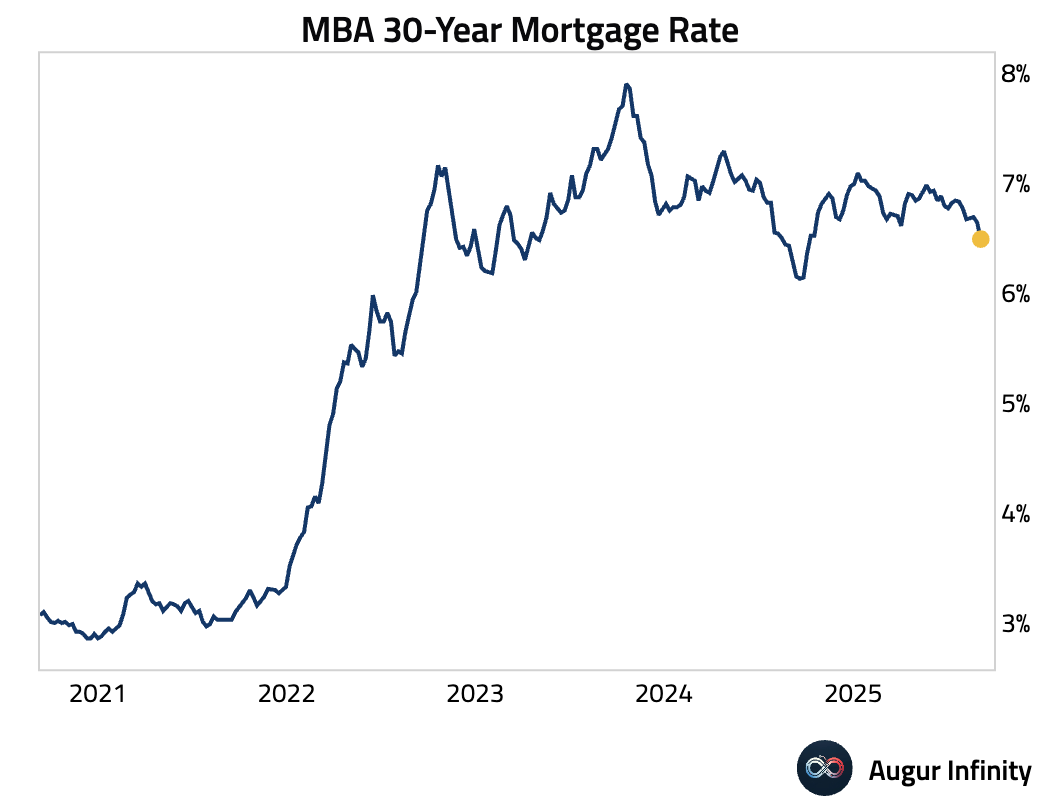

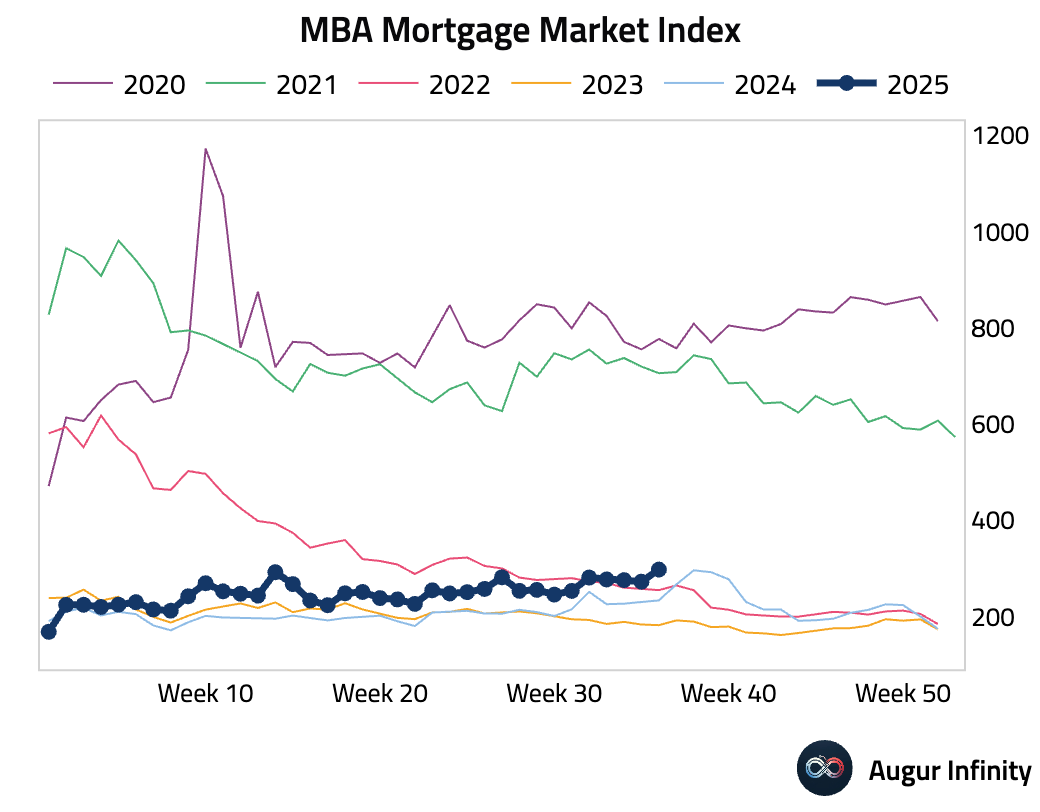

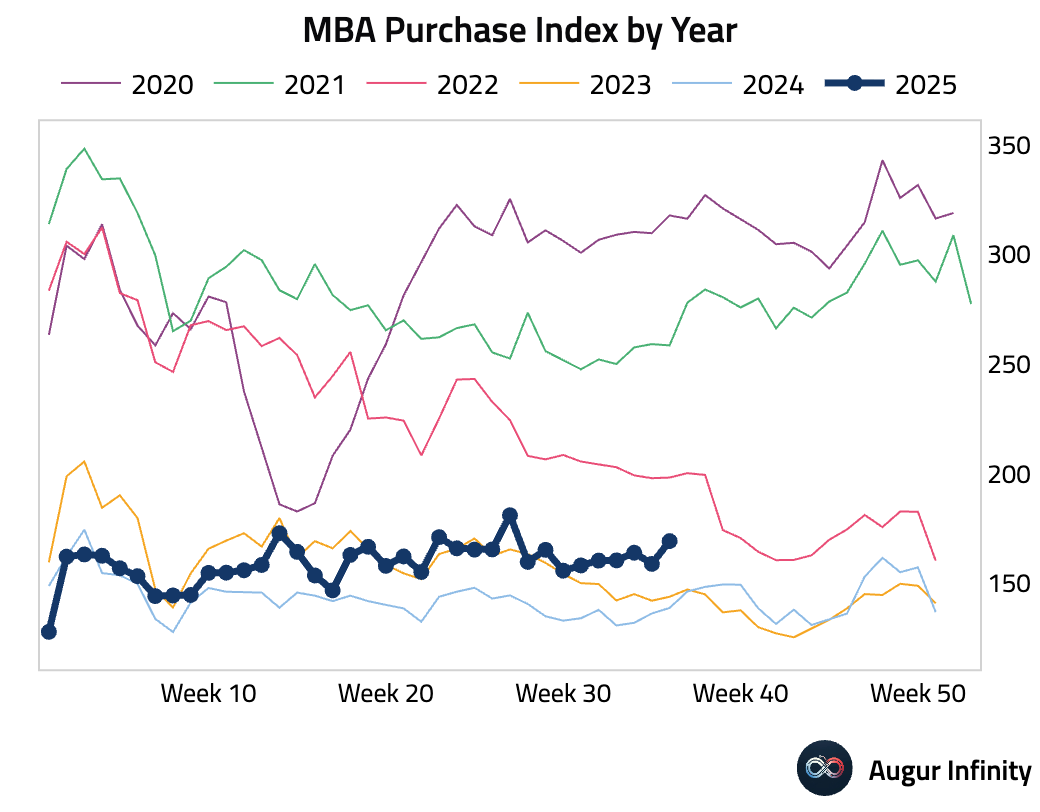

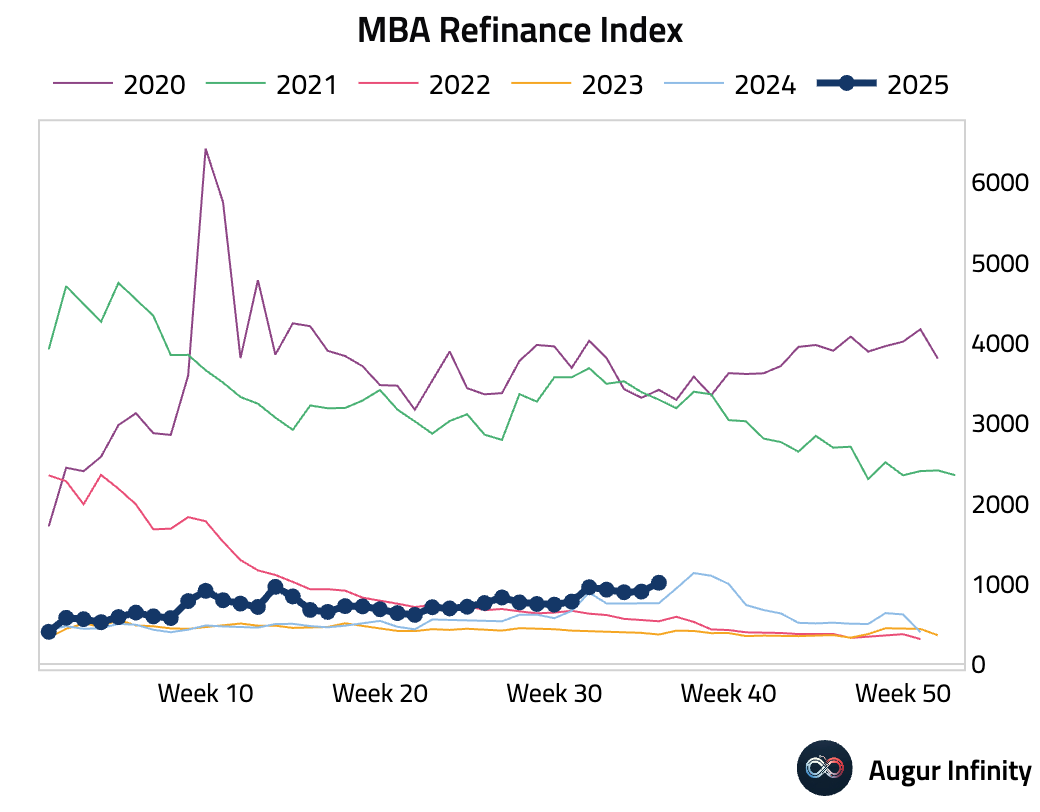

- MBA Mortgage Applications jumped 9.2% week-over-week, reversing the prior week’s 1.2% decline. The rebound was driven by a drop in the 30-year mortgage rate to 6.49% from 6.64%. The overall market index rose to 297.7, its highest level since July 2022, with the Refinance Index up 12.2% and the Purchase Index up 6.5%.

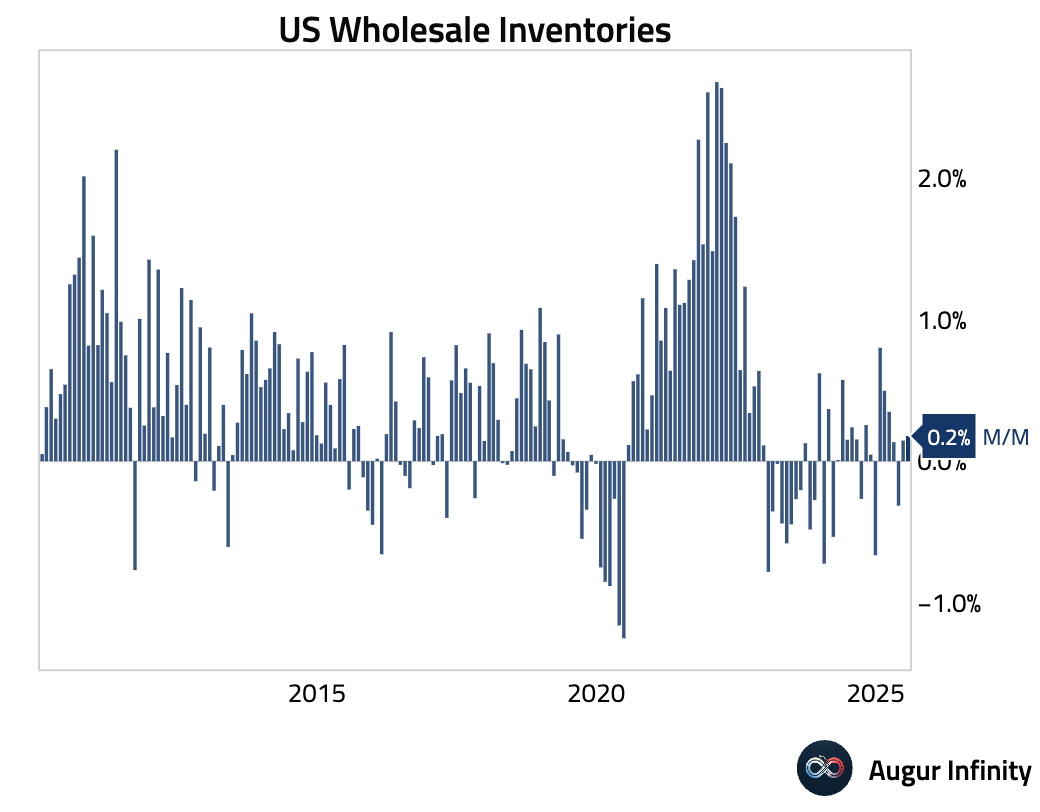

- Wholesale inventories rose 0.1% M/M, matching the prior month’s pace and coming in below the 0.2% consensus. This suggests a cautious approach to inventory management from businesses.

Europe

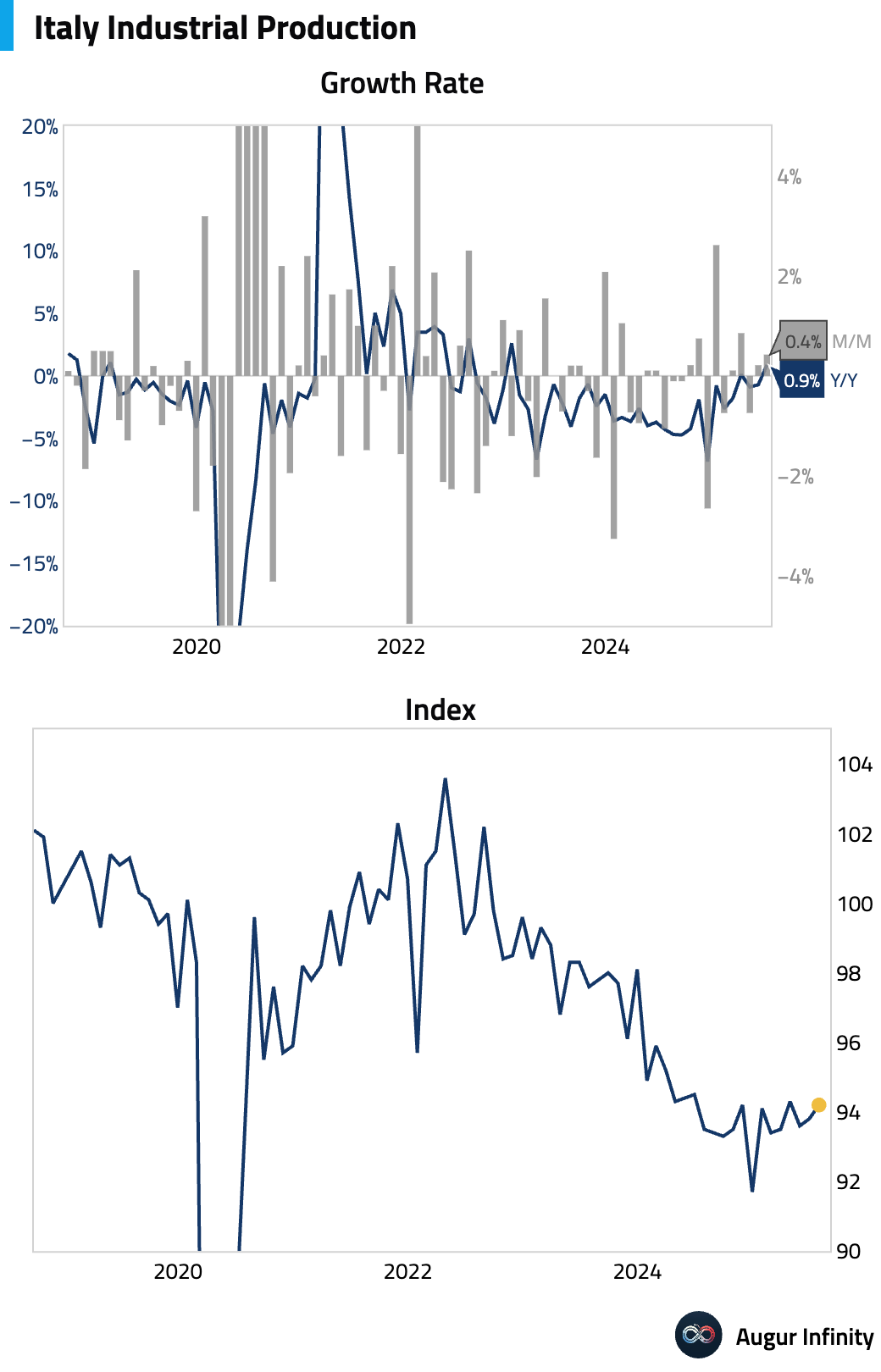

- Italy’s industrial production rose 0.4% M/M in July, beating expectations for a 0.1% decline and accelerating from the previous 0.2% gain. The year-over-year figure turned positive for the first time since January 2023, increasing 0.9% after a 0.7% fall previously.

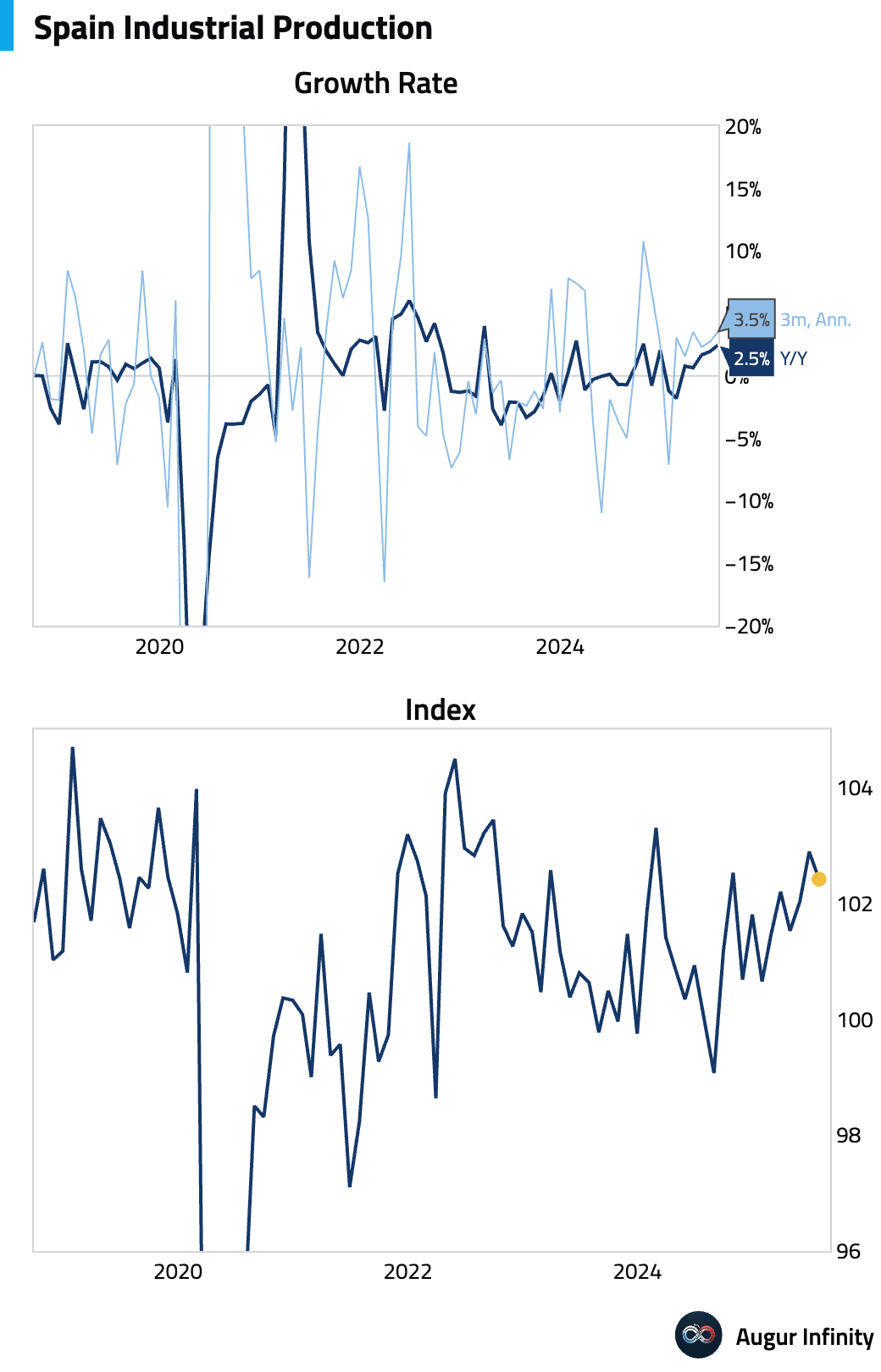

- Spanish industrial production grew by 2.5% Y/Y, accelerating from the prior 1.9% increase and marking the fastest pace of expansion since October 2024.

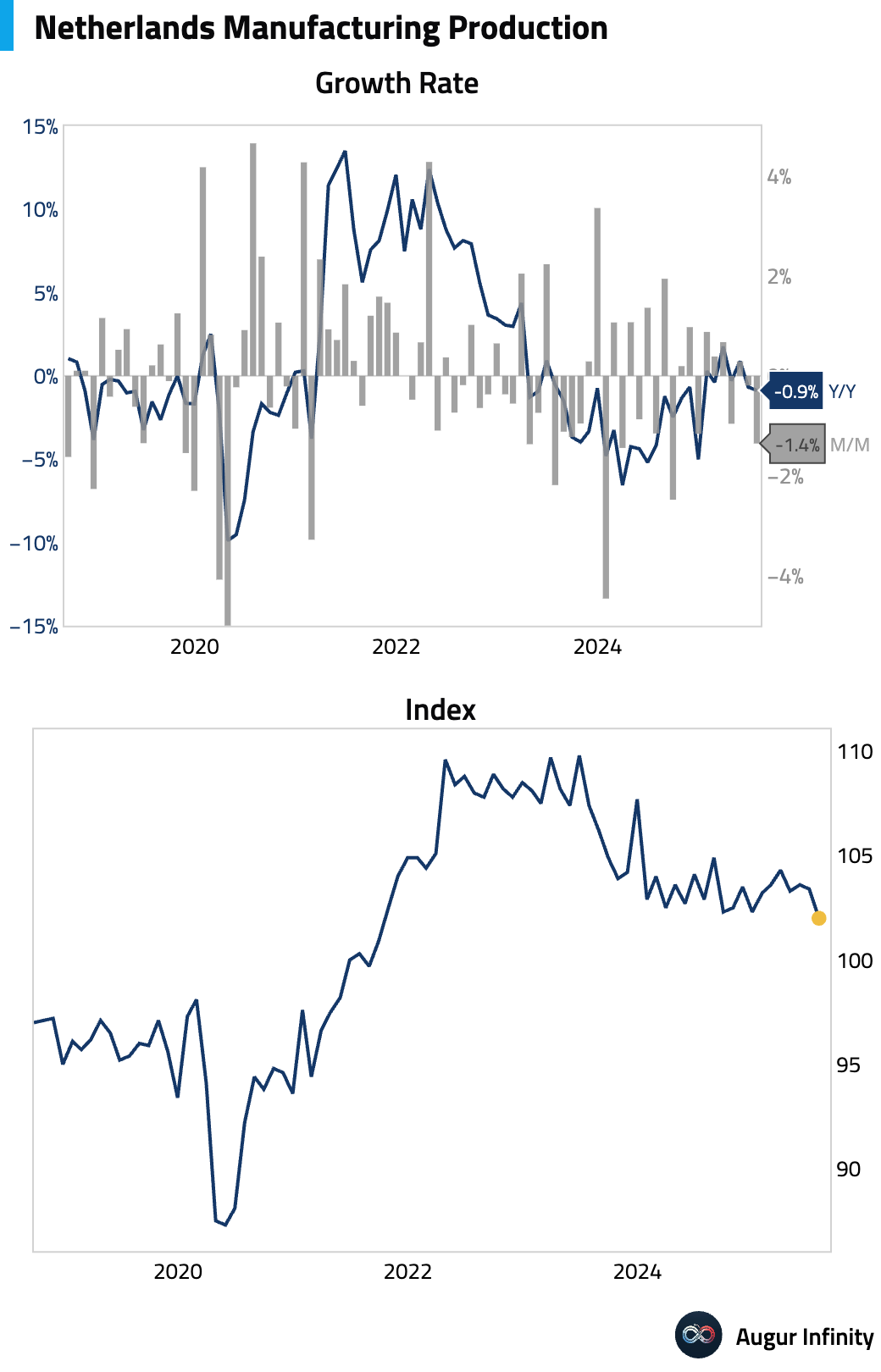

- Dutch manufacturing production fell 1.4% M/M, a significant downturn from the 0.1% dip in the prior month and the largest contraction in nearly a year.

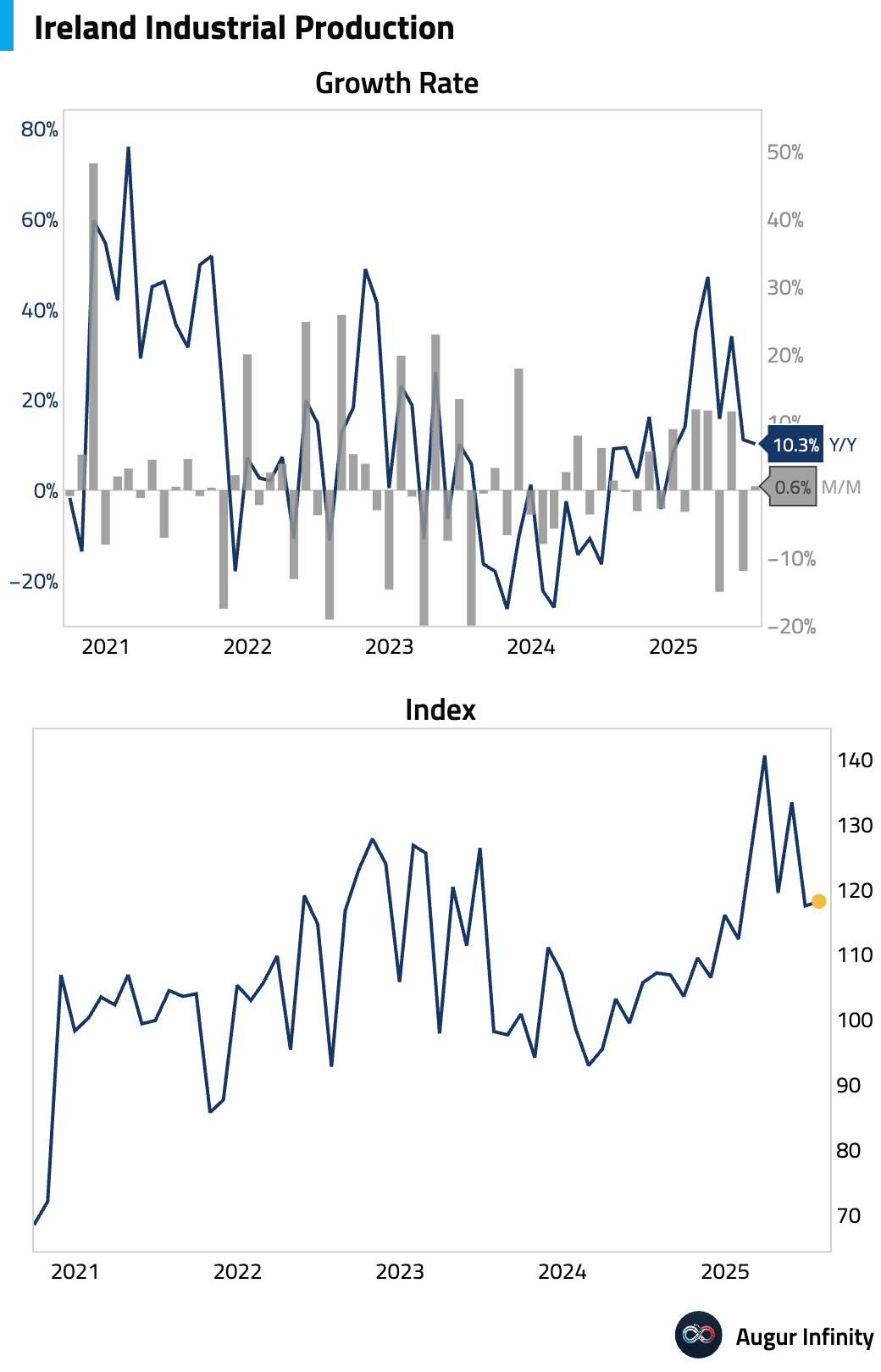

- Irish industrial production growth moderated to 10.3% Y/Y from 11.2% previously, continuing its trend of strong but volatile expansion.

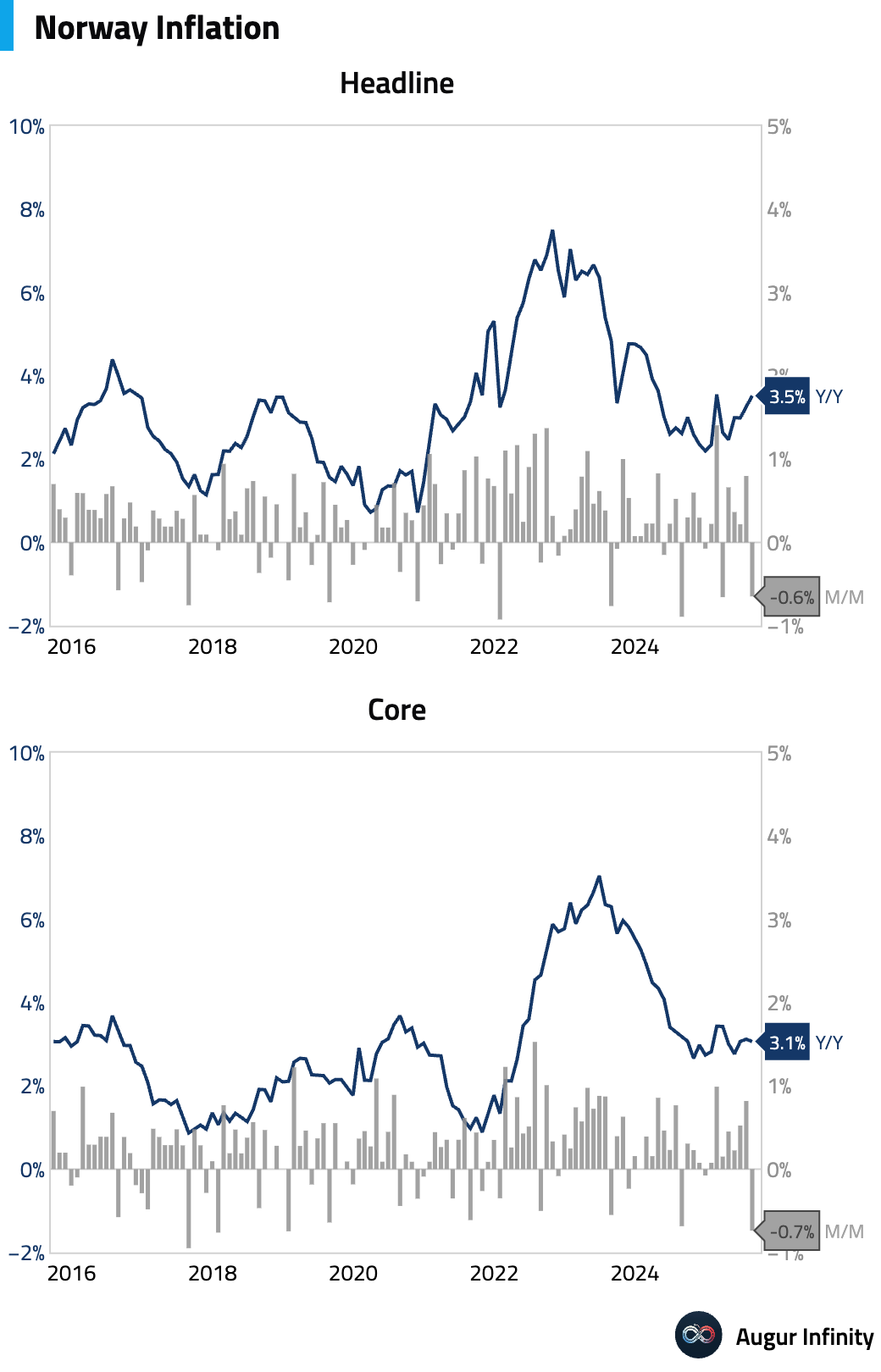

- Norway’s headline inflation accelerated to 3.5% Y/Y from 3.3%, matching consensus, while the core rate held steady at 3.1%. On a monthly basis, prices fell, with the headline and core CPI declining 0.6% and 0.7%, respectively. The monthly core drop was the largest since January 2019.

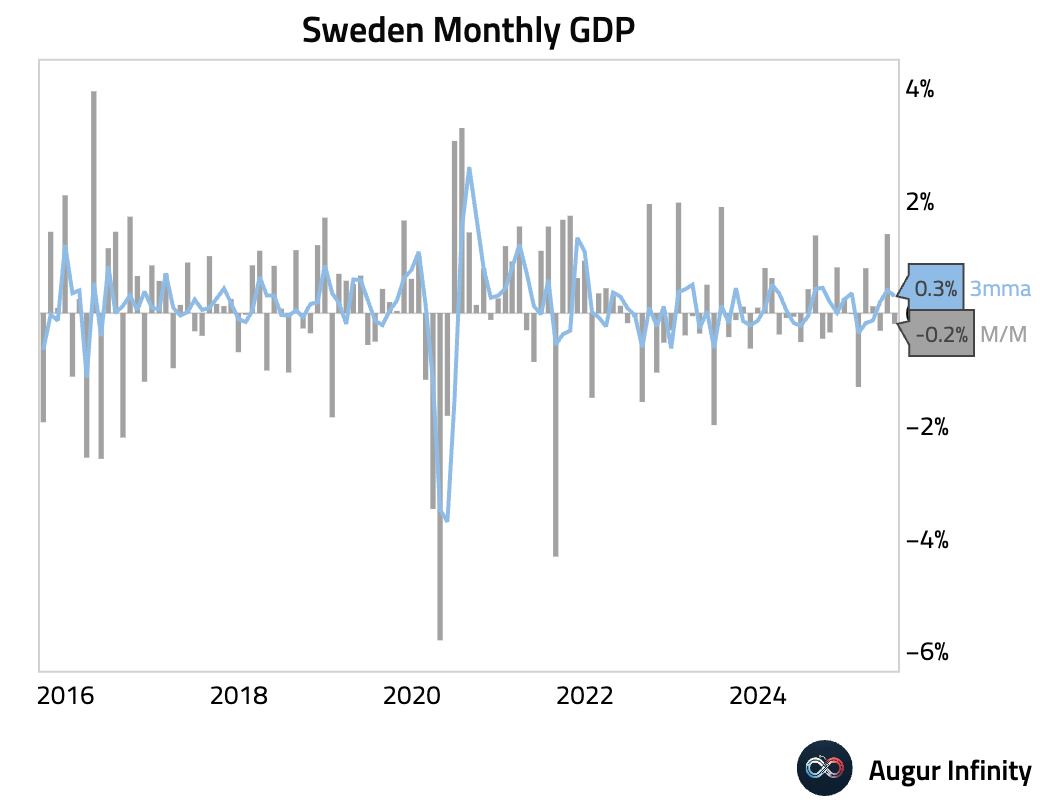

- Sweden’s economy contracted 0.2% M/M, a sharp deceleration from the 1.4% expansion recorded in the previous month.

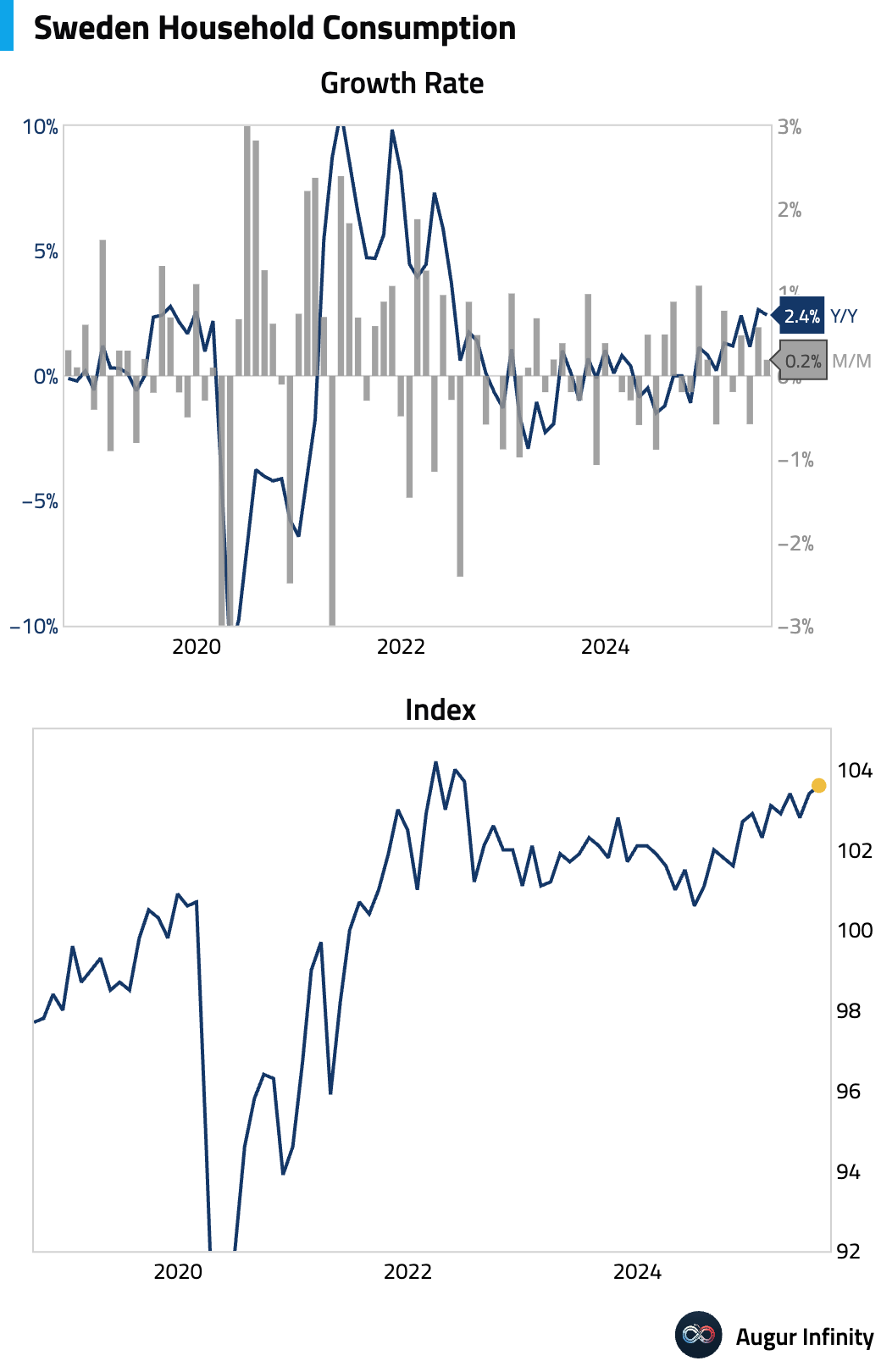

- Swedish household consumption growth slowed to 0.2% M/M from 0.6% previously. The annual rate also decelerated to 2.4% Y/Y from 2.6%.

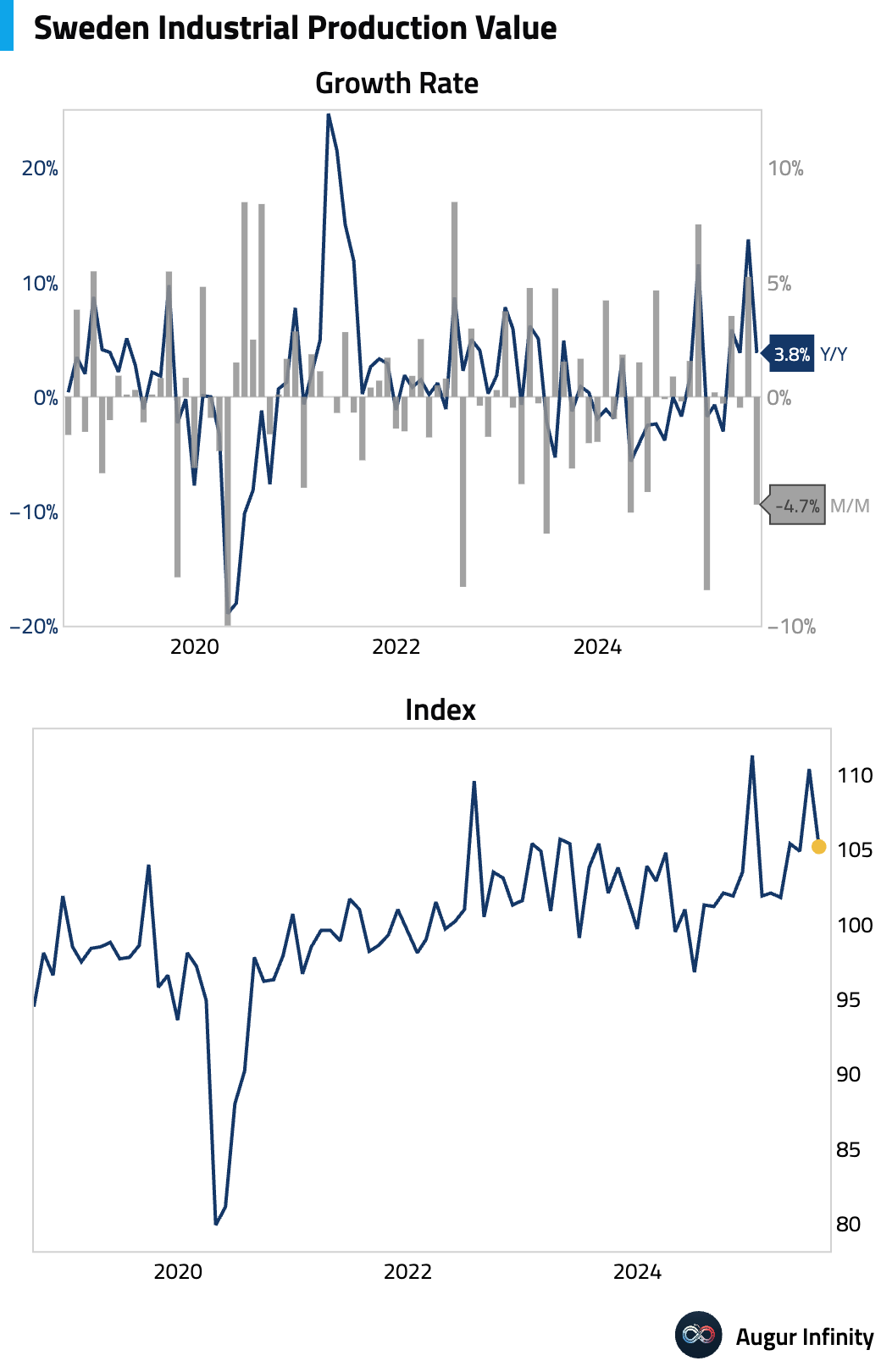

- Swedish industrial production fell 4.7% M/M, more than reversing the prior month's 5.2% gain. Year-over-year growth slowed sharply to 3.8% from 13.8%.

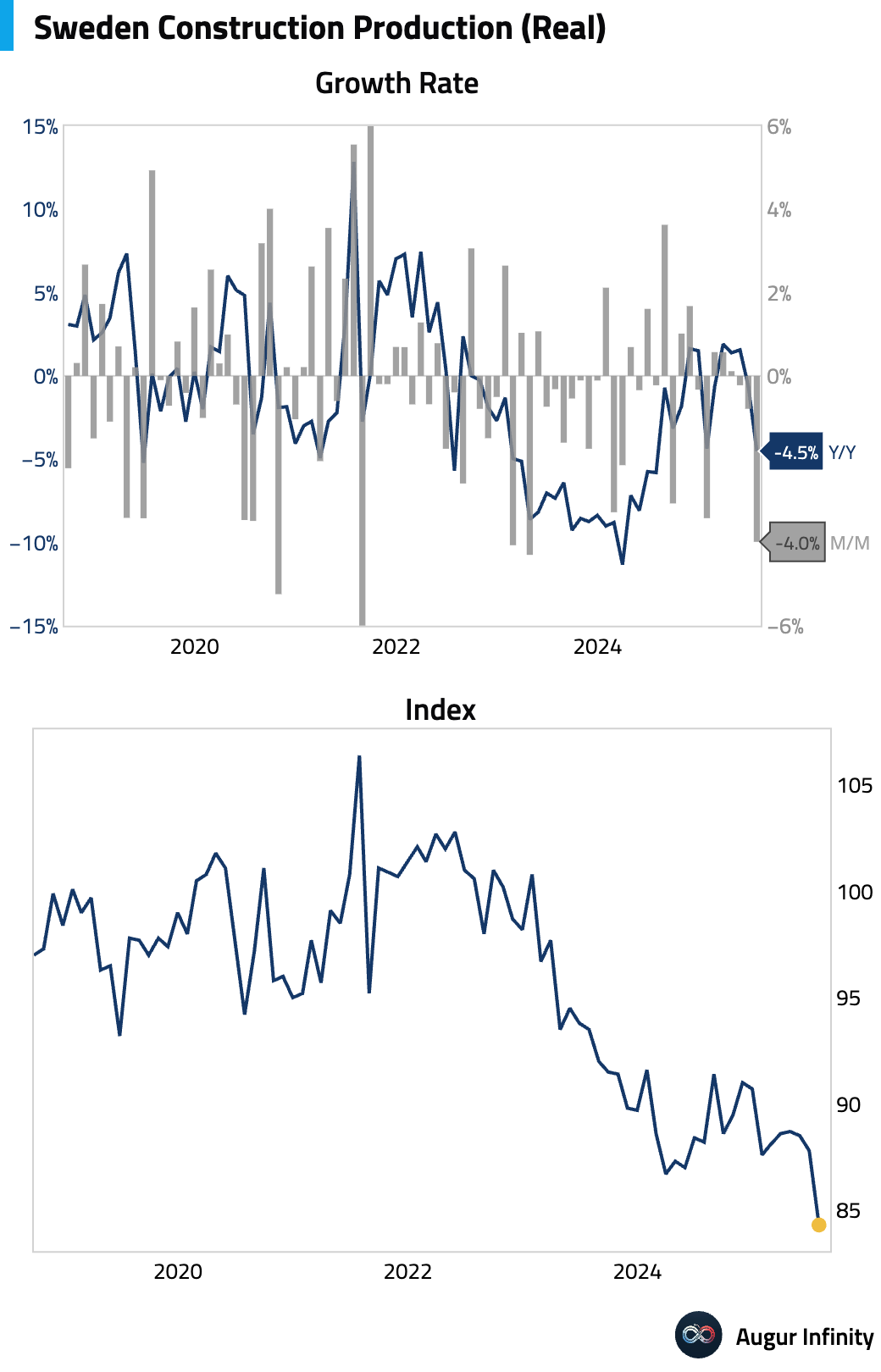

- Swedish construction output dropped 4.5% Y/Y, a steep decline from the previous 0.3% fall and the weakest reading in over a year.

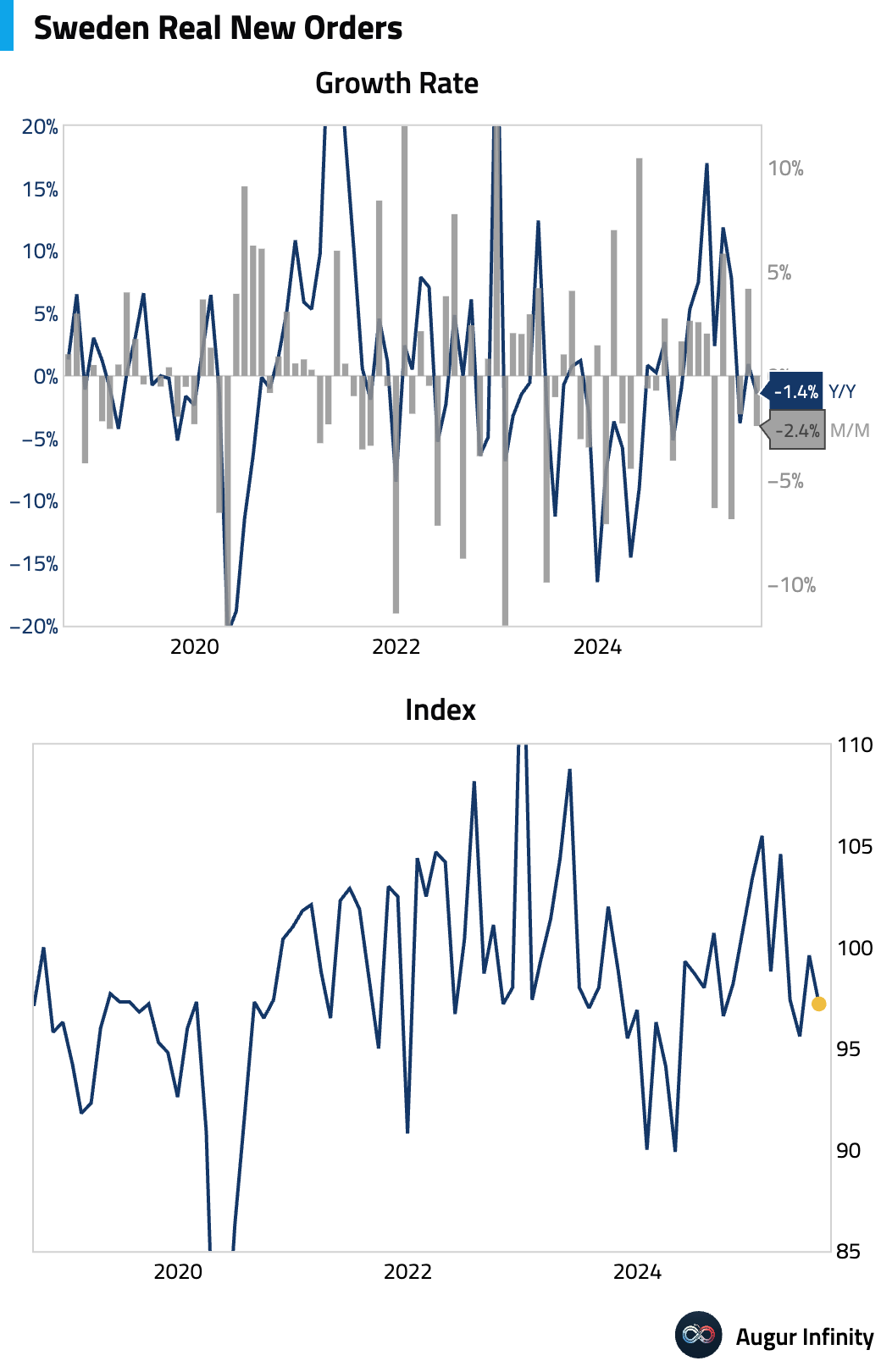

- New industrial orders in Sweden fell 1.4% Y/Y, reversing from a 0.9% gain in the prior period.

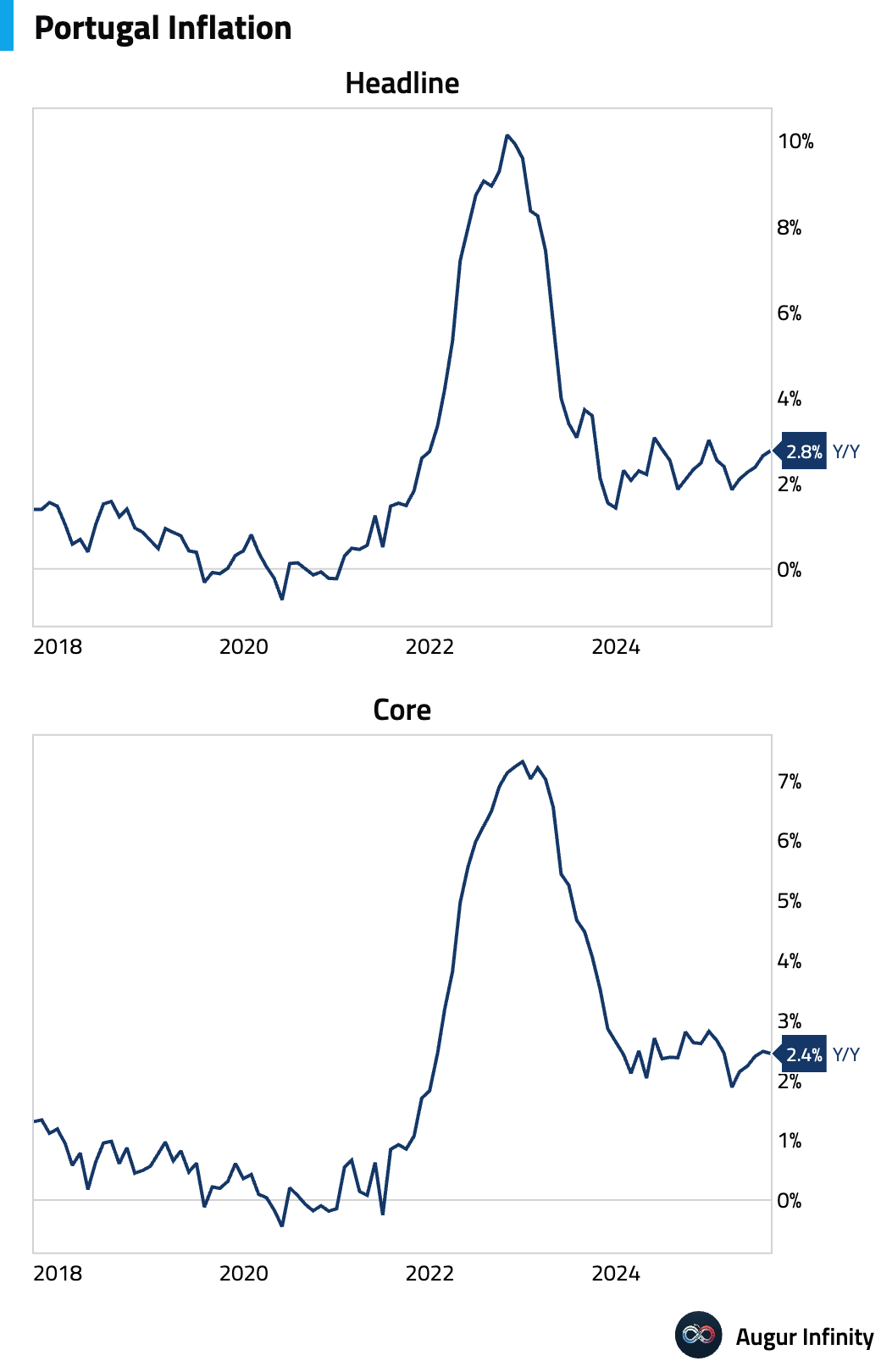

- Portugal’s final inflation figures confirmed the preliminary estimates, with the Y/Y rate rising to 2.8% from 2.6% and the M/M rate showing a 0.2% decline.

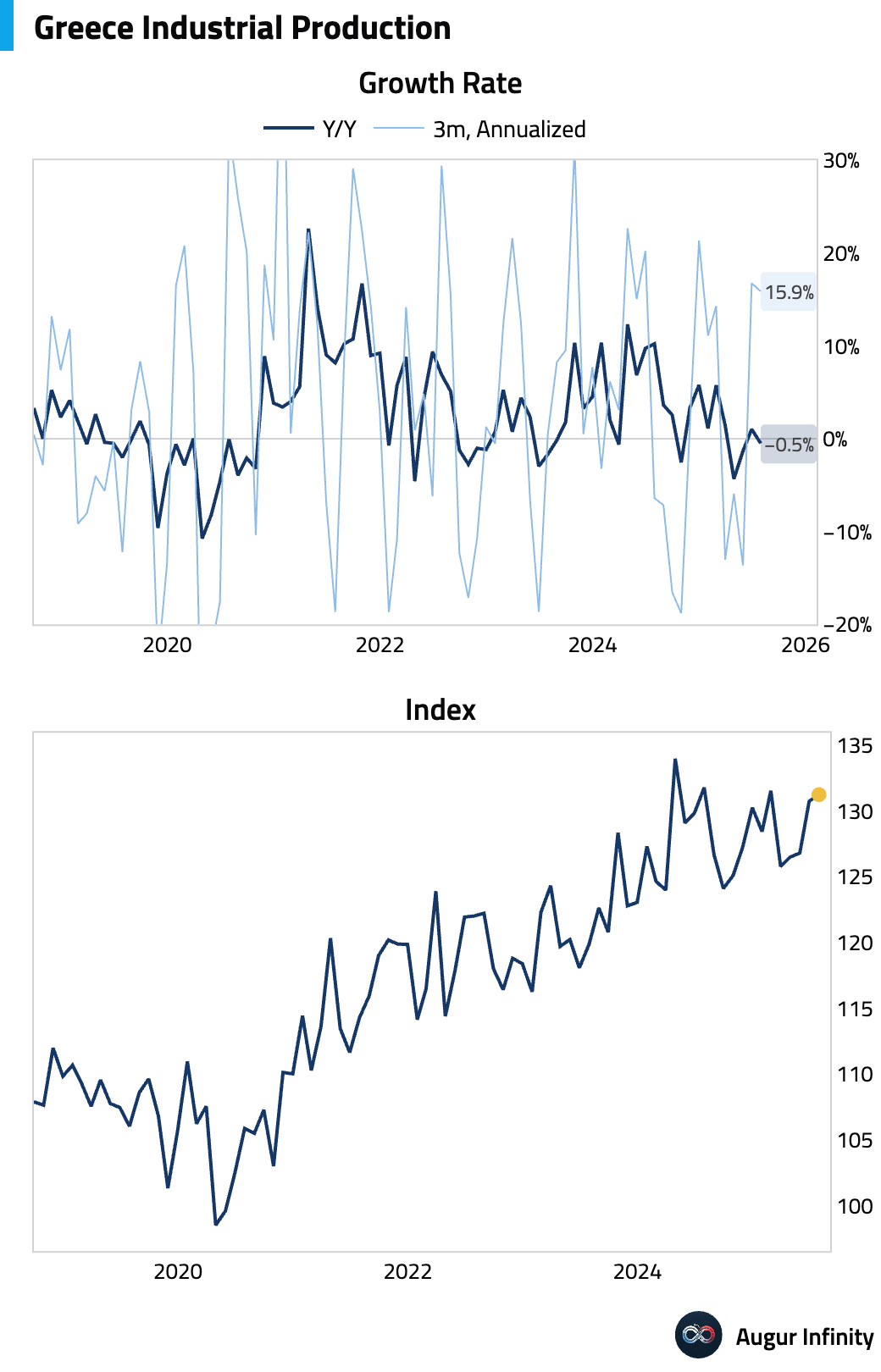

- Greek industrial production contracted 0.5% Y/Y, reversing a 1.0% gain in the previous period.

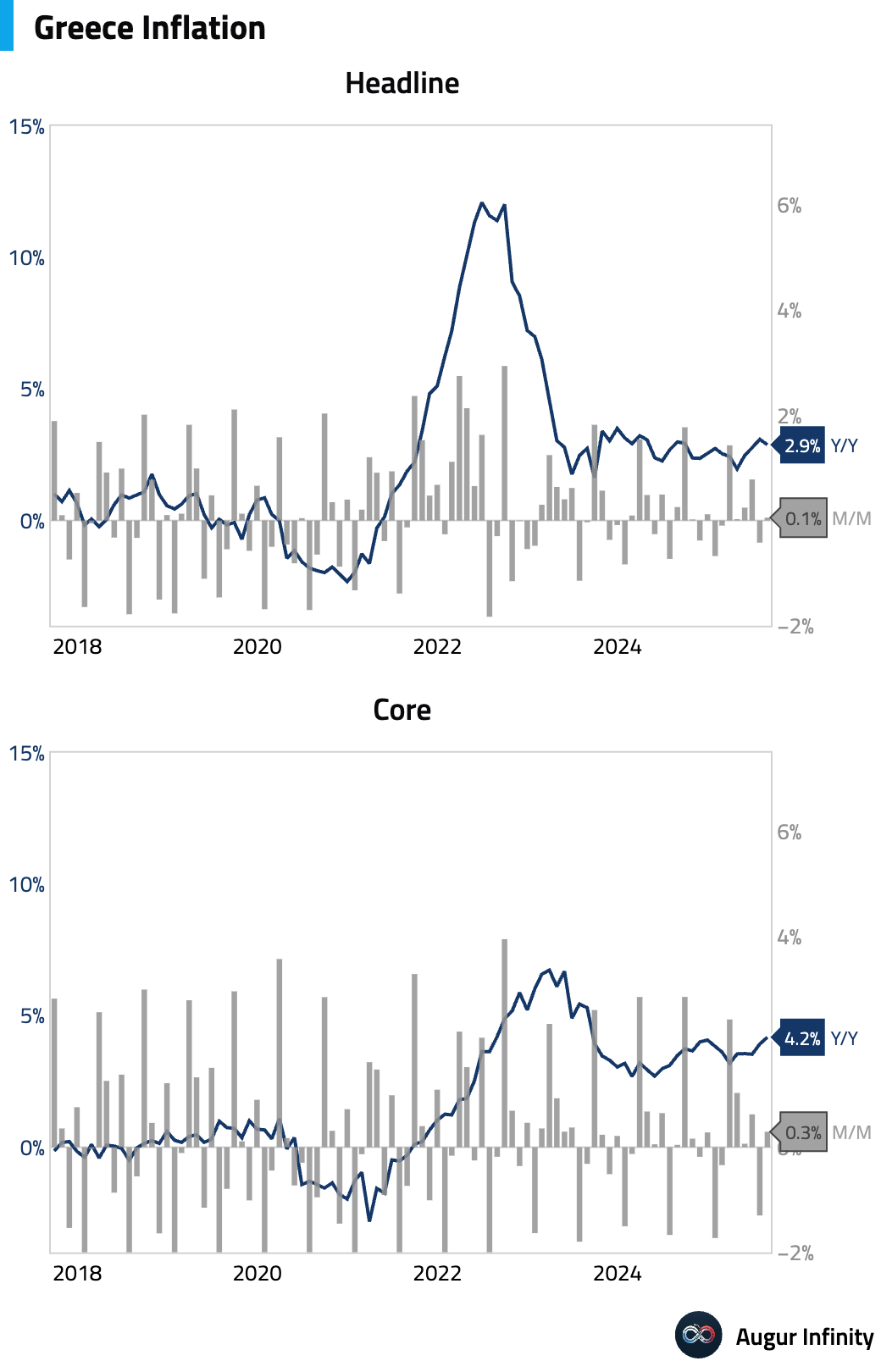

- Greek inflation eased to 2.9% Y/Y from 3.1% in the prior month. Month-over-month, prices rose 0.1%, reversing a 0.4% decline.

Asia-Pacific

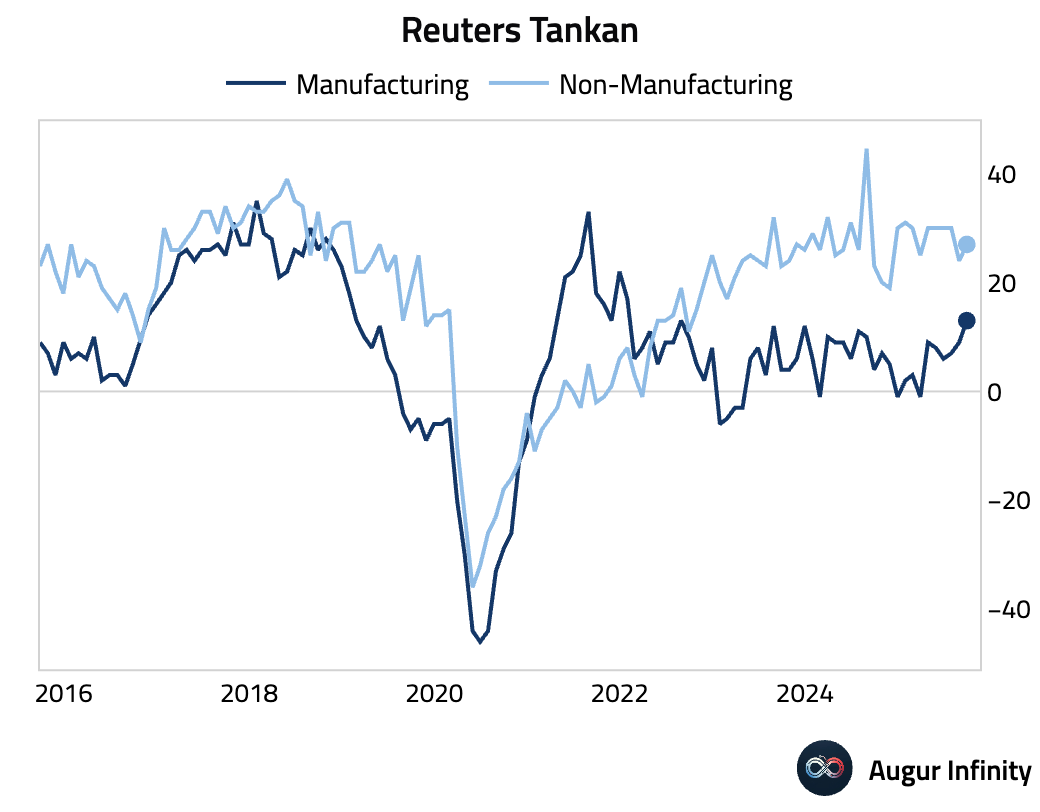

- Japan’s Reuters Tankan Index rose for a third consecutive month to 13, its highest level since January 2022. The gain was driven by strength in both manufacturers (+4 to +13), led by transport equipment and chemicals, and non-manufacturers (+3 to +27), led by real estate. However, the outlook for December dipped to +11, with transport equipment manufacturers signaling caution. The non-manufacturing recovery also appears to be losing momentum, suggesting the recovery may be peaking.

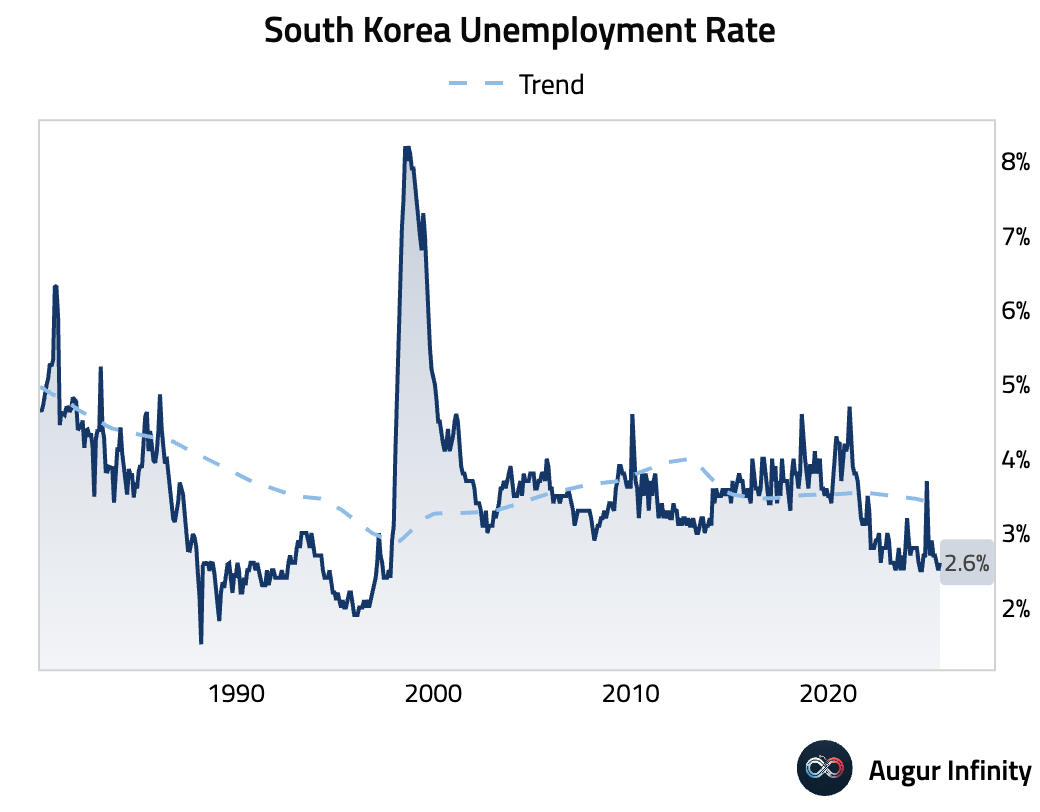

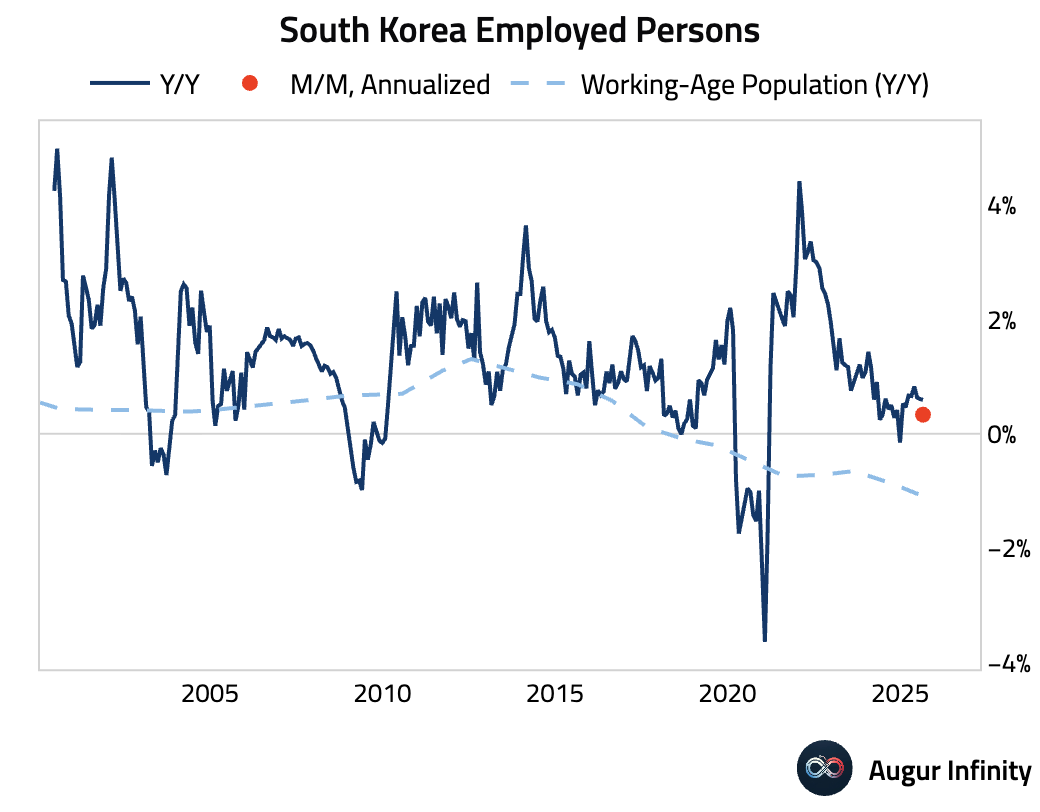

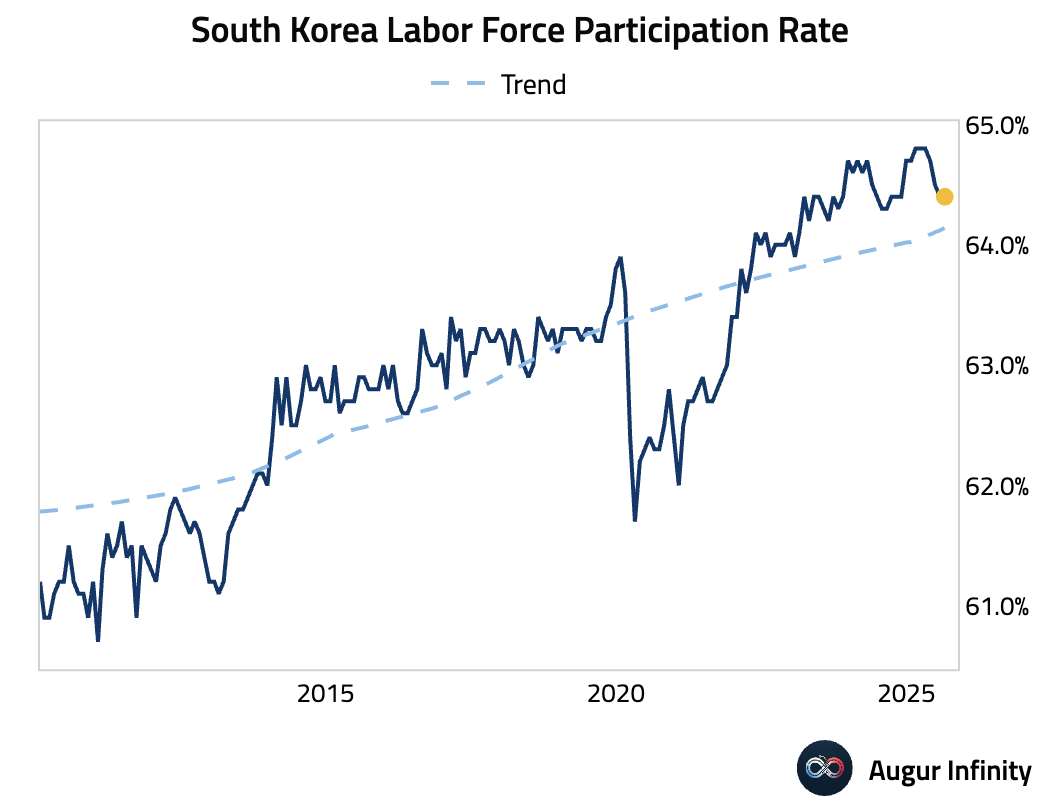

- South Korea’s unemployment rate edged up to 2.6% from 2.5% in the prior month. Despite the small increase, the labor market remains tight, with the participation rate holding steady and the number of employed persons continuing to rise.

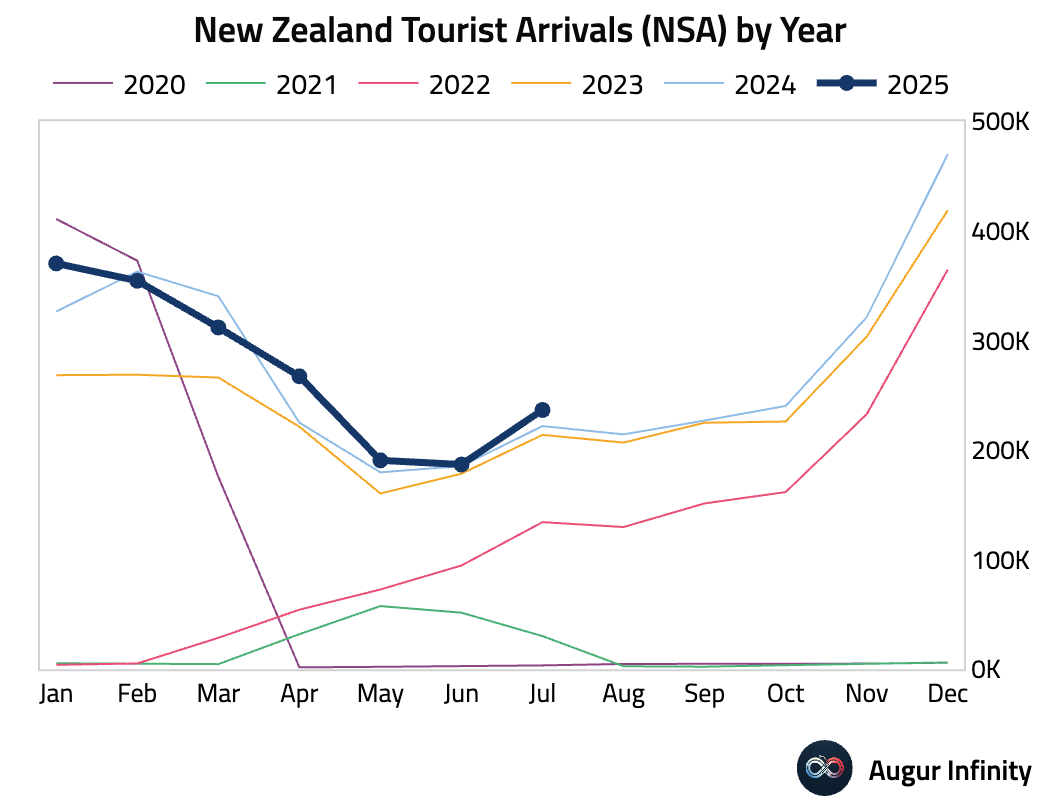

- New Zealand’s visitor arrivals increased by 6.6% Y/Y, a significant acceleration from the previous 0.8% rise, indicating a continued recovery in the tourism sector.

China

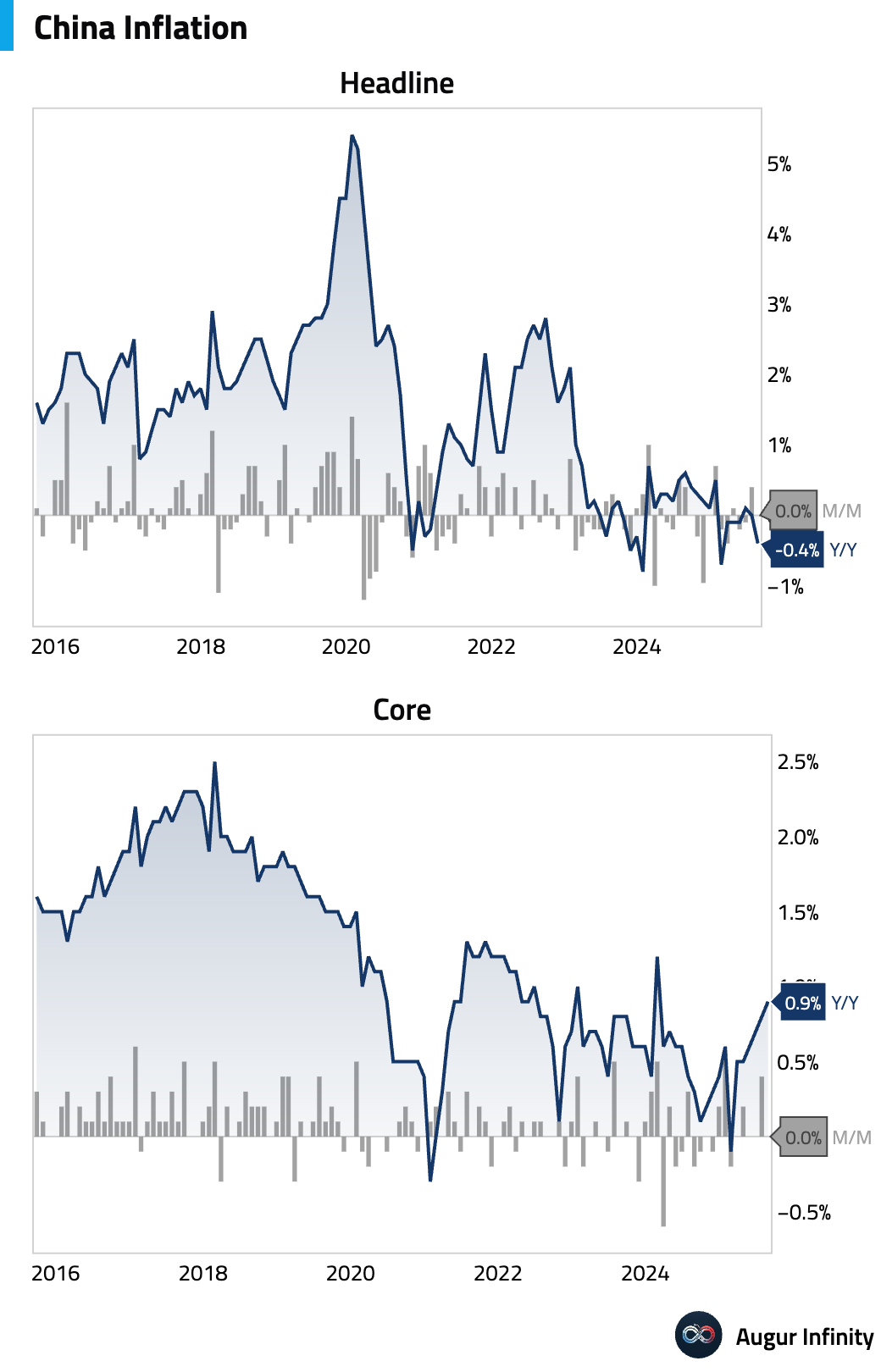

- China’s consumer price index (CPI) fell into deflation, posting a 0.4% Y/Y decline after a flat reading in July. The drop was driven by deepening food deflation (-4.3% Y/Y), particularly from lower pork and vegetable prices amid high base effects and increased supply. However, core CPI, which excludes food and energy, accelerated to 0.9% Y/Y, pointing to underlying strength in services and non-food goods demand. On a monthly basis, prices were flat, missing the 0.1% consensus.

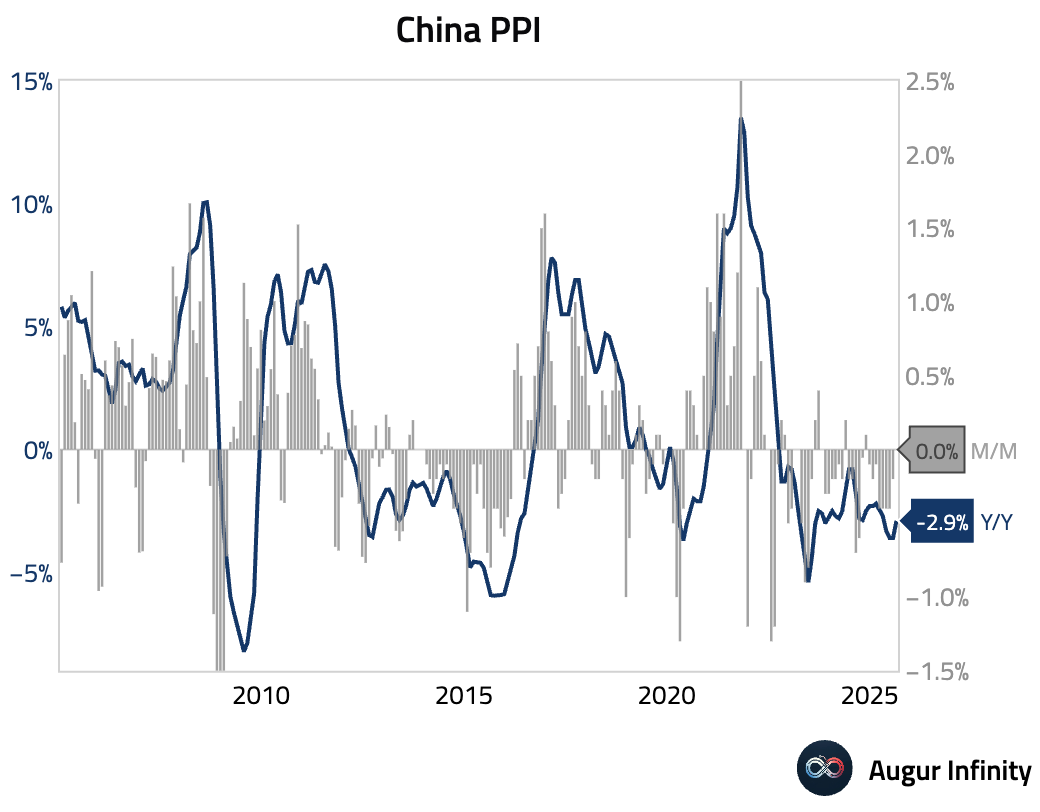

- China’s Producer Price Index (PPI) deflation eased for a second consecutive month, with prices falling 2.9% Y/Y compared to -3.6% in July. The improvement was better than expected and reflected narrower price declines in upstream sectors like ferrous metals, suggesting factory-gate price pressures are beginning to moderate.

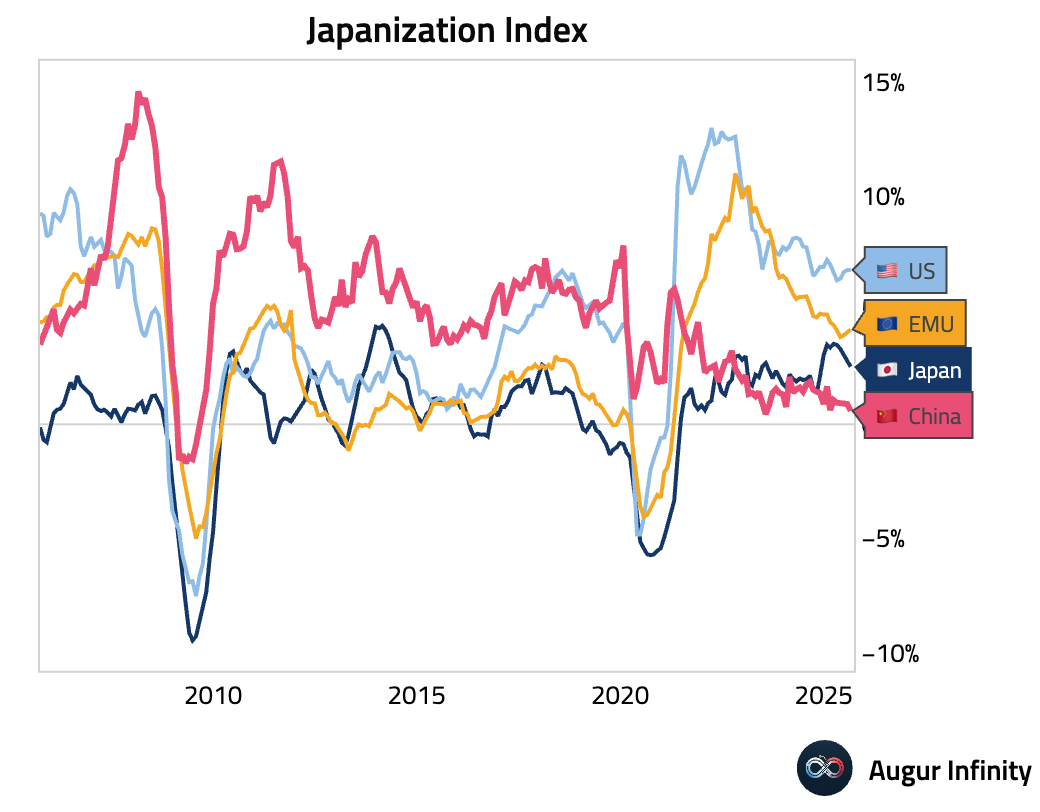

- According to Professor Takatoshi Ito's Japanization indices, China remains more Japanized than Japan.

Emerging Markets ex China

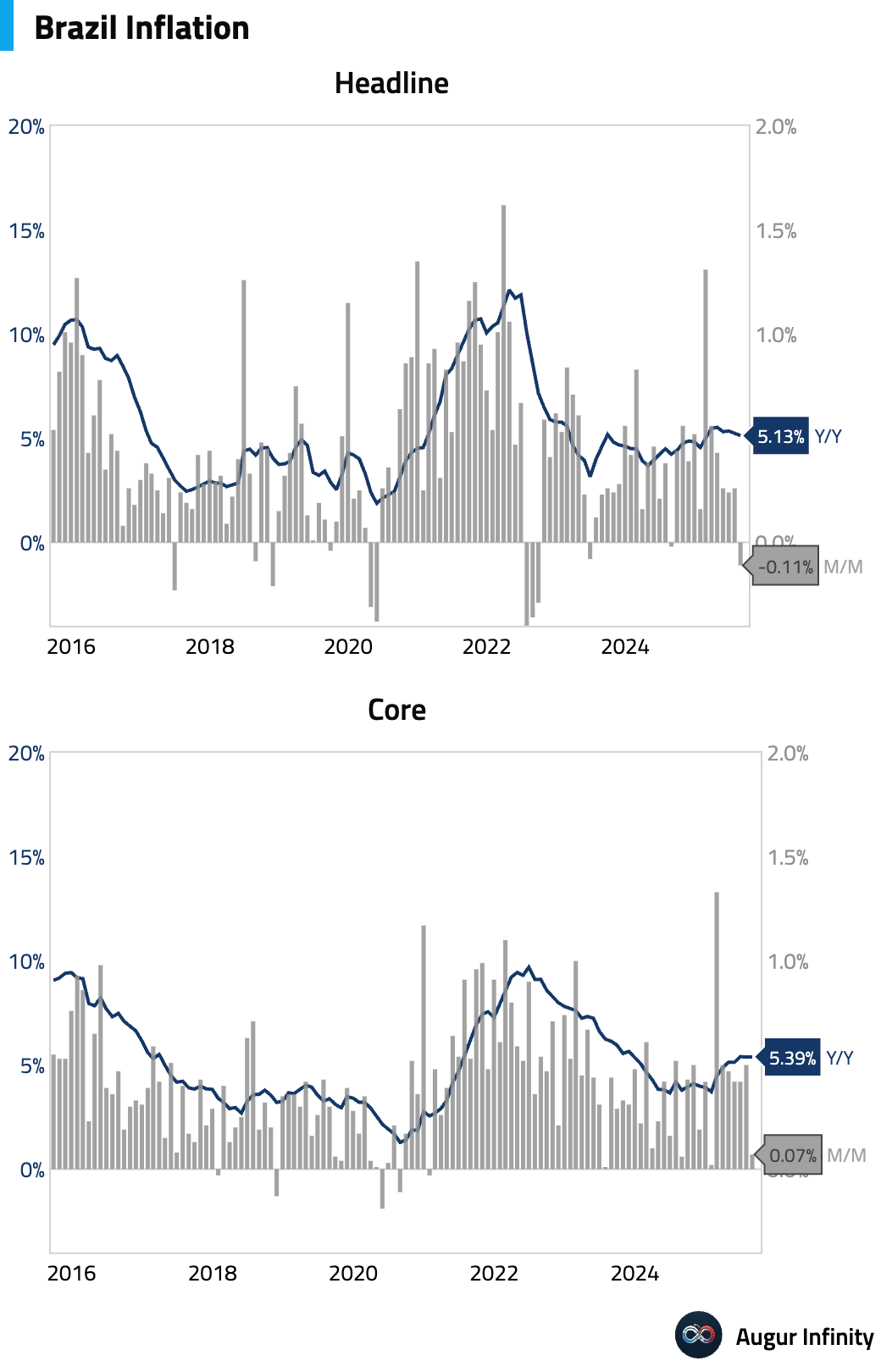

- Brazil’s IPCA inflation registered -0.11% M/M, a deeper deflation than the -0.15% consensus, pulling the annual rate down to 5.13%. The monthly decline was driven by a temporary electricity tariff rebate and lower airfares. However, underlying price pressures accelerated, with core inflation rising to 0.30% M/M and the three-month moving average for services inflation quickening to 6.7%, signaling the need for a continued hawkish policy stance.

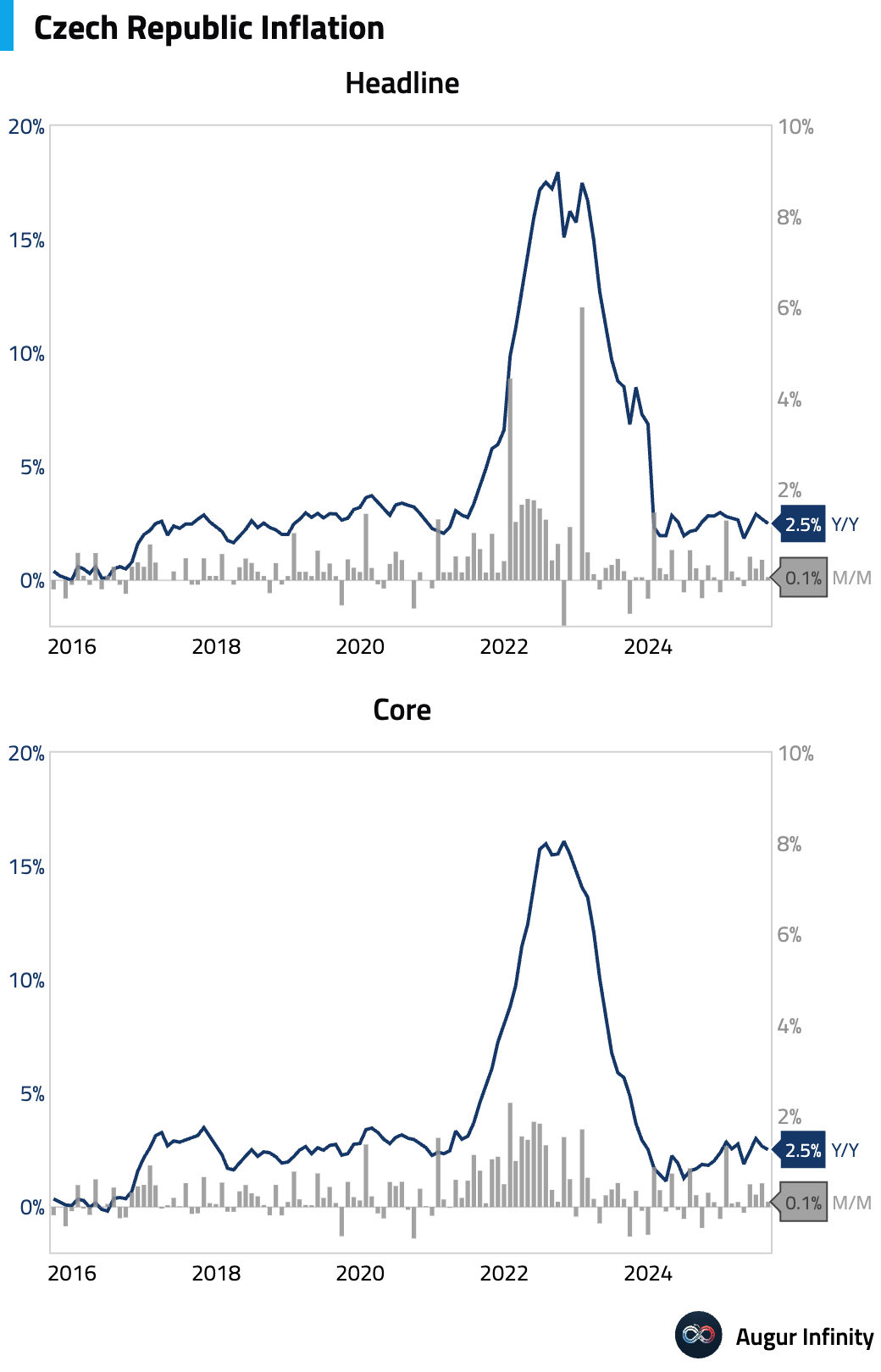

- The Czech Republic’s final August CPI was confirmed at 2.5% Y/Y, down from 2.7% and in line with consensus. The decline was driven by moderating food inflation. However, the central bank’s preferred measure of core inflation rose slightly to 2.8% Y/Y. Despite a hawkish official tone, the disinflationary trend is expected to continue, likely allowing for further rate cuts this year.

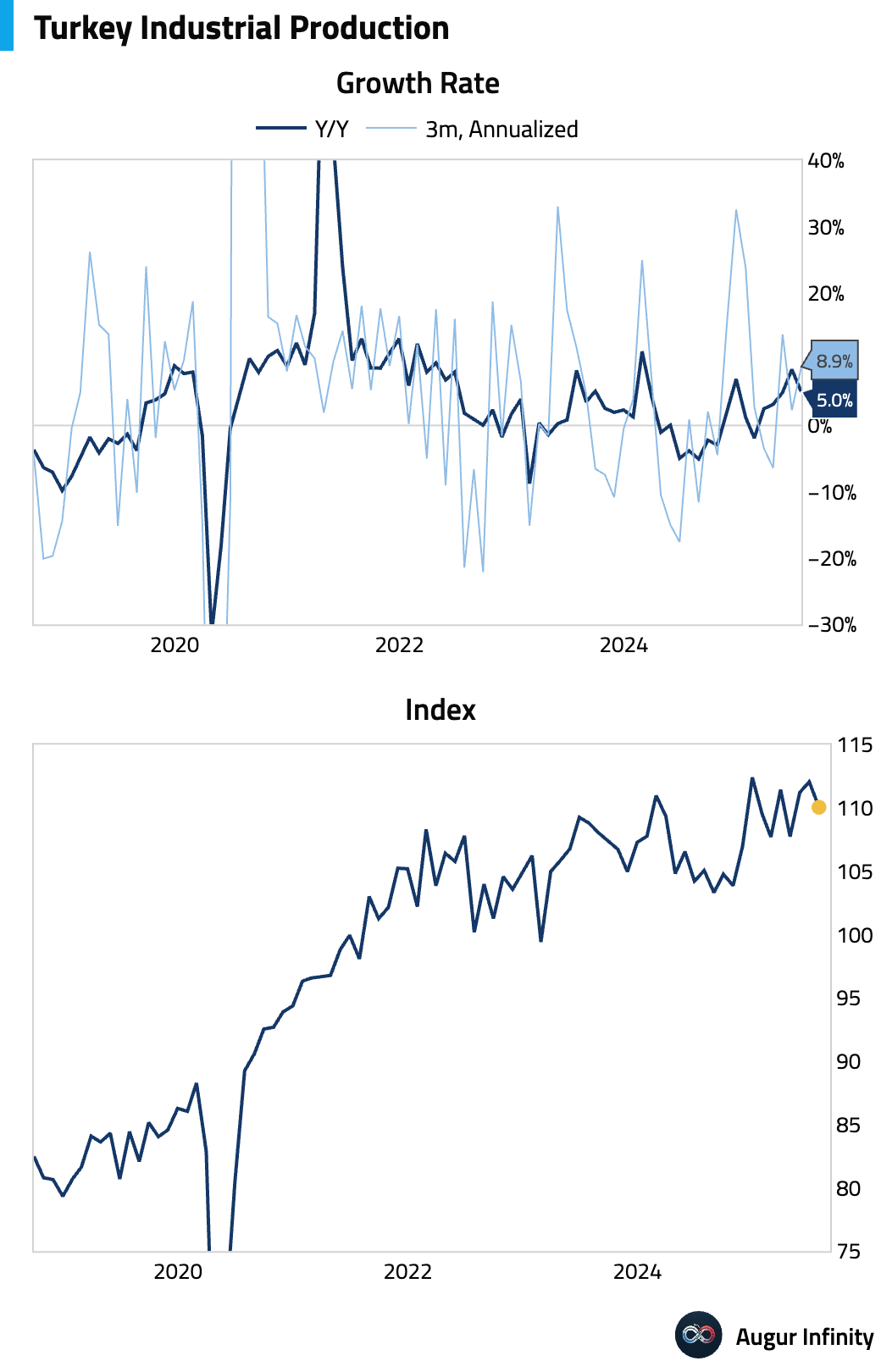

- Turkey’s industrial production growth decelerated to 5.0% Y/Y from 8.5% previously. On a monthly basis, output contracted by 1.8%, reversing a 0.8% gain.

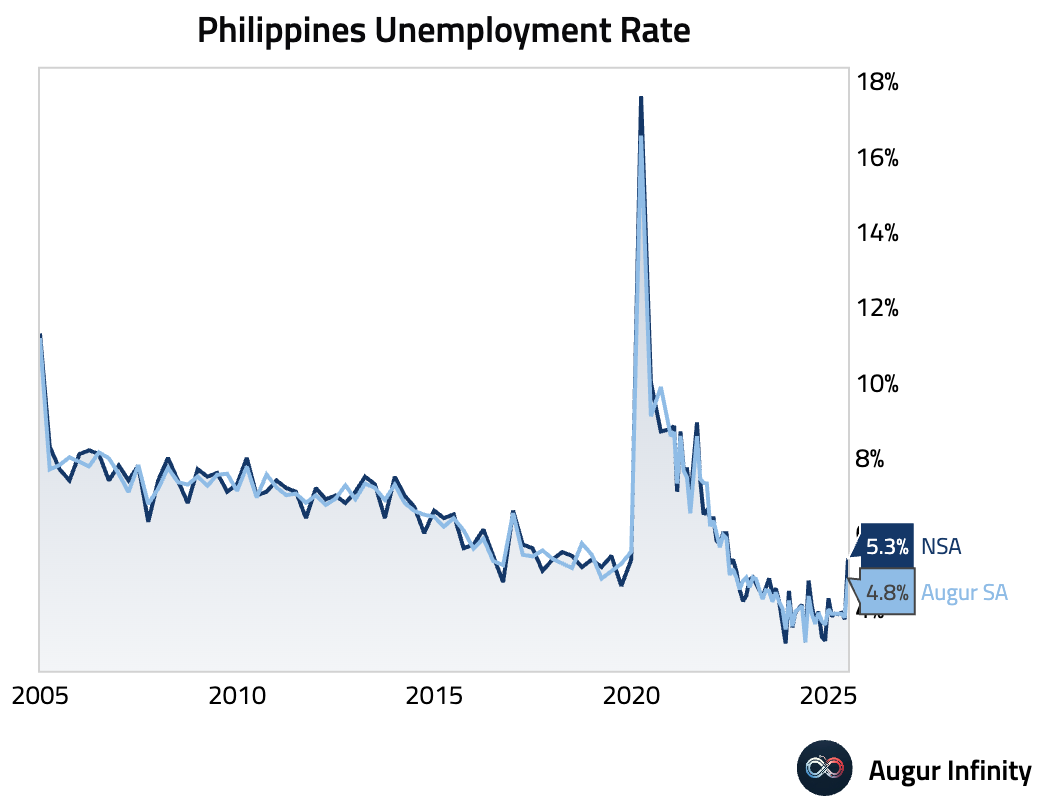

- The unemployment rate in the Philippines jumped to 5.3% from 3.7%, reaching its highest level since June 2022.

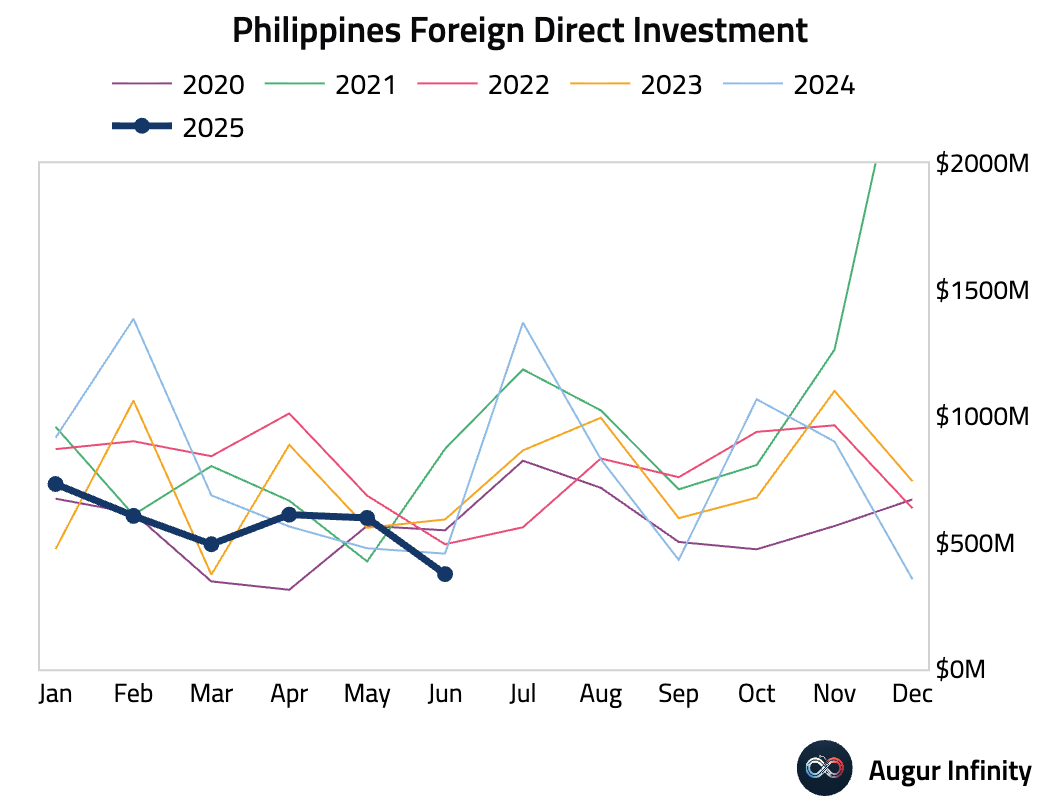

- Foreign direct investment into the Philippines fell to $400 million from $600 million in the prior period.

- Indonesian consumer confidence edged down to 117.2 from 118.1, reaching its lowest point since April 2022.

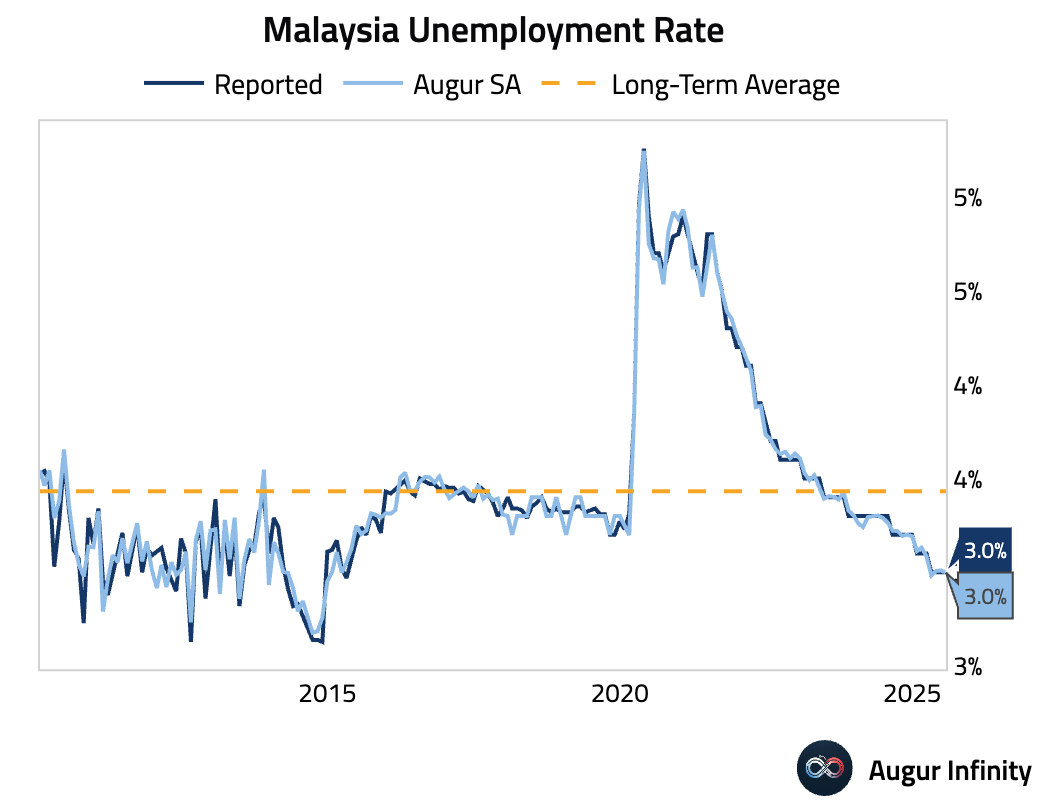

- Malaysia's unemployment rate held steady at 3.0%, a level it has maintained for several months.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.