Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- Mexico announced it will increase its tariff on vehicle imports from Asia to 50 percent from 20 percent.

- The Bank of Japan is reportedly preparing to sell exchange-traded funds as part of its portfolio unwind.

Global Economics

United States

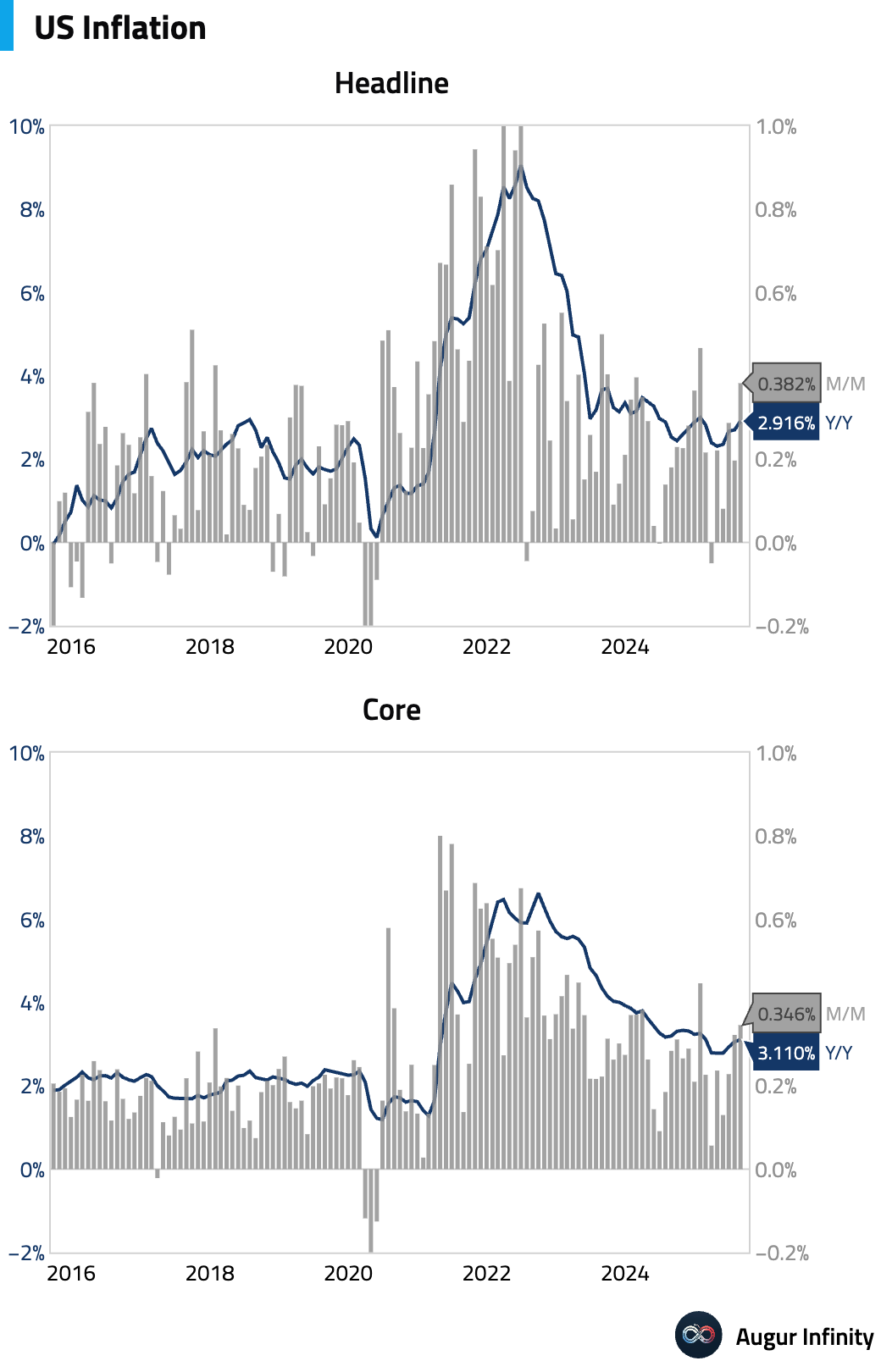

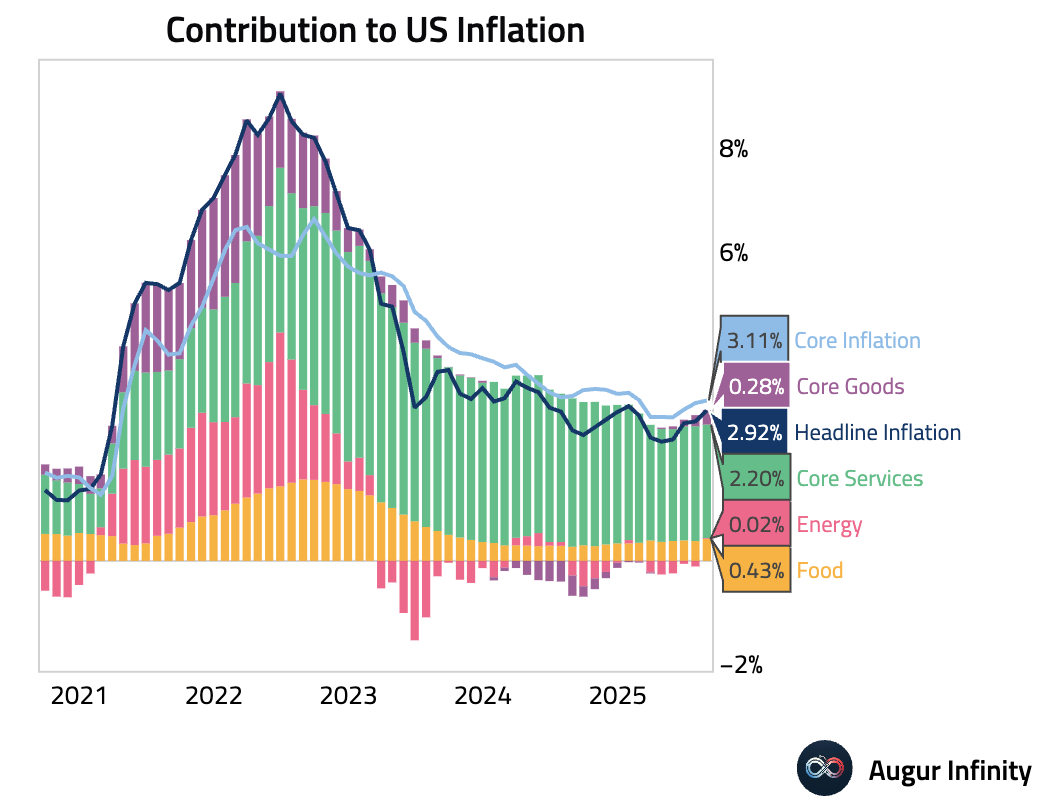

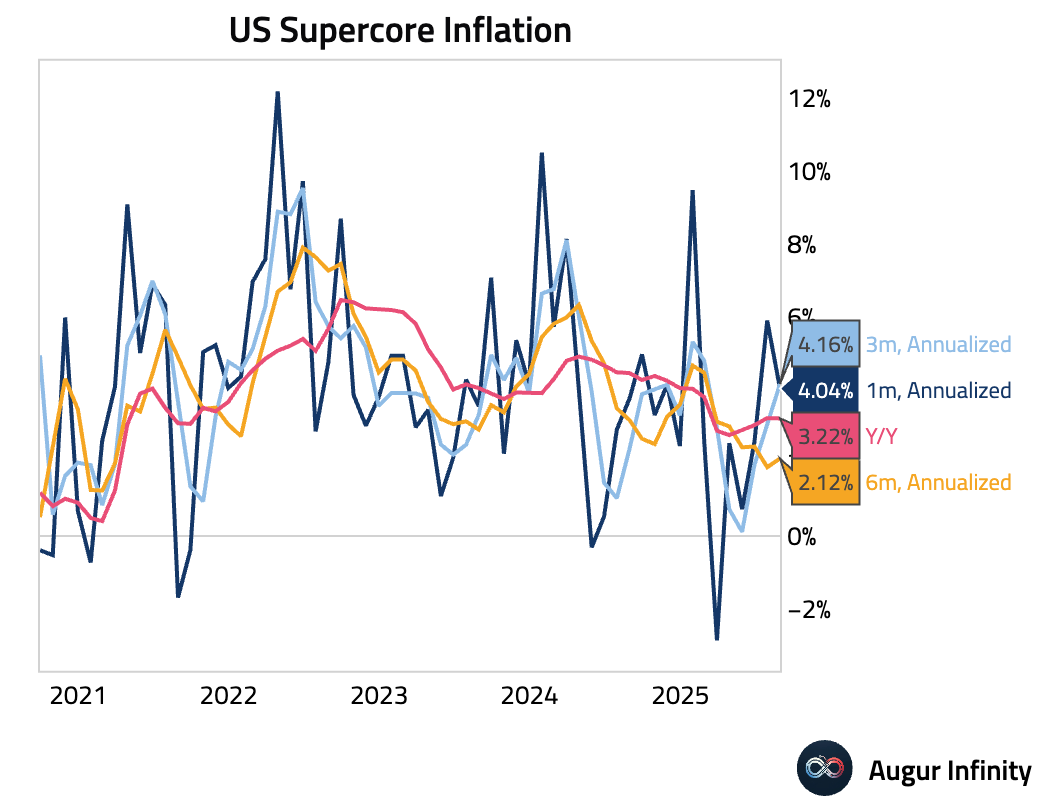

- The August Consumer Price Index rose 0.4% M/M and 2.9% Y/Y, accelerating from July and slightly topping the consensus monthly estimate. Core CPI increased 0.3% M/M and held steady at 3.1% Y/Y, both in line with expectations. The monthly core increase was driven by volatile airfares (+5.9%) and used cars (+1.0%), which together added 8 basis points to the reading. Shelter inflation also reaccelerated to 0.44%, with rent and owners' equivalent rent increases concentrated in smaller southern cities.

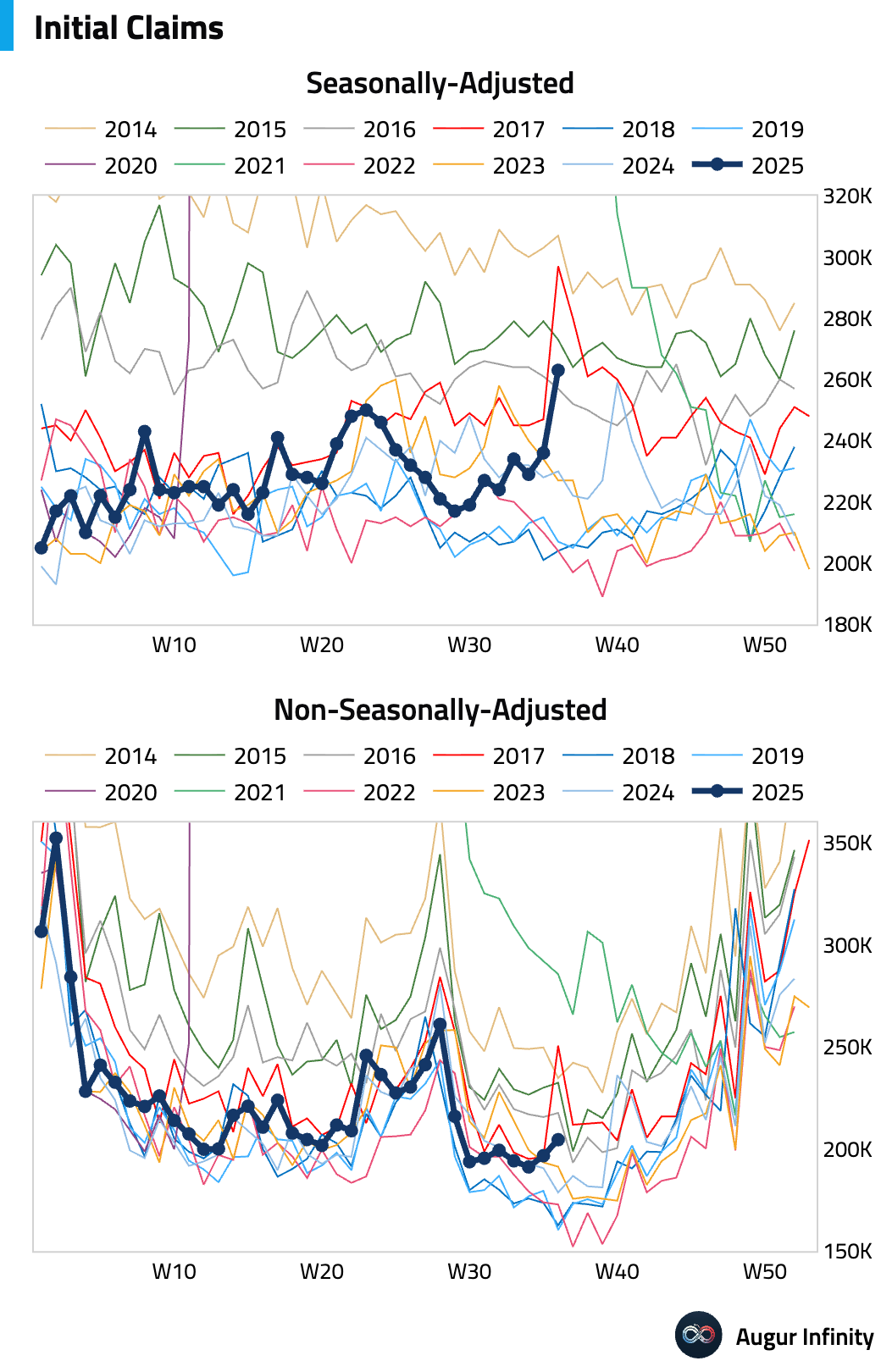

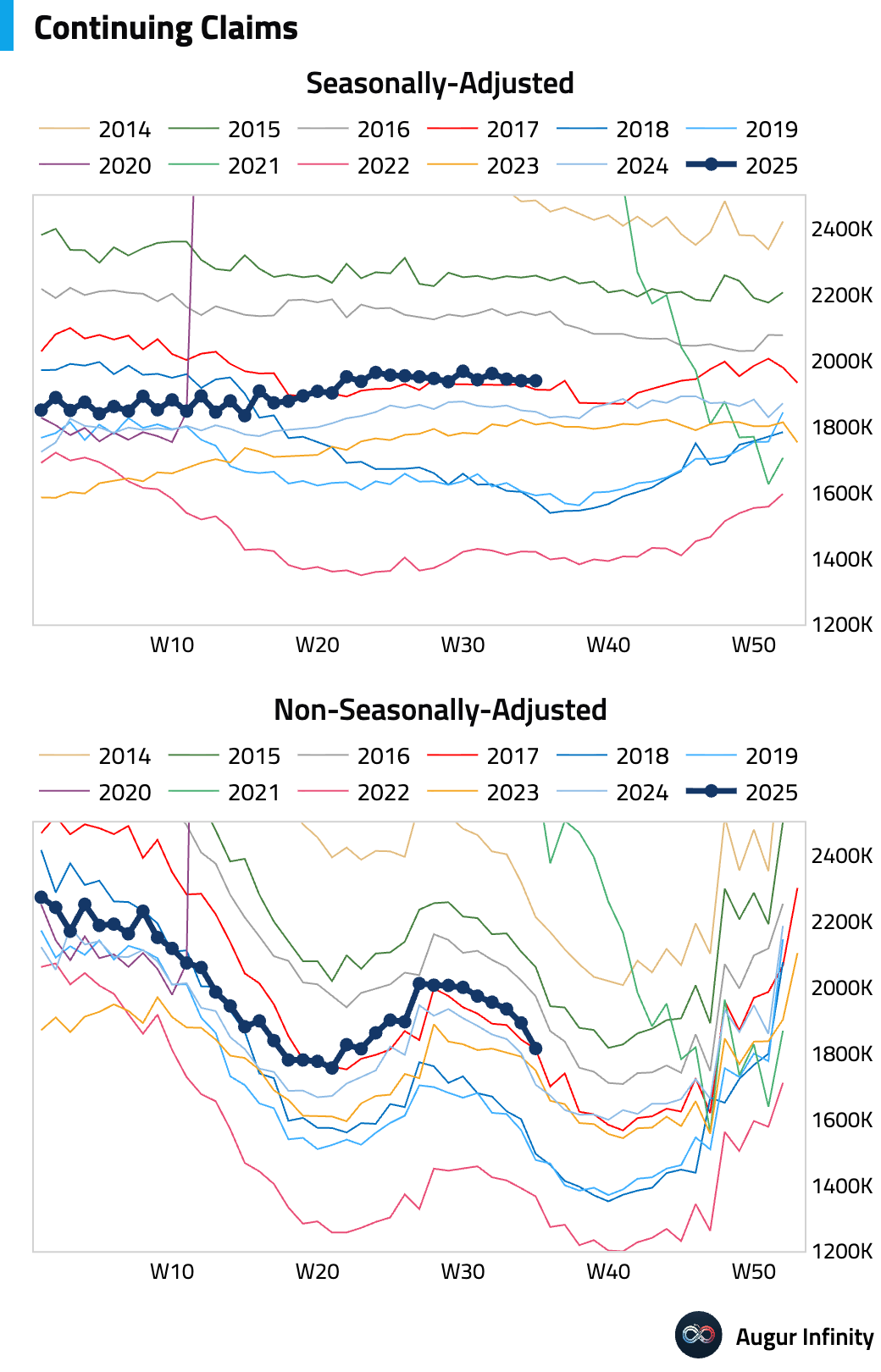

- Initial jobless claims rose more than expected to 263,000 for the week ending September 6, the highest level since October 2021. The increase was heavily concentrated in Texas, which accounted for 75% of the total rise. While some distortion from the Labor Day holiday is possible, the underlying trend points to a steady increase in claims in recent weeks. Continuing claims were unchanged at 1.939 million.

Europe

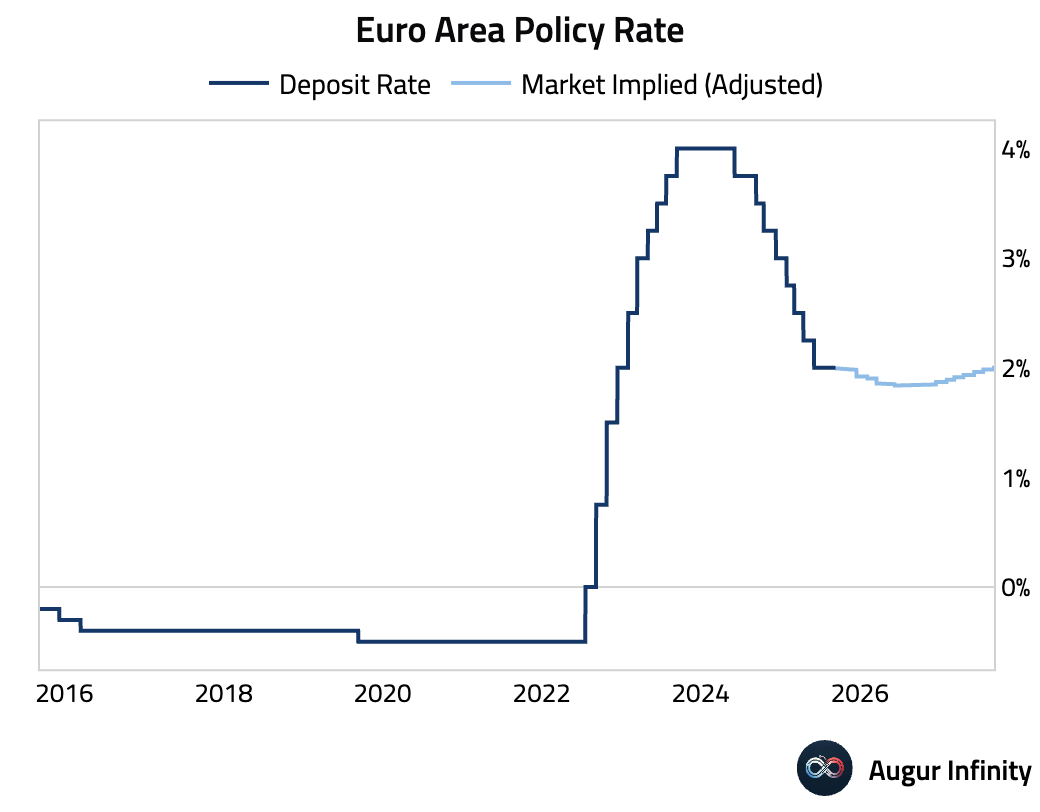

- The European Central Bank held its main deposit facility rate steady at 2.0%, a widely expected decision. President Lagarde signaled a high bar for future policy moves, stating that policy “continues to be in a good place.” The decision was unanimous, reinforcing the on-hold stance. The central bank raised its 2025 GDP forecast to 1.2% from 0.9% and upgraded its assessment of growth risks from “tilted to the downside” to “becoming more balanced.” Staff inflation projections were broadly unchanged, with core inflation still seen at 2.4% in 2025 and 1.9% in 2026, underpinning the ECB's confidence in its current policy path.

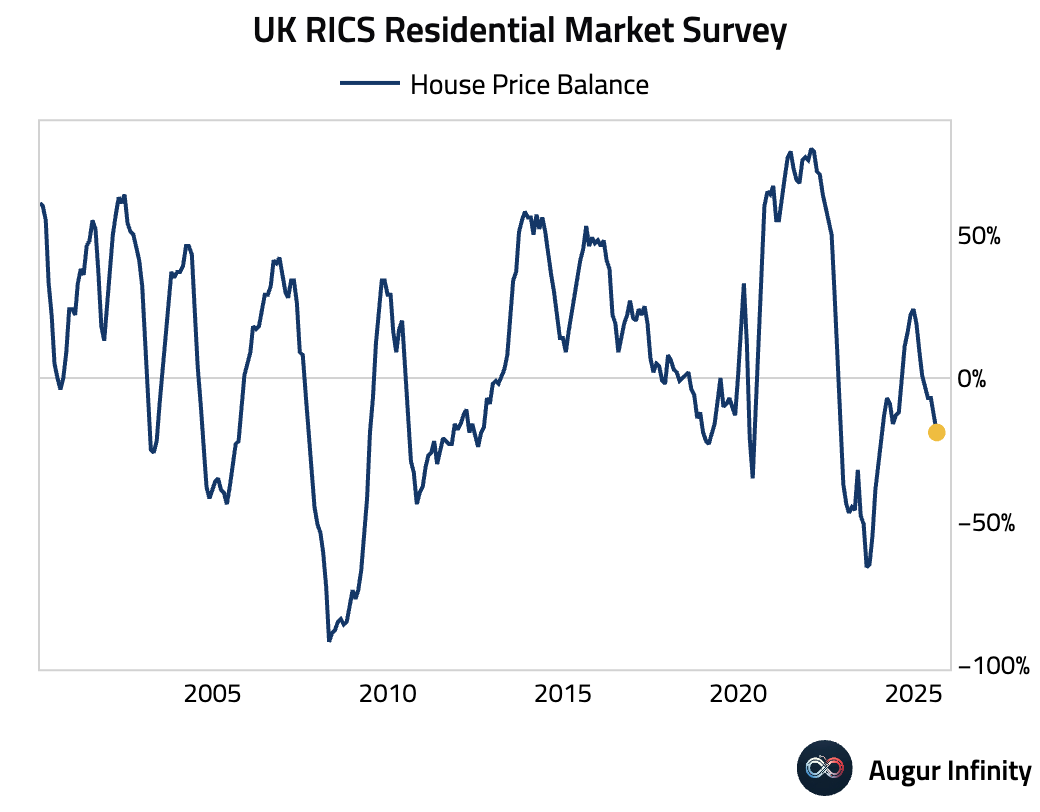

- The UK's RICS House Price Balance fell to -19 in August from -13, missing the consensus forecast of -10. The reading is the lowest since January 2024, indicating a further cooling in the housing market.

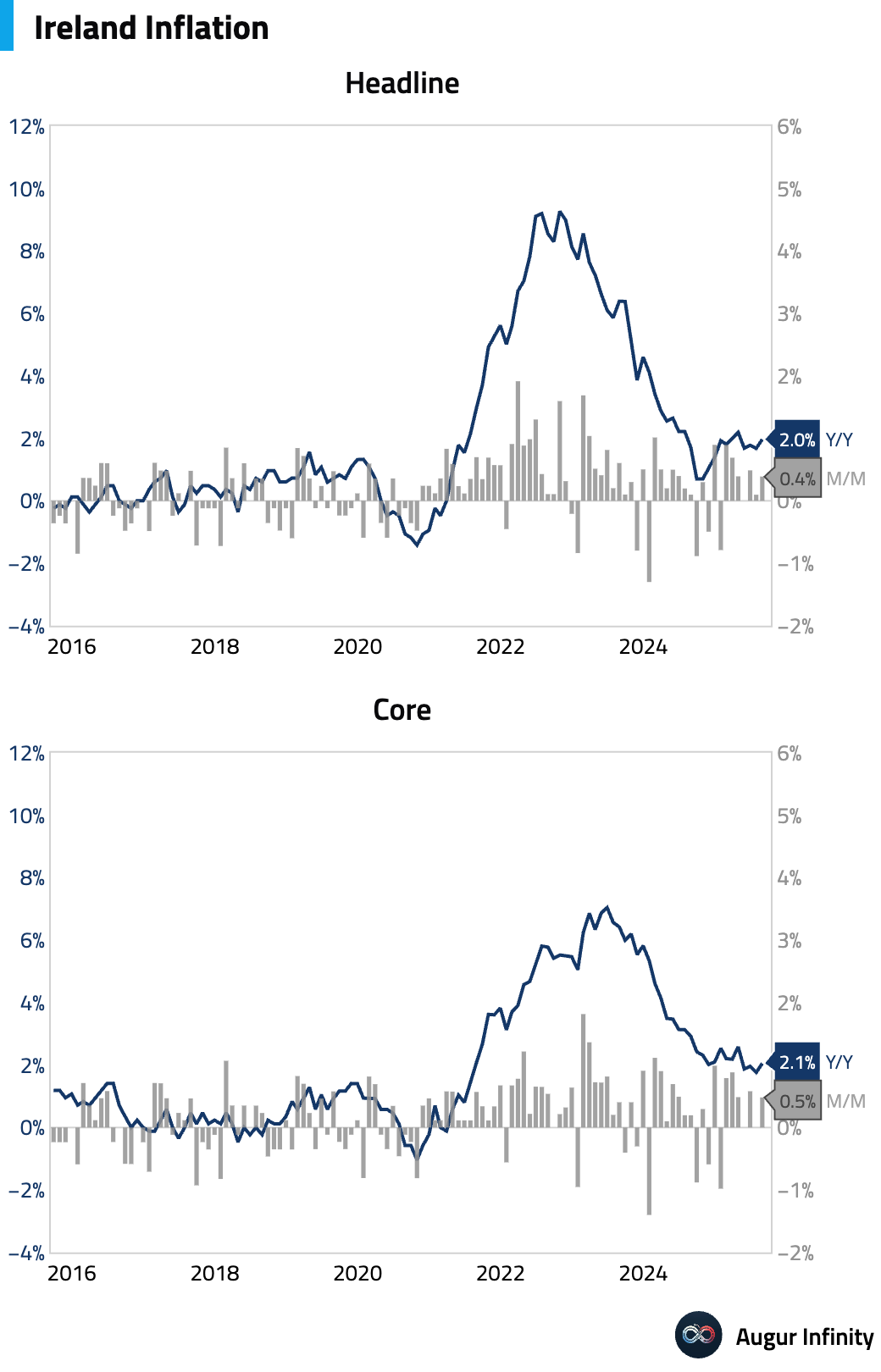

- Irish inflation accelerated in August, with the headline rate rising to 2.0% Y/Y from 1.7% in July. The EU-harmonised HICP rate also increased, reaching 1.9% Y/Y from 1.6%.

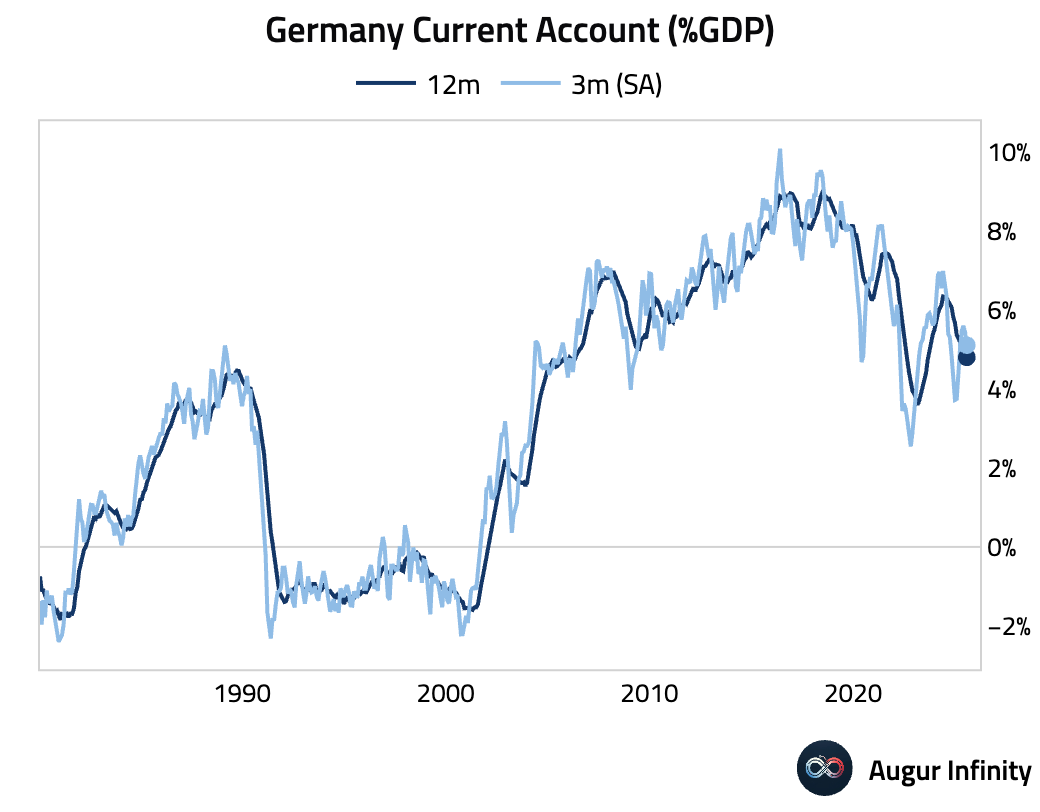

- Germany's current account surplus narrowed to €14.8 billion in July from €17.1 billion in June.

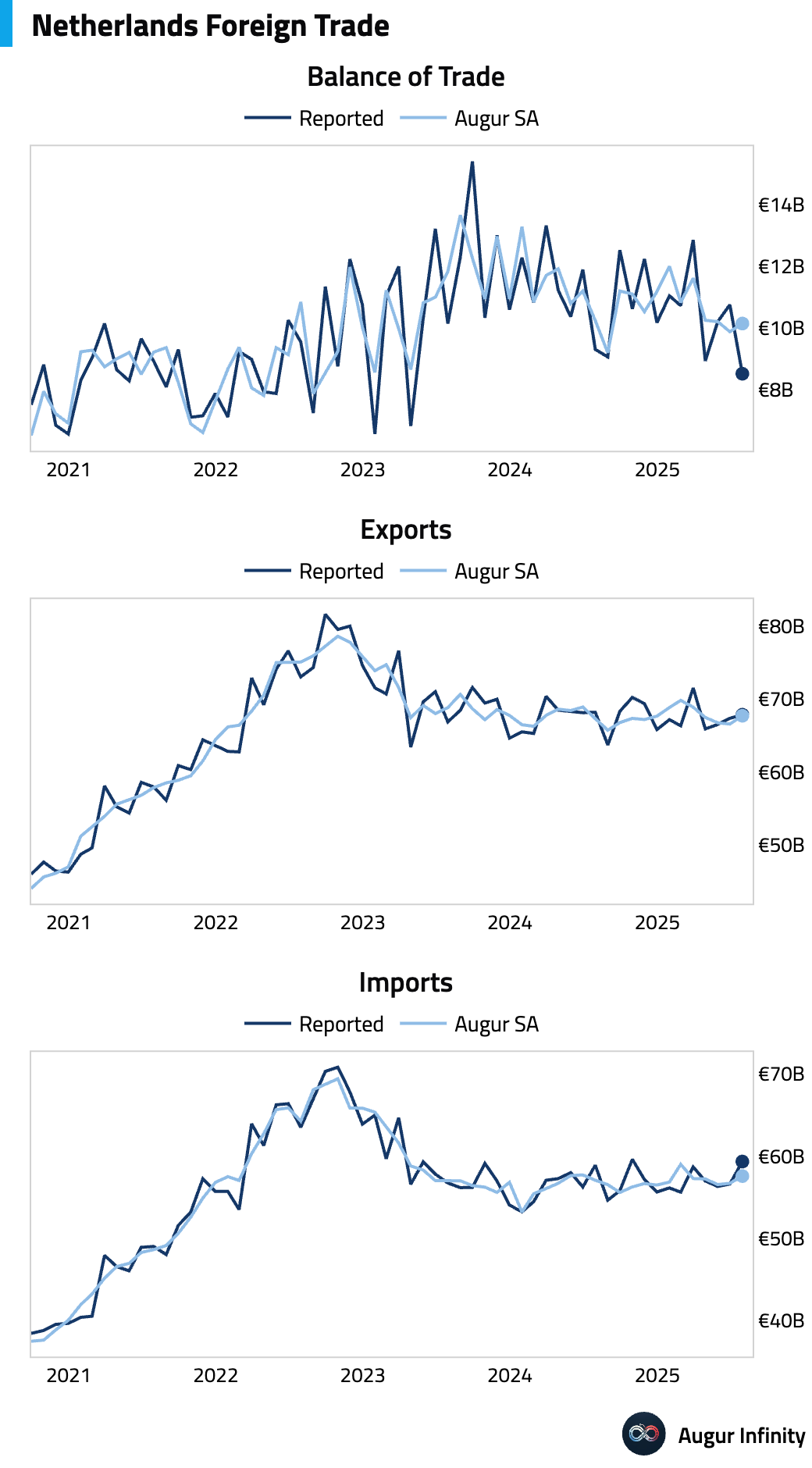

- The Netherlands' trade surplus decreased to €8.52 billion in July, down from €10.76 billion the prior month. However, the seasonally-adjusted trade balance ticked up a tad.

Asia-Pacific

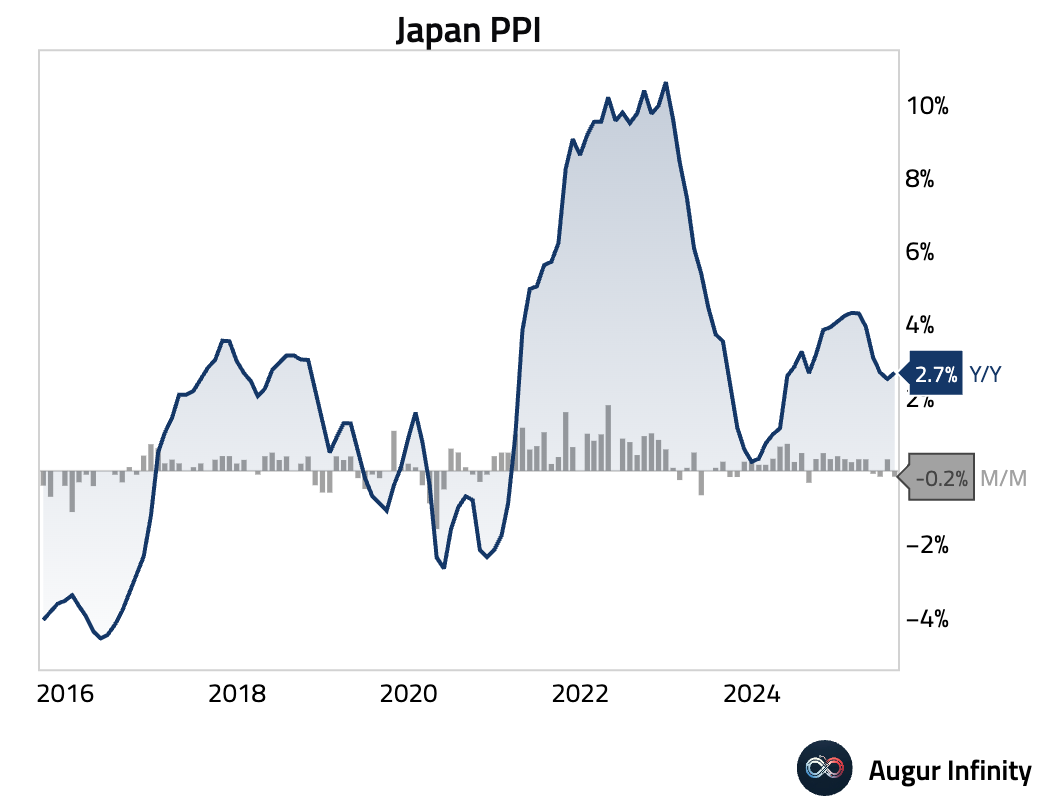

- Japan's producer prices fell 0.2% M/M in August, the first monthly decline in two months. The drop was driven by the resumption of government electricity and gas subsidies, which caused utility prices to fall 3.4%. Year-over-year, producer price inflation accelerated to 2.7% from 2.5%.

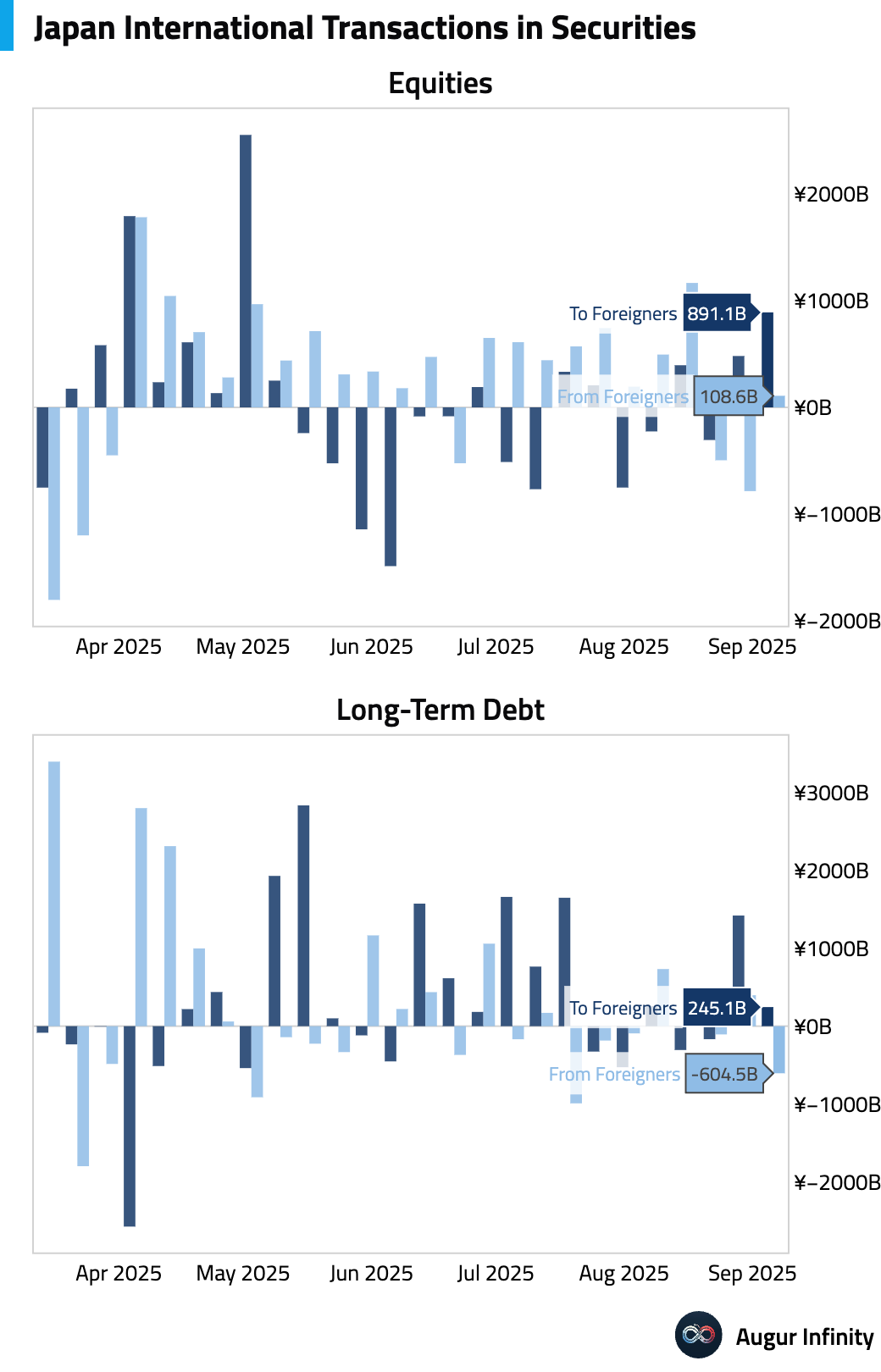

- Japanese investors purchased a net ¥245.1 billion of foreign bonds in the week ending September 6, a significant slowdown from the ¥1.42 trillion purchased in the prior week. Meanwhile, foreign investors returned to Japanese equities, buying a net ¥108.6 billion after selling ¥785.7 billion the week before.

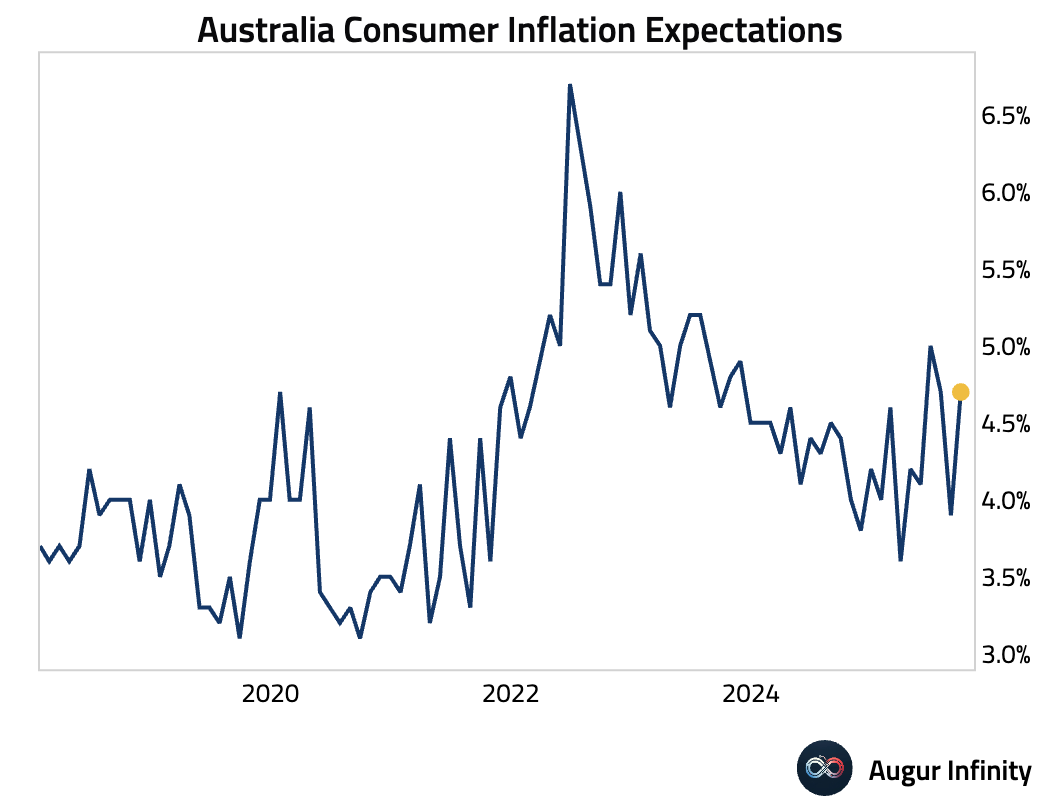

- Australian consumer inflation expectations for September jumped to 4.7% from 3.9% in August, reaching a three-month high.

China

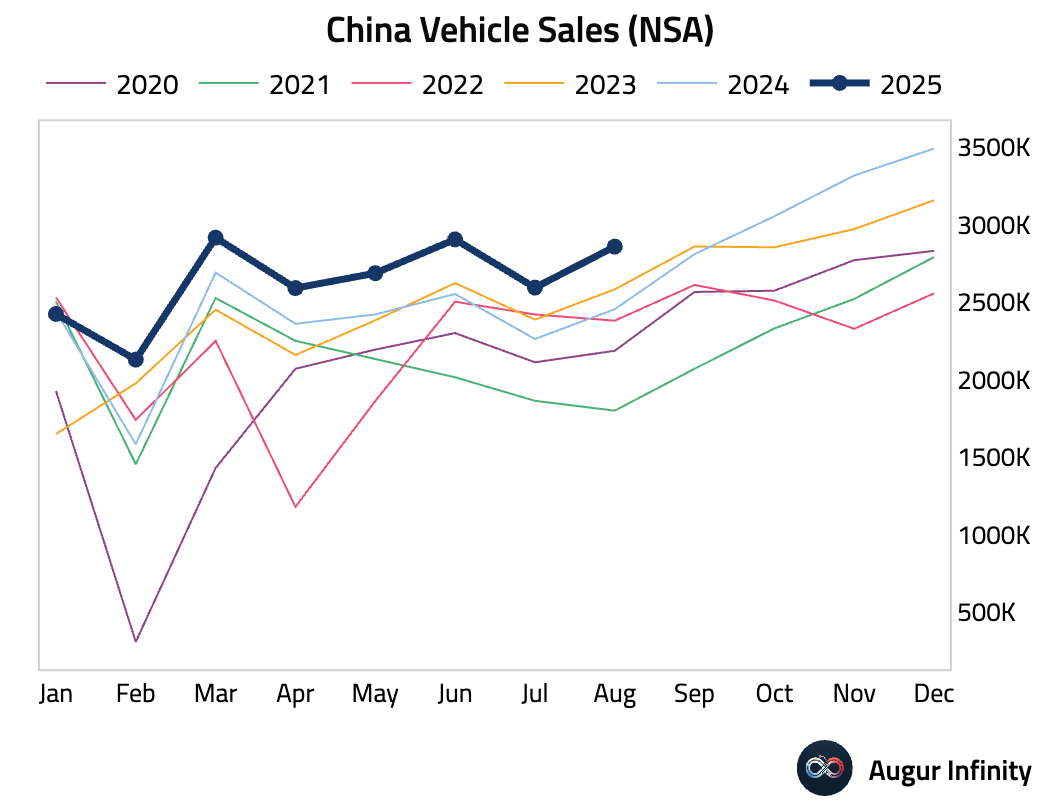

- Chinese vehicle sales growth accelerated to 16.4% Y/Y in August from 14.7% in July, marking the strongest pace in six months.

Emerging Markets ex China

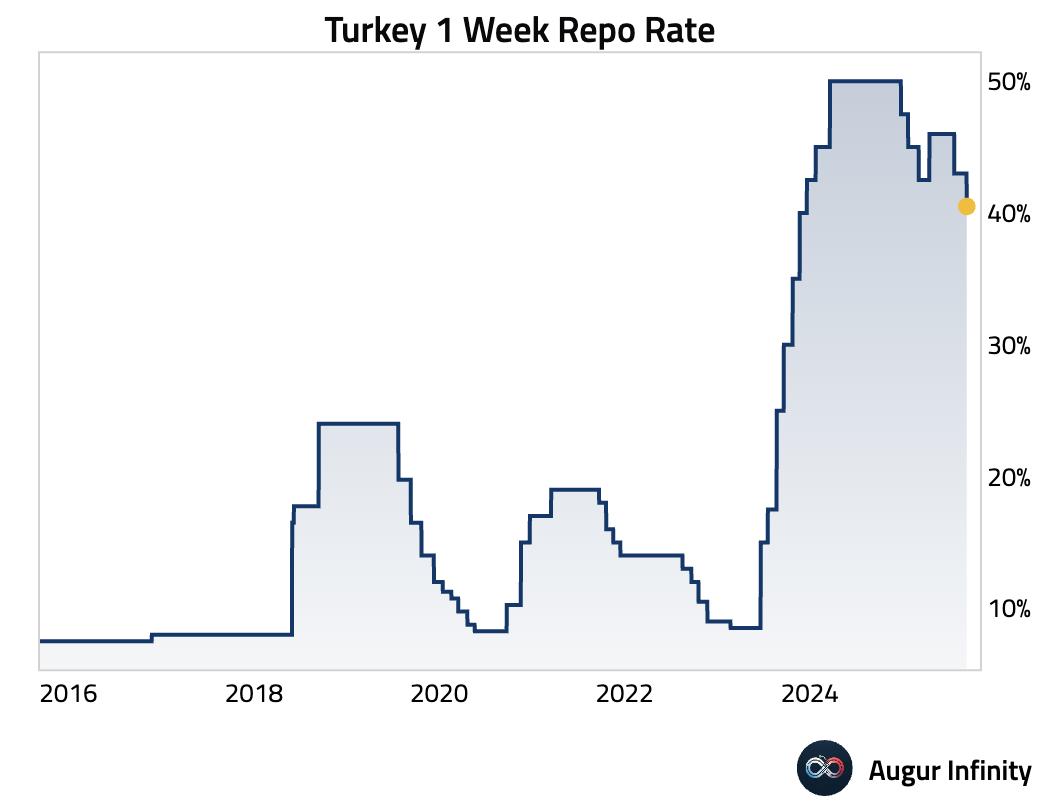

- The Central Bank of the Republic of Turkey cut its benchmark one-week repo rate by 250 basis points to 40.5%, a larger-than-expected reduction compared to the 200 bps consensus. While the pace of cuts has slowed, the move signals a policy shift towards greater reliance on future rate hikes, rather than lira appreciation, to manage inflation.

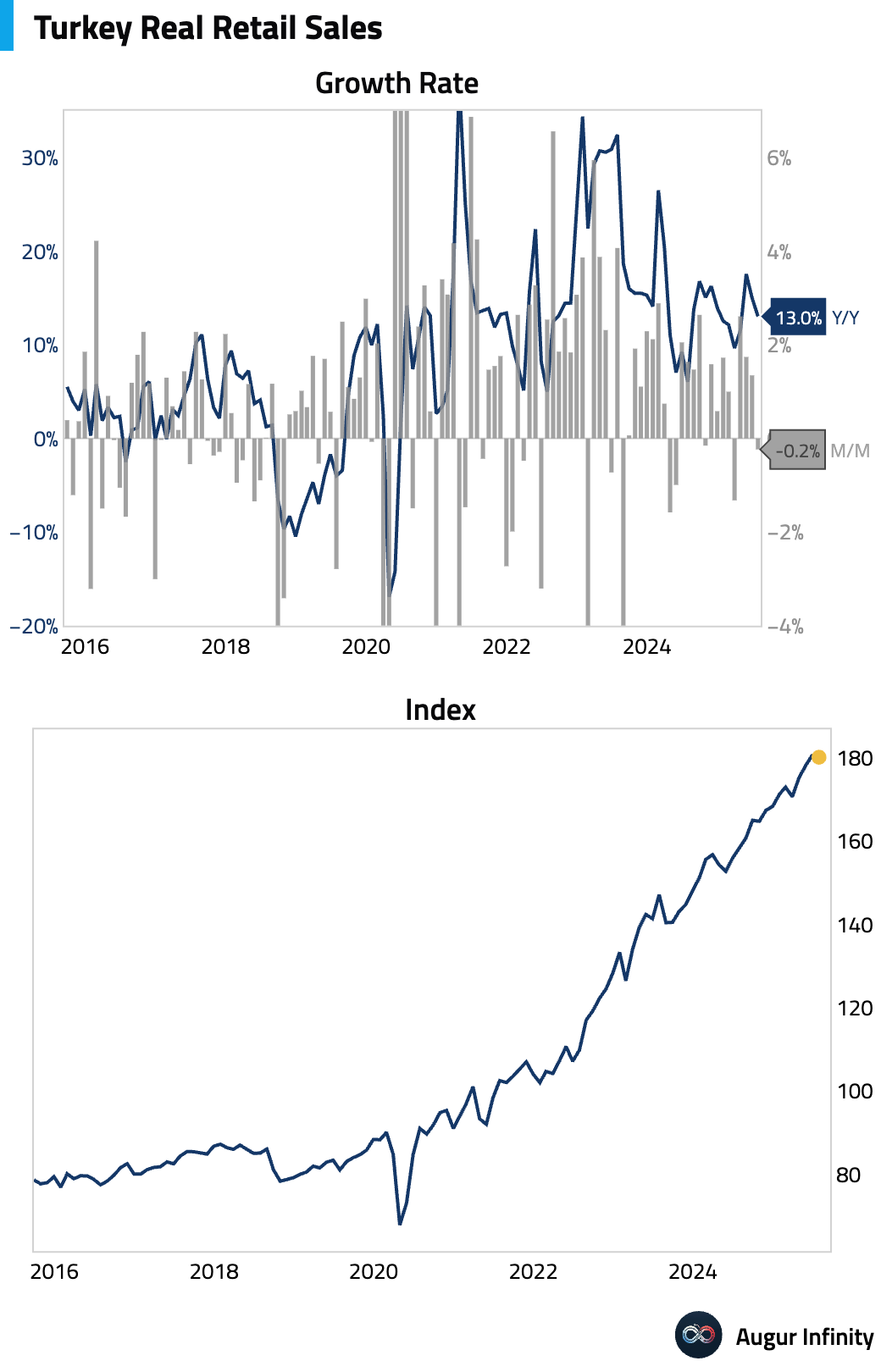

- Turkish retail sales volume contracted by 0.2% M/M in July, while the annual growth rate slowed to 13.0% from 15.0%.

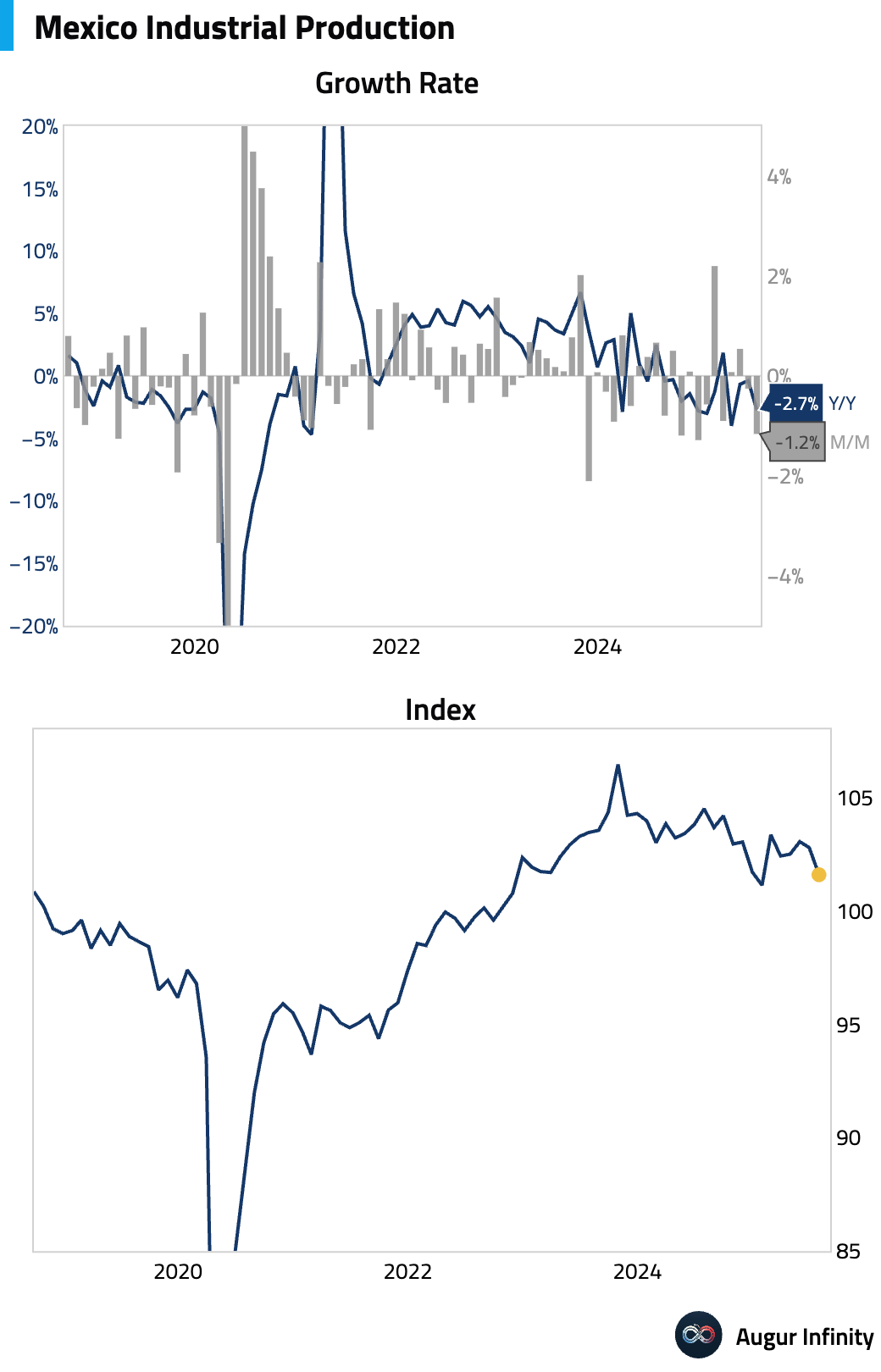

- Mexican industrial production contracted sharply in July, falling 1.2% M/M and 2.7% Y/Y, significantly weaker than consensus estimates of -0.2% M/M and -0.9% Y/Y. The downturn was broad-based, driven by sharp declines in both manufacturing (-1.6%) and construction (-1.2%), with only mining showing a partial offset. The weak print creates a negative carryover for third-quarter growth prospects.

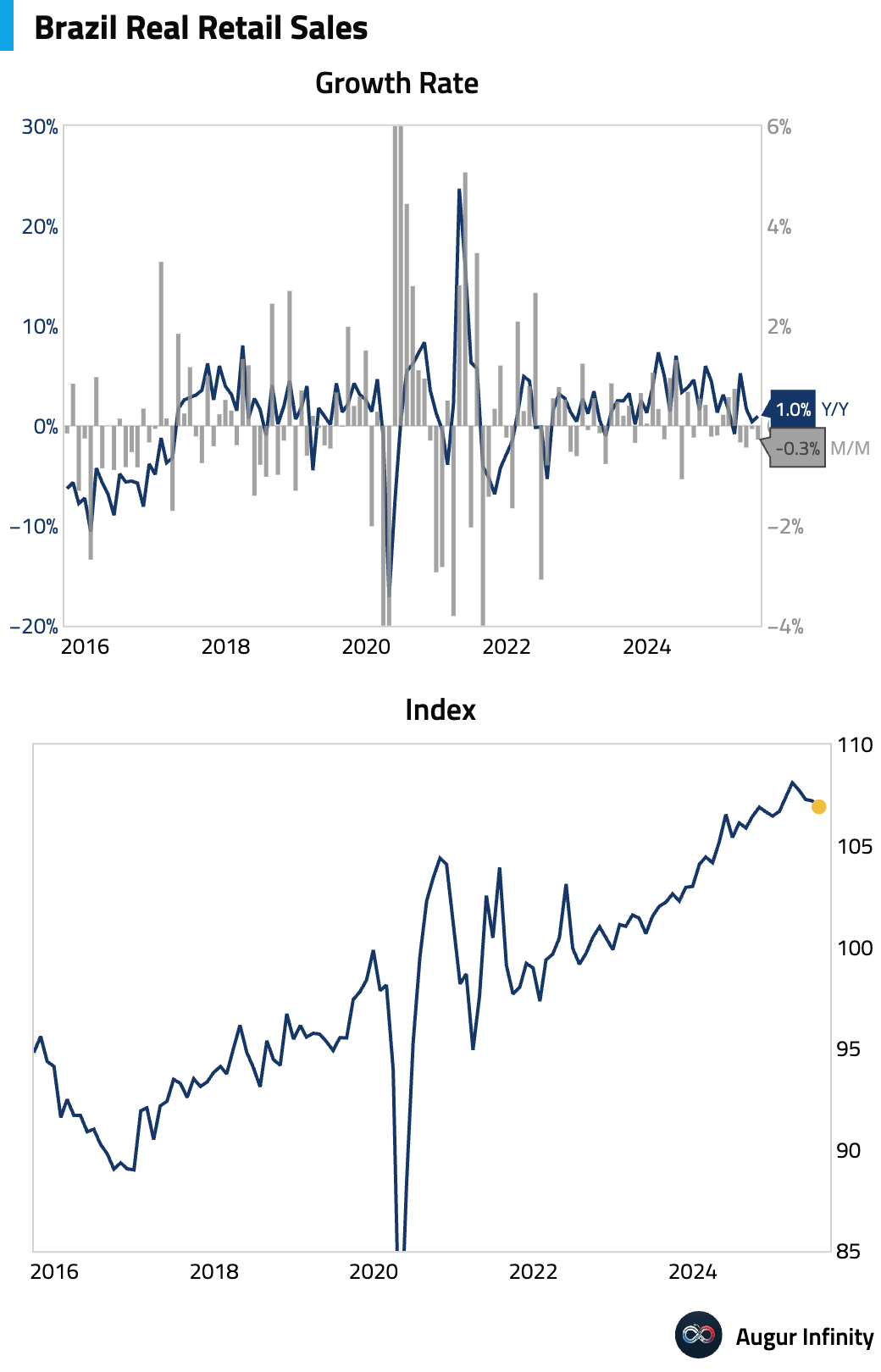

- Brazil's July retail sales presented a mixed picture. Core retail sales fell 0.3% M/M, in line with consensus and marking the fourth consecutive monthly decline. The weakness was concentrated in income-sensitive sectors. In contrast, broad retail sales, which include autos and construction materials, beat expectations by rising 1.0% Y/Y, supported by credit-sensitive categories.

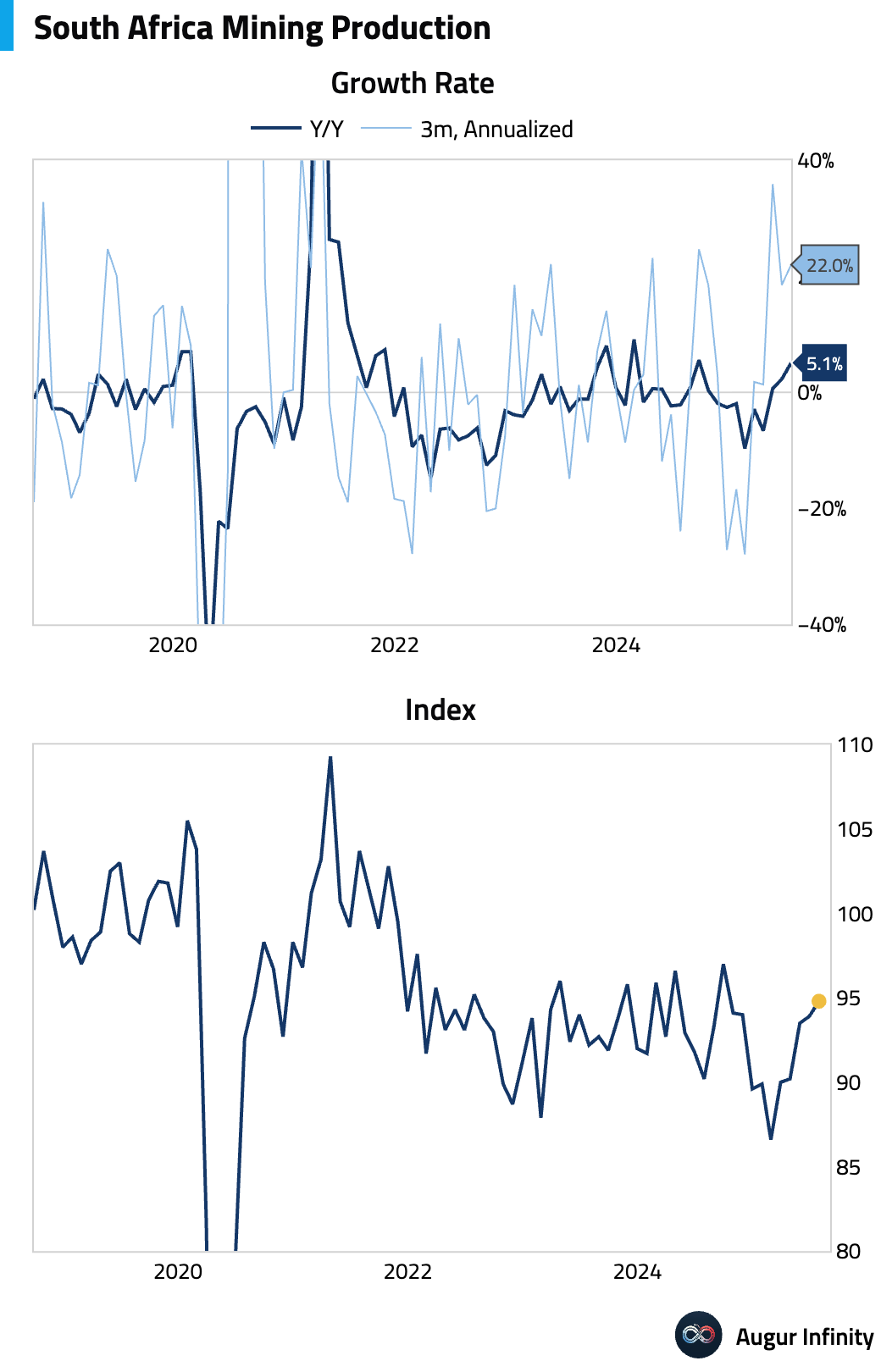

- South African mining production accelerated in July, rising 1.0% M/M and 4.4% Y/Y, well above the 3.2% consensus for the annual figure.

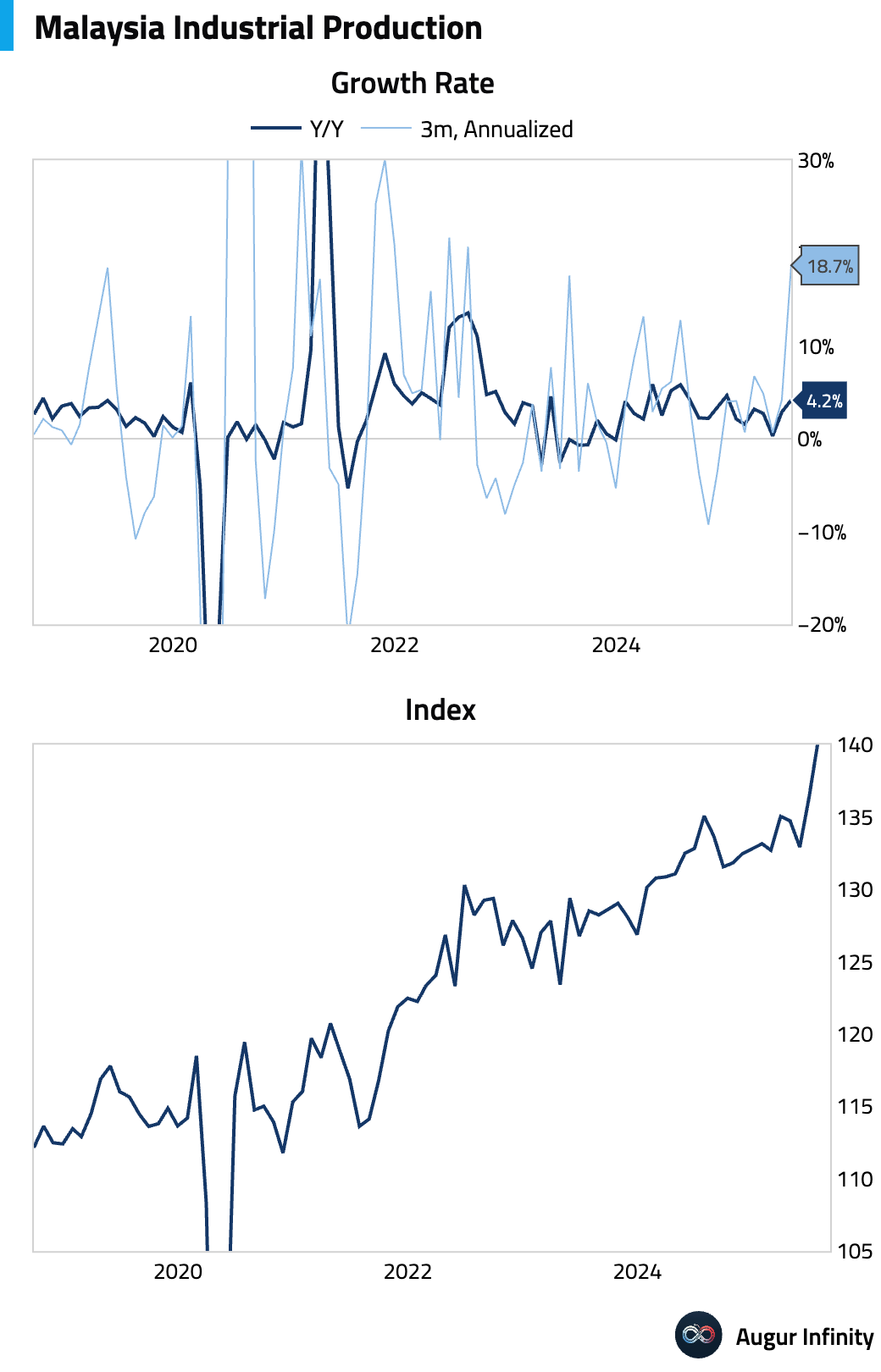

- Malaysian industrial production growth surprised to the upside, accelerating to 4.2% Y/Y in July from 2.9% previously, crushing the 1.7% consensus forecast. The reading was the strongest since December 2024.

- Indonesian retail sales grew 4.7% Y/Y in July, a sharp acceleration from the 1.3% pace seen in June.

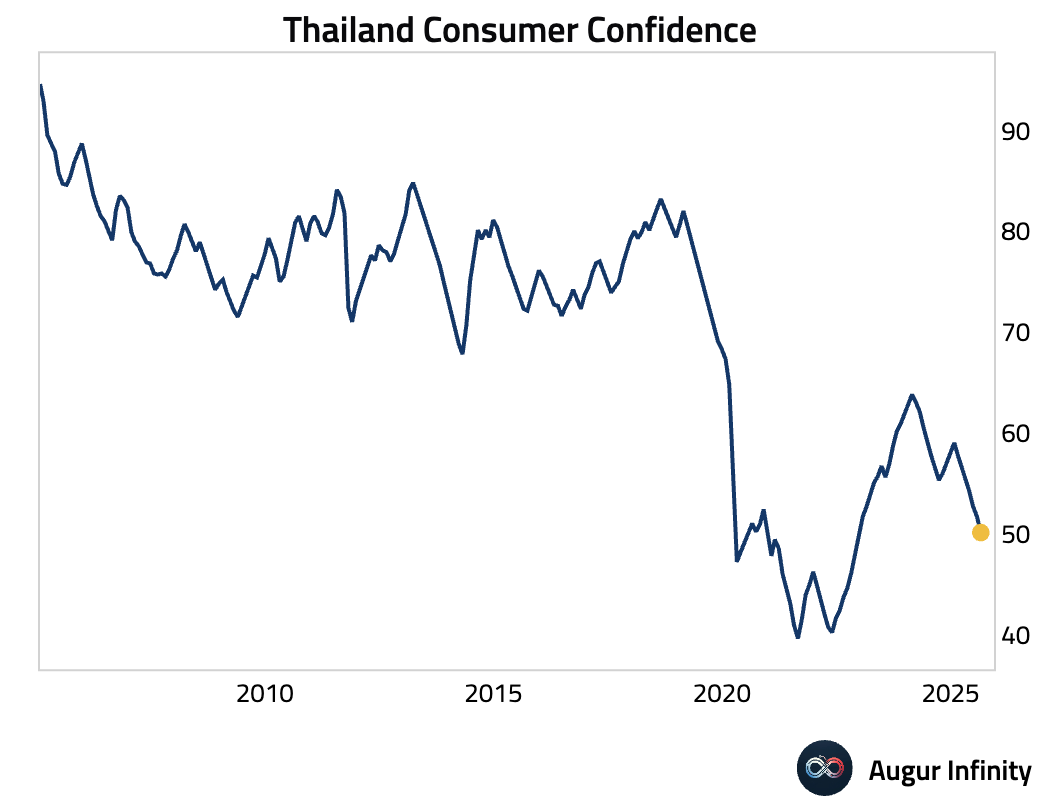

- Thai consumer confidence fell to 50.1 in August from 51.7, its lowest level since December 2022.

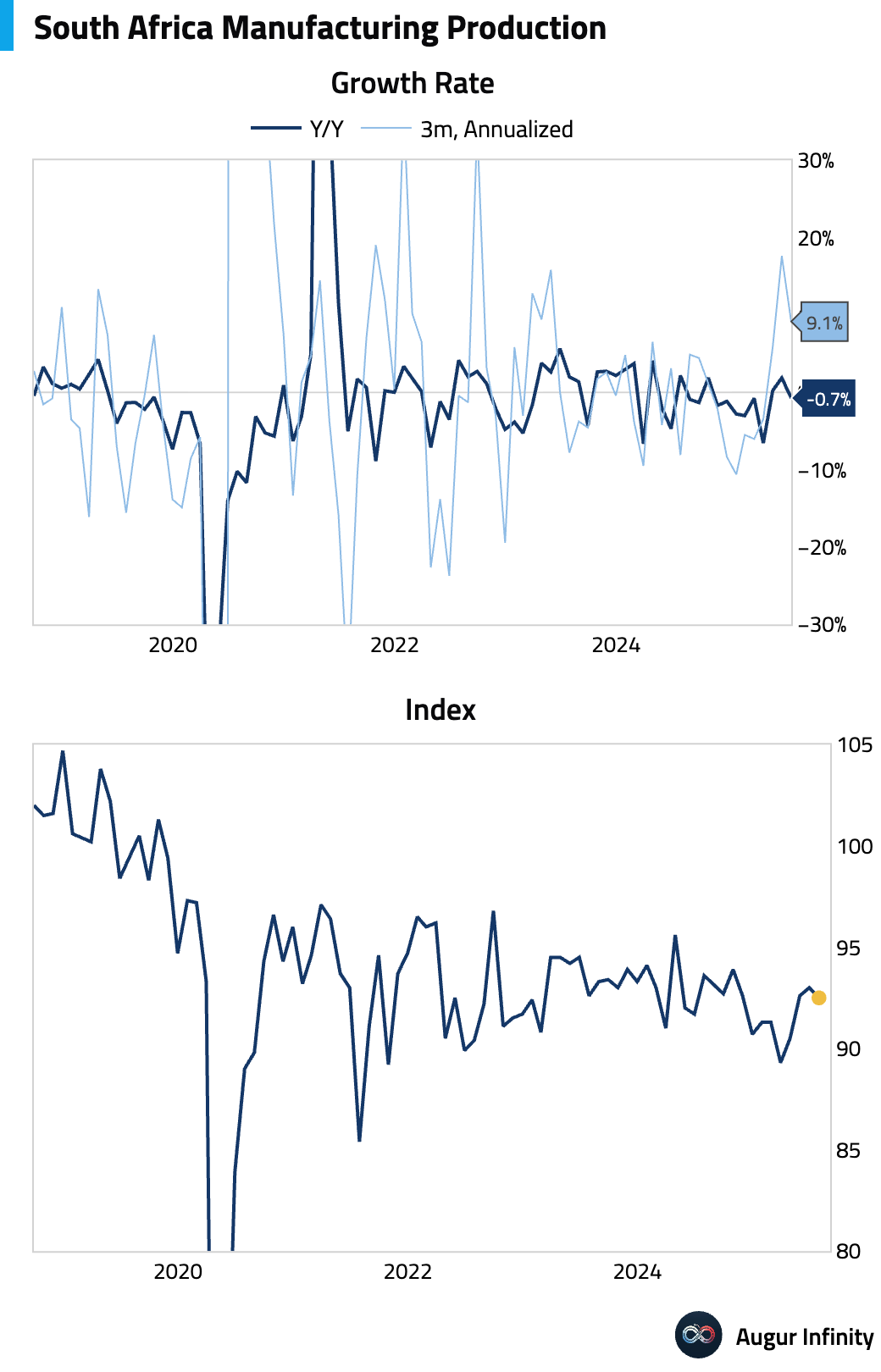

- South Africa's manufacturing output declined in July, falling 0.5% M/M and 0.7% Y/Y, slightly missing consensus expectations.

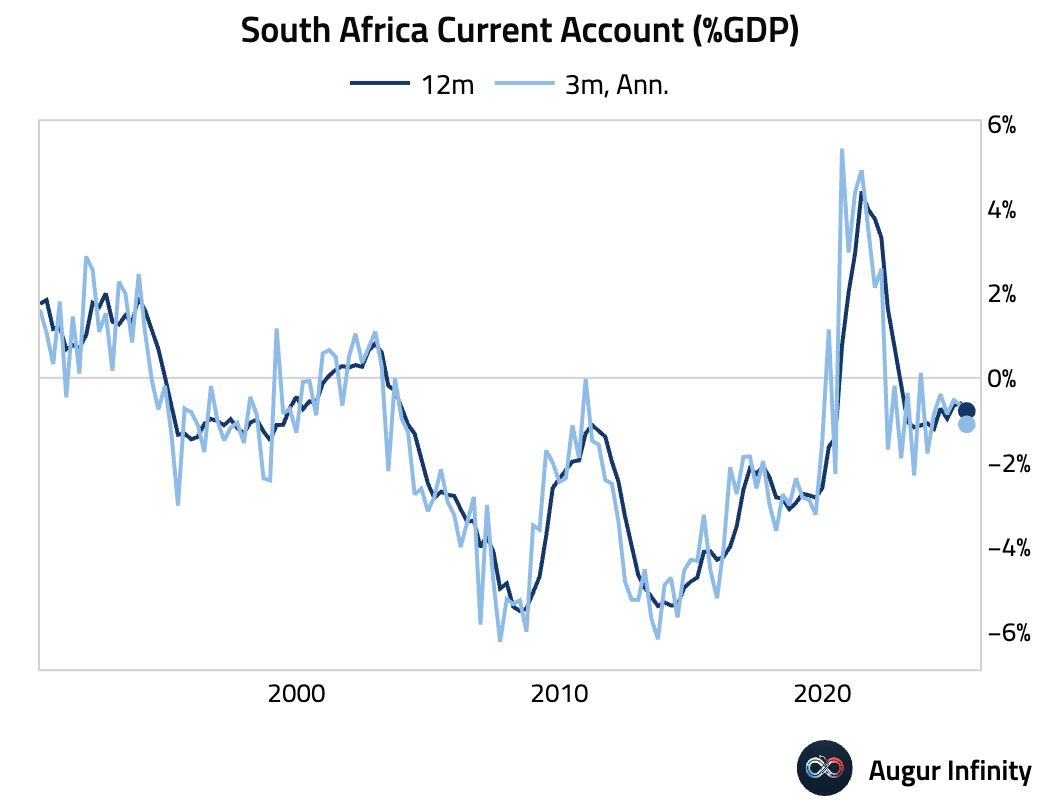

- South Africa's current account deficit widened significantly to ZAR 82.8 billion in the second quarter from a revised ZAR 47.8 billion in the first quarter.

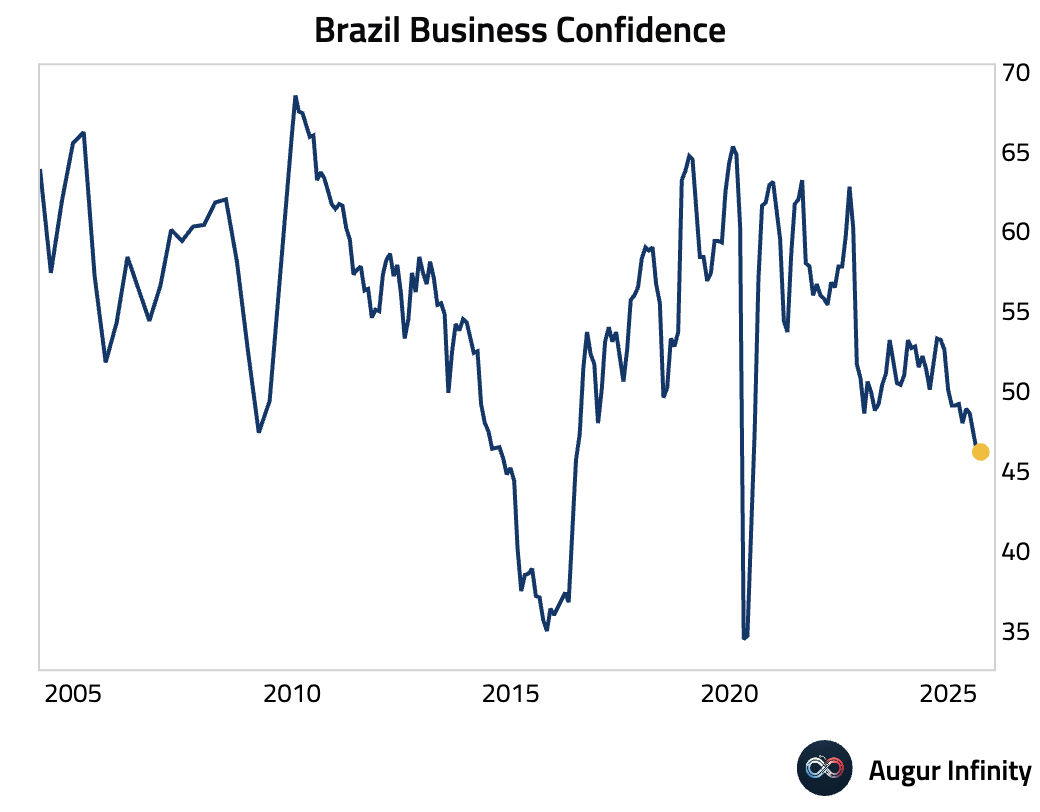

- Brazilian business confidence edged up to 46.2 in September from 46.1 in August.

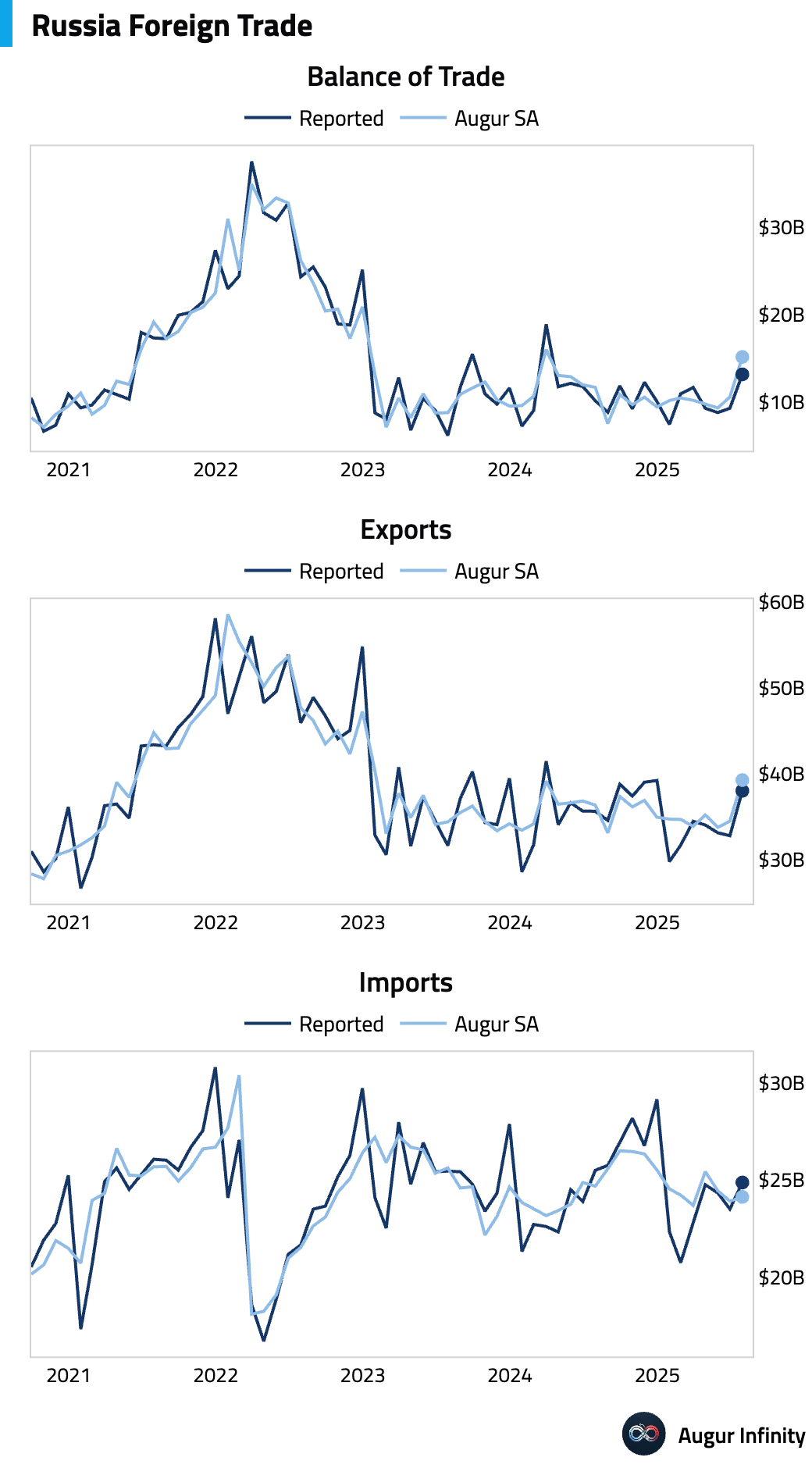

- Russia's trade surplus expanded to $13.17 billion in August from $9.3 billion in July, the largest surplus in over a year.

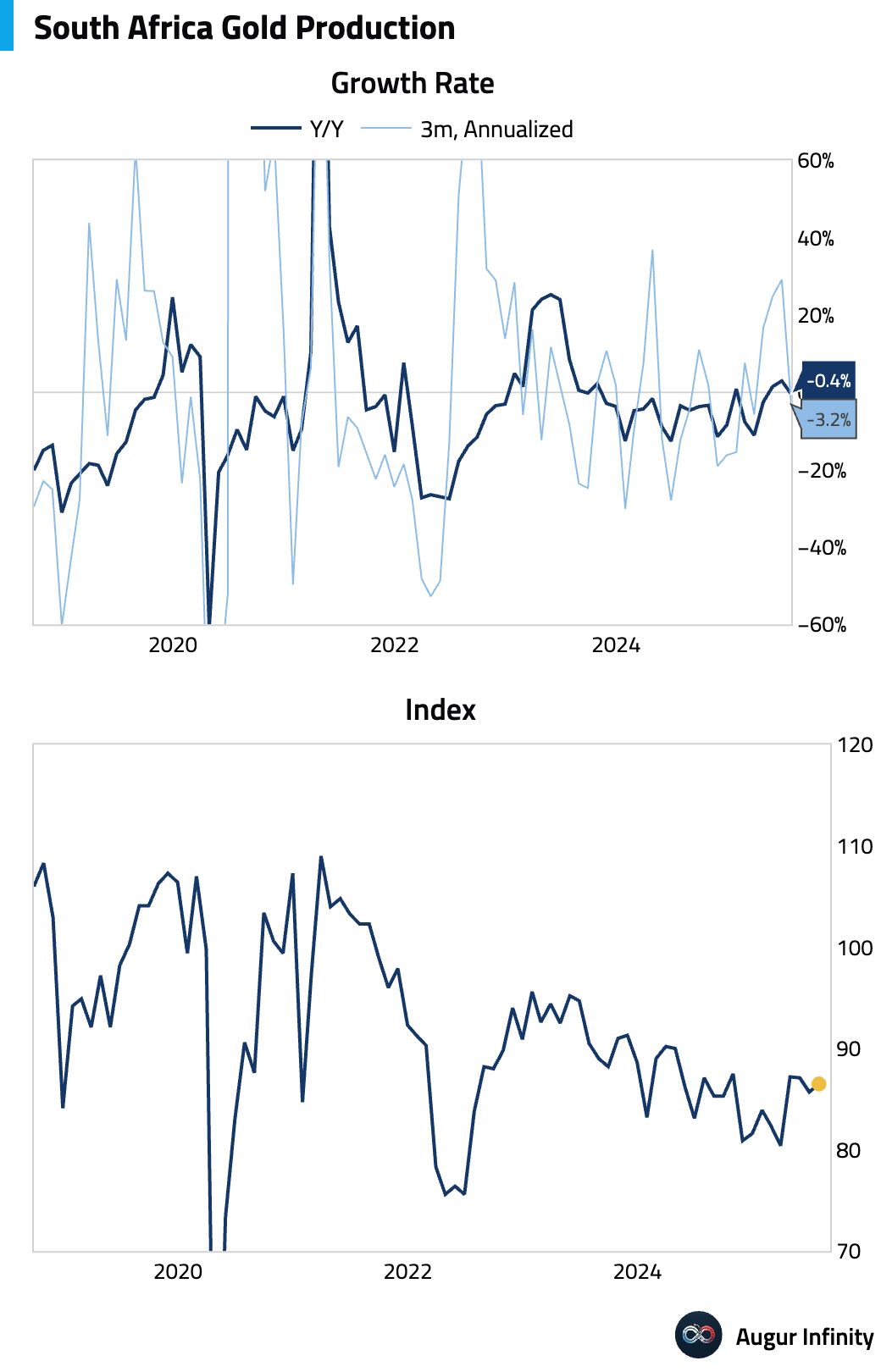

- South African gold production fell by 0.4% Y/Y in July, reversing a 2.9% gain from June.

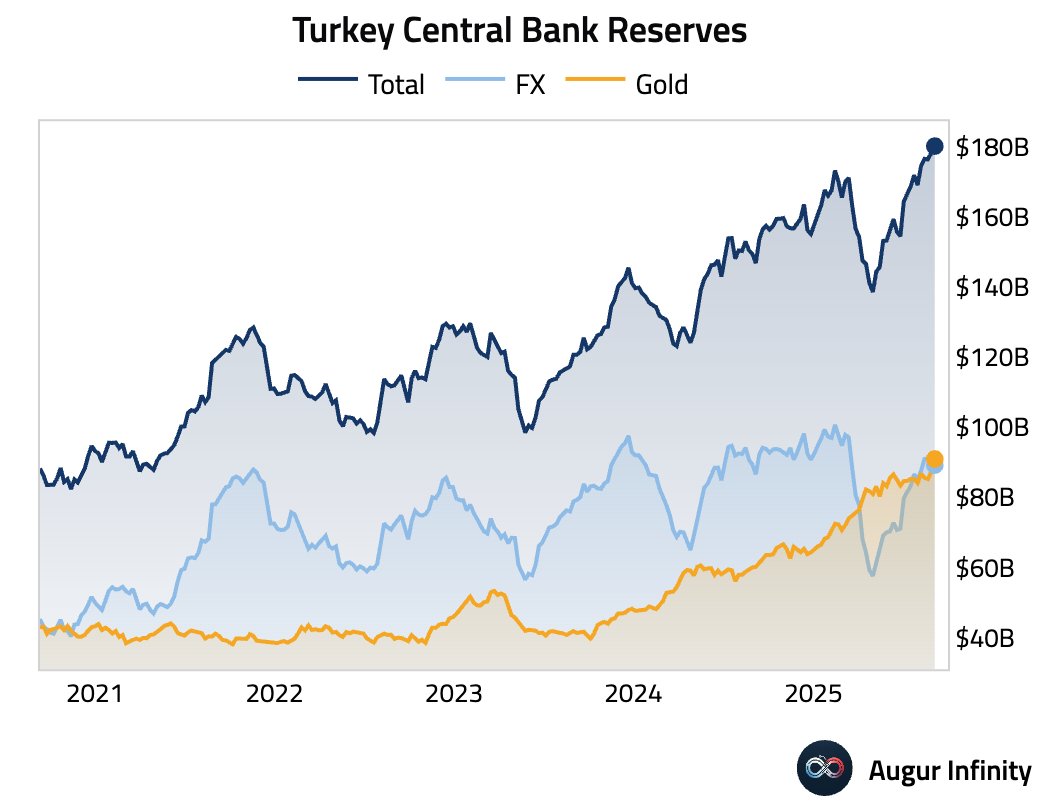

- Turkey's gross foreign exchange reserves declined to $89.18 billion in the week ending September 5 from $91.03 billion the prior week.

Global Markets

Equities

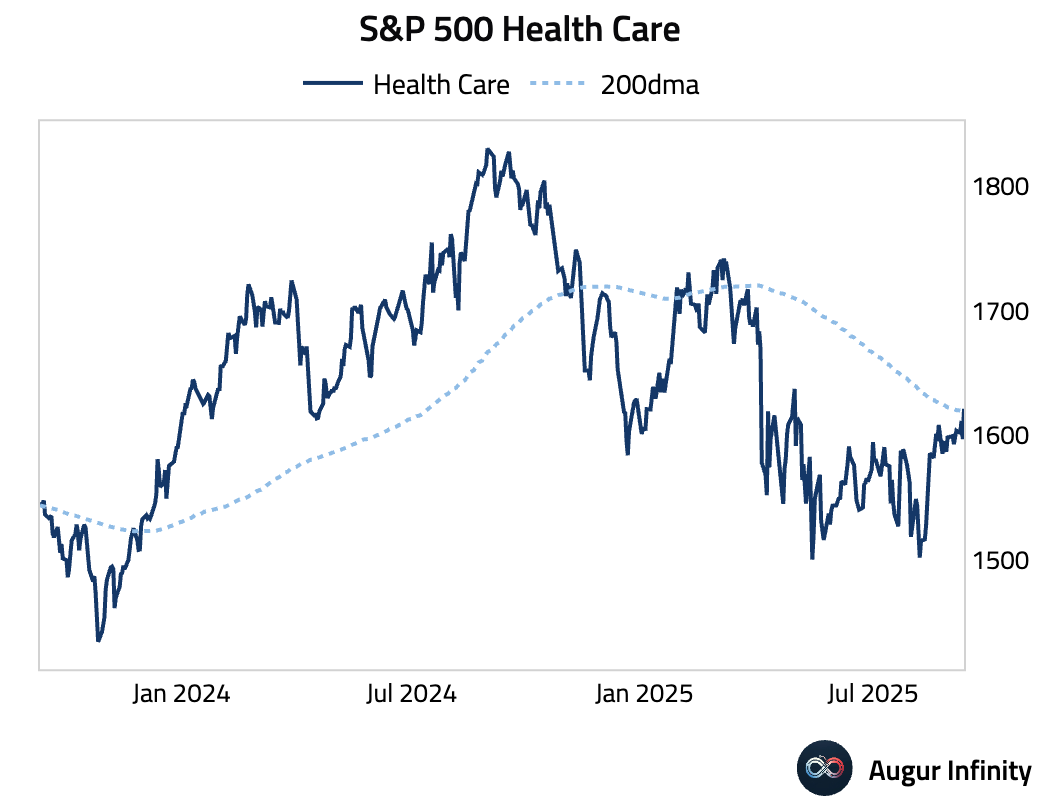

- S&P 500 Health Care rose above its 200-day moving average.

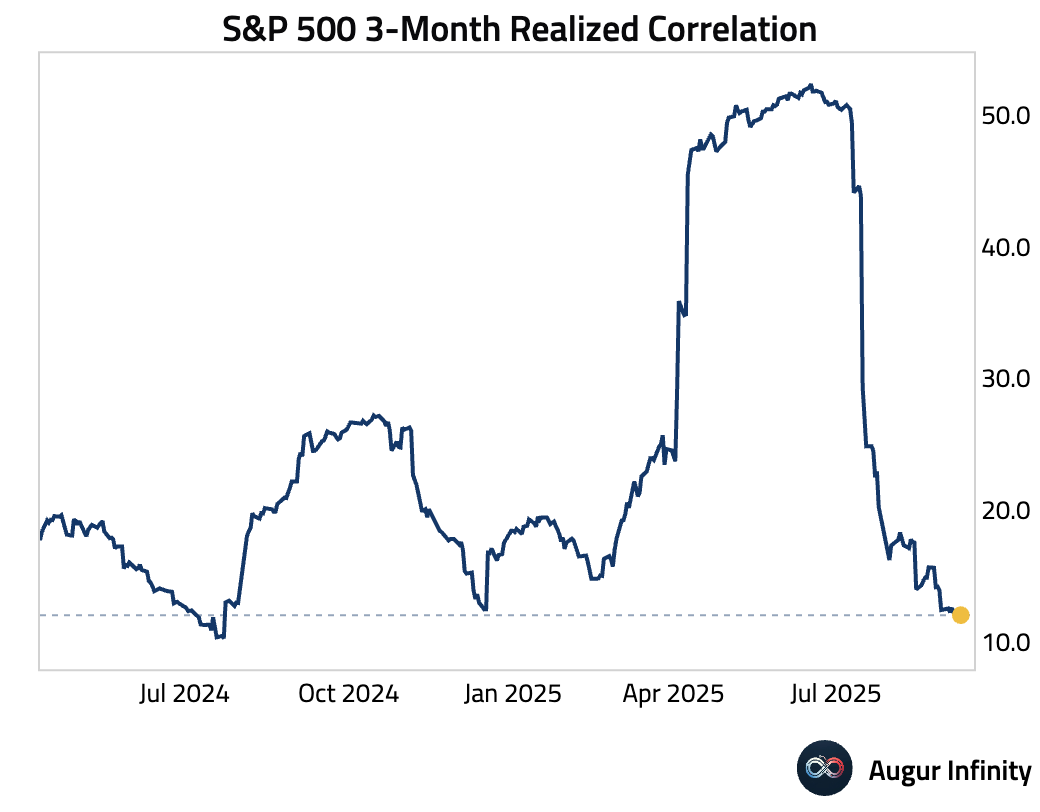

- 3-month realized correlation amongst S&P 500 members is at the lowest level since July 2024.

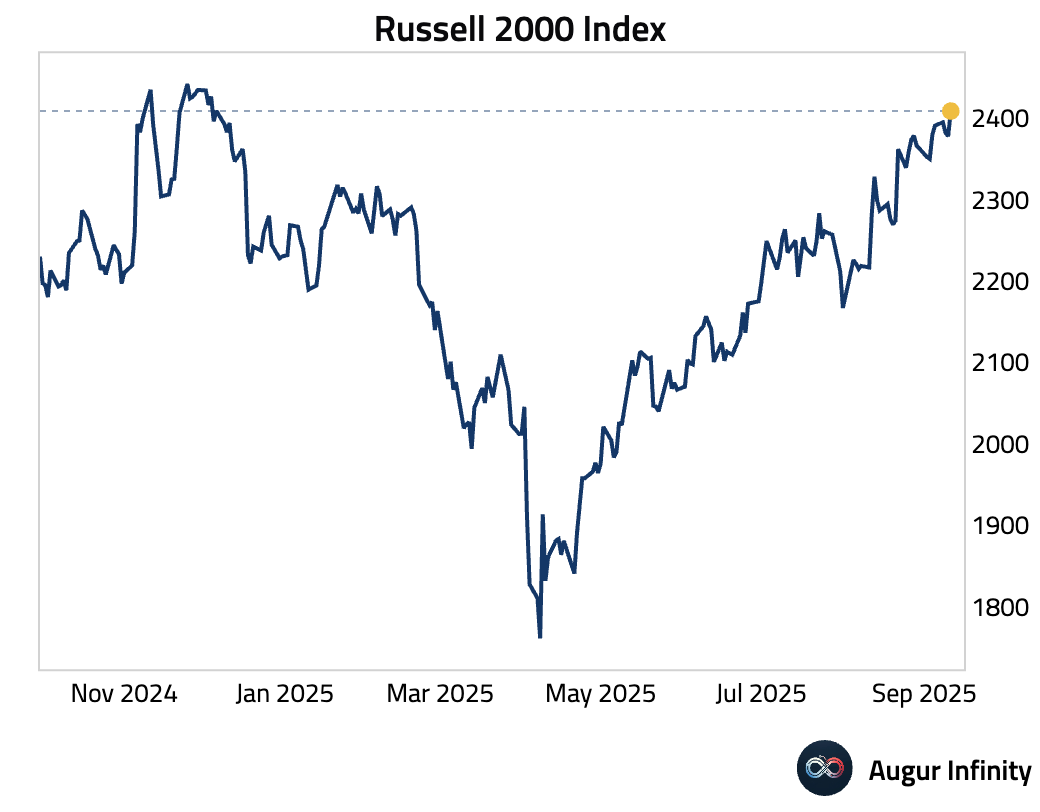

- Russell 2000 Index is trading at the highest level since December 2024.

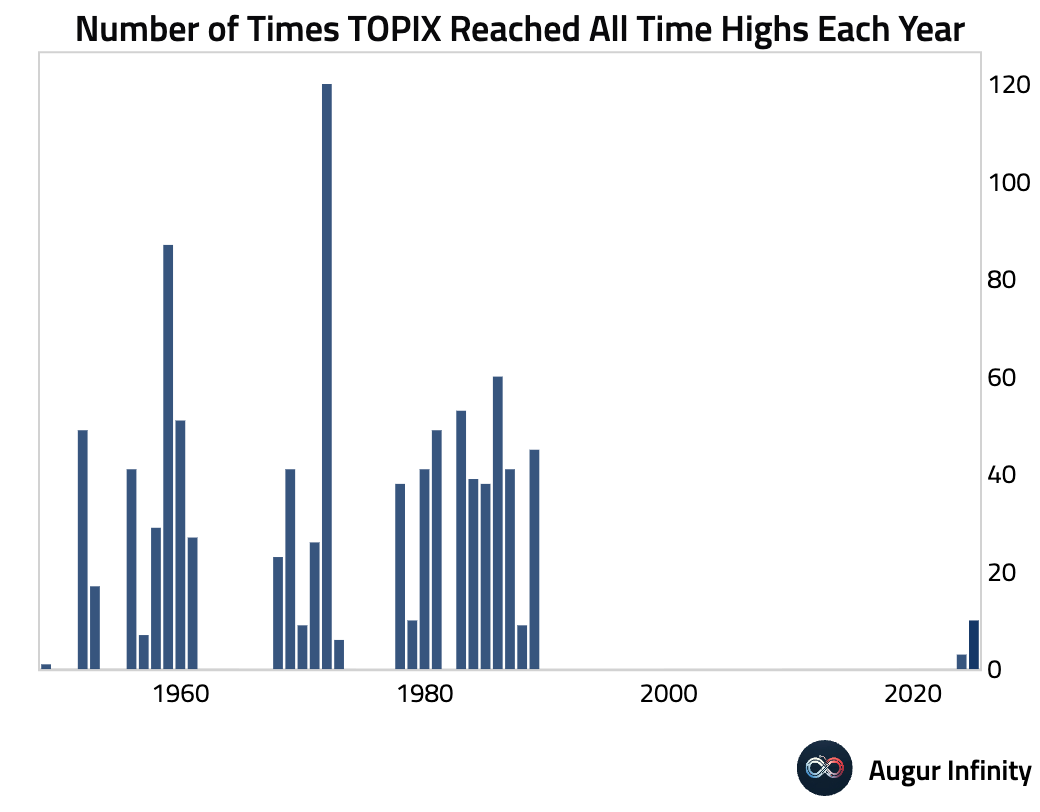

- Japan's TOPIX Index continues its ascent, having reached its tenth all-time-high in 2025.

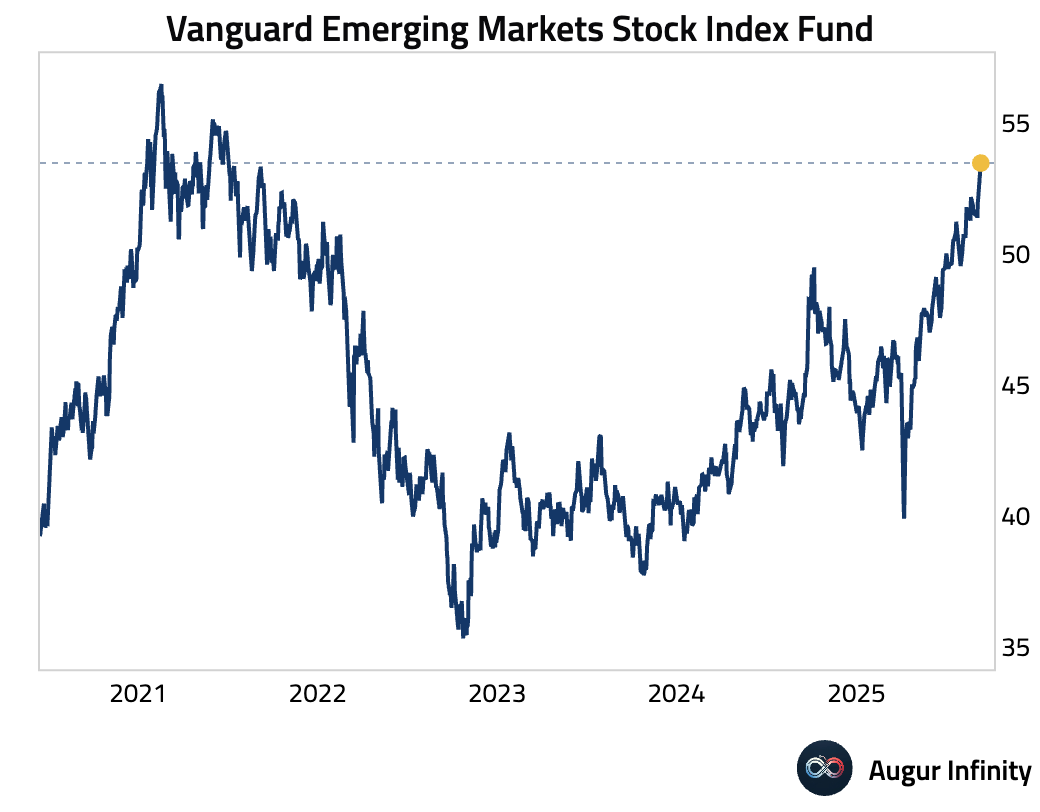

- Vanguard Emerging Markets Stock Index Fund rallied for the fifth consecutive day to reach the highest level since July 2021.

- Shanghai Shenzhen CSI 300 jumped by 2.3% today, the best one-day return since March 2025 and pushing the index to the highest level since March 2022.

Fixed Income

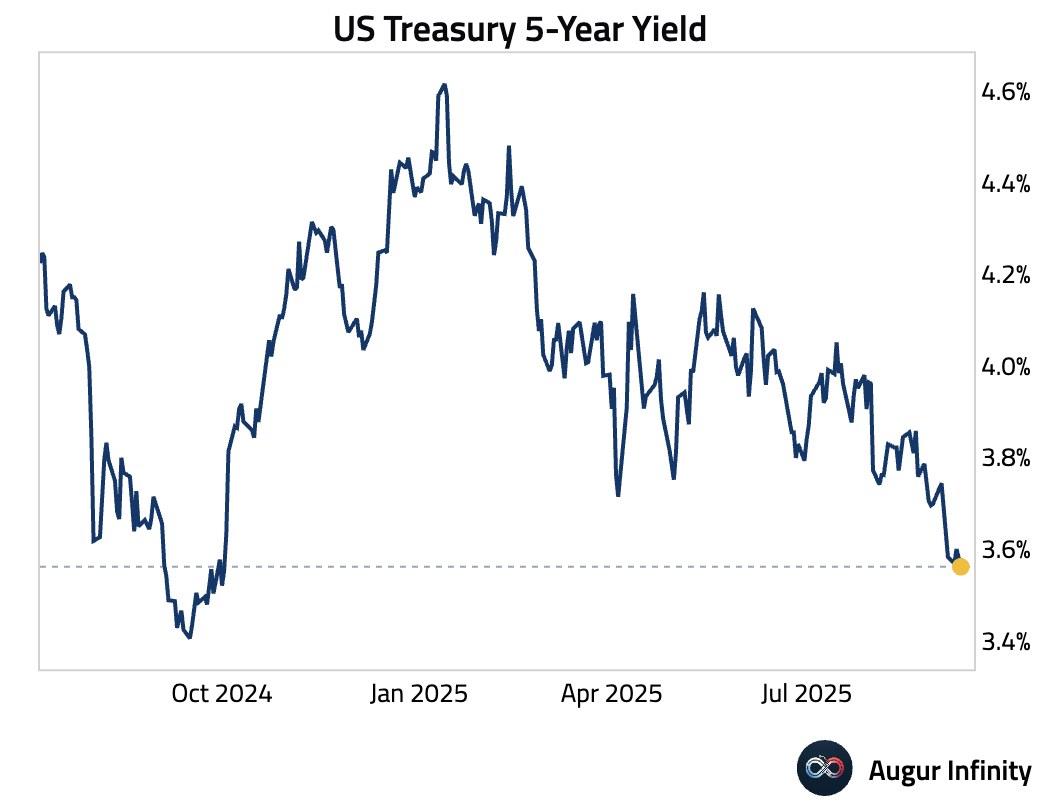

- US Treasury 5-year yield is at the lowest level since October 2024.

FX

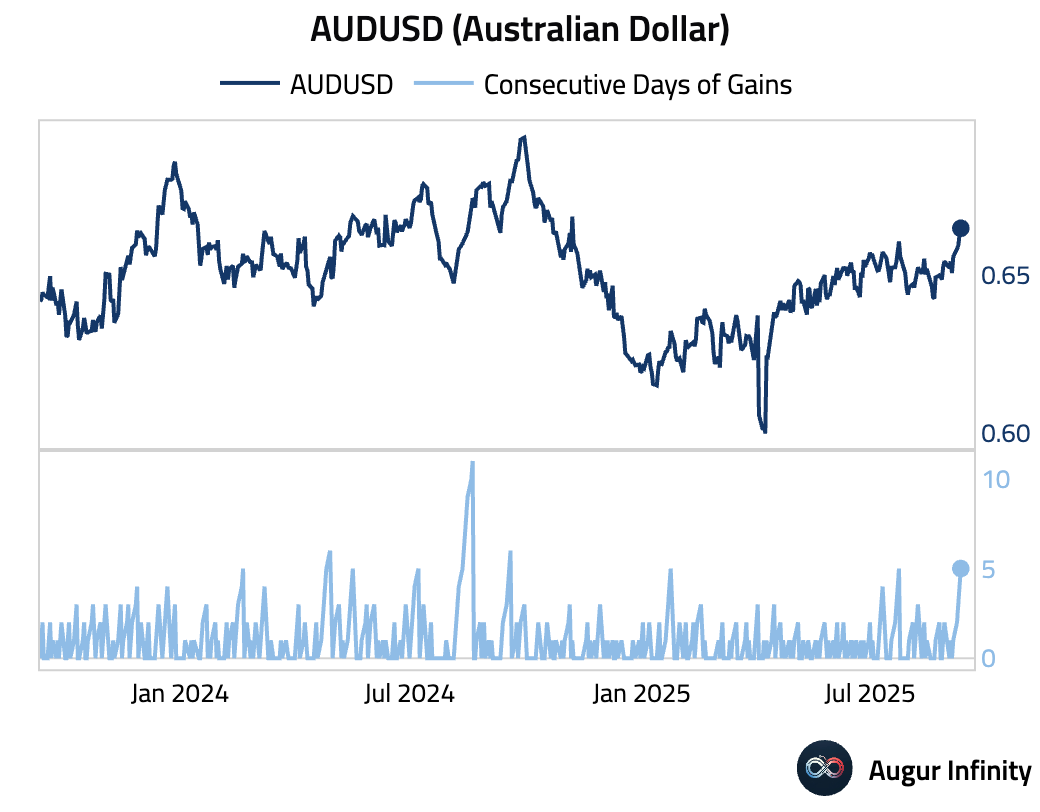

- AUD appreciated for the fifth consecutive day against the dollar, reaching the highest level since November 2024.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.