Headlines

• A 50 percent tariff increase on steel and aluminum became effective today; the United Kingdom has a five-week exemption.

• President Trump stated that the debt limit should be "entirely scrapped."

• The German government approved a EUR 46 billion corporate tax relief plan.

• Automakers expressed concern over potential production disruptions due to China's export restrictions.

Charts of the Day

• Mentions of “uncertainty” in the Fed’s Beige Book remained very elevated.

Mentions of “trade” and “tariff” reached a new high.

United States

• The ADP Employment Change for May showed an increase of 37,000 jobs, below the consensus of 115,000 and down from a revised 60,000 in April (originally 62,000). This marks its lowest level since March 2023. The services sector added 36,000 jobs, mainly in leisure and hospitality (+38,000) and financial services (+20,000). Goods-producing industries lost 2,000 jobs, as a 6,000 rise in construction was offset by a 5,000 decline in natural resources and mining. Median annual pay for job stayers rose 4.5 percent Y/Y, unchanged from April.

• The S&P Global Services PMI final for May was revised up 1.4 points to 53.7, from a previous 50.8. The new business component was revised to 53.2 (+0.9 points) and employment to 51.8 (+2.4 points).

• The ISM Services PMI for May fell by 1.7 points to 49.9, below the consensus of 52.0 and down from 51.6 in April. Business activity decreased by 3.7 points to 50.0, and new orders fell 5.9 points to 46.4, its lowest level since December 2022. The employment component improved by 1.7 points to 50.7. Supplier deliveries rose 1.2 points to 52.5. New export orders edged down 0.1 points to 48.5, while imports rose 3.9 points to 48.2. The prices paid measure increased 3.6 points to 68.7, its highest level since November 2022. The ISM press release noted 14 mentions of tariffs, with respondents indicating increased costs and supply chain disruptions.

• MBA Mortgage Applications fell 3.9 percent Week-over-week for the week ending May 30, following a 1.2 percent decrease in the previous week. The 30-year mortgage rate was 6.92 percent, down from 6.98 percent.

Canada

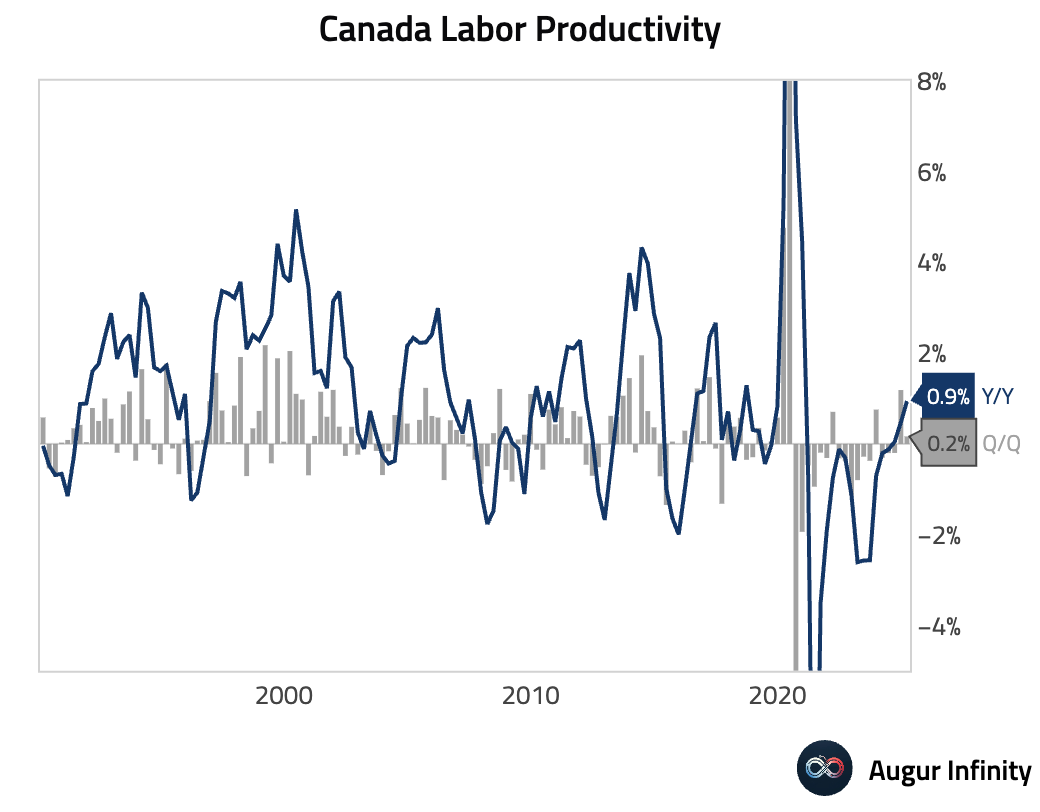

• Labor Productivity Q/Q for Q1 2025 rose 0.2 percent, compared to 1.2 percent in Q4 2024.

• The S&P Global Services PMI for May increased to 45.6 from 41.5 in April.

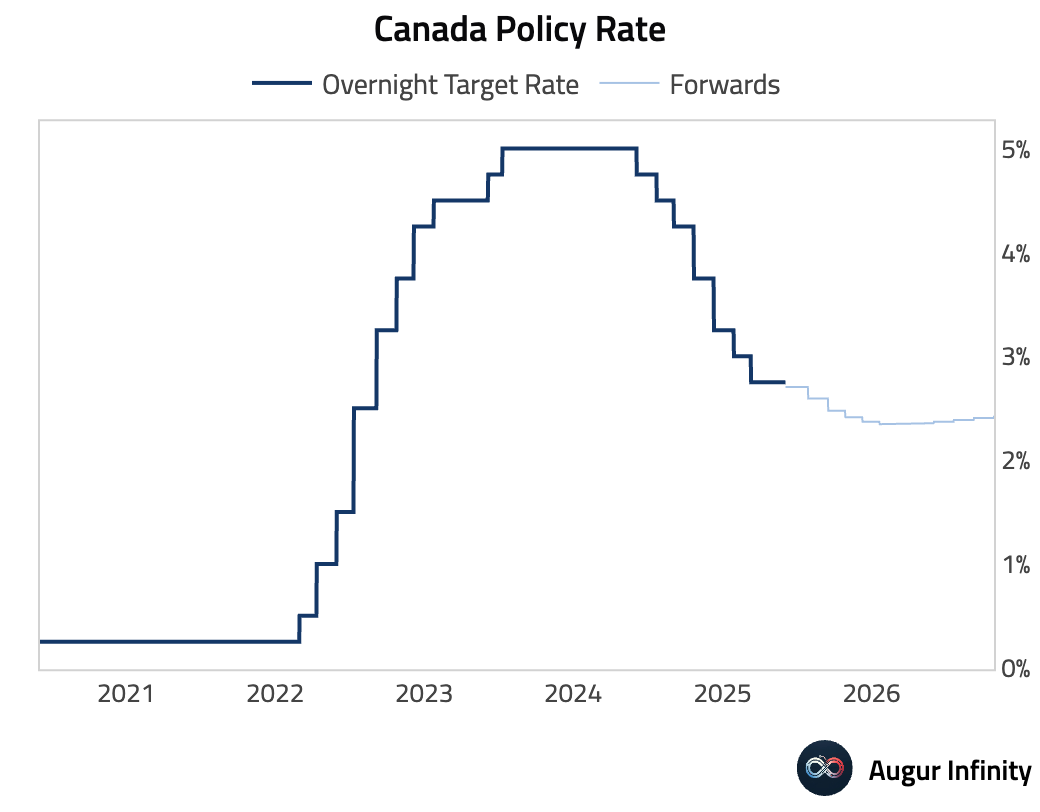

• The Bank of Canada maintained its key interest rate at 2.75 percent.

Europe

• Norway's Current Account surplus for Q1 2025 was NOK 286.5 billion, up from NOK 203.7 billion in Q4 2024.

• Sweden's Services PMI for May rose to 50.8 from 48.7 in April.

• Spain's Industrial Production Y/Y for April slowed to 0.6 percent from 0.9 percent in March.

• The HCOB Services PMI final for May showed varied results across the Eurozone: the aggregate index for the Eurozone fell to 49.7 (previous 50.1, consensus 48.9). Germany's Services PMI declined to 47.1 (previous 49.0, consensus 47.2), its lowest level since November 2022. France's Services PMI rose to 48.9 (previous 47.3, consensus 47.4). Italy's increased to 53.2 (previous 52.9, consensus 52.3). Spain's Services PMI decreased to 51.3 (previous 53.4, consensus 52.9).

• The UK's S&P Global Services PMI final for May increased to 50.9, up from 49.0 in April and beating the consensus of 50.2.

• Germany's New Car Registrations Y/Y for May rose to 1.2 percent, from -0.2 percent in April.

Japan

• The Jibun Bank Services PMI final for May was 51.0, down from 52.4 in April and below the consensus of 50.8.

Asia-Pacific

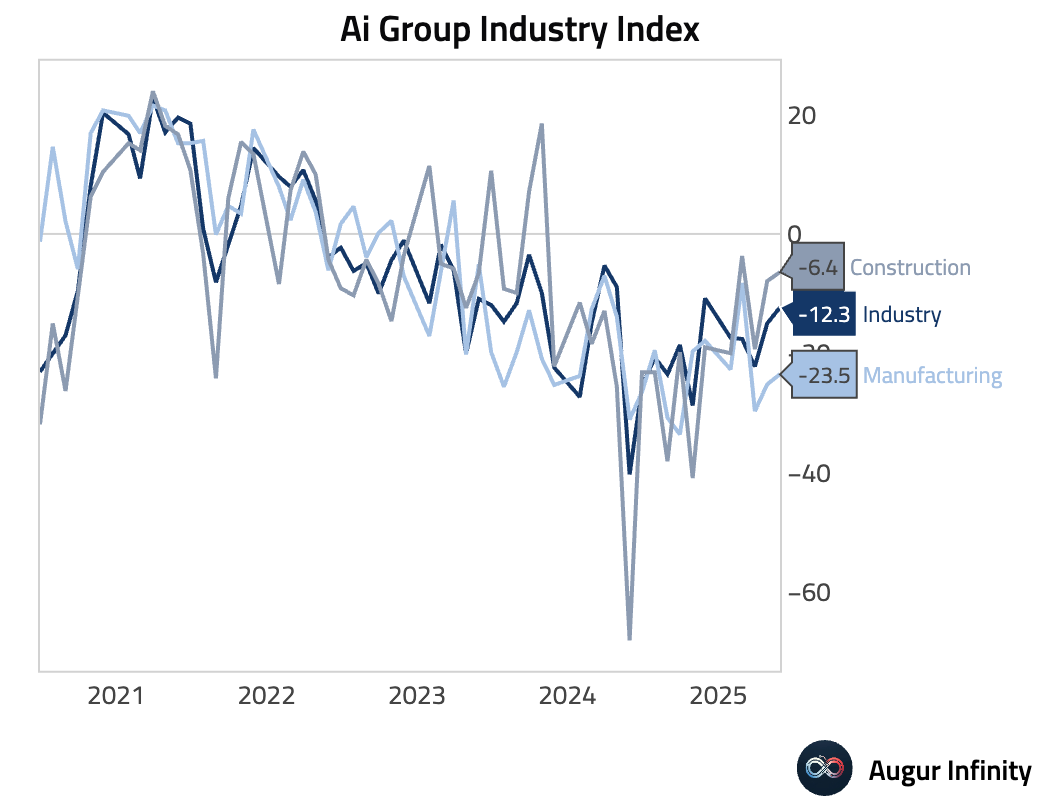

• Australian Ai Group indexes for May showed: the Industry Index improved to -12.3 (previous -15.0), the Construction Index rose to -6.4 (previous -7.9), and the Manufacturing Index increased to -23.5 (previous -25.2).

• Australia's S&P Global Services PMI final for May was 50.6, slightly down from 51.0 in April and above the consensus of 50.5.

• Australia's GDP Growth Rate for Q1 2025 was 0.2 percent Q/Q (previous 0.6 percent, consensus 0.4 percent) and 1.3 percent Y/Y (previous 1.3 percent, consensus 1.5 percent).

• South Korea's Inflation Rate for May eased to 1.9 percent Y/Y (previous 2.1 percent, consensus 2.1 percent) and -0.1 percent M/M (previous 0.1 percent, consensus 0.1 percent).

• Hong Kong's S&P Global PMI for May rose to 49.0 from 48.3 in April.

• Singapore's S&P Global PMI for May decreased to 51.5 from 52.8 in April.

Emerging Markets ex China

• Thailand's S&P Global Manufacturing PMI for May rose to 51.2 from 49.5 in April.

• Thailand's Business Confidence for May edged down to 46.7 from 47.1 in April.

• India's HSBC Services PMI final for May was 58.8, slightly up from 58.7 in April but below the consensus of 61.2.

• Russia's S&P Global Services PMI for May increased to 52.2 from 50.1 in April.

• Russia's Unemployment Rate for April was 2.3 percent, unchanged from March, matching an all-time low.

• Russia's Real Wage Growth Y/Y for March slowed to 0.1 percent from 3.2 percent in February, missing the consensus of 3.0 percent. This is its lowest level since September 2022.

• Russia's Retail Sales Y/Y for April rose to 1.9 percent from 1.3 percent in March.

• The Czech Republic's preliminary Inflation Rate for May was 2.4 percent Y/Y (previous 1.8 percent, consensus 2.1 percent) and 0.5 percent M/M (previous -0.1 percent, consensus 0.4 percent).

• The Czech Republic's Real Wages Y/Y for Q1 2025 decreased to 3.9 percent from 4.2 percent in Q4 2024.

• The Czech Republic's Retail Sales ex Auto for April rose 1.2 percent M/M (previous 0.8 percent) and 5.8 percent Y/Y (previous 3.9 percent, consensus 3.2 percent).

• South Africa's S&P Global PMI for May increased to 50.8 from 50.0 in April.

• South Africa's BER Business Confidence for Q2 2025 fell to 40.0 from 45.0 in Q1 2025.

• Mexico's Gross Fixed Investment for March rose 0.3 percent M/M (previous 0.1 percent) and fell 0.2 percent Y/Y (previous -7.8 percent).

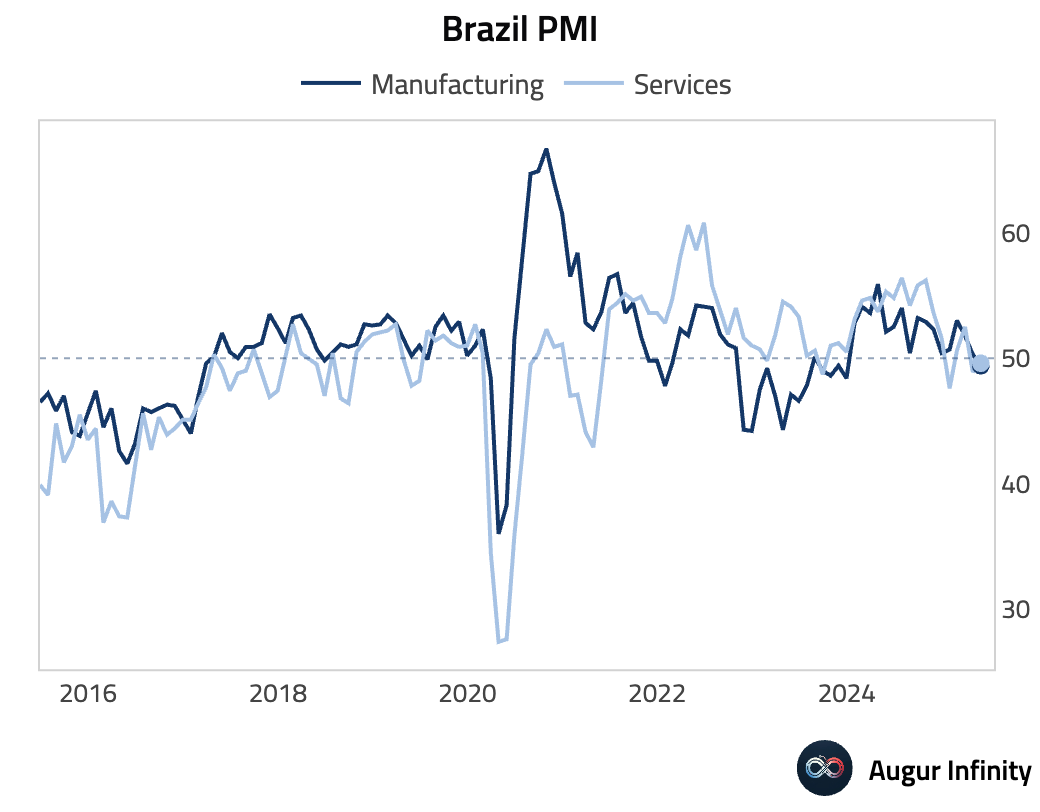

• Brazil's S&P Global Services PMI for May rose to 49.6 from 48.9 in April.

• Poland's central bank kept its interest rate unchanged at 5.25 percent, as expected.

Equities

US equities finished roughly flat (+0.01%), while the Nasdaq gained 0.3 percent. South Korea was a notable outperformer, up 3.4 percent. China rose 1.8 percent, and Australia gained 1.1 percent. Conversely, Brazil fell 0.4 percent and Mexico was down 0.1 percent.

Fixed Income

US Treasury yields fell across the curve, with the 2-year yield down 8.3 bps, and the 5-year, 10-year, and 30-year yields down approximately 9.7-9.8 bps.

FX

The US dollar weakened against all G10 currencies. The Swiss franc (CHF) was the strongest performer, up 0.6 percent, while the Australian dollar (AUD), New Zealand dollar (NZD), and Norwegian krone (NOK) all gained 0.5 percent.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.