Headlines

- China launched two investigations into US trade policy ahead of a scheduled meeting between Chinese and US officials in Spain.

- Fitch Ratings lowered France’s sovereign credit rating to A+ from AA−, citing high debt and political uncertainty; separately, Fitch upgraded Portugal’s rating to A, and Standard & Poor’s raised Spain’s rating to A+.

United States

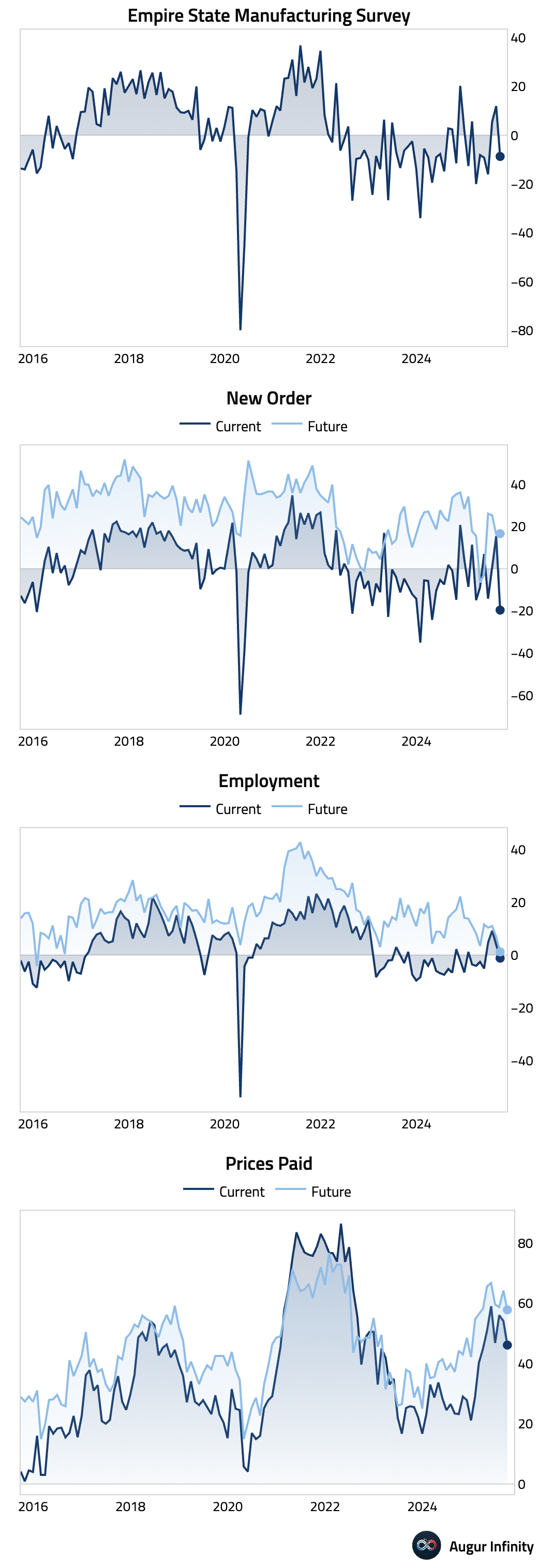

- The NY Empire State Manufacturing Index unexpectedly plunged into contractionary territory at -8.7, a stark reversal from the prior month’s 11.9 reading and a significant miss of the 5.0 consensus estimate.The sharp 21-point drop was driven by a collapse in new orders and shipments, pointing to a material drop in demand. The future employment index fell to near zero, a rare signal suggesting firms expect no job growth over the next six months.

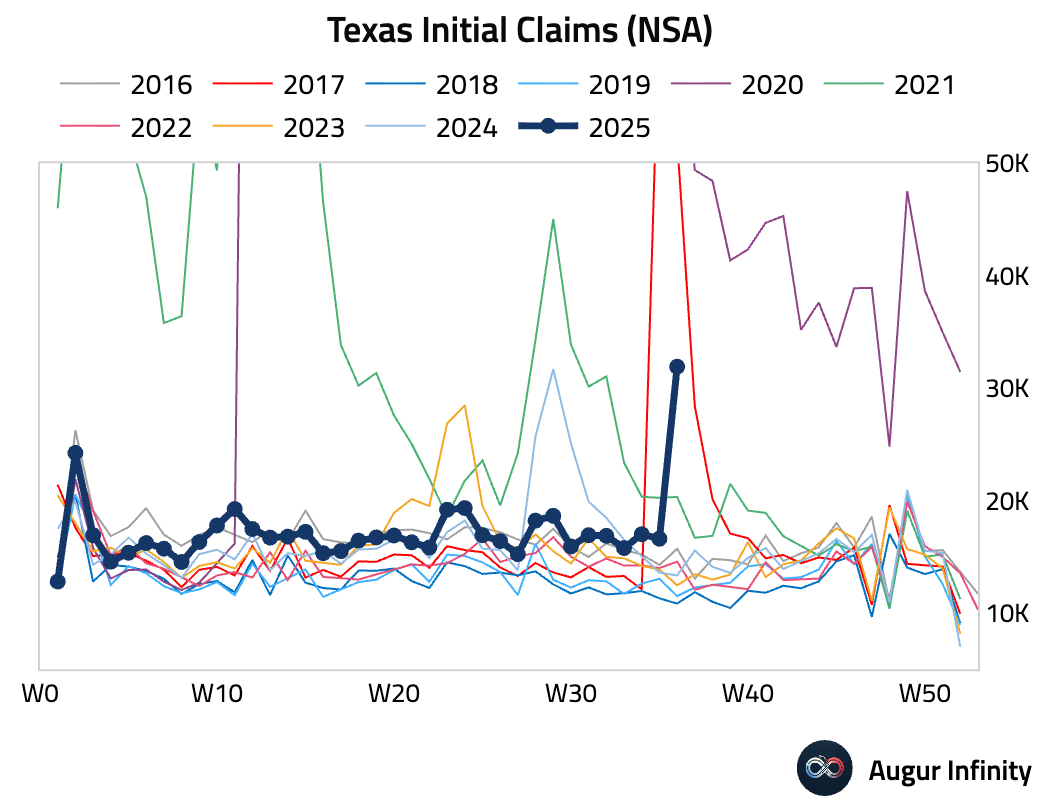

- Last week's unusual surge in Texas initial claims, which pushed the national series to a four-year high, was due to "an increased volume of fraudulent claim attempts."

Source: Axios

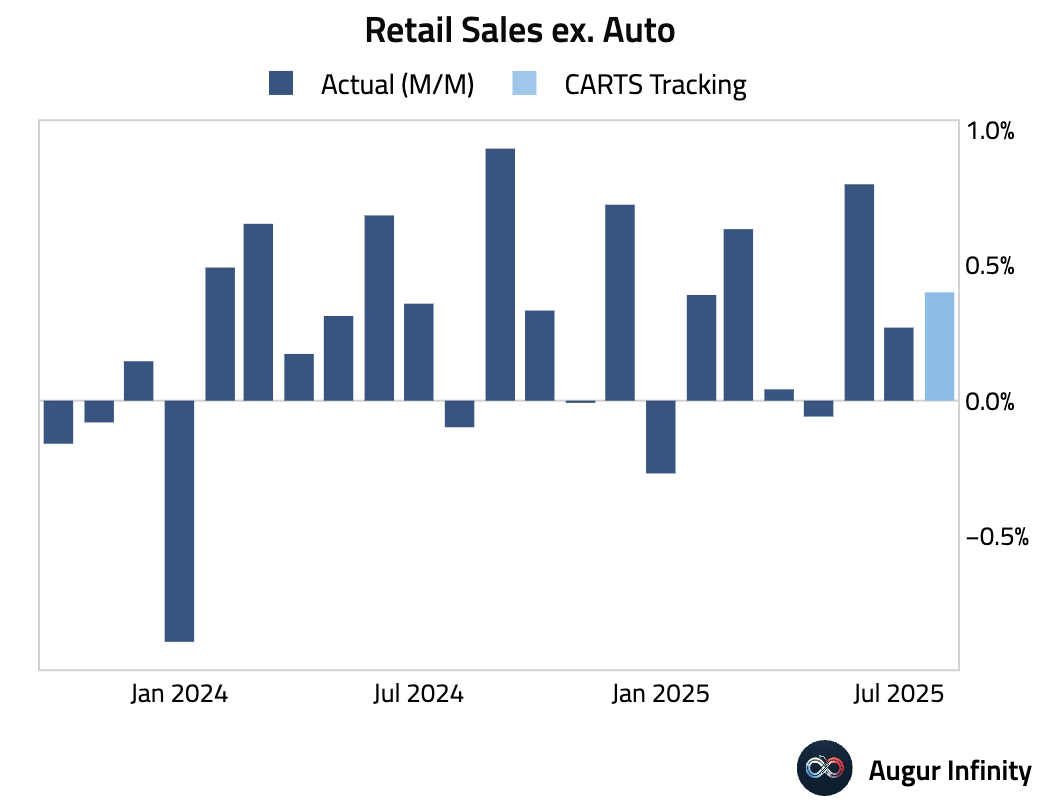

- August retail sales data will be released tomorrow (Tuesday). The Chicago Fed CARTS is projecting retail sales ex auto to rise by 0.4% M/M.

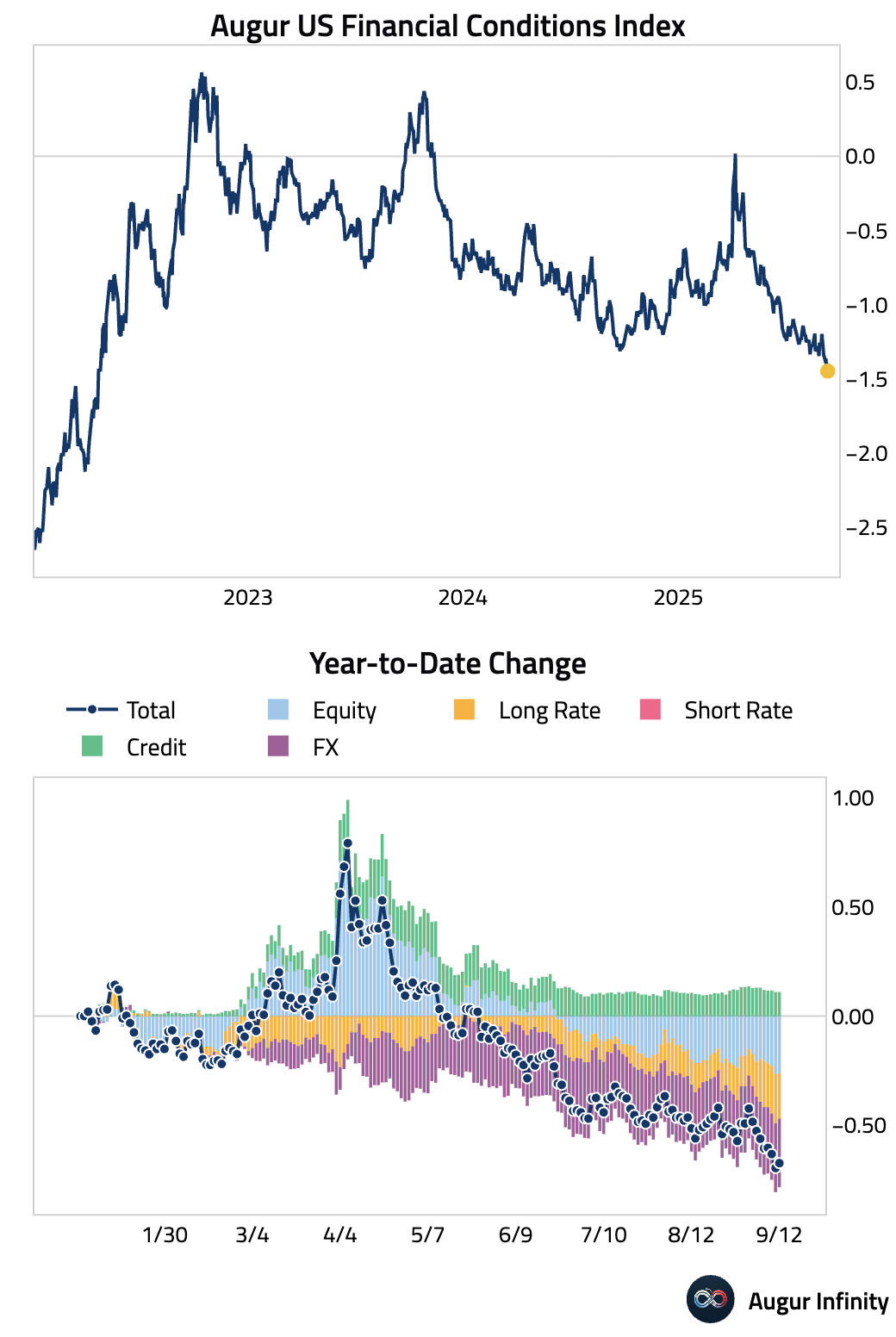

- US financial conditions have reached the easiest level since April 2022.

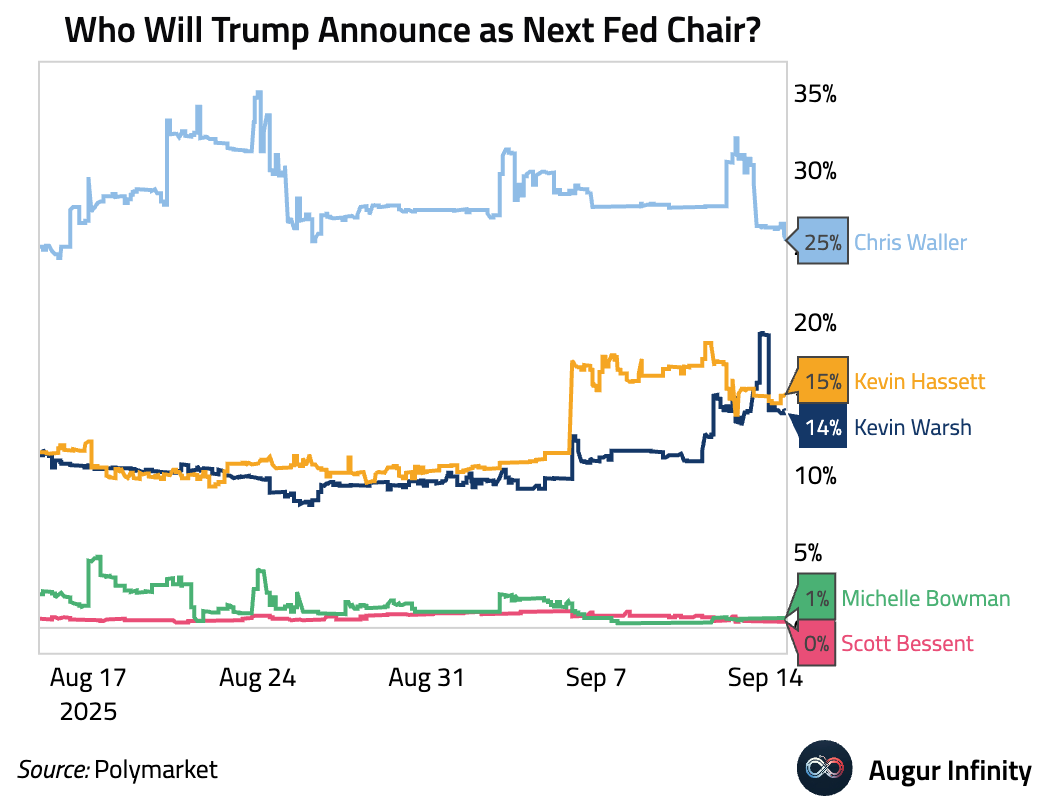

- Chris Waller continues to have a commanding lead in the race to become the next Fed chair, based on betting markets.

Canada

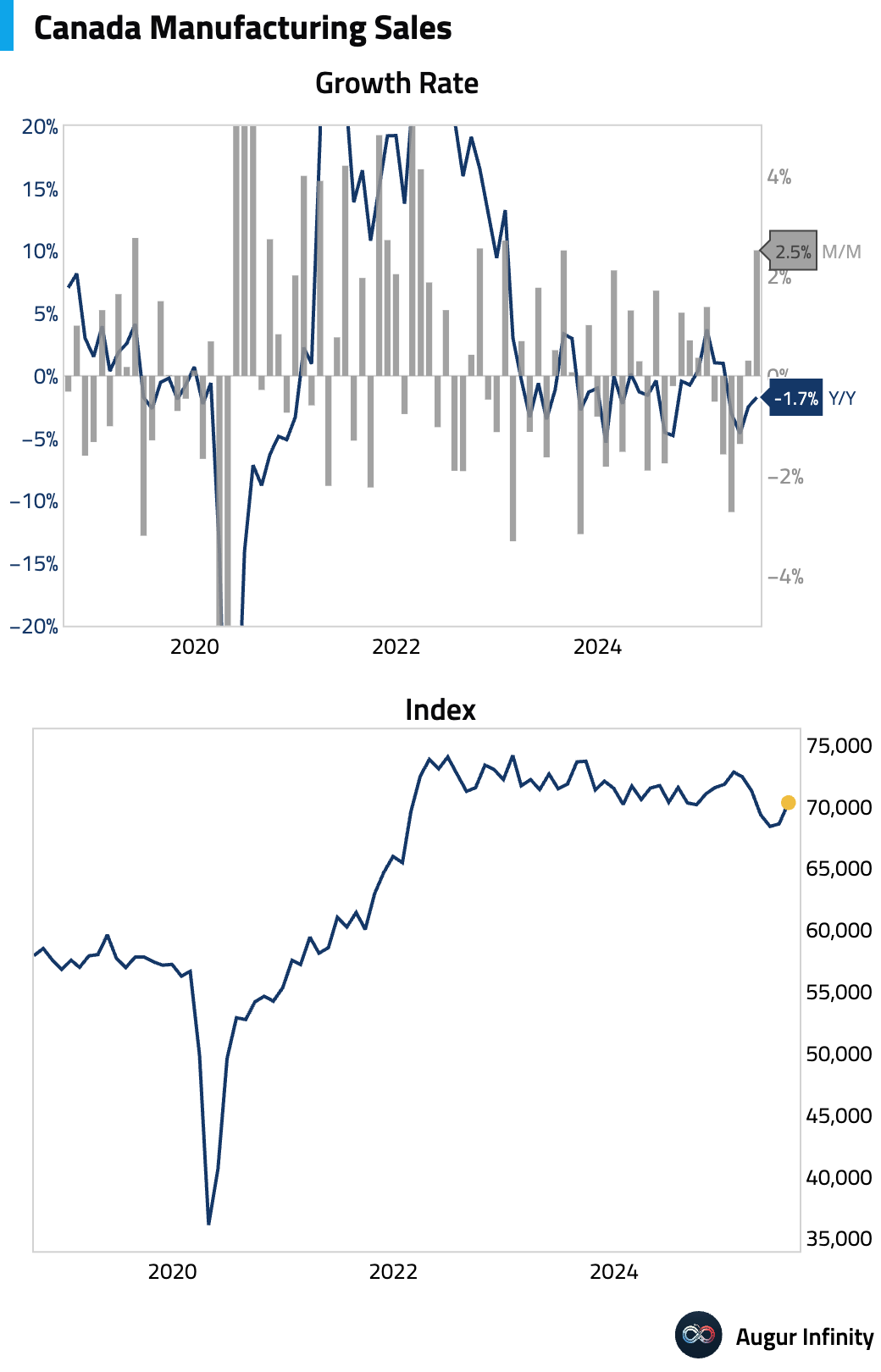

- Manufacturing sales in Canada rebounded strongly in July, rising 2.5% M/M and beating the 1.8% consensus estimate. This marks the strongest monthly growth since January 2023.

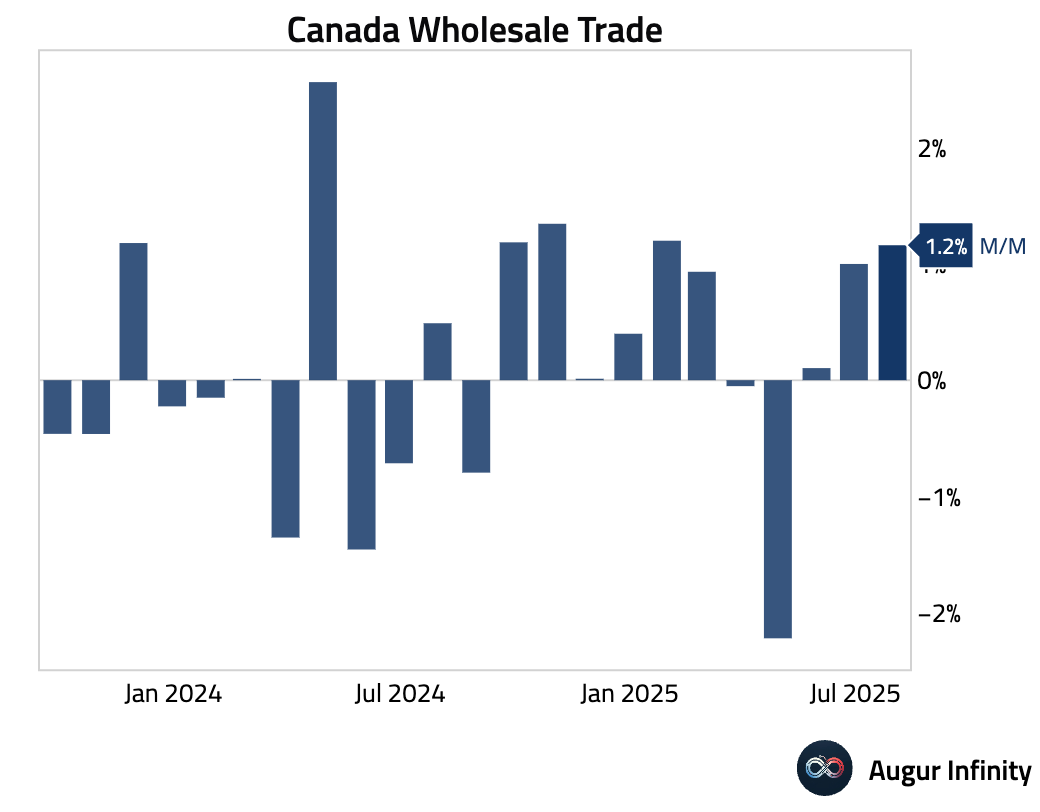

- Canadian wholesale sales grew 1.2% M/M in July (est: 1.3%, prev: 1.0%), indicating steady activity in the sector.

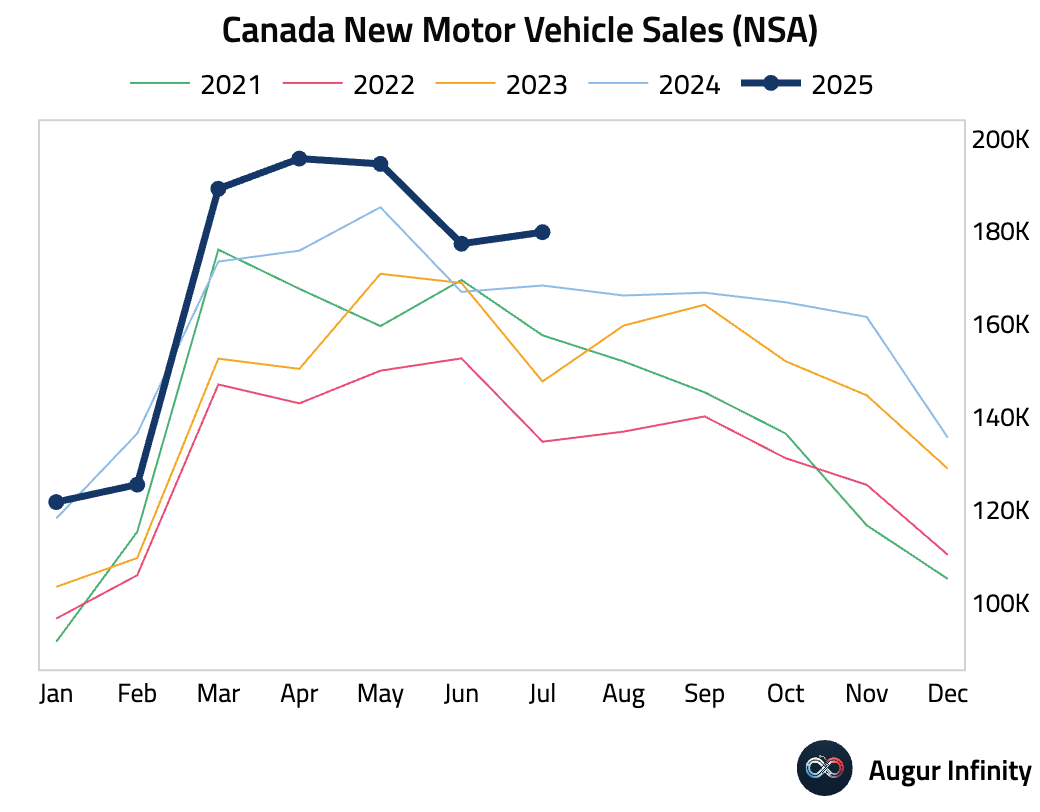

- New motor vehicle sales rose modestly in July to 179.8k from 177.2k in the prior month.

Europe

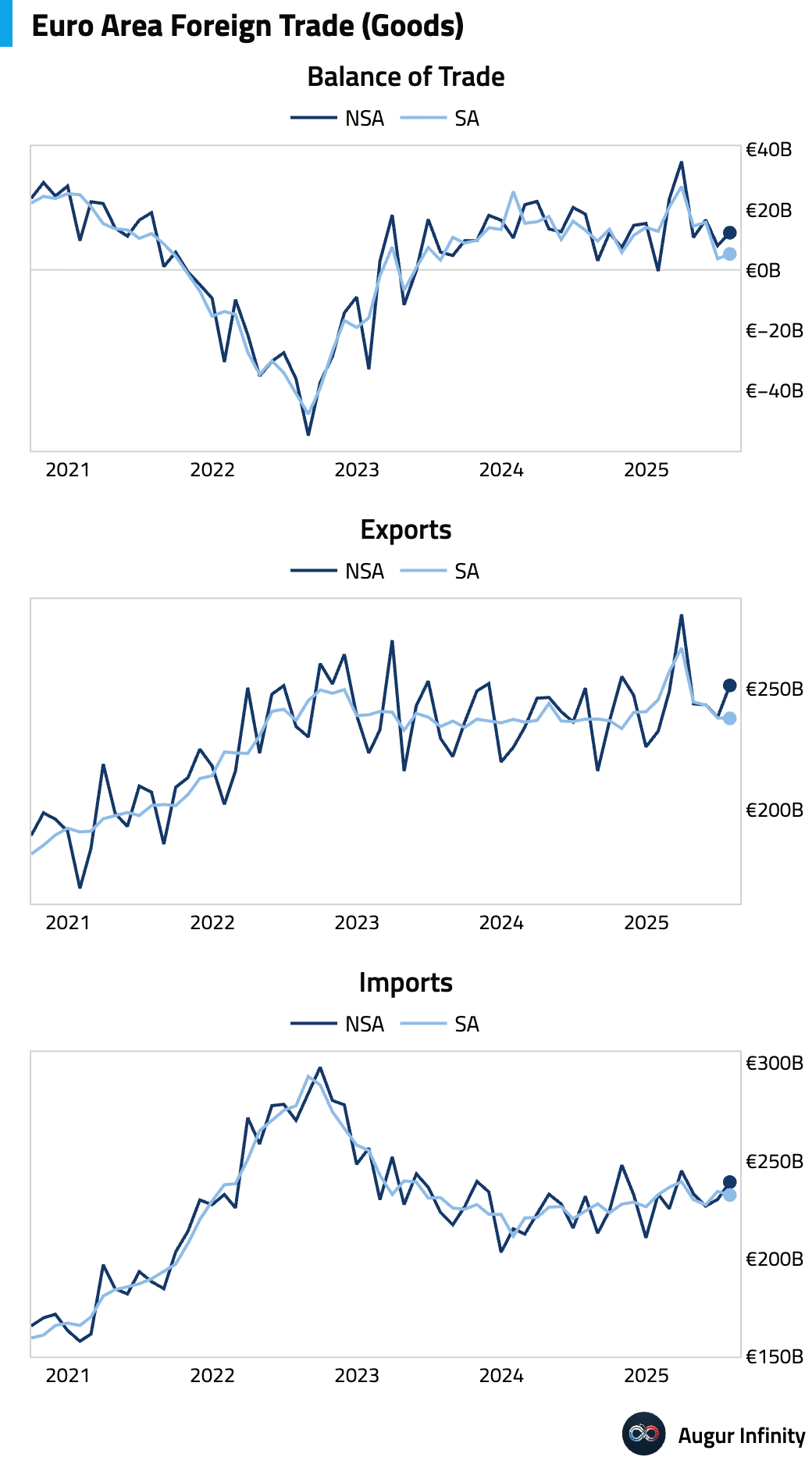

- The Euro Area’s goods trade surplus widened to €12.4B in July, beating the €11.7B consensus and up from €8.0B in June.

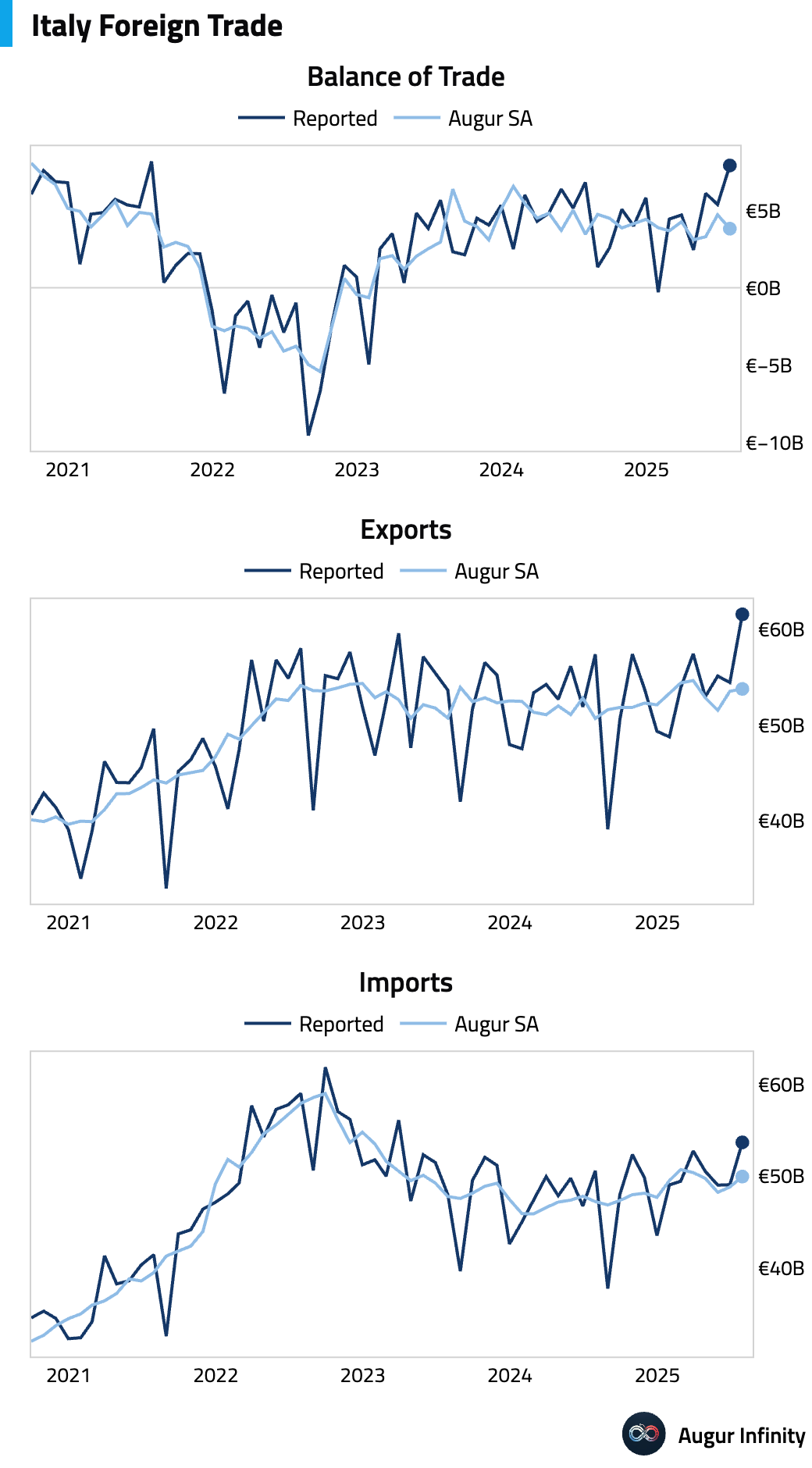

- Italy’s trade surplus expanded to €7.91B in July, well above the €5.50B consensus. After seasonal adjustment, trade balance declined.

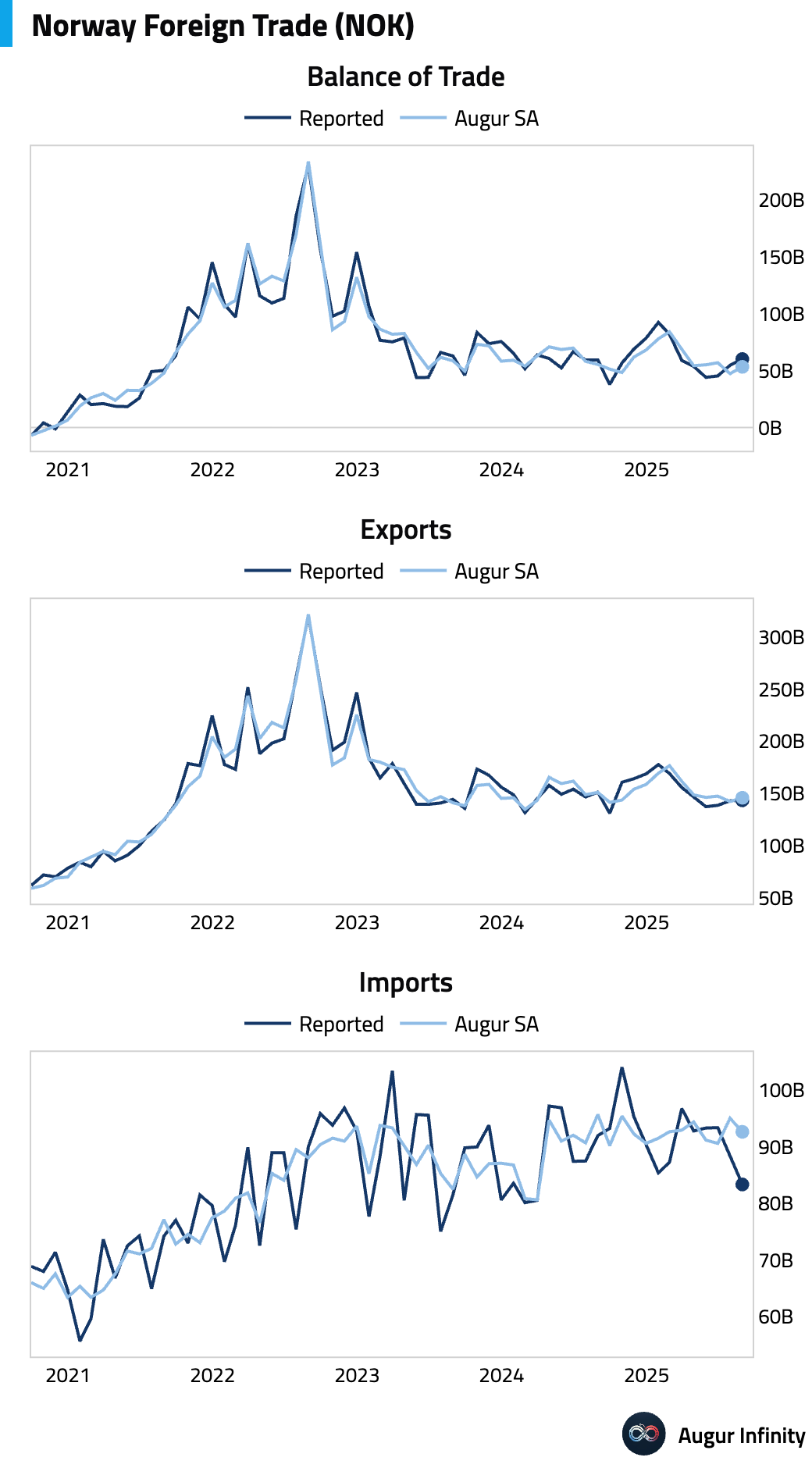

- Norway’s trade surplus widened to NOK 60.1B in August from NOK 54.6B, reaching its highest level since February.

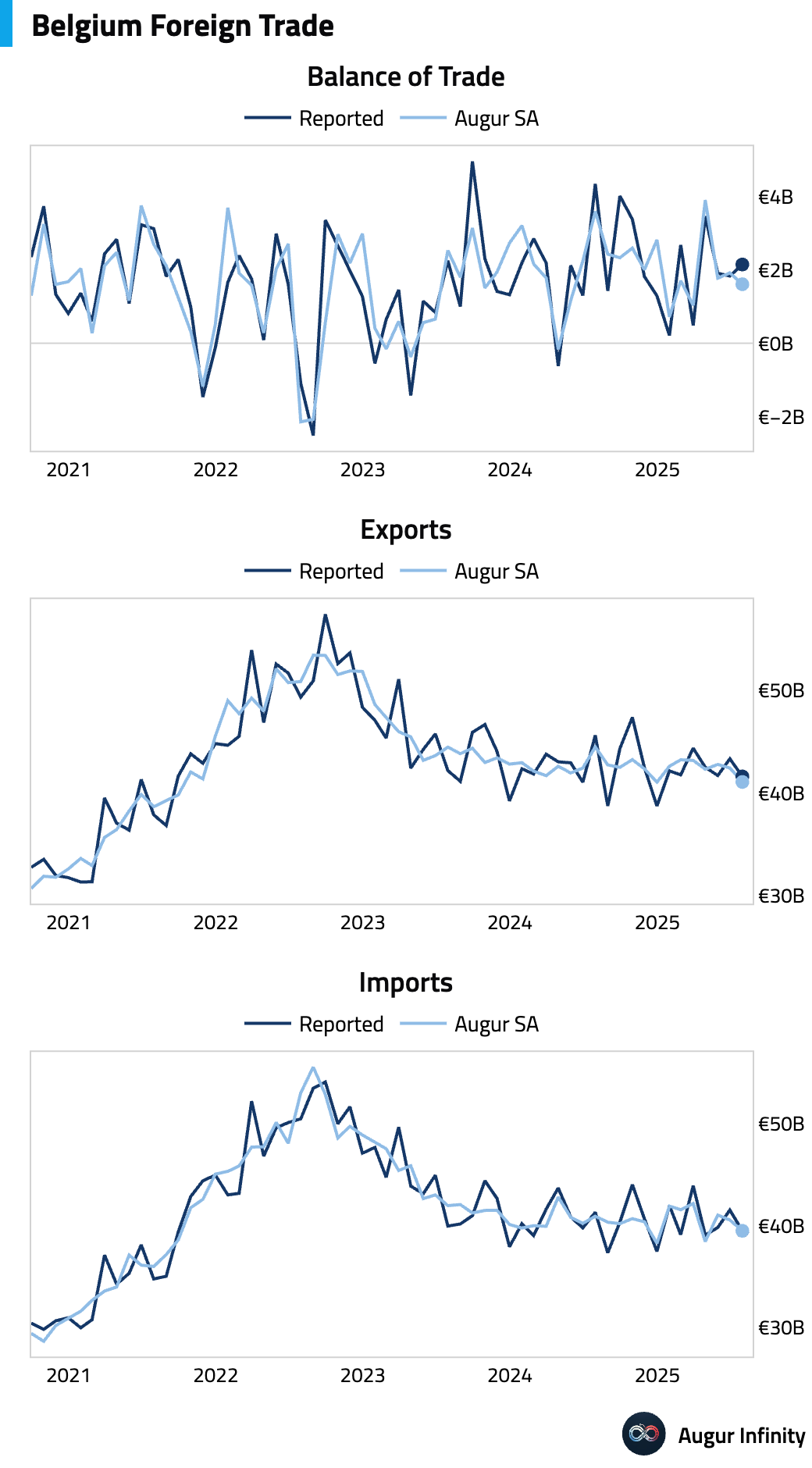

- Belgium’s trade surplus increased to €2.15B in July from €1.83B in June.

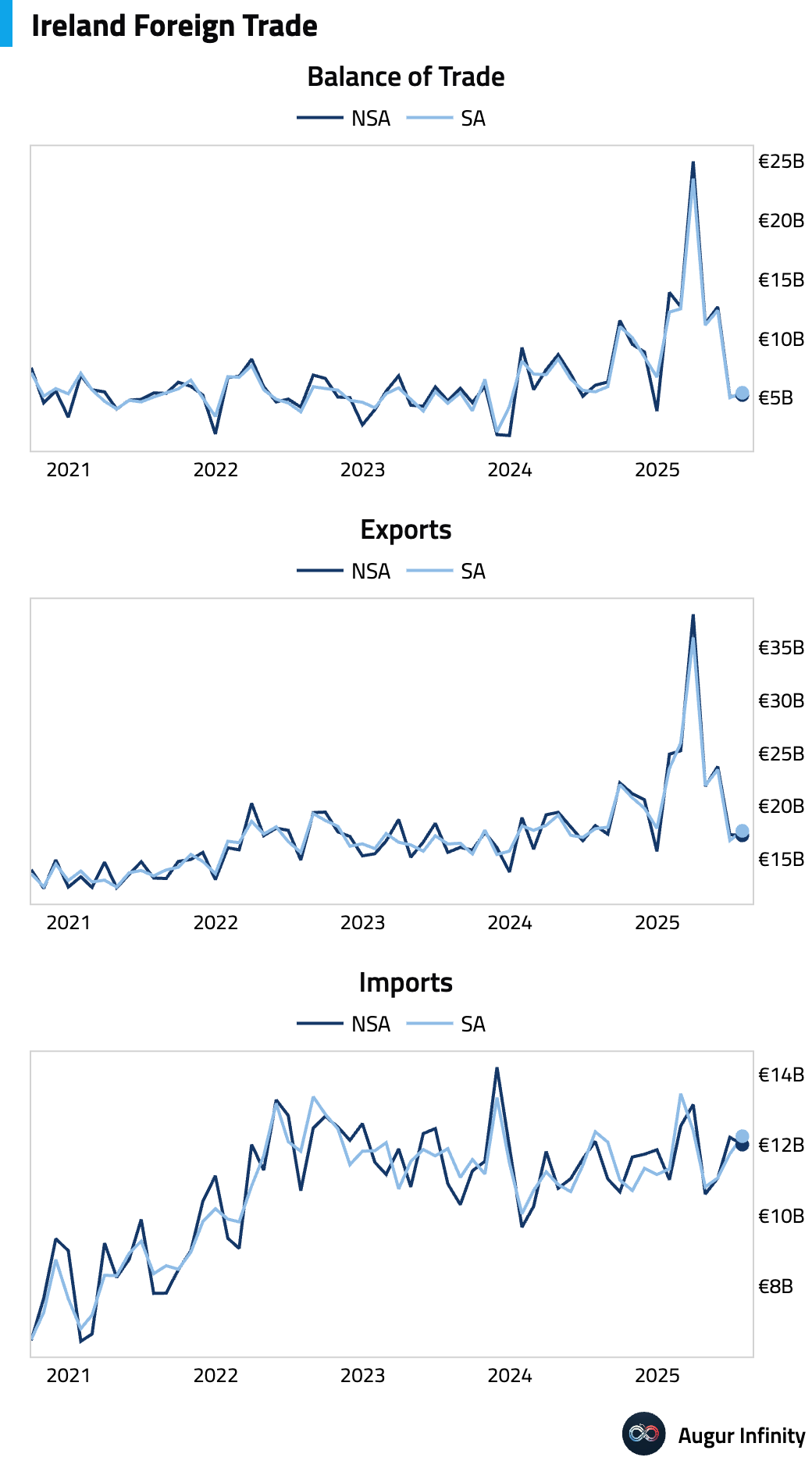

- Ireland's trade surplus edged up to €5.2B in July from €5.1B in the previous month.

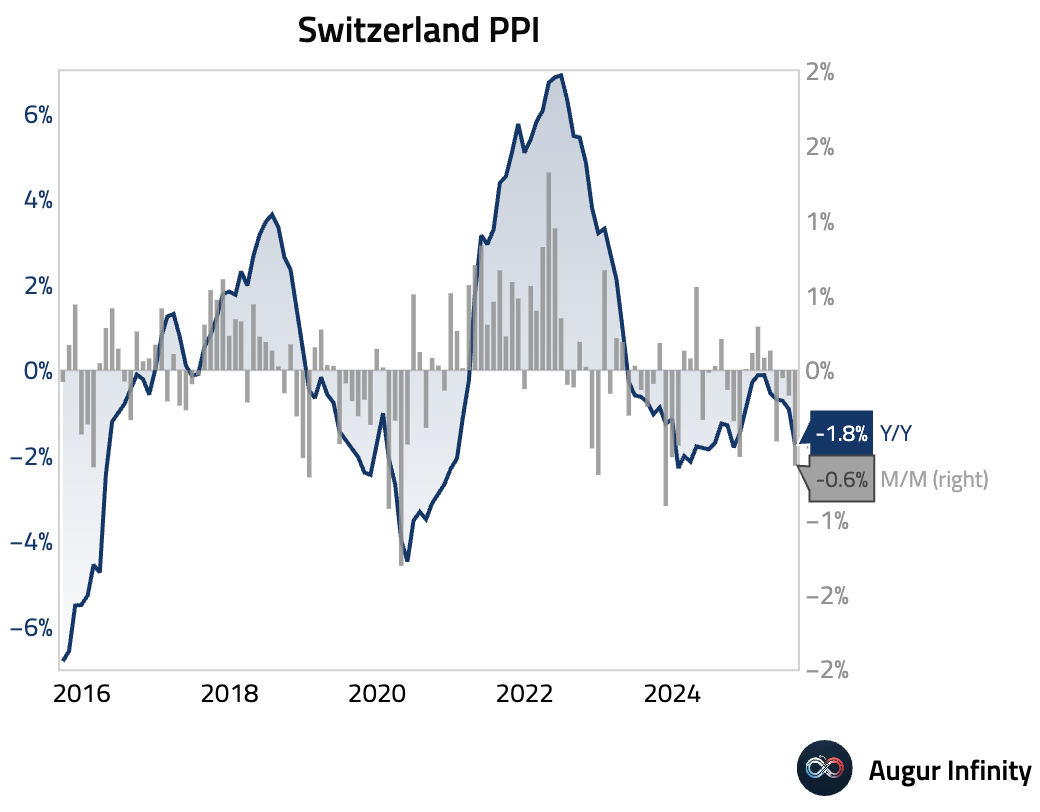

- Swiss producer and import prices fell more than expected in August, declining 0.6% M/M (est: -0.1%, prev: -0.2%). Year-over-year, prices were down 1.8% (prev: -0.9%), the largest drop since October 2024.

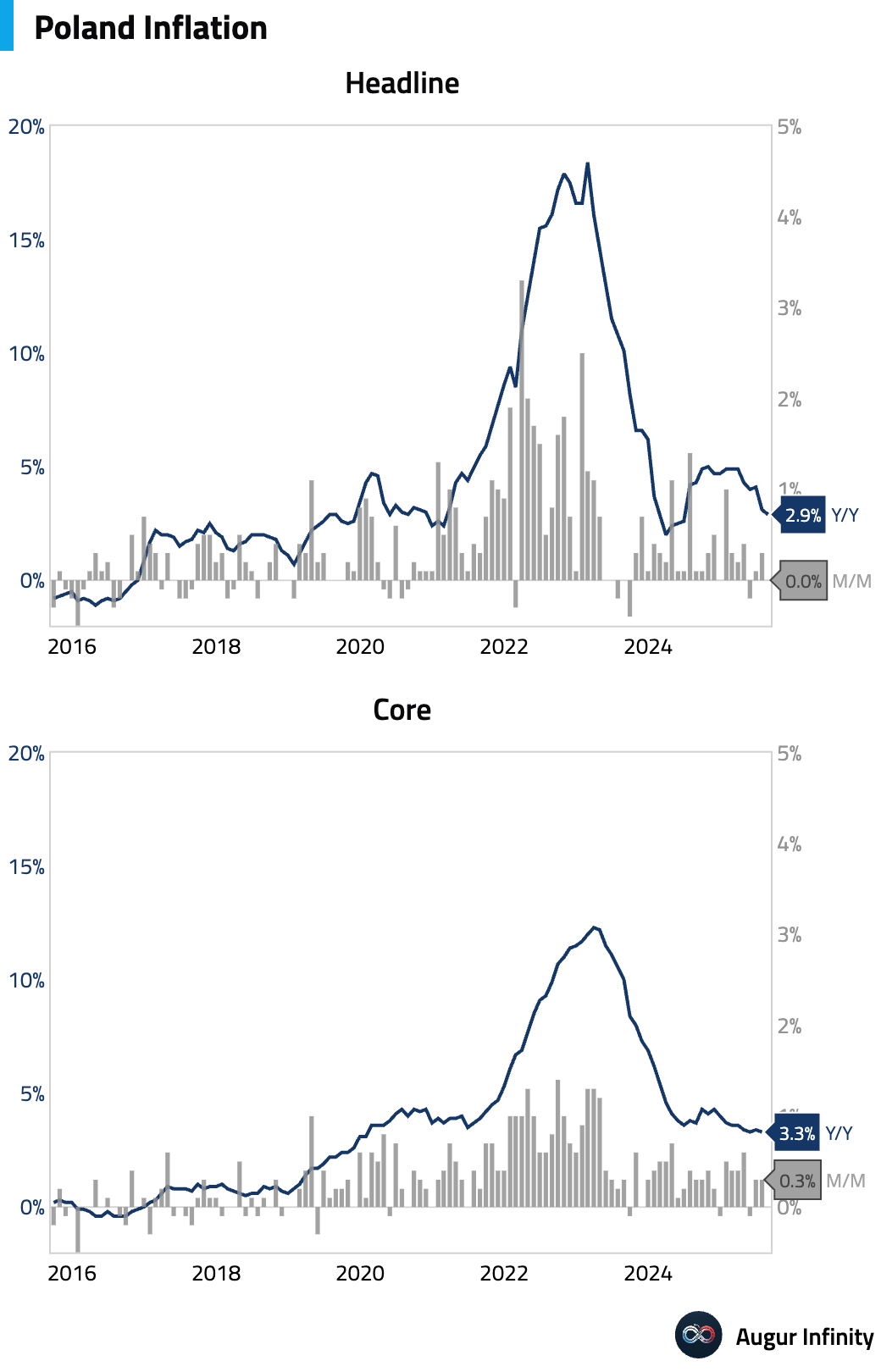

- Poland’s final August inflation confirmed a further cooling of price pressures. The CPI fell to 2.9% Y/Y from 3.1% (est: 2.8%), the lowest since June 2024, while prices were flat month-over-month (act: 0.0%, est: -0.1%).

Asia-Pacific

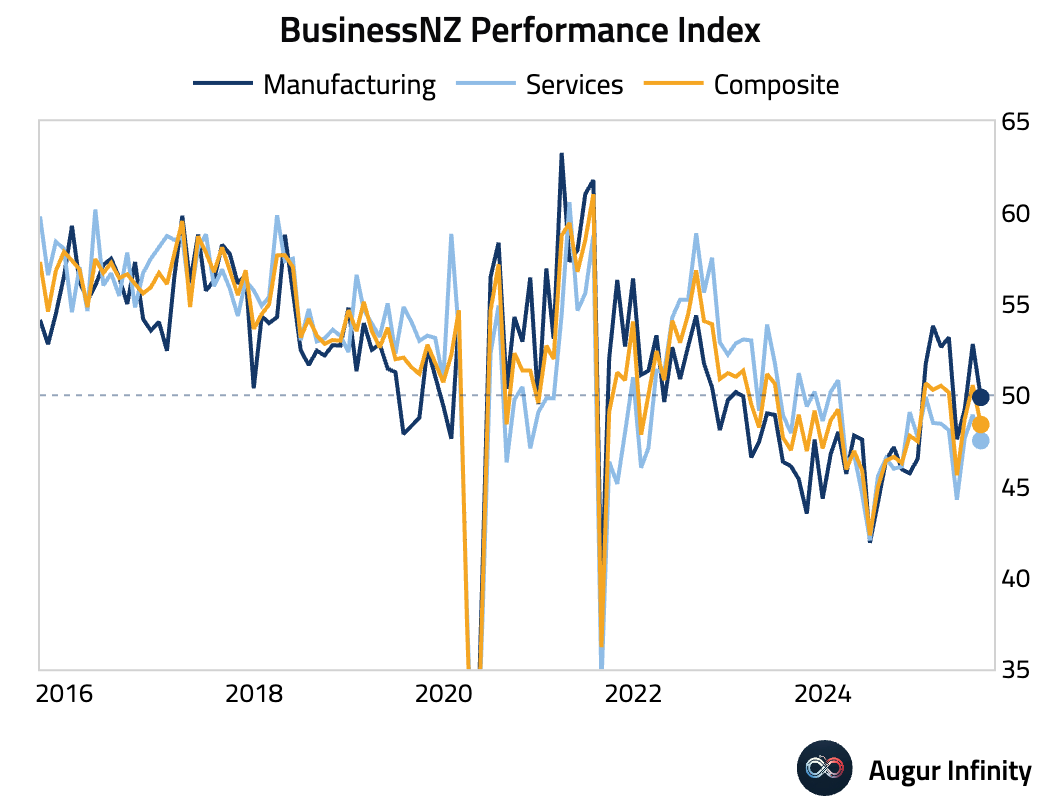

- New Zealand's services sector slump deepened in August, with the PSI falling to 47.5 from 48.9. This marks 18 straight months of contraction, driven by weak demand from high interest rates and poor consumer confidence. Key sub-indices like activity/sales and new orders both worsened, signaling persistent weakness and a potentially slower-than-expected economic recovery.

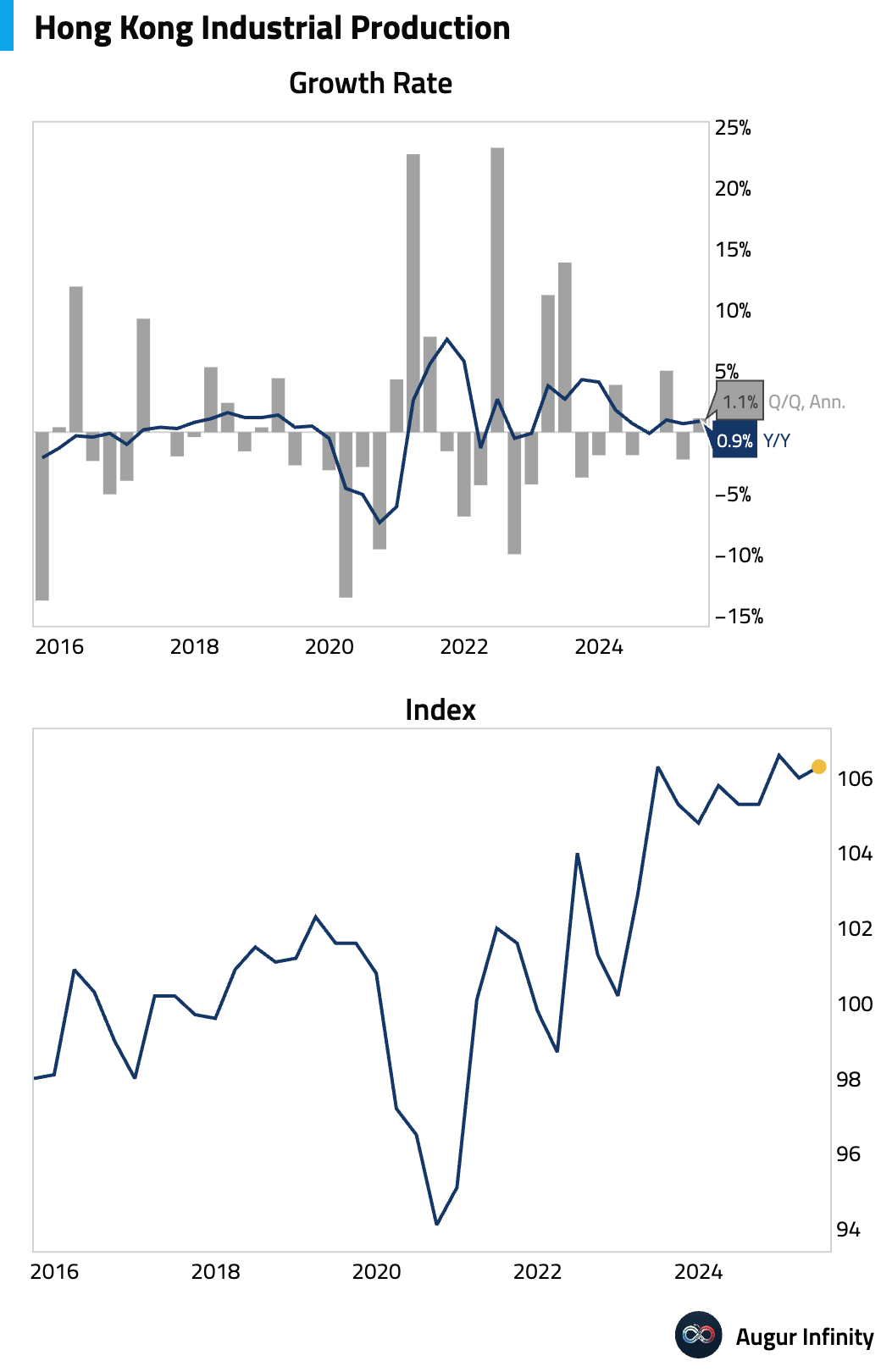

- Hong Kong's industrial production rose 0.9% Y/Y in the second quarter, accelerating from a 0.7% pace in Q1.

China

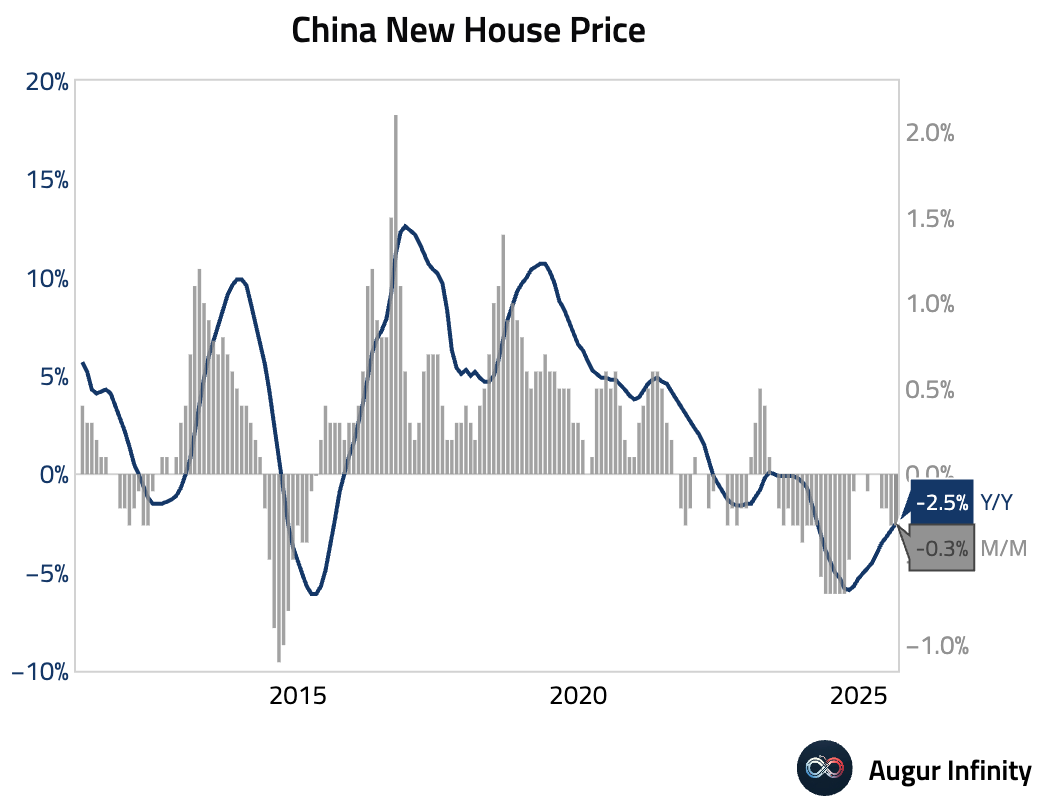

- Chinese house prices fell 2.5% Y/Y in August, a slight improvement from the 2.8% decline in July but marking the 26th consecutive month of Y/Y declines. The decline in new home prices was driven by lower-tier cities, while Tier-1 cities remained stable.

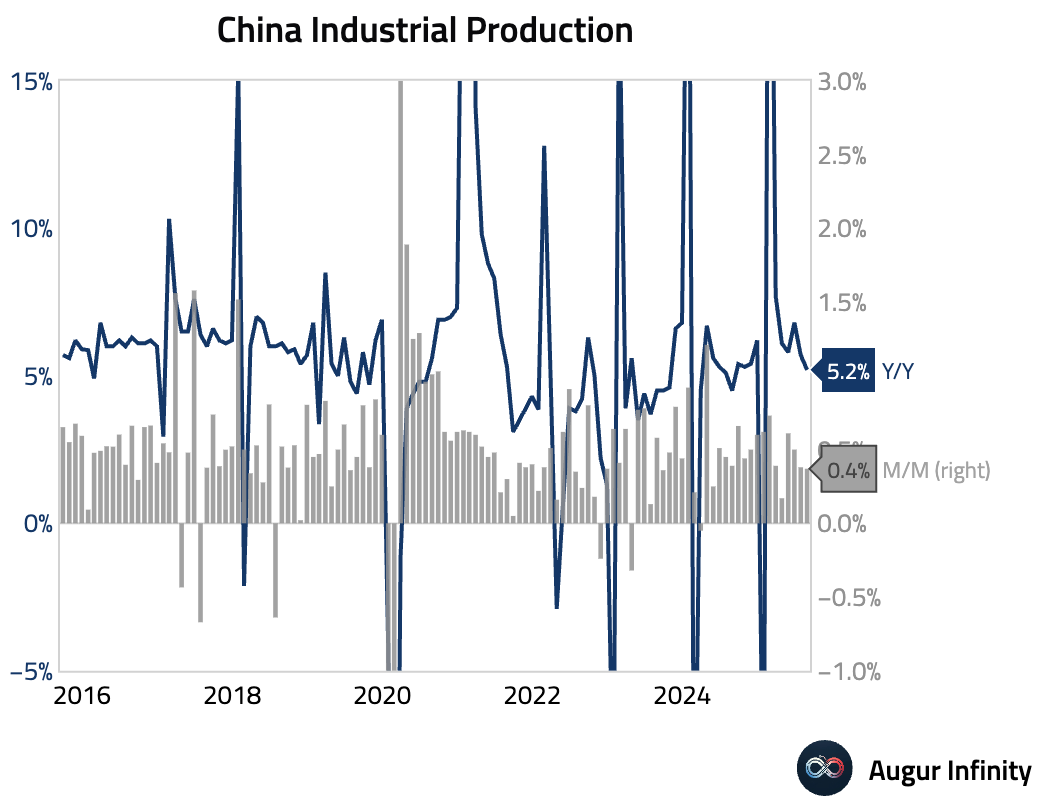

- Industrial production growth in China slowed to 5.2% Y/Y in August, missing the 5.8% consensus and decelerating from 5.7% in July.The slowdown was driven by weaker exports and slowing metals and power output.

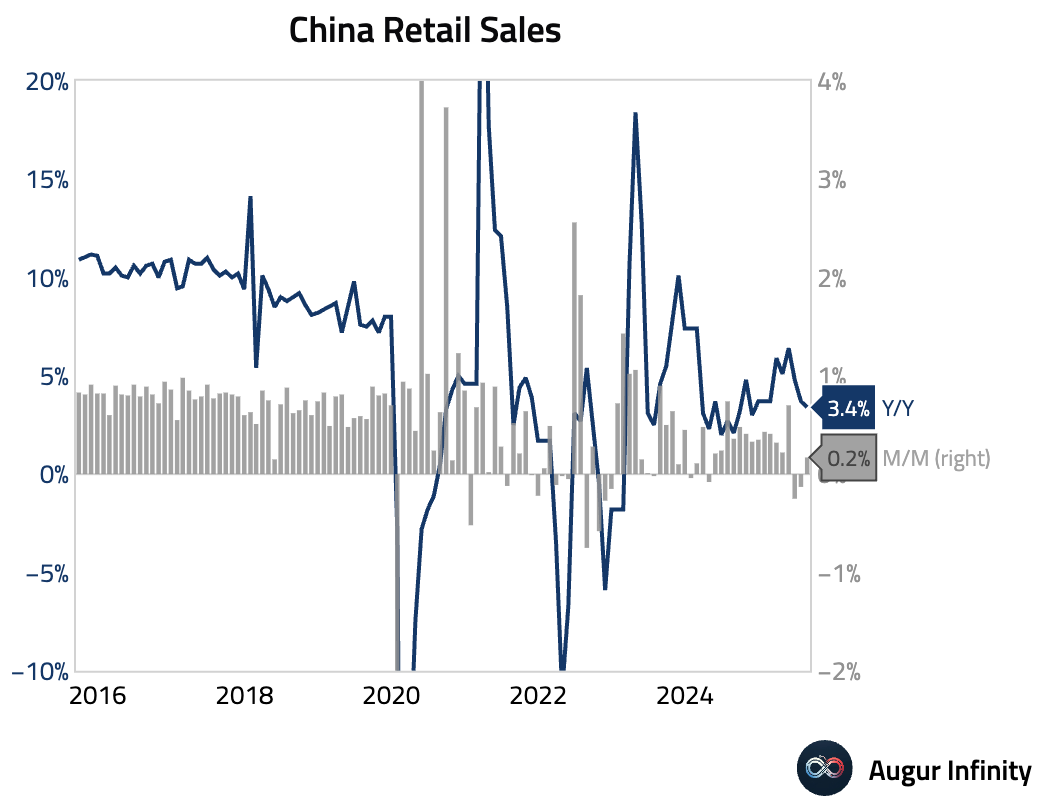

- Retail sales growth decelerated in August to 3.4% Y/Y, missing the 3.8% consensus and slowing from July’s 3.7% pace. The slowdown was driven by weaker online goods sales. In the auto sector, sales value rose while volumes fell, suggesting less discounting. Growth is expected to slow further due to unfavorable base effects from September onwards.

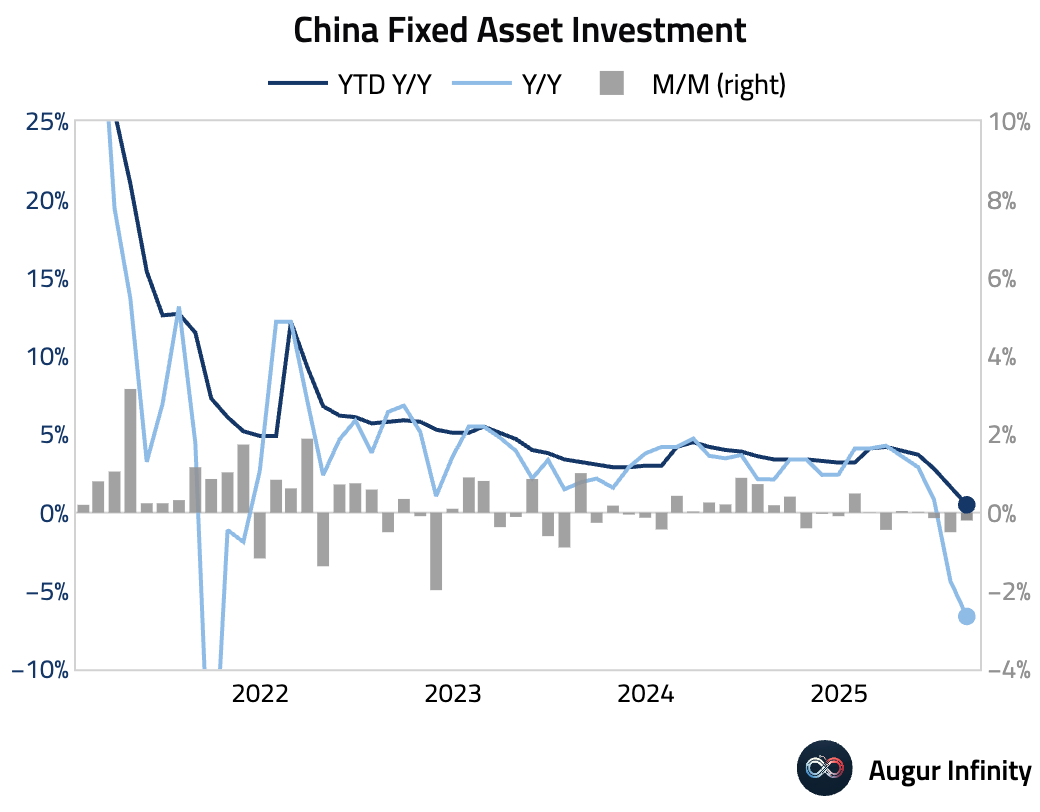

- Fixed asset investment growth slowed sharply to just 0.5% Y/Y year-to-date, a significant miss of the 1.5% consensus and a new low since March 2020. August single month Y/Y, based on our estimate, declined sharply to -6.6%.

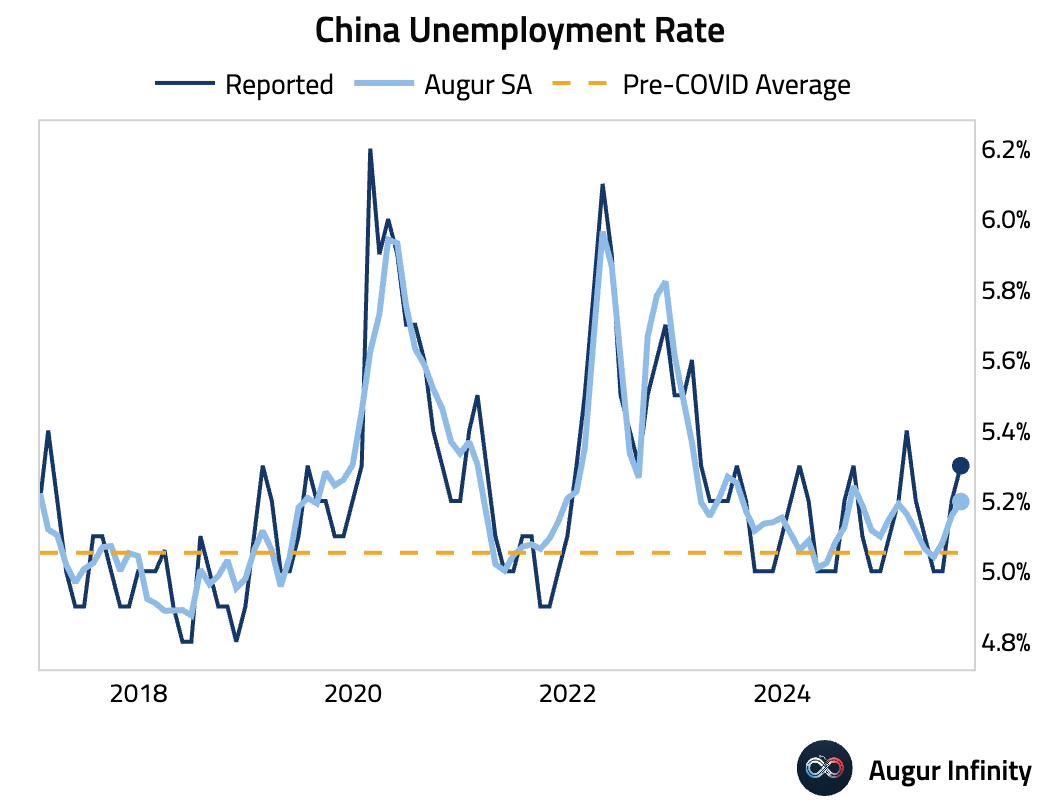

- China’s surveyed unemployment rate ticked up to 5.3% in August from 5.2% in July.

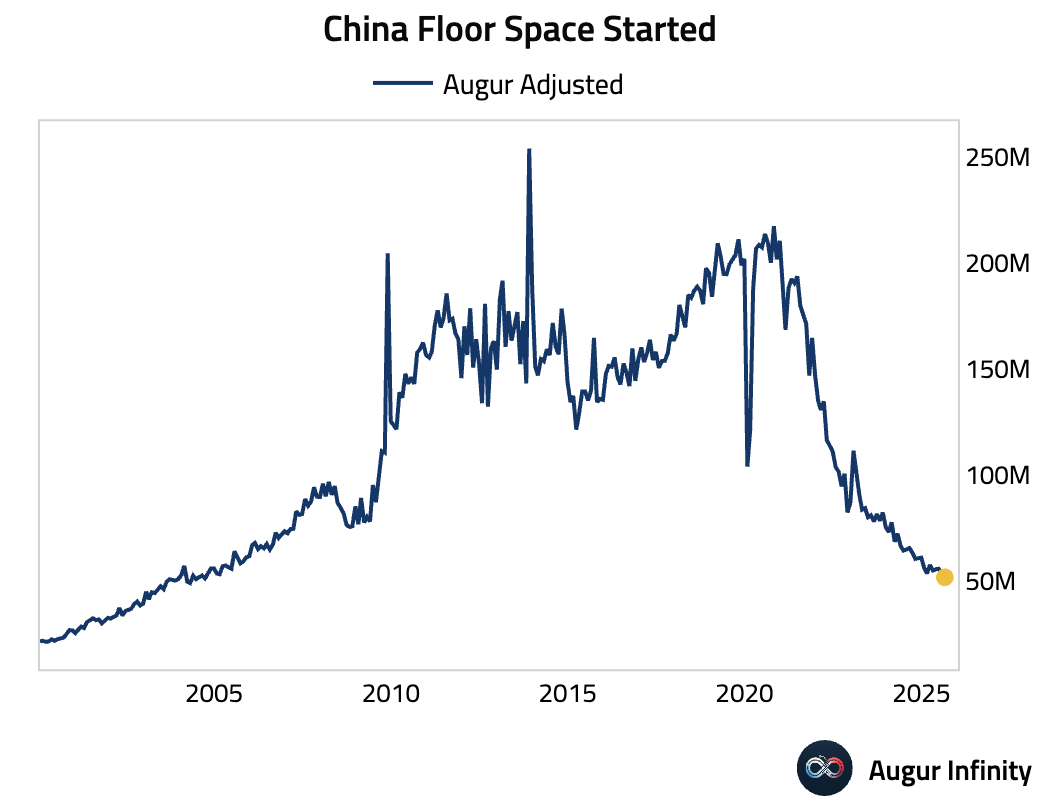

- China floor space started fell to the lowest level since 2004.

- Our economic surprises index for China plunged today.

Emerging Markets ex China

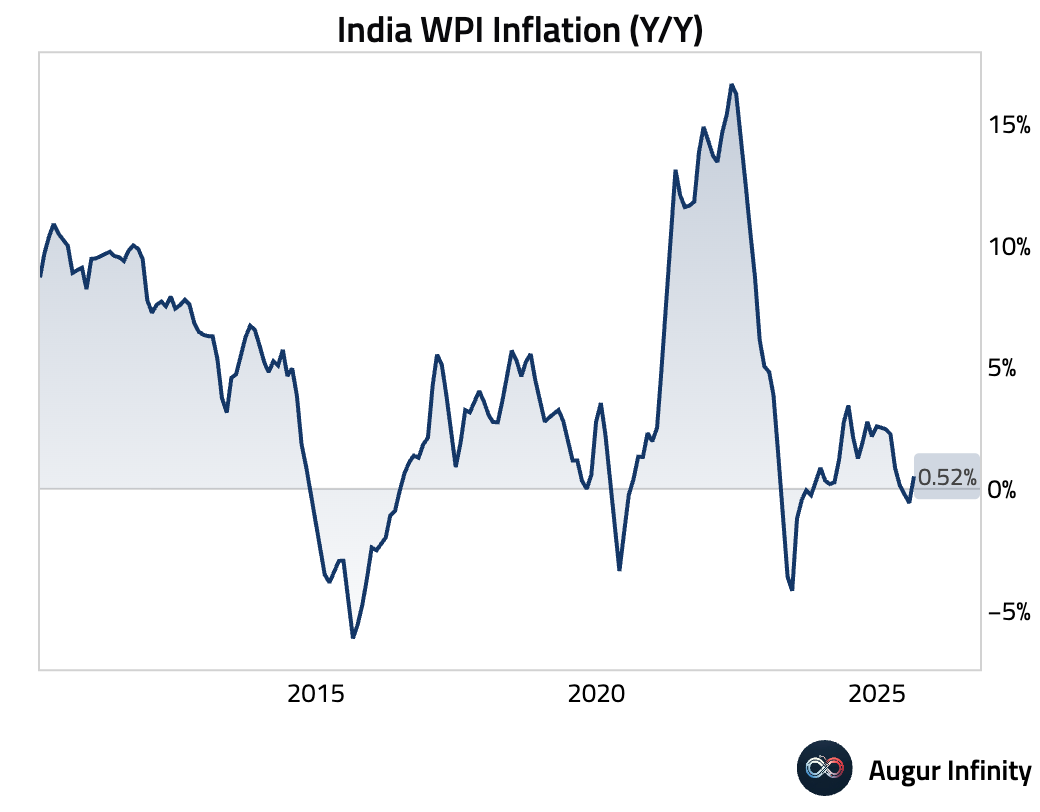

- India’s wholesale price inflation returned to positive territory, rising 0.52% Y/Y in August (est: 0.3%, prev: -0.58%), its first increase since April. The move was driven by a sharp rebound in food prices (act: 0.21% Y/Y, prev: -2.15%) and accelerating manufacturing inflation (act: 2.55% Y/Y, prev: 2.05%), while fuel prices continued to fall (act: -3.17% Y/Y, prev: -2.43%).

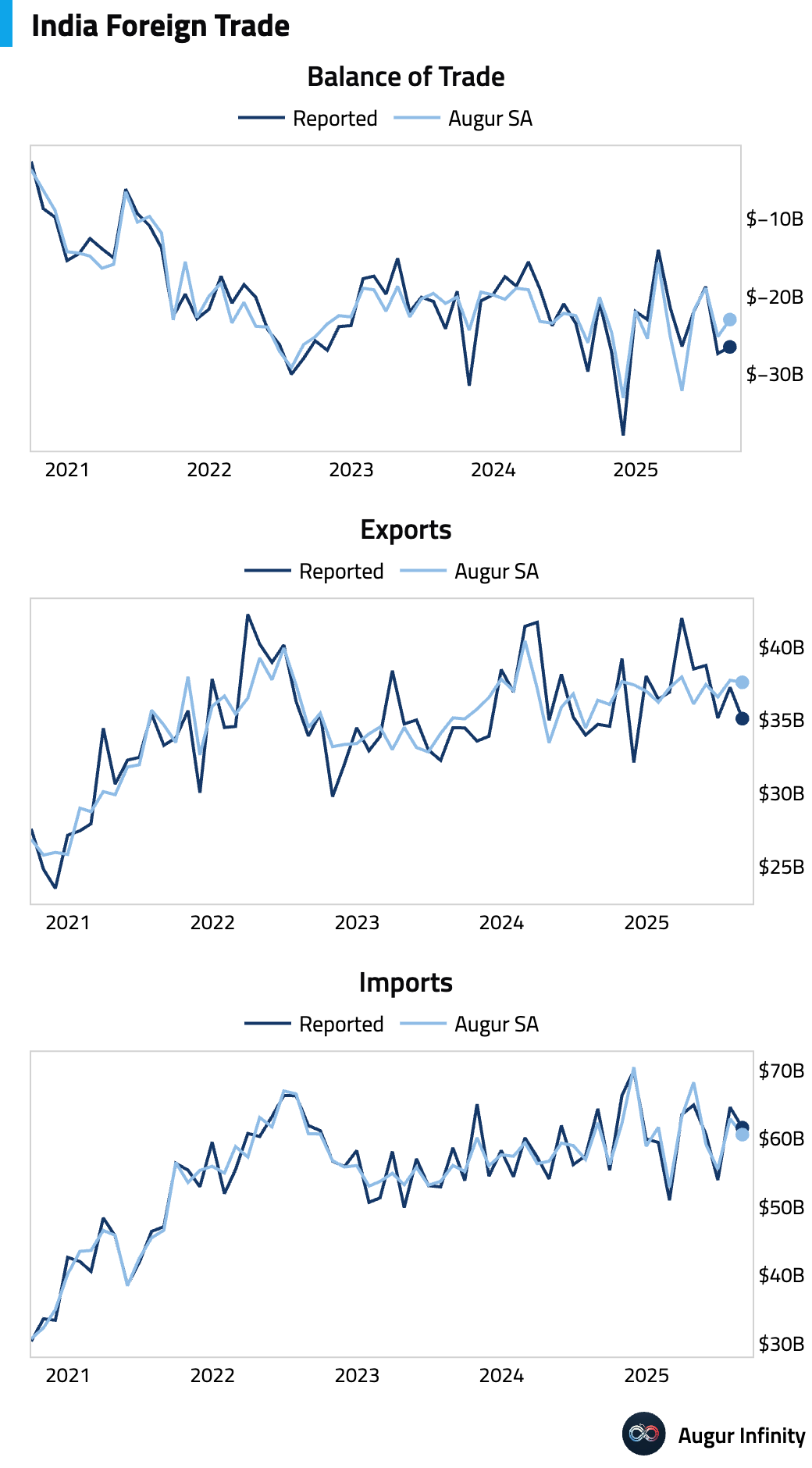

- India’s trade deficit narrowed slightly to $26.49B in August from $27.35B in July, as both exports and imports declined during the month.

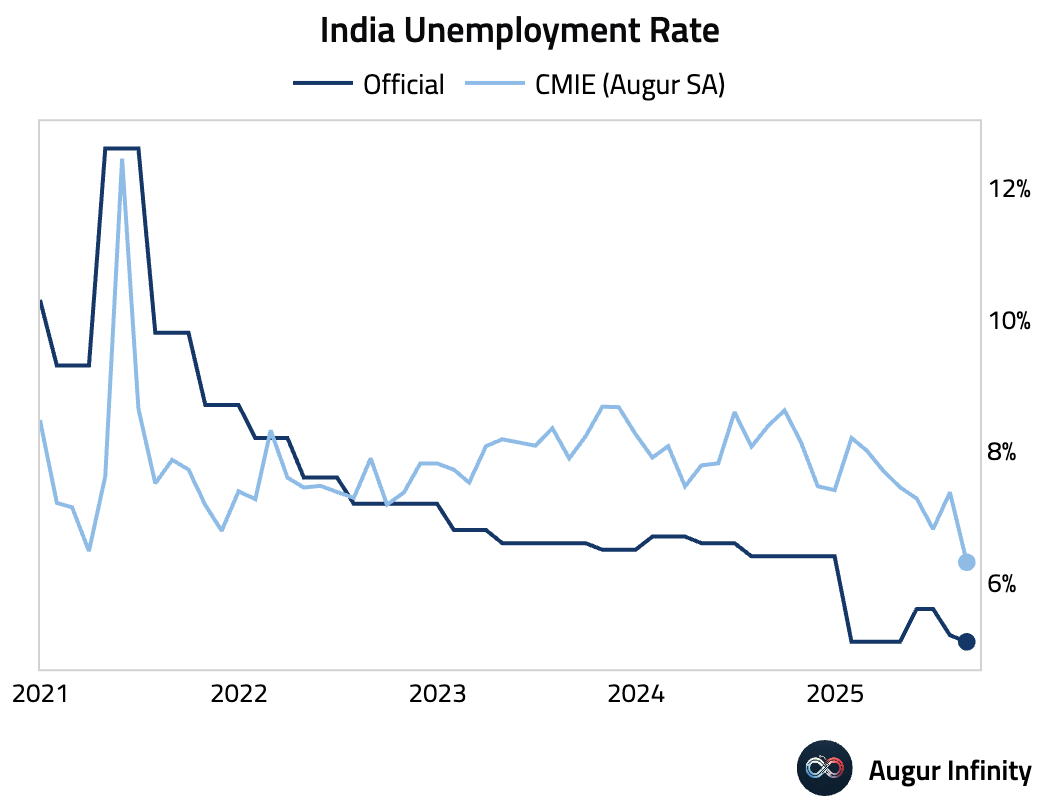

- India’s unemployment rate fell to 5.1% in August, beating estimates of 5.3% and reaching an all-time low. The previous rate was 5.2%.

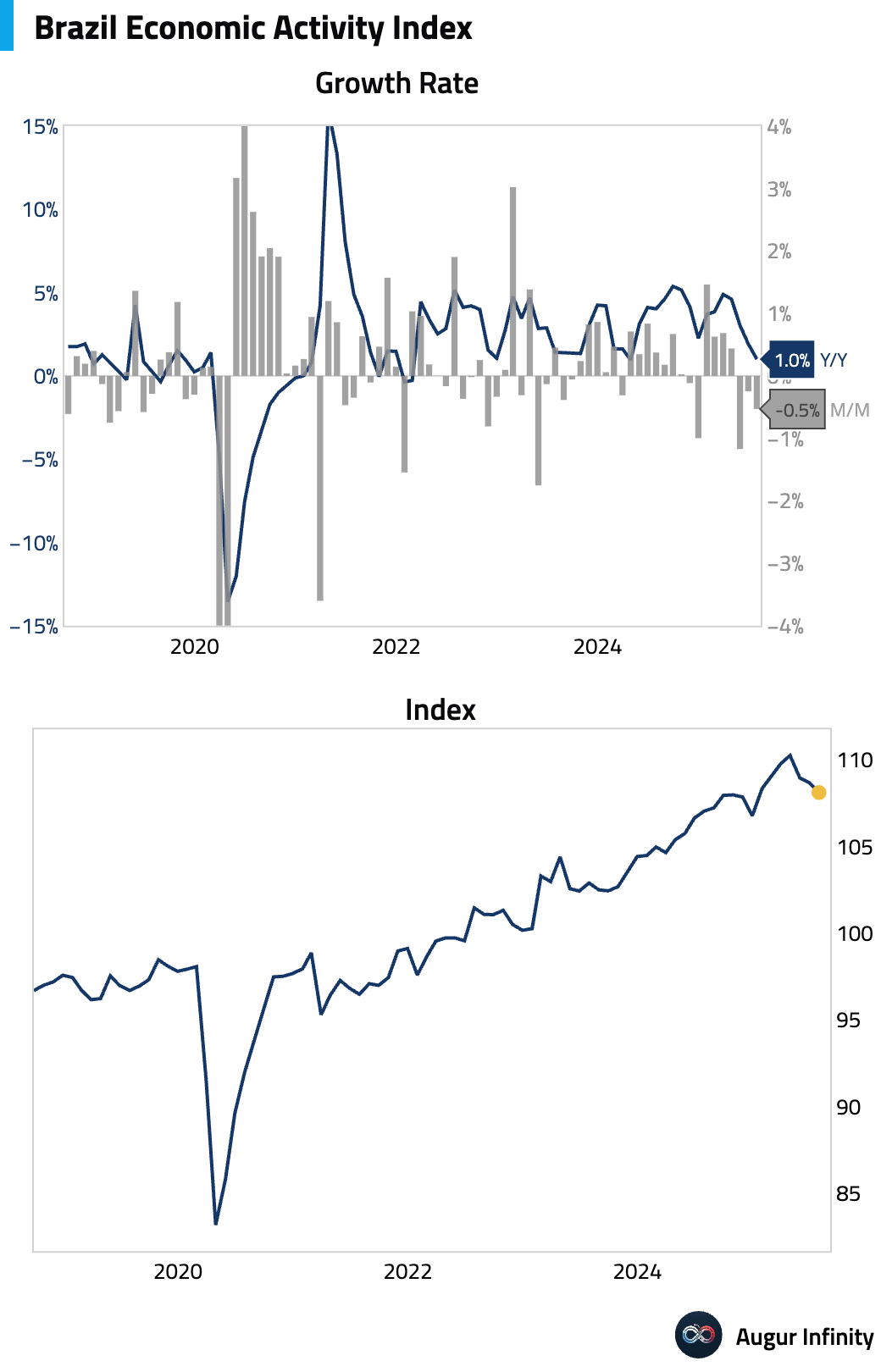

- Brazil’s economic activity index, a proxy for GDP, contracted by 0.5% M/M in July, worse than the -0.2% consensus.

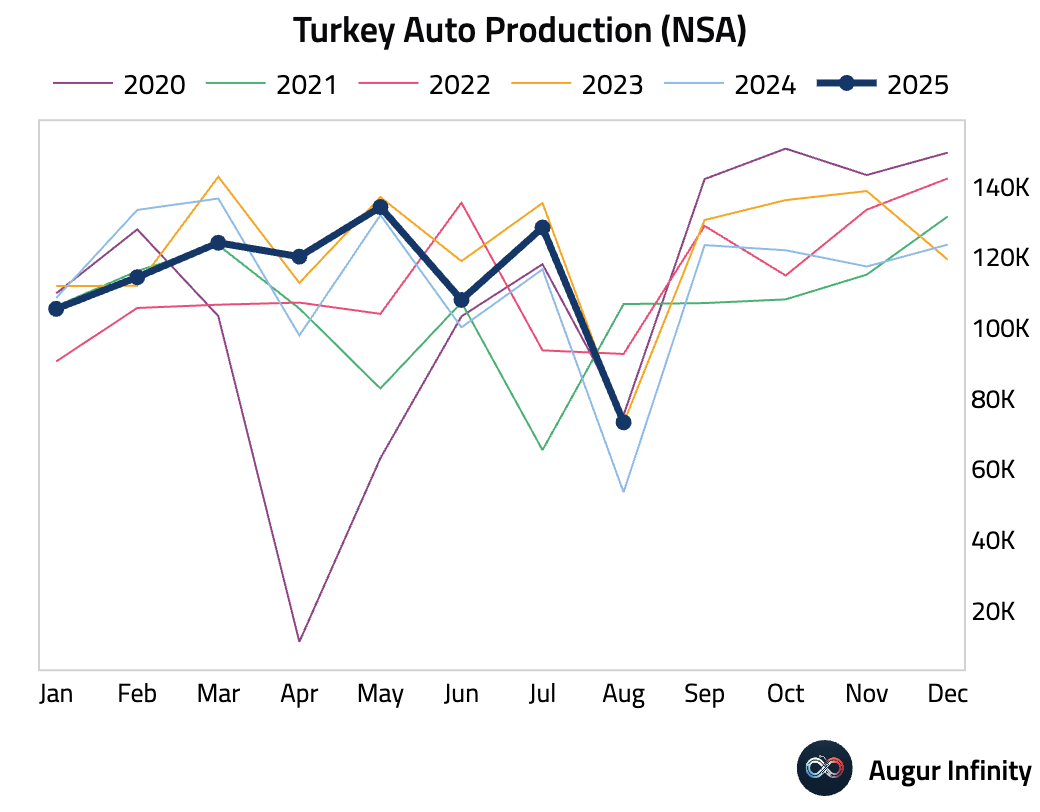

- Turkish auto production surged 37.0% Y/Y in August, a sharp acceleration from July's 10.1% growth and the fastest pace in over two years.

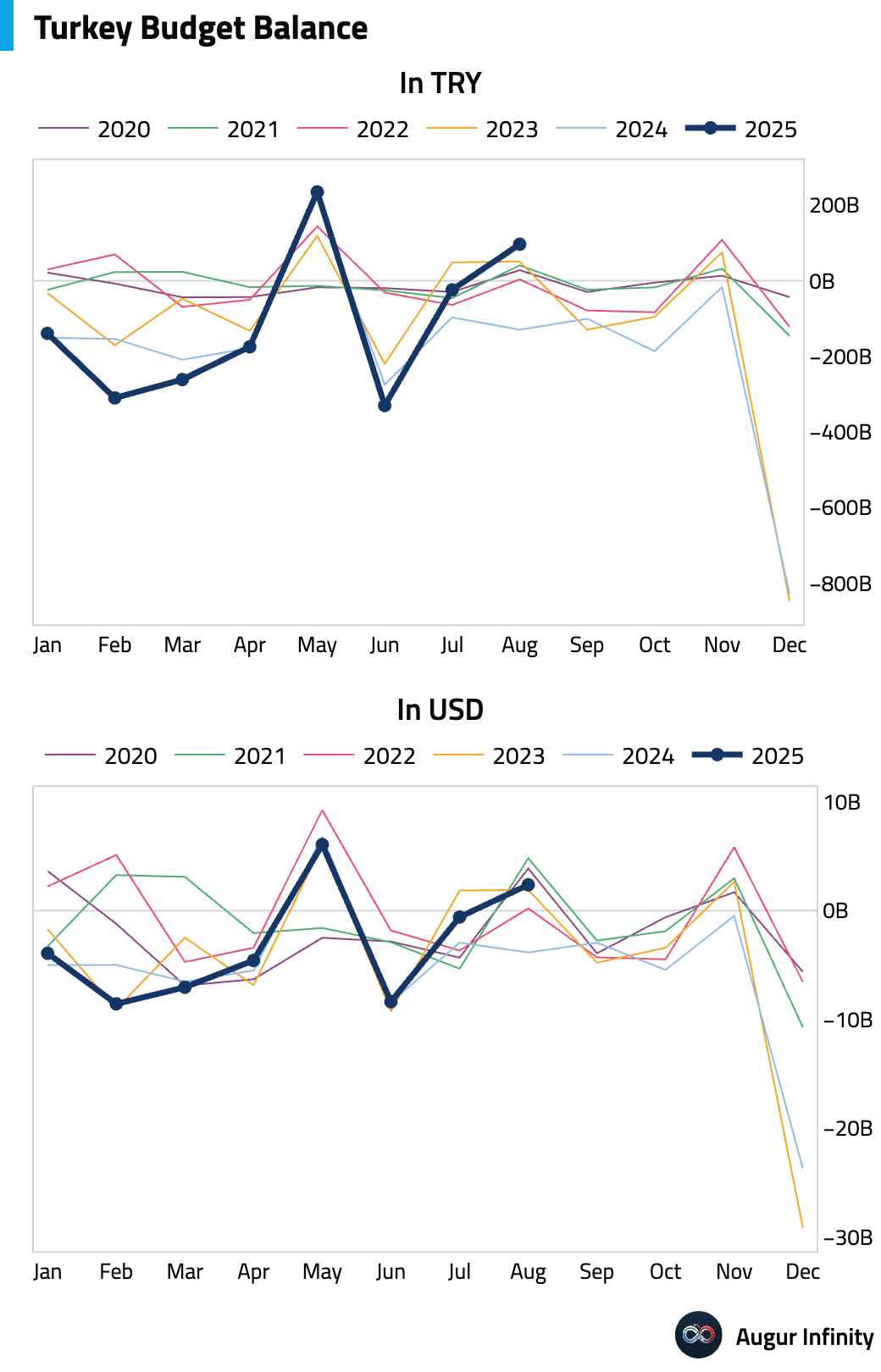

- Turkey's central government budget recorded a surplus of TRY 96.7B in August, a sharp swing from the TRY 23.9B deficit seen in July.

Global Markets

Equities

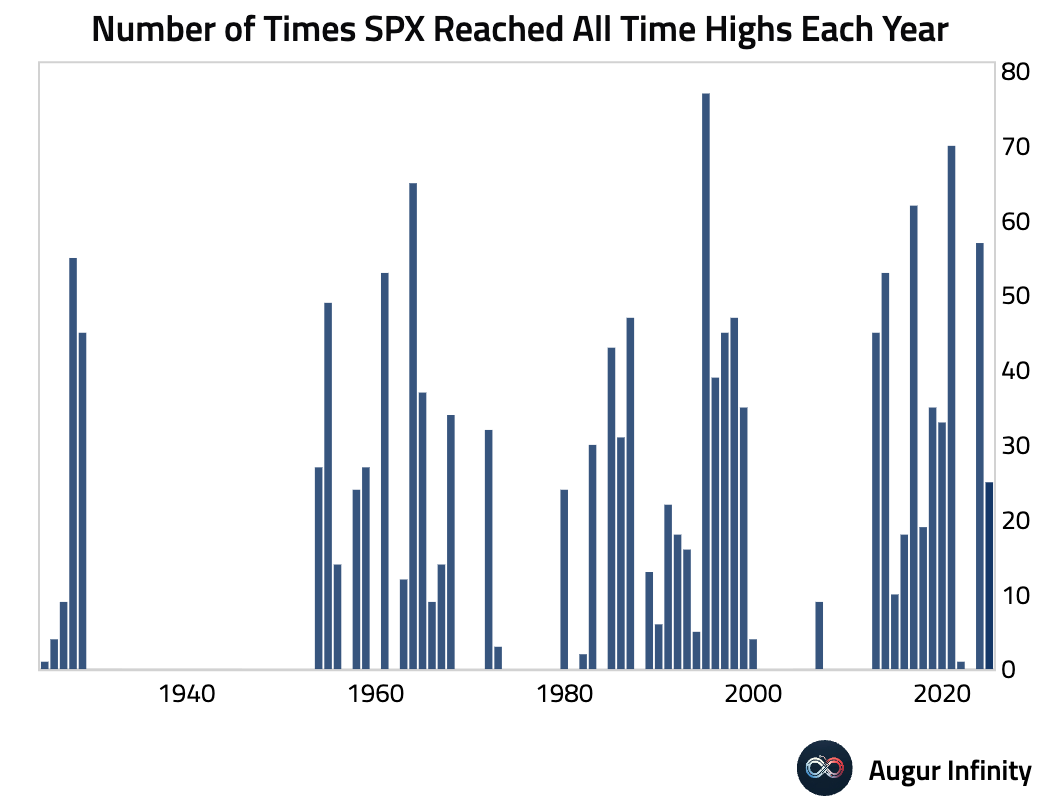

- S&P 500 has reached all-time highs 25 times this year.

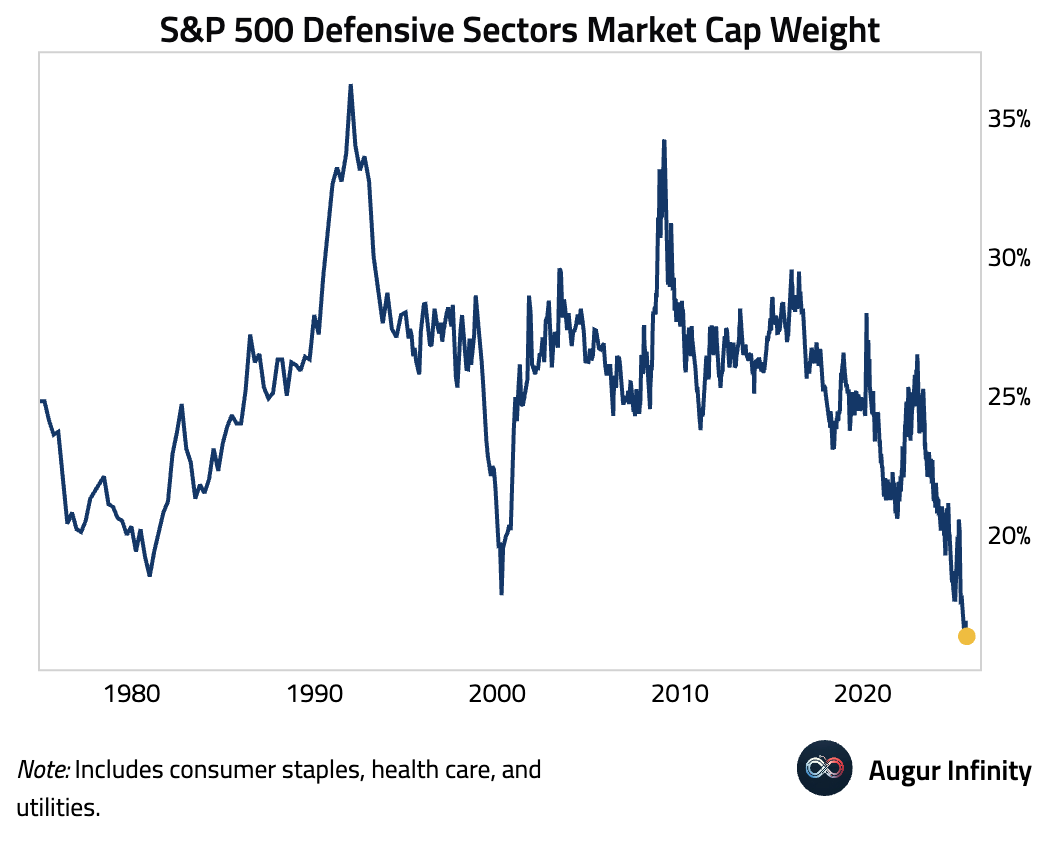

- The weight of defensive sectors in S&P 500 has declined to secularly low levels.

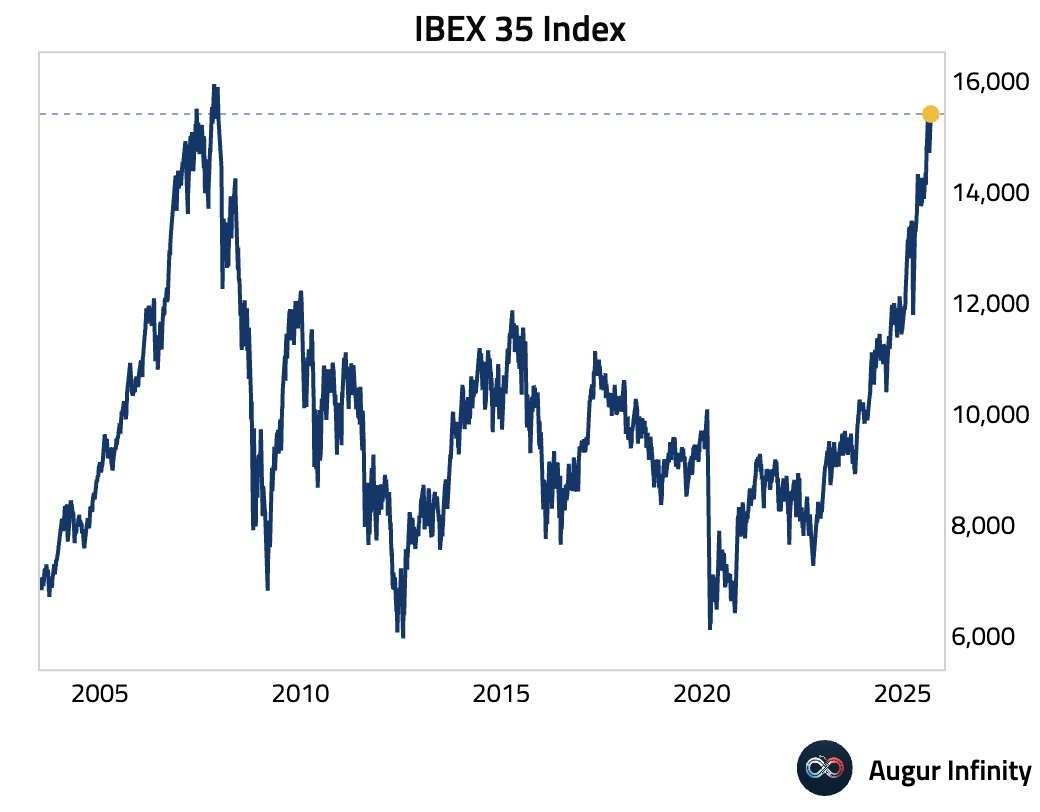

- IBEX 35 is now at the highest level since December 2007.

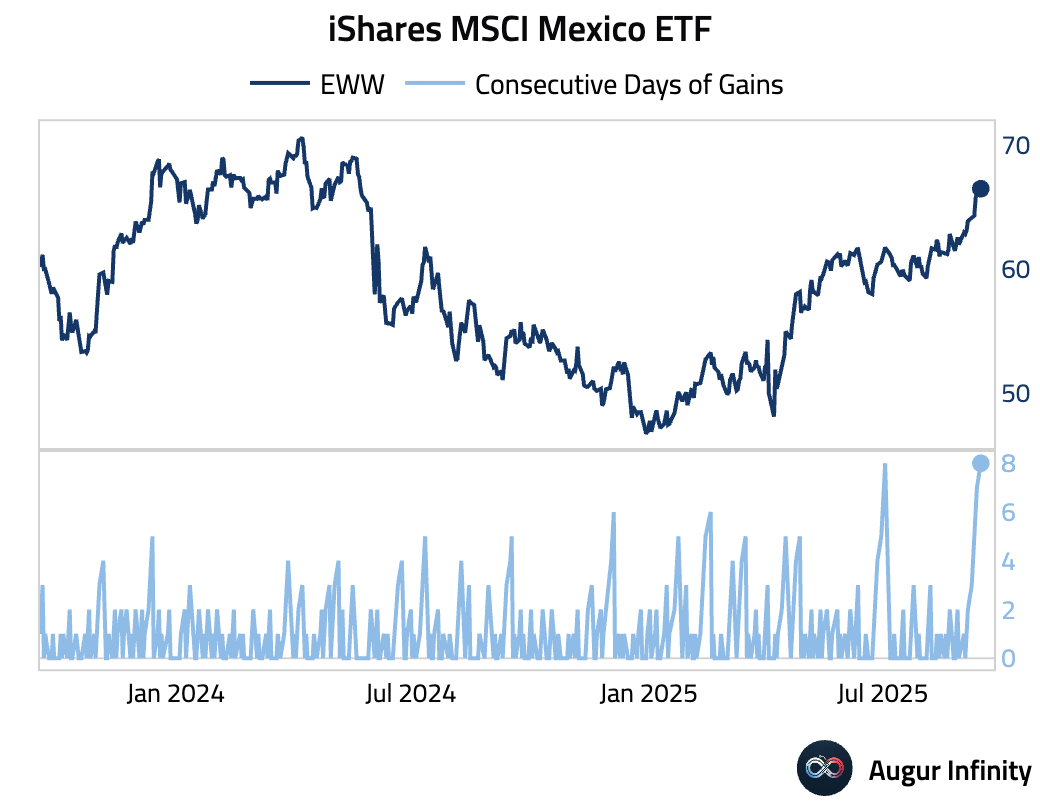

- The iShares MSCI Mexico ETF notched its eighth consecutive gain to reach the highest level since May 2024.

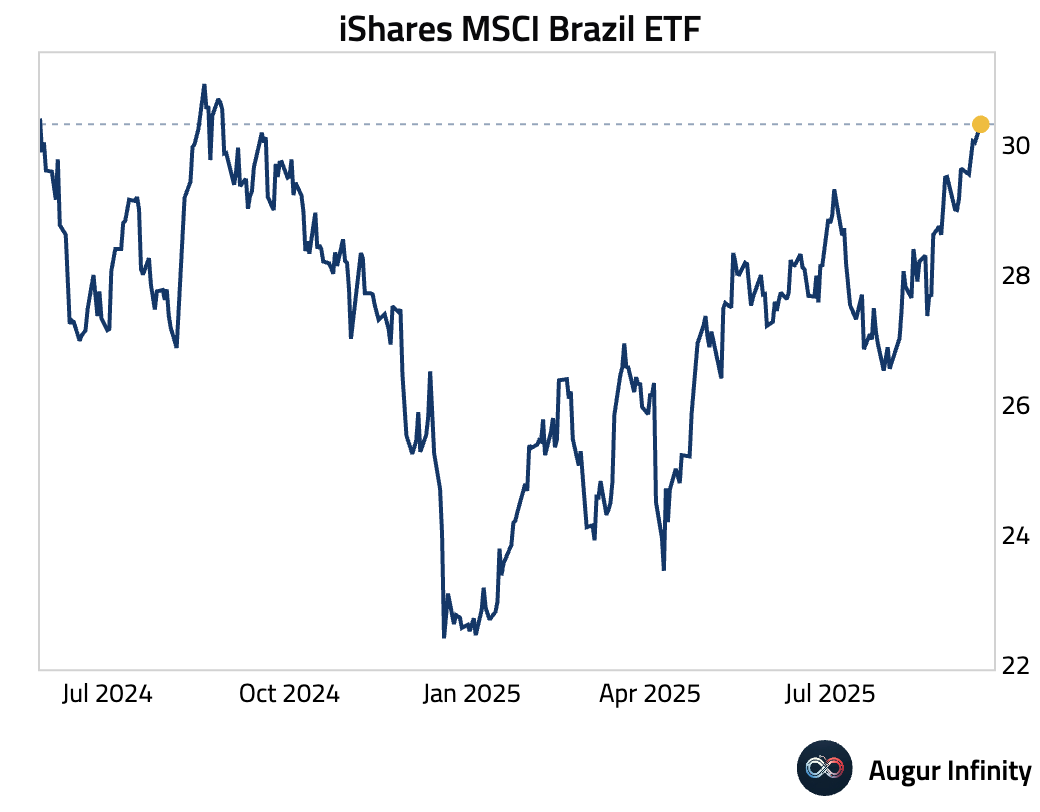

- Brazil stocks have also performed well, trading at the best level since August 2024.

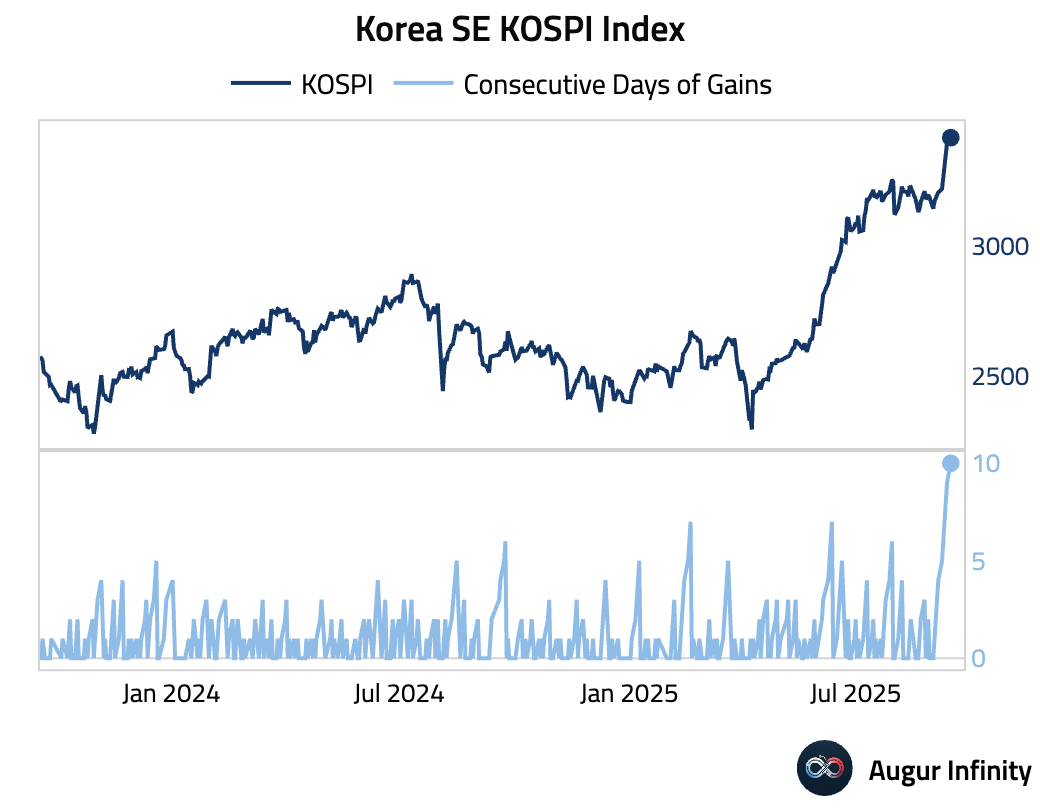

- Korea's KOSPI Index has rallied for ten straight days.

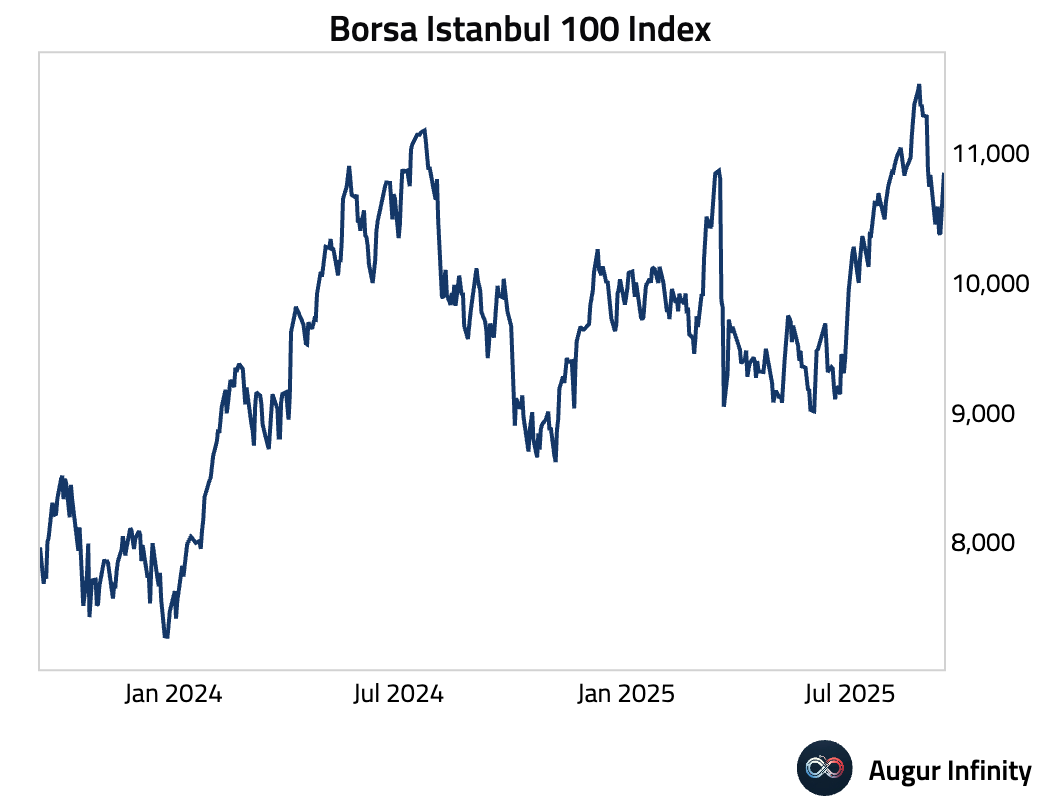

- The Borsa Istanbul 100 Index for Turkey jumped by nearly 6%.

Fixed Income

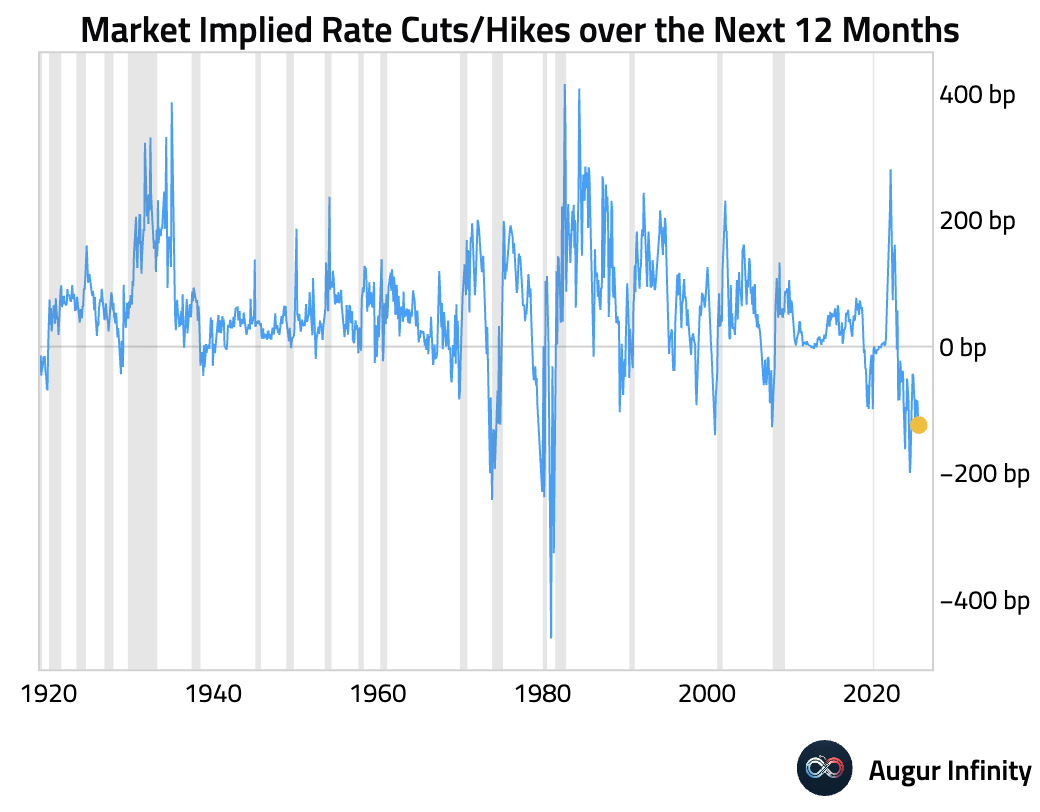

- The market now expects the Fed to deliver around 125 bps of rate cuts over the next twelve months, similar to pricing around prior recessions.

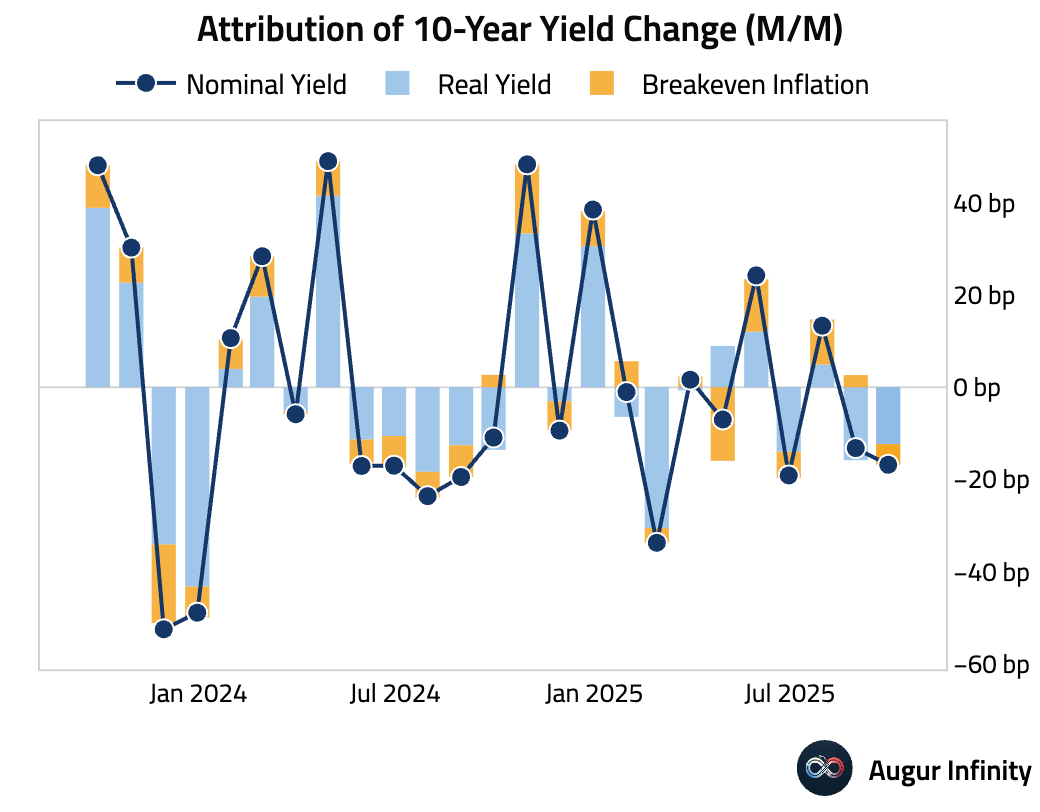

- 10-year Treasury yield is down 20 bps this month so far, driven primarily by a decline in real yield.

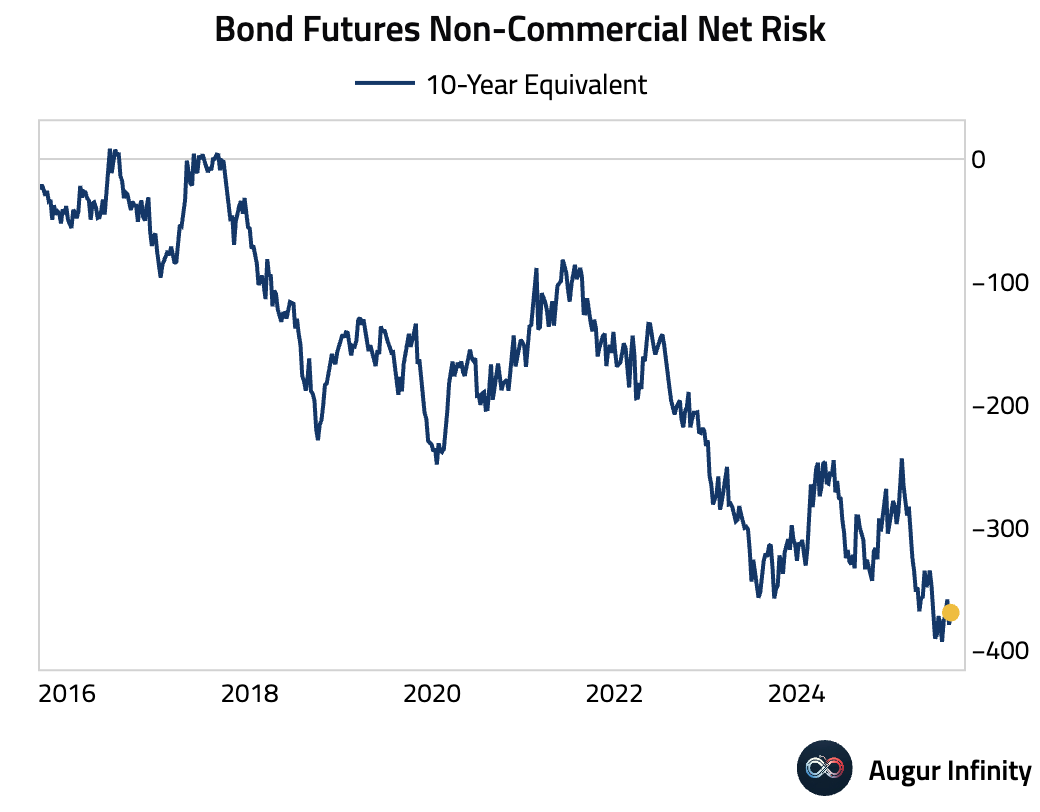

- Speculative accounts are still very short Treasury futures.

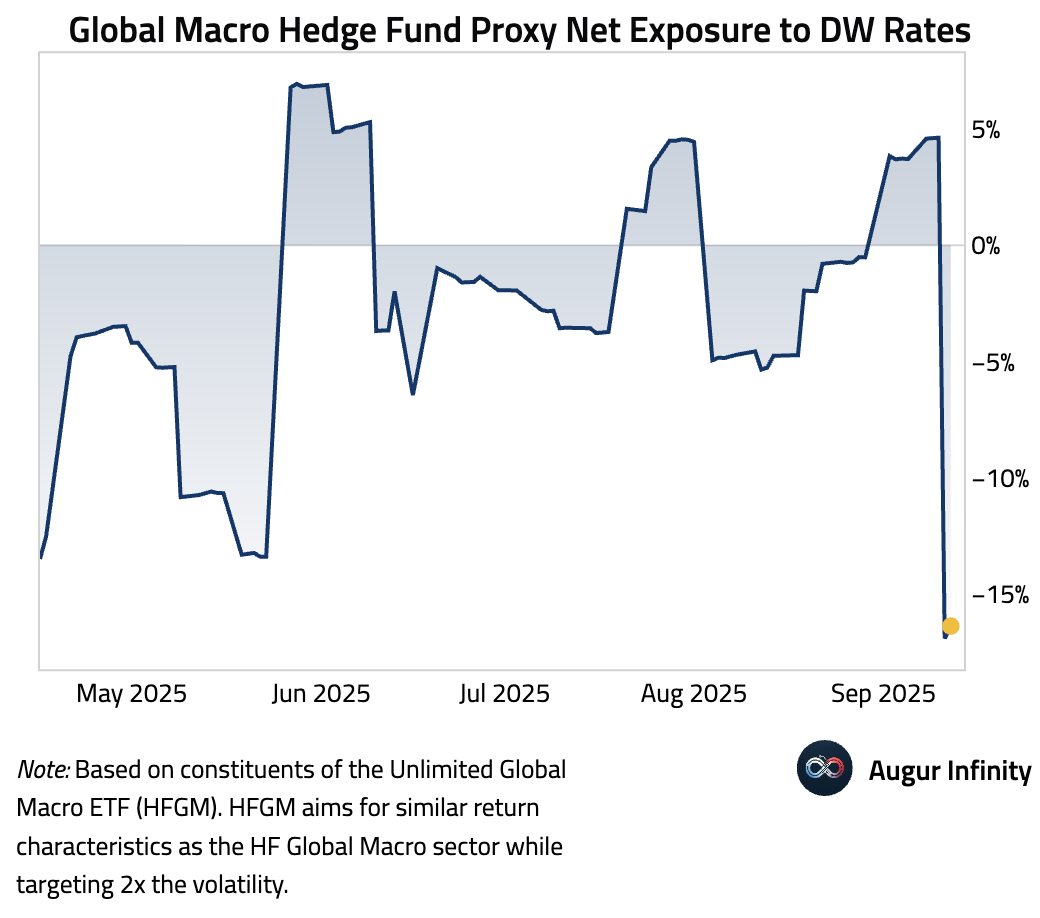

- HFGM, the ETF we use as a proxy for global macro hedge funds, has also turned net short in developed world government bonds, driven by a large short in 5-year US Treasuries.

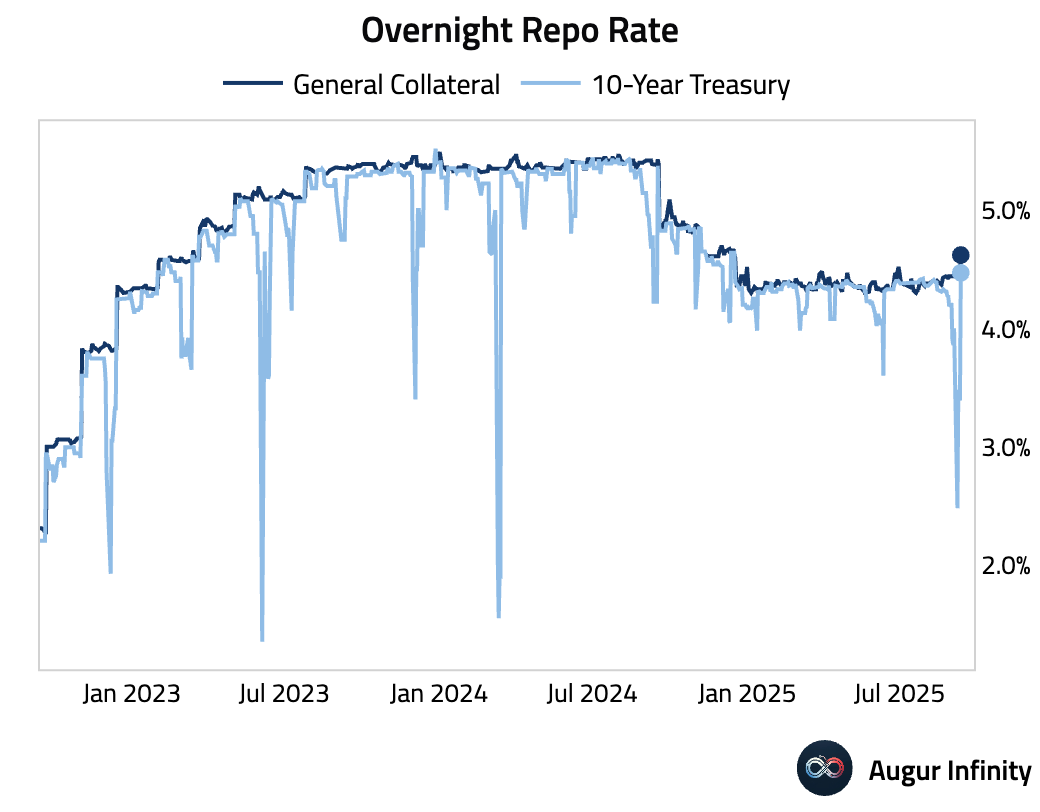

- The specialness of 10-year on-the-run Treasuries in the repo market has faded.

FX

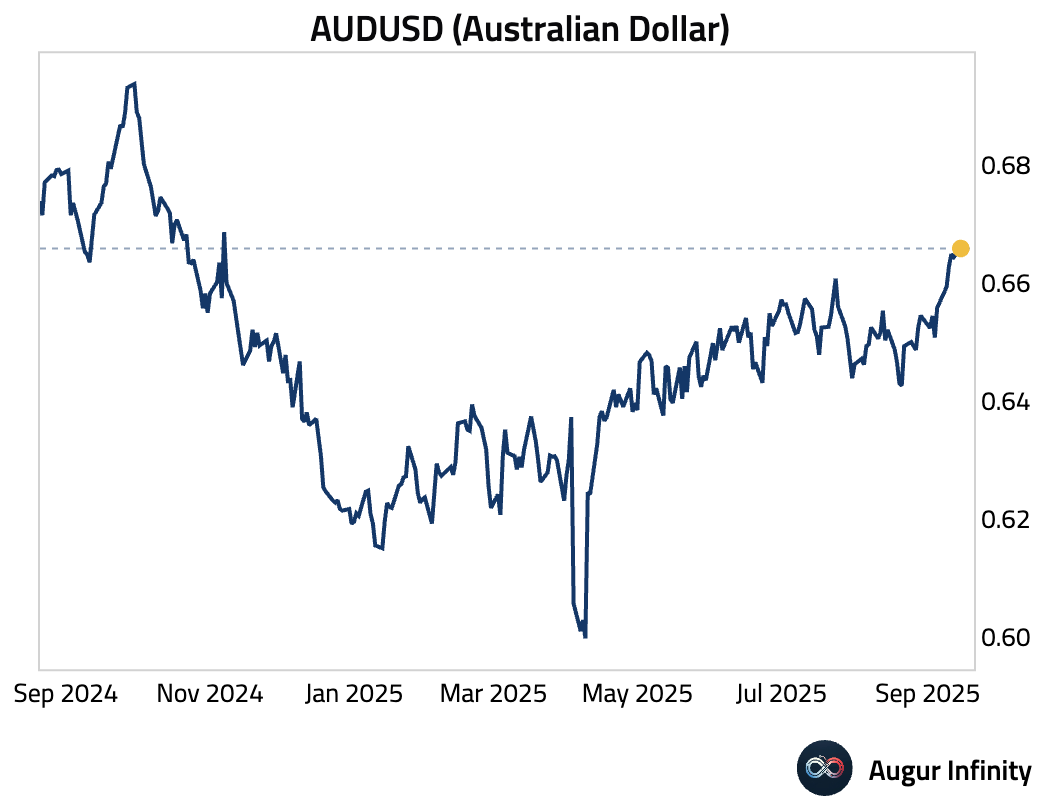

- Aussie dollar climbed to the highest level against USD since November 2024.

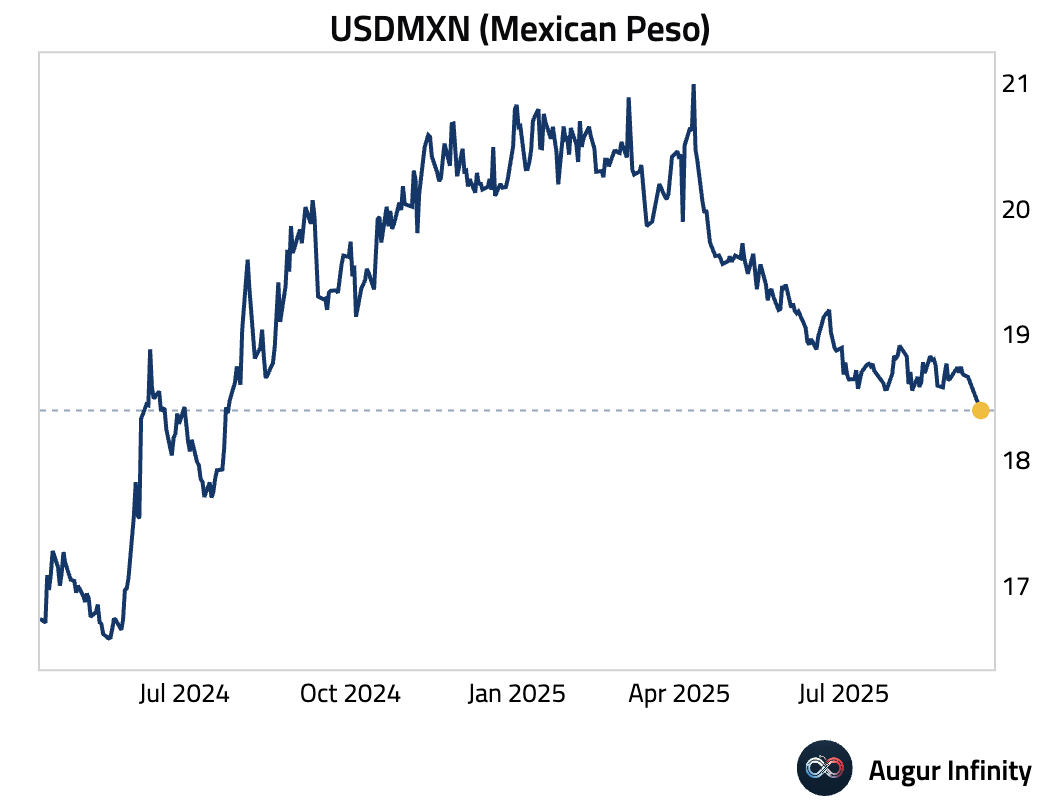

- Mexican peso has also strengthened, now at the best level against USD since July 2024.

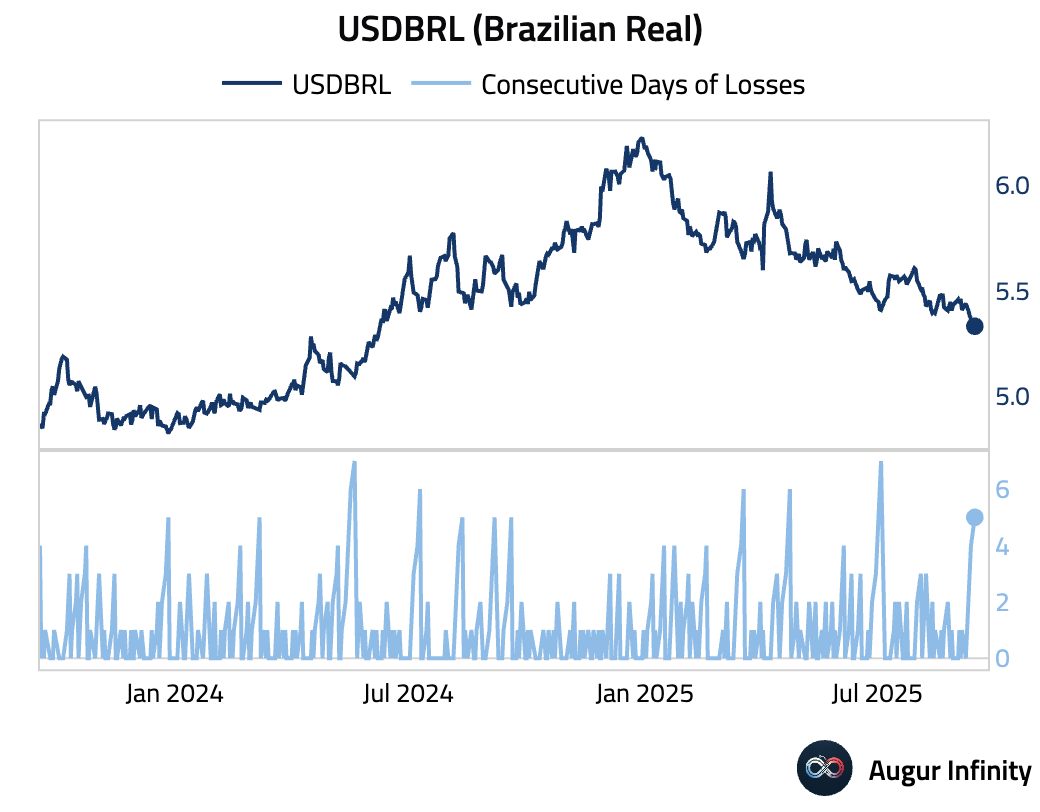

- Brazilian real has appreciated for five sessions.

Commodities

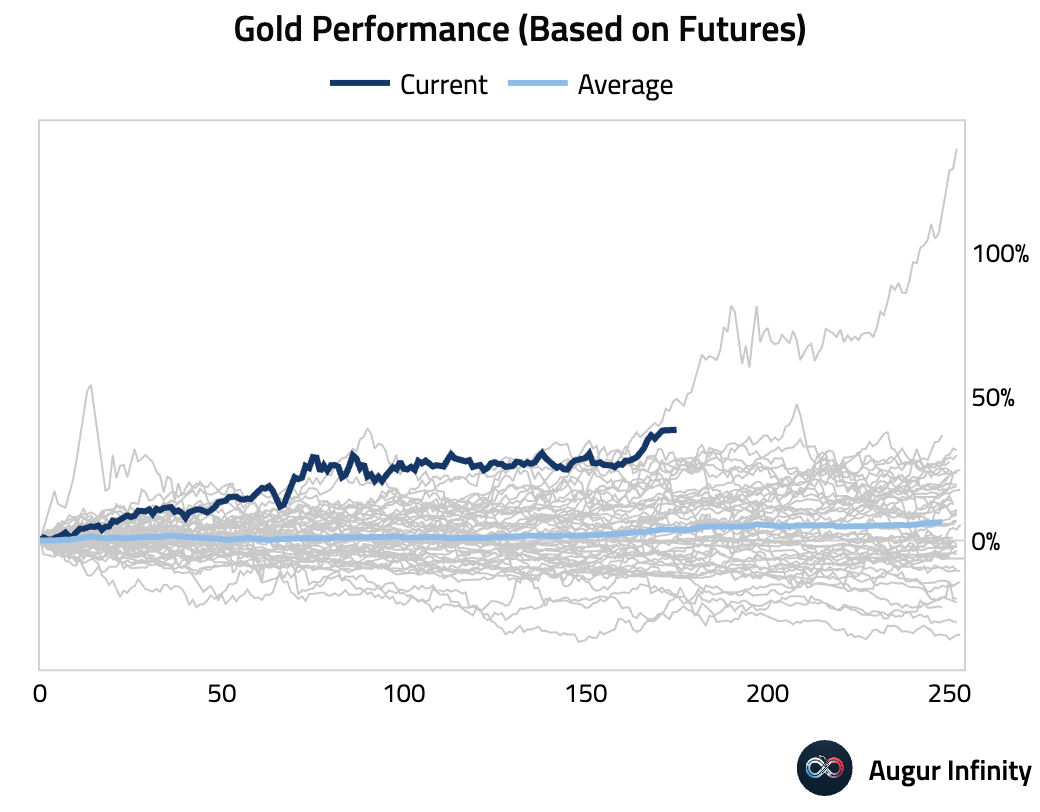

- The YTD performance of gold is the best since 1979.

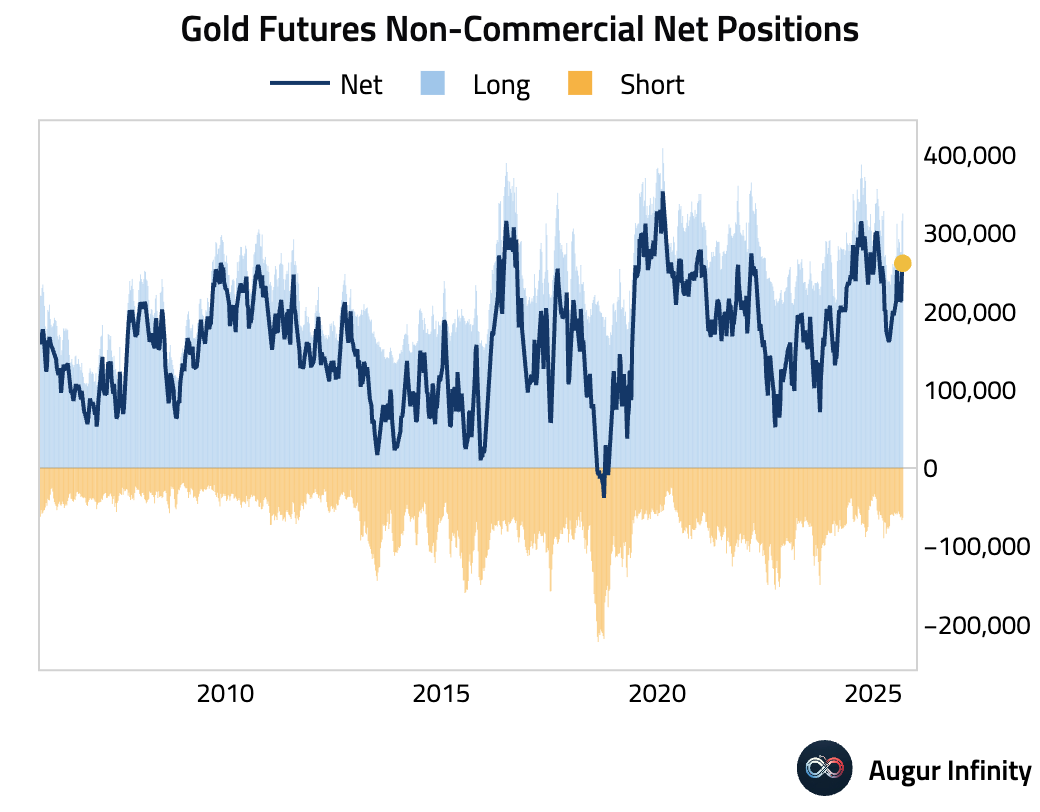

- Speculative net positions in gold are getting longer.

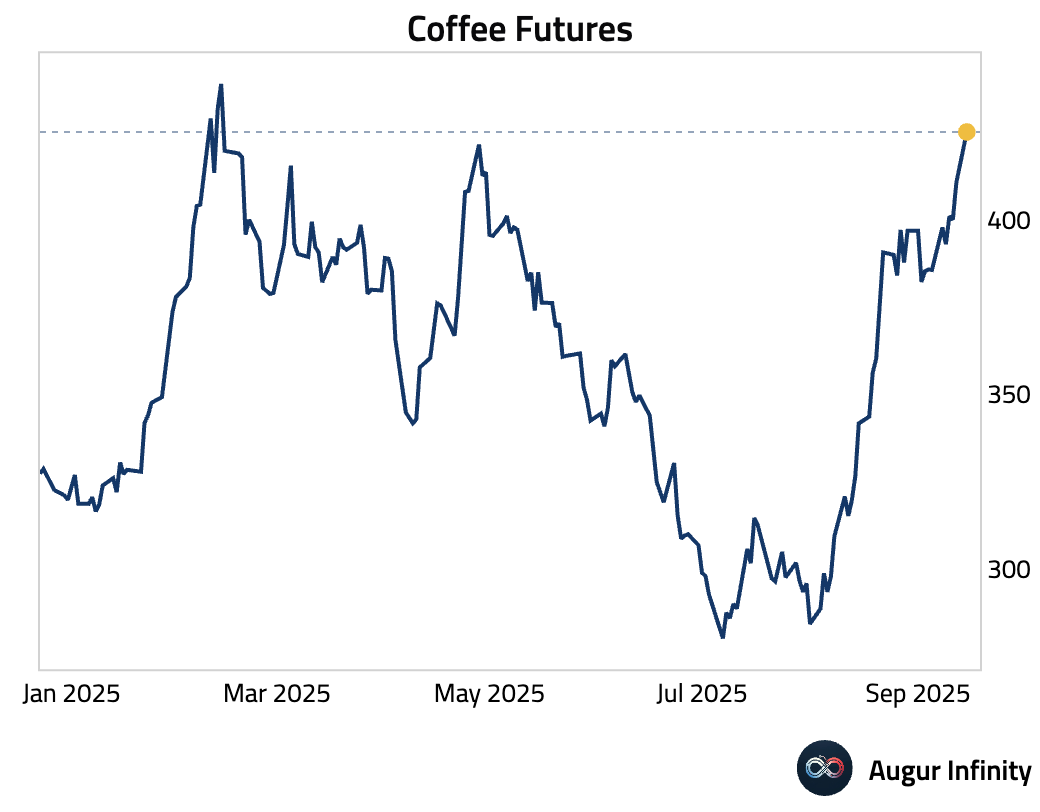

- Coffee futures have rallied.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.