Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- The United States implemented a reduced tariff rate of 15 percent, down from 27.5 percent, on imported Japanese vehicles and auto parts.

- Treasury Secretary Bessent stated his confidence that the Supreme Court will uphold the president’s authority on tariffs.

- President Trump is scheduled to begin a state visit to the United Kingdom.

Global Economics

United States

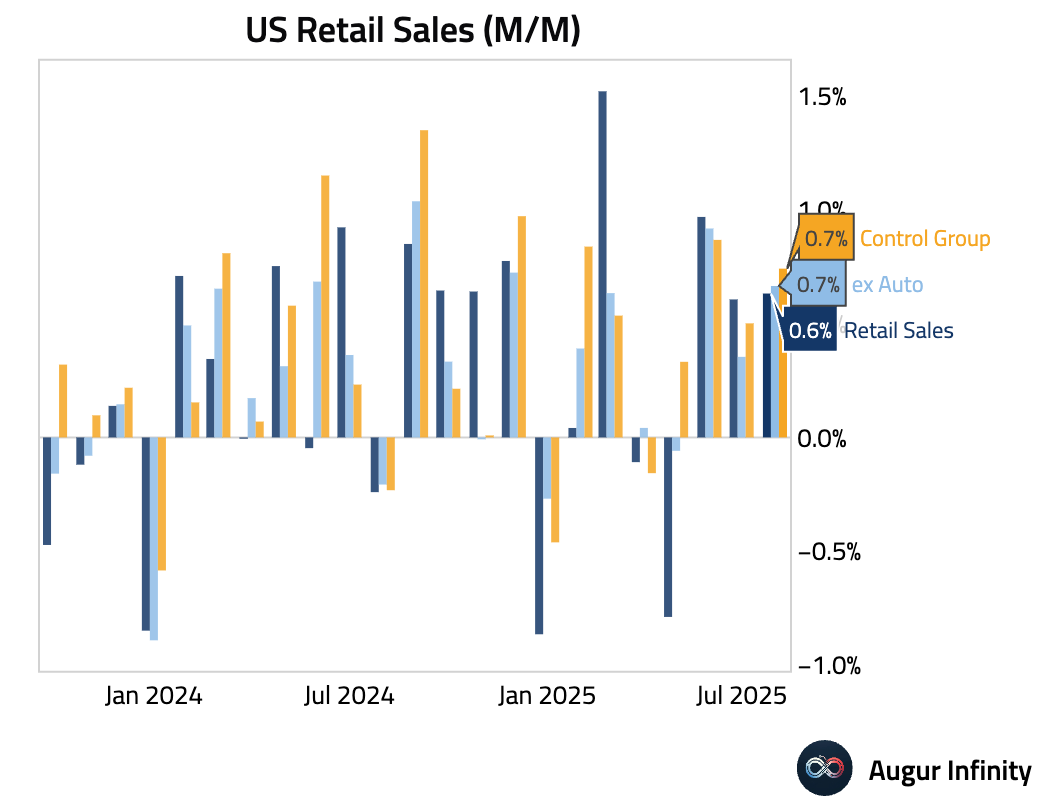

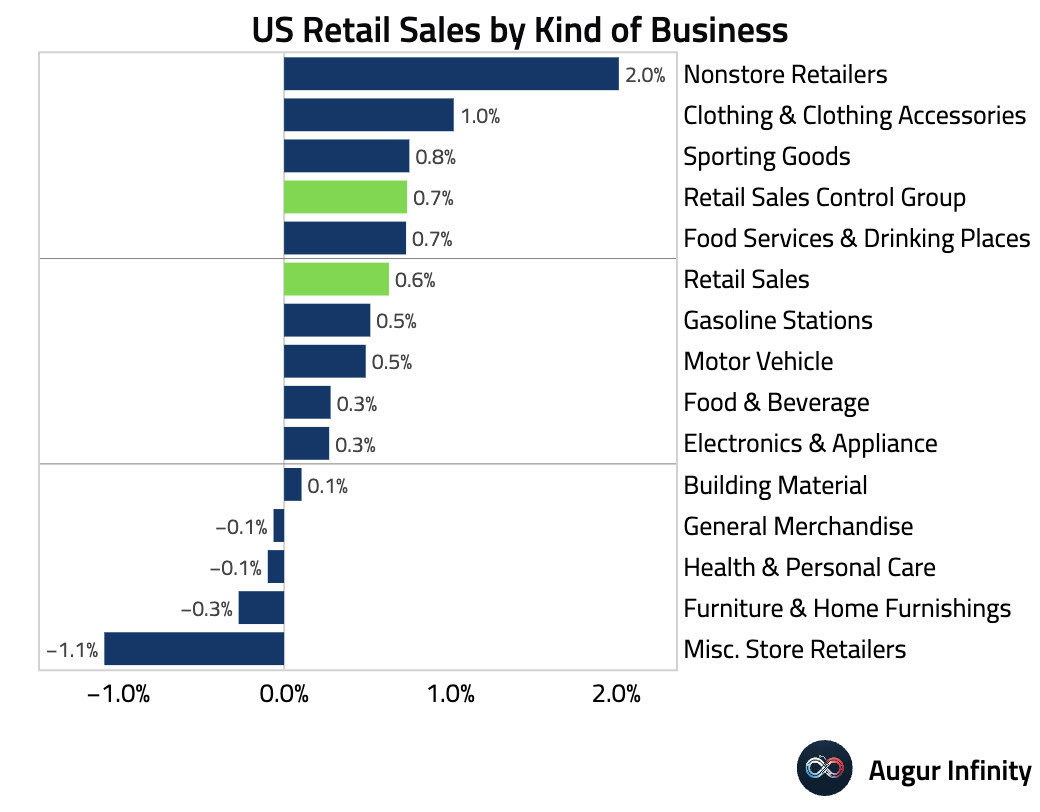

- August retail sales demonstrated robust consumer spending, handily beating expectations across the board. The headline figure rose 0.6% M/M(est: 0.2%), while the crucial control group, which feeds into GDP calculations, surged 0.7% M/M(est: 0.4%). Growth was broad-based and led by a 2.0% jump at nonstore retailers.

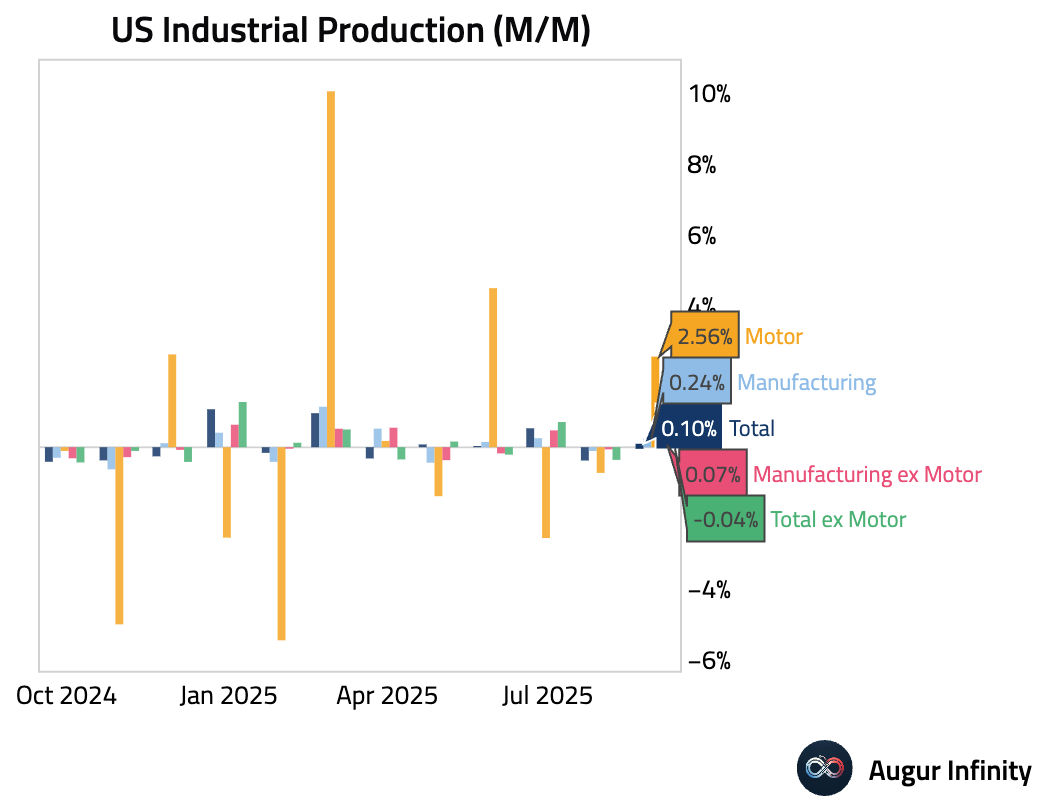

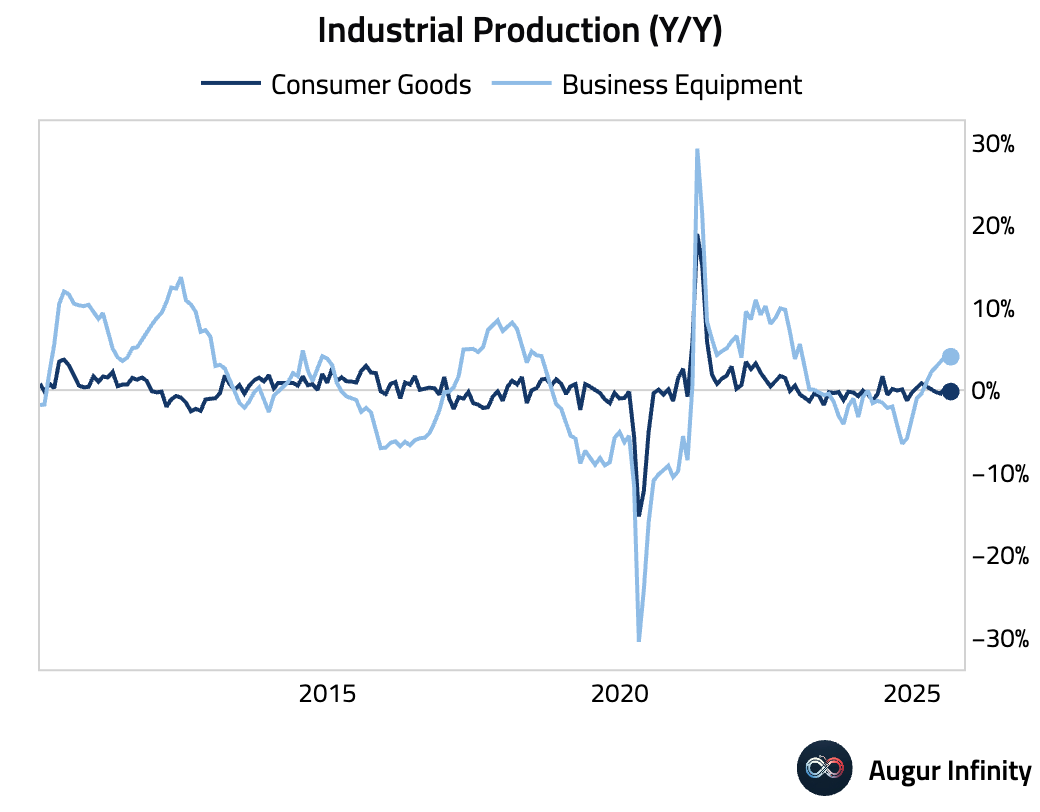

- Industrial production edged up 0.1% M/M in August(est: -0.1%), a weak rebound after a downwardly revised 0.4% drop in July. The gain was narrowly driven by a 2.6% surge in auto manufacturing, which was largely offset by a sharp 2.0% drop in utilities output. Manufacturing production rose 0.2% M/M.

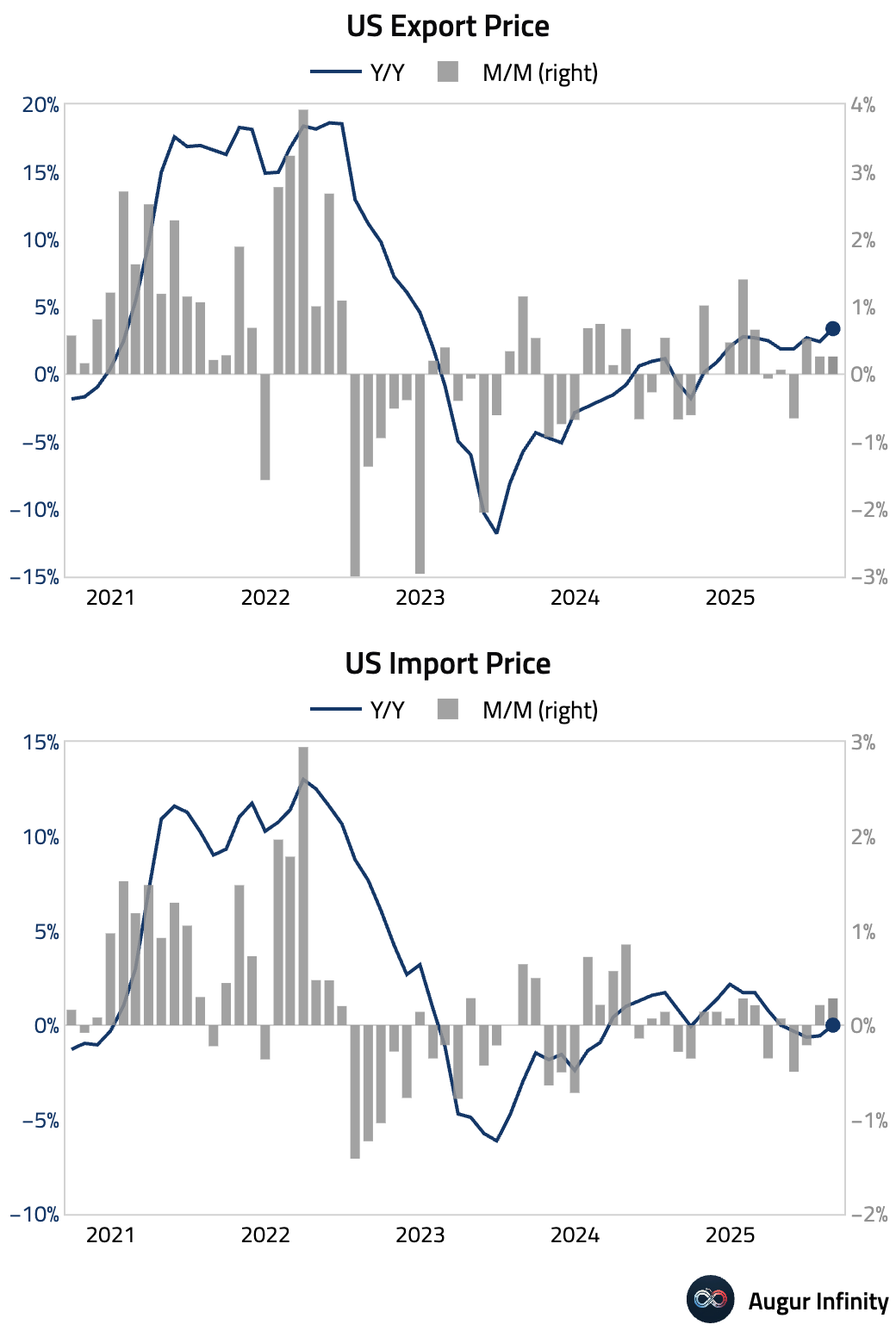

- August trade prices came in firmer than expected, particularly on the import side. Import prices rose 0.3% M/M (est: -0.1%), turning the year-over-year rate flat from -0.2% previously. A key inflationary detail was a significant 4.5% jump in the international airfares component, a direct input for the Core PCE price index. Export prices also firmed, rising 0.3% M/M and accelerating to 3.4% Y/Y from 2.4%.

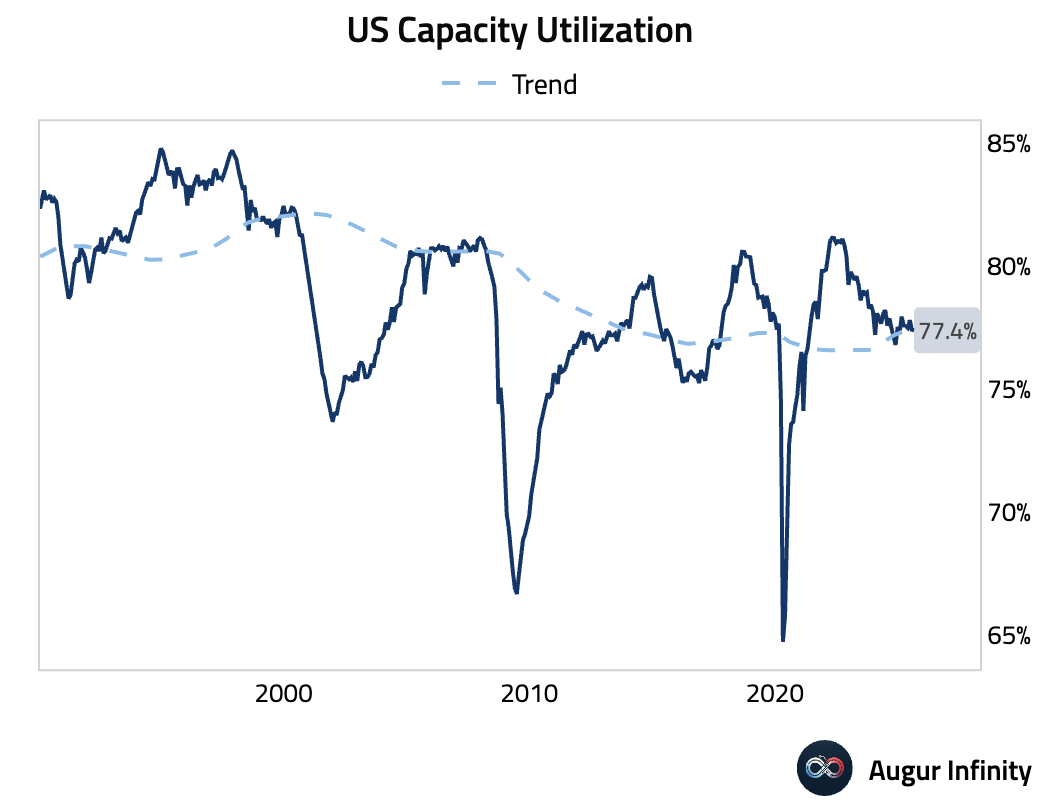

- Capacity utilization was unchanged in August (act: 77.4%, prev: 77.4%).

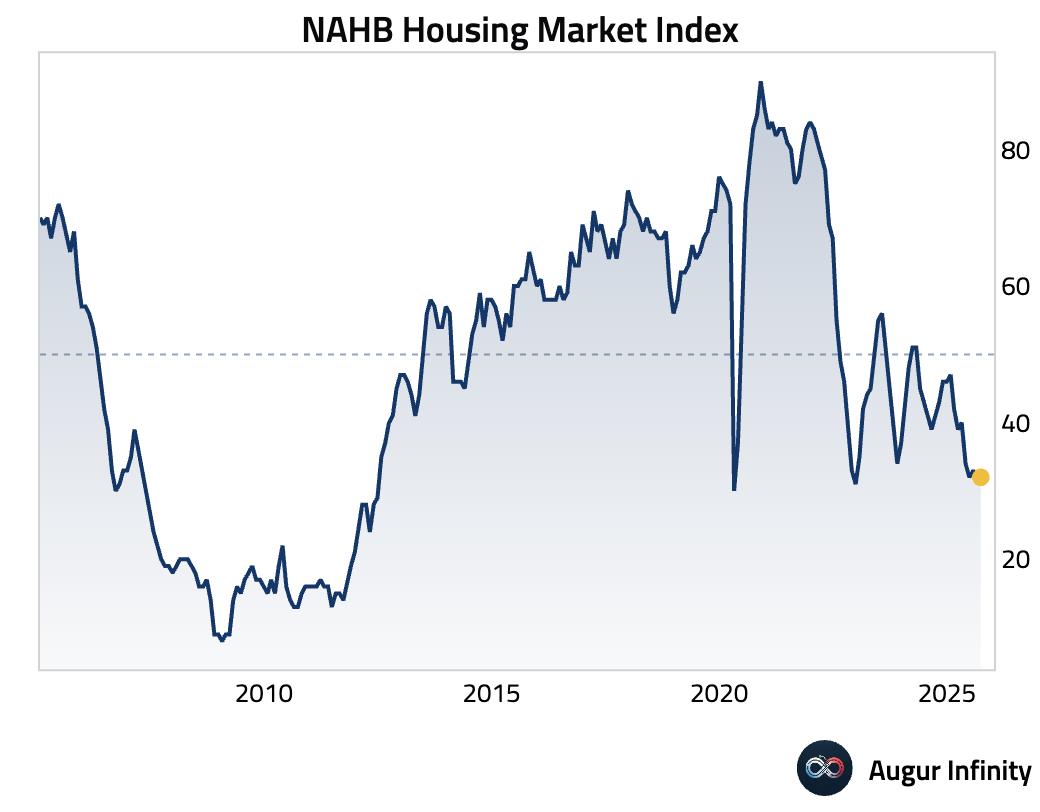

- The NAHB Housing Market Index was unchanged at 32 in September (est: 33), suggesting homebuilder sentiment remains subdued.

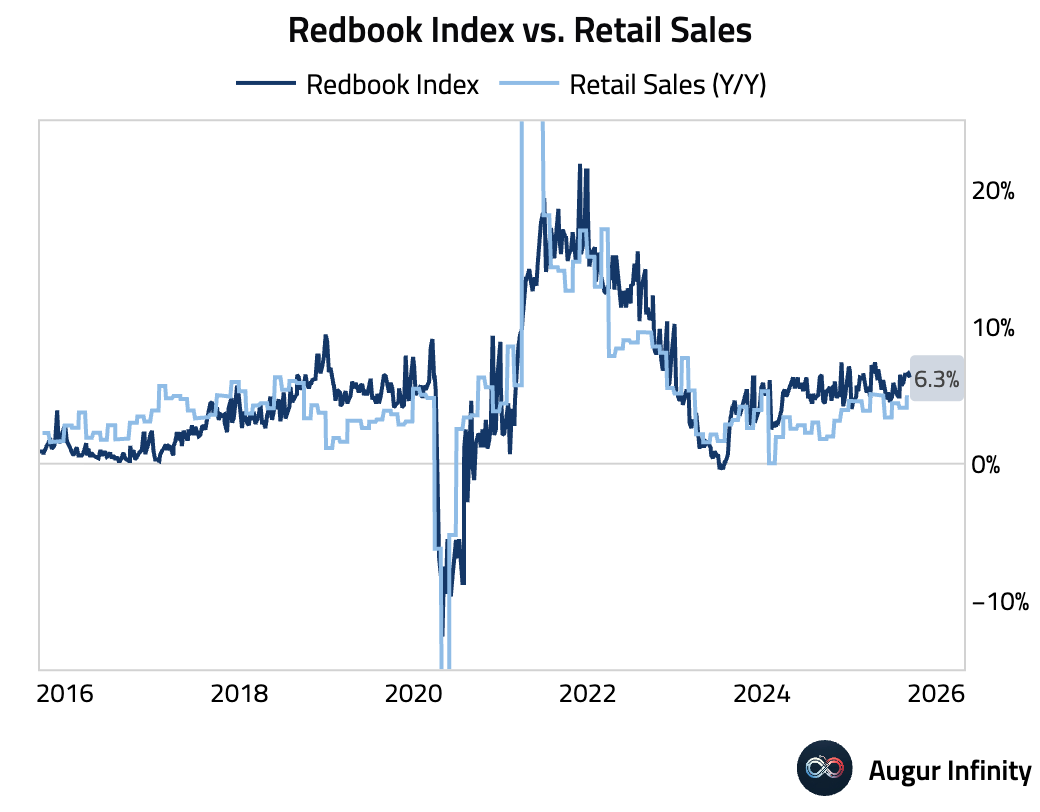

- The Redbook index of same-store sales growth softened slightly to 6.3% Y/Y for the week ending September 13 (prev: 6.6%).

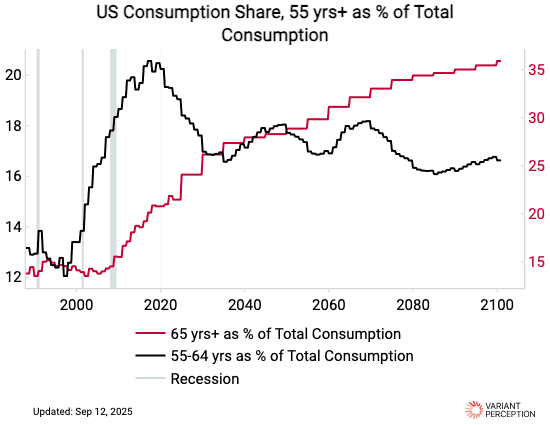

- Retirees continue to make up more and more of US consumption, a trend expected to continue.

Source: Variant Perception

Canada

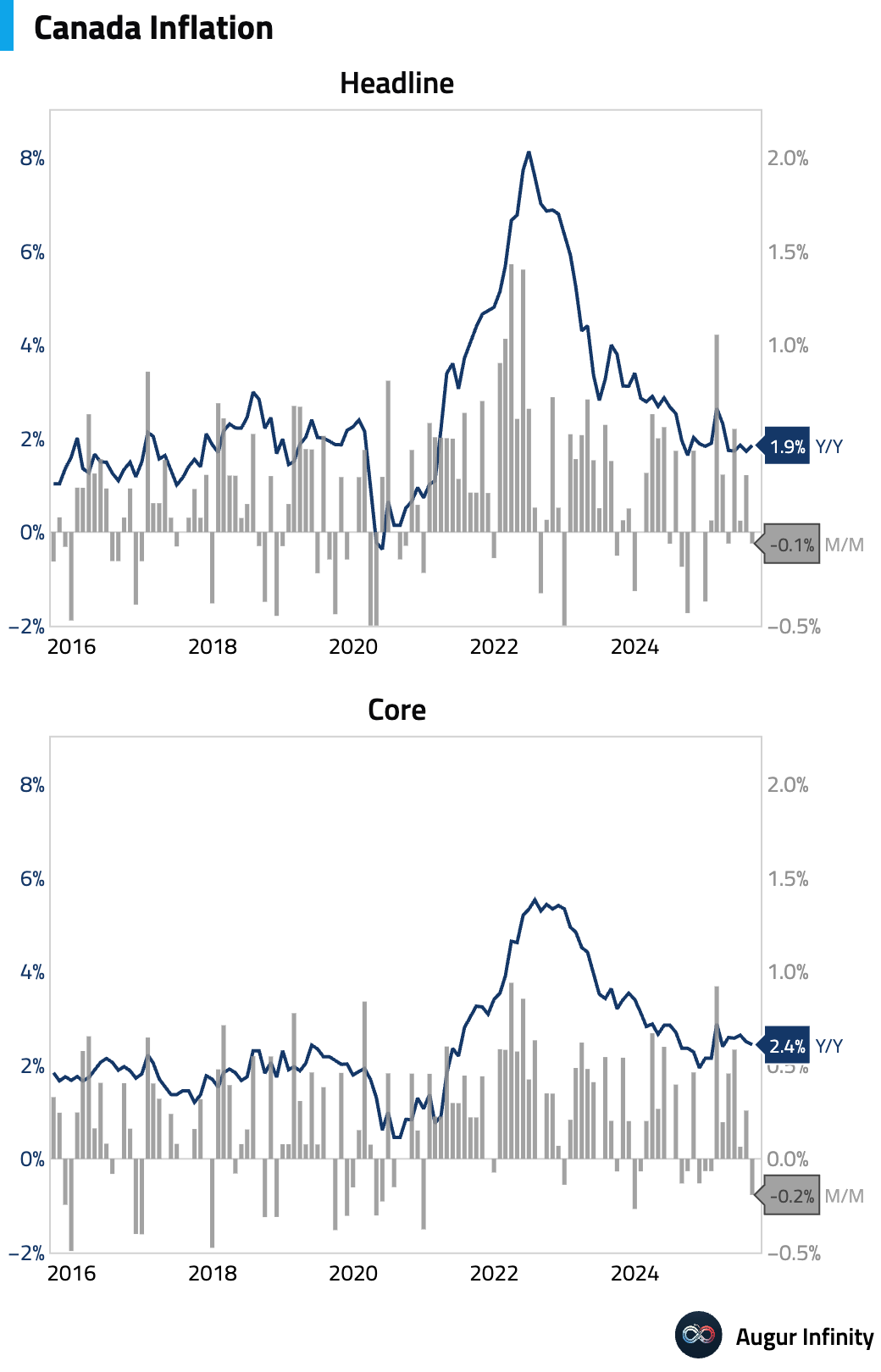

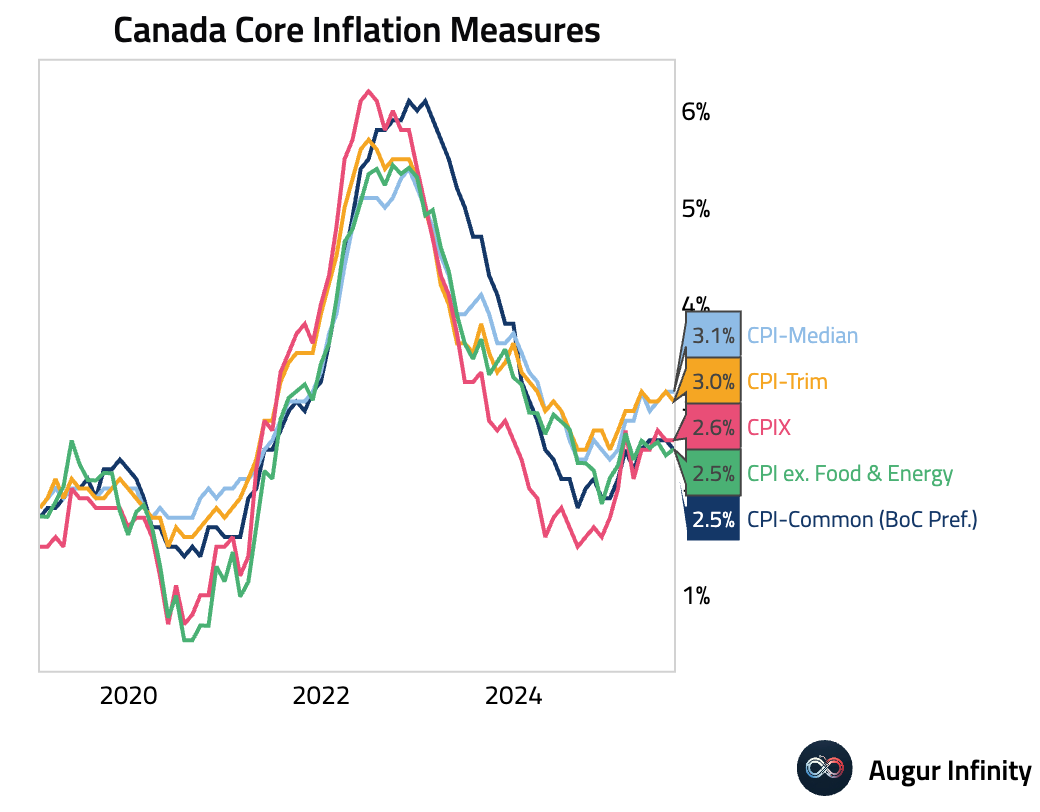

- Canada’s headline inflation rate ticked up in August but missed consensus, rising to 1.9% Y/Y (est: 2.0%, prev: 1.7%). The Bank of Canada’s preferred core measures showed some moderation, with CPI-Trim decelerating to 3.0% Y/Y (prev: 3.1%) and CPI-Median holding steady at 3.1% Y/Y.

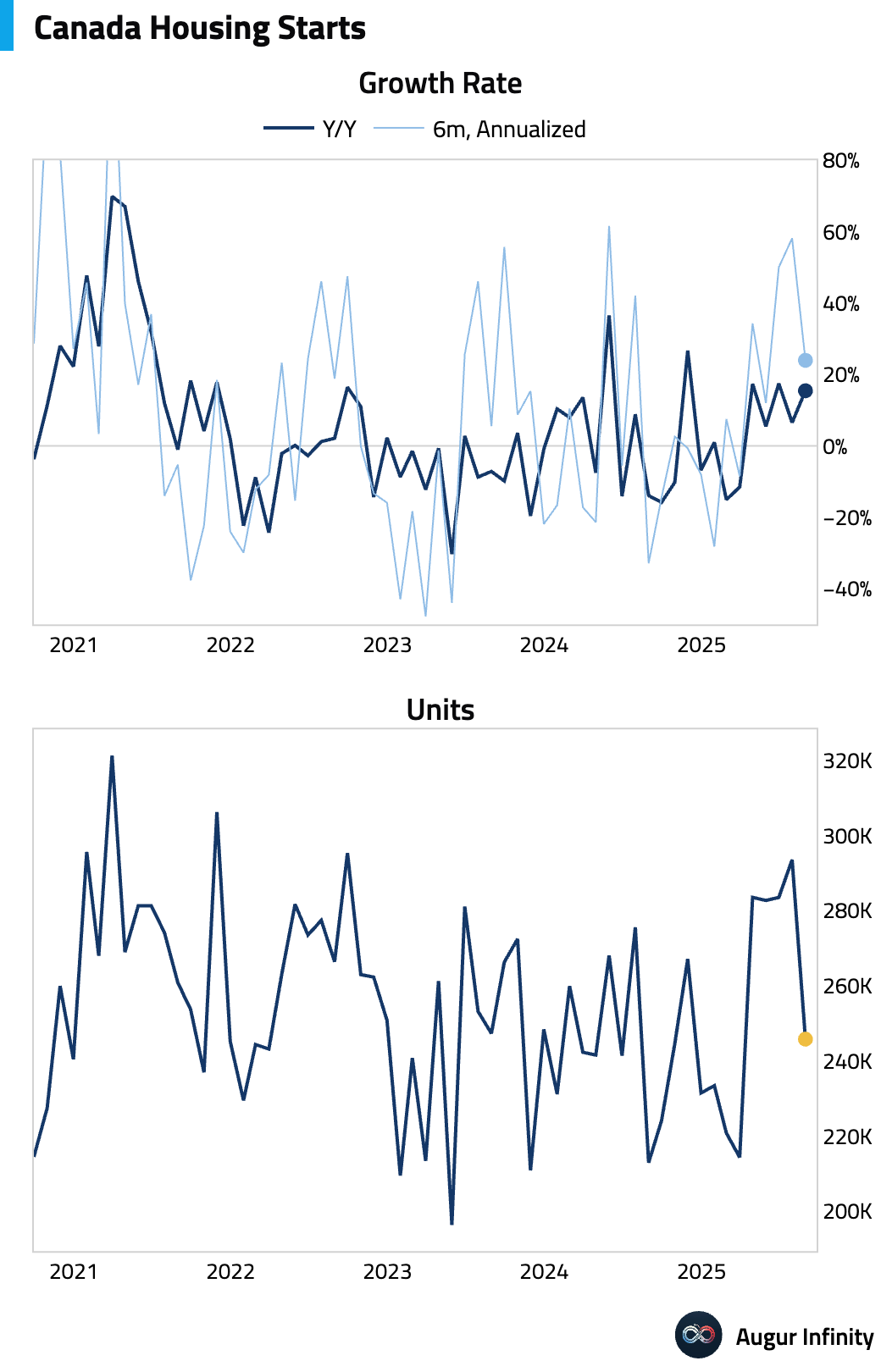

- Housing starts slowed significantly in August, falling to a 245.8k annualized rate from 293.5k in July and missing estimates (est: 277.5k).

Europe

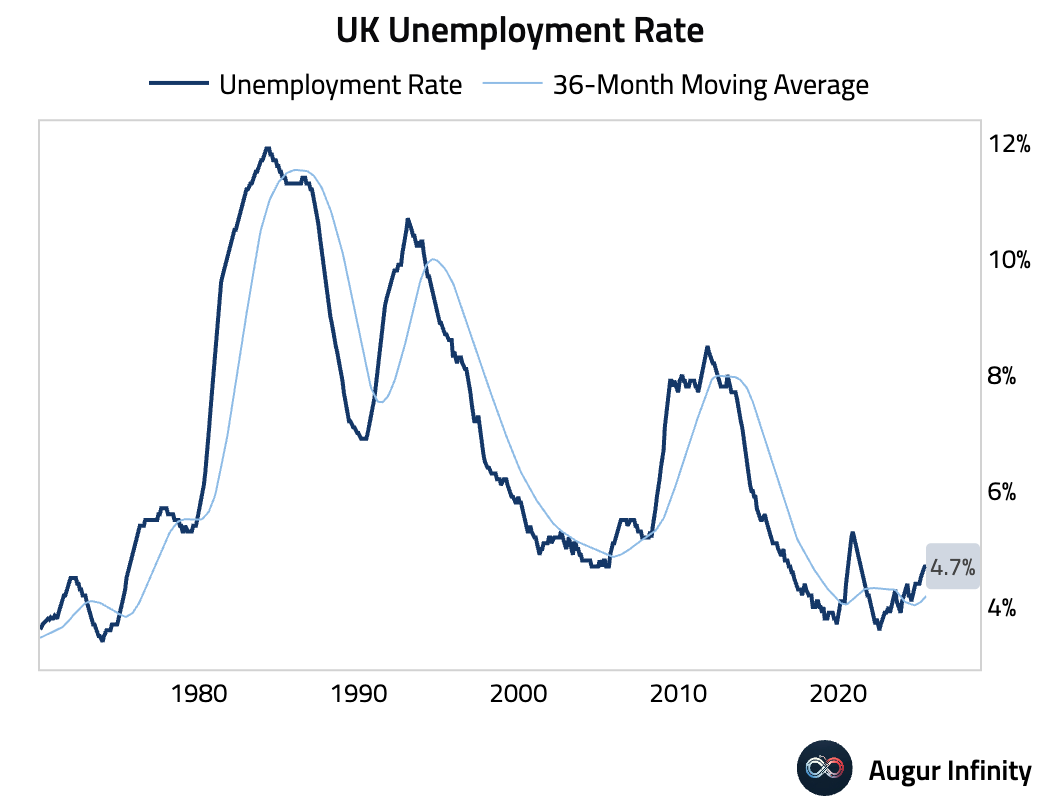

- The UK unemployment rate for the three months to July held steady at 4.7%(est: 4.7%).

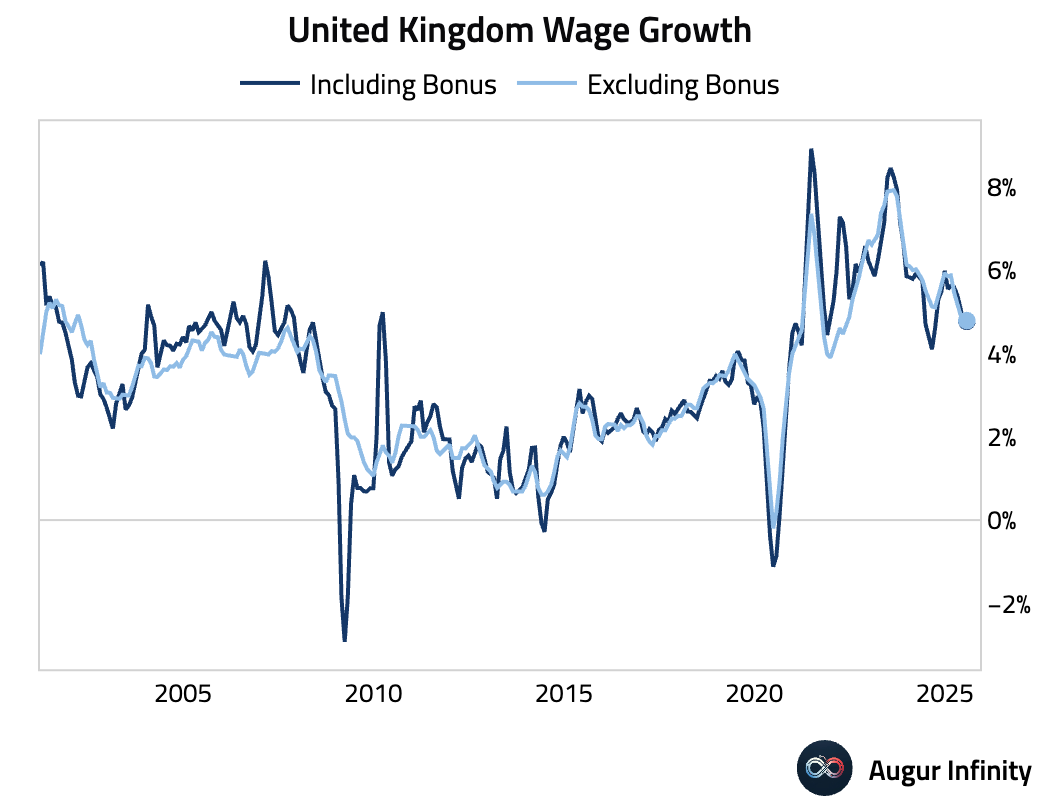

- UK wage growth presented a mixed picture for July. Average earnings including bonuses accelerated slightly to 4.7% Y/Y(est: 4.7%, prev: 4.6%). However, regular pay excluding bonuses, a key data point for the Bank of England, moderated to 4.8% Y/Y(est: 4.8%, prev: 5.0%).

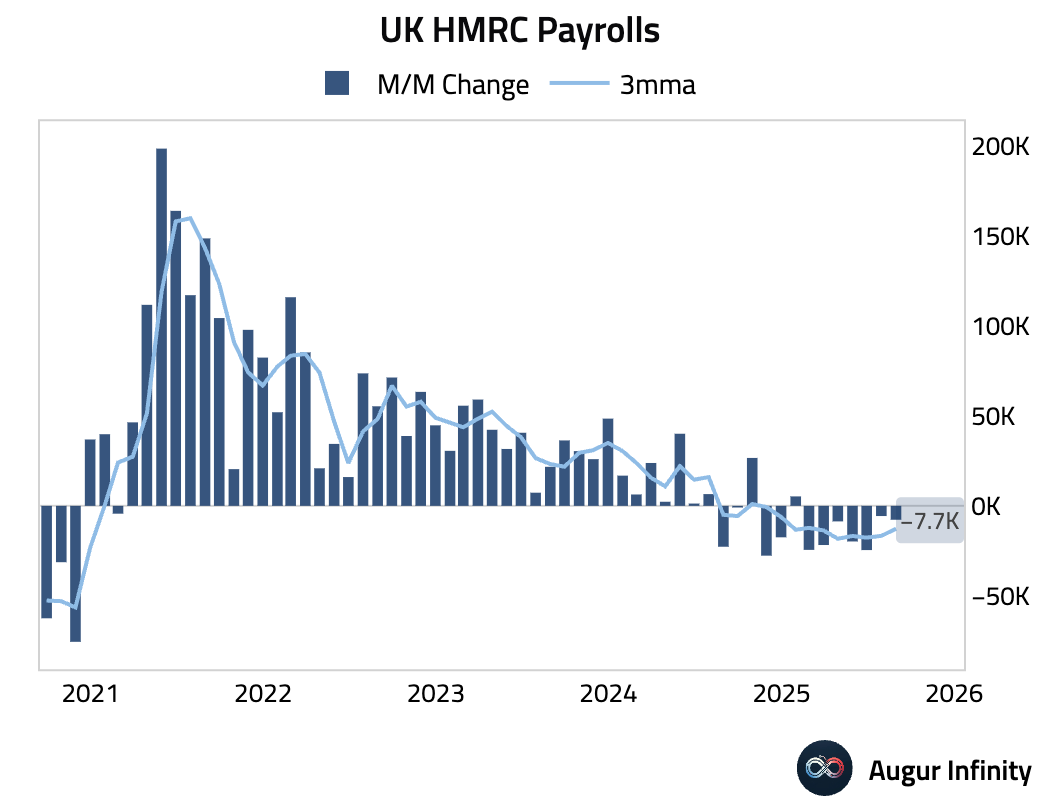

- The flash estimate for UK payrolled employees in August showed a contraction of 8k (prev: -6k). While this marks a second consecutive monthly decline, the fall was smaller than some had feared, and the prior month's reading was revised upward. This data is often subject to significant revision.

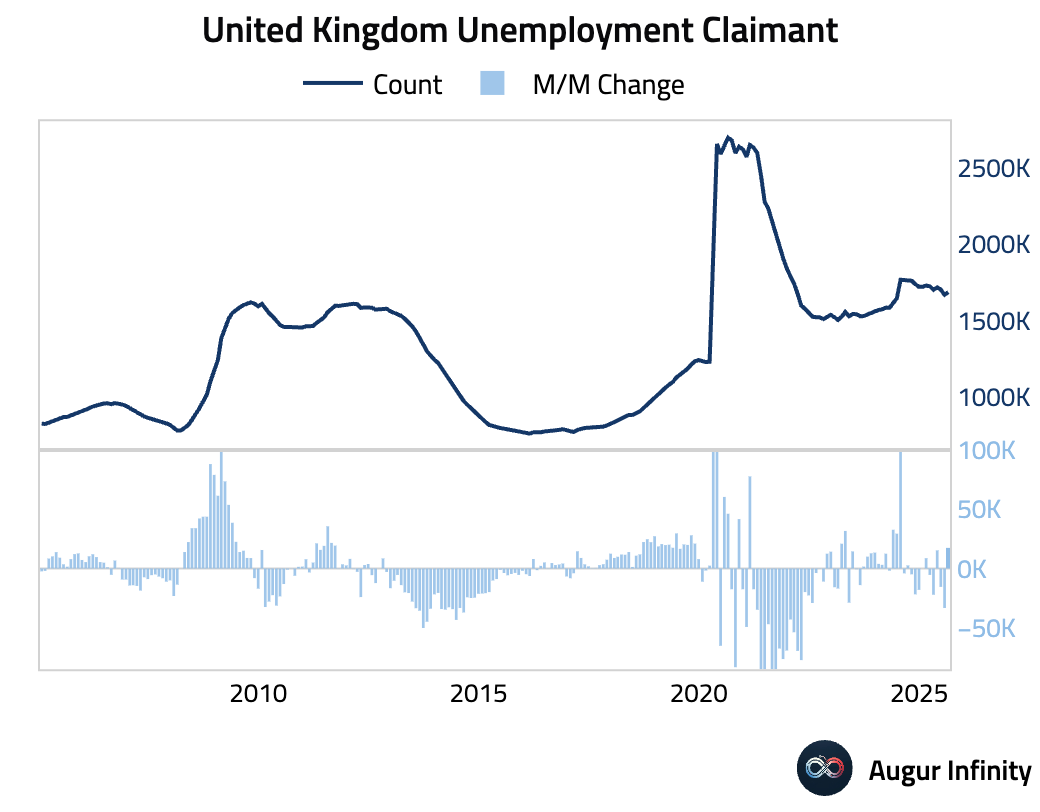

- The UK claimant count rose by 17.4k in August, missing consensus expectations for a 20.3k increase (prev: -33.3k).

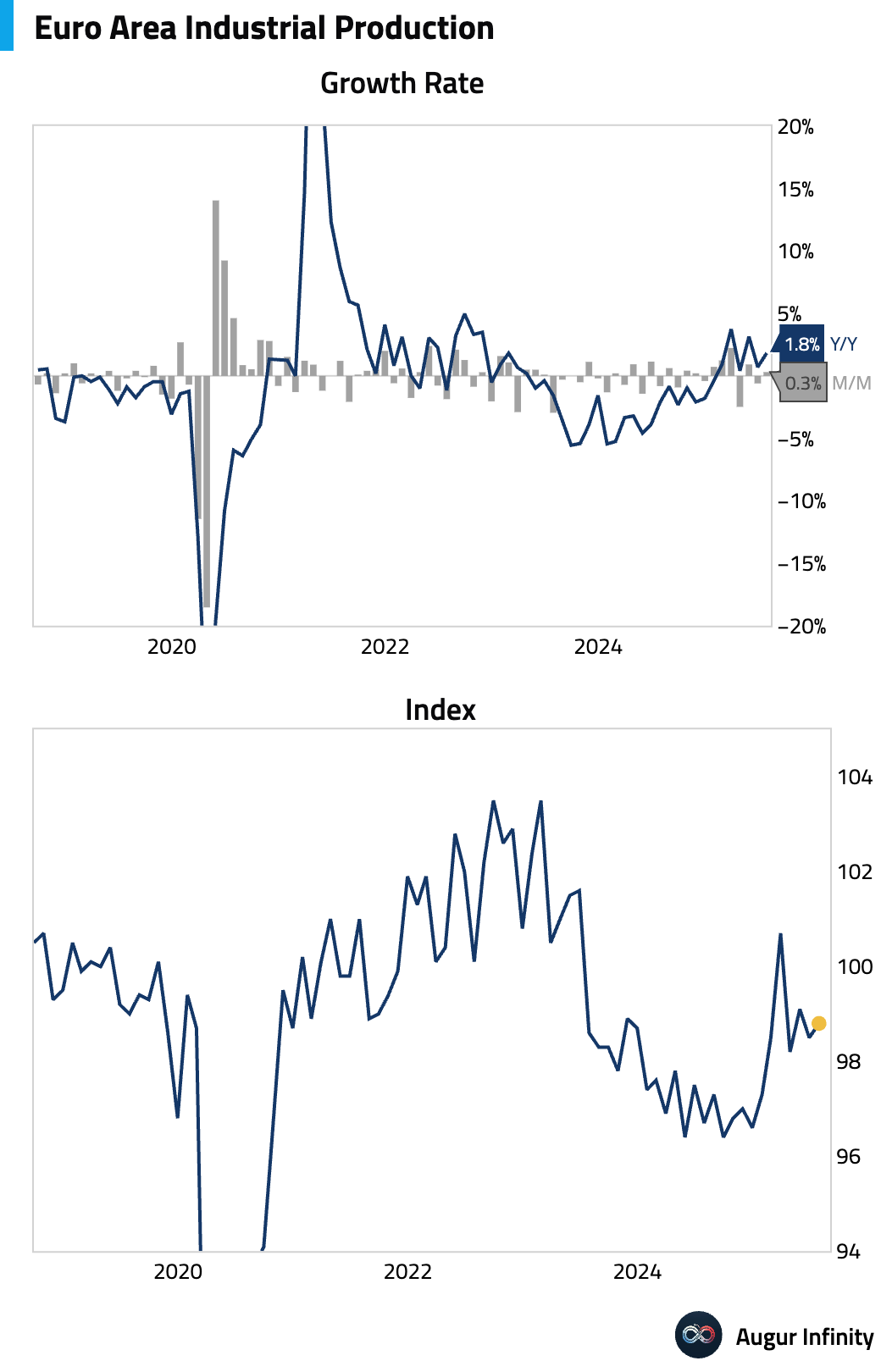

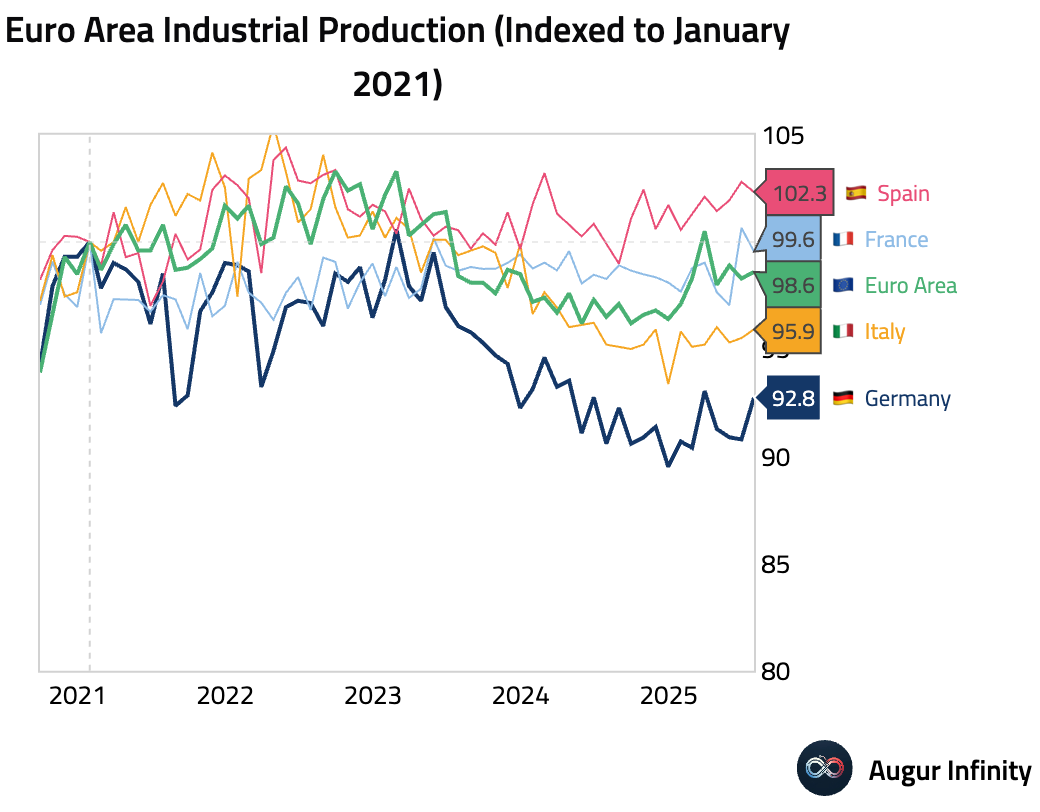

- Eurozone industrial production rebounded in July, rising 0.3% M/M, though this was slightly below the 0.4% consensus estimate. Year-over-year, production accelerated to 1.8% (est: 1.7%, prev: 0.7%).

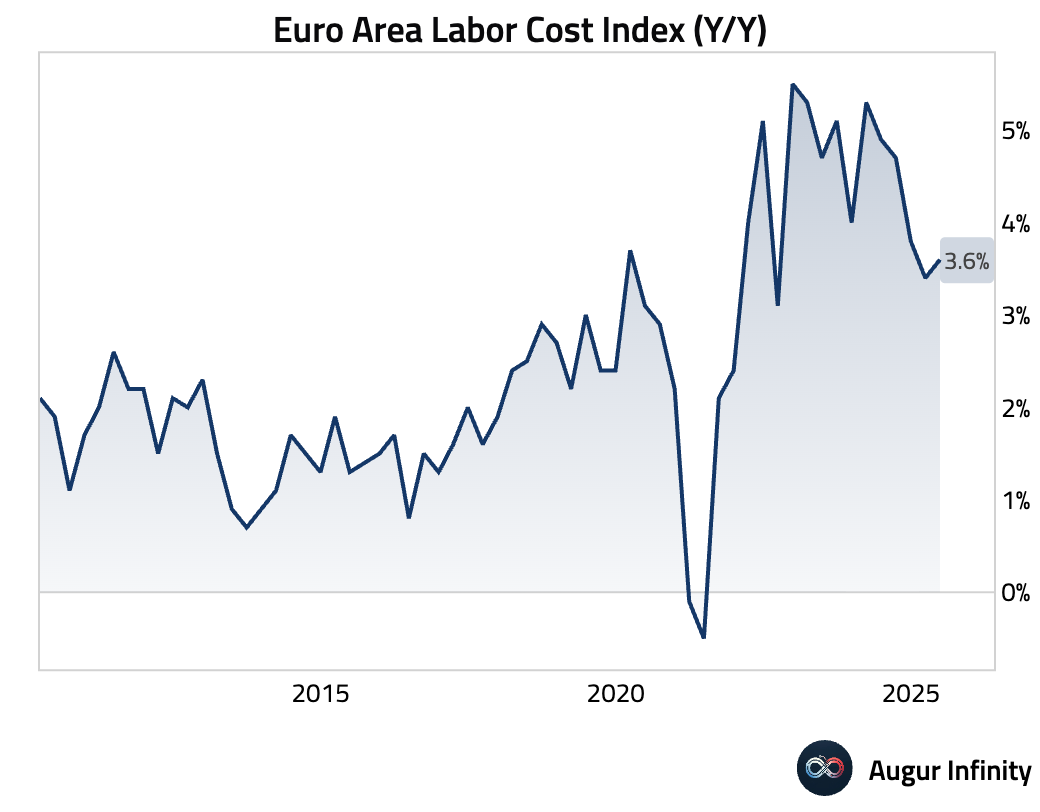

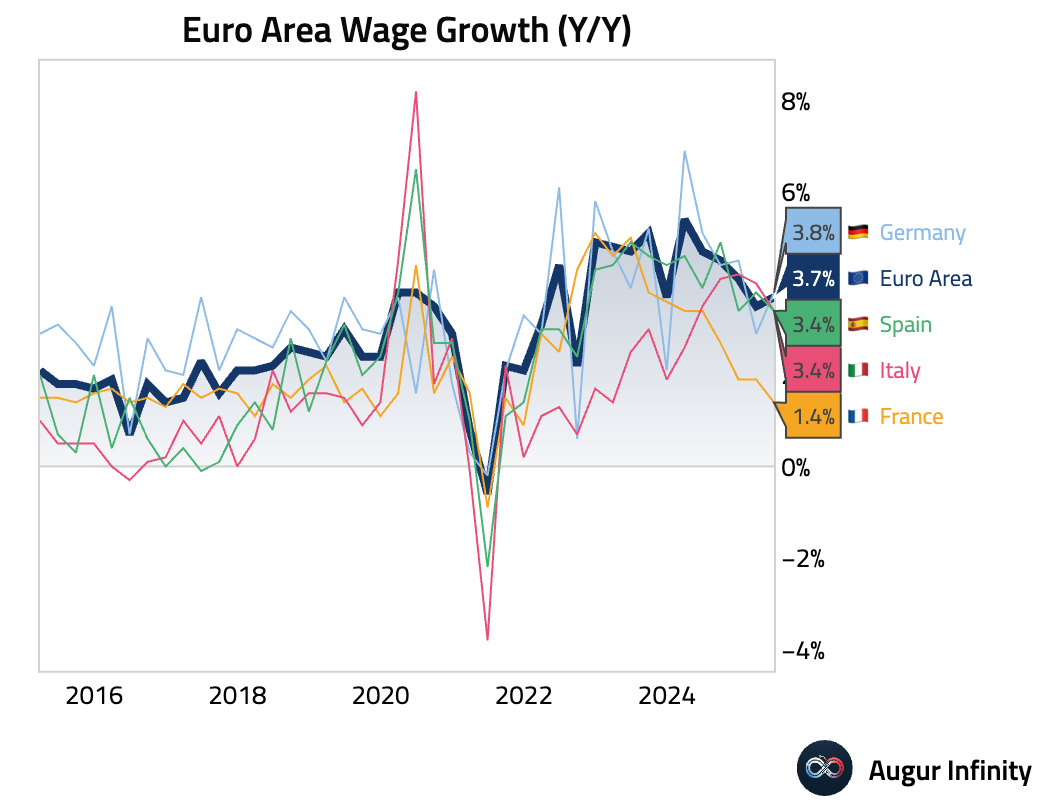

- Eurozone labor costs accelerated in Q2, with the final Labour Cost Index rising 3.6% Y/Y (est: 3.7%, prev: 3.4%). Wage growth also ticked up to 3.7% Y/Y.

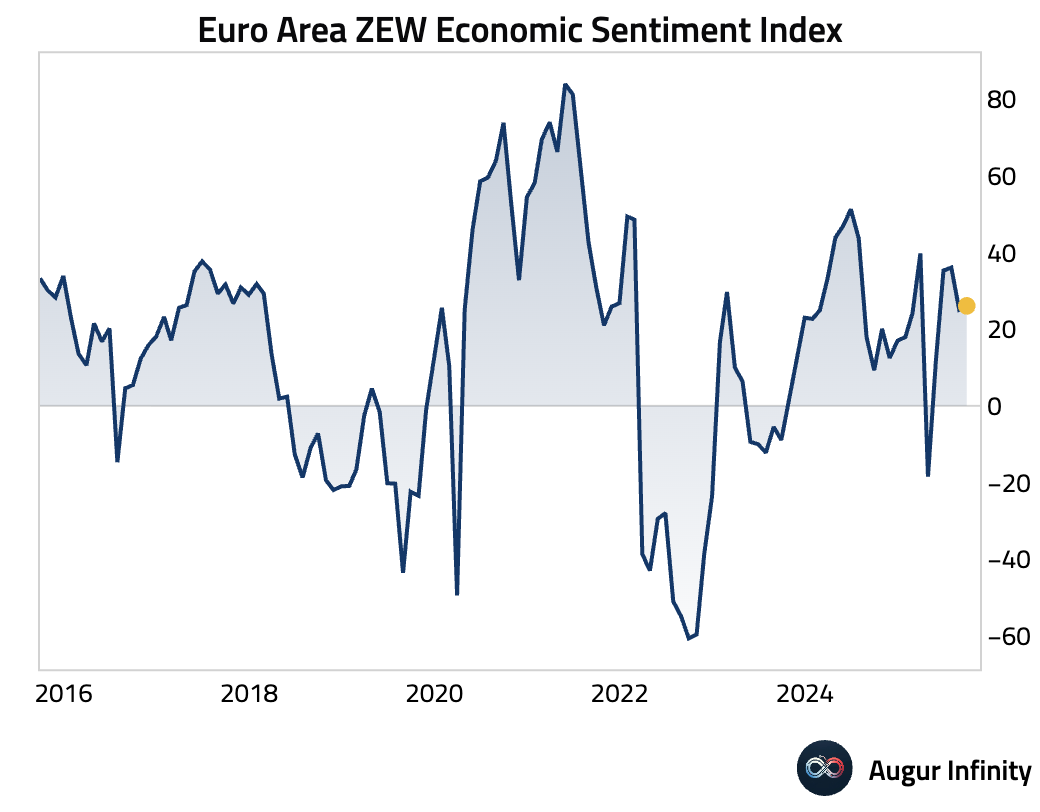

- The ZEW Economic Sentiment Index for the Eurozone improved to 26.1 in September, beating forecasts (est: 20.3, prev: 25.1).

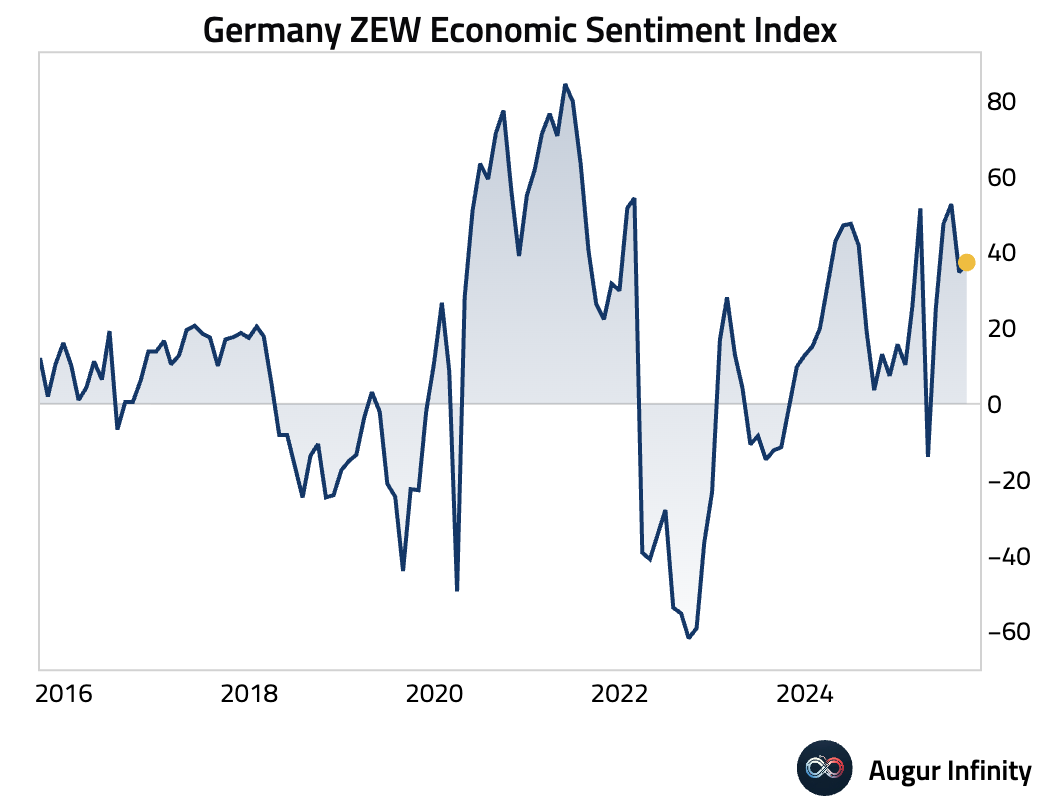

- Germany’s ZEW Economic Sentiment index for September jumped to 37.3, significantly beating expectations and marking its highest level since July (est: 26.3, prev: 34.7). However, the assessment of current conditions deteriorated more than anticipated, falling to -76.4 (est: -75.0, prev: -68.6).

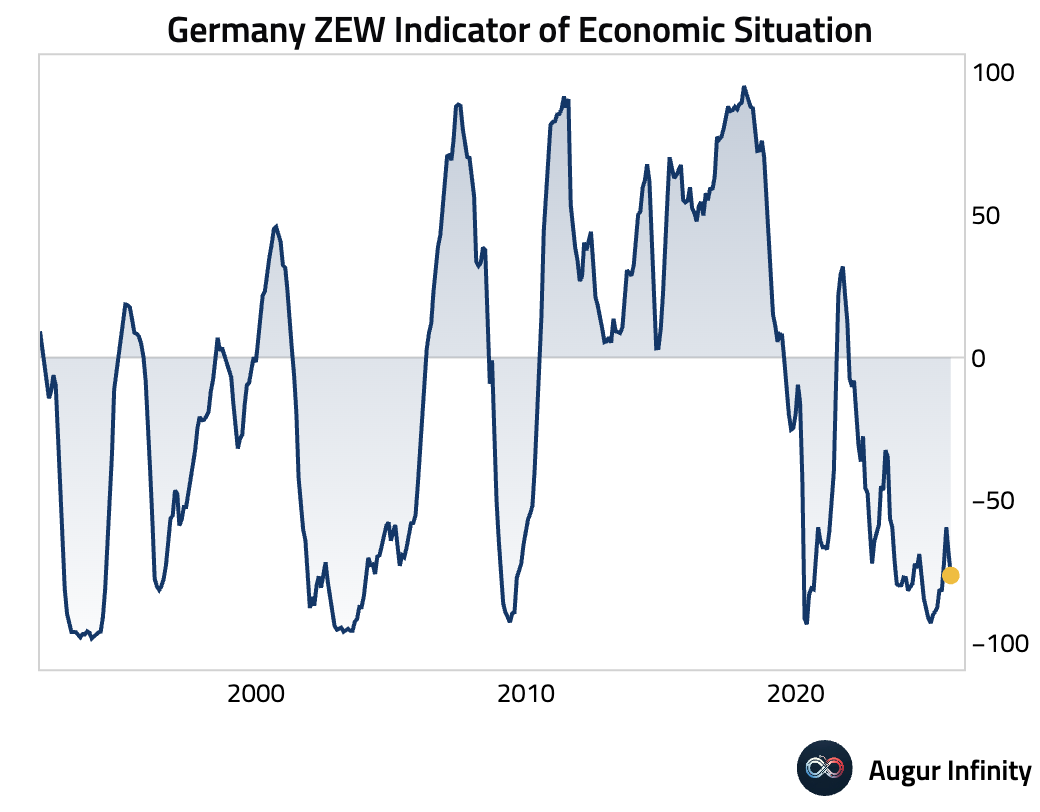

- Germany's ZEW Current Conditions index deteriorated further in September, falling to -76.4 from -68.6 (est: -75.0).

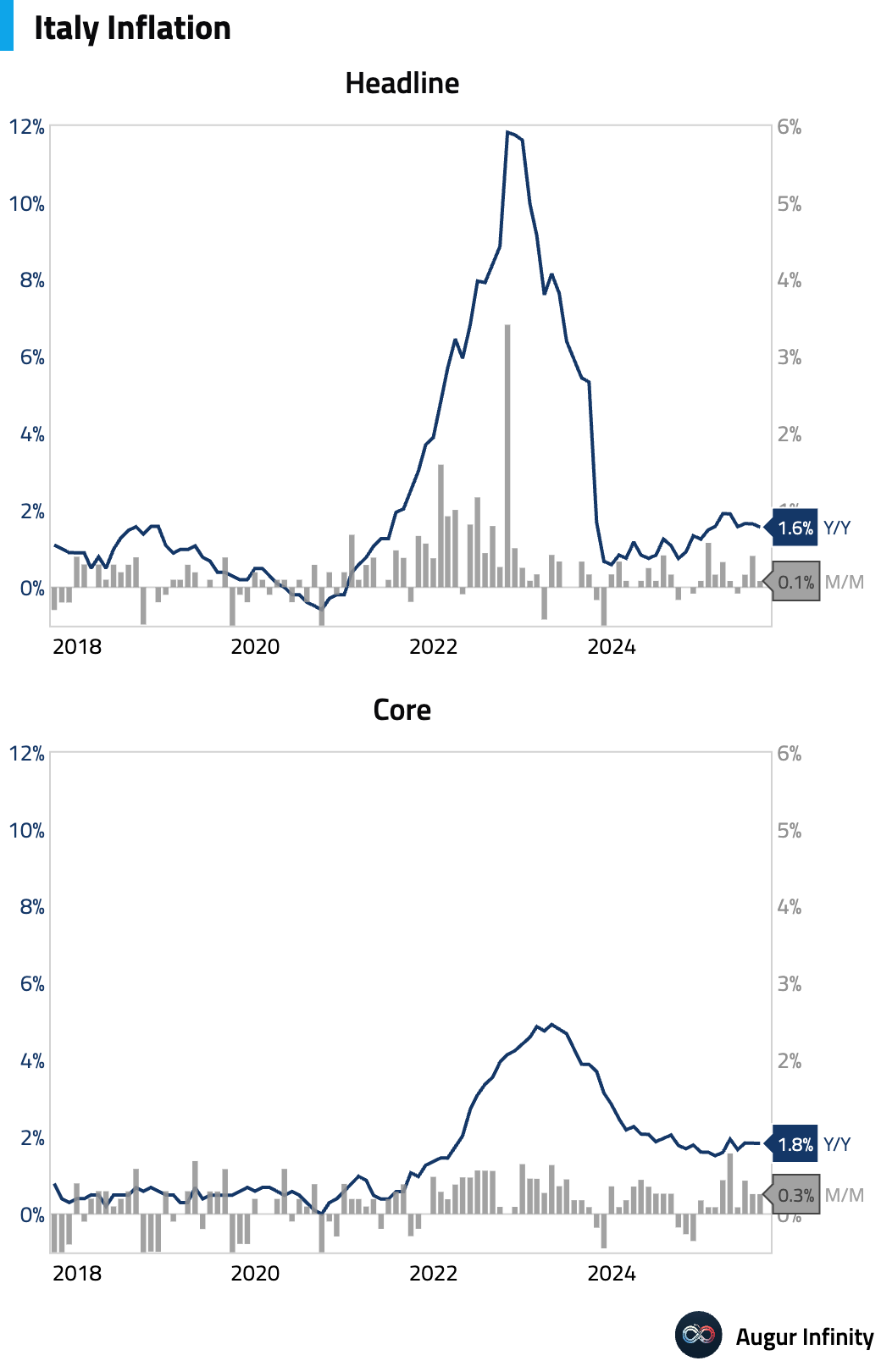

- Italy’s final national inflation figures for August confirmed a disinflationary trend, with the CPI rising 0.1% M/M and decelerating to 1.6% Y/Y (prev: 1.7%), both in line with estimates.

Asia-Pacific

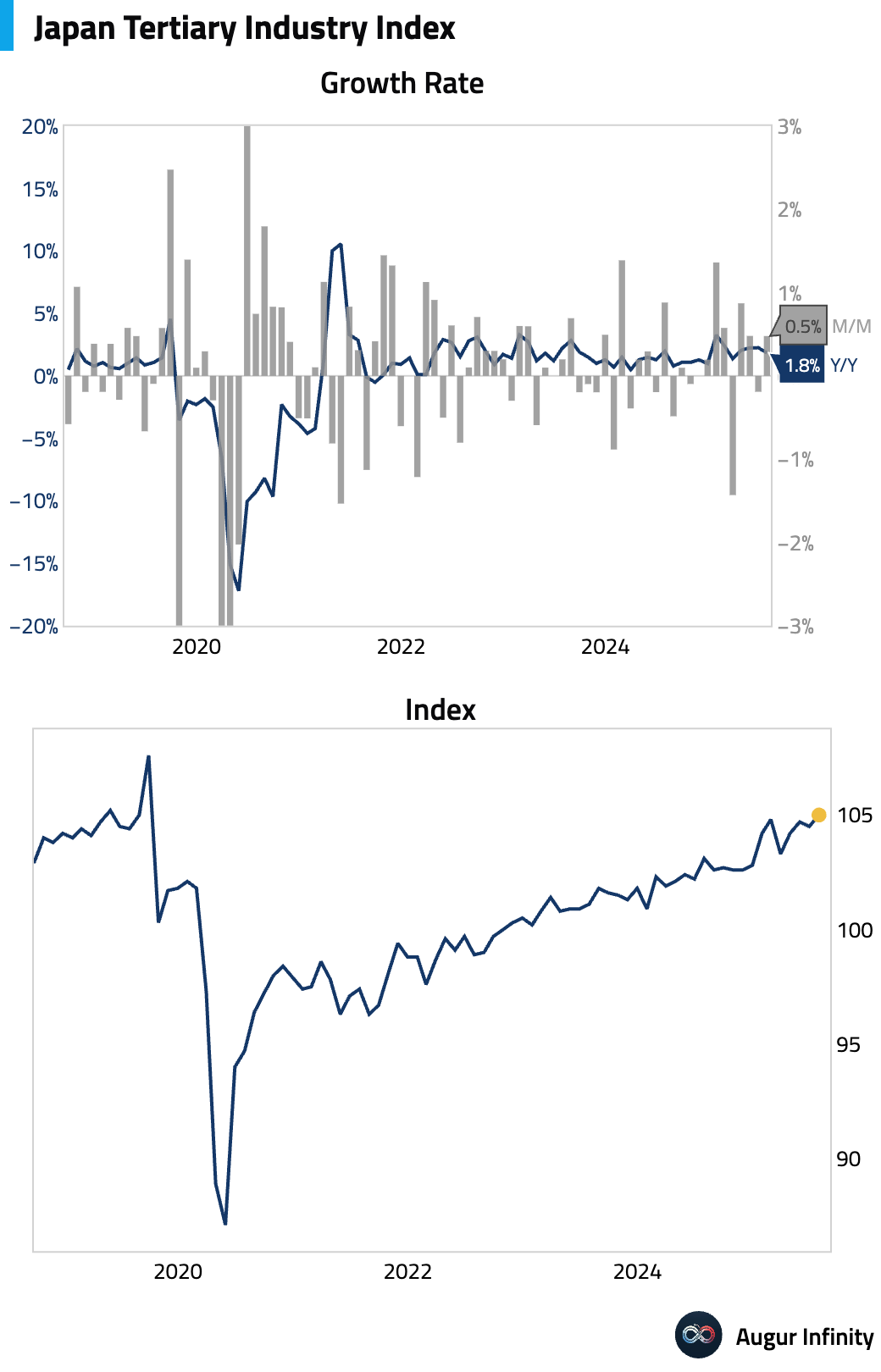

- Japan’s Tertiary Industry Index, a measure of service sector activity, rebounded 0.5% M/M in July, beating expectations (est: 0.2%, prev: -0.2%).

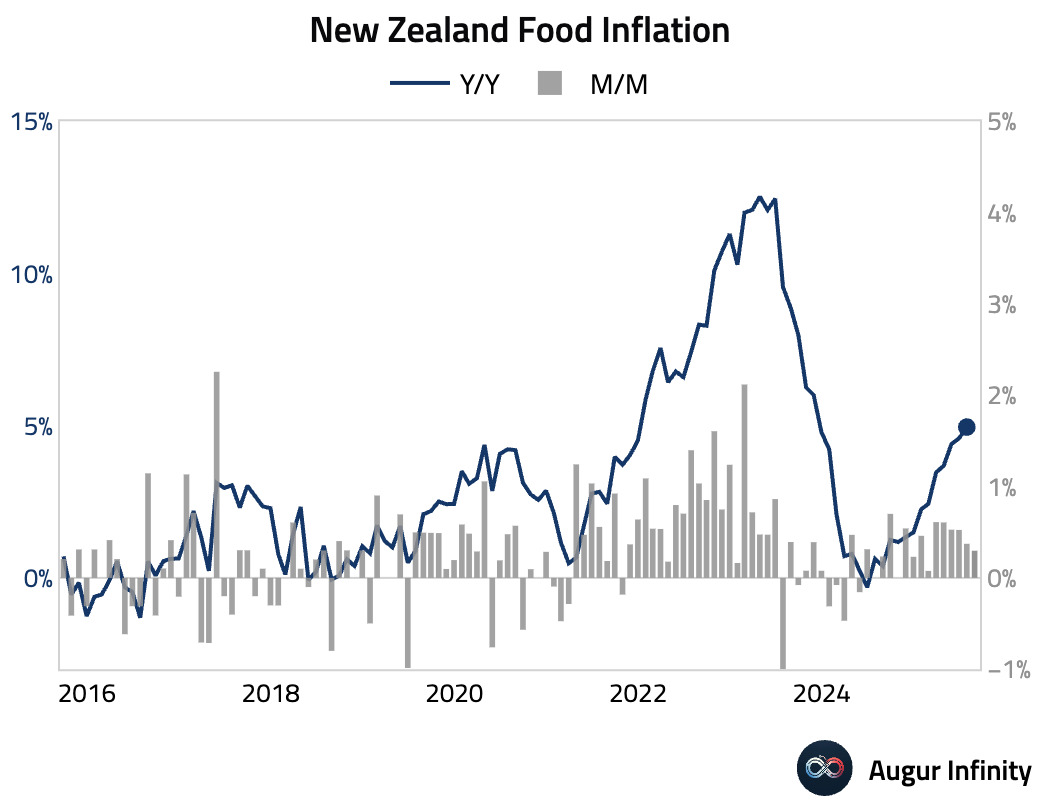

- New Zealand's food inflation remained steady at 5.0% Y/Y in August (prev: 5.0%).

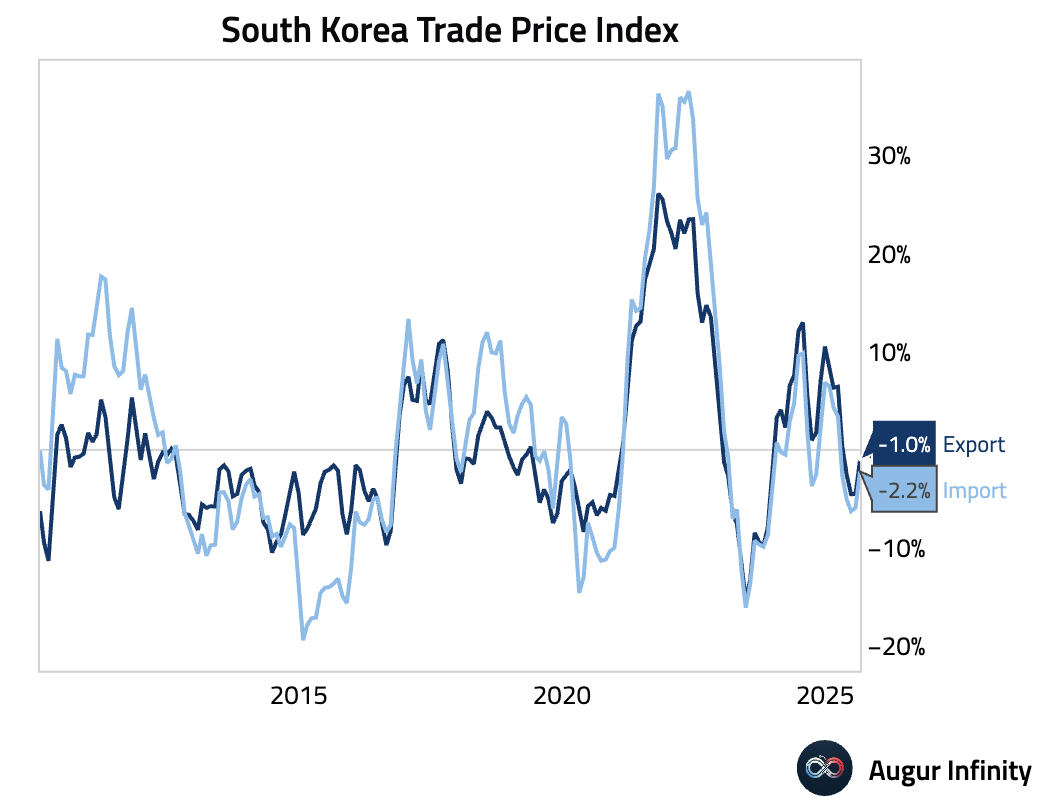

- South Korean trade price deflation eased in August. Export prices fell 1.0% Y/Y (prev: -4.5%), while import prices declined 2.2% Y/Y (prev: -5.9%).

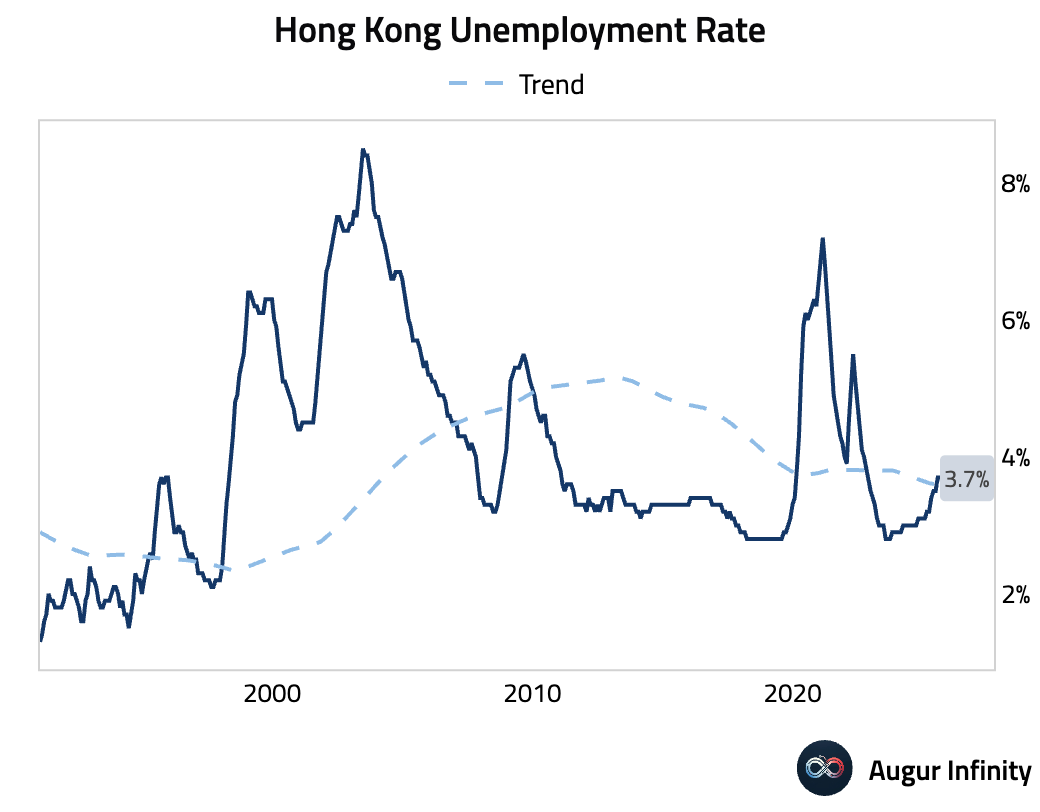

- Hong Kong's unemployment rate was unchanged at 3.7% in the three months to August.

Emerging Markets ex China

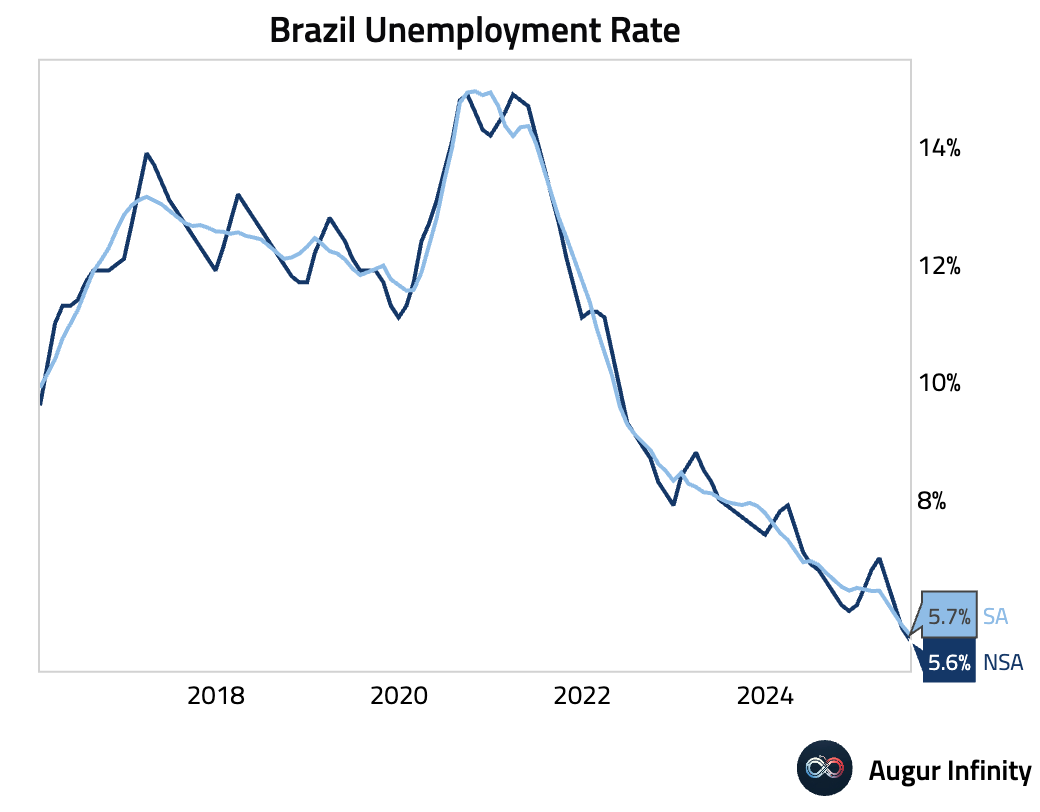

- Brazil's unemployment rate unexpectedly fell to 5.6% in July, a record low that was below consensus forecasts (est: 5.7%, prev: 5.8%). The labor market remains tight, not just from modest job growth but also from a declining labor participation rate. Generous fiscal transfers are thought to be discouraging some informal workers from seeking jobs, helping to keep the unemployment rate low.

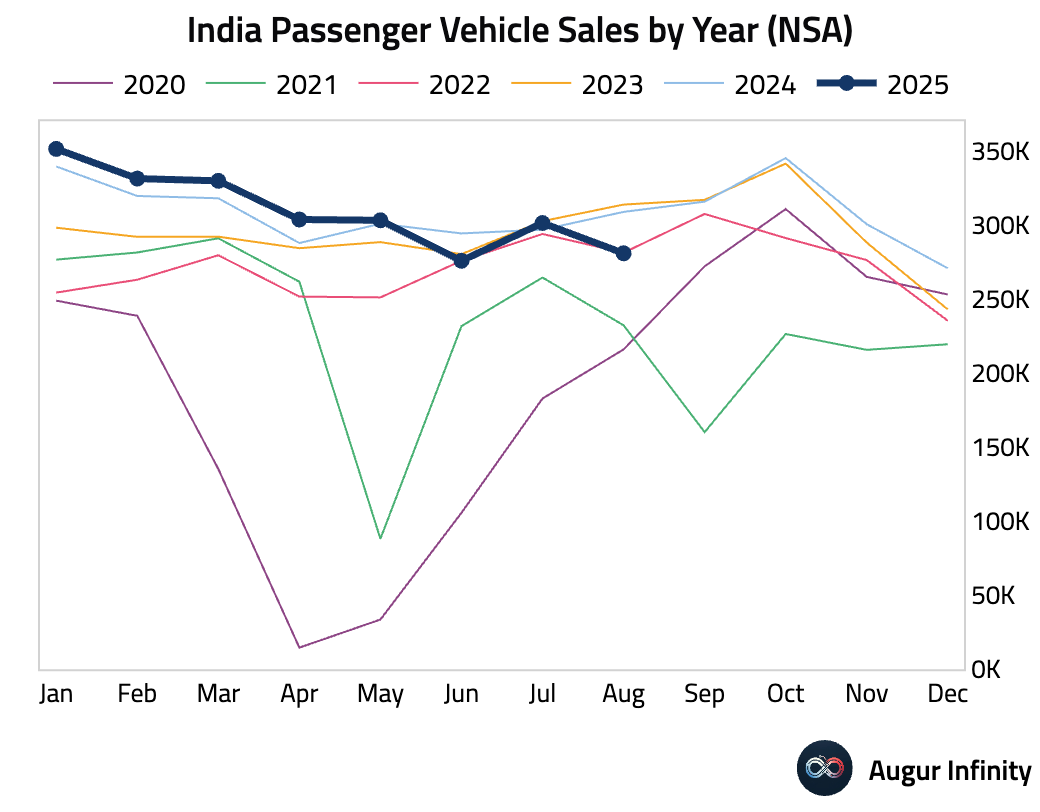

- Indian passenger vehicle sales declined sharply in August, falling 9.0% Y/Y after a 1.5% rise in July.

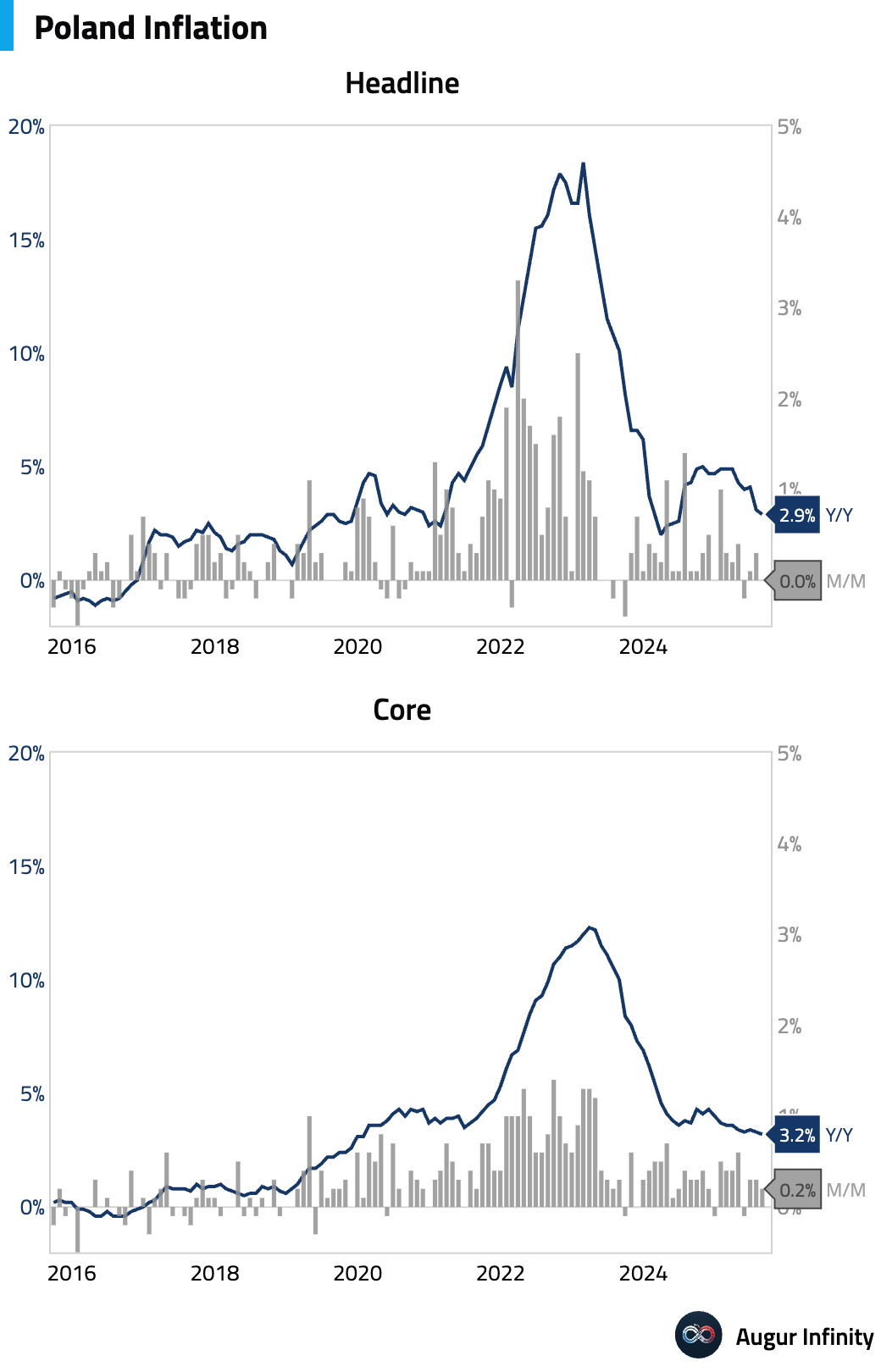

- Poland’s core inflation rate eased slightly to 3.2% Y/Y in August (est: 3.1%, prev: 3.3%). Broader inflation data showed a slowdown driven by deeper deflation in transport fuels, supporting a dovish outlook for the National Bank of Poland.

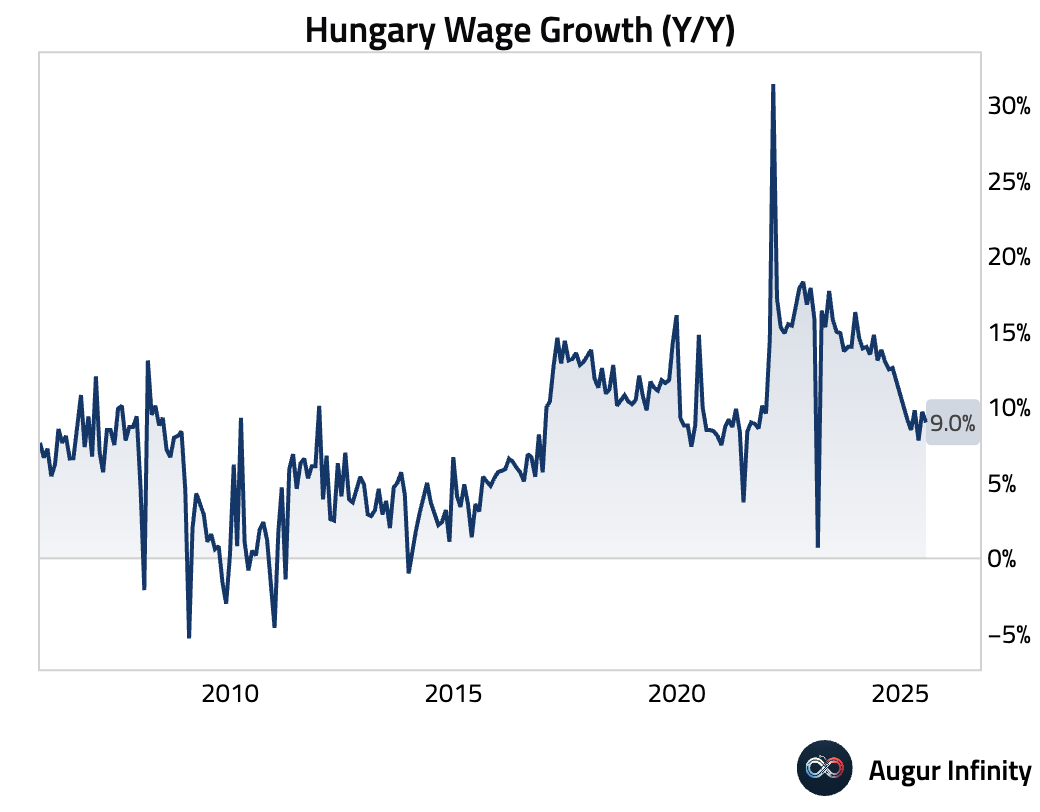

- Hungarian gross wage growth decelerated in July, rising 9.0% Y/Y (prev: 9.7%).

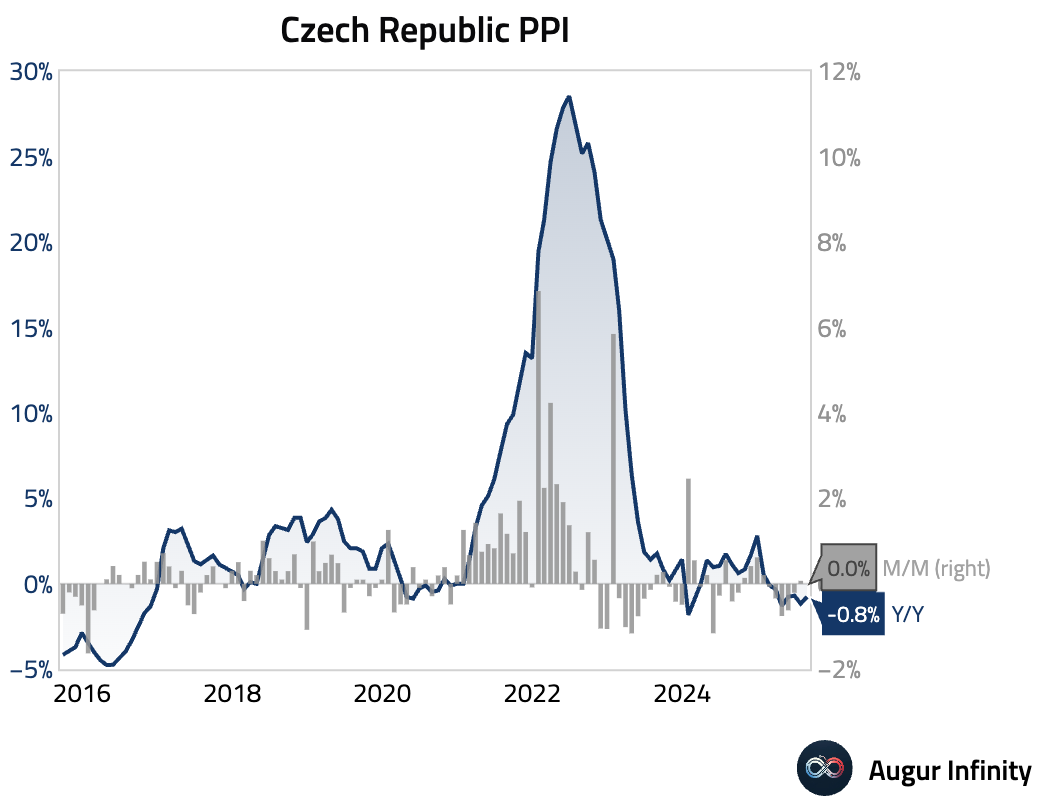

- Czech producer prices were flat in August, beating expectations for a slight decline (act: 0.0% M/M, est: -0.1%). The year-over-year deflationary trend eased, with prices down 0.8% (est: -0.9%, prev: -1.2%).

Global Markets

Equities

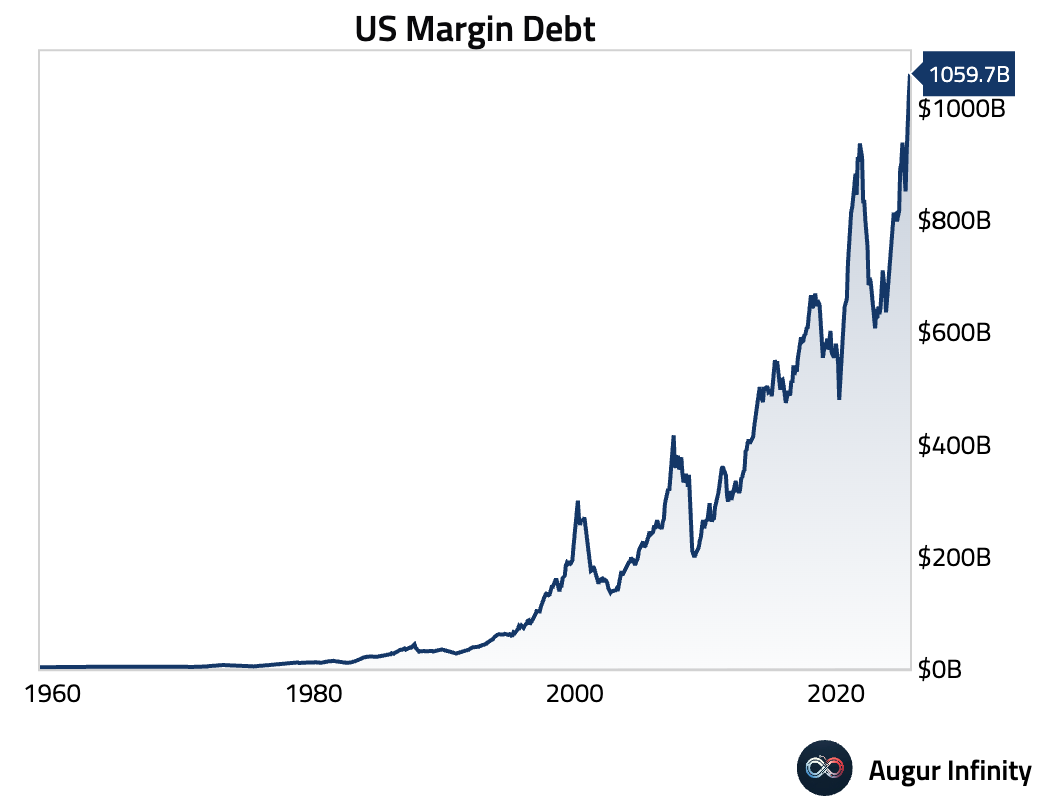

- After surpassing $1 trillion in June, US margin debt climbed further over the past two months.

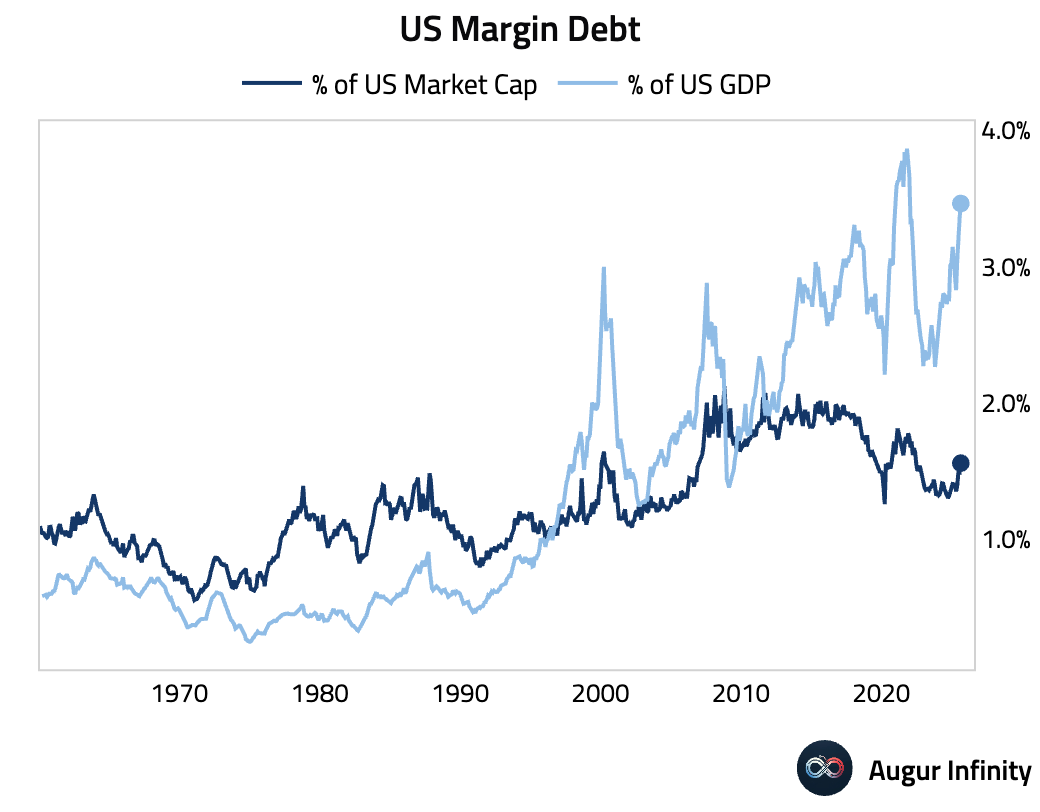

Here's margin debt as percentages of total US market cap and US GDP.

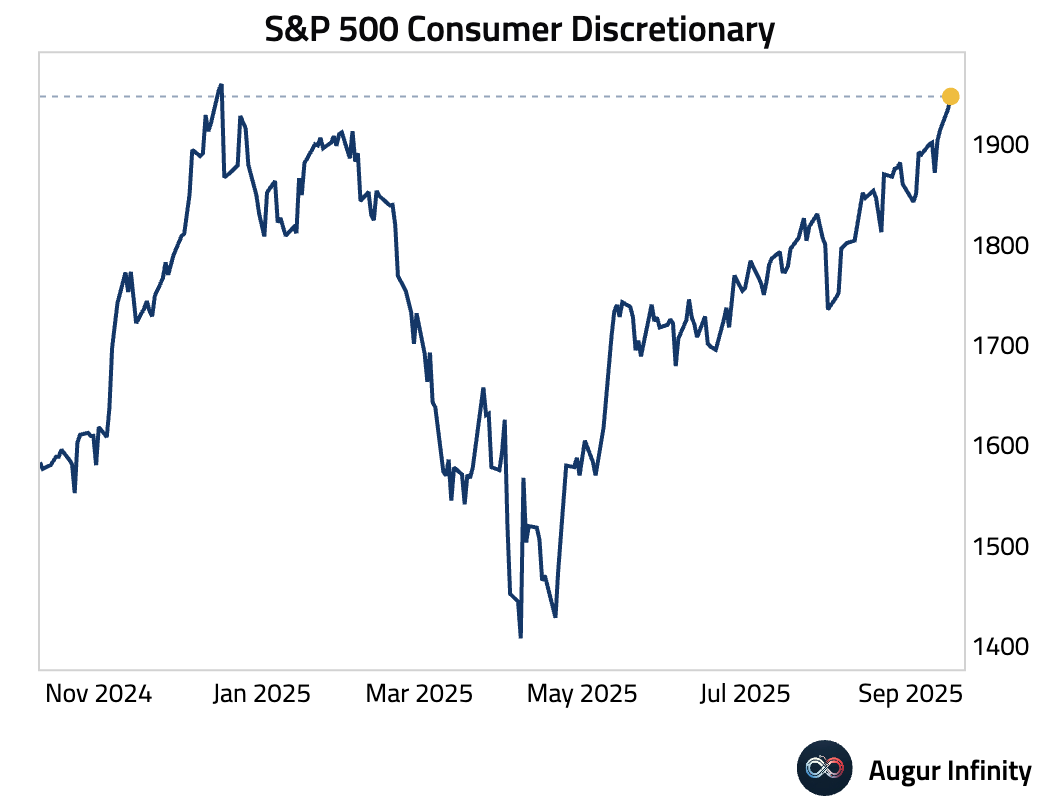

- S&P 500 Consumer Discretionary is about to surpass its previous all-time high established in December 2024. 2024.

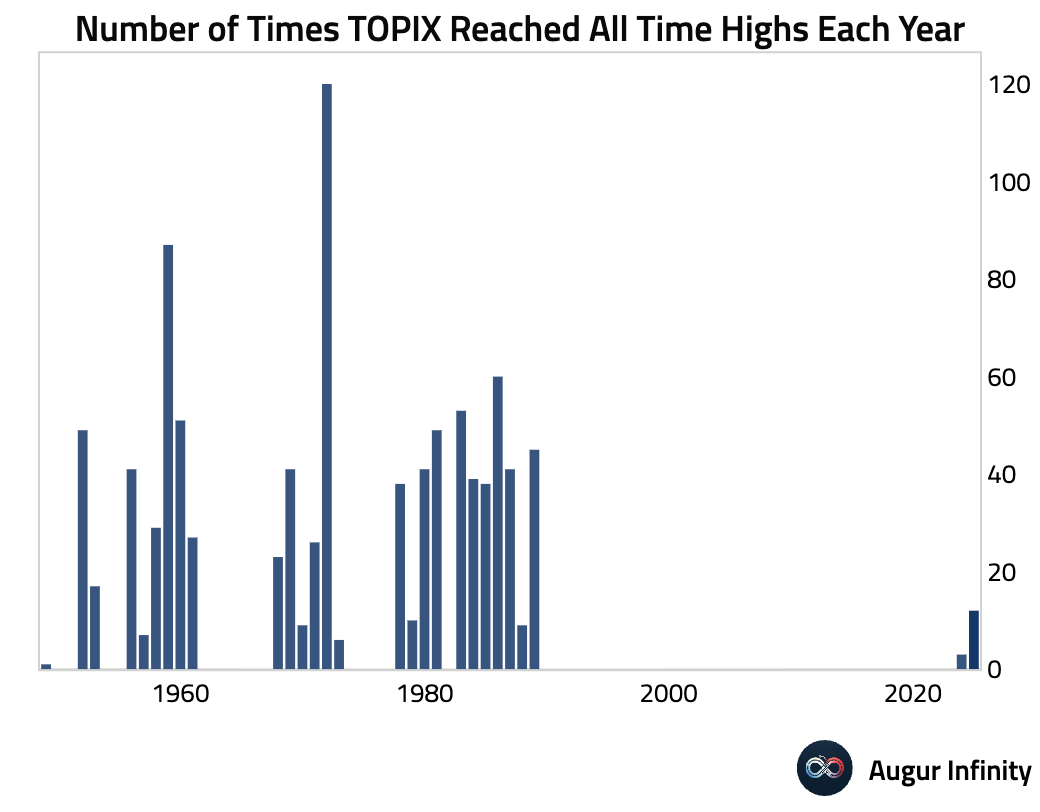

- The TOPIX Index has reached all-time highs 12 times this year.

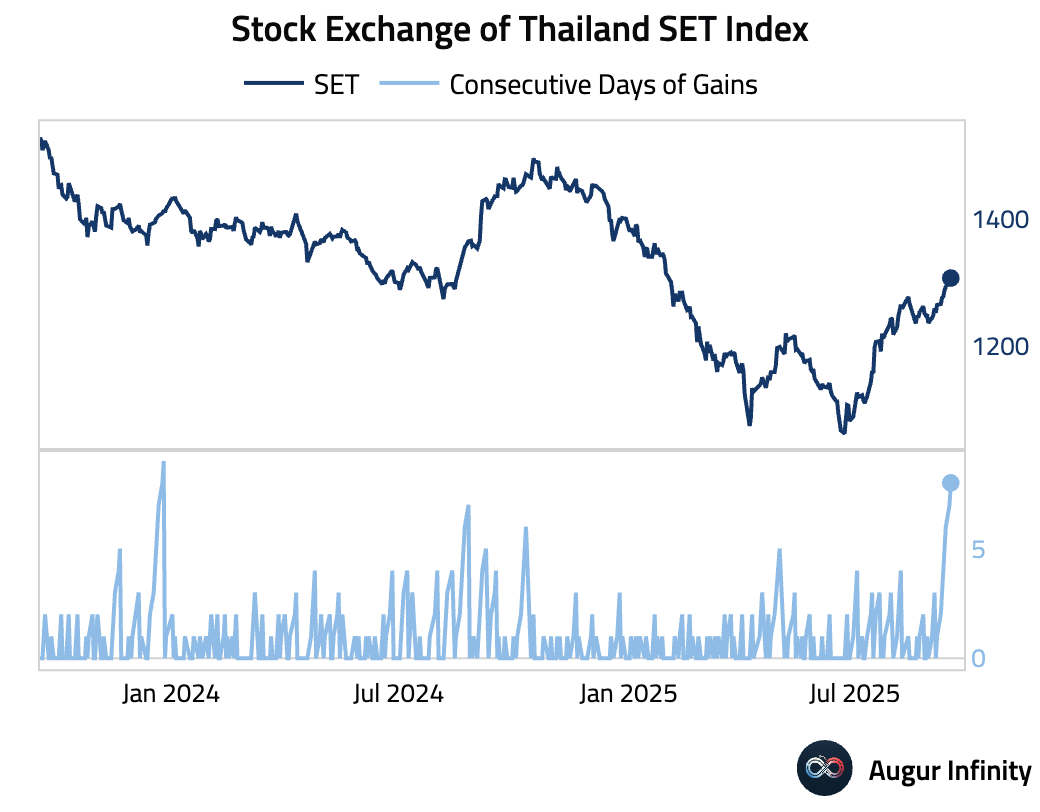

- Stock Exchange of Thailand SET Index has rallied for eight consecutive days to the highest level since January.

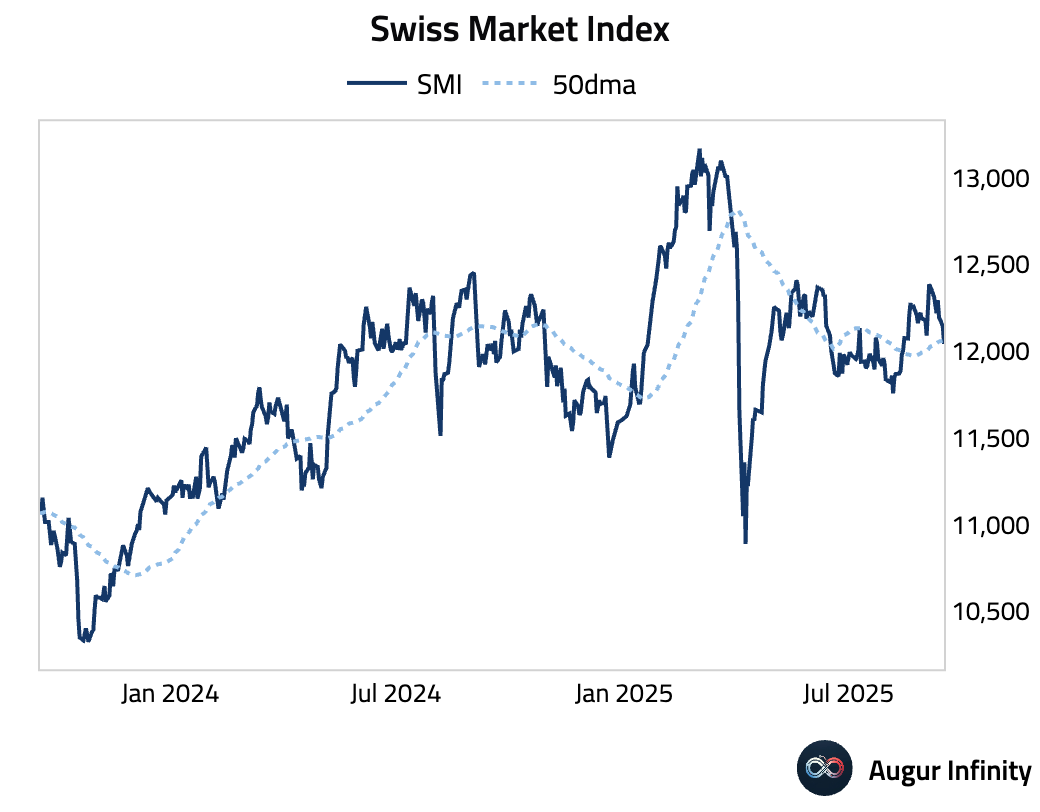

- Swiss Market Index dipped below its 50-day moving average.

Fixed Income

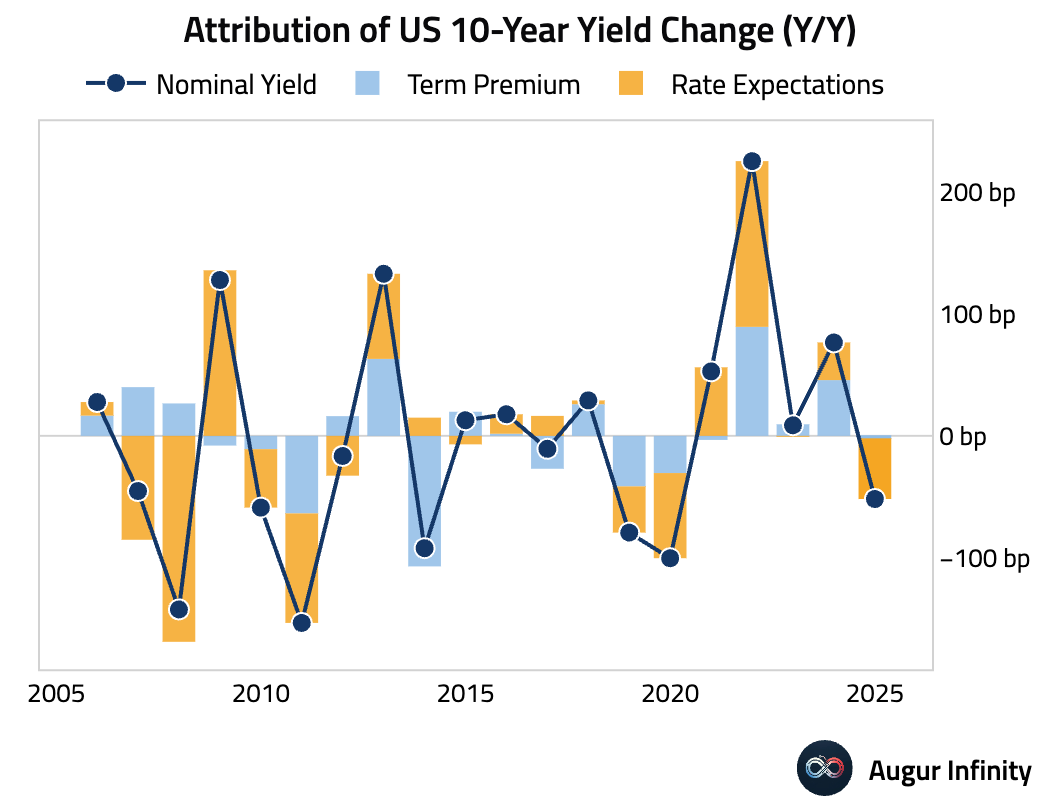

- The decline in 10-year yield this year has been driven by a decline in rate expectations, while term premium held steady.

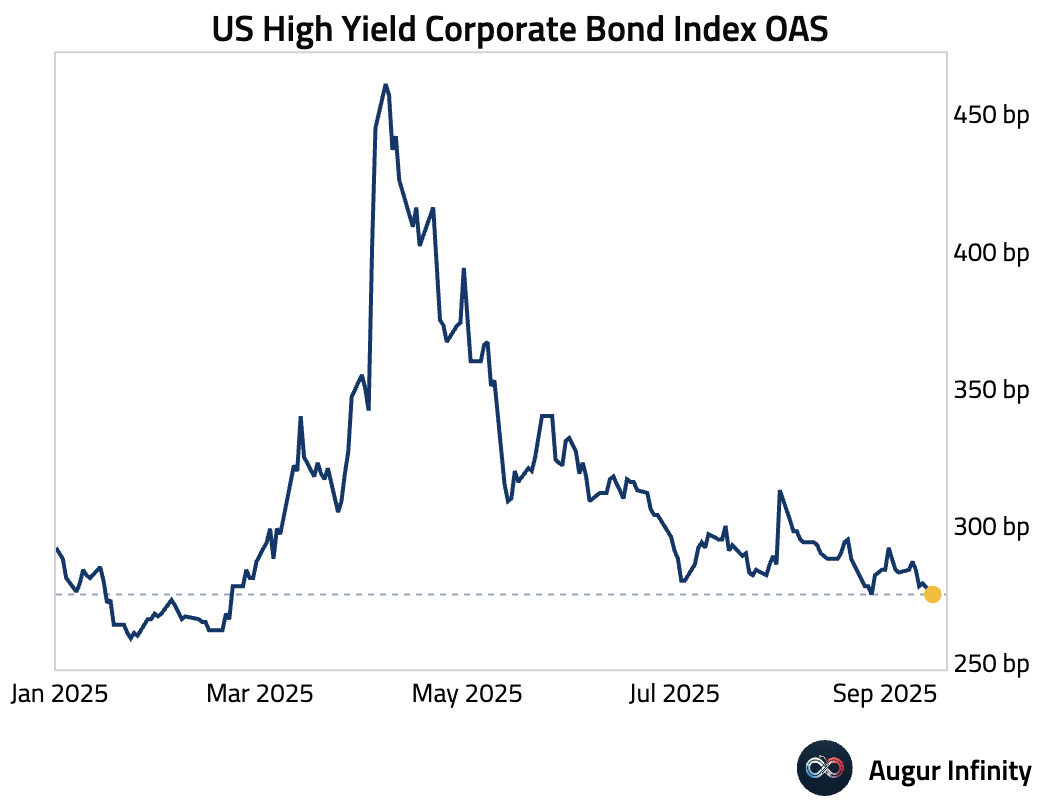

- US High Yield Corporate Bond Index OAS is at the lowest level since February.

FX

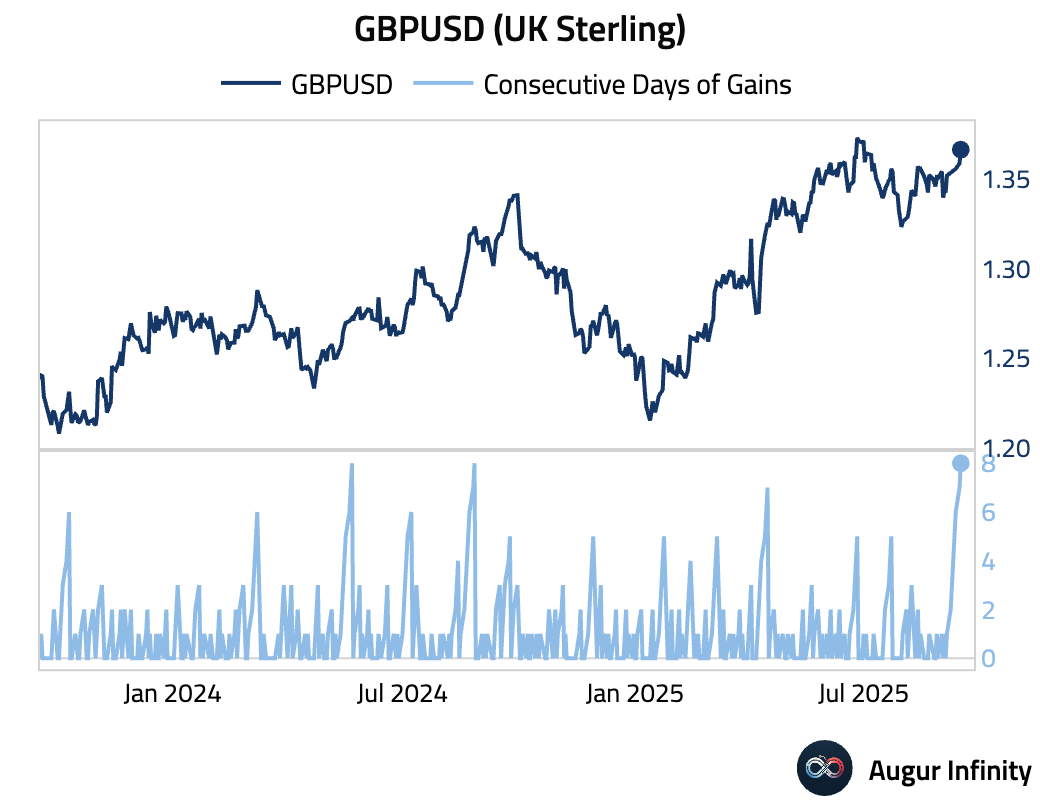

- The pound has gained against the dollar for eight straight days.

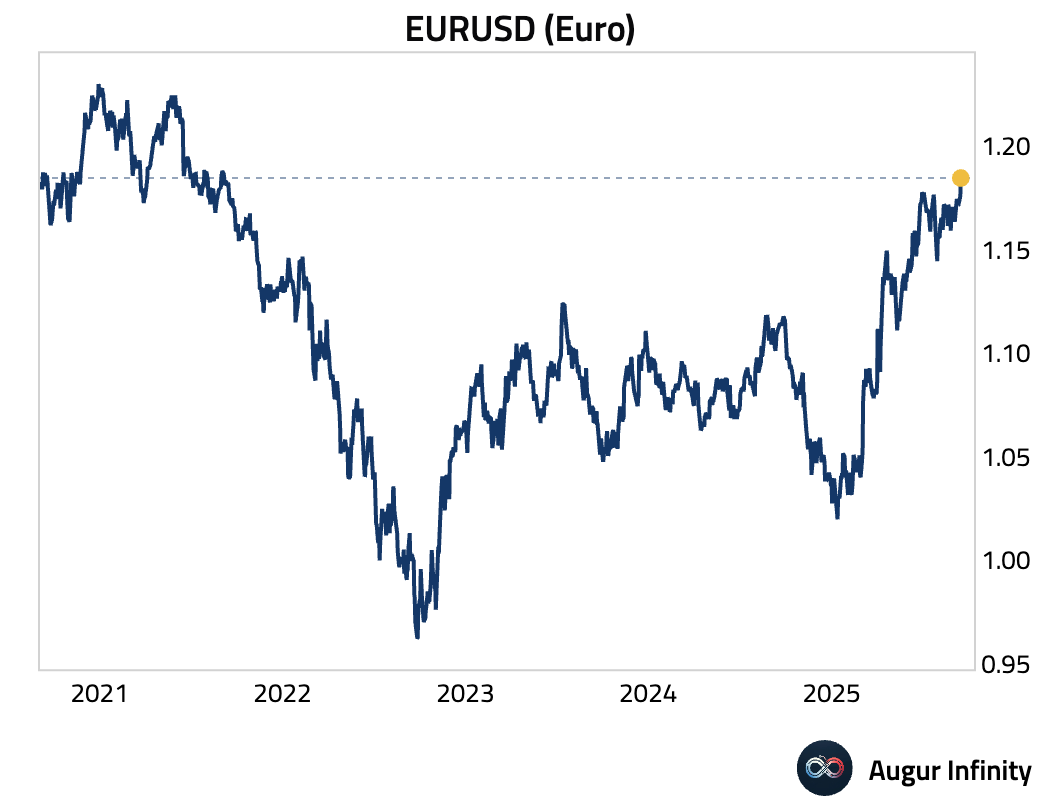

- The euro is trading at the best level against USD since September 2021.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.