Global Economics

United States

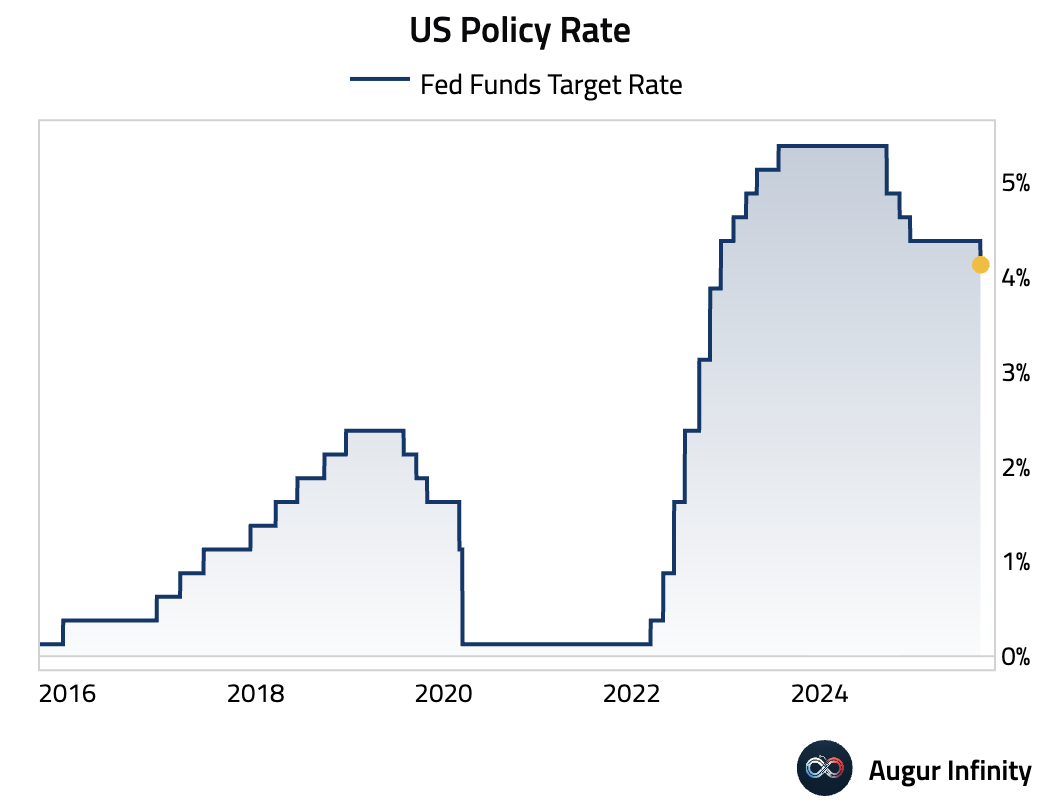

- The FOMC cut rates by 25 bps to 4%–4.25%, signaling a pivot to focus on rising "downside risks to employment." This is the first cut since December 2024.

Today’s FOMC statement was the most dovish since 2021.

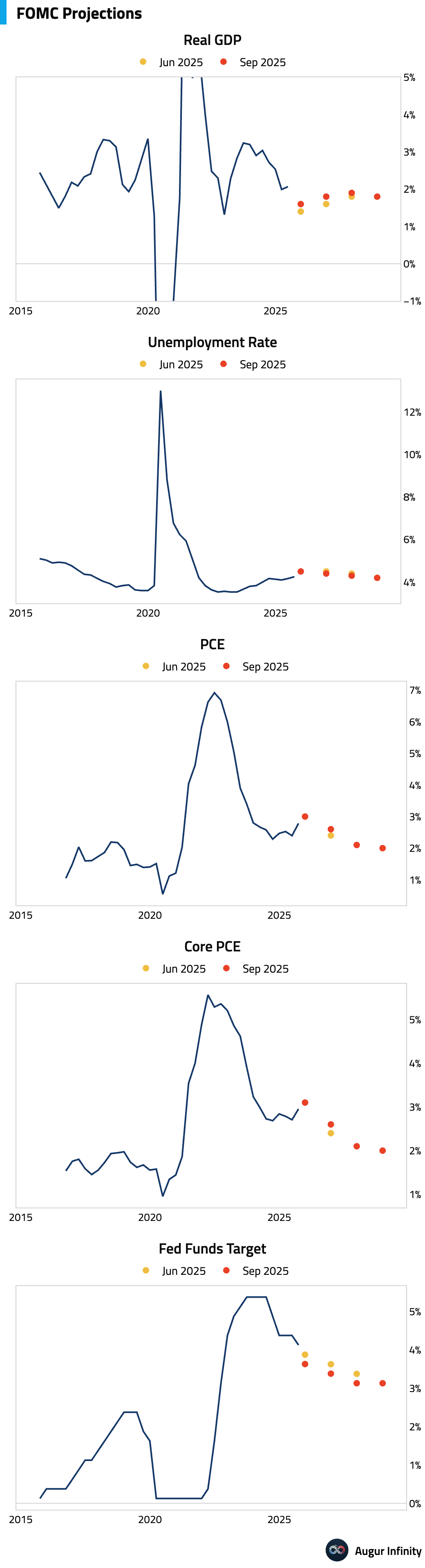

Paradoxically, the Fed's projections are penciling in higher growth (all horizons), lower unemployment (in 2026–27), higher inflation (in 2026), and more rate cuts (three cuts for 2025 and one each in 2026 and 2027).

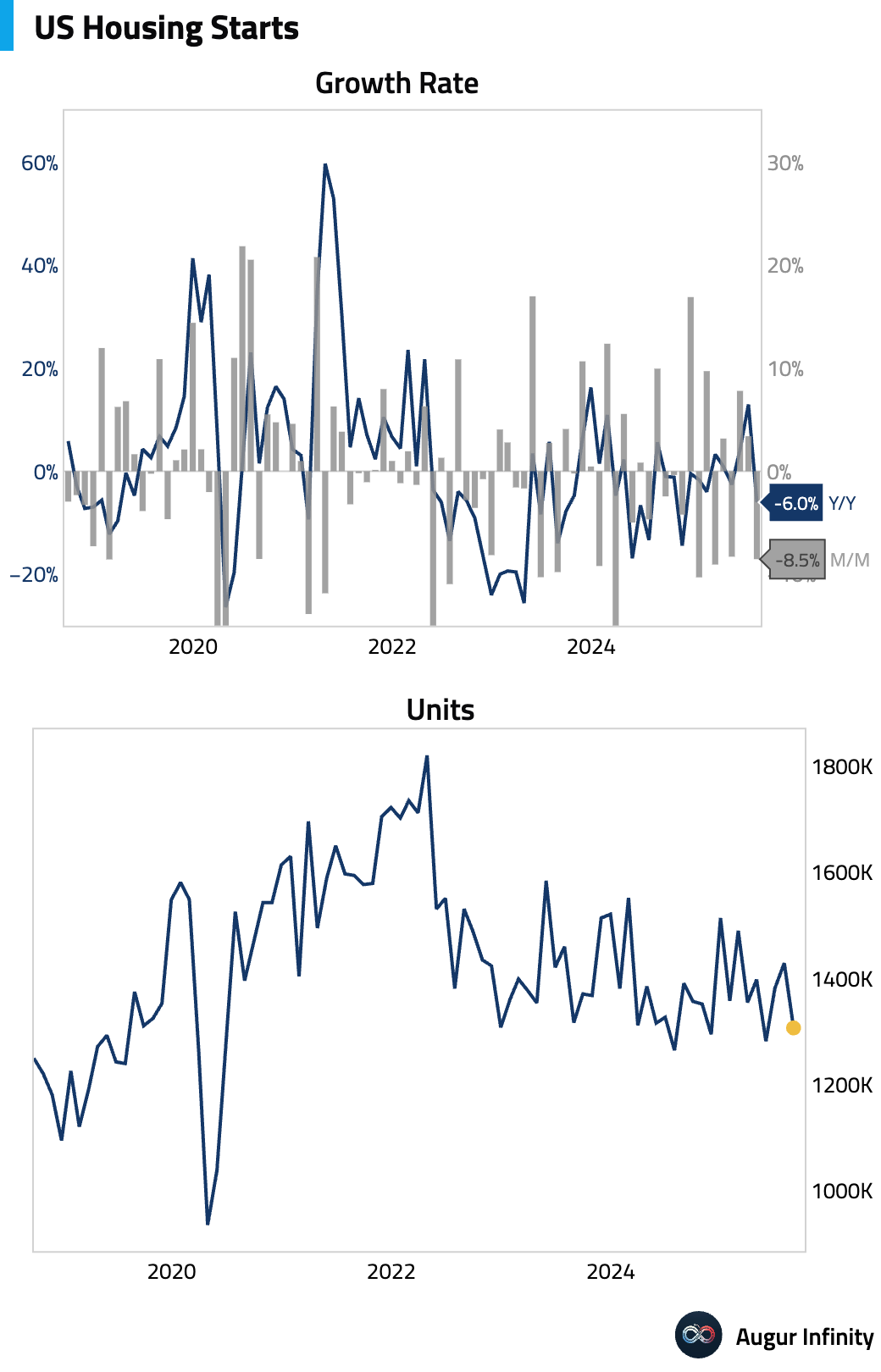

- US housing starts dropped a sharp 8.5% M/M in August to a 1.307 million annualized pace, significantly missing consensus expectations (est: 1.370M). The decline was broad-based, with both single-family (-7.0%) and multi-family (-11.7%) starts falling. The miss was partially cushioned by upward revisions to the prior two months.

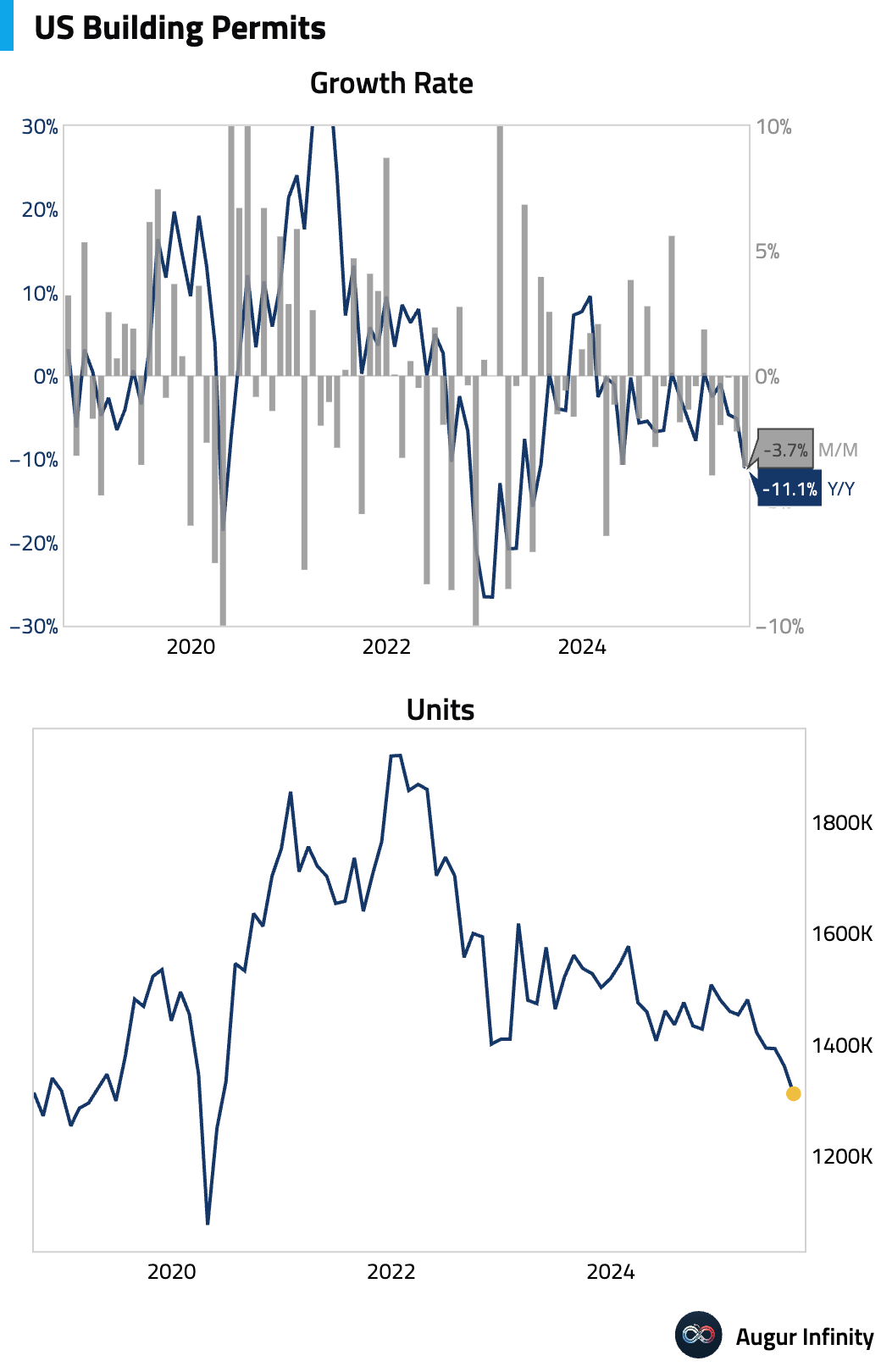

- Forward-looking building permits fell 3.7% M/M in August to an annualized 1.312 million units (est: 1.370M), the lowest level since June 2020.

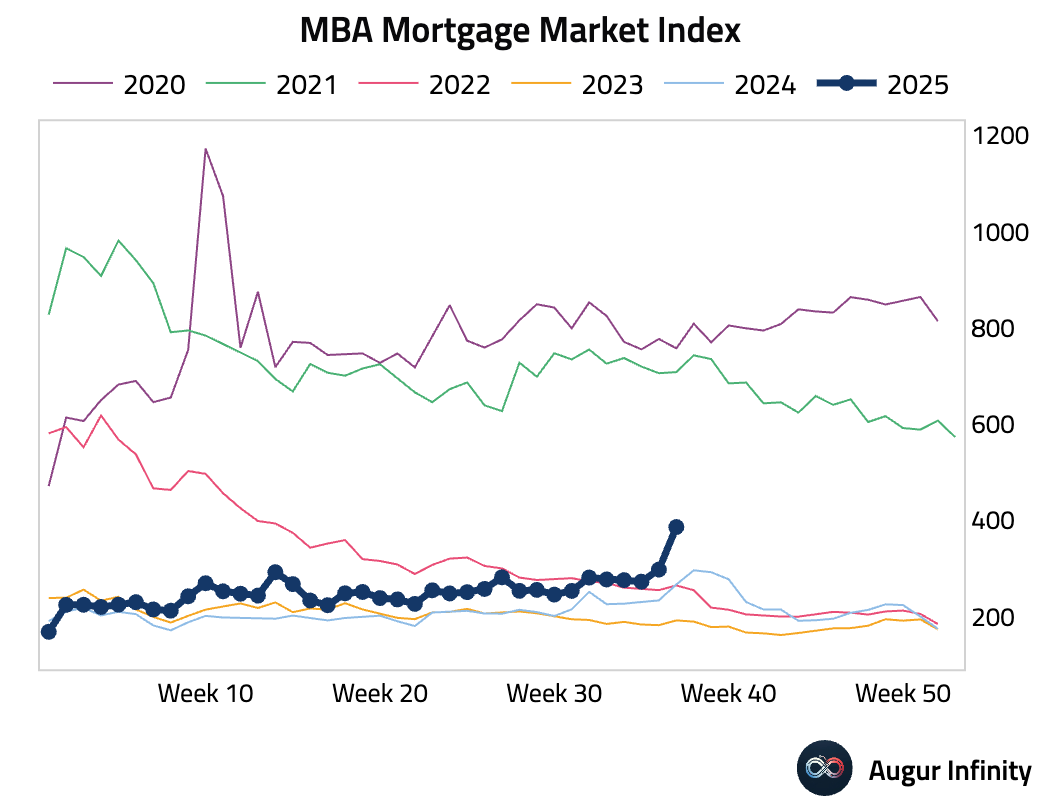

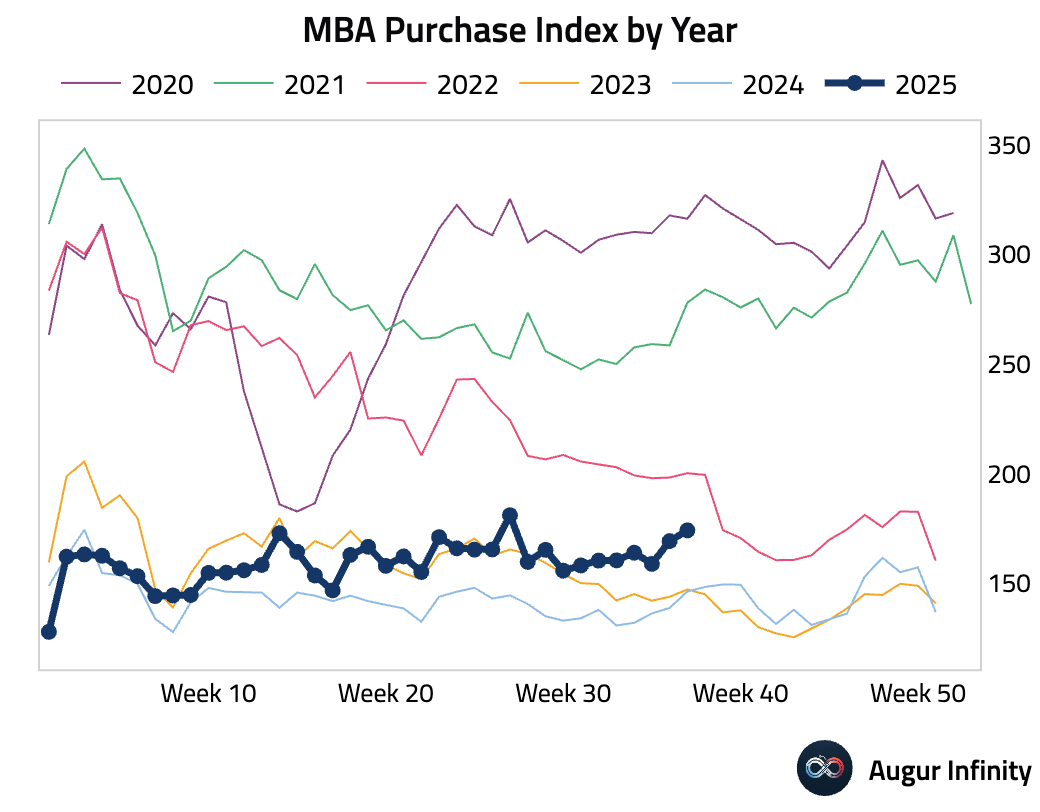

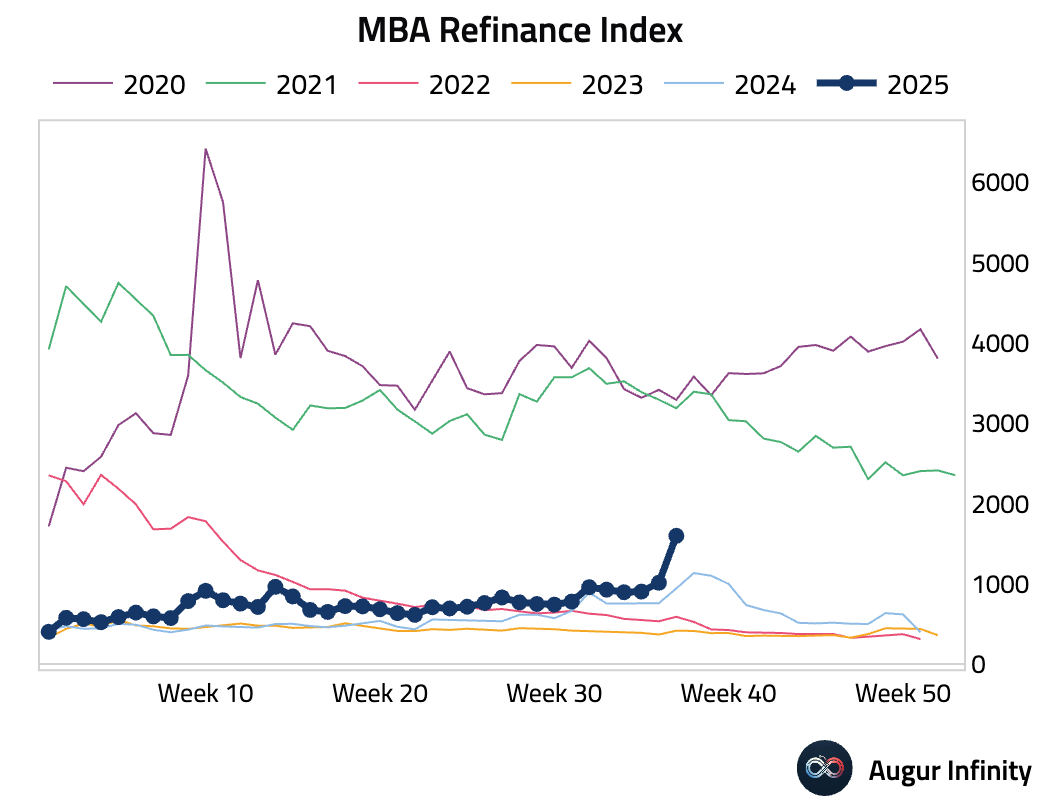

- US mortgage applications surged 29.7% week-over-week, driven by a significant jump in refinancing activity as mortgage rates fell. The MBA Refinance Index leaped 57.7%, while the Purchase Index saw a more modest 2.9% gain.

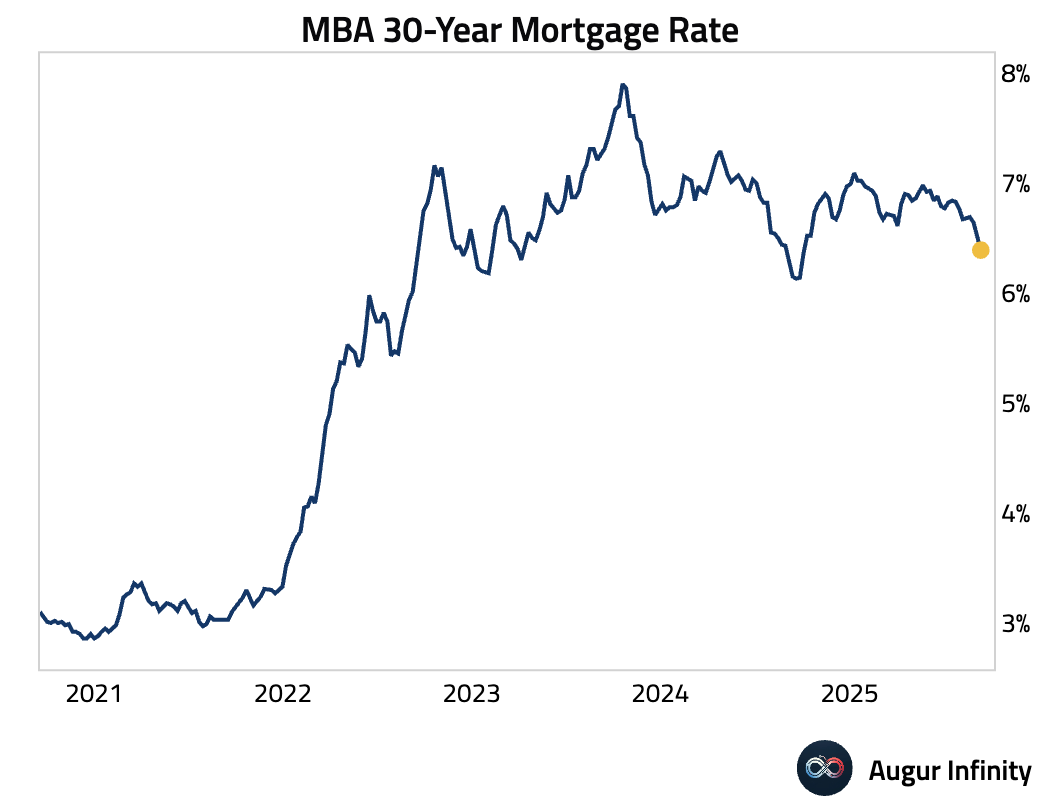

- The average 30-year fixed mortgage rate fell 10 bps to 6.39% for the week ending September 12, marking the second consecutive weekly decline.

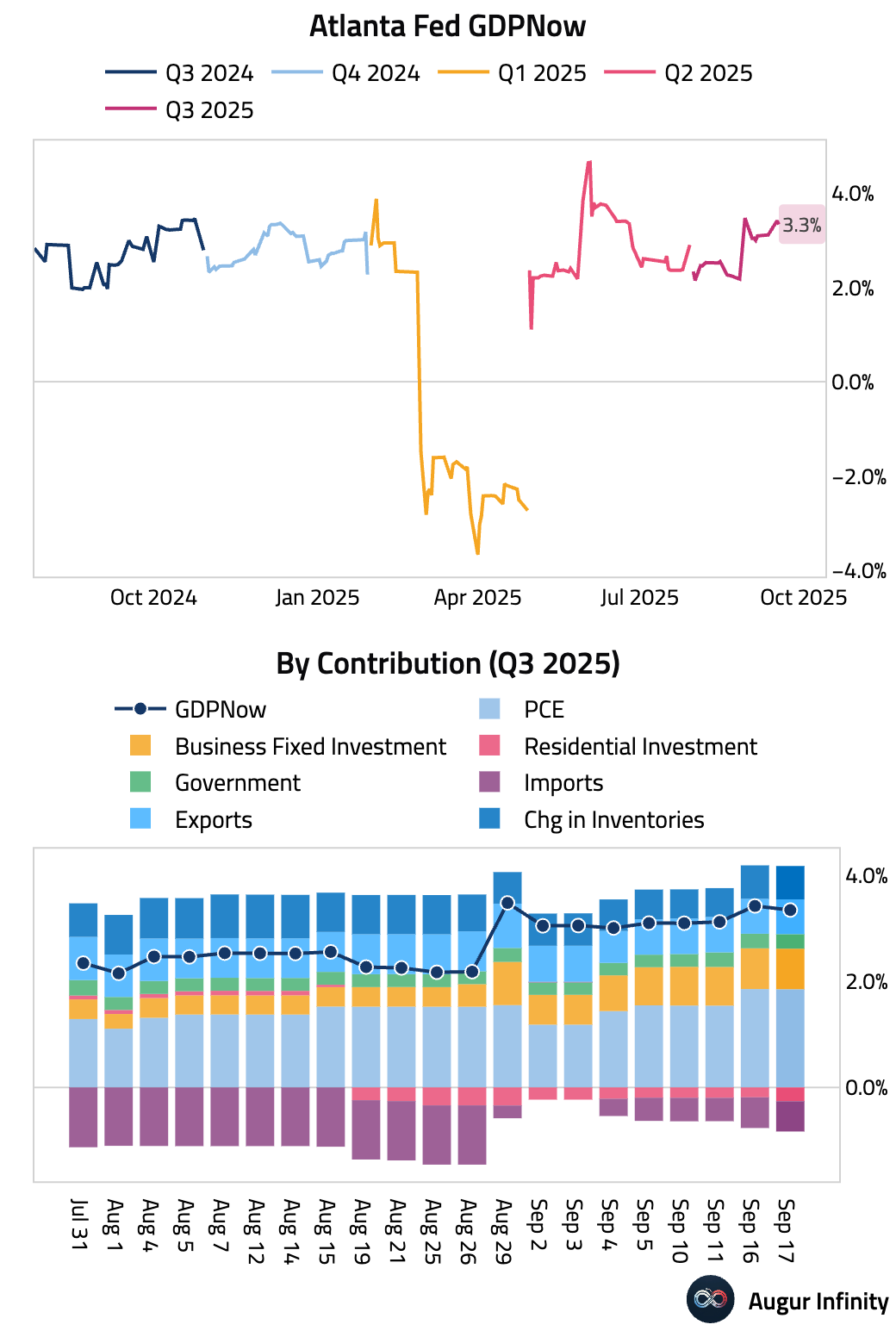

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 3.3%, down from 3.4% yesterday.

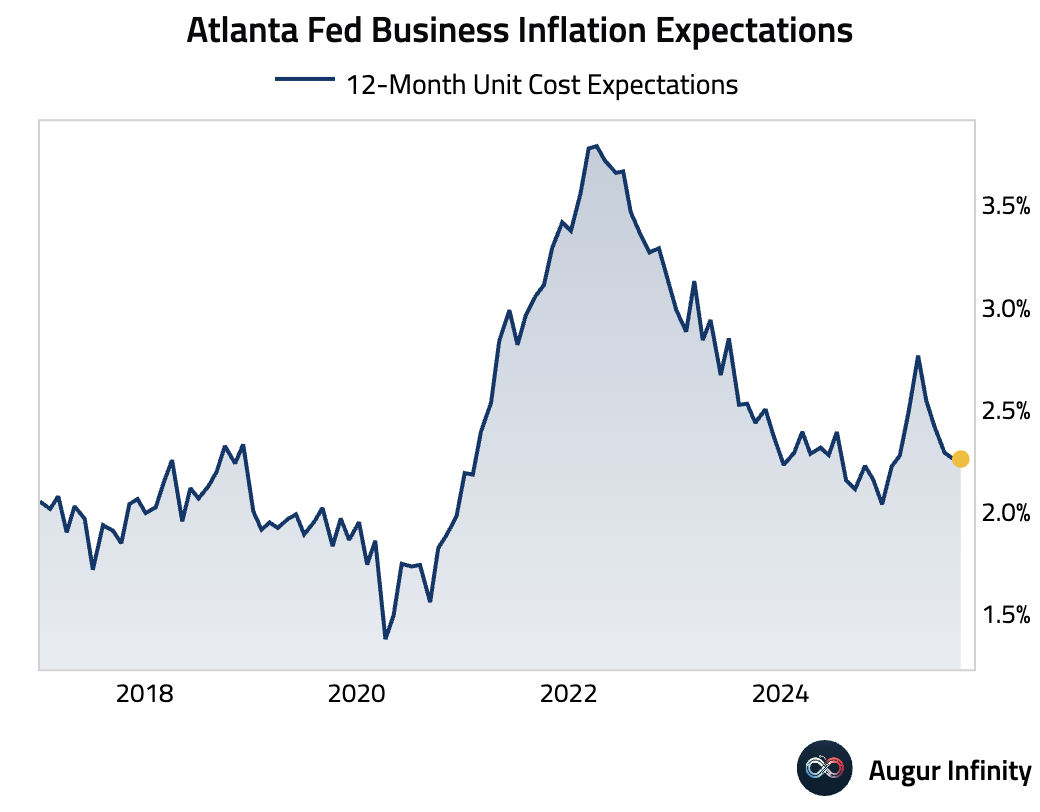

- Business inflation expectations for the coming year held steady at 2.3%.

Canada

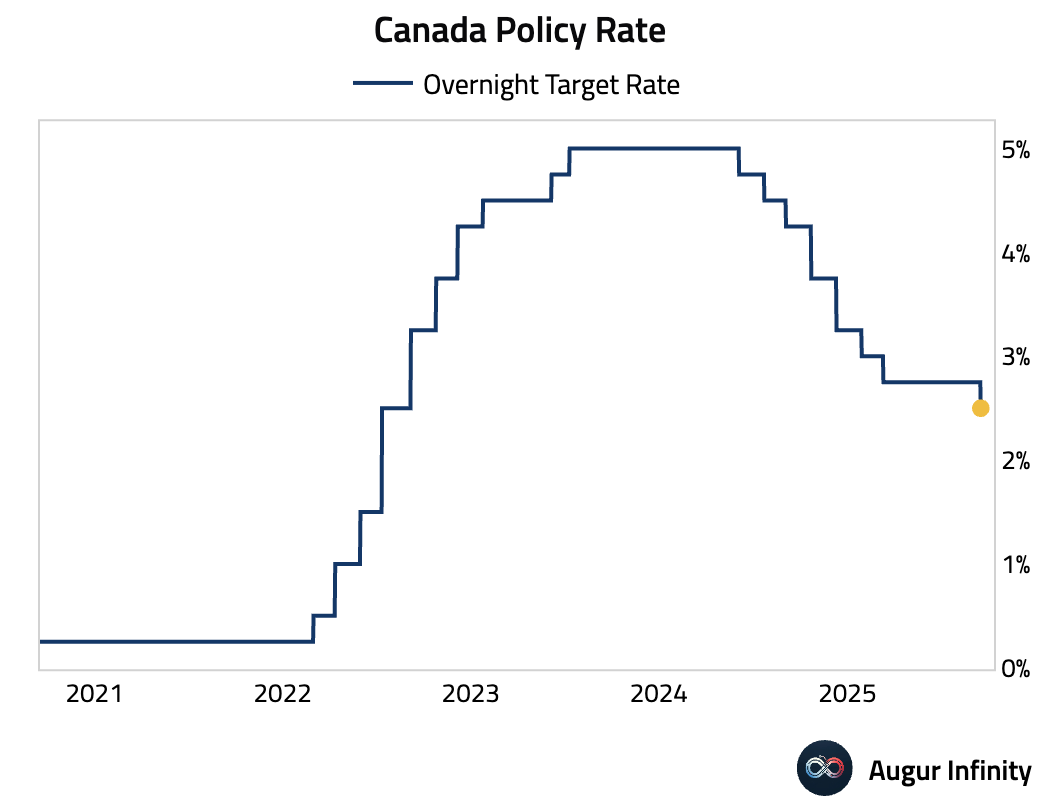

- Bank of Canada cut its policy rate by 25 bps to 2.5%, in line with consensus.

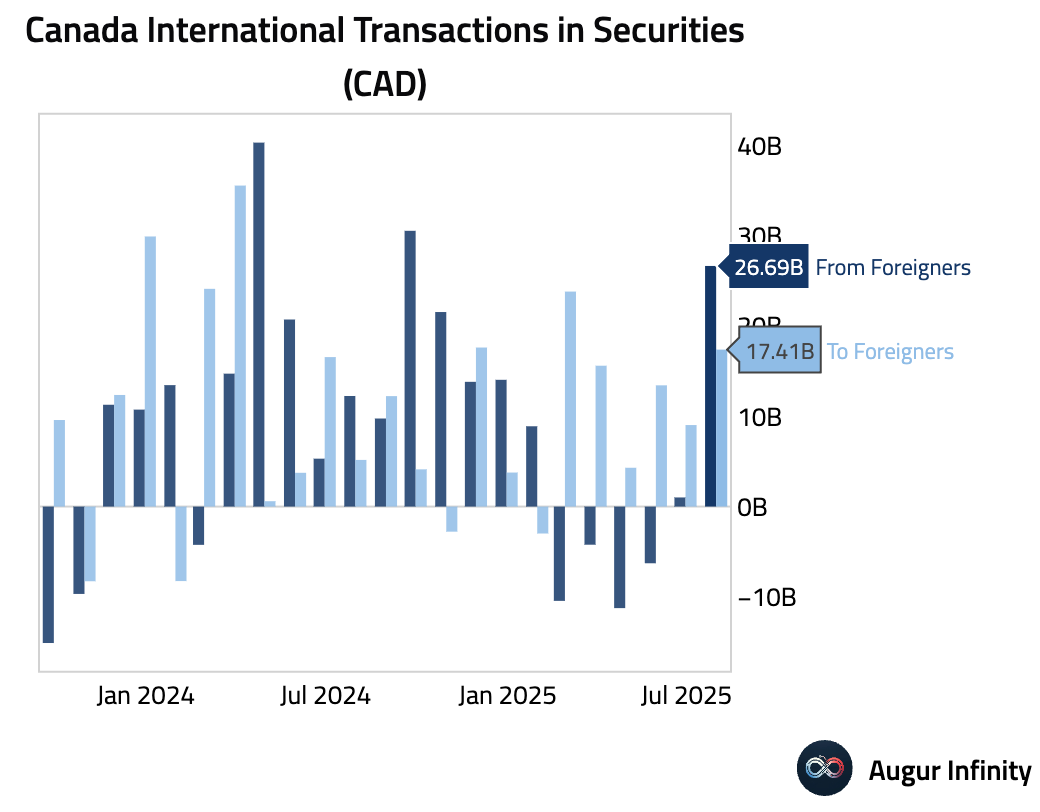

- Foreign investment in Canadian securities surged to C$26.7B in July (prev: C$1.0B), while Canadian investment in foreign securities also jumped to C$17.4B (prev: C$9.0B).

Europe

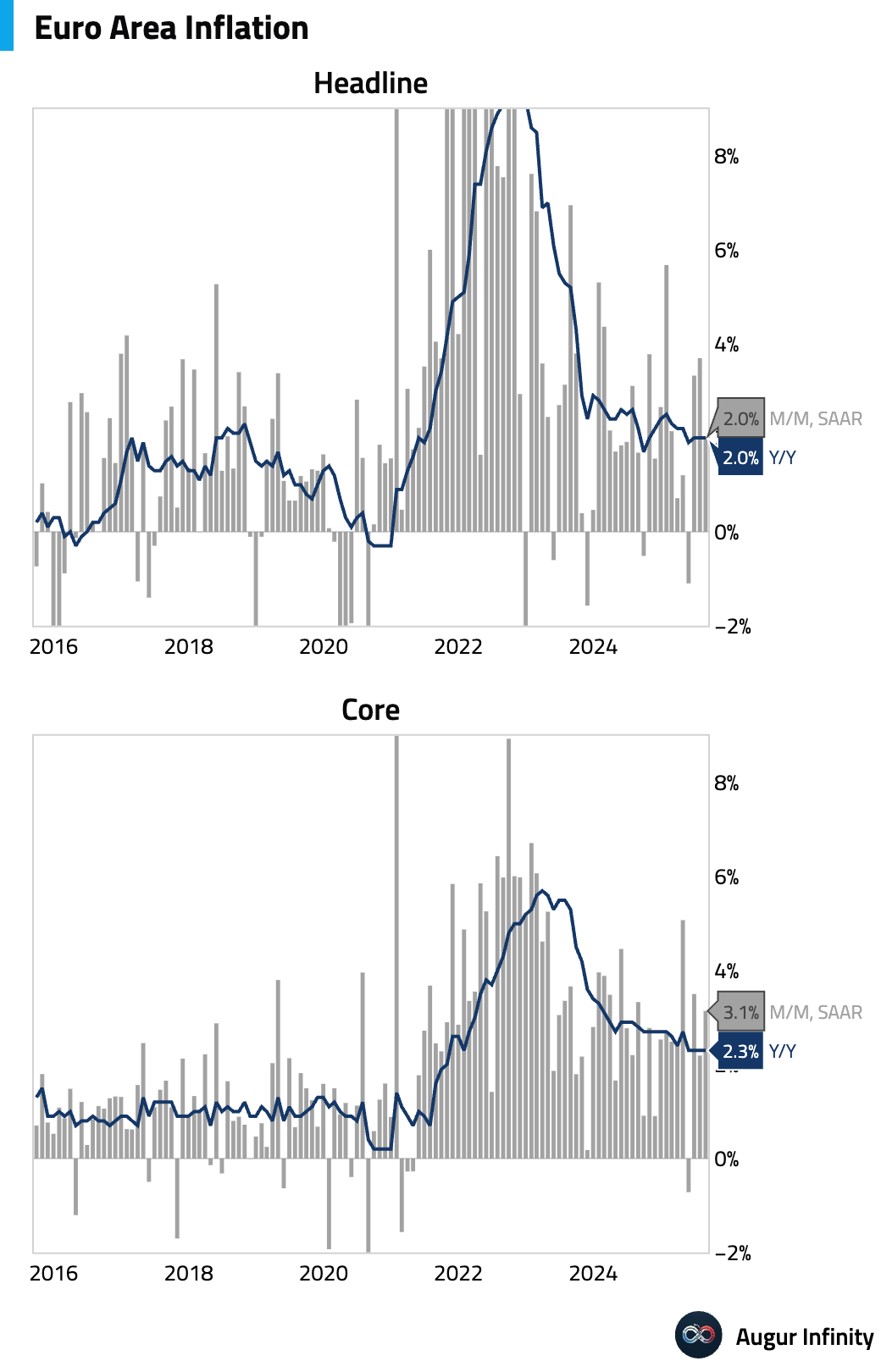

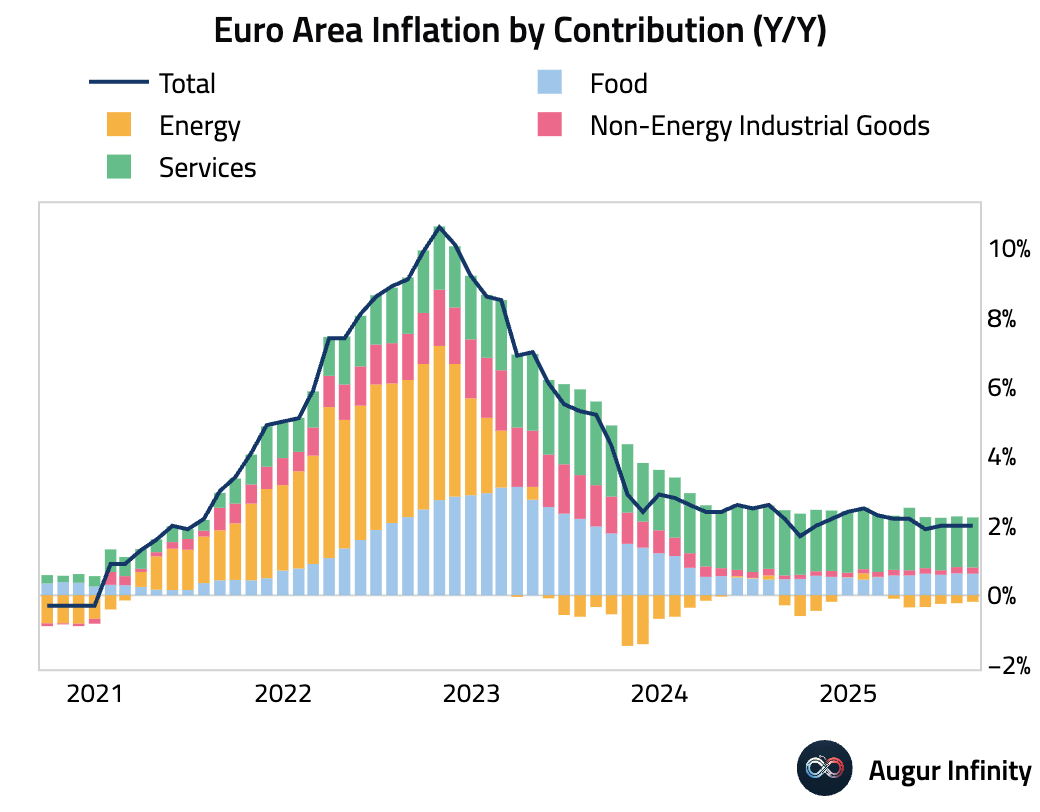

- The final estimate for Euro Area August inflation was unrevised, with headline HICP at 2.0% Y/Y and core at 2.3% Y/Y. Services remain the primary driver of inflation, contributing 1.44pp to the headline figure. While year-over-year figures were stable, sequential measures of underlying inflation ticked higher, signaling persistent price pressures.

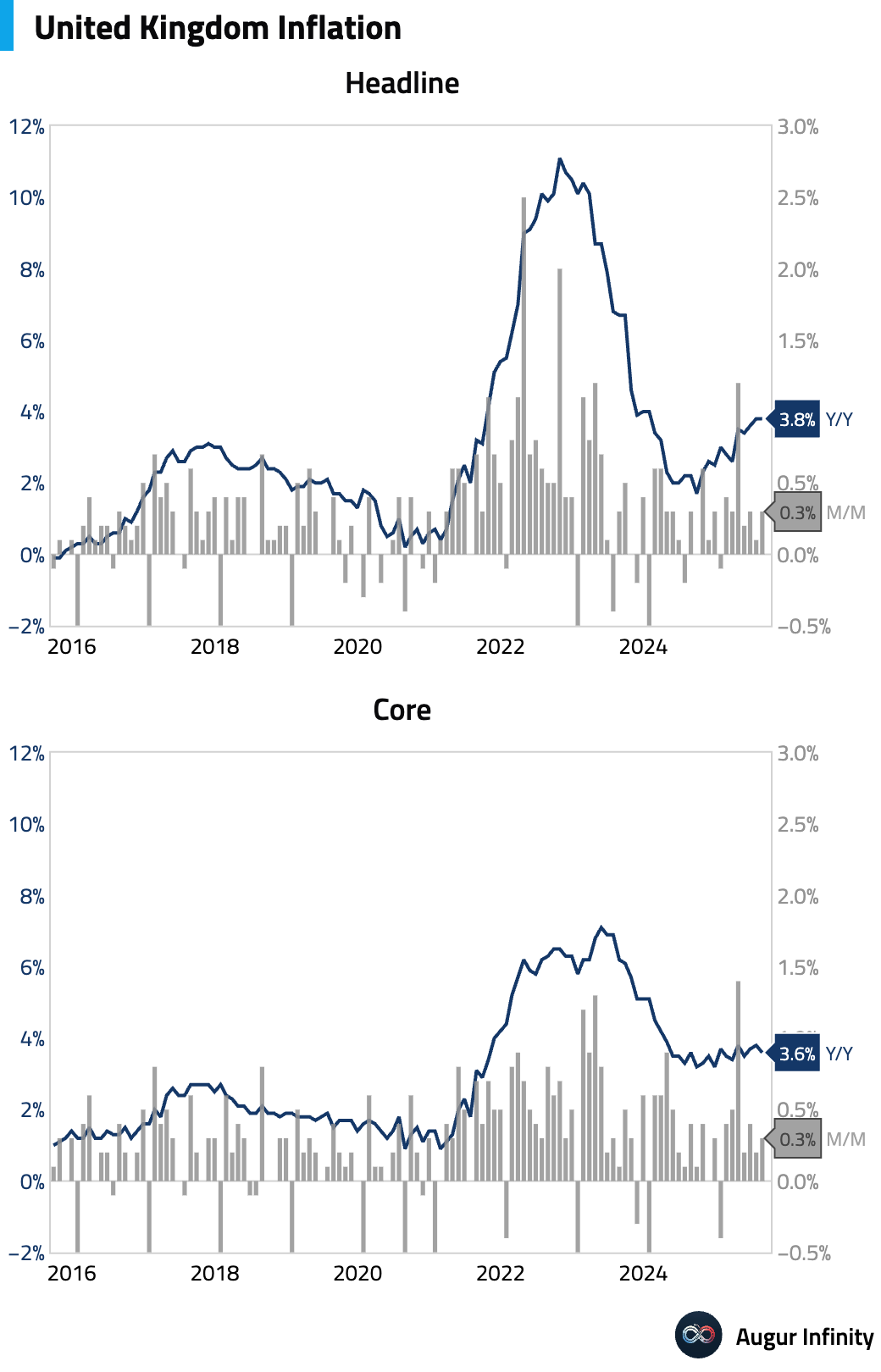

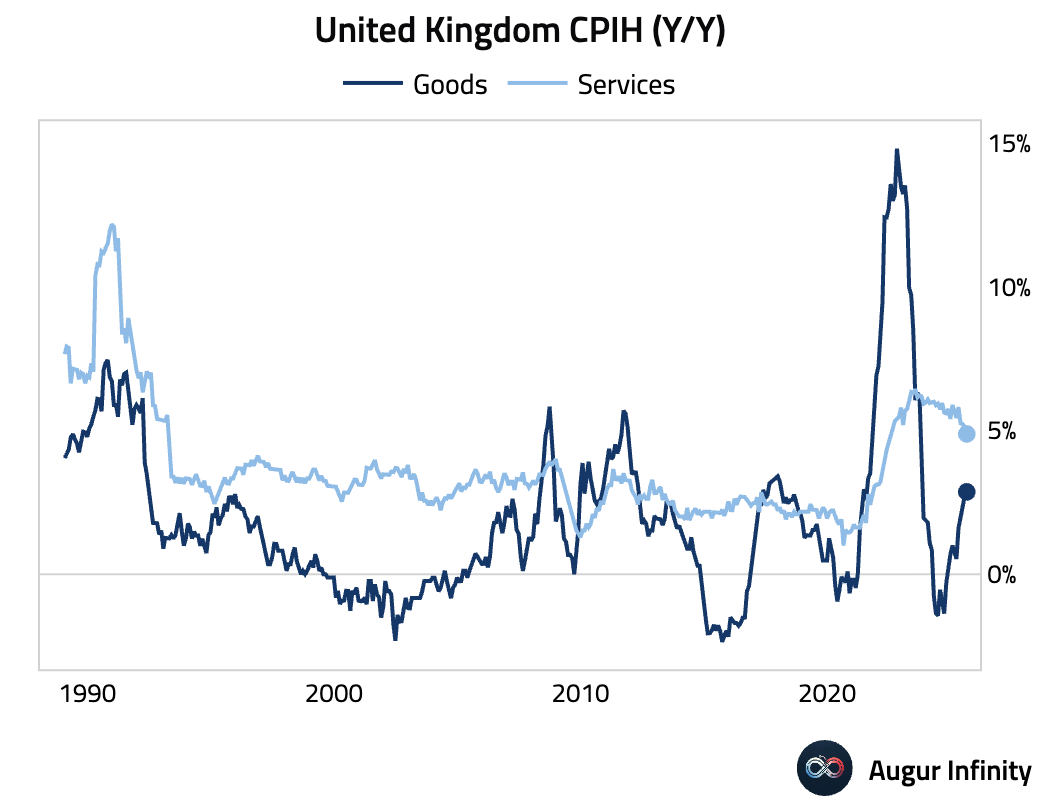

- UK headline inflation was stable in August at 3.8% Y/Y, meeting consensus estimates. Core inflation decelerated to 3.6% Y/Y from 3.8%. A modest dip in headline was driven by lower core inflation, largely offset by higher food and energy prices. Services inflation fell more than expected to 4.7% Y/Y, driven by a normalization in airfare inflation after a July spike, although underlying services inflation metrics were estimated to be unchanged.

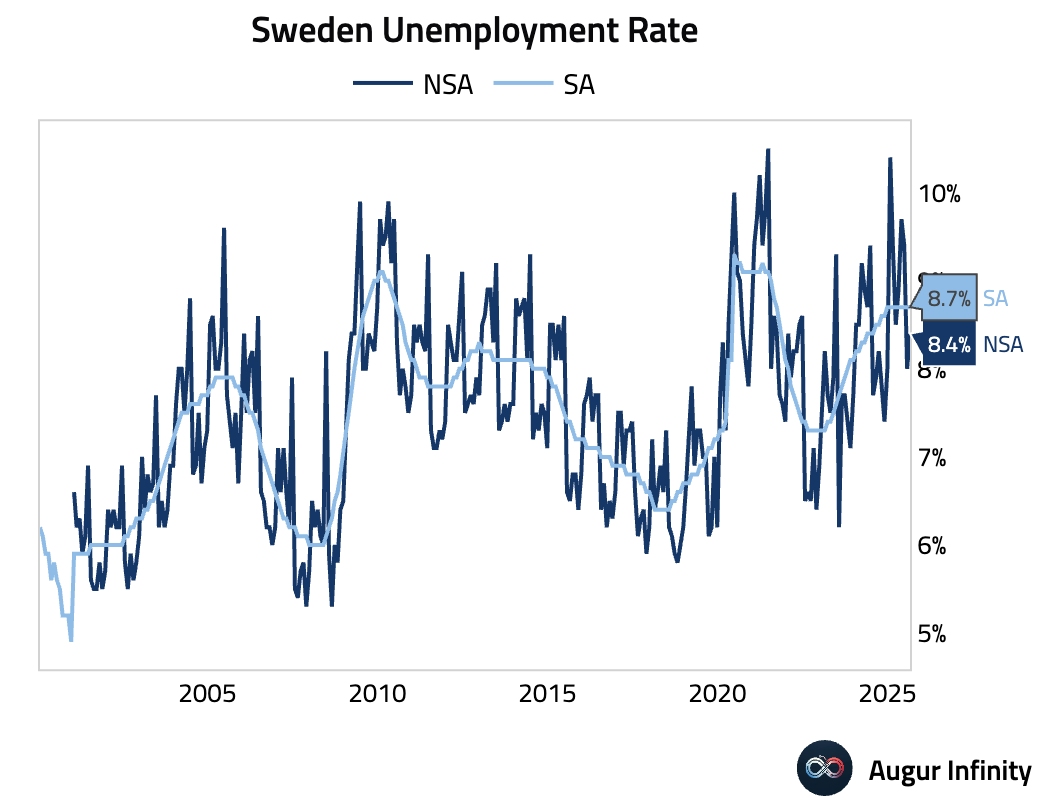

- Sweden’s unemployment rate rose to 8.4% in August (prev: 8.0%). On a seasonally adjusted basis, unemployment rate was unchanged.

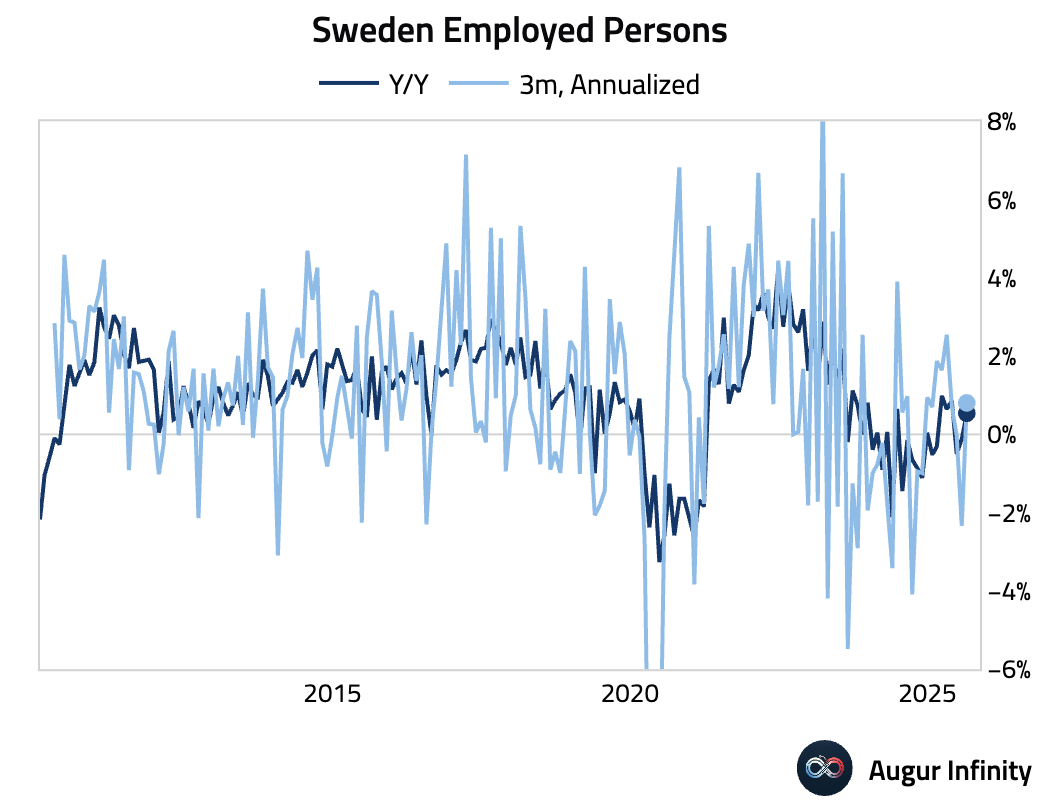

- The number of employed persons in Sweden fell to 5.32 million in August from 5.44 million in July.

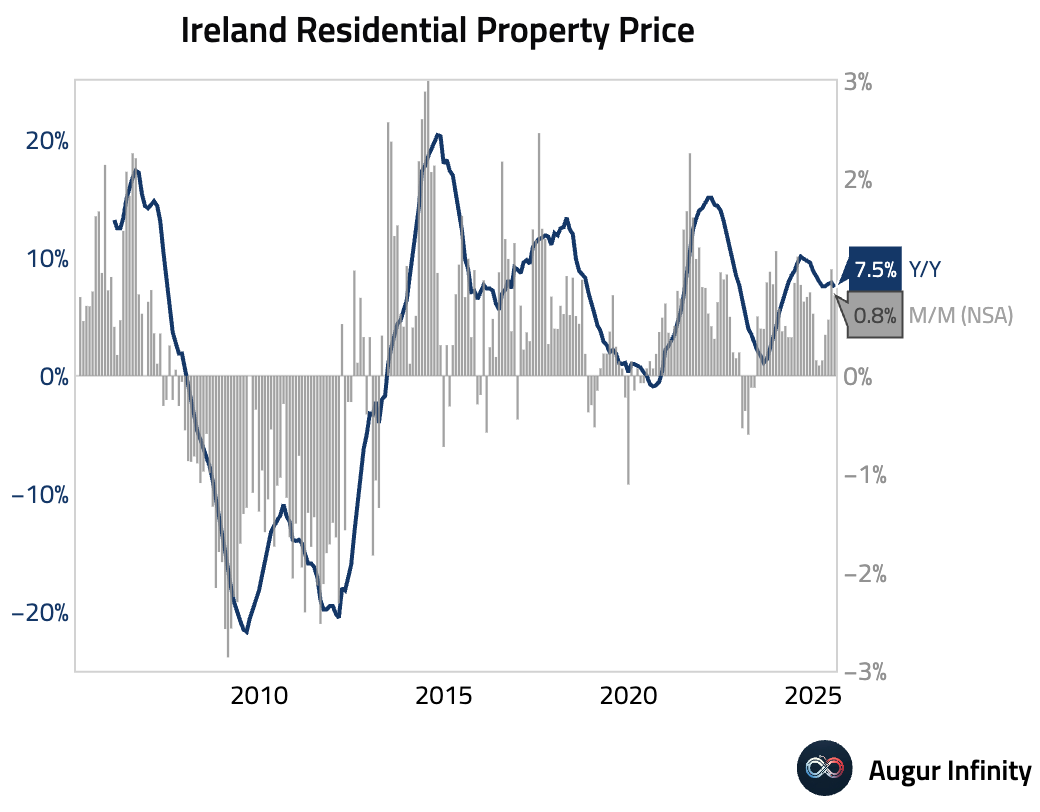

- Irish residential property prices continued to climb in July, rising 0.8% M/M and 7.5% Y/Y, though the annual pace of appreciation has slowed from June.

Asia-Pacific

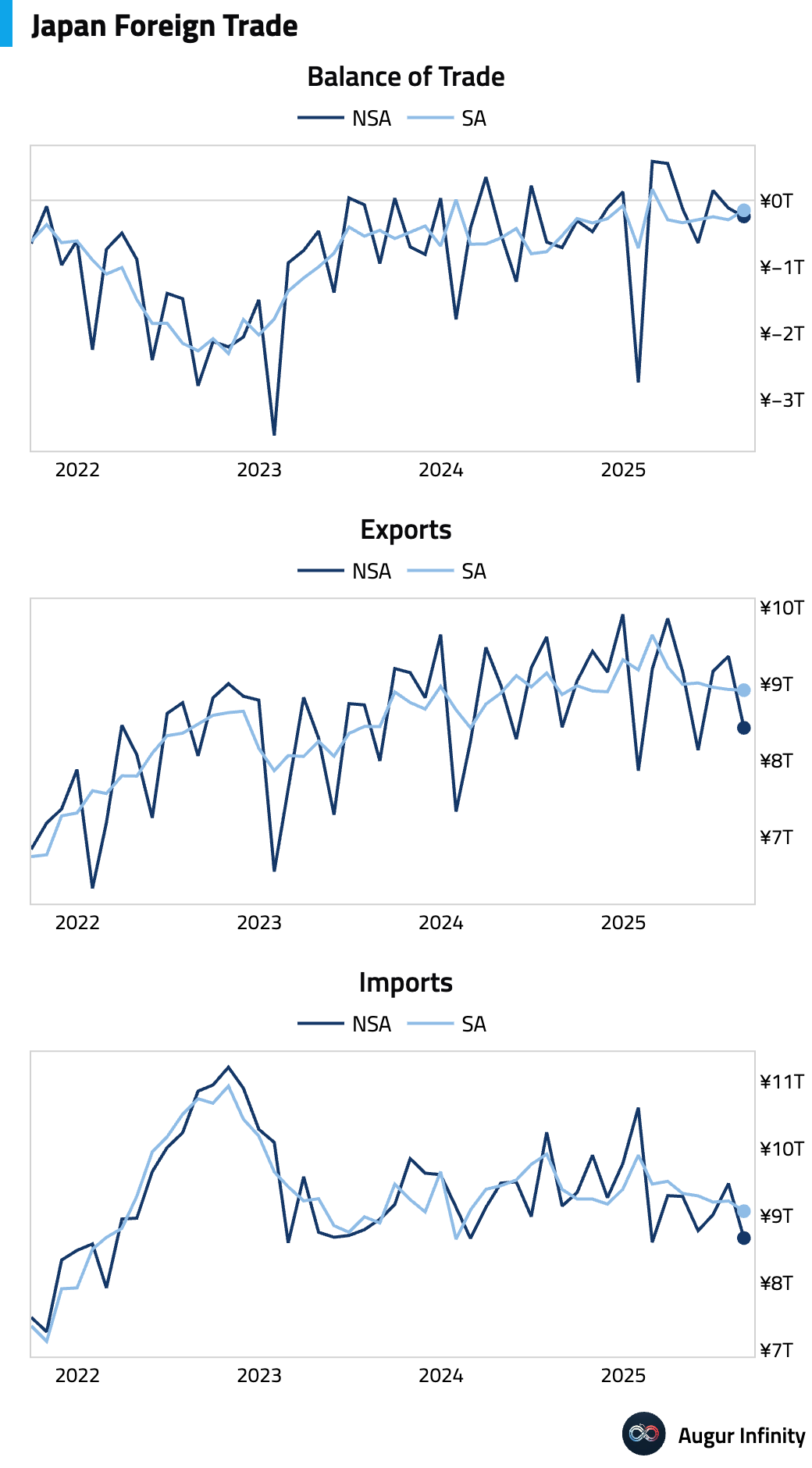

- Japan’s August trade deficit narrowed sharply to -¥242.5B, significantly beating forecasts (est: -¥513.6B), as exports declined less than expected at -0.1% Y/Y (est: -1.9%). However, the headline masks underlying weakness, as export volumes fell for a second straight month, driven by declines to the US and China. The weakness was attributed to automakers potentially holding back on low-profitability exports amid tariffs, rather than a drop in US demand.

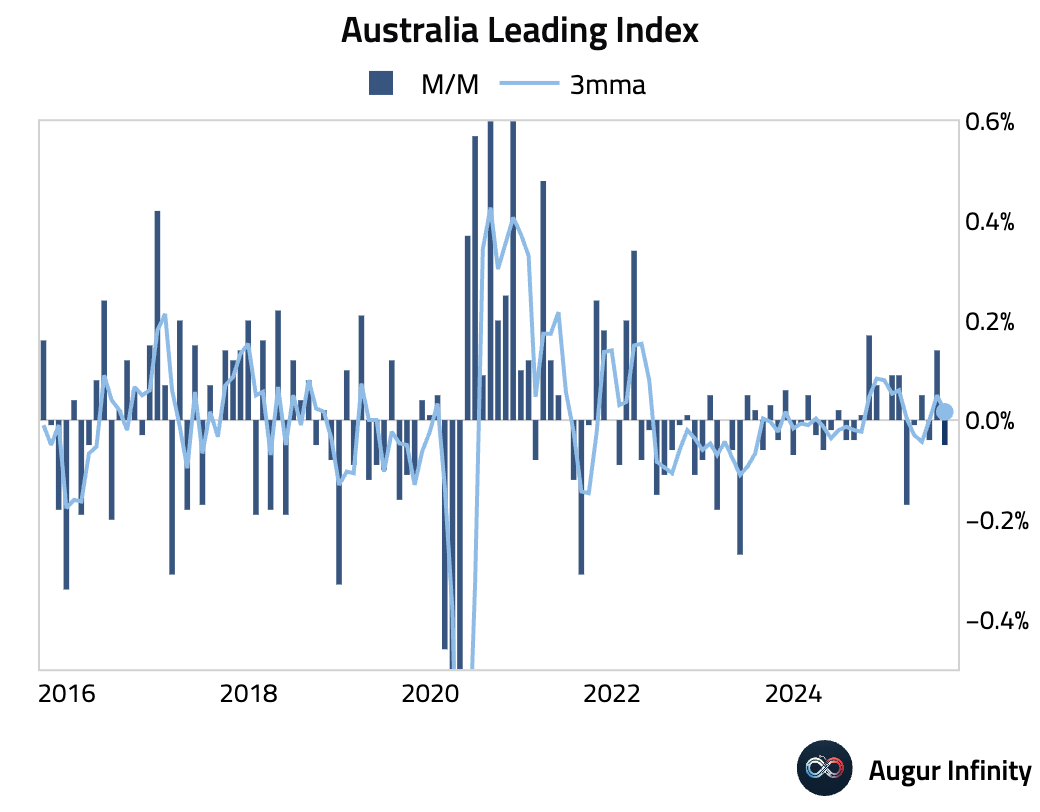

- Australia’s Westpac Leading Index slipped into negative territory in August, falling 0.1% M/M (prev: 0.1%).

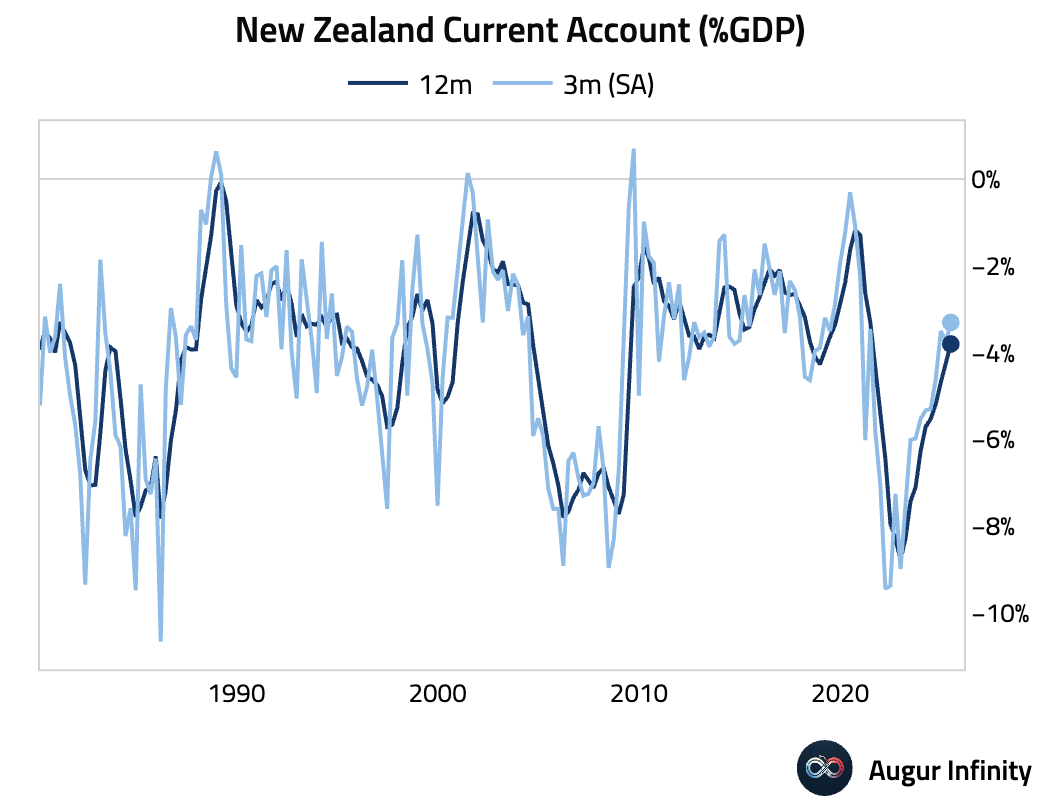

- New Zealand’s current account deficit for Q2 was significantly smaller than anticipated at -NZ$1.0B (est: -NZ$2.7B). The data included substantial downward revisions to deficits over the prior six quarters, reframing the country's historical balance of payments position.

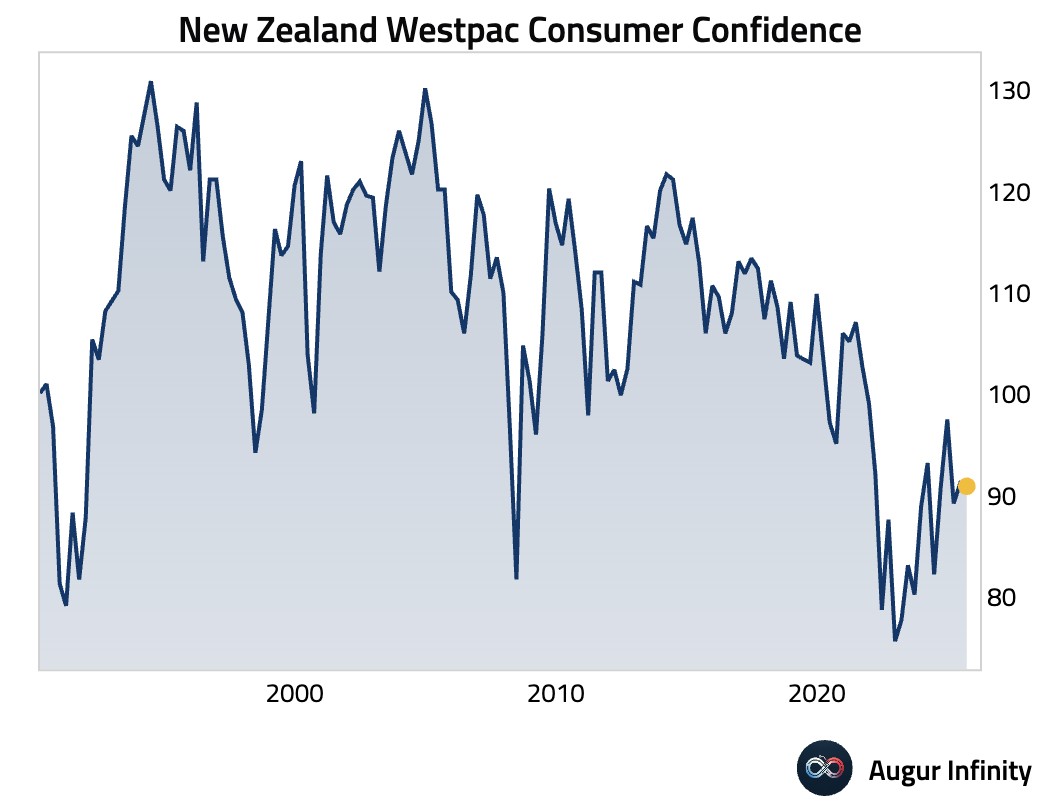

- New Zealand's consumer confidence edged slightly lower in Q3 (act: 90.9, prev: 91.2).

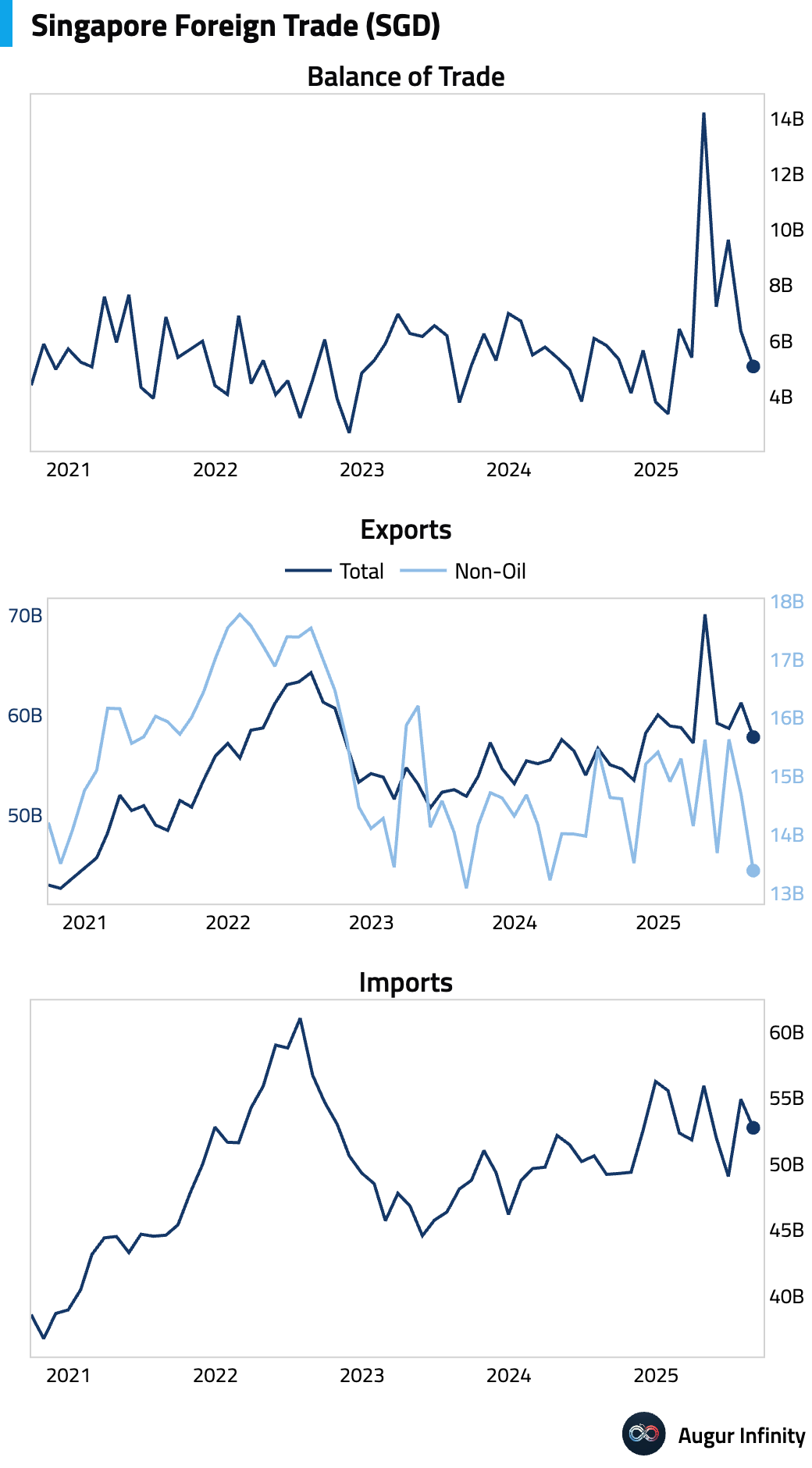

- Singapore's non-oil exports plunged in August, falling 8.9% M/M and 11.3% Y/Y (est: 1.0%), driven by a sharp fall in non-electronics. Exports to the US were the primary drag, suggesting US tariff impacts are now materializing.

Emerging Markets ex China

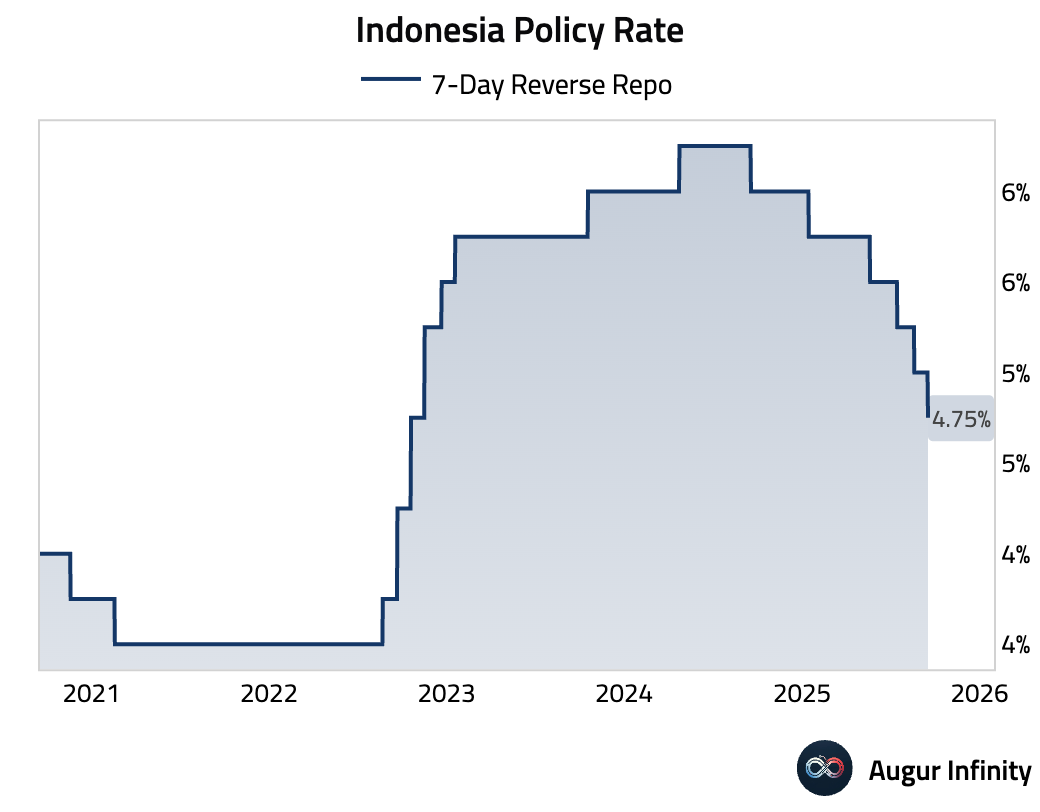

- Bank Indonesia unexpectedly cut its policy rate by 25 bps to 4.75% (est: 5.00%), citing the need to support growth amid low inflation. The surprise move came despite recent weakness in the rupiah. To further encourage bank lending, the deposit facility rate was cut by a larger 50 bps to 3.75%, as the transmission of previous cuts has been sluggish.

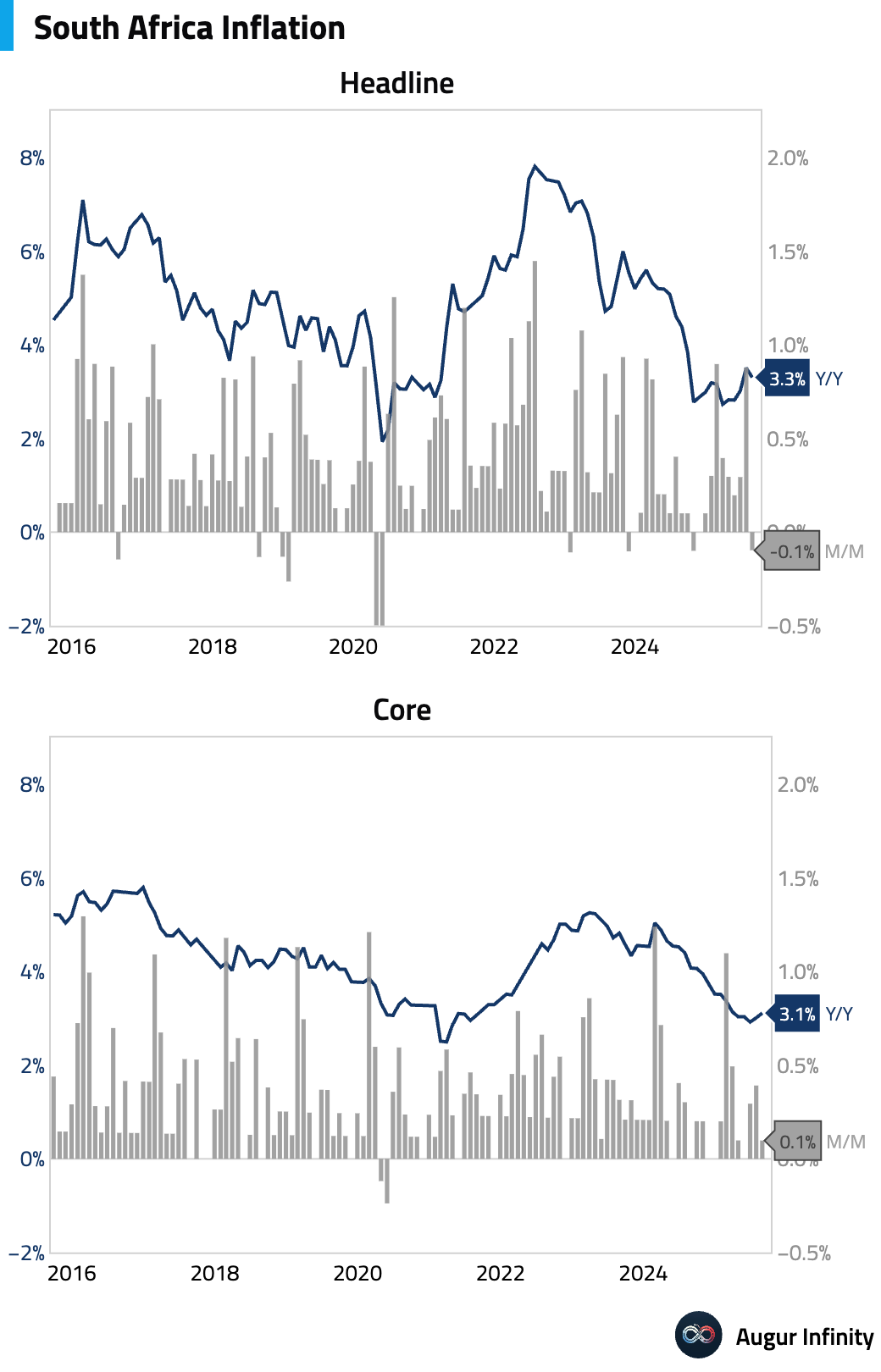

- South African inflation cooled more than expected in August, with headline CPI falling to 3.3% Y/Y (est: 3.6%). The downside surprise was driven by a sharp slowdown in food inflation, a result of favorable rainfall and harvests.

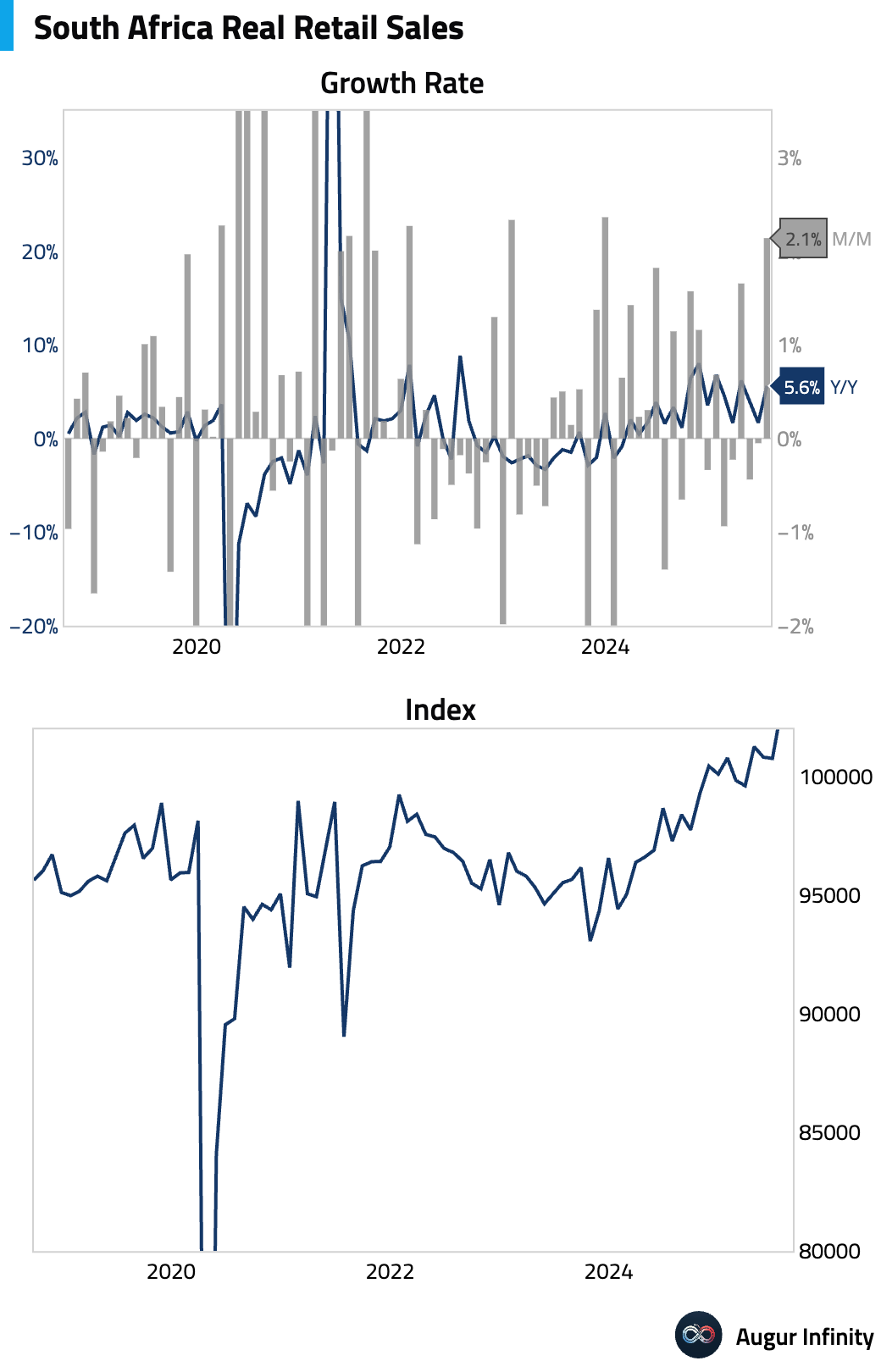

- South African retail sales posted a strong rebound in July, rising 2.1% M/M and 5.6% Y/Y.

Global Markets

Equities

- Global equities were mixed following the Federal Reserve’s rate cut. US markets were down slightly, with the S&P 500 falling 0.1% and the Nasdaq Composite slipping 0.3%. Emerging markets outperformed, rising 0.8% for a third consecutive day of gains. Chinese and Brazilian equities also extended their rallies to three days, climbing 1.5% and 1.0%, respectively. In Europe, French and UK stocks declined for a second straight session.

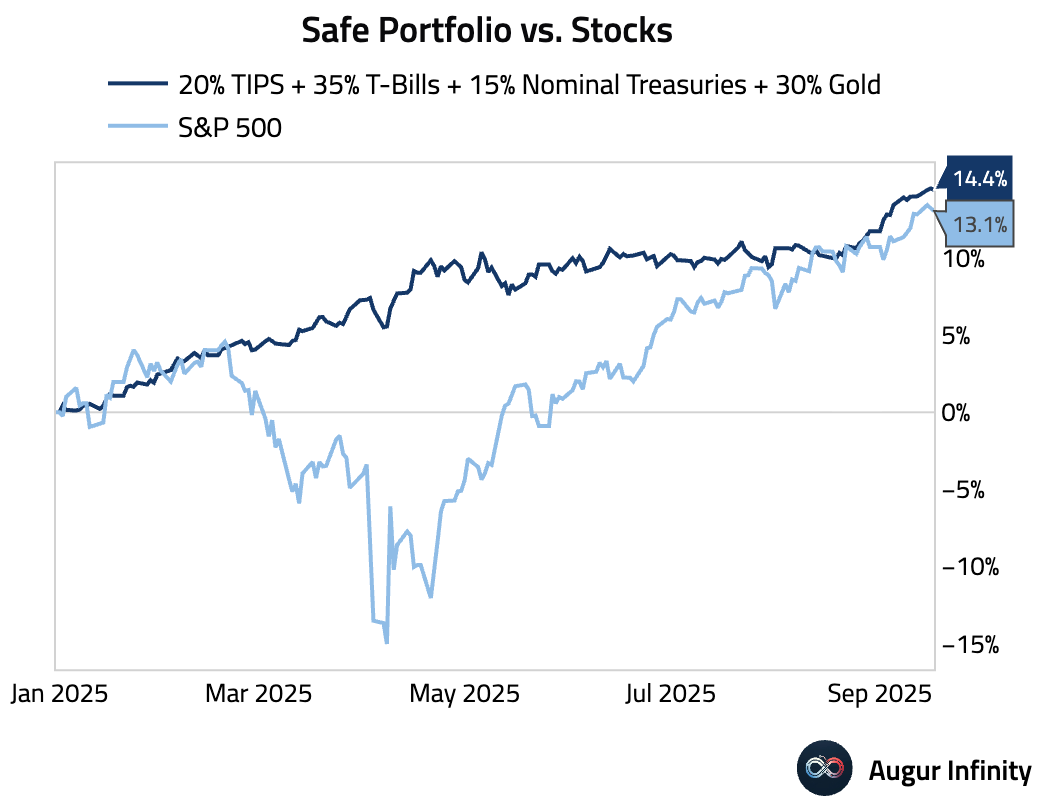

- A portfolio of "safe" assets continue to outperform the S&P 500 this year.

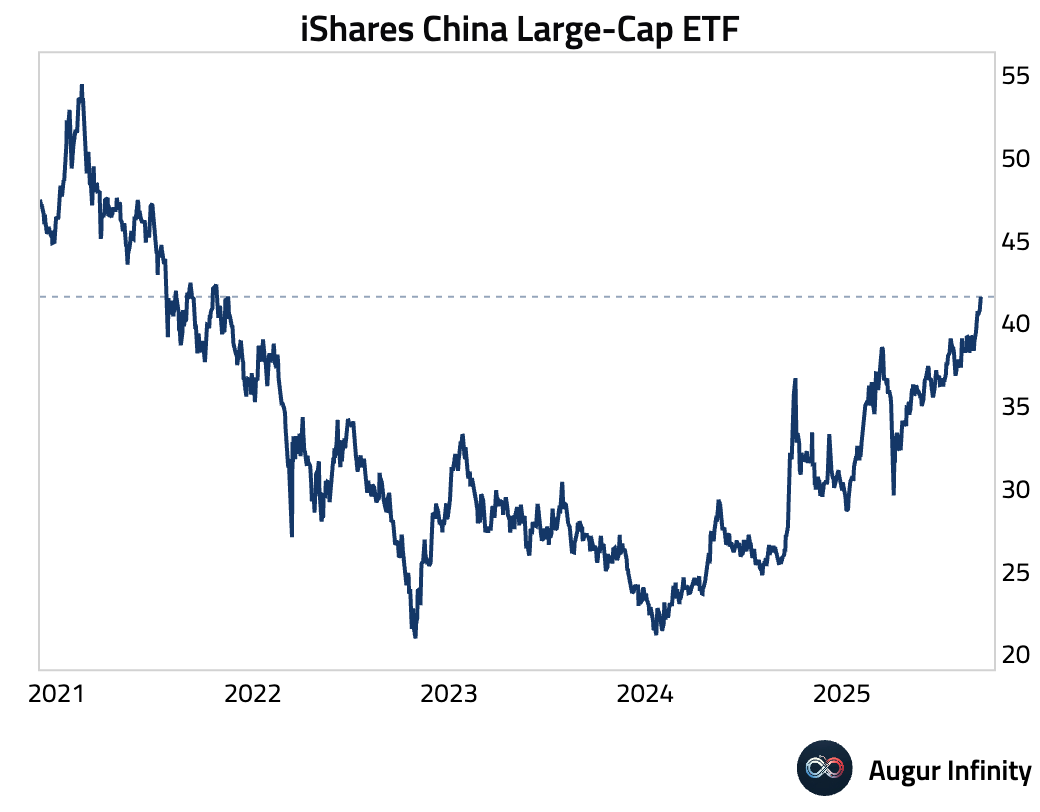

- iShares China Large-Cap ETF has reached the highest level since November 2021.

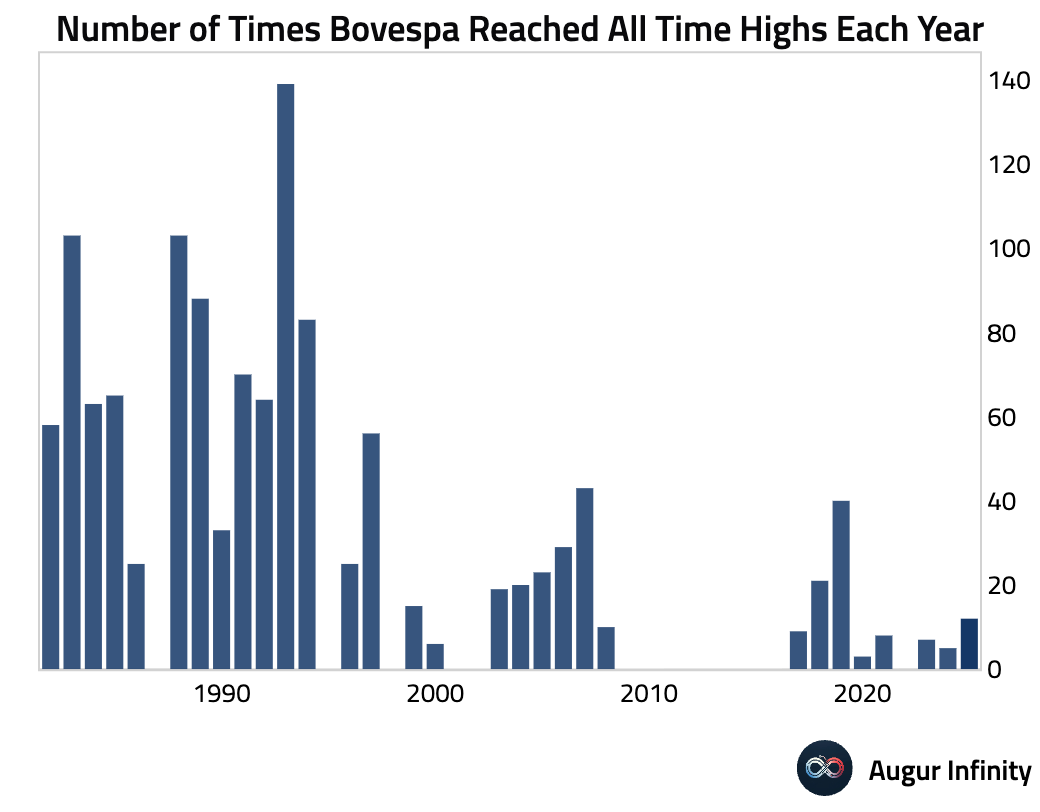

- Brazil's BOVESPA Index has reached all-time highs 12 times so far this year.

Fixed Income

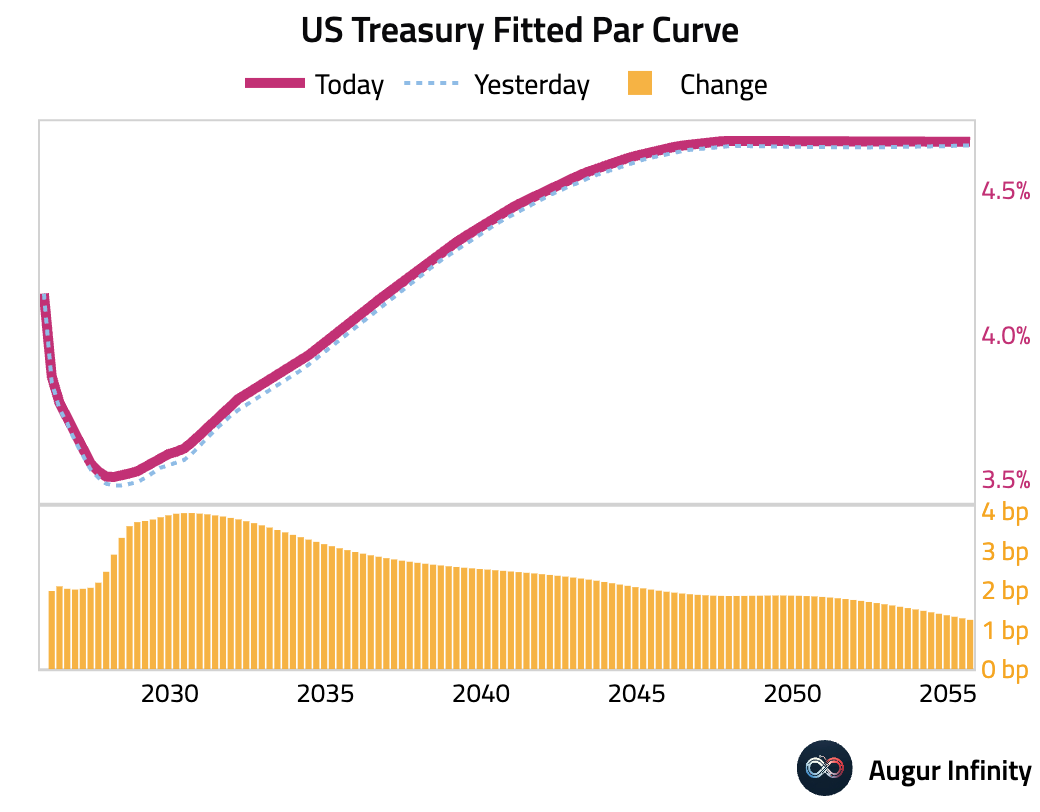

- US Treasury yields rose across the curve, with the 5-year yield leading the increase with a 5.5 bps climb. The 2-year and 10-year yields added 3.7 bps and 4.3 bps, respectively.

Commodities

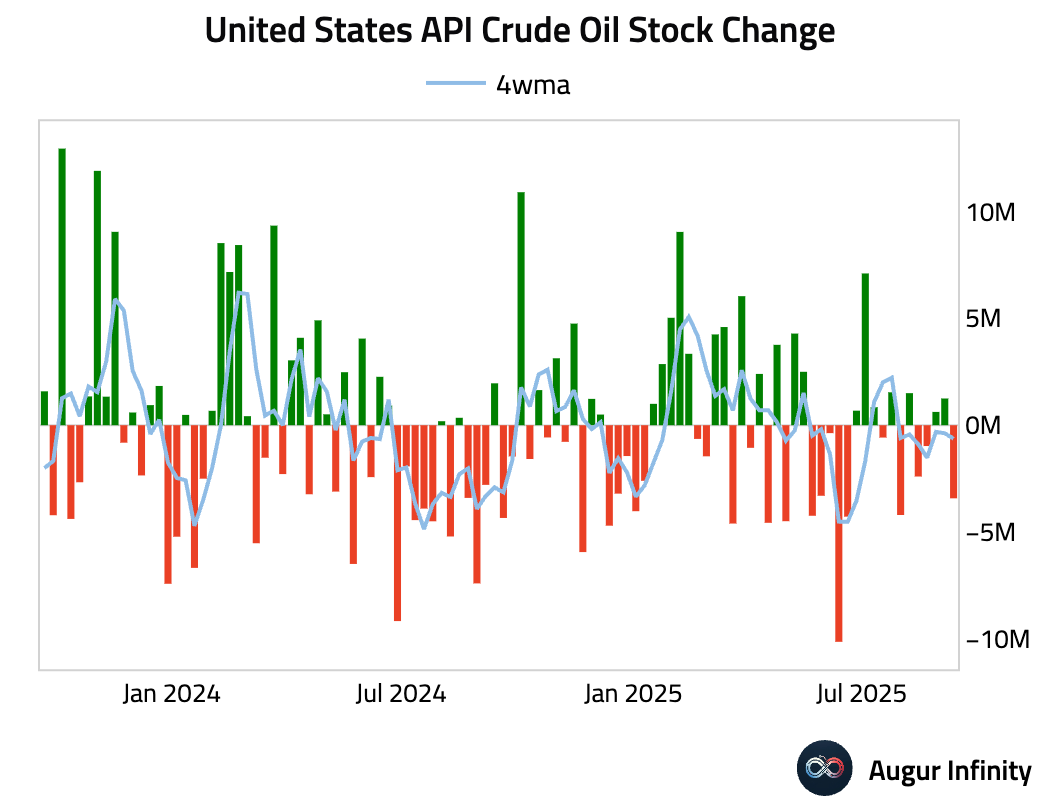

- API data showed a larger-than-expected draw in US crude oil inventories last week (act: -3.42M, est: -1.60M).

FX

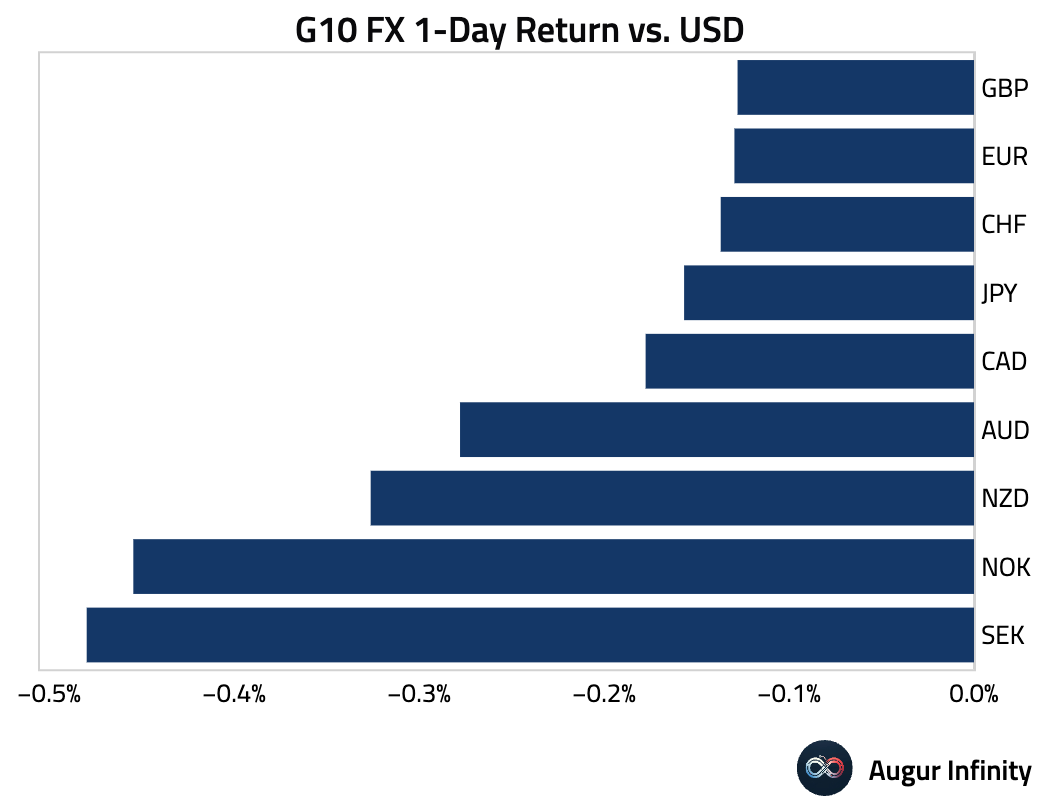

- The US dollar strengthened against all its G10 peers. The Scandinavian currencies were the primary underperformers, with both the Swedish krona and Norwegian krone falling 0.5% against the dollar. The Australian dollar also weakened, declining by 0.3%.

- The renminbi has appreciated to the highest level (against USD) since October 2024.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.