Global Economics

United States

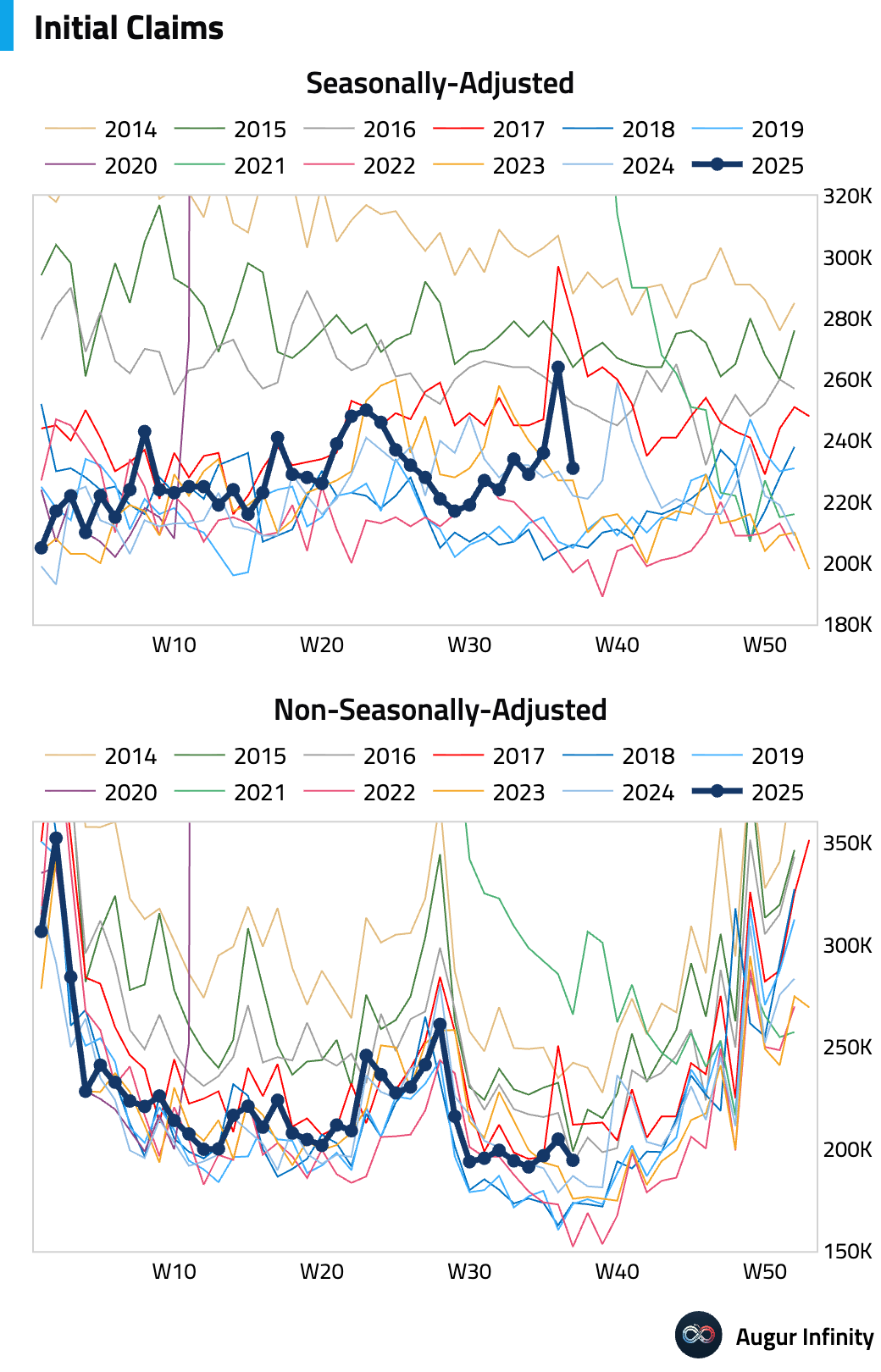

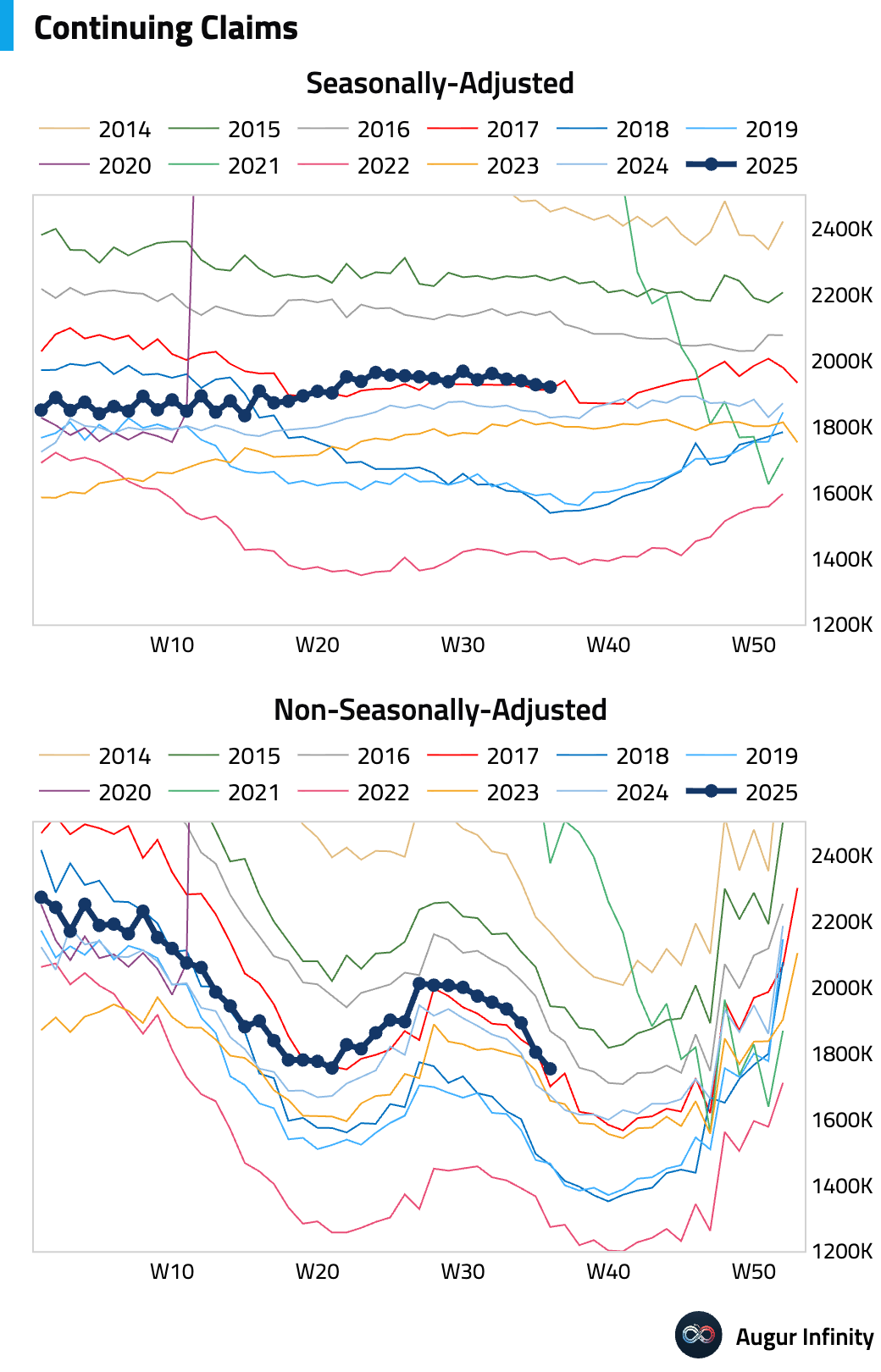

- Initial jobless claims fell more than expected last week to 231k, reversing a recent spike (est: 240k). The drop was driven by a normalization in Texas, where last week’s jump was attributed to fraudulent filings. Continuing claims also edged down to 1.92 million.

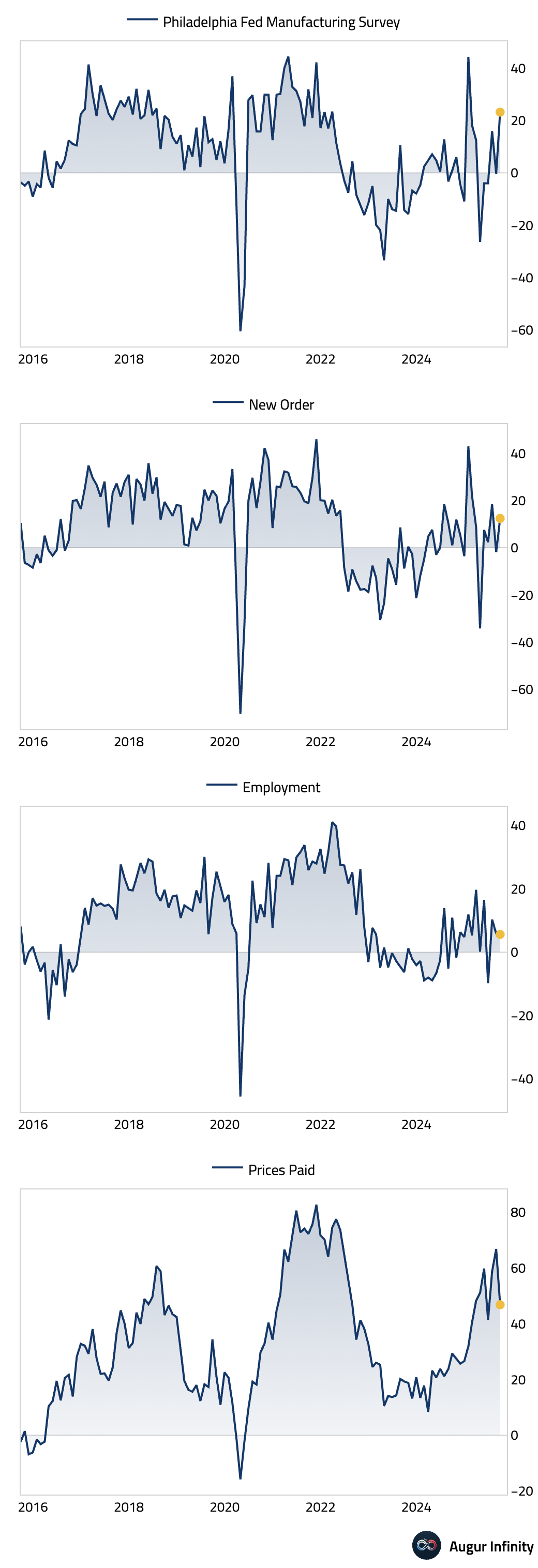

- The Philadelphia Fed Manufacturing Index surged in September, crushing expectations and signaling a rebound in regional factory activity (act: 23.2, est: 2.3). The beat was driven by strong increases in the new orders and shipments components. However, the employment sub-index edged down slightly. Both prices paid and prices received components declined, a positive signal for easing inflationary pressures.

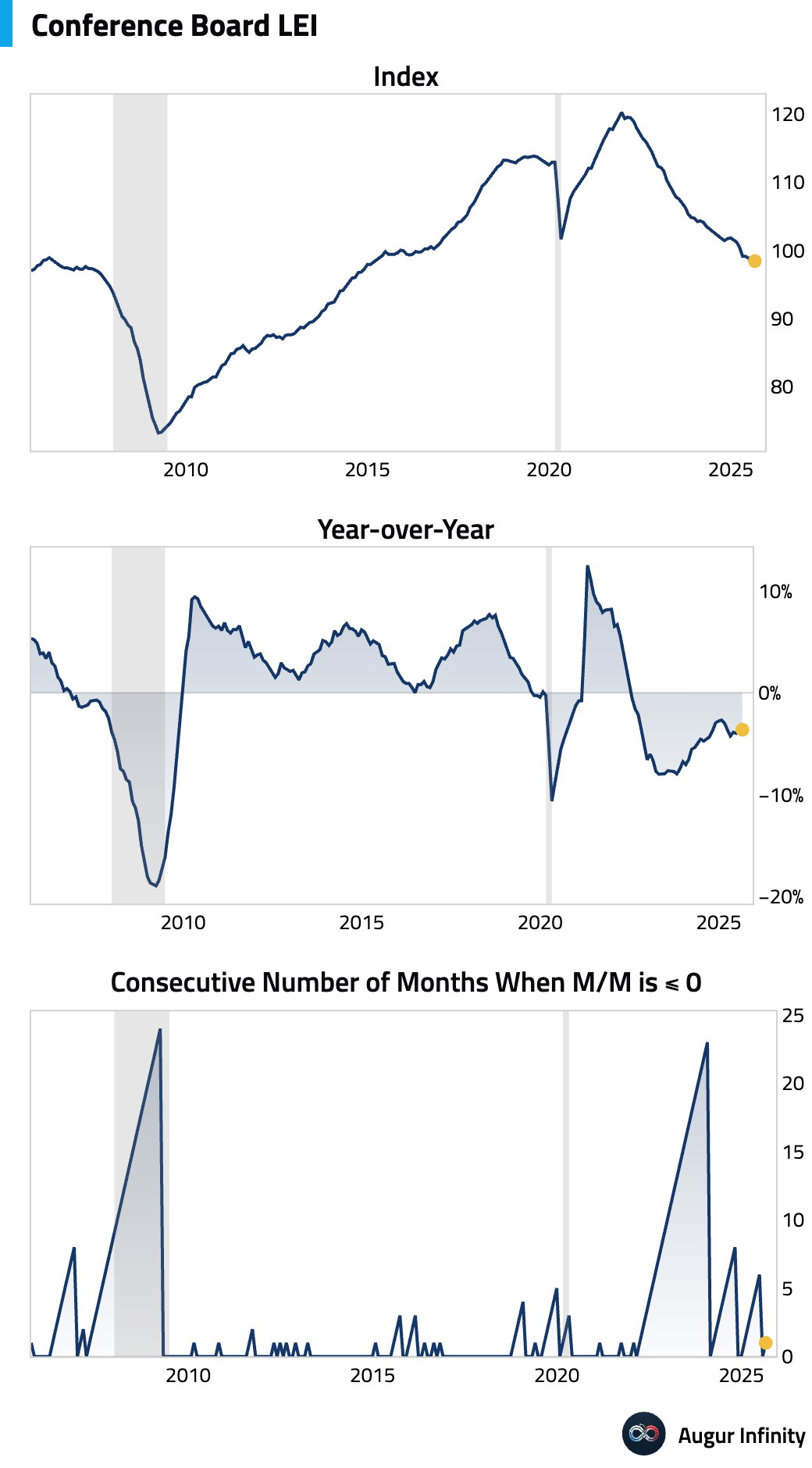

- The Conference Board’s Leading Economic Index fell more than anticipated in August, resuming its downward trend after a slight rise in July (act: -0.5% M/M, est: -0.2%).

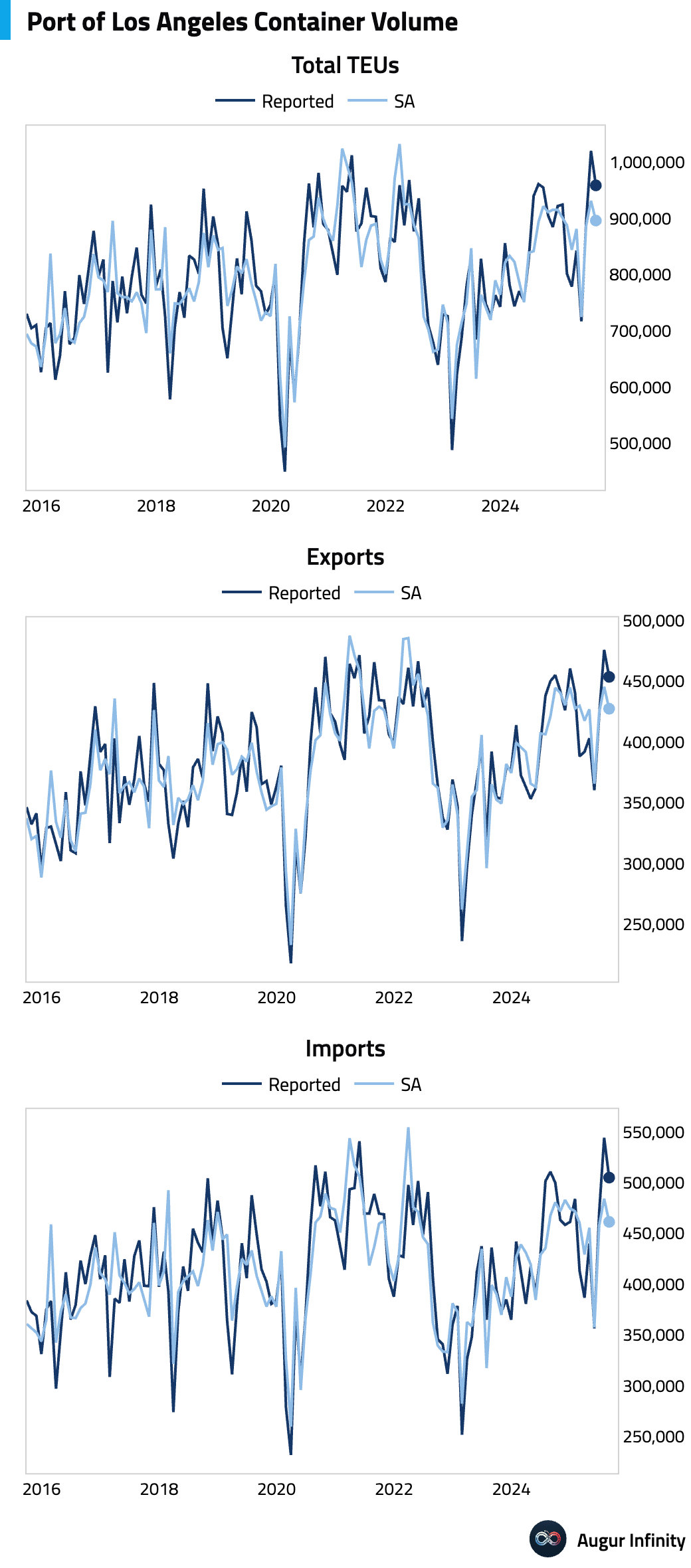

- Container volume at the Port of Los Angeles declined in August, with both exports and imports falling.

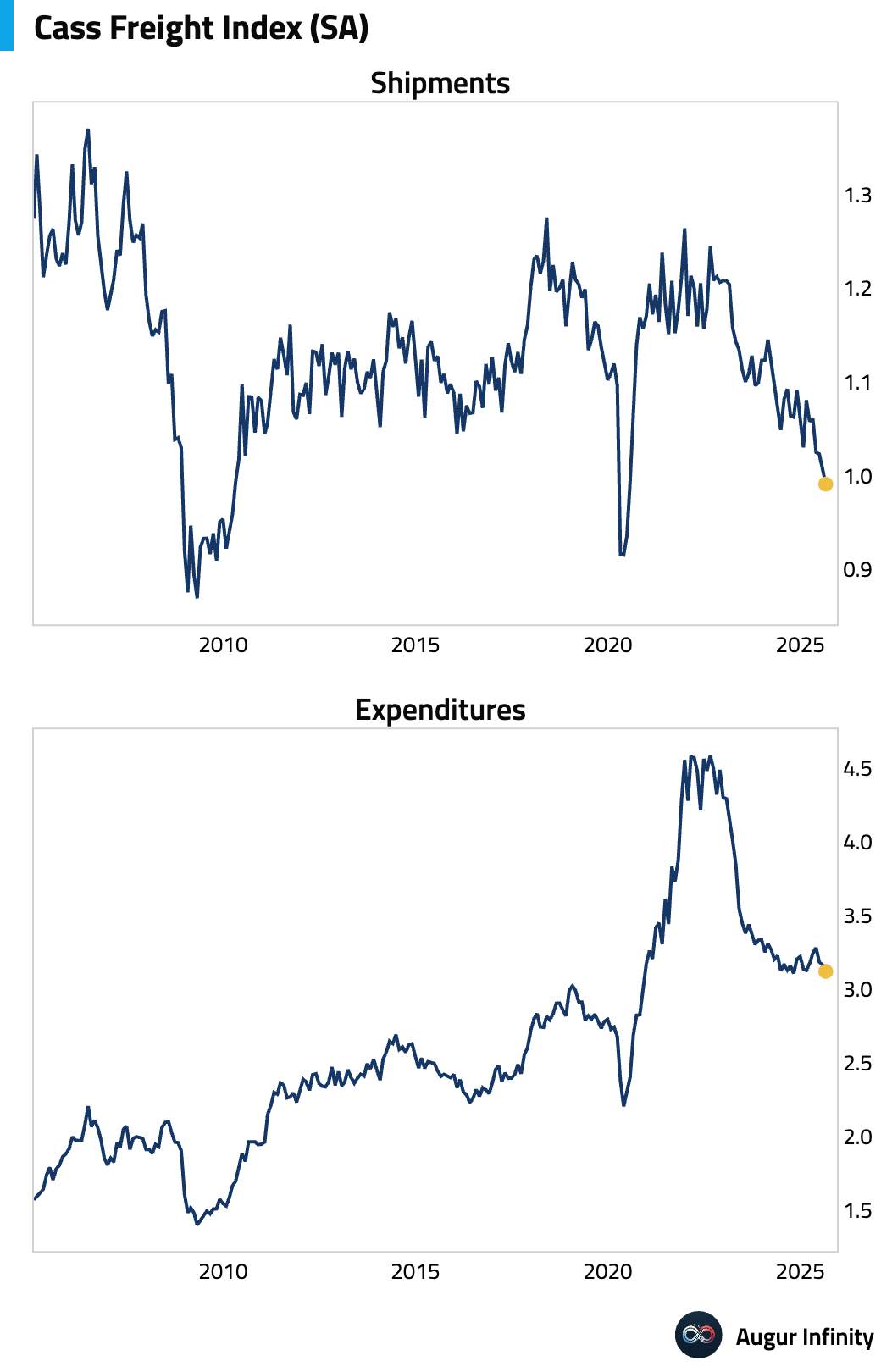

- According to Cass Freight Indices, Shipments declined to the lowest level since the pandemic.

Canada

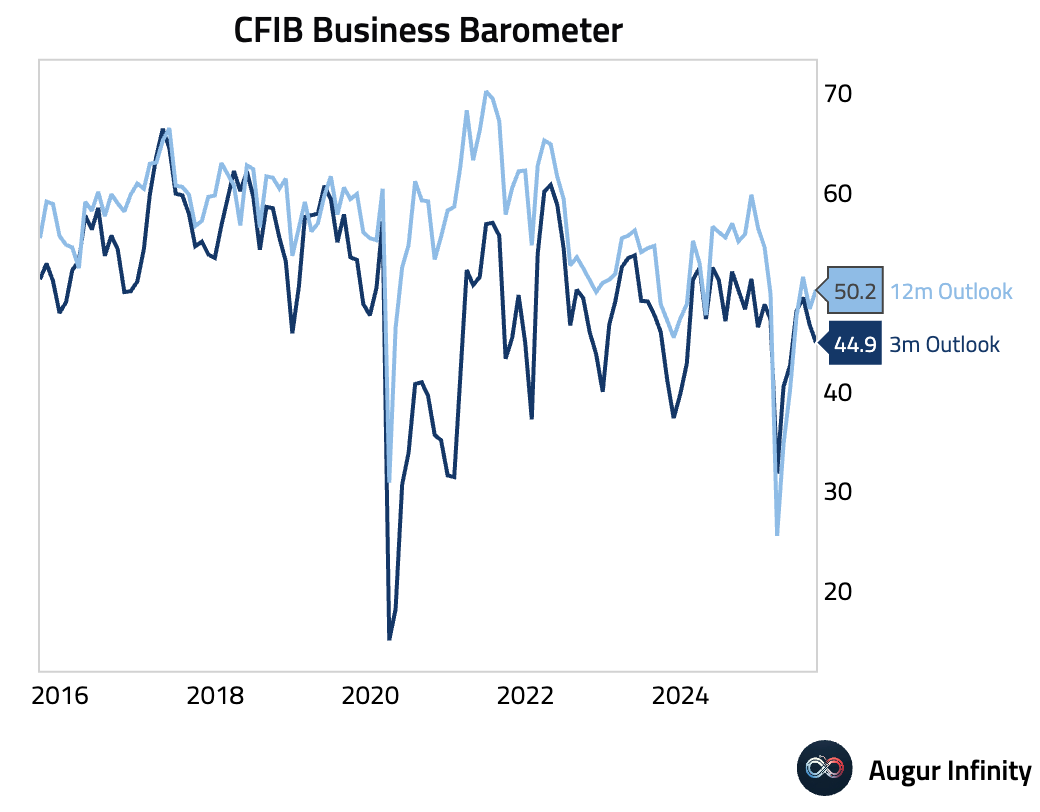

- Canadian small business confidence improved in September but remained subdued, with the 12-month outlook rising back above the 50-mark (act: 50.2, prev: 48.3).

Europe

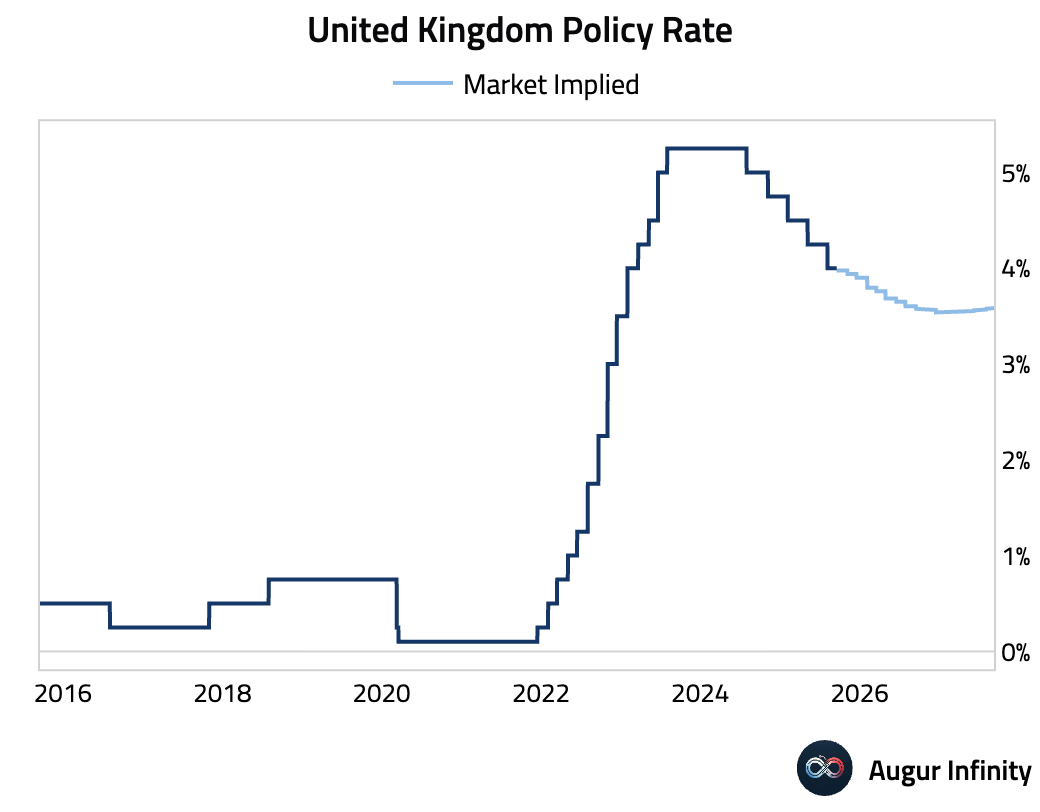

- The Bank of England held its Bank Rate at 4.0% in a 7-2 vote, meeting expectations. The two dissenters favored a 25bp cut. The majority cited unchanged risks since August, reiterating that a “gradual and careful” approach to easing is appropriate amid upside inflation risks. Concurrently, the BoE slowed its annual quantitative tightening (QT) pace to £70 billion from £100 billion. However, due to lower redemptions, this means active sales will increase. The bank also reduced the share of long-maturity gilts in its sales mix, signaling a more cautious approach to selling longer-dated debt.

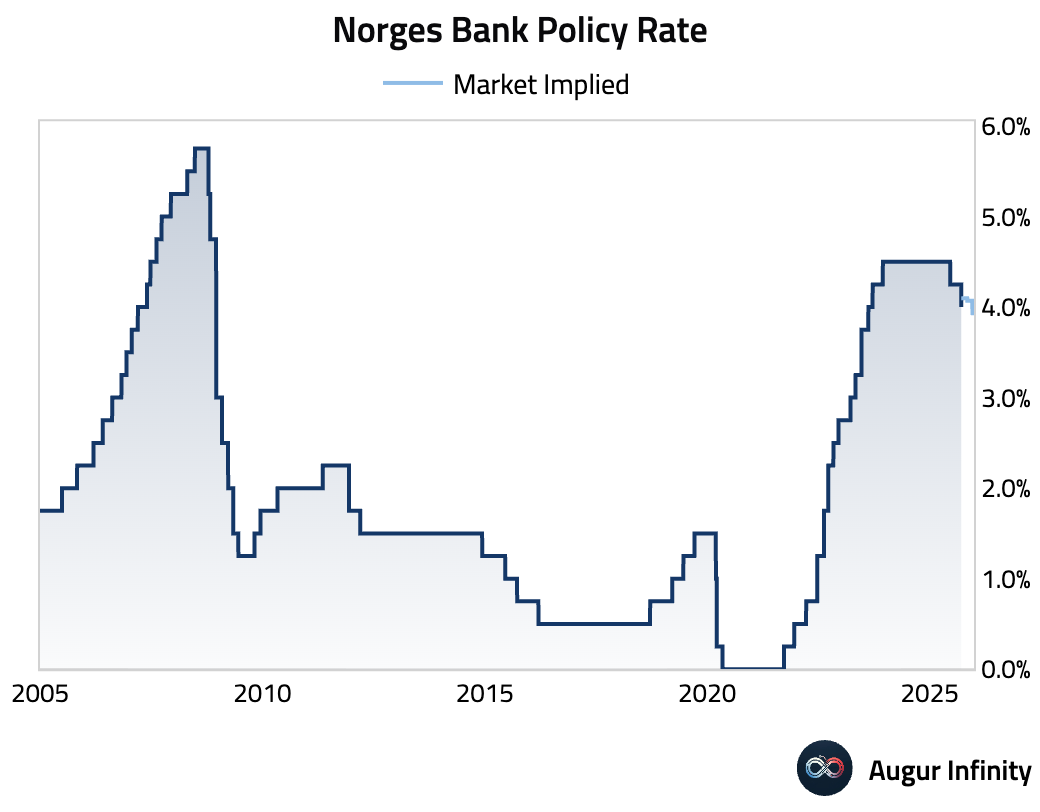

- Norges Bank delivered a “hawkish cut,” lowering its policy rate by 25 bps to 4.0%, in line with expectations. The bank upgraded its own future rate path forecast, citing stronger domestic demand and inflation, and signaled that rates would “not be reduced as quickly as envisaged.” The move prompted a reassessment of the future easing cycle, with analysts now seeing a higher terminal rate.

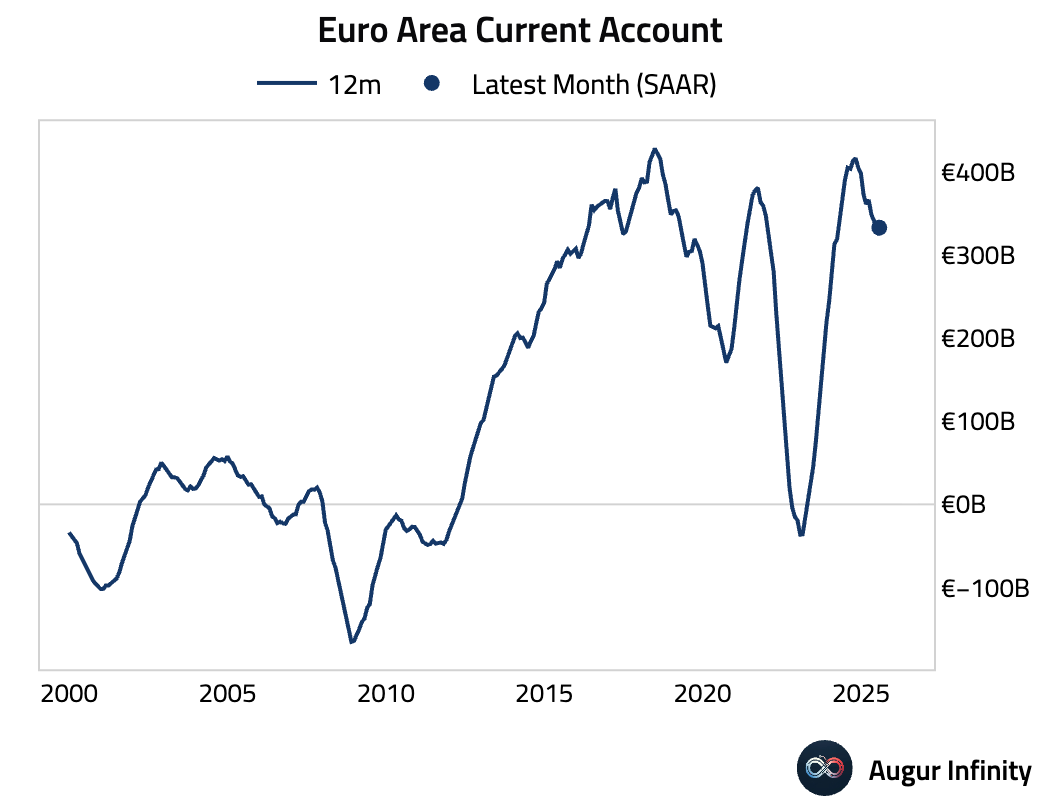

- The Euro Area's current account surplus narrowed in July to €35.0 billion from a revised €38.9 billion in June.

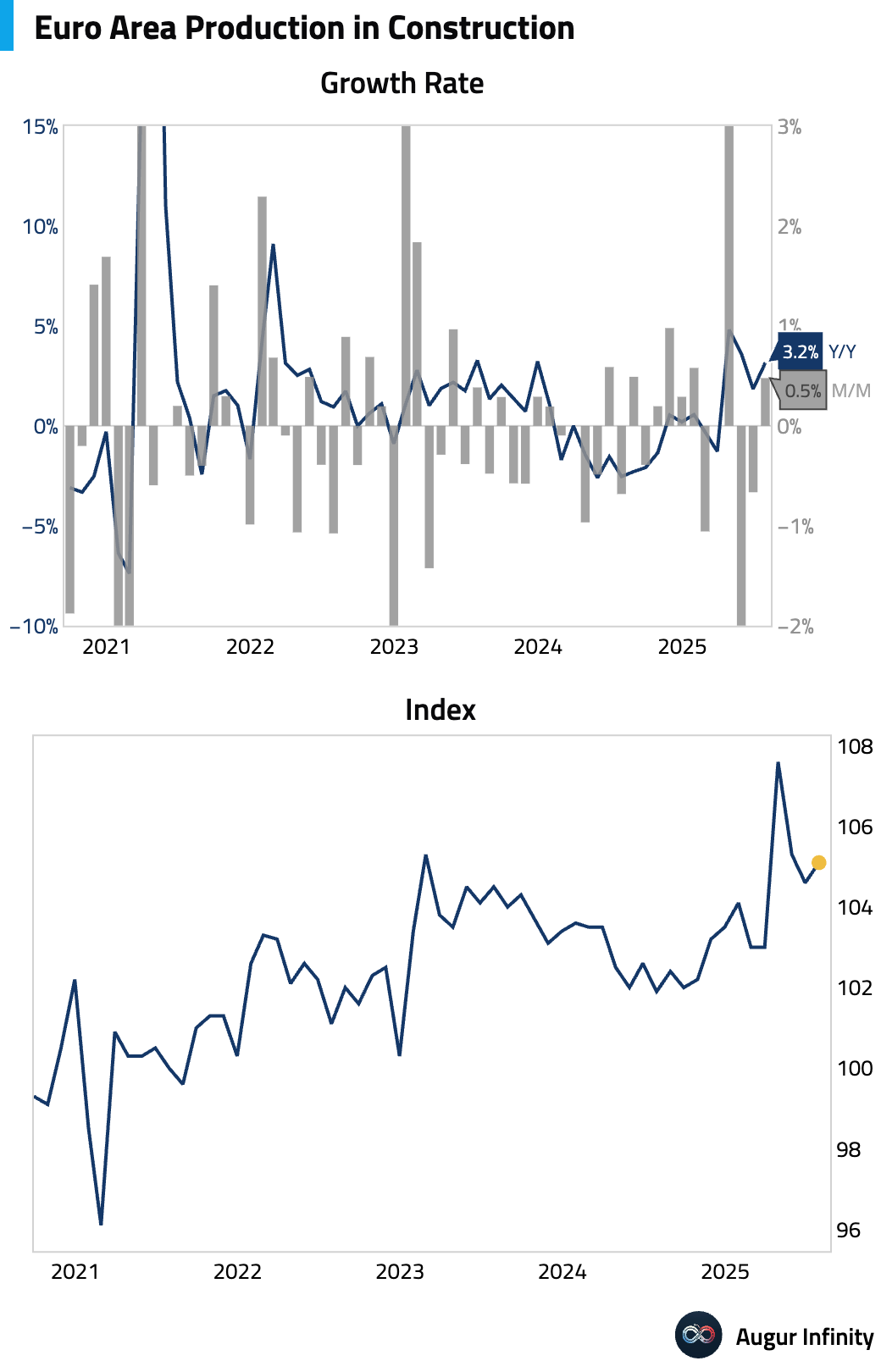

- Production in construction for the Euro Area accelerated in July, rising 3.2% Y/Y (prev: 1.8%).

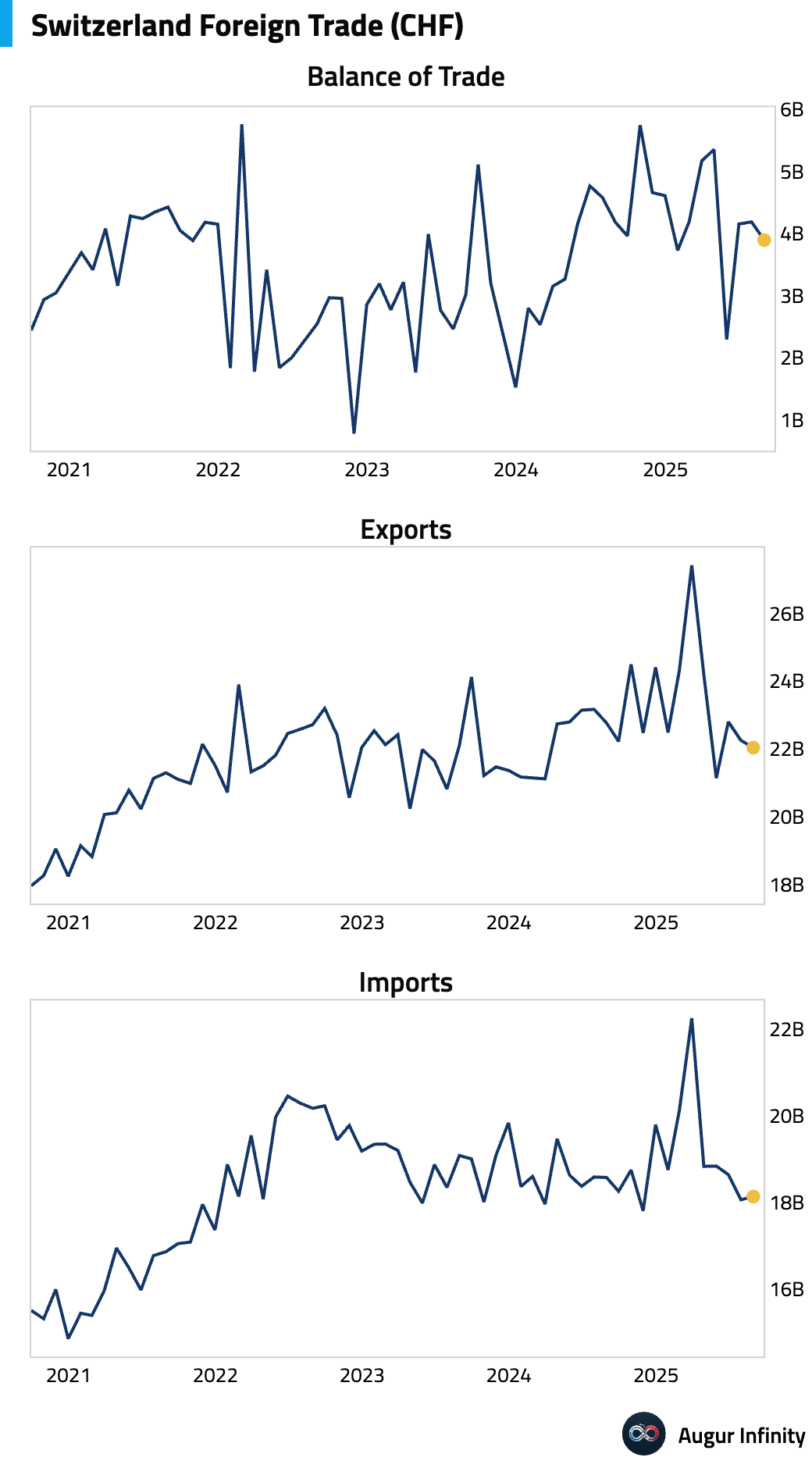

- Switzerland’s trade surplus narrowed in July (act: CHF 3.9B, prev: CHF 4.2B).

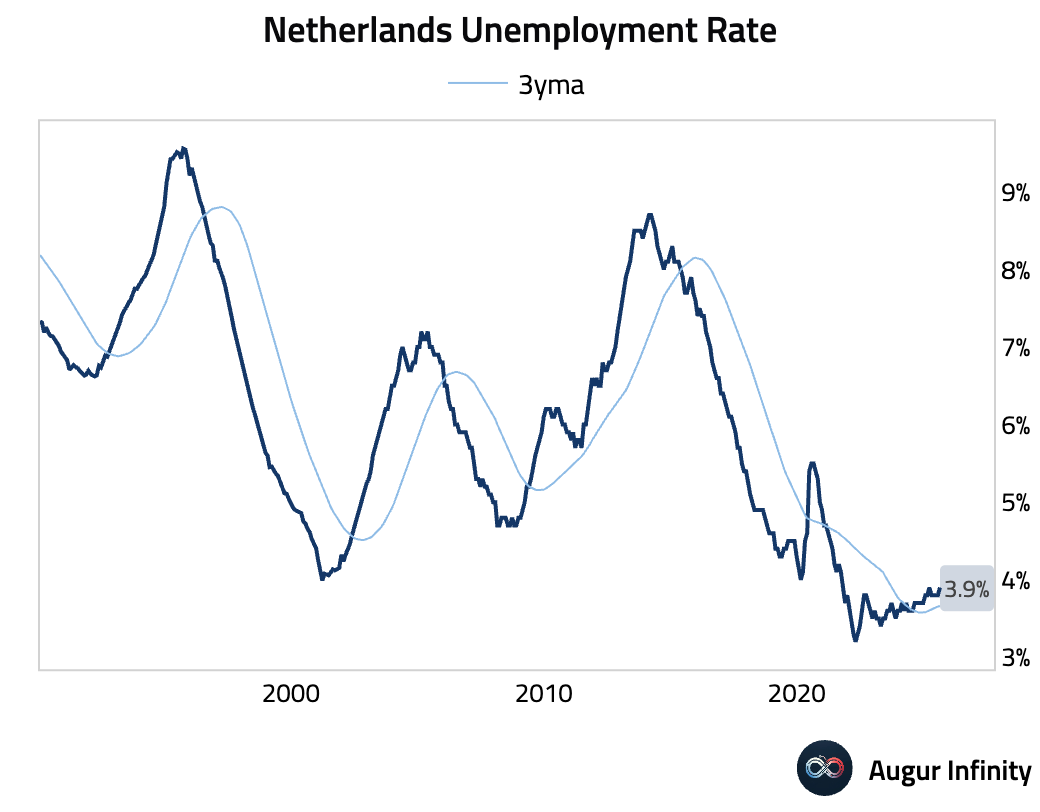

- The unemployment rate in the Netherlands ticked up to 3.9% in August, its highest level since September 2021.

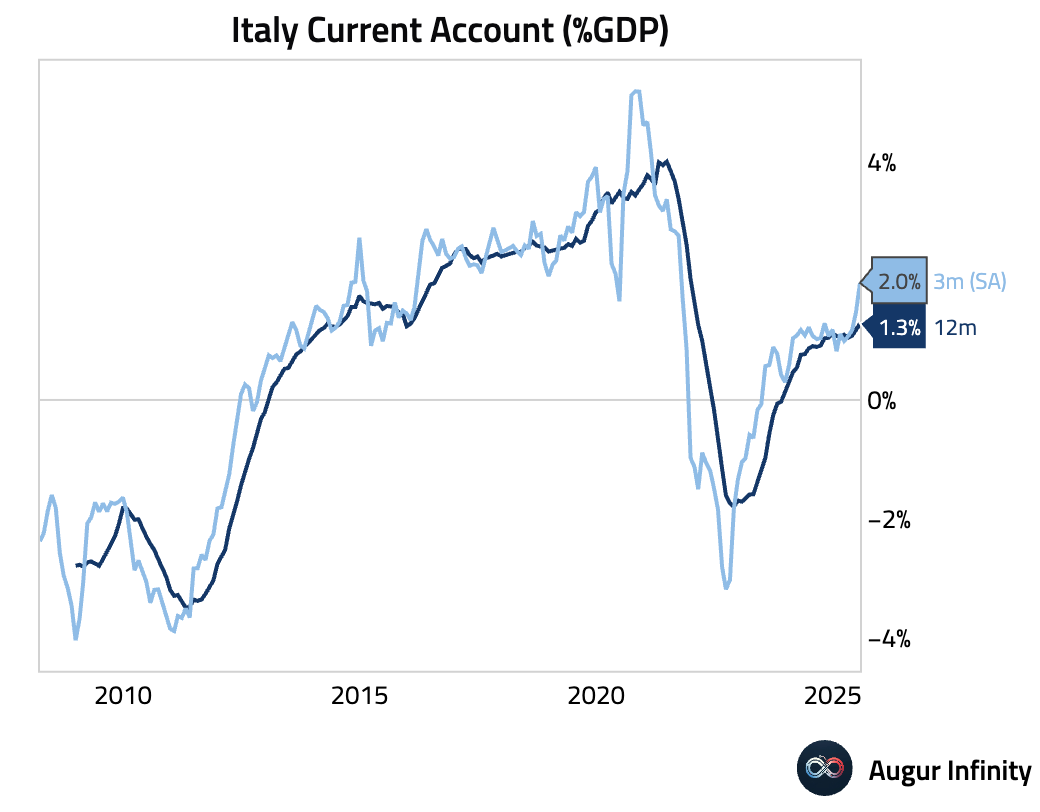

- Italy’s current account surplus widened to €8.69 billion in July, its largest since October 2020.

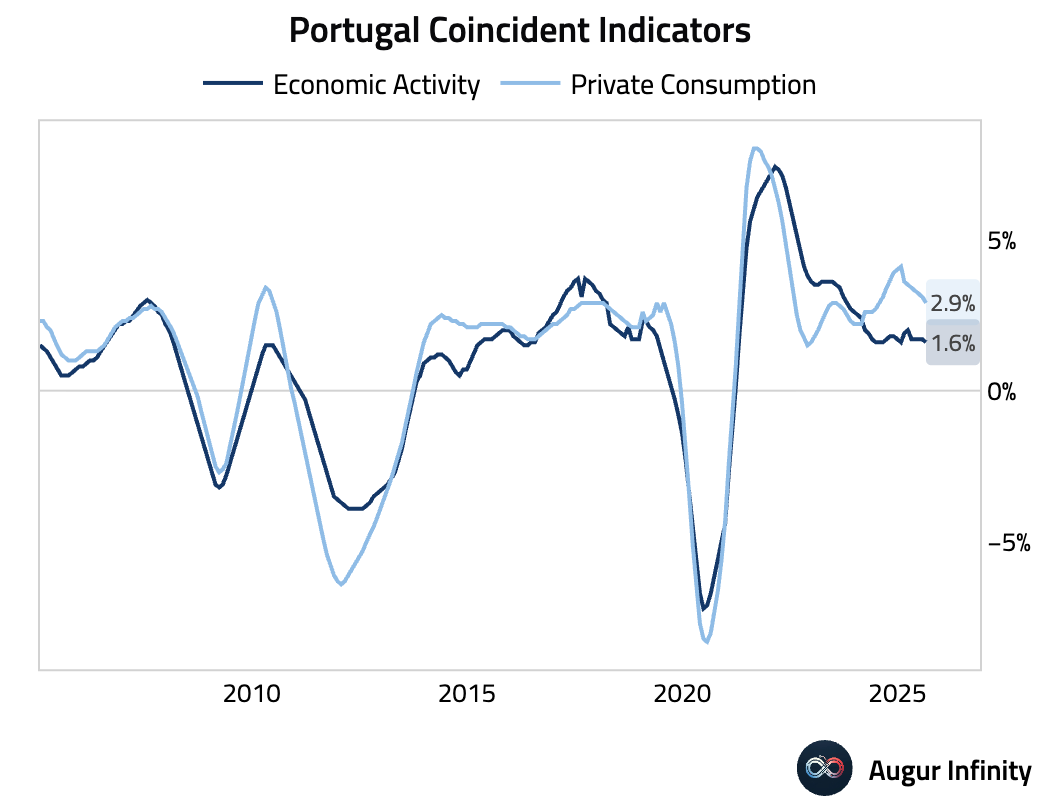

- Portugal's Economic Activity for August eased to 1.6% from 1.7%, marking its lowest reading since March 2021. Private Consumption also fell to 2.9% from 3.1%, the lowest since June 2024.

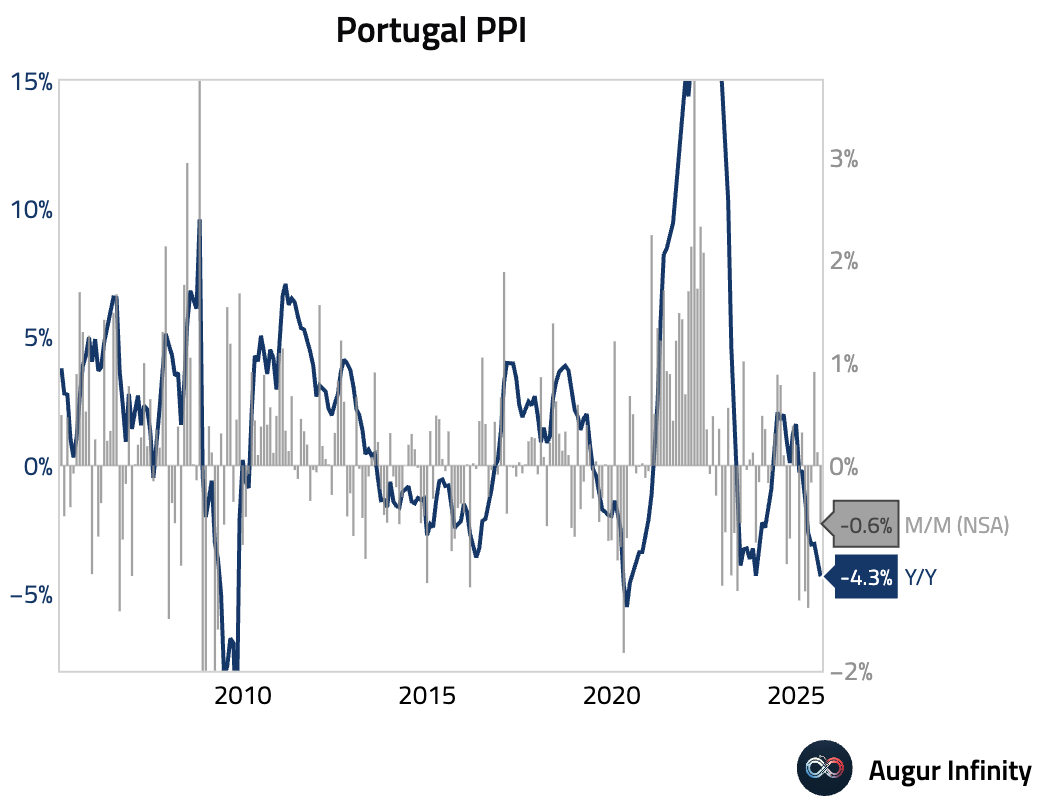

- Portuguese producer prices fell 0.6% M/M in August, pushing the annual deflation rate to -4.3% Y/Y from -3.7% previously.

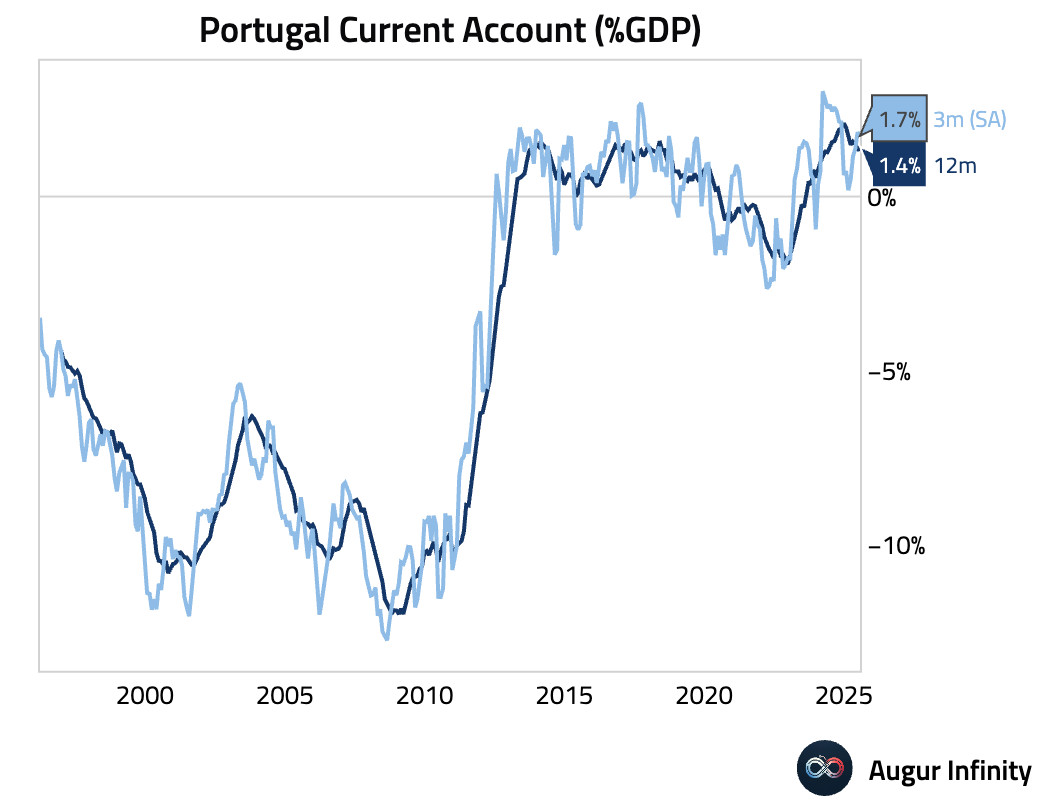

- Portugal posted a current account surplus of €1.41 billion in July.

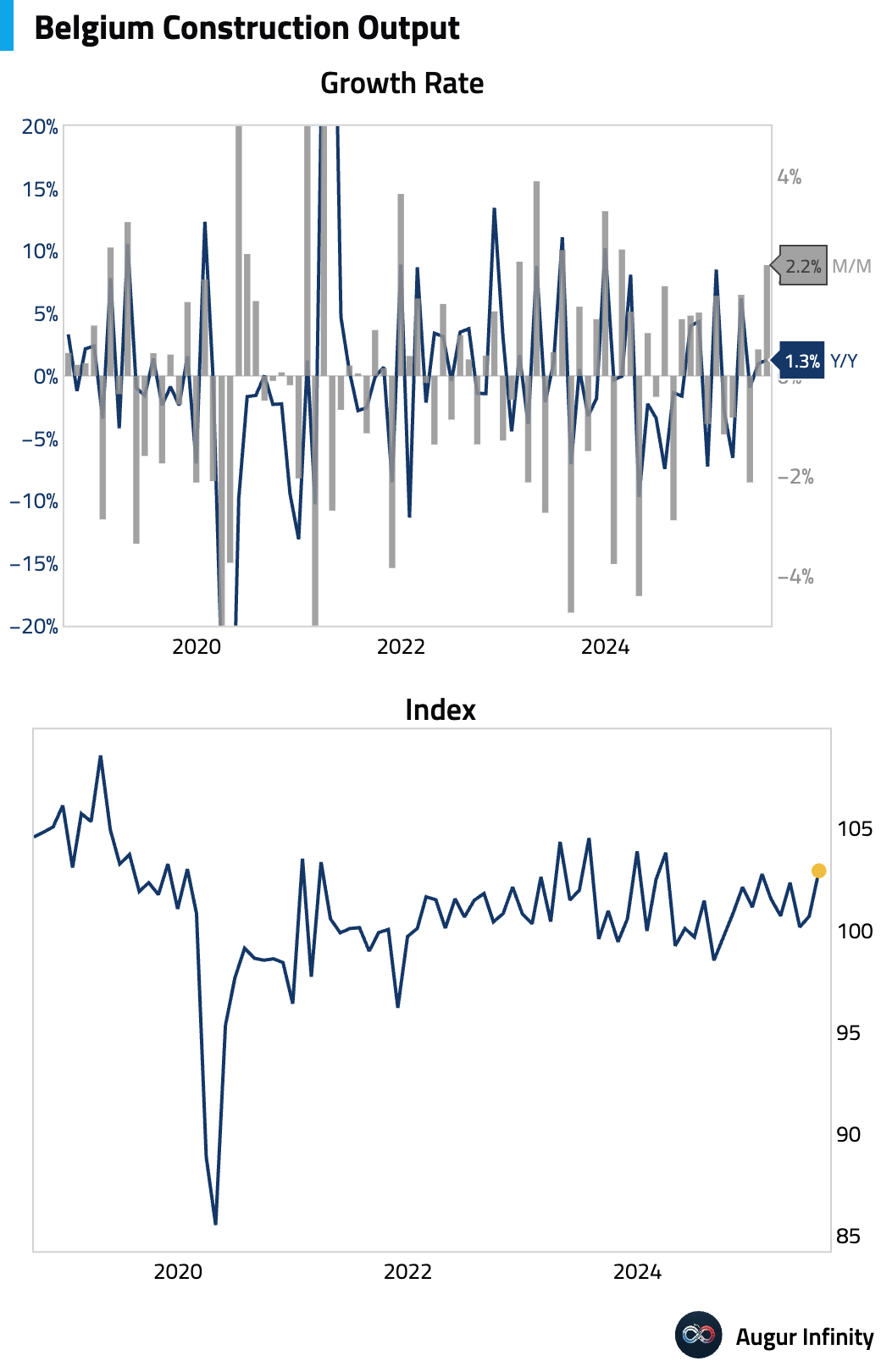

- Belgian construction output growth accelerated in July (act: 1.3%, prev: 1.0%).

Asia-Pacific

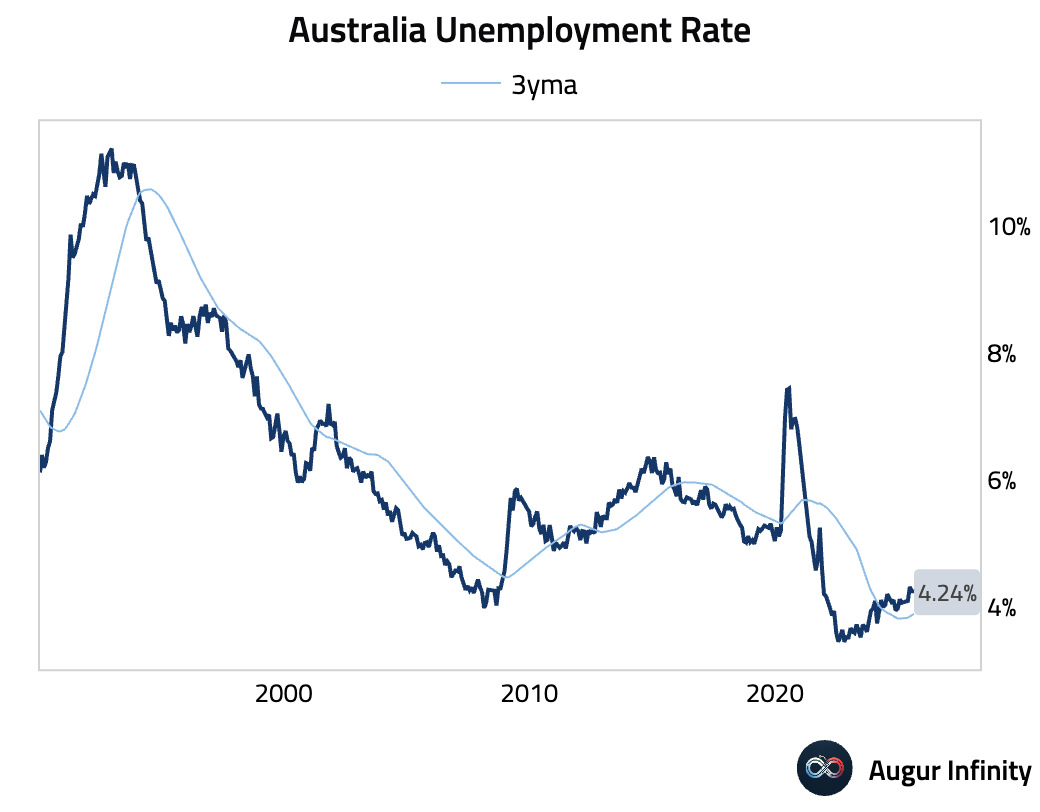

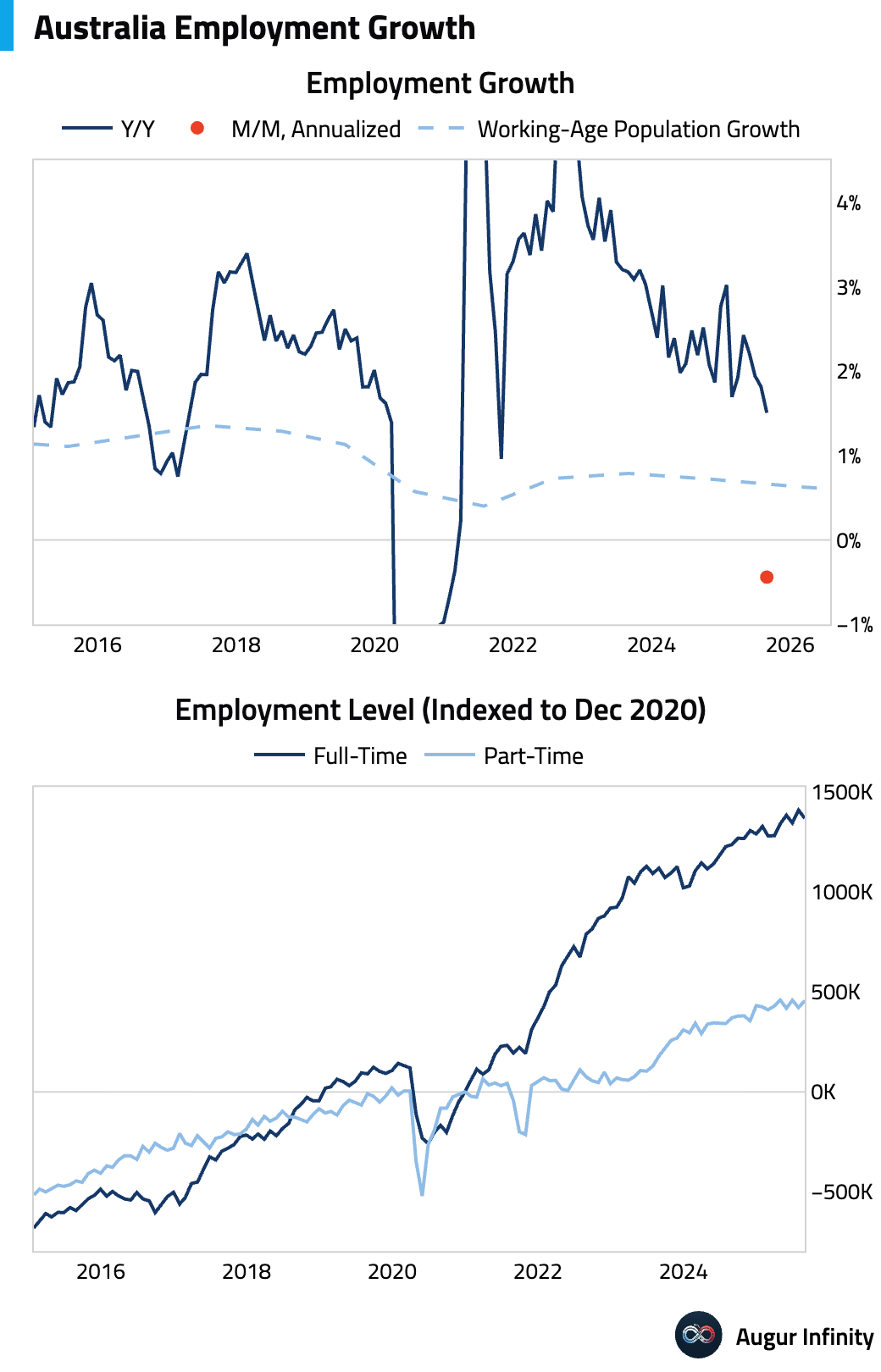

- Australia’s labor market showed signs of softening in August despite a stable unemployment rate of 4.2%. Employment unexpectedly fell by 5,400, well below the consensus for a 22,000 gain, driven by a sharp 40,900 drop in full-time roles. The stable headline unemployment rate was due to a 0.2 percentage point decline in the participation rate to 66.8%. The soft details are likely to increase pressure on the RBA to cut rates.

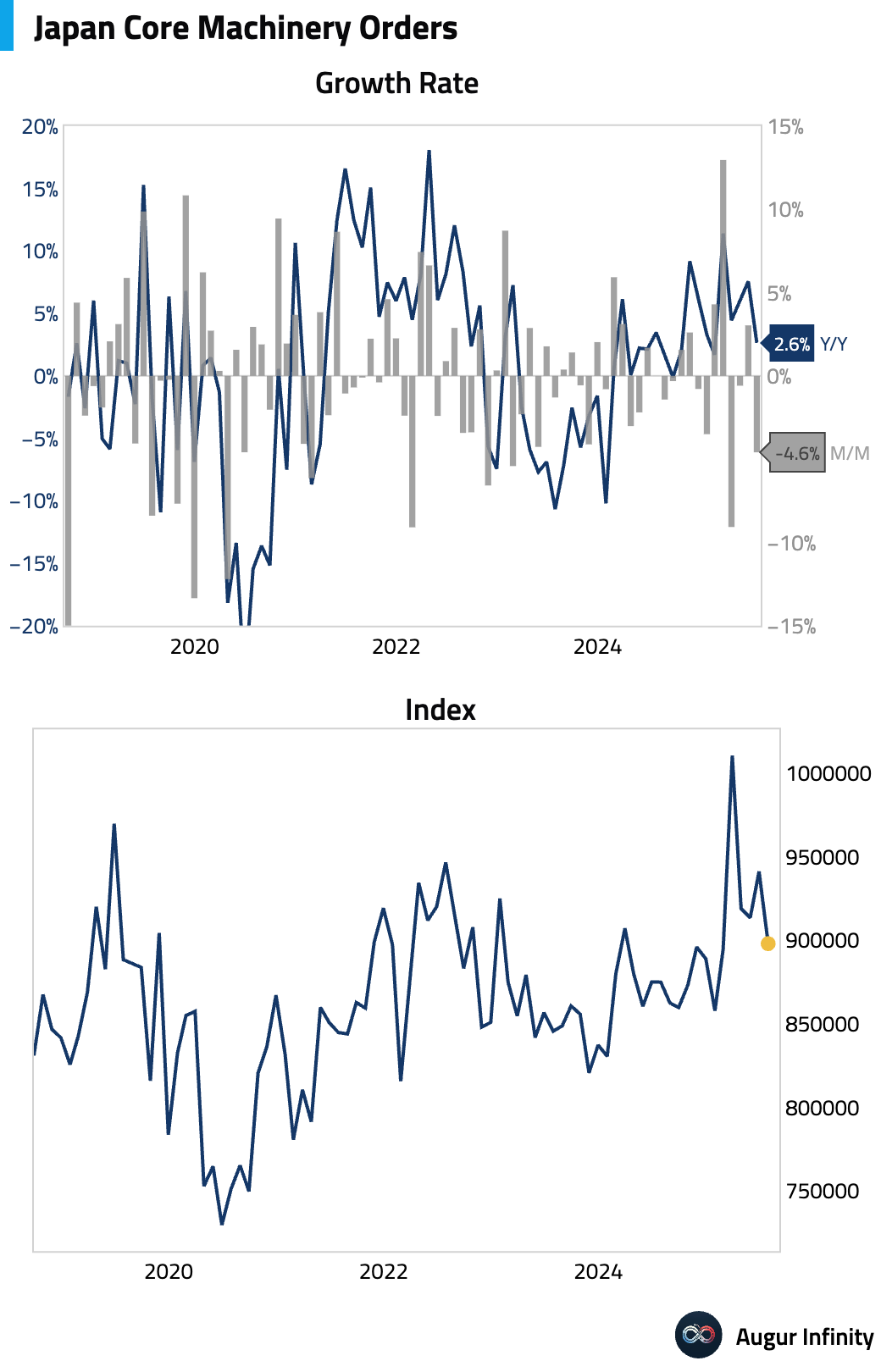

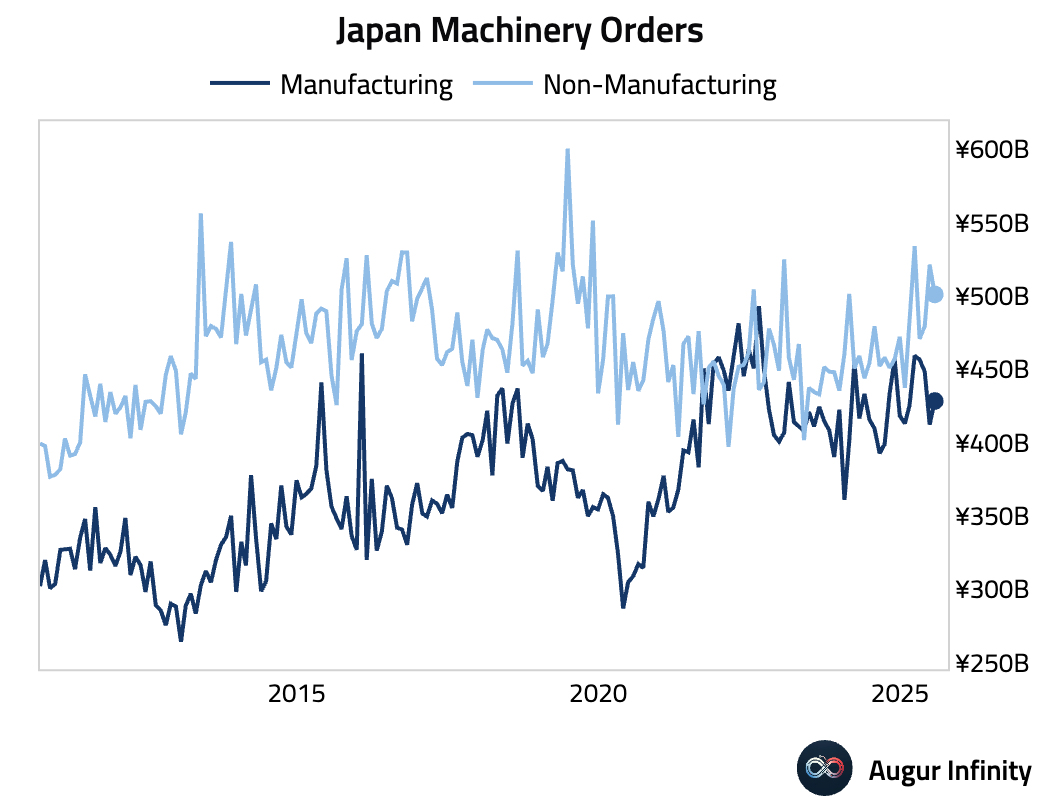

- Japan's core machinery orders, a key indicator of capital expenditure, fell sharply in July, missing expectations on both a monthly and annual basis (act: -4.6% M/M, est: -1.7%; act: 4.9% Y/Y, est: 5.4%). The decline was driven by weakness in the non-manufacturing sector.

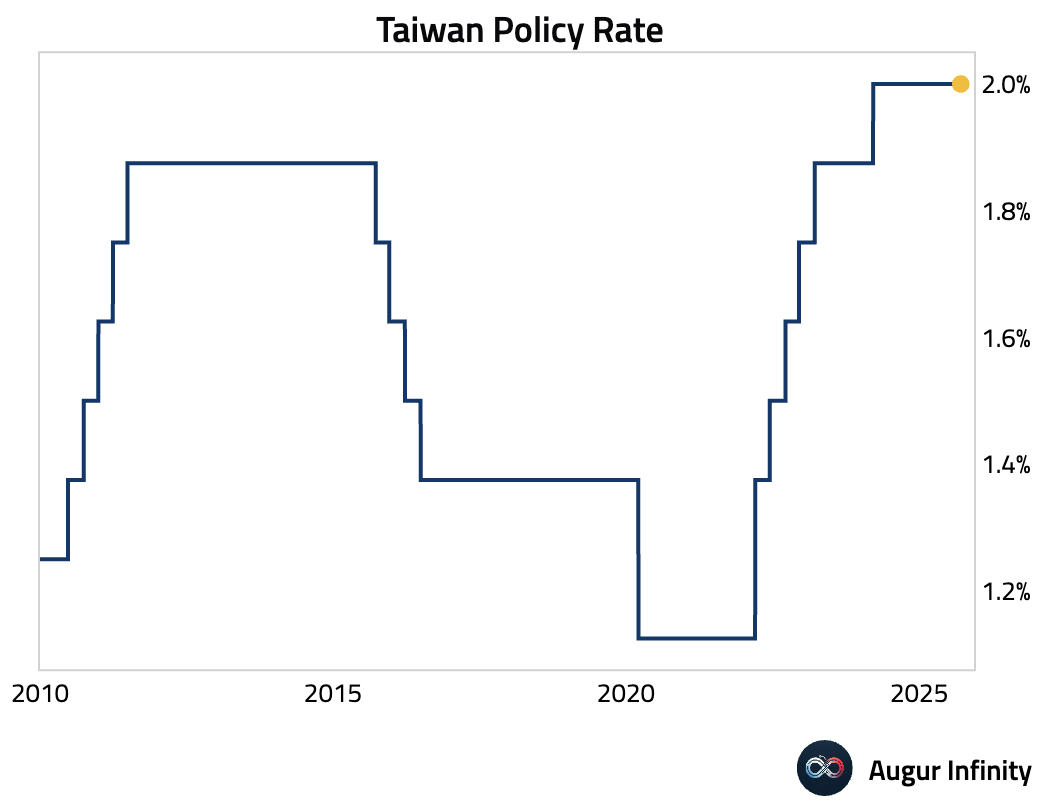

- Taiwan's central bank held its benchmark interest rate at 2.0%, as expected. The governor described the stance as “moderate easing” and signaled increased flexibility by moving away from a rigid inflation threshold for future cuts. The bank also sharply upgraded its 2025 GDP growth forecast to 4.55% from 3.05%, citing strong export performance, while keeping its inflation forecast largely unchanged at 1.75%.

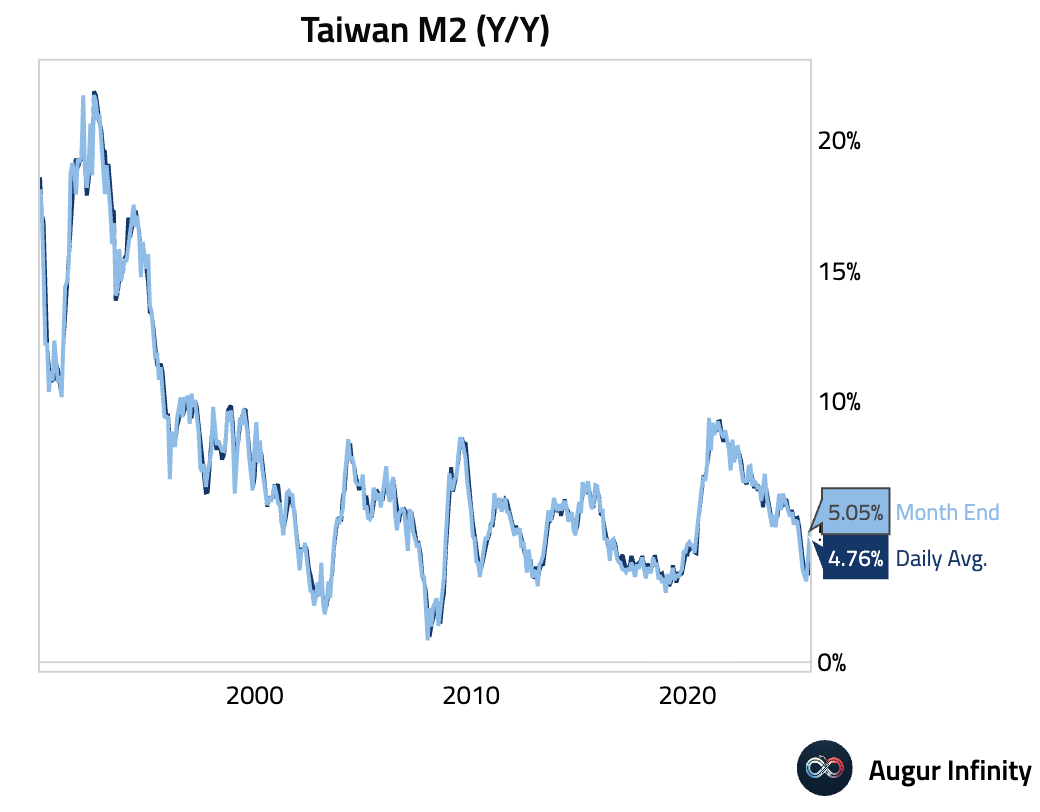

- Taiwan's M2 money supply growth accelerated in August (act: 4.76%, prev: 3.42%).

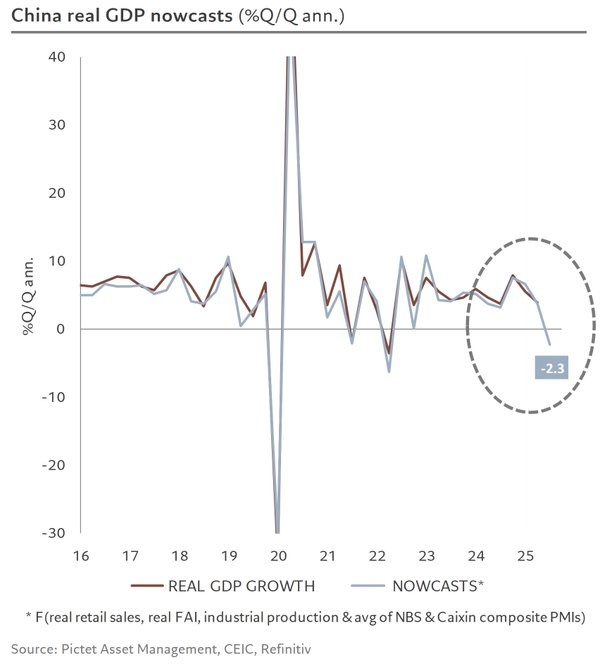

China

- Pictet's GDP nowcast for China points to a contraction in Q3.

Source: Patrick Zweifel

Emerging Markets ex China

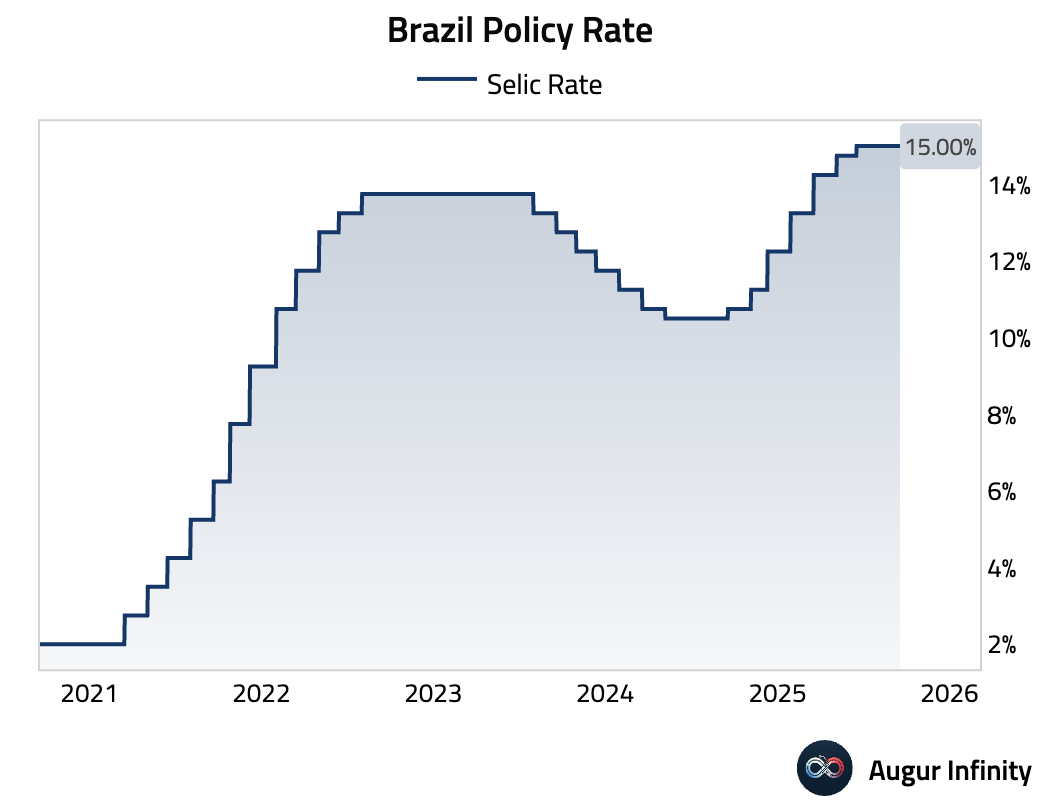

- Brazil's central bank unanimously kept its Selic policy rate at 15.00%, in line with consensus. The accompanying statement remained hawkish, signaling a readiness to hold the restrictive rate for a “very prolonged period” and even resume hiking if necessary to combat unmoored inflation expectations.

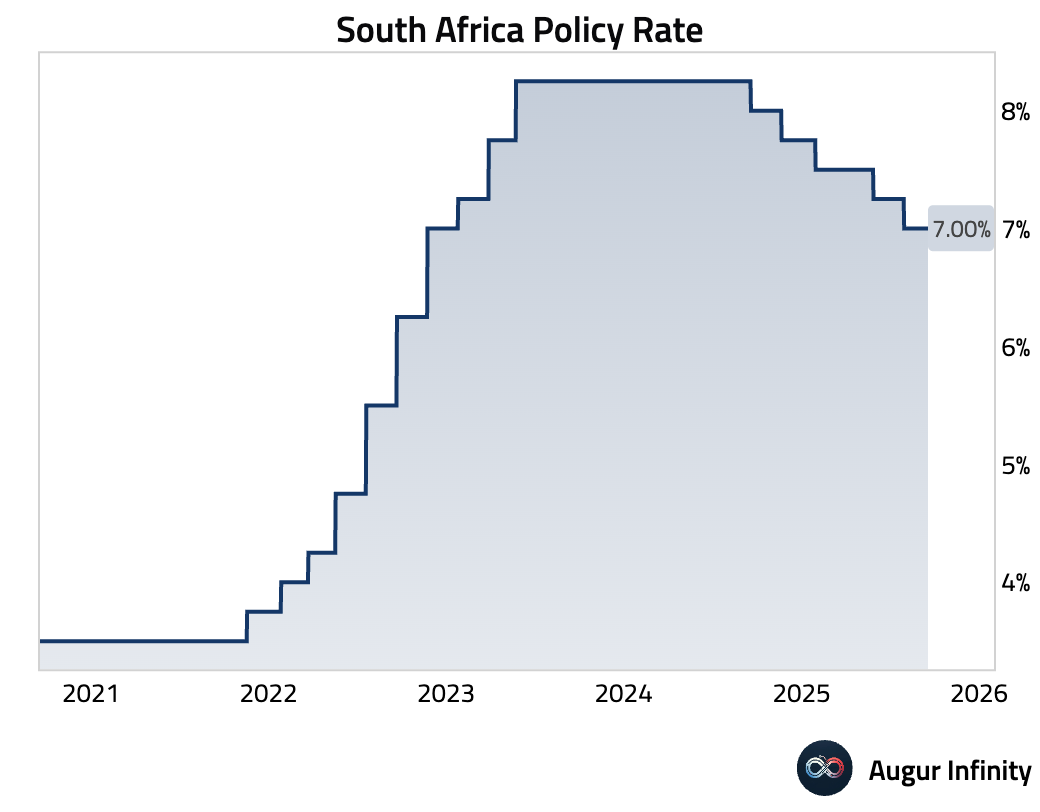

- The South African Reserve Bank held its benchmark interest rate steady (act: 7.0%, prev: 7.0%).

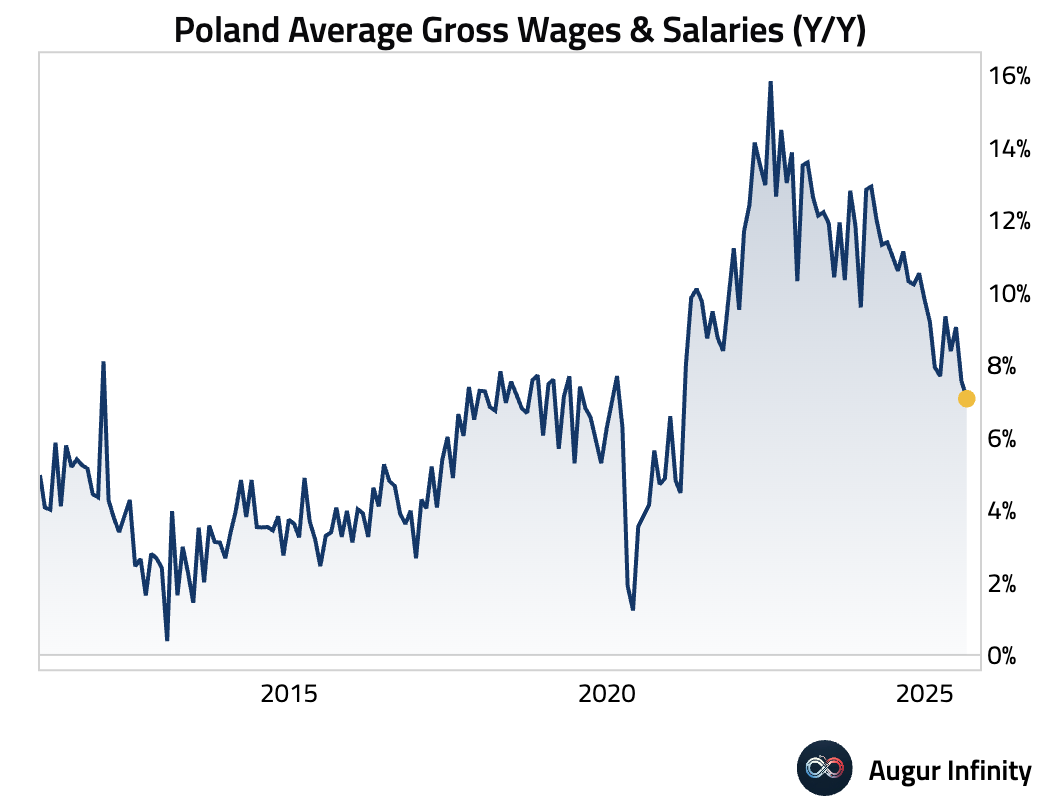

- Wage growth in Poland’s corporate sector slowed more than expected in August (act: 7.1%, est: 7.8%). This is the slowest pace of wage gains since February 2021.

- Polish employment growth remained in negative territory (act: -0.8%, prev: -0.9%).

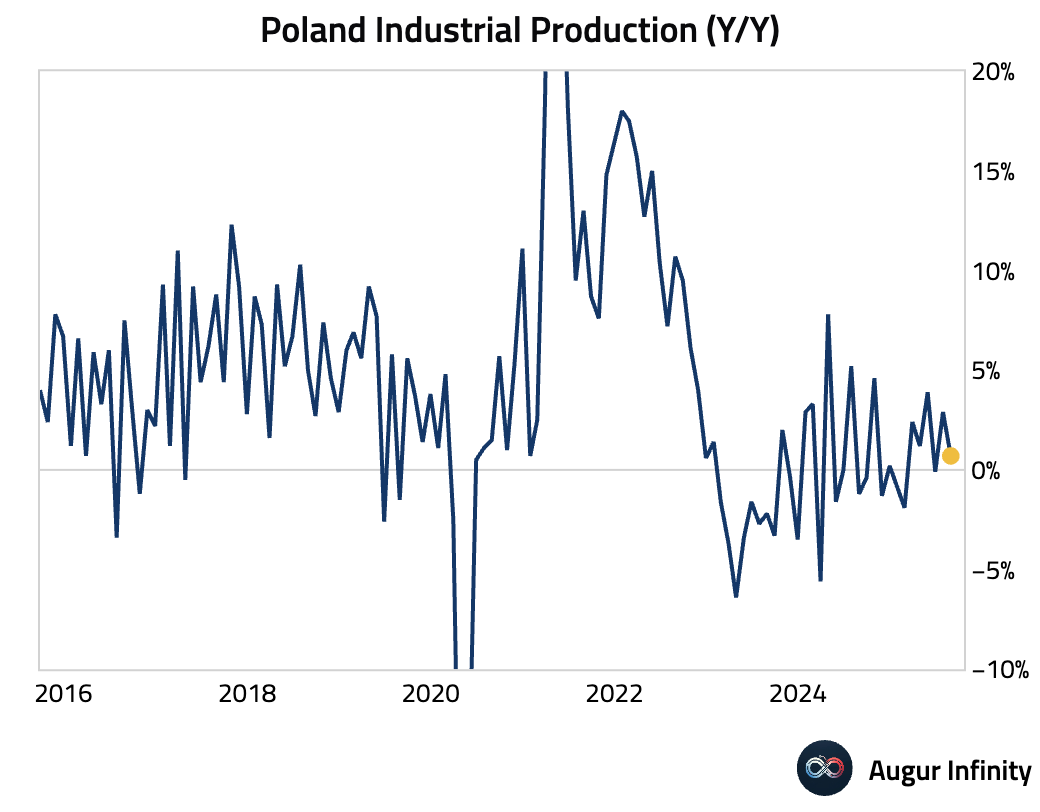

- Poland’s industrial production growth slowed sharply to 0.7% Y/Y in August, though this was better than the 0.3% consensus forecast.

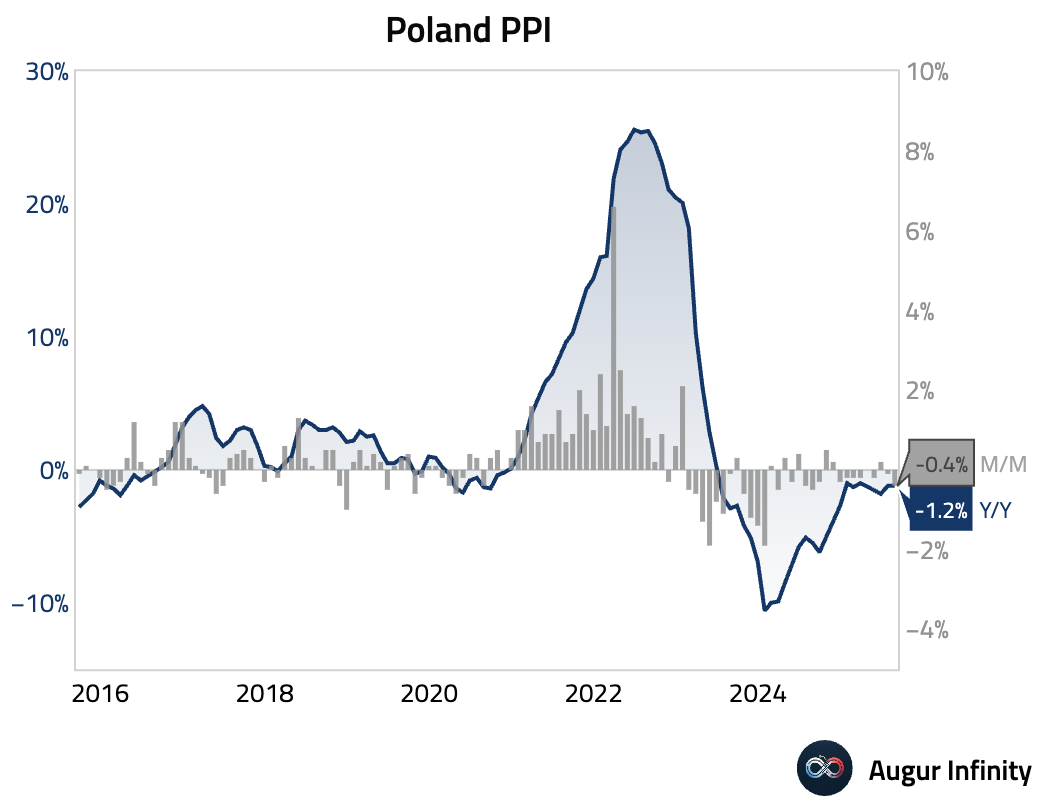

- Producer price deflation in Poland eased slightly in August (act: -1.2%, prev: -1.3%).

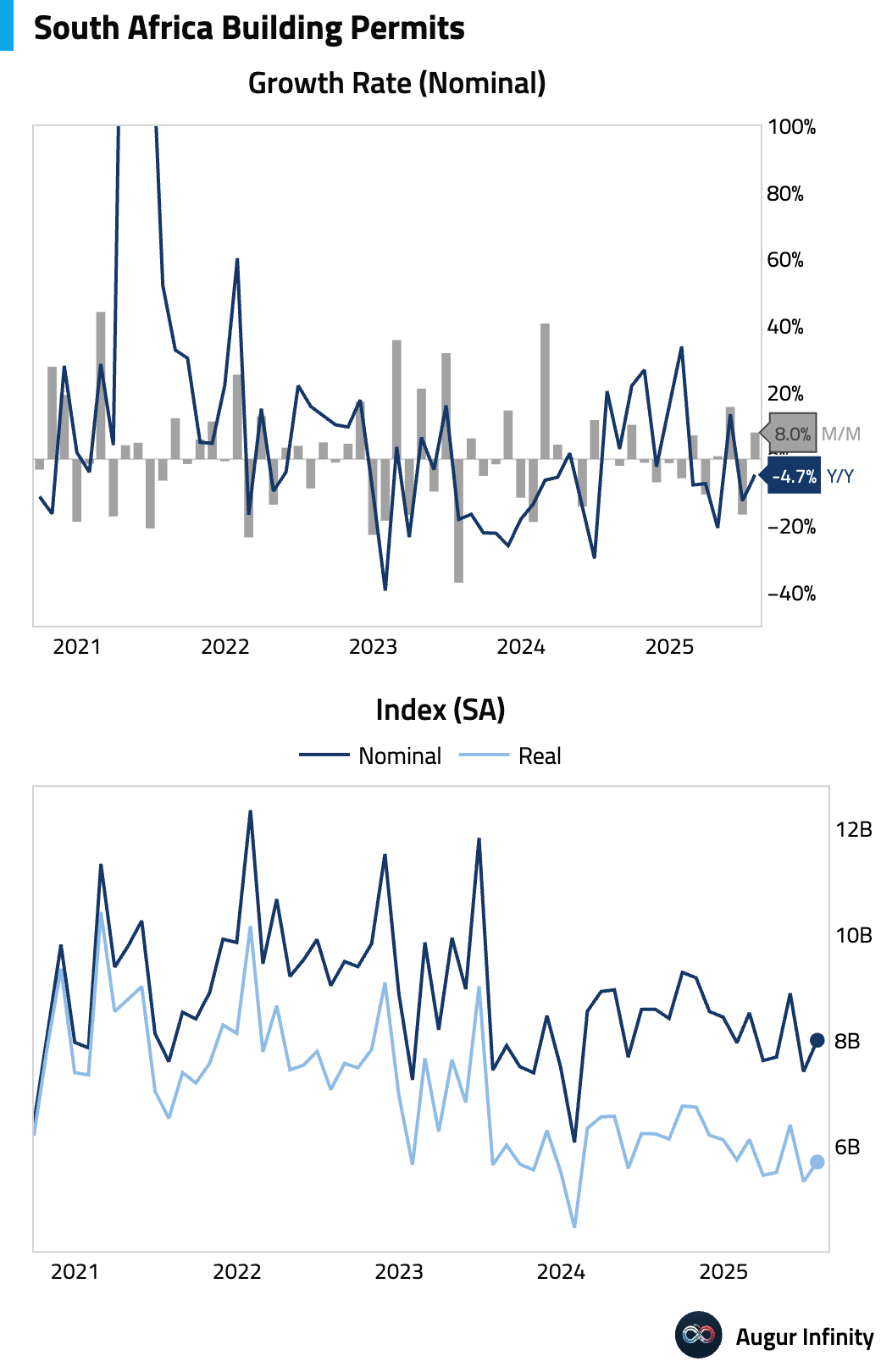

- South African building permits continued to decline in July, though the pace of contraction eased to -4.7% Y/Y from -12.5% in June.

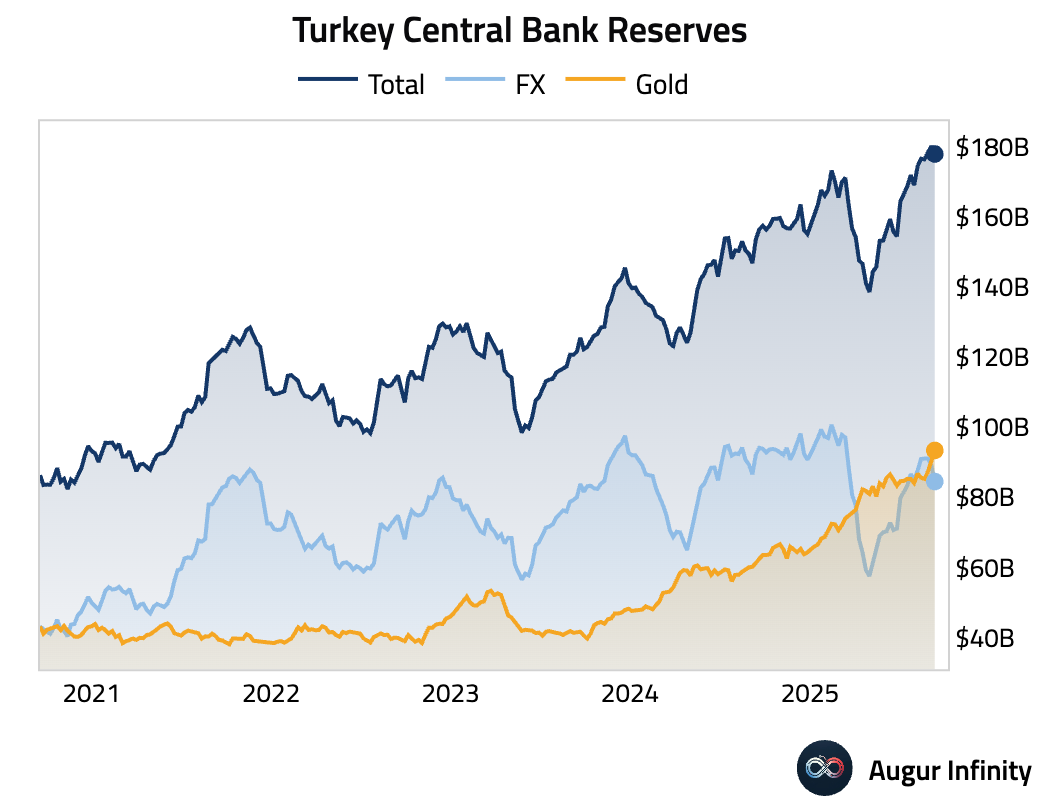

- Turkey's foreign exchange reserves declined for the week ending September 12 (act: $84.5B, prev: $89.2B).

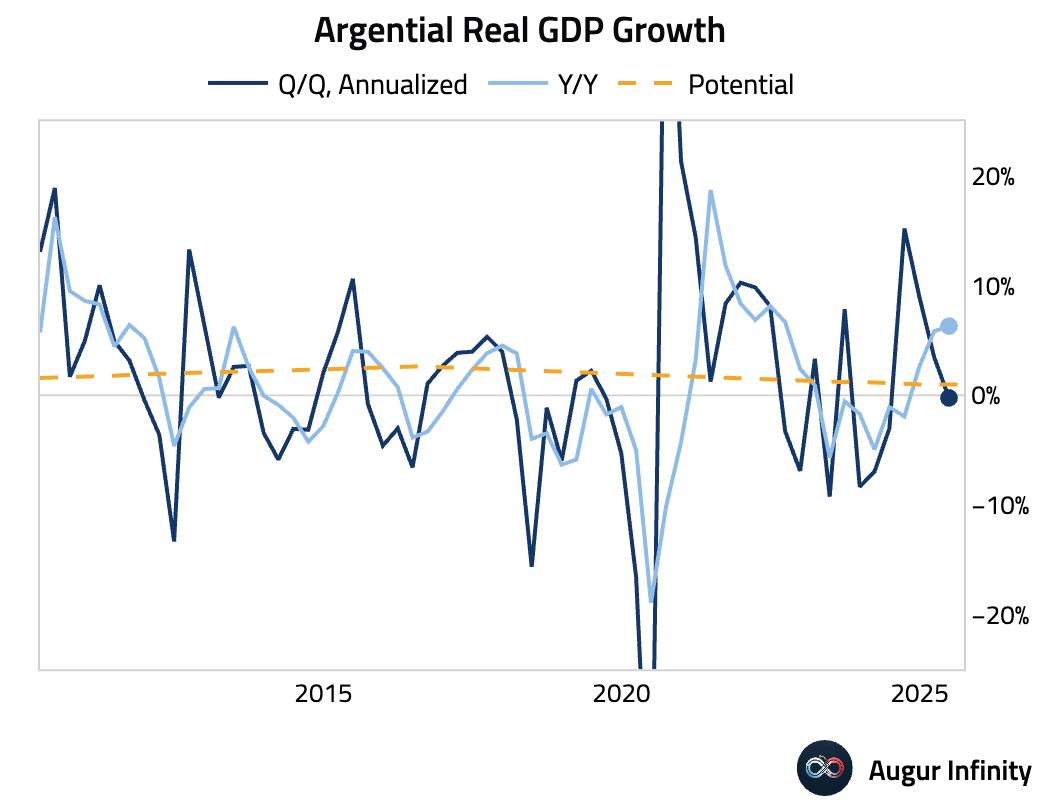

- Argentina's GDP unexpectedly contracted -0.1% Q/Q (est: 0.1%), stalling the recovery that began in H2 2024. The miss was driven by declines in private consumption and investment.

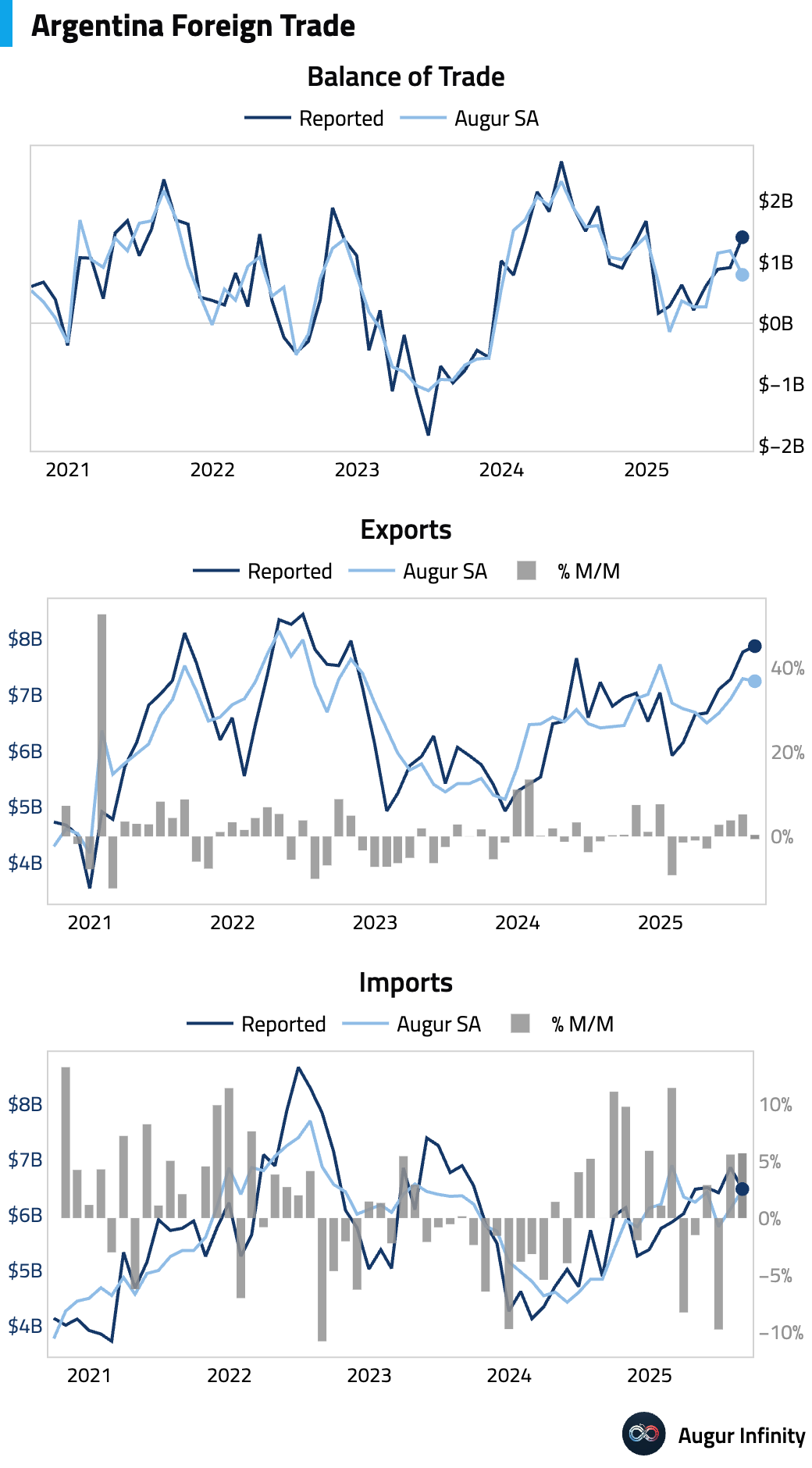

- Argentina's trade balance was a surplus of $1.402 billion, significantly exceeding consensus expectations of $800 million.

- Argentina's unemployment rate for Q2 2025 fell to 7.6% from 7.9%.

Global Markets

Equities

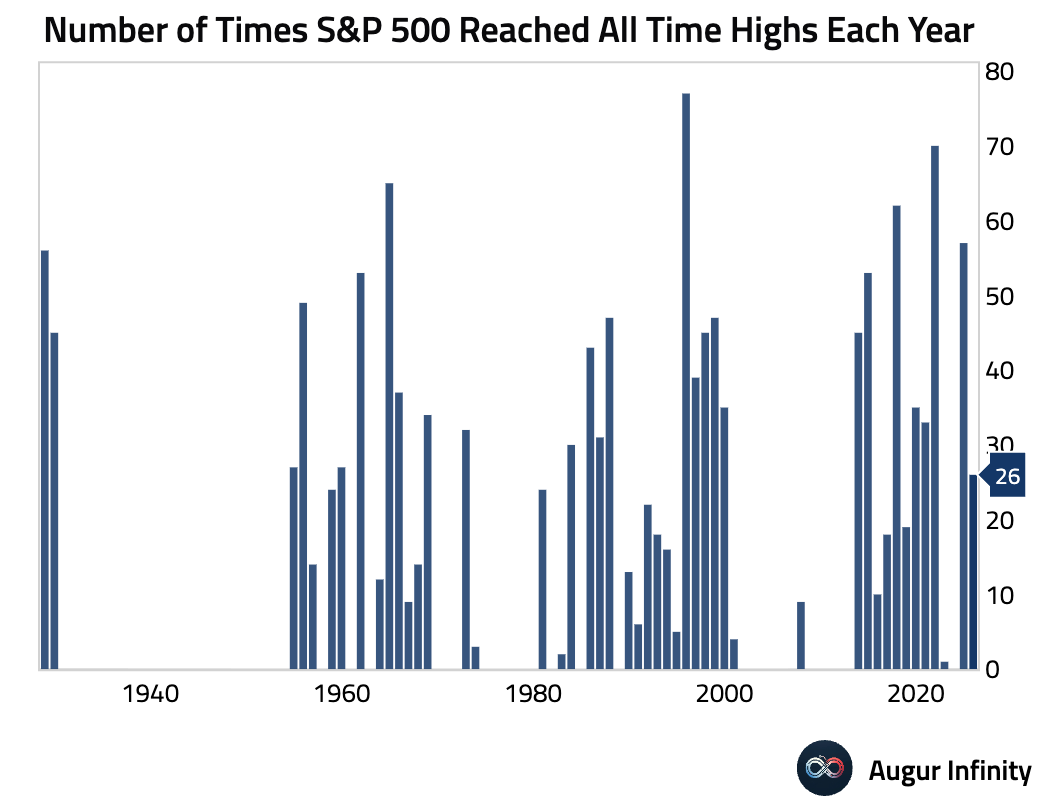

- US equity indices are making all time highs. The S&P 500 reached its 26th all-time high of the year.

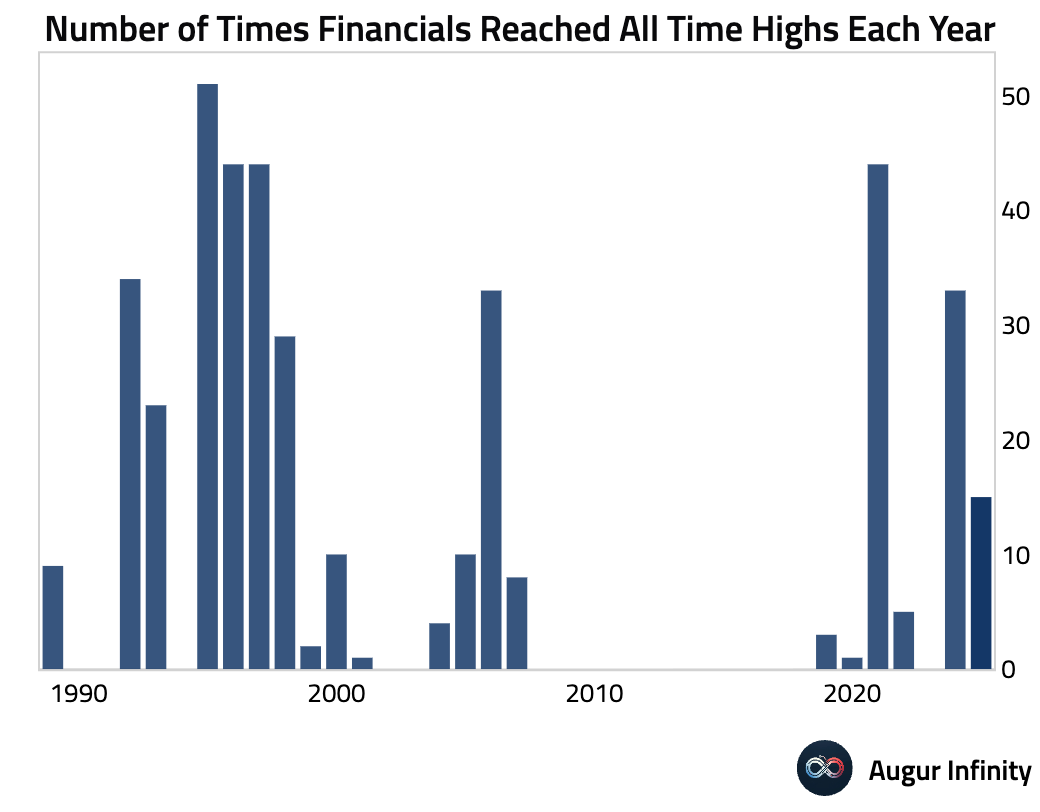

S&P 500 Financials hit its 15th all-time high this year.

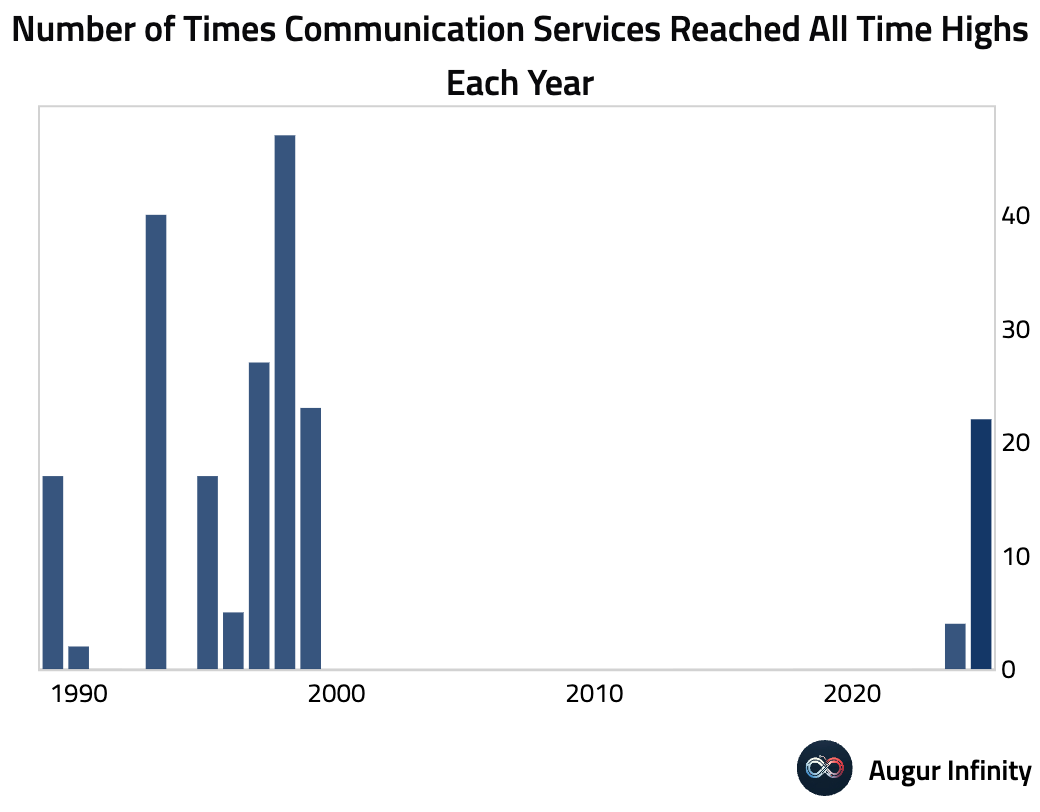

S&P 500 Communication Services has reached its 22nd all-time high so far this year.

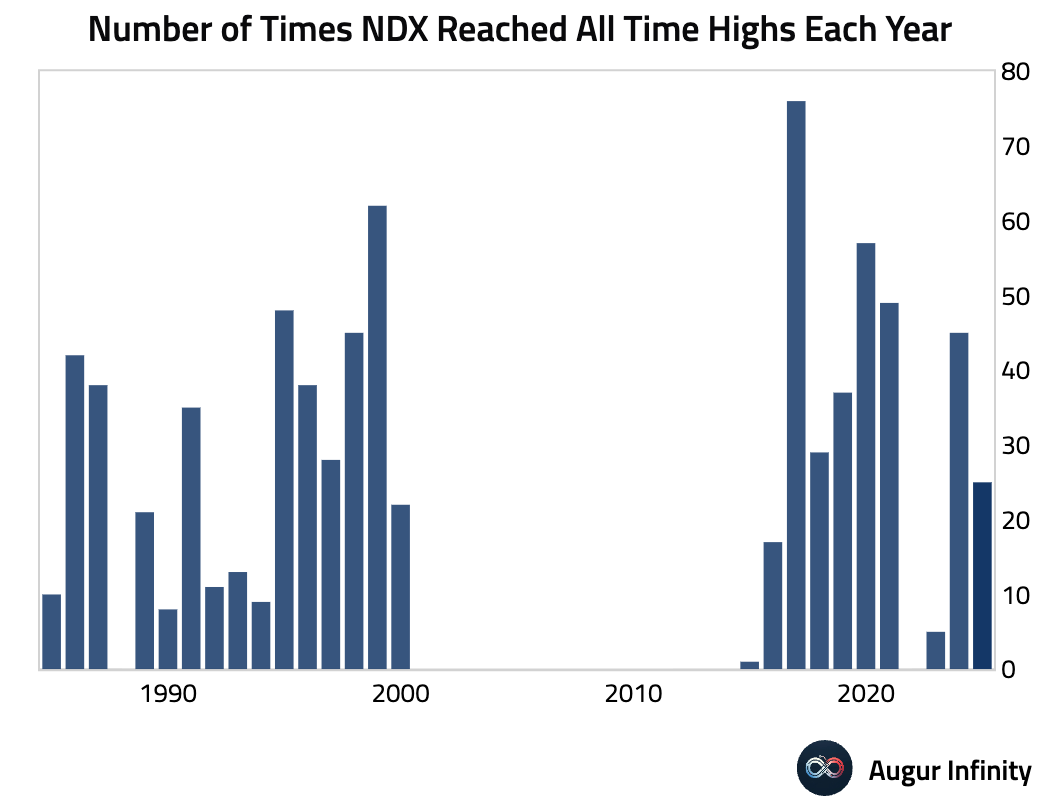

- NASDAQ 100 Index has made 25 all-time highs in 2025.

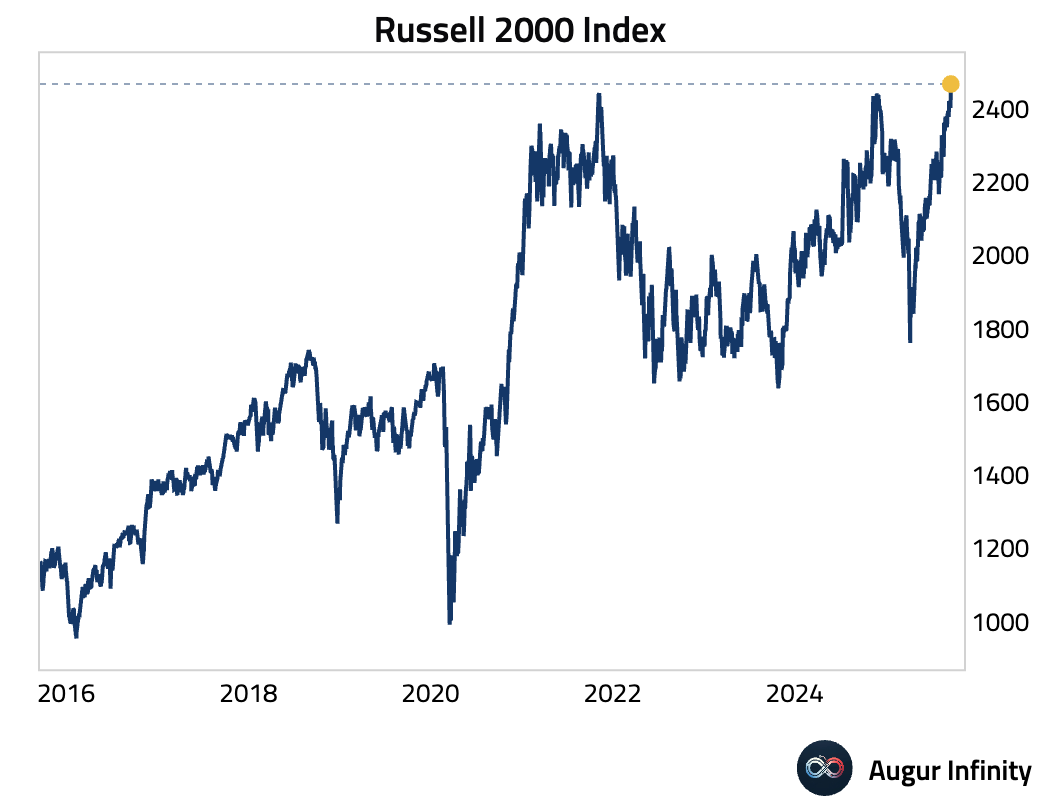

Even the Russell 2000 Index has reached an all-time high, the first time this year.

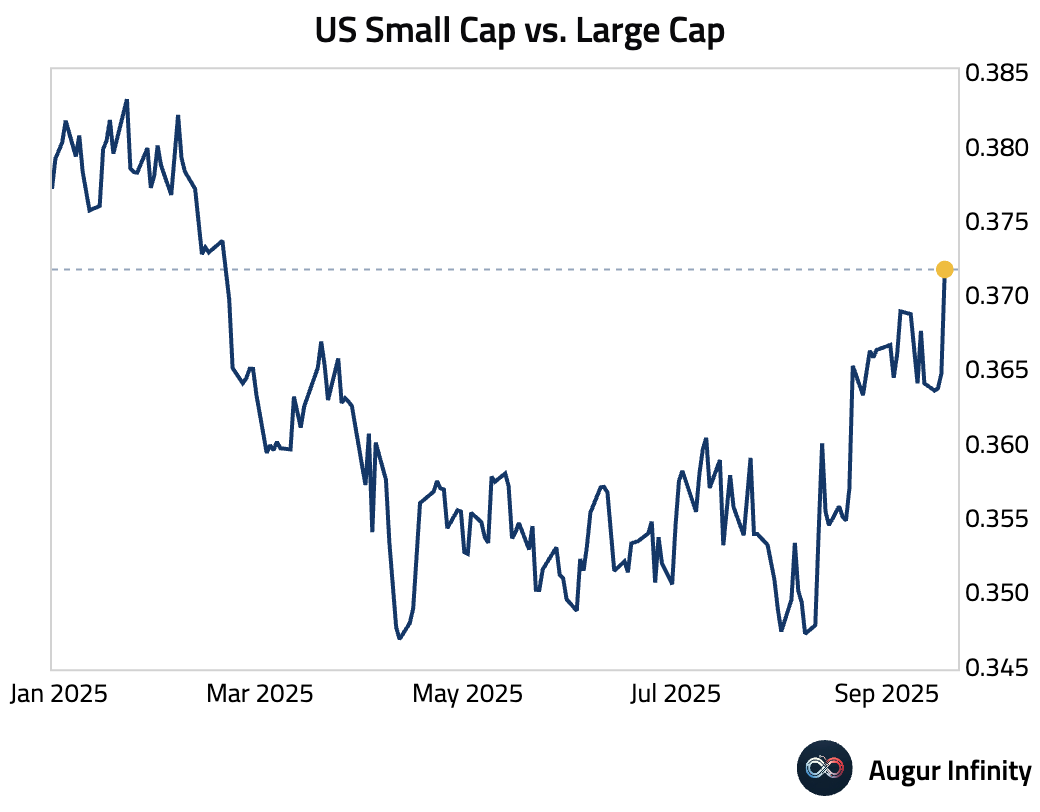

- US Small Cap vs. Large Cap rallied by 1.8% today (a 2.4σ move), reaching the highest level since February.

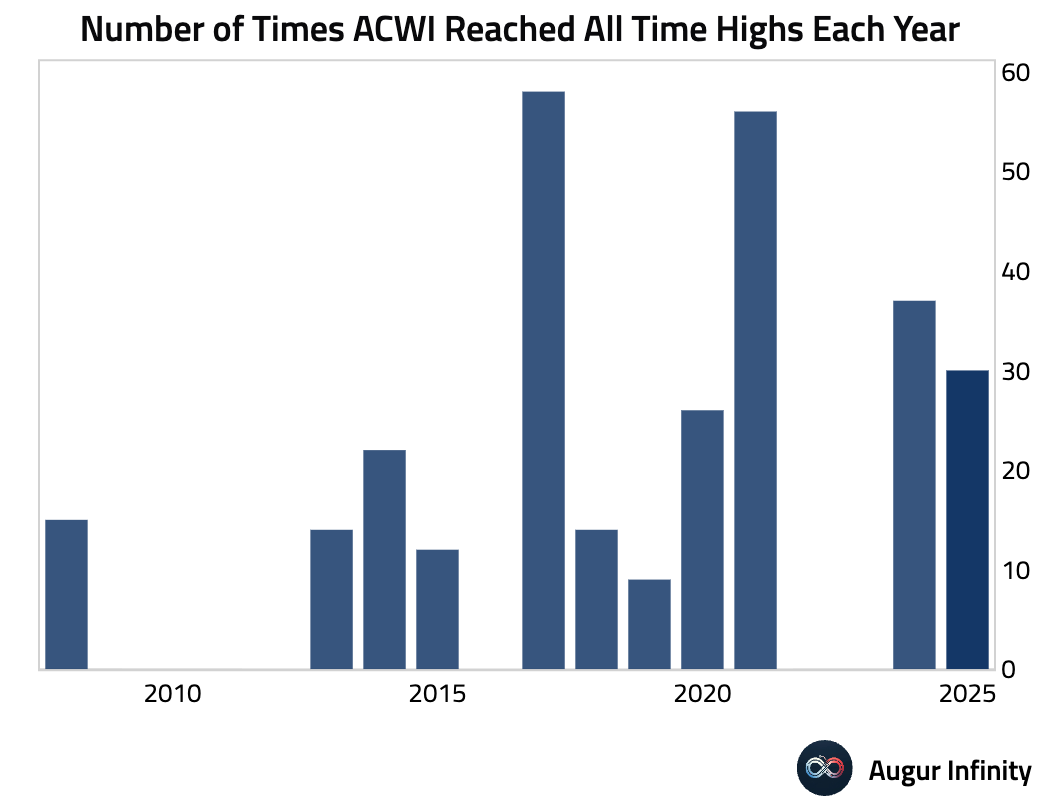

- Globally, the iShares MSCI ACWI ETF has reached all-time highs 30 times this year.

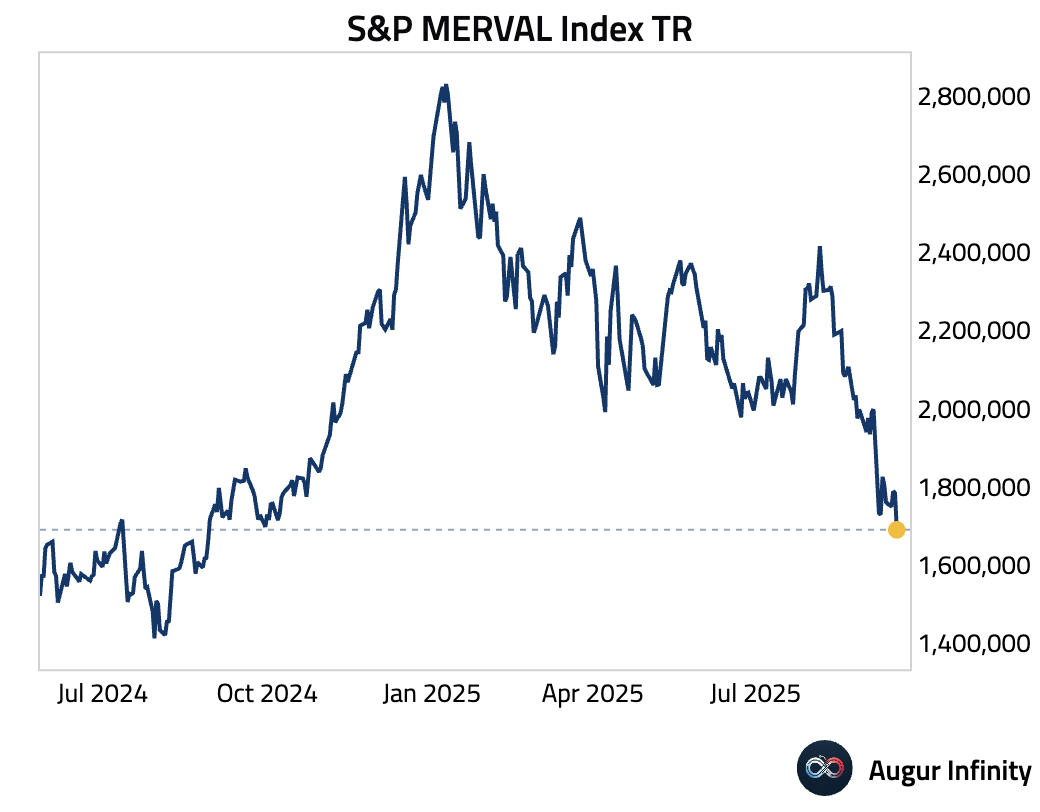

- Not all markets are rosy, however. The S&P MERVAL Index for Argentina fell to the lowest level since August 2024.

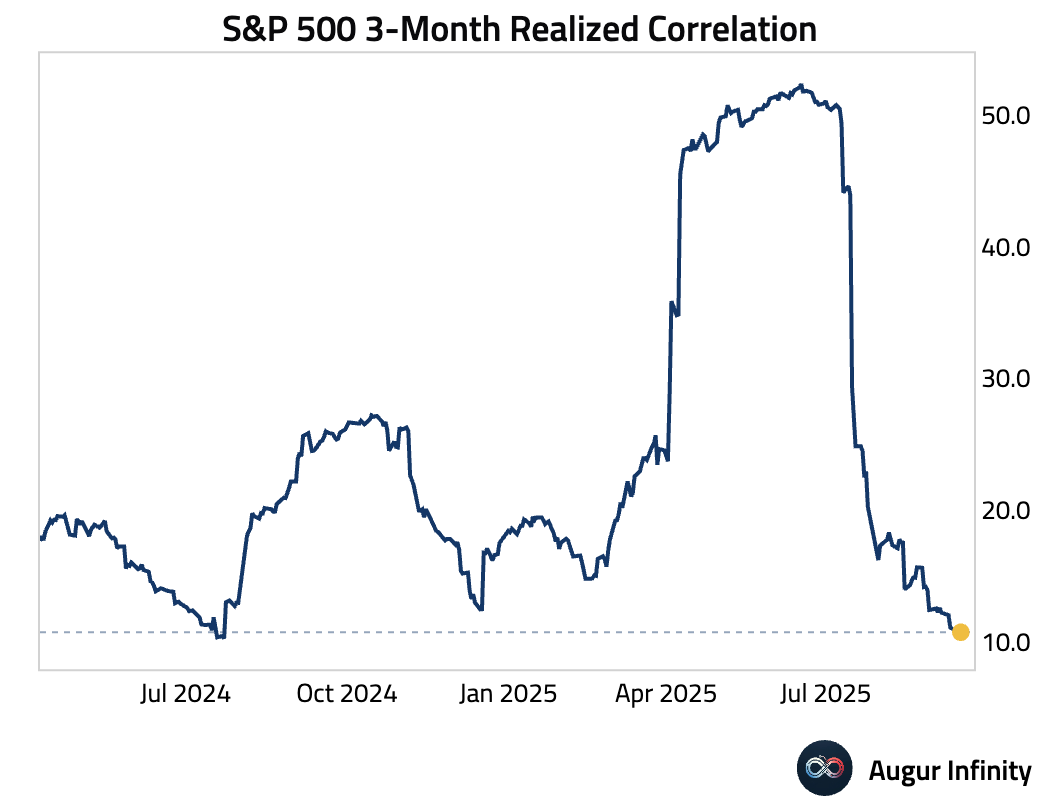

- S&P 500 3-Month Realized Correlation is at the lowest level since July 2024.

Fixed Income

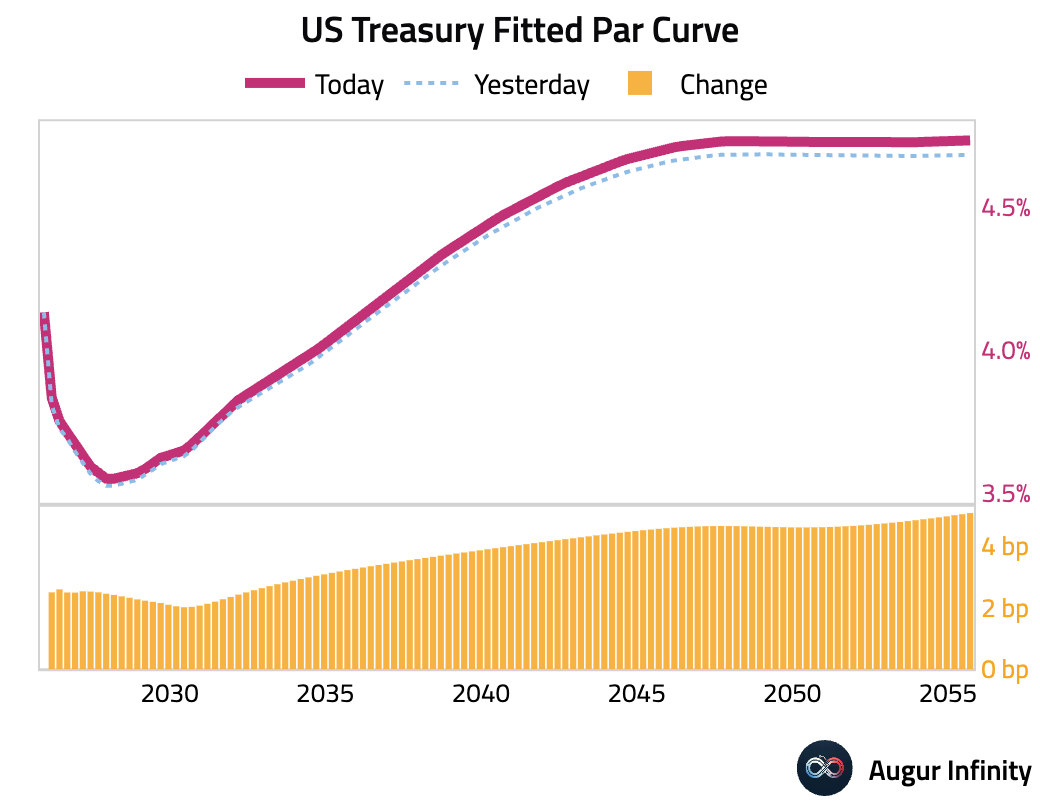

- US Treasury yields rose across the curve, with the 30-year yield up 5.9 bps and the 10-year yield up 4.1 bps. The move came as investors digested the Federal Reserve’s recent quarter-point rate cut, which was framed by officials as a risk-management adjustment rather than the start of an aggressive easing cycle.

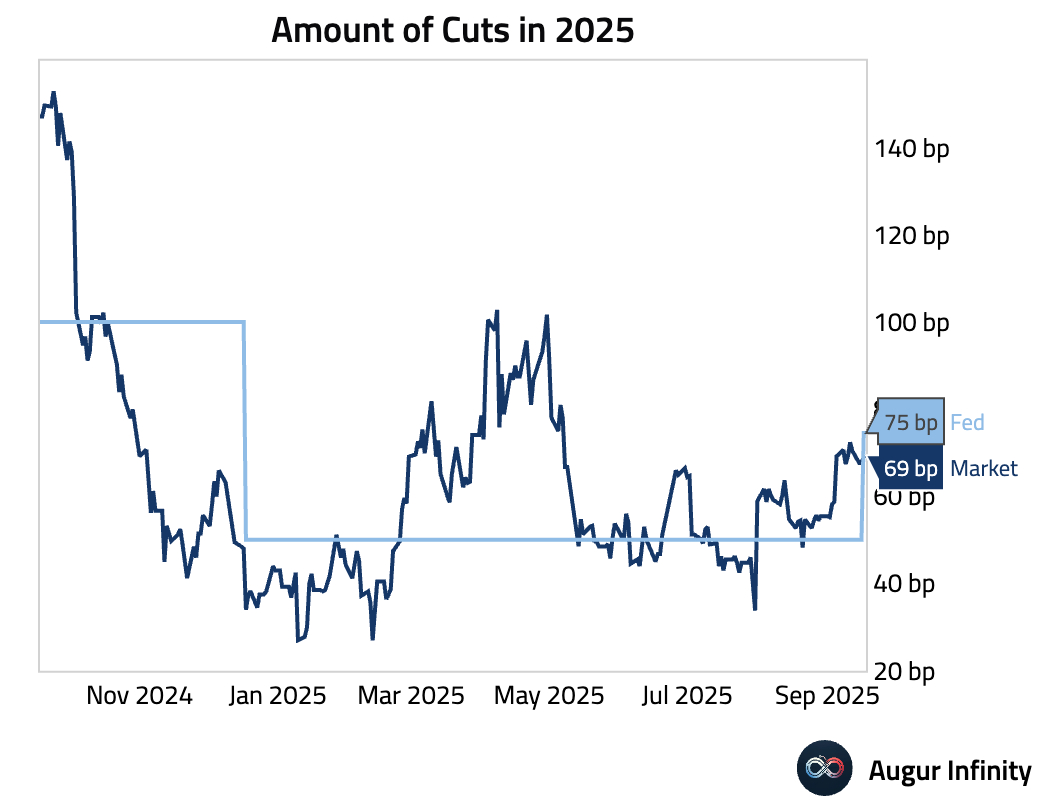

- After yesterday's 25 bps rate cut, the market is pricing for an additional 44 bps in cuts over the next two meetings.

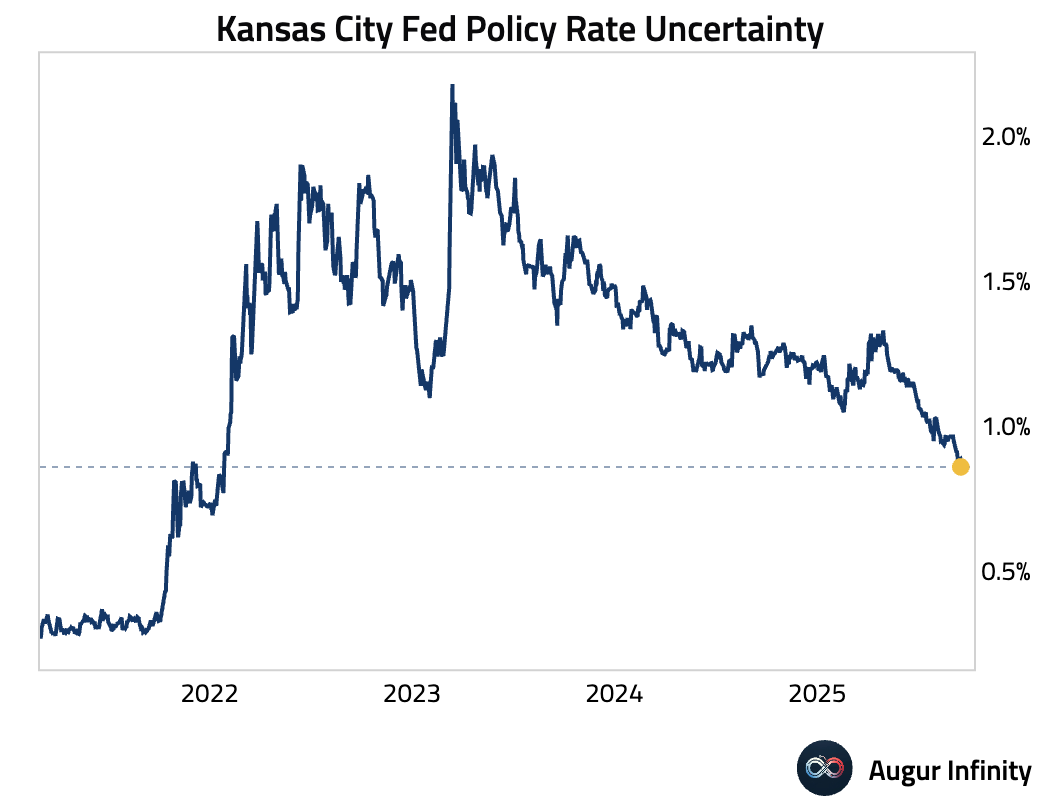

- Kansas City Fed Policy Rate Uncertainty is at the lowest level since January 27, 2022.

FX

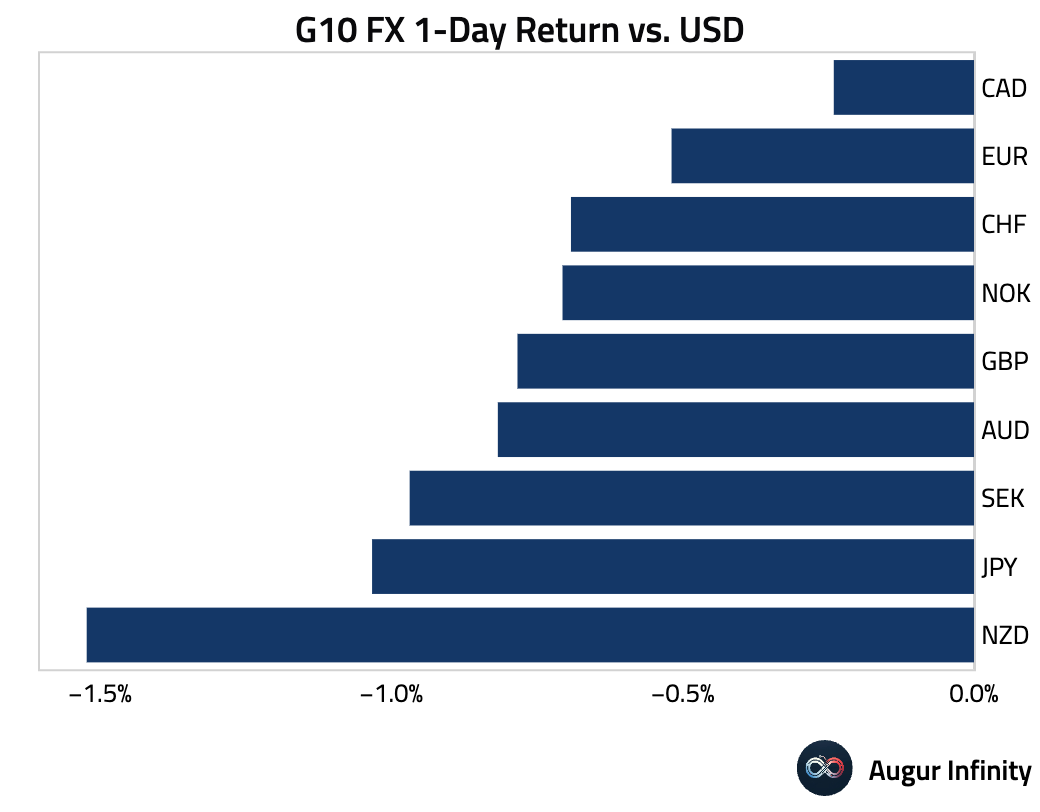

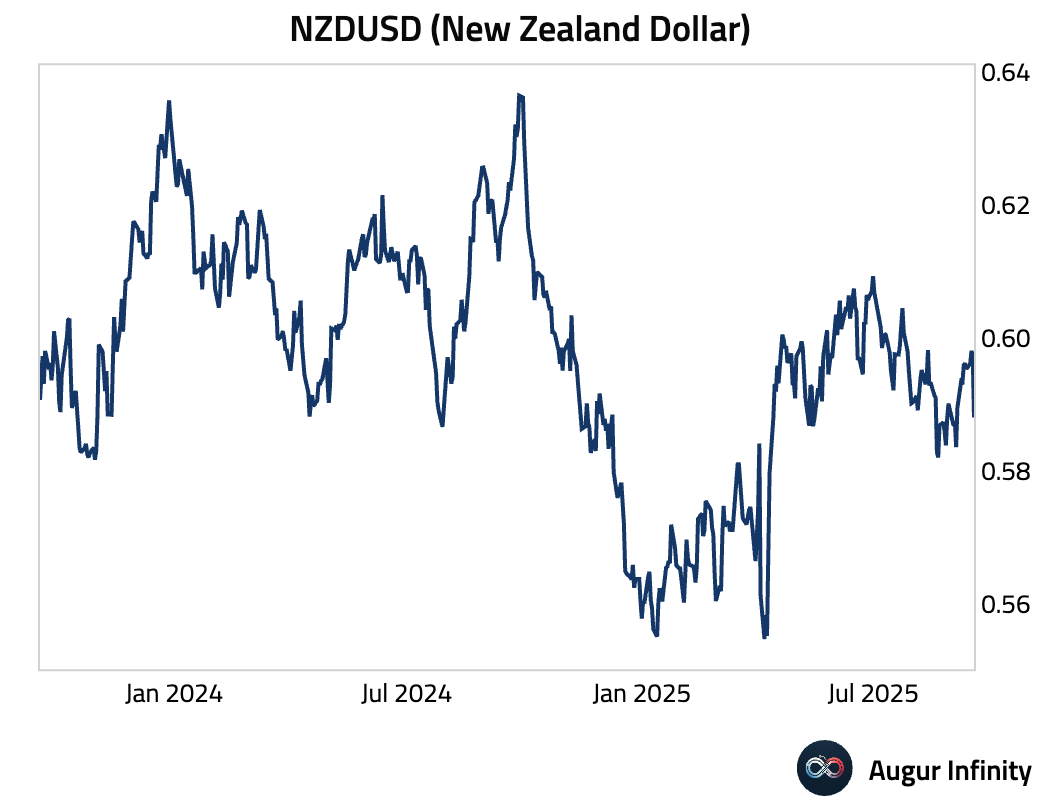

- The US dollar strengthened against all G10 currencies. The New Zealand dollar was the most significant underperformer, falling 1.5%, followed by the Japanese yen and Swedish krona, which both declined 1.0%. The Canadian dollar proved most resilient, down only 0.2% against the dollar.

- Here's the performance of NZDUSD.

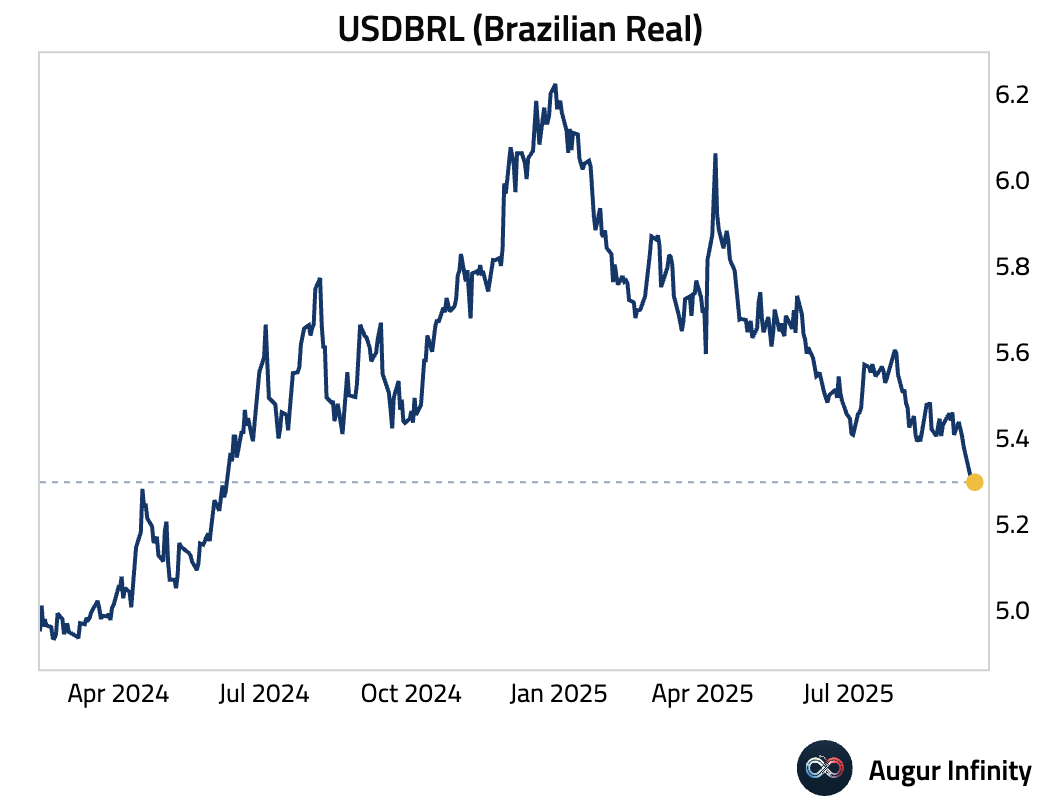

- USDBRL is at the lowest level since June 2024 after the Brazilian Real appreciated for eight consecutive days.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.