Headlines

- President Trump held a call with Chinese president Xi Jinping and announced plans to meet at next year’s APEC Summit, to be followed by a visit to China.

- The Bank of Japan announced a plan to sell its holdings of exchange-traded funds and Japanese real estate investment trusts at an annual pace of ¥330 billion and ¥5.5 billion, respectively.

- Spain’s economy minister called for the European Union to engage with China in an effort to reduce the bloc’s trade deficit.

Global Economics

United States

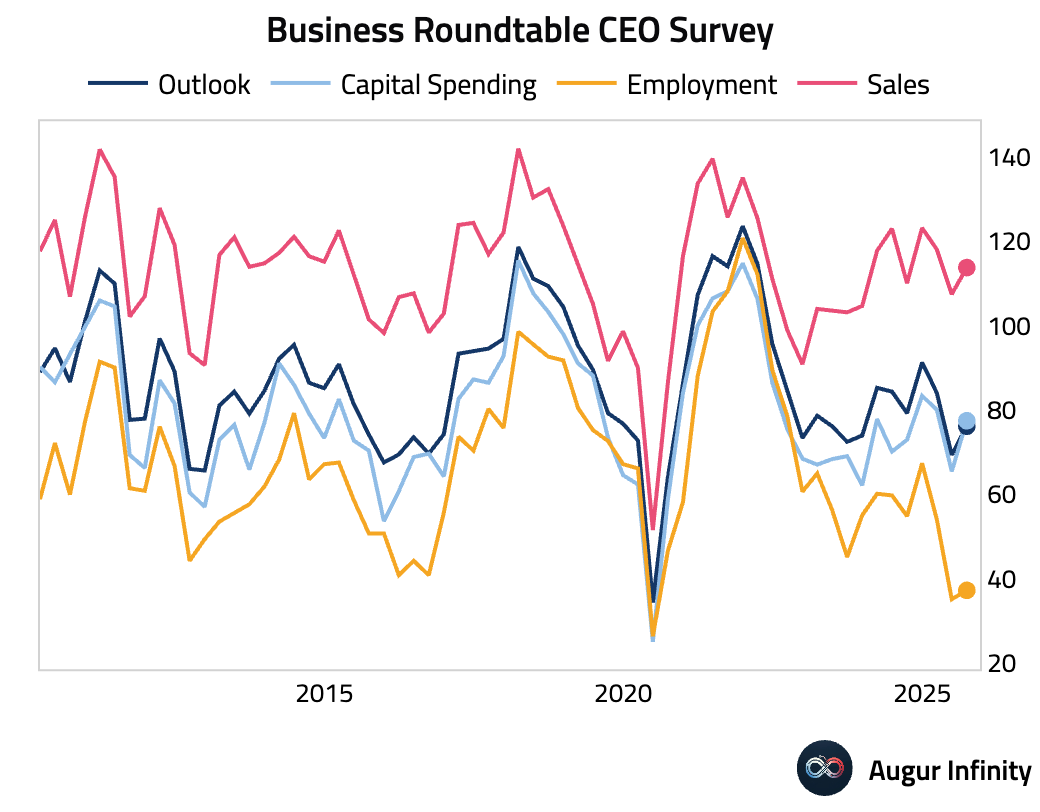

- The Q3 CEO Outlook Index rose 7 pts to 76, still below average. The gain was driven by a jump in capex plans, fueled by optimism over recent tax legislation. However, the hiring subindex remained in contraction territory for a second quarter, with CEOs citing headwinds for trade-exposed sectors like manufacturing.

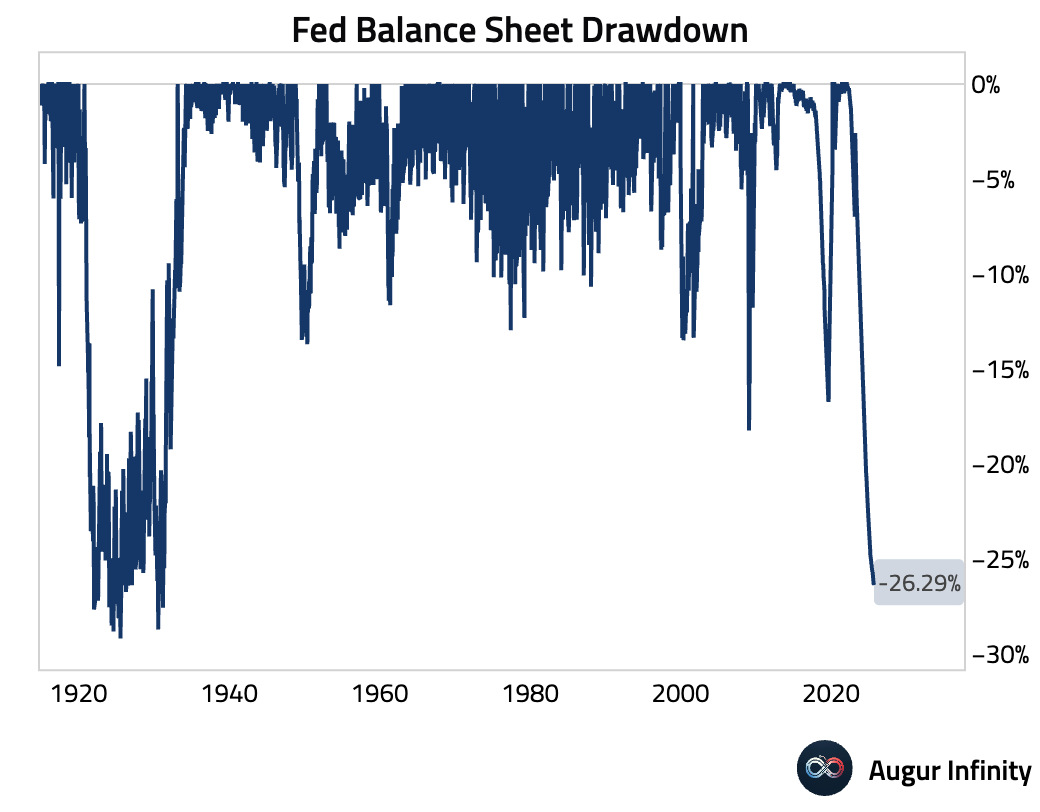

- The Federal Reserve’s balance sheet ticked up to $6.61 trillion last week from $6.60 trillion the week prior.

Canada

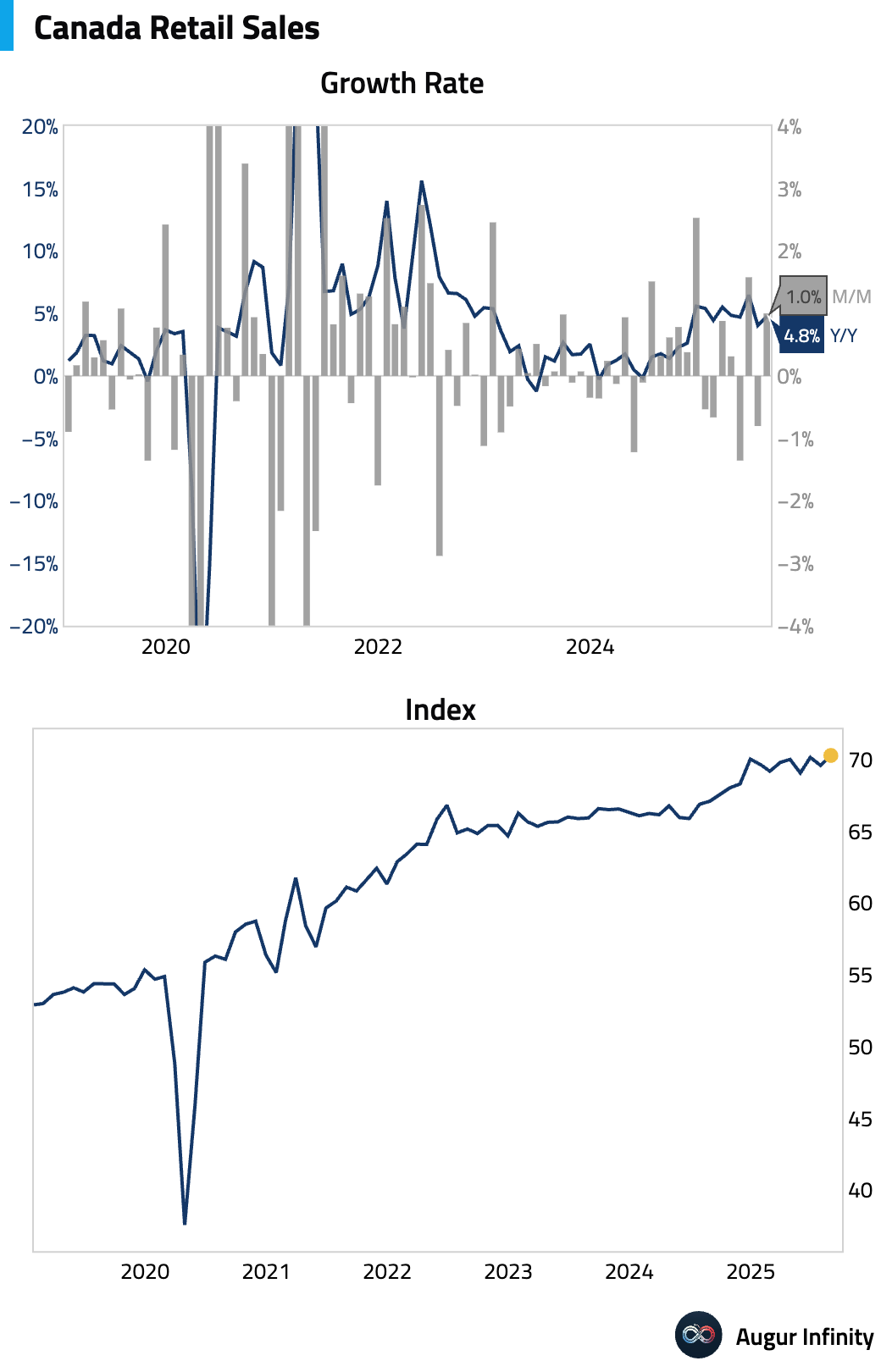

- Canadian retail sales contracted in July, in line with consensus, while sales ex-autos fell more sharply than expected (MoM act: -0.8%, est: -0.8%; ex-autos MoM act: -1.2%, est: -0.7%). The preliminary estimate for August points to a 1.0% rebound in sales. Year-over-year sales growth slowed to 4.0%.

Europe

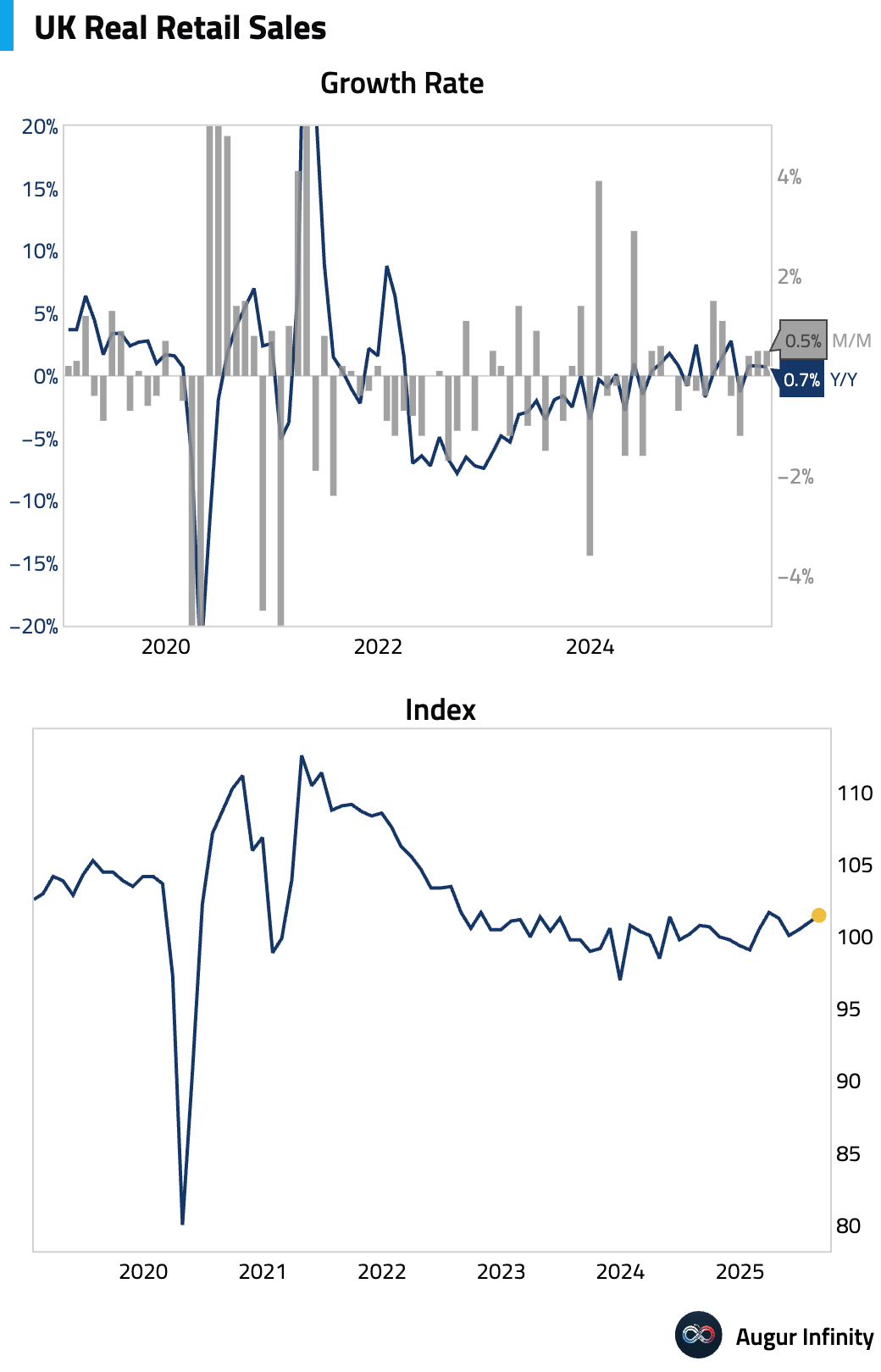

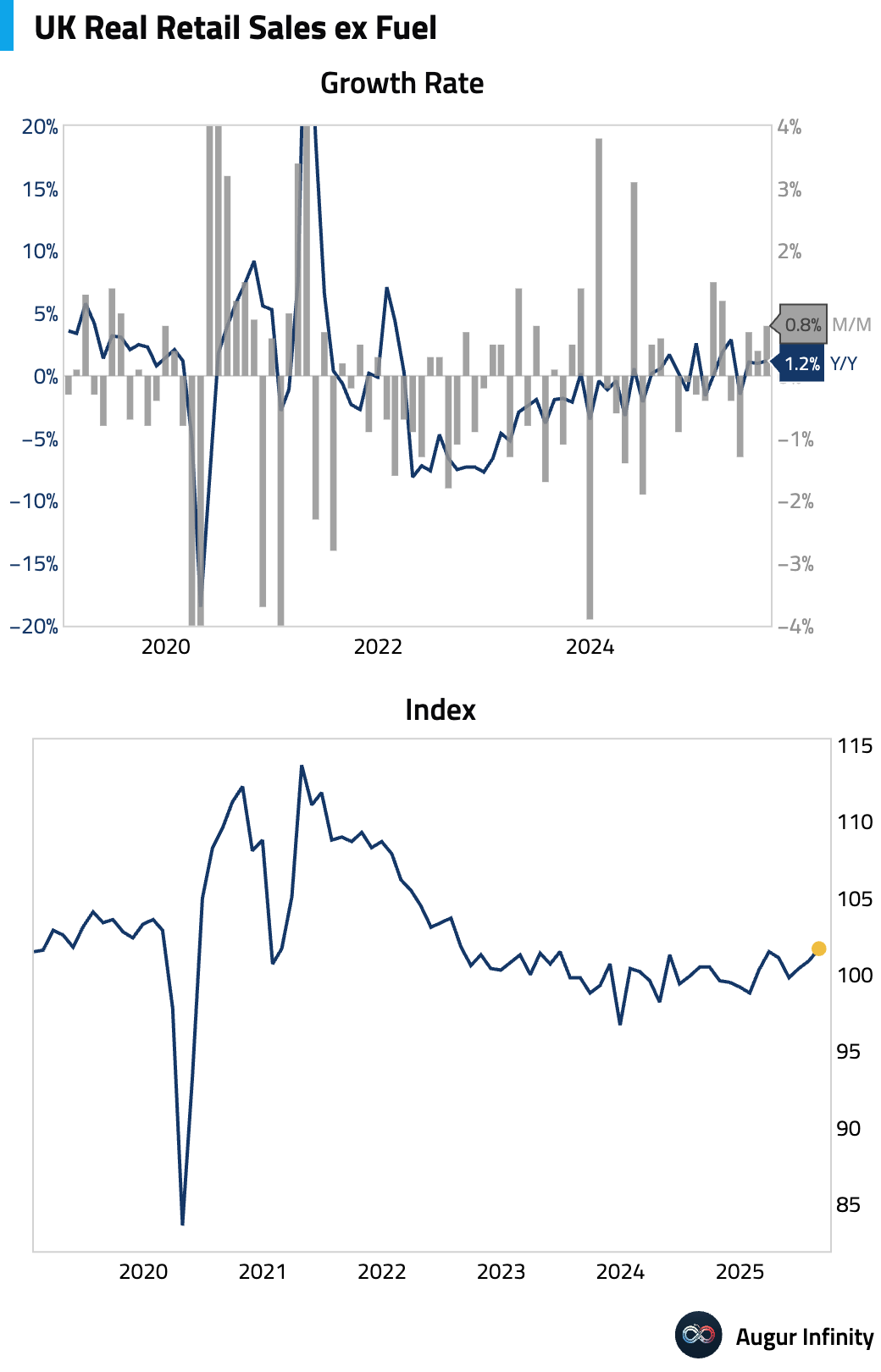

- UK retail sales rose for a second consecutive month in August, beating expectations and suggesting continued consumer resilience (MoM act: 0.5%, est: 0.3%). Year-over-year, sales growth edged down to 0.7% from 0.8%.

- Core UK retail sales, excluding fuel, also posted a strong gain that surpassed consensus forecasts (MoM act: 0.8%, est: 0.7%).

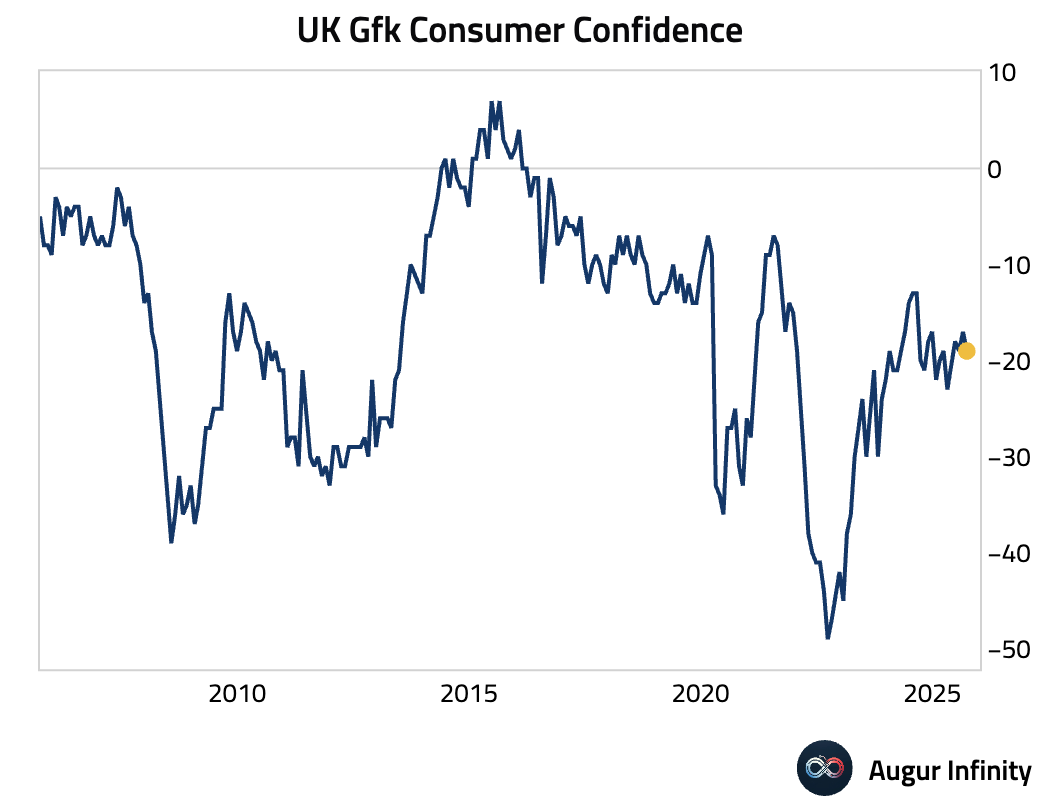

- UK consumer confidence deteriorated slightly in September, missing expectations for an unchanged reading (act: -19, est: -18).

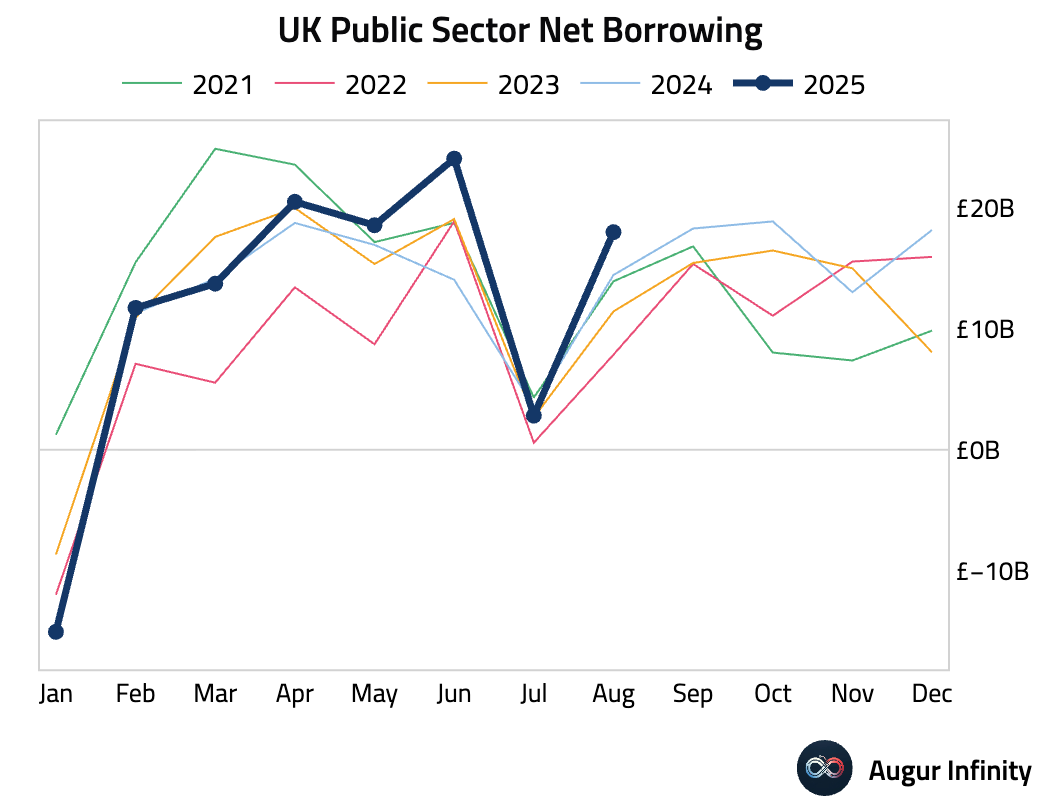

- UK public sector net borrowing was significantly higher than anticipated in August, driven by increased debt interest payments and social benefits (act: £18.0B, est: £12.8B).

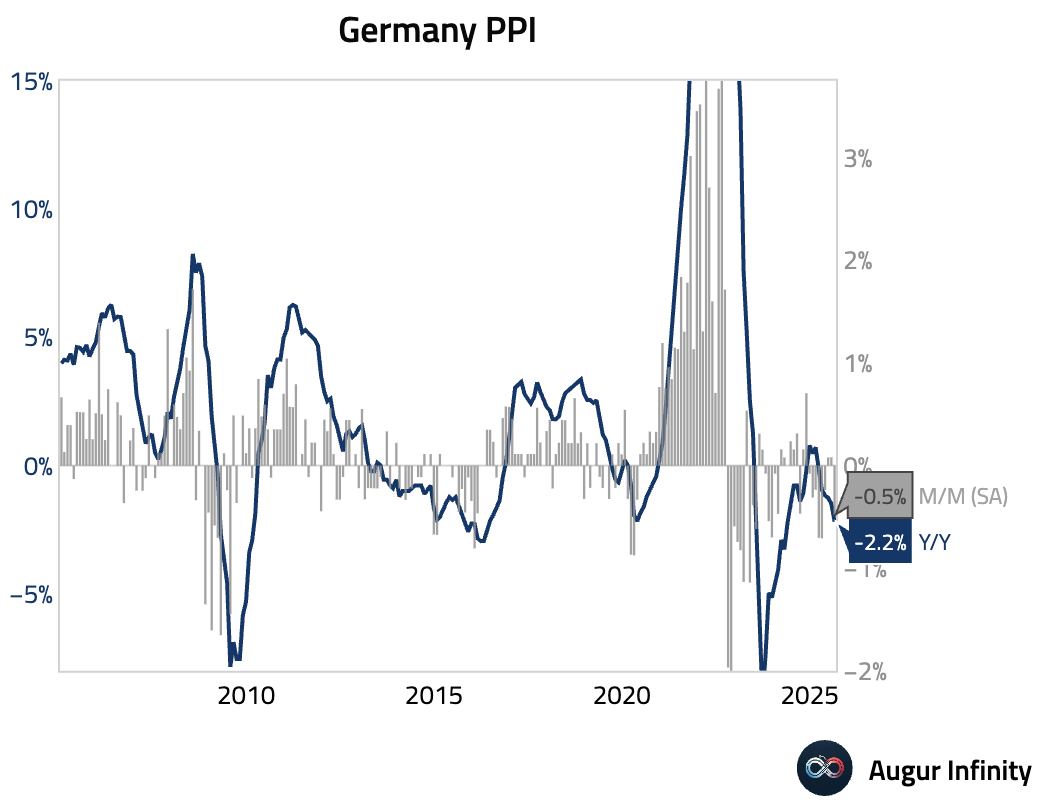

- German producer price deflation deepened in August, with prices falling 0.5% M/M and 2.2% Y/Y, both significantly weaker than consensus estimates of -0.1% M/M and -1.7% Y/Y, respectively. The monthly decline was the largest in four months.

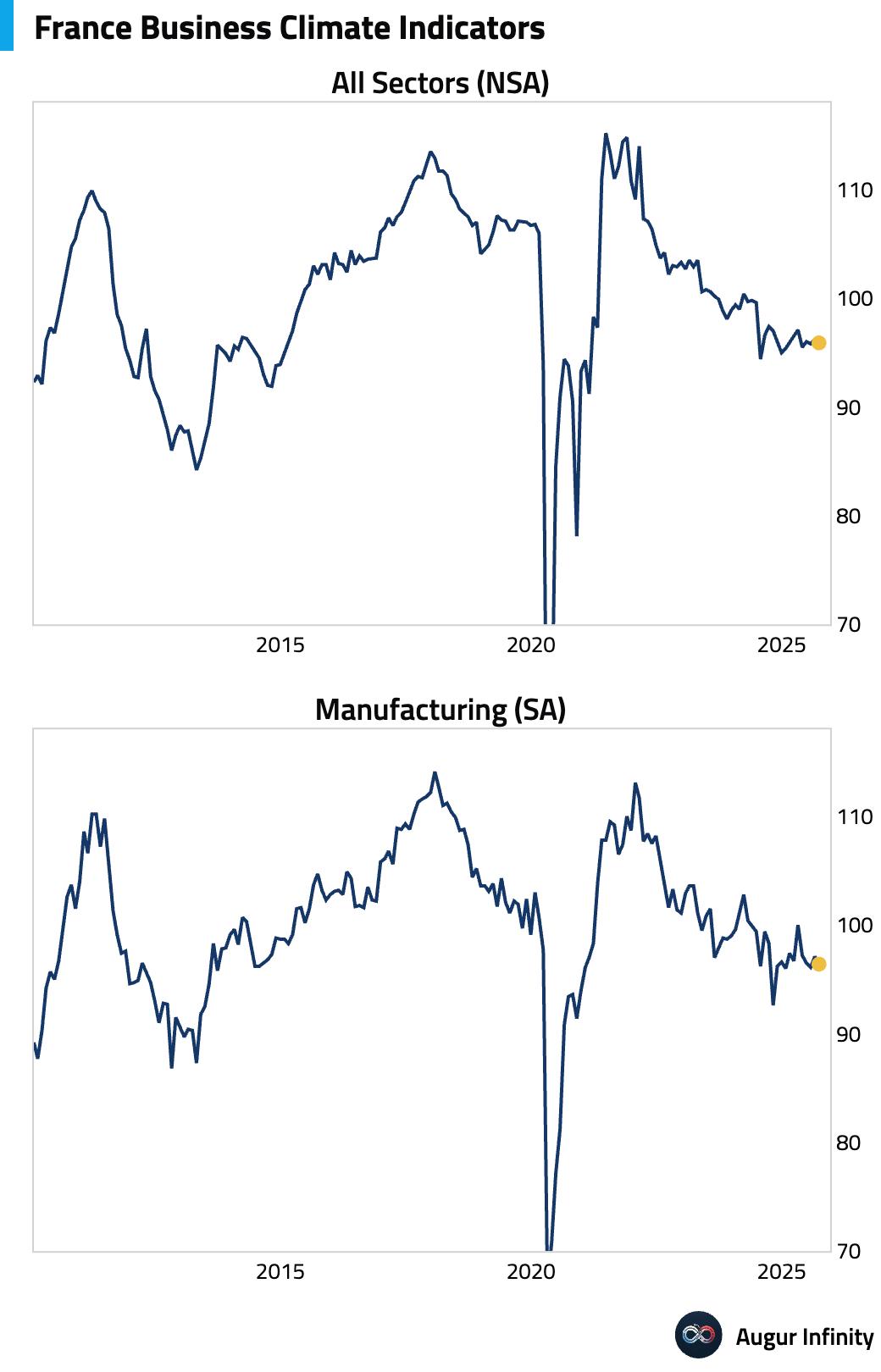

- French business confidence edged down in September but met market expectations (act: 96, est: 96).

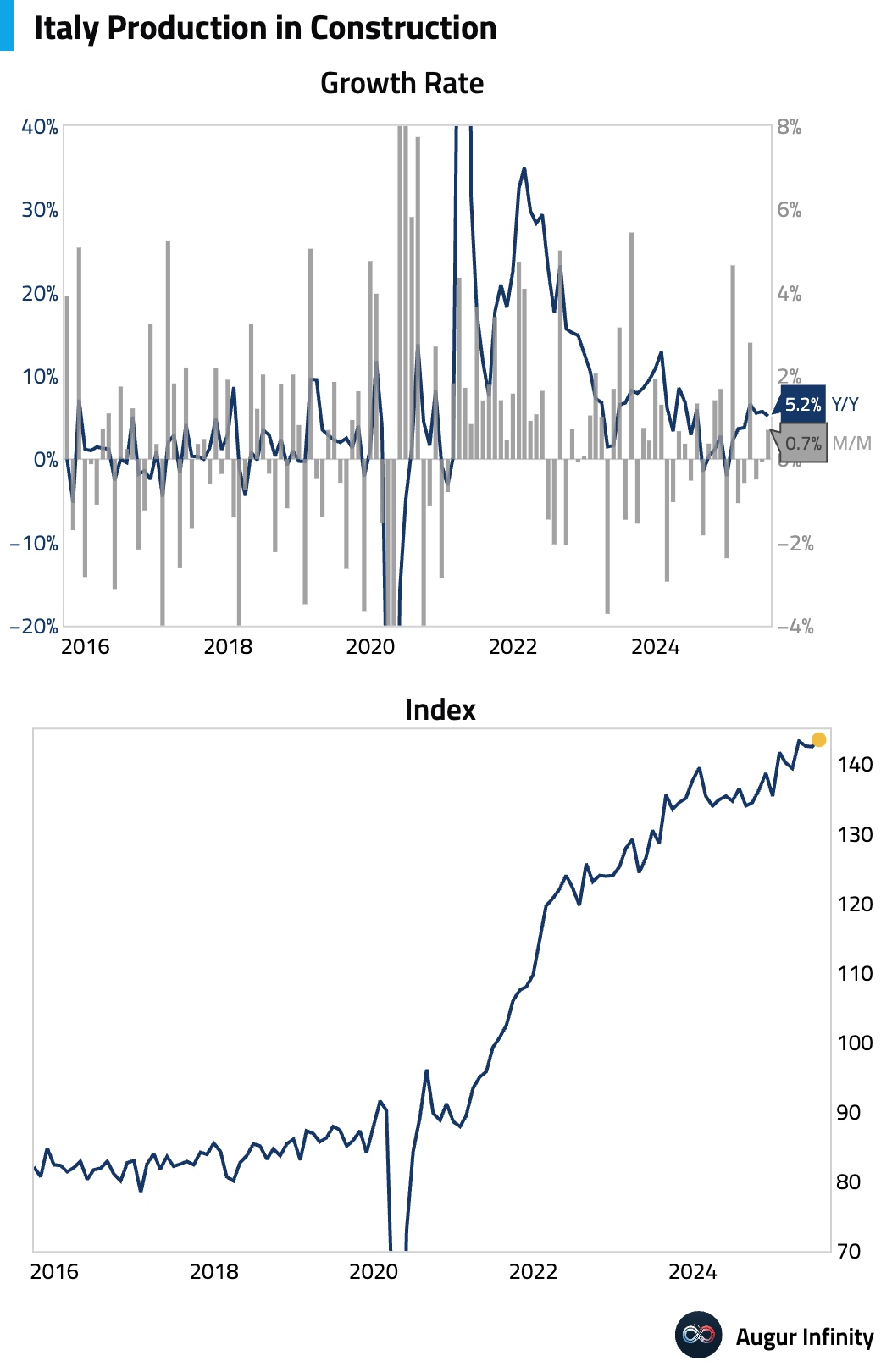

- Italian construction output growth accelerated to 5.7% Y/Y in July from 5.5% in the prior month.

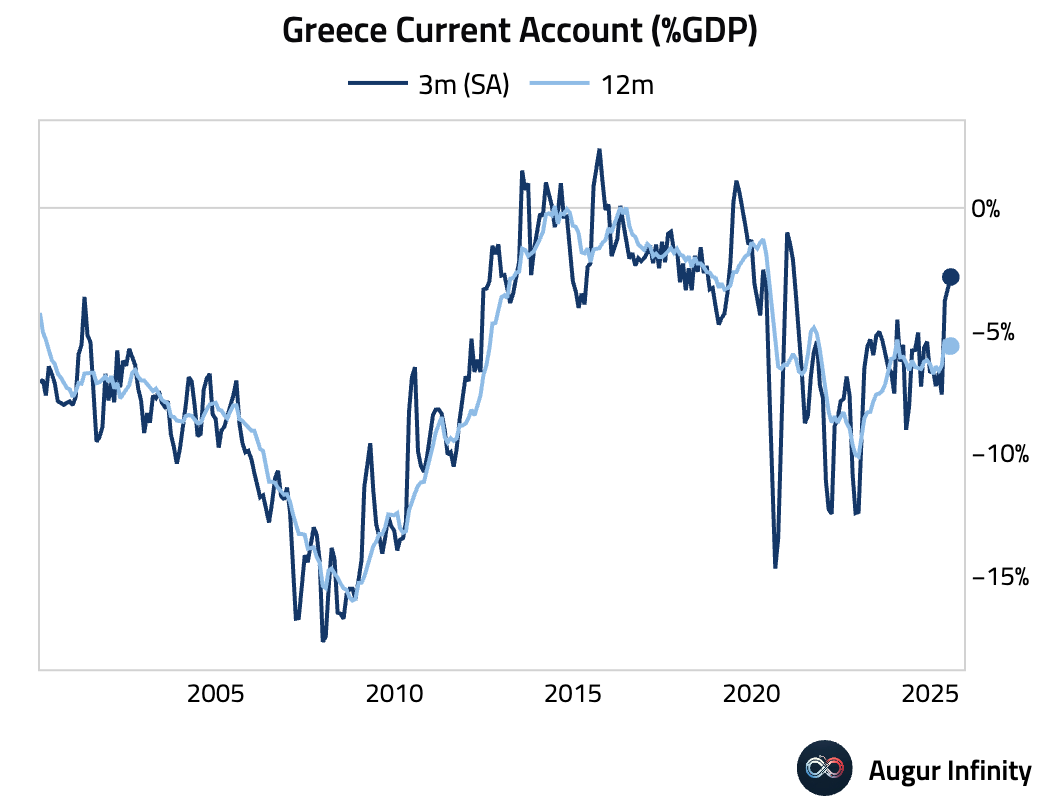

- Greece’s current account surplus widened in July (act: €938M, prev: €196M).

Asia-Pacific

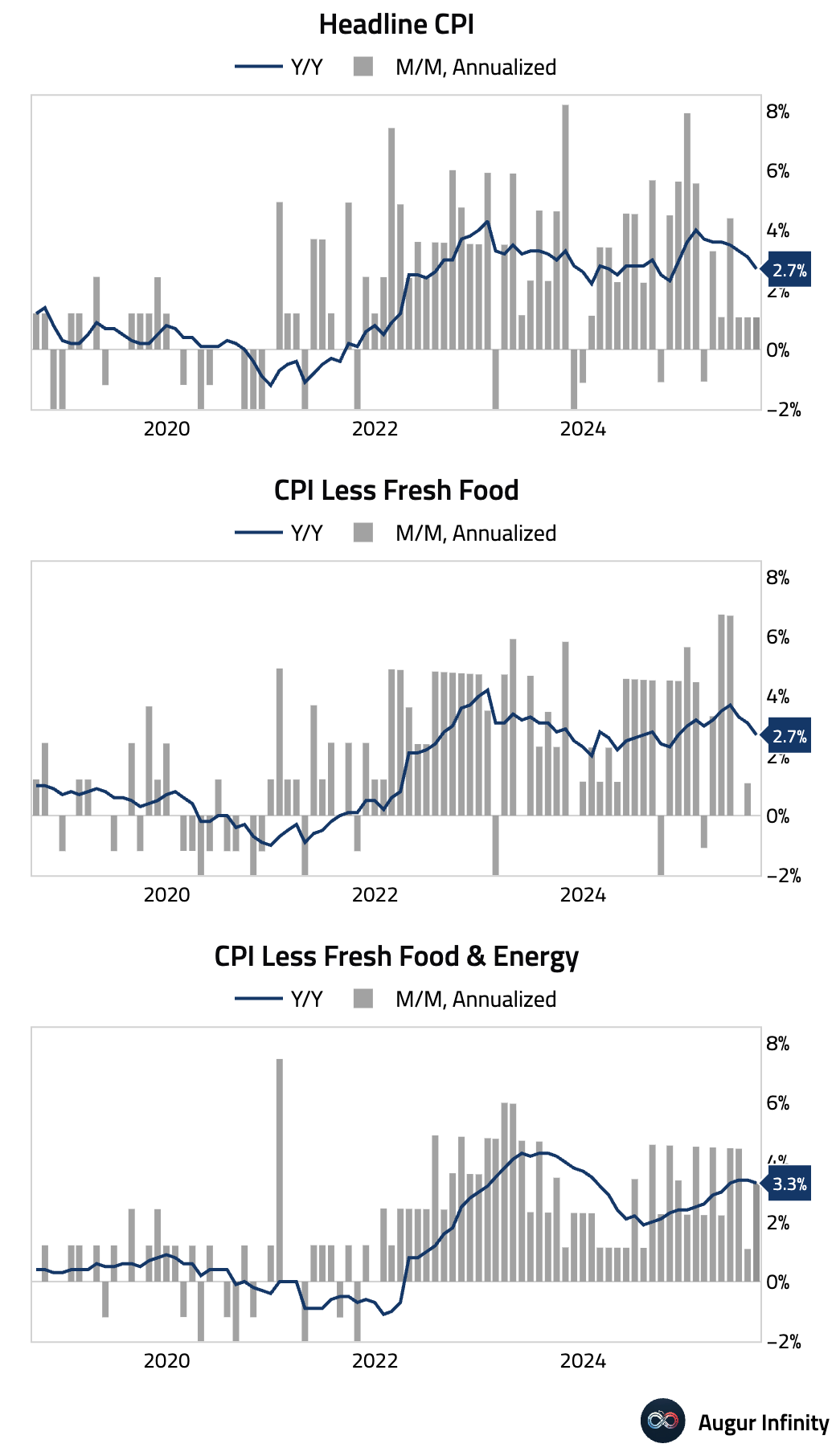

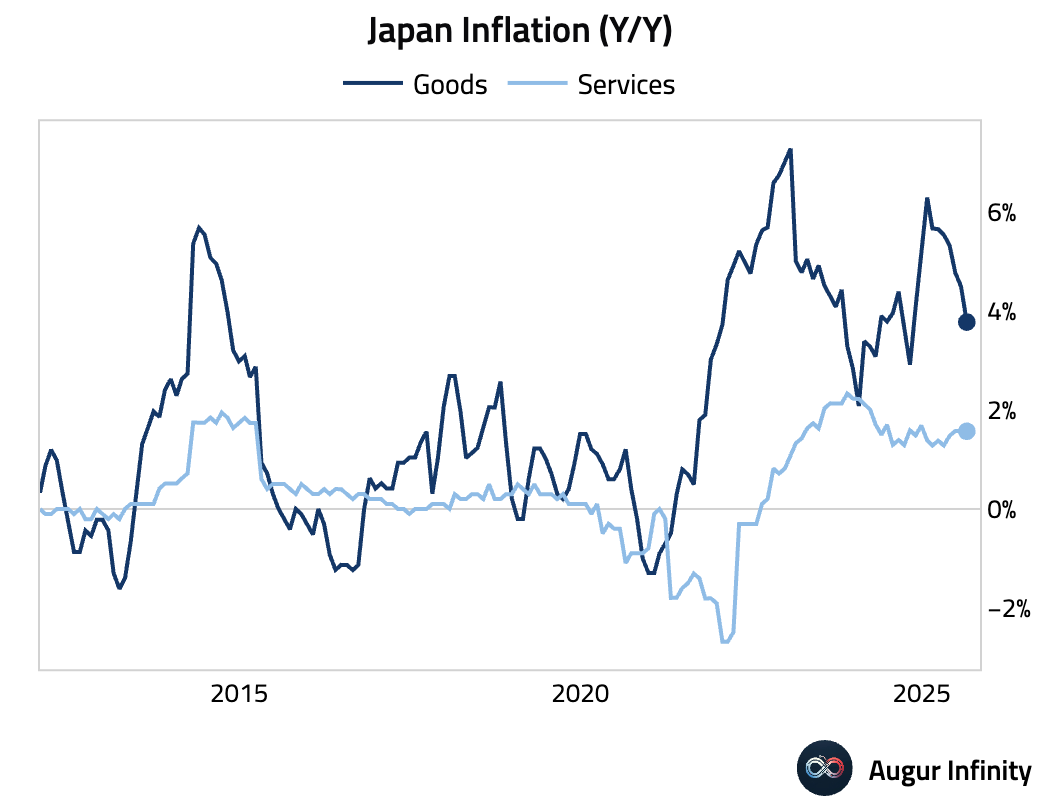

- Japanese inflation cooled in August, with the headline rate slowing to 2.7% Y/Y from 3.1% in July. Core inflation, which excludes fresh food, also decelerated to 2.7% Y/Y, meeting consensus, while the “core-core” measure, excluding both fresh food and energy, eased to 3.3% from 3.4%. The slowdown provides the Bank of Japan with more leeway as it considers normalizing policy.

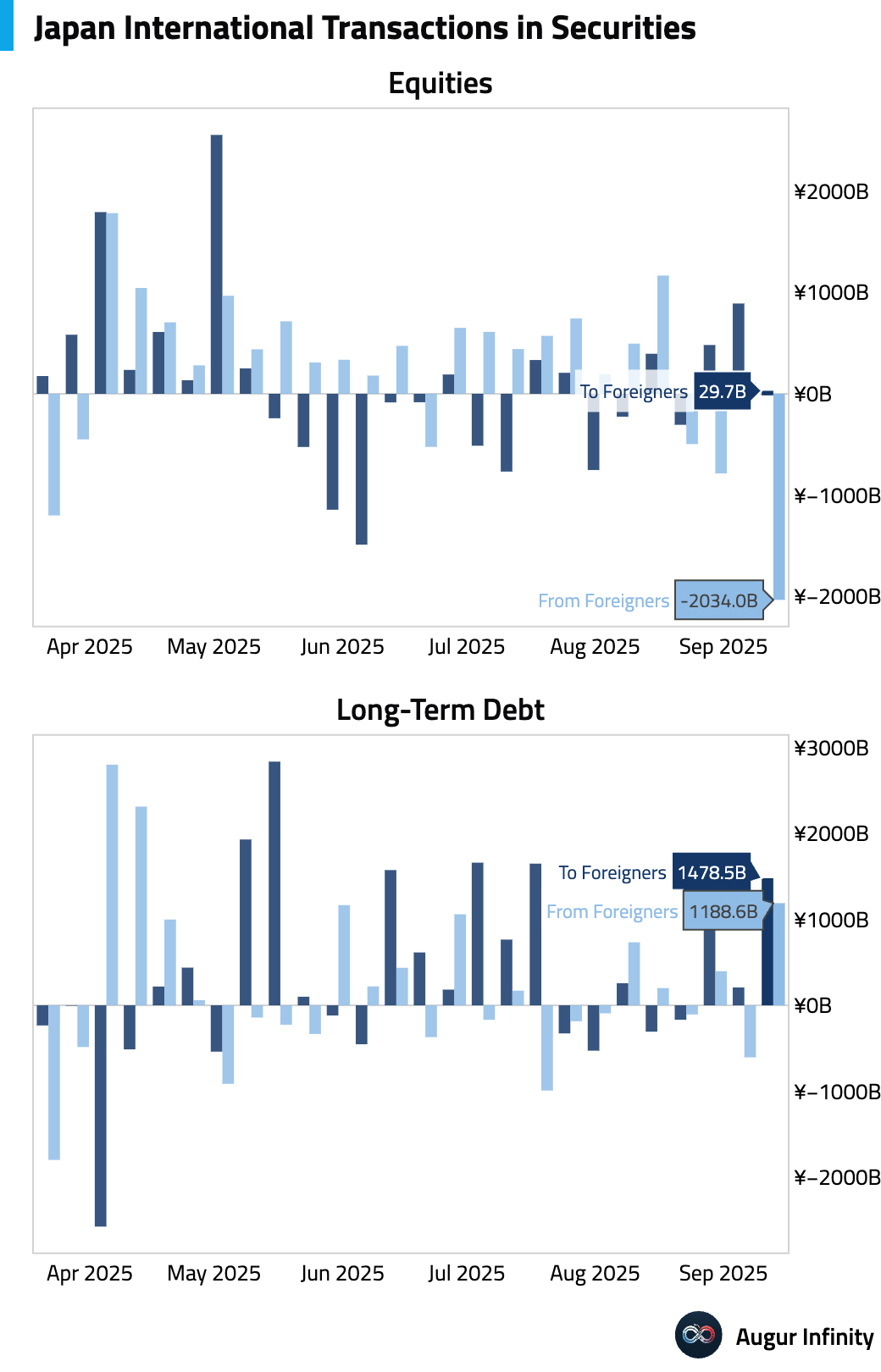

- Foreign investors sold a net ¥2.03 trillion of Japanese stocks in the week ending September 13, the largest weekly outflow in a year. Meanwhile, Japanese investors were net buyers of foreign bonds for a second consecutive week.

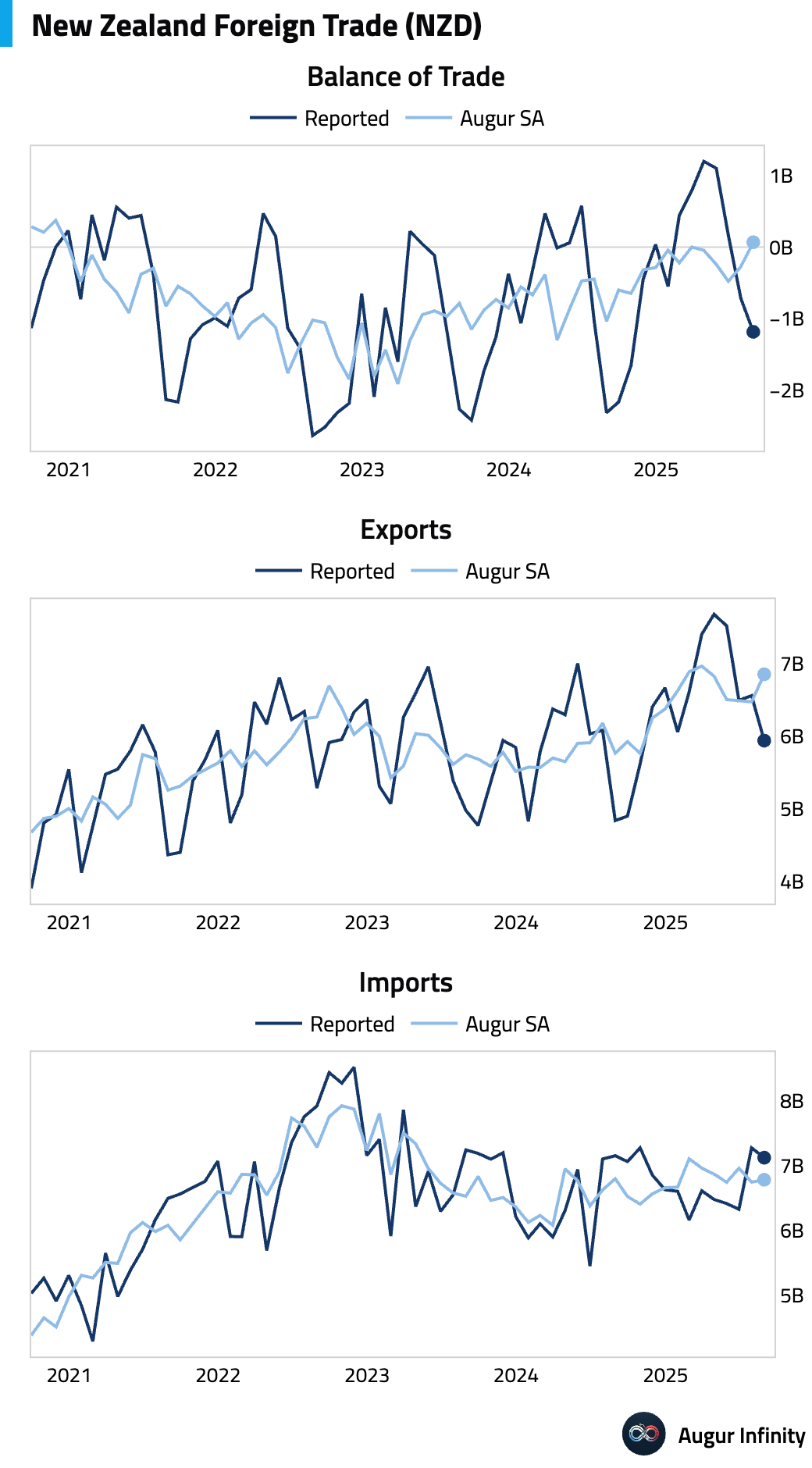

- New Zealand’s trade deficit widened more than expected in August as both exports and imports declined (act: -NZ$1.19B, est: -NZ$0.75B).

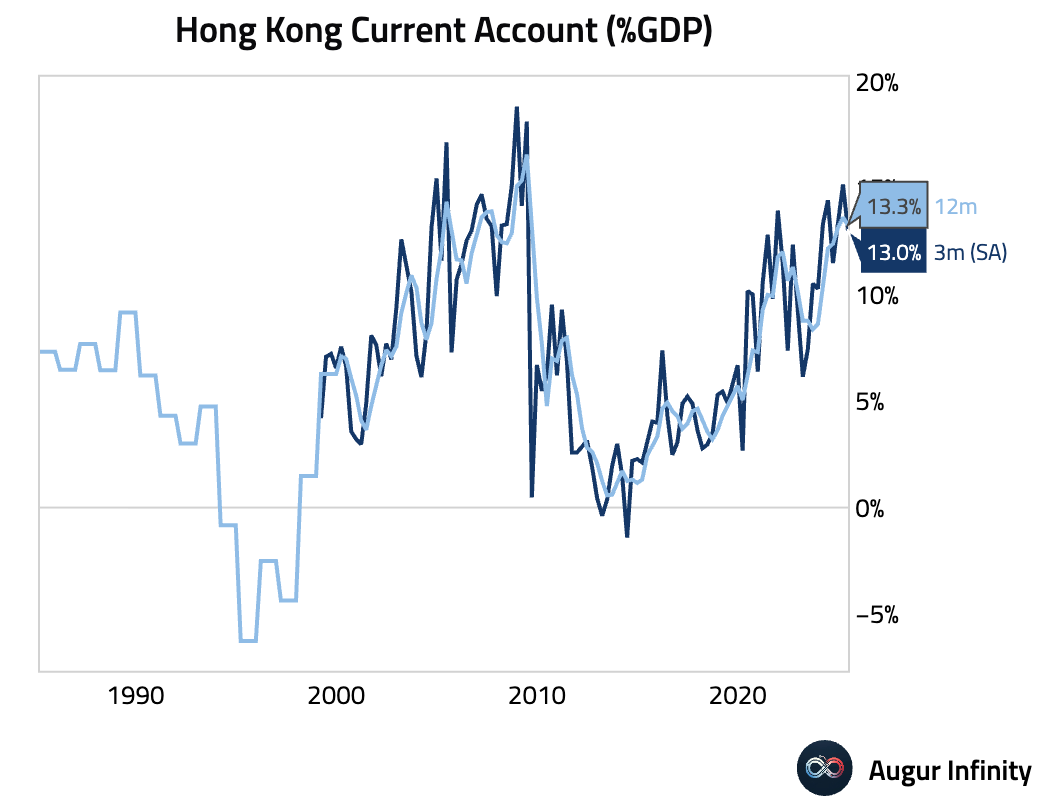

- Hong Kong's current account surplus narrowed in the second quarter (act: HK$92.6B, prev: HK$126.9B).

China

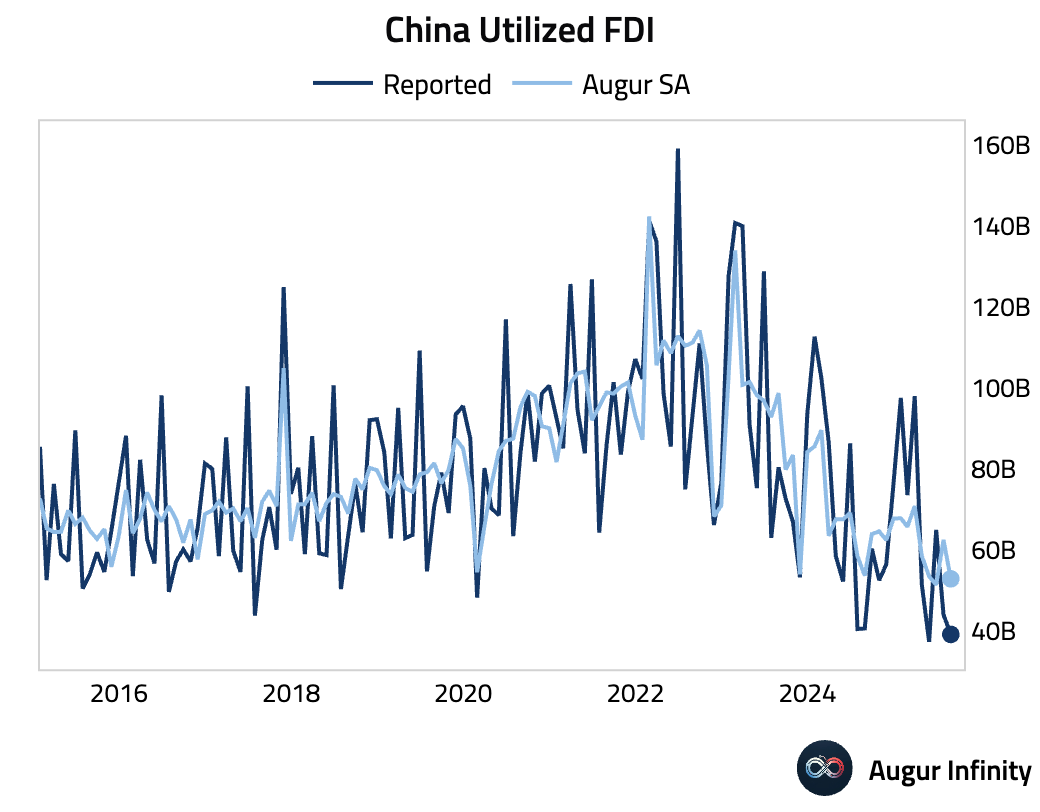

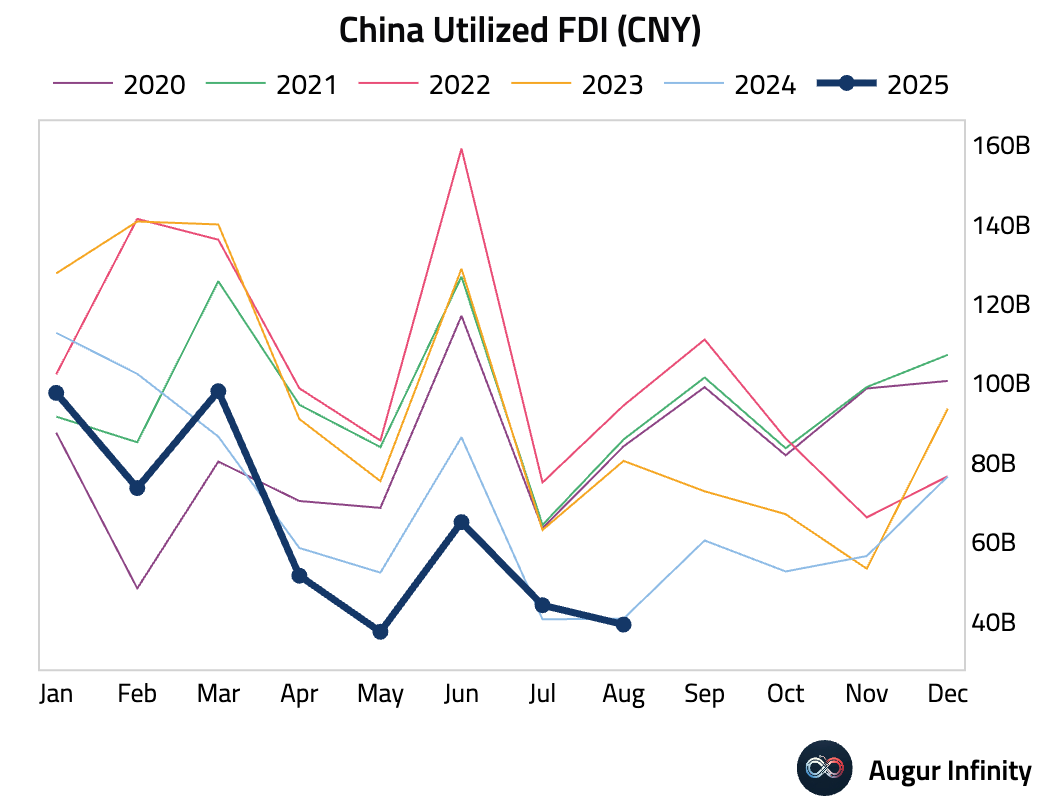

- Utilized foreign direct investment in China fell 12.7% Y/Y in the January-August period, a slight moderation from the 13.4% decline seen through July but still indicative of weak foreign investor sentiment.

Emerging Markets ex China

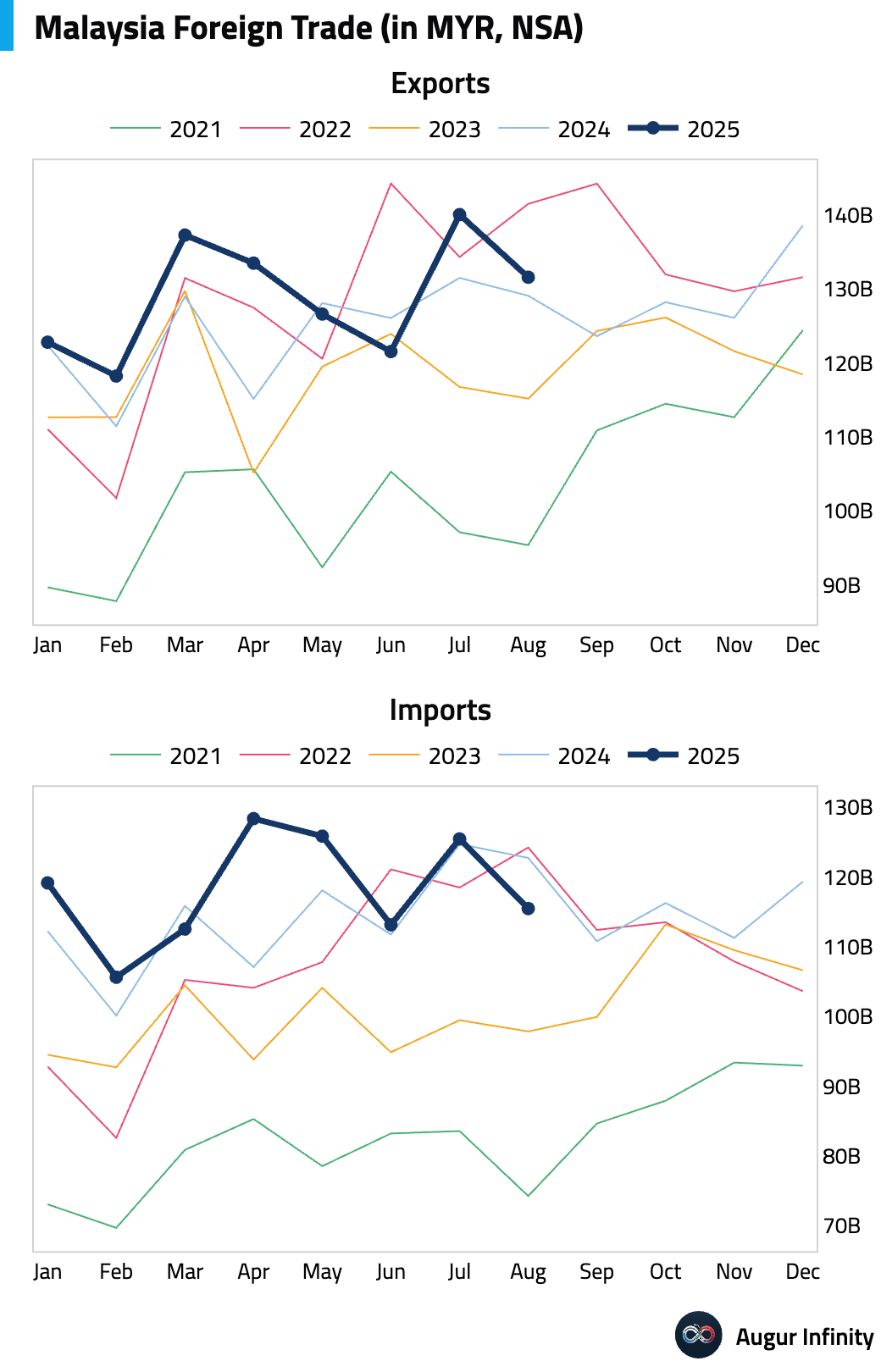

- Malaysia’s trade surplus widened in August, as imports fell 5.9% Y/Y while export growth slowed to 1.9% Y/Y.

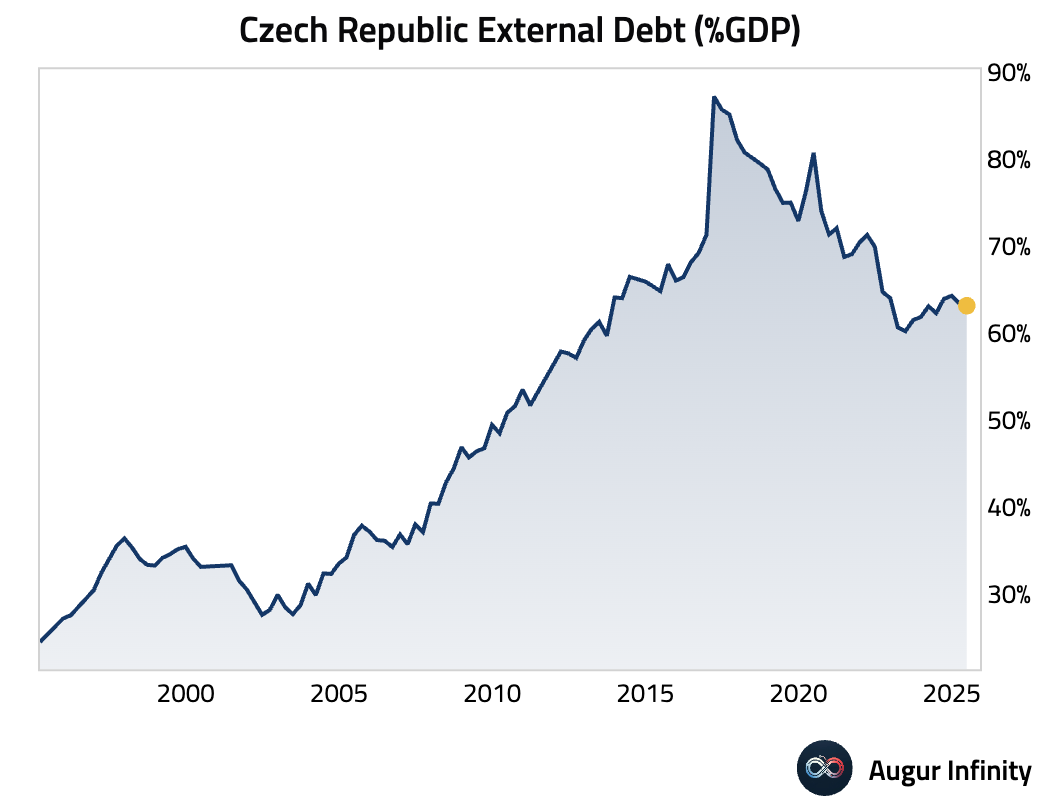

- The Czech Republic's external debt climbed to an all-time high in the second quarter (act: €216.4B, prev: €211.7B).

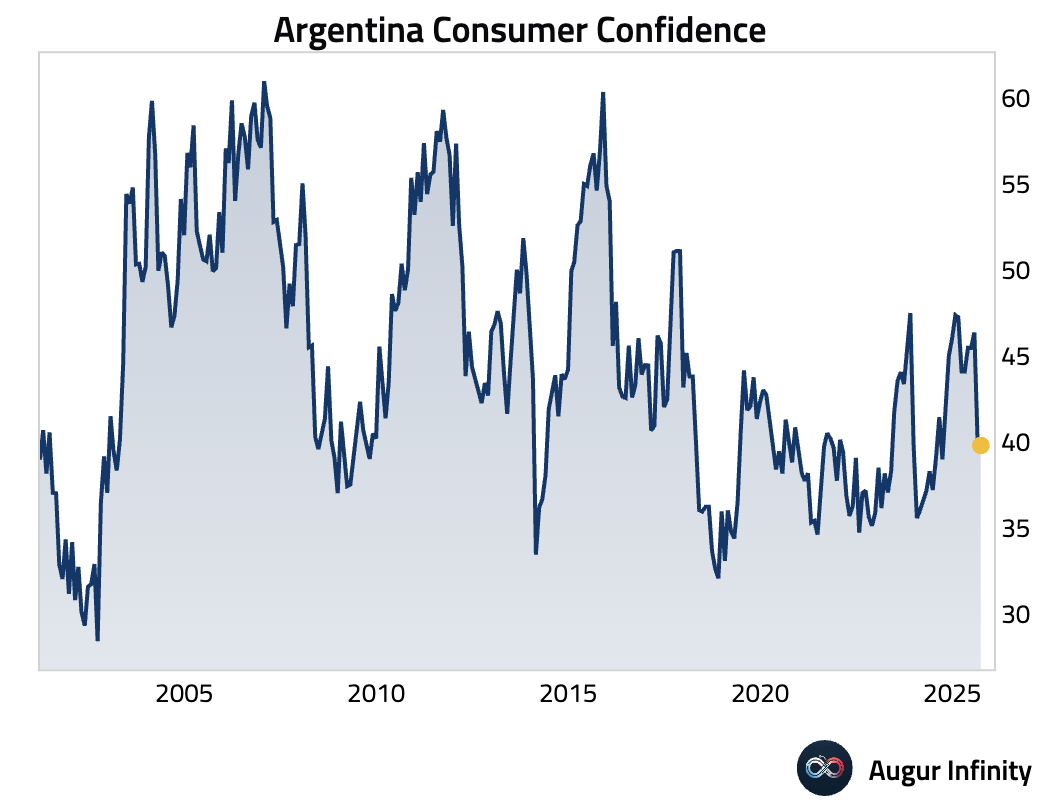

- Argentine consumer confidence ticked down in September (act: 39.81, prev: 39.94).

Global Markets

Equities

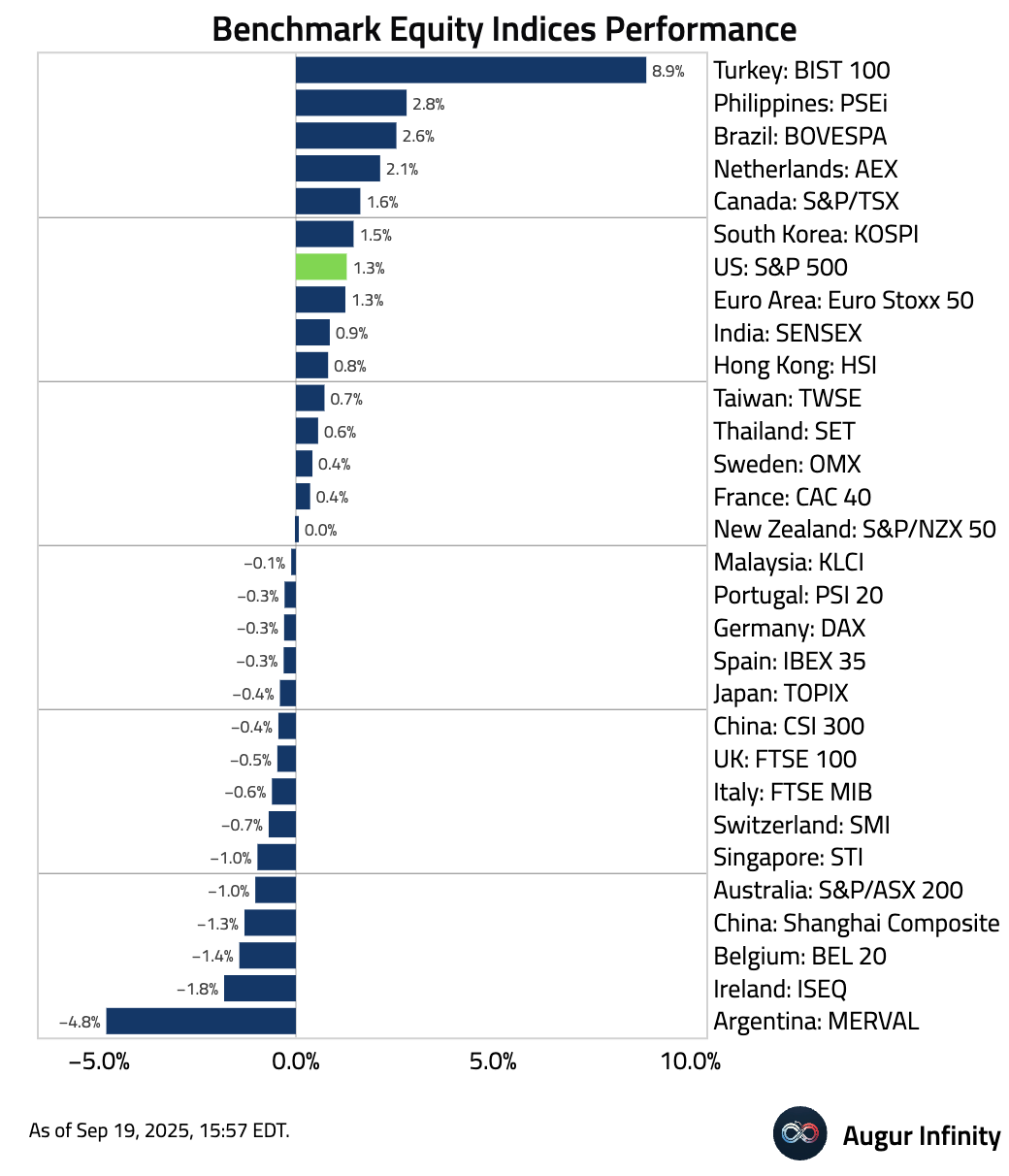

- Here's how global equity benchmarks performed this week …

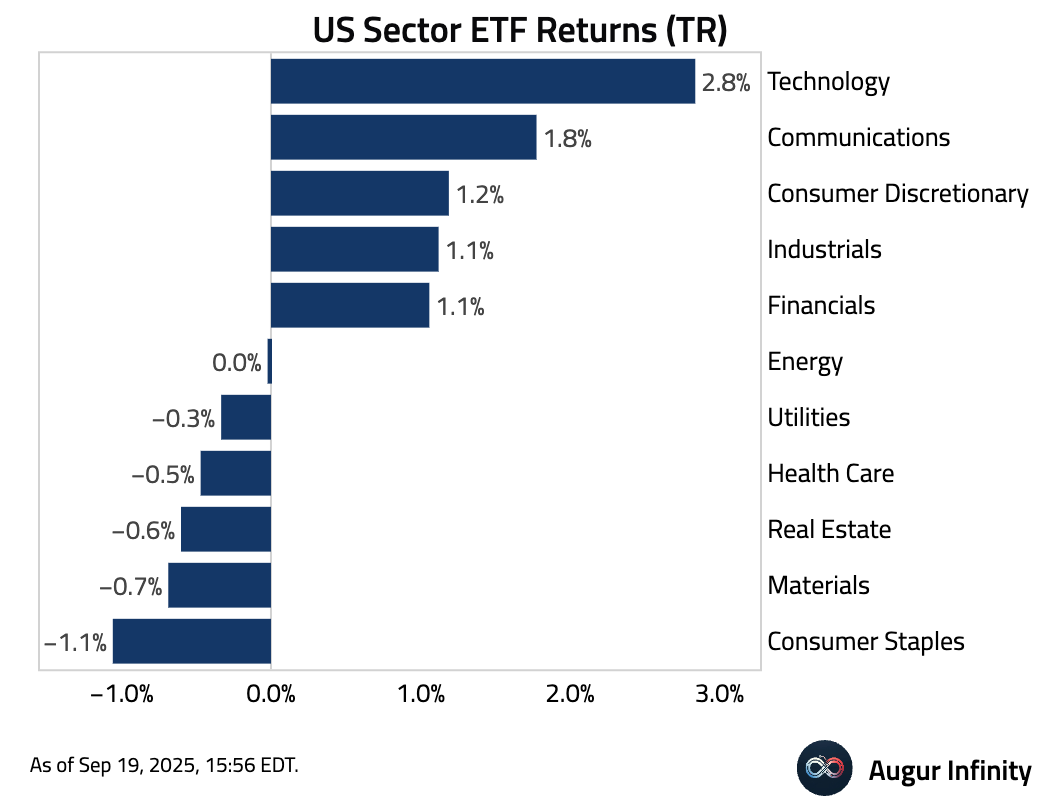

… and here's the weekly performance of US equity sectors.

Fixed Income

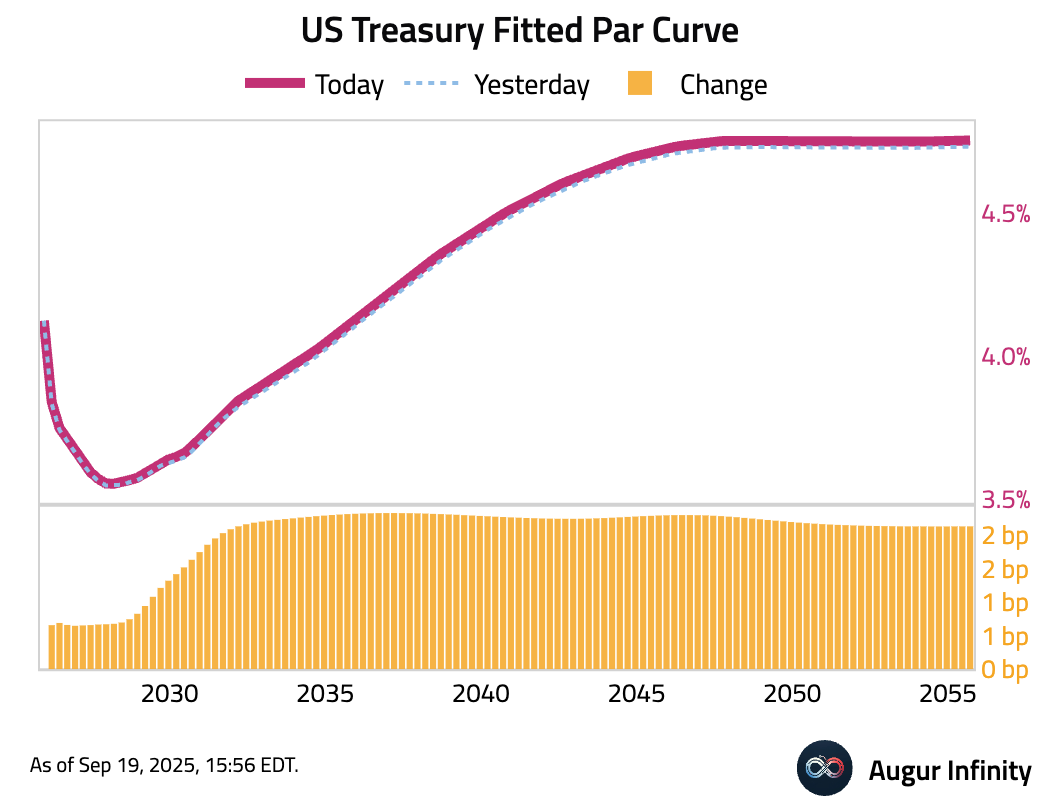

- The 10-year yield increased by 0.9 basis points, while the 2-year yield was down 0.5 basis points.

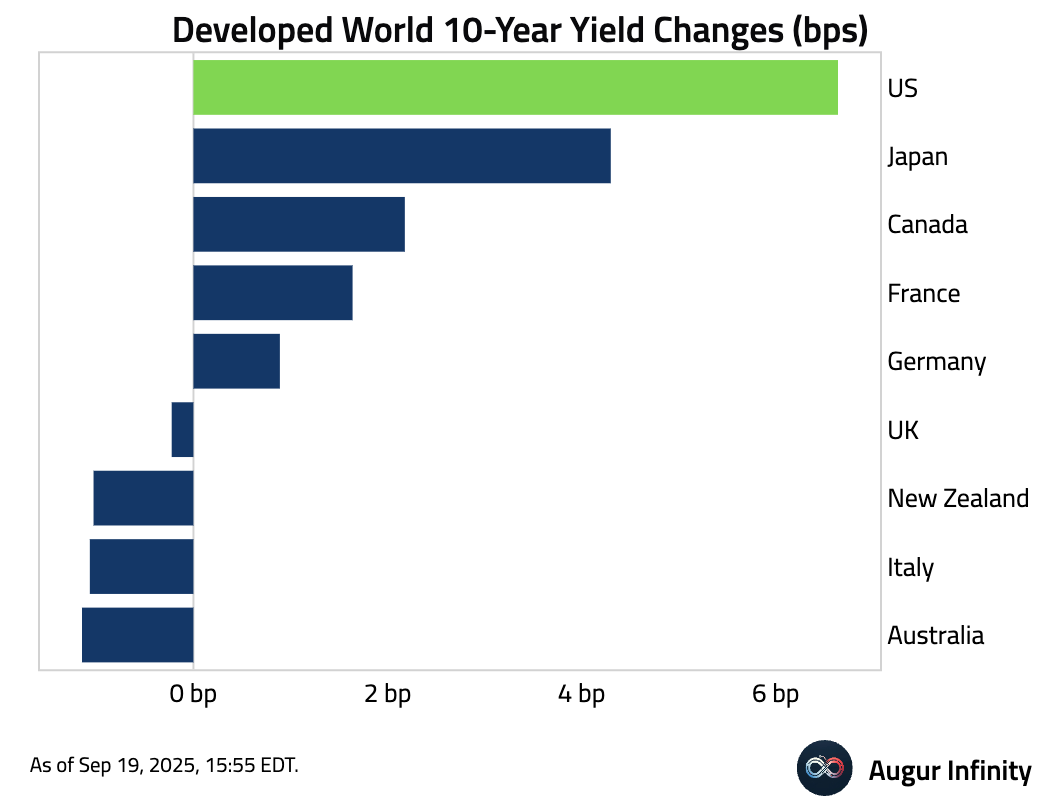

- Developed world bond yields either rose over the course of the week or remained largely unchanged.

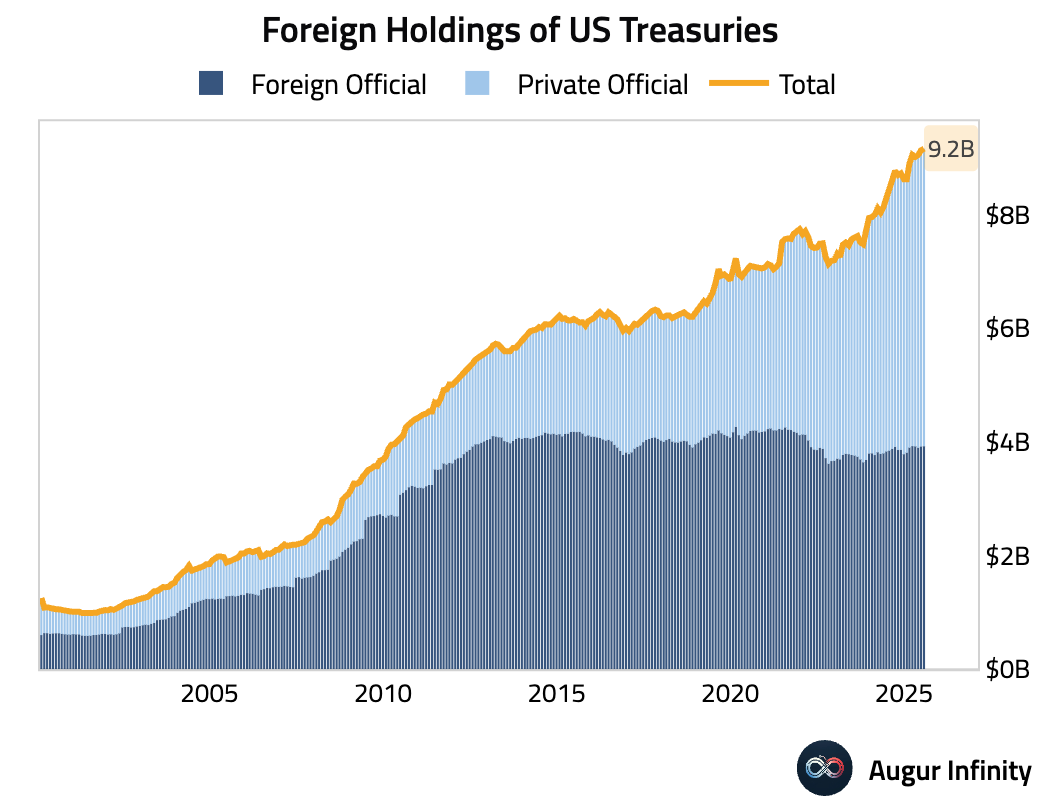

- Foreign holdings of US Treasuries reached a new record high of $9.2 trillion in July.

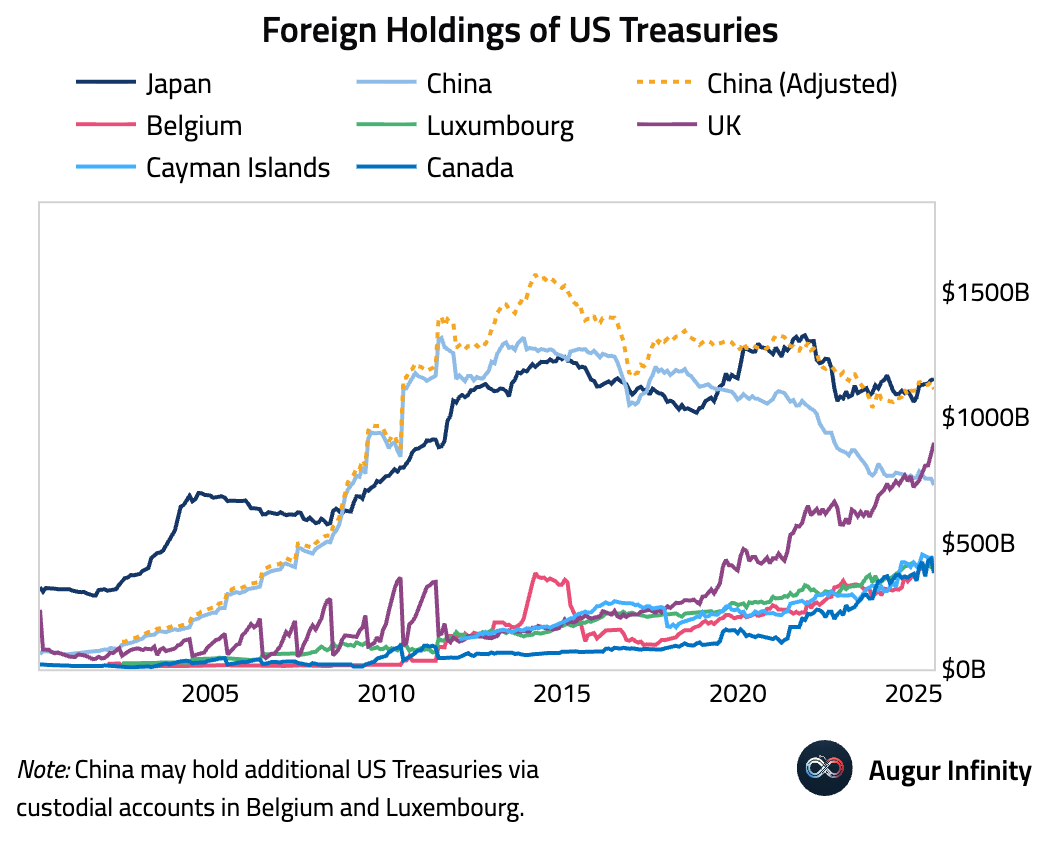

- Here's foreign holdings of US Treasuries by country. Notice that our adjusted China holdings, which account for holdings in Belgium and Luxembourg, have dipped below that of Japan.

FX

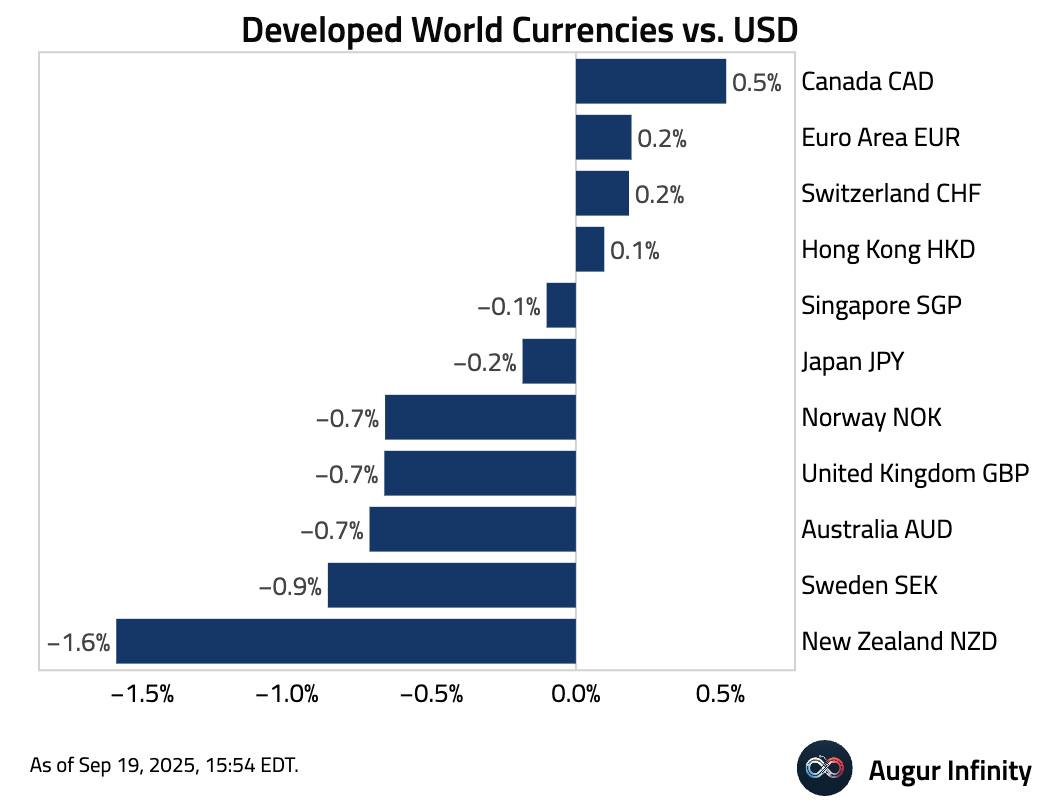

- Here's some performance data for developed world currencies against USD.

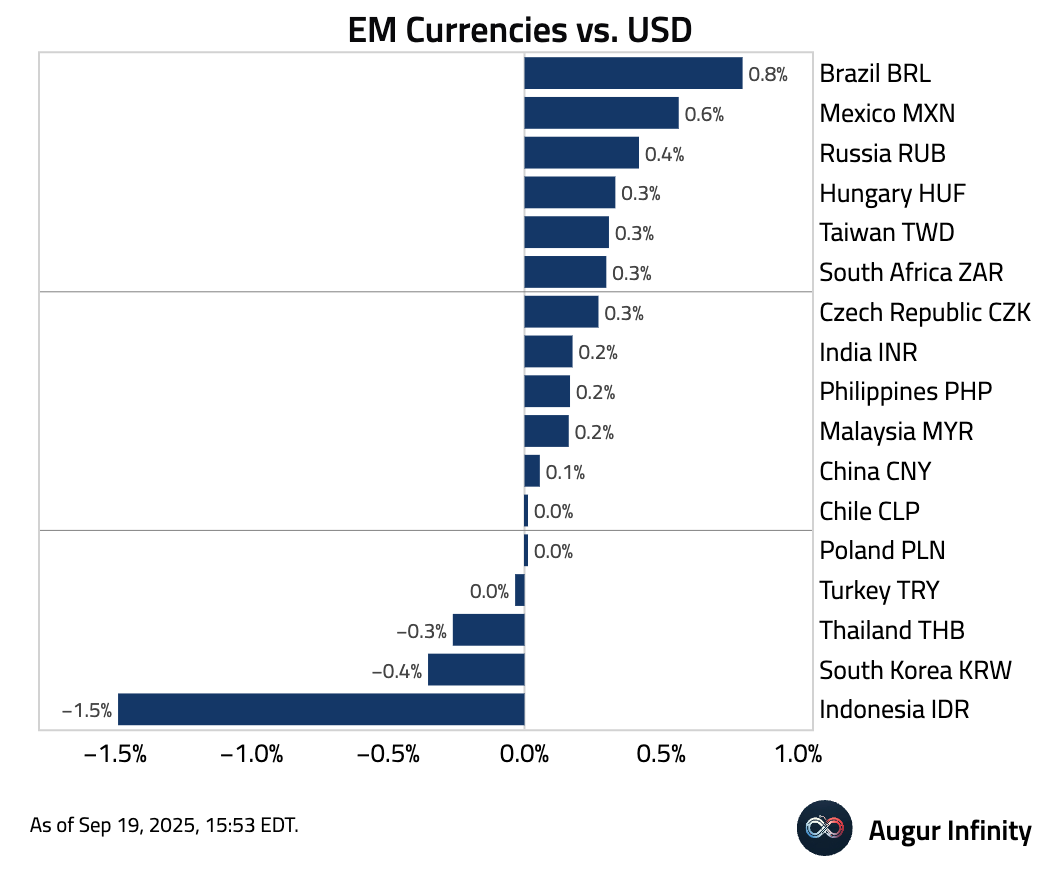

- Most EM FX strengthened against the dollar this week.

Commodities

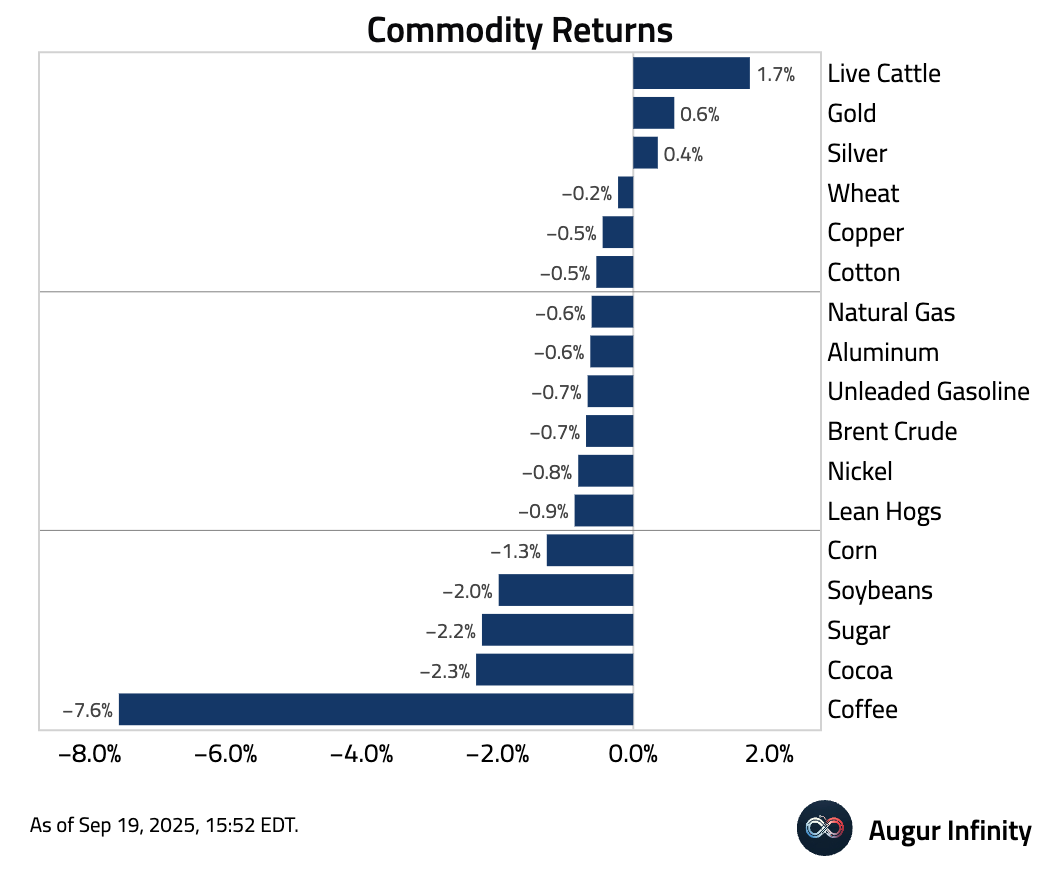

- Here is a look at this week's performance across key commodity markets.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.