Headlines

- President Trump is scheduled to address the United Nations General Assembly, with his speech reportedly set to focus on the “failures of globalism” and “American strength.”

- The White House will engage in fiscal negotiations this week as President Trump plans to meet with Democratic leadership to avert a potential government shutdown.

- Turkey announced plans to purchase hundreds of fighter jets from US defense contractors Boeing and Lockheed Martin.

Global Economics

United States

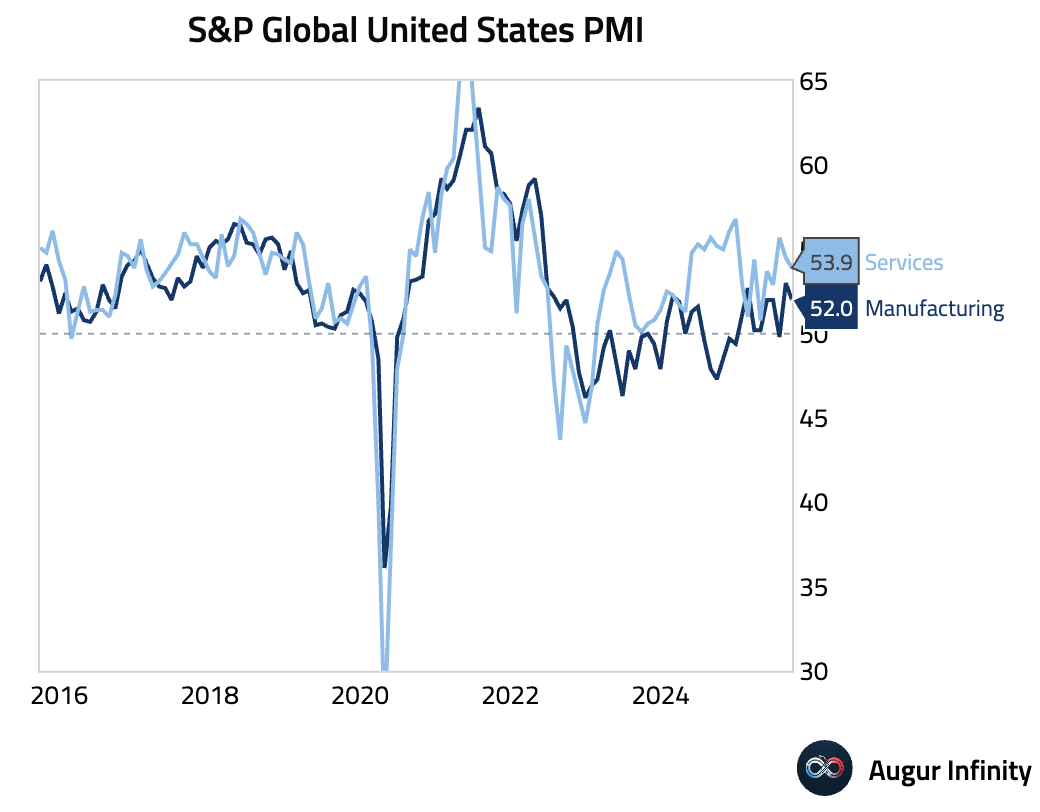

- The flash manufacturing index fell to 52.0, while the services index declined to 53.9. Disappointing sales led to the largest build-up of unsold finished goods in the manufacturing survey's history, signaling downside risk for future production. In services, rising input costs and competitive pressures are squeezing margins.

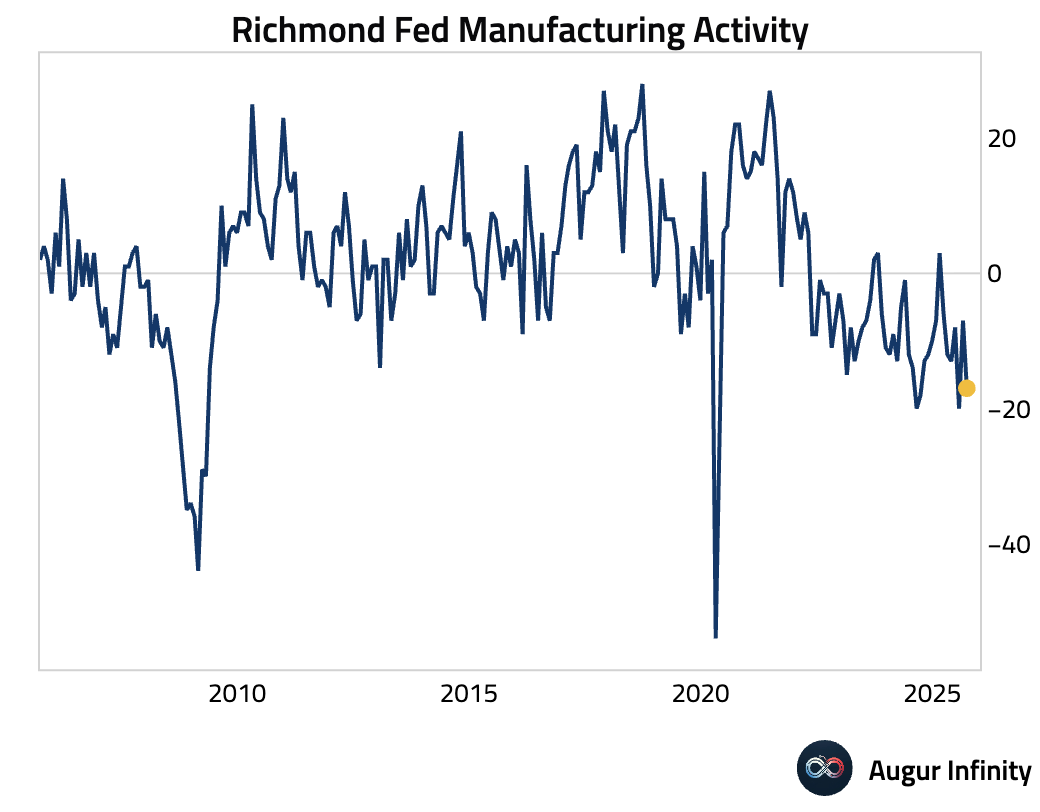

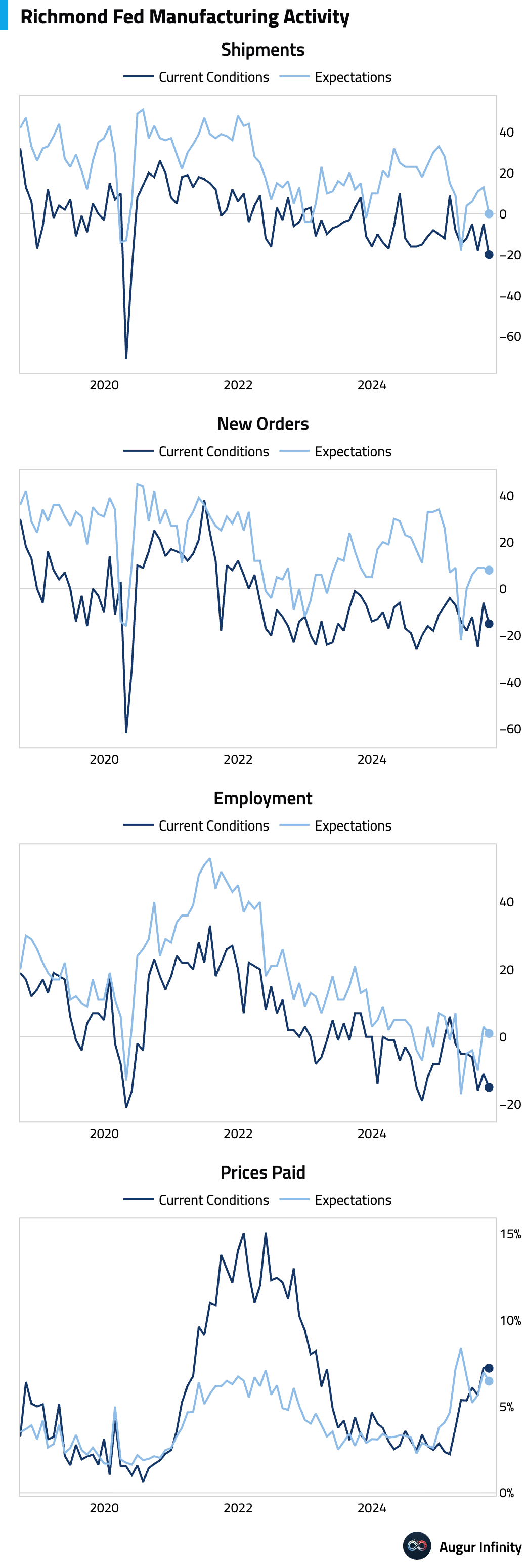

- The Richmond Fed Manufacturing Index plunged 10 points to -17 in September, well below consensus. The decline was broad-based, driven by steep drops in shipments and new orders.

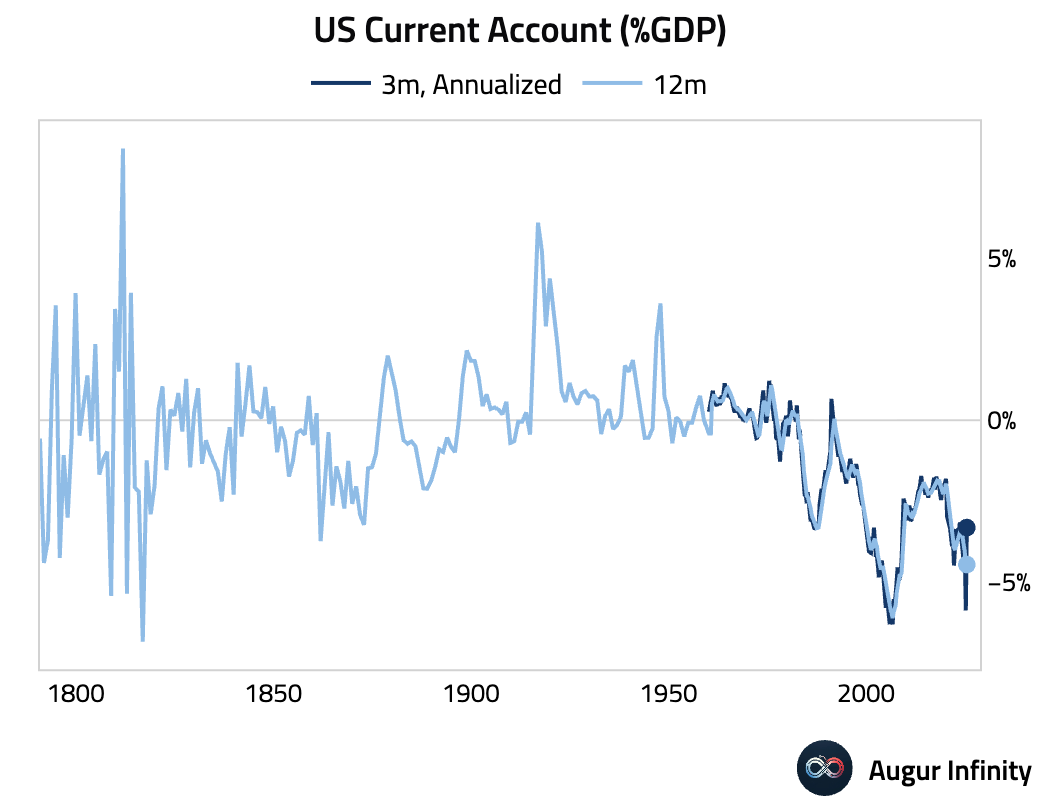

- The US current account deficit narrowed more than expected in the second quarter to its smallest level in over a year (act: -$251.3B, est: -$256.3B).

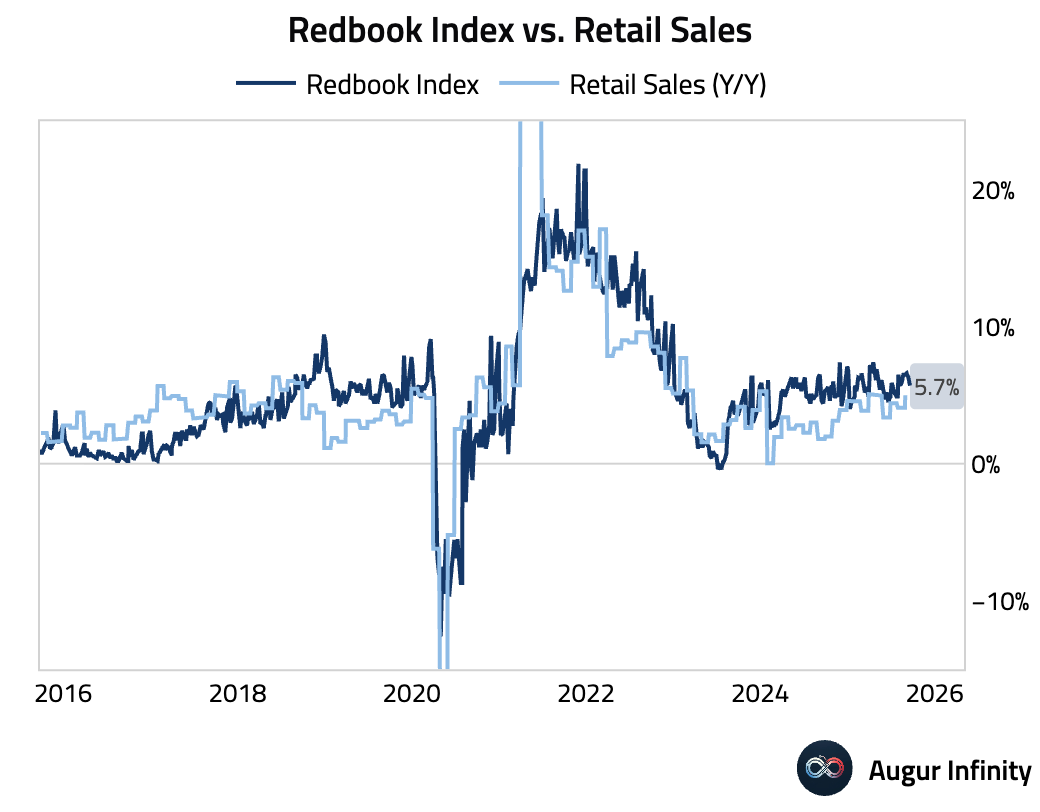

- Weekly retail sales growth according to the Redbook index decelerated.

Canada

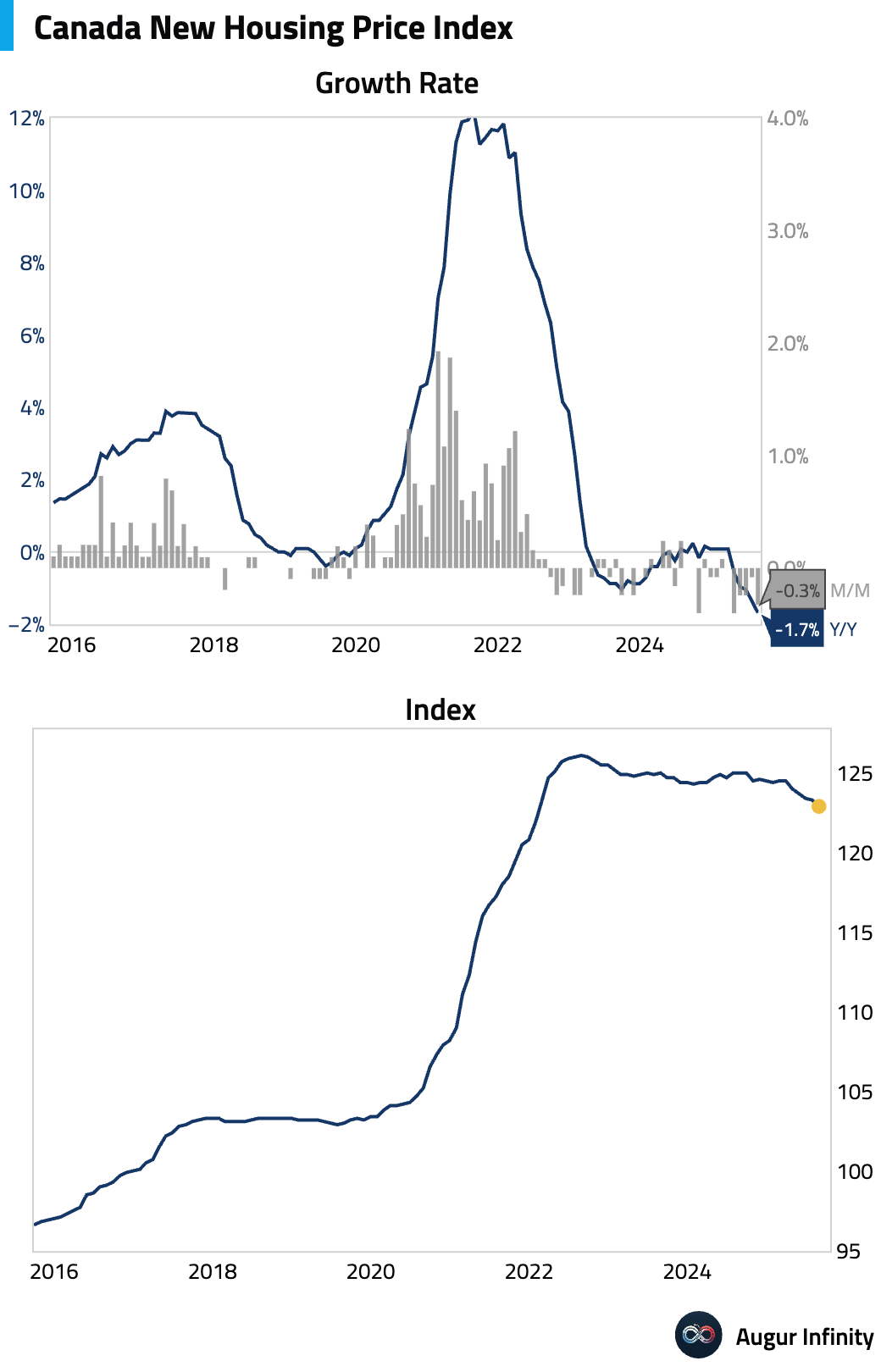

- New housing prices declined for a fifth consecutive month in July, falling more than anticipated (act: -0.3% M/M, est: 0.0%).

Europe

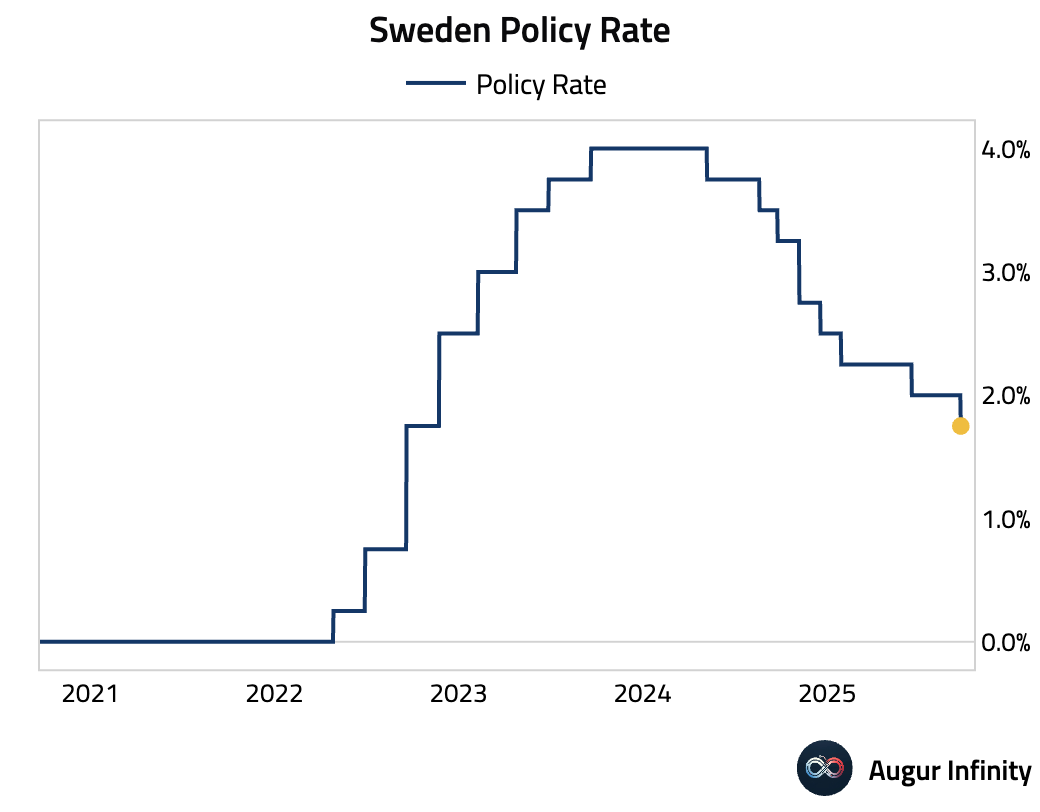

- Sweden’s Riksbank unexpectedly cut its policy rate by 25 basis points to 1.75%, against consensus expectations for a hold. The bank cited a weak recovery as the reason for the move, though the decision was not unanimous. The central bank's updated forecasts show the policy rate holding at 1.75% for the next year, while the 2026 inflation forecast was sharply lowered due to a temporary tax cut on food.

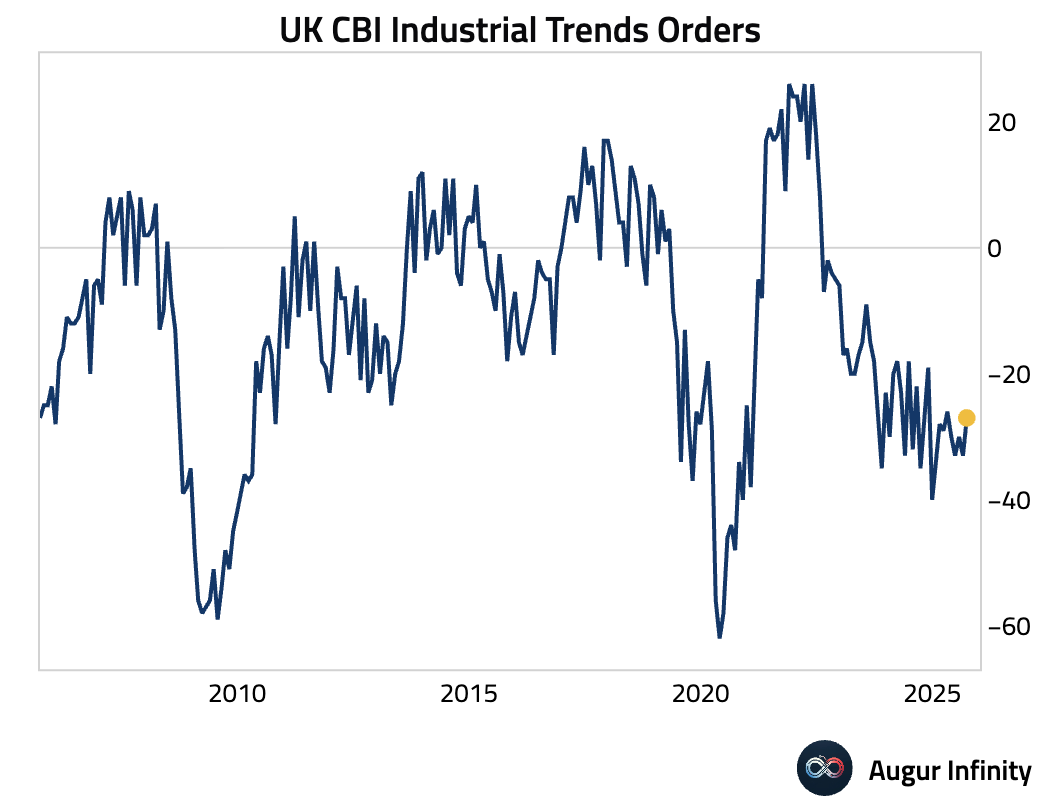

- The UK's CBI industrial orders balance improved in September but remained deeply in negative territory, though it beat expectations (act: -27, est: -30.0).

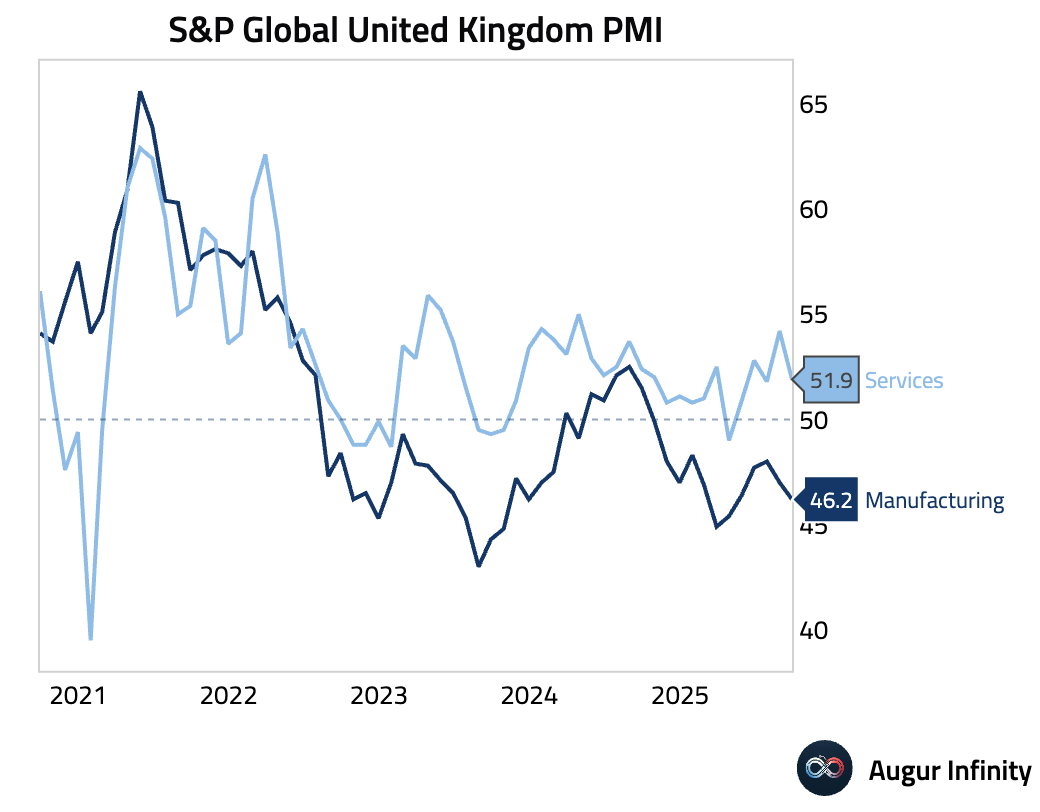

- Flash PMI data for the UK pointed to a near-stalling of economic growth in September. The manufacturing PMI fell to a 5-month low of 46.2, while the services index dropped to 51.9, both missing expectations. The slowdown was driven by subdued demand, weak client confidence, and political uncertainty, with firms cutting employment for the fifth consecutive month.

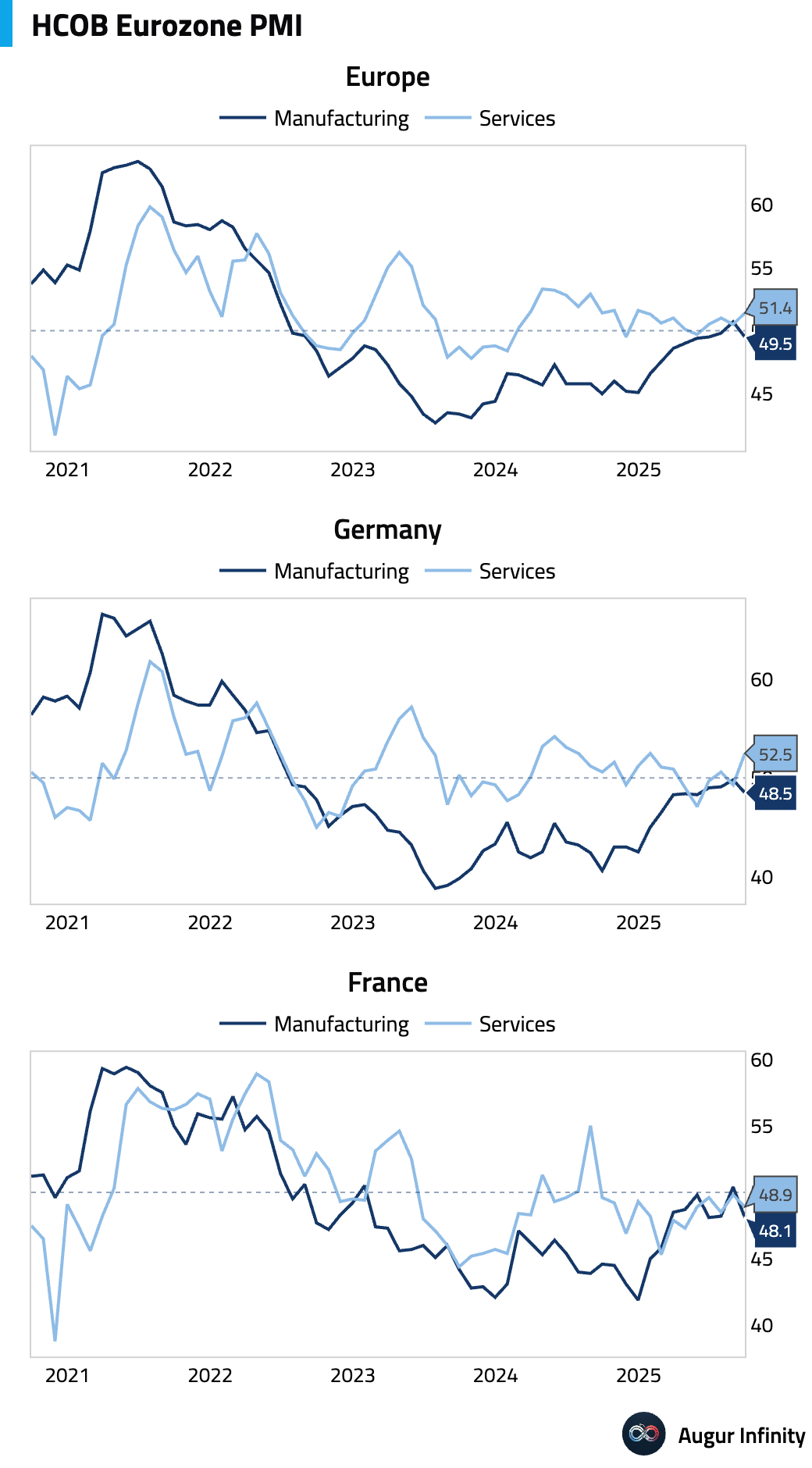

- The flash Eurozone manufacturing PMI fell back into contraction in September. The deterioration was broad-based, with Germany’s index falling to a 4-month low of 48.5 and France’s dropping to 48.1. Critically, new orders fell across the board, with firms supporting output by depleting backlogs rather than through new business.

The services sector showed improvement, with the flash PMI rising to 51.4 from 50.5. However, the strength was concentrated in Germany, where the index jumped to an 8-month high of 52.5. In contrast, France’s services activity contracted further to 48.9, with firms attributing weak demand to domestic political uncertainty.

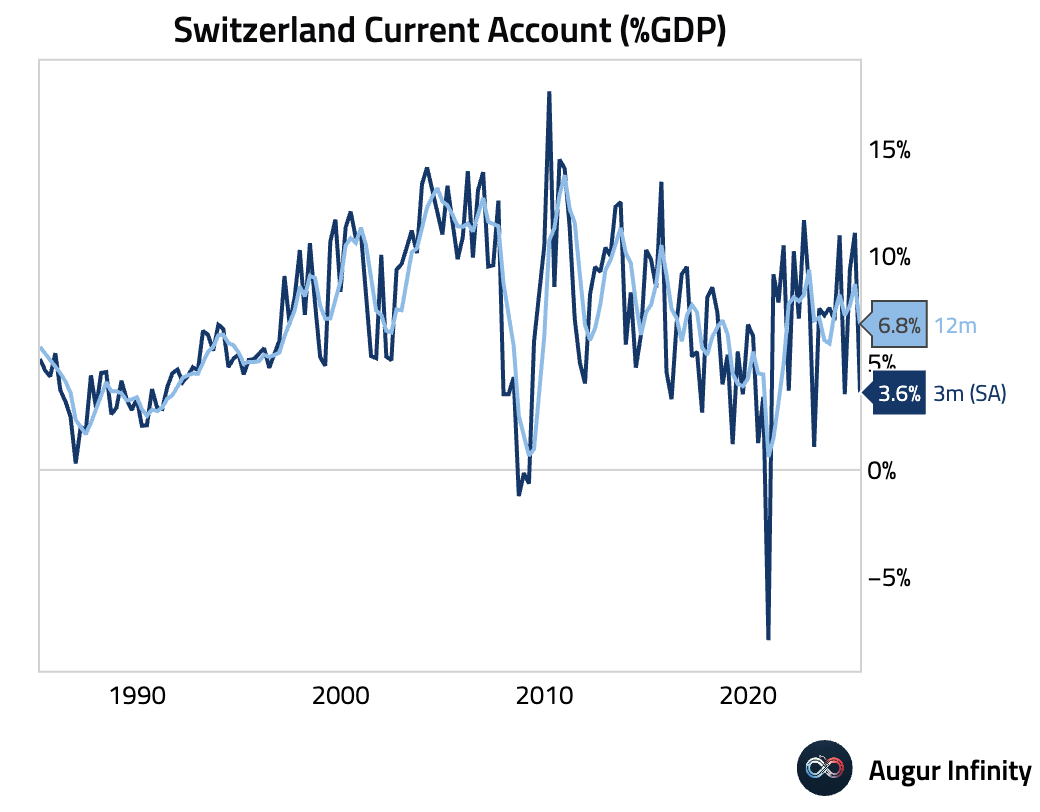

- Switzerland’s current account surplus narrowed sharply in the second quarter (act: CHF 10.2B, prev: CHF 23.5B).

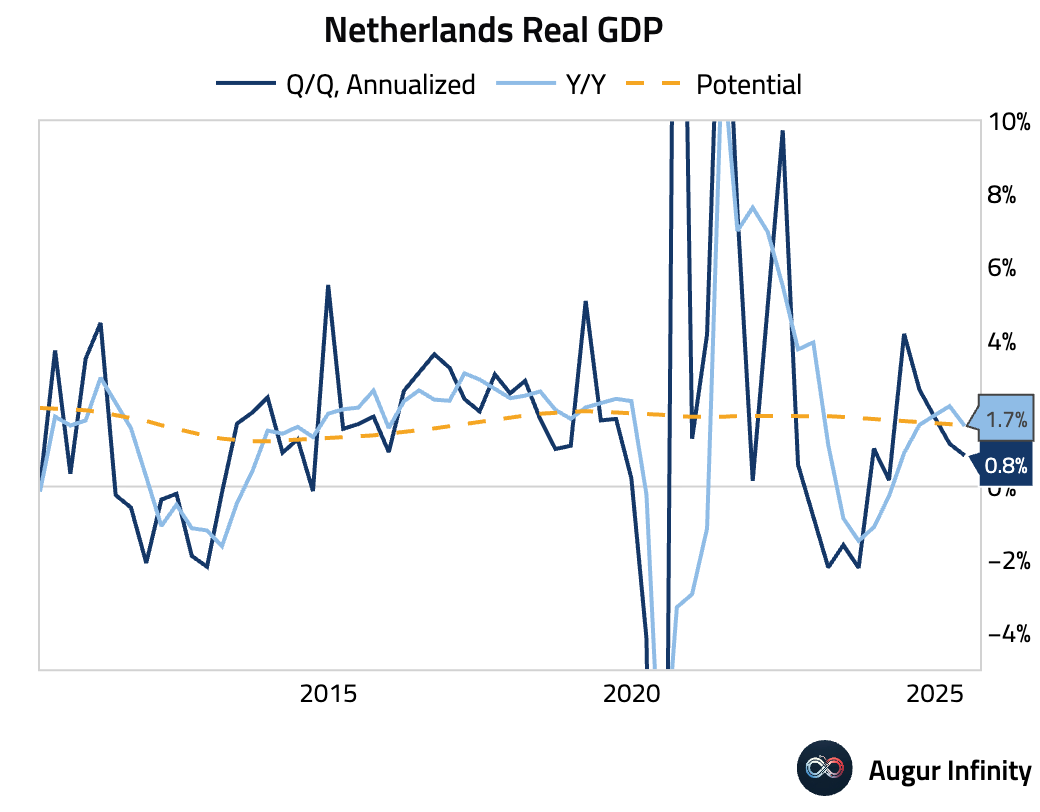

- The Netherlands' second-quarter GDP growth was confirmed at 0.2% Q/Q and 1.7% Y/Y, with both figures beating preliminary estimates.

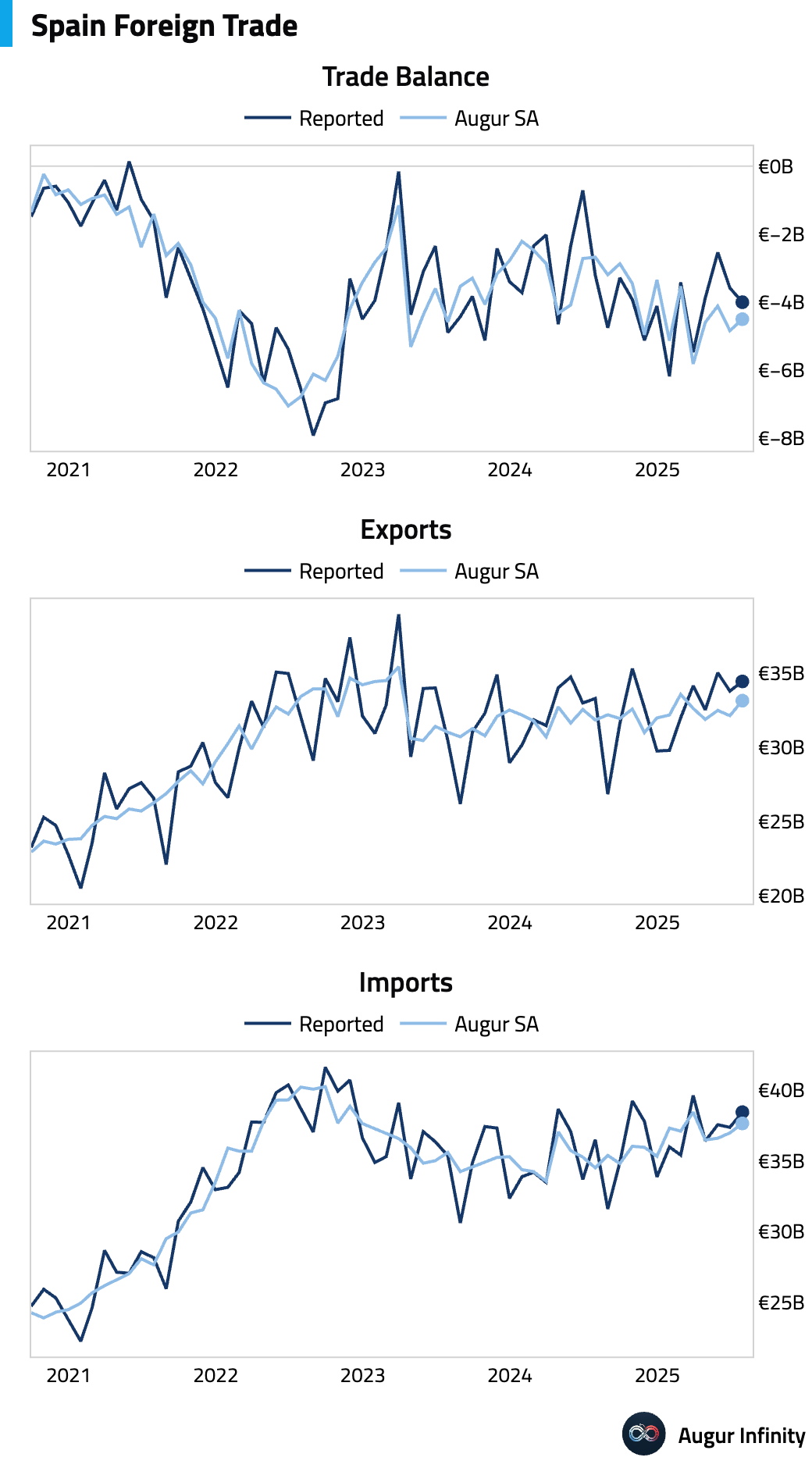

- Spain's trade deficit widened in July (act: -€4.01B, prev: -€3.59B).

Asia-Pacific

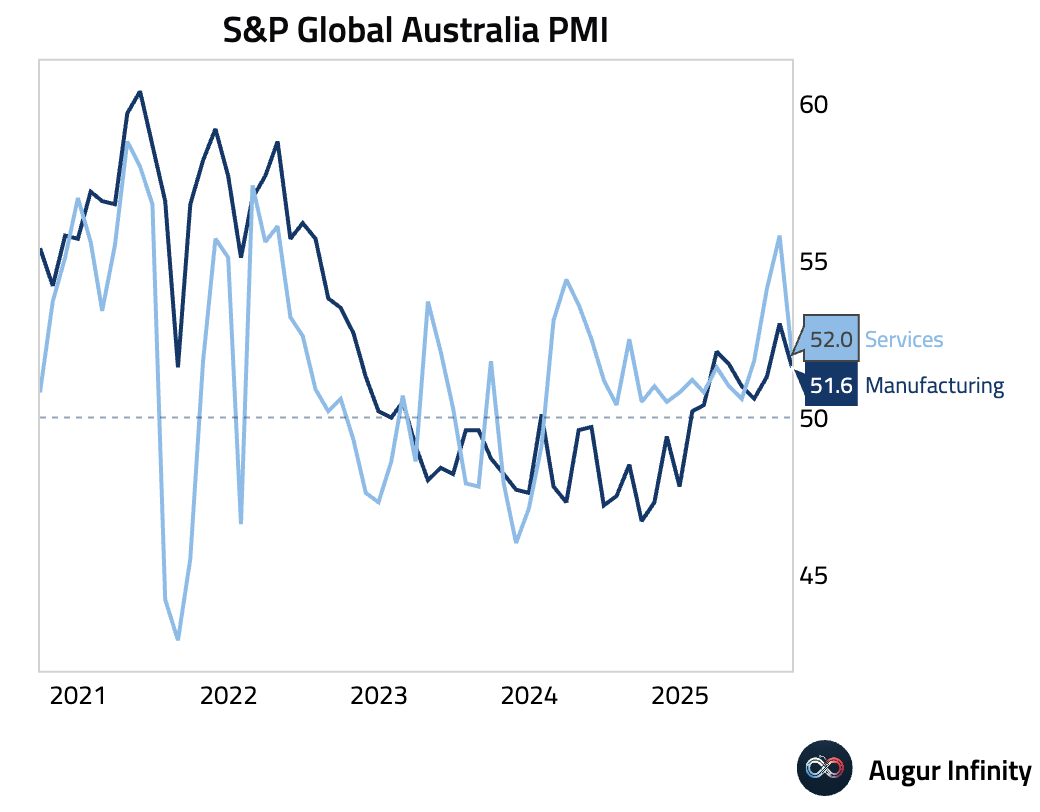

- Australia’s economic growth slowed significantly in September, with the flash composite PMI falling to a 3-month low of 52.1. While services activity remained resilient (act: 52.0, prev: 55.8), the manufacturing sector softened (act: 51.6, prev: 53.0). Firms explicitly attributed a slump in new manufacturing orders to the negative impact of US tariffs on exports, and overall business confidence dropped to a one-year low.

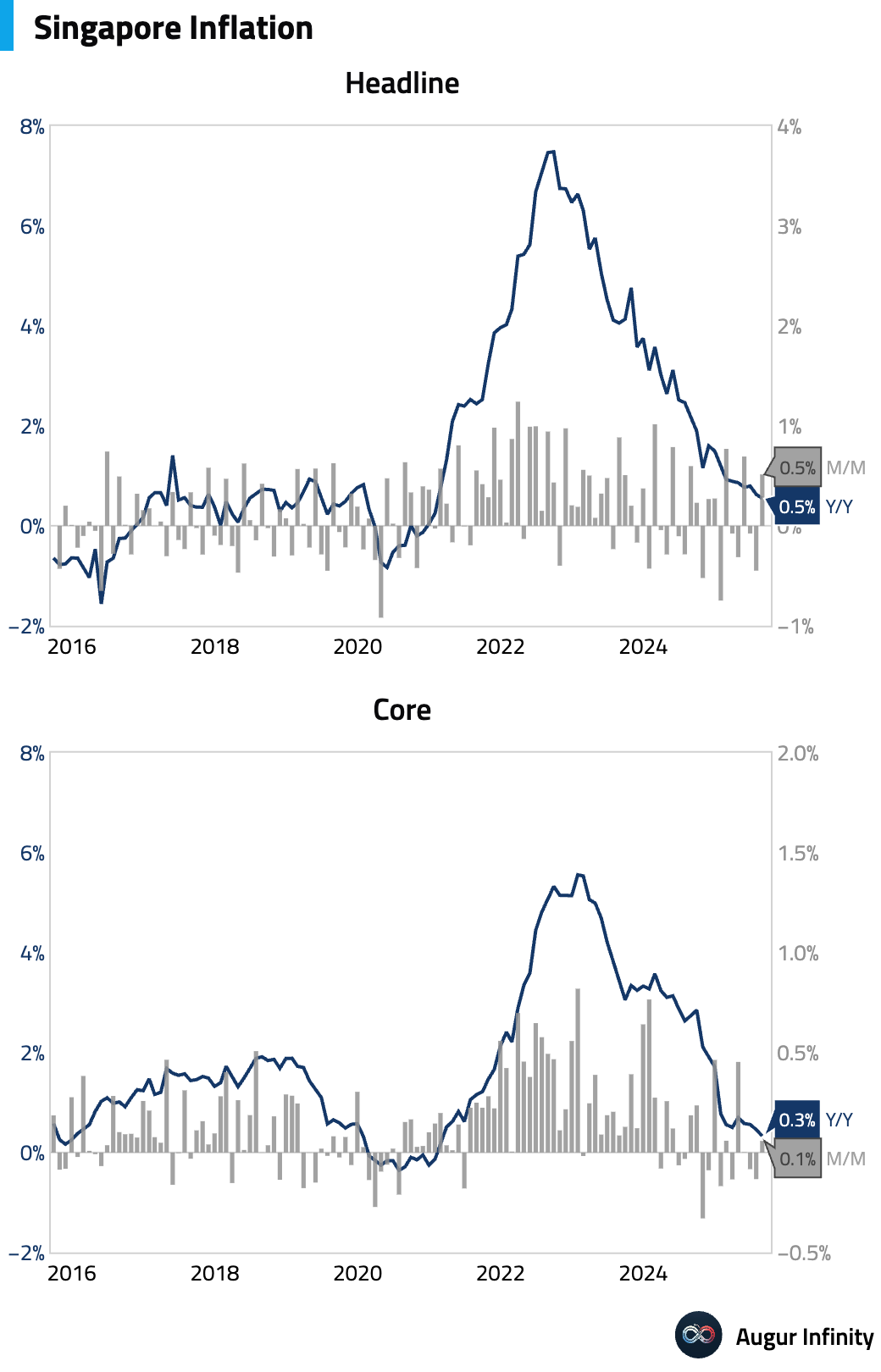

- Singapore's inflation cooled more than expected in August. Headline CPI eased to 0.5% Y/Y (vs. 0.6% est.), while core CPI slowed to 0.3% Y/Y (vs. 0.4% est.). The deceleration was largely driven by a sharp drop in holiday expenses. The soft print has led to expectations that the Monetary Authority of Singapore may flatten the currency's appreciation slope at its October meeting.

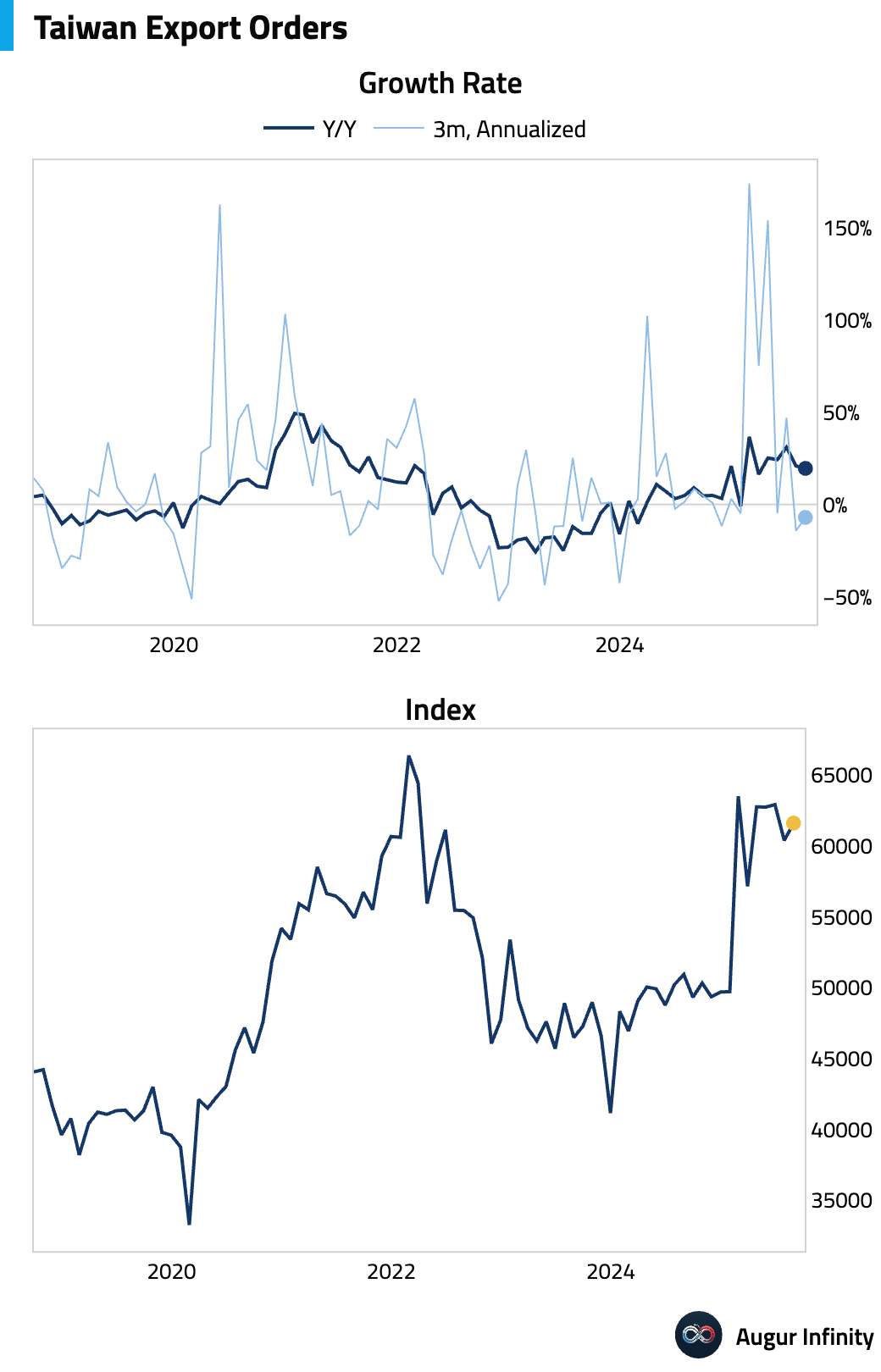

- Taiwan's export order growth moderated in August (act: 19.5% Y/Y, est: 13.0%).

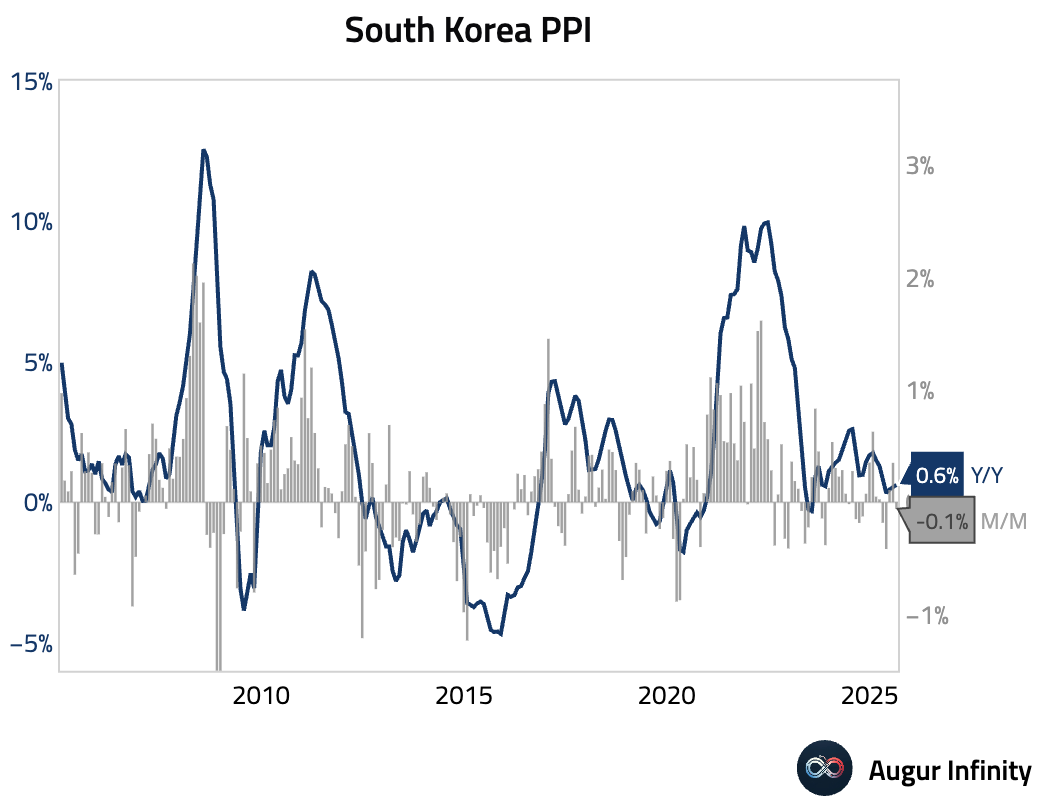

- South Korean producer prices fell 0.1% M/M in August, but the annual rate of PPI inflation accelerated to 0.6% Y/Y from 0.5%.

Emerging Markets ex China

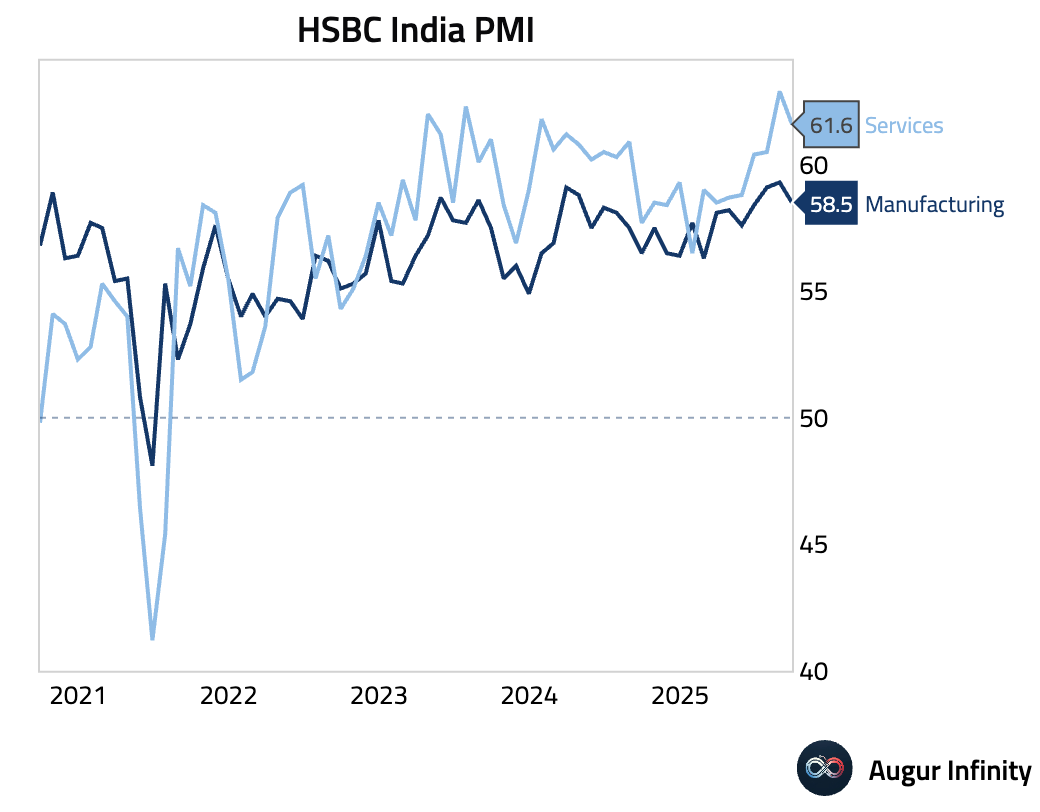

- India's private sector growth cooled in September but remains robust. The flash manufacturing PMI fell to 58.5 from 59.3, while the services PMI declined to 61.6 from 62.9. A slowdown in new export orders, attributed to US tariffs, created a headwind for manufacturers, but this was partly offset by strong domestic demand.

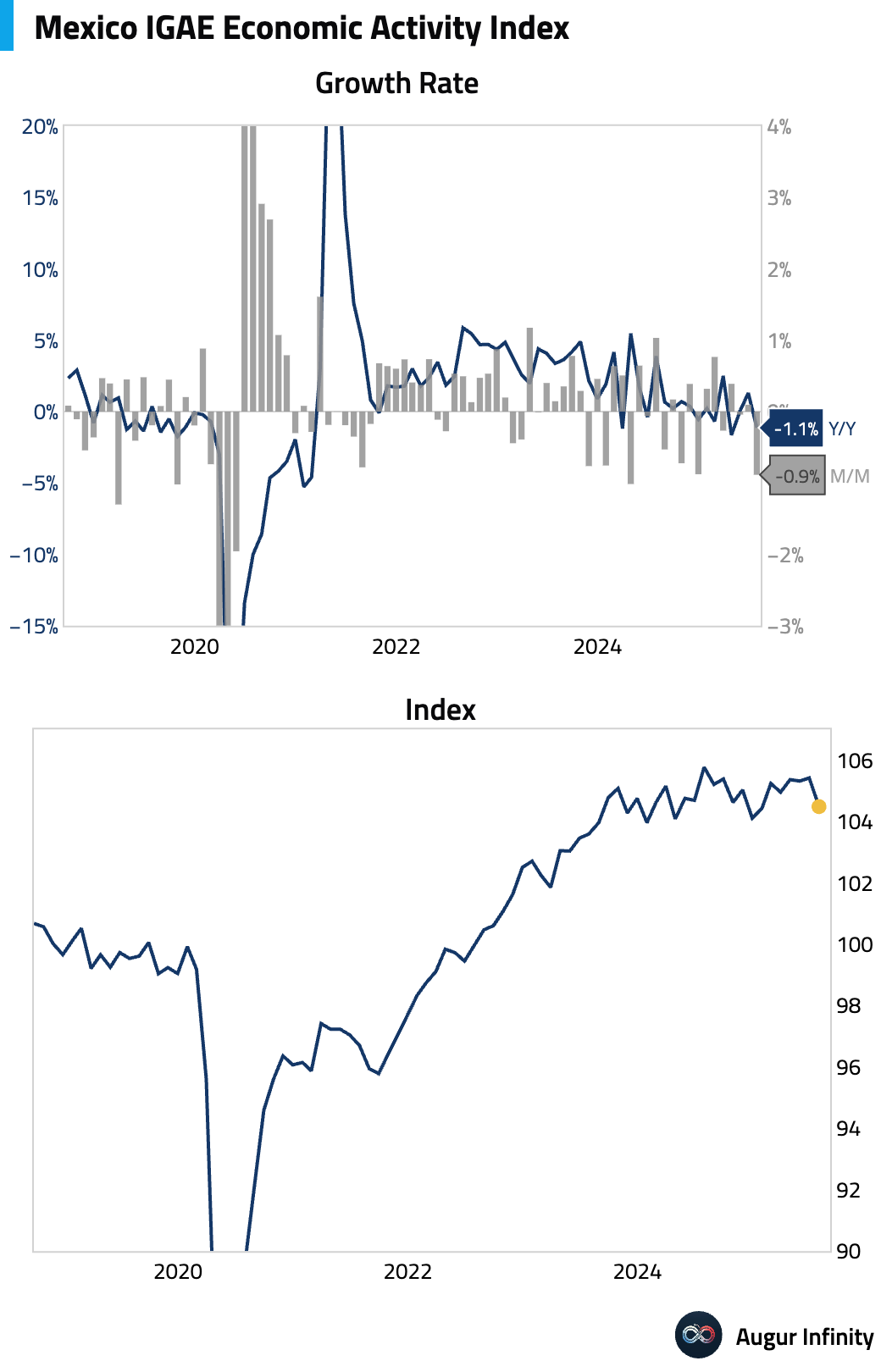

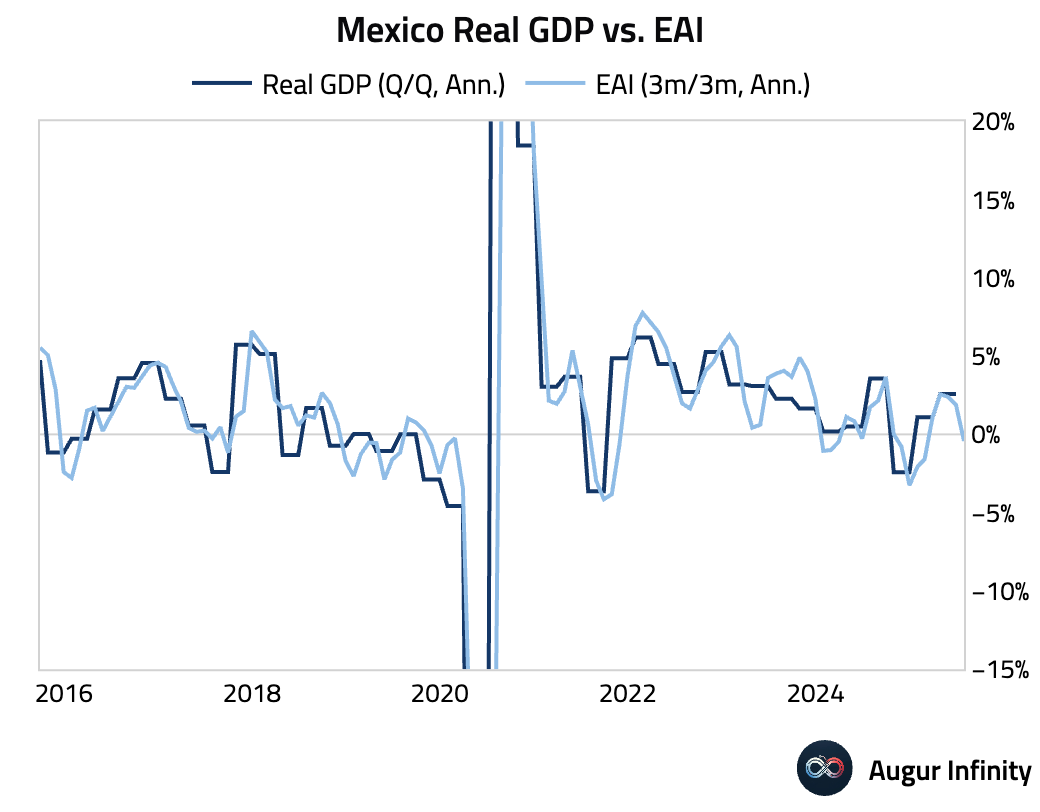

- Mexico's economic activity contracted by a much larger-than-expected 0.9% M/M in July, with the annual rate falling to -1.1%. The weakness was broad-based across all sectors. Combined with downward revisions to June data, the report implies a negative carry-over for third-quarter GDP growth.

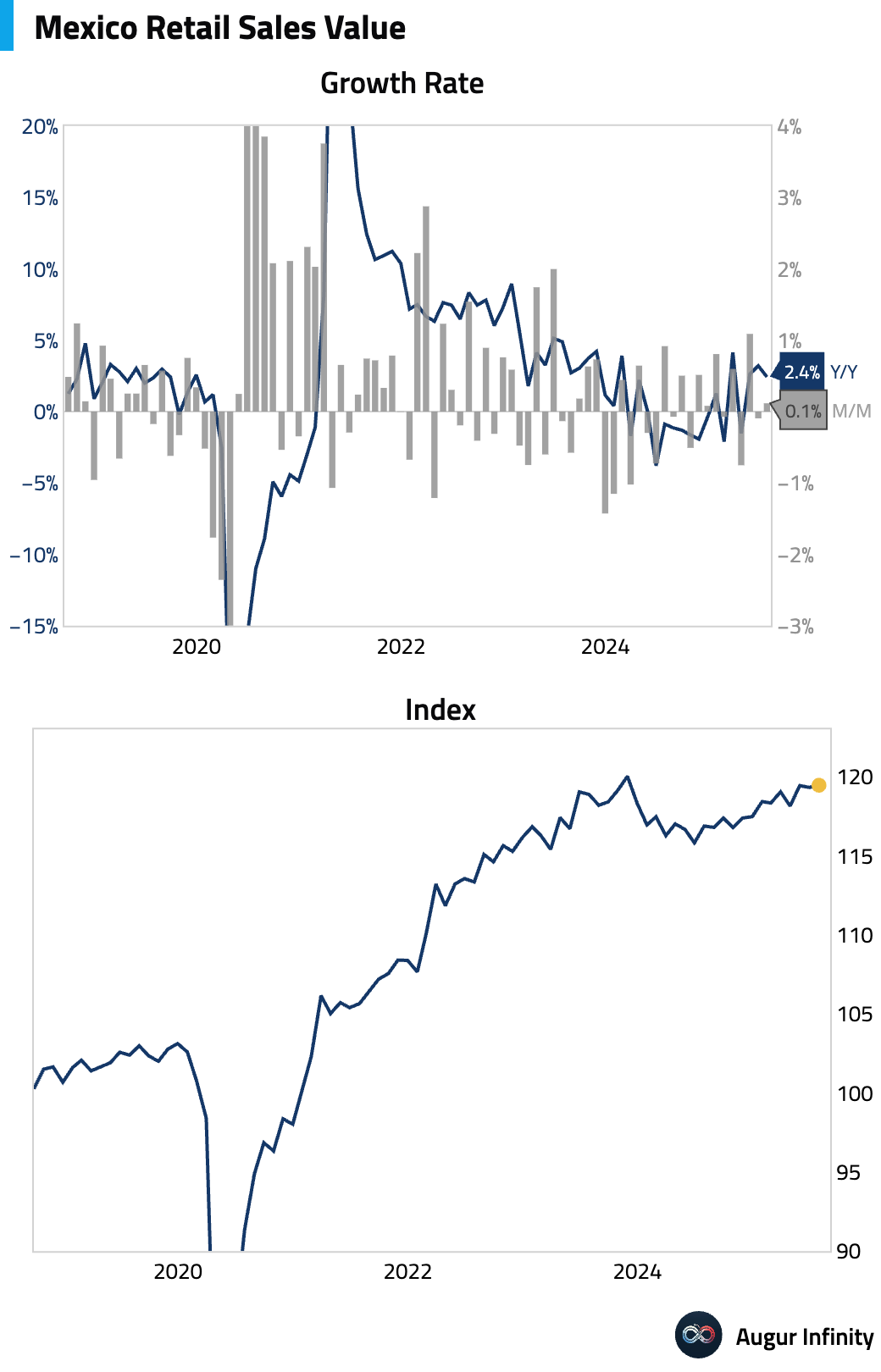

- Mexican retail sales rebounded in July, beating expectations on both a monthly and annual basis (act: 0.1% M/M, est: -0.1%). Despite the headline beat, underlying weakness persists, as both employment and real wages in the retail sector fell, casting a shadow on the outlook for future consumption.

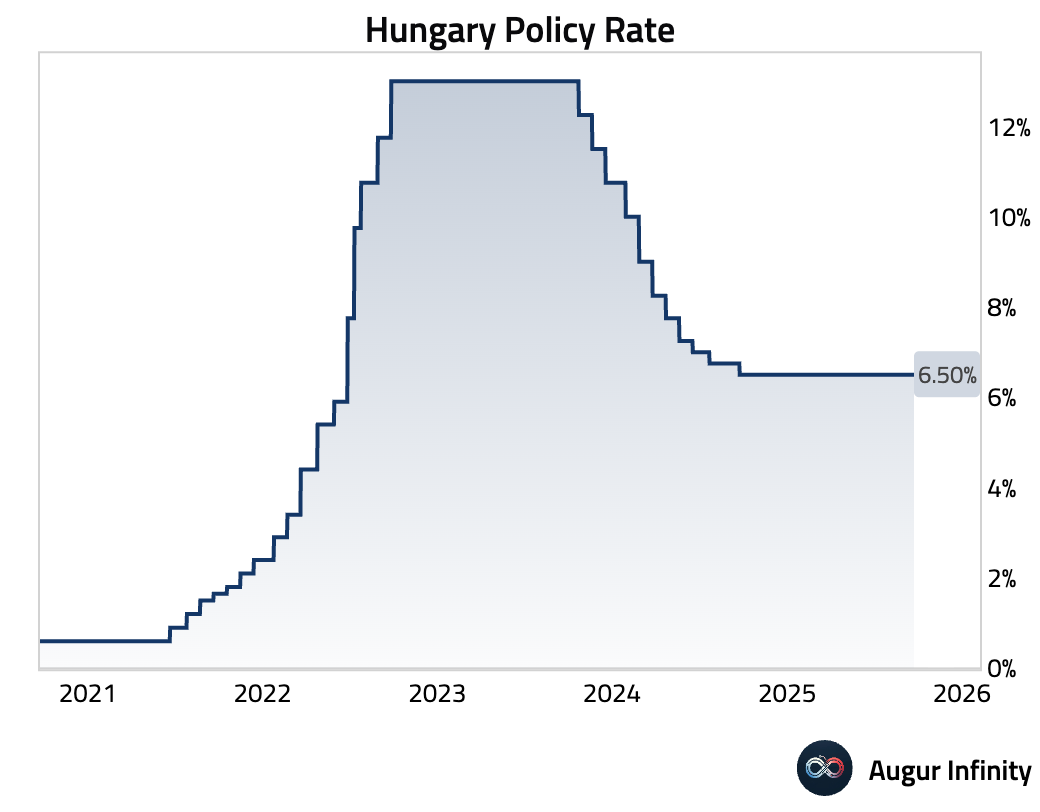

- Hungary's central bank held its key interest rate steady at 6.5%, as widely expected.

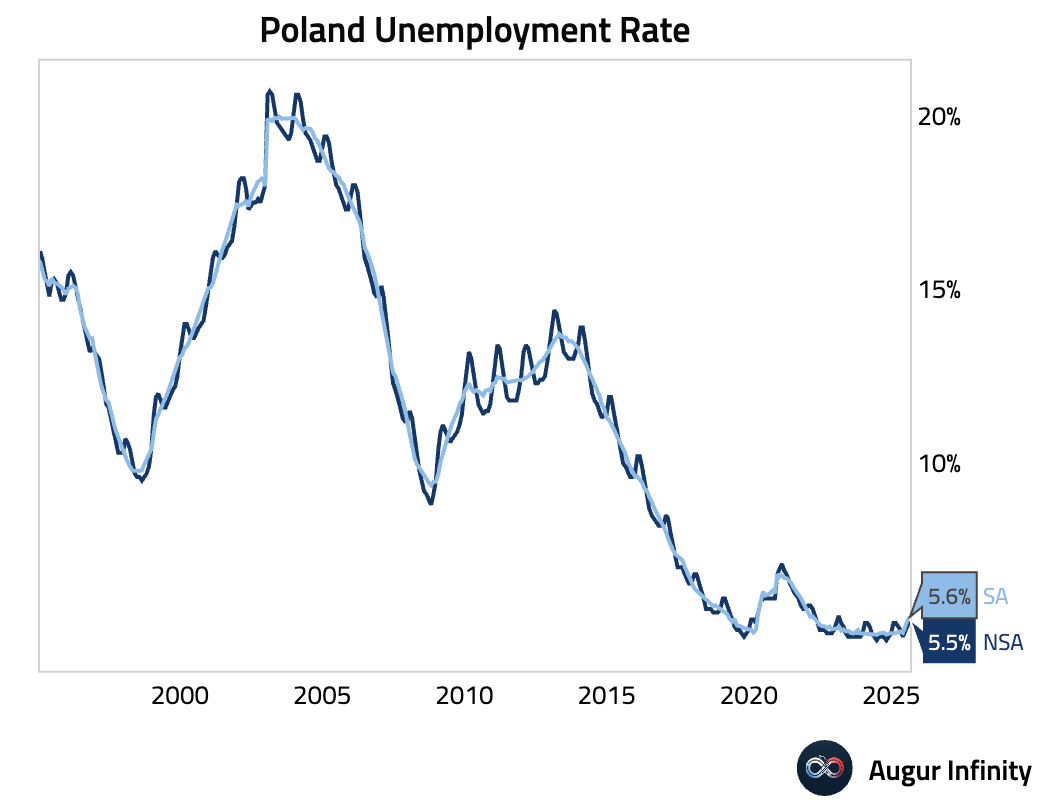

- Poland’s unemployment rate edged up to 5.5% in August, matching consensus forecasts.

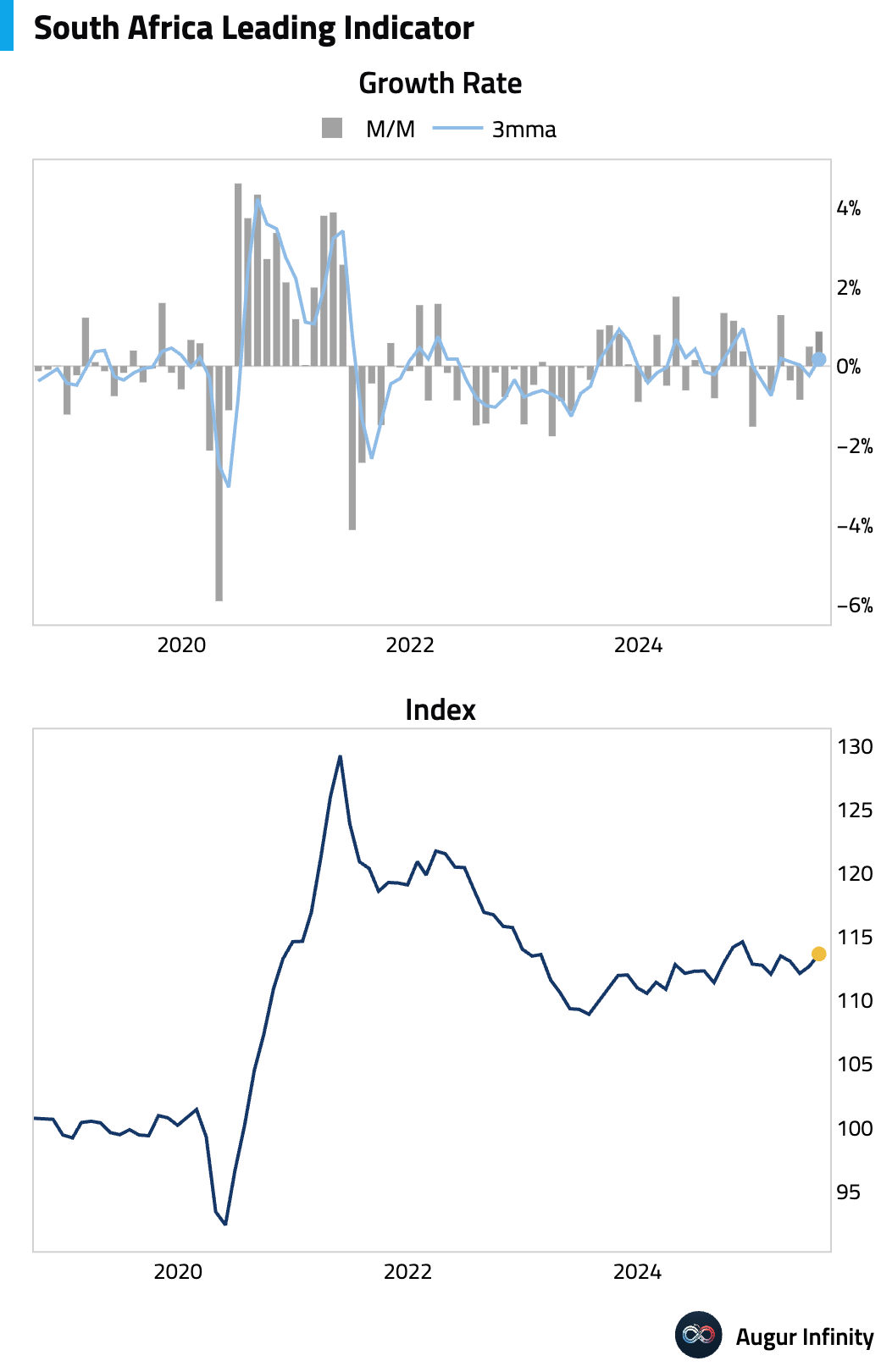

- South Africa’s leading indicator rose at a faster pace in July (act: 0.9% M/M, prev: 0.5%), suggesting an improving economic outlook.

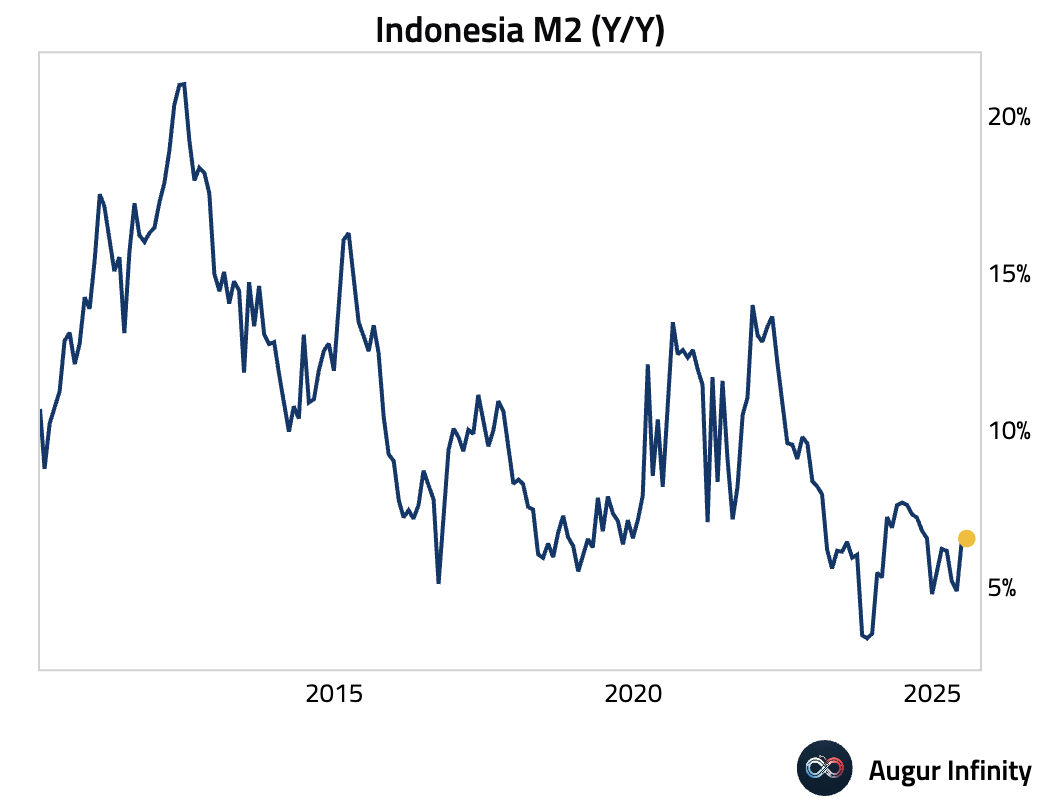

- Indonesia's M2 money supply growth accelerated in August (act: 7.6% Y/Y, prev: 6.6%).

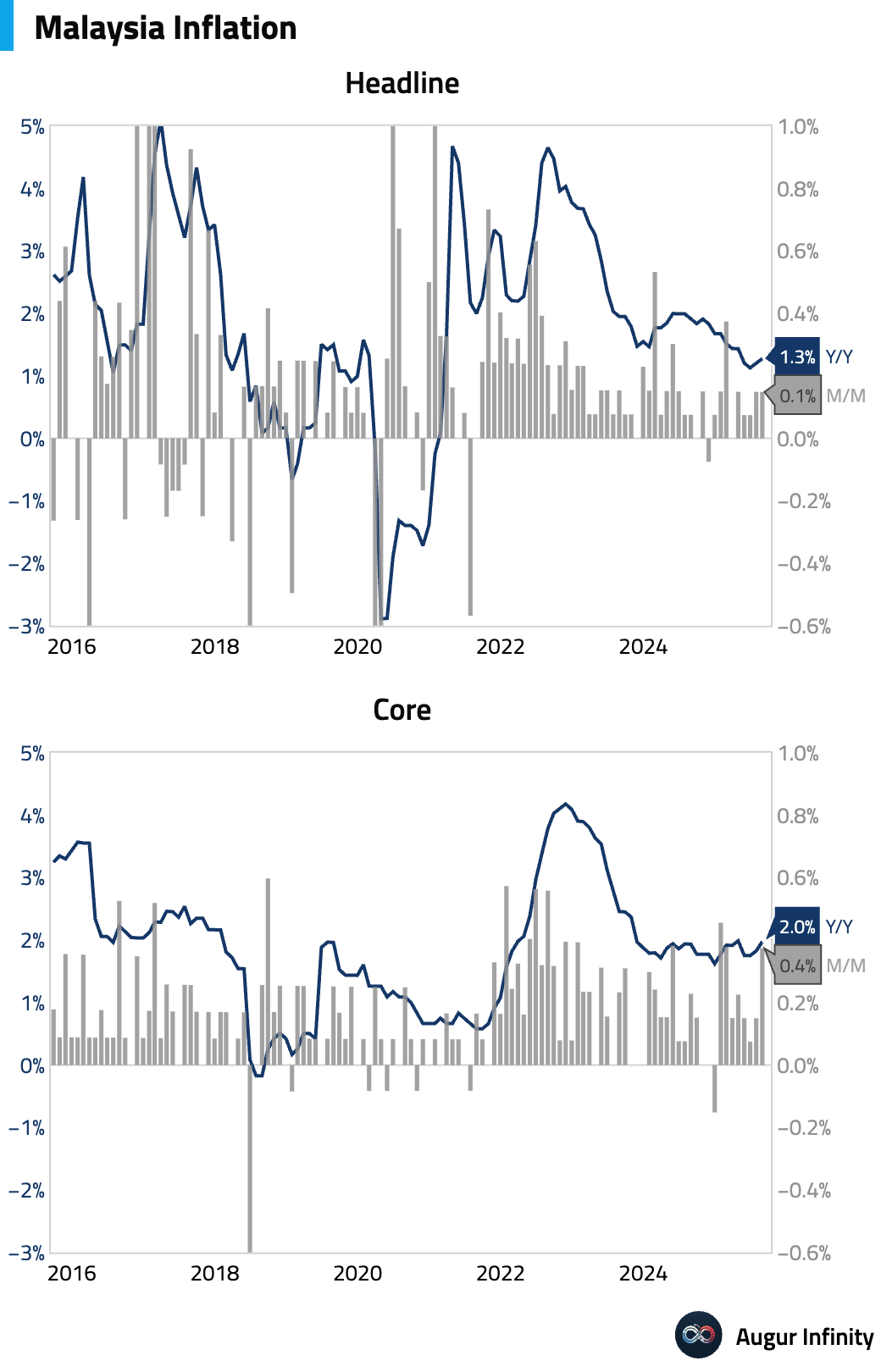

- Malaysia's headline inflation accelerated slightly to 1.3% Y/Y in August, in line with expectations, up from 1.2% in July. The increase was primarily due to a smaller price drag from the information & communication sector, while food inflation remained the largest positive contributor.

Global Markets

Equities

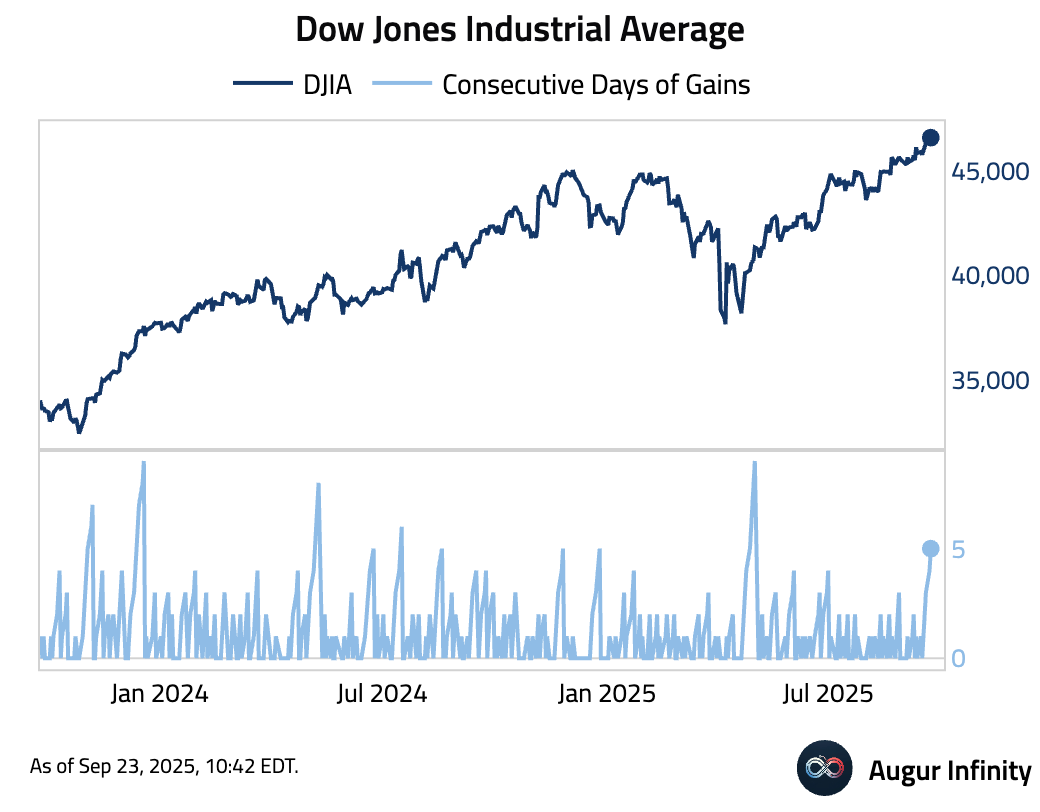

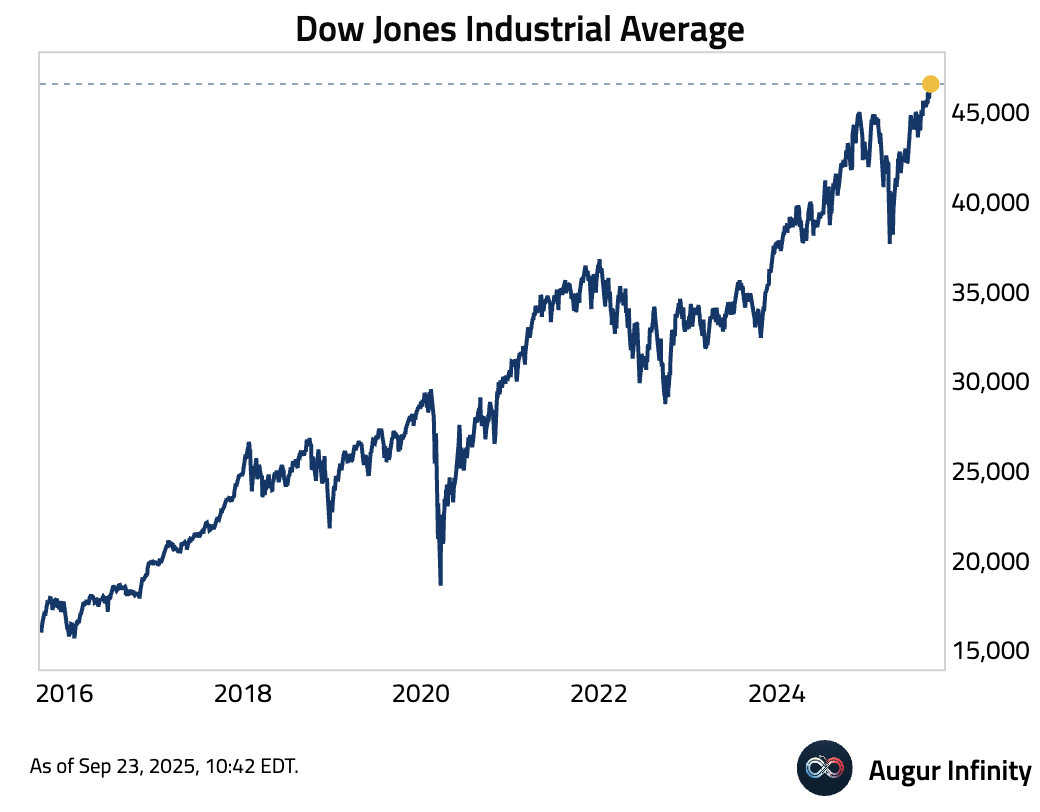

- Dow Jones Industrial Average consecutive number of gains: 5.

… to reach another all-time high.

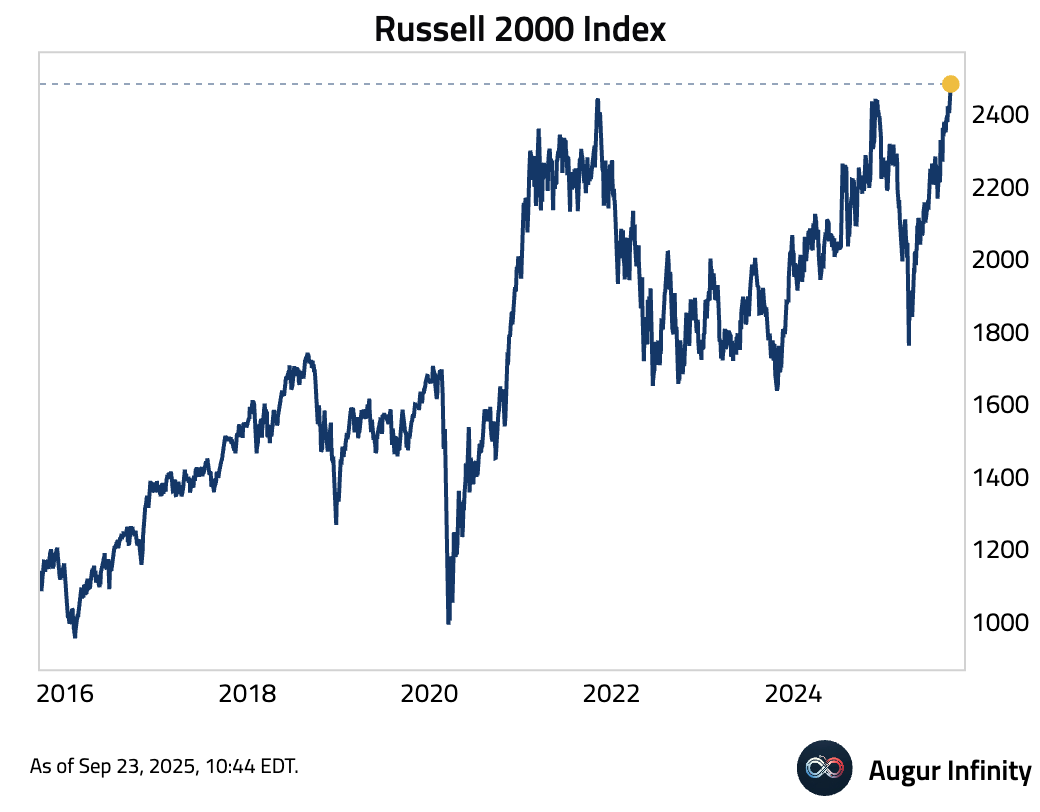

- Russell 2000 Index claimed its second all-time high of 2025.

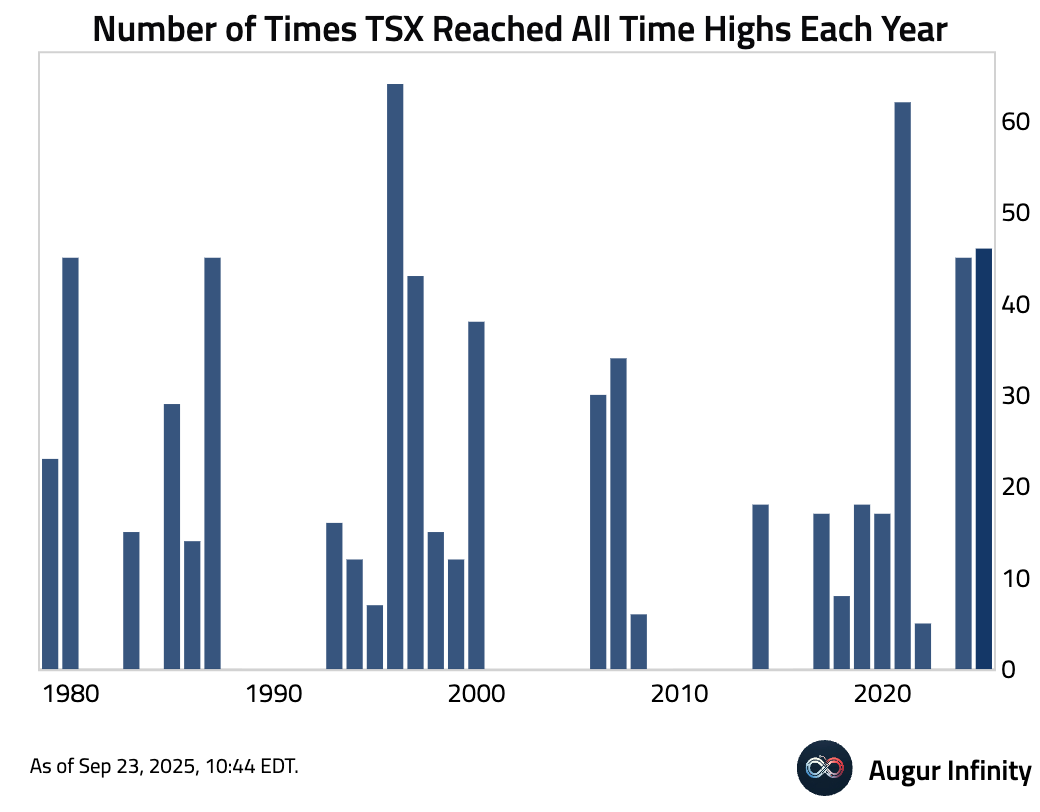

- S&P/TSX Composite has reached all-time highs 46 times this year.

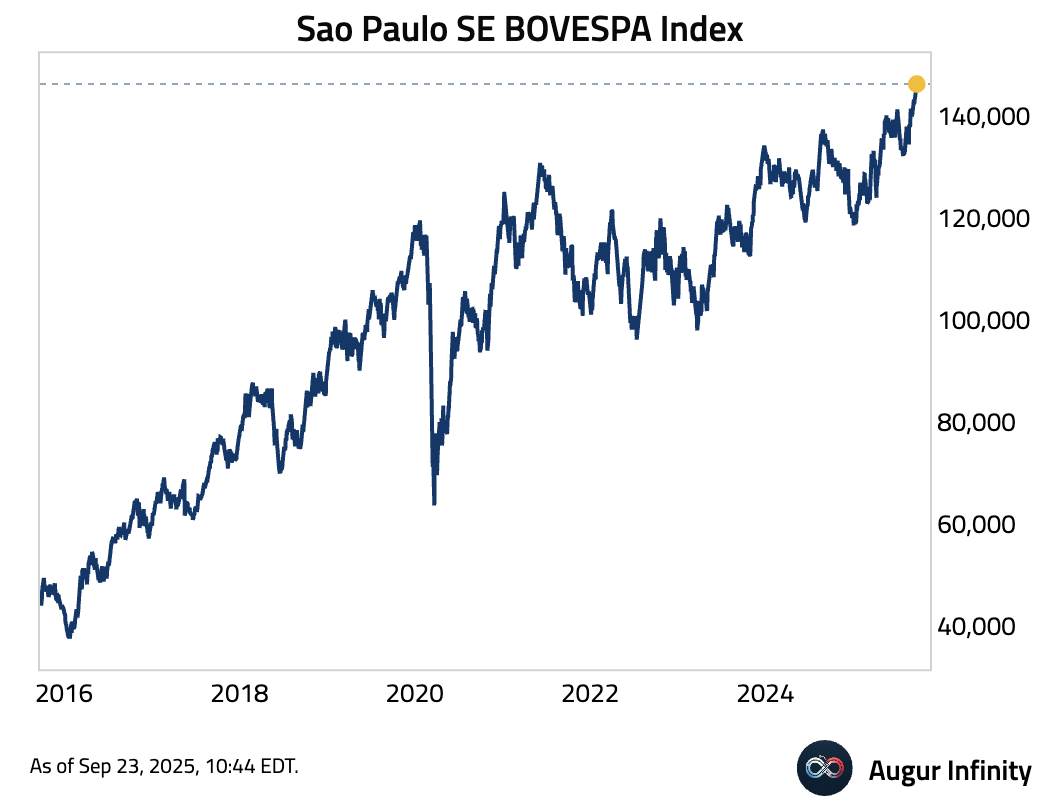

- Brazil's BOVESPA Index rallied to its 14th all-time high of the year.

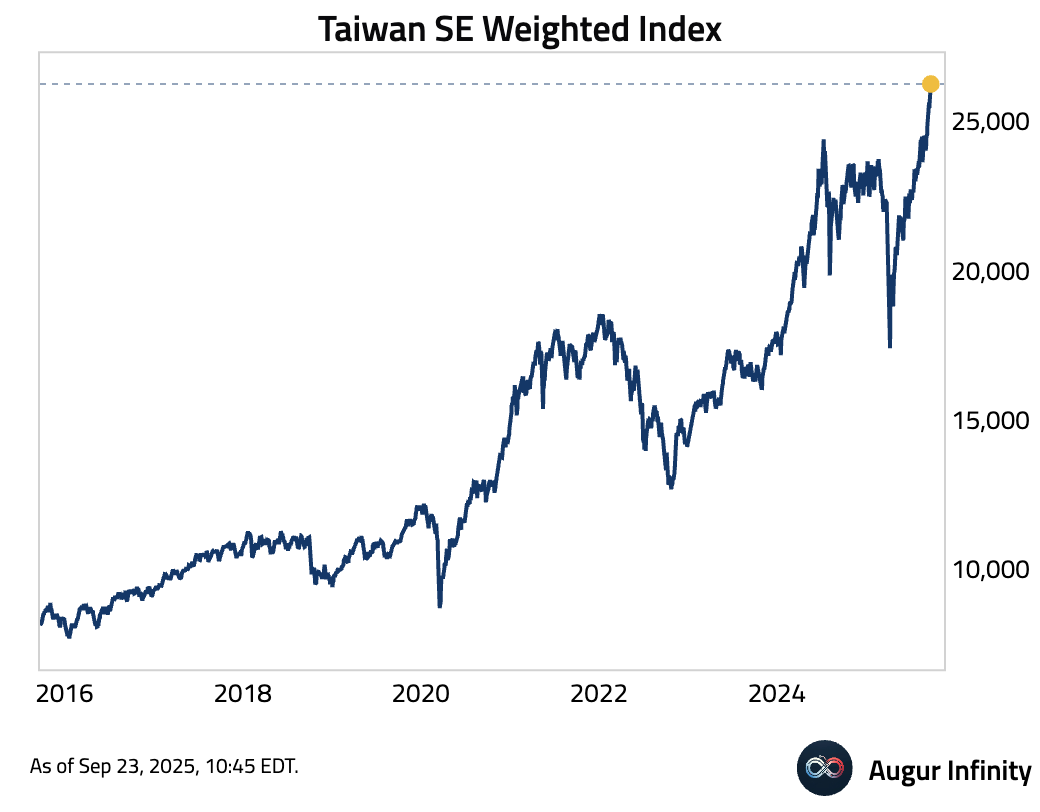

- Taiwan SE Weighted Index has surged.

Fixed Income

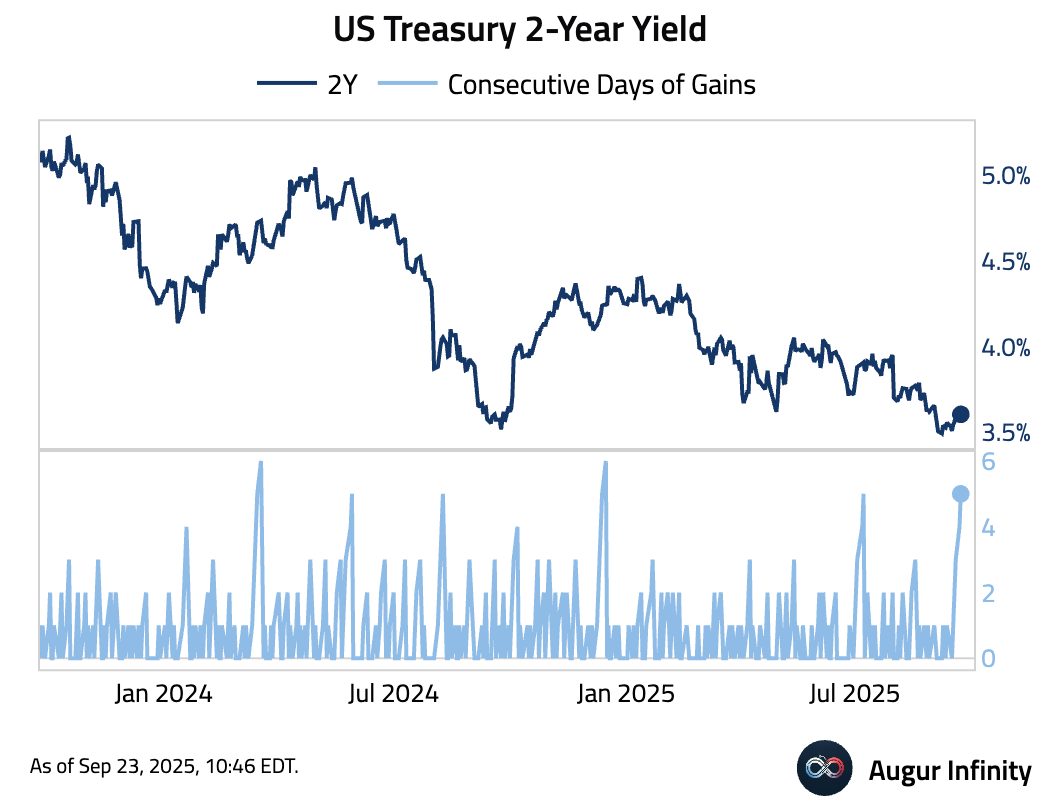

- US Treasury 2-year yield has risen for five consecutive days.

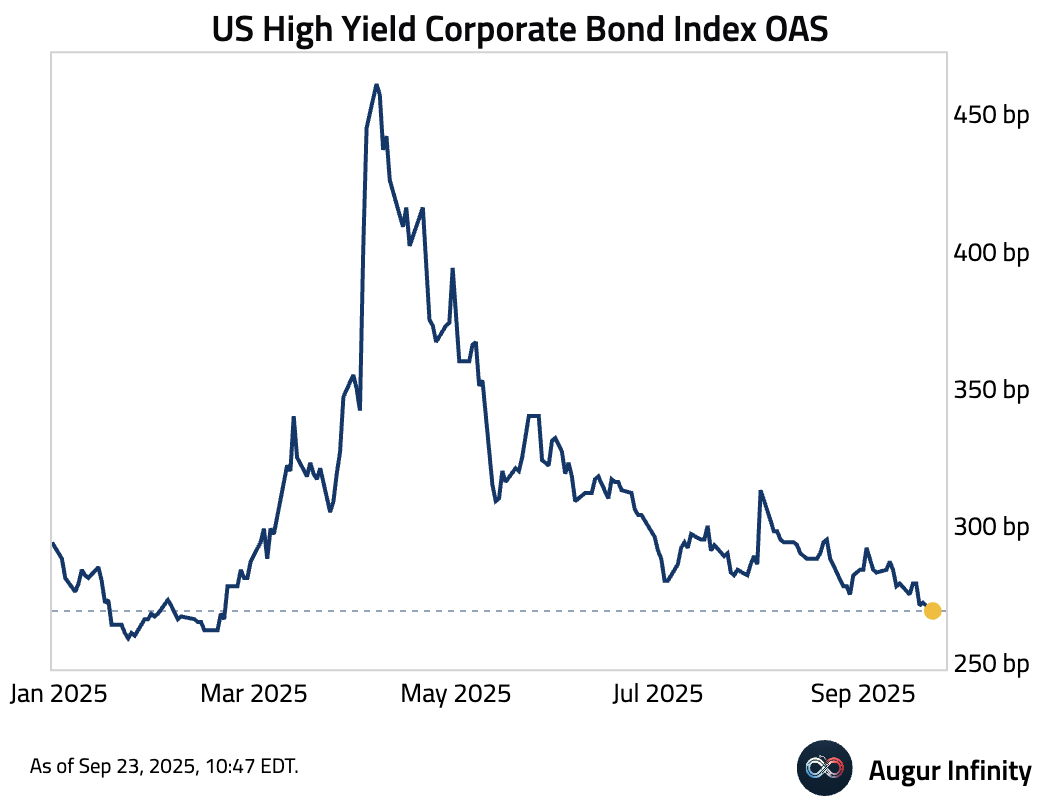

- US High Yield Corporate Bond Index OAS is at the lowest level since February 2025.

Commodities

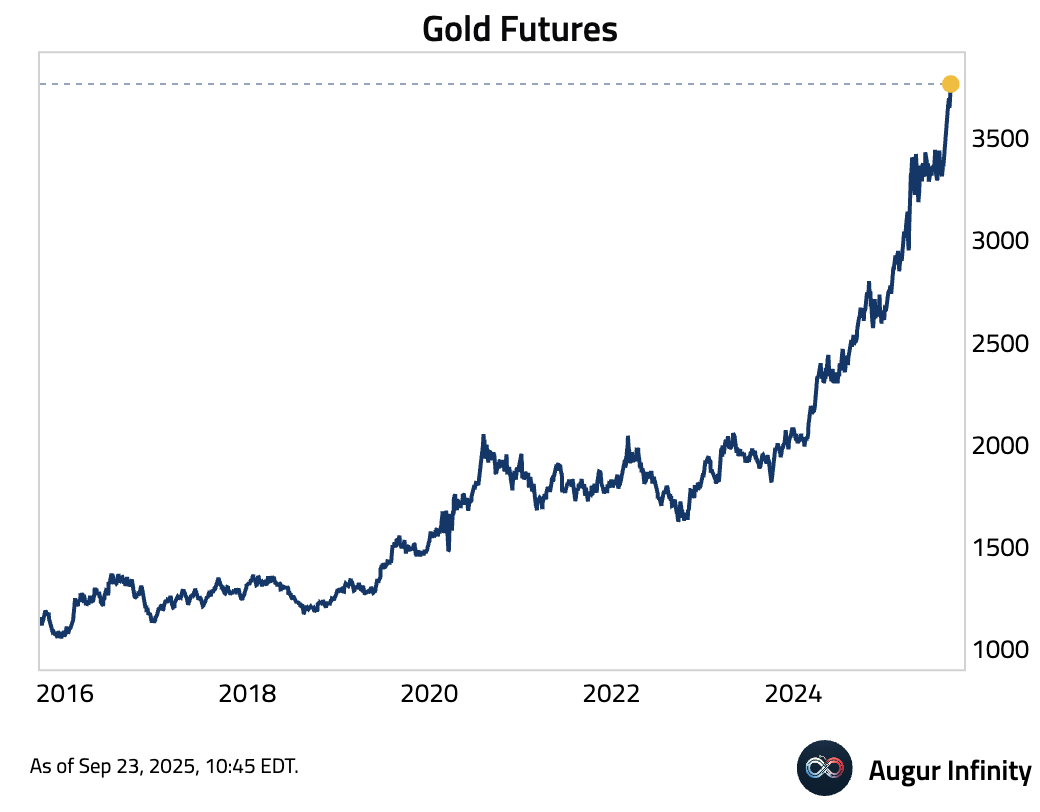

- Gold continues its advance.

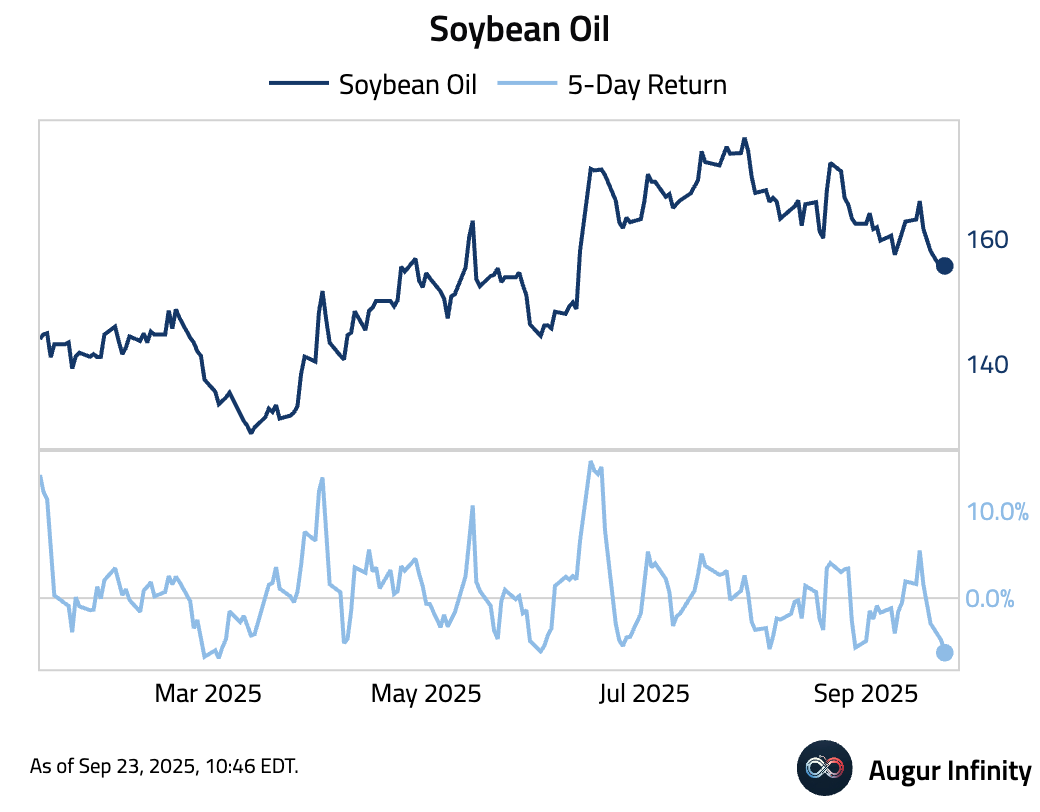

- Soybean oil had the worst 5-day return since March 2025.

FX

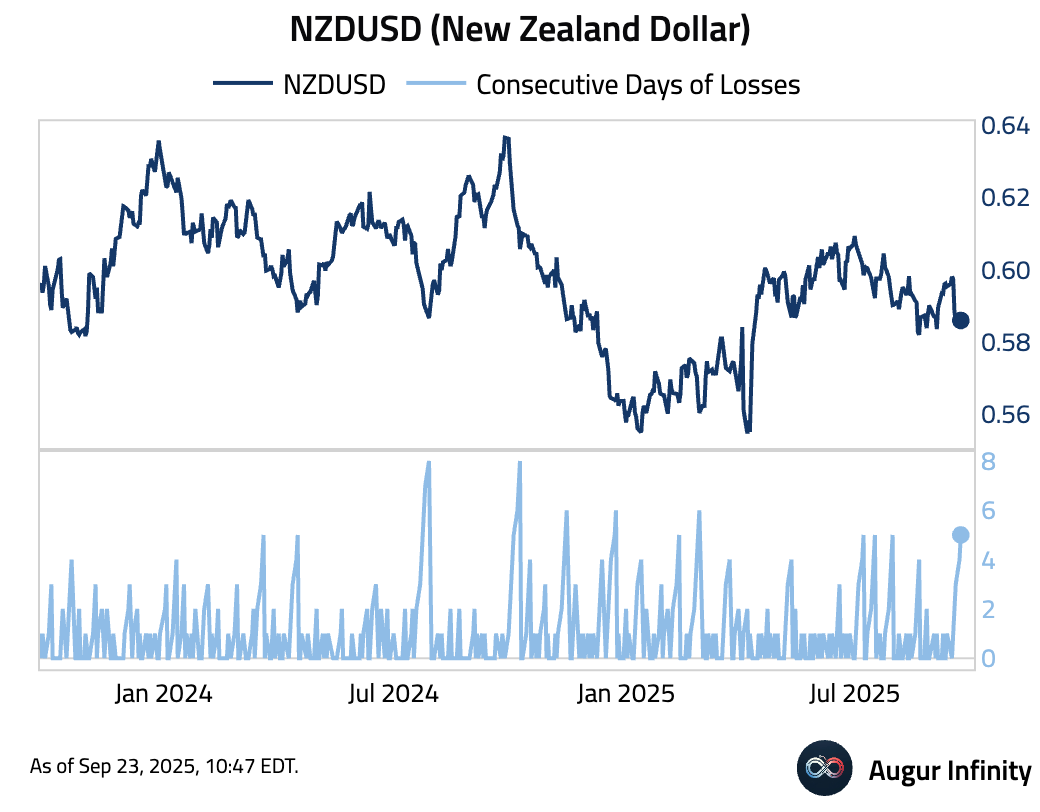

- NZDUSD (New Zealand Dollar) has depreciated against the dollar for five consecutive sessions.

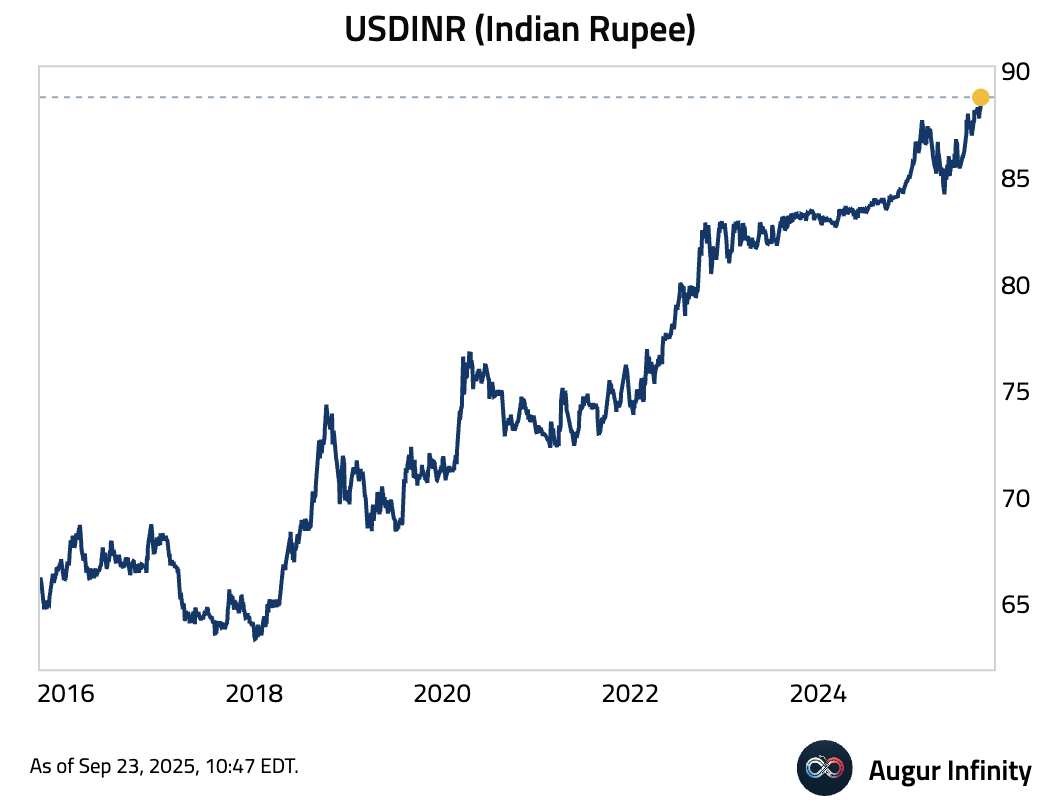

- Indian Rupee continues to lose value against the greenback.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.