Headlines

- President Trump, speaking at the UN General Assembly, threatened to impose a “powerful round” of new tariffs on Russia if the war in Ukraine does not end and criticized China, India, and the European Union for purchasing Russian oil.

- The president has also declined to meet with Democratic leadership this week ahead of the government funding deadline.

- South Korea’s finance minister is expected to meet with the US treasury secretary in New York.

Global Economics

United States

- New home sales surged unexpectedly in August, jumping to their highest level since January 2022 and crushing consensus estimates (act: 800k, est: 650k).The strong print was amplified by significant upward revisions to both June and July data. Sales increased in all regions, led by huge gains in the Northeast (+72%) and the South (+25%).

- The MBA 30-year mortgage rate fell for a second consecutive week to 6.34% (prev: 6.39%).

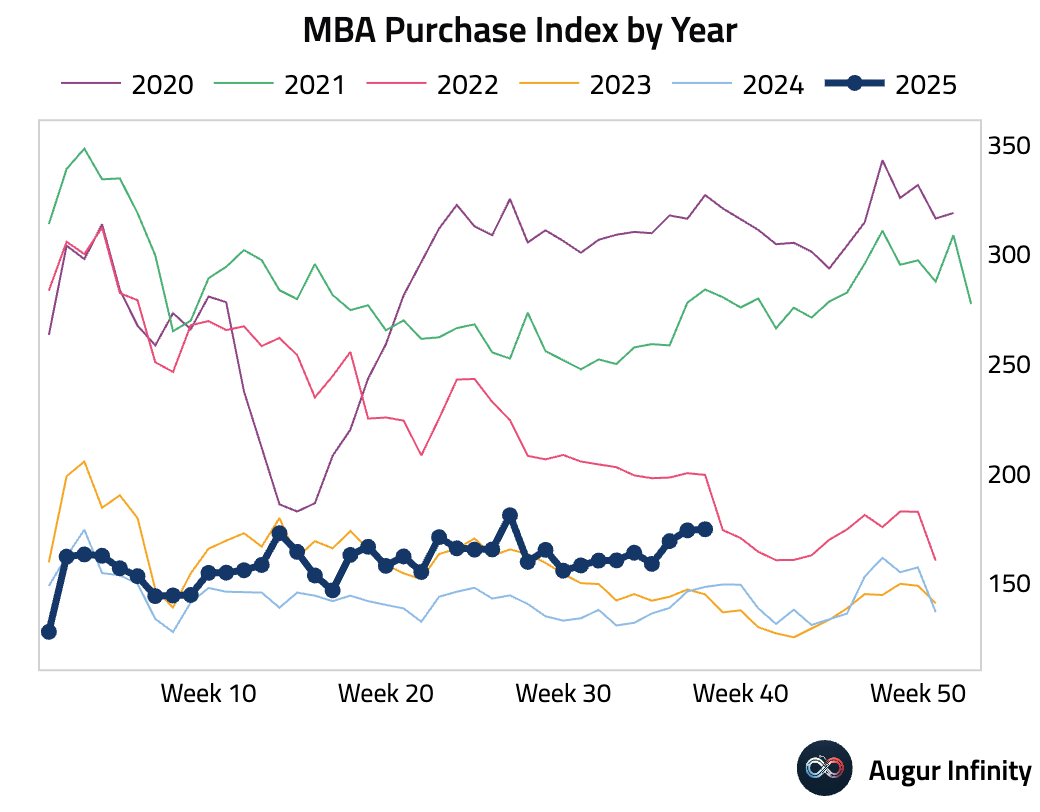

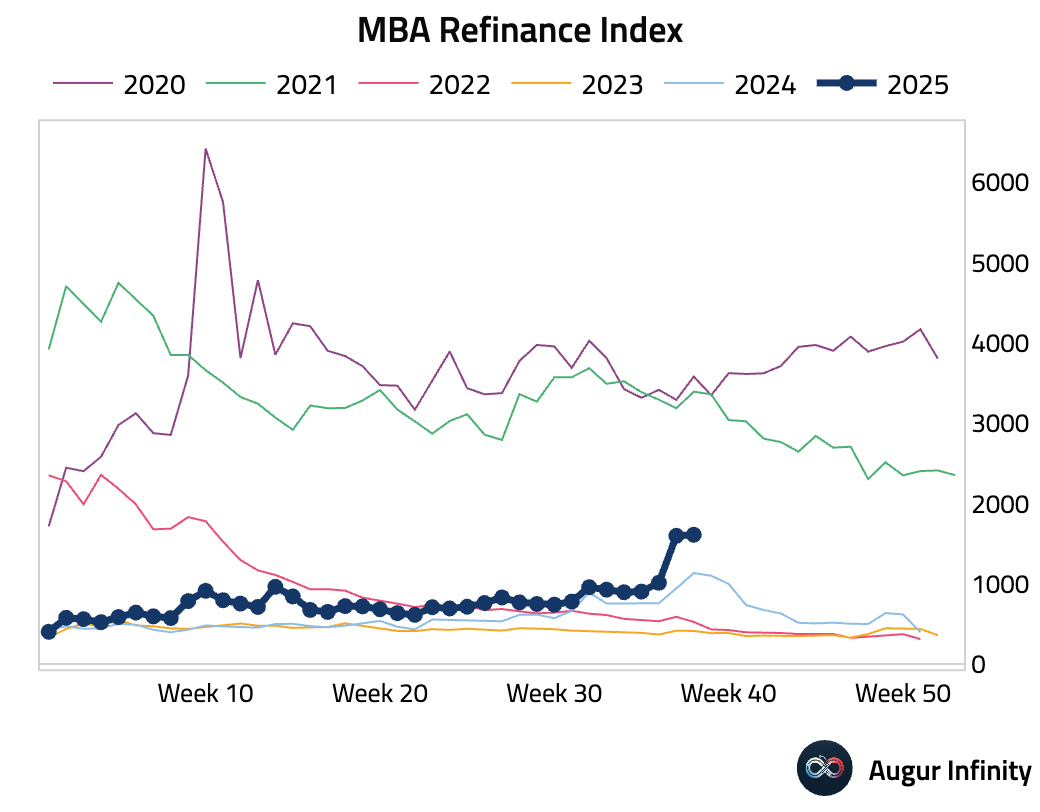

- US mortgage applications rose slightly last week, a sharp deceleration from the prior week’s jump, as a modest increase in both purchase and refinance activity drove the headline market index higher (act: 0.6% W/W, prev: 29.7%).

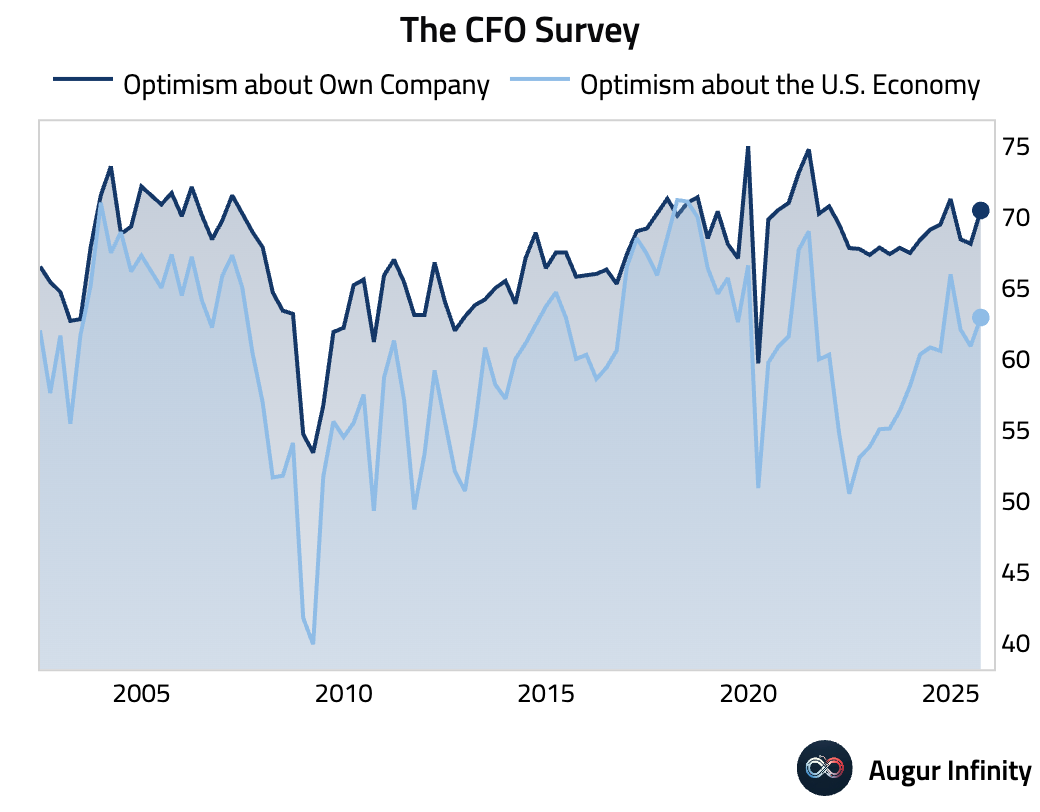

- CFO optimism improved somewhat in Q3, as uncertainty declined. However, concerns about the impact of tariffs on prices and business performance continued to weigh on firms.

- The American Petroleum Institute reported a larger-than-expected drawdown in crude oil inventories for the week (act: -3.821M, prev: -3.420M).

Canada

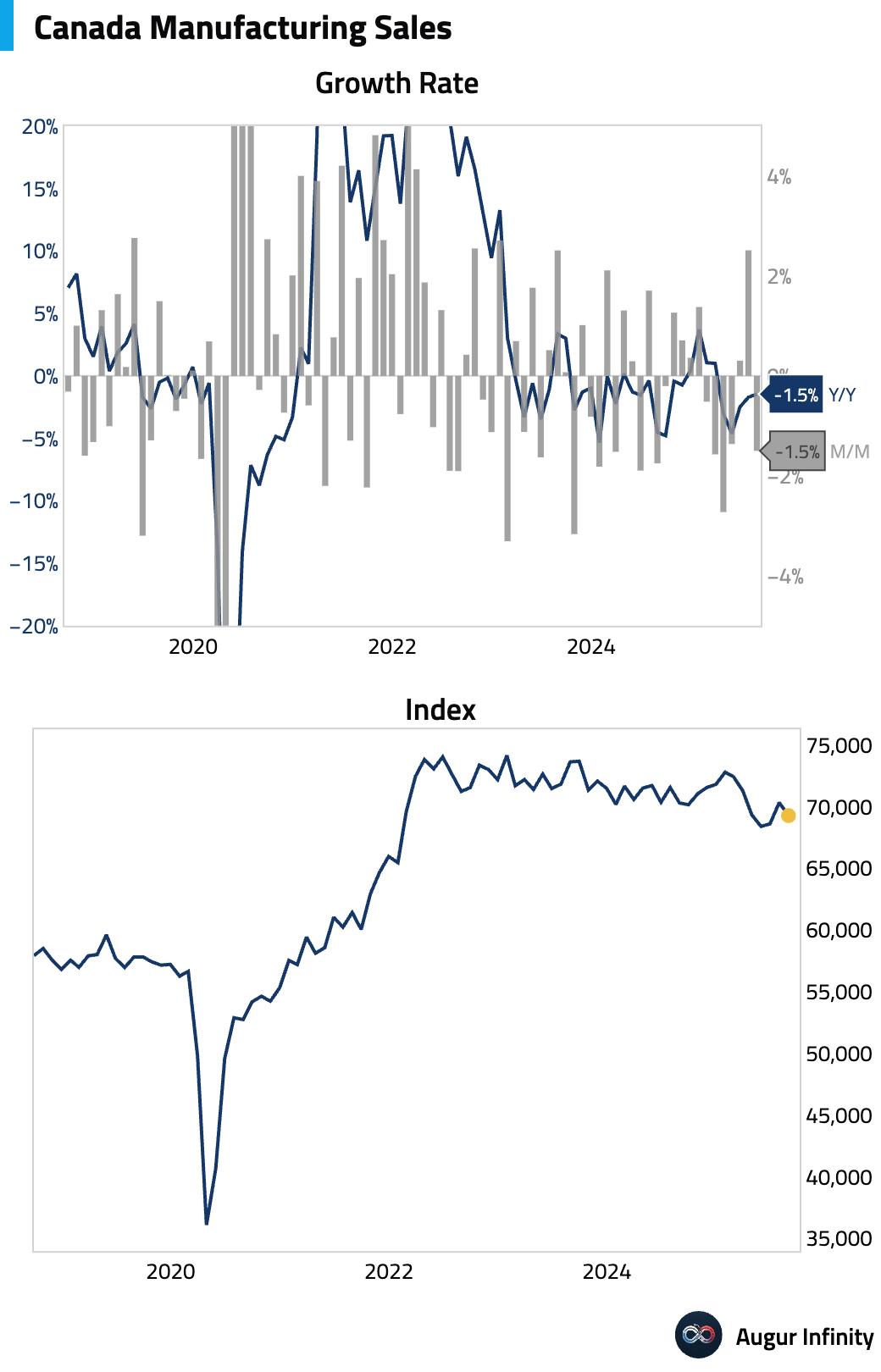

- The preliminary estimate for Canadian manufacturing sales pointed to a contraction in August, reversing July’s gain (act: -1.5% M/M, prev: 2.5%).

Europe

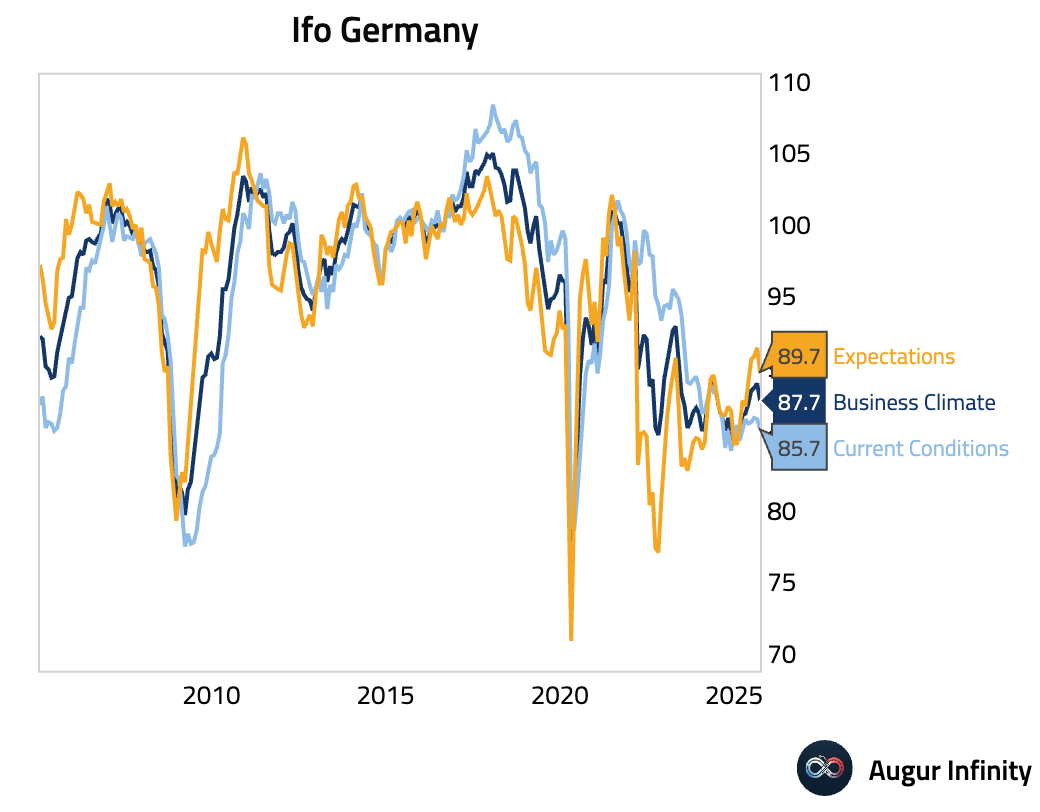

- German business sentiment deteriorated more than expected in September, with the Ifo Business Climate index falling to 87.7 from 88.9 (est: 89.3). Both the current conditions and expectations components weakened, pointing to ongoing pessimism about the economic outlook.

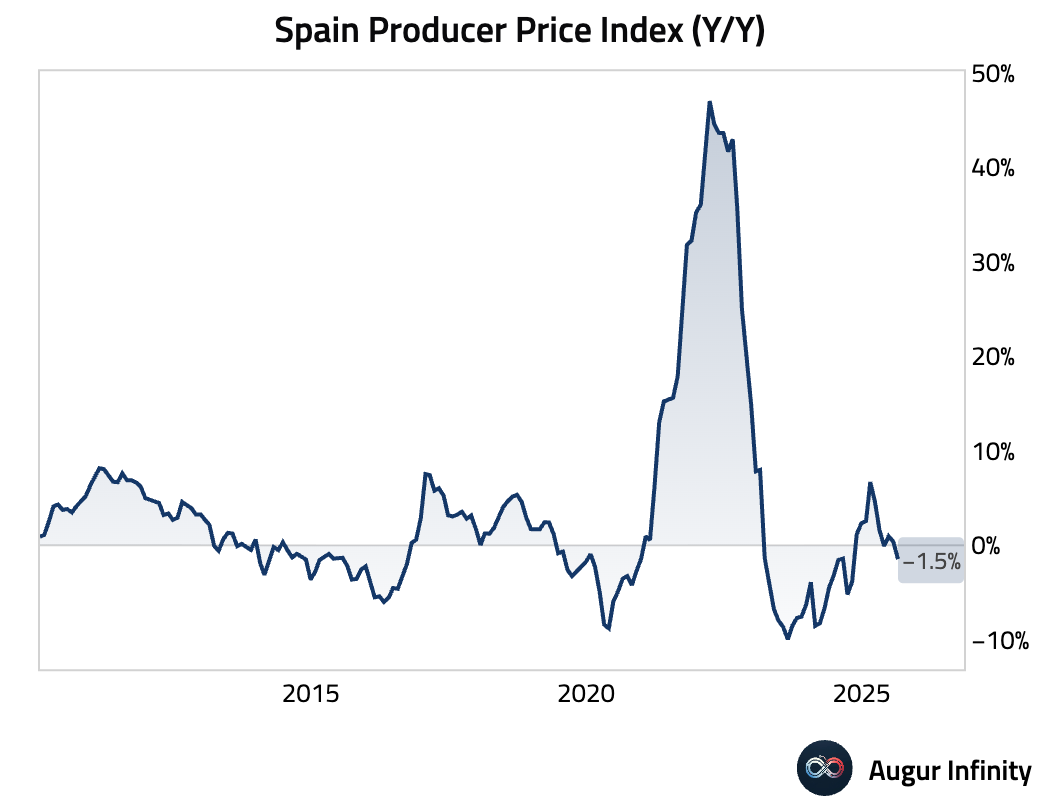

- Spanish producer prices fell back into deflationary territory, declining 1.5% Y/Y in August after a brief rise into positive territory in July (prev: 0.4%).

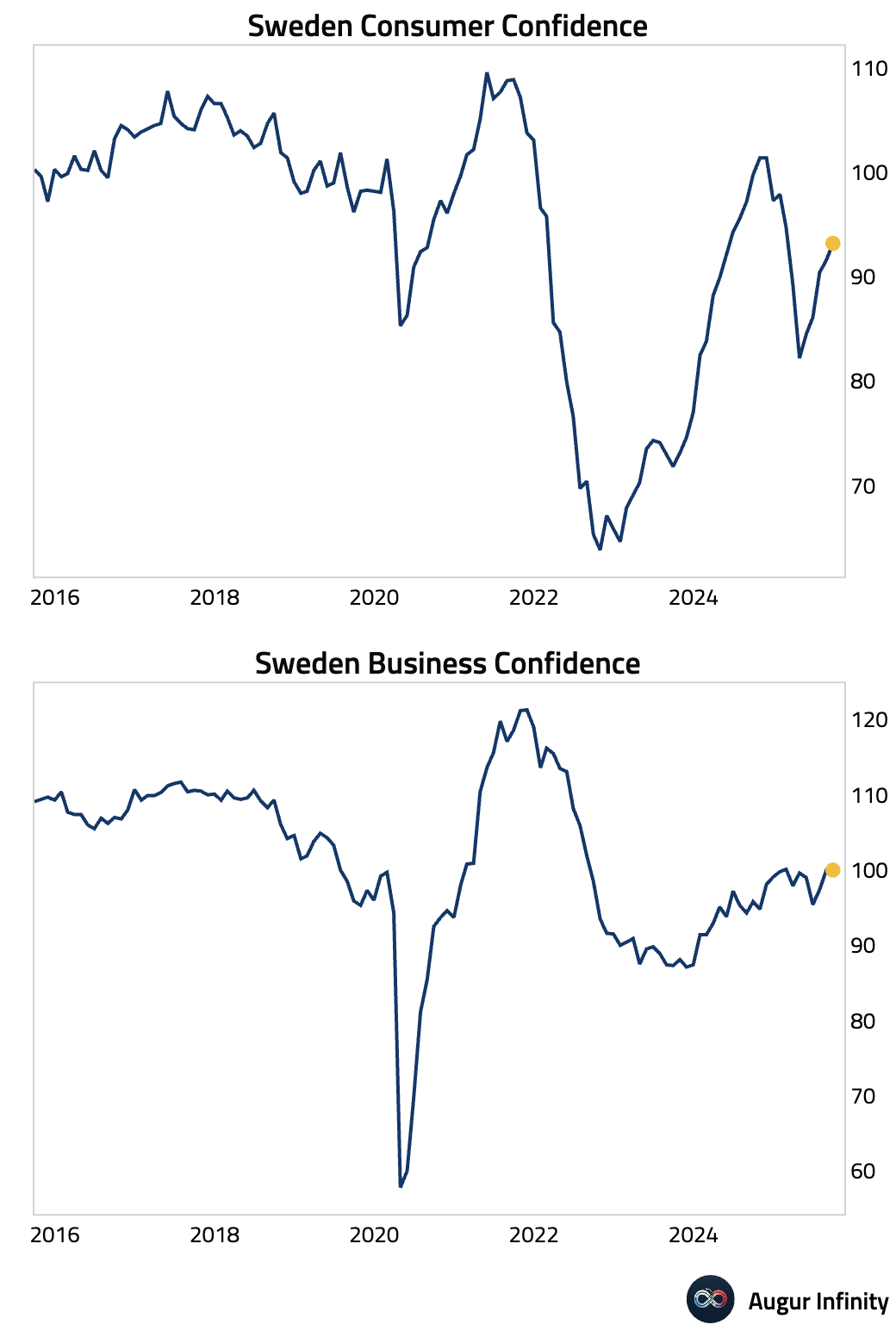

- Swedish consumer confidence improved in September but remained pessimistic, while business confidence was unchanged.

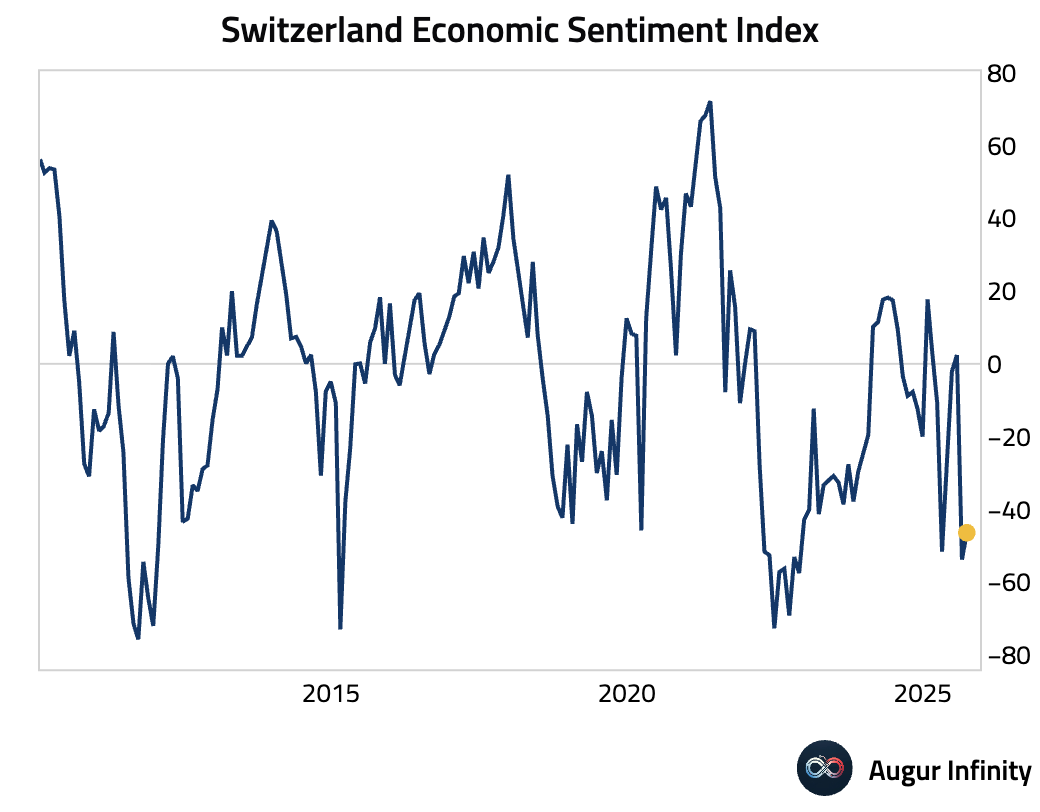

- The Swiss Economic Sentiment Index improved in September but remains deeply negative, indicating a pessimistic outlook for the economy (act: -46.4, prev: -53.8).

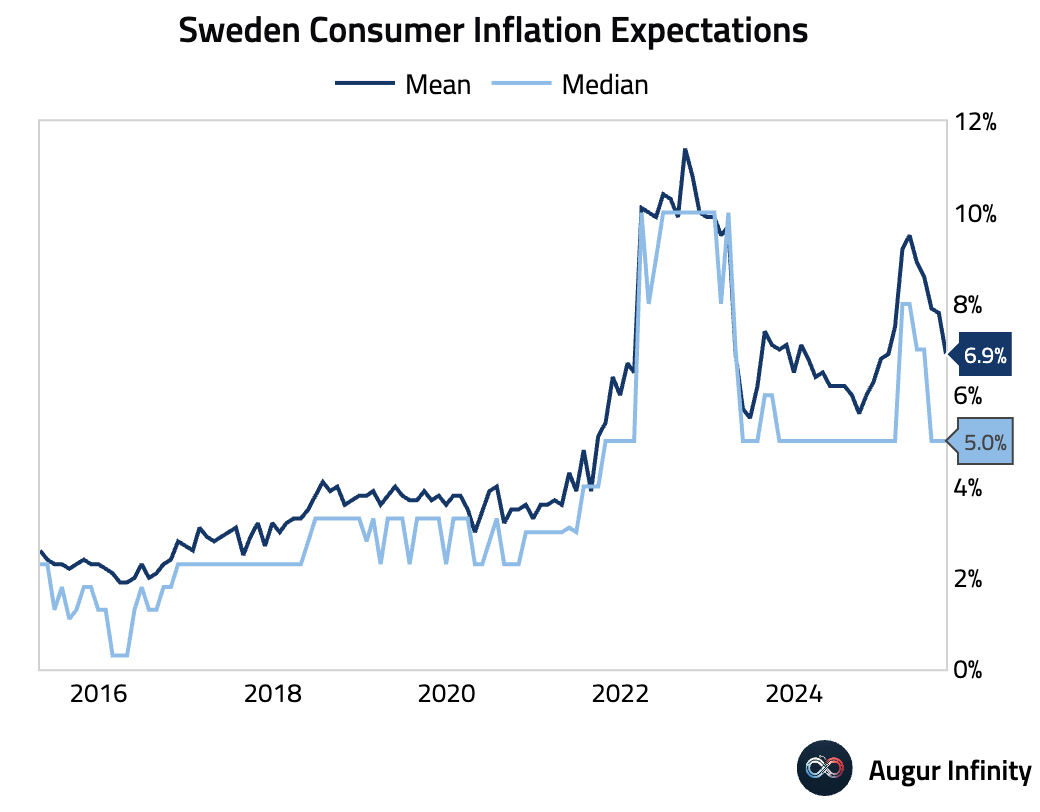

- Swedish consumer inflation expectations for the year ahead cooled significantly in September (act: 6.9%, prev: 7.8%).

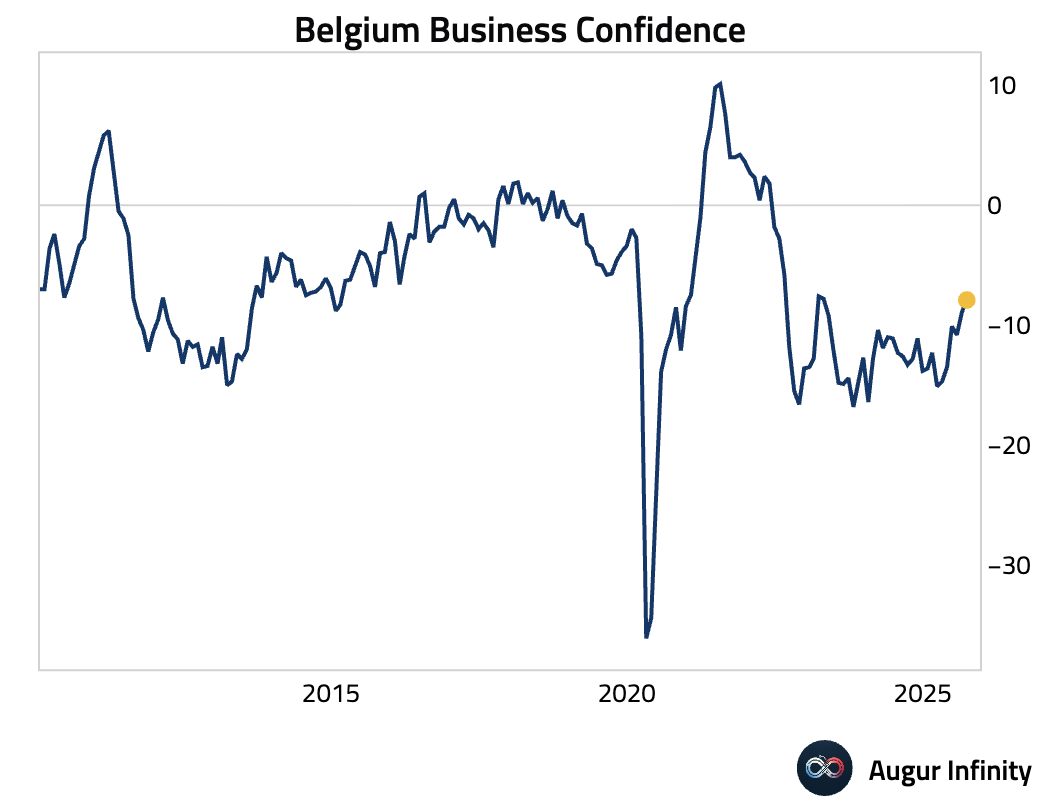

- Belgian business confidence improved for a second month in September but remains in pessimistic territory (act: -7.9, est: -8.0).

Asia-Pacific

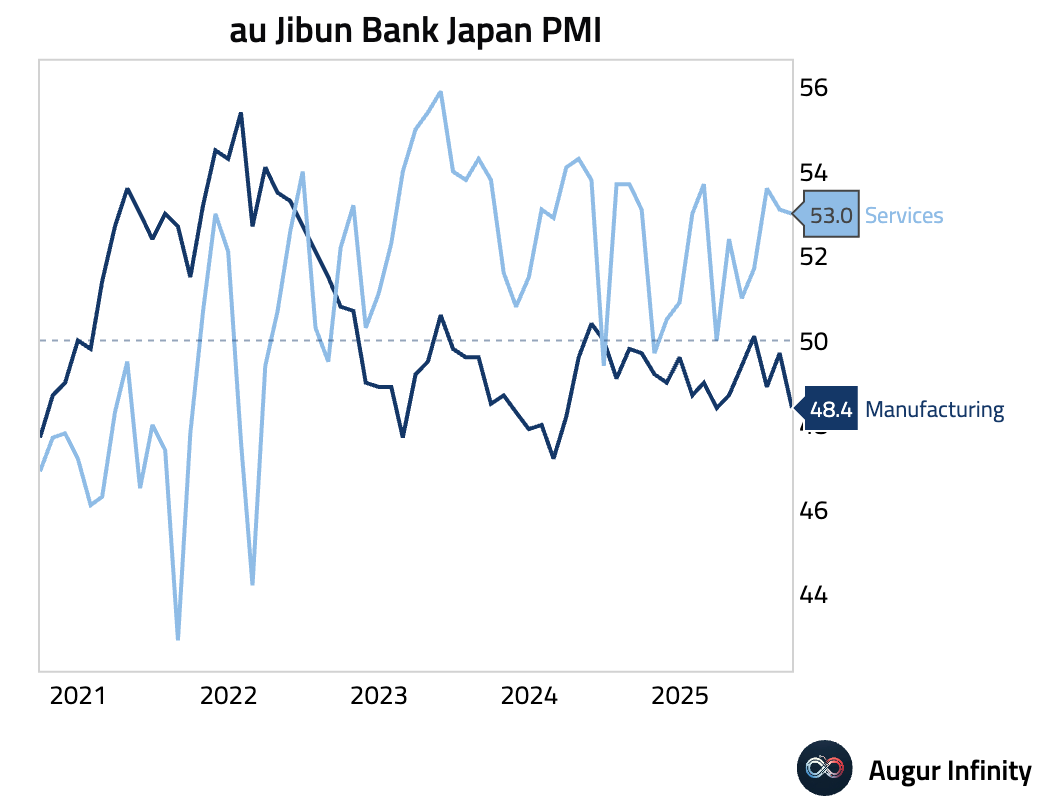

- Japan’s flash PMIs for September signaled slowing private sector growth, as a deepening manufacturing downturn offset solid expansion in services. The Composite PMI fell to a 4-month low of 51.1. The Manufacturing PMI sank further into contraction at 48.4 (est: 50.2), its lowest level since March 2024, driven by the sharpest drop in new orders since April. In contrast, the Services PMI remained strong at 53.0, supported by robust domestic demand that helped counter a continued decline in new export business.

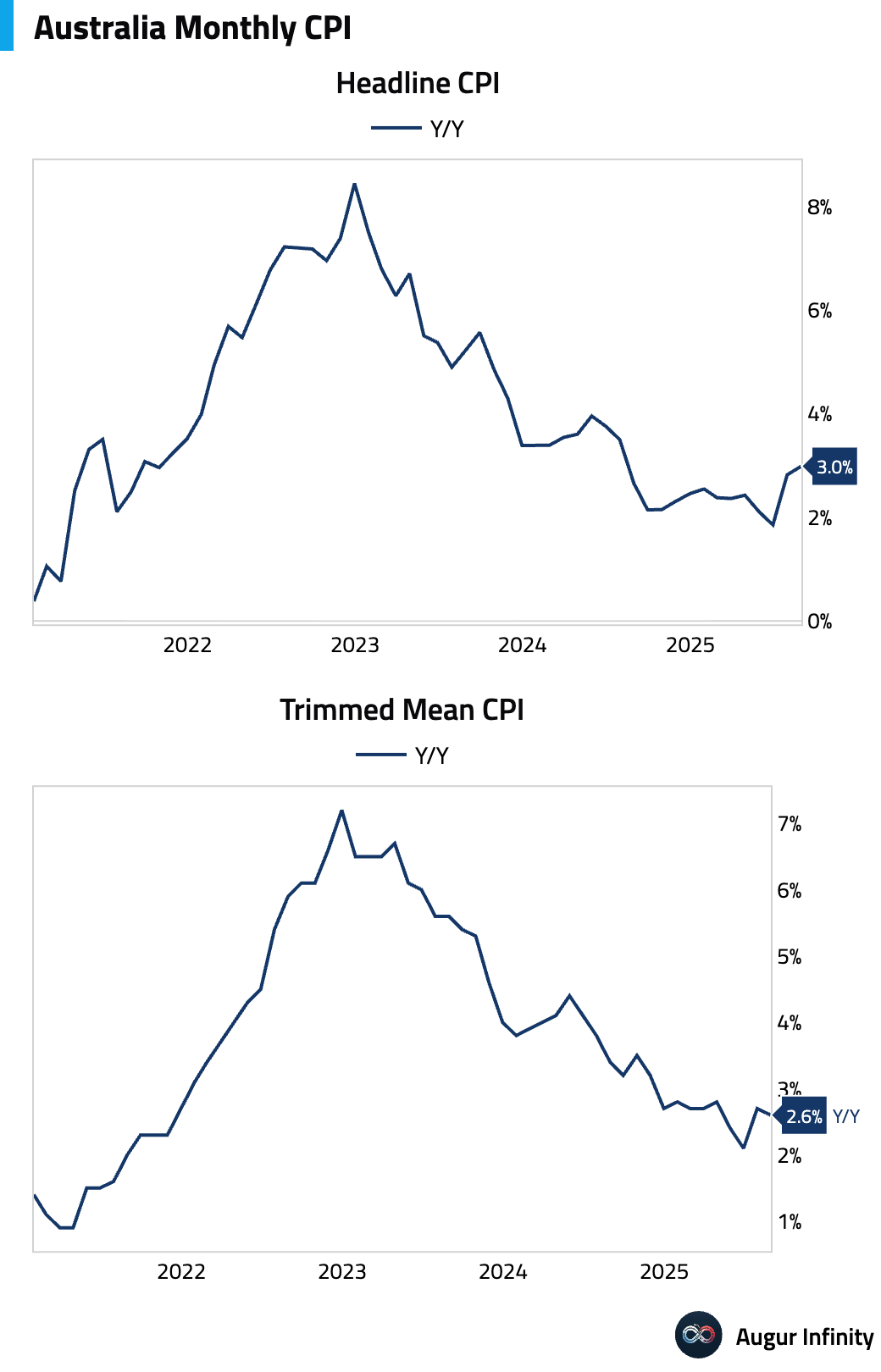

- Australia's monthly headline CPI accelerated to 3.0% Y/Y in August from 2.8% in July, coming in above consensus expectations of 2.9%. While the underlying trimmed mean measure eased to 2.6%, the print revealed sticky services inflation. The headline increase was partly driven by base effects from expiring electricity subsidies, masking some underlying trends. Rent growth decelerated to its slowest pace since November 2022, providing a key disinflationary signal.

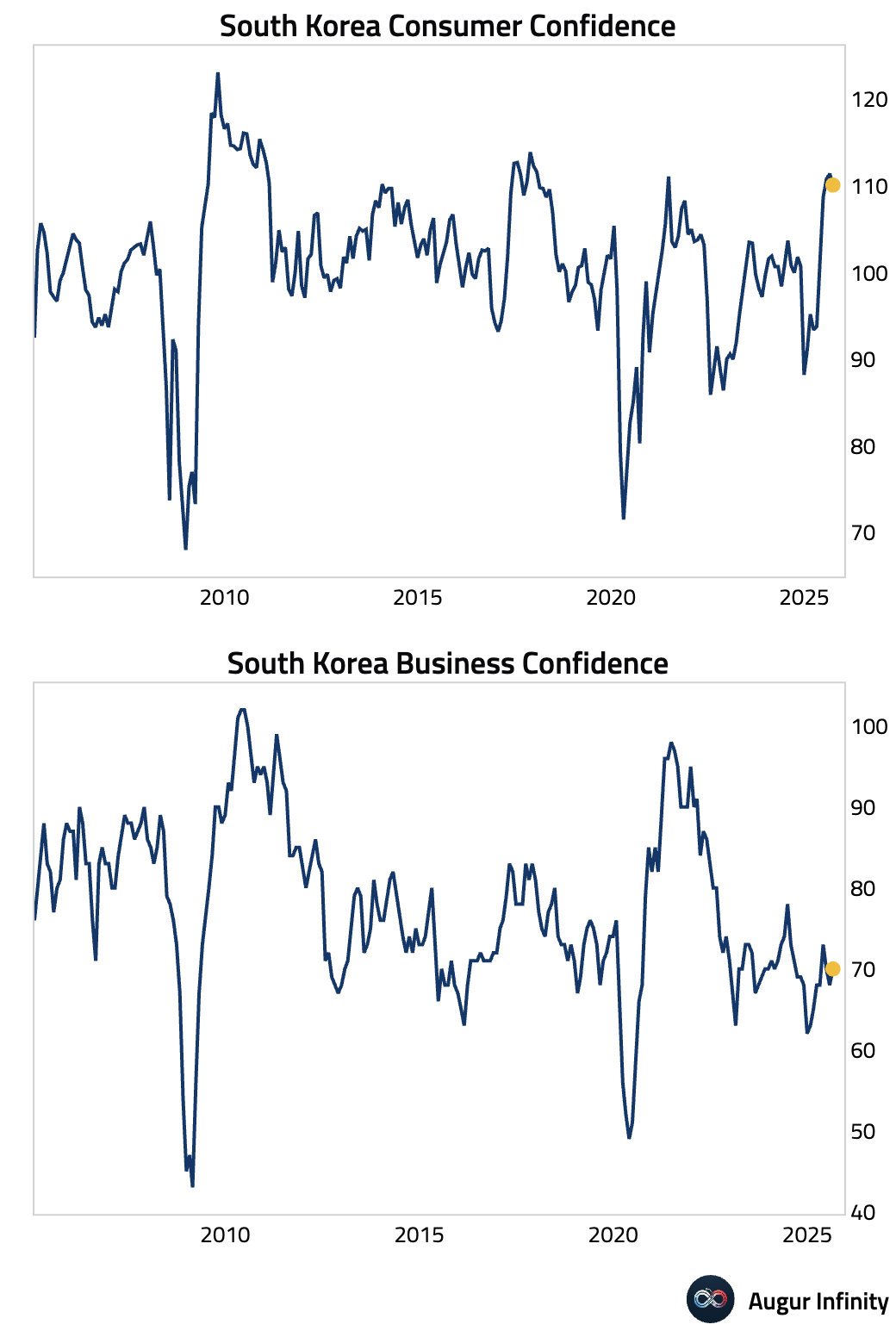

- South Korean consumer confidence edged lower for the second consecutive month in September, falling to 110.1 from 111.4.

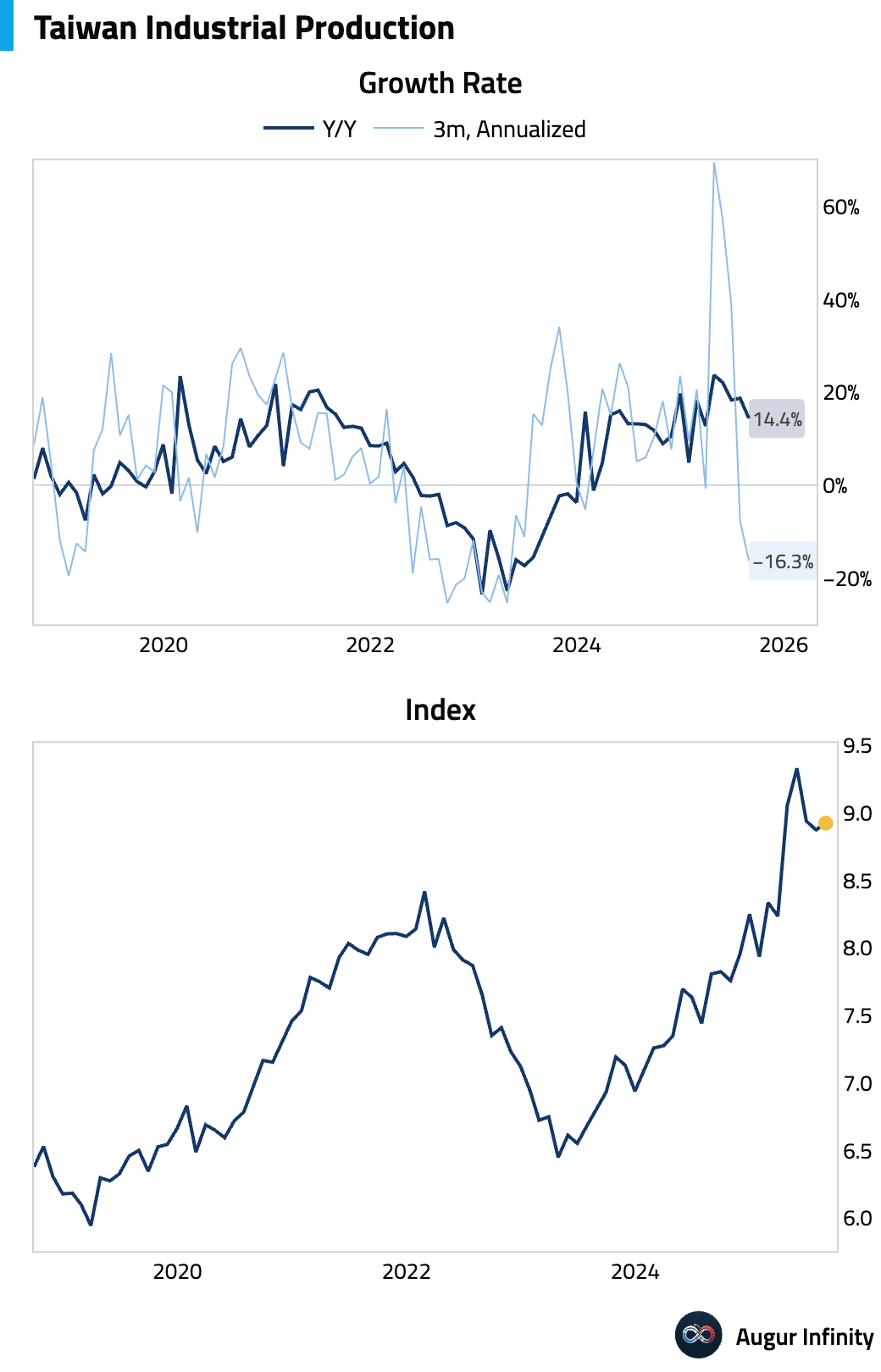

- Taiwan’s industrial production grew 14.4% Y/Y in August, a moderation from July's pace but in line with expectations. The result reflected a divergence between a sharp drop in computer and optical products, which normalized after prior gains, and a solid 2.2% M/M rise in the crucial electronic components sector that is dominated by semiconductors.

- New Zealand appointed Dr. Anna Breman, currently the First Deputy Governor of Sweden's Riksbank, as the next RBNZ Governor. Her five-year term begins December 1, 2025.

Emerging Markets ex China

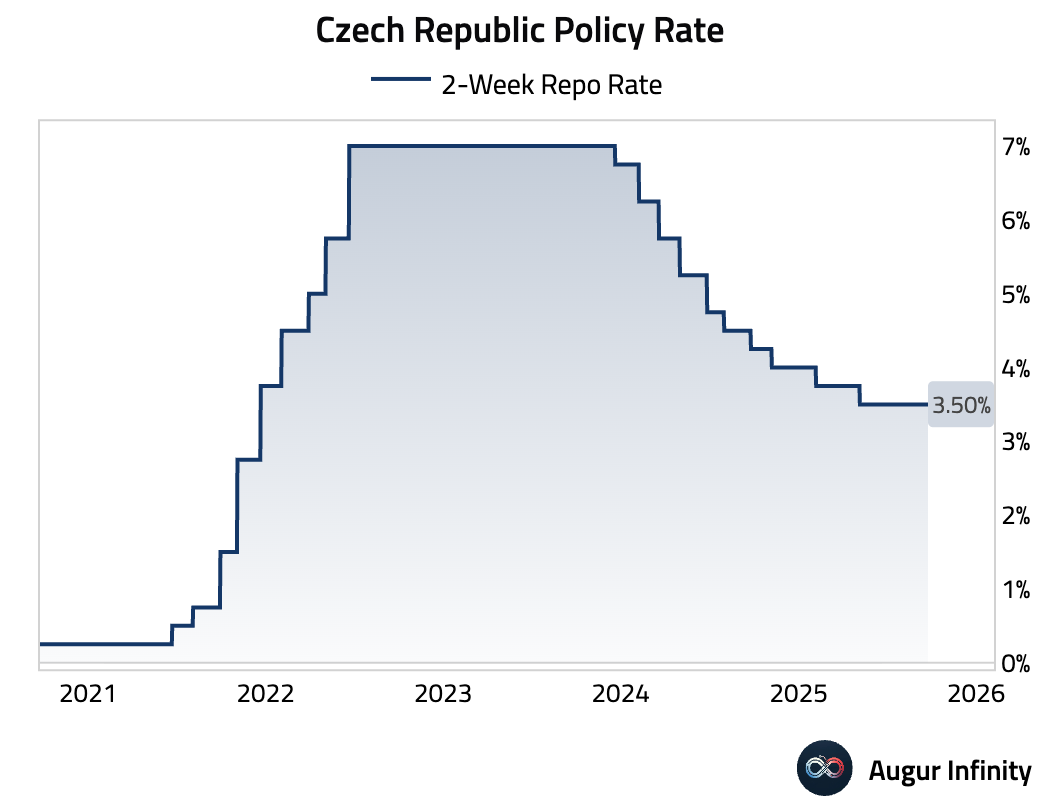

- The CNB unanimously held its key policy rate at 3.50%, in line with expectations. The bank maintained hawkish guidance, stating that ongoing domestic inflation pressures preclude further rate cuts.

- Czech consumer confidence saw a notable improvement in September, while business sentiment was little changed (Consumer act: 103.5, prev: 99.0; Business act: 101.6, prev: 101.5).

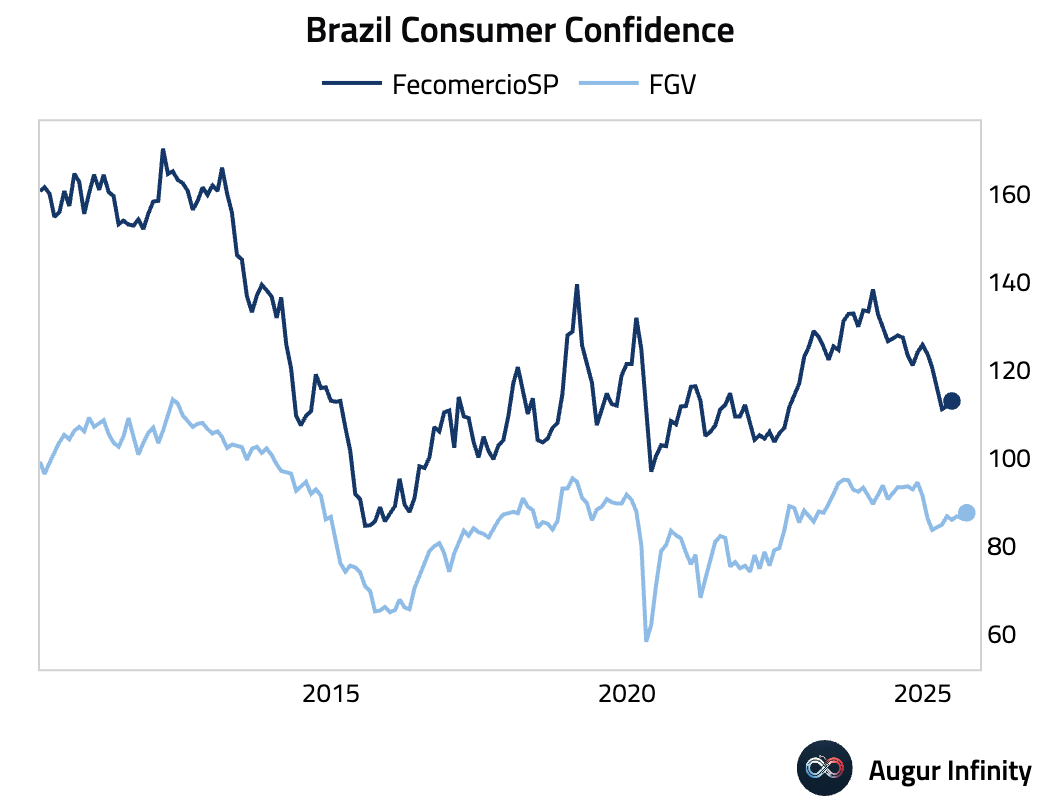

- Brazilian consumer confidence improved in September, rising to 87.5 from 86.2. The gain was driven entirely by a brighter outlook, as the expectations component rose 3.7 points, while the assessment of current conditions declined. Both components remain in pessimistic territory.

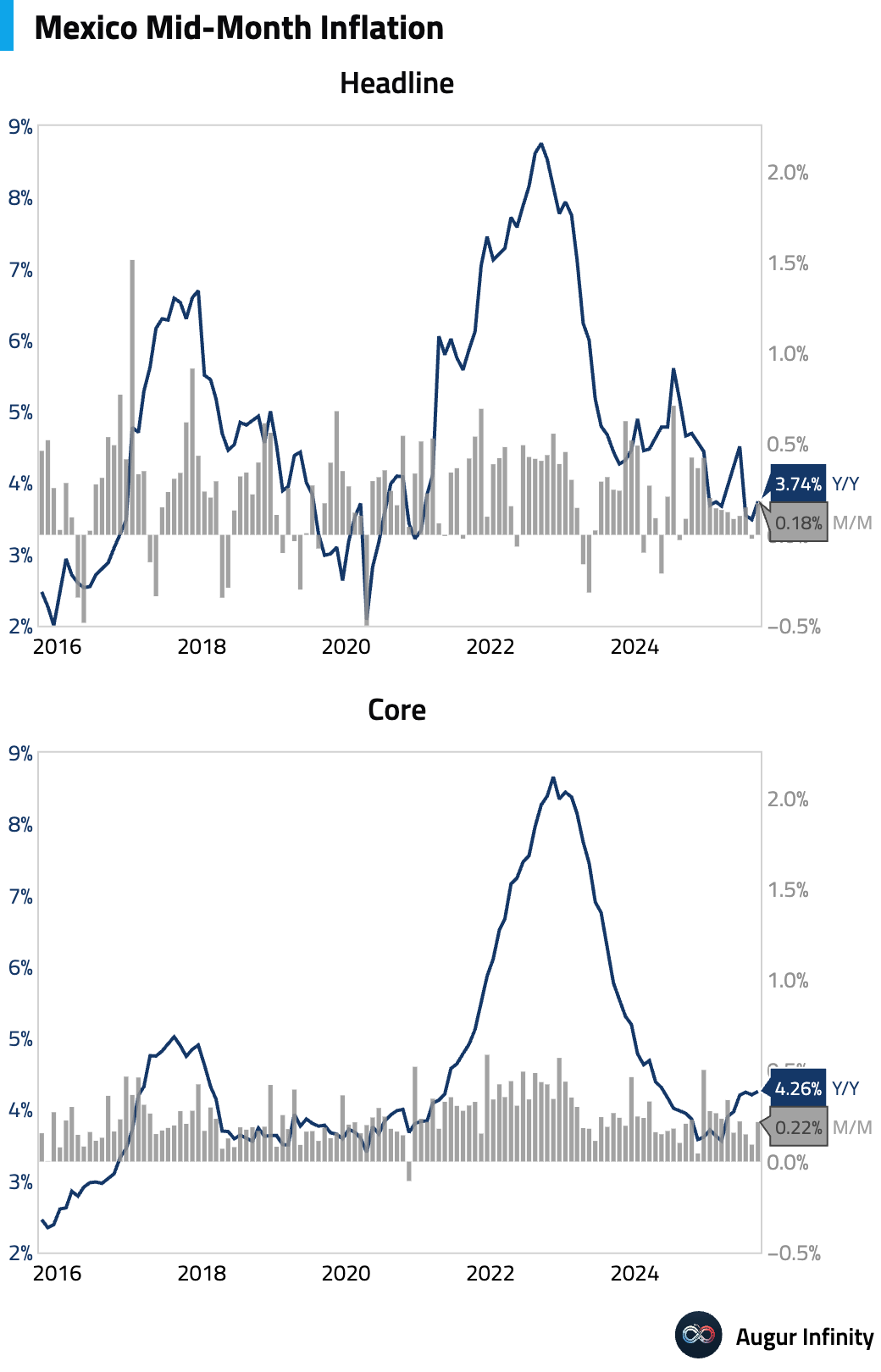

- Mexico’s mid-month inflation for September was hotter than expected, with the headline rate rising to 3.74% Y/Y and the core rate ticking up to 4.26% Y/Y. The increase in the core reading was driven by non-food goods and education fees, while services inflation remains sticky at 4.32% Y/Y.

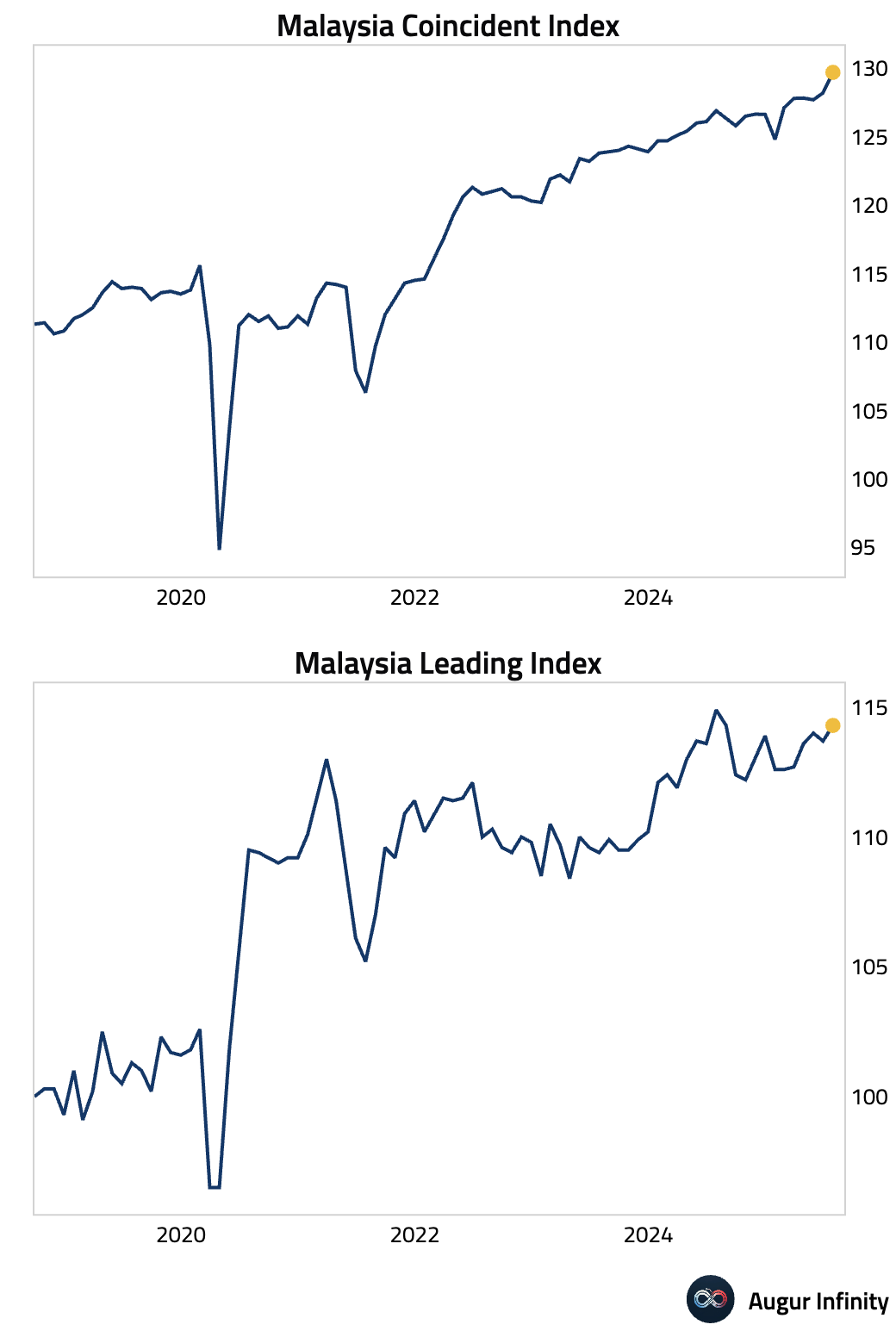

- Malaysia's Leading Index, a gauge of future economic activity, returned to positive territory in July, while the Coincident Index, which measures the current state of the economy, accelerated (Leading act: 0.5% M/M, prev: -0.3%; Coincident act: 1.2% M/M, prev: 0.4%).

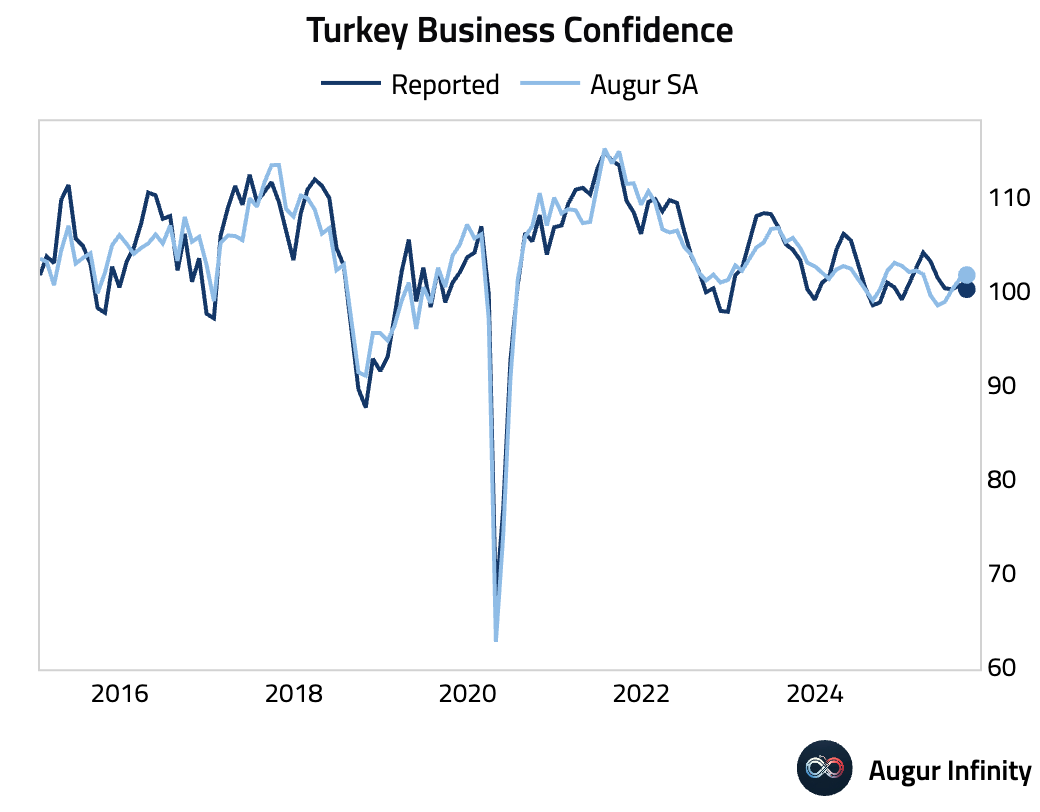

- Turkish business confidence eased slightly in September but remains in optimistic territory (act: 100.2, prev: 100.6).

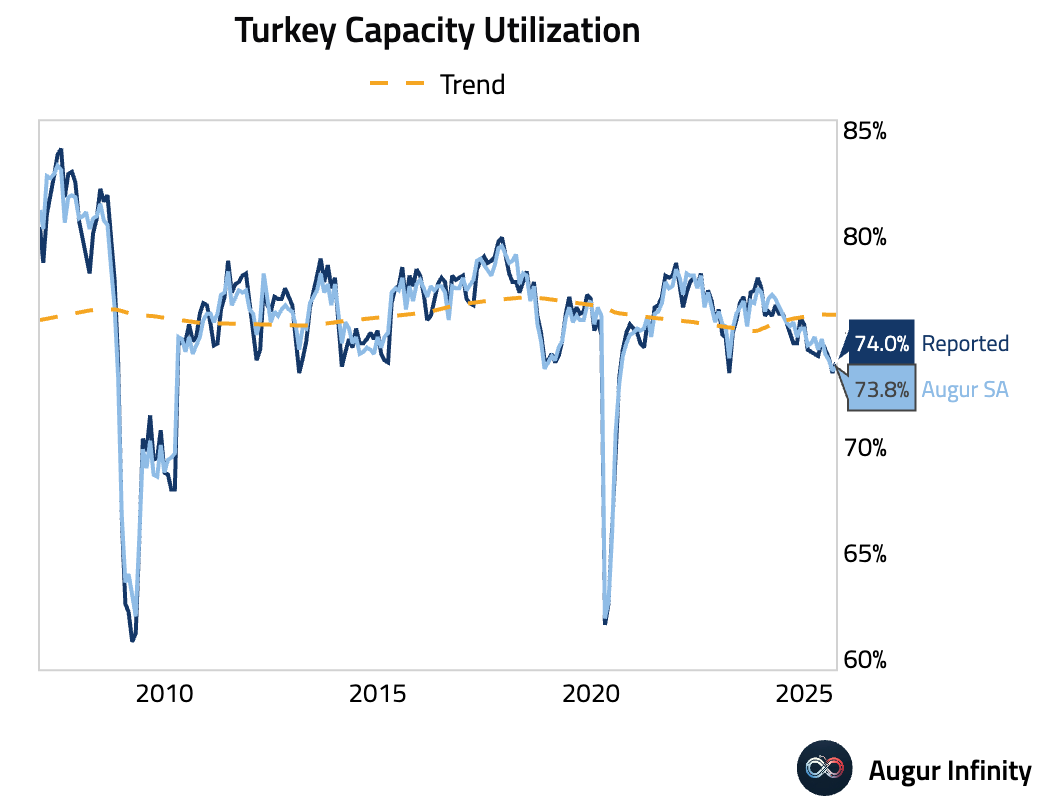

- Capacity utilization in Turkey’s manufacturing sector ticked up in September (act: 74.0%, prev: 73.5%).

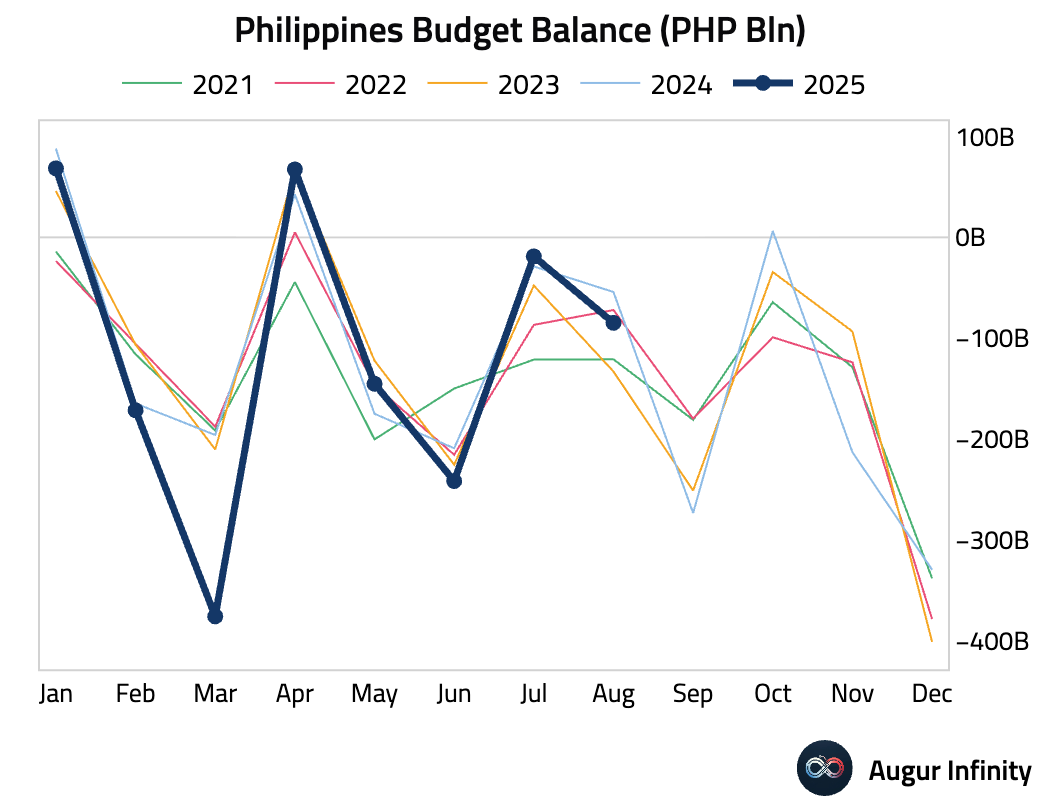

- The Philippines posted a wider budget deficit in August (act: -84.8B, prev: -18.9B).

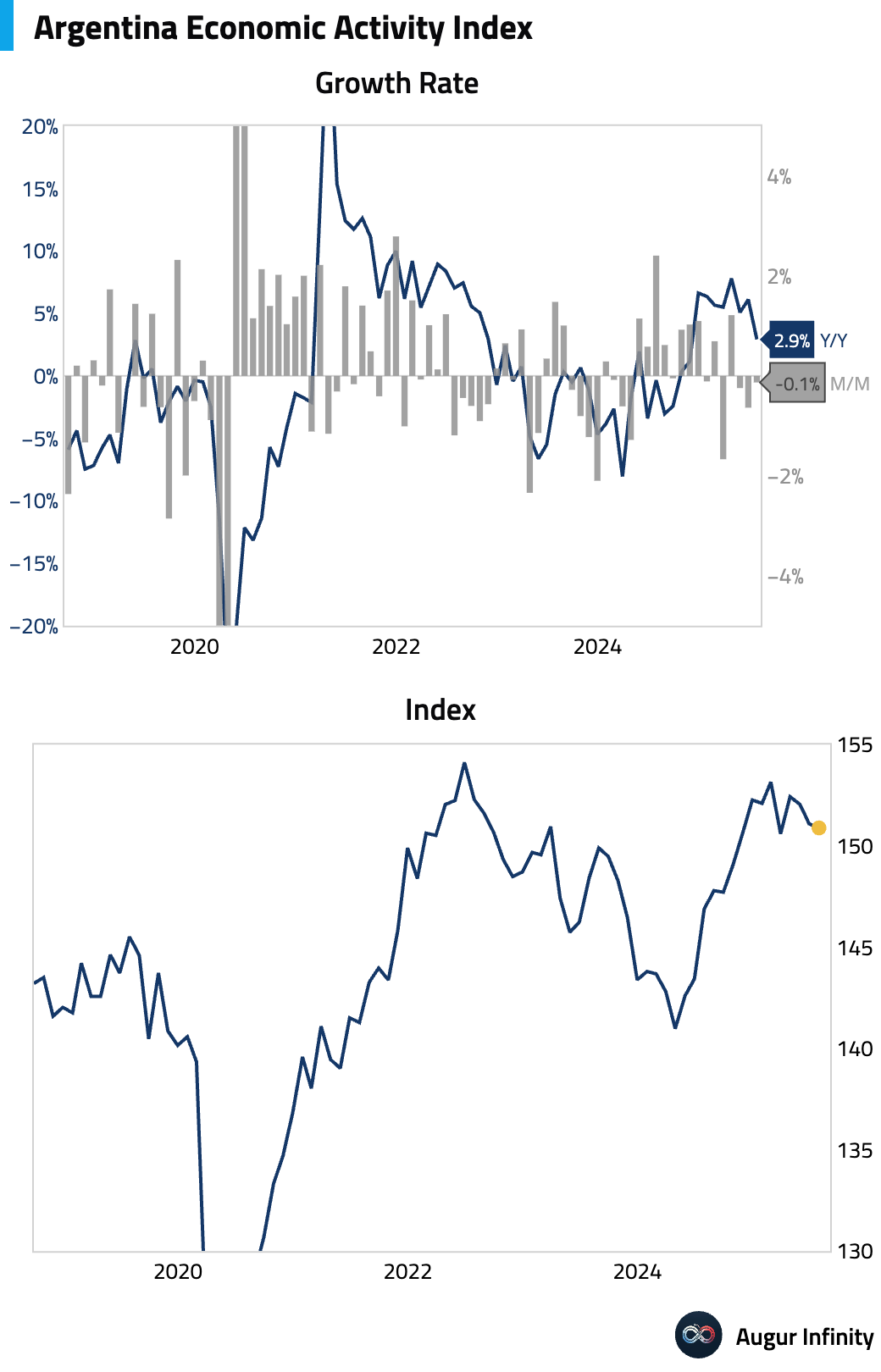

- Argentina's Economic Activity Index rose by 2.9% Y/Y in July, slowing from 6.1%. Month-over-month, growth was negative for the third straight month.

Global Markets

Equities

- US equities declined for a second consecutive session, with the S&P 500 and Nasdaq Composite each down 0.3%. Asian markets saw notable losses, particularly in South Korea (-1.7%) and Australia (-1.5%), while Chinese equities bucked the regional trend, rising 1.2%.

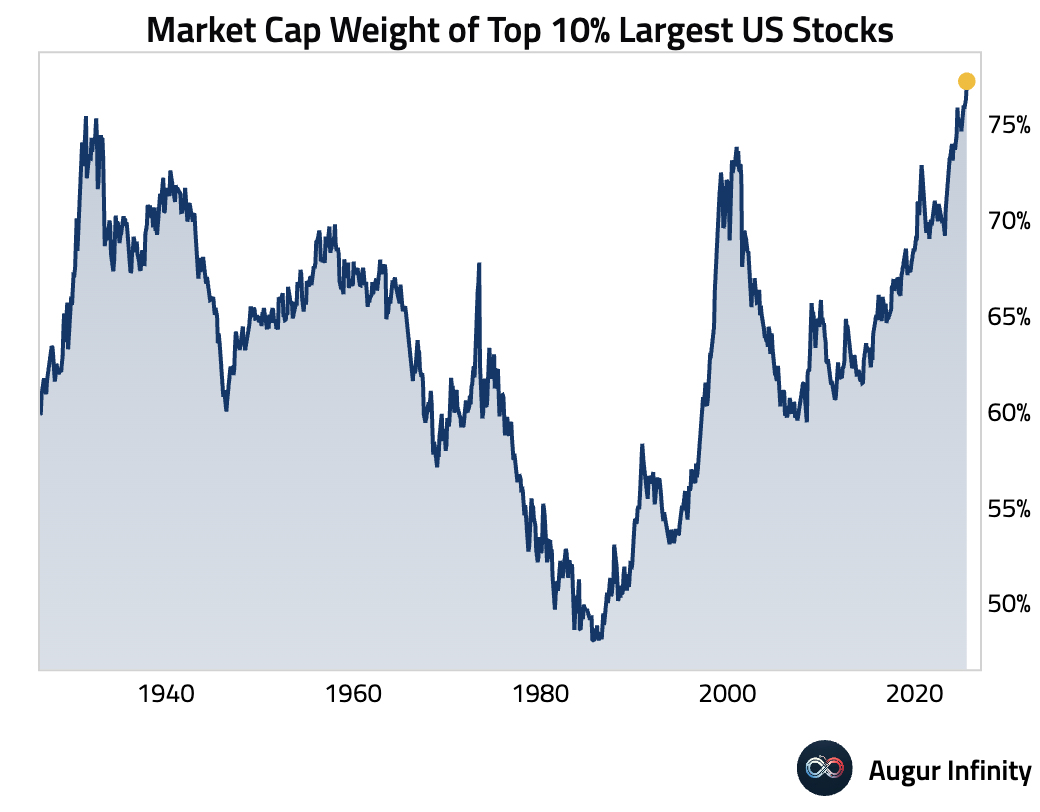

- The market cap weight of the top 10% of largest US stocks has reached a new record high.

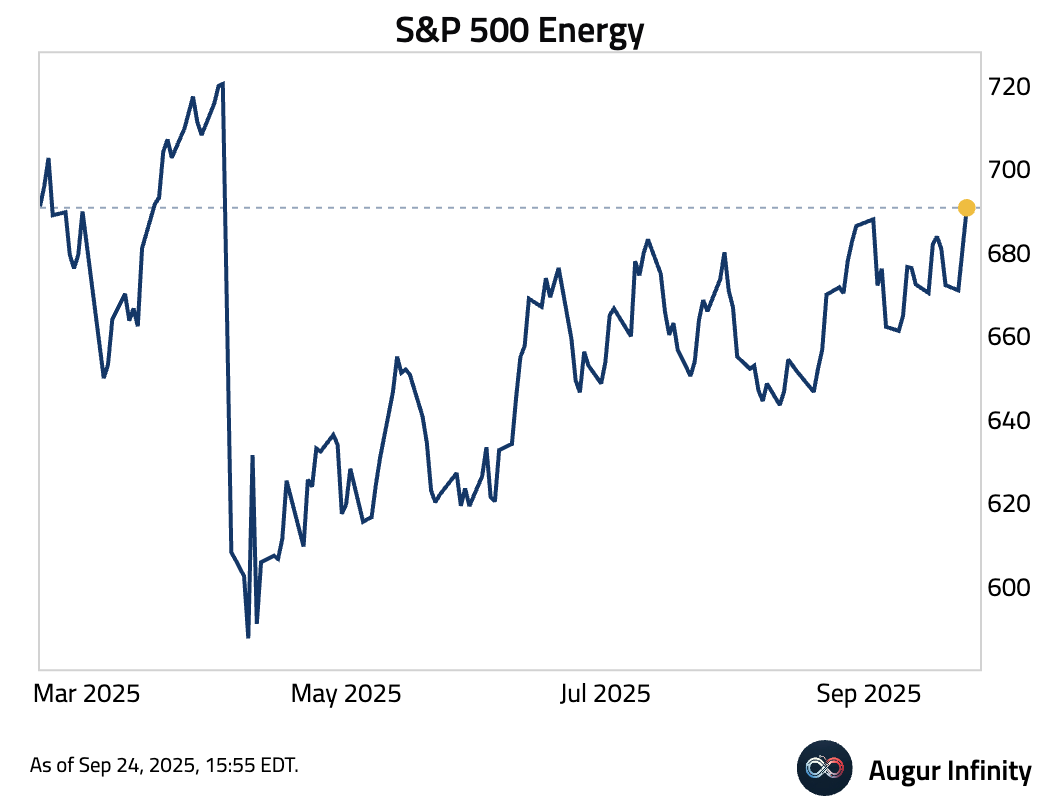

- The energy sector of the S&P 500 Index has reached the highest level since April.

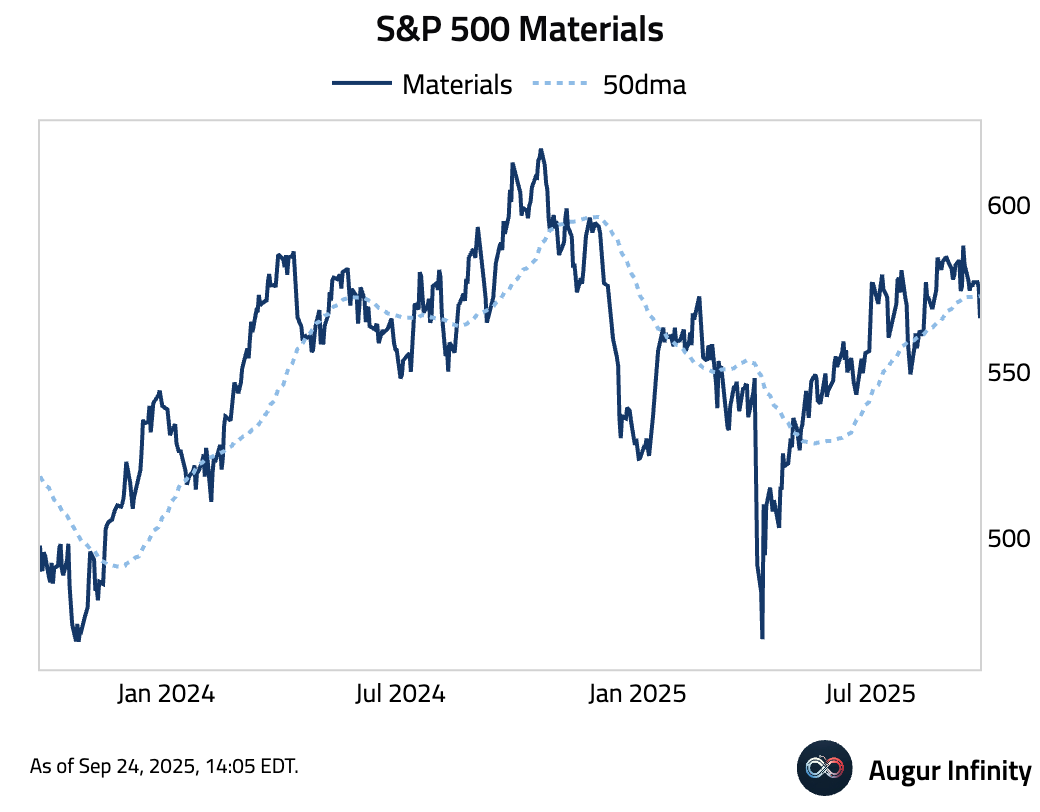

- The materials sector, by contrast, fell below its 50-day moving average.

Fixed Income

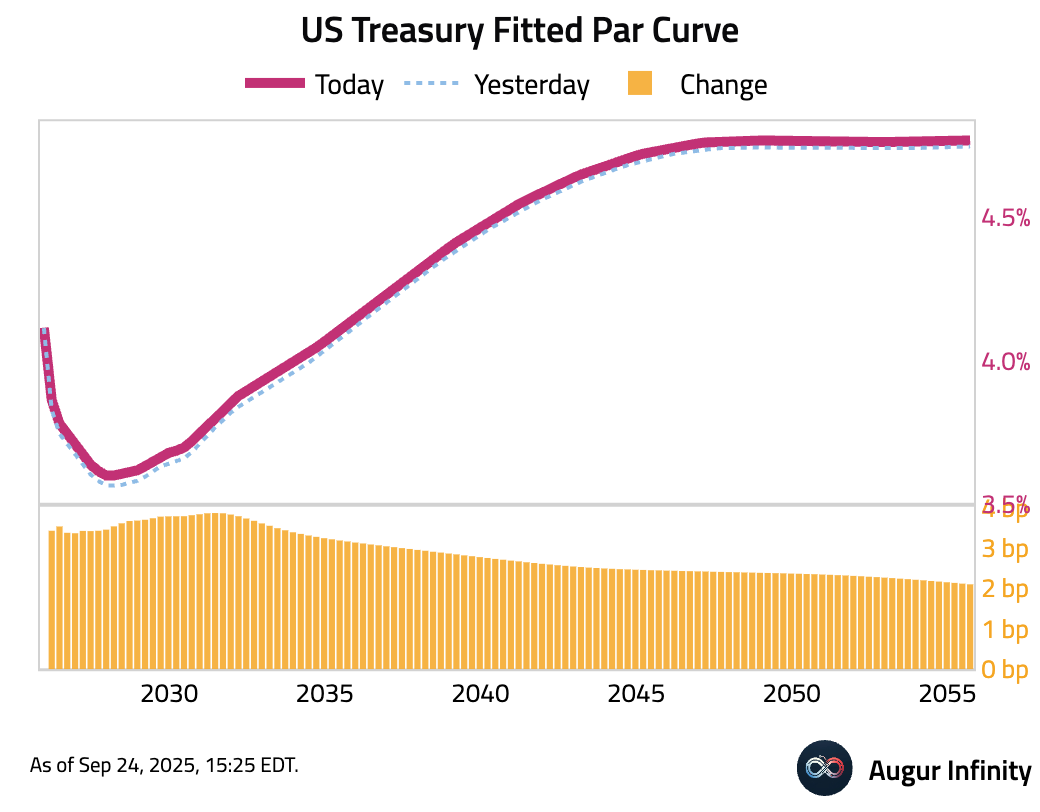

- US Treasury yields rose across the curve. The 2-year yield increased by 3.5 bps, while the 10-year yield climbed 2.7 bps.

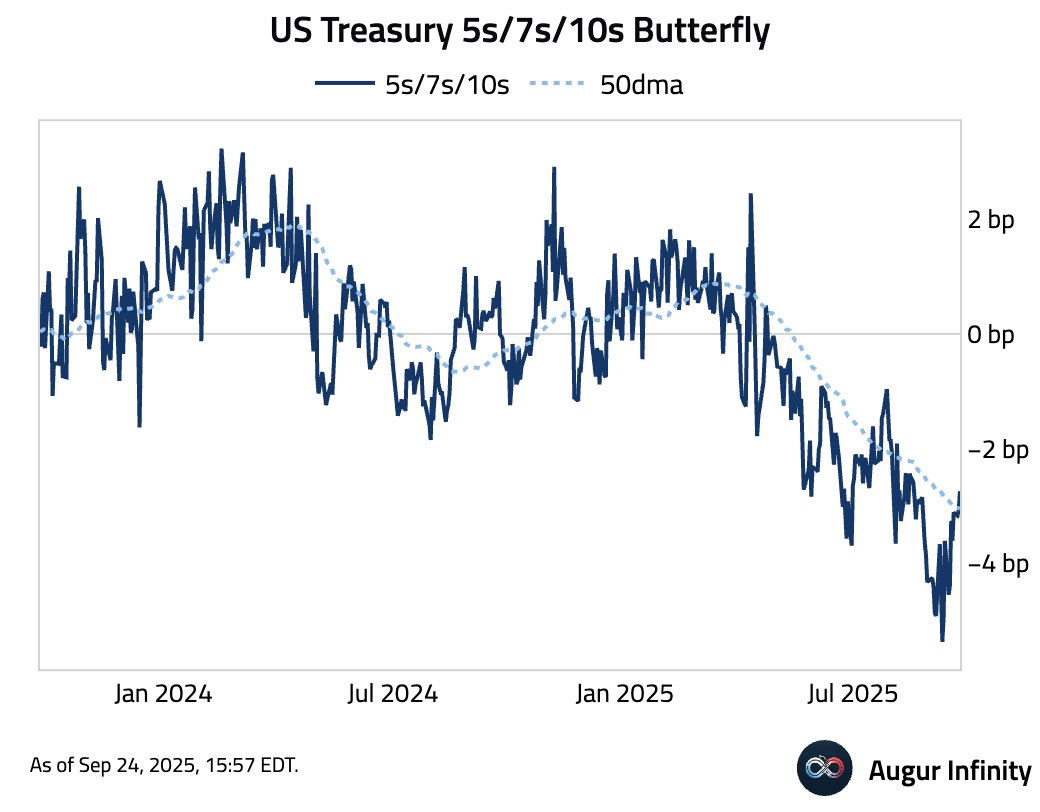

- US Treasury 5s/7s/10s butterfly is now trading above its 50-day moving average.

Commodities

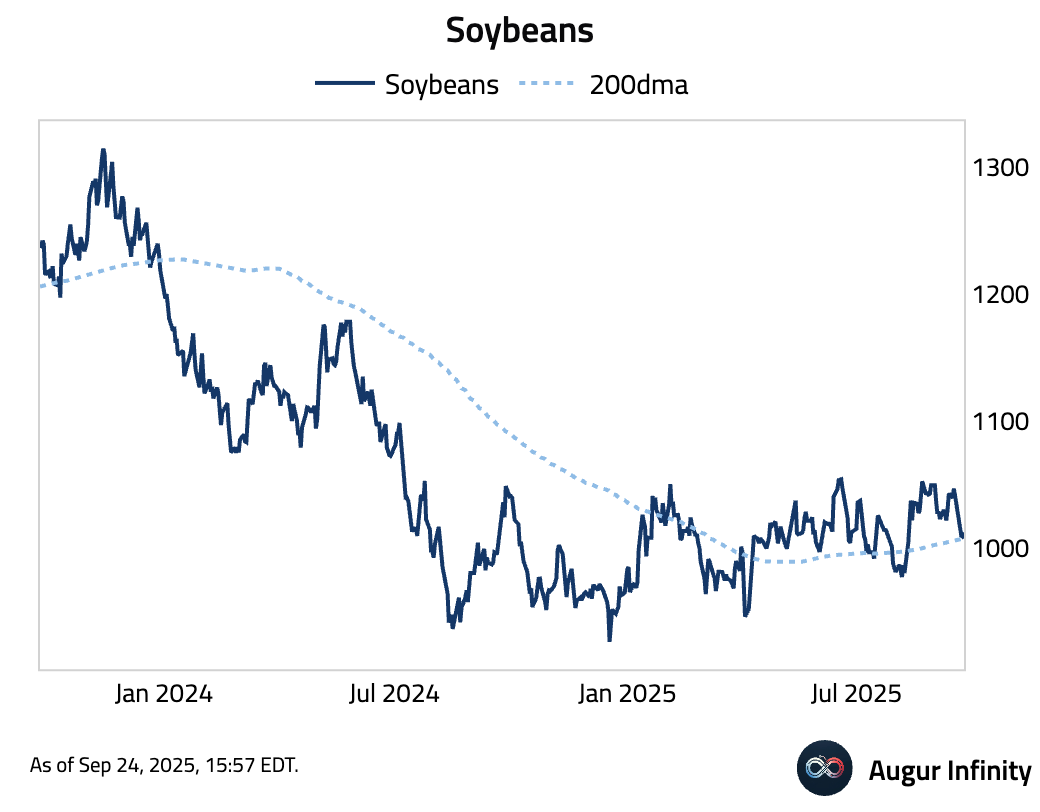

- Soybeans fell below its 200-day moving average.

FX

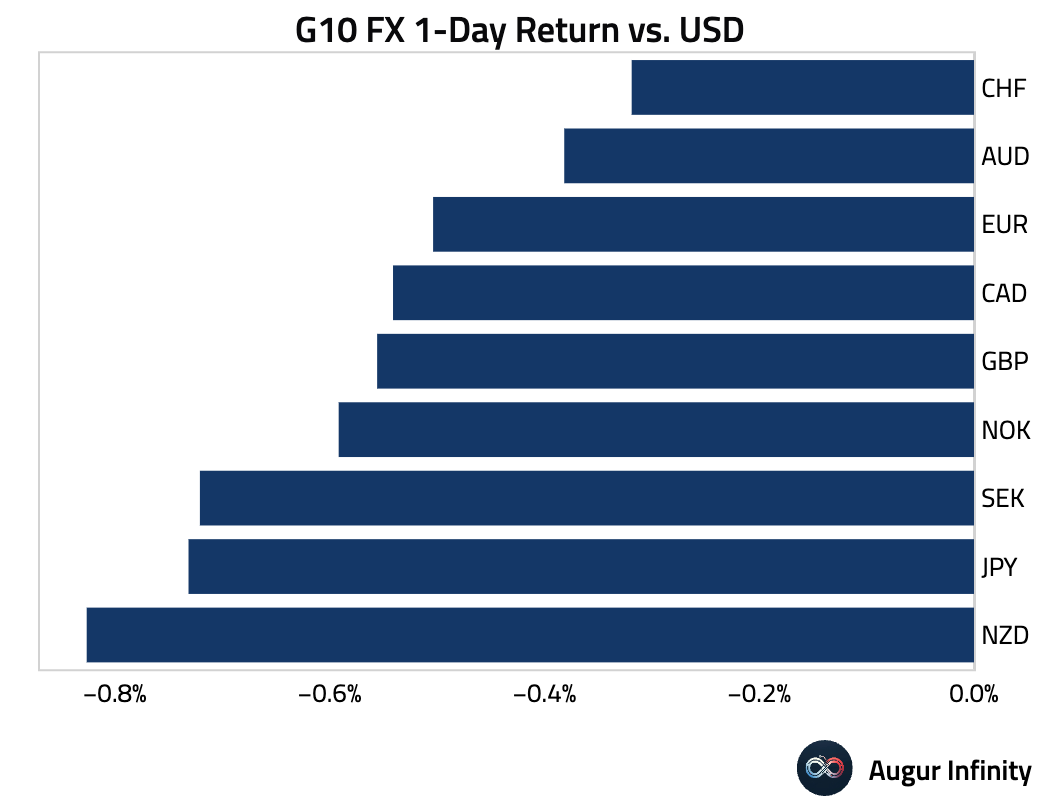

- The US dollar strengthened broadly against its G10 peers amid risk-averse flows. The New Zealand dollar (-0.8%) was the weakest performer, extending its losing streak to six days. The Canadian dollar (-0.5%) also weakened, marking its third consecutive daily decline.

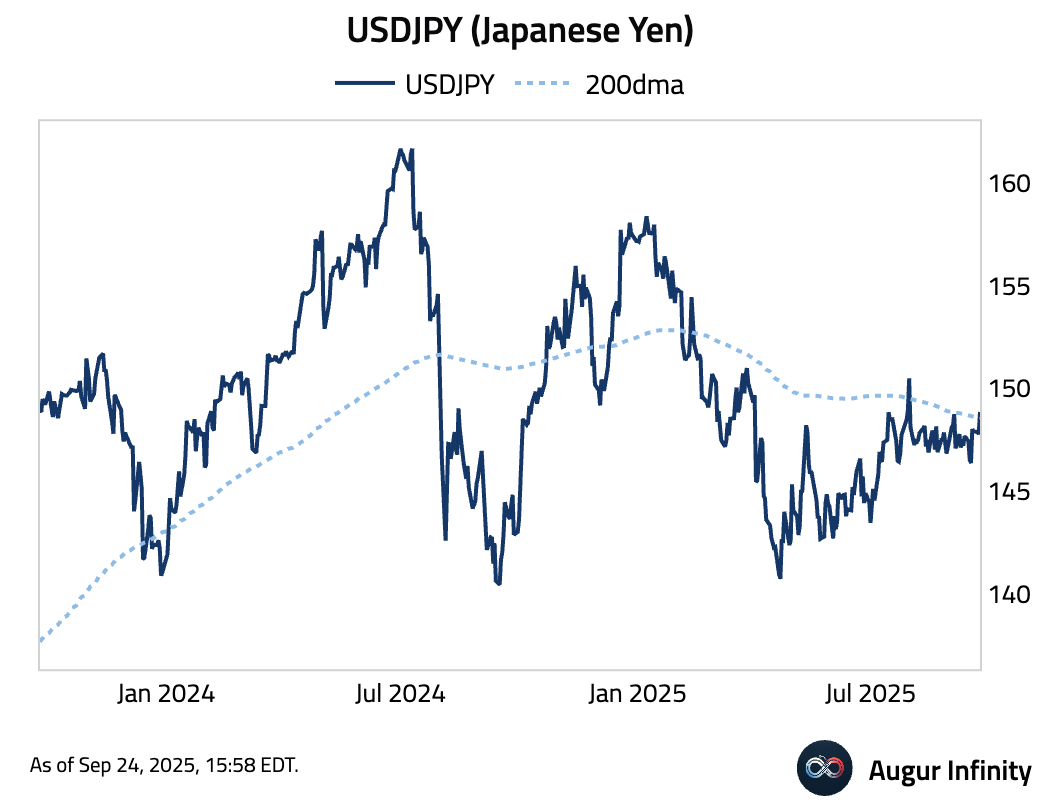

- USDJPY climbed above its 200-day moving average.

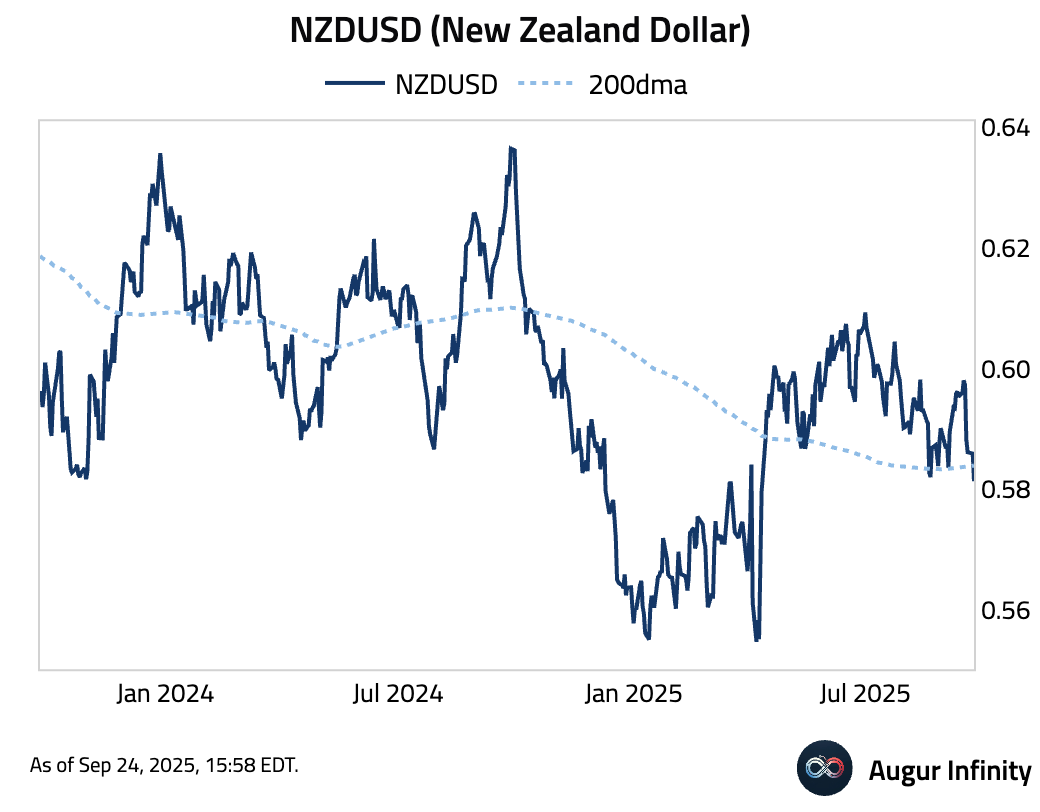

- NZDUSD, by contrast, fell below its 200-day moving average.

- Chinese Yuan depreciated by 0.4% against the dollar today, a 2.4σ move.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.