Headlines

- South Korean officials indicated hesitation in finalizing an investment deal with the United States, seeking the implementation of safeguards like currency swaps before proceeding.

- Japan revealed its intention to reduce the issuance of longer-dated government bonds, signaling a prospective shift in the country’s debt management strategy.

Global Economics

United States

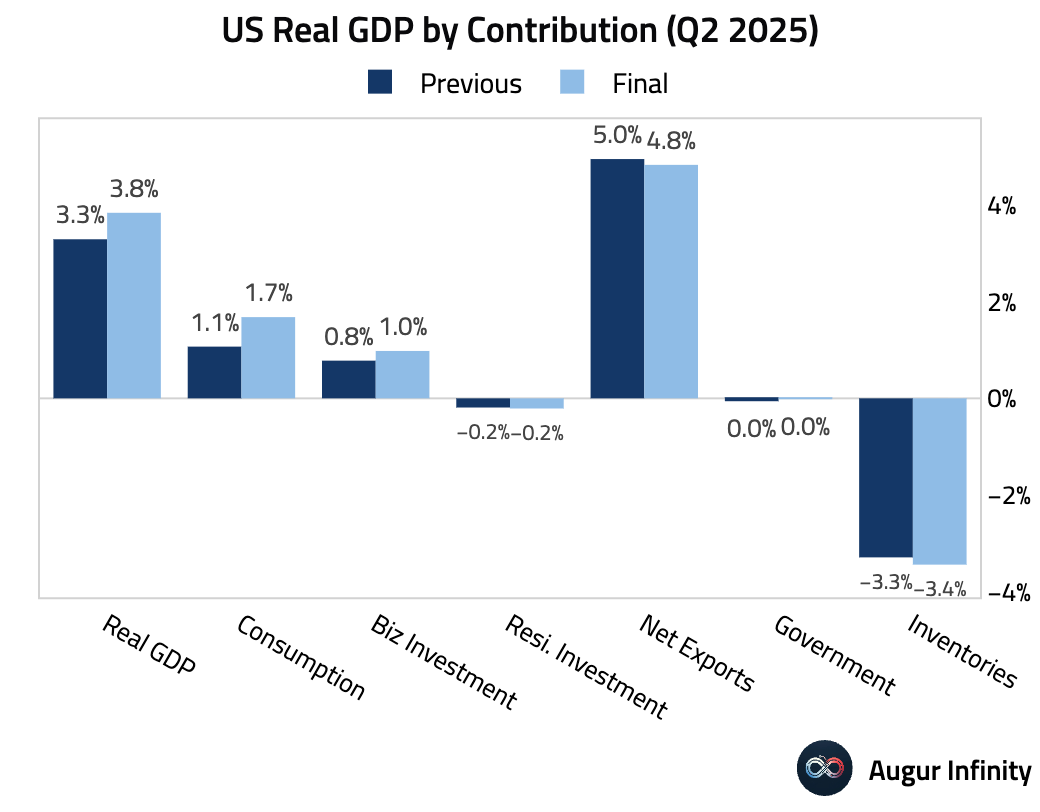

- The final estimate for Q2 GDP was revised up sharply to 3.8% Q/Q SAAR from 3.3%. The surprise was driven by a large upward revision to consumption (+2.5%), particularly in services.

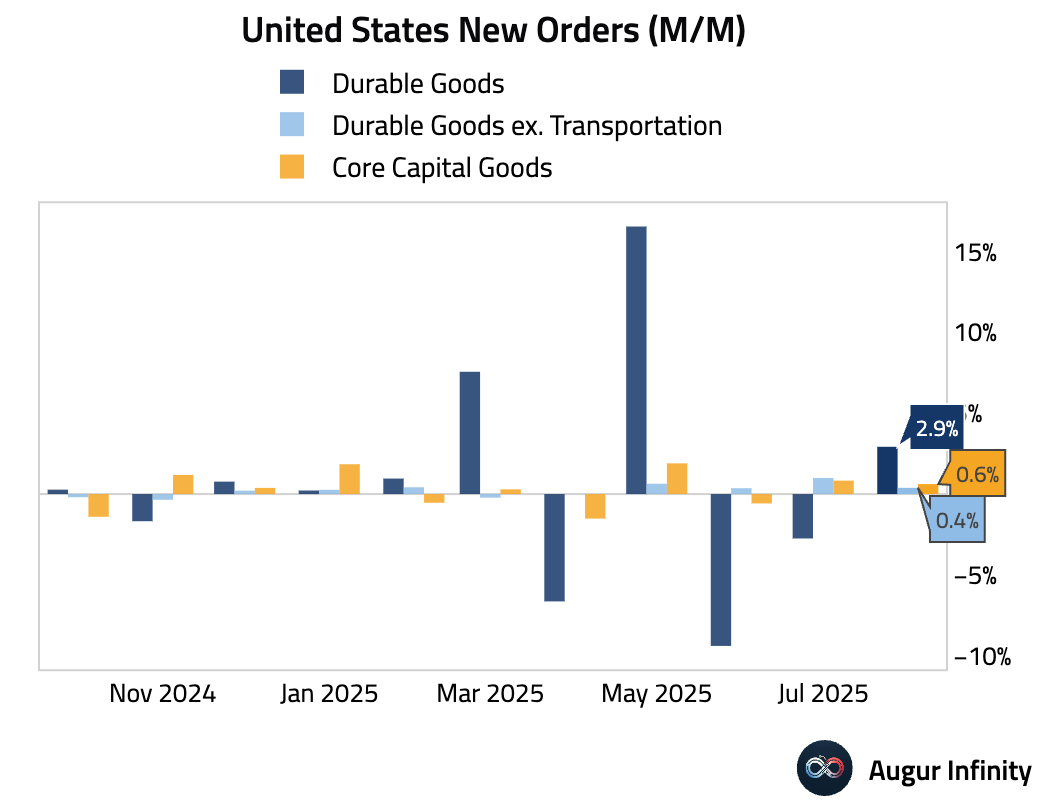

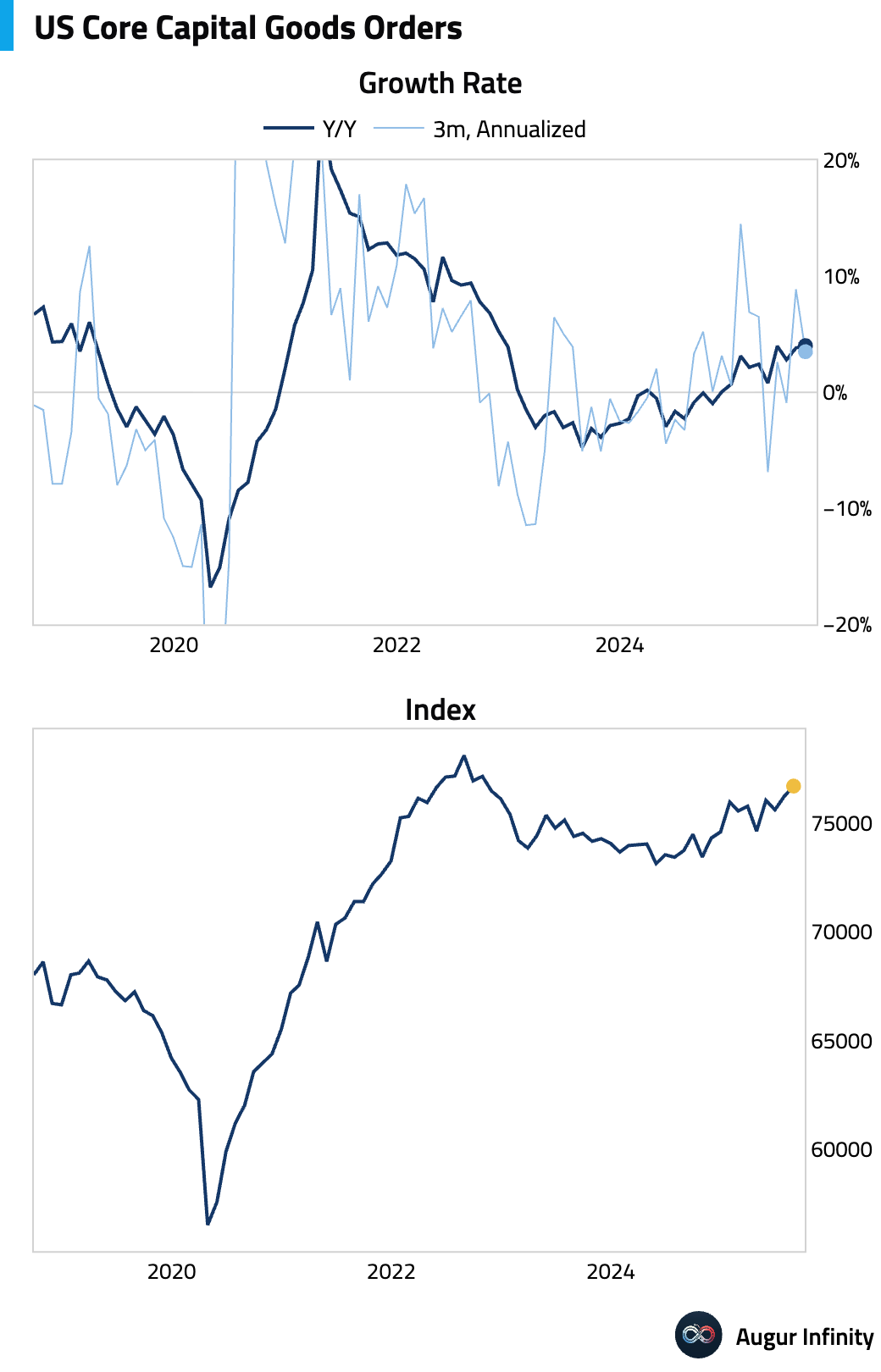

- Durable goods orders surged 2.9% M/M, a massive beat compared to the -0.5% consensus expectation, driven by a rebound in volatile aircraft orders. Core capital goods orders rose by 0.6% and also beating estimates.

- The advance goods trade deficit narrowed significantly, driven by a sharp reversal in imports that was likely an unwind of tariff-related frontloading (act: -$85.5B, est: -$95.7B). However, exports also softened, falling 1.3%, which indicates weaker external demand.

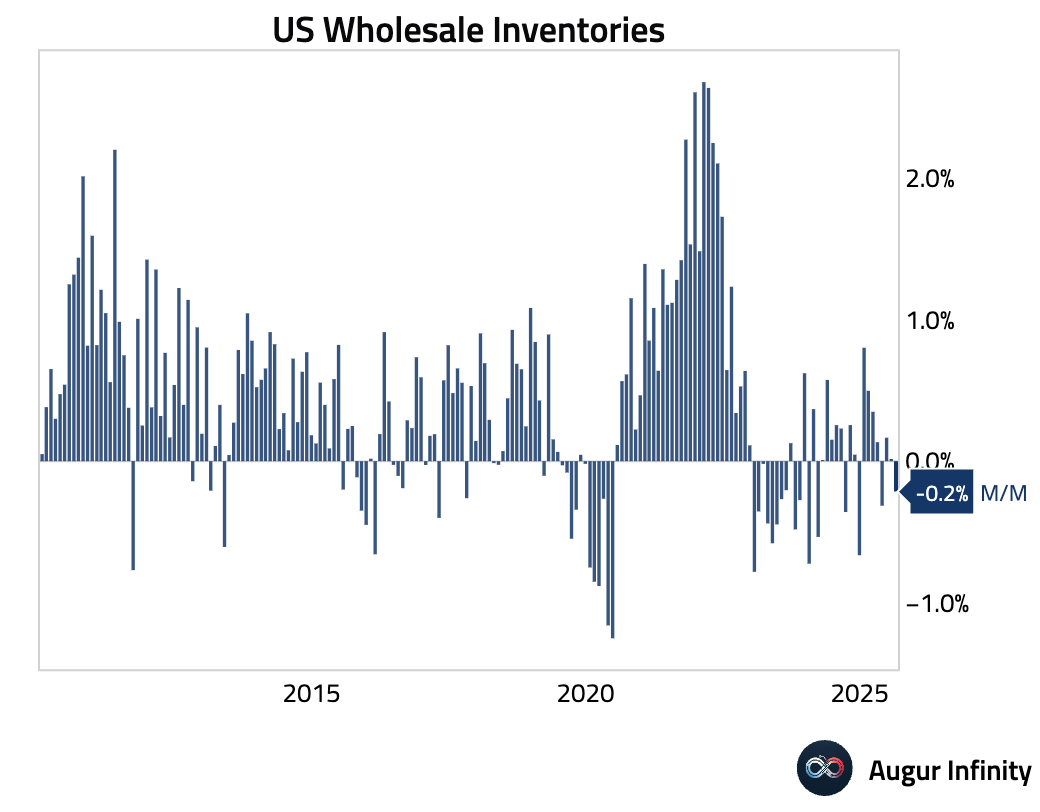

- Wholesale inventories unexpectedly fell in the advance August report (act: -0.2% M/M, est: 0.1%).

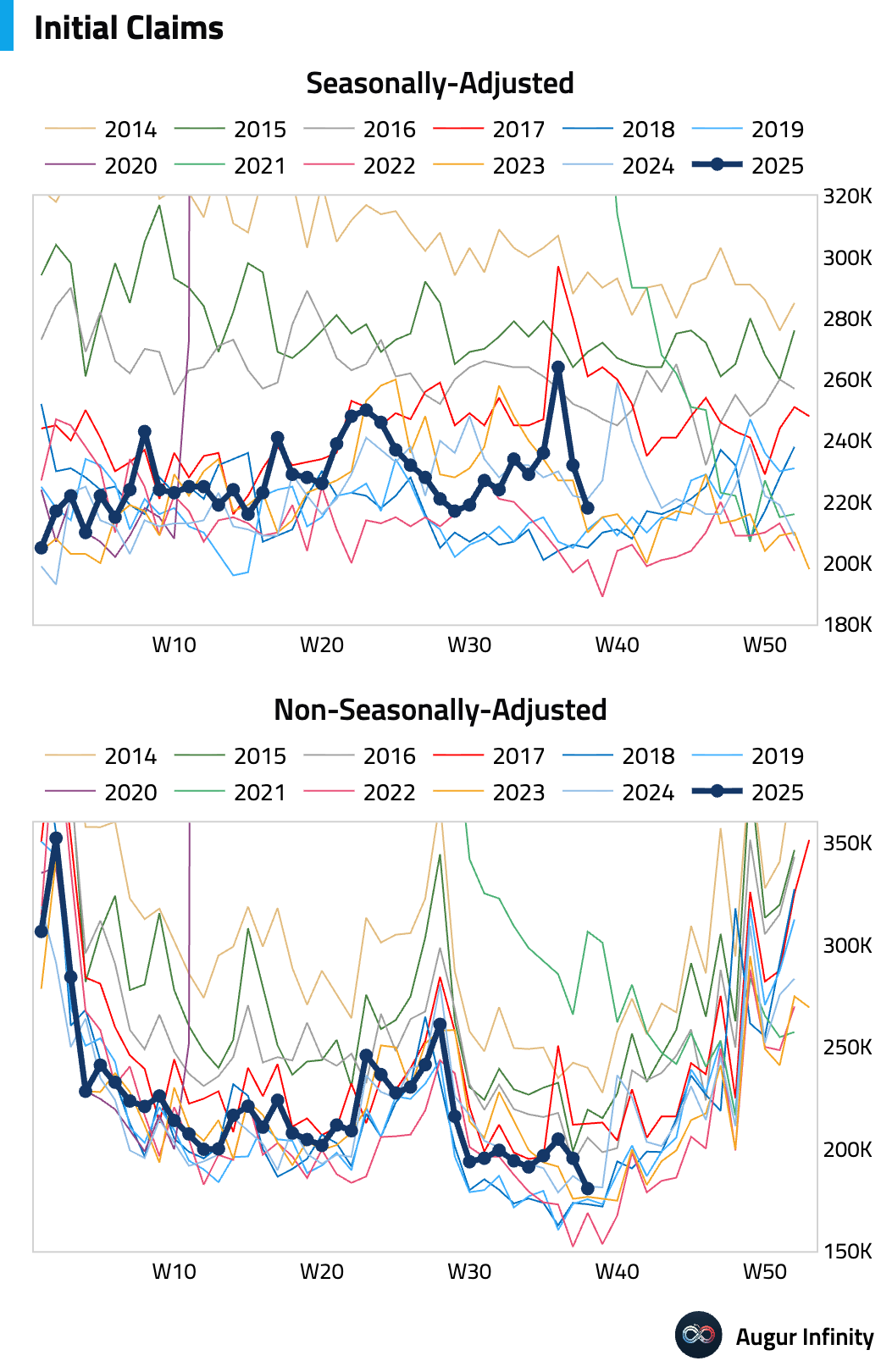

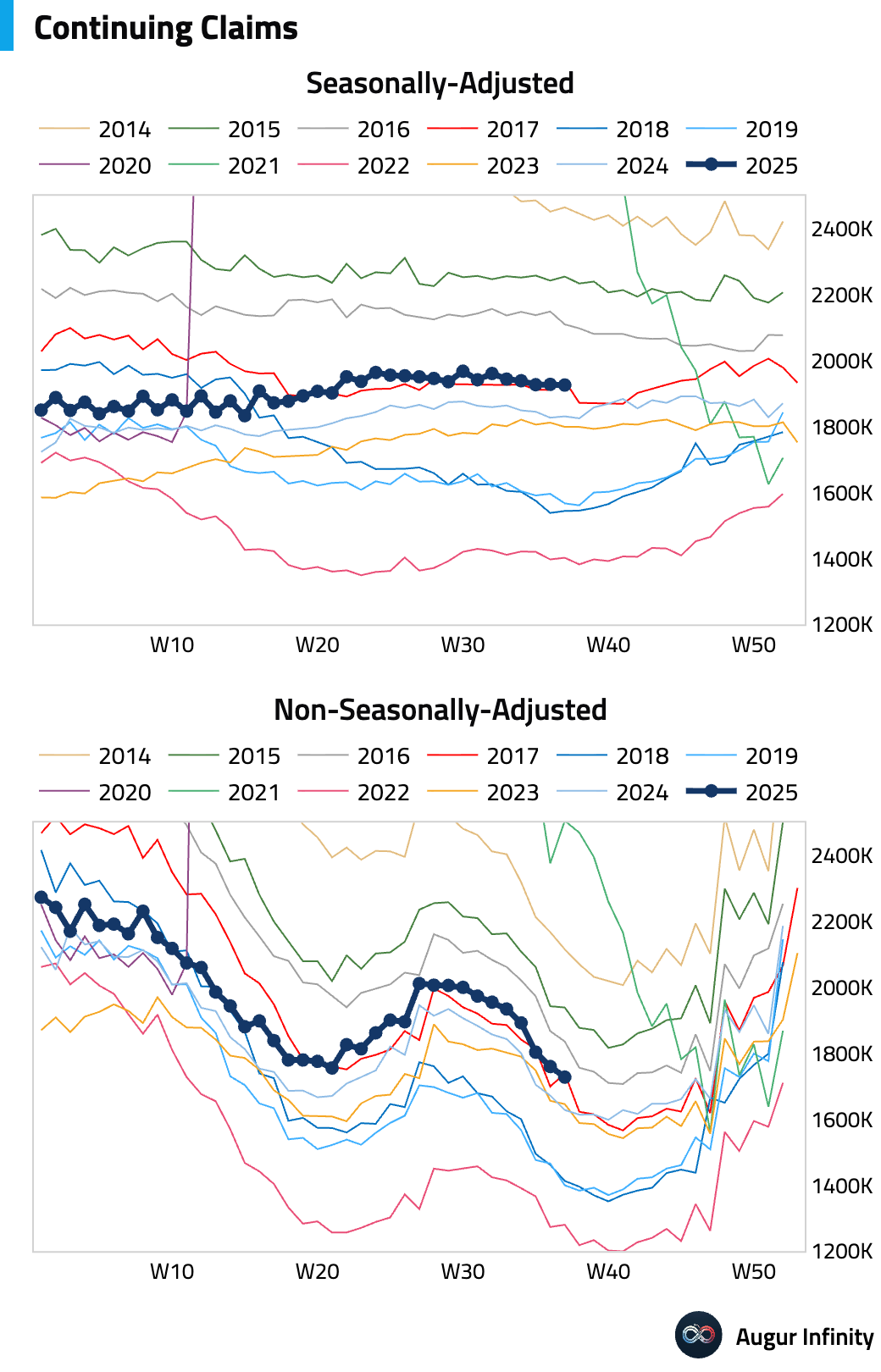

- Initial jobless claims fell to 218k, well below expectations. The decline was partly due to a reversal of recent fraudulent filings in Texas. Note that continuing claims for the prior week were revised higher due to a technical error, slightly tempering the positive headline number.

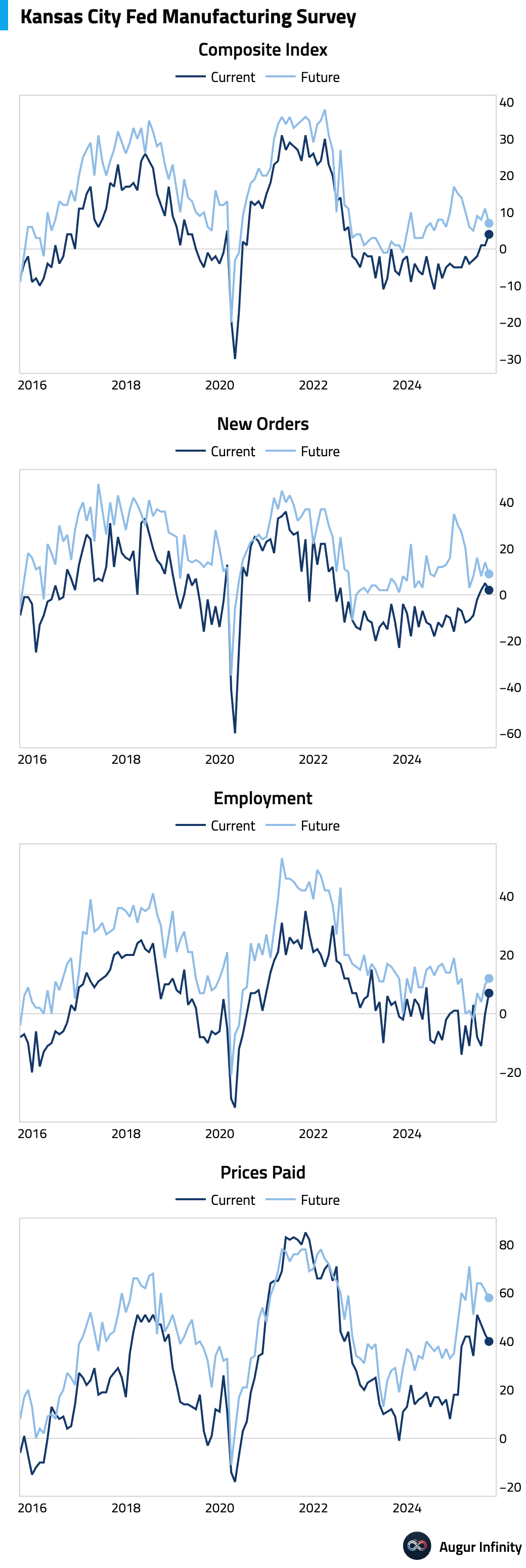

- The Kansas Fed’s composite index returned to expansionary territory for the first time in three years (act: 4, prev: 1).

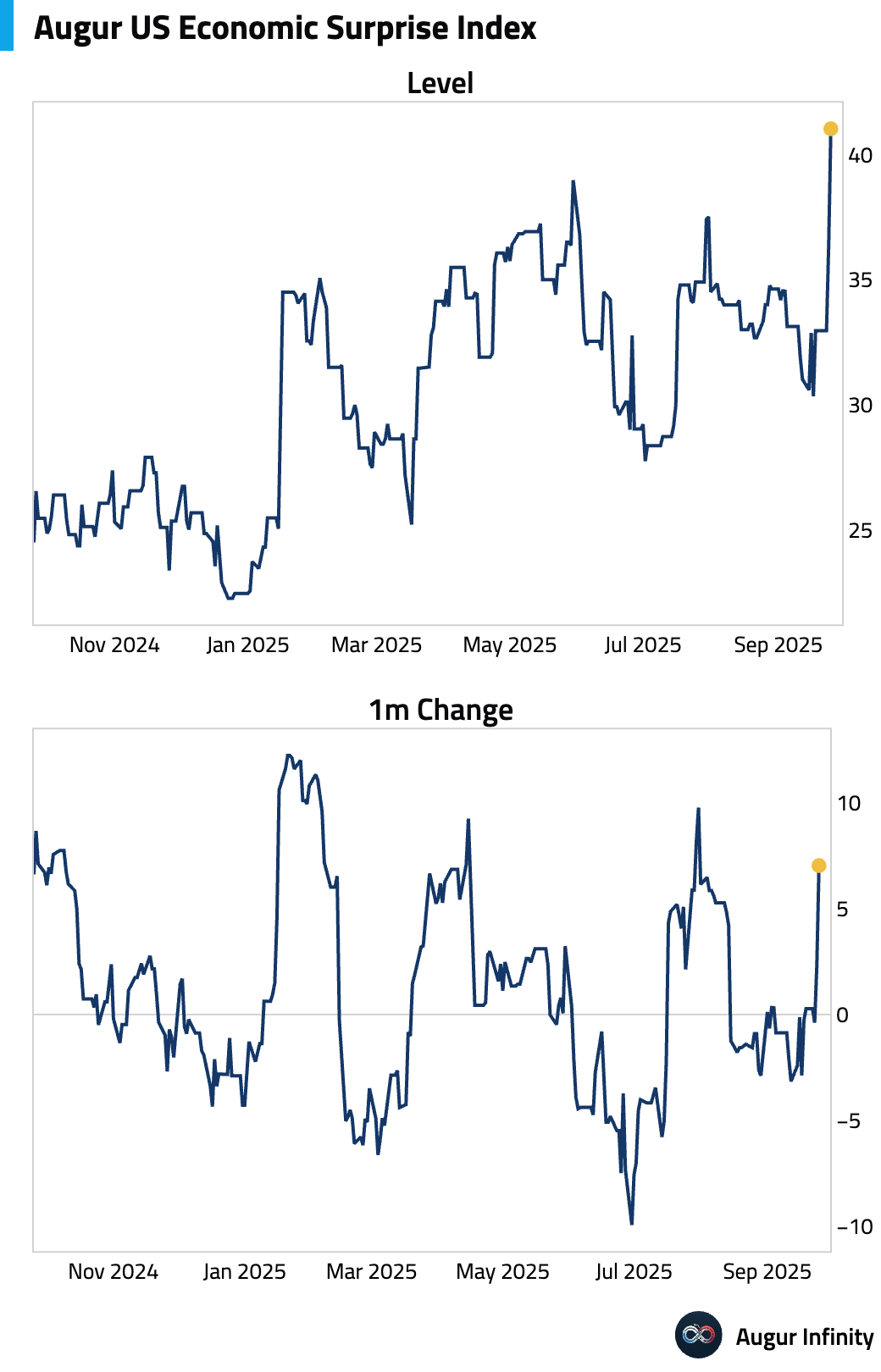

- US growth data meaningfully surprised to the upside over the past few days.

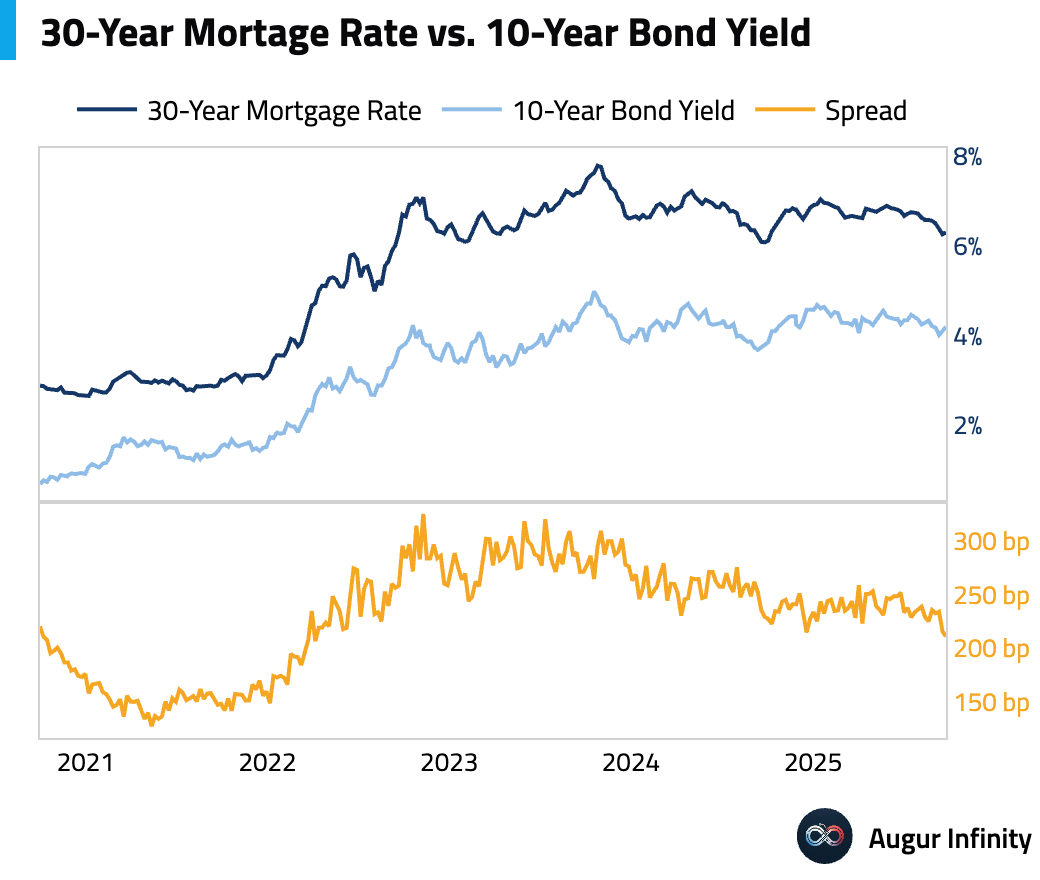

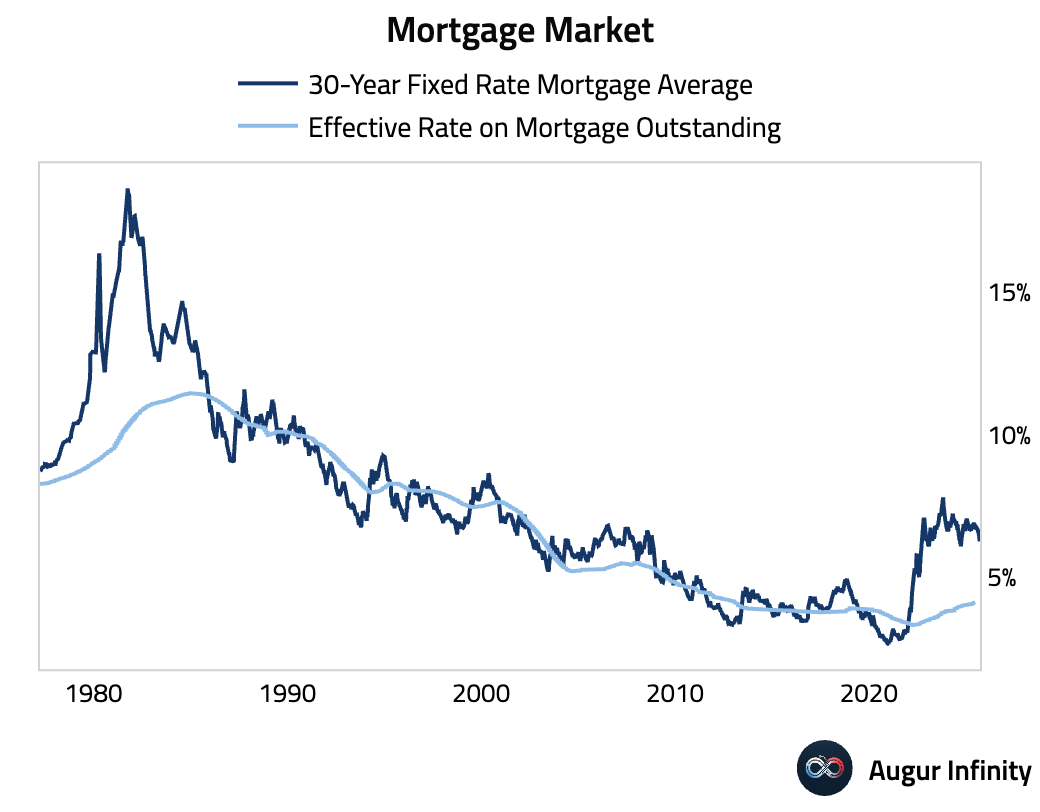

- Mortgage rates continued to climb, with the average 30-year fixed rate rising to 6.30% and the 15-year rate increasing to 5.49%.

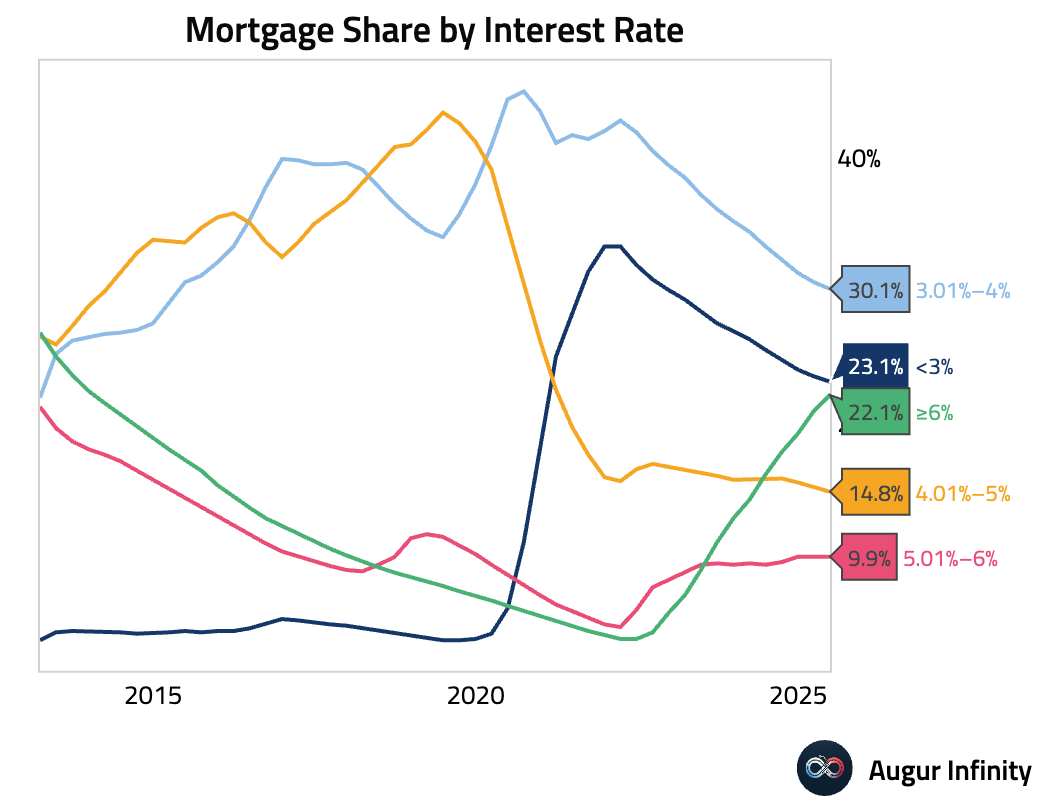

- The share of mortgages with rates above 6% is climbing rapidly.

Canada

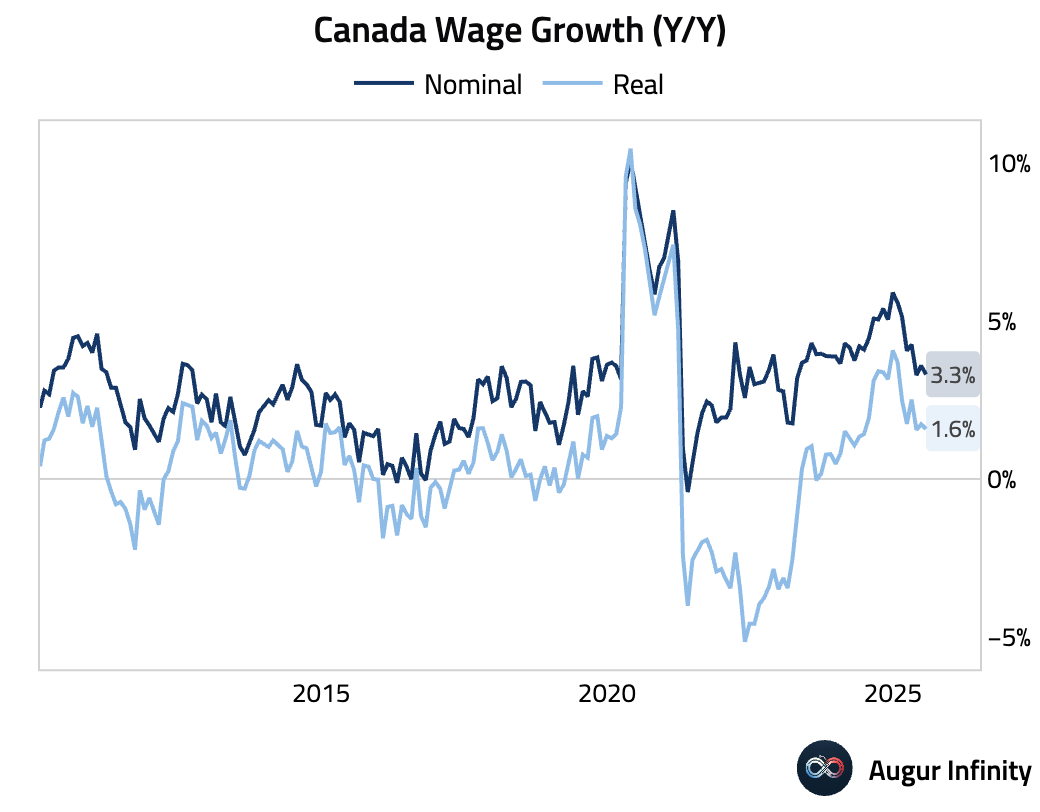

- Growth in average weekly earnings decelerated to 3.3% Y/Y from a revised 3.6% in the prior month.

Europe

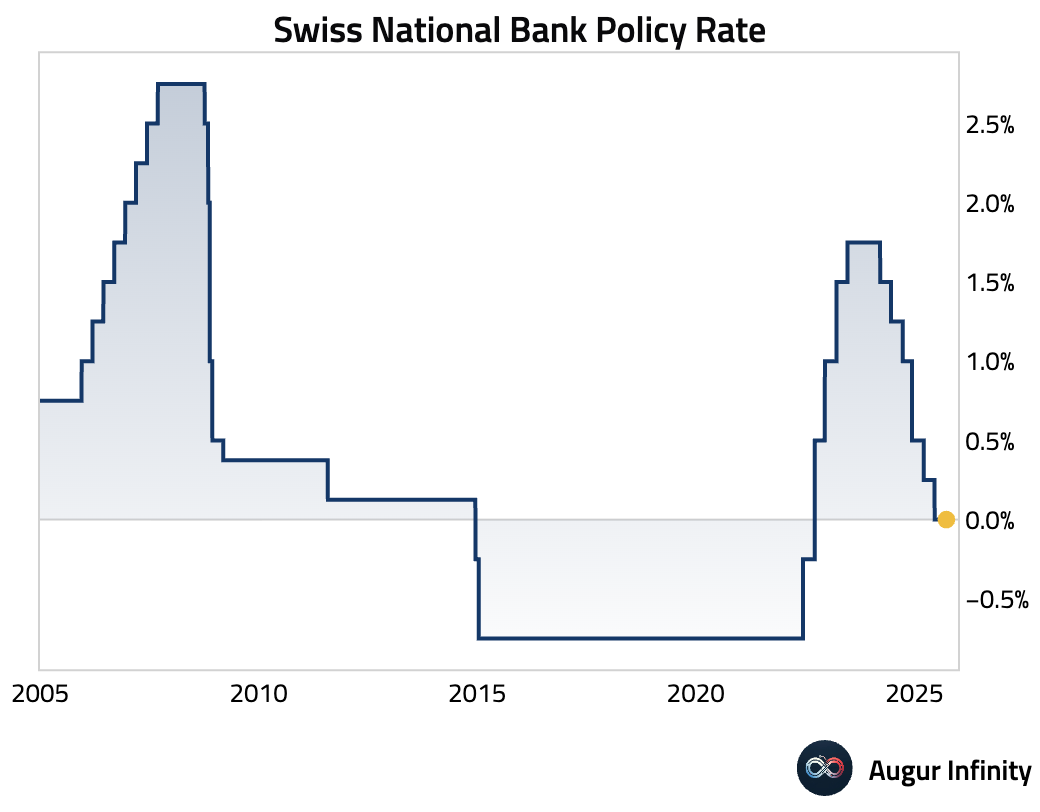

- The Swiss National Bank held its policy rate at 0.0%, as expected. The decision was driven by slightly higher near-term inflation forecasts, though the 2026 GDP growth outlook was downgraded. SNB Chair Schlegel signaled a high bar for a cut into negative territory, reinforcing expectations of a prolonged hold. In a move toward greater transparency, the SNB will begin publishing meeting minutes next month.

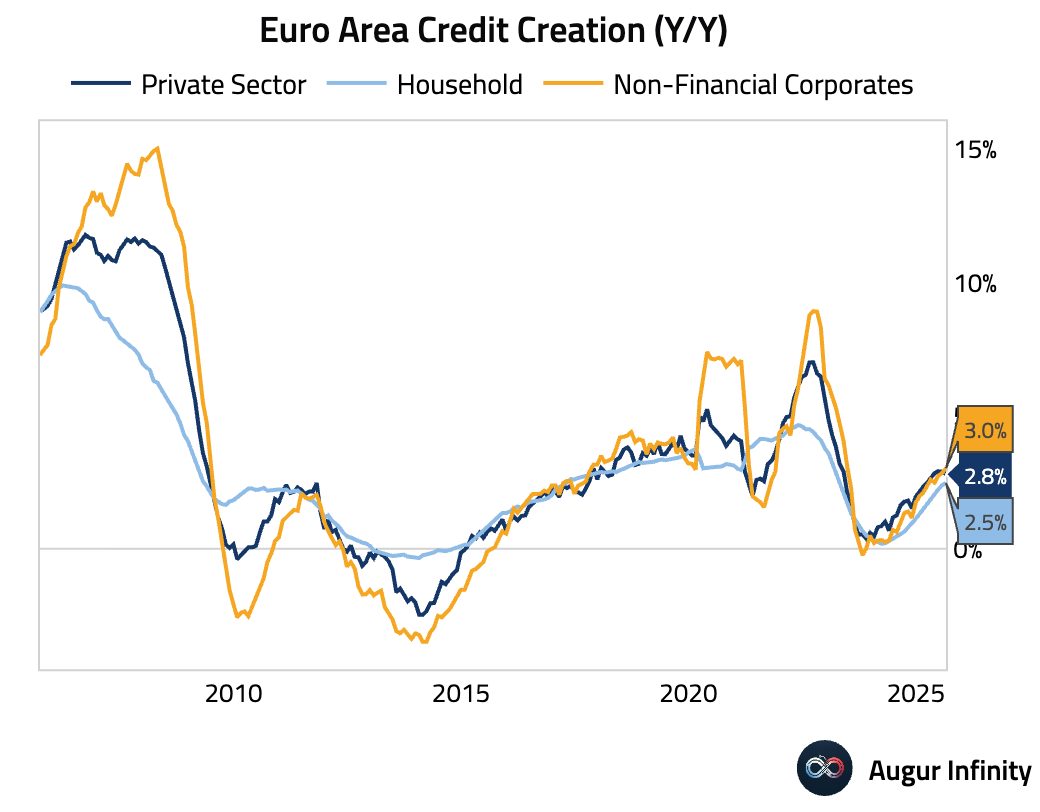

- Eurozone credit creation accelerated slightly in August, with annual growth in loans to companies rising to 3.0% and loans to households picking up to 2.5%.

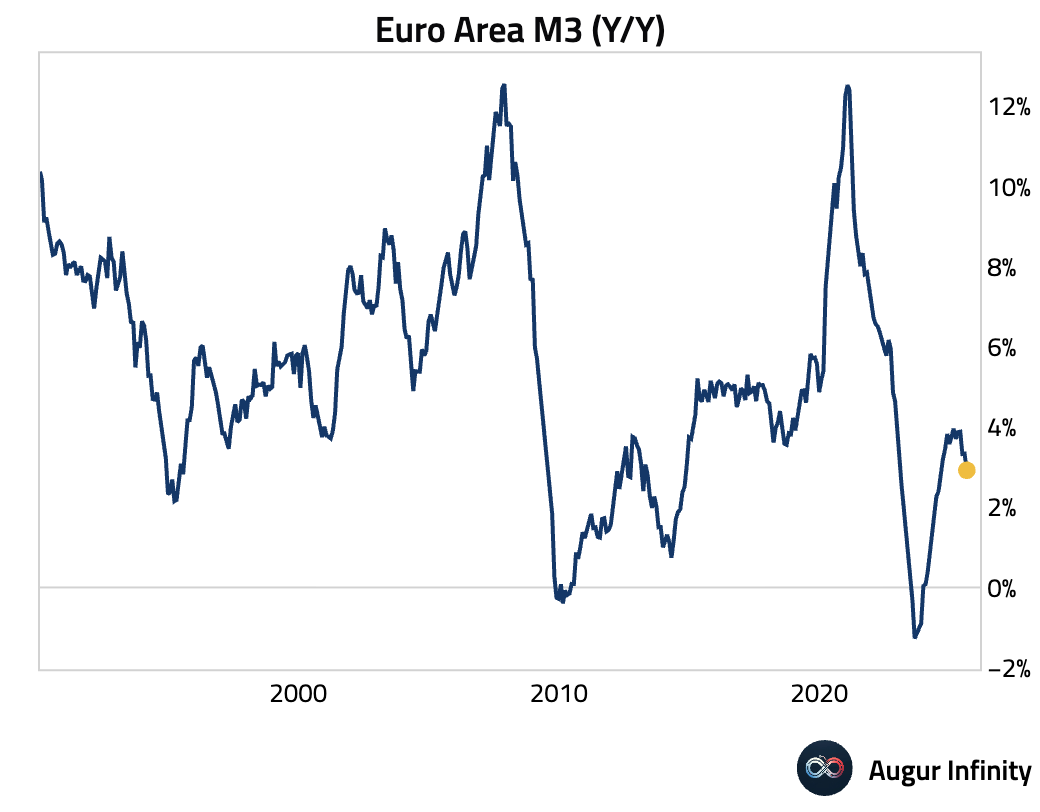

- Eurozone M3 money supply growth decelerated to 2.9% Y/Y, below consensus of 3.3%, reaching its lowest level in over a year.

- German GfK consumer confidence improved slightly but remained deeply pessimistic at -22.3, though this was better than the consensus forecast of -23.3.

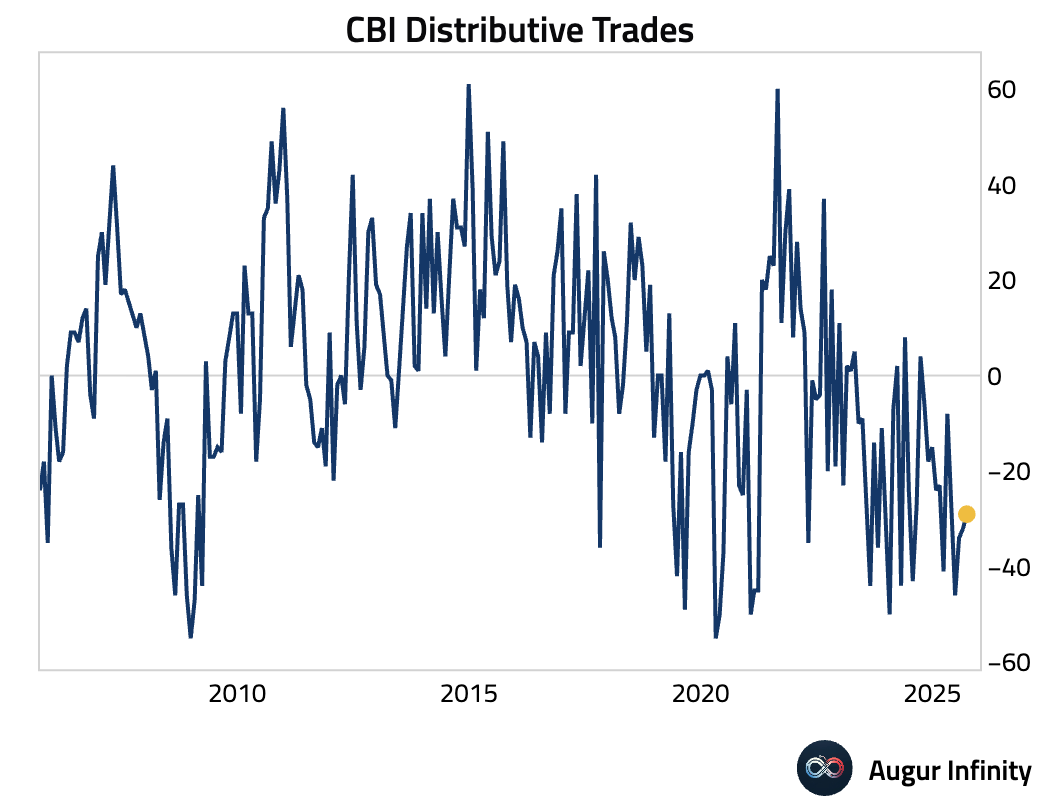

- The UK’s CBI Distributive Trades survey showed a slight improvement but remained deeply in contractionary territory, indicating a continued sharp decline in retail sales volumes (act: -29, est: -26).

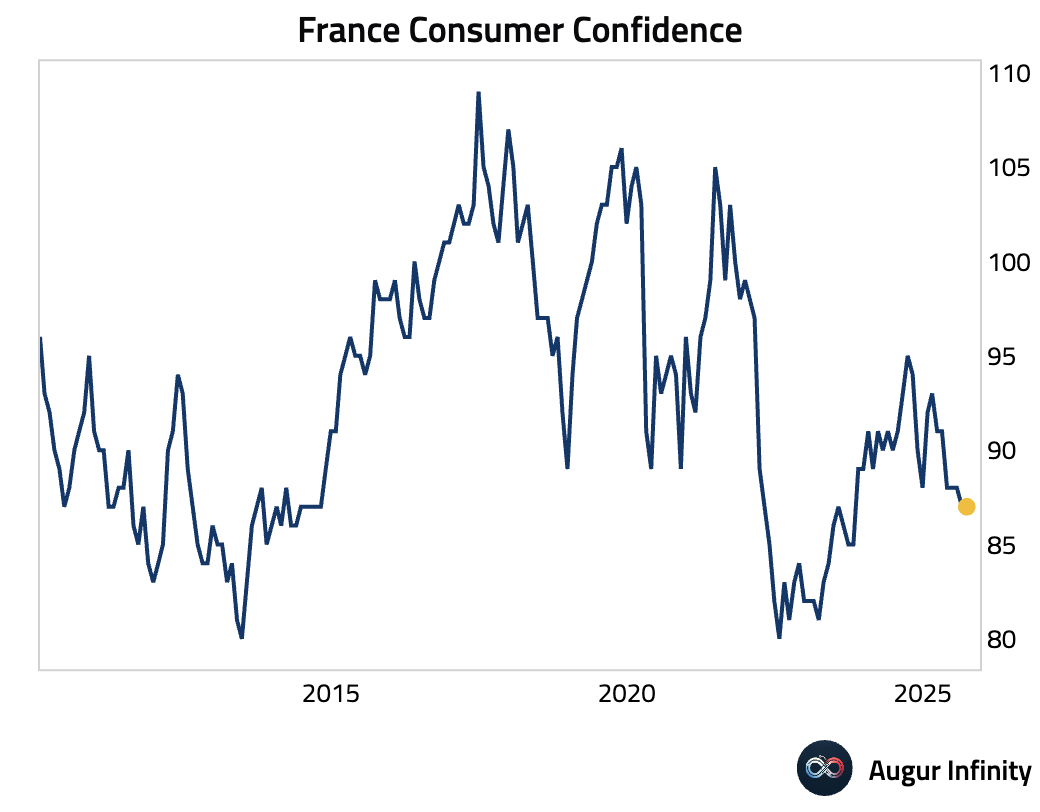

- French consumer confidence was unchanged and in line with expectations, remaining well below its long-term average (act: 87, est: 87).

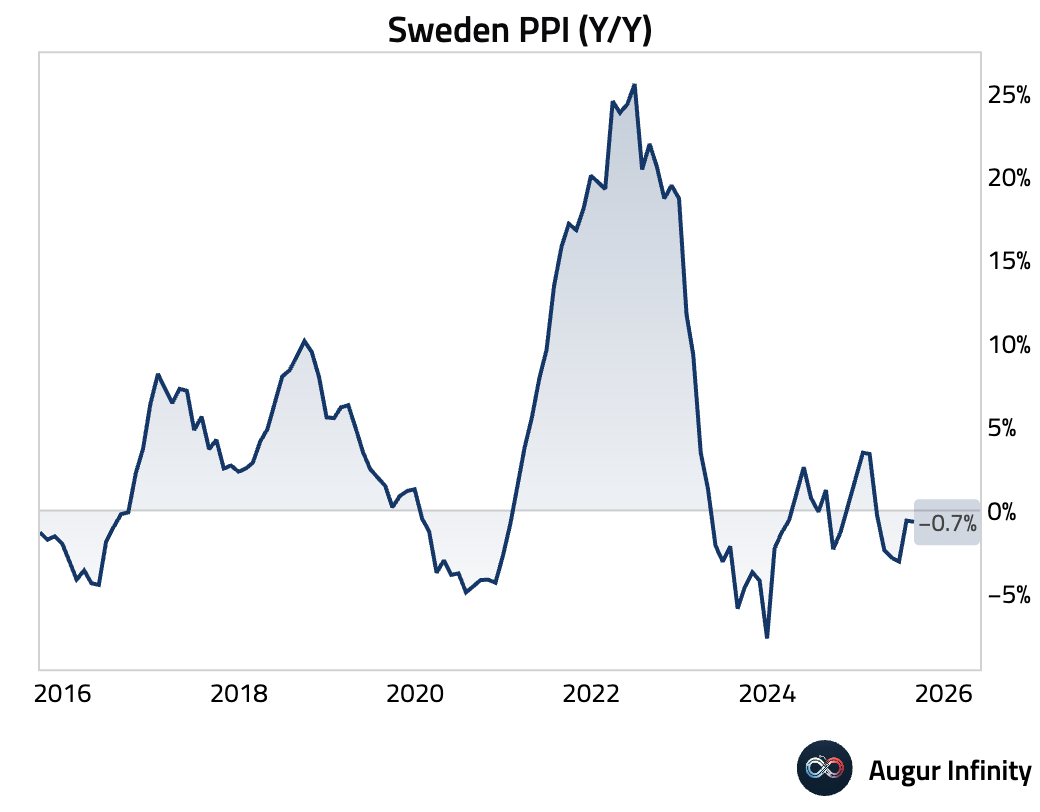

- Swedish producer prices rose 0.5% M/M, but the annual rate of deflation deepened to -0.7% Y/Y.

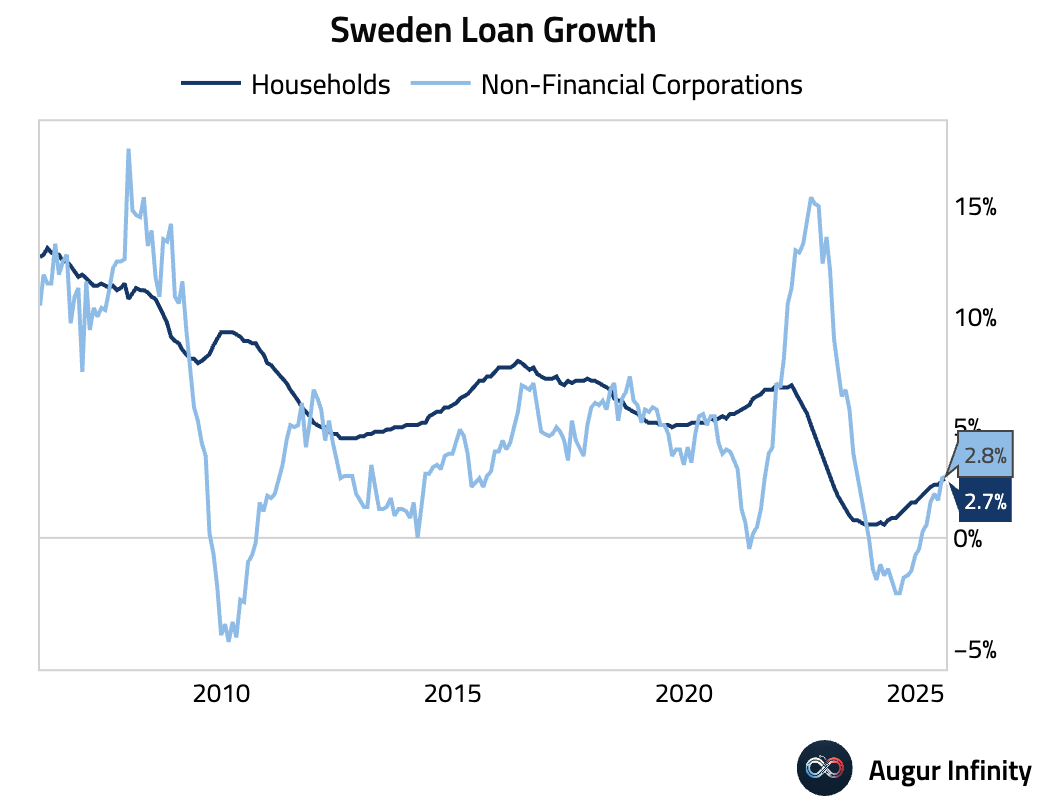

- Swedish household lending growth picked up to 2.7% Y/Y, its fastest pace in over two years.

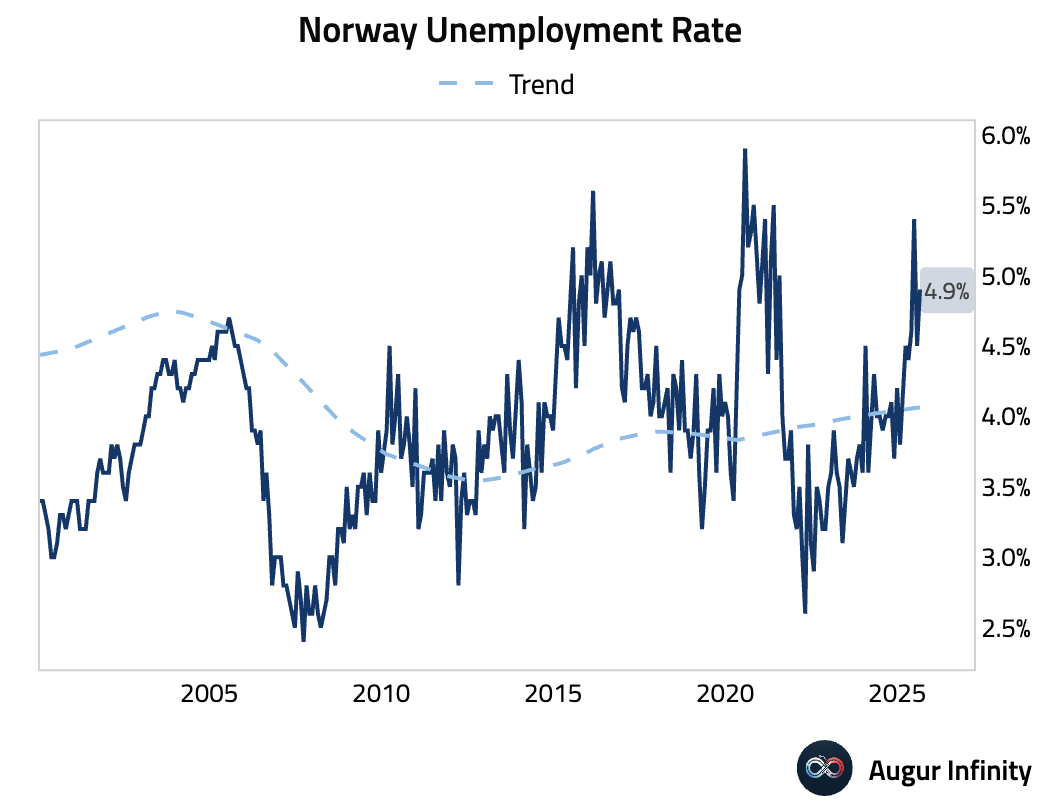

- Norway’s unemployment rate edged higher to 4.9% from 4.5%.

Asia-Pacific

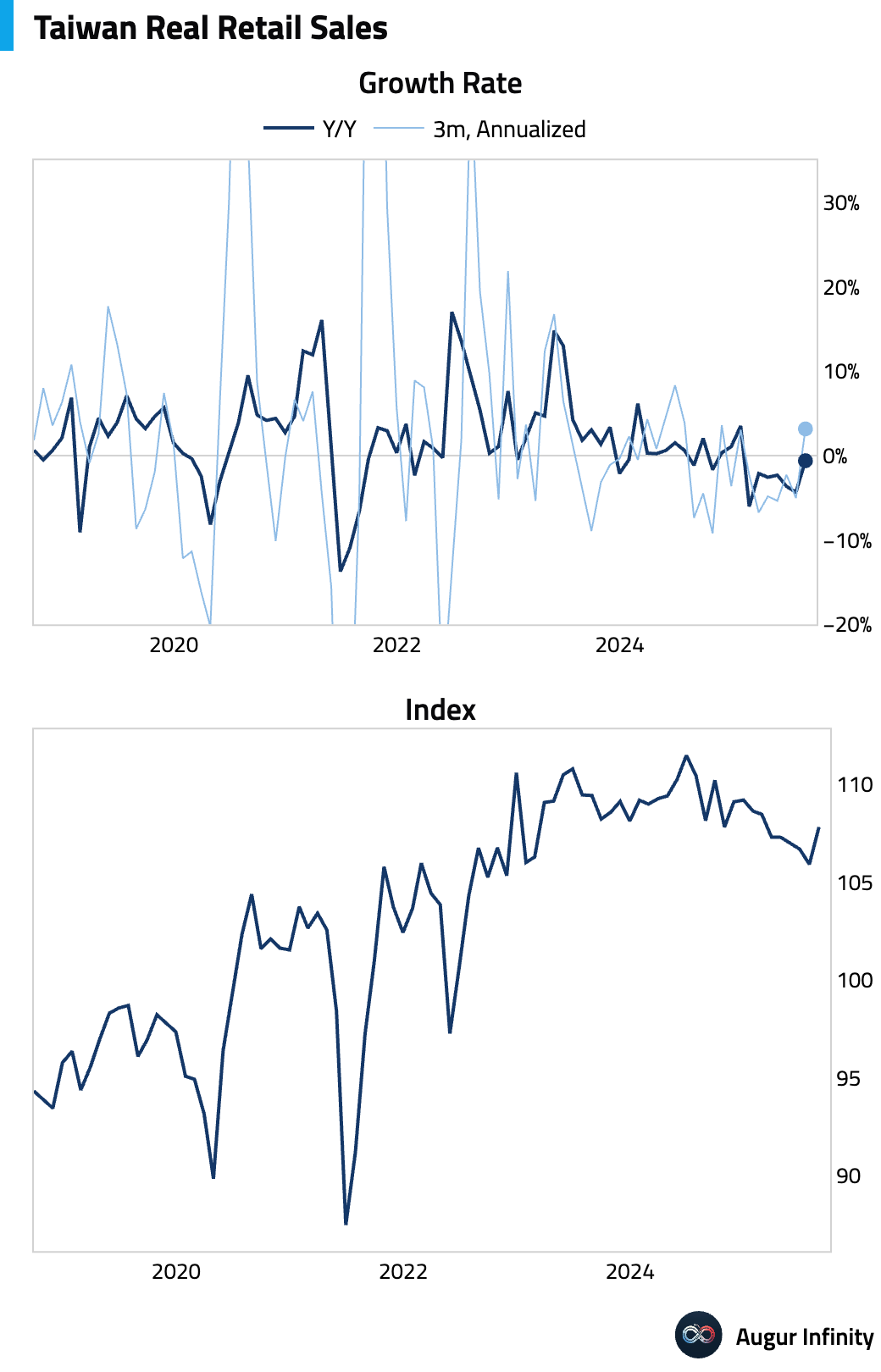

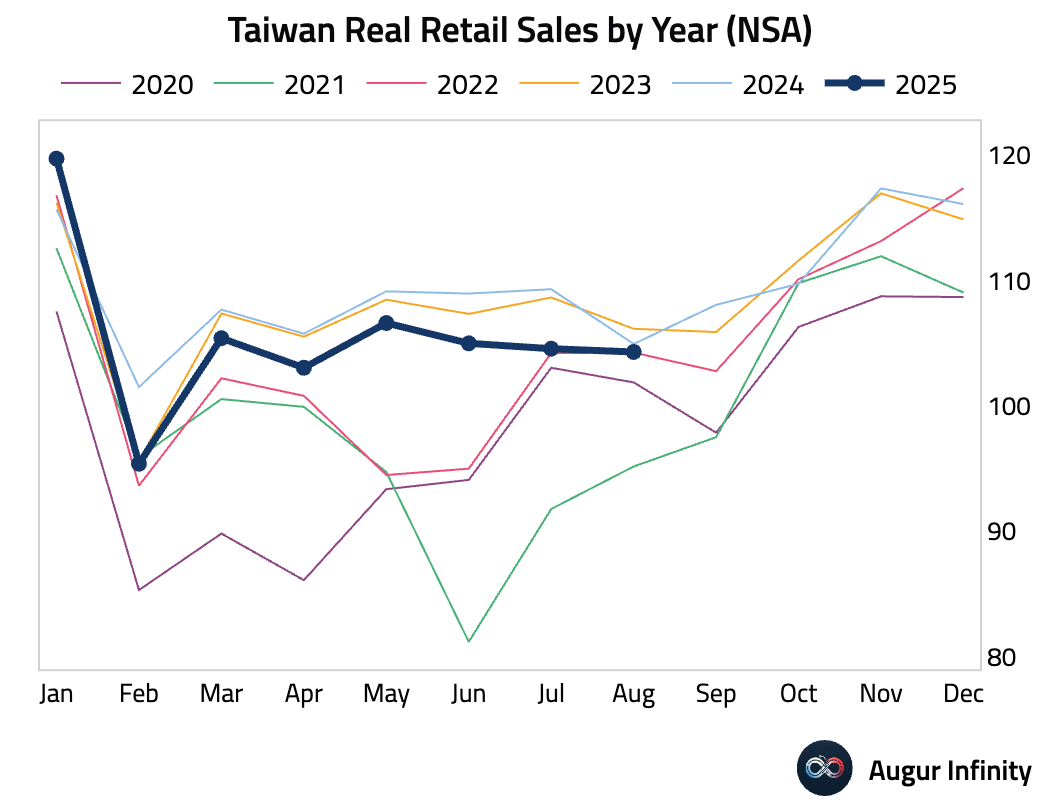

- Taiwan’s retail sales rebounded, growing 0.4% Y/Y after contracting by 3.6% in the prior month.

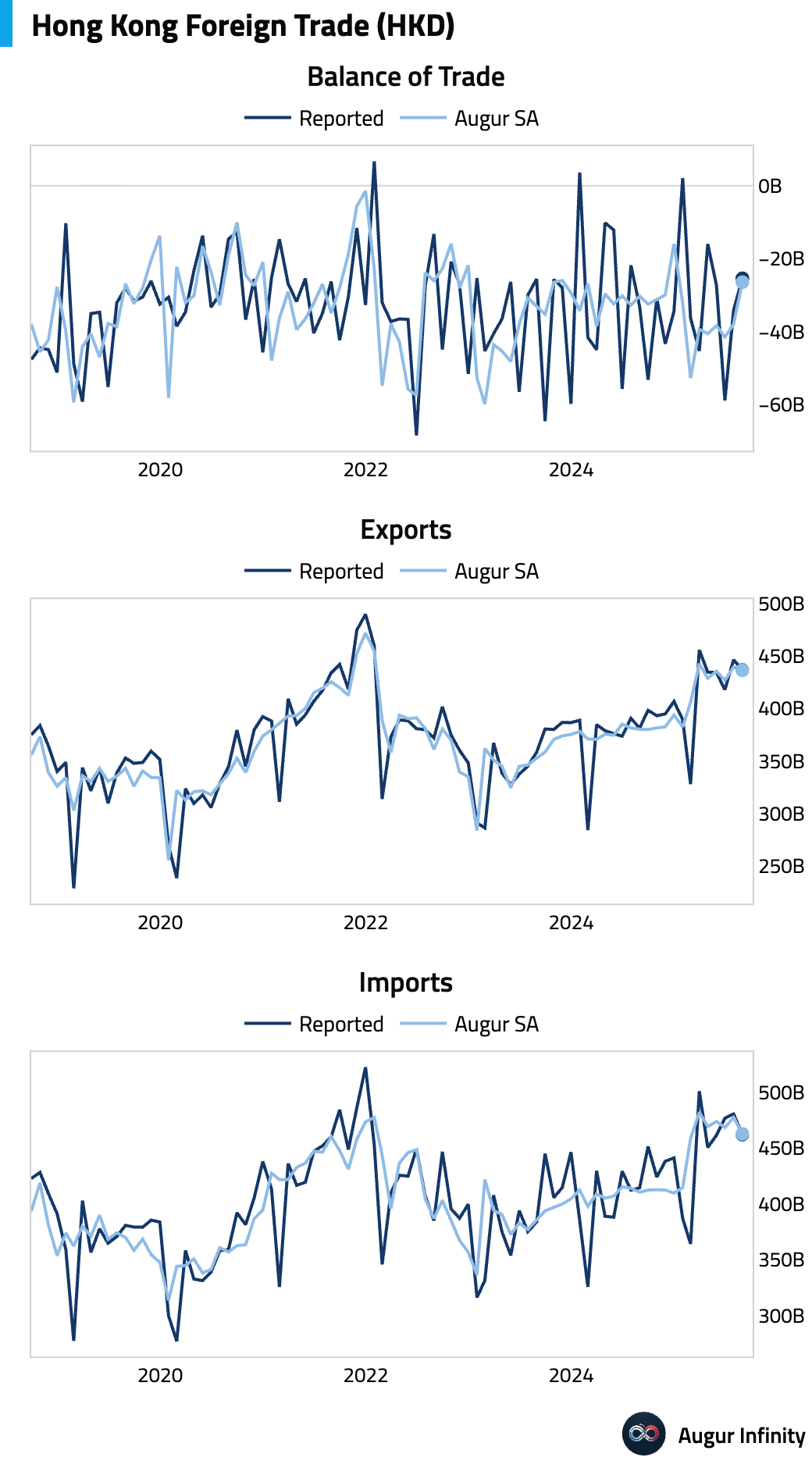

- Hong Kong’s trade deficit narrowed as export growth edged up to 14.5% Y/Y while import growth moderated to 11.5% Y/Y.

Emerging Markets ex China

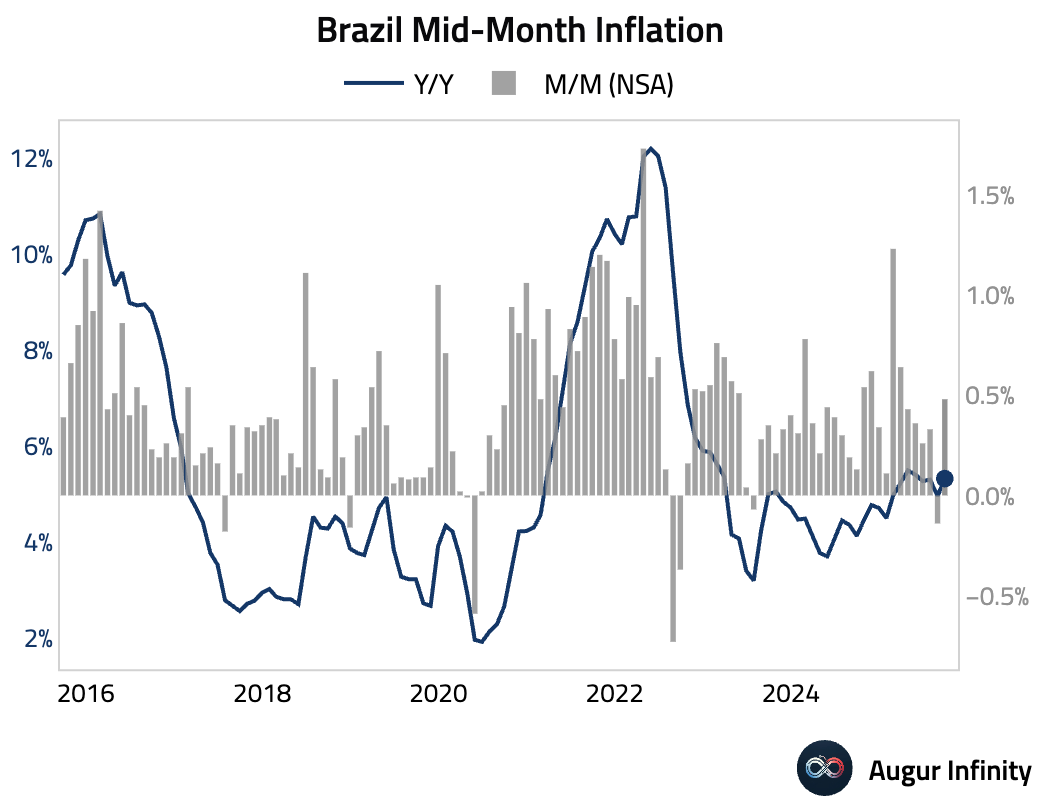

- Brazil’s mid-month IPCA inflation came in at 0.48% M/M, slightly below consensus, bringing the annual rate to 5.32% Y/Y. The miss was driven by a fading seasonal impact from school tuition and an unexpected drop in airfares, partially offset by a spike in electricity tariffs.

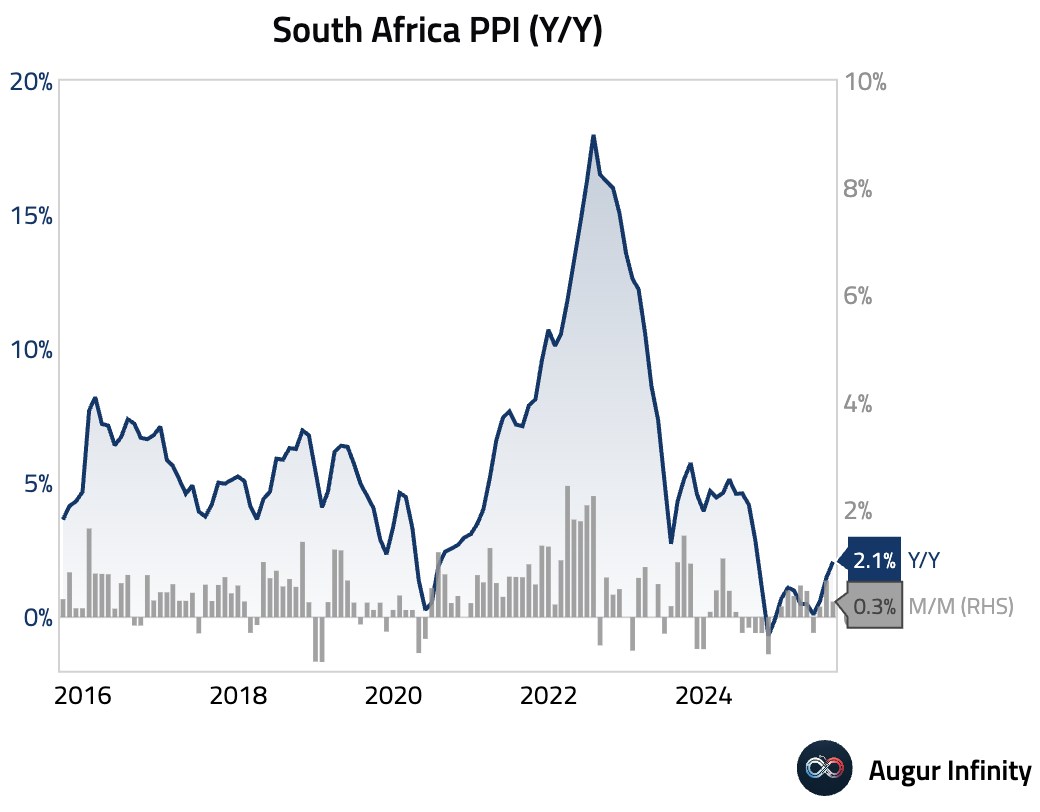

- South African producer price inflation accelerated more than expected, with the annual rate jumping to 2.1% Y/Y from 1.5%, well above the 1.8% consensus.

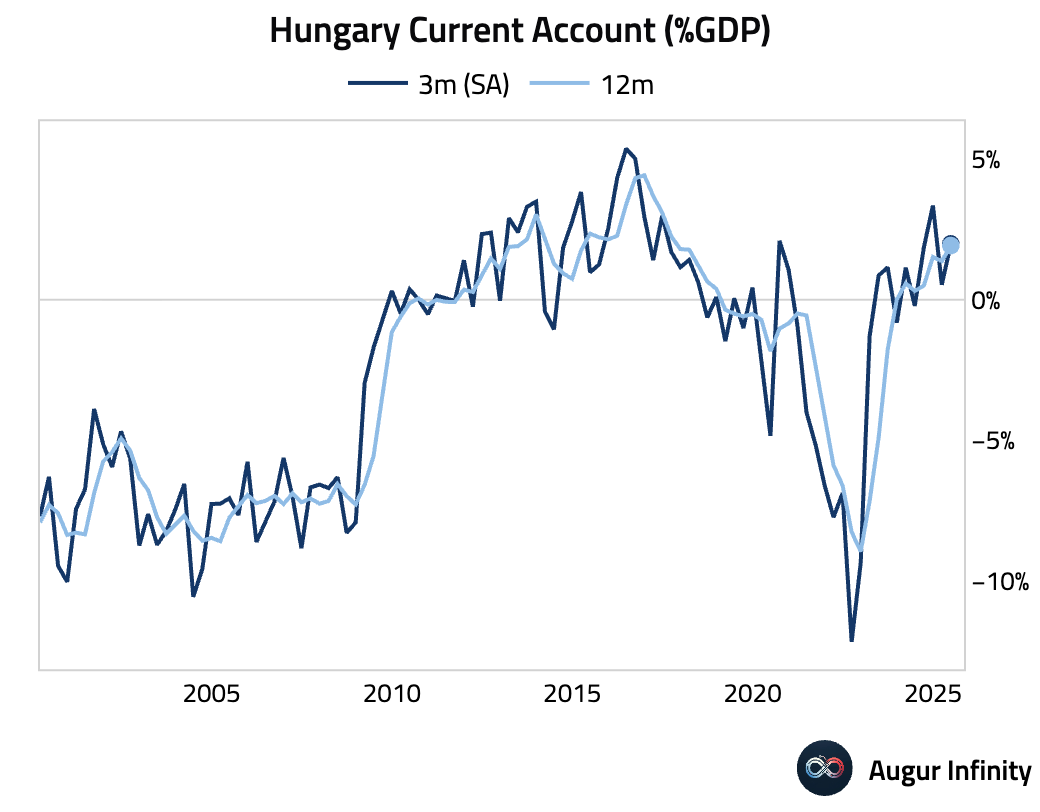

- Hungary's current account surplus widened more than expected in the second quarter (act: €1.39B, est: €0.80B).

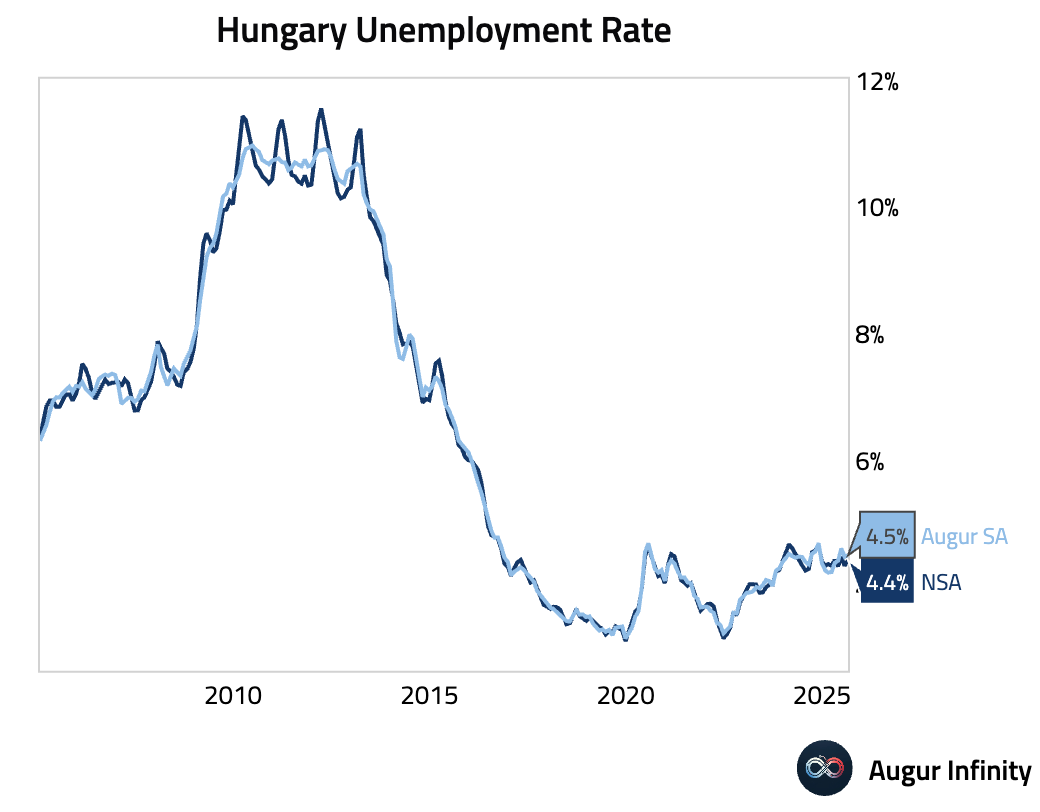

- Hungary's unemployment rate ticked up slightly to 4.4% from 4.3%.

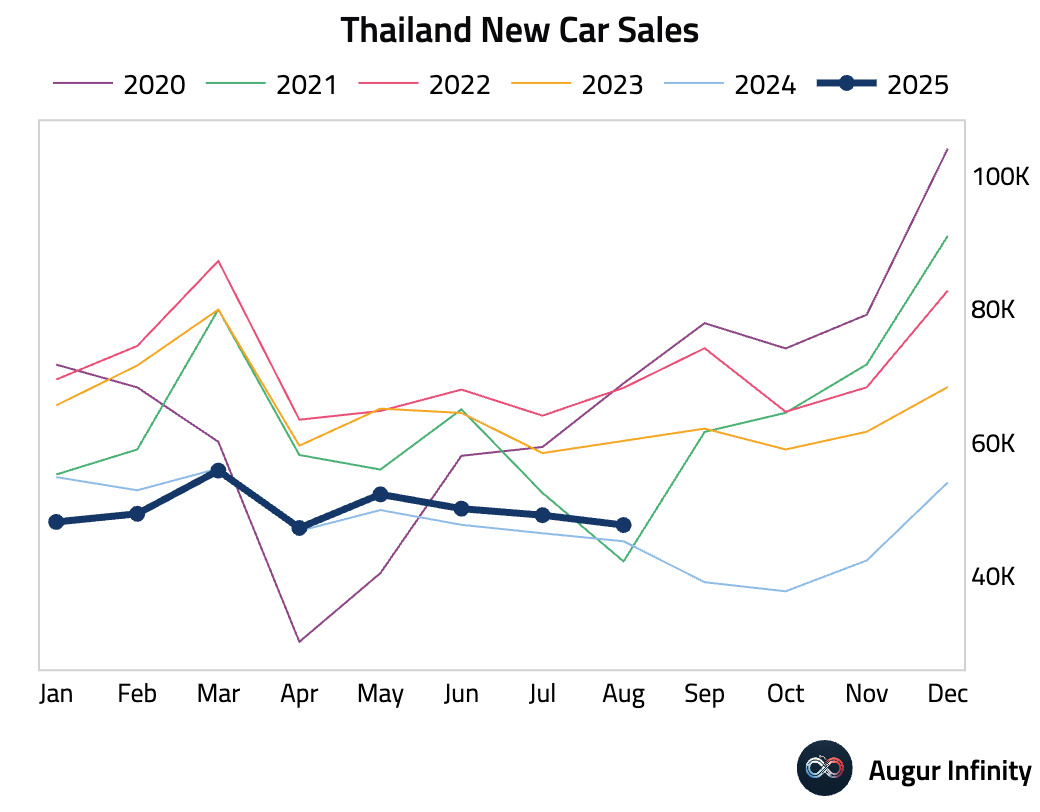

- New car sales growth in Thailand slowed to 5.4% Y/Y from 5.8% previously.

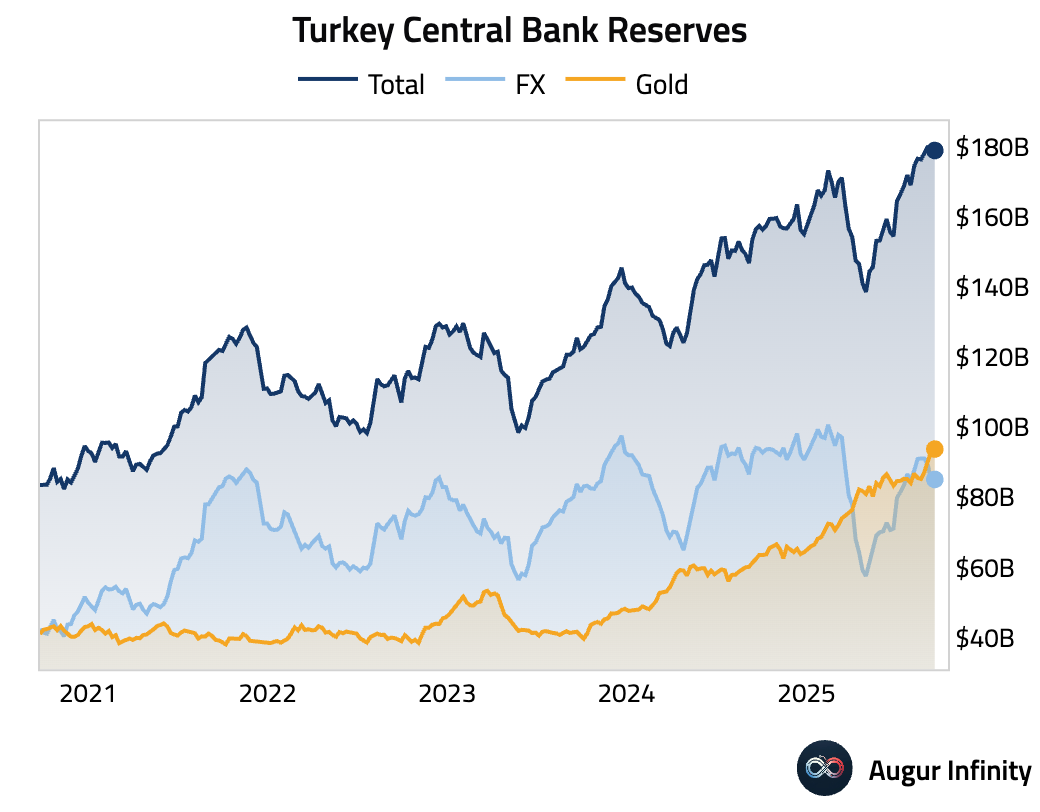

- Turkey's central bank foreign exchange reserves increased slightly (act: $85.1B, prev: $84.5B).

Global Markets

Equities

- US equities declined for a third consecutive session, with the S&P 500 falling 0.5%. European markets saw steeper losses, with Germany down 1.3% and France down 0.8%. In contrast, Chinese equities edged up 0.1%.

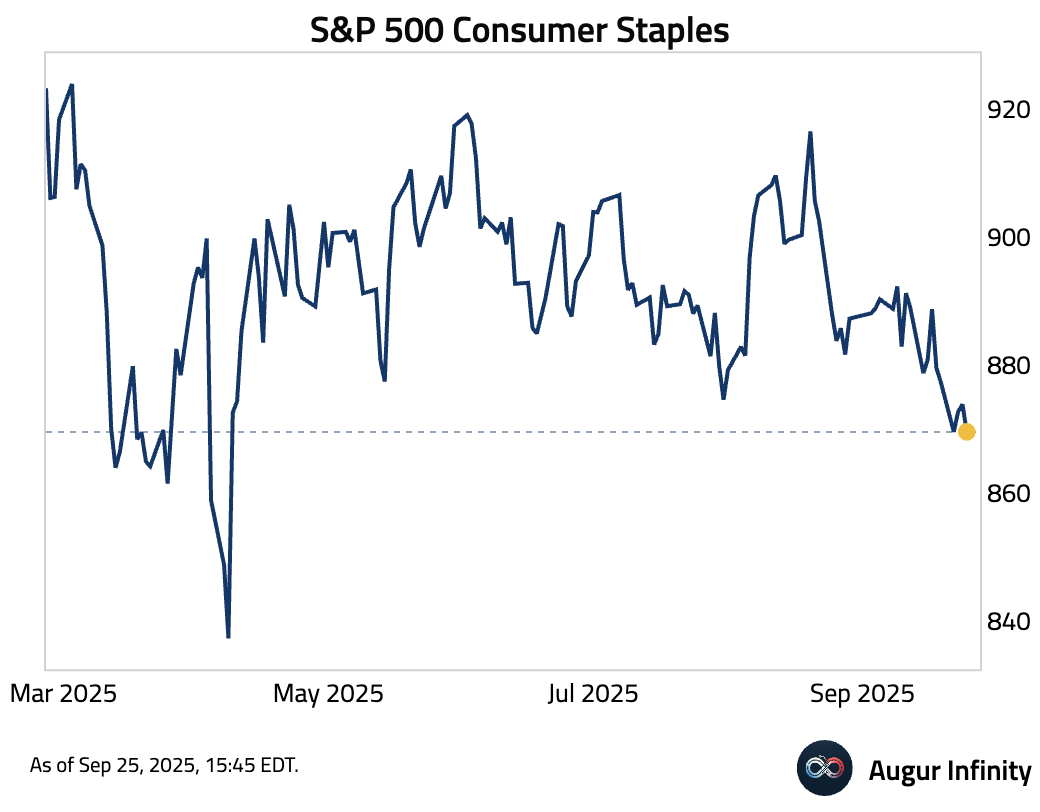

- S&P 500 Consumer Staples is at the lowest level since April.

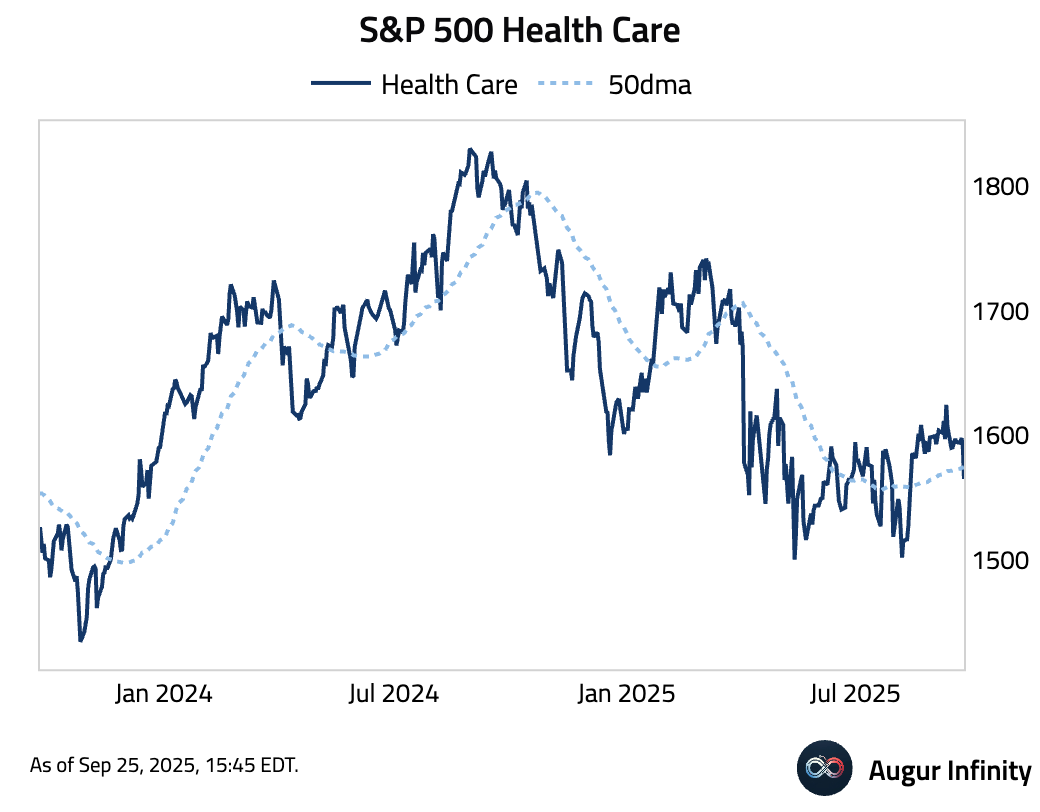

- S&P 500 Health Care fell below its 50-day moving average.

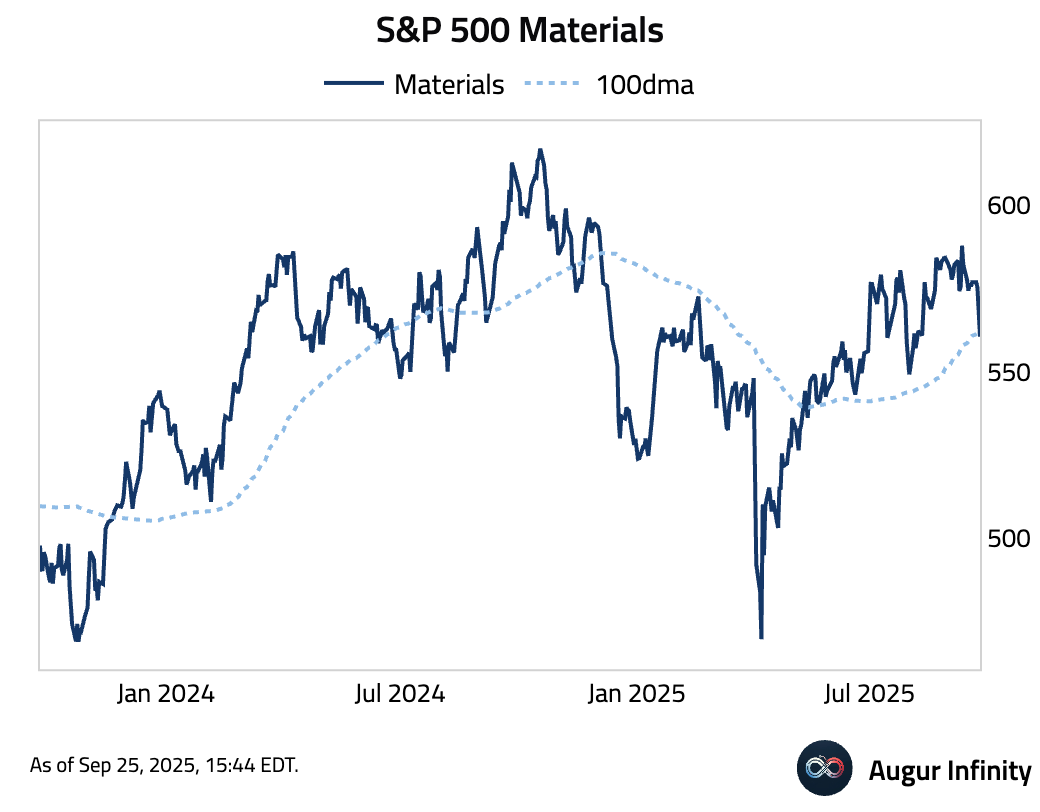

- The Materials sector of the S&P 500 Index flirts with its 100-day moving average.

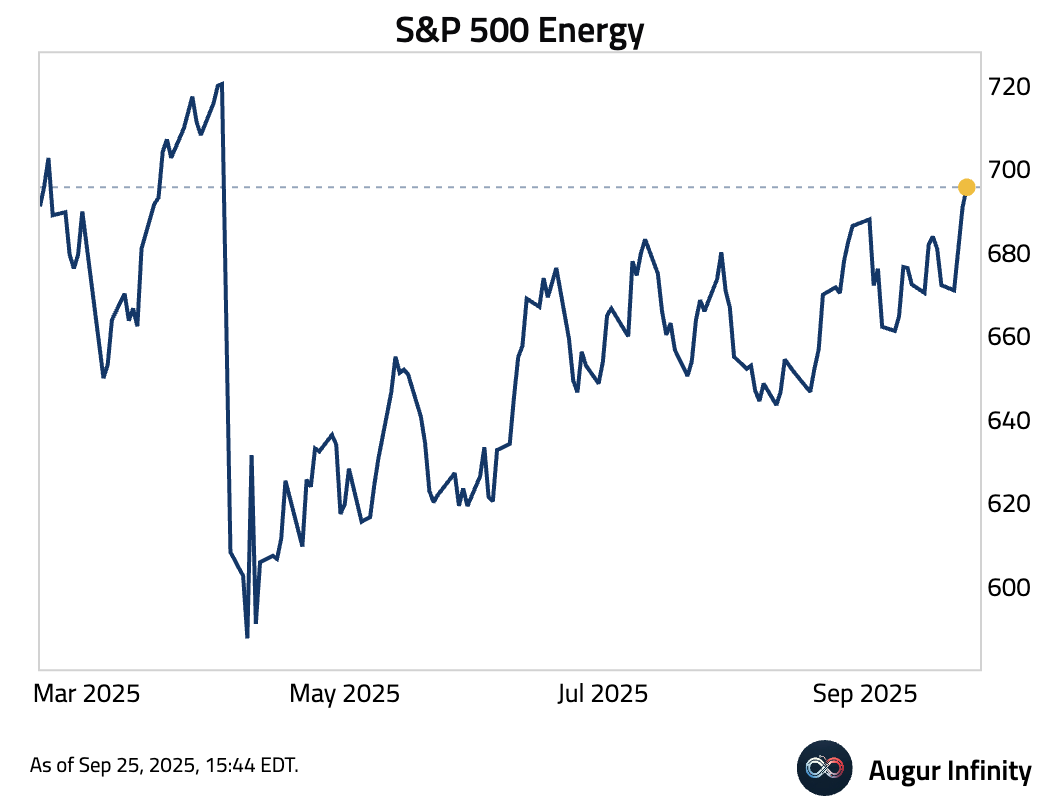

- However, S&P 500 Energy reached its highest level since April.

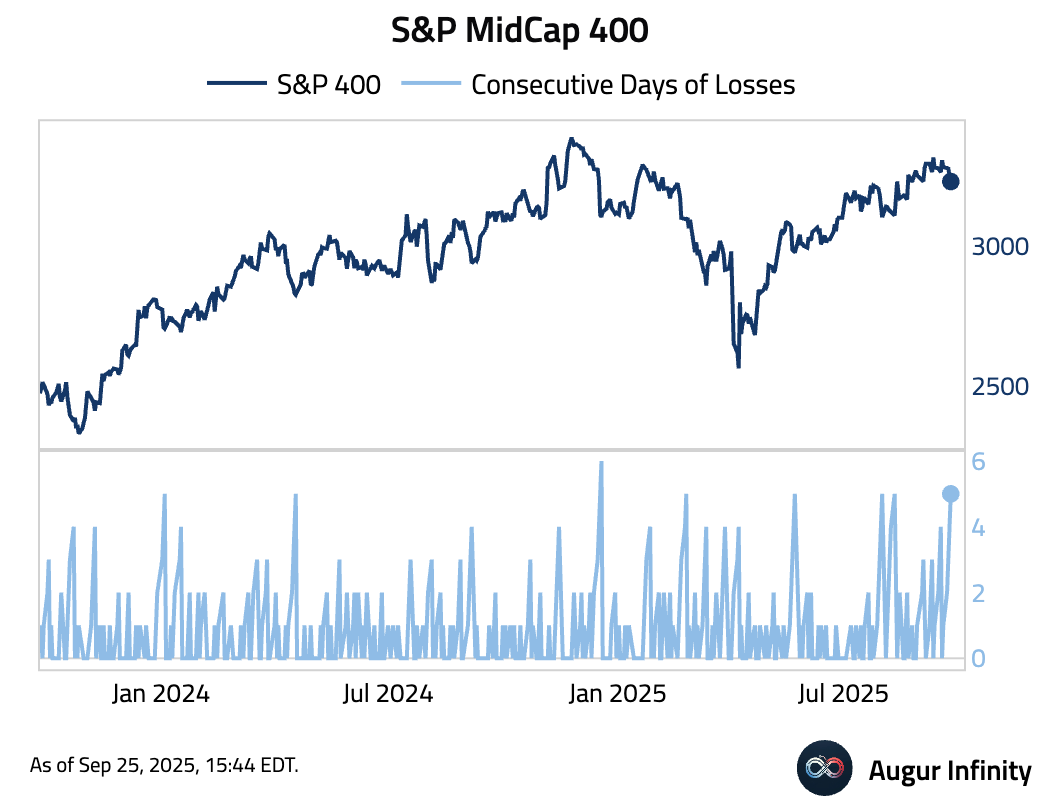

- S&P MidCap 400 has declined for five straight days.

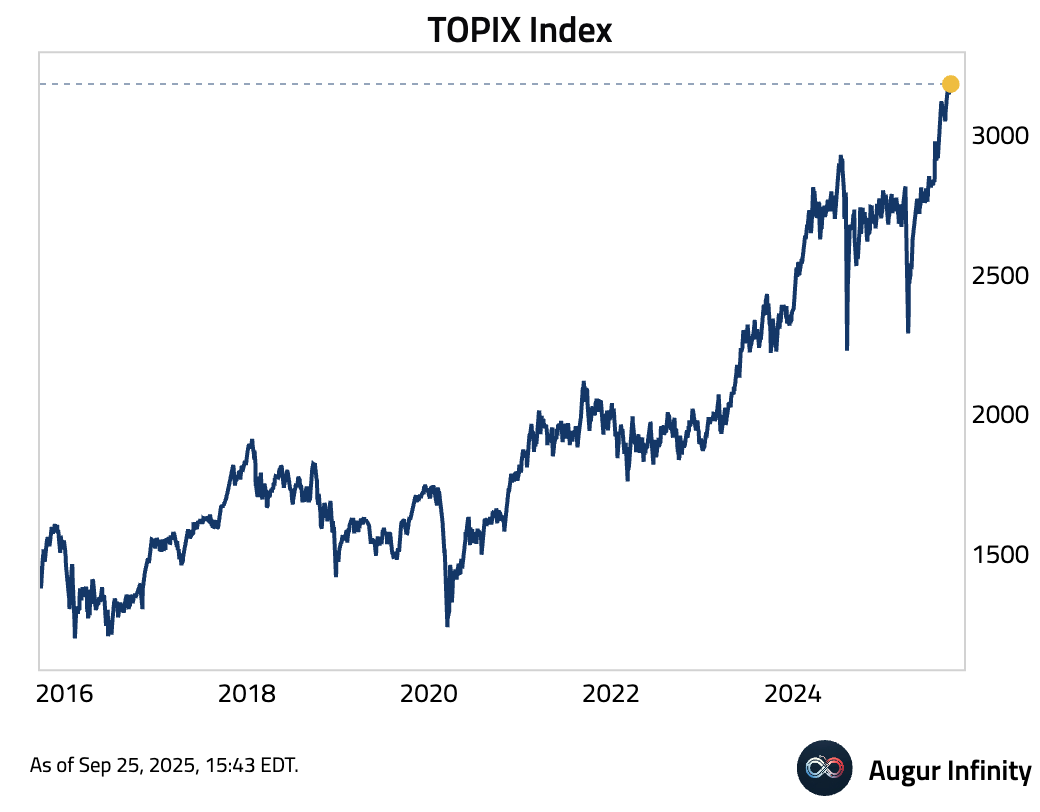

- TOPIX Index has reached an all-time high today, the 14th time of 2025.

Fixed Income

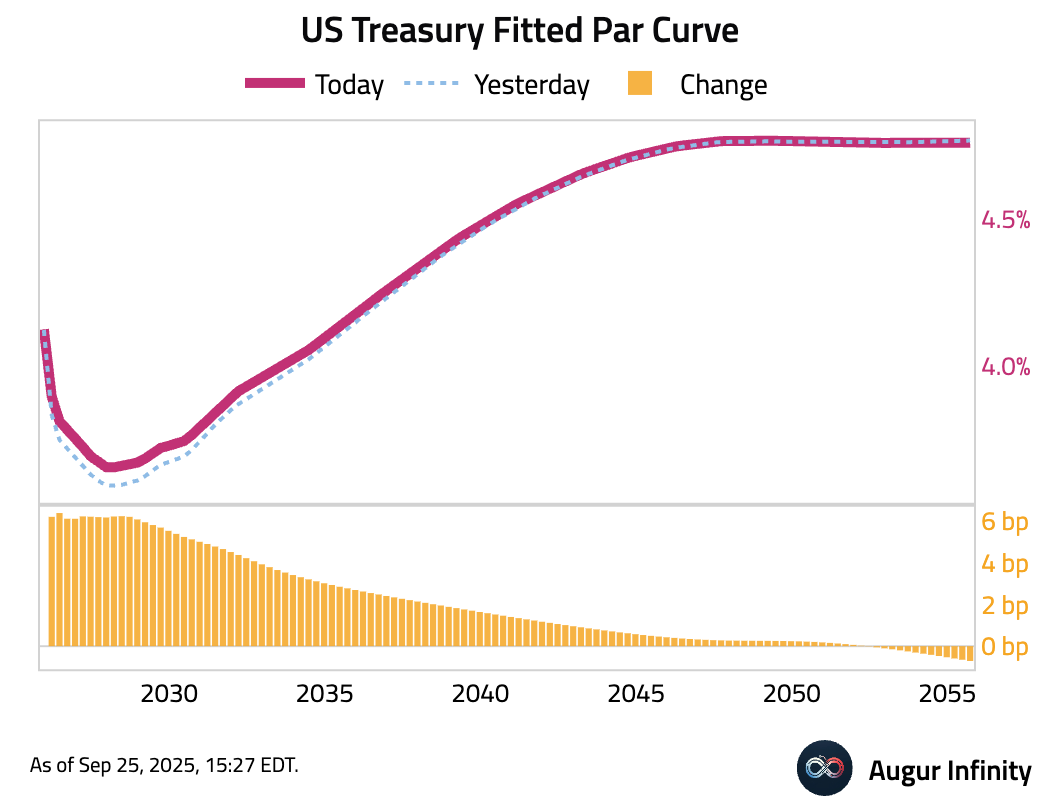

- US Treasury yields rose across the front-end and belly of the curve, with the 2-year yield up 6.2 bps and the 10-year yield adding 2.7 bps. The 30-year yield bucked the trend, dipping 0.6 bps, resulting in a flatter yield curve.

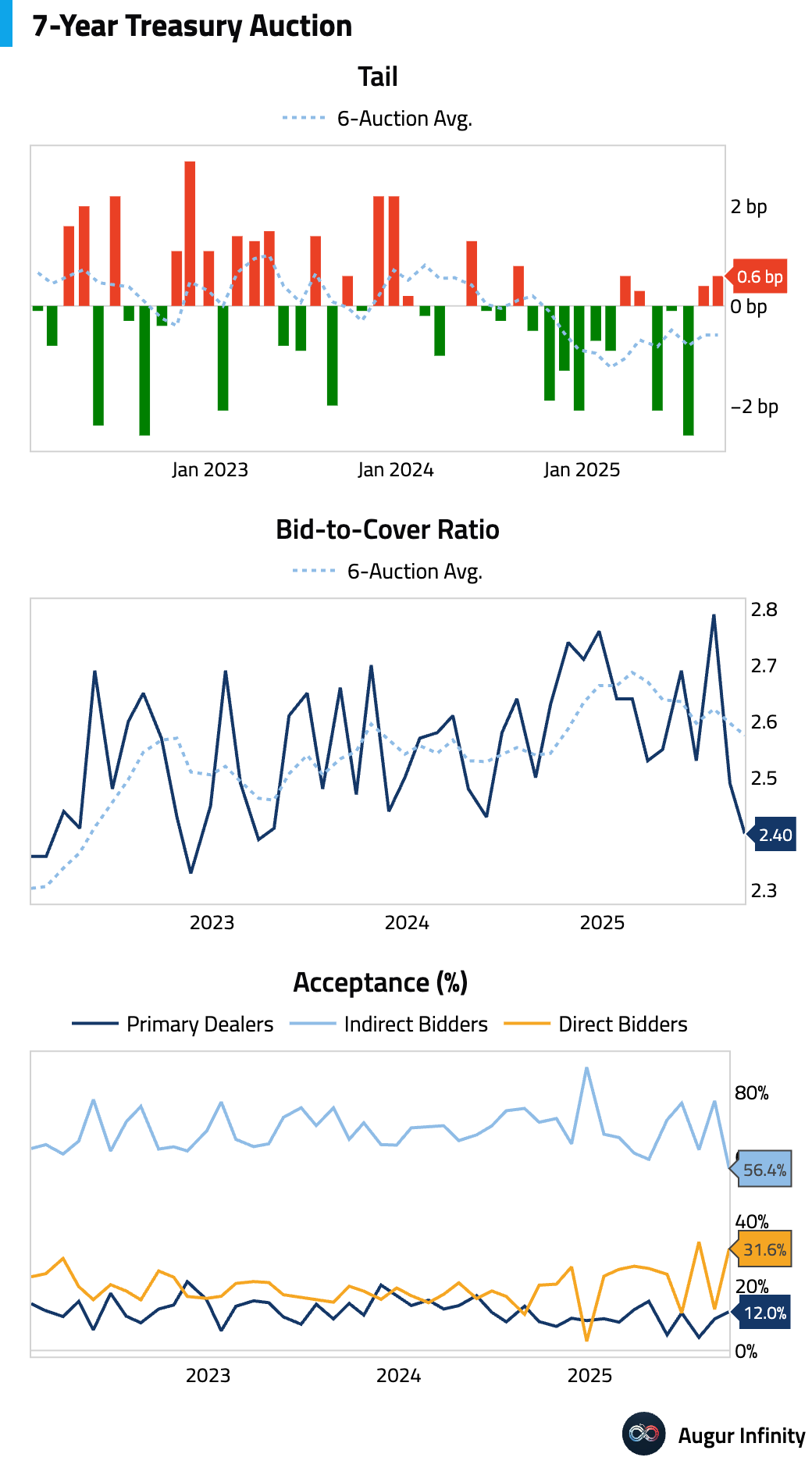

- The 7-year Treasury auction drew weak demand, tailing by 0.6 bps. The bid-to-cover ratio slipped to 2.4, the lowest since March 2023, while indirect bidder participation dropped sharply to 56.4%.

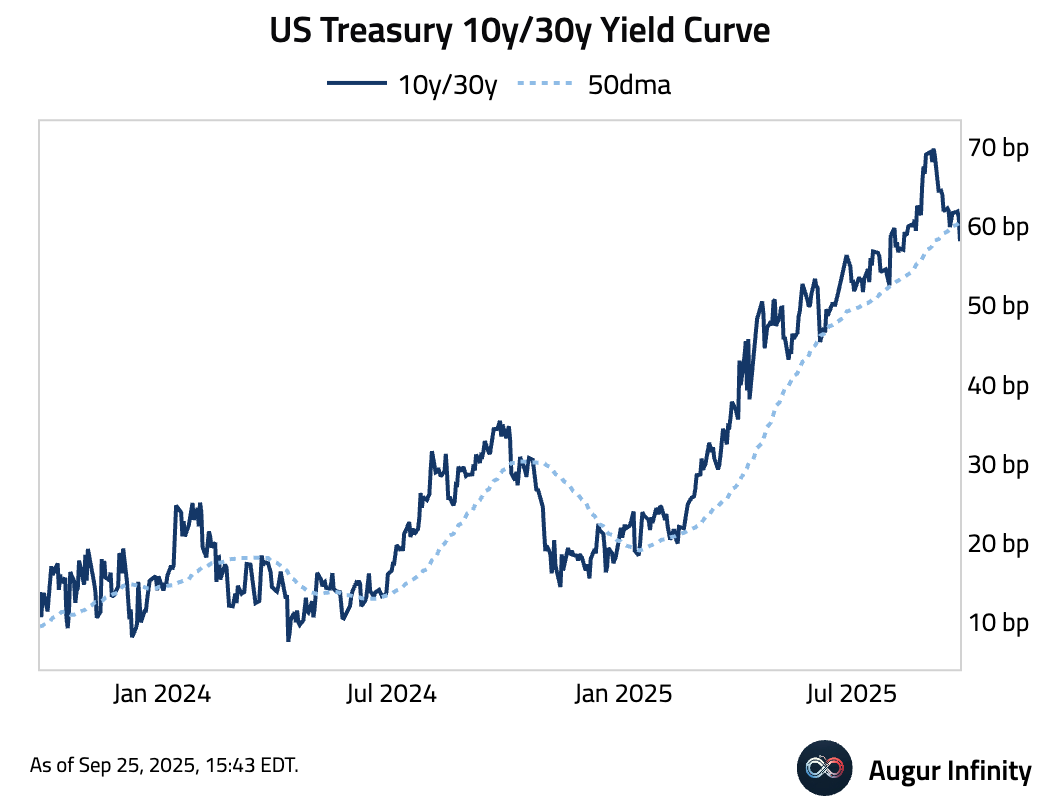

- US Treasury 10y/30y curve flattened below its 50-day moving average.

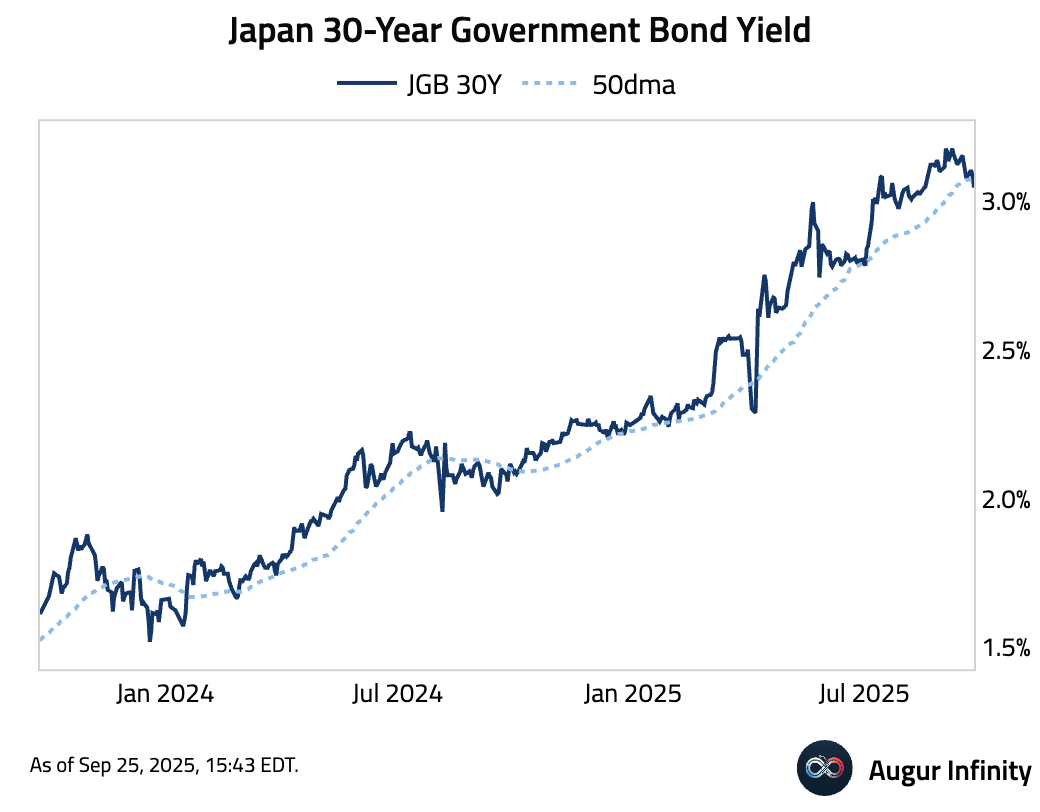

- Japans 30-year yield also fell below the 50-day moving average.

FX

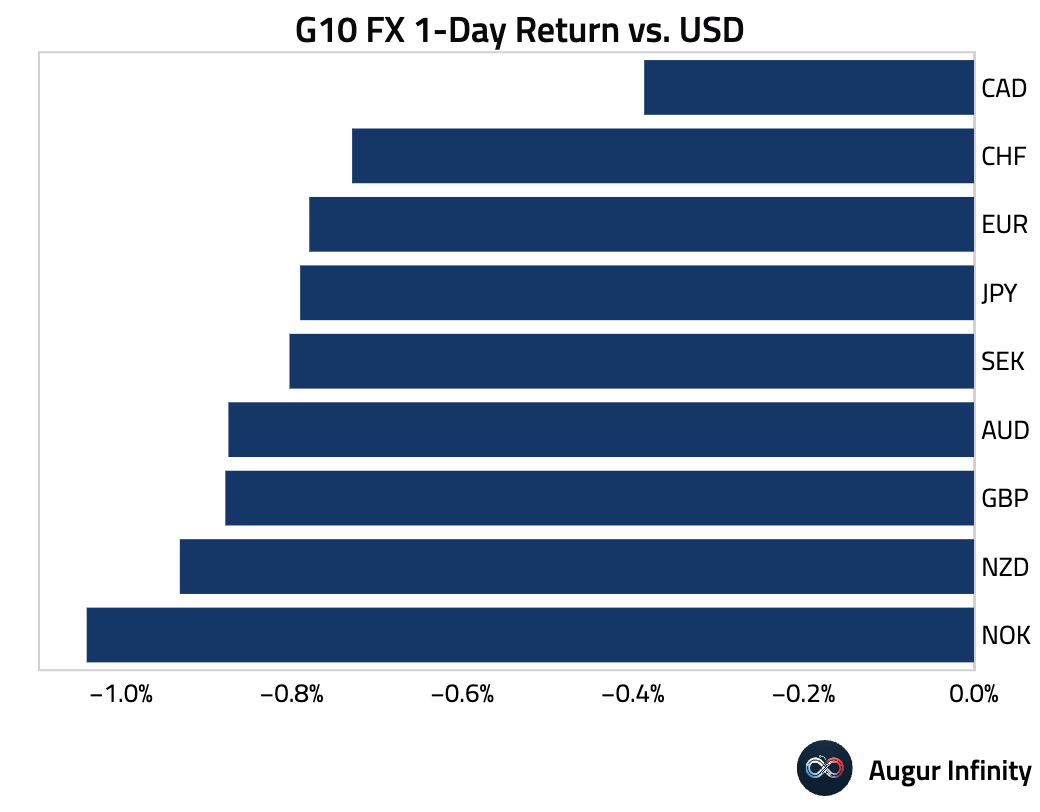

- The US dollar strengthened against all its G10 peers. The Norwegian krone was the weakest performer, falling 1.0%.

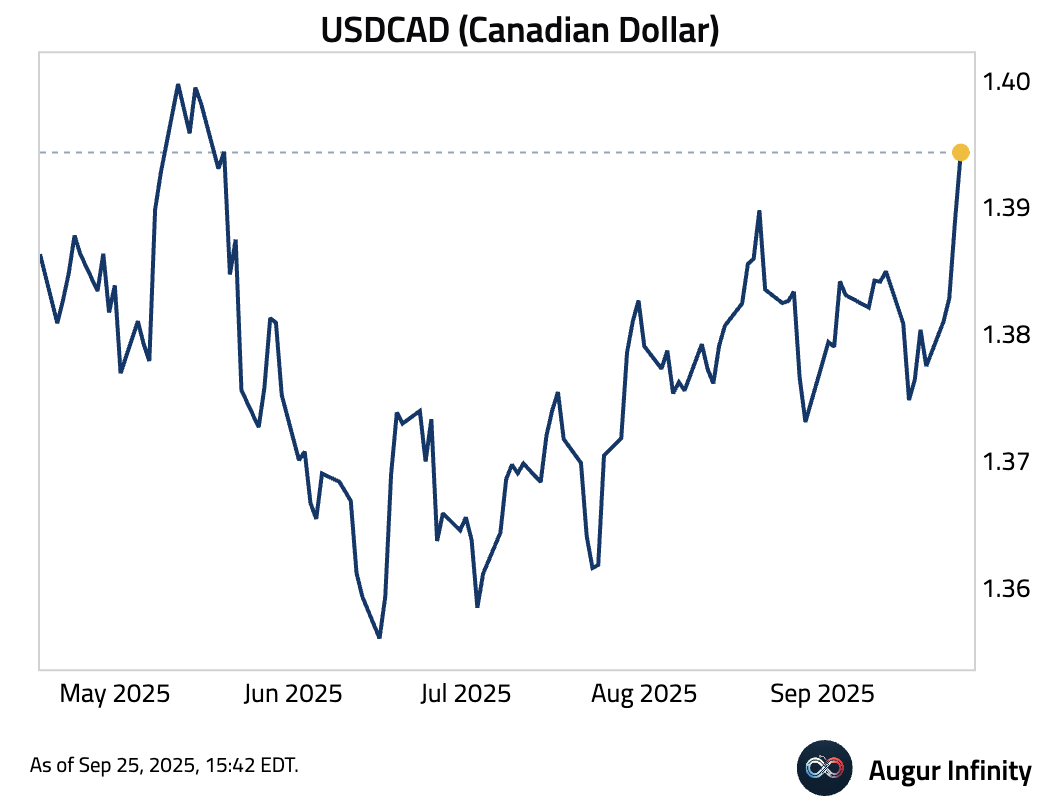

- Canadian dollar is at the weakest level against the dollar since May.

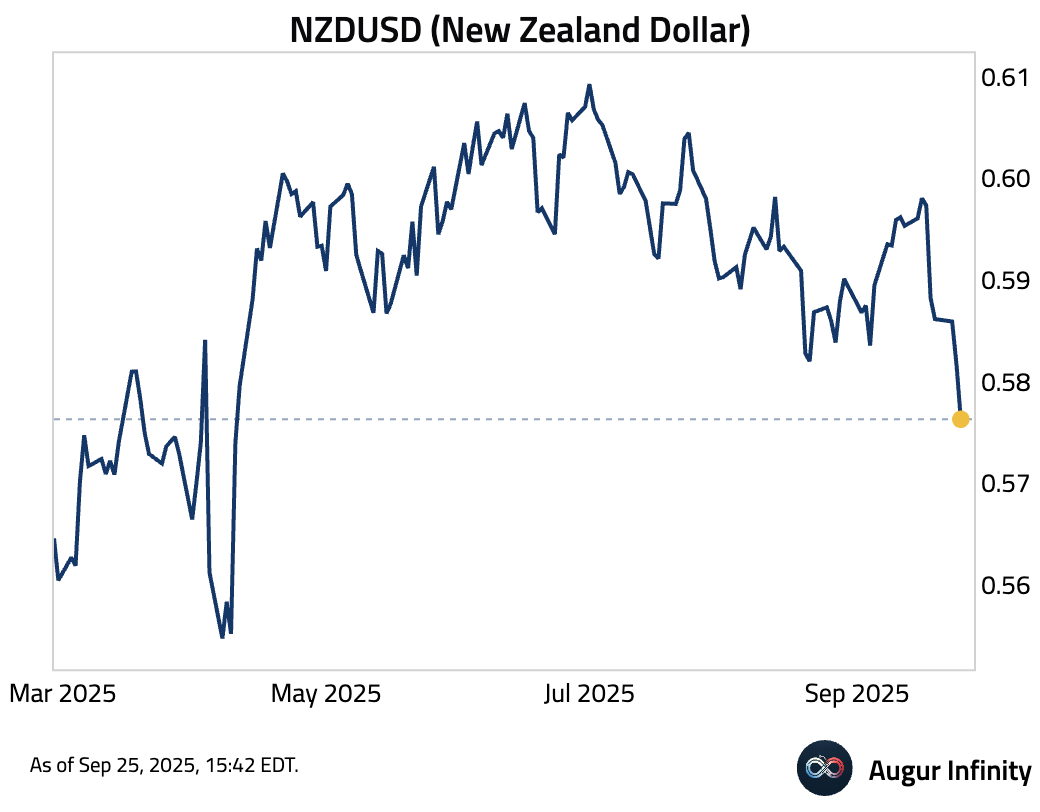

- New Zealand dollar continues to depreciate against the dollar as well, now at the worst level since April.

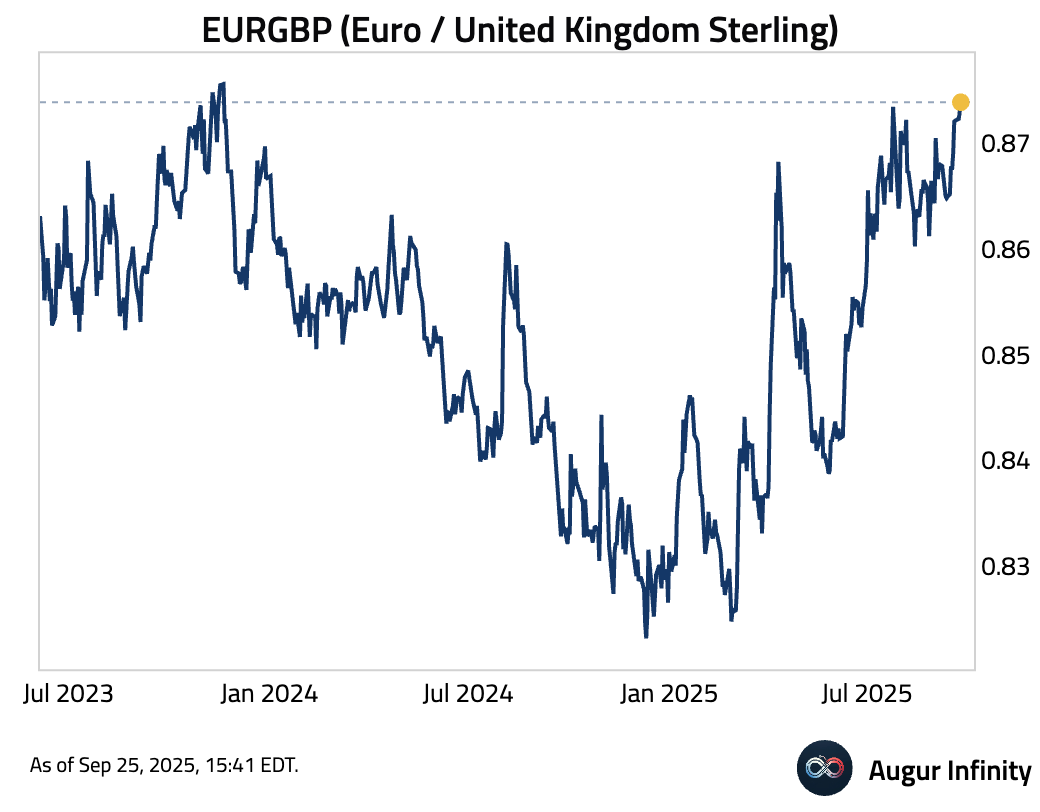

- The euro is trading at the strongest level against GBP since November 2023.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.