Table of Contents

- Headlines

- Charts of the Day

- United States

- Canada

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- President Trump and President Xi of China held a phone call and agreed that their respective teams would resume trade negotiations.

- The administration’s major reconciliation bill faces significant political challenges, including public criticism from business leader Elon Musk and reported policy disagreements between the Senate and the White House.

- The United States is reportedly holding secret trade and security negotiations with a delegation led by Prime Minister Carney, aiming for a bilateral agreement by the fall.

- New trade frictions have emerged as China’s restrictions on the export of rare earth minerals reportedly threaten global auto production, while the administration signed a new travel ban for twelve countries.

Charts of the Day

- The US has the lowest equity risk premium amongst major developed economies.

- Implied correlation has decoupled from realized correlations for members of the S&P 500 Index.

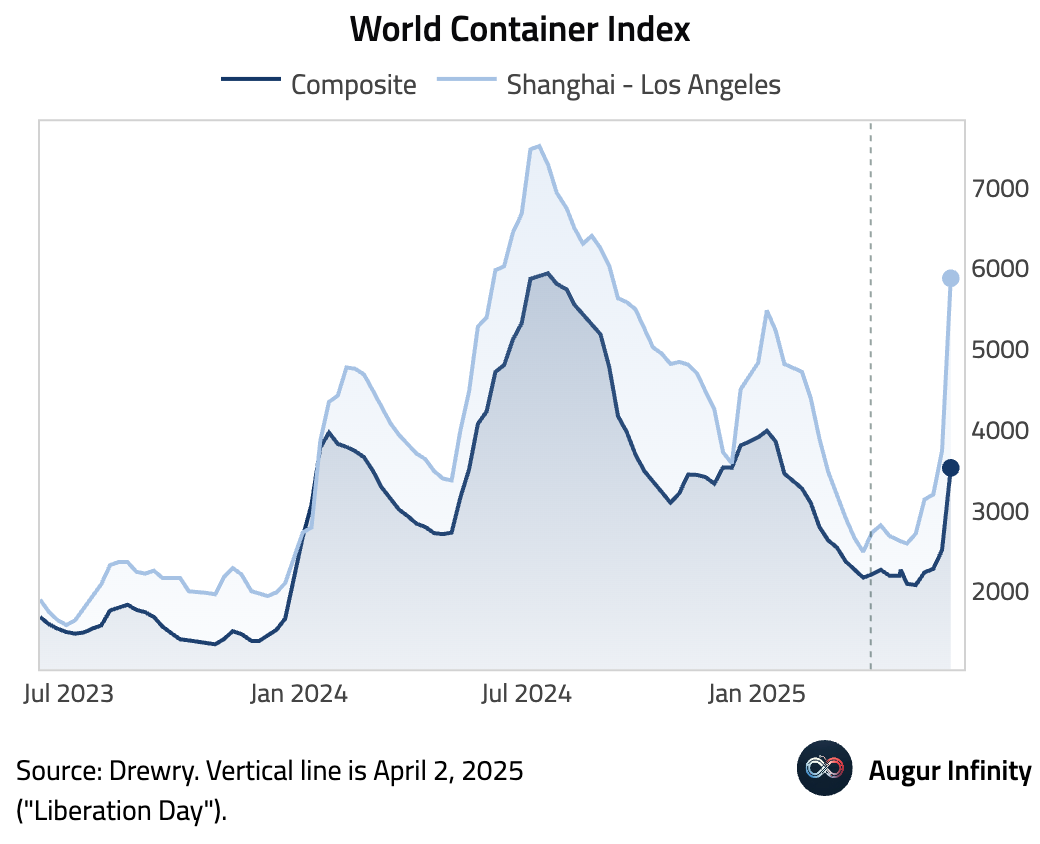

- Drewry's World Container Index jumped last week. In particular, freight rates from Shanghai to Los Angeles jumped 57% last week.

United States

- The Atlanta Fed's GDPNow model is now tracking Q2 GDP at 3.8%, down from 4.6% on June 2.

- Both hard data and soft data in the US have generally surprised to the downside (i.e., worse than expectations) this month.

- Challenger reported 93,816 job cuts in May, a decrease from 105,441 in the prior month.

- The US trade deficit in goods and services narrowed significantly to $61.6 billion in April from $138.3 billion in March, beating the consensus estimate of a $94.0 billion deficit. The improvement was driven by a sharp drop in imports to $351.0 billion and a rise in exports to an all-time high of $289.4 billion. This was partly due to a drop in pharmaceutical and gold imports, alongside a rebound in travel.

- Initial jobless claims for the week ending May 31 rose to 247,000, above the expected 235,000. The four-week moving average also increased to 235,000. Continuing claims for the week ending May 24 were stable at 1.904 million. Note that claims data can be volatile around holidays.

- The final estimate for Q1 nonfarm productivity was revised down to a -1.5% annualized rate from a previous 1.7%, falling short of the -0.8% consensus.

- Final Q1 unit labor costs were revised up to a 6.6% annualized rate, higher than the 5.7% consensus and the prior quarter's 2.0%. This reflects upward revisions to compensation per hour, which grew at a 5.0% rate.

- The average 30-year fixed mortgage rate fell to 6.85% from 6.89%, while the 15-year rate declined to 5.99% from 6.03%.

Canada

- Canada's trade deficit widened to an all-time low of C$7.14 billion in April, a significant miss from the C$1.5 billion deficit expected and down from C$2.26 billion in March. The deterioration was caused by a sharp fall in exports to C$60.44 billion while imports saw a smaller decline to C$67.58 billion.

- The Ivey PMI for May rose to 48.9 from 47.9, beating expectations of 48.3, but remained in contractionary territory for the second consecutive month.

Europe

- The European Central Bank cut its key interest rates by 25 basis points, as expected. The deposit facility rate now stands at 2.00%, down from 2.25%.

- Eurozone's Producer Price Index (PPI) fell 2.2% M/M in May, a larger drop than the -1.8% consensus. Year-over-year, PPI slowed to 0.7% from 1.9%.

- Germany's factory orders unexpectedly rose by 0.6% M/M in April, against expectations of a 1.0% decline. This follows a 3.4% rise in March.

- UK new car sales rose 1.6% Y/Y in May, rebounding from a 10.4% drop in April.

- The S&P Global UK Construction PMI for May improved to 47.9 from 46.6, beating the consensus of 47.2, but still indicating contraction in the sector.

- Italian retail sales rose 0.7% M/M in April, well above the 0.2% consensus and recovering from a 0.4% fall in March. On a Y/Y basis, sales surged 3.7%.

- Sweden's preliminary inflation rate for May came in at 0.2% Y/Y, below the 0.4% forecast and down from 0.3% previously. The CPIF gauge, which the Riksbank targets, was stable at 2.3% Y/Y.

- Sweden posted a current account surplus of SEK 119.3 billion in Q1, up from SEK 81.2 billion in the previous quarter.

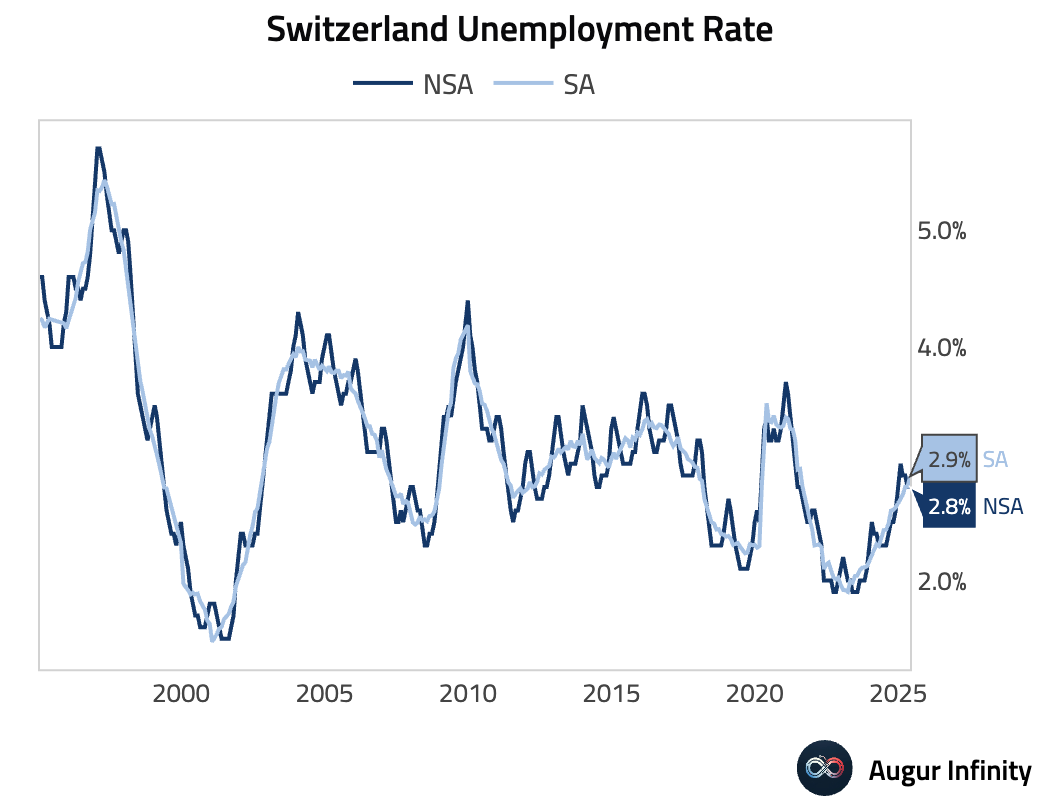

- Switzerland's unemployment rate held steady at 2.8% in May, matching expectations.

- Ireland's AIB Services PMI climbed to 54.7 in May from 52.8 in April, signaling stronger expansion in the services sector.

- Ireland's unemployment rate edged down to 4.0% in May from 4.1% in April.

- Ireland's final Q1 GDP growth was a stunning 9.7% Q/Q, far exceeding the 3.2% consensus. This took the Y/Y growth rate to 22.2%.

- Ireland's final Q1 Gross National Product (GNP) contracted by 2.1% Q/Q, resulting in a Y/Y decline of 5.0%.

Japan

- Japan's average cash earnings grew 2.3% Y/Y in April, in line with the previous month but slightly below the 2.6% consensus.

- Japanese investors were net sellers of foreign bonds to the tune of ¥118 billion in the week ending May 31, while foreign investors were net buyers of Japanese stocks, purchasing ¥336.1 billion.

Asia-Pacific

- South Korea's foreign exchange reserves edged down to $404.60 billion in May from $404.67 billion in April.

- South Korea's final Q1 GDP confirmed a contraction of 0.2% Q/Q, unchanged from the preliminary estimate. The Y/Y growth rate was confirmed at 0.0%.

- Australia's trade surplus narrowed to A$5.41 billion in April from A$6.89 billion previously. The change was driven by a 2.4% M/M fall in exports and a 1.1% M/M rise in imports.

- Singapore's retail sales rebounded with a 0.3% M/M increase in April, following a 2.7% decline in March. The Y/Y growth rate slowed to 0.3% from 1.3%.

- Taiwan's annual inflation rate eased to 1.55% in May from 2.03% in April, its lowest level since March 2021.

- Taiwan's foreign exchange reserves rose to an all-time high of $592.95 billion in May from $582.83 billion in April.

China

- China's Caixin Services PMI for May rose to 51.1, matching expectations and up from 50.7 in April, indicating a slight acceleration in services sector growth.

Emerging Markets ex China

- The Philippines' inflation rate was 1.3% Y/Y in May, meeting consensus and slightly down from 1.4% in April. Core inflation was stable at 2.2% Y/Y.

- South Africa's current account deficit narrowed to ZAR 35.6 billion in Q1 from a ZAR 39.3 billion deficit in the previous quarter.

- Turkey's central bank foreign exchange reserves increased to $70.03 billion as of May 30, up from $69.09 billion a week earlier.

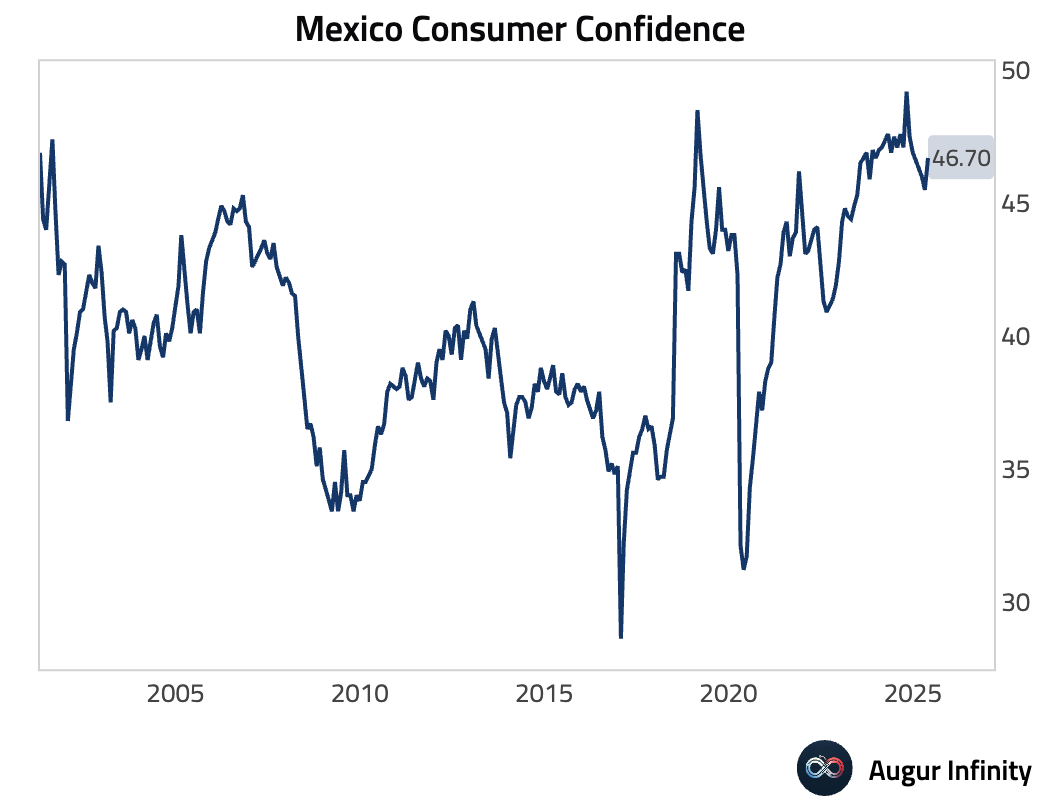

- Mexico's consumer confidence index improved to 46.7 in May from 45.5 in April, indicating rising optimism among consumers.

- Brazil's new car registrations increased by 8.1% M/M in May, accelerating from a 6.7% rise in April.

- Brazil's trade surplus for May was $7.24 billion, below the consensus of $8.4 billion and down from $7.64 billion in April.

Equities

- US markets were mixed, with the S&P 500 down 0.5% while the Nasdaq declined 0.8%. European markets were broadly positive. In Asia, South Korean equities surged 2.2%, marking a strong outperformance.

Fixed Income

- The 2-year yield increased by 5.7 basis points, and the 5-year yield rose by 6.2 basis points. The 10-year yield was up 3.6 basis points, while the 30-year yield edged down 0.5 basis points.

FX

- The US dollar was broadly weaker against its G10 peers. The New Zealand and Norwegian currencies were the top performers, gaining 0.4% each. The Japanese yen and Swiss franc were the laggards, both down 0.2% against the dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.