Headlines

- The US administration announced new tariffs effective October 1, including a 100 percent tariff on certain imported pharmaceuticals, a 50 percent tariff on kitchen cabinets and bathroom vanities, and a 30 percent tariff on upholstered furniture.

- The probability of a US government shutdown has reportedly increased, as legislative leaders remain at an impasse over the terms of a continuing resolution needed to fund government operations.

Global Economics

United States

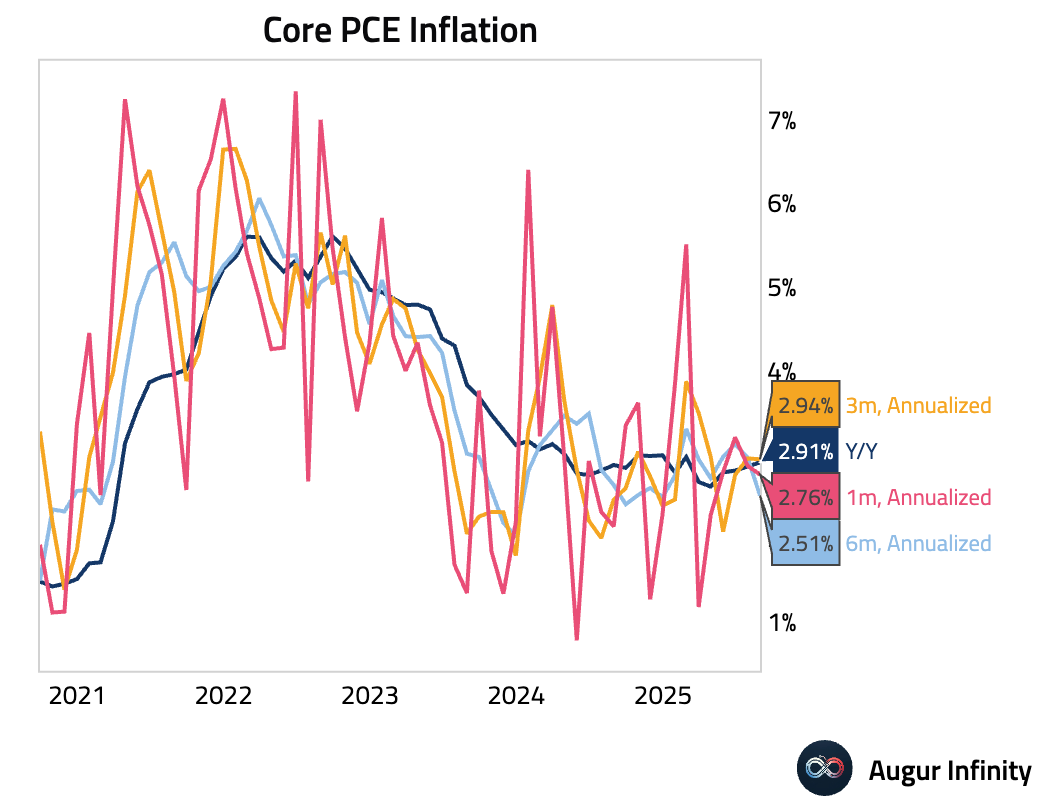

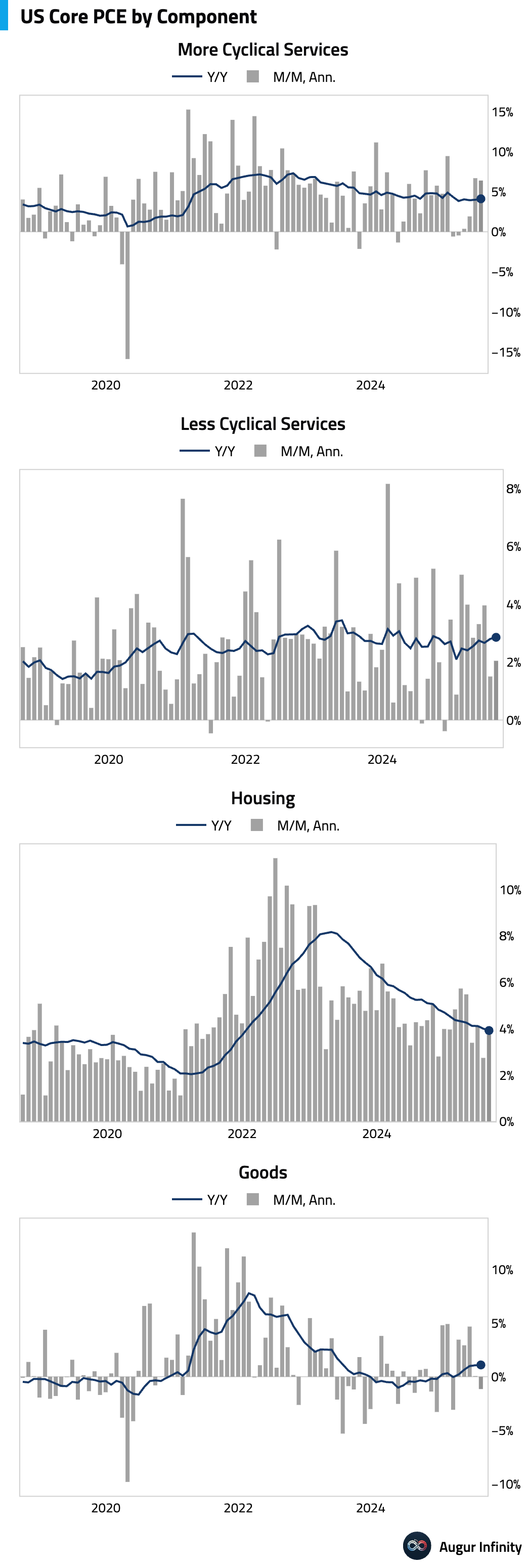

- August Core PCE was in line with expectations at +0.23% M/M. This was driven by a continued split between falling core goods prices and rising core services prices. The year-over-year rate rose to 2.91%, meeting the median forecast.

Interactive chart on Augur Infinity

Here's our aggregation of core PCE components.

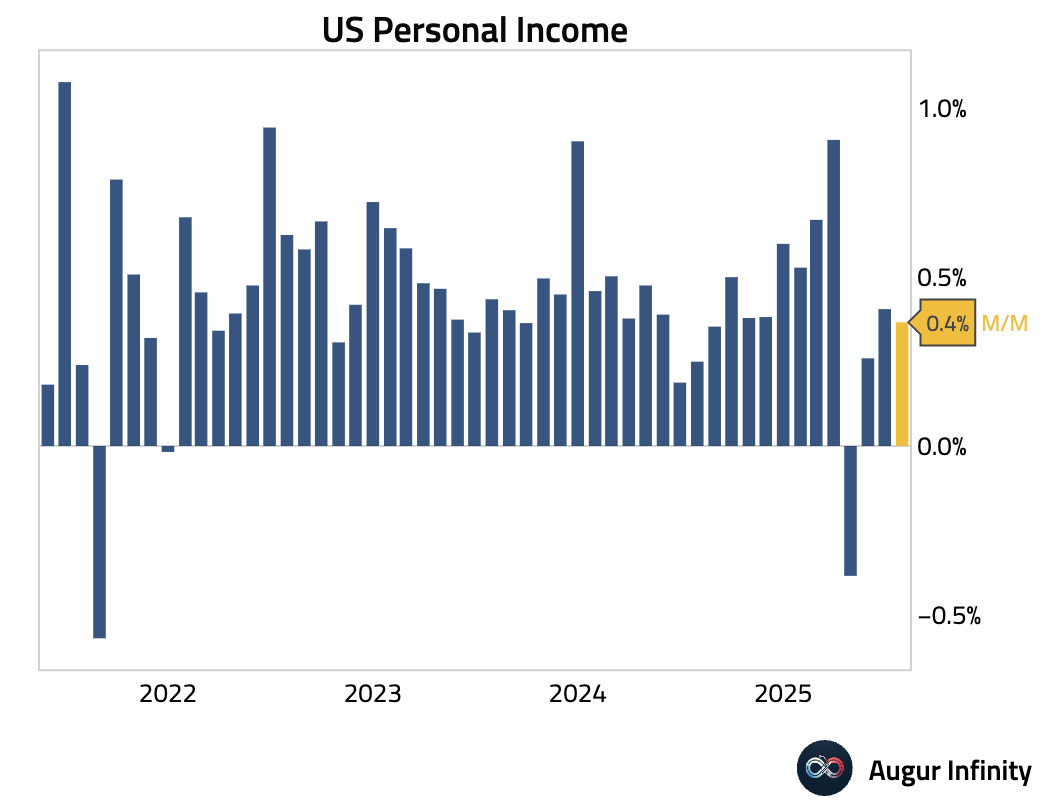

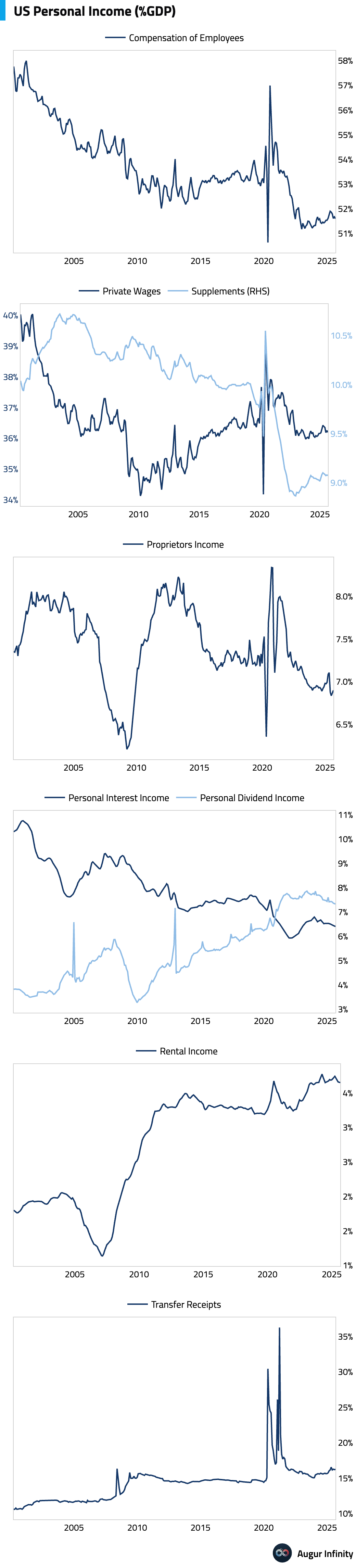

- Personal income rose +0.4%, slightly above consensus. The increase was largely driven by volatile components, including a surge in farm income and a 12.7% increase in transfer receipts from business insurance payouts. Employee compensation, a core component, rose a more modest +0.3%.

Interactive chart on Augur Infinity

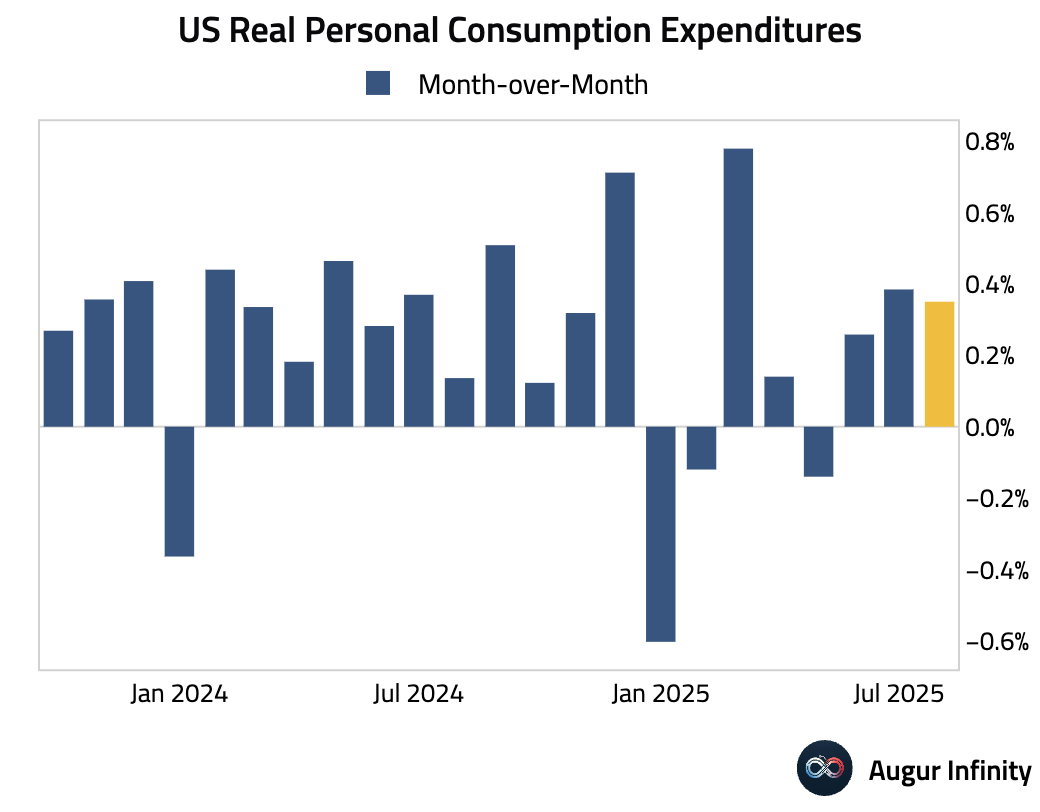

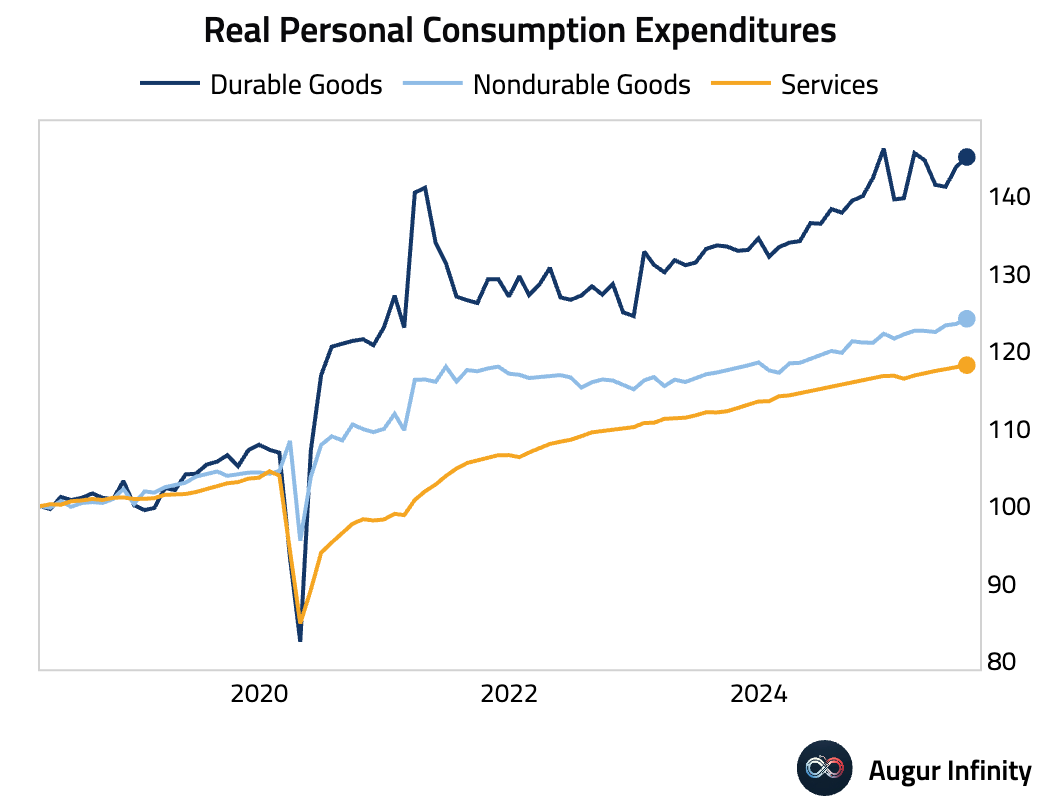

- Personal spending was strong, beating expectations at +0.6%. Real spending rose +0.3%, driven by a robust +0.7% increase in real goods spending.

Interactive chart on Augur Infinity

Interactive chart on Augur Infinity

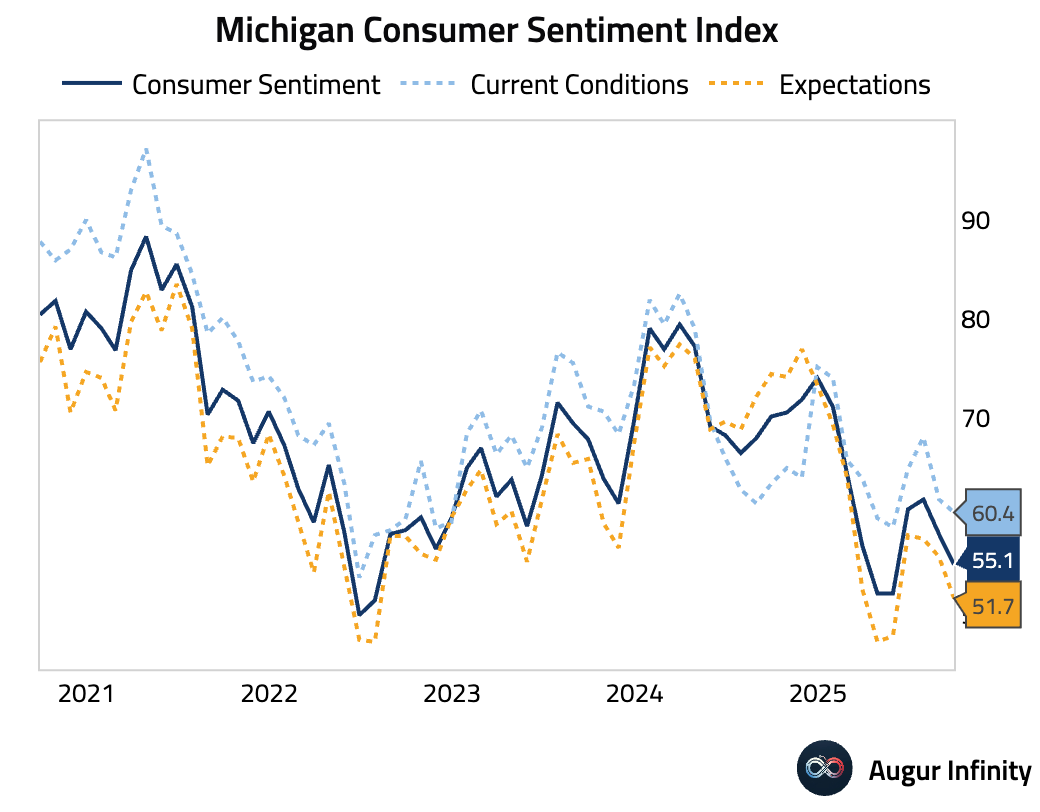

- The University of Michigan's final consumer sentiment reading for September was revised lower from the preliminary estimate, declining to its lowest level in four months (act: 55.1, est: 55.4, prev: 58.2). Both the current conditions and expectations components weakened.

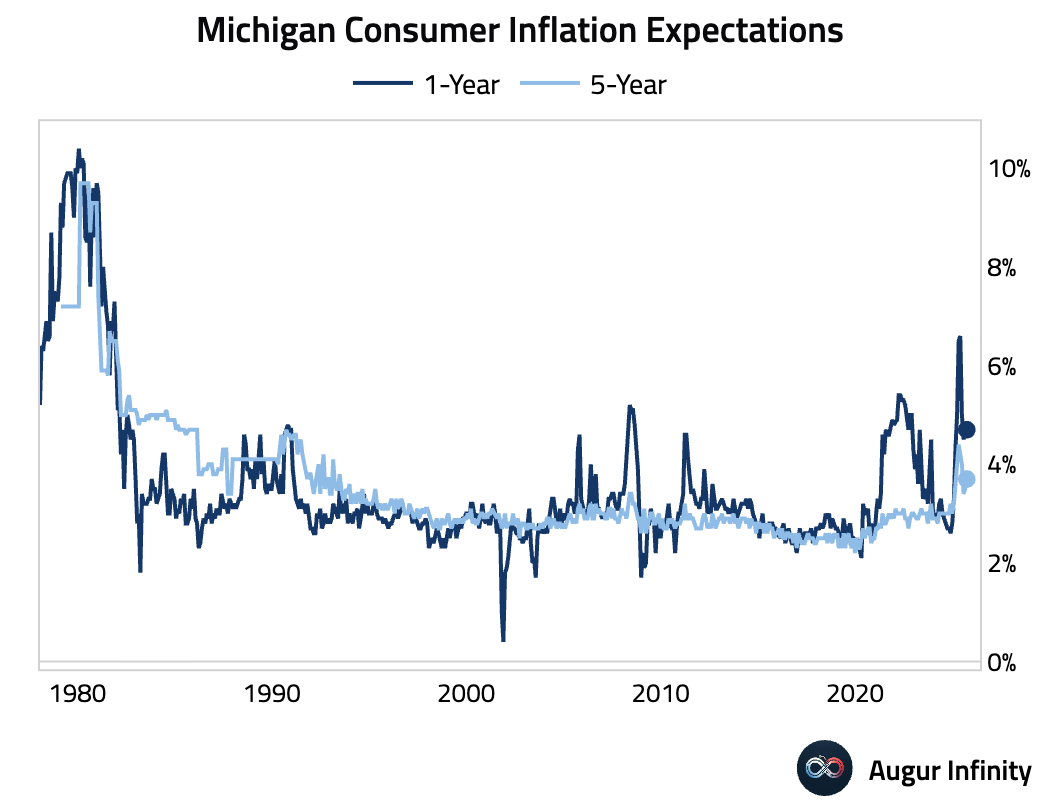

- The University of Michigan's final survey for September showed a divergence in consumer inflation expectations. The 1-year outlook eased slightly to 4.7% (est: 4.8%), while the 5-year outlook edged higher to 3.7% (est: 3.9%).

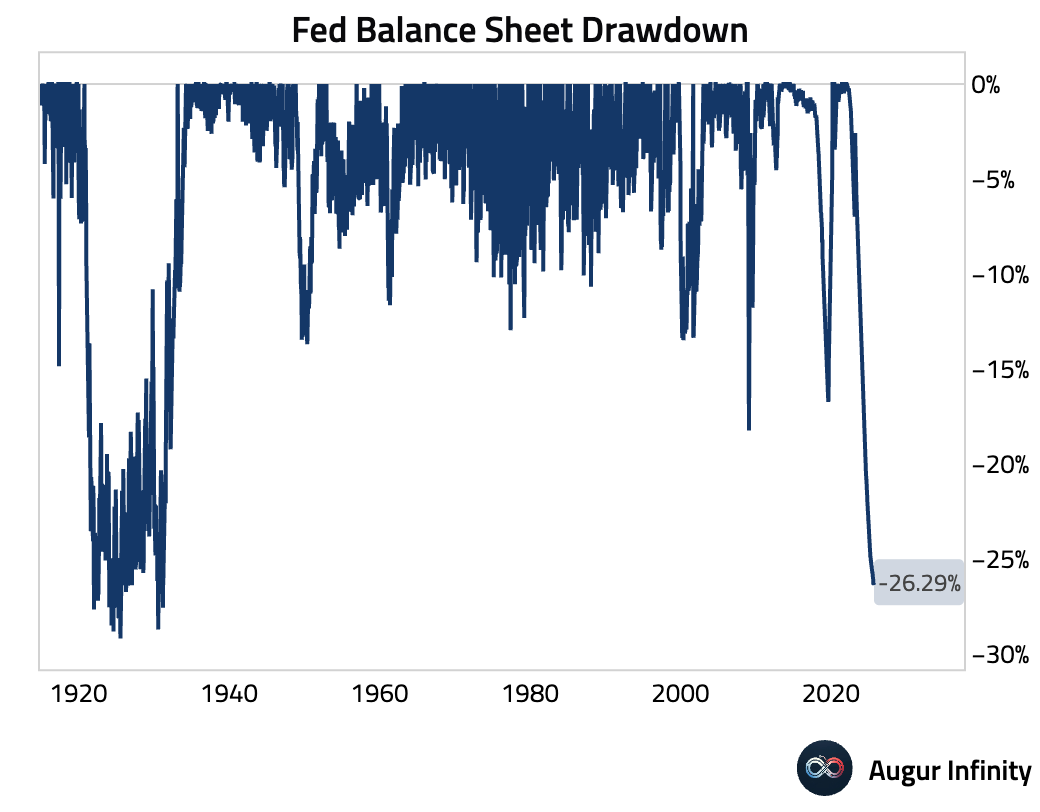

- The Federal Reserve’s balance sheet was unchanged at $6.61 trillion for the week ending September 25.

Interactive chart on Augur Infinity

Canada

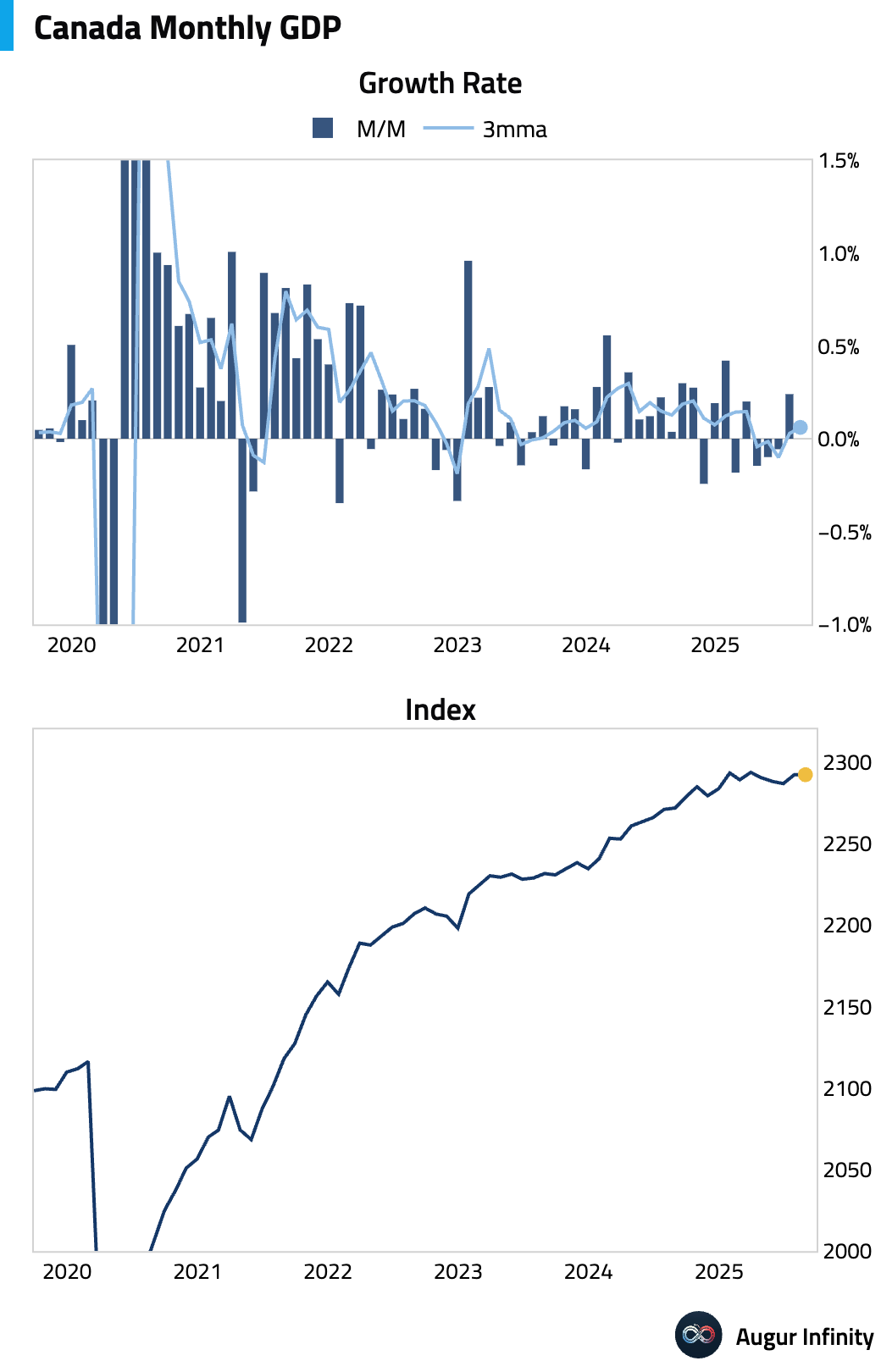

- Canada's economy grew by 0.2% M/M in July, beating expectations for a 0.1% expansion. However, the preliminary estimate for August points to flat growth (0.0% M/M), suggesting a loss of momentum.

Interactive chart on Augur Infinity

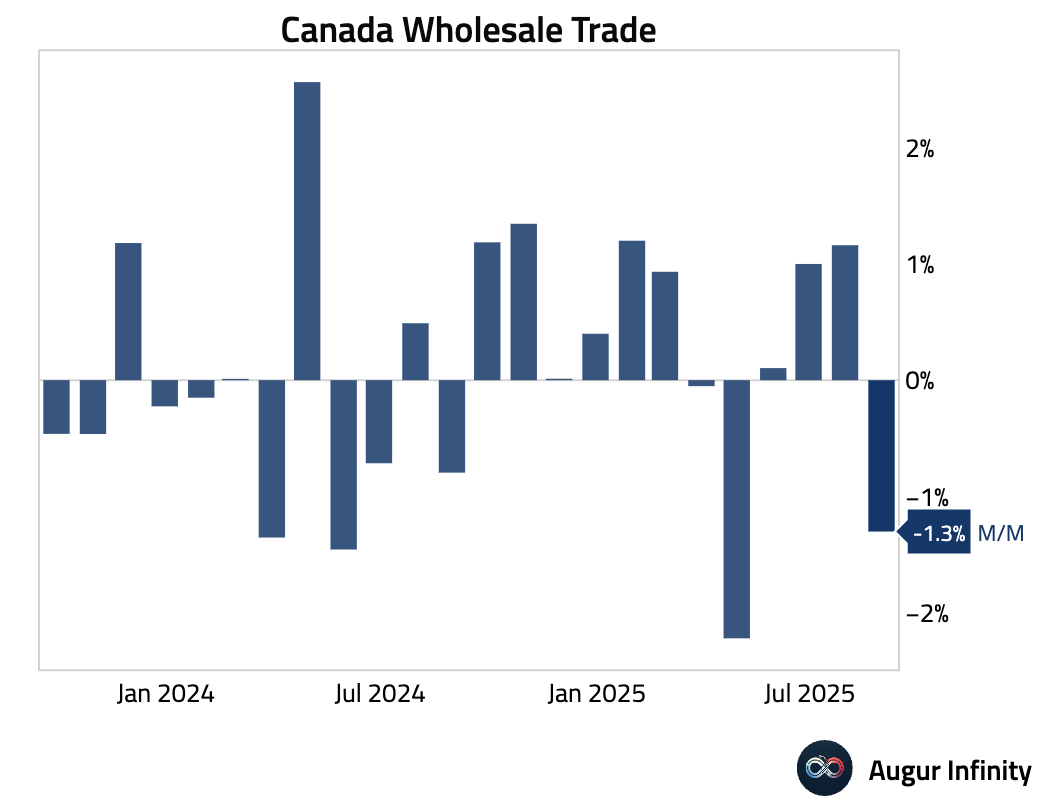

- Preliminary data showed Canadian wholesale sales fell in August, reversing the prior month's gain (act: -1.3% M/M, prev: 1.2%).

Interactive chart on Augur Infinity

Europe

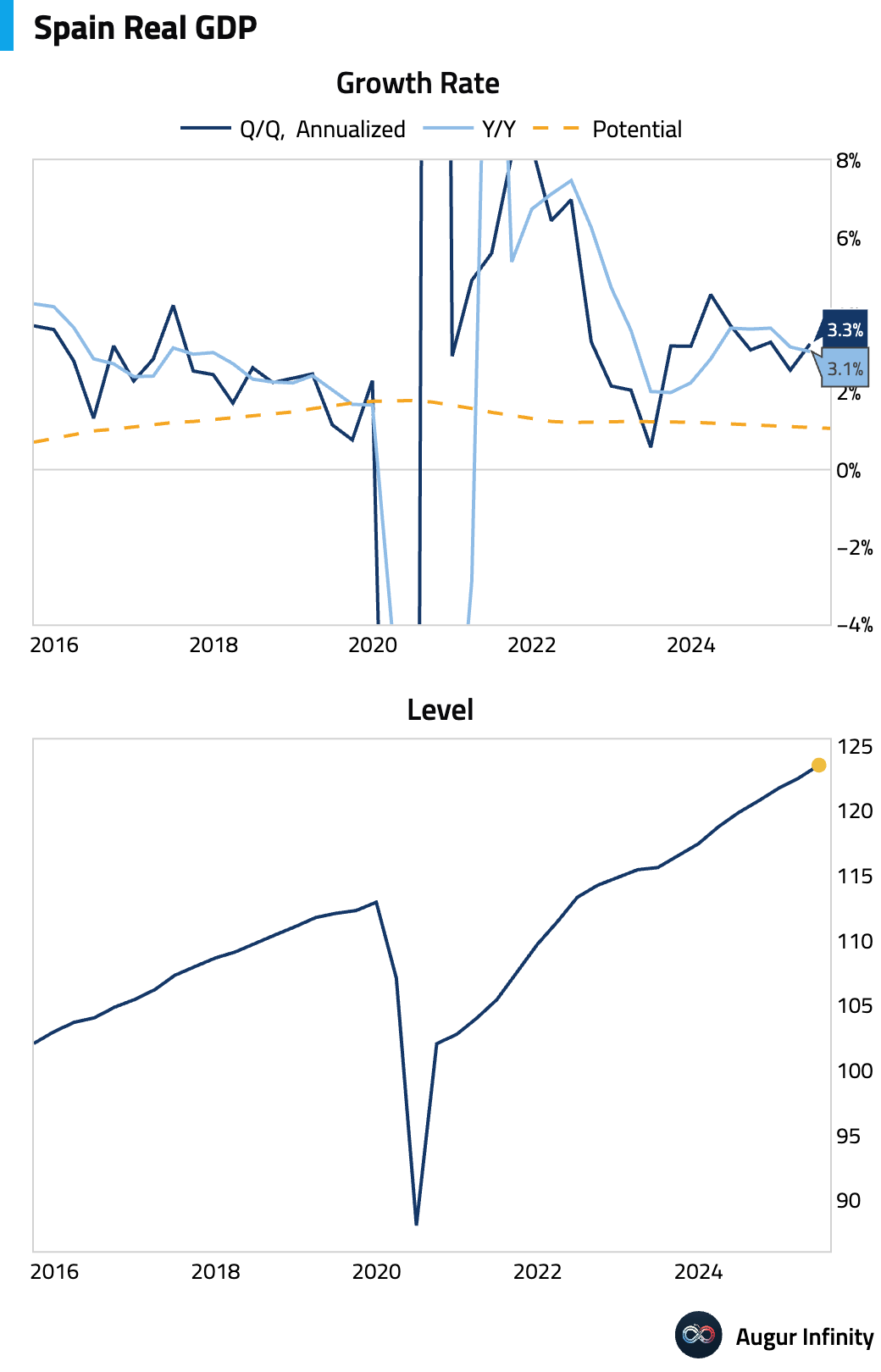

- Spain's final Q2 GDP figures confirmed an acceleration in economic activity, with growth revised up to 0.8% Q/Q (or 3.3% annualized) from 0.6% and 3.1% Y/Y, both beating expectations.

Interactive chart on Augur Infinity

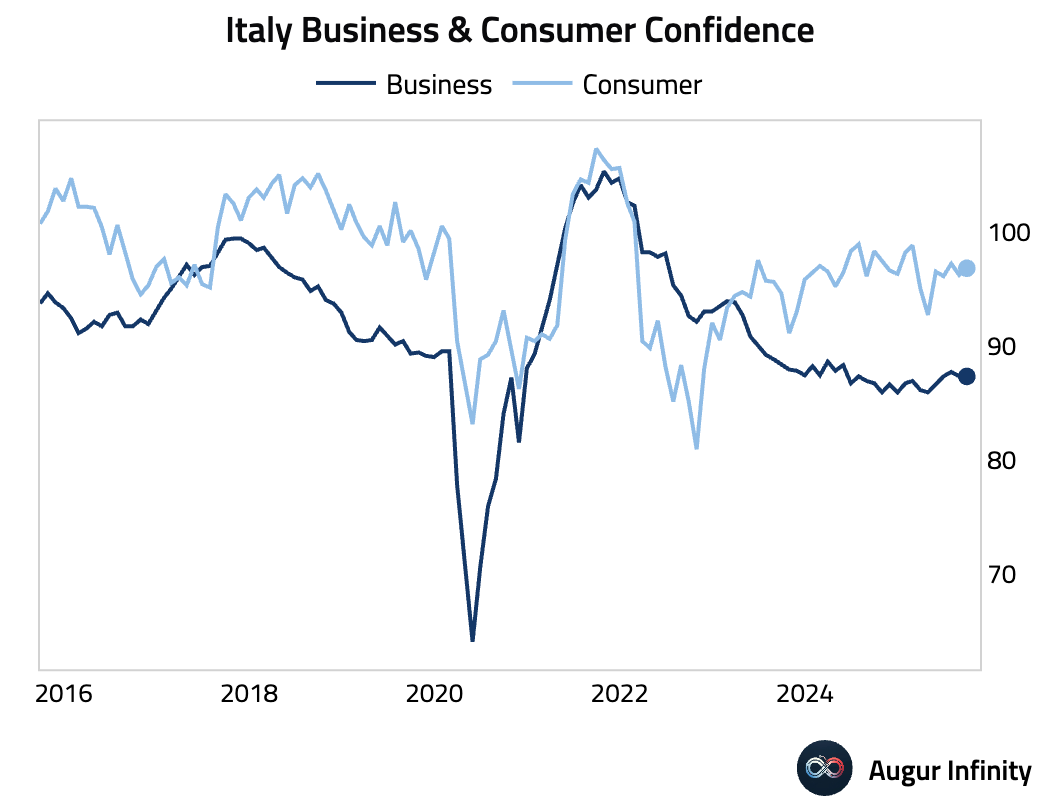

- Italian consumer confidence improved in September, rising slightly more than expected (act: 96.8, est: 96.5), while business sentiment was unchanged and marginally missed estimates (act: 87.3, est: 87.5).

Interactive chart on Augur Infinity

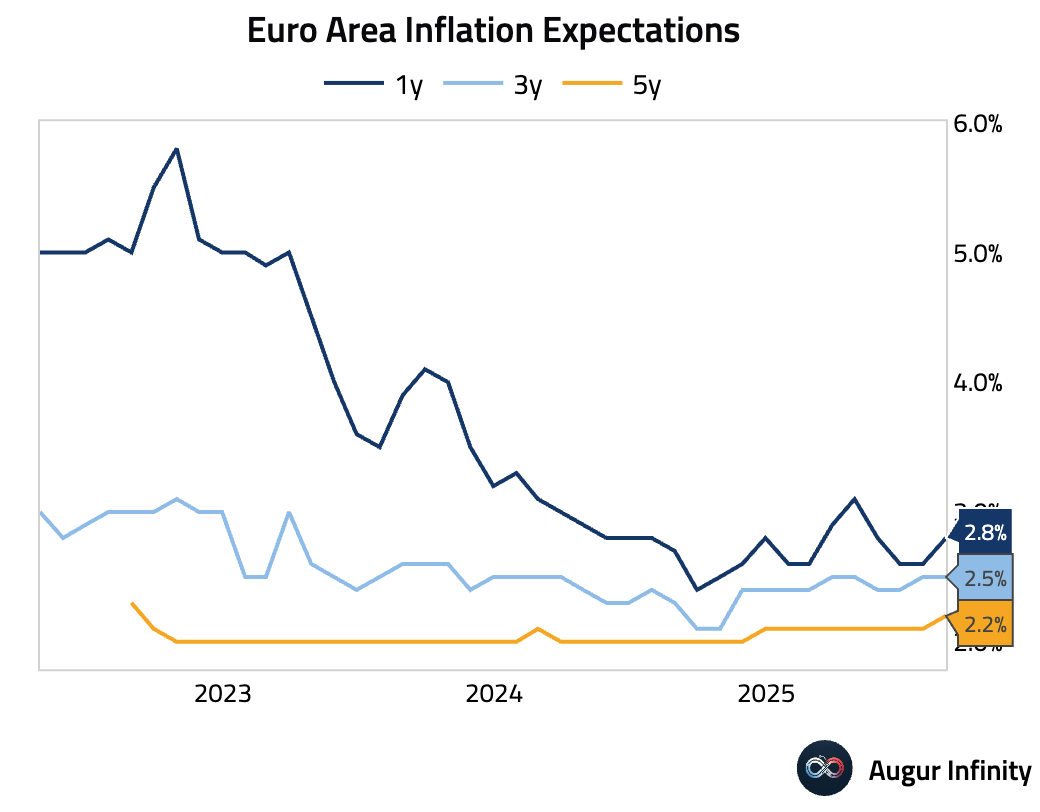

- Euro Area consumer inflation expectations for the next 12 months rose to 2.8% in August from 2.6% in July, moving further away from the ECB’s 2% target.

Interactive chart on Augur Infinity

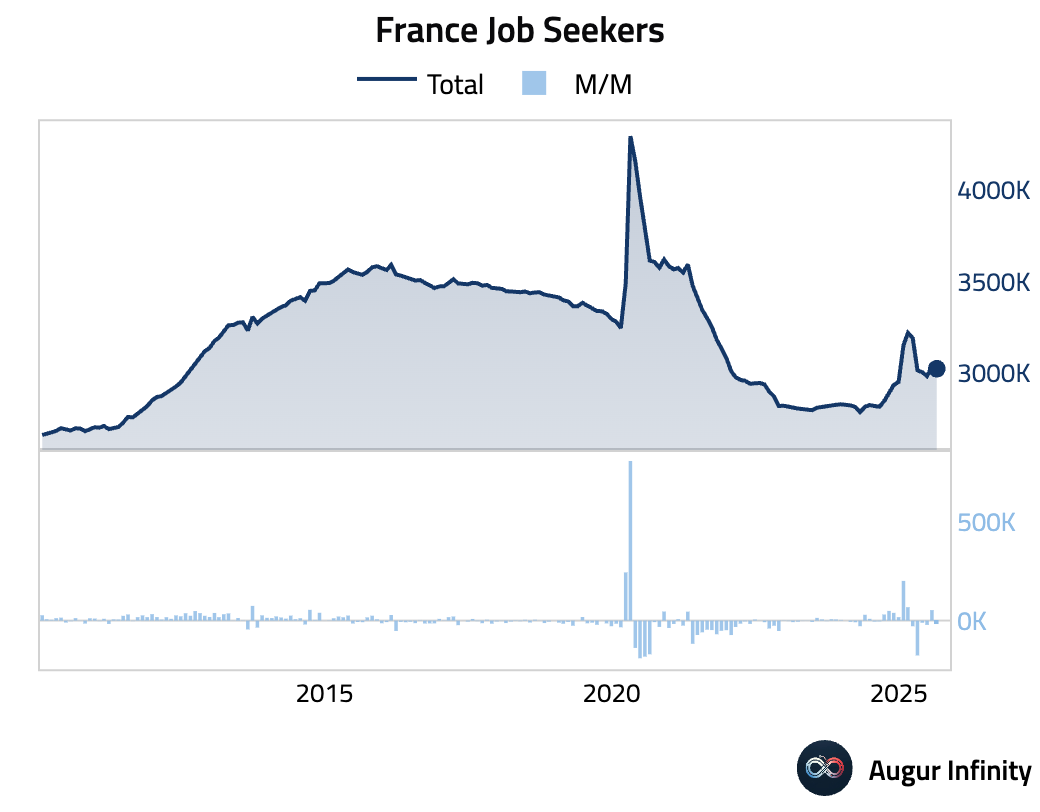

- The French labor market showed signs of improvement as the number of jobseekers fell in August, reversing a sharp increase from the prior month. Unemployment benefit claims decreased by 11,700, while the total number of jobseekers declined to 3.02 million.

Interactive chart on Augur Infinity

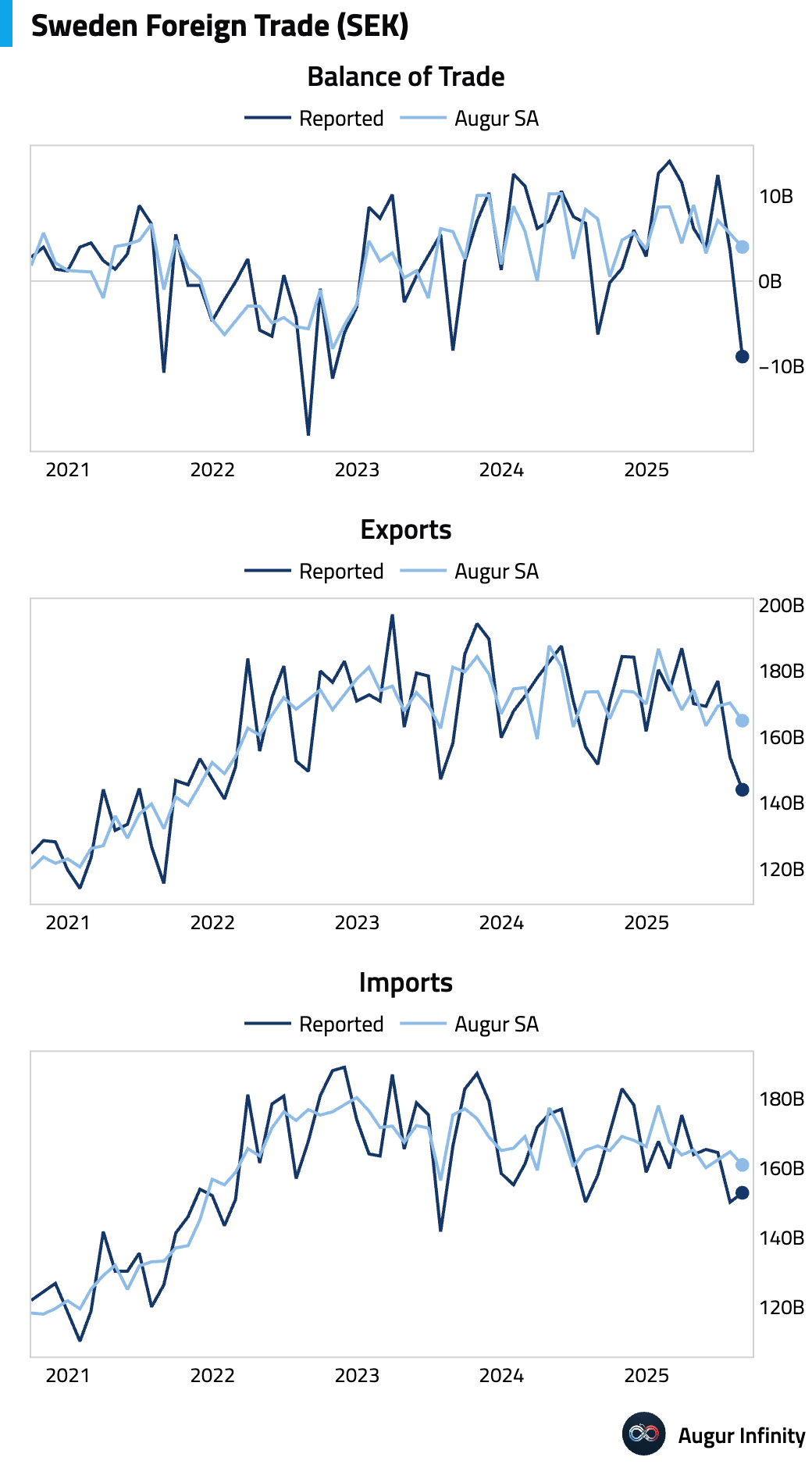

- Sweden's trade balance swung to a deficit in August from a surplus in July (act: -8.9B, prev: 3.6B), reaching its worst level in nearly three years.

Interactive chart on Augur Infinity

Asia-Pacific

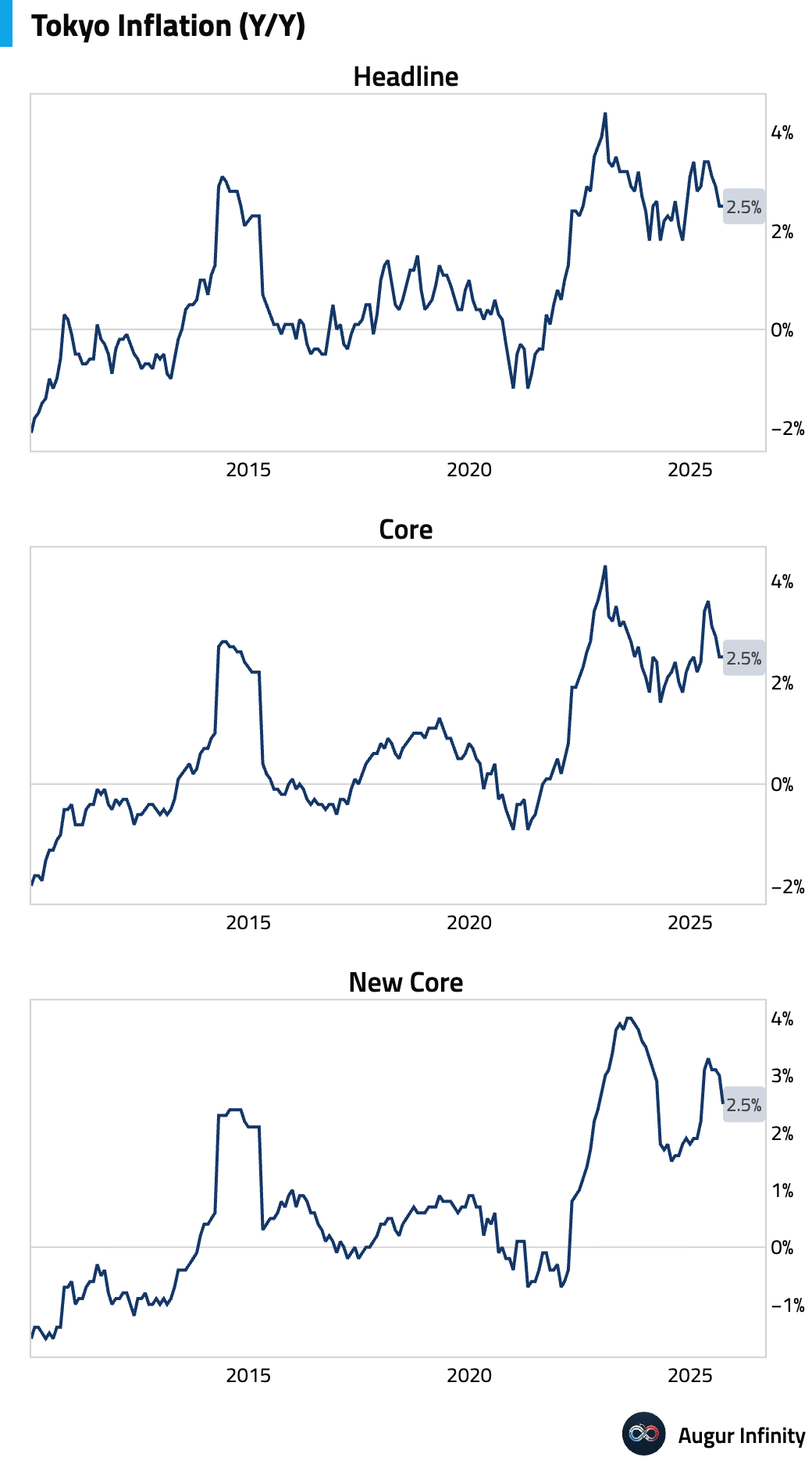

- Tokyo’s core inflation (ex-fresh food) was 2.5% Y/Y in September, below the 2.8% consensus, while headline inflation was also 2.5% Y/Y. The core-core rate (ex-food and energy) decelerated sharply to 2.5% from 3.0%, largely due to a one-off factor: a new free childcare policy in Tokyo. Excluding this distortion, underlying inflation is estimated to be significantly stronger at around 3.0% Y/Y.

Interactive chart on Augur Infinity

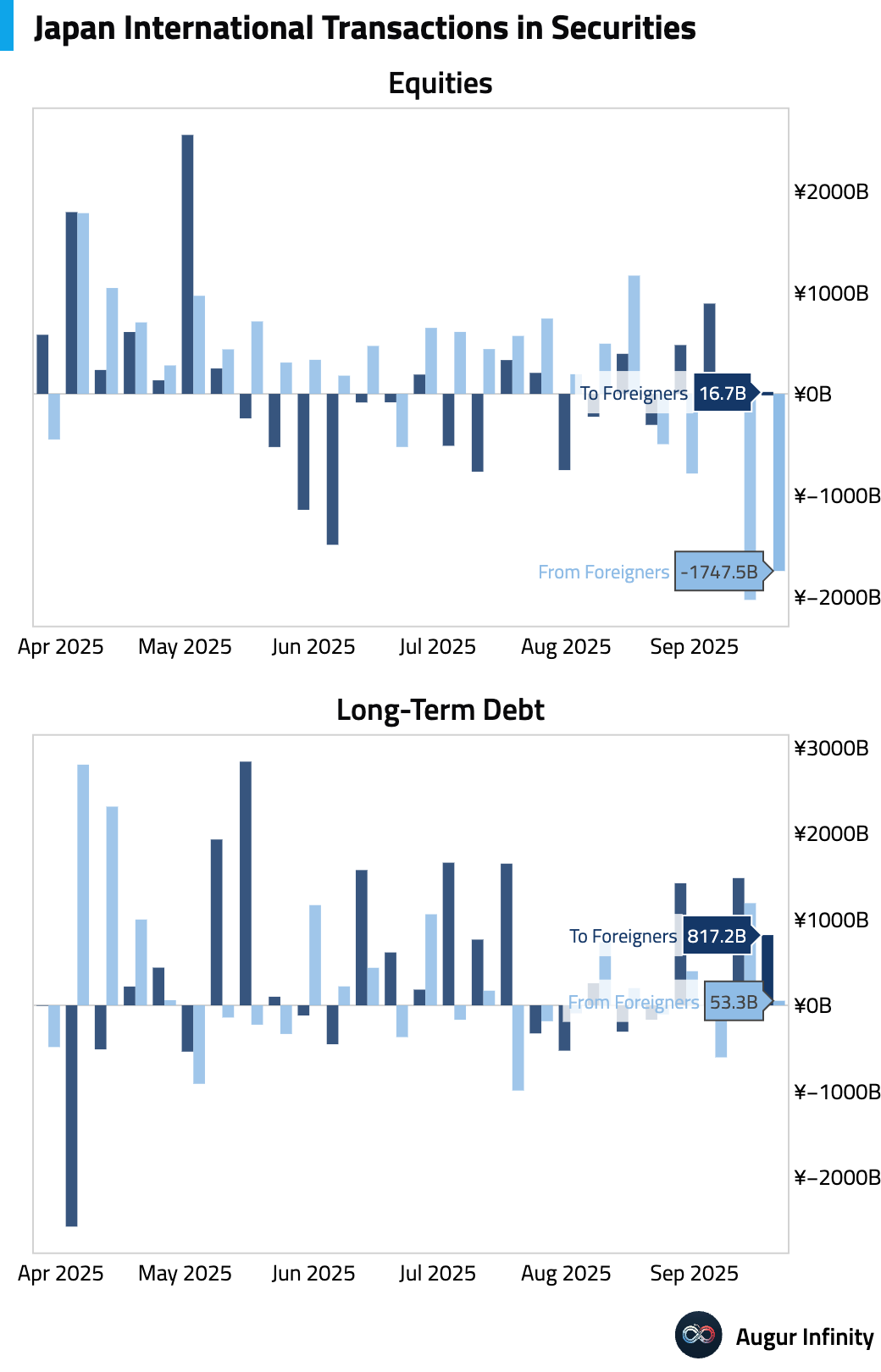

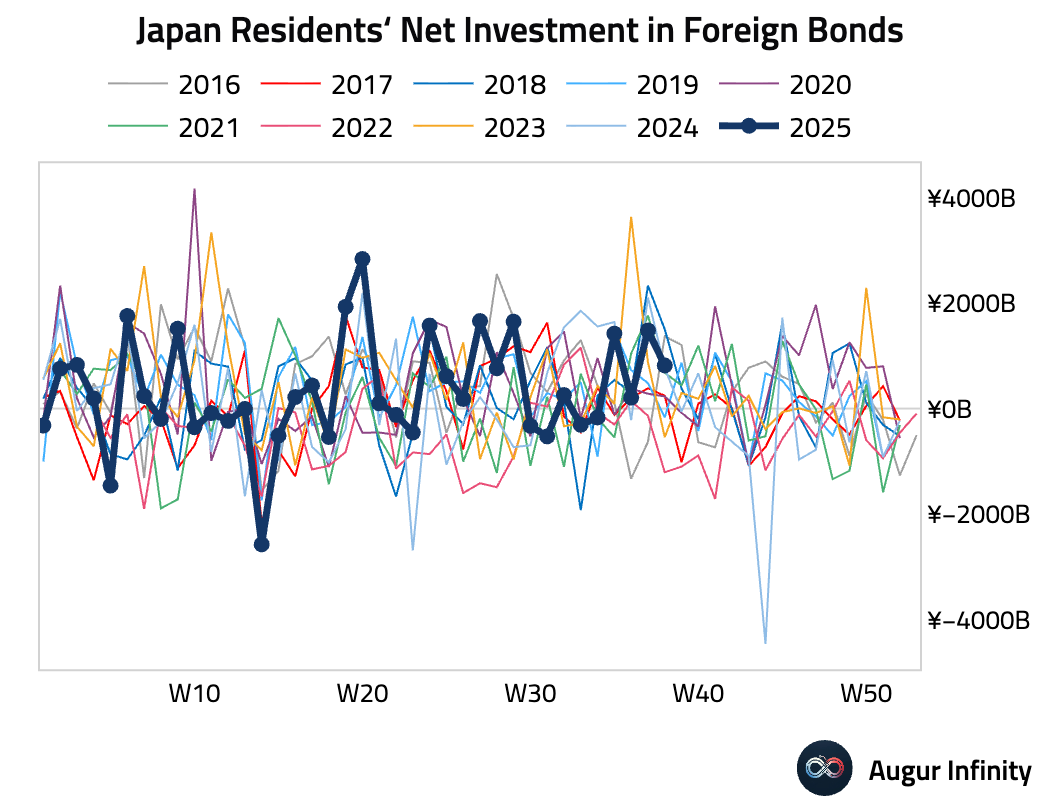

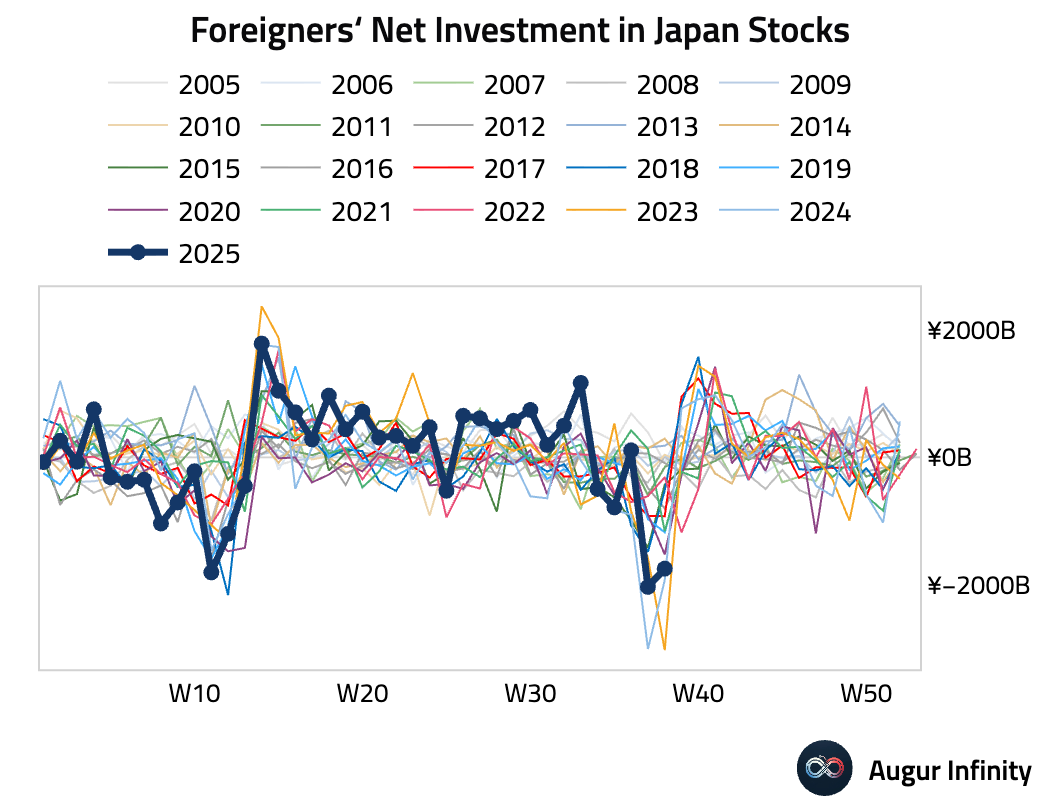

- Japanese investors continued to purchase foreign bonds last week, though at a slower pace, while foreign investors moderated their selling of Japanese stocks.

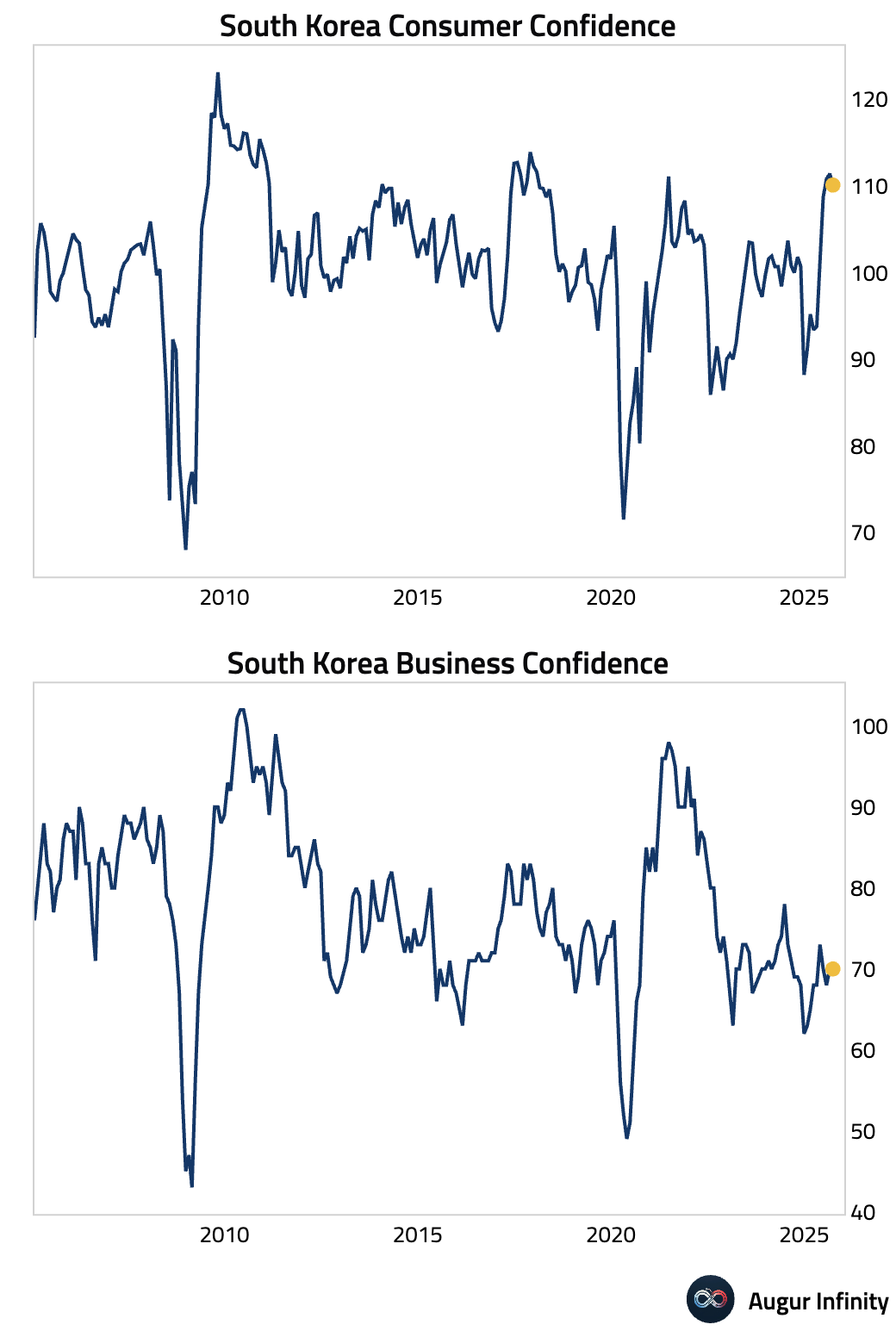

- South Korean business confidence was unchanged in September (act: 70, prev: 70), remaining at pessimistic levels.

Interactive chart on Augur Infinity

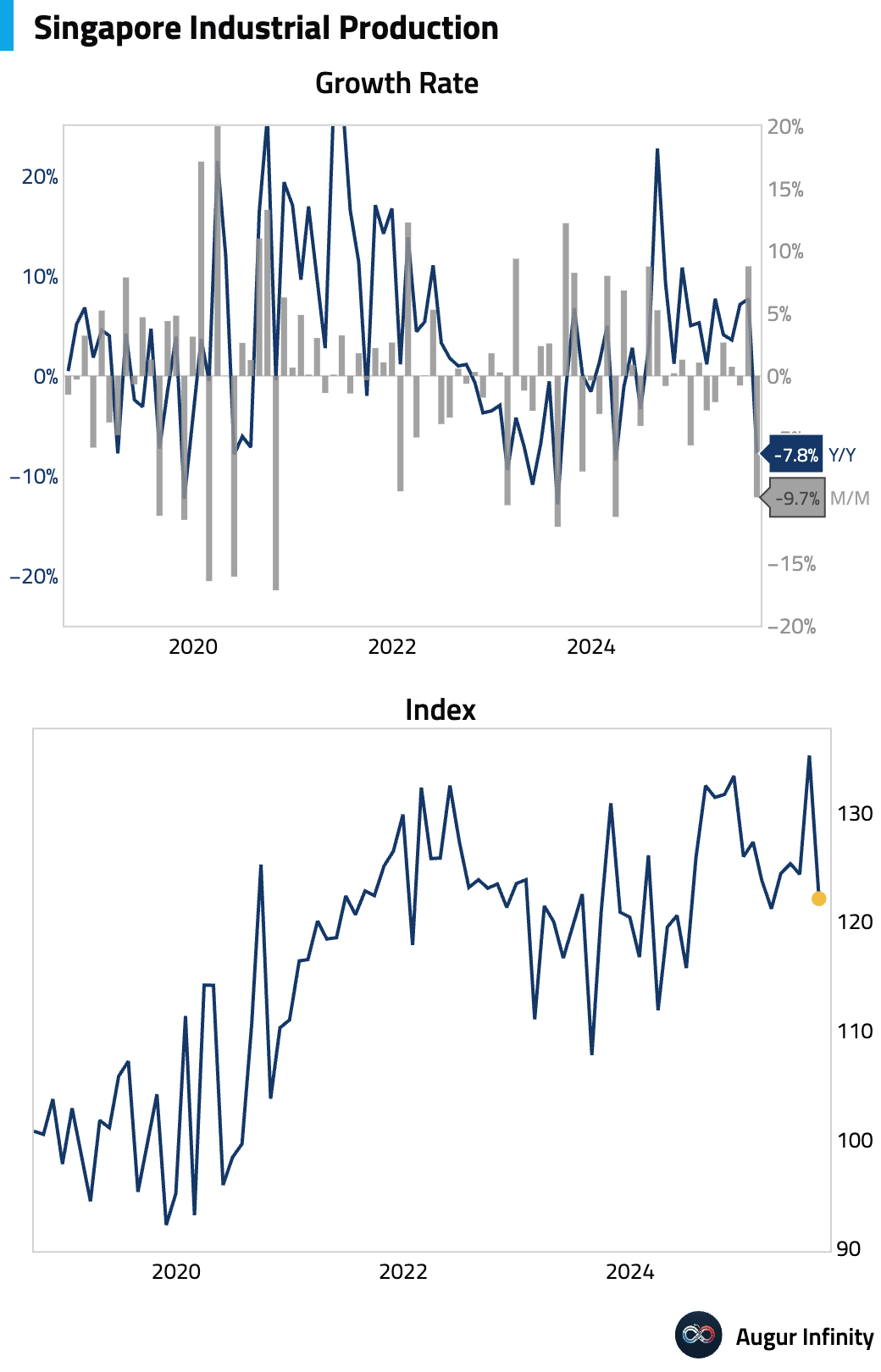

- Singapore's industrial production plunged unexpectedly in August, falling 9.7% M/M and 7.8% Y/Y. The results were significantly worse than consensus estimates of -4.6% M/M and -2.5% Y/Y, respectively, signaling a sharp downturn in the manufacturing sector.

Interactive chart on Augur Infinity

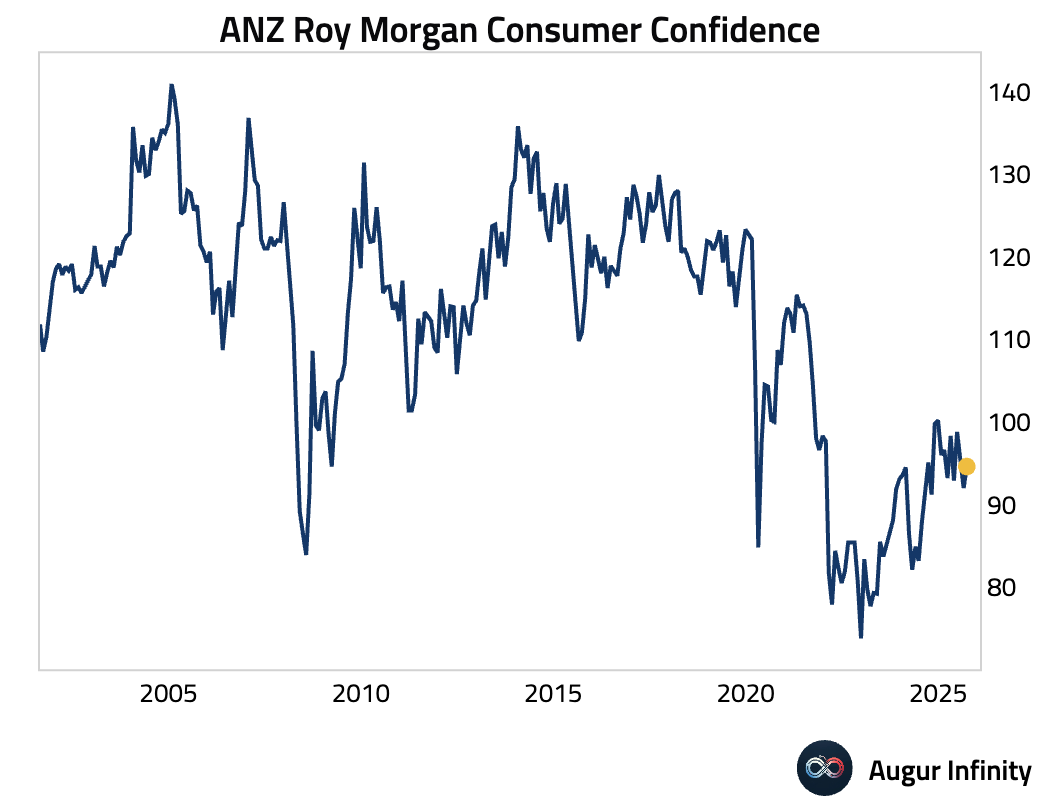

- New Zealand consumer confidence improved in September but remains subdued (act: 94.6, prev: 92.0).

Emerging Markets ex China

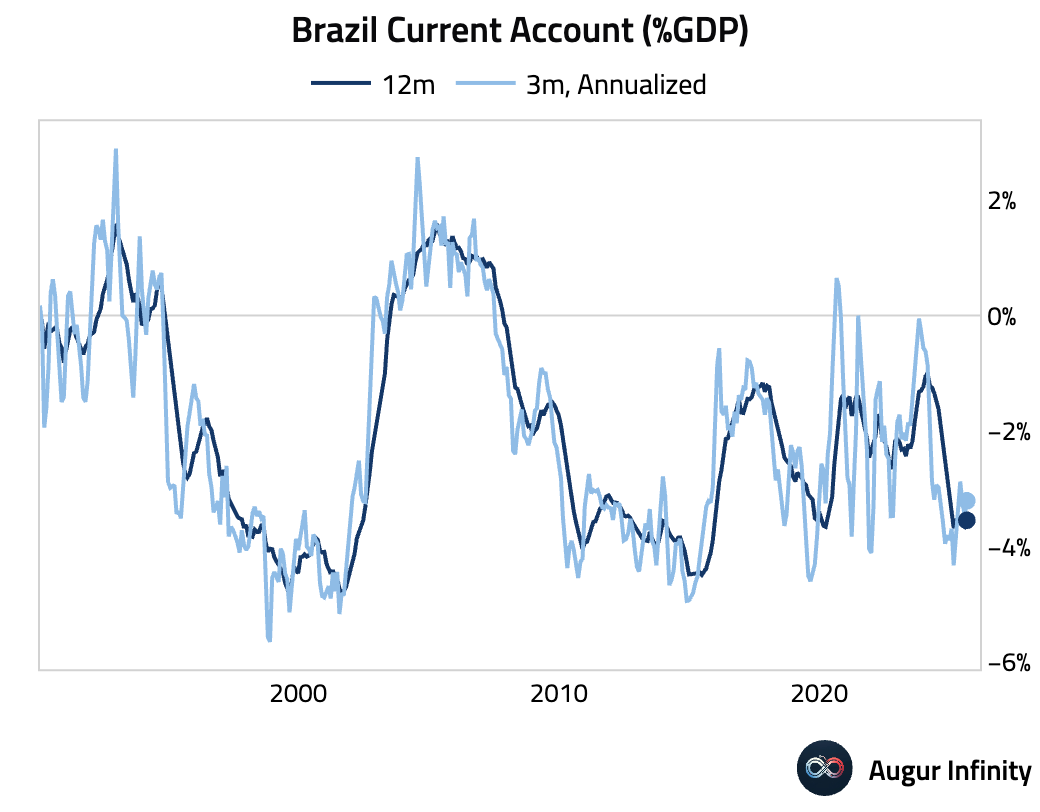

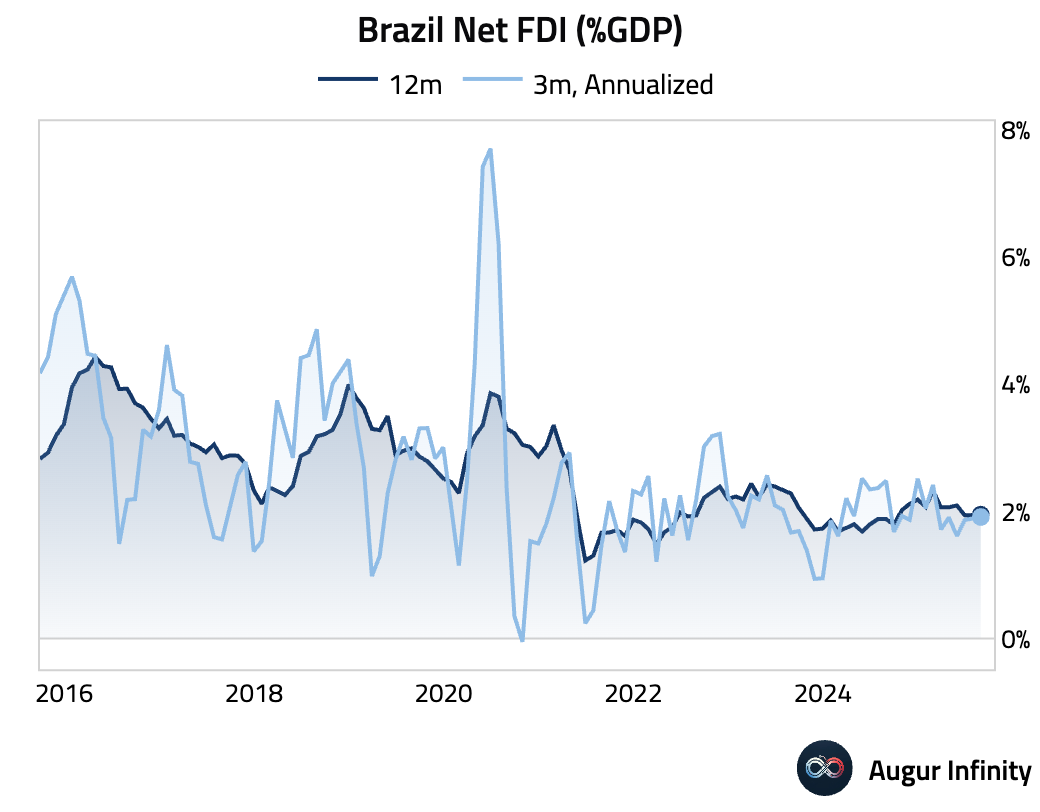

- Brazil’s current account deficit narrowed more than expected in August (act: -$4.7B, est: -$5.4B), helped by a strong trade surplus. Foreign direct investment remained robust, easily beating consensus (act: $8.0B, est: $6.1B). However, the improving headline numbers mask a deteriorating underlying trend; on a 12-month rolling basis, FDI no longer fully covers the current account deficit, signaling increasing external vulnerability due to loose fiscal policy.

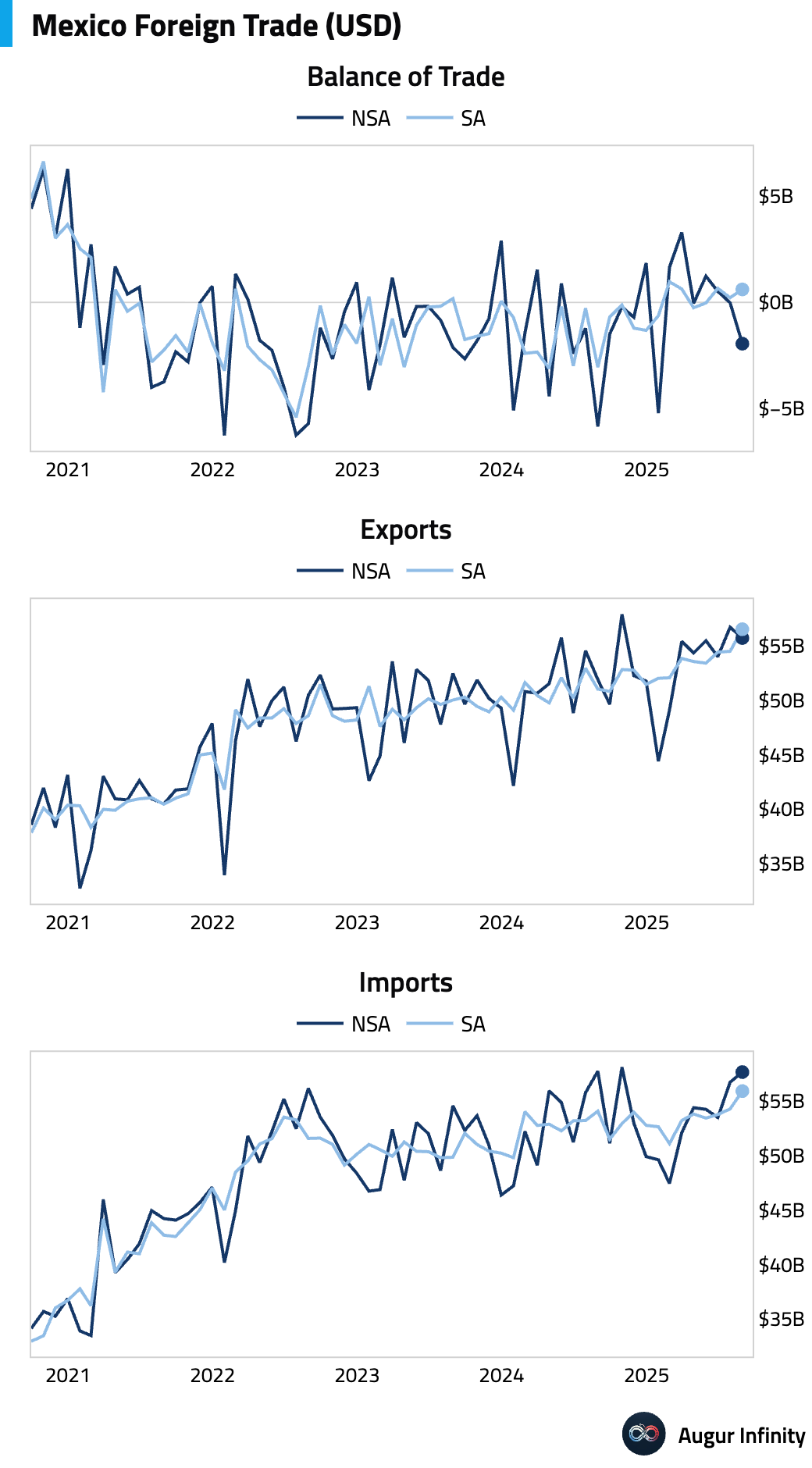

- Mexico’s trade deficit widened in August but was much smaller than anticipated (act: -$1.94B, est: -$2.60B). The beat was driven by strong manufacturing exports, although a seventh consecutive monthly decline in capital goods imports points to softening business investment.

Interactive chart on Augur Infinity

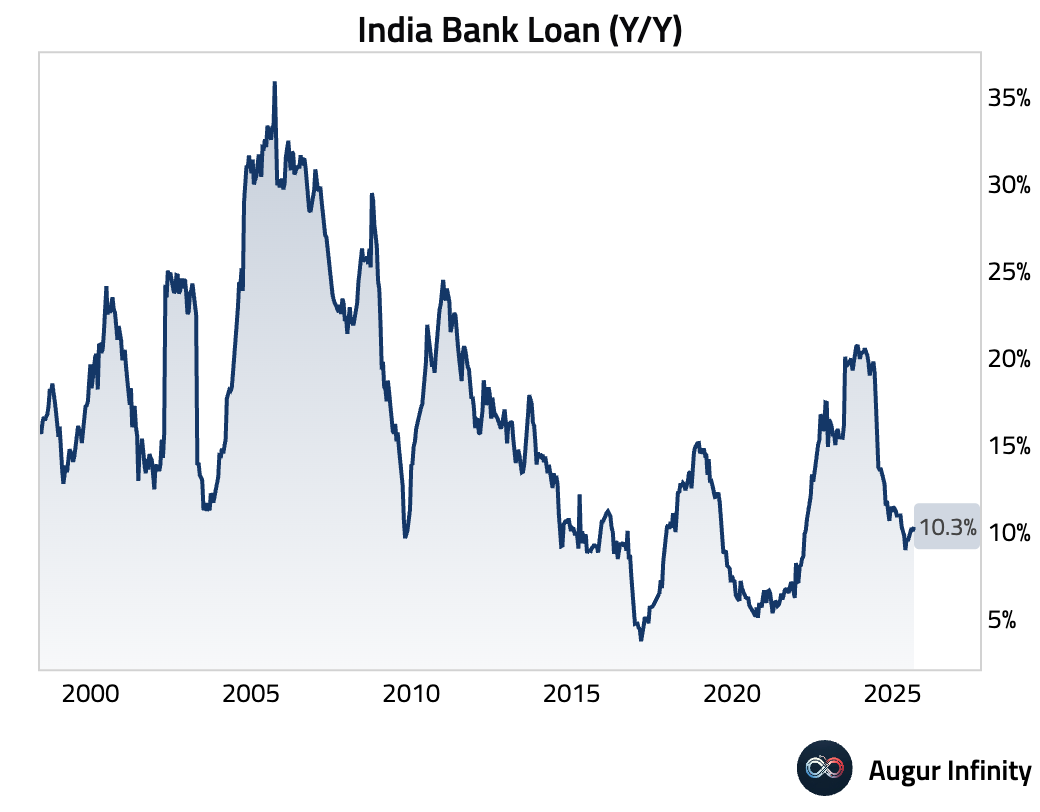

- Bank loan growth in India accelerated slightly in early September (act: 10.3% Y/Y, prev: 10.0%).

Interactive chart on Augur Infinity

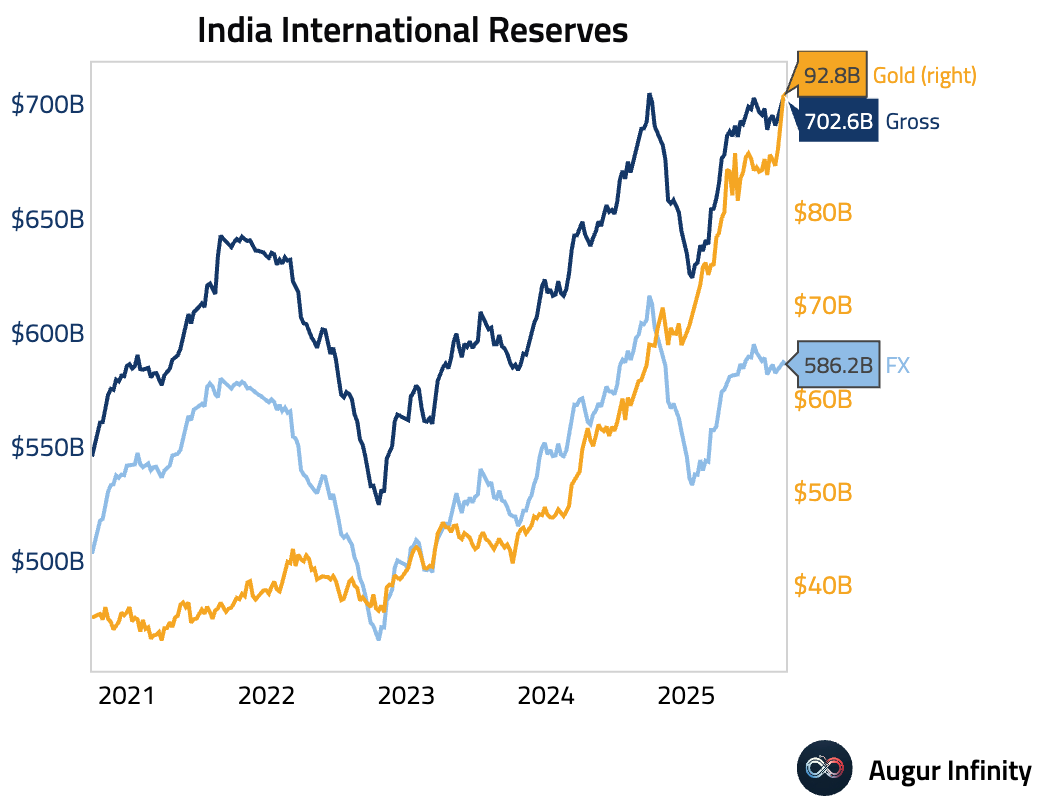

- India's foreign exchange reserves edged down last week (act: $702.57B, prev: $702.97B).

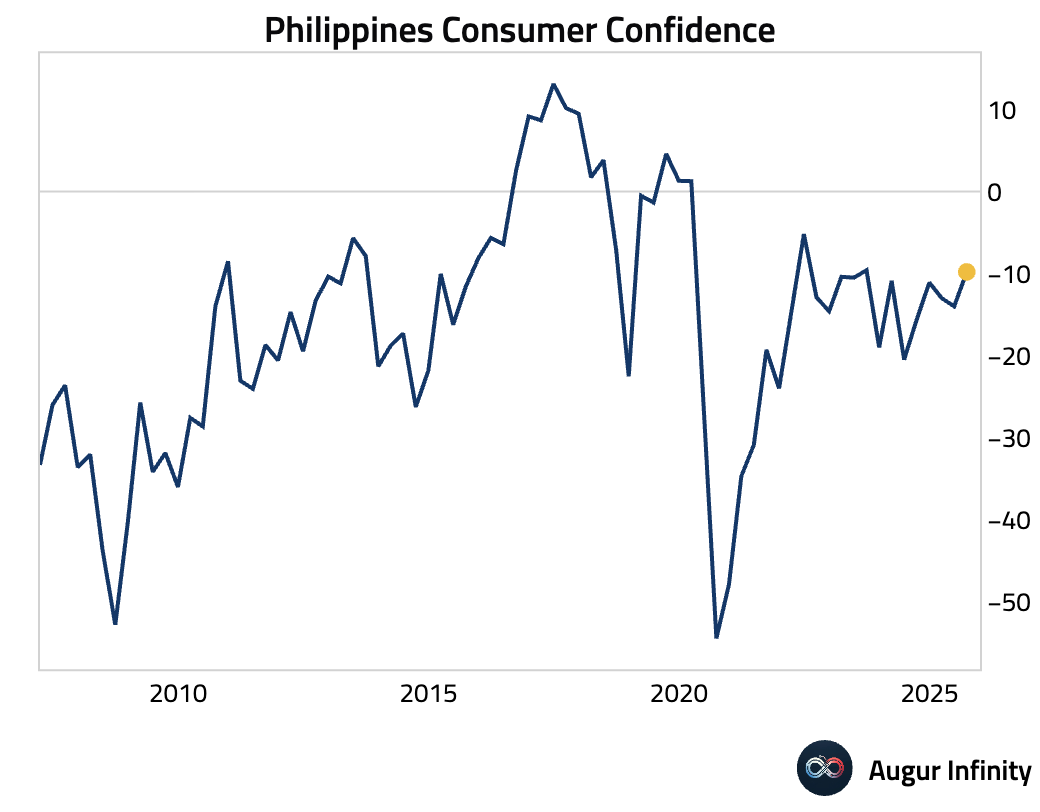

- Consumer confidence in the Philippines improved in the third quarter but remained deeply pessimistic (act: -9.8, prev: -14.0).

Interactive chart on Augur Infinity

Global Markets

Equities

- US equities advanced 0.6% on Friday, shrugging off the announcement of new tariffs. European markets posted stronger gains, with Germany, France, and the United Kingdom all rising by more than 1%. In contrast, emerging markets fell 0.2%, marking a fourth consecutive day of losses.

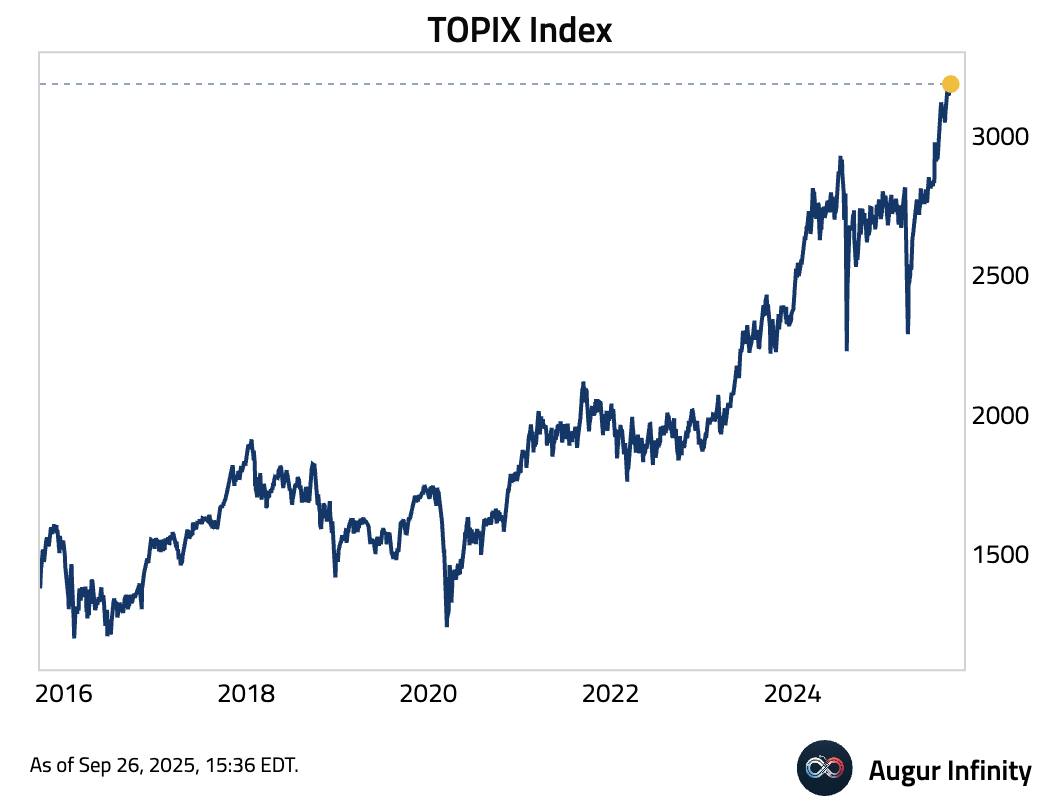

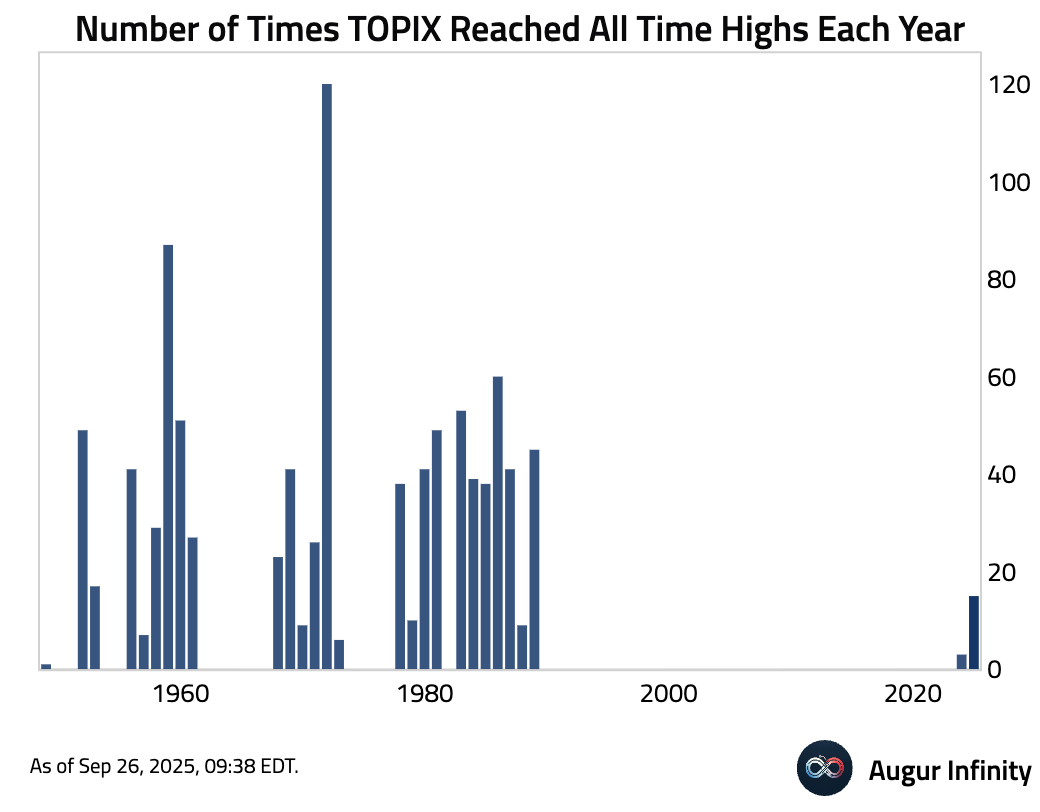

- The TOPIX Index has reached its 15th all-time high of the year.

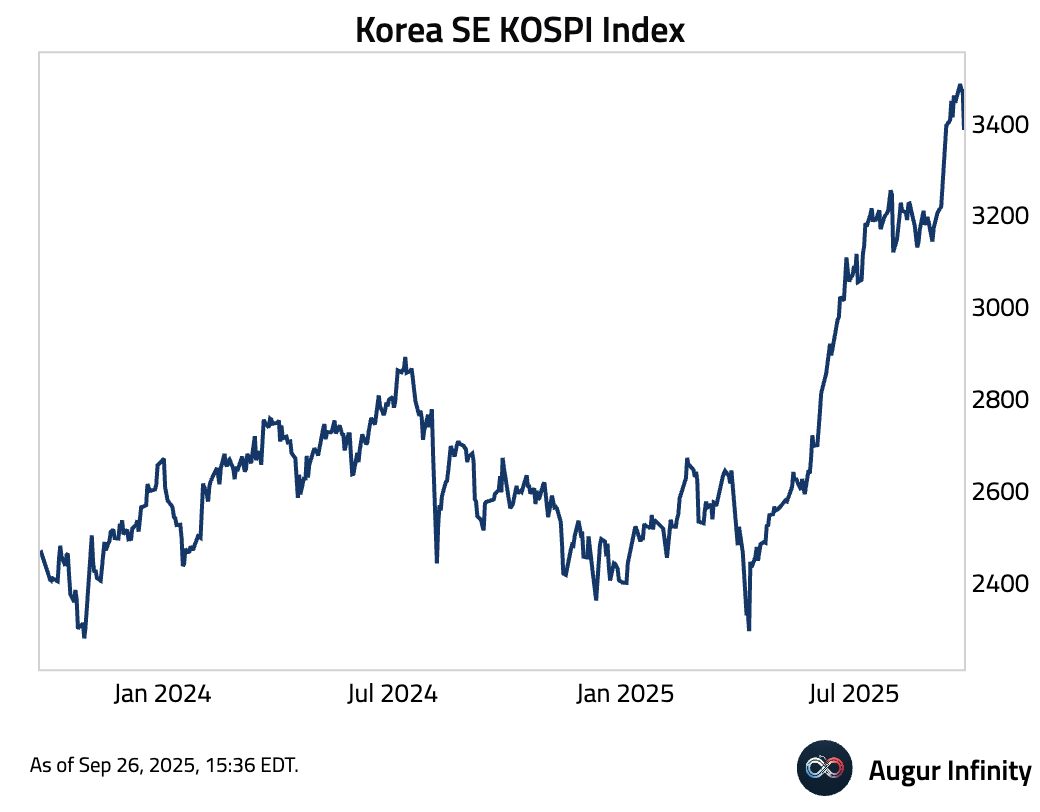

- Korea's KOSPI Index sold off by 2.5% today.

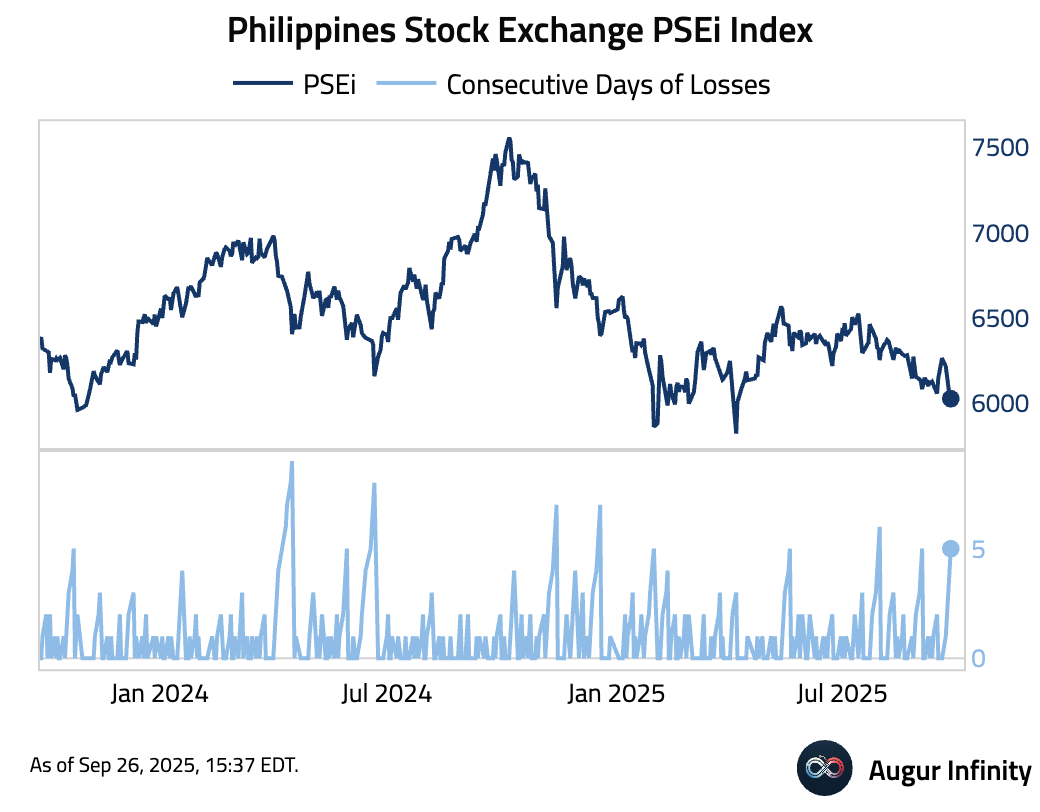

- Philippines Stock Exchange PSEi Index registered its fifth consecutive day of losses, closing at the lowest level since April.

Fixed Income

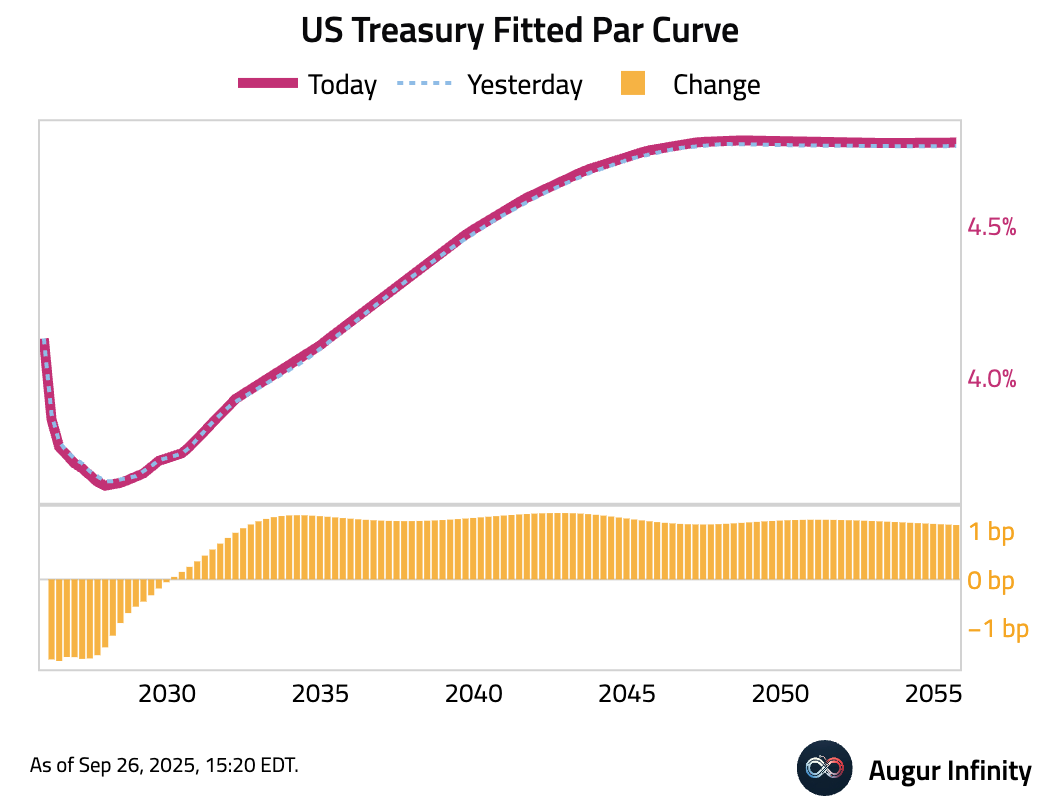

- The US Treasury curve bear-steepened as yields on the front-end declined while the belly and long-end rose. The 2-year yield fell 1.7 bps, while the 5-year and 10-year yields increased by 0.1 bps and 1.0 bps, respectively.

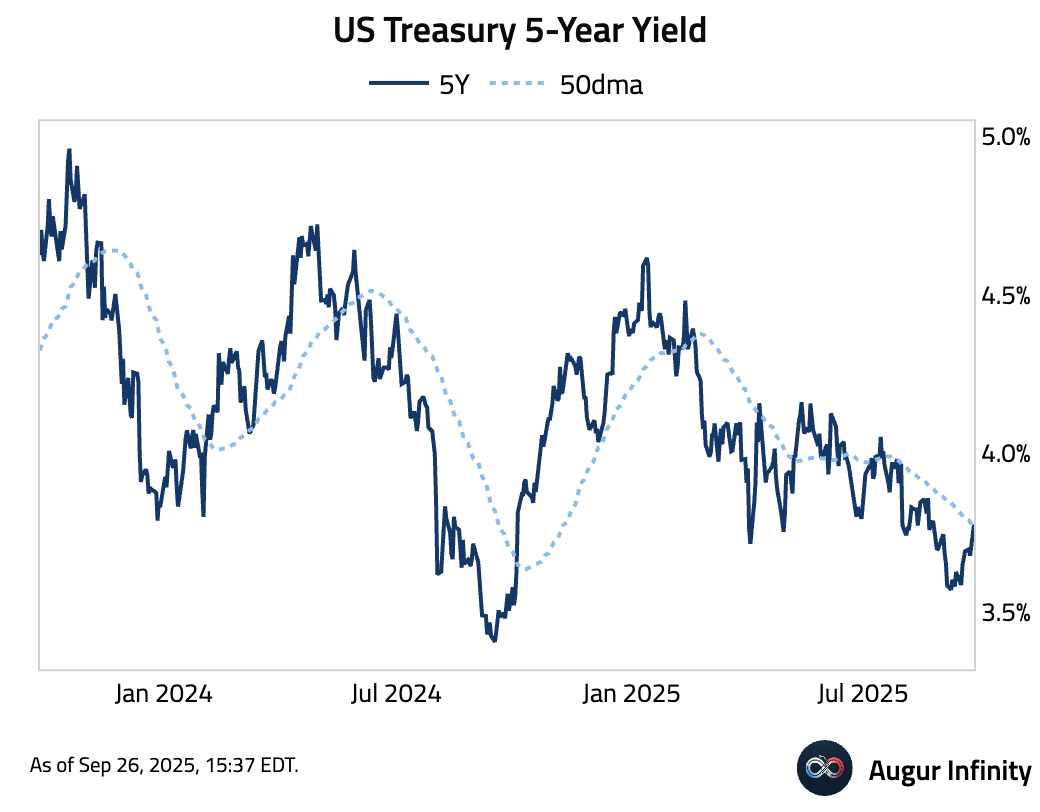

- US Treasury 5-year yield moved above its 50-day moving average.

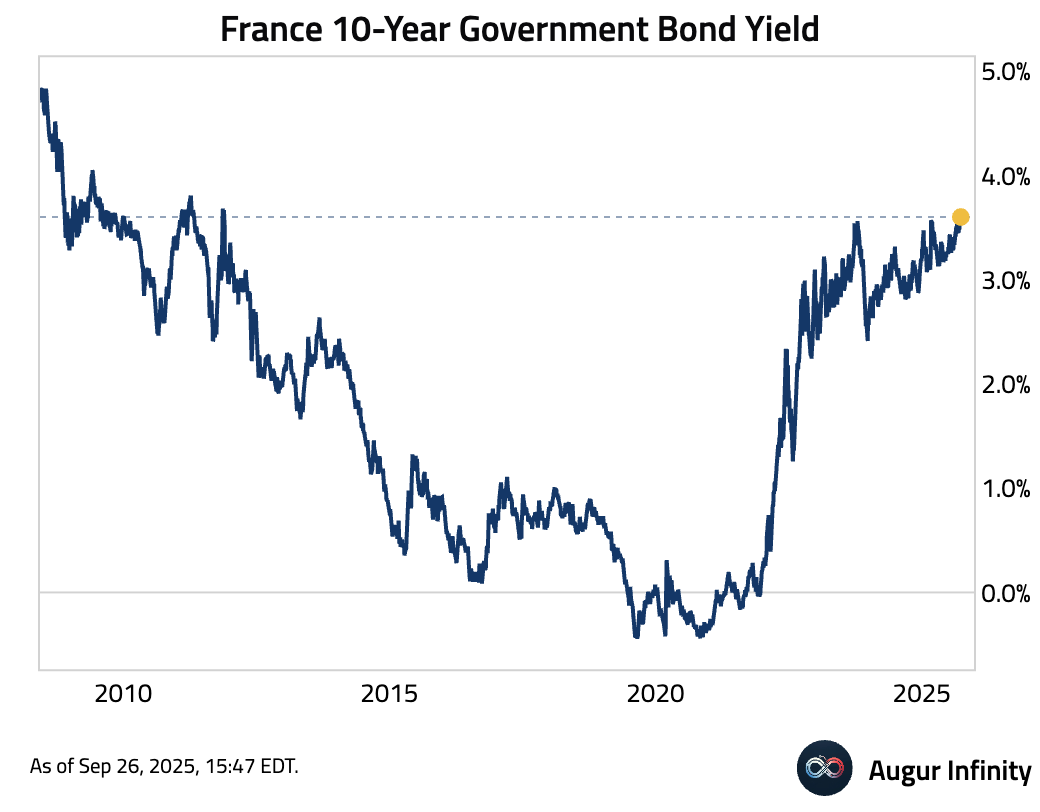

- France 10-year bond yield is at the highest level since November 2011.

FX

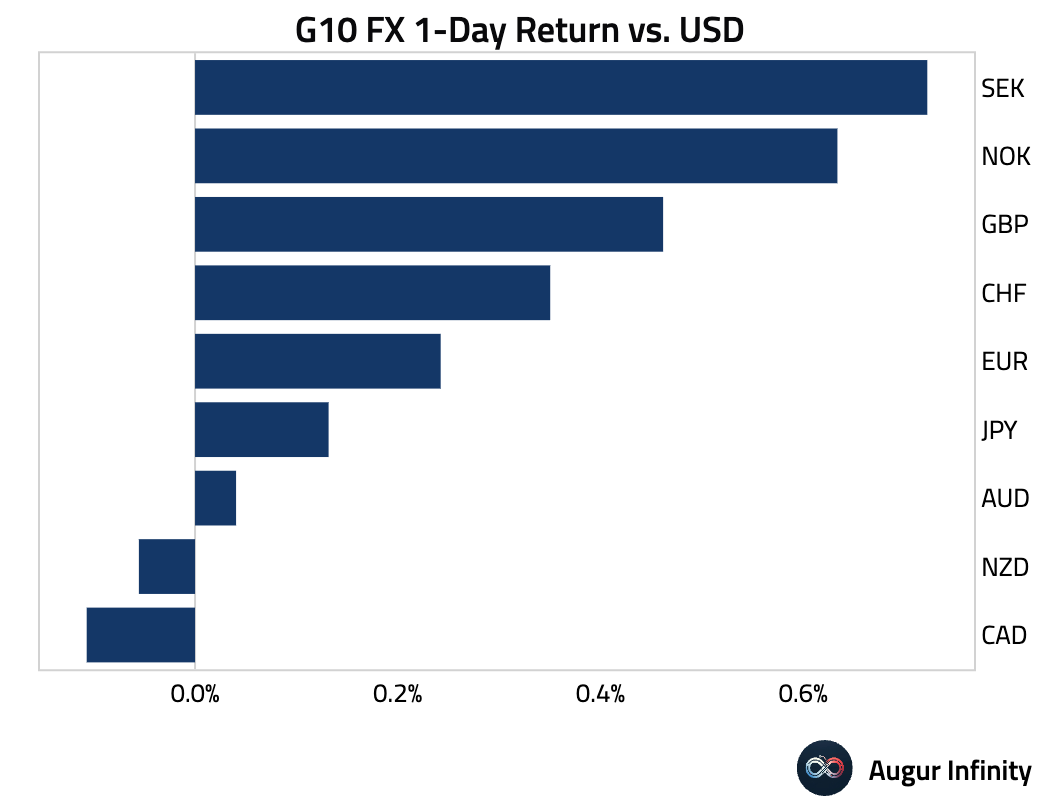

- The US dollar weakened against most G10 currencies, led by the Swedish krona (+0.7%) and Norwegian krone (+0.6%). The British pound also gained 0.5%. The Canadian and New Zealand dollars were notable underperformers, with the CAD extending its losing streak to five days and the NZD falling for an eighth consecutive session.

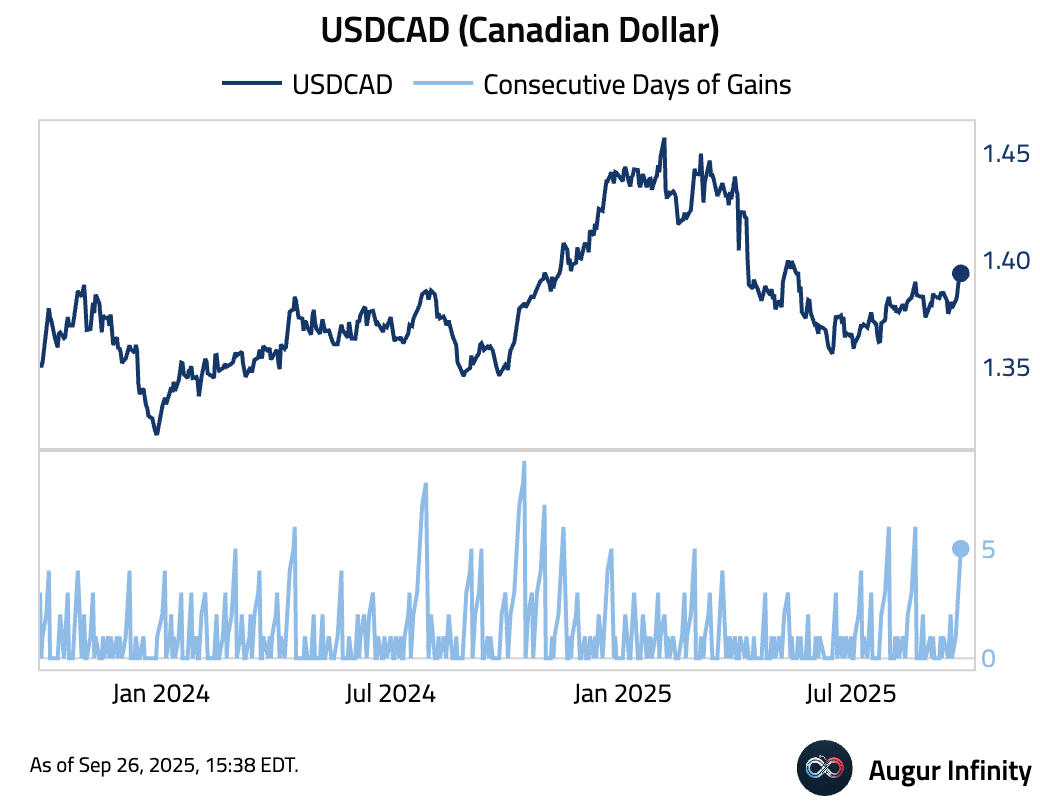

- The Canadian dollar has depreciated against USD for five consecutive sessions.

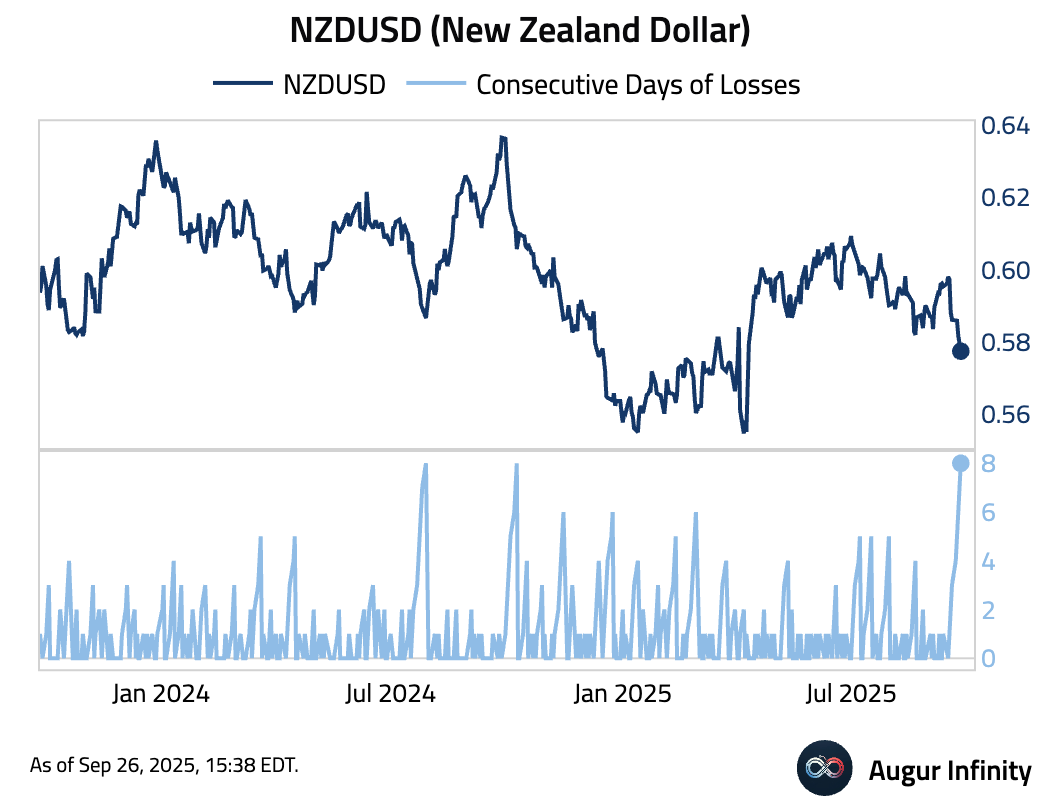

- The New Zealand dollar weakened for the eighth session against the dollar.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.