Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- The US Senate is scheduled to vote on a continuing resolution to fund the government, with a potential shutdown looming on October 1.

- France is reportedly considering an increase to its flat tax as part of the country’s upcoming budget proposal.

- The Spanish government lowered its net debt issuance target for the year by €5 billion, citing stronger-than-expected economic growth.

Global Economics

United States

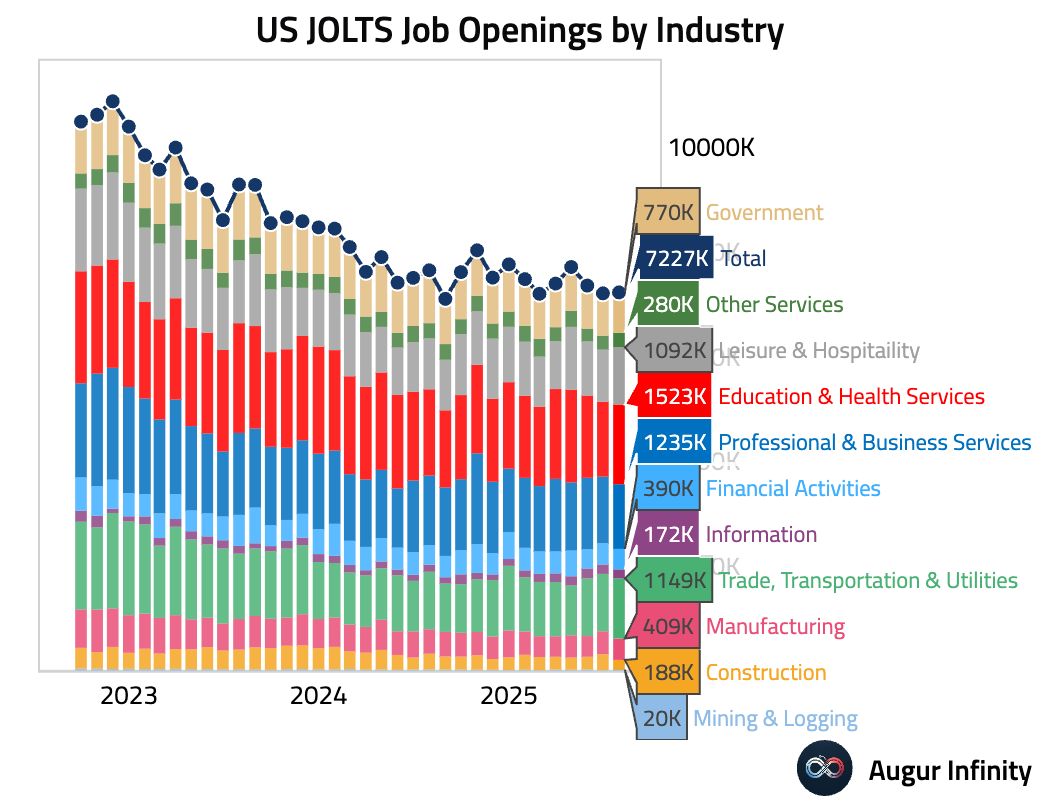

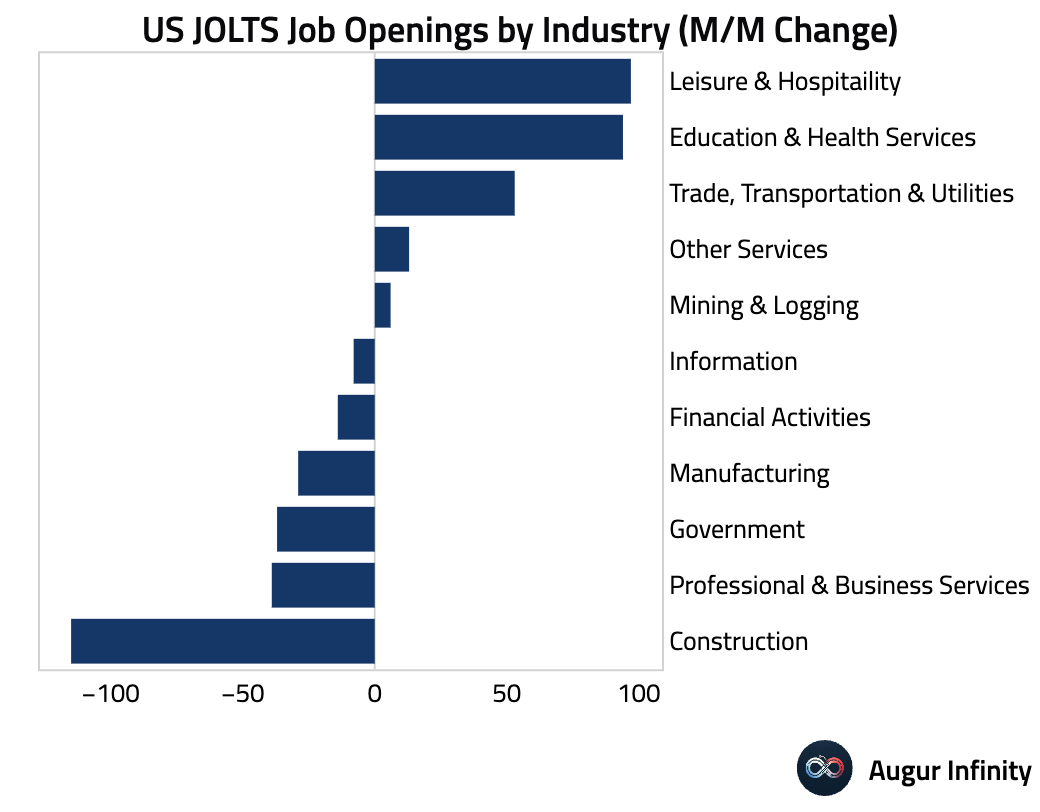

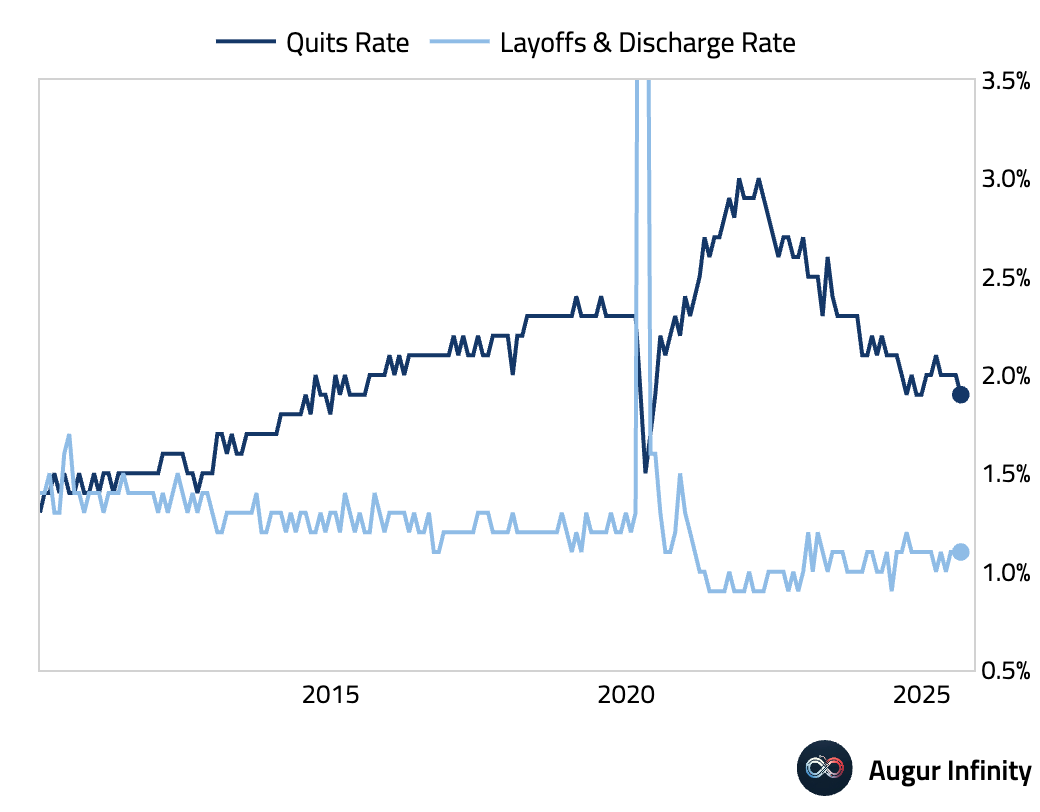

- US JOLTS job openings held steady at 7.2 million, broadly in line with expectations. Job openings increased the most in leisure & hospitality, followed by education & health services, offset by losses in construction and business services. The number of workers quitting their jobs edged down to 3.1 million, with a notable decrease in the accommodation and food services sector.

Interactive chart on Augur Infinity

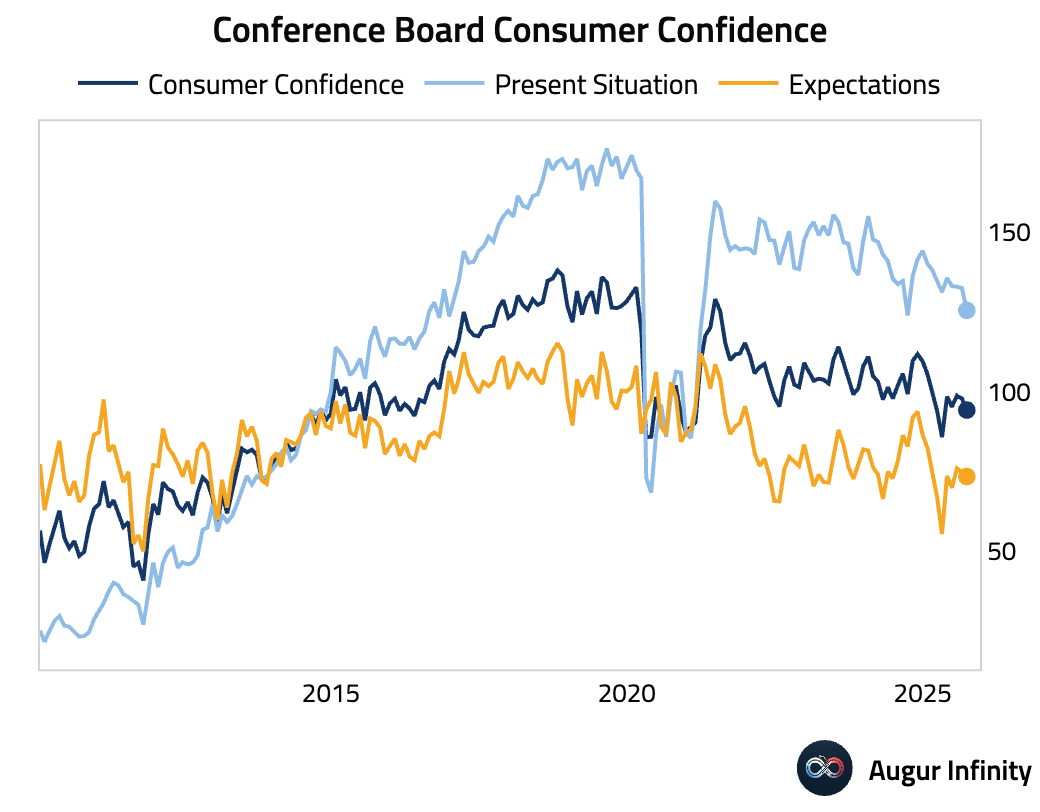

- Consumer confidence unexpectedly weakened in September, with the headline index falling to 94.2, well below the prior month’s 97.4 and consensus expectations of 96.0. The drop was driven by a sharp deterioration in views of the present situation, as consumers’ assessment of job availability hit a new multiyear low. The Expectations Index remains below the recession-warning threshold for the eighth consecutive month, with inflation regaining its position as the top concern for consumers.

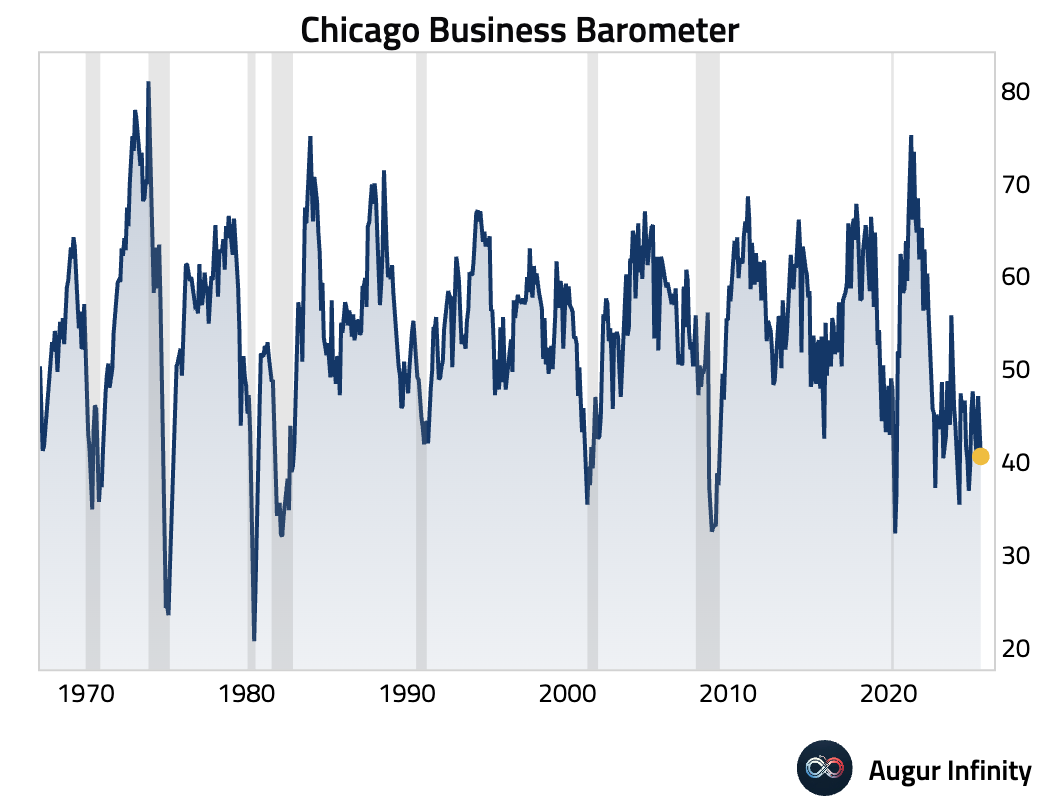

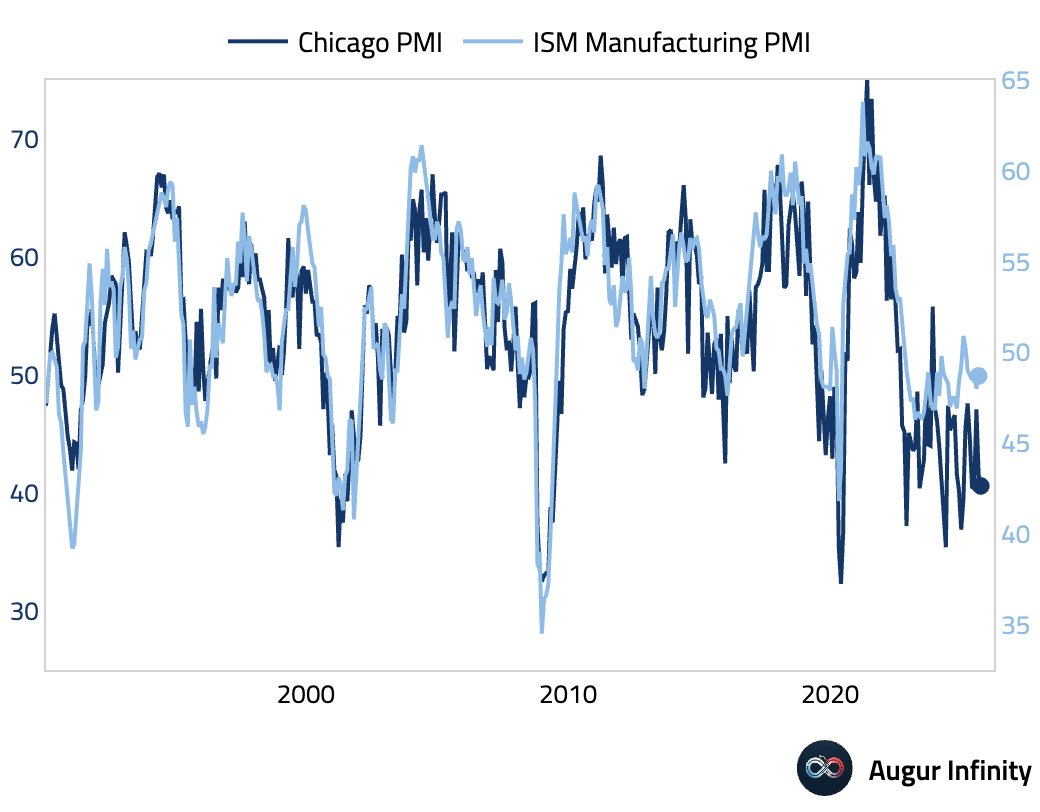

- The Chicago PMI fell to 40.6 in September, missing expectations and indicating a faster pace of contraction in regional manufacturing activity.

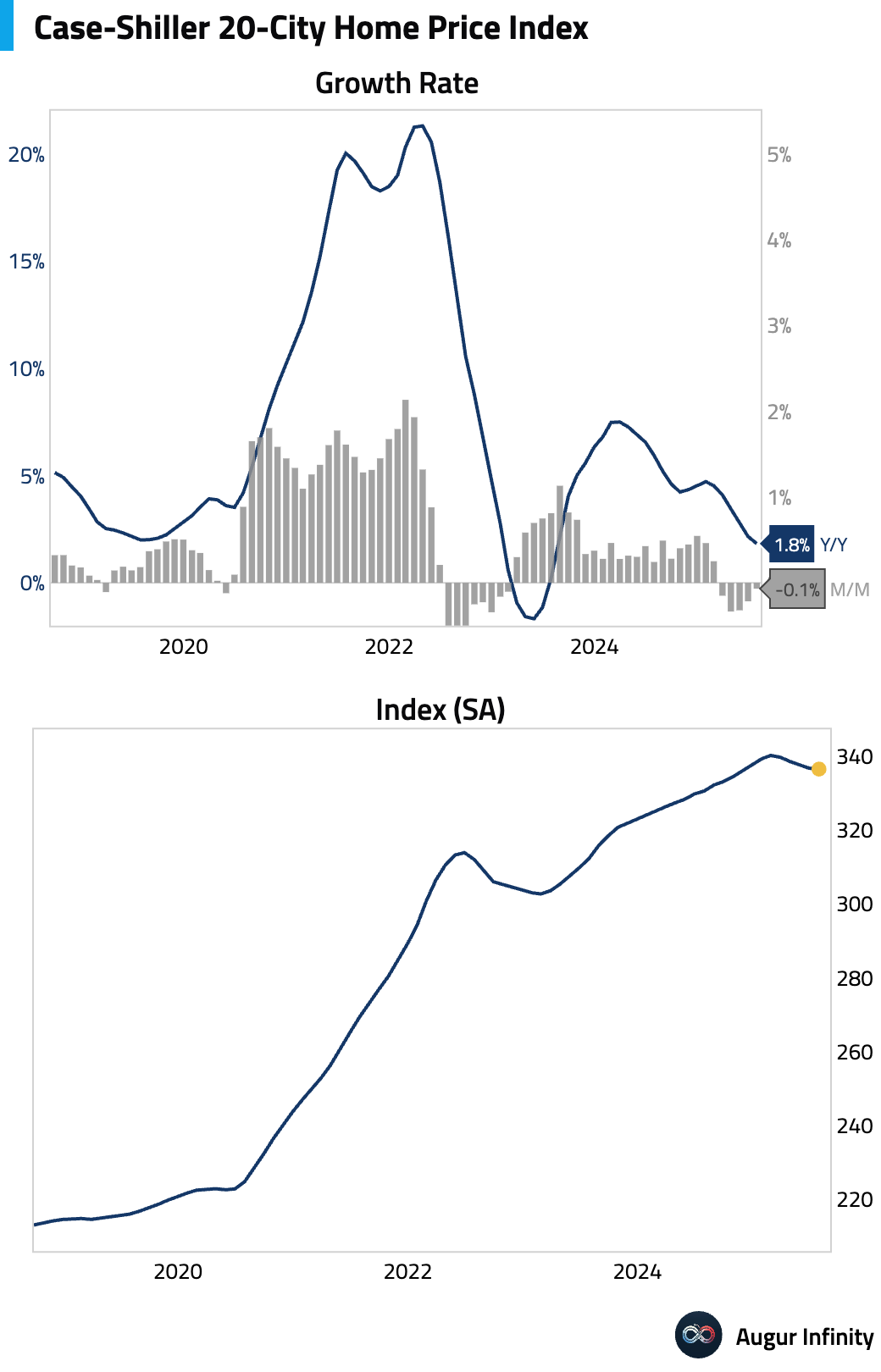

- The S&P/Case-Shiller 20-city home price index rose 1.8% Y/Y in July, above the 1.6% consensus but slowing from the prior month. On a monthly basis, prices fell for the first time in nearly a year.

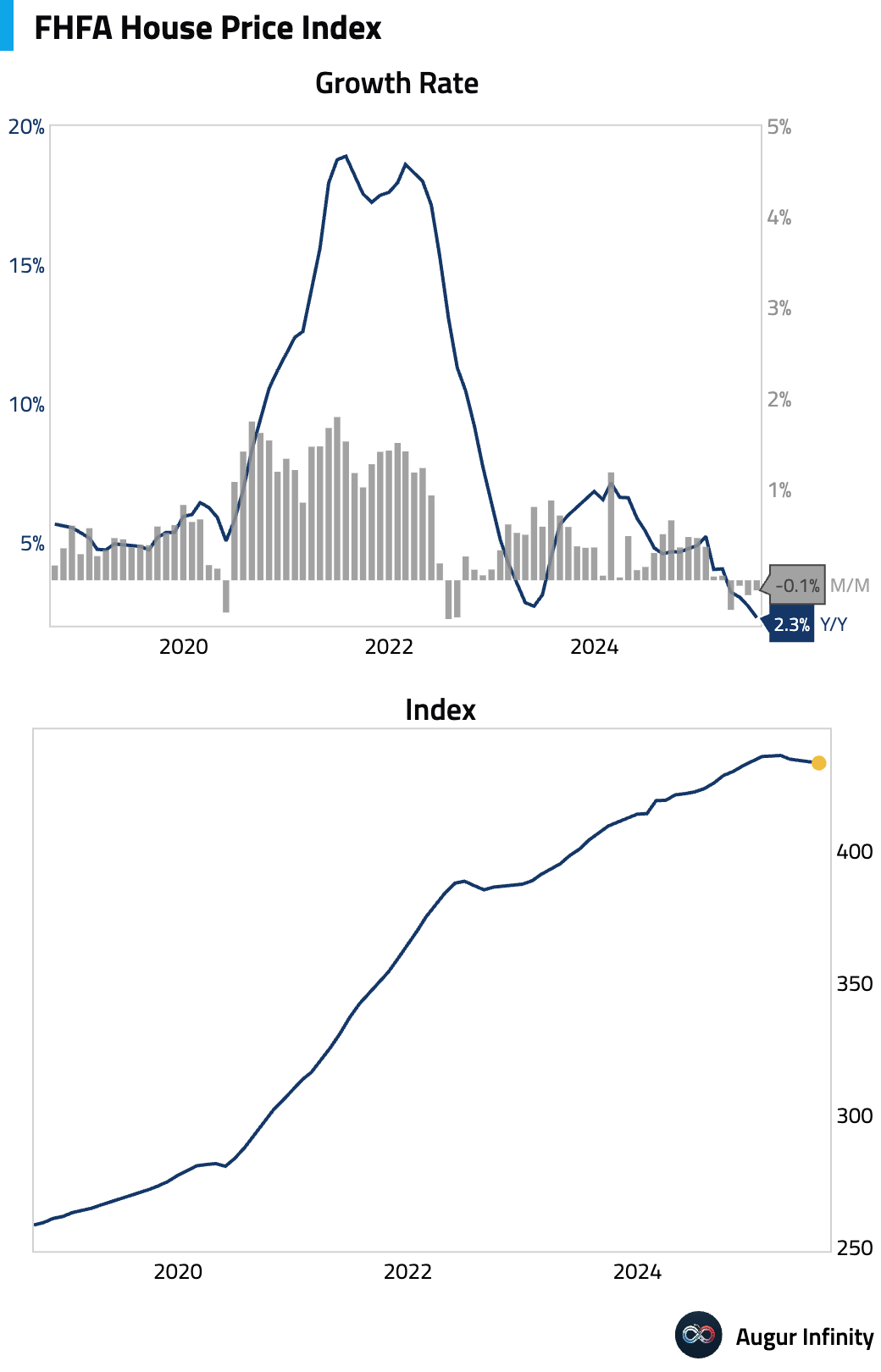

- The FHFA House Price Index showed a modest cooling, with prices falling month-over-month for the second consecutive month in July.

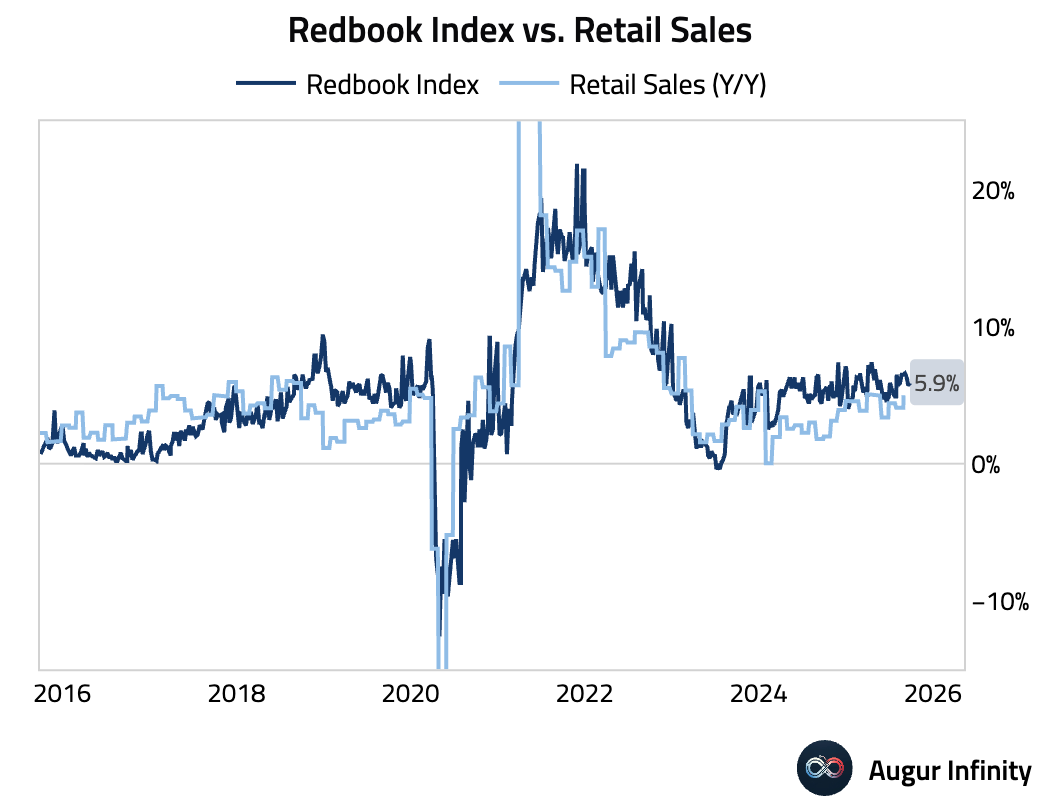

- The Redbook index of same-store sales growth accelerated slightly last week (act: 5.9% Y/Y, prev: 5.7%).

Europe

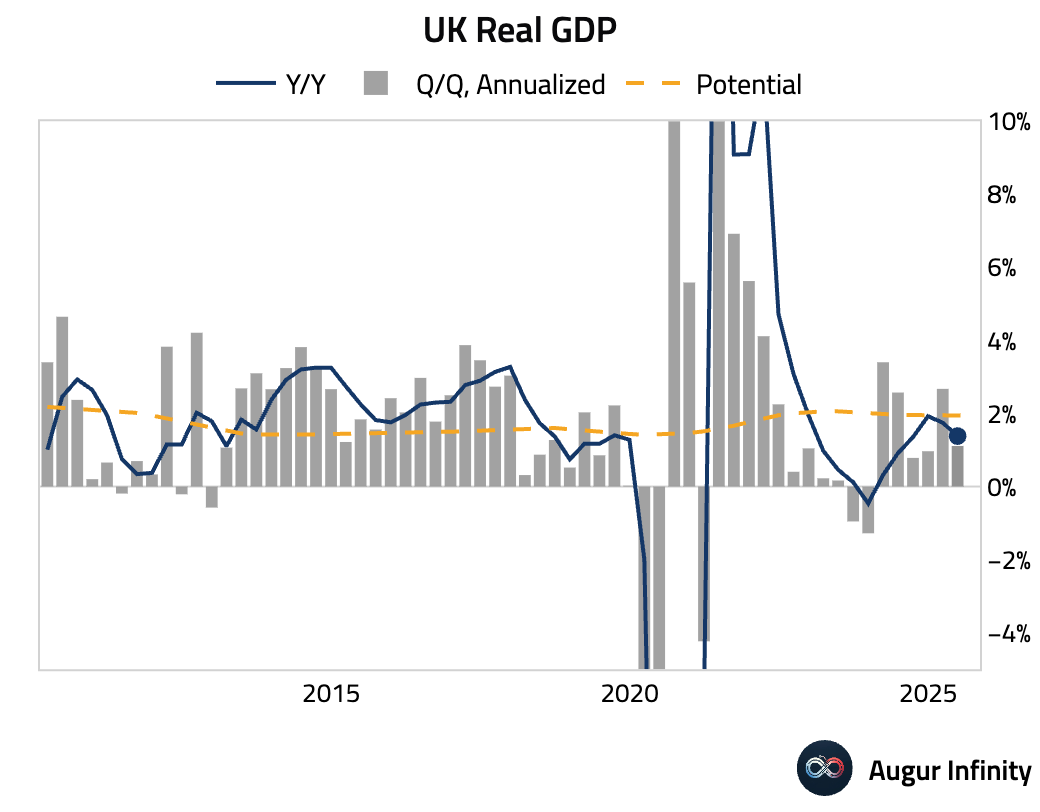

- The final estimate for UK Q2 GDP showed the economy grew 0.3% Q/Q (or 1.4% annualized).

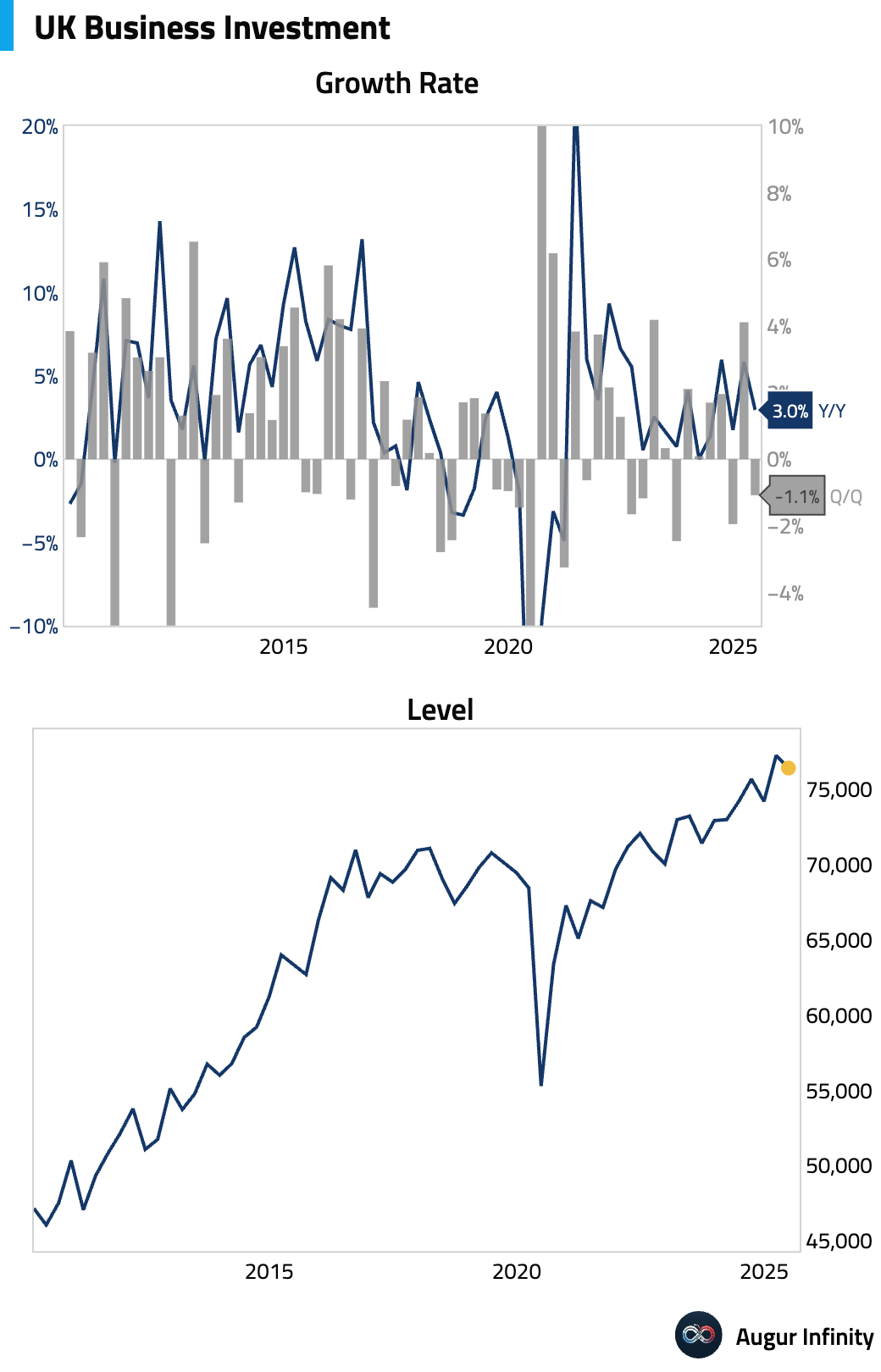

- Final data for UK business investment in Q2 showed a larger contraction than previously estimated, though it beat consensus forecasts (act: -1.1% Q/Q, est: -4.0%).

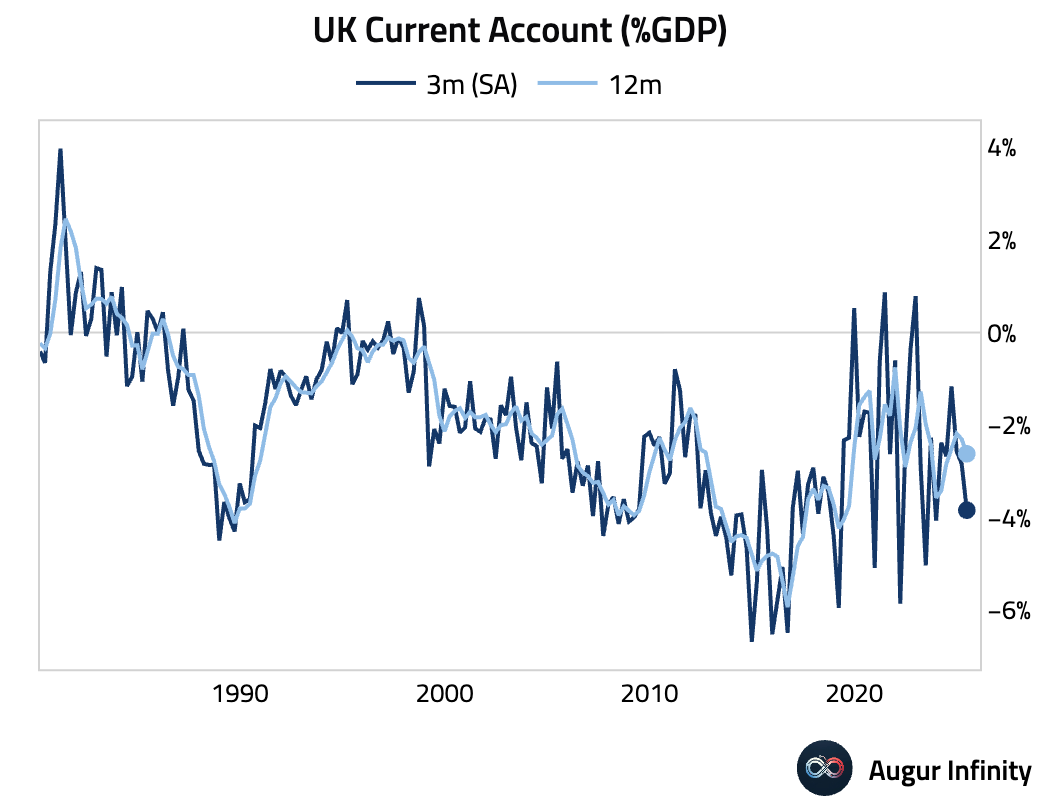

- The UK’s current account deficit widened more than expected in the second quarter (act: -£28.9B, est: -£24.9B), driven by a larger trade deficit.

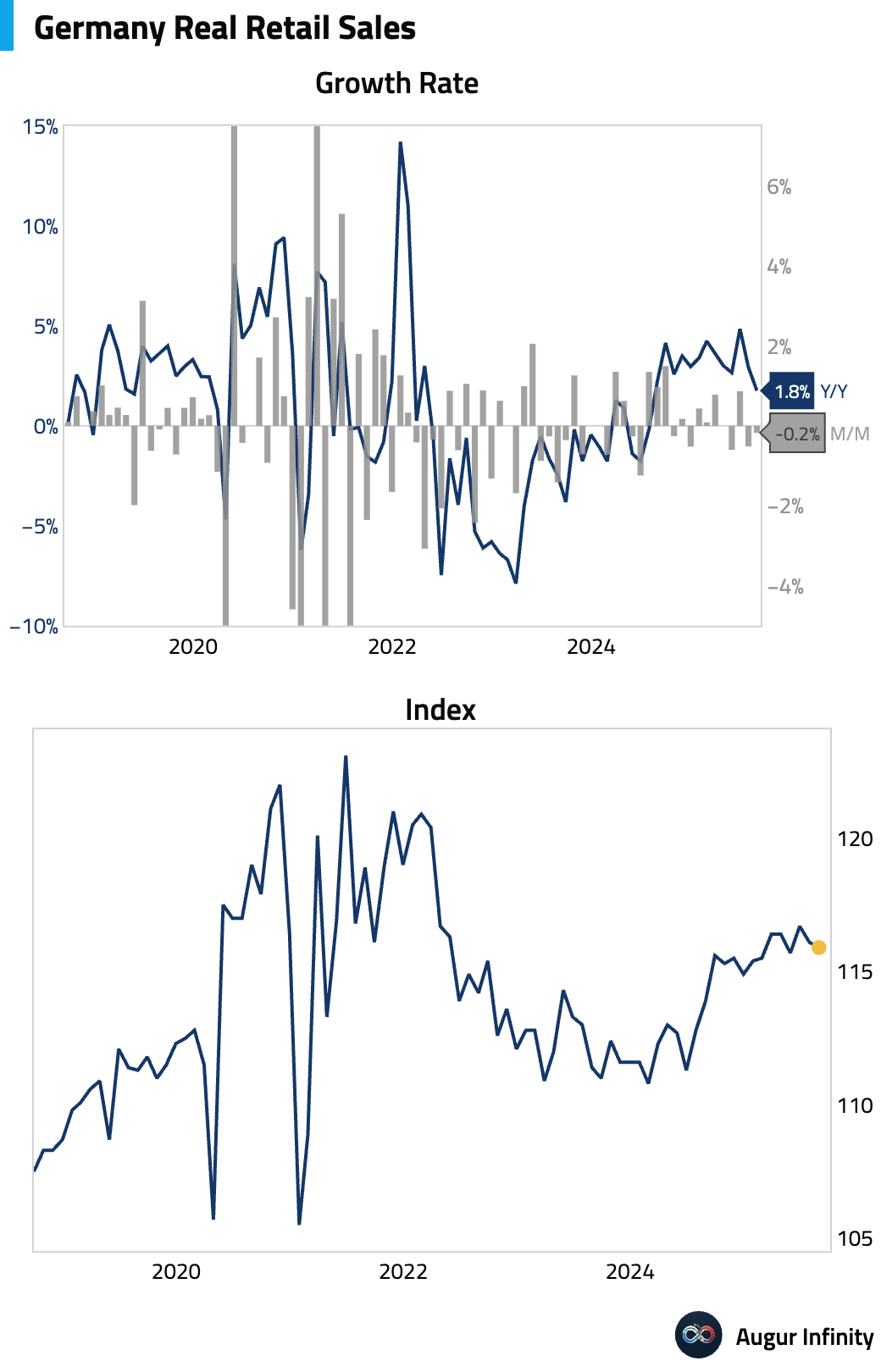

- German retail sales contracted for a second consecutive month in August, falling short of expectations for a rebound (act: -0.2% M/M, est: 0.5%).

Interactive chart on Augur Infinity

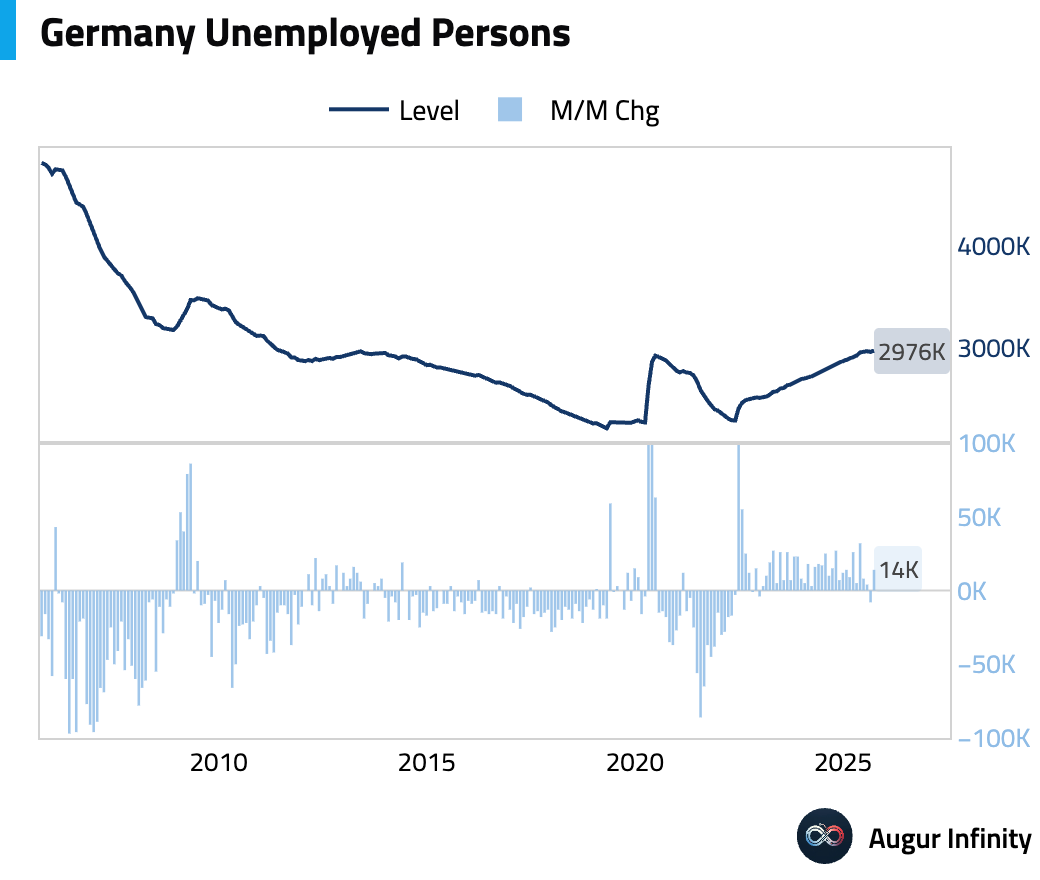

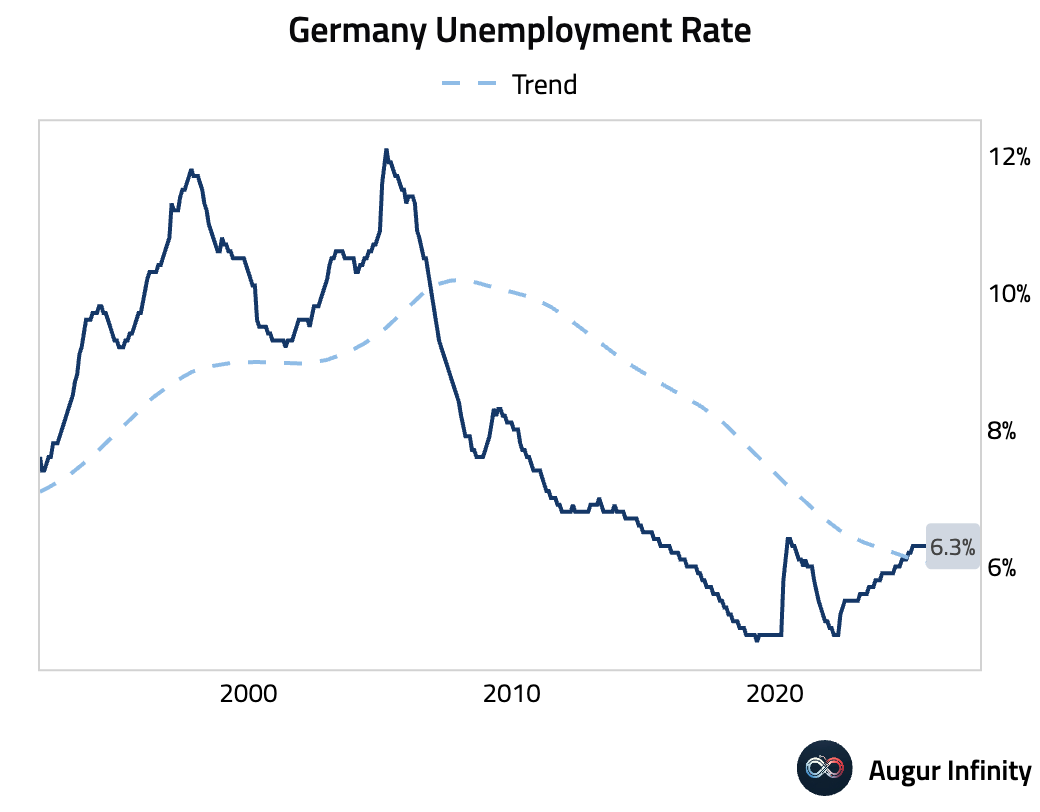

- Germany’s unemployment rate held steady at 6.3% in September, but the number of unemployed persons rose by 14,000, double the consensus estimate and signaling some softening in the labor market.

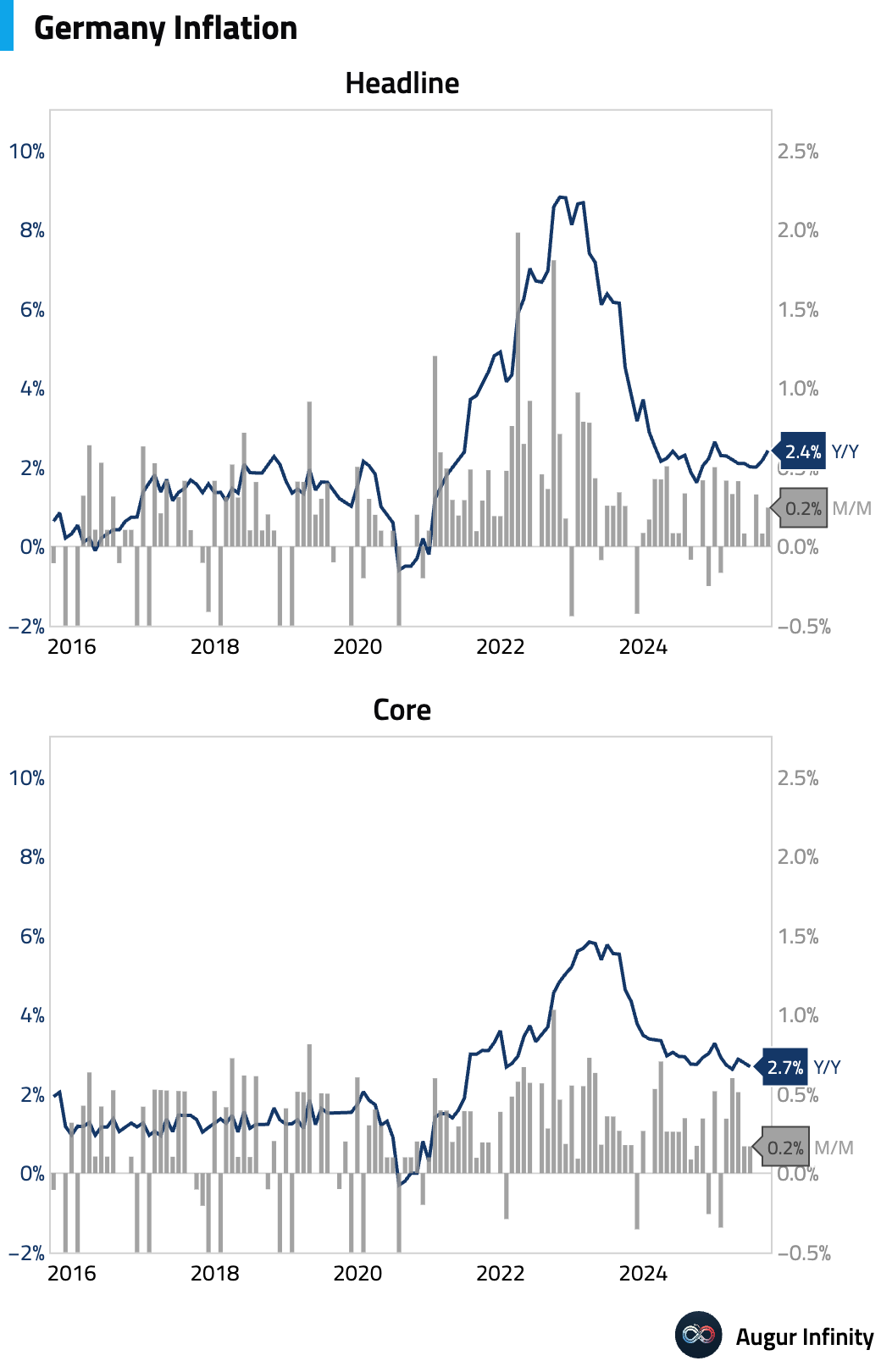

- Preliminary German inflation for September came in hotter than expected, with the headline CPI rising to 2.4% Y/Y from 2.2% previously, above the 2.3% consensus. Based on regional data, the strength appears broad-based, driven by firmer-than-expected energy and core inflation.

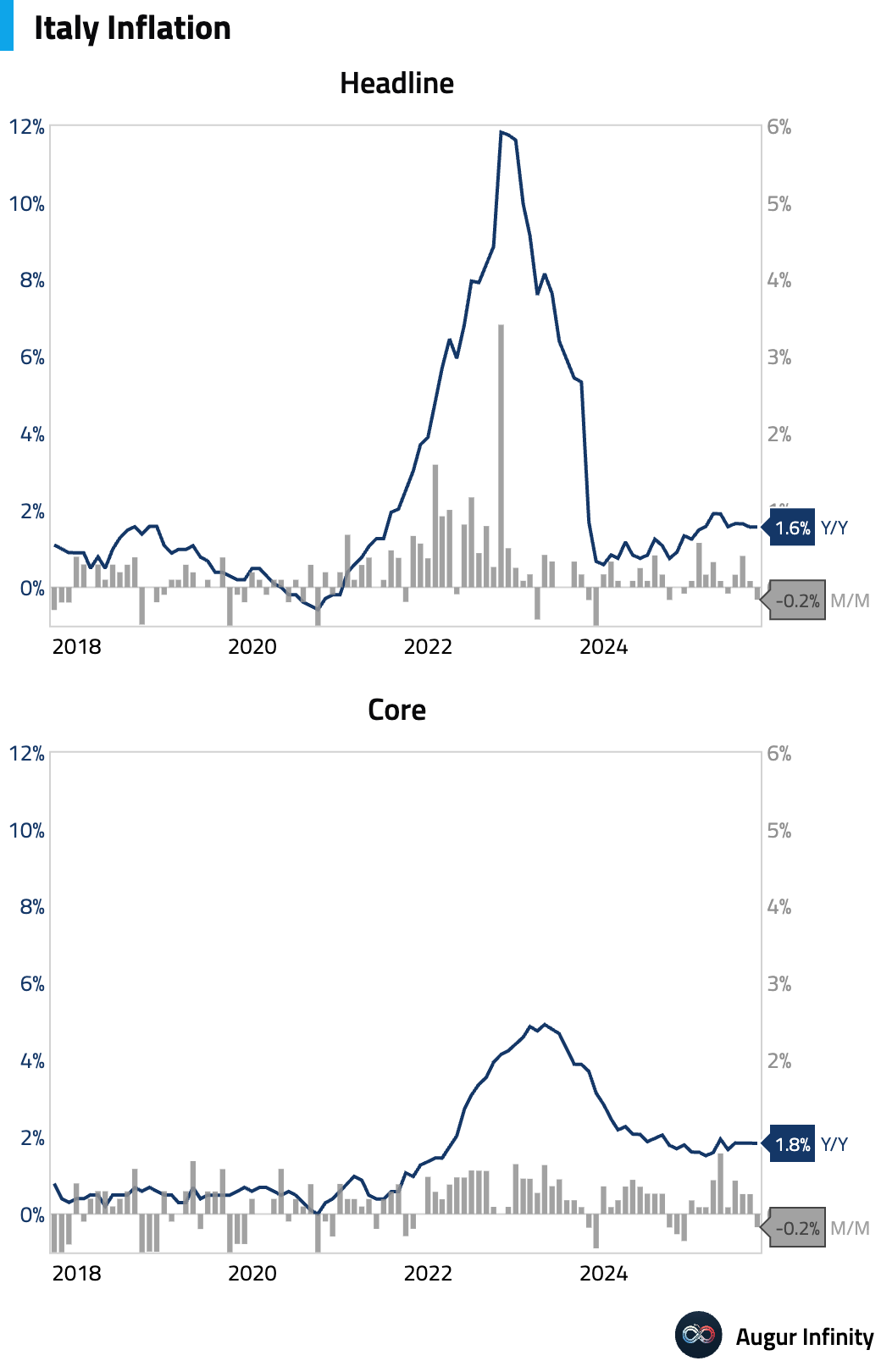

- Italian headline HICP inflation beat estimates at 1.8% Y/Y in September, compared to a 1.7% consensus. The surprise was driven by energy prices declining less than expected, while core inflation ticked up to 2.1%. However, sequential momentum decelerated, suggesting easing underlying pressures.

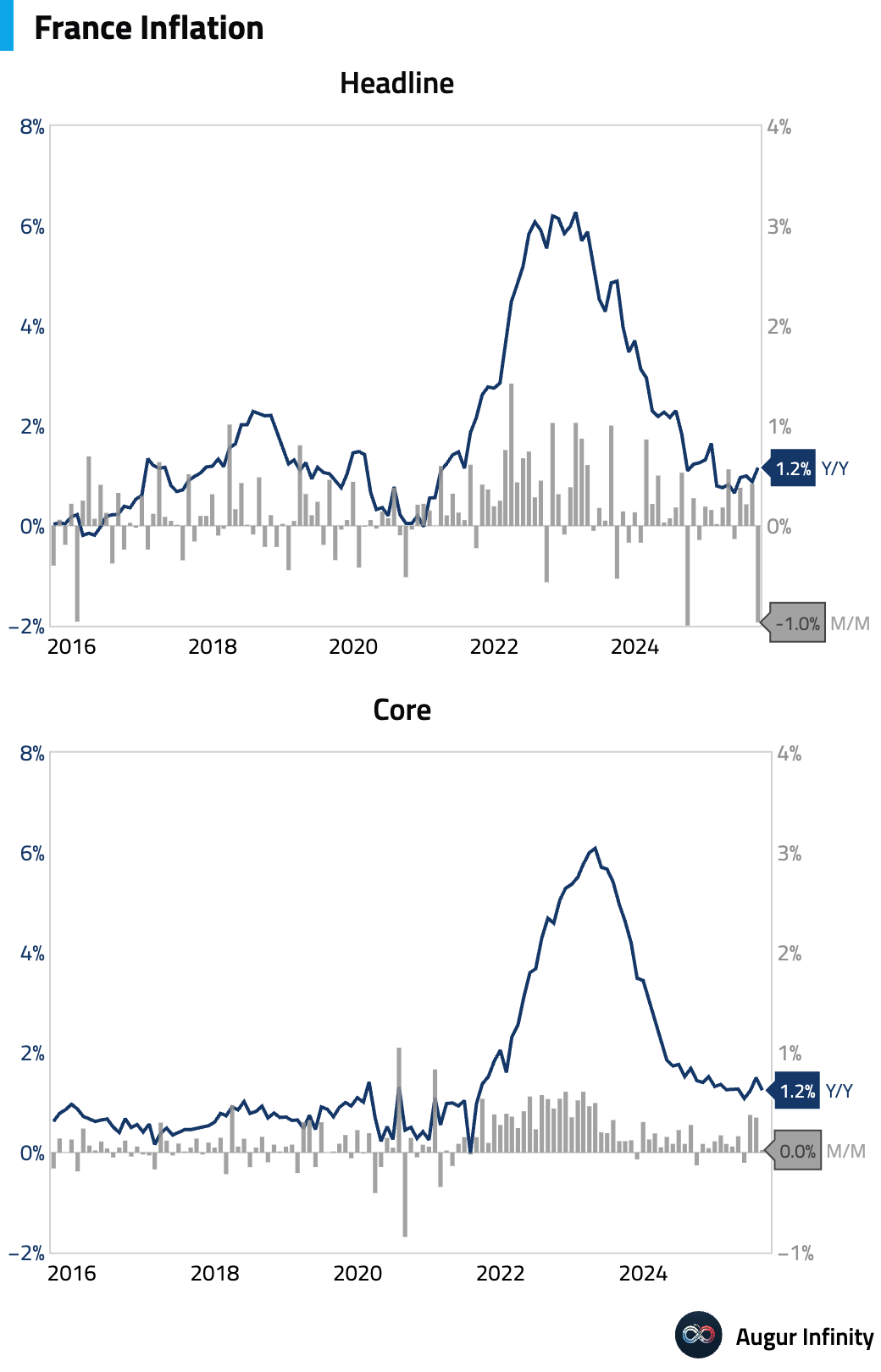

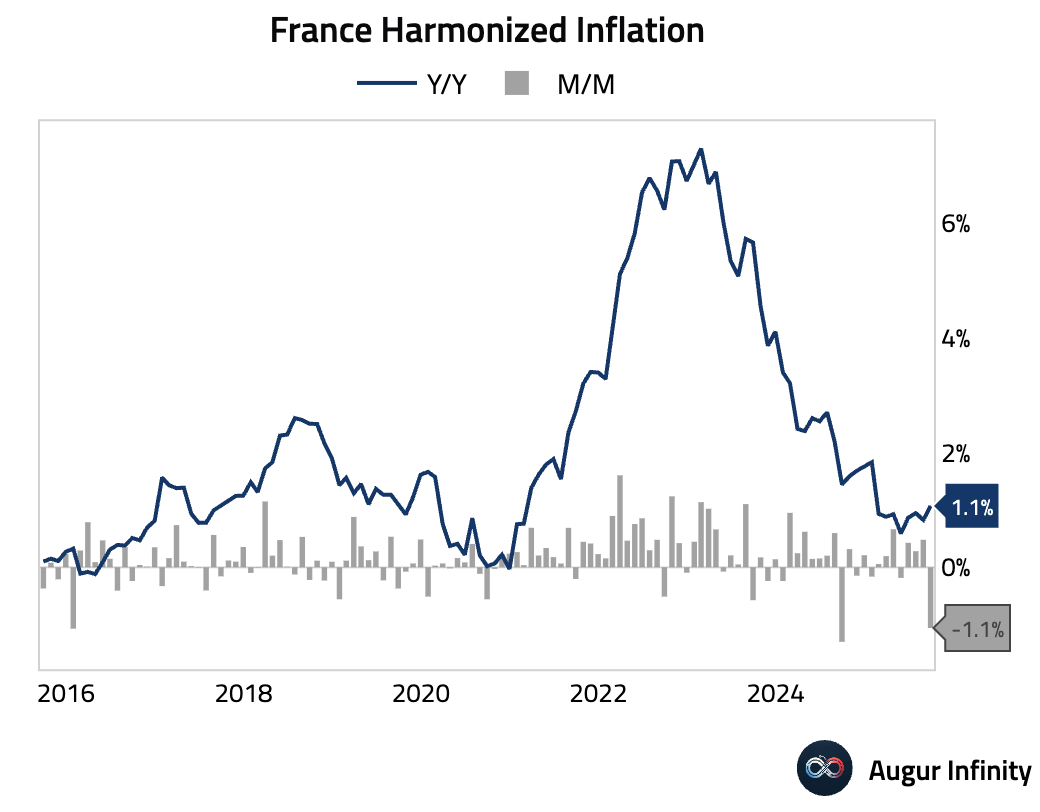

- French headline HICP inflation unexpectedly slowed to 1.1% Y/Y in September, missing consensus of 1.3%. The downside surprise was driven by a larger-than-expected slowdown in manufactured goods prices, which offset an acceleration in services and a smaller decline in energy costs.

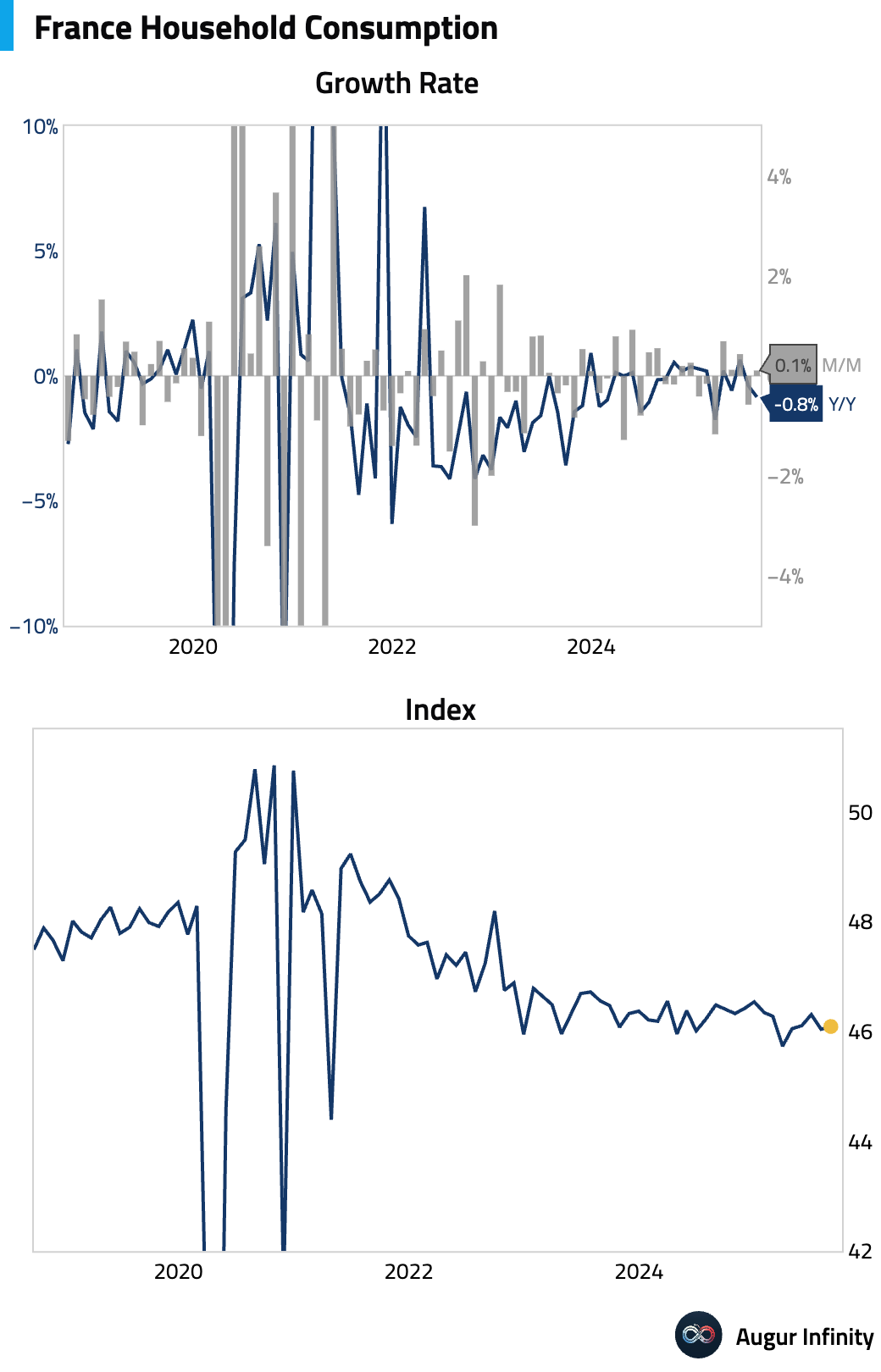

- French household consumption posted a slight rebound in August but missed expectations (act: 0.1% M/M, est: 0.3%).

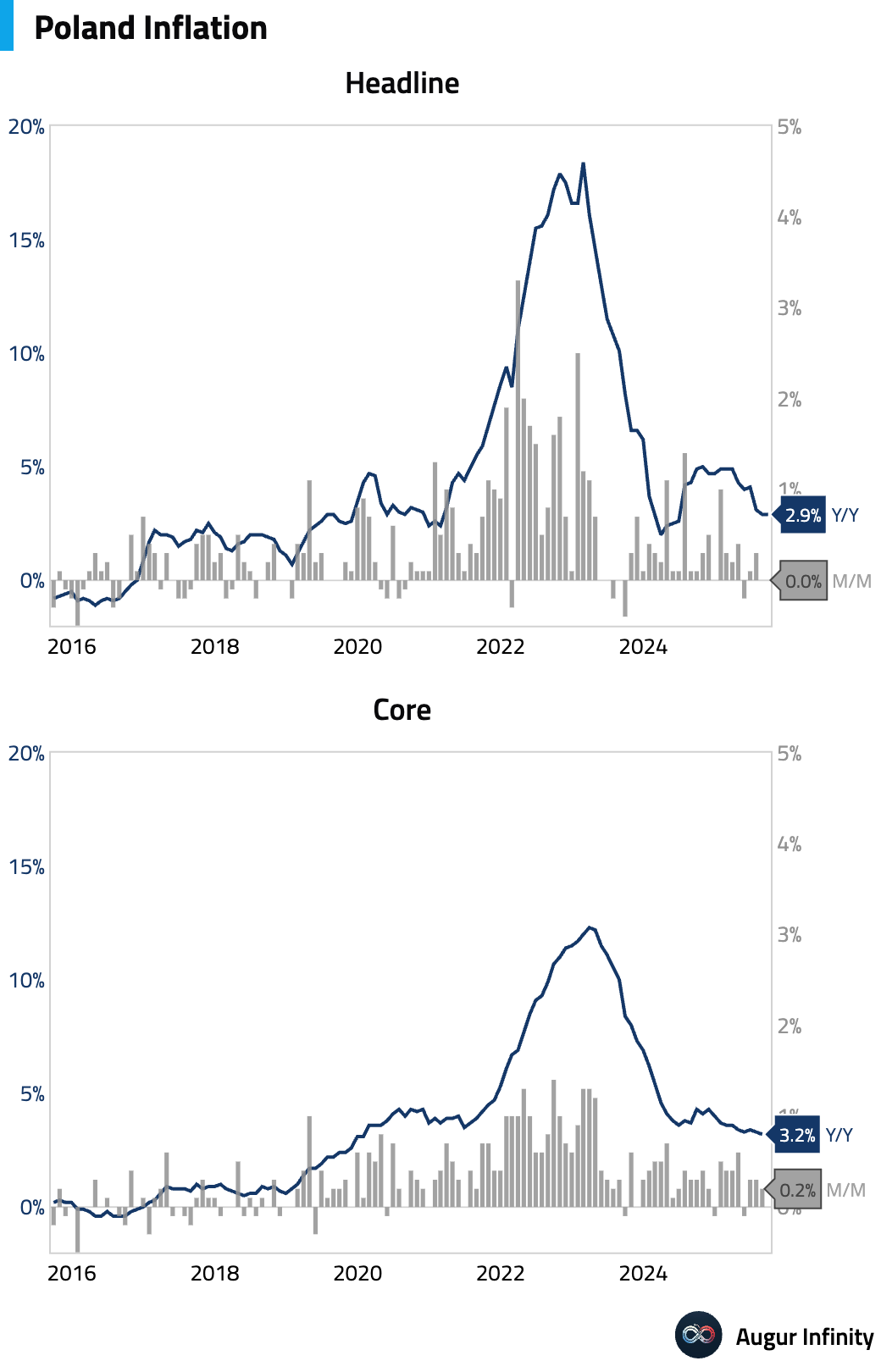

- Poland's headline CPI inflation was unchanged at 2.9% Y/Y in September. A decline in food inflation was offset by a smaller drag from fuel prices. The benign print, along with a planned freeze in power prices for the fourth quarter, solidifies expectations for a rate cut from the National Bank of Poland next week.

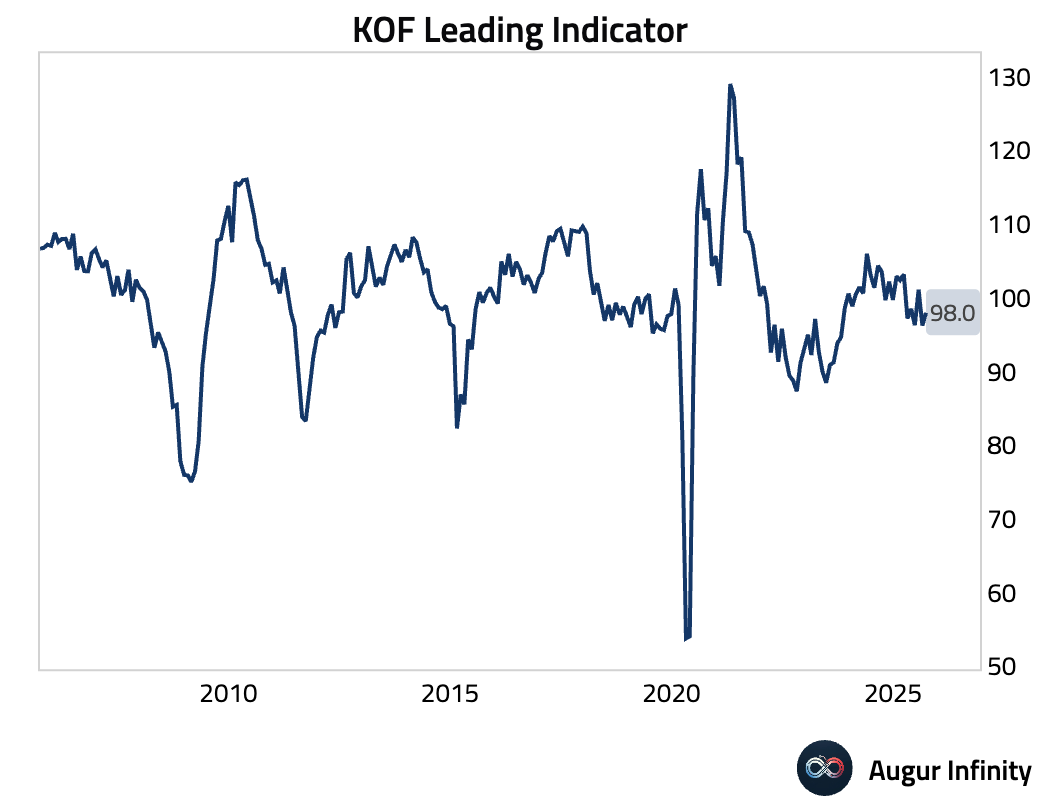

- Switzerland's KOF leading indicator rose more than expected in September, suggesting an improving economic outlook (act: 98.0, est: 97.3).

Asia-Pacific

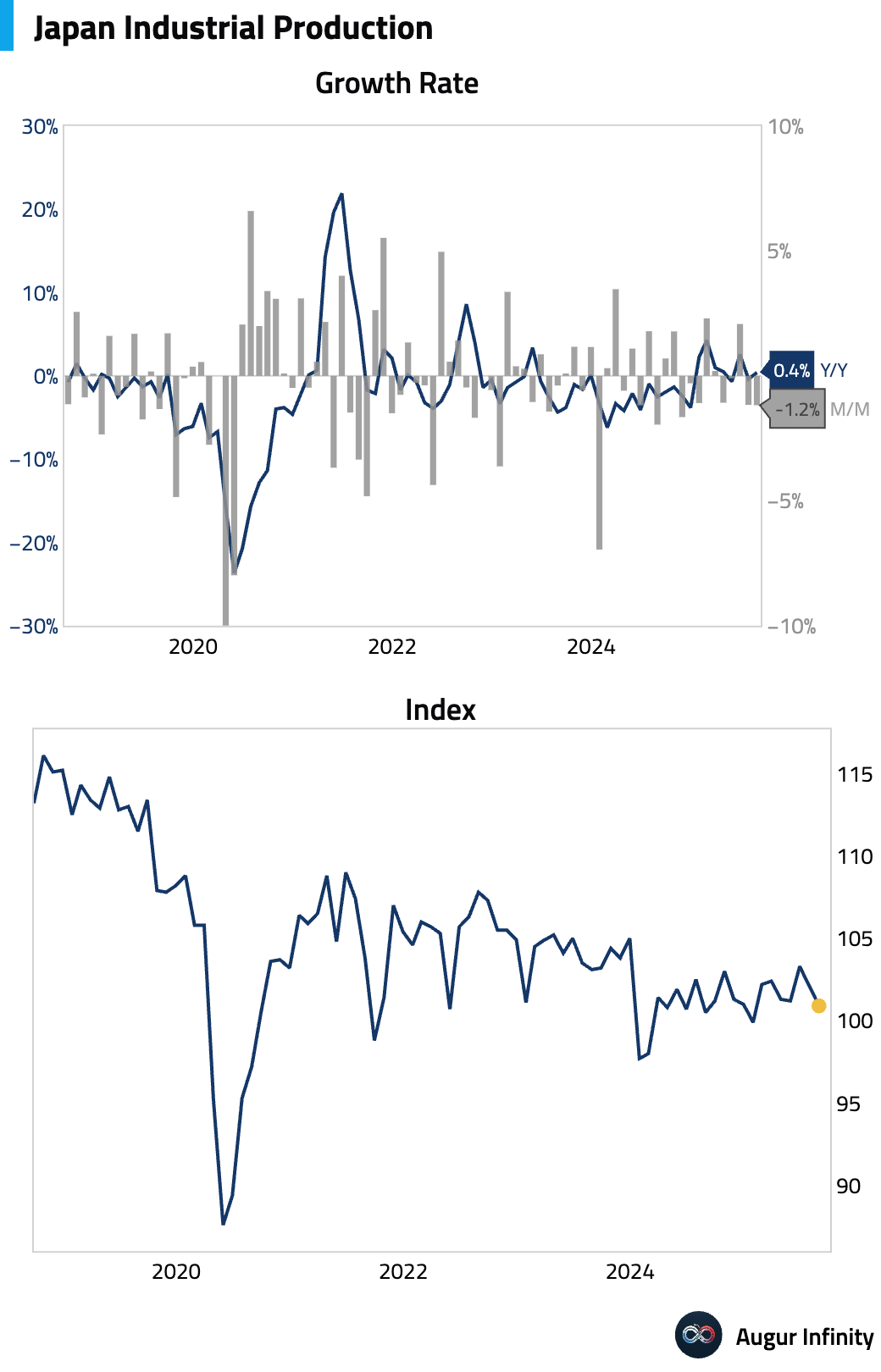

- Japan’s preliminary industrial production fell 1.2% M/M in August, a larger drop than the -0.8% consensus and the second straight monthly decline. The fall was broad-based, led by electronics and business machinery, which overshadowed a strong contribution from autos. The Ministry of Economy, Trade and Industry (METI) forecasts a rebound in September.

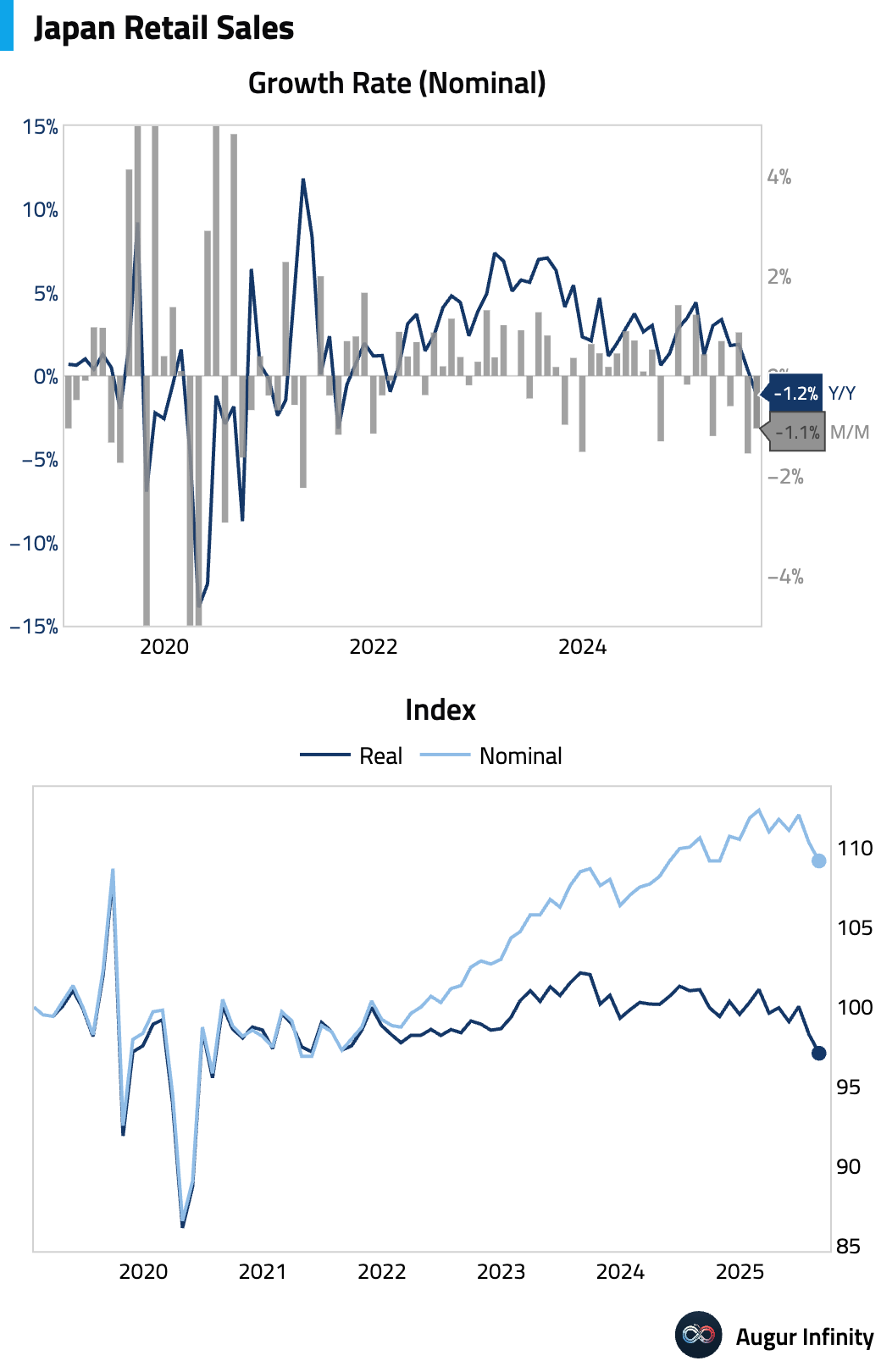

- Japanese retail sales fell 1.1% Y/Y in August, a significant miss against the +1.0% consensus and the first year-over-year decline in over three years. On a seasonally adjusted basis, sales also fell for the second consecutive month, indicating broad consumer weakness exacerbated by a sharp drop in auto sales.

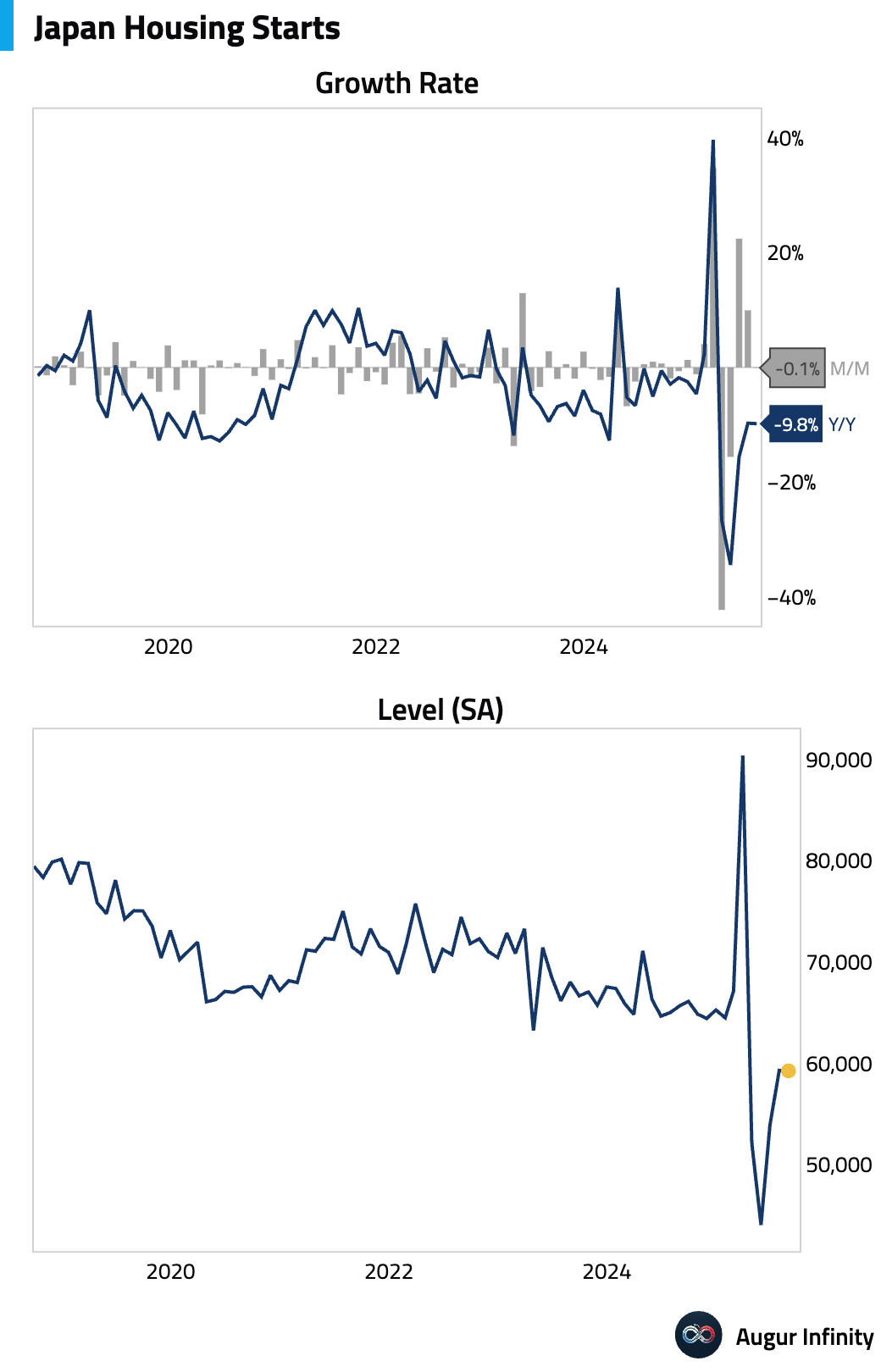

- Japanese housing starts plummeted 9.8% Y/Y in August, far worse than the -4.8% consensus forecast, extending the construction sector's weakness.

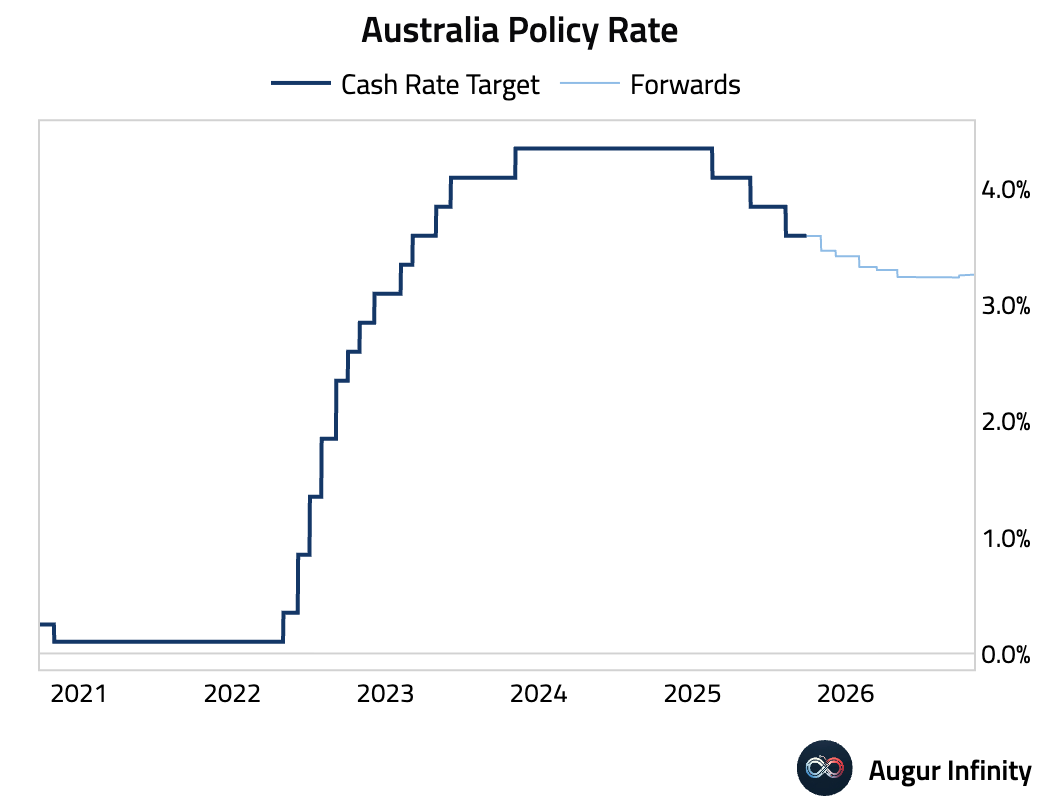

- The Reserve Bank of Australia held its cash rate steady at 3.6%, as widely expected.

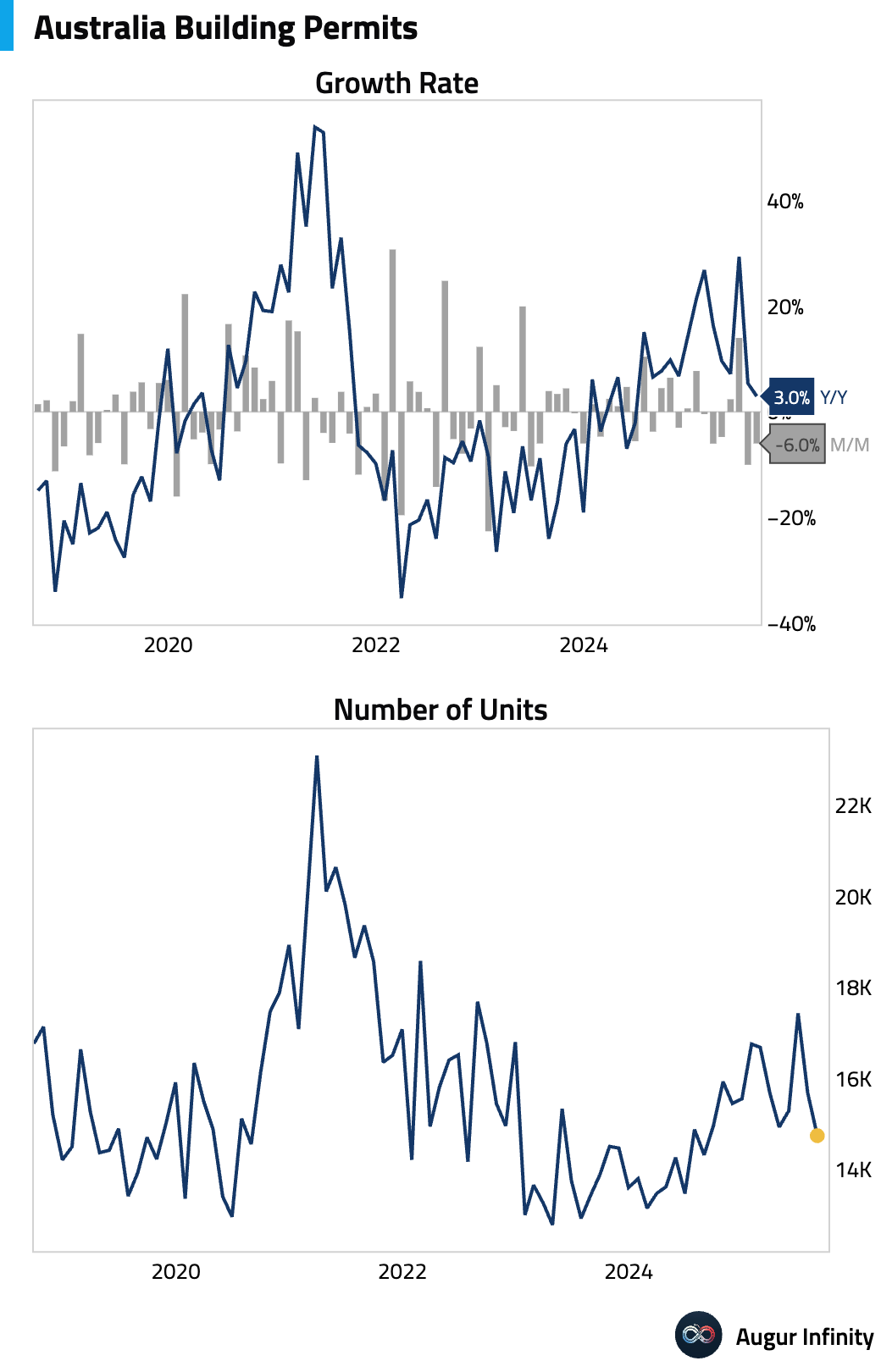

- Australian building permits unexpectedly fell 6.0% M/M in August, confounding expectations for a 3.0% rise. The decline was driven by a steep drop in the volatile high-density sector, but more concerningly, approvals for detached houses also fell, signaling a weaker construction pipeline.

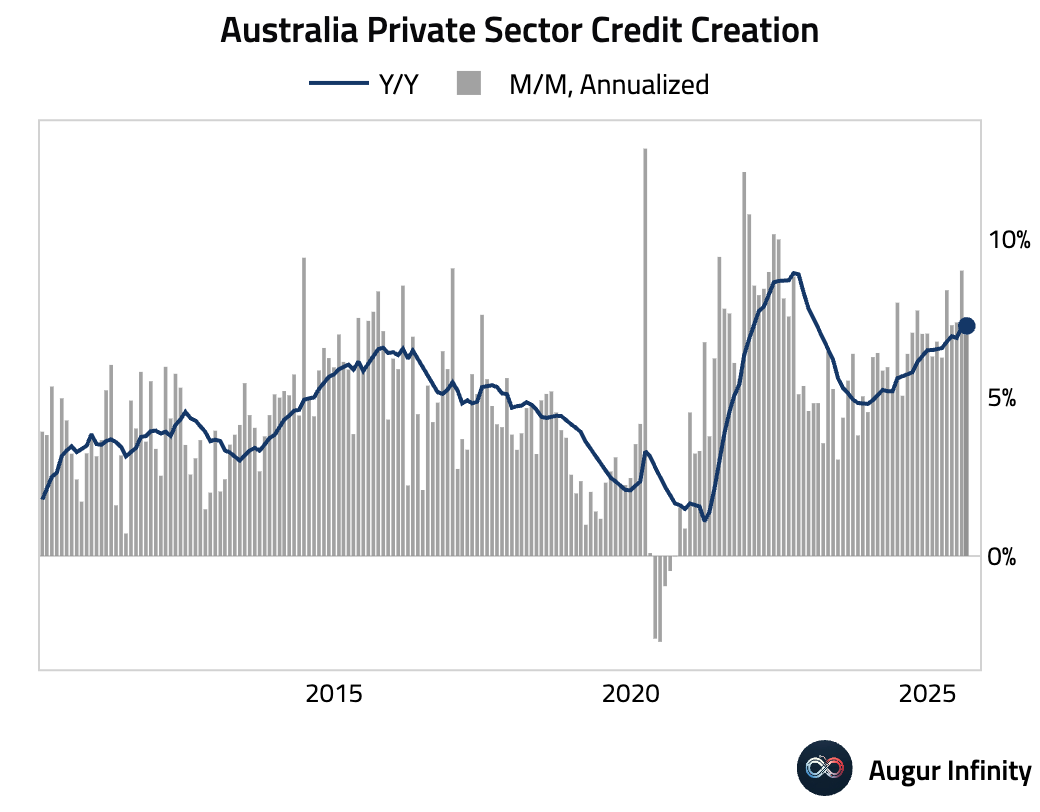

- Australian private sector credit growth was stable in August, rising in line with expectations (act: 0.6% M/M, est: 0.6%). The annual rate held firm at 7.2% Y/Y, the fastest pace since February 2023, with growth broad-based across housing, business, and personal loans.

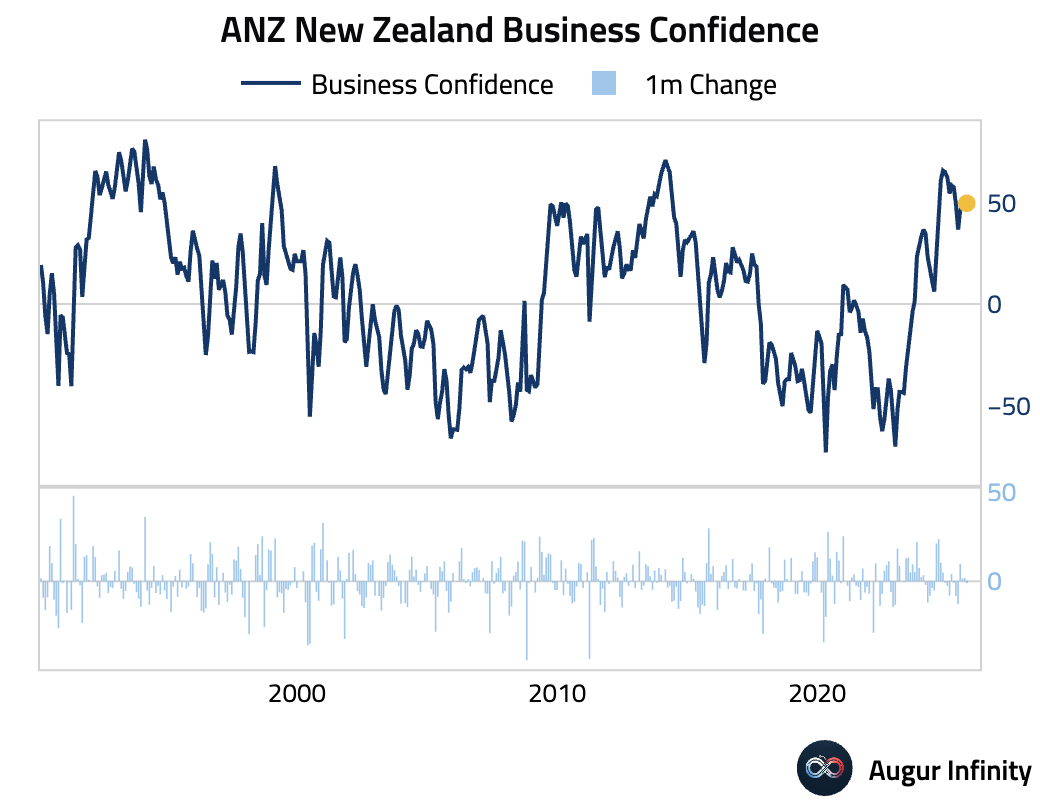

- New Zealand business confidence edged down slightly in September but remained near recent highs (act: 49.6, prev: 49.7).

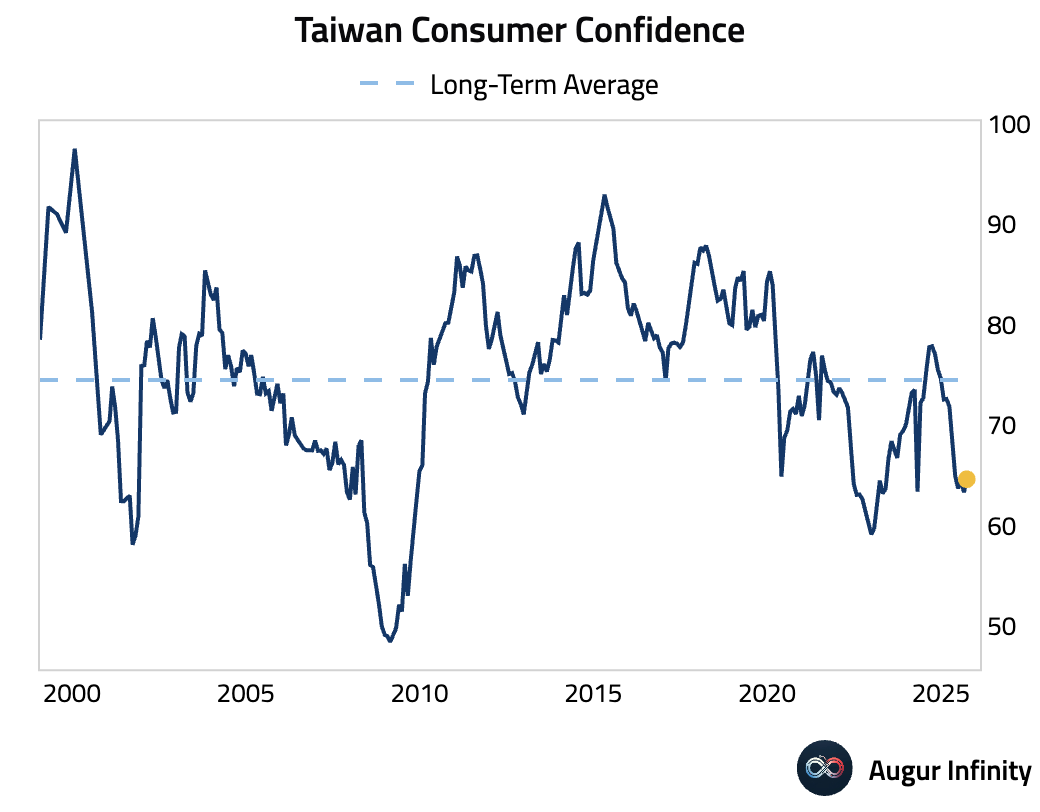

- Taiwanese consumer confidence improved in September (act: 64.69, prev: 63.31).

China

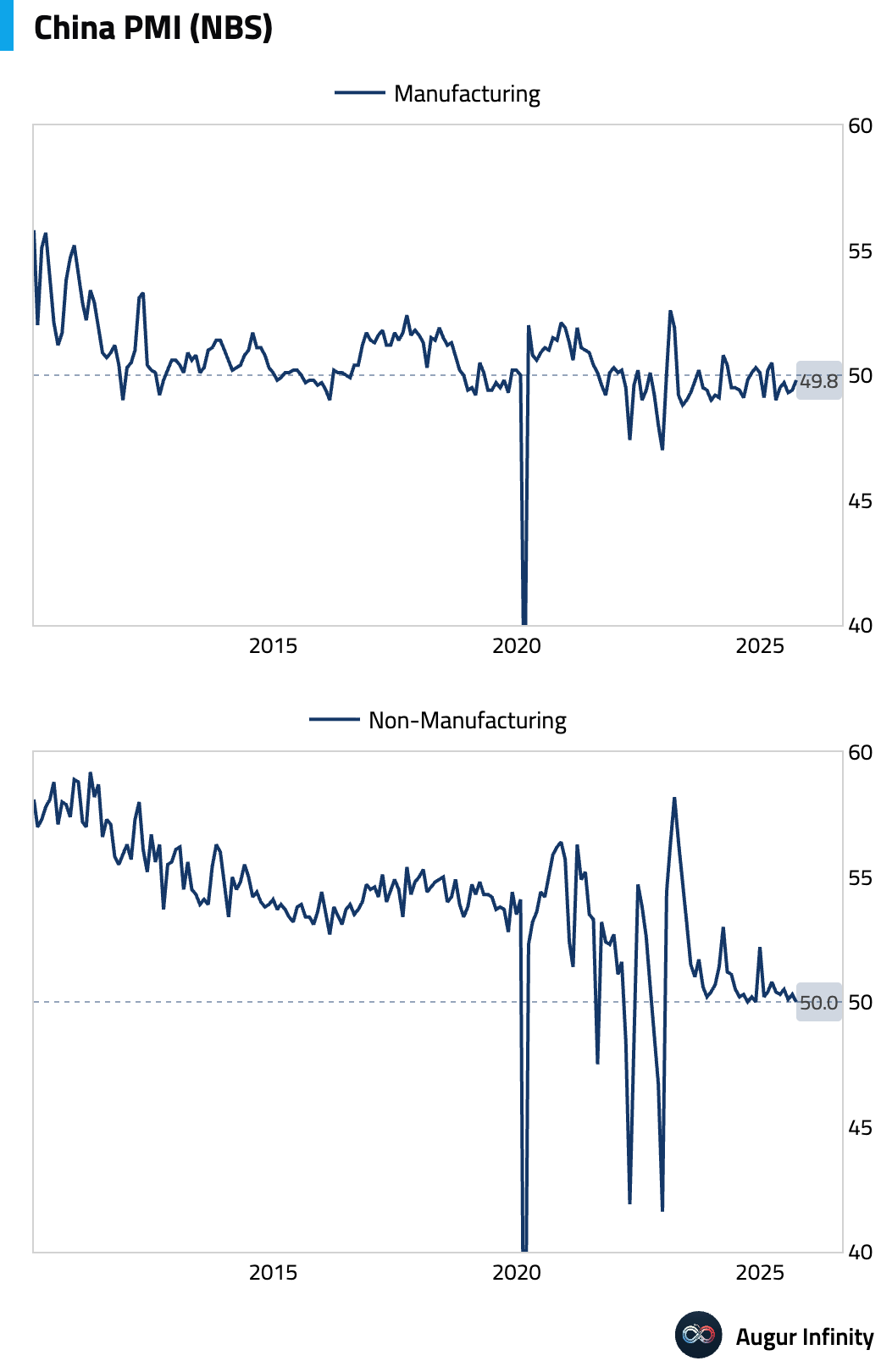

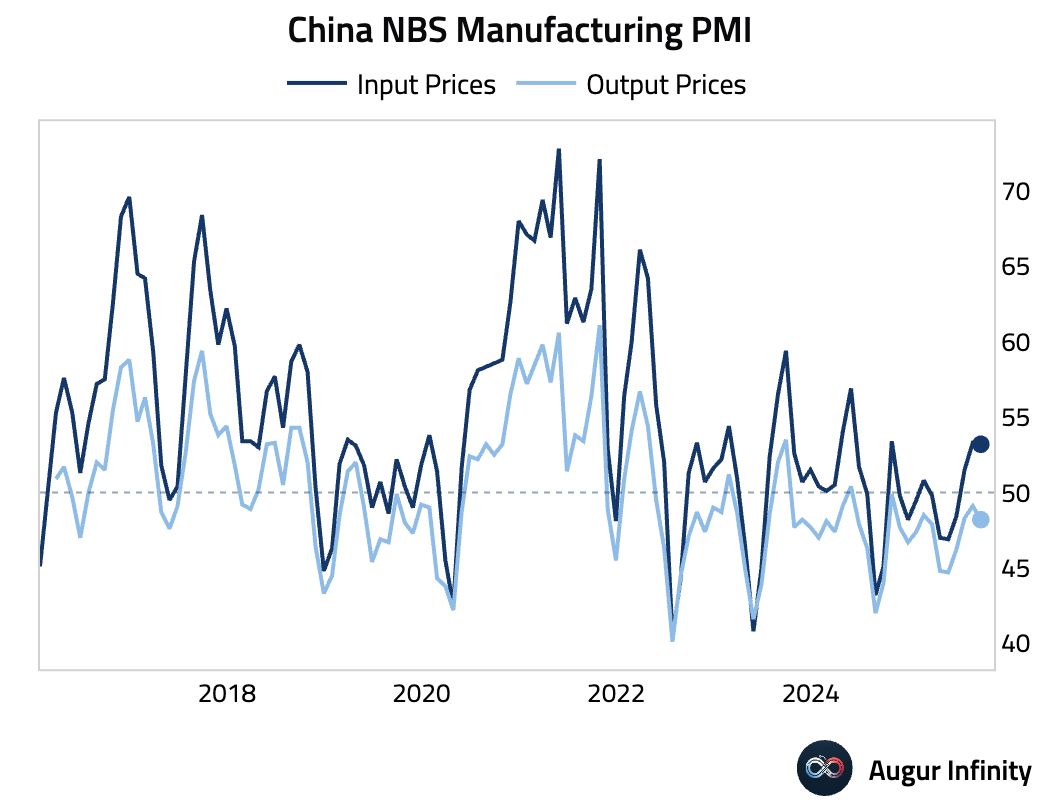

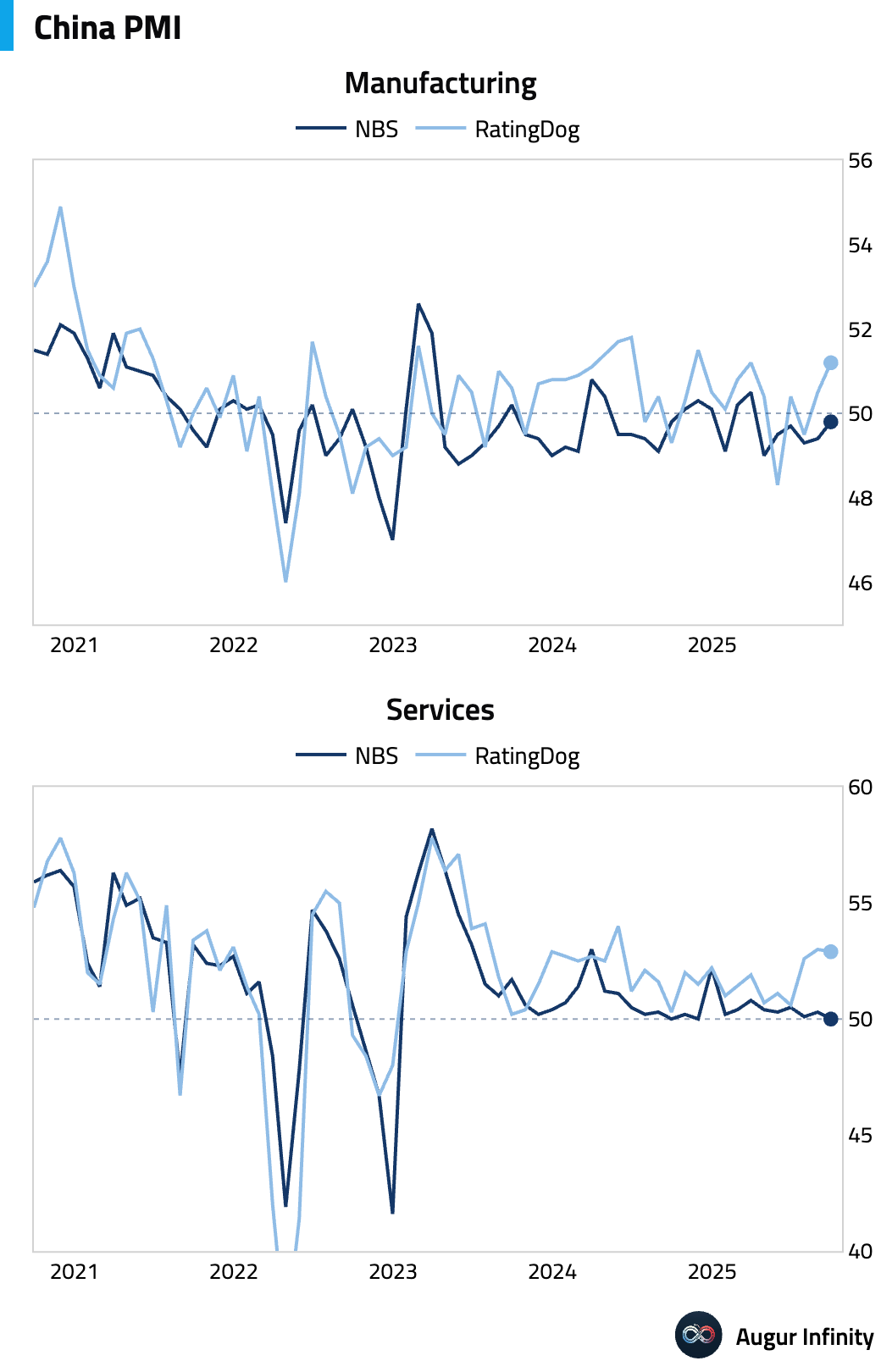

- China's official NBS Manufacturing PMI rose to 49.8 in September from 49.4, beating the consensus of 49.7. The improvement was driven by higher output, but the index remains just inside contractionary territory. Firms continue to face a margin squeeze, with the input price sub-index significantly higher than the output price sub-index, indicating rising costs are being absorbed amid weak final demand. The official NBS Non-Manufacturing PMI unexpectedly slipped to 50.0, missing forecasts of 50.3. The decline was driven entirely by the services sector as the summer travel season ended, while the construction sub-index remained in contraction, showing continued weakness despite improved weather.

- The RatingDog (Caixin) Manufacturing PMI showed a more substantial increase, rising to 51.2 in September and beating consensus of 50.3. This signals an accelerating expansion, driven by the quickest increase in new business since February and a return to growth for export orders. The stronger reading, compared to the official PMI, is attributed to RatingDog's sample which covers more export-oriented firms. The RatingDog (Caixin) Services PMI fell slightly to 52.9 from 53.0 but still indicated a solid expansion. Growth was supported by strong new business and a seven-month high in export orders from a tourism recovery. However, employment contracted at the fastest pace since April 2024 due to cost-cutting, creating a significant headwind despite rising business confidence.

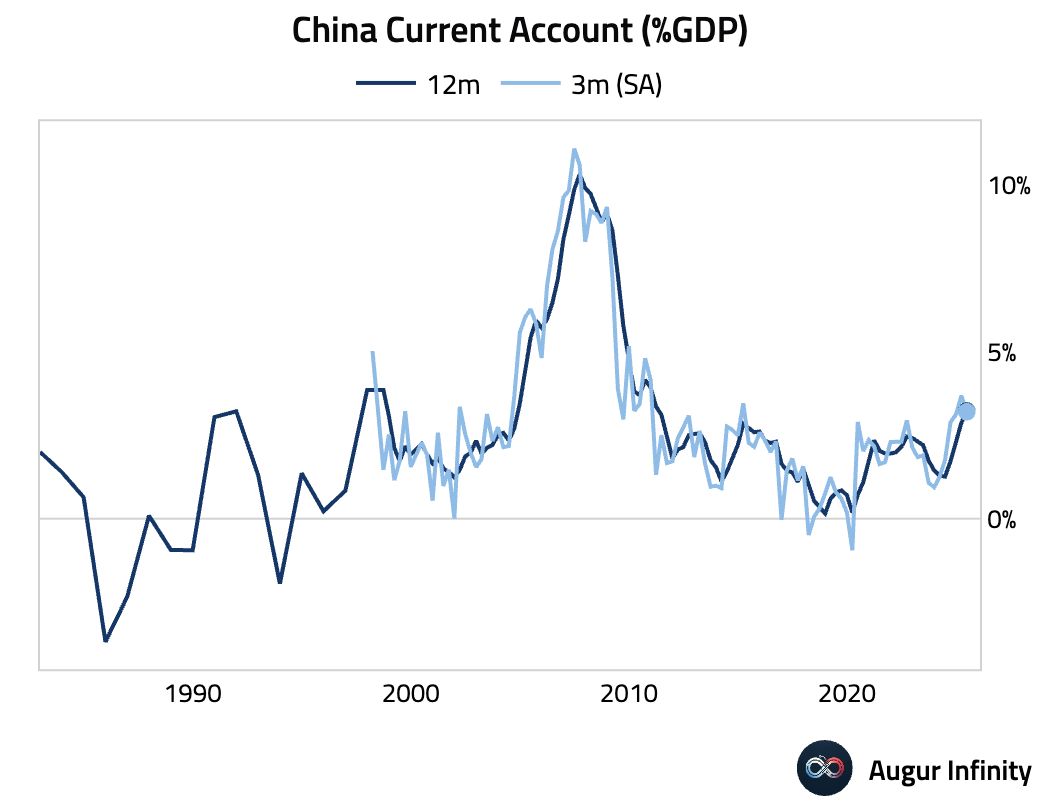

- China's final current account surplus for Q2 was revised lower (act: $128.7B, prev: $165.4B).

Emerging Markets ex China

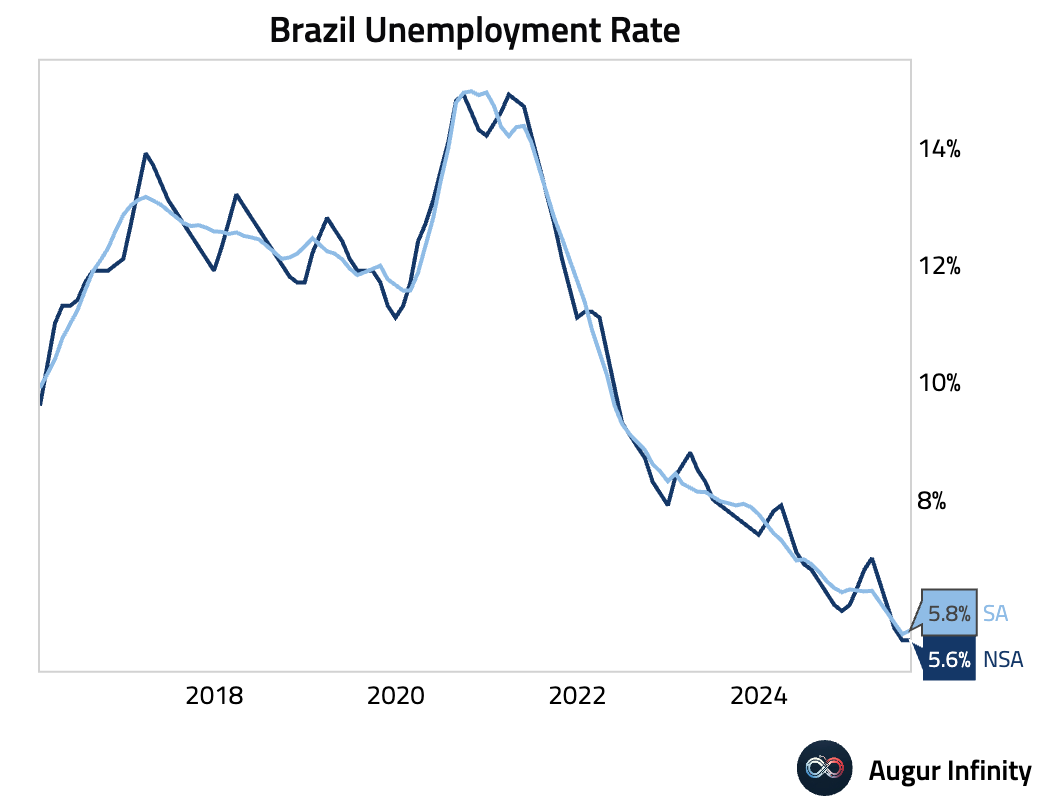

- Brazil’s unemployment rate held at 5.6% in August, matching a record low. The stability masks underlying weakness, as both employment and the labor force contracted by 0.3% M/M on a seasonally adjusted basis. The labor force participation rate fell, possibly reflecting the impact of fiscal transfers. While the labor market remains tight, moderating wage growth and the decline in participation suggest a gradual cooling.

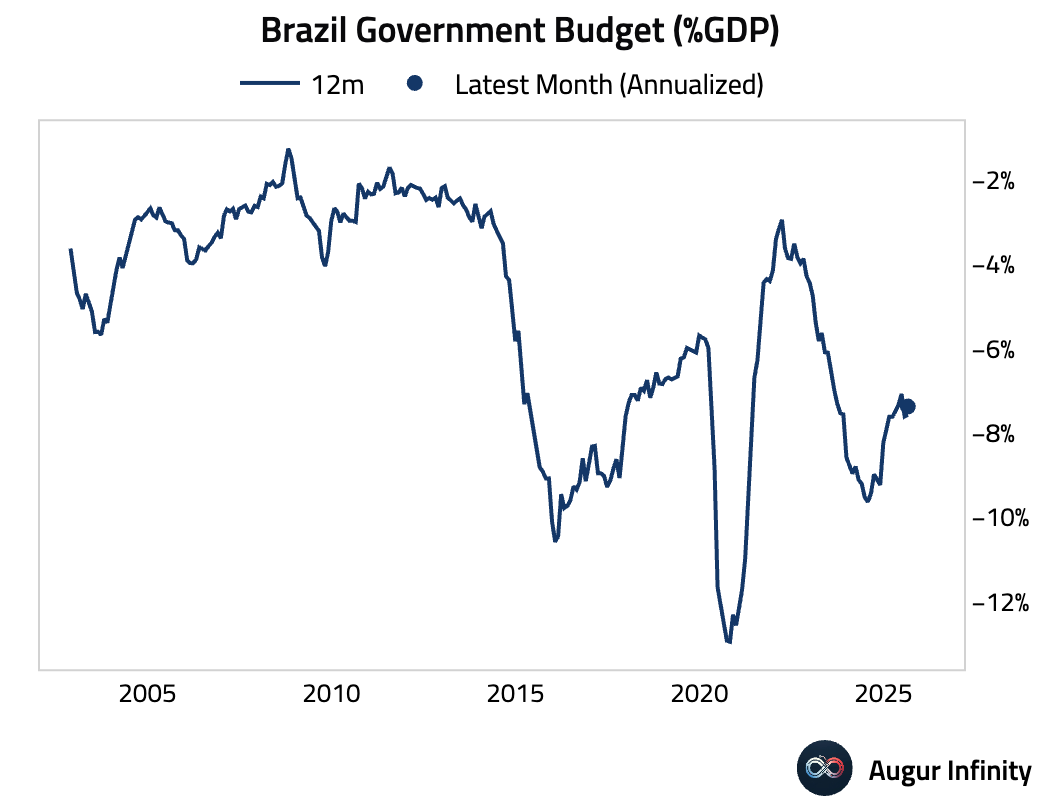

- Brazil's public sector posted a smaller-than-expected primary deficit in August. However, the 12-month overall deficit remains high at 7.8% of GDP due to a large interest bill. A pro-cyclical fiscal stance and reluctance to control spending are seen as undermining fiscal targets and anchoring inflation.

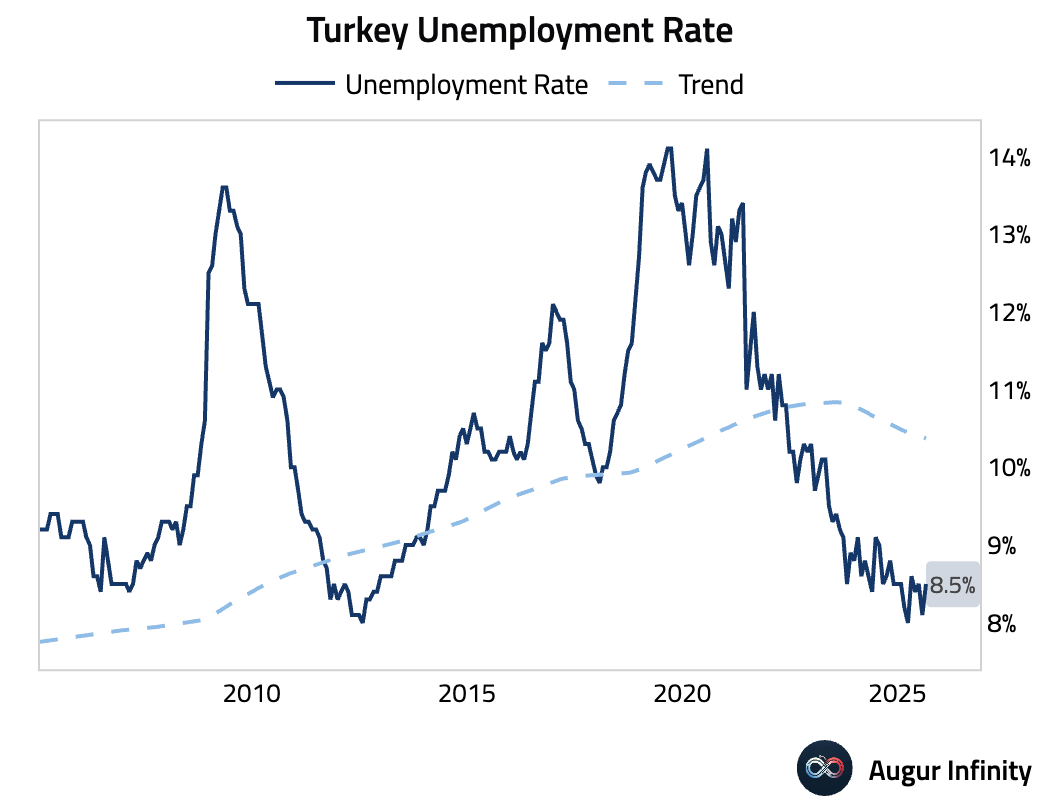

- Turkey's unemployment rate ticked up in August, rising from a multi-year low (act: 8.5%, prev: 8.1%).

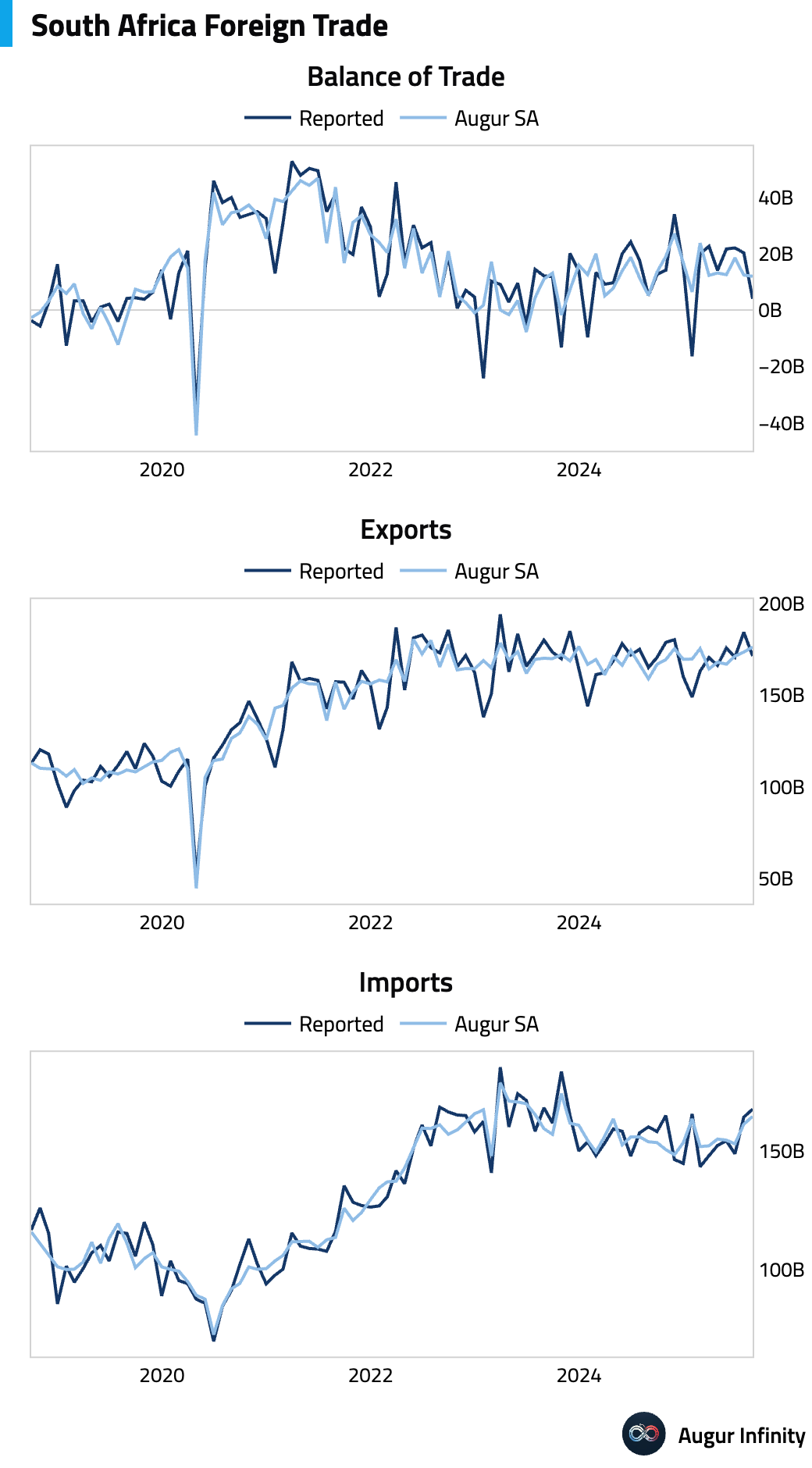

- South Africa's trade surplus narrowed significantly in August (act: ZAR 4.0B, prev: ZAR 19.6B).

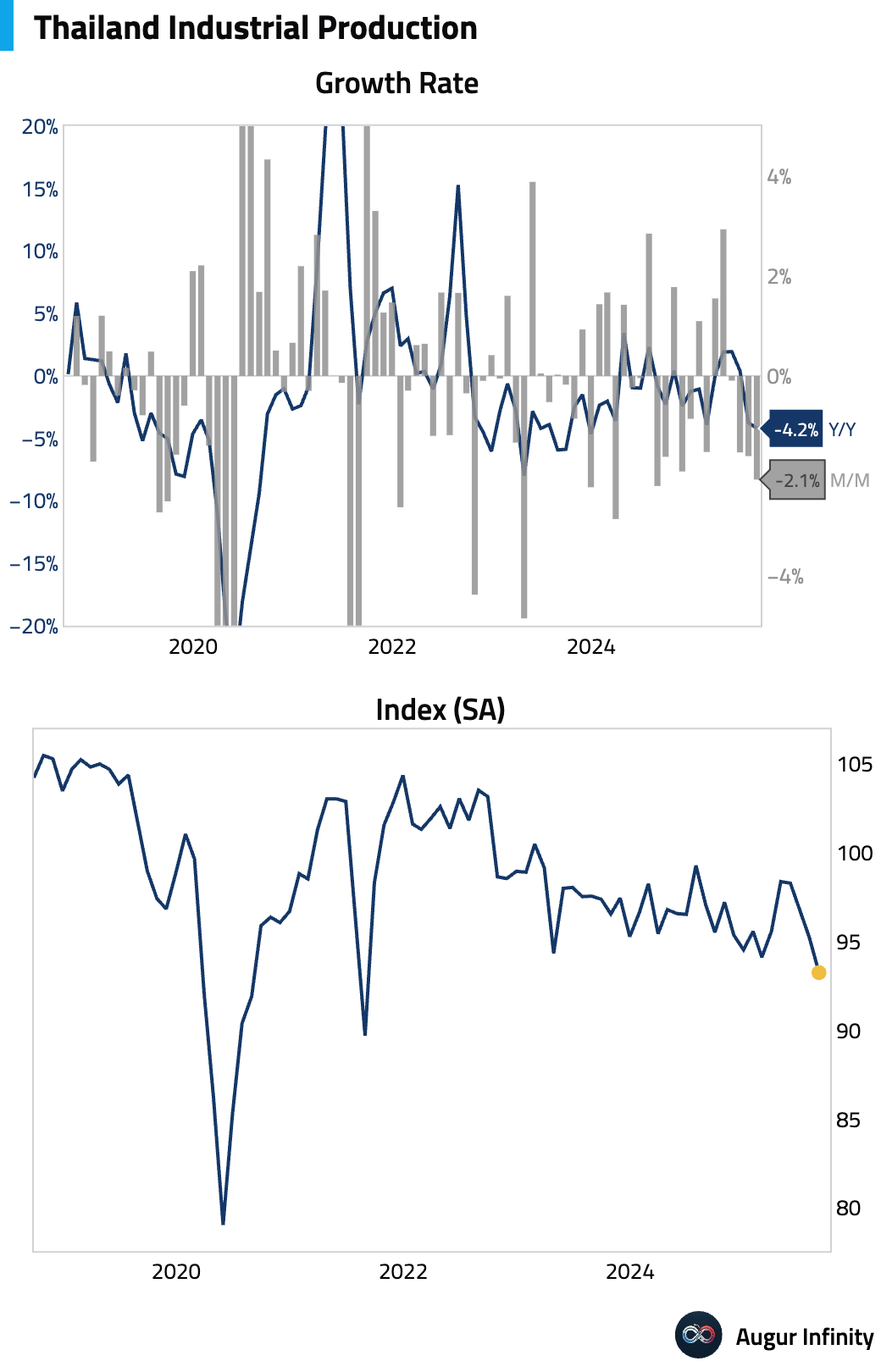

- Thailand's industrial production fell more than expected in August (act: -4.19% Y/Y, est: -2.1%), contracting for the fourth consecutive month.

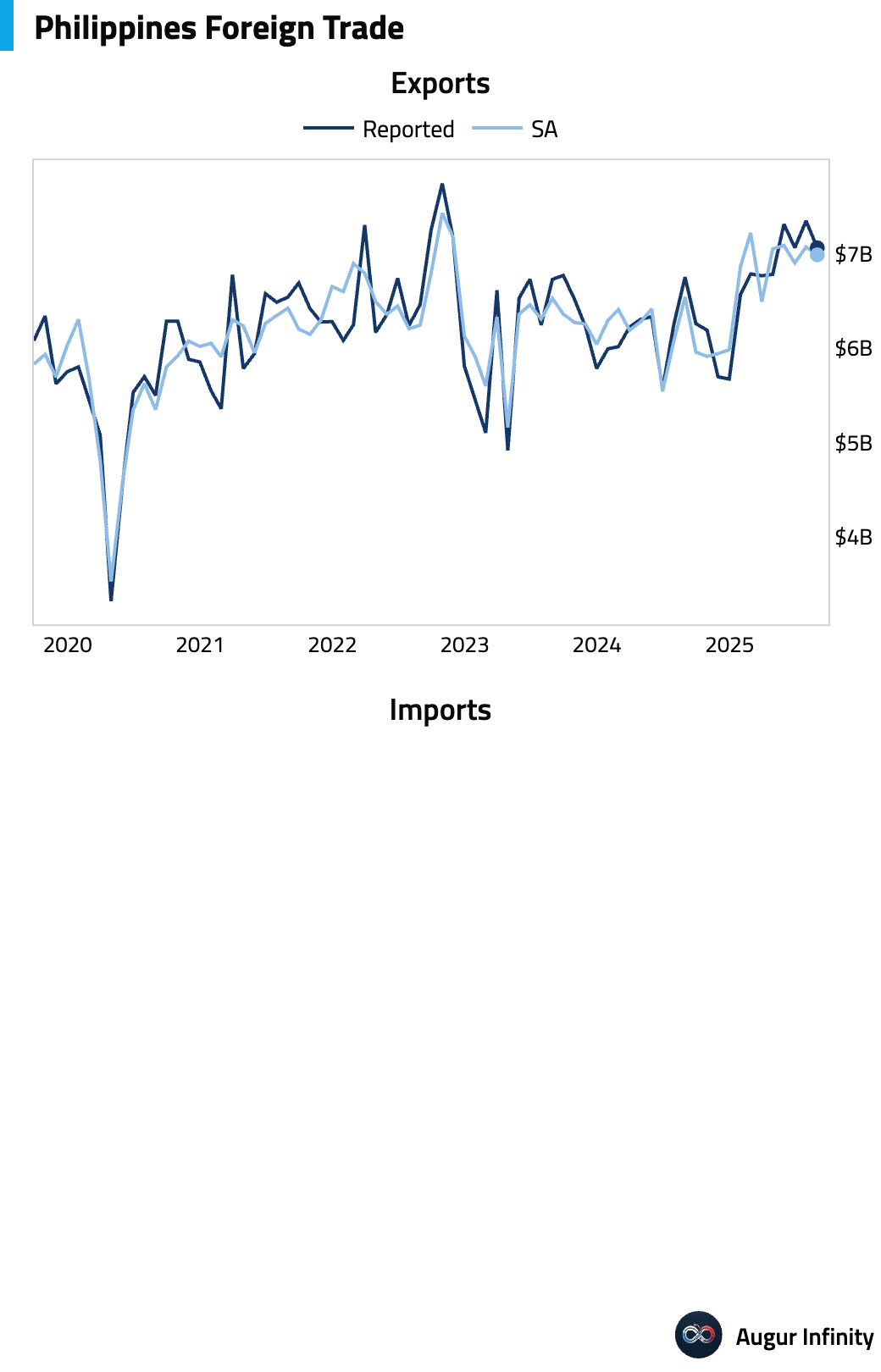

- The Philippines' trade deficit narrowed in August as export growth outpaced a decline in imports.

Global Markets

Equities

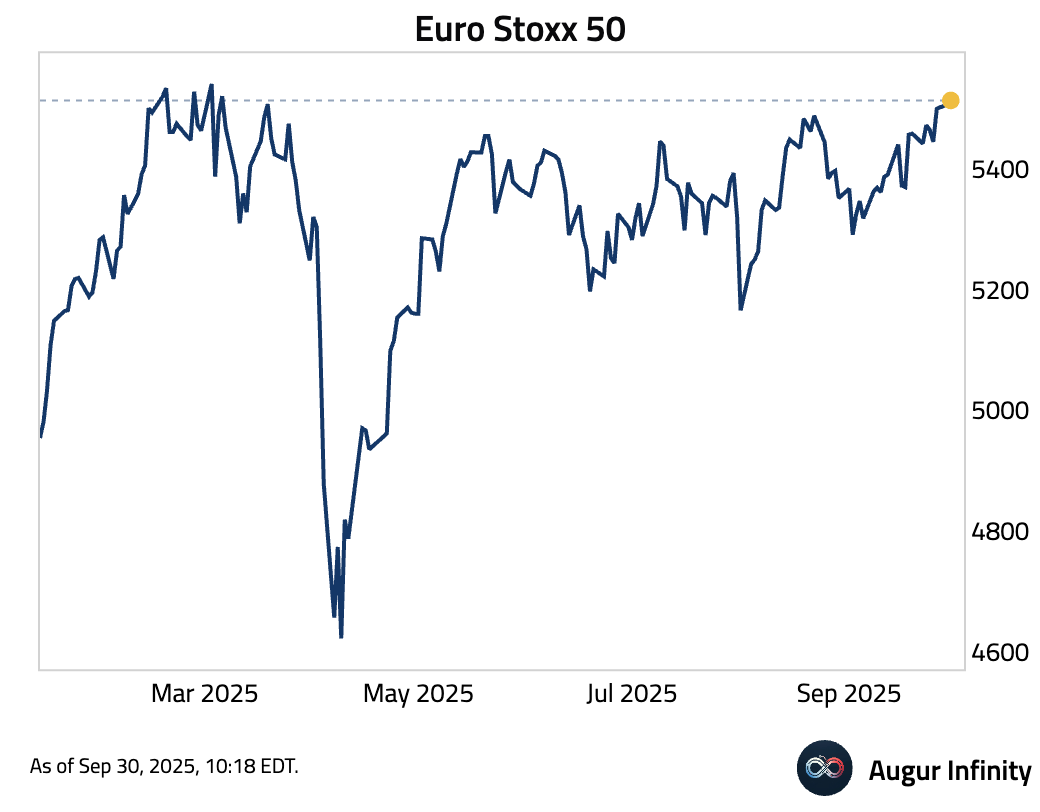

- Euro Stoxx 50 is at the highest level since March.

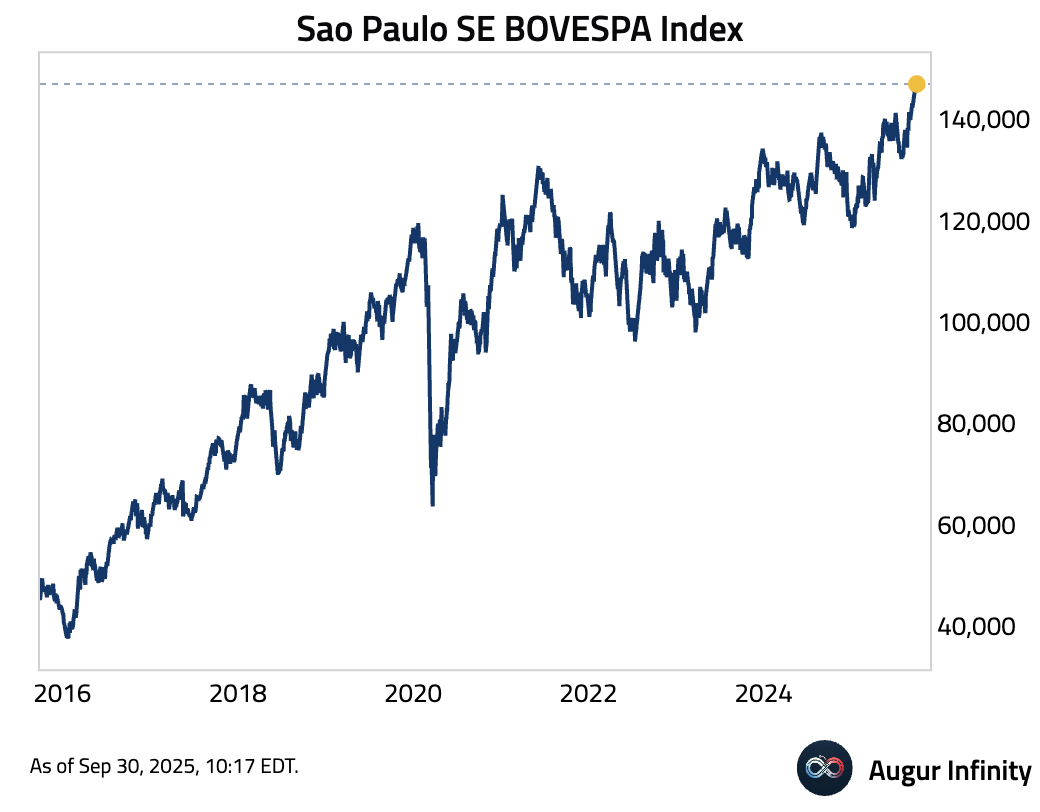

- Brazi's BOVESPA Index has reached its 16th all-time high of the year.

- Shanghai Shenzhen CSI 300 is trading at the best level since February 2022.

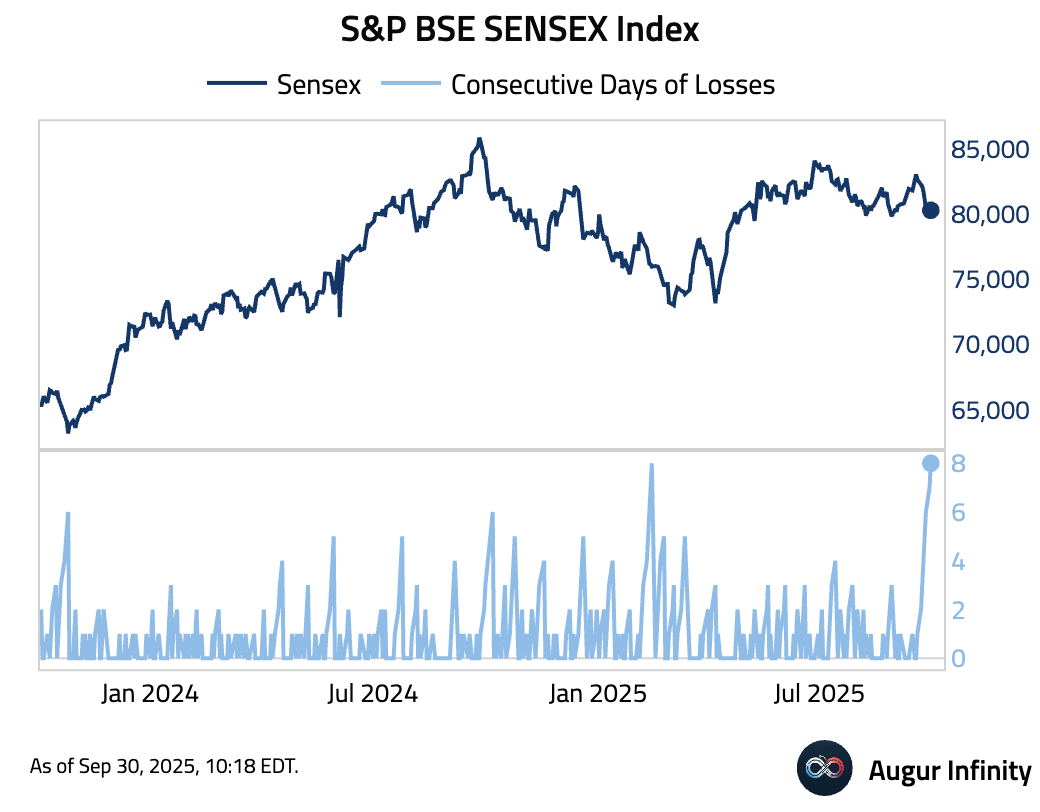

- The SENSEX Index for India has declined for eight consecutive sessions.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.