Note: This is the August Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- The US government entered a shutdown at midnight after failing to pass a funding resolution.

- The European Commission announced plans to increase tariffs on steel imports to approximately 50 percent.

- Taiwan rejected a US request to split semiconductor production evenly between the two countries.

Global Economics

United States

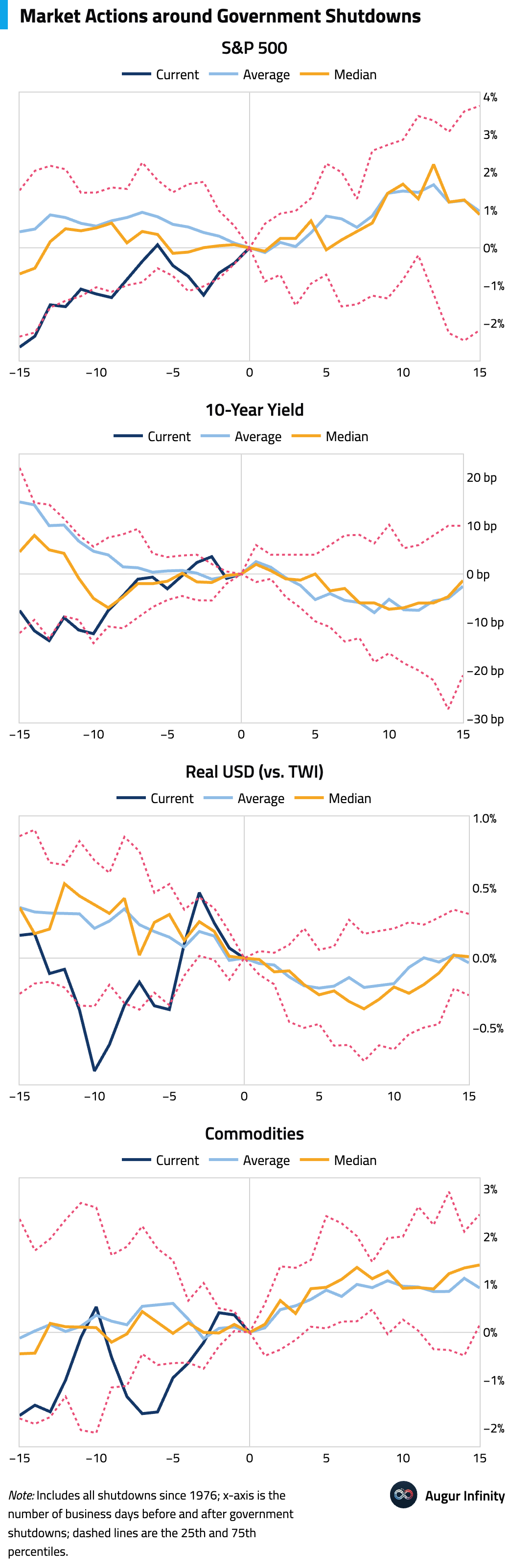

- Here's the typical market actions around government shutdowns since 1976.

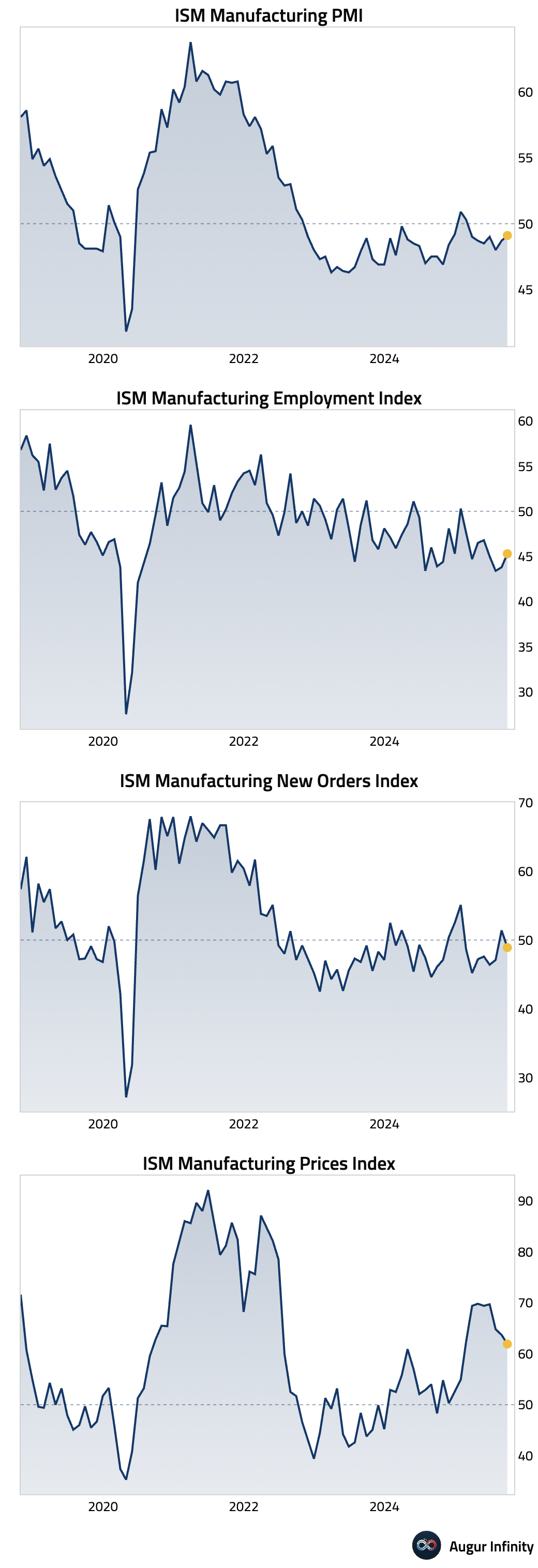

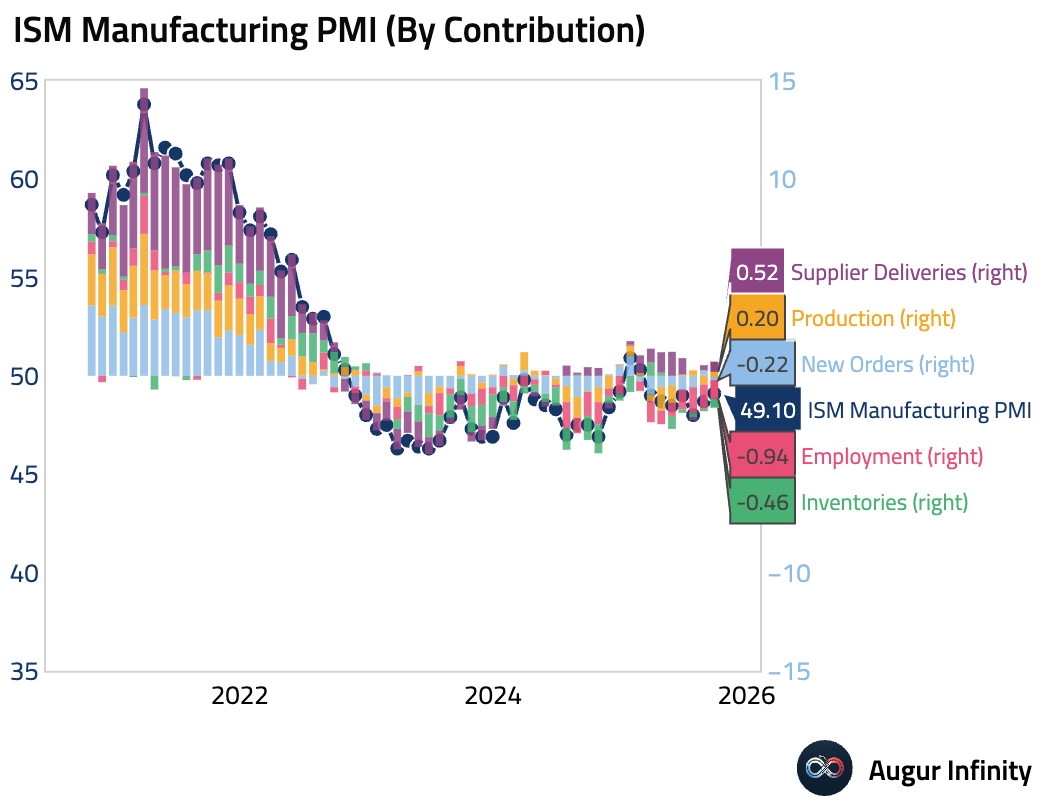

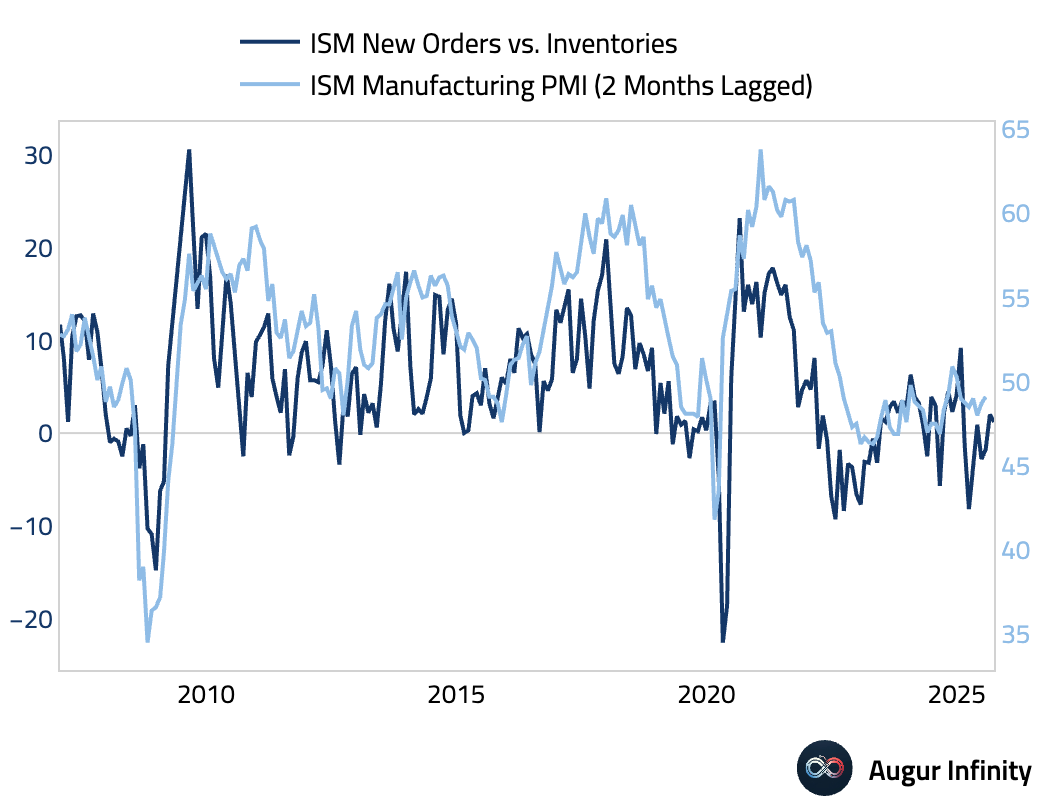

- The ISM Manufacturing PMI rose slightly to 49.1 in September but remained in contractionary territory for the seventh consecutive month. While the production sub-index moved back into expansion, the forward-looking new orders component fell sharply back into contraction at 48.9. The employment index also remained deeply negative at 45.3, with survey comments on staff reductions outnumbering hiring comments by a ratio of three to one. Survey respondents overwhelmingly cited tariffs as the primary driver of both weak demand and persistent price pressures, with the prices paid index remaining elevated at 61.9.

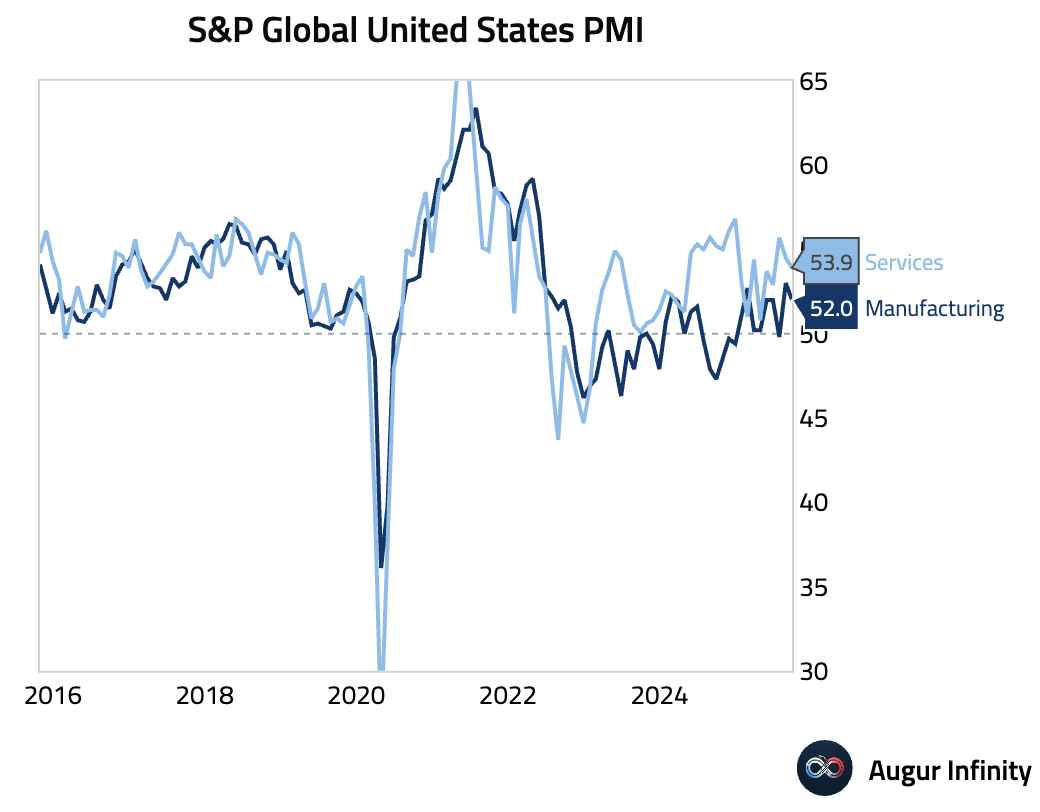

- The final September S&P Global Manufacturing PMI registered 52.0, revised down from the flash estimate and below the prior month's 53.0. The report indicated a slower expansion as tariffs hit new export orders. Production growth was supported by firms drawing down pre-tariff stockpiles, leading to a concerning buildup of unsold inventory that poses a downside risk to future production.

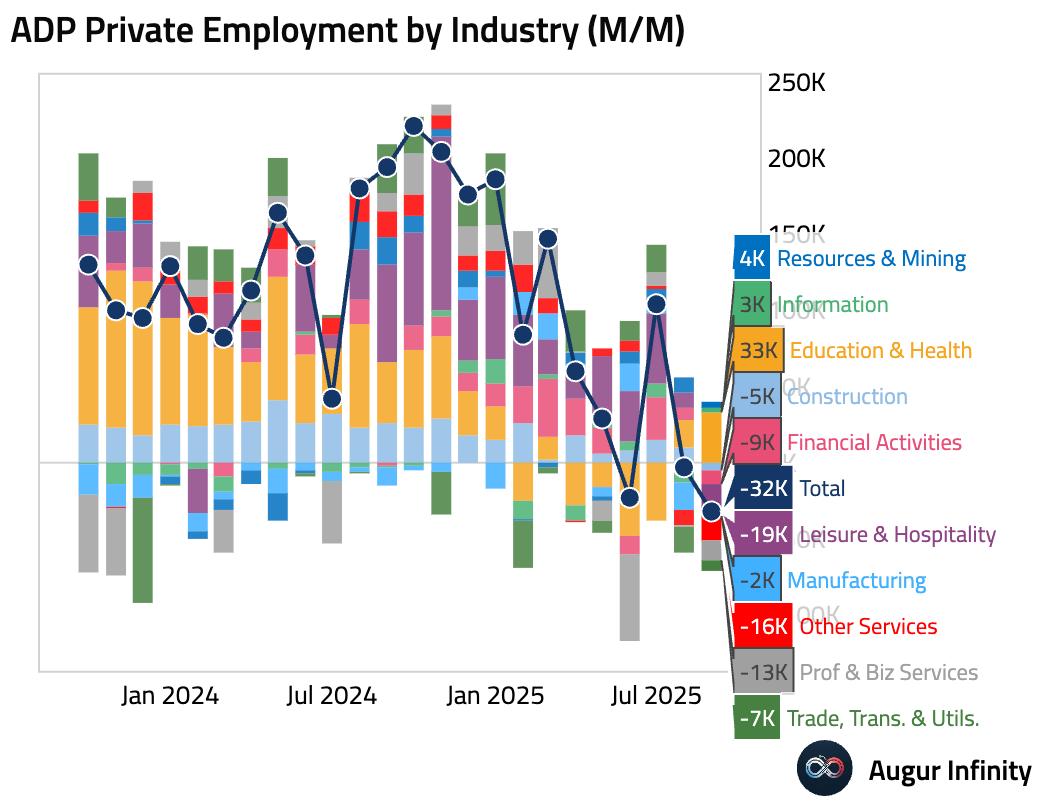

- Private payrolls unexpectedly contracted in September, a significant miss against consensus expectations of a modest gain (act: -32k, est: 50k). The prior month was also revised lower. A key driver was a one-off benchmarking to QCEW data, creating a 43k drag on September's number and causing a large downward revision to August.

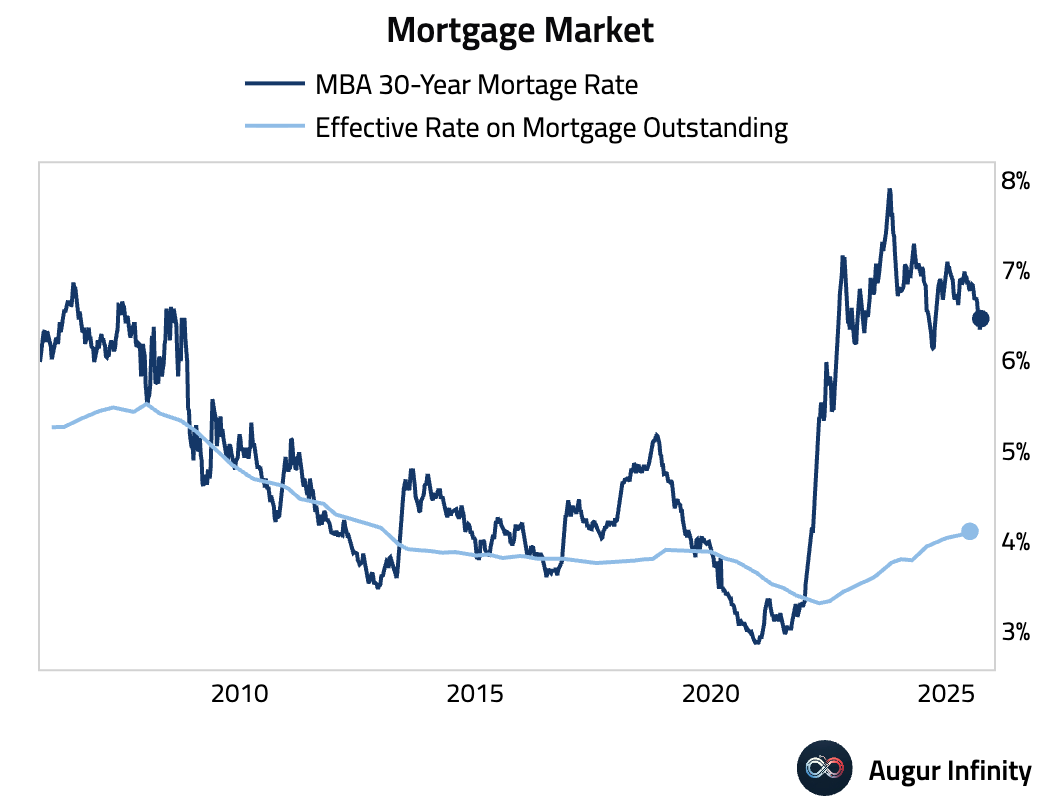

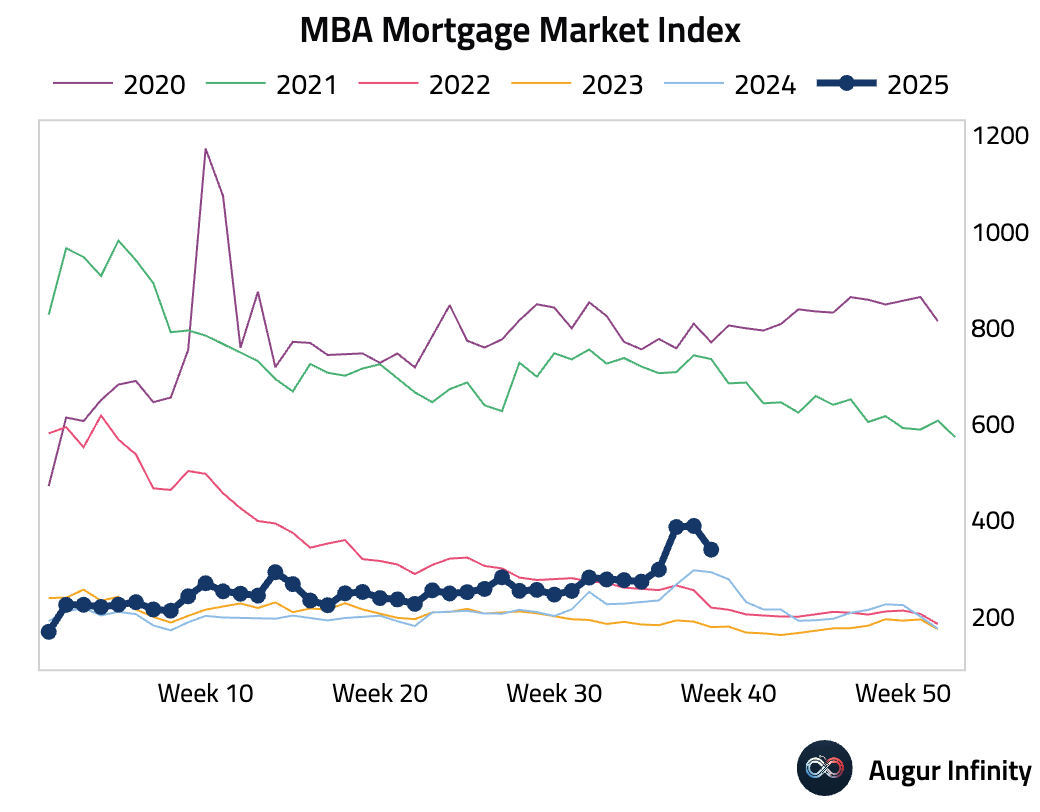

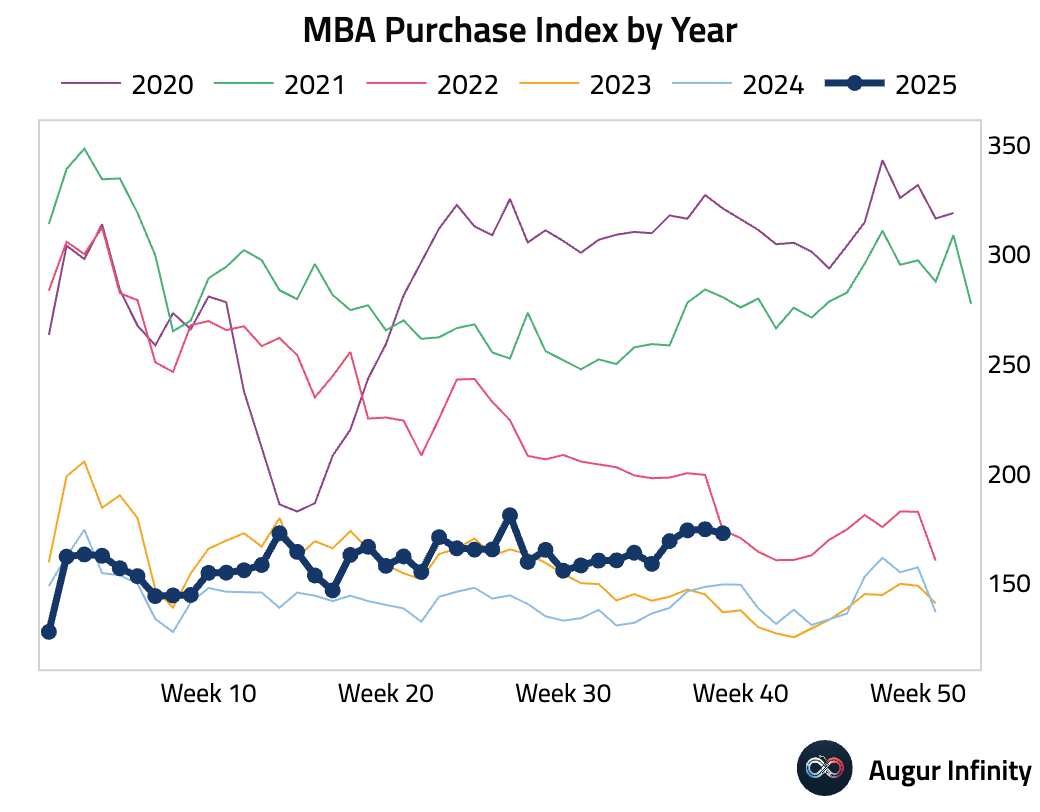

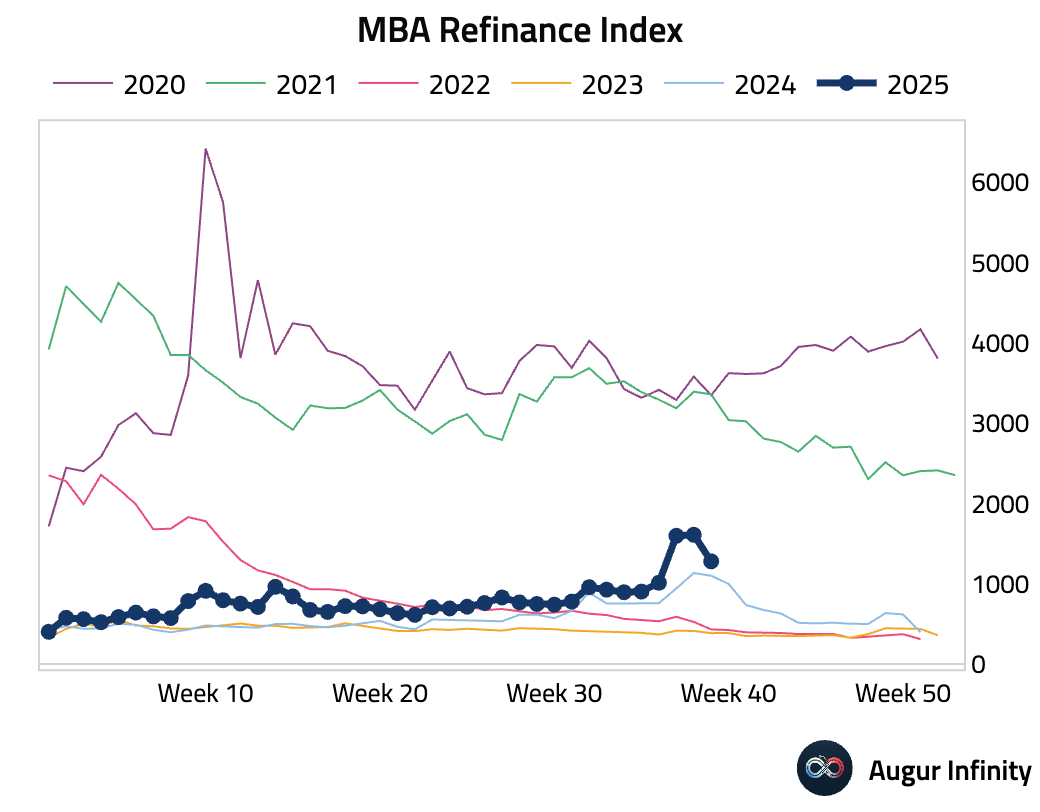

- The MBA 30-year mortgage rate rose (act: 6.46%, prev: 6.34%).

As a result, mortgage applications tumbled (Applications act: -12.7% w/w, prev: 0.6%). The decline was broad-based across both purchasing and refinancing activity.

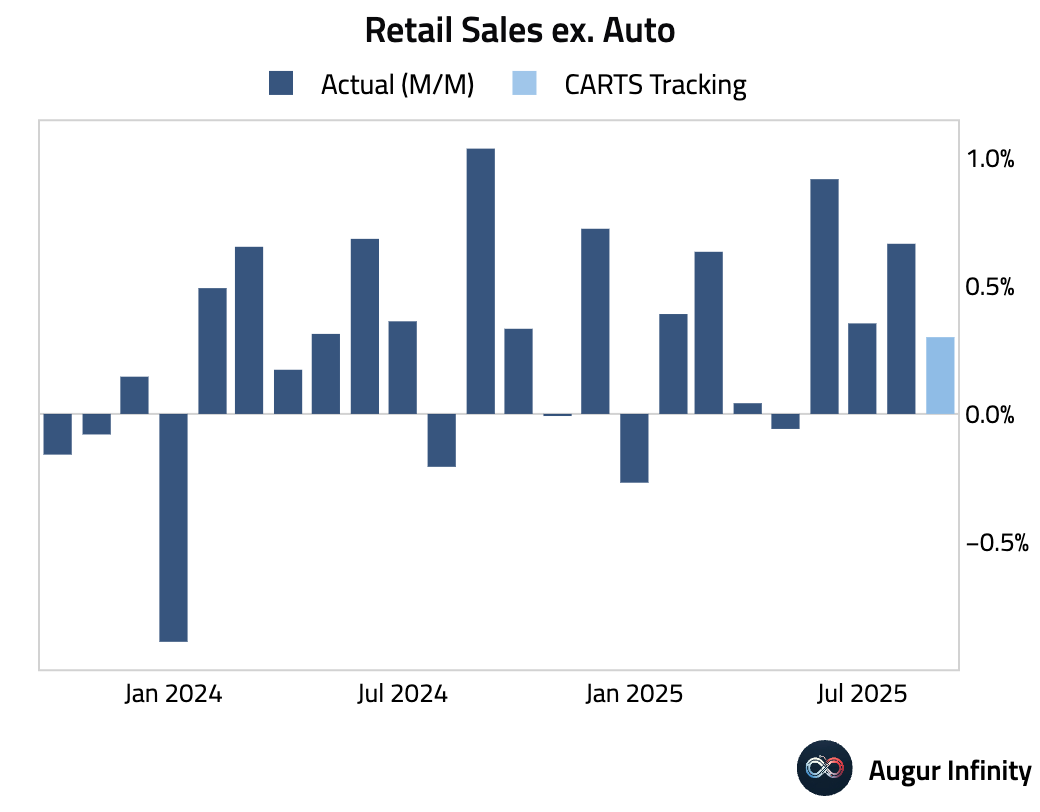

- The Chicago Fed CARTS is projecting retail sales ex auto for September to rise by 0.3% M/M.

Canada

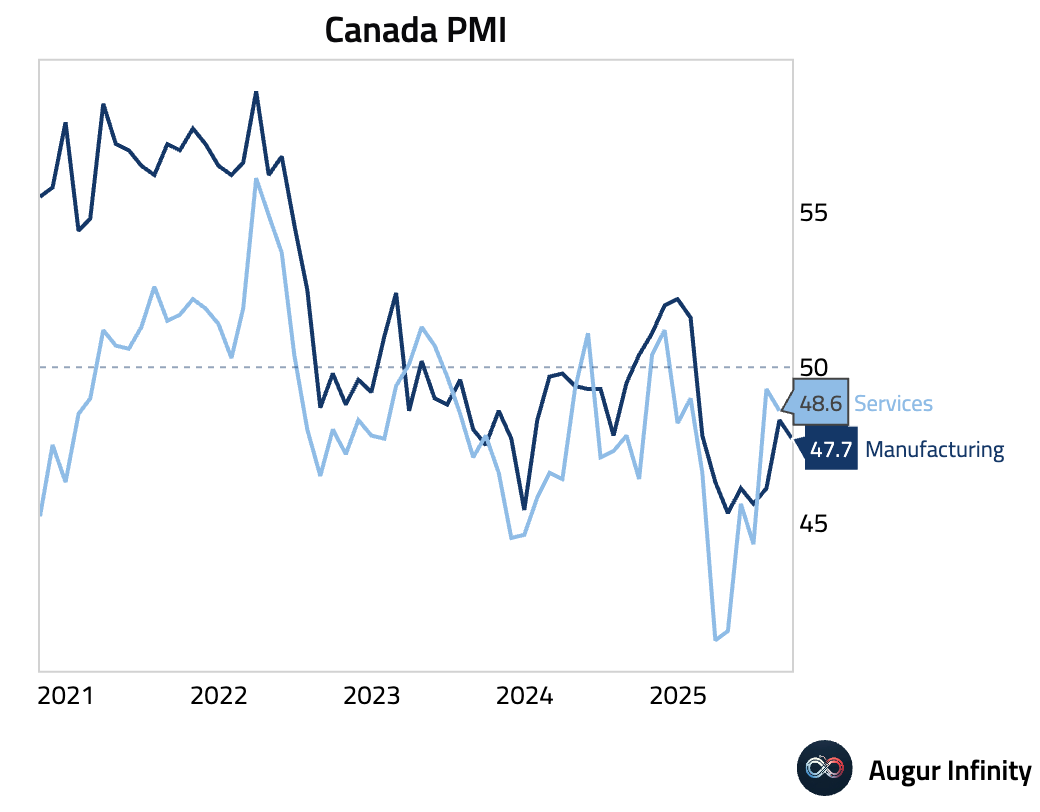

- Canada's manufacturing sector deteriorated at a faster pace in September, with the S&P Global PMI falling to 47.7. This marked the eighth consecutive month of contraction, driven by quicker declines in both output and new orders. Firms cited adverse tariff effects and weak demand from the United States.

Europe

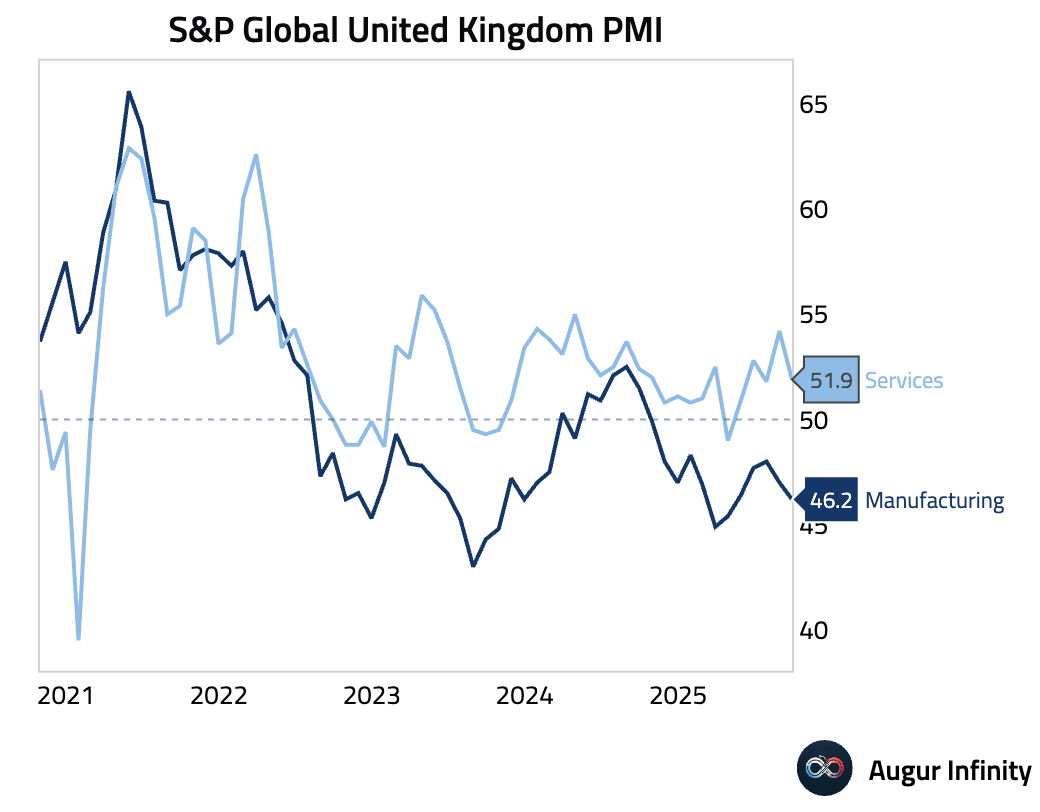

- The UK's manufacturing sector contraction deepened in September, with the S&P Global PMI falling to a five-month low of 46.2. This marks the 12th consecutive month of contraction. Faster downturns in output and new orders, particularly a steep drop in export business, drove the decline, with production shutdowns at a major automaker cited as a key disruption.

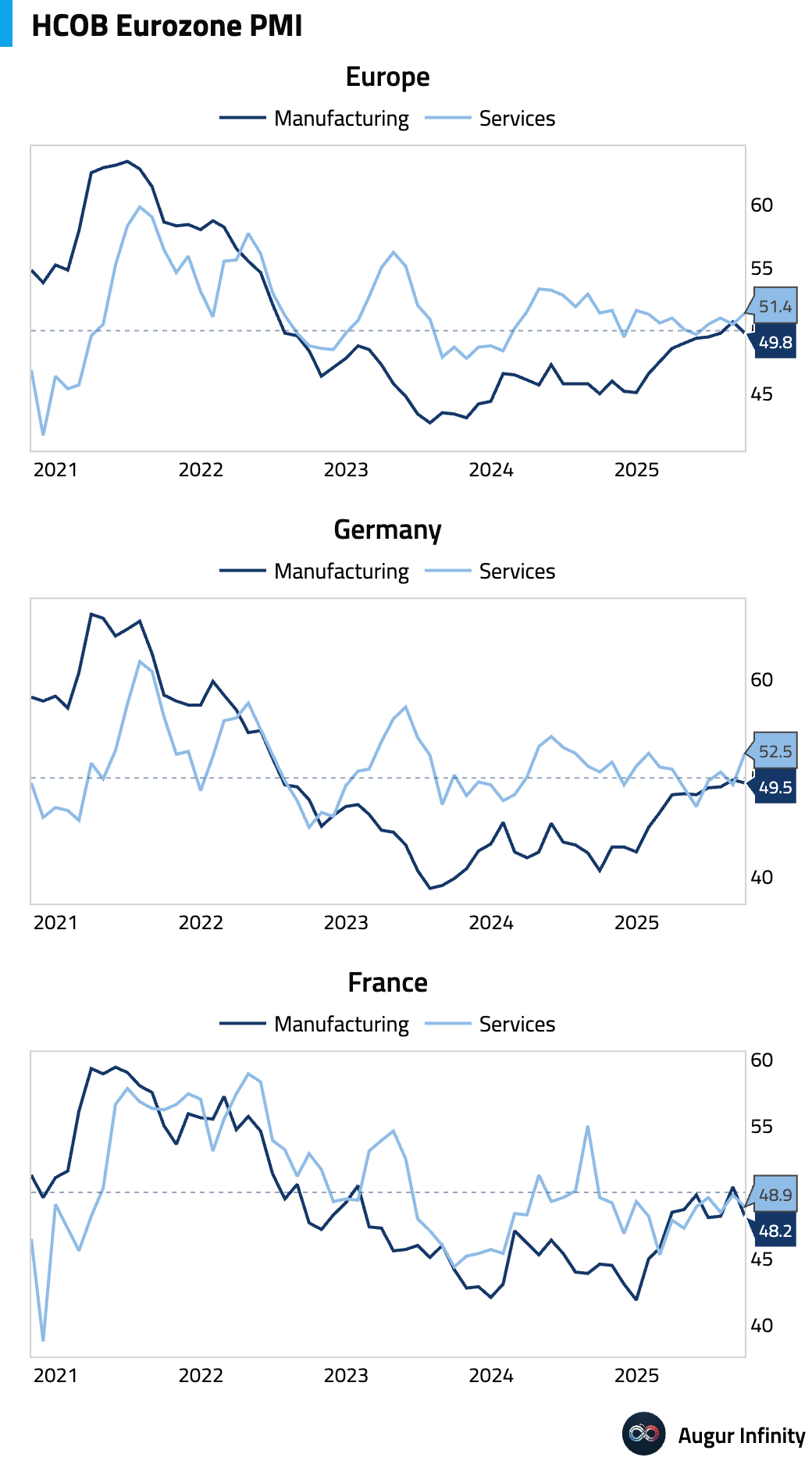

- The HCOB Eurozone Manufacturing PMI fell back into contraction, declining to 49.8 in September. The downturn was led by the bloc's largest economies, with Germany's PMI at 49.5 and France's at 48.2, both signaling contraction. The drop was driven by new orders declining at the fastest pace in six months. While German output growth hit a 42-month high as firms worked through backlogs, forward-looking indicators like new orders and business expectations deteriorated, pointing to future weakness.

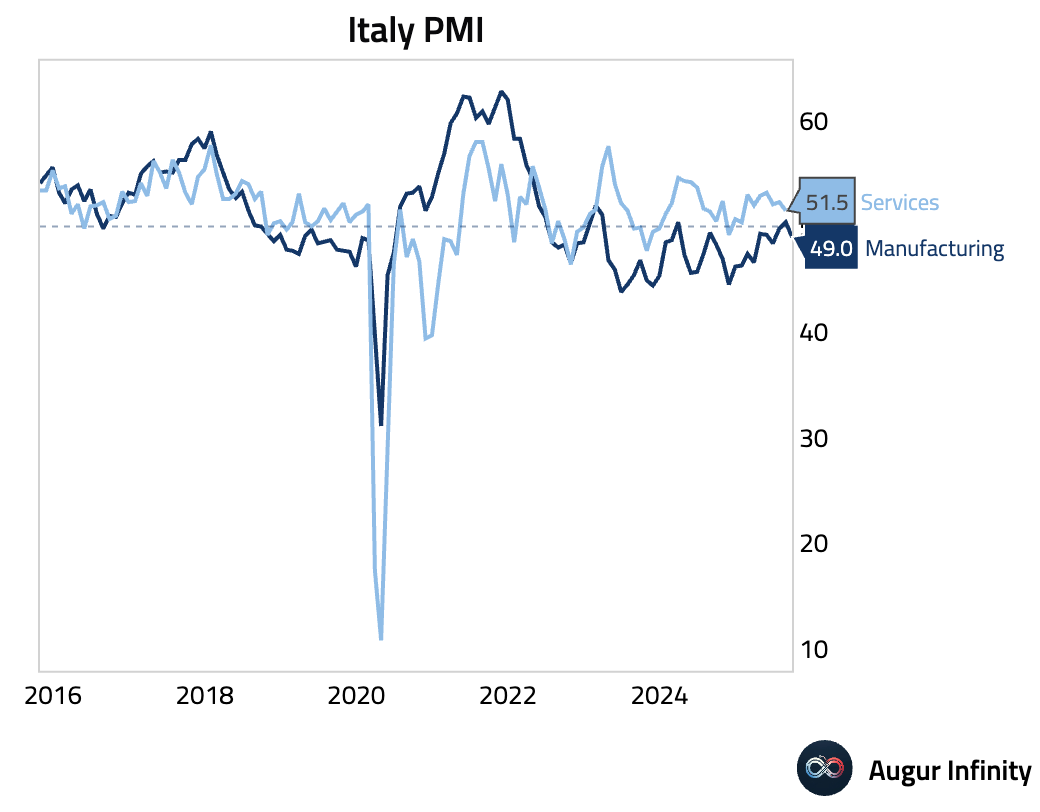

- Italian manufacturing activity contracted in September, with the HCOB PMI falling to 49.0. The downturn was driven by a solid drop in new orders amid economic uncertainty. Input costs rose at the fastest pace in six months, but intense competition squeezed margins by preventing firms from raising selling prices.

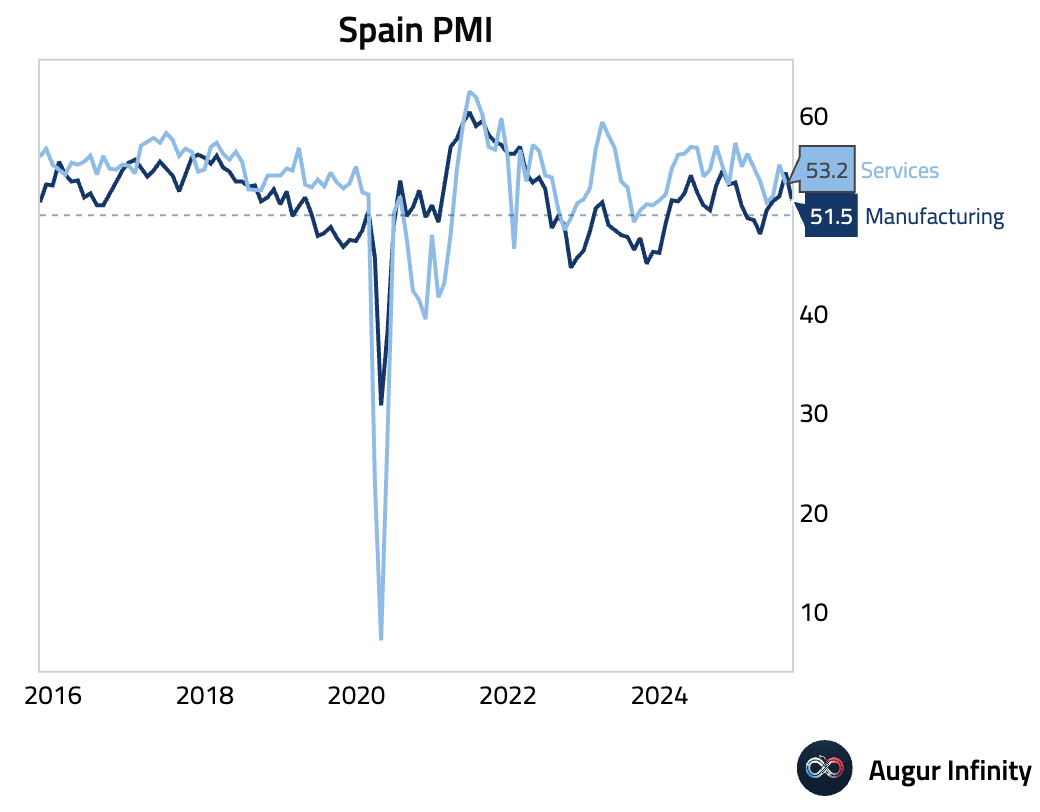

- Spain’s manufacturing sector growth slowed sharply in September, with the HCOB PMI falling to 51.5. Weaker output and new orders drove the slowdown, with exports contracting for the first time in three months.

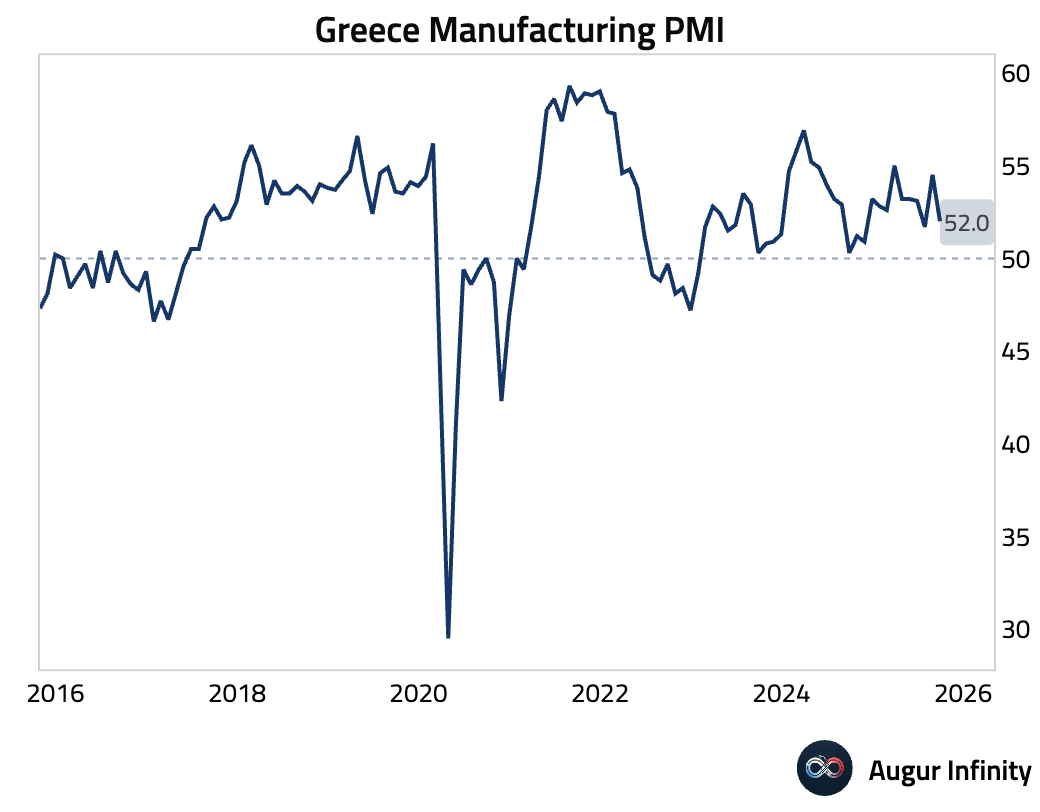

- Greece's manufacturing PMI fell to 52.0, its second-slowest expansion in 10 months, as plunging exports offset solid domestic demand.

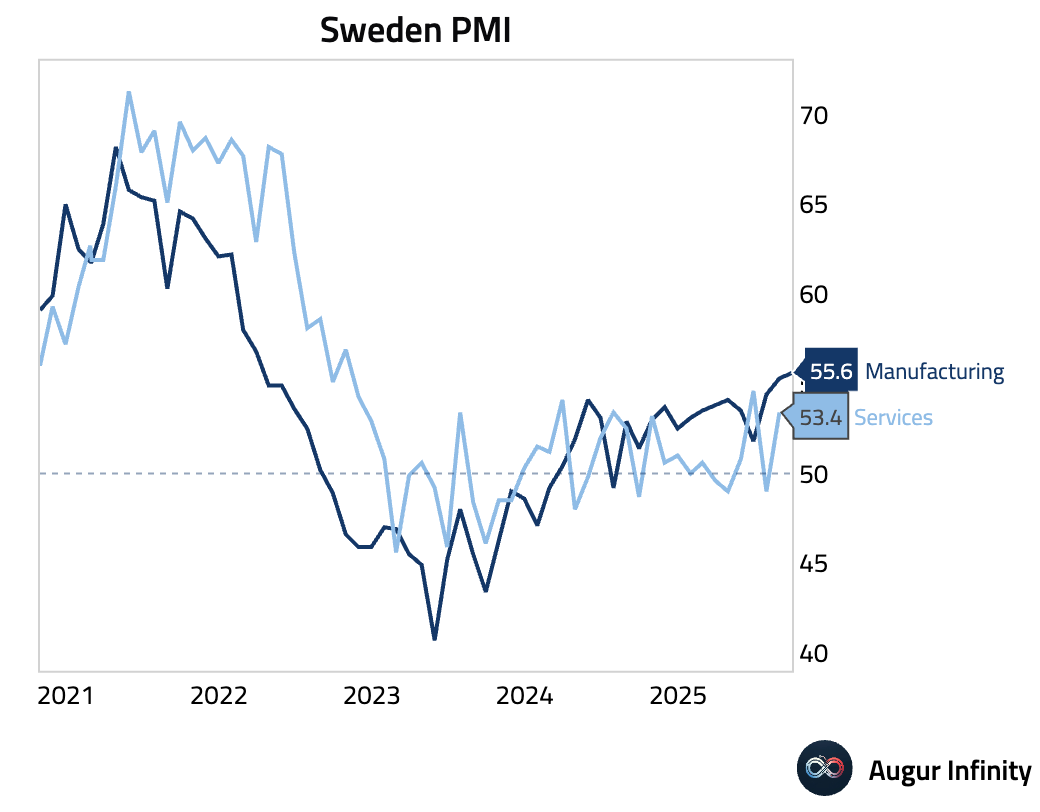

- Sweden's manufacturing PMI rose to 55.6, continuing its expansion.

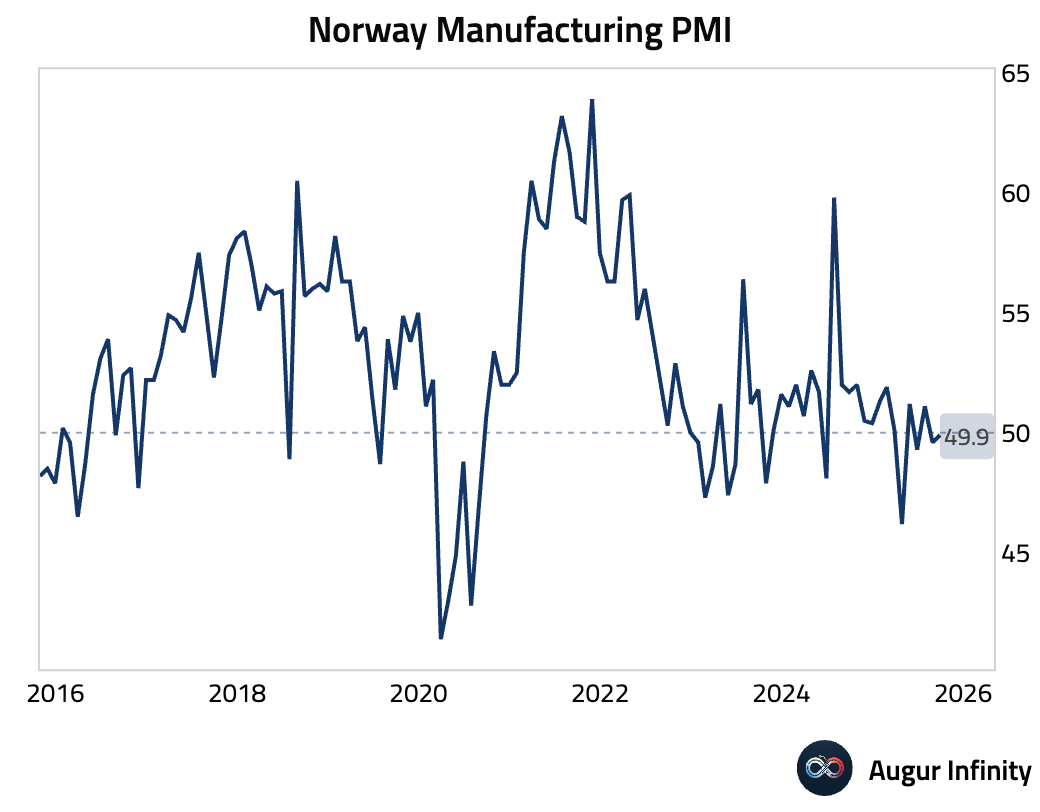

- Norway's manufacturing PMI ticked up to 49.9 but remained just below the neutral 50-mark.

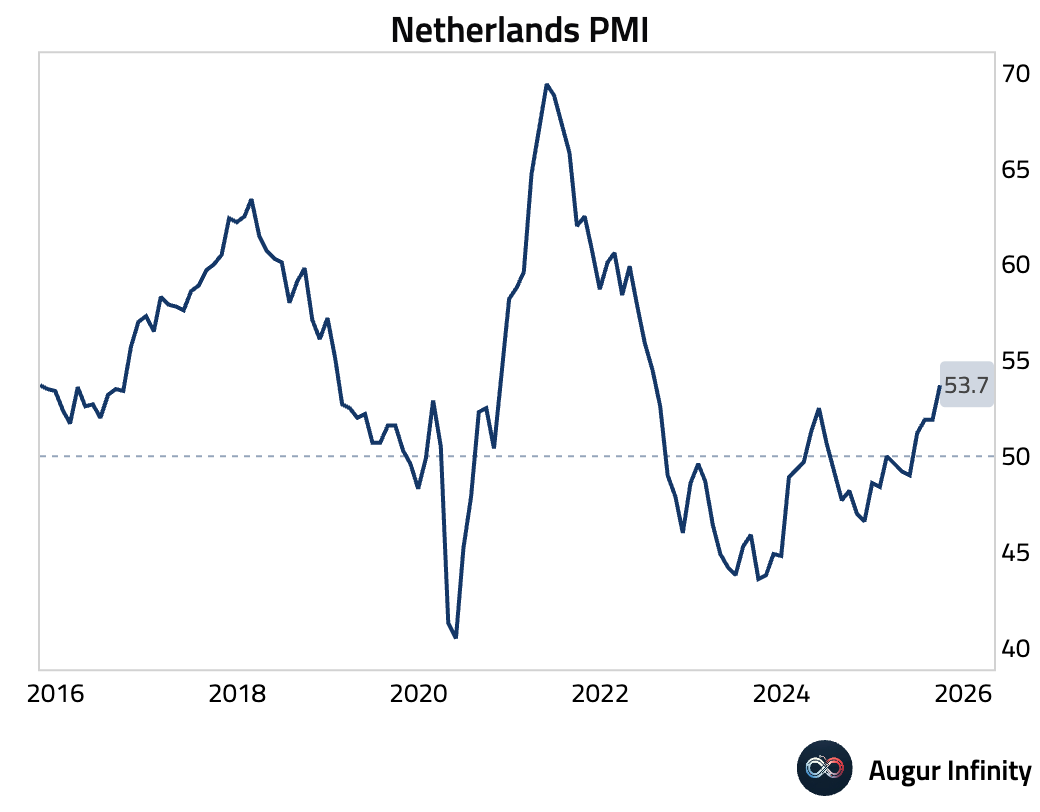

- The Dutch manufacturing sector showed robust growth, with the NEVI PMI jumping to 53.7, its strongest reading since July 2022, driven entirely by strong domestic demand.

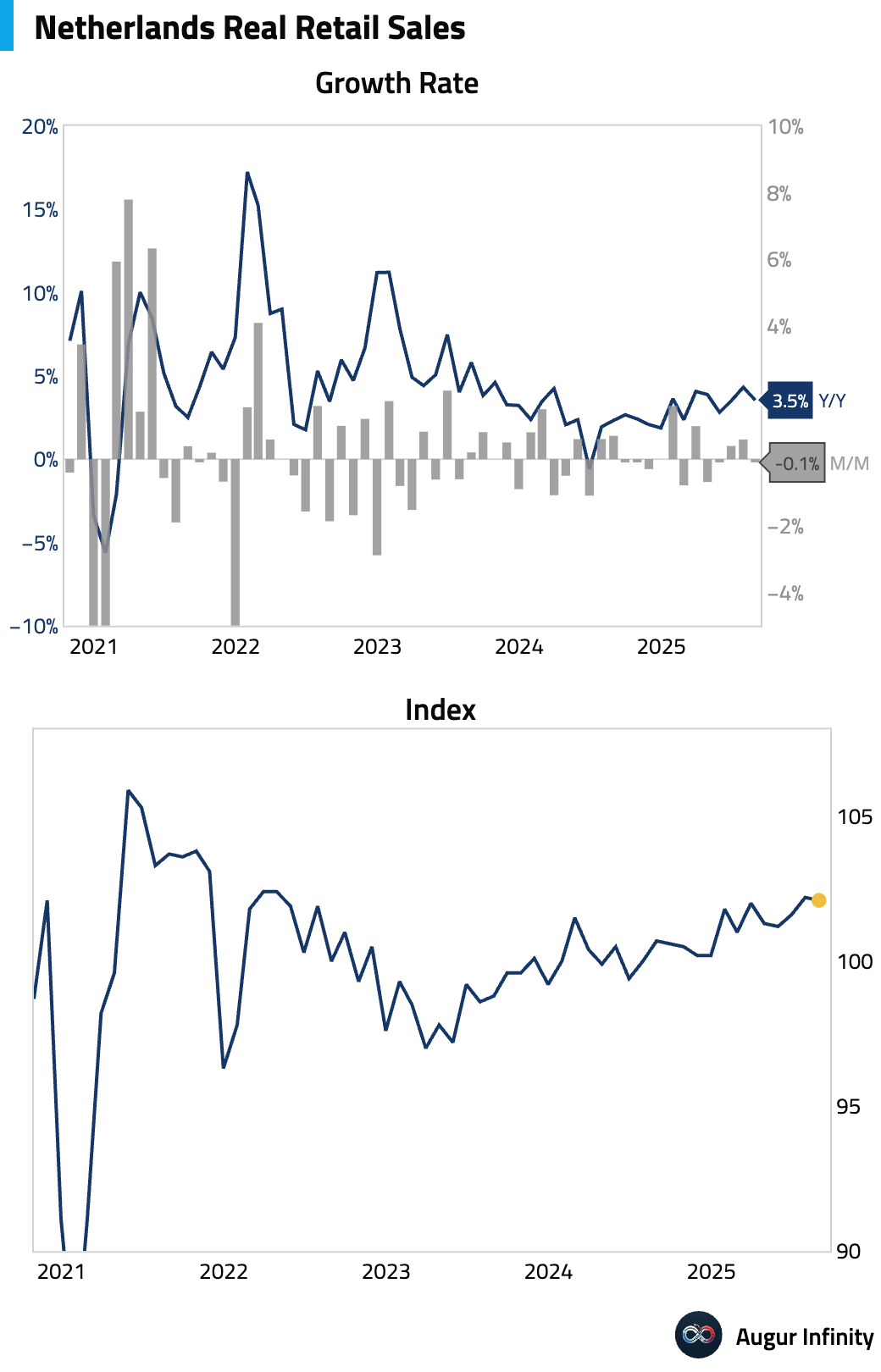

- Dutch retail sales growth slowed in August (act: 3.6% Y/Y, prev: 4.3%).

Interactive chart on Augur Infinity

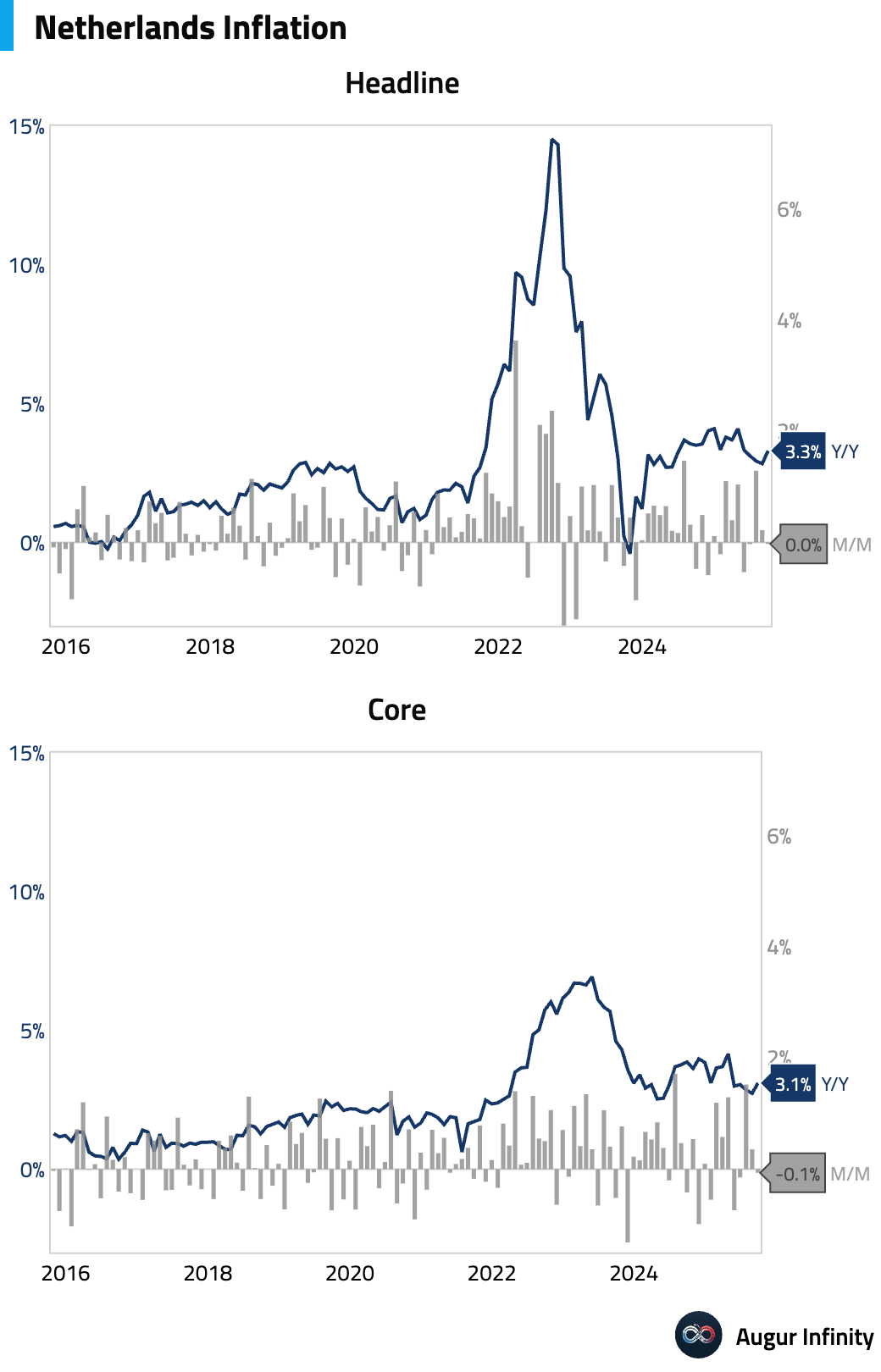

- Preliminary data showed Dutch inflation accelerated to 3.3% Y/Y in September from 2.8% previously.

Interactive chart on Augur Infinity

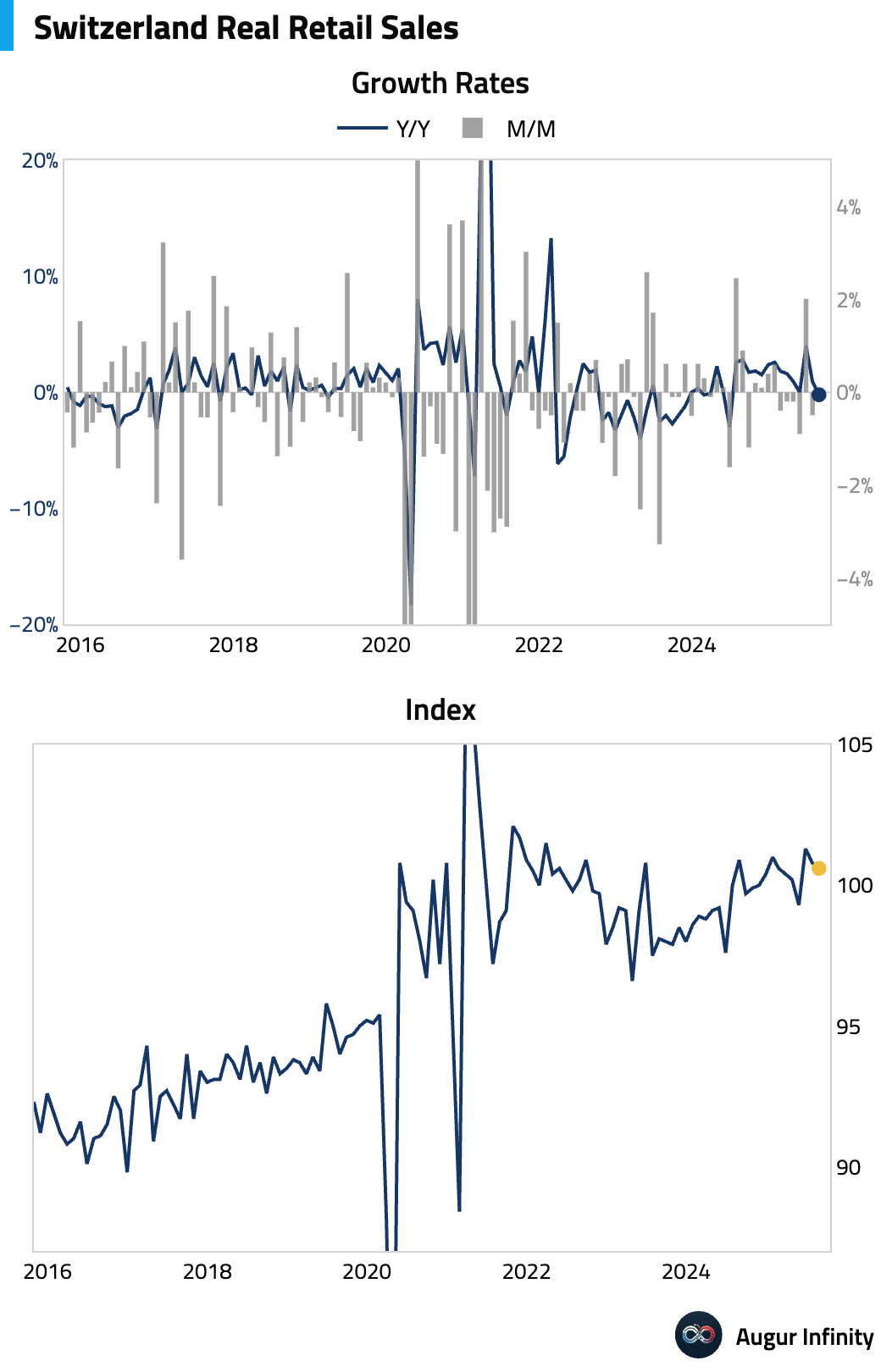

- Swiss retail sales unexpectedly contracted year-over-year in August, missing consensus forecasts (YoY act: -0.2%, est: 0.5%).

Interactive chart on Augur Infinity

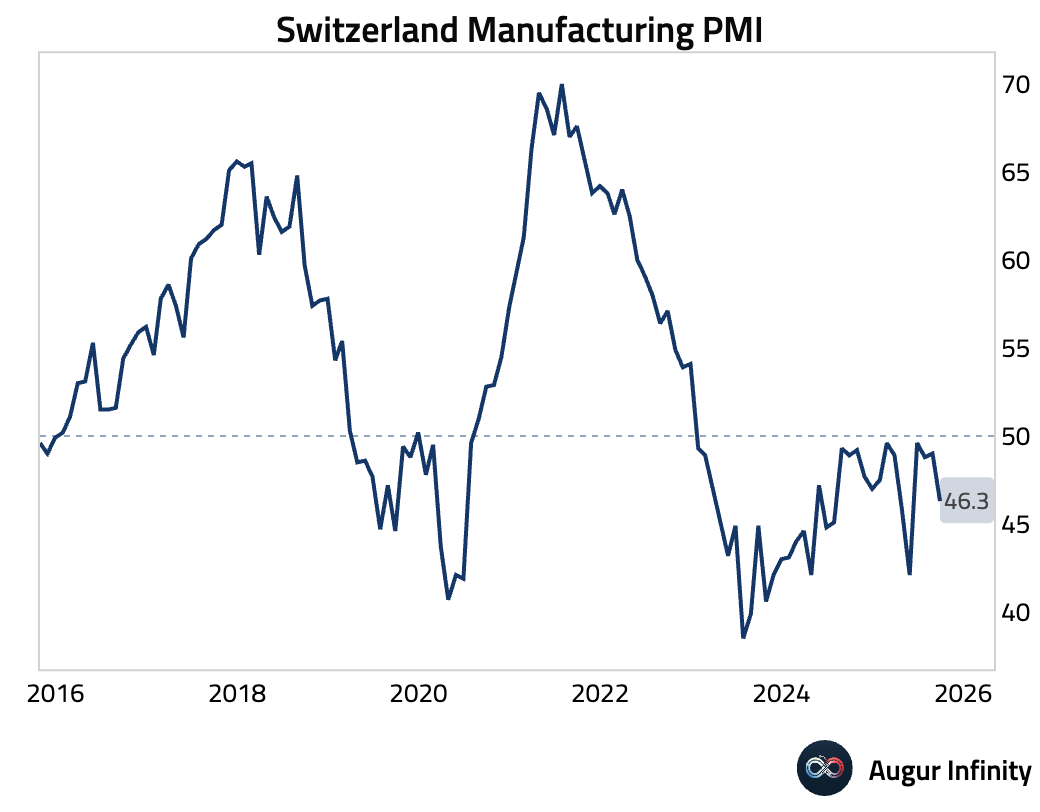

- Switzerland's procure.ch Manufacturing PMI slumped deeper into contraction territory, falling to 46.3 and missing estimates.

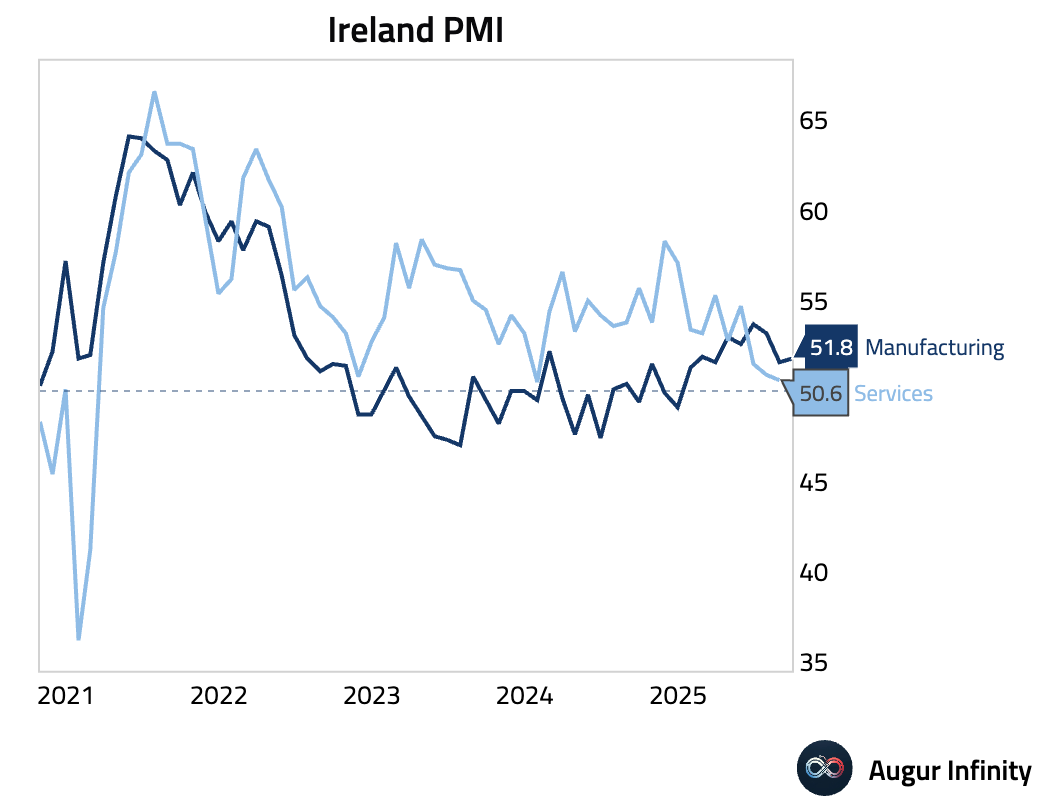

- Ireland's manufacturing PMI edged higher to 51.8, though output stalled as firms used inventories to meet demand.

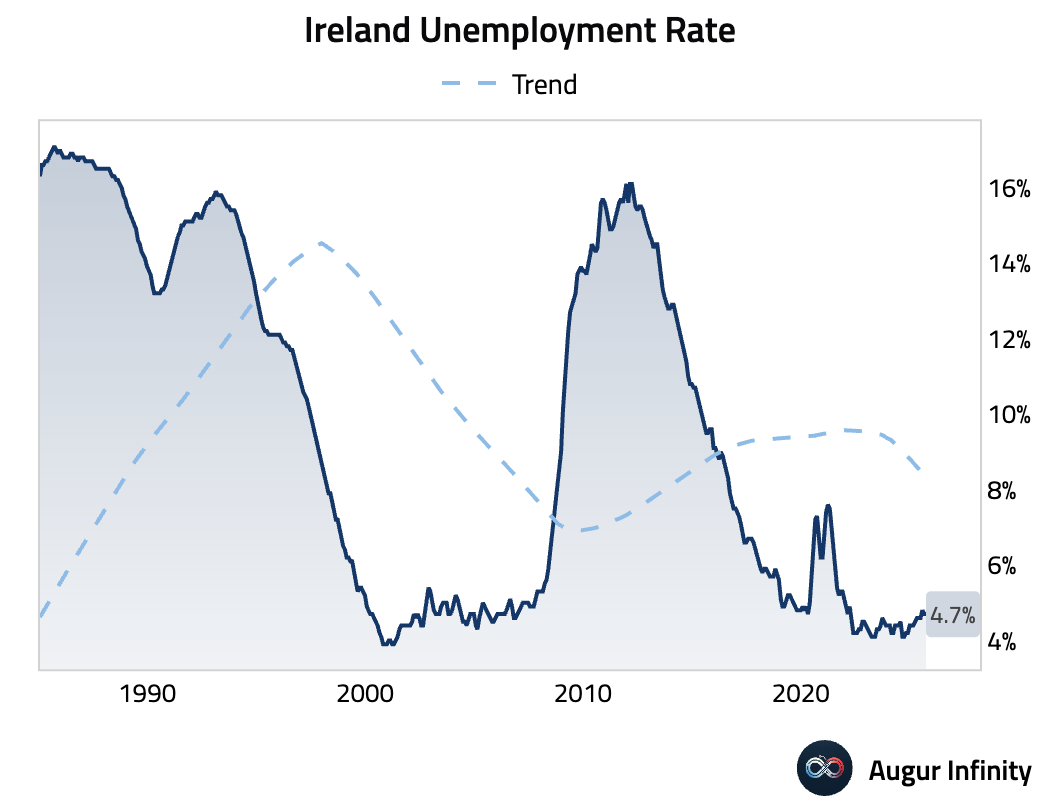

- Ireland's unemployment rate held steady at 4.7% in September.

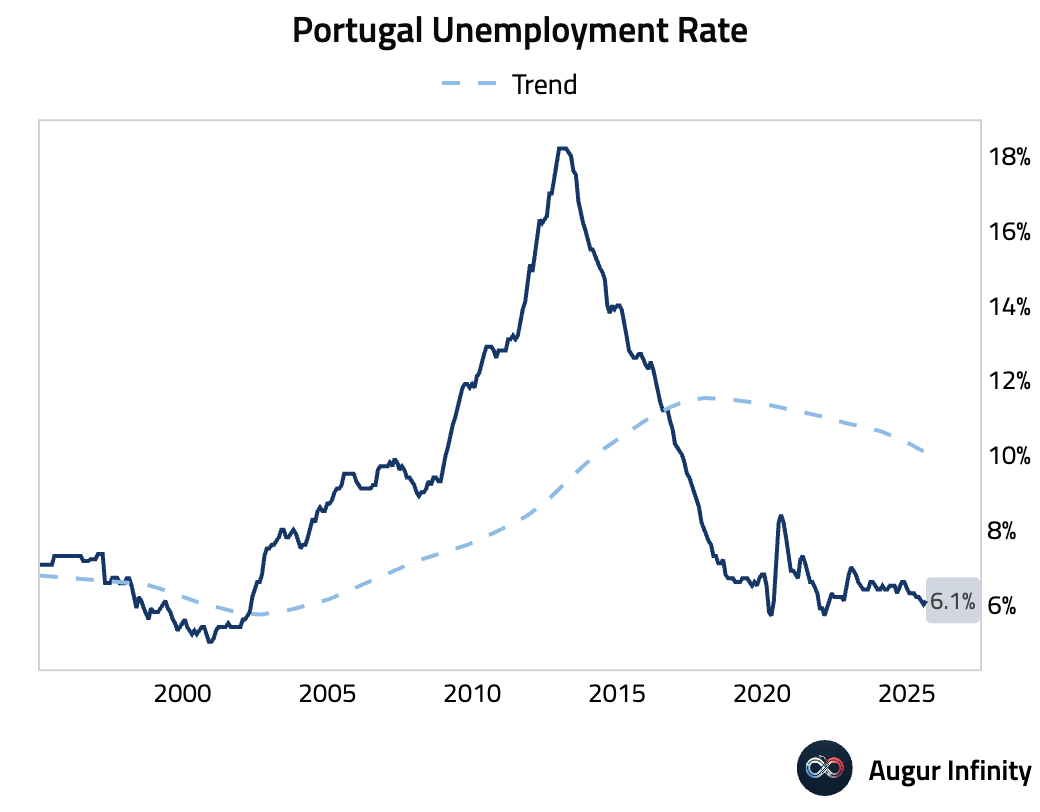

- Portugal's unemployment rate ticked up in August (act: 6.1%, prev: 5.8%).

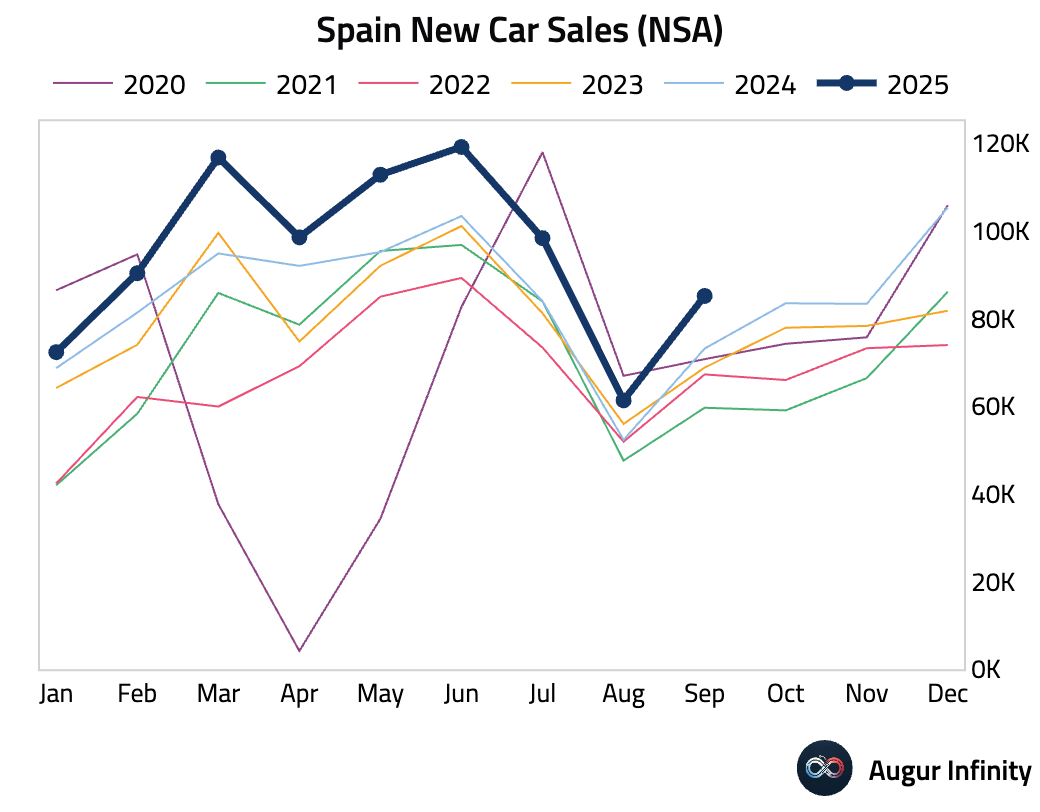

- Spanish new car sales remained robust in September, though growth moderated slightly from the prior month (act: 16.4% Y/Y, prev: 17.2%).

Asia-Pacific

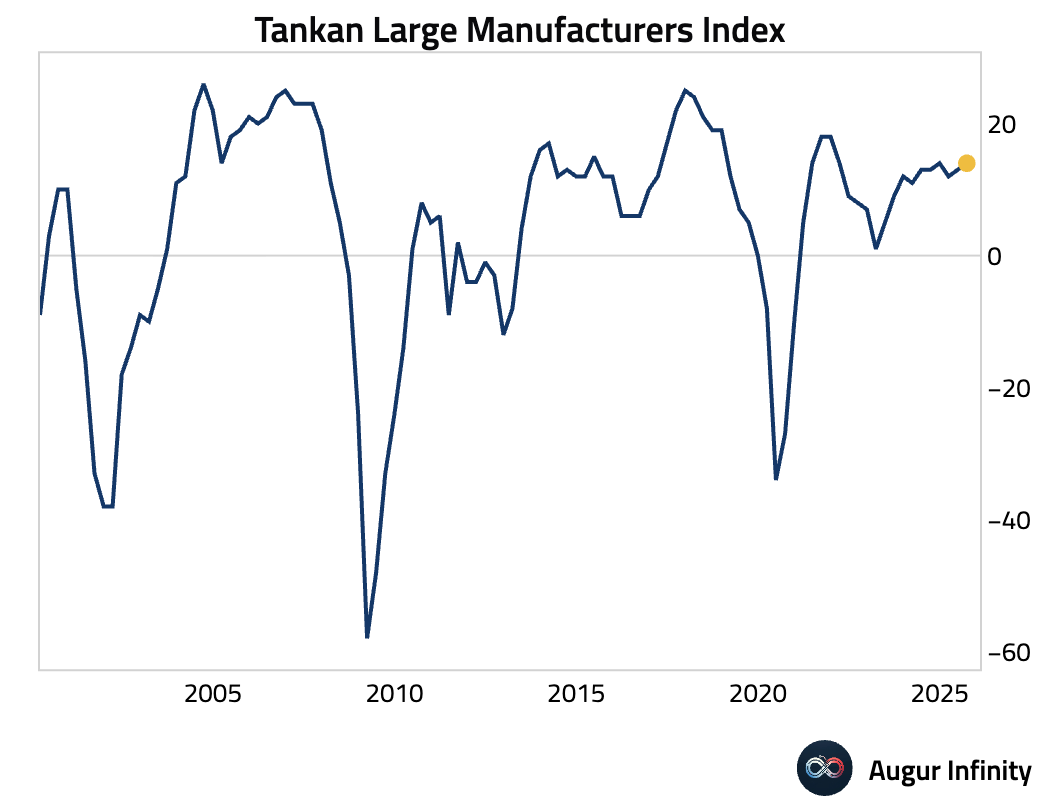

- The Q3 Tankan survey showed sentiment among Japan's large manufacturers improved to +14, its second straight quarterly gain, though it missed consensus by a point. A key positive was the upward revision of corporate capital expenditure plans, which signals investment resilience despite a worsening profit outlook. However, price DIs for both inputs and outputs declined, suggesting inflationary pressures may be peaking.

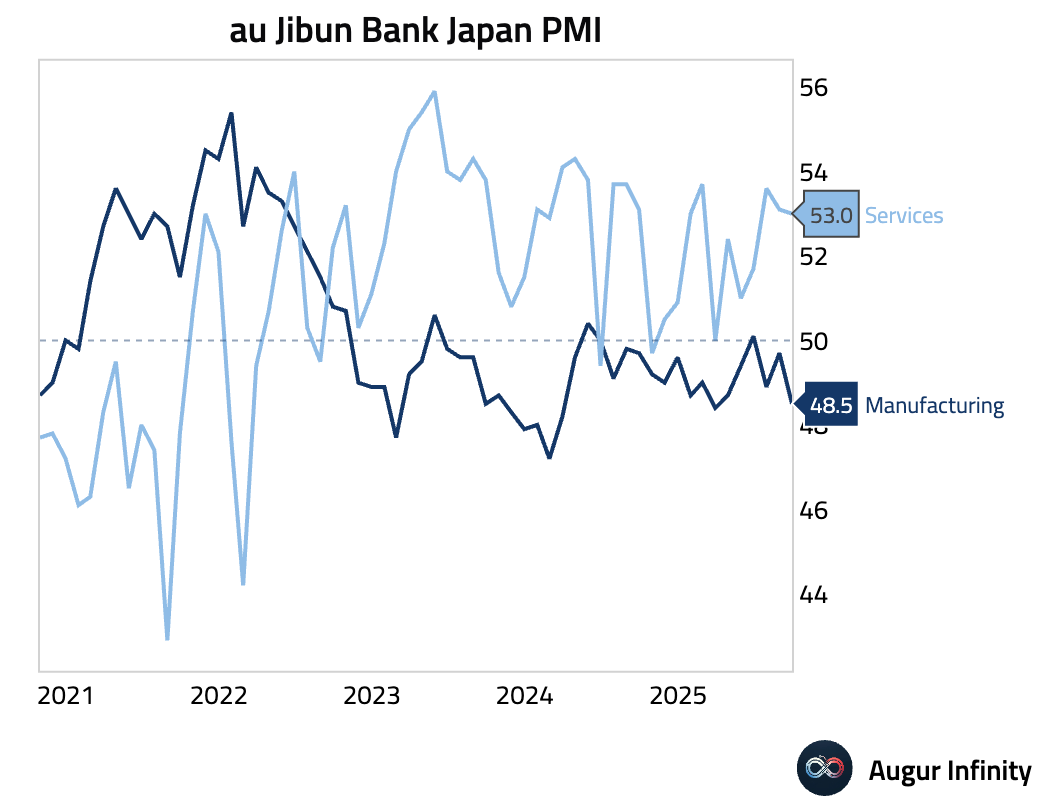

- Japan's final S&P Global Manufacturing PMI for September fell to 48.5, its lowest since March. The contraction was driven by weaker demand from key markets like China and the impact of US tariffs, which caused new orders to fall at the fastest pace since April.

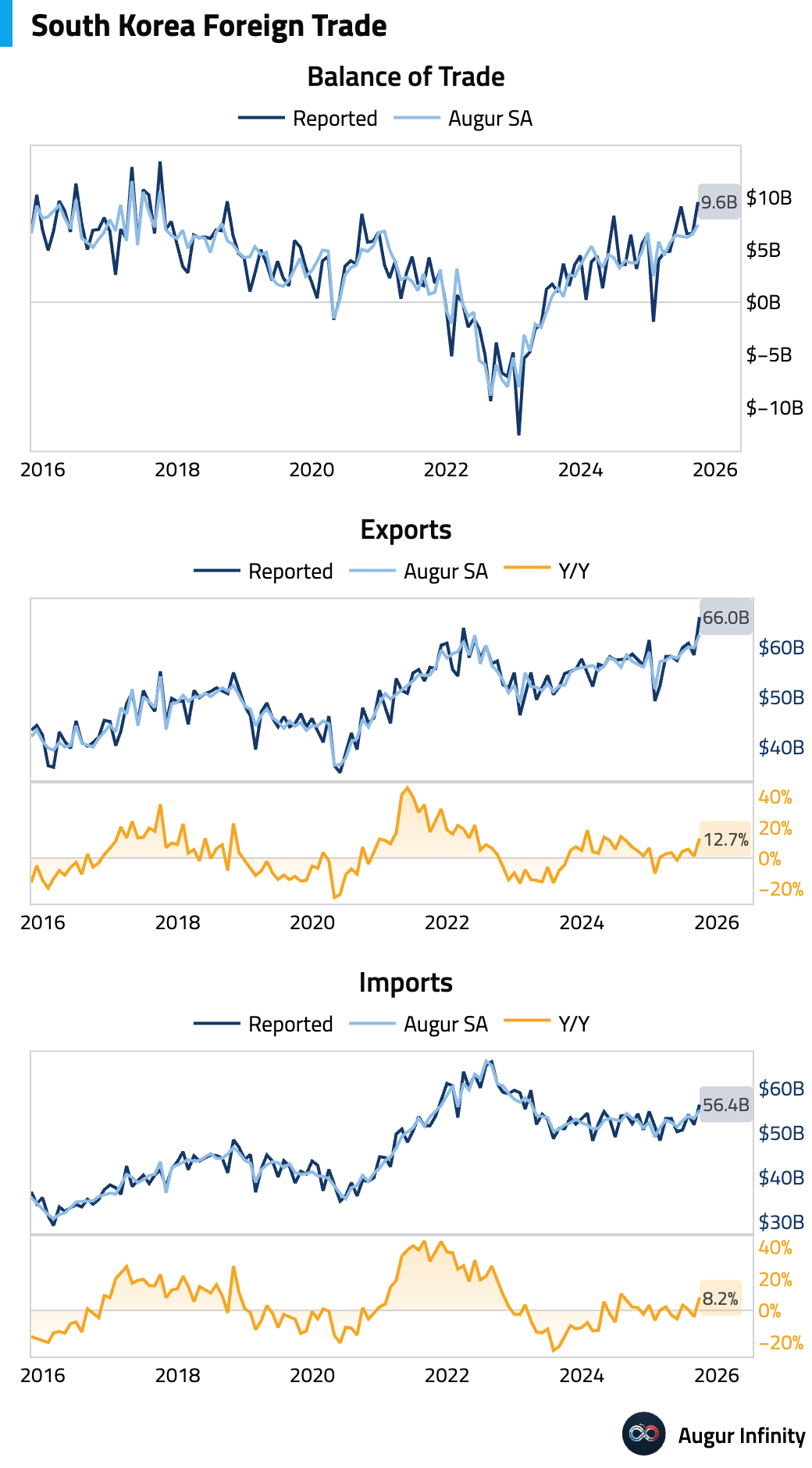

- South Korea’s exports surged 12.7% Y/Y in September, well above consensus, while imports also grew faster than expected at 8.2% Y/Y. This resulted in the trade surplus widening significantly to $9.6 billion, the largest since September 2018. The headline export strength was driven entirely by a rebound in non-tech exports, as tech exports, led by weaker semiconductors, continued to contract.

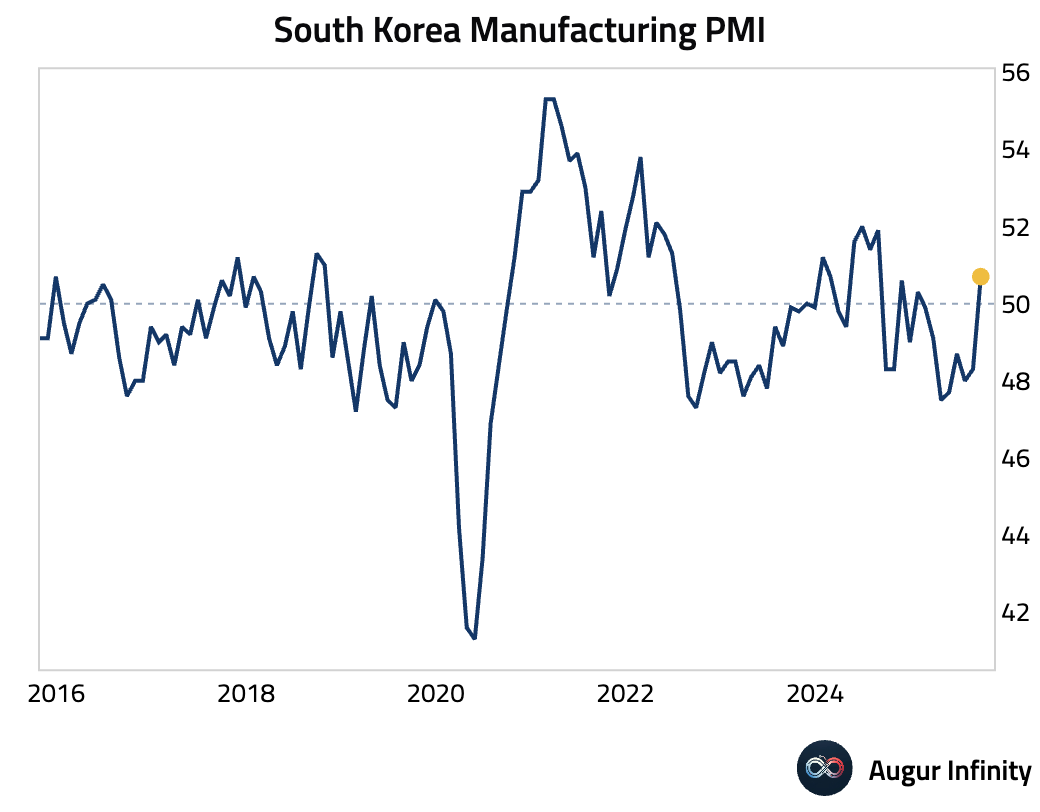

- South Korea's S&P Global Manufacturing PMI rose to 50.7, moving into expansionary territory for the first time since January. The improvement was driven by the strongest output growth in 13 months, supported by a rebound in export orders.

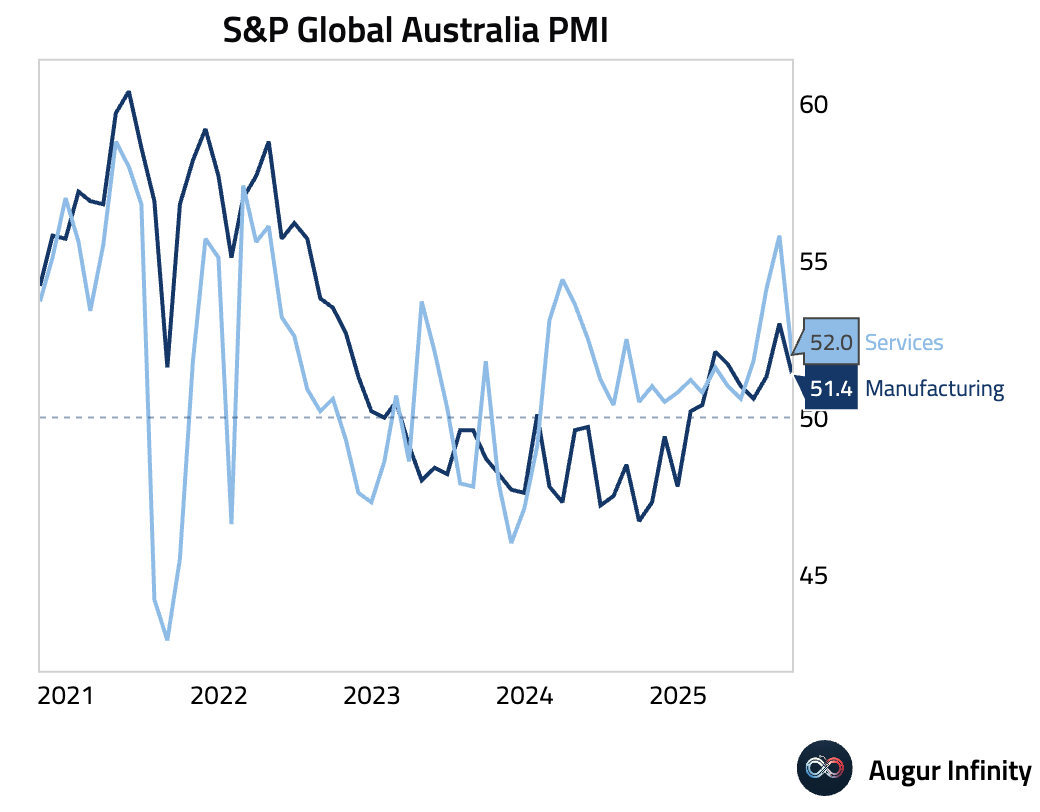

- Australia's S&P Global Manufacturing PMI eased to 51.4 in September but remained in expansionary territory.

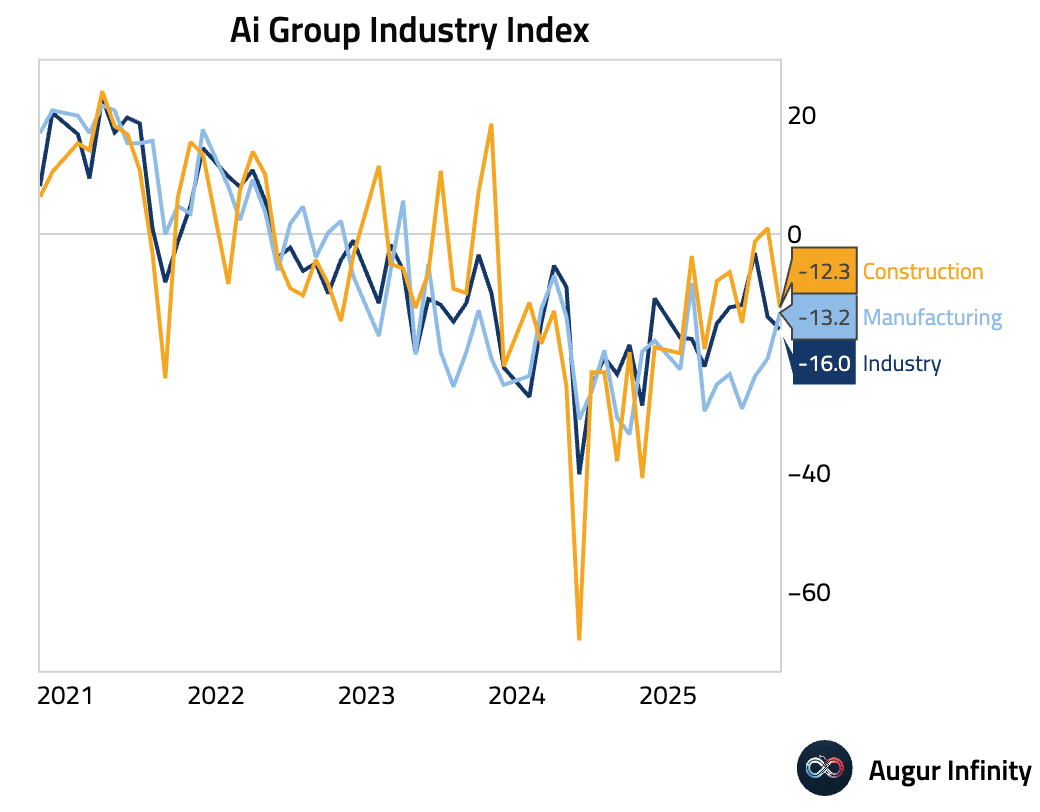

- The Ai Group's performance indices for September showed continued deep contraction across Australia's industry, manufacturing, and construction sectors.

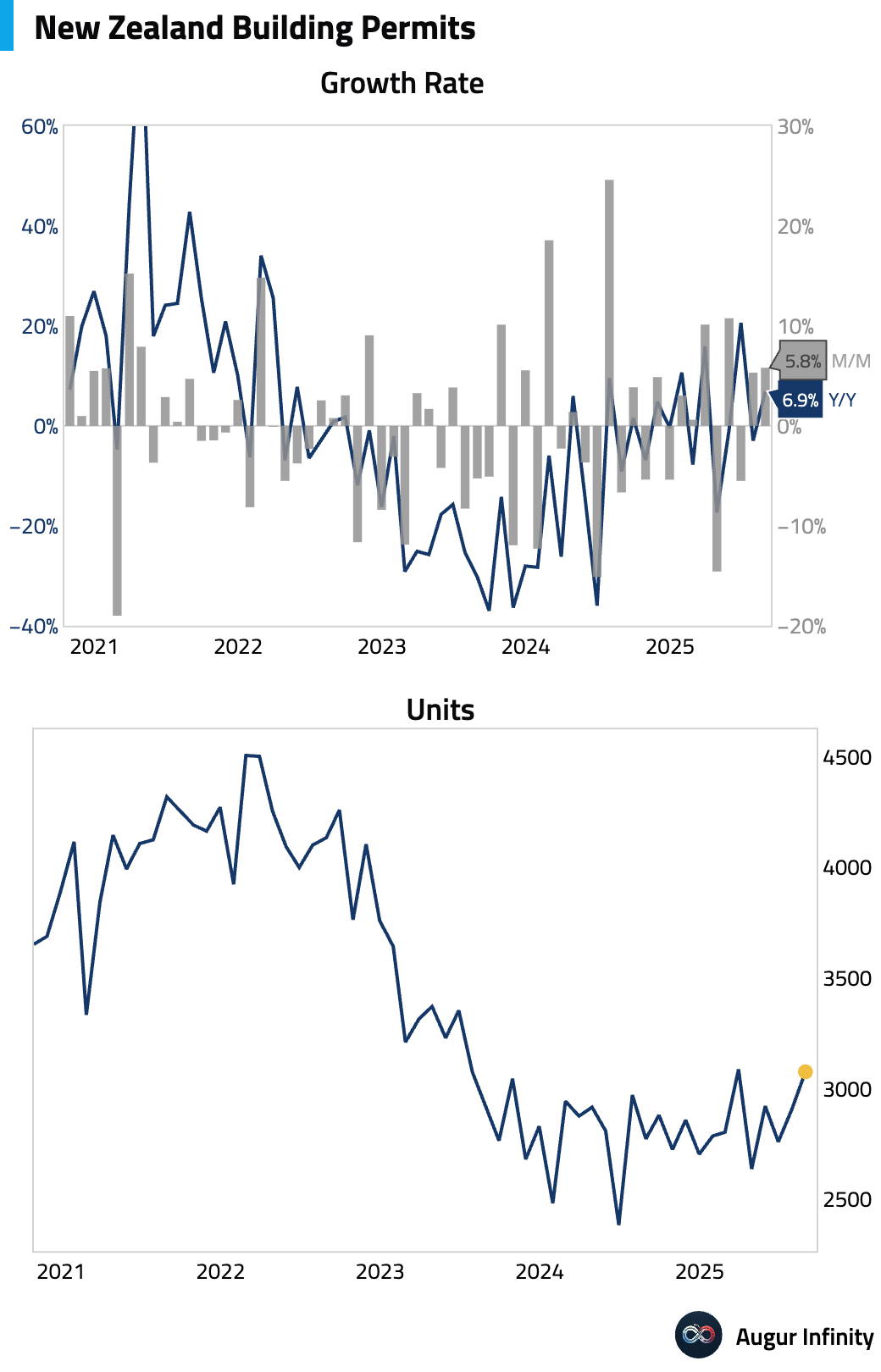

- New Zealand building permits rose for a second consecutive month in August (act: 5.8% M/M, prev: 5.3%).

Emerging Markets ex China

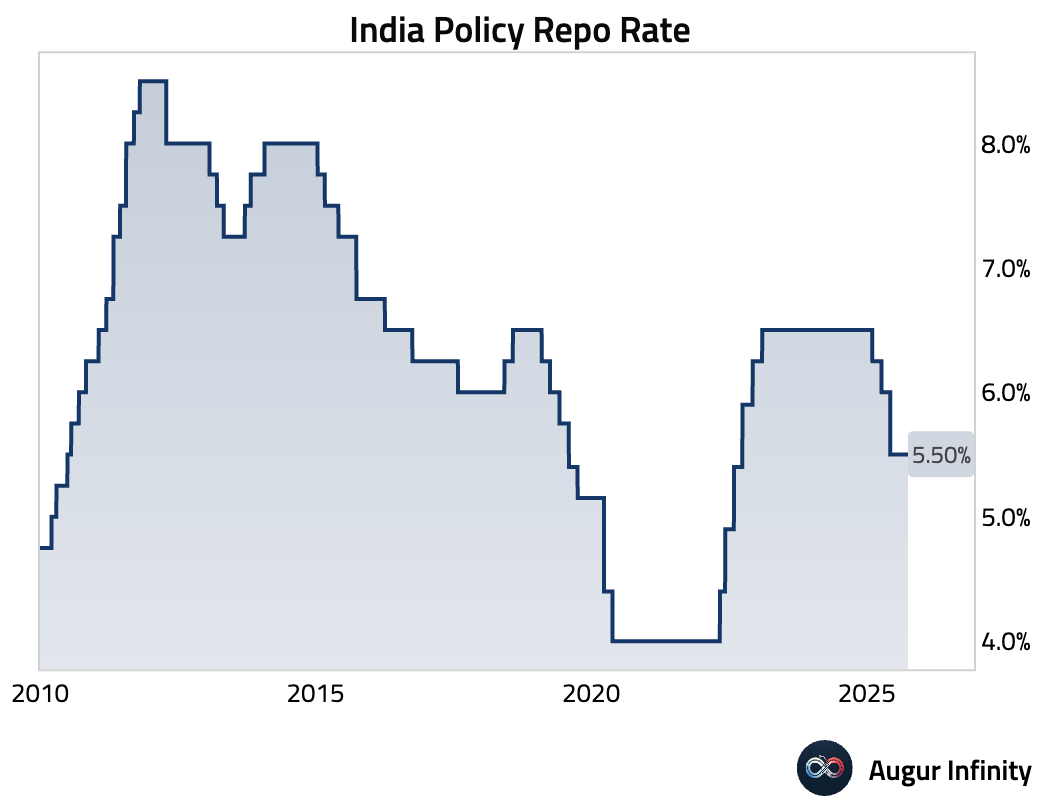

- The Reserve Bank of India held its policy repo rate at 5.50%, as expected. However, the commentary was notably dovish, with two external members voting for a more accommodative stance. The RBI significantly lowered its FY26 headline inflation forecast to 2.6% while slightly raising its GDP growth forecast to 6.8%, giving it policy space to support growth.

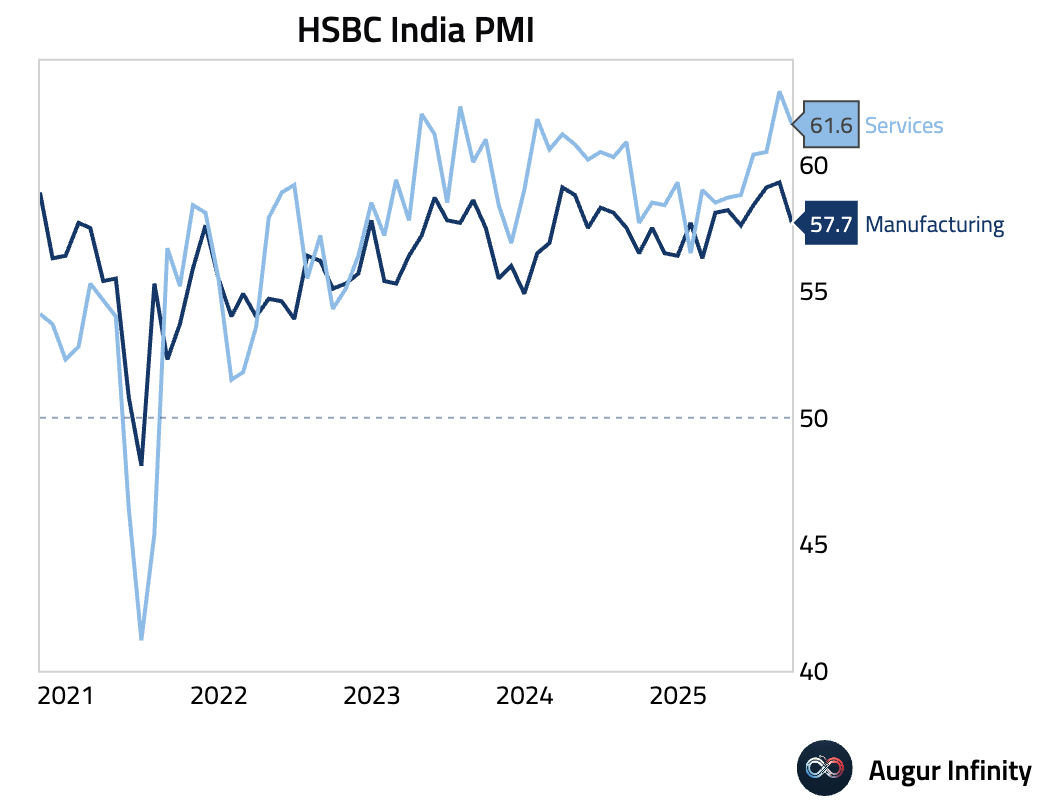

- The HSBC Manufacturing PMI for India declined to a four-month low of 57.7 but remained strongly expansionary. Growth in new orders and production moderated, but firms raised selling prices at the fastest pace in nearly 12 years to pass on higher input costs. New export orders accelerated, offsetting potential weakness from US tariffs.

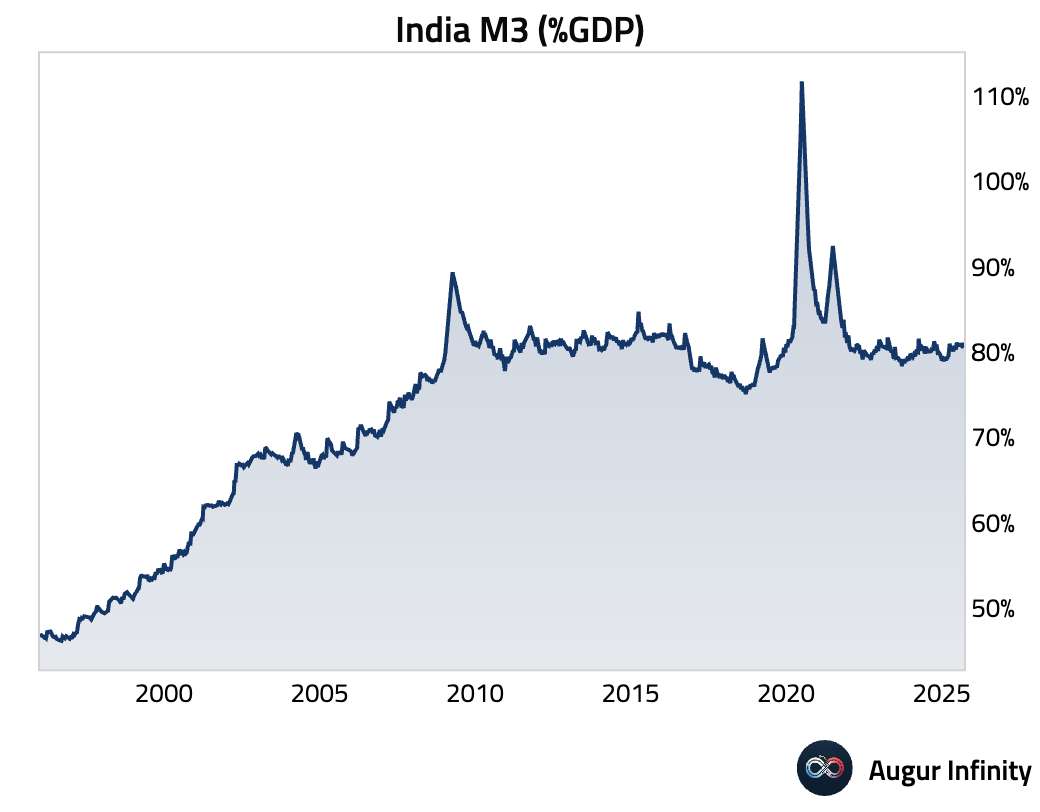

- India's M3 money supply growth slowed slightly in the latest reading (act: 9.2% Y/Y, prev: 9.5%).

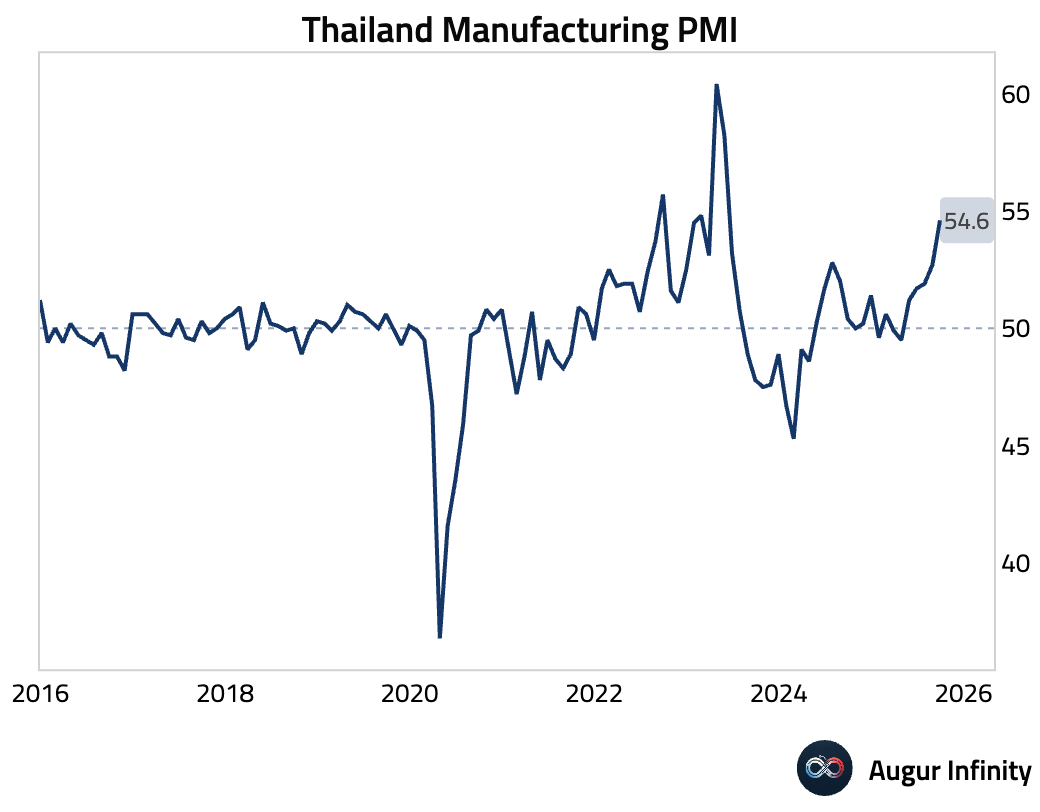

- Thailand's S&P Global Manufacturing PMI surged to 54.6, the fastest growth since May 2023, on strong domestic orders.

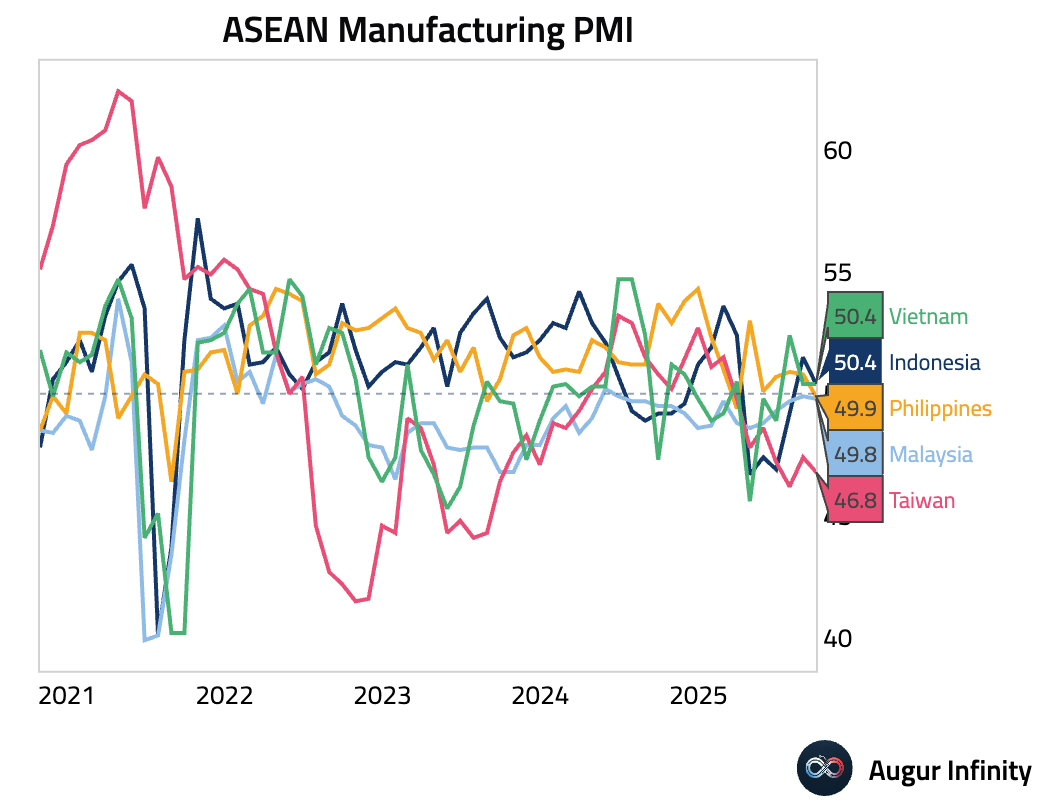

- Taiwan's S&P Global Manufacturing PMI fell to 46.8, marking a seventh straight month of contraction due to weak global demand linked to US tariff uncertainty.

Indonesia's manufacturing PMI slowed to 50.4, as a rise in new orders was offset by a fall in output.

Malaysia's manufacturing PMI edged down to 49.8, signaling broadly stable conditions as rising domestic demand was offset by falling export orders.

The Philippines' manufacturing PMI slipped into contraction at 49.9 for only the third time in over four years, driven by new drops in output and orders.

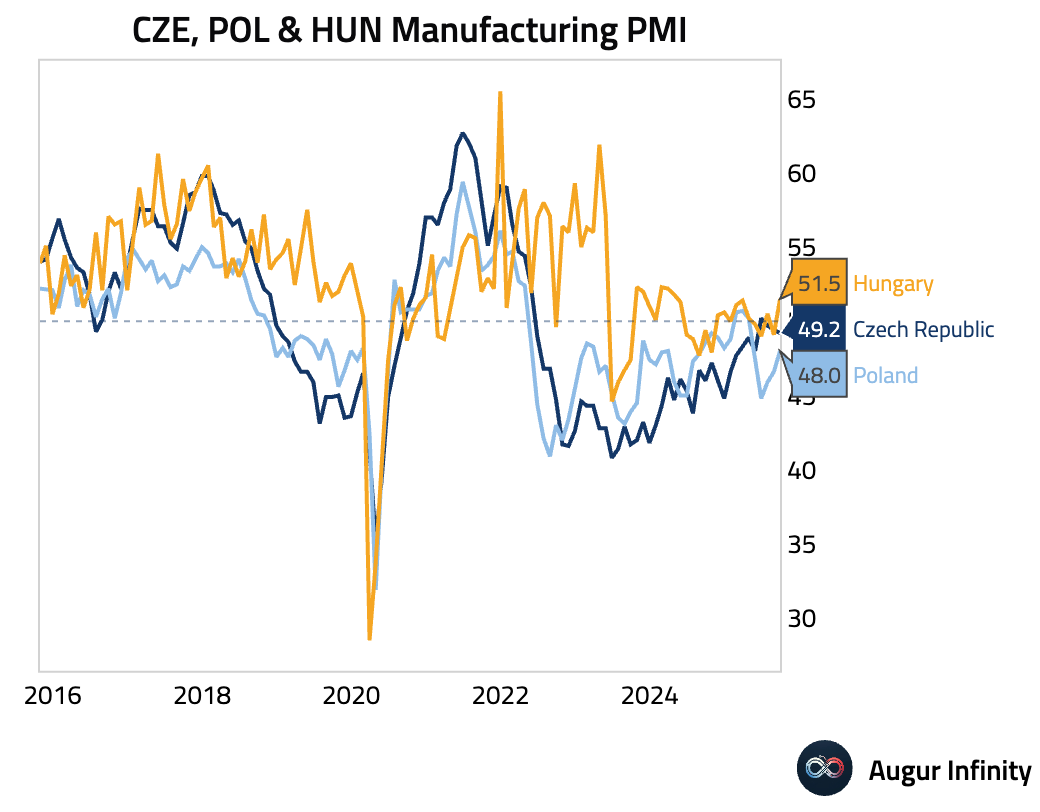

- The Czech Republic's manufacturing PMI fell further into contraction, declining to 49.2 as new orders contracted for the first time in four months. Poland's manufacturing PMI rose to a 5-month high of 48.0. Hungary's manufacturing PMI jumped back into expansion at 51.5.

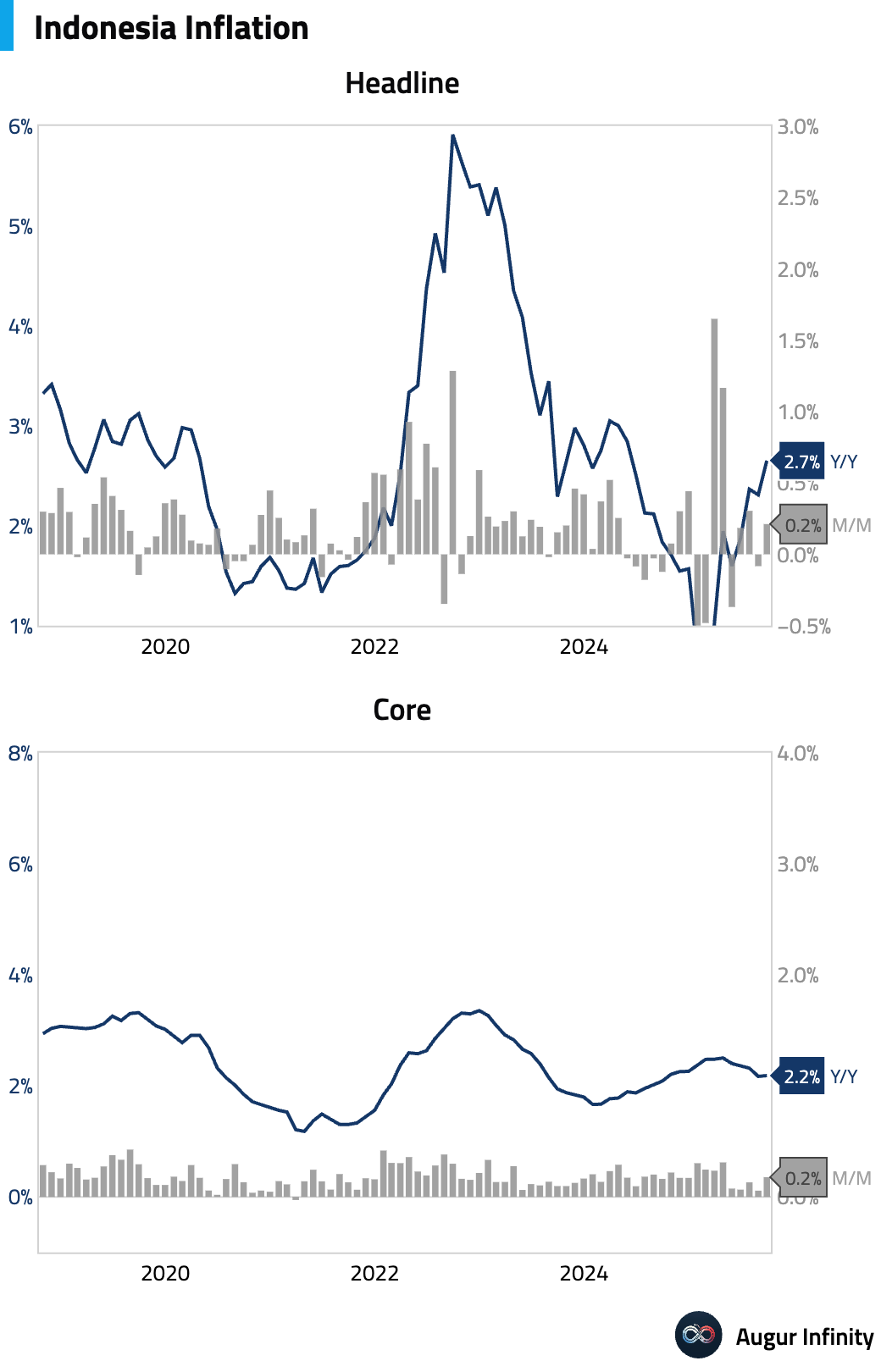

- Indonesia's headline inflation accelerated to 2.65% Y/Y in September, beating consensus expectations of 2.5%. The increase was driven by volatile food and gold prices. Core inflation, however, remained stable and in line with expectations at 2.19% Y/Y, suggesting underlying pressures are contained.

Interactive chart on Augur Infinity

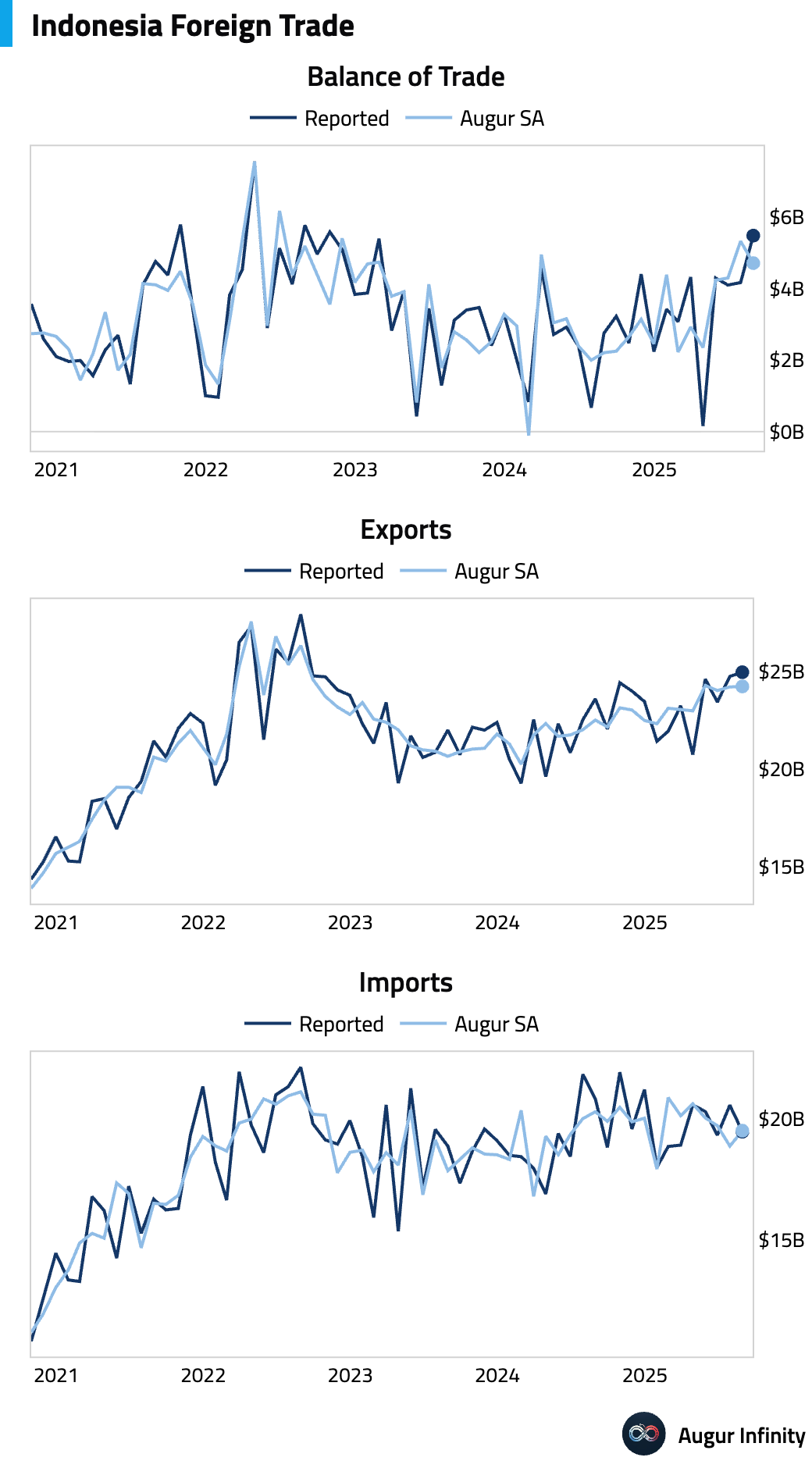

- Indonesia export growth outpaced expectations while imports contracted more than forecast.

- Tourist arrivals growth in Indonesia remained solid in August (act: 12.33% Y/Y, prev: 13.01%).

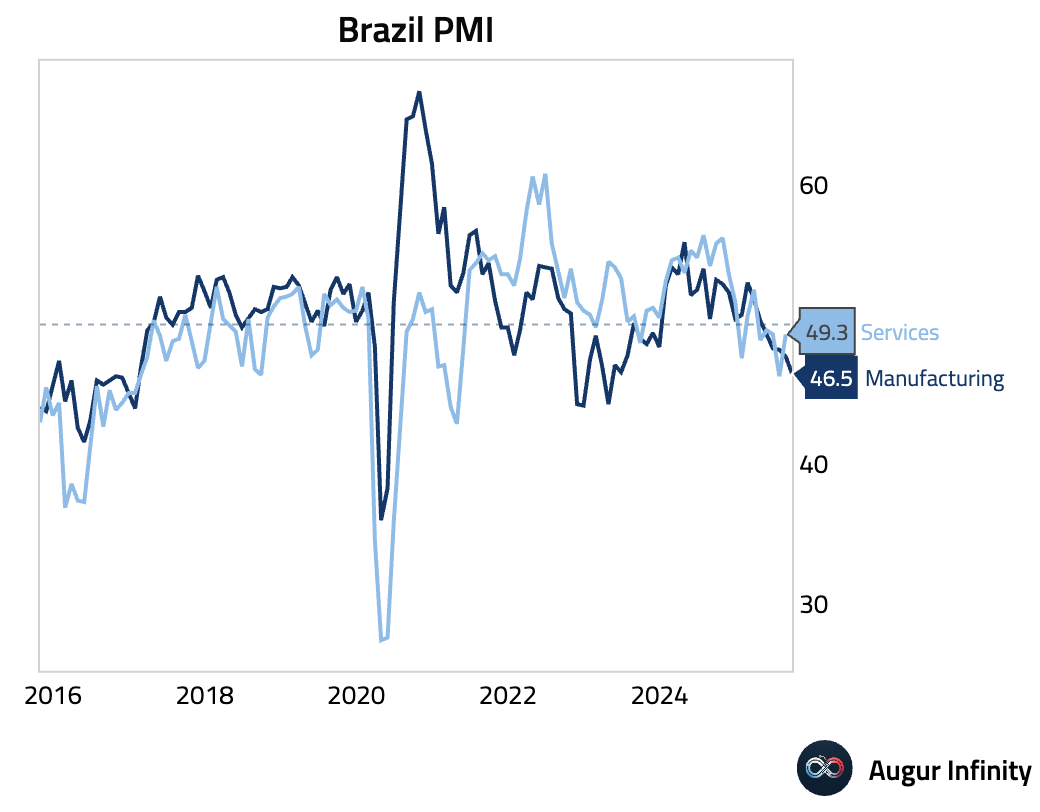

- Brazil's manufacturing sector contracted at the fastest pace in 29 months, with the S&P Global PMI falling to 46.5. Weak domestic demand drove a sharp drop in new orders and output. In a key shift, input costs fell for the first time since late 2023, allowing firms to cut selling prices.

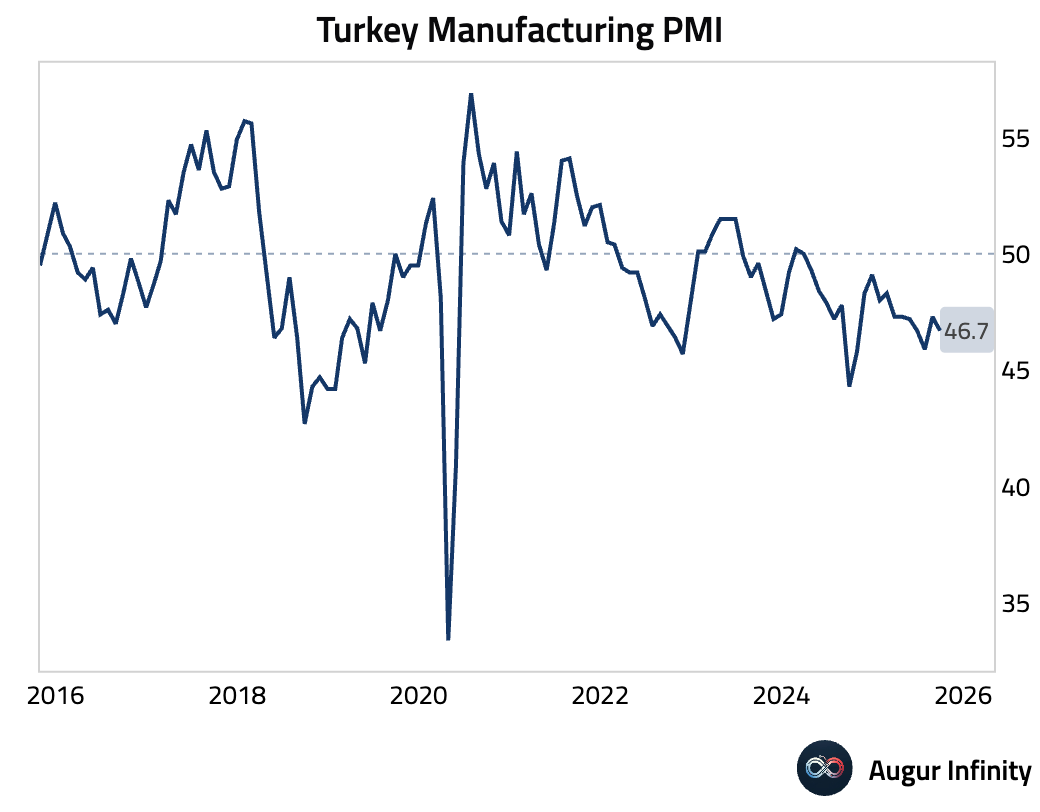

- Turkey's manufacturing PMI fell to 46.7, marking 18 consecutive months of contraction. Weak demand continued to weigh on new orders and output, while inflationary pressures accelerated due to currency weakness.

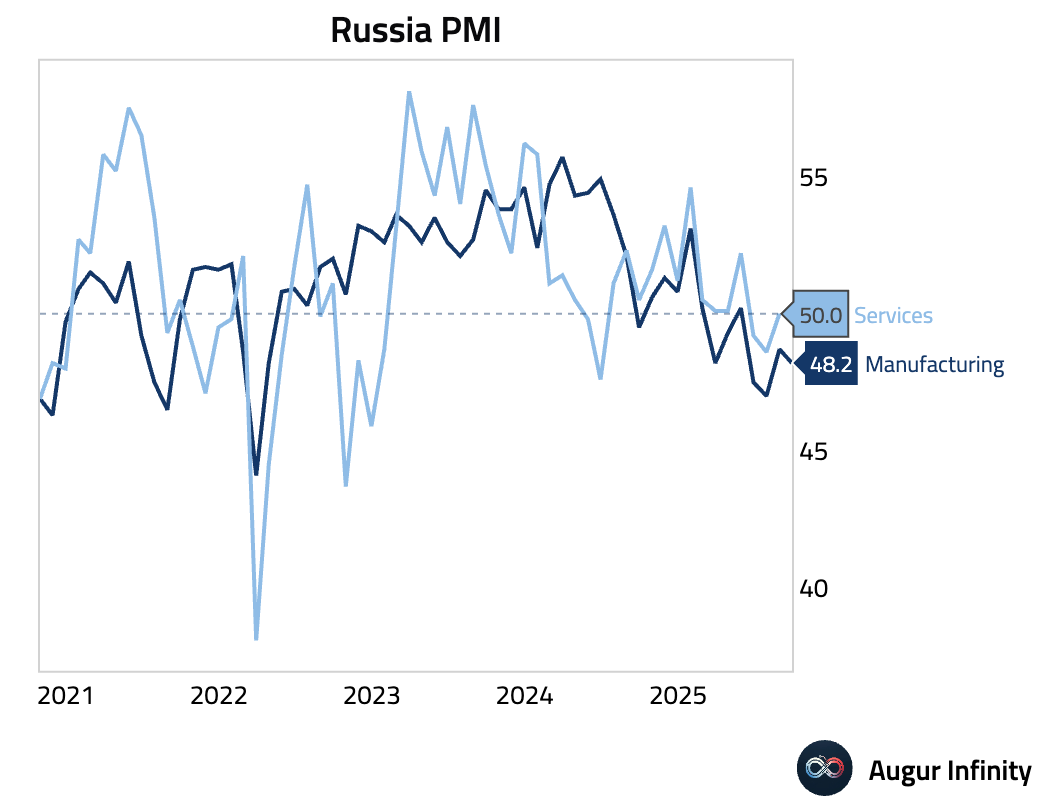

- Russia's S&P Global Manufacturing PMI fell to 48.2, its fourth consecutive month of contraction, driven by faster falls in output and new orders. Export sales saw their steepest decline since November 2022.

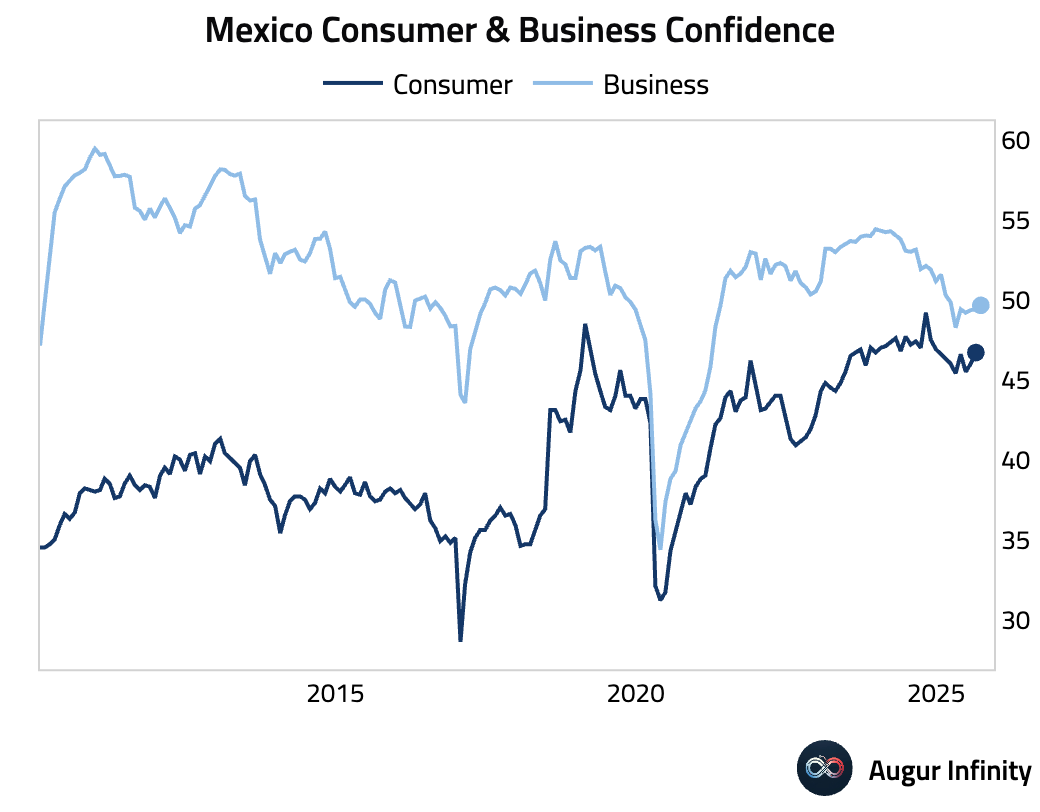

- Mexico's business confidence edged slightly higher but remained in contractionary territory for a seventh consecutive month (act: 49.7, prev: 49.4).

Interactive chart on Augur Infinity

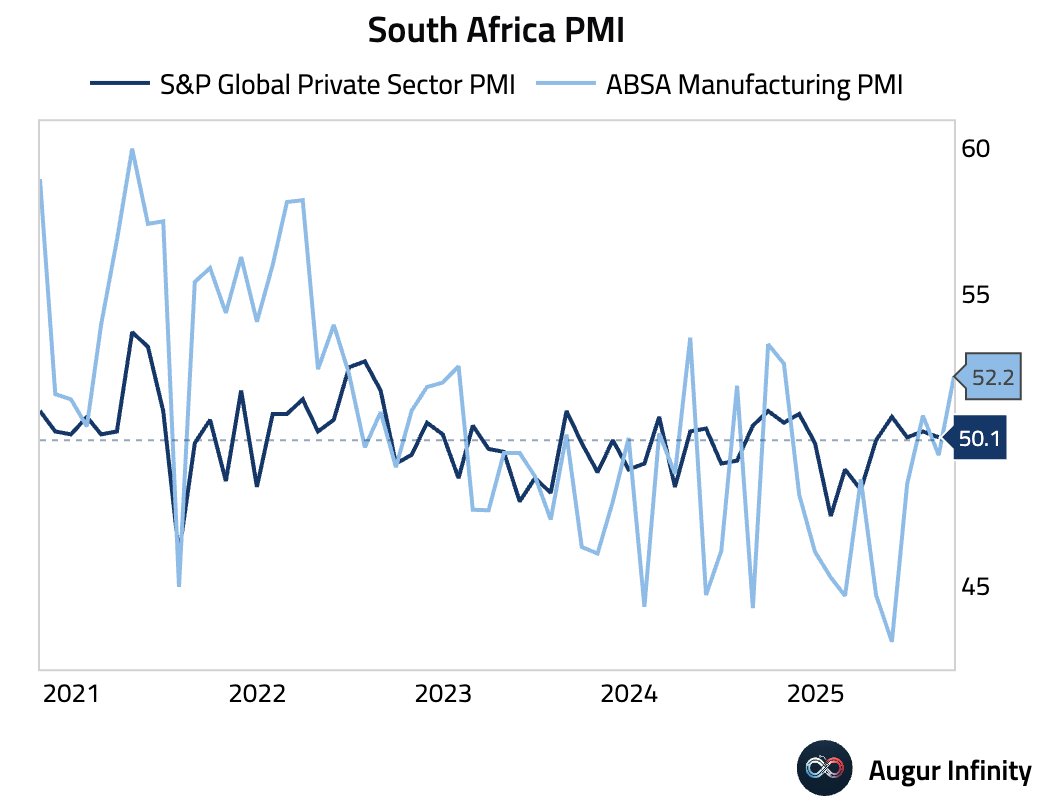

- South Africa's ABSA Manufacturing PMI jumped back into expansionary territory, rising to 52.2.

Global Markets

Equities

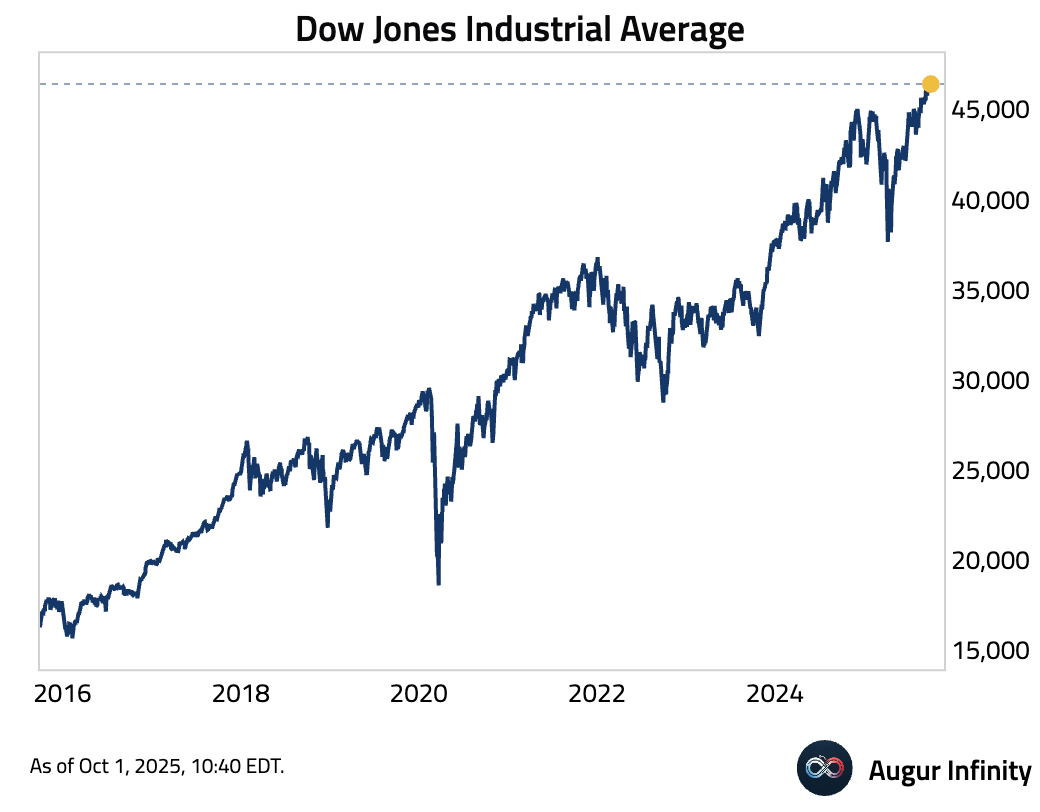

- Dow Jones Industrial Average reached another all-time high.

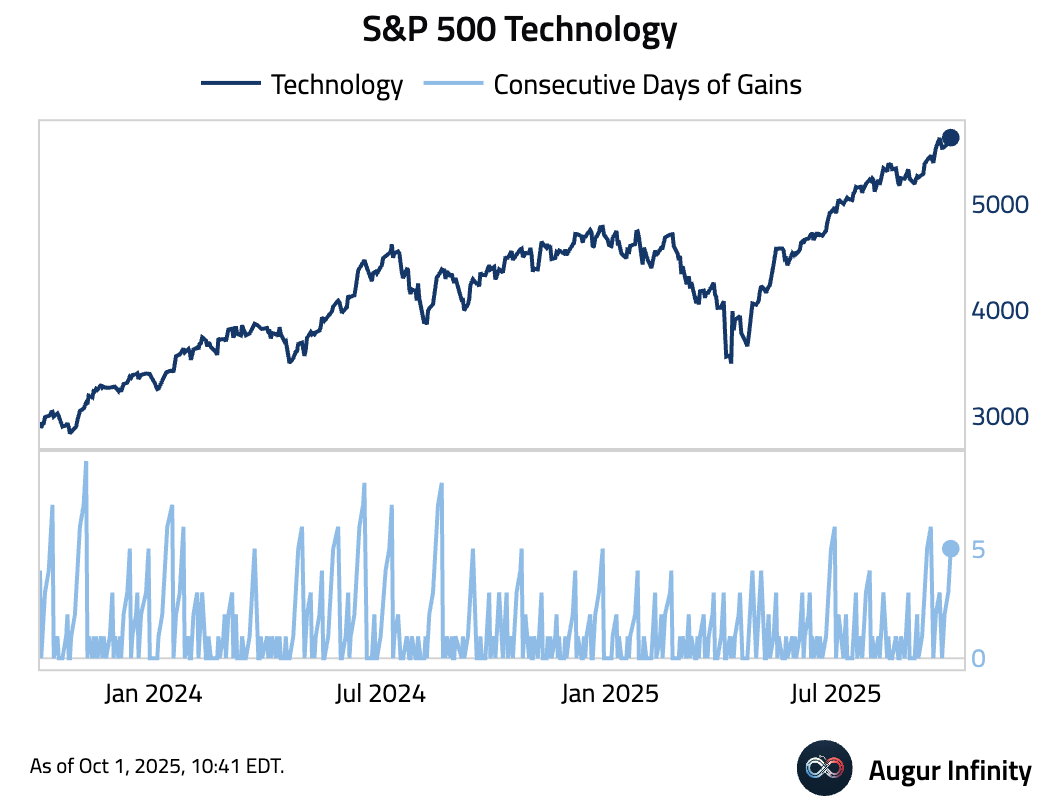

- S&P 500 Technology has gained for five consecutive days.

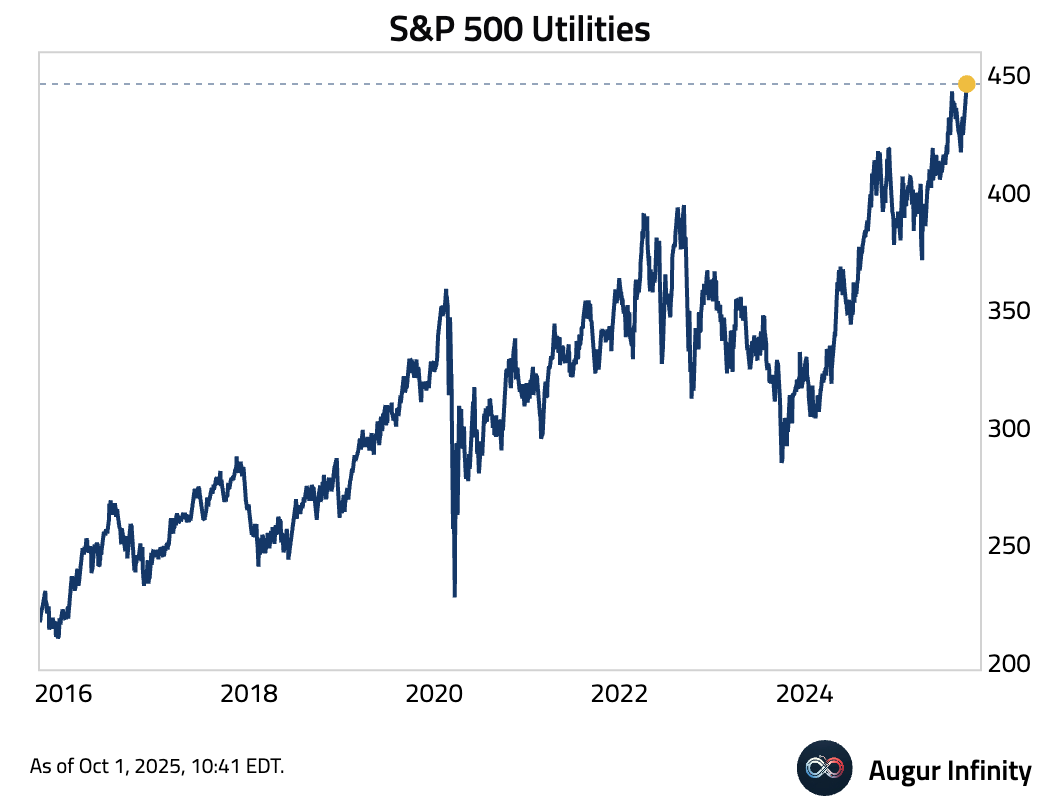

- The utilities sector reached the 12th all-time high of 2025.

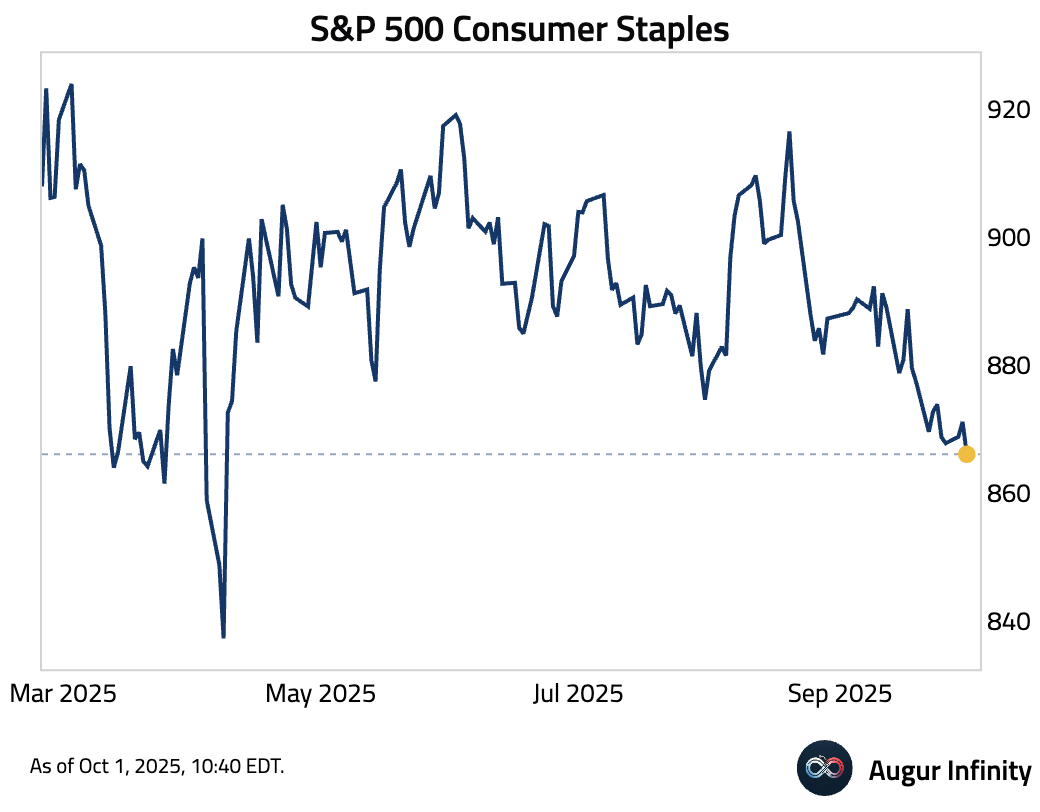

- But consumer Staples are now trading at the lowest level since April 2025.

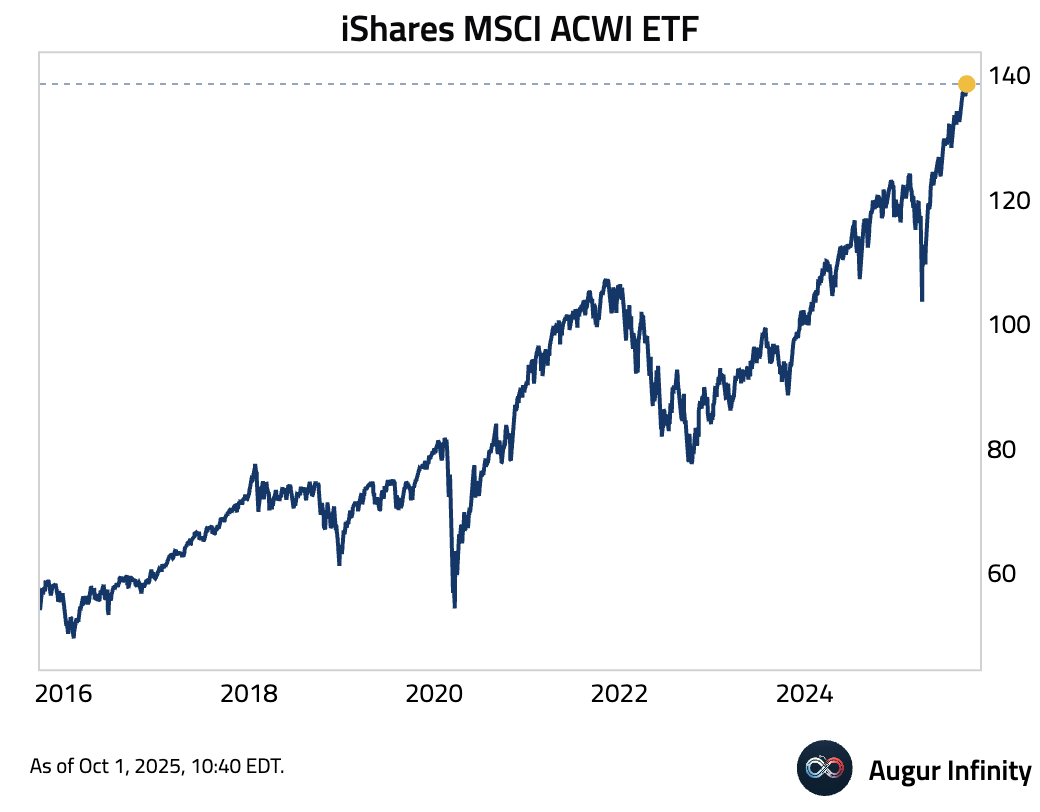

- Globally, the iShares MSCI ACWI ETF has reached an all-time high as well.

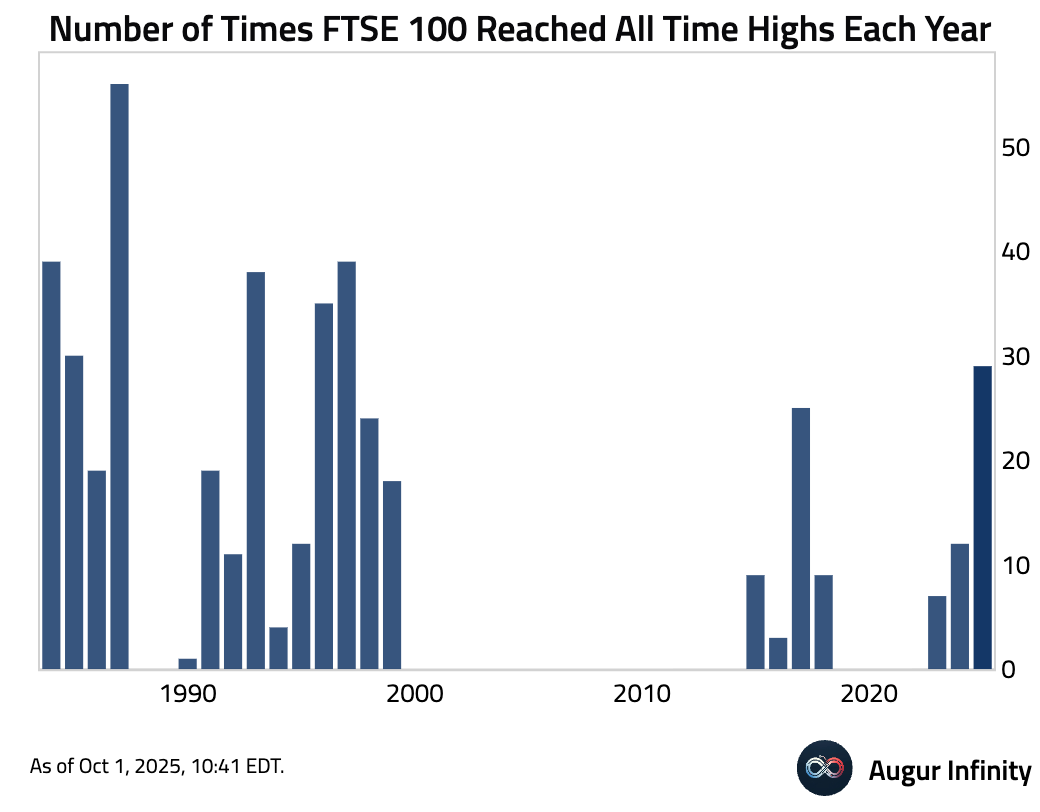

- Impressively, the FTSE 100 Index claimed its 29th all-time high this year.

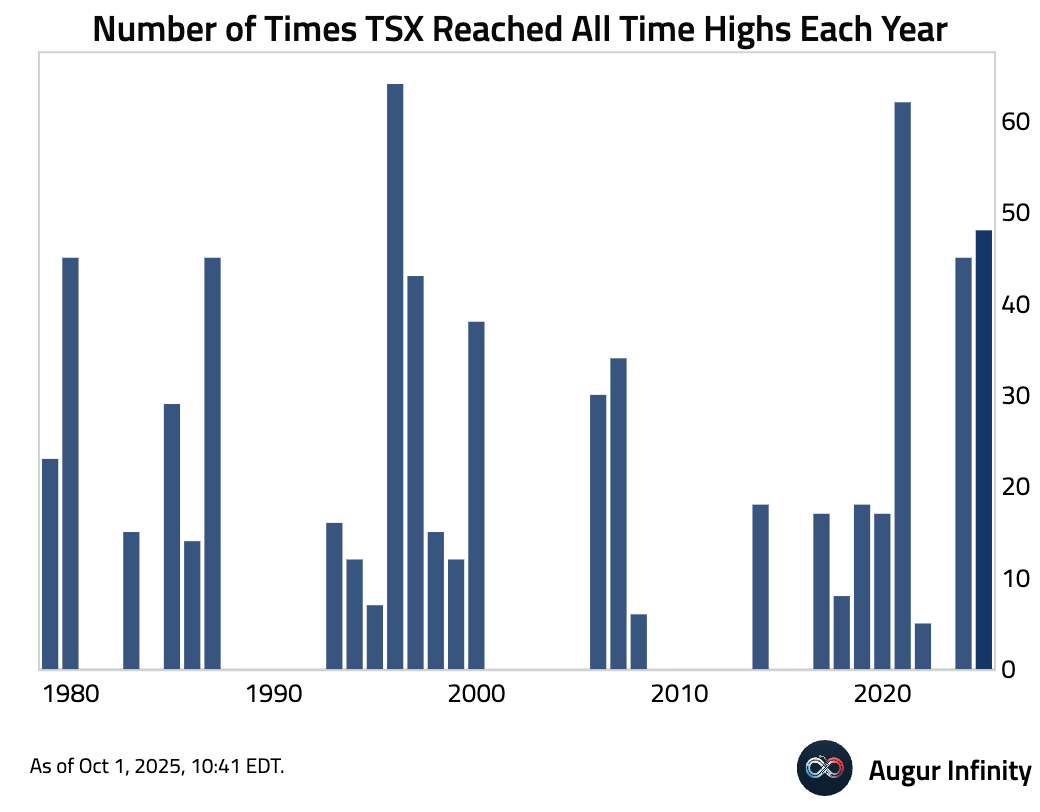

- Canada's S&P/TSX Composite is faring even better, eraching the 48th all-time high of the year.

Commodities

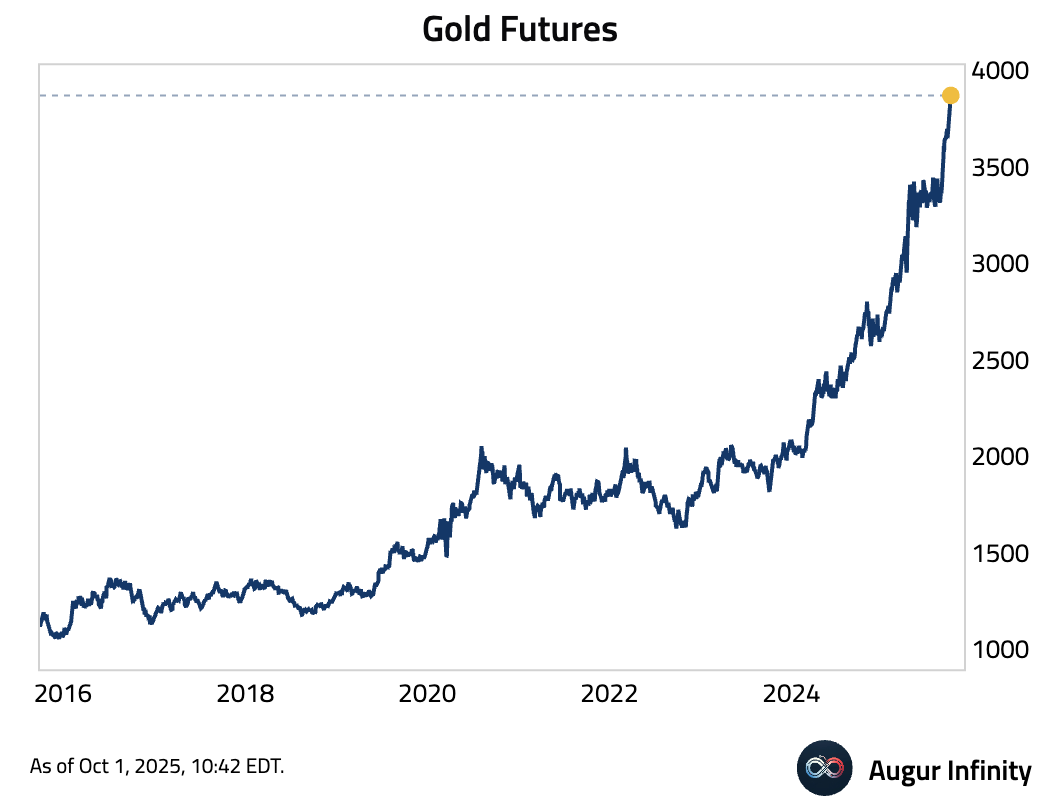

- Gold continues to surge.

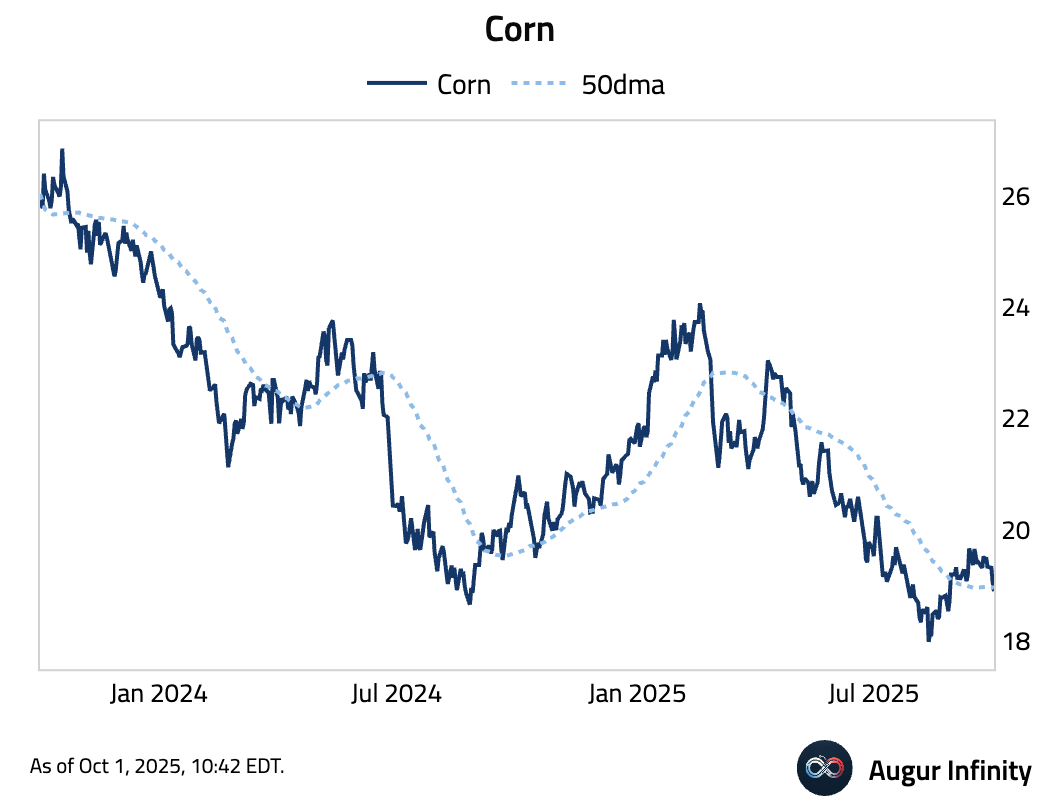

- Corn fell below its 50-day moving average.

FX

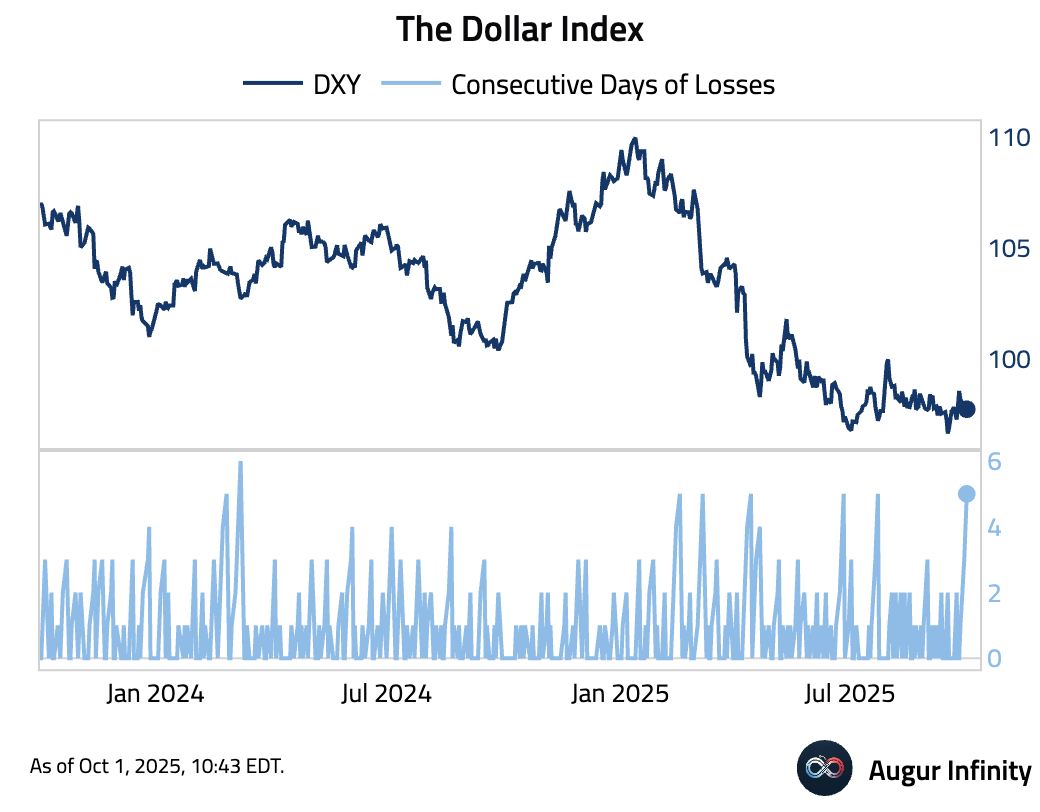

- The Dollar Index has declined for five consecutive sessions.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.