Note: This is the Augur Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- OPEC+ is expected to announce an oil production increase at its meeting this Sunday.

- Japan’s ruling Liberal Democratic Party will hold its leadership election on Saturday, with the outcome potentially influencing future economic policy.

Global Economics

United States

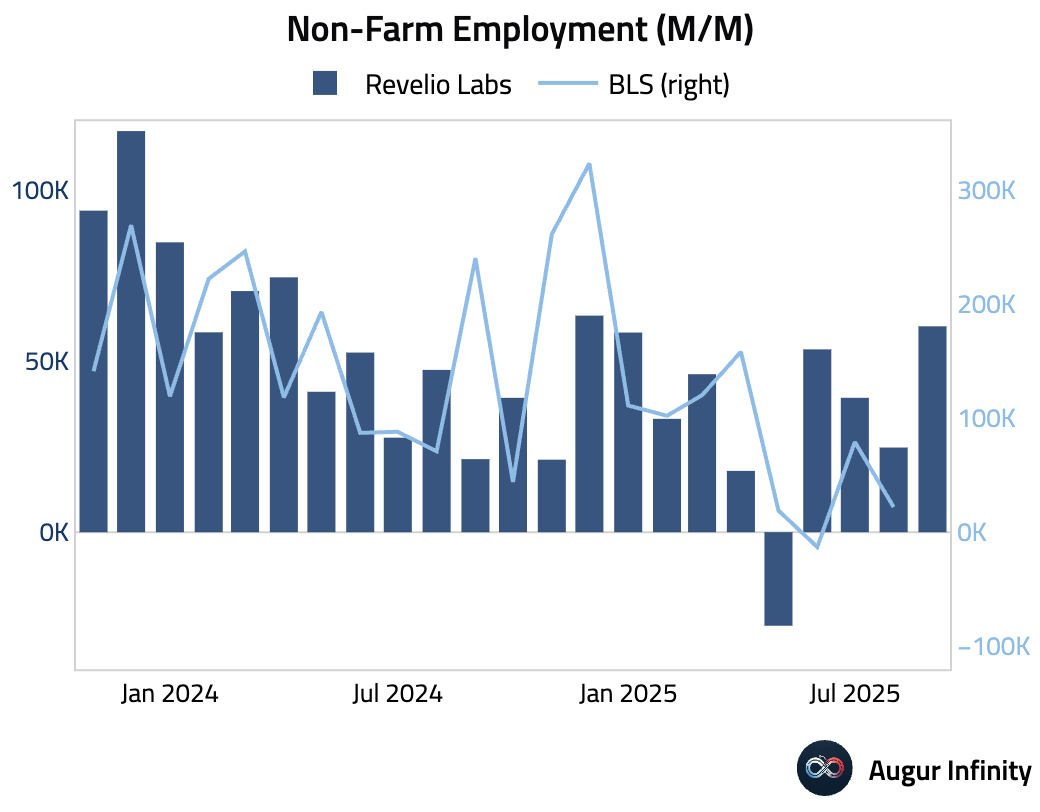

- Nonfarm payroll data was not released today due to the government shutdown. In lieu, Revelio Public Labor Statistics point to job gains that are slightly above expectations for September.

Source: Revelio Labs, Inc.

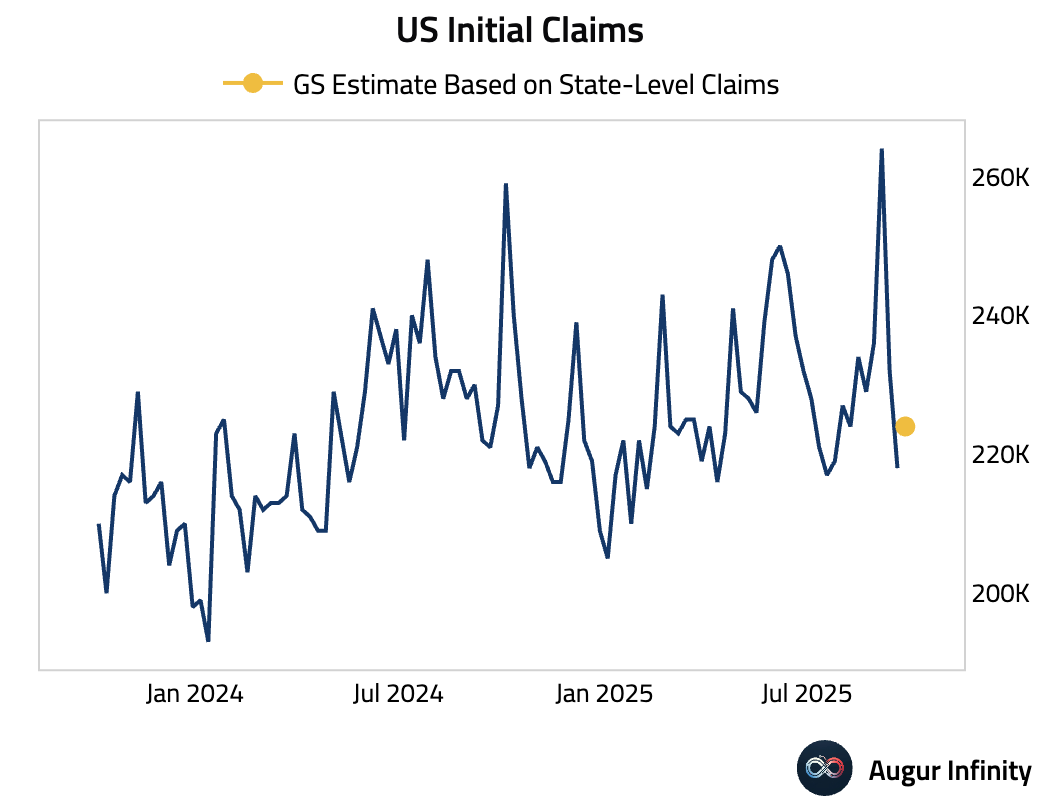

- Using state-level data, Goldman estimates initial claims rose to 224k for the week ended September 27.

Source: Goldman Sachs

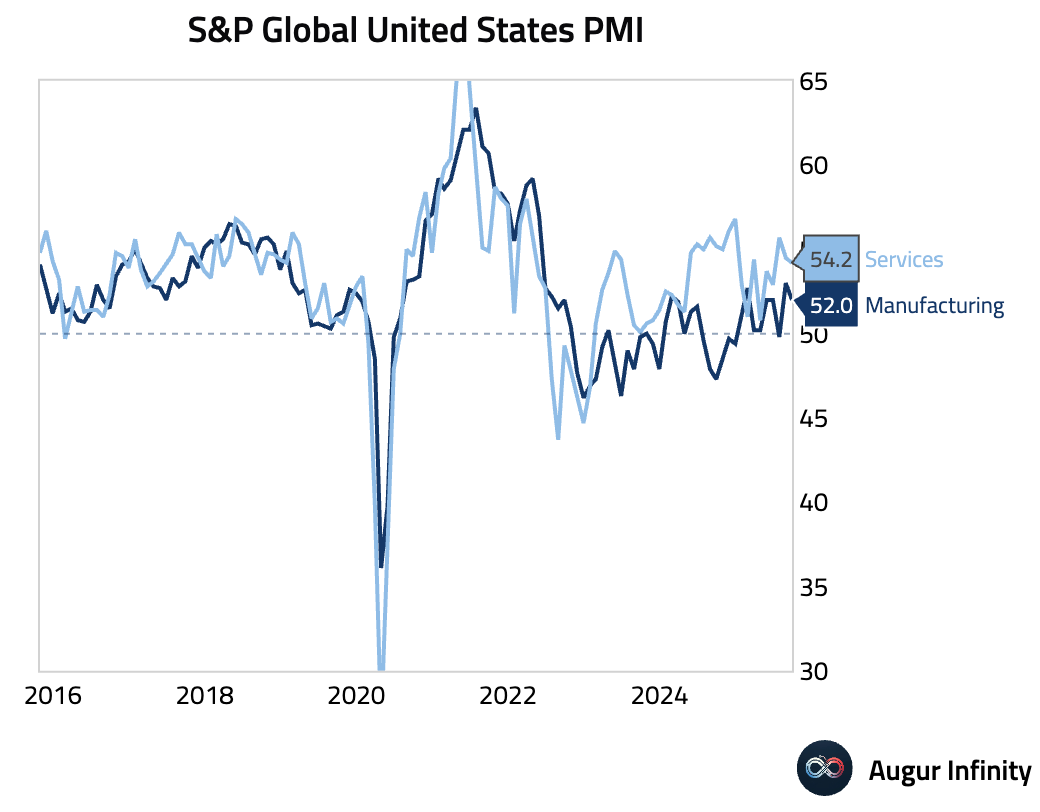

- The S&P Global Services PMI moderated slightly to 54.2 in September but continued to signal a robust expansion. The slowdown was driven by softer new business growth, with some firms citing tariffs as a headwind. Despite this, business confidence rose to a four-month high, though hiring nearly stalled.

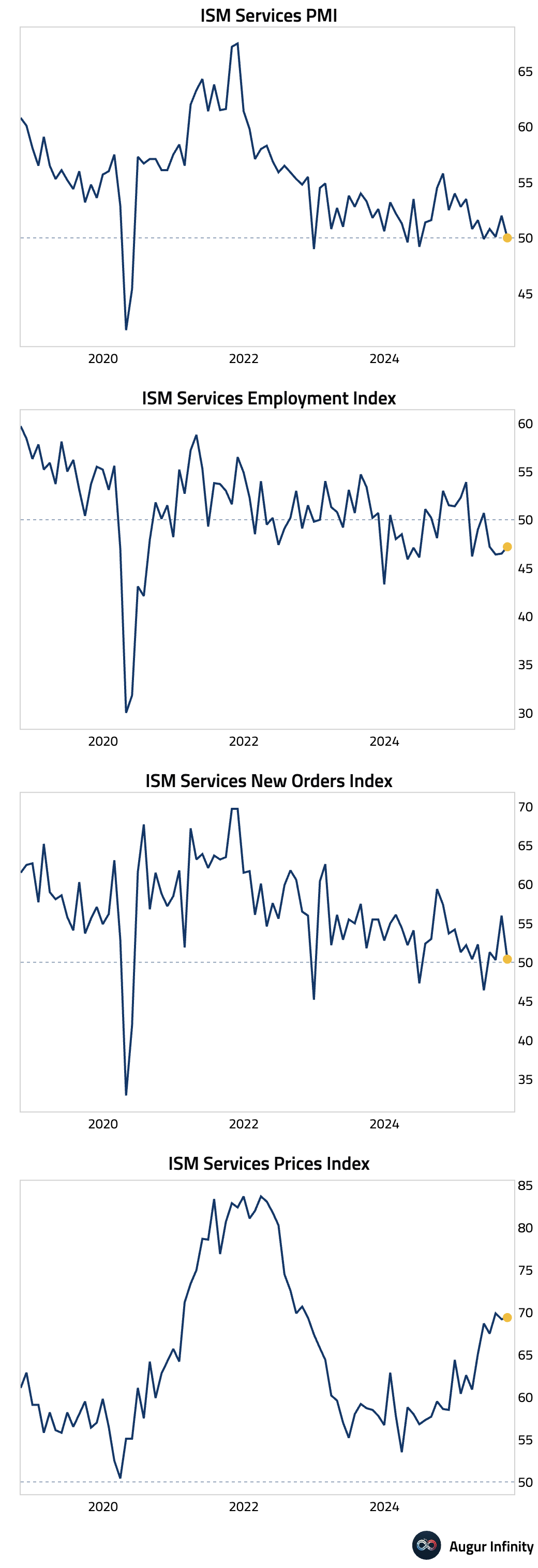

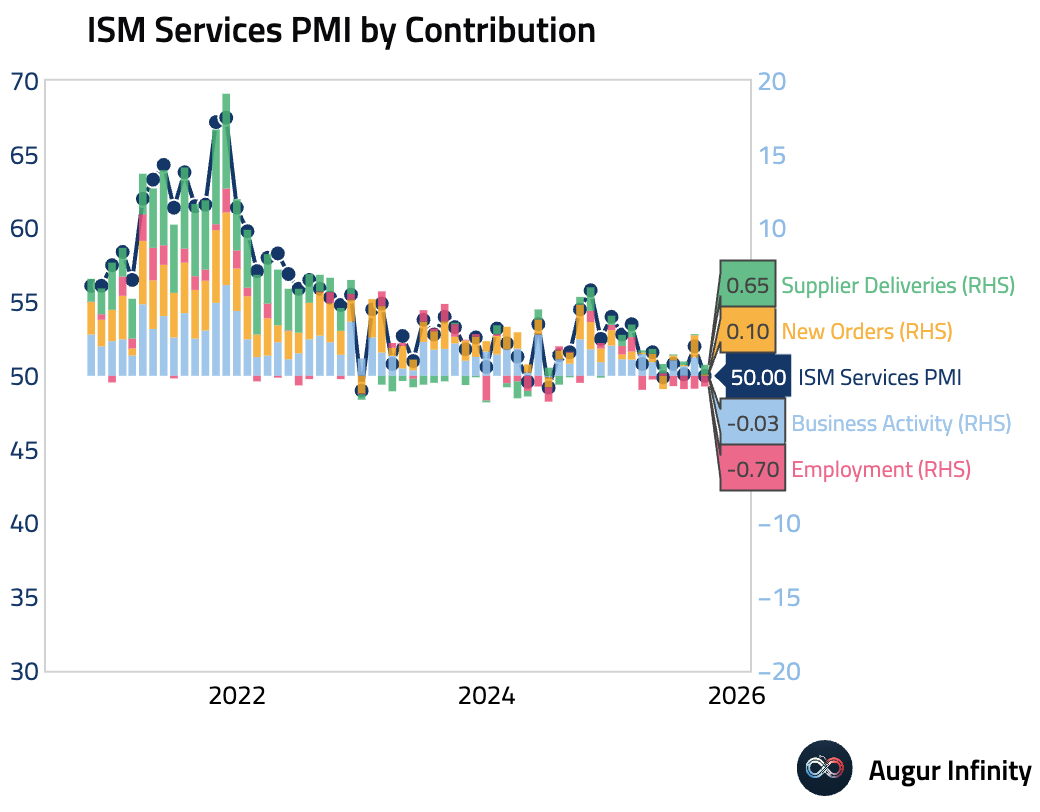

- The US ISM Services PMI unexpectedly stalled at 50.0 in September, a significant drop from 52.0 and well below the consensus of 51.7. The details were weak across the board: the Business Activity index plunged 5.1 points into contraction at 49.9 for the first time since May 2020, and the New Orders index fell a steep 5.6 points to 50.4. The Employment sub-index remained in contraction for the fourth consecutive month at 47.2. In a sign of stagflationary pressures, the Prices Paid index ticked higher to a near two-year high of 69.4, with tariffs cited as a key cost driver.

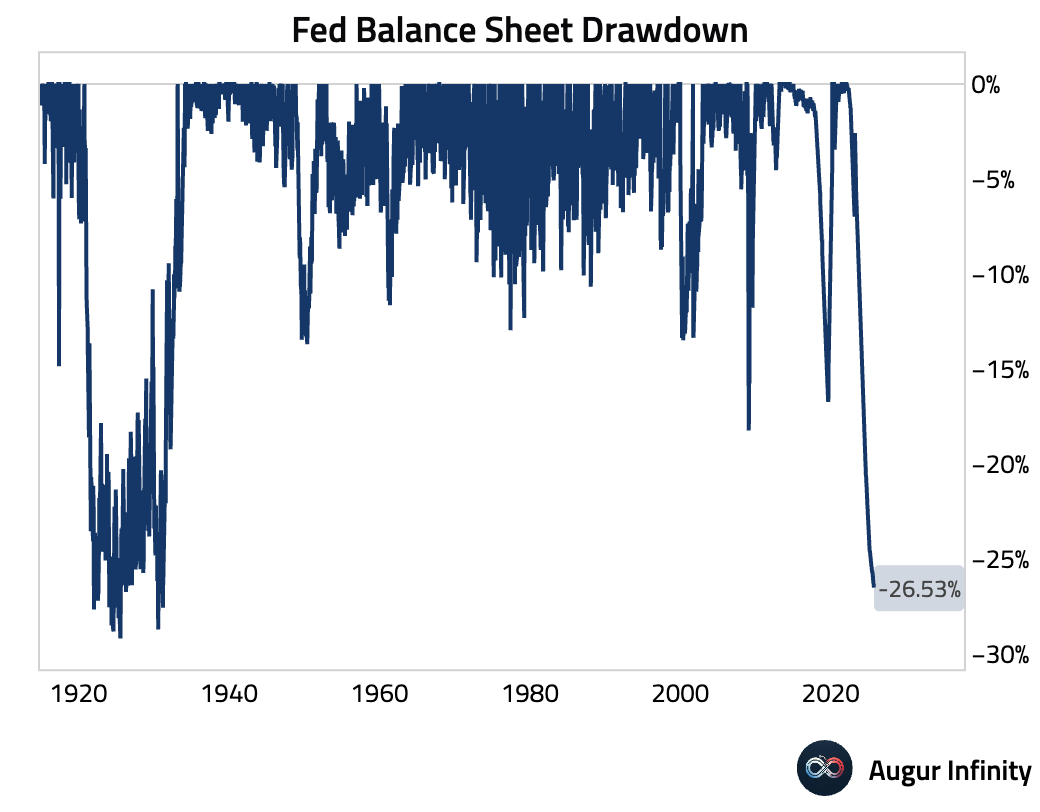

- The Federal Reserve’s balance sheet continued its decline, falling to its lowest level since April 2020 as quantitative tightening proceeds (act: $6.59T, prev: $6.61T).

Interactive chart on Augur Infinity

Canada

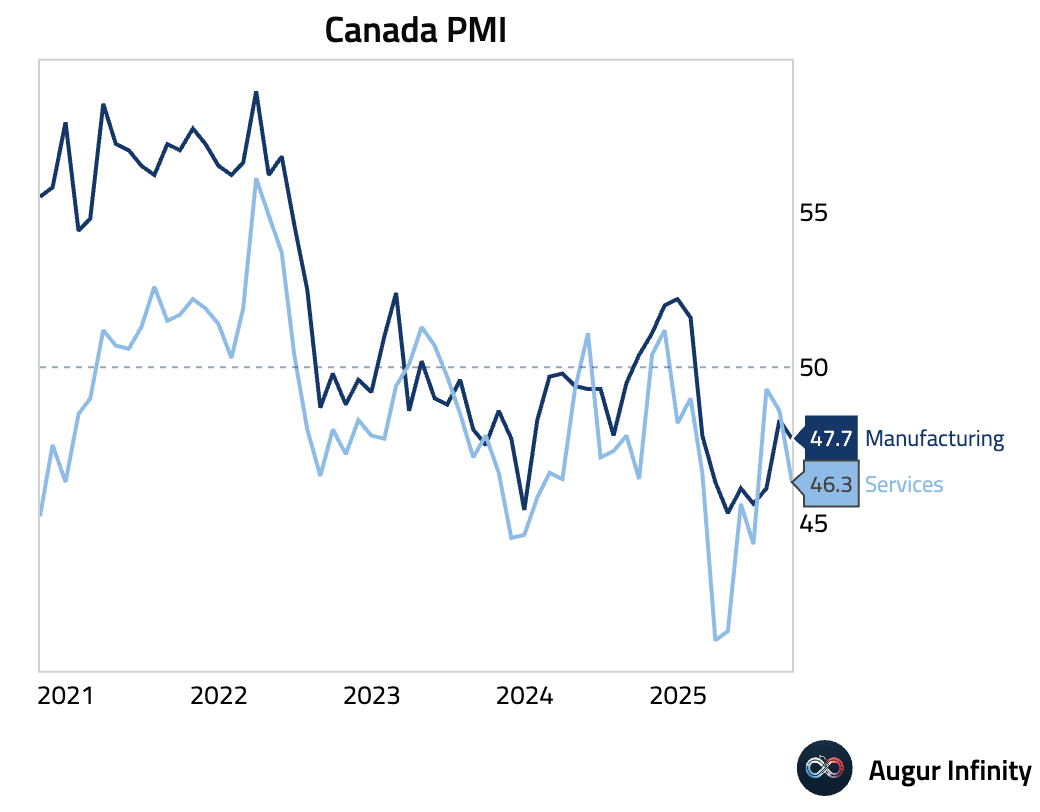

- Canada’s service sector activity contracted for the 10th consecutive month, with the S&P Global Services PMI falling to a three-month low of 46.3 in September. A lack of new business drove the downturn and led to the first reduction in staffing in five months. While input costs accelerated, weak demand suppressed selling prices, indicating margin pressure and supporting the recent Bank of Canada rate cut.

Europe

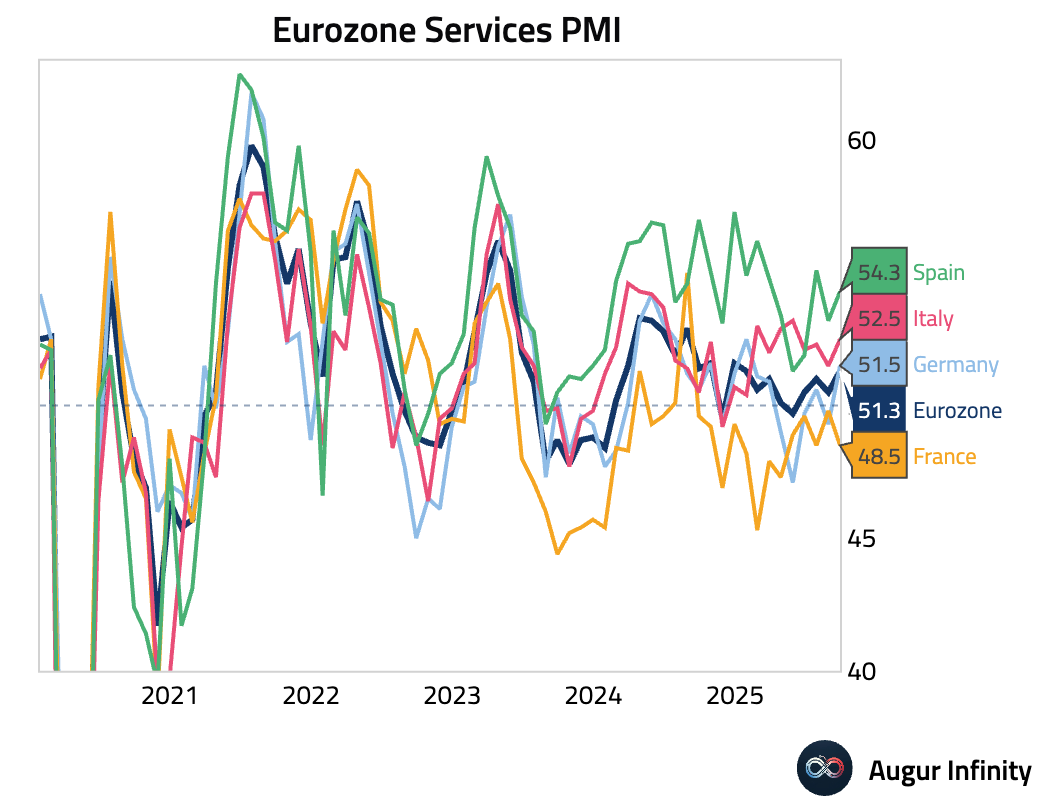

- The Eurozone’s services sector expansion gained momentum in September, with the final HCOB Services PMI rising to 51.3 from 50.5. Growth was uneven across the region. Spain’s PMI rose to 54.3, fueled by strong domestic orders, while Italy’s PMI increased to a four-month high of 52.5. Germany’s PMI returned to expansion at 51.5, an eight-month high, but masked underlying fragility as growth was driven by clearing backlogs while new orders fell and jobs were cut at the steepest rate since June 2020. France’s services sector fell back into contraction at 48.5.

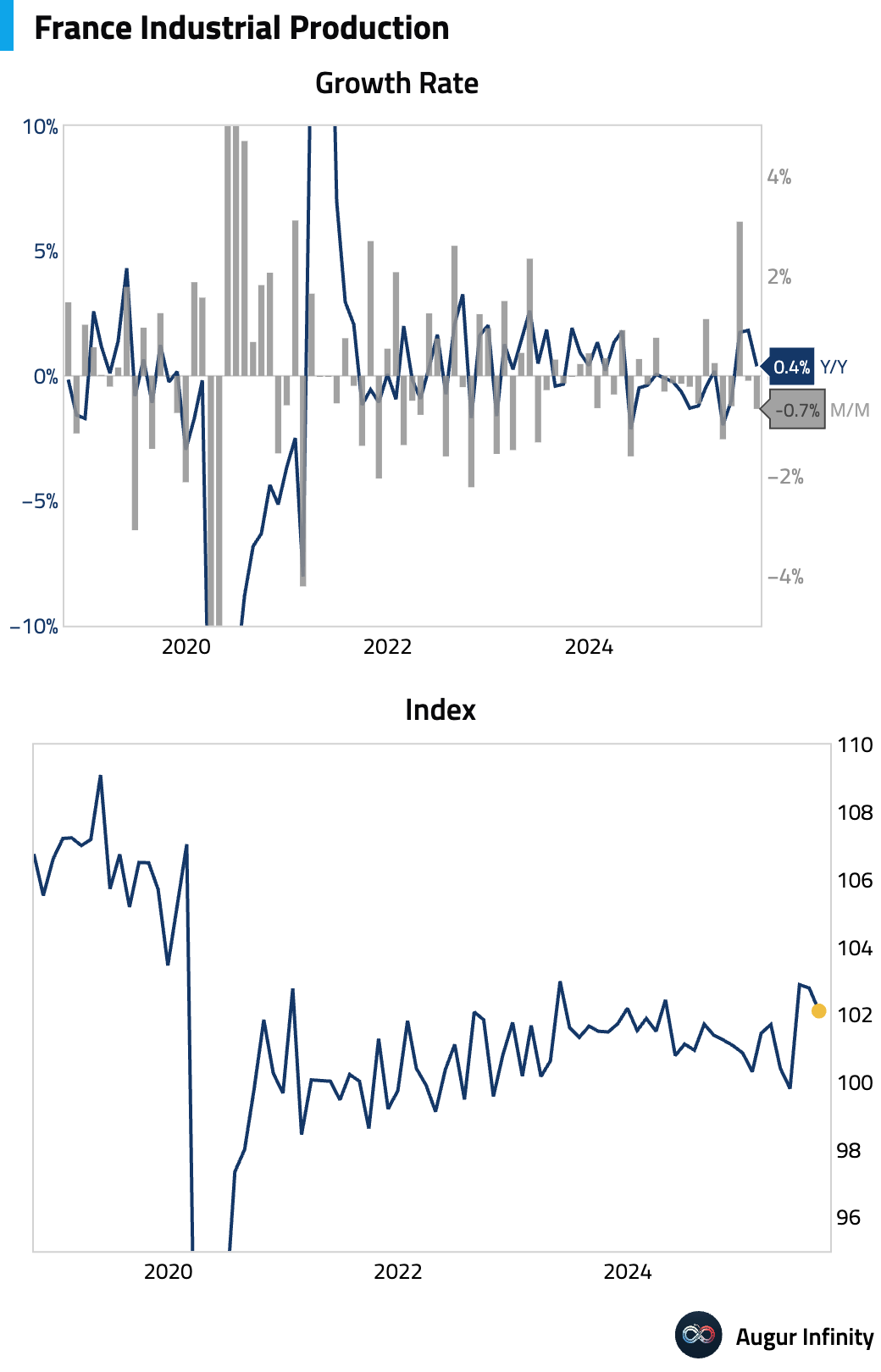

- French industrial production unexpectedly contracted in August for a second consecutive month, missing market expectations for a modest rebound (act: -0.7% M/M, est: 0.3%).

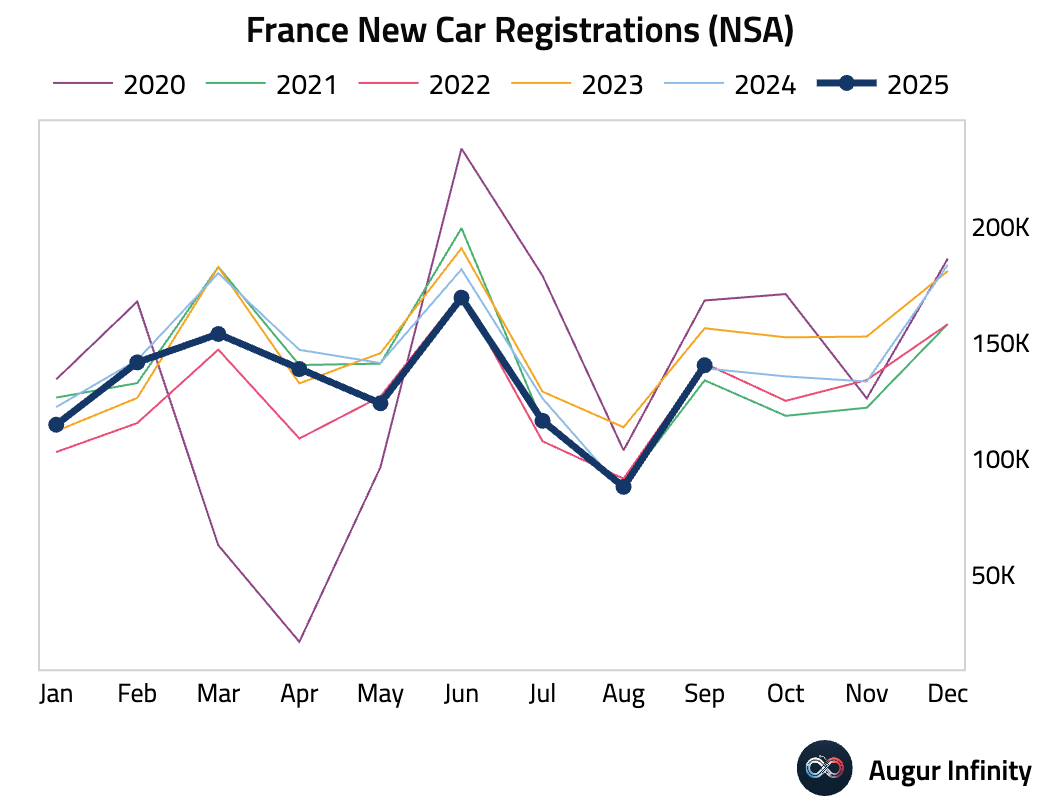

- French new car registrations slowed in September, with year-over-year growth moderating (act: 1.0% Y/Y, prev: 2.2%).

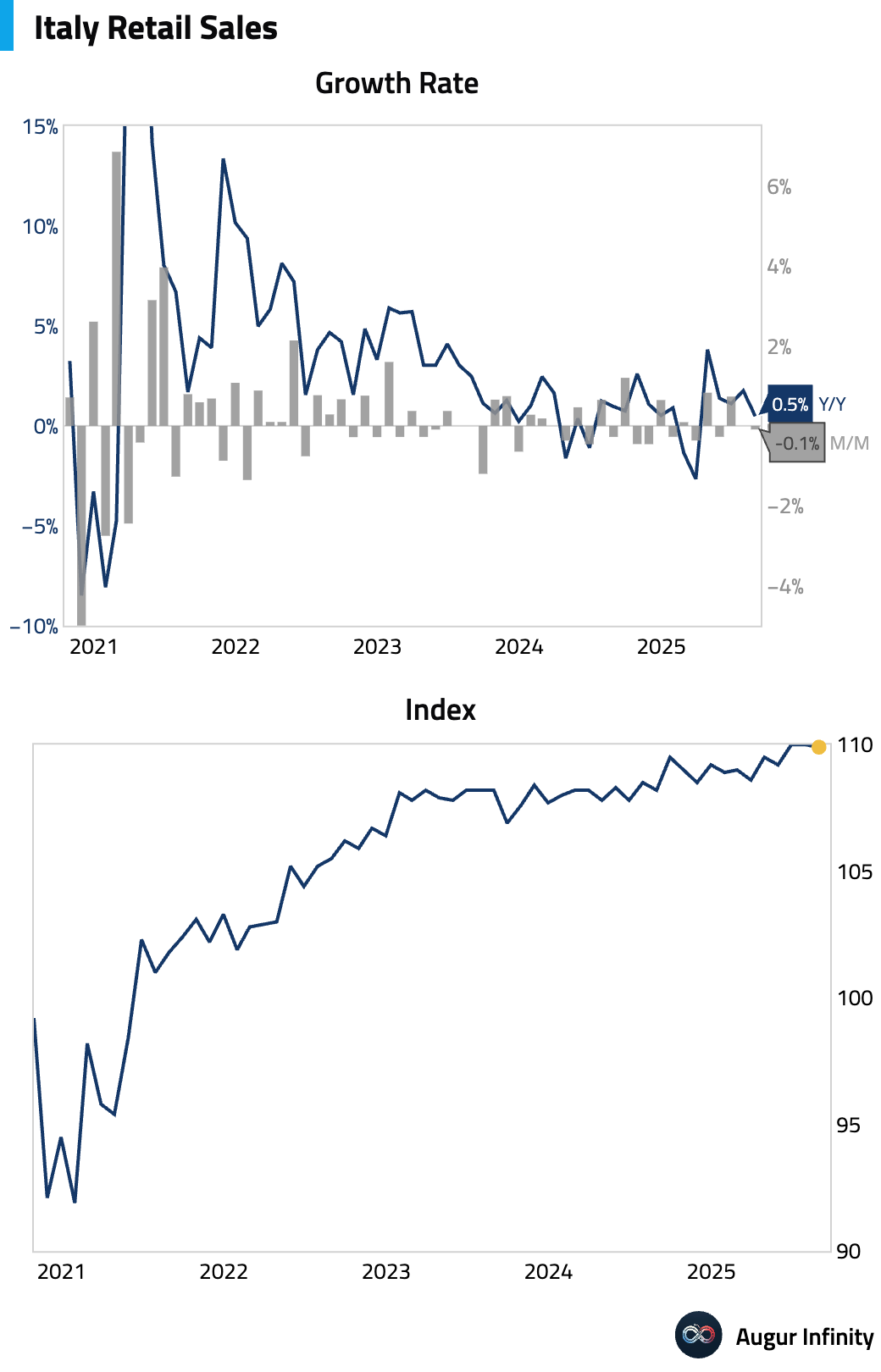

- Italian retail sales contracted slightly in August following a flat reading in July, while the annual growth rate slowed significantly (M/M act: -0.1%, prev: 0.0%; Y/Y act: 0.5%, prev: 1.8%).

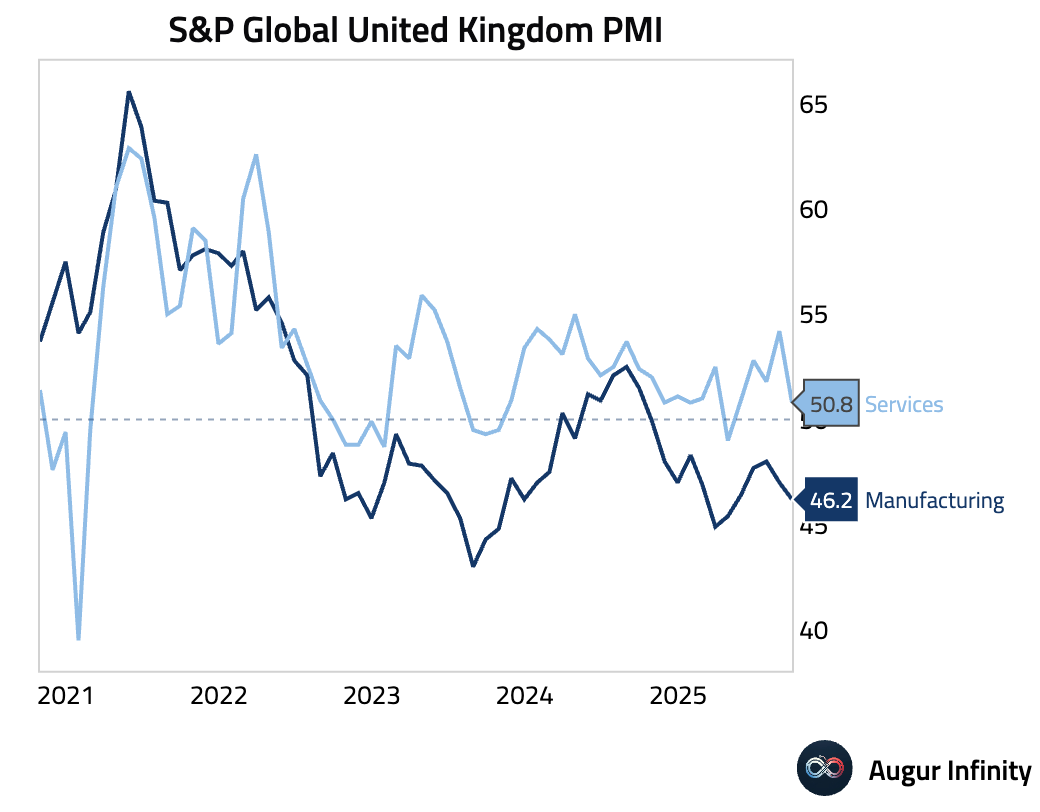

- The UK Services PMI fell sharply to a five-month low of 50.8 in September from 54.2, suggesting the summer’s recovery was short-lived. The slowdown was attributed to weak demand, as political uncertainty and the upcoming budget led clients to delay spending. Employment fell for the 12th consecutive month, signaling a softer labor market that could support a more dovish stance from the Bank of England.

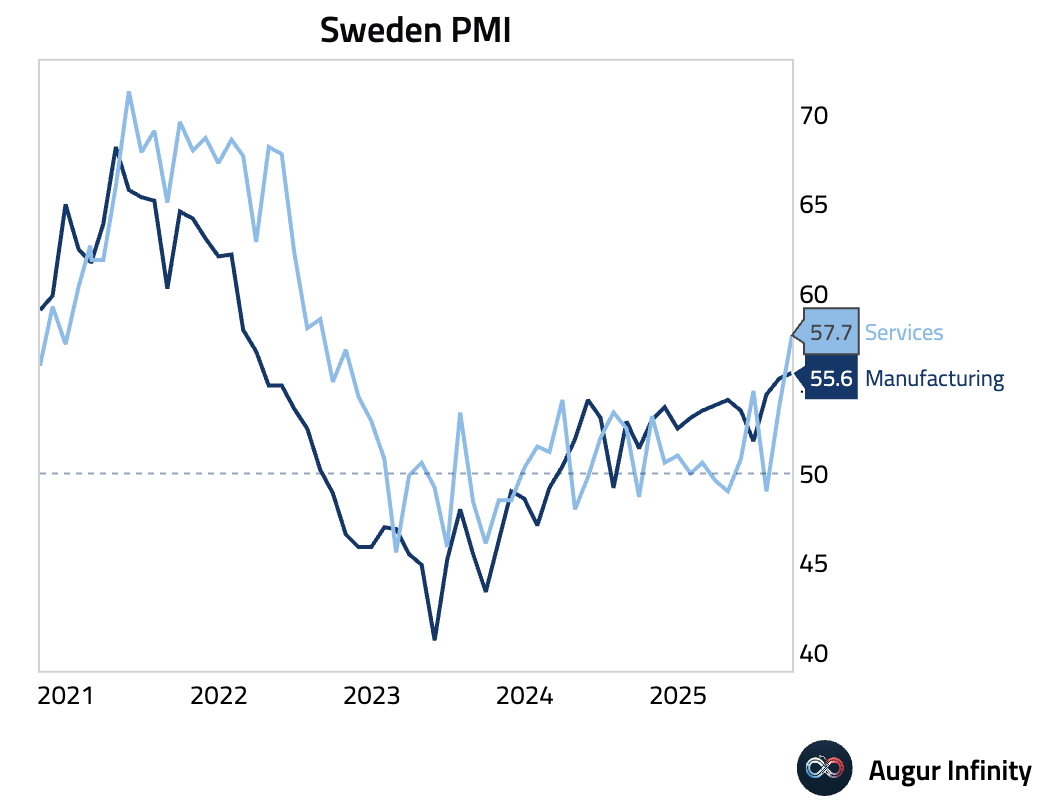

- Sweden’s services sector expanded at its fastest pace in over three years, with the PMI jumping to 57.7 in September (prev: 53.8).

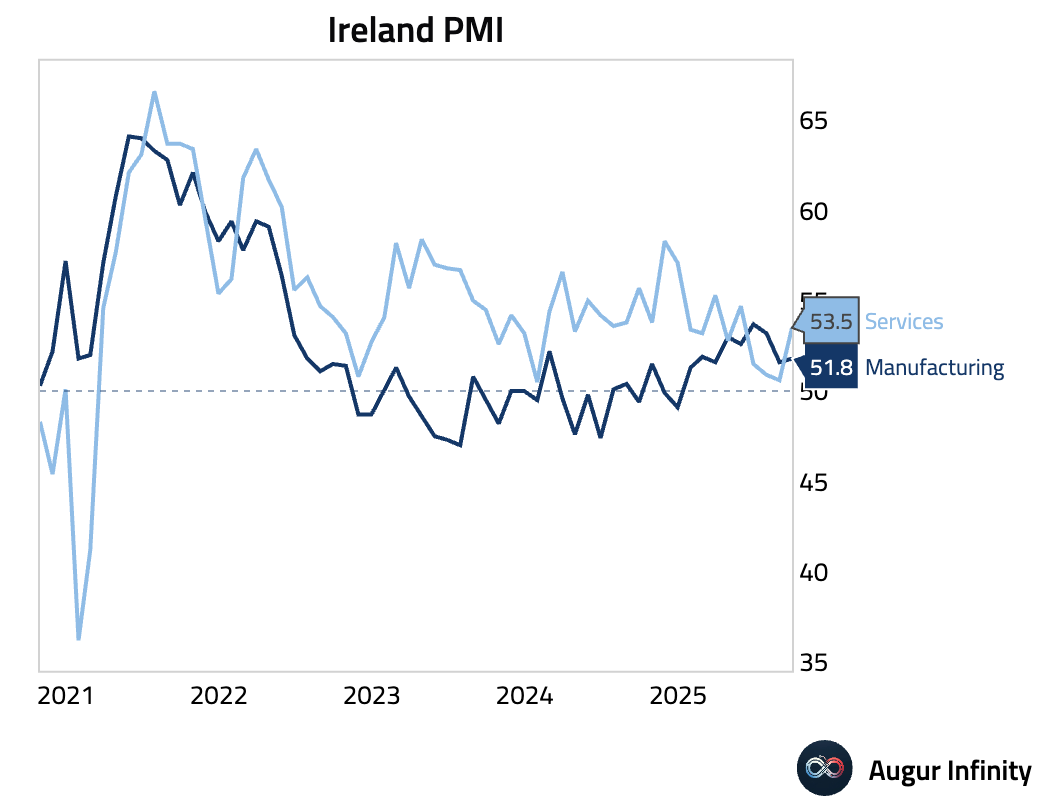

- Ireland’s Services PMI rebounded sharply to 53.5, its fastest growth in four months, driven by stronger new business and a solid return to job creation. A major sector divergence continues, with Technology booming at 60.9 while Transport & Tourism declined for a seventh straight month to 46.8. Input cost inflation accelerated to a six-month high on wage and energy pressures.

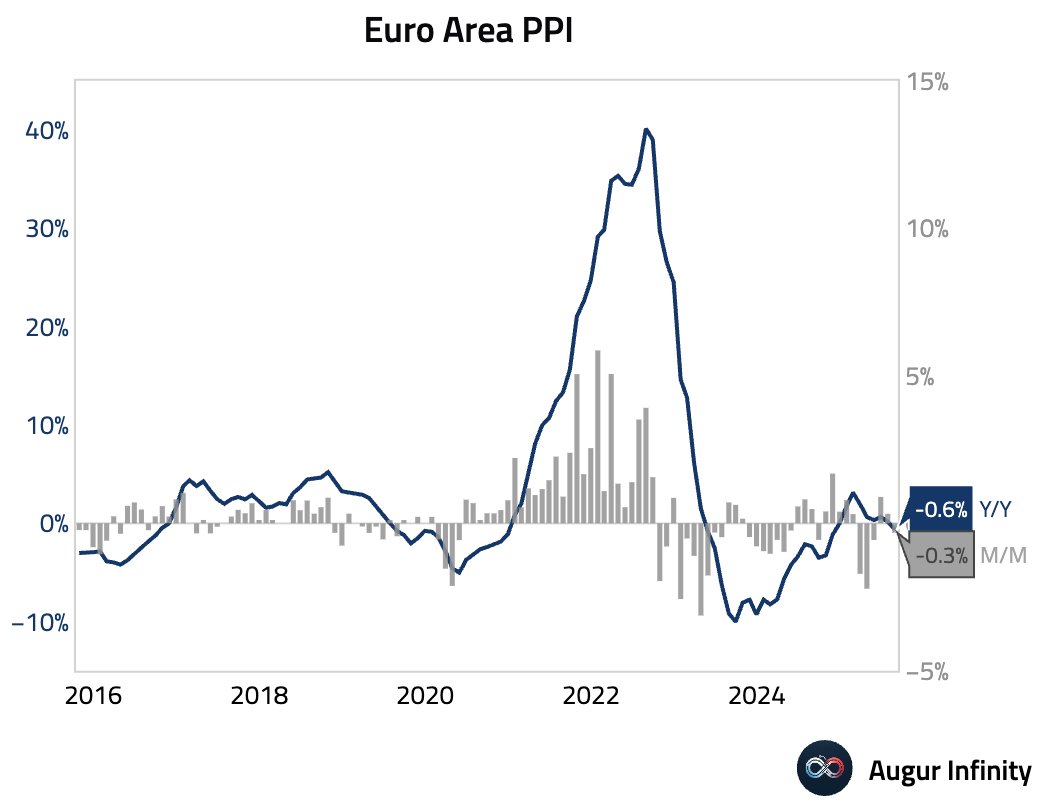

- Eurozone producer prices fell more than expected in August, returning to deflation on an annual basis (Y/Y act: -0.6%, est: -0.4%). The monthly decline also accelerated (M/M act: -0.3%, est: -0.1%).

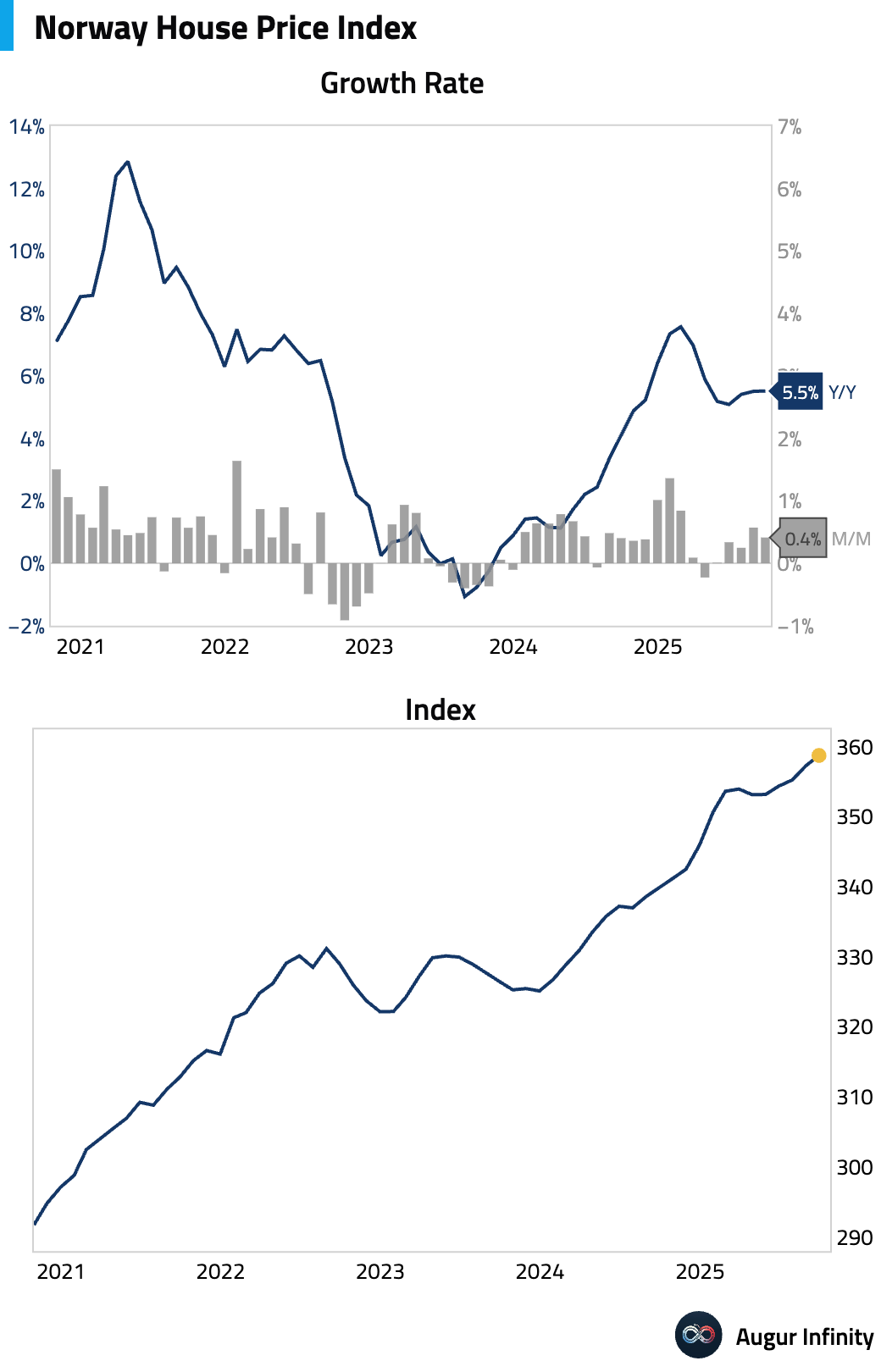

- Norwegian house price growth moderated on a monthly basis in September, while the annual rate of appreciation held steady (M/M act: 0.4%, prev: 0.6%; Y/Y act: 5.5%, prev: 5.5%).

Asia-Pacific

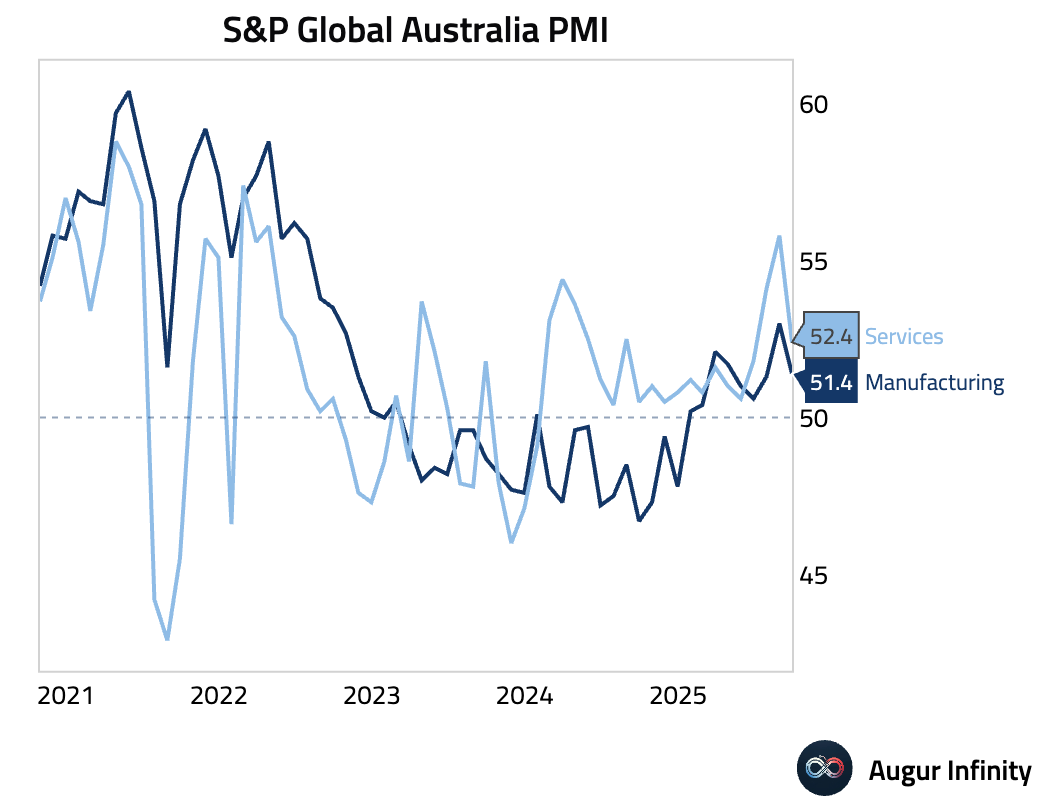

- Australia’s services sector expansion slowed in September, with the S&P Global Services PMI falling to 52.4 from 55.8. Despite the moderation in new business growth, firms accelerated hiring to a five-month high. Notably, both input and output price inflation eased, which may provide the Reserve Bank of Australia with room for further monetary policy loosening.

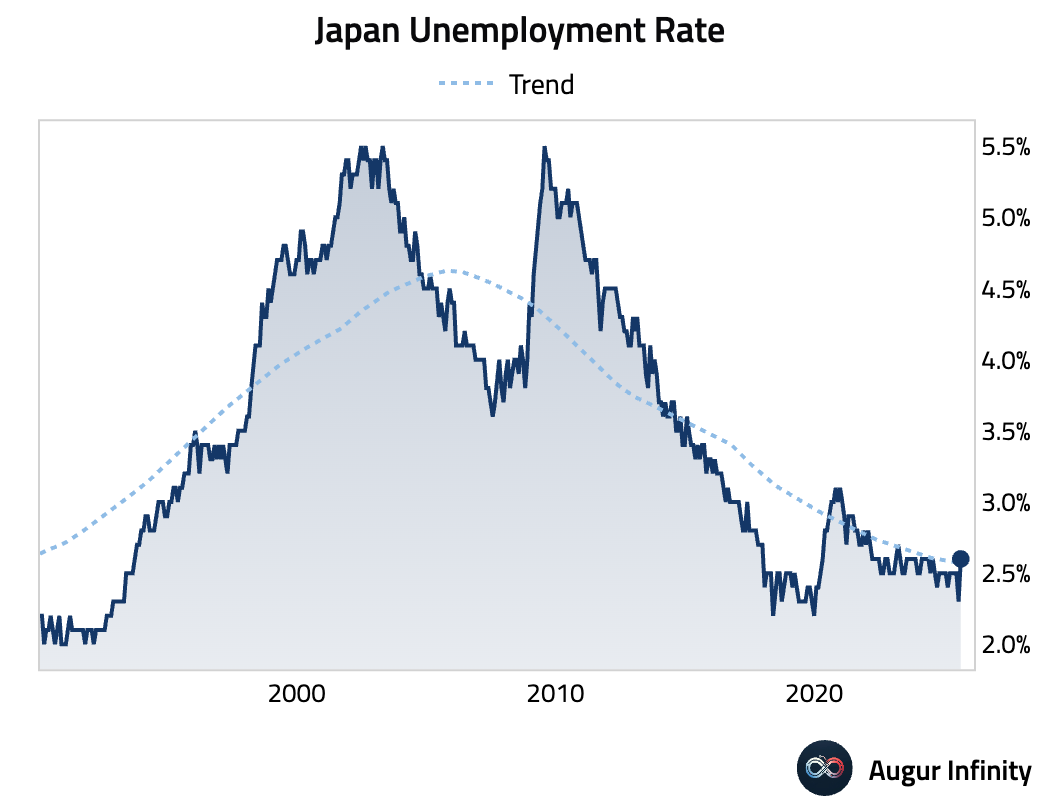

- Japan’s unemployment rate unexpectedly rose to 2.6% in August, its highest level in over two years (est: 2.4%, prev: 2.3%).

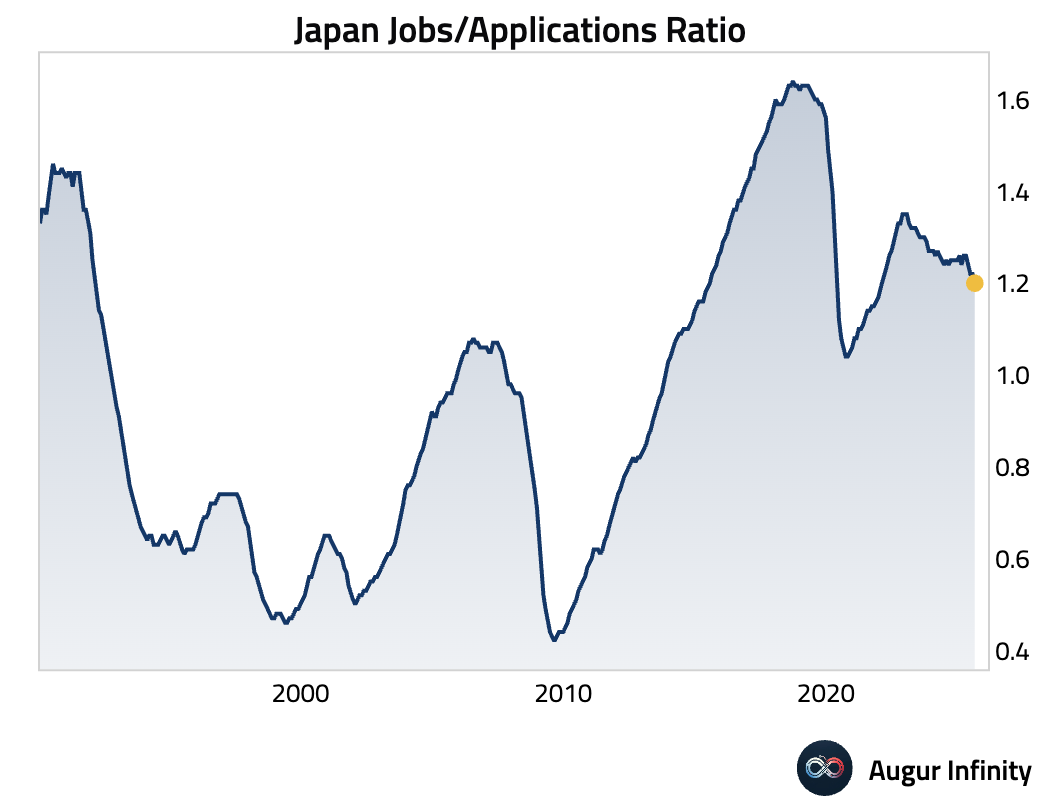

- The jobs-to-applications ratio in Japan edged down slightly, signaling a marginal loosening in labor market tightness (act: 1.20, est: 1.22).

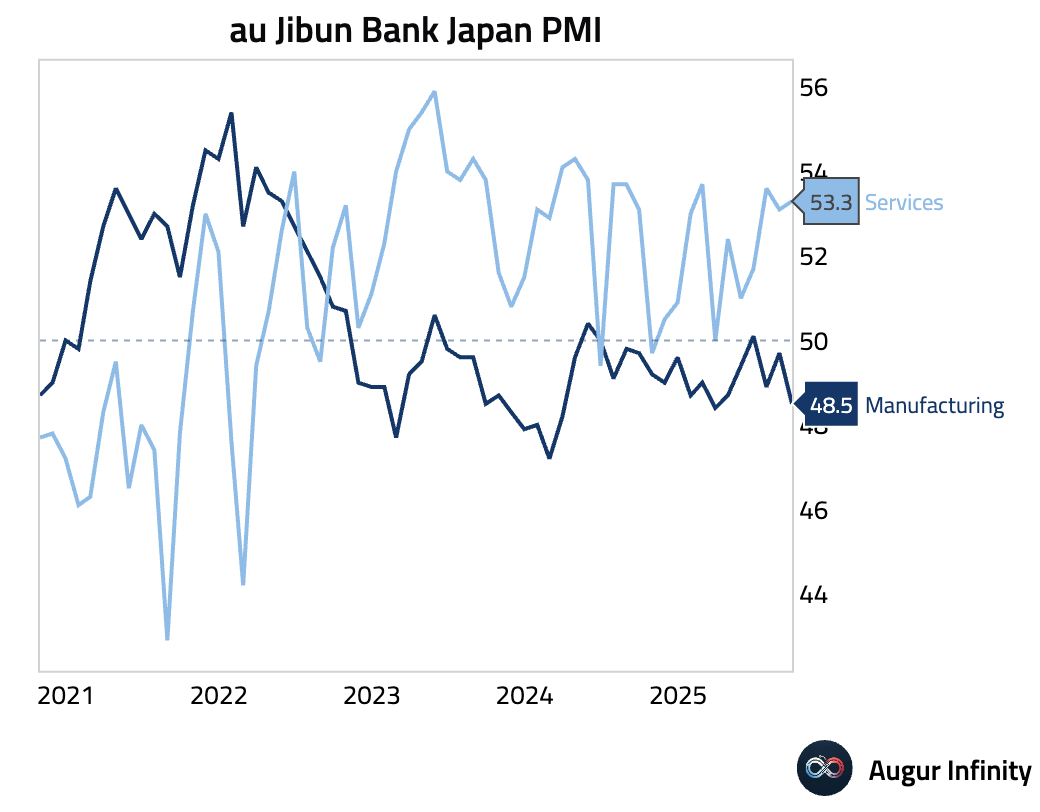

- Japan’s Services PMI ticked up to 53.3 in September, marking the second-steepest growth rate since February. The expansion was driven by strong domestic demand, as foreign demand continued to decline. Encouragingly, employment expanded for the first time in three months and business confidence hit an eight-month high.

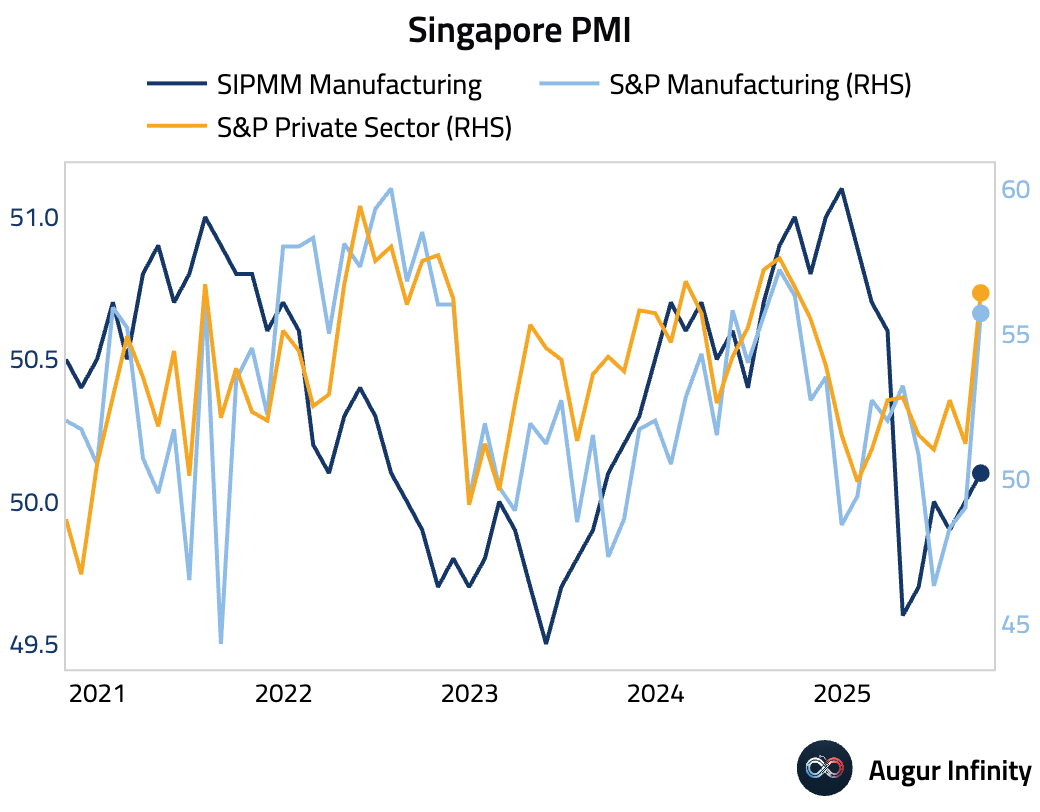

- Singapore’s private sector activity surged to a one-year high of 56.4 in September, indicating a sharp rebound from August's 51.2. The jump was driven by the fastest growth in new orders and output in nearly a year, fueled by better demand. Employment also rose at its quickest pace since February 2024, but rising backlogs and input costs suggest intensifying capacity and price pressures.

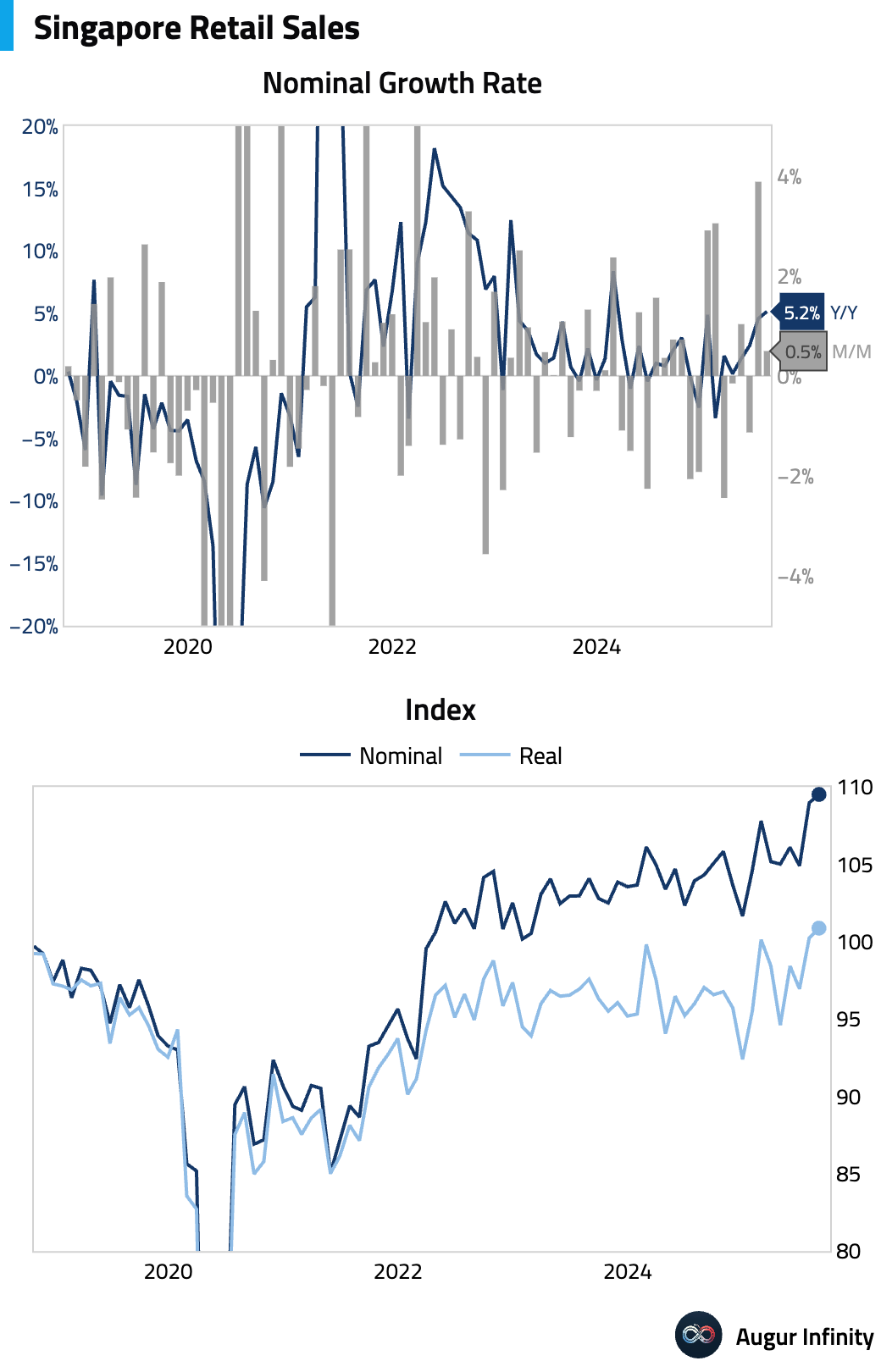

- Retail sales growth in Singapore moderated on a monthly basis while accelerating from a year ago (M/M act: 0.5%, prev: 3.9%; Y/Y act: 5.2%, prev: 4.6%).

Emerging Markets ex China

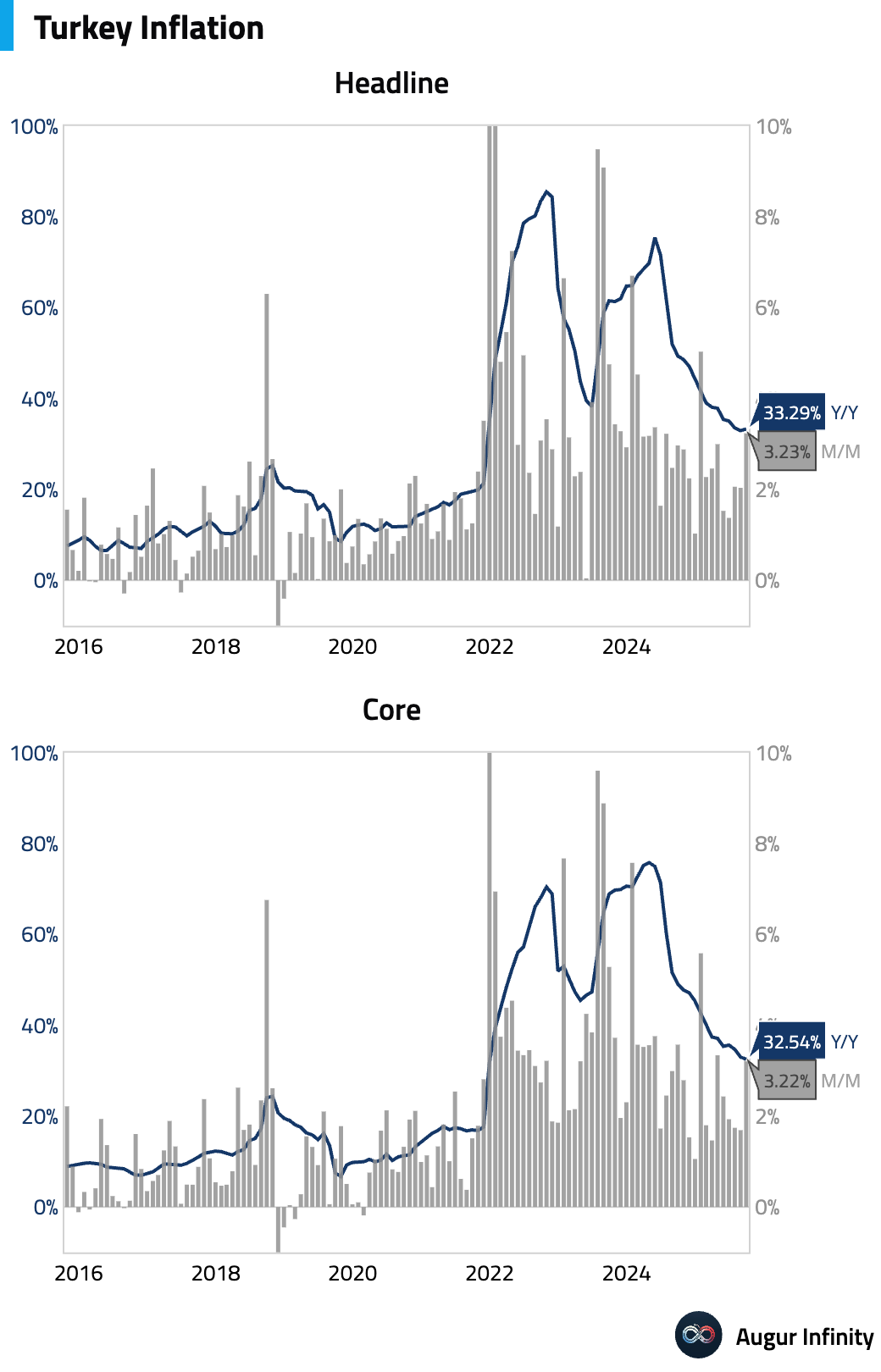

- Turkey's annual inflation rate accelerated to 33.29% in September from 32.95%, beating the 32.5% consensus forecast. On a monthly basis, prices rose 3.23%, also above expectations of 2.6%.

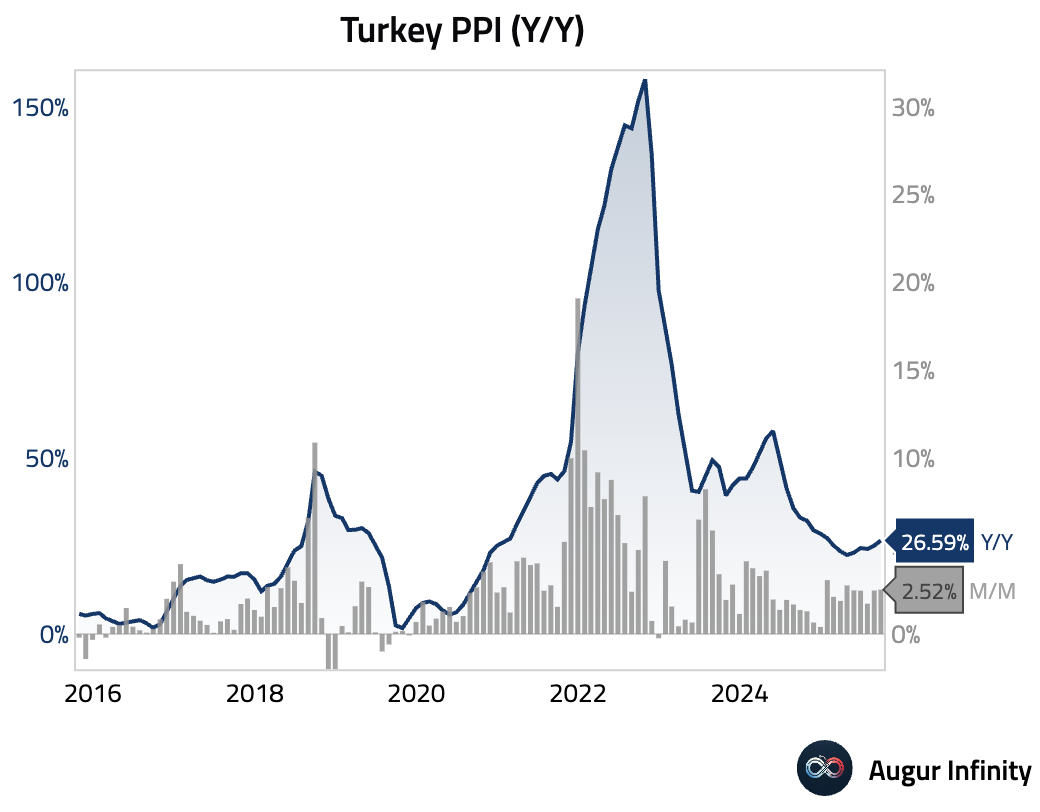

- Turkish producer prices continued to rise, with the annual rate climbing to 26.59% in September from 25.16% in August.

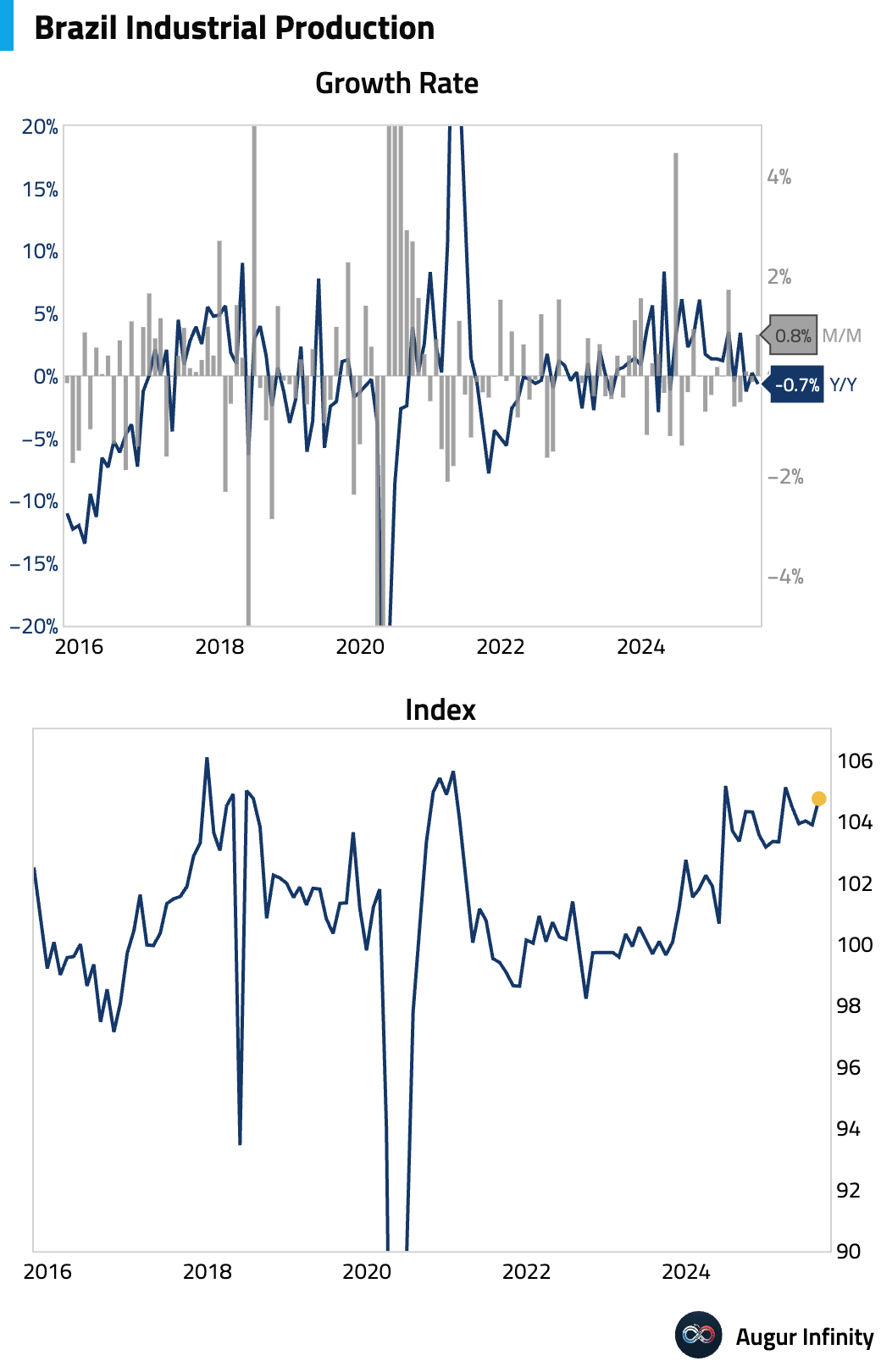

- Brazilian industrial production expanded by a stronger-than-expected 0.8% M/M in August, rebounding from July's decline (est: 0.3%). The expansion was driven by intermediate and consumer goods, but the underlying data revealed narrow breadth, as 16 of the 25 industrial segments recorded output decreases. The year-over-year figure fell back into contraction (Y/Y act: -0.7%, prev: 0.2%).

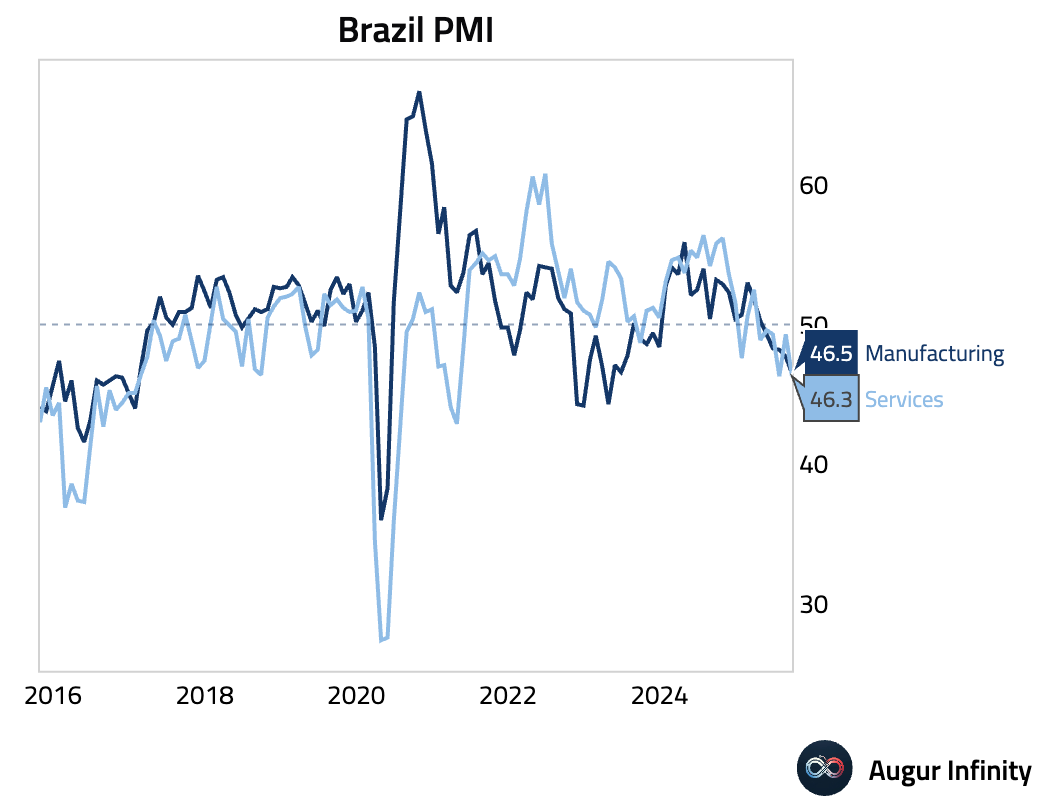

- Brazil’s service sector activity plunged in September, with the S&P Global Services PMI falling sharply to 46.3 from 49.3, a joint 4.5-year low. The contraction was driven by weak demand and a lack of new work for the sixth straight month. Despite the severe activity plunge, firms marginally increased employment, pointing to some underlying business confidence.

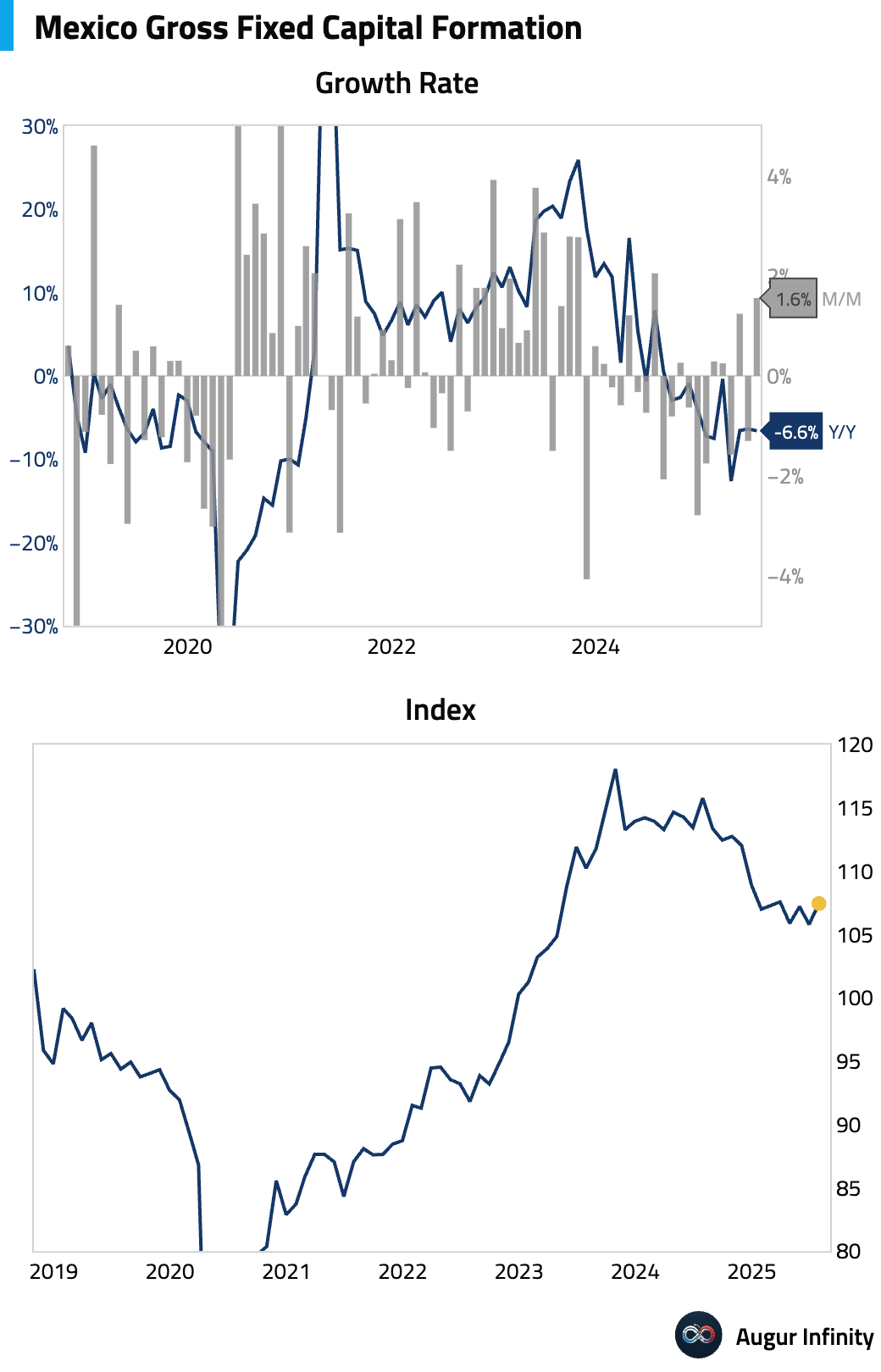

- Mexico's gross fixed investment rose more than expected in July, driven by strong machinery and equipment investment that offset persistent weakness in construction (M/M act: 1.6%, est: 1.0%). The year-over-year contraction moderated slightly (Y/Y act: -6.6%, prev: -6.4%).

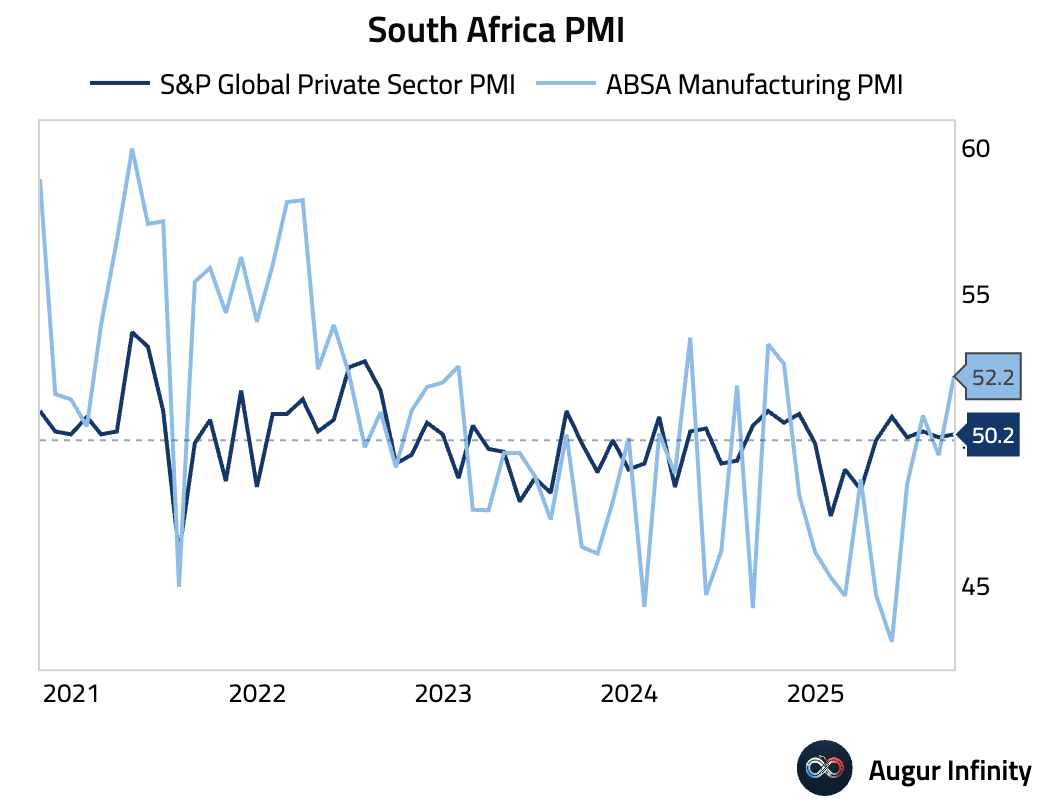

- South Africa's private sector activity expanded for a third consecutive month in September, with the S&P Global PMI edging up to 50.2 (prev: 50.1).

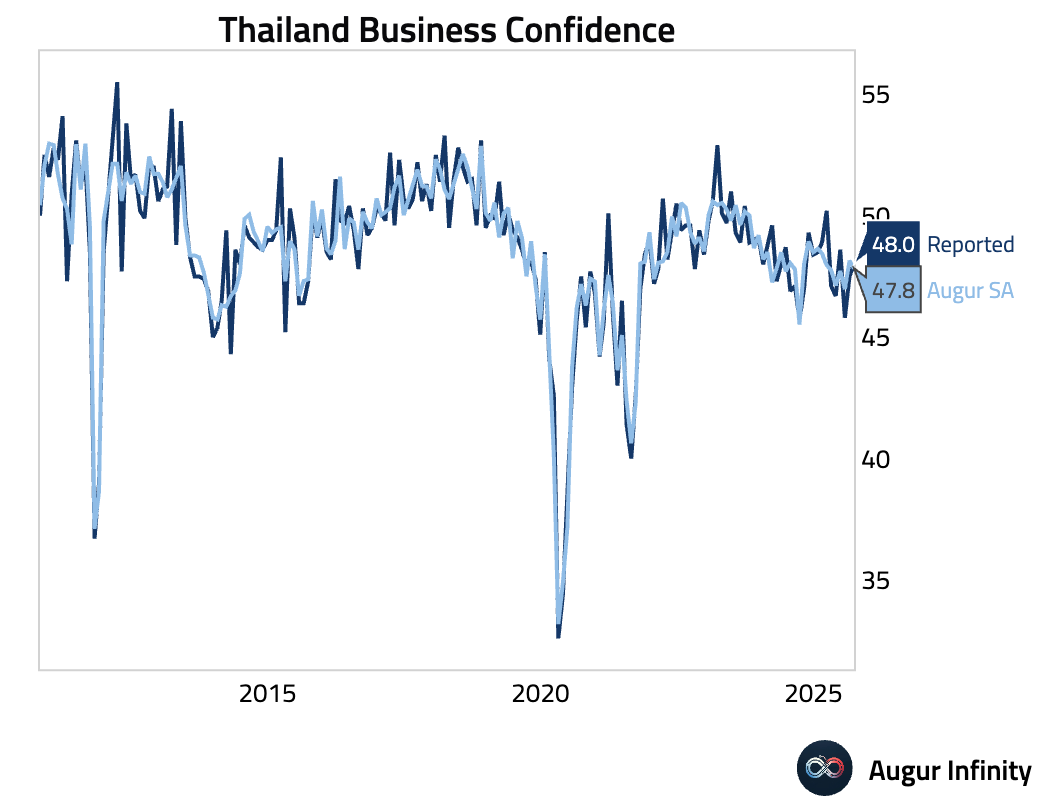

- Business confidence in Thailand improved slightly in September but remained in pessimistic territory (act: 48.0, prev: 47.5).

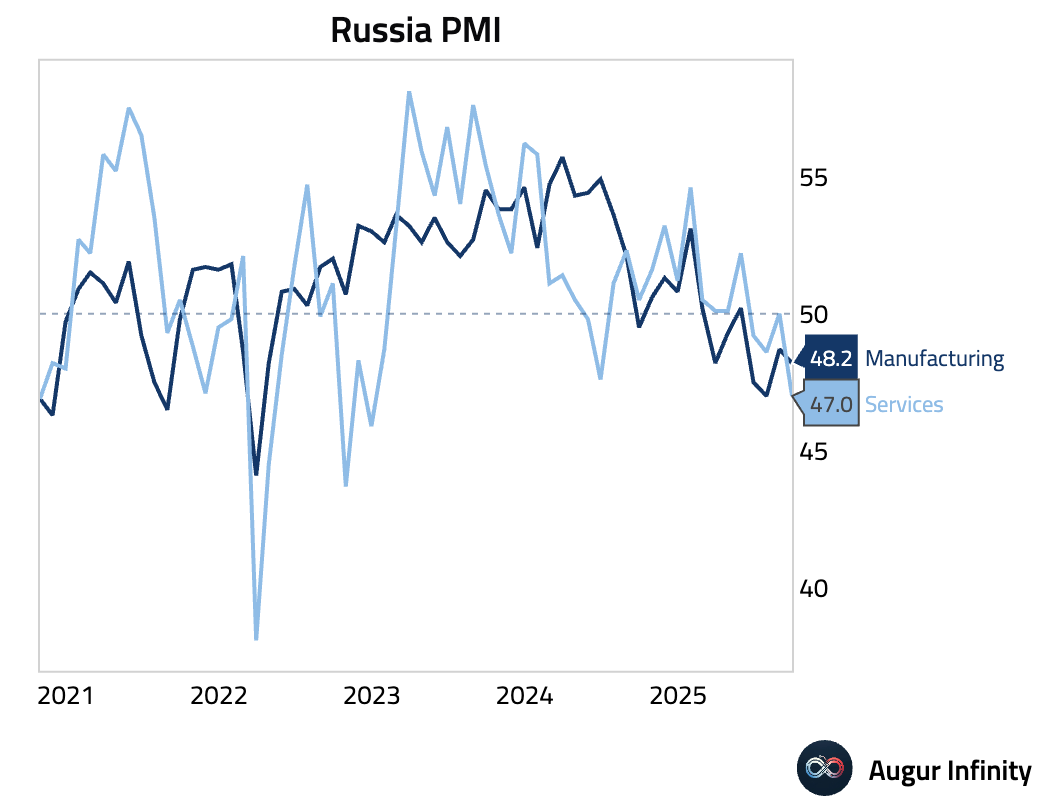

- Russia's services sector activity contracted at the fastest pace since December 2022, with the S&P Global PMI dropping to 47.0 in September from 50.0. The fall was driven by the sharpest decline in new orders in the same period. Despite this, firms hired at the quickest pace since January 2024 to clear backlogs.

Global Markets

Equities

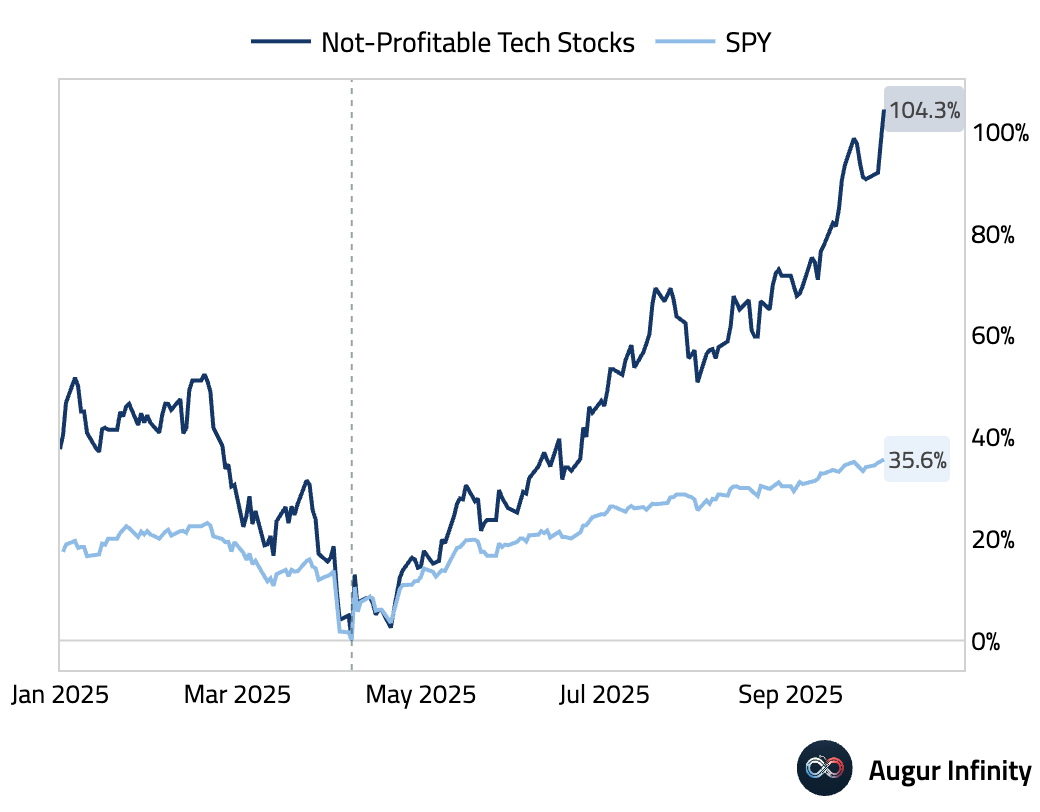

- Stocks of tech companies that are not profitable have more than doubled since the April 8 low.

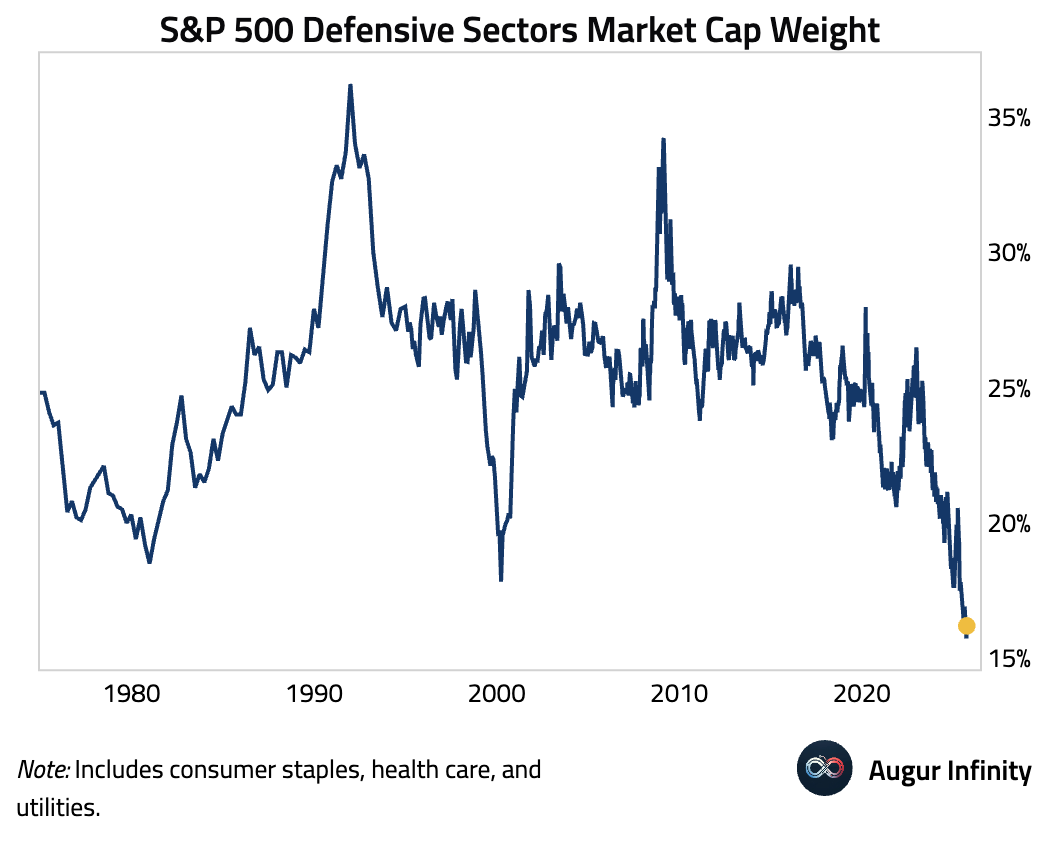

- The weight of defensive sectors in the S&P 500 has declined to secularly low levels.

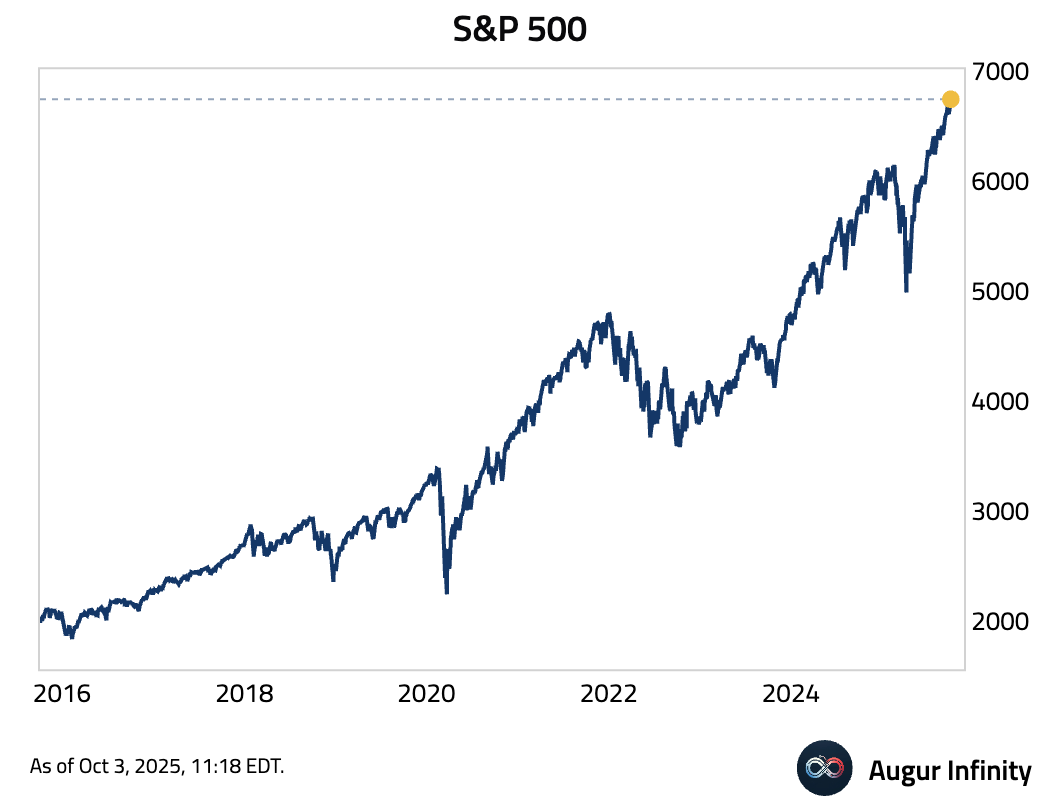

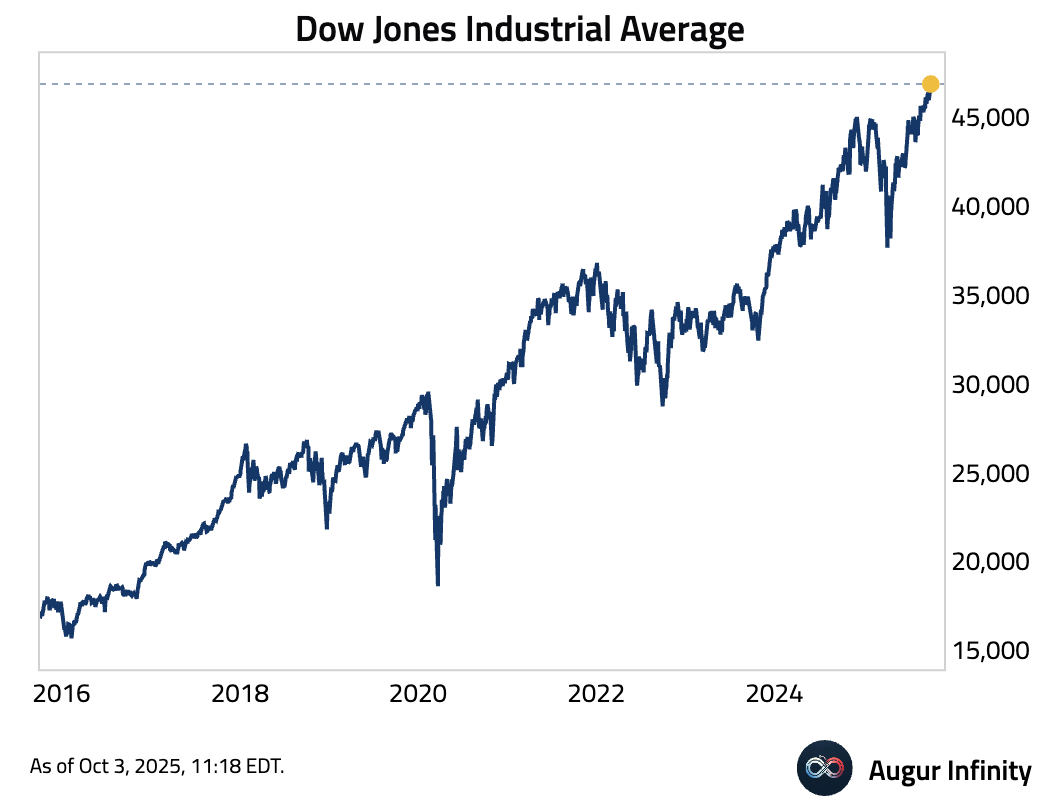

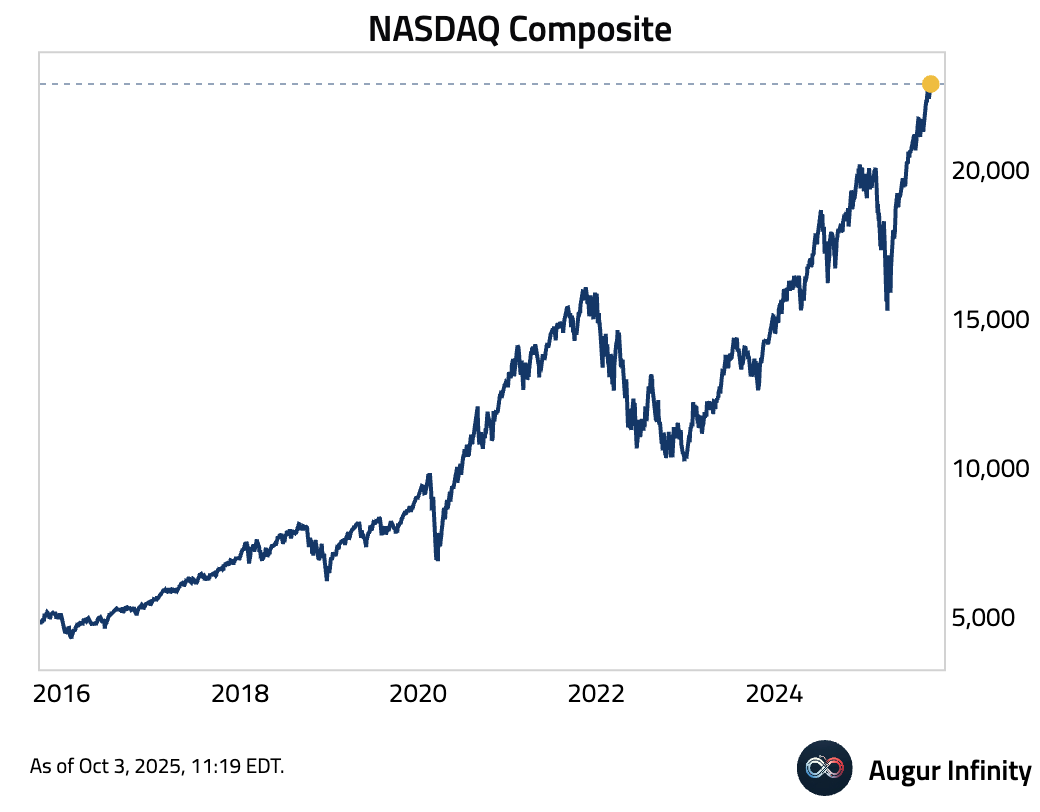

- All the major US equity indices are making new all-time-highs. Here's S&P 500 ...

... and the Dow Jones Industrial Average ...

... and the NASDAQ Composite.

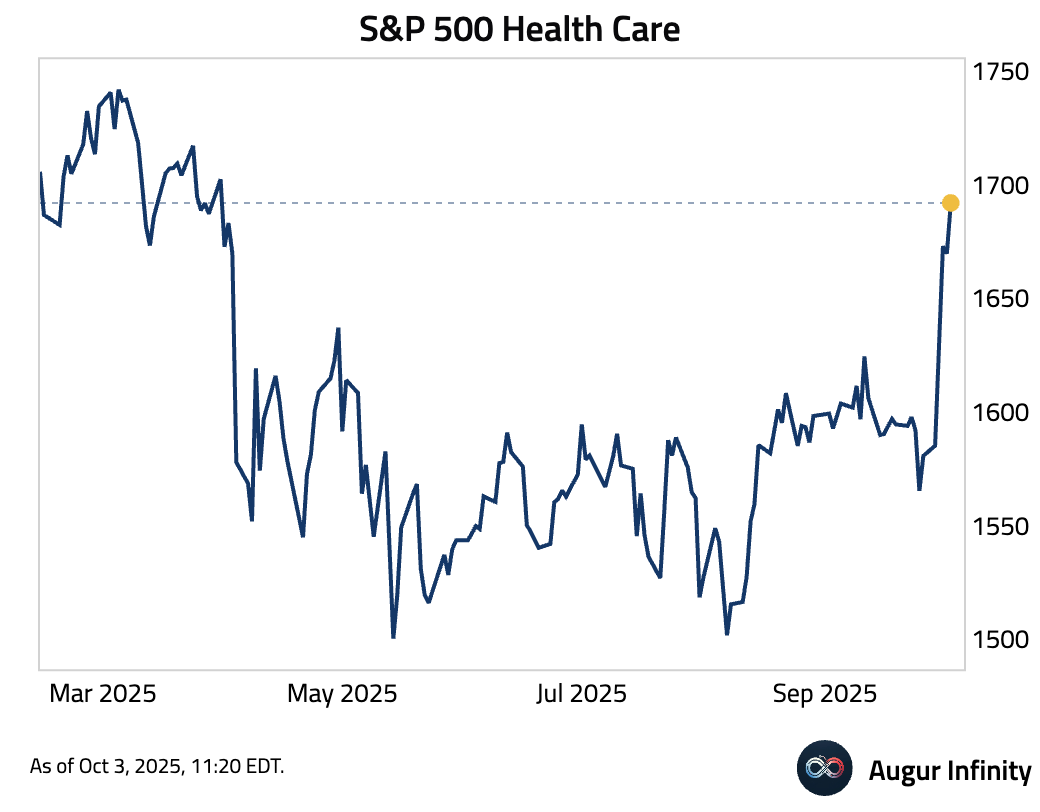

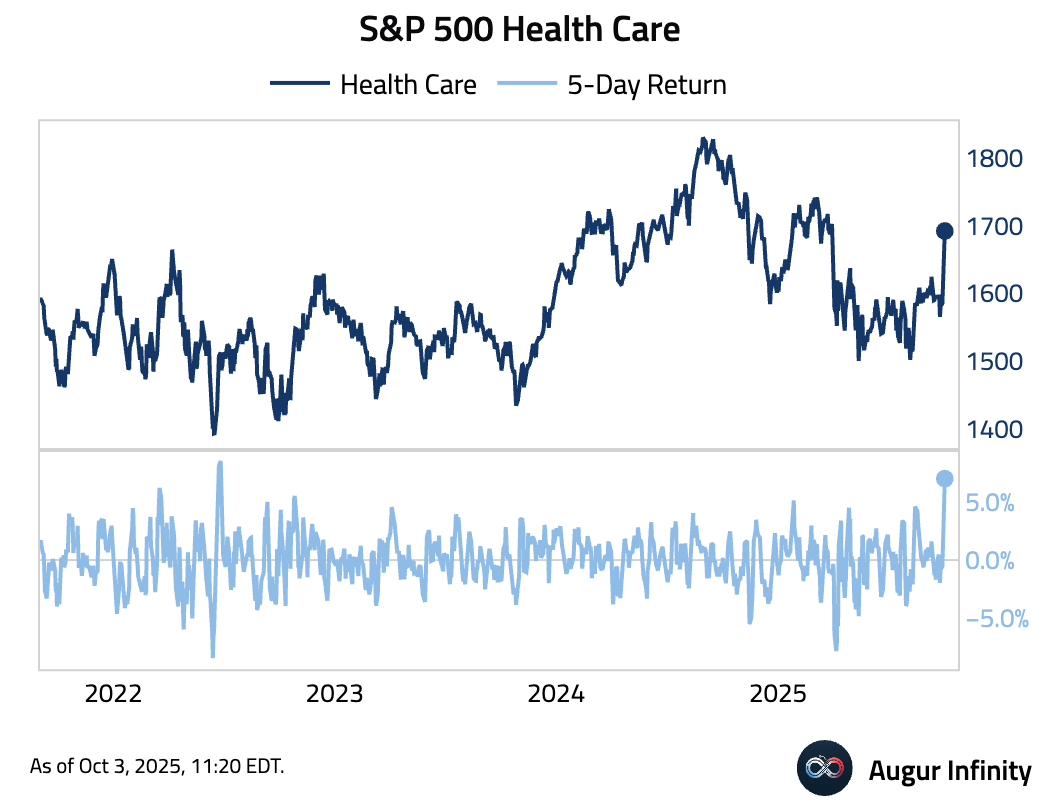

- S&P 500 Health Care is trading at the highest level since March ...

... with the best 5-day performance since June 2022.

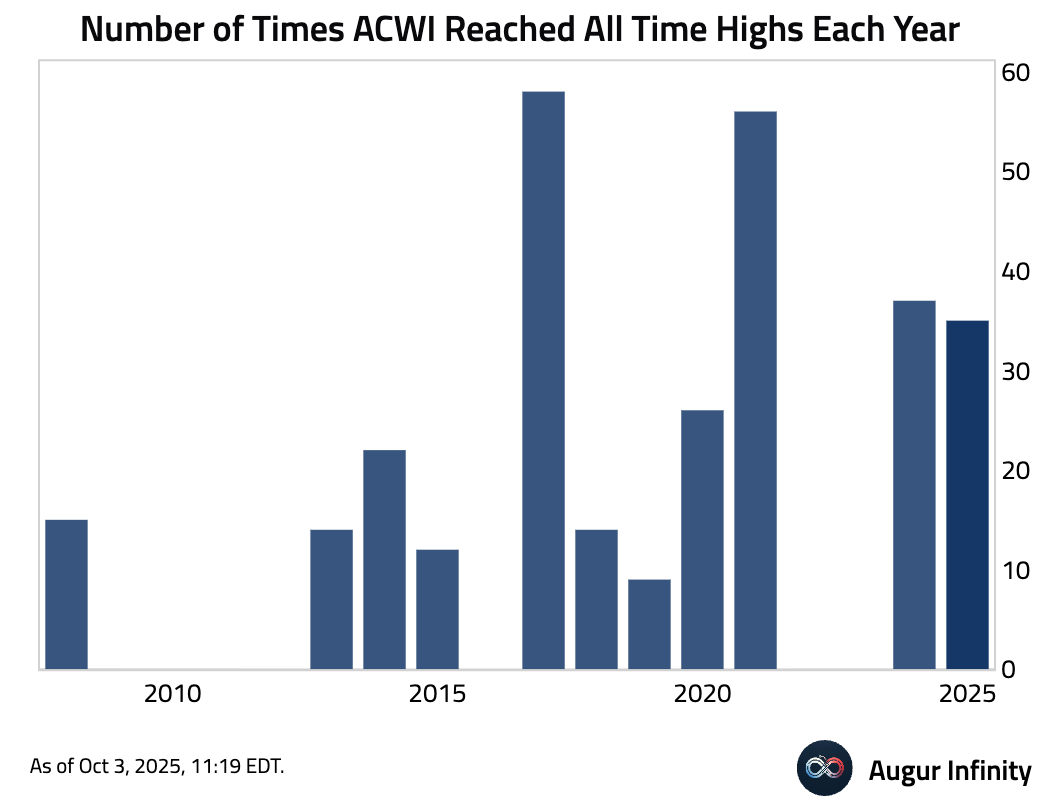

- iShares MSCI ACWI ETF has reached all-time highs 35 times this year.

Fixed Income

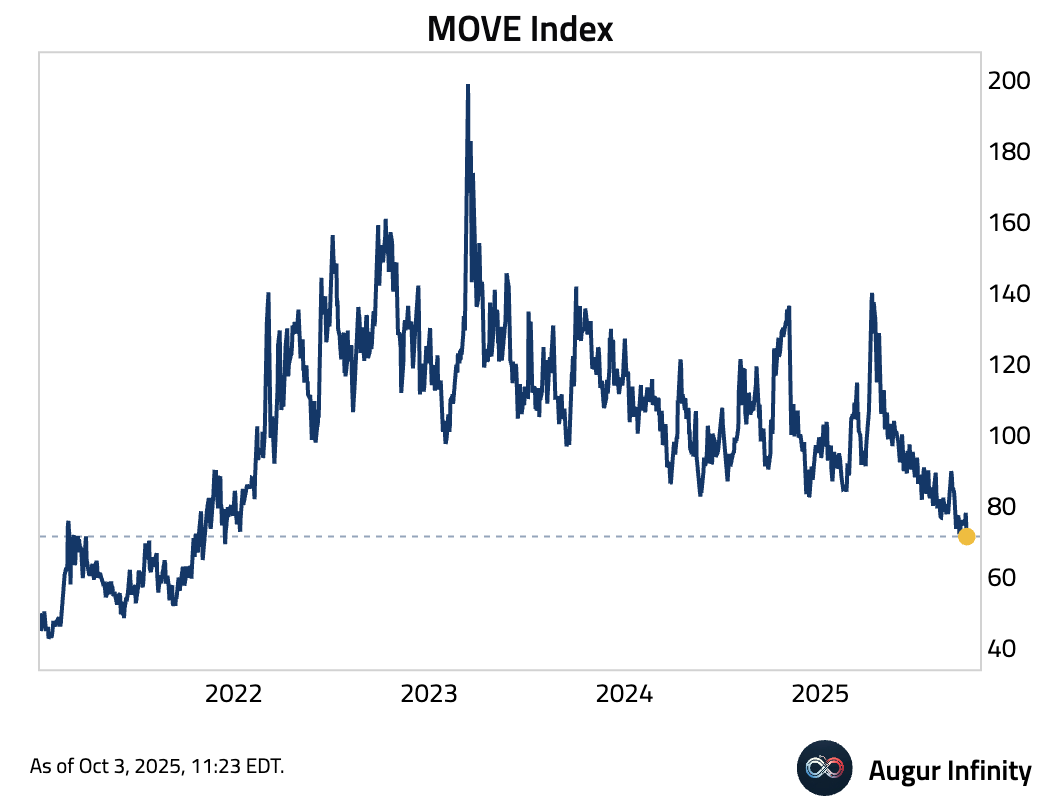

- MOVE Index has come down to the lowest level since December 2021.

Commodities

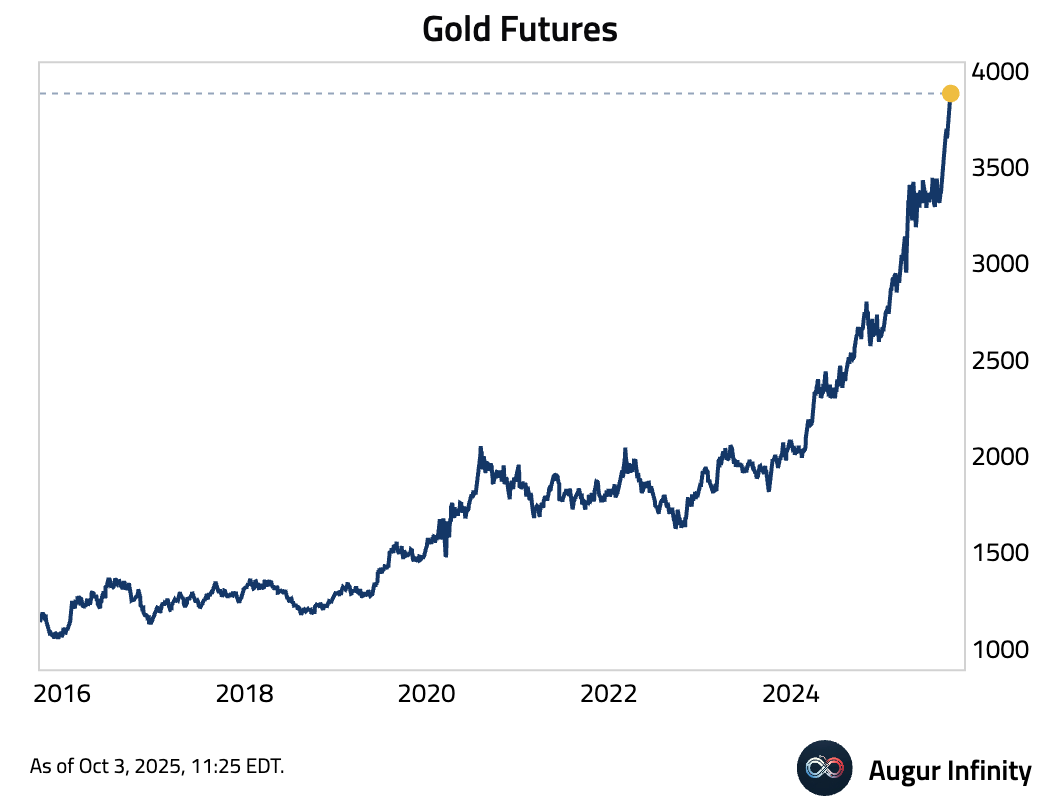

- Gold continues to push higher.

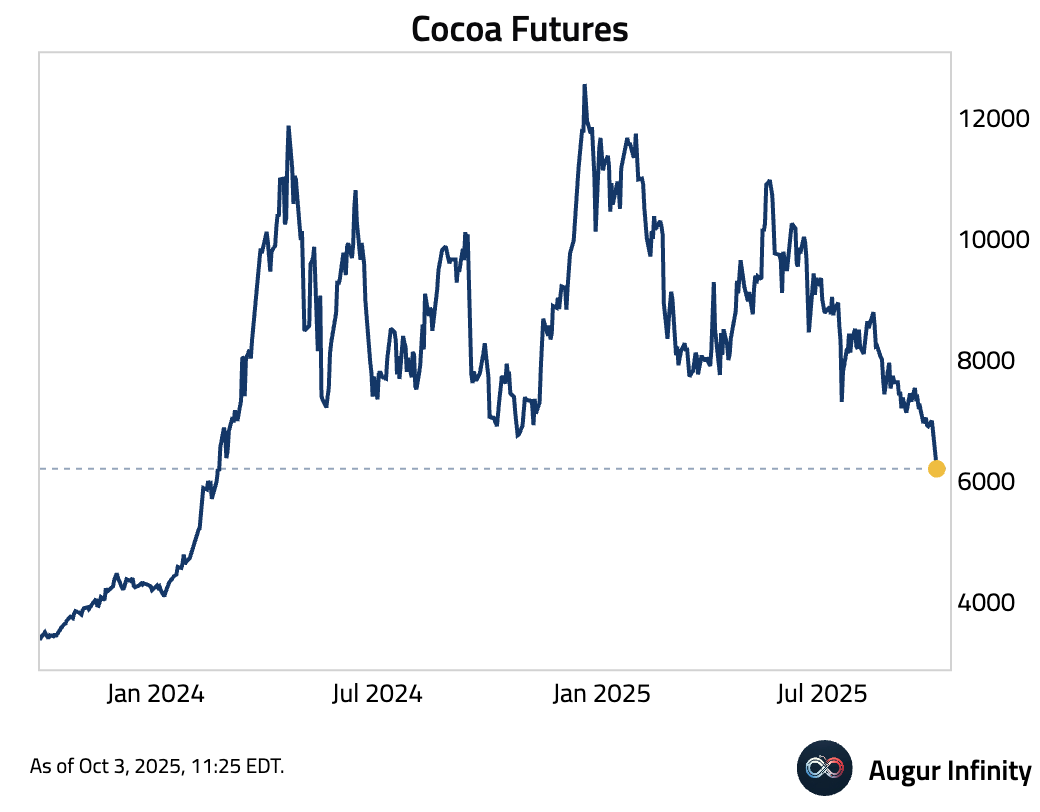

- Cocoa Futures is at the lowest level since February 2024.

FX

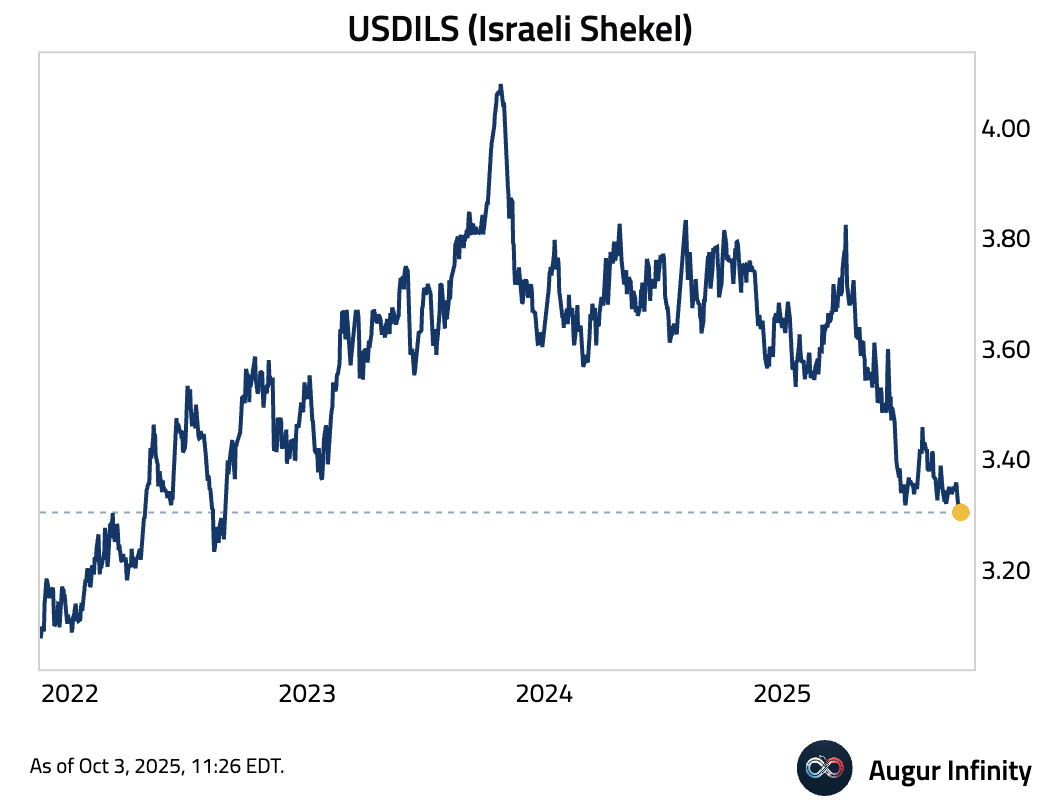

- USDILS (Israeli Shekel) has appreciated to the strongest level against USD since August 2022.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.