Headlines

- Sanae Takaichi unexpectedly won the leadership race for Japan’s ruling Liberal Democratic Party, creating a potential shift in the country’s economic policy direction.

- The French prime minister, Sébastien Lecornu, resigned over disagreements regarding fiscal policy, generating political uncertainty for the eurozone’s second-largest economy.

- OPEC+ announced a daily oil output increase of 137,000 barrels for November, in line with previous reports.

Global Economics

United States

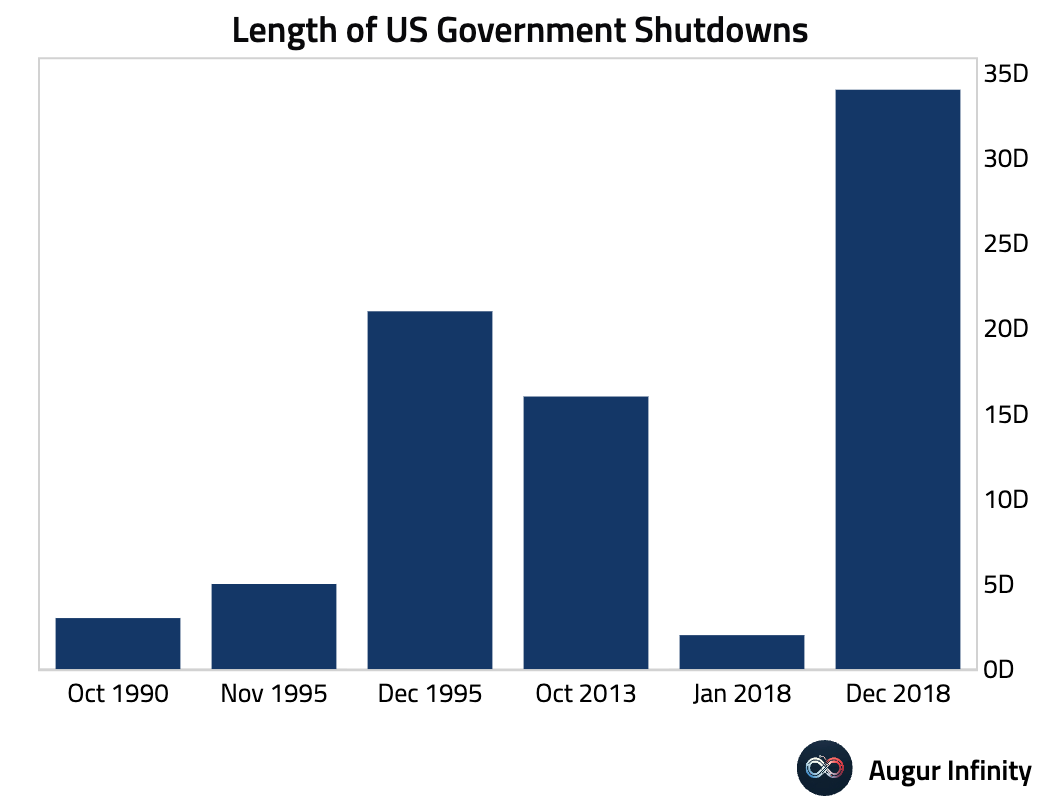

- The US government has been shut down for six days. Here’s how that compares with past shutdowns.

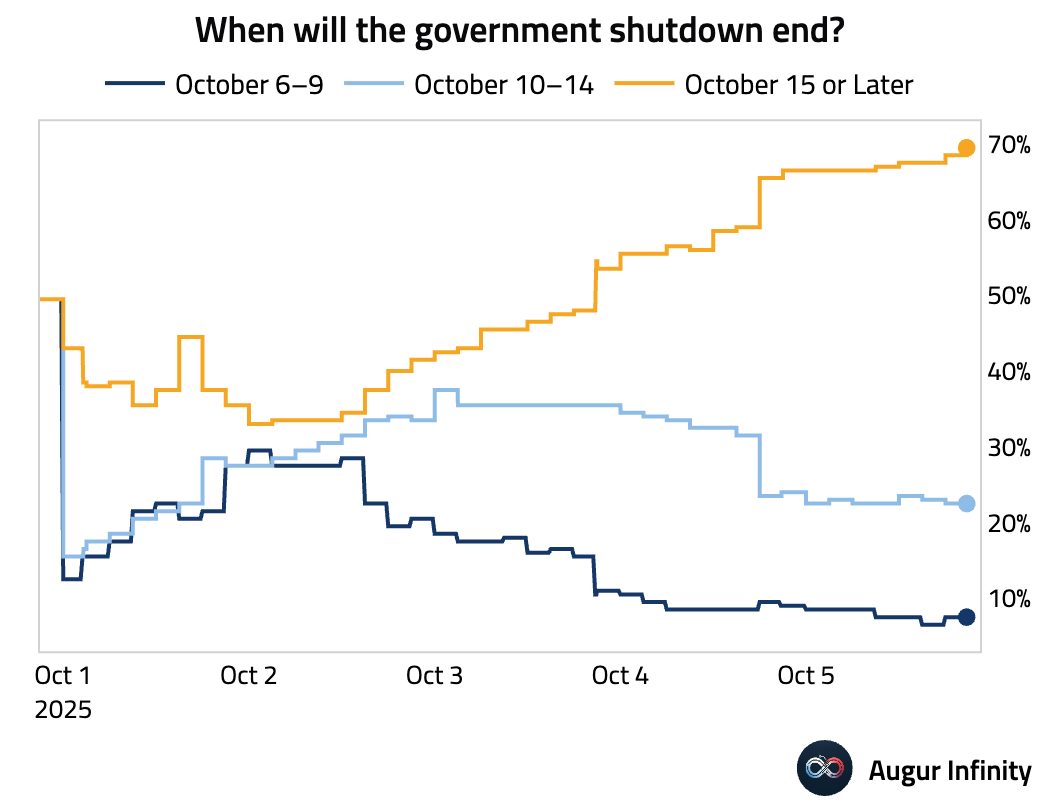

Betting markets currently see the highest odds of the government shutdown ending after October 15.

Source: Polymarket

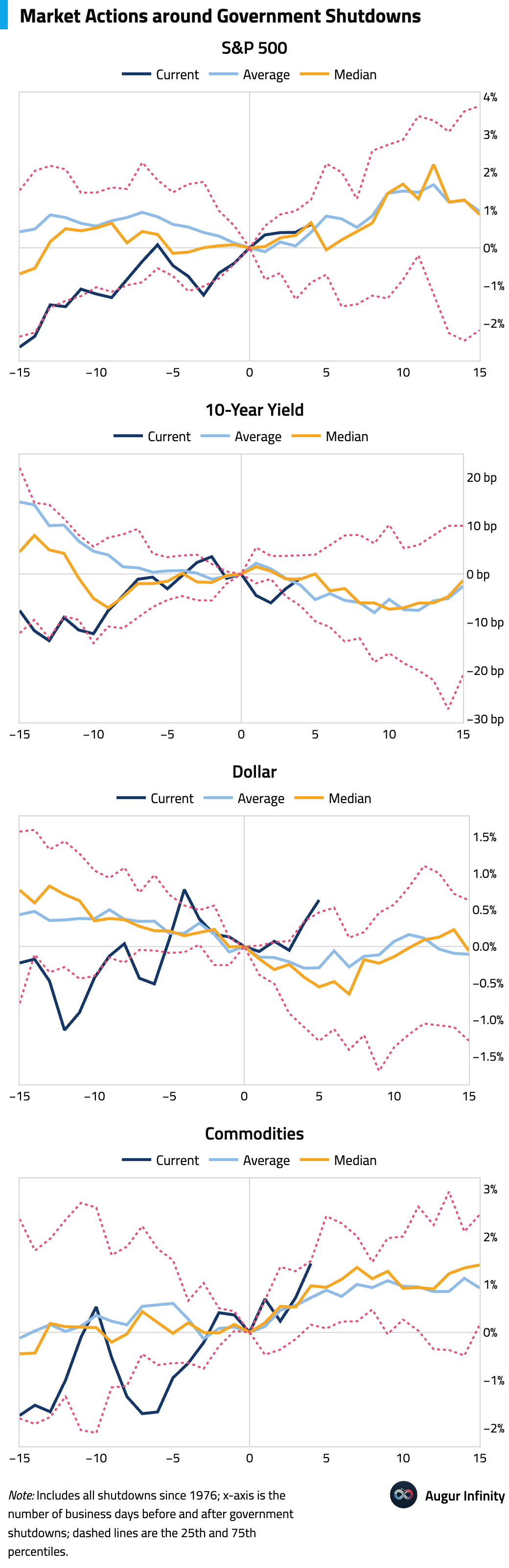

- Here’s how markets are moving compared to their typical patterns following past government shutdowns.

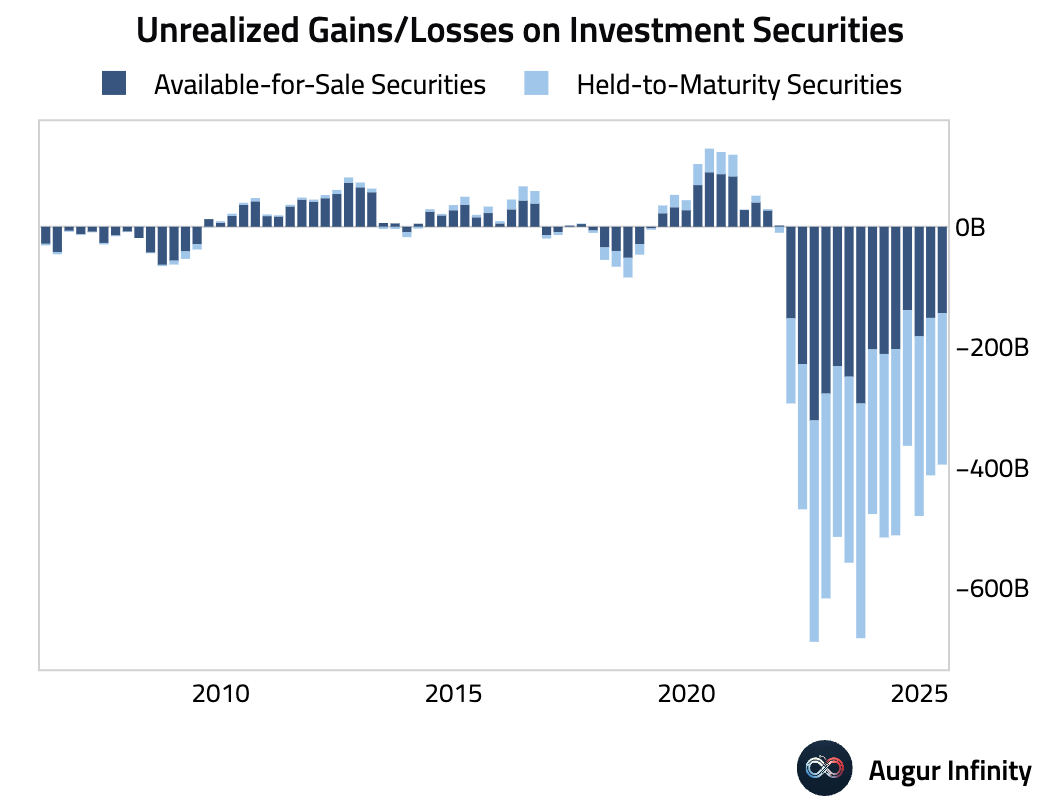

- Unrealized losses on investment securities at US banks totaled $395 billion as of Q2.

Interactive chart on Augur Infinity

Asia-Pacific

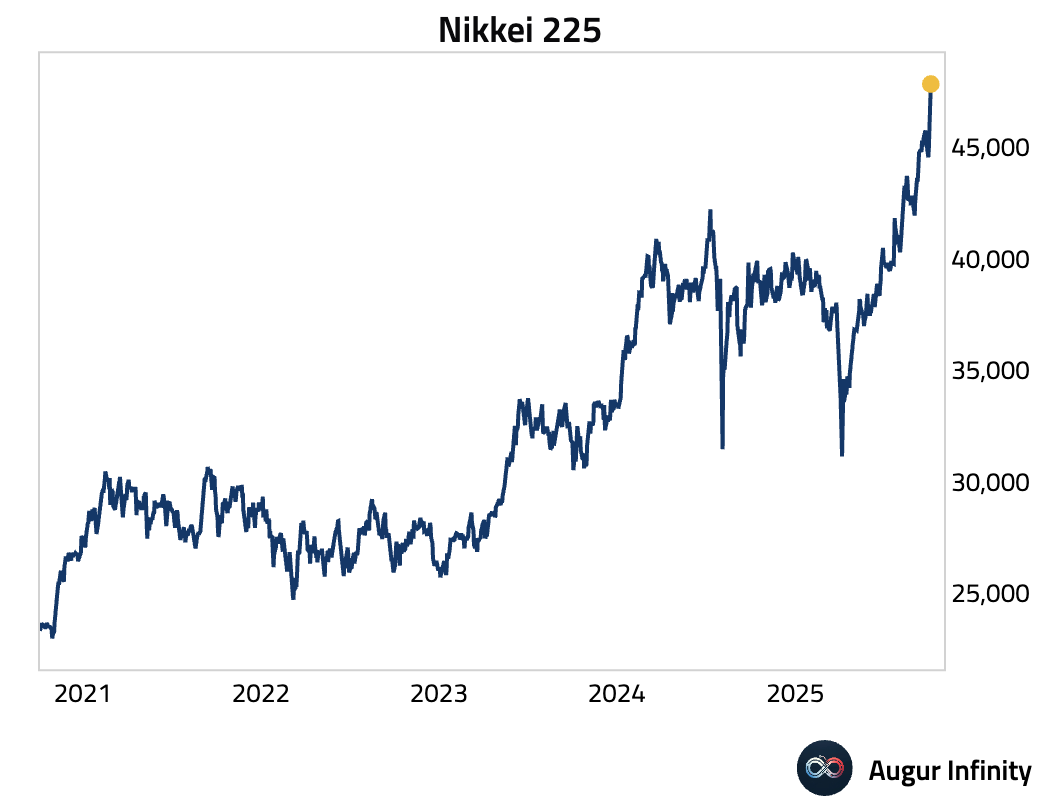

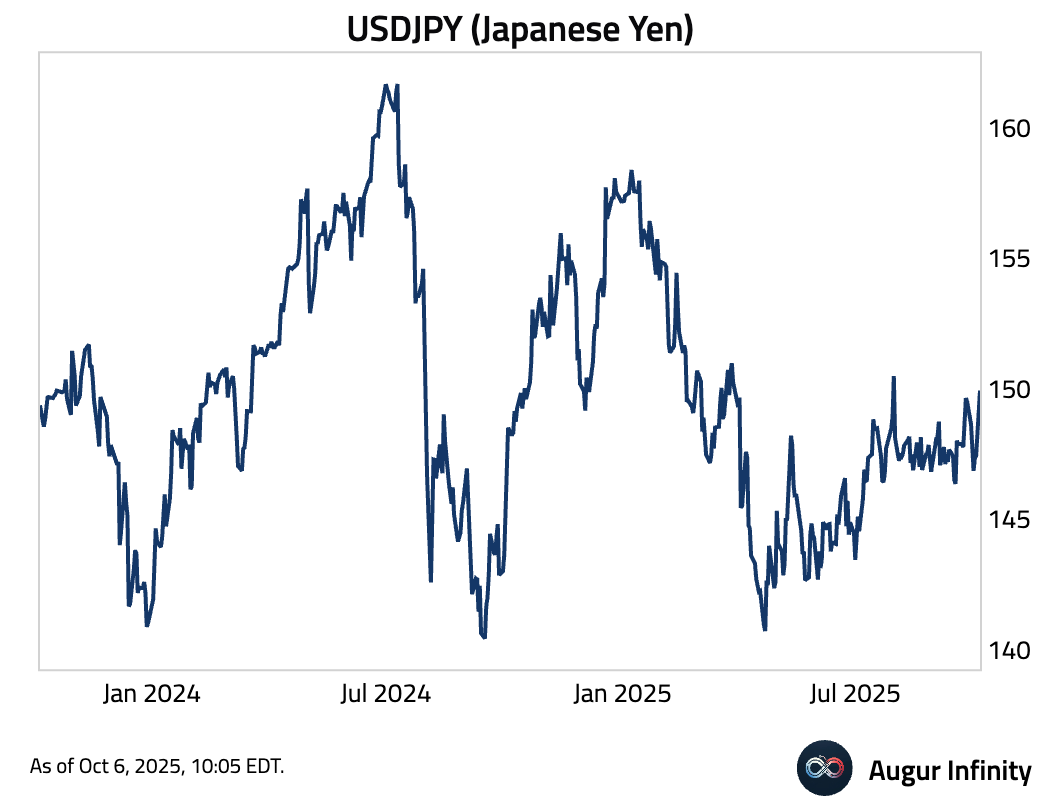

- Sanae Takaichi's surprise election as LDP president introduces "Sanaenomics," made up of three core policies: 1) emphasis on national crisis management and growth, 2) expansionary fiscal policy centered on measures to tackle inflation, and 3) an approach involving the government being responsible for monetary policy, while the BOJ determines the best means of carrying out this policy. The Nikkei 225 jumped by 4.75% on the day.

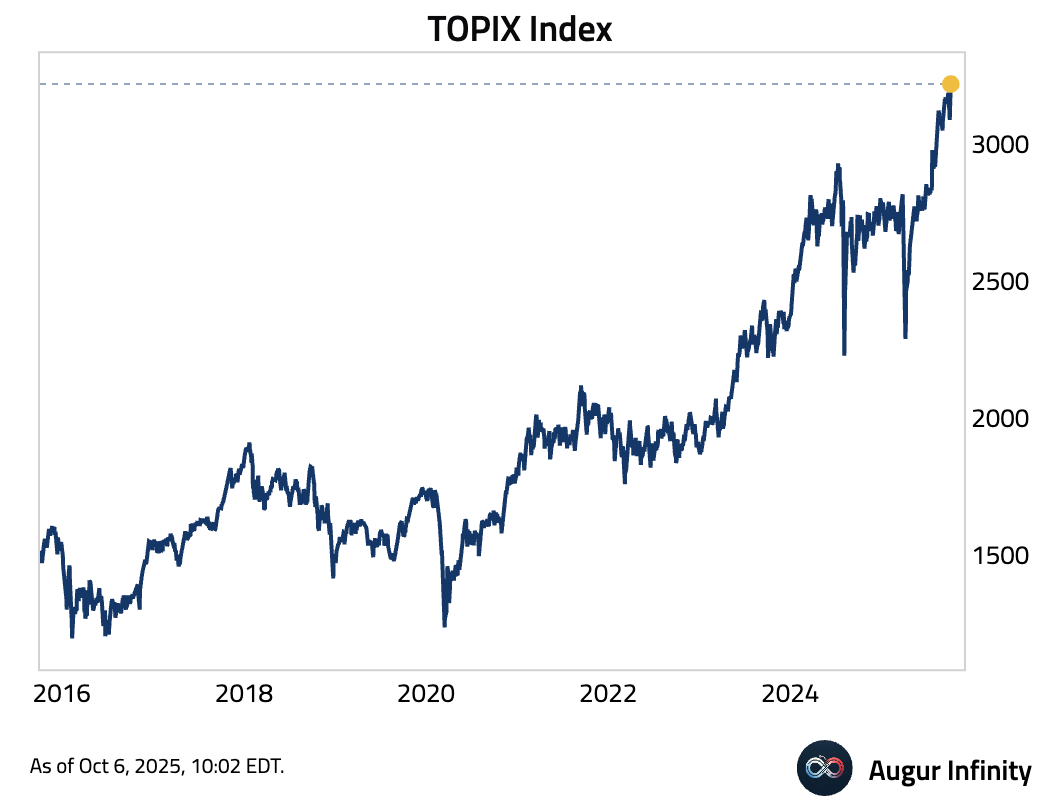

The TOPIX Index rallied by 3% to its 16th all-time high of 2025.

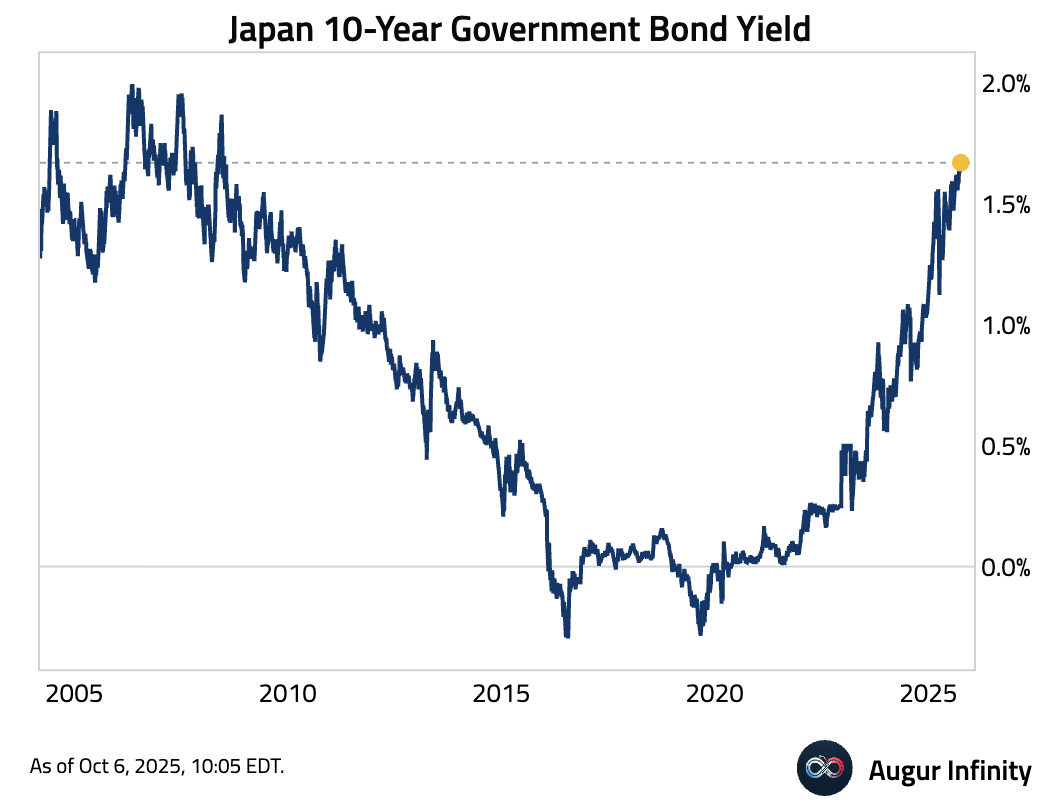

The JGB curve steepened sharply. 10-year yield rose by 2.7 bps to the highest level since July 2008 …

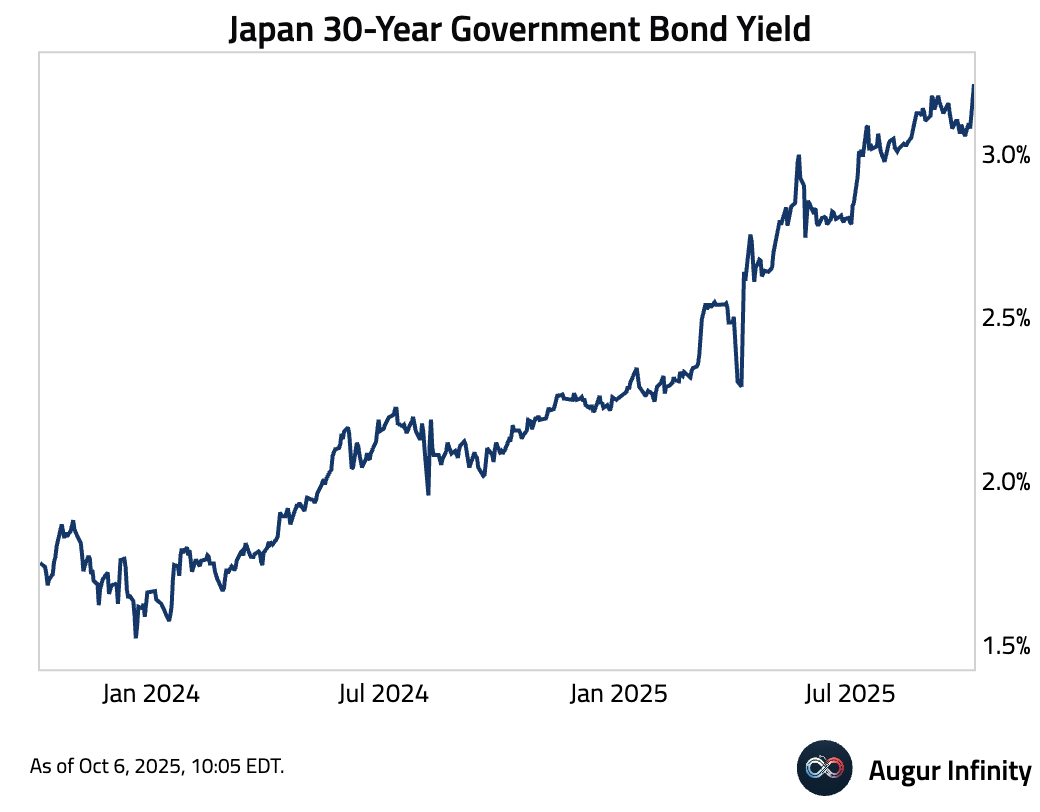

… while 30-year JGB yield jumped by 13.6 bps, a 3.0σ move.

Japanese yen depreciated by 1.6% aginst USD.

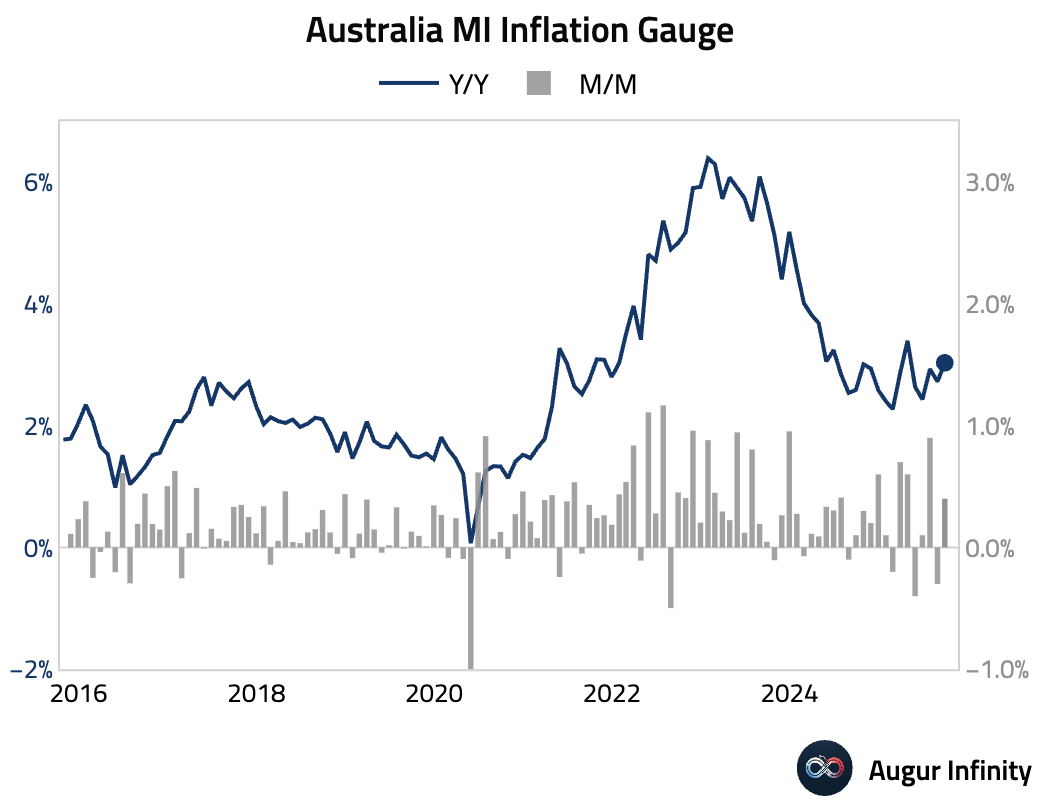

- Australia’s Inflation Gauge rose in September (act: 0.4% M/M, prev: -0.3%), reversing the prior month’s decline.

Source: Melbourne Institute

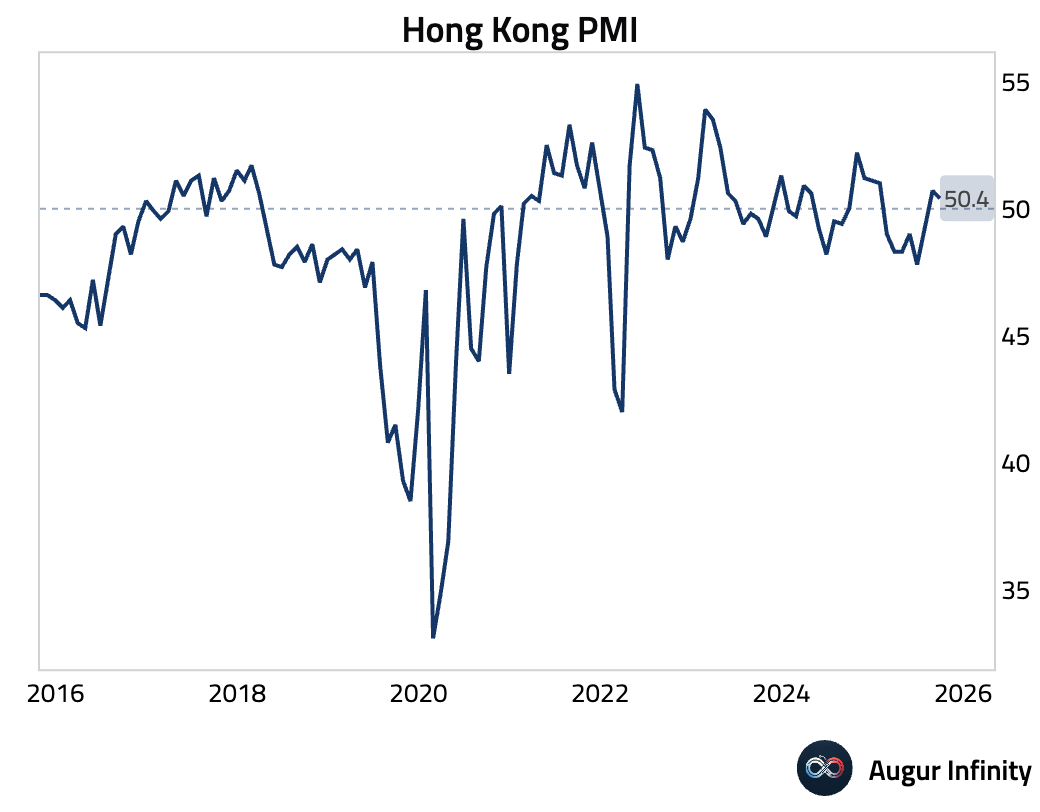

- Hong Kong’s PMI edged down to 50.4 in September, signaling a modest slowdown. The headline figure masked a sharp divergence between resilient domestic activity, which hit a 10-month high, and collapsing external demand. New export orders plunged at the fastest rate in three and a half years, with firms citing US tariffs and weak demand from mainland China. A surge in input costs to a nearly two-year high, combined with stagnant output prices, points to a severe margin squeeze for businesses.

Source: S&P Global

Europe

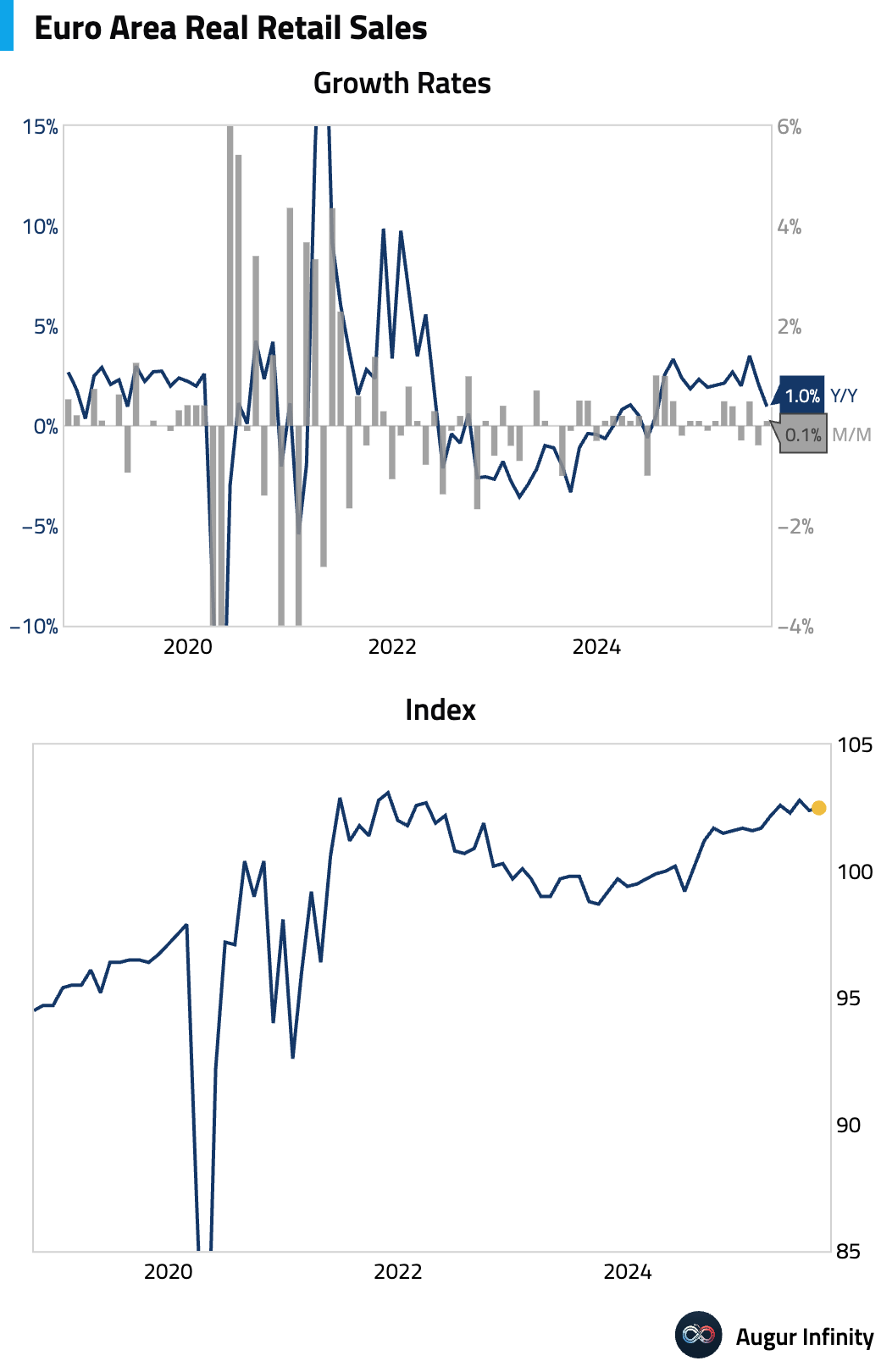

- Eurozone retail sales edged up in August but the year-over-year growth rate slowed significantly, indicating continued weakness in consumer spending (act: 0.1% M/M, prev: -0.4%; act: 1.0% Y/Y, prev: 2.1%).

Interactive chart on Augur Infinity

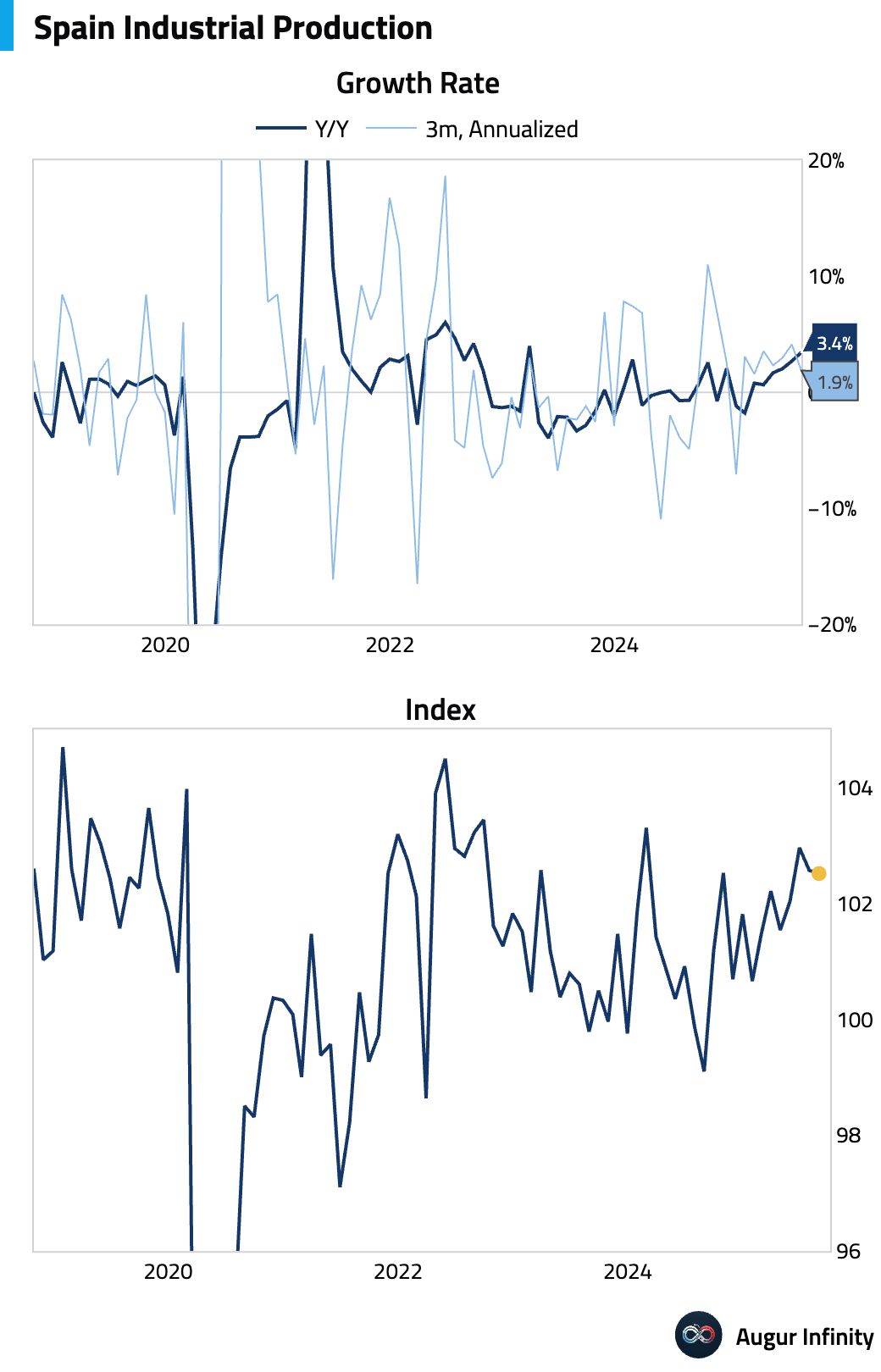

- Spanish industrial production growth accelerated in August to its fastest pace since March 2023 (act: 3.4% Y/Y, prev: 2.7%).

Interactive chart on Augur Infinity

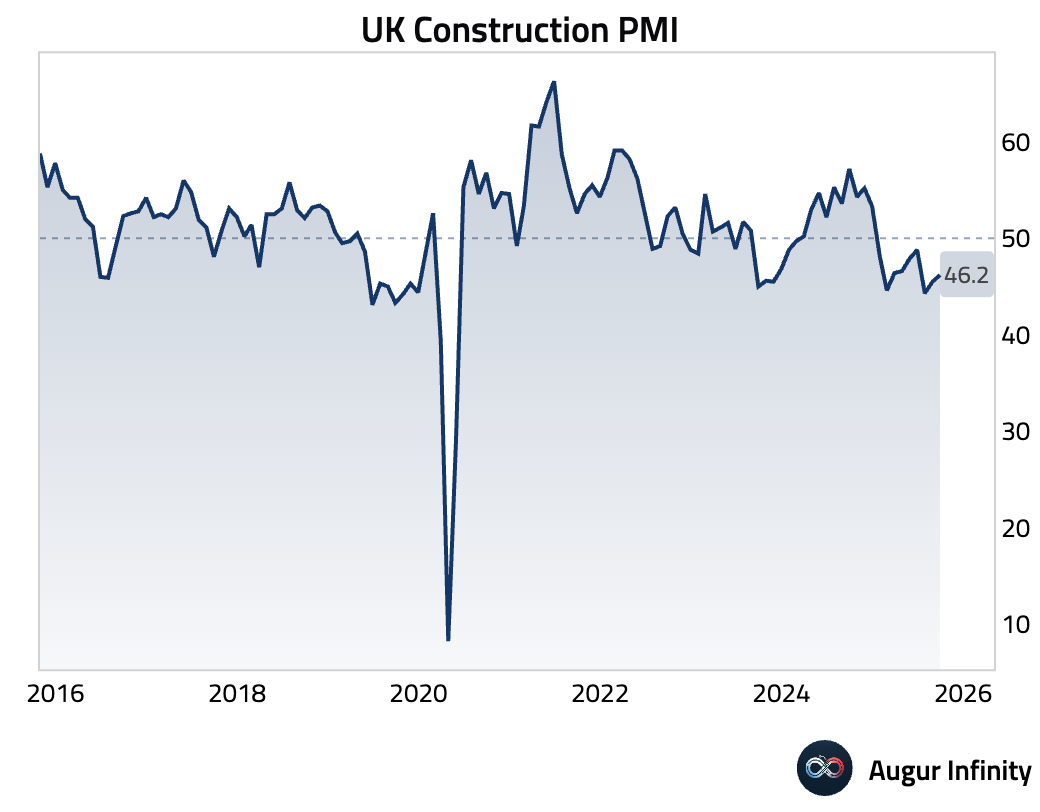

- The UK construction PMI rose in September but remained in contractionary territory for a fourth consecutive month (act: 46.2, prev: 45.5).

Source: S&P Global

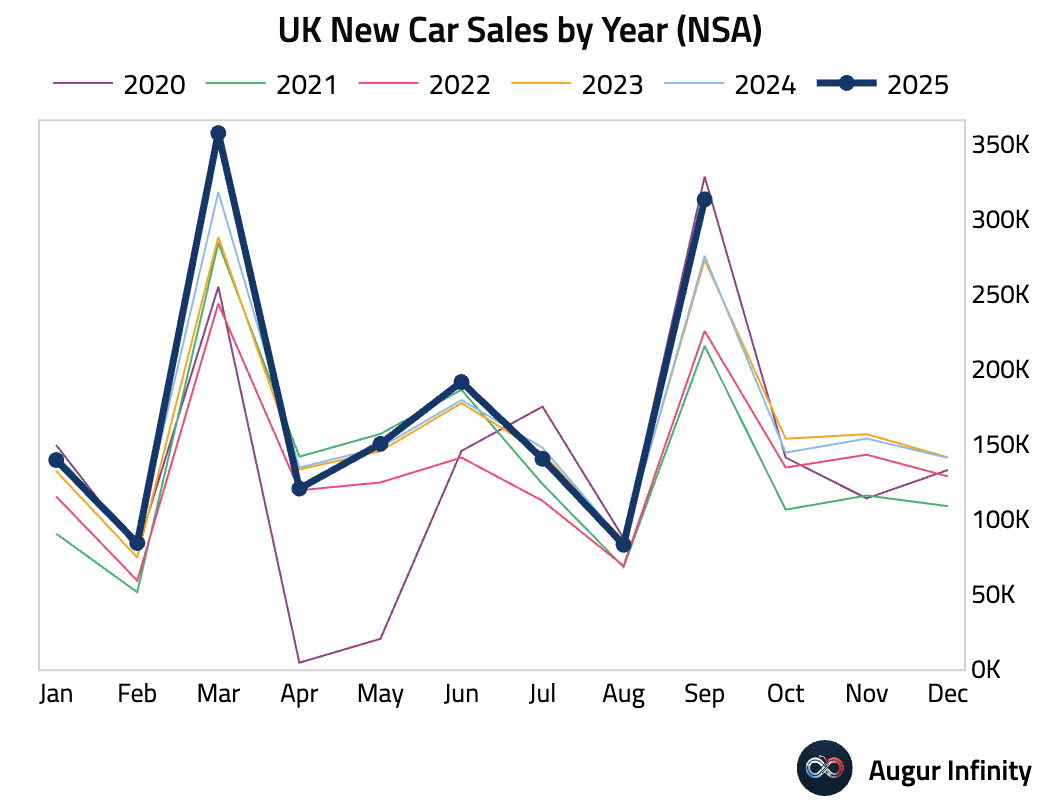

- UK new car sales rebounded sharply in September (act: 13.7% Y/Y, prev: -2.0%).

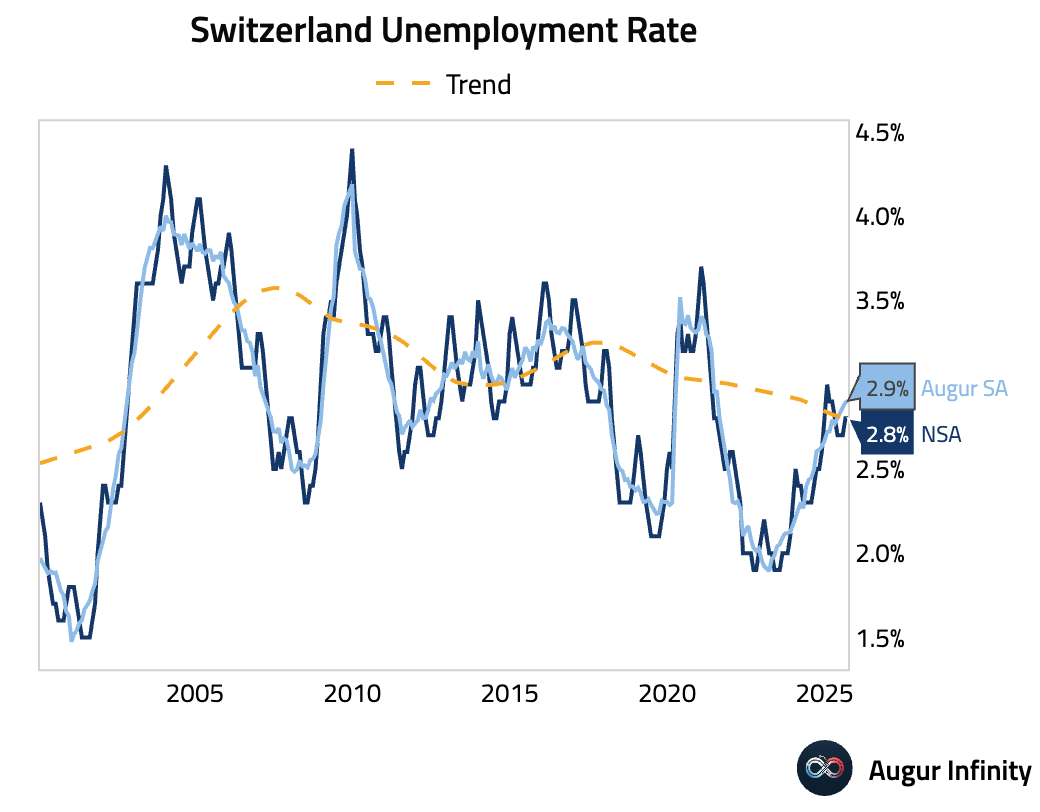

- Switzerland's unemployment rate held steady in September (act: 2.8%, prev: 2.8%).

Emerging Markets ex China

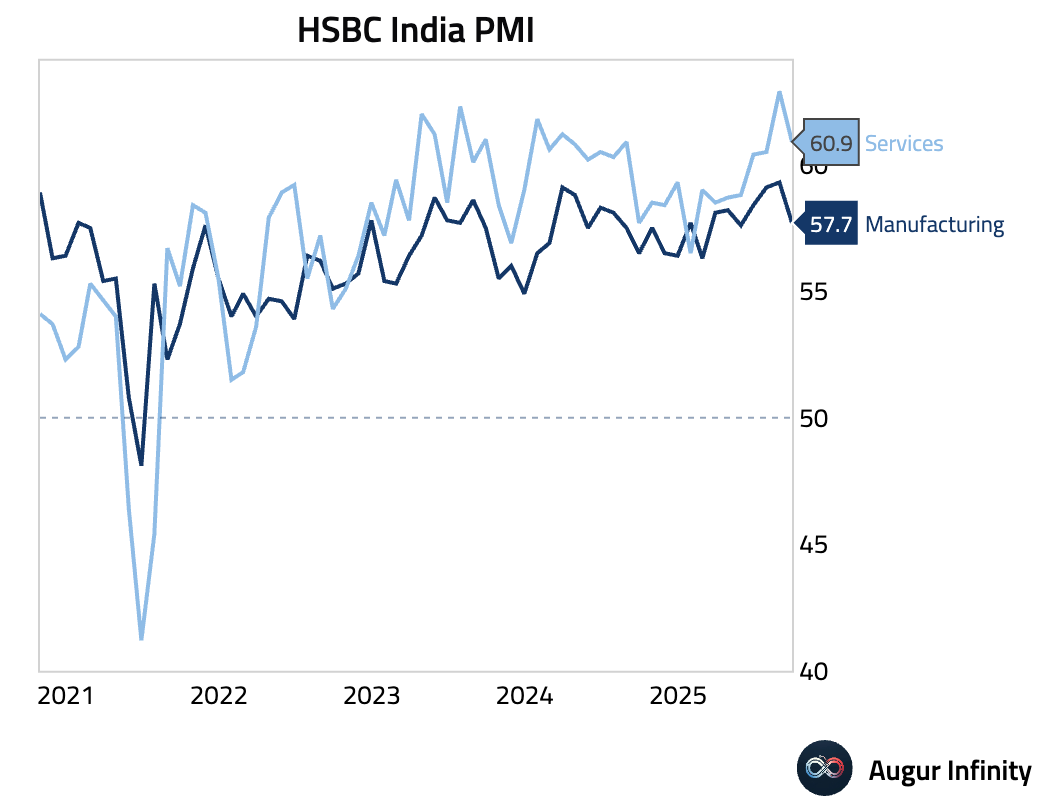

- India's Services PMI moderated to 60.9 in September from 62.9, remaining firmly in expansionary territory. The slowdown was driven by a sharp drop in new export orders to a six-month low, reflecting softer international demand. However, robust domestic demand continues to support overall activity. Price pressures also showed signs of easing, with both input and output price inflation cooling to six-month lows.

Source: S&P Global

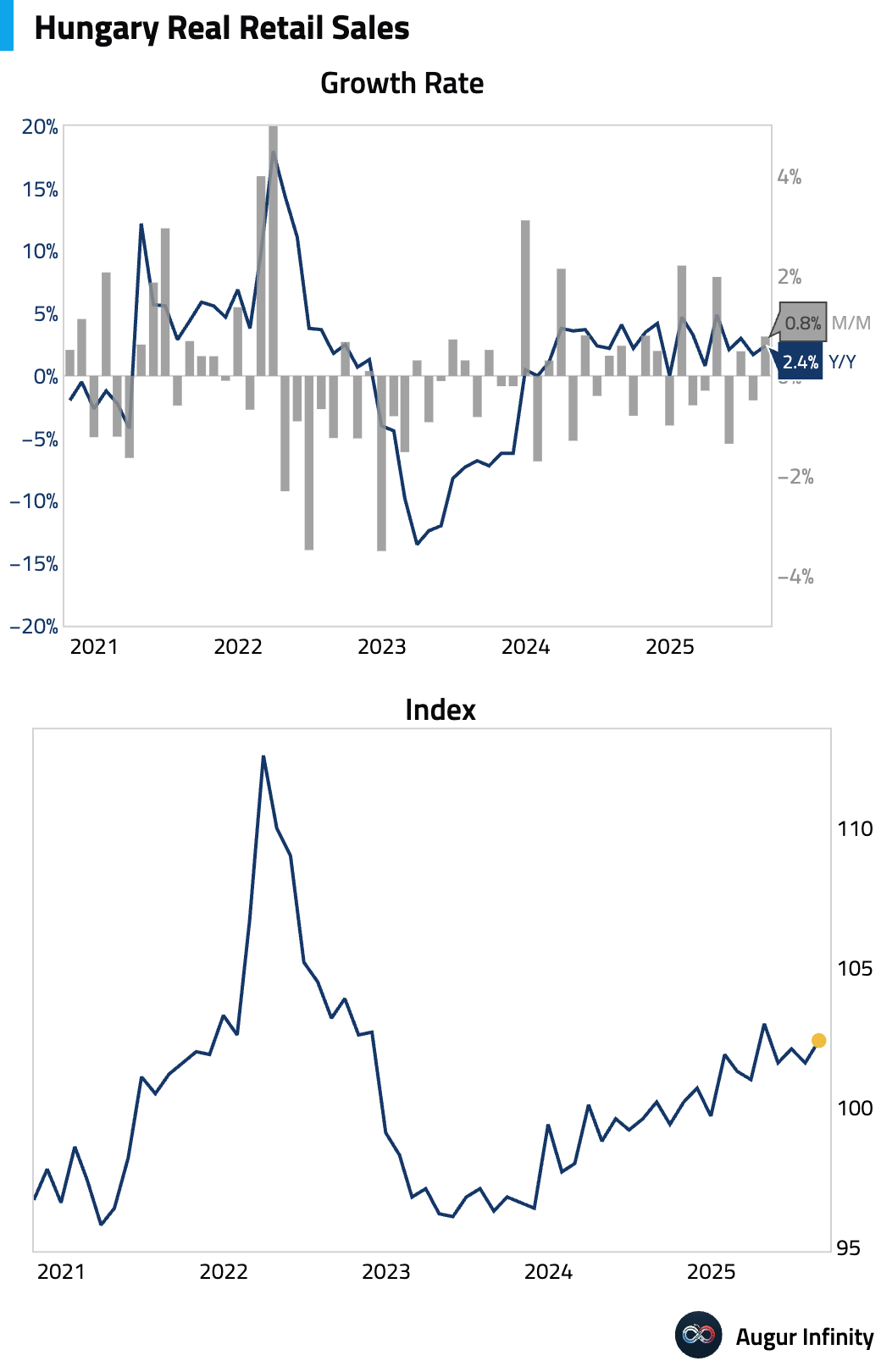

- Hungarian retail sales growth accelerated in August (act: 2.4% Y/Y, prev: 1.7%).

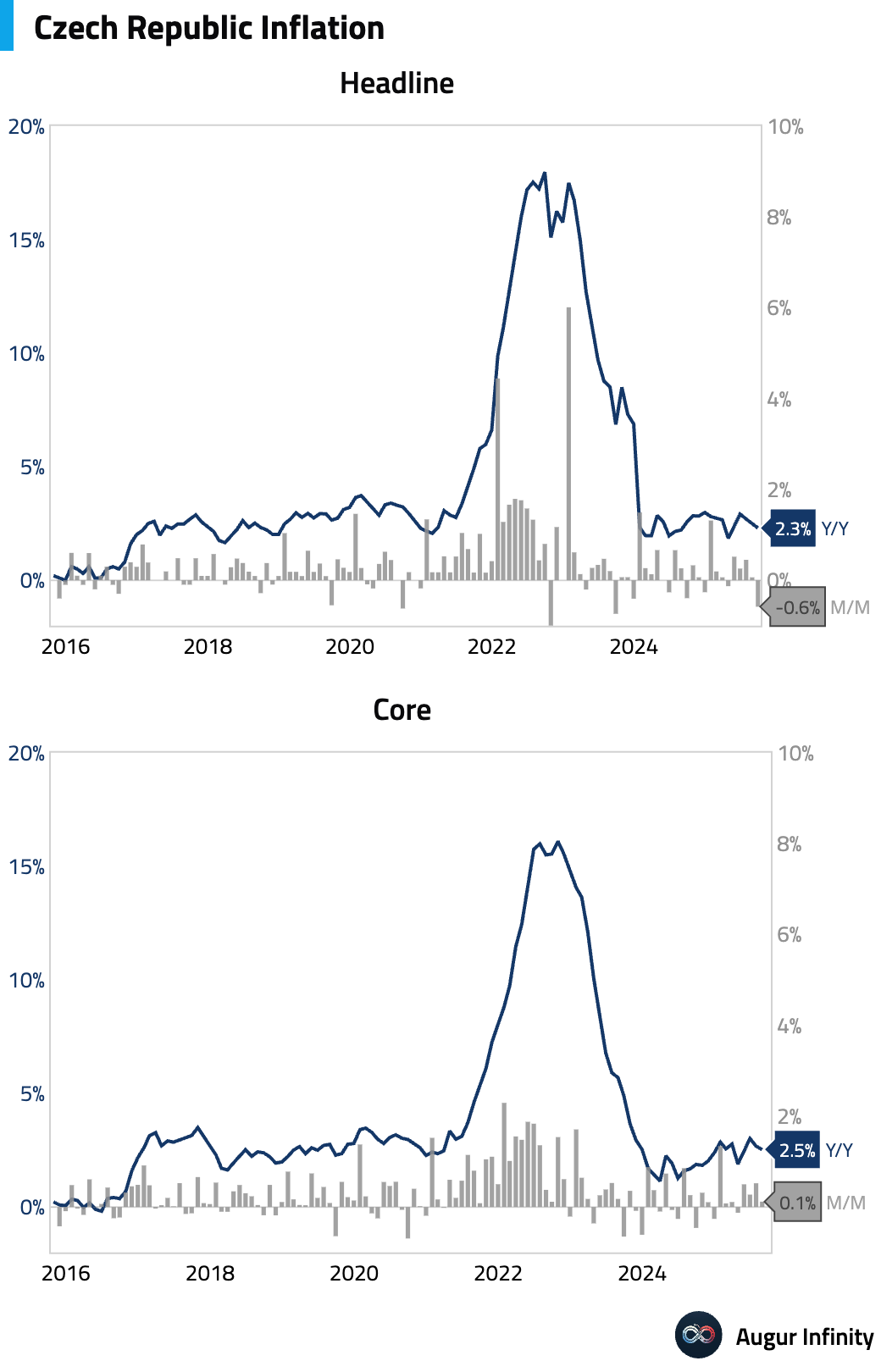

- The Czech Republic's preliminary inflation rate for September surprised to the downside, easing to 2.3% Y/Y from 2.5%, below the 2.6% consensus. Month-over-month, prices fell by 0.6%. The disinflation was primarily driven by a sharp fall in unprocessed food inflation, while core inflation was broadly unchanged. The soft print reduces the prospect of a near-term rate hike from the central bank.

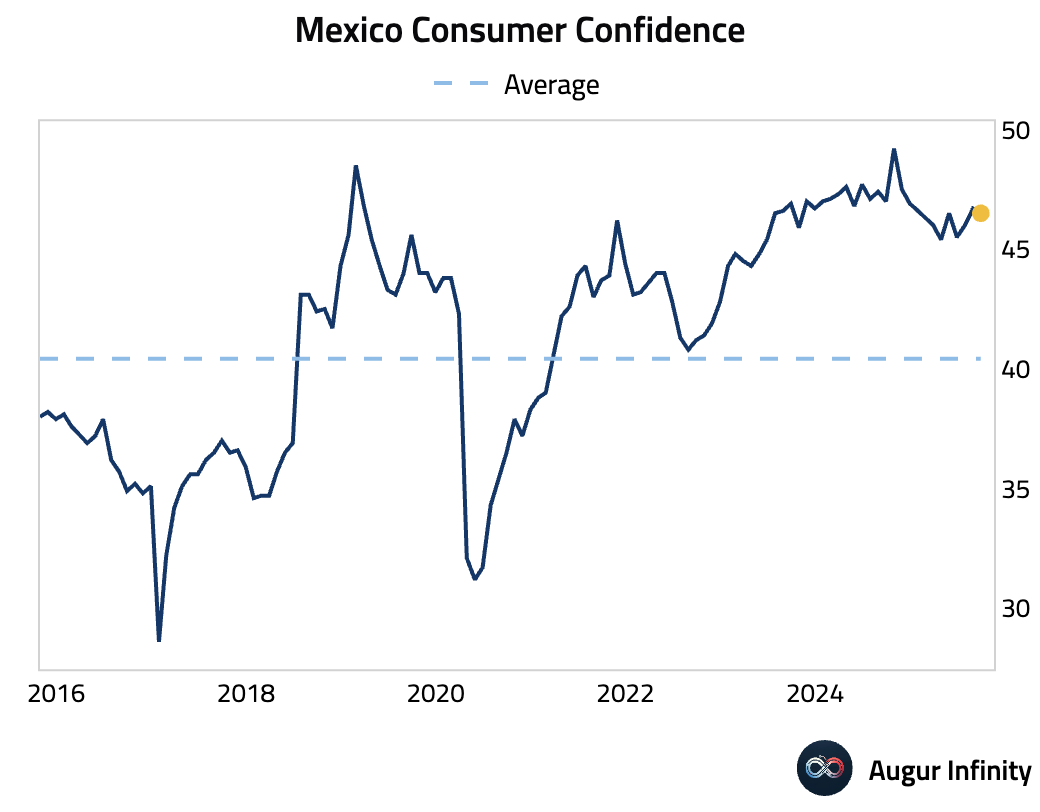

- Mexican consumer confidence fell for the eighth time in 11 months, declining slightly in September (act: 46.5, prev: 46.7). The drop was driven by weaker expectations for the broader economy and a sharp fall in consumers' capacity to purchase durable goods. Despite the recent downtrend, the index remains above its historical average.

Interactive chart on Augur Infinity

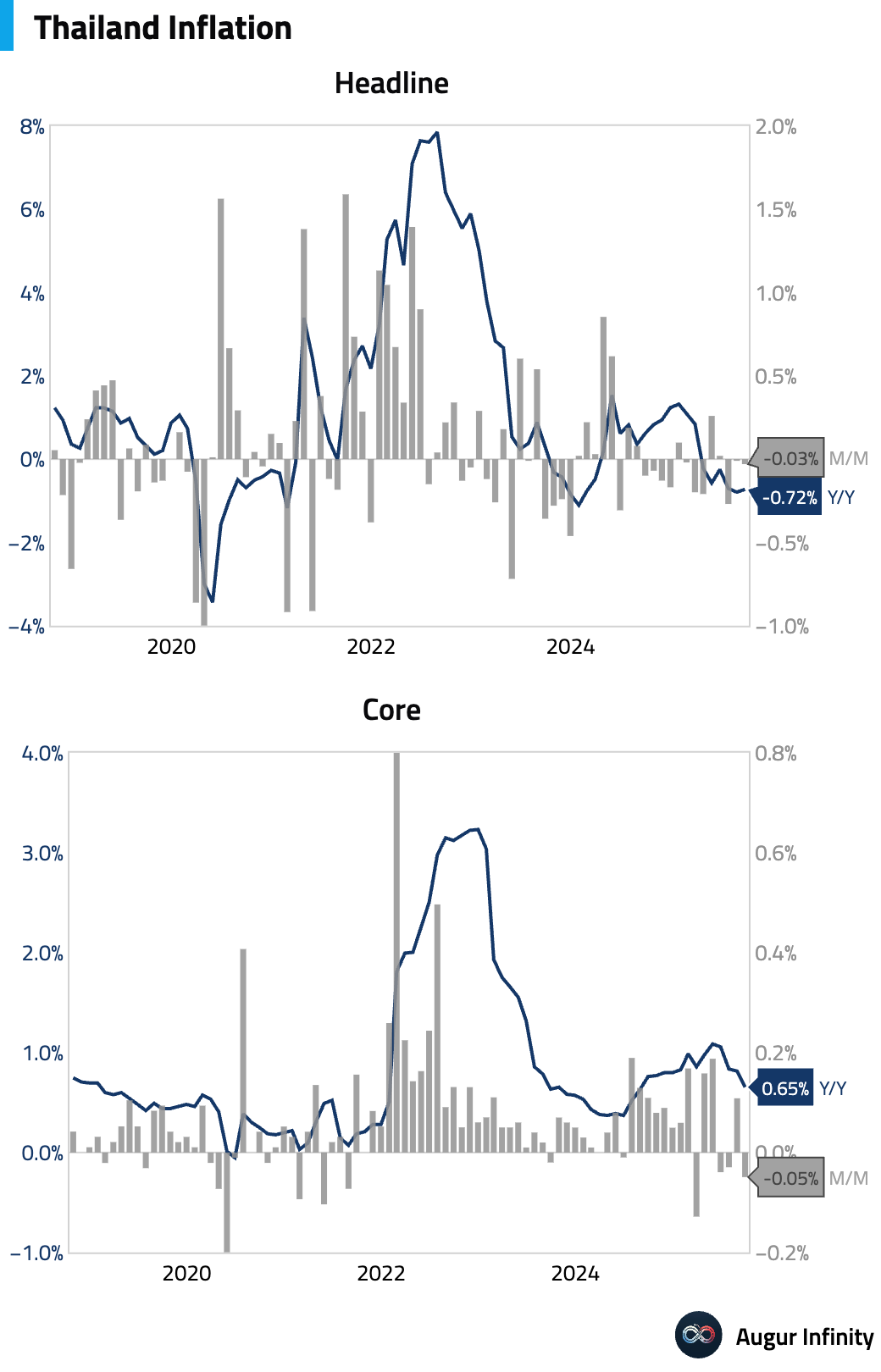

- Thailand’s headline deflation moderated to -0.72% Y/Y in September from -0.79% previously, driven by higher gasoline prices but missing consensus expectations of -0.6%. Core inflation slowed to 0.65% from 0.81%, a sign of muted underlying price pressures.

Interactive chart on Augur Infinity

Global Markets

Equities

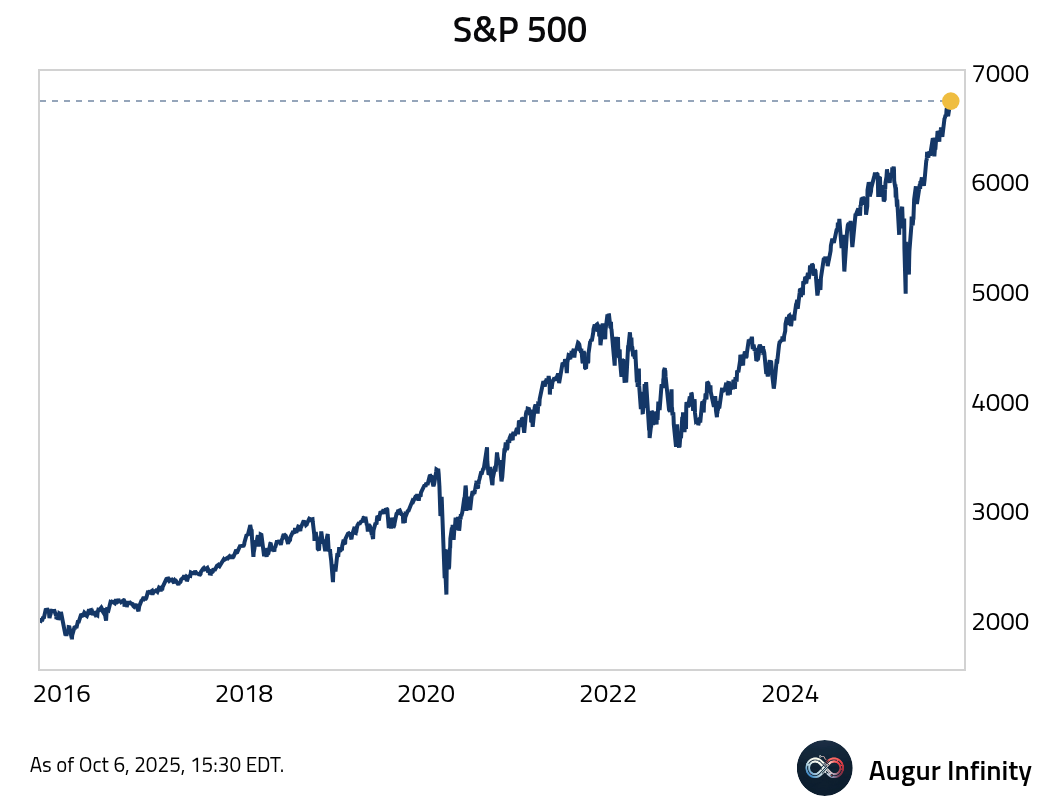

- S&P 500 continues to make new all-time highs.

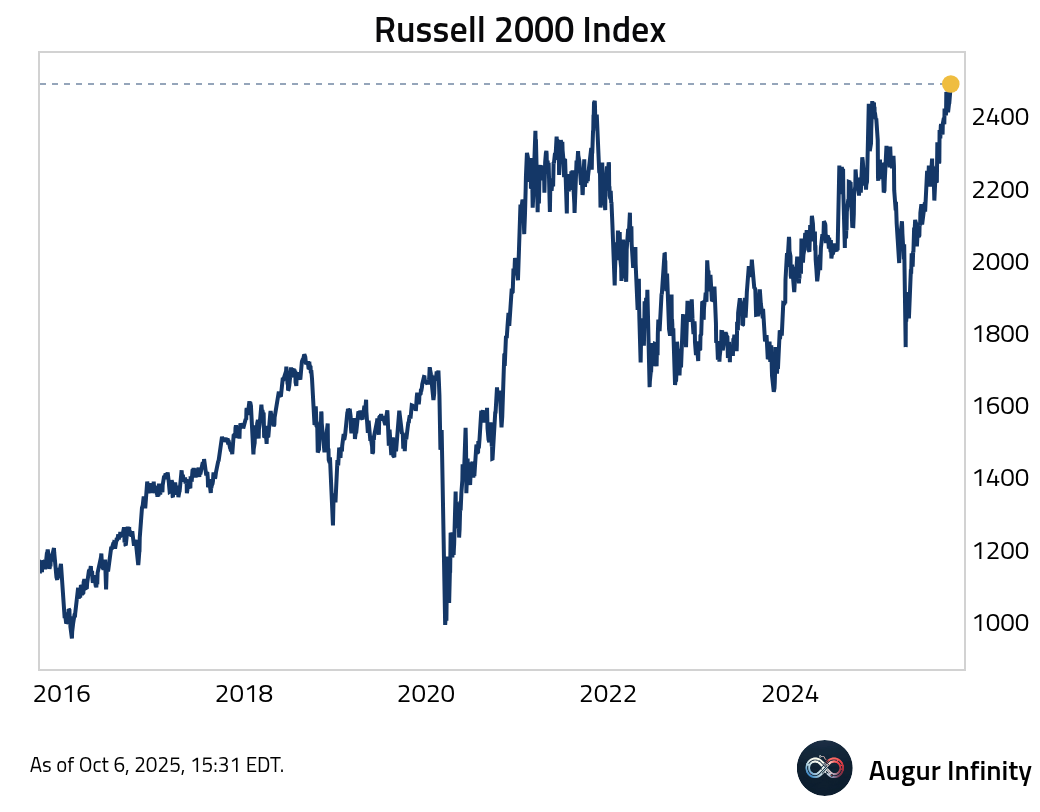

- Russell 2000 also gained, reaching the third all-time high of the year.

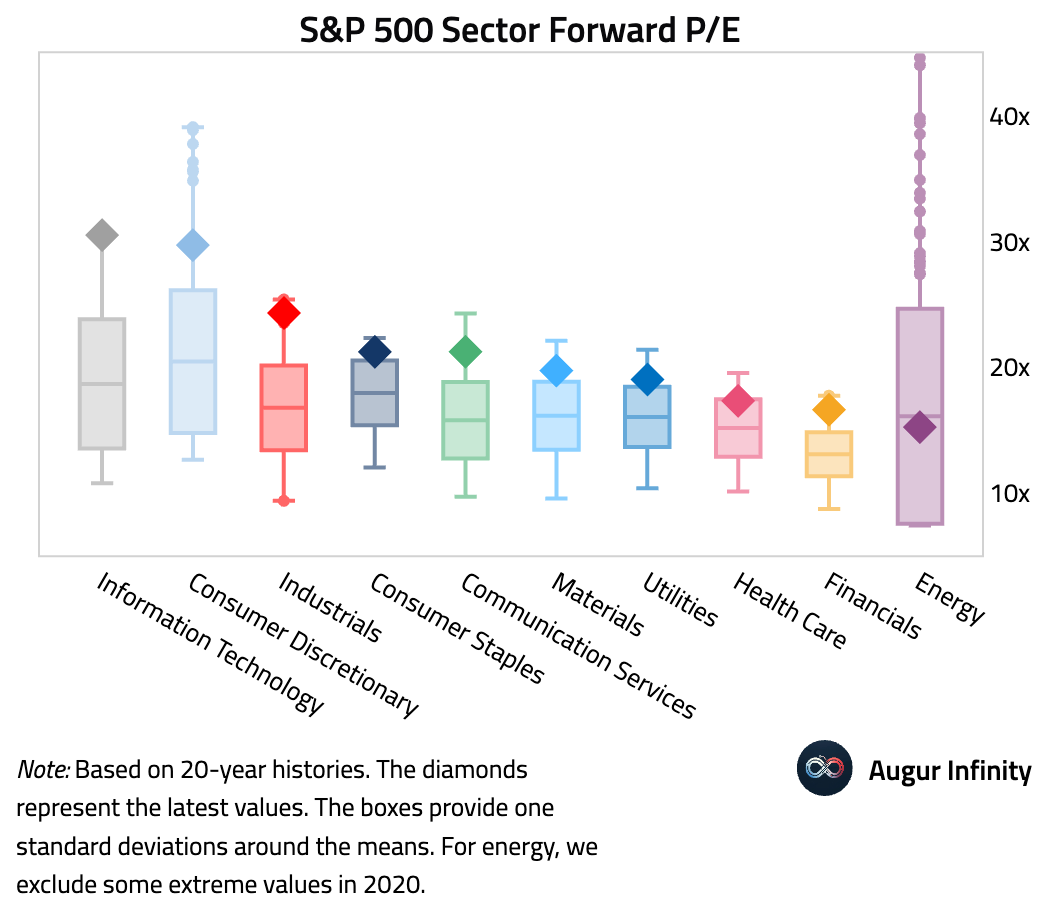

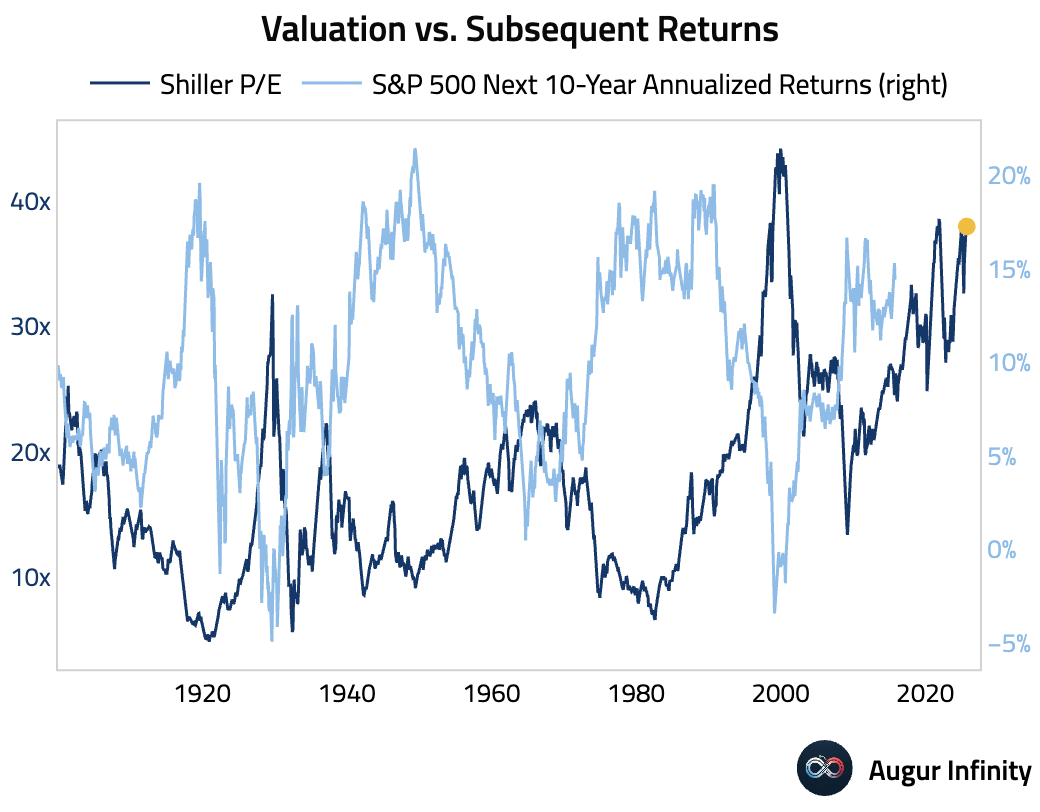

- Here's an overview of S&P 500 sector forward P/E, summarized over the past 20 years.

- A reminder that high starting valuation is correlated with low future returns.

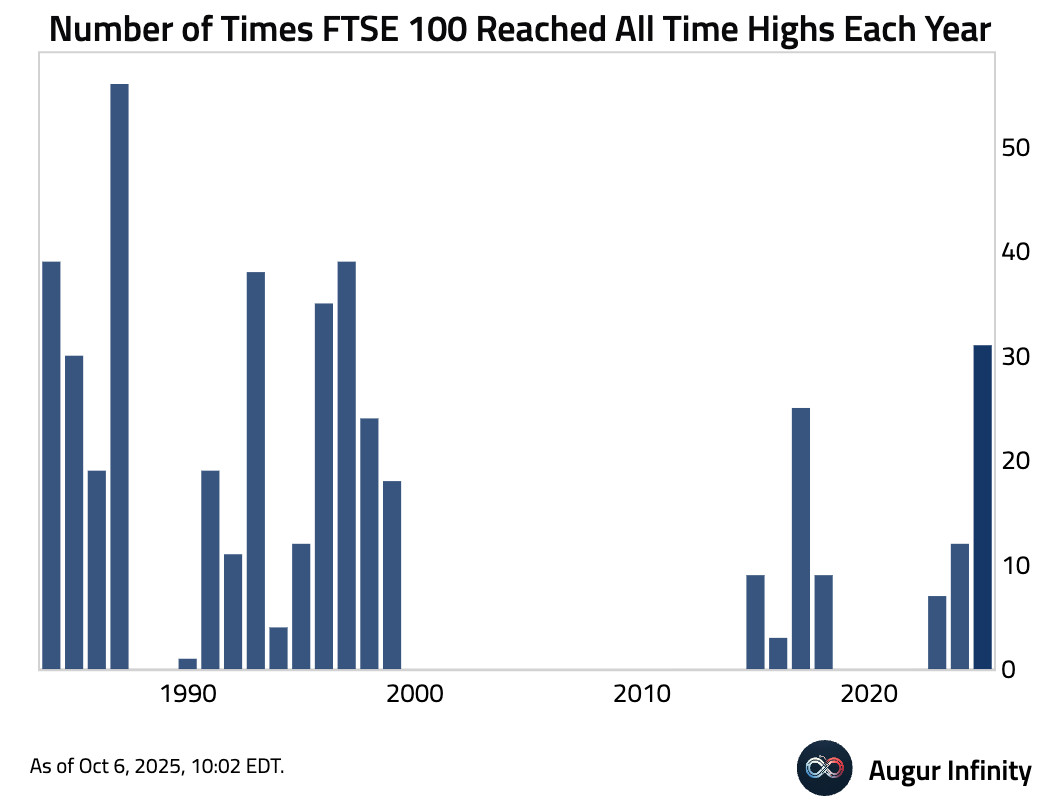

- Outside the US, the FTSE 100 Index has reached all-time highs 31 times this year …

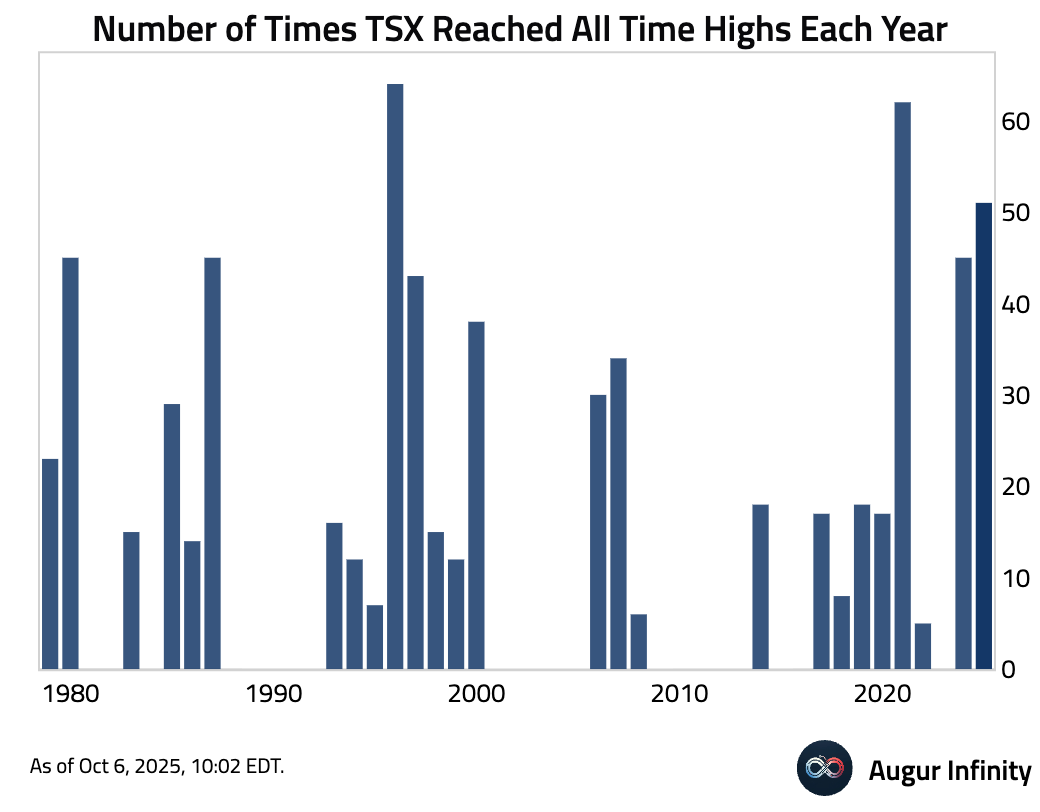

… while the S&P/TSX Composite climbed to its 51st all-time high of 2025.

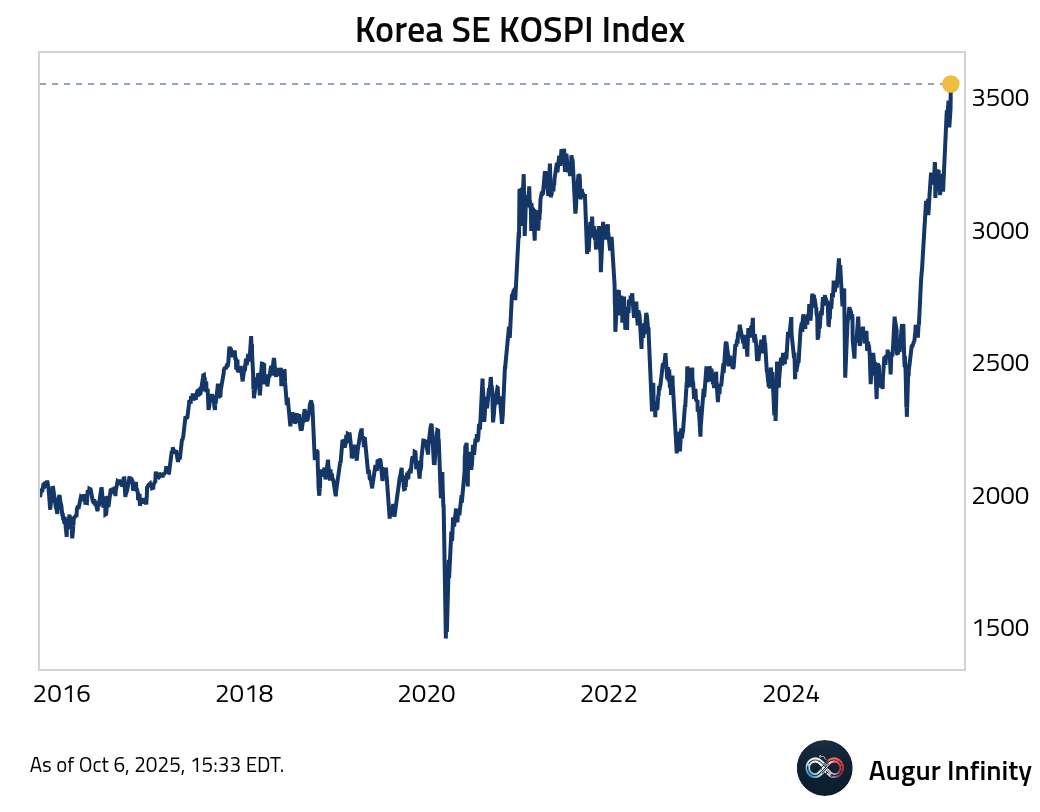

- Som emerging market equities are soaring as well. Here's Korea's KOSPI Index …

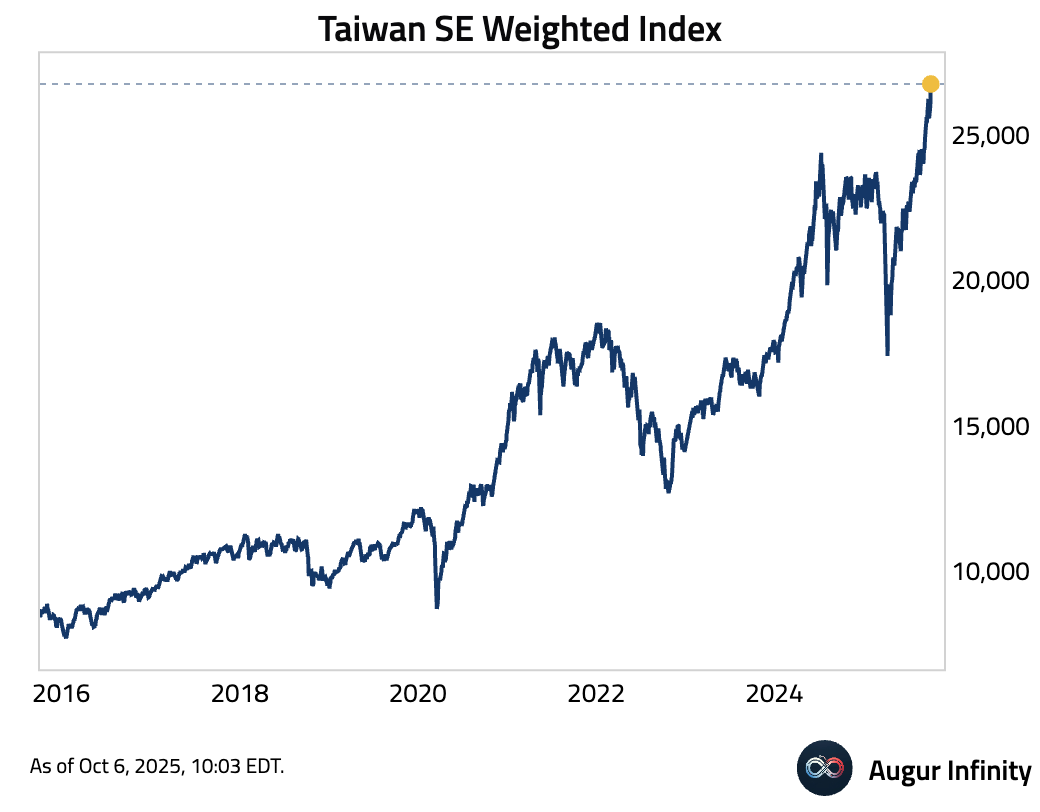

… and Taiwan's Cap-Weighted Index.

Fixed Income

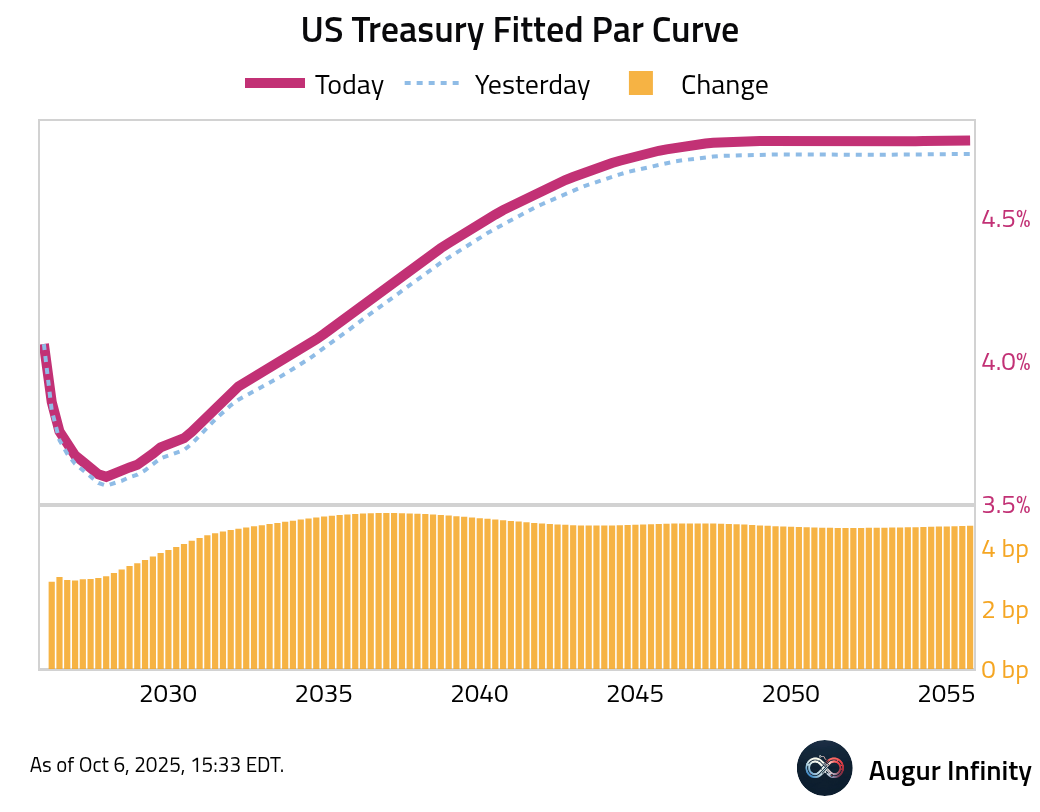

- US Treasury yields shifted higher across the curve. The 2-year yield rose 2.8 bps, marking its third consecutive daily increase, while the 10-year yield climbed 4.8 bps.

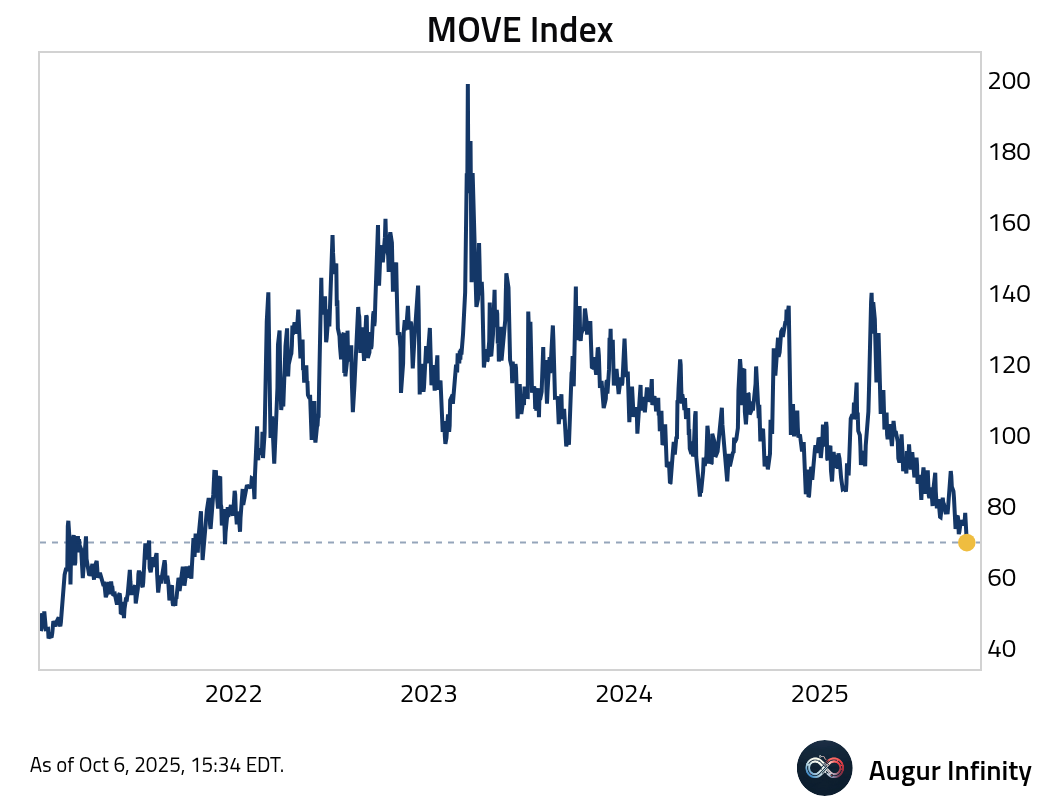

- The MOVE Index has declined to the lowest level since December 2021.

FX

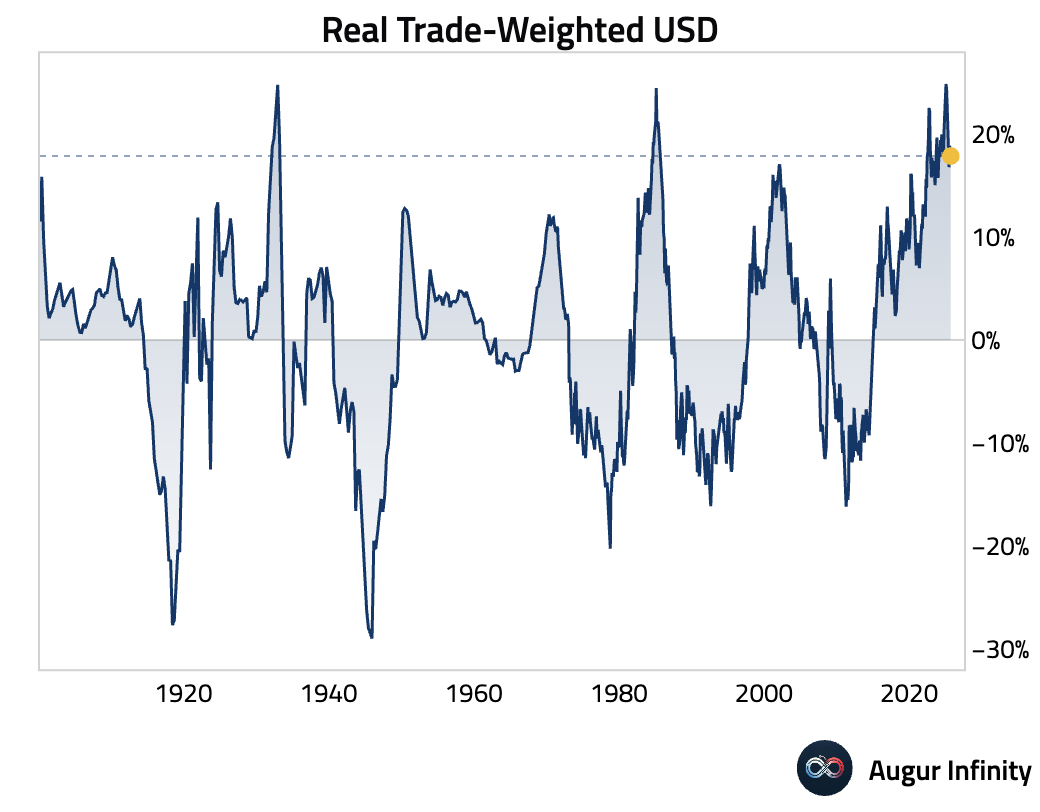

- Our trade-weighted real dollar index is down 7.6pp since the peak, but remains well above long-term average levels.

- FX implied volatility has declined meaningfully.

Commodities

- Gold continues to surge.

- The chart below shows the stunning decoupling between gold and real yield.

Interactive chart on Augur Infinity

- Sugar moved above its 50-day moving average.

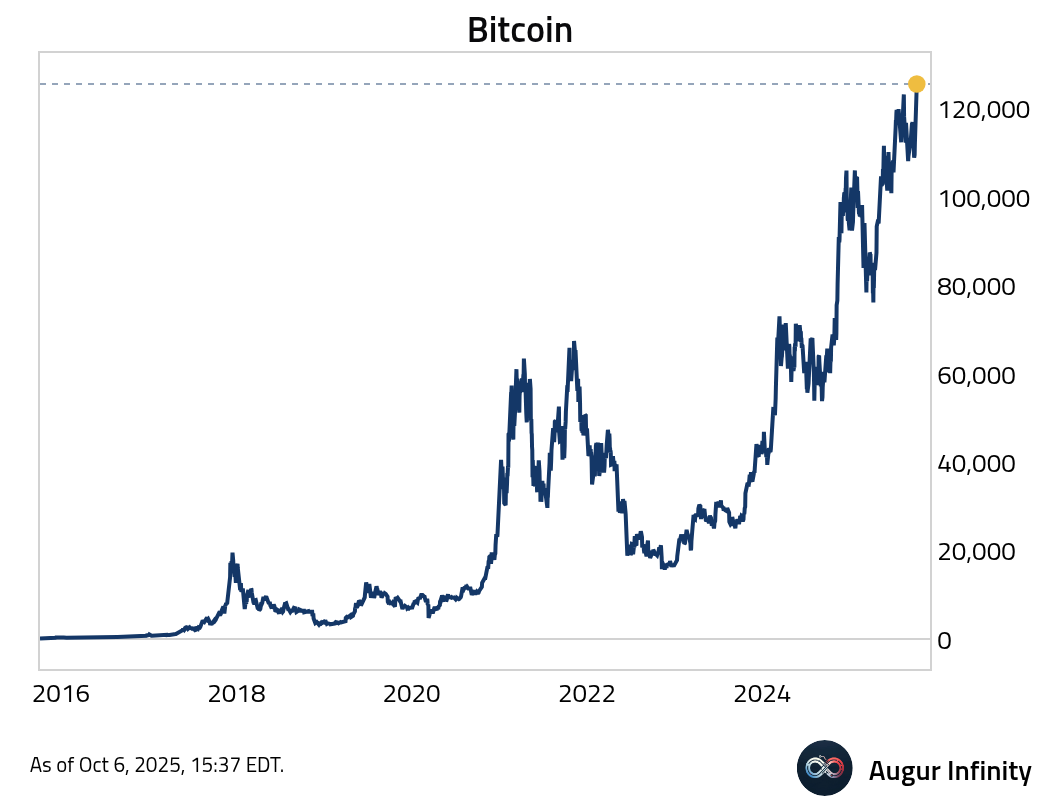

Crypto

- Bitcoin has reached a new all-time high.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.