Global Economics

United States

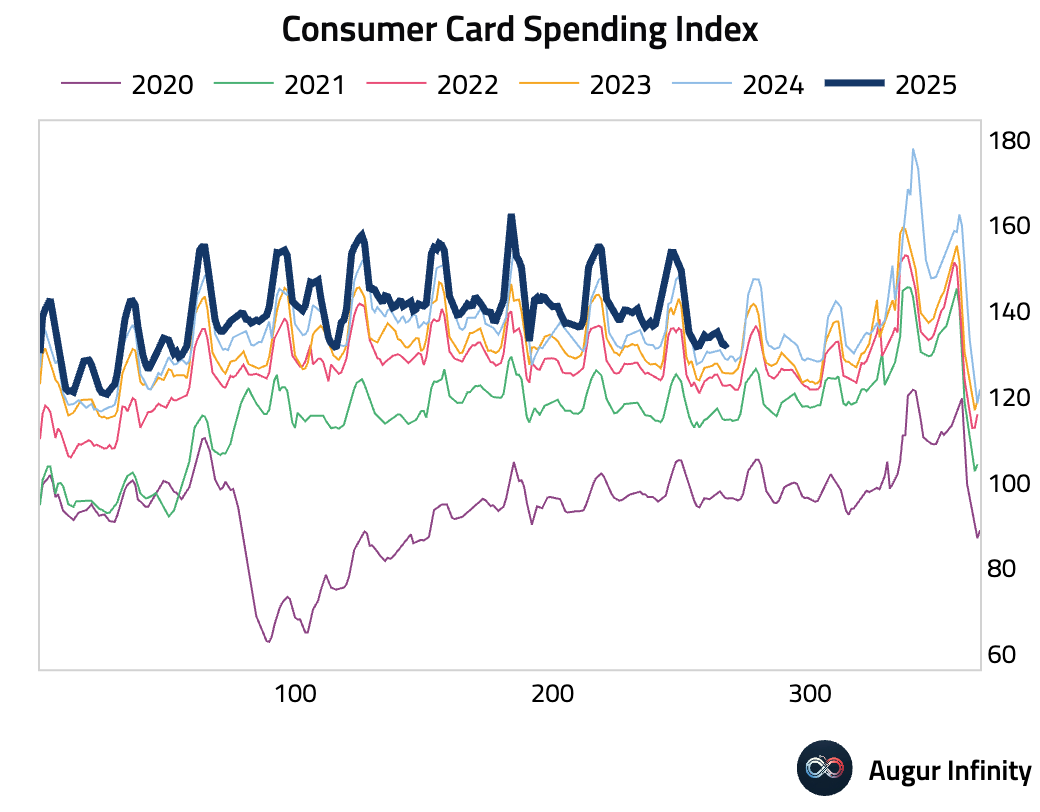

- Consumer spending, based on credit card data, is running about 2% higher than the same period last year.

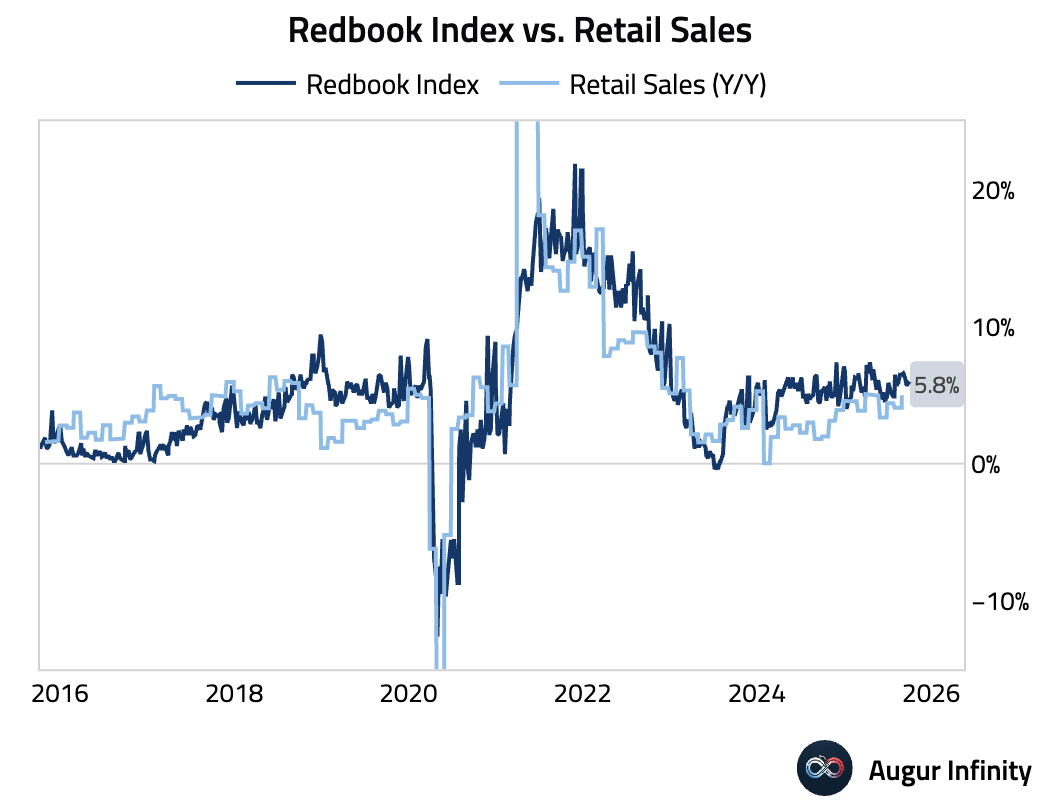

- The Redbook Index eased to 5.8% for the week ending October 4.

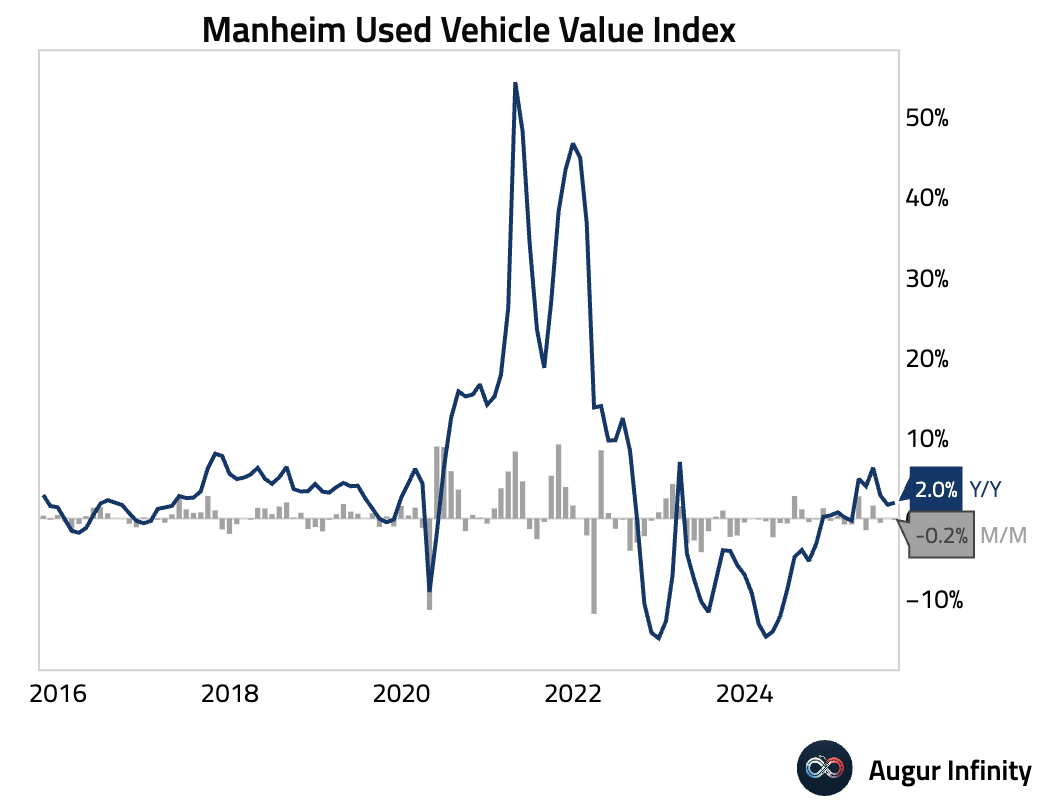

- The Manheim Used Vehicle Value Index fell 0.2% M/M but remains up 2.0% Y/Y. The monthly dip was driven by seasonal adjustments; non-adjusted prices actually rose 0.1%, beating the historical trend for September.

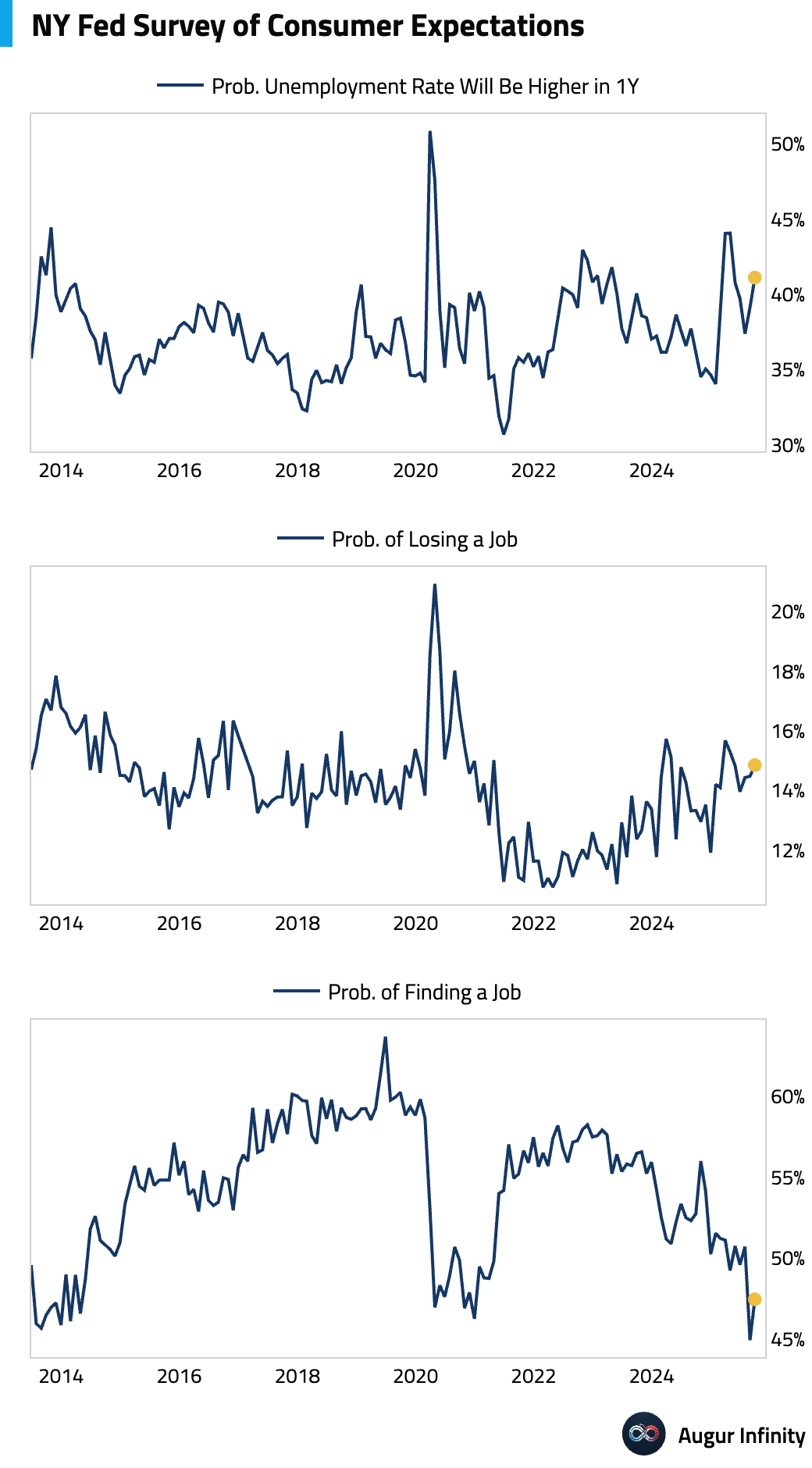

- Labor market expectations weakened in September. The perceived probability that unemployment will be higher one year from now rose, while the chance of losing one’s job increased slightly. The probability of finding a job if displaced rebounded, but remains well below its recent average.

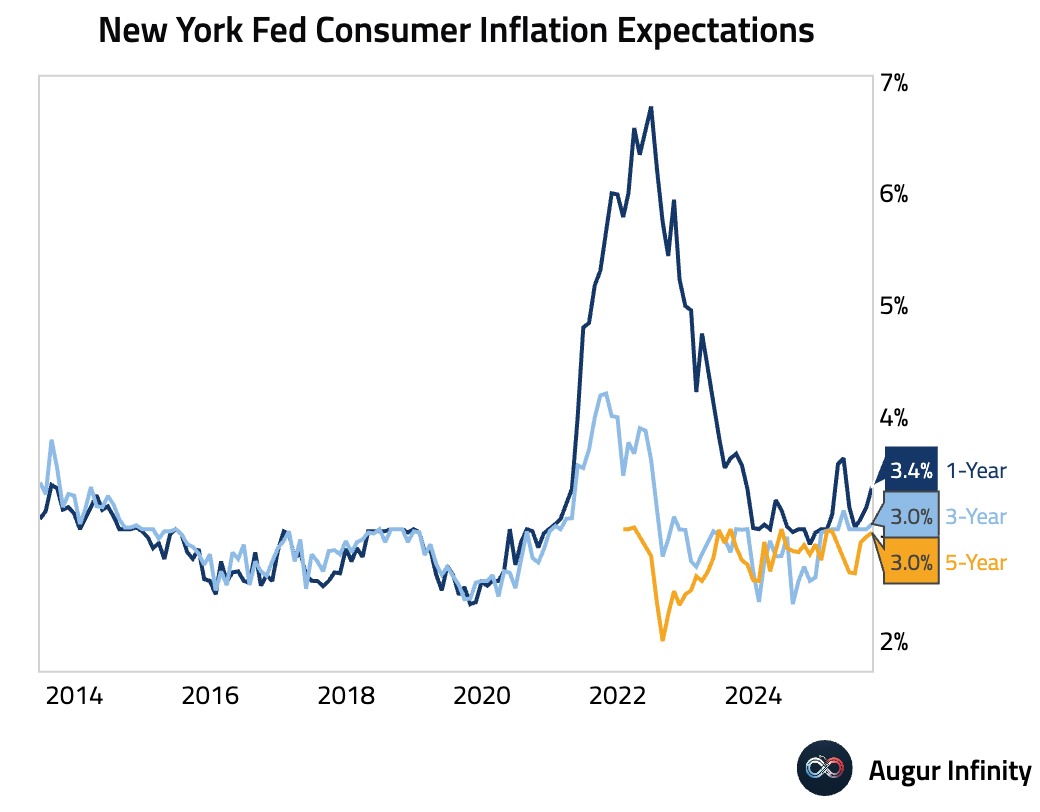

- Consumer inflation expectations in September increased at the 1-year and 5-year horizons, but remained steady at the 3-year horizon.

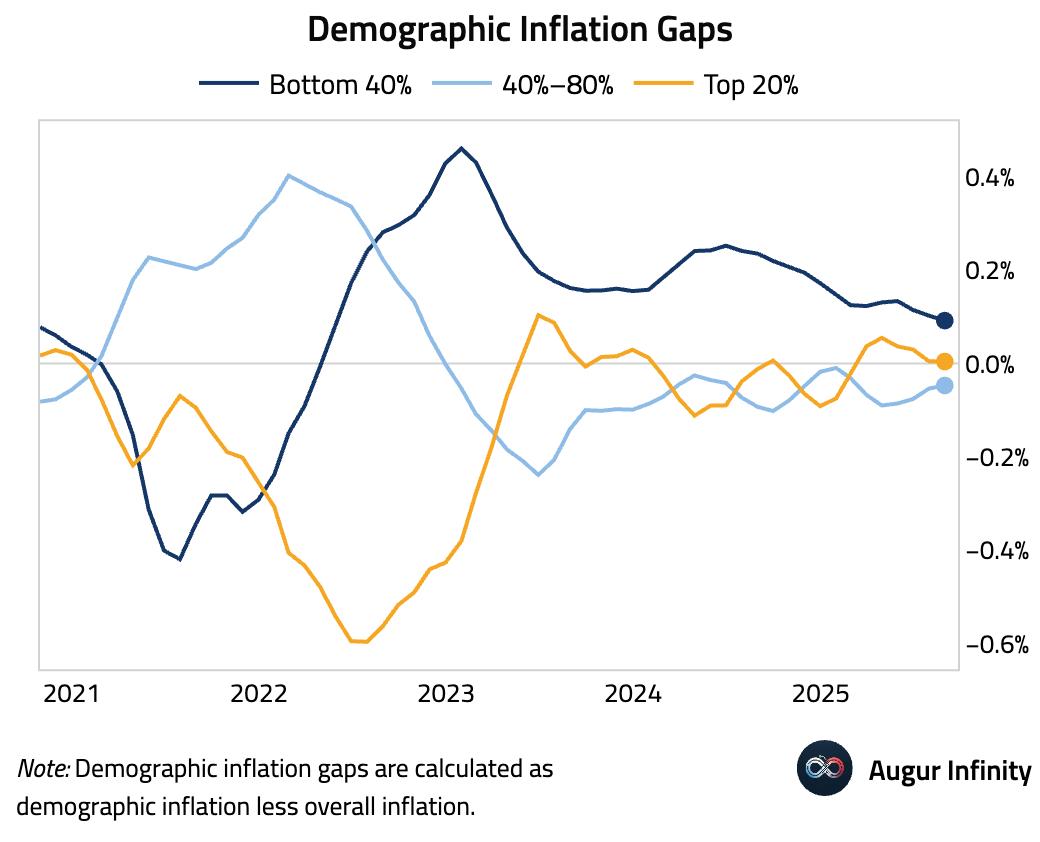

- The bottom 40% by income has experienced higher inflation than the national average.

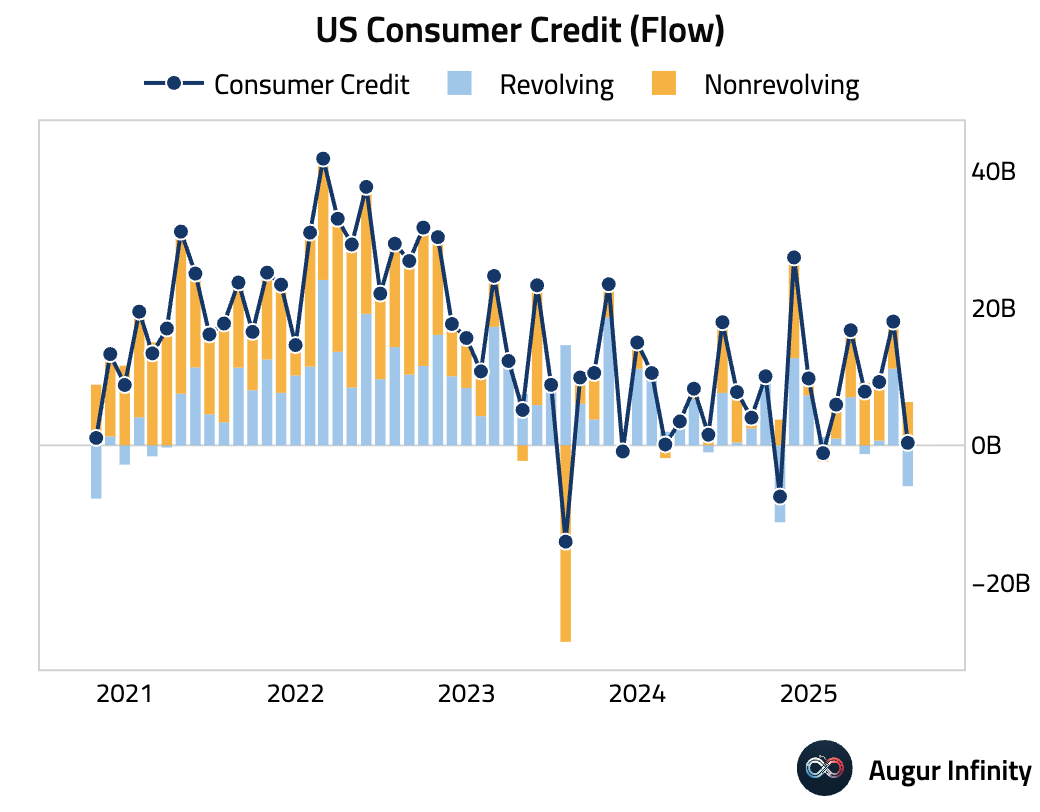

- US consumer credit rose by just $0.36B in August, well below consensus of $13.5B.

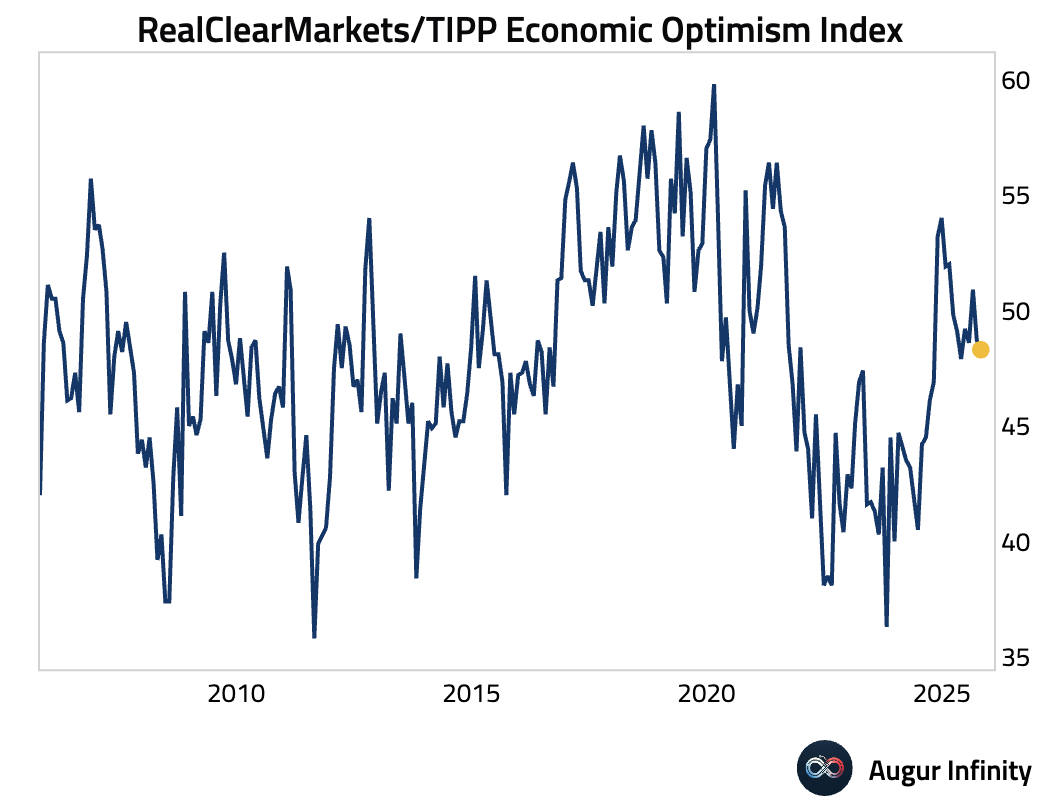

- The RCM/TIPP Economic Optimism Index declined in October.

Canada

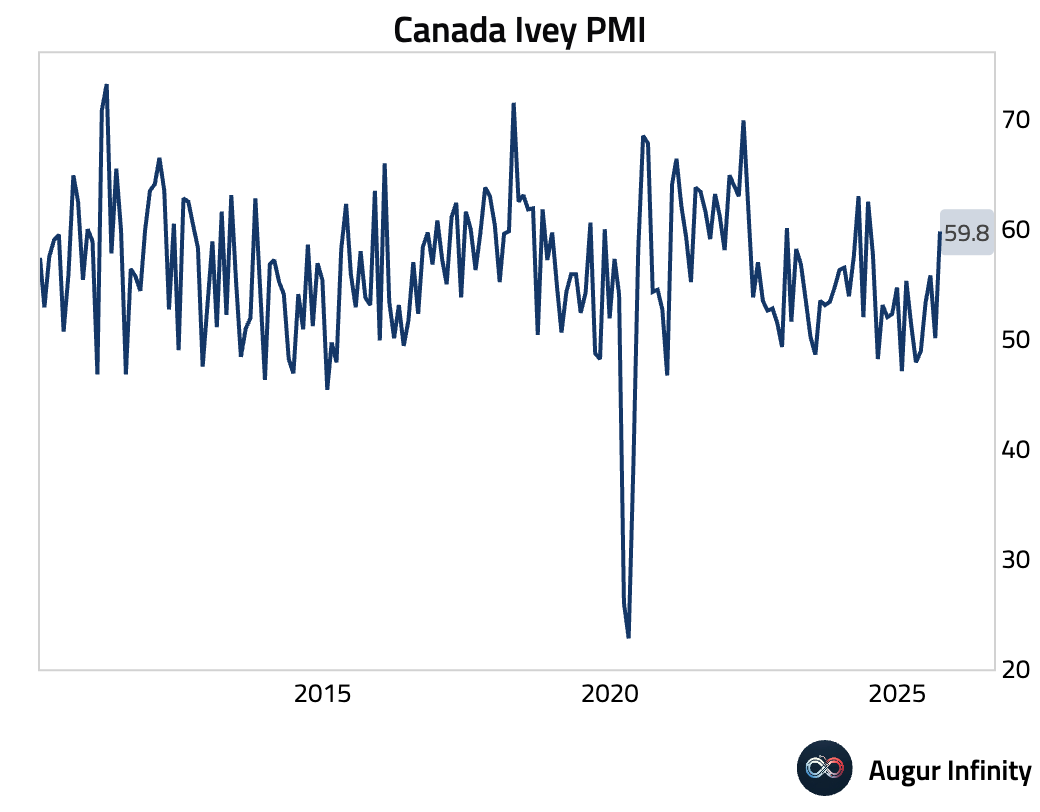

- Ivey PMI for September jumped to 59.8, significantly above the 51.2 consensus. This marks the strongest reading since June 2024.

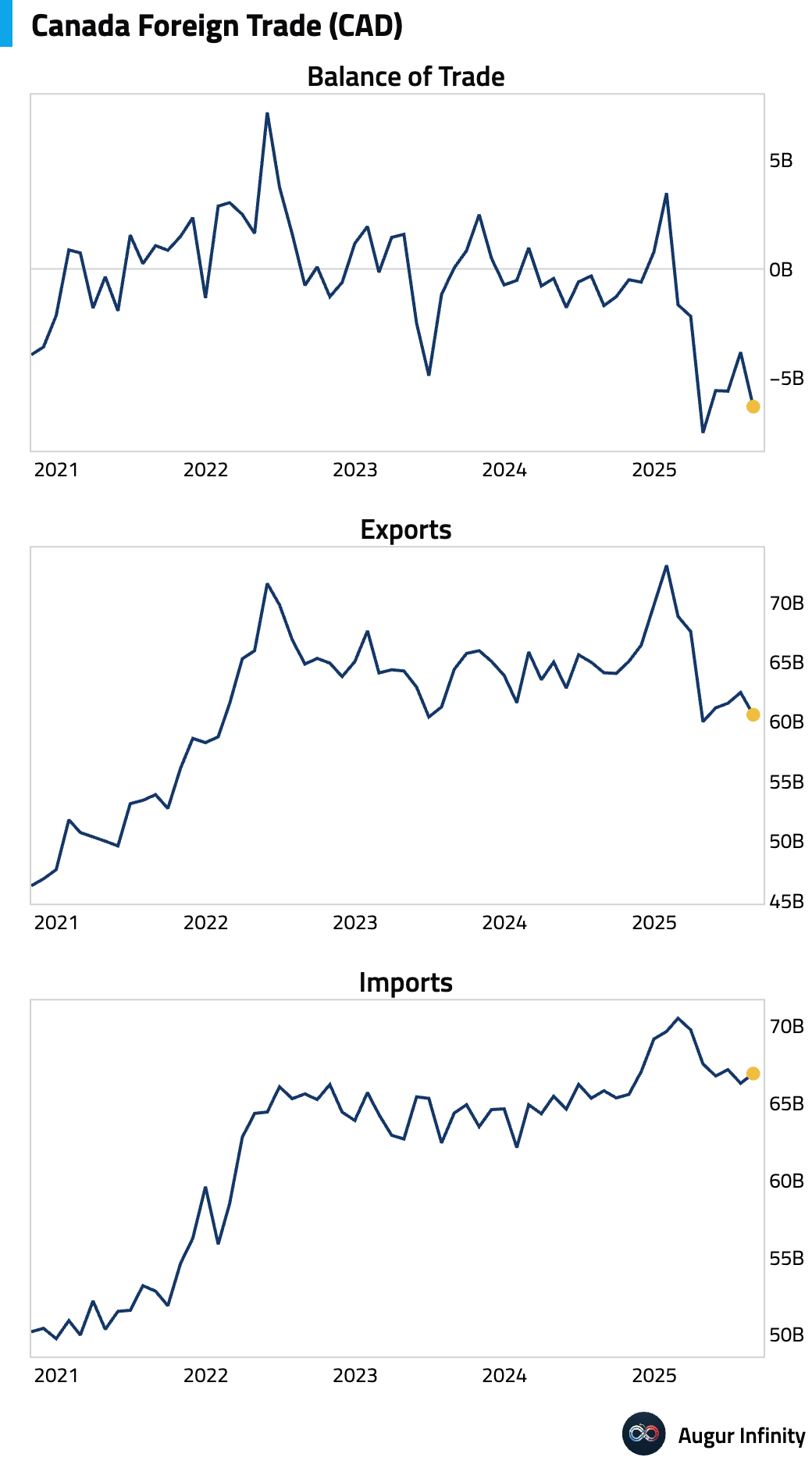

- Canada's trade deficit widened more than expected in August, driven by a drop in exports while imports saw a slight increase.

Europe

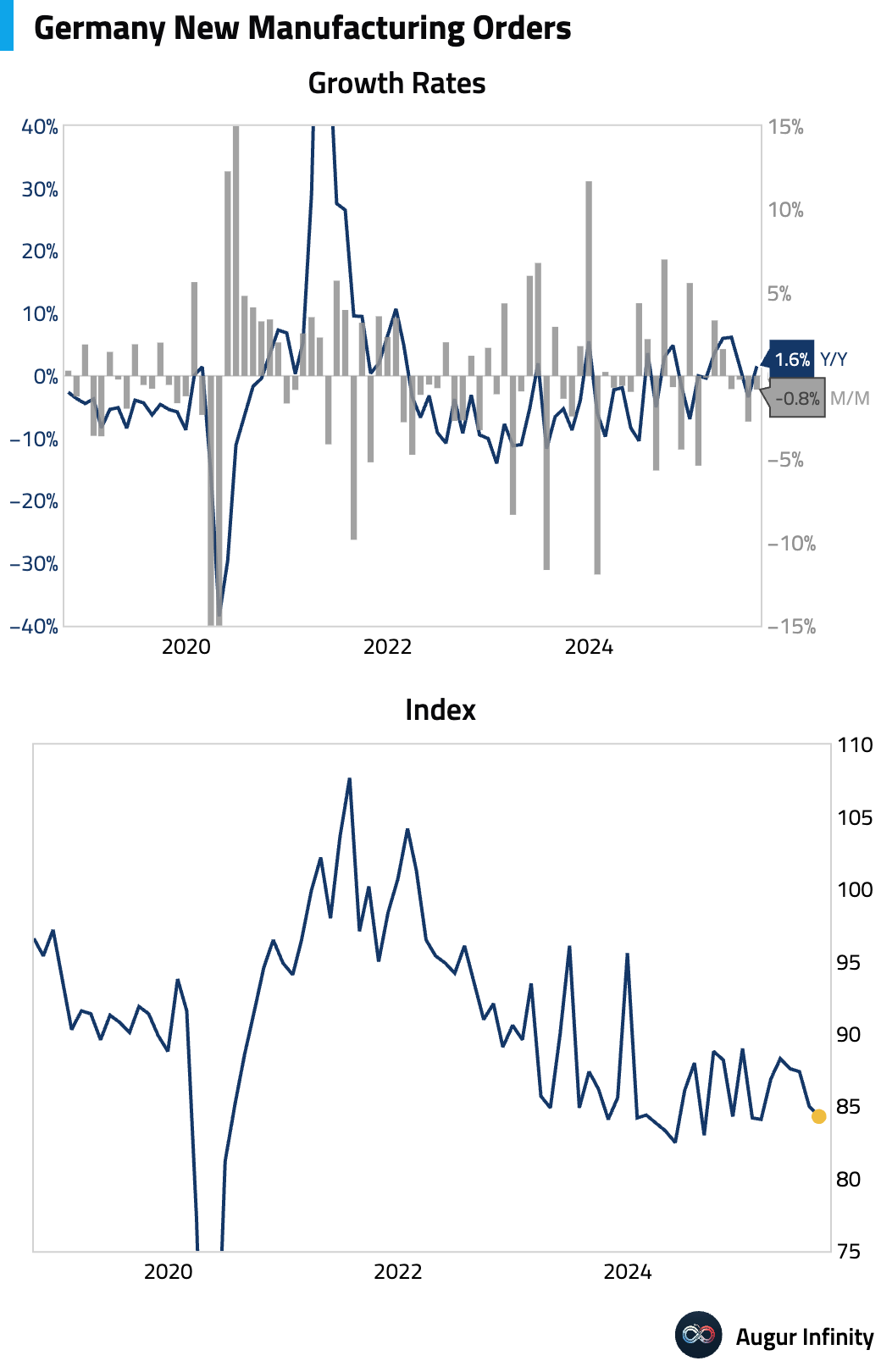

- German factory orders unexpectedly declined in August, falling 0.8% M/M against expectations for a 1.4% rise, suggesting persistent weakness in the industrial sector.

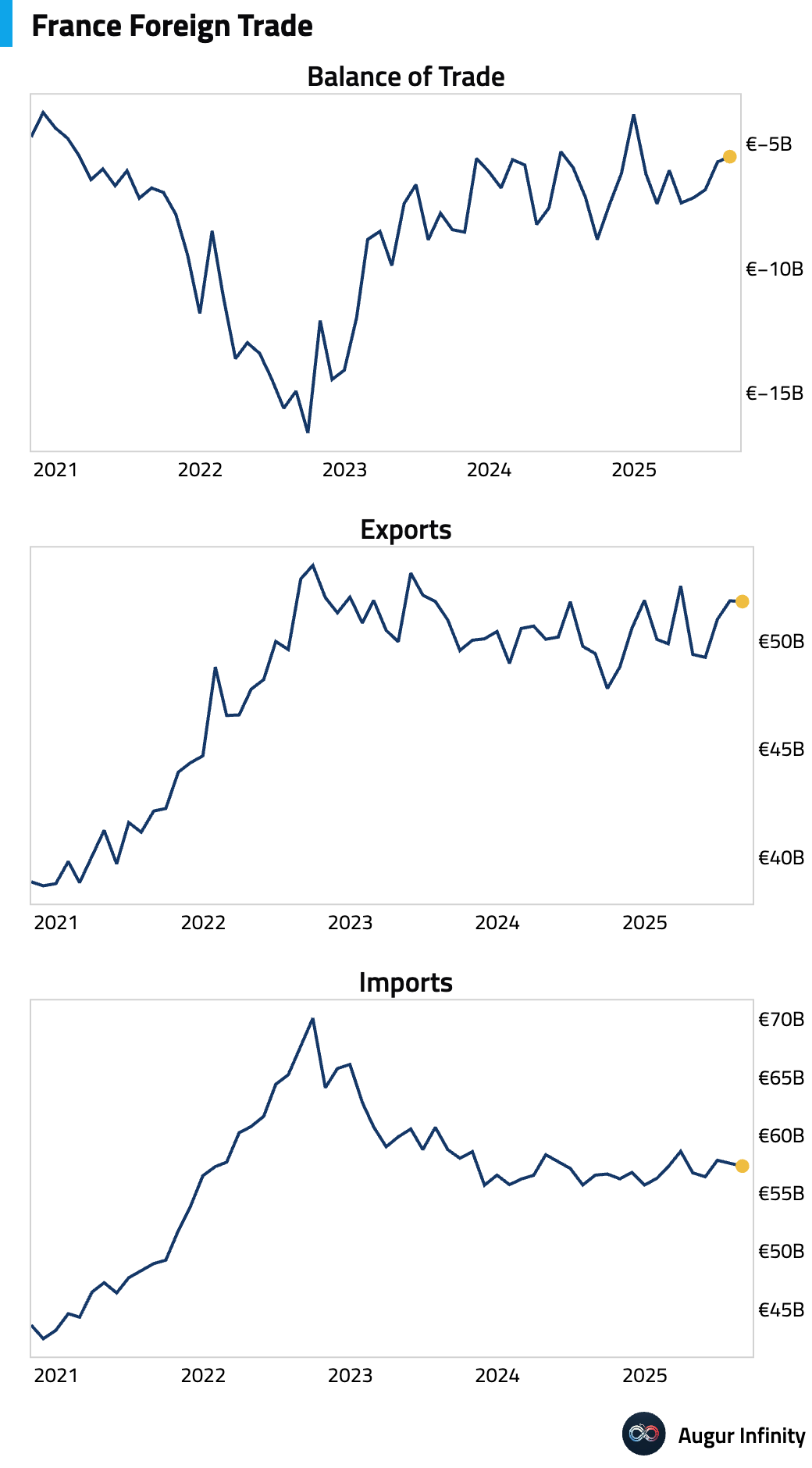

- France's trade deficit narrowed slightly in August as imports fell more than exports. The deficit was €5.5 billion, a modest improvement from the previous month's €5.7 billion and better than the consensus of €5.2 billion.

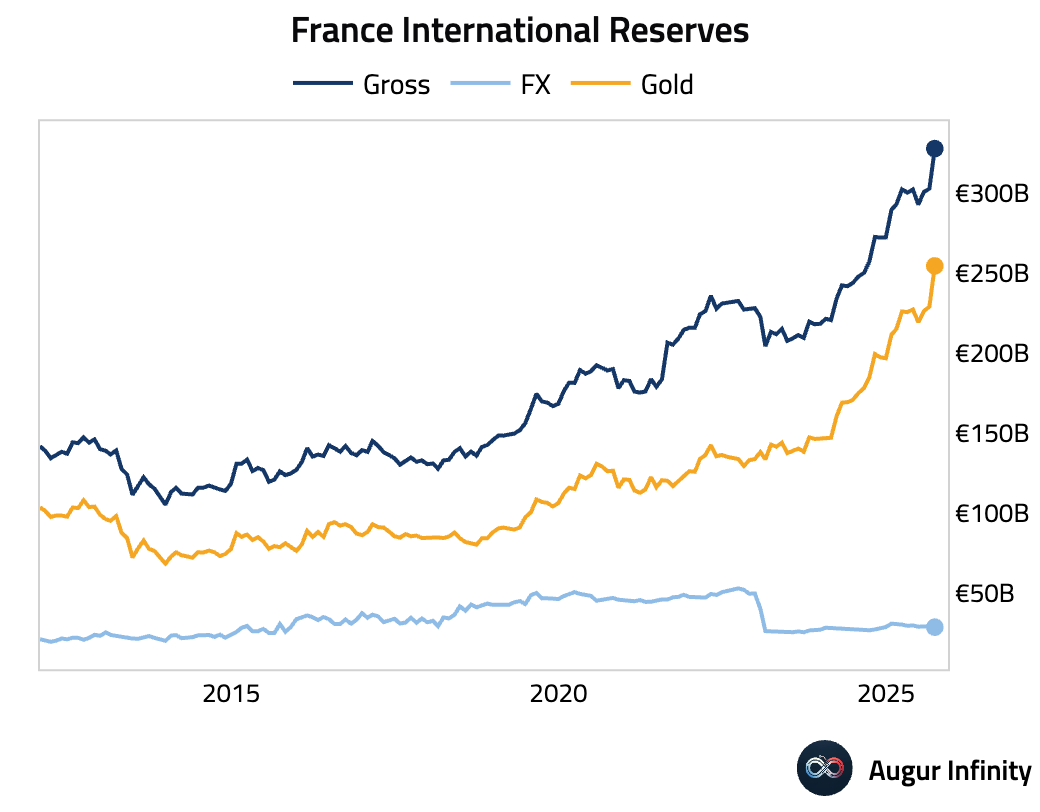

- France's official reserve assets increased to a new all-time high in September (act: €330.27B, prev: €304.80B).

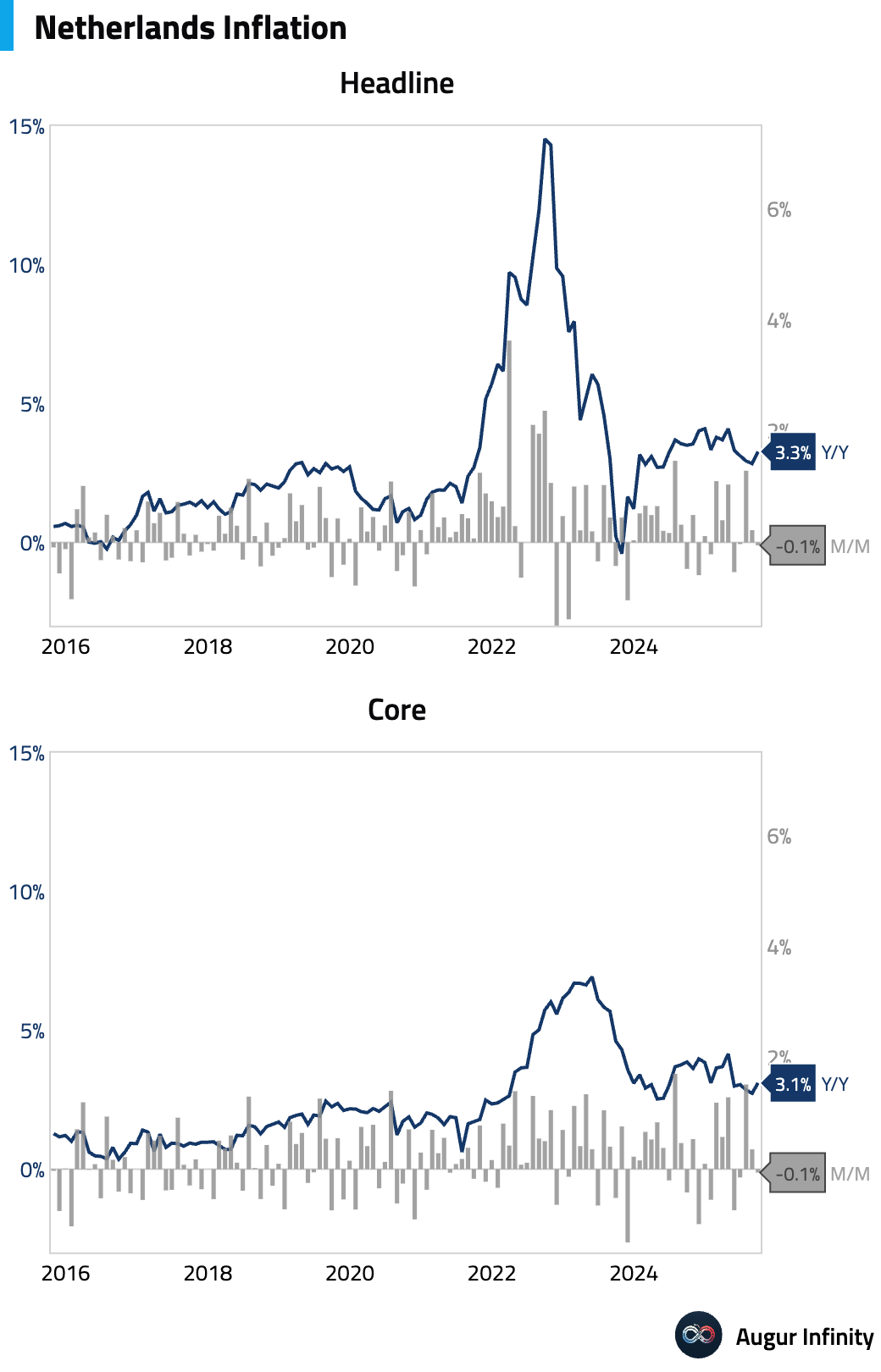

- The final estimate for Dutch inflation in September confirmed an acceleration to 3.3% Y/Y from 2.8% in August. On a monthly basis, prices fell 0.1%.

Interactive chart on Augur Infinity

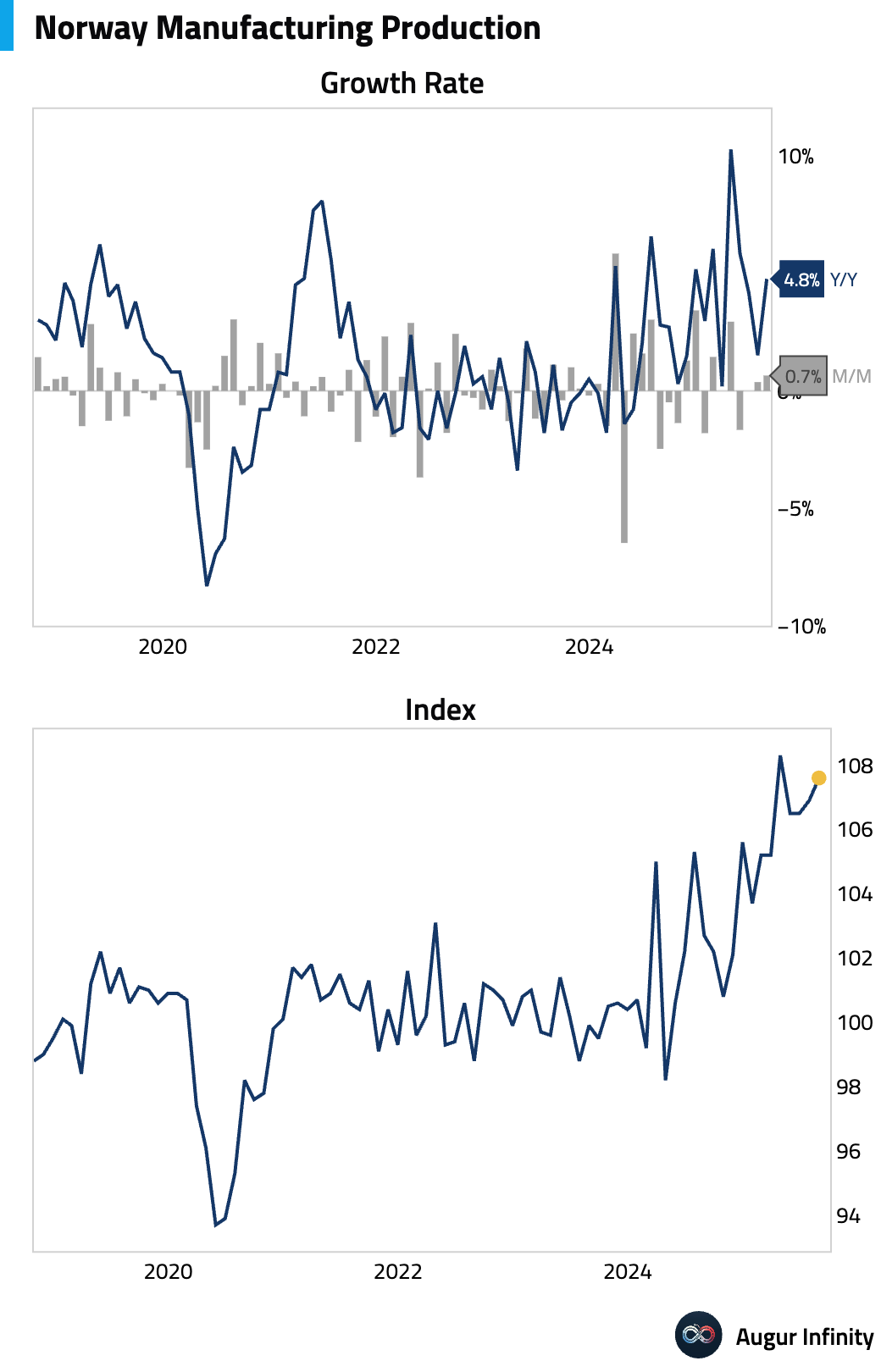

- Norwegian manufacturing production picked up in August, rising by a solid 0.7% M/M after a 0.4% increase in July.

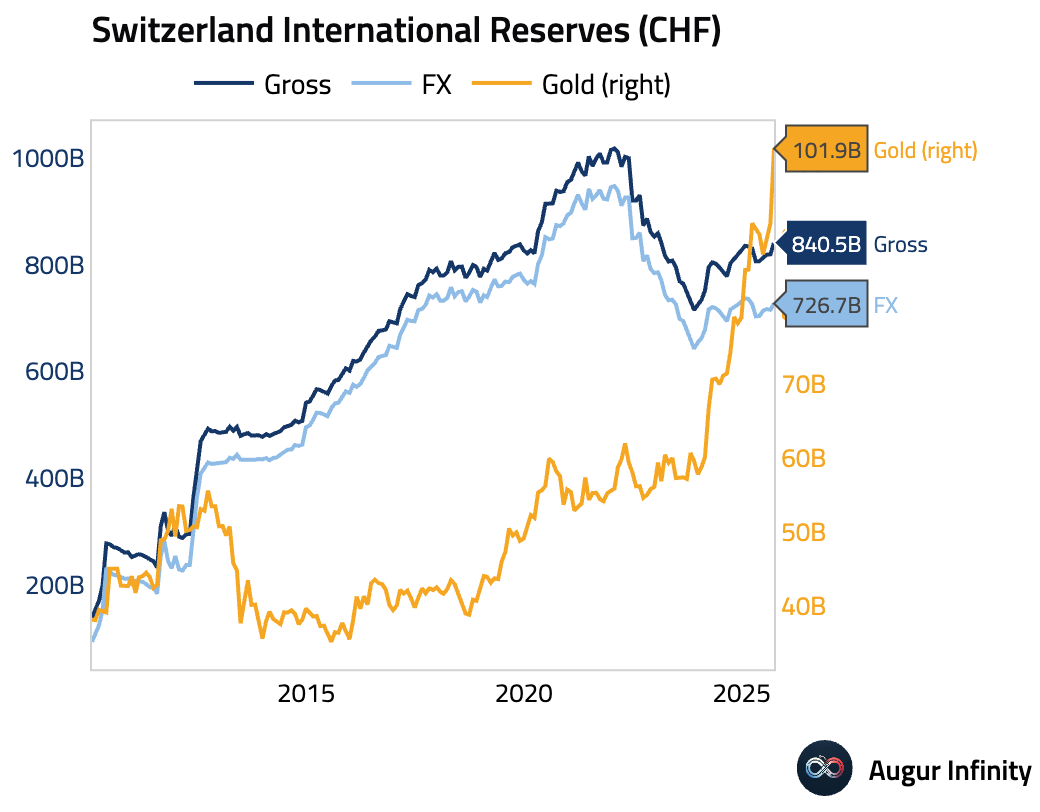

- Switzerland's international reserves rose in September.

Asia-Pacific

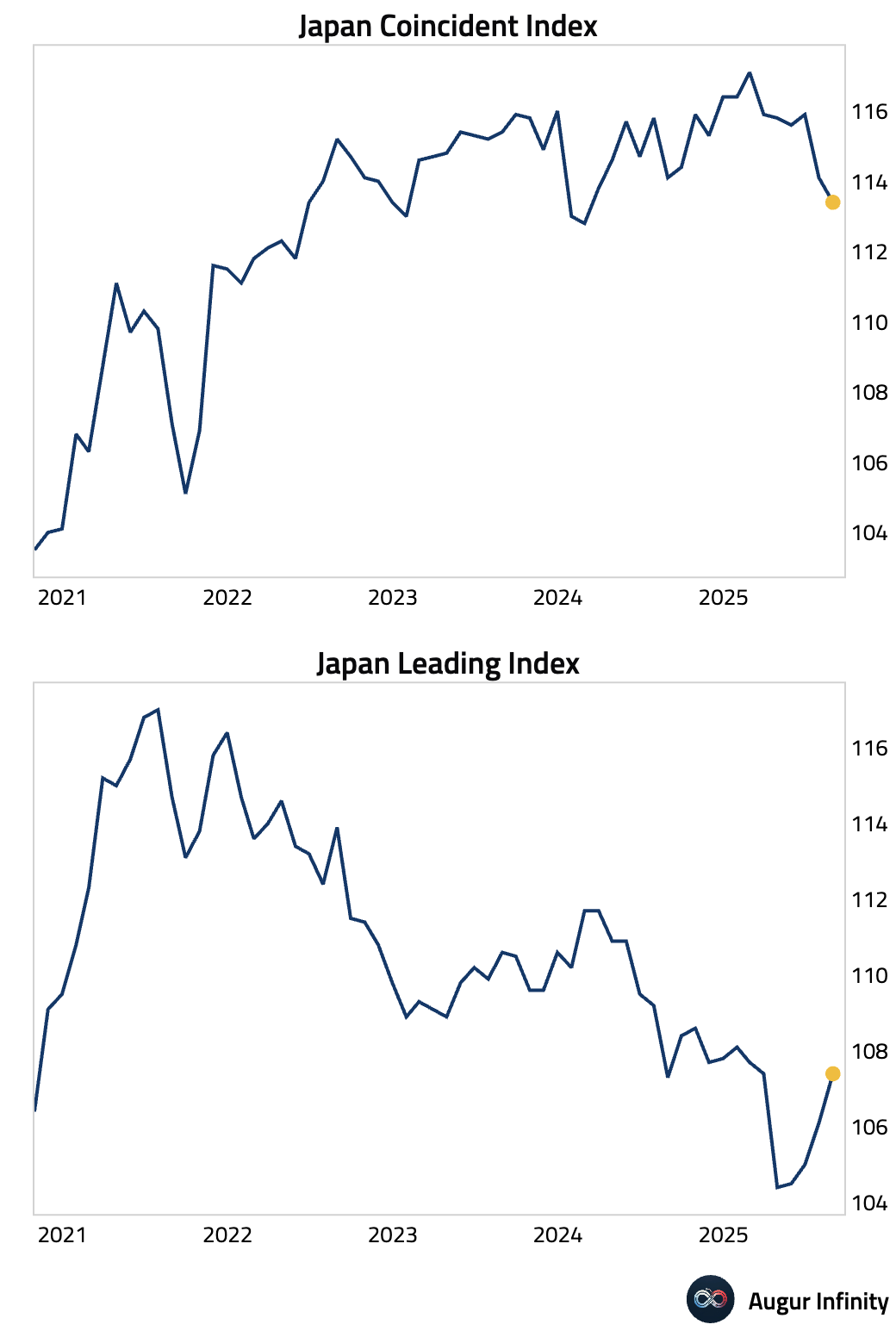

- Japan's preliminary leading economic index rose in August, while the coincident index fell (Leading act: 107.4, est: 107.1; Coincident act: 113.4, prev: 114.1).

Interactive chart on Augur Infinity

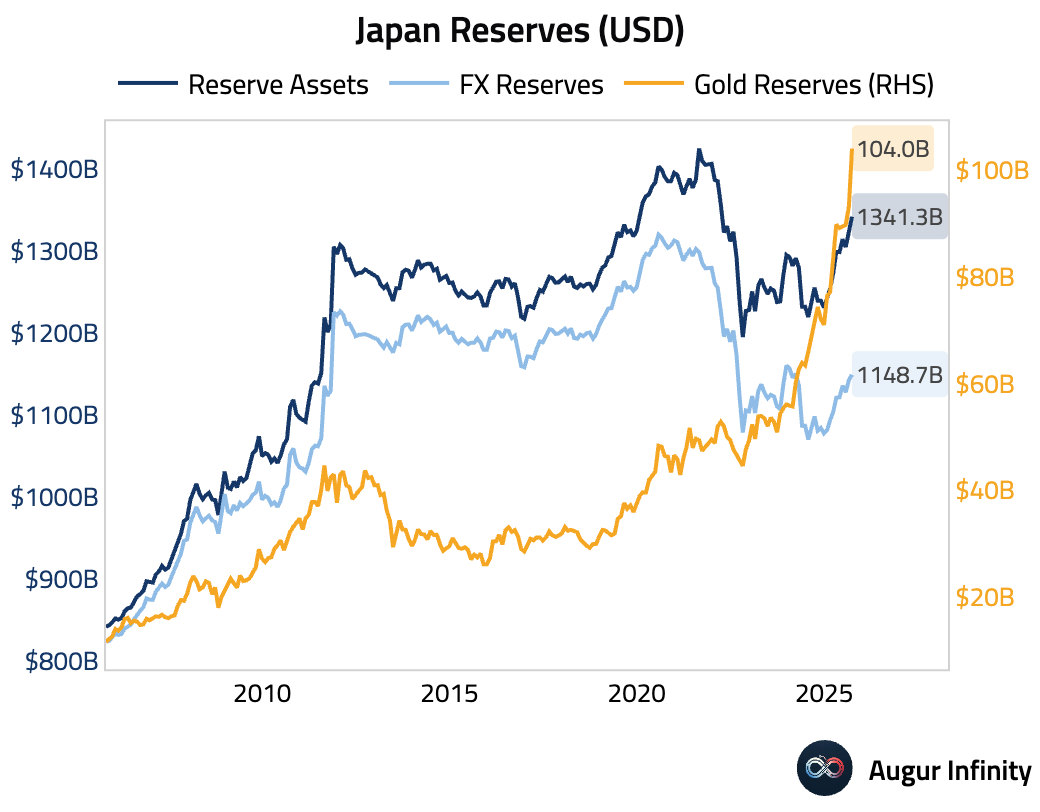

- Japan's official reserve assets increased in September (act: $1.341T, prev: $1.324T).

Interactive chart on Augur Infinity

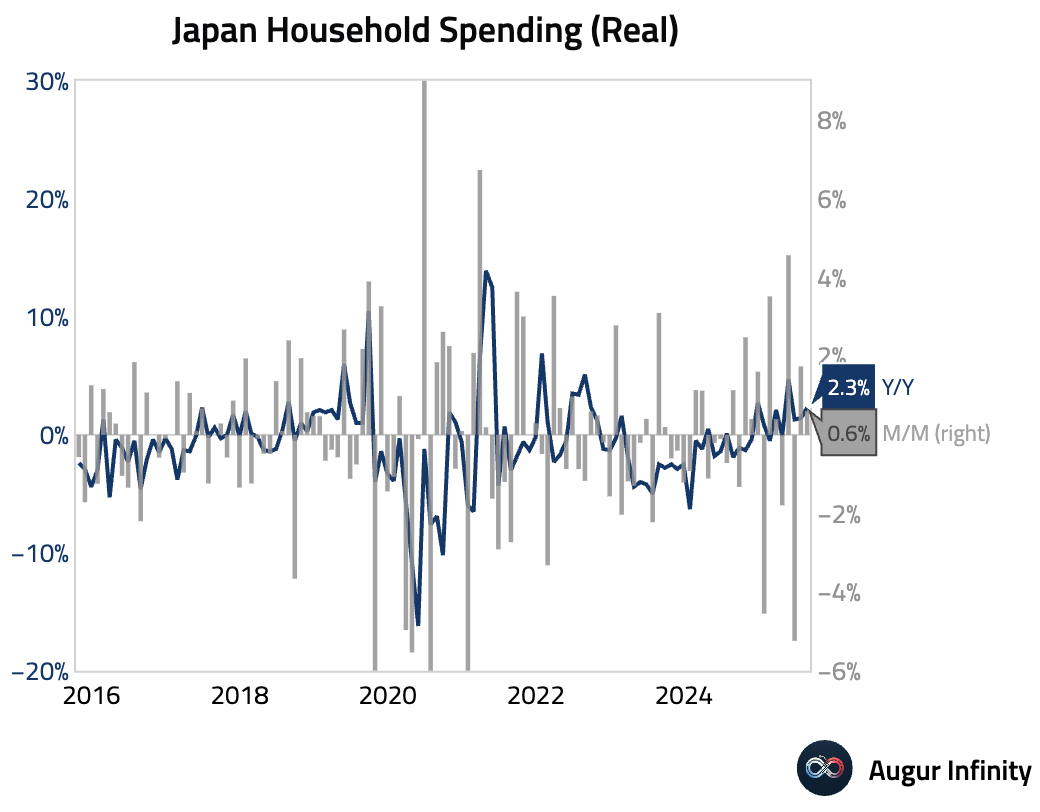

- Japanese household spending significantly beat expectations in August. Spending rose 2.3% Y/Y, well above the 1.2% consensus, while the M/M increase was a solid 0.6%. The data points to resilient consumer demand despite ongoing economic uncertainty.

Interactive chart on Augur Infinity

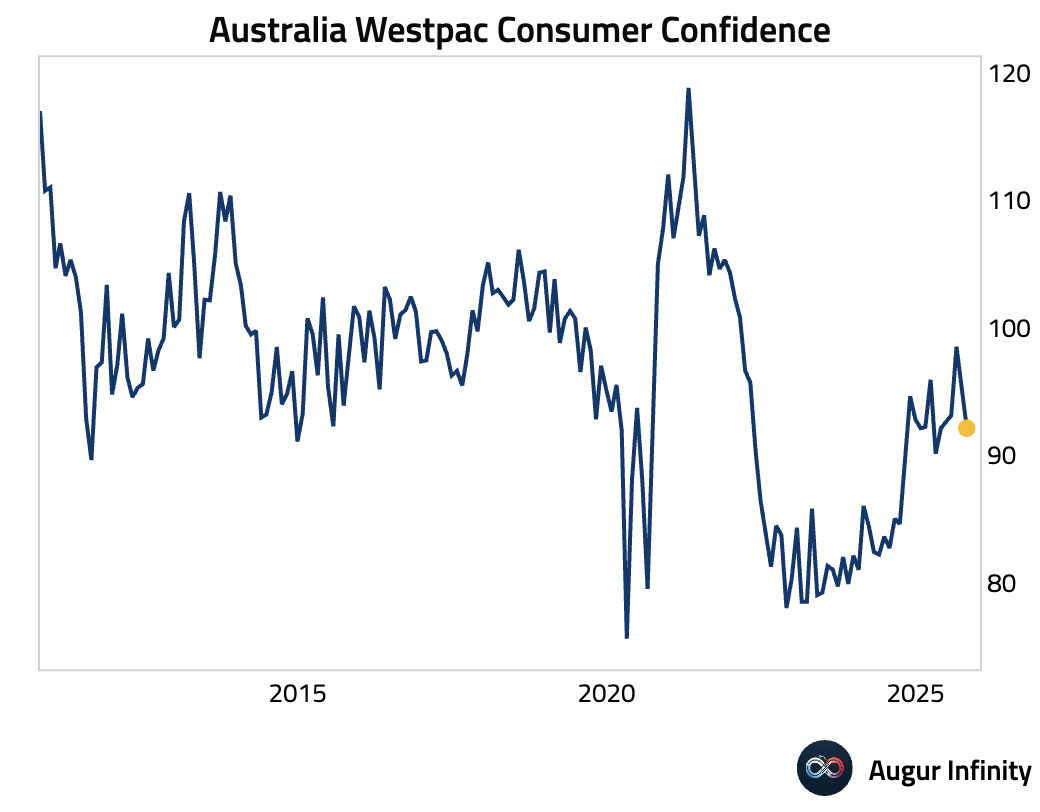

- Australian consumer sentiment fell for the second straight month in October, declining by 3.5% to an index level of 92.1, now 9% below its long-run average. The drop was driven by renewed inflation and interest rate uncertainty, which erased the boost from earlier RBA rate cuts. Perceptions of future family finances plunged 9.9%, though housing sentiment and expectations for rate hikes rose after the recent strong inflation report.

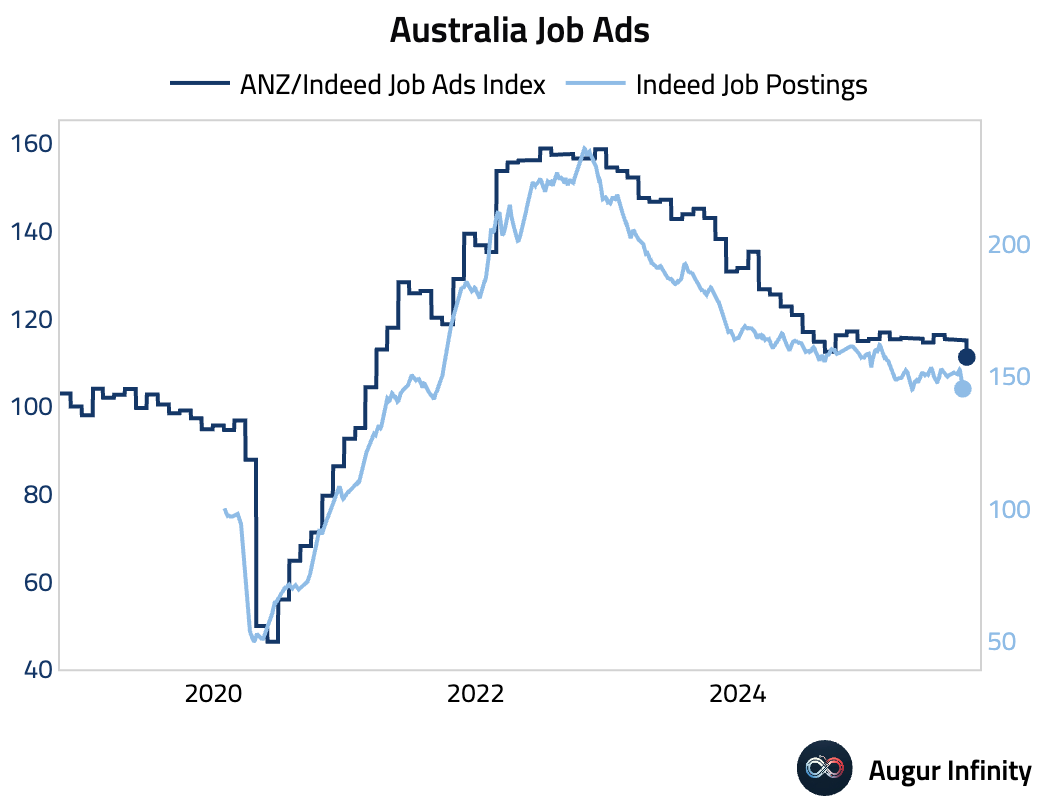

- Australian job advertisements fell sharply in September, dropping 3.3% M/M. The decline, which follows a smaller 0.3% dip in August, suggests continued cooling in the labor market.

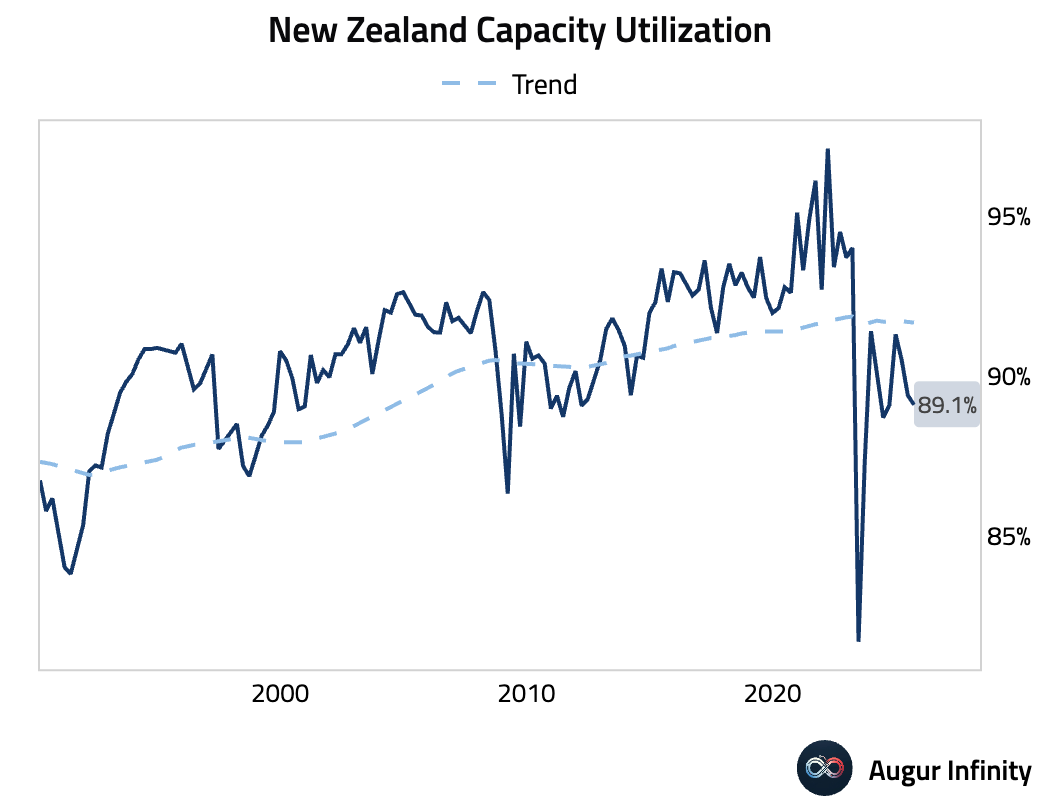

- New Zealand business conditions remained weak in the third quarter, with capacity utilization easing slightly to 89.1% from 89.4%.

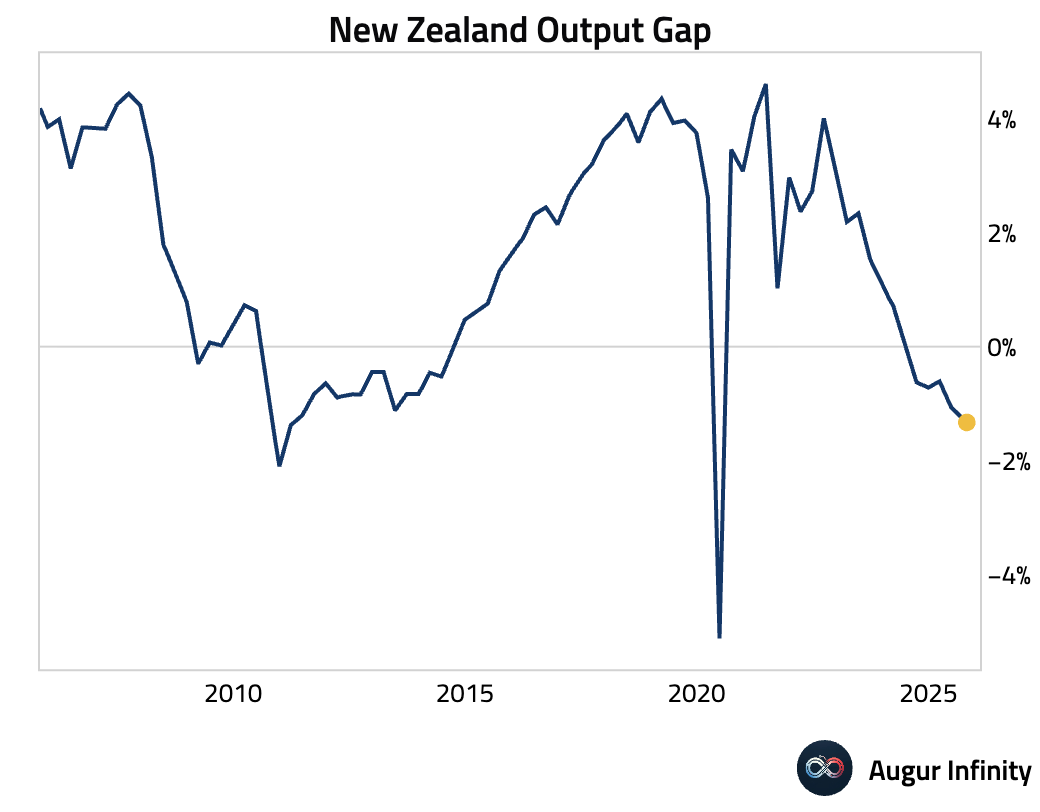

Here's our estimate of New Zealand's output gap, which shows that the economy is operating at well below potential levels.

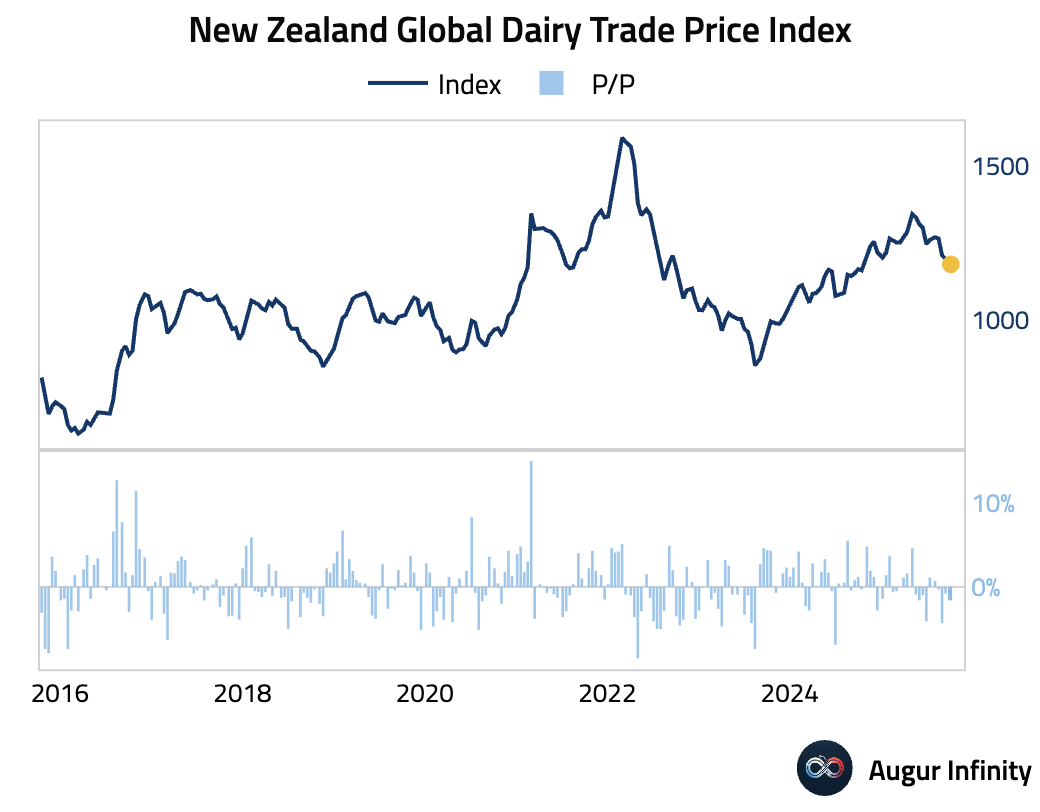

- New Zealand Global Dairy Trade Price Index declined further.

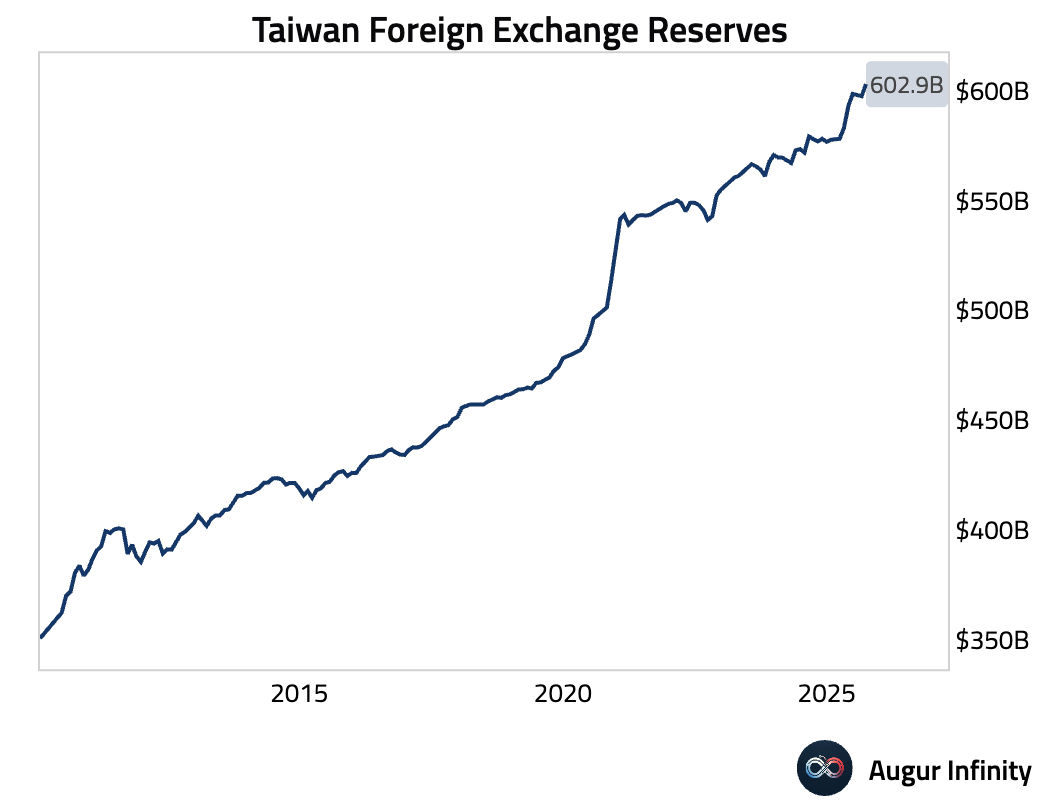

- Taiwan's foreign exchange reserves reached an all-time high in September (act: $602.94B, prev: $597.43B).

China

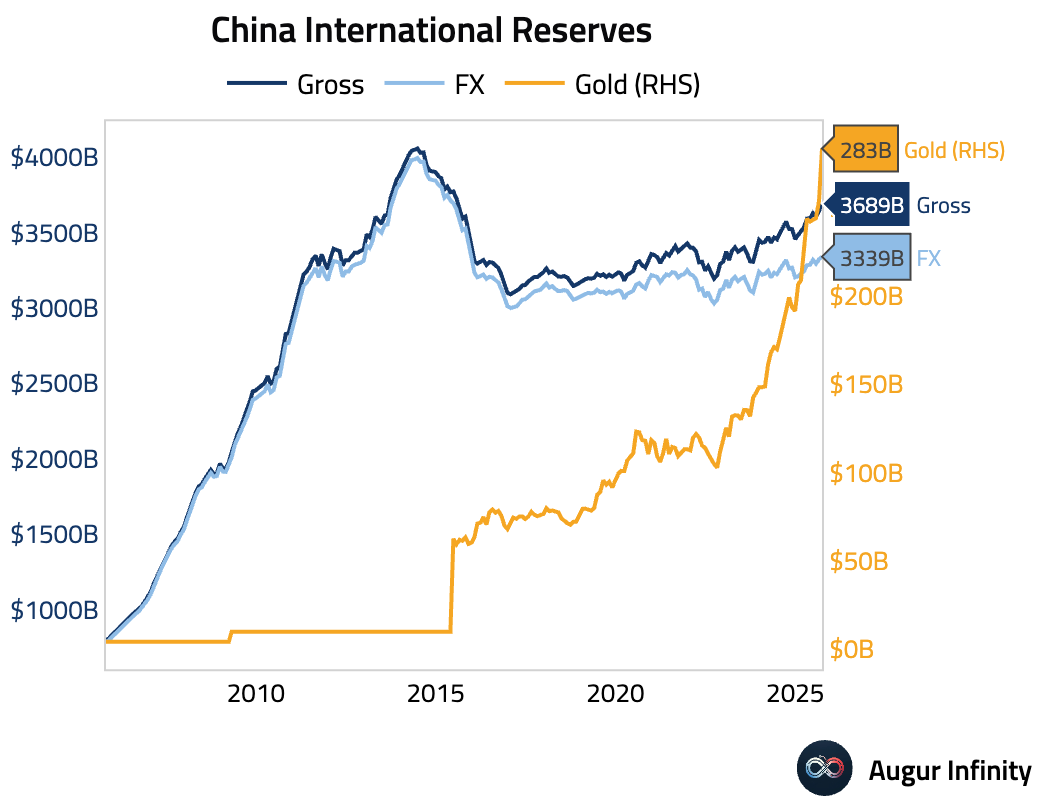

- China's foreign exchange reserves edged higher in September, rising to $3.339 trillion from $3.322 trillion in the previous month.

Emerging Markets ex China

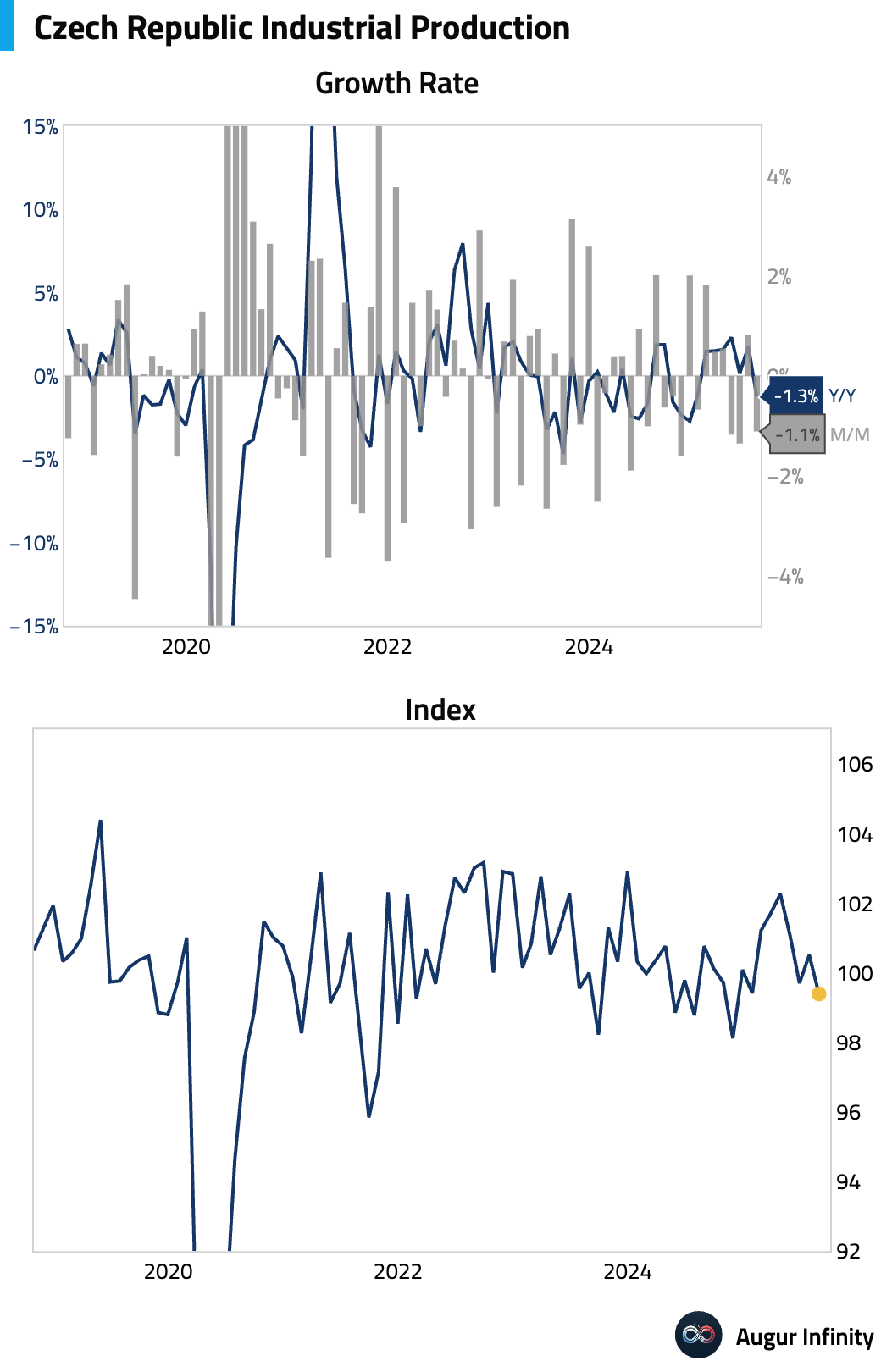

- Czech industrial production unexpectedly contracted in August, falling 1.3% Y/Y versus expectations for a 0.6% gain.

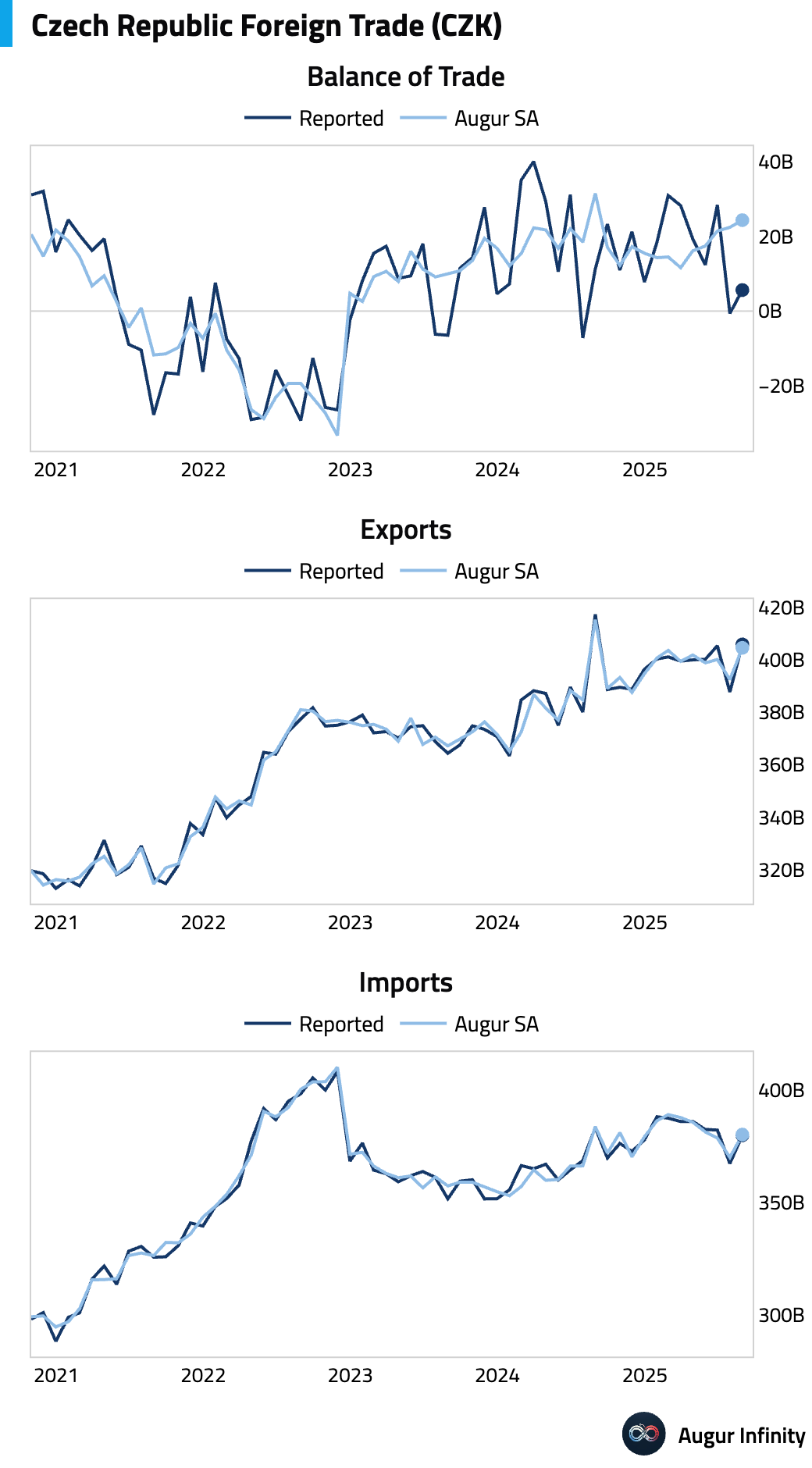

- The Czech Republic's trade surplus expanded significantly in August, beating consensus expectations (act: CZK 5.6B, est: CZK 3.8B).

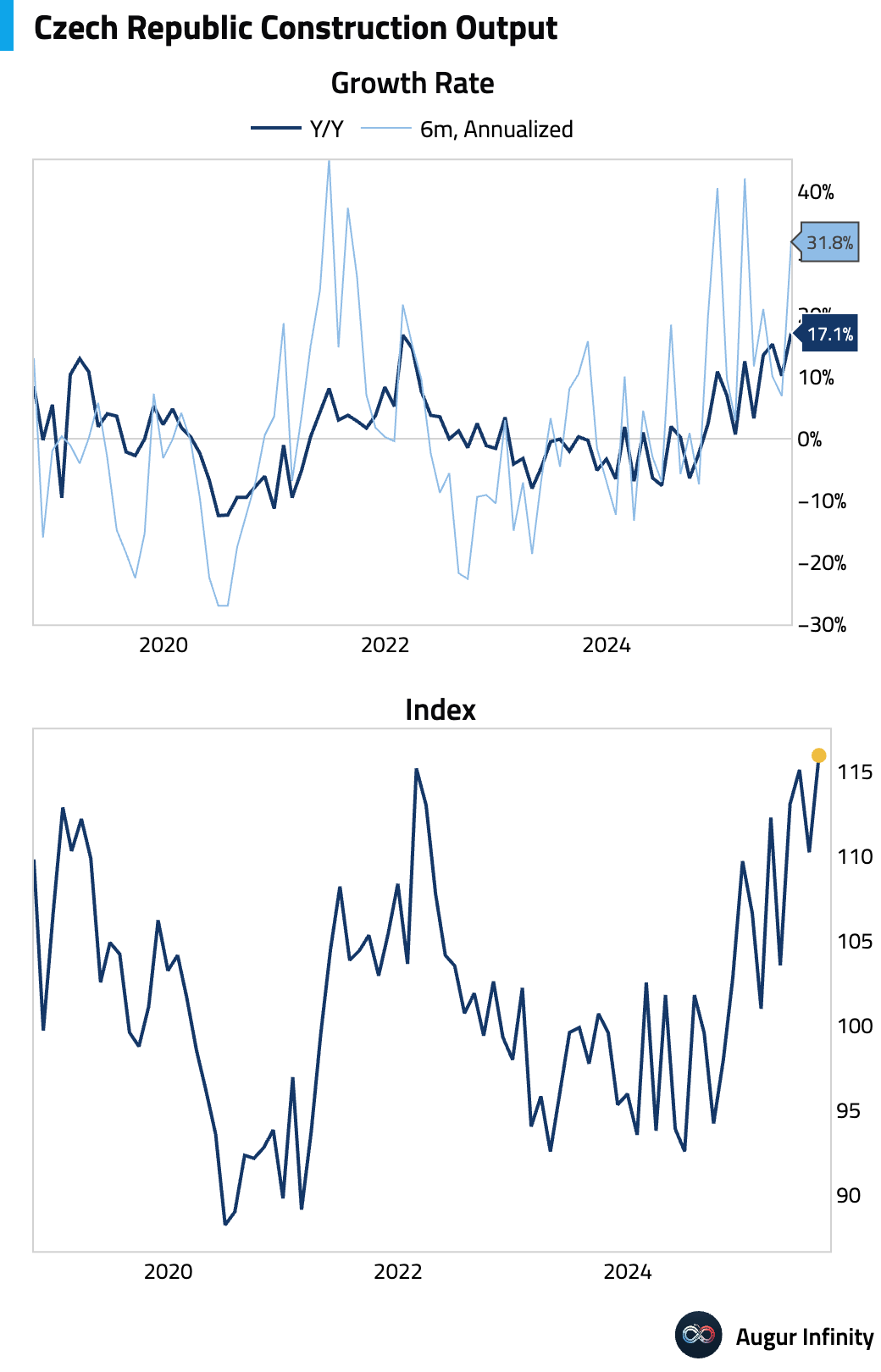

- Czech construction output surged in August, growing 17.1% Y/Y, the fastest pace since January 2018.

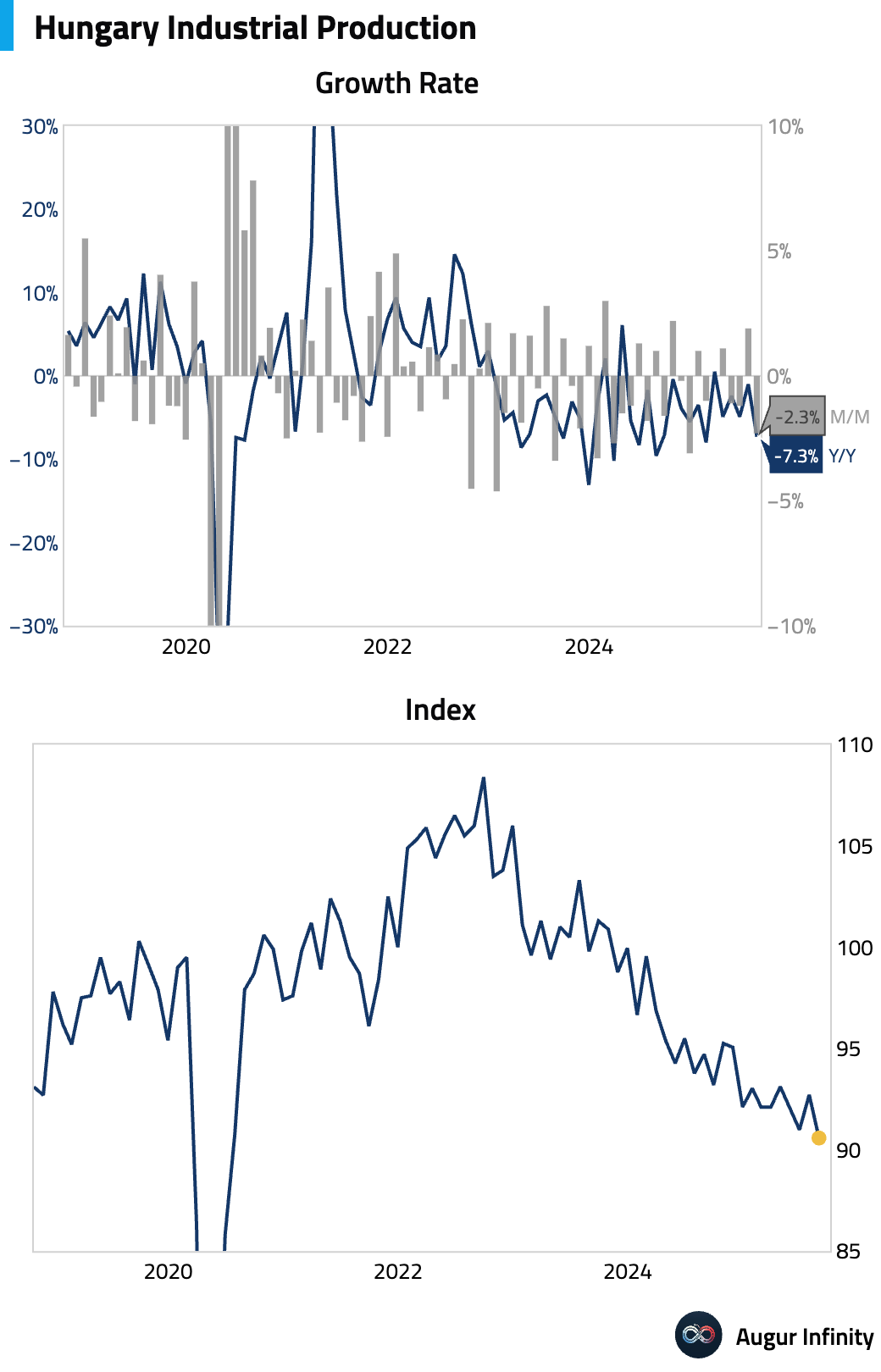

- Hungarian industrial output declined sharply in August, falling 7.3% Y/Y compared to a 1.0% drop in the prior month.

- Poland's foreign exchange reserves reached an all-time high in September (act: $262.5B, prev: $260.9B).

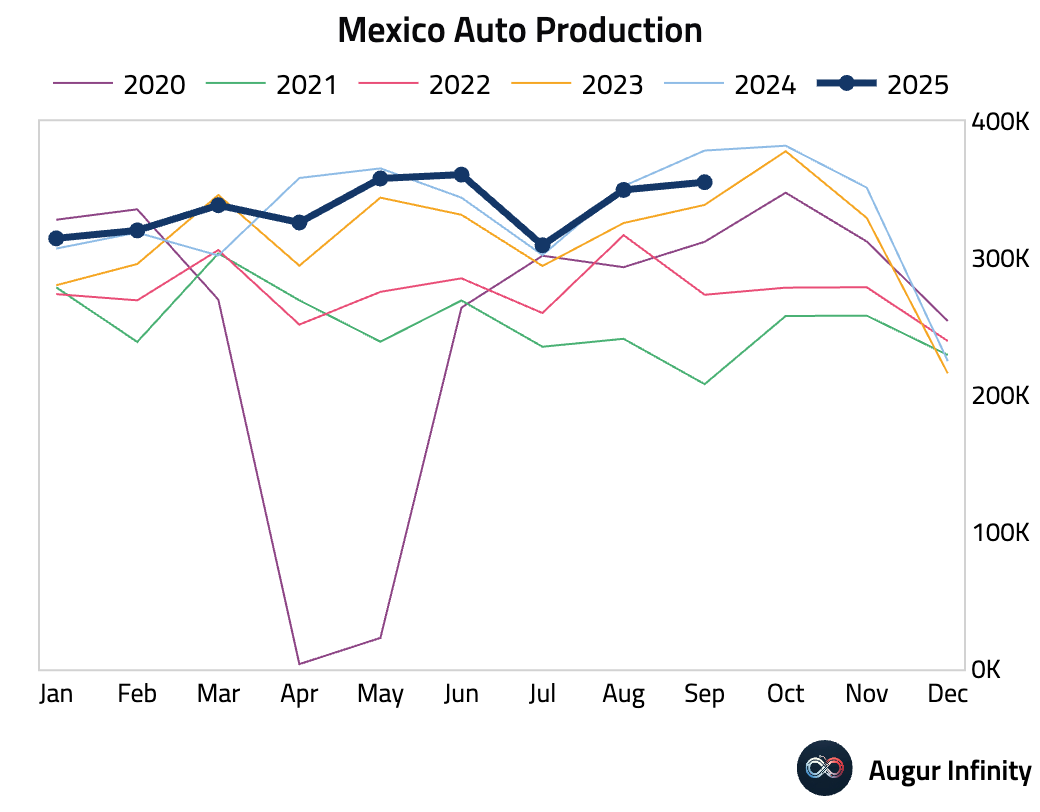

- Mexico's auto production contracted further in September, with the year-over-year decline worsening to 6.1% from 0.8% in August.

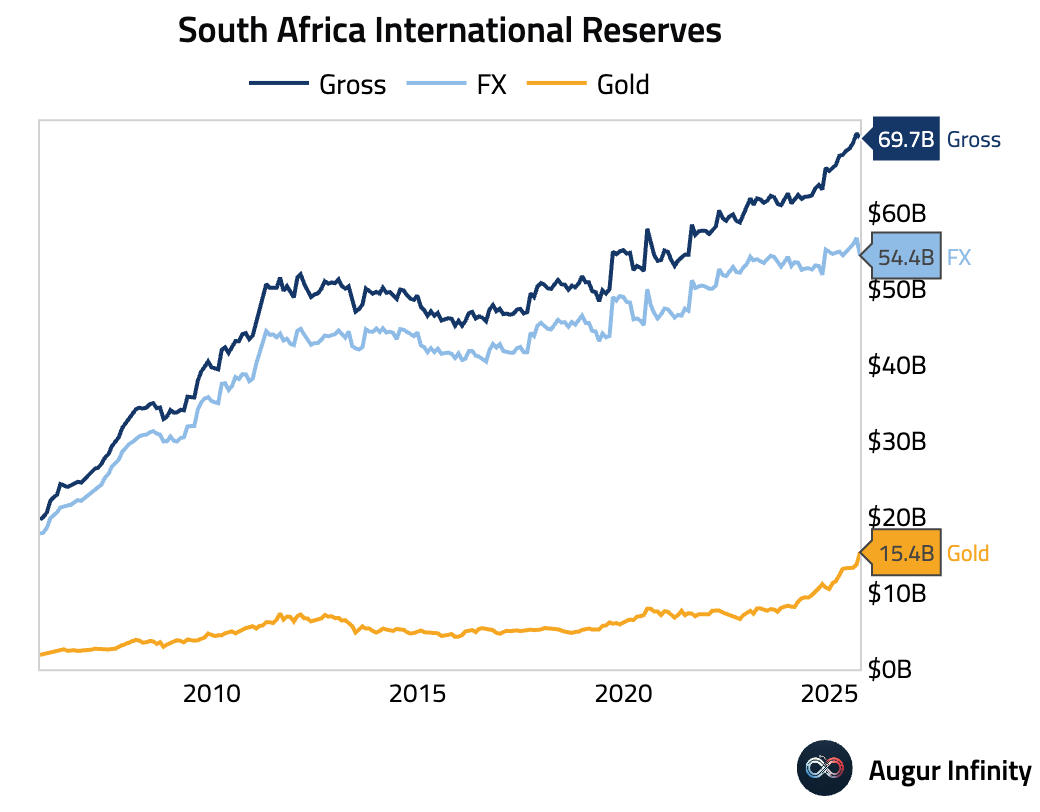

- South Africa's official reserve assets fell in September (act: $69.74B, prev: $70.42B).

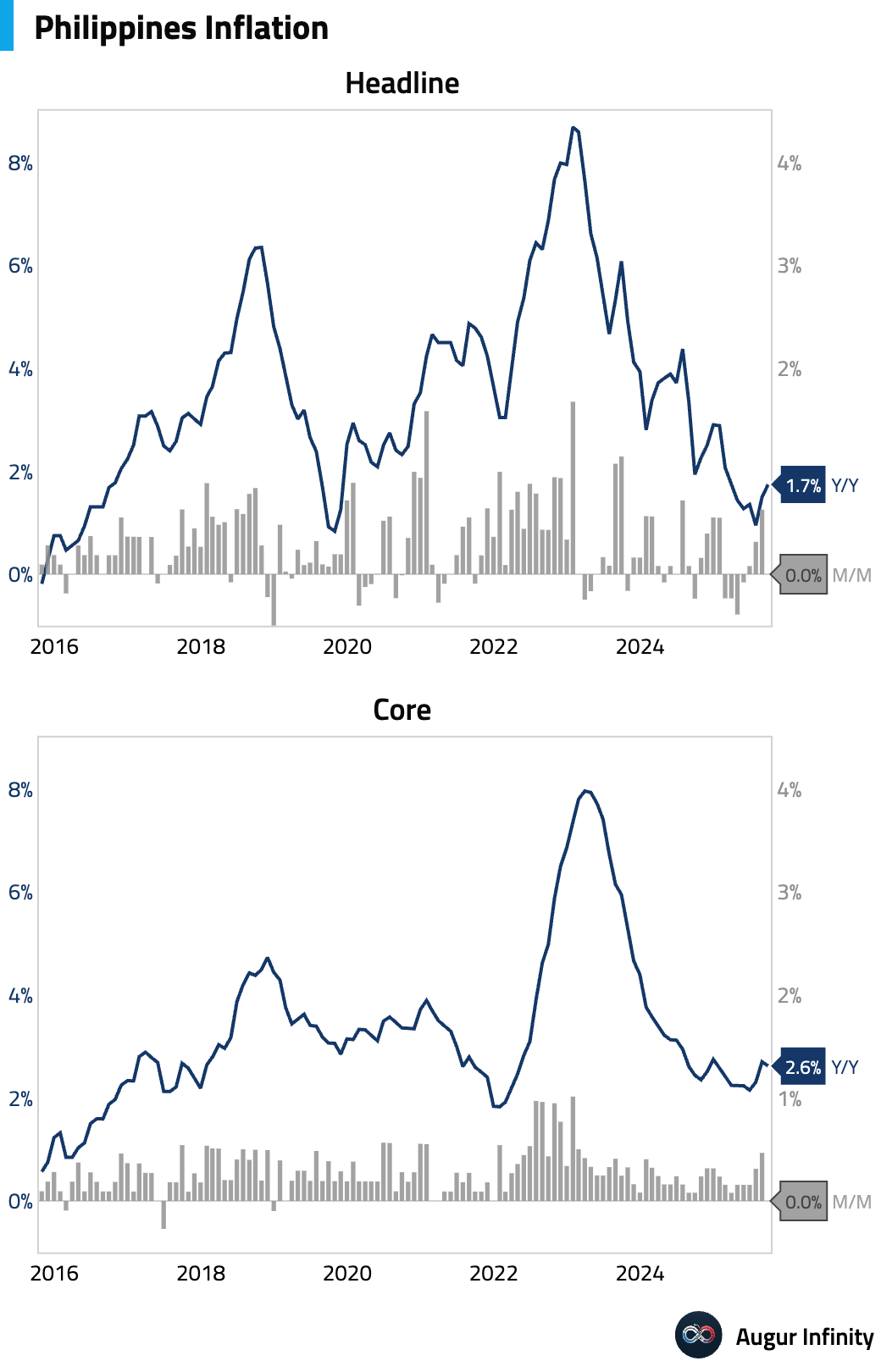

- Philippine headline inflation rose to 1.7% Y/Y in September but missed consensus expectations of 2.0%, driven by higher transport costs. Critically for the central bank, core CPI slowed to 2.6% Y/Y from 2.7%. The headline print came in at the low end of the central bank's forecast range, supporting the case for further rate cuts through the first quarter of 2026.

Interactive chart on Augur Infinity

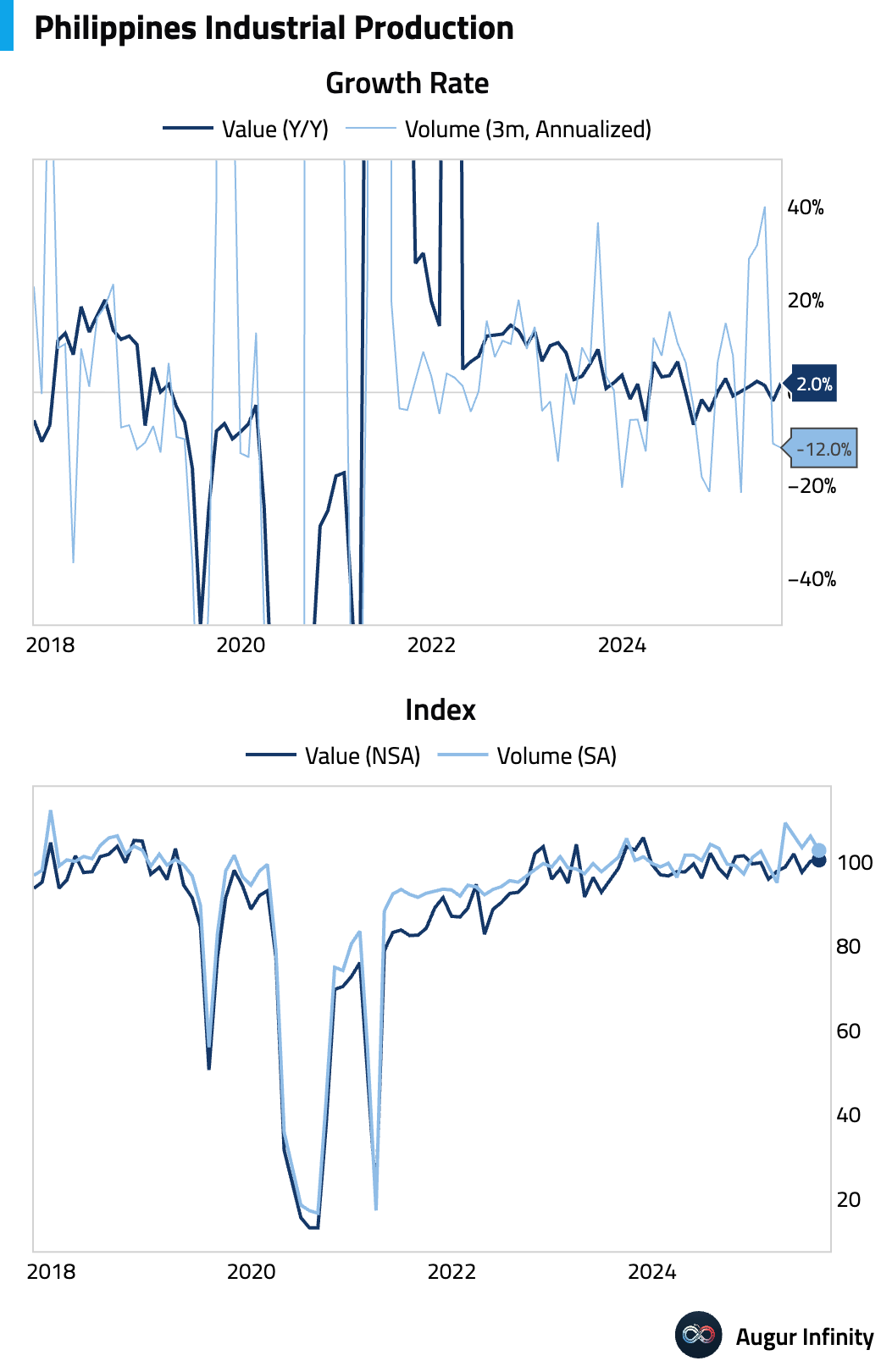

- Philippine industrial production rebounded in August, rising 2.0% Y/Y after contracting 1.9% in July. However, the 3-month rate of change in the volume index remains deeply negative.

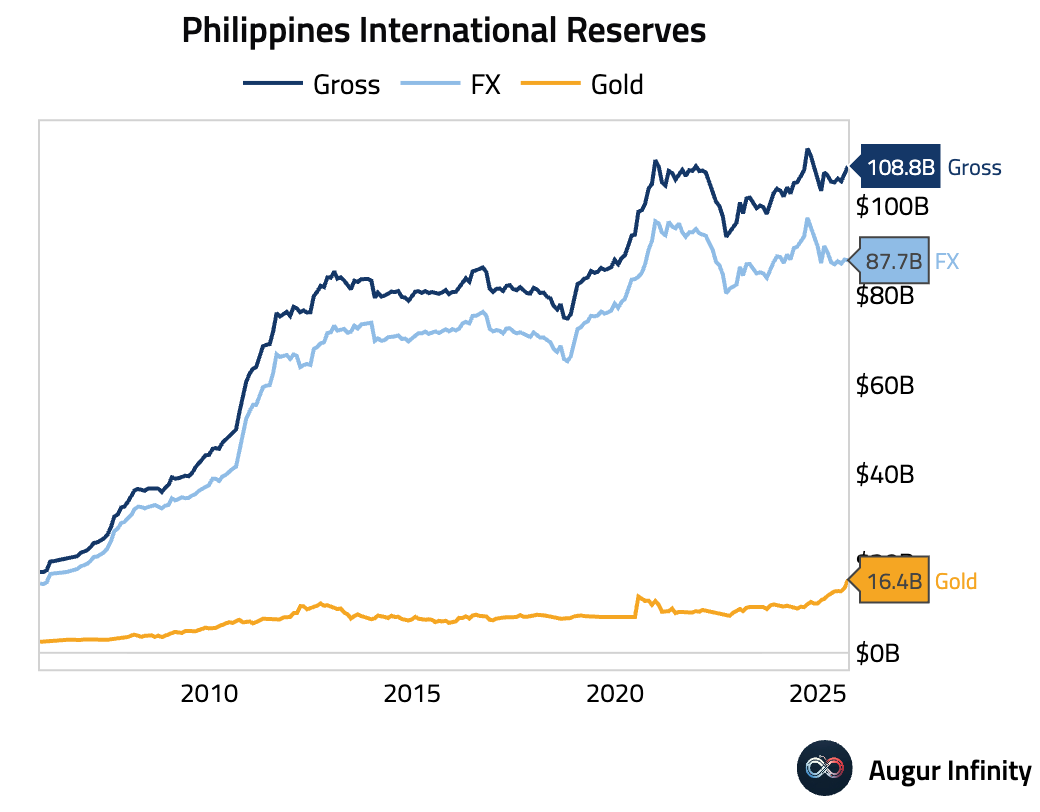

- The Philippines saw its official reserve assets increase in September (act: $108.8B, prev: $107.1B).

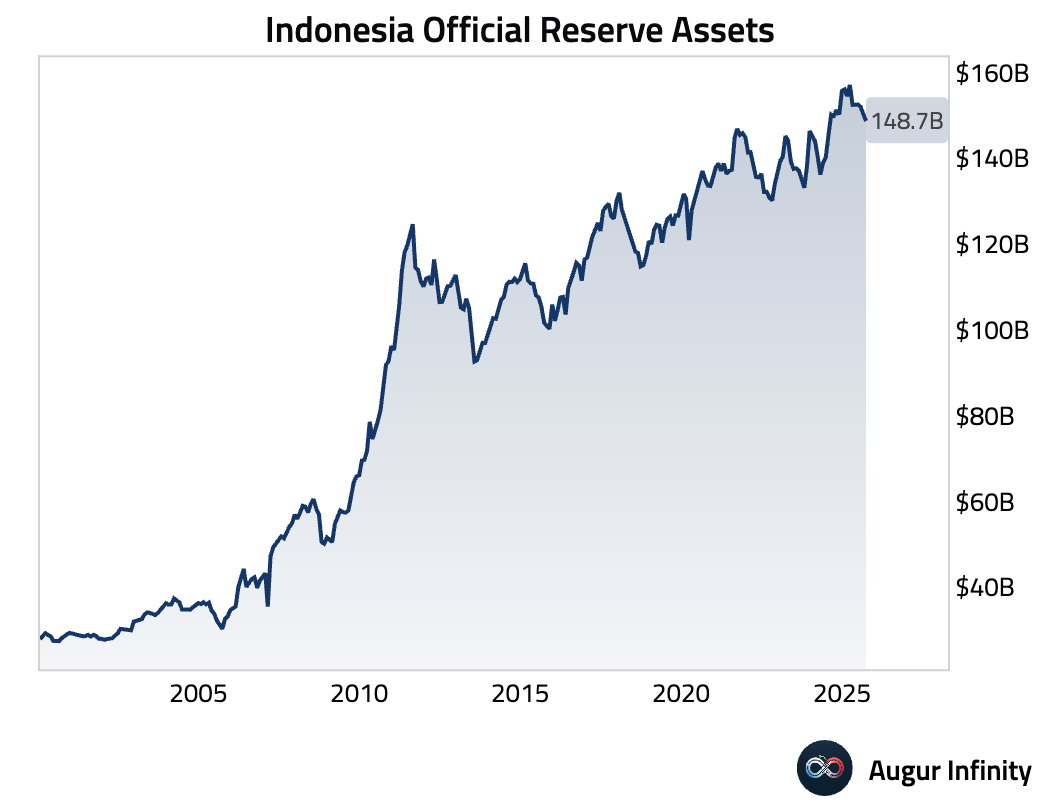

- Indonesia's official reserve assets declined in September (act: $148.7B, prev: $150.7B).

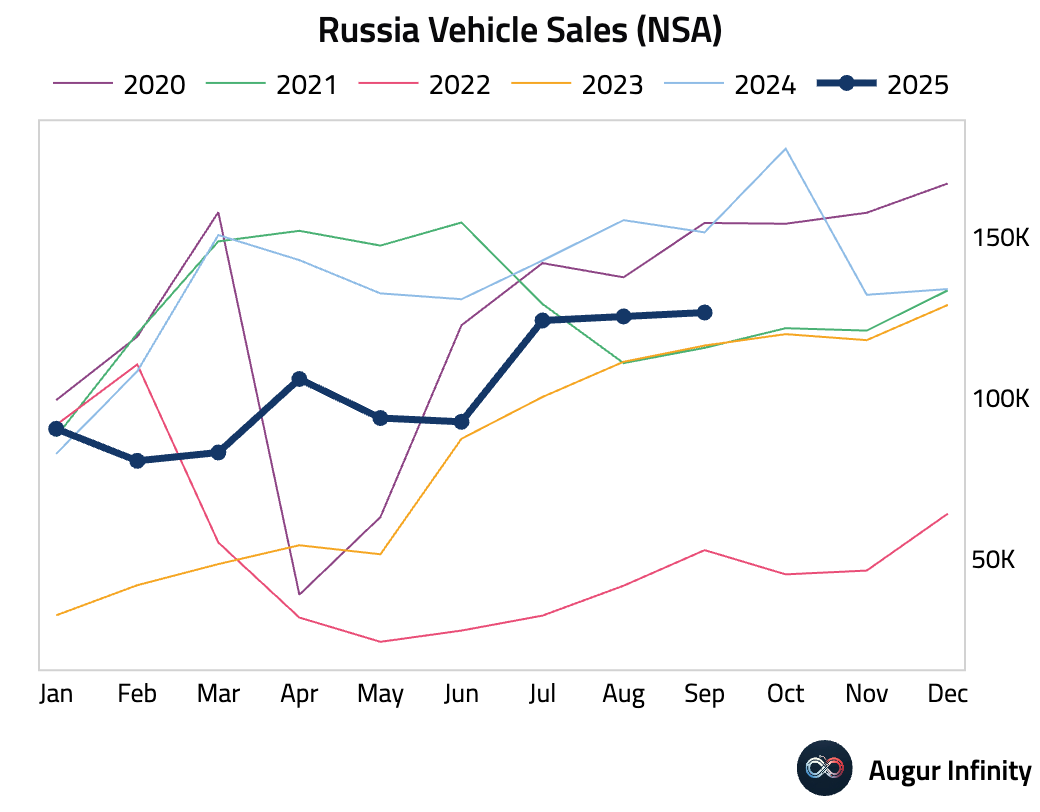

- Russian vehicle sales continued to fall in September, declining 20% Y/Y after an 19% drop in August.

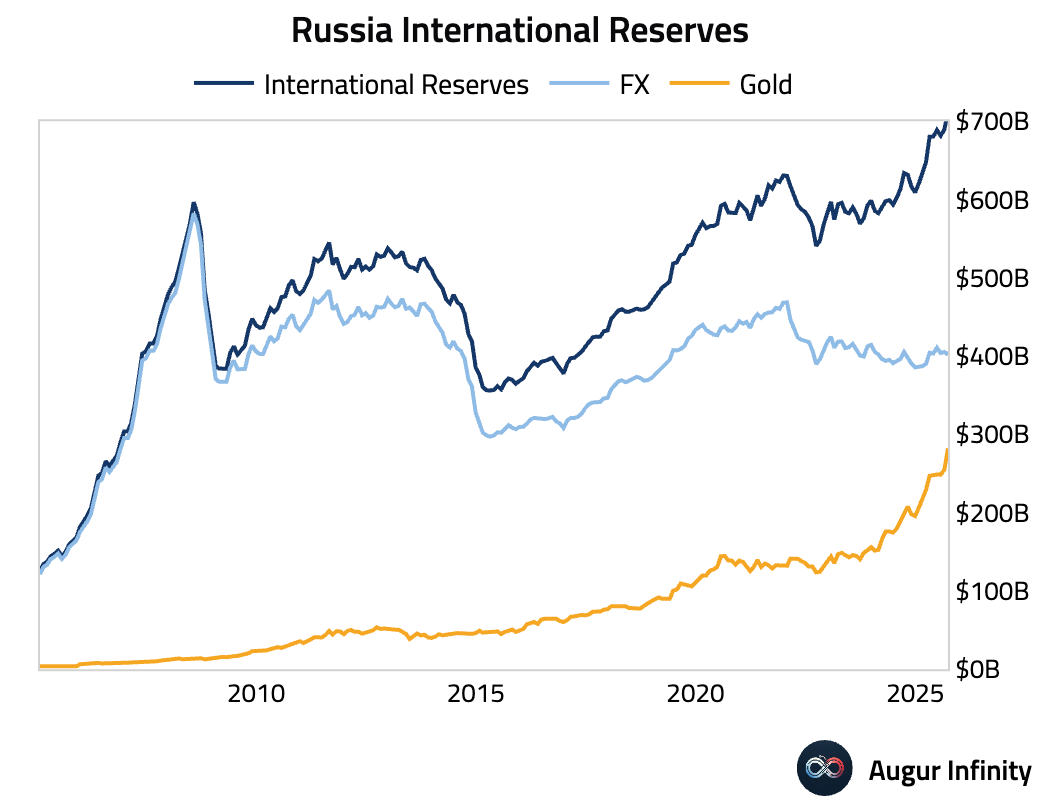

- Russia's official reserve assets reached a new all-time high in September (act: $713.3B, prev: $689.4B).

Global Markets

Equities

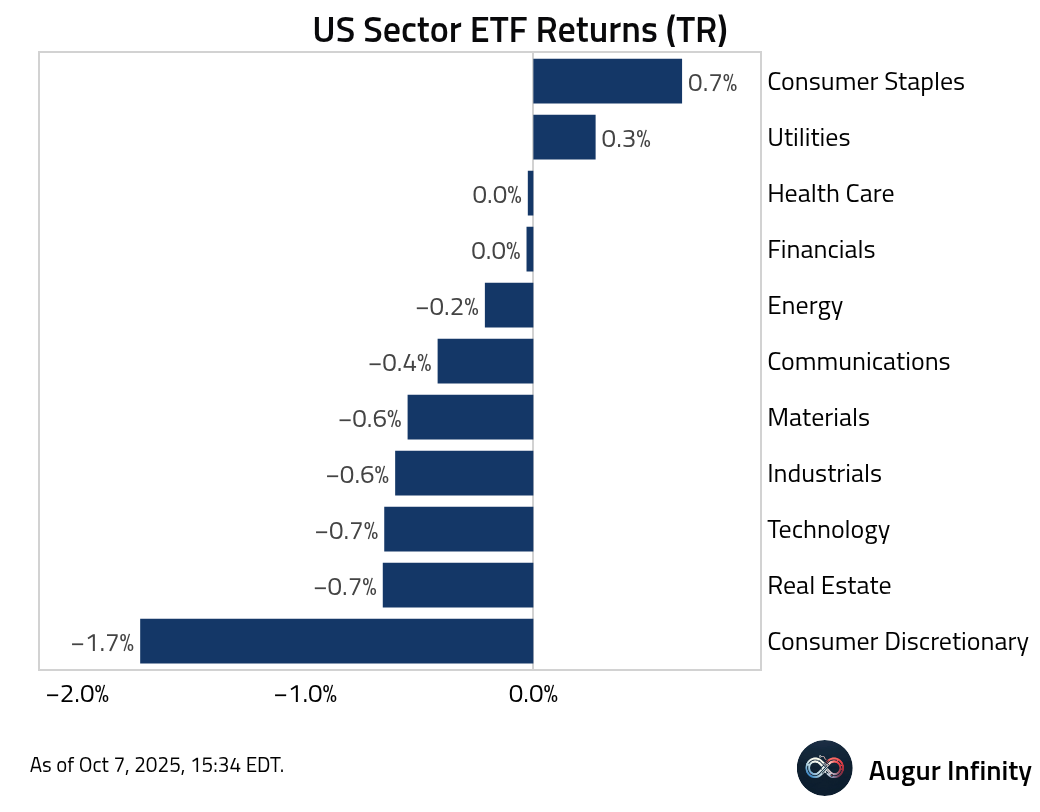

- Global equity markets retreated amid concerns over AI margins & political instability in key economies. US stocks fell, with the S&P 500 down 0.4%. The sell-off was broad-based, with notable declines in Brazil (-1.9%), South Korea (-1.7%), and China (-1.2%). The German, Chinese, and Mexican markets all extended their losing streaks to three consecutive sessions.

- Here's how US equity sectors performed today.

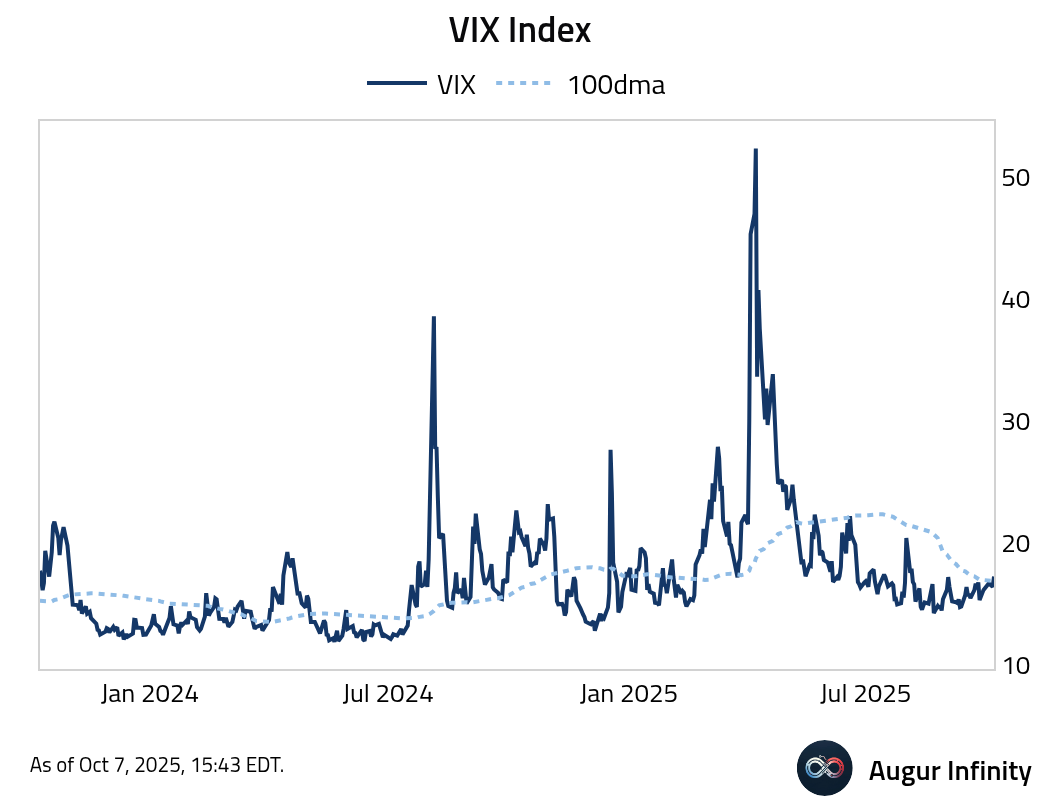

- VIX Index jumped above its 100-day moving average.

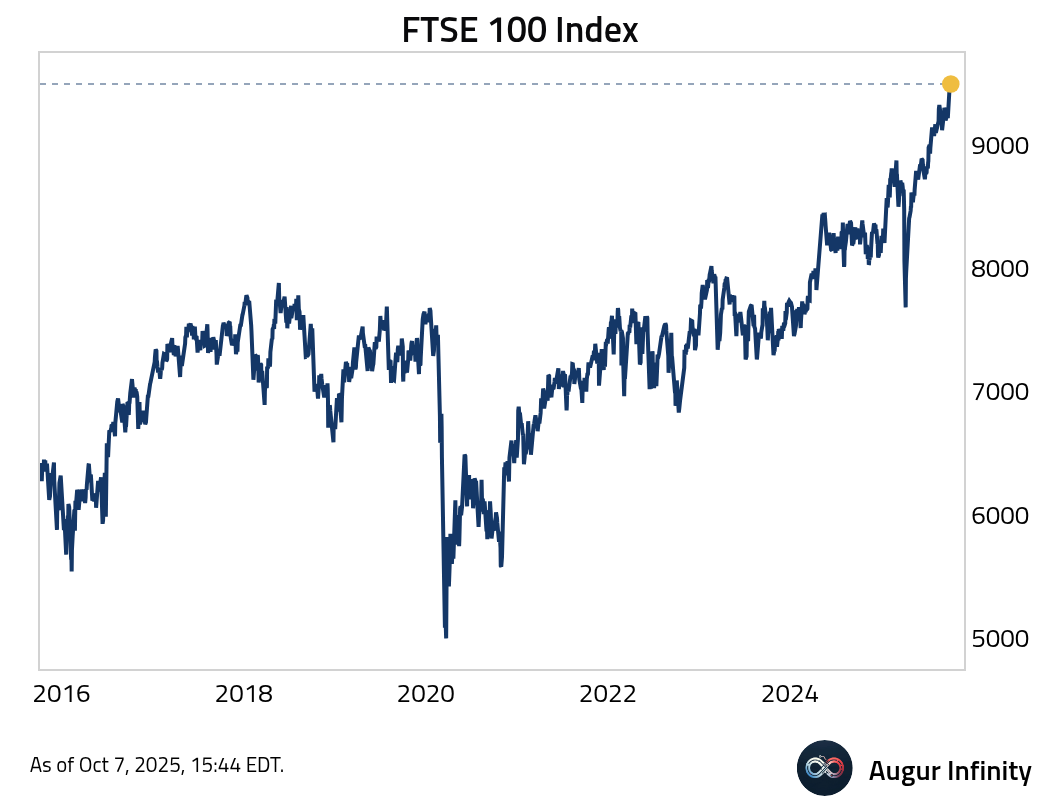

- FTSE 100 Index continued to push higher, reaching the 31st all-time high of 2025.

- Shanghai Shenzhen CSI 300 is trading at the highest level since February 2022.

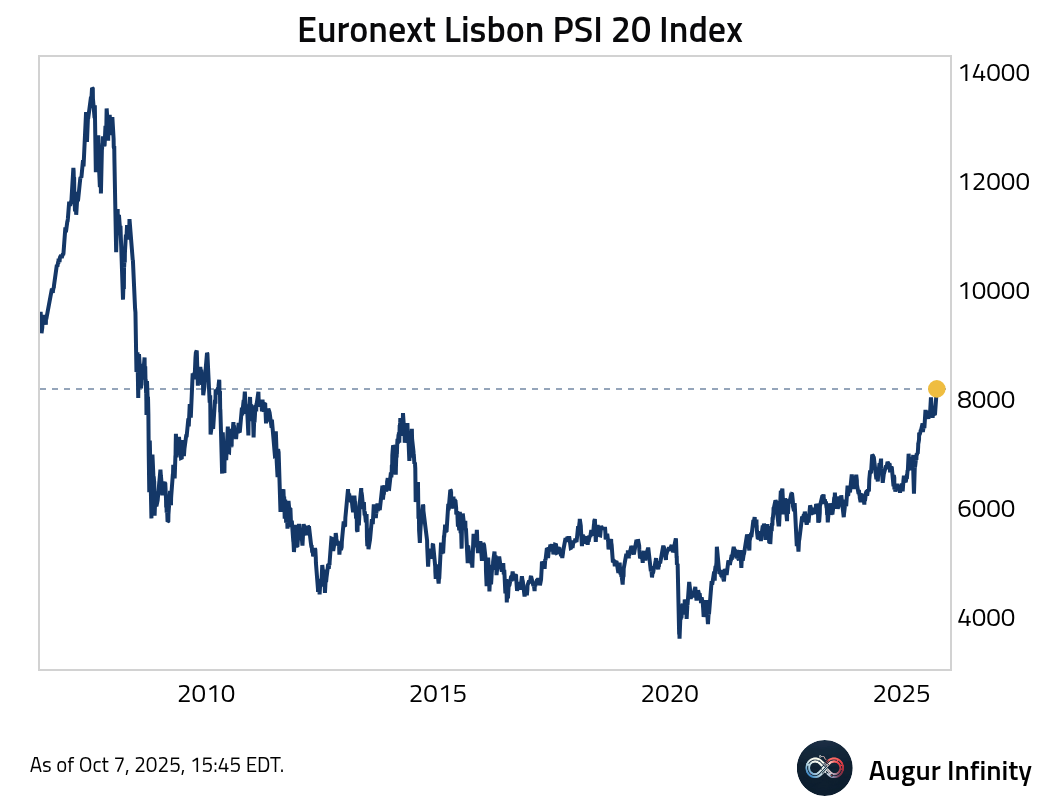

- The Euronext Lisbon PSI 20 Index has reached its best level since April 2010.

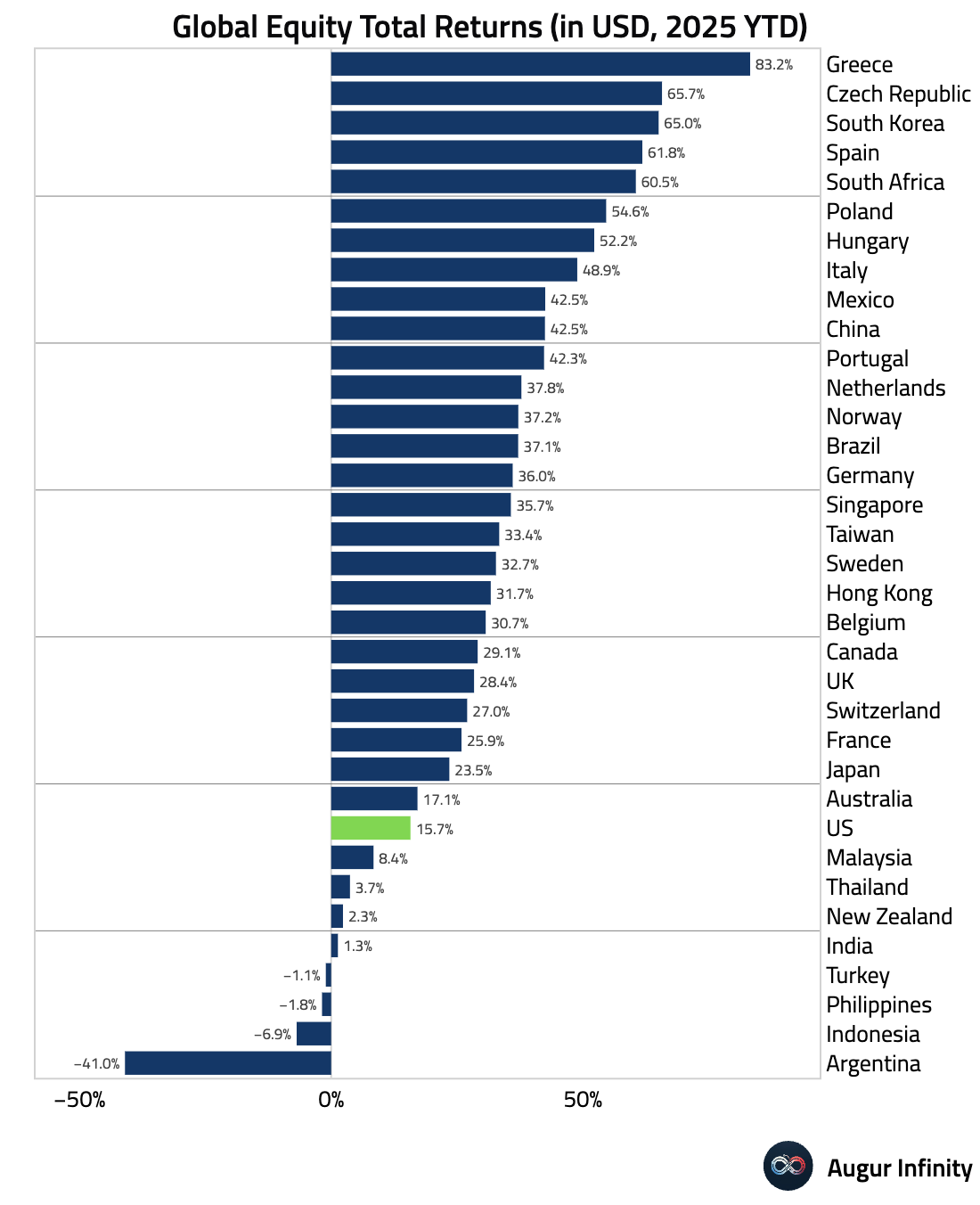

- Below we have the year-to-date returns of global equity markets (in USD). Greece equities toped the leaderboard, returning nearly 83%, while Argentina equities lagged far behind at -41%.

Fixed Income

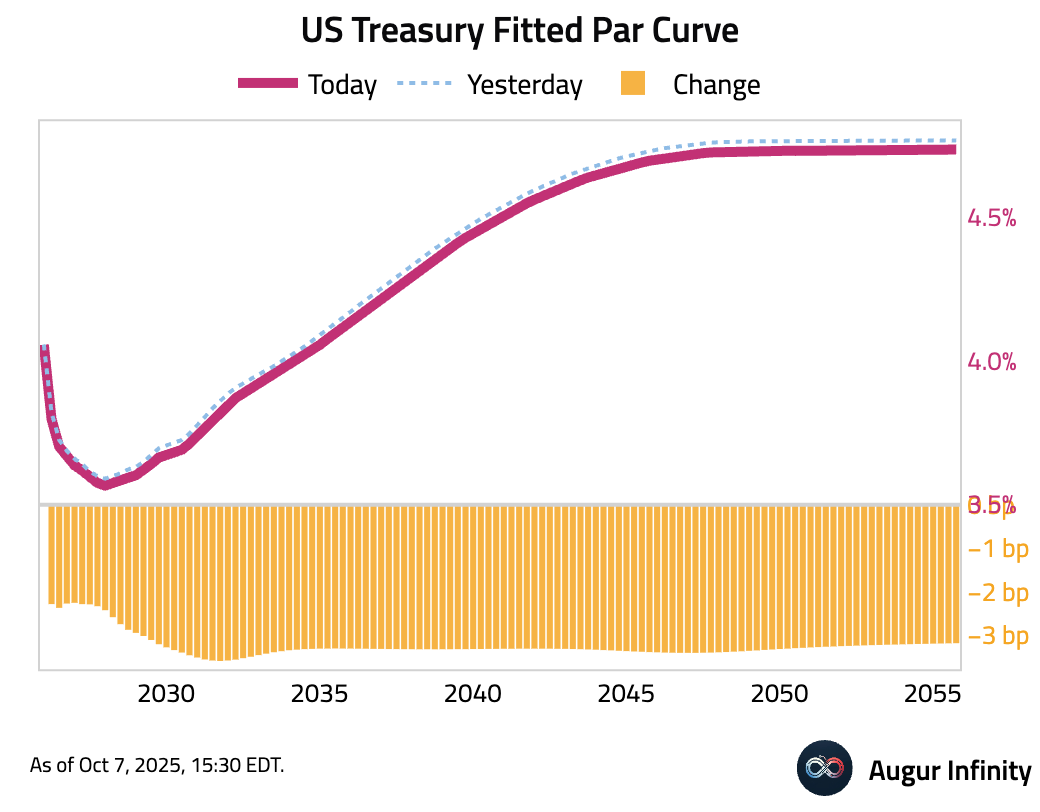

- US Treasury yields declined across the curve in a flight-to-safety move. The 5-year yield saw the largest drop, falling 3.2 basis points, while the 10-year yield decreased by 2.8 basis points.

FX

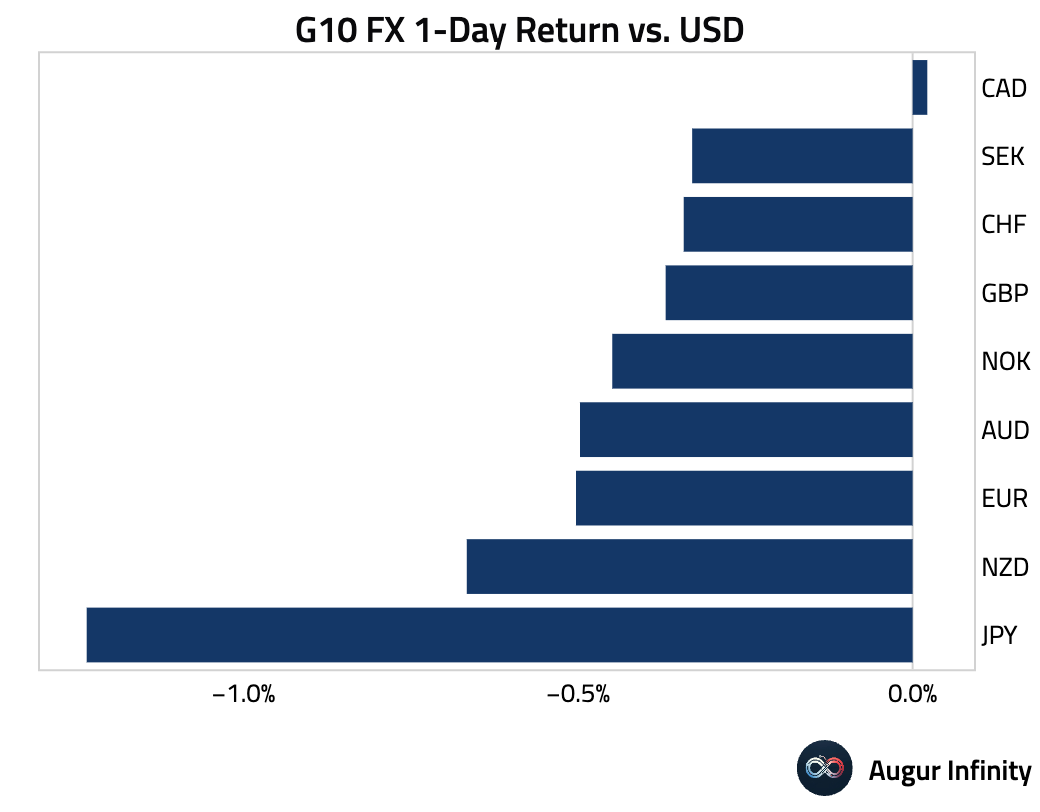

- The US dollar strengthened against most G10 currencies as political turmoil in Europe and Japan fueled haven demand. The Japanese yen was the primary underperformer, weakening 1.2% against the dollar and marking its fourth consecutive day of losses amid reports of difficulties in forming a new governing coalition.

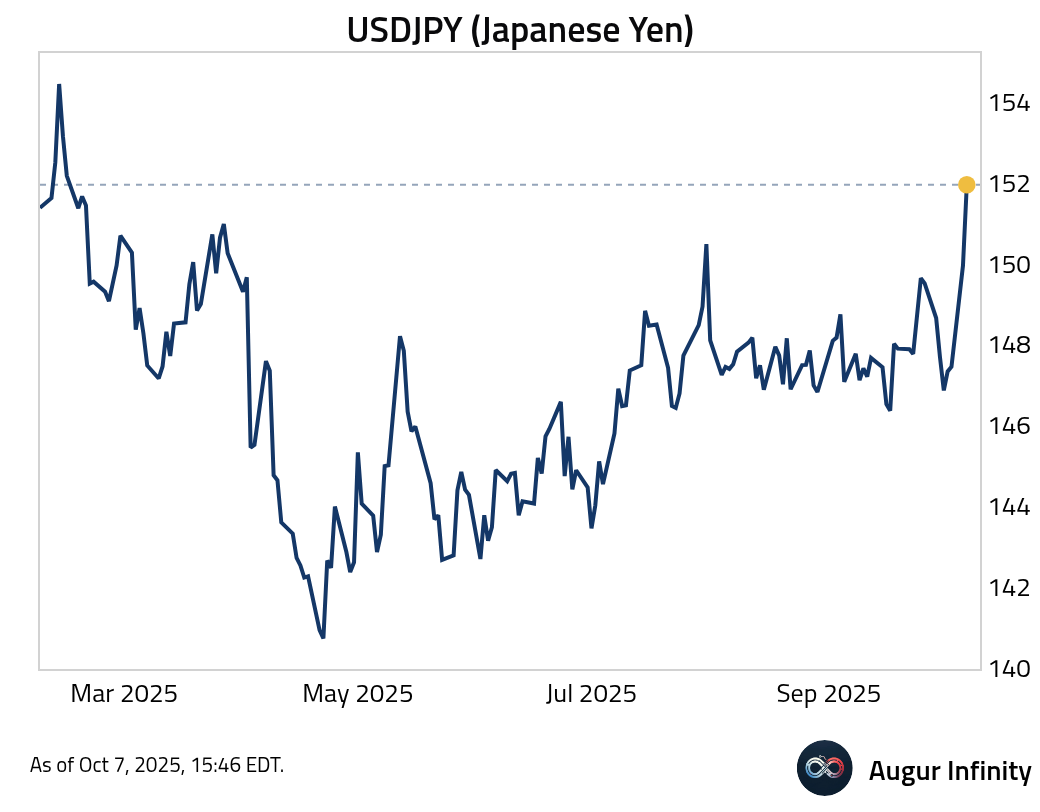

- The yen is trading at the weakest level against USD since March 2025.

- The yuan depreciated by 0.3% today, a 2.2σ move.

Commodities

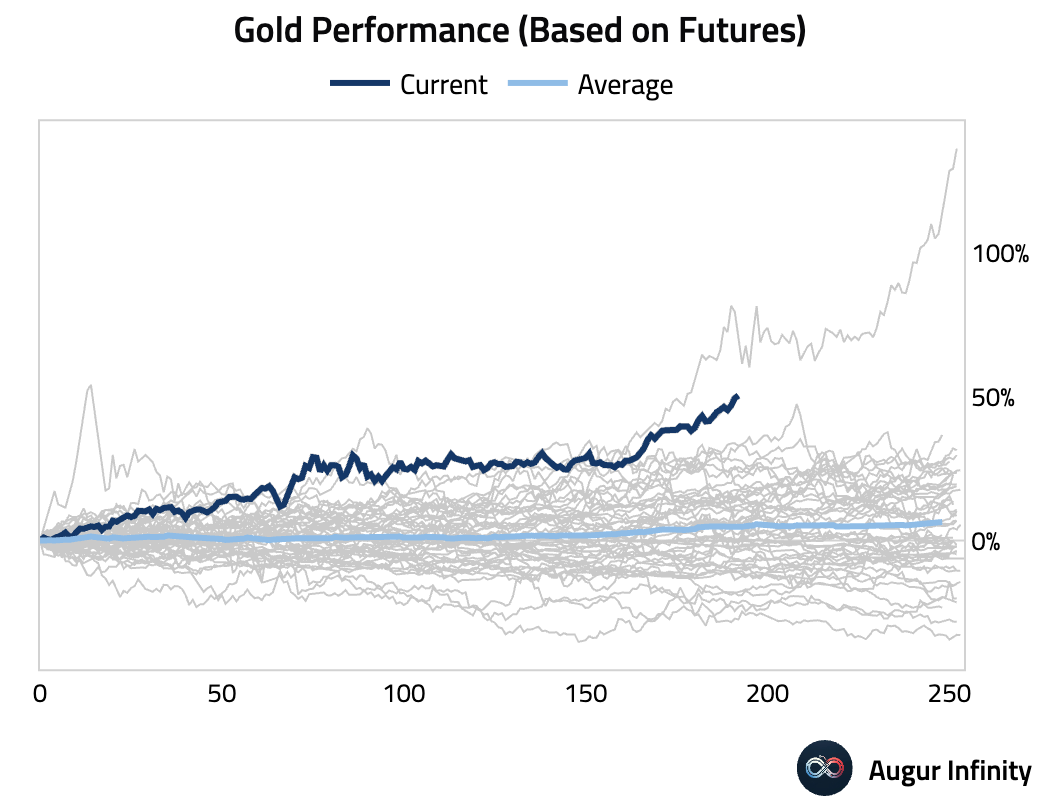

- The YTD performance of gold is the best since 1979.

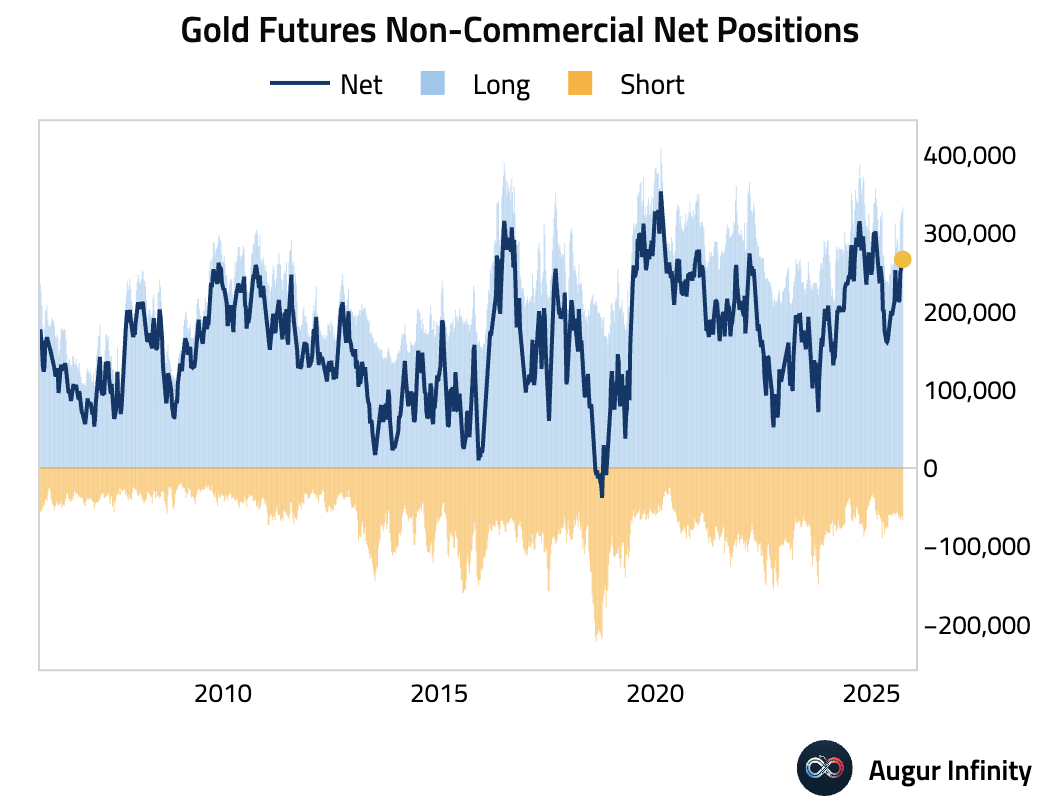

- Speculative net positions in gold are getting longer.

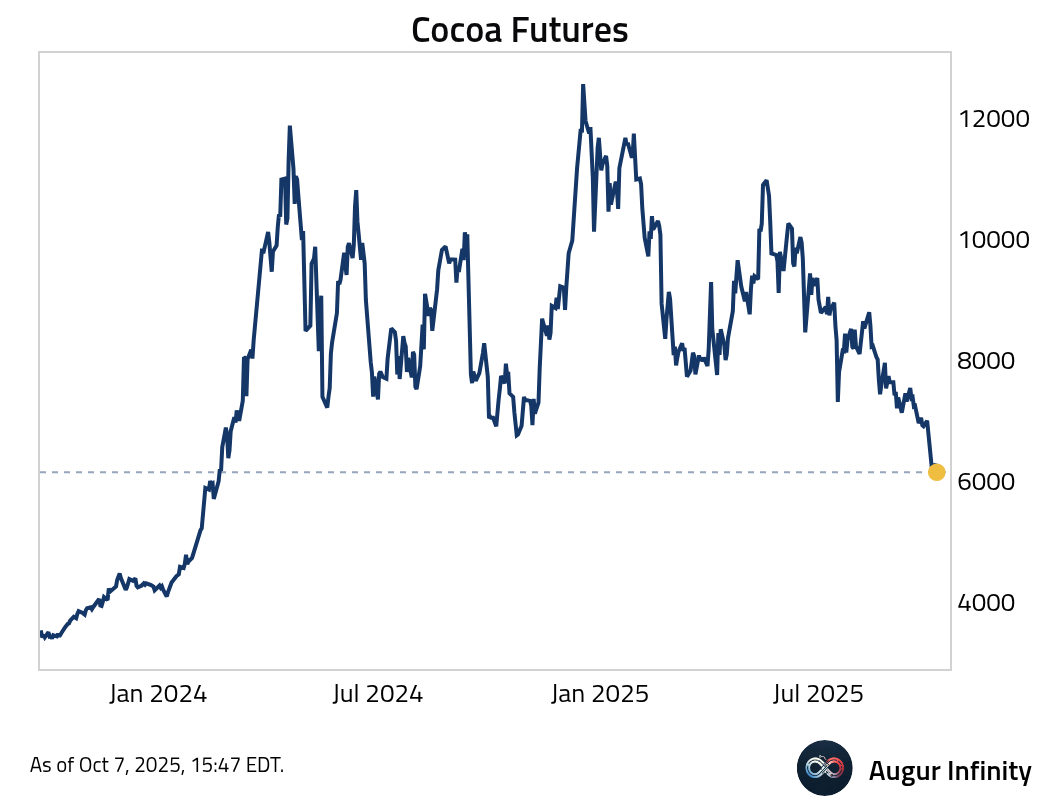

- Cocoa fell to the lowest level since February 2024.

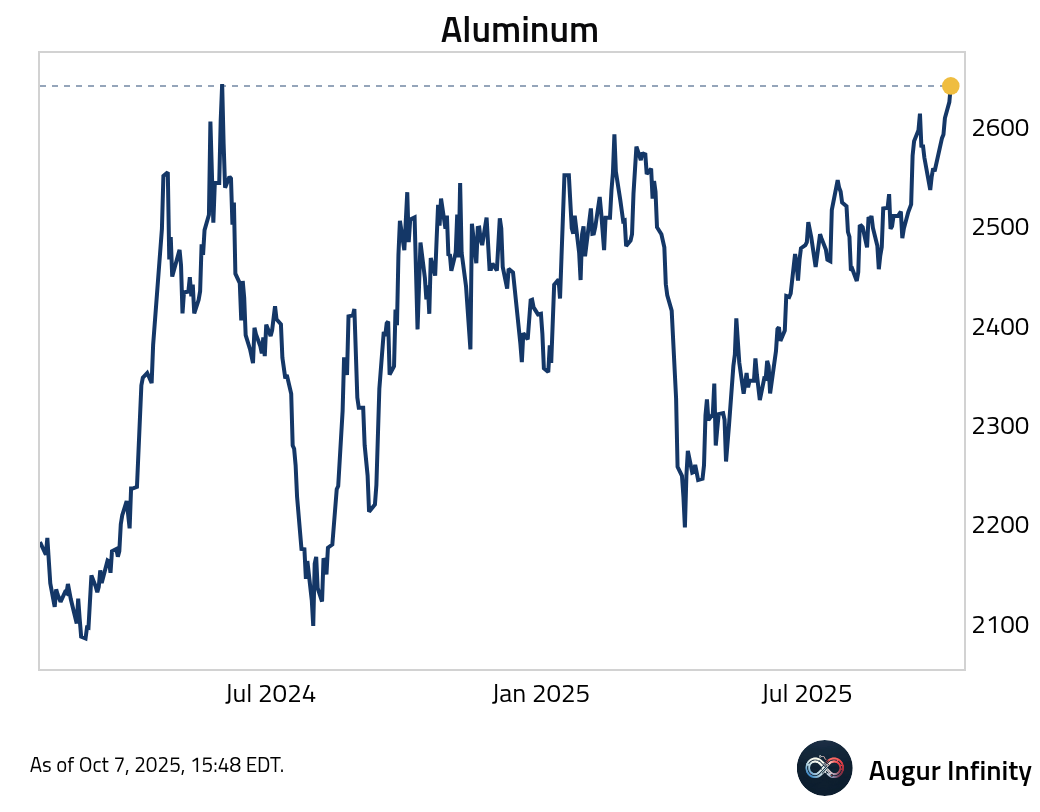

- Aluminum futures, on a roll-adjusted basis, hit the best level since May 2024.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.