Headlines

- Concern is growing that ongoing political paralysis in France may cause the country to miss its deadline for submitting a 2026 budget.

- Reports from China following the Golden Week holiday indicate that while travel volume was high, consumer spending was restrained.

- FOMC minutes show that Fed officials are divided, but saw another two interest rate cuts by the end of 2025.

Global Economics

United States

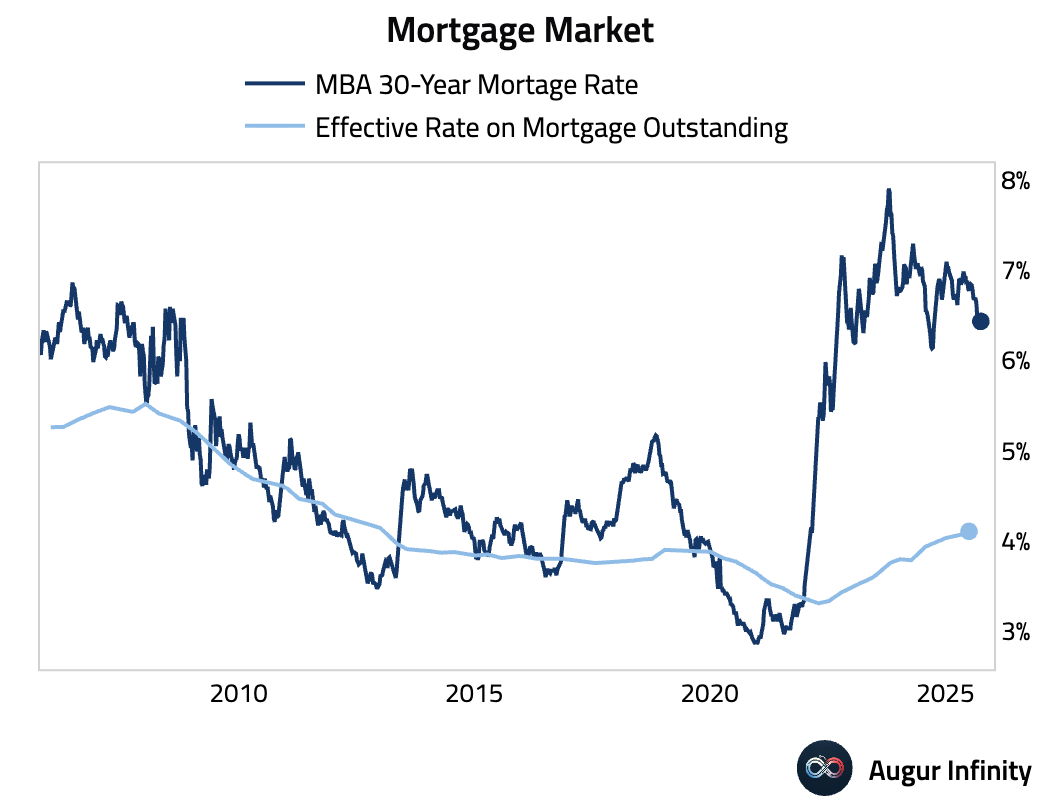

- The 30-year fixed mortgage rate edged down slightly to 6.43% from 6.46%.

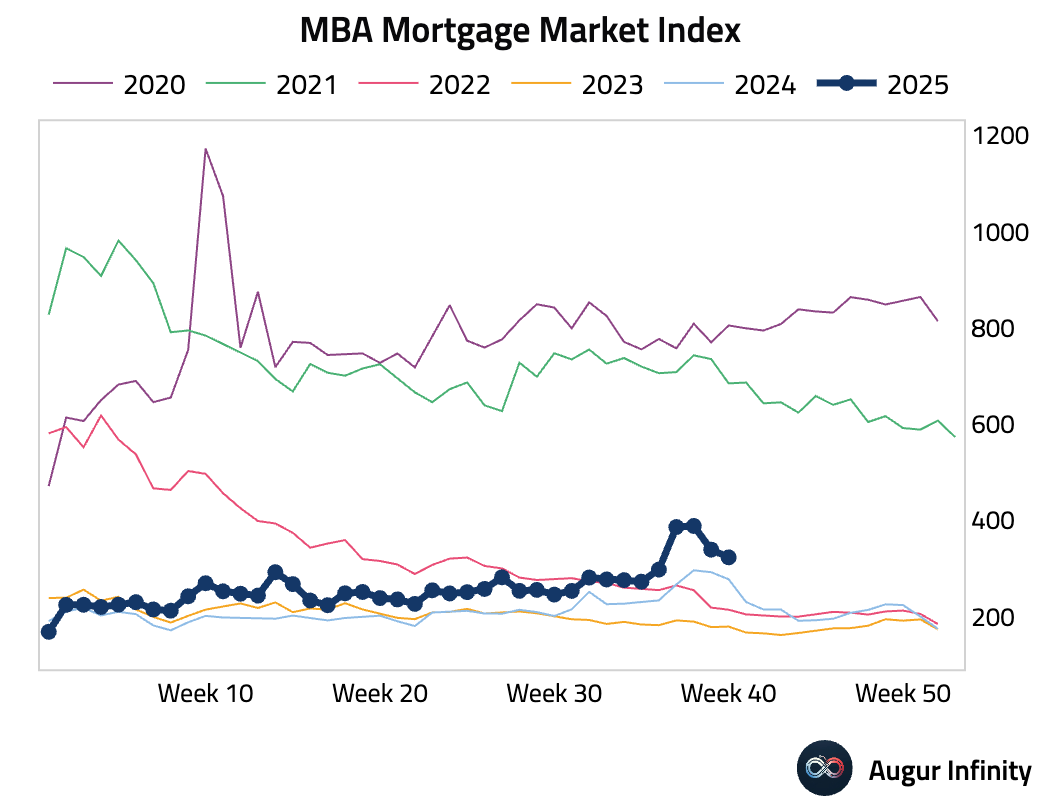

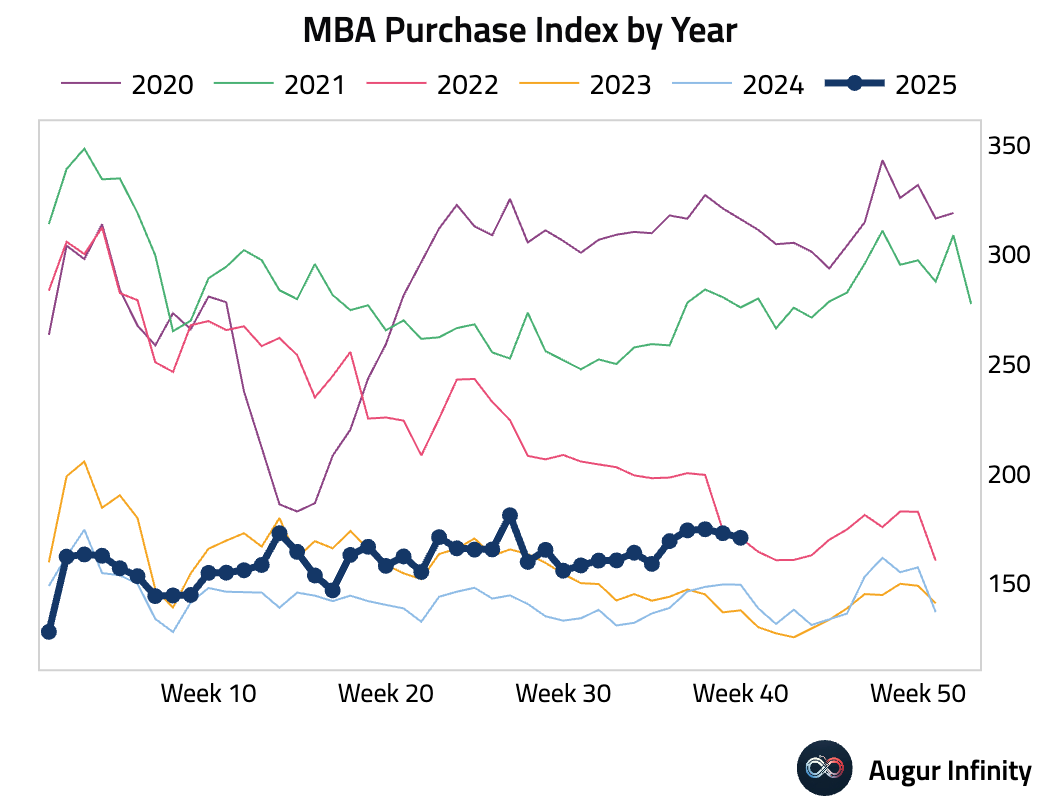

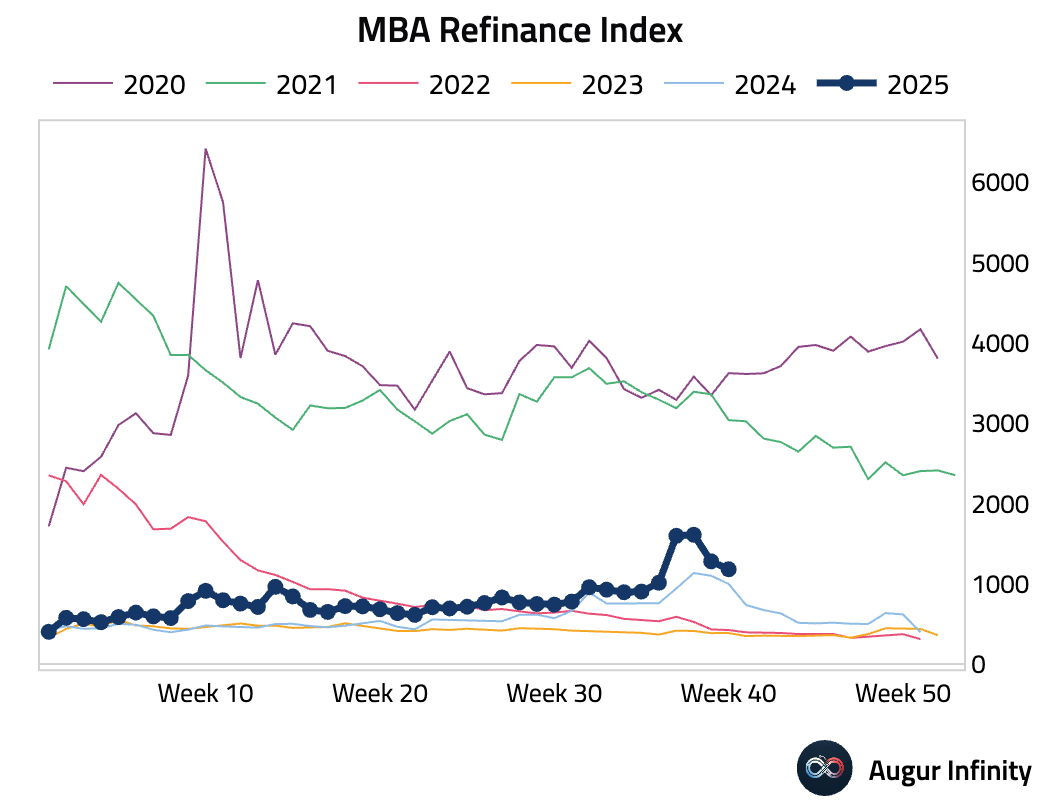

- US Mortgage Market Index fell for a fourth consecutive week, driven by a sharp decline in refinancing activity (Mortgage Applications: -4.7%, Refinance Index: -7.7%). The purchase index saw a smaller dip (-1.2%).

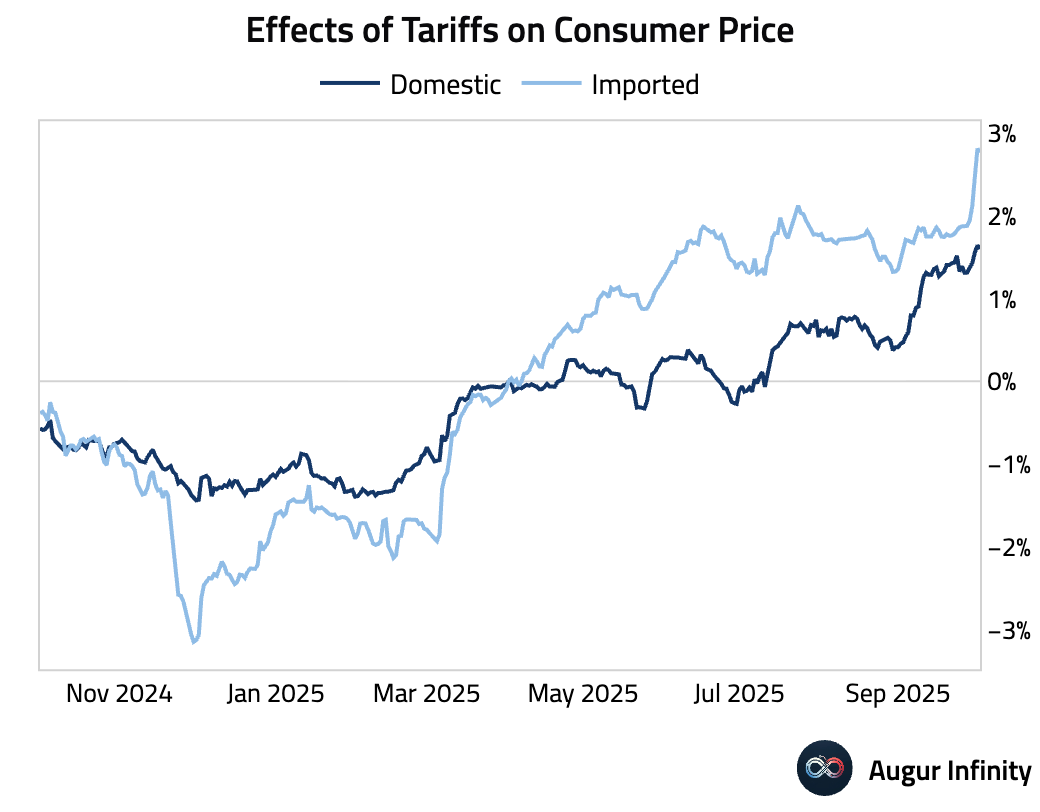

- The Tariff Tracker from HBS Pricing Lab suggests the 10% lumber and 25% wood furniture tariffs announced on September 29th are already affecting retail prices.

Source: Cavallo, Llamas & Vazquez (2025)

Europe

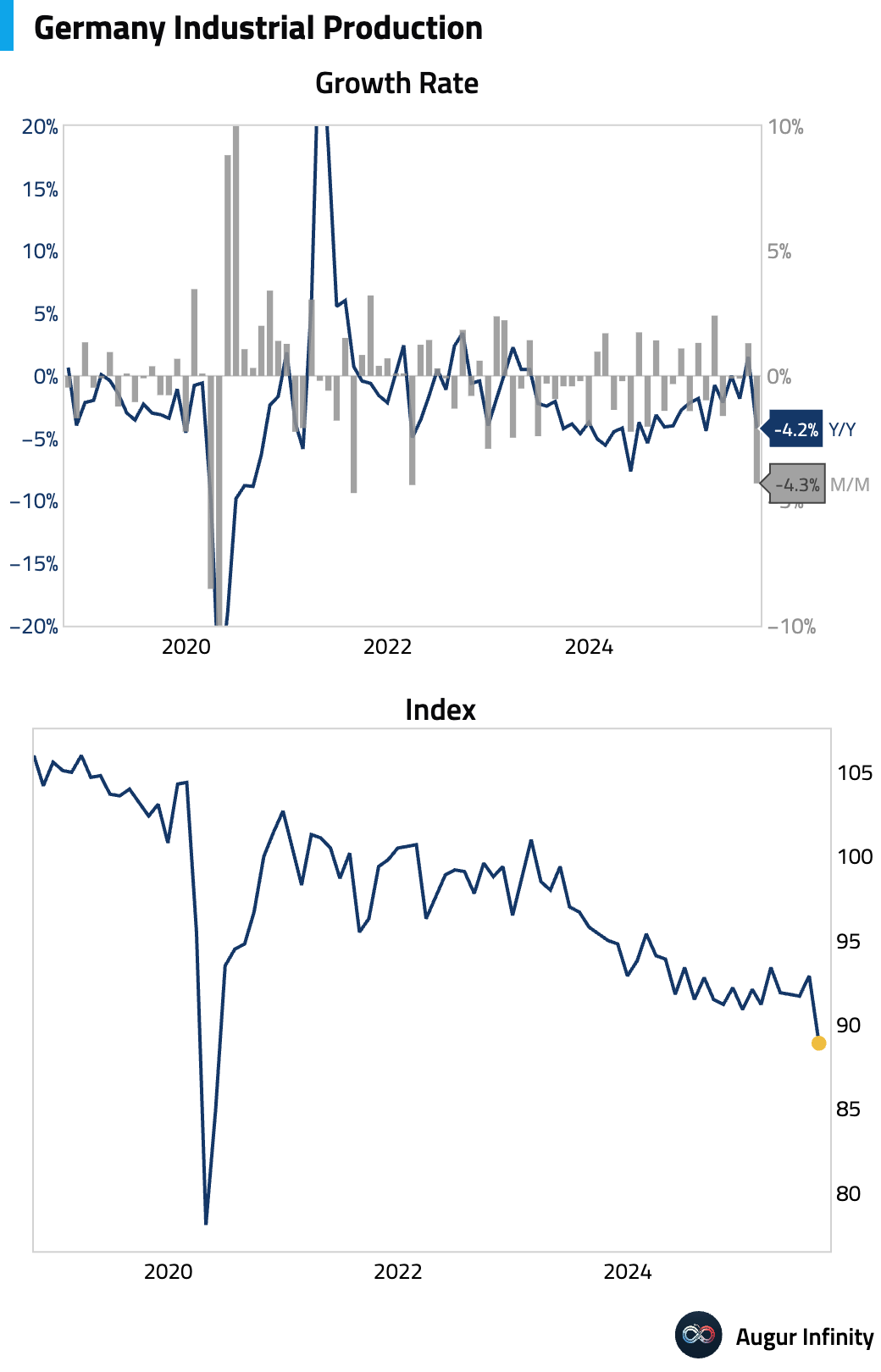

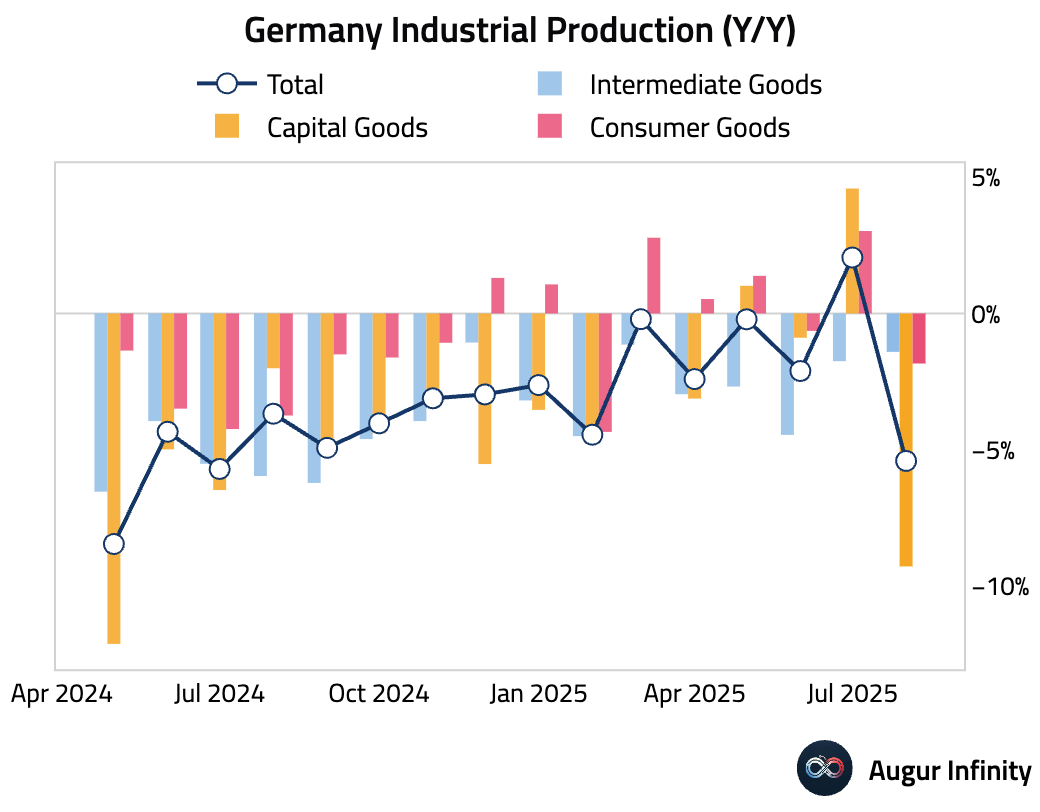

- German industrial production plunged 4.3% M/M in August, drastically missing expectations for a 1.0% decline and reversing a 1.3% gain from July. The downturn was broad-based, with significant contractions in capital goods (-6.3%), intermediate goods (-3.8%), and consumer goods (-2.1%). The energy sector also saw a steep drop of 6.6%.

Interactive chart on Augur Infinity

Interactive chart on Augur Infinity

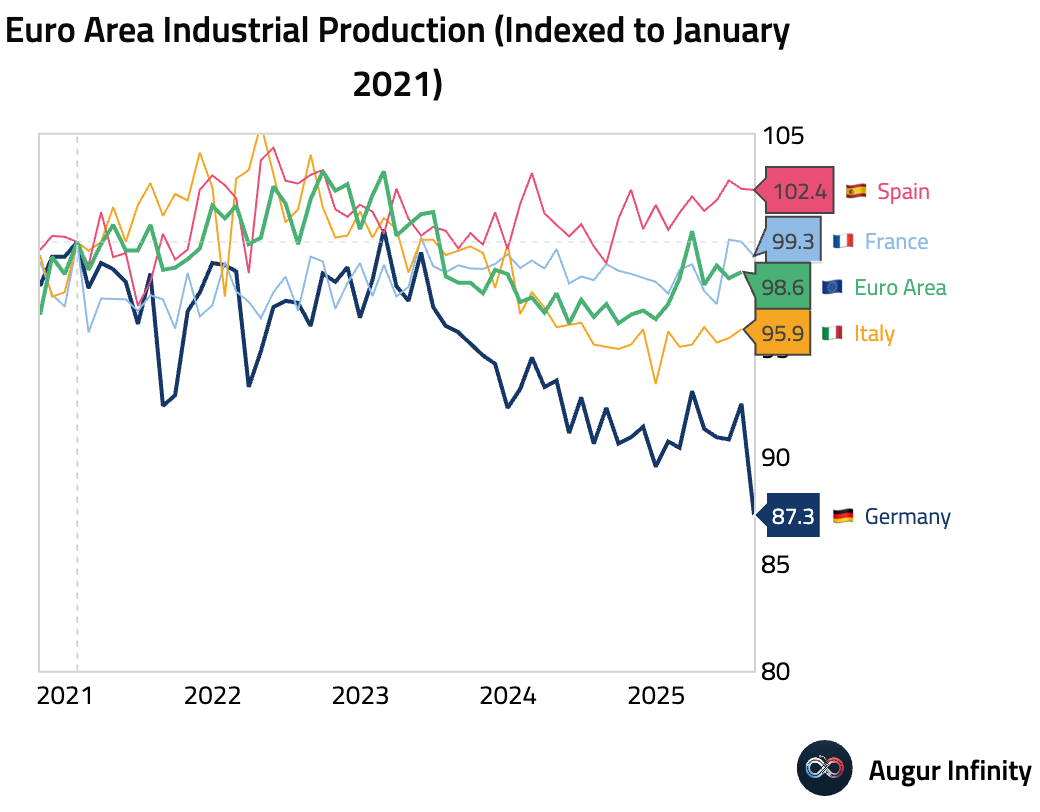

Germany's industrial production has meaningfully underperformed that of its peers over the past few years.

Interactive chart on Augur Infinity

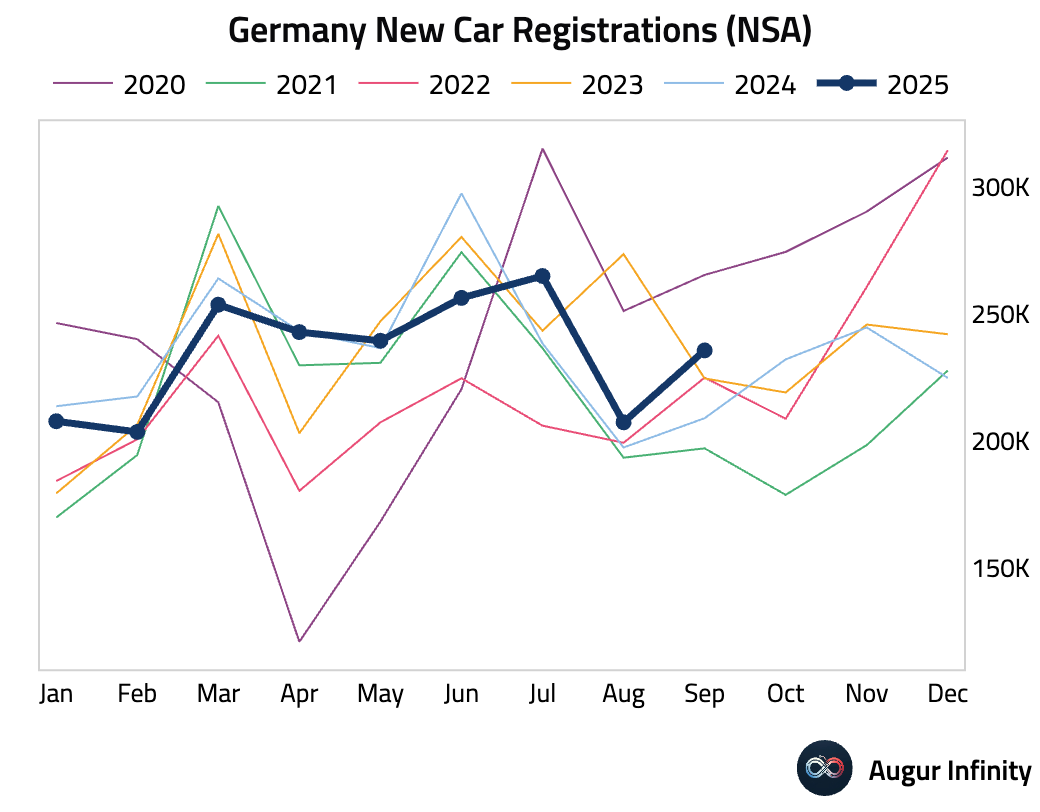

- New car registrations in Germany accelerated in September, growing at the fastest pace in 17 months (act: 12.8% Y/Y, prev: 5.0%).

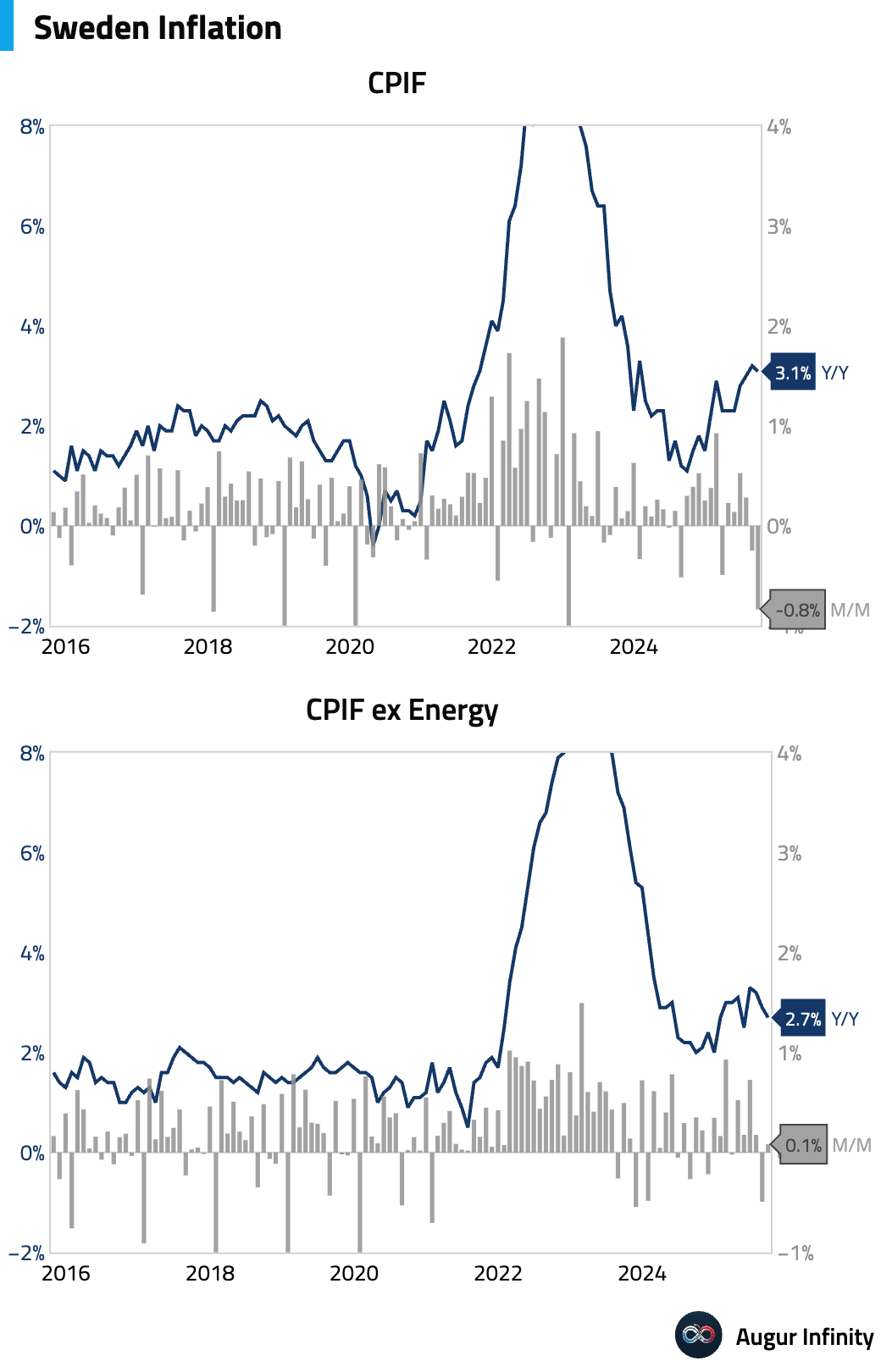

- Swedish inflation eased slightly in September. The headline CPIF rate fell to 3.1% Y/Y from 3.2%, just below the consensus of 3.2%. The monthly CPIF reading was 0.1%, also missing estimates.

Interactive chart on Augur Infinity

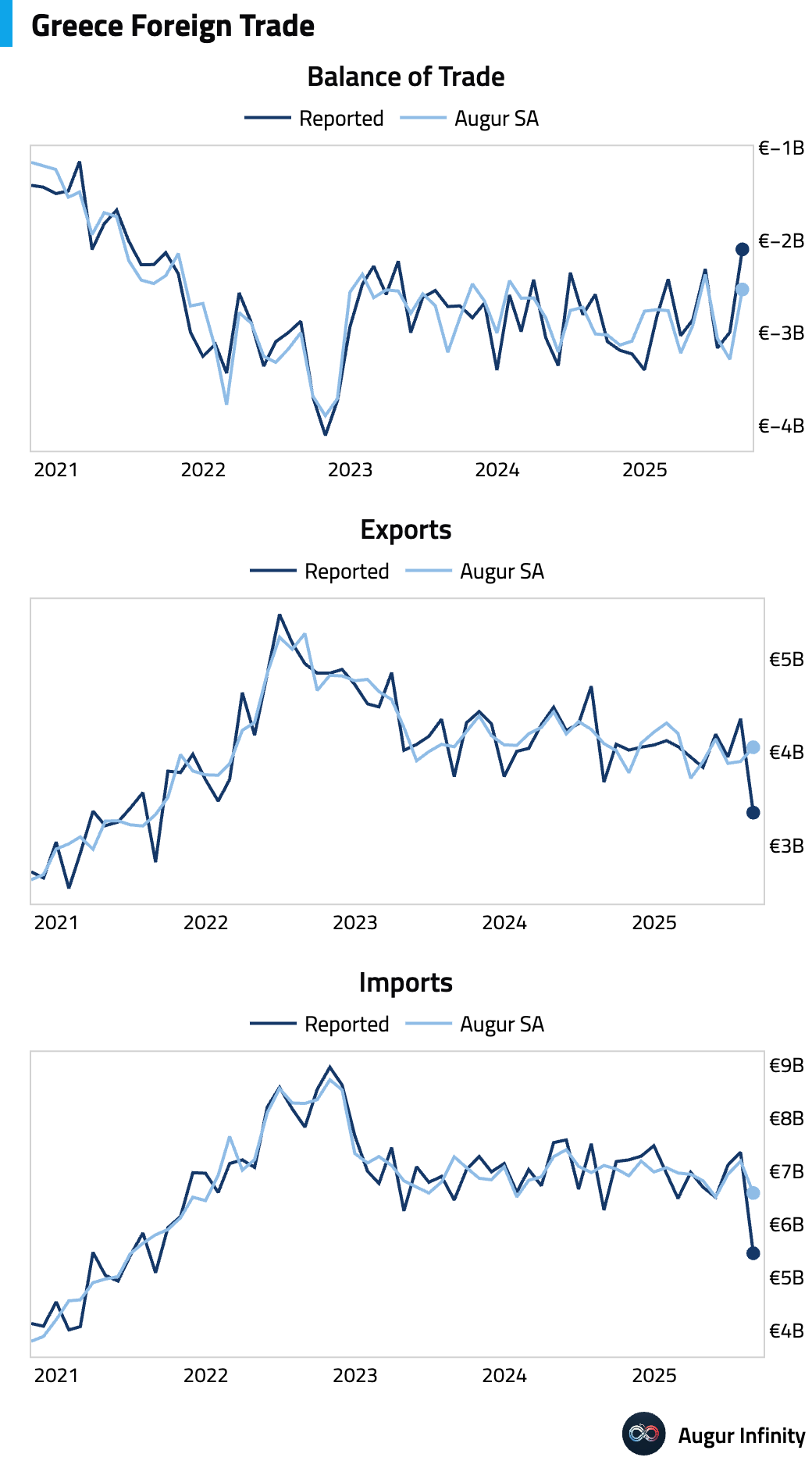

- Greece’s trade deficit narrowed in August to its smallest level in over four years, driven by a surge in exports and a decline in imports (act: -€2.1B, prev: -€3.0B).

Asia-Pacific

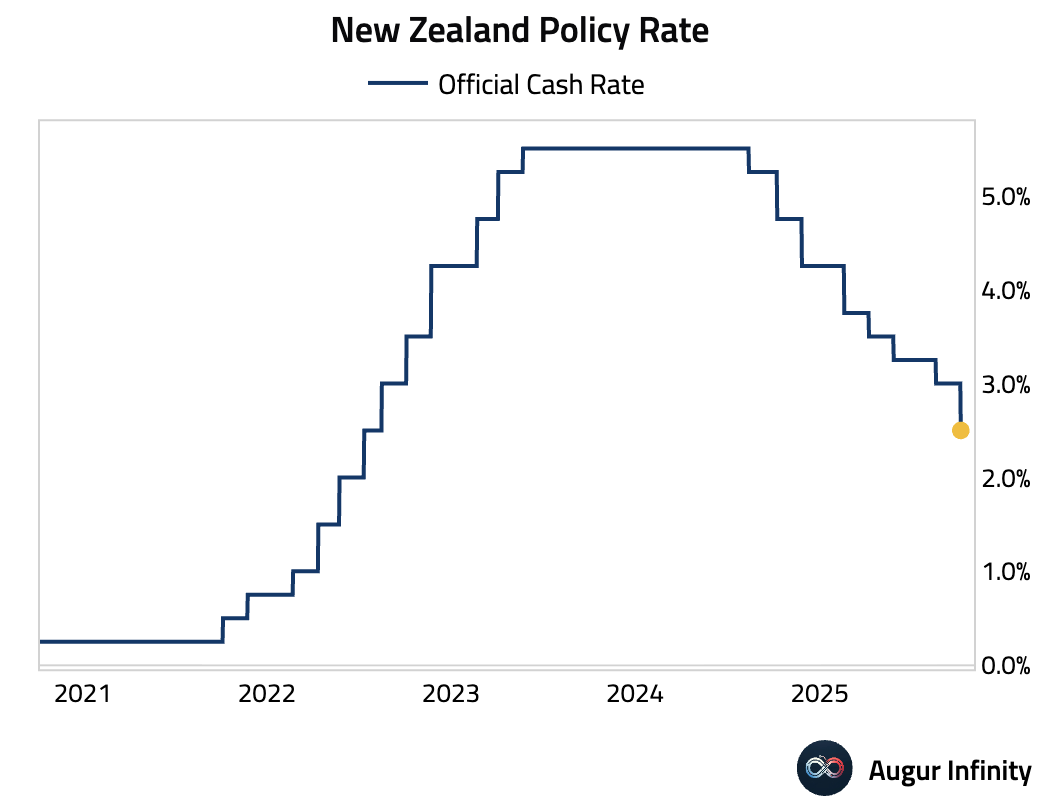

- The Reserve Bank of New Zealand cut its official cash rate by 50 bps to 2.50%, a larger move than the 25 bps cut anticipated by markets. This marks the first rate reduction since July 2022 and follows a period of holding rates at 3.00%.

Interactive chart on Augur Infinity

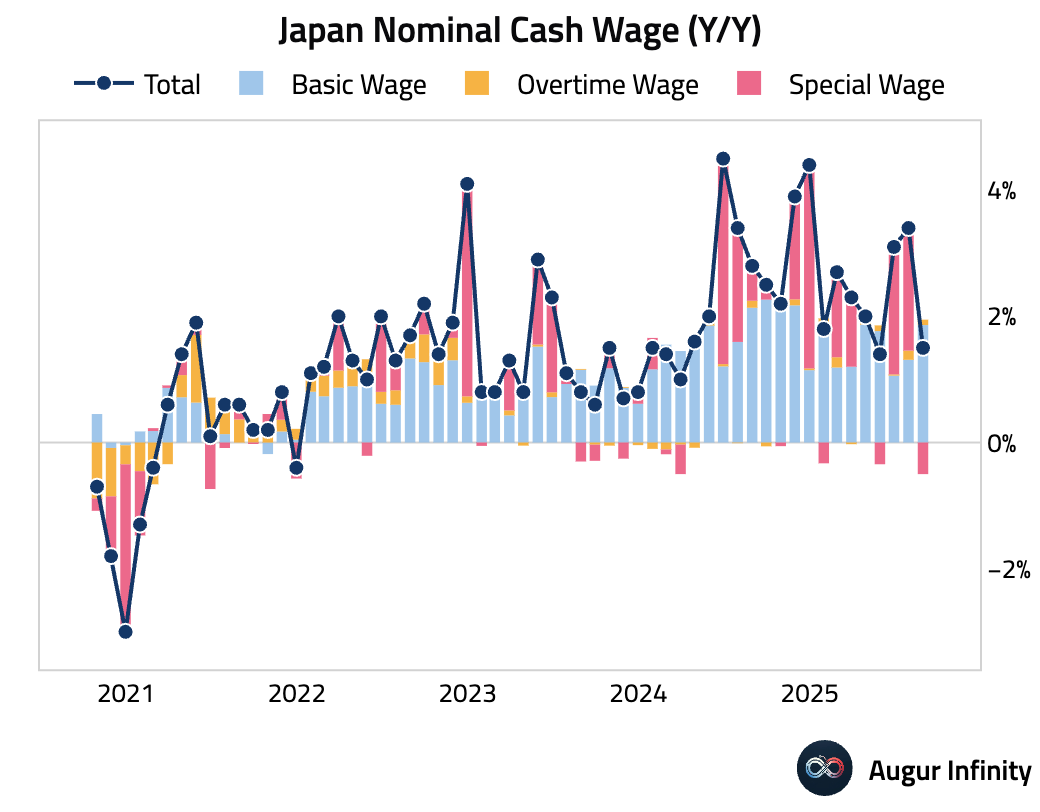

- Japanese nominal cash wage growth slowed sharply to 1.5% Y/Y in August from 3.4% in July, missing consensus of 2.6% by a wide margin. The slowdown was primarily due to a drop in special wages as summer bonus effects faded. The decline in real wages widened to -1.4%.

Interactive chart on Augur Infinity

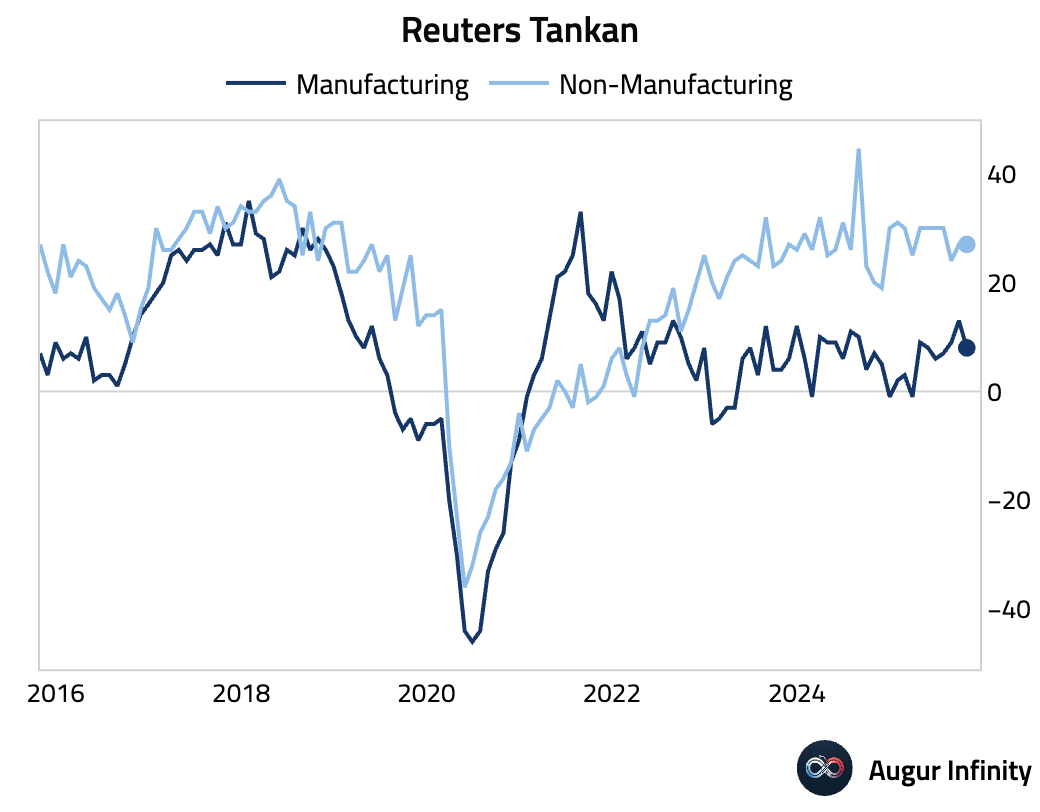

- The Reuters Tankan Manufacturing index fell in October, snapping a two-month streak of improvements (act: 8, prev: 13). The non-manufacturing index remained stable.

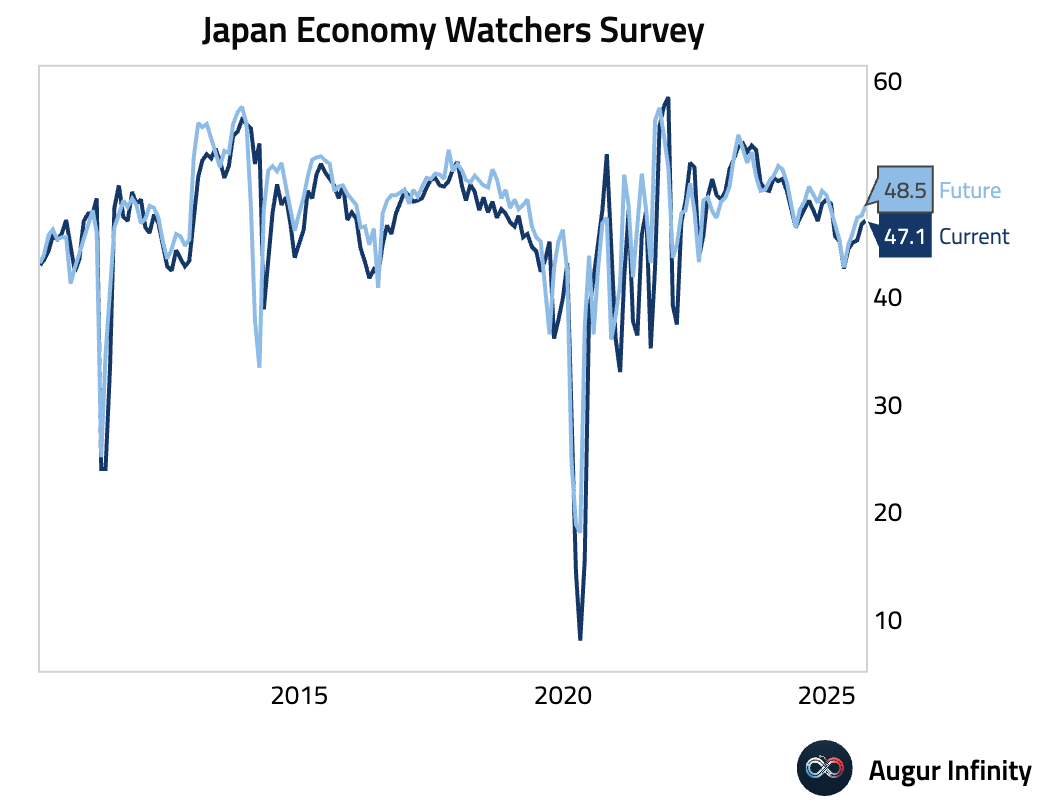

- Japan's Economy Watchers Survey for September showed a slight improvement in both current conditions and the outlook, though both indices remain below the neutral 50-mark, indicating prevailing pessimism (Current: 47.1, Outlook: 48.5).

Interactive chart on Augur Infinity

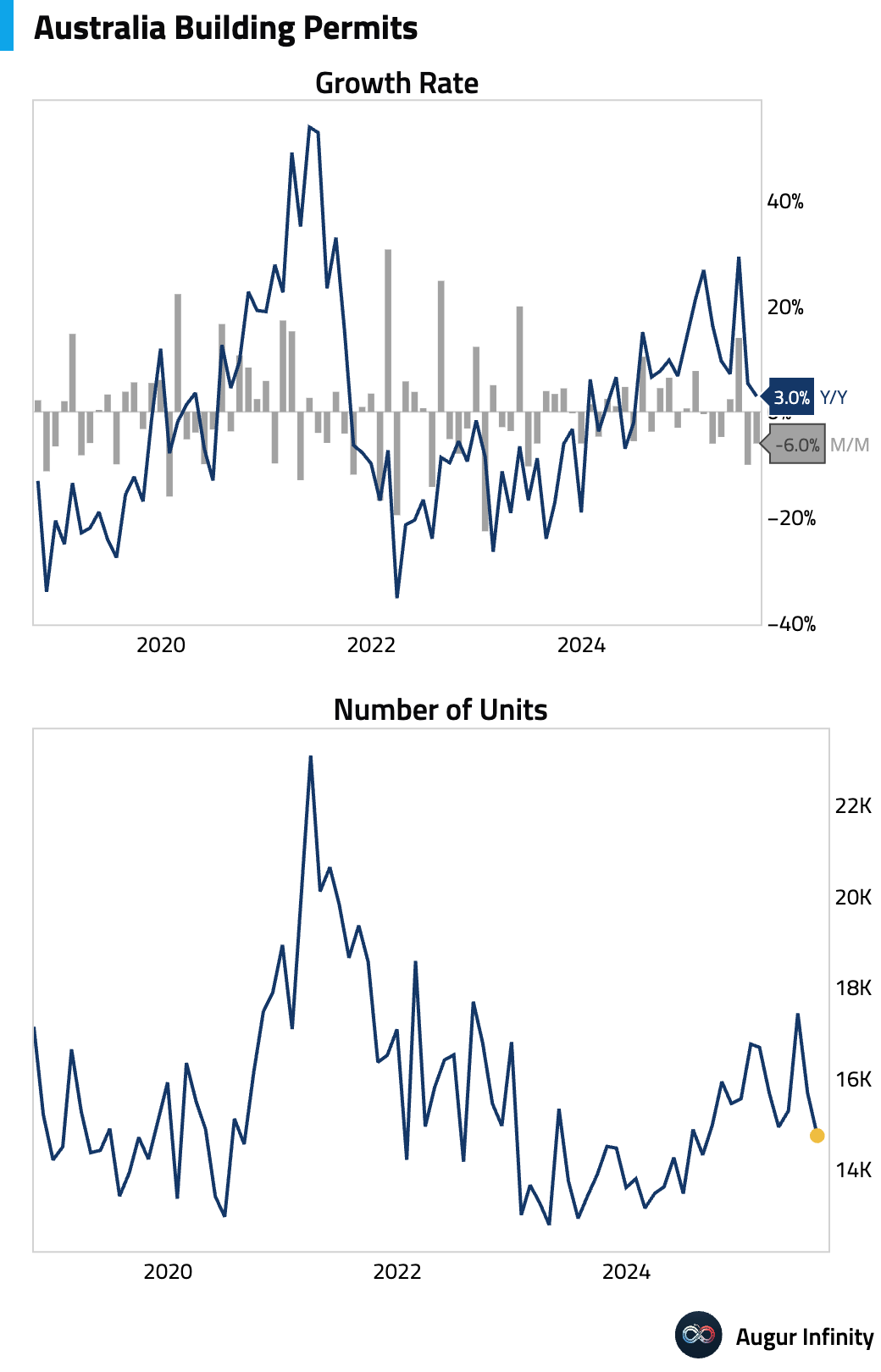

- Final data for Australian building permits confirmed a contraction for the third consecutive month in August, though the pace of decline eased from the prior month (act: -6.0% M/M, prev: -10.0%).

Interactive chart on Augur Infinity

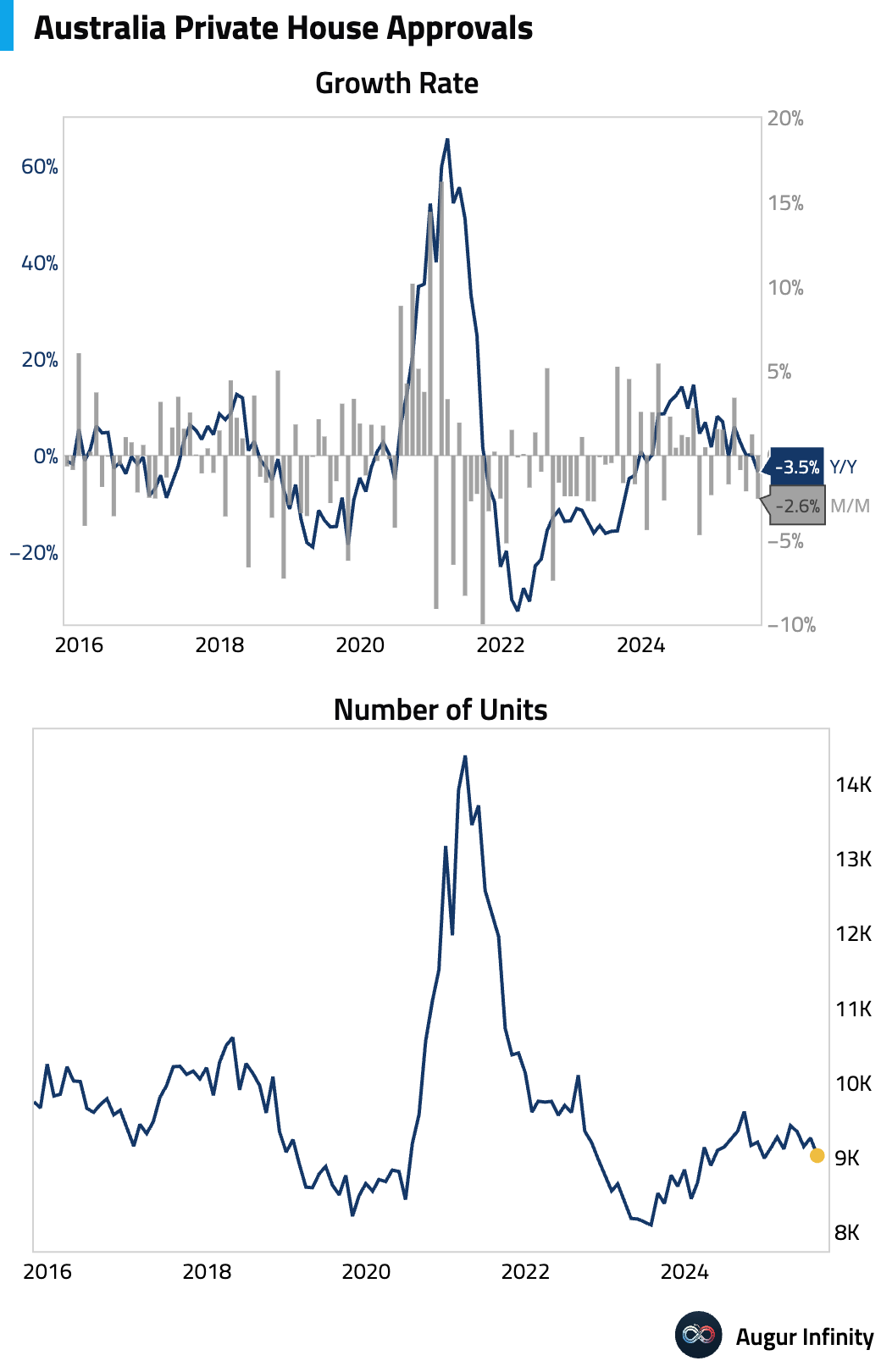

- Approvals for private sector houses in Australia fell in August, reversing the gain seen in July and marking the largest decline in nearly a year (act: -2.6% M/M, prev: 1.3%).

Interactive chart on Augur Infinity

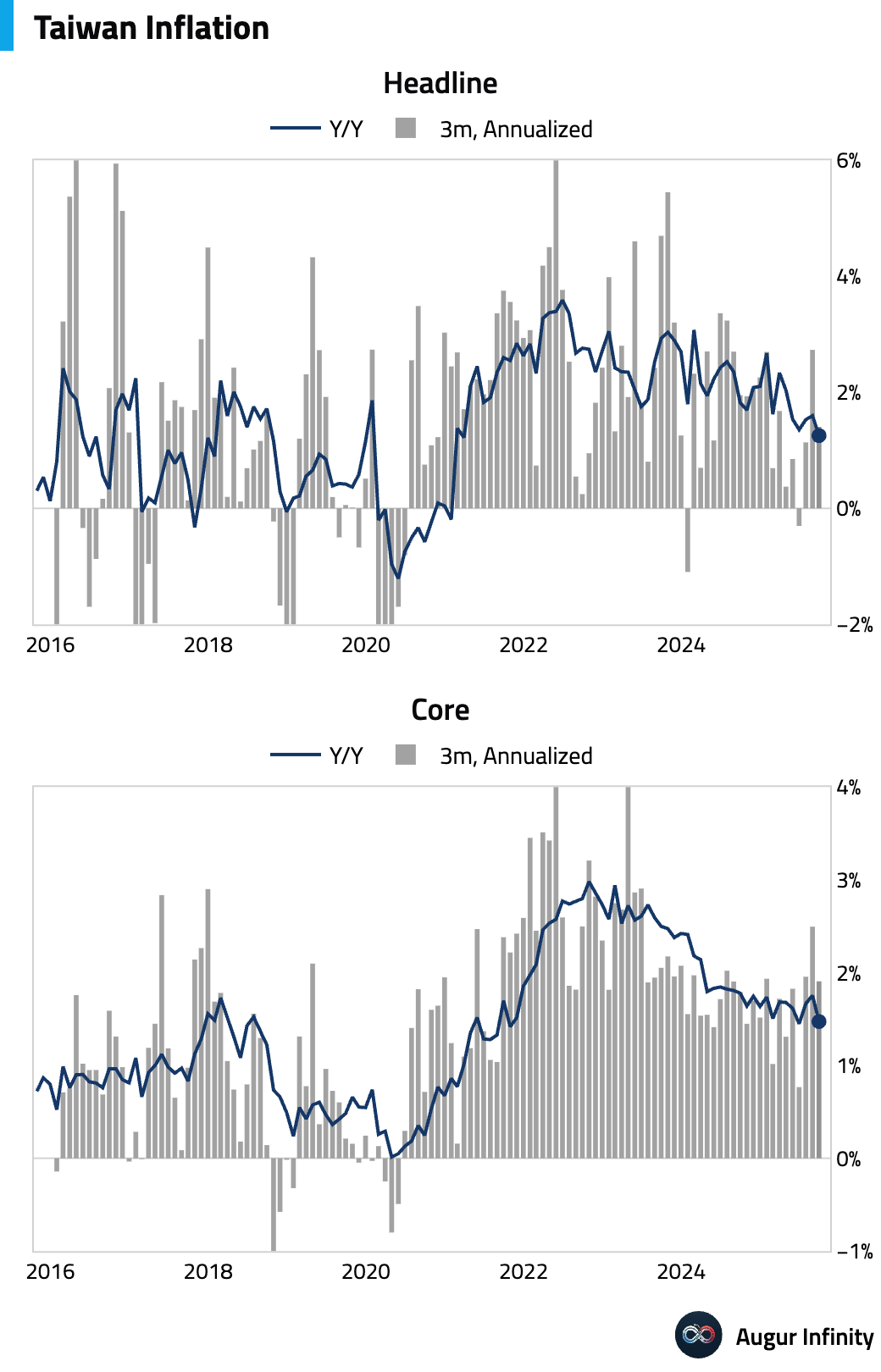

- Taiwan's annual inflation rate cooled to 1.25% in September from 1.6% in August, hitting its lowest level since March 2021.

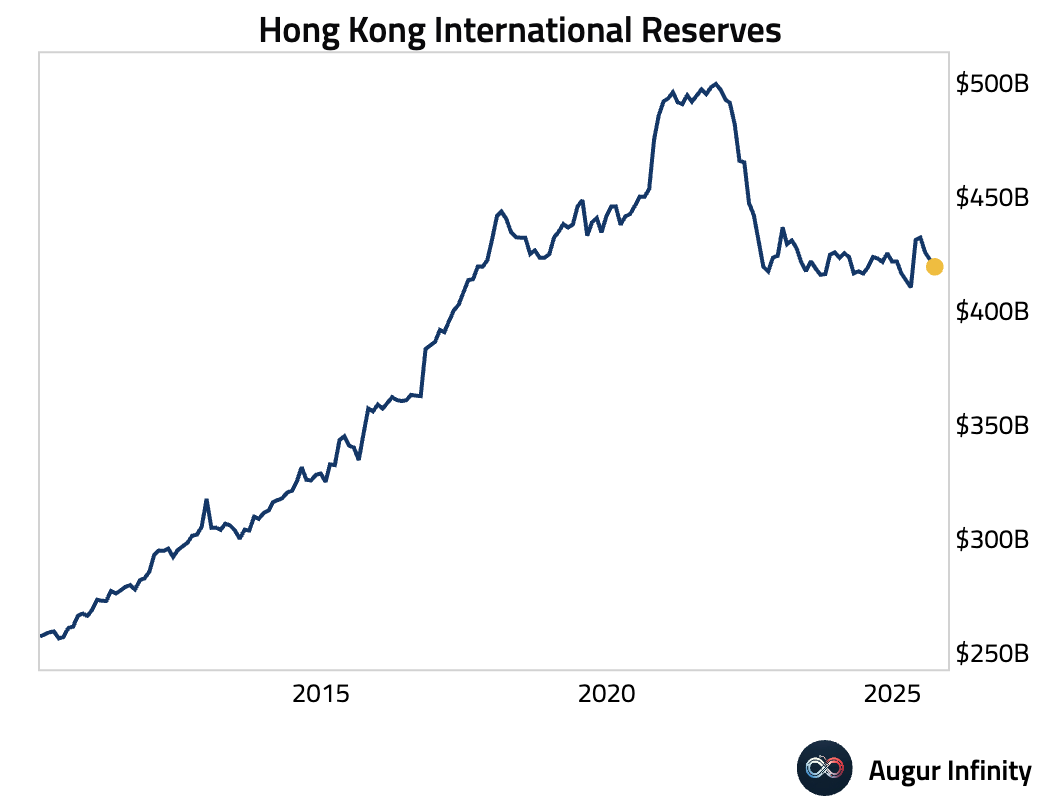

- Hong Kong's official reserve assets edged down slightly in September (act: $419.2B, prev: $421.6B).

Emerging Markets ex China

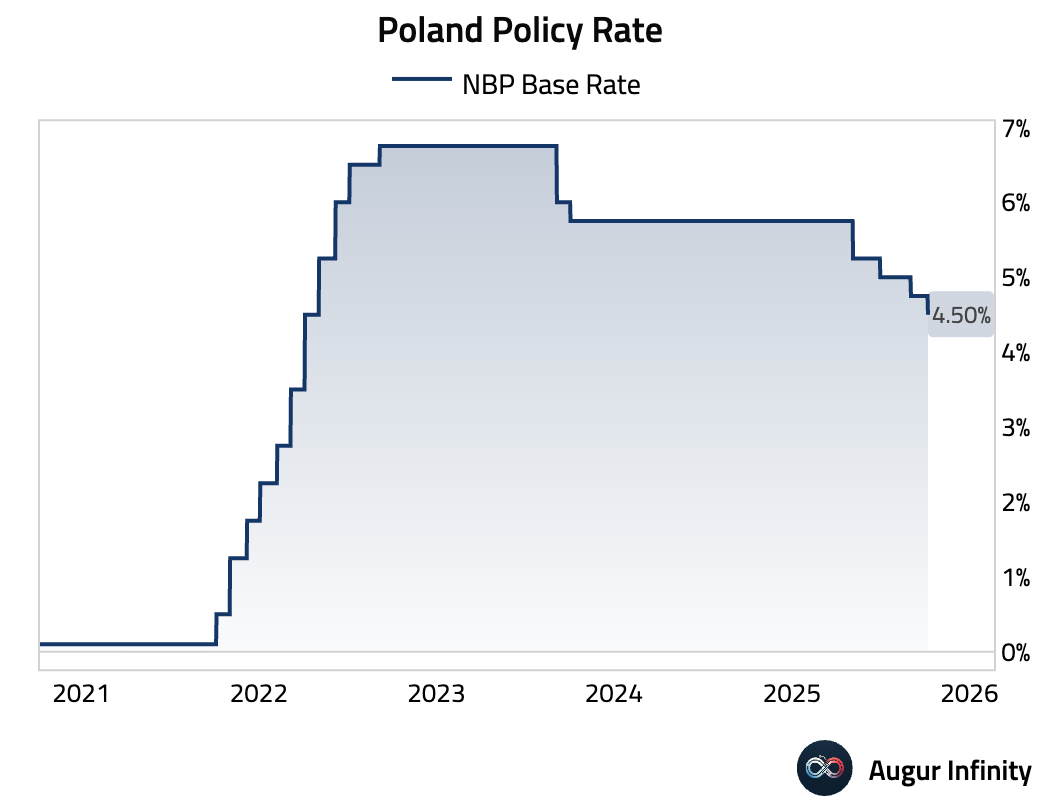

- The National Bank of Poland delivered a surprise 25 bps interest rate cut, lowering its key policy rate to 4.50%. Markets had expected the rate to remain on hold at 4.75%.

Interactive chart on Augur Infinity

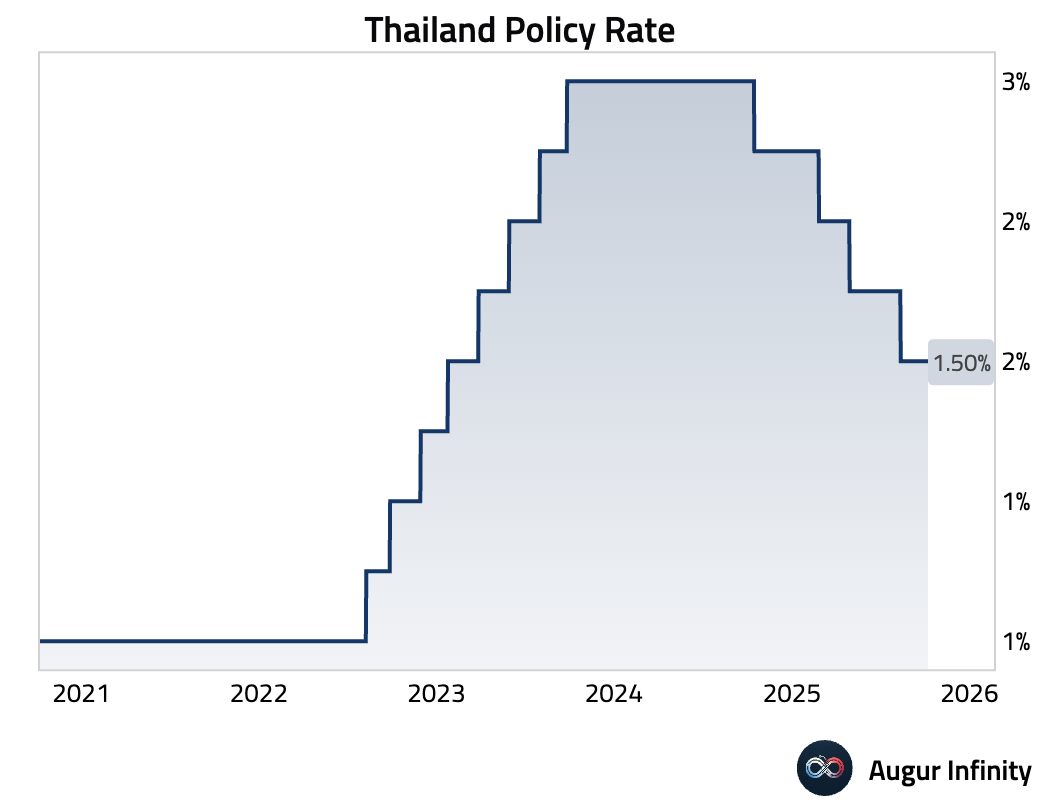

- The Bank of Thailand held its benchmark interest rate steady at 1.50%.

Interactive chart on Augur Infinity

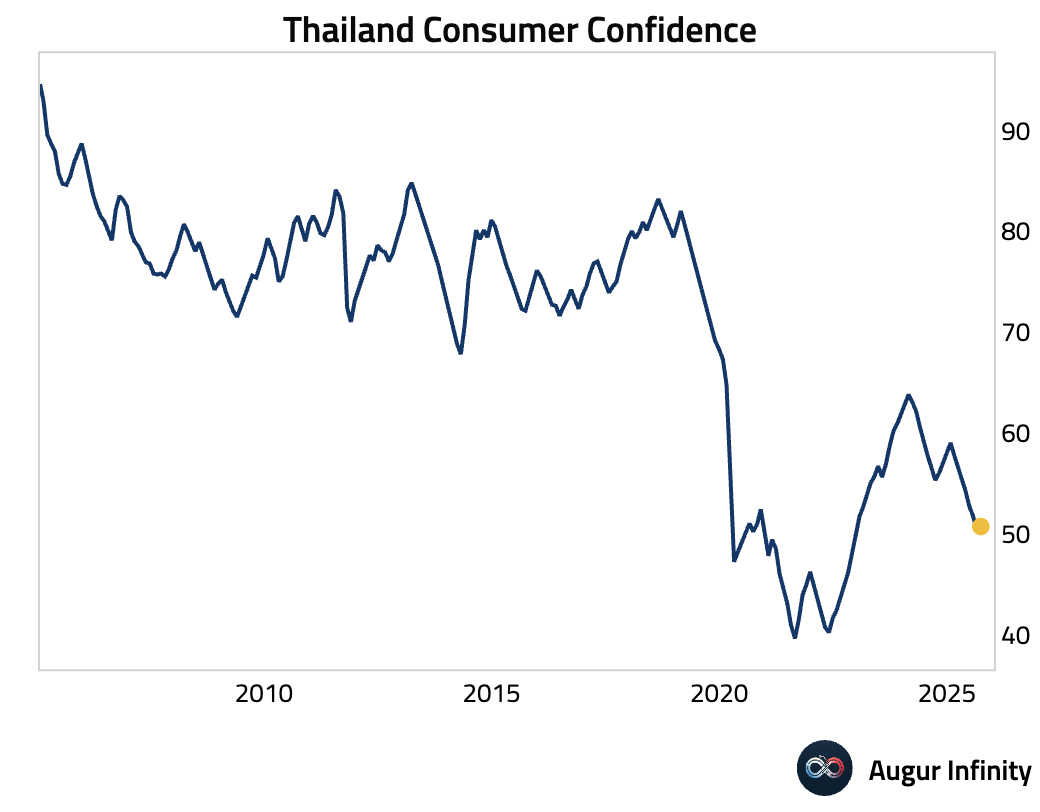

- Consumer confidence in Thailand improved for a second straight month in September, reaching its highest level since July (act: 50.7, prev: 50.1).

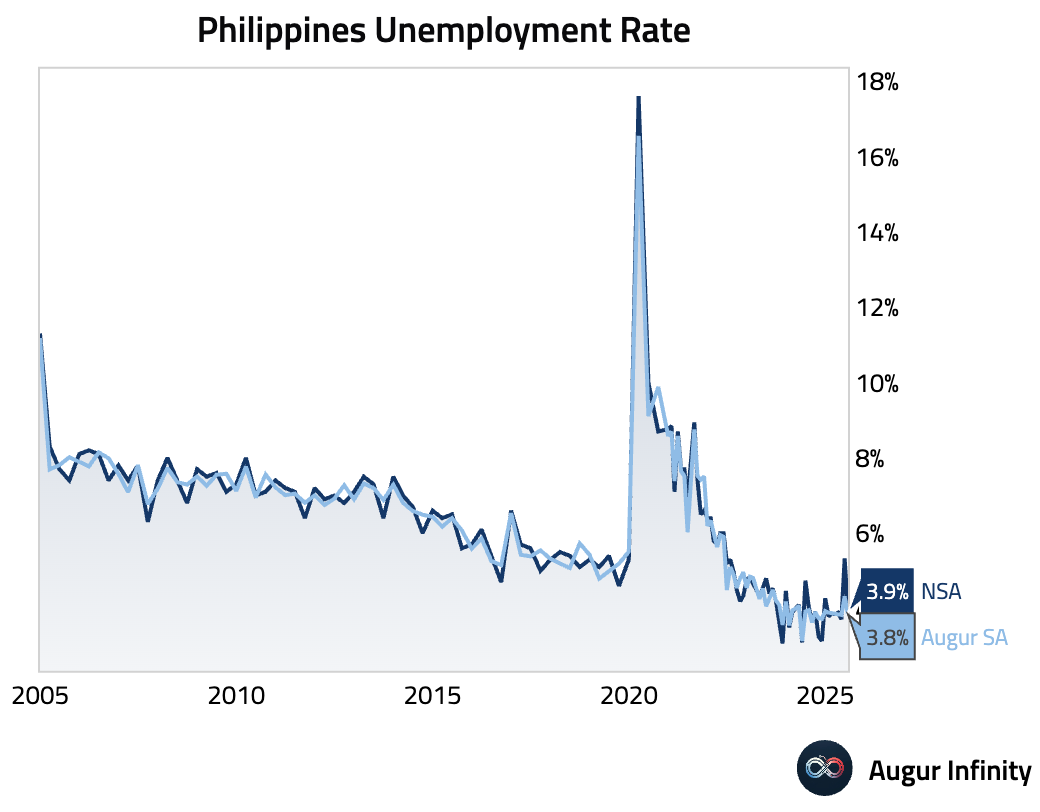

- The unemployment rate in the Philippines dropped sharply in August, falling to its lowest level in three months (act: 3.9%, prev: 5.3%).

- Indonesian consumer confidence edged lower in September but remained firmly in optimistic territory (act: 115.0, prev: 117.2).

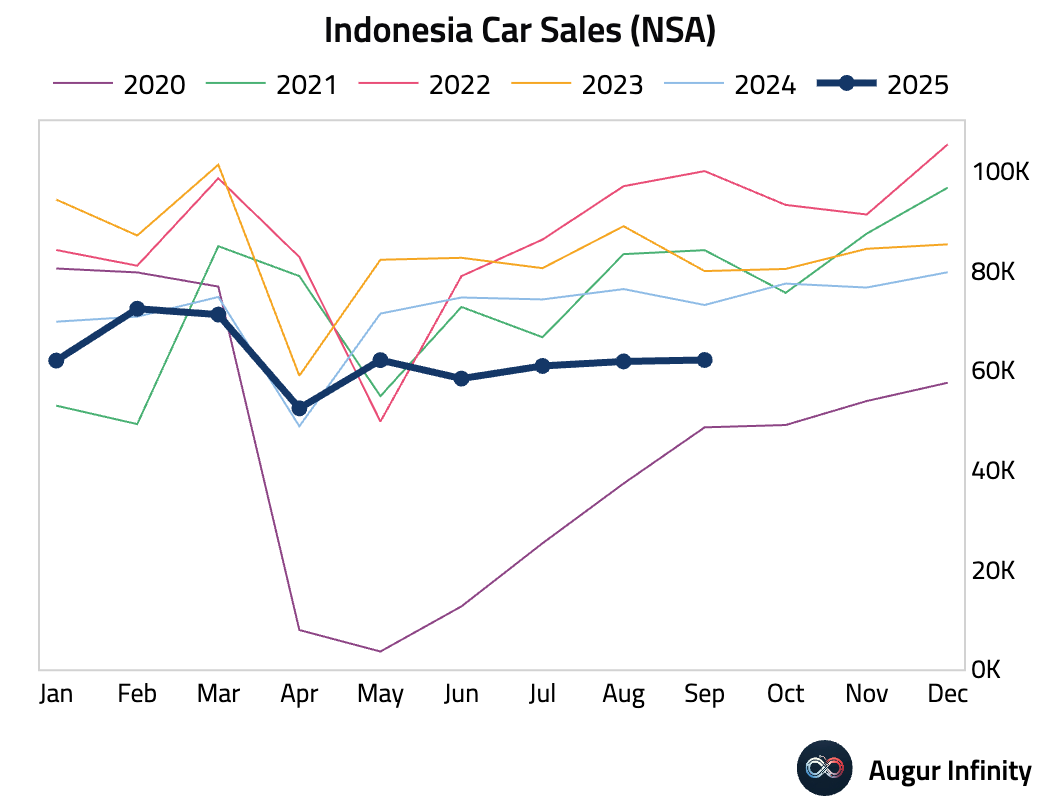

- Indonesian car sales continued to contract on a year-over-year basis in September, though the pace of decline lessened from the previous month (act: -15.1% Y/Y, prev: -19.0%).

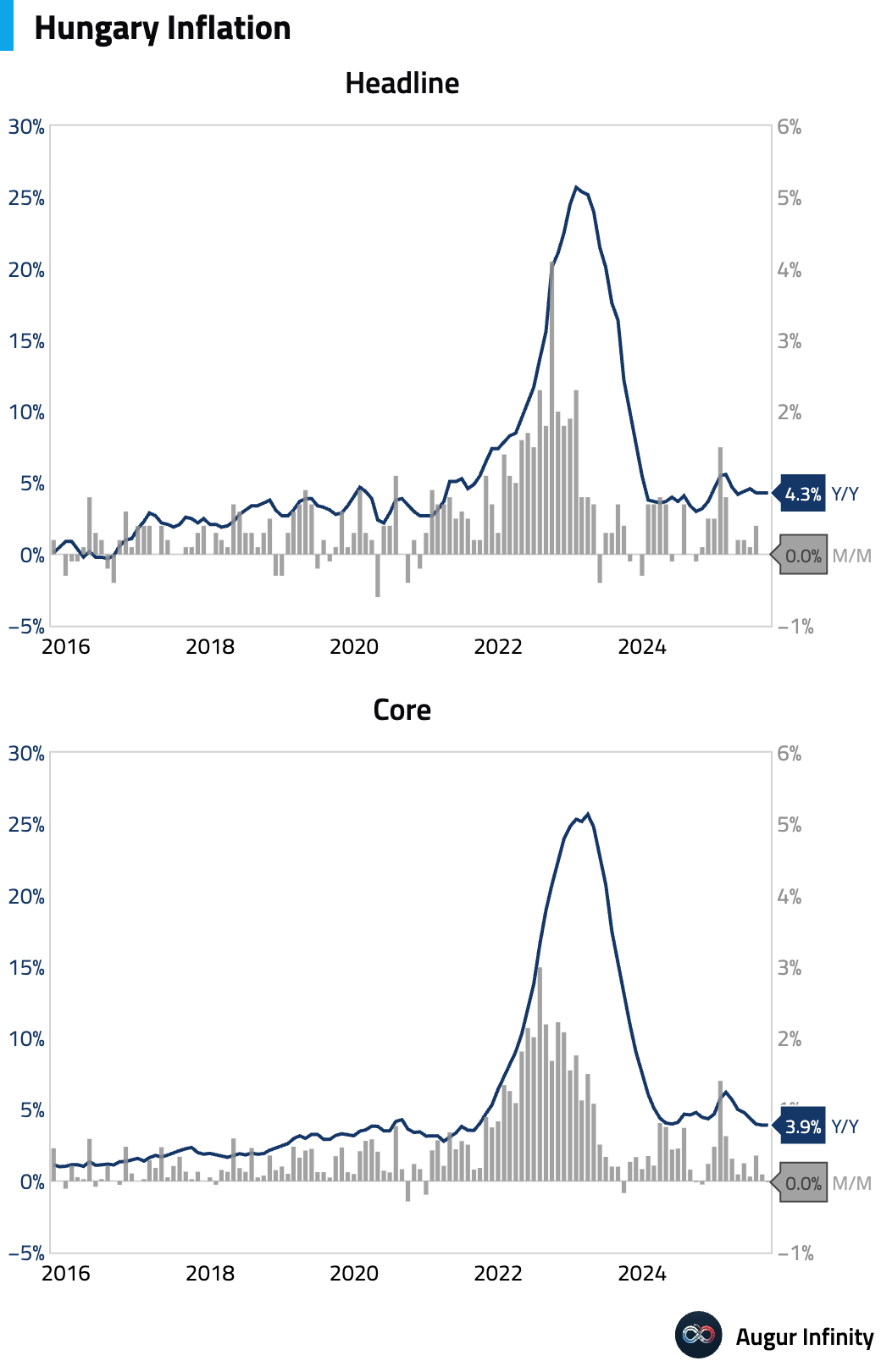

- Hungary's annual inflation rate was stable at 4.3% Y/Y in September, matching the previous month's reading and coming in slightly below consensus. Core inflation was also unchanged at 3.9% Y/Y.

Interactive chart on Augur Infinity

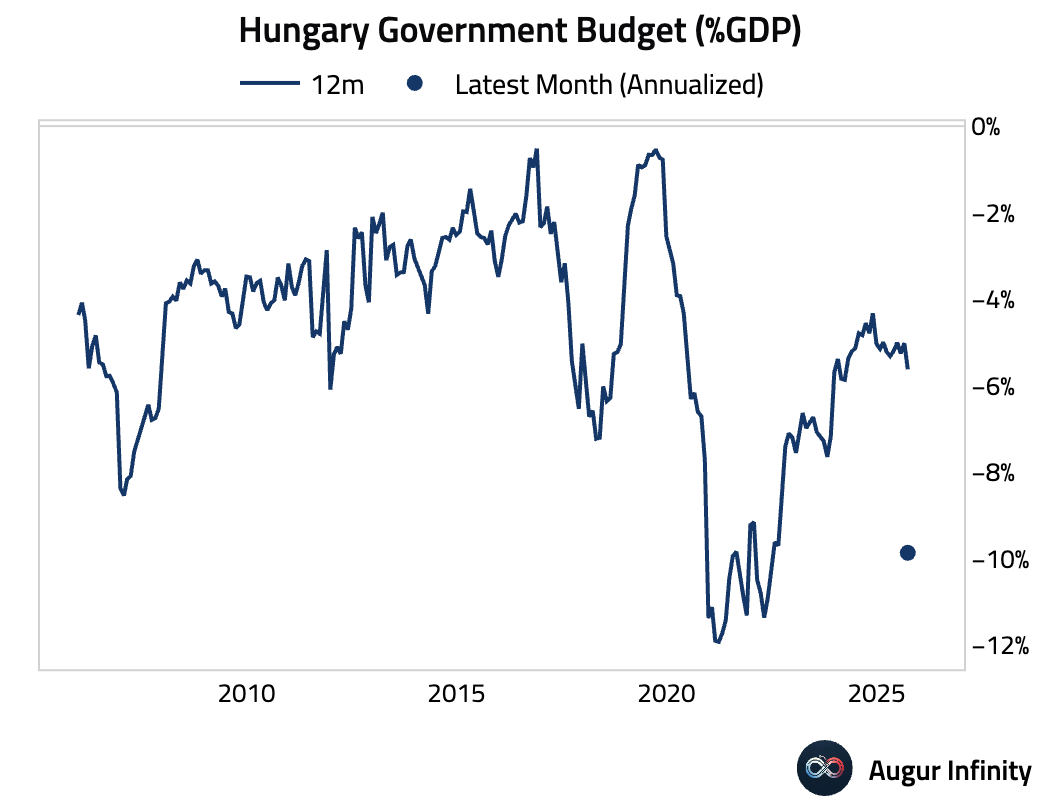

- Hungary's central government budget deficit widened in September (act: -HUF 303.2B, prev: -HUF 239.1B).

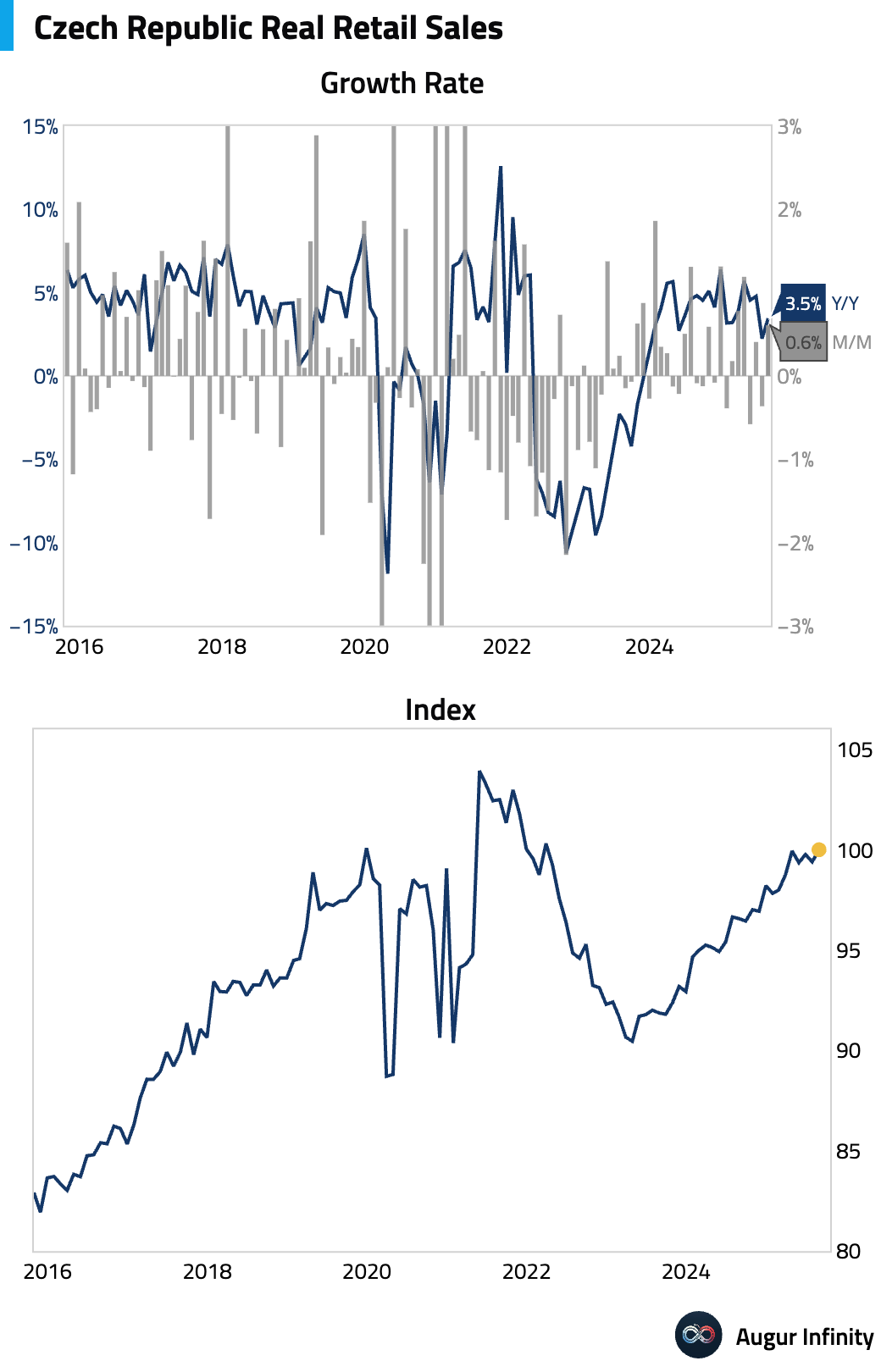

- Czech retail sales (excluding autos) grew more than expected in August, rising on both a monthly and annual basis (act: 0.6% M/M, est: n/a; act: 3.5% Y/Y, est: 3.2%).

Interactive chart on Augur Infinity

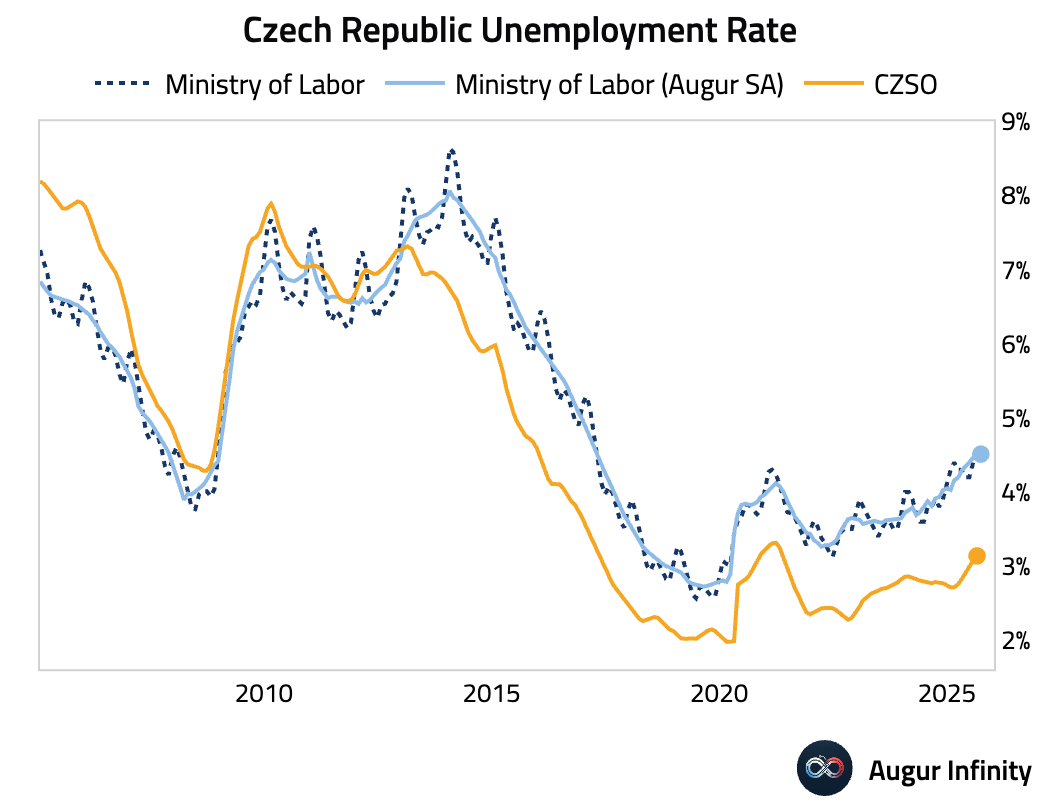

- The unemployment rate in the Czech Republic held steady at 4.5% in September, matching the prior month's reading.

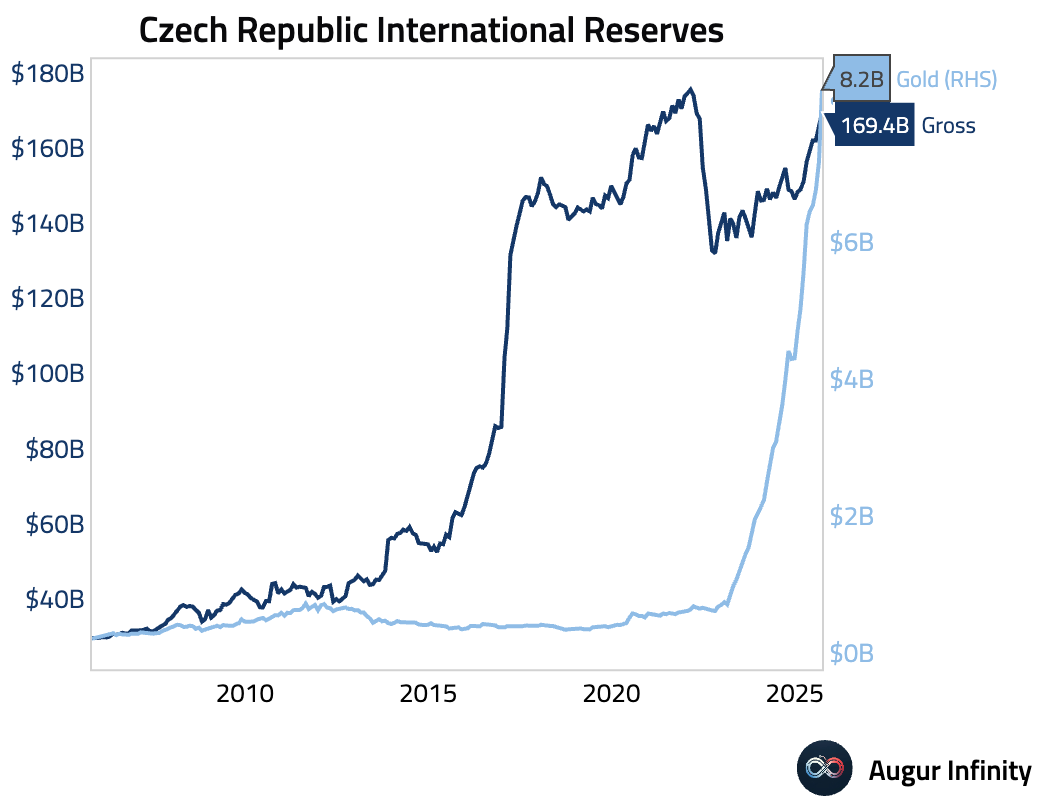

- The Czech Republic's official reserve assets increased in September, reaching their highest level since March 2022 (act: $169.4B, prev: $166.2B).

Global Markets

Cross Asset

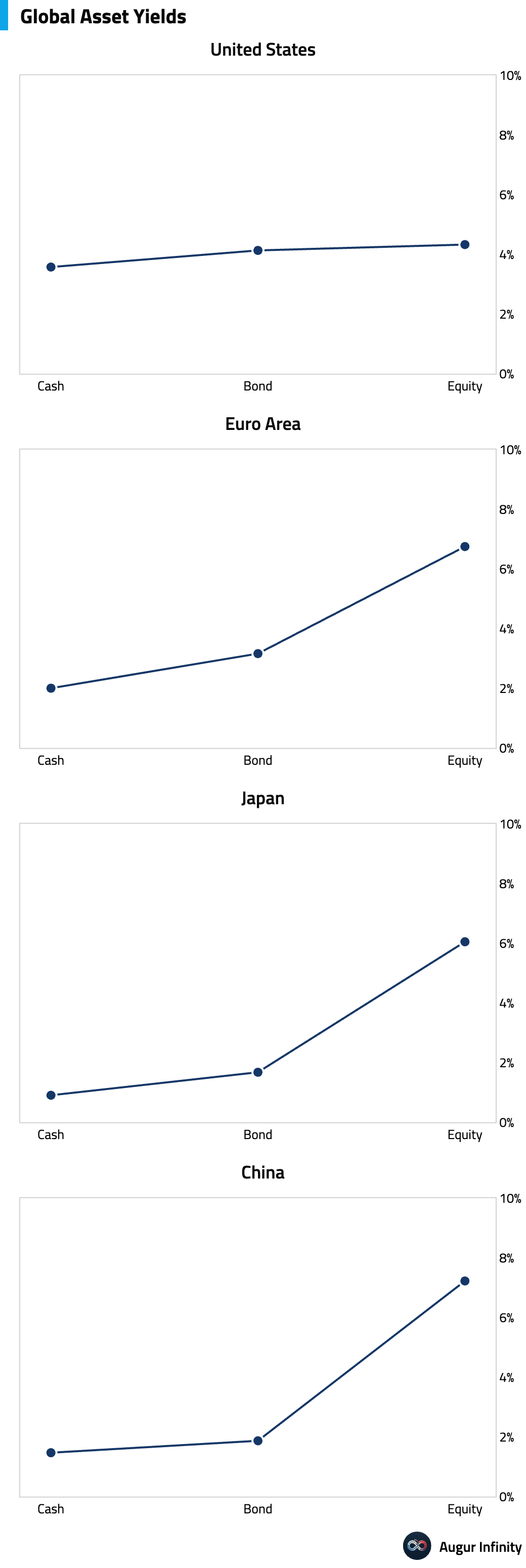

- The "risk curve"—comparing cash rates, bond yields, and equity earnings yields—is much flatter in the US than the rest of the world, suggesting limited risk premia offered by US assets.

Equities

- Global equities advanced on Tuesday, with US markets leading the gains. The tech-heavy Nasdaq Composite rose 1.0%, and the broader S&P 500 gained 0.6%, reportedly supported by dovish sentiment from recent Federal Reserve minutes. Elsewhere, France and South Korea were also strong performers, with both markets climbing 1.0%.

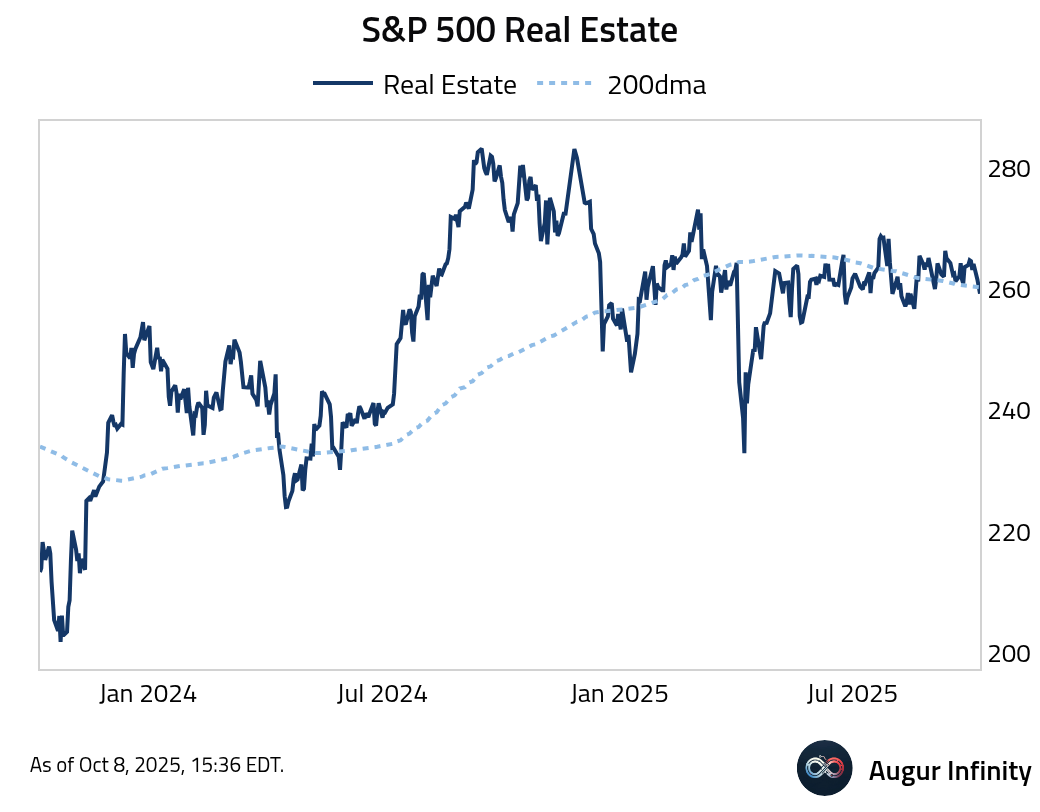

- S&P 500 Real Estate sector fell below its 200-day moving average.

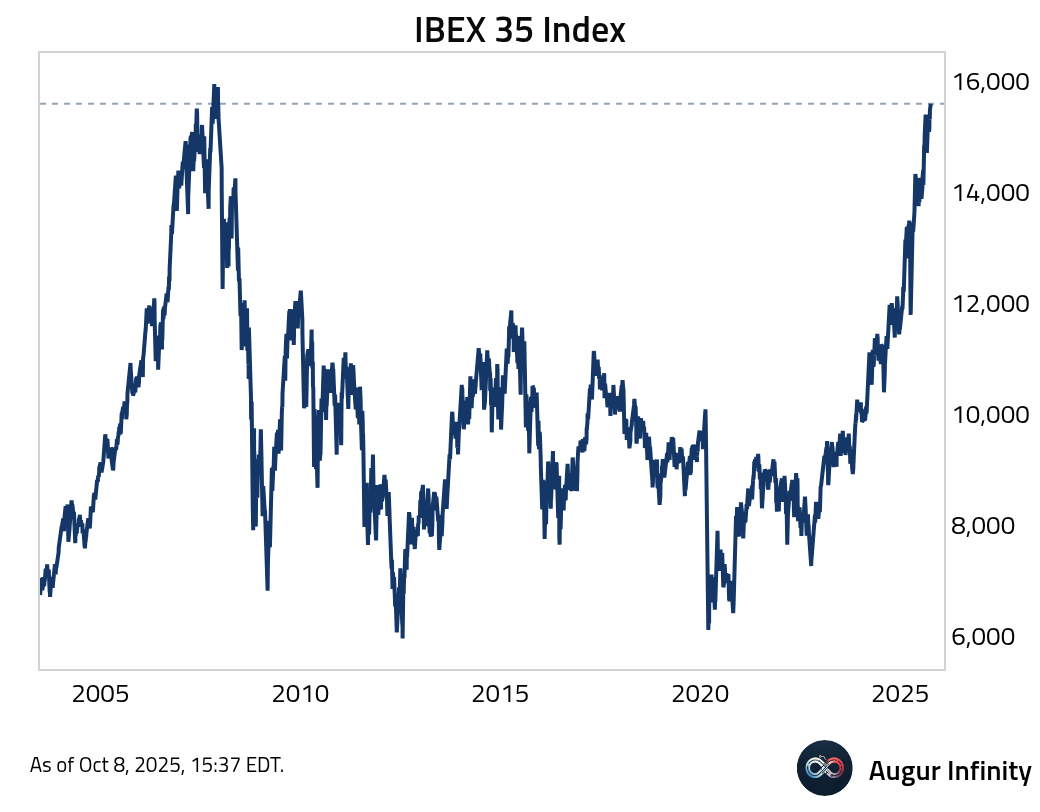

- IBEX 35 Index is at the highest level since December 2007.

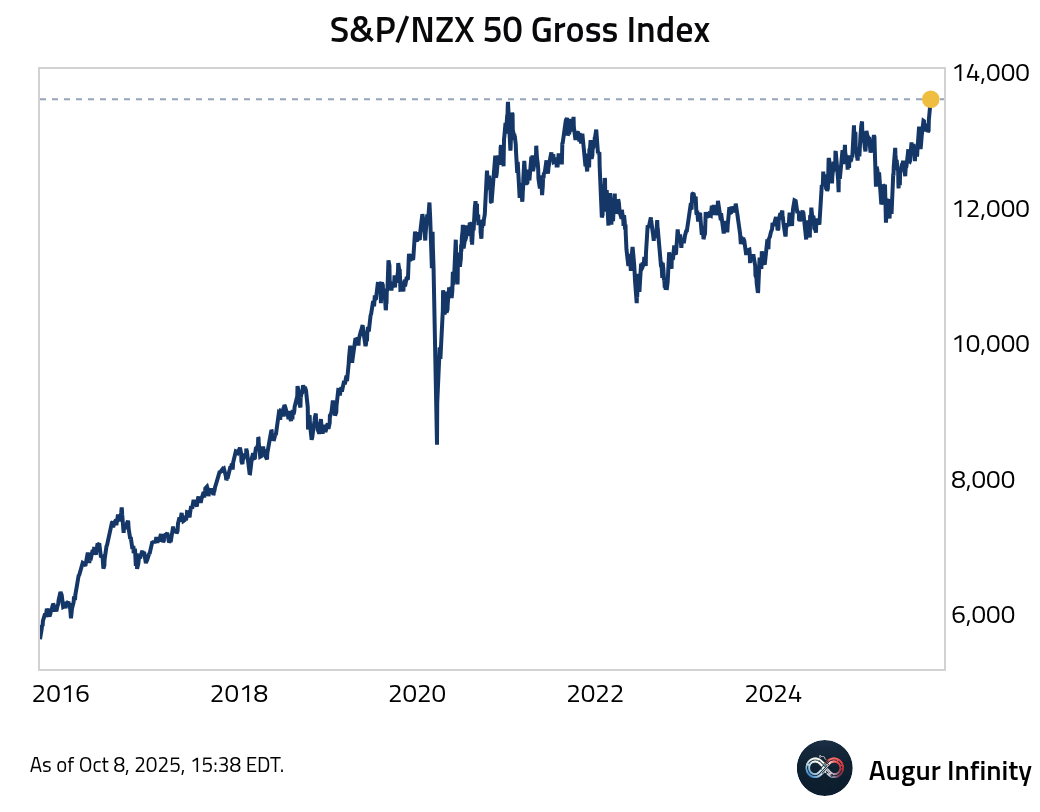

- S&P/NZX 50 Gross Index has reached an all-time high.

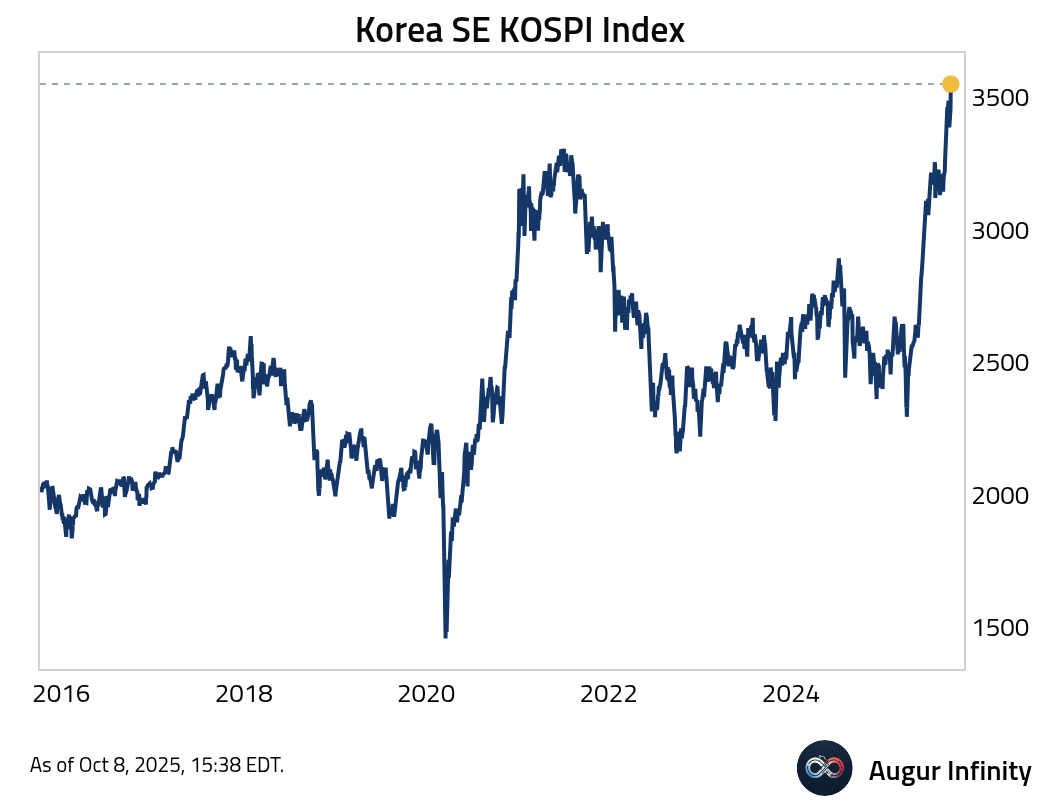

- Korea's KOSPI Index continues to advance.

Fixed Income

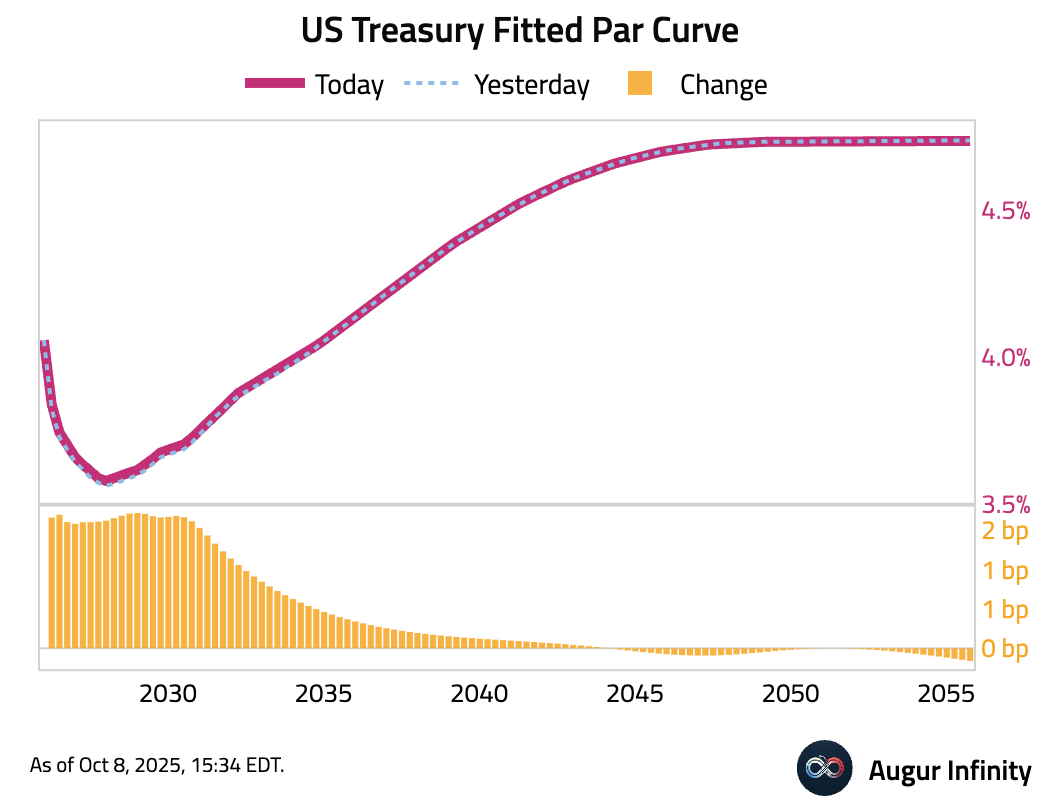

- The US Treasury curve flattened as yields on the front end and belly rose while the long end saw a slight decline. The 2-year yield increased by 1.8 bps, and the 10-year yield edged up by 0.7 bps. In contrast, the 30-year yield fell by 0.1 bps.

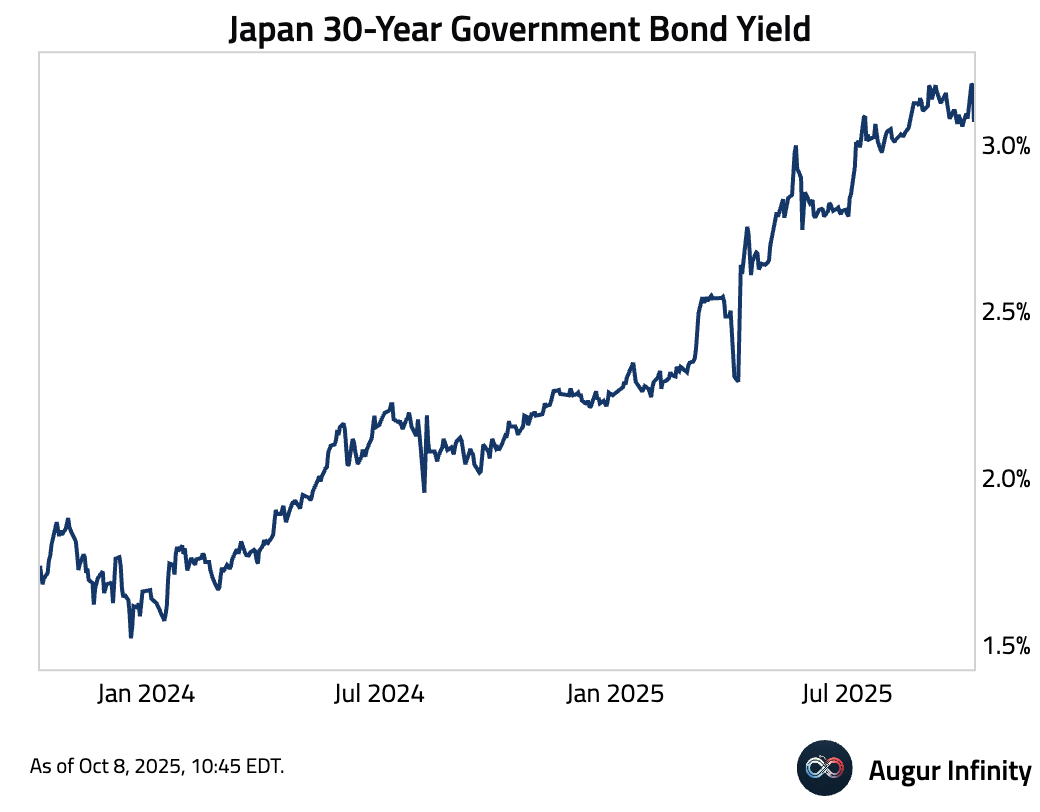

- Japan 30-year government bond yield declined by 11 bps today. Rumors are that Japan may have intervened in the bond market.

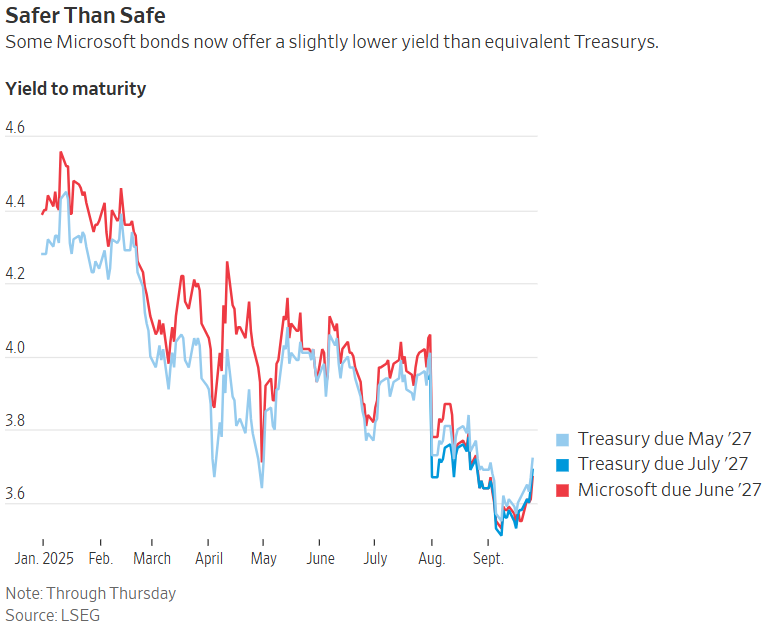

- Microsoft's bonds are trading at a lower yield than Treasuries.

Source: Charlie Bilello

FX

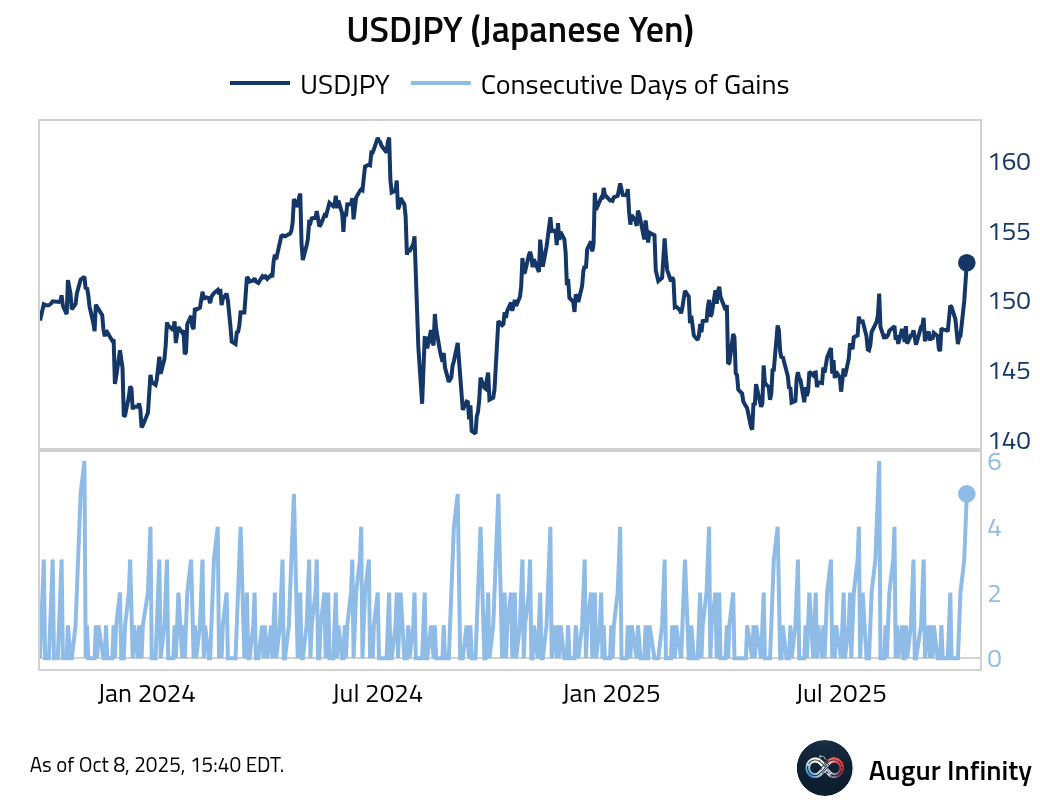

- The yen has depreciated against the dollar for five consecutive days.

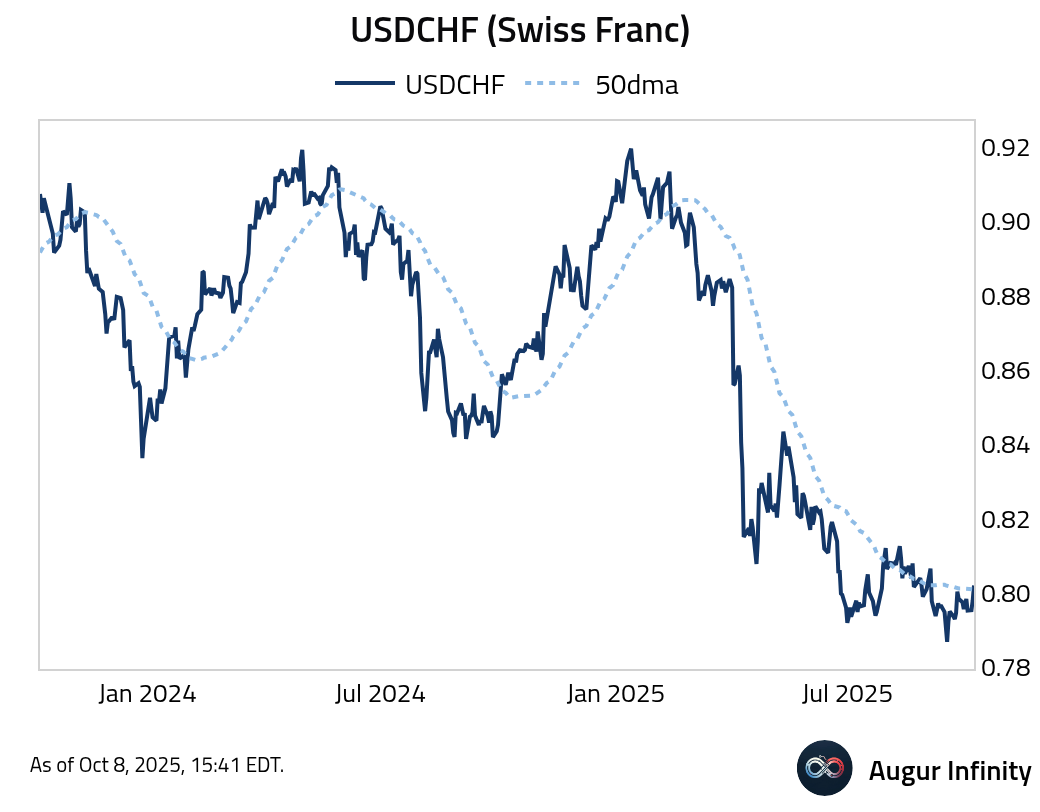

- USDCHF (Swiss Franc) is above its 50-day moving average.

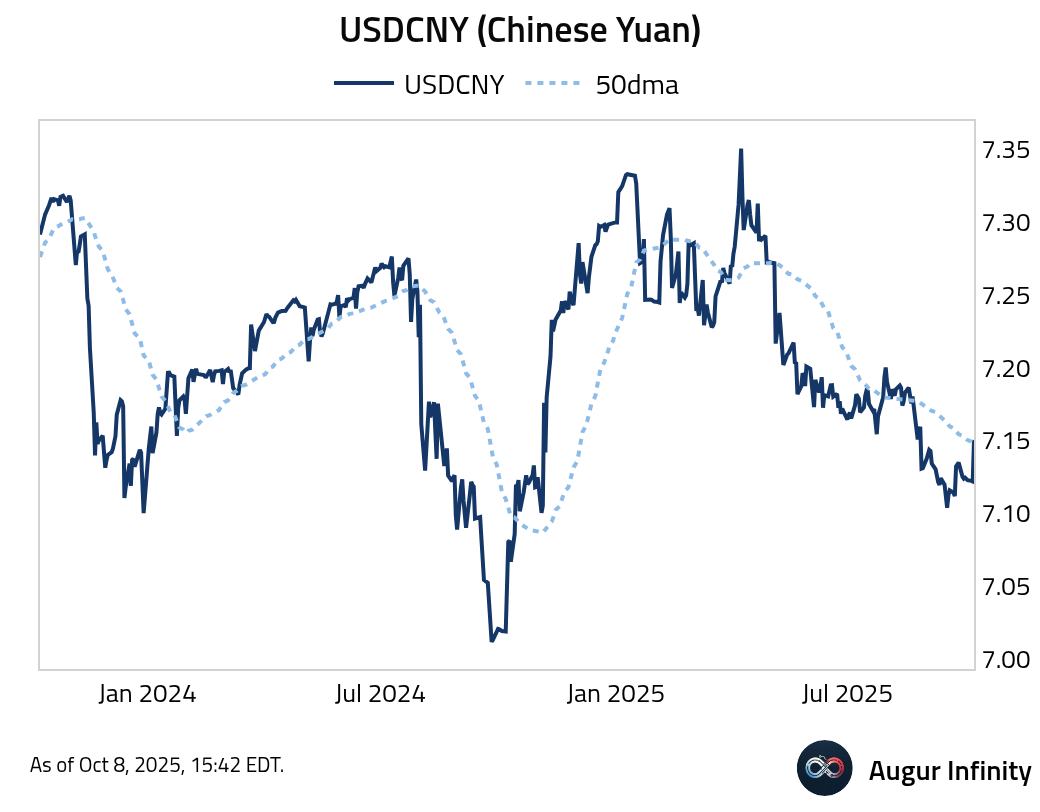

- Similarly, USDCNY also moved above its 50-day moving average.

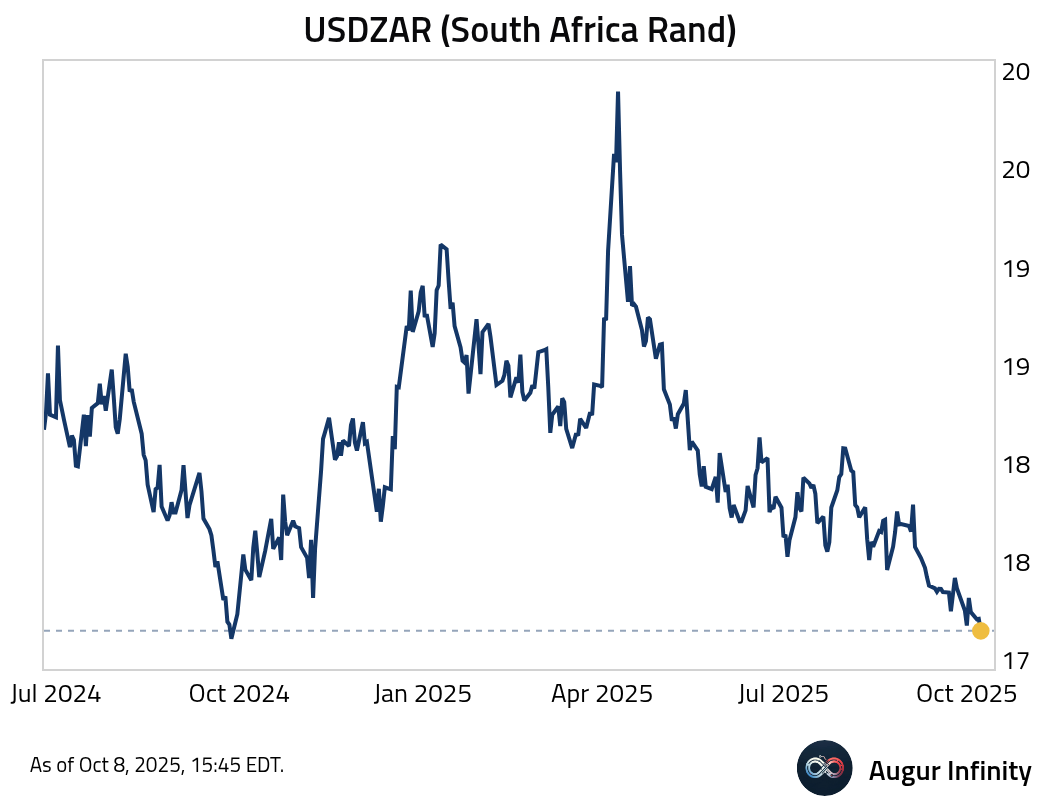

- The South Africa Rand has rallied to the best level against the dollar since September 2024.

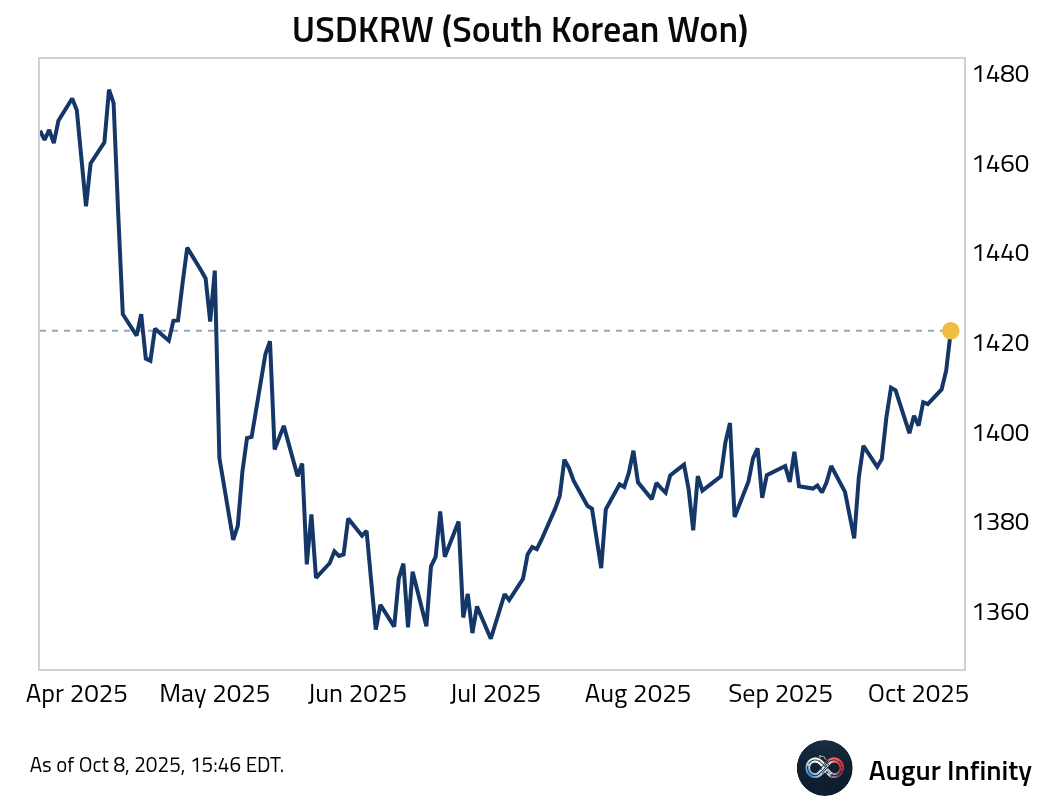

- By contrast, the South Korean Won has sunk to the worst level against USD since May 2025.

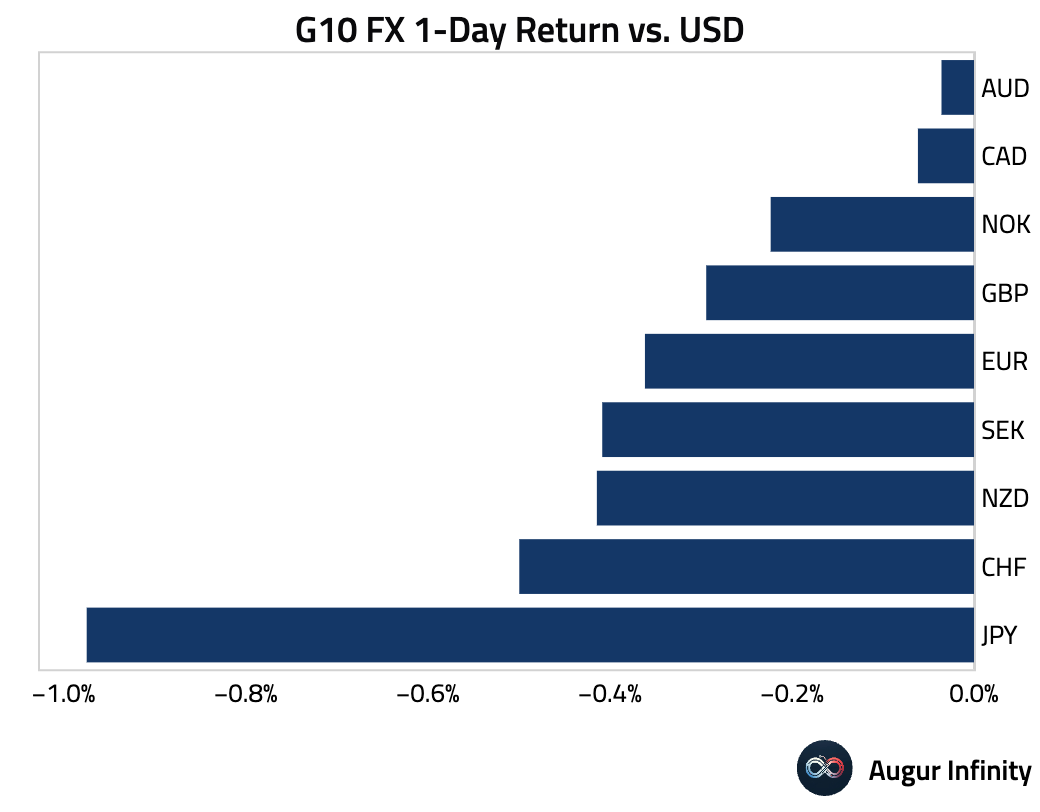

- The US dollar strengthened against all its G10 counterparts. The Japanese yen was the most significant underperformer, declining 1.0% for its fifth consecutive day of losses amid renewed carry-trade interest. The euro, Swiss franc, and Swedish krona all marked their third straight day of declines, with the euro’s weakness partly attributed to political uncertainty in France.

Commodities

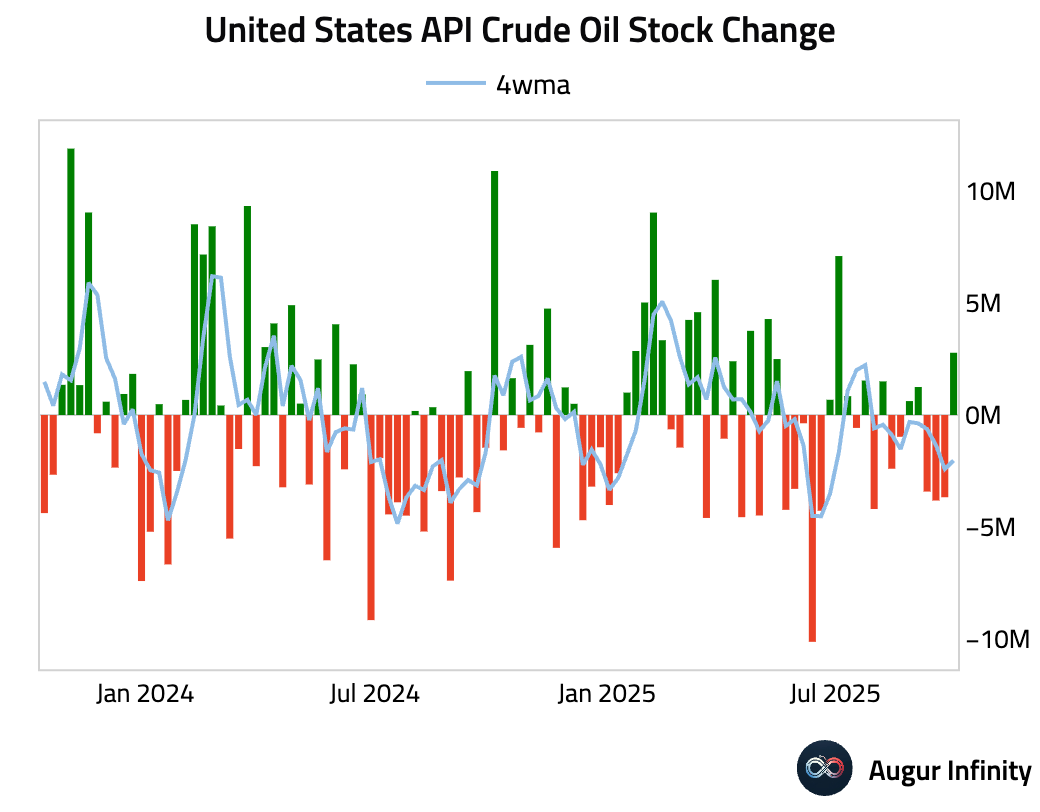

- US crude oil inventories saw a larger-than-expected build last week, rising for the second consecutive week (act: 2.78M barrels, est: 2.25M). This followed a significant drawdown in the prior period.

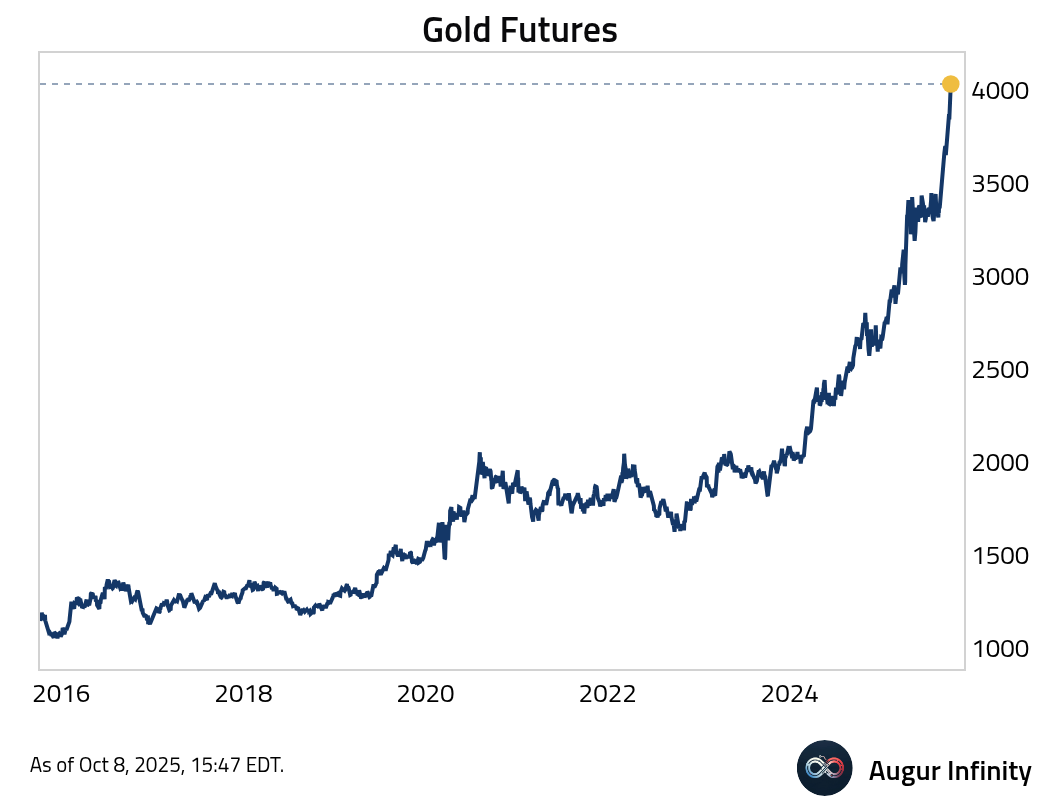

- Gold surged past $4000 for the first time.

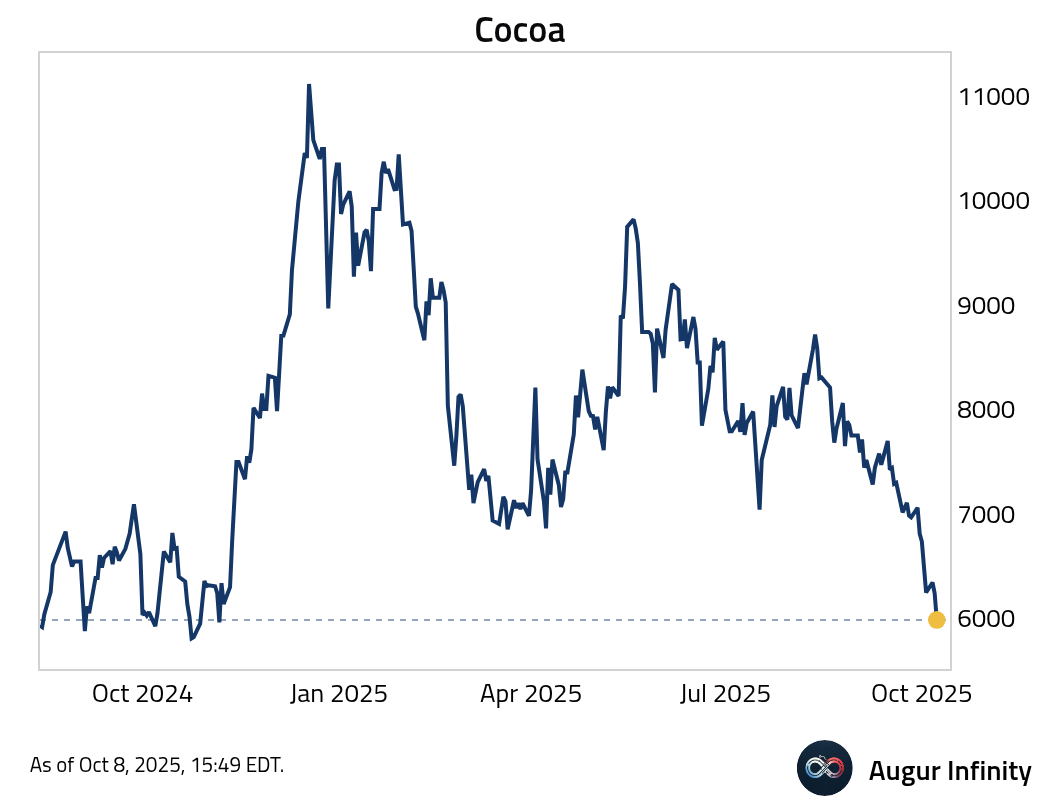

- Cocoa continues to trade down.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.