Note: This is the Augur Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- China’s Ministry of Commerce announced it has tightened export restrictions on rare earth materials used in high-technology products and military applications.

- The US federal government shutdown has entered its ninth day, while President Trump is reportedly expected to exclude generic drugs from planned pharmaceutical tariffs.

- A phase one peace agreement between Israel and Hamas has been reached, according to overnight reports.

Global Economics

United States

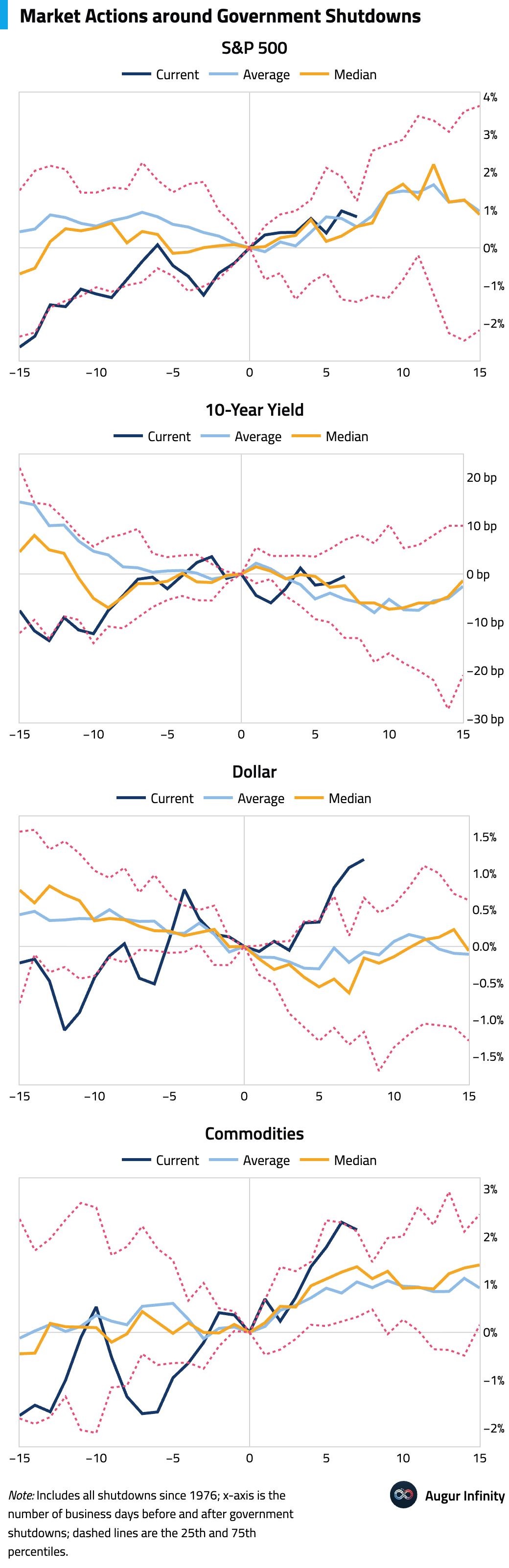

- Here’s how markets are moving compared to their typical patterns following past government shutdowns.

Europe

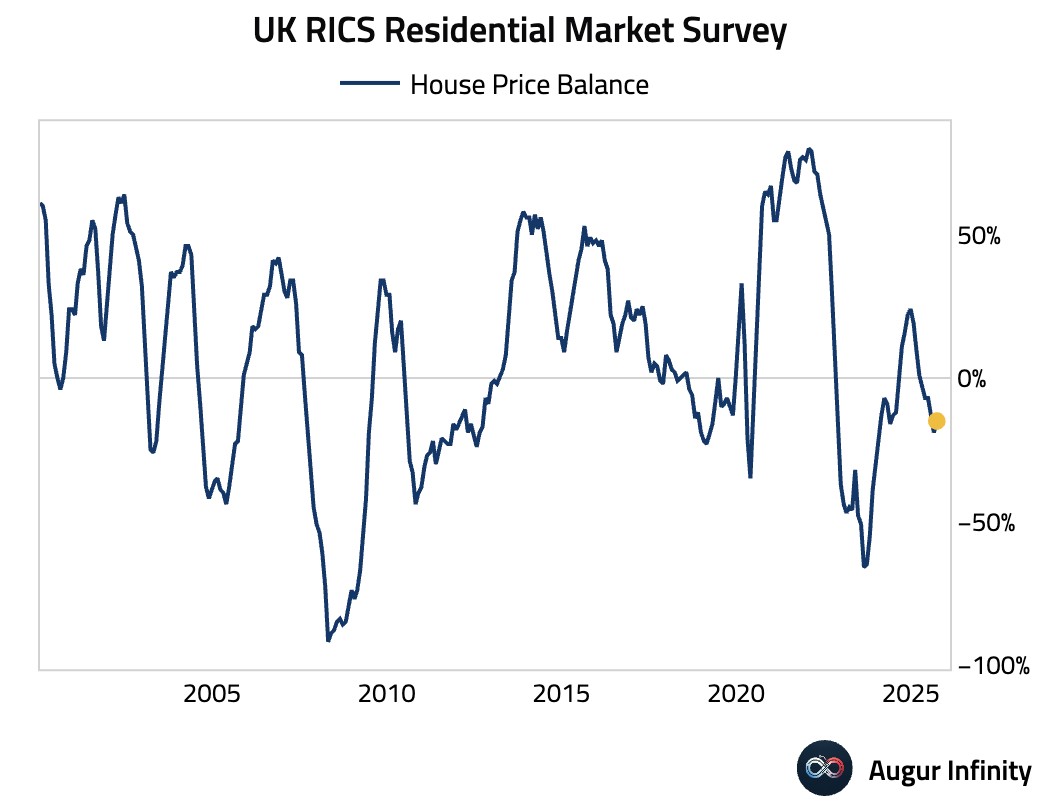

- The UK RICS House Price Balance improved in September but remained in negative territory, beating expectations (act: -15, est: -18, prev: -19).

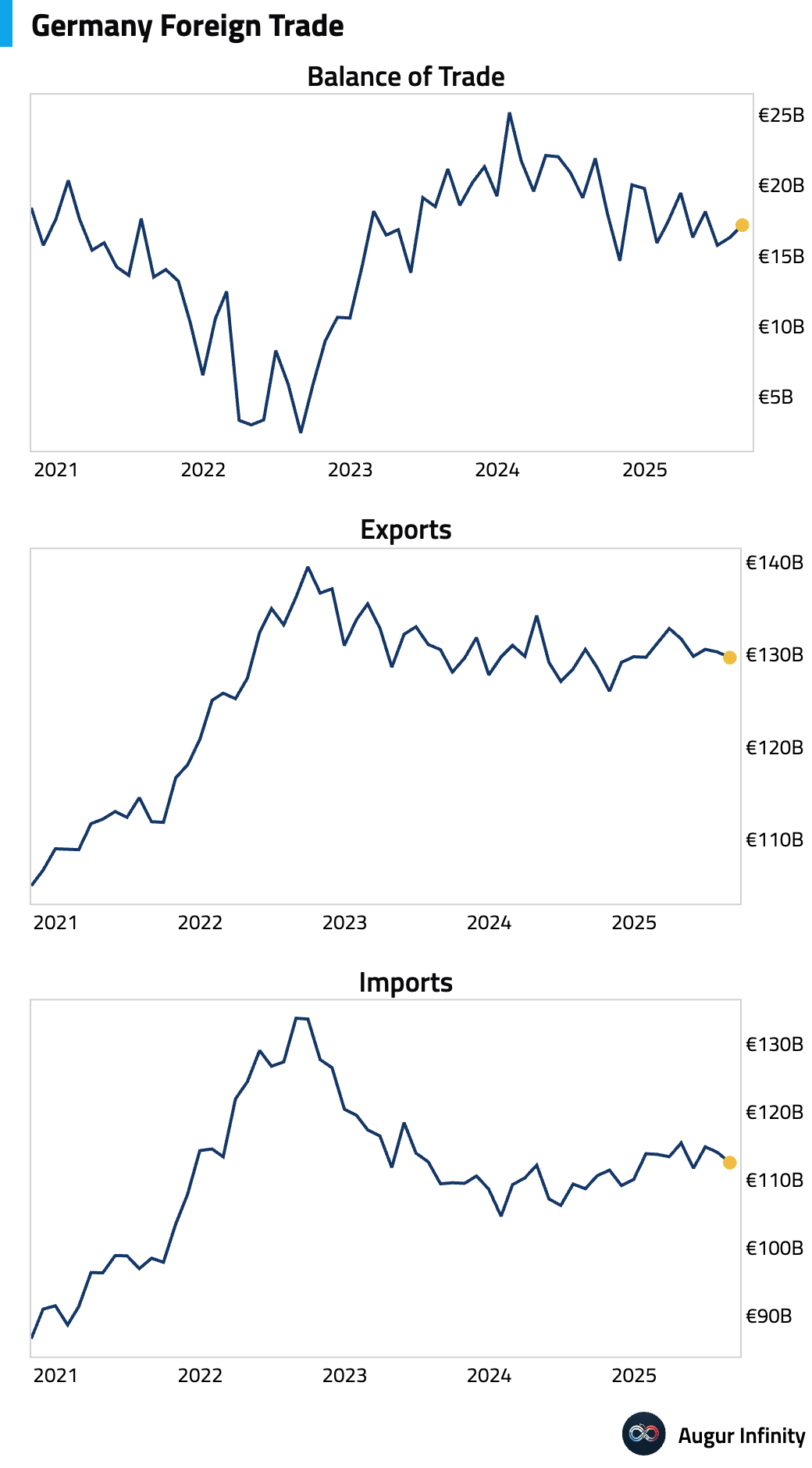

- Germany’s trade surplus widened to €17.2 billion in August, surpassing consensus estimates of €15.2 billion and the prior month's €16.3 billion. However, the details revealed underlying weakness, as exports fell by 0.5% M/M against expectations of a 0.3% rise. The larger surplus was driven by an even sharper, unexpected 1.3% M/M drop in imports, pointing to weak domestic demand.

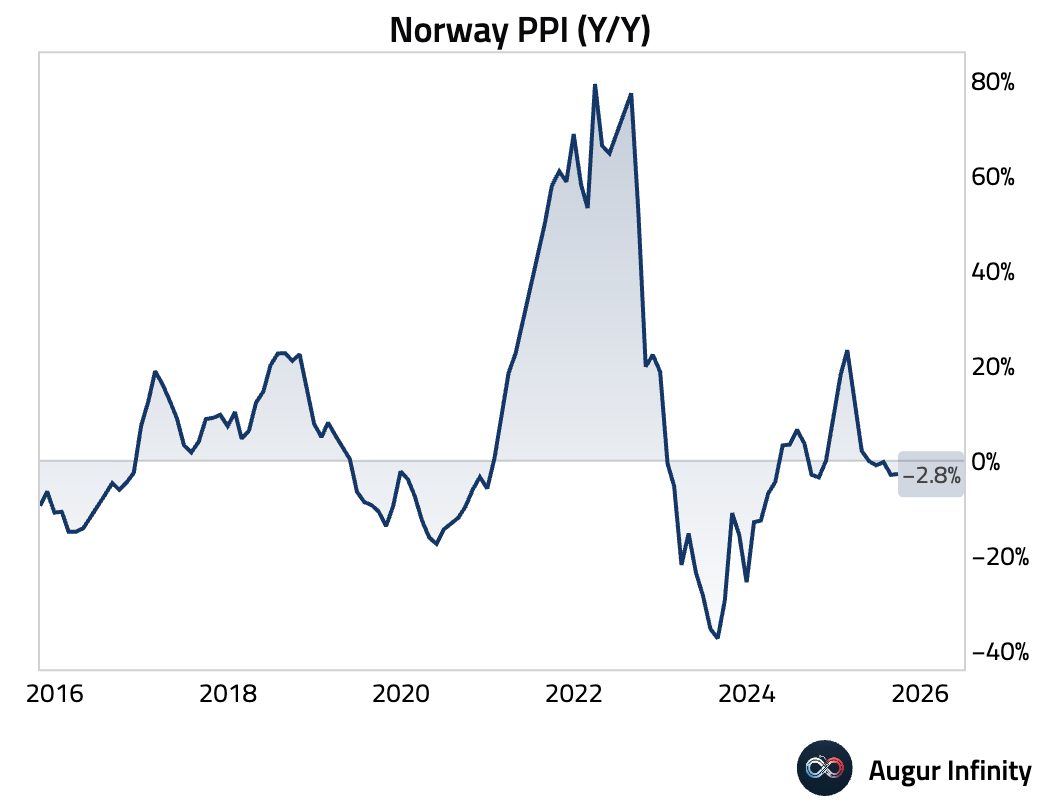

- Norwegian producer price deflation moderated in September, with the index falling 2.8% Y/Y compared to -3.0% previously.

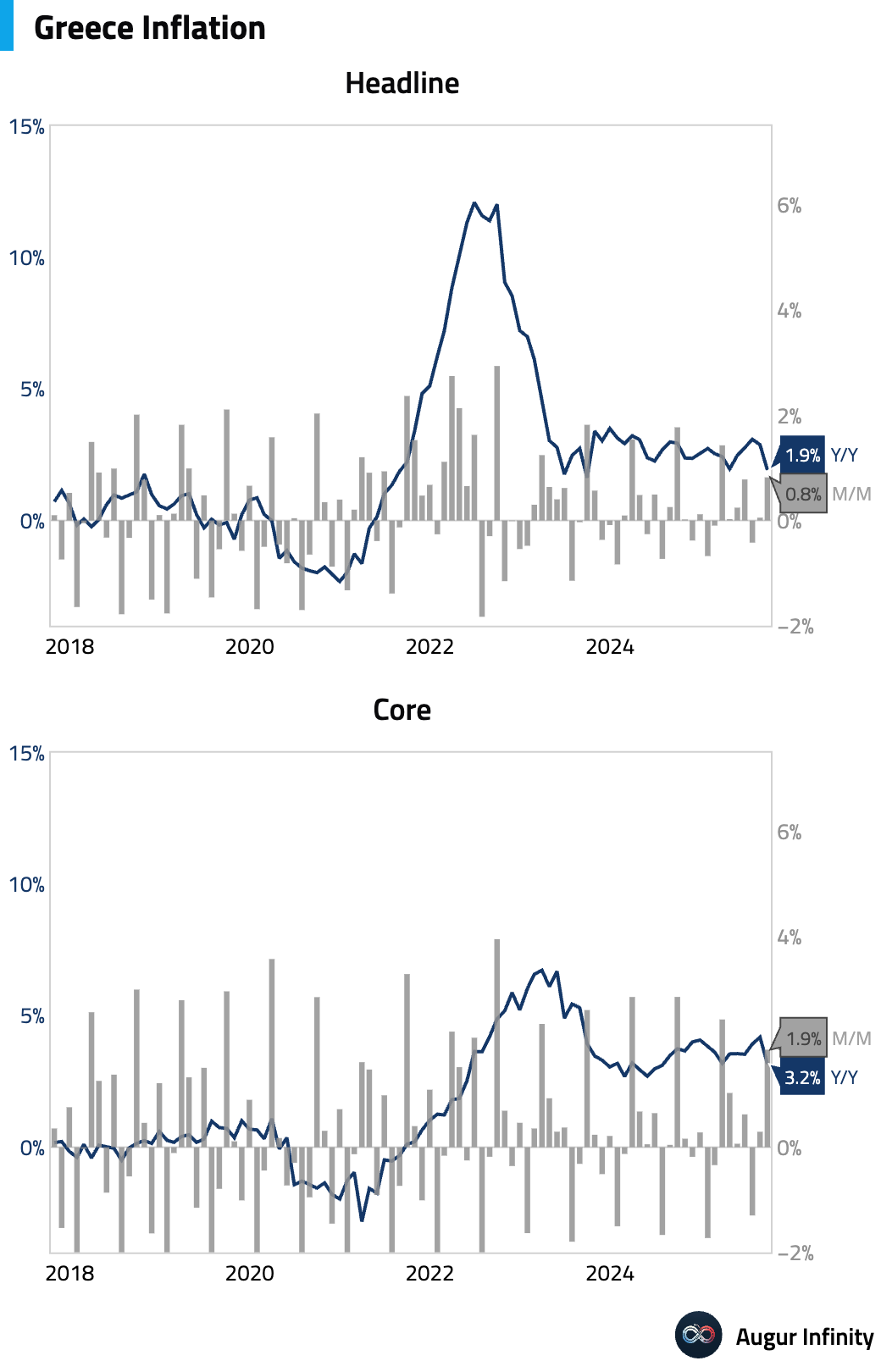

- Greek inflation decelerated sharply in September, with the annual rate falling to 1.9% from 2.9% in August. On a monthly basis, prices rose 0.8%.

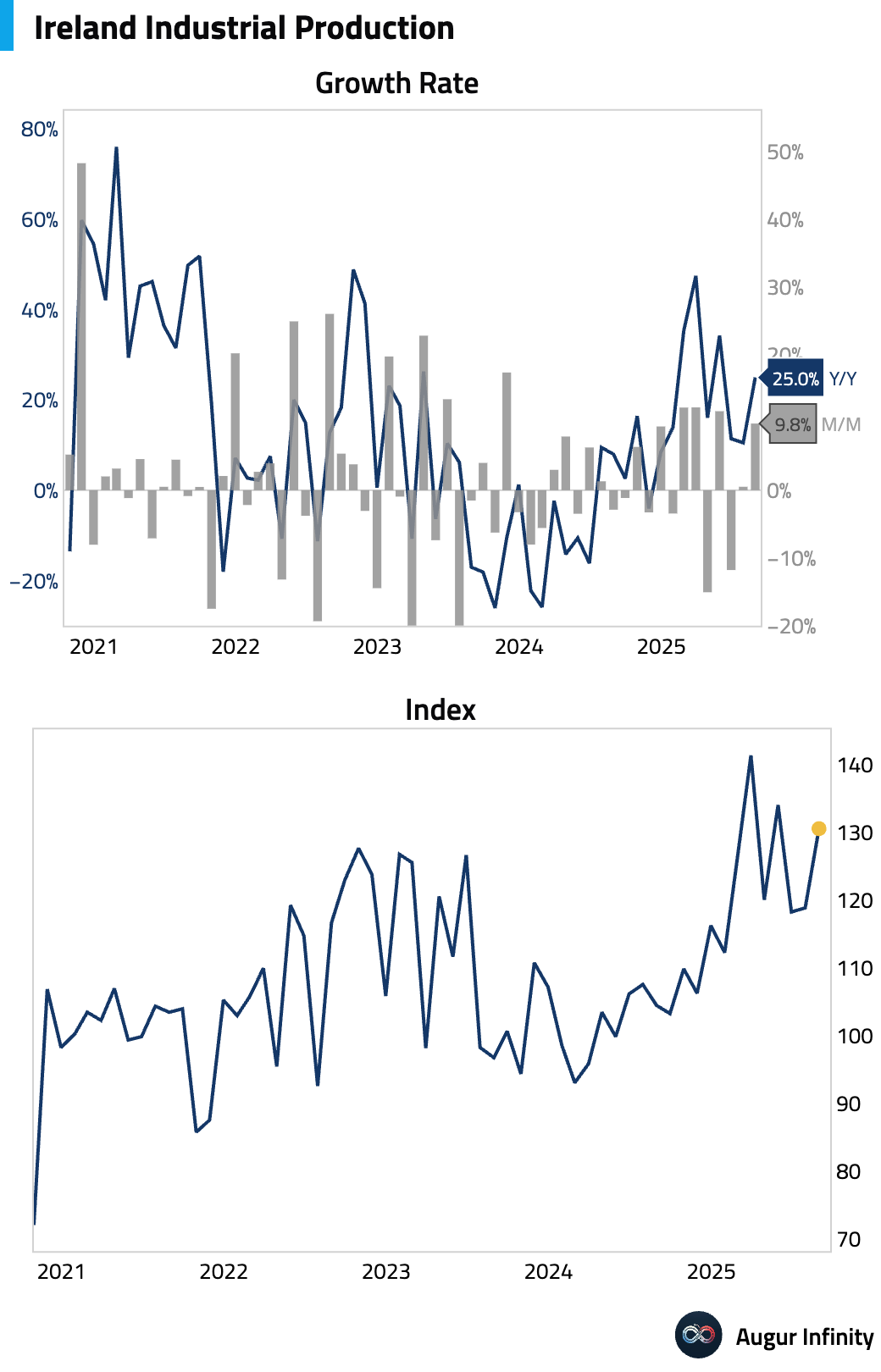

- Irish industrial production surged in August, rebounding strongly with a 25.0% Y/Y increase after a 10.5% rise in July.

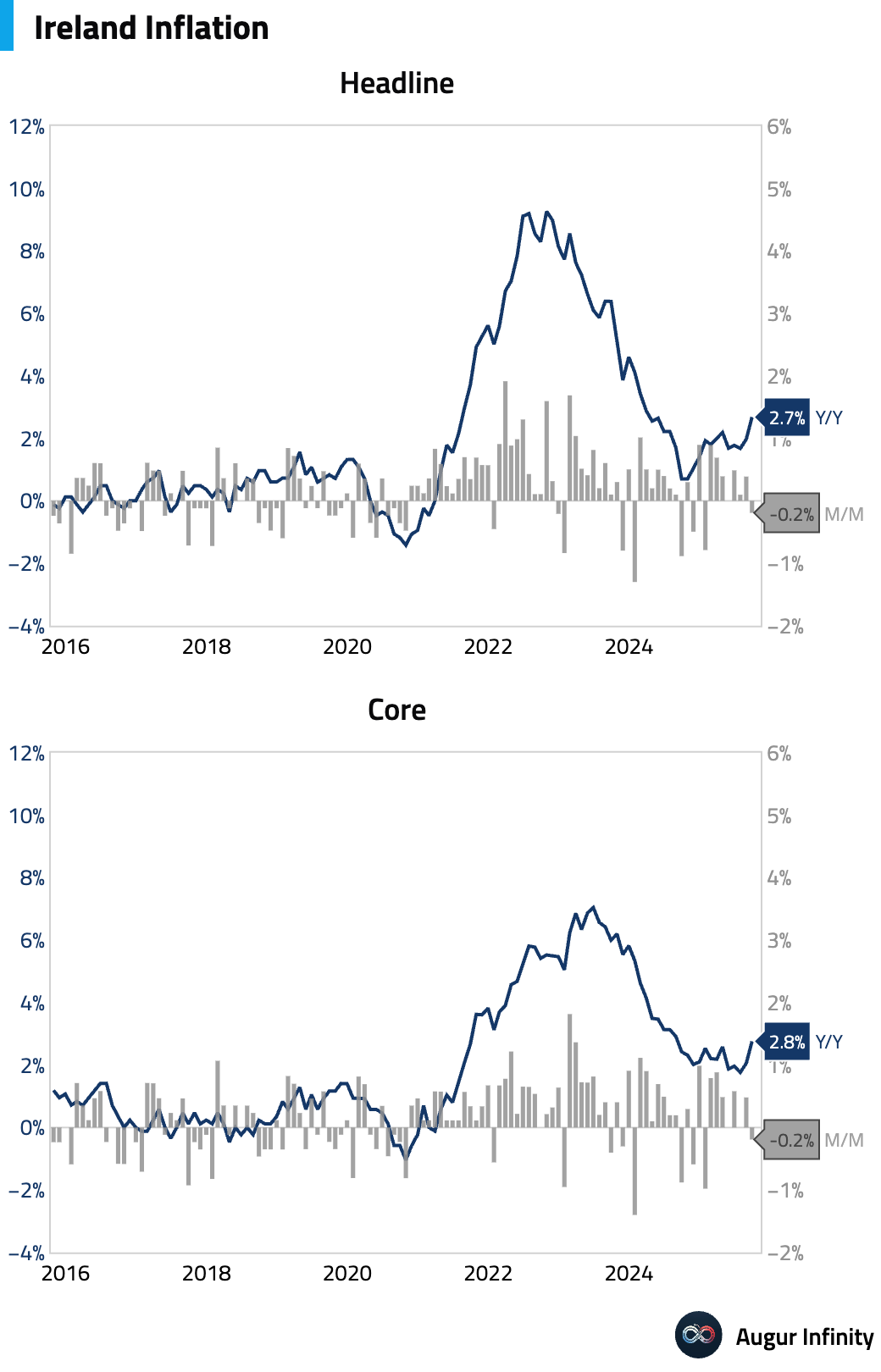

- Ireland’s national CPI measure for September showed annual inflation accelerating to 2.7% Y/Y from 2.0% in August. Month-over-month, prices declined by 0.2%.

Asia-Pacific

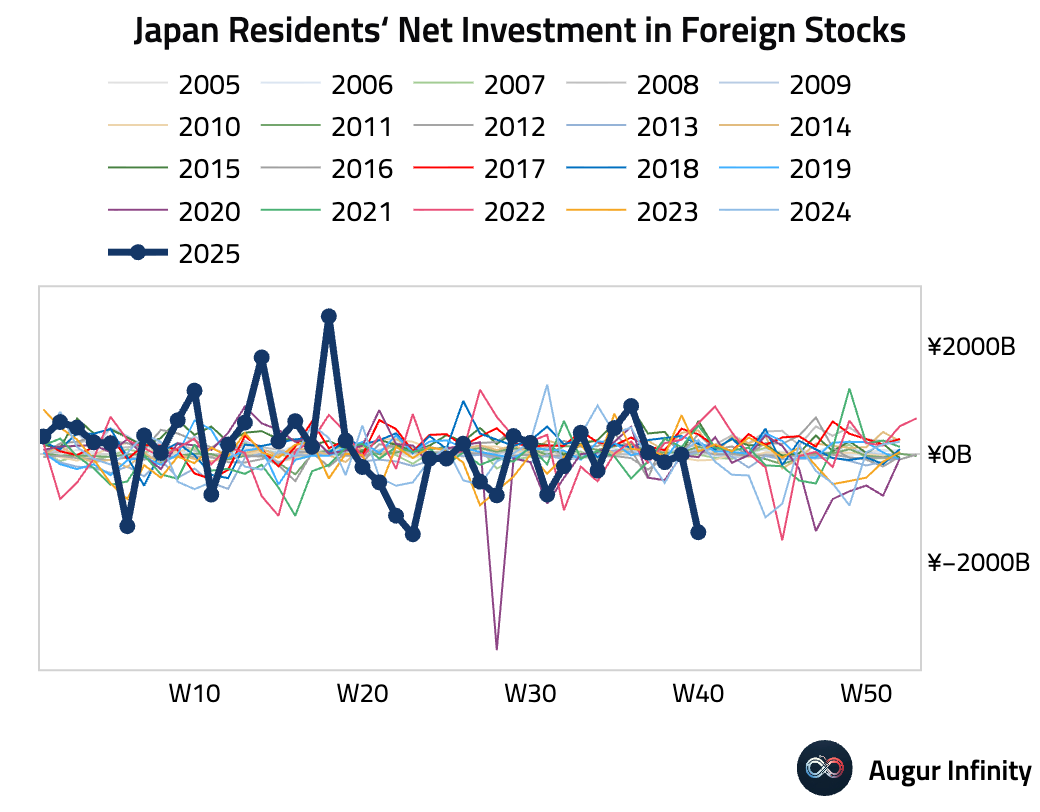

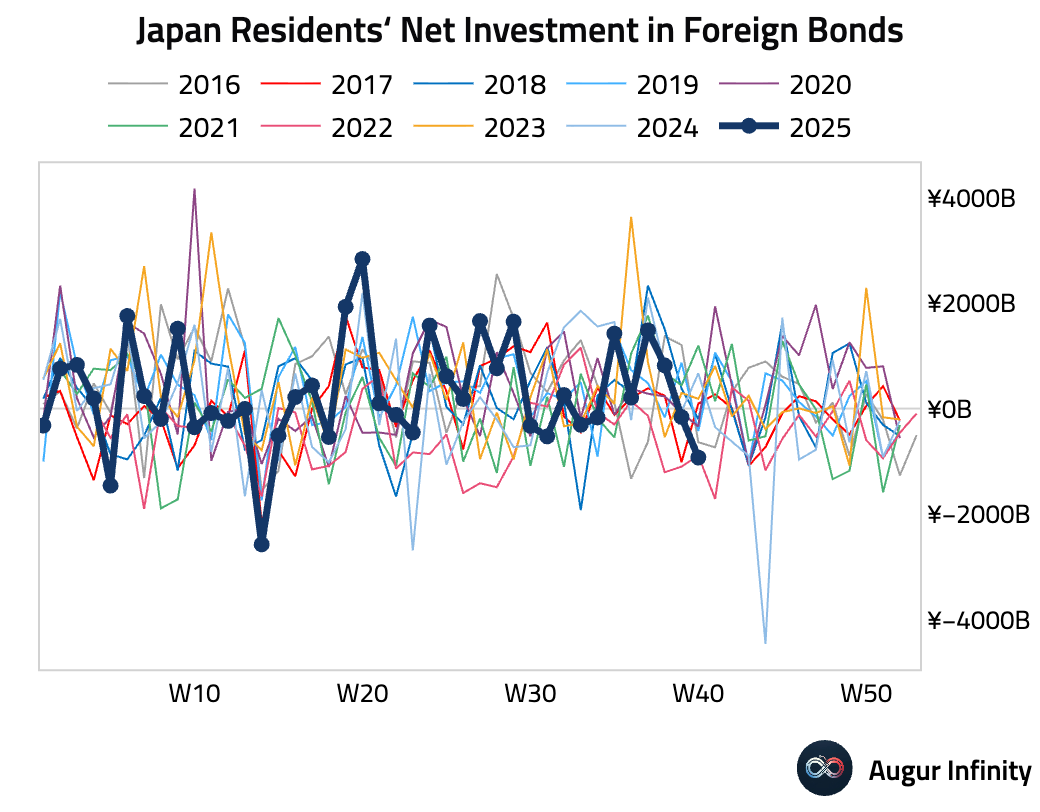

- Japanese investors were significant net sellers of foreign stocks and bonds in the latest week.

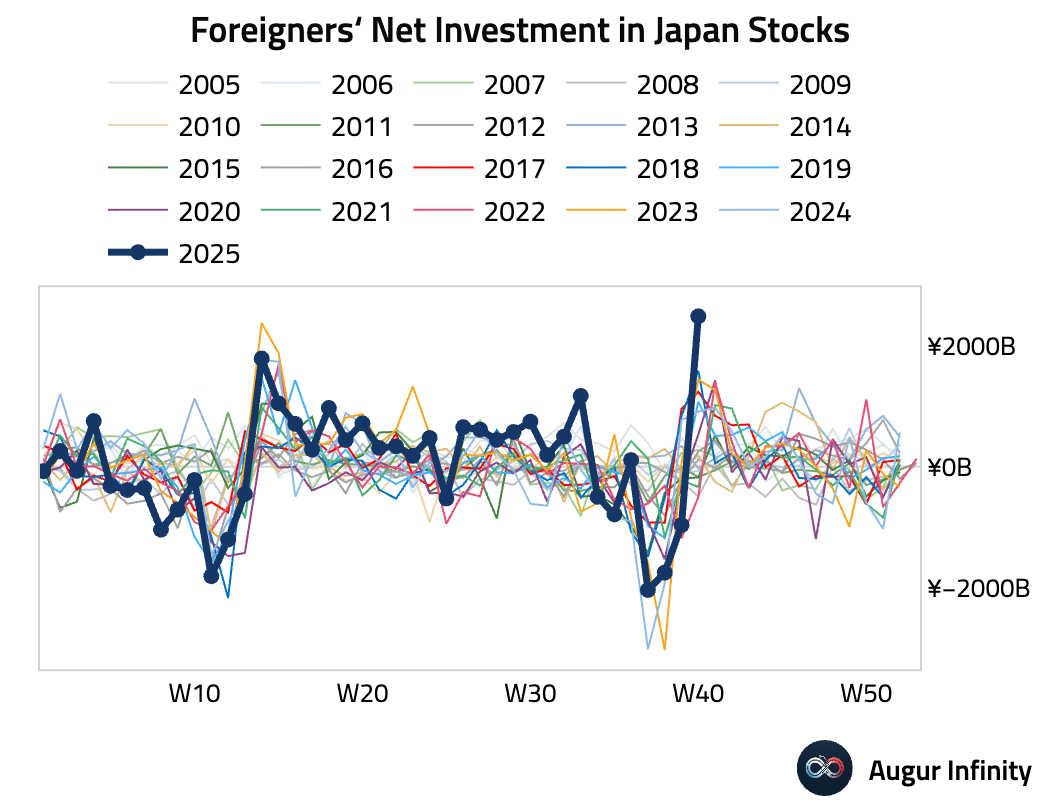

- Foreign investment in Japanese stocks surged to a record high of ¥2.48 trillion in the latest week.

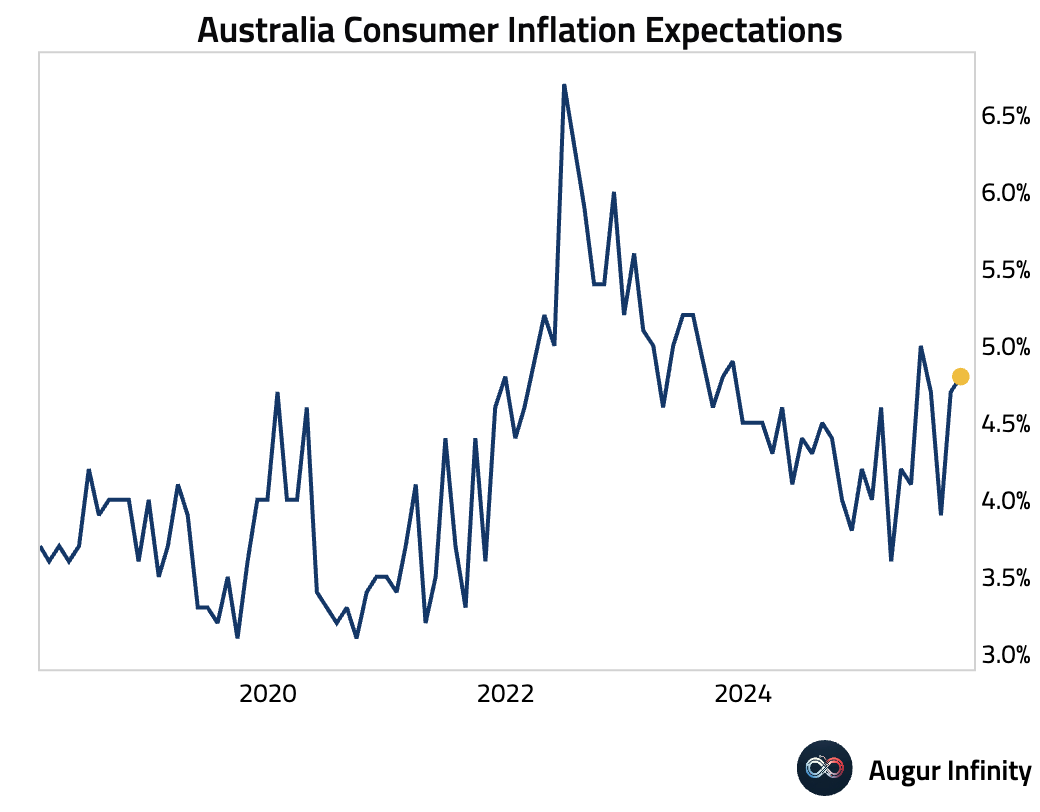

- Australian consumer inflation expectations for October ticked up to 4.8% from 4.7% in the prior month.

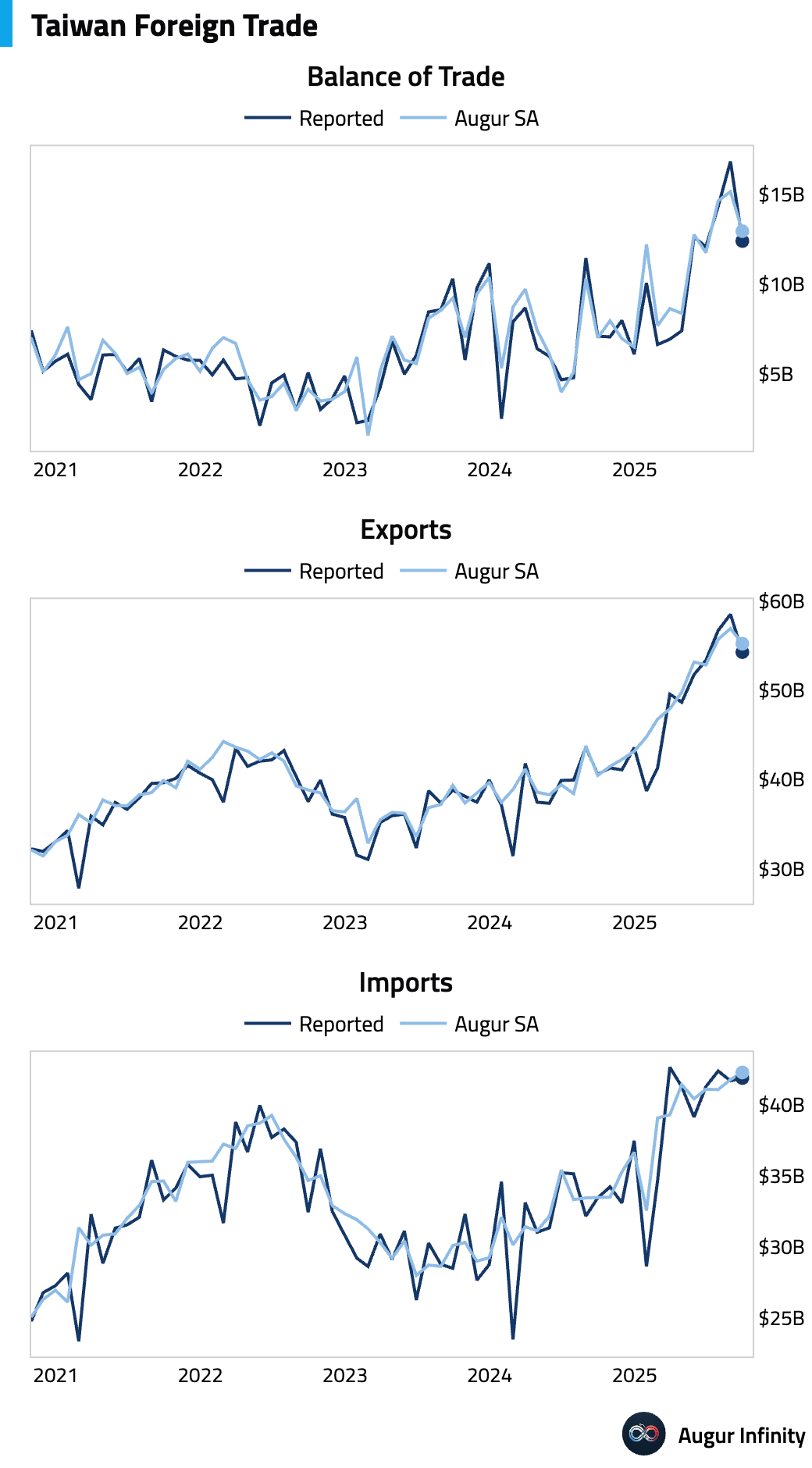

- Taiwan’s export growth moderated to 33.8% Y/Y in September from 34.1% previously, missing expectations for the first time since January. The disappointment was driven by a sharp pullback in tech demand, particularly a 23.4% M/M plunge in US-bound exports, which broke a seven-month streak of gains. The trade surplus narrowed to $12.4 billion from last month's record high as import growth also remained strong at 25.1% Y/Y.

Emerging Markets ex China

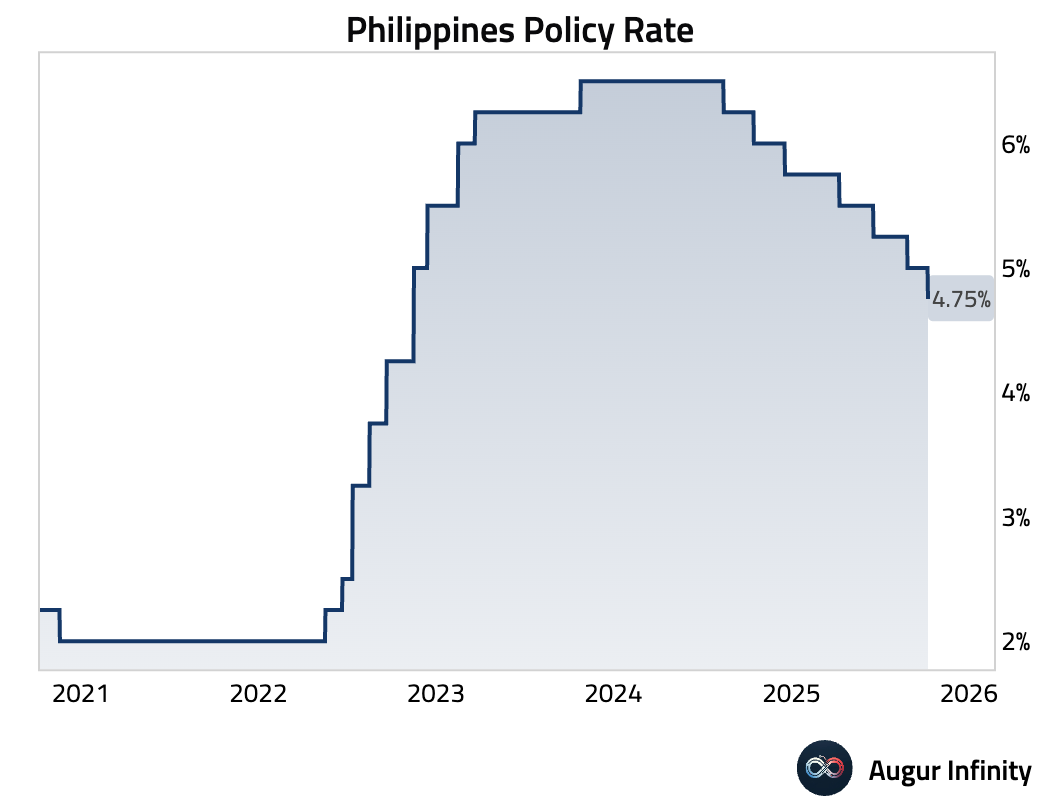

- The Bangko Sentral ng Pilipinas (BSP) unexpectedly cut its policy rate by 25 basis points to 4.75%, defying consensus expectations for a hold. The dovish surprise was driven by a lowered growth forecast for 2025 due to weaker business confidence. The central bank also reduced its estimate of the neutral policy rate, signaling room for further easing.

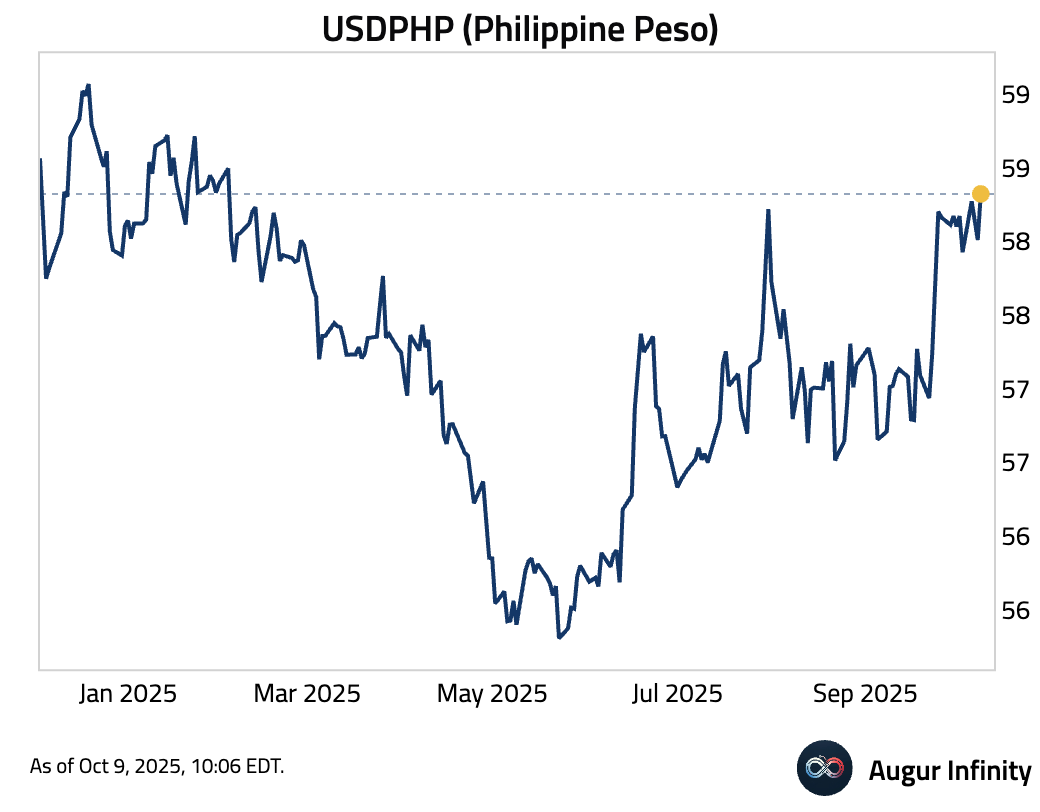

- The Philippine Peso depreciated against USD, reaching the weakest level since February 2025.

- Indonesian retail sales growth slowed in August, rising 3.5% Y/Y compared to 4.7% in July.

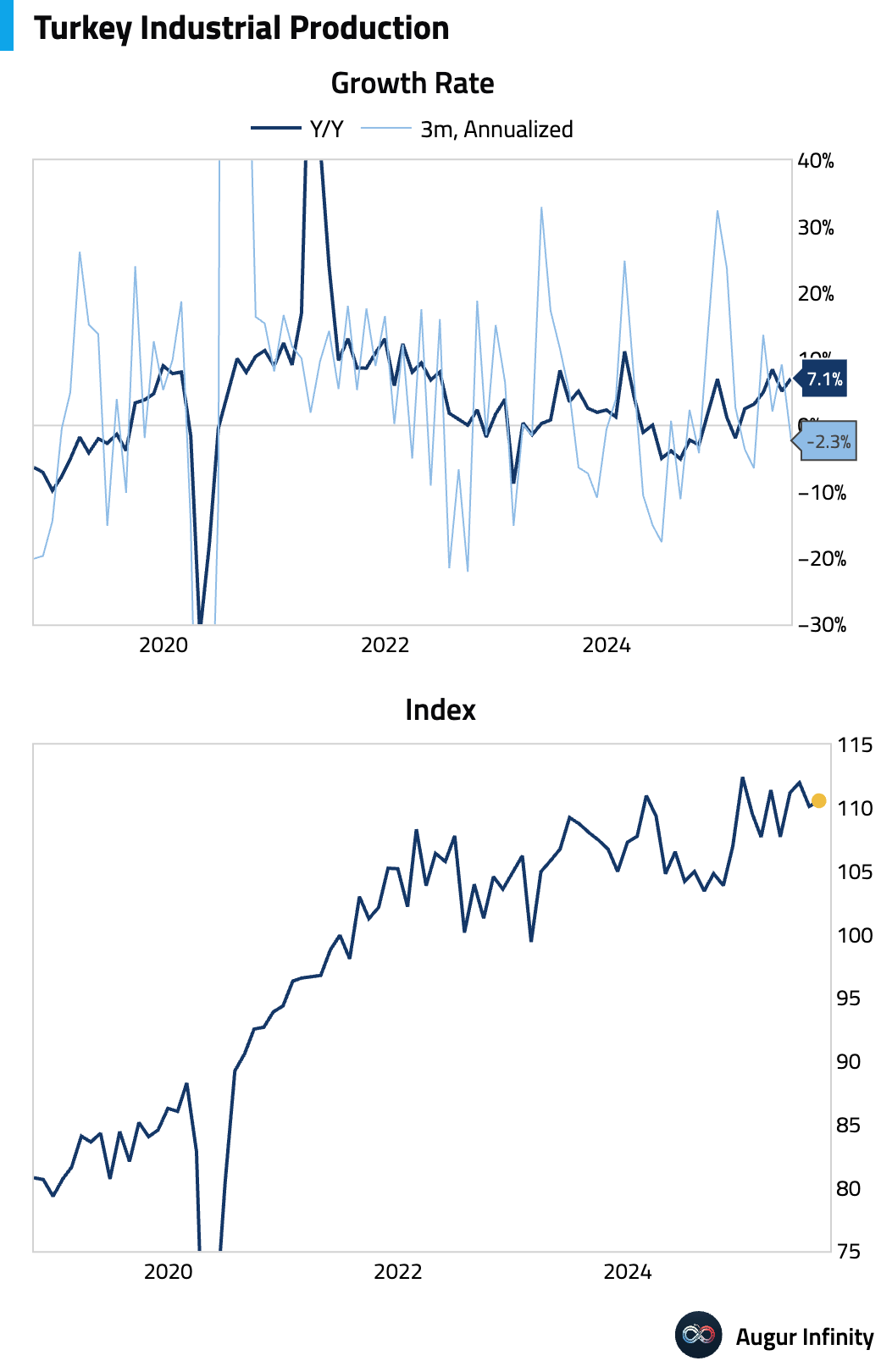

- Turkish industrial production accelerated in August, rising 7.1% Y/Y, well above the prior month's 5.2% expansion.

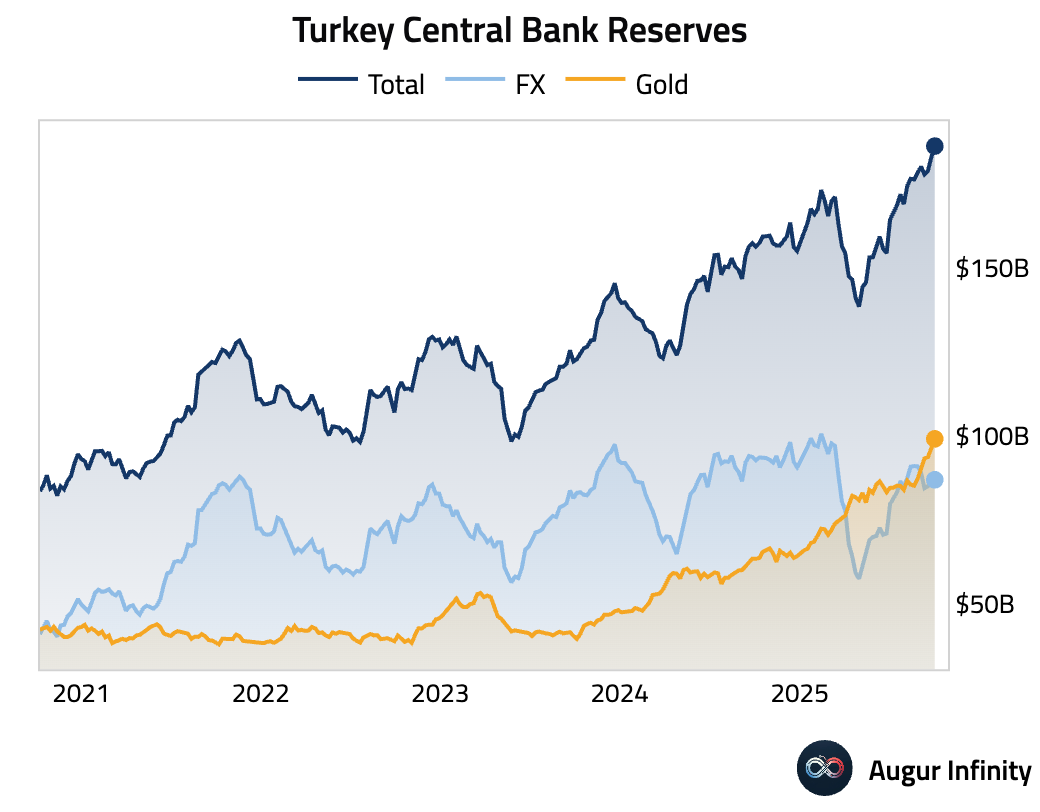

- Turkey's gross foreign exchange reserves edged higher in the first week of October (act: $87.03B, prev: $86.70B).

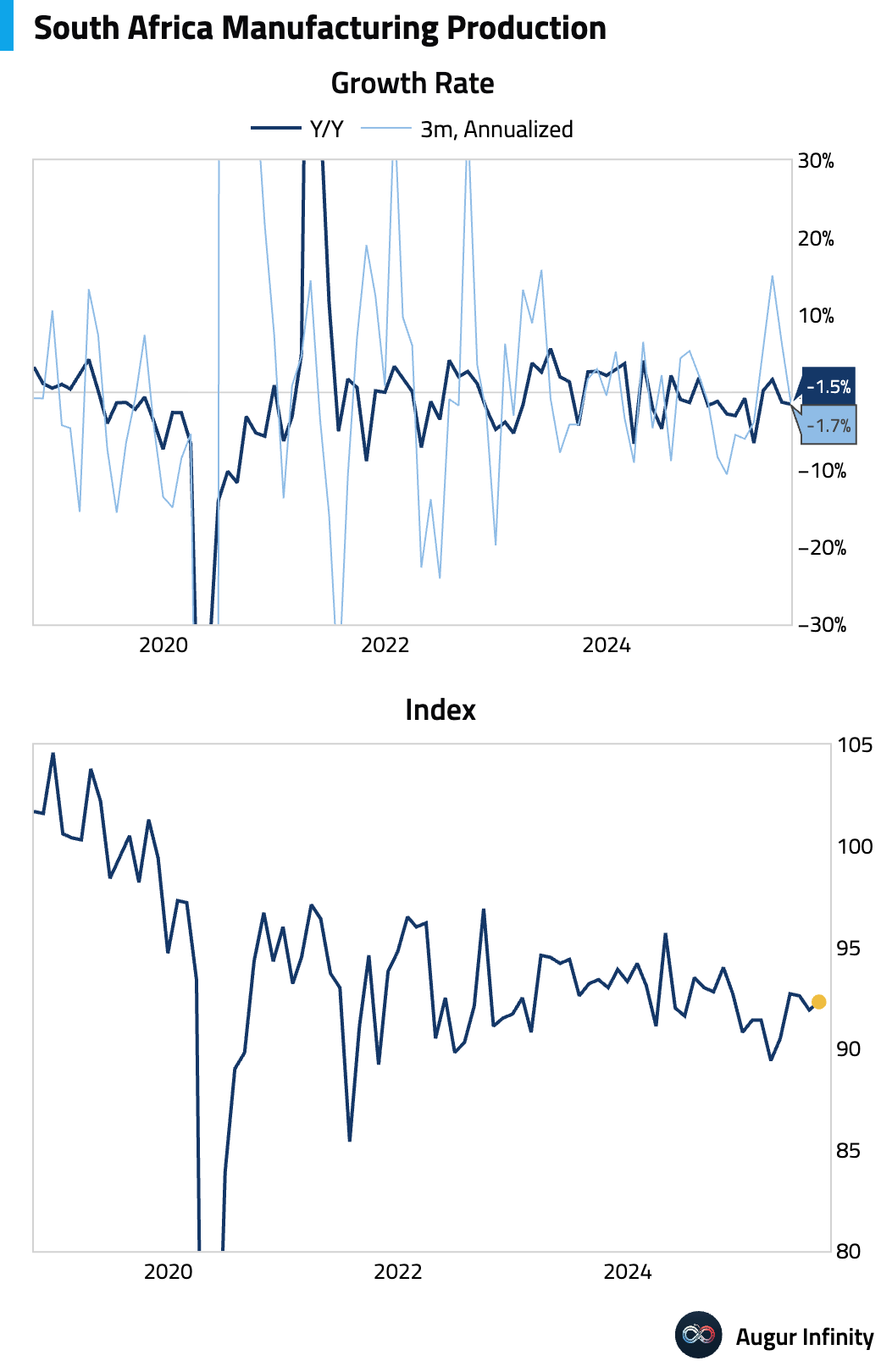

- South African manufacturing production contracted for a fifth consecutive month in August, falling 1.5% Y/Y, slightly worse than the previous 1.3% decline.

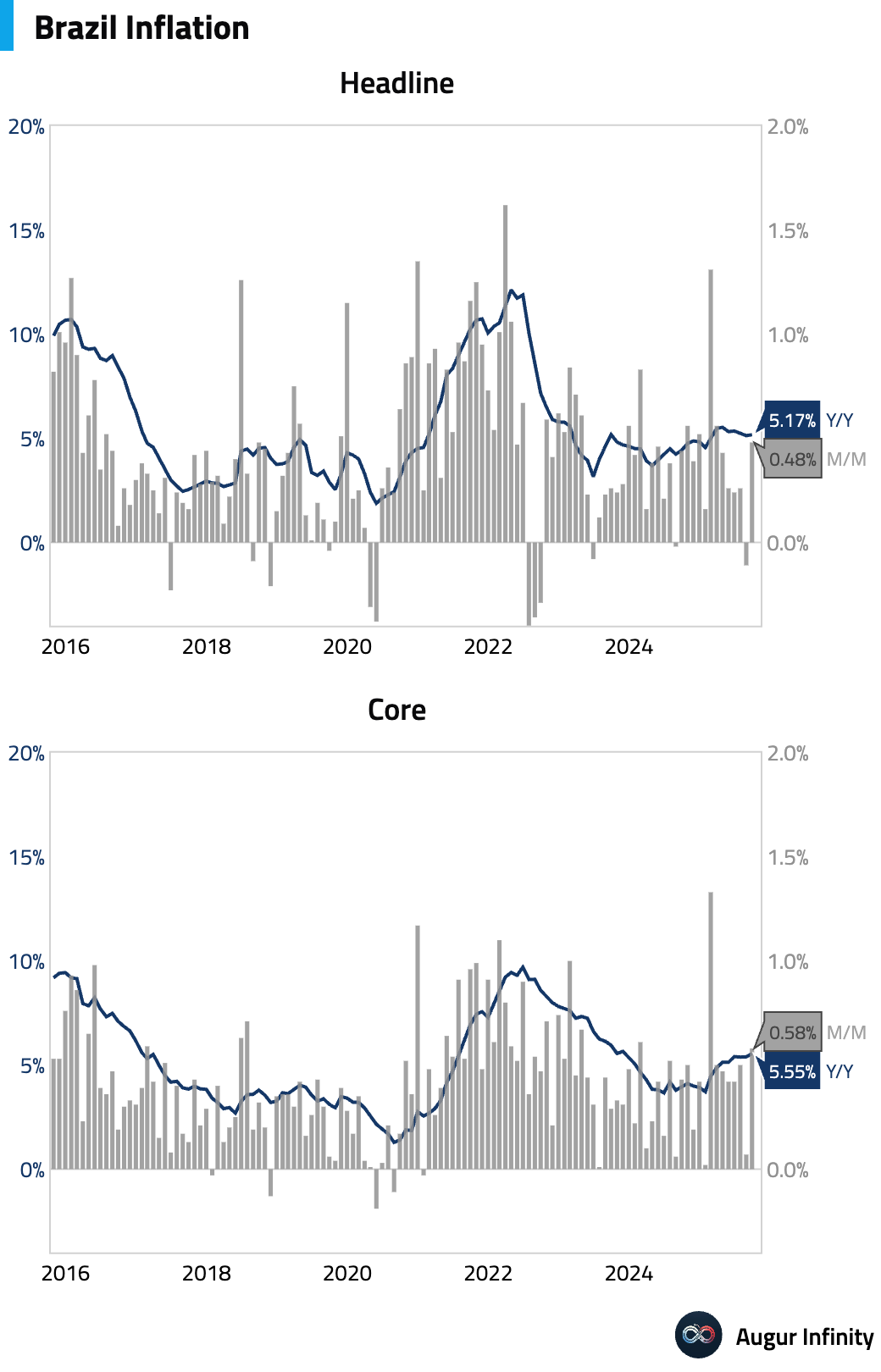

- Brazil's September headline inflation was softer than expected, rising 0.48% M/M (5.17% Y/Y), below the 0.52% consensus. The downside surprise was driven by lower services prices, particularly airfares, which offset pressure from higher electricity and fuel costs. Core inflation also missed estimates at 0.19% M/M (5.09% Y/Y), though underlying labor-sensitive services momentum remains elevated, warranting a cautious monetary policy outlook.

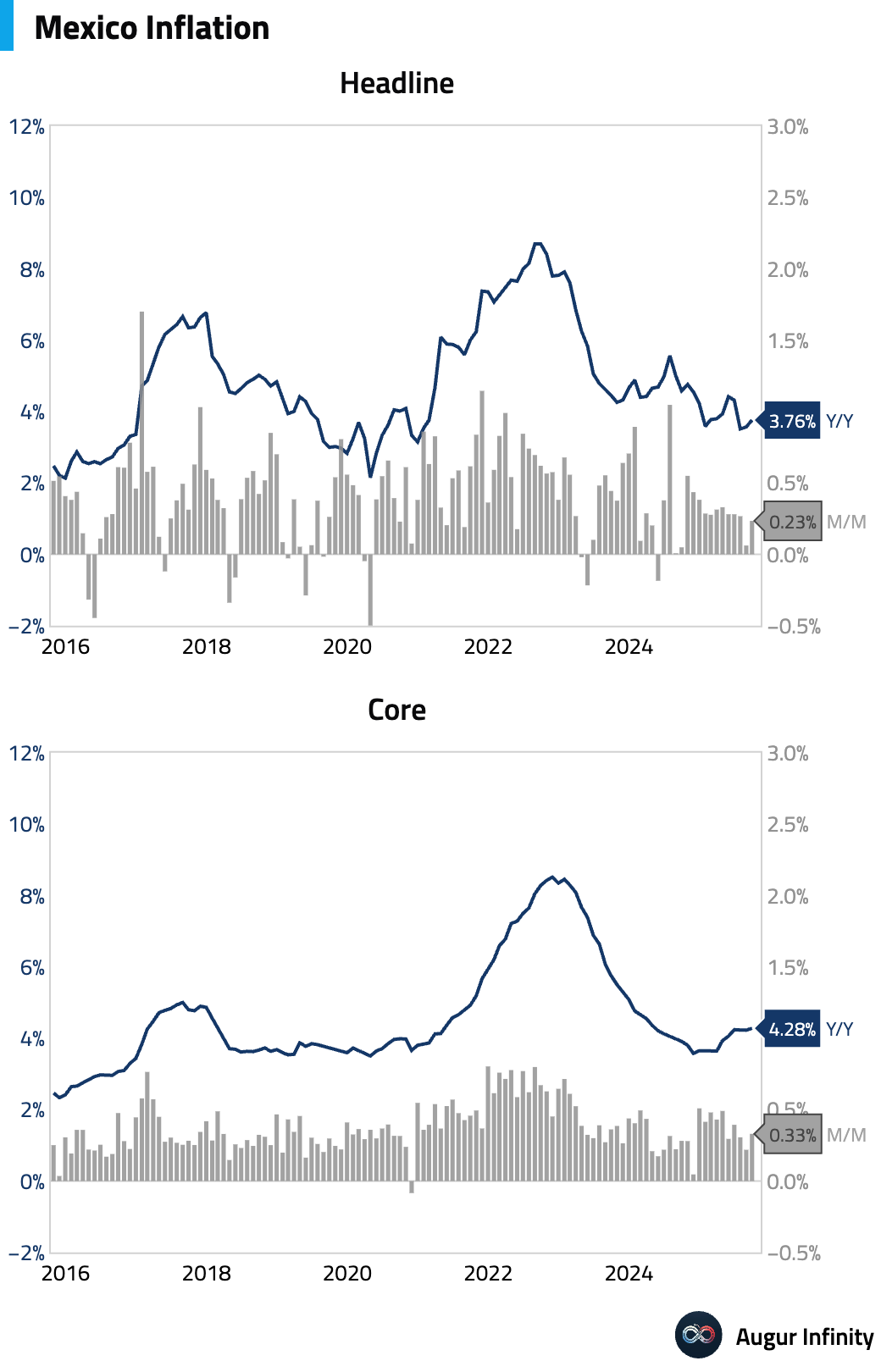

- Mexican headline inflation came in cooler than expected in September, rising 0.23% M/M for an annual rate of 3.76%, helped by falling non-core food prices. However, core inflation met consensus at a hotter 0.33% M/M (4.28% Y/Y), with services inflation remaining stubbornly high. A sharp drop in fruit and vegetable prices contributed to the soft headline figure, but this presents an upside risk for future inflation as these prices normalize.

Global Markets

Equities

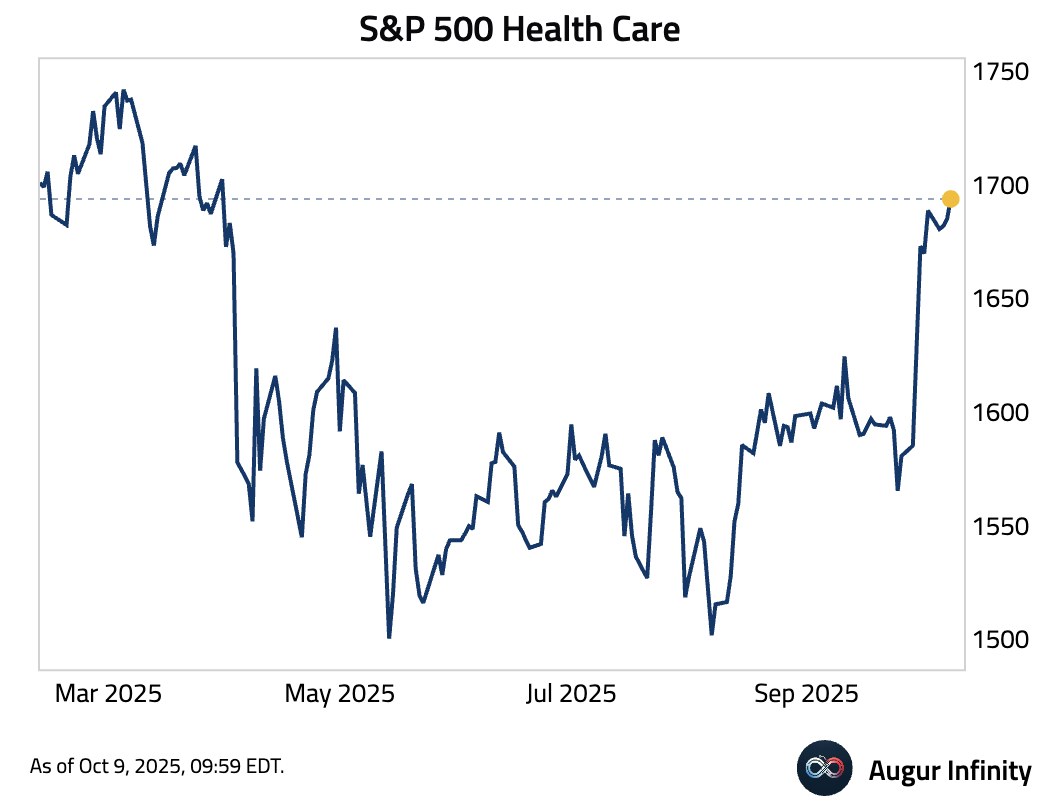

- S&P 500 Health Care rose to the highest level since March 2025

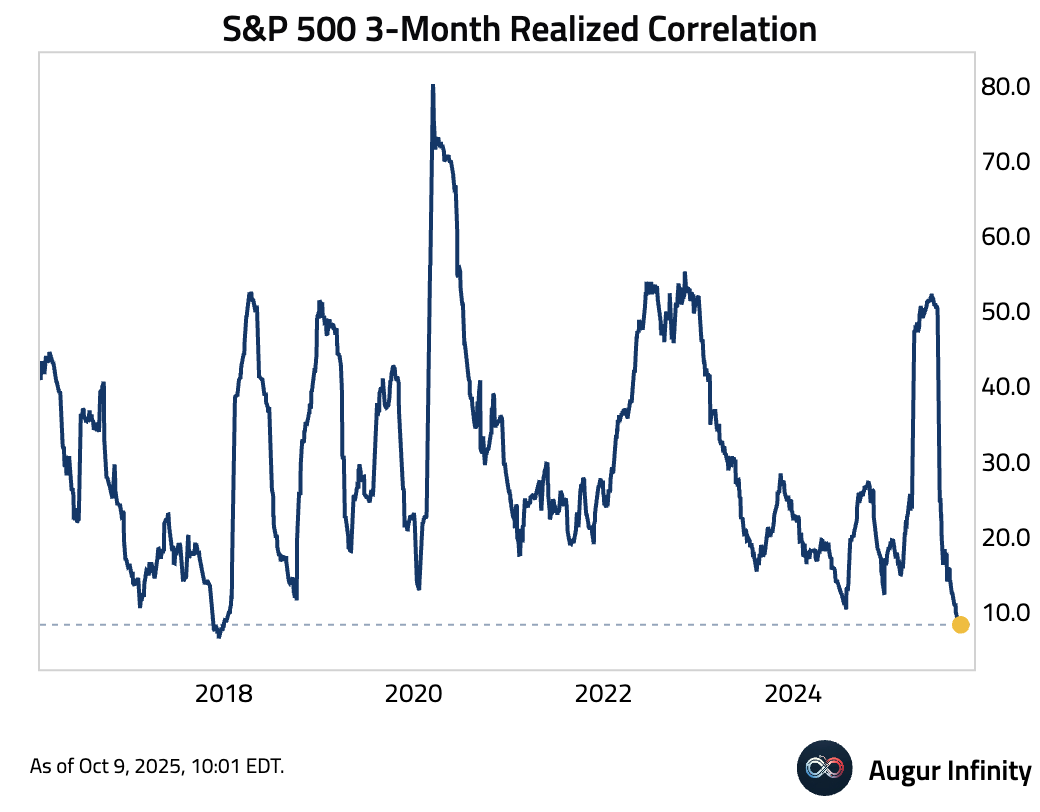

- The 3-month realized correlations amongst S&P 500 members declined to the lowest level since January 2018.

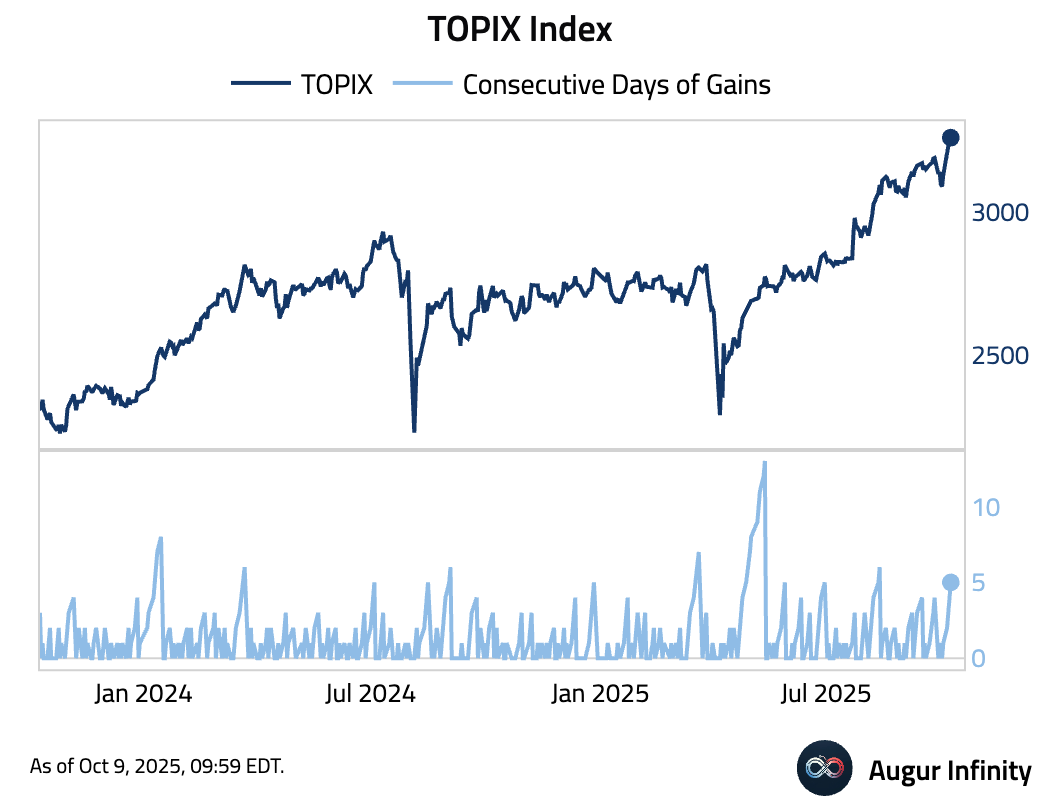

- The TOPIX Index gained for the fifth consecutive session, closing at the 19th all-time high of the year.

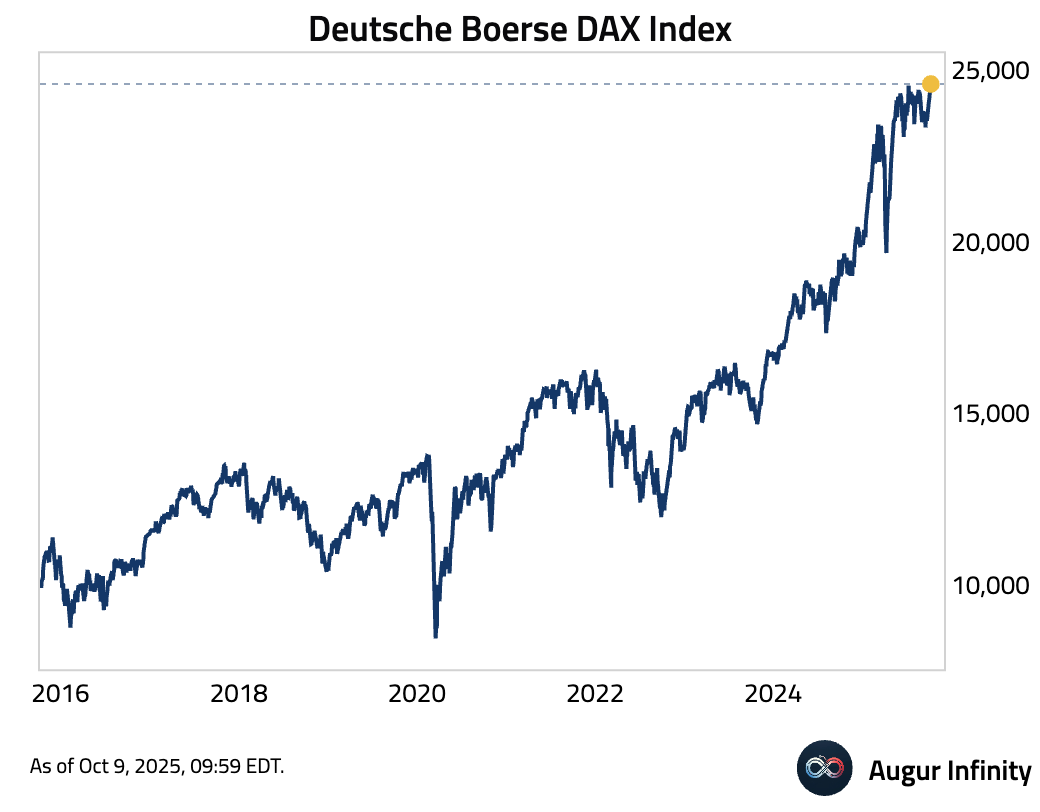

- The Deutsche Boerse DAX Index has also reached an all-time high.

- The Shanghai Composite Index rallied by 1.3% on the day, closing at the best level since August 2015.

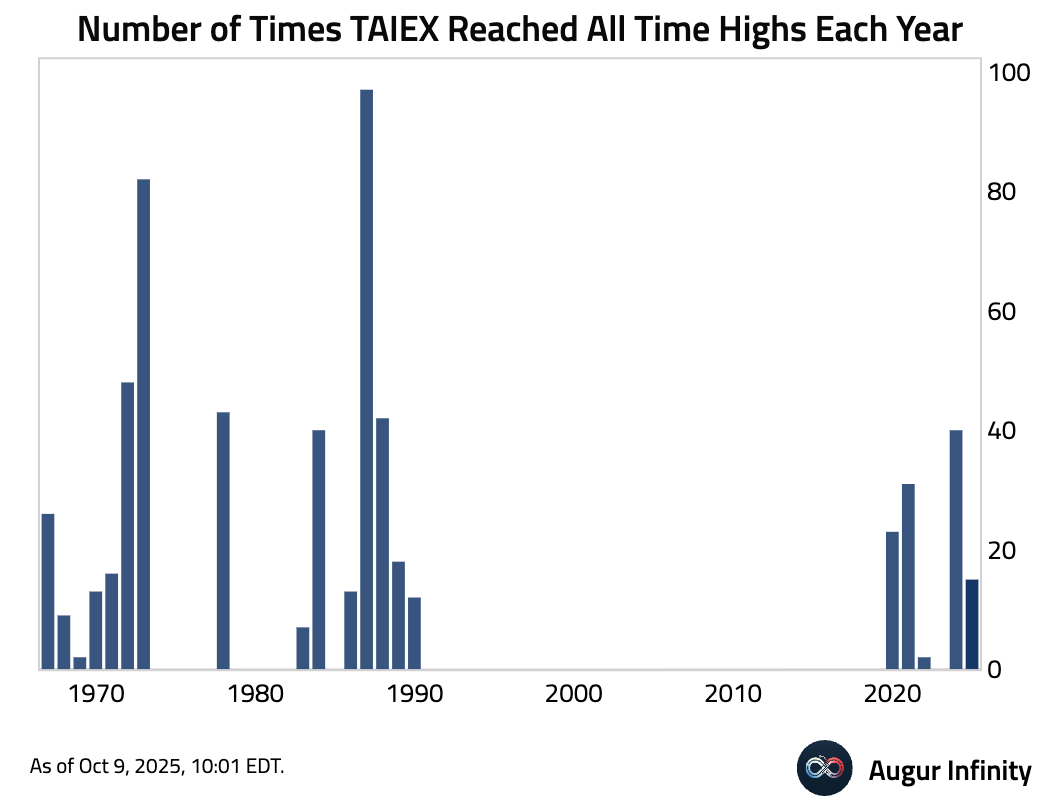

- The Taiwan SE Weighted Index has reached all-time highs 15 times this year.

Fixed Income

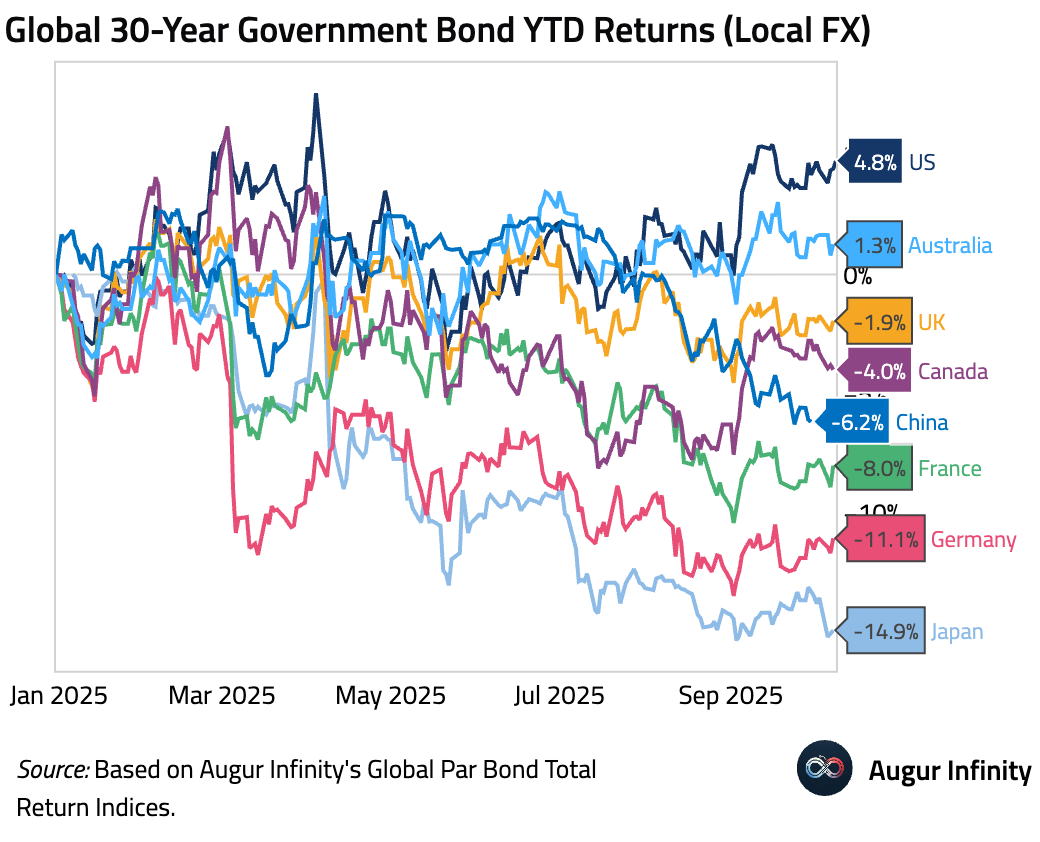

- Japan's 30-year government bonds are down nearly 15% year-to-date, significantly underperforming global peers.

FX

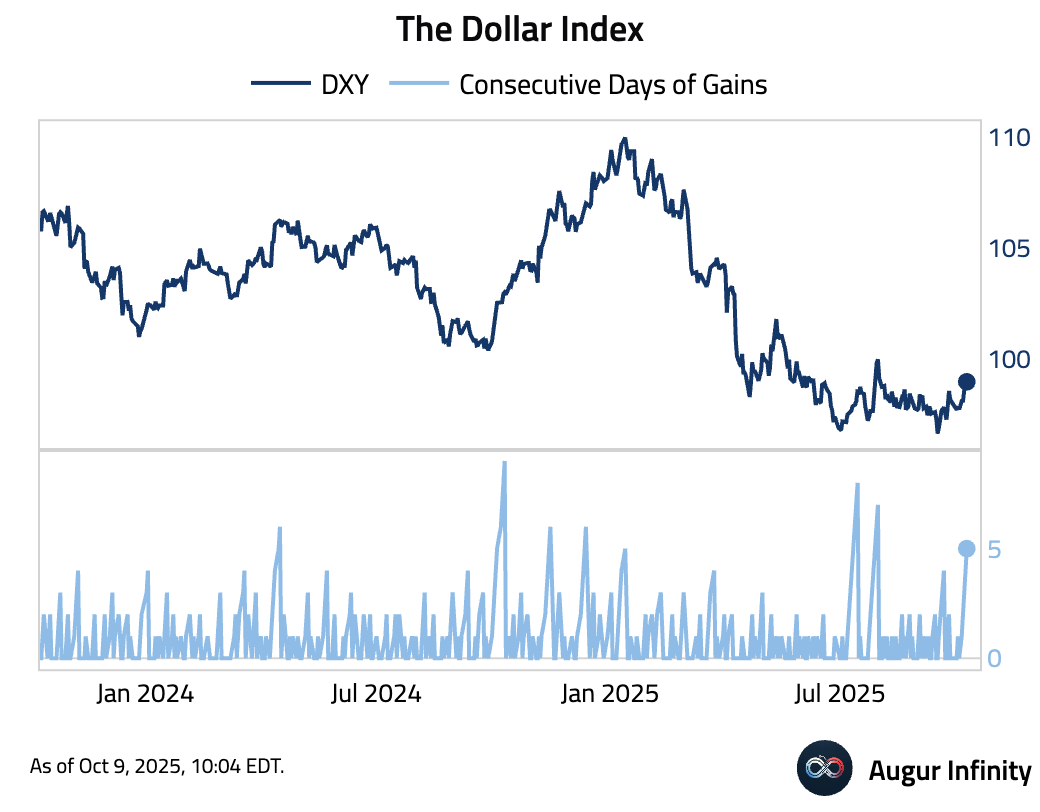

- The Dollar Index gained for the fifth consecutive session.

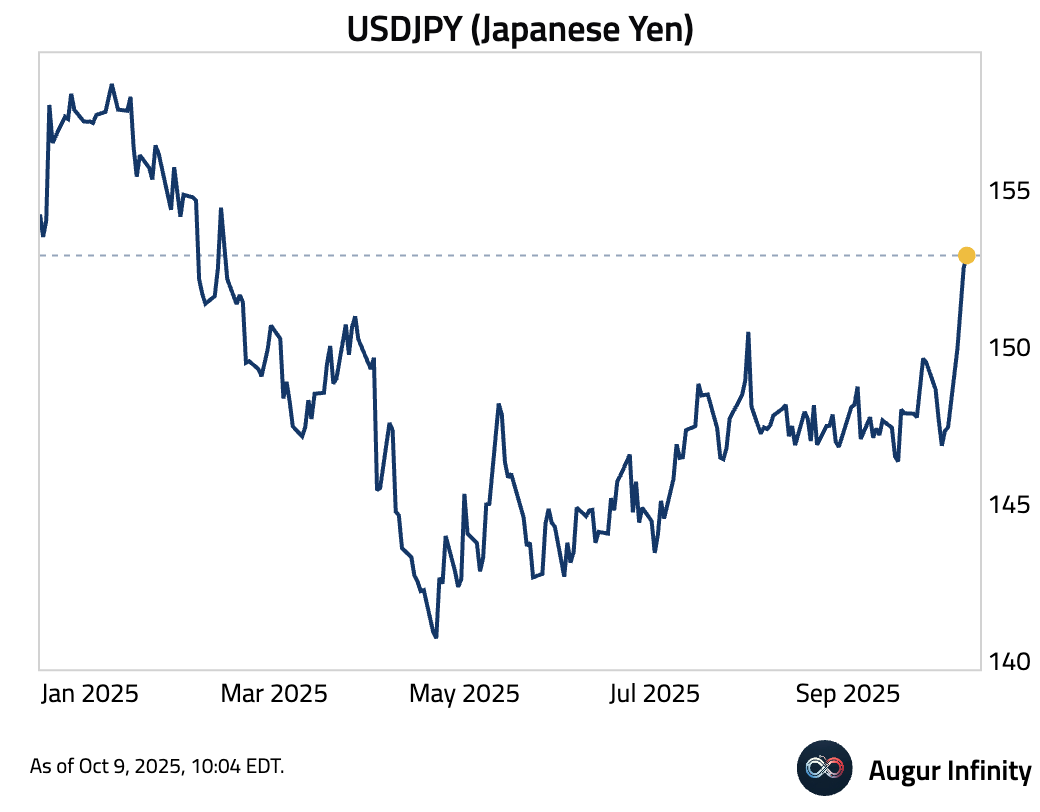

- The Japanese yen depreciated to the weakest level against USD since February 2025.

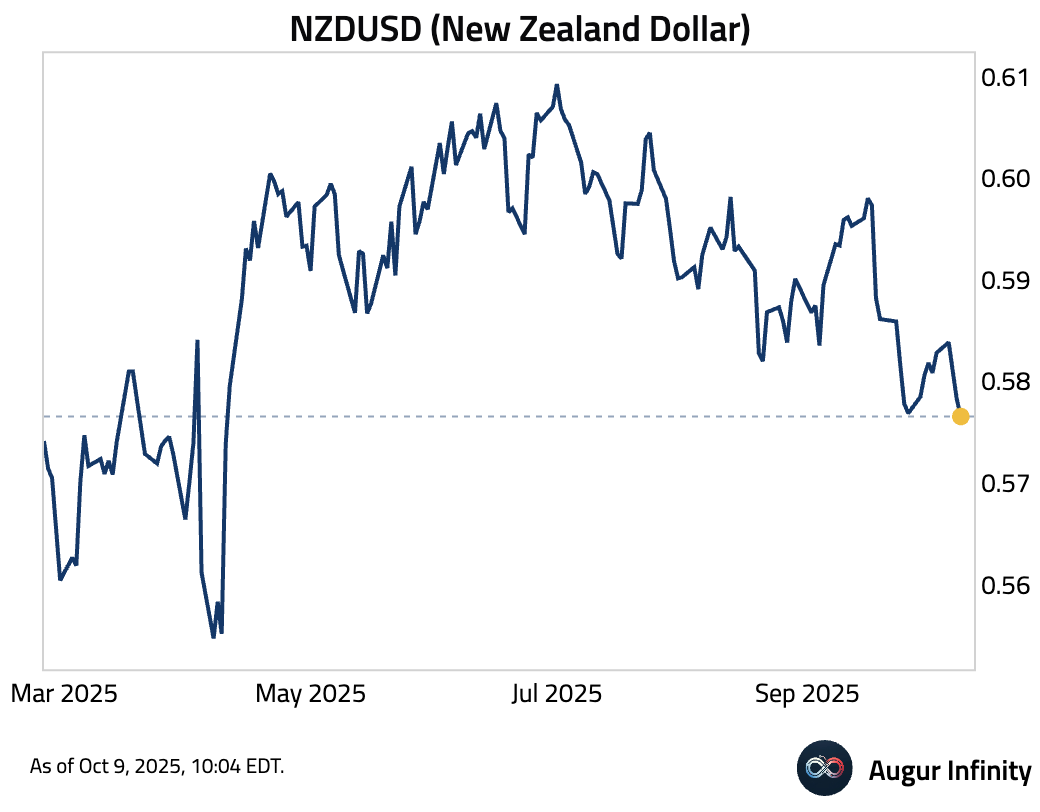

- NZDUSD slumped to the worst level since April 2025.

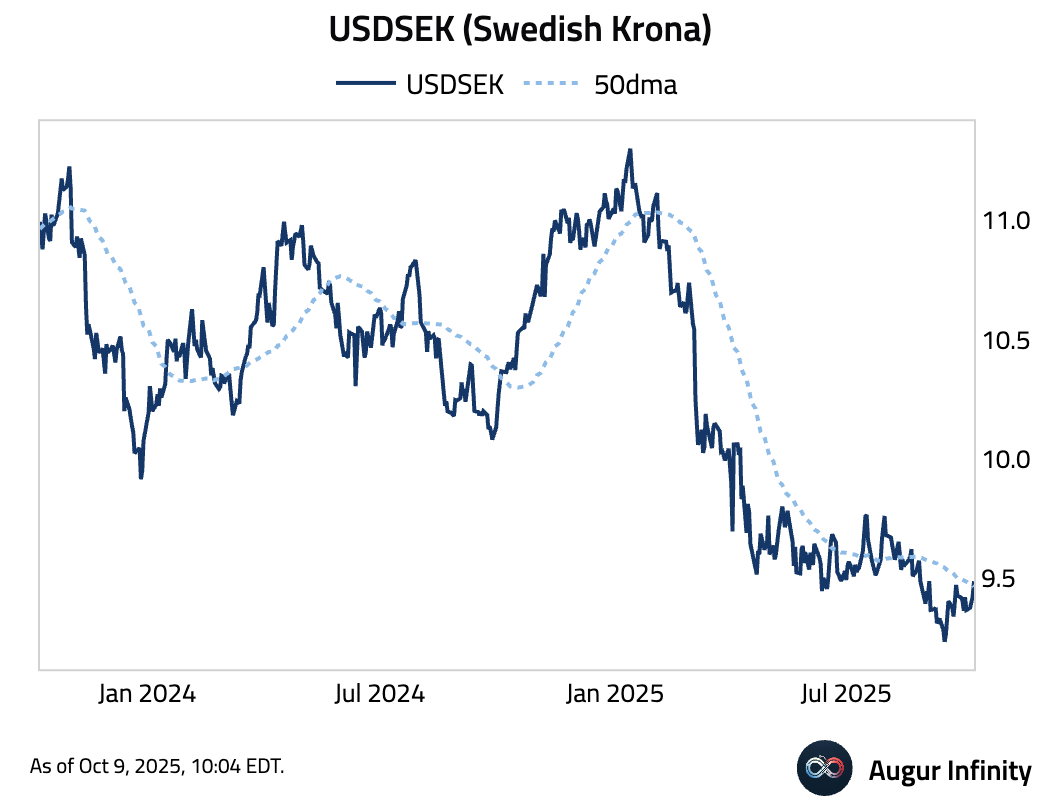

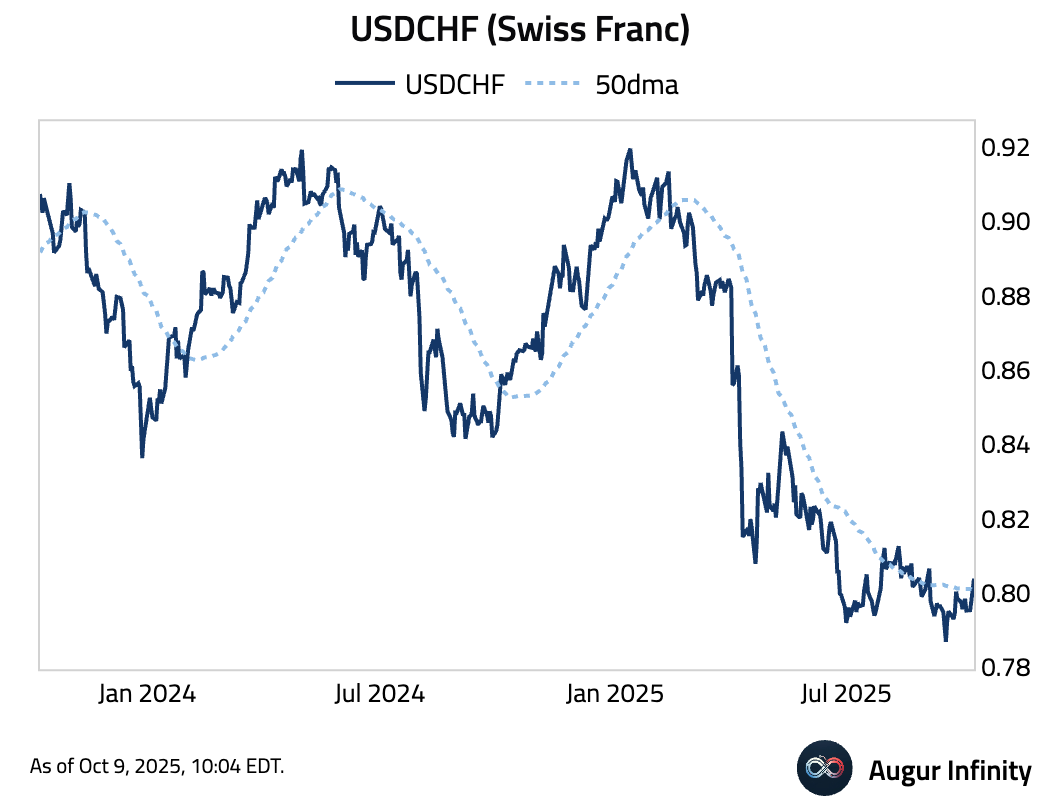

- USDSEK edged above its 50-day moving average …

… same for USDCHF.

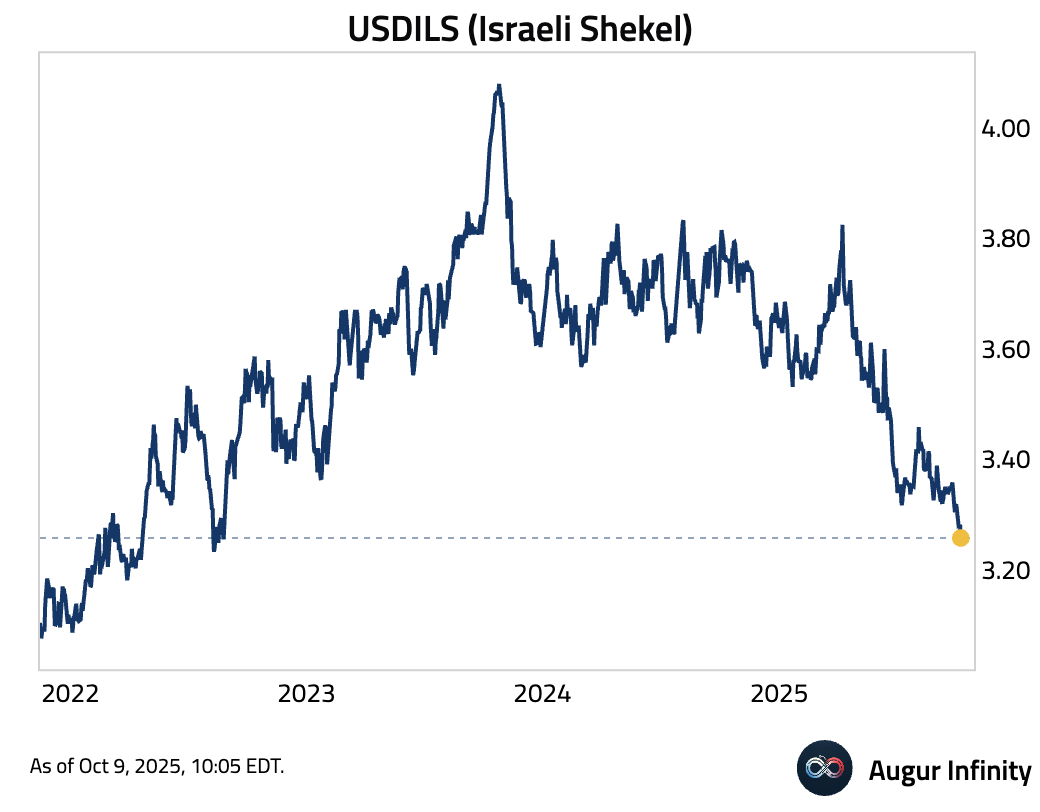

- The Israeli Shekel reached the strongest level against USD since August 2022.

Commodities

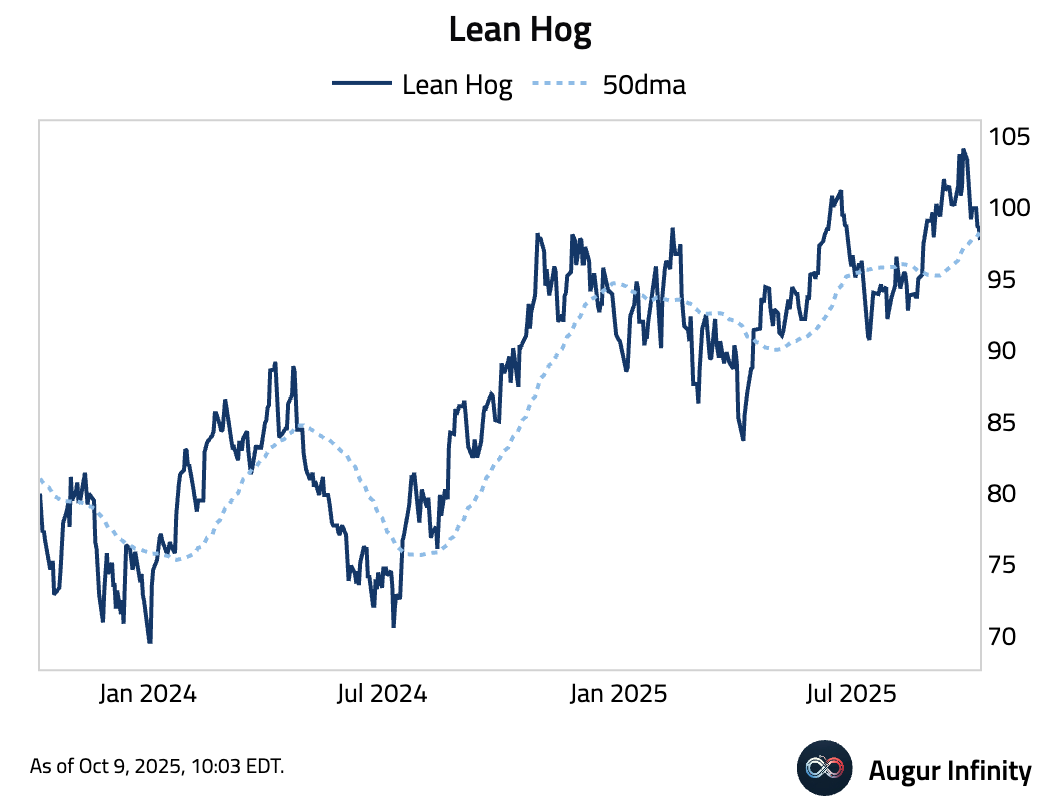

- Lean Hog fell below its 50-day moving average.

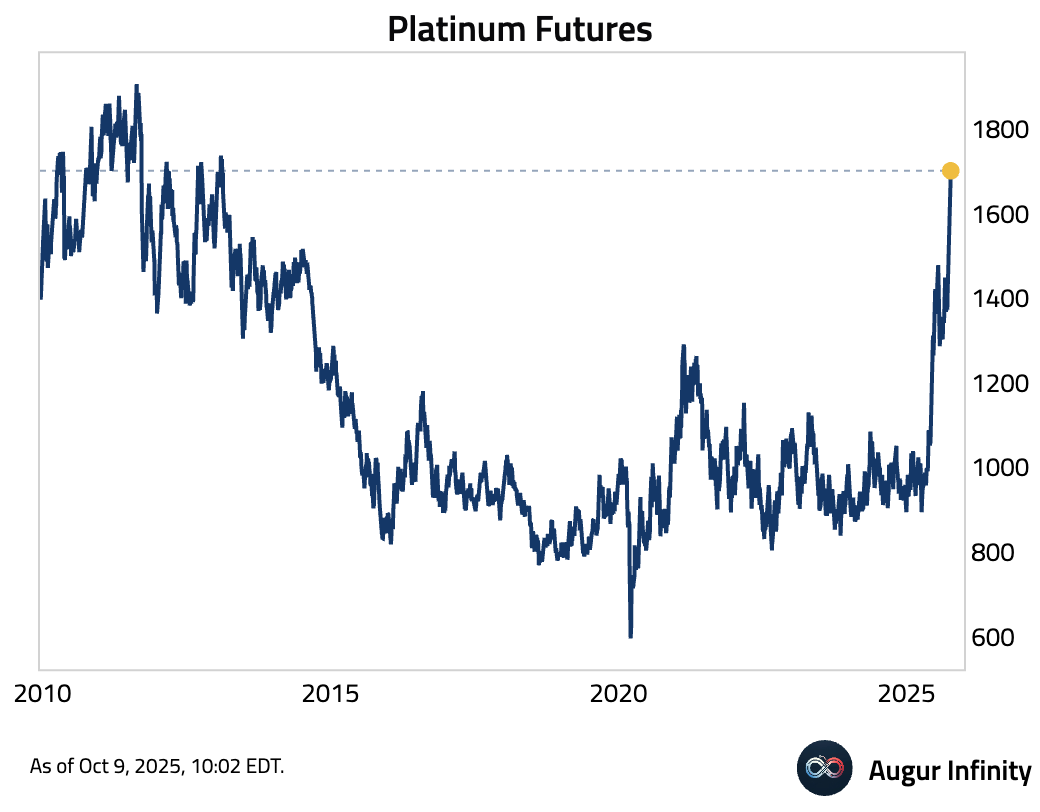

- Platinum is trading at the highest level in over a decade.

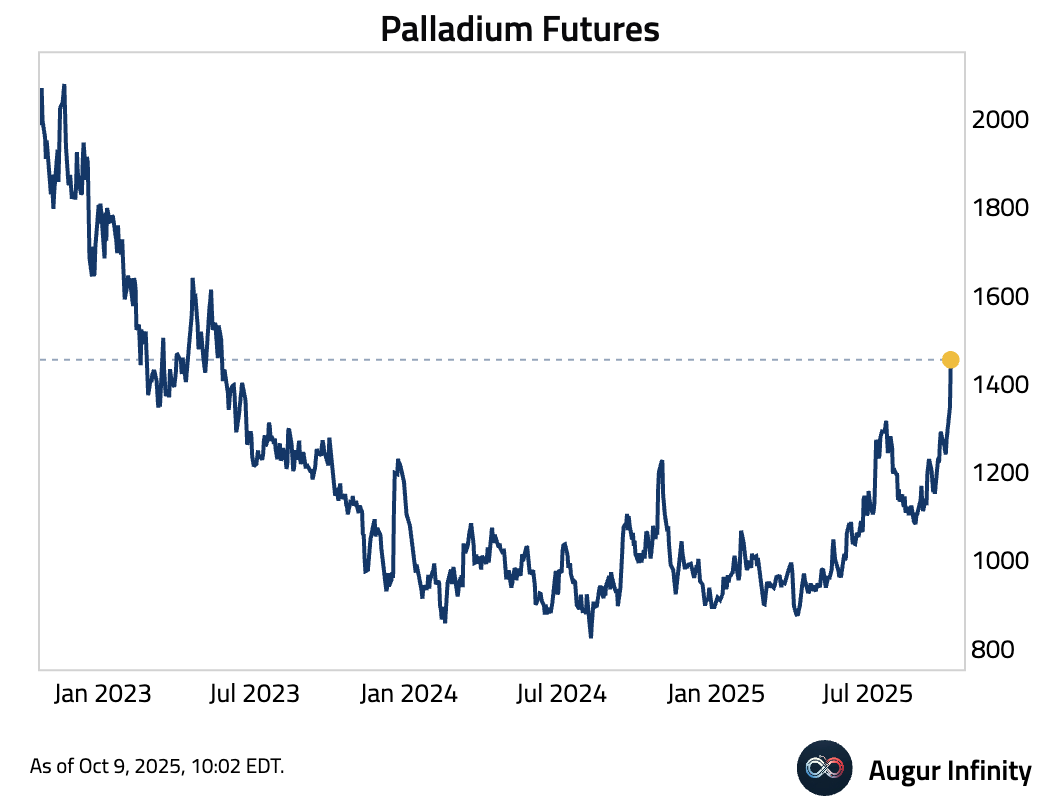

- Palladium jumped to the best level since May 2023.

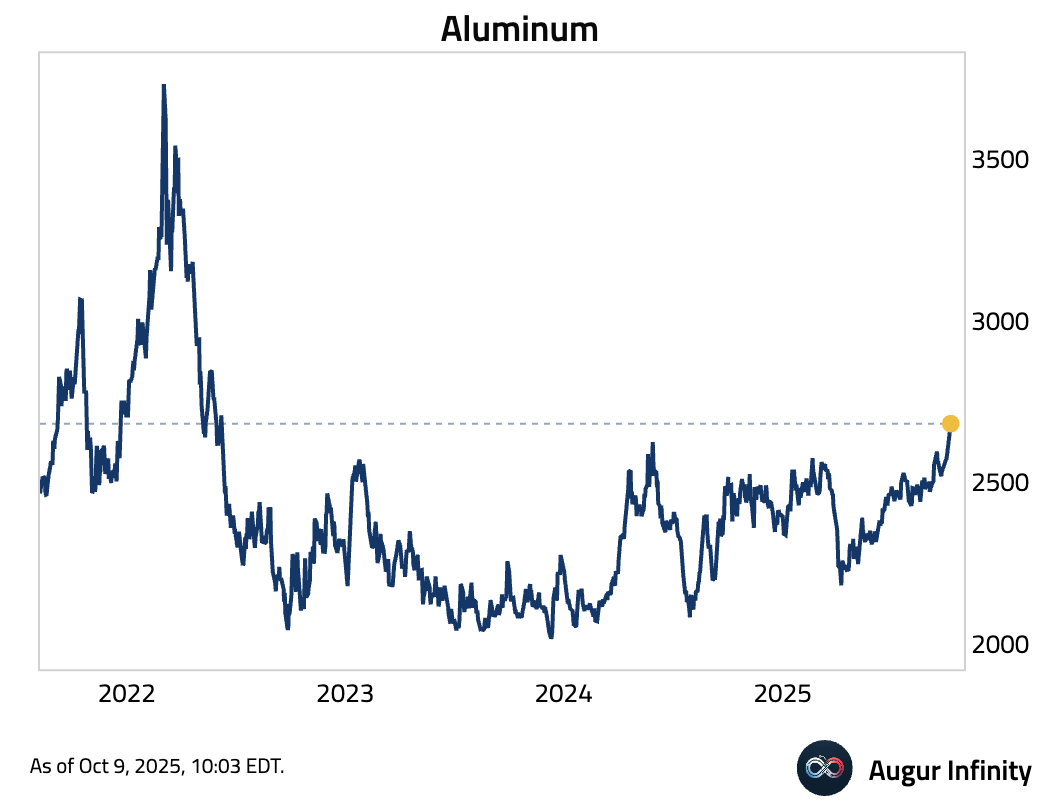

- Aluminum, on a roll-adjusted basis, hit the best level since June 2022.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.